TAX EVASION AND AVOIDANCE: Questions and Answers

|

|

|

- Verity Hannah Nash

- 6 years ago

- Views:

Transcription

1 EUROPEAN COMMISSION MEMO Brussels, 6 December 2012 TAX EVASION AND AVOIDANCE: Questions and Answers See also IP/12/1325 Tax Evasion Why has the Commission presented an Action Plan on Tax fraud and evasion? Every year, an estimated 1 trillion 1 in public money is lost in the EU due to tax evasion and avoidance. Member States suffer a serious loss of revenue, and a dent to the efficiency and fairness of their tax systems. Some businesses find themselves at a competitive disadvantage compared to those that find ways to avoid paying their fair share. The cross-border nature of tax evasion and avoidance, along with Member States' concerns to maintain competitiveness, make it very difficult for purely national measures to have the full desired effect. Tax evasion is a multi-facetted problem requiring a multi-pronged approach, at national, EU and international level. In March 2012, the 27 EU Heads of State asked the Commission to develop ideas and solutions to improve the fight against tax fraud and tax evasion. In April, the European Parliament also called for urgent action in this area. As a first response, the Commission adopted a Communication in June 2012 outlining how tax compliance could be improved and announced the preparation of today's Action Plan (see IP/12/697 and MEMO/12/492). The Action Plan today contains over 30 measures to be developed now and in years to come. If all 27 EU Member States cooperate together, it will help to increase the fairness of their tax systems, secure much needed tax revenues and help to improve the proper functioning of the Single Market. In addition, the "strength in numbers" of the EU acting as a united block can carry much more weight in achieving faster and more ambitious progress at international level and in discussions with OECD and G MEMO/12/949

2 What measures are already in place in the EU to fight tax fraud and evasion? The EU has built its standards of good governance in taxation on 3 pillars: transparency, information exchange, and fair tax competition. These are principles that must be respected by the Member States, and that the EU also seeks to promote internationally to the widest extent possible. In terms of transparency and information exchange, administrative cooperation between Member States has been considerably strengthened in recent years. Thanks to EU rules in this field, national tax authorities benefit greatly from their mutual exchange of data, information and experiences, in order to better identify and address tax evasion and fraud. Important new legislation has been adopted in recent years to further strengthen administrative cooperation, including a new Directive on Administrative Cooperation which will enter into force on 1 January The EU Savings Directive is proof of the benefits of intra-eu cooperation. On average, information on 20 billion euros of taxable income is exchanged between Member States each year and five non-eu countries (including Switzerland and Liechtenstein) as well as ten dependent or associated territories of MS outside the EU (including Jersey, Guernsey, the Isle of Man, the Cayman Islands and Aruba) participate in the EU network of cooperation in this field through agreements providing for equivalent or the same measures as those of the EU Savings Directive. To promote fair tax competition, the EU has the Code of Conduct on Business Taxation (see below). The Commission is currently in discussions with Switzerland and Liechtenstein to promote the principles of the Code beyond EU borders. In June 2012, the Commission set out 25 concrete measures to fight more effectively, at national and EU level, against tax fraud and evasion (see IP/12/697). Some of these measures are already underway e.g. in July the Commission proposed a Quick Reaction Mechanism (QRM) against VAT fraud. The VAT strategy presented last December also looked specifically at how to tackle VAT fraud in better way. In the Country Specific Recommendations for 2012, 10 Member States were encouraged to do more at national level to fight tax evasion and improve compliance. The Commission is always ready to provide targeted support and technical assistance to any Member State that needs it to strengthen its tax system against evasion, and improve tax collection. What is set out in the Action Plan to strengthen the EU stance on evasion and avoidance? As a starting point, Member States are urged to use, to full effect, the powerful tools already at their disposal. They should properly apply EU rules on administrative cooperation and information exchange, and rapidly agree on key proposals that could help recapture billions of euros. These include the revision of the EU Savings Tax Directive, a negotiating mandate to update the existing EU savings taxation agreements with Switzerland and other European third countries, and the Quick Reaction Mechanism to fight VAT fraud. The Code of Conduct on Business Taxation should also be reinvigorated, to better address instances of harmful tax competition. Its scope could also be widened e.g. to cover wealthy individuals. In the short term, EU measures will include a Taxpayers' Code to improve compliance and standardised forms for information exchange. The Commission will review the anti-abuse provisions in the Directives on Parent-Subsidiary, Mergers and Interest and Royalties. 2

3 In the medium and long term, measures will include an EU Tax Identification Number (TIN), an EU tax web portal, guidelines for tracing money flows and possibly common sanctions for tax offences. What is the Code of Conduct on Business Taxation? The Code of Conduct is the EU's main tool for ensuring fair tax competition in the area of business taxation. It sets out clear criteria for assessing whether or not a tax regime can be considered harmful. All Member States have committed to adhering to the principles of the Code. This means refraining from introducing tax measures deemed to be harmful and changing those that are found to be so. The Code of Conduct Group oversees the application of the Code, assesses regimes to determine whether or not they are harmful, and reports back to the EU's Council of Finance Ministers on developments in this area at the end of each Presidency. Since the Code of Conduct was established in 1997, over 400 tax regimes have been assessed within the EU and the overseas countries and territories and around 100 have been eliminated when assessed as harmful. The Code's criteria for identifying harmful measures include: A significantly lower level of effective taxation than the general level of taxation in the country concerned (a tax benefit) Tax benefits reserved for non-residents or transactions with non-residents Tax benefits for activities which are isolated from the domestic economy and have no impact on the national tax base (ring-fencing) Tax benefits granted despite the absence of any real economic activity (substance) Departure from internationally accepted rules (especially OECD) in setting the basis of profit determination for companies in a multinational group Lack of transparency What does the Action Plan say about the Code of Conduct in improving the EU's fight against tax evasion and avoidance? The criteria to be used to determine if a non-eu country is a "tax haven" or not will largely reflect those set out in the EU's Code of Conduct (in addition to the OECD's requirements on transparency and information exchange). This would send a clear signal that the EU expects its international partners to comply with the same minimum standards of good governance as Member States themselves comply with. Beyond this, the Action Plan also calls on Member States to use the Code of Conduct to better effect, as part of the effort to tackle evasion and avoidance. To ensure that the Code meets its original goal of preventing harmful tax competition, the Commission recommends that, for example, Member States refer topics more quickly to Council for political decisions when necessary. In addition, the scope of the Code of Conduct should be expanded to include special tax regimes for wealthy individuals and which could be considered harmful to the Single Market. 3

4 How does the Commission intend to follow-up to the Action Plan? The Commission will proceed in preparing the upcoming proposals and initiatives within the timeframe set out in the Action Plan. Already in the first half of 2013, it will launch consultations on the Taxpayers' Code and work to promote EU good governance standards internationally, notably through the OECD. The Commission will also continue to push for rapid agreement amongst Member States of the important proposals already on the table, most notably the revised Savings Directive, negotiating mandates for stronger savings taxation agreements with Switzerland and others, and the Quick Reaction Mechanism for VAT fraud. Beyond this, the Commission also intends to closely monitor the progress made by Member States in the implementation of today's Recommendations and the work in relation to tax evasion, avoidance and tax havens. The Platform for Tax Good Governance will be established to provide the opportunity for regular feedback by Member States, and the Commission will maintain pressure when the momentum is considered to be insufficient. This continuous monitoring will feed into an official report within 3 years on the application of the recommended measures and their impact. Tax Havens What is the added value of a common EU approach to tax havens? The criteria for identifying tax havens and measures to address them vary greatly from one Member State to another. This means that, in a Single Market, business and transactions involving tax havens can be routed through the Member States with the most lenient provisions. As a result, the real level of protection automatically coincides with the lowest common denominator i.e. those with a more ambitious approach are easily undermined in their efforts to clamp down on tax havens. A common EU approach to defining and reacting to "tax havens" would therefore be much more effective than a patchwork of national approaches. A minimum standard applied by all Member States would prevent tax evaders and avoiders from taking advantage of different national approaches in order to access the "tax havens". Added to this, a common EU approach has "more bite". It leaves third countries with no doubt about what is considered by Member States to be uncooperative behaviour, and the consequences of this. Acting as a block of 27 undoubtedly, representing 500 million citizens, has more weight than a series of unilateral measures. Finally, with a strong, common approach the EU can continue to be a central player in the good governance campaign internationally. With the high standards it applies internally, and the robust criteria it applies in its relations with non-eu countries, it can push for more ambitious measures to be agreed globally through international forums such as the OECD. 4

5 What does the Commission recommend for a stronger, common approach on tax havens? Member States are encouraged to adopt a common set of criteria to identify countries which do not respect minimum standards of good governance ("tax havens"). These criteria would help Member States to determine whether a non-eu country should be added to their national blacklists. Such common listing by all Member States in itself will send a strong signal. Additional measures which could be used in relation to non-compliant jurisdictions are also set out as part of the recommended common approach to tax havens. The Commission also recommends positive measures that should be taken in relation to non-eu countries (particularly developing ones) committed to complying with the EU minimum standards of good governance. What standards would apply in assessing whether a non-eu country should be considered a tax haven or not? A non-eu country would be considered to comply with minimum standards of good governance if it effectively applied the OECD standards on transparency and information exchange, and did not operate harmful tax measures. The criteria used by EU Code of Conduct on Business Taxation would be the basis for assessing whether a non-eu country's tax measures are harmful or not. Tax measures which give more favourable treatment to non-resident taxpayers than what is generally applied within that country would be considered potentially harmful, but there are other criteria as well. Examples would be offering a lower rate of corporate tax to foreign investors, or giving tax advantages to business operations that require no real economic activity or substantial presence within that country. What would be the consequences for countries on Member States' blacklists? First of all, appearing on Member States' blacklists would seriously undermine a jurisdiction's reputation as a trustworthy and recognised international partner. Furthermore, Member States are encouraged to renegotiate, suspend or even terminate the Double Tax Convention (DTC) that they have with a blacklisted country. This could have serious consequences for the non-compliant jurisdiction. DTCs help to avoid double taxation and are valued highly by potential foreign investors, so a state without a DTC is much less attractive for investors. Essentially, it could become much less attractive for people and companies to use these jurisdictions to avoid taxes at home. Beyond this, Member States are also advised to avoid promoting business with uncooperative jurisdictions and to take additional complementary actions where appropriate. 5

6 What positive measures does the Commission recommend Member States take to encourage compliance with EU good governance standards? The Commission encourages Member States to use "carrots" as well as "sticks" in encouraging non-eu countries to comply with the EU good governance criteria. Countries which comply with the EU criteria should be removed from national blacklists, if they are on them, and Member States should consider concluding a DTC with these countries. They should also consider cooperating more closely with non-eu countries committed to complying with the EU standards, especially developing countries. This could include offering technical assistance e.g. by seconding tax experts, to those countries that want and would benefit from it. How would the proposed EU approach differ from the current international (OECD) approach to tax havens? The EU approach, which the Commission recommends, is based on three pillars of good governance: transparency, information exchange and fair competition. This goes further than the criteria currently applied internationally, which focus mainly just on the first two pillars. On transparency and information exchange, the criteria in the Recommendation are the same as those applied within the OECD Global Forum on transparency and exchange of information. The Global Forum set certain standards and requirements for transparency and information exchange, which should be respected in order for a country to be considered as meeting the international standards. Through the Global Forum, an international peer review process is carried out to see whether the necessary rules and regulations are in place and working in each state. This peer review process is still ongoing. The main difference in the recommended EU approach lies in the criteria linked to "fair competition". Member States would examine whether a non-eu country's tax regime was in line with the principles of the EU's Code of Conduct (see above), in assessing whether or not it should be blacklisted as a tax haven. This would encourage non-eu countries to respect the same high standards of good governance that apply within the EU itself. Aggressive Tax Planning What is "aggressive tax planning"? Aggressive tax planning is when individuals or companies exploit legal technicalities of a tax system or mismatches between national tax systems with a deliberate intent to minimise the tax they pay. For example, aggressive tax planners may "treaty shop", using the DTCs between different countries to escape taxation in any of these countries. Aggressive tax planning is usually done within the letter of the law, but does not respect the spirit of the law. It tends to stretch the interpretation of what is "legal" to the maximum extent, and minimise the taxes paid by the "planner" to a level below what could be seen as a fair share. 6

7 Why is the Commission putting specific focus on this problem? Aggressive tax planning has become increasingly problematic for Member States for a number of reasons. First, tax planning has taken on an inherently cross-border nature, and the changing shape of the economy has allowed tax planning to become ever more sophisticated. In a globalised economy, where tax bases are less tangible and more mobile, it has become impossible to impose effective national provisions against aggressive tax planning without the risk of businesses relocating. This is a cross-border problem that requires cross-border solutions. Second, tax planners exploit mismatches and loopholes between national systems and different DTCs. Coordinated action is needed to close these loopholes and strengthen common defences. Third, the economic crisis has led Member States and their citizens to re-examine their national tax systems closely. With ordinary citizens facing tax hikes and spending cuts across Europe, it is difficult to justify the fact that some manage to avoid paying their fair share simply because they have the means to engage in complex tax planning. Tackling aggressive tax planning can contribute to the overall fairness of a tax system. Example: Profit participating loans are a type of loan which is often considered as debt in its country of source and as share capital in the country where the payment is made. This is a typical case of mismatch whereby two tax systems characterise the same payment differently for tax purposes. Taxpayers commonly arrange their tax affairs in a way that allows them to take advantage of this mismatch to benefit from (i) having the 'interest' deductible on one side of the border (state of source); and (ii) receiving a tax exempt 'dividend' on the other side of the border (state of residence). What common measures could Member States apply to help to tackle aggressive tax planning? Member States are encouraged to review their DTCs to ensure that they do not create opportunities to escape taxation completely. They should seek to include a clause in their DTCs (with each other and with non-eu countries) saying that they will only refrain from taxing certain income if it is taxed by the other contracting party. This would prevent double non-taxation. Member States are also encouraged to adopt a common General Anti-Abuse Rule. This would allow them to ignore artificial arrangements used essentially for tax avoidance purposes and to tax on the basis of actual economic substance. In addition, the Commission will seek to review the anti-abuse provisions in the Parent- Subsidiary, Interest and Royalties and Merger Directives to determine whether it should take action to strengthen these clauses in

8 Does corporate social responsibility have a role in reducing aggressive tax planning? Corporate Social Responsibility (CSR) refers to actions taken by companies beyond their purely legal obligations, to contribute to society. The economic crisis and its social consequences have made Member States and citizens more aware of the need for fair burden sharing in consolidation efforts. Public attention has also become increasingly focused on the social and ethical performance of enterprises, including on issues such as the level of taxes they pay, bonuses and executive pay. The perception is that recovery efforts must take place on a two way street: Member States should support businesses in getting through the hard times, but equally businesses must contribute fairly to the recovery efforts. Aggressive tax avoidance can be considered contrary to the principles of corporate social responsibility (CSR). Paying taxes is one of the important positive impacts that enterprises have on the rest of society. Last year the Commission presented a package on CSR with measures to improve transparency and promote sustainable business among multinationals. This included more openness about taxes, royalties and bonuses paid worldwide (see IP/11/1238 and MEMO/11/730). 8

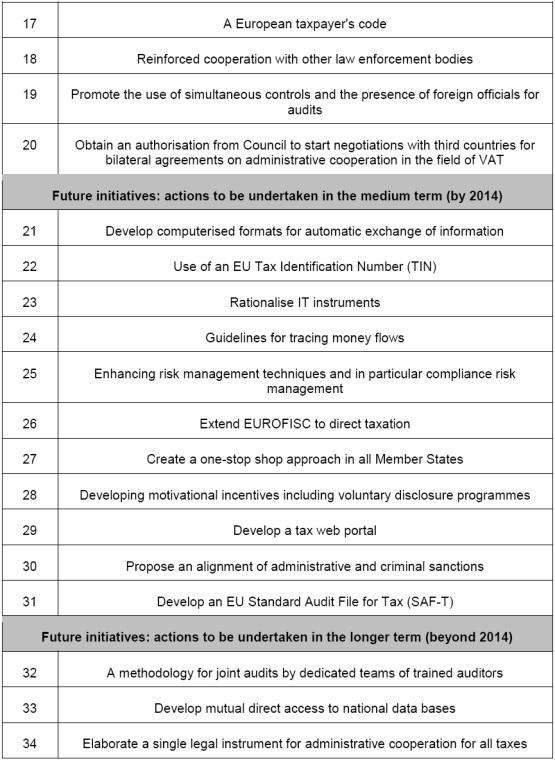

9 Annex: List of measures foreseen in the EU Action Plan 9

10 10

The Anti Tax Avoidance Package Questions and Answers (Updated)

") European Commission - Fact Sheet The Anti Tax Avoidance Package Questions and Answers (Updated) Brussels, 21 June 2016 1. Why has the Commission made the fight against corporate tax avoidance a priority?

European Commission - Fact Sheet The Anti Tax Avoidance Package Questions and Answers (Updated) Brussels, 21 June 2016 1. Why has the Commission made the fight against corporate tax avoidance a priority?

The Anti Tax Avoidance Package Questions and Answers

European Commission - Fact Sheet The Anti Tax Avoidance Package Questions and Answers Brussels, 28 January 2016 1. Why has the Commission made the fight against corporate tax avoidance a priority? Corporate

European Commission - Fact Sheet The Anti Tax Avoidance Package Questions and Answers Brussels, 28 January 2016 1. Why has the Commission made the fight against corporate tax avoidance a priority? Corporate

A FAIR SHARE. Taxation in the EU for the 21st century

A FAIR SHARE Taxation in the EU for the 21st century CONTENT I want Europeans to wake up to a Europe where we have managed to agree on a strong pillar of social standards. Where companies profits will

A FAIR SHARE Taxation in the EU for the 21st century CONTENT I want Europeans to wake up to a Europe where we have managed to agree on a strong pillar of social standards. Where companies profits will

Base erosion & profit shifting (BEPS) 25 May 2016

25 May 2016") Base erosion & profit shifting (BEPS) 25 May 2016 Introduction Important to distinguish between: Tax avoidance Using legal provisions to minimise tax liability Covers interventions that are referred to

Base erosion & profit shifting (BEPS) 25 May 2016 Introduction Important to distinguish between: Tax avoidance Using legal provisions to minimise tax liability Covers interventions that are referred to

Commissioner Algirdas Šemeta EU Commissioner for Taxation, Customs, Anti-Fraud and Audit

Commissioner Algirdas Šemeta EU Commissioner for Taxation, Customs, Anti-Fraud and Audit Speech to Australian Taxation Industry Roundtable 2 December 2013 1 ATI ROUNDTABLE SPEECH Ladies and Gentlemen,

Commissioner Algirdas Šemeta EU Commissioner for Taxation, Customs, Anti-Fraud and Audit Speech to Australian Taxation Industry Roundtable 2 December 2013 1 ATI ROUNDTABLE SPEECH Ladies and Gentlemen,

COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL. Building a fair, competitive and stable corporate tax system for the EU

EUROPEAN COMMISSION Strasbourg, 25.10.2016 COM(2016) 682 final COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL Building a fair, competitive and stable corporate tax system

EUROPEAN COMMISSION Strasbourg, 25.10.2016 COM(2016) 682 final COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL Building a fair, competitive and stable corporate tax system

EUROPEAN COMMISSION PRESENTS ANTI-TAX AVOIDANCE PACKAGE

EUROPEAN COMMISSION PRESENTS ANTI-TAX AVOIDANCE PACKAGE tax.thomsonreuters.com On January 28, 2016, the European Commission presented its Communication on the Anti-Tax Avoidance Package (ATA Package).

EUROPEAN COMMISSION PRESENTS ANTI-TAX AVOIDANCE PACKAGE tax.thomsonreuters.com On January 28, 2016, the European Commission presented its Communication on the Anti-Tax Avoidance Package (ATA Package).

Speech: Priorities for EU tax policy

EUROPEAN COMMISSION Algirdas Šemeta Commissioner responsible for Taxation and Customs Union, Audit and Anti-fraud Speech: Priorities for EU tax policy Irish Parliament Committee on Finance / Dublin 10

EUROPEAN COMMISSION Algirdas Šemeta Commissioner responsible for Taxation and Customs Union, Audit and Anti-fraud Speech: Priorities for EU tax policy Irish Parliament Committee on Finance / Dublin 10

5. Ireland is Countering Aggressive Tax Planning

CONTENTS 1. Foreword by the Minister for Finance 2. Introduction 3. Ireland s International Tax Charter 4. Ireland s Corporate Tax Strategy 5. Ireland is Countering Aggressive Tax Planning 6. Conclusion

CONTENTS 1. Foreword by the Minister for Finance 2. Introduction 3. Ireland s International Tax Charter 4. Ireland s Corporate Tax Strategy 5. Ireland is Countering Aggressive Tax Planning 6. Conclusion

Delegations will find attached the abovementioned opinion. Please note that other language versions should be available at :

Council of the European Union Brussels, 17 October 2017 (OR. en) 13306/17 FISC 227 COVER NOTE From: To: Subject: General Secretariat of the Council Delegations OPINION of the European Economic and Social

Council of the European Union Brussels, 17 October 2017 (OR. en) 13306/17 FISC 227 COVER NOTE From: To: Subject: General Secretariat of the Council Delegations OPINION of the European Economic and Social

AMENDMENTS EN United in diversity EN. European Parliament 2016/0011(CNS) Draft report Hugues Bayet (PE578.

Draft report Hugues Bayet (PE578.") European Parliament 2014-2019 Committee on Economic and Monetary Affairs 2016/0011(CNS) 18.4.2016 AMDMTS 40-237 Draft report Hugues Bayet (PE578.569v01-00) Rules against tax avoidance practices that directly

European Parliament 2014-2019 Committee on Economic and Monetary Affairs 2016/0011(CNS) 18.4.2016 AMDMTS 40-237 Draft report Hugues Bayet (PE578.569v01-00) Rules against tax avoidance practices that directly

The OECD report on base erosion and profit shifting (BEPS) and EU measures against aggressive tax planning and tax fraud

and EU measures against aggressive tax planning and tax fraud") The OECD report on base erosion and profit shifting (BEPS) and EU measures against aggressive tax planning and tax fraud Pere M. Pons New York, May 6 th, 2013 Agenda I. Background II. Key pressure areas

The OECD report on base erosion and profit shifting (BEPS) and EU measures against aggressive tax planning and tax fraud Pere M. Pons New York, May 6 th, 2013 Agenda I. Background II. Key pressure areas

Official Journal of the European Union. (Legislative acts) DIRECTIVES

DIRECTIVES") 5.6.2018 L 139/1 I (Legislative acts) DIRECTIVES COUNCIL DIRECTIVE (EU) 2018/822 of 25 May 2018 amending Directive 2011/16/EU as regards mandatory automatic exchange of information in the field of taxation

5.6.2018 L 139/1 I (Legislative acts) DIRECTIVES COUNCIL DIRECTIVE (EU) 2018/822 of 25 May 2018 amending Directive 2011/16/EU as regards mandatory automatic exchange of information in the field of taxation

COMMISSION RECOMMENDATION. of on aggressive tax planning

EUROPEAN COMMISSION Brussels, 6.12.2012 C(2012) 8806 final COMMISSION RECOMMENDATION of 6.12.2012 on aggressive tax planning EN EN COMMISSION RECOMMENDATION of 6.12.2012 on aggressive tax planning THE

EUROPEAN COMMISSION Brussels, 6.12.2012 C(2012) 8806 final COMMISSION RECOMMENDATION of 6.12.2012 on aggressive tax planning EN EN COMMISSION RECOMMENDATION of 6.12.2012 on aggressive tax planning THE

COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL

EUROPEAN COMMISSION Brussels, 21.3.2018 COM(2018) 146 final COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL Time to establish a modern, fair and efficient taxation standard

EUROPEAN COMMISSION Brussels, 21.3.2018 COM(2018) 146 final COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL Time to establish a modern, fair and efficient taxation standard

Report by Finance Ministers of the Euro Plus Pact on Tax Policy Coordination. European Council (comments by Nouwen)

") Highlights & Insights on European Taxation, Report by Finance Ministers of the Euro Plus Pact on Tax Policy Coordination. European Council (comments by Nouwen) Vindplaats H&I 2012/2.2 Bijgewerkt tot 01-01-2012

Highlights & Insights on European Taxation, Report by Finance Ministers of the Euro Plus Pact on Tax Policy Coordination. European Council (comments by Nouwen) Vindplaats H&I 2012/2.2 Bijgewerkt tot 01-01-2012

Moving Forward on the Global Transparency and Tax Information Exchange Agenda. Remarks by Angel Gurría, Secretary-General OECD

Moving Forward on the Global Transparency and Tax Information Exchange Agenda Remarks by Angel Gurría, Secretary-General OECD Berlin, 23 June 2009 Ladies and Gentlemen, distinguished Ministers: The last

Moving Forward on the Global Transparency and Tax Information Exchange Agenda Remarks by Angel Gurría, Secretary-General OECD Berlin, 23 June 2009 Ladies and Gentlemen, distinguished Ministers: The last

G8/G20 TAXATION ISSUES : Tax Training Day, ODI, London 16 September 2013

G8/G20 TAXATION ISSUES : Tax Training Day, ODI, London 16 September 2013 BASE EROSION AND PROFIT SHIFTING 2 OECD Work on Taxation Focus has historically been on the development of common standards to eliminate

G8/G20 TAXATION ISSUES : Tax Training Day, ODI, London 16 September 2013 BASE EROSION AND PROFIT SHIFTING 2 OECD Work on Taxation Focus has historically been on the development of common standards to eliminate

Proposal for a COUNCIL DIRECTIVE. amending Directive (EU) 2016/1164 as regards hybrid mismatches with third countries. {SWD(2016) 345 final}

2016/1164 as regards hybrid mismatches with third countries. {SWD(2016) 345 final}") EUROPEAN COMMISSION Strasbourg, 25.10.2016 COM(2016) 687 final 2016/0339 (CNS) Proposal for a COUNCIL DIRECTIVE amending Directive (EU) 2016/1164 as regards hybrid mismatches with third countries {SWD(2016)

EUROPEAN COMMISSION Strasbourg, 25.10.2016 COM(2016) 687 final 2016/0339 (CNS) Proposal for a COUNCIL DIRECTIVE amending Directive (EU) 2016/1164 as regards hybrid mismatches with third countries {SWD(2016)

COMMUNICATION FROM THE COMMISSION

EUROPEAN COMMISSION Brussels, 21.3.2018 C(2018) 1756 final COMMUNICATION FROM THE COMMISSION on new requirements against tax avoidance in EU legislation governing in particular financing and investment

EUROPEAN COMMISSION Brussels, 21.3.2018 C(2018) 1756 final COMMUNICATION FROM THE COMMISSION on new requirements against tax avoidance in EU legislation governing in particular financing and investment

The OECD s 3 Major Tax Initiatives

The OECD s 3 Major Tax Initiatives 1. The Global Forum on Transparency and Exchange of Information for Tax Purposes Peer review of ~ 100 countries International standard for transparency and exchange of

The OECD s 3 Major Tax Initiatives 1. The Global Forum on Transparency and Exchange of Information for Tax Purposes Peer review of ~ 100 countries International standard for transparency and exchange of

COMMISSION STAFF WORKING DOCUMENT Accompanying the document. Proposal for a Council Directive

EUROPEAN COMMISSION Strasbourg, 25.10.2016 SWD(2016) 345 final COMMISSION STAFF WORKING DOCUMENT Accompanying the document Proposal for a Council Directive amending Directive (EU) 2016/1164 as regards

EUROPEAN COMMISSION Strasbourg, 25.10.2016 SWD(2016) 345 final COMMISSION STAFF WORKING DOCUMENT Accompanying the document Proposal for a Council Directive amending Directive (EU) 2016/1164 as regards

A8-0189/ Proposal for a directive (COM(2016)0026 C8-0031/ /0011(CNS)) Text proposed by the Commission

0026 C8-0031/ /0011(CNS)) Text proposed by the Commission") 3.6.2016 A8-0189/ 001-091 AMDMTS 001-091 by the Committee on Economic and Monetary Affairs Report Hugues Bayet Rules against tax avoidance practices A8-0189/2016 (COM(2016)0026 C8-0031/2016 2016/0011(CNS))

3.6.2016 A8-0189/ 001-091 AMDMTS 001-091 by the Committee on Economic and Monetary Affairs Report Hugues Bayet Rules against tax avoidance practices A8-0189/2016 (COM(2016)0026 C8-0031/2016 2016/0011(CNS))

Committee on Economic and Monetary Affairs

European Parliament 2014-2019 Committee on Economic and Monetary Affairs 2015/0065(CNS) 17.9.2015 * DRAFT REPORT on the proposal for a Council directive repealing Council Directive 2003/48/EC (COM(2015)0129

European Parliament 2014-2019 Committee on Economic and Monetary Affairs 2015/0065(CNS) 17.9.2015 * DRAFT REPORT on the proposal for a Council directive repealing Council Directive 2003/48/EC (COM(2015)0129

COMMISSION STAFF WORKING DOCUMENT

EUROPEAN COMMISSION Brussels, 18.3.2015 SWD(2015) 60 final COMMISSION STAFF WORKING DOCUMENT Technical analysis of focus and scope of the legal proposal Accompanying the document Proposal for a Council

EUROPEAN COMMISSION Brussels, 18.3.2015 SWD(2015) 60 final COMMISSION STAFF WORKING DOCUMENT Technical analysis of focus and scope of the legal proposal Accompanying the document Proposal for a Council

International regulation and transparency to support Domestic Budget Revenues

International regulation and transparency to support Domestic Budget Revenues Issue brief Prepared by the SDSN Secretariat May 18, 2015 This issue brief summarizes the key propositions put forward in the

International regulation and transparency to support Domestic Budget Revenues Issue brief Prepared by the SDSN Secretariat May 18, 2015 This issue brief summarizes the key propositions put forward in the

Questions and Answers: Value Added Tax (VAT)

") MEMO/11/874 Brussels, 6 December 2011 Questions and Answers: Value Added Tax (VAT) 1. General background What is VAT? VAT is a consumption tax, charged on most goods and services traded for use or consumption

MEMO/11/874 Brussels, 6 December 2011 Questions and Answers: Value Added Tax (VAT) 1. General background What is VAT? VAT is a consumption tax, charged on most goods and services traded for use or consumption

Speech at the International tax symposium "Dynamics of International Tax Competition: Opportunity or Threat?"

Speech at the International tax symposium "Dynamics of International Tax Competition: Opportunity or Threat?" Tax policy coordination for more growth and employment the EU agenda Introduction Ladies and

Speech at the International tax symposium "Dynamics of International Tax Competition: Opportunity or Threat?" Tax policy coordination for more growth and employment the EU agenda Introduction Ladies and

Council of the European Union Brussels, 6 July 2016 (OR. en) Mr Jeppe TRANHOLM-MIKKELSEN, Secretary-General of the Council of the European Union

Mr Jeppe TRANHOLM-MIKKELSEN, Secretary-General of the Council of the European Union") Council of the European Union Brussels, 6 July 2016 (OR. en) 10977/16 FISC 119 COVER NOTE From: date of receipt: 6 July 2016 To: No. Cion doc.: Subject: Secretary-General of the European Commission, signed

Council of the European Union Brussels, 6 July 2016 (OR. en) 10977/16 FISC 119 COVER NOTE From: date of receipt: 6 July 2016 To: No. Cion doc.: Subject: Secretary-General of the European Commission, signed

THE OECD S REPORT ON HARMFUL TAX COMPETITION JOANN M. WEINER * & HUGH J. AULT **

THE OECD S REPORT ON HARMFUL TAX COMPETITION THE OECD S REPORT ON HARMFUL TAX COMPETITION JOANN M. WEINER * & HUGH J. AULT ** Abstract - In response to pressures created by the increasing globalization

THE OECD S REPORT ON HARMFUL TAX COMPETITION THE OECD S REPORT ON HARMFUL TAX COMPETITION JOANN M. WEINER * & HUGH J. AULT ** Abstract - In response to pressures created by the increasing globalization

Automatic exchange of information: frequently asked questions

EUROPEAN COMMISSION MEMO Brussels, 12 June 2013 Automatic exchange of information: frequently asked questions (see also : IP/13/530) What is the automatic exchange of information, for tax purposes? The

EUROPEAN COMMISSION MEMO Brussels, 12 June 2013 Automatic exchange of information: frequently asked questions (see also : IP/13/530) What is the automatic exchange of information, for tax purposes? The

The UAE has joined the Inclusive Framework on BEPS

The UAE has joined the Inclusive Framework on BEPS May 2018 In brief The United Arab Emirates ( UAE ) joined the OECD Inclusive Framework on Base Erosion and Profit Shifting ( BEPS ) on 16 May 2018, bringing

The UAE has joined the Inclusive Framework on BEPS May 2018 In brief The United Arab Emirates ( UAE ) joined the OECD Inclusive Framework on Base Erosion and Profit Shifting ( BEPS ) on 16 May 2018, bringing

COMMISSION OF THE EUROPEAN COMMUNITIES. Proposal for a COUNCIL DIRECTIVE

COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 17.10.2003 COM(2003) 613 final 2003/0239 (CNS) Proposal for a COUNCIL DIRECTIVE amending Directive 90/434/EEC of 23 July 1990 on the common system of taxation

COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 17.10.2003 COM(2003) 613 final 2003/0239 (CNS) Proposal for a COUNCIL DIRECTIVE amending Directive 90/434/EEC of 23 July 1990 on the common system of taxation

9452/16 FC/df 1 DG G 2B

Council of the European Union Brussels, 25 May 2016 (OR. en) 9452/16 FISC 85 ECOFIN 502 OUTCOME OF PROCEEDINGS From: On: 25 May 2016 To: General Secretariat of the Council Delegations No. prev. doc.: 8792/1/16

Council of the European Union Brussels, 25 May 2016 (OR. en) 9452/16 FISC 85 ECOFIN 502 OUTCOME OF PROCEEDINGS From: On: 25 May 2016 To: General Secretariat of the Council Delegations No. prev. doc.: 8792/1/16

EU JOINT TRANSFER PRICING FORUM

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Direct taxation, Tax Coordination, Economic Analysis and Evaluation Company Taxation Initiatives Brussels, June 2013 Taxud/D1/ DOC: JTPF/007/FINAL/2013/EN

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Direct taxation, Tax Coordination, Economic Analysis and Evaluation Company Taxation Initiatives Brussels, June 2013 Taxud/D1/ DOC: JTPF/007/FINAL/2013/EN

COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE COUNCIL AND THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE

EUROPEAN COMMISSION Brussels, 4.10.2017 COM(2017) 566 final COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE COUNCIL AND THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE On the follow-up to

EUROPEAN COMMISSION Brussels, 4.10.2017 COM(2017) 566 final COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE COUNCIL AND THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE On the follow-up to

a) Title of proposal Proposal for a Council Directive amending Council Regulation (EU) 2016/1164 as regards hybrid mismatches with third countries

Title of proposal Proposal for a Council Directive amending Council Regulation (EU) 2016/1164 as regards hybrid mismatches with third countries") Unofficial translation of the assessment by the Dutch government of the proposal of the European Commission regarding hybrid mismatches with third countries Leaflet 2: Directive on hybrid mismatches with

Unofficial translation of the assessment by the Dutch government of the proposal of the European Commission regarding hybrid mismatches with third countries Leaflet 2: Directive on hybrid mismatches with

A Guide To Changes In Irish Tax Rules

A Guide To Changes In Irish Tax Rules - The Global Tax Reform Agenda 6 September 2016 THE FACTS YOU NEED TO KNOW ON IRISH TAX CHANGES 1 INTERNATIONAL TAX RULES HAVE BEEN CHANGING - IRELAND HAS BEEN PARTICIPATING

A Guide To Changes In Irish Tax Rules - The Global Tax Reform Agenda 6 September 2016 THE FACTS YOU NEED TO KNOW ON IRISH TAX CHANGES 1 INTERNATIONAL TAX RULES HAVE BEEN CHANGING - IRELAND HAS BEEN PARTICIPATING

7148/16 HG/NT/kp,vm DGG 2B

Council of the European Union Brussels, 11 May 2016 (OR. en) Interinstitutional File: 2016/0010 (CNS) 7148/16 FISC 39 ECOFIN 231 LEGISLATIVE ACTS AND OTHER INSTRUMENTS Subject: COUNCIL DIRECTIVE amending

Council of the European Union Brussels, 11 May 2016 (OR. en) Interinstitutional File: 2016/0010 (CNS) 7148/16 FISC 39 ECOFIN 231 LEGISLATIVE ACTS AND OTHER INSTRUMENTS Subject: COUNCIL DIRECTIVE amending

European Commission publishes Anti Tax Avoidance Package

28 January 2016 - Number 65 Brazil Desk e-mail bulletin European Commission publishes Anti Tax Avoidance Package On 28 January 2016 the European Commission published an Anti Tax Avoidance Package containing

28 January 2016 - Number 65 Brazil Desk e-mail bulletin European Commission publishes Anti Tax Avoidance Package On 28 January 2016 the European Commission published an Anti Tax Avoidance Package containing

- ReportbyFinance MinistersonTaxPolicyCoordination

ConseilUE COUNCILOF THEEUROPEANUNION Brussels,17November2011 17084/1 PUBLIC LIMITE FISC 145 ECOFIN 783 NOTE from: to: Subject: GeneralSecretariat Delegations EuroPlusPact - ReportbyFinance MinistersonTaxPolicyCoordination

ConseilUE COUNCILOF THEEUROPEANUNION Brussels,17November2011 17084/1 PUBLIC LIMITE FISC 145 ECOFIN 783 NOTE from: to: Subject: GeneralSecretariat Delegations EuroPlusPact - ReportbyFinance MinistersonTaxPolicyCoordination

WORKING PAPER. Financial Counsellors - ECOFIN preparation Presidency Issues Note on 'Tax Certainty in a Changing Environment'

Brussels, 29 March 2017 WK 3787/2017 INIT LIMITE ECOFIN WORKING PAPER This is a paper intended for a specific community of recipients. Handling and further distribution are under the sole responsibility

Brussels, 29 March 2017 WK 3787/2017 INIT LIMITE ECOFIN WORKING PAPER This is a paper intended for a specific community of recipients. Handling and further distribution are under the sole responsibility

COMMISSION OF THE EUROPEAN COMMUNITIES

COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 19.12.2006 COM(2006) 824 final COMMUNICATION FROM THE COMMISSION TO THE COUNCIL, THE EUROPEAN PARLIAMENT AND THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE

COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 19.12.2006 COM(2006) 824 final COMMUNICATION FROM THE COMMISSION TO THE COUNCIL, THE EUROPEAN PARLIAMENT AND THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE

OECD releases final BEPS package

6 October 2015 Tax Flash OECD releases final BEPS package On 5 October 2015, the OECD published the final reports of the OECD/G20 Base Erosion and Profit Shifting ( BEPS ) project, which consist of a package

6 October 2015 Tax Flash OECD releases final BEPS package On 5 October 2015, the OECD published the final reports of the OECD/G20 Base Erosion and Profit Shifting ( BEPS ) project, which consist of a package

Delegations will find attached the text of the draft Directive, resulting from the discussions held at the ECOFIN Council of 8 March 2016.

Council of the European Union Brussels, 15 March 2016 (OR. en) Interinstitutional File: 2016/0010 (CNS) 6949/16 FISC 38 ECOFIN 216 NOTE From: To: General Secretariat of the Council Delegations No. prev.

Council of the European Union Brussels, 15 March 2016 (OR. en) Interinstitutional File: 2016/0010 (CNS) 6949/16 FISC 38 ECOFIN 216 NOTE From: To: General Secretariat of the Council Delegations No. prev.

BELGIUM GLOBAL GUIDE TO M&A TAX: 2018 EDITION

BELGIUM 1 BELGIUM INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? A major corporate income tax reform has been published

BELGIUM 1 BELGIUM INTERNATIONAL DEVELOPMENTS 1. WHAT ARE RECENT TAX DEVELOPMENTS IN YOUR COUNTRY WHICH ARE RELEVANT FOR M&A DEALS AND PRIVATE EQUITY? A major corporate income tax reform has been published

Report from the EU Code of Conduct Group (Business Taxation) to the ECOFIN Council of 4 December European Council (comments by Nouwen)

to the ECOFIN Council of 4 December European Council (comments by Nouwen)") Vindplaats H&I 2013/1.6 Auteur Council of the European Union 23 November 2012, no. 16488/12 Report from the EU Code of Conduct Group (Business Taxation) to the ECOFIN Council of 4 December 2012. European

Vindplaats H&I 2013/1.6 Auteur Council of the European Union 23 November 2012, no. 16488/12 Report from the EU Code of Conduct Group (Business Taxation) to the ECOFIN Council of 4 December 2012. European

AmCham EU s position on the Commission Anti-Tax Avoidance Package

AmCham EU s position on the Commission Anti-Tax Avoidance Package Executive summary AmCham EU welcomes attempts to ensure that adoption of the OECD s recommendations is consistent across the EU and with

AmCham EU s position on the Commission Anti-Tax Avoidance Package Executive summary AmCham EU welcomes attempts to ensure that adoption of the OECD s recommendations is consistent across the EU and with

VAT Tax Evasion. Measures undertaken by the Portuguese Government. The Brussels Tax Forum th of November, 2013

VAT Tax Evasion Measures undertaken by the Portuguese Government The Brussels Tax Forum 2013 18 th of November, 2013 Agenda European context Measures undertaken by the Portuguese Government to curb tax

VAT Tax Evasion Measures undertaken by the Portuguese Government The Brussels Tax Forum 2013 18 th of November, 2013 Agenda European context Measures undertaken by the Portuguese Government to curb tax

Tackling Aggressive Tax Planning in the European Union - Recent Developments

Tackling Aggressive Tax Planning in the European Union - Recent Developments Dr Christiana HJI Panayi Senior Lecturer in Tax Law Queen Mary University of London 1 Important recent developments Digital

Tackling Aggressive Tax Planning in the European Union - Recent Developments Dr Christiana HJI Panayi Senior Lecturer in Tax Law Queen Mary University of London 1 Important recent developments Digital

the procedural aspects of its future Work Package (as contained in Annex I); the final version of the future WorkPackage (as contained in Annex II);

; the final version of the future WorkPackage (as contained in Annex II);") COUNCIL OF THE EUROPEAN UNION Brussels, 26 November 2008 16410/08 FISC 174 "A" ITEM NOTE from: General Secretariat to: Council Subject:: Code of Conduct (Business Taxation) = Draft Council Conclusions

COUNCIL OF THE EUROPEAN UNION Brussels, 26 November 2008 16410/08 FISC 174 "A" ITEM NOTE from: General Secretariat to: Council Subject:: Code of Conduct (Business Taxation) = Draft Council Conclusions

Impact of BEPS and Other International Tax Risks on the Jersey Funds Industry

www.pwc.com/jg November 2015 Impact of BEPS and Other International Tax Risks on the Jersey Funds Industry Current International Tax Environment 1 2 The current environment The ability to achieve tax certainty

www.pwc.com/jg November 2015 Impact of BEPS and Other International Tax Risks on the Jersey Funds Industry Current International Tax Environment 1 2 The current environment The ability to achieve tax certainty

INCEPTION IMPACT ASSESSMENT

TITLE OF THE INITIATIVE LEAD DG RESPONSIBLE UNIT AP NUMBER LIKELY TYPE OF INITIATIVE INCEPTION IMPACT ASSESSMENT Re-launch of the Common Consolidated Corporate Tax Base (CCCTB) DG TAXUD.D DATE OF ROADMAP

TITLE OF THE INITIATIVE LEAD DG RESPONSIBLE UNIT AP NUMBER LIKELY TYPE OF INITIATIVE INCEPTION IMPACT ASSESSMENT Re-launch of the Common Consolidated Corporate Tax Base (CCCTB) DG TAXUD.D DATE OF ROADMAP

How BEPS fits in with the EU s tax agenda. The European Union (EU) has actively participated in the entire

has actively participated in the entire") How BEPS fits in with the EU s tax agenda Klaus von Brocke and Jurjan Wouda Kuipers look at how BEPS recommendations interact with EU tax laws. The European Union (EU) has actively participated in the

How BEPS fits in with the EU s tax agenda Klaus von Brocke and Jurjan Wouda Kuipers look at how BEPS recommendations interact with EU tax laws. The European Union (EU) has actively participated in the

PUBLIC INTRODUCTION /15 AS/FC/mpd 1 DG G 2B LIMITE EN. Council of the European Union Brussels, 23 November 2015 (OR. en) 14302/15 LIMITE

14302/15 LIMITE") Conseil UE Council of the European Union Brussels, 23 November 2015 (OR. en) PUBLIC 14302/15 LIMITE FISC 159 ECOFIN 883 REPORT From: To: Subject: Code of Conduct Group (Business Taxation) Permanent Representatives

Conseil UE Council of the European Union Brussels, 23 November 2015 (OR. en) PUBLIC 14302/15 LIMITE FISC 159 ECOFIN 883 REPORT From: To: Subject: Code of Conduct Group (Business Taxation) Permanent Representatives

Proposal for amending the Parent-Subsidiary Directive: European Commission is waging war against double non-taxation

Proposal for amending the Parent-Subsidiary Directive: European Commission is waging war against double non-taxation David Ledure/Frederik Boulogne/Pieter Deré On 25 November 2013, the European Commission

Proposal for amending the Parent-Subsidiary Directive: European Commission is waging war against double non-taxation David Ledure/Frederik Boulogne/Pieter Deré On 25 November 2013, the European Commission

Intellectual Property Box Regimes

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT A: ECONOMIC AND SCIENTIFIC POLICY Intellectual Property Box Regimes Tax Planning, Effective Tax Burdens and Tax Policy Options IN-DEPTH ANALYSIS

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT A: ECONOMIC AND SCIENTIFIC POLICY Intellectual Property Box Regimes Tax Planning, Effective Tax Burdens and Tax Policy Options IN-DEPTH ANALYSIS

Answer-to-Question- 1

Answer-to-Question- 1 The arm's length principle is the standard used by all OECD parties in setting and testing prices between related parties. It aims to assess the level of profits which would have

Answer-to-Question- 1 The arm's length principle is the standard used by all OECD parties in setting and testing prices between related parties. It aims to assess the level of profits which would have

TEXTS ADOPTED. having regard to the Commission proposal to the Council (COM(2016)0683),

0683),") European Parliament 2014-2019 TEXTS ADOPTED P8_TA(2018)0087 Common Consolidated Corporate Tax Base * European Parliament legislative resolution of 15 March 2018 on the proposal for a Council directive

European Parliament 2014-2019 TEXTS ADOPTED P8_TA(2018)0087 Common Consolidated Corporate Tax Base * European Parliament legislative resolution of 15 March 2018 on the proposal for a Council directive

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration Value Added Tax VEG N O 042

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration Value Added Tax VAT Expert Group 10 th meeting 31 March 2015 taxud.c.1(2015)1342130 EN Brussels,

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration Value Added Tax VAT Expert Group 10 th meeting 31 March 2015 taxud.c.1(2015)1342130 EN Brussels,

A holding company belonging to an equity investor group was not considered as an equity investor

Tax news PwC Finland 2.10.2014 Corporate Income Tax FINLAND A holding company belonging to an equity investor group was not considered as an equity investor Decision 14/1367/3 of the Administrative Court

Tax news PwC Finland 2.10.2014 Corporate Income Tax FINLAND A holding company belonging to an equity investor group was not considered as an equity investor Decision 14/1367/3 of the Administrative Court

WORKING PAPER. Brussels, 15 February 2019 WK 2235/2019 INIT LIMITE ECOFIN FISC

Brussels, 15 February 2019 WK 2235/2019 INIT LIMITE ECOFIN FISC WORKING PAPER This is a paper intended for a specific community of recipients. Handling and further distribution are under the sole responsibility

Brussels, 15 February 2019 WK 2235/2019 INIT LIMITE ECOFIN FISC WORKING PAPER This is a paper intended for a specific community of recipients. Handling and further distribution are under the sole responsibility

Government response to House of Lords Select Committee on Economic Affairs 1 st report of Session :

Government response to House of Lords Select Committee on Economic Affairs 1 st report of Session 2013-14: Tackling corporate tax avoidance in a global economy: is a new approach needed? Chapter 1: 136.

Government response to House of Lords Select Committee on Economic Affairs 1 st report of Session 2013-14: Tackling corporate tax avoidance in a global economy: is a new approach needed? Chapter 1: 136.

A package to tackle harmful tax competition in the European Union

COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 05.11.1997 COM(97) 564 final COMMUNICATION FROM THE COMMISSION TO THE COUNCIL AND THE EUROPEAN PARLIAMENT A package to tackle harmful tax competition in

COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 05.11.1997 COM(97) 564 final COMMUNICATION FROM THE COMMISSION TO THE COUNCIL AND THE EUROPEAN PARLIAMENT A package to tackle harmful tax competition in

European Investment Bank. EIB Policy towards weakly regulated, non-transparent and uncooperative jurisdictions

EIB Policy towards weakly regulated, non-transparent and uncooperative jurisdictions EIB Policy towards weakly regulated, non-transparent and uncooperative jurisdictions 15 December 2010 page 1 / 11 EIB

EIB Policy towards weakly regulated, non-transparent and uncooperative jurisdictions EIB Policy towards weakly regulated, non-transparent and uncooperative jurisdictions 15 December 2010 page 1 / 11 EIB

Committee on Economic and Monetary Affairs

+European Parliament 2014-2019 Committee on Economic and Monetary Affairs 2016/0337(CNS) 13.7.2017 * DRAFT REPORT on the proposal for a Council directive on a Common Corporate Tax Base (COM(2016)0685 C8-0472/2016

+European Parliament 2014-2019 Committee on Economic and Monetary Affairs 2016/0337(CNS) 13.7.2017 * DRAFT REPORT on the proposal for a Council directive on a Common Corporate Tax Base (COM(2016)0685 C8-0472/2016

15/09/2017. Conseil des barreaux européens Council of Bars and Law Societies of Europe

Conseil des barreaux européens Council of Bars and Law Societies of Europe Association internationale sans but lucratif Rue Joseph II, 40 /8 1000 Bruxelles T. : +32 (0)2 234 65 10 Email : ccbe@ccbe.eu

Conseil des barreaux européens Council of Bars and Law Societies of Europe Association internationale sans but lucratif Rue Joseph II, 40 /8 1000 Bruxelles T. : +32 (0)2 234 65 10 Email : ccbe@ccbe.eu

EIB stakeholders engagement seminar

EIB stakeholders engagement seminar Non-Compliant Jurisdictions 29 November, 2017, Brussels Office of the Group Chief Compliance Officer European Investment Bank 29/11/2017 1 Table of contents EIB and

EIB stakeholders engagement seminar Non-Compliant Jurisdictions 29 November, 2017, Brussels Office of the Group Chief Compliance Officer European Investment Bank 29/11/2017 1 Table of contents EIB and

EUROPEAN COUNCIL - CONCLUSIONS. Brussels, 22/05/2013

EUROPEAN COMMISSION SECRETARIAT-GENERAL D/13/4 Brussels, 22/05/2013 EUROPEAN COUNCIL - CONCLUSIONS Brussels, 22/05/2013 EUCO 75/13 EN Delegations will find attached the conclusions of the European Council

EUROPEAN COMMISSION SECRETARIAT-GENERAL D/13/4 Brussels, 22/05/2013 EUROPEAN COUNCIL - CONCLUSIONS Brussels, 22/05/2013 EUCO 75/13 EN Delegations will find attached the conclusions of the European Council

Recent and expected tax changes in Bulgaria and Greece important for cross-border operations

Baker Tilly in South East Europe Cyprus, Bulgaria, Greece, Romania, Moldova Recent and expected tax changes in Bulgaria and Greece important for cross-border operations November 2016 Agenda Implementation

Baker Tilly in South East Europe Cyprus, Bulgaria, Greece, Romania, Moldova Recent and expected tax changes in Bulgaria and Greece important for cross-border operations November 2016 Agenda Implementation

BEPS: What does it mean for funds and asset managers?

BEPS: What does it mean for funds and asset managers? Client Seminar Martin Shah René van Eldonk Malcolm Richardson, M&G 10 March 2015 Overview Background to and progress to date of BEPS Action Plan More

BEPS: What does it mean for funds and asset managers? Client Seminar Martin Shah René van Eldonk Malcolm Richardson, M&G 10 March 2015 Overview Background to and progress to date of BEPS Action Plan More

European Economic and Social Committee OPINION. European Economic and Social Committee

European Economic and Social Committee ECO/442 VAT reform package (I) OPINION European Economic and Social Committee Communication from the Commission to the European Parliament, the Council and the European

European Economic and Social Committee ECO/442 VAT reform package (I) OPINION European Economic and Social Committee Communication from the Commission to the European Parliament, the Council and the European

Tax Havens: Tax Fairness Action Plan THE QUÉBEC ECONOMIC PLAN

Tax Havens: Tax Fairness Action Plan THE QUÉBEC ECONOMIC PLAN Tax Havens: Tax Fairness Action Plan The québec Economic Plan Tax Havens: Tax Fairness Action Plan The Québec Economic Plan Legal deposit November

Tax Havens: Tax Fairness Action Plan THE QUÉBEC ECONOMIC PLAN Tax Havens: Tax Fairness Action Plan The québec Economic Plan Tax Havens: Tax Fairness Action Plan The Québec Economic Plan Legal deposit November

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Direct taxation, Tax Coordination, Economic Analysis and Evaluation Direct Tax Policy & Cooperation Brussels, 3 September 2014 TAXUD.D.2

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Direct taxation, Tax Coordination, Economic Analysis and Evaluation Direct Tax Policy & Cooperation Brussels, 3 September 2014 TAXUD.D.2

BACKGROUND 1 ECONOMIC and FINANCIAL AFFAIRS COUNCIL Tuesday 4 March in Brussels

Brussels, 29 February 2008 BACKGROUND 1 ECONOMIC and FINANCIAL AFFAIRS COUNCIL Tuesday 4 March in Brussels The Council will be preceded as usual by a meeting of the eurogroup, on Monday, 3 March, starting

Brussels, 29 February 2008 BACKGROUND 1 ECONOMIC and FINANCIAL AFFAIRS COUNCIL Tuesday 4 March in Brussels The Council will be preceded as usual by a meeting of the eurogroup, on Monday, 3 March, starting

Flash News. PwC Luxembourg BEPS Series- What it means for the Luxembourg Asset Management industry

www.pwc.lu/tax Flash News PwC Luxembourg BEPS Series- What it means for the Luxembourg Asset Management industry On Monday 5 October 2015, the Organisation for Economic Cooperation and Development (OECD)

www.pwc.lu/tax Flash News PwC Luxembourg BEPS Series- What it means for the Luxembourg Asset Management industry On Monday 5 October 2015, the Organisation for Economic Cooperation and Development (OECD)

Tax harmonisation versus tax competition in Europe

SPEECH/05/624 László Kovács European Commissioner for Taxation and Customs Tax harmonisation versus tax competition in Europe Conference «Tax harmonisation and legal uncertainty in Central and Eastern

SPEECH/05/624 László Kovács European Commissioner for Taxation and Customs Tax harmonisation versus tax competition in Europe Conference «Tax harmonisation and legal uncertainty in Central and Eastern

Standard contractual clauses for the transfer of personal data to third countries - Frequently asked questions

MEMO/05/3 Brussels, 7 January 2005 Standard contractual clauses for the transfer of personal data to third countries - Frequently asked questions Directive 95/46/EC, on the protection of individuals with

MEMO/05/3 Brussels, 7 January 2005 Standard contractual clauses for the transfer of personal data to third countries - Frequently asked questions Directive 95/46/EC, on the protection of individuals with

IMF Revenue Mobilizations and Development Conference: Session on Business Taxation. Alan Carter (ITD) Washington DC, April 18, 2011

Washington DC, April 18, 2011") IMF Revenue Mobilizations and Development Conference: Session on Business Taxation Alan Carter (ITD) Washington DC, April 18, 2011 International Business Tax Issues - Why are international tax issues important?

IMF Revenue Mobilizations and Development Conference: Session on Business Taxation Alan Carter (ITD) Washington DC, April 18, 2011 International Business Tax Issues - Why are international tax issues important?

TAX STRATEGY AND APPROACH TO TAX

TAX STRATEGY AND APPROACH TO TAX We are not just a British bank we take pride in being a bank for Britain, at the heart of the UK s economy. This document summarises our approach to tax. In line with our

TAX STRATEGY AND APPROACH TO TAX We are not just a British bank we take pride in being a bank for Britain, at the heart of the UK s economy. This document summarises our approach to tax. In line with our

Proposal for a COUNCIL DIRECTIVE

EUROPEAN COMMISSION Brussels, 21.6.2017 COM(2017) 335 final 2017/0138 (CNS) Proposal for a COUNCIL DIRECTIVE amending Directive 2011/16/EU as regards mandatory automatic exchange of information in the

EUROPEAN COMMISSION Brussels, 21.6.2017 COM(2017) 335 final 2017/0138 (CNS) Proposal for a COUNCIL DIRECTIVE amending Directive 2011/16/EU as regards mandatory automatic exchange of information in the

10472/18 JC/NC/jk ECOMP.2.B. Council of the European Union Brussels, 14 September 2018 (OR. en) 10472/18. Interinstitutional File: 2017/0248 (CNS)

10472/18. Interinstitutional File: 2017/0248 (CNS)") Council of the European Union Brussels, 14 September 2018 (OR. en) Interinstitutional File: 2017/0248 (CNS) 10472/18 FISC 276 ECOFIN 667 LEGISLATIVE ACTS AND OTHER INSTRUMTS Subject: COUNCIL REGULATION

Council of the European Union Brussels, 14 September 2018 (OR. en) Interinstitutional File: 2017/0248 (CNS) 10472/18 FISC 276 ECOFIN 667 LEGISLATIVE ACTS AND OTHER INSTRUMTS Subject: COUNCIL REGULATION

General Comments. Action 6 on Treaty Abuse reads as follows:

OECD Centre on Tax Policy and Administration Tax Treaties Transfer Pricing and Financial Transactions Division 2, rue André Pascal 75775 Paris France The Confederation of Swedish Enterprise: Comments on

OECD Centre on Tax Policy and Administration Tax Treaties Transfer Pricing and Financial Transactions Division 2, rue André Pascal 75775 Paris France The Confederation of Swedish Enterprise: Comments on

Transparent, sophisticated, tax neutral

Transparent, sophisticated, tax neutral The truth about offshore alternative investment funds www.aima.org Executive Summary Collective investment is good for investors. Investors such as pension funds,

Transparent, sophisticated, tax neutral The truth about offshore alternative investment funds www.aima.org Executive Summary Collective investment is good for investors. Investors such as pension funds,

CORPORATE TAX AND THE DIGITAL ECONOMY

ICAEW REPRESENTATION 12/18 CORPORATE TAX AND THE DIGITAL ECONOMY 2 February ICAEW welcomes the opportunity to comment on the position paper Corporate Tax and the Digital Economy published by HM Treasury

ICAEW REPRESENTATION 12/18 CORPORATE TAX AND THE DIGITAL ECONOMY 2 February ICAEW welcomes the opportunity to comment on the position paper Corporate Tax and the Digital Economy published by HM Treasury

Tax Information Exchange Arrangements

Tax Information Exchange Arrangements Draft TJN Briefing Paper April 2009: comments welcome to markus@taxjustice.net In March 2009, many states which had been identified as tax havens or secrecy jurisdictions

Tax Information Exchange Arrangements Draft TJN Briefing Paper April 2009: comments welcome to markus@taxjustice.net In March 2009, many states which had been identified as tax havens or secrecy jurisdictions

Reform of the EU Statutory Audit Market - Frequently Asked Questions

EUROPEAN COMMISSION MEMO Brussels, 3 April 2014 Reform of the EU Statutory Audit Market - Frequently Asked Questions WHERE DOES THE REFORM STAND? On 17 December 2013, the European Parliament and the Member

EUROPEAN COMMISSION MEMO Brussels, 3 April 2014 Reform of the EU Statutory Audit Market - Frequently Asked Questions WHERE DOES THE REFORM STAND? On 17 December 2013, the European Parliament and the Member

Council of the European Union Brussels, 22 October 2015 (OR. en) Mr Jeppe TRANHOLM-MIKKELSEN, Secretary-General of the Council of the European Union

Mr Jeppe TRANHOLM-MIKKELSEN, Secretary-General of the Council of the European Union") Council of the European Union Brussels, 22 October 2015 (OR. en) Interinstitutional File: 2015/0244 (NLE) 13299/15 PROPOSAL From: date of receipt: 21 October 2015 To: No. Cion doc.: Subject: FISC 133 ECOFIN

Council of the European Union Brussels, 22 October 2015 (OR. en) Interinstitutional File: 2015/0244 (NLE) 13299/15 PROPOSAL From: date of receipt: 21 October 2015 To: No. Cion doc.: Subject: FISC 133 ECOFIN

EU Anti-Tax Avoidance Package: impacts on the real estate industry

EUDTG/RE March 2016 EU Anti-Tax Avoidance Package: impacts on the real estate industry On 28 January 2016, the EU Commission (EC) presented its EU Anti-Tax Avoidance Package (ATAP). The below provides

EUDTG/RE March 2016 EU Anti-Tax Avoidance Package: impacts on the real estate industry On 28 January 2016, the EU Commission (EC) presented its EU Anti-Tax Avoidance Package (ATAP). The below provides

Contents. The tax policy is mandatory and applies to all Glencore Group entities.

Group Tax Policy The tax policy is mandatory and applies to all Glencore Group entities. Contents 1. Purpose and Scope 2 2. Group Approach to Tax 2 3. Prevention of Facilitation of Tax Evasion 3 4. Tax

Group Tax Policy The tax policy is mandatory and applies to all Glencore Group entities. Contents 1. Purpose and Scope 2 2. Group Approach to Tax 2 3. Prevention of Facilitation of Tax Evasion 3 4. Tax

Baker Tilly in South East Europe

Baker Tilly in South East Europe Cyprus, Bulgaria, Greece, Romania, Moldova Tax changes in Romania and internationally affecting substance Exchange of Information by banks March 2017 Agenda Changes in

Baker Tilly in South East Europe Cyprus, Bulgaria, Greece, Romania, Moldova Tax changes in Romania and internationally affecting substance Exchange of Information by banks March 2017 Agenda Changes in

The Commission s Study on Company

HOME STATE TAXATION VS. COMMON BASE TAXATION jurisdictions by an automatic formula, and taxed at the national tax rates, which member states will continue to establish themselves. A comprehensive solution

HOME STATE TAXATION VS. COMMON BASE TAXATION jurisdictions by an automatic formula, and taxed at the national tax rates, which member states will continue to establish themselves. A comprehensive solution

Contents. 1. Purpose and Scope Group Approach to Tax Prevention of Facilitation of Tax Evasion Tax Risk Management and Governance 3

GROUP TAX POLICY Contents 1. Purpose and Scope 2 2. Group Approach to Tax 2 3. Prevention of Facilitation of Tax Evasion 3 4. Tax Risk Management and Governance 3 5. Tax Compliance 3 6. Tax Authorities

GROUP TAX POLICY Contents 1. Purpose and Scope 2 2. Group Approach to Tax 2 3. Prevention of Facilitation of Tax Evasion 3 4. Tax Risk Management and Governance 3 5. Tax Compliance 3 6. Tax Authorities

Council of the European Union Brussels, 22 June 2015 (OR. en)

") Council of the European Union Brussels, 22 June 2015 (OR. en) 10162/15 FISC 82 ECOFIN 530 CO EUR-PREP 30 NOTE From: To: Subject: General Secretariat of the Council Delegations Report by Finance Ministers

Council of the European Union Brussels, 22 June 2015 (OR. en) 10162/15 FISC 82 ECOFIN 530 CO EUR-PREP 30 NOTE From: To: Subject: General Secretariat of the Council Delegations Report by Finance Ministers

Proposal for a COUNCIL DIRECTIVE

EUROPEAN COMMISSION Brussels, 25.5.2018 COM(2018) 298 final 2018/0150 (CNS) Proposal for a COUNCIL DIRECTIVE amending Directive 2006/112/EC on the common system of value added tax as regards the period

EUROPEAN COMMISSION Brussels, 25.5.2018 COM(2018) 298 final 2018/0150 (CNS) Proposal for a COUNCIL DIRECTIVE amending Directive 2006/112/EC on the common system of value added tax as regards the period

Protecting the Tax Base of Developing Countries: An Overview

Papers on Selected Topics in Protecting the Tax Base of Developing Countries Draft Paper No. 1 May 2013 Protecting the Tax Base of Developing Countries: An Overview Hugh J. Ault Professor Emeritus of Tax

Papers on Selected Topics in Protecting the Tax Base of Developing Countries Draft Paper No. 1 May 2013 Protecting the Tax Base of Developing Countries: An Overview Hugh J. Ault Professor Emeritus of Tax

The International Tax and Regulatory Landscape for Small State IFCs

December 2016 \ 1 The International Tax and Regulatory Landscape for Small State IFCs Overview This brief is aimed at officials working in small states that host international financial centres (IFCs)

December 2016 \ 1 The International Tax and Regulatory Landscape for Small State IFCs Overview This brief is aimed at officials working in small states that host international financial centres (IFCs)

PUBLIC INTRODUCTION. 9620/15 AS/FC/df 1 DG G 2B LIMITE EN. Council of the European Union. Brussels, 11 June 2015 (OR. en) 9620/15 LIMITE

9620/15 LIMITE") Conseil UE Council of the European Union PUBLIC Brussels, 11 June 2015 (OR. en) 9620/15 LIMITE FISC 60 ECOFIN 443 REPORT From: To: Subject: Code of Conduct Group (Business Taxation) Permanent Representatives

Conseil UE Council of the European Union PUBLIC Brussels, 11 June 2015 (OR. en) 9620/15 LIMITE FISC 60 ECOFIN 443 REPORT From: To: Subject: Code of Conduct Group (Business Taxation) Permanent Representatives

Proposal for a COUNCIL DIRECTIVE. on Double Taxation Dispute Resolution Mechanisms in the European Union. {SWD(2016) 343 final} {SWD(2016) 344 final}

343 final} {SWD(2016) 344 final}") EUROPEAN COMMISSION Strasbourg, 25.10.2016 COM(2016) 686 final 2016/0338 (CNS) Proposal for a COUNCIL DIRECTIVE on Double Taxation Dispute Resolution Mechanisms in the European Union {SWD(2016) 343 final}

EUROPEAN COMMISSION Strasbourg, 25.10.2016 COM(2016) 686 final 2016/0338 (CNS) Proposal for a COUNCIL DIRECTIVE on Double Taxation Dispute Resolution Mechanisms in the European Union {SWD(2016) 343 final}

(Legislative acts) DIRECTIVES

DIRECTIVES") 11.3.2011 Official Journal of the European Union L 64/1 I (Legislative acts) DIRECTIVES COUNCIL DIRECTIVE 2011/16/EU of 15 February 2011 on administrative cooperation in the field of taxation and repealing

11.3.2011 Official Journal of the European Union L 64/1 I (Legislative acts) DIRECTIVES COUNCIL DIRECTIVE 2011/16/EU of 15 February 2011 on administrative cooperation in the field of taxation and repealing