TAXREP 35/15 (ICAEW REPRESENTATION 97/15)

|

|

|

- Morgan Hill

- 5 years ago

- Views:

Transcription

1 TAXREP 35/15 (ICAEW REPRESENTATION 97/15) RENEWALS BASIS FOR UNFURNISHED RENTAL PROPERTY- ASSESSING THE IMPACT This representation of 30 June 2015 has been prepared on behalf of ICAEW by the Tax Faculty and CIOT. Internationally recognised as a source of expertise, the Faculty is a leading authority on taxation. It is responsible for making submissions to tax authorities on behalf of ICAEW and does this with support from over 130 volunteers, many of whom are well-known names in the tax world. Appendix 1 sets out the ICAEW Tax Faculty s Ten Tenets for a Better Tax System, by which we benchmark proposals for changes to the tax system. We should be happy to discuss any aspect of our comments with HM Revenue & Customs and to take part in all further consultations on this area. The Institute of Chartered Accountants in England and Wales T +44 (0) Chartered Accountants Hall F +44 (0) Moorgate Place London EC2R 6EA UK E taxfac@icaew.com icaew.com/taxfac

2 ICAEW is a world-leading professional accountancy body. We operate under a Royal Charter, working in the public interest. ICAEW s regulation of its members, in particular its responsibilities in respect of auditors, is overseen by the UK Financial Reporting Council. We provide leadership and practical support to over 144,000 member chartered accountants in more than 160 countries, working with governments, regulators and industry in order to ensure that the highest standards are maintained. ICAEW members operate across a wide range of areas in business, practice and the public sector. They provide financial expertise and guidance based on the highest professional, technical and ethical standards. They are trained to provide clarity and apply rigour, and so help create long-term sustainable economic value. Copyright ICAEW 2015 All rights reserved. This document may be reproduced without specific permission, in whole or part, free of charge and in any format or medium, subject to the conditions that: it is appropriately attributed, replicated accurately and is not used in a misleading context; the source of the extract or document is acknowledged and the title and ICAEW reference number are quoted. Where third-party copyright material has been identified application for permission must be made to the copyright holder. For more information, please contact ICAEW Tax Faculty: taxfac@icaew.com icaew.com 2

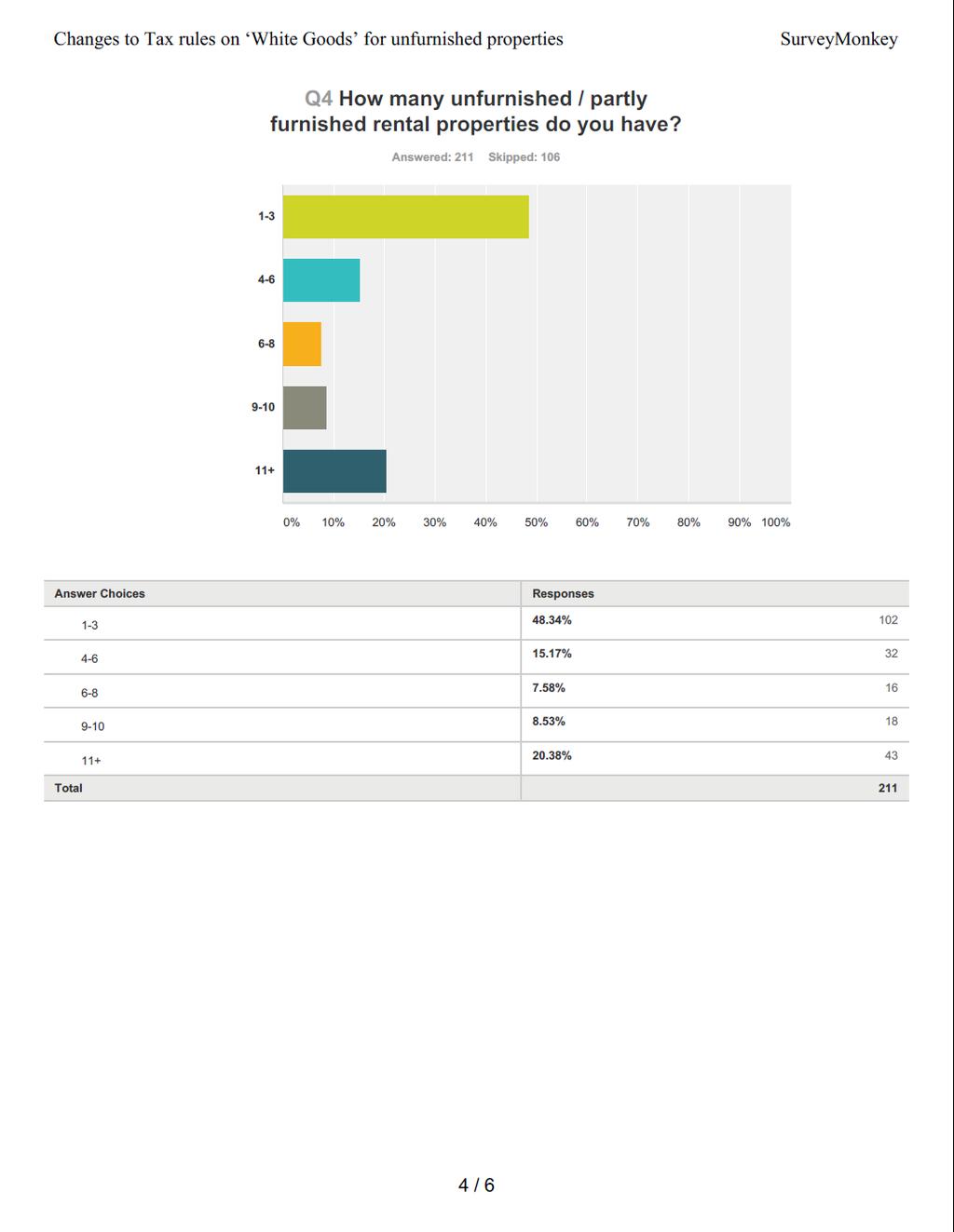

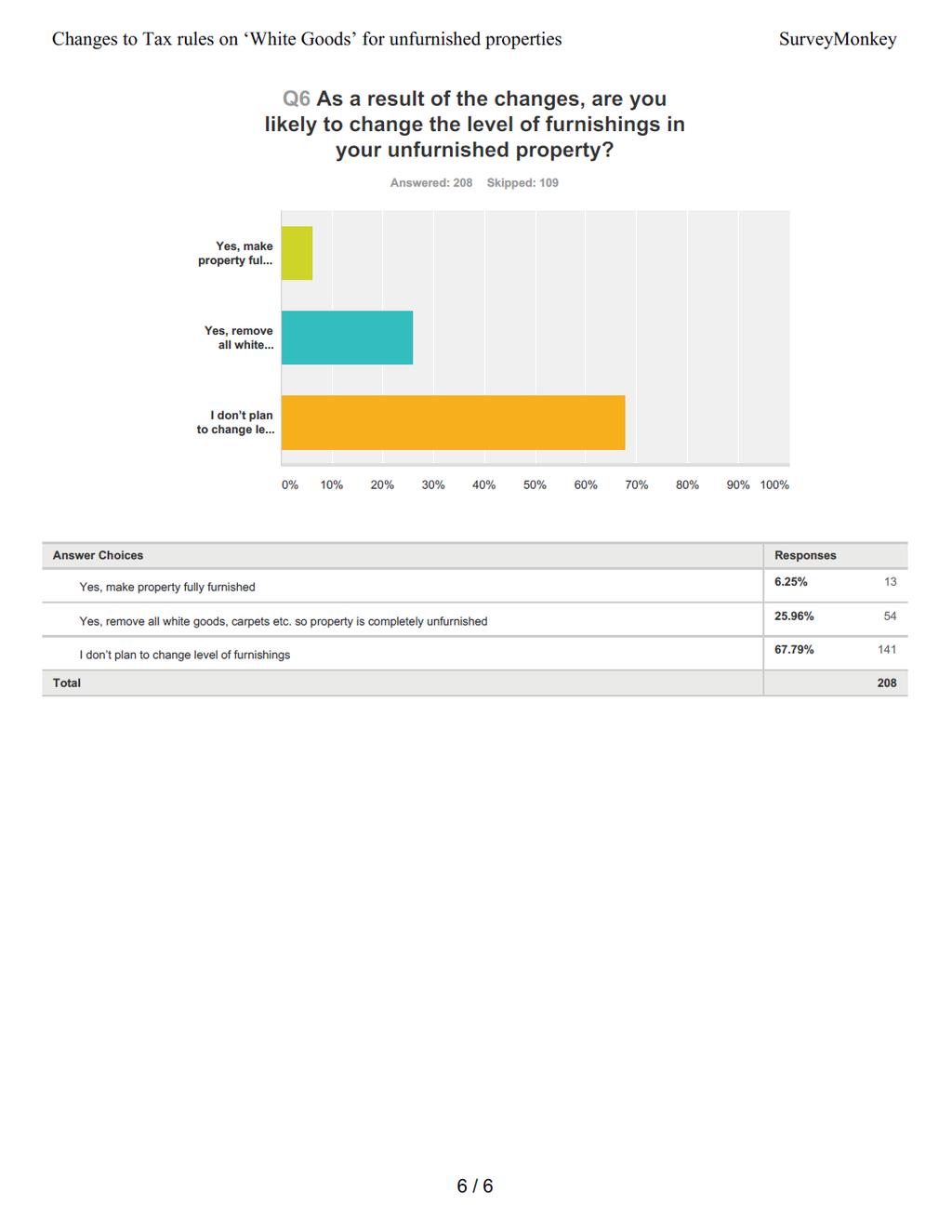

3 MAJOR POINTS Further to the correspondence ICAEW and CIOT had with HMRC in 2014, see TAXGuide 04/14, we have been receiving comments on the change to the tax rules from members expressing their concern about the lack of tax relief for what is seen as a pure business expense. In the final paragraph of the response from HMRC they said they would review the impact of the change and as a result we liaised with the Residential Landlords Association to survey their members regarding the change. We sent the results of that survey (pages 8-13) and a similar one run by the Scottish Landlords Association (pages 14-19) together with a summary of comments from ICAEW and CIOT members (page 7) to HMRC on 13 June. We have asked HMRC to let us know the conclusion of their review of the impact of the changes. 3

4 Megan Shaw Product Owner - Property Income & REITs HMRC Room 3/ Parliament Street London SW1A 2BQ via megan.shaw@hmrc.gsi.gov.uk 13 June 2015 Dear Megan RENEWALS BASIS RESIDENTIAL PROPERTY ASSESSING THE IMPACT As you know we wrote to HMRC regarding the changes to the taxation of unfurnished residential property income following the withdrawal of Extra-Statutory Concession B1 (ESC B1 and ESC B47) concerning the renewals basis for residential let property, copy enclosed. The reply we received from Jas Bhangu said that HMRC would be reviewing the impact of the change; we have been collating evidence of the impact of the change, some of which is anecdotal and some the result of a survey that the Residential Landlords Association (RLA) ran for us. The Scottish Association of Landlords ran a similar survey for their members. When the consultation on the withdrawal of the ESC was announced it was stated that the withdrawal would not have any material impact. Our research indicates that is not the case and therefore consideration should be given to reinstating by statute the relief previously afforded to landlords of unfurnished residential lets by the ESC. Residential letting is a business and accounts have to be prepared under generally accepted accounting practices (GAAP). Expenditure on white goods, carpets and curtains for an unfurnished residential rental property is quite clearly a business expense and should therefore be allowable for tax. The quantum of expenditure on these goods is frequently below the level that a business would be advised to capitalise the cost and charge depreciation through the accounts, so to include the cost in the profit and loss account would be following GAAP. The rental market appears to have shifted; we understand that no longer do people rent an unfurnished property for life, they are rented on short term rentals just like furnished property. Whilst the tenant wishes to use their own furniture in terms of beds, chairs, tables, sofas etc. they 4

5 do not want to provide floor coverings, curtains or white goods; these items are not as transferable between properties. If landlords are denied tax relief for what are essentially business costs, they may stop supplying them altogether (as the results indicate) with wider implications for the rented sector. We enclose with this letter the evidence we have collated and trust that consideration will be given to a change to the legislation to restore the status quo enjoyed before the withdrawal of the ESC. Yours sincerely Lisa Spearman Chairman, Private Client Committee ICAEW Tax Faculty Brian Slater Chairman, CIOT Property Taxes Sub-Committee cc Jas Bhangu, Policy and Technical Specialist, HMRC, jasbir.bhangu@hmrc.gsi.gov.uk The Institute of Chartered Accountants in England and Wales ICAEW is a world-leading professional accountancy body. We operate under a Royal Charter, working in the public interest. ICAEW s regulation of its members, in particular its responsibilities in respect of auditors, is overseen by the UK Financial Reporting Council. We provide leadership and practical support to over 144,000 member chartered accountants in more than 160 countries, working with governments, regulators and industry in order to ensure that the highest standards are maintained. ICAEW members operate across a wide range of areas in business, practice and the public sector. They provide financial expertise and guidance based on the highest professional, technical and ethical standards. They are trained to provide clarity and apply rigour, and so help create long-term sustainable economic value. The Tax Faculty is the voice of tax within ICAEW and is a leading authority on taxation. Internationally recognised as a source of expertise, the faculty is responsible for submissions to tax authorities on behalf of ICAEW as a whole. It also provides a range of tax services, including TAXline, a monthly journal sent to more than 8,200 members, a weekly newswire and a referral scheme. The Chartered Institute of Taxation The Chartered Institute of Taxation (CIOT) is the leading professional body in the United Kingdom concerned solely with taxation. The CIOT is an educational charity, promoting education and study of the administration and practice of taxation. One of our key aims is to work for a better, more efficient, tax system for all affected by it taxpayers, their advisers and the authorities. The CIOT s work covers all aspects of taxation, including direct and indirect taxes and duties. Through our Low Incomes Tax Reform Group (LITRG), the CIOT has a particular focus on improving the tax system, including tax credits and benefits, for the unrepresented taxpayer. The CIOT draws on our members experience in private practice, commerce and industry, government and academia to improve tax administration and propose and explain how tax policy objectives can most effectively be achieved. We also link to, and draw on, similar leading 5

6 professional tax bodies in other countries. The CIOT s comments and recommendations on tax issues are made in line with our charitable objectives: we are politically neutral in our work. The CIOT s 17,000 members have the practising title of Chartered Tax Adviser and the designatory letters CTA, to represent the leading tax qualification. 6

7 REMOVAL OF ESC B47 EFFECTS 2014/15- TAX FACULTY FORUM RESPONSES INCORPORATING CIOT MEMBERS' COMMENTS FROM TAX ADVISER ARTICLE No of clients with unfurnished lettings Number of landlords affected 2014/15 Did clients know of changes Average unrelieved expenditure for renewals per client affected Will this change behaviour re renewals White goods Carpets and curtains 15 3 No 950 Yes No 100% No Yes Yes No 2,500 Yes Yes 2 2 No 1500 No Yes Supply carpets but not curtains 1 1 No No 1 1 Yes 1500 Yes Yes 200 (800 properties) Only after advised 500 Yes Yes Yes Yes 50 2,000 Mixed Mixed Points raised on Forum and by CIOT members 15 I think the loss of trust with the perceived unfairness is the more important issue here, rather than the actual values involved. Nearly every landlord we have discussed this point with has been taken aback by the whole notion of being unable to obtain basic tax relief on a routine business expense which is unquestionably wholly and exclusively for the purpose of the rental business. 16 Landlords may offer new tenants a rent free period and leave it to the tenant to decide whether to purchase the items themselves. 17 Some landlords have decided to continue to claim under s68, CTA 2009 and make the appropriate disclosures, others say the threat of no tax relief means they won t renew as often others will repair rather than replace. 18 I have three property rental clients letting in total 19 properties. Each is unfurnished but carpets, curtains, light fittings and white goods ( not integral) are included Rental is a business and all expenses incurred in earning rent should be allowable for tax Letting agents require floor coverings and curtains. Health and safety risk of tenants providing own white goods and not replacing damaged carpets. Not everyone can afford to fully furnish a property. Will try to repair rather than replace Government should encourage good standard rental properties May reduce supply of properties with white goods suitable for families. White goods are 'tools'. Fitted carpets should be allowed on same basis as fitted furniture. Will reduce quality of items supplied. New rules unclear, confusing and illogical. Clients want to ignore and carry on as before. Consider writing down cost of carpets, curtains and white goods over 4-5 years. Clients coached along the lines that "this is an unintended consequence, HMRC will change their mind" and most are carrying on as before, albeit deferring spends if possible until this area is cleared up With our larger landlords we have discussed setting up a rental business to buy the goods and lease to the landlord and so claim the deduction, and I know some letting agents are mooting similar proposals but I don't think anyone wants to do this until we know if HMRC will change their minds given the general time and cost of such arrangements. Some lettings agents already rent furniture to landlords and/or tenants, so this would be a general extension of such services These changes (are) illogical and confusing. In particular please could you ask them to clarify their following statement "However landlords may be able to get some relief on carpets if the expenditure qualifies as a revenue expense" (page 3 of their letter, middle of page). Is replacing a worn or damaged carpet or part of a carpet a revenue expense? Carpets are after all attached to a floor by carpet grippers i.e. they are fitted and are not freestanding which totally contradicts why they should not be allowed under this new renewals basis. Numerous rental properties (>30 or so) in London. Most of the rental properties are "unfurnished" and a few "part-furnished" but are being phased out slowly so will eventually become unfurnished. The vocabulary "unfurnished" commonly refers to "white goods" which is standard for all lets these days and this means quite often even "dishwasher" and soft furnishings like curtains or blinds etc (In the case of )old houses where the kitchen was refitted with latest design and style i.e as part of a refurbishment, these white goods can be stand alone but are treated as part of kitchen and slotted into the gaps under the worktop as part of kitchen - basics to be supplied by landlord for renting and treated as part of standard kitchen. All the above is still is classified "unfurnished" Under current standards and market practice, certain fittings and equipments are standard requirements by tenants of unfurnished properties such as curtains, floorings/carpets, oven and hob, washing machine and fridge/ freezer. HMRC seem to acknowledge the first two items in their letter of 7 April 2014, page 10. By definition, the great majority of properties are not new build and do not typically include integral fittings. Functionally, the white goods do the same thing whether free standing or integral. Therefore, it seems unjust that they should have different tax treatments. HMRC said in their letter that "legislation could provide unforeseen opportunities for avoidance in a way that concessions do not." They have provided no evidence for this belief and no examples. Further, they said in their letter: "I can assure you that HMRC is continuing to review the impacts of the change." without explaining how they are doing this. 7

8 8

9 9

10 10

11 11

12 12

13 13

14 14

15 15

16 16

17 17

18 18

19 19

20 APPENDIX 1 ICAEW TAX FACULTY S TEN TENETS FOR A BETTER TAX SYSTEM The tax system should be: 1. Statutory: tax legislation should be enacted by statute and subject to proper democratic scrutiny by Parliament. 2. Certain: in virtually all circumstances the application of the tax rules should be certain. It should not normally be necessary for anyone to resort to the courts in order to resolve how the rules operate in relation to his or her tax affairs. 3. Simple: the tax rules should aim to be simple, understandable and clear in their objectives. 4. Easy to collect and to calculate: a person s tax liability should be easy to calculate and straightforward and cheap to collect. 5. Properly targeted: when anti-avoidance legislation is passed, due regard should be had to maintaining the simplicity and certainty of the tax system by targeting it to close specific loopholes. 6. Constant: Changes to the underlying rules should be kept to a minimum. There should be a justifiable economic and/or social basis for any change to the tax rules and this justification should be made public and the underlying policy made clear. 7. Subject to proper consultation: other than in exceptional circumstances, the Government should allow adequate time for both the drafting of tax legislation and full consultation on it. 8. Regularly reviewed: the tax rules should be subject to a regular public review to determine their continuing relevance and whether their original justification has been realised. If a tax rule is no longer relevant, then it should be repealed. 9. Fair and reasonable: the revenue authorities have a duty to exercise their powers reasonably. There should be a right of appeal to an independent tribunal against all their decisions. 10. Competitive: tax rules and rates should be framed so as to encourage investment, capital and trade in and with the UK. These are explained in more detail in our discussion document published in October 1999 as TAXGUIDE 4/99 (see via 20

FINANCE BILL 2012 DRAFT CLAUSES: INFORMATION POWERS

TAXREP 11/12 ICAEW TAX REPRESENTATION FINANCE BILL 2012 DRAFT CLAUSES: INFORMATION POWERS Comments submitted in February 2012 by ICAEW Tax Faculty to HM Revenue & Customs in response to the draft Finance

TAXREP 11/12 ICAEW TAX REPRESENTATION FINANCE BILL 2012 DRAFT CLAUSES: INFORMATION POWERS Comments submitted in February 2012 by ICAEW Tax Faculty to HM Revenue & Customs in response to the draft Finance

ICAEW REPRESENTATION 94/16 TAX REPRESENTATION

ICAEW REPRESENTATION 94/16 TAX REPRESENTATION Finance Bill (No 2) 2016 Clause 117: SDLT:higher rates for additional dwellings etc ICAEW welcomes the opportunity to comment on the Finance Bill published

ICAEW REPRESENTATION 94/16 TAX REPRESENTATION Finance Bill (No 2) 2016 Clause 117: SDLT:higher rates for additional dwellings etc ICAEW welcomes the opportunity to comment on the Finance Bill published

Implementation of International Tax Compliance (United States of America) Regulations 2013

Regulations 2013") TAXREP 25/13 (ICAEW REP 38/13) ICAEW TAX REPRESENTATION Implementation of International Tax Compliance (United States of America) Regulations 2013 Comments submitted on 27 February 2013 by ICAEW Tax Faculty

TAXREP 25/13 (ICAEW REP 38/13) ICAEW TAX REPRESENTATION Implementation of International Tax Compliance (United States of America) Regulations 2013 Comments submitted on 27 February 2013 by ICAEW Tax Faculty

TAXREP 11/15 (ICAEW REPRESENTATION 28/15)

") TAXREP 11/15 (ICAEW REPRESENTATION 28/15) PAID AND REIMBURSED EMPLOYEE EXPENSES DRAFT FINANCE BILL CLAUSES ICAEW welcomes the opportunity to comment on the draft Finance Bill 2015 legislation Administration

TAXREP 11/15 (ICAEW REPRESENTATION 28/15) PAID AND REIMBURSED EMPLOYEE EXPENSES DRAFT FINANCE BILL CLAUSES ICAEW welcomes the opportunity to comment on the draft Finance Bill 2015 legislation Administration

ICAEW REPRESENTATION132/17 TAX REPRESENTATION

ICAEW REPRESENTATION132/17 TAX REPRESENTATION LARGE BUSINES COMPLIANCE ENHANCING OUR RISK ASSESSMENT APPROACH ICAEW welcomes the opportunity to comment on the consultation document Large Business compliance

ICAEW REPRESENTATION132/17 TAX REPRESENTATION LARGE BUSINES COMPLIANCE ENHANCING OUR RISK ASSESSMENT APPROACH ICAEW welcomes the opportunity to comment on the consultation document Large Business compliance

RESEARCH AND DEVELOPMENT TAX CREDITS: RESPONSE AND FURTHER CONSULTATION

TAXREP 46/11 ICAEW TAX REPRESENTATION RESEARCH AND DEVELOPMENT TAX CREDITS: RESPONSE AND FURTHER CONSULTATION Comments submitted in August 2011 by the Tax Faculty of the Institute of Chartered Accountants

TAXREP 46/11 ICAEW TAX REPRESENTATION RESEARCH AND DEVELOPMENT TAX CREDITS: RESPONSE AND FURTHER CONSULTATION Comments submitted in August 2011 by the Tax Faculty of the Institute of Chartered Accountants

ICAEW REPRESENTATION 166/16 TAX REPRESENTATION

ICAEW REPRESENTATION 166/16 TAX REPRESENTATION Lease Accounting Changes: Tax Response ICAEW welcomes the opportunity to comment on the discussion draft Lease Accounting Changes: Tax Response published

ICAEW REPRESENTATION 166/16 TAX REPRESENTATION Lease Accounting Changes: Tax Response ICAEW welcomes the opportunity to comment on the discussion draft Lease Accounting Changes: Tax Response published

Introduction 1-3. Who we are 4-6. Key point summary / Major points Responses to specific questions 13-48

TAXREP 57/11 ICAEW TAX REPRESENTATION VAT: COST SHARING EXEMPTION Comments submitted in September 2011 by ICAEW Tax Faculty in response to the HM Revenue & Customs consultation document, VAT: Cost Sharing

TAXREP 57/11 ICAEW TAX REPRESENTATION VAT: COST SHARING EXEMPTION Comments submitted in September 2011 by ICAEW Tax Faculty in response to the HM Revenue & Customs consultation document, VAT: Cost Sharing

Contents Paragraph Introduction 1-4. Who we are 5-7. Response to consultation 8. Appendix Ten Tenets for a Better Tax System 1

TAXREP 40/12 (ICAEW REP 119/12) ICAEW TAX REPRESENTATION UNAUTHORISED UNIT TRUSTS ANTI-AVOIDANCE Comments submitted on 20 August 2012 by ICAEW Tax Faculty in response to HMRC consultation document High-risk

TAXREP 40/12 (ICAEW REP 119/12) ICAEW TAX REPRESENTATION UNAUTHORISED UNIT TRUSTS ANTI-AVOIDANCE Comments submitted on 20 August 2012 by ICAEW Tax Faculty in response to HMRC consultation document High-risk

TAXREP 34/15 (ICAEW REPRESENTATION 92/15)

") TAXREP 34/15 (ICAEW REPRESENTATION 92/15) PREVENT TREATY ABUSE: OECD PUBLIC DISCUSSION DRAFT ICAEW welcomes the opportunity to comment on the public discussion draft Prevent Treaty Abuse published by OECD

TAXREP 34/15 (ICAEW REPRESENTATION 92/15) PREVENT TREATY ABUSE: OECD PUBLIC DISCUSSION DRAFT ICAEW welcomes the opportunity to comment on the public discussion draft Prevent Treaty Abuse published by OECD

TAXREP 49/13 (ICAEWREP 132/13)

") TAXREP 49/13 (ICAEWREP 132/13) ICAEW TAX REPRESENTATION SUPPORTING THE EMPLOYEE-OWNERSHIP SECTOR Comments submitted in September 2013 by the Tax Faculty of the Institute of Chartered Accountants in England

TAXREP 49/13 (ICAEWREP 132/13) ICAEW TAX REPRESENTATION SUPPORTING THE EMPLOYEE-OWNERSHIP SECTOR Comments submitted in September 2013 by the Tax Faculty of the Institute of Chartered Accountants in England

ATTRIBUTION OF GAINS TO MEMBERS OF CLOSELY CONTROLLED NON- RESIDENT COMPANIES AND THE TRANSFER OF ASSETS ABROAD

TAXREP 53/12 (ICAEW REP 160/12) ICAEW TAX REPRESENTATION ATTRIBUTION OF GAINS TO MEMBERS OF CLOSELY CONTROLLED NON- RESIDENT COMPANIES AND THE TRANSFER OF ASSETS ABROAD Comments submitted on 22 October

TAXREP 53/12 (ICAEW REP 160/12) ICAEW TAX REPRESENTATION ATTRIBUTION OF GAINS TO MEMBERS OF CLOSELY CONTROLLED NON- RESIDENT COMPANIES AND THE TRANSFER OF ASSETS ABROAD Comments submitted on 22 October

STAMP DUTY LAND TAX: CONSULTATION ON THE POTENTIAL IMPACTS OF DEVOLVING TO THE NATIONAL ASSEMBLY FOR WALES AND WELSH GOVERNMENT

TAXREP 44/13 (ICAEW REP 121/13) ICAEW TAX REPRESENTATION STAMP DUTY LAND TAX: CONSULTATION ON THE POTENTIAL IMPACTS OF DEVOLVING TO THE NATIONAL ASSEMBLY FOR WALES AND WELSH GOVERNMENT Comments submitted

TAXREP 44/13 (ICAEW REP 121/13) ICAEW TAX REPRESENTATION STAMP DUTY LAND TAX: CONSULTATION ON THE POTENTIAL IMPACTS OF DEVOLVING TO THE NATIONAL ASSEMBLY FOR WALES AND WELSH GOVERNMENT Comments submitted

FINANCE (No 4) BILL BRIEFING CONTROLLED FOREIGN COMPANIES - CLAUSE 180 AND SCHEDULE 20

BILL BRIEFING CONTROLLED FOREIGN COMPANIES - CLAUSE 180 AND SCHEDULE 20") TAXREP 31/12 (ICAEW REP 107/12) ICAEW TAX REPRESENTATION FINANCE (No 4) BILL 2012 - BRIEFING CONTROLLED FOREIGN COMPANIES - CLAUSE 180 AND SCHEDULE 20 Briefing submitted in June 2012 by ICAEW Tax Faculty

TAXREP 31/12 (ICAEW REP 107/12) ICAEW TAX REPRESENTATION FINANCE (No 4) BILL 2012 - BRIEFING CONTROLLED FOREIGN COMPANIES - CLAUSE 180 AND SCHEDULE 20 Briefing submitted in June 2012 by ICAEW Tax Faculty

Contents Paragraphs Introduction. 1 4 Key point summary Detailed comments on the draft legislation

TAXREP 16/15 (ICAEW REPRESENTATION 35/15) DRAFT FINANCE BILL 2015 CLAUSES: ENFORCEMENT BY DEDUCTION FROM ACCOUNTS ICAEW welcomes the opportunity to comment on the draft legislation and the Tax Information

TAXREP 16/15 (ICAEW REPRESENTATION 35/15) DRAFT FINANCE BILL 2015 CLAUSES: ENFORCEMENT BY DEDUCTION FROM ACCOUNTS ICAEW welcomes the opportunity to comment on the draft legislation and the Tax Information

TAXREP 12/15 (ICAEW REPRESENTATION 29/15)

") TAXREP 12/15 (ICAEW REPRESENTATION 29/15) FINANCE BILL 2015 DRAFT CLAUSES DIVERTED PROFITS TAX ICAEW welcomes the opportunity to comment on the draft clauses on Diverted Profits Tax published for consultation

TAXREP 12/15 (ICAEW REPRESENTATION 29/15) FINANCE BILL 2015 DRAFT CLAUSES DIVERTED PROFITS TAX ICAEW welcomes the opportunity to comment on the draft clauses on Diverted Profits Tax published for consultation

TAXREP 42/14 (ICAEW REPRESENTATION 111/14)

") TAXREP 42/14 (ICAEW REPRESENTATION 111/14) VAT RELIEF ON SUBSTANTIALLY AND PERMANENTLY ADAPTED MOTOR VEHICLES FOR DISABLED WHEELCHAIR USERS ICAEW welcomes the opportunity to comment on the consultation

TAXREP 42/14 (ICAEW REPRESENTATION 111/14) VAT RELIEF ON SUBSTANTIALLY AND PERMANENTLY ADAPTED MOTOR VEHICLES FOR DISABLED WHEELCHAIR USERS ICAEW welcomes the opportunity to comment on the consultation

TAXREP 56/14 (ICAEW REPRESENTATION 136/14)

") TAXREP 56/14 (ICAEW REPRESENTATION 136/14) STRENGTHENING THE TAX AVOIDANCE DISCLOSURE REGIMES ICAEW welcomes the opportunity to comment on the consultation document Strengthening the tax avoidance disclosure

TAXREP 56/14 (ICAEW REPRESENTATION 136/14) STRENGTHENING THE TAX AVOIDANCE DISCLOSURE REGIMES ICAEW welcomes the opportunity to comment on the consultation document Strengthening the tax avoidance disclosure

Introduction 1 5. Who we are 6 8. General Comments Further contact 32. Ten Tenets for a Better Tax System Appendix 1

TAXREP 7/12 ICAEW TAX REPRESENTATION PATENT BOX: CORPORATION TAX REFORM Comments submitted on 10 February 2012 by ICAEW Tax Faculty in response to the publication on 6 December 2011 of draft clauses Profits

TAXREP 7/12 ICAEW TAX REPRESENTATION PATENT BOX: CORPORATION TAX REFORM Comments submitted on 10 February 2012 by ICAEW Tax Faculty in response to the publication on 6 December 2011 of draft clauses Profits

TAXREP 39/11 ICAEW TAX REPRESENTATION CONSULTATION ON THE ABOLITION OF 36 TAX RELIEFS

TAXREP 39/11 ICAEW TAX REPRESENTATION CONSULTATION ON THE ABOLITION OF 36 TAX RELIEFS Comments submitted in August 2011 by the Tax Faculty of the Institute of Chartered Accountants in England & Wales (ICAEW)

TAXREP 39/11 ICAEW TAX REPRESENTATION CONSULTATION ON THE ABOLITION OF 36 TAX RELIEFS Comments submitted in August 2011 by the Tax Faculty of the Institute of Chartered Accountants in England & Wales (ICAEW)

TAX RELIEF FOR TRAINING: SUGGESTIONS FOR CHANGE

ICAEW REPRESENTATION 30/18 TAX RELIEF FOR TRAINING: SUGGESTIONS FOR CHANGE This briefing of 9 January 2018 has been prepared on behalf of ICAEW by the Tax Faculty. Internationally recognised as a source

ICAEW REPRESENTATION 30/18 TAX RELIEF FOR TRAINING: SUGGESTIONS FOR CHANGE This briefing of 9 January 2018 has been prepared on behalf of ICAEW by the Tax Faculty. Internationally recognised as a source

FINANCE (No 4) BILL BRIEFING VAT - NON-ESTABLISHED TAXABLE PERSONS - CLAUSE 201 AND SCHEDULE 27 AND FACE VALUE VOUCHERS - NEW CLAUSE

BILL BRIEFING VAT - NON-ESTABLISHED TAXABLE PERSONS - CLAUSE 201 AND SCHEDULE 27 AND FACE VALUE VOUCHERS - NEW CLAUSE") TAXREP 32/12 (ICAEW REP 108/12) ICAEW TAX REPRESENTATION FINANCE (No 4) BILL 2012 - BRIEFING VAT - NON-ESTABLISHED TAXABLE PERSONS - CLAUSE 201 AND SCHEDULE 27 AND FACE VALUE VOUCHERS - NEW CLAUSE Briefing

TAXREP 32/12 (ICAEW REP 108/12) ICAEW TAX REPRESENTATION FINANCE (No 4) BILL 2012 - BRIEFING VAT - NON-ESTABLISHED TAXABLE PERSONS - CLAUSE 201 AND SCHEDULE 27 AND FACE VALUE VOUCHERS - NEW CLAUSE Briefing

Contents Paragraph Introduction 1-3. Who we are 4-6. Key point summary Major points Responses to consultation questions 21

TAXREP 17/14 (ICAEW REP 48/14) ICAEW TAX REPRESENTATION SIMPLIFICATION OF INTRASTAT Comments submitted on 7 April 2014 by ICAEW Tax Faculty in response to HMRC consultation document Simplification of Intrastat

TAXREP 17/14 (ICAEW REP 48/14) ICAEW TAX REPRESENTATION SIMPLIFICATION OF INTRASTAT Comments submitted on 7 April 2014 by ICAEW Tax Faculty in response to HMRC consultation document Simplification of Intrastat

ROYALTIES WITHHOLDING TAX

ICAEW REPRESENTATION 26/18 ROYALTIES WITHHOLDING TAX ICAEW welcomes the opportunity to comment on the consultation document Royalties Withholding Tax https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/663889/royalti

ICAEW REPRESENTATION 26/18 ROYALTIES WITHHOLDING TAX ICAEW welcomes the opportunity to comment on the consultation document Royalties Withholding Tax https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/663889/royalti

Introduction 1 2. Who we are 3-5 Comments 6-15 Further contact 16. Ten Tenets for a Better Tax System Appendix 1

TAXREP 13/12 ICAEW TAX REPRESENTATION CONTROLLED FOREIGN COMPANIES (CFC) REFORM Comments submitted on 24 February 2012 by ICAEW Tax Faculty in response to the publication on 31 January 2012 of further

TAXREP 13/12 ICAEW TAX REPRESENTATION CONTROLLED FOREIGN COMPANIES (CFC) REFORM Comments submitted on 24 February 2012 by ICAEW Tax Faculty in response to the publication on 31 January 2012 of further

TAXREP 38/14 (ICAEW REPRESENTATION 95/14)

") TAXREP 38/14 (ICAEW REPRESENTATION 95/14) PAYE CODE NUMBERS HMRC S OBLIGATION TO NOTIFY EMPLOYEES ICAEW welcomes the opportunity to comment on the draft secondary legislation The Income Tax (Pay As You

TAXREP 38/14 (ICAEW REPRESENTATION 95/14) PAYE CODE NUMBERS HMRC S OBLIGATION TO NOTIFY EMPLOYEES ICAEW welcomes the opportunity to comment on the draft secondary legislation The Income Tax (Pay As You

CALL FOR EVIDENCE RENT A ROOM RELIEF

ICAEW REPRESENTATION 25/18 CALL FOR EVIDENCE RENT A ROOM RELIEF ICAEW welcomes the opportunity to comment on the call for evidence Rent a room relief published by HM Treasury on 1 December 2017. This response

ICAEW REPRESENTATION 25/18 CALL FOR EVIDENCE RENT A ROOM RELIEF ICAEW welcomes the opportunity to comment on the call for evidence Rent a room relief published by HM Treasury on 1 December 2017. This response

Introduction 1-3. Who we are 4-6. Our comments Ten Tenets for a Better Tax System Appendix 1

TAXREP 6/13 (ICAEW REP 10/13) ICAEW TAX REPRESENTATION GENERAL ANTI-ABUSE RULE Comments submitted on 6 February 2013 by ICAEW Tax Faculty to introduce a General Anti-Abuse Rule (GAAR) and HMRC s draft

TAXREP 6/13 (ICAEW REP 10/13) ICAEW TAX REPRESENTATION GENERAL ANTI-ABUSE RULE Comments submitted on 6 February 2013 by ICAEW Tax Faculty to introduce a General Anti-Abuse Rule (GAAR) and HMRC s draft

REFORMS TO THE TAXATION OF NON DOMICILES MEETING NOTES

TECHNICAL RELEASE REFORMS TO THE TAXATION OF NON DOMICILES MEETING NOTES Note of meeting with HMRC/HMT on 26 October 2015 published by ICAEW Tax Faculty on 5 November 2015 ABOUT ICAEW ICAEW is a world-leading

TECHNICAL RELEASE REFORMS TO THE TAXATION OF NON DOMICILES MEETING NOTES Note of meeting with HMRC/HMT on 26 October 2015 published by ICAEW Tax Faculty on 5 November 2015 ABOUT ICAEW ICAEW is a world-leading

TAXREP 22/14 (ICAEW REPRESENTATION 56/14)

") TAXREP 22/14 (ICAEW REPRESENTATION 56/14) ICAEW TAX REPRESENTATION REVIEW OF EXISTING VAT LEGISLATION ON PUBLIC BODIES AND TAX EXEMPTIONS IN THE PUBLIC INTEREST ICAEW welcomes the opportunity to comment

TAXREP 22/14 (ICAEW REPRESENTATION 56/14) ICAEW TAX REPRESENTATION REVIEW OF EXISTING VAT LEGISLATION ON PUBLIC BODIES AND TAX EXEMPTIONS IN THE PUBLIC INTEREST ICAEW welcomes the opportunity to comment

CAPITAL GAINS TAX: PAYMENT WINDOW FOR RESIDENTIAL PROPERTY GAINS (PAYMENT ON ACCOUNT) Issued 6 June 2018

Issued 6 June 2018") ICAEW REPRESENTATION 64/18 CAPITAL GAINS TAX: PAYMENT WINDOW FOR RESIDENTIAL PROPERTY GAINS (PAYMENT Issued 6 June 2018 ICAEW welcomes the opportunity to respond to the Capital gains tax: Payment window

ICAEW REPRESENTATION 64/18 CAPITAL GAINS TAX: PAYMENT WINDOW FOR RESIDENTIAL PROPERTY GAINS (PAYMENT Issued 6 June 2018 ICAEW welcomes the opportunity to respond to the Capital gains tax: Payment window

Contents Paragraph Introduction 1-3. Who we are 4-6. Key point summary Major points 17-36

TAXREP 28/13 (ICAEW REP 66/13) ICAEW TAX REPRESENTATION OECD INTERNATIONAL VAT/GST GUIDELINES Comments submitted on 2 May 2013 by ICAEW Tax Faculty in response to the OECD consultation document OECD International

TAXREP 28/13 (ICAEW REP 66/13) ICAEW TAX REPRESENTATION OECD INTERNATIONAL VAT/GST GUIDELINES Comments submitted on 2 May 2013 by ICAEW Tax Faculty in response to the OECD consultation document OECD International

Contents Paragraph Introduction 1-4. Who we are 5-7. Key point summary Detailed comments 13-18

TAXREP 16/12 (ICAEW REP 39/12) ICAEW TAX REPRESENTATION REFORM OF THE TAXATION OF NON-DOMICILED INDIVIDUALS Comments submitted on 9 March 2012 by ICAEW Tax Faculty in response to HM Revenue and Customs

TAXREP 16/12 (ICAEW REP 39/12) ICAEW TAX REPRESENTATION REFORM OF THE TAXATION OF NON-DOMICILED INDIVIDUALS Comments submitted on 9 March 2012 by ICAEW Tax Faculty in response to HM Revenue and Customs

ICAEW TAX REPRESENTATION 128/17

ICAEW TAX REPRESENTATION 128/17 MAKING TAX DIGITAL FOR VAT: LEGISLATION OVERVIEW ICAEW welcomes the opportunity to comment on the Making Tax Digital for VAT: legislation overview published by HMRC on 13

ICAEW TAX REPRESENTATION 128/17 MAKING TAX DIGITAL FOR VAT: LEGISLATION OVERVIEW ICAEW welcomes the opportunity to comment on the Making Tax Digital for VAT: legislation overview published by HMRC on 13

Finance (No.3) Bill Clause 10: Exemption for expenses relating to travel

Bill Clause 10: Exemption for expenses relating to travel") Finance (No.3) Bill 2017-19 Clause 10: Exemption for expenses relating to travel Briefing for MPs by ICAEW Tax Faculty WHO WE ARE 1. Please see Appendix 1. EXECUTIVE SUMMARY 2. The new relaxed checking

Finance (No.3) Bill 2017-19 Clause 10: Exemption for expenses relating to travel Briefing for MPs by ICAEW Tax Faculty WHO WE ARE 1. Please see Appendix 1. EXECUTIVE SUMMARY 2. The new relaxed checking

Contents Paragraphs. Introduction 1 3. Key point summary 4

COMPLIANCE CHECKS: THE NEXT STAGE: DRAFT LEGISLATION AND COMMENTARY Comments submitted in March 2009 by the Tax Faculty of the Institute of Chartered Accountants in England & Wales in response to the consultation

COMPLIANCE CHECKS: THE NEXT STAGE: DRAFT LEGISLATION AND COMMENTARY Comments submitted in March 2009 by the Tax Faculty of the Institute of Chartered Accountants in England & Wales in response to the consultation

SIMPLIFICATION REVIEW: THE ASSOCIATED COMPANY RULES AS THEY APPLY TO THE SMALL COMPANIES RATE OF CORPORATION TAX

SIMPLIFICATION REVIEW: THE ASSOCIATED COMPANY RULES AS THEY APPLY TO THE SMALL COMPANIES RATE OF CORPORATION TAX Memorandum submitted on 22 January 2010 by the Tax Faculty of the Institute of Chartered

SIMPLIFICATION REVIEW: THE ASSOCIATED COMPANY RULES AS THEY APPLY TO THE SMALL COMPANIES RATE OF CORPORATION TAX Memorandum submitted on 22 January 2010 by the Tax Faculty of the Institute of Chartered

ICAEW TAX REPRESENTATION 68/17

ICAEW TAX REPRESENTATION 68/17 Making Tax Digital: sanctions for late submission and late payment ICAEW welcomes the opportunity to comment on the Making Tax Digital: sanctions for late submission and

ICAEW TAX REPRESENTATION 68/17 Making Tax Digital: sanctions for late submission and late payment ICAEW welcomes the opportunity to comment on the Making Tax Digital: sanctions for late submission and

ICAEW REPRESENTATION 108/16 TAX REPRESENTATION

ICAEW REPRESENTATION 108/16 TAX REPRESENTATION STRENGTHENING THE TAX AVOIDANCE DISCLOSURE REGIMES FOR INDIRECT TAXES ICAEW welcomes the opportunity to comment on the consultation document Strengthening

ICAEW REPRESENTATION 108/16 TAX REPRESENTATION STRENGTHENING THE TAX AVOIDANCE DISCLOSURE REGIMES FOR INDIRECT TAXES ICAEW welcomes the opportunity to comment on the consultation document Strengthening

TAXREP 50/14 (ICAEW REPRESENTATION 121/14)

") TAXREP 50/14 (ICAEW REPRESENTATION 121/14) TAX-ADVANTAGED VENTURE CAPITAL SCHEMES: ENSURING CONTINUED SUPPORT FOR SMALL AND GROWING BUSINESSES ICAEW welcomes the opportunity to comment on the consultation

TAXREP 50/14 (ICAEW REPRESENTATION 121/14) TAX-ADVANTAGED VENTURE CAPITAL SCHEMES: ENSURING CONTINUED SUPPORT FOR SMALL AND GROWING BUSINESSES ICAEW welcomes the opportunity to comment on the consultation

WRITTEN SUBMISSION TO THE HMRC BUSINESS INTERNATIONAL TAX TREATY TEAM ON THE ANNUAL REVIEW OF DOUBLE TAXATION TREATIES

TAXREP 18/09 DOUBLE TAXATION AGREEMENTS WRITTEN SUBMISSION TO THE HMRC BUSINESS INTERNATIONAL TAX TREATY TEAM ON THE ANNUAL REVIEW OF DOUBLE TAXATION TREATIES 2009-10 Contents Introduction Strategic Issues

TAXREP 18/09 DOUBLE TAXATION AGREEMENTS WRITTEN SUBMISSION TO THE HMRC BUSINESS INTERNATIONAL TAX TREATY TEAM ON THE ANNUAL REVIEW OF DOUBLE TAXATION TREATIES 2009-10 Contents Introduction Strategic Issues

MEETING THE OBLIGATIONS TO FILE RETURNS AND PAY TAX ON TIME

MEETING THE OBLIGATIONS TO FILE RETURNS AND PAY TAX ON TIME DRAFT LEGISLATION AND COMMENTARY Memorandum submitted on 3 March 2010 by the Tax Faculty of the Institute of Chartered Accountants in England

MEETING THE OBLIGATIONS TO FILE RETURNS AND PAY TAX ON TIME DRAFT LEGISLATION AND COMMENTARY Memorandum submitted on 3 March 2010 by the Tax Faculty of the Institute of Chartered Accountants in England

REVIEW OF DOUBLE TAXATION TREATIES AND DOUBLE CONTRIBUTION AGREEMENTS

REVIEW OF DOUBLE TAXATION TREATIES AND DOUBLE CONTRIBUTION AGREEMENTS 2010-11 Memorandum submitted on 1 February 2010 by the Tax Faculty of the Institute of Chartered Accountants in England and Wales to

REVIEW OF DOUBLE TAXATION TREATIES AND DOUBLE CONTRIBUTION AGREEMENTS 2010-11 Memorandum submitted on 1 February 2010 by the Tax Faculty of the Institute of Chartered Accountants in England and Wales to

VOLUNTARY DISCLOSURE OF ERRORS ON INDIRECT TAX RETURNS

VOLUNTARY DISCLOSURE OF ERRORS ON INDIRECT TAX RETURNS A submission made on 29 October 2007 by the Tax Faculty of the Institute of Chartered Accountants in England and Wales in response to a consultation

VOLUNTARY DISCLOSURE OF ERRORS ON INDIRECT TAX RETURNS A submission made on 29 October 2007 by the Tax Faculty of the Institute of Chartered Accountants in England and Wales in response to a consultation

ICAEW REPRESENTATION 16/17 TAX REPRESENTATION

ICAEW REPRESENTATION 16/17 TAX REPRESENTATION OPTIONAL REMUNERATION ARRANGEMENTS (INCLUDING SALARY SACRIFICE) DRAFT FINANCE BILL 2017 LEGISLATION: CLAUSE 2 & SCHEDULE 2 ICAEW welcomes the opportunity to

ICAEW REPRESENTATION 16/17 TAX REPRESENTATION OPTIONAL REMUNERATION ARRANGEMENTS (INCLUDING SALARY SACRIFICE) DRAFT FINANCE BILL 2017 LEGISLATION: CLAUSE 2 & SCHEDULE 2 ICAEW welcomes the opportunity to

SHARES ACQUIRED BEFORE 10 APRIL 2003 BY EXERCISING EMPLOYEE SHARE OPTIONS ALLOWABLE DEDUCTIONS: REVENUE & CUSTOMS BRIEF 30/09:

SHARES ACQUIRED BEFORE 10 APRIL 2003 BY EXERCISING EMPLOYEE SHARE OPTIONS ALLOWABLE DEDUCTIONS: REVENUE & CUSTOMS BRIEF 30/09: Text of a letter submitted on 4 June 2009 to HM Revenue & Customs by the Tax

SHARES ACQUIRED BEFORE 10 APRIL 2003 BY EXERCISING EMPLOYEE SHARE OPTIONS ALLOWABLE DEDUCTIONS: REVENUE & CUSTOMS BRIEF 30/09: Text of a letter submitted on 4 June 2009 to HM Revenue & Customs by the Tax

Introduction 1-2. Key point summary Comments Who we are. Ten Tenets for a Better Tax System

INTRASTAT A submission made on 30 August 2007 by the Tax Faculty of the Institute of Chartered Accountants in England and Wales in response to a consultation paper issued on 27 June 2007 by HM Revenue

INTRASTAT A submission made on 30 August 2007 by the Tax Faculty of the Institute of Chartered Accountants in England and Wales in response to a consultation paper issued on 27 June 2007 by HM Revenue

MODERN WORKING PRACTICES: EMPLOYMENT STATUS RULES FOR EMPLOYMENT RIGHTS AND TAX/NIC

L ICAEW REPRESENTATION 45/18 MODERN WORKING PRACTICES: EMPLOYMENT STATUS RULES FOR EMPLOYMENT RIGHTS AND TAX/NIC ICAEW welcomes the opportunity to respond to the Employment status rules for employment

L ICAEW REPRESENTATION 45/18 MODERN WORKING PRACTICES: EMPLOYMENT STATUS RULES FOR EMPLOYMENT RIGHTS AND TAX/NIC ICAEW welcomes the opportunity to respond to the Employment status rules for employment

REVIEW OF DOUBLE TAXATION TREATIES AND DOUBLE CONTRIBUTION AGREEMENTS

ICAEW TAX FACULTY REPRESENTATION REVIEW OF DOUBLE TAXATION TREATIES AND DOUBLE CONTRIBUTION AGREEMENTS 2011-12 Memorandum submitted in January 2011 by the Tax Faculty of the Institute of Chartered Accountants

ICAEW TAX FACULTY REPRESENTATION REVIEW OF DOUBLE TAXATION TREATIES AND DOUBLE CONTRIBUTION AGREEMENTS 2011-12 Memorandum submitted in January 2011 by the Tax Faculty of the Institute of Chartered Accountants

Introduction 1-2. Key point summary 3-4. Comments Answers to questions 16-20

APPROVED MILEAGE ALLOWANCE PAYMENTS Memorandum submitted in July 2007 by the Tax Faculty of the Institute of Chartered Accountants in England and Wales in response to an invitation to comment published

APPROVED MILEAGE ALLOWANCE PAYMENTS Memorandum submitted in July 2007 by the Tax Faculty of the Institute of Chartered Accountants in England and Wales in response to an invitation to comment published

Introduction 1-2. Key point summary 3 7. General comments Detailed comments 18-31

BUSINESS EXPENDITURE ON CARS Representations submitted on 26 February 2009 by the Tax Faculty of the Institute of Chartered Accountants in England and Wales in response to a consultation document Modernising

BUSINESS EXPENDITURE ON CARS Representations submitted on 26 February 2009 by the Tax Faculty of the Institute of Chartered Accountants in England and Wales in response to a consultation document Modernising

TECHNICAL RELEASE TAXGUIDE 02/15 (TECH 03/15TAX) HMRC CAPITAL TAXES LIAISON GROUP MINUTES

HMRC CAPITAL TAXES LIAISON GROUP MINUTES") TECHNICAL RELEASE TAXGUIDE 02/15 (TECH 03/15TAX) HMRC CAPITAL TAXES LIAISON GROUP MINUTES Minutes of meeting of 1 May 2015 of HMRC Capital Taxes Liaison Group published by ICAEW Tax Faculty in July 2015

TECHNICAL RELEASE TAXGUIDE 02/15 (TECH 03/15TAX) HMRC CAPITAL TAXES LIAISON GROUP MINUTES Minutes of meeting of 1 May 2015 of HMRC Capital Taxes Liaison Group published by ICAEW Tax Faculty in July 2015

AVOIDANCE INVOLVING PROFIT FRAGMENTATION ARRANGEMENTS (CL10, SCH 6) Issued 30 August 2018

Issued 30 August 2018") ICAEW REPRESENTATION 106/18 AVOIDANCE INVOLVING PROFIT FRAGMENTATION ARRANGEMENTS (CL10, SCH 6) Issued 30 August 2018 ICAEW welcomes the opportunity to comment on the consultation on draft Finance (No.3)

ICAEW REPRESENTATION 106/18 AVOIDANCE INVOLVING PROFIT FRAGMENTATION ARRANGEMENTS (CL10, SCH 6) Issued 30 August 2018 ICAEW welcomes the opportunity to comment on the consultation on draft Finance (No.3)

CORPORATE TAX AND THE DIGITAL ECONOMY

ICAEW REPRESENTATION 12/18 CORPORATE TAX AND THE DIGITAL ECONOMY 2 February ICAEW welcomes the opportunity to comment on the position paper Corporate Tax and the Digital Economy published by HM Treasury

ICAEW REPRESENTATION 12/18 CORPORATE TAX AND THE DIGITAL ECONOMY 2 February ICAEW welcomes the opportunity to comment on the position paper Corporate Tax and the Digital Economy published by HM Treasury

ICAEW REPRESENTATION 10/16

ICAEW REPRESENTATION 10/16 Uncertainty over Income Tax Treatments ICAEW welcomes the opportunity to comment on the IASB s DI/2015/1 Uncertainty over Income Tax Treatments, published in October 2015, a

ICAEW REPRESENTATION 10/16 Uncertainty over Income Tax Treatments ICAEW welcomes the opportunity to comment on the IASB s DI/2015/1 Uncertainty over Income Tax Treatments, published in October 2015, a

ICAEW TAX REPRESENTATION 110/17

ICAEW TAX REPRESENTATION 110/17 DELIVERING A TAX CUT FOR SMALL BUSINESSES: A NEW SMALL BUSINESS RATES RELIEF SCHEME FOR WALES ICAEW welcomes the opportunity to comment on the delivering a tax cut for small

ICAEW TAX REPRESENTATION 110/17 DELIVERING A TAX CUT FOR SMALL BUSINESSES: A NEW SMALL BUSINESS RATES RELIEF SCHEME FOR WALES ICAEW welcomes the opportunity to comment on the delivering a tax cut for small

ICAEW is pleased to respond to your request for comments on ED/2013/1 Recoverable amount disclosures for non-financial assets.

19 March 2013 Our ref: ICAEW Rep 47/13 Your ref: ED/2013/1 Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London EC4M 6XH Dear Hans ED/2013/1 Recoverable amount disclosures

19 March 2013 Our ref: ICAEW Rep 47/13 Your ref: ED/2013/1 Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London EC4M 6XH Dear Hans ED/2013/1 Recoverable amount disclosures

TAXREP 37/13 (ICAEWREP 105/13)

") TAXREP 37/13 (ICAEWREP 105/13) ICAEW TAX REPRESENTATION COMMUNITY AMATEUR SPORTS CLUBS (CASCS) SCHEME Comments submitted in August 2013 by the Tax Faculty of the Institute of Chartered Accountants in England

TAXREP 37/13 (ICAEWREP 105/13) ICAEW TAX REPRESENTATION COMMUNITY AMATEUR SPORTS CLUBS (CASCS) SCHEME Comments submitted in August 2013 by the Tax Faculty of the Institute of Chartered Accountants in England

ICAEW REPRESENTATION 168/14

ICAEW REPRESENTATION 168/14 EFRAG DRAFT ENDORSEMENT ADVICE ON IFRS 15 REVENUE FROM CONTRACTS WITH CUSTOMERS ICAEW welcomes the opportunity to respond to the draft endorsement advice and effects study report

ICAEW REPRESENTATION 168/14 EFRAG DRAFT ENDORSEMENT ADVICE ON IFRS 15 REVENUE FROM CONTRACTS WITH CUSTOMERS ICAEW welcomes the opportunity to respond to the draft endorsement advice and effects study report

SELF-FUNDED WORK-RELATED TRAINING FOR EMPLOYEES AND THE SELF EMPLOYED

L ICAEW REPRESENTATION 66/18 SELF-FUNDED WORK-RELATED TRAINING FOR EMPLOYEES AND THE SELF EMPLOYED ICAEW welcomes the opportunity to respond to the consultation Taxation of self-funded workrelated training:

L ICAEW REPRESENTATION 66/18 SELF-FUNDED WORK-RELATED TRAINING FOR EMPLOYEES AND THE SELF EMPLOYED ICAEW welcomes the opportunity to respond to the consultation Taxation of self-funded workrelated training:

ICAEW REPRESENTATION 92/16

ICAEW REPRESENTATION 92/16 Exposure Draft 60 Public Sector Combinations ICAEW welcomes the opportunity to comment on the Public Sector Combinations exposure draft published by the International Public

ICAEW REPRESENTATION 92/16 Exposure Draft 60 Public Sector Combinations ICAEW welcomes the opportunity to comment on the Public Sector Combinations exposure draft published by the International Public

Introduction 1 4. Who we are 5-7. Detailed Comments Further contact 29

TAXREP 8/12 ICAEW TAX REPRESENTATION CONTROLLED FOREIGN COMPANIES (CFC) REFORM Comments submitted on 10 February 2012 by ICAEW Tax Faculty in response to the publication on 6 December 2011 of draft clauses

TAXREP 8/12 ICAEW TAX REPRESENTATION CONTROLLED FOREIGN COMPANIES (CFC) REFORM Comments submitted on 10 February 2012 by ICAEW Tax Faculty in response to the publication on 6 December 2011 of draft clauses

1 Introduction. 1.4 Our stated objectives for the tax system include:

HMRC Technical Consultation: The Value Added Tax (Section 55A) (Specified Services and Excepted Supplies) Order 2019 Response by the Chartered Institute of Taxation 1 Introduction 1.1 The Chartered Institute

HMRC Technical Consultation: The Value Added Tax (Section 55A) (Specified Services and Excepted Supplies) Order 2019 Response by the Chartered Institute of Taxation 1 Introduction 1.1 The Chartered Institute

ICAEW REPRESENTATION 07/18

ICAEW REPRESENTATION 07/18 Occupational Pension Schemes (Master Trusts) Regulations 2018 ICAEW welcomes the opportunity to comment on the Occupational Pension Schemes (Master Trusts) Regulations 2018 published

ICAEW REPRESENTATION 07/18 Occupational Pension Schemes (Master Trusts) Regulations 2018 ICAEW welcomes the opportunity to comment on the Occupational Pension Schemes (Master Trusts) Regulations 2018 published

ICAEW REPRESENTATION 26/17 TAX REPRESENTATION

ICAEW REPRESENTATION 26/17 TAX REPRESENTATION Reforms to the taxation of non-domiciliaries and offshore trusts ICAEW welcomes the opportunity to comment on the revised draft Finance Bill 2017 legislation

ICAEW REPRESENTATION 26/17 TAX REPRESENTATION Reforms to the taxation of non-domiciliaries and offshore trusts ICAEW welcomes the opportunity to comment on the revised draft Finance Bill 2017 legislation

HOMES OUTSIDE THE UK OWNED THROUGH A COMPANY

HOMES OUTSIDE THE UK OWNED THROUGH A COMPANY Memorandum submitted in October 2007 by the Tax Faculty of the Institute of Chartered Accountants in England and Wales in response to an invitation dated 17

HOMES OUTSIDE THE UK OWNED THROUGH A COMPANY Memorandum submitted in October 2007 by the Tax Faculty of the Institute of Chartered Accountants in England and Wales in response to an invitation dated 17

EQUITY METHOD: SHARE OF OTHER NET ASSET CHANGES (PROPOSED AMENDMENTS TO IAS 28)

") 28 February 2013 Our ref: ICAEW Rep 41/13 Your ref: ED/2012/3 Mr Hans Hoogervorst International Accounting Standards Board 30 Canon Street London EC4M 6XH Dear Hans EQUITY METHOD: SHARE OF OTHER NET ASSET

28 February 2013 Our ref: ICAEW Rep 41/13 Your ref: ED/2012/3 Mr Hans Hoogervorst International Accounting Standards Board 30 Canon Street London EC4M 6XH Dear Hans EQUITY METHOD: SHARE OF OTHER NET ASSET

ICAEW REPRESENTATION 103/17

ICAEW REPRESENTATION 103/17 ASSET SALES IN COMPETITION WITH AN OFFER AND OTHER MATTERS ICAEW welcomes the opportunity to comment on PCP 2017/1 Asset sales in competition with an offer and other matters,

ICAEW REPRESENTATION 103/17 ASSET SALES IN COMPETITION WITH AN OFFER AND OTHER MATTERS ICAEW welcomes the opportunity to comment on PCP 2017/1 Asset sales in competition with an offer and other matters,

MAKING TAX DIGITAL: INTEREST HARMONISATION AND SANCTIONS FOR LATE PAYMENT

ICAEW REPRESENTATION 29/18 MAKING TAX DIGITAL: INTEREST HARMONISATION AND ICAEW welcomes the opportunity to comment on the Making Tax Digital: interest harmonisation and sanctions for late payment consultation

ICAEW REPRESENTATION 29/18 MAKING TAX DIGITAL: INTEREST HARMONISATION AND ICAEW welcomes the opportunity to comment on the Making Tax Digital: interest harmonisation and sanctions for late payment consultation

VAT POSTPONED ACCOUNTING LETTER TO FST

ICAEW REPRESENTATION 31/18 VAT POSTPONED ACCOUNTING LETTER TO FST This letter of 28 February 2018 has been prepared on behalf of ICAEW by the Tax Faculty. Internationally recognised as a source of expertise,

ICAEW REPRESENTATION 31/18 VAT POSTPONED ACCOUNTING LETTER TO FST This letter of 28 February 2018 has been prepared on behalf of ICAEW by the Tax Faculty. Internationally recognised as a source of expertise,

TAXREP 43/14 (ICAEW REPRESENTATION 112/14)

") TAXREP 43/14 (ICAEW REPRESENTATION 112/14) EMPLOYEE BENEFITS AND EXPENSES EXEMPTION FOR PAID OR REIMBURSED EXPENSES ICAEW welcomes the opportunity to comment on the consultation paper Employee benefits

TAXREP 43/14 (ICAEW REPRESENTATION 112/14) EMPLOYEE BENEFITS AND EXPENSES EXEMPTION FOR PAID OR REIMBURSED EXPENSES ICAEW welcomes the opportunity to comment on the consultation paper Employee benefits

ICAEW REPRESENTATION 60/15

ICAEW REPRESENTATION 60/15 DISCLOSURE INITIATIVE: PROPOSED AMENDMENTS TO IAS 7 ICAEW welcomes the opportunity to comment on ED/2014/6 Disclosure Initiative Proposed amendments to IAS 7 published by the

ICAEW REPRESENTATION 60/15 DISCLOSURE INITIATIVE: PROPOSED AMENDMENTS TO IAS 7 ICAEW welcomes the opportunity to comment on ED/2014/6 Disclosure Initiative Proposed amendments to IAS 7 published by the

NATIONAL INSURANCE CONTRIBUTIONS: IMPROVING COLLECTION FROM THE SELF EMPLOYED

NATIONAL INSURANCE CONTRIBUTIONS: IMPROVING COLLECTION FROM THE SELF EMPLOYED Memorandum submitted in June 2008 by the Tax Faculty of the Institute of Chartered Accountants in England and Wales in response

NATIONAL INSURANCE CONTRIBUTIONS: IMPROVING COLLECTION FROM THE SELF EMPLOYED Memorandum submitted in June 2008 by the Tax Faculty of the Institute of Chartered Accountants in England and Wales in response

Non-resident companies chargeable to Income Tax and non-resident CGT Response by the Chartered Institute of Taxation

Non-resident companies chargeable to Income Tax and non-resident CGT Response by the Chartered Institute of Taxation 1 Introduction 1.1 The CIOT responds to this Stage 1 1 consultation exploring the case

Non-resident companies chargeable to Income Tax and non-resident CGT Response by the Chartered Institute of Taxation 1 Introduction 1.1 The CIOT responds to this Stage 1 1 consultation exploring the case

Capital Gains Tax: Payment window for residential property gains (payment on account) Response by the Chartered Institute of Taxation

Response by the Chartered Institute of Taxation") Capital Gains Tax: Payment window for residential property gains (payment on account) Response by the Chartered Institute of Taxation 1 Introduction 1.1 This Stage Two 1 consultation follows the government

Capital Gains Tax: Payment window for residential property gains (payment on account) Response by the Chartered Institute of Taxation 1 Introduction 1.1 This Stage Two 1 consultation follows the government

Contents Paragraph Introduction 1-3. Who we are 4-6. Key point summary The consultation process in relation to the partnership proposals 14-20

TAXREP 05/14 (ICAEW REP 16/14) ICAEW TAX REPRESENTATION DRAFT FINANCE BILL 2014 PARTNERSHIPS PARTS 1-4 Comments submitted on 3 February 2014 by ICAEW Tax Faculty in response to Draft Finance Bill 2014

TAXREP 05/14 (ICAEW REP 16/14) ICAEW TAX REPRESENTATION DRAFT FINANCE BILL 2014 PARTNERSHIPS PARTS 1-4 Comments submitted on 3 February 2014 by ICAEW Tax Faculty in response to Draft Finance Bill 2014

Improving engagement practices between companies and institutional investors

20 December 2012 Our ref: ICAEW Rep 190/12 Seamus Gillen Director of Policy ICSA 16 Park Crescent London W1B 1AH By email: policy@icsaglobal.com Dear Mr Gillen Improving engagement practices between companies

20 December 2012 Our ref: ICAEW Rep 190/12 Seamus Gillen Director of Policy ICSA 16 Park Crescent London W1B 1AH By email: policy@icsaglobal.com Dear Mr Gillen Improving engagement practices between companies

ICAEW REPRESENTATION 30/15

ICAEW REPRESENTATION 30/15 Nullification of Ban on Invoice Assignment Clauses ICAEW welcomes the opportunity to comment on the consultation paper Nullification of Ban on Invoice Assignment Clauses published

ICAEW REPRESENTATION 30/15 Nullification of Ban on Invoice Assignment Clauses ICAEW welcomes the opportunity to comment on the consultation paper Nullification of Ban on Invoice Assignment Clauses published

ICAEW REPRESENTATION 191/16

ICAEW REPRESENTATION 191/16 Practice Note 20 (Revised): The Audit of Insurers in the United Kingdom ICAEW welcomes the opportunity to comment on the Practice Note 20 (Revised): The Audit of Insurers in

ICAEW REPRESENTATION 191/16 Practice Note 20 (Revised): The Audit of Insurers in the United Kingdom ICAEW welcomes the opportunity to comment on the Practice Note 20 (Revised): The Audit of Insurers in

Please contact me should you wish to discuss any of the points raised in the attached response.

10 September 2010 Our ref: ICAEW Rep 87/10 Your ref: ED/2010/7 Ms Hilary Eastman Senior Technical Manager International Accounting Standards Board 30 Cannon Street London EC4M 6XH Dear Hilary MEASUREMENT

10 September 2010 Our ref: ICAEW Rep 87/10 Your ref: ED/2010/7 Ms Hilary Eastman Senior Technical Manager International Accounting Standards Board 30 Cannon Street London EC4M 6XH Dear Hilary MEASUREMENT

17 June Our ref: ICAEW Rep 86/13. Mme Françoise Flores Chair European Financial Reporting Advisory Group Avenue des Arts B-1210 Brussels

17 June 2013 Our ref: ICAEW Rep 86/13 Mme Françoise Flores Chair European Financial Reporting Advisory Group 13-14 Avenue des Arts B-1210 Brussels Chère Mme Flores ED/2013/3 Financial Instruments: Expected

17 June 2013 Our ref: ICAEW Rep 86/13 Mme Françoise Flores Chair European Financial Reporting Advisory Group 13-14 Avenue des Arts B-1210 Brussels Chère Mme Flores ED/2013/3 Financial Instruments: Expected

Stakeholder Consultation: Review of Double Taxation Treaties 2018

Ref: IT 30 November 2018 David Price Tax Treaty Team BAI International Relations and Capacity Building Zone C, Floor 9 10 South Colonnade Canary Wharf E14 4PU Via email: taxtreaty.team@hmrc.gsi.gov.uk

Ref: IT 30 November 2018 David Price Tax Treaty Team BAI International Relations and Capacity Building Zone C, Floor 9 10 South Colonnade Canary Wharf E14 4PU Via email: taxtreaty.team@hmrc.gsi.gov.uk

ICAEW REPRESENTATION 96/15

ICAEW REPRESENTATION 96/15 EFRAG draft endorsement advice on IFRS 9 Financial Instruments ICAEW welcomes the opportunity to respond to the draft endorsement advice and effects study report on IFRS 9 Financial

ICAEW REPRESENTATION 96/15 EFRAG draft endorsement advice on IFRS 9 Financial Instruments ICAEW welcomes the opportunity to respond to the draft endorsement advice and effects study report on IFRS 9 Financial

1 Introduction. Background

Revenue Scotland Scottish Landfill Tax guidance on how to determine the rate of tax chargeable on waste fines A Consultation Paper Response by the Chartered Institute of Taxation 1 Introduction 1.1 This

Revenue Scotland Scottish Landfill Tax guidance on how to determine the rate of tax chargeable on waste fines A Consultation Paper Response by the Chartered Institute of Taxation 1 Introduction 1.1 This

HMRC Consultation Landfill Tax: improving clarity and certainty for taxpayers Response by the Chartered Institute of Taxation

HMRC Consultation Landfill Tax: improving clarity and certainty for taxpayers Response by the Chartered Institute of Taxation 1 Introduction 1.1 The Chartered Institute of Taxation (CIOT) presents its

HMRC Consultation Landfill Tax: improving clarity and certainty for taxpayers Response by the Chartered Institute of Taxation 1 Introduction 1.1 The Chartered Institute of Taxation (CIOT) presents its

(07 th October 2015) 39492/35 DOC 4113 Page 1

39492/35 DOC 4113 Page 1") RESIDENTIAL LANDLORDS ASSOCIATION RESPONSE TO THE CONSULTATION ON THE HMRC CONSULTATION REPLACING WEAR AND TEAR ALLOWANCE WITH TAX RELIEF FOR REPLACING FURNISHINGS IN LET RESIDENTIAL DWELLING HOUSES (07

RESIDENTIAL LANDLORDS ASSOCIATION RESPONSE TO THE CONSULTATION ON THE HMRC CONSULTATION REPLACING WEAR AND TEAR ALLOWANCE WITH TAX RELIEF FOR REPLACING FURNISHINGS IN LET RESIDENTIAL DWELLING HOUSES (07

ICAEW welcomes the opportunity to comment on the VAT and Vouchers consultation document published by HMRC on 1 December 2017.

ICAEW REPRESENTATION 24/18 VAT AND VOUCHERS 21 February ICAEW welcomes the opportunity to comment on the VAT and Vouchers consultation document published by HMRC on 1 December 2017. This response of 21

ICAEW REPRESENTATION 24/18 VAT AND VOUCHERS 21 February ICAEW welcomes the opportunity to comment on the VAT and Vouchers consultation document published by HMRC on 1 December 2017. This response of 21

TREASURY SELECT COMMITTEE VAT INQUIRY Issued 29 June 2018

ICAEW REPRESENTATION 74/18 TREASURY SELECT COMMITTEE VAT INQUIRY Issued 29 June 2018 ICAEW (Institute of Chartered Accountants in England & Wales) welcomes the opportunity to respond to the VAT Inquiry

ICAEW REPRESENTATION 74/18 TREASURY SELECT COMMITTEE VAT INQUIRY Issued 29 June 2018 ICAEW (Institute of Chartered Accountants in England & Wales) welcomes the opportunity to respond to the VAT Inquiry

SHARES ACQUIRED BEFORE 10 APRIL 2003 BY EXERCISING EMPLOYEE SHARE OPTIONS ALLOWABLE DEDUCTIONS AND CAPITAL LOSSES

Tax Guide MANSWORTH V JELLEY REVISITED SHARES ACQUIRED BEFORE 10 APRIL 2003 BY EXERCISING EMPLOYEE SHARE OPTIONS ALLOWABLE DEDUCTIONS AND CAPITAL LOSSES GUIDANCE ON THE PRACTICAL IMPLICATIONS OF HMRC S

Tax Guide MANSWORTH V JELLEY REVISITED SHARES ACQUIRED BEFORE 10 APRIL 2003 BY EXERCISING EMPLOYEE SHARE OPTIONS ALLOWABLE DEDUCTIONS AND CAPITAL LOSSES GUIDANCE ON THE PRACTICAL IMPLICATIONS OF HMRC S

HMRC Consultation Document Tackling Offshore Tax Evasion: A Requirement to Correct Response by the Chartered Institute of Taxation

HMRC Consultation Document Tackling Offshore Tax Evasion: A Requirement to Correct Response by the Chartered Institute of Taxation 1 Introduction 1.1 This is the latest in a series of consultations by

HMRC Consultation Document Tackling Offshore Tax Evasion: A Requirement to Correct Response by the Chartered Institute of Taxation 1 Introduction 1.1 This is the latest in a series of consultations by

Assessment of the suitability of the International Public Sector Accounting Standards for the Member States Public consultation

Our ref: ICAEW Rep 70/12 European Commission - Eurostat Directorate D: Government Finance Statistics Joseph Bech building 5 Rue Alphonse Weicker L-2721 Luxembourg By email: ESTAT-IPSASconsultation@ec.europa.eu

Our ref: ICAEW Rep 70/12 European Commission - Eurostat Directorate D: Government Finance Statistics Joseph Bech building 5 Rue Alphonse Weicker L-2721 Luxembourg By email: ESTAT-IPSASconsultation@ec.europa.eu

A Review of the Conceptual Framework for Financial Reporting: draft EFRAG comment letter

24 December 2013 Our ref: ICAEW Rep 179/13 Ms Françoise Flores Chairman EFRAG 35 Square de Meeûs B-1000 Brussels Belgium Dear Françoise A Review of the Conceptual Framework for Financial Reporting: draft

24 December 2013 Our ref: ICAEW Rep 179/13 Ms Françoise Flores Chairman EFRAG 35 Square de Meeûs B-1000 Brussels Belgium Dear Françoise A Review of the Conceptual Framework for Financial Reporting: draft

ICAEW REPRESENTATION 36/15

ICAEW REPRESENTATION 36/15 SEPARATE BUSINESS RULE ICAEW welcomes the opportunity to comment on the Consultation paper, Separate Business Rule, published by the Solicitors Regulation Authority (SRA) on

ICAEW REPRESENTATION 36/15 SEPARATE BUSINESS RULE ICAEW welcomes the opportunity to comment on the Consultation paper, Separate Business Rule, published by the Solicitors Regulation Authority (SRA) on

The ICAEW is pleased to respond to your request for comments on Tracing employers liability insurers.

14 September 2010 Our ref: ICAEW Rep 86/10 Your ref: CP 10/13 Trevor Cooke Prudential Insurance Policy Financial Services Authority 25 The North Colonnade Canary Wharf London E14 5HS Dear Trevor Tracing

14 September 2010 Our ref: ICAEW Rep 86/10 Your ref: CP 10/13 Trevor Cooke Prudential Insurance Policy Financial Services Authority 25 The North Colonnade Canary Wharf London E14 5HS Dear Trevor Tracing

Proposed Revisions to IVSC Exposure Draft: The Valuation of Equity Derivatives

30 September 2013 Our ref: ICAEW Rep 134/13 IVSC 1 King Street London EC2V 8AU United Kingdom CommentLetters@ivsc.org Dear Ms Castaneda Proposed Revisions to IVSC Exposure Draft: The Valuation of Equity

30 September 2013 Our ref: ICAEW Rep 134/13 IVSC 1 King Street London EC2V 8AU United Kingdom CommentLetters@ivsc.org Dear Ms Castaneda Proposed Revisions to IVSC Exposure Draft: The Valuation of Equity

National Insurance and Self-employed Entertainers Response by the Chartered Institute of Taxation

National Insurance and Self-employed Entertainers Response by the Chartered Institute of Taxation 1 Introduction 1.1 The Chartered Institute of Taxation (CIOT) is pleased to comment on the proposals to

National Insurance and Self-employed Entertainers Response by the Chartered Institute of Taxation 1 Introduction 1.1 The Chartered Institute of Taxation (CIOT) is pleased to comment on the proposals to

Penalties for enablers of defeated tax avoidance HMRC s draft guidance Comments from the Chartered Institute of Taxation

1 Introduction Penalties for enablers of defeated tax avoidance HMRC s draft guidance Comments from the Chartered Institute of Taxation 1.1 We set out below our comments on HMRC s draft guidance on the

1 Introduction Penalties for enablers of defeated tax avoidance HMRC s draft guidance Comments from the Chartered Institute of Taxation 1.1 We set out below our comments on HMRC s draft guidance on the

Revised scheme for registration of charges created by companies and limited liability partnerships: proposed revision of Part 25, Companies Act 2006

30 September 2011 Our ref: ICAEW Rep 94/11 Anne Scrope, Business Environment, Department for Business, Innovation and Skills, Spur 2, 3rd floor, 1 Victoria Street, London SW1H 0ET By email: anne.scrope@bis.gsi.gov.uk

30 September 2011 Our ref: ICAEW Rep 94/11 Anne Scrope, Business Environment, Department for Business, Innovation and Skills, Spur 2, 3rd floor, 1 Victoria Street, London SW1H 0ET By email: anne.scrope@bis.gsi.gov.uk

ICAEW REPRESENTATION 57/17

ICAEW REPRESENTATION 57/17 Security and Sustainability in Defined Benefit Pension Schemes ICAEW welcomes the opportunity to comment on the Security and Sustainability in Defined Benefit Pension Schemes

ICAEW REPRESENTATION 57/17 Security and Sustainability in Defined Benefit Pension Schemes ICAEW welcomes the opportunity to comment on the Security and Sustainability in Defined Benefit Pension Schemes

Introduction Paragraphs 1-6

ICAEW TAX FACULTY, CIOT AND STEP GUIDANCE NOTE TAXGUIDE 3/10 TRUSTEE RESIDENCE Guidance note agreed by HM Revenue & Customs issued in August 2010 by the Tax Faculty of the Institute of Chartered Accountants

ICAEW TAX FACULTY, CIOT AND STEP GUIDANCE NOTE TAXGUIDE 3/10 TRUSTEE RESIDENCE Guidance note agreed by HM Revenue & Customs issued in August 2010 by the Tax Faculty of the Institute of Chartered Accountants