Introduction to U.S. Taxation An Overview of Key Concepts and Considerations for Non-U.S. Investors. October 2017

|

|

|

- George Bryan Thompson

- 5 years ago

- Views:

Transcription

1 Introduction to U.S. Taxation An Overview of Key Concepts and Considerations for Non-U.S. Investors October 2017

2 Agenda Framework of the U.S. Tax System Structures for Entering the U.S. Market Non-Income Tax Considerations Transfer Pricing and BEPS Employee & Executive Considerations U.S. Tax Reform Proposals

3 Framework of the U.S. Tax System

4 What Type of Tax System? Progressive as a taxpayer s tax base increases, the taxpayer s tax increases proportionally the more money you make, the more taxes you pay

5 Types of Taxes Federal Taxes Treaty State & Local Taxes No Treaty

6 Types of Taxes Federal Taxes Income taxes Employment and unemployment taxes Excise taxes Estate and Gift taxes State & Local Taxes Sales and use taxes Property taxes Income taxes Excise taxes

Courts (judicial branch)")

7 Framework of U.S. Tax System Congress (legislative branch) President (executive branch) Courts (judicial branch) Writes tax laws included within IRC Approves or vetoes tax law/acts passed by Congress Dispute resolution interprets IRC and decides how Congress intended its application Agency within U.S. Dept. of Treasury IRC authorizes IRS to collect federal taxes enforce tax rules issue tax refunds

8 Structures for Entering the U.S. Market

9 U.S. Taxation on Foreign Investment Foreigners (NRAs or Corporations) are generally subject to income tax on two buckets of income OR Fixed or Determinable Annual or Periodic Income ( FDAPI ) Types (wages, interest, dividends, rents, royalties, etc.) Must be derived from U.S. sources 30% withholding tax on GROSS income by payor (treaty can reduce) Income Effectively Connected with a U.S. Trade or Business ( ECI ) Business income derived from U.S. trade or business Subject to graduated rates topping out at 35% on NET income Business activities of a U.S. partnership (e.g., U.S. LLC) will be attributed to the partners/investors which triggers a withholding obligation by the U.S. LLC/partnership

10 Structures for Entering the U.S. Market Direct Presence Branch Generally not recommended Tax issues Liability/asset exposure Agents? Activities carried out by agents may be attributable to the principal No tax regulations on point Law set forth in a number of rulings and cases

11 Structures for Entering the U.S. Market Corporation (Inc. or Corp.) Most common Establishment is convenient and straight forward Limited liability No audited financial statement requirement for private companies Financial results for private companies are confidential Ownership generally confidential Importance of proper capitalization and maintenance Corporation subject to U.S. federal, state and local income (and possibly other) taxes Benefits under Income Tax Treaty with the U.S. may be available (at federal level)

12 Structures for Entering the U.S. Market Limited Liability Company (LLC) Similar liability protection to a corporation Less common for non-u.s. owners Tax treatment LLC, in general, is treated the same for tax purposes as a branch, so the non-u.s. owner files tax returns and pays U.S. federal, state and local taxes Treaty benefits may NOT be available

13 Non-Income Tax Considerations

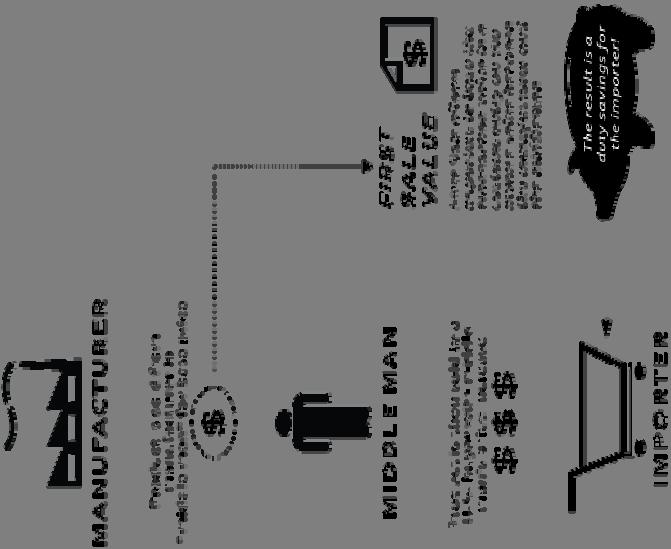

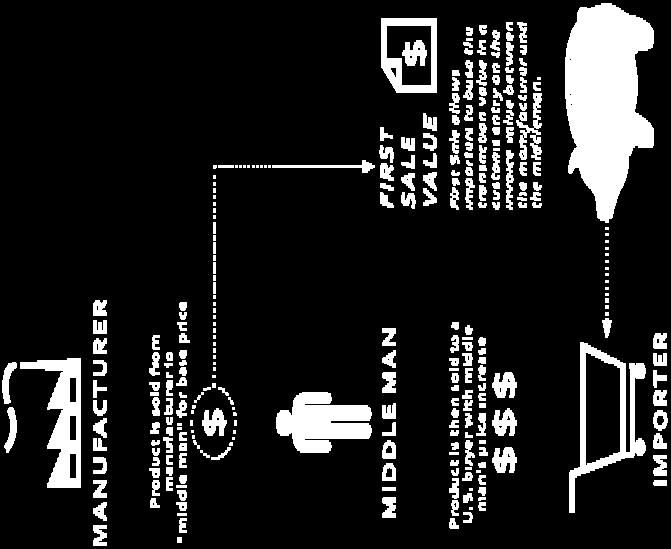

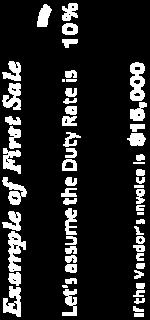

14 Non-Income Tax Considerations First-Sale Rule

15 Transfer Pricing and Base Erosion Profit Shifting ( BEPS )

16 Transfer Pricing and BEPS Transfer pricing Worldwide standard governing transactions between related parties Such transactions must be arms length Transfer of profits Generally, if a U.S. company has retained earnings, a transfer of profits will attract a 30% withholding tax (unless reduced by a tax treaty) The U.S. corporation does not receive a tax deduction for the transfer of profits Be aware of corporate law limitations on dividend payments

17 Transfer Pricing and BEPS U.S. persons that are the ultimate parent entity of a U.S. multinational enterprise (U.S. MNE) group with annual revenue for the preceding reporting period of $850 million or more are required to file Form 8975 Form 8975 and Schedules A (Form 8975) are used by those filers required to report annually certain information with respect to the filer s U.S. MNE group on a CbC basis The filer must report the U.S. MNE group s constituent entities, indicating each entity s: IRS Form 8975, Country-by-Country Report Tax jurisdiction (if any) Country of organization Main business activity Financial and employee information for each tax jurisdiction in which the U.S. MNE does business (including revenues, profits, income taxes paid and accrued, stated capital, accumulated earnings, and tangible assets other than cash) Form 8975 and Schedules A (Form 8975) must be filed with the IRS with the income tax return of the ultimate parent entity of a U.S. MNE group for the tax year in or within which the reporting period covered by the Form 8975 ends

18 Employee & Executive Considerations

19 Pre-Arrival Tax Planning Checklist Key U.S. Tax Considerations Consider establishing a foreign or U.S. trust for estate planning purposes Determine if accelerating gift planning or contemplated sales of assets prior to entering the U.S. will save global tax Explore tax strategies that will step up the tax basis of assets to their FMV so only appreciation after becoming a U.S. resident will be taxable in the U.S. Review existing investment structures to determine whether there will be adverse tax impacts under U.S. tax laws Stock options, when exercised, usually generate ordinary income in the U.S. that is taxable at the top rate consider exercising prior to arrival Review deferred compensation and retirement benefits, to determine how to efficiently access these sources with minimum tax before and after arrival If you have a foreign stock plan, check whether vesting will be taxable to you after entering the U.S. Plan the proper timing for arrival Arriving in the last half of the calendar year will usually result in nonresident status for the full year (thus exempting from U.S. tax foreign income and capital gains) If you are being relocated, consider whether you should be employed by the U.S. or foreign affiliate and whether you should be covered by social security in the U.S. or home country

20 U.S. Tax Reform Proposals

= 39.")

21 U.S. Tax Reform Highlights Unified Framework For Fixing Our Broken Tax Code Current Top Corporate Tax Rate = 35% Top Individual Tax Rate = 39.6% Top Pass-Through Tax Rate (S Corps, Partnerships, Sole Proprietors) = 39.6% Worldwide Taxation Estate and Gift Taxes Proposed Top Corporate Tax Rate = 20% Top Individual Tax Rate = 35% Top Pass-Through Tax Rate (S Corps, Partnerships, Sole Proprietors) = 25% Territorial Taxation NO Estate and Gift Taxes

22 U.S. Tax Reform Highlights Border Adjustability Tax NOT Included

23 THANK YOU For the Opportunity to Present to You Today Rocco Totino Partner Sarre Baldassarri Tax Principal Tim Larson International Tax Services Practice Leader

KIRKLAND ALERT. e First BEPS Changes Come to the U.S.: e IRS Issues Proposed Regulations on Country-by-Country Reporting. Attorney Advertising

KIRKLAND ALERT January 2016 e First BEPS Changes Come to the U.S.: e IRS Issues Proposed Regulations on Country-by-Country Reporting On December 21, 2015, the U.S. Treasury and the Internal Revenue Service

KIRKLAND ALERT January 2016 e First BEPS Changes Come to the U.S.: e IRS Issues Proposed Regulations on Country-by-Country Reporting On December 21, 2015, the U.S. Treasury and the Internal Revenue Service

Tax FAQs for US Inbound Transactions

Tax FAQs for US Inbound Transactions By Robert M. Finkel and Diana C. Española mbbp.com Corporate IP Licensing & Strategic Alliances Employment & Immigration Taxation Litigation 781-622-5930 3 Tax FAQs

Tax FAQs for US Inbound Transactions By Robert M. Finkel and Diana C. Española mbbp.com Corporate IP Licensing & Strategic Alliances Employment & Immigration Taxation Litigation 781-622-5930 3 Tax FAQs

QUESTIONNAIRE ON THE TREATMENT OF INTEREST PAYMENTS AND RELATED TAX BASE EROSION ISSUES

QUESTIONNAIRE ON THE TREATMENT OF INTEREST PAYMENTS AND RELATED TAX BASE EROSION ISSUES This questionnaire should be completed by participants in United Nations capacity development programs on protecting

QUESTIONNAIRE ON THE TREATMENT OF INTEREST PAYMENTS AND RELATED TAX BASE EROSION ISSUES This questionnaire should be completed by participants in United Nations capacity development programs on protecting

US Tax Information for Diplomatic Families at the Australian Embassy

US Tax Information for Diplomatic Families at the Australian Rick Ward LLC January 25, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of

US Tax Information for Diplomatic Families at the Australian Rick Ward LLC January 25, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of

OECD/G20 Base Erosion and Profit Shifting Project

OECD/G20 Base Erosion and Profit Shifting Project Action 13: Guidance on Transfer Pricing Documentation and Country-by-Country Reporting Country-by-Country Report Instructions Manual 24 June 2015 Page

OECD/G20 Base Erosion and Profit Shifting Project Action 13: Guidance on Transfer Pricing Documentation and Country-by-Country Reporting Country-by-Country Report Instructions Manual 24 June 2015 Page

US Tax Information for Diplomatic Families at the German Embassy

US Tax Information for Diplomatic Families at the German Rick Ward LLC February 26, 2018 Disclosure This presentation has been prepared for employees of the World Bank by LLC. The information in this presentation

US Tax Information for Diplomatic Families at the German Rick Ward LLC February 26, 2018 Disclosure This presentation has been prepared for employees of the World Bank by LLC. The information in this presentation

US Tax Information for Diplomatic Families at the Canadian Embassy

US Tax Information for Diplomatic Families at the Canadian Rick Ward LLC January 16, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of January

US Tax Information for Diplomatic Families at the Canadian Rick Ward LLC January 16, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of January

US Tax Information for Diplomatic Families at the Swiss Embassy

US Tax Information for Diplomatic Families at the Swiss Rick Ward LLC October 18, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of October

US Tax Information for Diplomatic Families at the Swiss Rick Ward LLC October 18, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of October

Tax & Estate Planning for Snowbirds

Tax & Estate Planning for Snowbirds Amin Mawani Schulich School of Business York University amawani@schulich.yorku.ca Taxes do influence behaviour Windowless Castles Narrow frontages SIN & gasoline taxes

Tax & Estate Planning for Snowbirds Amin Mawani Schulich School of Business York University amawani@schulich.yorku.ca Taxes do influence behaviour Windowless Castles Narrow frontages SIN & gasoline taxes

Red Light: Dealing with the IRS Enforcement Action

SESSION 4.3 Red Light: Dealing with the IRS Enforcement Action Michael Guerra, EASi Lori Nichols, Internal Revenue Service Carol Rutlen, Partner, GTN/Rutlen Associates LLC B SESSION 4.3 Red Light: Dealing

SESSION 4.3 Red Light: Dealing with the IRS Enforcement Action Michael Guerra, EASi Lori Nichols, Internal Revenue Service Carol Rutlen, Partner, GTN/Rutlen Associates LLC B SESSION 4.3 Red Light: Dealing

FINANCIAL RESEARCH ASSOCIATES PRIVATE INVESTMENT FUND TAX MASTER CLASS

FINANCIAL RESEARCH ASSOCIATES PRIVATE INVESTMENT FUND TAX MASTER CLASS EFFECTIVELY MANAGING TAX IMPLICATIONS OF FOREIGN INVESTMENTS Steven D. Bortnick May 24, 2017 Princeton Club, New York City #43410091

FINANCIAL RESEARCH ASSOCIATES PRIVATE INVESTMENT FUND TAX MASTER CLASS EFFECTIVELY MANAGING TAX IMPLICATIONS OF FOREIGN INVESTMENTS Steven D. Bortnick May 24, 2017 Princeton Club, New York City #43410091

Coming to America. U.S. Tax Planning for Foreign-Owned U.S. Operations. By Len Schneidman. Andersen Tax LLC, U.S.

Coming to America U.S. Tax Planning for Foreign-Owned U.S. Operations By Len Schneidman Andersen Tax LLC, U.S. June 2017 Table of Contents Introduction... 2 Tax Checklist for Foreign-Owned U.S. Operations...

Coming to America U.S. Tax Planning for Foreign-Owned U.S. Operations By Len Schneidman Andersen Tax LLC, U.S. June 2017 Table of Contents Introduction... 2 Tax Checklist for Foreign-Owned U.S. Operations...

26th Annual Health Sciences Tax Conference

26th Annual Health Sciences Tax Conference International and offshore captive issues for exempt December 5, 2016 Disclaimer EY refers to the global organization, and may refer to one or more, of the member

26th Annual Health Sciences Tax Conference International and offshore captive issues for exempt December 5, 2016 Disclaimer EY refers to the global organization, and may refer to one or more, of the member

International Tax Update. Friday, December 1, 2017 Grant Thornton's Year End taxguide Event Brandon Joseph Senior Manager, International Tax

International Tax Update Friday, December 1, 2017 Grant Thornton's Year End taxguide Event Brandon Joseph Senior Manager, International Tax Presenters Brandon Joseph Senior Manager International Tax Services

International Tax Update Friday, December 1, 2017 Grant Thornton's Year End taxguide Event Brandon Joseph Senior Manager, International Tax Presenters Brandon Joseph Senior Manager International Tax Services

OECD Country by Country Reporting with HFM. Alex Znyk Ingersoll Rand

OECD Country by Country Reporting with HFM Alex Znyk Ingersoll Rand Introduction This presentation is organized in two parts: Walkthrough of the OECD BEPS Action 13 Country-by-Country Reporting requirements

OECD Country by Country Reporting with HFM Alex Znyk Ingersoll Rand Introduction This presentation is organized in two parts: Walkthrough of the OECD BEPS Action 13 Country-by-Country Reporting requirements

US Tax Information for Diplomatic Families at the British Embassy

US Tax Information for Diplomatic Families at the British Rick Ward LLC February 22, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of February

US Tax Information for Diplomatic Families at the British Rick Ward LLC February 22, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of February

Coming to America. U.S. Tax Planning for Foreign-Owned U.S. Operations. By Len Schneidman. Andersen Tax LLC, U.S.

Coming to America U.S. Tax Planning for Foreign-Owned U.S. Operations By Len Schneidman Andersen Tax LLC, U.S. January 2018 Table of Contents Introduction... 2 Tax Checklist for Foreign-Owned U.S. Operations...

Coming to America U.S. Tax Planning for Foreign-Owned U.S. Operations By Len Schneidman Andersen Tax LLC, U.S. January 2018 Table of Contents Introduction... 2 Tax Checklist for Foreign-Owned U.S. Operations...

FDU: U.S. International Corporate Tax

190 Controlled Foreign Corporations 191 CFCs: Introduction Subpart F designed to prevent deferral of portable income Applies to US Shareholders of Controlled Foreign Corporations earning Subpart F income

190 Controlled Foreign Corporations 191 CFCs: Introduction Subpart F designed to prevent deferral of portable income Applies to US Shareholders of Controlled Foreign Corporations earning Subpart F income

Global Tax Alert. OECD releases report under BEPS Action 13 on Transfer Pricing Documentation and Country-by-Country Reporting.

23 September 2014 EY Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser: http://www.ey.com/gl/en/ Services/Tax/International- Tax/Tax-alert-library#date

23 September 2014 EY Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser: http://www.ey.com/gl/en/ Services/Tax/International- Tax/Tax-alert-library#date

EXPAT TAX HANDBOOK. Non-Citizens and U.S. Tax Residency. Tax Year Ephraim Moss, Esq Ext 101

EXPAT TAX HANDBOOK Non-Citizens and U.S. Tax Residency Tax Year 2018 Ephraim Moss, Esq. 718-887-9933 Ext 101 emoss@expattaxprofessionals.com Joshua Ashman, CPA 718-887-9933 Ext 102 jashman@expattaxprofessionals.com

EXPAT TAX HANDBOOK Non-Citizens and U.S. Tax Residency Tax Year 2018 Ephraim Moss, Esq. 718-887-9933 Ext 101 emoss@expattaxprofessionals.com Joshua Ashman, CPA 718-887-9933 Ext 102 jashman@expattaxprofessionals.com

U.S. Tax Legislation Corporate and International Provisions. Corporate Law Provisions

U.S. Tax Legislation Corporate and International Provisions On December 20, 2017, Congress enacted comprehensive tax legislation (the Act ). This memorandum highlights some of the important provisions

U.S. Tax Legislation Corporate and International Provisions On December 20, 2017, Congress enacted comprehensive tax legislation (the Act ). This memorandum highlights some of the important provisions

Bill of Tax Amendments for 2014 approved by the Lower House of the Mexican Congress

TAX FLASH Tax Consulting 2013-7 Bill of Tax Amendments for 2014 approved by the Lower House of the Mexican Congress The Bill of Tax Amendments submitted by the Executive Branch to the Mexican Congress

TAX FLASH Tax Consulting 2013-7 Bill of Tax Amendments for 2014 approved by the Lower House of the Mexican Congress The Bill of Tax Amendments submitted by the Executive Branch to the Mexican Congress

Chapter 24. Taxation of International Transactions. Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe

Chapter 24 Taxation of International Transactions Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004 South-Western/Thomson Learning Overview Of International Taxation

Chapter 24 Taxation of International Transactions Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004 South-Western/Thomson Learning Overview Of International Taxation

CROSS-BORDER INCOME TAX ISSUES IN OUTBOUND ESTATE PLANNING. Jenny Coates Law, PLLC, International Tax Lawyer

CROSS-BORDER INCOME TAX ISSUES IN OUTBOUND ESTATE PLANNING Jenny Coates Law, PLLC, International Tax Lawyer jenny@jennycoateslaw.com Increased Tax Complexity Whether between the US and Canada or the US

CROSS-BORDER INCOME TAX ISSUES IN OUTBOUND ESTATE PLANNING Jenny Coates Law, PLLC, International Tax Lawyer jenny@jennycoateslaw.com Increased Tax Complexity Whether between the US and Canada or the US

Table of Contents. Part I La Brienza Winery: Tax Trouble in Wine Country. Chapter 1 Introduction: The Vital Role of Tax in Global Management

Table of Contents Part I La Brienza Winery: Tax Trouble in Wine Country Chapter 1 Introduction: The Vital Role of Tax in Global Management La Brienza Winery, Present Day...3 The Two Objectives of International

Table of Contents Part I La Brienza Winery: Tax Trouble in Wine Country Chapter 1 Introduction: The Vital Role of Tax in Global Management La Brienza Winery, Present Day...3 The Two Objectives of International

International Tax Netherlands Highlights 2018

International Tax Netherlands Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control No Accounting principles/financial statements IAS/IFRS/Dutch GAAP. Financial statements must

International Tax Netherlands Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control No Accounting principles/financial statements IAS/IFRS/Dutch GAAP. Financial statements must

Taxation of International Transactions

Taxation of International Transactions General Tax Provisions US Individuals Gross Income Business Deductions Personal Deductions Personal Exemptions = Taxable Income X Tax Rates (about 40%) = Basic Tax

Taxation of International Transactions General Tax Provisions US Individuals Gross Income Business Deductions Personal Deductions Personal Exemptions = Taxable Income X Tax Rates (about 40%) = Basic Tax

Tax Guide For Foreign Investors In U.S. Residential Real Estate

A T T O R N E Y S A T L A W Tax Guide For Foreign Investors In U.S. Residential Real Estate 2018 Edition In this guide I. Introduction 2 II. The U.S. Tax System 3 A. U.S. Persons 3 1. Basic Rules 3 2.

A T T O R N E Y S A T L A W Tax Guide For Foreign Investors In U.S. Residential Real Estate 2018 Edition In this guide I. Introduction 2 II. The U.S. Tax System 3 A. U.S. Persons 3 1. Basic Rules 3 2.

SPECIAL CONCERNS FOR CROSS-BORDER TAX PLANNING. Jenny Coates Law, PLLC Seattle Tax Group - Sept. 17, 2012

SPECIAL CONCERNS FOR CROSS-BORDER TAX PLANNING 1 Jenny Coates Law, PLLC www.jennycoateslaw.com; Seattle Tax Group - Sept. 17, 2012 Increased Tax Complexity Whether between the US and Canada or the US and

SPECIAL CONCERNS FOR CROSS-BORDER TAX PLANNING 1 Jenny Coates Law, PLLC www.jennycoateslaw.com; Seattle Tax Group - Sept. 17, 2012 Increased Tax Complexity Whether between the US and Canada or the US and

Foreign-Owned U.S. Real Estate: To Rent Or Not To Rent By: Dina Kapur Sanna and Stephen Ziobrowski Day Pitney LLP

Foreign-Owned U.S. Real Estate: To Rent Or Not To Rent By: Dina Kapur Sanna and Stephen Ziobrowski 2015 Day Pitney LLP To avoid U.S. estate tax, the most common structure used by non-residence aliens to

Foreign-Owned U.S. Real Estate: To Rent Or Not To Rent By: Dina Kapur Sanna and Stephen Ziobrowski 2015 Day Pitney LLP To avoid U.S. estate tax, the most common structure used by non-residence aliens to

HONG KONG. 1. Introduction. Contact Information Henry Fung Candice Ng

HONG KONG Contact Information Henry Fung +852 2969 4054 hernyfung@pkf-hk.com Candice Ng +852 2969 4016 candiceng@pkf-hk.com 1. Introduction 1.1. Legal context Currently, the Hong Kong Inland Revenue Ordinance

HONG KONG Contact Information Henry Fung +852 2969 4054 hernyfung@pkf-hk.com Candice Ng +852 2969 4016 candiceng@pkf-hk.com 1. Introduction 1.1. Legal context Currently, the Hong Kong Inland Revenue Ordinance

International Tax South Africa Highlights 2018

International Tax South Africa Highlights 2018 Investment basics: Currency South African Rand (ZAR) Foreign exchange control Exchange control is administered by the South African Reserve Bank, which has

International Tax South Africa Highlights 2018 Investment basics: Currency South African Rand (ZAR) Foreign exchange control Exchange control is administered by the South African Reserve Bank, which has

American Citizens Abroad. Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION

American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation 5 December 2016; 1 November 2017; 1 December 2017; 18 January 2018; 19 April 2018 INTRODUCTION This side-by-side analysis

American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation 5 December 2016; 1 November 2017; 1 December 2017; 18 January 2018; 19 April 2018 INTRODUCTION This side-by-side analysis

Guidance on Transfer Pricing Documentation and Country-by-Country Reporting

OECD/G20 Base Erosion and Profit Shifting Project Guidance on Transfer Pricing Documentation and Country-by-Country Reporting ACTION 13: 2014 Deliverable ANNEX III TO CHAPTER V. A MODEL TEMPLATE FOR THE

OECD/G20 Base Erosion and Profit Shifting Project Guidance on Transfer Pricing Documentation and Country-by-Country Reporting ACTION 13: 2014 Deliverable ANNEX III TO CHAPTER V. A MODEL TEMPLATE FOR THE

All you ever wanted to know about the BEAT and other exciting but ignored provisions of the Tax Cuts and Jobs Act

All you ever wanted to know about the BEAT and other exciting but ignored provisions of the Tax Cuts and Jobs Act by Ian Shane, Esq. Prime Global 2019 Tax Conference January 6-9, 2019 BEAT BEAT imposes

All you ever wanted to know about the BEAT and other exciting but ignored provisions of the Tax Cuts and Jobs Act by Ian Shane, Esq. Prime Global 2019 Tax Conference January 6-9, 2019 BEAT BEAT imposes

Global Mobility of Employees: Practical Strategies

Global Mobility of Employees: Practical Strategies Tax Executives Institute Carolinas Chapter Charlotte, NC Jodi Epstein (202) 662-3468 JEpstein@ipbtax.com Douglas Andre (202) 662-3471 DAndre@ipbtax.com

Global Mobility of Employees: Practical Strategies Tax Executives Institute Carolinas Chapter Charlotte, NC Jodi Epstein (202) 662-3468 JEpstein@ipbtax.com Douglas Andre (202) 662-3471 DAndre@ipbtax.com

IRAS e-tax Guide. Country-by-Country Reporting

IRAS e-tax Guide Country-by-Country Reporting Published by Inland Revenue Authority of Singapore Published on 10 October 2016 Disclaimers: IRAS shall not be responsible or held accountable in any way for

IRAS e-tax Guide Country-by-Country Reporting Published by Inland Revenue Authority of Singapore Published on 10 October 2016 Disclaimers: IRAS shall not be responsible or held accountable in any way for

Chairman Camp s Discussion Draft of Tax Reform Act of 2014 and President Obama s Fiscal Year 2015 Revenue Proposals

Chairman Camp s Discussion Draft of Tax Reform Act of 2014 and President Obama s Fiscal Year 2015 Proposals Relating to International Taxation SUMMARY On February 26, 2014, Ways and Means Committee Chairman

Chairman Camp s Discussion Draft of Tax Reform Act of 2014 and President Obama s Fiscal Year 2015 Proposals Relating to International Taxation SUMMARY On February 26, 2014, Ways and Means Committee Chairman

Tax Reform and U.S. Foreign Reporting for Individuals: New Cross-Border Repatriation and Inclusion Provisions

Tax Reform and U.S. Foreign Reporting for Individuals: FOR LIVE PROGRAM ONLY New Cross-Border Repatriation and Inclusion Provisions THURSDAY, FEBRUARY 15, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Tax Reform and U.S. Foreign Reporting for Individuals: FOR LIVE PROGRAM ONLY New Cross-Border Repatriation and Inclusion Provisions THURSDAY, FEBRUARY 15, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

CORPORATE INVERSIONS. Jack Miles, Esq. Kelley Drye & Warren LLP 101 Park Avenue New York, NY (212)

") CORPORATE INVERSIONS Jack Miles, Esq. Kelley Drye & Warren LLP 101 Park Avenue New York, NY 10178 (212) 808-7574 jmiles@kelleydrye.com Background In a typical inversion, a U.S. multinational combines with

CORPORATE INVERSIONS Jack Miles, Esq. Kelley Drye & Warren LLP 101 Park Avenue New York, NY 10178 (212) 808-7574 jmiles@kelleydrye.com Background In a typical inversion, a U.S. multinational combines with

Transition Tax DEEMED REPATRIATION OVERVIEW

Transition Tax DEEMED REPATRIATION OVERVIEW Basic Framework A 10% U.S. shareholder (a US SH ) of a specified foreign corporation ( SFC ) must recognize its pro rata share of the SFC s post-1986 accumulated

Transition Tax DEEMED REPATRIATION OVERVIEW Basic Framework A 10% U.S. shareholder (a US SH ) of a specified foreign corporation ( SFC ) must recognize its pro rata share of the SFC s post-1986 accumulated

Tax Cuts & Jobs Act: Considerations for U.S. Multinationals

Tax Cuts & Jobs Act: Considerations for U.S. Multinationals January 2, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts & Jobs Act (the

Tax Cuts & Jobs Act: Considerations for U.S. Multinationals January 2, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts & Jobs Act (the

International Income Taxation Chapter 1: INTRODUCTION

Presentation: International Income Taxation Chapter 1: INTRODUCTION Professors Wells January 20, 2016 Chapter One: Introduction Problem of Primary versus Secondary Taxing Jurisdiction: 1) Inbound investment

Presentation: International Income Taxation Chapter 1: INTRODUCTION Professors Wells January 20, 2016 Chapter One: Introduction Problem of Primary versus Secondary Taxing Jurisdiction: 1) Inbound investment

Selected Issues for Canadians Holding and Disposing of US Vacation Property. Carol A. Fitzsimmons, Hodgson Russ LLP Philip Friedlan, Friedlan Law

Holding and Disposing of US Vacation Property, Hodgson Russ LLP, Friedlan Law Toronto Where Are We Going Introduction Overview of US Tax Issues for Nonresident Aliens ( NRAs ) The Case Studies Conclusion

Holding and Disposing of US Vacation Property, Hodgson Russ LLP, Friedlan Law Toronto Where Are We Going Introduction Overview of US Tax Issues for Nonresident Aliens ( NRAs ) The Case Studies Conclusion

1. New decree on transfer-pricing documentation requirements

THE NETHERLANDS 1. New decree on transfer-pricing documentation requirements 1.1. Introduction As from 1 January 2016, Netherlands-resident entities (and Netherlands permanent establishments) that are

THE NETHERLANDS 1. New decree on transfer-pricing documentation requirements 1.1. Introduction As from 1 January 2016, Netherlands-resident entities (and Netherlands permanent establishments) that are

Tax Reform Highlights for Employers

Tax Reform Highlights for Employers Northstar Statewide Conference October 2018 Employer Credit for Paid Family and Medical Leave This is a new non-refundable general business credit that will be reported

Tax Reform Highlights for Employers Northstar Statewide Conference October 2018 Employer Credit for Paid Family and Medical Leave This is a new non-refundable general business credit that will be reported

U.S. Tax Reform International Corporate Tax Provisions: The Good, the Bad and the Extremely Complex

U.S. Tax Reform International Corporate Tax Provisions: The Good, the Bad and the Extremely Complex On December 22, 2017, President Trump signed into law the 2017 U.S. tax reform bill An Act to provide

U.S. Tax Reform International Corporate Tax Provisions: The Good, the Bad and the Extremely Complex On December 22, 2017, President Trump signed into law the 2017 U.S. tax reform bill An Act to provide

US Tax Reform Update. 30 January 2018

US Tax Reform Update Introduction Aaron Topol Partner and Leader EY Asia-Pacific Tax Desk (US) Hong Kong Ernst & Young Tax Services Limited Robert King Partner and Leader Business Tax Advisory Vietnam

US Tax Reform Update Introduction Aaron Topol Partner and Leader EY Asia-Pacific Tax Desk (US) Hong Kong Ernst & Young Tax Services Limited Robert King Partner and Leader Business Tax Advisory Vietnam

Country Tax Guide.

Country Tax Guide www.bakertillyinternational.com Facts and figures as presented are correct as of 18 August 2014. Corporate Income Taxes Resident companies, defined as those companies which are incorporated

Country Tax Guide www.bakertillyinternational.com Facts and figures as presented are correct as of 18 August 2014. Corporate Income Taxes Resident companies, defined as those companies which are incorporated

TECHNICAL EXPLANATION OF THE SENATE COMMITTEE ON FINANCE CHAIRMAN S STAFF DISCUSSION DRAFT OF PROVISIONS TO REFORM INTERNATIONAL BUSINESS TAXATION

TECHNICAL EXPLANATION OF THE SENATE COMMITTEE ON FINANCE CHAIRMAN S STAFF DISCUSSION DRAFT OF PROVISIONS TO REFORM INTERNATIONAL BUSINESS TAXATION Prepared by the Staff of the JOINT COMMITTEE ON TAXATION

TECHNICAL EXPLANATION OF THE SENATE COMMITTEE ON FINANCE CHAIRMAN S STAFF DISCUSSION DRAFT OF PROVISIONS TO REFORM INTERNATIONAL BUSINESS TAXATION Prepared by the Staff of the JOINT COMMITTEE ON TAXATION

Switzerland. Investment basics

Switzerland Diego Weder Director Tel: +1 212 492 4432 diweder@deloitte.com Investment basics Currency Swiss Franc (CHF) Foreign exchange control restrictions are imposed on the import or export of capital.

Switzerland Diego Weder Director Tel: +1 212 492 4432 diweder@deloitte.com Investment basics Currency Swiss Franc (CHF) Foreign exchange control restrictions are imposed on the import or export of capital.

*Brackets adjusted for inflation in future years Long Term Capital Gains & Dividends Taxable income up to $413,200/$457,600 0% - 15%*

Income Tax Planning Overview The American Taxpayer Relief Act of 2012 extended prior law for certain income tax rates; however, it also increased income tax rates on upper income earners. Specifically,

Income Tax Planning Overview The American Taxpayer Relief Act of 2012 extended prior law for certain income tax rates; however, it also increased income tax rates on upper income earners. Specifically,

Tax Law Certification Exam Sample Questions

Tax Law Certification Exam Sample Questions Disclaimer: The following questions are provided to the public as examples of the types of questions that appear on Tax Law certification exams, as well as the

Tax Law Certification Exam Sample Questions Disclaimer: The following questions are provided to the public as examples of the types of questions that appear on Tax Law certification exams, as well as the

Index. [Current to Release ]

![Index. [Current to Release ]](/thumbs/95/123104163.jpg "Index. [Current to Release ]") 50-1 Index Abbreviations, xix to xx [Current to Release 2016-1] Accelerated cost recovery system (ACRS), see also Depreciation. generally, VII-402 to VII-406. percentage tables, VII-413 to VII-419 Accounting

50-1 Index Abbreviations, xix to xx [Current to Release 2016-1] Accelerated cost recovery system (ACRS), see also Depreciation. generally, VII-402 to VII-406. percentage tables, VII-413 to VII-419 Accounting

VILLAGE OF NEW LONDON, OHIO INCOME TAX RETURN AND DECLARATION

VILLAGE OF NEW LONDON Return Service Requested TO: INCOME TAX DEPARTMENT 115 EAST MAIN STREET NEW LONDON, OHIO 44851 PRE-SORTED FIRST CLASS MAIL U.S. POSTAGE PAID NEW LONDON, OHIO Permit No. 5 VILLAGE

VILLAGE OF NEW LONDON Return Service Requested TO: INCOME TAX DEPARTMENT 115 EAST MAIN STREET NEW LONDON, OHIO 44851 PRE-SORTED FIRST CLASS MAIL U.S. POSTAGE PAID NEW LONDON, OHIO Permit No. 5 VILLAGE

International Tax Reform. March 19, 2018 Nicole R. Suk, CPA

International Tax Reform March 19, 2018 Nicole R. Suk, CPA Why International Reform? Shift to territorial system Protect the U.S. tax base from perceived crossborder erosion Incentive for economic investment

International Tax Reform March 19, 2018 Nicole R. Suk, CPA Why International Reform? Shift to territorial system Protect the U.S. tax base from perceived crossborder erosion Incentive for economic investment

Setting up your Business in Georgia Issues to consider

Georgia is one of the world s fastest growing economies and in the region is leading location for global investment. As a result of innovative reforms implemented in Georgia, the World Bank rated Georgia

Georgia is one of the world s fastest growing economies and in the region is leading location for global investment. As a result of innovative reforms implemented in Georgia, the World Bank rated Georgia

International Tax Primer. Third Edition. Brian J. Arnold

International Tax Primer Third Edition Brian J. Arnold Wolters Kluwer Preface xi CHARTER 1 Introduction 1 1.1 Objectives of This Primer 1 1.2 What Is International Tax? 2 1.3 Goals of International Tax

International Tax Primer Third Edition Brian J. Arnold Wolters Kluwer Preface xi CHARTER 1 Introduction 1 1.1 Objectives of This Primer 1 1.2 What Is International Tax? 2 1.3 Goals of International Tax

Federal Tax Reform Idaho Impact

Federal Tax Reform Idaho Impact The potential effect of federal tax reform for Idaho On December 22, 2017, the President signed into law the Tax Cuts and Jobs Act. This legislation includes provisions

Federal Tax Reform Idaho Impact The potential effect of federal tax reform for Idaho On December 22, 2017, the President signed into law the Tax Cuts and Jobs Act. This legislation includes provisions

An Overview of Foreign (Non-U.S.) Investment in U.S. Real Estate

Investment in U.S. Real Estate") TTN Conference Miami 2015 An Overview of Foreign (Non-U.S.) Investment in U.S. Real Estate Presented By: Todd N. Rosenberg, Esq. 1500 San Remo Ave. Suite 125 Coral Gables, Florida 33146 (305) 665-3311

TTN Conference Miami 2015 An Overview of Foreign (Non-U.S.) Investment in U.S. Real Estate Presented By: Todd N. Rosenberg, Esq. 1500 San Remo Ave. Suite 125 Coral Gables, Florida 33146 (305) 665-3311

Administrative measures

August 2018 A special report from Policy and Strategy, Inland Revenue Administrative measures DEFINITION OF LARGE MULTINATIONAL GROUP Section YA 1 The new legislation introduces the term large multinational

August 2018 A special report from Policy and Strategy, Inland Revenue Administrative measures DEFINITION OF LARGE MULTINATIONAL GROUP Section YA 1 The new legislation introduces the term large multinational

SUMMARY: This document contains proposed regulations that would require annual

This document is scheduled to be published in the Federal Register on 12/23/2015 and available online at http://federalregister.gov/a/2015-32145, and on FDsys.gov [4830-01-p] DEPARTMENT OF THE TREASURY

This document is scheduled to be published in the Federal Register on 12/23/2015 and available online at http://federalregister.gov/a/2015-32145, and on FDsys.gov [4830-01-p] DEPARTMENT OF THE TREASURY

International Tax Slovenia Highlights 2018

International Tax Slovenia Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control Bank accounts may be held and repatriation payments made in any currency. Accounting principles/financial

International Tax Slovenia Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control Bank accounts may be held and repatriation payments made in any currency. Accounting principles/financial

International Tax Georgia Highlights 2018

International Tax Georgia Highlights 2018 Investment basics: Currency Georgian Lari (GEL) Foreign exchange control There generally are no foreign exchange controls and no restrictions on the import or

International Tax Georgia Highlights 2018 Investment basics: Currency Georgian Lari (GEL) Foreign exchange control There generally are no foreign exchange controls and no restrictions on the import or

TAX CONSEQUENCES FOR CANADIANS DOING BUSINESS IN THE U.S.

TAX CONSEQUENCES FOR CANADIANS DOING BUSINESS IN THE U.S. Has your Canadian business expanded into the U.S.? Do you have dealings with U.S. customers? If so, have you considered the U.S. tax implications?

TAX CONSEQUENCES FOR CANADIANS DOING BUSINESS IN THE U.S. Has your Canadian business expanded into the U.S.? Do you have dealings with U.S. customers? If so, have you considered the U.S. tax implications?

US Taxation- A Primer

WIRC of the ICAI- Seminar Series on Global Updates- I US Taxation- A Primer Presented by : 7 th May, 2011 CA. Shishir Lagu Session Overview Introduction Corporate Tax Overview Federal Income Tax State

WIRC of the ICAI- Seminar Series on Global Updates- I US Taxation- A Primer Presented by : 7 th May, 2011 CA. Shishir Lagu Session Overview Introduction Corporate Tax Overview Federal Income Tax State

International tax implications of US tax reform

Arm s Length Standard Global views within reach. International tax implications of US tax reform Congress has approved and President Trump has signed into law a massive tax reform package that lowers tax

Arm s Length Standard Global views within reach. International tax implications of US tax reform Congress has approved and President Trump has signed into law a massive tax reform package that lowers tax

Instructions for Form 4891 Corporate Income Tax (CIT) Annual Return

Annual Return") Instructions for Form 4891 Corporate Income Tax (CIT) Annual Return Purpose To calculate the Corporate Income Tax for standard taxpayers. Insurance companies should file the Insurance Company Annual Return

Instructions for Form 4891 Corporate Income Tax (CIT) Annual Return Purpose To calculate the Corporate Income Tax for standard taxpayers. Insurance companies should file the Insurance Company Annual Return

Tax Cuts & Jobs Act: Considerations for Funds

Tax Cuts & Jobs Act: Considerations for Funds December 22, 2017 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts & Jobs Act (the TCJA ).

Tax Cuts & Jobs Act: Considerations for Funds December 22, 2017 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts & Jobs Act (the TCJA ).

OECD Publishes Guidance on Transfer Pricing Documentation and Country-by-Country Reporting

17 September 2014 OECD Publishes Guidance on Transfer Pricing Documentation and Country-by-Country Reporting Action 13 On 16 September 2014, the Organization for Economic Co-operation and Development (

17 September 2014 OECD Publishes Guidance on Transfer Pricing Documentation and Country-by-Country Reporting Action 13 On 16 September 2014, the Organization for Economic Co-operation and Development (

Doing Business Guide. United States. 1st Edition. Marks Paneth LLP

Doing Business Guide United States 1st Edition Marks Paneth LLP About This Booklet This booklet has been produced by Marks Paneth LLP to provide an introduction to foreign investors on the various aspects

Doing Business Guide United States 1st Edition Marks Paneth LLP About This Booklet This booklet has been produced by Marks Paneth LLP to provide an introduction to foreign investors on the various aspects

PAPER 2.03 CYPRUS OPTION

THE ADVANCED DIPLOMA IN INTERNATIONAL TAXATION June 2017 PAPER 2.03 CYPRUS OPTION SUGGESTED SOLUTIONS PART A Question 1 Part 1 Tax residency of physical persons is determined by reference to physical presence

THE ADVANCED DIPLOMA IN INTERNATIONAL TAXATION June 2017 PAPER 2.03 CYPRUS OPTION SUGGESTED SOLUTIONS PART A Question 1 Part 1 Tax residency of physical persons is determined by reference to physical presence

International Tax Germany Highlights 2018

International Tax Germany Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control No restrictions are imposed on the import or export of capital; however, a declaration must be

International Tax Germany Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control No restrictions are imposed on the import or export of capital; however, a declaration must be

2017 Tax Reconciliation Bill Selected Provisions Impacting Real Estate (As of January 11, 2018)

") (As of January 11, 2018) Overview Tax Reform Impact on REITs and Other Investors in Real Estate The enactment of tax reform legislation will have far-reaching consequences and create new planning considerations

(As of January 11, 2018) Overview Tax Reform Impact on REITs and Other Investors in Real Estate The enactment of tax reform legislation will have far-reaching consequences and create new planning considerations

CHOICE OF ENTITY FOR INTERNATIONAL OPERATIONS AFTER THE 2017 TAXACT

CHOICE OF ENTITY FOR INTERNATIONAL OPERATIONS AFTER THE 2017 TAXACT John R. Wilson Partner, Holland & Hart LLP Holland & Hart Denver Tax Conference December 5, 2018 Copyright 2018 by John R. Wilson INBOUND

CHOICE OF ENTITY FOR INTERNATIONAL OPERATIONS AFTER THE 2017 TAXACT John R. Wilson Partner, Holland & Hart LLP Holland & Hart Denver Tax Conference December 5, 2018 Copyright 2018 by John R. Wilson INBOUND

The United States Government defines an alien as any individual who is not

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

Tax Cuts & Jobs Act: Considerations for Funds

A LERT M EM OR A N D UM Tax Cuts & Jobs Act: Considerations for Funds January 25, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts &

A LERT M EM OR A N D UM Tax Cuts & Jobs Act: Considerations for Funds January 25, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts &

Session Report: US Model Treaty 2015 Proposals

Session Report: US Model Treaty 2015 Proposals By Christie Galinski Session: The New Model Treaty and Treasury Explanation: What Is Proposed and What Is Needed September 18, 2015: 2015 Joint Fall Meeting:

Session Report: US Model Treaty 2015 Proposals By Christie Galinski Session: The New Model Treaty and Treasury Explanation: What Is Proposed and What Is Needed September 18, 2015: 2015 Joint Fall Meeting:

IMPACT OF THE NEW TAX LAW ON NONPROFIT HOSPITALS AND HEALTH SYSTEMS OVERVIEW

Catherine E. Livingston Gerald Griffith Amy Bibby, CPA clivingston@jonesday.com ggriffith@jonesday.com amy.bibby@dhgllp.com 202-879-3756 312-269-1507 828-236-5797 313.230.7907 IMPACT OF THE NEW TAX LAW

Catherine E. Livingston Gerald Griffith Amy Bibby, CPA clivingston@jonesday.com ggriffith@jonesday.com amy.bibby@dhgllp.com 202-879-3756 312-269-1507 828-236-5797 313.230.7907 IMPACT OF THE NEW TAX LAW

Practical issues with regard to business operations and investment in Myanmar. June 2015

Practical issues with regard to business operations and investment in Myanmar June 2015 Disclaimer This brief presentation on Myanmar Taxes managed by Internal Revenue Department is intended to provide

Practical issues with regard to business operations and investment in Myanmar June 2015 Disclaimer This brief presentation on Myanmar Taxes managed by Internal Revenue Department is intended to provide

The OECD s 3 Major Tax Initiatives

The OECD s 3 Major Tax Initiatives 1. The Global Forum on Transparency and Exchange of Information for Tax Purposes Peer review of ~ 100 countries International standard for transparency and exchange of

The OECD s 3 Major Tax Initiatives 1. The Global Forum on Transparency and Exchange of Information for Tax Purposes Peer review of ~ 100 countries International standard for transparency and exchange of

International Tax Reform - Practical Impacts and Considerations. 30 November 2017

International Tax Reform - Practical Impacts and Considerations 30 November 2017 Agenda Transition tax Territorial system Limitation on deductions of net interest Foreign high return amount / Global intangible

International Tax Reform - Practical Impacts and Considerations 30 November 2017 Agenda Transition tax Territorial system Limitation on deductions of net interest Foreign high return amount / Global intangible

Option 2: How to avoid double taxation? Tax treaty 101

Option 2: How to avoid double taxation? Tax treaty 101 Stefano Mariani TEP, Deacons Steven Sieker TEP, Baker & McKenzie Kindly sponsored by Background of international taxation 1. The power to make tax

Option 2: How to avoid double taxation? Tax treaty 101 Stefano Mariani TEP, Deacons Steven Sieker TEP, Baker & McKenzie Kindly sponsored by Background of international taxation 1. The power to make tax

American Citizens Abroad. Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION

1 November 2017; 1 December 2017; 19 January 2018 American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION This side-by-side analysis compares Current Law (i.e.,

1 November 2017; 1 December 2017; 19 January 2018 American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION This side-by-side analysis compares Current Law (i.e.,

LEARNING OBJECTIVES TRANSFER PRICING DOCUMENTATION. THE ROLE OF TPD Showing Compliance. Fundamentals of Transfer Pricing Documentation

UN-ATAF Workshop on Transfer Pricing Administrative Aspects and Recent Developments Ezulwini, Swaziland 4-8 December 2017 LEARNING OBJECTIVES Understanding and Reviewing Transfer Pricing Documentation

UN-ATAF Workshop on Transfer Pricing Administrative Aspects and Recent Developments Ezulwini, Swaziland 4-8 December 2017 LEARNING OBJECTIVES Understanding and Reviewing Transfer Pricing Documentation

Tax Cuts & Jobs Act: Considerations for M&A

A LERT M EM OR A N D UM Tax Cuts & Jobs Act: Considerations for M&A January 12, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts & Jobs

A LERT M EM OR A N D UM Tax Cuts & Jobs Act: Considerations for M&A January 12, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts & Jobs

Adam Williams. Anthony Licavoli. Principal Tax Manager

1 2 Adam Williams Principal 734.302.4179 adam.williams@rehmann.com Anthony Licavoli Tax Manager 248.463.4598 anthony.licavoli@rehmann.com 3 4 5 What is your impression about the speed at which Congress

1 2 Adam Williams Principal 734.302.4179 adam.williams@rehmann.com Anthony Licavoli Tax Manager 248.463.4598 anthony.licavoli@rehmann.com 3 4 5 What is your impression about the speed at which Congress

FIRPTA, Section 892 and REITS

FIRPTA, Section 892 and REITS ABA Tax Section: Real Estate Committee May 8, 2015 Alan I. Appel, Professor, New York Law School Charles Besecky, Branch Chief for Branch 4, IRS, ACCI Philip R. Hirschfeld,

FIRPTA, Section 892 and REITS ABA Tax Section: Real Estate Committee May 8, 2015 Alan I. Appel, Professor, New York Law School Charles Besecky, Branch Chief for Branch 4, IRS, ACCI Philip R. Hirschfeld,

International Tax Primer Andrew D. Oppenheimer, Esq. October 31, 2017

International Tax Primer Andrew D. Oppenheimer, Esq. October 31, 2017 Agenda International tax concepts Taxation of foreign earnings Sourcing of income and expenses Foreign tax credits Subpart F income

International Tax Primer Andrew D. Oppenheimer, Esq. October 31, 2017 Agenda International tax concepts Taxation of foreign earnings Sourcing of income and expenses Foreign tax credits Subpart F income

Nonresident Alien Tax Compliance

www.arcticintl.com ARCTIC INTERNATIONAL LLC Nonresident Alien Tax Compliance A Closer Look The Who, What When, How and Why... NACUBO Tax Forum 2013 Who... is required to withhold and report?... is a Nonresident

www.arcticintl.com ARCTIC INTERNATIONAL LLC Nonresident Alien Tax Compliance A Closer Look The Who, What When, How and Why... NACUBO Tax Forum 2013 Who... is required to withhold and report?... is a Nonresident

KEY INDIVIDUAL PROVISIONS Rule Present Law (2018 Rate Schedule) House Senate Differences and Observations

House Senate Differences and Observations") KEY INDIVIDUAL PROVISIONS Rule Present Law (2018 Rate Schedule) House Senate Differences and Observations Rates Single Filers Rates Joint Filers Alternative Minimum Tax Standard Personal Exemption Estate

KEY INDIVIDUAL PROVISIONS Rule Present Law (2018 Rate Schedule) House Senate Differences and Observations Rates Single Filers Rates Joint Filers Alternative Minimum Tax Standard Personal Exemption Estate

Provisions affecting private equity funds in tax reform bills House bill and Senate Finance Committee bill

Provisions affecting private equity funds in tax reform bills House bill and Senate Finance Committee bill November 22, 2017 1 The U.S. House of Representatives on November 16, 2017, passed H.R. 1, the

Provisions affecting private equity funds in tax reform bills House bill and Senate Finance Committee bill November 22, 2017 1 The U.S. House of Representatives on November 16, 2017, passed H.R. 1, the

Colombian Tax Reform Unveiled. October, DC3 - Información altamente confidencial

Colombian Tax Reform Unveiled October, 2016 Background 1. As recently as October 19 th, 2016 the Government released the set of draft tax rules which Congress will now consider. 2. The Government s expectation

Colombian Tax Reform Unveiled October, 2016 Background 1. As recently as October 19 th, 2016 the Government released the set of draft tax rules which Congress will now consider. 2. The Government s expectation

Chapter 13. Taxation of Companies and Shareholders Doing Business in Malta 99

Chapter 13 Taxation of Companies and Shareholders 2012 Doing Business in Malta 99 Company tax system Companies are subject to income tax and tax on capital gains in terms of the Income Tax Act and there

Chapter 13 Taxation of Companies and Shareholders 2012 Doing Business in Malta 99 Company tax system Companies are subject to income tax and tax on capital gains in terms of the Income Tax Act and there

Taxation of Trusts on Divorce: Interception of Section 682 in Divorce. Presented to ABA RPTE Section Meeting. May 12, Boston, Massachusetts

Taxation of Trusts on Divorce: Interception of Section 682 in Divorce Presented to ABA RPTE Section Meeting May 12, 2016 Boston, Massachusetts By Leigh-Alexandra Basha Partner/Private Client Group McDermott

Taxation of Trusts on Divorce: Interception of Section 682 in Divorce Presented to ABA RPTE Section Meeting May 12, 2016 Boston, Massachusetts By Leigh-Alexandra Basha Partner/Private Client Group McDermott

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A VANILLA APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A VANILLA APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION October 15, 2017 Congress and the Administration are expected to consider changes in US tax

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A VANILLA APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION October 15, 2017 Congress and the Administration are expected to consider changes in US tax

2. Name (print or type) 3. Federal Employer Identification Number (FEIN)

3. Federal Employer Identification Number (FEIN)") Michigan Department of Treasury 4891 (Rev. 07-12), Page 1 2012 MICHIGAN Corporate Income Tax Annual Return Issued under authority of Public Act 38 of 2011. MM-DD-YYYY This form cannot be used as an amended

Michigan Department of Treasury 4891 (Rev. 07-12), Page 1 2012 MICHIGAN Corporate Income Tax Annual Return Issued under authority of Public Act 38 of 2011. MM-DD-YYYY This form cannot be used as an amended

Ch International Tax- Free Exchanges P.814

Ch. 10 - International Tax- Free Exchanges P.814 Cross-border entity structuring options: 1) Corporation: domestic, foreign (destination country) or other (intermediary) foreign country, including special

Ch. 10 - International Tax- Free Exchanges P.814 Cross-border entity structuring options: 1) Corporation: domestic, foreign (destination country) or other (intermediary) foreign country, including special

Tax Incentives for Renewable Energy Investments Under the American Recovery and Reinvestment Act of 2009 ( ARRA )

") Tax Incentives for Renewable Energy Investments Under the American Recovery and Reinvestment Act of 2009 ( ARRA ) March 18, 2009 Copyright 2009 Shearman & Sterling LLP. As used herein Shearman & Sterling

Tax Incentives for Renewable Energy Investments Under the American Recovery and Reinvestment Act of 2009 ( ARRA ) March 18, 2009 Copyright 2009 Shearman & Sterling LLP. As used herein Shearman & Sterling

Table of Contents Personal Income Tax... 3 Tax-Free Savings Account ( TFSA )... 3 Home Accessibility Tax Credit... 3 Qualifying Individuals...

... 3 Home Accessibility Tax Credit... 3 Qualifying Individuals...") 2015 Federal Budget April 21, 2015 Table of Contents Personal Income Tax... 3 Tax-Free Savings Account ( TFSA )... 3 Home Accessibility Tax Credit... 3 Qualifying Individuals... 3 Eligible Dwellings...

2015 Federal Budget April 21, 2015 Table of Contents Personal Income Tax... 3 Tax-Free Savings Account ( TFSA )... 3 Home Accessibility Tax Credit... 3 Qualifying Individuals... 3 Eligible Dwellings...