The Practical Considerations and Impact of Addressing Country-by-Country Reporting

|

|

|

- Gerald Robbins

- 6 years ago

- Views:

Transcription

1 The Practical Considerations and Impact of Addressing Country-by-Country Reporting Country-by-Country Reporting has come into effect. Any multinational enterprises within the UK & Rebublic of Ireland, which have a collective turnover of greater than 750 million, will be required to submit Country-by-Country Reporting (CbCR) to HMRC or the Irish Revenue. With the implementation of any new process, there are likely to be questions which must be addressed, such as: Who is providing accurate data across the whole business? Where is the allocation of resources? And what is the impact of managing data across different regions in various formats? But, the toughest question of all; Are your existing processes and resources able to support the level of detail and data exchange required to support Country-by- Country Reporting? 1

2 Companies are asking these questions and considering whether implementing automated Country-by-Country software technology across their global business is a valid option, or whether adopting an outsourced service is an appropriate answer. They realise that there is a need for processes to be linked, information to be readily available and used across multiple teams within an organisation. It will also mean detailed data being provided from different sources and applications across multiple platforms all needing to be delivered in one cohesive electronic report for HMRC or the Irish Revenue. Tax compliance is moving at a rapid pace, with almost constant new schemas being released changing existing legislation and, on occasion, creating completely new reporting requirements. An example of this is HMRC and the Irish Revenue initiatives which follow BEPS (Base Erosion and Profit Shifting) action 13. This has led to the requirement of large multinational companies with a group revenue in excess of 750 million Euros, which have a presence in the UK or Ireland, to submit a Country-by-Country Report (CbCR) with the first filing deadlines starting in Developments within HMRC and the Irish Revenue, around the initial schema, are currently in motion with the ultimate goal of having greater transparency. This means that multinational corporations will need to deliver accurate reports. This white paper is drawn from our customer experiences and describes the practical considerations of Country-by- Country Reporting detailing: What is Country-by-Country Reporting? Which enterprises are affected? A process guide for submitting a Country-by-Country Report What are the challenges? What will happen if an error occurs? What should you be doing now? By the end of this white paper, you will gain an understanding of the practicalities, available options and timelines which need to be considered when addressing the impact of Country-by-Country Reporting. Tax compliance is moving at a rapid pace, with almost constant new schemas being released changing existing legislation and, on occasion, creating completely new reporting requirements. 2

3 Background What is Country-by-Country Reporting? As part of Action 13 of the Base Erosion and Profit Sharing ( BEPS ) Action Plan, there have been calls for regulations to be introduced to provide more tax transparency, to address tax avoidance. To meet this requirement, HMRC and the Irish Revenue has introduced mandatory Country-by-Country Reporting for all multinational enterprises within the UK & Republic of Ireland, which have a collective turnover of greater than 750 million. Where It Started There has been an increasing amount of discussion and press coverage around the amount of tax that large organisations are paying and where they are paying it. These large organisations, or multinational enterprises ( MNEs ), have evolved much faster than the international tax rules, which are not suitable for business in the modern world, therefore creating opportunity for BEPS with greater tax visibility across the global enterprise. This led to a package of 15 Actions to address the principal causes of the lost tax revenue, these being: Aggressive tax planning Interaction of domestic tax rules Co-ordination between tax administrations Limited country enforcement resources Harmful tax practices Lack of transparency. MNEs will say they are playing by the rules, and in most cases they are. However, individual countries are identifying that there are significant amounts of tax revenues they are entitled to claim. The OECD has estimated that the annual global lost tax revenues amount to $100-$240 billion, notwithstanding the fact that this creates an unfair playing field for domestic businesses which do not have the ability to shift profits across borders and therefore have difficulty competing with the MNEs. To address this problem and provide a level playing field across the enterprise required global cooperation. In September 2013, G20 leaders endorsed action to be taken on BEPS. Once these Actions are put into practice, the expected result is that profits will be taxed where economic activities take place and the business value is created. In the interest of balance, while this may seem like an attack on large businesses, part of the aim of this project was to initiate change while not harming MNEs, given the contribution they make to global trade and investment. The OECD Actions themselves do not create any change, it is up to the global tax administrations to implement them within each of their respective jurisdictions. Many of these actions have already been implemented by local country tax authorities and the requirement to file a Country-by-Country Report (part of BEPS Action 13 Transfer Pricing Documentation) is one of the first adopted by many. 3

4 The New Country-by-Country Report Many of the BEPS Actions will change the international tax rules for multinationals and they do need to be aware of their impact, but Action 13 includes a reporting requirement which will be new for most. The concept of businesses reporting the amount of tax paid by country has been around for a few years. Other initiatives, such as the Capital Requirements Directive IV and the Extractive Industries Transparency Initiative have placed the requirement on certain industries to report similar information, however Country-by-Country Reporting is not confined to any one industry. Another differentiator is that it has a defined template provided by the OECD, one which tax administrations implementing Country-by-Country Reporting have so far stuck to using the OECD s published template. The OECD report is specifically referred to within HMRC and the Irish Revenue s legislation, and appears as follows: Table 1: An overview of allocation of income, taxes and assets by jurisdiction 4

5 Table 2: A list of constituent entities, by jurisdiction and their business activities Table 3: Additional explanation you consider necessary for the report 5

6 The objective of Country-by- Country Reporting is to improve Tax Transparency. It will provide tax administrations with a consistent global picture of where MNE profits, tax and economic activities are reported. What do HMRC, the Irish Revenue and Other Tax Authorities want to get out of this? The objective of Country-by-Country Reporting is to improve Tax Transparency. It will provide tax administrations with a consistent global picture of where MNE profits, tax and economic activities are reported. This report will enable tax administrations to have the information they need to conduct transfer pricing and BEPS risk assessments and subsequently focus their resources appropriately. BEPS Action 13 also provides standards for Master and Local transfer pricing files, which may be requested or submitted (depending on jurisdiction) to provide a more comprehensive picture for the risk assessment. The requirement for these files is also in various stages of implementation across tax administrations and does not necessarily follow the implementation timetable of Country-by-Country Reporting. Which Businesses are Affected? The Legislative Bit. Most tax administrations, including HMRC and the Irish Revenue, have taken directly from the OECD recommendations in Action 13 and implemented them into legislation. However, there are some variations that create an additional challenge, which we will discuss later. 6

7 A Practical Process Guide for Submitting a Country-by-Country Report All the above probably looks like many other tax filings when reading legislative requirements, but what does trying to create and submit the new Country-by-Country Report look like in practice? We can summarise the process for creating the report in five stages: 1. Identify your source data 2. Transform that information into entity/country level reports for review 3. Aggregate all data into the OECD format reports for group review 4. Convert data to extensible Markup Language ( XML ) format 5. Submit to relevant tax authorities. SOURCE DATA ENTITY - COUNTRY LEVEL REPORTS COUNTRY-BY- COUNTRY REPORT XML COUNTRY-BY- COUNTRY REPORT POST SUBMISSION Local accounts data e.g. Financial statements OR ERP system POPULATE EXTRACT & POPULATE REVIEW AGGREGATE OECD TEMPLATE GROUP LEVEL EDITS CONVERT XML TAGGED REPORT SUBMIT ONLINE Local TAX AUTHORITY SHARED Overseas TAX AUTHORITY ENQUIRIES It would be inappropriate to end this process with the submission of the report to the tax authorities. A high-level summary global picture of your group in this format is something which tax authorities may not have had access to before, so it is reasonable to expect enquiries to result from the report. Accordingly, we have added that as a potential final step in this process which you would have to address, particularly in year one. 7

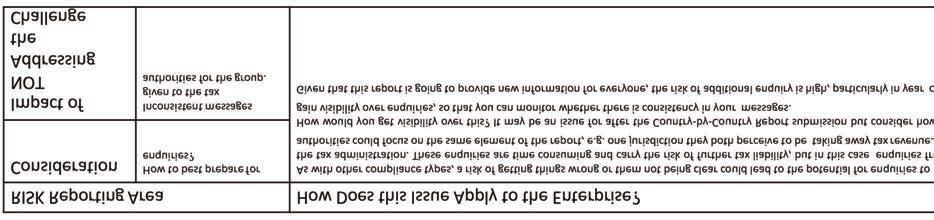

8 The Challenges of Country-by-Country Reporting Many of our clients have come to us to discuss the challenge of Country-by-Country Reporting, and we have worked with them to understand some of the emerging practical issues. We have set them out below, discussing where the impact of the issue lies, the questions which should be asked around the reporting area, the impact of not addressing the issue and then the ways in which the process could affect a business. 8

9 9

10 10

11 What are the Consequences of an Inaccurate Submission? Penalties There are penalties associated with not filing a Countryby-Country Report. For example, HMRC has penalties ranging from 300 for failing to file a report on time up to 3,000 for providing inaccurate information. The Irish equivalent is 19,045 for late submission or inaccuracies. However, other tax authorities have more significant fines, e.g. Luxembourg is proposing fines of up to 250,000 for similar failures. Aside from the straight fines, the cost could be associated in the time spent responding to enquiries related to the figures reported and possibly further tax liabilities should a tax authority successfully challenge your business based on the new information provided. Risk to Brand Named & Shamed For the time being, this information is only reported to the tax authorities and is intended for their eyes only, so late or incorrect information could impact on your relationship with HMRC, the Irish Revenue or other tax authorities, but not public reputation. There is the looming threat of Public Country-by- Country Reporting. The EU Commission has proposed public reporting and, interestingly, their proposals cover a reduced set of the OECD Country-by-Country Reporting data. Should this proceed, the practices you put in place now may leave you well placed for future public reporting. The UK has also added a provision in the 2016 Finance Bill to bring forward regulations which require Public Country-by-Country Reporting as part of the recent tax strategy publication requirement. This definition of Country-by-Country Reporting is the same as the OECD model. The discussion on public reporting continues and it is not possible to say for sure whether it will come into force, but many believe it to be only a matter of time! The discussion on public reporting continues and it is not possible to say for sure whether it will come into force, but many believe it to be only a matter of time! 11

12 What are the benefits of Country-by-Country Reporting as an organisation? Clearly there is a lot to think about in preparation for meeting the Country-by- Country Reporting requirements, but it does present interesting opportunities for you. When looking at some of the challenges which need to be met, there is an opportunity to introduce new or improved methods for co-ordinated group reporting. Not just Country-by-Country Reporting, but also the way that other compliance types and risks, such as enquiries, or tax amounts at stake, are reported. The data gathered in the report can also provide new perspectives and analysis of your group, which may not have been available before. This will allow you to critically analyse your group prior to any information being made public in future years. Additionally, the data gathering being performed for Country-by-Country Reporting could be combined with work you may already be doing for CRD IV or any other group reporting requirements. To take advantage of the above opportunities, now is the time to consider what technology you have, whether you could make better use of it or whether something more comprehensive is required to address the challenges presented by Country-by-Country Reporting. When looking at some of the challenges which need to be met, there is an opportunity to introduce new or improved methods for co-ordinated group reporting. 12

13 Addressing the new process to avoid inaccuracies later If you have not done so already, consider which of the challenges are going to apply to the business and how each of them will be addressed. It is clear from our conversations with our clients to date that the groups impacted by the requirement are at different stages of readiness for Country-by-Country Reporting. There are a lot of variations in terms of how these issues affect different groups - because of the differences in the way they are structured. That is structure in terms of entity global presence, but also where their tax and financial teams are based and how their reporting technology is structured, i.e. whether they can reliably extract all or most of what they need from one place. Before CbCR was introduced, many of the groups we spoke to were reviewing their data sources for the report. This is perhaps the key call to make now so you can identify which review approach is required to get the source data through in an acceptable standard. Many look to ERP extraction or circulating a spreadsheet as a solution, although that does not address the requirement for the electronic XML conversion part of the process. So, you should also be considering the lead time for your software now. For example, it could take three months to choose the software which fits your approach, then a further three months to get through contracting and completing the implementation. This could leave you with little time to go through an advisable dry-run with your software. If possible, the best way to test your approach and learn what works is by conducting a dry-run. This will allow you to test the data, technology, compliance, risk and resource elements of your solution. The sooner you can do this the more time you will have to adjust before the filing deadline arrives. We are aware that a small number have done dry-runs already, purely with the data, to see what results it brings. This, in turn, helps you to consider the level of explanation you may want to provide. You should also check the notification requirements within the jurisdictions you have a presence in. It is common that jurisdictions have a requirement for entities to send a notification to their local tax authority to inform who will be the reporting entity for the whole group and which jurisdiction that entity is in. Some, such as Ireland, required this notification to be made by the entity s fiscal year end, which could have been 31 December The OECD released some further guidance in December 2016 to recommend transitional relief, as not all data exchange frameworks are in place between tax authorities yet, so many groups are yet to choose in which jurisdiction to file their Country-by- Country Report. 13

14 Related to this you may want to look at the broader picture of how you manage your master and local files which, as we referred to earlier, can be requested by the authorities and used with the Country-by-Country Report to provide a clear tax understanding across the enterprise. The first mandatory reports were required at the end of 2017, so we would advise that in order to make an accurate, risk-averse Country-by-Country Report you will need to find a solution which will work for your business. Those affected by the requirements are: Multinational Enterprises, i.e. a presence in more than one country With annual consolidated revenues of greater than 750 million. They are required to report: Periods starting from 1 January 2016 With the first Country-by-Country Reports due to be submitted one year after the period end. So, for example, many periods starting on 1 January 2016 ended on 31 December 2016 and were required to file their first Country-by-Country Report on 31 December The filing then becomes an annual requirement. The report is expected to be submitted by the Ultimate Parent Entity ( UPE ) for the group, or otherwise a nominated Surrogate Parent. The report should only need to be submitted once and then would be shared between tax authorities who have a Qualifying Competent Authority Agreement ( QCAA ) in place. There is a Multilateral Competent Authority Agreement ( MCAA ) which currently includes 49 countries. The list of the signatories of the agreement on the exchange of country-by-country reports is published by the OECD. Even though you will choose to file in one jurisdiction (most likely the country of your UPE) the tax authorities within the jurisdictions in which you are present globally, may require informing. HMRC and the Irish Revenue expect you to inform them of which group entity will be filing the report, and which jurisdiction it is available from, if not their own. 14

15 Tax Systems and Country-by-Country Reporting At Tax Systems (TS), we are constantly monitoring new tax reporting requirements and considering which solutions will be needed to address them. With the new reporting methods and guidelines being issued by HMRC and the Irish Revenue, which include the need for transparency, automation and the increased use of technology, it is crucial that both TS and our customers are prepared for any inclusions and modifications to taxation processes which arise from any of the global authorities, and that internal processes are put in place before the filing deadline. Our solutions allow you to prepare and submit accurate and transparent XML Country-by-Country reports to the relevant tax authorities. Our customers approach us because they recognise our experience in providing solutions for a variety of compliance requirements and for creating documents which can be submitted directly to HMRC, the Irish Revenue or other tax authorities. For Country-by-Country Reporting there are significant changes to the reporting processes and so a software solution or an outsourced solution will be necessary to ensure that the report is submitted in the accepted electronic format ( XML ). Our solutions allow you to prepare and submit accurate XML Country-by-Country reports to the relevant tax authorities while providing a clear audit trail of where all data was sourced from and a PDF containing a human-readable summary of what has been included in the final XML submission. 15

16 Country-by-Country Reporting (part of the Alpha Compliance Suite) Option 1: software solution Tax Systems automated Country-by-Country Reporting software delivers a secure cloud-based solution which manages the collection and aggregation of relevant data across each country within a global business. The intuitive dashboard delivers live updates which provide the examination of data management, workloads and a realtime analysis of the global business situation, allowing the business to understand any areas of risk which may appear, bringing all relevant tax and compliance information into a single location. It supports the global implementation of HRMC and the Irish Revenue Country-by-Country Reporting schema, and will deliver an accurate report within the required electronic format ready for submission. The solution has been developed specifically for Tax and Compliance departments to replace spreadsheets and to automate processes previously based on information consolidation by or phone call. Features Efficient Accumulation Automated collection of all the relevant information from each jurisdiction is compiled into the required OECD format in a chosen base currency. Risk Analysis Comprehensive checks are done in the system so you can effectively identify any areas of risk and action these before submission. Event Tracking More than just an audit trail, CbCR can identify who, what and when information has been amended, constantly monitoring changes throughout the entire processes, giving you the maximum amount of visibility on the data. Real-time Updates Information is updated across the whole process instantly so all users can see live updates on the data progress. Single Repository Everything can be held in one location. CbCR is designed to hold all relevant information in one place. This is especially useful for global teams to input and review data without the need to send anything via . Personalisation Each user can have a personalised dashboard to show only the relevant information snapshots to their particular role. This helps the entire team as a whole from a management/ review level to those who will be managing the CbCR process. Automatic updates We constantly review the schema requirements so you don t have to. Any update to legislation is reviewed and built into the CbCR product and released to you accordingly, ensuring you always have the most up-to-date software platform....delivering a secure cloud-based solution which manages the collection and aggregation of relevant data across each country within a global business. 16

17 Option 2: Outsourced XML conversion solution Where you have already aggregated your data, we can convert it to XML for you. Our Professional Services team provides you with our Excel template, which has been designed to capture all information required to be reported by the group. Our tax experts provide a fresh pair of eyes, familiar with what should be included in your CbCR XML, to check the Excel template for any obvious errors or missing information. We then import your data into our CbCR engine, which will validate the data against the latest tax authority rules, such as whether all key information is included and whether it is formatted correctly. All we need from you is a complete set of data to be provided in the template as a means of confirming what you want to be reported to your relevant tax authority, and confirmation of which tax authority you will be submitting your report to. Whichever solution works for you, you will benefit from time and cost savings around internal resourcing as you will be able to redeploy your tax professionals to focus on value add tasks. In addition, quality is assured and takes away risks around submission because validation is made against latest rules and data is checked for completeness....you will benefit from time and cost savings around internal resourcing as you will be able to redeploy your tax professionals to focus on value add tasks. Data Gathering (TCS/Client) Review (TCS) Convert (TCS) Output Returned (TCS) Client upload (Client) EXCEL TEMPLATE Check for completeness Imported into AlphaCbCR, converted & validated XML and PDF returned Upload 17

Country-by-Country Reporting: Data Access & Usage. TDM Part

Tax and Duty Manual Part 38-03-20 Country-by-Country Reporting: Data Access & Usage TDM Part 38-03-20 This document should be read in conjunction with section 891H of the Taxes Consolidation Act 1997 Document

Tax and Duty Manual Part 38-03-20 Country-by-Country Reporting: Data Access & Usage TDM Part 38-03-20 This document should be read in conjunction with section 891H of the Taxes Consolidation Act 1997 Document

Your complete guide to submitting with HMRC. Country by Country. Reporting

Your complete guide to submitting with HMRC Country by Country Reporting Contents The First Deadline 3 Country by Country Reporting Submission Tips 5 Your Reporting Checklist 6 4 Common Filling Errors

Your complete guide to submitting with HMRC Country by Country Reporting Contents The First Deadline 3 Country by Country Reporting Submission Tips 5 Your Reporting Checklist 6 4 Common Filling Errors

New post-beps three-tiered documentation requirements Impact for Kazakhstan s multinational enterprises

New post-beps three-tiered documentation requirements Impact for Kazakhstan s multinational enterprises Kazakhstan, 2016 Brochure / report title goes here Section title goes here Documentation requirements

New post-beps three-tiered documentation requirements Impact for Kazakhstan s multinational enterprises Kazakhstan, 2016 Brochure / report title goes here Section title goes here Documentation requirements

Photo credits: Cover MIND AND I Shutterstock.com OECD 2017

This document and any map included herein are without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any

This document and any map included herein are without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any

On October , the OECD released its final report on

New TP documentation rules: update and CbCR example Maik Heggmair and Tobias Faltlhauser of WTS summarise the new transfer pricing (TP) documentation rules to be implemented in Germany and provide an example

New TP documentation rules: update and CbCR example Maik Heggmair and Tobias Faltlhauser of WTS summarise the new transfer pricing (TP) documentation rules to be implemented in Germany and provide an example

Country-By-Country Reporting. Some Frequently Asked Questions (FAQs)

") Country-By-Country Reporting Some Frequently Asked Questions (FAQs) These Frequently Asked Questions (FAQs) are designed to provide information in relation to the introduction of Country-by-Country Reporting

Country-By-Country Reporting Some Frequently Asked Questions (FAQs) These Frequently Asked Questions (FAQs) are designed to provide information in relation to the introduction of Country-by-Country Reporting

Luxembourg transfer pricing legislation at a glance

2017 EY TAX Alert Luxembourg Luxembourg transfer pricing legislation at a glance Executive summary The law of 23 December 2016 on the budget for the year 2017 ( Budget Law ) has introduced a new article

2017 EY TAX Alert Luxembourg Luxembourg transfer pricing legislation at a glance Executive summary The law of 23 December 2016 on the budget for the year 2017 ( Budget Law ) has introduced a new article

A Guide To Changes In Irish Tax Rules

A Guide To Changes In Irish Tax Rules - The Global Tax Reform Agenda 6 September 2016 THE FACTS YOU NEED TO KNOW ON IRISH TAX CHANGES 1 INTERNATIONAL TAX RULES HAVE BEEN CHANGING - IRELAND HAS BEEN PARTICIPATING

A Guide To Changes In Irish Tax Rules - The Global Tax Reform Agenda 6 September 2016 THE FACTS YOU NEED TO KNOW ON IRISH TAX CHANGES 1 INTERNATIONAL TAX RULES HAVE BEEN CHANGING - IRELAND HAS BEEN PARTICIPATING

Guidance on the Implementation of Country-by-Country Reporting BEPS ACTION 13

Guidance on the Implementation of Country-by-Country Reporting BEPS ACTION 13 Updated February 2018 Guidance on the Implementation of Country-by-Country Reporting: BEPS Action 13 Updated February 2018

Guidance on the Implementation of Country-by-Country Reporting BEPS ACTION 13 Updated February 2018 Guidance on the Implementation of Country-by-Country Reporting: BEPS Action 13 Updated February 2018

Pakistan implements formal transfer pricing documentation and Country-by- Country Reporting requirements

7 August 2017 Global Tax Alert News from Transfer Pricing Pakistan implements formal transfer pricing documentation and Country-by- Country Reporting requirements EY Global Tax Alert Library Access both

7 August 2017 Global Tax Alert News from Transfer Pricing Pakistan implements formal transfer pricing documentation and Country-by- Country Reporting requirements EY Global Tax Alert Library Access both

Exchange of information on Tax Rulings

Exchange of information on Tax Rulings 24 November 2016 Jean-Michel Hamelle Partner Tax and Accounting Agenda 2 Exchange of Information on Tax Rulings OECD BEPS Action 5 EU Directive 2015/2376/EU Luxembourg

Exchange of information on Tax Rulings 24 November 2016 Jean-Michel Hamelle Partner Tax and Accounting Agenda 2 Exchange of Information on Tax Rulings OECD BEPS Action 5 EU Directive 2015/2376/EU Luxembourg

The OECD s 3 Major Tax Initiatives

The OECD s 3 Major Tax Initiatives 1. The Global Forum on Transparency and Exchange of Information for Tax Purposes Peer review of ~ 100 countries International standard for transparency and exchange of

The OECD s 3 Major Tax Initiatives 1. The Global Forum on Transparency and Exchange of Information for Tax Purposes Peer review of ~ 100 countries International standard for transparency and exchange of

Transfer Pricing Documentation

2017 Transfer Pricing Documentation BRIEF ON SRO 1191(I)/2017 DATED NOVEMBER 16, 2017 BACKGROUND Transfer Pricing is not a new subject in Pakistan. Provisions in taxation law, dealing with determination

2017 Transfer Pricing Documentation BRIEF ON SRO 1191(I)/2017 DATED NOVEMBER 16, 2017 BACKGROUND Transfer Pricing is not a new subject in Pakistan. Provisions in taxation law, dealing with determination

Ireland s Country-by- Country reporting notification deadline is 31 December 2016

12 December 2016 Global Tax Alert News from Transfer Pricing Ireland s Country-by- Country reporting notification deadline is 31 December 2016 EY Global Tax Alert Library Access both online and pdf versions

12 December 2016 Global Tax Alert News from Transfer Pricing Ireland s Country-by- Country reporting notification deadline is 31 December 2016 EY Global Tax Alert Library Access both online and pdf versions

1. Codifies transfer pricing rules, relief and provides for advance pricing arrangement (APA) regime to cater for unilateral,

regime to cater for unilateral,") JANUARY 2018 WWW.BDO.COM.HK HONG KONG TAX HONG KONG INTRODUCES TAX BILL TO IMPLEMENT MINIMUM STANDARDS OF THE BASE EROSION AND PROFIT SHIFTING TRANSFER PRICING REGULATORY REGIME AND DOCUMENTATION REQUIREMENTS

JANUARY 2018 WWW.BDO.COM.HK HONG KONG TAX HONG KONG INTRODUCES TAX BILL TO IMPLEMENT MINIMUM STANDARDS OF THE BASE EROSION AND PROFIT SHIFTING TRANSFER PRICING REGULATORY REGIME AND DOCUMENTATION REQUIREMENTS

Delegations will find attached the text of the draft Directive, resulting from the discussions held at the ECOFIN Council of 8 March 2016.

Council of the European Union Brussels, 15 March 2016 (OR. en) Interinstitutional File: 2016/0010 (CNS) 6949/16 FISC 38 ECOFIN 216 NOTE From: To: General Secretariat of the Council Delegations No. prev.

Council of the European Union Brussels, 15 March 2016 (OR. en) Interinstitutional File: 2016/0010 (CNS) 6949/16 FISC 38 ECOFIN 216 NOTE From: To: General Secretariat of the Council Delegations No. prev.

7148/16 HG/NT/kp,vm DGG 2B

Council of the European Union Brussels, 11 May 2016 (OR. en) Interinstitutional File: 2016/0010 (CNS) 7148/16 FISC 39 ECOFIN 231 LEGISLATIVE ACTS AND OTHER INSTRUMENTS Subject: COUNCIL DIRECTIVE amending

Council of the European Union Brussels, 11 May 2016 (OR. en) Interinstitutional File: 2016/0010 (CNS) 7148/16 FISC 39 ECOFIN 231 LEGISLATIVE ACTS AND OTHER INSTRUMENTS Subject: COUNCIL DIRECTIVE amending

The global tax disputes environment

The global tax disputes environment How the tax disputes teams of multinational corporations are managing, responding and evolving Global Tax Disputes benchmarking survey 2016 KPMG International kpmg.com/tax

The global tax disputes environment How the tax disputes teams of multinational corporations are managing, responding and evolving Global Tax Disputes benchmarking survey 2016 KPMG International kpmg.com/tax

Denmark. WTS Global Country TP Guide Last Update: December Legal Basis. 2. Master File (MF) Yes

Yes") Denmark WTS Global Country TP Guide Last Update: December 2017 1. Legal Basis Is there a legal requirement to prepare TP documentation? Since when does a TP documentation requirement exist in your country?

Denmark WTS Global Country TP Guide Last Update: December 2017 1. Legal Basis Is there a legal requirement to prepare TP documentation? Since when does a TP documentation requirement exist in your country?

Statement for the Record

Statement for the Record of Dorothy Coleman Vice President, Tax & Domestic Economic Policy National Association of Manufacturers For the Hearing of the Senate Finance Committee on International Tax: OECD

Statement for the Record of Dorothy Coleman Vice President, Tax & Domestic Economic Policy National Association of Manufacturers For the Hearing of the Senate Finance Committee on International Tax: OECD

Transfer Pricing Documentation

2018 Transfer Pricing Documentation BRIEF ON FURTHER AMENDMENTS MADE THROUGH S.R.O. 144(I)/2018 DATED FEBRUARY 9, 2018 ON THE DOCUMENTATION AND COUNTRY-BY-COUNTRY REPORTING REQUIREMENTS FOREWORD This document

2018 Transfer Pricing Documentation BRIEF ON FURTHER AMENDMENTS MADE THROUGH S.R.O. 144(I)/2018 DATED FEBRUARY 9, 2018 ON THE DOCUMENTATION AND COUNTRY-BY-COUNTRY REPORTING REQUIREMENTS FOREWORD This document

OECD publishes BEPS peer review documents for exchanges of tax rulings and country-by-country reports

OECD publishes BEPS peer review documents for exchanges of tax rulings and country-by-country reports 7 February 2017 In brief On 1 February 2017, the Organisation for Economic Cooperation and Development

OECD publishes BEPS peer review documents for exchanges of tax rulings and country-by-country reports 7 February 2017 In brief On 1 February 2017, the Organisation for Economic Cooperation and Development

Managing operational tax risk through technology

Managing operational tax risk through technology EY Africa Tax Conference September 2014 Panel Daryl Blakeway Director Tax Performance Advisory Leader EY South Africa Anthony Davis Director Tax Performance

Managing operational tax risk through technology EY Africa Tax Conference September 2014 Panel Daryl Blakeway Director Tax Performance Advisory Leader EY South Africa Anthony Davis Director Tax Performance

Guidance on the Implementation of Country-by-Country Reporting BEPS ACTION 13

Guidance on the Implementation of Country-by-Country Reporting BEPS ACTION 13 Updated November 2017 Guidance on the Implementation of Country-by-Country Reporting: BEPS Action 13 Updated November 2017

Guidance on the Implementation of Country-by-Country Reporting BEPS ACTION 13 Updated November 2017 Guidance on the Implementation of Country-by-Country Reporting: BEPS Action 13 Updated November 2017

THE FUTURE OF TAX PLANNING: TRANSPARENCY AND SUBSTANCE FOR ALL? Friday, 26 February AM PM Conrad Hotel, Hong Kong

THE FUTURE OF TAX PLANNING: TRANSPARENCY AND SUBSTANCE FOR ALL? Friday, 26 February 2016 9.00AM - 12.00PM Conrad Hotel, Hong Kong THE DRIVE TOWARDS TRANSPARENCY: CHALLENGES AND OPPORTUNITIES IN INTERNATIONAL

THE FUTURE OF TAX PLANNING: TRANSPARENCY AND SUBSTANCE FOR ALL? Friday, 26 February 2016 9.00AM - 12.00PM Conrad Hotel, Hong Kong THE DRIVE TOWARDS TRANSPARENCY: CHALLENGES AND OPPORTUNITIES IN INTERNATIONAL

User guide «Country-by-Country Reporting»

User guide «Country-by-Country Reporting» The Country-by-Country Report (hereafter CbCR ) is created and sent to the Luxembourg Tax Administration (hereafter ACD ) via the platform MyGuichet. This platform

User guide «Country-by-Country Reporting» The Country-by-Country Report (hereafter CbCR ) is created and sent to the Luxembourg Tax Administration (hereafter ACD ) via the platform MyGuichet. This platform

FLC Guidance. Page 1. Version. September *Disclaimer: This is a living document and further content will be developed at a later stage.

FLC Guidance Version September 2017 *Disclaimer: This is a living document and further content will be developed at a later stage. Page 1 Table of Contents... 1 CHAPTER 1 General principles... 3 1.1 Introduction...

FLC Guidance Version September 2017 *Disclaimer: This is a living document and further content will be developed at a later stage. Page 1 Table of Contents... 1 CHAPTER 1 General principles... 3 1.1 Introduction...

2017 Global BEPS Survey Report

1 November 2017 2 Executive Summary Respondent Breakout BEPS comes into focus For the third consecutive year, Thomson Reuters sought to determine corporations compliance with the OECD s BEPS recommendations.

1 November 2017 2 Executive Summary Respondent Breakout BEPS comes into focus For the third consecutive year, Thomson Reuters sought to determine corporations compliance with the OECD s BEPS recommendations.

Navigating BEPS: Keeping track of the tax changes for internationally mobile employees

Navigating BEPS: Keeping track of the tax changes for internationally mobile employees Across a number of countries, the way internationally mobile employees are taxed is being shaken-up. This follows

Navigating BEPS: Keeping track of the tax changes for internationally mobile employees Across a number of countries, the way internationally mobile employees are taxed is being shaken-up. This follows

Newsletter October 2018

Tax Newsletter BEPS Series Kuala Lumpur Newsletter October 2018 In This Issue 1. What is BEPS? 2. BEPS Action 13 Transfer Pricing Documentation and Reporting 3. Malaysia Response and Implementation 4.

Tax Newsletter BEPS Series Kuala Lumpur Newsletter October 2018 In This Issue 1. What is BEPS? 2. BEPS Action 13 Transfer Pricing Documentation and Reporting 3. Malaysia Response and Implementation 4.

South African Revenue Service issues Country-by Country reporting, master file and local file guidance

26 June 2017 Global Tax Alert News from Transfer Pricing South African Revenue Service issues Country-by Country reporting, master file and local file guidance EY Global Tax Alert Library Access both online

26 June 2017 Global Tax Alert News from Transfer Pricing South African Revenue Service issues Country-by Country reporting, master file and local file guidance EY Global Tax Alert Library Access both online

Transfer pricing in the post-beps age The challenge to convert mere compliance into good governance

Transfer pricing in the post-beps age The challenge to convert mere compliance into good governance Transfer Pricing Compliance versus Transfer Pricing Governance Are Transfer Pricing Compliance and Transfer

Transfer pricing in the post-beps age The challenge to convert mere compliance into good governance Transfer Pricing Compliance versus Transfer Pricing Governance Are Transfer Pricing Compliance and Transfer

HONG KONG. 1. Introduction. Contact Information Henry Fung Candice Ng

HONG KONG Contact Information Henry Fung +852 2969 4054 hernyfung@pkf-hk.com Candice Ng +852 2969 4016 candiceng@pkf-hk.com 1. Introduction 1.1. Legal context Currently, the Hong Kong Inland Revenue Ordinance

HONG KONG Contact Information Henry Fung +852 2969 4054 hernyfung@pkf-hk.com Candice Ng +852 2969 4016 candiceng@pkf-hk.com 1. Introduction 1.1. Legal context Currently, the Hong Kong Inland Revenue Ordinance

Transfer Pricing Alert

Transfer Pricing Alert EY Han Young newsletter December 2016 Transfer Pricing Current issue. Hong Kong, Dutch Hong Kong Hong Kong publishes consultation paper on measures to counter BEPS Executive summary

Transfer Pricing Alert EY Han Young newsletter December 2016 Transfer Pricing Current issue. Hong Kong, Dutch Hong Kong Hong Kong publishes consultation paper on measures to counter BEPS Executive summary

Flash News. PwC Luxembourg BEPS Series- What it means for the Luxembourg Asset Management industry

www.pwc.lu/tax Flash News PwC Luxembourg BEPS Series- What it means for the Luxembourg Asset Management industry On Monday 5 October 2015, the Organisation for Economic Cooperation and Development (OECD)

www.pwc.lu/tax Flash News PwC Luxembourg BEPS Series- What it means for the Luxembourg Asset Management industry On Monday 5 October 2015, the Organisation for Economic Cooperation and Development (OECD)

EUROPEAN COMMISSION PRESENTS ANTI-TAX AVOIDANCE PACKAGE

EUROPEAN COMMISSION PRESENTS ANTI-TAX AVOIDANCE PACKAGE tax.thomsonreuters.com On January 28, 2016, the European Commission presented its Communication on the Anti-Tax Avoidance Package (ATA Package).

EUROPEAN COMMISSION PRESENTS ANTI-TAX AVOIDANCE PACKAGE tax.thomsonreuters.com On January 28, 2016, the European Commission presented its Communication on the Anti-Tax Avoidance Package (ATA Package).

Bilateral Advance Pricing Agreement Guidelines

September 2016 Bilateral Advance Pricing Agreement Guidelines Page 1 Contents PART 1 INTRODUCTION...5 PART 2 BILATERAL APA PROGRAMME OVERVIEW...5 PART 3 PURPOSE AND SCOPE OF APA...7 What is an APA?...7

September 2016 Bilateral Advance Pricing Agreement Guidelines Page 1 Contents PART 1 INTRODUCTION...5 PART 2 BILATERAL APA PROGRAMME OVERVIEW...5 PART 3 PURPOSE AND SCOPE OF APA...7 What is an APA?...7

Transfer Pricing Country Summary Austria

Page 1 of 6 Transfer Pricing Country Summary Austria April 2018 Page 2 of 6 Legislation Existence of Transfer Pricing Laws/Guidelines On July 6, 2016, the Transfer Pricing Documentation Act (TPDA) has

Page 1 of 6 Transfer Pricing Country Summary Austria April 2018 Page 2 of 6 Legislation Existence of Transfer Pricing Laws/Guidelines On July 6, 2016, the Transfer Pricing Documentation Act (TPDA) has

Base Erosion Profit Shifting (BEPS)

") Base Erosion Profit Shifting (BEPS) Base Erosion Profit Shifting (BEPS) The world continues to evolve and nations are becoming increasingly connected. Domestic tax laws have not kept pace with the evolution

Base Erosion Profit Shifting (BEPS) Base Erosion Profit Shifting (BEPS) The world continues to evolve and nations are becoming increasingly connected. Domestic tax laws have not kept pace with the evolution

Technology revs up regulatory complexity and drives deeper data demands

Technology revs up regulatory complexity and drives deeper data demands KPMG International kpmg.com/gcms For large international companies, compliance means a lot more than preparing tax forms and meeting

Technology revs up regulatory complexity and drives deeper data demands KPMG International kpmg.com/gcms For large international companies, compliance means a lot more than preparing tax forms and meeting

SWIFT for SECURITIES. How the world s post-trade experts can help you improve efficiency, and prepare for tomorrow

SWIFT for SECURITIES How the world s post-trade experts can help you improve efficiency, and prepare for tomorrow 2 1 2 3 4 Your global automation partner A complex and changing landscape Solutions across

SWIFT for SECURITIES How the world s post-trade experts can help you improve efficiency, and prepare for tomorrow 2 1 2 3 4 Your global automation partner A complex and changing landscape Solutions across

Technology Builds Transparency: Achieving Justified Trust

Technology Builds Transparency: Achieving Justified Trust INTRODUCTION A fair international tax system is one of the Organisation for Economic Co-operation and Development s (OECD s) main focus areas.

Technology Builds Transparency: Achieving Justified Trust INTRODUCTION A fair international tax system is one of the Organisation for Economic Co-operation and Development s (OECD s) main focus areas.

Submission of ixbrl Financial Statements as part of Corporation Tax Returns

Submission of ixbrl Financial Statements as part of Corporation Tax Returns Document last updated July 2018. This instruction provides details of the obligations of certain Corporation Tax (CT) filers

Submission of ixbrl Financial Statements as part of Corporation Tax Returns Document last updated July 2018. This instruction provides details of the obligations of certain Corporation Tax (CT) filers

BEPS Country-by-Country Reporting Rules and New Documentation Requirements

BEPS Country-by-Country Reporting Rules and New Documentation Requirements, EY LLP, Couzin Taylor LLP 67 th Annual Tax Conference 67e Conférence fiscale annuelle 2015 Agenda 1. The BEPS project: Action

BEPS Country-by-Country Reporting Rules and New Documentation Requirements, EY LLP, Couzin Taylor LLP 67 th Annual Tax Conference 67e Conférence fiscale annuelle 2015 Agenda 1. The BEPS project: Action

Guide to Making Tax Digital

Guide to Making Tax Digital Making Tax Digital - what does it mean for you? Making Tax Digital is a government initiative that sets out a bold vision for a digital tax system to make it easier for individuals

Guide to Making Tax Digital Making Tax Digital - what does it mean for you? Making Tax Digital is a government initiative that sets out a bold vision for a digital tax system to make it easier for individuals

Implementation of the XML structure to meet legal requirements within the framework of the CbCR

wts CbCR-2-XML Implement the XML structure to meet the legal requirements of Country-by-Country-Reporting Secure access No data storage Web-based service Implementation of the XML structure to meet legal

wts CbCR-2-XML Implement the XML structure to meet the legal requirements of Country-by-Country-Reporting Secure access No data storage Web-based service Implementation of the XML structure to meet legal

IBFD Course Programme International Tax Planning after BEPS and the MLI

IBFD Course Programme International Tax Planning after BEPS and the MLI Summary Recent developments such as the BEPS project and the Multilateral Instrument in international taxation, but also unilateral

IBFD Course Programme International Tax Planning after BEPS and the MLI Summary Recent developments such as the BEPS project and the Multilateral Instrument in international taxation, but also unilateral

Online filing of Corporation Tax returns with statutory accounts in XBRL from 2011

1 November 2010 Online filing of Corporation Tax returns with statutory accounts in XBRL from 2011 Online filing requirement Online filing to HMRC will be mandatory for all UK companies from 1 April 2011.

1 November 2010 Online filing of Corporation Tax returns with statutory accounts in XBRL from 2011 Online filing requirement Online filing to HMRC will be mandatory for all UK companies from 1 April 2011.

Hong Kong SAR Government s Roadmap following the outcomes of the BEPS Consultation

News Flash Transfer Pricing Hong Kong SAR Government s Roadmap following the outcomes of the BEPS Consultation August 2017 In brief On 31 July 2017, the Hong Kong SAR Government (the Government) released

News Flash Transfer Pricing Hong Kong SAR Government s Roadmap following the outcomes of the BEPS Consultation August 2017 In brief On 31 July 2017, the Hong Kong SAR Government (the Government) released

Transfer Pricing Alert

Transfer Pricing Alert EY Han Young newsletter July 2016 Transfer Pricing Current issue. Republic of Korea, United Kingdom, Belgium 2 Republic of Korea Korean Government Signed Multilateral Competent Authority

Transfer Pricing Alert EY Han Young newsletter July 2016 Transfer Pricing Current issue. Republic of Korea, United Kingdom, Belgium 2 Republic of Korea Korean Government Signed Multilateral Competent Authority

Step by step guide to auto enrolment

Step by step guide to auto enrolment The legislation surrounding auto enrolment can be quite tricky. When faced with an overwhelming set of tasks, rules, regulations and jargon it is difficult to fully

Step by step guide to auto enrolment The legislation surrounding auto enrolment can be quite tricky. When faced with an overwhelming set of tasks, rules, regulations and jargon it is difficult to fully

THE KNOWLEDGE DEVELOPMENT BOX Public Consultation JANUARY 2015

THE KNOWLEDGE DEVELOPMENT BOX Public Consultation JANUARY 2015 Public Consultation Paper: The Knowledge Development Box Department of Finance January 2015 Tax Policy Division Department of Finance Government

THE KNOWLEDGE DEVELOPMENT BOX Public Consultation JANUARY 2015 Public Consultation Paper: The Knowledge Development Box Department of Finance January 2015 Tax Policy Division Department of Finance Government

Submission of ixbrl Financial Statements as part of Corporation Tax Returns. Part 41A-03-01

Submission of ixbrl Financial Statements as part of Corporation Tax Returns Part 41A-03-01 Updated October 2017 This Instruction provides details of the obligations of certain Corporation Tax (CT) filers

Submission of ixbrl Financial Statements as part of Corporation Tax Returns Part 41A-03-01 Updated October 2017 This Instruction provides details of the obligations of certain Corporation Tax (CT) filers

Hong Kong introduces tax and transfer pricing legislation to counter Base Erosion and Profit Shifting

5 January 2018 Global Tax Alert Hong Kong introduces tax and transfer pricing legislation to counter Base Erosion and Profit Shifting EY Global Tax Alert Library Access both online and pdf versions of

5 January 2018 Global Tax Alert Hong Kong introduces tax and transfer pricing legislation to counter Base Erosion and Profit Shifting EY Global Tax Alert Library Access both online and pdf versions of

Reporting transparency information to the FCA. Questions and answers

Reporting transparency information to the FCA Questions and answers December 2017 Introduction... 3 Section 1 - Introduction to AIFMD Reporting Requirements... 4 Section 2 - AIFMD Submission through Gabriel...

Reporting transparency information to the FCA Questions and answers December 2017 Introduction... 3 Section 1 - Introduction to AIFMD Reporting Requirements... 4 Section 2 - AIFMD Submission through Gabriel...

The UAE has joined the Inclusive Framework on BEPS

The UAE has joined the Inclusive Framework on BEPS May 2018 In brief The United Arab Emirates ( UAE ) joined the OECD Inclusive Framework on Base Erosion and Profit Shifting ( BEPS ) on 16 May 2018, bringing

The UAE has joined the Inclusive Framework on BEPS May 2018 In brief The United Arab Emirates ( UAE ) joined the OECD Inclusive Framework on Base Erosion and Profit Shifting ( BEPS ) on 16 May 2018, bringing

CONTENTS. Introduction 2. Survey Highlights 3. Survey Demographics 5. Processes 10. Challenges 17

CONTENTS Introduction 2 Survey Highlights 3 Survey Demographics 5 Processes 10 Challenges 17 INTRODUCTION Solvency II is the most significant regulatory change ever to be implemented throughout the European

CONTENTS Introduction 2 Survey Highlights 3 Survey Demographics 5 Processes 10 Challenges 17 INTRODUCTION Solvency II is the most significant regulatory change ever to be implemented throughout the European

User guide for employers not using our system for assessment

For scheme administrators User guide for employers not using our system for assessment Workplace pensions CONTENTS Welcome... 6 Getting started... 8 The dashboard... 9 Import data... 10 How to import a

For scheme administrators User guide for employers not using our system for assessment Workplace pensions CONTENTS Welcome... 6 Getting started... 8 The dashboard... 9 Import data... 10 How to import a

Country-by-country reporting Adapting to a changing documentation regime

Country-by-country reporting Adapting to a changing documentation regime Setting the context The base erosion and profit shifting (BEPS) project of the Organisation for Economic Co-operation and Development

Country-by-country reporting Adapting to a changing documentation regime Setting the context The base erosion and profit shifting (BEPS) project of the Organisation for Economic Co-operation and Development

OECD/G20 Base Erosion and Profit Shifting Project

OECD/G20 Base Erosion and Profit Shifting Project Action 13: Guidance on Transfer Pricing Documentation and Country-by-Country Reporting Country-by-Country Report Instructions Manual 24 June 2015 Page

OECD/G20 Base Erosion and Profit Shifting Project Action 13: Guidance on Transfer Pricing Documentation and Country-by-Country Reporting Country-by-Country Report Instructions Manual 24 June 2015 Page

Why Legal Entity Management Matters IV

Why Legal Entity Management Matters IV Collating and reporting legal entity information in today s environment: are you prepared? Issue 4.0 Q3 2015 Collating and reporting legal entity information in today

Why Legal Entity Management Matters IV Collating and reporting legal entity information in today s environment: are you prepared? Issue 4.0 Q3 2015 Collating and reporting legal entity information in today

Belgium. WTS Global Country TP Guide Last Update: December Legal Basis. 2. Master File (MF) Yes

Yes") Belgium WTS Global Country TP Guide Last Update: December 2017 1. Legal Basis Is there a legal requirement to prepare TP documentation? Since when does a TP documentation requirement exist in your country?

Belgium WTS Global Country TP Guide Last Update: December 2017 1. Legal Basis Is there a legal requirement to prepare TP documentation? Since when does a TP documentation requirement exist in your country?

White Paper. Taming Your Workers Compensation Compliance Challenges

White Paper Taming Your Workers Compensation Compliance Challenges November 2015 Contents Introduction 3 FEDERAL MANDATES 3 CMS & MMSEA Section 111 STATE MANDATES 5 Key Requirements That Vary by State

White Paper Taming Your Workers Compensation Compliance Challenges November 2015 Contents Introduction 3 FEDERAL MANDATES 3 CMS & MMSEA Section 111 STATE MANDATES 5 Key Requirements That Vary by State

Employment intermediaries: reporting requirements

Employment intermediaries: reporting requirements Guidance about reports intermediaries may have to send to HMRC for agency workers where they didn't operate PAYE. An intermediary is any person who makes

Employment intermediaries: reporting requirements Guidance about reports intermediaries may have to send to HMRC for agency workers where they didn't operate PAYE. An intermediary is any person who makes

22 January 2018 January 2018 Special Edition

22 January 2018 January 2018 Special Edition Indonesia releases implementation regulation on Country-by-Country Reports (CbCR) that provides detailed instructions on the procedure and filing of the Country-by-Country

22 January 2018 January 2018 Special Edition Indonesia releases implementation regulation on Country-by-Country Reports (CbCR) that provides detailed instructions on the procedure and filing of the Country-by-Country

Understanding Pension Auto Enrolment. Essentials Guide

Understanding Pension Auto Enrolment Essentials Guide Contents Introduction 3 Employer responsibilities in a nutshell 4 How can KPMG Small Business Accounting help you? 5 Staging date checker and tracking

Understanding Pension Auto Enrolment Essentials Guide Contents Introduction 3 Employer responsibilities in a nutshell 4 How can KPMG Small Business Accounting help you? 5 Staging date checker and tracking

5 KEY THINGS YOUR POLICIES POLICY MUST HAVE (And the One Secret to Bringing Them All Together)

") 5 KEY THINGS YOUR POLICIES POLICY MUST HAVE (And the One Secret to Bringing Them All Together) PROCESSUNITY WHITE PAPER Many eyes are turning to your policies and procedures. Are you prepared for what

5 KEY THINGS YOUR POLICIES POLICY MUST HAVE (And the One Secret to Bringing Them All Together) PROCESSUNITY WHITE PAPER Many eyes are turning to your policies and procedures. Are you prepared for what

Transfer Pricing: The New Frontier Transfer Pricing Documentation in a Post-BEPS World: Evolution or Revolution? November 8, 2018

Transfer Pricing: The New Frontier Transfer Pricing Documentation in a Post-BEPS World: Evolution or Revolution? November 8, 2018 Today s Speakers Astrid Pieron Partner, Brussels apieron@mayerbrown.com

Transfer Pricing: The New Frontier Transfer Pricing Documentation in a Post-BEPS World: Evolution or Revolution? November 8, 2018 Today s Speakers Astrid Pieron Partner, Brussels apieron@mayerbrown.com

Tax and Legal Newsletter

16 June 2016 Newsletter Tax and Legal Newsletter EY CbCR.WEB The new tool for effective and timely management of Countryby-Country Reporting http://www.ey.com/serv ices/tax/tax- Performance-Advisory Contacts

16 June 2016 Newsletter Tax and Legal Newsletter EY CbCR.WEB The new tool for effective and timely management of Countryby-Country Reporting http://www.ey.com/serv ices/tax/tax- Performance-Advisory Contacts

Making Tax Digital for VAT. Main issues for consideration

Making Tax Digital for VAT Main issues for consideration Businesses whose taxable turnover exceeds the VAT registration threshold will need to keep their records digitally, using MTD functional compatible

Making Tax Digital for VAT Main issues for consideration Businesses whose taxable turnover exceeds the VAT registration threshold will need to keep their records digitally, using MTD functional compatible

Common Reporting Standard A work in progress requiring high reactivity. Alain Verbeken Director Cross-border Tax Deloitte

Common Reporting Standard A work in progress requiring high reactivity Pascal Eber Partner Operations Excellence & Human Capital Deloitte Alain Verbeken Director Cross-border Tax Deloitte Alexandre Havard

Common Reporting Standard A work in progress requiring high reactivity Pascal Eber Partner Operations Excellence & Human Capital Deloitte Alain Verbeken Director Cross-border Tax Deloitte Alexandre Havard

The definitive source of actionable intelligence on hedge fund law and regulation

By Dmitri Semenov, Jun Li, Lucas Rachuba and Carter Vinson Ernst & Young LLP FATCA Steps That Alternative Investment Fund Managers Need to Take Today to Comply With the Global Trend Toward Tax Transparency

By Dmitri Semenov, Jun Li, Lucas Rachuba and Carter Vinson Ernst & Young LLP FATCA Steps That Alternative Investment Fund Managers Need to Take Today to Comply With the Global Trend Toward Tax Transparency

IBFD Course Programme Transfer Pricing: Compliance and Audit Management in Southeast Asia

IBFD Course Programme Transfer Pricing: Compliance and Audit Management in Southeast Asia Summary This course will provide you with the best practices for implementing transfer pricing documentation requirements

IBFD Course Programme Transfer Pricing: Compliance and Audit Management in Southeast Asia Summary This course will provide you with the best practices for implementing transfer pricing documentation requirements

IBFD Course Programme BEPS Country Implementation

IBFD Course Programme BEPS Country Implementation Summary On 5 October 2015, the OECD published the final reports of its 15-point base erosion and profit shifting (BEPS) project. A bit more than a year

IBFD Course Programme BEPS Country Implementation Summary On 5 October 2015, the OECD published the final reports of its 15-point base erosion and profit shifting (BEPS) project. A bit more than a year

Engaging title in Green Descriptive element in Blue 2 lines if needed

BEPS Impact on TMT Sector January 2016 Engaging title in Green Descriptive element in Blue 2 lines if needed Second line optional lorem ipsum B Subhead lorem ipsum, date quatueriure Let s be crystal clear:

BEPS Impact on TMT Sector January 2016 Engaging title in Green Descriptive element in Blue 2 lines if needed Second line optional lorem ipsum B Subhead lorem ipsum, date quatueriure Let s be crystal clear:

German Ministry of Finance publishes draft bill to implement countryby-country. other measures against base erosion and profit shifting

2 June 2016 Global Tax Alert German Ministry of Finance publishes draft bill to implement countryby-country reporting and other measures against base erosion and profit shifting EY Global Tax Alert Library

2 June 2016 Global Tax Alert German Ministry of Finance publishes draft bill to implement countryby-country reporting and other measures against base erosion and profit shifting EY Global Tax Alert Library

Transfer Pricing Country Summary Brazil

Page 1 of 8 Transfer Pricing Country Summary Brazil June 2018 Page 2 of 8 Legislation Existence of Transfer Pricing Laws/Guidelines Brazil has a specific transfer pricing regime governed by the Law 9,430/96,

Page 1 of 8 Transfer Pricing Country Summary Brazil June 2018 Page 2 of 8 Legislation Existence of Transfer Pricing Laws/Guidelines Brazil has a specific transfer pricing regime governed by the Law 9,430/96,

Brazil: BEPS Action Plan 13 Country-by-Country Reporting

Brazil: BEPS Action Plan 13 Country-by-Country Reporting December, 2016 Fernando Retzler Martins WFaria Advogados BEPS Base Erosion and Profit Shifting The Base Erosion and Profit Shifting (BEPS) Action

Brazil: BEPS Action Plan 13 Country-by-Country Reporting December, 2016 Fernando Retzler Martins WFaria Advogados BEPS Base Erosion and Profit Shifting The Base Erosion and Profit Shifting (BEPS) Action

SPECIAL REPORT BEPS FILING REQUIREMENTS FOR MULTINATIONALS UNDER COUNTRY-BY-COUNTRY REPORTING

SPECIAL REPORT BEPS FILING REQUIREMENTS FOR MULTINATIONALS UNDER COUNTRY-BY-COUNTRY REPORTING 2 BEPS FILING REQUIREMENTS FOR MULTINATIONALS UNDER CbC REPORTING FILING REQUIREMENTS FOR MULTINATIONALS UNDER

SPECIAL REPORT BEPS FILING REQUIREMENTS FOR MULTINATIONALS UNDER COUNTRY-BY-COUNTRY REPORTING 2 BEPS FILING REQUIREMENTS FOR MULTINATIONALS UNDER CbC REPORTING FILING REQUIREMENTS FOR MULTINATIONALS UNDER

Significant tax changes: UK implications for captive insurers

Tax Services Significant tax changes: UK implications for captive insurers Executive summary This alert sets out how recent developments in the global tax environment may impact UK-connected groups with

Tax Services Significant tax changes: UK implications for captive insurers Executive summary This alert sets out how recent developments in the global tax environment may impact UK-connected groups with

The OECD s Discussion Draft on Transfer Pricing Documentation and Country-by-Country Reporting: A work in progress

Global Transfer Pricing Arm s Length Standard (Special Edition) In this issue: The OECD s Discussion Draft on Transfer Pricing Documentation and Country-by-Country Reporting: A work in progress... 1 The

Global Transfer Pricing Arm s Length Standard (Special Edition) In this issue: The OECD s Discussion Draft on Transfer Pricing Documentation and Country-by-Country Reporting: A work in progress... 1 The

Indirect tax alert. EU VAT refunds for non-eu businesses. Are you preparing your 2012 EU VAT refund application?

May 2013 Indirect tax alert EU VAT refunds for non-eu businesses Are you preparing your 2012 EU VAT refund application? According to an Organization for Economic Cooperation and Development (OECD) survey

May 2013 Indirect tax alert EU VAT refunds for non-eu businesses Are you preparing your 2012 EU VAT refund application? According to an Organization for Economic Cooperation and Development (OECD) survey

TAX UPDATES FEBRUARY SUBMISSIONS of CORPORATE INCOME TAX RETURNS for FISCAL YEAR 2017 is APPROACHING ARE YOU AWARE of THE KEY ISSUES?

FEBRUARY 2018 J A K A R T A O F F I C E M e n a r a I m p e r ium, 27 th F l o o r J l. H R R a s u n a S a id K a v. 1, 1 2 9 8 0 P h. + 6 2 2 1 8 3 5 6 3 6 3 F x. + 6 2 2 1 8 3 7 9 3 9 3 9 c o n ta c

FEBRUARY 2018 J A K A R T A O F F I C E M e n a r a I m p e r ium, 27 th F l o o r J l. H R R a s u n a S a id K a v. 1, 1 2 9 8 0 P h. + 6 2 2 1 8 3 5 6 3 6 3 F x. + 6 2 2 1 8 3 7 9 3 9 3 9 c o n ta c

OECD releases additional implementation guidance on CbC reporting and appropriate use of information in CbC reports

Arm s Length Standard Global views within reach. In this issue: OECD releases additional implementation guidance on CbC reporting and appropriate use of information in CbC reports... 1 Argentina issues

Arm s Length Standard Global views within reach. In this issue: OECD releases additional implementation guidance on CbC reporting and appropriate use of information in CbC reports... 1 Argentina issues

Christian Aid submission on COM(2016)198 - Proposal for a Directive of the European Parliament and of the Council amending Directive 2013/34/EU

198 - Proposal for a Directive of the European Parliament and of the Council amending Directive 2013/34/EU") 23.05.2016 Christian Aid submission on COM(2016)198 - Proposal for a Directive of the European Parliament and of the Council amending Directive 2013/34/EU 1. Introduction Christian Aid welcomes the opportunity

23.05.2016 Christian Aid submission on COM(2016)198 - Proposal for a Directive of the European Parliament and of the Council amending Directive 2013/34/EU 1. Introduction Christian Aid welcomes the opportunity

Making Tax Digital A roadmap for small businesses

blow abbott chartered accountants Making Tax Digital A roadmap for small businesses www.blowabbott.com Index Page What is Making Tax Digital? 3 When is it happening? 4 What are the upsides and downsides?

blow abbott chartered accountants Making Tax Digital A roadmap for small businesses www.blowabbott.com Index Page What is Making Tax Digital? 3 When is it happening? 4 What are the upsides and downsides?

Hong Kong SAR Government previews forthcoming BEPS legislation

Hong Kong SAR Government previews forthcoming BEPS legislation August 11, 2017 In brief On 31 July 2017, the Hong Kong SAR Government (the Government) released its consultation report on measures to implement

Hong Kong SAR Government previews forthcoming BEPS legislation August 11, 2017 In brief On 31 July 2017, the Hong Kong SAR Government (the Government) released its consultation report on measures to implement

Transfer Pricing Country Summary Belgium

Page 1 of 8 Transfer Pricing Country Summary Belgium July 2018 Page 2 of 8 Legislation Existence of Transfer Pricing Laws/Guidelines The arm s length principle is codified in Article 185, Par 2, of the

Page 1 of 8 Transfer Pricing Country Summary Belgium July 2018 Page 2 of 8 Legislation Existence of Transfer Pricing Laws/Guidelines The arm s length principle is codified in Article 185, Par 2, of the

The Hidden Costs of Paper-Based Payments. How Electronic Payments Save You Time, Cut Your Costs and Improve Your Customer Relationships

The Hidden Costs of Paper-Based Payments How Electronic Payments Save You Time, Cut Your Costs and Improve Your Customer Relationships The Hidden Costs of a Simple Check B2B payment methods are slow and

The Hidden Costs of Paper-Based Payments How Electronic Payments Save You Time, Cut Your Costs and Improve Your Customer Relationships The Hidden Costs of a Simple Check B2B payment methods are slow and

China s SAT issues new rules on reporting of related-party transactions and contemporaneous documentation

Arm s Length Standard Global views within reach. China s SAT issues new rules on reporting of related-party transactions and contemporaneous documentation China s State Administration of Taxation (SAT)

Arm s Length Standard Global views within reach. China s SAT issues new rules on reporting of related-party transactions and contemporaneous documentation China s State Administration of Taxation (SAT)

ASOS plc Group Tax Strategy

ASOS plc Group Tax Strategy Updated October 2016 ASOS plc Group Tax Strategy Introduction The aim of this document is to set out the strategic objectives of the ASOS plc ( The Group ) with regard to tax,

ASOS plc Group Tax Strategy Updated October 2016 ASOS plc Group Tax Strategy Introduction The aim of this document is to set out the strategic objectives of the ASOS plc ( The Group ) with regard to tax,

Making Tax Digital for Businesses and Landlords. Helping clients understand and prepare for Making Tax Digital

Making Tax Digital for Businesses and Landlords Helping clients understand and prepare for Making Tax Digital Making Tax Digital explained Making Tax Digital for Businesses and Landlords (referred to as

Making Tax Digital for Businesses and Landlords Helping clients understand and prepare for Making Tax Digital Making Tax Digital explained Making Tax Digital for Businesses and Landlords (referred to as

Country by country (CbC) reporting reaches Indian shores. By Paresh Parekh, Partner, EY March 2, 2016

reporting reaches Indian shores. By Paresh Parekh, Partner, EY March 2, 2016") Country by country (CbC) reporting reaches Indian shores By aresh arekh, artner, EY March 2, 2016 Contents CbC reporting BES Action 13 - background Budget 2016 proposals Global overview age 2 BES - What

Country by country (CbC) reporting reaches Indian shores By aresh arekh, artner, EY March 2, 2016 Contents CbC reporting BES Action 13 - background Budget 2016 proposals Global overview age 2 BES - What

Deliver Transparent and Effective Budgets. SAPPHIRE NOW Orlando May 16, 2013

Deliver Transparent and Effective Budgets SAPPHIRE NOW Orlando May 16, 2013 Common issues faced in public sector budgeting Heavily dependent on Microsoft Excel workbooks Multiple legacy budgeting and financial

Deliver Transparent and Effective Budgets SAPPHIRE NOW Orlando May 16, 2013 Common issues faced in public sector budgeting Heavily dependent on Microsoft Excel workbooks Multiple legacy budgeting and financial

Ireland updates international tax strategy

14 October 2016 Issue 06/2016 Tax alert Ireland Ireland updates international tax strategy Contacts If you require further information, please call your regular contact in EY or contact any of the following:

14 October 2016 Issue 06/2016 Tax alert Ireland Ireland updates international tax strategy Contacts If you require further information, please call your regular contact in EY or contact any of the following:

Transparent, sophisticated, tax neutral

Transparent, sophisticated, tax neutral The truth about offshore alternative investment funds www.aima.org Executive Summary Collective investment is good for investors. Investors such as pension funds,

Transparent, sophisticated, tax neutral The truth about offshore alternative investment funds www.aima.org Executive Summary Collective investment is good for investors. Investors such as pension funds,

Sage 50 Payroll. New. Payroll software for small to medium sized businesses who need complete control and confidence in their payroll process.

New Payroll software for small to medium sized businesses who need complete control and confidence in their payroll process. 1 What is Sage 50 Payroll? Sage 50 Payroll provides you with the confidence

New Payroll software for small to medium sized businesses who need complete control and confidence in their payroll process. 1 What is Sage 50 Payroll? Sage 50 Payroll provides you with the confidence

The new BEPS and transfer pricing law passed in Hong Kong

News Flash Hong Kong Tax The new BEPS and transfer pricing law passed in Hong Kong July 2018 Issue 9 In brief The Legislative Council passed the base erosion and profit shifting (BEPS) and transfer pricing

News Flash Hong Kong Tax The new BEPS and transfer pricing law passed in Hong Kong July 2018 Issue 9 In brief The Legislative Council passed the base erosion and profit shifting (BEPS) and transfer pricing

Advent Direct. Harnessing the power of technology for data management. Tackling the global challenges of fund regulations

October 2013 Advent Direct Harnessing the power of technology for data management Tackling the global challenges of fund regulations Integrated framework for data processing One-stop workflow solution

October 2013 Advent Direct Harnessing the power of technology for data management Tackling the global challenges of fund regulations Integrated framework for data processing One-stop workflow solution

MODULE Tax Transparency

MODULE Tax Transparency When you have to be right CCH Integrator: Tax Transparency Module Background On 3 May 2016, the Government released the Board of Taxation s (BoT s) final report on a voluntary Tax

MODULE Tax Transparency When you have to be right CCH Integrator: Tax Transparency Module Background On 3 May 2016, the Government released the Board of Taxation s (BoT s) final report on a voluntary Tax