February 20, 2018 LEGAL STRUCTURES FOR SOCIAL ENTREPRENEURS

|

|

|

- Rosemary Moody

- 6 years ago

- Views:

Transcription

1 February 20, 2018 LEGAL STRUCTURES FOR SOCIAL ENTREPRENEURS UC Berkeley, February 20, 2018

2 Speakers Jennifer Barnette Cooley LLP Jesse Finfrock Morrison & Foerster LLP 1

3 How do non-profits and for-profits differ?

4

5 What is a non-profit?

6 Non-Profit: Charitable Organizations Typically incorporated in the state where they are located In CA, three types: Public benefit corporation Mutual benefit corporation Religious corporation Charitable or public purpose Incorporation process: File Articles of Incorporation with Secretary of State Charitable or public purpose Appoint Board of Directors (independence requirements 51% non-interested) Board adopts Bylaws and appoints Officers Tax exemption: federal and state filings 5

7 Non-Profit: 501(c)(3) Federal tax exemption: 501(c)(3) Why? Donations to 501(c)(3)s are generally tax deductible. Exempt purpose: religious, charitable, scientific, testing for public safety, literary, education, fostering national and international sports competition, or the prevention of cruelty to children or animals Apply to IRS file form 1023 or 1023-EZ and wait for determination letter 1023-EZ: ~3-12 weeks 1023: ~3-12 months Exemption is retroactive to date of incorporation (if filed within 18 months) Two types: Public charity v. Private foundation Public charity must meet public support test 6

8 Non-Profit: Charity Public Charity Most common for operating organizations (e.g., American Cancer Society, World Wildlife Federation) No private inurement Must ensure that earnings do not inure to the benefit of any private shareholder or individual (loss of exemption; excise taxes) No stock/stock options (public assets) No private benefit Not operate for the benefit of private interests such as those of its founder, the founder's family or other controlling parties Operated for exempt purpose Not operate for the primary purpose of conducting a trade or business that is not related to its exempt purpose No lobbying Refrain from participating in political campaigns and restrict lobbying activities to an insubstantial part of total activities 7

9 Non-Profit Forms: Two basic types Private Foundation Often associated with a family or corporation (Gates Foundation, Google.org) Generally grant-making organizations All requirements of public charity No private inurement No private benefit Exempt purpose No self-dealing between private foundations and their substantial contributors or other disqualified persons (people who give the money or are involved in senior management) Requirements that the foundation annually distribute income for charitable purposes 8

10 What are the common for-profit structures?

11 For-Profit Forms: LLC Limited Liability Company (LLC) is a very flexible entity Governed by contract law (rather than statutory/corporate law) Governing document: Operating Agreement Specifies how the LLC will be governed, the financial obligations of the members and how profits, losses and distributions are shared Either Member-managed or Manager/Board-managed No requirement for a Board of Directors (unlike corporations) Custom-tailored to suit the needs of the members Formation: Certificate of Formation (DE) or Articles of Organization (CA) Pass-through taxation: profits/losses taxed at member level; no separate entity tax LLC is not suitable for VC investments because of tax restrictions on the funds partners Some states permit adjusting fiduciary duties, which would allow pursuit of mission over pursuit of profit Relatively easy to convert from LLC to corporation 10

12 For-Profit Forms: L3C Low-Profit Limited Liability Company (L3C) is a statutory variant of the LLC, currently adopted in 9 states Designed to assist for-profit companies that have a primarily charitable purpose Members agree that the purpose of the organization is social or charitable, not maximizing income Created with hope that this structure would spur L3Cs to obtain program-related investments (PRIs) from foundations PRIs must have primary purpose to accomplish the foundation s exempt purpose and production of income cannot be a significant purpose of the investment Generally very fact-intensive inquiries; foundations have typically been reluctant to use PRIs, though this is changing slowly Still have all of the issues of the LLC from an investment perspective You can arguably create this same structure with a traditional LLC 11

13 For-Profit Forms: Corporation Corporations - less flexible than LLCs; governed by statutory law Corporations are governed by a Board of Directors Governing documents: Certificate of Incorporation (DE); Articles of Incorporation (CA) + Bylaws Tax: Corporations are separate taxable entities; franchise taxes (state) and corporate income taxes (state and federal) Fiduciary Duties: Board must act in the best interests of the stockholders Corporations have significant leeway to pursue social/environmental goals as long as rationale is the long-term benefit of stockholders In a sale, the short-term pay-out to stockholders controls, so board must take the highest offer on the table 12

14 For-Profit Forms: Benefit Corporation Benefit Corporations New form of corporation; adopted in 30+ states (though with significant variations among state laws) Arose to accommodate social enterprises that pursue a dual purpose: public benefit + profit Corporate purpose: to create a general public benefit Optional specific public benefit purpose (e.g. providing low-income or underserved with beneficial products or services, promoting economic opportunity, improving human health, protecting or restoring the environment) Fiduciary Duties: Requires directors to consider a broad range of non-stockholder interests (employees, customers, local and global environment, community and societal factors, etc) Transparency and Accountability: Many states require a benefit director accountable solely to the public benefit Required annual benefit report using an independent third-party assessment Benefit enforcement proceeding: Special lawsuit to enforce public benefit purpose Benefit corporations B Corps 13

15 Benefit Corp. v. Traditional Corp. Traditional Corporation Benefit Corporation Purpose The purpose of the corporation is to create value for its stockholders. In addition to stockholder value, benefit corporations must commit to producing a general public benefit and to operate in a responsible and sustainable manner. Governance Directors have a fiduciary duty to manage the corporation in the best interests of the stockholders. Directors must consider the interests of chosen constituencies other than shareholders that are affected by the company s conduct (e.g. employees, local community, the environment). Transparency Shareholders have limited rights to inspect the corporation s books and records. The corporation must report on its overall social and environmental performance to shareholders, and in some jurisdictions, to the public. Accountability Stockholders can sue for breach of fiduciary duties, generally for failure to maximize economic return for shareholders. In addition to standard shareholder rights, shareholders can sue to enforce the company s public benefit mission. In some states, stakeholders affected by the corporation s conduct can also sue to enforce the corporation s public benefit mission. 14

16 For-Profit Forms: PBC/SPC Public Benefit Corp. (DE) & Social Purpose Corp. (CA) PBC is a for-profit corporation intended to produce a public benefit and operate in a responsible and sustainable manner Corporate Purpose: Requires a specific public benefit/social or charitable purpose (clearly stated in charter) in addition to the other purposes of the corporation Fiduciary Duties: Requires boards and management to consider environmental and social factors in addition to shareholder value and protects them from related shareholder liability PBC: Board must balance the public benefit purpose, the interests of the stockholders and the interests of those materially affected by the corporation s conduct. No benefit director Transparency/Accountability: Benefit report has no third-party standard requirement PBC: biannual report to shareholders SPC: annual report made public No benefit enforcement proceeding 15

17 For-Profit Social Enterprise Forms LLC & L3C Benefit Corp. PBC & SPC C Corp. Challenges & Opportunities These forms are still new! First benefit corporation legislation adopted 2010; DE PBC in 2013 Many CEOs report having to explain these to investors Lack of guidance No case law on benefit corporations, PBCs or SPCs Little guidance from authorities on how conflicting fiduciary duties should be handled Confusion over nomenclature B Corps is often used as a catch-all, but each of these have distinct legal differences State law variations Some state benefit corp. legislation does not fit within broader corporate codes CA has a benefit corporation and the SPC Lack of compliance? Many companies may not be strictly adhering to the benefit reporting requirements in the statutes 16

18 What is a hybrid/tandem structure?

19 Hybrid/Tandem Corporate Structures A close relationship via equity ownership, funding, or contract between a non-profit and for-profit entity Five general types For-profit with contractual relationship with non-profit Non-profit as minority investor in for-profit For-profit as wholly owned subsidiary of non-profit Non-profit with for-profit as sole member Non-profit investment in for-profit impact fund 18

20 Why choose a hybrid/tandem structure?

21 Hybrid/Tandem Corporate Structures Substantial flexibility in the types of activities that can be engaged in out of the various entities. Ability to raise both investment and philanthropic capital. Credibility in impact circles by including nonprofit arm to engage in charitable activities. Cost-shifting strategies related to nonprofit research that benefits the for-profit s activities. [Note that the nonprofit s research products should be made public to avoid a private inurement issue.] But it s not all positive 20

22 Hybrid/Tandem Corporate Structures Management of the two entities is complicated, costly and time-consuming (largely because of the private inurement issue), and includes: Tracking/documenting the flow of funds, assets (including IP), services and resources between the non-profit and the for-profit Monitoring Unrelated Business Income Tax ( UBIT ) Ensuring that the for-profit always pays at least market rates to the nonprofit Appointing disinterested directors on the governing bodies of both the nonprofit and for-profit. The non-profit and for-profit must have clearly separate functions and must avoid offering competing goods and/or services. 21

23 Legal Issues Surrounding Hybrid/Tandem Structures

24 Hybrid/Tandem Corporate Structures In each of these models, the non-profit, for-profit and investors must consider the following: Both entities must track and document the flow of funds, the flow of services and resources and the flow of IP between the non-profit and the for-profit. One entity can make loans to the other; the interest on loans may be unrelated business taxable income ( UBTI ) to the non-profit. Alternatives include dividends on the equity held by the non-profit in a profit subsidiary and royalties on license agreements. Documentation takes the form of intercompany agreements including an IP license agreement, services agreement and/or resource sharing agreement. Both entities must have separate functions and avoid offering competing goods/services. 23

25 Hybrid/Tandem Corporate Structures The documentation must ensure that the for-profit always pays at least fair value or market rates (for funding, services/resources and IP). There also must be good governance, specifically disinterested or independent directors on the boards of both the non-profit and for-profit. Management is required to report on the flow of funds, services and IP to the special committee on a quarterly basis; amendments to the intercompany agreements are usually required as the hybrid evolves over time. 24

26 Contract-Based Relationship A frequently used hybrid corporate structure involves a specific contractual relationship between a nonprofit entity and a for-profit entity. Among other items, the two entities may contract for the provision of specific services or products, the sharing of resources, or use of IP, at fair value or market rates. Key aspects defining the relationship: No ownership of equity in for-profit by the nonprofit. Often no overlapping board members. 25

(3) charity). Several key advantages including the relative ease of structuring and clear corporate governance mission alignment through oversight by the nonprofit.")

27 Non-Profit Forms Wholly Owned For-Profit Subsidiary This form of hybrid/tandem structure occurs where a for-profit entity is held as a wholly owned subsidiary by a nonprofit entity (usually a 501(c)(3) charity). Several key advantages including the relative ease of structuring and clear corporate governance mission alignment through oversight by the nonprofit. Key structural, strategic and corporate governance best practices include: The entities should not be in competition with one another. Must carefully consider potential employment, UBTI and compensation issues. All flow of funds, services/resources and IP is documented. Independent/disinterested directors to evaluate potential self-dealing and conflicts of interest. 26

28 Non-Profit as Minority Investor in For- Profit Involves a non-profit with a minority ownership stake (for private foundations, typically 20% or less) in a for-profit. May be structured as a PRI. Non-profit minority ownership implicates several challenges: Greater difficulty to ensure alignment with the non-profit s mission. Potential conflicts between the non-profit and for-profit investors, and careful management of UBTI issues. Redemption rights for a non-profit investor with a PRI can dampen enthusiasm of mainstream investors. Impact on exit opportunities for the forprofit investors. Increased importance of independence. 27

29 For-Profit Establishment of a Non-Profit A for-profit entity may establish a non-profit entity (structured often as a 501(c)(3) private foundation). Although the for-profit cannot formally own the non-profit, it can maintain control through funding and governance of the entity. Typically favored by large corporations rather than mission-driven social enterprises. Key corporate governance best practices: Maintenance of corporate governance independence board member overlap should be kept to a minimum. Issues raised by resource and employee sharing. Awareness of potential private benefit issues. 28

30 Additional Legal and Practical Issues Maintaining tax-exempt status of non-profit Unrelated business income tax Exposure to/insulation from liability Governance and control Protection against mission drift Funding and sustainability Double taxation vs. pass-through entity Branding/credibility of the charity 29

31 Additional Resources MoFo Impact MoFo Impact Blog: MoFo Impact Resource Center: Cooley: ~ The End ~ 30

Starting a Nonprofit Frequently Asked Questions

Starting a Nonprofit Frequently Asked Questions Q. Are nonprofit and tax-exempt the same thing? A. No. A nonprofit is a type of corporation that is formed at the state level. Nonprofit and notfor-profit

Starting a Nonprofit Frequently Asked Questions Q. Are nonprofit and tax-exempt the same thing? A. No. A nonprofit is a type of corporation that is formed at the state level. Nonprofit and notfor-profit

INTRODUCING THE ILLINOIS L 3 C

INTRODUCING THE ILLINOIS L 3 C Marc J. Lane Hosted by: COMMUNITY ECONOMIC DEVELOPMENT LAW PROJECT Copyright 2009, by Marc J. Lane. All rights reserved. The 1-2 Punch Mission-related investing Program-related

INTRODUCING THE ILLINOIS L 3 C Marc J. Lane Hosted by: COMMUNITY ECONOMIC DEVELOPMENT LAW PROJECT Copyright 2009, by Marc J. Lane. All rights reserved. The 1-2 Punch Mission-related investing Program-related

TAX-EXEMPT ORGANIZATIONS: EFFECTIVE GOVERNANCE AND LEGAL COMPLIANCE VICTOR J. FERGUSON SUZANNE R. GALYARDT VORYS, SATER, SEYMOUR AND PEASE LLP

TAX-EXEMPT ORGANIZATIONS: EFFECTIVE GOVERNANCE AND LEGAL COMPLIANCE VICTOR J. FERGUSON SUZANNE R. GALYARDT VORYS, SATER, SEYMOUR AND PEASE LLP OVERVIEW 1. Organizational Test 2. Operational Test 3. Private

TAX-EXEMPT ORGANIZATIONS: EFFECTIVE GOVERNANCE AND LEGAL COMPLIANCE VICTOR J. FERGUSON SUZANNE R. GALYARDT VORYS, SATER, SEYMOUR AND PEASE LLP OVERVIEW 1. Organizational Test 2. Operational Test 3. Private

(c)(3) Applying for 501(c)(3) Tax-Exempt Status,

(3) Applying for 501(c)(3) Tax-Exempt Status,") Tax Exempt and Government Entities EXEMPT ORGANIZATIONS Applying for 501(c)(3) Tax-Exempt Status, Inside: Why apply for 501(c)(3) status? Who is eligible for 501(c)(3) status? What responsibilities accompany

Tax Exempt and Government Entities EXEMPT ORGANIZATIONS Applying for 501(c)(3) Tax-Exempt Status, Inside: Why apply for 501(c)(3) status? Who is eligible for 501(c)(3) status? What responsibilities accompany

Copyright 2018, James M. McCarten, Burr & Forman LLP, all rights reserved

Prepared for Stetson 2018 National Conference on Special Needs Planning and Special Needs Trusts Pre-Conference Pooled Trusts Intensive St. Petersburg, Florida Wednesday, October 17, 2018 Presented by:

Prepared for Stetson 2018 National Conference on Special Needs Planning and Special Needs Trusts Pre-Conference Pooled Trusts Intensive St. Petersburg, Florida Wednesday, October 17, 2018 Presented by:

Knowledge Share. Alternative. Navigating New choices for business formations

Knowledge Share Alternative ENTITIES Navigating New choices for business formations 2016 SEMINAR REFERENCE BOOK NAVIGATING NEW CHOICES FOR BUSINESS FORMATIONS Seminar Reference Book TABLE OF CONTENTS INTRODUCTION

Knowledge Share Alternative ENTITIES Navigating New choices for business formations 2016 SEMINAR REFERENCE BOOK NAVIGATING NEW CHOICES FOR BUSINESS FORMATIONS Seminar Reference Book TABLE OF CONTENTS INTRODUCTION

Obtaining and Retaining Tax-Exempt Status

Obtaining and Retaining Tax-Exempt Status Becky Seidel Primer on Advising Nonprofit Organizations May 4, 2016 2016 Leaffer Law Group 1 Agenda 1. Overview of Tax-Exempt Status 2. Requirements for a 501(c)(3)

Obtaining and Retaining Tax-Exempt Status Becky Seidel Primer on Advising Nonprofit Organizations May 4, 2016 2016 Leaffer Law Group 1 Agenda 1. Overview of Tax-Exempt Status 2. Requirements for a 501(c)(3)

RUNNING A SOCIAL ENTERPRISE: LEGAL STRUCTURE AND TAX CONSIDERATIONS

RUNNING A SOCIAL ENTERPRISE: LEGAL STRUCTURE AND TAX CONSIDERATIONS Mission Edge: San Diego Accelerator + Impact Lab (SAIL) September 25, 2017 0 Questions for audience What are you hoping to learn? Is

RUNNING A SOCIAL ENTERPRISE: LEGAL STRUCTURE AND TAX CONSIDERATIONS Mission Edge: San Diego Accelerator + Impact Lab (SAIL) September 25, 2017 0 Questions for audience What are you hoping to learn? Is

An Overview of the Tax Treatment of Nonprofits. Trina Griffin Research Division, NCGA October 22, 2008

An Overview of the Tax Treatment of Nonprofits Trina Griffin Research Division, NCGA October 22, 2008 Outline Basics Statistics Tax Treatment Trends Issues Nonprofit Basics What Is A Nonprofit? An organization

An Overview of the Tax Treatment of Nonprofits Trina Griffin Research Division, NCGA October 22, 2008 Outline Basics Statistics Tax Treatment Trends Issues Nonprofit Basics What Is A Nonprofit? An organization

Unrelated Business Income. Preston C. Worley & John-Paul Volk

Unrelated Business Income Preston C. Worley & John-Paul Volk What is Unrelated Business Income Tax (UBIT)? UBIT: Unrelated Business Income Tax Unrelated Business Income Tax (UBIT) in the U.S. Internal

Unrelated Business Income Preston C. Worley & John-Paul Volk What is Unrelated Business Income Tax (UBIT)? UBIT: Unrelated Business Income Tax Unrelated Business Income Tax (UBIT) in the U.S. Internal

CRS Report for Congress Received through the CRS Web

Order Code RL30877 CRS Report for Congress Received through the CRS Web Characteristics of and Reporting Requirements for Selected Tax-Exempt Organizations March 8, 2001 Marie B. Morris Legislative Attorney

Order Code RL30877 CRS Report for Congress Received through the CRS Web Characteristics of and Reporting Requirements for Selected Tax-Exempt Organizations March 8, 2001 Marie B. Morris Legislative Attorney

T A X A B L E F O U N D A T I O N S

T A X A B L E F O U N D A T I O N S Sarah D. McDaniel, Andrea Sanft, Beth Smith and Paul Stam 2016 While limited liability companies (LLC) have been used for years to house funds earmarked for philanthropy,

T A X A B L E F O U N D A T I O N S Sarah D. McDaniel, Andrea Sanft, Beth Smith and Paul Stam 2016 While limited liability companies (LLC) have been used for years to house funds earmarked for philanthropy,

The First European Benefit Corporation: blurring the lines between social and business

The First European Benefit Corporation: blurring the lines between social and business Alissa Pelatan Roberto Randazzo A. Introduction In December 2015, the Italian parliament passed the Stability Act

The First European Benefit Corporation: blurring the lines between social and business Alissa Pelatan Roberto Randazzo A. Introduction In December 2015, the Italian parliament passed the Stability Act

PRIVATE FOUNDATION CAUTION: The purposes of this memorandum are to assist you, the directors of your private foundation, and your accountant in:

CHERRY CREEK CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM CORPORATE DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

CHERRY CREEK CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM CORPORATE DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

Legal Issues Unique to Social Enterprise

Legal Issues Unique to Social Enterprise Marc J. Lane March 9, 2011 Copyright 2011, by Marc J. Lane Advisors, L3C. All rights reserved. How can the for-profit social enterprise meet its shareholder primacy

Legal Issues Unique to Social Enterprise Marc J. Lane March 9, 2011 Copyright 2011, by Marc J. Lane Advisors, L3C. All rights reserved. How can the for-profit social enterprise meet its shareholder primacy

Public Benefit Corporations: An Overview of the Delaware Benefit Corporation Statute

Public Benefit Corporations: An Overview of the Delaware Benefit Corporation Statute Sara Mattern and Sharon C. Lincoln 1 What is a Benefit Corporation? A unique, hybrid corporate form that combines characteristics

Public Benefit Corporations: An Overview of the Delaware Benefit Corporation Statute Sara Mattern and Sharon C. Lincoln 1 What is a Benefit Corporation? A unique, hybrid corporate form that combines characteristics

Alternative Operating Structures, Governance Best Practices and Fraud Risk Management

THE UNIVERSITY OF TEXAS SCHOOL OF LAW Presented: 2015 Nonprofit Organizations Primer and 32 nd Annual Nonprofit Organizations Institute January 14, 15-16, 2015 Austin, Texas Alternative Operating Structures,

THE UNIVERSITY OF TEXAS SCHOOL OF LAW Presented: 2015 Nonprofit Organizations Primer and 32 nd Annual Nonprofit Organizations Institute January 14, 15-16, 2015 Austin, Texas Alternative Operating Structures,

Last Updated: November SOUTH CAROLINA FORMS OF ORGANIZATION Wyche, P.A. Eric K. Graben, Esquire

Last Updated: November 2013 SOUTH CAROLINA FORMS OF ORGANIZATION Wyche, P.A. Eric K. Graben, Esquire Table of Contents 1. Nonprofit Corporations 2. For-Profit Corporations 3. Benefit Corporations 4. Limited

Last Updated: November 2013 SOUTH CAROLINA FORMS OF ORGANIZATION Wyche, P.A. Eric K. Graben, Esquire Table of Contents 1. Nonprofit Corporations 2. For-Profit Corporations 3. Benefit Corporations 4. Limited

Comparison of 501(c)(3) and 501(c)(4) and 501(c)(6) Compiled from multiple publicly available web and printed resources**

(3) and 501(c)(4) and 501(c)(6) Compiled from multiple publicly available web and printed resources**") Comparison of 501(c)(3) and 501(c)(4) and 501(c)(6) Compiled from multiple publicly available web and printed resources** Purposes 501(c)(3) 501(c)(4) 501(c)(6) Social Welfare: An organization must be

Comparison of 501(c)(3) and 501(c)(4) and 501(c)(6) Compiled from multiple publicly available web and printed resources** Purposes 501(c)(3) 501(c)(4) 501(c)(6) Social Welfare: An organization must be

COMPARISON OF LEGAL STRUCTURES FOR SOCIAL ENTERPRISES 1

COMPARISON OF LEGAL STRUCTURES FOR SOCIAL ENTERPRISES 1 INDEX 1. Comparison of HK, UK and Singapore legal structures... 2 2. Principal Legal Forms in US... 8 3. Legal Innovations in US and UK... 11 3.1

COMPARISON OF LEGAL STRUCTURES FOR SOCIAL ENTERPRISES 1 INDEX 1. Comparison of HK, UK and Singapore legal structures... 2 2. Principal Legal Forms in US... 8 3. Legal Innovations in US and UK... 11 3.1

Form 990 Tax Exempt Reporting

Form 990 Tax Exempt Reporting CLAconnect.com Speaker Introductions Amanda Treml, CPA Amanda is a Manager with CliftonLarsonAllen and provides assurance and tax compliance services to non-profit organizations.

Form 990 Tax Exempt Reporting CLAconnect.com Speaker Introductions Amanda Treml, CPA Amanda is a Manager with CliftonLarsonAllen and provides assurance and tax compliance services to non-profit organizations.

Nonprofits and Social Enterprise: Finding the Right Fit for Your Organization

Nonprofits and Social Enterprise: Finding the Right Fit for Your Organization Karen Leaffer 25th Annual Institute on Advising Nonprofit Organizations May 5, 2016 2016 Leaffer Law Group 1 Agenda 1. What

Nonprofits and Social Enterprise: Finding the Right Fit for Your Organization Karen Leaffer 25th Annual Institute on Advising Nonprofit Organizations May 5, 2016 2016 Leaffer Law Group 1 Agenda 1. What

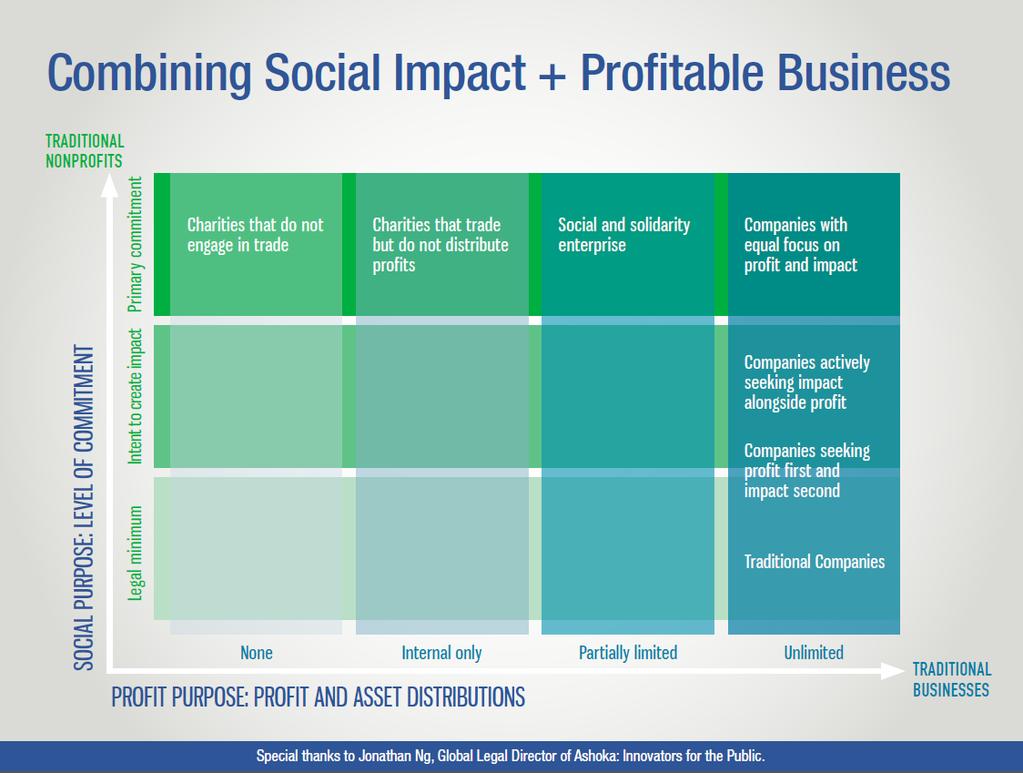

STRUCTURE FOR

STRUCTURE FOR IMPACT form follows function how do you define success? what is your Business model? profit purpose tension zero sum game increasing purpose at the expense of profit often beneficiaries are

STRUCTURE FOR IMPACT form follows function how do you define success? what is your Business model? profit purpose tension zero sum game increasing purpose at the expense of profit often beneficiaries are

LEGAL & FINANCIAL GUIDELINES

LEGAL & FINANCIAL GUIDELINES I. Introduction 1. National League for Nursing (NLN) must be aware of the activities carried on by Constituent Leagues (CLs) in its name. A court could deem an act by a CL

LEGAL & FINANCIAL GUIDELINES I. Introduction 1. National League for Nursing (NLN) must be aware of the activities carried on by Constituent Leagues (CLs) in its name. A court could deem an act by a CL

Resources for Starting a 501(c)(3) Peter Shaw Assistant School District Attorney

(3) Peter Shaw Assistant School District Attorney") Resources for Starting a 501(c)(3) Peter Shaw Assistant School District Attorney Disclaimer School Board Regulation 801.3AR Membership shall be primarily made up of parents and community members, though

Resources for Starting a 501(c)(3) Peter Shaw Assistant School District Attorney Disclaimer School Board Regulation 801.3AR Membership shall be primarily made up of parents and community members, though

Philanthropy as a Family Affair: Using a Private Foundation to Achieve Your Charitable Goals ~ Susan B. Hecker

Philanthropy as a Family Affair: Using a Private Foundation to Achieve Your Charitable Goals ~ Susan B. Hecker Establishing a private foundation can be a fulfilling way to work with charities, but be prepared

Philanthropy as a Family Affair: Using a Private Foundation to Achieve Your Charitable Goals ~ Susan B. Hecker Establishing a private foundation can be a fulfilling way to work with charities, but be prepared

Chapter 22. Exempt Entities. Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe

Chapter 22 Exempt Entities Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004 South-Western/Thomson Learning Requirements For Exempt Status (slide 1 of 3) Serve

Chapter 22 Exempt Entities Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004 South-Western/Thomson Learning Requirements For Exempt Status (slide 1 of 3) Serve

Understanding the Revised Form 990 and Governance Disclosures Enhancing Transparency and Compliance

Understanding the Revised Form 990 and Governance Disclosures Enhancing Transparency and Compliance March 20, 2009 9:30 am 11:15 am North County Philanthropy Council Lake San Marcos Country Club 1750 San

Understanding the Revised Form 990 and Governance Disclosures Enhancing Transparency and Compliance March 20, 2009 9:30 am 11:15 am North County Philanthropy Council Lake San Marcos Country Club 1750 San

June Private Foundation

June 2017 Private Foundation A private foundation is a legal entity created, funded and operated for the primary purpose of making grants to charities. Because of its charitable mission, a private foundation

June 2017 Private Foundation A private foundation is a legal entity created, funded and operated for the primary purpose of making grants to charities. Because of its charitable mission, a private foundation

Questions and Answers for Chapters on National Unification With Society for Social Work Leadership In Health Care

Questions and Answers for Chapters on National Unification With Society for Social Work Leadership In Health Care Updates: 3/31/09 4/1/09 4/2/09 Disclosure Statement: The following question and answer

Questions and Answers for Chapters on National Unification With Society for Social Work Leadership In Health Care Updates: 3/31/09 4/1/09 4/2/09 Disclosure Statement: The following question and answer

Social Enterprise Part 2: What Can 501(c)(3)s Do?

(3)s Do?") Social Enterprise Part 2: What Can 501(c)(3)s Do? Robyn Miller Corporate/Tax Counsel, Pro Bono Partnership of Atlanta May 4, 2016 Mission of Pro Bono Partnership of Atlanta: To provide free legal assistance

Social Enterprise Part 2: What Can 501(c)(3)s Do? Robyn Miller Corporate/Tax Counsel, Pro Bono Partnership of Atlanta May 4, 2016 Mission of Pro Bono Partnership of Atlanta: To provide free legal assistance

An Overview of Current NonProfit Status as it Relates to the Amateur Radio Community. Lynn T Baxter, CPA WØLTB NEAR-Fest 2016

An Overview of Current NonProfit Status as it Relates to the Amateur Radio Community Lynn T Baxter, CPA WØLTB NEAR-Fest 2016 This presentation was made at the NEARfest Oct 15,2016 forums, and this presentation

An Overview of Current NonProfit Status as it Relates to the Amateur Radio Community Lynn T Baxter, CPA WØLTB NEAR-Fest 2016 This presentation was made at the NEARfest Oct 15,2016 forums, and this presentation

MAY Private Foundation

MAY 2016 Private Foundation A private foundation is a legal entity created, funded and operated for the primary purpose of making grants to charities. Because of its charitable mission, a private foundation

MAY 2016 Private Foundation A private foundation is a legal entity created, funded and operated for the primary purpose of making grants to charities. Because of its charitable mission, a private foundation

Tax Requirements for Student Clubs

Tax Reporting Tax Requirements for Student Clubs FOLLOW-UP Prepared by Office of the Controller, Department of Tax Reporting August 2016 1 Tax Reporting All income from whatever source derived is taxable

Tax Reporting Tax Requirements for Student Clubs FOLLOW-UP Prepared by Office of the Controller, Department of Tax Reporting August 2016 1 Tax Reporting All income from whatever source derived is taxable

HOW TO APPLY FOR TAX-EXEMPT STATUS. Table of Contents

HOW TO APPLY FOR TAX-EXEMPT STATUS Table of Contents Basics of Tax Exemption Who Must File a Form 1023 501(c)(3) Requirements Organizational Test Operational Test Form 1023 Part I. Basic Information about

HOW TO APPLY FOR TAX-EXEMPT STATUS Table of Contents Basics of Tax Exemption Who Must File a Form 1023 501(c)(3) Requirements Organizational Test Operational Test Form 1023 Part I. Basic Information about

. This return is a consolidation from multiple entities, for use as an informational tool only.

. This return is a consolidation from multiple entities, for use as an informational tool only. 1 2 3 4 5 6 Susie Q. Smart, Exec. Director 40 X 165,000 0 5,500 (See Sched J for addl info) 7 8 9 10 11 12

. This return is a consolidation from multiple entities, for use as an informational tool only. 1 2 3 4 5 6 Susie Q. Smart, Exec. Director 40 X 165,000 0 5,500 (See Sched J for addl info) 7 8 9 10 11 12

Non-profit Organizations. Steps for establishing and for meeting Federal filing requirements

Non-profit Organizations Steps for establishing and for meeting Federal filing requirements US Income Taxes: A Brief Primer Definition of 'Federal Income Tax' A tax levied by the United States Internal

Non-profit Organizations Steps for establishing and for meeting Federal filing requirements US Income Taxes: A Brief Primer Definition of 'Federal Income Tax' A tax levied by the United States Internal

Walk Like An Exemption: Fast-Track and Maintain the Right Tax Exemption

Walk Like An Exemption: Fast-Track and Maintain the Right Tax Exemption California Charter Schools Conference March 17, 2015 Kevin M. Davis Greta A. Proctor 1 What We Will Cover in This Program What Is

Walk Like An Exemption: Fast-Track and Maintain the Right Tax Exemption California Charter Schools Conference March 17, 2015 Kevin M. Davis Greta A. Proctor 1 What We Will Cover in This Program What Is

Getting Tax-exempt. Linnea R. Michel, Esq. Legal Center for Nonprofits, Inc.

Getting Tax-exempt Linnea R. Michel, Esq. Legal Center for Nonprofits, Inc. 2014 Legal Center for Nonprofits, Inc. Information provided herein is not legal advice and is intended for informational purposes

Getting Tax-exempt Linnea R. Michel, Esq. Legal Center for Nonprofits, Inc. 2014 Legal Center for Nonprofits, Inc. Information provided herein is not legal advice and is intended for informational purposes

Shoreline Neighborhood Association Presentation. City of Shoreline, Washington March 19, 2008

Shoreline Neighborhood Association Presentation City of Shoreline, Washington March 19, 2008 Susan Schalla, Attorney Davis Wright Tremaine LLP 1201 Third Avenue, Suite 2200 Seattle, WA 98101 (206) 757-7700

Shoreline Neighborhood Association Presentation City of Shoreline, Washington March 19, 2008 Susan Schalla, Attorney Davis Wright Tremaine LLP 1201 Third Avenue, Suite 2200 Seattle, WA 98101 (206) 757-7700

CORPORATE ENTITY MANAGEMENT

CORPORATE ENTITY MANAGEMENT Melinda Brown Former General Counsel, Draper Laboratory Jesse R. Moore Deputy General Counsel, Corporate & Regional INC Research/inVentiv Health Maggie Palen Director, Subsidiary

CORPORATE ENTITY MANAGEMENT Melinda Brown Former General Counsel, Draper Laboratory Jesse R. Moore Deputy General Counsel, Corporate & Regional INC Research/inVentiv Health Maggie Palen Director, Subsidiary

Private Foundations Deeper Dive

Private Foundations Deeper Dive David Lawson, Davis Wright Tremaine November 2, 2017 Seattle, Washington What is a private foundation? Can be a nonprofit corporation or a charitable trust Nonprofit corporation

Private Foundations Deeper Dive David Lawson, Davis Wright Tremaine November 2, 2017 Seattle, Washington What is a private foundation? Can be a nonprofit corporation or a charitable trust Nonprofit corporation

BEST PRACTICES. Best Practices #125: 501(c)(3) Chapter Organization Cover Letter and Structure

(3) Chapter Organization Cover Letter and Structure") BEST PRACTICES Best Practices #125: 501(c)(3) Chapter Organization Cover Letter and Structure A lot has changed since the original Best Practices Article for Tax-Exempt Status was posted in 2009. Most

BEST PRACTICES Best Practices #125: 501(c)(3) Chapter Organization Cover Letter and Structure A lot has changed since the original Best Practices Article for Tax-Exempt Status was posted in 2009. Most

Frequently Asked Questions About Company Foundations and Corporate Giving

Welcome to Our 2006 Seminar Series: Frequently Asked Questions About Company Foundations and Corporate Giving May 23, 2006 1 Speakers: Victoria Bjorklund David Shevlin 2006 Simpson Thacher & Bartlett LLP.

Welcome to Our 2006 Seminar Series: Frequently Asked Questions About Company Foundations and Corporate Giving May 23, 2006 1 Speakers: Victoria Bjorklund David Shevlin 2006 Simpson Thacher & Bartlett LLP.

OVERVIEW OF PRIVATE FOUNDATIONS

OVERVIEW OF PRIVATE FOUNDATIONS BERNARD J. SMITH BRIAN W. FITZSIMONS INTRODUCTION A private foundation is a charitable corporation or trust which receives financial support from a limited number of sources.

OVERVIEW OF PRIVATE FOUNDATIONS BERNARD J. SMITH BRIAN W. FITZSIMONS INTRODUCTION A private foundation is a charitable corporation or trust which receives financial support from a limited number of sources.

Economic Development as a Charitable Activity April 5, Lara Kalwinski, Esq. Council on Foundations

Economic Development as a Charitable Activity April 5, 2017 Lara Kalwinski, Esq. Council on Foundations Agenda Legal Background and Why This is Important Meeting Charitability Standards What We Know What

Economic Development as a Charitable Activity April 5, 2017 Lara Kalwinski, Esq. Council on Foundations Agenda Legal Background and Why This is Important Meeting Charitability Standards What We Know What

National Network of Fiscal Sponsors. Guidelines for Pre-Approved Grant Relationship Fiscal Sponsorship

Introduction National Network of Fiscal Sponsors Guidelines for Pre-Approved Grant Relationship Fiscal Sponsorship Fiscal sponsorship has evolved as an effective and efficient mode of starting new nonprofits,

Introduction National Network of Fiscal Sponsors Guidelines for Pre-Approved Grant Relationship Fiscal Sponsorship Fiscal sponsorship has evolved as an effective and efficient mode of starting new nonprofits,

FREQUENTLY ASKED QUESTIONS ABOUT PRIVATE FOUNDATIONS. Investments, Governance, and Compliance

FREUENTLY ASKED UESTIONS ABOUT PRIVATE FOUNDATIONS Investments, Governance, and Compliance INTRODUCTION For those seeking philanthropic flexibility and impact, the vehicle of choice has always been the

FREUENTLY ASKED UESTIONS ABOUT PRIVATE FOUNDATIONS Investments, Governance, and Compliance INTRODUCTION For those seeking philanthropic flexibility and impact, the vehicle of choice has always been the

MODEL BENEFIT CORPORATION LEGISLATION With Explanatory Comments 1

Version of April 17, 2017 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 MODEL BENEFIT CORPORATION LEGISLATION With Explanatory Comments 1 [Chapter] Benefit

Version of April 17, 2017 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 MODEL BENEFIT CORPORATION LEGISLATION With Explanatory Comments 1 [Chapter] Benefit

Connecticut Benefit Corporation How-To Guide

1 Benefit Corporation Connecticut Benefit Corporation How-To Guide Overview Unlike traditional corporations that make business decisions primarily to maximize shareholder value, benefit corporations aim

1 Benefit Corporation Connecticut Benefit Corporation How-To Guide Overview Unlike traditional corporations that make business decisions primarily to maximize shareholder value, benefit corporations aim

THE IMPACT SECURITY. A Novel Financial Product That Links Financial Returns With Social & Environmental Impact WRITTEN BY

THE IMPACT SECURITY A Novel Financial Product That Links Financial Returns With Social & Environmental Impact WRITTEN BY Lindsay Beck, Co-Founder & Co-CEO, NPX With assistance from: Anna Pinedo, Partner,

THE IMPACT SECURITY A Novel Financial Product That Links Financial Returns With Social & Environmental Impact WRITTEN BY Lindsay Beck, Co-Founder & Co-CEO, NPX With assistance from: Anna Pinedo, Partner,

WikiLeaks Document Release

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS21892 Application Process for Seeking Section 501(c)(3) Tax Exempt Status Erika Lunder, American Law Division December

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS21892 Application Process for Seeking Section 501(c)(3) Tax Exempt Status Erika Lunder, American Law Division December

Nonprofit Essentials Conference, August 10, 2017 LEGAL REQUIREMENTS & THE IMPORTANCE OF BEING TRANSPARENT

Nonprofit Essentials Conference, August 10, 2017 LEGAL REQUIREMENTS & THE IMPORTANCE OF BEING TRANSPARENT About the Presenters Heidi Christianson Attorney Nilan Johnson Lewis, PA Kris Kewitsch Executive

Nonprofit Essentials Conference, August 10, 2017 LEGAL REQUIREMENTS & THE IMPORTANCE OF BEING TRANSPARENT About the Presenters Heidi Christianson Attorney Nilan Johnson Lewis, PA Kris Kewitsch Executive

Time for a Legal Tune-Up: Compliance Issues for Nonprofit and Tax-Exempt Organizations

Time for a Legal Tune-Up: Compliance Issues for Nonprofit and Tax-Exempt Organizations presented by Corinne H. Gartner October 5, 2017 500 Capitol Mall, Suite 1550 Sacramento, CA 95814 p. (916) 661-5700

Time for a Legal Tune-Up: Compliance Issues for Nonprofit and Tax-Exempt Organizations presented by Corinne H. Gartner October 5, 2017 500 Capitol Mall, Suite 1550 Sacramento, CA 95814 p. (916) 661-5700

Nonprofit Tax Update. September 22,

Nonprofit Tax Update September 22, 2016 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company BDO KNOWLEDGE limited by guarantee, Webinar

Nonprofit Tax Update September 22, 2016 BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company BDO KNOWLEDGE limited by guarantee, Webinar

IRS Form 990: Who Sees it Besides the IRS?

IRS Form 990: Who Sees it Besides the IRS? State Tax Authorities. Attorney General. Public Inspection. www.guidestar.org Newspapers and Media. Donors. Anyone! 2 Purpose of New IRS Form 990 Enhance Transparency

IRS Form 990: Who Sees it Besides the IRS? State Tax Authorities. Attorney General. Public Inspection. www.guidestar.org Newspapers and Media. Donors. Anyone! 2 Purpose of New IRS Form 990 Enhance Transparency

Staying Legal: General Guidelines. for Operating a 501(c)(3) Nonprofit Corporation in Georgia

(3) Nonprofit Corporation in Georgia") Staying Legal: General Guidelines for Operating a 501(c)(3) Nonprofit Corporation in Georgia Originally Prepared By: Tax Subcommittee of Pro Bono Partnership of Atlanta, chaired by Ed Manigault (formerly

Staying Legal: General Guidelines for Operating a 501(c)(3) Nonprofit Corporation in Georgia Originally Prepared By: Tax Subcommittee of Pro Bono Partnership of Atlanta, chaired by Ed Manigault (formerly

Tax-Exempt Status and IRS Reporting Obligations. 1. All Undergraduate Organizations

Tax-Exempt Status and IRS Reporting Obligations All undergraduate organizations are expected to comply with the Undergraduate Regulations, and must also comply with Federal and State tax laws. The purpose

Tax-Exempt Status and IRS Reporting Obligations All undergraduate organizations are expected to comply with the Undergraduate Regulations, and must also comply with Federal and State tax laws. The purpose

MODEL BENEFIT CORPORATION LEGISLATION With Explanatory Comments 1

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 Version of June 24, 2014 MODEL BENEFIT CORPORATION LEGISLATION With Explanatory Comments 1 [Chapter]

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 Version of June 24, 2014 MODEL BENEFIT CORPORATION LEGISLATION With Explanatory Comments 1 [Chapter]

Social Enterprise Empowering Mission-Driven Entrepreneurs Marc J. Lane

Social Enterprise Empowering Mission-Driven Entrepreneurs Marc J. Lane AMEMCANBAa ASSOCIATION Defending Liberty Pursuing justice Contents Preface: A Word to My Colleagues xiii ** Chapter One Empowering

Social Enterprise Empowering Mission-Driven Entrepreneurs Marc J. Lane AMEMCANBAa ASSOCIATION Defending Liberty Pursuing justice Contents Preface: A Word to My Colleagues xiii ** Chapter One Empowering

(c)(3) Compliance Guide for 501(c)(3) Public Charities,

(3) Compliance Guide for 501(c)(3) Public Charities,") Tax Exempt and Government Entities EXEMPT ORGANIZATIONS Compliance Guide for 501(c)(3) Public Charities, Inside: Activities that may jeopardize a charity s exempt status, Federal information returns, tax

Tax Exempt and Government Entities EXEMPT ORGANIZATIONS Compliance Guide for 501(c)(3) Public Charities, Inside: Activities that may jeopardize a charity s exempt status, Federal information returns, tax

Colleges and Universities: Investing for Impact

EDITED BY STEPHANIE PETIT, J.D. EXEMPT e Colleges and Universities: Investing for Impact ALEXANDER L. REID When making impact investments, colleges and universities should give due consideration to the

EDITED BY STEPHANIE PETIT, J.D. EXEMPT e Colleges and Universities: Investing for Impact ALEXANDER L. REID When making impact investments, colleges and universities should give due consideration to the

ANNUAL TAX UPDATE & FORM 990 CHANGES

ANNUAL TAX UPDATE & FORM 990 CHANGES May 2, 2017 Aaron Hershberger, CPA Director ahershberger@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are

ANNUAL TAX UPDATE & FORM 990 CHANGES May 2, 2017 Aaron Hershberger, CPA Director ahershberger@bkd.com 1 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are

Doug Jones. Partner. 600 Congress Ave., Ste Austin, TX O F. mcginnislaw.

PRACTICE AREAS Tax Planning & Controversy 600 Congress Ave., Ste. 2100 Austin, TX 78701 512-495-6013 O 512-505-6313 F mcginnislaw.com Tax Exempt / NonProfit Organizations Corporate & Business Transactions

PRACTICE AREAS Tax Planning & Controversy 600 Congress Ave., Ste. 2100 Austin, TX 78701 512-495-6013 O 512-505-6313 F mcginnislaw.com Tax Exempt / NonProfit Organizations Corporate & Business Transactions

Federal Tax-Exempt Status 501(c)(3) Organizations

(3) Organizations") Federal Tax-Exempt Status 501(c)(3) Organizations Most PTAs are classified as tax-exempt 501(c)(3) public charities under the Internal Revenue Code (IRC). One major advantage for organizations that are

Federal Tax-Exempt Status 501(c)(3) Organizations Most PTAs are classified as tax-exempt 501(c)(3) public charities under the Internal Revenue Code (IRC). One major advantage for organizations that are

[26 CFR ]: Returns by exempt organizations and returns by certain nonexempt

![[26 CFR ]: Returns by exempt organizations and returns by certain nonexempt](/thumbs/82/85277399.jpg "[26 CFR ]: Returns by exempt organizations and returns by certain nonexempt") Part III Administrative, Procedural, and Miscellaneous [26 CFR 1.6033-2]: Returns by exempt organizations and returns by certain nonexempt organizations (Also: 6001, 6033, and 1.6001-1) Rev. Proc. 2018-38

Part III Administrative, Procedural, and Miscellaneous [26 CFR 1.6033-2]: Returns by exempt organizations and returns by certain nonexempt organizations (Also: 6001, 6033, and 1.6001-1) Rev. Proc. 2018-38

Start Smart Law Presents: Social Enterprise - Profit with A Purpose

Start Smart Law Presents: Social Enterprise - Profit with A Purpose This is Not Legal Advice! Stephanie I do NOT practice law Purpose of Tonight s Session: To Make You a Better Consumer of Legal Services,

Start Smart Law Presents: Social Enterprise - Profit with A Purpose This is Not Legal Advice! Stephanie I do NOT practice law Purpose of Tonight s Session: To Make You a Better Consumer of Legal Services,

Keeping it Legal: The Dos and DON Ts of Managing Your 501(c)3

3") Keeping it Legal: The Dos and DON Ts of Managing Your 501(c)3 Women s Collective Giving Grantmakers Network 2014 Leadership Forum April 9, 2014 Presented by: Dianne Chipps Bailey A Few Introductory Thoughts

Keeping it Legal: The Dos and DON Ts of Managing Your 501(c)3 Women s Collective Giving Grantmakers Network 2014 Leadership Forum April 9, 2014 Presented by: Dianne Chipps Bailey A Few Introductory Thoughts

ISAO SP Forming a Tax-Exempt Entity. Draft Document Request For Comment. ISAO SO 2017 v0.01. ISAO Standards Organization

ISAO SP 1000 Forming a Tax-Exempt Entity Draft Document Request For Comment ISAO SO 2017 v0.01 ISAO Standards Organization April 19, 2017 Copyright 2017, ISAO SO (Information Sharing and Analysis Organization

ISAO SP 1000 Forming a Tax-Exempt Entity Draft Document Request For Comment ISAO SO 2017 v0.01 ISAO Standards Organization April 19, 2017 Copyright 2017, ISAO SO (Information Sharing and Analysis Organization

PRIVATE FOUNDATION VERSUS PUBLIC CHARITY (Non Profit Advisory No. 5)

") PRIVATE FOUNDATION VERSUS PUBLIC CHARITY (Non Profit Advisory No. 5) Most nonprofit entities -- and especially their primary donors -- want to insure that they have public charity status for the 50% deduction

PRIVATE FOUNDATION VERSUS PUBLIC CHARITY (Non Profit Advisory No. 5) Most nonprofit entities -- and especially their primary donors -- want to insure that they have public charity status for the 50% deduction

Corporate Social Responsibility, Social Impact Investing and Green Bonds December 2014

Corporate Social Responsibility, Social Impact Investing and Green Bonds December 2014 mofo.com Alternative Corporate Forms 2 Introduction How can business use Corporate Form to help achieve a positive

Corporate Social Responsibility, Social Impact Investing and Green Bonds December 2014 mofo.com Alternative Corporate Forms 2 Introduction How can business use Corporate Form to help achieve a positive

New Guidelines for Tax Exempt Organizations A Look at IRS Compliance Readiness for 2012 and Beyond

New Guidelines for Tax Exempt Organizations A Look at IRS Compliance Readiness for 2012 and Beyond Executive Directors Roundtable Fall Leadership Network Meeting Las Cruces, NM October 4, 2013 Eduardo

New Guidelines for Tax Exempt Organizations A Look at IRS Compliance Readiness for 2012 and Beyond Executive Directors Roundtable Fall Leadership Network Meeting Las Cruces, NM October 4, 2013 Eduardo

Comments related to any information in this Note should be addressed to Mai El-Sadany.

USIG Country Note: Israel Current as of January 2017 Comments related to any information in this Note should be addressed to Mai El-Sadany. Table of Contents I. Summary A. Types of Organizations B. Tax

USIG Country Note: Israel Current as of January 2017 Comments related to any information in this Note should be addressed to Mai El-Sadany. Table of Contents I. Summary A. Types of Organizations B. Tax

Comments related to any information in this Note should be addressed to Lily Liu.

ISRAEL Current as of December 2018 Comments related to any information in this Note should be addressed to Lily Liu. TABLE OF CONTENTS I. Summary A. Types of Organizations B. Tax Laws II. Applicable Laws

ISRAEL Current as of December 2018 Comments related to any information in this Note should be addressed to Lily Liu. TABLE OF CONTENTS I. Summary A. Types of Organizations B. Tax Laws II. Applicable Laws

MBA for Non-Profits Understanding Non-Profit Financial Statements Part I

MBA for Non-Profits Understanding Non-Profit Financial Statements Part I Corporate Counsel Women of Color Thirteenth Annual Career Strategies Conference September 27, 2017 Copyright 2017 Deloitte Development

MBA for Non-Profits Understanding Non-Profit Financial Statements Part I Corporate Counsel Women of Color Thirteenth Annual Career Strategies Conference September 27, 2017 Copyright 2017 Deloitte Development

A GUIDE TO MINNESOTA S CHARITIES LAWS

A GUIDE TO MINNESOTA S CHARITIES LAWS FROM THE OFFICE OF MINNESOTA ATTORNEY GENERAL LORI SWANSON www.ag.state.mn.us This brochure is intended to be used as a source for general information and is not provided

A GUIDE TO MINNESOTA S CHARITIES LAWS FROM THE OFFICE OF MINNESOTA ATTORNEY GENERAL LORI SWANSON www.ag.state.mn.us This brochure is intended to be used as a source for general information and is not provided

KING GEORGE GRAND LODGE / QUEEN VASHTI GRAND CHAPTER FOUNDATION

KING GEORGE GRAND LODGE / QUEEN VASHTI GRAND CHAPTER FOUNDATION Established in 2014 Founded under the direction of King George Grand Lodge Grand Master Jonathan Dearbone Meeting the Needs of the Community

KING GEORGE GRAND LODGE / QUEEN VASHTI GRAND CHAPTER FOUNDATION Established in 2014 Founded under the direction of King George Grand Lodge Grand Master Jonathan Dearbone Meeting the Needs of the Community

ANNUAL TAX UPDATE & 2014 FORM 990 CHANGES

THURSDAY MARCH 5, 2015 10 11 AM CENTRAL TIME ANNUAL TAX UPDATE & 2014 FORM 990 CHANGES Jessica Freeman Manager BKD, LLP jfreeman@bkd.com Wendy Budde Manager BKD, LLP wbudde@bkd.com TO RECEIVE CPE CREDIT

THURSDAY MARCH 5, 2015 10 11 AM CENTRAL TIME ANNUAL TAX UPDATE & 2014 FORM 990 CHANGES Jessica Freeman Manager BKD, LLP jfreeman@bkd.com Wendy Budde Manager BKD, LLP wbudde@bkd.com TO RECEIVE CPE CREDIT

Forever Young Foundation (FYF) Conflict of Interest Policy And Annual Statement

Conflict of Interest Policy And Annual Statement") Forever Young Foundation (FYF) Conflict of Interest Policy And Annual Statement For Directors and Officers and Members of a Committee with Board Delegated Powers Article I -- Purpose 1. The purpose of

Forever Young Foundation (FYF) Conflict of Interest Policy And Annual Statement For Directors and Officers and Members of a Committee with Board Delegated Powers Article I -- Purpose 1. The purpose of

THE IMPACT SECURITY. A Novel Financial Product That Links Financial Returns With Social & Environmental Impact WRITTEN BY

THE IMPACT SECURITY A Novel Financial Product That Links Financial Returns With Social & Environmental Impact WRITTEN BY Lindsay Beck, Co-Founder & Co-CEO, NPX With assistance from: Anna Pinedo, Partner,

THE IMPACT SECURITY A Novel Financial Product That Links Financial Returns With Social & Environmental Impact WRITTEN BY Lindsay Beck, Co-Founder & Co-CEO, NPX With assistance from: Anna Pinedo, Partner,

CCCIA Ways & Means Committee 501c3 Assessment. Kate Tallman, John Stevens, Jay Schaller, & Ashley Roberts

CCCIA Ways & Means Committee 501c3 Assessment Kate Tallman, John Stevens, Jay Schaller, & Ashley Roberts Problem Statement Over the past 5 years CCCIA expenses have exceeded revenues by an average of

CCCIA Ways & Means Committee 501c3 Assessment Kate Tallman, John Stevens, Jay Schaller, & Ashley Roberts Problem Statement Over the past 5 years CCCIA expenses have exceeded revenues by an average of

I. Summary. A. Types of Organizations. Table of Contents. Country Note: Israel. Current as of August 2013 Download print version (in PDF)

") Country Note: Israel Current as of August 2013 Download print version (in PDF) Comments related to any information in this note should be addressed to Brittany Grabel. Table of Contents I. Summary A. Types

Country Note: Israel Current as of August 2013 Download print version (in PDF) Comments related to any information in this note should be addressed to Brittany Grabel. Table of Contents I. Summary A. Types

8.1 Entrepreneurs 8.2 Sole Proprietorships and Partnerships 8.3 Corporations and Other Organizations

CHAPTER 8 Businesses 8.1 Entrepreneurs 8.2 Sole Proprietorships and Partnerships 8.3 Corporations and Other Organizations 1 CONTEMPORARY ECONOMICS: LESSON 8.1 Consider CHAPTER 8 Businesses Why do some

CHAPTER 8 Businesses 8.1 Entrepreneurs 8.2 Sole Proprietorships and Partnerships 8.3 Corporations and Other Organizations 1 CONTEMPORARY ECONOMICS: LESSON 8.1 Consider CHAPTER 8 Businesses Why do some

IRS Definition of a Business. A business is where goods and services are exchanged for money

Business Structures IRS Definition of a Business A business is where goods and services are exchanged for money Business Structure Importance Choosing the proper legal organizational structure for a business

Business Structures IRS Definition of a Business A business is where goods and services are exchanged for money Business Structure Importance Choosing the proper legal organizational structure for a business

RESEARCHED AND WRITTEN BY:

PROGRAM RELATED INVESTMENTS: AN INTRODUCTORY GUIDE RESEARCHED AND WRITTEN BY: JULY 206 Program Related Investments are used as high impact tools to stimulate private-sector driven innovation, encourage

PROGRAM RELATED INVESTMENTS: AN INTRODUCTORY GUIDE RESEARCHED AND WRITTEN BY: JULY 206 Program Related Investments are used as high impact tools to stimulate private-sector driven innovation, encourage

EXECUTIVE COMPENSATION POLICY California Nonprofit Public Benefit Corporation Exempt from Taxation Under Internal Revenue Code Section 501(c)(3)

(3)") PUBLIC COUNSEL COMMUNITY DEVELOPMENT PROJECT ANNOTATED EXECUTIVE COMPENSATION POLICY AUGUST 2017 EXECUTIVE COMPENSATION POLICY California Nonprofit Public Benefit Corporation Exempt from Taxation Under

PUBLIC COUNSEL COMMUNITY DEVELOPMENT PROJECT ANNOTATED EXECUTIVE COMPENSATION POLICY AUGUST 2017 EXECUTIVE COMPENSATION POLICY California Nonprofit Public Benefit Corporation Exempt from Taxation Under

2015 CliftonLarsonAllen LLP CliftonLarsonAllen LLP. Form 990-PF Update. CLAconnect.com

Form 990-PF Update CLAconnect.com Form 990-PF Filings Importance of filings is identified by requirements All foundations regardless of income or assets Must be made available to the public All pages no

Form 990-PF Update CLAconnect.com Form 990-PF Filings Importance of filings is identified by requirements All foundations regardless of income or assets Must be made available to the public All pages no

SHOULD CHARITABLE GIVING BE A PART OF MY ESTATE PLAN?

by Layne T. Rushforth Summary Charitable contributions not only entitle the donor to an income-tax deduction, but may also accomplish certain estate-planning objectives. Such contributions can be made

by Layne T. Rushforth Summary Charitable contributions not only entitle the donor to an income-tax deduction, but may also accomplish certain estate-planning objectives. Such contributions can be made

BMET5103 ENTREPRENEURSHIP. Topic 5 Forms of Business Ownership and Franchising

BMET5103 ENTREPRENEURSHIP Topic 5 Forms of Business Ownership and Franchising 19 February 2017 Content 5.0 Introduction 5.1 Issues to Consider When Setting up Business Ownership 5.2 Sole Proprietorship

BMET5103 ENTREPRENEURSHIP Topic 5 Forms of Business Ownership and Franchising 19 February 2017 Content 5.0 Introduction 5.1 Issues to Consider When Setting up Business Ownership 5.2 Sole Proprietorship

Private foundations Establishing a vehicle for your charitable vision

Private foundations Establishing a vehicle for your charitable vision I didn t know where to start. The advice I received on creating a private foundation pointed me in the right direction, and now I m

Private foundations Establishing a vehicle for your charitable vision I didn t know where to start. The advice I received on creating a private foundation pointed me in the right direction, and now I m

Some Structures for Social Enterprise

Some Structures for Social Enterprise Presentation to the Schulich School of Business (York University) October 29, 2013 Mark Blumberg (mark@blumbergs.ca) Blumberg Segal LLP 1 Blumberg Segal LLP Blumberg

Some Structures for Social Enterprise Presentation to the Schulich School of Business (York University) October 29, 2013 Mark Blumberg (mark@blumbergs.ca) Blumberg Segal LLP 1 Blumberg Segal LLP Blumberg

The Path To University Startups. A Launchpad for Innovators at the University of Alaska Fairbanks

The Path To University Startups A Launchpad for Innovators at the University of Alaska Fairbanks Success of Inventions Worked on in 2012 Inventors Engaged New Invention Disclosures File Closures Provisional

The Path To University Startups A Launchpad for Innovators at the University of Alaska Fairbanks Success of Inventions Worked on in 2012 Inventors Engaged New Invention Disclosures File Closures Provisional

ANSWERS TO END-OF-CHAPTER QUESTIONS

This is a sample of the instructor resources for Louis C. Gapenski, PhD, Fundamentals of Healthcare Finance, Second Edition. The complete instructor resources include Test Bank PowerPoint slides Sample

This is a sample of the instructor resources for Louis C. Gapenski, PhD, Fundamentals of Healthcare Finance, Second Edition. The complete instructor resources include Test Bank PowerPoint slides Sample

Federal Financial Requirements

American Society of Health-System Pharmacists Federal Financial Requirements ASHP s Financial Toolkit for Affiliates Kimberlee Berry [Pick the date] FEDERAL REQUIREMENTS NOTE: All IRS forms can be accessed

American Society of Health-System Pharmacists Federal Financial Requirements ASHP s Financial Toolkit for Affiliates Kimberlee Berry [Pick the date] FEDERAL REQUIREMENTS NOTE: All IRS forms can be accessed

New United States-Japan Tax Treaty Enters Into Force: New Withholding Rates Take Effect on July 1, 2004

New United States-Japan Tax Treaty Enters Into Force: New Withholding Rates Take Effect on July 1, 2004 4/2/2004 Client Alert On March 30, 2004, the Governments of the United States and Japan exchanged

New United States-Japan Tax Treaty Enters Into Force: New Withholding Rates Take Effect on July 1, 2004 4/2/2004 Client Alert On March 30, 2004, the Governments of the United States and Japan exchanged

ALTERNATIVES TO STARTING A NEW NONPROFIT

ALTERNATIVES TO STARTING A NEW NONPROFIT While many people are tempted to incorporate first, there are a number of options for undertaking a new activity without starting a new organization. Because most

ALTERNATIVES TO STARTING A NEW NONPROFIT While many people are tempted to incorporate first, there are a number of options for undertaking a new activity without starting a new organization. Because most

Get By With a Little Legal Help For Your Friends

Get By With a Little Legal Help For Your Friends Presented for the 2014 New York Library Association Conference Friday, November 7, 2014 Judy Siegel, Staff Attorney Courtney Darts, Senior Staff Attorney

Get By With a Little Legal Help For Your Friends Presented for the 2014 New York Library Association Conference Friday, November 7, 2014 Judy Siegel, Staff Attorney Courtney Darts, Senior Staff Attorney

Seminar for Not-For Profit Organizations. Scott Rodgville, CPA

Seminar for Not-For Profit Organizations Scott Rodgville, CPA Copyright, 2009 Core Form Changes Which Form do you have to file and when? Form 990-N, 990-EZ or 990 Phase in Schedule for revised Form 990

Seminar for Not-For Profit Organizations Scott Rodgville, CPA Copyright, 2009 Core Form Changes Which Form do you have to file and when? Form 990-N, 990-EZ or 990 Phase in Schedule for revised Form 990

SOCIAL PURPOSE CORPORATIONS AND BENEFIT CORPORATIONS NEW BUSINESS ENTITIES AUTHORIZED BY FLORIDA LAW

SOCIAL PURPOSE CORPORATIONS AND BENEFIT CORPORATIONS NEW BUSINESS ENTITIES AUTHORIZED BY FLORIDA LAW Jane D. Callahan, Esq. Dean, Mead, Egerton, Bloodworth, Capouano & Bozarth, P.A. A. Introduction 1.

SOCIAL PURPOSE CORPORATIONS AND BENEFIT CORPORATIONS NEW BUSINESS ENTITIES AUTHORIZED BY FLORIDA LAW Jane D. Callahan, Esq. Dean, Mead, Egerton, Bloodworth, Capouano & Bozarth, P.A. A. Introduction 1.

HOUSE BILL (1lr2906) ENROLLED BILL Economic Matters/Judicial Proceedings. Read and Examined by Proofreaders:

ENROLLED BILL Economic Matters/Judicial Proceedings. Read and Examined by Proofreaders:") C Introduced by Delegate Feldman HOUSE BILL ENROLLED BILL Economic Matters/Judicial Proceedings (lr0) Read and Examined by Proofreaders: Proofreader. Proofreader. Sealed with the Great Seal and presented

C Introduced by Delegate Feldman HOUSE BILL ENROLLED BILL Economic Matters/Judicial Proceedings (lr0) Read and Examined by Proofreaders: Proofreader. Proofreader. Sealed with the Great Seal and presented