Study Support. Business Tax (BTX) The Association of Accounting Technicians

|

|

|

- Alexander Hudson

- 6 years ago

- Views:

Transcription

. There are some topic similarities between the 2003/2006 standards and the AAT Accounting Qualification (launched July 2010).")

1 Study Support Business Tax (BTX) Disclaimer Study Support materials comprise non live assessments that were created for the 2003/2006 standards and do not resemble assessments designed for the AAT Accountancy Qualification (launched July 2010). There are some topic similarities between the 2003/2006 standards and the AAT Accounting Qualification (launched July 2010). Practice assessments, guidance and standards for the AAT Accountancy Qualification (launched July 2010) can be found on the AAT website. The Association of Accounting Technicians 1

2 Contents Support book Part 1 Unit 18: Business Tax Computations (BTC) 2003/2006 standards exam; June 2009 sitting, FA2008 Support book Part 2 Unit 18: Business Tax Computations (BTC) 2003/2006 standards exam; December 2009 sitting

3 Support book Part 1 Questions Source: 2003/2006 standards exam; June 2009 sitting, FA2008 Contents: Unit 18: Business Tax Computations (BTC) AAT Level 4 Technician Pathway (2003/2006 standards) This exam paper is in TWO sections. You must show competence in BOTH sections. So, try to complete EVERY task in BOTH sections. Section 1 contains 5 tasks and Section 2 contains 5 tasks. You should spend about 90 minutes on each section. Against each task is the recommended time for that task, but please note that these times are guidelines only. There is blank space for your workings on pages 2, 10, 18 and 19, but you should include all essential calculations and workings in your answers.

4 BTC Unit 18 FA2008 Tuesday 16 June 2009 (morning) Time allowed - 3 hours plus 15 minutes reading time Taxation tables for business tax 2008/09 Capital allowances: Annual investment allowance 50,000 Writing down allowance Plant and machinery 20% First year allowance Low emission cars 100% Energy efficient and water saving plant 100% Capital gains Entrepreneurs relief Lifetime limit 1,000,000 Relieving fraction 4/9 Annual exemption 9,600 Tax rate 18% Indexation allowance: April 1992 to November National insurance rates: Class 2 contributions: Small earnings exemption 2.30 per week 4,825 p.a. Class 4 contributions: Main rate 8% Additional rate 1% Lower earnings limit 5,435 Upper earnings limit 40,040 Corporation tax: Financial year Small companies rate 21% 20% Marginal relief: Lower limit 300, ,000 Upper limit 1,500,000 1,500,000 Marginal relief fraction 7/400 1/40 Full rate 28% 30% Formula: Fraction x (M P) x I/P

5 Section 1 Data You work in the tax department of a firm of chartered accountants. Emily Wilson has traded as a sole trader for many years. On 1 October 2008, Ismail Ali joined Emily as a partner. You have been asked by your supervisor to do the tax computations for the business for the year ended 31 March The accounting department has given you the following information: 1. Adjusted trading profits, before deducting capital allowances, for the year ended 31 March 2009 were 198, Fixed asset information: Balances brought forward on 1 April 2008: General pool 56,995 Emily s car 40% private usage 14,500 Additions: Machinery 27,050 Delivery van 12,400 Water saving plant 8,700 Office furniture 14,225 Car for Ismail Ali 20% private usage 18,370 Disposal: Machinery original cost higher than disposal value 11, Since 1 October 2008, Emily has received an annual salary of 20,000. Emily and Ismail have agreed to share the profits equally. 2

6 Task 1.1 (40 minutes) Calculate the capital allowances for the year ended 31 March

7 Task 1.2 (5 minutes) Calculate the assessable trading profits for the year ended 31 March Task 1.3 (15 minutes) Allocate the assessable trading profits to each partner for the year ended 31 March

8 Data You have received the following from Emily. From: To: Sent: 11 June 2009 Subject: Retirement As you know, I have recently gone into partnership with Ismail, who is really successful in the business. As I have run the business for so long, I am thinking of retiring and selling the business to Ismail. However, I think the business is worth quite a lot possibly in excess of 1,500,000 and I am concerned that if I go ahead, I will end up with a really large capital gains tax liability. Please advise me on how the sale would be taxed and what, if any, reliefs I could claim to reduce any gain as much as possible. Any information or advice would be much appreciated. Emily Task 1.4 (15 minutes) Reply to Emily s , explaining the capital gains tax implications if she sells the business. From: AATstudent@boxmail.net To: e.wilson@heads.com Sent: 16 June 2009 Subject: Re: Retirement 5

9 This page is for the continuation of your . You may not need all of it. 6

10 Data You have received a query from Ismail. It is the first time that he has been self-employed and he doesn t know how the deadlines, forms or payments of tax operate for self-employed people. Task 1.5 (15 minutes) Provide Ismail with the following information: (a) the dates by which he must pay his tax liabilities for 2008/09 and 2009/10 (b) the dates by which he must submit his tax return for 2008/09. 7

11 Section 2 Data Shatter Ltd is a new client to your firm. The company has traded for many years. The following information is available for the year ended 31 December 2008: 1. A summary of the accounts show: Gross profit 994,290 Depreciation 128,195 Expenses 243,780 Salaries 334, ,170 Net profit 288,120 The expenses include: Speeding fines incurred by a director 340 Customer entertaining 1,190 Political donation 2,500 Subscription to the trade association 450 Gift aid payment 750 Lease payments on a car costing 15,600 2, The capital allowances on plant and machinery have already been calculated at 74, In October 2008, Shatter Ltd received a dividend of 5,400 from a company not associated with it. 4. Shatter Ltd owns 20 acres of land, which it bought in April 1992 for 100,000. In November 2008, Shatter Ltd sold 5 acres for 150,000, when the remaining 15 acres had a market value of 500, There is a capital loss of 9,345 brought forward from the year ended 31 December Shatter Ltd has two associated companies. 8

12 Task 2.1 (20 minutes) Calculate the adjusted trading profits, after capital allowances, for the year ended 31 December

13 Task 2.2 (10 minutes) Calculate the chargeable gain on the land for the year ended 31 December 2008 Task 2.3 (10 minutes) Calculate the profits chargeable to corporation tax (PCTCT) for the year ended 31 December

14 Task 2.4 (35 minutes) Calculate the corporation tax payable for the year ended 31 December State the due date for payment. 11

15 Data You have received the following from the Managing Director of Shatter Ltd. From: To: Sent: 12 June 2009 Subject: Tax returns We are new clients to your firm, as we had some problems with our previous accountant. As a result, we have not submitted the tax return form for the year ended 31 December I am quite concerned about this, but I have no idea about the implications. I don t even know when the return should have been submitted. I suspect that we are late, and that penalties or fines may have to be paid. We are really busy here, and don t have the time to complete the return this month. I am hoping to complete it with the information provided by the previous accountant sometime in July. Any advice or information that you can provide would be most welcome. Thank you. Neil Task 2.5 (15 minutes) Reply to Neil s , providing all the information he needs. From: AATstudent@boxmail.net To: Neil.George@shatter.co.uk Sent: 16 June 2009 Subject: Re: Tax returns 12

16 This page is for the continuation of your . You may not need all of it. 13

17 Model Answers Note: The model answers may, in parts, be longer than would be expected of candidates in the exam. The fuller version is given for teaching purposes. Section 1 Task 1.1 (a) General Pool Car (40%) Car (20%) Total Balance b/f 56,995 14,500 Non-AIA additions: Car 18,370 AIA additions: Machinery 27,050 Van 12,400 Furniture 14,225 53,675 AIA 50,000 3,675 50,000 Disposals: Machinery (11,660) 49,010 WDA 20% 9,802 9,802 WDA 20% or 3,000 2,900 1,740 WDA 20% or 3,000 3,000 2,400 FYA additions: Plant 8, % 8,700 8,700 Total allowances 72,642 Balance c/f 39,208 11,600 15,370 14

18 Task 1.2 Adjusted profits 198,370 Capital allowances (task 1.1) 72,642 Trading profits 125,728 Task 1.3 Total Emily Ismail Period to 30 September ,728 / 2 62,864 62,864 Period to 31 March 2009 Salary - 20,000 / 2 10,000 10,000 Balance of profits 52,864 26,432 26, ,728 / 2 62,864 36,432 26,432 Trading profits 125,728 99,296 26,432 Task 1.4 From: AATstudent@boxmail.net To: e.wilson@heads.com Sent: 16 June 2009 Subject: Re: Retirement If you sell the business to Ismail, you will almost definitely be liable for capital gains tax. This is worked out as the difference between the proceeds received and the cost of the business. This will result in a gain. Fortunately, as you will be selling a business, you will be eligible to claim the Entrepreneurs Relief. This relief reduces any gain by 4/9, leaving 5/9 chargeable. It is restricted to lifetime gains of 1,000,000, so if the gain made exceeds this, the maximum relief that you can claim will be 444,444. Any gain after this will be reduced by your annual exemption, and the resultant net gain is taxed at a flat rate of 18%. The impact of the 4/9 relief is that it effectively reduces the tax rate, on the first 1,000,000 of gain, to 10%, so if you work out roughly what your gain is, 10% of that figure will give you an approximation of your tax liability. I hope this is clear, but please feel free to contact me again if you need any further information. AAT student

19 Task 1.5 (a) (b) Ismail will need to pay the tax liability from 2008/09 by 31 January For 2009/10, he will need to make two payments on account (POA) on 31 January 2010 and 31 July A final balancing payment on 31 January 2011 may also need to be made. If he is submitting a paper based return, this needs to be filed by 31 October If the return is to be filed online, this needs to be done by 31 January

20 Section 2 Task 2.1 Net profit 288,120 Add: Depreciation 128,195 Speeding fines 340 Customer entertaining 1,190 Political donation 2,500 Gift aid 750 Lease payments: ½ x (15,600 12,000) x 2, ,229 15, ,349 Less: Capital allowances 74,430 Adjusted profits 346,919 Task 2.2 Proceeds 150,000 Cost: 100,000 x 150, , , , ,923 IA - 23,077 x ,177 Gain 113,746 Task 2.3 Trading profits (task 2.1) 346,919 Chargeable gain ( 113,746-9,345) 104,401 Gift aid (750) PCTCT 450,570

21 Task months 9 months PCTCT 3 / 9 112, ,928 Dividends 5,400 x 100/90 1,500 4,500 Profits 114, ,428 SCMR lower limit 300,000 / 3 3 / 9 25,000 75,000 SCMR upper limit - 1,500,000 / 3 3 / 9 125, ,000 CT Payable: PCTCT x 30% / 28% 33, , Less: SCMR 1/40 X (125, ,142) X 112,642 / 114, , /400 X (375, ,428) X 337,928 / 342, , Total payable: 127, Date of payment 1 October 2009 Task 2.5 From: AATstudent@boxmail.net To: Neil.George@shatter.co.uk Sent: 16 June 2009 Subject: Re: Tax returns You are right to be concerned over this matter. The date that the tax return was due for the year ended 31 December 2007 was 31 December As it is over five months late, there will be a penalty of 200. It is quite urgent that this return is submitted by the end of this month, otherwise it will be over six months late. In such a case, HMRC may impose a tax geared penalty, which is 10% of the unpaid tax. I am sure that my firm would be able to assist you in the completion of the outstanding tax return. If you wish us to do so, please contact the office to discuss this further. Regards AAT student

22 Chief Assessor s report AAT Accounting Qualification NVQ/SVQ Level 4 Preparing Business Taxation Computations (BTC) 2003 Standards AAT Accounting Qualification Diploma pathway Diploma level Preparing Business Taxation Computations (BTC) 2003 Standards June 2009 General comments This paper is the first one to cover the changes made to some aspects of the Standards in the 2008 Finance Act. As such, if a student did not fully prepare for the new rules, then they could struggle on some of the tasks that specifically targeted these changes. As usual, Section 1 covered the aspects of a sole trader, and Section 2 covered taxation aspects of a limited company. There should have been no surprises in the paper to a well prepared student, especially as a detailed article has been written about the impact of these changes and several notices placed in both the Accounting Technician magazine and on the AAT website. Despite this, there was evidence that some students had failed to fully grasp the new rules, and this must be avoided for the December 2009 paper. Section 1 Task 1.1 Capital allowances have seen quite a drastic change in the tax rules and the majority of these rules were tested in this task. Many students performed well, clearly appreciating that this topic would be assessed in this paper. The key to success in this task is the appreciation of the order of events that need to be placed in the computation, and what attracts annual investment allowance (AIA), and what does not. Following a logical structure and layout is vital in order to avoid confusion over which items attract what allowances. Most students understood that the water saving plant attracted 100% first year allowance, and not AIA, and that Emily s car did not automatically attract 3,000 written down allowance. Having one car at a cost below 15,000 and one car at a cost above 15,000 was deliberately incorporated into the question to ensure that candidates demonstrated full understanding of the impact of the change of WDA to 20%. Generally, this was all well handled. Tasks 1.2 This was a very straightforward task, requiring students only to adjust the given profits for the capital allowances computed in task 1.1. Whilst straightforward, this task was vital in preparation for the next task.

23 Task 1.3 Given how well students coped with task 1.1, it was to be hoped that they had covered the whole syllabus in full. This is clearly not the case and it was a rare student who gained full marks for this task. Given that apportionment of profits for partners was examined in June 2008 and the comment was made then on the poor quality of answers, it was hoped that students and tutors had noted this and covered this area thoroughly. This is clearly not the case. As in June 2008, the main area of confusion is over the treatment of the salary for Emily. Students must understand how to tackle partnership accounts the principles are the same as assessed in the FRA paper, yet they seem incapable of transferring that knowledge to the taxation issues. The most common error made was: Trading profits 125,728 (or student equivalent) Salary 10, ,728 6 months to Emily 57,864 Balance ½ to Emily 28,932 Balance ½ to Ismail 28,932 57,864 The problem with this is that Emily only started receiving the salary once the partnership was formed on 1 October If you compare the above answer to the correct one, you will see that Emily received: Correct answer 99,296 As above, including 10,000 salary 96,796 Difference 2,500 It is therefore vital that students fully appreciate how to handle appropriation of profits for partnerships. Task 1.4 This task covered the other major change to the tax rules, being the introduction of a relief for capital gains, entrepreneur s relief. Generally, this task was well handled, and it appeared that students were prepared for a complex computational question. Traditionally, students do not like discursive tasks, but this one was well answered, with students taking time to structure their answers logically and sensibly. Task 1.5 As with task 1.3, the answers to these types of questions tend to be poorly answered, and this task was no exception. Students tended to repeat rote learnt answers, stating 31 January and 31 July, but failing to put these dates into context. Far too many students stated that there would be three payment dates for 2008/09, the payments on account being based on his tax liability for 2007/08. As Ismail only started trading in the partnership on 1 October 2008, it is clear that students are not applying logic to their answers; they are not reading the data carefully to appreciate the context in which the tasks are written. Also, as the question specifically asked for which dates apply to which tax year, giving dates without allocating them to the right year will affect the marks that can be awarded. Part (b), however, tended to be well answered. 3

24 Section 2 Task 2.1 This is a staple task in this section and generally, with one major exception, it was answered well by the majority of students. The layouts used were appropriate and virtually 100% of candidates started correctly with the net profit of 288,120. The major issue with the task was the handling of the lease payments for the car. There were two consistently wrong answers used by nearly all students it was either totally ignored or the full 2,200 was added back. It would appear that this topic was not covered by students in their studies. Task 2.2 Part disposal of assets tends to be rather poorly handled by students, but seems to have been solved in this paper. The vast majority gained full marks, although there was a tendency to deduct 9,600 from the net gain. In previous papers, the computation of the cost has been the issue, but at this sitting it was not. Task 2.3 This was a straightforward task, similar to 1.2, in that, although it just brings together previous figures, it is a necessary stage before tackling the next task. In the main, it was well handled. Task 2.4 Computationally, this was the most complex task of the whole paper. One of the biggest issues was students not understanding how best to lay out their answer. As their own workings were confusingly written, so they seemed to struggle with how to use these workings. Logically splitting all the necessary figures was needed in the first instance and then pulling together those figures followed. Unfortunately, many students failed to realise that the accounting period straddled 31 March, with different rates applying pre and post this date. Unlike income tax, which applies the rates applicable in the tax year in which the accounting period ends, corporation tax needs to apply the rates as applicable for the period in which the months fall. Hence, the period 1 January 2008 to 31 March 2008 falls in the finance year 2007, and the period 1 April 2008 to 31 December 2008 falls in the finance year As ever, there were the usual errors of deducting the dividends from the PCTCT, or calculating SCMR and deducting that from the PCTCT, then applying the tax rate. However, these tended to come from the weaker students who also failed to demonstrate ability in other tasks. Task 2.5 As with task 1.5, this task was not well handled. Many students seemed confused over the penalties that would apply to a sole trader or limited company, and gave the answer as if the former. A common wrong answer would be: The tax return would be due, in paper form, on 31 October 2008 and in electronic form, on 31 January Therefore, the tax return is 5 months late and so there will be a penalty of 200. There would be part credit for the 200, but nothing else. Students must cover this topic in depth and fully appreciate the implications of late returns and late payments. Not only must they learn the rules, they must be able to apply those rules to the question in hand to provide clients with concrete, direct advice and not vague, general answers that could be given to anyone in any situation. Markers are looking for the answer that applies to the given task and students must develop this skill. 4

25 Support book Part 2 Questions Source: 2003/2006 standards exam; December 2009 sitting Contents: Unit 18: Business Tax Computations (BTC) AAT Level 4 Technician Pathway (2003/2006 standards) Tuesday 1 December 2009 (morning) Time allowed - 3 hours plus 15 minutes reading time Please complete the following information in BLOCK CAPITALS: This exam paper is in TWO sections. You must show competence in BOTH sections. So, try to complete EVERY task in BOTH sections. Section 1 contains 6 tasks and Section 2 contains 5 tasks. You should spend about 80 minutes on Section 1 and 100 minutes on Section 2. There is blank space for your workings on pages 21-23, but you should include all workings and essential calculations in your answers.

26 Taxation tables for business tax 2008/09 Capital allowances Annual investment allowance 50,000 Writing down allowance Plant and machinery 20% First year allowance Low emission cars 100% Energy efficient and water saving plant 100% Capital gains Entrepreneurs relief Lifetime limit 1,000,000 Relieving fraction 4/9 Annual exemption 9,600 Tax rate 18% Indexation allowance: August 2000 to November National insurance rates Class 2 contributions: Small earnings exemption 2.30 per week 4,825 p.a. Class 4 contributions: Main rate 8% Additional rate 1% Lower earnings limit 5,435 Upper earnings limit 40,040 Corporation tax Financial year Small companies rate 21% 20% Marginal relief: Lower limit 300, ,000 Upper limit 1,500,000 1,500,000 Marginal relief fraction 7/400 1/40 Full rate 28% 30% Formula: Fraction x (M P) x I/P

27 Section 1 You should spend about 80 minutes on this section. Against each task is the recommended time for that task, but please note that these times are guidelines only. Data You work in the tax department of a firm of chartered accountants. Businessman Mr Zhang has been a client of the firm for many years, making up his company s accounts to 30 April each year. His business ceased trading on 31 January 2009, and the accounts department has provided you with the following details: 1. Profit and loss account for the nine-month period 31 January 2009 Turnover 1,210,210 Cost of sales 808,480 Gross profit 401,730 Wages and salaries 125,778 Rent, rates and insurance 59,221 Repairs to plant 8,215 Advertising and entertaining 19,077 Accountancy and legal costs 5,710 Motor expenses 53,018 Telephone and office costs 14,017 Depreciation 28,019 Other expenses 92, ,515 Loss (3,785) 2. Wages and salaries include: Mr Zhang 30,000 Mr Zhang s wife, who works in the marketing department 18, Advertising and entertaining includes: Gifts to customers: Bottles of wine costing 15 each 2,250 Diaries carrying the business s logo, costing 10 each 400 Staff Christmas party for 20 employees 1, Motor expenses include: Delivery vans 10,403 Sales Manager s car 6,915 Mr Zhang s car, total expense (70% business usage) 5, Other expenses include: Cost of staff training 3,550 Subscription to a trade association 220 Data continues over the page

28 6. The written down values of the pools on 1 May 2008 for capital allowance purposes are: General pool 19,450 Mr Zhang s car (30% private usage) 8,080 Sales Manager s car (no private usage) 10,400 On 31 January 2009, the proceeds or market value for each pool were: General pool proceeds 11,803 Mr Zhang s car market value 9,750 Sales Manager s car proceeds 7, Information from the previous tax years show that the net trading taxable profits were: Year ended 30 April ,000 Year ended 30 April , Mr Zhang has overlap profits of 8,316 from when he commenced trading. 9. In February 2009, Mr Zhang sold what was left of his business to a rival company. This was mainly the goodwill, relating to his customer base. The capital gain from this sale was 400,000.

29 Task 1.1 (10 minutes) Calculate the capital allowances for the period ended 31 January Task 1.2 (15 minutes) Calculate the net trading profits of the business for the period ended 31 January 2009, after capital allowances.

30 Task 1.3 (10 minutes) Calculate the taxable profits for the tax year 2008/09. Task 1.4 (10 minutes) Calculate the total National Insurance contributions payable by Mr Zhang for 2008/09.

31 Task 1.5 (10 minutes) (a) Calculate the net capital gain arising from the sale of Mr Zhang s business. You do not need to calculate the tax payable. (b) State the date that the tax liability arising from this sale would be payable. Task 1.6 (25 minutes) As far as possible, complete the tax return for Mr Zhang s business on pages

32

33

34

35 Section 2 You should spend about 100 minutes on this section. Against each task is the recommended time for that task, but please note that these times are guidelines only. Data You work in the tax department of a manufacturing company trading as Toner Ltd. The following information is available for the year ended 31 March The adjusted trading profits, before capital allowances, have been calculated at 2,951, Fixed asset information: Balances brought forward as at 1 April 2008: General pool: 265,400 Managing Director s car (BMW) 70% private usage 18,705 Finance Director s car 13,600 Additions: Machinery 32,230 Energy saving plant 13,900 Office furniture 22,405 Managing Director s car (Ford) 32,100 Disposals: Machinery 11,250 Managing Director s car (BMW) 15, In November 2008, Toner Ltd sold a picture for 12,000. This was bought for 4,000 in August 2000.

36 Task 2.1 (35 minutes) Calculate the capital allowance for the year ended 31 March 2009, clearly showing the balance of the pools to carry forward.

37 Task 2.2 (15 minutes) Calculate the chargeable gain arising from the picture. Task 2.3 (10 minutes) Calculate the profits chargeable to corporation tax (PCTCT) for the year ended 31 March 2009.

38 Task 2.4 (20 minutes) (a) Calculate the corporation tax payable for the year ended 31 March (b) State the due dates of payment for the above tax liability. Briefly explain how these payments would be calculated.

39 Data You have received the following from the Managing Director of Toner Ltd. From: To: Sent: 27 November 2009 Subject: Losses I am really pleased with the profit we made for the year ended 31 March However, we are eight months into the new financial year, and the general economic downturn seems to have badly affected our company. Our budget for the next three years shows the following: Y/e 31/03/10 Y/e 31/03/11 Y/e 31/03/12 Trading profit / (loss) 500,000 (750,000) 200,000 Chargeable gain / (loss) 10,000 12,000 (15,000) I am hoping that you can provide some information on the various options we have regarding these losses. James

40 Task 2.5 (20 minutes) Reply to James , clearly describing: (a) (b) (c) The ways in which the trading loss can be relieved The considerations that need to be taken into account when deciding how to relieve such a loss The ways in which the chargeable loss can be relieved Note: You do not need to calculate any figures. From: AATstudent@toner.com To: James.Toner@toner.com Sent: 1 December 2009 Subject: Re: Losses

41 This page is for the continuation of your . You may not need all of it.

42 Model Answers December 2009 Note: The model answers may, in parts, be longer than would be expected of candidates in the exam. The fuller version is given for teaching purposes.

43 Section 1 Task 1.1 General Car pool (30%) Car Total WDV b/f 19,450 8,080 10,400 Proceeds / Market value 11,803 9,750 7,000 Balancing allowance 7,647 3,400 11,047 Balancing charge 1,670 (1,169) Total allowances 9,878 Task 1.2 Net loss (3,785) Add: Depreciation 28,019 Mr Zhang s salary 30,000 Gifts to customers 2,250 Motor expenses for Mr Zhang s car - 5,700 x 30% 1,710 61,979 58,194 Less: Capital allowances 9,878 Adjusted trading profits 48,316 Task 1.3 Profits for year ended 30 April ,000 Profits for period ended 31 January ,316 78,316 Less: Overlap profits 8,316 Taxable profits 70,000 Task 1.4 Class 2: 2.30 x Class 4: ( 40,040 5,435) x 8% 2, ( 70,000 40,040) x 1% Total NIC 3,187.60

44 Task 1.5 Gain from sale 400, ,000 x 4/9 177,778 Gain 222,222 Date payable: 31 January 2010 Task 1.6 Box 7 31/01/09 Box 14 1,210,210 Box ,480 Box ,778 Box 33 30,000 Box 19 53,018 Box 34 1,710 Box 20 59,221 Box 21 8,215 Box 22 14,017 Box 23 19,077 Box 38 2,250 Box 27 5,710 Box 28 28,019 Box 43 28,019 Box 29 92,460 Box 30 1,213,995 Box 45 61,979 Box 47 3,785 Box 54 9,878 Box 55 9,878 Box 59 61,979 Box 61 9,878 Box 62 48,316

45 Section 2 Task 2.1 General MD s FD s Pool car car Total WDV b/f 265,400 18,705 13,600 Disposal 15,400 Balancing allowance 3,305 3,305 Non-AIA additions: Managing Director s car 32,100 AIA additions: Machinery 32,230 Furniture 22,405 54,635 AIA 50,000 4,635 50, ,035 Disposals 11, ,785 WDA 20% 51,757 51,757 WDA 20% / 3,000 3,000 3,000 WDA 20% / 3,000 2,720 2,720 FYA additions: Plant 13, % 13,900 13,900 Total allowances 124,682 Balance c/f 207,028 29,100 10,880 Task 2.2 Proceeds 12,000 Cost 4,000 8,000 IA 4,000 x ,116 Gain 6,884 Restricted to 5/3 x (12,000 6,000) = 10,000 Task 2.3 Adjusted profit 2,951,100 Less: Capital allowances 124,682 Adjusted trading profit 2,826,418 Chargeable gain 6,884 PCTCT 2,833,302

46 Task 2.4 (a) 2,833,302 x 28% 793, (b) Dates of payment: 14 October 2009; 14 January 2010; 14 April 2010; 14 July 2010 First three payments are based on estimates of the taxable profit for that year that will be revised as the accounting period progresses. The tax liability is a quarter of the total expected. Differences between revised estimates and original estimates will be added or deducted from the instalment. Task 2.5 From: AATstudent@toner.com To: James.Toner@toner.com Sent: 1 December 2009 Subject: Losses This is a very sad state of affairs, but I am sure we are not the only company badly affected by the economic situation. Fortunately, there is good news in the way that this loss can be handled for tax purposes. There are three ways in which a company can relieve trade losses: by carrying forward against trading profits in future periods by setting off against any other profits made in the year of the loss by setting off against any profits made in the preceding 12 months As we are not expecting the profits in 2012 to be able to fully relieve the 2011 loss, my recommendation would be that we would carry back the loss against ,000 can then be relieved against 2012, leaving a further 50,000 loss to carry forward. The reason for doing this is twofold: we will be able to get a tax rebate for 2010, which will improve our cash flow. Given our projected financial position at this time, this would be advantageous. The situation for the chargeable loss is different. Such losses can only be carried forward to be relieved against future chargeable gains. I hope this information is useful. AAT student

2003 Standards June 2009 General comments This paper is the first one to cover the changes made to some aspects of the Standards in the 2008 Finance Act.")

47 Chief Assessor s report AAT Accounting Qualification NVQ/SVQ Level 4 Preparing Business Taxation Computations (BTC) 2003 Standards AAT Accounting Qualification Diploma pathway Diploma level Preparing Business Taxation Computations (BTC) 2003 Standards June 2009 General comments This paper is the first one to cover the changes made to some aspects of the Standards in the 2008 Finance Act. As such, if a student did not fully prepare for the new rules, then they could struggle on some of the tasks that specifically targeted these changes. As usual, Section 1 covered the aspects of a sole trader, and Section 2 covered taxation aspects of a limited company. There should have been no surprises in the paper to a well prepared student, especially as a detailed article has been written about the impact of these changes and several notices placed in both the Accounting Technician magazine and on the AAT website. Despite this, there was evidence that some students had failed to fully grasp the new rules, and this must be avoided for the December 2009 paper. Section 1 Task 1.1 Capital allowances have seen quite a drastic change in the tax rules and the majority of these rules were tested in this task. Many students performed well, clearly appreciating that this topic would be assessed in this paper. The key to success in this task is the appreciation of the order of events that need to be placed in the computation, and what attracts annual investment allowance (AIA), and what does not. Following a logical structure and layout is vital in order to avoid confusion over which items attract what allowances. Most students understood that the water saving plant attracted 100% first year allowance, and not AIA, and that Emily s car did not automatically attract 3,000 written down allowance. Having one car at a cost below 15,000 and one car at a cost above 15,000 was deliberately incorporated into the question to ensure that candidates demonstrated full understanding of the impact of the change of WDA to 20%. Generally, this was all well handled. Tasks 1.2 This was a very straightforward task, requiring students only to adjust the given profits for the capital allowances computed in task 1.1. Whilst straightforward, this task was vital in preparation for the next task.

48 Task 1.3 Given how well students coped with task 1.1, it was to be hoped that they had covered the whole syllabus in full. This is clearly not the case and it was a rare student who gained full marks for this task. Given that apportionment of profits for partners was examined in June 2008 and the comment was made then on the poor quality of answers, it was hoped that students and tutors had noted this and covered this area thoroughly. This is clearly not the case. As in June 2008, the main area of confusion is over the treatment of the salary for Emily. Students must understand how to tackle partnership accounts the principles are the same as assessed in the FRA paper, yet they seem incapable of transferring that knowledge to the taxation issues. The most common error made was: Trading profits 125,728 (or student equivalent) Salary 10, ,728 6 months to Emily 57,864 Balance ½ to Emily 28,932 Balance ½ to Ismail 28,932 57,864 The problem with this is that Emily only started receiving the salary once the partnership was formed on 1 October If you compare the above answer to the correct one, you will see that Emily received: Correct answer 99,296 As above, including 10,000 salary 96,796 Difference 2,500 It is therefore vital that students fully appreciate how to handle appropriation of profits for partnerships. Task 1.4 This task covered the other major change to the tax rules, being the introduction of a relief for capital gains, entrepreneur s relief. Generally, this task was well handled, and it appeared that students were prepared for a complex computational question. Traditionally, students do not like discursive tasks, but this one was well answered, with students taking time to structure their answers logically and sensibly. Task 1.5 As with task 1.3, the answers to these types of questions tend to be poorly answered, and this task was no exception. Students tended to repeat rote learnt answers, stating 31 January and 31 July, but failing to put these dates into context. Far too many students stated that there would be three payment dates for 2008/09, the payments on account being based on his tax liability for 2007/08. As Ismail only started trading in the partnership on 1 October 2008, it is clear that students are not applying logic to their answers; they are not reading the data carefully to appreciate the context in which the tasks are written. Also, as the question specifically asked for which dates apply to which tax year, giving dates without allocating them to the right year will affect the marks that can be awarded. Part (b), however, tended to be well answered.

49 Section 2 Task 2.1 This is a staple task in this section and generally, with one major exception, it was answered well by the majority of students. The layouts used were appropriate and virtually 100% of candidates started correctly with the net profit of 288,120. The major issue with the task was the handling of the lease payments for the car. There were two consistently wrong answers used by nearly all students it was either totally ignored or the full 2,200 was added back. It would appear that this topic was not covered by students in their studies. Task 2.2 Part disposal of assets tends to be rather poorly handled by students, but seems to have been solved in this paper. The vast majority gained full marks, although there was a tendency to deduct 9,600 from the net gain. In previous papers, the computation of the cost has been the issue, but at this sitting it was not. Task 2.3 This was a straightforward task, similar to 1.2, in that, although it just brings together previous figures, it is a necessary stage before tackling the next task. In the main, it was well handled. Task 2.4 Computationally, this was the most complex task of the whole paper. One of the biggest issues was students not understanding how best to lay out their answer. As their own workings were confusingly written, so they seemed to struggle with how to use these workings. Logically splitting all the necessary figures was needed in the first instance and then pulling together those figures followed. Unfortunately, many students failed to realise that the accounting period straddled 31 March, with different rates applying pre and post this date. Unlike income tax, which applies the rates applicable in the tax year in which the accounting period ends, corporation tax needs to apply the rates as applicable for the period in which the months fall. Hence, the period 1 January 2008 to 31 March 2008 falls in the finance year 2007, and the period 1 April 2008 to 31 December 2008 falls in the finance year As ever, there were the usual errors of deducting the dividends from the PCTCT, or calculating SCMR and deducting that from the PCTCT, then applying the tax rate. However, these tended to come from the weaker students who also failed to demonstrate ability in other tasks. Task 2.5 As with task 1.5, this task was not well handled. Many students seemed confused over the penalties that would apply to a sole trader or limited company, and gave the answer as if the former. A common wrong answer would be: The tax return would be due, in paper form, on 31 October 2008 and in electronic form, on 31 January Therefore, the tax return is 5 months late and so there will be a penalty of 200. There would be part credit for the 200, but nothing else. Students must cover this topic in depth and fully appreciate the implications of late returns and late payments. Not only must they learn the rules, they must be able to apply those rules to the question in hand to provide clients with concrete, direct advice and not vague, general answers that could be given to anyone in any situation. Markers are looking for the answer that applies to the given task and students must develop this skill.

Tuesday 5 December 2006 (morning) EXAM QUESTION PAPER. Time allowed 3 hours plus 15 minutes reading time

EXAM QUESTION PAPER. Time allowed 3 hours plus 15 minutes reading time") NVQ/SVQ Level 4 in Accounting Preparing Business Taxation Computations (FA 2005) (BTC) (2003 standards) Tuesday 5 December 2006 (morning) EXAM QUESTION PAPER Time allowed 3 hours plus 15 minutes reading

NVQ/SVQ Level 4 in Accounting Preparing Business Taxation Computations (FA 2005) (BTC) (2003 standards) Tuesday 5 December 2006 (morning) EXAM QUESTION PAPER Time allowed 3 hours plus 15 minutes reading

Technician/ Level 4 Diploma (QCF) Preparing personal taxation computations (PTC)

Preparing personal taxation computations (PTC)") Accounting Qualification Question paper Technician/ Level 4 Diploma (QCF) Preparing personal taxation computations (PTC) Friday 18 June 2010 (morning) Time allowed - 3 hours plus 15 minutes reading time

Accounting Qualification Question paper Technician/ Level 4 Diploma (QCF) Preparing personal taxation computations (PTC) Friday 18 June 2010 (morning) Time allowed - 3 hours plus 15 minutes reading time

Advanced Taxation Northern Ireland

Advanced Taxation Northern Ireland 2 nd Year Examination May 2012 Exam Paper, Solutions & Examiner s Report NOTES TO USERS ABOUT THESE SOLUTIONS The solutions in this document are published by Accounting

Advanced Taxation Northern Ireland 2 nd Year Examination May 2012 Exam Paper, Solutions & Examiner s Report NOTES TO USERS ABOUT THESE SOLUTIONS The solutions in this document are published by Accounting

Examiner s report P6 Advanced Taxation (UK) December 2017

December 2017") Examiner s report P6 Advanced Taxation (UK) December 2017 General Comments The exam was in its standard format; section A consisting of the compulsory questions 1 and 2, worth 35 marks and 25 marks respectively,

Examiner s report P6 Advanced Taxation (UK) December 2017 General Comments The exam was in its standard format; section A consisting of the compulsory questions 1 and 2, worth 35 marks and 25 marks respectively,

Accounting Qualification

Accounting Qualification Business Tax Reference material Finance Act 2016 for assessments 1 January 31 December 2018 The Association of Accounting Technicians Copyright 2016 AAT All rights reserved. Reproduction

Accounting Qualification Business Tax Reference material Finance Act 2016 for assessments 1 January 31 December 2018 The Association of Accounting Technicians Copyright 2016 AAT All rights reserved. Reproduction

Friday 9 December 2005 (morning) EXAMINATION

EXAMINATION") NVQ/SVQ Level 4 in Accounting Preparing Personal Taxation Computations (FA 2004) (PTC) Friday 9 December 2005 (morning) EXAMINATION Time allowed 3 hours plus 15 minutes reading time Please complete the

NVQ/SVQ Level 4 in Accounting Preparing Personal Taxation Computations (FA 2004) (PTC) Friday 9 December 2005 (morning) EXAMINATION Time allowed 3 hours plus 15 minutes reading time Please complete the

ACCA. Paper F6 Taxation. June 2015 to March 2016 examination sittings FA2014. Interim Assessment Answers

ACCA Paper F6 Taxation June 2015 to March 2016 examination sittings FA2014 Interim Assessment Answers To gain maximum benefit, do not refer to these answers until you have completed the interim assessment

ACCA Paper F6 Taxation June 2015 to March 2016 examination sittings FA2014 Interim Assessment Answers To gain maximum benefit, do not refer to these answers until you have completed the interim assessment

Fundamentals Level Skills Module, Paper F6 (UK)

") Answers Fundamentals Level Skills Module, Paper F6 (UK) Taxation (United Kingdom) December 2009 Answers 1 (a) 200506 (1 January 2006 to 5 April 2006) 25,200 x /6 12,600 200607 (1 January 2006 to 1 December

Answers Fundamentals Level Skills Module, Paper F6 (UK) Taxation (United Kingdom) December 2009 Answers 1 (a) 200506 (1 January 2006 to 5 April 2006) 25,200 x /6 12,600 200607 (1 January 2006 to 1 December

Normal Dividend rates rates % % Basic rate 1 35, Higher rate 35,001 to 150, Additional rate 150,001 and over

RELEVANT TO ACCA QUALIFICATION PAPERS F6 (UK), P6 (UK) FOUNDATIONS IN ACCOUNTANCY PAPER FTX (UK) AND PERFORMANCE OBJECTIVES 19 AND 20 Finance Act 2011 This article summarises the changes made by the Finance

RELEVANT TO ACCA QUALIFICATION PAPERS F6 (UK), P6 (UK) FOUNDATIONS IN ACCOUNTANCY PAPER FTX (UK) AND PERFORMANCE OBJECTIVES 19 AND 20 Finance Act 2011 This article summarises the changes made by the Finance

Billy Income Tax Computation 2014/15 Non-savings income Savings income Total

December 2015 Examinations 165 ANSWERS TO EXAMPLES Chapter 1 (a) (b) (c) (d) (e) (f) Income Tax and NIC - both direct taxes Corporation tax on profits and NIC in respect of employees - both direct taxes.

December 2015 Examinations 165 ANSWERS TO EXAMPLES Chapter 1 (a) (b) (c) (d) (e) (f) Income Tax and NIC - both direct taxes Corporation tax on profits and NIC in respect of employees - both direct taxes.

Technician/Level 4 Diploma (QCF) Preparing business taxation computations South Africa (BTC-SA)

Preparing business taxation computations South Africa (BTC-SA)") Accounting Qualification Question paper Technician/Level 4 Diploma (QCF) Preparing business taxation computations South Africa (BTC-SA) Tuesday 30 November 2010 (morning) Time allowed - 3 hours plus 15

Accounting Qualification Question paper Technician/Level 4 Diploma (QCF) Preparing business taxation computations South Africa (BTC-SA) Tuesday 30 November 2010 (morning) Time allowed - 3 hours plus 15

Taxation of an unincorporated business. Part 1 The new business

RELEVANT TO ACCA QUALIFICATION PAPER P6 (UK) AND PERFORMANCE OBJECTIVES 19 AND 20 Taxation of an unincorporated business Part 1 The new business This is the Finance Act 2011 version of this article. It

RELEVANT TO ACCA QUALIFICATION PAPER P6 (UK) AND PERFORMANCE OBJECTIVES 19 AND 20 Taxation of an unincorporated business Part 1 The new business This is the Finance Act 2011 version of this article. It

Paper F6 (UK) Taxation (United Kingdom) Monday 7 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (United Kingdom) Monday 7 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (United Kingdom) Monday 7 June 2010 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Rates

Fundamentals Level Skills Module Taxation (United Kingdom) Monday 7 June 2010 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Rates

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting November 2011 Principal Examiner Report for Teachers

ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 B 16 C 2 D 17 A 3 C 18 C 4 B 19 D 5 A 20 A 6 A 21 B 7 B 22 C 8 A 23 C 9 D 24 B 10 C 25 D 11 B 26

ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 B 16 C 2 D 17 A 3 C 18 C 4 B 19 D 5 A 20 A 6 A 21 B 7 B 22 C 8 A 23 C 9 D 24 B 10 C 25 D 11 B 26

Examiner s report F6 (UK) Taxation September 2015

Taxation September 2015") Examiner s report F6 (UK) Taxation September 2015 General Comments There were two sections to the examination paper and all of the questions were compulsory. Section A consisted of 15 multiple choice questions

Examiner s report F6 (UK) Taxation September 2015 General Comments There were two sections to the examination paper and all of the questions were compulsory. Section A consisted of 15 multiple choice questions

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting June 2015 Principal Examiner Report for Teachers

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 D 16 A 2 C 17 A 3 D 18 B 4 B 19 A 5 D 20 D 6 A 21

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 D 16 A 2 C 17 A 3 D 18 B 4 B 19 A 5 D 20 D 6 A 21

Advanced Taxation. Northern Ireland. 2 nd Year Examination. August Exam Paper, Solutions & Examiner s Report

Advanced Taxation Northern Ireland nd Year Examination August 04 Exam Paper, Solutions & Examiner s Report Advanced Taxation (NI) August 04 nd Year Paper NOTES TO USERS ABOUT THESE SOLUTIONS The solutions

Advanced Taxation Northern Ireland nd Year Examination August 04 Exam Paper, Solutions & Examiner s Report Advanced Taxation (NI) August 04 nd Year Paper NOTES TO USERS ABOUT THESE SOLUTIONS The solutions

The Chartered Tax Adviser Examination

MODULE E Candidate Number The Chartered Tax Adviser Examination 4 May 2017 AWARENESS Module E Taxation of Unincorporated Businesses (Ensure this number matches your candidate number on your desk label

MODULE E Candidate Number The Chartered Tax Adviser Examination 4 May 2017 AWARENESS Module E Taxation of Unincorporated Businesses (Ensure this number matches your candidate number on your desk label

Taxation Northern Ireland. Sample Paper 1 Questions & Suggested Solutions

Taxation Northern Ireland Sample Paper 1 Questions & Suggested Solutions INSTRUCTIONS TO CANDIDATES PLEASE READ CAREFULLY For candidates answering in accordance with the law and practice of the Northern

Taxation Northern Ireland Sample Paper 1 Questions & Suggested Solutions INSTRUCTIONS TO CANDIDATES PLEASE READ CAREFULLY For candidates answering in accordance with the law and practice of the Northern

Examiner s report ATX Advanced Taxation (UK) September 2018

September 2018") Examiner s report ATX Advanced Taxation (UK) September 2018 General Comments The exam was the second in its new format comprising wholly compulsory questions. Section A consisted of the compulsory questions

Examiner s report ATX Advanced Taxation (UK) September 2018 General Comments The exam was the second in its new format comprising wholly compulsory questions. Section A consisted of the compulsory questions

Paper FTX (UK) Foundations in Taxation (United Kingdom) FOUNDATIONS IN ACCOUNTANCY. Pilot Paper. The Association of Chartered Certified Accountants

Foundations in Taxation (United Kingdom) FOUNDATIONS IN ACCOUNTANCY. Pilot Paper. The Association of Chartered Certified Accountants") FOUNDATIONS IN ACCOUNTANCY Foundations in Taxation (United Kingdom) Pilot Paper Time allowed: Writing: 2 hours This paper is divided into two sections: Section A ALL TEN questions are compulsory and MUST

FOUNDATIONS IN ACCOUNTANCY Foundations in Taxation (United Kingdom) Pilot Paper Time allowed: Writing: 2 hours This paper is divided into two sections: Section A ALL TEN questions are compulsory and MUST

Paper F6 (UK) Taxation (United Kingdom) Specimen Exam applicable from September Fundamentals Level Skills Module

Taxation (United Kingdom) Specimen Exam applicable from September Fundamentals Level Skills Module") Fundamentals Level Skills Module Taxation (United Kingdom) Specimen Exam applicable from September 2016 Time allowed: 3 hours 15 minutes This question paper is divided into three sections: Section A ALL

Fundamentals Level Skills Module Taxation (United Kingdom) Specimen Exam applicable from September 2016 Time allowed: 3 hours 15 minutes This question paper is divided into three sections: Section A ALL

Business Tax: Maria s scenario Answer book

Business Tax: Maria s scenario Answer book May 2017 AAT is a registered charity. No. 1050724 Business Tax: Maria s scenario Maria de Sousa operated as a sole trader for three years running a food stall

Business Tax: Maria s scenario Answer book May 2017 AAT is a registered charity. No. 1050724 Business Tax: Maria s scenario Maria de Sousa operated as a sole trader for three years running a food stall

Examiner s report P6 Advanced Taxation (UK) June 2017

June 2017") Examiner s report P6 Advanced Taxation (UK) June 2017 General Comments The exam was in its standard format; section A consisting of the compulsory questions 1 and 2, worth 35 marks and 25 marks respectively,

Examiner s report P6 Advanced Taxation (UK) June 2017 General Comments The exam was in its standard format; section A consisting of the compulsory questions 1 and 2, worth 35 marks and 25 marks respectively,

CGT is a tax on the profit you make from selling certain assets such as property, shares or other investments e.g. antiques and fine art.

Capital Gains Tax A brief history CGT was first introduced in 1965. Until then capital gains were not subject to tax. This had led many people to avoid Income Tax by converting (taxable) income into (tax

Capital Gains Tax A brief history CGT was first introduced in 1965. Until then capital gains were not subject to tax. This had led many people to avoid Income Tax by converting (taxable) income into (tax

CHAPTER 4 LONG PERIODS OF ACCOUNT

CHAPTER 4 LONG PERIODS OF ACCOUNT This chapter demonstrates how to calculate the corporation tax liability of a company that draws up accounts for a period more than 12 months long. 4.1 Introduction A

CHAPTER 4 LONG PERIODS OF ACCOUNT This chapter demonstrates how to calculate the corporation tax liability of a company that draws up accounts for a period more than 12 months long. 4.1 Introduction A

F6 (MLA) Taxation. Presentation to tutors. Mark Grech (Examiner)

Taxation. Presentation to tutors. Mark Grech (Examiner)") 1 2 F6 (MLA) Taxation Presentation to tutors Mark Grech (Examiner) 7th November 2008 A large number of candidates possess sufficiently good knowledge of the principles required to compute a basic personal

1 2 F6 (MLA) Taxation Presentation to tutors Mark Grech (Examiner) 7th November 2008 A large number of candidates possess sufficiently good knowledge of the principles required to compute a basic personal

Annual Qualification Review

LCCI International Qualifications Level 2 Certificate in Book-Keeping and Accounts Annual Qualification Review 2008 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com

LCCI International Qualifications Level 2 Certificate in Book-Keeping and Accounts Annual Qualification Review 2008 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com

This exam paper is in two sections. You should try to complete every task in both sections.

Exam NVQ/SVQ Level 3 in Accounting Maintaining Financial Records and Preparing Accounts (FRA) 2003 Standards Advanced Certificate in Accounting (Diploma Pathway) Financial Accounting (FRA) 2003 Standards

Exam NVQ/SVQ Level 3 in Accounting Maintaining Financial Records and Preparing Accounts (FRA) 2003 Standards Advanced Certificate in Accounting (Diploma Pathway) Financial Accounting (FRA) 2003 Standards

ACCA F4 Corporate & Business Law (ENG) Exam Evaluation June 2014

Exam Evaluation June 2014") ACCA F4 Corporate & Business Law (ENG) Exam Evaluation June 2014 Question 1 An anticipated question about civil law and criminal law in part (a). For students who knew this, it was a gift in the exam.

ACCA F4 Corporate & Business Law (ENG) Exam Evaluation June 2014 Question 1 An anticipated question about civil law and criminal law in part (a). For students who knew this, it was a gift in the exam.

ACCA Fundamentals Level Paper F6 (FA 2012) Taxation (UK) Final Mock Examination

Taxation (UK) Final Mock Examination") ACCA Fundamentals Level Paper F6 (FA 2012) Taxation (UK) Final Mock Examination Question Paper Time allowed Reading and Planning Writing 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be

ACCA Fundamentals Level Paper F6 (FA 2012) Taxation (UK) Final Mock Examination Question Paper Time allowed Reading and Planning Writing 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be

ACCA Paper F6 Taxation December 2015 Revision Mock

REVISION MOCK SCRIPT SUBMISSION FORM Script marking is only available to Classroom, Live Online and Distance Learning students enrolled on appropriate Kaplan courses. Name:...... Address:..............

REVISION MOCK SCRIPT SUBMISSION FORM Script marking is only available to Classroom, Live Online and Distance Learning students enrolled on appropriate Kaplan courses. Name:...... Address:..............

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting June 2014 Principal Examiner Report for Teachers

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 C 16 B 2 B 17 D 3 C 18 C 4 C 19 A 5 B 20 A 6 C 21

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 C 16 B 2 B 17 D 3 C 18 C 4 C 19 A 5 B 20 A 6 C 21

Director s remuneration 25,000 ½ Dividend income 75, ,000 Personal allowance (11,000) Taxable income 89,000 Income tax

Taxable income 89,000 Income tax") Answers Fundamentals Level Skills Module, Paper F6 (UK) Taxation (United Kingdom) Section C September/December 2017 Sample Answers and Marking Scheme Marks 31 Alimag Ltd (1) Gamila s income tax liability

Answers Fundamentals Level Skills Module, Paper F6 (UK) Taxation (United Kingdom) Section C September/December 2017 Sample Answers and Marking Scheme Marks 31 Alimag Ltd (1) Gamila s income tax liability

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting November 2014 Principal Examiner Report for Teachers

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice 1 B 16 B 2 B 17 B 3 B 18 D 4 C 19 D 5 C 20 C 6 D 21 C 7 B 22 C 8 B 23

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice 1 B 16 B 2 B 17 B 3 B 18 D 4 C 19 D 5 C 20 C 6 D 21 C 7 B 22 C 8 B 23

5 IBTX. Business Taxation. Intermediate Level. 25 May 2004 Tuesday afternoon INSTRUCTIONS TO CANDIDATES

Intermediate Level Business Taxation 5 IBTX INSTRUCTIONS TO CANDIDATES 25 Tuesday afternoon Read this page before you look at the questions You are allowed three hours to answer this question paper. Answer

Intermediate Level Business Taxation 5 IBTX INSTRUCTIONS TO CANDIDATES 25 Tuesday afternoon Read this page before you look at the questions You are allowed three hours to answer this question paper. Answer

Institute of Certified Bookkeepers Level III Diploma in Self-Assessment Tax Returns Completion

Institute of Certified Bookkeepers Level III Diploma in Self-Assessment Tax Returns Completion 1 Level III Diploma in Self-Assessment Tax Returns Completion Course Code L3SAT Introduction This qualification

Institute of Certified Bookkeepers Level III Diploma in Self-Assessment Tax Returns Completion 1 Level III Diploma in Self-Assessment Tax Returns Completion Course Code L3SAT Introduction This qualification

TX CYP. Taxation Cyprus (TX CYP) Applied Skills. Tuesday 4 December 2018 TX CYP ICPAC. Time allowed: 3 hours 15 minutes

Applied Skills. Tuesday 4 December 2018 TX CYP ICPAC. Time allowed: 3 hours 15 minutes") Applied Skills Taxation Cyprus (TX CYP) Tuesday 4 December 2018 TX CYP ICPAC Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A ALL 15 questions are compulsory

Applied Skills Taxation Cyprus (TX CYP) Tuesday 4 December 2018 TX CYP ICPAC Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A ALL 15 questions are compulsory

RELEVANT TO ACCA QUALIFICATION PAPER P6 (UK)

") RELEVANT TO ACCA QUALIFICATION PAPER P6 (UK) Taxation of the unincorporated business Part 2 the existing business This is the Finance Act 2012 version of this article. It is relevant for candidates sitting

RELEVANT TO ACCA QUALIFICATION PAPER P6 (UK) Taxation of the unincorporated business Part 2 the existing business This is the Finance Act 2012 version of this article. It is relevant for candidates sitting

Examiner s report P6 (UK) Advanced Taxation March 2017

Advanced Taxation March 2017") Examiner s report P6 (UK) Advanced Taxation March 2017 General Comments The exam was in its standard format; section A consisting of the compulsory questions 1 and 2, worth 35 marks and 25 marks respectively,

Examiner s report P6 (UK) Advanced Taxation March 2017 General Comments The exam was in its standard format; section A consisting of the compulsory questions 1 and 2, worth 35 marks and 25 marks respectively,

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting June 2011 Principal Examiner Report for Teachers

ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice (Core) Question Number Key Question Number Key 1 D 16 C 2 D 17 C 3 C 18 C 4 B 19 B 5 D 20 D 6 A 21 C 7 D 22 B 8 A 23 D 9 A 24 A 10 C 25 A 11

ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice (Core) Question Number Key Question Number Key 1 D 16 C 2 D 17 C 3 C 18 C 4 B 19 B 5 D 20 D 6 A 21 C 7 D 22 B 8 A 23 D 9 A 24 A 10 C 25 A 11

Advanced Taxation Republic of Ireland

Advanced Taxation Republic of Ireland 2 nd Year Examination May 2015 Exam Paper, Solutions & Examiner s Comments Page 1 of 16 NOTES TO USERS ABOUT THESE SOLUTIONS The solutions in this document are published

Advanced Taxation Republic of Ireland 2 nd Year Examination May 2015 Exam Paper, Solutions & Examiner s Comments Page 1 of 16 NOTES TO USERS ABOUT THESE SOLUTIONS The solutions in this document are published

Fundamentals Level Skills Module, Paper F6 (UK) Marks 1 (a) Richard Feast Trading profit for the year ended 5 April 2013

Marks 1 (a) Richard Feast Trading profit for the year ended 5 April 2013") Answers Fundamentals Level Skills Module, Paper F6 (UK) Taxation (United Kingdom) December 03 Answers and Marking Scheme Marks (a) Richard Feast Trading profit for the year ended 5 April 03 Net profit

Answers Fundamentals Level Skills Module, Paper F6 (UK) Taxation (United Kingdom) December 03 Answers and Marking Scheme Marks (a) Richard Feast Trading profit for the year ended 5 April 03 Net profit

Notes. ACCA Paper F6 (UK) Taxation (UK) DEMO PAGES - FREE FULL SET AT theexpgroup.com. For exams from June 2015 to March 2016

Taxation (UK) DEMO PAGES - FREE FULL SET AT theexpgroup.com. For exams from June 2015 to March 2016") ACCA Paper F6 (UK) Taxation (UK) Notes For exams from June 2015 to March 2016 theexpgroup.com Contents About ExPress Notes 3 1. Introduction 7 2. Income tax an introduction 9 3. Income Tax Employment Income

ACCA Paper F6 (UK) Taxation (UK) Notes For exams from June 2015 to March 2016 theexpgroup.com Contents About ExPress Notes 3 1. Introduction 7 2. Income tax an introduction 9 3. Income Tax Employment Income

Paper P6 (UK) Advanced Taxation (United Kingdom) Monday 1 June Professional Level Options Module

Advanced Taxation (United Kingdom) Monday 1 June Professional Level Options Module") Professional Level Options Module Advanced Taxation (United Kingdom) Monday 1 June 2009 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A

Professional Level Options Module Advanced Taxation (United Kingdom) Monday 1 June 2009 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A

Accounting Technicians Ireland. Paper: ADVANCED TAXATION (Northern Ireland) Thursday 17 August p.m. to 5.30 p.m.

Thursday 17 August p.m. to 5.30 p.m.") Accounting Technicians Ireland 2 nd Year Examination: August 2017 Paper: ADVANCED TAXATION (Northern Ireland) Thursday 17 August 2017 2.30 p.m. to 5.30 p.m. INSTRUCTIONS TO CANDIDATES PLEASE READ CAREFULLY

Accounting Technicians Ireland 2 nd Year Examination: August 2017 Paper: ADVANCED TAXATION (Northern Ireland) Thursday 17 August 2017 2.30 p.m. to 5.30 p.m. INSTRUCTIONS TO CANDIDATES PLEASE READ CAREFULLY

Foundations in Taxation FTX (UK) June and December 2018

June and December 2018") Foundations in Taxation FTX (UK) June and December 2018 This syllabus and study guide is designed to help with teaching and learning and is intended to provide detailed information on what could be assessed

Foundations in Taxation FTX (UK) June and December 2018 This syllabus and study guide is designed to help with teaching and learning and is intended to provide detailed information on what could be assessed

emission rate in excess of 160 grams per kilometre, so 15% of the leasing costs are not allowed. (ii) Bayle Defender Income tax computation

Bayle Defender Income tax computation") Answers Fundamentals Level Skills Module, Paper F6 (UK) Taxation (United Kingdom) June 2011 Answers 1 (a) (i) Bayle Defender Trading profit for the year ended 30 September 2010 Net profit 172,400 Impairment

Answers Fundamentals Level Skills Module, Paper F6 (UK) Taxation (United Kingdom) June 2011 Answers 1 (a) (i) Bayle Defender Trading profit for the year ended 30 September 2010 Net profit 172,400 Impairment

2,320 at 10% ,950 at 20% 17,270 Income tax liability 3,222

Answers Fundamentals Level Skills Module, Paper F6 (UK) Taxation (United Kingdom) June 2009 Answers 1 (a) (i) Domingo Gomez Income tax computation 2008 09 Pensions (4,500 + 2,00) 6,800 Building society

Answers Fundamentals Level Skills Module, Paper F6 (UK) Taxation (United Kingdom) June 2009 Answers 1 (a) (i) Domingo Gomez Income tax computation 2008 09 Pensions (4,500 + 2,00) 6,800 Building society

Fundamentals Level Skills Module, Paper F6 (UK) Marks 1 (a) John Beach Income tax computation

Marks 1 (a) John Beach Income tax computation") Answers Fundamentals Level Skills Module, Paper F6 (UK) Taxation (United Kingdom) June 203 Answers and Marking Scheme Marks (a) John Beach Income tax computation 202 3 Employment income Director s remuneration

Answers Fundamentals Level Skills Module, Paper F6 (UK) Taxation (United Kingdom) June 203 Answers and Marking Scheme Marks (a) John Beach Income tax computation 202 3 Employment income Director s remuneration

Advanced Taxation Northern Ireland. Sample Paper 2 Questions & Suggested Solutions

Advanced Taxation Northern Ireland Sample Paper 2 Questions & Suggested Solutions NOTES TO USERS ABOUT SAMPLE PAPERS Sample papers are published by Accounting Technicians Ireland. They are intended to

Advanced Taxation Northern Ireland Sample Paper 2 Questions & Suggested Solutions NOTES TO USERS ABOUT SAMPLE PAPERS Sample papers are published by Accounting Technicians Ireland. They are intended to

ACCA Paper F6 Taxation June 2015 to March 2016 sittings FA2014 Interim Assessment

INTERIM ASSESSMENT SCRIPT SUBMISSION FORM Script marking is only available to Classroom, Live Online and Distance Learning students enrolled on appropriate Kaplan courses. Name:...... Address:..............

INTERIM ASSESSMENT SCRIPT SUBMISSION FORM Script marking is only available to Classroom, Live Online and Distance Learning students enrolled on appropriate Kaplan courses. Name:...... Address:..............

Examiner s report P6 Advanced Taxation (MLA) June 2013

June 2013") Examiner s report P6 Advanced Taxation (MLA) June 2013 General Comments The examination consisted of two compulsory questions and three optional questions from which two were to be chosen. Section A contained

Examiner s report P6 Advanced Taxation (MLA) June 2013 General Comments The examination consisted of two compulsory questions and three optional questions from which two were to be chosen. Section A contained

ACCA P6 Advanced Taxation Mock Examination 2. Mock Examination Submission Form. This front sheet should be attached to your submitted answers.

Mock Examination Submission Form This front sheet should be attached to your submitted answers Name: Email address: For HTFT Partnership to complete Date received: Marker: Date returned: Overall mark:

Mock Examination Submission Form This front sheet should be attached to your submitted answers Name: Email address: For HTFT Partnership to complete Date received: Marker: Date returned: Overall mark:

ACCA F6 UK Taxation Finance ACT 2016

ACCA F6 UK Taxation Finance ACT 2016 These Notes are relevant for Exam in Jun 2017, Sep 2017, Dec 2017 & Mar 2018 Please Use these notes along with Online Free Lectures to fully benefit from the notes.

ACCA F6 UK Taxation Finance ACT 2016 These Notes are relevant for Exam in Jun 2017, Sep 2017, Dec 2017 & Mar 2018 Please Use these notes along with Online Free Lectures to fully benefit from the notes.

ACCA P6 UK Advanced Taxation Mock Exam Friday 25th May, 2018

Page 1 ACCA P6 UK Advanced Taxation Mock Exam Friday 25th May, 2018 Please attempt this mock exam under exam conditions in 3 hours and 15 minutes and send scanned answers to admin@accountancytube.com by

Page 1 ACCA P6 UK Advanced Taxation Mock Exam Friday 25th May, 2018 Please attempt this mock exam under exam conditions in 3 hours and 15 minutes and send scanned answers to admin@accountancytube.com by

Fundamentals Level Skills Module, Paper F6 (UK) Marks 1 (a) Richard Tryer Income tax computation

Marks 1 (a) Richard Tryer Income tax computation") Answers Fundamentals Level Skills Module, Paper F6 (UK) Taxation (United Kingdom) June 204 Answers and Marking Scheme Marks (a) Richard Tryer Income tax computation 203 4 Trading profit (working ),592

Answers Fundamentals Level Skills Module, Paper F6 (UK) Taxation (United Kingdom) June 204 Answers and Marking Scheme Marks (a) Richard Tryer Income tax computation 203 4 Trading profit (working ),592

The Chartered Tax Adviser Examination

The Chartered Tax Adviser Examination May 2015 AWARENESS MODULE E TAXATION OF UNINCORPORATED BUSINESSES Suggested Solutions Q1) 1. 2013/14 Year 1 1 July 2013 to 5 April 2014 9/15 x (45,000) (27,000) 1

The Chartered Tax Adviser Examination May 2015 AWARENESS MODULE E TAXATION OF UNINCORPORATED BUSINESSES Suggested Solutions Q1) 1. 2013/14 Year 1 1 July 2013 to 5 April 2014 9/15 x (45,000) (27,000) 1

Paper F6 (UK) Taxation (United Kingdom) September/December 2017 Sample Questions. Fundamentals Level Skills Module

Taxation (United Kingdom) September/December 2017 Sample Questions. Fundamentals Level Skills Module") Fundamentals Level Skills Module Taxation (United Kingdom) September/December 2017 Sample Questions Time allowed: 3 hours 15 minutes This question paper is divided into three sections: Section A ALL 15

Fundamentals Level Skills Module Taxation (United Kingdom) September/December 2017 Sample Questions Time allowed: 3 hours 15 minutes This question paper is divided into three sections: Section A ALL 15

The Chartered Tax Adviser Examination

The Chartered Tax Adviser Examination May 2017 Suggested solutions Application and Interaction Question 3 From: Bowham on Sea Tax Consultancy To: Aaron Amies (`Aaron`); Bill Bowles (`Bill`); Chloe Cowen

The Chartered Tax Adviser Examination May 2017 Suggested solutions Application and Interaction Question 3 From: Bowham on Sea Tax Consultancy To: Aaron Amies (`Aaron`); Bill Bowles (`Bill`); Chloe Cowen

Advanced Taxation. Advanced Taxation. Specimen Exam applicable from June Strategic Professional Options

Strategic Professional Options Advanced Taxation Specimen Exam applicable from June 2018 Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH questions are

Strategic Professional Options Advanced Taxation Specimen Exam applicable from June 2018 Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH questions are

Partnership Tax Return Guide Tax year 6 April 2011 to 5 April 2012

Partnership Tax Return Guide Tax year 6 April 2011 to 5 April 2012 How to fill in the Partnership Tax Return This guide has step-by-step instructions to help you fill in the Partnership Tax Return. The

Partnership Tax Return Guide Tax year 6 April 2011 to 5 April 2012 How to fill in the Partnership Tax Return This guide has step-by-step instructions to help you fill in the Partnership Tax Return. The

Cambridge International Advanced Subsidiary and Advanced Level 9706 Accounting June 2016 Principal Examiner Report for Teachers

ACCOUNTING Cambridge International Advanced Subsidiary and Advanced Level Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 D 16 C 2 A 17 A 3 C 18 B 4 D 19 B 5 B 20 A 6 C 21 C 7 C

ACCOUNTING Cambridge International Advanced Subsidiary and Advanced Level Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 D 16 C 2 A 17 A 3 C 18 B 4 D 19 B 5 B 20 A 6 C 21 C 7 C

Fundamentals Level Skills Module, Paper F6 (UK) 1 (a) (i) Vanessa Serve Income tax computation

1 (a) (i) Vanessa Serve Income tax computation") Answers Fundamentals Level Skills Module, Paper F6 (UK) Taxation (United Kingdom) December 2007 Answers 1 (a) (i) Vanessa Serve Income tax computation 200607 Trading profit 52,400 Capital allowances (10,400

Answers Fundamentals Level Skills Module, Paper F6 (UK) Taxation (United Kingdom) December 2007 Answers 1 (a) (i) Vanessa Serve Income tax computation 200607 Trading profit 52,400 Capital allowances (10,400

Paper F6 (UK) Taxation (United Kingdom) March/June 2017 Sample Questions. Fundamentals Level Skills Module

Taxation (United Kingdom) March/June 2017 Sample Questions. Fundamentals Level Skills Module") Fundamentals Level Skills Module Taxation (United Kingdom) March/June 2017 Sample Questions Time allowed: 3 hours 15 minutes This question paper is divided into three sections: Section A ALL 15 questions

Fundamentals Level Skills Module Taxation (United Kingdom) March/June 2017 Sample Questions Time allowed: 3 hours 15 minutes This question paper is divided into three sections: Section A ALL 15 questions

Paper F6 (CYP) Taxation (Cyprus) Tuesday 2 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (Cyprus) Tuesday 2 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (Cyprus) Tuesday 2 June 2015 Time allowed Reading and planning: 15 minutes Writing: 3 hours This paper is divided into two sections: Section A ALL 15 questions

Fundamentals Level Skills Module Taxation (Cyprus) Tuesday 2 June 2015 Time allowed Reading and planning: 15 minutes Writing: 3 hours This paper is divided into two sections: Section A ALL 15 questions

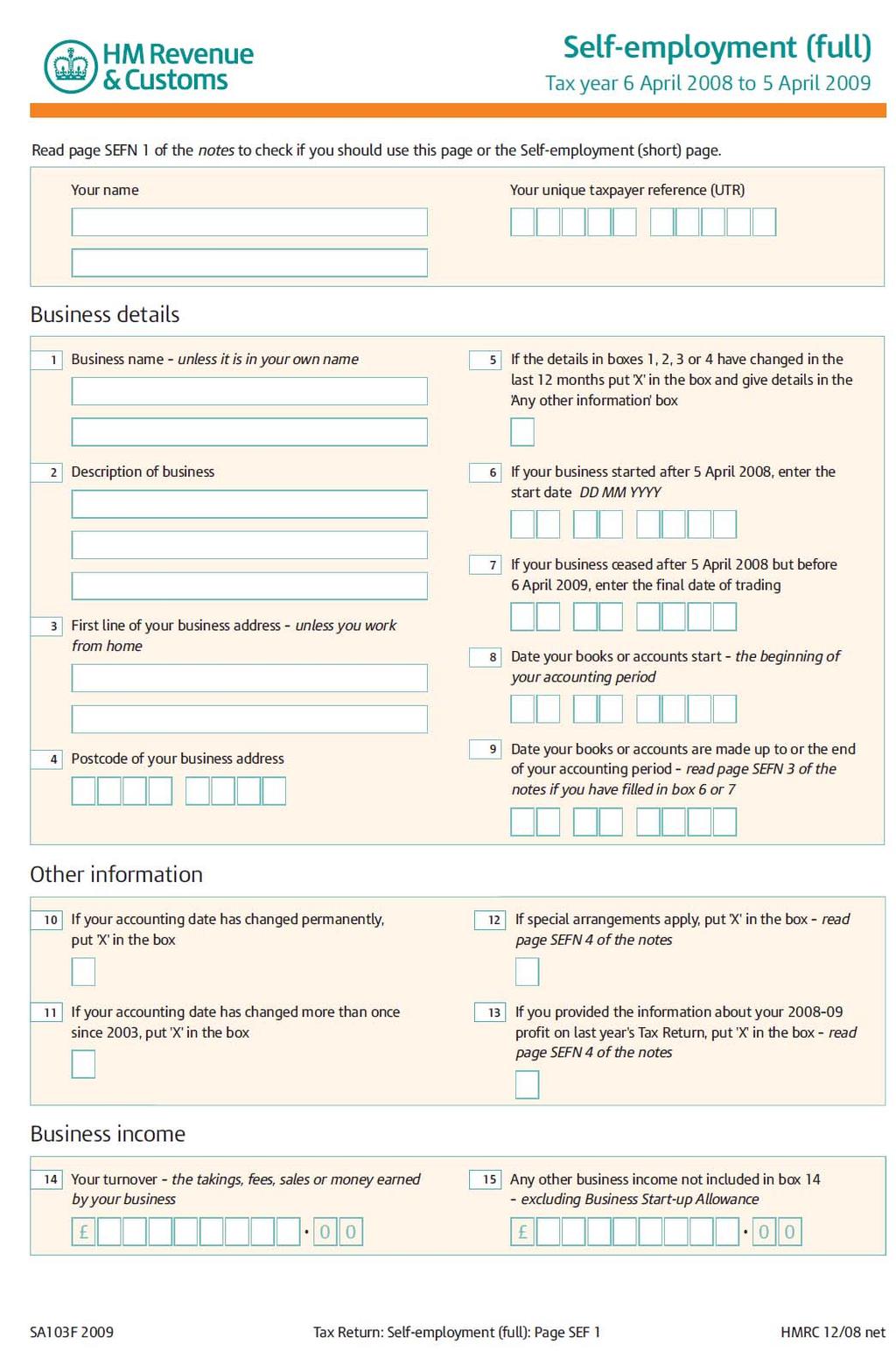

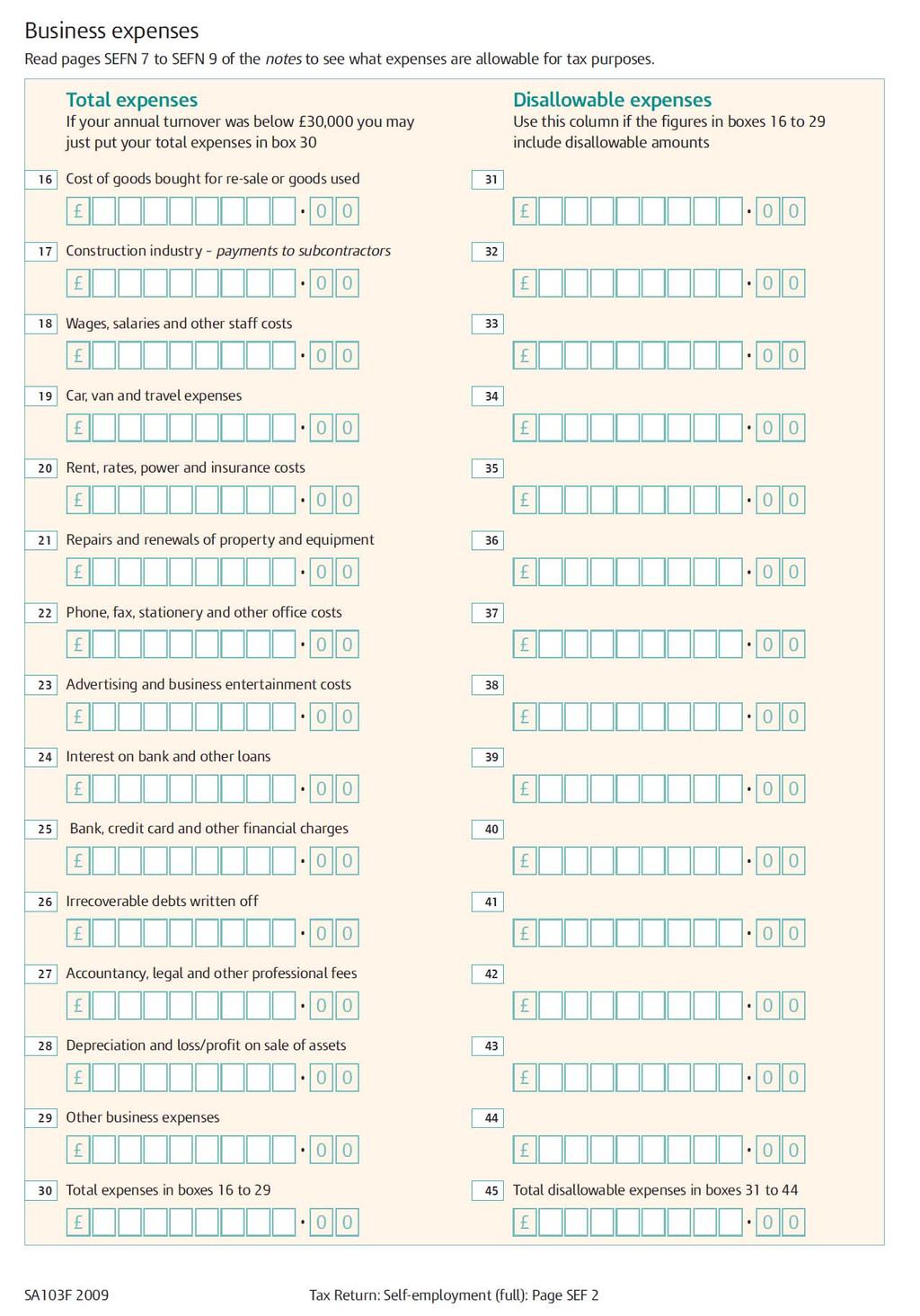

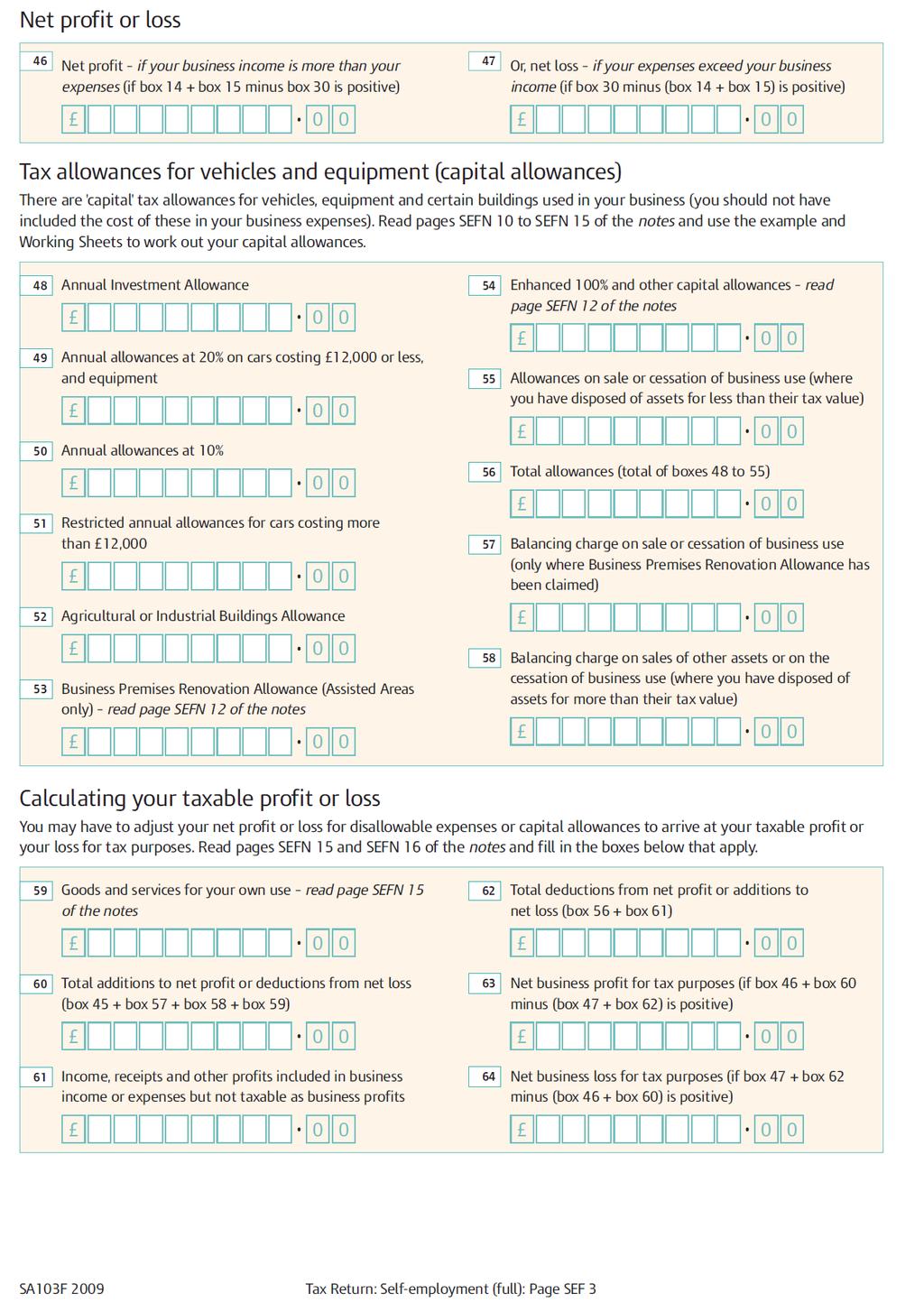

This Section contains a selection of pages from Tax forms, both for reference and also for use in student activities and practice assessments.

TAX FORMS This Section contains a selection of pages from Tax forms, both for reference and also for use in student activities and practice assessments. The forms may also be downloaded from www.hmrc.gov.uk

TAX FORMS This Section contains a selection of pages from Tax forms, both for reference and also for use in student activities and practice assessments. The forms may also be downloaded from www.hmrc.gov.uk

NOVEMBER 2016 PROFESSIONAL EXAMINATION FINANCIAL ACCOUNTING (PAPER 1.1) CHIEF EXAMINER S REPORT, QUESTIONS AND MARKING SCHEME

CHIEF EXAMINER S REPORT, QUESTIONS AND MARKING SCHEME") NOVEMBER 2016 PROFESSIONAL EXAMINATION FINANCIAL ACCOUNTING (PAPER 1.1) CHIEF EXAMINER S REPORT, QUESTIONS AND MARKING SCHEME GENERAL COMMENTS The standard of the question paper was good and candidates

NOVEMBER 2016 PROFESSIONAL EXAMINATION FINANCIAL ACCOUNTING (PAPER 1.1) CHIEF EXAMINER S REPORT, QUESTIONS AND MARKING SCHEME GENERAL COMMENTS The standard of the question paper was good and candidates

2016/17 Edition ebook by JF Financial Management Ltd

2016/17 Edition ebook by JF Financial Management Ltd Contents Disclaimer... 4 Introduction... 5 Self employed sole traders general information... 6 What is a self employed sole trader?... 6 Sole trader

2016/17 Edition ebook by JF Financial Management Ltd Contents Disclaimer... 4 Introduction... 5 Self employed sole traders general information... 6 What is a self employed sole trader?... 6 Sole trader

Partnership Tax Return 2018 for the year ended 5 April 2018 ( )

") Partnership Tax Return 2018 for the year ended 5 April 2018 (2017 18) Tax reference Date Issue address HM Revenue and Customs office address Telephone For Reference This notice requires you by law to send

Partnership Tax Return 2018 for the year ended 5 April 2018 (2017 18) Tax reference Date Issue address HM Revenue and Customs office address Telephone For Reference This notice requires you by law to send

F2 - Financial Management Post Exam Guide May 2010 Exam. F2 FINANCIAL MANAGEMENT Examiner s general comments

F2 FINANCIAL MANAGEMENT Examiner s general comments The new format adopted in F2 appeared to cause little problem with candidates. There was no evidence of any time pressure and few incomplete scripts.

F2 FINANCIAL MANAGEMENT Examiner s general comments The new format adopted in F2 appeared to cause little problem with candidates. There was no evidence of any time pressure and few incomplete scripts.

TX UK. Taxation United Kingdom (TX UK) Applied Skills. September/December 2018 Sample Questions. The Association of Chartered Certified Accountants

Applied Skills. September/December 2018 Sample Questions. The Association of Chartered Certified Accountants") Applied Skills Taxation United Kingdom (TX UK) September/December 2018 Sample Questions TX UK ACCA Time allowed: 3 hours 15 minutes This question paper is divided into three sections: Section A ALL 15

Applied Skills Taxation United Kingdom (TX UK) September/December 2018 Sample Questions TX UK ACCA Time allowed: 3 hours 15 minutes This question paper is divided into three sections: Section A ALL 15

Taxation of investment

Taxation of investment Introduction This section explains how different investments are subject to income tax and capital gains tax (CGT), and includes some ideas for tax planning. The general principles

Taxation of investment Introduction This section explains how different investments are subject to income tax and capital gains tax (CGT), and includes some ideas for tax planning. The general principles

Paper F6 (UK) Taxation (United Kingdom) Monday 1 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (United Kingdom) Monday 1 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (United Kingdom) Monday 1 June 2009 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Rates

Fundamentals Level Skills Module Taxation (United Kingdom) Monday 1 June 2009 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Rates

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting November 2013 Principal Examiner Report for Teachers

ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 D 16 D 2 C 17 B 3 C 18 B 4 B 19 A 5 C 20 B 6 B 21 C 7 C 22 D 8 C 23 D 9 C 24 C 10 A 25 B 11 A 26

ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 D 16 D 2 C 17 B 3 C 18 B 4 B 19 A 5 C 20 B 6 B 21 C 7 C 22 D 8 C 23 D 9 C 24 C 10 A 25 B 11 A 26

TAX NEWSLETTER DECEMBER 2015