COMMENTARY JONES DAY. Under Ohio law, an individual is a resident for Ohio income tax purposes if he or she is domiciled in Ohio.

|

|

|

- Nickolas Arnold

- 6 years ago

- Views:

Transcription

. Outgoing Ohio Governor Bob Taft signed the bill into law on January 2, 2007.")

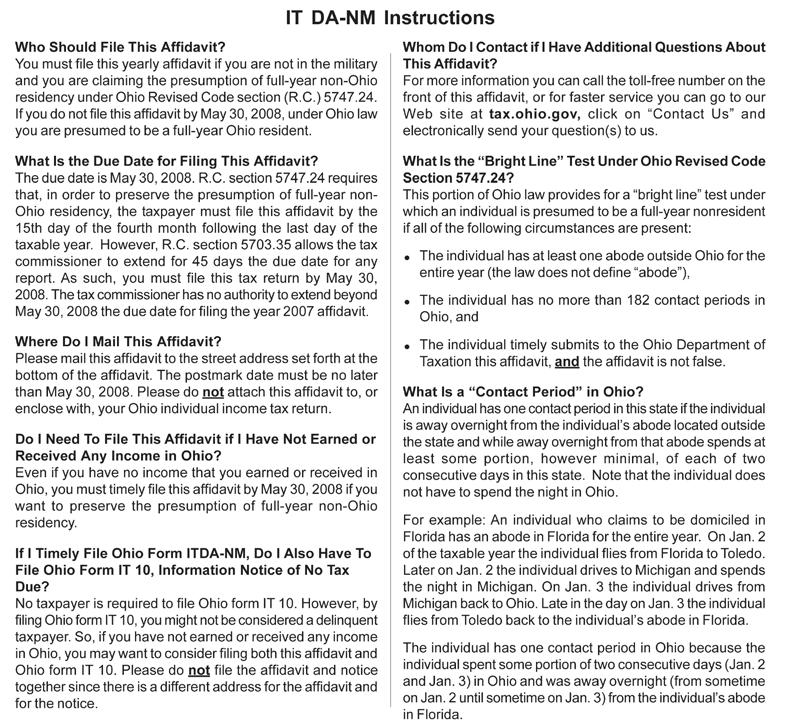

1 January 2008 JONES DAY COMMENTARY Wealth Management Ohio s New Residency Requirements for Individual Income Tax Purposes On December 14, 2006, the Ohio General Assembly passed Sub. H.B. 73, which changed Ohio s residency requirements for Ohio income tax purposes (the socalled snowbird rules). Outgoing Ohio Governor Bob Taft signed the bill into law on January 2, It is effective for tax years after The Ohio Department of Taxation recently published the Affidavit of Non-Ohio Domicile for Taxable Year 2007 form. Why Does Residency Status Matter? An Ohio resident must pay Ohio income tax on his or her worldwide income, subject to credits for taxes paid in other jurisdictions. A nonresident, however, only pays Ohio income tax on income earned or received in Ohio. Who Is a Resident? Under Ohio law, an individual is a resident for Ohio income tax purposes if he or she is domiciled in Ohio. Whether an individual is domiciled in Ohio depends upon the number of contact periods the individual has in Ohio during the taxable year (for most people, the calendar year). A contact period occurs when an individual is away from his or her out-of-state abode and spends a portion of two consecutive days in Ohio. ( Abode typically means a place where one lives.) In most circumstances, this will be the number of nights spent in Ohio. Old Law Under the old Ohio residency rules, an individual who had 120 or fewer contact periods during a taxable year and at least one abode outside Ohio during the entire taxable year was presumed not to be domiciled in Ohio for that taxable year. This presumption was irrebuttable (meaning it could not be challenged), unless the taxpayer received a request from the Ohio Tax Commissioner ( Commissioner ) for a statement verifying facts concerning the individual s domicile, 2008 Jones Day. All rights reserved. Printed in the USA.

2 and the individual failed to submit the statement within 60 days of receipt. Failure to submit the requested statement resulted in a presumption that the individual was domiciled in Ohio for the entire taxable year. This presumption was rebuttable (or challengeable) by the individual upon presentation of sufficient evidence. Moreover, Ohio domicile was presumed to exist for an individual with more than 121 contact periods with Ohio during the taxable year. The individual could rebut the presumption with sufficient evidence, but the burden of proof was much higher if the individual had more than 182 contact periods with Ohio during the taxable year. Certain contact periods were exempt from these determinations. For instance, a contact period did not count for 2006 if the individual spent any portion of a contact period: (i) providing services or raising funds for a not-for-profit organization, (ii) attending to his or her own, or an immediate or extended family member s, medical hardship, or (iii) attending an immediate or extended family member s funeral. Also, under prior law, an individual could elect nonresident status by filing a written statement with the Commissioner during the taxable year immediately preceding the taxable year to which the election applied. For instance, an individual who made this election in 2005 would have been considered a nonresident for all of taxable year New Law The new law increases the number of contact periods an individual can have with Ohio and still be presumed not to be domiciled in Ohio for income tax purposes from 120 to 182. Ohio domicile is presumed for individuals with more than 182 contact periods (and like the old law, this presumption can be rebutted by the individual, but the burden of proof is high). The new law brings several other significant changes. It requires an individual wishing to take advantage of the non- Ohio domicile presumption for tax year 2007 to file Ohio Tax Form IT DA-NM (the Form ) (attached hereto), verifying that the individual is not domiciled in Ohio and specifying the location of each non-ohio abode (in contrast, under the old law, such a statement was required only if requested by the Commissioner). The Form needs to be filed by May 30, Failure to file, or filing a false Form, will result in a presumption that the individual was domiciled in Ohio during tax year The individual would then need to rebut this presumption by presenting sufficient evidence to the contrary. As was the case under the old law, only certain types of evidence regarding domicile will be considered by the Commissioner. For instance, the Commissioner will not consider: the location of financial institutions in which the individual has accounts, the location of professional services (accounting, legal, health care) utilized by the individual, the location or place of formation of a business entity with which the individual is associated, the place of residency or domicile listed in the individual s estate planning documents, and the location of not-for-profit organizations to which the individual makes contributions. On the other hand, the Commissioner will consider evidence of: the forwarding of mail from an Ohio address to a non-ohio address by the individual, the use of club facilities outside of Ohio by the individual, utility shut-off notices related to the individual s Ohio residence, and the individual s out-of-state voting records. Another important change is that the new law no longer includes the so-called charitable, medical hardship, or funeral exemptions from contact periods. Thus, individuals must now take into account all time spent in Ohio for purposes of computing contact periods. Lastly, under the new law, individuals can no longer affirmatively elect nonresident status in the current year for application in the subsequent year. Residency for Ohio Estate Tax Purposes The new law only applies for Ohio income tax purposes. For Ohio estate tax purposes, facts and circumstances are analyzed in order to determine where the decedent intended to have his or her domicile. An individual s domicile depends upon a variety of factors, including location(s) of the individual s home(s), location(s) of the individual s valuable possessions and personal property, where the individual votes, where the individual is involved in civic activities, etc. 2

3 Conclusion Under the new law, snowbirds can spend more time in Ohio while maintaining a presumption of nonresidency status for Ohio income tax purposes, but they must file the requisite Form with the Commissioner. (Although the Form is valid only for tax year 2007, presumably the Ohio Department of Taxation will publish a similar form for subsequent tax years.) Also, individuals must now take into account time spent in Ohio for charitable or medical reasons, or to attend a funeral. For individuals wishing to establish residency outside Ohio, or wishing to establish nonresidency for estate tax purposes, it is still important to take steps such as forwarding mail, changing Ohio club memberships from resident to nonresident status, and registering to vote outside of Ohio (and to keep good records of these steps), as they will provide evidence of nonresidency if needed. Lawyer Contacts For further information, please contact your principal Firm representative or one of the lawyers listed below. General messages may be sent using our Contact Us form, which can be found at Kenneth G. Hochman kghochman@jonesday.com Lisa A. Roberts-Mamone larobertsmamone@jonesday.com Michael J. Horvitz mjhorvitz@jonesday.com Ellen E. Halfon eehalfon@jonesday.com J. Joseph Korpics jkorpics@jonesday.com Joseph F. Verciglio jfverciglio@jonesday.com 3

4 Jones Day publications should not be construed as legal advice on any specific facts or circumstances. The contents are intended for general information purposes only and may not be quoted or referred to in any other publication or proceeding without the prior written consent of the Firm, to be given or withheld at our discretion. To request reprint permission for any of our publications, please use our Contact Us form, which can be found on our web site at The mailing of this publication is not intended to create, and receipt of it does not constitute, an attorney-client relationship. The views set forth herein are the personal views of the authors and do not necessarily reflect those of the Firm.

5 5

6 6

COMMENTARY WHAT A RELIEF? CONGRESS FINALLY PASSES PENSION FUNDING LEGISLATION JONES DAY

JULY 2010 JONES DAY COMMENTARY WHAT A RELIEF? CONGRESS FINALLY PASSES PENSION FUNDING LEGISLATION Congress has passed much-anticipated legislation providing funding relief for pension plan sponsors. The

JULY 2010 JONES DAY COMMENTARY WHAT A RELIEF? CONGRESS FINALLY PASSES PENSION FUNDING LEGISLATION Congress has passed much-anticipated legislation providing funding relief for pension plan sponsors. The

COMMENTARY JONES DAY. Importantly, the Notice provides generous transitional relief for correcting certain document failures in 2010.

February 2010 JONES DAY COMMENTARY IRS Releases Section 409A Documentary Correction Program Recently issued Notice 2010-6 ( Notice 2010-6 or the Notice ) provides taxpayers with the opportunity to voluntarily

February 2010 JONES DAY COMMENTARY IRS Releases Section 409A Documentary Correction Program Recently issued Notice 2010-6 ( Notice 2010-6 or the Notice ) provides taxpayers with the opportunity to voluntarily

COMMENTARY. Recent Changes in the Registered Capital System in China. Certain Registered Capital Requirements Have Been Eliminated

MAY 2014 COMMENTARY Recent Changes in the Registered Capital System in China On December 28, 2013, the Standing Committee of the National People s Congress passed certain amendments to the PRC Company

MAY 2014 COMMENTARY Recent Changes in the Registered Capital System in China On December 28, 2013, the Standing Committee of the National People s Congress passed certain amendments to the PRC Company

COMMENTARY. Potential Impact of the U.S. Dodd-Frank Act JONES DAY

March 2013 JONES DAY COMMENTARY Potential Impact of the U.S. Dodd-Frank Act and Global OTC Derivatives Regulations In connection with any over-the-counter ( OTC ) derivatives transactions you execute with

March 2013 JONES DAY COMMENTARY Potential Impact of the U.S. Dodd-Frank Act and Global OTC Derivatives Regulations In connection with any over-the-counter ( OTC ) derivatives transactions you execute with

COMMENTARY JONES DAY. Section 409A operates in three steps. First, it identifies compensation it considers nonqualified deferred

February 2006 JONES DAY COMMENTARY Employee Benefits & Executive Compensation Section 409A s Impact on Private Companies Section 409A was added to the Internal Revenue Code in October 2004 to provide strict

February 2006 JONES DAY COMMENTARY Employee Benefits & Executive Compensation Section 409A s Impact on Private Companies Section 409A was added to the Internal Revenue Code in October 2004 to provide strict

COMMENTARY. Update on Qualified Small Business Stock: New Federal Legislation and Status of California Rules JONES DAY

March 2013 JONES DAY COMMENTARY Update on Qualified Small Business Stock: New Federal Legislation and Status of California Rules Eligible investors in qualified small businesses are entitled to certain

March 2013 JONES DAY COMMENTARY Update on Qualified Small Business Stock: New Federal Legislation and Status of California Rules Eligible investors in qualified small businesses are entitled to certain

COMMENTARY JONES DAY. Italian law provides for three main types of mandatory tender offers:

May 2007 JONES DAY COMMENTARY Tender Offers in Italy Italy has not yet implemented the Directive on Takeover Bids (Directive 2004/25/EC, the Directive ) in its internal legal system. 1 However, Italian

May 2007 JONES DAY COMMENTARY Tender Offers in Italy Italy has not yet implemented the Directive on Takeover Bids (Directive 2004/25/EC, the Directive ) in its internal legal system. 1 However, Italian

COMMENTARY. Grandfathered Plans JONES DAY

March 2010 JONES DAY COMMENTARY Health Care Reform Upcoming Effective Dates for Employer-Sponsored Group Health Plans Introduction On March 23, 2010, President Obama signed into law the Patient Protection

March 2010 JONES DAY COMMENTARY Health Care Reform Upcoming Effective Dates for Employer-Sponsored Group Health Plans Introduction On March 23, 2010, President Obama signed into law the Patient Protection

Maine Revenue Services

Maine Revenue Services Guidance to Residency Safe Harbors for Residents Spending Time Outside Maine 1 As explained in the Maine Revenue Services Guidance to Residency Status, an individual who is domiciled

Maine Revenue Services Guidance to Residency Safe Harbors for Residents Spending Time Outside Maine 1 As explained in the Maine Revenue Services Guidance to Residency Status, an individual who is domiciled

COMMENTARY ICC Rules of Arbitration Come Into Force. Changes to Achieve Greater Speed and Cost-Efficiency JONES DAY

January 2012 JONES DAY COMMENTARY 2012 ICC Rules of Arbitration Come Into Force On January 1, 2012, a new version of the ICC Rules of Arbitration (the 2012 ICC Rules ) came into force. They will apply

January 2012 JONES DAY COMMENTARY 2012 ICC Rules of Arbitration Come Into Force On January 1, 2012, a new version of the ICC Rules of Arbitration (the 2012 ICC Rules ) came into force. They will apply

COMMENTARY. General Solicitation Now Permitted in Rule 144a Offerings: Are Foreign Private Issuers Free to Talk?

October 2013 JONES DAY COMMENTARY General Solicitation Now Permitted in Rule 144a Offerings: Are Foreign Private Issuers Free to Talk? On July 10, the SEC adopted final rules under Section 201(a) of the

October 2013 JONES DAY COMMENTARY General Solicitation Now Permitted in Rule 144a Offerings: Are Foreign Private Issuers Free to Talk? On July 10, the SEC adopted final rules under Section 201(a) of the

June 2010 State Tax Return. Georgia (and New York) Reexamine their IRC 338(h)(10) Election for S Corporations

Reexamine their IRC 338(h)(10) Election for S Corporations") June 2010 State Tax Return Volume 17 Number 2 Georgia (and New York) Reexamine their IRC 338(h)(10) Election for S Corporations E. Kendrick Smith Dan Conner Atlanta Atlanta 1.404.581.8343 1.404.581.8629

June 2010 State Tax Return Volume 17 Number 2 Georgia (and New York) Reexamine their IRC 338(h)(10) Election for S Corporations E. Kendrick Smith Dan Conner Atlanta Atlanta 1.404.581.8343 1.404.581.8629

Non-Resident Inheritance Tax Frequently Asked Questions

Non-Resident Inheritance Tax Frequently Asked Questions General Information 1. Where should I send my completed forms? 2. I need to overnight a package. What is the street address? 3. I sent in a non-resident

Non-Resident Inheritance Tax Frequently Asked Questions General Information 1. Where should I send my completed forms? 2. I need to overnight a package. What is the street address? 3. I sent in a non-resident

Employee Stock Plans: 2016 Year-End International Reporting Requirements

WHITE PAPER January 2017 Employee Stock Plans: 2016 Year-End International Reporting Requirements Year-end reporting requirements vary by jurisdiction for U.S. companies that provide stock plans to their

WHITE PAPER January 2017 Employee Stock Plans: 2016 Year-End International Reporting Requirements Year-end reporting requirements vary by jurisdiction for U.S. companies that provide stock plans to their

Rulings of the Tax Commissioner

Rulings of the Tax Commissioner Tax Type: Individual Income Tax Brief Description: Guidelines for Pass Through Entity Withholding Topics: Pass Through Entities Persons Subject to Tax Withholding of Tax

Rulings of the Tax Commissioner Tax Type: Individual Income Tax Brief Description: Guidelines for Pass Through Entity Withholding Topics: Pass Through Entities Persons Subject to Tax Withholding of Tax

State & Local Tax Alert Breaking state and local tax developments from Grant Thornton LLP

State & Local Tax Alert Breaking state and local tax developments from Grant Thornton LLP Ohio Enacts Municipal Income Tax Reform Concluding a process that spanned several years, Ohio Governor John Kasich

State & Local Tax Alert Breaking state and local tax developments from Grant Thornton LLP Ohio Enacts Municipal Income Tax Reform Concluding a process that spanned several years, Ohio Governor John Kasich

COMMENTARY. CREdit FOR CONsuMERs ANd BusiNEsses

March 2009 JONES DAY COMMENTARY The FedERAl ResERve s TERM AssET-BACked securities loan FACiliTY ( TALF ) ExpANding New CREdit FOR CONsuMERs ANd BusiNEsses In 2008, issuances of asset-backed securities

March 2009 JONES DAY COMMENTARY The FedERAl ResERve s TERM AssET-BACked securities loan FACiliTY ( TALF ) ExpANding New CREdit FOR CONsuMERs ANd BusiNEsses In 2008, issuances of asset-backed securities

COMMENTARY. Is Unlawful JONES DAY. prior to the time such interlock arises.

July 2006 JONES DAY COMMENTARY Energy FERC Interlocking Director Rules A Guide to Compliance FERC has recently stepped up enforcement of many provisions of the Federal Power Act ( FPA ), including Section

July 2006 JONES DAY COMMENTARY Energy FERC Interlocking Director Rules A Guide to Compliance FERC has recently stepped up enforcement of many provisions of the Federal Power Act ( FPA ), including Section

State Tax Return PENALTIES FOR GEORGIA TAX RETURN PREPARERS

June 2009 State Tax Return Volume 16 Number 2 PENALTIES FOR GEORGIA TAX RETURN PREPARERS E. Kendrick Smith Shane A. Lord Atlanta Atlanta (404) 581-8343 (404) 581-8055 On March 30, 2009, the Georgia General

June 2009 State Tax Return Volume 16 Number 2 PENALTIES FOR GEORGIA TAX RETURN PREPARERS E. Kendrick Smith Shane A. Lord Atlanta Atlanta (404) 581-8343 (404) 581-8055 On March 30, 2009, the Georgia General

COMMENTARY JONES DAY. 1 Reportedly, the Amended Act is expected to become enforceable on January 1, 2010, at the earliest.

September 2009 JONES DAY COMMENTARY Amendment of the Anti-Monopoly Act of Japan and its Impact on Mergers and Acquisitions On June 3, 2009, the Japanese Diet enacted a bill to amend the Act on Prohibition

September 2009 JONES DAY COMMENTARY Amendment of the Anti-Monopoly Act of Japan and its Impact on Mergers and Acquisitions On June 3, 2009, the Japanese Diet enacted a bill to amend the Act on Prohibition

Guidelines for Pass-Through Entity Withholding

Article 16.1 of Chapter 3 of Title 58.1 ( 58.1-486.1 et seq.) enacted by 2007 Senate Bill 1238 (Chapter 796) requires pass-through entities doing business in the Commonwealth and having taxable income

Article 16.1 of Chapter 3 of Title 58.1 ( 58.1-486.1 et seq.) enacted by 2007 Senate Bill 1238 (Chapter 796) requires pass-through entities doing business in the Commonwealth and having taxable income

COMMENTARY. Interference With the Tax Preferences JONES DAY

June 2009 JONES DAY COMMENTARY Colleges and Universities: Is There Impending Interference With the Tax Preferences Applicable to Intercollegiate Sports? In May 2009, the Congressional Budget Office of

June 2009 JONES DAY COMMENTARY Colleges and Universities: Is There Impending Interference With the Tax Preferences Applicable to Intercollegiate Sports? In May 2009, the Congressional Budget Office of

COMMENTARY. Dodd-Frank Derivatives 101: What In-House. The Basics JONES DAY

November 2012 JONES DAY COMMENTARY Dodd-Frank Derivatives 101: What In-House Counsel Needs to Know Now So you are in-house counsel to a company that, either occasionally or on a regular basis, enters into

November 2012 JONES DAY COMMENTARY Dodd-Frank Derivatives 101: What In-House Counsel Needs to Know Now So you are in-house counsel to a company that, either occasionally or on a regular basis, enters into

COMMENTARY. Navigating the Treacherous Waters of California s Expanded Anti-Indemnity Laws for Construction Projects JONES DAY

April 2013 JONES DAY COMMENTARY Navigating the Treacherous Waters of California s Expanded Anti-Indemnity Laws for Construction Projects California s long-standing anti-indemnity laws prohibit a public

April 2013 JONES DAY COMMENTARY Navigating the Treacherous Waters of California s Expanded Anti-Indemnity Laws for Construction Projects California s long-standing anti-indemnity laws prohibit a public

IN THE COURT OF APPEALS OF IOWA. No / Filed September 19, Appeal from the Iowa District Court for Black Hawk County, David F.

IN THE COURT OF APPEALS OF IOWA No. 2-583 / 12-0100 Filed September 19, 2012 JAMES G. SCHMITZ and VICKIE J. SCHMITZ, Husband and Wife, Petitioners-Appellants, vs. IOWA DEPARTMENT OF REVENUE, Respondent-Appellee.

IN THE COURT OF APPEALS OF IOWA No. 2-583 / 12-0100 Filed September 19, 2012 JAMES G. SCHMITZ and VICKIE J. SCHMITZ, Husband and Wife, Petitioners-Appellants, vs. IOWA DEPARTMENT OF REVENUE, Respondent-Appellee.

EXPAT TAX HANDBOOK. Tax Considerations For Remote Workers Living Abroad

EXPAT TAX HANDBOOK Tax Considerations For Remote Workers Living Abroad Tax Year 2017 Expat Tax Handbook Tax Considerations for Remote Workers Living Abroad Table of Contents: Introduction / 3 U.S. Federal

EXPAT TAX HANDBOOK Tax Considerations For Remote Workers Living Abroad Tax Year 2017 Expat Tax Handbook Tax Considerations for Remote Workers Living Abroad Table of Contents: Introduction / 3 U.S. Federal

Department of Revenue

Page 1 of 6 The Official Website of the Department of Revenue (DOR) Mass.Gov Department of Revenue Home > Businesses > Help & Resources > Legal Library > Technical Information Releases > TIRs - By Year(s)

Page 1 of 6 The Official Website of the Department of Revenue (DOR) Mass.Gov Department of Revenue Home > Businesses > Help & Resources > Legal Library > Technical Information Releases > TIRs - By Year(s)

Lancaster County Tax Collection Bureau Earned Income and Net Profits Tax Regulations Effective January 1, 2017

These Regulations supplement the Local Tax Enabling Act, 53 P.S. 6924.501 et seq. (LTEA), and Regulations of the Pennsylvania Department of Community and Economic Development promulgated thereunder. These

These Regulations supplement the Local Tax Enabling Act, 53 P.S. 6924.501 et seq. (LTEA), and Regulations of the Pennsylvania Department of Community and Economic Development promulgated thereunder. These

Issues for Employers as Health Care Legislation Moves to the Senate

WHITE PAPER May 2017 Issues for Employers as Health Care Legislation Moves to the Senate Although the American Health Care Act, as passed by the U.S. House of Representatives, mainly affects the individual

WHITE PAPER May 2017 Issues for Employers as Health Care Legislation Moves to the Senate Although the American Health Care Act, as passed by the U.S. House of Representatives, mainly affects the individual

COMMENTARY JONES DAY. 1) To clarify the legal interpretation of the Act. As

To clarify the legal interpretation of the Act. As") November 2005 JONES DAY COMMENTARY Personal Information Protection Law in Japan The Personal Information Protection Act (Law No. 57 of 2003) (hereinafter referred to as Act ), which was promulgated on

November 2005 JONES DAY COMMENTARY Personal Information Protection Law in Japan The Personal Information Protection Act (Law No. 57 of 2003) (hereinafter referred to as Act ), which was promulgated on

"US recipients of gifts and bequests from Covered Expatriates will now incur gift and estate tax"

Steve Leimberg's Estate Planning Email Newsletter - Archive Message #1324 Date: 23-Jul-08 From: Steve Leimberg's Estate Planning Newsletter Subject: HEART Legislation Enacts New Expatriation Rules "US

Steve Leimberg's Estate Planning Email Newsletter - Archive Message #1324 Date: 23-Jul-08 From: Steve Leimberg's Estate Planning Newsletter Subject: HEART Legislation Enacts New Expatriation Rules "US

Second Reading: Adopted: Defeated: CITY OF NORWALK, OHIO ORDINANCE NO

First Reading: Tabled: Referred: Second Reading: Adopted: Defeated: CITY OF NORWALK, OHIO ORDINANCE NO. 2015- Item No. 15-110a AN ORDINANCE AMENDING AND RESTATING CHAPTER 181 OF THE CODIFIED ORDINANCES

First Reading: Tabled: Referred: Second Reading: Adopted: Defeated: CITY OF NORWALK, OHIO ORDINANCE NO. 2015- Item No. 15-110a AN ORDINANCE AMENDING AND RESTATING CHAPTER 181 OF THE CODIFIED ORDINANCES

Taxation of Illinois nonresident taxpayers / Illinois 'sourcing' not based on workdays

Taxation of Illinois nonresident taxpayers / Illinois 'sourcing' not based on workdays This document is to clarify nonresident individual income tax filing positions in Illinois. Summary - The Illinois

Taxation of Illinois nonresident taxpayers / Illinois 'sourcing' not based on workdays This document is to clarify nonresident individual income tax filing positions in Illinois. Summary - The Illinois

DOMICILE TAX ISSUES FOR INDIVIDUALS AND ESTATES

DOMICILE TAX ISSUES FOR INDIVIDUALS AND ESTATES Tracy J. Roberts, Esq. Wealth Management Group - Bangor Savings Bank Jennifer L. Eastman, Esq. Rudman Winchell 19th Annual Maine Tax Forum -Nov2015 1 What

DOMICILE TAX ISSUES FOR INDIVIDUALS AND ESTATES Tracy J. Roberts, Esq. Wealth Management Group - Bangor Savings Bank Jennifer L. Eastman, Esq. Rudman Winchell 19th Annual Maine Tax Forum -Nov2015 1 What

COMMENTARY JONES DAY. House Bill 301 contains provisions, discussed in more detail herein, that:

September 2006 JONES DAY COMMENTARY Amendments to Ohio s Business Entity Statutes Effective in October 2006 Ohio House Bill 301, which will become law on October 9, 2006, is intended to improve Ohio s

September 2006 JONES DAY COMMENTARY Amendments to Ohio s Business Entity Statutes Effective in October 2006 Ohio House Bill 301, which will become law on October 9, 2006, is intended to improve Ohio s

State Tax Return CAT SITUSING RULES FOR CERTAIN SERVICES FINAL RULE EFFECTIVE DECEMBER 28, 2006

January 2007 Volume 14 Number 1 State Tax Return Update On Ohio Commercial Activity Tax: Final Rules And Revised Information Releases Charles M. Steines Phyllis J. Shambaugh Cleveland Columbus (216) 586-7211

January 2007 Volume 14 Number 1 State Tax Return Update On Ohio Commercial Activity Tax: Final Rules And Revised Information Releases Charles M. Steines Phyllis J. Shambaugh Cleveland Columbus (216) 586-7211

Texas Enforcement Sweep Finds Widespread Fraud in Cryptocurrency Offerings

WHITE PAPER May 2018 Texas Enforcement Sweep Finds Widespread Fraud in Cryptocurrency Offerings The surge in cryptocurrency activity has led to an increase in attention from enforcement authorities at

WHITE PAPER May 2018 Texas Enforcement Sweep Finds Widespread Fraud in Cryptocurrency Offerings The surge in cryptocurrency activity has led to an increase in attention from enforcement authorities at

Ohio Tax. Workshop DD. Major Developments in Ohio Pass-Through Entity & Personal Income Taxation. Wednesday, January 24, :00 a.m. to 12:30 p.m.

27th Annual Tuesday & Wednesday, January 23 24, 2018 Hya Regency Columbus, Columbus, Ohio Ohio Tax Workshop DD Major Developments in Ohio Pass-Through Entity & Personal Income Taxation Wednesday, January

27th Annual Tuesday & Wednesday, January 23 24, 2018 Hya Regency Columbus, Columbus, Ohio Ohio Tax Workshop DD Major Developments in Ohio Pass-Through Entity & Personal Income Taxation Wednesday, January

JONES DAY COMMENTARY

October 2007 JONES DAY COMMENTARY U.S. Bankruptcy Court Denies Failed Hedge Funds Request for Chapter 15 Recognition Two hedge funds affiliated with Bear Stearns & Co., Inc., the fifth-largest investment

October 2007 JONES DAY COMMENTARY U.S. Bankruptcy Court Denies Failed Hedge Funds Request for Chapter 15 Recognition Two hedge funds affiliated with Bear Stearns & Co., Inc., the fifth-largest investment

COMMENTARY JONES DAY. Pitfalls loom when applying for patent term extensions

February 2011 JONES DAY COMMENTARY No Clear Pointer in the Right Direction: Validity Issues in Europe of Patent Term Extensions Covering Fixed-Combination Medicinal Products Pitfalls loom when applying

February 2011 JONES DAY COMMENTARY No Clear Pointer in the Right Direction: Validity Issues in Europe of Patent Term Extensions Covering Fixed-Combination Medicinal Products Pitfalls loom when applying

ADMINISTRATIVE DECISION

STATE OF ARKANSAS DEPARTMENT OF FINANCE AND ADMINISTRATION OFFICE OF HEARINGS & APPEALS ADMINISTRATIVE DECISION IN THE MATTER OF (ACCT. NO.: ) INDIVIDUAL INCOME TAX ASSESSMENT DOCKET NO.: 17-061 TAX YEAR

STATE OF ARKANSAS DEPARTMENT OF FINANCE AND ADMINISTRATION OFFICE OF HEARINGS & APPEALS ADMINISTRATIVE DECISION IN THE MATTER OF (ACCT. NO.: ) INDIVIDUAL INCOME TAX ASSESSMENT DOCKET NO.: 17-061 TAX YEAR

JONES DAY COMMENTARY

May 2009 JONES DAY COMMENTARY The Helping Families Save Their Homes Act of 2009 Significantly Changes the TARP, PPIP, and TALF Programs and FDIC Insurance On May 19, the U.S. Congress overwhelmingly approved

May 2009 JONES DAY COMMENTARY The Helping Families Save Their Homes Act of 2009 Significantly Changes the TARP, PPIP, and TALF Programs and FDIC Insurance On May 19, the U.S. Congress overwhelmingly approved

JONES DAY COMMENTARY

April 2012 JONES DAY COMMENTARY CIETAC Issues New Arbitration Rules: Interim Measures and Consolidation Among the Highlights On February 3, 2012, the China Council for the Promotion of International Trade

April 2012 JONES DAY COMMENTARY CIETAC Issues New Arbitration Rules: Interim Measures and Consolidation Among the Highlights On February 3, 2012, the China Council for the Promotion of International Trade

American Citizens Abroad. Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION

1 November 2017; 1 December 2017; 19 January 2018 American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION This side-by-side analysis compares Current Law (i.e.,

1 November 2017; 1 December 2017; 19 January 2018 American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION This side-by-side analysis compares Current Law (i.e.,

CHAPTER 367 PDF p. 1 of 7 CHAPTER 367 (HB 457) AN ACT relating to income taxation. Be it enacted by the General Assembly of the Commonwealth of

AN ACT relating to income taxation. Be it enacted by the General Assembly of the Commonwealth of") CHAPTER 367 PDF p. 1 of 7 CHAPTER 367 (HB 457) AN ACT relating to income taxation. Be it enacted by the General Assembly of the Commonwealth of Kentucky: Section 1. KRS 141.010 is amended to read as follows:

CHAPTER 367 PDF p. 1 of 7 CHAPTER 367 (HB 457) AN ACT relating to income taxation. Be it enacted by the General Assembly of the Commonwealth of Kentucky: Section 1. KRS 141.010 is amended to read as follows:

COMMENTARY. Amendment to Japanese Real Estate Joint Enterprise Act Will It Benefit Overseas Investors? Yes, It Will JONES DAY

January 2014 JONES DAY COMMENTARY Amendment to Japanese Real Estate Joint Enterprise Act Will It Benefit Overseas Investors? Yes, It Will An amendment to the Joint Enterprise Act, 1 which was enacted on

January 2014 JONES DAY COMMENTARY Amendment to Japanese Real Estate Joint Enterprise Act Will It Benefit Overseas Investors? Yes, It Will An amendment to the Joint Enterprise Act, 1 which was enacted on

Title 36: TAXATION. Chapter 801: DEFINITIONS. Table of Contents Part 8. INCOME TAXES... Section SHORT TITLE... 3 Section DEFINITIONS...

Title 36: TAXATION Chapter 801: DEFINITIONS Table of Contents Part 8. INCOME TAXES... Section 5101. SHORT TITLE... 3 Section 5102. DEFINITIONS... 3 i Text current through November 1, 2018, see disclaimer

Title 36: TAXATION Chapter 801: DEFINITIONS Table of Contents Part 8. INCOME TAXES... Section 5101. SHORT TITLE... 3 Section 5102. DEFINITIONS... 3 i Text current through November 1, 2018, see disclaimer

Be it enacted by the General Assembly of the Commonwealth of Kentucky: Section 1. KRS is amended to read as follows:

AN ACT relating to taxation. Be it enacted by the General Assembly of the Commonwealth of Kentucky: 0 Section. KRS.0 is amended to read as follows: As used in KRS.0 to.0, unless the context requires otherwise:

AN ACT relating to taxation. Be it enacted by the General Assembly of the Commonwealth of Kentucky: 0 Section. KRS.0 is amended to read as follows: As used in KRS.0 to.0, unless the context requires otherwise:

COMMENTARY. Partnership Program JONES DAY

October 2009 JONES DAY COMMENTARY U.S. Department of Energy Announces Loan Guarantee Program To Help Accelerate Financing of Conventional Renewable Energy Projects On October 7, 2009, the U.S. Department

October 2009 JONES DAY COMMENTARY U.S. Department of Energy Announces Loan Guarantee Program To Help Accelerate Financing of Conventional Renewable Energy Projects On October 7, 2009, the U.S. Department

As Introduced. 132nd General Assembly Regular Session S. B. No Senator Jordan A B I L L

132nd General Assembly Regular Session S. B. No. 176 2017-2018 Senator Jordan A B I L L To amend sections 709.023, 718.01, 718.02, 718.03, 718.04, 718.05, and 718.16 and to repeal sections 718.011 and

132nd General Assembly Regular Session S. B. No. 176 2017-2018 Senator Jordan A B I L L To amend sections 709.023, 718.01, 718.02, 718.03, 718.04, 718.05, and 718.16 and to repeal sections 718.011 and

Absolute Liability for a Failure to Prevent Foreign Bribery: Significant Change Ahead in Australia?

WHITE PAPER December 2017 Absolute Liability for a Failure to Prevent Foreign Bribery: Significant Change Ahead in Australia? Australia s Federal Government has tabled the Crimes Legislation Amendment

WHITE PAPER December 2017 Absolute Liability for a Failure to Prevent Foreign Bribery: Significant Change Ahead in Australia? Australia s Federal Government has tabled the Crimes Legislation Amendment

Ohio House Ways and Means Considers Substantially Watered-Down Municipal Income Tax Reform

November 5, 2013 No. 401 Fiscal Fact Ohio House Ways and Means Considers Substantially Watered-Down Municipal Income Tax Reform By Chris Stephens & Scott Drenkard This year, the Ohio House Ways and Means

November 5, 2013 No. 401 Fiscal Fact Ohio House Ways and Means Considers Substantially Watered-Down Municipal Income Tax Reform By Chris Stephens & Scott Drenkard This year, the Ohio House Ways and Means

U.S. Government Takes Steps Toward Implementation of Sanctions on Russia

WHITE PAPER November 2017 U.S. Government Takes Steps Toward Implementation of Sanctions on Russia The United States has taken significant steps toward fully implementing the sanctions imposed on Russia

WHITE PAPER November 2017 U.S. Government Takes Steps Toward Implementation of Sanctions on Russia The United States has taken significant steps toward fully implementing the sanctions imposed on Russia

PAPER 2.02 CHINA OPTION

THE ADVANCED DIPLOMA IN INTERNATIONAL TAXATION June 2015 PAPER 2.02 CHINA OPTION ADVANCED INTERNATIONAL TAXATION (JURISDICTION) Suggested solutions PART I Question 1 Mr Wing s tax liability for 2014 is

THE ADVANCED DIPLOMA IN INTERNATIONAL TAXATION June 2015 PAPER 2.02 CHINA OPTION ADVANCED INTERNATIONAL TAXATION (JURISDICTION) Suggested solutions PART I Question 1 Mr Wing s tax liability for 2014 is

JONES DAY COMMENTARY

December 2007 JONES DAY COMMENTARY Implementation Regulations for the New Enterprise Income Tax Law of China On March 16, 2007, China passed the new Enterprise Income Tax Law (the EIT Law ), which will

December 2007 JONES DAY COMMENTARY Implementation Regulations for the New Enterprise Income Tax Law of China On March 16, 2007, China passed the new Enterprise Income Tax Law (the EIT Law ), which will

Secretary of State Update

Secretary of State Update 2011 LLCs, LPs AND PARTNERSHIPS July 14-15, 2011 Austin, Texas Lorna Wassdorf, Director Business & Public Filings Division 512 463-5591 lwassdorf@sos.state.tx.us New Texas Business

Secretary of State Update 2011 LLCs, LPs AND PARTNERSHIPS July 14-15, 2011 Austin, Texas Lorna Wassdorf, Director Business & Public Filings Division 512 463-5591 lwassdorf@sos.state.tx.us New Texas Business

Recent Developments in Transfer Pricing and the Taxation of Multinational Companies in Australia

WHITE PAPER November 2017 Recent Developments in Transfer Pricing and the Taxation of Multinational Companies in Australia As part of a wide-ranging crackdown on multinational tax avoidance, the Australian

WHITE PAPER November 2017 Recent Developments in Transfer Pricing and the Taxation of Multinational Companies in Australia As part of a wide-ranging crackdown on multinational tax avoidance, the Australian

As Introduced. 131st General Assembly Regular Session S. B. No

131st General Assembly Regular Session S. B. No. 12 2015-2016 Senator Hottinger A B I L L To amend sections 5747.08 and 5747.98 and to enact sections 3333.51 and 5747.82 of the Revised Code to grant an

131st General Assembly Regular Session S. B. No. 12 2015-2016 Senator Hottinger A B I L L To amend sections 5747.08 and 5747.98 and to enact sections 3333.51 and 5747.82 of the Revised Code to grant an

State Tax Return. A Federal Treaty and Approximately $2.00 Will Get You A Ride on the New York Subway

April 2008 State Tax Return Volume 15 Number 2 Peter Leonardis New York (212) 326-3770 A Federal Treaty and Approximately $2.00 Will Get You A Ride on the New York Subway Tax directors of corporations

April 2008 State Tax Return Volume 15 Number 2 Peter Leonardis New York (212) 326-3770 A Federal Treaty and Approximately $2.00 Will Get You A Ride on the New York Subway Tax directors of corporations

November 8 th, Not Your Typical Tax Update

November 8 th, 2016 Not Your Typical Tax Update Discla im e r This document and information is provided by Ary Roepcke Mulchaey, P.C. and the presenter for general guidance only, and does not constitute

November 8 th, 2016 Not Your Typical Tax Update Discla im e r This document and information is provided by Ary Roepcke Mulchaey, P.C. and the presenter for general guidance only, and does not constitute

****** requests that its sales of services be considered non-marketing services and

,:~}~~{) l, ~ti!'jstate of California chair John Chiang I member Jerome E. Horton I member Michael Cohen '\~franchise Tax Board Legal Division MS A260 PO Box 1720 Rancho Cordova, CA 95741-1720 tel: 916.845.7831

,:~}~~{) l, ~ti!'jstate of California chair John Chiang I member Jerome E. Horton I member Michael Cohen '\~franchise Tax Board Legal Division MS A260 PO Box 1720 Rancho Cordova, CA 95741-1720 tel: 916.845.7831

Direct Contracting 101: Collaborations Between Employers and Health Care Providers

WHITE PAPER May 2018 Direct Contracting 101: Collaborations Between Employers and Health Care Providers As employers continue to encounter escalating health care costs, many are exploring the direct contracting

WHITE PAPER May 2018 Direct Contracting 101: Collaborations Between Employers and Health Care Providers As employers continue to encounter escalating health care costs, many are exploring the direct contracting

Thinking Beyond Borders

INTERNATIONAL EXECUTIVE SERVICES Thinking Beyond Borders France kpmg.com France Introduction Income tax in France is assessed on a family/household basis. Income tax liability is determined by applying

INTERNATIONAL EXECUTIVE SERVICES Thinking Beyond Borders France kpmg.com France Introduction Income tax in France is assessed on a family/household basis. Income tax liability is determined by applying

Vermont Tax Seminar. December 8, Mark A. Langan, Esq. Dinse Knapp & McAndrew, PC 209 Battery Street, PO Box 988 Burlington, VT 05402

Vermont Tax Seminar December 8, 2016 Mark A. Langan, Esq. Dinse Knapp & McAndrew, PC 209 Battery Street, PO Box 988 Burlington, VT 05402 802-864-5751 mlangan@dinse.com www.dinse.com 2016 Vermont Laws No.

Vermont Tax Seminar December 8, 2016 Mark A. Langan, Esq. Dinse Knapp & McAndrew, PC 209 Battery Street, PO Box 988 Burlington, VT 05402 802-864-5751 mlangan@dinse.com www.dinse.com 2016 Vermont Laws No.

PROPOSED REGULATION 830 CMR

830 CMR: DEPARTMENT OF REVENUE PROPOSED REGULATION 830 CMR 63.38.1 830 CMR 63:00: TAXATION OF CORPORATIONS 830 CMR 63.38.1 is repealed and replaced with the following: 830 CMR 63.38.1: Apportionment of

830 CMR: DEPARTMENT OF REVENUE PROPOSED REGULATION 830 CMR 63.38.1 830 CMR 63:00: TAXATION OF CORPORATIONS 830 CMR 63.38.1 is repealed and replaced with the following: 830 CMR 63.38.1: Apportionment of

Thank you for the opportunity to comment on the Department s draft Article 9-A and Article 32 regulations regarding combined reports.

TO: John W. Bartlett, Director of Regulations, NYS Department of Taxation and Finance FROM: Kenneth J. Pokalsky SUBJECT: Draft Combined Report Regulation DATE: 11/7/08 Thank you for the opportunity to

TO: John W. Bartlett, Director of Regulations, NYS Department of Taxation and Finance FROM: Kenneth J. Pokalsky SUBJECT: Draft Combined Report Regulation DATE: 11/7/08 Thank you for the opportunity to

A Look at the Final Section 2053 Regulations

A PROFESSIONAL CORPORATION ATTORNEYS AT LAW A Look at the Final Section 2053 Regulations 2009 by Jonathan G. Blattmachr & Mitchell M. Gans All Rights Reserved. Introduction As a general rule, expenses

A PROFESSIONAL CORPORATION ATTORNEYS AT LAW A Look at the Final Section 2053 Regulations 2009 by Jonathan G. Blattmachr & Mitchell M. Gans All Rights Reserved. Introduction As a general rule, expenses

CLERK OF COURT AMECOURTM BET'TY L. LUNN, ET AL., BTA CASE No

IN THE SUPREME COIJRT OF OHIO BET'TY L. LUNN, ET AL., NO. ^ ;^ r ; ^ ^, APPELLEES ON APPEAL FROM THE OHIO BOARD OF TAX APPEALS V. BTA CASE No. 2013-2661 LORAIN COUNTY BOARD OF REVISION, LORAIN COUNTY AUDITOR,

IN THE SUPREME COIJRT OF OHIO BET'TY L. LUNN, ET AL., NO. ^ ;^ r ; ^ ^, APPELLEES ON APPEAL FROM THE OHIO BOARD OF TAX APPEALS V. BTA CASE No. 2013-2661 LORAIN COUNTY BOARD OF REVISION, LORAIN COUNTY AUDITOR,

Tenth Circuit Finds IRS Followed Procedures and Could Proceed with Levy Action. Cropper v. Comm., (CA 10 6/22/2016) 117 AFTR 2d

117 AFTR 2d") Tenth Circuit Finds IRS Followed Procedures and Could Proceed with Levy Action Cropper v. Comm., (CA 10 6/22/2016) 117 AFTR 2d 2016-794 The Court of Appeals for the Tenth Circuit concluded that because

Tenth Circuit Finds IRS Followed Procedures and Could Proceed with Levy Action Cropper v. Comm., (CA 10 6/22/2016) 117 AFTR 2d 2016-794 The Court of Appeals for the Tenth Circuit concluded that because

Consumer Taxes INTERPRETATION AND ADMINISTRATIVE BULLETIN CONCERNING THE LAWS AND REGULATIONS

INTERPRETATION AND ADMINISTRATIVE BULLETIN CONCERNING THE LAWS AND REGULATIONS Consumer Taxes ADM. 7-1 Reduction in source deductions of income tax in respect of a payment for services rendered in Québec

INTERPRETATION AND ADMINISTRATIVE BULLETIN CONCERNING THE LAWS AND REGULATIONS Consumer Taxes ADM. 7-1 Reduction in source deductions of income tax in respect of a payment for services rendered in Québec

STATE OF MICHIGAN COURT OF APPEALS

STATE OF MICHIGAN COURT OF APPEALS HUSSEIN SAID and JAMELAH SAID, Petitioners-Appellants, FOR PUBLICATION April 27, 2001 9:20 a.m. v No. 216994 Tax Tribunal DEPARTMENT OF TREASURY, LC No. 00-223448 Respondent-Appellee.

STATE OF MICHIGAN COURT OF APPEALS HUSSEIN SAID and JAMELAH SAID, Petitioners-Appellants, FOR PUBLICATION April 27, 2001 9:20 a.m. v No. 216994 Tax Tribunal DEPARTMENT OF TREASURY, LC No. 00-223448 Respondent-Appellee.

Occupational License Tax ORDINANCE

Occupational License Tax ORDINANCE 2013-09 AN ORDINANCE AMENDING ORDINANCE 2007-11 TO INCREASE THE OCCUPATIONAL LICENSE TAX FROM.5% (ONE-HALF PERCENT) TO 1% (ONE PERCENT) Now, therefore, be it ordained

Occupational License Tax ORDINANCE 2013-09 AN ORDINANCE AMENDING ORDINANCE 2007-11 TO INCREASE THE OCCUPATIONAL LICENSE TAX FROM.5% (ONE-HALF PERCENT) TO 1% (ONE PERCENT) Now, therefore, be it ordained

As Introduced. Regular Session H. B. No

132nd General Assembly Regular Session H. B. No. 333 2017-2018 Representatives Becker, Leland Cosponsors: Representatives Vitale, Retherford, Keller, Duffey, Thompson, Brinkman, Hambley, Henne, Dean, Roegner,

132nd General Assembly Regular Session H. B. No. 333 2017-2018 Representatives Becker, Leland Cosponsors: Representatives Vitale, Retherford, Keller, Duffey, Thompson, Brinkman, Hambley, Henne, Dean, Roegner,

State Tax Return. Sooner Rather Than Later: Oklahoma Court of Civil Appeals Upholds Distinct Withholding Requirements For Nonresident Royalty Owners

September 2007 Volume 14 Number 9 State Tax Return Sooner Rather Than Later: Oklahoma Court of Civil Appeals Upholds Distinct Withholding Requirements For Nonresident Royalty Owners Laura A. Kulwicki Columbus

September 2007 Volume 14 Number 9 State Tax Return Sooner Rather Than Later: Oklahoma Court of Civil Appeals Upholds Distinct Withholding Requirements For Nonresident Royalty Owners Laura A. Kulwicki Columbus

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014 Federal Income Tax Withholding 14.1-1 U.S. citizens & resident aliens are subject to income tax withholding

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014 Federal Income Tax Withholding 14.1-1 U.S. citizens & resident aliens are subject to income tax withholding

As Introduced. Regular Session H. B. No

131st General Assembly Regular Session H. B. No. 232 2015-2016 Representatives Grossman, Scherer Cosponsors: Representatives Ryan, Burkley, Reineke, Hackett, Sheehy A B I L L To amend sections 5741.01

131st General Assembly Regular Session H. B. No. 232 2015-2016 Representatives Grossman, Scherer Cosponsors: Representatives Ryan, Burkley, Reineke, Hackett, Sheehy A B I L L To amend sections 5741.01

CHAPTER 194 Municipal Income Tax Effective January 1, 2016 For taxable years beginning with taxable year 2016

CHAPTER 194 Municipal Income Tax Effective January 1, 2016 For taxable years beginning with taxable year 2016 194.01 AUTHORITY TO LEVY TAX; PURPOSES OF TAX; RATE 194.011 AUTHORITY TO LEVY TAX 194.012 PURPOSES

CHAPTER 194 Municipal Income Tax Effective January 1, 2016 For taxable years beginning with taxable year 2016 194.01 AUTHORITY TO LEVY TAX; PURPOSES OF TAX; RATE 194.011 AUTHORITY TO LEVY TAX 194.012 PURPOSES

INSTRUCTIONS FOR SUMMARY RELEASE FROM ADMINISTRATION

INSTRUCTIONS FOR SUMMARY RELEASE FROM ADMINISTRATION These instructions are intended as a guideline only and should not be relied upon as a comprehensive list of duties in the summary release from administration

INSTRUCTIONS FOR SUMMARY RELEASE FROM ADMINISTRATION These instructions are intended as a guideline only and should not be relied upon as a comprehensive list of duties in the summary release from administration

ALIYAH FROM THE USA. STEP ISRAEL Annual Conference Tel Aviv, Israel June 20, 21, 2017

Washington, DC New York, NY New Haven, CT Chicago, IL ALIYAH FROM THE USA STEP ISRAEL Annual Conference Tel Aviv, Israel June 20, 21, 2017 Stanley A. Barg Kozusko Harris Duncan Email: sbarg@kozlaw.com

Washington, DC New York, NY New Haven, CT Chicago, IL ALIYAH FROM THE USA STEP ISRAEL Annual Conference Tel Aviv, Israel June 20, 21, 2017 Stanley A. Barg Kozusko Harris Duncan Email: sbarg@kozlaw.com

Tax Planning for High Net Worth Individuals Immigrating to the United States

The Tax Adviser Tax Planning for High Net Worth Individuals Immigrating to the United States By Rolando Garcia, CPA, J.D., Houston 7 hours 42 minutes ago Editor: Mindy Tyson Weber, CPA, M.Tax. For generations,

The Tax Adviser Tax Planning for High Net Worth Individuals Immigrating to the United States By Rolando Garcia, CPA, J.D., Houston 7 hours 42 minutes ago Editor: Mindy Tyson Weber, CPA, M.Tax. For generations,

American Citizens Abroad. Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION

American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation 5 December 2016; 1 November 2017; 1 December 2017; 18 January 2018; 19 April 2018 INTRODUCTION This side-by-side analysis

American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation 5 December 2016; 1 November 2017; 1 December 2017; 18 January 2018; 19 April 2018 INTRODUCTION This side-by-side analysis

Individual Income and Estate Taxation Residence, Domicile, and Taxation

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp INFORMATION BRIEF Research

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp INFORMATION BRIEF Research

ESTATE & TRUST CONSIDER UTILIZING YOUR LIFETIME GIFT EXEMPTION BY FUNDING A SPOUSAL LIFETIME ACCESS TRUST BE IN A POSITION OF STRENGTH SM

BE IN A POSITION OF STRENGTH SM WithumSmith+Brown s Tax Services Team Newsletter ESTATE & TRUST 04-06 DON T FORGET ABOUT STATE TAXES IN YOUR ESTATE PLAN CONSIDER UTILIZING YOUR LIFETIME GIFT EXEMPTION

BE IN A POSITION OF STRENGTH SM WithumSmith+Brown s Tax Services Team Newsletter ESTATE & TRUST 04-06 DON T FORGET ABOUT STATE TAXES IN YOUR ESTATE PLAN CONSIDER UTILIZING YOUR LIFETIME GIFT EXEMPTION

][Form 23 ][SUN FDEATH ][01/24/06 ][Page 1 of 12 ][000: ][TT33][/ Frequency: Monthly Quarterly Semi-Annually Annually

![][Form 23 ][SUN FDEATH ][01/24/06 ][Page 1 of 12 ][000: ][TT33][/ Frequency: Monthly Quarterly Semi-Annually Annually](/thumbs/80/80751311.jpg "][Form 23 ][SUN FDEATH ][01/24/06 ][Page 1 of 12 ][000: ][TT33][/ Frequency: Monthly Quarterly Semi-Annually Annually") Death Benefit Claim Request 401(a) Plan Refer to the Death Benefit Claim Guide while completing this form. Use blue or black ink only. If you have questions regarding the completion of this form, please

Death Benefit Claim Request 401(a) Plan Refer to the Death Benefit Claim Guide while completing this form. Use blue or black ink only. If you have questions regarding the completion of this form, please

HOUSE BILL K1, K2 9lr1542 CF SB 912 By: Delegate Davis Introduced and read first time: February 13, 2009 Assigned to: Economic Matters

HOUSE BILL 0 K, K lr CF SB By: Delegate Davis Introduced and read first time: February, 0 Assigned to: Economic Matters A BILL ENTITLED AN ACT concerning Labor and Employment Misclassification of Employees

HOUSE BILL 0 K, K lr CF SB By: Delegate Davis Introduced and read first time: February, 0 Assigned to: Economic Matters A BILL ENTITLED AN ACT concerning Labor and Employment Misclassification of Employees

T.C. Memo UNITED STATES TAX COURT. RAYMOND S. MCGAUGH, Petitioner v. COMMISSIONER OF INTERNAL REVENUE, Respondent

T.C. Memo. 2016-28 UNITED STATES TAX COURT RAYMOND S. MCGAUGH, Petitioner v. COMMISSIONER OF INTERNAL REVENUE, Respondent Docket No. 13665-14. Filed February 24, 2016. P had a self-directed IRA of which

T.C. Memo. 2016-28 UNITED STATES TAX COURT RAYMOND S. MCGAUGH, Petitioner v. COMMISSIONER OF INTERNAL REVENUE, Respondent Docket No. 13665-14. Filed February 24, 2016. P had a self-directed IRA of which

][A01: ][Form 17 ][FRPS FDEATH ][04/24/13 ][Page 1 of 19 [401K Plan] ][GP33/ ][STD_INST

![][A01: ][Form 17 ][FRPS FDEATH ][04/24/13 ][Page 1 of 19 [401K Plan] ][GP33/ ][STD_INST](/thumbs/82/86983989.jpg "][A01: ][Form 17 ][FRPS FDEATH ][04/24/13 ][Page 1 of 19 [401K Plan] ][GP33/ ][STD_INST") Death Benefit Claim Request Refer to the Death Benefit Claim Guide while completing this form. Use blue or black ink only. A certified death certificate must accompany this form. TAYLOR TRUCK LINE INC.

Death Benefit Claim Request Refer to the Death Benefit Claim Guide while completing this form. Use blue or black ink only. A certified death certificate must accompany this form. TAYLOR TRUCK LINE INC.

Thursday, 15 February 2018 #WRM TOPIC: Moving On: Changing State Tax Residency Easier Said than Done?

The WR Marketplace is created exclusively for AALU members by experts at Greenberg Traurig and the AALU staff, led by Jonathan M. Forster, Steven B. Lapidus, Martin Kalb, Richard A. Sirus, and Rebecca

The WR Marketplace is created exclusively for AALU members by experts at Greenberg Traurig and the AALU staff, led by Jonathan M. Forster, Steven B. Lapidus, Martin Kalb, Richard A. Sirus, and Rebecca

][Form 23 ][C401K FDEATH ][01/17/12 ][Page 1 of 16 ][A01: ][GP19][/

![][Form 23 ][C401K FDEATH ][01/17/12 ][Page 1 of 16 ][A01: ][GP19][/](/thumbs/89/98512675.jpg "][Form 23 ][C401K FDEATH ][01/17/12 ][Page 1 of 16 ][A01: ][GP19][/") Death Benefit Claim Request 401(k) Plan Refer to the Death Benefit Claim Guide while completing this form. Use blue or black ink only. Cargo Express, Inc. 401(k) Profit Sharing Plan 939200-01 Decedent

Death Benefit Claim Request 401(k) Plan Refer to the Death Benefit Claim Guide while completing this form. Use blue or black ink only. Cargo Express, Inc. 401(k) Profit Sharing Plan 939200-01 Decedent

State Tax Return. Out With The Old And In With The New: Ohio Abandons Its Corporate Franchise Tax And Enacts A Commercial Activities Tax

June 2005 Volume 12 Number 6 State Tax Return Out With The Old And In With The New: Ohio Abandons Its Corporate Franchise Tax And Enacts A Commercial Activities Tax Maryann B. Gall Jason R. Grove Columbus

June 2005 Volume 12 Number 6 State Tax Return Out With The Old And In With The New: Ohio Abandons Its Corporate Franchise Tax And Enacts A Commercial Activities Tax Maryann B. Gall Jason R. Grove Columbus

ARTICLES OF INCORPORATION OF ANTIQUE PHONOGRAPH SOCIETY

ARTICLES OF INCORPORATION OF ANTIQUE PHONOGRAPH SOCIETY The undersigned, acting as incorporator under the provisions of the Washington Nonprofit Corporation Act (Chapter 24.03 of the Revised Code of Washington),

ARTICLES OF INCORPORATION OF ANTIQUE PHONOGRAPH SOCIETY The undersigned, acting as incorporator under the provisions of the Washington Nonprofit Corporation Act (Chapter 24.03 of the Revised Code of Washington),

STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. S951201A On December

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. S951201A On December

Internal Revenue Service Number: Release Date: 3/2/2007 Index Number:

Internal Revenue Service Number: 200709036 Release Date: 3/2/2007 Index Number: 1031.06-00 ---------------- ------------------------------------------------------- -------------------------------------------------

Internal Revenue Service Number: 200709036 Release Date: 3/2/2007 Index Number: 1031.06-00 ---------------- ------------------------------------------------------- -------------------------------------------------

Copyright (c) 2002 American Bar Association The Tax Lawyer. Summer, Tax Law. 961

2002 American Bar Association The Tax Lawyer. Summer, Tax Law. 961") Page 1 LENGTH: 4515 words SECTION: NOTE. Copyright (c) 2002 American Bar Association The Tax Lawyer Summer, 2002 55 Tax Law. 961 TITLE: THE REAL ESTATE EXCEPTION TO THE PASSIVE ACTIVITY RULES IN MOWAFI

Page 1 LENGTH: 4515 words SECTION: NOTE. Copyright (c) 2002 American Bar Association The Tax Lawyer Summer, 2002 55 Tax Law. 961 TITLE: THE REAL ESTATE EXCEPTION TO THE PASSIVE ACTIVITY RULES IN MOWAFI

FLORIDA BAR ETHICS OPINION OPINION 93-2 October 1, Advisory ethics opinions are not binding.

FLORIDA BAR ETHICS OPINION OPINION 93-2 October 1, 1993 Advisory ethics opinions are not binding. Earned fees, including true retainers, must not be placed in the trust account. Unearned fees and advances

FLORIDA BAR ETHICS OPINION OPINION 93-2 October 1, 1993 Advisory ethics opinions are not binding. Earned fees, including true retainers, must not be placed in the trust account. Unearned fees and advances

A BILL IN THE COUNCIL OF DISTRICT OF COLUMBIA

A BILL IN THE COUNCIL OF DISTRICT OF COLUMBIA To amend Title 47, Chapter 18 of the District of Columbia Official Code by adding thereto new sections, designated 47-1805.02A, 47-1810.04, 47-1810.05, 47-1810.06,

A BILL IN THE COUNCIL OF DISTRICT OF COLUMBIA To amend Title 47, Chapter 18 of the District of Columbia Official Code by adding thereto new sections, designated 47-1805.02A, 47-1810.04, 47-1810.05, 47-1810.06,

NOTICE OF RULE MAKING. Arizona Commerce Authority Rule Notice of Rule Making No

NOTICE OF RULE MAKING Arizona Commerce Authority Rule Notice of Rule Making No. 19-01 1. Rule(s): Quality Jobs Tax Credit Program (the Program ) 2. Preamble. A. A.R.S. 41-1525 B. The proposed Rules will

NOTICE OF RULE MAKING Arizona Commerce Authority Rule Notice of Rule Making No. 19-01 1. Rule(s): Quality Jobs Tax Credit Program (the Program ) 2. Preamble. A. A.R.S. 41-1525 B. The proposed Rules will

BRIEF. A Snowbird Must Carefully Plan Its Flight. Establishing Tax Residency under the Laws of New York and Florida TAX

TAX TAXATION I state & local taxation A Snowbird Must Carefully Plan Its Flight Establishing Tax Residency under the Laws of New York and Florida By Mark Klein and Dan Kelly IN BRIEF New York residents

TAX TAXATION I state & local taxation A Snowbird Must Carefully Plan Its Flight Establishing Tax Residency under the Laws of New York and Florida By Mark Klein and Dan Kelly IN BRIEF New York residents

The New York WARN Act

August 2008 The New York WARN Act BY ALLAN S. BLOOM, STEPHEN H. HARRIS, ETHAN LIPSIG AND GLENN S. GRINDLINGER On August 5, 2008, Governor David Patterson signed legislation enacting the New York State

August 2008 The New York WARN Act BY ALLAN S. BLOOM, STEPHEN H. HARRIS, ETHAN LIPSIG AND GLENN S. GRINDLINGER On August 5, 2008, Governor David Patterson signed legislation enacting the New York State