ASSET PROTECTION PLANNING WITH OFFSHORE TRUSTS

|

|

|

- Austin Robbins

- 5 years ago

- Views:

Transcription

1 ASSET PROTECTION PLANNING WITH OFFSHORE TRUSTS PRESENTED BY HOWARD ROSEN, ATTORNEY, CPA 2016, by DONLEVY-ROSEN & ROSEN, P.A. Coral Gables, Florida (305) WEB SITE: PROTECTYOU.COM

2 HOWARD ROSEN is an "AV Preeminent" rated Attorney and Certified Public Accountant practicing law in Miami, Florida, as a shareholder (partner) in the firm of Donlevy-Rosen & Rosen, P.A. (the "AV Preeminent" rating is the highest rating accorded by Martindale-Hubbell, an internationally recognized independent attorney rating organization). Donlevy-Rosen & Rosen, P.A. is listed in Martindale-Hubbell's Bar Register of Preeminent Lawyers. Mr. Rosen served as an Adjunct Professor and lecturer at law at the University of Miami School of Law for twenty years ( ), a guest lecturer at the University of Miami School of Business Administration, and is an internationally recognized authority and frequent lecturer on the subjects of asset protection, taxation, and estate planning. Mr. Rosen is the Chairman of the Asset Protection Committee of the American Association of Attorney - Certified Public Accountants ( Present). Mr. Rosen is the co-author of "ASSET PROTECTION: A GUIDE FOR PROFESSIONALS" (2014), a contributing author of the ABA Practical Guide To Estate Planning: Chapter Title: "ASSET PROTECTION TRUSTS - WHAT YOU SHOULD KNOW" (2011 American Bar Association), and was the co-author of BNA Tax Management Portfolio, U.S. TAXATION OF FOREIGN ESTATES, TRUSTS, and BENEFICIARIES (2008) and the founding author of "ASSET PROTECTION PLANNING" (1994; 2002), used by lawyers, CPA's, and estate planners nationwide in researching asset protection and offshore trust issues. Mr. Rosen is the co-author of ASSET PROTECTION (2007; 2008), ASSET PROTECTION IN FLORIDA (2005, 2006), ASSET PROTECTION IN VIRGINIA (2005), "ASSET PROTECTION IN TEXAS" (2004; 2005), and "ASSET PROTECTION IN GEORGIA" (2004), all published by Lorman Education Services. Mr. Rosen is also co-author of ASSET PROTECTION WITH OFFSHORE TRUSTS (2008), DEMYSTIFYING ASSET PROTECTION VEHICLES (2007), AN A TO Z GUIDE TO THE FUNDAMENTALS OF ASSET PROTECTION IN FLORIDA (2005), "UNRAVELING THE MYSTERY OF ASSET PROTECTION VEHICLES IN FLORIDA" (2004), "ASSET PROTECTION TECHNIQUES IN FLORIDA" (2001; 2003), and "ASSET PRESERVATION TECHNIQUES IN FLORIDA" (1996), all published by the National Business Institute. Mr. Rosen is the Editor/Publisher of THE ASSET PROTECTION NEWS, and has also published numerous articles in professional and academic journals such as the University of Miami Law Review, the Asset Protection Journal, Journal of Asset Protection, Taxes Magazine, Journal of Taxation of Investments, University of Miami Business Law Journal, Offshore Finance USA, CCH Financial and Estate Planning, Tax Management's Estates, Gifts and Trusts Journal, BNA Tax Management Portfolios, Estate Planning, Taxation for Lawyers, Taxation for Accountants, International Tax Report, Small Business Taxation, and others. Mr. Rosen is a member of BNA Tax Management's Advisory Board on Estates, Gifts and Trusts ( Present), the Board of Advisors of the Southpac Offshore Planning Institute (SOPI), the Asset Protection Planning Committee of the Real Property, Probate and Trust Law Section of the ABA, the Tax and International Law Sections of the Florida Bar, and the American Association of Attorney - Certified Public Accountants. Mr. Rosen served as a member of the Board of Advisors of Aspen Publishers Asset Protection Journal ( ), the Board of Advisors of Warren, Gorham & Lamont s Journal of Asset Protection ( ), the Board of Governors of the Florida Institute of CPA's ( ), as the President ( ) and as a Director ( ) of its South Dade Chapter, and has received the Outstanding Discussion Leader award from the Florida Institute of CPA's. Mr. Rosen also served as a charter member of the Planned Giving Advisory Council of the Baptist Hospital of Miami Foundation. Mr. Rosen's educational achievements include a Juris Doctor degree from the University of Miami (Summa Cum Laude - #2 in his class) where he was a Reid Scholar, and a Bachelor of Business Administration degree (in Accounting) from the University of Miami (Magna Cum Laude). Mr. Rosen concentrates his law practice in asset protection planning and related matters. Admitted to practice law in 1974, his experience includes estate planning, corporate and personal tax planning, foreign tax planning, and other tax related matters. His law offices are located at 2121 Ponce de Leon Boulevard - Suite 320, Coral Gables, Florida 33134; Telephone (direct): (305) ; Web Site:

3 I. INTRODUCTION ASSET PROTECTION PLANNING WITH OFFSHORE TRUSTS PRESENTED BY HOWARD ROSEN, ATTORNEY, CPA A. Who needs this type of planning? 2016, by DONLEVY-ROSEN & ROSEN, P.A. 1. Real Estate Developers / Investors. 2. Business owners; Businesses; Sellers of businesses. 3. Health care providers. 4. Accountants (see article in July 1991 Journal of Accountancy), auditors, and actuaries. 5. Architects, engineers, and appraisers. 6. Parents of teenage drivers. 7. Officers and Directors of public companies. 8. ANY HIGH INCOME/HIGH NET WORTH INDIVIDUAL B. Trust concept in our legal system. C. Use of trusts in asset protection planning - A proper use: 1. Since the time of the Crusades 2. Treas. Reg (a) provides: "... the term "trust" as used in the Internal Revenue Code refers to an arrangement created either by a will or by an inter vivos declaration whereby trustees take title to property for the purpose of protecting or conserving it for the beneficiaries under the ordinary rules applied in chancery or probate courts. Usually the beneficiaries of such a trust do no more than accept the benefits thereof and are not the voluntary planners or creators of the trust arrangement. However, the beneficiaries of such a trust may be the persons who create it and it will be recognized as a trust under the Internal Revenue Code if it was created for the purpose of protecting or conserving the trust property for beneficiaries who stand in the same relation to the trust as they would if the trust had been created by others for them. Generally speaking, an arrangement will be treated as a trust under the Internal Revenue Code if it can be shown that the purpose of the arrangement is to vest in trustees responsibility for the protection and conservation of property for beneficiaries who cannot share in the

4 discharge of this responsibility and, therefore, are not associates in a joint enterprise for the conduct of business for profit."(emphasis added). D. Limitations on the asset protection facilities of domestic trusts: 1. Settlor retained benefits and controls can result in determination that the trust is invalid, although the laws of some states do repudiate this common law trust principal to a limited extent. 2. In general, the ability of a domestic trust to provide effective asset protection depends upon the relationship to the trust of the person for whom protection is sought (i.e., settlor-beneficiary or nonsettlorbeneficiary), and the nature and extent of that person's interest in and/or controls over the trust. 3. If the trust is otherwise valid, public policy in the US (and in many other countries) permits a creditor of the settlor-beneficiary to reach the trust assets to the extent of the maximum property interest potentially available to the settlor-defendant under the instrument. EXAMPLE: X settles trust which provides that he is one of several discretionary income beneficiaries, remainder to Z. X's creditor can reach all of the income, but none of the principal of the trust. 4. Similarly, public policy in the US (and in many other countries) will not allow a self-settled spendthrift trust to afford protection for a settlorbeneficiary. 5. ALASKA, DELAWARE, ETC., TRUSTS: STATE LEGISLATION A. U.S. CONSTITUTIONAL ISSUES: a. Full Faith & Credit Clause b. Supremacy Clause c. Contract Clause B. PRACTICALITIES: A COMPARISON a. Enforcement of Judgments a. Location of Assets - 2 -

5 b. Statute of Limitations c. Standard of Proof e. invalidity Basis of Attack f. fees C BANKRUPTCY LEGISLATION - THE END? 6. In summary, in order to obtain complete protection for assets settled in a domestic trust, the settlor must retain no control over and no beneficial interest in the trust - essentially no different than an outright gift. E. Working Definitions: 1. ASSET PROTECTION PLANNING: The adoption of advance planning techniques which tend to place assets beyond the reach of future potential creditors. APP must not involve hiding assets or committing fraud or perjury. 2. OFFSHORE TRUST: A trust under which at least one trustee is resident outside of the United States (and its territories and possessions), and some aspects of which are construed, interpreted, and otherwise subject to the laws of a foreign country (usually, but not necessarily, the same country where the non-u.s. trustee is resident). The term "offshore trust", in this outline, unless indicated to the contrary, does not define or refer to the U.S. tax status of the trust. II. FACTORS IN SELECTING AN OFFSHORE JURISDICTION A. Legal System - Common Law vs. Civil Law B. Protective Legislation - What to look for: 1. First and Foremost: Lack of Comity 2. Repudiation of certain public policy based rules in US a. Retained Controls b. Spendthrift Trust - 3 -

6 3. Repealing the Statute of Elizabeth; Replaced With Specific Rules 4. Favorable tax laws - no tax on international trusts 5. No exchange controls on international trusts 6. Bankruptcy rule - absent a fraudulent transfer, the settlor's bankruptcy should not affect the validity of the trust or any transfers to it. C. Economic Health of Country D. Political and Social Stability E. Language - English? & Communications Facilities F. Track Record! III. PROTECTIVE ASPECTS A. General: 1. Jurisdiction over trust by US court 2. Implications of Lack of Comity a. Commence litigation de novo b. Utilize unfamiliar local lawyer c. Can't pay lawyer a contingency fee d. Bond usually required by court - "loser pays" rules usually applicable e. Sole basis of litigation: fraudulent transfer issues B. Comparison of Fraudulent Transfer Rules 1. Overview of Domestic Rules: a. Level of Proof in US: Preponderance of the evidence - does the - 4 -

7 greater weight of the evidence tend to show that a fraudulent transfer occurred? b. Creditor must prove: that a transfer was fraudulent as to any creditor. Thus, if a creditor can prove that a transfer was fraudulent as to another creditor, he can set aside the transfer, even though it may not have been fraudulent as to him. c. Limitations: Somewhat open-ended under the UFTA: a transfer can be set aside within four years after the transfer was made, or, if later, within one year after the transfer was or could reasonably have been discovered by the plaintiff. d. Elements of a fraudulent transfer under the UFTA: A transfer is fraudulent, as to present and subsequent creditors, if it is made with actual intent to hinder, delay or defraud any creditor of the debtor. The debtor's actual intent may be determined by a US court by giving consideration to the following factors, among others: i. The transfer or obligation was to an insider. ii. iii. iv. The debtor retained possession or control of the property transferred after the transfer. The transfer or obligation was disclosed or concealed. Before the transfer was made or obligation was incurred, the debtor had been sued or threatened with suit. v. The transfer was of substantially all the debtor's assets. vi. vii. viii. ix. The debtor absconded. The debtor removed or concealed assets. The value of the consideration received by the debtor was reasonably equivalent to the value of the asset transferred or the amount of the obligation incurred. The debtor was insolvent or became insolvent shortly after the transfer was made or the obligation was incurred. x. The transfer occurred shortly before or shortly after a - 5 -

8 substantial debt was incurred. e. A transfer is also fraudulent under the UFTA (almost identical under the UFCA), regardless of the debtor's intent, if it was made: i. Without receiving a reasonably equivalent value for the transfer, and the debtor was engaged or was about to engage in a business or transaction for which the debtor's remaining assets were unreasonably small in relation to the business or transaction, or if the debtor intended to incur, or believed or reasonably should have believed that he would incur, debts beyond his ability to pay as they became due, or ii. iii. As to present creditors, if the transfer was made while the debtor was insolvent or if it rendered him insolvent. These are sometimes referred to as "constructive" fraudulent transfers. f. What You Should Know About Solvency Under State Law 2. Overview of Cook Islands and Nevis Rules: a. Level of Proof Required: Beyond a reasonable doubt - the same standard utilized in this country to convict a person of a capital offense. b. Creditor must prove: that a transfer was fraudulent as to him - whether the transfer was fraudulent as to any other creditor is not relevant. c. Elements: The complaining creditor must prove beyond a reasonable doubt that establishment of the trust or the transfer of property to the trust was done with the principal intent to defraud that particular creditor and that the establishment or transfer rendered the settlor insolvent or without property by which the creditor's claim could be satisfied. i. If the settlor was solvent immediately after the establishment or transfer he is deemed not to have the requisite intent. ii. In addition, even if the settlor was rendered insolvent, the requisite intent cannot be imputed to him by reason of the fact that he: - 6 -

9 (A) (B) (C) established the trust or transferred property to it within two years from the date the creditor's cause of action arose, Retains significant powers over the trust (including powers to amend or revoke the trust), or Is a beneficiary of the trust. d. Limitations: i. The establishment of the trust or a transfer of property to it cannot be fraudulent if done more than two years after the creditor's cause of action accrued, or ii. iii. If same occurs within the two year period mentioned above, the creditor fails to commence an action within one year after such establishment or transfer, and Cannot be fraudulent as to subsequent creditor (i.e., where cause of action arose after the establishment or transfer). 3. When can a US planner ethically utilize the foreign fraudulent transfer laws? C. Comparison of Other Rules: Retained Controls/Benefits 1. Domestic: Extensive retained controls can result in a trust being declared invalid, and extensive retained benefits will the "property" a court can award to a creditor of the settlor-beneficiary because of public policy based rules. 2. Offshore: Certain offshore jurisdictions have enacted specific legislation which provides that a trust will not be rendered invalid by reason of extensive retained controls, and a self-settled spendthrift trust will be given effect as such - thereby authorizing asset protection trusts. In addition, the laws of several jurisdictions provide that a trust may establish the position of "trust protector", and the protector shall have (at a minimum, unless contravened in the instrument) the power to remove and replace trustees - a very significant control which might render a US trust invalid or a mere agent of the settlor. D. Protective Trust Clauses - 7 -

10 1. Trust Protector Clause: Enables a designated person to exercise certain powers over a trust, EXAMPLES: removal and replacement of trustees, veto of discretionary actions of trustees, consent to trust amendments. 2. Duress Clause: Should be drafted in a manner which will result in the nullification of the exercise of a power by any person acting under specified situations of duress. EXAMPLES: Trust protector's power to remove and replace a trustee is nullified if he is ordered by a court to do so; Trust protector's power to veto discretionary actions of trustees is nullified if acting under duress. 3. Flight Clause: Permits the trustee to change trust situs (can incorporate power to change applicable law of trust, as well) in order to protect the trust from a potential threat; especially useful if coupled with a power of attorney held by trust protector to effect title changes in such circumstances. 4. Discretionary Distribution/Allocation Provisions 5. Spendthrift Clause and progeny IV. PLANNING TECHNIQUES A. Utilizing Holding Entities - overcoming client's "loss of control" objections to offshore trusts B. Entity & Group Trust Planning Strategies V. US TAX CONSEQUENCES A. Income Tax B. Estate & Gift Taxes C. Is Tax Planning Possible With An Offshore Trust? VI. OTHER CONSIDERATIONS A. Risk and Nonrisk Assets B. Contempt of Court Issues - 8 -

11 ASSET PROTECTION PLANNING WITH OFFSHORE TRUSTS 2016 DONLEVY-ROSEN & ROSEN, P.A.

12 HOWARD ROSEN, ESQ. DONLEVY-ROSEN & ROSEN, P.A. CORAL GABLES, FLORIDA

13 PROTECTYOU.COM

14 ASSET PROTECTION NEWS.

15 ASK YOUR QUESTIONS PLEASE!

16 BUT FIRST, TWO QUESTIONS FOR YOU.

17 ARE YOUR CLIENTS CONFIDENT THAT THEY WILL NEVER BE SUED?

18 ARE YOUR CLIENTS CONFIDENT THAT THEY WILL NEVER BE SUED? ARE YOUR CLIENTS CONFIDENT THAT IF THEY ARE SUED, THEY WILL BE TREATED FAIRLY BY OUR LEGAL SYSTEM?

19 OK, So Who Needs Asset Protection Planning? Real Estate Investors / Developers Business Owners, Sellers (& Businesses) Health Care Providers Accountants Attorneys Architects, Engineers, Appraisers Parents of Teen-Age Drivers ANY HIGH INCOME/HIGH NET WORTH INDIVIDUAL Rule of Thumb?

20

21

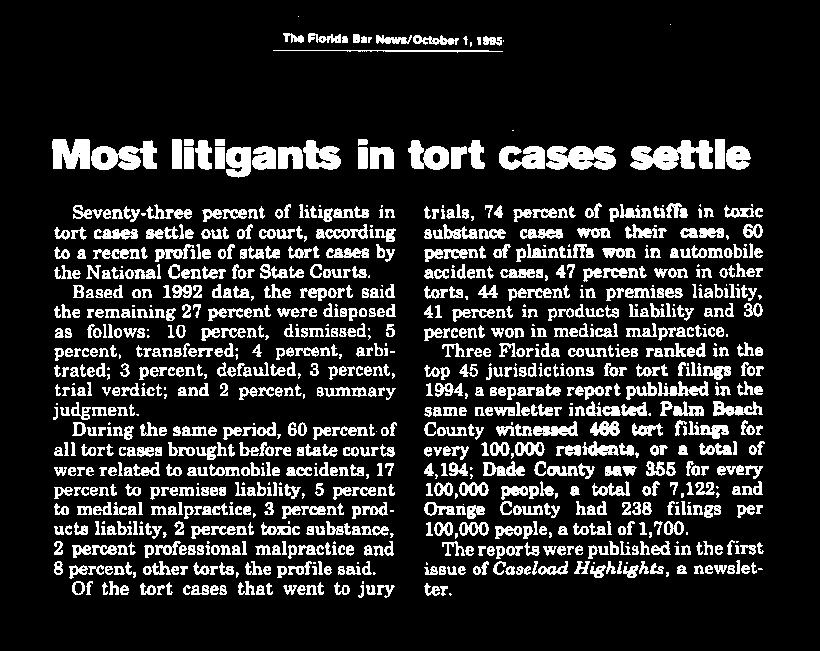

22 TWO REASONS MOST LITIGANTS...SETTLE THE SAME PRIMARY REASONS UPON WHICH THE IRS BASES ITS ACCEPTANCE OF AN OFFER IN COMPROMISE

23 TWO REASONS MOST LITIGANTS...SETTLE DOUBT AS TO LIABILITY

24 TWO REASONS MOST LITIGANTS...SETTLE DOUBT AS TO LIABILITY DOUBT AS TO COLLECTIBILITY

25 WHAT WE LL COVER IN THIS PRESENTATION:

26 WHAT WE LL COVER IN THIS PRESENTATION: SELECTING THE OFFSHORE JURISDICTION

27 WHAT WE LL COVER IN THIS PRESENTATION: SELECTING THE OFFSHORE JURISDICTION PROTECTIVE ASPECTS

28 WHAT WE LL COVER IN THIS PRESENTATION: SELECTING THE OFFSHORE JURISDICTION PROTECTIVE ASPECTS TYPICAL CLIENT CONCERNS

29 WHAT WE LL COVER IN THIS PRESENTATION: SELECTING THE OFFSHORE JURISDICTION PROTECTIVE ASPECTS TYPICAL CLIENT CONCERNS U.S. TAX COMPLIANCE

30 WHAT WE LL COVER IN THIS PRESENTATION: SELECTING THE OFFSHORE JURISDICTION PROTECTIVE ASPECTS TYPICAL CLIENT CONCERNS U.S. TAX COMPLIANCE OTHER STRATEGIES: Real Estate Special Strategies ENTITY TRUSTS; GROUP TRUSTS

31 Let s start with some background material.....

32 LET S START WITH SOME DEFINITIONS: ASSET PROTECTION PLANNING AN ESTATE PLANNING TOOL..

33 LET S START WITH SOME DEFINITIONS: ASSET PROTECTION PLANNING THE ARRANGEMENT OF ONE S FINANCIAL AFFAIRS IN A SUCH A WAY AS TO PLACE ASSETS BEYOND THE REACH OF FUTURE POTENTIAL CREDITORS, WHILE YOUR CLIENT CONTINUES TO ENJOY AND BENEFIT FROM THEM DOES NOT INVOLVE SECRET TRANSFERS, TAX EVASION, FRAUD OR SIMILAR SCHEMES

34 LET S START WITH SOME DEFINITIONS: OFFSHORE TRUST A TRUST WHICH: 1. HAS AT LEAST ONE TRUSTEE RESIDENT IN ANOTHER COUNTRY, AND 2. IS GOVERNED BY THE LAWS OF ANOTHER COUNTRY (NOT NECESSARILY A FOREIGN TRUST FOR U.S. INCOME TAX PURPOSES)

35 CONTINUING WITH DEFINITIONS: CREDITOR ANY PERSON WITH A CLAIM AGAINST YOUR CLIENT Could be Amex Could be spouse Could be a customer/patient Could be the EPA Could be ANYONE

36 A TRUST WILL BE THE CORNERSTONE OF ANY EFFECTIVE ASSET PROTECTION SOLUTION

37 BECAUSE TRUSTS HAVE BEEN USED SINCE THE CRUSADES TO PROTECT ASSETS...

38 EVEN THE IRS REGULATIONS DEFINE A TRUST BY RECOGNIZING THIS ANCIENT CORE PURPOSE: A TRUST IS AN ARRANGEMENT WHEREBY TRUSTEES TAKE TITLE TO PROPERTY FOR THE PURPOSE OF CONSERVING AND PROTECTING IT FOR THE BENEFIT OF THE BENEFICIARIES OF THE TRUST (WHO MAY BE THE PERSON(S) WHO CREATED THE TRUST)

39 GREAT! I LL SET UP MY TRUST RIGHT HERE! UNFORTUNATELY....

40 OVER THE PAST SEVERAL HUNDRED YEARS LIMITATIONS ON THE PROTECTIVE USE OF TRUSTS FOR SETTLORS (AS BENEFICIARIES) HAVE EVOLVED: Retained Controls Maximum Potential Property Interest Self-Settled Spendthrift Trusts

41 WHAT S THE SOLUTION? ESTABLISH THE TRUST IN A PLACE WHERE THE LAWS WILL NOT PERMIT A CREDITOR TO REACH TRUST ASSETS UNDER THE GENERAL RULES

42 WHAT S THE SOLUTION? WHERE WOULD THAT BE? WOULD IT BE A DOMESTIC (US) JURISDICTION OR WOULD IT BE AN OFFSHORE JURISDICTION?

43 DOMESTIC JURISDICTIONS: ALASKA DELAWARE RHODE ISLAND NEVADA MISSOURI UTAH OKLAHOMA SOUTH DAKOTA TENNESSEE WYOMING HAWAII OHIO

44 DOMESTIC JURISDICTIONS: DO THEY ACCOMPLISH OUR GOAL? THERE ARE PROBLEMS..

45 DOMESTIC JURISDICTIONS: CONSTITUTIONAL ISSUES: FULL FAITH & CREDIT CLAUSE SUPREMACY CLAUSE CONTRACT CLAUSE PRACTICAL CONSIDERATIONS: ENFORCEMENT OF JUDGMENTS ASSET PRESENCE RETAINED POWERS/CONTROLS ISSUES STANDARD OF PROOF/ STATUTE OF LIM FEES

46 WHAT S A MAJOR PROBLEM? 2005 BANKRUPTCY ACT s 10 YEAR SET ASIDE RULE:

47 548(e)(1) the [bankruptcy] trustee may avoid any transfer of an interest of the debtor in property that was made on or within 10 years before the date of the filing of the petition, if- (A) such transfer was made to a self-settled trust or similar device; (B) such transfer was by the debtor; (C) the debtor is a beneficiary of such trust or similar device; and (D) the debtor made such transfer with actual intent to hinder, delay, or defraud any entity to which the debtor was or became, on or after the date that such transfer was made, indebted.

48 WHY DOESN T THIS RULE APPLY TO THE OFFSHORE TRUST?

49 A SIMPLE EXAMPLE WILL ILLUSTRATE WHY..

50 SUPPOSE I MAKE A GIFT TO SOMEONE IN A COUNTRY WHICH DOESN T RECOGNIZE US COURT JUDGMENTS

51 AND THE US COURT ORDERS ME TO GET IT BACK HOW CAN I GET IT BACK?

52 WHAT S THE BIGGEST PROBLEM WITH U.S. BASED TRUSTS? THEY ARE ALL STILL PART OF THE UNITED STATES!

53 A BETTER APPROACH: USE AN APPROPRIATE OFFSHORE JURISDICTION AS THE TRUST SITUS TO BE CERTAIN THAT YOUR PLANNING WILL BE EFFECTIVE

54 AND HOW WOULD WE SELECT THE APPROPRIATE JURISDICTION?

55

56 SITUS SELECTION FACTORS: LEGAL SYSTEM: COMMON LAW or???

57 SITUS SELECTION FACTORS: LEGAL SYSTEM PROTECTIVE LEGISLATION

58 SITUS SELECTION FACTORS: LEGAL SYSTEM PROTECTIVE LEGISLATION (BIG 3) REPUDIATION OF CERTAIN RULES FAVORABLE FRAUDULENT TRANSFER RULES LACK OF COMITY

59 SITUS SELECTION FACTORS: LEGAL SYSTEM PROTECTIVE LEGISLATION ECONOMIC HEALTH

60 SITUS SELECTION FACTORS: LEGAL SYSTEM PROTECTIVE LEGISLATION ECONOMIC HEALTH POLITICAL/SOCIAL STABILITY

61 SITUS SELECTION FACTORS: LEGAL SYSTEM PROTECTIVE LEGISLATION ECONOMIC HEALTH POLITICAL/SOCIAL STABILITY LANGUAGE

62 SITUS SELECTION FACTORS: LEGAL SYSTEM PROTECTIVE LEGISLATION ECONOMIC HEALTH POLITICAL/SOCIAL STABILITY LANGUAGE TRACK RECORD

63 IN ORDER TO UNDERSTAND HOW A PROTECTIVE TRUST WORKS. WE MUST FIRST UNDERSTAND HOW CLAIMANTS NORMALLY REACH TRUST ASSETS

64 THERE ARE ONLY TWO WAYS...

65 THE CLAIMANT BRINGS HIS/HER CASE IN A COURT WHICH HAS: JURISDICTION OVER THE TRUSTEE OR JURISDICTION OVER TRUST ASSETS

66 HOW DOES AN OFFSHORE TRUST WORK? FIRST: AT THE CRITICAL TIME: THERE WILL BE A COMPLETE LACK OF US COURT JURISDICTION OVER THE TRUSTEE & THE TRUST ASSETS...

67 HOW DOES AN OFFSHORE TRUST WORK? THAT MEANS THERE WILL BE NO POWER IN ANY US COURT TO REACH THE TRUST THE US COURT: CAN T FORCE THE TRUSTEE TO DO ANYTHING CAN T SEIZE TRUST ASSETS

68 HOW DOES AN OFFSHORE TRUST WORK? SO WHERE DOES THAT LEAVE THE JUDGMENT CREDITOR? TRYING TO HAVE THE JUDGMENT ENFORCED IN THE TRUST SITUS JURISDICTION.. HOW WELL IS THAT GOING TO WORK?

69 HOW DOES AN OFFSHORE TRUST WORK? SO WHERE DOES THAT LEAVE THE JUDGMENT CREDITOR? TRYING TO HAVE THE JUDGMENT ENFORCED IN THE TRUST SITUS JURISDICTION.. REMEMBER LACK OF COMITY???

70 HOW DOES AN OFFSHORE TRUST WORK? WHAT ARE THE IMPLICATIONS OF LACK OF COMITY?

71 HOW DOES AN OFFSHORE TRUST WORK? IMPLICATIONS OF LACK OF COMITY COMMENCE LITIGATION DE NOVO

72 HOW DOES AN OFFSHORE TRUST WORK? IMPLICATIONS OF LACK OF COMITY COMMENCE LITIGATION DE NOVO UTILIZE UNFAMILIAR LAWYER

73 HOW DOES AN OFFSHORE TRUST WORK? IMPLICATIONS OF LACK OF COMITY COMMENCE LITIGATION DE NOVO UTILIZE UNFAMILIAR LAWYER CONTINGENCY FEE

74 HOW DOES AN OFFSHORE TRUST WORK? IMPLICATIONS OF LACK OF COMITY COMMENCE LITIGATION DE NOVO UTILIZE UNFAMILIAR LAWYER CONTINGENCY FEE BOND & LOSER PAYS RULES

75 HOW DOES AN OFFSHORE TRUST WORK? IMPLICATIONS OF LACK OF COMITY COMMENCE LITIGATION DE NOVO UTILIZE UNFAMILIAR LAWYER CONTINGENCY FEE BOND & LOSER PAYS RULES BASIS OF LITIGATION? A FRAUDULENT TRANSFER ASSERTION

76 HOW DOES AN OFFSHORE TRUST WORK? LET S COMPARE THE TWO MAJOR FACTORS OF THE FRAUDULENT TRANSFER RULES - US vs. OFFSHORE STATUTE OF LIMITATIONS LEVEL OF PROOF

77 HOW DOES AN OFFSHORE TRUST WORK? LET S COMPARE THE TWO MAJOR FACTORS OF THE FRAUDULENT TRANSFER RULES - US vs. OFFSHORE 4YRS+ vs. ZERO to 2yrs LEVEL OF PROOF

78 HOW DOES AN OFFSHORE TRUST WORK? LET S COMPARE THE TWO MAJOR FACTORS OF THE FRAUDULENT TRANSFER RULES - US vs. OFFSHORE 4YRS+ vs. ZERO to 2yrs CIVIL PREPONDERANCE STD vs. BEYOND REASONABLE DOUBT

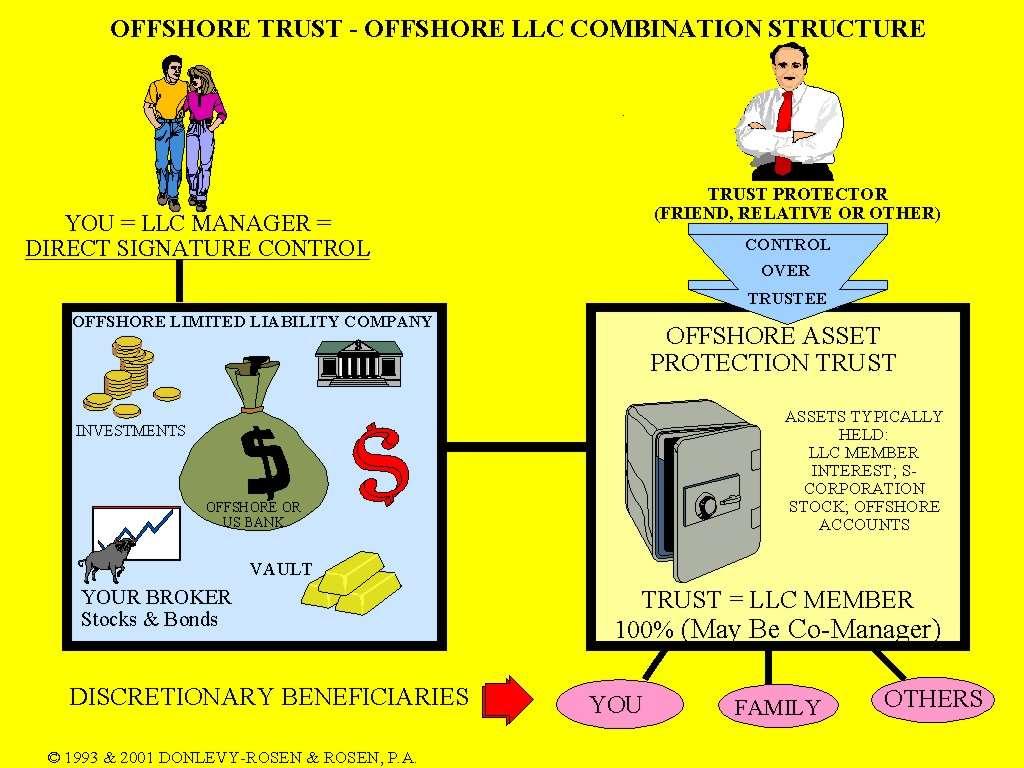

79 HOW DOES AN OFFSHORE TRUST WORK? WE VE SEEN HOW THE LAWS OF AN APPROPRIATE OFFSHORE JURISDICTION CAN AFFORD FOUNDATION PROTECTION FOR OUR CLIENTS TRUSTS. LET S SEE HOW WE CAN ENHANCE THAT PROTECTION WITH PROTECTIVE TRUST PROVISIONS

80 HOW DOES AN OFFSHORE TRUST WORK? TYPICAL PROTECTIVE CLAUSES TRUST PROTECTOR DURESS CLAUSE FLIGHT CLAUSE

81 HOW DOES AN OFFSHORE TRUST WORK? TYPICAL PROTECTIVE CLAUSES TRUST PROTECTOR: AN INDEPENDENT COMPANY HAVING THE POWER TO: VETO ANY DISCRETIONARY ACT OF THE TRUSTEE, AND REMOVE AND REPLACE ANY TRUSTEE WITH OR WITHOUT CAUSE

82 HOW DOES AN OFFSHORE TRUST WORK? TYPICAL PROTECTIVE CLAUSES DURESS CLAUSE: NULIFIES THE ATTEMPTED EXERCISE OF ANY POWER UNLESS EXERCISED BY THE POWER HOLDER OF HIS/HER OWN FREE WILL (A MECHANISM BY WHICH THE TRUSTEE CAN BE CERTAIN THAT A POWER IS BEING FREELY EXERCISED IS ESSENTIAL)

83 HOW DOES AN OFFSHORE TRUST WORK? TYPICAL PROTECTIVE CLAUSES FLIGHT CLAUSE: ALLOWS THE TRUST TO MOVE TO ANOTHER JURISDICTION IF APPROPRIATE (WE MUST INCLUDE A MECHANISM TO BE CERTAIN THAT THE FLIGHT CLAUSE CAN BE EFFECTED UNDER ALL CIRCUMSTANCES WE LL SEE HOW LATER)

84 WHAT CONCERN DO CLIENTS MOST OFTEN EXPRESS?

85 I DON T WANT TO LOSE CONTROL... SO HOW DO WE ADDRESS THAT CONCERN?

86 LOSS OF CONTROL CONCERNS... WE USE HOLDING ENTITIES: FOR PROTECTION OF LIQUID ASSETS (CASH AND PUBLICLY TRADED SECURITIES)

87 OFFSHORE TRUST OFFSHORE LLC COMBINATION STRUCTURE YOU = LLC MANAGER = DIRECT SIGNATURE CONTROL OFFSHORE LIMITED LIABILITY COMPANY INVESTMENTS OFFSHORE OR US BANK IMPLEMENTATION OPERATION CRISIS TRUST PROTECTOR (INDEPENDENT COMPANY) CONTROL OVER TRUSTEE OFFSHORE ASSET PROTECTION TRUST ASSETS TYPICALLY HELD: LLC MEMBER INTEREST; S- CORPORATION STOCK; OFFSHORE ACCOUNTS US TRUSTEE FOREIGN TRUSTEE YOUR BROKER Stocks & Bonds VAULT TRUST = LLC MEMBER 100% (May Be Co-Manager) DISCRETIONARY BENEFICIARIES YOU FAMILY OTHERS 1993 & 2001 DONLEVY-ROSEN & ROSEN, P.A.

88

89 (INDEPENDENT COMPANY)

90 GREAT. THE ASSETS ARE PROTECTED, BUT MY CLIENT NEEDS THE INCOME AND/OR PRINCIPAL TO LIVE ON

DISCRETIONARY BENEFICIARIES YOU FAMILY OTHERS 1993 & 2001 DONLEVY-ROSEN & ROSEN, P.")

91 OFFSHORE TRUST OFFSHORE LLC COMBINATION STRUCTURE TRUST PROTECTOR (INDEPENDENT COMPANY) CONTROL OVER TRUSTEE OFFSHORE ASSET PROTECTION TRUST ASSETS TYPICALLY HELD: LLC MEMBER INTEREST; S- CORPORATION STOCK; OFFSHORE ACCOUNTS TRUST = LLC MEMBER 100% (May Be Co-Manager) DISCRETIONARY BENEFICIARIES YOU FAMILY OTHERS 1993 & 2001 DONLEVY-ROSEN & ROSEN, P.A.

92 CONTINUING WITH LOSS OF CONTROL CONCERNS... ADVISOR AGREEMENTS ACCOUNT SIGNATURES POWER OF ATTORNEY IRREVOCABLE DIRECTION TRUSTEE INSURANCE

93 OK. WE VE BEEN DISCUSSING HOW TO PROTECT FINANCIAL ASSETS (CASH & PUBLICLY TRADED SECURITIES). HOW DO WE PROTECT IMMOVABLE ASSETS: REAL ESTATE - WHICH CANNOT BE MOVED OFFSHORE???

94 PROTECTING IMMOVABLE ASSETS MAKE THE ASSET UNATTRACTIVE TO A CREDITOR HOW DO WE MAKE AN ASSET UNATTRACTIVE? WE REMOVE ITS VALUE

95 HOW DO WE REMOVE AN ASSET S VALUE? WE ENCUMBER IT WE USE THE ASSET AS COLLATERAL FOR A LOAN OK. WHAT DO WE DO WITH THE LOAN PROCEEDS? WE PROTECT THE LOAN PROCEEDS WITH THE OTHER FINANCIAL ASSETS.

96 PROTECTING FIXED ASSETS - PART ONE OFFSHORE LENDER UNRELATED TO SETTLOR LOAN TO CLIENT (INVESTED IN CD) PLEDGE OF COLLATERAL (MORTGAGE OR OTHER LIEN) CD TRANSFERRED TO TRUST CLIENT=S OFFSHORE TRUST DONLEVY-ROSEN & ROSEN, P.A.

97 PROTECTING FIXED ASSETS - PART TWO OFFSHORE LENDER UNRELATED TO SETTLOR INTEREST PAYMENTS FROM TRUST OFFSHORE BANK ISSUER OF CD CLIENT=S OFFSHORE TRUST INTEREST PAYMENTS TO TRUST DONLEVY-ROSEN & ROSEN, P.A.

98 SUMMARY OF LOAN STRUCTURE Interest earned on CD held in Trust is reportable. Interest paid on Loan by Trustee on behalf of Borrower is deductible as Investment Interest under Section 163. Other Loan Fees & Costs are deductible as Miscellaneous Itemized deductions under Section 212.

99 SUMMARY OF LOAN STRUCTURE LOAN AMOUNT: 95% OF ASSET VALUE (=SIGNIFICANT PROTECTION) PAYMENTS: QUARTERLY INTEREST ONLY PAYMENTS PAID BY TRUST FROM EARNINGS ON INVESTED LOAN PROCEEDS LOAN STRUCTURE COST (UNDER 10,000,000): ORIGINATION FEE IS 1.35% OF LOAN AMOUNT OR MINIMUM FEE (PLUS LOCAL RECORDING COSTS) NET-NET ANNUAL COST OF LOAN STRUCTURE IS 1.2% OF LOAN AMOUNT NO RISK

100 ENTITY PROTECTION

101 ENTITY TRUSTS

102 ENTITY TRUSTS Definition: A trust settled (created) by an entity or by an appropriate group of entities.

103 ENTITY TRUSTS What are the Typical Appropriate Uses? Business - commonly used to hold proceeds of borrowing against receivables and equipment Nonqualified deferred compensation (can be structured to avoid 409A) Entity owner being sued - make his ownership interest uninteresting by eliminating the availability of entity assets (equity) for litigation settlement Any entity with assets to protect

104 ENTITY TRUSTS Construction Who will be the Settlor? A single entity or A group of entities (similar to a group trust)

105 ENTITY TRUSTS Construction Dispositive provisions Discretionary Income Discretionary Principal Special Power in Governing Board

106 ENTITY TRUSTS Construction Who Will Be The DISCRETIONARY Beneficiaries? The Entity or Entities Settling the Trust The Owners of the Entity (ies) Officers, Directors, Managers, Etc. Any trust settled by any of the foregoing Any trust under which any of the foregoing is or may be a beneficiary to any extent Charitable organizations

107 ENTITY TRUST EXAMPLE: CPA FIRM A 65 PARTNER CPA FIRM HAD A LARGE FUND OF CASH AND SECURITIES TO BE HELD TO FUND THE RETIREMENT OF PARTNERS THEY WERE WELL AWARE OF THE LITIGATION ISSUES FACING CPA S TODAY

108 EXAMPLE: CPA FIRM THE FIRM ESTABLISHED AN ENTITY TRUST TO HOLD AND PROTECT THE RETIREMENT FUND AMONG THE DISCRETIONARY BENEFICIARIES WERE ANY TRUST ESTABLISHED BY ANY PARTNER

109 EXAMPLE: CPA FIRM ON RETIREMENT, A PARTNER WAS FACING LITIGATION; HIS RETIREMENT DISTRIBUTION WAS MADE DIRECTLY TO HIS ASSET PROTECTION TRUST NEVER BEING EXPOSED TO US COURT JURISDICTION TO SATISFY HIS CREDITOR S CLAIM

110 GROUP TRUST STRATEGIES WHAT IS A GROUP TRUST? A group trust is a trust created by 4 or more individuals (who typically know each other) under a single trust document. For this purpose (only), a married couple is counted as one individual

111 GROUP TRUST STRATEGIES Appropriate Uses: Business practice groups (typical) Other homogeneous groups

112 GROUP TRUST STRATEGIES Construction

113 GROUP TRUST STRATEGIES Standardized dispositive provisions, i.e., credit shelter, qtip, children s provisions Each settlor has his/her own separate subtrust Separate accounting is required; thus gains, losses, dividends and other income/expense items are strictly allocated to the settlor/contributor of the asset generating same - avoids investment company issues of IRC Subchapter K

114 GROUP TRUST STRATEGIES Single trustee; single protector Strict financial confidentiality maintained as between settlors Each subtrust unaffected by another s lawsuits/issues A settlor can upgrade to an individually designed plan, but no additional settlors can be added

115 GROUP TRUST STRATEGIES COMPARISON TO INDIVIDUALIZED PLANNING: 40% LOWER FEES/COSTS STANDARDIZED vs. INDIVIDUALIZED DISPOSITIVE PROVISIONS FIXED TRUSTEE & PROTECTOR vs. LIMITED SELECTION BY CLIENT PROTECTION: NO DIFFERENCE! LET S TAKE A LOOK.

116 GROUP TRUST STRATEGIES

117 REMEMBER.. ONE OF THE QUESTIONS I ASKED AT THE BEGINNING OF THIS PROGRAM: ARE YOUR CLIENTS CONFIDENT THAT IF THEY ARE SUED, THEY WILL BE TREATED FAIRLY BY OUR LEGAL SYSTEM?

118 UNDERSTAND: THE PROTECTION UNDER ANY U.S. BASED PLAN DEPENDS UPON A US COURT TREATING YOUR CLIENT FAIRLY: I.E., UPHOLDING THE PLANNING IN YOUR CLIENT S FAVOR..

119 UNDERSTAND: ANY U.S. BASED PLAN CAN BE SUCCESSFULLY ATTACKED WITH THE RESULT THAT THE ASSETS ARE LOST

120 THE QUESTION BECOMES: DO I LEAVE MY CLIENT AT THE MERCY OF A U.S. COURT WITH A DOMESTIC PLAN, OR DO WE SET UP A PLAN THAT A U.S. COURT CAN T DISRUPT?

121 ASSET PROTECTION NEWS.

122 PROTECTYOU.COM

ASSET PROTECTION PLANNING & STRATEGIES FOR LAWYERS ACCOUNTANTS, FINANCIAL PLANNING AND INVESTMENT PROFESSIONALS

EPC Diablo Valley September 21, 2016 ASSET PROTECTION PLANNING & STRATEGIES FOR LAWYERS ACCOUNTANTS, FINANCIAL PLANNING AND INVESTMENT PROFESSIONALS Presented by Jeffrey M. Verdon, Esq. Managing Partner

EPC Diablo Valley September 21, 2016 ASSET PROTECTION PLANNING & STRATEGIES FOR LAWYERS ACCOUNTANTS, FINANCIAL PLANNING AND INVESTMENT PROFESSIONALS Presented by Jeffrey M. Verdon, Esq. Managing Partner

HONEY WE CAN CANCEL OUR TRIP TO THE COOK ISLANDS MICHIGAN HAS AN ASSET PROTECTION TRUST STATUTE!

HONEY WE CAN CANCEL OUR TRIP TO THE COOK ISLANDS MICHIGAN HAS AN ASSET PROTECTION TRUST STATUTE! By: Geoffrey N. Taylor, Esq. I. INTRODUCTION A. On my list of favorite estate planning myths, number one

HONEY WE CAN CANCEL OUR TRIP TO THE COOK ISLANDS MICHIGAN HAS AN ASSET PROTECTION TRUST STATUTE! By: Geoffrey N. Taylor, Esq. I. INTRODUCTION A. On my list of favorite estate planning myths, number one

Offshore Asset Protection Trusts vs. Onshore Asset Protection Trusts

Offshore Asset Protection Trusts vs. Onshore Asset Protection Trusts Same trust concepts govern both Both support estate planning and wealth transfer Same benefits re: probate and avoidance of estate delays

Offshore Asset Protection Trusts vs. Onshore Asset Protection Trusts Same trust concepts govern both Both support estate planning and wealth transfer Same benefits re: probate and avoidance of estate delays

Appendices Sample domestic asset protection trust clauses Sample irrevocable trust clauses Sample solvency letter State liability systems rankings Sta

PLANNING WITH DOMESTIC AND FOREIGN ASSET PR0TECTION TRUSTS Robert G. Alexander, JD, LL.M., EPLS, AEP Copyright 2009 Our Two Study Goals To Understand the Dynamics of Assets Protection Planning To Examine

PLANNING WITH DOMESTIC AND FOREIGN ASSET PR0TECTION TRUSTS Robert G. Alexander, JD, LL.M., EPLS, AEP Copyright 2009 Our Two Study Goals To Understand the Dynamics of Assets Protection Planning To Examine

Searching for Favorable DAPT Legislation: Tennessee Enters the Arena

Steve Leimberg's Asset Protection Planning Email Newsletter - Archive Message #105 Date: From: Subject: 1-June-07 Steve Leimberg's Asset Protection Planning Newsletter Searching for Favorable DAPT Legislation:

Steve Leimberg's Asset Protection Planning Email Newsletter - Archive Message #105 Date: From: Subject: 1-June-07 Steve Leimberg's Asset Protection Planning Newsletter Searching for Favorable DAPT Legislation:

Introduction to Asset Protection Planning. Objective of Asset Protection Planning Remove individual and family wealth from the attacks of :

Introduction to Asset Protection Planning Thomas P. Langdon, Esq. Objective of Asset Protection Planning Remove individual and family wealth from the attacks of : & Creditors Predators (IRS) Asset Protection

Introduction to Asset Protection Planning Thomas P. Langdon, Esq. Objective of Asset Protection Planning Remove individual and family wealth from the attacks of : & Creditors Predators (IRS) Asset Protection

Asset Protection Overview

Asset Protection Overview Leslie C. Giordani Michael H. Ripp, Jr. 100 CONGRESS AVENUE, SUITE 1440 AUSTIN, TEXAS 78701 phone 512.767.7100 fax 512.767.7101 WWW.GSRP.COM 2009 Giordani, Swanger, Ripp & Phillips,

Asset Protection Overview Leslie C. Giordani Michael H. Ripp, Jr. 100 CONGRESS AVENUE, SUITE 1440 AUSTIN, TEXAS 78701 phone 512.767.7100 fax 512.767.7101 WWW.GSRP.COM 2009 Giordani, Swanger, Ripp & Phillips,

PROTECTING YOUR ASSETS Release No. 7

PROTECTING YOUR ASSETS Release No. 7 Everything you need... New Section on Property Agreements Includes Prenuptial and Post-Marital Property Agreements for Community Property & Separate Property States

PROTECTING YOUR ASSETS Release No. 7 Everything you need... New Section on Property Agreements Includes Prenuptial and Post-Marital Property Agreements for Community Property & Separate Property States

Presented By: Jeffrey R. Matsen. November, 2009, Jeffrey R. Matsen

INTRODUCTION TO ASSET PROTECTION PLANNING Presented By: Jeffrey R. Matsen November, 2009, Jeffrey R. Matsen 1 What Is Fully Integrated Estate Planning? Planning for the orderly disposition of assets at

INTRODUCTION TO ASSET PROTECTION PLANNING Presented By: Jeffrey R. Matsen November, 2009, Jeffrey R. Matsen 1 What Is Fully Integrated Estate Planning? Planning for the orderly disposition of assets at

PLANNING TECHNIQUES FOR LARGE ESTATES PLANNING WITH DOMESTIC ASSET PROTECTION TRUSTS

PLANNING TECHNIQUES FOR LARGE ESTATES PLANNING WITH DOMESTIC ASSET PROTECTION TRUSTS Richard W. Nenno, Esquire Managing Director and Trust Counsel Wilmington Trust Company Rodney Square North 1100 North

PLANNING TECHNIQUES FOR LARGE ESTATES PLANNING WITH DOMESTIC ASSET PROTECTION TRUSTS Richard W. Nenno, Esquire Managing Director and Trust Counsel Wilmington Trust Company Rodney Square North 1100 North

Asset Protection Planning (With Audit Checklist)

") Asset Protection Planning (With Audit Checklist) Gideon Rothschild Gideon Rothschild, J.D., CPA, is with Moses & Singer LLP, in New York, New York. A. Introduction 1. Litigation environment creates greater

Asset Protection Planning (With Audit Checklist) Gideon Rothschild Gideon Rothschild, J.D., CPA, is with Moses & Singer LLP, in New York, New York. A. Introduction 1. Litigation environment creates greater

Asset Protection and Retention of Control: Is Peaceful Co-Existence Possible?

University of Miami Law School Institutional Repository University of Miami Business Law Review 10-1-1992 Asset Protection and Retention of Control: Is Peaceful Co-Existence Possible? Howard D. Rosen Follow

University of Miami Law School Institutional Repository University of Miami Business Law Review 10-1-1992 Asset Protection and Retention of Control: Is Peaceful Co-Existence Possible? Howard D. Rosen Follow

Revocable Trust Vs. Irrevocable Trust

I am not an attorney but here to help you undertand what things are... Speak to An Asset protection Attorney and find the best solution for you... Revocable Trust Vs. Irrevocable Trust Trusts are relatively

I am not an attorney but here to help you undertand what things are... Speak to An Asset protection Attorney and find the best solution for you... Revocable Trust Vs. Irrevocable Trust Trusts are relatively

WILLMS, S.C. LAW FIRM

WILLMS, S.C. LAW FIRM TO: FROM: Clients and Friends of Willms, S.C. Attorney Maureen L. O Leary DATE: December 5, 2011 RE: Asset Protection Planning Asset protection planning refers to arranging an individual

WILLMS, S.C. LAW FIRM TO: FROM: Clients and Friends of Willms, S.C. Attorney Maureen L. O Leary DATE: December 5, 2011 RE: Asset Protection Planning Asset protection planning refers to arranging an individual

Integrating Asset Protection Planning Into Your Estate Planning Practice. Douglass S. Lodmell, J.D., LL.M. Managing Partner Lodmell & Lodmell, P.

Integrating Asset Protection Planning Into Your Estate Planning Practice Douglass S. Lodmell, J.D., LL.M. Managing Partner Lodmell & Lodmell, P.C Douglass is the Co-Founder and the managing partner of,

Integrating Asset Protection Planning Into Your Estate Planning Practice Douglass S. Lodmell, J.D., LL.M. Managing Partner Lodmell & Lodmell, P.C Douglass is the Co-Founder and the managing partner of,

THE NEW MICHIGAN DOMESTIC ASSET PROTECTION TRUST

THE NEW MICHIGAN DOMESTIC ASSET PROTECTION TRUST Presenter: Larry E. Powe, Esq., KELLER THOMA, P.C., Southfield, Michigan 2017 I. RATIONALE Until approximately 20 years ago, the laws throughout the United

THE NEW MICHIGAN DOMESTIC ASSET PROTECTION TRUST Presenter: Larry E. Powe, Esq., KELLER THOMA, P.C., Southfield, Michigan 2017 I. RATIONALE Until approximately 20 years ago, the laws throughout the United

Saving Your Clients Assets: Asset Protection Planning

Saving Your Clients Assets: Asset Protection Planning June 21, 2016 SABA Family Law Section-CLE Presented by: Ivan Ramirez, Esq. Legal Disclaimer - The information provided is designed for general information

Saving Your Clients Assets: Asset Protection Planning June 21, 2016 SABA Family Law Section-CLE Presented by: Ivan Ramirez, Esq. Legal Disclaimer - The information provided is designed for general information

L A N R U O J tm Utah Bar Volume 23 No. 2 March/April 2010

Utah Bartm J O U R N A L Volume 23 No. 2 March/April 2010 Table of Contents Letters to the Editor 7 President-Elect & Bar Commission Candidates 8 President s Message: Helping Unemployed/Underemployed Lawyers

Utah Bartm J O U R N A L Volume 23 No. 2 March/April 2010 Table of Contents Letters to the Editor 7 President-Elect & Bar Commission Candidates 8 President s Message: Helping Unemployed/Underemployed Lawyers

Asset Protection Planning for Arizona Residents

ESTATE PLANNING INHERITANCE PROTECTION 7650 E. BROADWAY BLVD. #108 PHONE (520) 546-3558 TUCSON, AZ 85710 TOM@TOMBOUMANLAW.COM Asset Protection Planning for Arizona Residents 1. What is Asset Protection

ESTATE PLANNING INHERITANCE PROTECTION 7650 E. BROADWAY BLVD. #108 PHONE (520) 546-3558 TUCSON, AZ 85710 TOM@TOMBOUMANLAW.COM Asset Protection Planning for Arizona Residents 1. What is Asset Protection

NC General Statutes - Chapter 39 Article 3A 1

Article 3A. Uniform Voidable Transactions Act. 39-23.1. Definitions. In this Article, the following definitions apply: (1) Affiliate. Any of the following: a. A person that directly or indirectly owns,

Article 3A. Uniform Voidable Transactions Act. 39-23.1. Definitions. In this Article, the following definitions apply: (1) Affiliate. Any of the following: a. A person that directly or indirectly owns,

Creditor Protection for High Net Worth Individuals and Business Owners

Creditor Protection for High Net Worth Individuals and Business Owners Presented by Maritess T. Bott of Bott & Associates, Ltd. Attorneys at Law Helping people preserve their wealth The Family Business

Creditor Protection for High Net Worth Individuals and Business Owners Presented by Maritess T. Bott of Bott & Associates, Ltd. Attorneys at Law Helping people preserve their wealth The Family Business

Asset Protection Advance Planning is Key

Partners Office for Women s Careers at MGH Presents Asset Protection Advance Planning is Key Barbara Freedman Wand, Esq. Estate Planning Group Bingham McCutchen LLP Boston Asset Protection Planning is

Partners Office for Women s Careers at MGH Presents Asset Protection Advance Planning is Key Barbara Freedman Wand, Esq. Estate Planning Group Bingham McCutchen LLP Boston Asset Protection Planning is

1/19/2012. J. Grant Coleman

J. Grant Coleman jcoleman@kingkrebs.com www.kingkrebs.com 1 Consideration and implementation of advance planning techniques designed to place assets outside the reach of potential future creditors (not

J. Grant Coleman jcoleman@kingkrebs.com www.kingkrebs.com 1 Consideration and implementation of advance planning techniques designed to place assets outside the reach of potential future creditors (not

September /October Some strings attached Stretching your legacy Don t underestimate the power of Crummey trusts Estate Planning Red Flag

The Estate Planner September/October 2007 Some strings attached Maintaining control over your charitable contributions without losing your deduction Stretching your legacy Dynasty trusts benefit many generations

The Estate Planner September/October 2007 Some strings attached Maintaining control over your charitable contributions without losing your deduction Stretching your legacy Dynasty trusts benefit many generations

STEALTH WEALTH HIDING ASSETS FROM THE PUBLIC by Layne T. Rushforth 1

HIDING ASSETS FROM THE PUBLIC by Layne T. Rushforth 1 1. OVERVIEW 1.1 Overview: Many people are concerned about having other people know about their assets 2. Some worry about lawsuits and other creditors

HIDING ASSETS FROM THE PUBLIC by Layne T. Rushforth 1 1. OVERVIEW 1.1 Overview: Many people are concerned about having other people know about their assets 2. Some worry about lawsuits and other creditors

Weller Group LLC January 30, 2017

Weller Group LLC Timothy Weller, CFP CERTIFIED FINANCIAL PLANNER 6206 Slocum Road Ontario, NY 14519 315-524-8000 tim@wellergroupllc.com www.wellergroupllc.com Asset Protection Page 1 of 6, see disclaimer

Weller Group LLC Timothy Weller, CFP CERTIFIED FINANCIAL PLANNER 6206 Slocum Road Ontario, NY 14519 315-524-8000 tim@wellergroupllc.com www.wellergroupllc.com Asset Protection Page 1 of 6, see disclaimer

Offshore Protection with Domestic Simplicity

Spokane Estate Planning Council 2017 Annual Seminar The Bridge Trust Offshore Protection with Domestic Simplicity Douglass S. Lodmell, J.D., LL.M. Managing Partner Lodmell & Lodmell, P.C. Douglass Lodmell,

Spokane Estate Planning Council 2017 Annual Seminar The Bridge Trust Offshore Protection with Domestic Simplicity Douglass S. Lodmell, J.D., LL.M. Managing Partner Lodmell & Lodmell, P.C. Douglass Lodmell,

Leimberg s Think About It

Leimberg s Think About It Think About It is written by Stephan R. Leimberg, JD, CLU and co-authored by Linas Sudzius MAY 2009 # 399 Diversity of opinion helps us to be more successful? Your Success Matters!

Leimberg s Think About It Think About It is written by Stephan R. Leimberg, JD, CLU and co-authored by Linas Sudzius MAY 2009 # 399 Diversity of opinion helps us to be more successful? Your Success Matters!

Using Advanced Irrevocable Trusts for Income and Estate Tax Savings: Making 2012 Count

Using Advanced Irrevocable Trusts for Income and Estate Tax Savings: Making 2012 Count The next nine months are an exceptional window of opportunity for your clients to make family wealth transfers. The

Using Advanced Irrevocable Trusts for Income and Estate Tax Savings: Making 2012 Count The next nine months are an exceptional window of opportunity for your clients to make family wealth transfers. The

White Paper: Asset Protection

White Paper: www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 Introduction...

White Paper: www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 Introduction...

Law Offices of Jack S. Johal. Fall 2016 Bulletin DYNASTY TRUSTS MAY BE EVEN MORE POWERFUL AFTER CHANGES IN TRANSFER TAX

The tax and creditor protection advantages of dynasty trusts will make these trusts more attractive as family wealth preservation tools in the event of repeal of the estate and GST taxes, or if the estate

The tax and creditor protection advantages of dynasty trusts will make these trusts more attractive as family wealth preservation tools in the event of repeal of the estate and GST taxes, or if the estate

An Overview of the Asset Protection Spectrum By: Leah Del Percio, Esq.

An Overview of the Asset Protection Spectrum By: Leah Del Percio, Esq. In our increasingly litigious society, the threat of lawsuits, debt and liability is at an all-time high for individuals and their

An Overview of the Asset Protection Spectrum By: Leah Del Percio, Esq. In our increasingly litigious society, the threat of lawsuits, debt and liability is at an all-time high for individuals and their

Lifetime Asset Protection Strategies for Arizona Residents

ESTATE PLANNING INHERITANCE PROTECTION 7650 E. BROADWAY BLVD. #108 PHONE (520) 546-3558 TUCSON, AZ 85710 TOM@TOMBOUMANLAW.COM Lifetime Asset Protection Strategies for Arizona Residents Asset protection

ESTATE PLANNING INHERITANCE PROTECTION 7650 E. BROADWAY BLVD. #108 PHONE (520) 546-3558 TUCSON, AZ 85710 TOM@TOMBOUMANLAW.COM Lifetime Asset Protection Strategies for Arizona Residents Asset protection

Introduction to Asset Protection Planning

Introduction to Asset Protection Planning FPA of Phoenix, Arizona September 2011 Thomas P. Langdon, Esq. Asset Protection Planning Defined Protecting wealth from creditors & predators Lifetime/multi-generational

Introduction to Asset Protection Planning FPA of Phoenix, Arizona September 2011 Thomas P. Langdon, Esq. Asset Protection Planning Defined Protecting wealth from creditors & predators Lifetime/multi-generational

SAMPLE DECLARATION OF TRUST. The John Doe Living Trust (the Trust )

") DECLARATION OF TRUST The John Doe Living Trust (the Trust ) This DECLARATION OF TRUST (this Declaration ) is made and executed on the date below by and between the herein-named grantors and trustees. This

DECLARATION OF TRUST The John Doe Living Trust (the Trust ) This DECLARATION OF TRUST (this Declaration ) is made and executed on the date below by and between the herein-named grantors and trustees. This

Chapter 24 PROTECTING YOUR ASSETS

Chapter 24 PROTECTING YOUR ASSETS Practice and business owners pay much attention to and spend much of their time building their practices and businesses in an effort to obtain and accumulate wealth. The

Chapter 24 PROTECTING YOUR ASSETS Practice and business owners pay much attention to and spend much of their time building their practices and businesses in an effort to obtain and accumulate wealth. The

Affordable Asset Protection Strategies for Arizona Residents

ESTATE PLANNING INHERITANCE PROTECTION 7650 E. BROADWAY BLVD. #108 PHONE (520) 546-3558 TUCSON, AZ 85710 TOM@TOMBOUMANLAW.COM Affordable Asset Protection Strategies for Arizona Residents My first exposure

ESTATE PLANNING INHERITANCE PROTECTION 7650 E. BROADWAY BLVD. #108 PHONE (520) 546-3558 TUCSON, AZ 85710 TOM@TOMBOUMANLAW.COM Affordable Asset Protection Strategies for Arizona Residents My first exposure

ASSET PROTECTION PLANNING

I. INTRODUCTION ASSET PROTECTION PLANNING Gideon Rothschild Moses & Singer LLP grothschild@mosessinger.com A. The Current Litigation Environment Creates Greater Exposure to Risk of Loss Than Ever Before:

I. INTRODUCTION ASSET PROTECTION PLANNING Gideon Rothschild Moses & Singer LLP grothschild@mosessinger.com A. The Current Litigation Environment Creates Greater Exposure to Risk of Loss Than Ever Before:

Estate Planning. Insight on. Decanting breathes new life into an old trust. Choosing a trustee for your living trust

Insight on Estate Planning August/September 2012 Decanting breathes new life into an old trust Estate planning 101 Choosing a trustee for your living trust Is your estate liquid enough to cover estate

Insight on Estate Planning August/September 2012 Decanting breathes new life into an old trust Estate planning 101 Choosing a trustee for your living trust Is your estate liquid enough to cover estate

CHAPTER 245 INTERNATIONAL TRUSTS

1 L.R.O. 1998 International Trusts CAP. 245 CHAPTER 245 INTERNATIONAL TRUSTS ARRANGEMENT OF SECTIONS SECTION Citation 1. Short title. 2. Definitions. 3. Trust described. 4. Application of Act. PART I Interpretation

1 L.R.O. 1998 International Trusts CAP. 245 CHAPTER 245 INTERNATIONAL TRUSTS ARRANGEMENT OF SECTIONS SECTION Citation 1. Short title. 2. Definitions. 3. Trust described. 4. Application of Act. PART I Interpretation

ASSET PROTECTION SHIELDING ASSETS FROM CREDITORS AND CLAIMANTS by Layne T. Rushforth 1

SHIELDING ASSETS FROM CREDITORS AND CLAIMANTS by Layne T. Rushforth 1 1. OVERVIEW 1.1 Overview: Many people are concerned about having their assets 2 taken from them by creditors. This memo briefly outlines

SHIELDING ASSETS FROM CREDITORS AND CLAIMANTS by Layne T. Rushforth 1 1. OVERVIEW 1.1 Overview: Many people are concerned about having their assets 2 taken from them by creditors. This memo briefly outlines

New York Enacts Important New Law Governing a Trustee s Power to Pay Trust Assets to a New Trust

PAMELA EHRENKRANZ (PEhrenkranz@wlrk.com) is chair of the Trusts and Estates Practice Group at Wachtell, Lipton, Rosen & Katz in New York. Her practice is focused on developing estate plans for individual

PAMELA EHRENKRANZ (PEhrenkranz@wlrk.com) is chair of the Trusts and Estates Practice Group at Wachtell, Lipton, Rosen & Katz in New York. Her practice is focused on developing estate plans for individual

Taddei, Ludwig & Associates, Inc.

Taddei, Ludwig & Associates, Inc. Kirk Ludwig, ChFC, CFP Scot Elrod Diane McCracken, ChFC Matt Taddei, CLU, CFP 999 Fifth Ave., Suite 230 San Rafael, CA 94901 415-456-2292 scot@tlafinancial.com www.tlafinancial.com

Taddei, Ludwig & Associates, Inc. Kirk Ludwig, ChFC, CFP Scot Elrod Diane McCracken, ChFC Matt Taddei, CLU, CFP 999 Fifth Ave., Suite 230 San Rafael, CA 94901 415-456-2292 scot@tlafinancial.com www.tlafinancial.com

ACTEC COMPARISON OF THE. EDITED BY DAVID G. SHAFTEL Copyright 2012, David G. Shaftel. All Rights Reserved.

ACTEC COMPARISON OF THE DOMESTIC ASSET PROTECTION TRUST STATUTES UPDATED THROUGH DECEMBER 2011 EDITED BY DAVID G. SHAFTEL Copyright 2012, David G. Shaftel. All Rights Reserved. This 2012 version of the

ACTEC COMPARISON OF THE DOMESTIC ASSET PROTECTION TRUST STATUTES UPDATED THROUGH DECEMBER 2011 EDITED BY DAVID G. SHAFTEL Copyright 2012, David G. Shaftel. All Rights Reserved. This 2012 version of the

THE USE OF ASSET PROTECTION TRUSTS FOR TAX PLANNING PURPOSES

THE USE OF ASSET PROTECTION TRUSTS FOR TAX PLANNING PURPOSES Presented by: Michael M. Gordon Gordon, Fournaris & Mammarella, P.A. 1925 Lovering Avenue Wilmington, Delaware 19806 302-652-2900 mgordon@gfmlaw.com

THE USE OF ASSET PROTECTION TRUSTS FOR TAX PLANNING PURPOSES Presented by: Michael M. Gordon Gordon, Fournaris & Mammarella, P.A. 1925 Lovering Avenue Wilmington, Delaware 19806 302-652-2900 mgordon@gfmlaw.com

ASSET PROTECTION PLANNING LIKE THE AMERICAN EXPRESS CARD COMMERCIAL SAYS "DON'T LEAVE HOME WITHOUT IT"

I. The Problem. ASSET PROTECTION PLANNING LIKE THE AMERICAN EXPRESS CARD COMMERCIAL SAYS "DON'T LEAVE HOME WITHOUT IT" Maurice Offit, Esquire Offit Kurman (301) 575-0308 moffit@offitkurman.com A. We live

I. The Problem. ASSET PROTECTION PLANNING LIKE THE AMERICAN EXPRESS CARD COMMERCIAL SAYS "DON'T LEAVE HOME WITHOUT IT" Maurice Offit, Esquire Offit Kurman (301) 575-0308 moffit@offitkurman.com A. We live

Strafford Publications Webinar. October 6, 2011 THE DELAWARE DECANTING STATUTE

Strafford Publications Webinar October 6, 2011 THE DELAWARE DECANTING STATUTE Thomas R. Pulsifer Morris Nichols Arsht & Tunnell LLP 1201 North Market Street P. O. Box 1347 Wilmington, DE 19899-1347 Telephone:

Strafford Publications Webinar October 6, 2011 THE DELAWARE DECANTING STATUTE Thomas R. Pulsifer Morris Nichols Arsht & Tunnell LLP 1201 North Market Street P. O. Box 1347 Wilmington, DE 19899-1347 Telephone:

White Paper Use of Trusts and Creditor Implications

White Paper Use of Trusts and Creditor Implications www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC,

White Paper Use of Trusts and Creditor Implications www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC,

Estate Planning. Insight on. The Crummey trust: Still relevant after all these years. Now s the time for a charitable lead trust

Insight on Estate Planning October/November 2014 The Crummey trust: Still relevant after all these years Now s the time for a charitable lead trust Good intentions Don t let asset transfers run afoul of

Insight on Estate Planning October/November 2014 The Crummey trust: Still relevant after all these years Now s the time for a charitable lead trust Good intentions Don t let asset transfers run afoul of

Rush University Case: Impact on Self-Settled Trusts. By Gideon Rothschild, Esq. and Martin M. Shenkman, Esq.

Rush University Case: Impact on Self-Settled Trusts By Gideon Rothschild, Esq. and Martin M. Shenkman, Esq. A recent Illinois case that ruled unfavorably on the use of self-settled trusts, Rush Univ. Med.

Rush University Case: Impact on Self-Settled Trusts By Gideon Rothschild, Esq. and Martin M. Shenkman, Esq. A recent Illinois case that ruled unfavorably on the use of self-settled trusts, Rush Univ. Med.

Changing Trust Situs. Thomas M. Forrest. President, U.S. Trust Company of Delaware

Changing Trust Situs Thomas M. Forrest President, U.S. Trust Company of Delaware Changing Trust Situs Choice of law: When creating a new trust, a grantor can and should designate the law of the trust state

Changing Trust Situs Thomas M. Forrest President, U.S. Trust Company of Delaware Changing Trust Situs Choice of law: When creating a new trust, a grantor can and should designate the law of the trust state

Frederick N. Widen Partner

216.583.7340 1660 West 2nd Street, Suite 1100 Cleveland, OH 44113-1406 fwiden@ulmer.com Practices/Industries General Taxation Tax Controversy Succession Planning Education Cleveland State University (B.B.A.,

216.583.7340 1660 West 2nd Street, Suite 1100 Cleveland, OH 44113-1406 fwiden@ulmer.com Practices/Industries General Taxation Tax Controversy Succession Planning Education Cleveland State University (B.B.A.,

Estate Planning Through an Asset Protection Lens

Estate Planning Through an Asset Protection Lens Gideon Rothschild, J.D., C.P.A. Moses & Singer LLP 405 Lexington Avenue New York, NY 10174 Telephone: 212.554.7806 grothschild@mosessinger.com www.mosessinger.com

Estate Planning Through an Asset Protection Lens Gideon Rothschild, J.D., C.P.A. Moses & Singer LLP 405 Lexington Avenue New York, NY 10174 Telephone: 212.554.7806 grothschild@mosessinger.com www.mosessinger.com

MARYLAND STATUTORY FORM PERSONAL FINANCIAL POWER OF ATTORNEY IMPORTANT INFORMATION AND WARNING

MARYLAND STATUTORY FORM PERSONAL FINANCIAL POWER OF ATTORNEY IMPORTANT INFORMATION AND WARNING You should be very careful in deciding whether or not to sign this document. The powers granted by you (the

MARYLAND STATUTORY FORM PERSONAL FINANCIAL POWER OF ATTORNEY IMPORTANT INFORMATION AND WARNING You should be very careful in deciding whether or not to sign this document. The powers granted by you (the

Estate Planning. Insight on. Protecting your assets without a prenup. The ABLE account: A good alternative to a special needs trust?

Insight on Estate Planning August/September 2015 Premarital planning Protecting your assets without a prenup The ABLE account: A good alternative to a special needs trust? Make net gifts to reduce your

Insight on Estate Planning August/September 2015 Premarital planning Protecting your assets without a prenup The ABLE account: A good alternative to a special needs trust? Make net gifts to reduce your

The 2014 Florida Statutes. Title XLI STATUTE OF FRAUDS, FRAUDULENT TRANSFERS, AND GENERAL ASSIGNMENTS. Chapter 726 FRAUDULENT TRANSFERS

The 2014 Florida Statutes Title XLI STATUTE OF FRAUDS, FRAUDULENT TRANSFERS, AND GENERAL ASSIGNMENTS Chapter 726 FRAUDULENT TRANSFERS View Entire Chapter CHAPTER 726 FRAUDULENT TRANSFERS 726.101 Short

The 2014 Florida Statutes Title XLI STATUTE OF FRAUDS, FRAUDULENT TRANSFERS, AND GENERAL ASSIGNMENTS Chapter 726 FRAUDULENT TRANSFERS View Entire Chapter CHAPTER 726 FRAUDULENT TRANSFERS 726.101 Short

PLANNING AND DEFENDING DOMESTIC ASSET-PROTECTION TRUSTS

PLANNING AND DEFENDING DOMESTIC ASSET-PROTECTION TRUSTS Richard W. Nenno, Esquire Wilmington Trust Company Wilmington, Delaware John E. Sullivan, III, Esquire Sullivan & Sullivan, Ltd. Beachwood, Ohio

PLANNING AND DEFENDING DOMESTIC ASSET-PROTECTION TRUSTS Richard W. Nenno, Esquire Wilmington Trust Company Wilmington, Delaware John E. Sullivan, III, Esquire Sullivan & Sullivan, Ltd. Beachwood, Ohio

GUIDE TO TRUSTS IN MAURITIUS

GUIDE TO TRUSTS IN MAURITIUS CONTENTS PREFACE 1 1. Introduction 2 2. What is a Trust? 2 3. Settlors 2 4. Beneficiaries 3 5. Why a Mauritius Trust? 3 6. Creating a Trust 3 7. Trust Duration 4 8. Trustees

GUIDE TO TRUSTS IN MAURITIUS CONTENTS PREFACE 1 1. Introduction 2 2. What is a Trust? 2 3. Settlors 2 4. Beneficiaries 3 5. Why a Mauritius Trust? 3 6. Creating a Trust 3 7. Trust Duration 4 8. Trustees

In these times, with the real estate bust and economic downturn, it is likely

Asset Protection Planning: An Important Resource For Clients in Difficult Times By Richard M. Guerard In these times, with the real estate bust and economic downturn, it is likely that most attorneys have

Asset Protection Planning: An Important Resource For Clients in Difficult Times By Richard M. Guerard In these times, with the real estate bust and economic downturn, it is likely that most attorneys have

Asset Protection Planning (With Audit Checklist)

") Asset Protection Planning (With Audit Checklist) Gideon Rothschild A. Introduction 1. Litigation environment creates greater exposure to risk of loss. a. Expanded theories of liability (such as McDonald

Asset Protection Planning (With Audit Checklist) Gideon Rothschild A. Introduction 1. Litigation environment creates greater exposure to risk of loss. a. Expanded theories of liability (such as McDonald

Estate Planning. Insight on. Saving for college is also good for your estate plan. Will your estate plan benefit from a trust protector?

Insight on Estate Planning Year End 2014 Saving for college is also good for your estate plan Will your estate plan benefit from a trust protector? Charitable deductions Substantiate them or lose them

Insight on Estate Planning Year End 2014 Saving for college is also good for your estate plan Will your estate plan benefit from a trust protector? Charitable deductions Substantiate them or lose them

WCI Communities, Inc., and certain related Debtors FORM OF CHINESE DRYWALL PROPERTY DAMAGE AND PERSONAL INJURY SETTLEMENT TRUST AGREEMENT

WCI Communities, Inc., and certain related Debtors FORM OF CHINESE DRYWALL PROPERTY DAMAGE AND PERSONAL INJURY SETTLEMENT TRUST AGREEMENT WCI Communities, Inc., and certain related Debtors CHINESE DRYWALL

WCI Communities, Inc., and certain related Debtors FORM OF CHINESE DRYWALL PROPERTY DAMAGE AND PERSONAL INJURY SETTLEMENT TRUST AGREEMENT WCI Communities, Inc., and certain related Debtors CHINESE DRYWALL

Taming the Planning B.E.A.S.T.

Taming the Planning B.E.A.S.T. Tulsa Estate Planning Forum October 9 th, 2017 James M. Duggan, M.B.A., J.D. DUGGAN BERTSCH, LLC 303 West Madison, Suite 1000 Chicago, Illinois 60606-3321 e-mail: jduggan@dugganbertsch.com

Taming the Planning B.E.A.S.T. Tulsa Estate Planning Forum October 9 th, 2017 James M. Duggan, M.B.A., J.D. DUGGAN BERTSCH, LLC 303 West Madison, Suite 1000 Chicago, Illinois 60606-3321 e-mail: jduggan@dugganbertsch.com

Special Drafting Considerations For Asset Protection Trusts - The Offspring of Offshore Trusts

THE LAW FIRM OF BOVE & LANGA A PROFESSIONAL CORPORATION TEN TREMONT STREET, SUITE 600 BOSTON, MASSACHUSETTS 02108 Telephone: 617.720.6040 Facsimile: 617.720.1919 www.bovelanga.com Trusts and Estates Forum

THE LAW FIRM OF BOVE & LANGA A PROFESSIONAL CORPORATION TEN TREMONT STREET, SUITE 600 BOSTON, MASSACHUSETTS 02108 Telephone: 617.720.6040 Facsimile: 617.720.1919 www.bovelanga.com Trusts and Estates Forum

USING A SPECIAL NEEDS TRUST FOR CHARITABLE GIVING

I. BACKGROUND The Special Needs Trust or Supplemental Needs Trust ( SNT ) is a form of discretionary spendthrift trust designed to protect a disabled beneficiary s government benefits while providing a

I. BACKGROUND The Special Needs Trust or Supplemental Needs Trust ( SNT ) is a form of discretionary spendthrift trust designed to protect a disabled beneficiary s government benefits while providing a

AFFILIATED HEALTHCARE SYSTEMS NONQUALIFIED DEFERRED COMPENSATION PLAN ARTICLE I PURPOSE

AFFILIATED HEALTHCARE SYSTEMS NONQUALIFIED DEFERRED COMPENSATION PLAN ARTICLE I PURPOSE 1.1 Purpose of Plan. Effective as of the 1st day of January, 2018, Affiliated Healthcare Systems ( AHS ), a Maine

AFFILIATED HEALTHCARE SYSTEMS NONQUALIFIED DEFERRED COMPENSATION PLAN ARTICLE I PURPOSE 1.1 Purpose of Plan. Effective as of the 1st day of January, 2018, Affiliated Healthcare Systems ( AHS ), a Maine

DIVIDING A TRUST INTO SUBTRUSTS

AFTER A SETTLOR S DEATH Funding Separate Subtrusts Created under a Trust by Layne T. Rushforth Section 1. Overview: This memo is directed to the trustee of a revocable trust where the trust requires the

AFTER A SETTLOR S DEATH Funding Separate Subtrusts Created under a Trust by Layne T. Rushforth Section 1. Overview: This memo is directed to the trustee of a revocable trust where the trust requires the

THE ESTATE PLANNER S SIX PACK

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 SPECIAL REPORT www.disinherit-irs.com For persons with taxable estates, there is an assortment

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 SPECIAL REPORT www.disinherit-irs.com For persons with taxable estates, there is an assortment

CHAPTER 13 INCOME TAXATION OF TRUSTS AND ESTATES LECTURE NOTES

CHAPTER 13 INCOME TAXATION OF TRUSTS AND ESTATES LECTURE NOTES 13.1 AN OVERVIEW OF SUBCHAPTER J What is a Trust? 1. A trust is an arrangement created by a will or by a lifetime declaration, through which

CHAPTER 13 INCOME TAXATION OF TRUSTS AND ESTATES LECTURE NOTES 13.1 AN OVERVIEW OF SUBCHAPTER J What is a Trust? 1. A trust is an arrangement created by a will or by a lifetime declaration, through which

Real Estate Investment Newsletter November 2004

Primer on Legal Structures for Asset Protection In our society, once you have sufficient assets, people will try to take them away from you; lawsuits and taxes are a threat to your wealth. While my business

Primer on Legal Structures for Asset Protection In our society, once you have sufficient assets, people will try to take them away from you; lawsuits and taxes are a threat to your wealth. While my business

Estate Planning. Insight on. Defective by design Weighing the ins and outs of income defective and estate defective trusts

Insight on Estate Planning June/July 2009 Defective by design Weighing the ins and outs of income defective and estate defective trusts Don t let your Crummey trust crumble Bankruptcy and your estate plan

Insight on Estate Planning June/July 2009 Defective by design Weighing the ins and outs of income defective and estate defective trusts Don t let your Crummey trust crumble Bankruptcy and your estate plan

Directed Trusts: Delaware v. Florida Estate Planning Council of Greater Miami March 19, 2015

Directed Trusts: Delaware v. Florida Estate Planning Council of Greater Miami March 19, 2015 Gail Cohen Vice Chairman and General Trust Counsel 212.632.3253 gcohen@ftci.com 1 Directed Trusts: An Overview

Directed Trusts: Delaware v. Florida Estate Planning Council of Greater Miami March 19, 2015 Gail Cohen Vice Chairman and General Trust Counsel 212.632.3253 gcohen@ftci.com 1 Directed Trusts: An Overview

Asset Protection Planning After the 2005 Bankruptcy Act

THE LAW FIRM OF BOVE & LANGA A PROFESSIONAL CORPORATION TEN TREMONT STREET, SUITE 600 BOSTON, MASSACHUSETTS 02108 Telephone: 617.720.6040 Facsimile: 617.720.1919 www.bovelanga.com Trusts and Estates Forum

THE LAW FIRM OF BOVE & LANGA A PROFESSIONAL CORPORATION TEN TREMONT STREET, SUITE 600 BOSTON, MASSACHUSETTS 02108 Telephone: 617.720.6040 Facsimile: 617.720.1919 www.bovelanga.com Trusts and Estates Forum

Understanding Dynasty Trusts

Understanding Dynasty Trusts Understanding Dynasty Trusts DISCUSSION TOPICS What is a Dynasty Trust? How to Set Up a Dynasty Trust What are the Benefits of a Charitable Lead Trust? INVEST Trust Services

Understanding Dynasty Trusts Understanding Dynasty Trusts DISCUSSION TOPICS What is a Dynasty Trust? How to Set Up a Dynasty Trust What are the Benefits of a Charitable Lead Trust? INVEST Trust Services

U.S. Tax Considerations for Multi-Jurisdictional Family Trust Planning

Slide 1 Slide 2 Estate Planning Council of Greater Miami February 19, 2015 U.S. Tax Considerations for Multi-Jurisdictional Family Trust Planning Presented by Todd N. Rosenberg, Esq. of Packman, Neuwahl

Slide 1 Slide 2 Estate Planning Council of Greater Miami February 19, 2015 U.S. Tax Considerations for Multi-Jurisdictional Family Trust Planning Presented by Todd N. Rosenberg, Esq. of Packman, Neuwahl

Morris, Nichols, Arsht & Tunnell LLP. Eliminate a Trust's State Income Tax. June An update from our Trusts & Estates Group

June 2006 Morris, Nichols, Arsht & Tunnell LLP An update from our Trusts & Estates Group Eliminate a Trust's State Income Tax A Delaware non-grantor/incomplete gift trust can help you do it. That is, if

June 2006 Morris, Nichols, Arsht & Tunnell LLP An update from our Trusts & Estates Group Eliminate a Trust's State Income Tax A Delaware non-grantor/incomplete gift trust can help you do it. That is, if

Fixing Old B Trusts. by Steve Oshins, J.D., AEP (Distinguished)

") Fixing Old B Trusts by Steve Oshins, J.D., AEP (Distinguished) PROGRAM DETAILS Date: Thursday, March 16, 2017 Start Time: 9am Pacific Time (10am MT, 11am CT, 12pm ET) Duration: 60 minutes (including Q&A)

Fixing Old B Trusts by Steve Oshins, J.D., AEP (Distinguished) PROGRAM DETAILS Date: Thursday, March 16, 2017 Start Time: 9am Pacific Time (10am MT, 11am CT, 12pm ET) Duration: 60 minutes (including Q&A)

State Income Tax On Trusts: How to improve the trust s total return.

State Income Tax On Trusts: How to improve the trust s total return. J a n et Nava B a n d e ra, J. D. r a t e d AV P r e e m i n e n t BA N DERA L AW F IRM, P. A. 9 4 1-345- 4 0 7 3 j b a n d e ra @ b

State Income Tax On Trusts: How to improve the trust s total return. J a n et Nava B a n d e ra, J. D. r a t e d AV P r e e m i n e n t BA N DERA L AW F IRM, P. A. 9 4 1-345- 4 0 7 3 j b a n d e ra @ b

Asset Protection Introduction. The Wealth Preservation Institute 139 N. Whittaker New Buffalo, MI

Asset Protection Introduction The Wealth Preservation Institute 139 N. Whittaker New Buffalo, MI 49117 269-469-0537 www.thewpi.org Are your clients asset protection plans put together? Help your clients

Asset Protection Introduction The Wealth Preservation Institute 139 N. Whittaker New Buffalo, MI 49117 269-469-0537 www.thewpi.org Are your clients asset protection plans put together? Help your clients

ADVANTAGES OF A LIVING TRUST

ADVANTAGES OF A LIVING TRUST By: Sol S. Reifer, Director, Wealth Preservation Planning, Coats Rose, P.C. Are you interested in creating a revocable trust (commonly referred to as a "Living Trust") that

ADVANTAGES OF A LIVING TRUST By: Sol S. Reifer, Director, Wealth Preservation Planning, Coats Rose, P.C. Are you interested in creating a revocable trust (commonly referred to as a "Living Trust") that

Who Should Consider Medicaid Planning?

Who Should Consider Medicaid Planning? Relevant Law vs. Plan Design 2014, LWP Who Should Consider Mediciad Planning? 1 Summary of What We Covered Week 1 Medicaid Planning Profile Qualification Standards

Who Should Consider Medicaid Planning? Relevant Law vs. Plan Design 2014, LWP Who Should Consider Mediciad Planning? 1 Summary of What We Covered Week 1 Medicaid Planning Profile Qualification Standards

Recent Developments in Estate Planning

ESTATE PLANNING INHERITANCE PROTECTION 7650 E. BROADWAY BLVD. #108 PHONE (520) 546-3558 TUCSON, AZ 85710 TOM@TOMBOUMANLAW.COM Recent Developments in Estate Planning 1. Estate Tax Summary: Federal estate

ESTATE PLANNING INHERITANCE PROTECTION 7650 E. BROADWAY BLVD. #108 PHONE (520) 546-3558 TUCSON, AZ 85710 TOM@TOMBOUMANLAW.COM Recent Developments in Estate Planning 1. Estate Tax Summary: Federal estate

Steve Leimberg's Asset Protection Planning Newsletter - Archive Message #109

Steve Leimberg's Asset Protection Planning Email Newsletter - Archive Message #109 Date: 19-Jul-07 From: Steve Leimberg's Asset Protection Planning Newsletter Subject: Wyoming Enters DAPT Legislation Arena

Steve Leimberg's Asset Protection Planning Email Newsletter - Archive Message #109 Date: 19-Jul-07 From: Steve Leimberg's Asset Protection Planning Newsletter Subject: Wyoming Enters DAPT Legislation Arena

5 Strategies to Resolve Your IRS Tax Problem. By Nehemiah Jefferson, Esq., EA.

5 Strategies to Resolve Your IRS Tax Problem By Nehemiah Jefferson, Esq., EA This mini book is provided for information purposes only, does not create an attorney-client relationship, and should not be

5 Strategies to Resolve Your IRS Tax Problem By Nehemiah Jefferson, Esq., EA This mini book is provided for information purposes only, does not create an attorney-client relationship, and should not be

TEXAS TRUST BASICS Once you have a basic understanding of trusts, you may find that a trust would make an excellent addition to your own estate plan.

TEXAS TRUST BASICS Once you have a basic understanding of trusts, you may find that a trust would make an excellent addition to your own estate plan. STEPHEN A MENDEL Houston Texas Estate Planning Attorney

TEXAS TRUST BASICS Once you have a basic understanding of trusts, you may find that a trust would make an excellent addition to your own estate plan. STEPHEN A MENDEL Houston Texas Estate Planning Attorney

THE NING NEVADA INCOMPLETE GIFT, NONGRANTOR TRUST by Layne T. Rushforth 1

THE NING NEVADA INCOMPLETE GIFT, NONGRANTOR TRUST by Layne T. Rushforth 1 1. OVERVIEW 1.1 Overview: It is understandable that people living in a state with a state income tax want to avoid paying that

THE NING NEVADA INCOMPLETE GIFT, NONGRANTOR TRUST by Layne T. Rushforth 1 1. OVERVIEW 1.1 Overview: It is understandable that people living in a state with a state income tax want to avoid paying that

REVISED STATUTES OF ANGUILLA CHAPTER I16 INSURANCE ACT. Showing the Law as at 15 December 2014

ANGUILLA REVISED STATUTES OF ANGUILLA CHAPTER I16 INSURANCE ACT Showing the Law as at 15 December 2014 This Edition was prepared under the authority of the Revised Statutes and Regulations Act, R.S.A.

ANGUILLA REVISED STATUTES OF ANGUILLA CHAPTER I16 INSURANCE ACT Showing the Law as at 15 December 2014 This Edition was prepared under the authority of the Revised Statutes and Regulations Act, R.S.A.

Sprint Session A 2:40-3:10 p.m. Salon 3. Bankruptcy 101. Panelists: Ryan J. Richmond Attorney at Law Baton Rouge

Sprint Session A 2:40-3:10 p.m. Salon 3 Bankruptcy 101 Panelists: Ryan J. Richmond Attorney at Law Baton Rouge Lacey E. Rochester Baker Donelson New Orleans Ryan J. Richmond Ryan is a 2006 graduate of

Sprint Session A 2:40-3:10 p.m. Salon 3 Bankruptcy 101 Panelists: Ryan J. Richmond Attorney at Law Baton Rouge Lacey E. Rochester Baker Donelson New Orleans Ryan J. Richmond Ryan is a 2006 graduate of

S Corporation Planning

S Corporation Planning Details Written by Martin M. Shenkman, CPA, MBA, PFS, AEP, JD The income tax is the new estate tax. With a federal estate tax exemption at over $5 million and increasing by an inflation

S Corporation Planning Details Written by Martin M. Shenkman, CPA, MBA, PFS, AEP, JD The income tax is the new estate tax. With a federal estate tax exemption at over $5 million and increasing by an inflation

Chapter XX TRUSTEES CONDENSED OUTLINE

Chapter XX TRUSTS CONDENSED OUTLINE I. INTRODUCTION B. Other Relationships Distinguished. C. Tentative Trust in Bank Deposit. D. Conflict of Laws. E. The Trust Law. II. CREATION OF EXPRESS TRUST B. Statute

Chapter XX TRUSTS CONDENSED OUTLINE I. INTRODUCTION B. Other Relationships Distinguished. C. Tentative Trust in Bank Deposit. D. Conflict of Laws. E. The Trust Law. II. CREATION OF EXPRESS TRUST B. Statute

BASICS * Irrevocable Life Insurance Trusts

KAREN S. GERSTNER & ASSOCIATES, P.C. 5615 Kirby Drive, Suite 306 Houston, Texas 77005-2448 Telephone (713) 520-5205 Fax (713) 520-5235 www.gerstnerlaw.com BASICS * Irrevocable Life Insurance Trusts Synopsis

KAREN S. GERSTNER & ASSOCIATES, P.C. 5615 Kirby Drive, Suite 306 Houston, Texas 77005-2448 Telephone (713) 520-5205 Fax (713) 520-5235 www.gerstnerlaw.com BASICS * Irrevocable Life Insurance Trusts Synopsis

The Republic of China Arbitration Law

The Republic of China Arbitration Law Amended on June 24, 1998 Effective as of December 24, 1998 Articles 8, 54, and 56 are as amended and effective as of July 10, 2002 In case of any discrepancies between

The Republic of China Arbitration Law Amended on June 24, 1998 Effective as of December 24, 1998 Articles 8, 54, and 56 are as amended and effective as of July 10, 2002 In case of any discrepancies between

THE PETER JONES IRREVOCABLE TRUST