China Tax & Investment News. The long-awaited tax agreement between the China Mainland - Taiwan Straits was signed. Background

|

|

|

- Roy Chandler

- 5 years ago

- Views:

Transcription

1 Issue No.CTIN Sep 2015 China Tax & Investment News The long-awaited tax agreement between the China Mainland - Taiwan Straits was signed Background A bilateral tax treaty, known as an agreement for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income, refers to an agreement that is entered into between two jurisdictions to allocate their taxing rights on revenues as well as other tax-related matters. Due to differences in political, economic and cultural environments, plus the gap in their tax systems, to protect the interests of respective jurisdictions, bilateral negotiations between two jurisdictions would be relatively efficient and can reach the purposes of providing tax residents with relief from double taxation; appropriate distribution of taxing rights and tax revenue; saving administrative costs as well as prevention of tax evasion. In addition to tax treaties, the bilateral tax arrangements entered into under specific circumstances, e.g., the agreements between Mainland China (the Mainland) and the special administration regions (SARs), have similar functionality to the double tax treaties (hereby collectively referred as DTA). The DTA plays a key role in international taxation coordination and cooperation and is a significant regulatory framework to promote and facilitate cross-border business activities. Nevertheless, the Mainland and Taiwan had never entered into a DTA due to historical reasons; this inevitably resulted in double taxation on cross-strait economic activities, impeding the cross-strait trading flows and economic development. China Tax & Investment News 1

on 25 August 2015. Mr.")

2 After years of negotiations, Chairman Chen Deming of the Association for Relations across the Taiwan Straits (ARATS) and Chairman Lin Join-sane of the Straits Exchange Foundation (SEF) finally signed the Agreement on Avoidance of Double Taxation and Improvement of Tax Cooperation across the Taiwan Straits (hereinafter referred to as the Cross-strait DTA ) on 25 August Mr. Zhang Zhiyong, the vice-minister of the State Administration of Taxation (SAT) was invited to witness the signing ceremony. The Cross-strait DTA 1, according to its claims, aims to further improve cross-strait economic and trade cooperation, as well as reduce or eliminate double taxation. The Cross-strait DTA shall be ratified upon the completion of the respective internal procedures required by both the Mainland and Taiwan and shall take effect on the day following to the relevant notes being exchanged from both sides. It will apply to income derived on or after 1 January of the calendar year following that in which the Cross-strait DTA enters into force. The Cross-strait DTA stipulates the taxing jurisdictions over various incomes derived from cross-strait economic activities and available DTA relief mechanisms. It also clarifies the approaches to eliminate double taxation and promises a non-discrimination tax treatment for residents from both sides. It is expected that the DTA would reduce the tax burden of enterprises doing business across the Strait, enhance the competitiveness of both jurisdictions and facilitate investments between the Mainland and Taiwan. This issue of China Tax and Investment News is to discuss the Cross-strait DTA in detail. The Cross-strait DTA The Cross-strait DTA is similar to some standard DTAs and covers matters related to scope, permanent establishment, income derived from business and etc. We summarize certain key contents of the Cross-strait DTA as follows: Table 1 Note: 1. You can click this link to access the full content of the Cross-strait DTA: China Tax & Investment News 2

3 China Tax & Investment News 3

4 Our observations The Cross-strait DTA aims to reduce the tax burden of enterprises and individuals participating in cross-strait economic activities by taking into consideration the special cross-strait economic relationships and the respective tax schemes. The goal of the Cross-strait DTA is to create a certain and transparent tax environment for cross-strait investors with appropriate tax relief so as to improve the development of economic and trade across the Taiwan Strait. According to the official website of the SAT, as of the end of May 2015 China has entered into 100 DTAs with other jurisdictions, among which, 97 DTAs already became effective. On top of that, the Mainland has entered into double tax arrangements with the Hong Kong SAR and Macau SAR in 2006 and 2003 respectively. In the absence of a similar tax agreement/arrangement, enterprises and individuals of the Mainland and Taiwan engaging in cross-strait investments or trading were placed in comparatively disadvantageous positions. Based on the statistics released by the competent finance department of Taiwan, for the past 20 years, the accumulated investments in the Mainland from Taiwan have reached USD147 billion which accounts for 62% of total Taiwan s outbound investments. The conclusion of the Cross-strait DTA would not only reduce the tax burden of Taiwan enterprises investing in the Mainland but also encourage more Mainland enterprises to invest in Taiwan. Upon the ratification of the Cross-strait DTA, it is anticipated that positive impacts would arise in the following areas: 1. Elimination of double taxation Before the conclusion of the Cross-strait DTA, it is not impossible that some cross-strait economic activities may be double taxed. Within the effectiveness of the Cross-strait DTA, such a problem could be effectively addressed. For instance, where a Mainland/Taiwan enterprise engages in businesses with the other side without the constitution of a PE, then the relevant business profits derived shall not be taxable on the sourcing side. According to the Cross-strait DTA, where a resident of the Mainland/Taiwan does not constitute a PE in the other jurisdiction, this resident shall not be taxed on the other side (i.e. for a construction project, if the activities do not continue for a period of more than 12 months; or, for a service project, if the provision of services by an enterprise through employees or other personnel engaged by the enterprise does not continue for a period or periods aggregating more than 183 days within any 12-month period, no PE is constituted). 2. Indirect investment made by Taiwan Investors through a third jurisdiction may also enjoy benefits under the DTA In general, a DTA is not applicable to a situation where a resident of one jurisdiction invests in another jurisdiction through an entity incorporated under laws of a third jurisdiction. However, according to the statistics released by the competent finance department of Taiwan, 75% of investments in the Mainland by Taiwan investors are through their entities incorporated in a third jurisdiction. In this respect, the Cross-strait DTA specifically adds the provision that any entity incorporated under the law of a third jurisdiction which has its place of effective management in one of the jurisdictions, is regarded as resident for the purposes of this agreement, and hence any entity incorporated under the law of third jurisdiction may be deemed as residents of the Mainland/Taiwan and would therefore be eligible for enjoying benefits under the Cross-Strait DTA in future, as long as the places of effective management (PEM) of such an entity are in the Mainland/Taiwan. Pursuant to the Cross-strait DTA, the aforesaid places of effective management refer to enterprise which satisfies ALL of the following criteria: Substantial operation management, financial and human capital decisions are made or approved by personnel/head offices/organizations located in the Mainland/Taiwan. China Tax & Investment News 4

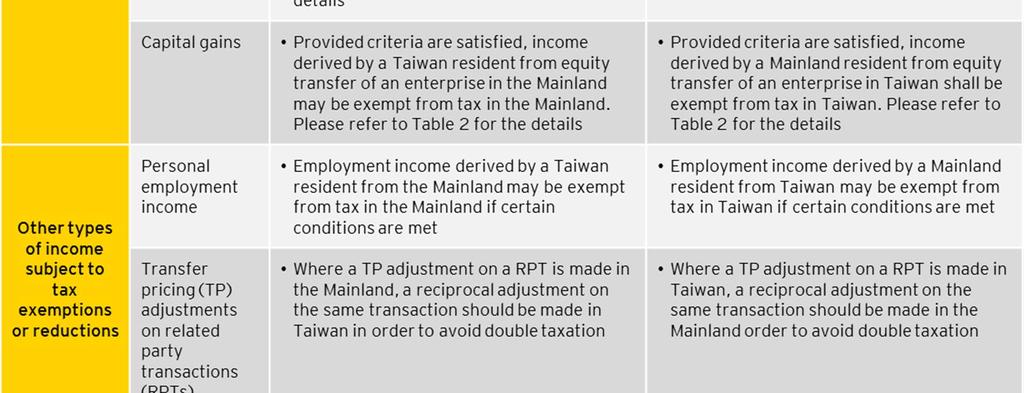

5 Financial statements, accounting records, board resolutions or shareholders resolutions are recorded or maintained in the Mainland/Taiwan. Organizations in charge of the major operation activities are located in the Mainland/Taiwan. 3. Reduction of withholding tax rates According to the prevailing PRC CIT Law, dividends, interests and royalties derived from the Mainland by Taiwan enterprises are subject to CIT at 10%. After the Cross-strait DAT becomes effective, the relevant withholding tax rates could be substantially reduced. The preferential tax treatments among the Cross-strait DTA, the Mainland - Hong Kong DTA and the Mainland Macao DTA are generally in line and details are laid out for your reference: Table 2 China Tax & Investment News 5

![Note: 2. According to Guishuihan [2008] No.](/docs-images/85/92106489/images/6-2.jpg "685, when implementing this provision, where a Hong Kong resident has directly or indirectly owned not less than 25% capital of the Mainland")

6 Upon the ratification of the Cross-strait DTA, it is anticipated that positive impacts would arise in the following areas: 1. Elimination of double taxation For dividends, interests and royalties, the preferential withholding tax rates as prescribed in the Cross-strait DTA are the same as that of the Mainland Hong Kong DTA and the Mainland Macau DTA. After the effectiveness of the Cross-strait DTA, the treaty relief would enhance the willingness of domestic enterprises to invest in Taiwan. Note: 2. According to Guishuihan [2008] No. 685, when implementing this provision, where a Hong Kong resident has directly or indirectly owned not less than 25% capital of the Mainland enterprise at any time within the 12 months before the alienation, the supervising tax authority in the Mainland is empowered to impose tax. China Tax & Investment News 6

7 For capital gains, prior to the effectiveness of the Cross-strait DTA, if a Taiwan enterprise directly transfers shares of a Mainland enterprise, the Taiwan enterprise shall be subject to CIT at 10% according to the prevailing PRC CIT Law and its Implementation Rules, regardless the percentage of ownership or other conditions. However, under the Cross-strait DTA, a resident of one jurisdiction derives gains from the alienation of shares or other rights of the resident company of the other jurisdiction may only be taxed in the jurisdiction where the transferor resides. For example, for non-land-rich equity transfer, unless such gains are exempt from tax in the jurisdiction where the transferor resides and such transferor directly or indirectly holds 25% capital of the company of the other jurisdiction at any time during the 12-month period preceding such alienation, upon the effectiveness of the DTA, gains so derived by a Taiwan resident may only be taxed in Taiwan and are exempt from tax in the Mainland. The same tax treatment will apply to a Mainland resident disposing shares of a Taiwan company. In addition, as aforesaid, if a Taiwan enterprise transfers shares of their Mainland subsidiaries through an intermediate company incorporated in a third jurisdiction, the relevant capital gain provisions in the Crossstrait DTA may also be applied, provided its PEM is located in Taiwan. 4. Improvement of cooperation Before announcement of the Cross-strait DTA, it was not rare that tax authorities of both sides could not agree on a transfer price for RPT by mutual consent, which accordingly may have lead to double taxation. Under the effectiveness of the DTA, the tax burden of taxpayers, especially for the business group, can be reduced and double taxation can be eliminated by adopting the mutual BAPA and signing an APA. When encountering any disputes, the Mainland domestic enterprises or Taiwan enterprises can take advantage of the Cross-strait DTA to protect the respective benefits. In the meantime, although the automatic EoI system has not been specified in the Cross-strait DTA, it is expected that tax authorities of both sides would work closer for the exchange of tax related information and would therefore disallow structure or actions that would abuse provisions under Cross-strait DTA. Conclusions Although the Cross-strait DTA was signed on 25 August 2015, it will not be effective until the respective ratification procedures are completed. The DTA shall then apply to income derived on or after 1 January of the calendar year when this Agreement enters into force. After the Cross-strait DTA is ratified successfully, it will bring about far-reaching positive impacts for thecross-strait investment environment. It is an encouraging change that the tax systems can finally catch up with the rapid business development driven by cross-strait entrepreneurs. It will clearly benefit entrepreneurs who ve been aiming atoptimizing their business operation structure in the globalized economy. Taiwanese enterprises that already have investments in the Mainland or intend to invest in the Mainland should review their existing or planned investment structures and transactional flows to determine whether proper adjustments need to be made to enhance operational and financial synergy. Meanwhile, it is important to note that the legislative ratification may not necessarily be a straight-forward process, especially considering the fact that the Service Trade Agreement between the Mainland and Taiwan signed in 2013 has not yet become effective due to unresolved legislative debates in Taiwan. The business community is advised to be patient and wait for the effective date of the Cross-strait DTA to be confirmed.. We will aim to always keep you abreast of the developments regarding this important Cross-strait Agreement. Analysis related to individual services as prescribed in the DTA shall be released separately in due course. If in doubt, consultations with tax professionals are recommended. China Tax & Investment News 7

8 Contact us For more information, please contact your usual EY contact or one of the following of EY s China tax leaders. Office Tax Leaders Margin Ngai (Beijing) martin.ngai@cn.ey.com Fisher Tian (Tianjin) fisher.tian@cn.ey.com Samuel Yan (Dalian/Shenyang) samuel.yan@cn.ey.com Lucy Wang (Qingdao) lucy-c.wang@cn.ey.com Joanne Su (Xi an) joanne.su@cn.ey.com Vickie Tan (Shanghai) vickie.tan@cn.ey.com Raymond Zhu (Wuhan) raymond.zhu@cn.ey.com Audrie Xia (Suzhou) audrie.xia@cn.ey.com Andrew Chen (Nanjing) andrew-jp.chen@cn.ey.com Patricia Xia (Hangzhou) patricia.xia@cn.ey.com Chuan Shi (Chengdu) chuan.shi@cn.ey.com Clement Yuen (Shenzhen) clement.yuen@cn.ey.com Rio Chan (Guangzhou/Changsha) rio.chan@cn.ey.com Jean Li (Xiamen) jean-n.li@cn.ey.com Tracy Ho (Hong Kong) tracy.ho@hk.ey.com Heidi Liu (Taipei) heidi.liu@tw.ey.com Service Line Tax Leaders Andrew Choy (International Tax & Transfer Pricing) andrew.choy@cn.ey.com Paul Wen (Human Capital) paul.wen@hk.ey.com Kenneth Leung (Indirect Tax) kenneth.leung@cn.ey.com Becky Lai (Tax Policy) becky.lai@hk.ey.com David Chan (Transaction Tax) david.chan@hk.ey.com Samuel Yan (Global Compliance & Reporting) samuel.yan@cn.ey.com Sector Leaders Henry Chan (Financial Services) henry.chan@cn.ey.com Alan Lan (Energy & Resources) alan.lan@cn.ey.com Martin Ngai (Technology, Media, Telecommunications) martin.ngai@cn.ey.com Vickie Tan (Life Science) vickie.tan@cn.ey.com Gary Chan (Real Estate) gary.chan@cn.ey.com Audrie Xia (Consumer Products) audrie.xia@cn.ey.com Walter Tong (Automotive & Transportation) walter.tong@cn.ey.com Raymond Zhu (Government& Public Sector) raymond.zhu@cn.ey.com Greater China Tax Leader Walter Tong walter.tong@cn.ey.com Author China Tax Center Jane Hui jane.hui@hk.ey.com China Tax & Investment News 8

9 EY Assurance Tax Transactions Advisory About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities. EY refers to the global organization and may refer to one or more of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com Ernst & Young (China) Advisory Limited All Rights Reserved. APAC no ED None. This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice. ey.com/china China Tax & Investment News 9

China enhances preferential income tax policies to encourage entrepreneurship and innovation

China enhances preferential income tax policies to encourage entrepreneurship and innovation Issue No.CTIN2016003 11 Oct 2016 Recently, Caishui [2016] No. 101 (Circular 101) was jointly issued by the Ministry

China enhances preferential income tax policies to encourage entrepreneurship and innovation Issue No.CTIN2016003 11 Oct 2016 Recently, Caishui [2016] No. 101 (Circular 101) was jointly issued by the Ministry

China announces detailed rule on withholding tax deferral treatment on direct reinvestment made by foreign investors

Issue No.CTIN2018001 China announces detailed rule on withholding tax deferral treatment on direct reinvestment made by foreign investors 2 January 2018 Our observations The WHT deferral treatment introduced

Issue No.CTIN2018001 China announces detailed rule on withholding tax deferral treatment on direct reinvestment made by foreign investors 2 January 2018 Our observations The WHT deferral treatment introduced

China s Fifth Tax Law

China s Fifth Tax Law Issue No.CTIN2017001 - Environmental Protection Tax Law will take effect from Year 2018 05 Jan 2017 After six years of studies and discussions and through two rounds deliberations,

China s Fifth Tax Law Issue No.CTIN2017001 - Environmental Protection Tax Law will take effect from Year 2018 05 Jan 2017 After six years of studies and discussions and through two rounds deliberations,

China Tax Center China Tax & Investment Express

Issue No. 2017039 13 Oct 2017 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2017039 13 Oct 2017 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center. China Tax & Investment Express. Tax circulars

Issue No. 2016046 2 Dec 2016 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2016046 2 Dec 2016 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax & Investment Express

China Tax Center China Tax & Investment Express Issue No. 2017002 13 Jan 2017 (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center China Tax & Investment Express Issue No. 2017002 13 Jan 2017 (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center China Tax & Investment Express

Issue No. 2017010 17 March 2017 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2017010 17 March 2017 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center China Tax & Investment Express

Issue No. 2017009 10 Mar 2017 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2017009 10 Mar 2017 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center China Tax & Investment Express

Issue No. 2018023 15 June 2018 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2018023 15 June 2018 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax & Investment News. Local incentives clean-up campaign shows a positive turn. Background

Issue No.CTIN2015004 14 May 2015 China Tax & Investment News Local incentives clean-up campaign shows a positive turn Background On 11 May 2015, the State Council announced Circular Guofa [2015] No. 25

Issue No.CTIN2015004 14 May 2015 China Tax & Investment News Local incentives clean-up campaign shows a positive turn Background On 11 May 2015, the State Council announced Circular Guofa [2015] No. 25

China Tax Center. China Tax & Investment Express. Tax circulars

Issue No. 2015025 26 June 2015 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2015025 26 June 2015 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center China Tax & Investment Express

Issue No. 2018046 30 November 2018 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2018046 30 November 2018 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center China Tax & Investment Express

Issue No. 2019002 11 January 2019 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2019002 11 January 2019 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax & Investment News. New implementation guideline on indirect transfers of China assets has just been issued. Background

Issue No.CTIN2015006 05 Jun 2015 China Tax & Investment News New implementation guideline on indirect transfers of China assets has just been issued Background In 2009, the State Administration of Taxation

Issue No.CTIN2015006 05 Jun 2015 China Tax & Investment News New implementation guideline on indirect transfers of China assets has just been issued Background In 2009, the State Administration of Taxation

China Tax Center. China Tax & Investment Express. Tax circulars

Issue No. 2015051 31 Dec 2015 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2015051 31 Dec 2015 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center. China Tax & Investment Express. Tax circulars

Issue No. 2015018 8 May 2015 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2015018 8 May 2015 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center. China Tax & Investment Express. Tax circulars

Issue No. 2015029 24 July 2015 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2015029 24 July 2015 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center. China Tax & Investment Express. Tax circulars

Issue No. 2015038 25 Sept 2015 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2015038 25 Sept 2015 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center. China Tax & Investment Express. Business circulars

Issue No. 2016040 21 Oct 2016 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2016040 21 Oct 2016 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center. China Tax & Investment Express. Tax circulars

Issue No. 2016038 30 September 2016 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2016038 30 September 2016 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center China Tax & Investment Express

Issue No. 2018014 13 April 2018 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2018014 13 April 2018 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center. China Tax & Investment Express. Tax circulars

Issue No. 2015036 11 Sept 2015 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2015036 11 Sept 2015 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center China Tax & Investment Express

Issue No. 2018005 2 Feb 2018 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2018005 2 Feb 2018 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center. China Tax & Investment Express. Tax circulars

Issue No. 2016007 26 February 2016 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2016007 26 February 2016 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center. China Tax & Investment Express. Tax circulars

Issue No. 2016016 29 April 2016 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2016016 29 April 2016 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center China Tax & Investment Express

Issue No. 2018021 1 June 2018 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2018021 1 June 2018 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center. China Tax & Investment Express. Tax circulars

Issue No. 2015040 16 Oct 2015 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2015040 16 Oct 2015 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center. China Tax & Investment Express. Tax circulars

Issue No. 2014052 31 Dec 2014 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2014052 31 Dec 2014 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax & Investment News. 23 approvals on tax matters are now removed yet, not sure if it is good news. Introduction

Issue No.CTIN2015005 25 May 2015 China Tax & Investment News 23 approvals on tax matters are now removed yet, not sure if it is good news Introduction In order to remove all of the approvals on non-administrative

Issue No.CTIN2015005 25 May 2015 China Tax & Investment News 23 approvals on tax matters are now removed yet, not sure if it is good news Introduction In order to remove all of the approvals on non-administrative

China Tax Center. China Tax & Investment Express. Tax circulars

Issue No. 2015004 30 January 2015 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2015004 30 January 2015 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center China Tax & Investment Express

Issue No. 2018025 29 June 2018 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2018025 29 June 2018 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center China Tax & Investment Express

Issue No. 2017044 17 Nov 2017 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2017044 17 Nov 2017 China Tax Center China Tax & Investment Express (CTIE)* brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

China Tax Center. China Tax & Investment Express. Tax circulars

Issue No. 2015015 17 April 2015 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Issue No. 2015015 17 April 2015 China Tax Center China Tax & Investment Express (CTIE) * brings you the latest tax and business announcements on a weekly basis. CTIE provides a synopsis of each announcement

Double taxation agreement (DTA) signed to benefit mutual trade and investment between mainland China and Taiwan

signed to benefit mutual trade and investment between mainland China and Taiwan") News Flash China Tax and Business Advisory Double taxation agreement (DTA) signed to benefit mutual trade and investment between mainland China and Taiwan August 2015 Issue 37 In brief On 25 August 2015,

News Flash China Tax and Business Advisory Double taxation agreement (DTA) signed to benefit mutual trade and investment between mainland China and Taiwan August 2015 Issue 37 In brief On 25 August 2015,

Human resource & Tax alert

September 2018 Human resource & Tax alert China launches individual income tax reform Executive summary The fifth session of the 13th National People's Congress Standing Committee passed the revisions

September 2018 Human resource & Tax alert China launches individual income tax reform Executive summary The fifth session of the 13th National People's Congress Standing Committee passed the revisions

China s SAT issues China advance pricing arrangement annual report for 2016

EY China TP Alert China s SAT issues China advance pricing arrangement annual report for 2016 On 8 October 2017, China s State Administration of Taxation ( SAT ) issued the China Advance Pricing Arrangement

EY China TP Alert China s SAT issues China advance pricing arrangement annual report for 2016 On 8 October 2017, China s State Administration of Taxation ( SAT ) issued the China Advance Pricing Arrangement

Human resource & Tax alert

October 2018 Human resource & Tax alert China releases draft implementation rules of individual income tax law and draft rules regarding specific additional tax deductions Executive summary On 20 October

October 2018 Human resource & Tax alert China releases draft implementation rules of individual income tax law and draft rules regarding specific additional tax deductions Executive summary On 20 October

China s new transfer pricing compliance requirements: impact on foreign headquarters

China s new transfer pricing compliance requirements: impact on foreign headquarters On 29 June 2016, China s State Administration of Taxation (SAT) issued SAT Bulletin [2016] No. 42 (Bulletin 42), which

China s new transfer pricing compliance requirements: impact on foreign headquarters On 29 June 2016, China s State Administration of Taxation (SAT) issued SAT Bulletin [2016] No. 42 (Bulletin 42), which

Profit monitoring and management system of multinational corporations launched in Jiangsu

EY China TP Alert Profit monitoring and management system of multinational corporations launched in Jiangsu Executive summary On 17 March 2017, the State Administration of Taxation (SAT) issued the Administrative

EY China TP Alert Profit monitoring and management system of multinational corporations launched in Jiangsu Executive summary On 17 March 2017, the State Administration of Taxation (SAT) issued the Administrative

Hong Kong Tax Alert. Hong Kong signs comprehensive double tax agreement with Latvia. 21 April Issue No. 7

Hong Kong Tax Alert 21 April 2016 2016 Issue No. 7 Hong Kong signs comprehensive double tax agreement with Latvia On 13 April 2016, Hong Kong signed a comprehensive avoidance of double taxation agreement

Hong Kong Tax Alert 21 April 2016 2016 Issue No. 7 Hong Kong signs comprehensive double tax agreement with Latvia On 13 April 2016, Hong Kong signed a comprehensive avoidance of double taxation agreement

Hong Kong Tax Alert. Hong Kong signs comprehensive double tax agreement with Saudi Arabia. 31 August Issue No. 13

Hong Kong Tax Alert 31 August 2017 2017 Issue No. 13 Hong Kong signs comprehensive double tax agreement with Saudi Arabia On 24 August 2017, Hong Kong signed a comprehensive avoidance of double taxation

Hong Kong Tax Alert 31 August 2017 2017 Issue No. 13 Hong Kong signs comprehensive double tax agreement with Saudi Arabia On 24 August 2017, Hong Kong signed a comprehensive avoidance of double taxation

China s SAT issues new guidance on administration of advance pricing agreements

21 October 2016 Global Tax Alert News from Transfer Pricing China s SAT issues new guidance on administration of advance pricing agreements EY Global Tax Alert Library Access both online and pdf versions

21 October 2016 Global Tax Alert News from Transfer Pricing China s SAT issues new guidance on administration of advance pricing agreements EY Global Tax Alert Library Access both online and pdf versions

Hong Kong Tax Alert. Hong Kong signs comprehensive double tax agreement with Latvia. 21 April Issue No. 7

Hong Kong Tax Alert 21 April 2016 2016 Issue No. 7 Hong Kong signs comprehensive double tax agreement with Latvia On 13 April 2016, Hong Kong signed a comprehensive avoidance of double taxation agreement

Hong Kong Tax Alert 21 April 2016 2016 Issue No. 7 Hong Kong signs comprehensive double tax agreement with Latvia On 13 April 2016, Hong Kong signed a comprehensive avoidance of double taxation agreement

The Latest Development in Mainland China Tax. 9 February 2015

The Latest Development in Mainland China Tax 9 February 2015 Today s rundown Overview of China s Tax Position Today and Future Development Valued Added Tax (VAT) Reform Overview of Pilot Zones in China

The Latest Development in Mainland China Tax 9 February 2015 Today s rundown Overview of China s Tax Position Today and Future Development Valued Added Tax (VAT) Reform Overview of Pilot Zones in China

China s Jiangsu provincial state tax authority updates its compliance plan for international tax administration

EY China TP Alert China s Jiangsu provincial state tax authority updates its compliance plan for international tax administration Following the first release of Compliance Plan for International Tax Administration

EY China TP Alert China s Jiangsu provincial state tax authority updates its compliance plan for international tax administration Following the first release of Compliance Plan for International Tax Administration

Tax Analysis. New Guidance Clarifies Rules Relating to EIT Withholding on China- Source Income Derived by Nonresident Enterprises

Tax Issue P265/2017 27 October 2017 Tax Analysis New Guidance Clarifies Rules Relating to EIT Withholding on China- Source Income Derived by Nonresident Enterprises Authors: Beijing Julie Zhang Tel: +86

Tax Issue P265/2017 27 October 2017 Tax Analysis New Guidance Clarifies Rules Relating to EIT Withholding on China- Source Income Derived by Nonresident Enterprises Authors: Beijing Julie Zhang Tel: +86

Tax Analysis. SAT updates guidance on application of capital gains article in China s tax treaties. PRC Tax. Tax Issue P178/ January 2013

Tax Issue P178/2013 24 January 2013 Tax Analysis Authors: Shanghai Hong Ye Tel: +86 21 6141 1171 Email: hoye@deloitte.com.cn PRC Tax SAT updates guidance on application of capital gains article in China

Tax Issue P178/2013 24 January 2013 Tax Analysis Authors: Shanghai Hong Ye Tel: +86 21 6141 1171 Email: hoye@deloitte.com.cn PRC Tax SAT updates guidance on application of capital gains article in China

Hong Kong Tax Alert. Hong Kong signs comprehensive double tax agreement with Romania. Who is covered by the CDTA. 27 November Issue No.

Hong Kong Tax Alert 27 November 2015 2015 Issue No. 19 Hong Kong signs comprehensive double tax agreement with Romania On 18 November 2015, Hong Kong signed a comprehensive avoidance of double taxation

Hong Kong Tax Alert 27 November 2015 2015 Issue No. 19 Hong Kong signs comprehensive double tax agreement with Romania On 18 November 2015, Hong Kong signed a comprehensive avoidance of double taxation

China Related Party Transactions and TP Documentation Rules Highlights. 10 August 2016

China Related Party Transactions and TP Documentation Rules Highlights 10 August 2016 Related Party Transactions and TP Documentation Rules Aligned with OECD recommendations and adapted for China Bulletin

China Related Party Transactions and TP Documentation Rules Highlights 10 August 2016 Related Party Transactions and TP Documentation Rules Aligned with OECD recommendations and adapted for China Bulletin

SAT releases new rules on corporate income tax for non- TREs bringing significant changes in the timing of withholding

News Flash China Tax and Business Advisory SAT releases new rules on corporate income tax for non- TREs bringing significant changes in the timing of withholding October 2017 Issue 32 In brief In October

News Flash China Tax and Business Advisory SAT releases new rules on corporate income tax for non- TREs bringing significant changes in the timing of withholding October 2017 Issue 32 In brief In October

Hong Kong Tax Alert. Inland Revenue Department (IRD) outlines its views on certain Salaries Tax and treaty-related issues relating to individuals

outlines its views on certain Salaries Tax and treaty-related issues relating to individuals") Hong Kong Tax Alert 15 January 2018 2018 Issue No. 4 Inland Revenue Department (IRD) outlines its views on certain Salaries Tax and treaty-related issues relating to individuals Issues discussed in the

Hong Kong Tax Alert 15 January 2018 2018 Issue No. 4 Inland Revenue Department (IRD) outlines its views on certain Salaries Tax and treaty-related issues relating to individuals Issues discussed in the

Intangible property transactions. International context

EY China TP Alert SAT s newly released Bulletin 6 strengthens MAP procedures in advance of peer reviews and enhances alignment of China s transfer pricing rules with OECD standards On 1 April 2017, China

EY China TP Alert SAT s newly released Bulletin 6 strengthens MAP procedures in advance of peer reviews and enhances alignment of China s transfer pricing rules with OECD standards On 1 April 2017, China

Further clarification of asset management VAT regulation

Further clarification of asset management VAT regulation July 2017 Synopsis On 30 June 2017, the Ministry of Finance (MOF) and the State Administration of Taxation (SAT) jointly released Caishui [2017]

Further clarification of asset management VAT regulation July 2017 Synopsis On 30 June 2017, the Ministry of Finance (MOF) and the State Administration of Taxation (SAT) jointly released Caishui [2017]

Hong Kong s OECD BEPS Associate status requires implementation of BEPS minimum standards

28 June 2016 International Tax and TP Alert Hong Kong s OECD BEPS Associate status requires implementation of BEPS minimum standards Executive summary On 20 June 2016, Hong Kong announced that it will

28 June 2016 International Tax and TP Alert Hong Kong s OECD BEPS Associate status requires implementation of BEPS minimum standards Executive summary On 20 June 2016, Hong Kong announced that it will

Hong Kong Tax Alert. Hong Kong signs comprehensive double tax agreement with the Russian Federation. Who is covered by the CDTA

Hong Kong Tax Alert 29 January 2016 2016 Issue No. 2 Hong Kong signs comprehensive double tax agreement with the Russian Federation On 18 January 2016, Hong Kong signed a comprehensive avoidance of double

Hong Kong Tax Alert 29 January 2016 2016 Issue No. 2 Hong Kong signs comprehensive double tax agreement with the Russian Federation On 18 January 2016, Hong Kong signed a comprehensive avoidance of double

Hong Kong and India sign income tax treaty

28 March 2018 Global Tax Alert Hong Kong and India sign income tax treaty EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser: www.ey.com/taxalerts

28 March 2018 Global Tax Alert Hong Kong and India sign income tax treaty EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser: www.ey.com/taxalerts

Transfer Pricing Alert

Transfer Pricing Alert July 2015 Journey to the future: BEPS and the fastevolving transfer pricing landscape in China On 6-7 July 2015, the Organisation for Economic Co-operation and Development (OECD)

Transfer Pricing Alert July 2015 Journey to the future: BEPS and the fastevolving transfer pricing landscape in China On 6-7 July 2015, the Organisation for Economic Co-operation and Development (OECD)

Hong Kong Tax Alert. Legislative bill detailing enhanced tax deductions for qualifying R&D activities introduced. 8 May Issue No.

Hong Kong Tax Alert 8 May 2018 2018 Issue No. 11 Legislative bill detailing enhanced tax deductions for qualifying R&D activities introduced On 20 April 2018, the Inland Revenue Amendment (No. 3) Bill

Hong Kong Tax Alert 8 May 2018 2018 Issue No. 11 Legislative bill detailing enhanced tax deductions for qualifying R&D activities introduced On 20 April 2018, the Inland Revenue Amendment (No. 3) Bill

Hong Kong Tax Alert. Hong Kong signs comprehensive double tax agreement with India. Who is covered by the CDTA law. 4 April Issue No.

Hong Kong Tax Alert 4 April 2018 2018 Issue No. 9 Hong Kong signs comprehensive double tax agreement with India On 19 March 2018, Hong Kong signed a comprehensive avoidance of double taxation agreement

Hong Kong Tax Alert 4 April 2018 2018 Issue No. 9 Hong Kong signs comprehensive double tax agreement with India On 19 March 2018, Hong Kong signed a comprehensive avoidance of double taxation agreement

Transfer Pricing Alert

Transfer Pricing Alert July 2016 SAT issues highly significant new rules on related party transactions disclosure and contemporaneous transfer pricing documentation to update China s transfer pricing rules

Transfer Pricing Alert July 2016 SAT issues highly significant new rules on related party transactions disclosure and contemporaneous transfer pricing documentation to update China s transfer pricing rules

Tax Analysis. IRD partially clarifies tax treatment of court-free amalgamations. Hong Kong Tax

Tax Issue H67/2016 20 January 2016 Tax Analysis Authors: Hong Kong Tax Hong Kong Davy Yun Tax Tel: +852 2852 6538 Email: dyun@deloitte.com.hk Doris Chik Senior Tax Manager Tel: +852 2852 6608 Email: dchik@deloitte.com.hk

Tax Issue H67/2016 20 January 2016 Tax Analysis Authors: Hong Kong Tax Hong Kong Davy Yun Tax Tel: +852 2852 6538 Email: dyun@deloitte.com.hk Doris Chik Senior Tax Manager Tel: +852 2852 6608 Email: dchik@deloitte.com.hk

Tax Analysis. SAT Issues Guidance on Tax Treatment of Share Transfers by Individuals. PRC Tax. Tax Issue P205/ December 2014.

Tax Issue P205/2014 30 December 2014 Tax Analysis Authors: Beijing Huan Wang Tel: +86 10 8520 7510 Email: huawang@deloitte.com.cn Shanghai Irene Yu Tel: +86 21 6141 1277 Email: iryu@deloitte.com.cn For

Tax Issue P205/2014 30 December 2014 Tax Analysis Authors: Beijing Huan Wang Tel: +86 10 8520 7510 Email: huawang@deloitte.com.cn Shanghai Irene Yu Tel: +86 21 6141 1277 Email: iryu@deloitte.com.cn For

Tax Analysis. Individual Income Tax Reform: Final implementation regulations for IIT law released. Tax Issue P287/ December 2018

Tax Issue P287/2018 24 December 2018 Tax Analysis Individual Income Tax Reform: Final implementation regulations for IIT law released Authors: Beijing Rebecca Wang Tel: +86 10 8520 7885 Email: rewang@deloitte.com.cn

Tax Issue P287/2018 24 December 2018 Tax Analysis Individual Income Tax Reform: Final implementation regulations for IIT law released Authors: Beijing Rebecca Wang Tel: +86 10 8520 7885 Email: rewang@deloitte.com.cn

IIT treatment for natural person partners of venture capital funds was finally released

IIT treatment for natural person partners of venture capital funds was finally released News Flash China Tax and Business Advisory January 2019 Issue 5 In brief On 12 December 2018, the State Council Executive

IIT treatment for natural person partners of venture capital funds was finally released News Flash China Tax and Business Advisory January 2019 Issue 5 In brief On 12 December 2018, the State Council Executive

Tax Analysis. PRC Tax. International and M&A Tax Services. PRC Foreign Tax Credit Regime - (II) Analysis of Caishui [2009] No. 125

![Tax Analysis. PRC Tax. International and M&A Tax Services. PRC Foreign Tax Credit Regime - (II) Analysis of Caishui [2009] No. 125](/thumbs/92/109983453.jpg "Tax Analysis. PRC Tax. International and M&A Tax Services. PRC Foreign Tax Credit Regime - (II) Analysis of Caishui [2009] No. 125") Tax Issue P97/2010 15 January 2010 Tax Analysis Authors: Beijing Andrew Zhu Tel: +852 8520 7508 Email: andzhu@deloitte.com.cn PRC Tax International and M&A Tax Services PRC Foreign Tax Credit Regime -

Tax Issue P97/2010 15 January 2010 Tax Analysis Authors: Beijing Andrew Zhu Tel: +852 8520 7508 Email: andzhu@deloitte.com.cn PRC Tax International and M&A Tax Services PRC Foreign Tax Credit Regime -

Tax Analysis. SAT Published New Rules on Beneficial Owners. Tax Issue P270/ February 2018

Tax Issue P270/2018 8 February 2018 Tax Analysis SAT Published New Rules on Beneficial Owners On 3 February 2018, China s State Administration of Taxation (SAT) published new rules on the concept of a

Tax Issue P270/2018 8 February 2018 Tax Analysis SAT Published New Rules on Beneficial Owners On 3 February 2018, China s State Administration of Taxation (SAT) published new rules on the concept of a

Hong Kong Tax alert. Inland Revenue (Amendment) Bill 2015 gazetted to extend Profits Tax Exemption for Offshore Funds to Private Equity Funds

Bill 2015 gazetted to extend Profits Tax Exemption for Offshore Funds to Private Equity Funds") 31 March 2015 2015 Issue No. 5 Hong Kong Tax alert Inland Revenue (Amendment) Bill 2015 gazetted to extend Profits Tax Exemption for Offshore Funds to Private Equity Funds Executive Summary The Budget

31 March 2015 2015 Issue No. 5 Hong Kong Tax alert Inland Revenue (Amendment) Bill 2015 gazetted to extend Profits Tax Exemption for Offshore Funds to Private Equity Funds Executive Summary The Budget

Draft Regulations Governing Controlled Foreign Companies and Regulations Governing Places of Effective Management

Taiwan Tax Update November 2016 Draft Regulations Governing Controlled Foreign Companies and Regulations Governing Places of Effective Management The Income Tax Act was amended in July 2016 to include

Taiwan Tax Update November 2016 Draft Regulations Governing Controlled Foreign Companies and Regulations Governing Places of Effective Management The Income Tax Act was amended in July 2016 to include

Setting up a Corporate Treasury Center in Hong Kong

Setting up a Corporate Treasury Center in Why a Corporate Treasury Center? A growing number of multinational corporations (MNCs) are setting up Corporate Treasury Centers (CTCs) in Asia The size and scale

Setting up a Corporate Treasury Center in Why a Corporate Treasury Center? A growing number of multinational corporations (MNCs) are setting up Corporate Treasury Centers (CTCs) in Asia The size and scale

Tax Analysis Authors:

Tax Issue H46/2012 27 July 2012 Tax Analysis Authors: Hong Kong Davy Yun Tel: +852 2852 6538 Email: dyun@deloitte.com.hk Hong Kong Tax Inland Revenue Department issues guidance on deduction of purchase

Tax Issue H46/2012 27 July 2012 Tax Analysis Authors: Hong Kong Davy Yun Tel: +852 2852 6538 Email: dyun@deloitte.com.hk Hong Kong Tax Inland Revenue Department issues guidance on deduction of purchase

Hong Kong Tax Analysis

Tax Issue H86/2018 3 October 2018 Hong Kong Tax Analysis Overview of Tax Law Changes Under New BEPS Law The Inland Revenue (Amendment) (No. 6) Ordinance 2018 (Amendment Ordinance), enacted on 13 July 2018,

Tax Issue H86/2018 3 October 2018 Hong Kong Tax Analysis Overview of Tax Law Changes Under New BEPS Law The Inland Revenue (Amendment) (No. 6) Ordinance 2018 (Amendment Ordinance), enacted on 13 July 2018,

Hong Kong Tax alert. Time limit for a section 70A application may not be as generous as it appears

4 March 2015 2015 Issue No. 4 Hong Kong Tax alert Time limit for a section 70A application may not be as generous as it appears Under section 70A of the Inland Revenue Ordinance (IRO), a taxpayer can apply

4 March 2015 2015 Issue No. 4 Hong Kong Tax alert Time limit for a section 70A application may not be as generous as it appears Under section 70A of the Inland Revenue Ordinance (IRO), a taxpayer can apply

Hong Kong introduces legislative bill for corporate treasury center incentives

11 December 2015 Global Tax Alert Hong Kong introduces legislative bill for corporate treasury center incentives EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts.

11 December 2015 Global Tax Alert Hong Kong introduces legislative bill for corporate treasury center incentives EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts.

Enhanced auditor s reporting

Enhanced auditor s reporting Assurance Special edition January 2016 A new foundation in auditor s reporting In January 2015, the International Auditing and Assurance Standards Board (IAASB) issued its

Enhanced auditor s reporting Assurance Special edition January 2016 A new foundation in auditor s reporting In January 2015, the International Auditing and Assurance Standards Board (IAASB) issued its

Hong Kong-India income tax treaty enters into force

6 December 2018 Global Tax Alert Hong Kong-India income tax treaty enters into force NEW! EY Tax News Update: Global Edition EY s new Tax News Update: Global Edition is a free, personalized email subscription

6 December 2018 Global Tax Alert Hong Kong-India income tax treaty enters into force NEW! EY Tax News Update: Global Edition EY s new Tax News Update: Global Edition is a free, personalized email subscription

Tax Analysis. Individual Income Tax Treatment of Contribution of Nonmonetary Assets Clarified. PRC Tax. Tax Issue P217/ May 2015

Tax Issue P217/2015 18 May 2015 Tax Analysis Authors: Huan Wang Tel: +86 10 8520 7510 Email: huawang@deloitte.com.cn Julie Zhang Tel: +86 10 8520 7511 Email: juliezhang@deloitte.com.cn PRC Tax Individual

Tax Issue P217/2015 18 May 2015 Tax Analysis Authors: Huan Wang Tel: +86 10 8520 7510 Email: huawang@deloitte.com.cn Julie Zhang Tel: +86 10 8520 7511 Email: juliezhang@deloitte.com.cn PRC Tax Individual

China s SAT issues fourth Advance Pricing Arrangement Annual Report

29 August 2013 Global Tax Alert News from Transfer Pricing China s SAT issues fourth Advance Pricing Arrangement Annual Report Executive summary On 13 August 2013, China s State Administration of Taxation

29 August 2013 Global Tax Alert News from Transfer Pricing China s SAT issues fourth Advance Pricing Arrangement Annual Report Executive summary On 13 August 2013, China s State Administration of Taxation

7 November Issue No. 14

Hong Kong Tax Alert 7 November 2017 2017 Issue No. 14 The IRD clarifies how it will interpret and administer the concessionary tax regime for qualifying aircraft leasing activities On 27 October 2017,

Hong Kong Tax Alert 7 November 2017 2017 Issue No. 14 The IRD clarifies how it will interpret and administer the concessionary tax regime for qualifying aircraft leasing activities On 27 October 2017,

Luxembourg-Cyprus double tax treaty enters into force

7 June 2018 Global Tax Alert Luxembourg-Cyprus double tax treaty enters into force NEW! EY Tax News Update: Global Edition EY s new Tax News Update: Global Edition is a free, personalized email subscription

7 June 2018 Global Tax Alert Luxembourg-Cyprus double tax treaty enters into force NEW! EY Tax News Update: Global Edition EY s new Tax News Update: Global Edition is a free, personalized email subscription

Hong Kong Tax Analysis

Tax Issue H82/2018 4 May 2018 Hong Kong Tax Analysis Enhanced Deduction for R&D Expenditures Introduced Author: Hong Kong Ryan Chang Tax Tel:+852 2852 6768 Email: ryanchang@deloitte.com Doris Chik Tax

Tax Issue H82/2018 4 May 2018 Hong Kong Tax Analysis Enhanced Deduction for R&D Expenditures Introduced Author: Hong Kong Ryan Chang Tax Tel:+852 2852 6768 Email: ryanchang@deloitte.com Doris Chik Tax

Hong Kong releases new practice note on concessionary tax regime for qualifying aircraft leasing activities

10 November 2017 Global Tax Alert Hong Kong releases new practice note on concessionary tax regime for qualifying aircraft leasing activities EY Global Tax Alert Library Access both online and pdf versions

10 November 2017 Global Tax Alert Hong Kong releases new practice note on concessionary tax regime for qualifying aircraft leasing activities EY Global Tax Alert Library Access both online and pdf versions

Tax Analysis. China CRS Rules Apply as from 1 July Tax Issue P259/ May 2017

Tax Issue P259/ 22 May Tax Analysis China CRS Rules Apply as from 1 July Long-awaited rules implementing the OECD common reporting standard (CRS) in China will apply as from 1 July. The final rules ( Due

Tax Issue P259/ 22 May Tax Analysis China CRS Rules Apply as from 1 July Long-awaited rules implementing the OECD common reporting standard (CRS) in China will apply as from 1 July. The final rules ( Due

Timing of deduction. Deduction must not be excessive

Tax Issue H53/2013 20 December 2013 Tax Analysis Authors: Hong Kong Raymond Tang, Tel: +852 2852 6661 Email: raytang@deloitte.com.hk Silent Li, Senior Tax Manager Tel: +852 2852 6399 Email: silli@deloitte.com.hk

Tax Issue H53/2013 20 December 2013 Tax Analysis Authors: Hong Kong Raymond Tang, Tel: +852 2852 6661 Email: raytang@deloitte.com.hk Silent Li, Senior Tax Manager Tel: +852 2852 6399 Email: silli@deloitte.com.hk

New Australia- Germany Tax Treaty enters into force

12 December 2016 Global Tax Alert New Australia- Germany Tax Treaty enters into force EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser:

12 December 2016 Global Tax Alert New Australia- Germany Tax Treaty enters into force EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser:

Tax Claus Schuermann Friedman Ji Stefan Zimmermann Comparison

Tax Issue P242/2016 4 August 2016 Tax Analysis New China - Germany Agreement on the Avoidance of Double Taxation and the Prevention of Fiscal Evasion The new tax treaty between China and Germany was already

Tax Issue P242/2016 4 August 2016 Tax Analysis New China - Germany Agreement on the Avoidance of Double Taxation and the Prevention of Fiscal Evasion The new tax treaty between China and Germany was already

SAT releases new rules on corporate income tax for non-tres bringing potential benefits to the financial services industry

www.pwccn.com SAT releases new rules on corporate income tax for non-tres bringing potential benefits to the financial services industry December 2017 Financial Services Tax News Flash In brief In October

www.pwccn.com SAT releases new rules on corporate income tax for non-tres bringing potential benefits to the financial services industry December 2017 Financial Services Tax News Flash In brief In October

Tax Analysis. SAT Issues Guidance on Registration of General VAT Payers. Tax Issue P269/ January 2018

Tax Issue P269/2018 17 January 2018 Tax Analysis SAT Issues Guidance on Registration of General VAT Payers Authors: Liqun Gao Tel: +86 21 6141 1053 Email: ligao@deloitte.com.cn China's State Administration

Tax Issue P269/2018 17 January 2018 Tax Analysis SAT Issues Guidance on Registration of General VAT Payers Authors: Liqun Gao Tel: +86 21 6141 1053 Email: ligao@deloitte.com.cn China's State Administration

An observation of the key fiscal and taxation task in China s Government Work Report in 2018

News Flash China Tax and Business Advisory An observation of the key fiscal and taxation task in China s Government Work Report in 2018 March 2018 Issue 8 In brief On 5 March 2018, the State Council Premier

News Flash China Tax and Business Advisory An observation of the key fiscal and taxation task in China s Government Work Report in 2018 March 2018 Issue 8 In brief On 5 March 2018, the State Council Premier

Mainland audit issues Q&As value-added tax

Mainland audit issues Q&As value-added tax The Questions and Answers (Q&As) below are developed by the Working Group on Mainland Audit Issues of the HKSA Auditing and Assurance Standards Committee (AASC)

Mainland audit issues Q&As value-added tax The Questions and Answers (Q&As) below are developed by the Working Group on Mainland Audit Issues of the HKSA Auditing and Assurance Standards Committee (AASC)

China further released new IIT preferential policies to benefit individuals investing in NEEQlisted companies as well as Venture Capital Funds

News Flash China Tax and Business Advisory China further released new IIT preferential policies to benefit individuals investing in NEEQlisted companies as well as Venture Capital Funds December 2018 Issue

News Flash China Tax and Business Advisory China further released new IIT preferential policies to benefit individuals investing in NEEQlisted companies as well as Venture Capital Funds December 2018 Issue

News Flash China Tax and Business Advisory. May 2016 Issue 16. In brief. In detail.

ews Flash China Tax and Business Advisory Administrative measures for VAT exemption on cross-border under the B2V Pilot Program detailed preferential policy conditions and standardised record filing procedure

ews Flash China Tax and Business Advisory Administrative measures for VAT exemption on cross-border under the B2V Pilot Program detailed preferential policy conditions and standardised record filing procedure

Initial steps on the IPO journey. April 2016

April 2016 Contents 1 2 3 Listing requirements About EY 3 16 19 IPO readiness Self-assessment Do you recognize these challenges in your company? Question Self-assessment Often Sometimes Never Do you understand

April 2016 Contents 1 2 3 Listing requirements About EY 3 16 19 IPO readiness Self-assessment Do you recognize these challenges in your company? Question Self-assessment Often Sometimes Never Do you understand

Enhanced deduction for qualifying R&D expenditure will be introduced in Hong Kong

News Flash Hong Kong Tax Enhanced deduction for qualifying R&D expenditure will be introduced in Hong Kong April 2018 Issue 7 In brief The bill proposing an enhanced tax deduction for research and development

News Flash Hong Kong Tax Enhanced deduction for qualifying R&D expenditure will be introduced in Hong Kong April 2018 Issue 7 In brief The bill proposing an enhanced tax deduction for research and development

Luxembourg publishes draft law ratifying Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS

4 September 2018 Global Tax Alert Luxembourg publishes draft law ratifying Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS NEW! EY Tax News Update: Global Edition EY s

4 September 2018 Global Tax Alert Luxembourg publishes draft law ratifying Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS NEW! EY Tax News Update: Global Edition EY s

A totally different tax landscape for offshore indirect transfer wider, clearer & more challenging

News Flash China Tax and Business Advisory A totally different tax landscape for offshore indirect transfer wider, clearer & more challenging February 2015 Issue 04 In brief According to the circular Guoshuihan

News Flash China Tax and Business Advisory A totally different tax landscape for offshore indirect transfer wider, clearer & more challenging February 2015 Issue 04 In brief According to the circular Guoshuihan

Tax Analysis. SAT Strengthens Management of VAT General Invoices. Tax Issue P261/ June 2017

Tax Issue P261/2017 28 June 2017 Tax Analysis SAT Strengthens Management of VAT General Invoices Authors: Liqun Gao Tel: +86 21 6141 1053 Email: ligao@deloitte.com.cn China s State Administration of Taxation

Tax Issue P261/2017 28 June 2017 Tax Analysis SAT Strengthens Management of VAT General Invoices Authors: Liqun Gao Tel: +86 21 6141 1053 Email: ligao@deloitte.com.cn China s State Administration of Taxation

Netherlands ratifies tax treaty with Sint Maarten

21 January 2016 Global Tax Alert Netherlands ratifies tax treaty with Sint Maarten EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser:

21 January 2016 Global Tax Alert Netherlands ratifies tax treaty with Sint Maarten EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser:

Hong Kong introduces tax and transfer pricing legislation to counter Base Erosion and Profit Shifting

5 January 2018 Global Tax Alert Hong Kong introduces tax and transfer pricing legislation to counter Base Erosion and Profit Shifting EY Global Tax Alert Library Access both online and pdf versions of

5 January 2018 Global Tax Alert Hong Kong introduces tax and transfer pricing legislation to counter Base Erosion and Profit Shifting EY Global Tax Alert Library Access both online and pdf versions of

Beneficial Ownership & Indirect Disposals

PRC Non-Resident Enterprise Tax Series: Beneficial Ownership & Indirect Disposals TAX Beneficial Ownership & Indirect Disposal Rules 1 Introduction Over recent months, the PRC tax authorities have introduced

PRC Non-Resident Enterprise Tax Series: Beneficial Ownership & Indirect Disposals TAX Beneficial Ownership & Indirect Disposal Rules 1 Introduction Over recent months, the PRC tax authorities have introduced

Tax Analysis. 2019/20 Budget Analysis. A conservative yet practical approach, with clear direction of Hong Kong's economic development

Tax Issue H87/2019 27 February 2019 Tax Analysis 2019/20 Budget Analysis A conservative yet practical approach, with clear direction of Hong Kong's economic development Author: Hong Kong Sarah Chan Tax

Tax Issue H87/2019 27 February 2019 Tax Analysis 2019/20 Budget Analysis A conservative yet practical approach, with clear direction of Hong Kong's economic development Author: Hong Kong Sarah Chan Tax