U.S. Inbound Investment. April 2017

|

|

|

- Sharyl Hodge

- 6 years ago

- Views:

Transcription

1 U.S. Inbound Investment April 2017

is not intended or written to be used, and cannot be used,")

2 Table of Contents About Frazier & Deeter Tax Considerations Structuring Alternatives Further Considerations Additional Inbound Planning Bio & Contact Information To ensure compliance with Treasury Department regulations, we wish to inform you that any tax advice that may be contained in this communication (including any attachments) is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or applicable state or local tax law provisions or (ii) promoting, marketing or recommending to another party any tax-related matters addressed herein. 2

3 Our Unique Approach About Our Firm Frazier & Deeter. All rights reserved.

4 Key Facts About Frazier & Deeter Frazier & Deeter is ranked in the Top 60 Largest Firms in the U.S professionals across offices in Atlanta, Alpharetta, Nashville, Philadelphia and Tampa. Fastest Growing Firms in the U.S Inside Public Accounting Top 25 Best Managed U.S. Firms Inside Public Accounting Named a 2015 Best Firm to Work For Accounting Today 9 time winner Best of the Best CPA firm Inside Public Accounting Member of PKF International and CPAmerica Full suite of audit, tax & advisory services Clients in all 50 states, Canada, Mexico, Central and South America, Europe, China and Australia 4

5 Qualifications Frazier & Deeter Highest level of credentials in the accounting industry PCAOB registered AICPA certified Audit methodologies developed by former PCAOB members Majority of partners have Big 4 backgrounds Recognized as a qualified firm by top financial institutions 5

6 Key Facts Member of PKF International PKF has 440 offices in 150 countries worldwide. NORTH AMERICA PKF International has 41 member firms in U.S. and Canada EUROPE PKF International has member firms in every EU country, the key emerging markets in Eastern and Central Europe, and in some of the Central Asian republics MIDDLE EAST PKF has a comprehensive representation across the Middle East from the Mediterranean states to the GCC states in the Gulf. AMERICAS 45,940 Professionals 59,428 PKF is represented in Mexico, all the Latin American countries and throughout the Caribbean Professionals AFRICA Our members extend from North Africa down through East Africa, across English and French speaking West Africa and throughout Southern Africa ASIA PACIFIC PKF members cover the region from the Indian sub-continent and South East Asia mainland to Oceania, Hong Kong and China 6

7 US Inbound Investments Various Tax Considerations Frazier & Deeter. All rights reserved.

8 Tax Considerations U.S. Inbound Investments Tax return filing threshold Entity selection/structure Non-business income reporting Owning real estate in the United States State & Local tax issues ( SALT ) Other planning items 8

9 Tax Considerations U.S. Trade or Business A nonresident alien individual or foreign corporation generally pays U.S. income tax at the regular U.S. rates on the income (including certain foreign-source income) that is effectively connected with a U.S. trade or business. Threshold for what constitutes a U.S. trade or business is low. No statutory definition; reliance on case law and IRS rulings. Determination of what income is effectively connected with the conduct of a U.S. trade or business. 9

. These treaties allow foreign persons to conduct limited commercial activities in the U.S. without being subject to U.S. tax (PE threshold higher than U.S. Trade or Business ).")

10 Tax Considerations Permanent Establishment Most income tax treaties exempt the business profits of a resident of a treaty country from U.S. tax unless those profits are attributable to a taxpayer's U.S. permanent establishment ( PE ). These treaties allow foreign persons to conduct limited commercial activities in the U.S. without being subject to U.S. tax (PE threshold higher than U.S. Trade or Business ). In general, a PE is a fixed place of business through which the business of an enterprise is carried on in whole or in part. Exceptions (subject to specific treaty provisions) if the facility is for: Storage, display or delivery of goods Storage for processing by another enterprise Purchasing or collecting information Advertising, supply of information, scientific or preparatory or auxiliary activities Activities of a dependent agent may also create a PE. 10

upon repatriation. Branch profits tax on dividend equivalent A branch will require the foreign owner(s) to file US tax returns.")

11 Tax Considerations Branch or Subsidiary Both are essentially subject to the same tax rates: up to 35% Federal corporate income tax plus State income tax plus dividend withholding tax (or branch profits tax) upon repatriation. Branch profits tax on dividend equivalent A branch will require the foreign owner(s) to file US tax returns. Allocation between US and worldwide income and expenses adds to the complexity of a branch return (especially at the State and local tax level). Corporate form provides for income deferral in home country. Check-the-box elections and hybrid entities. 11

12 Tax Considerations Limited Liability Company (LLC) Transparent for US tax purposes unless an election is made to treat the LLC as a corporation. Characterization may be difficult in the shareholder s jurisdiction. Check-the-box regime allows for substantial flexibility and sometimes planning opportunities. Single-member LLC is disregarded for US tax purposes. Transactions between single-member LLC and its owner are therefore also disregarded for US tax purposes. 12

13 Basic Structuring Alternatives A1 A2 A1 A2 A1 A2 AT Co AT Co AT LP US Sub US LLC US LLC US Sub files US tax return Dividend withholding tax No exposure for AT Co, A1 and A2 AT Co files US branch return Branch profits tax No exposure for A1 and A2 A1 and A2 file individual US tax returns AT LP files US partnership tax return No dividend withholding tax or BPT Individual income tax rates 13

14 Consolidated Returns Dos and Don ts NO YES YES A1 A2 A1 A2 A1 A2 AT Co AT Co AT Co US Sub US Sub US Holding Co US Sub US Sub US LLC US LLC 14

income from U.S. sources.")

15 Tax Considerations Non-Business Income/Withholding Generally, there is a 30% U.S. withholding tax from certain types of (non-business) income from U.S. sources paid to foreign persons. This applies to payments of fixed or determinable annual or periodical ( FDAP ) income from U.S. sources. FDAP income generally includes interest, dividends, rents, royalties and any other annual or periodical gain, profit or income. Income tax treaties between the U.S. and foreign countries may reduce or eliminate withholding tax on various types of FDAP income. Reduced withholding rate under treaty through withholding certificate provided by beneficial owner to payor (US withholding agent). Generally, this will be Form W-8BEN-E. No requirement to submit the withholding certificates to the IRS. 15

is generally required to disclose such position on a U.S. tax return.")

16 Tax Considerations Treaty-based Return Positions A taxpayer who, with respect to any tax imposed, takes the position that a treaty of the U.S. overrules (or otherwise modifies U.S. tax law) is generally required to disclose such position on a U.S. tax return. If no tax return filing is otherwise required, disclosure is made by filing a return. Return need only include required disclosure, taxpayers name, address, and taxpayer identification number. The required disclosure is made on Form 8833, attached to the return. Exceptions from the Form 8833 reporting requirement include certain amounts that are reported on Form 1042-S (e.g. dividends) and that do not total more than $500,000 for the tax year. 16

17 Tax Considerations Foreign Investment In U.S. Real Property Tax Act ( FIRPTA ) Rules Foreign persons are not generally subject to U.S. tax on gains from dispositions of capital assets. However, under the FIRPTA rules, a nonresident alien individual or foreign corporation disposing of a U.S. real property interest ( USRPI ), will be taxed on the net gains from such a disposition as if such gains or losses were effectively connected with the conduct of the U.S. business. Special withholding regime under FIRPTA: 15% of amount realized; or 35% of gain. Complex interplay with corporate reorganization rules. 17

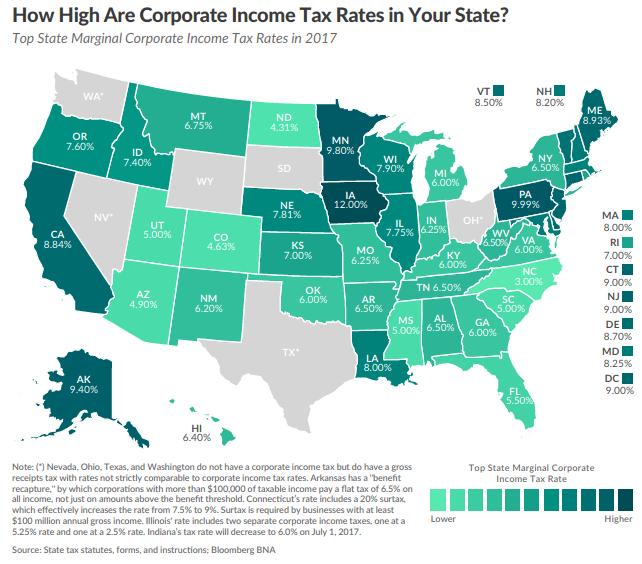

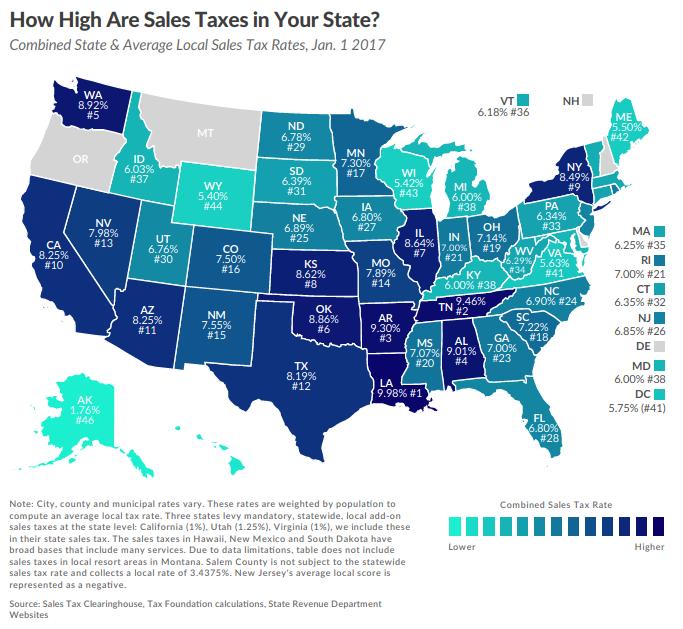

18 Tax Considerations SALT Issues Impacting Foreign Entities There are 50 states, 3,007 counties in addition to cities in the United States (Wikipedia 2013) States and localities (counties, cities) are not obligated to honor tax treaties State income tax has some protections under P.L Sales & Use tax ( SUT ) liability has extremely low thresholds Nexus concept (similar to PE concept) Beware of taxes based on items other than net income SUT per above Texas gross margin tax, Ohio CAT tax, Washington B&O tax 18

19 19

20 20

Sales tax matrix Intellectual property ( IP")

21 Additional Inbound Planning Items Organize Capital Structure SALT Planning Transfer Pricing Debt vs. equity Interest rate planning Interest deductibility planning Nexus analysis (SUT and Income/Franchise tax) Sales tax matrix Intellectual property ( IP ) Management services Intercompany product sales 21

22 USA Tax Reform Change on the Way >Trump Plan >House GOP Plan >Current Law >Border Adjusted Tax 22

23 Proposal Comparisons - Business Tax Reform Proposal Trump Plan House GOP Plan Current Law Corporate Tax Rate 15 percent 20 percent Depreciation If election is make, immediate deduction of capital expenditures by manufacturers Interest on debt used to acquire such assets would not be deductible Immediate deduction of capital expenditures 35 percent (excluding state income tax) Business Tax Rate Income form S corporations, partnerships, disregarded entities and sole proprietorships would be taxed at 15% Income from S corporations, partnerships, disregarded entities and sole proprietorships would be taxed at 25% Income from S corporations, partnerships, disregarded entities and sole proprietorships taxed at regarded tax owner s tax rate Limited to interest income Interest Deduction Reasonable cap on the deductibility of business interest expenses* Excess interest expense carries over to following years Exceptions to be developed for financial businesses (e.g., banks insurers, etc.) 23

24 Proposal Comparisons Business Cont. Tax Reform Proposal Trump Plan House GOP Plan Current Law Net Operating Losses Silent Unlimited carryforward Carryforwards will be increased by interest factor Carryback two years Carry forward 20 years Income that may be offset in any year limited to 90% of income Section 199 Gross Production Activities Silent Repeal Domestic production activities deduction equal to 9 % of taxable income or qualified production activities Business Tax Credits Largely repeal, but retain the research and development credit and business tax credit for onsite child care Largely repeal specialinterest credits and deductions, but retain the research and development credit Small business health care credit, research credits, hybrid vehicle credits, etc. 24

25 Proposal Comparisons International Tax Reform Proposal Trump Plan House GOP Plan Current Law Taxation of International Income Silent Territorial system based on consumption Subpart F Regime Earnings of Foreign Subsidiaries One-time 10% deemed repatriation tax on cash held abroad that represents earnings of foreign subsidiaries of U.S. companies payable over 10 years Future earnings of foreign subsidiaries of U.S. corporations are taxable as earned One-time deemed repatriation tax on earnings of foreign subsidiaries of U.S. companies of 8.75% to the extent held in cash or cash equivalent and 3.5 % otherwise, payable over 8 years Subject to Corporate Income Tax Rate Dividends from Foreign Subsidiaries Silent Excluded from income of U.S. parent Subject to Corporate Income Tax Rate Subpart F Income Silent Largely repeal Subject to Corporate Income Tax Rate 25

26 Border Adjusted Tax The House plan provides for border adjustments exempting exports and taxing imports designed to reflect a consumption based tax. The belief is that it will eliminate incentives created by the current U.S. tax system to move or locate operations outside the U.S. Generally operate by excluding from tax the gross receipts earned from exports while effectively taxing imports by disallowing a deduction for the cost of the imported good. In addition, all capital expenses are fully expensed and net interest payments are no longer deductible. Active foreign earnings of U.S. multinationals would not be subject to tax upon repatriation. The border adjusted tax should raise U.S. tax revenue through the broadening of the tax base. 26

27 Border Adjusted Tax - Example Tax Without Borders Adjustment Tax With Borders Adjustment Domestic Sales $1,000 $1,000 Domestic Inputs $300 $300 Foreign Inputs $300 $300 Pre-tax Income $400 $400 Taxable Income $400 $700 20% $80 $140 After-Tax Income $320 $260 27

28 Michael R. Whitacre Partner, Tax Services 30+ years in auditing and taxation in public accounting Mike has worked proactively with a variety of businesses including clients in the technology, service and manufacturing/distribution sectors. He has assisted clients with federal, state and international tax issues including mergers and acquisitions, controversy and tax minimization. Mike s areas of specialization include: corporate taxation, cross border taxation, mergers and acquisitions, and taxation of pass-through entities. Formerly Regional Head of Tax North America for a Top 5 international accounting firm. Professional Affiliations: American Institute of Certified Public Accountants Association for Corporate Growth Technology Executives Roundtable [TER] Board of Directors Financial Executives Institute (FEI) Georgia Society of Certified Public Accountants B.S., Accounting, Indiana University Kelley School of Business 28

29 Contact Information Michael R. Whitacre office

Michael R. Whitacre & Dr. Jan Wendland. Tax Structuring and Compliance Issues when July 2017 German companies enter the U.S.

Michael R. Whitacre & Dr. Jan Wendland Tax Structuring and Compliance Issues when July 2017 German companies enter the U.S. Table of Contents About PKF Frazier & Deeter and PKF Fasselt Schlage Tax Considerations

Michael R. Whitacre & Dr. Jan Wendland Tax Structuring and Compliance Issues when July 2017 German companies enter the U.S. Table of Contents About PKF Frazier & Deeter and PKF Fasselt Schlage Tax Considerations

Optimizing Asian Operations Through Hong Kong s Double Tax Agreement Network

Volume 61, Number 11 March 14, 2011 Optimizing Asian Operations Through s Double Tax Agreement Network by Paul Previtera, Brandon Boyle, and Michael Kent Reprinted from Tax Notes Int l, March 14, 2011,

Volume 61, Number 11 March 14, 2011 Optimizing Asian Operations Through s Double Tax Agreement Network by Paul Previtera, Brandon Boyle, and Michael Kent Reprinted from Tax Notes Int l, March 14, 2011,

International Tax Reporting and Opportunities

International Tax Reporting and Opportunities Justin Hobson May 16, 2017 2017 Lane Powell PC 1 Agenda 1. Objective 2. Acronyms 3. Common Outbound Structures 4. Common Inbound Structures 5. Current Tax

International Tax Reporting and Opportunities Justin Hobson May 16, 2017 2017 Lane Powell PC 1 Agenda 1. Objective 2. Acronyms 3. Common Outbound Structures 4. Common Inbound Structures 5. Current Tax

TECHNICAL EXPLANATION OF THE SENATE COMMITTEE ON FINANCE CHAIRMAN S STAFF DISCUSSION DRAFT OF PROVISIONS TO REFORM INTERNATIONAL BUSINESS TAXATION

TECHNICAL EXPLANATION OF THE SENATE COMMITTEE ON FINANCE CHAIRMAN S STAFF DISCUSSION DRAFT OF PROVISIONS TO REFORM INTERNATIONAL BUSINESS TAXATION Prepared by the Staff of the JOINT COMMITTEE ON TAXATION

TECHNICAL EXPLANATION OF THE SENATE COMMITTEE ON FINANCE CHAIRMAN S STAFF DISCUSSION DRAFT OF PROVISIONS TO REFORM INTERNATIONAL BUSINESS TAXATION Prepared by the Staff of the JOINT COMMITTEE ON TAXATION

TAX CONSEQUENCES FOR CANADIANS DOING BUSINESS IN THE U.S.

TAX CONSEQUENCES FOR CANADIANS DOING BUSINESS IN THE U.S. Has your Canadian business expanded into the U.S.? Do you have dealings with U.S. customers? If so, have you considered the U.S. tax implications?

TAX CONSEQUENCES FOR CANADIANS DOING BUSINESS IN THE U.S. Has your Canadian business expanded into the U.S.? Do you have dealings with U.S. customers? If so, have you considered the U.S. tax implications?

NAVIGATING US TAX REFORM:

NAVIGATING US TAX REFORM: What Businesses Need to Know March 20, 2018 2018 Morgan, Lewis & Bockius LLP Agenda Topic Slides Overview...3 Domestic Provisions...4-13 International Provisions...14-29 Immediate

NAVIGATING US TAX REFORM: What Businesses Need to Know March 20, 2018 2018 Morgan, Lewis & Bockius LLP Agenda Topic Slides Overview...3 Domestic Provisions...4-13 International Provisions...14-29 Immediate

Chairman Camp s Discussion Draft of Tax Reform Act of 2014 and President Obama s Fiscal Year 2015 Revenue Proposals

Chairman Camp s Discussion Draft of Tax Reform Act of 2014 and President Obama s Fiscal Year 2015 Proposals Relating to International Taxation SUMMARY On February 26, 2014, Ways and Means Committee Chairman

Chairman Camp s Discussion Draft of Tax Reform Act of 2014 and President Obama s Fiscal Year 2015 Proposals Relating to International Taxation SUMMARY On February 26, 2014, Ways and Means Committee Chairman

Presented to: NRF Canadian Tax Clients. New U.S. tax legislation Impact on Selected Cross-Border Transactions

January 11, 2018 Presented to: NRF Canadian Tax Clients New U.S. tax legislation Impact on Selected Cross-Border Transactions Adrienne Oliver Tel: (416) 216-1854 email: adrienne.oliver@nortonrosefulbright.com

January 11, 2018 Presented to: NRF Canadian Tax Clients New U.S. tax legislation Impact on Selected Cross-Border Transactions Adrienne Oliver Tel: (416) 216-1854 email: adrienne.oliver@nortonrosefulbright.com

What Entity Do You Want To Be?

What Entity Do You Want To Be? Presenters: Carla M. Smaston, Plante Moran Chip Chambley, Dixon Hughes Goodman, LLP Agenda I. Choice of Entity for Foreign Operations Overview of U.S. System Tax Classifications

What Entity Do You Want To Be? Presenters: Carla M. Smaston, Plante Moran Chip Chambley, Dixon Hughes Goodman, LLP Agenda I. Choice of Entity for Foreign Operations Overview of U.S. System Tax Classifications

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 25, 2016 Presented by

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 25, 2016 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 25, 2016 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

Introduction to the Taxation of Foreign Investment in U.S. Real Estate

Introduction to the Taxation of Foreign Investment in U.S. Real Estate October 2009 Contents Introduction 1 Taxation of Income from U.S. Real Estate 2 Taxation of U.S. Entities and Individuals 2 Taxation

Introduction to the Taxation of Foreign Investment in U.S. Real Estate October 2009 Contents Introduction 1 Taxation of Income from U.S. Real Estate 2 Taxation of U.S. Entities and Individuals 2 Taxation

Tax Cuts & Jobs Act: Considerations for Funds

A LERT M EM OR A N D UM Tax Cuts & Jobs Act: Considerations for Funds January 25, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts &

A LERT M EM OR A N D UM Tax Cuts & Jobs Act: Considerations for Funds January 25, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts &

NAVIGATING US TAX REFORM:

NAVIGATING US TAX REFORM: WHAT BUSINESSES NEED TO KNOW Inbound Investment: Non-U.S. Taxpayers Investing Into the U.S. Market January 23, 2018 Presenters: Richard LaFalce, Partner Daniel Nelson, Partner

NAVIGATING US TAX REFORM: WHAT BUSINESSES NEED TO KNOW Inbound Investment: Non-U.S. Taxpayers Investing Into the U.S. Market January 23, 2018 Presenters: Richard LaFalce, Partner Daniel Nelson, Partner

US Corporate Taxation

Overview and Learning Objectives This course provides participants with an essential overview and comprehensive understanding of the complex US tax system, with particular emphasis on international aspects.

Overview and Learning Objectives This course provides participants with an essential overview and comprehensive understanding of the complex US tax system, with particular emphasis on international aspects.

Flipping the Switch on Foreign Corporation s Form of Doing Business in the U.S.

ABA Section of Taxation, U.S. Activities of Foreigners & Tax Treaties Committee 2014 Joint Fall CLE Meeting September 18-20, 2014 Denver, Colorado 35081157v2/1 Flipping the Switch on Foreign Corporation

ABA Section of Taxation, U.S. Activities of Foreigners & Tax Treaties Committee 2014 Joint Fall CLE Meeting September 18-20, 2014 Denver, Colorado 35081157v2/1 Flipping the Switch on Foreign Corporation

Doing Business in the U.S. Accounting and Tax Overview

Doing Business in the U.S. Accounting and Tax Overview November 8, 2016 MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2016 Wolf & Company, P.C. Agenda Introductions Initial entry

Doing Business in the U.S. Accounting and Tax Overview November 8, 2016 MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2016 Wolf & Company, P.C. Agenda Introductions Initial entry

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

Tax Considerations & Due Diligence for US Inbound Investors

Tax Considerations & Due Diligence for US Inbound Investors Timothy J. Hilligoss, CPA, MST June 23, 2016 Copyright 2017 Clayton & McKervey, All rights reserved. Today s Presenter Tim Hilligoss, CPA, MST

Tax Considerations & Due Diligence for US Inbound Investors Timothy J. Hilligoss, CPA, MST June 23, 2016 Copyright 2017 Clayton & McKervey, All rights reserved. Today s Presenter Tim Hilligoss, CPA, MST

Report on the United States of America

Arctic Circle This report provides helpful information on the current business environment in the United States of America. It is designed to assist companies in doing business and establishing effective

Arctic Circle This report provides helpful information on the current business environment in the United States of America. It is designed to assist companies in doing business and establishing effective

International Tax Primer Andrew D. Oppenheimer, Esq. October 31, 2017

International Tax Primer Andrew D. Oppenheimer, Esq. October 31, 2017 Agenda International tax concepts Taxation of foreign earnings Sourcing of income and expenses Foreign tax credits Subpart F income

International Tax Primer Andrew D. Oppenheimer, Esq. October 31, 2017 Agenda International tax concepts Taxation of foreign earnings Sourcing of income and expenses Foreign tax credits Subpart F income

Impact of recent U.S. tax legislation on Israeli Companies May 13, 2008 Doron Sadan, Tax Partner, PwC Israel Tel:

Doron Sadan, Tax Partner, PwC Israel Tel: 03-7954584 doron.sadan@il.pwc.com The information contained in this presentation is for general guidance on matters of interest only. As such, it should not be

Doron Sadan, Tax Partner, PwC Israel Tel: 03-7954584 doron.sadan@il.pwc.com The information contained in this presentation is for general guidance on matters of interest only. As such, it should not be

ARNOLD PORTER LLP. Special Edition: International Provisions of the American Jobs Creation Act. Overview INTERNATIONAL TAX HEADLINES DECEMBER 2004

INTERNATIONAL TAX HEADLINES Special Edition: International Provisions of the American Jobs Creation Act Overview The American Jobs Creation Act of 2004 (the AJCA or the Act ) was enacted on October 22nd,

INTERNATIONAL TAX HEADLINES Special Edition: International Provisions of the American Jobs Creation Act Overview The American Jobs Creation Act of 2004 (the AJCA or the Act ) was enacted on October 22nd,

MANAGING INTERNATIONAL TAX ISSUES

MANAGING INTERNATIONAL TAX ISSUES Starting A Business Retirement Strategies Operating A Business Marriage Investing Tax Smart Estate Planning Ending A Business Off to School Divorce And Separation Travel

MANAGING INTERNATIONAL TAX ISSUES Starting A Business Retirement Strategies Operating A Business Marriage Investing Tax Smart Estate Planning Ending A Business Off to School Divorce And Separation Travel

taxnotes U.S. Tax Reform: The End of the LLC? international by Elan Harper and Azam Rajan Reprinted from Tax Notes Interna onal, July 30, 2018, p.

taxnotes U.S. Tax Reform: The End of the LLC? by Elan Harper and Azam Rajan Reprinted from Tax Notes Interna onal, July 30, 2018, p. 465 international Volume 91, Number 5 July 30, 2018 U.S. Tax Reform:

taxnotes U.S. Tax Reform: The End of the LLC? by Elan Harper and Azam Rajan Reprinted from Tax Notes Interna onal, July 30, 2018, p. 465 international Volume 91, Number 5 July 30, 2018 U.S. Tax Reform:

Tax Planning for U.S. Real Estate After the Tax Cuts and Jobs Act May 31, 2018

Tax Planning for U.S. Real Estate After the Tax Cuts and Jobs Act May 31, 2018 Moderator and Speaker: Professor Alan I. Appel Director, International Tax Program Director, Center for International Law

Tax Planning for U.S. Real Estate After the Tax Cuts and Jobs Act May 31, 2018 Moderator and Speaker: Professor Alan I. Appel Director, International Tax Program Director, Center for International Law

M&A ACADEMY: TAX ISSUES IN M&A TRANSACTIONS

M&A ACADEMY: TAX ISSUES IN M&A TRANSACTIONS Daniel Nelson, Partner Casey August, Partner February 12, 2019 2019 Morgan, Lewis & Bockius LLP Introductory Notes Focus on domestic transactions Cross-border

M&A ACADEMY: TAX ISSUES IN M&A TRANSACTIONS Daniel Nelson, Partner Casey August, Partner February 12, 2019 2019 Morgan, Lewis & Bockius LLP Introductory Notes Focus on domestic transactions Cross-border

Tax Executives Institute Houston Chapter Tax accounting considerations of recent U.S. tax reform proposals May 4, 2017

www.pwc.com Tax Executives Institute Houston Chapter Tax accounting considerations of recent U.S. tax reform proposals Introductions Bret Oliver Tax Partner, (713) 356-8564 Bret.Oliver@pwc.com John Swilling

www.pwc.com Tax Executives Institute Houston Chapter Tax accounting considerations of recent U.S. tax reform proposals Introductions Bret Oliver Tax Partner, (713) 356-8564 Bret.Oliver@pwc.com John Swilling

Taxation of International Transactions

Taxation of International Transactions General Tax Provisions US Individuals Gross Income Business Deductions Personal Deductions Personal Exemptions = Taxable Income X Tax Rates (about 40%) = Basic Tax

Taxation of International Transactions General Tax Provisions US Individuals Gross Income Business Deductions Personal Deductions Personal Exemptions = Taxable Income X Tax Rates (about 40%) = Basic Tax

TAX ISSUES IN M&A TRANSACTIONS

MORGAN LEWIS 2018 M&A ACADEMY PRESENTS: TAX ISSUES IN M&A TRANSACTIONS Daniel Nelson, Partner Casey August, Partner March 6, 2018 2018 Morgan, Lewis & Bockius LLP Introductory Notes Focus on domestic transactions

MORGAN LEWIS 2018 M&A ACADEMY PRESENTS: TAX ISSUES IN M&A TRANSACTIONS Daniel Nelson, Partner Casey August, Partner March 6, 2018 2018 Morgan, Lewis & Bockius LLP Introductory Notes Focus on domestic transactions

WELCOME TO OUR WEBINAR

WELCOME TO OUR WEBINAR International Franchise Structures Tuesday, September 15, 2015 1:00 p.m. EDT If you cannot hear us speaking, please make sure you have called into the teleconference number on your

WELCOME TO OUR WEBINAR International Franchise Structures Tuesday, September 15, 2015 1:00 p.m. EDT If you cannot hear us speaking, please make sure you have called into the teleconference number on your

Coming to America. U.S. Tax Planning for Foreign-Owned U.S. Operations. By Len Schneidman. Andersen Tax LLC, U.S.

Coming to America U.S. Tax Planning for Foreign-Owned U.S. Operations By Len Schneidman Andersen Tax LLC, U.S. January 2018 Table of Contents Introduction... 2 Tax Checklist for Foreign-Owned U.S. Operations...

Coming to America U.S. Tax Planning for Foreign-Owned U.S. Operations By Len Schneidman Andersen Tax LLC, U.S. January 2018 Table of Contents Introduction... 2 Tax Checklist for Foreign-Owned U.S. Operations...

Company vs. enterprise

Agenda: Corporate structure, fund repatriation & management relocation 2008 PRC CIT Law Alfred K. K. Chan Singapore 25th June 2008 1.Legal and tax rules 2.Change in scope of resident enterprise; 3.Re-location

Agenda: Corporate structure, fund repatriation & management relocation 2008 PRC CIT Law Alfred K. K. Chan Singapore 25th June 2008 1.Legal and tax rules 2.Change in scope of resident enterprise; 3.Re-location

62 ASSOCIATION OF CORPORATE COUNSEL

62 ASSOCIATION OF CORPORATE COUNSEL CHEAT SHEET Foreign corporate earnings. Under the recently created Tax Cuts and Jobs Act, taxation and participation exemption of foreign corporate earnings have significantly

62 ASSOCIATION OF CORPORATE COUNSEL CHEAT SHEET Foreign corporate earnings. Under the recently created Tax Cuts and Jobs Act, taxation and participation exemption of foreign corporate earnings have significantly

Doing Business Guide. United States. 1st Edition. Marks Paneth LLP

Doing Business Guide United States 1st Edition Marks Paneth LLP About This Booklet This booklet has been produced by Marks Paneth LLP to provide an introduction to foreign investors on the various aspects

Doing Business Guide United States 1st Edition Marks Paneth LLP About This Booklet This booklet has been produced by Marks Paneth LLP to provide an introduction to foreign investors on the various aspects

Issue One Americas Region and PKF NAN February Chairman s Note

Issue One Americas Region and PKF NAN February 2009 Chairman s Note Welcome to the first edition of the PKF International Tax Alert, a publication designed to summarise key tax changes from around the

Issue One Americas Region and PKF NAN February 2009 Chairman s Note Welcome to the first edition of the PKF International Tax Alert, a publication designed to summarise key tax changes from around the

2013 U.S. Tax Policy Update

2013 U.S. Tax Policy Update Insert client logo here (or delete box) Frank Landreneau Director, International Tax Services PKF Texas, P.C. International Tax Policy Debate Reason for consensus for change:

2013 U.S. Tax Policy Update Insert client logo here (or delete box) Frank Landreneau Director, International Tax Services PKF Texas, P.C. International Tax Policy Debate Reason for consensus for change:

Tax Executives Institute

Tax Executives Institute International Tax Update (Detroit) Dates: October 26, 2017 Presenter: Seth Green Partner WNT International Tax Notice The following information is not intended to be written advice

Tax Executives Institute International Tax Update (Detroit) Dates: October 26, 2017 Presenter: Seth Green Partner WNT International Tax Notice The following information is not intended to be written advice

US-Canada Tax Strategies for US Entities Expanding to Canada

US-Canada Tax Strategies for US Entities Expanding to Canada Allinial Global Summit Conference Charleston, SC November 17, 2015 Bill Macaulay, CPA, CA Expanding Business into Canada Overview Key issues

US-Canada Tax Strategies for US Entities Expanding to Canada Allinial Global Summit Conference Charleston, SC November 17, 2015 Bill Macaulay, CPA, CA Expanding Business into Canada Overview Key issues

INTERNATIONAL TAX PLANNING. Singapore Domestic Law And Treaties SHANKER IYER FCA

INTERNATIONAL TAX PLANNING Singapore Domestic Law And Treaties SHANKER IYER FCA Contents Singapore Tax System Corporate & personal Recent tax developments What makes Singapore an attractive centre for

INTERNATIONAL TAX PLANNING Singapore Domestic Law And Treaties SHANKER IYER FCA Contents Singapore Tax System Corporate & personal Recent tax developments What makes Singapore an attractive centre for

New US income tax treaty and protocol with Italy enters into force

22 December 2009 International Tax Alert News and views from Foreign Tax Desks New US income tax treaty and protocol with Italy enters into force Executive summary On 16 December 2009, the United States

22 December 2009 International Tax Alert News and views from Foreign Tax Desks New US income tax treaty and protocol with Italy enters into force Executive summary On 16 December 2009, the United States

Income Tax Treaties. Fundamentals of International Taxation. Stanley C. Ruchelman The Ruchelman Law Firm New York, New York

Fundamentals of International Taxation Income Tax Treaties Stanley C. Ruchelman The Ruchelman Law Firm New York, New York The Association of the Bar of the City of New York February 23, 2003 Treaty Benefits

Fundamentals of International Taxation Income Tax Treaties Stanley C. Ruchelman The Ruchelman Law Firm New York, New York The Association of the Bar of the City of New York February 23, 2003 Treaty Benefits

Tax Reform and U.S. Foreign Reporting for Individuals: New Cross-Border Repatriation and Inclusion Provisions

Tax Reform and U.S. Foreign Reporting for Individuals: FOR LIVE PROGRAM ONLY New Cross-Border Repatriation and Inclusion Provisions THURSDAY, FEBRUARY 15, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Tax Reform and U.S. Foreign Reporting for Individuals: FOR LIVE PROGRAM ONLY New Cross-Border Repatriation and Inclusion Provisions THURSDAY, FEBRUARY 15, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

U.S. Tax Reform. Webinar for Australian MNC & Institutional Investors. Carol Kulish, Justin Davis, Patrick Jackman and Peter Madden.

U.S. Tax Reform Webinar for Australian MNC & Institutional Investors Carol Kulish, Justin Davis, Patrick Jackman and Peter Madden December 2017 With us today Patrick Jackman US - Washington National Tax

U.S. Tax Reform Webinar for Australian MNC & Institutional Investors Carol Kulish, Justin Davis, Patrick Jackman and Peter Madden December 2017 With us today Patrick Jackman US - Washington National Tax

Foreign Investment in U.S. Real Estate: Impact of Tax Reform

Presenting a live 90-minute webinar with interactive Q&A Foreign Investment in U.S. Real Estate: Impact of Tax Reform Entity Selection, FIRPTA, Tax Concerns When Acquiring or Disposing of Ownership Interests

Presenting a live 90-minute webinar with interactive Q&A Foreign Investment in U.S. Real Estate: Impact of Tax Reform Entity Selection, FIRPTA, Tax Concerns When Acquiring or Disposing of Ownership Interests

Tax Cuts & Jobs Act: The Road to Reform Reform Results of Reform

Tax Cuts & Jobs Act: The Road to Reform Reform Results of Reform Mindy Herzfeld University of Florida Levin College of Law UF Law Summer Tax Course July 23, 2018 7/17/2018 1 30 Years in the Making The

Tax Cuts & Jobs Act: The Road to Reform Reform Results of Reform Mindy Herzfeld University of Florida Levin College of Law UF Law Summer Tax Course July 23, 2018 7/17/2018 1 30 Years in the Making The

International Planning

International Planning Presentation for Members and Friends of the Swiss-American Chamber of Commerce April 14, 2005 Company LLP Accountants International Tax Consultants San Francisco 415-433-1177 Palo

International Planning Presentation for Members and Friends of the Swiss-American Chamber of Commerce April 14, 2005 Company LLP Accountants International Tax Consultants San Francisco 415-433-1177 Palo

SENATE TAX REFORM PROPOSAL INTERNATIONAL

The following chart sets forth some of the international tax provisions in the Senate Finance Committee s version of the Tax Cuts and Jobs Act bill, as approved by the Senate Finance Committee on November

The following chart sets forth some of the international tax provisions in the Senate Finance Committee s version of the Tax Cuts and Jobs Act bill, as approved by the Senate Finance Committee on November

U.S. Tax Reform Legislative Updates

U.S. Tax Reform Legislative Updates Fred Gander 12 May 2014 Notice ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY KPMG TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY OTHER PERSON

U.S. Tax Reform Legislative Updates Fred Gander 12 May 2014 Notice ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY KPMG TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY OTHER PERSON

February Introduction to the taxation of foreign investment in U.S. real estate

February 2014 Introduction to the taxation of foreign investment in U.S. real estate Contents Introduction 1 Taxation of income from U.S. real estate 2 U.S. tax implications of specific investment vehicles

February 2014 Introduction to the taxation of foreign investment in U.S. real estate Contents Introduction 1 Taxation of income from U.S. real estate 2 U.S. tax implications of specific investment vehicles

INTERNATIONAL TAX. Contacts. Professionals

Hodgson Russ tax attorneys provide guidance on the full range of U.S. business and personal tax issues for clients around the world, including multinational companies, public companies, privately held

Hodgson Russ tax attorneys provide guidance on the full range of U.S. business and personal tax issues for clients around the world, including multinational companies, public companies, privately held

International Tax Italy Highlights 2018

International Tax Italy Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control There are no foreign exchange controls or restrictions on repatriating funds. Residents and nonresidents

International Tax Italy Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control There are no foreign exchange controls or restrictions on repatriating funds. Residents and nonresidents

International Tax Update. Friday, December 1, 2017 Grant Thornton's Year End taxguide Event Brandon Joseph Senior Manager, International Tax

International Tax Update Friday, December 1, 2017 Grant Thornton's Year End taxguide Event Brandon Joseph Senior Manager, International Tax Presenters Brandon Joseph Senior Manager International Tax Services

International Tax Update Friday, December 1, 2017 Grant Thornton's Year End taxguide Event Brandon Joseph Senior Manager, International Tax Presenters Brandon Joseph Senior Manager International Tax Services

Mastering the Effectively Connected Income Rules for Foreign Persons Engaged in Inbound Transactions

Mastering the Effectively Connected Income Rules for Foreign Persons Engaged in Inbound Transactions TUESDAY, SEPTEMBER 22, 2015 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Mastering the Effectively Connected Income Rules for Foreign Persons Engaged in Inbound Transactions TUESDAY, SEPTEMBER 22, 2015 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for

Cyprus - Iran. The gateway to Iranian business

Cyprus - Iran CYPRUS - IRAN CONTENT Introduction 3 Cyprus: Tax Benefits 4 New Treaty Cyprus - Iran 5 Cyprus Holding Company 6 Cyprus Holding Company in International 7 Investments Cyprus Back-to-Back Financing

Cyprus - Iran CYPRUS - IRAN CONTENT Introduction 3 Cyprus: Tax Benefits 4 New Treaty Cyprus - Iran 5 Cyprus Holding Company 6 Cyprus Holding Company in International 7 Investments Cyprus Back-to-Back Financing

CONFERENCE AGREEMENT PROPOSAL INTERNATIONAL

The following chart sets forth some of the international tax provisions in the Conference Agreement version of the Tax Cuts and Jobs Act, as made available on December 15, 2017. This chart highlights only

The following chart sets forth some of the international tax provisions in the Conference Agreement version of the Tax Cuts and Jobs Act, as made available on December 15, 2017. This chart highlights only

CYPRUS AS A GATEWAY FOR INDIAN CROSS BORDER TRANSACTIONS

CONTENT Introduction 3 Cyprus: tax benefits Cyprus-India double tax treaty Cyprus Holding Company Cyprus Holding In International Investments Back-to-Back financing structures Cyprus royalties company

CONTENT Introduction 3 Cyprus: tax benefits Cyprus-India double tax treaty Cyprus Holding Company Cyprus Holding In International Investments Back-to-Back financing structures Cyprus royalties company

2007 Update to Doing Business in China via the Cayman Islands

2007 Update to Doing Business in China via the Cayman Islands by fred greguras and bart bassett Many companies doing business in China are using a structure which includes a company formed under the laws

2007 Update to Doing Business in China via the Cayman Islands by fred greguras and bart bassett Many companies doing business in China are using a structure which includes a company formed under the laws

SENATE TAX REFORM PROPOSAL INTERNATIONAL

The following chart sets forth some of the international tax provisions in the Senate s version of the Tax Cuts and Jobs Act, as approved by the Senate on December 2, 2017. This chart highlights only some

The following chart sets forth some of the international tax provisions in the Senate s version of the Tax Cuts and Jobs Act, as approved by the Senate on December 2, 2017. This chart highlights only some

Tax Cuts & Jobs Act: Considerations for Funds

Tax Cuts & Jobs Act: Considerations for Funds December 22, 2017 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts & Jobs Act (the TCJA ).

Tax Cuts & Jobs Act: Considerations for Funds December 22, 2017 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts & Jobs Act (the TCJA ).

Provisions affecting private equity funds in tax reform bills House bill and Senate Finance Committee bill

Provisions affecting private equity funds in tax reform bills House bill and Senate Finance Committee bill November 22, 2017 1 The U.S. House of Representatives on November 16, 2017, passed H.R. 1, the

Provisions affecting private equity funds in tax reform bills House bill and Senate Finance Committee bill November 22, 2017 1 The U.S. House of Representatives on November 16, 2017, passed H.R. 1, the

International Tax Slovakia Highlights 2019

International Tax Updated January 2019 Investment basics: Currency Euro (EUR) Foreign exchange control No restrictions are imposed on the import or export of capital, and repatriation payments may be made

International Tax Updated January 2019 Investment basics: Currency Euro (EUR) Foreign exchange control No restrictions are imposed on the import or export of capital, and repatriation payments may be made

International Tax Egypt Highlights 2018

International Tax Egypt Highlights 2018 Investment basics: Currency Egyptian Pound (EGP) Foreign exchange control Following the floatation of the EGP on 3 November 2016, the central bank relaxed some restrictions

International Tax Egypt Highlights 2018 Investment basics: Currency Egyptian Pound (EGP) Foreign exchange control Following the floatation of the EGP on 3 November 2016, the central bank relaxed some restrictions

Overview of the Major International Tax Provisions Of the Tax Cuts and Jobs Act

Overview of the Major International Tax Provisions Of the Tax Cuts and Jobs Act Gutter Chaves Josepher Rubin Forman Fleisher Miller P.A. On December 20, 2017, Congress passed H.R.1, known as the Tax Cuts

Overview of the Major International Tax Provisions Of the Tax Cuts and Jobs Act Gutter Chaves Josepher Rubin Forman Fleisher Miller P.A. On December 20, 2017, Congress passed H.R.1, known as the Tax Cuts

US Tax Reform For Canadian Companies

For Canadian Companies 1 Agenda Domestic Changes Income Tax Rate Reduction Update for Certain Deductions NOL, Interest, Depreciation, DPAD (Section 199) Credits and Incentives International Changes Migration

For Canadian Companies 1 Agenda Domestic Changes Income Tax Rate Reduction Update for Certain Deductions NOL, Interest, Depreciation, DPAD (Section 199) Credits and Incentives International Changes Migration

SUMMARY OF INTERNATIONAL TAX LAW DEVELOPMENTS

SUMMARY OF INTERNATIONAL TAX LAW DEVELOPMENTS SIMPSON THACHER & BARTLETT LLP FEBRUARY 12, 1998 In the past year there have been many developments affecting the United States taxation of international transactions.

SUMMARY OF INTERNATIONAL TAX LAW DEVELOPMENTS SIMPSON THACHER & BARTLETT LLP FEBRUARY 12, 1998 In the past year there have been many developments affecting the United States taxation of international transactions.

Tax Cuts & Jobs Act: Considerations for Multinationals

ALE R T MEM ORAN D UM Tax Cuts & Jobs Act: Considerations for Multinationals February 5, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax

ALE R T MEM ORAN D UM Tax Cuts & Jobs Act: Considerations for Multinationals February 5, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax

Challenges Facing NGOs Operating Internationally

Challenges Facing NGOs Operating Internationally Tuesday, August 1, 2017 2:00 pm 3:30 pm ET InterAction 1400 16th Street NW, Suite 210 Washington, DC 20036 Speakers Lindsay B. Meyer, Esq. Partner and Chair

Challenges Facing NGOs Operating Internationally Tuesday, August 1, 2017 2:00 pm 3:30 pm ET InterAction 1400 16th Street NW, Suite 210 Washington, DC 20036 Speakers Lindsay B. Meyer, Esq. Partner and Chair

Gary P. Tober Principal

Principal Second & Seneca Building 1191 Second Avenue 18th Floor Seattle, WA 98101-2939 T 206. 816.1415 F 206.464.0125 gtober@gsblaw.com Gary P. Tober has been practicing law for over thirty-five years.

Principal Second & Seneca Building 1191 Second Avenue 18th Floor Seattle, WA 98101-2939 T 206. 816.1415 F 206.464.0125 gtober@gsblaw.com Gary P. Tober has been practicing law for over thirty-five years.

U.S. Tax Legislation Corporate and International Provisions. Corporate Law Provisions

U.S. Tax Legislation Corporate and International Provisions On December 20, 2017, Congress enacted comprehensive tax legislation (the Act ). This memorandum highlights some of the important provisions

U.S. Tax Legislation Corporate and International Provisions On December 20, 2017, Congress enacted comprehensive tax legislation (the Act ). This memorandum highlights some of the important provisions

Foreign-Owned U.S. Real Estate: To Rent Or Not To Rent By: Dina Kapur Sanna and Stephen Ziobrowski Day Pitney LLP

Foreign-Owned U.S. Real Estate: To Rent Or Not To Rent By: Dina Kapur Sanna and Stephen Ziobrowski 2015 Day Pitney LLP To avoid U.S. estate tax, the most common structure used by non-residence aliens to

Foreign-Owned U.S. Real Estate: To Rent Or Not To Rent By: Dina Kapur Sanna and Stephen Ziobrowski 2015 Day Pitney LLP To avoid U.S. estate tax, the most common structure used by non-residence aliens to

Tax Cuts & Jobs Act: Considerations for M&A

A LERT M EM OR A N D UM Tax Cuts & Jobs Act: Considerations for M&A January 17, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts & Jobs

A LERT M EM OR A N D UM Tax Cuts & Jobs Act: Considerations for M&A January 17, 2018 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts & Jobs

Comparison of the House and Senate Tax Bills

Comparison of the House and Senate Tax Bills LJPR Financial Advisors Leon C. LaBrecque, JD, CPA, CFP, CFA Item House Senate Individual brackets 12%, 25%, 35% and 39.6% ( bump ) 10%, 12%, 22%, 24%, 32%,

Comparison of the House and Senate Tax Bills LJPR Financial Advisors Leon C. LaBrecque, JD, CPA, CFP, CFA Item House Senate Individual brackets 12%, 25%, 35% and 39.6% ( bump ) 10%, 12%, 22%, 24%, 32%,

Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding

Form W-8BEN Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding (Rev. February 2006) OMB No. 1545-1621 Department of the Treasury Section references are to the Internal

Form W-8BEN Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding (Rev. February 2006) OMB No. 1545-1621 Department of the Treasury Section references are to the Internal

TAX REFORM ACT - IMPACT ON INTERNATIONAL OPERATIONS

TAX REFORM ACT - IMPACT ON INTERNATIONAL OPERATIONS December 20, 2017 BAKER BOTTS 1 View it as a Web Page. December 20, 2017 Tax Reform Act Impact on Taxpayers with International Operations Jon Lobb, Michael

TAX REFORM ACT - IMPACT ON INTERNATIONAL OPERATIONS December 20, 2017 BAKER BOTTS 1 View it as a Web Page. December 20, 2017 Tax Reform Act Impact on Taxpayers with International Operations Jon Lobb, Michael

Tax planning for U.S. business operations of Indian enterprises

D:\ALL DATA OF ANIL\ANIL\IT MAG 2011\IT FROM JANUARY 2011\IT V5P5 (NOVEMBER 2011)\IT V5P5-ART 3 (TOPICS) MAK\CORR 24-10-2011/2-11-2011 70 USA- TAX PLANNING FOR INDIAN ENTERPRISES Tax planning for U.S.

D:\ALL DATA OF ANIL\ANIL\IT MAG 2011\IT FROM JANUARY 2011\IT V5P5 (NOVEMBER 2011)\IT V5P5-ART 3 (TOPICS) MAK\CORR 24-10-2011/2-11-2011 70 USA- TAX PLANNING FOR INDIAN ENTERPRISES Tax planning for U.S.

Chapter 24. Taxation of International Transactions. Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe

Chapter 24 Taxation of International Transactions Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004 South-Western/Thomson Learning Overview Of International Taxation

Chapter 24 Taxation of International Transactions Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004 South-Western/Thomson Learning Overview Of International Taxation

Recent developments in international tax

Recent developments in international tax Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate

Recent developments in international tax Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate

Index. [Current to Release ]

![Index. [Current to Release ]](/thumbs/95/123104163.jpg "Index. [Current to Release ]") 50-1 Index Abbreviations, xix to xx [Current to Release 2016-1] Accelerated cost recovery system (ACRS), see also Depreciation. generally, VII-402 to VII-406. percentage tables, VII-413 to VII-419 Accounting

50-1 Index Abbreviations, xix to xx [Current to Release 2016-1] Accelerated cost recovery system (ACRS), see also Depreciation. generally, VII-402 to VII-406. percentage tables, VII-413 to VII-419 Accounting

BEPS Beyond Fortune 1000 October Armanino LLP amllp.com Armanino LLP amllp.com

BEPS Beyond Fortune 1000 October 2016 1 Armanino LLP amllp.com Armanino LLP amllp.com 1 BEPS Overview Timeline Pre-2013 - Organization for Economic Cooperation and Development (OECD) concern that existing

BEPS Beyond Fortune 1000 October 2016 1 Armanino LLP amllp.com Armanino LLP amllp.com 1 BEPS Overview Timeline Pre-2013 - Organization for Economic Cooperation and Development (OECD) concern that existing

US Tax Reform: Impact on Private Funds

2018 INVESTMENT MANAGEMENT CONFERENCE CHICAGO US Tax Reform: Impact on Private Funds Adam J. Tejeda, New York Frank W. Dworak, Orange County January 31, 2018 Copyright 2018 by K&L Gates LLP. All rights

2018 INVESTMENT MANAGEMENT CONFERENCE CHICAGO US Tax Reform: Impact on Private Funds Adam J. Tejeda, New York Frank W. Dworak, Orange County January 31, 2018 Copyright 2018 by K&L Gates LLP. All rights

Doing Business in Canada: Key Canadian Tax Considerations

Doing Business in Canada: Key Canadian Tax Considerations Foreign enterprises have long been attracted to investment opportunities in Canada. Canada has led the G7 in growth in total inbound investment

Doing Business in Canada: Key Canadian Tax Considerations Foreign enterprises have long been attracted to investment opportunities in Canada. Canada has led the G7 in growth in total inbound investment

Bank Tax Planning: A New Era of Taxation?

Bank Tax Planning: A New Era of Taxation? Eric D. Budreau, CPA, M.T. Partner ebudreau@eidebailly.com 303.770.5700 Andy Kaiser, CPA Partner akaiser@eidebailly.com 303.770.5700 Agenda Tax Reform Overview

Bank Tax Planning: A New Era of Taxation? Eric D. Budreau, CPA, M.T. Partner ebudreau@eidebailly.com 303.770.5700 Andy Kaiser, CPA Partner akaiser@eidebailly.com 303.770.5700 Agenda Tax Reform Overview

Please any questions for Robert to: Thank you.

EXPLORING THE NEW TERRITORIAL TAX SYSTEM PORTLAND TAX FORUM SHORT TOPIC PRESENTATION JANUARY 18, 2018 ROBERT J. WOLFER, CPA Robert is a Senior Tax Manager with DiLorenzo & Company, LLC, where his duties

EXPLORING THE NEW TERRITORIAL TAX SYSTEM PORTLAND TAX FORUM SHORT TOPIC PRESENTATION JANUARY 18, 2018 ROBERT J. WOLFER, CPA Robert is a Senior Tax Manager with DiLorenzo & Company, LLC, where his duties

Mergers & Acquisitions

Mergers & Acquisitions Mergers & Acquisitions Our Signature Story Since 1926, we have been a trusted business partner to our clients and have earned our reputation as one of the most respected and socially

Mergers & Acquisitions Mergers & Acquisitions Our Signature Story Since 1926, we have been a trusted business partner to our clients and have earned our reputation as one of the most respected and socially

Setting up your Business in Georgia Issues to consider

Georgia is one of the world s fastest growing economies and in the region is leading location for global investment. As a result of innovative reforms implemented in Georgia, the World Bank rated Georgia

Georgia is one of the world s fastest growing economies and in the region is leading location for global investment. As a result of innovative reforms implemented in Georgia, the World Bank rated Georgia

Tax Guide For Foreign Investors In U.S. Residential Real Estate

A T T O R N E Y S A T L A W Tax Guide For Foreign Investors In U.S. Residential Real Estate 2018 Edition In this guide I. Introduction 2 II. The U.S. Tax System 3 A. U.S. Persons 3 1. Basic Rules 3 2.

A T T O R N E Y S A T L A W Tax Guide For Foreign Investors In U.S. Residential Real Estate 2018 Edition In this guide I. Introduction 2 II. The U.S. Tax System 3 A. U.S. Persons 3 1. Basic Rules 3 2.

US Tax Information for Diplomatic Families at the Canadian Embassy

US Tax Information for Diplomatic Families at the Canadian Rick Ward LLC January 16, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of January

US Tax Information for Diplomatic Families at the Canadian Rick Ward LLC January 16, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of January

U.S. TAX REFORM: INTERNATIONAL IMPLICATIONS

DID YOU GET YOUR BADGE SCANNED? U.S. TAX REFORM: INTERNATIONAL IMPLICATIONS #TaxLaw #FBA Username: taxlaw Password: taxlaw18 PanelistS Jorge Castro, Castro Strategies LLC Alan Granwell, Sharp Partners

DID YOU GET YOUR BADGE SCANNED? U.S. TAX REFORM: INTERNATIONAL IMPLICATIONS #TaxLaw #FBA Username: taxlaw Password: taxlaw18 PanelistS Jorge Castro, Castro Strategies LLC Alan Granwell, Sharp Partners

International Income Taxation Chapter 1: INTRODUCTION

Presentation: International Income Taxation Chapter 1: INTRODUCTION Professors Wells January 20, 2016 Chapter One: Introduction Problem of Primary versus Secondary Taxing Jurisdiction: 1) Inbound investment

Presentation: International Income Taxation Chapter 1: INTRODUCTION Professors Wells January 20, 2016 Chapter One: Introduction Problem of Primary versus Secondary Taxing Jurisdiction: 1) Inbound investment

Hot Tax and Investment Issues when Structuring Investment into Myanmar

Hot Tax and Investment Issues when Structuring Investment into Myanmar At a Glance Myanmar Laos Cambodia Vietnam Singapore 6 countries More than 50 professional staff Indonesia Our Vision Southeast Asia

Hot Tax and Investment Issues when Structuring Investment into Myanmar At a Glance Myanmar Laos Cambodia Vietnam Singapore 6 countries More than 50 professional staff Indonesia Our Vision Southeast Asia

U.S. tax reforms prevention of base erosion. S. Krishnan

U.S. tax reforms prevention of base erosion S. Krishnan 2 U.S. tax regime prior to 2018 Amongst the large economies in the world, the United States had the highest statutory corporate income tax rate upwards

U.S. tax reforms prevention of base erosion S. Krishnan 2 U.S. tax regime prior to 2018 Amongst the large economies in the world, the United States had the highest statutory corporate income tax rate upwards

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features:

Presenting a live 90-minute webinar with interactive Q&A Nonresident Alien Tax Compliance: Challenges and Planning Techniques for Tax Professionals Recent IRS Compliance Campaign, ECI vs. FDAP Income,

Presenting a live 90-minute webinar with interactive Q&A Nonresident Alien Tax Compliance: Challenges and Planning Techniques for Tax Professionals Recent IRS Compliance Campaign, ECI vs. FDAP Income,

International Provisions in U.S. Tax Reform A Closer Look

December 22, 2017 International Provisions in U.S. Tax Reform A Closer Look by Peter Connors John Narducci Stephen Jackson Barbara De Marigny Michael Rodgers On December 15, the U.S. Congress issued its

December 22, 2017 International Provisions in U.S. Tax Reform A Closer Look by Peter Connors John Narducci Stephen Jackson Barbara De Marigny Michael Rodgers On December 15, the U.S. Congress issued its

Doing business in the UK. Expansion into the UK - Considerations for US investors. Nick Farmer ACA CTA ATII

Expansion into the UK - Considerations for US investors Nick Farmer ACA CTA ATII London: http://www.youtube.com/watch?v=45etz1xvhs0 Expansion into the UK Doing business in the UK United Kingdom Economy

Expansion into the UK - Considerations for US investors Nick Farmer ACA CTA ATII London: http://www.youtube.com/watch?v=45etz1xvhs0 Expansion into the UK Doing business in the UK United Kingdom Economy

United States Tax Alert

International Tax United States Tax Alert 6 February 2015 On February 2, 2015, the Obama Administration (the Administration) released its FY2016 Budget and the Treasury Department released the General

International Tax United States Tax Alert 6 February 2015 On February 2, 2015, the Obama Administration (the Administration) released its FY2016 Budget and the Treasury Department released the General

CORPORATE INVERSIONS. Jack Miles, Esq. Kelley Drye & Warren LLP 101 Park Avenue New York, NY (212)

") CORPORATE INVERSIONS Jack Miles, Esq. Kelley Drye & Warren LLP 101 Park Avenue New York, NY 10178 (212) 808-7574 jmiles@kelleydrye.com Background In a typical inversion, a U.S. multinational combines with

CORPORATE INVERSIONS Jack Miles, Esq. Kelley Drye & Warren LLP 101 Park Avenue New York, NY 10178 (212) 808-7574 jmiles@kelleydrye.com Background In a typical inversion, a U.S. multinational combines with

US tax reform and the impact on cross-border individuals

US tax reform and the impact on cross-border individuals January 2018 Tax Alert The Tax Cuts and Jobs Act was signed into law on December 22, 2017. Several significant changes arose out of this tax legislation.

US tax reform and the impact on cross-border individuals January 2018 Tax Alert The Tax Cuts and Jobs Act was signed into law on December 22, 2017. Several significant changes arose out of this tax legislation.

Comparison of Key Anti-Base Erosion Rules in the Tax Reform Act of 2017 and under UK Tax Law Calum Dewar, PwC Mike Williams, HM Treasury

Comparison of Key Anti-Base Erosion Rules in the Tax Reform Act of 2017 and under UK Tax Law Calum Dewar, PwC Mike Williams, HM Treasury International Tax Policy Forum and Institute of Economic Law Conference

Comparison of Key Anti-Base Erosion Rules in the Tax Reform Act of 2017 and under UK Tax Law Calum Dewar, PwC Mike Williams, HM Treasury International Tax Policy Forum and Institute of Economic Law Conference

CROSS-BORDER INCOME TAX ISSUES IN OUTBOUND ESTATE PLANNING. Jenny Coates Law, PLLC, International Tax Lawyer

CROSS-BORDER INCOME TAX ISSUES IN OUTBOUND ESTATE PLANNING Jenny Coates Law, PLLC, International Tax Lawyer jenny@jennycoateslaw.com Increased Tax Complexity Whether between the US and Canada or the US

CROSS-BORDER INCOME TAX ISSUES IN OUTBOUND ESTATE PLANNING Jenny Coates Law, PLLC, International Tax Lawyer jenny@jennycoateslaw.com Increased Tax Complexity Whether between the US and Canada or the US

FATCA considerations for multinational non-financial corporate groups

19 July 2013 International Tax Alert News from the Global Tax Desk Network FATCA considerations for multinational non-financial corporate groups Executive summary On 17 January 2013, the US Treasury (Treasury)

19 July 2013 International Tax Alert News from the Global Tax Desk Network FATCA considerations for multinational non-financial corporate groups Executive summary On 17 January 2013, the US Treasury (Treasury)