Fiduciary and Investment Risk Management Association 28 th National Risk Management Training Conference

|

|

|

- Rachel Heath

- 5 years ago

- Views:

Transcription

1 Fiduciary and Investment Risk Management Association 28 th National Risk Management Training Conference Foreign Account Tax Compliance Act: Considerations for Trusts April 30, 2014 Michael Shepard Principal Deloitte Transactions and Business Analytics LLP Andrea Garcia Castelao Manager Deloitte Tax LLP

2 DISCLAIMER This document contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this document. 1

3 Foreign Account Tax Compliance Act Overview

4 Foreign Account Tax Compliance Act Overview What is FATCA? The Foreign Account Tax Compliance Act (FATCA) was enacted as part of the Hiring Incentives to Restore Employment (HIRE) Act on March 18, FATCA creates a new information reporting and withholding regime for payments made to individuals and entities that do not provide certain documentation that evidences their FATCA status. The FATCA rules generally become effective with respect to certain payments made on or after July 1, U.S. withholding agents (USWAs) and participating Foreign Financial Institutions (FFIs) are required to document account holders and withhold and/or report on non-compliant accounts. 3

with respect to U.S. persons that may be investing and earning income through non-u.s. institutions. While the primary goal of FATCA is to gain information about U.S. persons, FATCA imposes tax withholding where the applicable documentation and reporting requirements are not met.")

5 Foreign Account Tax Compliance Act Overview What is the Intent of FATCA? FATCA is intended to increase transparency for the Internal Revenue Service (IRS) with respect to U.S. persons that may be investing and earning income through non-u.s. institutions. While the primary goal of FATCA is to gain information about U.S. persons, FATCA imposes tax withholding where the applicable documentation and reporting requirements are not met. FATCA aims to identify U.S. persons trying to avoid U.S. tax obligations by holding assets in non-u.s. structures and products 4

6 Foreign Account Tax Compliance Act Overview Who does FATCA Impact? While FATCA affects U.S. withholding agents and U.S. multinational companies, its greatest impact will likely be to Foreign Financial Institutions (FFIs) 5 Main FATCA impact US US Financial Institutions Due diligence processes according to Chapter 4 (FATCA) New documentation requirements for payees New Standards of Knowledge s rules New presumption rules Withholding 30% on withholdable payments to NPFFIs New reporting obligations US Non Financial Entities Classify entities within the group Identify withholdable payments Withholding 30% on withholdable payments to NPFFIs New reporting obligations

7 Foreign Account Tax Compliance Act Overview Who does FATCA Impact? (cont.) While FATCA affects U.S. withholding agents and U.S. multinational companies, its greatest impact will likely be to Foreign Financial Institutions (FFIs) 6 Main FATCA impact - Foreign Foreign Financial Institutions Sign an Agreement with the IRS Due diligence processes according to Chapter 4 (FATCA) - New documentation requirements for payees Withholding 30% on withholdable payments to NPFFIs/ Recalcitrant account holders Closing accounts New reporting obligations Compliance program - Responsible Officer Registration with the IRS Non Financial Foreign Entities Non-Financial Foreign Entities (NFFEs) are required to report substantial U.S. owners or certify no U.S. ownership Classify entities within the group They may opt to register with the IRS as Direct Reporting NFFEs

8 Foreign Account Tax Compliance Act Overview What are the Withholding Requirements? In general, a withholding agent is required to withhold 30% on a withholdable payment made to a FFI or to a Non-Financial Foreign Entity (NFFE), unless the FFI or NFFE meets certain requirements. In addition, an FFI must withhold 30% on any pass through payment it makes to a recalcitrant account holder, as well as to payments it makes to another FFI unless that FFI meets certain requirements 7

9 Foreign Account Tax Compliance Act Overview Who Needs to Comply? U.S. Withholding Agents U.S. entity that has control, receipt, custody, disposal or makes a payment of any withholdable payment FFIs potential relevant categories Accepts deposits in the ordinary course of a banking or similar business (depository institution) Holds financial assets for the account of others as a substantial part of its business (custodial institution) Engages primarily in the business of investing or trading securities, commodities, partnerships or any interests in such positions, individual or collective portfolio management or otherwise invests, administers, or manages funds, money, or financial assets on behalf of other persons (investment entity) Primarily holds the shares of other related entities (holding company) 8

10 Foreign Account Tax Compliance Act Overview Who Needs to Comply? (Cont.) Specified U.S. persons U.S. citizens, U.S. residents (i.e., Green card holder), non-u.s. persons who meet the substantial presence test, U.S. partnerships, U.S. trusts, U.S. estates and U.S. corporations that are not publicly traded 9

11 Foreign Account Tax Compliance Act Overview Implications of Non-Compliance Financial, commercial and reputational risks May be forced to comply even where no U.S. source payments as many third parties will require FATCA compliance Uncertain degree of foreign government regulatory enforcement under the bilateral intergovernmental agreements (IGA) with IRS Non-Compliance is Not an Option Although FATCA is technically voluntary, institutions who ignore it may find themselves frozen out of the global financial market 10

12 Foreign Account Tax Compliance Act Overview The Cost of Getting Caught as a Taxpayer Filing Requirement Any taxpayer with an aggregate total of at least $50,000 in foreign assets has to follow this tax reporting measure. Failure to complete Form 8938 by the reporting deadline leads to a minimum $10,000 penalty, which may go as high as $50,000 over time. Further, all assets must be reported or a 40 percent understatement penalty will be issued In addition to civil penalties, there could be criminal penalties for willful violations as much as $250,000 for individuals and $500,000 for corporations FBAR Penalties Failure to file a FBAR comes with its own penalties in addition to those associated with Form Civil penalties can be up to $10,000 per non-willful violation. Willful violation penalties can exceed $100,000 or be equal to 50 percent of the account amount for each violation 11

13 Foreign Account Tax Compliance Act Overview What is an Intergovernmental Agreement ( IGA )? Under the Model IGA, FFIs in partner jurisdictions will report information on U.S. account holders to their national tax authorities, which in turn will provide this information into the U.S. under an automatic exchange of information IGAs provide reduced compliance burdens for FFIs in the partner country jurisdiction in exchange for instituting the FATCA requirements into local law or relaxing local laws that would preclude FATCA compliance IGAs are still a moving target! Many new agreements are already in negotiation and will be signed IGAs open for renegotiation in the future and may be terminated IGAs may be modified by the contracting authorities (Favored Nation Clause) 12

14 Foreign Account Tax Compliance Act Overview 26 Intergovernmental Agreements signed (as of April 17, 2014) Model 1 United Kingdom Denmark Ireland Spain Germany Norway France Guernsey Isle of Man Jersey Netherlands Malta Italy Hungary Finland Luxembourg Model 2 Switzerland Model 1 No IGA currently in place Model 2 Japan Model 1 Mexico Costa Rica Cayman Islands (Model 1B) Canada Honduras Model 2 Bermuda Chile Model 1 No IGA currently in place Model 2 No IGA currently in place Model 1 Republic of Mauritius Model 2 No IGA currently in place 13 IGAs status - 4/21/2014

15 Foreign Account Tax Compliance Act Overview 24 Jurisdictions that have reached agreements in substance and have consented to being included on IRS list (Announcement , April 2, 2014) Model 1 Australia ( ) Belgium ( ) Brazil ( ) British Virgin Islands ( ) Croatia ( ) Czech Republic ( ) Estonia ( ) Gibraltar ( ) India ( ) Jamaica ( ) Kosovo ( ) Latvia ( ) Liechtenstein ( ) Lithuania ( ) New Zealand ( ) Poland ( ) Portugal ( ) Qatar ( ) Slovak Republic ( ) Slovenia ( ) South Africa ( ) South Korea ( ) Romania ( ) Model 2 Austria ( ) There are more than 100 IGAs being negotiated today 14 IGAs status - 4/21/2014

16 Foreign Account Tax Compliance Act Overview Characteristics of the Model I IGA Model I FIs will be required to register with the IRS but will not be required to enter into an FFI Agreement Further, Model I FIs will not report directly to the IRS pursuant to the standard FATCA regulations, but rather to the domestic tax authority, which will then pass on the information on an automatic basis to the IRS Model I FIs are relieved of the requirement to close accounts belonging to recalcitrant account holders. However, Model I FIs will report to the domestic tax authority the names of recalcitrant account holders and nonparticipating FFIs and the amounts of all payments made to them No payments to Model I FIs are subject to withholding. Exception: substantial non-compliance clause. Model I FIs are relieved of the responsibility to withhold 30% of certain U.S.- sourced payments to recalcitrant account holders. However, if the withholding implicates a nonparticipating FFI located outside an IGA partner country, the Model I FI must report the amount to an upstream withholding agent who will withhold on the payment (or assume withholding responsibility) 15

17 Foreign Account Tax Compliance Act Overview Characteristics of the Model II IGA Under Model 2 IGA, Reporting Financial Institutions (RFIs) enter into an FFI Agreement and report directly to the IRS pursuant to the standard FATCA regulations RFIs are relieved of the requirement to close accounts belonging to recalcitrant account holders. However, for account holders (with U.S. indicia) and nonparticipating FFIs (NPFFIs) which do not consent to have their account information reported to the IRS (non-consenting accounts), the detailed account information must be transmitted to the local tax authority, while aggregated information will be reported to the IRS, which may result in a group administrative request. Upon its receipt, the domestic tax authority is allotted eight months to exchange this information with IRS 16

18 Foreign Account Tax Compliance Act Overview Characteristics of the Model II IGA (Cont.) No payments to RFIs are subject to withholding. Exception: substantial non-compliance clause. In general, RFIs are relieved of the responsibility to withhold 30% of certain U.S.-sourced payments to non-consenting U.S. account holders. However, the withholding requirement still remains for certain non-consenting accounts and payments made to Nonparticipating FFIs Note: Should the suspension of the duty to withhold be revoked because the domestic tax authority does not comply with the U.S. request within eight months, the cost of the withholding falls on the customer, not the financial institution However, amounts paid to NPFFIs not located in a country with an IGA will be subject to withholding 17

19 Foreign Account Tax Compliance Act Impacts to the Trust Industry

20 How Does FATCA Impact the Trust Industry? How will you ensure the FATCA compliance of this structure? 19

21 How Does FATCA Impact the Trust Industry? Trust Company s Legal Entities Location of entity determines set of governing rules Depending on governing rules and classification type, entity may need to register and possibly sign an FFI Agreement by 25 April 2014 FATCA requires classification of all legal entities, including trust companies, corporate directors and nominee shareholders Generally operations of trust companies and typical related entities qualify as FFIs 20

22 How Does FATCA Impact the Trust Industry? Clients: Trust or Fiduciary Structures Including Underlying Companies FATCA treats all trusts and other structures as entities regardless of legal form, and therefore requires all to be classified FATCA does not oblige trust companies to comply on behalf of the fiduciary structures they administer, but it is very likely part of the fiduciary duty Typically, structures holding financial assets will qualify as FFIs 21

23 How Does FATCA Impact the Trust Industry? Beneficiaries U.S. tax rules dictate the owner of the trust or other structure As part of the diligence obligations, the trust or other structure will identify its owner and U.S. persons will generally be reported 22

24 Foreign Account Tax Compliance Act Considerations

25 Considerations for use of AML/KYC Information Optional Considerations Example Identify substantial U.S. owners of certain Passive NFFEs Requires: Integrated systems between AML and Onboarding Consistent data quality Tracking of account balance information Mandatory Requirements Example Reason To Know: Determine if inconsistencies exist between KYC and Tax certification Requires: Closely linked processes and controls between onboarding, Tax and AML Documented Policies and Procedures Compliance monitoring Both optional and mandatory considerations should be addressed throughout your FATCA implementation 24

26 Asset Management Compliance Model Determine impact of KYC/FATCA mandatory and optional considerations through gap assessment between current capabilities under chapter 3 and the new chapter 4 requirements Map current AML/KYC fields that would need to be cross referenced for U.S. Indicia such as: Phone Number, Address, Place of Birth Tax forms and documentation on file providing residency and citizenship information Align solutions with impact, consider current and future state Govern centrally with common standards and guidelines and execute locally 25

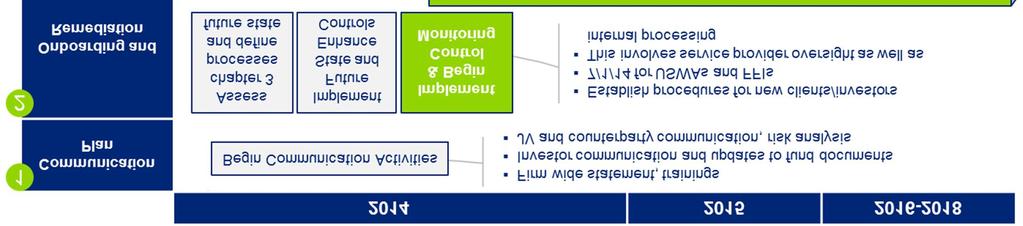

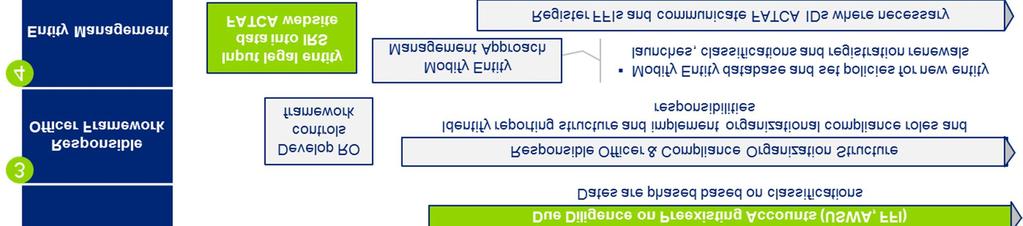

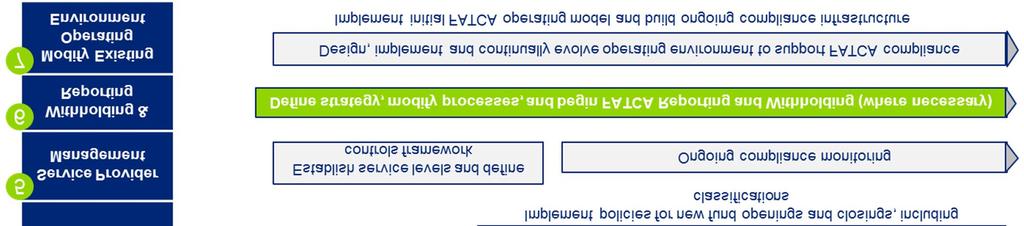

27 Mandatory AML/KYC compliance considerations Ongoing FATCA Compliance 1 Communication Plan Website updates, internal educations and awareness, investor communications, and counterparty verifications Onboarding and Remediation Responsible Officer Framework Registration Strategy Service Provider Management Withholding & Reporting 7 Update fund documents (subscription, prospectus, and offering) Enhance KYC/AML procedures and systems (onboarding) Implement controls for incomplete and expired information Begin due diligence of pre-existing accounts Develop an oversight and responsible officer strategy that fits the segregated business lines and geographic regions, while inclusive of IGA requirements Engage resources to govern the compliance sub structure Implement solutions` Build data management solution Develop registration strategy and identify resources Document policies and process for classifying and implementing new entities or funds Supply registration information to counterparties to prevent withholding Modify Existing Operating Environment Outline support model and finalize zone of responsibility Discuss and finalize any impacts to commercial terms Manage service provider process and system changes Develop ongoing governance and service level metrics Assign scope of responsibilities, adopt common practices, and enhance capability to manage performance across regions/businesses, investment strategies and portfolio companies Define global withholding model and reporting framework once regulations are finalized (adaptable for IGAs) Draft business requirements for systematic and process updates Implement solutions 26

28 Illustrative FATCA Governance Roles 27

29 Illustrative FATCA Timeline Key Activities`` Role Description 1 Legal Considerations Support the assessment of legal considerations impacting compliance with FATCA. Frame and develop analysis, impact and go forward approach across legal considerations such as: Intergovernmental Approach Data Protection/storage and reuse of AML/KYC data 2 Tax SME Provide Tax Subject Matter support to provide refresh to the tools and education materials in alignment with the release of the final FATCA regulations. Provide guidance on Withholding and Reporting approach and planning considerations. Take part in enterprise solutioning providing support on FATCA remediation and implementation considerations. Develop tracking dashboard for key milestones. 3 Compliance Support approach and framework development to support monitoring of Blackstone compliance initiatives. Development of a FATCA control framework AML/KYC considerations Remediation strategy support 4 Entity Classification/FFI Framework Support entity classification initiatives including special purpose entities. Develop FFI Agreement framework to build off requirements support. 5 Initiative Support Provide overall management and coordination of activities of resources while supporting each stream with subject matter knowledge of FATCA and coordinating additional support from areas where needed. 6 Business Unit Liaison Liaise with Business Unit s to cross pollinate issue discovery and resolution and share best practices across Business Unit and to PMO. Work with the Business Unit Lead to identify specific enterprise FATCA compliance issues and coordinate resolution Track and report progress by Business Unit; provide recommendations for escalation 28

30 Foreign Account Tax Compliance Act Reporting

31 Foreign Account Tax Compliance Act Reporting Reporting will be phased in gradually between 2015 and Foreign Financial Institutions (FFIs) are required to report name, address, TIN, account number and account balance on U.S. accounts (U.S. Account Reporting), in line with IGA requirements The effective date of the FFI Agreement is June 30,201 for all those entities that have obtained a Global Intermediary Identification Number (GIIN) before July 1 st, The agreement requires reporting U.S. accounts identified during 2014 under the FFI Agreement due diligence requirements. An FFI can elect Form 1099 reporting Reporting is required to be filed electronically on March 31,

32 Foreign Account Tax Compliance Act Reporting Reporting will be phased in gradually between 2015 and FFIs are required to add income payments made in the prior year to its U.S. Account Reporting, again in line with IGA requirements FFI is required to complete Forms 1042-S allocating the income and withholding paid to its recalcitrant account holder pools. New 1042-S form has been released. Reporting is required regardless of whether the FFI made a payment of a chapter 4 reportable amount to each such account holder FFI must aggregate report on NPFFI accounts opened in 2015, as under IGA approach 31

33 Foreign Account Tax Compliance Act Reporting Reporting will be phased in gradually between 2015 and FFI are required to add gross proceed payments made in the prior year to its U.S. Account Reporting, aligning with IGA approach FFI is required to complete Forms 1042-S allocating the income and withholding paid to its recalcitrant account holder pools FFI must aggregate report on NPFFI payments made in 2016, as under IGA approach 32

34 Foreign Account Tax Compliance Act Reporting Highlights The FFI that maintains the account is generally responsible for reporting the account The final regulations add a rule to determine when the FFI is treated as maintaining an account FFIs will be issued a GIIN that will be used for FATCA reporting purposes The GIIN is provided by the IRS. The entities need to be registered with the IRS to obtain the GIIN (generally, before May 5 th, 2014). The IRS will release a list of participating FFIs by June 2 nd, Reporting does not need to be performed in U.S. currency The character of payments may be determined under the same principles that the FFI uses to report information to the tax authorities in their own country The amount and character of items of income need not be determined in accordance with U.S. federal income tax principles In the UK, a consistent and verifiable approach must be adopted to valuation 33

35 Foreign Account Tax Compliance Act Reporting Form 8966 The IRS has released a new version of draft Form 8966 on March 2014, FATCA Report, that will be used by FFIs (including Qualified Intermediaries (QI), Withholding Foreign Partnerships (WP), and Withholding Foreign Trusts (WT)) and withholding agents to comply with their chapter 4 reporting obligations This new Form 8966 will set forth all the information that must be reported with respect to financial accounts Will be used to report Certain information regarding U.S. accounts Substantial U.S. owners of passive NFFEs and owner documented FFIs Aggregate recalcitrant account information Form 8966 will be filed electronically with the IRS on or before March 31 of each year reporting prior year information 34

36 Foreign Account Tax Compliance Act What is Coming Next?

37 Final FATCA Regulations Timeline AG2 36 Highlights *Form 8966 **Form 1042-S

38 Slide 37 AG2 I have updated this table Garcia Castelao, Andrea, 4/17/2014

39 Foreign Account Tax Compliance Act More Coming On February 20, 2014, the Treasury and the IRS released temporary regulations that revise and clarify the final FATCA regulations Temporary Regulations On the same date, the government also released temporary regulations coordinating the final regulations under Chapters 3 and 61 of the Internal Revenue Code with the final FATCA (Chapter 4) regulations Coordination Regulations The new rules do not provide any further extensions to the effective date of FATCA FFI Agreement: on December 27, 2013, the IRS published Revenue Procedure containing the final FFI Agreement Forms W-8 s: W-8BEN, W-8BEN-E forms have been released. However, new form W-8IMY as well as Instructions to W-8BEN-E are still pending Draft 1042 instructions have been released. However, by now only final form 1042-S has been released Final form 8966 Additional IGAs 37

40 Foreign Account Tax Compliance Act Registration Process All FFIs will go through a paperless registration process using a secure online web system from anywhere in the world FFIs will need to respond to 15 questions Form 8957 will be used in rare cases where FFI must register manually Upon registration participating and deemed compliant FFIs will be issued a GIIN that will identify them as Participating FFIs or Model 1 Reporting FFIs. Registered FFIs designated as leads of an expanded affiliated group will use the System to manage the registration status of group members The registration system is used by Financial Institutions in IGA jurisdictions to obtain a GIIN reporting purposes Sponsoring entities will need to be registered by May 5 th, However, an extension is granted to Sponsored entities. This scheme is applicable to Investment entities meeting certain requirements. Registering entities will also use the System to manage their information, and, as appropriate, agree to the terms of or make the representations required for their status and communicate with the IRS Due by May 5 th, 2014 (some exceptions in IGA countries may apply) 38

41 Questions & Answers

299-5260 About Deloitte As used in this document, Deloitte means Deloitte Transactions and Business Analytics LLP, an affiliate of Deloitte Financial Advisory Services LLP.")

42 Michael Shepard Principal Deloitte Transactions and Business Analytics LLP (215) About Deloitte As used in this document, Deloitte means Deloitte Transactions and Business Analytics LLP, an affiliate of Deloitte Financial Advisory Services LLP. Deloitte Transactions and Business Analytics LLP is not a certified public accounting firm. Please see for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting.

Foreign Account Tax Compliance Act (FATCA)

") Foreign Account Tax Compliance Act (FATCA) Andrea Garcia Castelao November 18, 2013 Foreign Account Tax Compliance Act (FATCA) 0 2013 Deloitte Tax LLP FATCA Update Final FATCA regulations were released

Foreign Account Tax Compliance Act (FATCA) Andrea Garcia Castelao November 18, 2013 Foreign Account Tax Compliance Act (FATCA) 0 2013 Deloitte Tax LLP FATCA Update Final FATCA regulations were released

FATCA Update May 2014

www.pwc.com The Basics Foreign Account Tax Compliance Act Purpose of Prevent and detect offshore tax evasion by US citizens Increased information reporting Enforced by withholding tax Effective begins

www.pwc.com The Basics Foreign Account Tax Compliance Act Purpose of Prevent and detect offshore tax evasion by US citizens Increased information reporting Enforced by withholding tax Effective begins

FATCA: THE 2014 HORIZON

FATCA: THE 2014 HORIZON Breakout Session 5C FIBA 2014 AML Compliance Conference February 21, 2014 Gabriel Caballero, Esq. Gunster, Yoakley & Stewart, P.A. 2 South Biscayne Boulevard Suite #3400 Miami,

FATCA: THE 2014 HORIZON Breakout Session 5C FIBA 2014 AML Compliance Conference February 21, 2014 Gabriel Caballero, Esq. Gunster, Yoakley & Stewart, P.A. 2 South Biscayne Boulevard Suite #3400 Miami,

Implications of FATCA for legal entities

Implications of FATCA for legal entities April 2015 Introduction FATCA and its context Page 3 Section 1 Application variants and entities concerned Page 4 Section 2 Classification of entities under FATCA

Implications of FATCA for legal entities April 2015 Introduction FATCA and its context Page 3 Section 1 Application variants and entities concerned Page 4 Section 2 Classification of entities under FATCA

FATCA: The final regulations have landed let the games begin

FATCA: The final regulations have landed let the games begin By Anthony Quinn In January the United States Treasury Department released the final regulations relating to the U.S. Foreign Account Tax Compliance

FATCA: The final regulations have landed let the games begin By Anthony Quinn In January the United States Treasury Department released the final regulations relating to the U.S. Foreign Account Tax Compliance

Update on Jurisdictions Treated as Having an IGA in Effect and on FATCA Financial Institution Registration

Part IV Items of General Interest Update on Jurisdictions Treated as Having an IGA in Effect and on FATCA Financial Institution Registration Announcement 2014-17 Since the 2012 release of the Model 1 and

Part IV Items of General Interest Update on Jurisdictions Treated as Having an IGA in Effect and on FATCA Financial Institution Registration Announcement 2014-17 Since the 2012 release of the Model 1 and

UPDATE. COMMON REPORTING STANDARD IN THE CAYMAN ISLANDS. What is CRS? Participating Jurisdictions

www.kensington-trust.com UPDATE COMMON REPORTING STANDARD IN THE CAYMAN ISLANDS The Cayman Islands Tax Information Authority (International Tax Compliance) (Common Reporting Standard) Regulations, 2015

www.kensington-trust.com UPDATE COMMON REPORTING STANDARD IN THE CAYMAN ISLANDS The Cayman Islands Tax Information Authority (International Tax Compliance) (Common Reporting Standard) Regulations, 2015

General introduction on FATCA

General introduction on FATCA By Dr. Zhan Hao and He Shan from AnJie Law Firm At present, most Chinese financial institutions are paying quite close attention to the ongoing process of Chinese participation

General introduction on FATCA By Dr. Zhan Hao and He Shan from AnJie Law Firm At present, most Chinese financial institutions are paying quite close attention to the ongoing process of Chinese participation

FOREIGN ACCOUNT TAX COMPLIANCE ACT: FINAL REGULATIONS AND CURRENT DEVELOPMENTS

FOREIGN ACCOUNT TAX COMPLIANCE ACT: FINAL REGULATIONS AND CURRENT DEVELOPMENTS J.P. Morgan Corporate & Investment Bank Presented by Client Tax Services April 2013 S T R I C T L Y P R I V A T E A N D C

FOREIGN ACCOUNT TAX COMPLIANCE ACT: FINAL REGULATIONS AND CURRENT DEVELOPMENTS J.P. Morgan Corporate & Investment Bank Presented by Client Tax Services April 2013 S T R I C T L Y P R I V A T E A N D C

FATCA Update: Final Regulations, IGAs and their Impact on Trusts and Trust Companies

FATCA Update: Final Regulations, IGAs and their Impact on Trusts and Trust Companies June 2013 Background On March 18, 2010, President Obama signed the Hiring Incentives to Restore Employment Act of 2010

FATCA Update: Final Regulations, IGAs and their Impact on Trusts and Trust Companies June 2013 Background On March 18, 2010, President Obama signed the Hiring Incentives to Restore Employment Act of 2010

Foreign Account Tax Compliance Act (FATCA)

") Foreign Account Tax Compliance Act (FATCA) Impact Assessment on the Financial Services (Banking and Insurance) sectors and businesses in Trinidad and Tobago Presentation by the Bankers Association of Trinidad

Foreign Account Tax Compliance Act (FATCA) Impact Assessment on the Financial Services (Banking and Insurance) sectors and businesses in Trinidad and Tobago Presentation by the Bankers Association of Trinidad

FATCA: Developments & Perspective

www.pwc.de FATCA: Developments & Perspective Luxembourg May 5, 2014 Agenda Section 1: Section 2: Section 3: Section 4: Section 5: Introduction Update to the Financial Account Tax Compliance Act Update

www.pwc.de FATCA: Developments & Perspective Luxembourg May 5, 2014 Agenda Section 1: Section 2: Section 3: Section 4: Section 5: Introduction Update to the Financial Account Tax Compliance Act Update

Ifat Ginsburg, Adv. Ginsburg and Co Advocates

Ifat Ginsburg, Adv. Ginsburg and Co Advocates ifat@gac-law.com 073-707-3737 Stuart M. Schabes, Esq. Ober, Kaler, Grimes & Shriver smschabes@ober.com 410-347-7696 Tel Aviv December 18, 2012 FATCA introduction

Ifat Ginsburg, Adv. Ginsburg and Co Advocates ifat@gac-law.com 073-707-3737 Stuart M. Schabes, Esq. Ober, Kaler, Grimes & Shriver smschabes@ober.com 410-347-7696 Tel Aviv December 18, 2012 FATCA introduction

Ninth Annual Domestic Tax Conference. 24 April 2014 New York City

Ninth Annual Domestic Tax Conference 24 April 2014 New York City Information reporting and withholding Impact of FATCA on USWA IRS Circular 230 disclosure Any US tax advice contained herein was not intended

Ninth Annual Domestic Tax Conference 24 April 2014 New York City Information reporting and withholding Impact of FATCA on USWA IRS Circular 230 disclosure Any US tax advice contained herein was not intended

IMAS 7 December FATCA New definitions New classifications New rules New ideas

IMAS 7 December 2012 FATCA New definitions New classifications New rules New ideas Contents 1 FATCA - the principles 2 Model IGAs 3 Ernst & Young Benchmarking survey - approaches to interpreting and delivering

IMAS 7 December 2012 FATCA New definitions New classifications New rules New ideas Contents 1 FATCA - the principles 2 Model IGAs 3 Ernst & Young Benchmarking survey - approaches to interpreting and delivering

THE COMMON REPORTING STANDARD ("CRS") UPDATE FOR OCORIAN CLIENTS

UPDATE FOR OCORIAN CLIENTS") JERSEY BRIEFING November 2015 THE COMMON REPORTING STANDARD ("CRS") UPDATE FOR OCORIAN CLIENTS At present 93 countries will implement CRS over a two year period commencing 1 January 2016. The CRS initiative

JERSEY BRIEFING November 2015 THE COMMON REPORTING STANDARD ("CRS") UPDATE FOR OCORIAN CLIENTS At present 93 countries will implement CRS over a two year period commencing 1 January 2016. The CRS initiative

Intercontinental Trust Ltd COMMON REPORTING STANDARD

Intercontinental Trust Ltd COMMON REPORTING STANDARD 1 Conspectus The OECD, working in collaboration with G20 and in close co-operation with the EU, has developed a global standard for automatic exchange

Intercontinental Trust Ltd COMMON REPORTING STANDARD 1 Conspectus The OECD, working in collaboration with G20 and in close co-operation with the EU, has developed a global standard for automatic exchange

Tax certification for Entities FATCA and CRS

Schroder Investment Management Australia Limited Level 20, Angel Place 123 Pitt Street Sydney, NSW 2000 www.schroders.com.au AFSL 226473 ABN 22 000 443 274 Tax certification for Entities FATCA and CRS

Schroder Investment Management Australia Limited Level 20, Angel Place 123 Pitt Street Sydney, NSW 2000 www.schroders.com.au AFSL 226473 ABN 22 000 443 274 Tax certification for Entities FATCA and CRS

What Impact Will FATCA Have on Offshore Hedge Funds and How Should Such Funds Prepare for FATCA Compliance?

hedge LAW REPORT fund law and regulation FATCA What Impact Will FATCA Have on Offshore s and How Should Such Funds Prepare for FATCA Compliance? By Michele Gibbs Itri, Tannenbaum Helpern Syracuse & Hirschtritt,

hedge LAW REPORT fund law and regulation FATCA What Impact Will FATCA Have on Offshore s and How Should Such Funds Prepare for FATCA Compliance? By Michele Gibbs Itri, Tannenbaum Helpern Syracuse & Hirschtritt,

FATCA considerations for multinational non-financial corporate groups

19 July 2013 International Tax Alert News from the Global Tax Desk Network FATCA considerations for multinational non-financial corporate groups Executive summary On 17 January 2013, the US Treasury (Treasury)

19 July 2013 International Tax Alert News from the Global Tax Desk Network FATCA considerations for multinational non-financial corporate groups Executive summary On 17 January 2013, the US Treasury (Treasury)

FATCA, Foreign Trusts and Estate Planning: Navigating Complex Reporting and Withholding Requirements

Presenting a live 90-minute webinar with interactive Q&A FATCA, Foreign Trusts and Estate Planning: Navigating Complex Reporting and Withholding Requirements TUESDAY, SEPTEMBER 22, 2015 1pm Eastern 12pm

Presenting a live 90-minute webinar with interactive Q&A FATCA, Foreign Trusts and Estate Planning: Navigating Complex Reporting and Withholding Requirements TUESDAY, SEPTEMBER 22, 2015 1pm Eastern 12pm

TRUST AND SETTLEMENT DETAILS FORM

FOR USE IN CAYMAN, DUBLIN AND JERSEY TRUST AND SETTLEMENT DETAILS FORM IMPORTANT: ALL SECTIONS MUST BE COMPLETED Name of proposed new entity: (if known) Name of trust: Date trust established: Proper law

FOR USE IN CAYMAN, DUBLIN AND JERSEY TRUST AND SETTLEMENT DETAILS FORM IMPORTANT: ALL SECTIONS MUST BE COMPLETED Name of proposed new entity: (if known) Name of trust: Date trust established: Proper law

Attorneys at Law. 11th Annual International Estate Planning Institute New York City, 12 & 13 March 2015

FATCA Implementation Attorneys at Law 11th Annual International Estate Planning Institute New York City, 12 & 13 March 2015 Presenters: Anthony Cetta: Citi Trust Wealth Planner, Citigroup (New York, NY)

FATCA Implementation Attorneys at Law 11th Annual International Estate Planning Institute New York City, 12 & 13 March 2015 Presenters: Anthony Cetta: Citi Trust Wealth Planner, Citigroup (New York, NY)

PARTNERSHIP DETAILS FORM

FOR USE IN SINGAPORE PARTNERSHIP DETAILS FORM IMPORTANT: ALL SECTIONS MUST BE COMPLETED Name of proposed new entity (if known) Name of applicant partnership Form of applicant partnership Partnership Limited

FOR USE IN SINGAPORE PARTNERSHIP DETAILS FORM IMPORTANT: ALL SECTIONS MUST BE COMPLETED Name of proposed new entity (if known) Name of applicant partnership Form of applicant partnership Partnership Limited

COMPANY DETAILS FORM

FOR USE IN MAURITIUS COMPANY DETAILS FORM IMPORTANT: ALL SECTIONS MUST BE COMPLETED Name of proposed new entity: (if known) Name of applicant company: Company type: (please tick one box) Quoted on a stock

FOR USE IN MAURITIUS COMPANY DETAILS FORM IMPORTANT: ALL SECTIONS MUST BE COMPLETED Name of proposed new entity: (if known) Name of applicant company: Company type: (please tick one box) Quoted on a stock

When will CbC reports need to be filled?

Who will be subject to CbCR? Country by Country Reporting (CbCR) applies to multinational companies (MNCs) with a combined revenue of euros 750 million or more When will CbC reports need to be filled?

Who will be subject to CbCR? Country by Country Reporting (CbCR) applies to multinational companies (MNCs) with a combined revenue of euros 750 million or more When will CbC reports need to be filled?

FATCA: More than a Five Letter Word NACUBO Tax Forum 2014

FATCA: More than a Five Letter Word NACUBO Tax Forum 2014 Presented by: Nicole Bencik, Partner, Crowe Horwath LLP John Kelleher, Partner Crowe Horwath LLP Joel Levenson, Associate Director: Tax Compliance,

FATCA: More than a Five Letter Word NACUBO Tax Forum 2014 Presented by: Nicole Bencik, Partner, Crowe Horwath LLP John Kelleher, Partner Crowe Horwath LLP Joel Levenson, Associate Director: Tax Compliance,

FATCA, an American law applied starting July 1 st, 2014 to fight offshore tax evasion by US Taxpayers

Communication on June 19 th 2014 last update: July 23 rd 2018 FATCA, an American law applied starting July 1 st, 2014 to fight offshore tax evasion by US Taxpayers Goal and legal framework of FATCA The

Communication on June 19 th 2014 last update: July 23 rd 2018 FATCA, an American law applied starting July 1 st, 2014 to fight offshore tax evasion by US Taxpayers Goal and legal framework of FATCA The

COMPANY DETAILS FORM

FOR USE IN JERSEY COMPANY DETAILS FORM IMPORTANT: ALL SECTIONS MUST BE COMPLETED Name of proposed new entity: (if known) Name of applicant company: Company type: (please tick one box) Quoted on a stock

FOR USE IN JERSEY COMPANY DETAILS FORM IMPORTANT: ALL SECTIONS MUST BE COMPLETED Name of proposed new entity: (if known) Name of applicant company: Company type: (please tick one box) Quoted on a stock

Sight FATCA. line of. Frequently asked questions. table of contents. November 2, 2012

line of Sight FATCA Frequently asked questions FOR INSTITUTIONAL INVESTORS table of contents November 2, 2012 PART I PROPOSED REGULATIONS and IRS Announcement OVERVIEW 1. What is the objective of the Foreign

line of Sight FATCA Frequently asked questions FOR INSTITUTIONAL INVESTORS table of contents November 2, 2012 PART I PROPOSED REGULATIONS and IRS Announcement OVERVIEW 1. What is the objective of the Foreign

Introduction to FATCA (Foreign Account Tax Compliance Act) Introduction to FATCA

Introduction to FATCA") (Foreign Account Tax Compliance Act) Jim Browne 214.651.4420 jim.browne@strasburger.com Joe Perera 210.250.6119 joe.perera@strasburger.com Agenda Background Rules for Withholding Agents Classification

(Foreign Account Tax Compliance Act) Jim Browne 214.651.4420 jim.browne@strasburger.com Joe Perera 210.250.6119 joe.perera@strasburger.com Agenda Background Rules for Withholding Agents Classification

COMBATTING OFFSHORE TAX EVASION FROM THE FINANCIAL INSTITUTION S PERSPECTIVE

GLOBAL INVESTIGATIONS & COMPLIANCE ELLEN ZIMILES Financial Services Advisory and Compliance Segment Leader Head of Global Investigations and Compliance +1.212.554.2602 ellen.zimiles@navigant.com RICHARD

GLOBAL INVESTIGATIONS & COMPLIANCE ELLEN ZIMILES Financial Services Advisory and Compliance Segment Leader Head of Global Investigations and Compliance +1.212.554.2602 ellen.zimiles@navigant.com RICHARD

FATCA. Its Implications for the Financial Services Industry in Belize (A Banking Perspective) February 19, 2015 Aldo J. Salazar

February 19, 2015 Aldo J. Salazar") FATCA Its Implications for the Financial Services Industry in Belize (A Banking Perspective) February 19, 2015 Aldo J. Salazar Introduction The Foreign Account Tax Compliance Act (FATCA) was signed into

FATCA Its Implications for the Financial Services Industry in Belize (A Banking Perspective) February 19, 2015 Aldo J. Salazar Introduction The Foreign Account Tax Compliance Act (FATCA) was signed into

Rev. Proc Implementation of Nonresident Alien Deposit Interest Regulations

Rev. Proc. 2012-24 Implementation of Nonresident Alien Deposit Interest Regulations SECTION 1. PURPOSE Sections 1.6049-4(b)(5) and 1.6049-8 of the Income Tax Regulations, as revised by TD 9584, require

Rev. Proc. 2012-24 Implementation of Nonresident Alien Deposit Interest Regulations SECTION 1. PURPOSE Sections 1.6049-4(b)(5) and 1.6049-8 of the Income Tax Regulations, as revised by TD 9584, require

OECD Common Reporting Standard Getting into the Detail STEP / GAT

OECD Common Reporting Standard Getting into the Detail STEP / GAT Jo Huxtable Martin Popplewell 11 February 2016 Agenda Introduction CRS and the wider regulatory environment CRS latest developments and

OECD Common Reporting Standard Getting into the Detail STEP / GAT Jo Huxtable Martin Popplewell 11 February 2016 Agenda Introduction CRS and the wider regulatory environment CRS latest developments and

Introduction to FATCA. Introduction to FATCA

Presented by: Joe Perera Strasburger & Price, LLP July 1, 2014 Agenda Legislative Purpose and Approach To Whom and To What Payments Does FATCA Apply? Rules Regarding Foreign Financial Institutions (FFIs)

Presented by: Joe Perera Strasburger & Price, LLP July 1, 2014 Agenda Legislative Purpose and Approach To Whom and To What Payments Does FATCA Apply? Rules Regarding Foreign Financial Institutions (FFIs)

IRS Reporting Rules. Reference Guide. serving the people who serve the world

IRS Reporting Rules Reference Guide serving the people who serve the world The United States has and continues to maintain a policy of not taxing the deposit interest earned by United States (US) nonresidents

IRS Reporting Rules Reference Guide serving the people who serve the world The United States has and continues to maintain a policy of not taxing the deposit interest earned by United States (US) nonresidents

Webinar: Common Reporting Standard. Game Plan for Compliance December 10, 2015

Webinar: Common Reporting Standard Game Plan for Compliance December 10, 2015 Presenters Moderator: Sara Pereda Director DMS Offshore Investment Services Roman Ipfling Director DMS International Tax Compliance

Webinar: Common Reporting Standard Game Plan for Compliance December 10, 2015 Presenters Moderator: Sara Pereda Director DMS Offshore Investment Services Roman Ipfling Director DMS International Tax Compliance

Roundtable Discussion Foreign Account Tax Compliance Act (FATCA) Andrew Mitchel, Bob Rinninsland, Stan Ruchelman

Andrew Mitchel, Bob Rinninsland, Stan Ruchelman") Roundtable Discussion Foreign Account Tax Compliance Act (FATCA) Andrew Mitchel, Bob Rinninsland, Stan Ruchelman FATCA Introduction/Base Case Issues Effective March 18, 2010 enacted as part of the HIRE

Roundtable Discussion Foreign Account Tax Compliance Act (FATCA) Andrew Mitchel, Bob Rinninsland, Stan Ruchelman FATCA Introduction/Base Case Issues Effective March 18, 2010 enacted as part of the HIRE

Instructions to the Entity Self Certification Form

Section A General Instructions to the Entity Self Certification Form 1. Foreign Account Tax Compliance Act (FATCA) FATCA is a component of the Hiring Incentives to Restore Employment Act (the HIRE Act),

Section A General Instructions to the Entity Self Certification Form 1. Foreign Account Tax Compliance Act (FATCA) FATCA is a component of the Hiring Incentives to Restore Employment Act (the HIRE Act),

Tax Management International Journal

Tax Management International Journal Reproduced with permission from Tax Management International Journal, 43 TMIJ 540, 09/12/2014. Copyright 2014 by The Bureau of National Affairs, Inc. (800-372- 1033)

Tax Management International Journal Reproduced with permission from Tax Management International Journal, 43 TMIJ 540, 09/12/2014. Copyright 2014 by The Bureau of National Affairs, Inc. (800-372- 1033)

MEXICO - INTERNATIONAL TAX UPDATE -

TTN Conference May 2017 MEXICO - INTERNATIONAL TAX UPDATE - Arturo G. Brook Main Taxes Income Tax Value Added Tax Others Agenda DTTs and TIEAs FATCA (IGA) and CRS Choice of Vehicles Income Tax - General

TTN Conference May 2017 MEXICO - INTERNATIONAL TAX UPDATE - Arturo G. Brook Main Taxes Income Tax Value Added Tax Others Agenda DTTs and TIEAs FATCA (IGA) and CRS Choice of Vehicles Income Tax - General

Key provisions of FATCA proposed regulations. Anastasia Urias Senior Manager

Key provisions of FATCA proposed regulations Anastasia Urias Senior Manager 1. Overview of keypoints 1 2 Significant highlights of FATCA FATCA was worked out by the United States of America in 2010. The

Key provisions of FATCA proposed regulations Anastasia Urias Senior Manager 1. Overview of keypoints 1 2 Significant highlights of FATCA FATCA was worked out by the United States of America in 2010. The

TAXATION (IMPLEMENTATION) (CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS) (AMENDMENT OF REGULATIONS No. 3) (JERSEY) ORDER 2017

(CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS) (AMENDMENT OF REGULATIONS No. 3) (JERSEY) ORDER 2017") Taxation (Implementation) (Convention on Mutual Regulations No. 3) (Jersey) Order 2017 Article 1 TAXATION (IMPLEMENTATION) (CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS) (AMENDMENT OF

Taxation (Implementation) (Convention on Mutual Regulations No. 3) (Jersey) Order 2017 Article 1 TAXATION (IMPLEMENTATION) (CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS) (AMENDMENT OF

Common Reporting Standard (CRS) The road continues

The road continues") Common Reporting Standard (CRS) The road continues The information exchange landscape Coming years will see increasing global transparency of account holder information requiring global scalable solutions

Common Reporting Standard (CRS) The road continues The information exchange landscape Coming years will see increasing global transparency of account holder information requiring global scalable solutions

FATCA FAQS FATCA AND THE MOVEMENT TO HARMONISE INTERNATIONAL TAX COMPLIANCE AND TRANSPARENCY

FATCA FAQS FATCA AND THE MOVEMENT TO HARMONISE INTERNATIONAL TAX COMPLIANCE AND TRANSPARENCY The last decade has seen an extraordinary number of tax information exchange agreements (TIEAs), which the Organisation

FATCA FAQS FATCA AND THE MOVEMENT TO HARMONISE INTERNATIONAL TAX COMPLIANCE AND TRANSPARENCY The last decade has seen an extraordinary number of tax information exchange agreements (TIEAs), which the Organisation

SAINT CHRISTOPHER AND NEVIS STATUTORY RULES AND ORDERS. No. 32 of 2016

1 SAINT CHRISTOPHER AND NEVIS STATUTORY RULES AND ORDERS No. 32 of 2016 Common Reporting Standard (Automatic Exchange of Financial Account Information) Regulations The Minister, in exercise of the powers

1 SAINT CHRISTOPHER AND NEVIS STATUTORY RULES AND ORDERS No. 32 of 2016 Common Reporting Standard (Automatic Exchange of Financial Account Information) Regulations The Minister, in exercise of the powers

FATCA: Impact on Cayman Islands Entities

FATCA: Impact on Cayman Islands Entities Preface This publication provides a brief overview of the impact on entities incorporated in the Cayman Islands of the foreign account tax compliance provisions

FATCA: Impact on Cayman Islands Entities Preface This publication provides a brief overview of the impact on entities incorporated in the Cayman Islands of the foreign account tax compliance provisions

FATCA:INVESTMENT REPORTING AND IMPLICATIONS FOR CARIBBEAN FINANCIAL INSTITUTIONS

FATCA:INVESTMENT REPORTING AND IMPLICATIONS FOR CARIBBEAN FINANCIAL INSTITUTIONS Barbados International Business Association Conference October 26, 2012 Bruce Zagaris Partner Berliner, Corcoran, & Rowe

FATCA:INVESTMENT REPORTING AND IMPLICATIONS FOR CARIBBEAN FINANCIAL INSTITUTIONS Barbados International Business Association Conference October 26, 2012 Bruce Zagaris Partner Berliner, Corcoran, & Rowe

FATCA: Impact on Mauritius Entities

FATCA: Impact on Mauritius Entities Foreword This publication provides a brief overview of the expected impact on entities resident in the Republic of Mauritius ( Mauritius ) of the foreign account tax

FATCA: Impact on Mauritius Entities Foreword This publication provides a brief overview of the expected impact on entities resident in the Republic of Mauritius ( Mauritius ) of the foreign account tax

AUTOMATIC EXCHANGE OF INFORMATION (AEOI)

") AUTOMATIC EXCHANGE OF INFORMATION (AEOI) As the world becomes increasingly globalised, money can be transferred from one jurisdiction to another with ease. While this may help to facilitate trade and boost

AUTOMATIC EXCHANGE OF INFORMATION (AEOI) As the world becomes increasingly globalised, money can be transferred from one jurisdiction to another with ease. While this may help to facilitate trade and boost

Frequently Asked Questions (FAQ) CRS

CRS") Frequently Asked Questions (FAQ) CRS Contents General... 1 Accounts of Individuals... 3 Accounts of Legal Entities... 6 Glossary... 9 General What is the Standard for Automatic Exchange of Financial Information

Frequently Asked Questions (FAQ) CRS Contents General... 1 Accounts of Individuals... 3 Accounts of Legal Entities... 6 Glossary... 9 General What is the Standard for Automatic Exchange of Financial Information

APA & MAP COUNTRY GUIDE 2017 DENMARK

APA & MAP COUNTRY GUIDE 2017 DENMARK Managing uncertainty in the new tax environment DENMARK KEY FEATURES Competent authority Danish Tax Office ( SKAT ) APA provisions/ guidance Types of APAs available

APA & MAP COUNTRY GUIDE 2017 DENMARK Managing uncertainty in the new tax environment DENMARK KEY FEATURES Competent authority Danish Tax Office ( SKAT ) APA provisions/ guidance Types of APAs available

FATCA: Why all Cayman Islands domiciled Investment Entities should act before the registration deadline of 31 December 2014

FATCA: Why all Cayman Islands domiciled Investment Entities should act before the registration deadline of 31 December 2014 Registration with the IRS The broad scope of the Foreign Account Tax Compliance

FATCA: Why all Cayman Islands domiciled Investment Entities should act before the registration deadline of 31 December 2014 Registration with the IRS The broad scope of the Foreign Account Tax Compliance

RSM AND HFMWEEK CRS/FATCA SURVEY HOW DO FUNDS INTEND TO ADDRESS CRS AND FATCA COMPLIANCE CHALLENGES?

RSM AND HFMWEEK CRS/FATCA SURVEY HOW DO FUNDS INTEND TO ADDRESS CRS AND FATCA COMPLIANCE CHALLENGES? During the third quarter of 2016, RSM and Hedge Fund Management Week (HFMWeek) surveyed chief operating

RSM AND HFMWEEK CRS/FATCA SURVEY HOW DO FUNDS INTEND TO ADDRESS CRS AND FATCA COMPLIANCE CHALLENGES? During the third quarter of 2016, RSM and Hedge Fund Management Week (HFMWeek) surveyed chief operating

FACT SHEET. Automatic exchange of information (AEOI)

") FACT SHEET Automatic exchange of information (AEOI) In a joint statement, a number of countries, including all major financial centres and Liechtenstein, have announced that they will introduce the new

FACT SHEET Automatic exchange of information (AEOI) In a joint statement, a number of countries, including all major financial centres and Liechtenstein, have announced that they will introduce the new

GUERNSEY. Sections 75C and 75CC of the Income Tax (Guernsey) Law, 1975

Law, 1975") GUERNSEY Sections 75C and 75CC of the Income Tax (Guernsey) Law, 1975 75C. Notices under section 75A and 75B: requests for information. 75CC. Implementation of approved international agreements by regulation.

GUERNSEY Sections 75C and 75CC of the Income Tax (Guernsey) Law, 1975 75C. Notices under section 75A and 75B: requests for information. 75CC. Implementation of approved international agreements by regulation.

FACT SHEET. Automatic exchange of information (AEOI)

") FACT SHEET Automatic exchange of information (AEOI) In a joint statement, a number of countries, including all major financial centres and Liechtenstein, have announced that they will introduce the new

FACT SHEET Automatic exchange of information (AEOI) In a joint statement, a number of countries, including all major financial centres and Liechtenstein, have announced that they will introduce the new

STANDARD FOR AUTOMATIC EXCHANGE OF FINANCIAL ACCOUNT INFORMATION. Philip Kerfs, OECD

STANDARD FOR AUTOMATIC EXCHANGE OF FINANCIAL ACCOUNT INFORMATION Philip Kerfs, OECD Overview Background, context and timeline The Standard: basic approach and key features Next steps: implementing the

STANDARD FOR AUTOMATIC EXCHANGE OF FINANCIAL ACCOUNT INFORMATION Philip Kerfs, OECD Overview Background, context and timeline The Standard: basic approach and key features Next steps: implementing the

The Final FATCA Regulations Are Out What Does It Mean for the Swiss Economy

The Final FATCA Regulations Are Out What Does It Mean for the Swiss Economy Erick C. Christensen Capgemini Financial Services Alan Winston Granwell DLA Piper This presentation is offered for information

The Final FATCA Regulations Are Out What Does It Mean for the Swiss Economy Erick C. Christensen Capgemini Financial Services Alan Winston Granwell DLA Piper This presentation is offered for information

CRS Form for Tax Residency Self Certification For Individuals, Joint Accounts (CRS I)

") For Individuals, Joint Accounts (CRS I) Please read these instructions carefully before completing the form Chapter XIIA of Income Tax Rules, 2002 and Regulations based on the OECD Common Reporting Standard

For Individuals, Joint Accounts (CRS I) Please read these instructions carefully before completing the form Chapter XIIA of Income Tax Rules, 2002 and Regulations based on the OECD Common Reporting Standard

Foreign Account Tax Compliance Act ( FATCA )

") Foreign Account Tax Compliance Act (FATCA) What Is It & Why Should I Care? Presented by: Cynthia J. Hoffman, CPA, J.D. Director of International Tax Advisory Services Schneider Downs & Co., Inc. April

Foreign Account Tax Compliance Act (FATCA) What Is It & Why Should I Care? Presented by: Cynthia J. Hoffman, CPA, J.D. Director of International Tax Advisory Services Schneider Downs & Co., Inc. April

A guide to FACTA and the new Common Reporting Standard. For advisers use only.

A guide to FACTA and the new Common Reporting Standard For advisers use only. Contents 01 Introduction 01 Background 02 How are we complying with FACTA in the UK? 02 How are we complying with FACTA in

A guide to FACTA and the new Common Reporting Standard For advisers use only. Contents 01 Introduction 01 Background 02 How are we complying with FACTA in the UK? 02 How are we complying with FACTA in

THE MULTILATERAL CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS AND THE PATH TO THE OECD-STANDARD ON AUTOMATIC EXCHANGE OF INFORMATION

THE MULTILATERAL CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS AND THE PATH TO THE OECD-STANDARD ON AUTOMATIC EXCHANGE OF INFORMATION Dr. Achim Pross Head of International Cooperation and

THE MULTILATERAL CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS AND THE PATH TO THE OECD-STANDARD ON AUTOMATIC EXCHANGE OF INFORMATION Dr. Achim Pross Head of International Cooperation and

FATCA: Developments & perspectives

FATCA: Developments & perspectives Automatic Exchange of Information 22 May 2014 FATCA evolves into CRS a multilateral automatic exchange of information 2010 The Foreign Account Tax Compliance Act (FATCA)

FATCA: Developments & perspectives Automatic Exchange of Information 22 May 2014 FATCA evolves into CRS a multilateral automatic exchange of information 2010 The Foreign Account Tax Compliance Act (FATCA)

Tax Game Changers Yair Zorea, Tax Partner, PwC Israel Yitzhak Zahavy, Tax Supervisor, PwC Israel November 2015

www.pwc.com/il Tax Game Changers Yair Zorea, Tax Partner, Yitzhak Zahavy, Tax Supervisor, November 2015 Agenda FATCA Common Reporting Standard IRS Audit Trends A look under the hood 2 FATCA 3 Foreign Account

www.pwc.com/il Tax Game Changers Yair Zorea, Tax Partner, Yitzhak Zahavy, Tax Supervisor, November 2015 Agenda FATCA Common Reporting Standard IRS Audit Trends A look under the hood 2 FATCA 3 Foreign Account

Vinodh & Muthu. Tax Alert. Insight. Chartered Accountants. Country by Country Reporting & Master File

Vinodh & Muthu Chartered Accountants Tax Alert Country by Country Reporting & Master File Insight The Organisation for Economic Cooperation and Development ( OECD ) report on Action 13 of Base Erosion

Vinodh & Muthu Chartered Accountants Tax Alert Country by Country Reporting & Master File Insight The Organisation for Economic Cooperation and Development ( OECD ) report on Action 13 of Base Erosion

The Global Tax Reset 2017 Audit Committee Symposium

The Global Tax Reset Copyright 2017 Deloitte Development LLC. All rights reserved. 2017 Audit Committee Symposium Anticipate. Navigate. Focus. 1 The Global Tax Reset General context Multinational companies

The Global Tax Reset Copyright 2017 Deloitte Development LLC. All rights reserved. 2017 Audit Committee Symposium Anticipate. Navigate. Focus. 1 The Global Tax Reset General context Multinational companies

US Regulations

January 2015 Tax alert Cayman Islands FATCA tax alert Get the facts on FATCA! You can access current FATCA news and thought leadership. Type into your web browser: www.ey.com/fatca. On 4 July 2014, the

January 2015 Tax alert Cayman Islands FATCA tax alert Get the facts on FATCA! You can access current FATCA news and thought leadership. Type into your web browser: www.ey.com/fatca. On 4 July 2014, the

Offshore Tax Evasion: IRS Tax Compliance FATCA/FBAR. By Gary S. Wolfe, Esq. Special Contribution by Ryan L. Losi, CPA, Piascik.com

Offshore Tax Evasion: IRS Tax Compliance FATCA/FBAR By Gary S. Wolfe, Esq. Special Contribution by Ryan L. Losi, CPA, Piascik.com Other Books by Gary S. Wolfe: Asset Protection 2013: The Gathering Storm

Offshore Tax Evasion: IRS Tax Compliance FATCA/FBAR By Gary S. Wolfe, Esq. Special Contribution by Ryan L. Losi, CPA, Piascik.com Other Books by Gary S. Wolfe: Asset Protection 2013: The Gathering Storm

Abuse that Spawned FATCA

IFA USA Young IFA Network (YIN) International Tax Webinar April 27, 2012 FATCA Impact on International Business Transactions: Proposed Regulations and Other New Issues SPEAKERS Michael Hirschfeld Partner,

IFA USA Young IFA Network (YIN) International Tax Webinar April 27, 2012 FATCA Impact on International Business Transactions: Proposed Regulations and Other New Issues SPEAKERS Michael Hirschfeld Partner,

TRANS WORLD COMPLIANCE, INC. CARIBBEAN ASSOCIATION OF BANKS, INC. & BARBADOS INTERNATIONAL BUSINESS ASSOC. Presents: FATCA compliance update

TRANS WORLD COMPLIANCE, INC. IN PARTNERSHIP WITH CARIBBEAN ASSOCIATION OF BANKS, INC. & BARBADOS INTERNATIONAL BUSINESS ASSOC. Presents: FATCA compliance update AGENDA Current FATCA status / update FATCA

TRANS WORLD COMPLIANCE, INC. IN PARTNERSHIP WITH CARIBBEAN ASSOCIATION OF BANKS, INC. & BARBADOS INTERNATIONAL BUSINESS ASSOC. Presents: FATCA compliance update AGENDA Current FATCA status / update FATCA

FATCA Impact of FATCA and the planned Intergovernmental Agreement on the Private Banking sector in Luxembourg Private Banker Luxembourg 14 March 2013

FATCA Impact of FATCA and the planned Intergovernmental Agreement on the Private Banking sector in Luxembourg Private Banker Luxembourg 14 March 2013 Final Regulations Highlights Notices Hire Act What

FATCA Impact of FATCA and the planned Intergovernmental Agreement on the Private Banking sector in Luxembourg Private Banker Luxembourg 14 March 2013 Final Regulations Highlights Notices Hire Act What

Argentina Tax amnesty: the day after

Argentina Tax amnesty: the day after Walter C. Keiniger December 2016 YES to amnesty: exchange of Information DTTs (Art. 26 OECD Model) Provisions or agreements signed by Argentina Bilateral Agreements

Argentina Tax amnesty: the day after Walter C. Keiniger December 2016 YES to amnesty: exchange of Information DTTs (Art. 26 OECD Model) Provisions or agreements signed by Argentina Bilateral Agreements

Q&A. 1. Q: Why did the company feel the need to move to Ireland?

Q&A 1. Q: Why did the company feel the need to move to Ireland? A: As we continue to grow the international portion of our business, we believe that moving to a member state of the European Union (EU)

Q&A 1. Q: Why did the company feel the need to move to Ireland? A: As we continue to grow the international portion of our business, we believe that moving to a member state of the European Union (EU)

TAXATION (IMPLEMENTATION) (INTERNATIONAL TAX COMPLIANCE) (COMMON REPORTING STANDARD) (JERSEY) REGULATIONS 2015

(INTERNATIONAL TAX COMPLIANCE) (COMMON REPORTING STANDARD) (JERSEY) REGULATIONS 2015") Arrangement TAXATION (IMPLEMENTATION) (INTERNATIONAL TAX COMPLIANCE) (COMMON REPORTING STANDARD) (JERSEY) REGULATIONS 2015 Arrangement Regulation 1 Interpretation... 3 2 Meaning of relevant date and relevant

Arrangement TAXATION (IMPLEMENTATION) (INTERNATIONAL TAX COMPLIANCE) (COMMON REPORTING STANDARD) (JERSEY) REGULATIONS 2015 Arrangement Regulation 1 Interpretation... 3 2 Meaning of relevant date and relevant

FATCA Update and its Global Reach

FATCA Update and its Global Reach Sally Miller, Chief Executive Officer Institute of International Bankers FIRMA s 27 th National Risk Management Training Conference Las Vegas, Nevada May 2, 2013 1 Background

FATCA Update and its Global Reach Sally Miller, Chief Executive Officer Institute of International Bankers FIRMA s 27 th National Risk Management Training Conference Las Vegas, Nevada May 2, 2013 1 Background

Country-by-Country Reporting:

-by- Reporting: Notifications Last updated: December 5, 2017 Notifications OECD Model Rule, Article 3. Notifications. Where a Constituent Entity of an MNE Group that is... not the Ultimate Parent Entity

-by- Reporting: Notifications Last updated: December 5, 2017 Notifications OECD Model Rule, Article 3. Notifications. Where a Constituent Entity of an MNE Group that is... not the Ultimate Parent Entity

STEP Lausanne / Luncheon Meeting FATCA and the Trust Industry - Current Practical Issues. Erol Baruh

STEP Lausanne / Luncheon Meeting FATCA and the Trust Industry - Current Practical Issues Erol Baruh Table of Contents 1. Introduction 2. Classification of entities (FFI vs. NFFE) 3. Compliance method 4.

STEP Lausanne / Luncheon Meeting FATCA and the Trust Industry - Current Practical Issues Erol Baruh Table of Contents 1. Introduction 2. Classification of entities (FFI vs. NFFE) 3. Compliance method 4.

FATCA What is the impact to you?

www.pwc.com FATCA What is the impact to you? Citi Global Banks Forum April 18, 2012 Agenda Background What does it mean? How does it work? So what are people doing now? What else is going on? This document

www.pwc.com FATCA What is the impact to you? Citi Global Banks Forum April 18, 2012 Agenda Background What does it mean? How does it work? So what are people doing now? What else is going on? This document

FATCA Intergovernmental Agreements

FATCA Intergovernmental Agreements And Dispute Resolution Alternatives Tax Treaties: Advanced Topics and Strategic Planning Tax Executives Institute Houston Chapter May 7, 2013 Joshua D. Odintz (Washington)

FATCA Intergovernmental Agreements And Dispute Resolution Alternatives Tax Treaties: Advanced Topics and Strategic Planning Tax Executives Institute Houston Chapter May 7, 2013 Joshua D. Odintz (Washington)

CRS Self-Certification Form for Controlling Persons

Instructions Please read these instructions carefully before completing the form. Citi offices located in countries that have adopted the Common Reporting Standard (CRS) are required to collect certain

Instructions Please read these instructions carefully before completing the form. Citi offices located in countries that have adopted the Common Reporting Standard (CRS) are required to collect certain

- Act Nr. XXXVII of 2013 on certain regulation connected with the international administrative cooperation on tax and other public burdens.

Dear Customer, The Hungarian Parliament introduced the Common Reporting Standards, CRS on the automatic financial data exchange with the effect of 01.01.2016. The aim of the regulation is to hinder the

Dear Customer, The Hungarian Parliament introduced the Common Reporting Standards, CRS on the automatic financial data exchange with the effect of 01.01.2016. The aim of the regulation is to hinder the

Impact of FATCA on Cayman Islands Entities

Impact of FATCA on Cayman Islands Entities This publication provides a brief overview of the expected impact on entities incorporated in the Cayman Islands of (a) the foreign account tax compliance provisions

Impact of FATCA on Cayman Islands Entities This publication provides a brief overview of the expected impact on entities incorporated in the Cayman Islands of (a) the foreign account tax compliance provisions

TAXATION OF TRUSTS IN ISRAEL. An Opportunity For Foreign Residents. Dr. Avi Nov

TAXATION OF TRUSTS IN ISRAEL An Opportunity For Foreign Residents Dr. Avi Nov Short Bio Dr. Avi Nov is an Israeli lawyer who represents taxpayers, individuals and entities. Areas of Practice: Tax Law,

TAXATION OF TRUSTS IN ISRAEL An Opportunity For Foreign Residents Dr. Avi Nov Short Bio Dr. Avi Nov is an Israeli lawyer who represents taxpayers, individuals and entities. Areas of Practice: Tax Law,

Common Reporting Standard (CRS) The road continues

The road continues") Common Reporting Standard (CRS) The road continues The information exchange landscape Coming years will see increasing global transparency of account holder information requiring global scalable solutions

Common Reporting Standard (CRS) The road continues The information exchange landscape Coming years will see increasing global transparency of account holder information requiring global scalable solutions

Corrigendum. OECD Pensions Outlook 2012 DOI: ISBN (print) ISBN (PDF) OECD 2012

ISBN (PDF) OECD 2012") OECD Pensions Outlook 2012 DOI: http://dx.doi.org/9789264169401-en ISBN 978-92-64-16939-5 (print) ISBN 978-92-64-16940-1 (PDF) OECD 2012 Corrigendum Page 21: Figure 1.1. Average annual real net investment

OECD Pensions Outlook 2012 DOI: http://dx.doi.org/9789264169401-en ISBN 978-92-64-16939-5 (print) ISBN 978-92-64-16940-1 (PDF) OECD 2012 Corrigendum Page 21: Figure 1.1. Average annual real net investment

Approach to Employment Injury (EI) compensation benefits in the EU and OECD

compensation benefits in the EU and OECD") Approach to (EI) compensation benefits in the EU and OECD The benefits of protection can be divided in three main groups. The cash benefits include disability pensions, survivor's pensions and other short-

Approach to (EI) compensation benefits in the EU and OECD The benefits of protection can be divided in three main groups. The cash benefits include disability pensions, survivor's pensions and other short-

GENERAL ANTI AVOIDANCE RULE RECENT CASE LAW IN ARGENTINA

GENERAL ANTI AVOIDANCE RULE RECENT CASE LAW IN ARGENTINA Leandro M. Passarella Passarella Abogados TTN Conferences Latin America 2014 Buenos Aires November 17, 2014 Background Past structures Case Law

GENERAL ANTI AVOIDANCE RULE RECENT CASE LAW IN ARGENTINA Leandro M. Passarella Passarella Abogados TTN Conferences Latin America 2014 Buenos Aires November 17, 2014 Background Past structures Case Law

Global Tax Reset Transfer Pricing Documentation Summary. February 2018

Global Tax Reset Transfer Pricing Summary February 2018 Global Tax Reset Transfer Pricing Summary Overview The Global Tax Reset Transfer Pricing Summary ( Guide ) compiles essential country-by-country

Global Tax Reset Transfer Pricing Summary February 2018 Global Tax Reset Transfer Pricing Summary Overview The Global Tax Reset Transfer Pricing Summary ( Guide ) compiles essential country-by-country

PENTA CLO 2 B.V. (the "Issuer")

") THIS NOTICE CONTAINS IMPORTANT INFORMATION OF INTEREST TO THE REGISTERED AND BENEFICIAL OWNERS OF THE NOTES (AS DEFINED BELOW). IF APPLICABLE, ALL DEPOSITARIES, CUSTODIANS AND OTHER INTERMEDIARIES RECEIVING

THIS NOTICE CONTAINS IMPORTANT INFORMATION OF INTEREST TO THE REGISTERED AND BENEFICIAL OWNERS OF THE NOTES (AS DEFINED BELOW). IF APPLICABLE, ALL DEPOSITARIES, CUSTODIANS AND OTHER INTERMEDIARIES RECEIVING

TAX TRANSPARENCY THE NEW GLOBAL REPORTING STANDARD

TAX TRANSPARENCY THE NEW GLOBAL REPORTING STANDARD 2 TAX TRANSPARENCY THE NEW GLOBAL REPORTING STANDARD A COMMON REPORTING STANDARD ACROSS THE WORLD The goalposts in international tax reporting are moving

TAX TRANSPARENCY THE NEW GLOBAL REPORTING STANDARD 2 TAX TRANSPARENCY THE NEW GLOBAL REPORTING STANDARD A COMMON REPORTING STANDARD ACROSS THE WORLD The goalposts in international tax reporting are moving

Global IRW Newsbrief Information reporting and withholding (IRW)

") Global IRW Newsbrief Information reporting and withholding (IRW) 9 January 2013 HMRC issues Draft Guidance Notes - Implementation of International Tax Compliance (United States of America) Regulations

Global IRW Newsbrief Information reporting and withholding (IRW) 9 January 2013 HMRC issues Draft Guidance Notes - Implementation of International Tax Compliance (United States of America) Regulations

A closer look at the final regulations and the path forward

www.pwc.com FATCA A closer look at the final regulations and the path forward 19 February 2013 Circular 230: This document was not intended or written to be used, and it cannot be used, for the purpose

www.pwc.com FATCA A closer look at the final regulations and the path forward 19 February 2013 Circular 230: This document was not intended or written to be used, and it cannot be used, for the purpose

Select Tax Developments (Affecting Financial Products)

") Select Tax Developments (Affecting Financial Products) March 27, 2014 Remmelt A. Reigersman 2014 Morrison & Foerster LLP mofo.com Agenda HIRE Act Dividend Equivalents FATCA Update Tax Reform Financial

Select Tax Developments (Affecting Financial Products) March 27, 2014 Remmelt A. Reigersman 2014 Morrison & Foerster LLP mofo.com Agenda HIRE Act Dividend Equivalents FATCA Update Tax Reform Financial

Global Forum on Transparency and Exchange of Information for Tax Purposes. Statement of Outcomes

Global Forum on Transparency and Exchange of Information for Tax Purposes Statement of Outcomes 1. On 25-26 October 2011, over 250 delegates from 84 jurisdictions and 9 international organisations and

Global Forum on Transparency and Exchange of Information for Tax Purposes Statement of Outcomes 1. On 25-26 October 2011, over 250 delegates from 84 jurisdictions and 9 international organisations and

FATCA the final countdown

www.pwc.co.uk TISA FATCA the final countdown 3 June 2013 Current state of play Year March 2010 What has been published? 2010 March 2010 Foreign Account Tax Compliance Act 2010 2010-2011 Aug 2010, April

www.pwc.co.uk TISA FATCA the final countdown 3 June 2013 Current state of play Year March 2010 What has been published? 2010 March 2010 Foreign Account Tax Compliance Act 2010 2010-2011 Aug 2010, April

(Rev. June 2017) General Instructions. Purpose of Form. What s New

General Instructions. Purpose of Form. What s New") Department of the Treasury Instructions for Form W-8IMY Internal Revenue Service (Rev. June 2017) Certificate of Foreign Intermediary, Foreign Flow-Through Entity, or Certain U.S. Branches for United States

Department of the Treasury Instructions for Form W-8IMY Internal Revenue Service (Rev. June 2017) Certificate of Foreign Intermediary, Foreign Flow-Through Entity, or Certain U.S. Branches for United States

Information reporting and withholding: the impact of Foreign Account Tax Compliance Act (FATCA) on multinational organizations.

on multinational organizations.") Information reporting and withholding: the impact of Foreign Account Tax Compliance Act (FATCA) on multinational organizations 1 May 2013 Disclaimer Ernst & Young refers to the global organization of member

Information reporting and withholding: the impact of Foreign Account Tax Compliance Act (FATCA) on multinational organizations 1 May 2013 Disclaimer Ernst & Young refers to the global organization of member

FATCA: An Update for STEP

FATCA: An Update for STEP N I C O L A V I R G I L L - R O L L E, P H D D I R E C T O R O F F I N A N C I A L S E R V I C E S M I N I S T R Y O F F I N A N C I A L S E R V I C E S 29 TH J A N U A R Y, 2

FATCA: An Update for STEP N I C O L A V I R G I L L - R O L L E, P H D D I R E C T O R O F F I N A N C I A L S E R V I C E S M I N I S T R Y O F F I N A N C I A L S E R V I C E S 29 TH J A N U A R Y, 2