What is a disclaimer? A disclaimer is an irrevocable statement that the beneficiary/recipient of an asset does not wish to receive the asset.

|

|

|

- Berenice Shepherd

- 6 years ago

- Views:

Transcription

1 What is a disclaimer? A disclaimer is an irrevocable statement that the beneficiary/recipient of an asset does not wish to receive the asset. The disclaimed asset passes as if the disclaimant had predeceased the person transferring the asset.

2 Inheritance under Will or Trust Intestacy Non-probate property Powers of Appointment Jointly owned property Effect of a qualified disclaimer: The disclaimed interest is treated as passing directly from the transferor of the property to the person entitled to receive the property as a result of the disclaimer The person making the disclaimer is not treated as making a gift. If an estate disclaims an interest it would otherwise receive, the decedent's estate does not include the value of the disclaimed property

3 Requirements for Disclaimer : Section 2518(b) and Treasury Reg and 20 Pa.C.S provide the requirements for a qualified disclaimer. If the disclaimer is not a qualified disclaimer, it typically is treated as a gift. The disclaimer must be irrevocable and unqualified The disclaimer must be in writing The writing must be delivered within nine (9) months from the date of death The disclaimant cannot accept any of the interest being disclaimed or any of its benefits The interest disclaimed must pass without any direction on the part of the person making the disclaimer. Specific Rules Commencement of 9 month period from which to make the disclaimer: Lifetime transfers: the transfer creating the interest occurs when there is a completed gift for Federal gift tax purposes, regardless of whether a gift tax is imposed on the completed gift. Transfers at death: the transfer creating the interest occurs on the date of the decedent's death. Nine Month Time Limit - The disclaimer must be filed within nine months after the later of the date on which the transfer creating the interest is made or the date on which the disclaimant attains age twenty-one (federal rule).

4 Acceptance of Interest or its Benefits A qualified disclaimer cannot be made if the disclaimant has accepted the interest or its benefits Acceptance can be either express or implied Acceptance is manifested by an affirmative act which is consistent with ownership of the interest in property Acts indicative of acceptance include using the property or the interest in property; accepting dividends, interest, or rents from the property; and directing others to act with respect to the property or interest in property Taking delivery of an instrument of title, alone, does not constitute acceptance Disclaimed interest must pass without direction of the disclaimant. Exception for surviving spouse in certain cases where it passes to a trust under which the surviving spouse still is a beneficiary, provided access is limited by an ascertainable standard.

5 The regulations provide that the interest of a joint tenant with rights of survivorship or a tenant by the entireties (other than in a bank, brokerage and other investment accounts), regardless of whether it can be unilaterally severed, is deemed to be a one-half interest. This is the case regardless of whether the disclaimant contributed any of the property and regardless of the portion of property includable in the decedent s estate under Reg (c)(4)(I) Special rule for joint bank, brokerage and other investment accounts: Transfer creating the survivor s interest occurs on the death of the deceased cotenant. Therefore, the disclaimer must be made within nine (9) months of the decedent s death. Surviving joint tenant may not disclaim any portion of the joint account attributable to contribution or consideration furnished by that surviving joint tenant

6 Right to Disclaim: The recipients of interests by whatever means can disclaim such interests. Such interests include: a beneficiary under a will an appointee under the exercise of a power of appointment a person entitled to take by intestacy a joint tenant with right of survivorship a donee of an inter vivos transfer beneficiaries of life insurance, annuities, and retirement assets Disclaimer Requirements (PA Law): Must be in writing and shall: describe the interest disclaimed declare the disclaimer and extent thereof; and be signed by the disclaimant (A disclaimer can be made on behalf of another person through the authority contained in a power of attorney or by the personal representative of an estate) Must be delivered and filed in some instances (see below)

7 The acceptance of part of a single interest shall be considered as only a partial acceptance and will not be a bar to a subsequent disclaimer of any part or all of the balance of the interest if the part of the interest is accepted before the expiration of six months from: The death of the decedent in the case of an interest that would have devolved by will or intestacy; or the effective date of the transfer in the case of an interest that would have devolved by an inter vivos transfer or third-party beneficiary contract. The acceptance of a part of a single interest after the expiration of such six-month period shall be considered an acceptance of the entire interest and a bar to any subsequent disclaimer thereof but shall not be an acceptance of any separate interest given under the same instrument.

8 Interests passing through Will or intestacy Inter vivos transfers Assets passing through contractual arrangements Powers of appointment Real Estate Disclaimers by Fiduciaries or Agents Personal Representative if authorized by Will or otherwise requires court approval Guardian of minor Court appointed guardian of incapacitated person if authorized by court Agent under Power of Attorney if power of attorney specifically authorizes

refers to a renunciation of right to receive a distributive share of an estate, whether under an inter vivos trust, a will or the intestate law for no consideration.")

9 72 P.S. 9116(c) provides separate requirements for a disclaimer to be effective for Inheritance Tax Purposes. 9116(c) refers to a renunciation of right to receive a distributive share of an estate, whether under an inter vivos trust, a will or the intestate law for no consideration. The tax shall then be computed as though the persons who benefit by such renunciation were originally designated to be the distributees The renunciation shall be made within nine months after the death of the decedent. Note that 9116(c) applies to the inheritance tax effect of making a disclaimer within 9 months. Ch. 62 of Title 20, addresses the transfer effects when a disclaimer is made. Therefore even though a disclaimer that is made 10 months after death will not be effective for inheritance tax purposes, as long as the requirements of Ch.62 are met, the transfer may be effective for PA purposes. Compare Federal law, which will not recognize a dislcaimer not made within 9 months. For Federal tax law, an untimely disclaimer is instead treated as a gift. There are planning opportunities for disclaimers to pass wealth to younger generation without gifting Consider when death of beneficiary may be within short time of decedent and there is no survivorship provision in Will Be careful making disclaimer if beneficiary is Medicaid recipient or may be applying for Medicaid can cause ineligibility period

10 Federal Estate Tax 40% Tax Date of death value $5,490,000 basic exclusion amount (2017) $5,600,000 basic exclusion amount (2018)* Marital Deduction Charitable Deduction *subject to tax reform bill House and Senate Bills: $11,000,000 basic exclusion House Bill only: Estate tax repeal 2025 and beyond

11 Must Reduce the size of the gross estate Reduce the federal estate tax No federal estate tax Marital Charitable Portability Stock - Date of death is 1/2/2017 Google, Inc. = Mean Value on 1/2/2017 $44 (High $46; Low $42) Alternate Value: Sell Google, Inc. on 3/2/2017 for $42 Distribute to Beneficiary on 4/2/2017 value $41 Hold on 7/2/2017 mean value is $45

12 Alternate value=sum of all asset values Elect on Federal Estate Tax Return Alternate Value MUST Reduce the value of the Gross Estate AND Reduce Federal Estate Tax -Marital Deduction / no tax estates Elect on timely return Elect on late return (up to 1 year after due date) Irrevocable Form 706 (Rev ) Estate of: Barney Fife Part 3 Elections by the Executor Decedent s social security number Note: For information on electing portability of the decedent's DSUE amount, including how to opt out of the election, see Part 6 Portability of Deceased Spousal Unused Exclusion. Note: Some of the following elections may require the posting of bonds or liens. Yes No Please check Yes or No box for each question (see instructions). 1 Do you elect alternate valuation?

13 Date of death on or after 1/1/2011 Deceased Spousal Unused Exclusion Used by surviving spouse Election Timely filed Federal Estate Tax Return

14 Complete and properly prepared Portability filing only no value needed for Marital Deduction Items Charitable Deduction Items Timely filed federal estate tax return however Rev. Proc provides relief for certain late filed returns Form 706 (Rev ) Decedent s social security number Estate of: Barney Fife Part 6 Portability of Deceased Spousal Unused Exclusion (DSUE) Portability Election A decedent with a surviving spouse elects portability of the deceased spousal unused exclusion (DSUE) amount, if any, by completing and timely-filing this return. No further action is required to elect portability of the DSUE amount to allow the surviving spouse to use the decedent's DSUE amount. Section A. Opting Out of Portability The estate of a decedent with a surviving spouse may opt out of electing portability of the DSUE amount. Check here and do not complete Sections B and C of Part 6 only if the estate opts NOT to elect portability of the DSUE amount.

15 Tim dies 2017 Leaves $1,000,000 to son Everything else to wife Tim s Basic Exclusion $5,490,000 Used $1,000,000 DSUE to wife $4,490,000 Section C. DSUE Amount Portable to the Surviving Spouse (To be completed by the estate of a decedent making a portability election.) Complete the following calculation to determine the DSUE amount that can be transferred to the surviving spouse. 1 Enter the amount from line 9d, Part 2 Tax Computation Reserved Enter the value of the cumulative lifetime gifts on which tax was paid or payable (see instructions)... 4 Add lines 1 and Enter amount from line 10, Part 2 Tax Computation Divide amount on line 5 by 40% (0.40) (do not enter less than zero) Subtract line 6 from line Enter the amount from line 5, Part 2 Tax Computation Subtract line 8 from line 7 (do not enter less than zero) DSUE amount portable to surviving spouse (Enter lesser of line 9 or line 9a, Part 2 Tax Computation).. 1 5,490, ,490, ,490, ,000, ,490, ,490,000

16 DSUE applies to Surviving spouse lifetime gifting first Then to surviving spouse s estate Wife can shield $4,490,000 (DSUE) $5,490,000 (Exclusion) $9,980,000 Filing for portability only: Page 1 box 11: If you are estimating the value of assets included in the gross estate on line 1 pursuant to the special rule of Reg. section T(a)(7)(ii) check here

17

18 Taxable Gifts of survivor use DSUE first. Portability does not apply to GST Portability election is irrevocable. Executor can supersede a previous election by filing due date of return (Reg (a)(4)).

19 Late Portability Election Rev. Proc Decedent survived by spouse Died after 12/31/2010 Was a US citizen or resident Executor was not required to file because gross estate was less than the basic exclusion amount ($5,490,000) Executor did not file a timely return (9 months) Late Portability Election Rev. Proc File a complete and properly prepared Form 706 on or before the later of: January 2, 2018, OR Second annual anniversary of Decedent s death Write on Return: FILED PURSUANT TO REV PROC TO ELECT PORTABILITY UNDER 2010(c)(5)(A)

20 Trusts for surviving spouse that qualify for marital deduction: Withdrawal right General power to appoint to estate, creditors, or creditors of estate I give the residue of my estate to the Trustees to be held in trust as follows: Pay all income to my husband quarterly; Pay principal to husband for health, support, maintenance; At husband s death, pay all remaining principal and income to my children. (a) (b) (c)

21 I give the residue of my estate to the Trustees to be held in trust as follows: Pay all income to my husband quarterly; Pay principal to husband for health, support, maintenance; At husband s death, husband has limited power to appoint to my issue. In default of appointment, pay all remaining principal and income to my children. (a) (b) (c) I.R.C. 2056(b)(7)(B) qualified terminable interest property passes from the decedent Surviving spouse has a qualifying income interest for life Income payable at least annually No person has a power to appoint property to anyone other than surviving spouse Election made under 2056(b)(7)(B)

22 Non-productive property Surviving spouse must have right to convert Local law Instrument Stub income does not have to be paid to surviving spouse s estate

23 WHEN: Gift tax Timely filed gift tax return 6 month extension Estate Tax Timely filed return, with extensions On first estate tax return filed late CONSEQUENCE: Marital Deduction No tax at first death Trust subject to Federal Estate Tax when surviving spouse dies Federal estate due paid from Trust unless surviving spouse specifically exonerates under 2207A

24 Percentage or fraction Numerator the amount necessary to reduce federal estate tax to zero Administration: Divide trust into QTIP and non-qtip parts Transferor Decedent Donor (gifts) QTIP trusts surviving spouse Skip person Two or more generations below transferor grandchildren A trust with beneficiaries of all skipped persons

25 Lineal descendants of Transferor s grandparent Non-lineal descendants A person more than 37 and ½ years younger than transferor Tax rate of 40% Generation-skipping tax exemption 2017 $5,490, $5,600,000

26 Direct Skip I give $1,000,000 to my granddaughter, Jenna

27 $1,000,000 in trust for my wife. Income and principal to wife during her lifetime. At wife s death, in trust for son. Income and principal to son during his lifetime. At son s death, outright to granddaughter.

28 Unlimited estate tax marital deduction Surviving spouse must be a US citizen No marital deduction if surviving spouse is not a US citizen Exception Qualified Domestic Trust

29 One trustee a US citizen or corporation Created/maintained under US state law No distributions of principal unless US trustee can withhold QDOT tax Distributions except for hardship and income are subject to estate tax Property at survivor s death subject to estate tax Irrevocable election made List trust on Schedule M Marital Deduction Name of Trustee Description of Transfer EIN

30 File Form 706-QDT on 4/15: Distribution of principal to surviving spouse Death of surviving spouse Disqualification of Trust No tax if: Distribution of income Corpus on account of hardship Administrative dispositions

Must be postmarked (or hand delivered) on or before the 3 month")

31 PRE-PAYMENT OF INHERITANCE TAX 72 PA.C.S Estimated payments of inheritance tax within 3 months of the date of decedent s death 5% discount of amount of actual tax (owed vs. paid) Must be postmarked (or hand delivered) on or before the 3 month anniversary of decedent s death

32 Rates 0% to surviving spouse 4.5% to lineal heirs 12% to siblings 15% everyone else No tax on charities Date of Death: 12/1/17 Discount payment due: 3/1/2018 $100,000 payment Divide payment by.95 to calculate discount $105, credit

33 72 P.S "Transfer of property for the sole use." A transfer to or for the use of a transferee if, during the transferee's lifetime, the transferee is entitled to all income and principal distributions from the property and no person, including the transferee, possesses an inter vivos power of appointment over the property. 72 P.S (a) In the case of a transfer of property for the sole use of the transferor's surviving spouse during the surviving spouse's entire lifetime, all succeeding interests which follow the interest of the surviving spouse shall not be subject to tax as transfers by the transferor if the transfer was made by a decedent dying on or after January 1, 1995; provided that the transferor's personal representative may elect, on a timely filed inheritance tax return, to have this section not apply to a trust or similar arrangement or portion of a trust or similar arrangement

34 72 P.S (b) Succeeding interests not subject to tax as transfers by the transferor by reason of subsection (a) shall be deemed to be transfers subject to tax by the surviving spouse of the property held in the trust or similar arrangement at the death of the surviving spouse. The tax on that property shall be based upon its value at the death of the surviving spouse, the tax rates applicable to dispositions by the surviving spouse or by the transferor, whichever are lower, and any exemptions relating to the kind or location of property held in the trust or similar arrangement at the surviving spouse's death I give the residue of my estate to the Trustees to be held in trust as follows: (a) (b) (c) Pay all income to my wife quarterly; Pay principal to wife for health, support, maintenance; At wife s death, pay all remaining principal and income to my children.

35 Election: Pay tax based on value at husband s death OR Pay tax when wife dies

36 Inheritance Tax Result on $3,332,517 trust To wife: Income $197,884 x 0% = $0 Principal $313,463 x 0% = $0 Remainder interest to children: $2,821,169 x 4.5% = $126,953

37 At Jane Doe s death value = $3,332,517 Tax = 4.5% x $3,332,517 $149,963 Compare tax with election to prepay: $126,953

38 Elect to prepay: Trust will appreciate Surviving spouse will not use funds Do not prepay: Will spouse move out of state? Will assets depreciate? Will surviving spouse deplete trust funds? A transfer of a qualified family-owned business to one or more qualified transferees is exempt from inheritance tax if It continues to be owned by a qualified transferee for seven years after decedent s death Is reported on a timely filed inheritance tax return* *Under recent legislation Act 43 of 2017, 72 P.S was amended to add a new provision treating any tax return filed after 12/31/12 which makes an election under 9111 (s), (s.1) or (t) considered timely filed if filed within 1 year of the tax return due date, and any extension

39 Fewer than fifty full time employees Net book value less than $5,000,000 Wholly owned by decedent and members of decedent s family that are qualified transferees Trade or business not management of investments or income producing assets Existed at least 5 years before death Husband or wife Lineal descendants Siblings and sibling s lineal descendants Ancestors and ancestor s siblings No in-laws

40 Annual certification to Department of Revenue: Continues to be owned by qualified transferee Disqualification Inheritance tax and interest due

41 WHO: Surviving spouse WHAT: 1/3 of certain property WHEN: Within six months of later of date of death, or probate HOW: In writing to Orphans court Copy to personal representative WHAT: 1/3 of: Probate property Intestacy Property Revocable Trusts Trusts with retained income interest

42 SURVIVING SPOUSE MUST OFFSET THE 1/3 RD WITH ITEMS HE/SHE MUST DISCLAIM: Property not awarded as part of election General power of appointment property Trusts created by decedent Life insurance Annuities Pension, profit sharing, retirement Spouse has 6 months to make election may need to consider an extension of time Election is irrevocable Consider property spouse may have to give up to make election Certain property is not subject to election need to understand what can elect against

provide an election to exclude certain real property that is")

Complete")

43 Decedents dying after 7/1/ P.S. 9111(s) and (s.1) provide an election to exclude certain real property that is used for farmland-other or agricultural use. Check box 4 on front of Inheritance Tax Return (Rev-1500) Complete Schedule AU and attach to the Return.

44 Fiscal year Begin: Date of death Short Fiscal Year Long Fiscal year

45 Decedent dies 3/5/2017 Longest Fiscal Year End: 2/28/ Due Date: 6/15/2018 Pay beneficiary income 9/30/2017 K1 issued 6/15/2018 Beneficiary reports on 2018 return due 4/15/19 Decedent dies 11/15/17 Longest Fiscal Year End: 10/31/2018 Significant capital gains: September 2018 Short fiscal year from 11/15/17 to 8/31/18 Initial 1041 Due Date: 12/15/2018 September 2018 gains reported on 9/1/18 to 8/31/19 year Return due 12/15/19

46 Decedent dies 12/9/17 Longest Fiscal Year End: 11/30/2018 $100,000 per year IRA payments due estate 2017 No IRA payment due 2018 IRA payment must be taken by 12/31/2018 Take 2018 IRA distribution in December 2018 December 2018 IRA distribution reported on 12/1/18 to 11/30/19 year Return and Tax due on 3/15/20 For Tax Years Beginning in 2017 If Taxable This Rate of Income is: This Amount PLUS of Excess Taxable Income $ - $ % $2,550. $ % $6,000. $1, % $9,150. $2, % $12,500. $3, %

47 3.8% Net investment income tax Estate/Trust threshold $12, Individual Amounts Single or Head of household $200,000 Married filing jointly $250,000 Married filing separately $125,000 Qualifying widow(er) with a child $250,000 Accrued Savings Bond Interest Decedent s Final 1040 Election under Section 454(a) Estate s Fiduciary Income Tax Return (1041) Beneficiary s 1040

48 Decedent s Final 1040 Election under Section 454(a) Itemized deduction offset Medical expenses Impact on taxability of social security Federal Estate Tax Deduction 40% Federal Estate Tax Rate Fiduciary Income Tax Deduction 39.6% Income Tax Rate 3.8% Net Investment Income Tax Deduction

49 Executor Fees Attorney Fees Appraisal Fees, etc. Deduct on Federal Estate Tax Return: Federal Estate Tax Deduct on Form 1041 Fiduciary Income Tax No Federal Estate Tax Return No Federal Estate Tax Estate Portability

50 The undersigned Executrix hereby certifies that the deductions used in computing the taxable income of the Estate for the fiscal year ending 10/31/17 have not been used as deductions from the gross estate of the decedent for federal estate tax purposes under IRC 2053 or The undersigned waives all rights to have such items allowed at any time as deductions under said Code Sections. Deduct on Federal Estate Tax Return: Federal Estate Tax 40% rate Deduct on Decedent s final 1040 Paid within one year of death Waiver filed Not allowed as estate tax deductions Waive right to take on Federal Estate Tax Return 10% AGI threshold

51 Trusts: Calendar year tax reporting Estates: Fiscal year tax reporting 645 Election Estate and Revocable Trust combined on Form 1041 Elect on Form 1041 for Estate Executor and Trustee File Form 8855

52 Distribution of property in kind to a beneficiary does not result in gain or loss to the trust or estate, unless the distribution is in satisfaction of a right to receive a distribution in a pecuniary amount or in specific property other than that distributed To avoid double taxation, federal estate tax paid on items of IRD can be deducted on Fiduciary Income Tax Return when recognized in income Amount of deduction is determined by calculating the amount of estate tax paid on the IRD items.

53 Direct Rollover of IRA Rollover of Eligible Rollover distribution made by a qualified plan If estate or trust is beneficiary surviving spouse does not have same rollover options unless certain requirements are met. Trusts must use a calendar year for income tax reporting A revocable trust may be treated as part of an estate for income tax reporting by making an election on Form 1041 Election permits the trust and estate income and deductions to be reported on one fiduciary income tax return

54 Requirements for Qualification: The decedent must be a citizen or resident of the United States. 6166(a)(1). The value of the decedent's interest in a closely held business must exceed 35% of the "adjusted gross estate" (defined in 6166(b)(6)). (Gifts made within three years of death are considered in determining whether the 35% requirement is satisfied, but not for purposes of determining the amount of tax that may be deferred. See 2035(d)(4).

55 The deferral only applies to an interest in a closely held business and does not apply to passive investments. There are specific objective tests to determine whether the business is closely held. If the IRS denies (or terminates) a 6166 election, the taxpayer has the right to petition the Tax Court for a declaratory judgment under See Rev. Proc , I.R.B The Internal Revenue Service conditions their approval of installment payment of estate taxes pursuant to IRC 6166 on the furnishing of a surety bond under IRC 6165 or the election to have a special lien placed on property that has a value equal to the amount of the deferred tax plus the first four years of deferred interest. IRC 6324A. Certain real property used by the decedent or a member of the decedent's family for farming or in a closely held business Personal representative can elect to value the real property on the basis of its value as a farm or in a closely held business, rather than the FMV of the property determined on the basis of its highest and best use

56 Decedent must be a US citizen or resident At least 50% of the adjusted value of the estate must consist of the adjusted value of the real and personal property used in the business At least 25% of the adjusted value of the estate must consist of the real property alone. The property must be qualified real property During at least 5 years of the last 8 years prior to the death of the decedent: The property was owned by the decedent or a family member and used for a qualified use (as a farm or in a trade or business) and The decedent or a member of the family materially participated in the farm or the business. Special attention should be made to any S corporation stock as part of an estate Executor may need to elect to treat trust as a Qualified Subchapter S Trust or Electing Small Business Trust

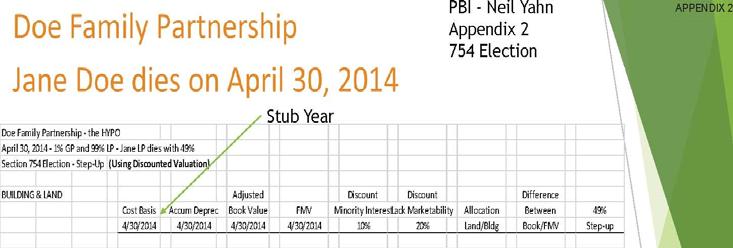

57 Determination must be made whether to make an election under Section 754 to adjust the basis of partnership property.

58 F-41

Estate Planning. Farm Credit East, ACA Stephen Makarevich

Estate Planning Farm Credit East, ACA Stephen Makarevich Farm Business Consultant 9 County Road 618 Lebanon, NJ 08833 1.800.787.3276 stephen.makarevich@farmcrediteast.com 1 What is Estate Planning? 2 Estate

Estate Planning Farm Credit East, ACA Stephen Makarevich Farm Business Consultant 9 County Road 618 Lebanon, NJ 08833 1.800.787.3276 stephen.makarevich@farmcrediteast.com 1 What is Estate Planning? 2 Estate

PREPARING GIFT TAX RETURNS

PREPARING GIFT TAX RETURNS I. Overview A sample 2014 gift tax return illustrating several different types of gifts is attached at Tab A. The instructions for the 2014 gift tax return can be found at Tab

PREPARING GIFT TAX RETURNS I. Overview A sample 2014 gift tax return illustrating several different types of gifts is attached at Tab A. The instructions for the 2014 gift tax return can be found at Tab

TRUST AND ESTATE PLANNING GLOSSARY

TRUST AND ESTATE PLANNING GLOSSARY What is estate planning? Estate planning is the process by which one protects and disposes of his or her wealth, sometimes during life and more often at death, in accordance

TRUST AND ESTATE PLANNING GLOSSARY What is estate planning? Estate planning is the process by which one protects and disposes of his or her wealth, sometimes during life and more often at death, in accordance

ALI-ABA Course of Study Estate Planning for the Family Business Owner. July 11-13, 2007 San Francisco, California

1041 ALI-ABA Course of Study Estate Planning for the Family Business Owner Cosponsored by the ABA Section of Real Property, Probate and Trust Law and the ABA Section of Taxation July 11-13, 2007 San Francisco,

1041 ALI-ABA Course of Study Estate Planning for the Family Business Owner Cosponsored by the ABA Section of Real Property, Probate and Trust Law and the ABA Section of Taxation July 11-13, 2007 San Francisco,

ALI-ABA Course of Study Planning Techniques for Large Estates November 17-21, 2008 San Francisco, California

1203 ALI-ABA Course of Study Planning Techniques for Large Estates November 17-21, 2008 San Francisco, California Postmortem Planning Considerations for the Family Business Owner: A Review of Income, Gift,

1203 ALI-ABA Course of Study Planning Techniques for Large Estates November 17-21, 2008 San Francisco, California Postmortem Planning Considerations for the Family Business Owner: A Review of Income, Gift,

ESTATE PLANNING. Estate Planning

ESTATE PLANNING Estate Planning 2 Why do you need estate planning? Estate planning is a way for your family to create a plan in case something happens to you. It may help you take care of both the financial

ESTATE PLANNING Estate Planning 2 Why do you need estate planning? Estate planning is a way for your family to create a plan in case something happens to you. It may help you take care of both the financial

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR SINGLE, DIVORCED, AND WIDOWED PEOPLE (New York)

") HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR SINGLE, DIVORCED, AND WIDOWED PEOPLE - 2018 (New York) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR SINGLE, DIVORCED, AND WIDOWED PEOPLE - 2018 (New York) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets

Annual Advanced ALI-ABA Course of Study Planning Techniques for Large Estates. November 17-21, 2003 San Francisco, California

Annual Advanced ALI-ABA Course of Study Planning Techniques for Large Estates November 17-21, 2003 San Francisco, California Estate Administration: A Review of Income, Gift, and Estate Tax Planning Issues

Annual Advanced ALI-ABA Course of Study Planning Techniques for Large Estates November 17-21, 2003 San Francisco, California Estate Administration: A Review of Income, Gift, and Estate Tax Planning Issues

ESTATE EVALUATION. John and Jane Doe

ESTATE EVALUATION John and Jane Doe Adam Advisor Investment Advisors 265 Anystreet Suite 123 AnyCity, AnyState, AnyZip (555) 555-5555 adam@investmentadvisors.inv Important Notes Estate Evaluation is a

ESTATE EVALUATION John and Jane Doe Adam Advisor Investment Advisors 265 Anystreet Suite 123 AnyCity, AnyState, AnyZip (555) 555-5555 adam@investmentadvisors.inv Important Notes Estate Evaluation is a

Recent Developments in the Estate and Gift Tax Area. Annual Business Plan and the Proposed Regulations under Section 2642

DID YOU GET YOUR BADGE SCANNED? Gift & Estate Tax Recent Developments in the Estate and Gift Tax Area Annual Business Plan and the Proposed Regulations under Section 2642 #TaxLaw #FBA Username: taxlaw

DID YOU GET YOUR BADGE SCANNED? Gift & Estate Tax Recent Developments in the Estate and Gift Tax Area Annual Business Plan and the Proposed Regulations under Section 2642 #TaxLaw #FBA Username: taxlaw

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond The Florida Bar Real Property Probate and Trust Law Section 2018 Wills, Trusts & Estates Certification and Practice Review

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond The Florida Bar Real Property Probate and Trust Law Section 2018 Wills, Trusts & Estates Certification and Practice Review

Tax Implications of Family Wealth Transfers

Tax Implications of Family Wealth Transfers Jill Choate Beier, Esq. Federal and Estate Gift Tax Overview Estate Tax Formula: Less: Plus: Equals: Decedent s Gross Estate Allowable Deductions Adjusted Taxable

Tax Implications of Family Wealth Transfers Jill Choate Beier, Esq. Federal and Estate Gift Tax Overview Estate Tax Formula: Less: Plus: Equals: Decedent s Gross Estate Allowable Deductions Adjusted Taxable

Federal Estate, Gift and GST Taxes

Federal Estate, Gift and GST Taxes 2018 Estate Law Institute November 2, 2018 Bradley D. Terebelo, Esquire Peter E. Moshang, Esquire Heckscher, Teillon, Terrill & Sager, P.C. 100 Four Falls, Suite 300

Federal Estate, Gift and GST Taxes 2018 Estate Law Institute November 2, 2018 Bradley D. Terebelo, Esquire Peter E. Moshang, Esquire Heckscher, Teillon, Terrill & Sager, P.C. 100 Four Falls, Suite 300

A Primer on Portability

A Primer on Portability Presentation to: Estate Planning Council of New York City, Inc. Estate Planners Day 2013 May 8, 2013 Ivan Taback, Esq. Proskauer Rose LLP Eleven Times Square New York, New York

A Primer on Portability Presentation to: Estate Planning Council of New York City, Inc. Estate Planners Day 2013 May 8, 2013 Ivan Taback, Esq. Proskauer Rose LLP Eleven Times Square New York, New York

ALI-ABA Course of Study Estate Planning for the Family Business Owner

1089 ALI-ABA Course of Study Estate Planning for the Family Business Owner Cosponsored by the ABA Section of Real Property, Trust and Estate Law - ABA Section of Taxation July 9-11, 2008 Boston, Massachusetts

1089 ALI-ABA Course of Study Estate Planning for the Family Business Owner Cosponsored by the ABA Section of Real Property, Trust and Estate Law - ABA Section of Taxation July 9-11, 2008 Boston, Massachusetts

ASPPA ANNUAL CONFERENCE TRUSTS AS BENEFICIARY ISSUES

ASPPA ANNUAL CONFERENCE TRUSTS AS BENEFICIARY ISSUES October 19, 2015 Leonard J. Witman, Esq. Witman Stadtmauer, P.A. 26 Columbia Turnpike, Suite 100 Florham Park, NJ 07932 (973) 822-0220 1 TABLE OF CONTENTS

ASPPA ANNUAL CONFERENCE TRUSTS AS BENEFICIARY ISSUES October 19, 2015 Leonard J. Witman, Esq. Witman Stadtmauer, P.A. 26 Columbia Turnpike, Suite 100 Florham Park, NJ 07932 (973) 822-0220 1 TABLE OF CONTENTS

United States Estate (and Generation-Skipping Transfer)

") United States Estate (and Generation-Skipping Transfer) Form 706 Tax Return OMB No. 1545-0015 G Estate of a citizen or resident of the United States (see instructions). To be filed for decedents dying

United States Estate (and Generation-Skipping Transfer) Form 706 Tax Return OMB No. 1545-0015 G Estate of a citizen or resident of the United States (see instructions). To be filed for decedents dying

Trusts That Affect Estate Administration

Trusts That Affect Estate Administration NBI Estate Administration Boot Camp September 22-23, 2016 Baltimore, Maryland By: Jill A. Snyder, Esq. Law Office of Jill A. Snyder, LLC 410-864- 8788 1 I. When

Trusts That Affect Estate Administration NBI Estate Administration Boot Camp September 22-23, 2016 Baltimore, Maryland By: Jill A. Snyder, Esq. Law Office of Jill A. Snyder, LLC 410-864- 8788 1 I. When

Estate, Gift and GST Tax Basics for the New Estate Planner Boston Bar Association Trusts & Estates Practice Fundamentals Committee November 4, 2015

Estate, Gift and GST Tax Basics for the New Estate Planner Boston Bar Association Trusts & Estates Practice Fundamentals Committee November 4, 2015 Danielle R. Greene Loring, Wolcott & Coolidge Trust,

Estate, Gift and GST Tax Basics for the New Estate Planner Boston Bar Association Trusts & Estates Practice Fundamentals Committee November 4, 2015 Danielle R. Greene Loring, Wolcott & Coolidge Trust,

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR SINGLE, DIVORCED, AND WIDOWED PEOPLE (Connecticut)

") HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR SINGLE, DIVORCED, AND WIDOWED PEOPLE - 2017 (Connecticut) I. Purposes of Estate Planning. II. A. Providing for the distribution and management of your

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR SINGLE, DIVORCED, AND WIDOWED PEOPLE - 2017 (Connecticut) I. Purposes of Estate Planning. II. A. Providing for the distribution and management of your

NC General Statutes - Chapter 31B 1

Chapter 31B. Renunciation of Property and Renunciation of Fiduciary Powers Act. 31B-1. Right to renounce succession. (a) A person who succeeds to a property interest as: (1) Heir; (2) Next of kin; (3)

Chapter 31B. Renunciation of Property and Renunciation of Fiduciary Powers Act. 31B-1. Right to renounce succession. (a) A person who succeeds to a property interest as: (1) Heir; (2) Next of kin; (3)

Probate in Florida. 1. What is probate?

Probate in Florida 1. What is probate? Probate is a court-supervised process for identifying and gathering the assets of a deceased person (decedent), paying the decedent s debts, and distributing the

Probate in Florida 1. What is probate? Probate is a court-supervised process for identifying and gathering the assets of a deceased person (decedent), paying the decedent s debts, and distributing the

EDWARD L. PERKINS, BA, JD, LLM (Tax), CPA Partner - Gibson&Perkins, PC Suite W Sixth St Media, PA Adjunct Professor - Villanova Law

, CPA Partner - Gibson&Perkins, PC Suite W Sixth St Media, PA Adjunct Professor - Villanova Law") EDWARD L. PERKINS, BA, JD, LLM (Tax), CPA Partner - Gibson&Perkins, PC Suite 204-100 W Sixth St Media, PA 19063 Adjunct Professor - Villanova Law School Graduate Tax Program Telephone : 610-565-1708 e-mail

EDWARD L. PERKINS, BA, JD, LLM (Tax), CPA Partner - Gibson&Perkins, PC Suite 204-100 W Sixth St Media, PA 19063 Adjunct Professor - Villanova Law School Graduate Tax Program Telephone : 610-565-1708 e-mail

ESTATE AND GIFT TAXATION

H Chapter Fourteen H ESTATE AND GIFT TAXATION INTRODUCTION AND STUDY OBJECTIVES Estate taxes are imposed on transfers of property by decedents, and gift taxes are imposed on the transfers by living individual

H Chapter Fourteen H ESTATE AND GIFT TAXATION INTRODUCTION AND STUDY OBJECTIVES Estate taxes are imposed on transfers of property by decedents, and gift taxes are imposed on the transfers by living individual

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2019 (New York)

") HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2019 (New York) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets after your death. B.

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2019 (New York) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets after your death. B.

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2018 (Connecticut)

") HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2018 (Connecticut) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets after your death.

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2018 (Connecticut) I. Purposes of Estate Planning. A. Providing for the distribution and management of your assets after your death.

Bypass Trust (also called B Trust or Credit Shelter Trust)

") Vertex Wealth Management, LLC Michael J. Aluotto, CRPC President Private Wealth Manager 1325 Franklin Ave., Ste. 335 Garden City, NY 11530 516-294-8200 mjaluotto@1stallied.com Bypass Trust (also called

Vertex Wealth Management, LLC Michael J. Aluotto, CRPC President Private Wealth Manager 1325 Franklin Ave., Ste. 335 Garden City, NY 11530 516-294-8200 mjaluotto@1stallied.com Bypass Trust (also called

GLOSSARY OF FIDUCIARY TERMS

The terminology used when discussing trusts and estates can often be unfamiliar and our glossary of fiduciary terms is designed to help you understand it better. If you have a question about the glossary

The terminology used when discussing trusts and estates can often be unfamiliar and our glossary of fiduciary terms is designed to help you understand it better. If you have a question about the glossary

Recent Developments in Estate & Gift Tax

Recent Developments in Estate & Gift Tax Disclaimer The information presented in this handout from the Internal Revenue Service is for educational purposes only and shall not be cited or relied upon as

Recent Developments in Estate & Gift Tax Disclaimer The information presented in this handout from the Internal Revenue Service is for educational purposes only and shall not be cited or relied upon as

Gift Planning Glossary of Terms

Gift Planning Glossary of Terms Annual Exclusion The amount of property (presently $14,000 or $28,000 for a married couple in 2013) that may annually be given to a donee, regardless of the donee s relationship

Gift Planning Glossary of Terms Annual Exclusion The amount of property (presently $14,000 or $28,000 for a married couple in 2013) that may annually be given to a donee, regardless of the donee s relationship

Creative Estate Planning for Clients Under $10 Million

Creative Estate Planning for Clients Under $10 Million Presented by Missia H. Vaselaney Taft Partner October, 2017 Created by Jeremiah W. Doyle, IV, Senior Vice President, BYN Mellon Wealth Management

Creative Estate Planning for Clients Under $10 Million Presented by Missia H. Vaselaney Taft Partner October, 2017 Created by Jeremiah W. Doyle, IV, Senior Vice President, BYN Mellon Wealth Management

NC General Statutes - Chapter 30 Article 1A 1

Article 1A. Elective Share. 30-3.1. Right of elective share. (a) Elective Share. The surviving spouse of a decedent who dies domiciled in this State has a right to claim an "elective share", which means

Article 1A. Elective Share. 30-3.1. Right of elective share. (a) Elective Share. The surviving spouse of a decedent who dies domiciled in this State has a right to claim an "elective share", which means

Preparing the PA Inheritance Tax Return

Preparing the PA Inheritance Tax Return Charles Bender, Esq. November 2, 2018 2018 Fox Rothschild Summary of PA Inheritance Tax PA is one of the few states that still has an inheritance tax NJ also has

Preparing the PA Inheritance Tax Return Charles Bender, Esq. November 2, 2018 2018 Fox Rothschild Summary of PA Inheritance Tax PA is one of the few states that still has an inheritance tax NJ also has

Estate Planning Client Guide

CLIENT GUIDE Advanced Markets Estate Planning Client Guide LIFE-5711 6/17 TABLE OF CONTENTS Why Create an Estate Plan?... 1 Basic Estate Planning Tools... 2 Funding an Irrevocable Life Insurance Trust

CLIENT GUIDE Advanced Markets Estate Planning Client Guide LIFE-5711 6/17 TABLE OF CONTENTS Why Create an Estate Plan?... 1 Basic Estate Planning Tools... 2 Funding an Irrevocable Life Insurance Trust

Revised through March 1, 2016

Pocket Tax Tables Revised through March, 206 POCKET TAX TABLES Revised through March, 206 Although care was taken to make these Pocket Tax Tables an accurate, handy reference, they should not be relied

Pocket Tax Tables Revised through March, 206 POCKET TAX TABLES Revised through March, 206 Although care was taken to make these Pocket Tax Tables an accurate, handy reference, they should not be relied

A Guide to Estate Planning

BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON, DC www.daypitney.com A Guide to Estate Planning THE IMPORTANCE OF ESTATE PLANNING The goal of estate planning is to direct the transfer and management

BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON, DC www.daypitney.com A Guide to Estate Planning THE IMPORTANCE OF ESTATE PLANNING The goal of estate planning is to direct the transfer and management

BASIC ESTATE PLANNING FOR YOU AND YOUR CLIENTS

BASIC ESTATE PLANNING FOR YOU AND YOUR CLIENTS I. INTRODUCTION The purpose of this manuscript is to revisit basic estate planning concepts and techniques. The manuscript will revisit basic estate planning

BASIC ESTATE PLANNING FOR YOU AND YOUR CLIENTS I. INTRODUCTION The purpose of this manuscript is to revisit basic estate planning concepts and techniques. The manuscript will revisit basic estate planning

Estate And Legacy Planning

Estate And Legacy Planning An Overview of the Estate Planning Process By: Samuel S. Stalsberg Sjoberg & Tebelius, P.A. 2145 Woodlane Drive, Suite 101 Woodbury, Minnesota 55125 Phone: 651-738-3433 sam@stlawfirm.com

Estate And Legacy Planning An Overview of the Estate Planning Process By: Samuel S. Stalsberg Sjoberg & Tebelius, P.A. 2145 Woodlane Drive, Suite 101 Woodbury, Minnesota 55125 Phone: 651-738-3433 sam@stlawfirm.com

Trusts and Other Planning Tools

Trusts and Other Planning Tools Today, We Will Discuss: Estate planning fundamentals Wills and probate Taxes Trusts Life insurance Alternate decision makers How we can help Preliminary Considerations Ask

Trusts and Other Planning Tools Today, We Will Discuss: Estate planning fundamentals Wills and probate Taxes Trusts Life insurance Alternate decision makers How we can help Preliminary Considerations Ask

Link Between Gift and Estate Taxes

Link Between Gift and Estate Taxes Each is necessary to enforce the other The taxes are assessed at essentially the same rates Though, the gift tax is measured exclusively while the estate tax is measured

Link Between Gift and Estate Taxes Each is necessary to enforce the other The taxes are assessed at essentially the same rates Though, the gift tax is measured exclusively while the estate tax is measured

Probate in Florida* 2. WHAT ARE PROBATE ASSETS?

Probate in Florida* Table of Contents What Is Probate? What Is A Will? Who Is Involved In The Probate Process? What Is A Personal Representative, And What Does The Personal Representative Do? What Are

Probate in Florida* Table of Contents What Is Probate? What Is A Will? Who Is Involved In The Probate Process? What Is A Personal Representative, And What Does The Personal Representative Do? What Are

1. Will 2. Trust 3. Durable Power of Attorney 4. Living Will / Health Care Power of Attorney

THE MECHANICS OF ESTATE AND GENERATION TRANSITION PLANNING Pamela Epp Olsen Cline Williams Wright Johnson & Oldfather, LLP Lincoln, Omaha, Aurora, and Scottsbluff, Nebraska Fort Collins and Holyoke, Colorado

THE MECHANICS OF ESTATE AND GENERATION TRANSITION PLANNING Pamela Epp Olsen Cline Williams Wright Johnson & Oldfather, LLP Lincoln, Omaha, Aurora, and Scottsbluff, Nebraska Fort Collins and Holyoke, Colorado

Important Notes. Version c May 9, of 57. Presented by: Joseph Davis, CLU, ChFC For Evaluation Purposes Only

Ed and Tina Allen Presented by: Joseph Davis, CLU, ChFC 215 Broad Street Charlotte, North Carolina 26292 Phone: 704-927-5555 Mobile Phone: 704-549-5555 Fax: 704-549-6666 Email: joseph.davis@aol.com Financial

Ed and Tina Allen Presented by: Joseph Davis, CLU, ChFC 215 Broad Street Charlotte, North Carolina 26292 Phone: 704-927-5555 Mobile Phone: 704-549-5555 Fax: 704-549-6666 Email: joseph.davis@aol.com Financial

MARITAL DEDUCTION TRUSTS

One Commerce Plaza Albany, New York 12260 P 518.487.7600 F 518.487.7777 www.woh.com QTIPS Unlimited Marital Deduction IRC 2056(a) Estate taxes are not imposed on any assets passing to a surviving spouse

One Commerce Plaza Albany, New York 12260 P 518.487.7600 F 518.487.7777 www.woh.com QTIPS Unlimited Marital Deduction IRC 2056(a) Estate taxes are not imposed on any assets passing to a surviving spouse

CHAPTER TEN Transfers to/for a Spouse

CHAPTER TEN Transfers to/for a Spouse Objective: Property transfers to the spouse to enable him/her to have financial support during survivorship period from the entire marital estate. Avoid dilution for

CHAPTER TEN Transfers to/for a Spouse Objective: Property transfers to the spouse to enable him/her to have financial support during survivorship period from the entire marital estate. Avoid dilution for

Keir Digest. with. Assessment Questions for HS 319. For use with text Applications In Financial Planning II 2 nd Edition TABLE OF CONTENTS

Keir Digest with Assessment Questions for HS 319 2015 TABLE OF CONTENTS Chapter Title Page 1 Overview of Federal Estate and GST Taxation 7 2 Overview of Federal Gift Taxation 34 3 Estate Planning Case

Keir Digest with Assessment Questions for HS 319 2015 TABLE OF CONTENTS Chapter Title Page 1 Overview of Federal Estate and GST Taxation 7 2 Overview of Federal Gift Taxation 34 3 Estate Planning Case

I. Basic Rules. Planning for the Non- Citizen Spouse: Tips and Traps 2/25/2016. Zena M. Tamler. March 11, 2016 New York, New York

Planning for the Non- Citizen Spouse: Tips and Traps Zena M. Tamler March 11, 2016 New York, New York Attorney Advertising Prior results do not guarantee a similar outcome. Copyright 2016 2015 Sullivan

Planning for the Non- Citizen Spouse: Tips and Traps Zena M. Tamler March 11, 2016 New York, New York Attorney Advertising Prior results do not guarantee a similar outcome. Copyright 2016 2015 Sullivan

2018 tax planning guide

Advanced Planning 2018 tax planning guide We are committed to helping you confirm that your current and future tax strategy supports your larger financial goals. Advice. Beyond investing. Your financial

Advanced Planning 2018 tax planning guide We are committed to helping you confirm that your current and future tax strategy supports your larger financial goals. Advice. Beyond investing. Your financial

TAX & TRANSACTIONS BULLETIN

Volume 25 U.S. Families have accumulated significant wealth in their IRA accounts Family goals are to preserve this IRA wealth Specific Family goals for IRAs include: keep assets within the Family protect

Volume 25 U.S. Families have accumulated significant wealth in their IRA accounts Family goals are to preserve this IRA wealth Specific Family goals for IRAs include: keep assets within the Family protect

SOLE USE TRUSTS 72 P.S. 9113

SOLE USE TRUSTS 72 P.S. 9113 9113. Trusts and similar arrangements for spouses (a) In the case of a transfer of property for the sole use of the transferor s surviving spouse during the surviving spouse

SOLE USE TRUSTS 72 P.S. 9113 9113. Trusts and similar arrangements for spouses (a) In the case of a transfer of property for the sole use of the transferor s surviving spouse during the surviving spouse

HOPKINS & CARLEY GUIDE TO BASIC ESTATE PLANNING TECHNIQUES FOR 2017

HOPKINS & CARLEY GUIDE TO BASIC ESTATE PLANNING TECHNIQUES FOR 2017 PART I: REVOCABLE TRUST vs. WILL A. Introduction In general, an estate plan can be implemented either by the use of wills or by the use

HOPKINS & CARLEY GUIDE TO BASIC ESTATE PLANNING TECHNIQUES FOR 2017 PART I: REVOCABLE TRUST vs. WILL A. Introduction In general, an estate plan can be implemented either by the use of wills or by the use

Post-Mortem Planning Steve R. Akers

Post-Mortem Planning Steve R. Akers Bessemer Trust Dallas, Texas akers@bessemer.com Copyright 2012 by Bessemer Trust Company, N.A. All rights reserved I. PLANNING ISSUES FOR 2010 DECEDENTS A. Default Rule

Post-Mortem Planning Steve R. Akers Bessemer Trust Dallas, Texas akers@bessemer.com Copyright 2012 by Bessemer Trust Company, N.A. All rights reserved I. PLANNING ISSUES FOR 2010 DECEDENTS A. Default Rule

Non-Citizen Spouse. Estate Planning Using Qualified Domestic Trusts (QDOTs) and Irrevocable Life Insurance Trusts (ILITs)

and Irrevocable Life Insurance Trusts (ILITs)") Guiding you through life. SALES STRATEGY NEEDS ANALYSIS Non-Citizen Spouse Estate Planning Using Qualified Domestic Trusts (QDOTs) and Irrevocable Life Insurance Trusts (ILITs) As large numbers of people

Guiding you through life. SALES STRATEGY NEEDS ANALYSIS Non-Citizen Spouse Estate Planning Using Qualified Domestic Trusts (QDOTs) and Irrevocable Life Insurance Trusts (ILITs) As large numbers of people

Probate in Flor ida 1

Probate in Florida 1 2 1. WHAT IS PROBATE? Probate is a court-supervised process for identifying and gathering the assets of a deceased person (decedent), paying the decedent s debts, and distributing

Probate in Florida 1 2 1. WHAT IS PROBATE? Probate is a court-supervised process for identifying and gathering the assets of a deceased person (decedent), paying the decedent s debts, and distributing

Revised through March 1, 2018

Pocket Tax Tables Revised through March 1, 2018 SELECTIVE TAX RETURN DUE DATES September 17, 2018 October 1, 2018 October 15, 2018 January 15, 2019 April 15, 2019 Third estimated installment. 2017 1041s

Pocket Tax Tables Revised through March 1, 2018 SELECTIVE TAX RETURN DUE DATES September 17, 2018 October 1, 2018 October 15, 2018 January 15, 2019 April 15, 2019 Third estimated installment. 2017 1041s

Contents. Foreword Acknowledgments Introduction

Contents Foreword Acknowledgments Introduction Chapter 1 Brief History Of The Estate Tax And The Marital Deduction 1 1.1 Historical Background Of The Federal Estate Tax And The Marital Deduction 1 1.2

Contents Foreword Acknowledgments Introduction Chapter 1 Brief History Of The Estate Tax And The Marital Deduction 1 1.1 Historical Background Of The Federal Estate Tax And The Marital Deduction 1 1.2

CHANGES IN ESTATE, GIFT & GENERATION SKIPPING TRANSFER TAX RULES

CHANGES IN ESTATE, GIFT & GENERATION SKIPPING TRANSFER TAX RULES Current Rules By: Christine J. Sylvester, Attorney at Law 2720 E. WT Harris Blvd., Suite 100 Charlotte, North Carolina 28213 (704) 597-7337

CHANGES IN ESTATE, GIFT & GENERATION SKIPPING TRANSFER TAX RULES Current Rules By: Christine J. Sylvester, Attorney at Law 2720 E. WT Harris Blvd., Suite 100 Charlotte, North Carolina 28213 (704) 597-7337

Gregory W. Sampson Looper Reed & McGraw, P.C

Gregory W. Sampson Looper Reed & McGraw, P.C 469-320-6097 GSampson@LRMLaw.com www.lrmlaw.com 2010 Looper Reed & McGraw, P.C. The information contained herein is subject to change without notice Basic Estate

Gregory W. Sampson Looper Reed & McGraw, P.C 469-320-6097 GSampson@LRMLaw.com www.lrmlaw.com 2010 Looper Reed & McGraw, P.C. The information contained herein is subject to change without notice Basic Estate

If you would like you can also add a picture of the church or church activity of your choice.

Please enter the name of your church and location on this page. If you would like you can also add a picture of the church or church activity of your choice. 1 2 Many people have not really thought about

Please enter the name of your church and location on this page. If you would like you can also add a picture of the church or church activity of your choice. 1 2 Many people have not really thought about

Instructions for Form 709

Instructions for Form 709 (Revised November 1993) United States Gift (and Generation-Skipping Transfer) Tax Return (For gifts made after December 31, 1991) For Privacy Act Notice, see the Instructions

Instructions for Form 709 (Revised November 1993) United States Gift (and Generation-Skipping Transfer) Tax Return (For gifts made after December 31, 1991) For Privacy Act Notice, see the Instructions

CHAPTER 14: ESTATE PLANNING

CHAPTER 14: ESTATE PLANNING MATCHING a. marital deduction b. charitable remainder c. gift splitting d. present interest e. legal life estate f. stepped-up basis g. general power of appointment h. term

CHAPTER 14: ESTATE PLANNING MATCHING a. marital deduction b. charitable remainder c. gift splitting d. present interest e. legal life estate f. stepped-up basis g. general power of appointment h. term

Recent Developments in Estate & Gift Tax

Recent Developments in Estate & Gift Tax Disclaimer The information presented in this handout from the Internal Revenue Service is for educational purposes only and shall not be cited or relied upon as

Recent Developments in Estate & Gift Tax Disclaimer The information presented in this handout from the Internal Revenue Service is for educational purposes only and shall not be cited or relied upon as

TABLE OF CONTENTS. Simple will with residue pouring over to inter vivos trust

TABLE OF CONTENTS Preface Form I Form II Form III Form IIIA Form IV Form V Form VI Form VII Form VIII Form IX Form IXA Form X Form XI Form XII Form XIII Form XIV Form XV Form XVI Form XVII Form XVIII Form

TABLE OF CONTENTS Preface Form I Form II Form III Form IIIA Form IV Form V Form VI Form VII Form VIII Form IX Form IXA Form X Form XI Form XII Form XIII Form XIV Form XV Form XVI Form XVII Form XVIII Form

Pensioners of the. Department of RETIREMENT OAS Staff. Human LECTURE. Resources SERIES. of Retirees Federal. of the OAS 2 2 Credit Union

Association of OAS Pensioners of the Retirement OAS Retirement and Pension and Pension Fund Fund (ASPEN) PRE- Department of RETIREMENT OAS Staff Human LECTURE Association Resources SERIES of the OAS Association

Association of OAS Pensioners of the Retirement OAS Retirement and Pension and Pension Fund Fund (ASPEN) PRE- Department of RETIREMENT OAS Staff Human LECTURE Association Resources SERIES of the OAS Association

Memorandum. LeBlanc & Young Clients DATE: January 2017 SUBJECT: Primer on Transfer Taxes. 1. Overview of Federal Transfer Tax System

LEBLANC & YOUNG FOUR CANAL PLAZA, PORTLAND, MAINE 04101 FAX (207)772-2822 TELEPHONE (207)772-2800 INFO@LEBLANCYOUNG.COM TO: LeBlanc & Young Clients DATE: January 2017 SUBJECT: Primer on Transfer Taxes

LEBLANC & YOUNG FOUR CANAL PLAZA, PORTLAND, MAINE 04101 FAX (207)772-2822 TELEPHONE (207)772-2800 INFO@LEBLANCYOUNG.COM TO: LeBlanc & Young Clients DATE: January 2017 SUBJECT: Primer on Transfer Taxes

SENATE BILL lr1198 A BILL ENTITLED. Estates and Trusts Elective Share Augmented Estate

N SENATE BILL lr By: Senator Frosh Introduced and read first time: February, 0 Assigned to: Judicial Proceedings A BILL ENTITLED 0 0 AN ACT concerning Estates and Trusts Elective Share Augmented Estate

N SENATE BILL lr By: Senator Frosh Introduced and read first time: February, 0 Assigned to: Judicial Proceedings A BILL ENTITLED 0 0 AN ACT concerning Estates and Trusts Elective Share Augmented Estate

29th Annual Elder Law Institute

TAX LAW AND ESTATE PLANNING SERIES Tax Law and Practice Course Handbook Series Number D-489 29th Annual Elder Law Institute Co-Chairs Jeffrey G. Abrandt Douglas J. Chu To order this book, call (800) 260-4PLI

TAX LAW AND ESTATE PLANNING SERIES Tax Law and Practice Course Handbook Series Number D-489 29th Annual Elder Law Institute Co-Chairs Jeffrey G. Abrandt Douglas J. Chu To order this book, call (800) 260-4PLI

FIDUCIARY INCOME TAXES

FIDUCIARY INCOME TAXES 12 Miscellaneous Itemized Deductions.............. 362 Qualified Revocable Trust.... 365 Case Study................. 367 Appendix: Treasury Regulation 1.67-4................ 389

FIDUCIARY INCOME TAXES 12 Miscellaneous Itemized Deductions.............. 362 Qualified Revocable Trust.... 365 Case Study................. 367 Appendix: Treasury Regulation 1.67-4................ 389

2010 and Beyond: Estate Planning and Administration Issues

2010 and Beyond: Estate Planning and Administration Issues Mickey R. Davis Bracewell & Giuliani LLP 711 Louisiana, Suite 2300 Houston, Texas 77002 713.221.1154 mickey.davis@bgllp.com Overview of 2010 Changes

2010 and Beyond: Estate Planning and Administration Issues Mickey R. Davis Bracewell & Giuliani LLP 711 Louisiana, Suite 2300 Houston, Texas 77002 713.221.1154 mickey.davis@bgllp.com Overview of 2010 Changes

Credit shelter trusts and portability

Credit shelter trusts and portability Comparing strategies to help manage estate taxes Married couples have two strategies to choose from to help protect their families from estate taxes. Choosing the

Credit shelter trusts and portability Comparing strategies to help manage estate taxes Married couples have two strategies to choose from to help protect their families from estate taxes. Choosing the

Understanding the Transfer Tax and Its Impact on Estate Planning

Understanding the Transfer Tax and Its Impact on Estate Planning 2016 Skills Training for Estate Planners Sponsored by the Real Property, Trust and Estate Law Section of the American Bar Association New

Understanding the Transfer Tax and Its Impact on Estate Planning 2016 Skills Training for Estate Planners Sponsored by the Real Property, Trust and Estate Law Section of the American Bar Association New

WILLS. a. If you die without a will you forfeit your right to determine the distribution of your probate estate.

WILLS 1. Do you need a will? a. If you die without a will you forfeit your right to determine the distribution of your probate estate. b. The State of Arkansas decides by statute how your estate is distributed.

WILLS 1. Do you need a will? a. If you die without a will you forfeit your right to determine the distribution of your probate estate. b. The State of Arkansas decides by statute how your estate is distributed.

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2019 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2019 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

Introduction to the Federal Income Tax Issues of Filing Form 1041 for Estates and Trusts

National Society of Tax Professionals presents Introduction to the Federal Income Tax Issues of Filing Form 1041 for Estates and Trusts Developed and Written by Paul La Monaca, CPA, MST NSTP Director of

National Society of Tax Professionals presents Introduction to the Federal Income Tax Issues of Filing Form 1041 for Estates and Trusts Developed and Written by Paul La Monaca, CPA, MST NSTP Director of

RBC Wealth Management Services

RBC Wealth Management Services The Navigator C HARLES W. C ULLEN III CFP(Canada and U.S.),CIM Associate Portfolio Manager & Wealth Advisor 902-424-1092 charles.cullen@rbc.com D AYNA P ARK Associate 902-421-0244

RBC Wealth Management Services The Navigator C HARLES W. C ULLEN III CFP(Canada and U.S.),CIM Associate Portfolio Manager & Wealth Advisor 902-424-1092 charles.cullen@rbc.com D AYNA P ARK Associate 902-421-0244

Effective Strategies for Wealth Transfer

Effective Strategies for Wealth Transfer The Prudential Insurance Company of America, Newark, NJ. 0265295-00002-00 Ed. 02/2016 Exp. 08/04/2017 UNDERSTANDING WEALTH TRANSFER What strategy to use and when?

Effective Strategies for Wealth Transfer The Prudential Insurance Company of America, Newark, NJ. 0265295-00002-00 Ed. 02/2016 Exp. 08/04/2017 UNDERSTANDING WEALTH TRANSFER What strategy to use and when?

MICKEY R. DAVIS AND MELISSA J. WILLMS DAVIS & WILLMS, PLLC HOUSTON, TEXAS APRIL 25, 2018

MICKEY R. DAVIS AND MELISSA J. WILLMS DAVIS & WILLMS, PLLC HOUSTON, TEXAS APRIL 25, 2018 Unified Transfer Tax System $10,000,000 exclusion/exemption for gift, estate and GST tax for years between 2018

MICKEY R. DAVIS AND MELISSA J. WILLMS DAVIS & WILLMS, PLLC HOUSTON, TEXAS APRIL 25, 2018 Unified Transfer Tax System $10,000,000 exclusion/exemption for gift, estate and GST tax for years between 2018

MARKET TREND: With the enactment of exemption portability, clients may dismiss the need for lifetime estate planning, to their detriment.

The trusted source of actionable technical and marketplace knowledge for AALU members the nation s most advanced life insurance professionals. TOPIC: Issuance of Temporary Portability Regulations - Practical

The trusted source of actionable technical and marketplace knowledge for AALU members the nation s most advanced life insurance professionals. TOPIC: Issuance of Temporary Portability Regulations - Practical

What is legal and tax planning for private clients?...2. What are assets?...3. How do individuals transfer assets?...4

About the Editors... vii Table of Chapters...ix...xi Acknowledgments... xli Chapter 1 Introduction...1 Definitions...2 Estate Planning...2 Q 1.1 What is legal and tax planning for private clients?...2

About the Editors... vii Table of Chapters...ix...xi Acknowledgments... xli Chapter 1 Introduction...1 Definitions...2 Estate Planning...2 Q 1.1 What is legal and tax planning for private clients?...2

ESTATE PLANNING 1 / 11

2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 What happens to my money and assets after I die? No matter what your age or income, you need to

2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 What happens to my money and assets after I die? No matter what your age or income, you need to

Internal Revenue Code Section 1022 (REPEALED) Treatment of property acquired from a decedent dying after December 31, 2009.

Treatment of property acquired from a decedent dying after December 31, 2009.") CLICK HERE to return to the home page Internal Revenue Code Section 1022 (REPEALED) Treatment of property acquired from a decedent dying after December 31, 2009. (a) In general. Except as otherwise provided

CLICK HERE to return to the home page Internal Revenue Code Section 1022 (REPEALED) Treatment of property acquired from a decedent dying after December 31, 2009. (a) In general. Except as otherwise provided

ESTATE PLANNING DICTIONARY

ESTATE PLANNING DICTIONARY Administrator For estates administered prior to April 1, 2012, the fiduciary appointed by the Probate Court to settle your estate if you die without a Will (intestate). Attorney-in-fact

ESTATE PLANNING DICTIONARY Administrator For estates administered prior to April 1, 2012, the fiduciary appointed by the Probate Court to settle your estate if you die without a Will (intestate). Attorney-in-fact

Individual Retirement Accounts as Estate Planning Tools: Opportunities and Pitfalls

Individual Retirement Accounts as Estate Planning Tools: Opportunities and Pitfalls December 2010 This material is provided for educational purposes only. This material is not intended to constitute legal,

Individual Retirement Accounts as Estate Planning Tools: Opportunities and Pitfalls December 2010 This material is provided for educational purposes only. This material is not intended to constitute legal,

Estate Taxation Made Simple (?) Monica Haven, E.A.

Monica Haven, E.A.") Estate Taxation Made Simple (?) 061403 Monica Haven, E.A. I. Types of Tax A. Estate Tax Assessed on the value of the decedent s estate on the date of death or the alternate valuation date 6 months later

Estate Taxation Made Simple (?) 061403 Monica Haven, E.A. I. Types of Tax A. Estate Tax Assessed on the value of the decedent s estate on the date of death or the alternate valuation date 6 months later

WHAT EVERY ATTORNEY AND CPA NEEDS TO KNOW TO PREPARE AND REVIEW GIFT AND ESTATE TAX RETURNS

WHAT EVERY ATTORNEY AND CPA NEEDS TO KNOW TO PREPARE AND REVIEW GIFT AND ESTATE TAX RETURNS Mark Scott, Principal Kaufman Rossin Miami, FL January 19, 2019 #1 KNOW YOUR STARTING POINT Analyze Prior Gift

WHAT EVERY ATTORNEY AND CPA NEEDS TO KNOW TO PREPARE AND REVIEW GIFT AND ESTATE TAX RETURNS Mark Scott, Principal Kaufman Rossin Miami, FL January 19, 2019 #1 KNOW YOUR STARTING POINT Analyze Prior Gift

ESTATE TRANSFER SUMMARY A Brief Summary of Estate Transfer Tools

ESTATE TRANSFER SUMMARY A Brief Summary of Estate Transfer Tools Field Staff Paper #0909- September 1, 2009 PROPERTY OWNERSHIP The form of ownership of an asset is a critical element in estate planning,

ESTATE TRANSFER SUMMARY A Brief Summary of Estate Transfer Tools Field Staff Paper #0909- September 1, 2009 PROPERTY OWNERSHIP The form of ownership of an asset is a critical element in estate planning,

2. What will happen to my property if I die without a will or trust?

1. What is estate planning? Estate planning is the accumulation, the preservation, and the distribution of your assets. It is accomplishing your personal family goals and easing the management of your

1. What is estate planning? Estate planning is the accumulation, the preservation, and the distribution of your assets. It is accomplishing your personal family goals and easing the management of your

Life insurance beneficiary designations

ADVANCED MARKETS Life insurance beneficiary designations BECAUSE YOU ASKED When designating a beneficiary of a life insurance policy, the policy owner should consider a multitude of factors, such as the

ADVANCED MARKETS Life insurance beneficiary designations BECAUSE YOU ASKED When designating a beneficiary of a life insurance policy, the policy owner should consider a multitude of factors, such as the

NOTATIONS FOR FORM 201

NOTATIONS FOR FORM 201 For a discussion of the advantages and disadvantages of the fractional share marital trust, see the INTRODUCTION. This form is designed for a settlor who will execute a will patterned

NOTATIONS FOR FORM 201 For a discussion of the advantages and disadvantages of the fractional share marital trust, see the INTRODUCTION. This form is designed for a settlor who will execute a will patterned

ESTATE PLANNING BASICS

ESTATE PLANNING BASICS Agricultural Law Project, Legal Aid of Nebraska and the Risk Management Agency, USDA Prepared by: Joe M. Hawbaker, Hawbaker Law Office, Omaha, Nebraska and Dave Goeller, University

ESTATE PLANNING BASICS Agricultural Law Project, Legal Aid of Nebraska and the Risk Management Agency, USDA Prepared by: Joe M. Hawbaker, Hawbaker Law Office, Omaha, Nebraska and Dave Goeller, University

Advisory. Will and estate planning considerations for Canadians with U.S. connections

Advisory Will and estate planning considerations for Canadians with U.S. connections Canadian citizens and residents may be exposed to U.S. estate, gift, and generation-skipping transfer tax (together,

Advisory Will and estate planning considerations for Canadians with U.S. connections Canadian citizens and residents may be exposed to U.S. estate, gift, and generation-skipping transfer tax (together,

Reporting GRATS, GRUTS, ILITS and IDGTs on Form 709: GST Exemption Allocation Calculations and Strategies

FOR LIVE PROGRAM ONLY Reporting GRATS, GRUTS, ILITS and IDGTs on Form 709: GST Exemption Allocation Calculations and Strategies WEDNESDAY, JULY 13, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

FOR LIVE PROGRAM ONLY Reporting GRATS, GRUTS, ILITS and IDGTs on Form 709: GST Exemption Allocation Calculations and Strategies WEDNESDAY, JULY 13, 2016, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR

ESTATE PLANNING 101:

Introduction ESTATE PLANNING 101: THE IMPORTANCE OF DEVELOPING AN ESTATE PLAN At some point, most people will contemplate estate planning. Often, this is prior to or shortly after a significant life event,

Introduction ESTATE PLANNING 101: THE IMPORTANCE OF DEVELOPING AN ESTATE PLAN At some point, most people will contemplate estate planning. Often, this is prior to or shortly after a significant life event,

Understanding TRUSTS. A Summary of Trusts for Estate Planning VLC

Understanding TRUSTS A Summary of Trusts for Estate Planning VLC0009-0417 TABLE OF CONTENTS What Is a Trust.... 1 Who s Who in a Trust.... 2 Types of Trusts... 3 Taxation.... 4 Frequently Asked Questions....

Understanding TRUSTS A Summary of Trusts for Estate Planning VLC0009-0417 TABLE OF CONTENTS What Is a Trust.... 1 Who s Who in a Trust.... 2 Types of Trusts... 3 Taxation.... 4 Frequently Asked Questions....

HOW TO DEAL WITH INCOME AND ESTATE TAX TIMEBOMBS

HOW TO DEAL WITH INCOME AND ESTATE TAX TIMEBOMBS Nicholas J. Houle CPA/PFS CFP 2010 Ag Summit Principal December, 2010 LarsonAllen Financial LLC Chicago, IL Minneapolis, MN 612-376-4760 nhoule@larsonallen.com

HOW TO DEAL WITH INCOME AND ESTATE TAX TIMEBOMBS Nicholas J. Houle CPA/PFS CFP 2010 Ag Summit Principal December, 2010 LarsonAllen Financial LLC Chicago, IL Minneapolis, MN 612-376-4760 nhoule@larsonallen.com

Please understand that this podcast is not intended to be legal advice. As always, you should contact your WEALTH TRANSFER STRATEGIES

WEALTH TRANSFER STRATEGIES Hello and welcome. Northern Trust is proud to sponsor this podcast, Wealth Transfer Strategies, the third in a series based on our book titled Legacy: Conversations about Wealth

WEALTH TRANSFER STRATEGIES Hello and welcome. Northern Trust is proud to sponsor this podcast, Wealth Transfer Strategies, the third in a series based on our book titled Legacy: Conversations about Wealth

ANITA J. SIEGEL, ESQ. Siegel & Bergman, LLC 365 South Street Morristown, NJ Fax

ANITA J. SIEGEL, ESQ. Siegel & Bergman, LLC 365 South Street Morristown, NJ 07960 973-285-5007 Fax 973-285-5008 ajs@sblawllc.com CHARITABLE PLANNING A PRIMER April 4, 2011 Planning for charitable gifts

ANITA J. SIEGEL, ESQ. Siegel & Bergman, LLC 365 South Street Morristown, NJ 07960 973-285-5007 Fax 973-285-5008 ajs@sblawllc.com CHARITABLE PLANNING A PRIMER April 4, 2011 Planning for charitable gifts

GLOSSARY. Compiled by Carolyn Paseneaux

GLOSSARY Compiled by Carolyn Paseneaux AB TRUST A trust giving a surviving spouse or mate a life estate interest in property of a deceased spouse or mate. It is used to save eventual taxes on the estate.

GLOSSARY Compiled by Carolyn Paseneaux AB TRUST A trust giving a surviving spouse or mate a life estate interest in property of a deceased spouse or mate. It is used to save eventual taxes on the estate.

UNIFORM ESTATE TAX APPORTIONMENT ACT

POST-MEETING DRAFT of October 001 UNIFORM ESTATE TAX APPORTIONMENT ACT NATIONAL CONFERENCE OF COMMISSIONERS ON UNIFORM STATE LAWS WITH COMMENTS Copyright 001 by the NATIONAL CONFERENCE OF COMMISSIONERS

POST-MEETING DRAFT of October 001 UNIFORM ESTATE TAX APPORTIONMENT ACT NATIONAL CONFERENCE OF COMMISSIONERS ON UNIFORM STATE LAWS WITH COMMENTS Copyright 001 by the NATIONAL CONFERENCE OF COMMISSIONERS

National Business Institute Key Issues in Estate Planning and Probate Tuesday September 11, 2007 Jeff Billings, Godfrey & Kahn, S.C.

National Business Institute Key Issues in Estate Planning and Probate Tuesday September 11, 2007 Jeff Billings, Godfrey & Kahn, S.C. I. SELECTED ISSUES IN PROBATE a. Introduction i. "Probate": Probate

National Business Institute Key Issues in Estate Planning and Probate Tuesday September 11, 2007 Jeff Billings, Godfrey & Kahn, S.C. I. SELECTED ISSUES IN PROBATE a. Introduction i. "Probate": Probate