Appeal Process Overview

|

|

|

- Esmond Bruce

- 5 years ago

- Views:

Transcription

1 Appeal Process Overview DISCLAIMER AND SCOPE The following discussion broadly outlines the process for the most common property-tax appeals appeals from local officials assessments. Slightly different procedures and deadlines apply in other instances, such as appeals from assessments made by the Department of Local Government Finance. For other appeal procedures, consult Indiana Code and Click here to link to the Indiana Code. The IBTR offers this discussion for informational purposes only and may revise its contents at any time without notice. The discussion is not intended, nor should it be construed, as a ruling on any specific appeal, and parties shall not cite it in any proceedings. The IBTR strongly advises parties to consult relevant statutes, court rules, administrative regulations, and case law to determine applicable deadlines and procedures. Relevant materials include, without limitation, Ind. Code ; Ind. Code and -5; 52 Ind. Admin. Code, rr. 1, 2 and 3; and the Indiana Tax Court Rules. APPEALS PROCESS Taxpayers can resolve many disputes through discussions with local assessing officials. But in some cases, they will have to pursue an appeal to obtain relief. To do so, a taxpayer must file written notice with the local official that made the disputed assessment. And the taxpayer must file that notice within statutorily prescribed timeframes. Those timeframes are described at Ind. Code The local official is statutorily required to forward that written notice to the county property tax assessment board of appeals ( PTABOA ), which will hear the taxpayer s appeal and issue a written determination. A taxpayer who believes the PTABOA s determination is wrong may petition the IBTR to review that determination. The taxpayer must file his or her petition no later than 45 days after the PTABOA gives notice of its determination. If the taxpayer initiated the appeal process at the local level after June 30, 2007, he or she can appeal to the IBTR without the PTABOA having issued a determination. But the taxpayer can do so only if PTABOA failed (1) to hear the case within 180 days after the taxpayer initiated the appeal process, or (2) to issue a determination within 120 days after holding its hearing. The IBTR will hear timely filed petitions that otherwise comply with statutory requirements. For appeals from assessments made in general-reassessment years, the IBTR must hold a hearing within one year of the petition being filed. For all other appeals, the IBTR must hold its hearing within 9 months of the petition being filed. After conducting its hearing and considering the parties evidence, the IBTR will issue a final determination. Once again, the IBTR must issue its determination within statutorily prescribed timeframes 9 months from the hearing for general-reassessment-year appeals, and 3 months from the hearing in all other appeals. The Board can extend those

2 timeframes up to 180 days. If the IBTR fails to issue a final determination within those timeframes, the petitioner may either wait for the IBTR to issue its determination or petition the Indiana Tax Court for judicial review. A party that is dissatisfied with the IBTR s final determination may, at its option, petition for rehearing or seek judicial review. If the party seeks rehearing, it must file its petition no later than 15 days after the IBTR gives notice of its final determination. Unless the IBTR grants the petition for rehearing, that petition does not toll the time for seeking judicial review. A party seeking judicial review must follow the procedures under applicable statutes and the Indiana Tax Court s rules. Due to amendments embodied in Public Law (Senate Enrolled Act 287), the procedures for obtaining judicial review of IBTR determinations issued after June 30, 2007, differ significantly from those applying to IBTR determinations issued before that date.

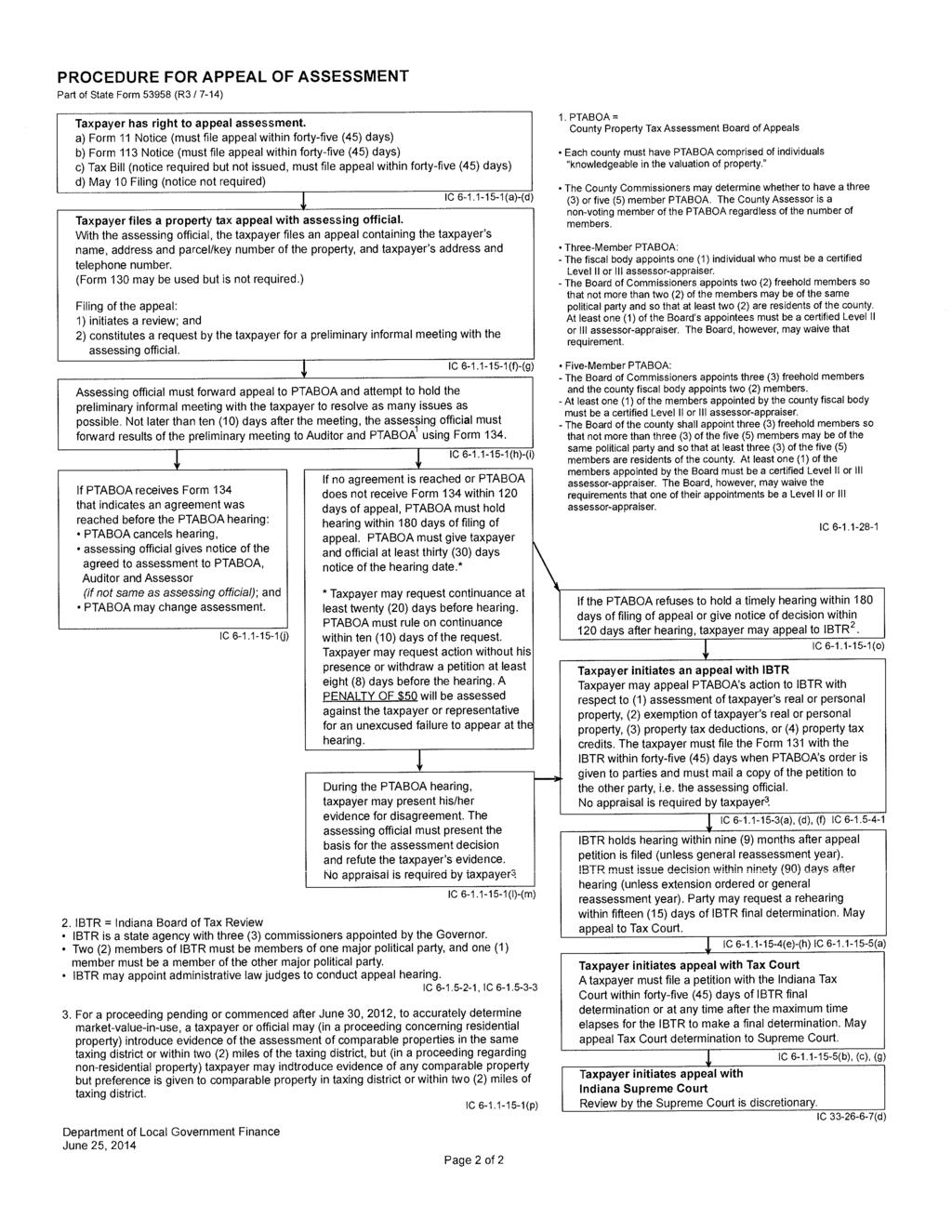

3 Procedure for Appeal of Assessment Taxpayer has right to appeal assessment. a) Form 11 Notice (must file appeal within 45 days) b) Form 113 Notice (must file appeal within 45 days) c) Tax Bill (notice required but not issued, must file appeal within 45 days) d) May 10 Filing (notice not required) Taxpayer files a property tax appeal with assessing official. With the assessing official, the taxpayer files an appeal containing the taxpayer's name, address and parcel/key number of the property, and taxpayer's address and telephone number. (Form 130 may be used but is not required.) Filing of the appeal: 1) initiates a review; and 2) constitutes a request by the taxpayer for a preliminary informal meeting with the assessing official. that indicates an agreement was assessing official gives notice of the agreed to assessment to PTABOA, Auditor and Assessor (if not same as assessing official); PTABOA may change assessment. 2. IBTR = Indiana Board of Tax Review by taxpayer. 3 IC (a)-(d) Assessing official must forward appeal to PTABOA and attempt to hold the preliminary informal meeting with the taxpayer to resolve as many issues as possible. Not later than 10 days after the meeting, the assessing official must forward results of the preliminary meeting to Auditor and PTABOA 1 using Form 134. If PTABOA receives Form 134 reached before the PTABOA hearing: PTABOA cancels hearing. and IC (j) If no agreement is reached or PTABOA does not receive Form 134 within 120 days of appeal, PTABOA must hold hearing within 180 days of filing of appeal. PTABOA must give taxpayer and official at least 30 days notice of the hearing date.* * Taxpayer may request continuance at least 20 days before hearing. PTABOA must rule on continuance within 10 days of the request. Taxpayer may request action without his presence or withdraw a petition at least 8 days before the hearing. A PENALTY OF $50 will be assessed against the taxpayer or representative for an unexcused failure to appear at the hearing. During the PTABOA hearing, taxpayer may present his/her evidence for disagreement. The assessing official must present the basis for the assessment decision and refute the taxpayer's evidence. No appraisal is required IBTR is a state agency with 3 commissioners appointed by the Governor. IC (f)-(g) IC (h)-(i) IC (l)-(m) 2 members of IBTR must be members of one major political party, and 1 member must be a member of the other major political party. IBTR may appoint administrative law judges to conduct appeal hearing. IC , IC For a proceeding pending or commenced after June 30, 2012, to accurately determine market-value-in-use, a taxpayer or official may (in a proceeding concerning residential property) introduce evidence of the assessment of comparable properties in the same taxing district or within 2 miles of the taxing district; but (in a proceeding regarding nonresidential property) taxpayer may introduce evidence of any comparable property but preference is given to comparable property in taxing district or within 2 miles of taxing district. 1. PTABOA= County Property Tax Assessment Board of Appeals Each county must have PTABOA comprised of individuals "knowledgeable in the valuation of property." The County Commissioners may determine whether to have a 3 or 5 member PTABOA. The County Assessor is a non-voting member of the PTABOA regardless of the number of members. Three-Member PTABOA: - The fiscal body appoints 1 individual who may be a certified Level II or III assessor-appraiser. - The Board of Commissioners appoints 2 freehold members so that not more than 2 of the members may be of the same political party and so that at lest 2 are residents of the county. At least 1 of the Board's appointees must be a certified Level II or III assessor-appraiser. The Board, however, may waive that requirement. Five-Member PTABOA: - The Board of Commissioners appoints 3 freehold members and the county fiscal body appoints 2 members. - At least 1 of the members appointed by the county fiscal body may be a certified Level II or III assessor-appraiser. - The Board of the county shall appoint 3 freehold members so that not more than 3 of the 5 members may be of the same political-party and so that at least 3 of the 5 members are residents of the county. At least 1 of the members appointed by the Board must be a certified Level II or III assessor-appraiser. The Board, however, may waive the requirements that one of their appointments be a Level II or III assessor-appraiser. If the PTABOA does not hold a timely hearing within 180 days of filing of appeal or give notice of decision within 120 days after hearing, taxpayer may appeal to IBTR. 2 Taxpayer initiates an appeal with IBTR IC IC (o) Taxpayer may appeal PTABOA's action to IBTR with respect to (1) assessment of taxpayer's real or personal property, (2) exemption of taxpayer's real or personal property, (3) property tax deductions, or (4) property tax credits. The taxpayer must file the Form 131 with the IBTR within 45 days when PTABOA's order is given to parties and must mail a copy of the petitiion to the other party, i.e. the assessing official. No appraisal is required by taxpayer. 3 IC (a), (d), (f); IC IBTR holds hearing within 9 months after appeal petition is filed (unless general reassessment year). IBTR must issue decision within 90 days after hearing (unless extension ordered or general reassessment year). Party may request a rehearing within 15 days of IBTR final determination. May appeal to Tax Court. maximum time elapses for the IBTR to make a final determination. May appeal Tax Court determination to Supreme Court. IC (e)-(h); IC (a) Taxpayer initiates appeal with Tax Court A taxpayer must file a petition with the Indiana Tax Court within 45 days of IBTR final determination or at any time after the IC (b), (c ), (g) Department of Local Government Finance June 25, 2014 IC Taxpayer initiates appeal with Indiana Supreme Court Review by the Supreme Court is discretionary. IC (d)

in the mail. How do I know if my assessed value is correct?")

4 STATE OF INDIANA DEPARTMENT OF LOCAL GOVERNMENT FINANCE INDIANA GOVERNMENT CENTER NORTH 100 NORTH SENATE AVENUE N1058(B) INDIANAPOLIS, IN PHONE (317) FAX (317) Frequently Asked Questions Assessment Appeals 101 July 28, Question: I received a Notice of Assessment (Form 11) in the mail. How do I know if my assessed value is correct? Answer: The assessed value should reflect the amount a willing buyer would pay for the property at the time of the assessment (March 1 is the assessment date. NOTE: The assessment/valuation date will change to January 1 st in 2016). When a property owner receives a notice of assessment, the best way to determine if it is accurate is to question if the property could have sold for approximately that amount. 2. Who should I contact to initiate an appeal of the assessed value of my home? Answer: The first step in the appeals process begins with written notification to the appropriate local official. A taxpayer may elect to do one of the following and submit the appeal to the appropriate local official: File an Appeal Form 130 with the local assessor - is for subjective appeals (e.g., you believe the assessed value is incorrect), File an Appeal Form 133 with the local assessor - is for objective appeals (e.g., I was assessed for a fireplace, and I do not have a fireplace) or, Submit a written appeal (including information such as the name of the taxpayer, the property address, parcel number, contact information, etc.) to the local assessor. A taxpayer has forty-five (45) days after the date of the notice of assessment to file an appeal. If a notice of assessment is not sent, then the taxpayer must file an appeal no later than May 10 or 45 days after the date of the tax statement (tax bill), whichever is later. Appeals begin at the local level and can be appealed to the state (Indiana Board of Tax Review) only after being reviewed locally. Page 1 of 4

5 3. I received my property tax bill and I think it is too high. What can I do? Answer: A person s property tax liability reflects the assessed value, deductions (e.g., the Homestead Standard Deduction and the Mortgage Deduction are the two most common deductions), and local government spending. Hence, the first thing a taxpayer should do is to make sure their assessment is correct. This can be done by getting a copy of their property record card from the local assessor s office to make sure all of the parcel characteristics (e.g. square footage, features like decks, detached garage, etc.) are correct. The next step is to make sure all of the deductions for which the taxpayer has applied and is eligible for are in place (see for a list of property tax benefits). Finally, taxpayers can check with their local government officials (e.g. city, town, or county council members, etc.) about local government spending decisions. 4. To whom do I speak about an appeal if my township no longer has an assessor? Answer: The county assessor is responsible for all assessment duties if you do not have a township assessor. Please visit the following link to locate your local assessing official: 5. Is an appraisal required as evidence when appealing an assessment? Answer: No, state law does not require a taxpayer to submit an appraisal of the subject property in order to appeal the assessment. Information about acceptable evidence to support an appeal is available at 6. What is the Property Tax Assessment Board of Appeals (PTABOA)? Answer: The PTABOA is either a three or five member board comprised of individuals knowledgeable in the valuation of property. The county commissioners determine whether to have a three or five member PTABOA. The county assessor is a non-voting member of the PTABOA regardless of the number of members. The members are appointed by the county commissioners and the county council. 7. So how does the appeal process work? Answer: Once a taxpayer has filed a written notice of appeal, the local assessing official is statutorily required to forward that written notice to the PTABOA and attempt to hold a preliminary meeting with the taxpayer to resolve as many issues as possible. The assessing official will forward a copy of the results of the preliminary meeting to the PTABOA. The PTABOA will review the agreement (if one is reached) and may change the assessment. If an agreement was not reached or if an informal meeting was not held, the PTABOA must hold a hearing within 180 days of the filing of the appeal. The PTABOA must give the taxpayer at least 30 days notice of the hearing date. After the hearing and a decision is rendered, the PTABOA will issue a written determination. If the taxpayer disagrees with the final determination, or the Page 2 of 4

6 PTABOA does not hold a timely hearing or give notice of the decision within 120 days after the hearing, the taxpayer may appeal to the Indiana Board of Tax Review (IBTR). 8. I think my assessment is incorrect and I am filing an appeal. Do I have to pay the full amount of my tax bill or can I wait for the results of my appeal? Answer: If you have filed an appeal, you may pay an amount based on the immediately preceding year's assessment of real property if an assessment, or increase in assessment, of real property is involved. The taxes resulting must be paid when the installments come due. 9. What if I can t attend the scheduled hearing? What is the timeframe to file a continuance? Answer: Effective July 1, 2012, the PTABOA must give at least thirty (30) days notice, by mail, of the date, time, and place of the hearing to the taxpayer and the county or township official with whom the taxpayer filed the notice for review. In some situations, a taxpayer may need to request an extension of time (i.e., a continuance) because of individual circumstances (for example, the taxpayer may be waiting for some information such as an appraisal [although an appraisal is not required in the appeal process] or there may be some urgent family or work issues that must be attended to on the date scheduled for the appeal hearing). A taxpayer may request a continuance of the hearing (that is, a postponement to a later date) by filing, at least twenty (20) days before the hearing date, a request for continuance with the PTABOA and the county or township official with evidence supporting just cause why the PTABOA should postpone the hearing. The PTABOA must, no later than ten (10) days after the date the request for continuance is filed, determine whether the taxpayer has demonstrated just cause for a continuance, at which point the PTABOA either must grant or deny the taxpayer s request for continuance. 10. Do I have to show up for the appeal hearing or can they review the information I submitted? Answer: A taxpayer may request that the PTABOA take action without the taxpayer being present and make a decision based on the evidence already submitted to the PTABOA. The taxpayer may make the request by filing it with the PTABOA and county or township official at least eight (8) days before the hearing date. 11. What if I do not attend my appeal hearing? Is there a penalty? Answer: If the taxpayer or representative fails to appear at the PTABOA hearing, and the taxpayer s request for a continuance was denied, a penalty of fifty dollars ($50) will be assessed against the taxpayer. The penalty will also be assessed if the taxpayer s request for a continuance, request for the PTABOA to take action without the taxpayer being present, or withdrawal is not timely filed. A taxpayer may appeal the assessment of the penalty to the IBTR or directly to the Tax Court. Page 3 of 4

7 12. I filed a property tax appeal, but now I decided I do not want to pursue it. What do I need to do? Answer: A taxpayer may withdraw a petition by filing a notice of withdrawal with the PTABOA and the county or township official at least eight (8) days before the hearing date. As a reminder, if it is after the eight (8) days, a penalty of fifty dollars ($50) will be assessed against the taxpayer. 13. What is the IBTR? Answer: The IBTR is the state administrative tax appeals board. A taxpayer who disagrees with the PTABOA s determination may petition the IBTR for further review. More information about the IBTR is available at If I am successful in my appeal, do I get a refund and is there interest? Answer: If a taxpayer is entitled to a property tax refund or credit because an assessment is decreased, the taxpayer shall also be paid, or credited with, interest on the excess taxes that the taxpayer paid at the rate established for excess tax payments by the Department of Revenue under IC Page 4 of 4

8 Department of Local Government Finance August 2014 Property Tax Assessment Appeals FACT SHEET Property Tax Assessment Appeals Process (Form 130) (Form 130 may be used but is not required.) A taxpayer has the right to initiate an appeal of the current year s assessed valuation. The first step in the appeals process begins with written notification to the local assessing official. Taxpayers have 45 days after the date of the notice of assessment to initiate an appeal. If no notice of assessment is given, the notice of appeal must be filed not later than the later of May 10 of the tax bill year or 45 days after the date of the tax bill. In other words, if no Form 11 is issued by the county assessor for the March 1, 2013 assessment date, the 2014 tax bill serves as the notice of assessment and the deadline to file an appeal is the later of May 10 or 45 days after the date of the 2014 tax bill. Evidence to support the taxpayer s case can be in the form of a sale of the subject property, sales of comparable properties, offers to purchase or an appraisal prepared by a licensed appraiser. Indiana law does not require a taxpayer to submit an appraisal of the subject property to appeal the assessment. While the Indiana Tax Court has held that an appraisal properly trended to the appropriate valuation date is the best evidence, it is not the only acceptable evidence. The county or township assessor has the burden of proof in an appeal where the assessment increased by more than 5% over the preceding assessment date. If the taxpayer and the assessing official do not agree on the resolution of all assessment issues or the results of the informal meeting are not forwarded to the Property Tax Assessment Board of Appeals (PTABOA) not later than 120 days after the date of the notice of review filed by the taxpayer, the PTABOA must hold a hearing on the appeal not later than 180 days after the date of the appeal. The taxpayer may request a continuance at least 20 days before the hearing. The PTABOA must rule on the continuance no later than ten days after the date the request for a continuance is filed. The taxpayer may, at least eight days before the hearing, request that the PTABOA take action without his presence. The taxpayer may withdraw a petition at least eight days before the hearing. A PENALTY OF $50 will be assessed against the taxpayer or his representative for failure to appear at the hearing and if the taxpayer s request for continuance, request for the PTABOA to take action without the taxpayer s presence, or withdrawal is not timely filed (a penalty may be appealed). At the PTABOA hearing, the taxpayer may present reasons for disagreement with the assessment. If a taxpayer is not satisfied with the decision of the PTABOA or if the PTABOA fails to hear the case not later than 180 days after the appeal was initiated or fails to issue a determination not later than 120 days after holding its hearing, the taxpayer has the right to appeal to the Indiana Board of Tax Review (IBTR) by filing a Form 131. Taxpayers may contact the IBTR directly at (317) or visit the IBTR Guide to Appeals at After being heard by the IBTR, taxpayers may also seek review by the Indiana Tax Court and, subsequently, the Indiana Supreme Court. Contact information is available for the Indiana Department of Local Government Finance at: Facts Form 130: aspx?id=4816 Related Memorandum: Indiana law does not require a taxpayer to submit an appraisal of the subject property in order to appeal the assessment. Memorandum on Use of Appraisals: dlgf/files/memo_appeals pdf Memorandum on Penalty to Taxpayer for Not Appearing: files/120522_assessment_and_ Appeal_Changes.pdf Appeals 101: dlgf/files/120618_assessment_ Appeals_101-final.pdf Memorandum on Legislative Changes to Procedures for Appeal of Assessment: Rushenberg_Memo_-_Appeals_ Process_and_PTABOA_ Composition.pdf Pertinent Evidence to Support a Taxpayer s Case: A sale of the subject property Sales of comparable properties Offers to purchase An appraisal prepared by a licensed appraiser For income producing property: capitalized income and expense information Burden of proof falls to the township or county assessor if the assessment has increased by more than 5% over the previous year s assessment Claim for Refund Form 17T: Taxpayers requesting refunds should also file a Claim for Refund Form 17T with the county auditor. Page 1

9 Frequently Asked Questions Q: How do I know if my new assessed value is correct? A: The assessed value should reflect the amount a willing buyer would pay for the property at the time of the assessment. When a property owner receives the notice of new assessment, the best way to determine if it is accurate is to ask if the property could have sold for approximately that amount during the valuation time period. For 2014 pay 2015 property taxes, the assessment and valuation date was March 1, Sales from 2013 and the first two months of 2014 were used to determine this assessed value. A correct assessed value should reflect the amount a willing buyer would pay for the property during 2013 and the first two months of Q. Who should I contact to initiate an appeal of the assessed value of my property? A: The appeals process begins with written notification to your local assessing official. Appeals begin at the local level and can be appealed to the state only after being reviewed locally. Q: To whom do I speak about an appeal if my township no longer has an assessor? A: The county assessor is responsible for all assessment duties if you do not have a township assessor. Please visit the following link to locate your local assessing official: Q: When should I initiate an appeal? A: If you receive a notice of assessment (Form 11), you should initiate an appeal not later than 45 days after the date of the notice. If no Form 11 is sent, the tax bill serves as the notice of assessment and you should initiate an appeal not later than May 10 of the year or 45 days after the date of the tax bill, whichever is later. Q: Do I need a Form 130 to initiate an appeal of my assessment and if not, what else can I use? A: You are not required to use the Form 130 to initiate an appeal. Indiana statute only requires written notification to the local assessing official. The notification should include the name of the taxpayer, the address and parcel or key number of the property, and the address and telephone number of the taxpayer. Q: Is an appraisal required as evidence when appealing an assessment? A: No. State law does not require a taxpayer to submit an appraisal of the subject property in order to appeal the assessment. Information about acceptable evidence to support an appeal is available at htm. If the value of the subject property has increased by more than 5% over the previous assessment date, the burden of proof rests with the local assessing official. Q: What happens if the Property Tax Assessment Board of Appeals (PTABOA) denies my appeal and I still disagree? A: A petitioner may appeal the PTABOA decision to the Indiana Board of Tax Review (IBTR). After being heard by the IBTR, taxpayers may then seek review by the Indiana Tax Court. Q: What is the PTABOA? A: Once a taxpayer has filed written notice of appeal, the local official is statutorily required to forward that written notice to the county PTABOA, which will hear the taxpayer s appeal and issue a written determination if the taxpayer and assessing official are unable to resolve the dispute. The board of county commissioners may determine whether to have a three or five member PTABOA. The county assessor is a non-voting member of the PTABOA regardless of the number of members. In a county with a five member PTABOA, the commissioners appoint three freehold members and the county council appoints two members. In a county with a three member PTABOA, the county council will appoint one individual and the commissioners will appoint two freehold members. See IC for more information. Q: What is the IBTR? A: The IBTR is the state agency charged with hearing appeals from the PTABOA. A taxpayer who disagrees with the PTABOA s determination may petition the IBTR for further review. More information about the IBTR is available online at: Q: I know my assessment is incorrect and I am filing an appeal. Do I have to pay the full amount of my tax bill, or can I wait for the results of my appeal? A: If you have initiated an appeal, you may pay only an amount of taxes based on the immediately preceding year s assessment pending a final determination of your appeal. If you do not pay this amount when the property tax installment is due, you will be considered delinquent and assessed penalties based on that delinquency. For example, your property was assessed at $200,000 this year. You file an appeal contesting this assessment. Last year your property was assessed at $100,000. You may pay taxes based on an assessed value of $100,000 during the pending appeal with no penalty. Page 2

10

11

12

13

14

15

16

17

18

19 Department of Local Government Finance March 2013 Petition for Correction of an Error FACT SHEET Appeal for Correction of an Error (Form 133): Indiana law provides two ways for taxpayers to contest the assessed value of their property. Both begin at the local level and can be appealed to the state only after being reviewed locally. Facts Objective Appeal: Objective issues are such things as mathematical miscalculations, factual errors or incorrect measurements. If a taxpayer believes the assessed valuation of a property is incorrect, a subjective appeal may be filed. This type of appeal is based on the taxpayer s judgement as to the correct market value of the property. (For more information on this process, see the Property Tax Assessment Appeals Process Fact Sheet.) The other appeal process addresses factual matters through an objective appeal. For example, if a taxpayer notices that his property tax card contains an incorrect description of his property, such as a garage listed that does not exist, the objective appeal is available to correct the problem. This simple process begins with the submission of a Petition for Correction of Error (Form 133) to the county auditor. This form may be used to appeal objective issues such as: The taxes are illegal as a matter of law. There is a math error in computing the assessment. Through error or omission by any state or county officer, the taxpayer was not given credit for an exemption or deduction as permitted by law. The description of the real property was in error. The assessment was against the wrong person. Taxes on the same property were charged more than one time in the same year. There was a mathematical error in computing the taxes or penalties on the taxes. There was an error in carrying delinquent taxes forward from one tax duplicate to another. If the appeal is successful and a refund is due, the taxpayer must file a Claim for Refund Form 17T with the county auditor. However, if the petition is denied, the county auditor will refer the matter to the county Property Tax Assessment Board of Appeals (PTABOA) for determination. The PTABOA then provides a copy of its determination to the petitioner and the auditor. If the PTABOA agrees with the local officials denial of the petition, the taxpayer may appeal the PTABOA decision to the Indiana Board of Tax Review (IBTR). The appeal must be made not later than 45 days after the date of the notice of the PTABOA determination. Form 133: aspx?id=4728 Successful Appeal Claims for Correction of an Error: Claims may be made for up to three years of assessments with the submission of the Form 133. Taxpayers requesting refunds must also file a Claim for Refund form (Form 17T) available from the county auditor. Appeal Contacts: Your Local Assessing Official: htm County Property Tax Assessment Board of Appeals (PTABOA) - (contact your county assessor.) Indiana Board of Tax Review (IBTR): ibtr/2330.htm Indiana Tax Court: in.gov/judiciary/tax Memorandum on Legislative Changes to Procedures for Appeal of Assessment: files/120618_assessment_ Appeals_101-final.pdf Page 1

20 Taxpayers may contact the IBTR directly at (317) or visit the IBTR website at the Guide to Appeals link: If the petition is denied after being heard by the IBTR, the taxpayer may seek review by the Indiana Tax Court (see Frequently Asked Questions Q: What is the difference between an objective appeal and a subjective appeal? A: Objective issues are such things as mathematical miscalculations, factual errors, or incorrect measurements (Form 133). Subjective issues generally relate to the determination of the assessed value of a property by an assessing official (Form 130). Q: What can I do if all the data on my property record card are accurate but my assessment is too high (incorrect)? A: You may file a Form 130 if you believe your assessment is too high and does not reflect market value. Information about the appeals process is available on the DLGF website at A fact sheet with Frequently Asked Questions is located at and a flowchart of the process is available at Q: Can I be refunded for a correction of an error for previous years? A: Claims must be filed within three years after the taxes were first due. Taxpayers requesting refunds must file a Claim for Refund form (Form 17T) available from the county auditor. Q: Where can I obtain a property tax card? A: Property tax cards can be obtained at the office of your local assessing official. Contact information for county officials is available online at Contact Information: For more information on an appeal for correction of an error, contact your county auditor. A complete listing of local government contact information is located at Contact information for the Indiana Department of Local Government Finance is available at Page 2

21

22

23

24

25

26

27

28

29

30

31

32

33

34

Disputing an assessment

IR776 June 2018 Disputing an assessment What to do if you dispute an assessment 2 DISPUTING AN ASSESSMENT Introduction While we make every effort to apply the tax laws fairly and correctly, there may be

IR776 June 2018 Disputing an assessment What to do if you dispute an assessment 2 DISPUTING AN ASSESSMENT Introduction While we make every effort to apply the tax laws fairly and correctly, there may be

IC Chapter 17. Procedures for Fixing and Reviewing Budgets, Tax Rates, and Tax Levies

IC 6-1.1-17 Chapter 17. Procedures for Fixing and Reviewing Budgets, Tax Rates, and Tax Levies IC 6-1.1-17-0.5 Exclusion by county auditor of certain assessed value on tax duplicate; county auditor reduction

IC 6-1.1-17 Chapter 17. Procedures for Fixing and Reviewing Budgets, Tax Rates, and Tax Levies IC 6-1.1-17-0.5 Exclusion by county auditor of certain assessed value on tax duplicate; county auditor reduction

2017 Salt Lake County Board of Equalization Administrative Rules

2017 Salt Lake County Board of Equalization Administrative Rules Adopted 18 July 2017 TABLE OF CONTENTS I. GENERAL PROVISIONS... 1 II. AUTHORITY OF THE BOARD OF EQUALIZATION... 1 III. APPLICATIONS FOR

2017 Salt Lake County Board of Equalization Administrative Rules Adopted 18 July 2017 TABLE OF CONTENTS I. GENERAL PROVISIONS... 1 II. AUTHORITY OF THE BOARD OF EQUALIZATION... 1 III. APPLICATIONS FOR

Procedures for Protest to New York State and City Tribunals

September 25, 1997 Procedures for Protest to New York State and City Tribunals By: Glenn Newman This new feature of the New York Law Journal will highlight cases involving New York State and City tax controversies

September 25, 1997 Procedures for Protest to New York State and City Tribunals By: Glenn Newman This new feature of the New York Law Journal will highlight cases involving New York State and City tax controversies

Indiana Property Taxation of Affordable Housing Overview and Update. Paul M. Jones, Jr. Maureen Hougland Mark Shublak

Indiana Property Taxation of Affordable Housing Overview and Update Paul M. Jones, Jr. Maureen Hougland Mark Shublak Indiana Property Tax Overview and Update Indiana Housing Conference August 15, 2017

Indiana Property Taxation of Affordable Housing Overview and Update Paul M. Jones, Jr. Maureen Hougland Mark Shublak Indiana Property Tax Overview and Update Indiana Housing Conference August 15, 2017

IC Chapter 17. Procedures for Fixing and Reviewing Budgets, Tax Rates, and Tax Levies

IC 6-1.1-17 Chapter 17. Procedures for Fixing and Reviewing Budgets, Tax Rates, and Tax Levies IC 6-1.1-17-0.5 Exclusion by county auditor of certain assessed value on tax duplicate; county auditor reduction

IC 6-1.1-17 Chapter 17. Procedures for Fixing and Reviewing Budgets, Tax Rates, and Tax Levies IC 6-1.1-17-0.5 Exclusion by county auditor of certain assessed value on tax duplicate; county auditor reduction

CHAPTER 56. SETOFF DEBT COLLECTION ACT

Disclaimer This statutory database is current through the 2003 Regular Session of the South Carolina General Assembly. Changes to the statutes enacted by the 2004 General Assembly, which will convene in

Disclaimer This statutory database is current through the 2003 Regular Session of the South Carolina General Assembly. Changes to the statutes enacted by the 2004 General Assembly, which will convene in

Abatements and Refunds

Abatements and Refunds Janeen Ogden Colorado Division of Property Taxation CCTA Conference Colorado Springs, Colorado June 29, 2010 1 Abatements & Refunds Definitions Need for Abatements History of Abatement

Abatements and Refunds Janeen Ogden Colorado Division of Property Taxation CCTA Conference Colorado Springs, Colorado June 29, 2010 1 Abatements & Refunds Definitions Need for Abatements History of Abatement

Title 36: TAXATION. Chapter 101: GENERAL PROVISIONS. Table of Contents Part 2. PROPERTY TAXES...

Title 36: TAXATION Chapter 101: GENERAL PROVISIONS Table of Contents Part 2. PROPERTY TAXES... Subchapter 1. POWERS AND DUTIES OF STATE TAX ASSESSOR... 3 Section 201. SUPERVISION AND ADMINISTRATION...

Title 36: TAXATION Chapter 101: GENERAL PROVISIONS Table of Contents Part 2. PROPERTY TAXES... Subchapter 1. POWERS AND DUTIES OF STATE TAX ASSESSOR... 3 Section 201. SUPERVISION AND ADMINISTRATION...

ALAMEDA COUNTY ASSESSMENT APPEALS BOARD AND EQUALIZATION HEARING OFFICER INSTRUCTION BOOKLET

ALAMEDA COUNTY ASSESSMENT APPEALS BOARD AND EQUALIZATION HEARING OFFICER INSTRUCTION BOOKLET OFFICE OF THE CLERK-ADMINISTRATOR ASSESSMENT APPEALS BOARD P. O. BOX 1499 OAKLAND, CA 94612-1499 (510) 272-3854

ALAMEDA COUNTY ASSESSMENT APPEALS BOARD AND EQUALIZATION HEARING OFFICER INSTRUCTION BOOKLET OFFICE OF THE CLERK-ADMINISTRATOR ASSESSMENT APPEALS BOARD P. O. BOX 1499 OAKLAND, CA 94612-1499 (510) 272-3854

IC Chapter 41. Cumulative Fund Tax Levy Procedures

IC 6-1.1-41 Chapter 41. Cumulative Fund Tax Levy Procedures IC 6-1.1-41-1 Application of chapter Sec. 1. This chapter applies to establishing and imposing a tax levy for cumulative funds under the following:

IC 6-1.1-41 Chapter 41. Cumulative Fund Tax Levy Procedures IC 6-1.1-41-1 Application of chapter Sec. 1. This chapter applies to establishing and imposing a tax levy for cumulative funds under the following:

Motor Vehicle Excise Information

Motor Vehicle Excise Information Our office has produced this booklet as a public service. There may be other offices to contact for specific information regarding your excise tax bill. The following offices

Motor Vehicle Excise Information Our office has produced this booklet as a public service. There may be other offices to contact for specific information regarding your excise tax bill. The following offices

SENATE, No. 673 STATE OF NEW JERSEY. 208th LEGISLATURE INTRODUCED FEBRUARY 23, 1998

SENATE, No. STATE OF NEW JERSEY 0th LEGISLATURE INTRODUCED FEBRUARY, Sponsored by: Senator PETER A. INVERSO District (Mercer and Middlesex) SYNOPSIS Adopts series of amendments dealing with Tax Court proceedings.

SENATE, No. STATE OF NEW JERSEY 0th LEGISLATURE INTRODUCED FEBRUARY, Sponsored by: Senator PETER A. INVERSO District (Mercer and Middlesex) SYNOPSIS Adopts series of amendments dealing with Tax Court proceedings.

H 5209 S T A T E O F R H O D E I S L A N D

LC000 0 -- H 0 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 0 A N A C T RELATING TO TAXATION - LEVY AND ASSESSMENT OF LOCAL TAXES Introduced By: Representative Michael

LC000 0 -- H 0 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 0 A N A C T RELATING TO TAXATION - LEVY AND ASSESSMENT OF LOCAL TAXES Introduced By: Representative Michael

Part VIII RULES GOVERNING PRACTICE IN THE TAX COURT OF NEW JERSEY TABLE OF CONTENTS

APPENDIX C - New Jersey Tax Court Rules Part VIII RULES GOVERNING PRACTICE IN THE TAX COURT OF NEW JERSEY Rule 8:1. Rule 8:2. Rule 8:3. Rule 8:4. Rule 8:5. TABLE OF CONTENTS Scope: Applicability Review

APPENDIX C - New Jersey Tax Court Rules Part VIII RULES GOVERNING PRACTICE IN THE TAX COURT OF NEW JERSEY Rule 8:1. Rule 8:2. Rule 8:3. Rule 8:4. Rule 8:5. TABLE OF CONTENTS Scope: Applicability Review

O.C.G.A GEORGIA CODE Copyright 2015 by The State of Georgia All rights reserved. *** Current Through the 2015 Regular Session ***

O.C.G.A. 48-5-311 GEORGIA CODE Copyright 2015 by The State of Georgia All rights reserved. *** Current Through the 2015 Regular Session *** TITLE 48. REVENUE AND TAXATION CHAPTER 5. AD VALOREM TAXATION

O.C.G.A. 48-5-311 GEORGIA CODE Copyright 2015 by The State of Georgia All rights reserved. *** Current Through the 2015 Regular Session *** TITLE 48. REVENUE AND TAXATION CHAPTER 5. AD VALOREM TAXATION

Senate Bill No. 818 CHAPTER 404

Senate Bill No. 818 CHAPTER 404 An act to amend Section 2924 of, to amend and repeal Sections 2923.4, 2923.5, 2923.6, 2923.7, 2924.12, 2924.15, and 2924.17 of, to add Sections 2923.55, 2924.9, 2924.10,

Senate Bill No. 818 CHAPTER 404 An act to amend Section 2924 of, to amend and repeal Sections 2923.4, 2923.5, 2923.6, 2923.7, 2924.12, 2924.15, and 2924.17 of, to add Sections 2923.55, 2924.9, 2924.10,

Motor Vehicle Excise Information

Motor Vehicle Excise Information William Francis Galvin Secretary of the Commonwealth updated 4/13/17 William Francis Galvin Secretary of the Commonwealth Citizen Information Service One Ashburton Place,

Motor Vehicle Excise Information William Francis Galvin Secretary of the Commonwealth updated 4/13/17 William Francis Galvin Secretary of the Commonwealth Citizen Information Service One Ashburton Place,

TRANSMITTAL MEMORANDUM DEPARTMENT OF REVENUE RULES. This transmittal memorandum contains changes to the Department of Revenue Rules.

T/M #12-29 Date: November 1, 2012 TRANSMITTAL MEMORANDUM DEPARTMENT OF REVENUE RULES PURPOSE: This transmittal memorandum contains changes to the Department of Revenue Rules. RULE CHAPTER TITLE: Rule Chapter

T/M #12-29 Date: November 1, 2012 TRANSMITTAL MEMORANDUM DEPARTMENT OF REVENUE RULES PURPOSE: This transmittal memorandum contains changes to the Department of Revenue Rules. RULE CHAPTER TITLE: Rule Chapter

Chapter WAC EMPLOYMENT SECURITY RULE GOVERNANCE

Chapter 192-01 WAC EMPLOYMENT SECURITY RULE GOVERNANCE WAC 192-01-001 Rule governance statement. The employment security department administers several distinct programs in Titles 50 and 50A RCW through

Chapter 192-01 WAC EMPLOYMENT SECURITY RULE GOVERNANCE WAC 192-01-001 Rule governance statement. The employment security department administers several distinct programs in Titles 50 and 50A RCW through

FREQUENTLY ASKED QUESTIONS ASSESSOR S OFFICE

FREQUENTLY ASKED QUESTIONS ASSESSOR S OFFICE Q: What do Assessors do? A: Assessors are required by Massachusetts law to value all real and personal property within their community. They value every property,

FREQUENTLY ASKED QUESTIONS ASSESSOR S OFFICE Q: What do Assessors do? A: Assessors are required by Massachusetts law to value all real and personal property within their community. They value every property,

IC Chapter 8. Taxation of Public Utility Companies

IC 6-1.1-8 Chapter 8. Taxation of Public Utility Companies IC 6-1.1-8-1 Property owned or used by public utility company Sec. 1. The property owned or used by a public utility company shall be taxed in

IC 6-1.1-8 Chapter 8. Taxation of Public Utility Companies IC 6-1.1-8-1 Property owned or used by public utility company Sec. 1. The property owned or used by a public utility company shall be taxed in

IN THE COMMONWEALTH COURT OF PENNSYLVANIA

IN THE COMMONWEALTH COURT OF PENNSYLVANIA Lawrence Lee and Victoria : Evstafieva, : Appellants : : v. : No. 1041 C.D. 2016 : ARGUED: March 6, 2017 Luzerne County Tax Claim Bureau : BEFORE: HONORABLE RENÉE

IN THE COMMONWEALTH COURT OF PENNSYLVANIA Lawrence Lee and Victoria : Evstafieva, : Appellants : : v. : No. 1041 C.D. 2016 : ARGUED: March 6, 2017 Luzerne County Tax Claim Bureau : BEFORE: HONORABLE RENÉE

BUSINESS PERSONAL PROPERTY

CONTACT INFORMATION Mailing Address: PO Box 7015 Indianapolis, IN 46207-7015 Office Location: 200 East Washington Street, Suite 1360 Indianapolis, IN 46204-3308 PHONE: 317-327-4631 FAX: 317-327-4639 EMAIL:

CONTACT INFORMATION Mailing Address: PO Box 7015 Indianapolis, IN 46207-7015 Office Location: 200 East Washington Street, Suite 1360 Indianapolis, IN 46204-3308 PHONE: 317-327-4631 FAX: 317-327-4639 EMAIL:

Significant State Statutes. For the Budget Season

Significant State Statutes For the 2016-2017 Budget Season Every effort has been made to have the State Statutes contained within to be verbatim and to reflect all changes made during the 2016 Legislative

Significant State Statutes For the 2016-2017 Budget Season Every effort has been made to have the State Statutes contained within to be verbatim and to reflect all changes made during the 2016 Legislative

Significant State Statutes. For the Budget Season

Significant State Statutes For the 2017-2018 Budget Season Every effort has been made to have the State Statutes contained within to be verbatim and to reflect all changes made during the 2017 Legislative

Significant State Statutes For the 2017-2018 Budget Season Every effort has been made to have the State Statutes contained within to be verbatim and to reflect all changes made during the 2017 Legislative

As Introduced. 132nd General Assembly Regular Session S. B. No

132nd General Assembly Regular Session S. B. No. 123 2017-2018 Senator Coley Cosponsors: Senators Eklund, Huffman A B I L L To amend sections 307.699, 3735.67, 5715.19, 5715.27, and 5717.01 of the Revised

132nd General Assembly Regular Session S. B. No. 123 2017-2018 Senator Coley Cosponsors: Senators Eklund, Huffman A B I L L To amend sections 307.699, 3735.67, 5715.19, 5715.27, and 5717.01 of the Revised

August 2017 Legal Calendar

1 Assessor On or before this date, the assessor must forward approved homestead exemption applications and a copy of the certification of disability status to the Tax Commissioner. 77-3517(1) 1 Assessor

1 Assessor On or before this date, the assessor must forward approved homestead exemption applications and a copy of the certification of disability status to the Tax Commissioner. 77-3517(1) 1 Assessor

STATE OF ARKANSAS DEPARTMENT OF FINANCE & ADMINISTRATION OFFICE OF HEARINGS & APPEALS ADMINISTRATIVE DECISION TODD EVANS, ADMINISTRATIVE LAW JUDGE

STATE OF ARKANSAS DEPARTMENT OF FINANCE & ADMINISTRATION OFFICE OF HEARINGS & APPEALS ADMINISTRATIVE DECISION IN THE MATTER OF LICENSE NO.: DOCKET NO.: 19-209 GROSS RECEIPTS (SALES) TAX REFUND CLAIM DENIAL

STATE OF ARKANSAS DEPARTMENT OF FINANCE & ADMINISTRATION OFFICE OF HEARINGS & APPEALS ADMINISTRATIVE DECISION IN THE MATTER OF LICENSE NO.: DOCKET NO.: 19-209 GROSS RECEIPTS (SALES) TAX REFUND CLAIM DENIAL

Rulemaking Hearing Rules of Tennessee Department of Finance and Administration. Bureau of TennCare. Chapter TennCare Medicaid.

Rulemaking Hearing Rules of Tennessee Department of Finance and Administration Bureau of TennCare Chapter 1200-13-13 TennCare Medicaid Amendments Parts 5. and 6. of subparagraph (a) of paragraph (1) of

Rulemaking Hearing Rules of Tennessee Department of Finance and Administration Bureau of TennCare Chapter 1200-13-13 TennCare Medicaid Amendments Parts 5. and 6. of subparagraph (a) of paragraph (1) of

Property Tax 101. Amy Koethe Dakota County Property Taxation & Records Jeanne Vogt - Ehlers

Property Tax 101 Amy Koethe Dakota County Property Taxation & Records Jeanne Vogt - Ehlers 1 Minnesota GFOA Conference Arrowwood Resort September 28, 2017 Overview Minnesota has one of the most complex

Property Tax 101 Amy Koethe Dakota County Property Taxation & Records Jeanne Vogt - Ehlers 1 Minnesota GFOA Conference Arrowwood Resort September 28, 2017 Overview Minnesota has one of the most complex

Subd. 5. "Health and Inspections Department" means the City of St. Cloud Health and

Section 441 - Lodging Establishments Section 441:00. Regulation of Lodging Establishments, Hotels, Motels, Bed and Breakfast and Board and Lodging Establishments. Subd. 1. Purpose. The purpose of this

Section 441 - Lodging Establishments Section 441:00. Regulation of Lodging Establishments, Hotels, Motels, Bed and Breakfast and Board and Lodging Establishments. Subd. 1. Purpose. The purpose of this

SUMMARY OF THE 2014 MISSISSIPPI TAXPAYER FAIRNESS ACT

SUMMARY OF THE 2014 MISSISSIPPI TAXPAYER FAIRNESS ACT This omnibus tax legislation, House Bill No. 799, was signed into law by Governor Phil Bryant on April 11, 2014, after passing the House of Representatives

SUMMARY OF THE 2014 MISSISSIPPI TAXPAYER FAIRNESS ACT This omnibus tax legislation, House Bill No. 799, was signed into law by Governor Phil Bryant on April 11, 2014, after passing the House of Representatives

Protest Procedure: A Primer

Protest Procedure: A Primer Marjorie Welch Interim General Counsel Oklahoma Tax Commission Agency s Mission Statement: To serve the people of Oklahoma by promoting tax compliance through quality service

Protest Procedure: A Primer Marjorie Welch Interim General Counsel Oklahoma Tax Commission Agency s Mission Statement: To serve the people of Oklahoma by promoting tax compliance through quality service

REAL PROPERTY ASSESSMENTS IN OHIO

REAL PROPERTY ASSESSMENTS IN OHIO Locally imposed real property taxes have traditionally been the principle financial bulwark of the local governments in Ohio. These taxes are locally collected, and virtually

REAL PROPERTY ASSESSMENTS IN OHIO Locally imposed real property taxes have traditionally been the principle financial bulwark of the local governments in Ohio. These taxes are locally collected, and virtually

Rule 006 Refunds & Credits

Rule 006 Refunds & Credits Refunds or credits are granted according to R.S. 47:337.77 through 47:337.81 and 47:337.86. When requesting a refund or credit, the taxpayer must first submit a formal written

Rule 006 Refunds & Credits Refunds or credits are granted according to R.S. 47:337.77 through 47:337.81 and 47:337.86. When requesting a refund or credit, the taxpayer must first submit a formal written

Comptroller Tax Process Improvements

Comptroller Tax Process Improvements Introduction Comptroller Susan Combs announces improvements to all phases of the Comptroller s tax process. After transferring the Administrative Law Judges (ALJs)

Comptroller Tax Process Improvements Introduction Comptroller Susan Combs announces improvements to all phases of the Comptroller s tax process. After transferring the Administrative Law Judges (ALJs)

SENIORS Clauses 41, 41B, 41C, 41C½

Michael J. Heffernan Commissioner of Revenue Sean R. Cronin Senior Deputy Commissioner TAXPAYER S GUIDE TO LOCAL PROPERTY TAX EXEMPTIONS SENIORS Clauses 41, 41B, 41C, 41C½ The Department of Revenue (DOR)

Michael J. Heffernan Commissioner of Revenue Sean R. Cronin Senior Deputy Commissioner TAXPAYER S GUIDE TO LOCAL PROPERTY TAX EXEMPTIONS SENIORS Clauses 41, 41B, 41C, 41C½ The Department of Revenue (DOR)

Duties of Department of Revenue. NC General Statutes - Chapter 105 Article 15 1

Article 15. Duties of Department and Property Tax Commission as to Assessments. 105-288. Property Tax Commission. (a) Creation and Membership. The Property Tax Commission is created. It consists of five

Article 15. Duties of Department and Property Tax Commission as to Assessments. 105-288. Property Tax Commission. (a) Creation and Membership. The Property Tax Commission is created. It consists of five

SEC. 5. SMALL CASE PROCEDURE FOR REQUESTING COMPETENT AUTHORITY ASSISTANCE.01 General.02 Small Case Standards.03 Small Case Filing Procedure

26 CFR 601.201: Rulings and determination letters. Rev. Proc. 96 13 OUTLINE SECTION 1. PURPOSE OF MUTUAL AGREEMENT PROCESS SEC. 2. SCOPE Suspension.02 Requests for Assistance.03 U.S. Competent Authority.04

26 CFR 601.201: Rulings and determination letters. Rev. Proc. 96 13 OUTLINE SECTION 1. PURPOSE OF MUTUAL AGREEMENT PROCESS SEC. 2. SCOPE Suspension.02 Requests for Assistance.03 U.S. Competent Authority.04

TRANSMITTAL MEMORANDUM PROPERTY TAX OVERSIGHT RULES

PTO TM #16-01 TRANSMITTAL MEMORANDUM PROPERTY TAX OVERSIGHT RULES PURPOSE: This transmittal memorandum contains changes to the Department of Revenue Rules within the Property Tax Oversight Program. RULE

PTO TM #16-01 TRANSMITTAL MEMORANDUM PROPERTY TAX OVERSIGHT RULES PURPOSE: This transmittal memorandum contains changes to the Department of Revenue Rules within the Property Tax Oversight Program. RULE

County Boards of Equalization: Creation, Duties, and Statutory Procedures

County Boards of Equalization: Creation, Duties, and Statutory Procedures Prepared and Presented By F. Barry Wilkes Clerk of the Superior Court of Liberty County General Provisions Laws specifically pertaining

County Boards of Equalization: Creation, Duties, and Statutory Procedures Prepared and Presented By F. Barry Wilkes Clerk of the Superior Court of Liberty County General Provisions Laws specifically pertaining

Taxpayers Guide to the 2018 Reassessment

Taxpayers Guide to the 2018 Reassessment Why is there a reassessment done? Lancaster County uses base year methodology to set assessed values. Lancaster County s base year will be set as January 1, 2015

Taxpayers Guide to the 2018 Reassessment Why is there a reassessment done? Lancaster County uses base year methodology to set assessed values. Lancaster County s base year will be set as January 1, 2015

TABLE OF CONTENTS. .03 Farmers cooperatives. .01 A request made during the course of an examination

Rev. Proc. 2000 2 TABLE OF CONTENTS SECTION 1. WHAT IS THE p. 77 PURPOSE OF THIS REVENUE PROCEDURE? SECTION 2. WHAT IS p. 78 TECHNICAL ADVICE? SECTION 3. ON WHAT ISSUES p. 78 MAY TECHNICAL ADVICE BE REQUESTED

Rev. Proc. 2000 2 TABLE OF CONTENTS SECTION 1. WHAT IS THE p. 77 PURPOSE OF THIS REVENUE PROCEDURE? SECTION 2. WHAT IS p. 78 TECHNICAL ADVICE? SECTION 3. ON WHAT ISSUES p. 78 MAY TECHNICAL ADVICE BE REQUESTED

Tammy L Smith, Sr. Residential Real Estate Appraisal Deputy Certified Level III Assessor Appraiser Certified Indiana Tax Representative

Tammy L Smith, Sr. Residential Real Estate Appraisal Deputy Certified Level III Assessor Appraiser Certified Indiana Tax Representative IMPORTANT CONTACT INFORMATION Tammy L Smith, Wayne Township Rental

Tammy L Smith, Sr. Residential Real Estate Appraisal Deputy Certified Level III Assessor Appraiser Certified Indiana Tax Representative IMPORTANT CONTACT INFORMATION Tammy L Smith, Wayne Township Rental

Legislative Information - LBDC

Page 1 of 9 PART A Section 1. Paragraph (a) of subdivision 6 of section 425 of the real property tax law, as amended by chapter 6 of the laws of 2010, and as further amended by subdivision (b) of section

Page 1 of 9 PART A Section 1. Paragraph (a) of subdivision 6 of section 425 of the real property tax law, as amended by chapter 6 of the laws of 2010, and as further amended by subdivision (b) of section

A Bill Regular Session, 2017 HOUSE BILL 1772

Stricken language would be deleted from and underlined language would be added to present law. Act of the Regular Session 0 State of Arkansas st General Assembly As Engrossed: H// A Bill Regular Session,

Stricken language would be deleted from and underlined language would be added to present law. Act of the Regular Session 0 State of Arkansas st General Assembly As Engrossed: H// A Bill Regular Session,

Summary of House Bill 202: Amendments to Georgia s Real Property Tax Assessment and Appeal System

Summary of House Bill 202: Amendments to Georgia s Real Property Tax Assessment and Appeal System After a wild finish, the Georgia Legislature passed House Bill 202 on the final day of the session, April

Summary of House Bill 202: Amendments to Georgia s Real Property Tax Assessment and Appeal System After a wild finish, the Georgia Legislature passed House Bill 202 on the final day of the session, April

APPEAL PROCEDURES, RULES and REGULATIONS

APPEAL PROCEDURES, RULES and REGULATIONS Rule # BOARD OF ASSESSMENT APPEALS OF CLEARFIELD COUNTY A. GENERAL RULES 1) TIME for FILING: All annual appeals from the assessment of real estate must be properly

APPEAL PROCEDURES, RULES and REGULATIONS Rule # BOARD OF ASSESSMENT APPEALS OF CLEARFIELD COUNTY A. GENERAL RULES 1) TIME for FILING: All annual appeals from the assessment of real estate must be properly

v No Wayne Circuit Court

S T A T E O F M I C H I G A N C O U R T O F A P P E A L S CITY OF DETROIT, Plaintiff-Appellant, UNPUBLISHED March 15, 2018 v No. 337705 Wayne Circuit Court BAYLOR LTD, LC No. 16-010881-CZ Defendant-Appellee.

S T A T E O F M I C H I G A N C O U R T O F A P P E A L S CITY OF DETROIT, Plaintiff-Appellant, UNPUBLISHED March 15, 2018 v No. 337705 Wayne Circuit Court BAYLOR LTD, LC No. 16-010881-CZ Defendant-Appellee.

Certificate of Insurance Individual Vision Indemnity Plan

Underwritten by SafeHealth Life Insurance Company Certificate of Insurance Individual Vision Indemnity Plan This certificate contains a deductible provision. SG SHL IND V - POL 1 POLICYHOLDER: POLICY NUMBER:

Underwritten by SafeHealth Life Insurance Company Certificate of Insurance Individual Vision Indemnity Plan This certificate contains a deductible provision. SG SHL IND V - POL 1 POLICYHOLDER: POLICY NUMBER:

Rights of the Taxpayer

State of Louisiana Department of Revenue Rights of the Taxpayer Louisiana Department of Revenue Post Office Box 201 Baton Rouge, LA 70821-0201 Additional copies of this pamphlet (R-20161) are available

State of Louisiana Department of Revenue Rights of the Taxpayer Louisiana Department of Revenue Post Office Box 201 Baton Rouge, LA 70821-0201 Additional copies of this pamphlet (R-20161) are available

IN THE COMMONWEALTH COURT OF PENNSYLVANIA

IN THE COMMONWEALTH COURT OF PENNSYLVANIA In Re: Petition of the Venango County : Tax Claim Bureau for Judicial : Sale of Lands Free and Clear : of all Taxes and Municipal Claims, : Mortgages, Liens, Charges

IN THE COMMONWEALTH COURT OF PENNSYLVANIA In Re: Petition of the Venango County : Tax Claim Bureau for Judicial : Sale of Lands Free and Clear : of all Taxes and Municipal Claims, : Mortgages, Liens, Charges

IC Chapter 5. Assessment of Taxes

IC 6-8.1-5 Chapter 5. Assessment of Taxes IC 6-8.1-5-1 Proposed assessment; notice; protest; hearing; letter of findings; rehearing; appeal; demand for payment Sec. 1. (a) As used in this section, "letter

IC 6-8.1-5 Chapter 5. Assessment of Taxes IC 6-8.1-5-1 Proposed assessment; notice; protest; hearing; letter of findings; rehearing; appeal; demand for payment Sec. 1. (a) As used in this section, "letter

BURNS INDIANA STATUTES ANNOTATED TITLE 34. CIVIL LAW AND PROCEDURE ARTICLE 50. SETTLEMENT OF CLAIMS CHAPTER 2. ANNUITY STRUCTURED SETTLEMENTS

For more information please visit Strategic Capital Corporation at www.strategiccapital.com, or contact us at Toll Free: 1-866-256-0088 or email us at info@strategiccapital.com. BURNS INDIANA STATUTES

For more information please visit Strategic Capital Corporation at www.strategiccapital.com, or contact us at Toll Free: 1-866-256-0088 or email us at info@strategiccapital.com. BURNS INDIANA STATUTES

State of Indiana Board of Tax Review

State of Indiana Board of Tax Review Evansville Lapidary Society, Inc., ) On Appeal from the Vanderburgh County ) Property Tax Assessment Board of Appeals Petitioner, ) ) ) Petition for Review of Exemption,

State of Indiana Board of Tax Review Evansville Lapidary Society, Inc., ) On Appeal from the Vanderburgh County ) Property Tax Assessment Board of Appeals Petitioner, ) ) ) Petition for Review of Exemption,

Chapter 2 Books, Records, Accounts and Vouchers

Public Records Authority Chapter 2 Books, Records, Accounts and Vouchers 1. Ch. 66, Ch. 4 7(26) and 950 CMR 32.01-32.09 regulate access to public records. 2. Public records include all books, papers, maps,

Public Records Authority Chapter 2 Books, Records, Accounts and Vouchers 1. Ch. 66, Ch. 4 7(26) and 950 CMR 32.01-32.09 regulate access to public records. 2. Public records include all books, papers, maps,

STATE OF ARKANSAS DEPARTMENT OF FINANCE & ADMINISTRATION OFFICE OF HEARINGS & APPEALS ADMINISTRATIVE DECISION

STATE OF ARKANSAS DEPARTMENT OF FINANCE & ADMINISTRATION OFFICE OF HEARINGS & APPEALS ADMINISTRATIVE DECISION IN THE MATTER OF (ACCT. NO.: INDIVIDUAL INCOME TAX ASSESSMENT LETTER ID.: DOCKET NO.: 17-045

STATE OF ARKANSAS DEPARTMENT OF FINANCE & ADMINISTRATION OFFICE OF HEARINGS & APPEALS ADMINISTRATIVE DECISION IN THE MATTER OF (ACCT. NO.: INDIVIDUAL INCOME TAX ASSESSMENT LETTER ID.: DOCKET NO.: 17-045

IC Chapter 5. Assessment of Taxes

IC 6-8.1-5 Chapter 5. Assessment of Taxes IC 6-8.1-5-1 Proposed assessment; notice; protest; hearing; letter of findings; rehearing; appeal; demand for payment Sec. 1. (a) As used in this section, "letter

IC 6-8.1-5 Chapter 5. Assessment of Taxes IC 6-8.1-5-1 Proposed assessment; notice; protest; hearing; letter of findings; rehearing; appeal; demand for payment Sec. 1. (a) As used in this section, "letter

06.07 ALTERNATE METHODS OF TAXATION

06.07 ALTERNATE METHODS OF TAXATION Overview There are methods of property taxation that differ from the normal calculations described elsewhere in this manual. This section provides an overview of three

06.07 ALTERNATE METHODS OF TAXATION Overview There are methods of property taxation that differ from the normal calculations described elsewhere in this manual. This section provides an overview of three

ORDINANCE NO. WHEREAS, Act , was approved and adopted May 5, 1998 by the General Assembly of the Commonwealth of Pennsylvania; and

ORDINANCE NO. AN ORDINANCE OF THE BOARD OF SUPERVISORS OF THE TOWNSHIP OF HANOVER, NORTHAMPTON COUNTY, IN THE COMMONWEALTH OF PENNSYLVANIA AMENDING THE CODE OF THE TOWNSHIP OF HANOVER CODE OF ORDINANCES

ORDINANCE NO. AN ORDINANCE OF THE BOARD OF SUPERVISORS OF THE TOWNSHIP OF HANOVER, NORTHAMPTON COUNTY, IN THE COMMONWEALTH OF PENNSYLVANIA AMENDING THE CODE OF THE TOWNSHIP OF HANOVER CODE OF ORDINANCES

COURT OF APPEALS PERRY COUNTY, OHIO FIFTH APPELLATE DISTRICT

[Cite as Owen v. Perry Cty. Bd. of Revision, 2013-Ohio-2303.] COURT OF APPEALS PERRY COUNTY, OHIO FIFTH APPELLATE DISTRICT CHARLES W. OWEN, JR., ET AL. : JUDGES: : Hon. W. Scott Gwin, P.J. Plaintiffs-Appellees

[Cite as Owen v. Perry Cty. Bd. of Revision, 2013-Ohio-2303.] COURT OF APPEALS PERRY COUNTY, OHIO FIFTH APPELLATE DISTRICT CHARLES W. OWEN, JR., ET AL. : JUDGES: : Hon. W. Scott Gwin, P.J. Plaintiffs-Appellees

Child Care Center Licensing Manual (August 2016)

") Child Care Center Licensing Manual (August 2016) for use with COMAR 13A.16 Child Care Centers (as amended effective 7/20/15) Table of Contents COMAR 13A.16.18 ADMINISTRATIVE HEARINGS.01 Scope...1.02 Definitions...1.03

Child Care Center Licensing Manual (August 2016) for use with COMAR 13A.16 Child Care Centers (as amended effective 7/20/15) Table of Contents COMAR 13A.16.18 ADMINISTRATIVE HEARINGS.01 Scope...1.02 Definitions...1.03

STATE OF ARKANSAS DEPARTMENT OF FINANCE & ADMINISTRATION OFFICE OF HEARINGS & APPEALS ADMINISTRATIVE DECISION

STATE OF ARKANSAS DEPARTMENT OF FINANCE & ADMINISTRATION OFFICE OF HEARINGS & APPEALS ADMINISTRATIVE DECISION IN THE MATTER OF GROSS RECEIPTS TAX & ALCOHOLIC BEVERAGE ACCT. NO.: TAX ASSESSMENTS AUDIT NO.:

STATE OF ARKANSAS DEPARTMENT OF FINANCE & ADMINISTRATION OFFICE OF HEARINGS & APPEALS ADMINISTRATIVE DECISION IN THE MATTER OF GROSS RECEIPTS TAX & ALCOHOLIC BEVERAGE ACCT. NO.: TAX ASSESSMENTS AUDIT NO.:

New Jersey Division of Taxation

New Jersey Division of Taxation Protest and Conference Guidebook Office of Counsel Services Conference and Appeals Branch October 2017 CAB-300 Protest and Conference Guidebook Page 2 Submitting a Protest

New Jersey Division of Taxation Protest and Conference Guidebook Office of Counsel Services Conference and Appeals Branch October 2017 CAB-300 Protest and Conference Guidebook Page 2 Submitting a Protest

LEGISLATIVE UPDATE. Association of Indiana Counties 2012 District Meetings

LEGISLATIVE UPDATE Association of Indiana Counties 2012 District Meetings Local Income Tax Under-Distribution Issue: Dept. of Revenue misclassified estimated payments that broke apart both county and state

LEGISLATIVE UPDATE Association of Indiana Counties 2012 District Meetings Local Income Tax Under-Distribution Issue: Dept. of Revenue misclassified estimated payments that broke apart both county and state

BLAIR COUNTY ASSESSMENT APPEALS RULES AND REGULATIONS

BLAIR COUNTY ASSESSMENT APPEALS RULES AND REGULATIONS I. FILING OF APPEAL 1. STANDING TO APPEAL: The Board of Assessment Revision/Board of Assessment Appeals (or such auxiliary appeal boards or alternates

BLAIR COUNTY ASSESSMENT APPEALS RULES AND REGULATIONS I. FILING OF APPEAL 1. STANDING TO APPEAL: The Board of Assessment Revision/Board of Assessment Appeals (or such auxiliary appeal boards or alternates

IN THE COMMONWEALTH COURT OF PENNSYLVANIA

IN THE COMMONWEALTH COURT OF PENNSYLVANIA In Re: Return and Report of an : Upset Tax Sale held by the : Cumberland County Tax Claim : Bureau on September 20, 2007 : No. 1829 C.D. 2008 : Re: Property of

IN THE COMMONWEALTH COURT OF PENNSYLVANIA In Re: Return and Report of an : Upset Tax Sale held by the : Cumberland County Tax Claim : Bureau on September 20, 2007 : No. 1829 C.D. 2008 : Re: Property of

APPEALS AND GRIEVANCES Section 6. Member Grievances / Complaints

Member Grievances / Complaints A grievance is an expression of dissatisfaction from a member, member s representative or provider on behalf of a member about any matter other than an action. A member may

Member Grievances / Complaints A grievance is an expression of dissatisfaction from a member, member s representative or provider on behalf of a member about any matter other than an action. A member may

SECTION 5. SMALL CASE PROCEDURE FOR REQUESTING COMPETENT AUTHORITY ASSISTANCE.01 General.02 Small Case Standards.03 Small Case Filing Procedure

Rev. Proc. 2002 52 SECTION 1. PURPOSE OF THE REVENUE PROCEDURE SECTION 2. SCOPE.01 In General.02 Requests for Assistance.03 Authority of the U.S. Competent Authority.04 General Process.05 Failure to Request

Rev. Proc. 2002 52 SECTION 1. PURPOSE OF THE REVENUE PROCEDURE SECTION 2. SCOPE.01 In General.02 Requests for Assistance.03 Authority of the U.S. Competent Authority.04 General Process.05 Failure to Request

TAX LITIGATION MEMORANDUM

LAW OFFICES DAVID L. SILVERMAN, J.D., LL.M. 2001 MARCUS AVENUE LAKE SUCCESS, NEW YORK 11042 (516) 466-5900 SILVERMAN, DAVID L. TELECOPIER (516) 437-7292 NYTAXATTY@AOL.COM AMINOFF, SHIRLEE AMINOFFS@GMAIL.COM

LAW OFFICES DAVID L. SILVERMAN, J.D., LL.M. 2001 MARCUS AVENUE LAKE SUCCESS, NEW YORK 11042 (516) 466-5900 SILVERMAN, DAVID L. TELECOPIER (516) 437-7292 NYTAXATTY@AOL.COM AMINOFF, SHIRLEE AMINOFFS@GMAIL.COM

Member Appeal and Grievance Process

Standard Member Appeal and Grievance Process Carefully read the information in this packet and keep it for future reference. It has important information about how to appeal/grieve decisions Blue Cross

Standard Member Appeal and Grievance Process Carefully read the information in this packet and keep it for future reference. It has important information about how to appeal/grieve decisions Blue Cross

THE UNFAIR CLAIMS SETTLEMENT PRACTICES REGULATION. AMENDATORY SECTION (Amending Order R 78-3, filed 7/27/78, effective 9/1/78)

") THE UNFAIR CLAIMS SETTLEMENT PRACTICES REGULATION WAC 284-30-300 Authority and purpose. RCW 48.30.010 authorizes the commissioner to define methods of competition and acts and practices in the conduct

THE UNFAIR CLAIMS SETTLEMENT PRACTICES REGULATION WAC 284-30-300 Authority and purpose. RCW 48.30.010 authorizes the commissioner to define methods of competition and acts and practices in the conduct

Busy Season. all year long. TRI Tax Resolution Institute. where your tax debt is your power!

1 TRI Tax Resolution Institute where your tax debt is your power! Busy Season all year long www.taxresolutioninstitute.org info@taxresolutioninstitute.org (877) 829-8370 2 Appeals www.taxresolutioninstitute.org

1 TRI Tax Resolution Institute where your tax debt is your power! Busy Season all year long www.taxresolutioninstitute.org info@taxresolutioninstitute.org (877) 829-8370 2 Appeals www.taxresolutioninstitute.org

EXTERNAL FREQUENTLY ASKED QUESTIONS DISPUTE ADMINISTRATION

EXTERNAL FREQUENTLY ASKED QUESTIONS Revision: 5 Page 1 of 9 1 PURPOSE These frequently asked questions (FAQ) deal with the basic principles of objections and appeals applicable to individual and corporate

EXTERNAL FREQUENTLY ASKED QUESTIONS Revision: 5 Page 1 of 9 1 PURPOSE These frequently asked questions (FAQ) deal with the basic principles of objections and appeals applicable to individual and corporate

REFORMS Overview of Reforms to Mortgage and Foreclosure Processing Standards in the Settlement

Office of WV Attorney General Darrell McGraw MORTGAGE FORECLOSURE SETTLEMENT REFORMS Overview of Reforms to Mortgage and Foreclosure Processing Standards in the Settlement As negotiated nationally I. RETURN

Office of WV Attorney General Darrell McGraw MORTGAGE FORECLOSURE SETTLEMENT REFORMS Overview of Reforms to Mortgage and Foreclosure Processing Standards in the Settlement As negotiated nationally I. RETURN

CALIFORNIA CODES CIVIL CODE SECTION This title may be cited as the "Song-Beverly Credit Card Act of 1971."

CALIFORNIA CODES CIVIL CODE SECTION 1747-1748.95 1747. This title may be cited as the "Song-Beverly Credit Card Act of 1971." 1747.01. It is the intent of the Legislature that the provisions of this title

CALIFORNIA CODES CIVIL CODE SECTION 1747-1748.95 1747. This title may be cited as the "Song-Beverly Credit Card Act of 1971." 1747.01. It is the intent of the Legislature that the provisions of this title

10 SB 346/AP A BILL TO BE ENTITLED AN ACT

SB 346/AP Senate Bill 346 By: Senators Rogers of the 21st, Williams of the 19th, Thompson of the 33rd, Seabaugh of the 28th, Butterworth of the 50th and others AS PASSED A BILL TO BE ENTITLED AN ACT 1

SB 346/AP Senate Bill 346 By: Senators Rogers of the 21st, Williams of the 19th, Thompson of the 33rd, Seabaugh of the 28th, Butterworth of the 50th and others AS PASSED A BILL TO BE ENTITLED AN ACT 1

Title 36: TAXATION. Chapter 914: 2003 TAX AMNESTY PROGRAM. Table of Contents Part 9. TAXPAYER BENEFIT PROGRAMS...

Title 36: TAXATION Chapter 914: 2003 TAX AMNESTY PROGRAM Table of Contents Part 9. TAXPAYER BENEFIT PROGRAMS... Section 6571. 2003 MAINE TAX AMNESTY PROGRAM ESTABLISHED... 3 Section 6572. ADMINISTRATION...

Title 36: TAXATION Chapter 914: 2003 TAX AMNESTY PROGRAM Table of Contents Part 9. TAXPAYER BENEFIT PROGRAMS... Section 6571. 2003 MAINE TAX AMNESTY PROGRAM ESTABLISHED... 3 Section 6572. ADMINISTRATION...

HOW THE 1998 TAX ACT AFFECTS YOUR DEALINGS WITH THE IRS APPEALS OFFICE. The IRS Restructuring and Reform Act of 1998.

HOW THE 1998 TAX ACT AFFECTS YOUR DEALINGS WITH THE IRS APPEALS OFFICE The IRS Restructuring and Reform Act of 1998 January 22, 1999 Robert M. Kane, Jr. LeSourd & Patten, P.S. 600 University Street, Ste

HOW THE 1998 TAX ACT AFFECTS YOUR DEALINGS WITH THE IRS APPEALS OFFICE The IRS Restructuring and Reform Act of 1998 January 22, 1999 Robert M. Kane, Jr. LeSourd & Patten, P.S. 600 University Street, Ste

BOARD OF ASSESSMENT REVIEW OF NEW CASTLE COUNTY RULES OF PROCEDURE

Revised: May 17, 2018 BOARD OF ASSESSMENT REVIEW OF NEW CASTLE COUNTY RULES OF PROCEDURE Article I. Authorization. The Board of Assessment Review of New Castle County (hereinafter referred to as the Board

Revised: May 17, 2018 BOARD OF ASSESSMENT REVIEW OF NEW CASTLE COUNTY RULES OF PROCEDURE Article I. Authorization. The Board of Assessment Review of New Castle County (hereinafter referred to as the Board

NOTICE OF PENDENCY OF CLASS ACTION, PROPOSED SETTLEMENT AND HEARING DATE FOR COURT APPROVAL

ATTENTION: NOTICE OF PENDENCY OF CLASS ACTION, PROPOSED SETTLEMENT AND HEARING DATE FOR COURT APPROVAL BANK BRANCH STORE MANAGERS EMPLOYED BY WELLS FARGO BANK, NA ( DEFENDANT ) WHO: WORKED IN A LEVEL 1

ATTENTION: NOTICE OF PENDENCY OF CLASS ACTION, PROPOSED SETTLEMENT AND HEARING DATE FOR COURT APPROVAL BANK BRANCH STORE MANAGERS EMPLOYED BY WELLS FARGO BANK, NA ( DEFENDANT ) WHO: WORKED IN A LEVEL 1

Arbitration Forums, Inc. Rules

Arbitration Forums, Inc. Rules Effective February 1, 2010 The following rules are made and administered by Arbitration Forums, Inc. (AF) under the authority of Article Fifth (a) of the various Arbitration

Arbitration Forums, Inc. Rules Effective February 1, 2010 The following rules are made and administered by Arbitration Forums, Inc. (AF) under the authority of Article Fifth (a) of the various Arbitration

All Home and Community Based Services Waiver Providers. Subject: HCBS Waiver Audit Process, Recoupment, and Appeals

P R O V I D E R B U L L E T I N B T 2 0 0 4 1 2 J U N E 1 1, 2 0 0 4 To: All Home and Community Based Services Waiver Providers Subject: Overview This bulletin informs all Home and Community Based Services

P R O V I D E R B U L L E T I N B T 2 0 0 4 1 2 J U N E 1 1, 2 0 0 4 To: All Home and Community Based Services Waiver Providers Subject: Overview This bulletin informs all Home and Community Based Services

Senate Substitute for HOUSE BILL No. 2026

Senate Substitute for HOUSE BILL No. 2026 AN ACT concerning the Kansas program of medical assistance; process and contract requirements; claims appeals. Be it enacted by the Legislature of the State of

Senate Substitute for HOUSE BILL No. 2026 AN ACT concerning the Kansas program of medical assistance; process and contract requirements; claims appeals. Be it enacted by the Legislature of the State of

FREEHOLD MINERAL RIGHTS TAX ACT

Province of Alberta FREEHOLD MINERAL RIGHTS TAX ACT Revised Statutes of Alberta 2000 Chapter F-26 Current as of November 30, 2015 Office Consolidation Published by Alberta Queen s Printer Alberta Queen

Province of Alberta FREEHOLD MINERAL RIGHTS TAX ACT Revised Statutes of Alberta 2000 Chapter F-26 Current as of November 30, 2015 Office Consolidation Published by Alberta Queen s Printer Alberta Queen

Mercantil Bank, N.A. Cardholder Agreement

Mercantil Bank, N.A. Cardholder Agreement This Agreement governs your credit card account ( Account ) with us. It consists of this document, a Pricing Information document, and other documents that we

Mercantil Bank, N.A. Cardholder Agreement This Agreement governs your credit card account ( Account ) with us. It consists of this document, a Pricing Information document, and other documents that we

CITY OF DOVER ORDINANCE # WITH AMENDMENT #1 BE IT ORDAINED BY THE MAYOR AND COUNCIL OF THE CITY OF DOVER, IN COUNCIL MET:

CITY OF DOVER ORDINANCE #2009-17 WITH AMENDMENT #1 BE IT ORDAINED BY THE MAYOR AND COUNCIL OF THE CITY OF DOVER, IN COUNCIL MET: That Chapter 2 Administration, Article IV - Officers and Employees, Division

CITY OF DOVER ORDINANCE #2009-17 WITH AMENDMENT #1 BE IT ORDAINED BY THE MAYOR AND COUNCIL OF THE CITY OF DOVER, IN COUNCIL MET: That Chapter 2 Administration, Article IV - Officers and Employees, Division

When Will They Stop Changing the Rules for Employee Benefits?

When Will They Stop Changing the Rules for Employee Benefits? Presented by: Daniel Kopti National Practice Employee Benefits Compliance Advisor Wells Fargo Insurance Services USA, Inc. January 10, 2017

When Will They Stop Changing the Rules for Employee Benefits? Presented by: Daniel Kopti National Practice Employee Benefits Compliance Advisor Wells Fargo Insurance Services USA, Inc. January 10, 2017

BOSTON WATER AND SEWER COMMISSION BILLING, TERMINATION AND APPEAL REGULATIONS

BOSTON WATER AND SEWER COMMISSION BILLING, TERMINATION AND APPEAL REGULATIONS TABLE OF CONTENTS CHAPTER 1 DEFINITIONS AND GENERAL PROVISIONS 1.1 Authority to Adopt Rules and Regulations 1.2 Application;

BOSTON WATER AND SEWER COMMISSION BILLING, TERMINATION AND APPEAL REGULATIONS TABLE OF CONTENTS CHAPTER 1 DEFINITIONS AND GENERAL PROVISIONS 1.1 Authority to Adopt Rules and Regulations 1.2 Application;

As Introduced. 132nd General Assembly Regular Session H. B. No

132nd General Assembly Regular Session H. B. No. 460 2017-2018 Representatives Patterson, Sheehy Cosponsors: Representatives Antonio, Smith, K., Kelly, O'Brien, West A B I L L To amend sections 321.24,

132nd General Assembly Regular Session H. B. No. 460 2017-2018 Representatives Patterson, Sheehy Cosponsors: Representatives Antonio, Smith, K., Kelly, O'Brien, West A B I L L To amend sections 321.24,

Appeal Process Guide. Property Valuation Services Corporation phone: fax:

Appeal Process Guide Property Valuation Services Corporation phone: 1-800-380-7775 fax: 1-888-339-4555 web: WWW.PVSC.CA Last Revised December 2012 Property Valuation Services Corporation Effective April

Appeal Process Guide Property Valuation Services Corporation phone: 1-800-380-7775 fax: 1-888-339-4555 web: WWW.PVSC.CA Last Revised December 2012 Property Valuation Services Corporation Effective April

STATE OF MISSISSIPPI DEPARTMENT OF BANKING AND CONSUMER FINANCE MORTGAGE DIVISION MISSISSIPPI MORTGAGE CONSUMER PROTECTION LAW REGULATIONS

STATE OF MISSISSIPPI DEPARTMENT OF BANKING AND CONSUMER FINANCE MORTGAGE DIVISION MISSISSIPPI MORTGAGE CONSUMER PROTECTION LAW REGULATIONS Compiled by the Department of Banking and Consumer Finance For

STATE OF MISSISSIPPI DEPARTMENT OF BANKING AND CONSUMER FINANCE MORTGAGE DIVISION MISSISSIPPI MORTGAGE CONSUMER PROTECTION LAW REGULATIONS Compiled by the Department of Banking and Consumer Finance For

DEFERRAL/WAIVER OF FEES & COSTS. Packet #2. Separate forms from packet before filing.

DEFERRAL/WAIVER OF FEES & COSTS Packet #2 Separate forms from packet before filing. SOUTHERN ARIZONA LEGAL AID, INC. DEFERRAL OR WAIVER OF COURT FEES AND COSTS INSTRUCTIONS AND FORMS USE AND DISCLAIMER

DEFERRAL/WAIVER OF FEES & COSTS Packet #2 Separate forms from packet before filing. SOUTHERN ARIZONA LEGAL AID, INC. DEFERRAL OR WAIVER OF COURT FEES AND COSTS INSTRUCTIONS AND FORMS USE AND DISCLAIMER

ADOPTED REGULATION OF THE DEPARTMENT OF TAXATION. LCB File No. R Effective April 30, 2004

ADOPTED REGULATION OF THE DEPARTMENT OF TAXATION LCB File No. R224-03 Effective April 30, 2004 EXPLANATION Matter in italics is new; matter in brackets [omitted material] is material to be omitted. AUTHORITY:

ADOPTED REGULATION OF THE DEPARTMENT OF TAXATION LCB File No. R224-03 Effective April 30, 2004 EXPLANATION Matter in italics is new; matter in brackets [omitted material] is material to be omitted. AUTHORITY:

Appeals for providers