Crucial Superyacht Knowledge for the Modern Trustee Alison Vassallo and Ann Fenech

|

|

|

- Anthony Douglas

- 6 years ago

- Views:

Transcription

1 Crucial Superyacht Knowledge for the Modern Trustee Alison Vassallo and Ann Fenech Partner Yachting Department Managing Partner

2 Info on next 8 slides - Martin Redman Chairman Superyacht Group, Marine Money Forum 2017

3

4

5

6

7

8

9

10

11

12

13 Type of legal Info sought Quality and Reputation of the flag Efficient Corporate solutions Strong package of tried and tested legal solutions for private and commercial yachts

14 Services required by a prospective owner Assistance with sale and purchase Registration of the yacht Corporate requirements Financing/Mortgage requirements VAT/Tax considerations relating to purchase of yacht VAT/Tax considerations relating to commercial operation of yacht

15 Flag choice - Malta Flag As of December 2017 Over 65 Million Tonnes 687 yachts over 24 metres 449 Private 238 Commercial

16 WHY THE IMPRESSIVE STATISTICS A European flag English is an official language Central European Time Zone Very efficient Maritime Administration White list of the Paris MOU Member of the IMO Legal Committee.

17 A Registry which is open 24/7 Very competitive fees Excellent rapport between the administration and service providers. Excellent pool of professional service providers Tonnage tax regime for commercial yachts A legal system which supports the mortgagee

18

19

20 Tax treatment depending on different scenarios EU/non EU resident Size and type of yacht Use - Private or commercial Location of shipyard/yacht at time of purchase Cruising area/s

21 Scenario 1 Private use EU Resident Purchasing yacht for private use Use in EU waters VAT due on hull VAT on supplies/services/fuel/refit etc. Irrespective of flag whether EU or non EU

22 Scenario 2 Private use Non EU Resident Private use Limited use in EU waters (18 months) Yacht built in non EU yard or exported after being built in EU No VAT on hull Owner may use Temporary Importation Regime Flag must be non EU

23 Scenario 3 commercial use EU/Non EU Residents Commercial Use EU waters Account for VAT on acquisition (Intracommunity/importation/local supply) VAT on charters Irrespective of whether the flag is EU or non EU Exemption/recovery of VAT due on supplies/services/fuel/refit etc

24 Application for a VAT number on the owning company Physical importation of the yacht into Malta Deferment of VAT on importation on the basis of a bank guarantee (20% of VAT due for four months)

25 Private Yachts Guidelines regarding the VAT Treatment of Yacht Leasing 2005 VAT payment for smaller yachts with limited geographical reach Efficient Temporary Importation Procedures

26 Payment of VAT on Hull Guidelines regarding the VAT Treatment of Yacht Leasing 2005 (i) Maltese lessor company as owner of yacht (ii) VAT registration in Malta and purchases yacht (iii) Yacht is delivered in Malta (iv) Enters into a lease agreement (12-36 months) with lessee in Malta. (v) Supply of service on which VAT is payable (vi) VAT accountable in Malta and a provisional VAT declaration

27 EC Directive 2006/112 Article 59a Member States may consider the place of supply of a means of transport as being situated outside the Community if the effective use and enjoyment of the services or part thereof takes place outside the Community

28

29

30 The Yachting Sector Progress through the years 1. From a few small yachts registered under the Malta flag to the Malta flag being used by the largest most glamorous yachts in the world.

31

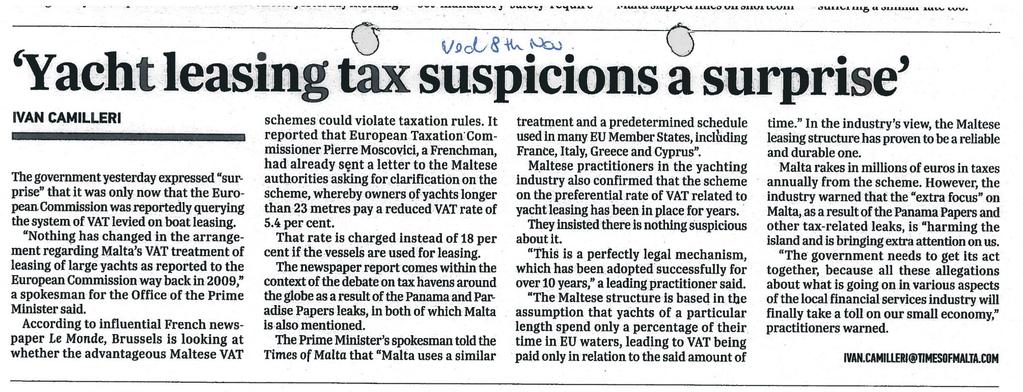

32

33 Supply of a Service v Supply of a Good Mercedez Benz Financial Services UK Judgement (Case C-164/16) 4 th October 2017

34 Mercedez Benz Financial Services UK Judgement (Case C-164/16) 4 th October 2017 Essentially - when is a leasing arrangement a supply of a good? Article 14(2)(b) Supply of a good includes The actual handing over of goods pursuant to a contract for the hire of goods for a certain period, or for the sale of goods on deferred terms, which provides that in the normal course of events ownership is to pass at the latest upon payment of the final instalment

35 Mercedez Benz Financial Services UK Judgement (Case C-164/16) Leasing agreement which excludes any transfer of ownership and sets a maximum mileage beyond which the customer has to pay a penalty; Hire Purchase agreement whereby the aggregate of the monthly payments represent as a rule the total sale price of the vehicle, including the cost of financing. A modest additional fee (the option fee) must be paid in order to acquire ownership of the vehicle at the end of the contract. An Agility agreement where the monthly instalments are as a rule lower than under a Hire Purchase agreement. The total installments represent only 60% of the vehicle sale price, including the cost of financing. If the user wishes to exercise the option to purchase the vehicle, he must therefore pay approximately 40% of the sale price.

36 Mercedez Benz Financial Services UK Judgement (Case C-164/16) Question put to the Court: Whether and to what extent, the words contract for hire which provides that in the normal course of events ownership is to pass at the latest upon payment of the final instalment used in Article 14(2)(b) of the VAT directive, must be interpreted as applying to a leasing contract with an option to purchase, such as the type of contract at issue in the main proceedings.

37 Mercedez Benz Financial Services UK Judgement (Case C-164/16) First condition: The agreement pursuant to which the goods are handed over contains a clause expressly relating to the transfer of ownership of those goods from the lessor to the lessee. An agreement may be considered to contain an express ownership transfer clause where that agreement contains an option to purchase the leased asset. AND Second condition: It must be clear from the terms of the contract, as objectively assessed at the time when it is signed, that ownership of the goods is intended to be acquired automatically by the lessee if performance of the contract proceeds normally, over the full term of the contract.

38 Mercedez Benz Financial Services UK Judgement (Case C-164/16) Conclusion: The words contract for hire which provides that in the normal course of events ownership is to pass at the latest upon payment of the final instalment used in Article 14(2)(b) of the VAT directive, must be interpreted as applying to a leasing contract with an option to purchase if it can be inferred from the financial terms of the contract that exercising the option appears to be the only economically rational choice that the lessee will be able to make at the appropriate time if the contract is performed for its full term, which is for the national court to ascertain.

39 Parallel Developments It was reported in the press in November 2017 that on same day of this judgement a letter was sent by EU Commissioner Moscovici to Minister Scicluna Malta s minister of finance

40

41 A Joint Communique was immediately released by local yachting associations as a specific reaction to articles reported in the press

42

43

44 Four months later on the 8 th March 2018 a Letter of Formal Notice is sent by the Commission to Malta, Greece and Cyprus

45 Letter of Formal Notice Commission acknowledges that Member States are allowed not to tax the supply of a service where the effective use and enjoyment is outside the EU however it is alleging that these rules do not allow for a general flat rate reduction without proof of the actual use Alleging incorrect taxation of purchases of yachts by means of a lease purchase whereby the leasing of a yacht is classified as a supply of a service rather than a good.

46 Reaction by Malta and Industry Initial reaction was indignation and surprise given that the system is fully compliant with Article 59a and fully respects EU regulation. France and Italy apply the same principles of effective use and enjoyment and no similar letter was sent to them Malta had based its schedule on the Italian system Disappointment at the inequality of treatment by the commission to different member states having the same structures. Task Force mobilised by Government involving the industry in order to work on a response to the Notice of Infringement

47 Maltese system has always been fully compliant with VAT Directive from its inception: Application of effective use and enjoyment in line with the VAT Directive that speaks of effective not actual Application of principle in line with other Member States What we have here is indeed a lease agreement not a purchase the supply is one of a service of a lease and not a sale of a good.

48 Application of principle by other jurisdictions: France: since 2005 applies a 50% reduction on the total lease amount irrespective of the category and size of the yacht and irrespective of the yacht s actual use and enjoyment within/outside EU waters. Official Tax Bulletin No 15, 24 th January 2005 Article 13 It is accepted that the hirers who find it difficult to carry out this assessment, shall determine, on a flat rate basis, the time spent outside community or French territorial waters by applying a 50% reduction in the total rental time whatever the category of the pleasure craft concerned.

49 Application of principle by other jurisdictions: Italy: applies article 59a of the VAT Directive by reference to the deemed used and enjoyment of the yacht inside/outside EU waters, with percentages for deemed use which are identical to those adopted by Malta

50 Fine tuning of Guidelines in November: Reinforcement of the fact that the lease agreement is a stand alone lease only of the yacht making it clear that the Guidelines relate to a supply of a service The VAT Department will review all lease agreements submitted to ensure compliance with Maltese law and recent case law, and to ensure that the leasing supply is one of a leasing services and not the supply of goods for VAT purposes. Upon the end of the lease term and re-delivery of the yacht, the Lessor company and the Lessee remain free to discuss and contract a possible eventual sale of the yacht in Malta.

51 The way forward: There are currently no infringement proceedings against Malta what has been received is a Letter of Formal Notice Continuity of the application of the guidelines - lease applications are being processed as per normal Malta is working hard to produce a reasoned reply to this letter within the 2 month deadline. In the meantime Malta remains open to and indeed encourages guidance from the EU on the further fine tuning of the product. Hopefully common sense will prevail and the matter will end there.

52 Commercial Yachts - VAT on Charters

53

54 Up until December 2010 No VAT on charters collected by owners and operators.

55 Council Directive 2006/112/EC Article 148 Member States shall exempt the following transactions: (a) the supply of goods for the fuelling and provisioning of vessels used for navigation on the high seas and carrying passengers for reward or used for the purpose of commercial, industrial or fishing activities, or for rescue or assistance at sea, or for inshore fishing, with the exception, in the case of vessels used for inshore fishing, of ships' provisions;.. (c) the supply, modification, repair, maintenance, chartering and hiring of the vessels referred to in point (a), and the supply, hiring, repair and maintenance of equipment, including fishing equipment, incorporated or used therein;

56 Etat du Grand-Duche de Luxembourg, Administration de l enregistrement et des demains v. Pierre Feltgen, Bacino Charter Company SA (C-116/10) 22 nd December 2010 In order for such a hiring service to be capable of exemption under that provision, the lessee of the vessel concerned must use it for an economic activity It follows that if, as in the main proceedings, the vessel is leased to persons who use it exclusively for leisure purposes and not for financial gain, outside the sphere of any economic activity, the hire service does not meet the explicit conditions for VAT exemption The exemption set out in Article 15(5) of the Sixth Directive cannot benefit vessel-hire services for charters who intend to use the vessel strictly for private purposes as final consumers.

57 EC Directive 2006/112 Article 56 (1) The place of short-term hiring of a means of transport is the place where the means of transport is actually placed at the disposal of the customer. (2) short-term shall, in the case of vessels, mean the continuous possession or use of the means of transport throughout a period of not more than ninety days.

Charterparty to specify area of cruising as touching international waters 5.")

58 Malta The Ministry of Finance launched Guidelines for the VAT treatment of Short-Term Chartering on the 29 th July 2013 Standard rate of 18% VAT is applied to the established percentage of the charter deemed to be related to the use of the yacht in EU waters Owner/Operator to be registered for VAT in Malta Application to Director General VAT for approval and confirmation of percentage of charter subject to VAT (i) Charterparty to indicate Malta as place of delivery (ii) Charterparty to specify area of cruising as touching international waters 5.4% (iii) Details of yacht and proof of payment of charter fee

59

60

61 Conclusions More and more international persons involved in yachting are looking at Malta as the base for their yachting activity whether it is for the purposes of registering their yacht, for the purposes of paying VAT or both. Malta appears to tick a number of boxes as there is an apparent growth in such persons wanting to fly a European flag. There is equally a growing percentage of persons who actually want to pay VAT rather than avoid it and Malta offers such persons the opportunity to do so.

62 Conclusions This is good news all round not only for Malta but for Europe. The prominence of Malta as an EU member state in the world of international yachting means that it is fulfilling the function and one of the key pillars of the European Integrated Maritime Policy pioneered by our own Commissioner, Commissioner Joe Borg in 2007 who heralded this important perspective of attempting to harness the mass exodus of maritime activity outside Europe and of making the Maritime sector important in Europe again by encouraging maritime activity, which in turn regenerates entire which provides maritime jobs.

63 Thank you Ann Fenech Managing Partner & Alison Vassallo Partner Fenech & Fenech Advocates

October 2017 kpmg.com.mt

Ship Registration in Malta October 2017 kpmg.com.mt Malta developed a strong legal and regulatory platform that enabled the Maltese Flag to become an established and reputable International Ship Register

Ship Registration in Malta October 2017 kpmg.com.mt Malta developed a strong legal and regulatory platform that enabled the Maltese Flag to become an established and reputable International Ship Register

Global Maritime Clusters Competitive Advantages & Business Development Opportunities (Malta) 9 th Annual Capital Link Forum Athens

9 th Annual Capital Link Forum Athens") Global Maritime Clusters Competitive Advantages & Business Development Opportunities (Malta) 9 th Annual Capital Link Forum Athens Disclaimer This material has been prepared by Gauci-Maistre Xynou ( GMX

Global Maritime Clusters Competitive Advantages & Business Development Opportunities (Malta) 9 th Annual Capital Link Forum Athens Disclaimer This material has been prepared by Gauci-Maistre Xynou ( GMX

Ship Registration in Malta

Ship Registration in Malta Your Flag of Confidence June 2018 kpmg.com.mt Malta developed a strong legal and regulatory platform that enabled the Maltese flag to become an established and reputable International

Ship Registration in Malta Your Flag of Confidence June 2018 kpmg.com.mt Malta developed a strong legal and regulatory platform that enabled the Maltese flag to become an established and reputable International

VALUE ADDED TAX COMMITTEE (ARTICLE 398 OF DIRECTIVE 2006/112/EC) WORKING PAPER NO 840

WORKING PAPER NO 840") EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration Value added tax taxud.c.1(2015)630069 EN Brussels, 10 February 2015 VALUE ADDED TAX COMMITTEE

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration Value added tax taxud.c.1(2015)630069 EN Brussels, 10 February 2015 VALUE ADDED TAX COMMITTEE

Cyprus VAT Yacht Leasing Scheme

Cyprus VAT Yacht Leasing Scheme We would like to inform you that the Tax Department of the Republic of Cyprus has issued on 25 November 2015, Circular No. 198, amending the provisions the Cyprus Yacht

Cyprus VAT Yacht Leasing Scheme We would like to inform you that the Tax Department of the Republic of Cyprus has issued on 25 November 2015, Circular No. 198, amending the provisions the Cyprus Yacht

Accessing Europe s Largest Registry. Dr. Jean-Pie Gauci-Maistre

Accessing Europe s Largest Registry Dr. Jean-Pie Gauci-Maistre The Two Maltese Registries Ships The continuous growth of the ship registry. Various factors that continue to contribute and new factors which

Accessing Europe s Largest Registry Dr. Jean-Pie Gauci-Maistre The Two Maltese Registries Ships The continuous growth of the ship registry. Various factors that continue to contribute and new factors which

SHIPPING IN MALTA. a strategic location since time immemorial. UHY BUSINESS ADVISORY SERVICES LIMITED Malta

SHIPPING IN MALTA a strategic location since time immemorial UHY BUSINESS ADVISORY SERVICES LIMITED Malta Shipping in Malta REGISTRATION - CLEAR BENEFITS The Merchant Shipping Act, which regulates the

SHIPPING IN MALTA a strategic location since time immemorial UHY BUSINESS ADVISORY SERVICES LIMITED Malta Shipping in Malta REGISTRATION - CLEAR BENEFITS The Merchant Shipping Act, which regulates the

JUDGMENT OF THE COURT (Fourth Chamber) 18 October 2007 *

18 October 2007 *") NAVICON JUDGMENT OF THE COURT (Fourth Chamber) 18 October 2007 * In Case C-97/06, REFERENCE for a preliminary ruling under Article 234 EC by the Tribunal Superior de Justicia de Madrid (Spain), made by

NAVICON JUDGMENT OF THE COURT (Fourth Chamber) 18 October 2007 * In Case C-97/06, REFERENCE for a preliminary ruling under Article 234 EC by the Tribunal Superior de Justicia de Madrid (Spain), made by

A yacht is a significant investment made up of time, effort and money; placing it in a carefully structured ownership entity can offer a number of

Yachts A yacht is a significant investment made up of time, effort and money; placing it in a carefully structured ownership entity can offer a number of benefits, including potential tax and VAT savings.

Yachts A yacht is a significant investment made up of time, effort and money; placing it in a carefully structured ownership entity can offer a number of benefits, including potential tax and VAT savings.

JUDGMENT OF THE COURT (Sixth Chamber) 7 March 1996 *

7 March 1996 *") JUDGMENT OF THE COURT (Sixth Chamber) 7 March 1996 * In Case C-334/94, Commission of the European Communities, represented by Gérard Rozet, Legal Adviser, and Xavier Lewis, of its Legal Service, acting

JUDGMENT OF THE COURT (Sixth Chamber) 7 March 1996 * In Case C-334/94, Commission of the European Communities, represented by Gérard Rozet, Legal Adviser, and Xavier Lewis, of its Legal Service, acting

CYPRUS YACHT REGISTRATION

CYPRUS YACHT REGISTRATION NEW PREFERABLE VAT TREATMENT realsubstance.com.cy ...the Cyprus VAT Authority has launched a scheme making Cyprus one of the most attractive EU jurisdictions for yacht registration.

CYPRUS YACHT REGISTRATION NEW PREFERABLE VAT TREATMENT realsubstance.com.cy ...the Cyprus VAT Authority has launched a scheme making Cyprus one of the most attractive EU jurisdictions for yacht registration.

JUDGMENT OF THE COURT (First Chamber) 4 October 2017 *

4 October 2017 *") JUDGMENT OF THE COURT (First Chamber) 4 October 2017 * (Reference for a preliminary ruling Value added tax (VAT) Directive 2006/112/EC Article 14(2)(b) Supply of goods Motor vehicles Finance lease with

JUDGMENT OF THE COURT (First Chamber) 4 October 2017 * (Reference for a preliminary ruling Value added tax (VAT) Directive 2006/112/EC Article 14(2)(b) Supply of goods Motor vehicles Finance lease with

Cyprus Yacht Leasing Scheme An Appealing VAT Regime

Cyprus Yacht Leasing Scheme An Appealing VAT Regime On 11th September 2014 by its Circular 188, the Tax Department amended its policy on the leasing of pleasure yachts. The Tax Department has reduced to

Cyprus Yacht Leasing Scheme An Appealing VAT Regime On 11th September 2014 by its Circular 188, the Tax Department amended its policy on the leasing of pleasure yachts. The Tax Department has reduced to

Professional Level Options Module, Paper P6 (MLA)

") Answers Professional Level Options Module, Paper P6 (MLA) Advanced Taxation (Malta) December 2014 Answers 1 (a) Tax Consultant 14, Main Street Valletta The Directors Borg Co 18, Main Street Mosta 3 December

Answers Professional Level Options Module, Paper P6 (MLA) Advanced Taxation (Malta) December 2014 Answers 1 (a) Tax Consultant 14, Main Street Valletta The Directors Borg Co 18, Main Street Mosta 3 December

THE MERCHANT SHIPPING (FEES AND TAXING PROVISIONS) LAW OF LAW No. 44 (I) OF 2010

LAW OF LAW No. 44 (I) OF 2010") DMS Version dated 15. 05.2010 Final THE MERCHANT SHIPPING (FEES AND TAXING PROVISIONS) LAW OF 2010 1 LAW No. 44 (I) OF 2010 Section 1. Short title. 2. Interpretation. 3. Delegation of powers and duties.

DMS Version dated 15. 05.2010 Final THE MERCHANT SHIPPING (FEES AND TAXING PROVISIONS) LAW OF 2010 1 LAW No. 44 (I) OF 2010 Section 1. Short title. 2. Interpretation. 3. Delegation of powers and duties.

YACHTING TRANSPORT AGREEMENT

YACHTING TRANSPORT AGREEMENT EXPLANATORY NOTICE P R O 1 I. Why a Transport and Services Agreement Because of changes in tax and customs regulations in Europe, and in particular the cancellation of the

YACHTING TRANSPORT AGREEMENT EXPLANATORY NOTICE P R O 1 I. Why a Transport and Services Agreement Because of changes in tax and customs regulations in Europe, and in particular the cancellation of the

UK News. UK Finance Bill. Compliance reviews. Interest compound or simple? On line filing of VAT returns. Payment handling fees

VAT Newsletter Welcome Welcome to the latest edition of our VAT Newsletter, which provides up to date detail of significant VAT changes over the past few months. In addition, we have noticed an increased

VAT Newsletter Welcome Welcome to the latest edition of our VAT Newsletter, which provides up to date detail of significant VAT changes over the past few months. In addition, we have noticed an increased

Aircraft Registration in Malta

Aircraft Registration in Malta Aircraft Registration in Malta Following the success in the Maltese Maritime sector, Malta launched an Aircraft registry. The Maltese Government has developed a comprehensive

Aircraft Registration in Malta Aircraft Registration in Malta Following the success in the Maltese Maritime sector, Malta launched an Aircraft registry. The Maltese Government has developed a comprehensive

REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL

EUROPEAN COMMISSION Brussels, 8.5.2015 COM(2015) 195 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL on the implementation of Regulation (EC) no 789/2004 on the transfer of

EUROPEAN COMMISSION Brussels, 8.5.2015 COM(2015) 195 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL on the implementation of Regulation (EC) no 789/2004 on the transfer of

Value Added Tax. Your frequently asked questions answered

Value Added Tax Your frequently asked questions answered Jan 2008 Introduction This document provides a comprehensive set of answers to the most frequently asked questions on the complex issue of VAT on

Value Added Tax Your frequently asked questions answered Jan 2008 Introduction This document provides a comprehensive set of answers to the most frequently asked questions on the complex issue of VAT on

The curious ECJ case of Eon Asset Management and its impact on finance leasing in the United Kingdom

August 2012 Recently, the European Court of Justice (ECJ) delivered its judgment in Eon Aset Menidjmunt OOD v Direktor na Direktsia Obzhalvane i upravlenie na izpalnenieto (C-118/11) which (save for capturing

August 2012 Recently, the European Court of Justice (ECJ) delivered its judgment in Eon Aset Menidjmunt OOD v Direktor na Direktsia Obzhalvane i upravlenie na izpalnenieto (C-118/11) which (save for capturing

Official Journal of the European Communities

L 188/35 COUNCIL DIRECTIVE 98/41/EC of 18 June 1998 on the registration of persons sailing on board passenger ships operating to or from ports of the Member States of the Community THE COUNCIL OF THE EUROPEAN

L 188/35 COUNCIL DIRECTIVE 98/41/EC of 18 June 1998 on the registration of persons sailing on board passenger ships operating to or from ports of the Member States of the Community THE COUNCIL OF THE EUROPEAN

Irish Tonnage Tax Delivering Global Competitive Advantage

1 Irish Tonnage Tax Delivering Global Competitive Advantage 1 Irish Tonnage Tax Delivering Global Competitive Advantage Irish Tonnage Tax has been introduced to support the development of a new, innovative,

1 Irish Tonnage Tax Delivering Global Competitive Advantage 1 Irish Tonnage Tax Delivering Global Competitive Advantage Irish Tonnage Tax has been introduced to support the development of a new, innovative,

Integrated text of Council Directive 2006/112/EC on the common system of value added tax

Integrated text of Council Directive 2006/112/EC on the common system of value added tax Title I Subject Matter and Scope Article 1 [Subject] 1. This Directive establishes the common system of value added

Integrated text of Council Directive 2006/112/EC on the common system of value added tax Title I Subject Matter and Scope Article 1 [Subject] 1. This Directive establishes the common system of value added

Consolidated act on taxation of shipping activities (the tonnage tax act (tonnageskatteloven))

)") Translation. Only the Danish document has legal validity Consolidated act no. 945 of 6 August 2015 issued by the Danish Ministry of Taxation Consolidated act on taxation of shipping activities (the tonnage

Translation. Only the Danish document has legal validity Consolidated act no. 945 of 6 August 2015 issued by the Danish Ministry of Taxation Consolidated act on taxation of shipping activities (the tonnage

VAT in the European Community APPLICATION IN THE MEMBER STATES, FACTS FOR USE BY ADMINISTRATIONS/TRADERS INFORMATION NETWORKS ETC.

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration VAT and other turnover taxes VAT in the European Community APPLICATION IN THE MEMBER STATES,

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration VAT and other turnover taxes VAT in the European Community APPLICATION IN THE MEMBER STATES,

SHIPPING AND MARITIME LAW

Issue No 17 February 2015 SHIPPING AND MARITIME LAW NEWSLETTER News Feature MSD Notices Legislative Developments Questions & Suggestions 2 Malta Flag is now sixth largest in the world IN THIS ISSUE 3 News

Issue No 17 February 2015 SHIPPING AND MARITIME LAW NEWSLETTER News Feature MSD Notices Legislative Developments Questions & Suggestions 2 Malta Flag is now sixth largest in the world IN THIS ISSUE 3 News

June 2018 kpmg.com.mt

Malta Tonnage Tax Rules June 2018 kpmg.com.mt Malta developed a strong legal and regulatory platform that enabled the Maltese flag to become an established and reputable International Ship Register which

Malta Tonnage Tax Rules June 2018 kpmg.com.mt Malta developed a strong legal and regulatory platform that enabled the Maltese flag to become an established and reputable International Ship Register which

Considerations on Introduction of Tonnage Tax Systems in the European Union

Maritime Transport & Navigation Journal, Vol. 2 (2010), No. 2 Considerations on Introduction of Tonnage Tax Systems in the European Union Ghiorghe Batrinca* Constanta Maritime University Abstract Shipping

Maritime Transport & Navigation Journal, Vol. 2 (2010), No. 2 Considerations on Introduction of Tonnage Tax Systems in the European Union Ghiorghe Batrinca* Constanta Maritime University Abstract Shipping

Introduction. Choose the language your prefer.

The United Arab Emirates Federal Decree-Law No. (8) of 2017 on the Value Added Tax Law August 2017 Introduction This document is an English version of The United Arab Emirates Federal Decree-Law No. (8)

The United Arab Emirates Federal Decree-Law No. (8) of 2017 on the Value Added Tax Law August 2017 Introduction This document is an English version of The United Arab Emirates Federal Decree-Law No. (8)

REPORT On the public consultation on new initiative regarding dismantling of ships

EUROPEAN COMMISSION DIRECTORATE-GENERAL ENVIRONMENT Directorate G - Sustainable Development and Integration ENV.G.4 - Sustainable Production & Consumption REPORT On the public consultation on new initiative

EUROPEAN COMMISSION DIRECTORATE-GENERAL ENVIRONMENT Directorate G - Sustainable Development and Integration ENV.G.4 - Sustainable Production & Consumption REPORT On the public consultation on new initiative

Tax Flash. Law on development investment tools, provision of credit and other provisions. Α. Individuals. Tax residence. Registry of Assets

Tax Flash Law on development investment tools, provision of credit and other provisions April 2013 A new law was ratified on 26.3.2013 (its publication in the Government Gazette is still pending). We hereby

Tax Flash Law on development investment tools, provision of credit and other provisions April 2013 A new law was ratified on 26.3.2013 (its publication in the Government Gazette is still pending). We hereby

Cyprus: A dynamic business and investment centre INTAX FORUM

Cyprus: A dynamic business and investment centre INTAX FORUM Kiev, 29 th May 2017 Cyprus Investment Promotion Agency Cyprus: an international business hub A destination of choice for doing business A reputable

Cyprus: A dynamic business and investment centre INTAX FORUM Kiev, 29 th May 2017 Cyprus Investment Promotion Agency Cyprus: an international business hub A destination of choice for doing business A reputable

Registration for service activation of Maritime Mobile Earth Station

Registration for service activation of Maritime Mobile Earth Station code Sections 1-4, 6 and 8 are to be completed by all customers Application number Tick Boxes as appropriate. Please write in block

Registration for service activation of Maritime Mobile Earth Station code Sections 1-4, 6 and 8 are to be completed by all customers Application number Tick Boxes as appropriate. Please write in block

JUDGMENT OF THE COURT (Second Chamber) 16 September 2004 *

16 September 2004 *") CIMBER AIR JUDGMENT OF THE COURT (Second Chamber) 16 September 2004 * In Case C-382/02, REFERENCE for a preliminary ruling under Article 234 EC from the Vestre Landsret (Denmark), made by decision of 9

CIMBER AIR JUDGMENT OF THE COURT (Second Chamber) 16 September 2004 * In Case C-382/02, REFERENCE for a preliminary ruling under Article 234 EC from the Vestre Landsret (Denmark), made by decision of 9

Bank finance and regulation. Multi-jurisdictional survey. Malta. Enforcement of security interests in banking transactions.

Bank finance and regulation Multi-jurisdictional survey Malta Enforcement of security interests in banking transactions Leonard Bonello Ganado & Associates Advocates lbonello@jmganado.com Part I - types

Bank finance and regulation Multi-jurisdictional survey Malta Enforcement of security interests in banking transactions Leonard Bonello Ganado & Associates Advocates lbonello@jmganado.com Part I - types

The Government of the Kingdom of the Netherlands. And. The Government of the Isle of Man

Agreement between the Kingdom of the Netherlands and the Isle of Man on the access to mutual agreements procedures in connection with the adjustment of profits of associated enterprises and the application

Agreement between the Kingdom of the Netherlands and the Isle of Man on the access to mutual agreements procedures in connection with the adjustment of profits of associated enterprises and the application

This is an unofficial translation

Federal Decree-Law No. (8) of 2017 on Value Added Tax We, Khalifa bin Zayed Al Nahyan, President of the United Arab Emirates, Having reviewed the Constitution, Federal Law No. (1) of 1972 on the Competencies

Federal Decree-Law No. (8) of 2017 on Value Added Tax We, Khalifa bin Zayed Al Nahyan, President of the United Arab Emirates, Having reviewed the Constitution, Federal Law No. (1) of 1972 on the Competencies

REPUBLIC OF THE MARSHALL ISLANDS

REPUBLIC OF THE MARSHALL ISLANDS MARITIME ADMINISTRATOR Marine Notice No. 2-011-45 Rev. 2/15 TO: SUBJECT: ALL SHIPOWNERS, OPERATORS, MASTERS AND OFFICERS OF MERCHANT SHIPS, AND RECOGNIZED ORGANIZATIONS

REPUBLIC OF THE MARSHALL ISLANDS MARITIME ADMINISTRATOR Marine Notice No. 2-011-45 Rev. 2/15 TO: SUBJECT: ALL SHIPOWNERS, OPERATORS, MASTERS AND OFFICERS OF MERCHANT SHIPS, AND RECOGNIZED ORGANIZATIONS

GLOBAL INDIRECT TAX. Malta. Country VAT/GST Essentials. kpmg.com TAX

GLOBAL INDIRECT TAX Malta Country VAT/GST Essentials kpmg.com TAX b Malta: Country VAT/GST Essentials Malta: Country VAT/GST Essentials Contents Scope and Rates 2 What supplies are liable to VAT? 2 What

GLOBAL INDIRECT TAX Malta Country VAT/GST Essentials kpmg.com TAX b Malta: Country VAT/GST Essentials Malta: Country VAT/GST Essentials Contents Scope and Rates 2 What supplies are liable to VAT? 2 What

The High Net Worth Individuals Rules will run in parallel to the Residents Scheme Regulations as amended.

High Net Worth Individuals Rules announced on the 15 th September 2011 The High Net Worth Individuals Rules will run in parallel to the Residents Scheme Regulations as amended. An application for special

High Net Worth Individuals Rules announced on the 15 th September 2011 The High Net Worth Individuals Rules will run in parallel to the Residents Scheme Regulations as amended. An application for special

Maritime Rules Part 21: Safe Ship Management Systems

Maritime Rules Part 21: Safe Ship Management Systems ISBN 978-0-478-44731-6 Published by Maritime New Zealand, PO Box 25620, Wellington 6146, New Zealand Maritime New Zealand Copyright 2015 Part 21: Safe

Maritime Rules Part 21: Safe Ship Management Systems ISBN 978-0-478-44731-6 Published by Maritime New Zealand, PO Box 25620, Wellington 6146, New Zealand Maritime New Zealand Copyright 2015 Part 21: Safe

Convention on Limitation of Liability for Maritime Claims, 1976 (London, 19 November 1976)

") Convention on Limitation of Liability for Maritime Claims, 1976 (London, 19 November 1976) THE STATES PARTIES TO THIS CONVENTION, HAVING RECOGNIZED the desirability of determining by agreement certain

Convention on Limitation of Liability for Maritime Claims, 1976 (London, 19 November 1976) THE STATES PARTIES TO THIS CONVENTION, HAVING RECOGNIZED the desirability of determining by agreement certain

REGULATION ON IMPLEMENTATION OF INTERNATIONAL SAFETY MANAGEMENT CODE FOR TURKISH FLAGGED VESSELS AND THEIR MANAGEMENT COMPANIES PART ONE

Official Journal Date: 27.10.2009 Official Journal No: 27389 REGULATION ON IMPLEMENTATION OF INTERNATIONAL SAFETY MANAGEMENT CODE FOR TURKISH FLAGGED VESSELS AND THEIR MANAGEMENT COMPANIES PART ONE Objective,

Official Journal Date: 27.10.2009 Official Journal No: 27389 REGULATION ON IMPLEMENTATION OF INTERNATIONAL SAFETY MANAGEMENT CODE FOR TURKISH FLAGGED VESSELS AND THEIR MANAGEMENT COMPANIES PART ONE Objective,

Tonnage Tax Part 24A

Tonnage Tax Part 24A This manual should be read in conjunction with sections 697(A) to 697(Q) and Schedule 18B Taxes Consolidation Act 1997 (TCA 1997) Document last reviewed December 2017 1 Introduction...2

Tonnage Tax Part 24A This manual should be read in conjunction with sections 697(A) to 697(Q) and Schedule 18B Taxes Consolidation Act 1997 (TCA 1997) Document last reviewed December 2017 1 Introduction...2

The European Union. DG MARE - EUROPEAN COMMISSION Explanatory meeting Serbia 30 September 2014

The European Union fisheries con ntrol system DG MARE - EUROPEAN COMMISSION Explanatory meeting Serbia 30 September 2014 A global EU fisheries control system The EU fisheries control system is composed

The European Union fisheries con ntrol system DG MARE - EUROPEAN COMMISSION Explanatory meeting Serbia 30 September 2014 A global EU fisheries control system The EU fisheries control system is composed

INTERNATIONAL CONVENTION ON CIVIL LIABILITY FOR BUNKER OIL POLLUTION DAMAGE, 2001

INTERNATIONAL CONVENTION ON CIVIL LIABILITY FOR BUNKER OIL POLLUTION DAMAGE, 2001 The States Parties to this Convention, RECALLING article 194 of the United Nations Convention on the Law of the Sea, 1982,

INTERNATIONAL CONVENTION ON CIVIL LIABILITY FOR BUNKER OIL POLLUTION DAMAGE, 2001 The States Parties to this Convention, RECALLING article 194 of the United Nations Convention on the Law of the Sea, 1982,

2: PROCEDURES CONCERNING REQUIREMENTS FOR MEMBERSHIP OF IACS

IACS PROCEDURES Volume 2: PROCEDURES CONCERNING REQUIREMENTS FOR MEMBERSHIP OF IACS Volume 2: PROCEDURES CONCERNING REQUIREMENTS FOR MEMBERSHIP OF IACS 1 of 76 Adopted at C60, December 2009 Add 1, April

IACS PROCEDURES Volume 2: PROCEDURES CONCERNING REQUIREMENTS FOR MEMBERSHIP OF IACS Volume 2: PROCEDURES CONCERNING REQUIREMENTS FOR MEMBERSHIP OF IACS 1 of 76 Adopted at C60, December 2009 Add 1, April

CONVENTION ON LIMITATION OF LIABILITY FOR MARITIME CLAIMS 1976

CONVENTION ON LIMITATION OF LIABILITY FOR MARITIME CLAIMS 1976 The States parties to this Convention, Having recognized the desirability of determining by agreement certain uniform rules relating to the

CONVENTION ON LIMITATION OF LIABILITY FOR MARITIME CLAIMS 1976 The States parties to this Convention, Having recognized the desirability of determining by agreement certain uniform rules relating to the

SYH GENERAL CONDITIONS

SYH GENERAL CONDITIONS 1 DEFINITIONS Where the following words appear in these Conditions, the Licence and the Company's Regulations they shall have these meanings: Company shall mean the Company or any

SYH GENERAL CONDITIONS 1 DEFINITIONS Where the following words appear in these Conditions, the Licence and the Company's Regulations they shall have these meanings: Company shall mean the Company or any

The Government of the Kingdom of the Netherlands. and. The Government of the Isle of Man,

AGREEMENT BETWEEN THE KINGDOM OF THE NETHERLANDS AND THE ISLE OF MAN FOR THE AVOIDANCE OF DOUBLE TAXATION WITH RESPECT TO ENTERPRISES OPERATING SHIPS OR AIRCRAFT IN INTERNATIONAL TRAFFIC The Government

AGREEMENT BETWEEN THE KINGDOM OF THE NETHERLANDS AND THE ISLE OF MAN FOR THE AVOIDANCE OF DOUBLE TAXATION WITH RESPECT TO ENTERPRISES OPERATING SHIPS OR AIRCRAFT IN INTERNATIONAL TRAFFIC The Government

Taxation on Hong Kong shipping companies, vessels and goods, and potential reforms

Taxation on Hong Kong shipping companies, vessels and goods, and potential reforms Hong Kong Tax System Simple, transparent, straightforward Territorial source principle Hong Kong has: Profits tax, salaries

Taxation on Hong Kong shipping companies, vessels and goods, and potential reforms Hong Kong Tax System Simple, transparent, straightforward Territorial source principle Hong Kong has: Profits tax, salaries

Printed by The BIMCO Charter Party Editor

1. Date of Agreement THE BALTIC AND INTERNATIONAL MARITIME COUNCIL (BIMCO) STANDARD CREW MANAGEMENT AGREEMENT (LUMP SUM) CODE NAME:"CREWMAN B - LUMP SUM" 2. Owners (state name, place of registered office

1. Date of Agreement THE BALTIC AND INTERNATIONAL MARITIME COUNCIL (BIMCO) STANDARD CREW MANAGEMENT AGREEMENT (LUMP SUM) CODE NAME:"CREWMAN B - LUMP SUM" 2. Owners (state name, place of registered office

The Accident Investigation Act (1990:712)

") This is a translation into English of the Swedish original text. In case of discrepancies between this translation and the Swedish text, the Swedish text shall prevail with respect to the meaning and interpretation

This is a translation into English of the Swedish original text. In case of discrepancies between this translation and the Swedish text, the Swedish text shall prevail with respect to the meaning and interpretation

VALUE ADDED TAX COMMITTEE (ARTICLE 398 OF DIRECTIVE 2006/112/EC) WORKING PAPER NO 850

WORKING PAPER NO 850") EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration Value added tax taxud.c.1(2015)2039564 EN Brussels, 28 April 2015 VALUE ADDED TAX COMMITTEE (ARTICLE

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration Value added tax taxud.c.1(2015)2039564 EN Brussels, 28 April 2015 VALUE ADDED TAX COMMITTEE (ARTICLE

Strasbourg Convention of on the Limitation of Liability in Inland Navigation

Strasbourg Convention of 2012 on the Limitation of Liability in Inland Navigation (CLNI 2012) The States Parties to this Convention, having recognised the desirability of determining by agreement certain

Strasbourg Convention of 2012 on the Limitation of Liability in Inland Navigation (CLNI 2012) The States Parties to this Convention, having recognised the desirability of determining by agreement certain

Shipping in Cyprus. July 2016

Shipping in Cyprus July 2016 Shipping in Cyprus Cyprus holds a leading role in the shipping industry and ship management activities in South East Europe and is considered to be as one of the most attractive

Shipping in Cyprus July 2016 Shipping in Cyprus Cyprus holds a leading role in the shipping industry and ship management activities in South East Europe and is considered to be as one of the most attractive

SEAFARER LEGAL OBLIGATION & SOLUTIONS

SEAFARER LEGAL OBLIGATION & SOLUTIONS APPLICATION OF THE FRENCH DECREE WITH EFFECT FROM 1 JANUARY 2018 (No retroactive effect). The amended version of the French social security obligations for seafarers

SEAFARER LEGAL OBLIGATION & SOLUTIONS APPLICATION OF THE FRENCH DECREE WITH EFFECT FROM 1 JANUARY 2018 (No retroactive effect). The amended version of the French social security obligations for seafarers

1/ ITALIAN TAX UPDATE

Notes from VAT conference: ********************** Speakers: Alex Mazzoni, es-fraser Yachts. Thierry Voisin, ECPY President. Ezzio, Italian lawyer. 1/ ITALIAN TAX UPDATE Alex Mazzoni / Ezzio. CUSTOMS ANSWERS

Notes from VAT conference: ********************** Speakers: Alex Mazzoni, es-fraser Yachts. Thierry Voisin, ECPY President. Ezzio, Italian lawyer. 1/ ITALIAN TAX UPDATE Alex Mazzoni / Ezzio. CUSTOMS ANSWERS

COMMISSION OF THE EUROPEAN COMMUNITIES REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 25.06.2007 COM(2007) 207 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL on certain issues relating to Motor Insurance

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 25.06.2007 COM(2007) 207 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL on certain issues relating to Motor Insurance

Exam Spring 2009: Marine Insurance

Exam Spring 2009: Marine Insurance Some general comments on the student group, the course and the material The course in marine insurance is very new, and has only been offered three times. It is not an

Exam Spring 2009: Marine Insurance Some general comments on the student group, the course and the material The course in marine insurance is very new, and has only been offered three times. It is not an

Malta 13 th Directive (86/560/EEC) VAT refunds

VAT refunds") Malta 13 th Directive (86/560/EEC) VAT refunds I. RECIPROCITY AGREEMENTS Article 2(2) 1. Does your country have any reciprocity agreements? No. 2. If yes, what countries are included in the reciprocity

Malta 13 th Directive (86/560/EEC) VAT refunds I. RECIPROCITY AGREEMENTS Article 2(2) 1. Does your country have any reciprocity agreements? No. 2. If yes, what countries are included in the reciprocity

JUDGMENT OF THE COURT 22 September 1988*

JUDGMENT OF THE COURT 22 September 1988* In Case 272/86 Commission of the European Communities, represented by Xénophon Yataganas, a member of its Legal Department, with an address for service in Luxembourg

JUDGMENT OF THE COURT 22 September 1988* In Case 272/86 Commission of the European Communities, represented by Xénophon Yataganas, a member of its Legal Department, with an address for service in Luxembourg

THE NEW SPANISH SHIPPING LAW

THE NEW SPANISH SHIPPING LAW Rio de Janeiro Maritime and Port Law Conference 26 and 27 August, 2015 The Spanish Law of July 2014 (Ley de Navegación Marítima) came into force on September 25, 2014. It s

THE NEW SPANISH SHIPPING LAW Rio de Janeiro Maritime and Port Law Conference 26 and 27 August, 2015 The Spanish Law of July 2014 (Ley de Navegación Marítima) came into force on September 25, 2014. It s

APPLICATION TO P&I CLUB FOR ATHENS 2002 PLR WAR BLUE CARD. IMO ship identification number(s): Port of registry: Flag:

: Port of registry: Flag:") APPLICATION TO P&I CLUB FOR ATHENS 2002 PLR WAR BLUE CARD Section 1: Ship/Blue Card Information Name of Ship(s): Distinctive number or letters: IMO ship identification number(s): Port of registry: Flag:

APPLICATION TO P&I CLUB FOR ATHENS 2002 PLR WAR BLUE CARD Section 1: Ship/Blue Card Information Name of Ship(s): Distinctive number or letters: IMO ship identification number(s): Port of registry: Flag:

SMALL TANKER OIL POLLUTION INDEMNIFICATION AGREEMENT (STOPIA)

") The Shipowners Protection Limited St Clare House, 30-33 Minories London EC3N 1BP TO ALL MEMBERS Managers of The Shipowners Mutual Protection and Indemnity Association (Luxembourg) June 2005 Dear Sirs,

The Shipowners Protection Limited St Clare House, 30-33 Minories London EC3N 1BP TO ALL MEMBERS Managers of The Shipowners Mutual Protection and Indemnity Association (Luxembourg) June 2005 Dear Sirs,

COMMISSION OF THE EUROPEAN COMMUNITIES COMMISSION STAFF WORKING DOCUMENT

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 19.12.2005 SEC(2005) 1777 COMMISSION STAFF WORKING DOCUMENT addressed to the European Parliament and to the Council on certain issues relating

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 19.12.2005 SEC(2005) 1777 COMMISSION STAFF WORKING DOCUMENT addressed to the European Parliament and to the Council on certain issues relating

State aid N 37/ Cyprus Introduction of a tonnage tax scheme in favour of international maritime transport

EUROPEAN COMMISSION Brussels, 24.03.2010 C (2010) 1727 final PUBLIC VERSION WORKING LANGUAGE This document is made available for information purposes only. Subject: Sir, State aid N 37/2010 - Cyprus Introduction

EUROPEAN COMMISSION Brussels, 24.03.2010 C (2010) 1727 final PUBLIC VERSION WORKING LANGUAGE This document is made available for information purposes only. Subject: Sir, State aid N 37/2010 - Cyprus Introduction

Paper P6 (MLA) Advanced Taxation (Malta) Friday 5 December Professional Level Options Module. Time allowed

Advanced Taxation (Malta) Friday 5 December Professional Level Options Module. Time allowed") Professional Level Options Module Advanced Taxation (Malta) Friday 5 December 2014 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

Professional Level Options Module Advanced Taxation (Malta) Friday 5 December 2014 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

Financial Penalties for Member States who fail to comply with Judgments of the European Court of Justice: European Commission clarifies rules

MEMO/05/482 Brussels, 14 December 2005 Financial Penalties for Member States who fail to comply with Judgments of the European Court of Justice: European Commission clarifies rules The European Commission

MEMO/05/482 Brussels, 14 December 2005 Financial Penalties for Member States who fail to comply with Judgments of the European Court of Justice: European Commission clarifies rules The European Commission

The Nairobi International Convention on the Removal of Wrecks. Dr. Matthew Attard GANADO ADVOCATES

The Nairobi International Convention on the Removal of Wrecks Dr. Matthew Attard GANADO ADVOCATES History behind the Convention The Torrey Canyon incident of 1967 This wreck demonstrated the inadequacies

The Nairobi International Convention on the Removal of Wrecks Dr. Matthew Attard GANADO ADVOCATES History behind the Convention The Torrey Canyon incident of 1967 This wreck demonstrated the inadequacies

Member Circular No November 2012

Member Circular No. 13-2012 November 2012 To the Members Dear Sirs, The Athens Convention/EU Passenger Liability Regulation Safeguard Guarantee Company Ltd as provider of financial security for War and

Member Circular No. 13-2012 November 2012 To the Members Dear Sirs, The Athens Convention/EU Passenger Liability Regulation Safeguard Guarantee Company Ltd as provider of financial security for War and

REPUBLIC OF THE MARSHALL ISLANDS. Fees for Official Documents and Services MARITIME ADMINISTRATOR

REPUBLIC OF THE MARSHALL ISLANDS Fees for Official Documents and Services MARITIME ADMINISTRATOR Jul/2018 MN-1-005-1 TABLE OF CONTENTS REFERENCES... 3 PURPOSE... 3 APPLICABILITY... 3 REQUIREMENTS... 3

REPUBLIC OF THE MARSHALL ISLANDS Fees for Official Documents and Services MARITIME ADMINISTRATOR Jul/2018 MN-1-005-1 TABLE OF CONTENTS REFERENCES... 3 PURPOSE... 3 APPLICABILITY... 3 REQUIREMENTS... 3

JUDGMENT OF THE COURT 24 November 1992 *

JUDGMENT OF 24. 11. 1992 CASE C-286/90 JUDGMENT OF THE COURT 24 November 1992 * In Case C-286/90, REFERENCE to the Court under Article 177 of the EEC Treaty by the Kriminal-og Skifteret (Criminal and Probate

JUDGMENT OF 24. 11. 1992 CASE C-286/90 JUDGMENT OF THE COURT 24 November 1992 * In Case C-286/90, REFERENCE to the Court under Article 177 of the EEC Treaty by the Kriminal-og Skifteret (Criminal and Probate

Regulation and Supervision of the Financial Services Sector. Mdina The Silent City, Malta

Regulation and Supervision of the Financial Services Sector Mdina The Silent City, Malta Contents Introduction... 3 1 Regulation and Supervision of Financial Services Companies... 4 1.1 Jurisdiction who

Regulation and Supervision of the Financial Services Sector Mdina The Silent City, Malta Contents Introduction... 3 1 Regulation and Supervision of Financial Services Companies... 4 1.1 Jurisdiction who

Excise. (a) Remission/Repayment of mineral oil tax on mineral oil used for the purpose of commercial sea navigation, including sea-fishing, and

Remission/Repayment of mineral oil tax on mineral oil used for the purpose of commercial sea navigation, including sea-fishing, and") Notice No 1884 (Revised Version September 2017) Excise Procedures relating to: (a) Remission/Repayment of mineral oil tax on mineral oil used for the purpose of commercial sea navigation, including sea-fishing,

Notice No 1884 (Revised Version September 2017) Excise Procedures relating to: (a) Remission/Repayment of mineral oil tax on mineral oil used for the purpose of commercial sea navigation, including sea-fishing,

Official Journal of the European Union L 172. Legislation. Non-legislative acts. Volume July English edition. Contents REGULATIONS

Official Journal of the European Union L 172 English edition Legislation Volume 61 9 July 2018 Contents II Non-legislative acts REGULATIONS Commission Implementing Regulation (EU) 2018/963 of 6 July 2018

Official Journal of the European Union L 172 English edition Legislation Volume 61 9 July 2018 Contents II Non-legislative acts REGULATIONS Commission Implementing Regulation (EU) 2018/963 of 6 July 2018

Section 1: General Definitions and Provisions Section 2: Supplies within Tax Scope Section 3: Place of Supply Chapter 1: Place of Goods Supply

GCC VAT Framework 1 Contents Section 1: General Definitions and Provisions... 6 Article 1: Definitions... 6 Article 2: Tax Scope... 8 Article 3: The Calculation of Tax Periods... 8 Article 4: Tax Group...

GCC VAT Framework 1 Contents Section 1: General Definitions and Provisions... 6 Article 1: Definitions... 6 Article 2: Tax Scope... 8 Article 3: The Calculation of Tax Periods... 8 Article 4: Tax Group...

WELCOME TO TAXING ISSUES THE QUARTERLY BULLETIN FROM CAPITAL GES

WELCOME TO TAXING ISSUES THE QUARTERLY BULLETIN FROM CAPITAL GES WELCOME TO TAXING ISSUES Welcome to the third issue of Taxing Issues in 2017. In this third issue of 2017 we provide an important article

WELCOME TO TAXING ISSUES THE QUARTERLY BULLETIN FROM CAPITAL GES WELCOME TO TAXING ISSUES Welcome to the third issue of Taxing Issues in 2017. In this third issue of 2017 we provide an important article

UK LEISURE, SUPERYACHT AND SMALL COMMERCIAL MARINE INDUSTRY KEY PERFORMANCE INDICATORS 2008/9

UK LEISURE, SUPERYACHT AND SMALL COMMERCIAL MARINE INDUSTRY KEY PERFORMANCE INDICATORS 2008/9 CONTENTS Introduction 01 Headline Figures 02 Revenue and Value Added 03 05 International Trade 06 07 Employment

UK LEISURE, SUPERYACHT AND SMALL COMMERCIAL MARINE INDUSTRY KEY PERFORMANCE INDICATORS 2008/9 CONTENTS Introduction 01 Headline Figures 02 Revenue and Value Added 03 05 International Trade 06 07 Employment

VAT in the European Community APPLICATION IN THE MEMBER STATES, INFORMATION FOR USE BY: ADMINISTRATIONS/TRADERS INFORMATION NETWORKS, ETC.

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration VAT and other turnover taxes Brussels, October 2010 TAXUD/C/1 VAT in the European Community APPLICATION

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration VAT and other turnover taxes Brussels, October 2010 TAXUD/C/1 VAT in the European Community APPLICATION

***I POSITION OF THE EUROPEAN PARLIAMENT

European Parliament 2014-2019 Consolidated legislative document 4.10.2017 EP-PE_TC1-COD(2016)0171 ***I POSITION OF THE EUROPEAN PARLIAMENT adopted at first reading on 4 October 2017 with a view to the

European Parliament 2014-2019 Consolidated legislative document 4.10.2017 EP-PE_TC1-COD(2016)0171 ***I POSITION OF THE EUROPEAN PARLIAMENT adopted at first reading on 4 October 2017 with a view to the

Insurance and premium conditions

CIRCULAR NO. 649 Insurance and premium conditions 2016 1 Introduction and overview p. 2 2 Conditional trading areas p. 4 3 Standard cover p. 5 4 Piracy p. 7 5 DNK Special covers p. 8 6 Vessels under construction

CIRCULAR NO. 649 Insurance and premium conditions 2016 1 Introduction and overview p. 2 2 Conditional trading areas p. 4 3 Standard cover p. 5 4 Piracy p. 7 5 DNK Special covers p. 8 6 Vessels under construction

Statistics: Fair taxation of the digital economy

Statistics: Fair taxation of the digital economy Your reply: can be published with your personal information (I consent to the publication of all information in my contribution in whole or in part including

Statistics: Fair taxation of the digital economy Your reply: can be published with your personal information (I consent to the publication of all information in my contribution in whole or in part including

VOLUNTARY GUIDELINES FOR FLAG STATE PERFORMANCE - A NEW TOOL AGAINST IUU FISHING

VOLUNTARY GUIDELINES FOR FLAG STATE PERFORMANCE - A NEW TOOL AGAINST IUU FISHING THE FOURTH GLOBAL FISHERIES ENFORCEMENT TRAINING WORKSHOP SAN JOSE, COSTA RICA Johann Augustyn Chair: FAO Technical Consultation

VOLUNTARY GUIDELINES FOR FLAG STATE PERFORMANCE - A NEW TOOL AGAINST IUU FISHING THE FOURTH GLOBAL FISHERIES ENFORCEMENT TRAINING WORKSHOP SAN JOSE, COSTA RICA Johann Augustyn Chair: FAO Technical Consultation

VALUE ADDED TAX COMMITTEE (ARTICLE 398 OF DIRECTIVE 2006/112/EC) WORKING PAPER NO 897

WORKING PAPER NO 897") EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration Value added tax taxud.c.1(2016)923028 EN Brussels, 10 February 2016 VALUE ADDED TAX COMMITTEE

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration Value added tax taxud.c.1(2016)923028 EN Brussels, 10 February 2016 VALUE ADDED TAX COMMITTEE

Terms and Conditions for Payment Services

Terms and Conditions for Payment Services Nordea Bank S.A. 1 Terms and Conditions for Payment Services January 2018 2 Terms and Conditions for Payment Services Nordea Bank S.A. Contents 1. General provisions

Terms and Conditions for Payment Services Nordea Bank S.A. 1 Terms and Conditions for Payment Services January 2018 2 Terms and Conditions for Payment Services Nordea Bank S.A. Contents 1. General provisions

COMMUNICATION FROM THE COMMISSION

EUROPEAN COMMISSION Brussels, 20.2.2019 C(2019) 1396 final COMMUNICATION FROM THE COMMISSION Modification of the calculation method for lump sum payments and daily penalty payments proposed by the Commission

EUROPEAN COMMISSION Brussels, 20.2.2019 C(2019) 1396 final COMMUNICATION FROM THE COMMISSION Modification of the calculation method for lump sum payments and daily penalty payments proposed by the Commission

(iii) for loss of or damage to the effects of any passengers on board an insured vessel;

for loss of or damage to the effects of any passengers on board an insured vessel;") Class 1 Protection & Indemnity and Other Risks Section 2A. Liability to passengers. Liability to pay damages or compensation:- for personal injury, illness or death of any passenger of an insured vessel

Class 1 Protection & Indemnity and Other Risks Section 2A. Liability to passengers. Liability to pay damages or compensation:- for personal injury, illness or death of any passenger of an insured vessel

UK and Norway after the Common Fisheries Policy BARRIE DEAS NATIONAL FEDERATION OF FISHERMEN S ORGANISATIONS

UK and Norway after the Common Fisheries Policy BARRIE DEAS NATIONAL FEDERATION OF FISHERMEN S ORGANISATIONS A presentation for the Norwegian Seafood Council UK leaves the EU March 2019 Transitional arrangements

UK and Norway after the Common Fisheries Policy BARRIE DEAS NATIONAL FEDERATION OF FISHERMEN S ORGANISATIONS A presentation for the Norwegian Seafood Council UK leaves the EU March 2019 Transitional arrangements

EUROPEAN COMMISSION. State aid SA (2012/E, 2011/CP) Tonnage tax scheme and other tax relieves provided in Law No 27 of 19 April 1975 as amended

Tonnage tax scheme and other tax relieves provided in Law No 27 of 19 April 1975 as amended") EUROPEAN COMMISSION Brussels, 18.12.2015 C(2015) 9019 final PUBLIC VERSION This document is made available for information purposes only. Subject: State aid SA.33828 (2012/E, 2011/CP) Tonnage tax scheme

EUROPEAN COMMISSION Brussels, 18.12.2015 C(2015) 9019 final PUBLIC VERSION This document is made available for information purposes only. Subject: State aid SA.33828 (2012/E, 2011/CP) Tonnage tax scheme

Shipping Services Piloting through calm waters and heavy seas. Shipping Services Piloting through calm waters and heavy seas

Shipping Services Piloting through calm waters and heavy seas October 2016 00 Contents Introduction 3 The economic value of the EU shipping industry 3 Supply overcapacity 3 The finance/refinance challenge

Shipping Services Piloting through calm waters and heavy seas October 2016 00 Contents Introduction 3 The economic value of the EU shipping industry 3 Supply overcapacity 3 The finance/refinance challenge

EUROPEAN COMMISSION AND COURTS DECISIONS ARE PRODUCING

6 JULY 2009 PRESS STATEMENT TAX DISCRIMINATION OF FOREIGN PENSION FUNDS EUROPEAN COMMISSION AND COURTS DECISIONS ARE PRODUCING TANGIBLE RESULTS EFRP is happy to note progress and considers it is an appropriate

6 JULY 2009 PRESS STATEMENT TAX DISCRIMINATION OF FOREIGN PENSION FUNDS EUROPEAN COMMISSION AND COURTS DECISIONS ARE PRODUCING TANGIBLE RESULTS EFRP is happy to note progress and considers it is an appropriate

Arianna. American Issue. Mets BIRD OF PARADISE DISTINCTIVE BUILDS SHOW WITHIN A SHOW

NETHERLANDS LEADING BUSINESS-TO-BUSINESS MAGAZINE FOR THE INTERNATIONAL SUPERYACHT INDUSTRY SYI 2012 volume 7 ISSUE 5 Arianna BIRD OF PARADISE American Issue DISTINCTIVE BUILDS Mets SHOW WITHIN A SHOW

NETHERLANDS LEADING BUSINESS-TO-BUSINESS MAGAZINE FOR THE INTERNATIONAL SUPERYACHT INDUSTRY SYI 2012 volume 7 ISSUE 5 Arianna BIRD OF PARADISE American Issue DISTINCTIVE BUILDS Mets SHOW WITHIN A SHOW

Carbon Fund Annual Report

Carbon Fund Annual Report 2016 REPORT AND ACCOUNTS OF THE CARBON FUND FOR THE YEAR ENDED 31 DECEMBER 2016 23 May 2017 Contents summary 3 Background 3 section one 4 Measuring Greenhouse Gas emissions 4

Carbon Fund Annual Report 2016 REPORT AND ACCOUNTS OF THE CARBON FUND FOR THE YEAR ENDED 31 DECEMBER 2016 23 May 2017 Contents summary 3 Background 3 section one 4 Measuring Greenhouse Gas emissions 4

(incorporated in Bermuda with limited liability) Stock Code: 2343

Stock Code: 2343") The Stock Exchange of Hong Kong Limited takes no responsibility for the contents of this announcement, makes no representation as to its accuracy or completeness and expressly disclaims any liability whatsoever

The Stock Exchange of Hong Kong Limited takes no responsibility for the contents of this announcement, makes no representation as to its accuracy or completeness and expressly disclaims any liability whatsoever

Maritime Cyprus Tax alert: New tonnage tax legislation introduced

Maritime Cyprus Tax alert: New tonnage tax legislation introduced May 2010 Kanaris Demetriades & Associates COMPLIANCE AUDIT TAX ADVISORY QUALITYSERVICEEXCELLENCE Cyprus: a well established shipping centre

Maritime Cyprus Tax alert: New tonnage tax legislation introduced May 2010 Kanaris Demetriades & Associates COMPLIANCE AUDIT TAX ADVISORY QUALITYSERVICEEXCELLENCE Cyprus: a well established shipping centre

Shipping Companies and Ship Registration in Bermuda

Shipping Companies and Ship Registration in Bermuda Preface This publication has been prepared for the assistance of those who are considering the incorporation of a Bermuda company to own or operate ships,

Shipping Companies and Ship Registration in Bermuda Preface This publication has been prepared for the assistance of those who are considering the incorporation of a Bermuda company to own or operate ships,

The Republic of Palau Palau International Ship Registry

The Republic of Palau Palau International Ship Registry A New Vision of Quality in Ship Registration Services MC 16-024 Revision No. 00 Issue Date: 24 August 2016 MARINE CIRCULAR 16-024 SUSPENSION AND

The Republic of Palau Palau International Ship Registry A New Vision of Quality in Ship Registration Services MC 16-024 Revision No. 00 Issue Date: 24 August 2016 MARINE CIRCULAR 16-024 SUSPENSION AND

Ghana Tax Guide 2012

Ghana Tax Guide 2012 I IMPORTANT DISCLAIMER: No person, entity or corporation should act or rely upon any matter or information as contained or implied within this publication without first obtaining advice

Ghana Tax Guide 2012 I IMPORTANT DISCLAIMER: No person, entity or corporation should act or rely upon any matter or information as contained or implied within this publication without first obtaining advice