TAX-RETURN MISTAKES AND ERROR PREVENTION. Bruce Brumberg, Editor-in-Chief & Co-Founder mystockoptions.com and mynqdc.

|

|

|

- Judith Fisher

- 5 years ago

- Views:

Transcription

1 TAX-RETURN MISTAKES AND ERROR PREVENTION Bruce Brumberg, Editor-in-Chief & Co-Founder mystockoptions.com and mynqdc.com March 8, 2018

2 Disclosure The following presentation and the views expressed by the presenters are not intended to provide legal, tax, accounting, investment, or other professional advice. The information contained in this presentation is general in nature and based on authorities that are subject to change. Applicability to specific situations should be determined through consultation with your investment, legal, and tax advisors. The information contained in these materials is only current as of the date produced. The materials have not been and will not be updated to incorporate any changes since the production date. 2

3 Asking Questions Enter your question into the Questions pane on the GoToWebinar control panel. 3

4 Housekeeping Eligible for CPE for Taxes credit - Must stay for entire presentation - Must participate in all three poll questions during presentation Presentation is being recorded - will be sent to all attendees with link to recording and presentation Please take our survey! 4

5 Today s presenter Bruce Brumberg, Editor-in-Chief and Co-Founder, mystockoptions.com Award-winning online resource center, has received a patent and has been featured in publications ranging from the San Francisco Chronicle to Money magazine. Human Resource Executive magazine featured mystockoptions.com as one of the 10 Best HR Products. Past President of the Boston NASPP chapter On the NASPP Advisory Board, and contributor to the Stock Plan Advisor. Producer of the Think Twice insider trading prevention videos ( Editor of another site on nonqualified deferred compensation at Bruce graduated from the University of Michigan and University of Virginia School of Law. 5

6 6

7 7

8 8

9 Computershare 2017 Tax Form Reference Guide Find it on the education section of Employee Online 9

Review")

10 Roadmap for presentation What s new for the 2018 tax-return season (reporting for tax year 2017) Review of rules for cost-basis reporting Common questions and errors Communication and education for employees and executives 10

11 Polling Question #1 How does the Tax Cuts & Jobs Act, adopted in late 2017, impact tax return reporting for 2017 income? a. The rates and rules under it fully apply b. It does not apply. It starts with 2018 income c. Only the tax bracket rates apply to 2017 income d. You can elect to apply the 2018 tax rates and rules 11

12 Polling Question #1 How does the Tax Cuts & Jobs Act, adopted in late 2017, impact tax return reporting for 2017 income? a. The rates and rules under it fully apply b. It does not apply. It starts with 2018 income c. Only the tax bracket rates apply to 2017 income d. You can elect to apply the 2018 tax rates and rules 12

13 Three main points for employees about the Tax Cuts & Jobs Act ( Tax Reform ) 1. No impact on tax-return reporting for 2017 income. Rules the same! 13

14 Three main points for employees about the Tax Cuts & Jobs Act ( Tax Reform ) 2. Flat rate used for stock compensation income withholding (what we pros call supplemental wage income) is now 22% (37% for amounts over $1 million per year). What this means: The 24% tax bracket starts with yearly income over $165,000 for joint filers and over $82,500 for singles. Most employees with stock compensation are in a higher tax bracket. Need to know the tax bracket for total income and assess need to put money aside or pay estimated taxes. 14

15 Three main points for employees about the Tax Cuts & Jobs Act ( Tax Reform ) 3. AMT or how it applies to ISOs is not repealed. New key numbers in the AMT calculation: - The AMT income exemption amount rises to $70,300 (from 54,300) for single filers and to $109,400 (from 84,500) for married joint filers. - AMT income exemption starts to phase out begins at $500,000 for individuals (up from $120,700 in 2017) and $1,000,000 (up from $160,900) for married filers. What this means: Much less likely to trigger AMT from ISO exercise and hold. 15

16 Key bracket thresholds for federal income tax Tax thresholds for 2017 ordinary income, capital gains, and dividends, along with phaseouts on personal exemptions and itemized deductions. TAX RATE YEARLY INCOME THRESHOLD Top ordinary income rate (39.6%) & capital gains/dividend rate (20%) Taxable income of $418,400 (single) or $470,700 (joint) Income where 25% rate for supplemental withholding will not cover taxes owed (28% bracket rate starts) $91,900 (single) or $153,100 (joint) Medicare surtax on investment income (3.8%) Additional Medicare tax on earned income (0.9%) Phaseout of limit itemized deductions and personal exemptions Modified adjusted gross income of $200,000 (single) or $250,000 (joint) Earned income of $200,000 (single) or $250,000 (joint) Adjusted gross income of $384,000 (single) or $436,300 (joint) 16

17 AMT: Important for ISOs Alternative minimum tax (AMT): The income exemption amounts, the phaseout ranges, and the threshold for the higher 28% rate are now all indexed for inflation. The table below, prepared by mystockoptions.com, shows the 2017 figures. Filer status AMT income exemption amount AMT income exemption phaseout starts AMT income exemption phaseout ends Threshold where AMT rate rises from 26% to 28% Single $54,300 $120,700 $337,900 $187,800 ($93,900 for married but filing separately) Joint $84,500 $160,900 $498,900 $187,800 17

18 No changes in the rules and forms for tax-return reporting this year Similar to last year: Form W-2, Form 1099-B, Form 8949, Schedule D Same restrictions in what brokers can report for the cost basis on Form 1099-B More good news: The core reporting rules for Form 8949 and Schedule D have not changed 18

19 Polling Question #2 What is the box on the 1099-B that reports cost basis? a. Box 3 b. Box 1e c. Box 1g d. Box CB 19

20 Polling Question #2 What is the box on the 1099-B that reports cost basis? a. Box 3 b. Box 1e c. Box 1g d. Box CB 20

21 Cost Basis Reporting: IRS Form 1099-B core boxes (brokers use substitute statement with columns)

22 What is the cost basis? Cost basis (also called the tax basis) is the total cost of an acquired security: Price paid to acquire shares + compensation recognized for acquiring them (reported on W-2) When you sell a security, you need to know the cost basis to determine whether you have a capital gain or a capital loss for tax purposes. NET PROCEEDS COST BASIS = CAPITAL GAIN OR LOSS Cost basis too low: you overpay taxes

23 Recap of regulations on cost-basis reporting Cost-basis-reporting regulations were implemented as part of the Emergency Economic Stabilization Act of 2008 IRS Goal: capture lost tax revenue from capital gains and losses 2011: regulations require brokers to compute and report on Form 1099-B the cost basis of covered securities Initially, broker had the choice to include compensation income amounts in the cost basis they reported on Form 1099-B

24 Covered and uncovered securities Key IRS distinction A covered security: acquired for cash on or after January 1, Securities acquired through stock plans Covered securities Noncovered securities 1. Option exercise 2. ESPP purchase 1. Restricted stock/rsus vesting 2. Performance share/psus vesting 3. Stock appreciation right (SAR) exercise

25 Final cost-basis regulations The IRS wanted to reduce inconsistency in cost-basis reporting among brokers. The final regulations, adopted April 18, 2013, include this statement: A broker may not increase initial basis for income recognized upon the exercise of a compensatory option or the vesting or exercise of other equity-based compensation arrangements, granted or acquired on or after January 1, Removed the flexibility to increase the basis to include compensation income. Consistency comes at a price: If the basis on Form 1099-B is not adjusted for the W-2 income, you risk over-reporting gains and overpaying taxes.

26 What this means for tax-return reporting Compensation income will not be included in the basis reported on Form 1099-B for grants made starting 1/2014 Compensation income recognized: The cost-basis value will be incomplete in every scenario Need to know: How will the broker report the cost basis of shares acquired between the start of 2011 and the end of 2013? Trend is standardization: not adding W-2 income to basis for option exercises or ESPP purchases that occurred during this period Brokers provide supplemental information on basis and tax guides to help with tax-return reporting

27 Risk of overpaying taxes There are only three disposition scenarios in which the cost basis will not be understated: - qualifying dispositions of ISOs (all capital gain) - disqualifying dispositions of ISOs, with shares sold at a loss (all capital loss) - qualifying dispositions of ESPPs, with shares sold at a loss (all capital loss) In other scenarios, the cost basis will be understated or omitted (i.e. the box will be blank). Unless participants and tax professionals are aware of this, taxpayers risk: - over-report of capital gains - paying more taxes than they owe!

28 Ten tax-return issues and errors 1. Not reporting stock sales on Form 8949/Schedule D 2. Not reporting tax basis correctly on Form Double-counting income from W-2 4. Forgetting about AMT calculation or AMT credits 5. Sell-to-cover exercises 6. Share withholding for restricted stock/rsus 7. Dividends with restricted stock 8. Not reporting ordinary income with ESPP sales 9. Netting of income 10. Extensions

29

30 Polling Question #3 If employees sold stock during the calendar year, which tax forms do they file with their IRS Form 1040 to report the sale? a. Form 1099-B and Schedule A b. Form 8949 and Schedule D c. Form 6251 and Schedule C d. Form 1099-MISC and Schedule C 30

31 Polling Question #3 If employees sold stock during the calendar year, which tax forms do they file with their IRS Form 1040 to report the sale? a. Form 1099-B and Schedule A b. Form 8949 and Schedule D c. Form 6251 and Schedule C d. Form 1099-MISC and Schedule C 31

.")

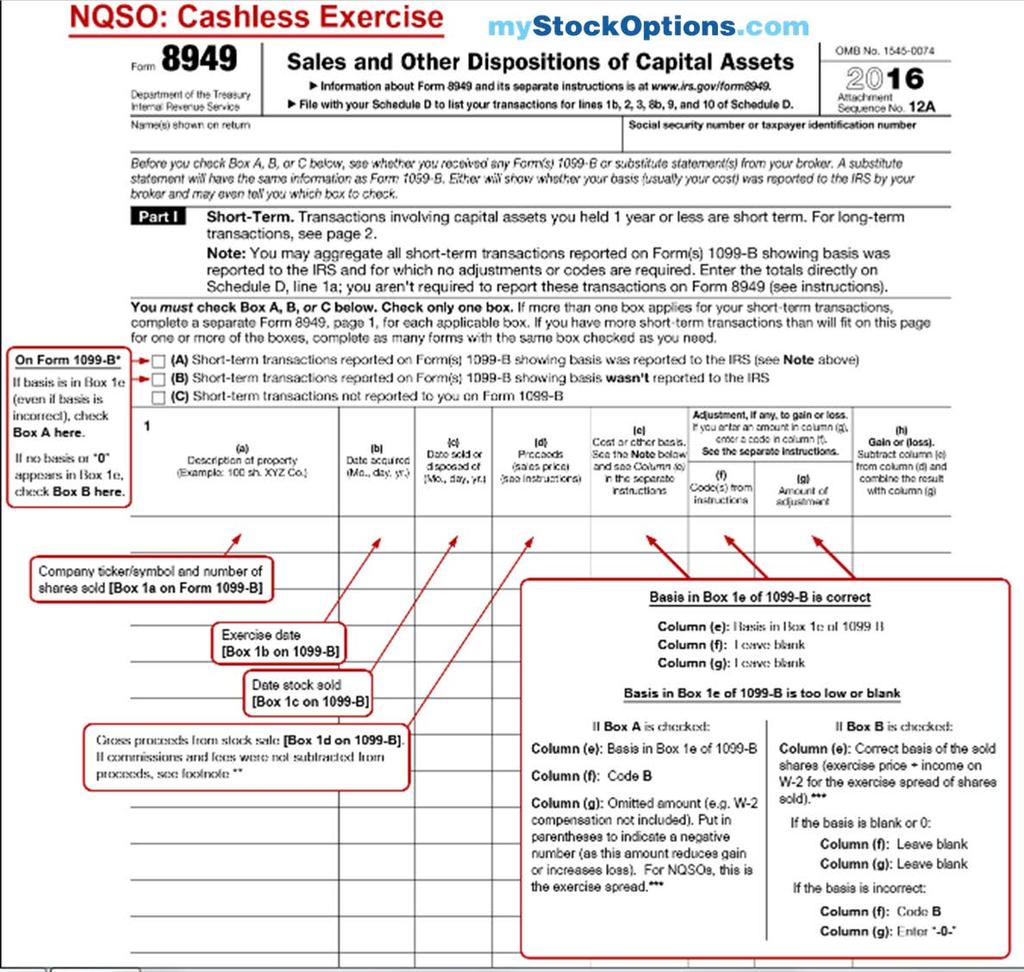

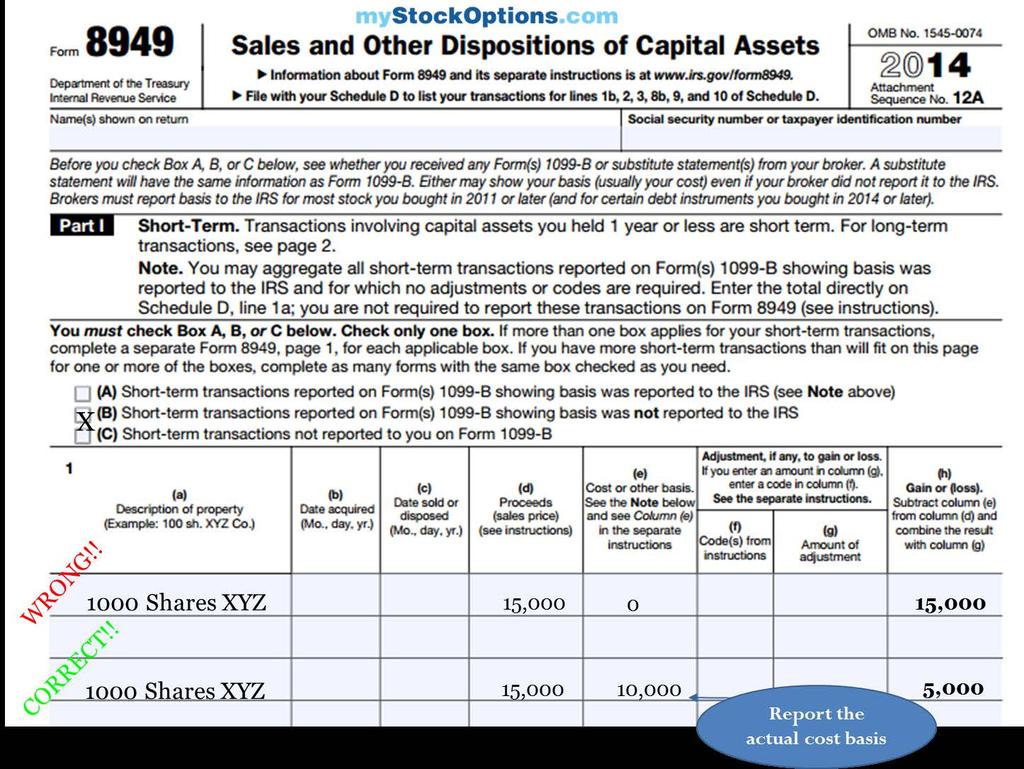

32 1. Not reporting stock sales on Form 8949 and Schedule D Event: Sell all stock at exercise (i.e. a cashless exercise), restricted stock/rsu vesting, or ESPP purchase. Employee may think: No gains beyond what s on W-2 for ordinary income. May not realize there are two reportable events. Result of incorrect thinking: employee does not report sale on Form 8949/Schedule D. IRS gets 1099-B from broker. IRS computers note no Form 8949/Schedule D reporting for it. Result: IRS sends notice for unreported income (CP-2000). For response to IRS, see the instructions at

33 1. Not reporting stock sales on Form 8949 and Schedule D Company and broker meet certain conditions: employee may not receive a Form 1099-B. Employee must still file Form 8949/Schedule D to report sale. Employee may even have small gains or losses for any commissions and fees for the stock sale.

34 1. Not reporting sales on Form 8949 and Schedule D Example: Exercised options and sold 2,000 shares on August 14. Exercise price $10 per share ($20,000 total) Stock price at exercise/sale: $35 $70,000 proceeds, minus $500 commission ($69,500 net on Form 1099-B What appears on Form W-2 $50,000 income [($35 - $10) x 2,000] Tax basis $70,000 ($20,000 + $50,000). But what is on 1099-B? $20,000 or $70,000? Schedule D (Part 1) Included as a $500 short-term capital loss If sale is not reported: IRS gets 1099-B with the $70,000 proceeds and sends employee letter looking for taxes on that full amount!

35

36

: Using exercise price only Mistake with ESPP: Using purchase price only Mistake with Restricted stock or")

37 2. Not reporting tax basis correctly Cost-basis reporting is now more complex, confusing, and vulnerable to errors! Error by type of grant that leads to OVERPAYING TAXES: Mistake with NQSOs, SARs, or ISO (DD) : Using exercise price only Mistake with ESPP: Using purchase price only Mistake with Restricted stock or Performance shares: Using purchase price of (usually $0). Grant type Mistake with reporting basis NQSOs, SARs, ISOs (DD) ESPP Restricted Stock/RSUs Exercise price only Purchase price only $0 as no purchase price

38 Amount of ordinary income recognized: reported on Form W-2 Grant type Income reported on W-2 NQSOs Spread at exercise Restricted stock, RSUs, performance shares Value at vesting and share delivery Section 423 (qualified) ESPP Depends on holding period ISO in disqualifying disposition Depends on the sales price relative to the market price at exercise

39 Cost-basis confusion: three situations 1. Stock purchases before 2011: No cost basis reported to IRS. 2. Securities not purchased with cash (restricted stock or RSUs): No cost basis reported to IRS. 3. Compensation part of cost basis for stock compensation: Cannot be part of basis reported to IRS for stock acquired or granted starting 1/2014.

40 Reporting tax basis on 1099-B: Timeline of changing IRS rules 40

41 What to do on Form 8949: Depends on 1099-B (mystockoptions.com Interpretation of Rules) correctly: reporting tax basis correctly: what The the cost rules basis say on rules do The on cost-basis Form 8949 box if on Form 1099-B is too low Form 1099-B is blank 1. Basis from 1099-B in column (e) 2. Adjustment in column (g) 3. Code B in column (f) 4. Check Box (A) or (D) near top 1. Put correct basis in column (e) 2. Check Box (B) or (E) near top 3. No adjustments or codes in other columns needed

42 Cost-basis example: RSUs Per share Total (1000 shares) Vesting date price $10 $10,000 Compensation income reported on Form W-2 $10 $10,000 Purchase price $0 $0 Cost basis $10 $10,000 (but $0 on the 1099-B) Sale price $15 $15,000 Taxable gain and capital gains tax Capital Gain: Overpaying using wrong cost basis $15 - $10 = $5 $15-$0 = $15 $15,000 - $10,000 = $5000 $5000 x 15% = $750 $15,000 - $0= $15,000 $15000 x 15% = $2250

43

44 Review: Reporting cost basis on Form 8949 depends on 1099-B 1. Basis just right Put number from 1099-B in column (e)

Adjustment amount in column (g)")

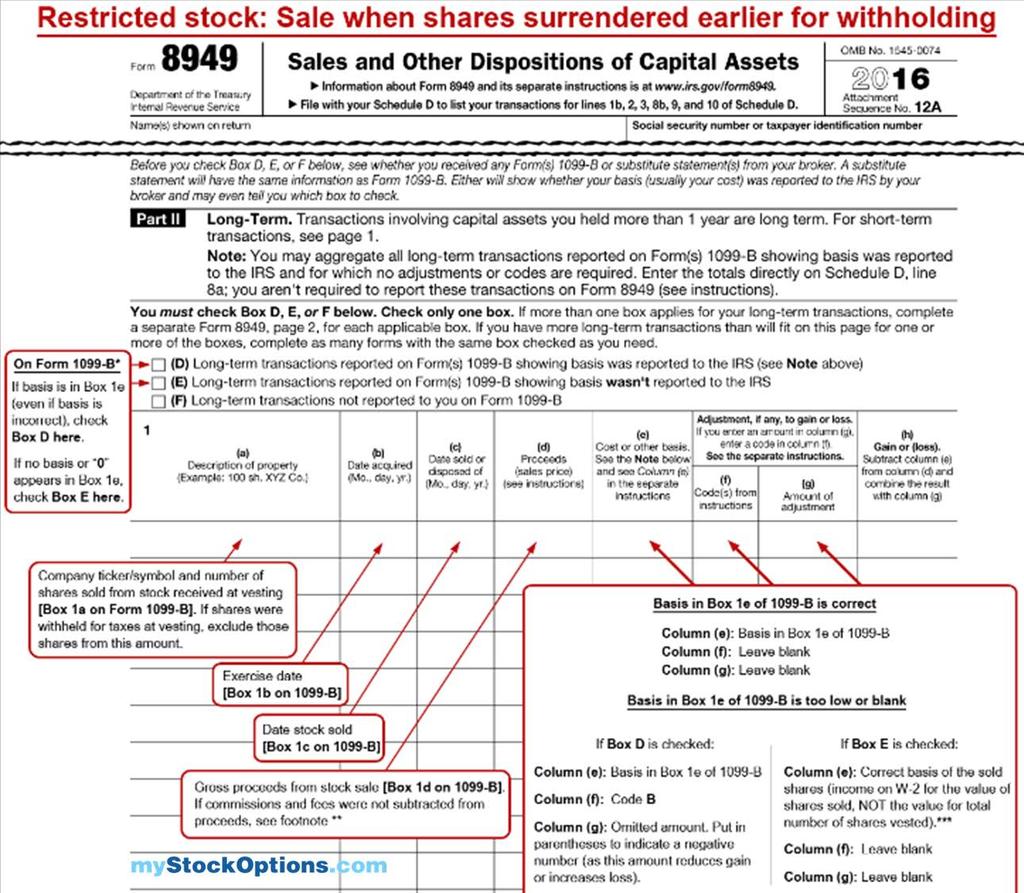

45 Review: Reporting cost basis on Form 8949 depends on 1099-B 2. Basis too low Put number from 1099-B in column (e) Adjustment amount in column (g) Code B in column (f) B ( )

46 Review: Reporting cost basis on Form 8949 depends on 1099-B 3. Basis blank Put correct basis In column (e), including W-2 income (columns (f) and (g) left blank)

47 2. Not reporting tax basis correctly: commission 1099-B does not subtract commissions or other fees from the proceeds (see what's checked in Box 6). Do not add it to your cost basis on Form 8949 Adjust the amount on Form 8949 in column (g) and add Code E in column (f). Starting with 2014 stock sales, less of an issue: IRS requires reporting sales proceeds net of transaction fees after January 1, 2013.

48 3. Double-counting income from W-2 in Box 12 or 14 W-2 income in Box 1 already includes stock compensation income, along with salary, wages. Put amount in Box 1 as part of income on line 7 of Form 1040 for Salary, wages Mistake: Using the amount in Box 12 (NQSOs) or Box 14 to report income on Form 1040 on the line for "Other income" (line 21). Alert: If you do this, you will be paying tax on the income twice as ordinary income. You use Line 21 only when the company mistakenly omits the stock compensation income from your W-2 or 1099-MISC. That can happen for sales of ESPPs in qualifying disposition.

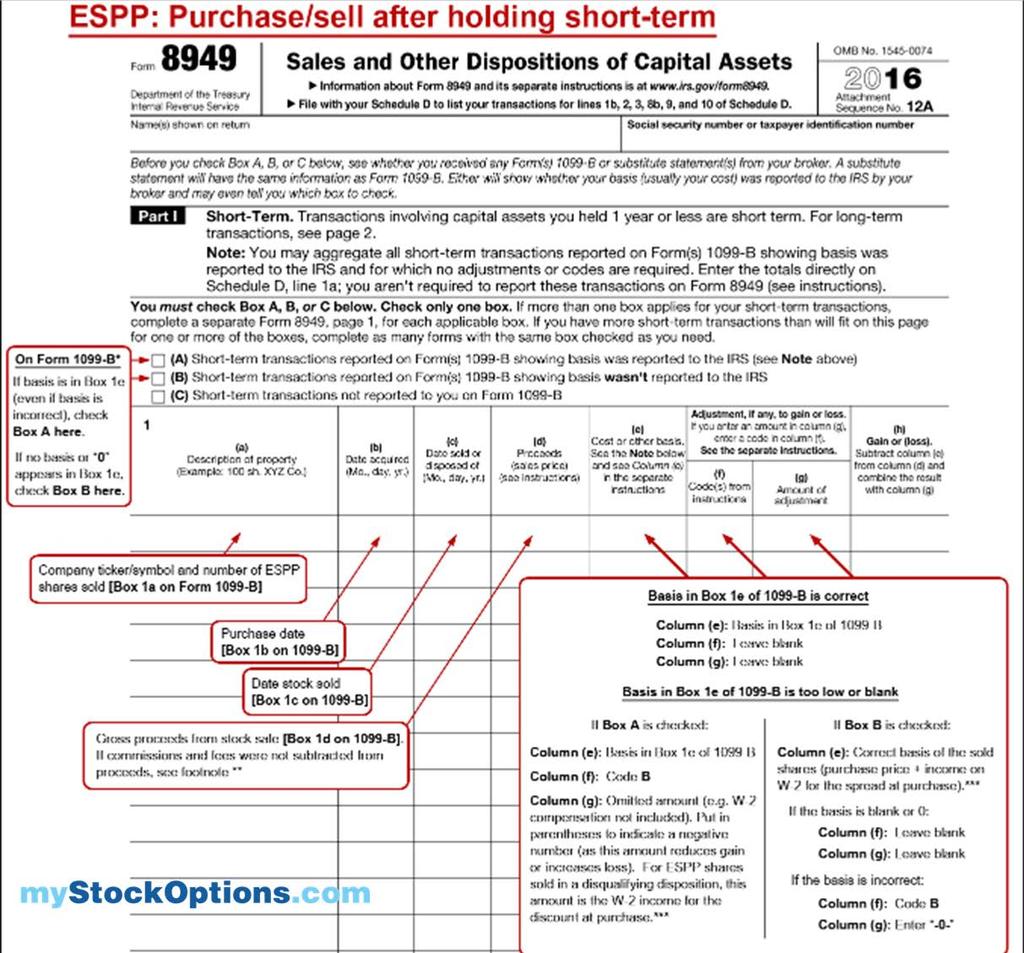

49

50 Remind employees about what they need for tax-return reporting IRS Forms to gather Form W-2 if shares were sold at exercise / vesting / purchase Form 1099-B from broker or transfer agent Form 3921 for ISO exercises; Form 3922 for ESPP purchases Additional Information & Forms Exercise/vesting/purchase income reported on Form 1040 if shares were acquired in a prior year. (Helps with cost-basis calculation.) Supplemental information (if any) provided by the broker to help with the cost basis. Exercise, purchase, vesting, and/or trade confirmations from the company or the stock plan provider. Alert: Understand how the basis is reported on the substitute statement and to the IRS (not the same). Taxpayer s responsibility to make adjustments on Form 8949.

51 4. AMT calculation and credits For AMT purposes, always complete IRS Form 6251 line 14 when ISOs are exercised & held through calendar year of exercise (not on W-2). Could be last year for AMT! ISO stock is dual-basis stock. Your gain or loss for the AMT system and the regular-tax system will differ when sell. For the year when you sell ISO stock, avoid paying or calculating more AMT than is required for your stock sale by reporting (as a negative amount) your adjusted gain or loss on line 17 of IRS Form This negative adjustment can reduce the AMT you would otherwise calculate and let you recover more of your AMT credit. The negative adjustment can't be greater than the capital gain for regular-tax purposes plus $3,000.

52 4. AMT and credits Once AMT has been triggered, you must complete Form 6251 every year, along with Form 8801 for the AMT credit. It can take years to benefit fully from the AMT credit if you are selling at a substantial loss. Will change starting in 2018 tax year. Use of AMT credit: In year when you do not trigger AMT, use credit against regular income tax up to amount of what would be your AMT. Does not require you sell the ISO stock. Example: Last year ISO exercise and hold triggered $14,000 of AMT This year, regular tax is $35,000, while AMT is only $30,000 $5,000 of the $14,000 credit used, and carry forward $9,000 to future

53 5. Sell-to-cover exercises Broker sells just enough shares from exercise to pay the exercise price, tax withholding, and the broker's transaction fees. Employee receives the remaining shares. For the year of sell-to-cover, report on your Form 8949 only the number of shares sold and their tax basis. Do not report the number and tax basis of all the options exercised that are part of W-2 income.

54 5. Sell-to-cover example: Exercise NQSOs for 2,000 shares on August 14 Exercise price $10 per share ($35 stock price) Exercise cost $20,000 Tax withholding $17,500 (combined 35% tax rate on $50,000) Brokerage commission $250 Total needed $37,750 What is included on Form W-2 $50,000 income [($35 - $10) x 2,000] Number of shares sold 1,079 (keep 921) Form 8949 reporting $37,515 ($37,765 - $250 commission) Tax basis on sold shares $37,765 (Schedule D includes a $250 short-term capital loss in Part I) In the future, when you sell any or all of the net shares (921 shares net): report the tax basis of $35 per share.

55 6. Share withholding for restricted stock and RSUs Definitely report a sale for taxes at vesting if you received a 1099-B that reports the proceeds. Sell-to-Cover for taxes. When the shares directly withheld by your company (often called net share withholding"), the situation is different. Report this "sale" back to company to cover the taxes if receive a 1099-B. Most companies do not issue these to employees. Rumor: IRS has informally approved this practice of not issuing 1099-Bs for share withholding. Common Mistake: Remember to exclude these tax shares when you calculate your capital gains on Form 8949 after you sell the remainder. See the sections Restricted Stock: Taxes and Restricted Stock: Taxes Advanced at mystockoptions.com or in the Knowledge Center

56 6. Share withholding with restricted stock and RSUs: Potential for confusion 2,000 shares of restricted stock vest on Aug. 15 Vesting value: $20 per share ($40,000) Shares surrender/net-settled to pay taxes 625 Amount your W-2 reports for the vested restricted stock $40,000 (2,000 x $20) Remaining 1,375 share sold the next year at $25 per share (after commissions) How you calculate capital gain $34,375 $34,375 proceeds $27,500 cost basis (1,375 x $20) Capital gain reported on Form 8949 = $6,875

57

election (not available for RSUs). Eligible for the lower 15%/20% rate for qualified dividends. Reported on 1099-DIV.")

58 7. Dividends with restricted stock Dividends paid: compensation during vesting period or at vesting. Reported on W-2. Exception: Employee makes a Section 83(b) election (not available for RSUs). Eligible for the lower 15%/20% rate for qualified dividends. Reported on 1099-DIV. Once the shares vest: dividends are no longer compensation and instead become dividend income.

59 7. Dividends: Complications Pre-vesting dividends included on W-2 + Double-reported on Form DIV. Can occur if the company's transfer agent routinely issues dividend payments and 1099-DIV as it does to shareholders. The IRS recommends: list these dividends on Schedule B ( Interest and Ordinary Dividends ) of Form Subtract them from the total with a note that you have already included them in wages. See IRS Publication 550, Investment Income and Expenses (Chapter 1), for more details on reporting restricted stock dividends

60 8. ESPP sales: Not reporting ordinary income Tax-qualified Section 423 ESPP: the purchase itself does not trigger taxreturn reporting. The sale does. At sale: need to include the discount from the year of purchase as income. Review of Tax Rules for QD: With qualifying disposition: Ordinary income in the year of sale equal to: the lesser of either the actual gain upon sale or the purchase price discount at the beginning of the offering. The discount at the beginning of the offering does not qualify for capital gains treatment regardless of holding period Beyond the discount, all additional gain is long-term capital gain. For details, examples, and videos see sections ESPPs: Taxes and ESPPs: Taxes Advanced at mystockoptions.com or in the Knowledge Center

61 8. Not reporting ordinary income with ESPP sales Example: 15% discount from the stock price on either first or last day of offering, whichever is lower. Stock price on first day of offering $10 Stock price on last day of offering (purchase date) $8 Purchase price $6.80 (85% of $8) Net at sale after commission $18 Income recognized at sale after meeting ESPP holding periods Cost basis $1.50 per share in ordinary income (15% of $10) $8.30 ($1.50 ordinary income + $6.80 purchase price) Long-term capital gain $9.70 per share ($18 minus cost basis of $8.30) What should be reported on Form W-2 $1.50 multiplied by the number of shares purchased (if this is not reported, still report that amount on your tax return, using the line Other ). Using Form 3922: Box 3 minus Box 8. If your sale gain is less than $1.50 per share (i.e. stock price of $8.30 per share or lower), you have just ordinary income for the amount of the actual gain. Sales below a stock price of $6.80 per share are all capital losses.

62

63 9. Netting of capital gain/loss Only same kinds of income net each other out. Only capital gains and losses net each other out on Schedule D. Stock compensation income is not capital gains income. Matching capital losses with gains is called tax-loss harvesting. Up to $3,000 (joint filers) in capital losses can be netted against ordinary income. Remainder carries forward. Example: You sold company stock early last year at $9,000 short-term capital loss. - You bought and sold this year at a short-term capital gain of $5, The loss carryforward and current year s gain net each other out on your Schedule D, leaving you $4,000 of unused losses. - $3,000 is used to offset against ordinary income on your current tax return. $1,000 is carried forward. Wash sale issues: purchase company stock at gain within 30 days of sale at loss. Easy mistake to make in down markets.

.")

64 10. Extensions IRS Form 4868: automatic six-month extension for the due date of your tax return (until mid-october). No explanation or signature is needed to get the automatic extension. To avoid the failure-to-file penalty on what you owe, you must file the extension no later than the original deadline of your return (for details, see IR ). Payment of the actual tax is not delayed (just the period for filing the return). Pay 100% of anticipated tax when file the extension to avoid interest and penalties. Extensions do not delay estimated tax payments for the current tax year. Complications for US expatriates: avoid double taxation by using the foreign earned income exclusion ($102,100 in 2017) or a US tax credit for taxes paid in a foreign country.

65

66

67 The video appears in the Tax Center

Tax-Return Mistakes And Error Prevention

Tax-Return Mistakes And Error Prevention Bruce Brumberg, Editor-in-Chief and Co-Founder, mystockoptions.com and mynqdc.com bruce@mystockoptions.com, 617-734-1979 Copyright 2018 mystockplan.com, Inc. Please

Tax-Return Mistakes And Error Prevention Bruce Brumberg, Editor-in-Chief and Co-Founder, mystockoptions.com and mynqdc.com bruce@mystockoptions.com, 617-734-1979 Copyright 2018 mystockplan.com, Inc. Please

YEAR-END FINANCIAL AND TAX PLANNING FOR EMPLOYEES IN 2018

YEAR-END FINANCIAL AND TAX PLANNING FOR EMPLOYEES IN 2018 Upcoming Events Webinar Series - All Things ESPP @ www.computershare.com/allthingsespp - All Things Equity Plans @ www.computershare.com/allthingsequityplans

YEAR-END FINANCIAL AND TAX PLANNING FOR EMPLOYEES IN 2018 Upcoming Events Webinar Series - All Things ESPP @ www.computershare.com/allthingsespp - All Things Equity Plans @ www.computershare.com/allthingsequityplans

Year-End Financial And Tax Planning For Employees In 2017

Year-End Financial And Tax Planning For Employees In 2017 Bruce Brumberg Editor-In-Chief and Co-Founder mystockoptions.com bruce@mystockoptions.com, 617-734-1979 Copyright mystockplan.com Inc. Please do

Year-End Financial And Tax Planning For Employees In 2017 Bruce Brumberg Editor-In-Chief and Co-Founder mystockoptions.com bruce@mystockoptions.com, 617-734-1979 Copyright mystockplan.com Inc. Please do

Year-End Financial And Tax Planning For Employees In 2015

Year-End Financial And Tax Planning For Employees In 2015 Bruce Brumberg Editor-In-Chief and Co-Founder mystockoptions.com bruce@mystockoptions.com, 617-734-1979 Copyright mystockplan.com Inc. Please do

Year-End Financial And Tax Planning For Employees In 2015 Bruce Brumberg Editor-In-Chief and Co-Founder mystockoptions.com bruce@mystockoptions.com, 617-734-1979 Copyright mystockplan.com Inc. Please do

2018 GUIDE TO TAX REPORTING FOR US EQUITY

2018 GUIDE TO TAX REPORTING FOR US EQUITY A PRACTICAL GUIDE TO TAX REPORTING FOR US-BASED EQUITY AWARDS - 2018 Introduction This guide is designed for US-based taxpayers who receive US equity awards. We

2018 GUIDE TO TAX REPORTING FOR US EQUITY A PRACTICAL GUIDE TO TAX REPORTING FOR US-BASED EQUITY AWARDS - 2018 Introduction This guide is designed for US-based taxpayers who receive US equity awards. We

2017 Tax Return Reporting Guide for Plan Participants in US Companies

2017 Tax Return Reporting Guide for Plan Participants in US Companies YOUR GUIDE TO 2017 TAX FORMS The 2017 Tax Return Reporting Guide for Plan Participants in US Companies (the Guide ) summarizes the

2017 Tax Return Reporting Guide for Plan Participants in US Companies YOUR GUIDE TO 2017 TAX FORMS The 2017 Tax Return Reporting Guide for Plan Participants in US Companies (the Guide ) summarizes the

Copyright mystockplan.com Inc. Please do not distribute or copy without permission. Questions? Contact us at

Copyright mystockplan.com Inc. Please do not distribute or copy without permission. Questions? Contact us at editors@mystockoptions.com. After reading this overview, see our ISO content section for more

Copyright mystockplan.com Inc. Please do not distribute or copy without permission. Questions? Contact us at editors@mystockoptions.com. After reading this overview, see our ISO content section for more

Don t overpay your taxes. Learn more about tax reporting and cost basis facts for stock plans.

Don t overpay your taxes. Learn more about tax reporting and cost basis facts for stock plans. As a participant in your company s stock plan program and/or employee stock purchase plan (ESPP), it s important

Don t overpay your taxes. Learn more about tax reporting and cost basis facts for stock plans. As a participant in your company s stock plan program and/or employee stock purchase plan (ESPP), it s important

Certified Equity Professional Institute

Exam Overview Webinars Certified Equity Professional Institute L1 Exam Overview Webinar Taxation Certified Equity Professional Institute 2011 http://cepi.scu.edu The information presented herein is of

Exam Overview Webinars Certified Equity Professional Institute L1 Exam Overview Webinar Taxation Certified Equity Professional Institute 2011 http://cepi.scu.edu The information presented herein is of

An Overview of Stock Compensation & Restricted Stock. Presented By: Incentive Stock Options. Disclaimer. Agenda. Meet John

An Overview of Stock Compensation & Restricted Stock February 13, 2018 Presented By: Scott Eichar, CPA, CFP, PFS Tax Senior Manager seichar@gbq.com 614.947.5233 Disclaimer Any material discussed in this

An Overview of Stock Compensation & Restricted Stock February 13, 2018 Presented By: Scott Eichar, CPA, CFP, PFS Tax Senior Manager seichar@gbq.com 614.947.5233 Disclaimer Any material discussed in this

Bruce Brumberg Editor-in-Chief & Co-Founder, mystockoptions.com

Bruce Brumberg Editor-in-Chief & Co-Founder, mystockoptions.com Employees enroll in plan Salary deduction: percentage or $ amount elected by employee for purchase Offering period when salary deducted Post

Bruce Brumberg Editor-in-Chief & Co-Founder, mystockoptions.com Employees enroll in plan Salary deduction: percentage or $ amount elected by employee for purchase Offering period when salary deducted Post

Back to Basics: Taxation

The 10th Annual New England NASPP Regional Conference co-hosted by the Boston and Connecticut NASPP Chapters July 11 th, 2018 Agenda 1. General Introduction to Tax Law Related to Equity Compensation 2.

The 10th Annual New England NASPP Regional Conference co-hosted by the Boston and Connecticut NASPP Chapters July 11 th, 2018 Agenda 1. General Introduction to Tax Law Related to Equity Compensation 2.

Stock option plan. Equity Plan Advisory Services tax filing guide. Last updated: December 2016

Last updated: December 2016 Stock option plan 2016 tax filing guide This guide will help you complete your annual U.S. tax forms if you participated in a stock option plan during 2016. We will go through

Last updated: December 2016 Stock option plan 2016 tax filing guide This guide will help you complete your annual U.S. tax forms if you participated in a stock option plan during 2016. We will go through

Back to Basics: Taxation

The 10th Annual New England NASPP Regional Conference co-hosted by the Boston and Connecticut NASPP Chapters July 11 th, 2018 Agenda 1. General Introduction to Concepts Related to Equity Compensation 2.

The 10th Annual New England NASPP Regional Conference co-hosted by the Boston and Connecticut NASPP Chapters July 11 th, 2018 Agenda 1. General Introduction to Concepts Related to Equity Compensation 2.

Determining your 2017 stock plan tax requirements a step-by-step guide

Determining your 2017 stock plan tax requirements a step-by-step guide Alert: The tax-reform legislation adopted in December 2017 does not affect the 2017 tax year or the federal tax return for 2017 that

Determining your 2017 stock plan tax requirements a step-by-step guide Alert: The tax-reform legislation adopted in December 2017 does not affect the 2017 tax year or the federal tax return for 2017 that

Stock Awards Keeping Pace with Equity Alternatives

Stock Awards Keeping Pace with Equity Alternatives Thursday, April 27, 2006 4:00pm 5:00pm Virginia L. Gibson White & Case LLP vgibson@whitecase.com Goals of Equity Compensation Recruit Motivate Retain

Stock Awards Keeping Pace with Equity Alternatives Thursday, April 27, 2006 4:00pm 5:00pm Virginia L. Gibson White & Case LLP vgibson@whitecase.com Goals of Equity Compensation Recruit Motivate Retain

Certified Equity Professional Institute

Exam Overview Webinars Certified Equity Professional Institute L2 Exam Overview Webinar Taxation Certified Equity Professional Institute 2011 http://cepi.scu.edu The information presented herein is of

Exam Overview Webinars Certified Equity Professional Institute L2 Exam Overview Webinar Taxation Certified Equity Professional Institute 2011 http://cepi.scu.edu The information presented herein is of

Determining your 2017 stock plan tax requirements a step-by-step guide

Determining your 2017 stock plan tax requirements a step-by-step guide Alert: The tax-reform legislation adopted in December 2017 does not affect the 2017 tax year or the federal tax return for 2017 that

Determining your 2017 stock plan tax requirements a step-by-step guide Alert: The tax-reform legislation adopted in December 2017 does not affect the 2017 tax year or the federal tax return for 2017 that

Medicare taxes for higher-income taxpayers

Medicare taxes for higher-income taxpayers Facts and planning considerations to help manage your tax liability Begin planning now You ll especially want to discuss these tax provisions with your Financial

Medicare taxes for higher-income taxpayers Facts and planning considerations to help manage your tax liability Begin planning now You ll especially want to discuss these tax provisions with your Financial

2018 tax planning tables

2018 tax planning tables Investment and Insurance Products: NOT FDIC Insured NO Bank Guarantee MAY Lose Value 2018 important deadlines Last day to January 16 Pay fourth-quarter 2017 federal individual

2018 tax planning tables Investment and Insurance Products: NOT FDIC Insured NO Bank Guarantee MAY Lose Value 2018 important deadlines Last day to January 16 Pay fourth-quarter 2017 federal individual

Understanding employer-granted stock options

Understanding employer-granted stock options Important information for option holders Employee stock options can be one of the most valuable benefits companies provide as part of a benefits package. However,

Understanding employer-granted stock options Important information for option holders Employee stock options can be one of the most valuable benefits companies provide as part of a benefits package. However,

2018 tax planning guide

Advanced Planning 2018 tax planning guide We are committed to helping you confirm that your current and future tax strategy supports your larger financial goals. Advice. Beyond investing. Your financial

Advanced Planning 2018 tax planning guide We are committed to helping you confirm that your current and future tax strategy supports your larger financial goals. Advice. Beyond investing. Your financial

Table of Contents Part I Preliminaries 11 Part II Dealing with Company Stock

Table of Contents About This Book 9 Part I Preliminaries 11 1 Equity Compensation 13 1.1 Six Categories of Equity Compensation 13 1.2 The Central Problem 14 2 Terminology 16 2.1 Recipients of Equity Compensation

Table of Contents About This Book 9 Part I Preliminaries 11 1 Equity Compensation 13 1.1 Six Categories of Equity Compensation 13 1.2 The Central Problem 14 2 Terminology 16 2.1 Recipients of Equity Compensation

BROAD-BASED EMPLOYEE INCENTIVE ARRANGEMENTS

I. Equity-Based Compensation BROAD-BASED EMPLOYEE INCENTIVE ARRANGEMENTS A. Nonqualified Stock Option ( NSO ) Right to purchase stock from the issuer at a fixed price. Holder may exercise at any time (after

I. Equity-Based Compensation BROAD-BASED EMPLOYEE INCENTIVE ARRANGEMENTS A. Nonqualified Stock Option ( NSO ) Right to purchase stock from the issuer at a fixed price. Holder may exercise at any time (after

Understanding Employee Stock Options

Understanding Employee Stock Options Family Office Resources Compensation in the form of employee stock options tends to carry a significant level of risk and a high degree of complexity. Investors who

Understanding Employee Stock Options Family Office Resources Compensation in the form of employee stock options tends to carry a significant level of risk and a high degree of complexity. Investors who

2016 Tax Information Guide

2016 Tax Information Guide To Our Clients: Please retain this booklet with your 2016 tax records. If you use the services of a tax advisor, please furnish this booklet to him or her. This Tax Information

2016 Tax Information Guide To Our Clients: Please retain this booklet with your 2016 tax records. If you use the services of a tax advisor, please furnish this booklet to him or her. This Tax Information

Medicare taxes for higher-income taxpayers

Medicare taxes for higher-income taxpayers Many changes from the 2010 health care reform are now in effect Begin planning now You ll especially want to discuss these tax provisions with your Financial

Medicare taxes for higher-income taxpayers Many changes from the 2010 health care reform are now in effect Begin planning now You ll especially want to discuss these tax provisions with your Financial

SOS Educational Webcast: Stock Admin Prep for Year-End and Some Things In-Between

SOS Educational Webcast: Stock Admin Prep for Year-End and Some Things In-Between Colin Bass, Stock & Option Solutions, Inc. Christopher Cox, Stock & Option Solutions, Inc. Disclaimer The following discussion

SOS Educational Webcast: Stock Admin Prep for Year-End and Some Things In-Between Colin Bass, Stock & Option Solutions, Inc. Christopher Cox, Stock & Option Solutions, Inc. Disclaimer The following discussion

Determining your 2017 stock plan tax requirements a step-by-step guide

Determining your 2017 stock plan tax requirements a step-by-step guide Alert: The tax-reform legislation adopted in December 2017 does not affect the 2017 tax year or the federal tax return for 2017 that

Determining your 2017 stock plan tax requirements a step-by-step guide Alert: The tax-reform legislation adopted in December 2017 does not affect the 2017 tax year or the federal tax return for 2017 that

2017 Tax Planning Tables

2017 Tax Planning Tables 2017 Important Deadlines Last day to January 17 Pay fourth-quarter 2016 federal individual estimated income tax January 25 Buy in to close a short-against-the-box position (regular-way

2017 Tax Planning Tables 2017 Important Deadlines Last day to January 17 Pay fourth-quarter 2016 federal individual estimated income tax January 25 Buy in to close a short-against-the-box position (regular-way

2017 Tax Information Guide

2017 Tax Information Guide Please retain this booklet with your 2017 tax records. If you use the services of a tax advisor, please furnish this booklet to him or her. This Tax Information Guide is provided

2017 Tax Information Guide Please retain this booklet with your 2017 tax records. If you use the services of a tax advisor, please furnish this booklet to him or her. This Tax Information Guide is provided

2016 Tax Planning Tables

2016 Tax Planning Tables 2016 Important Deadlines Last day to January 15 Pay fourth-quarter 2015 federal individual estimated income tax January 26 Buy in to close a short-against-the-box position (regular-way

2016 Tax Planning Tables 2016 Important Deadlines Last day to January 15 Pay fourth-quarter 2015 federal individual estimated income tax January 26 Buy in to close a short-against-the-box position (regular-way

Determining your 2017 stock plan tax requirements a step-by-step guide

Determining your 2017 stock plan tax requirements a step-by-step guide Alert: The tax-reform legislation adopted in December 2017 does not affect the 2017 tax year or the federal tax return for 2017 that

Determining your 2017 stock plan tax requirements a step-by-step guide Alert: The tax-reform legislation adopted in December 2017 does not affect the 2017 tax year or the federal tax return for 2017 that

planning tables Investment and Insurance Products: NOT FDIC Insured NO Bank Guarantee MAY Lose Value

2019 tax planning tables Investment and Insurance Products: NOT FDIC Insured NO Bank Guarantee MAY Lose Value 2019 important deadlines Last day to January 15 Pay fourth-quarter 2018 federal individual

2019 tax planning tables Investment and Insurance Products: NOT FDIC Insured NO Bank Guarantee MAY Lose Value 2019 important deadlines Last day to January 15 Pay fourth-quarter 2018 federal individual

Determining your 2016 stock plan tax requirements a step-by-step guide

Determining your 2016 stock plan tax requirements a step-by-step guide INSIDE How to use the Supplemental Form to avoid overpaying taxes Upon selling shares acquired from a nonqualified employee stock

Determining your 2016 stock plan tax requirements a step-by-step guide INSIDE How to use the Supplemental Form to avoid overpaying taxes Upon selling shares acquired from a nonqualified employee stock

Side-by-Side Summary of Current Tax Law and the Final Version of the Tax Reform Bill 1

Side-by-Side Summary of Current Tax Law and the Final Version of the Tax Reform Bill 1 Corporate Tax Provisions Tax rates C corporations pay tax on their income based on a graduated rate structure with

Side-by-Side Summary of Current Tax Law and the Final Version of the Tax Reform Bill 1 Corporate Tax Provisions Tax rates C corporations pay tax on their income based on a graduated rate structure with

Copyright mystockplan.com Inc. Please do not distribute or copy without permission.

Copyright mystockplan.com Inc. Please do not distribute or copy without permission. After reading this overview, see our NQSO content section for more detailed coverage. A nonqualified stock option, or

Copyright mystockplan.com Inc. Please do not distribute or copy without permission. After reading this overview, see our NQSO content section for more detailed coverage. A nonqualified stock option, or

TAX ASPECTS OF MUTUAL FUND INVESTING

Tax Guide for 2017 TAX ASPECTS OF MUTUAL FUND INVESTING INTRODUCTION I. Mutual Fund Distributions A. Distributions From All Mutual Funds 1. Net Investment Income and Short-Term Capital Gain Distributions

Tax Guide for 2017 TAX ASPECTS OF MUTUAL FUND INVESTING INTRODUCTION I. Mutual Fund Distributions A. Distributions From All Mutual Funds 1. Net Investment Income and Short-Term Capital Gain Distributions

Growing Your Practice With Equity Compensation and Executive Trading Plans

Growing Your Practice With Equity Compensation and Executive Trading Plans Joe Leighty, CFP, CWS VP Financial Consultant, Executive Services Branch Schwab Private Client Investment Advisory, Inc. (SPCIA)

Growing Your Practice With Equity Compensation and Executive Trading Plans Joe Leighty, CFP, CWS VP Financial Consultant, Executive Services Branch Schwab Private Client Investment Advisory, Inc. (SPCIA)

Tax Cuts and Jobs Act: Mobility and Rewards Comparison of current US tax reform proposals December 4, 2017

Tax Cuts and Jobs Act: Mobility and Rewards Comparison of current US tax reform proposals December 4, 2017 Overview The below summary highlights key provisions of current tax reform proposals that may

Tax Cuts and Jobs Act: Mobility and Rewards Comparison of current US tax reform proposals December 4, 2017 Overview The below summary highlights key provisions of current tax reform proposals that may

Tax Cuts and Jobs Act: Mobility and Rewards House and Senate proposals side-by-side comparison November 13, 2017

Tax Cuts and Jobs Act: Mobility and Rewards House and Senate proposals side-by-side comparison November 13, 2017 Overview On November 2, 2017, the House Ways and Means Committee released details of their

Tax Cuts and Jobs Act: Mobility and Rewards House and Senate proposals side-by-side comparison November 13, 2017 Overview On November 2, 2017, the House Ways and Means Committee released details of their

NOVEMBER (New Due Dates) 2016 Returns Due in 2017

2016 Returns Due in 2017") NOVEMBER 2016 EARLIER DUE DATES FOR 2016 RETURNS The filing due dates for all Forms W-2 and Forms 1099-MISC for non-employee compensation have been moved up to January 31, 2017. Reducing the time available

NOVEMBER 2016 EARLIER DUE DATES FOR 2016 RETURNS The filing due dates for all Forms W-2 and Forms 1099-MISC for non-employee compensation have been moved up to January 31, 2017. Reducing the time available

Tax Planning Considerations for 2015

Tax Planning Considerations for 2015 Most strategies that could have an impact on your taxes need to be made by December 31 if you want them reflected on your 2015 tax return. Executive summary As the

Tax Planning Considerations for 2015 Most strategies that could have an impact on your taxes need to be made by December 31 if you want them reflected on your 2015 tax return. Executive summary As the

Tax strategies for higher-income taxpayers

Tax strategies for higher-income taxpayers This overview summarizes some of the key areas that you and your tax advisor should assess. Your Financial Advisor can assist in evaluating investment decisions

Tax strategies for higher-income taxpayers This overview summarizes some of the key areas that you and your tax advisor should assess. Your Financial Advisor can assist in evaluating investment decisions

2017 tax planning tables

217 tax planning tables 217 important deadlines Last day to... January 31 Issue 199 to service providers, issue paper/e-filing of 199 s to IRS March 15 Establish and fund SEP plans for corporations for

217 tax planning tables 217 important deadlines Last day to... January 31 Issue 199 to service providers, issue paper/e-filing of 199 s to IRS March 15 Establish and fund SEP plans for corporations for

Stock & Option Solutions, Inc. November 18th, Cost Basis Confusion: What Do the New Regulations Mean for Stock Plan Professionals?

Cost Basis Confusion: What Do the New Regulations Mean for Stock Plan Professionals? Elizabeth Dodge, CEP Stock & Option Solutions, Inc. Andrew Schwartz, CEP, CPA BNY Mellon Shareowner Services Materials

Cost Basis Confusion: What Do the New Regulations Mean for Stock Plan Professionals? Elizabeth Dodge, CEP Stock & Option Solutions, Inc. Andrew Schwartz, CEP, CPA BNY Mellon Shareowner Services Materials

U.S. Global Investors Mutual Funds-Forms 1099 Guide for Tax Year 2009

U.S. Global Investors Funds U.S. Global Investors Mutual Funds-Forms 1099 Guide for Tax Year 2009 U.S. Global Investors is committed to providing accuracy in reporting tax information related to your mutual

U.S. Global Investors Funds U.S. Global Investors Mutual Funds-Forms 1099 Guide for Tax Year 2009 U.S. Global Investors is committed to providing accuracy in reporting tax information related to your mutual

2018 year-end tax guide

2018 year-end tax guide It s a new day for tax planning CONTENTS Year-to-date review 2 Executive compensation 8 Investing 11 Real estate 17 Business ownership 21 Charitable giving 24 Family and education

2018 year-end tax guide It s a new day for tax planning CONTENTS Year-to-date review 2 Executive compensation 8 Investing 11 Real estate 17 Business ownership 21 Charitable giving 24 Family and education

Year-End Tax Planning Letter

2013 Year-End Tax Planning Letter 54 North Country Road Miller Place, NY 11764 (877) 474-3747 or (631) 474-9400 www.ceschinipllc.com Introduction Tax planning is inherently complex, with the most powerful

2013 Year-End Tax Planning Letter 54 North Country Road Miller Place, NY 11764 (877) 474-3747 or (631) 474-9400 www.ceschinipllc.com Introduction Tax planning is inherently complex, with the most powerful

LAST CHANCE TO REDUCE 2018 INCOME TAXES

LAST CHANCE TO REDUCE 2018 INCOME TAXES Presented by: James J. Holtzman, CFP Wealth Advisor and Shareholder with Legend Financial Advisors, Inc. JAMES J. HOLTZMAN, CFP James J. Holtzman, CFP, is a Wealth

LAST CHANCE TO REDUCE 2018 INCOME TAXES Presented by: James J. Holtzman, CFP Wealth Advisor and Shareholder with Legend Financial Advisors, Inc. JAMES J. HOLTZMAN, CFP James J. Holtzman, CFP, is a Wealth

PART 1: CALCULATION OF SINGLE BUSINESS TAX (SBT) INVESTMENT TAX CREDIT (ITC) RECAPTURE BASES

INVESTMENT TAX CREDIT (ITC) RECAPTURE BASES") Michigan Department of Treasury 4585 (Rev. 07-12), Page 1 Attachment 05 2012 MICHIGAN Business Tax Investment Tax Credit Recapture From Sale of Assets Acquired Under Single Business Tax Issued under authority

Michigan Department of Treasury 4585 (Rev. 07-12), Page 1 Attachment 05 2012 MICHIGAN Business Tax Investment Tax Credit Recapture From Sale of Assets Acquired Under Single Business Tax Issued under authority

Glossary. 701(g)(3) Account Certification (Activation) 144K. Alternate Identification. Alternative Minimum Tax (AMT)

(3) Account Certification (Activation) 144K. Alternate Identification. Alternative Minimum Tax (AMT)") Glossary 144 SEC Rule 144 is a means by which restricted and control securities may be sold in compliance with federal law and regulations. Rule 144 requirements depend on who owns the security, the length

Glossary 144 SEC Rule 144 is a means by which restricted and control securities may be sold in compliance with federal law and regulations. Rule 144 requirements depend on who owns the security, the length

Tax strategies for higher-income taxpayers

Tax strategies for higher-income taxpayers This overview summarizes some of the key areas that you and your tax advisor should assess. Your Financial Advisor can assist in evaluating investment decisions

Tax strategies for higher-income taxpayers This overview summarizes some of the key areas that you and your tax advisor should assess. Your Financial Advisor can assist in evaluating investment decisions

2013 Tax Planning Guide Year-round strategies to make the tax laws work for you

2013 Tax Planning Guide Year-round strategies to make the tax laws work for you 2032 Caribou Drive, Suite 200 Fort Collins, CO 80525 970.223.2727 www.soukupbush.com Dear Clients and Friends, We wish we

2013 Tax Planning Guide Year-round strategies to make the tax laws work for you 2032 Caribou Drive, Suite 200 Fort Collins, CO 80525 970.223.2727 www.soukupbush.com Dear Clients and Friends, We wish we

PART 1: CALCULATION OF SINGLE BUSINESS TAX (SBT) INVESTMENT TAX CREDIT (ITC) RECAPTURE BASES

INVESTMENT TAX CREDIT (ITC) RECAPTURE BASES") Michigan Department of Treasury Attachment 05 4585 (Rev. 04-17), Page 1 of 2 2017 MICHIGAN usiness Tax Investment Tax Credit Recapture From Sale of Assets Acquired Under Single usiness Tax Issued under

Michigan Department of Treasury Attachment 05 4585 (Rev. 04-17), Page 1 of 2 2017 MICHIGAN usiness Tax Investment Tax Credit Recapture From Sale of Assets Acquired Under Single usiness Tax Issued under

2017 year-end tax guide Possible tax law changes on the horizon

2017 year-end tax guide Possible tax law changes on the horizon With Donald Trump in the White House and Republicans maintaining a majority in Congress comes the possibility of some dramatic changes in

2017 year-end tax guide Possible tax law changes on the horizon With Donald Trump in the White House and Republicans maintaining a majority in Congress comes the possibility of some dramatic changes in

alternative minimum tax

alternative minimum tax The alternative minimum tax ( AMT ) was designed to prevent wealthy taxpayers from using tax loopholes to avoid paying taxes. Because the exemption from the AMT is not automatically

alternative minimum tax The alternative minimum tax ( AMT ) was designed to prevent wealthy taxpayers from using tax loopholes to avoid paying taxes. Because the exemption from the AMT is not automatically

A Comprehensive Guide to your Composite Tax Statement

A Comprehensive Guide to your Composite Tax Statement Hilltop Securities does not provide tax advice. This material is presented for informational purposes only. You should consult your tax advisor on

A Comprehensive Guide to your Composite Tax Statement Hilltop Securities does not provide tax advice. This material is presented for informational purposes only. You should consult your tax advisor on

2. Name (print or type) 3. Federal Employer Identification Number (FEIN)

3. Federal Employer Identification Number (FEIN)") Michigan Department of Treasury 4891 (Rev. 07-12), Page 1 2012 MICHIGAN Corporate Income Tax Annual Return Issued under authority of Public Act 38 of 2011. MM-DD-YYYY This form cannot be used as an amended

Michigan Department of Treasury 4891 (Rev. 07-12), Page 1 2012 MICHIGAN Corporate Income Tax Annual Return Issued under authority of Public Act 38 of 2011. MM-DD-YYYY This form cannot be used as an amended

TAX PLANNING GUIDE YEAR-ROUND STRATEGIES TO MAKE THE TAX LAWS WORK FOR YOU

2017-2018 TAX PLANNING GUIDE YEAR-ROUND STRATEGIES TO MAKE THE TAX LAWS WORK FOR YOU Possible tax law changes on the horizon With Donald Trump in the White House and Republicans maintaining a majority

2017-2018 TAX PLANNING GUIDE YEAR-ROUND STRATEGIES TO MAKE THE TAX LAWS WORK FOR YOU Possible tax law changes on the horizon With Donald Trump in the White House and Republicans maintaining a majority

PART 1: CALCULATION OF SINGLE BUSINESS TAX (SBT) INVESTMENT TAX CREDIT (ITC) RECAPTURE BASES

INVESTMENT TAX CREDIT (ITC) RECAPTURE BASES") Michigan Department of Treasury 4585 (Rev. 07-12), Page 1 Attachment 05 2012 MICHIGAN Business Tax Investment Tax Credit Recapture From Sale of Assets Acquired Under Single Business Tax Issued under authority

Michigan Department of Treasury 4585 (Rev. 07-12), Page 1 Attachment 05 2012 MICHIGAN Business Tax Investment Tax Credit Recapture From Sale of Assets Acquired Under Single Business Tax Issued under authority

DESIGN YOUR ESPP FOR THE US AND THE WORLD

DESIGN YOUR ESPP FOR THE US AND THE WORLD Upcoming Events Webinar Series - All Things ESPP @ www.computershare.com/allthingsespp - All Things Equity Plans @ www.computershare.com/allthingsequityplans ESPP

DESIGN YOUR ESPP FOR THE US AND THE WORLD Upcoming Events Webinar Series - All Things ESPP @ www.computershare.com/allthingsespp - All Things Equity Plans @ www.computershare.com/allthingsequityplans ESPP

Executive Compensation

Executive Compensation Bulletin IRS Issues Two Final Rules With Implications for High-Income Taxpayers Russ Hall and Steve Seelig, Towers Watson January 13, 2014 Recently, the Internal Revenue Service

Executive Compensation Bulletin IRS Issues Two Final Rules With Implications for High-Income Taxpayers Russ Hall and Steve Seelig, Towers Watson January 13, 2014 Recently, the Internal Revenue Service

NQ An easy, step-by-step guide

Your Non-Qualified () Stock Options Reporting the exercise and related sale of shares on your 2017 tax return A tax This document provides information about US federal income tax reporting requirements

Your Non-Qualified () Stock Options Reporting the exercise and related sale of shares on your 2017 tax return A tax This document provides information about US federal income tax reporting requirements

Employee Stock Purchase Plan

Employee Stock Purchase Plan This document constitutes part of a Prospectus covering securities that have been registered under the Securities Act of 1933. The date of this Prospectus is November 1, 2015.

Employee Stock Purchase Plan This document constitutes part of a Prospectus covering securities that have been registered under the Securities Act of 1933. The date of this Prospectus is November 1, 2015.

ISO An easy, step-by-step guide

Your Incentive Stock Options () Reporting the exercise and related sale on your 2017 tax return A tax This document provides information about US federal income tax reporting requirements that may apply

Your Incentive Stock Options () Reporting the exercise and related sale on your 2017 tax return A tax This document provides information about US federal income tax reporting requirements that may apply

A Comprehensive Reference Guide to your Consolidated Tax Statement

Formerly Clearview Correspondent Services, LLC. 1099-Consolidated Tax Statement 2012 Guide A Comprehensive Reference Guide to your 2012 1099 Consolidated Tax Statement This comprehensive and informative

Formerly Clearview Correspondent Services, LLC. 1099-Consolidated Tax Statement 2012 Guide A Comprehensive Reference Guide to your 2012 1099 Consolidated Tax Statement This comprehensive and informative

Above lists are not all-inclusive. For more information, contact (937)

") In this packet you, will find general tax information about the City of Springboro Income Tax Return. We encourage you to bring your income tax information to our office and we will gladly prepare your

In this packet you, will find general tax information about the City of Springboro Income Tax Return. We encourage you to bring your income tax information to our office and we will gladly prepare your

2016 Year-End Tax Planning Letter

9NOV2016 2016 Year-End Tax Planning Letter Dear Vista Wealth Clients and Friends, As 2016 draws to a close, you should give consideration to year-end tax planning strategies. This letter highlights some

9NOV2016 2016 Year-End Tax Planning Letter Dear Vista Wealth Clients and Friends, As 2016 draws to a close, you should give consideration to year-end tax planning strategies. This letter highlights some

Tax Determination, Payments, and Reporting Procedures

CCH Essentials of Federal Income Taxation Tax Determination, Payments, and Reporting Procedures 2002, CCH INCORPORATED 4025 West Peterson Ave. Chicago, IL 60646-6085 http://tax.cchgroup.com Taxpayer Filing

CCH Essentials of Federal Income Taxation Tax Determination, Payments, and Reporting Procedures 2002, CCH INCORPORATED 4025 West Peterson Ave. Chicago, IL 60646-6085 http://tax.cchgroup.com Taxpayer Filing

2016 Tax Preparation Checklist. Documentation for Itemized Deductions

Essentials for Taxpayers For 2016 Federal Returns Due in April 2017 2016 Tax Preparation Checklist n Copy of 2015 tax return n Social Security number(s) taxpayers and dependents n W-2 forms from all employers

Essentials for Taxpayers For 2016 Federal Returns Due in April 2017 2016 Tax Preparation Checklist n Copy of 2015 tax return n Social Security number(s) taxpayers and dependents n W-2 forms from all employers

TAX GUIDE PLANNING YEAR-ROUND STRATEGIES TO MAKE THE TAX LAWS WORK FOR YOU

2018 2019 TAX PLANNING GUIDE YEAR-ROUND STRATEGIES TO MAKE THE TAX LAWS WORK FOR YOU It s a new day for tax planning On December 22, 2017, the most sweeping tax legislation since the Tax Reform Act of

2018 2019 TAX PLANNING GUIDE YEAR-ROUND STRATEGIES TO MAKE THE TAX LAWS WORK FOR YOU It s a new day for tax planning On December 22, 2017, the most sweeping tax legislation since the Tax Reform Act of

Tax Planning Guide. Year-round strategies to make the tax laws work for you

2018 2019 Tax Planning Guide Year-round strategies to make the tax laws work for you Dear Clients and Friends, Commitment influences behavior, and behavior determines results. That s a phrase from Even

2018 2019 Tax Planning Guide Year-round strategies to make the tax laws work for you Dear Clients and Friends, Commitment influences behavior, and behavior determines results. That s a phrase from Even

TECHNICAL CORRECTIONS ACT OF 2007 INCLUDES MANY SUBSTANTIVE CHANGES

Page 1 of 14 TECHNICAL CORRECTIONS ACT OF 2007 INCLUDES MANY SUBSTANTIVE CHANGES The Tax Technical Corrections Act of 2007 (TCA), was passed by Congress on December 19, 2007, and awaits the President's

Page 1 of 14 TECHNICAL CORRECTIONS ACT OF 2007 INCLUDES MANY SUBSTANTIVE CHANGES The Tax Technical Corrections Act of 2007 (TCA), was passed by Congress on December 19, 2007, and awaits the President's

A Comprehensive Reference Guide to Your Consolidated Tax Statement

1099-Consolidated Tax Statement 2013 Guide A Comprehensive Reference Guide to Your 2013 1099-Consolidated Tax Statement This comprehensive and informative guide is a tool to assist you and your tax professional

1099-Consolidated Tax Statement 2013 Guide A Comprehensive Reference Guide to Your 2013 1099-Consolidated Tax Statement This comprehensive and informative guide is a tool to assist you and your tax professional

5 Qualifying widow(er) (see instructions) 6a Yourself. If someone can claim you as a dependent, do not check box 6a...

(see instructions) 6a Yourself. If someone can claim you as a dependent, do not check box 6a...") Form 1040 Department of the Treasury Internal Revenue Service (99) US Individual Income Tax Return OMB No 1545-0074 IRS Use Only Do not write or staple in this space For the year Jan 1 Dec 31,, or other

Form 1040 Department of the Treasury Internal Revenue Service (99) US Individual Income Tax Return OMB No 1545-0074 IRS Use Only Do not write or staple in this space For the year Jan 1 Dec 31,, or other

Capital Asset Taxation Introduction

Capital Asset Taxation Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually 0% or 15% rate Could be 20% rate for very high incomes NTTC Training

Capital Asset Taxation Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually 0% or 15% rate Could be 20% rate for very high incomes NTTC Training

LAST CHANCE 2017 INCOME TAX MINIMIZATION TIPS

LAST CHANCE 2017 INCOME TAX MINIMIZATION TIPS Presented by: James J. Holtzman, CFP Wealth Advisor and Shareholder with Legend Financial Advisors, Inc. JAMES J. HOLTZMAN, CFP James J. Holtzman, CFP, is

LAST CHANCE 2017 INCOME TAX MINIMIZATION TIPS Presented by: James J. Holtzman, CFP Wealth Advisor and Shareholder with Legend Financial Advisors, Inc. JAMES J. HOLTZMAN, CFP James J. Holtzman, CFP, is

YEAR-END TAX PLANNING OPPORTUNITIES

YEAR-END TAX PLANNING OPPORTUNITIES These important tax and financial planning moves can help prepare you for the upcoming tax season and better align your portfolio with your short- and long-term goals.

YEAR-END TAX PLANNING OPPORTUNITIES These important tax and financial planning moves can help prepare you for the upcoming tax season and better align your portfolio with your short- and long-term goals.

Year-End Tax Moves for Income Tax Rates for 2015

Year-End Tax Moves for 2015 One of our major goals is to help our clients identify opportunities that coordinate tax reduction with their investment portfolios. In order to achieve this goal, we stay current

Year-End Tax Moves for 2015 One of our major goals is to help our clients identify opportunities that coordinate tax reduction with their investment portfolios. In order to achieve this goal, we stay current

2012 TO 2013 TAX TRANSITIONS SUMMARY

2012 TO 2013 TAX TRANSITIONS SUMMARY September 2012 Individual Income Tax 2012 Law Scheduled 2013 Law* Green Book Q3 and Q4 2012 and Q1 2013 General Overview Lower rates with special treatment of qualified

2012 TO 2013 TAX TRANSITIONS SUMMARY September 2012 Individual Income Tax 2012 Law Scheduled 2013 Law* Green Book Q3 and Q4 2012 and Q1 2013 General Overview Lower rates with special treatment of qualified

2017 Year-End Tax Planning

2017 Year-End Tax Planning If you've been following the news out of Washington, you probably know that for the first time in decades, tax reform is a real possibility. Given that both the House and the

2017 Year-End Tax Planning If you've been following the news out of Washington, you probably know that for the first time in decades, tax reform is a real possibility. Given that both the House and the

Mutual Funds Tax Guide 2017

Mutual Funds Tax Guide 2017 A guide to your year-end tax statements and forms When it comes to investing, we at Nuveen work to help investors build and sustain the wealth of a lifetime. For many, that

Mutual Funds Tax Guide 2017 A guide to your year-end tax statements and forms When it comes to investing, we at Nuveen work to help investors build and sustain the wealth of a lifetime. For many, that

7th Correction Run October 10. ***Prior year corrections are included in the above schedule if requested.

Tax Reporting Q: LPL mails the majority of the 1099-C forms on February 15. Isn t this considered late? A: No. In the fall of 2008, the IRS recognized that there was not sufficient time to make the necessary

Tax Reporting Q: LPL mails the majority of the 1099-C forms on February 15. Isn t this considered late? A: No. In the fall of 2008, the IRS recognized that there was not sufficient time to make the necessary

PROSPECTUS 626,600,000 SHARES COMMON STOCK 2003 KEY ASSOCIATE STOCK PLAN, AS AMENDED AND RESTATED EFFECTIVE APRIL 28, 2010

PROSPECTUS 626,600,000 SHARES BANK OF AMERICA CORPORATION COMMON STOCK 2003 KEY ASSOCIATE STOCK PLAN, AS AMENDED AND RESTATED EFFECTIVE APRIL 28, 2010 This Prospectus relates to the offer and sale of up

PROSPECTUS 626,600,000 SHARES BANK OF AMERICA CORPORATION COMMON STOCK 2003 KEY ASSOCIATE STOCK PLAN, AS AMENDED AND RESTATED EFFECTIVE APRIL 28, 2010 This Prospectus relates to the offer and sale of up

2017 YEAR-END TAX AND WEALTH TRANSFER PLANNING

2017 YEAR-END TAX AND WEALTH TRANSFER PLANNING Tax reform is in progress, and Congress and the White House are pushing for a historic tax overhaul. We have not seen major tax reform legislation since President

2017 YEAR-END TAX AND WEALTH TRANSFER PLANNING Tax reform is in progress, and Congress and the White House are pushing for a historic tax overhaul. We have not seen major tax reform legislation since President

Year-end Tax Moves for 2017

Year-end Tax Moves for 2017 Holloway Wealth Management One of our main goals as holistic financial advisors is to help our clients recognize tax reducing opportunities within their investment portfolios

Year-end Tax Moves for 2017 Holloway Wealth Management One of our main goals as holistic financial advisors is to help our clients recognize tax reducing opportunities within their investment portfolios

Form 1099 Consolidated Tax Statement

Understanding Your 2018 Form 1099 Consolidated Tax Statement The 2018 Tax Reporting Information Statement, Form 1099, is a record of activity in your account at Janney Montgomery Scott LLC. This statement

Understanding Your 2018 Form 1099 Consolidated Tax Statement The 2018 Tax Reporting Information Statement, Form 1099, is a record of activity in your account at Janney Montgomery Scott LLC. This statement

NOW ON TO TAX PLANNING. THERE IS A LOT HERE, SO HAPPY READING.

To Our Valued Clients, Tis the season of holidays and tax planning. We are excited about the upcoming tax season and wanted to update everyone on some year-end planning tips. Before we jump into the tax

To Our Valued Clients, Tis the season of holidays and tax planning. We are excited about the upcoming tax season and wanted to update everyone on some year-end planning tips. Before we jump into the tax

Tax Season Insights with Ernst & Young. March 29, 2019

Tax Season Insights with Ernst & Young March 29, 2019 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is

Tax Season Insights with Ernst & Young March 29, 2019 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is

Year-end Tax Moves for 2015

Year-end Tax Moves for 2015 PRESENTED BY: One of our major goals is to help our clients identify opportunities that coordinate tax reduction with their investment portfolios. In order to achieve this goal,

Year-end Tax Moves for 2015 PRESENTED BY: One of our major goals is to help our clients identify opportunities that coordinate tax reduction with their investment portfolios. In order to achieve this goal,

Year-End Planning 2017

Wealth Management Year-End Planning Executive Summary As we approach the end of, it is time to review traditional year-end planning decisions. We are aware of the significant changes in the tax code currently

Wealth Management Year-End Planning Executive Summary As we approach the end of, it is time to review traditional year-end planning decisions. We are aware of the significant changes in the tax code currently

Purpose. Important Dates. Tax Forms. Tax Topics

Mutual Fund Tax Guide 2017 Contents Purpose Important Dates Tax Forms What s included in the Mutual Fund Tax Guide? Will the Guide help me file my tax return? Who should I contact for tax advice? Who should

Mutual Fund Tax Guide 2017 Contents Purpose Important Dates Tax Forms What s included in the Mutual Fund Tax Guide? Will the Guide help me file my tax return? Who should I contact for tax advice? Who should

TIPS FOR TRADERS ON PREPARING 2018 TAX RETURNS

1/4/2019 Copyright 2019 @ GreenTraderTax.com TIPS FOR TRADERS ON PREPARING 2018 TAX RETURNS Jan. 9, 2019 @ 12:00 pm EST (Interactive Brokers Webinar) 1 1/4/2019 Copyright 2019 @ GreenTraderTax.com 2 CPA

1/4/2019 Copyright 2019 @ GreenTraderTax.com TIPS FOR TRADERS ON PREPARING 2018 TAX RETURNS Jan. 9, 2019 @ 12:00 pm EST (Interactive Brokers Webinar) 1 1/4/2019 Copyright 2019 @ GreenTraderTax.com 2 CPA

Tax Impact. Accelerating depreciation deductions A cost segregation study may reduce taxes. How basis planning can result in significant tax savings

Tax Impact September/October 2016 Accelerating depreciation deductions A cost segregation study may reduce taxes How basis planning can result in significant tax savings Watch out for the alternative minimum

Tax Impact September/October 2016 Accelerating depreciation deductions A cost segregation study may reduce taxes How basis planning can result in significant tax savings Watch out for the alternative minimum

Arthur Lander C.P.A., P.C. A professional corporation

A Arthur Lander C.P.A., P.C. A professional corporation 300 N. Washington St. #104 Alexandria, Virginia 22314 phone: (703) 486-0700 fax: (703) 527-7207 YEAR-END TAX PLANNING FOR INDIVIDUALS Once again,

A Arthur Lander C.P.A., P.C. A professional corporation 300 N. Washington St. #104 Alexandria, Virginia 22314 phone: (703) 486-0700 fax: (703) 527-7207 YEAR-END TAX PLANNING FOR INDIVIDUALS Once again,

2017 Year-End Tax Reminders

2017 Year-End Tax Reminders INCOME TAX Wealth Planning Income Tax Rates 1. The following federal tax rates now apply to most types of capital gains for taxpayers in the highest tax brackets: 39.6% (short-term),

2017 Year-End Tax Reminders INCOME TAX Wealth Planning Income Tax Rates 1. The following federal tax rates now apply to most types of capital gains for taxpayers in the highest tax brackets: 39.6% (short-term),

Executives Beware: States May Look To Equity Compensation for Revenue

Executives Beware: States May Look To Equity Compensation for Revenue by Cara Griffith Cara Griffith is a legal editor of State Tax Notes. Many public corporations and even some closely held businesses

Executives Beware: States May Look To Equity Compensation for Revenue by Cara Griffith Cara Griffith is a legal editor of State Tax Notes. Many public corporations and even some closely held businesses

Instructions for Form 4891 Corporate Income Tax (CIT) Annual Return

Annual Return") Instructions for Form 4891 Corporate Income Tax (CIT) Annual Return Purpose To calculate the Corporate Income Tax for standard taxpayers. Insurance companies should file the Insurance Company Annual Return

Instructions for Form 4891 Corporate Income Tax (CIT) Annual Return Purpose To calculate the Corporate Income Tax for standard taxpayers. Insurance companies should file the Insurance Company Annual Return

2017 Year-End Tax Memo

2017 Year-End Tax Memo An Annual Publication of Large & Gilbert, Inc. January 2018 Large & Gilbert, Inc., is a full service CPA firm specializing in Accounting, Tax, Consulting, Business Advisory, Wealth

2017 Year-End Tax Memo An Annual Publication of Large & Gilbert, Inc. January 2018 Large & Gilbert, Inc., is a full service CPA firm specializing in Accounting, Tax, Consulting, Business Advisory, Wealth