Privatisation and Infrastructure Australian Federal Tax Framework (January 2017 Draft)

|

|

|

- Hortense Peters

- 5 years ago

- Views:

Transcription

1 Privatisation and Infrastructure Australian Federal Tax Framework (January 2017 Draft) QUALIFICATION THIS DOCUMENT IS A DRAFT. IT IS INTENDED TO GENERATE FEEDBACK FROM STAKEHOLDERS ON THE ISSUES IT RAISES RELATING TO THE TAXATION OF INCOME FROM PRIVATISATION AND INFRASTRUCTURE ACTIVITY. 1

2 Contents Introduction Construction of social infrastructure using the securitised licence PPP model Background Structure of a social PPP Income tax treatment of a social PPP Variation involving a progressive securitisation Variations involving Government contributions GST interaction with PPPs Investor structure of the social PPP Tax treatment of the investor s investment into the social PPP Tax treatment upon exit for investors Privatisation of Government businesses into stapled structures Tax treatment of the asset-level structure Cross-staple loan variation The upstream/feeder-level structure Tax treatment of the upstream/feeder-level structure Restructuring and exiting of an investment Other infrastructure-related issues Customer cash contributions / reimbursements Government grants Gifted assets Capitalised Labour Undergrounding power lines Control for the purposes of Division 6C Areas of ATO compliance focus Abuse of PPP structures Illegitimate use of stapled structures Overshoot of land-rich privatisations into stapled structures Fracturing of control interests Satisfaction of MIT requirements Interposition of a Finance Co owned by a Charitable Trust

3 Introduction The Australian Taxation Office (ATO) recognises the increasing importance that infrastructure investment has to the Australian economy. The ATO plays an integral role in facilitating the continuation and expansion of this industry. For this reason, it is our intention to work collaboratively with industry and state governments to: maximise certainty about the way we administer the law; ensure that the tax system is administered in a sensible and pragmatic way, to the extent the law allows; provide assurance to the federal government that an appropriate amount of tax is collected from these transactions; and minimise the compliance costs of bidders, operators and state governments. What this framework is about This framework sets out our overall position on a range of infrastructure-related tax issues. It is not meant to provide the answer to all your questions or explain the tax treatment of every type of transaction you might enter into. Rather, it is a guide on how the tax law will apply in relation to a number of issues. This framework is also intended to be a living document. As new transactions and issues emerge, the framework may have to be updated to reflect them. The same can be said about changes to tax laws that may impact upon the analysis. Unless otherwise stated, all legislative references are to the Income Tax Assessment Act 1997 and any references to a government and its related entities are stylised as Government. How this framework differs to other ATO guidance products This document does not bind us to a particular view of the law. Only taxation rulings, taxation determinations or private rulings can do that. However, if you have transactions that are similar to the transactions outlined in this document, our officers would be expected to follow the overall views set out here. This includes officers that issue rulings as well as those conducting compliance activities. 3

4 Contents of the framework This framework is in four chapters: 1. Construction of social infrastructure using the securitised licence PPP model 2. Privatisation of Government businesses into stapled structures 3. Other infrastructure-related issues 4. Areas of ATO compliance focus 4

5 1. Construction of social infrastructure using the securitised licence PPP model This chapter sets out how the income tax and the Goods and Services Tax (GST) laws apply to a social PPP. This chapter is structured as follows: 1. Background 2. Structure of a social PPP 3. Income tax treatment of a social PPP 4. Variation involving a progressive securitisation 5. Variations involving Government contributions 6. GST interaction with PPPs 7. Investor structure of the social PPP 8. Tax treatment of the investor s investment into the social PPP 9. Tax treatment upon exit for investors 5

6 1.1 Background A social PPP involves a consortium and a Government agreeing that: the consortium will construct and maintain certain social infrastructure; the consortium will obtain the financing for that infrastructure; and the Government will obtain title to and repay the consortium for the infrastructure, plus interest, over a certain period. Examples of the type of infrastructure that may be subject to this arrangement include schools, hospitals, prisons, roads and public utilities. These are different to economic PPPs which involve user fees being used to repay the consortium s cost of construction and financing, rather than payments from the Government. These are not covered by this chapter. 1.2 Structure of a social PPP This part is about: 1. The substance of the commercial relations between the parties involved in a social PPP 2. The transactions actually undertaken between the parties 3. How the flow of funds operates between the parties The substance of the commercial relations The substance of the commercial relations between the parties involved in a social PPP is as follows: 1. An infrastructure asset is built for the Government by a private sector consortium. Depending on the terms of the PPP, the risks associated with the construction of this asset may be partially or completely borne by the private sector. The period of this construction is called the design and construction phase. The private sector also finances the cost of construction during this phase. 2. Once the design and construction phase is complete, the Government: a. owns the asset; and b. starts paying for the cost of construction, plus interest. It progressively pays down the principal and interest over a defined term, akin to an amortising loan. 6

7 3. During the term of the repayment, the private sector consortium also operates and maintains the infrastructure. The risks relating to this phase of the operation are also partially or completely borne by the private sector, depending upon the terms of the PPP. This phase is called the operations and maintenance phase. The consortium is compensated for providing this service by the Government. 4. The consortium may make profits in two ways: a. the amount it receives from the Government for the cost of construction is more than its actual cost of construction (plus the interest incurred while the construction happened); and b. the amount it receives from the Government to operate and maintain the infrastructure is more than its actual costs for these activities The transactions actually undertaken The transactions actually undertaken between the parties are as follows: 1. Two special purpose project entities are established. These are: a. Project Trust carries out the design, construction, operation and maintenance of the infrastructure asset. Project Trust is usually owned by the private sector consortium s members, and it is Project Trust that makes most of the profits from the project. b. Finance Co obtains senior debt for the project. Finance Co may be held by the consortium s members or by a charitable trust. Finance Co generally does not make profits from the project. 2. Finance Co raises external debt in the form of loans or facility agreements for the design and construction phase of the project. This external debt is repaid at the end of the design and construction phase. 3. Finance Co on-lends these funds to Project Trust (the D&C loan), which procures the design and construction of the asset. 4. In terms of Project Trust itself, a project deed is entered into which sets out its obligations to procure the design and construction of the asset and subsequently operate and maintain the asset. 5. Project Trust obtains consideration for entering into the project deed. Specifically: a. it obtains the construction payment from the Government at the end of the design and construction phase; and 7

8 b. it obtains availability payments from the Government during the term of the operations and maintenance phase. 6. At the end of the design and construction phase, Finance Co raises long-term debt for the duration of the operations and maintenance phase (the O&M loan). This is usually with a consortium of banks. 7. Finance Co enters into the securitisation agreement with the Government under which: a. it is assigned the licence payments that Project Trust pays to the Government in step 11(a); and b. Finance Co pays the receivables purchase payment which is financed by the longterm debt raised at step The Government finances the construction payment to Project Trust, described at step 5(a), from the receivables purchase payment it receives from Finance Co. 9. Project Trust uses the construction payment to repay the D&C loan, and Finance Co in turn uses these funds to repay the design and construction financiers (D&C financiers). In some circumstances, the D&C loan and the O&M loan could be the same loan, and in other cases it may be a different loan with different financiers. 10. The Government makes the availability payments, referred to in step 5(b), out of consolidated revenue. These payments are the mechanism by which the Government pays the consortium for the infrastructure asset, plus interest, over the life of the operations and maintenance phase. These payments also compensate the consortium for actually operating and maintaining the infrastructure, and provide the consortium a return on equity. 11. However, because it is Finance Co that actually raised the senior debt, and not Project Trust, a significant portion of the payments the Government made to Project Trust need to find their way back to Finance Co. This is done in two steps: a. The Project Trust enters into a licence agreement with the Government that gives Project Trust the right to access the Crown land the project is to be undertaken on. The licence payments are ostensibly the consideration for the licence agreement, but in reality are calculated to be sufficient for Finance Co to repay the debt it incurred to its external financiers. b. These licence payments are then immediately paid on to Finance Co under the securitisation agreement in step 7(a). In legal terms, the licence payments are securitised by the Government to Finance Co. 8

9 12. The securitisation agreement is important for another reason. It is the mechanism by which the Government originally financed the construction payments to Finance Co in step 5. The financing was done by Finance Co providing the receivables purchase payment to the Government. Legally, this is consideration for the securitised licence payments Finance Co pays to the Government. However, the substance of the securitisation agreement is similar to: a. Finance Co lending money to the Government to have the infrastructure asset designed and constructed - this is the role played by the receivables purchase payment b. once construction is complete, the Government repaying Finance Co for the cost of design and construction, plus interest, over the life of the operations and maintenance phase - this is the role of the securitised licence payments. 13. An equalisation swap confirmation is entered into between Project Trust and Finance Co, under the auspices of an ISDA master agreement, whereby: a. Finance Co s financing costs as modelled at the outset of the agreement are paid to Project Trust; and b. Finance Co s actual financing costs, taking into account any increased or decreased costs of financing as a result of the refinancing of the debt, are paid by Project Trust to Finance Co. The payments under (a) and (b) are netted off against each other. Another way of understanding a social PPP is illustrated in the cash flow diagrams below. 9

10 1.2.3 The design and construction stage 1. Finance Co borrows money from the external D&C financiers in the form of loans or facility agreements. The money may be borrowed entirely up-front or in stages, such as through a facility arrangement. 2. Finance Co uses that money to fund the D&C loan to Project Trust. The interest payments on this loan are capitalised. 3. Project Trust uses that money to fund the design and construction of the infrastructure asset, including payments to the D&C subcontractors. 10

. 5.")

11 1.2.4 End of design and construction Upon the completion of design and construction, the ownership of the infrastructure asset passes to the Government, existing financing unwinds, and new long-term financing put in place. The cash flows to give effect to this are: 4. Long-term loans or facility agreements are entered into with the operations and maintenance financiers (O&M financiers). 5. That financing is used to purchase the securitised licence payments from the Government. The receivables purchase payment is paid in exchange for this. That payment is financed from the borrowing with the O&M financiers. 6. The Government uses the receivables purchase payment to finance the construction payment to Project Trust. 7. Project Trust uses the construction payment to repay the D&C loan with Finance Co, plus interest. 8. Finance Co uses the repayment of the D&C loan to repay the D&C financiers. 11

12 1.2.5 Operations and maintenance stage 9. The Government pays availability payments (also known as service payments or quarterly service payments) to Project Trust over the life of the operations and maintenance phase. The amount of these payments are calculated to be sufficient to: a. cover Project Trust s cost of construction b. cover the interest payments incurred by Finance Co to the external financiers c. pay subcontractors to operate and maintain the infrastructure during the operations and maintenance phase d. provide a return on equity to the consortium members. 10. Project Trust pays some of the money received from the availability payments to subcontractors to operate and maintain the infrastructure and also to fund a return on equity. 11. An amount is paid to the Government in the form of licence payments, calculated by reference to the Government s obligations under the receivables purchase agreement. 12. The licence payments are securitised by the Government and passed straight through to Finance Co by way of a securitisation agreement. 13. Finance Co uses the securitised licence payments to fund the repayment of principal and interest to the O&M financiers. 14. Cash flows under the equalisation swap produce the result that any increase in Finance Co s cost of financing is paid by Project Trust to Finance Co. Any decrease in Finance Co s cost of financing is paid by Finance Co to Project Trust. 12

13 13

14 1.3 Income tax treatment of a social PPP In summary, the income tax treatment of a social PPP is as follows: the loans or facility agreements between the D&C and O&M financiers and Finance Co are financial arrangements to which Taxation of financial arrangements (TOFA) will apply. This means that any loss made by Finance Co from these agreements would generally be deductible on an accruals basis TOFA will also apply to the D&C loan with Project Trust and the securitisation agreement with the Government. This means the agreements will be treated similarly to the loans with the external financiers, and any gain made by Finance Co would generally be assessable on an accruals basis the construction payment and the availability payments will be assessable to Project Trust the licence payments and the payments made to both the D&C and O&M subcontractors are fully deductible to Project Trust TOFA will apply to the D&C loan but not to any of Project Trust s other transactions thin capitalisation will not apply to Finance Co even if the consortium members are nonresidents Project Trust will not be entitled to capital allowances the payments under the equalisation swap will be assessable and deductible to Finance Co and Project Trust subject to the provisos set out below, Part IVA of the Income Tax Assessment Act 1936 (ITAA 1936) would not be expected to apply Agreement between the D&C and O&M financiers and Finance Co TOFA applies to the loan or facility agreements with the D&C and O&M financiers because those agreements will be financial arrangements as set out in section There will be a loss from those arrangements under TOFA to the extent that the payments made to the financiers reflect a return on those financiers investment. Unless Finance Co makes an election under Division 230, the accruals or realisation method in Subdivision 230 B will apply to the loss. Except in unusual circumstances, such as the project s viability being unclear or the Government potentially defaulting on its obligations, the accruals method would apply to that loss. 14

15 We will generally accept that the TOFA accruals method could be satisfied by Finance Co relying on the outcome that the effective interest method as set out in AASB 139, as long as this is applied consistently by Finance Co across its financial arrangements The D&C loan TOFA will apply to the D&C loan between Finance Co and Project Trust. There will be a gain for Finance Co from that arrangement under TOFA to the extent that the payments made to Finance Co reflect a return on its investment. Unless Finance Co makes an election under Division 230, the accruals or realisation method in Subdivision 230 B will apply to the loss. Except in unusual circumstances, such as the project s viability being unclear or the Government potentially defaulting on its obligations, the accruals method would apply to that gain. We will generally accept that the TOFA accruals method could be satisfied by Finance Co relying on the outcome that the effective interest method as set out in AASB 139, as long as this is applied consistently by Finance Co across its financial arrangements Securitisation agreement between Finance Co and Government We accept that TOFA will apply to the securitisation agreement. It will apply as though: the receivables purchase payments were the equivalent of a principal investment; and the securitised licence payment was the equivalent of the repayment of that principal with interest. This means that there should be a gain to which the accruals method under TOFA will apply unless the circumstances mentioned above arise. As with the above, we generally accept that the TOFA accruals method could be satisfied by Finance Co relying on the outcome that the effective interest method as set out in AASB 139. This is if the agreement were treated as a loan under that standard, and if it is applied consistently by Finance Co across its financial arrangements Construction payment The construction payment made by the Government to Project Trust constitutes income according to ordinary concepts. It is not capital in nature. As a result, it is assessable income under section 6 5. TOFA will not apply to it because it involves the obligation to procure the design and construction of the infrastructure. 15

16 In determining the timing of the assessability of income, consistent with the ideas and principles set out in IT 2450, a method of accounting which has the effect of allocating, on a reasonable basis, the ultimate profit or loss made by Project Trust in relation to the construction over the years taken to complete the construction, will be acceptable. However, the conditions and provisos around the reasonability and consistency of the method chosen as set out in IT 2450 would similarly apply in this situation. To avoid doubt, the profit on the construction, if any, should emerge over the construction phase, not over the term of the overall project Availability payments Similarly, the availability payments made by the Government to Project Trust constitute income according to ordinary concepts. They are not capital in nature. As a result, they are assessable income under section 6 5. TOFA will, subject to the discussion at Chapter 4, not apply to them Payments to the D&C and O&M subcontractors The payments to the subcontractors are made for Project Trust to fulfil its contractual obligations to build the infrastructure assets, and thus earn the assessable income referred to above. Therefore, the expenditure falls within the first limb of section 8 1. Additionally, the incurring of the construction costs will not result in any tangible asset or enduring benefit for the Project Trust because they are not the legal owner of the infrastructure asset legally the State owns the relevant asset. Therefore, the expenditure does not fall within the capital-related negative limb of section 8 1. The determination of the timing of any deduction to the D&C contractor would need to be done consistently with the timing of the derivation of income as set out in section Construction payment Licence payments The licence payments are purportedly made periodically to secure Project Trust s ongoing right to access the land. Notwithstanding, the payments will be set at a level able to be sold by the state to fund the construction cost. In the context of a social PPP which structures its tax affairs consistently with the overall intent of this information, we will not seek to challenge the contractual characterisation. Project Trust requires access to fulfil its contractual obligations and thereby derive assessable income. Based on the contractual characterisation, the expenditure falls within the first limb of section

17 The recurrent payments meet Project Trust s continuous need to access the land. The payments do not enlarge Project Trust s profit-yielding structure or secure any enduring benefit. As a result, the expenditure does not fall within the capital-related negative limb of section Thin capitalisation Section Section exempts certain special purpose entities from the application of thin capitalisation. Consistent with TD 2014/18, this exemption will generally apply to Finance Co. See also: TD 2014/18 Income tax: can the exemption in section of the Income Tax Assessment Act 1997 apply to the special purpose finance entity established as part of the 'securitised licence structure' used in some social infrastructure Public Private Partnerships?; That said, as set out in Chapter 4, the ATO will generally regard a PPP as high risk if the Finance Co is financed using related party funding. This is because the thin capitalisation rules, due to the exemption in section , will not operate to control the quantum of related party debt the consortium will enter into The equalisation swap Under the equalisation swap, the net: receipts will be assessable to Project Trust and Finance Co payments will be deductible to Project Trust and Finance Co. We do not consider the payments under the equalisation swap from Finance Co to Project Trust to represent an application of income derived. For completeness, we have general concerns with the use of swaps which shift economic returns between entities. Specific guidance should be sought in relation to swaps outside of this limited context Capital allowances Project Trust will not be entitled to capital allowances under Division 40 because: it will not hold any depreciating asset under section 40 40; and even if it did, there would not be a cost for the asset. In relation to the hold question, the reason: item 2 does not apply is because the agreements do not give Project Trust a right to remove any of the infrastructure 17

18 item 3 does not apply is because Project Trust does not use the asset for its own use item 6 does not apply is because Project Trust will not have a right against the state to become the holder of the asset item 10 does not apply is because Project Trust has no legal title to the assets. There will be no cost for Division 40 purposes (section ) because none of the payments, either to the subcontractors or the Government, consists of an amount that is of a capital nature. Neither will there be deductions under Division 43, because the payments do not constitute capital expenditure (subsection 43 70(1)). The fact that there are no capital allowances also means that Division 250 has no application (paragraph (d)) Part IVA If taxpayers adopt the exact structure outlined above, Part IVA would not be generally expected to apply because no aspect of the transaction structure appears to be driven predominantly by tax considerations. There may, of course, be exceptions. In particular, the following aspects of the above transaction structure, without more, would not generally concern us from a Part IVA perspective: the application of the exemption for special purpose entities in section to Finance Co the fact that Project Trust secures greater deductions under section 8 1 than what would be available under Division 43 under a counterfactual in which Project Trust constructs the asset and retains title to it, and transfers it to the Government at the end of the operations and maintenance period. However, the ATO has seen a number of variations on this structure that it regards as high risk. These variations fall into three broad categories: 1. Arrangements attempting to bring forward deductions and/or defer income. 2. Arrangements attempting to disguise capital outgoings as deductible payments. 3. Arrangements which attempt to fragment integrated trading businesses in order to recharacterise trading income into more favourably taxed passive income. These variations are outlined in detail in Chapter 4. 18

19 The ATO discourages taxpayers from entering into structures or transactions that depart from the type set out in this Chapter. To be clear, this means that taxpayers should not enter into transactions of the type described above, or those that possess the features described above or in Chapter 4. However, the ATO acknowledges that there may be other variations that represent a low compliance risk. If such variations are to be proposed, the ATO would want to understand the nature and rationale for this, and expect that you would approach us to discuss your proposal. 19

20 1.4 Variation involving a progressive securitisation A variation on the securitised licence model outlined above is the progressive securitisation model under which: Government pays construction payments to Project Trust during the construction period, according to the achievement of certain milestones; and these construction payments are financed by the receivables purchase payment paid to the Government, and are similarly progressively over the course of the construction period. All of the other aspects of this model are materially the same as the model outlined above. The availability payments are similarly used by Project Trust to finance the licence payments, which in turn are securitised to Finance Co, with Finance Co using those funds to repay the external financiers. This approach minimises the extent to which the Project Trust incurs deductible capitalised interest expenses without having assessable income to set off against those expenses. This causes the Project Trust s carry-forward loss balance to be reduced. In the event there is a change of ownership in the D&C phase, it will reduce the adverse consequences if the Project Trust were to become disentitled to those carry-forward losses Tax treatment of Finance Co Consistent with the previous model, TOFA will apply to the securitisation agreement composed of: the receivables purchase payment that is paid in instalments (similar to a loan being gradually drawn-down); and the securitised licence payments (similar to that loan gradually being repaid with principal and interest). Note that consistent with the accounting treatment of the securitisation, it is not necessary for Finance Co to start accruing, under TOFA, the entire gain it will make from the securitisation agreement from the time the first receivables purchase payment is made. Rather, the gain under TOFA is worked out by applying a rate of return to an outstanding balance. An example of how this is done is provided below. It can be seen from the example below that an accrual only commences once the receivables purchase price is provided. The accrual is calculated only with reference to an outstanding balance rather than the entire gain that is predicted from the arrangement. 20

21 Example: TOFA accrual calculation on a 35-year progressive securitisation Financial model TOFA accrual calculation Year Receivables purchase payment provided ($) Securitised licence payments ($) Net cashflows ($) Opening value ($) TOFA accrual ($) Closing value ($) ,000, ,000, ,000, ,000, ,000,000 5,000, ,967 30,475, ,000, ,000,000 30,475,967 2,901,112 83,377, ,000, ,000,000 83,377,080 7,936, ,314, ,000,000 7,000, ,314,031 10,596, ,910, ,500,000 7,500, ,910,397 10,938, ,349, ,000,000 8,000, ,349,114 11,266, ,615, ,500,000 8,500, ,615,173 11,576, ,692, ,000,000 9,000, ,692,141 11,869, ,562, ,500,000 9,500, ,562,015 12,143, ,205, ,000,000 10,000, ,205,083 12,394, ,599, ,500,000 10,500, ,599,753 12,622, ,722, ,000,000 11,000, ,722,381 12,824, ,547, ,500,000 11,500, ,547,068 12,998, ,045, ,000,000 12,000, ,045,454 13,141, ,186, ,500,000 12,500, ,186,476 13,249, ,936, ,000,000 13,000, ,936,117 13,321, ,257, ,500,000 13,500, ,257,118 13,351, ,108, ,000,000 14,000, ,108,676 13,337, ,446, ,500,000 14,500, ,446,103 13,274, ,220, ,000,000 15,000, ,220,458 13,157, ,378, ,500,000 15,500, ,378,140 12,982, ,860, ,000,000 16,000, ,860,445 12,742, ,603, ,500,000 16,500, ,603,082 12,432, ,535, ,000,000 17,000, ,535,639 12,045, ,581, ,500,000 17,500, ,581,003 11,573, ,654, ,000,000 18,000, ,654,717 11,009, ,664, ,500,000 18,500, ,664,288 10,344, ,508, ,000,000 19,000, ,508,416 9,567,742 91,076, ,500,000 19,500,000 91,076,158 8,669,853 80,246, ,000,000 20,000,000 80,246,012 7,638,894 67,884, ,500,000 20,500,000 67,884,906 6,462,198 53,847, ,000,000 21,000,000 53,847,104 5,125,891 37,972, ,500,000 21,500,000 37,972,995 3,614,780 20,087, ,000,000 22,000,000 20,087,775 1,912,225 0 Totals $100,000,000 $449,500,000 $349,500,000 $349,500,000 21

22 This example assumes that the cash flows occur at the end of each income year. If they occur part way through an income year, there would be a need to apportion the accrual across two income years. It also assumes that Finance Co has chosen yearly accrual intervals under TOFA. This is not a formal election it is something done by Finance Co when filling out its income tax return in a certain way Tax treatment of Project Trust Consistent with the previous model, the construction payments are assessable income of Project Trust. 22

23 1.5 Variations involving Government contributions As part of a social PPP, the Government may provide its own contributions. Here we discuss the forms these contributions may take and their tax outcomes Cash payment that must be used for certain purposes The first type of Government contribution may be the provision of cash to Project Trust on condition that it be used for certain purposes. Contractually, the Project Trust will provide either goods or services to the Government in consideration for a cash payment. Taxation Ruling TR 2006/3 contains the principles for determining whether a cash payment by the Government to Project Trust, on condition that it be used for certain purposes, will be assessable income under sections 6 5 or While it is difficult to generalise, the cash payment is likely to be included in assessable income under sections 6 5 or on condition that it be used: as part of the design and construction of the asset; or as part of the operations and maintenance of the asset. In working out the timing of the recognition of this income, a method of accounting which has the effect of allocating, on a reasonable basis, the ultimate profit or loss made by Project Trust in relation to the construction over the years taken to complete the construction, consistent with the ideas and principles set out in IT 2450, will be acceptable. However, the conditions and provisos around the reasonability and consistency of the method chosen as set out in IT 2450 would similarly apply in this situation. There may be capital gains tax (CGT) implications if the payment is not assessable under sections 6 5 or See also: TR 2006/3 Income tax: government payments to industry to assist entities (including individuals) to continue, commence or cease business Payment on completion of design and construction Another type of contribution involves the Government contractually incurring part of the cost of construction on its own account. In this situation it will not include the value of that contribution in the availability payments made to the Project Trust. Examples of this would include the Government incurring the costs for the entry ramps on a toll way and the parking around a football stadium. The Project trust will then be responsible for the maintenance of both the part of the infrastructure funded by the Government and the part funded by itself. 23

24 Unlike example the amount of the Government contribution does not form part of the assessable income of the Project Trust. In these instances it is appropriate to treat the construction like a joint venture and the Project trust would only treat as part of its profit the amount attributable to its portion of the infrastructure. The critical point of distinction between and is that in the Government contribution is a contractual payment to Project Trust for goods or services whereas in the Government contribution is on the account of the Government and no tax benefits or attributes pass to the Project Trust as a consequence of the Government contribution Early completion payments In some circumstances the Government may agree to pay an amount to which provides an incentive for early completion of the design and construction phase. This is an amount that is usually prorated depending on the number of days or weeks the design and construction phase was completed in advance. The early completion payments would be assessable income under section Government lending to enable purchase of securitised licence receivables The last type of Government contribution is where the Government lends money to Finance Co to enable it to finance the receivables purchase payment. The tax treatment of the Government lending to Finance Co is the same as the treatment of the D&C and O&M loans Buy-back of securitised licence payments Under some social PPPs, the Government and Finance Co might agree that, after a few years following the commencement of the O&M phase, the Government will purchase a portion of the securitised licence payments and pay a lump sum to Finance Co as consideration for that. This lump sum payment will be, in turn, used by Finance Co to make an early repayment on the loan to the O&M financiers. The purchase of the securitised licence payments however will be usually on satisfaction of certain benchmarks for the O&M phase as set out in the project deed. The price paid for the buy-back may or may not vary depending upon prevailing interest rates or the need for the Government to use the price paid to provide the consortium with an incentive to satisfy certain benchmarks. As stated above, we will accept that Division 230 will apply to the securitised licence payments and the receivables purchase payments as though they were one financial arrangement. 24

25 The presence of the potential right to buy-back the securitised licence payments should be generally disregarded when working out whether the accruals method provided for in Subdivision 230-B, and the amount of any accrual, applies. However, once there is a buy-back, there may be additional implications under Division 230. We will accept that the approach provided for in AASB 139 in relation to partial transfers of financial assets that are a part of a larger financial asset would satisfy the requirements of Division 230, provided this is done consistently. Broadly, the approach in AASB 139 would firstly compare the carrying amount of the derecognised financial asset with what is received in respect of the buy-back. The extent of any difference would be profit or loss. The effective interest method then continues in relation to the part of the larger financial asset that was not transferred. The following page is a continuation of the example discussed previously, where 20% of the securitised licence receivables were bought-back at the end of $24,323,035 is paid by the Government to Finance Co representing the present value of the securitised licence receivables foregone, and discounted using the original rate of return of 9.52% that was initially calculated in the financial model. 25

26 Year Example: 20% of securitised licence receivables bought-back at end 2022 Receivables Purchase Payment ($) Original Financial Model Buy-back Securitise d Licence Payments ($) Net cash flows ($) Nominal value of rights disposed ($) Buy-back gain/loss PV of rights disposed using existing discount rate ($) Gain / loss on disposal ($) Calculating new accrual value Remaining cash flows after buyback ($) PV of remaining cash flows ($) TOFA Accrual Calculation Comparison of cash flows to TOFA gain/loss ,000, ,000, ,000,000-5,000, ,000, ,000,000 5,000, ,967 30,475,967-25,000, , ,000, ,000,000 30,475,967 2,901,112 83,377,080-50,000,000 2,901, ,000, ,000,000 83,377,080 7,936, ,314,031-20,000,000 7,936,951 Opening value ($) TOFA Accrual ($) Closing value ($) Net cash flows ($) Total TOFA gain/loss ($) ,000,000 7,000, ,314,031 10,596, ,910,397 7,000,000 10,596, ,500,000 7,500, ,910,397 10,938, ,349,114 7,500,000 10,938, ,323,035 8,000,000 32,323, ,349,114 11,266,060 97,292,139 32,323,035 11,266, ,800,000 6,800,000 1,700,000 1,552,237 6,800,000 6,208,949 97,292,139 9,261,574 99,753,713 6,800,000 9,261, ,200,000 7,200,000 1,800,000 1,500,689 7,200,000 6,002,758 99,753,713 9,495, ,049,612 7,200,000 9,495, ,600,000 7,600,000 1,900,000 1,446,376 7,600,000 5,785, ,049,612 9,714, ,164,066 7,600,000 9,714, ,000,000 8,000,000 2,000,000 1,390,166 8,000,000 5,560, ,164,066 9,915, ,079,803 8,000,000 9,915, ,400,000 8,400,000 2,100,000 1,332,800 8,400,000 5,331, ,079,803 10,098, ,777,905 8,400,000 10,098, ,800,000 8,800,000 2,200,000 1,274,905 8,800,000 5,099, ,777,905 10,259, ,237,655 8,800,000 10,259, ,200,000 9,200,000 2,300,000 1,217,004 9,200,000 4,868, ,237,655 10,398, ,436,363 9,200,000 10,398, ,600,000 9,600,000 2,400,000 1,159,537 9,600,000 4,638, ,436,363 10,512, ,349,181 9,600,000 10,512, ,000,000 10,000,000 2,500,000 1,102,865 10,000,000 4,411, ,349,181 10,599, ,948,893 10,000,000 10,599, ,400,000 10,400,000 2,600,000 1,047,285 10,400,000 4,189, ,948,893 10,656, ,205,694 10,400,000 10,656,801 26

27 ,800,000 10,800,000 2,700, ,035 10,800,000 3,972, ,205,694 10,681, ,086,941 10,800,000 10,681, ,200,000 11,200,000 2,800, ,303 11,200,000 3,761, ,086,941 10,669, ,556,883 11,200,000 10,669, ,600,000 11,600,000 2,900, ,236 11,600,000 3,556, ,556,883 10,619, ,576,367 11,600,000 10,619, ,000,000 12,000,000 3,000, ,942 12,000,000 3,359, ,576,367 10,526, ,102,512 12,000,000 10,526, ,400,000 12,400,000 3,100, ,500 12,400,000 3,169, ,102,512 10,385, ,088,356 12,400,000 10,385, ,800,000 12,800,000 3,200, ,959 12,800,000 2,987, ,088,356 10,194, ,482,465 12,800,000 10,194, ,200,000 13,200,000 3,300, ,347 13,200,000 2,813, ,482,465 9,946, ,228,511 13,200,000 9,946, ,600,000 13,600,000 3,400, ,674 13,600,000 2,646, ,228,511 9,636,291 97,264,802 13,600,000 9,636, ,000,000 14,000,000 3,500, ,931 14,000,000 2,487,724 97,264,802 9,258,972 92,523,774 14,000,000 9,258, ,400,000 14,400,000 3,600, ,098 14,400,000 2,336,392 92,523,774 8,807,657 86,931,430 14,400,000 8,807, ,800,000 14,800,000 3,700, ,143 14,800,000 2,192,574 86,931,430 8,275,302 80,406,733 14,800,000 8,275, ,200,000 15,200,000 3,800, ,026 15,200,000 2,056,105 80,406,733 7,654,194 72,860,927 15,200,000 7,654, ,600,000 $15,600,000 3,900, ,699 15,600,000 1,926,794 72,860,927 6,935,883 64,196,809 15,600,000 6,935, ,000,000 $16,000,000 4,000, ,107 16,000,000 1,804,430 64,196,809 6,111,115 54,307,925 16,000,000 6,111, ,400,000 $16,400,000 4,100, ,195 16,400,000 1,688,780 54,307,925 5,169,758 43,077,683 16,400,000 5,169, ,800,000 $16,800,000 4,200, ,900 16,800,000 1,579,602 43,077,683 4,100,713 30,378,396 16,800,000 4,100, ,200,000 $17,200,000 4,300, ,161 17,200,000 1,476,644 30,378,396 2,891,824 16,070,220 17,200,000 2,891, ,600,000 $17,600,000 4,400, ,913 17,600,000 1,379,651 16,070,220 1,529, ,600,000 1,529,780 Total 100,000,000 24,323, ,100,00 0 $288,423,035 85,400,000 24,323, ,600,000 97,292, ,423, ,423, ,423,035 27

28 In this example, the carrying amount of the financial asset disposed is $24,323,035. Because the amount paid for the buy-back exactly equals the carrying amount, there is no profit or loss, and therefore no assessable income or allowable deductions on the buy-back. The remaining financial asset is subject to an accrual on the remaining cash-flows. However, there may be scenarios under which the buy-back amount is based on the market value of the rights bought back, rather than the carrying amount. An example of this is where the buy-back amount is $20,000,000 because of changes in market interest rates. In such a situation, there would be a deduction of $4,323,035 in the year of buy-back. Additionally, there may be incentive payments built into the buy-back price in order to encourage the consortium to meet certain benchmarks. For example, if there was an incentive component in the buy-back price of $10,000,000, this would mean the buy-back amount would be $34,323,035. In such a case, the buy-back amount exceeds the carrying amount of the asset transferred by $10,000,000. This would result in profit, and therefore assessable income, of $10,000,000 in the year of the buy-back. In any case, the remaining financial asset will be subject to an accrual on the remaining cash-flows. We will accept that the approaches described above in relation to partial transfers of financial assets that are a part of a larger financial asset would satisfy the requirements of Division 230, provided this is done consistently. 28

29 1.6 GST interaction with PPPs In determining the particular taxable supplies and creditable acquisitions associated with PPP arrangements, careful consideration needs to be given to the precise terms of the relevant agreement General observations about GST and PPPs The following observations are made concerning GST issues that arise in typical PPP scenarios: where a government agency grants a development lease to allow a developer to undertake development works on the land, the government agency makes a supply of land to the developer by way of lease or licence. The developer also makes a corresponding acquisition of land by way of lease or licence in completing the development works on the land, in accordance with the terms of a development lease arrangement, the developer makes a supply of development services to the government agency. The government agency will make corresponding acquisitions on satisfactory and practical completion of the infrastructure project, the developer may be entitled to the grant of operating rights or lease over the completed development for a period. The grant of this lease or operating rights will be a supply of rights or real property made by the Government. The developer will make a corresponding acquisition the total consideration for the supply of the rights or lease over the land comprises any payment made by the developer for the rights or lease, plus a non-monetary component being the development works. Typically, regular rental payments associated with the rights or lease do not form part of the consideration for the supply of the operating rights or grant of lease for a specified period Description of PPPs from a GST perspective Not all arrangements will be the same and the creation of different rights and obligations can result in different GST implications. However, in relation to the infrastructure arrangement outlined in this framework, we note the following: it is assumed that the relevant infrastructure project being built or developed by the Government is not something that would be an input taxed supply or GST-free supply the PPP entities that are party to the arrangements are: o o registered for GST purposes; making supplies that are connected with the indirect tax zone in carrying on their enterprises; and 29

Act 1999 (GST Act), it is necessary to identify the relevant supplies being made.")

30 o in the case of Finance Co, exceeding the financial acquisition threshold. The diagrams below identify the cash flows that arise to give effect to a typical arrangement. However, in the context of the A New Tax System (Goods and Services Tax) Act 1999 (GST Act), it is necessary to identify the relevant supplies being made. To understand the GST consequences of the arrangements entered into, the diagrams below are relevant. They represent the same transactions as outlined in the income tax section of this chapter, but with an emphasis on the elements of the transactions that are pertinent for GST. The design and construction stage The steps in the transactions in the design and construction stage pertinent to GST are as follows: 1. D&C financiers provide a loan to Finance Co either entirely up-front, or in stages, such as through a facility arrangement. 2. Finance Co uses that money to provide a loan to Project Trust. 3. Project Trust uses that money to fund the design and construction of the infrastructure asset, including payments for the services. These services are provided by the D&C subcontractors to Project Trust. 4. Project Trust supplies design and construction services of the infrastructure asset to the Government. 30

31 Operations and maintenance stage The steps in the transactions in the operations and maintenance stage pertinent to GST are as follows: 5. The Government grants a licence to Project Trust for the right to access the Crown land that the project is to be undertaken on. As consideration, the Government receives the licence payments. 6. Project Trust also supplies ongoing operational and maintenance services to the Government. 7. The Government assigns their right to receive the licence payments to Finance Co. 8. Long-term loans or facilities are provided by the O&M financiers to Finance Co. 9. Finance Co and Project Trust are each exchanging rights to make a payment based on Finance Co s financing cost, which is the supply of a derivative. 31

32 1.6.3 GST treatment In summary, the typical GST treatment will be as follows: the loans or other financial facilities with the external financiers, or by Finance Co to Project Trust, are input taxed financial supplies by both the relevant lender and borrower the securitisation agreement involving the supply of the right to receive cash payments under an agreement will also be an input taxed financial supply by the Government the construction payments are consideration for a taxable supply made by Project Trust to the Government being the provision of design and construction of the infrastructure. As a result, GST is payable on the consideration for the supply by Project Trust, and the Government can claim a corresponding GST credit the supplies by the design and construction subcontractors to Project Trust are taxable supplies by those subcontractors. These supplies also constitute a creditable acquisition by Project Trust, and it is entitled to claim the GST credits the availability payments paid by the Government are a consideration for a taxable supply made by Project Trust to the Government being the operations and maintenance of the infrastructure. As a result, GST is payable on the consideration for the supply by Project Trust, and can be claimed back as a GST credit by the Government the licence granted by the Government is a taxable supply. Project Trust as the recipient makes a creditable acquisition from the Government. As a result Project Trust will be entitled to claim a GST credit for this acquisition the payment that arises from the equalisation swap represents consideration for an input taxed supply being made by either Finance Co or the Project Trust. Funding arrangements between Finance Co and the external financiers When Finance Co enters into debt funding arrangements (on either a short or long-term basis) with the external financiers, we accept that: Finance Co is acquiring an interest in a credit arrangement for consideration and is making an input taxed financial supply Finance Co is not liable to pay GST on this supply and generally has no entitlement to a GST credit for anything acquired or imported to make the supply (unless the thing acquired or imported qualifies as a reduced credit acquisition). This means that GST is not payable on the amounts loaned and repaid under these financial supplies (i.e. the principal), and is not paid on the consideration received for making those loans (i.e. the 32

33 interest or charges). As no GST is payable, there are no GST credits to claim in respect of the movements of principal, the interest or charges. Funding arrangement between Finance Co and Project Trust When Finance Co enters into the D&C loan with Project Trust, we accept that: Finance Co is providing an interest in a credit arrangement to Project Trust for consideration and is making an input taxed financial supply to Project Trust Finance Co is not liable to pay GST on this supply and generally has no entitlement to a GST credit for anything acquired or imported to make the supply (unless the thing acquired or imported qualifies as a reduced credit acquisition) Project Trust, in acquiring an interest in a credit arrangement from Finance Co for consideration, is also making an input taxed financial supply to Finance Co while Project Trust is not liable to pay GST on this supply, it may be entitled to a GST credit on things acquired or imported to make the supply. This is due to Project Trust being able to enjoy the benefit of either the financial acquisition threshold or borrowings rule concessions where Finance Co has a right against Project Trust to on-charge the costs it incurs (as a principal) in borrowing funds from the external financiers, the payment of this amount by Project Trust to Finance Co may be a further consideration for financial supplies depending on the documentation (see paragraphs of GSTR 2002/2). Securitisation arrangement between the Government and Finance Co When the Government enters into the securitisation agreement with Finance Co for the securitisation of the licence fee payments that Project Trust is required to make to the Government, we accept that: the Government is not liable to pay GST on this supply and will be entitled to a GST credit for anything acquired or imported to make the supply, where it is able to take advantage of the financial acquisition threshold concession where the Government is not able to access this concession, it will generally not be entitled to a GST credit for anything acquired or imported to make the supply (unless the thing acquired or imported qualifies as a reduced credit acquisition) the Government is entitled to GST credits on the acquisition of the asset being designed and constructed by Project Trust depending upon whether the acquisition is found (based on an objective assessment of the facts and surrounding circumstances) to have a sufficient 33

34 connection to the financial supply that the Government makes to Finance Co under the terms of the securitisation agreement GSTR 2008/1 provides our views on when an entity acquires or imports anything solely or partly for a creditable purpose. In this case, based on the facts and circumstances described, and the guidance provided by GSTR 2008/1, we consider that the Government would be entitled to a GST credit in respect of the asset as the acquisition does not have a sufficient connection to the financial supply that the Government makes to Finance Co Finance Co, in acquiring an interest in a debt from the Government for consideration, is also making an input taxed financial supply to the Government Finance Co is not liable to pay GST on this supply, and generally has no entitlement to a GST credit for anything acquired or imported to make the supply (unless the thing acquired or imported qualifies as a reduced credit acquisition) the assignment of the licence fee income stream does not change the underlying supply that the Government is providing to Project Trust for these payments. The Government retains the obligation to make this supply and remits any GST liability in respect of that supply. So long as the Government continues to make the underlying supply, it will be entitled to claim GST credits on its acquisitions to make that supply in much the same manner as before the assignment occurred. Equalisation swap agreement between Finance Co and Project Trust When Finance Co and Project Trust enter into an equalisation swap, under the auspices of the ISDA master agreement, the following observations are made: both parties are exchanging rights to make a payment dependent upon the value of Finance Co s financing costs. This constitutes to each party making an input taxed financial supply of a derivative to the other for the consideration of the rights exchanged Finance Co is not liable for GST on this supply and generally has no entitlement to a GST credit for anything acquired or imported to make the supply (unless the thing acquired or imported qualifies as a reduced credit acquisition) Project Trust is similarly not liable for GST on this supply, but will be entitled to a GST credit on things acquired or imported to make the supply if it is able to take advantage of the financial acquisition threshold concession no GST consequences arise from either party making a payment to the other in discharge of its equalisation swap obligation. 34

35 Attribution rules The timing of an entity s GST liabilities and GST credit entitlements is driven by the tax period, either monthly or quarterly, to which that obligation or entitlement is attributed. In the context of a PPP, where a party to the PPP accounts for GST on a non-cash basis, attribution of a GST liability or a corresponding GST credit entitlement is required in the earliest tax period in which either: a monetary payment is received some or part of the non-monetary consideration is received an invoice is issued. If the arrangement provides for the payment of rent for lease or the operating rights, then the rules in Division 156 of the GST Act about progressive and periodic supplies will apply to attribute any GST liability on a progressive basis. Understanding when a GST liability is triggered in these types of arrangements assists the developer to ensure that they have adequate cash flow for the life of the project. Valuation PPP arrangements can also raise issues regarding how to determine the appropriate market value of any non-monetary consideration provided. We accept that parties dealing with each other at arm s length can use a reasonable valuation method as agreed between them to determine the GST inclusive market value of any non-monetary consideration for supplies arising in the context of a PPP. Administration matters - offsetting We maintain running balance accounts for various taxes. These taxpayer accounts record obligations, payments and credit entitlements under tax laws. In general, where the taxpayer is due a credit entitlement or refund of payment, this amount may be reduced due to offsetting. Use of the term offsetting describes when an amount that we owe to the taxpayer is applied or allocated against another debt owed by the taxpayer, therefore reducing their refund. In circumstances where a taxpayer has no outstanding tax debts or other Commonwealth liabilities to offset, we are required to refund the credit to the taxpayer. However the taxpayer can request that this refund be offset against the taxation debt of another taxpayer. In the context of PPP arrangements, circumstances may arise where one party, for example Project Trust, becomes entitled to a GST refund after the lodgement of an activity statement. In such a 35

36 scenario, Project Trust can request that the amount to be refunded be offset against the debt of another taxpayer, such as the Government. We are under no obligation to act on the parties request. However, such a request may be agreed to, taking into account the following considerations: the recipient of the GST credit has no outstanding debt or other Commonwealth liabilities to offset the parties agree to coordinate the lodgment of their respective business activity statements the criteria set out in paragraph 40 of Law Administration Practice Statement PS LA 2011/21 Offsetting of refunds and credits against taxation and other debts, being: o o o the risk associated with granting the request is appropriate and in accordance with the requirements of PS LA 2011/6 Risk management in the enforcement of lodgment obligations and other debt collection activities paying the refund in this manner is an efficient, effective, economical and ethical use of public resources (section 15 of the Public Governance, Performance and Accountability Act 2013 (PGPA Act)) the offset satisfies our obligation to pay the refund the taxpayer is entitled to under Division 3A of Part IIB to the Taxation Administration Act In accordance with paragraph 41 of PS LA 2011/21, any such request must: be made by the taxpayer or an authorised representative of the entitled taxpayer include a statement by the taxpayer or an authorised representative of the entitled taxpayer that they understand the refundable amount will be offset against a different taxpayer s tax debt state how much of the refundable amount is to be offset against the other taxpayer s debt provide sufficient details to enable identification of the taxpayer and the debt against which the entitled taxpayer wants to have the refundable amount offset. See also: Reasons for offsetting explained PS LA 2011/21: Offsetting of refunds and credits against taxation and other debts 36

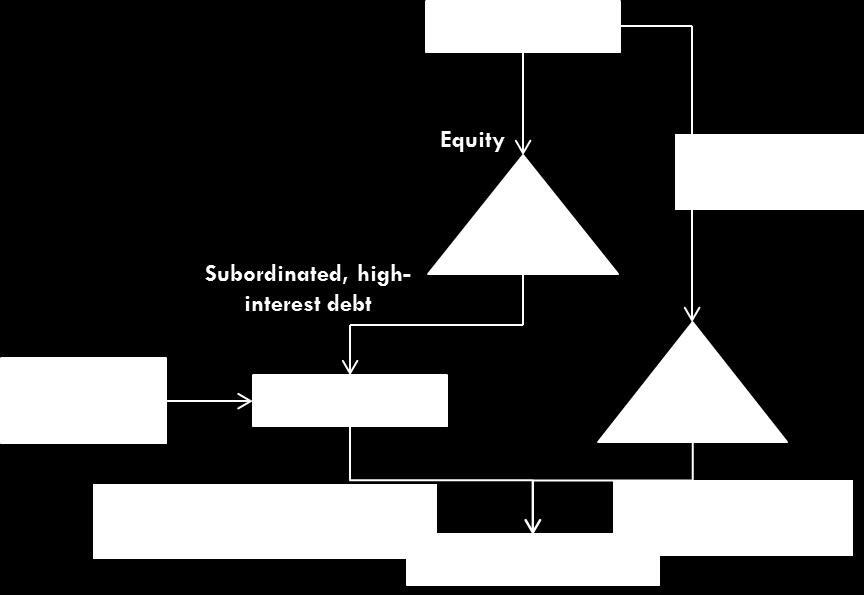

37 1.7 Investor structure of the social PPP Typically, the consortium members will subscribe to equity in a holding trust (Project Hold Trust), which will in turn subscribe to equity in Project Trust. Some of the consortium members may initially invest into Project Trust for the purpose of making a profit from the sale of their interests within a few years after the end of the design and construction phase. Other investors will have longer time horizons. These investors may also be non-residents. The non-residents would typically hold their investment through an Australian resident holding trust. In some structures, the equity in Finance Co would be held by a charitable trust via a holding company. 37

38 1.8 Tax treatment of the investor s investment into the social PPP This part will examine the tax treatment of the investors into the social PPP The charity In the event that Finance Hold Co makes a profit, there may be a distribution to the charity. A discussion on the taxation arrangements applying to charities is out of the scope of this framework and is dealt with in the relevant sections of our website. Where the taxable income allocated to the charity aligns with its economic result, for example the charity receives distributions broadly aligning with the profit of Finance Hold Co or its net income (where trusts are used), Part IVA is unlikely to apply The Australian long-term investor Assessability of distributions received from the Project Hold Trust. Where the Australian long-term investor is presently entitled to a distribution from Project Hold Trust, the assessable income of the Australian long-term investor will be a proportionate share of the net income of Project Hold Trust. The net income of Project Hold Trust is broadly defined to be its taxable income. These concepts are elaborated upon in Division 6 of the ITAA Tax deferred distributions In some income years, the trust distributions may be comprised of accounting income in excess of the net income of Project Hold Trust determined under Division 6. The extent to which the distribution is in excess of the net income is a tax deferred distribution (TDD). Broadly, under our compliance approach, on the assumption that the Australian long-term investor holds its investment on capital account, the TDDs will be treated as non-assessable amounts under the CGT cost base and reduced cost base rules. See also: Our compliance approach 38

39 1.8.3 The Australian short-term investor The Australian short-term investor purchases units in Project Hold Trust with a view to selling those units for a profit within a few years after purchasing them (usually after the end of the D&C phase). Often, one of the consortium members will also be the D&C contractor. It may be the case that their purpose in being a participant in the project is to make a short-term profit from the construction of the asset, with no intention of maintaining their ownership of the Project Trust during the O&M phase. In this circumstance, the units are held on revenue account and any gain or loss from the sale of them may be treated as ordinary income under section 6 5 or deductible under section 8 1. See Taxation Ruling TR 92/3 as to when this may occur. Additionally, if the Australian short-term investor receives a TDD (as explained above) under our compliance approach, the TDDs will not be assessed as ordinary income. This is provided that the TDDs, including CGT concessional amounts, are fully taken into account in working out revenue gains and losses on those units. See also: TR 92/3 Income tax: whether profits on isolated transactions are income Our compliance approach Hold Trust 1 and Hold Trust 2 The tax treatment of Hold Trust 1 and Hold Trust 2 will depend upon whether they are managed investment trusts (MITs). If the trusts are not managed investment trusts If Hold Trust 1 and Hold Trust 2 are not MITs, then Division 6 and CGT will apply similarly to the way those provisions applied to the Australian investors. However, as the beneficiaries of Hold Trust 1 and Hold Trust 2 are non-residents the trustee of Hold Trust 1 and Hold Trust 2 will be taxed in relation to the beneficiaries. The trustee is taxed to assist in the collection of Australian tax on relevant income. Specifically, under section 98 of the ITAA 1936, the trustee of the trusts will be liable to pay tax on the foreign resident investor s share of the net income of those trusts. If the foreign resident investors are companies, the current rate of tax is 30%. If it is an individual or a trustee of another trust, the current tax rate is 47.5%. If the trusts are managed investment trusts Hold Trust 1 and Hold Trust 2 may be MITs as defined in section See our publication What is an MIT under the new rules for the requirements for a trust to be an MIT. 39

40 If the trust is an MIT, then: a special MIT withholding rate may apply the trustee assessment mentioned above will not occur. Generally, the MIT withholding rate will be 15% for beneficiaries that are residents of tax information exchange countries. Details of the tax rates that apply to particular types of beneficiaries and types of investments are set out in withholding tax arrangements for MIT fund payments. However, one of the key issues whether Hold Trust 1 and 2 would qualify as MITs, relate to the requirement that these trusts not control, or not be able to control, a trading business. The business of the Project Trust is a trading business. If these trusts control the affairs and operations of the Project Trust, they will not qualify to be MITs. The concept of control is discussed in Chapter 3. Additionally, in determining whether Hold Trust 1 and 2 qualify as MITs, and/or are entitled to the MIT withholding rate of 15%, particular care should be taken to ensure that: the trust is a managed investment scheme (within the meaning of section 9 of the Corporations Act 2001) a requirement that may be difficult to satisfy where there is a single beneficiary of that trust; a substantial proportion of the investment management activities are in substance carried out in relation to the trust in respect of the assets of the trust are carried out in Australia. The ATO will be undertaking compliance resources in order to ascertain whether purported MITs or withholding MITs do actually satisfy these requirements The foreign resident investors If the foreign resident investor holds units in a trust that is not an MIT, the tax assessed to the trustee in relation to the foreign resident investor is generally not a final tax. If the trustee is assessed under subsection 98(3) of the ITAA 1936 in respect of an individual or company beneficiary, those beneficiaries are assessed under subsection 98A(1) and allowed a credit under subsection 98A(2) for tax paid by the trustee. If the trustee is assessed under subsection 98(4) in respect of a trustee beneficiary, the trustee beneficiary and any later trustee in the chain of trusts, is not assessed again on that amount under sections 98, 99 or 99A. However, an amount may be taxed to an ultimate individual or company beneficiary under section 97, subsection 98A(3) or section 100 and allowed a credit under section 98B. However, if the trust is an MIT and MIT withholding tax was applied to the payment, then the distribution to the foreign resident investor will be non-assessable, non-exempt income. 40

41 1.9 Tax treatment upon exit for investors Outlined below are the tax outcomes if an investor chooses to exit their investment The long-term Australian investor CGT event A1 will generally occur if the long-term Australian investor sells its units in the Project Hold Trust. In working out the capital gain from CGT event A1, any reduction in the cost base, as outlined above in relation to TDDs, would need to be taken into account The short-term Australian investor As the units are held on revenue account, any gain or loss from the sale of the units may be treated as ordinary income under section 6 5 or a deduction under section 8 1. However, for the short-term Australian investor to avail themselves of our administrative approach in relation to TDDs, as outlined above, those TDDs must be taken into account in working out revenue gains and losses on those interests The long-term foreign investor Generally, CGT will not apply to the long-term foreign investor selling its units in the Project Hold Trust, per subsection (1). This will be true so long as, consistent with the example being used, the assets of the Project Hold Trust do not constitute taxable Australian property as defined in section The short-term foreign investor However, the exemption for the gain upon the sale of the units in the Project Hold Trust will not apply if any income from their sale will be treated as ordinary income under section 6 5. In working out the amount of ordinary income, consistent with our administrative approach in relation to TDDs, the amount of any TDD should be taken into account. The fact that there is an amount of ordinary income does not automatically mean that the gain is taxable in Australia. As the short-term foreign investor is a foreign resident, any income from the sale will only be taxable in Australia to the extent that the income is from an Australian source. In determining whether the income from the sale is from an Australian source, the question is not dependent solely on where the purchase and sale contracts are executed in respect of the sale of the units. While issued in the context of the sale of the shares by a private equity fund, TD 2011/24 outlines some of the factors we will consider when determining the source of the income from the sale of the units. 41

42 Where the short-term foreign investor is a resident of a country with which Australia has a tax treaty, the business profits article will likely determine which country has the taxing rights in respect of any profit. It is generally the case that the country of residence of the profit maker will be entitled to tax those profits, although this may depend upon whether the interests of the short-term foreign investor are being held at or through a permanent establishment located in Australia. If there is no Australian permanent establishment, the short-term foreign investors in treaty countries will not usually be subject to tax on their Australian-sourced business profits, although this will depend upon the terms of the relevant business profits article. That said, if the gain on disposal is not assessed under section 6 5, any residual application of CGT, subject to the provisos outlined above, would need to be considered. See also: TD 2010/20 Income tax: treaty shopping - can Part IVA of the Income Tax Assessment Act 1936 apply to arrangements designed to alter the intended effect of Australia's International Tax Agreements network? TD 2011/24 Income tax: is an 'Australian source' in subsection 6-5(3) of the Income Tax Assessment Act 1997 dependent solely on where purchase and sale contracts are executed in respect of the sale of shares in an Australian corporate group acquired in a leveraged buyout by a private equity fund? TD 2011/25 Operation of the Business Profits Article can be traced through certain limited partnerships 42

43 2. Privatisation of Government businesses into stapled structures Taxpayer Alert 2017/1 sets out the ATO s concerns in relation to arrangements which attempt to fragment integrated trading businesses in order to re-characterise trading income into more favourably taxed passive income. One of the areas of concern stated in that Alert relates to the use of stapled structures. However, that Alert also states that it does not extend to privatisations, and that the ATO would be providing separate guidance in relation to those transactions/structures. This Chapter provides that guidance. It sets out: 1. the types of privatisation, 2. the structure that should be used in order to provide taxpayers certainty that the ATO will not apply compliance resources. The ATO will apply compliance resources to, and discourages taxpayers from: 1. relying on this Chapter for a privatisation into a stapled structure not of a type described in this Chapter; and 2. departing from the structure and tax treatments set out in this Chapter. The ATO will however engage on a transaction-by-transaction basis in relation to potential privatisations. This Chapter is structured as follows: 1. Privatisations to which this Chapter applies 2. The asset-level structure of a privatisation 3. Tax treatment of the asset-level structure 4. Cross-staple loan variation 5. The upstream/feeder-level structure 6. Tax treatment of the upstream/feeder-level structure 7. Restructuring and exiting of an investment. 43

44 2.1 Privatisations to which this Chapter applies The privatisation of a Government business into a stapled structure that the ATO will not apply compliance resources involves: 1 a Government business being privatised that is land rich. A Government business is land-rich if it is effectively land (and land improvement) based or heavily reliant on particular land holdings and related improvements for the purposes of section 102M (the Land Assets). These can include ports and electricity transmission and distribution networks. For the avoidance of doubt, a Government business will not be effectively land (and land improvement) if the assets of the business are moveable property said to be covered by subsection 102MB(1); the granting by the Government to a consortium of a long-term lease of the Government businesses Land Assets, and the consortium agreeing to pay a lease premium in return for that grant; the disposal of the other assets of the Government business that are not assets of the type mentioned above (the Non-Land Assets), including intangibles such as licences to operate the business, to that consortium (either directly or indirectly via a sale of an SPV entity that holds those rights) for consideration; the consortium using the assets acquired above to run the privatised Government business for the period of the lease (for which there may be a renewal at the end of the term); and in some cases, the consortium agreeing to operate, maintain, and sometimes upgrade or expand the assets of the business over the term of the lease. This Chapter does not apply to, and the ATO will apply compliance resources to, privatisations into a stapled structure not of the type described above. The ATO will however engage on a transactionby-transaction basis in relation to potential privatisations. 1 Provided taxpayers also do not depart from the structure and tax treatments set out in this Chapter. 44

45 2.2 The asset-level structure There are typically three stages of the privatisation of a land-rich Government business: 1. The initial construction and acquisition of the assets of the business by the Government. This may occur many years prior to privatisation. 2. The establishment of the stapled entities prior to privatisation. 3. The privatisation of the business into the stapled entities Initial construction of the asset Before the Government business is privatised, the assets would have been acquired and/or constructed by a government agency or body, or a government-owned corporation (the Government entity ), such as a port. The construction of the assets will likely involve the Government entity incurring construction expenditure, as well as salary and wages expenses. Additionally, the Government entity may have undertaken capital improvements to the asset prior to privatisation. If it was a government agency or body that acquired or constructed the assets, at some stage prior to privatisation, the Government entity may have vested ownership of the assets in a governmentowned corporation Establishment of consortium entities prior to privatisation In the lead-up to the privatisation, the Government and/or the consortium will set up a number of entities. These entities are: An Operating Trust (which actually may be a trust or a company but for present purposes will be referred to as a trust), whose role it is to operate and maintain the privatised business. Specifically, the Operating Trust will: o o o own the assets of Non-Land Assets; charge customers for the use of those assets (such as electricity tariffs, or port usage charges); and be vested with the assets or may pay consideration for the acquisition of these assets. 45

46 An Asset Trust, whose role it is to: o o o lease the Land Assets; pay a lease premium to the Government for the grant of the lease; and enter into an arrangement with the Operating Trust so that the Operating Trust can use the Land Assets. This is typically given effect through the execution of a sublease of the Land Assets leased from the Government for market value periodic rentals as will be outlined below. A Holding Trust (Operating), whose role it is to hold all of the units in the Operating Trust. A Holding Trust (Asset), whose role it is to hold all the units in Asset Trust. Finance Co whose role it is to raise debt finance for both the Operating Trust and the Asset Trust. Finance Co is a company whose shares may be owned by the consortium, or one of the entities listed above. Generally, the units in the Holding Trust (Asset) and the Holding Trust (Operating) are owned by investors in proportion to their equity contribution. The Asset Trust and the Operating Trust may also either be stapled entities, or there may be some agreement (typically a security holder s agreement and by restrictions in the Operating Trust and Asset Trust deeds), that is in substance the equivalent of stapling The Privatisation The structure of the privatisation is as follows: 1. Finance Co borrows funds from External Financiers. The External Financiers take security over all of the entities and assets in the structure. Asset Trust and Operating Trust would be obligors under the project finance documents. 2. Finance Co lends the money obtained under step 1 to the Asset Trust and the Operating Trust on back-to-back terms. 3. The Holding Trust (Asset) contributes equity to the Asset Trust. 4. The Holding Trust (Operating) contributes equity to the Operating Trust. 5. The Asset Trust and the Government enter into a long-term lease of the Land Assets under which: a. a lease premium is paid; and 46

47 b. as relevant - the Asset Trust has the ability to remove the Land Assets. This ability may arise by virtue of a right the Asset Trust has to remove the asset, conditional on an event such as obsolescence and/or an obligation the Asset Trust has, to replace the asset where necessary for the proper conduct of the facility. At the end of the lease, Asset Trust may or may not receive compensation from the Government for the value of the Land Assets that revert back to the Government. 6. The Asset Trust sub-leases the Land Assets to Operating Trust (the Sub-Lease). The Operating Trust agrees to pay market value periodic rentals to the Asset Trust in exchange. The Operating Trust operates the business, and charges end-user customers for the goods or services of the business, similar to a port usage charge. 7. The Operating Trust purchases or is vested with the Non-Land Assets and liabilities. These assets and contracts, in existence at the end of the sub-lease, typically revert to the Government for no consideration. 8. The Asset Trust uses the lease rentals to repay the borrowing to Finance Co and to fund a return to its unit holders (via the Holding Trust (Asset)). The Operating Trust similarly uses its funds after paying the sub-lease to fund repayments to Finance Co and a return to its unit holders (via the Holding Trust (Operating)). 9. Finance Co uses the funds it receives in step 8 to repay the debt to the external financiers. In this model there are no loans between the Asset Trust and the Operating Trust. A variation that includes such a loan is detailed in

48 48

49 2.3 Tax treatment of the asset-level structure This part will cover the following matters: 1. The staple as a single unified business 2. Purchase Price allocation between the Asset Trust and the Operating Trust 3. Approach to the pricing of the cross-staple lease 4. Levels of gearing 5. Application of Division 6C of the ITAA 1936 to the Asset Trust Rent from land 6. Application of Division 6C to the Operating Trust 7. Tracing for the purposes of Division 6C 8. Holder for the purposes of Division Application of Division 250 to the holder 10. Application of Division 58 to the holder 11. Capital character of lease premium paid to the Government 12. Application of Division Application of Division 57 of Schedule 2D to the ITAA Deductibility of rentals paid by Operating Trust 15. Stamp Duty 16. Part IVA 49