ARIZONA TRANSACTION PRIVILEGE AND USE TAX

|

|

|

- Kristopher West

- 6 years ago

- Views:

Transcription

1 ARIZONA TRANSACTION PRIVILEGE AND USE TAX

2 DEFINITION TRANSACTION PRIVILEGE TAX (TPT) Commonly referred to as sales tax, TPT is tax on the retail sale of tangible personal property AND services. Retail Sale sale to end user End user each state defines it differently Special case - in AZ, a MRRA contractor is an end user Tangible in AZ, something that can be perceived by the senses (touch, taste, sight, sound) Special case in AZ, software is tangible personal property regardless of delivery method Personal Property not land or building or attached to land or building Special case in AZ, counters in a bank, although attached, are considered personal property Services intangible, cannot be stored or transported, come into existence at time of purchase Special case - in AZ, professional and personal service occupations are usually exempt

3 THE GENERAL RULES The University of Arizona is not a non-profit organization and is not exempt from sales and use tax!!! Sales to a non-profit organization Generally taxable Sales by a non-profit organization Generally exempt Goods Generally taxable unless specifically exempt Services Generally taxable unless specifically exempt such as: Professional and personal service occupations Transfers of TPP are inconsequential elements i.e.: CPAs, lawyers Services in addition to selling TPP at retail i.e.: delivery of TPP Examples of taxable services include: transportation, utilities, telecommunications, a photographer s services, and amusements

4 SALES TAX RATES For transactions involving retail, restaurants, utilities, communications, job printing, publication, rent of personal property, amusements, etc AZ State 5.6% Pima County 0.5% Tucson 0% when UA is seller UA is exempt from collecting city tax from its customers, but: Tucson % when UA is buyer UA pays 2.5% to vendors retail, restaurants, communications, job printing, publication, rent of personal property and amusements UA pays 4.5% to vendors public utilities

5 SALES TAX RATES - SUMMARY Description Tax % (when selling) Tax % (when buying) AZ State 5.60% 5.60% Pima County* 0.50% 0.50% Tucson City* 0% % Total 6.10% 8.60%-10.60% *These rates may vary when buying or selling from or to different counties or cities/towns

6 UNIVERSITY AS A SELLER We work together to properly collect and remit TPT Department s responsibilities: Identify taxable sales for Arizona customers Collect and file customer s tax exemption certificates Collect the correct tax Use proper object codes (refer to Financial Services Manual 8.11) Taxable vs. non-taxable Deposit revenue and tax in University accounts Maintain detailed records of sales activities FSO s responsibilities: Prepare TPT return Remit tax receipts to the State of Arizona Provide guidance to Departments

7 UNIVERSITY AS A SELLER No Is the customer in Arizona? Yes Does the customer take possession of the good or service in Arizona? Yes Is the transaction taxable in Arizona? No Do not collect Arizona TPT No Yes Do not collect any sales tax No Is the transaction taxable in the other state? Is there an available Arizona exemption for the purchase? Yes Collect applicable Arizona Form 5000 from customer Yes/Maybe No CONTACT FSO IMMEDIATELY! Collect Arizona TPT

8 DEFINITION USE TAX Self-assessed tax on the use, storage, or consumption of tangible personal property where: Sales tax was not levied by the vendor, and The purchase is otherwise taxable in Arizona Example: Purchase from an out of state vendor who does not have an Arizona TPT license

9 USE TAX RATE AZ State 5.60% Counties generally do not impose use tax The University of Arizona is not subject to city tax

10 SALES OR USE TAX? How do you know if it s sales tax or use tax, and, does it make a difference? Sales and use tax are complementary Pay only sales tax or use tax Vendors charge sales tax Use tax is self-assessed USE TAX OR NO USE TAX? Test tubes shipped to AZ from FL, vendor did not charge sales tax Cab fare in Boston, not sure if tax was charged Software accessed on a CA vendor s website, vendor did not charge sales tax Restaurant in Portland, vendor did not charge sales tax -USE TAX -NO USE TAX -USE TAX -NO USE TAX

11 WHAT IS SALES TAX NEXUS? Nexus means connection, or linkage. Factors that can create nexus: Renting or owning property Business presence in the state Trade shows (except Nevada/Florida) Presence of agents/contractors/employees Consequence of having nexus Register as a retailer in that state Collect taxes (University wide) File returns (Minimum 1 year) Remit payment to the state Departmental responsibility Talk with FSO before you plan to: Travel out of state to make sales Have a distributor or warehouse in another state

12 NON-TAXABLE SERVICES Professional/personal services where sales of TPP is an inconsequential element Remember, many services are specifically taxable, such as: Transportation, utilities, telecommunications, and photographer s services Services rendered in addition to selling TPP at retail i.e.: Repair/maintenance and installation services, unless: Taxable if not separately disclosed on invoice Taxable if installation is to be attached to real property Shipping services/freight charges, unless: Taxable if handling is included (Use object code 3880 for Shipping & Handling) Warranty services/service contracts Be careful, if related to software or other tangible personal property, it MAY be taxable

consumption Medically prescribed drugs, equipment or devices Purchases for resale where tax will be collected at sale to end user (Use Arizona Form")

13 NON-TAXABLE TANGIBLE PERSONAL PROPERTY Textbooks/required course materials purchased/sold by UA Bookstores Printed and other media materials made available to the public by UA Libraries Unprepared food for home (human) consumption Medically prescribed drugs, equipment or devices Purchases for resale where tax will be collected at sale to end user (Use Arizona Form 5000A)

14 MORE NON-TAXABLE TRANSACTIONS Conference registration fees Professional membership dues Machinery and equipment used for research and development Chemicals used for research and development Others as set forth in statutes such as ARS or ARS

15 ARIZONA S RESEARCH & DEVELOPMENT DEFINITION What it is: Research and development means basic and applied research in the sciences and engineering, and designing, developing or testing prototypes, processes or new products, including research and development of computer software that is embedded in or an integral part of the prototype or new product or that is required for machinery or equipment otherwise exempt under this section to function effectively. What it isn t: Research and development do not include manufacturing quality control, routine consumer product testing, market research, sales promotion, sales service, research in social sciences or psychology, computer software research that is not included in the definition of research and development, or other non-technological activities or technical services.

16 MACHINERY & EQUIPMENT USED FOR RESEARCH Machinery or equipment used for research as defined is tax exempt Must be 100% research use Dollar amount is not a factor Machinery or equipment does not include: Expendable materials and supplies Office equipment, furniture or supplies Hand tools Janitorial equipment Licensed motor vehicles Shops, buildings, depots A repair or replacement part of tax-exempt research equipment is also exempt Leases and rentals of tax-exempt research equipment are exempt

(14) to claim exemption from sales tax Use exemption ARS 42-5159(B)(14) to claim exemption")

17 MACHINERY & EQUIPMENT USED FOR RESEARCH Research does not include: Social sciences Psychology Routine consumer product testing Computer software development Non-technological activities or technical services PCs, laptops and portable devices are almost never tax exempt Computers used in research of computer software Not tax exempt Use exemption ARS (B)(14) to claim exemption from sales tax Use exemption ARS (B)(14) to claim exemption from use tax

(38) to claim exemption from sales tax Use exemption ARS 42-5159(A)(35) to claim exemption from use tax")

18 CHEMICALS USED FOR RESEARCH Chemicals used directly in research as defined are tax exempt Exempt chemicals cannot be used or consumed in: Packaging Storage Transportation Researcher who orders the item must determine whether it is chemical Use exemption ARS (A)(38) to claim exemption from sales tax Use exemption ARS (A)(35) to claim exemption from use tax

")

19 COMPUTER HARDWARE & SOFTWARE Purchase of hardware and standard, pre-written or canned software: Almost never* exempt Purchase of tangible, regardless of delivery *Purchase of customized software: Designed exclusively to the specifications of a UA unique application Modification of standard software at installation does not make it custom Not taxable Purchase of professional/personal services *Purchase (by a State community college or university) of remote software applications that either: Are designed to assess or test student learning, or Promote curriculum design and enhancement Not taxable ARS (53) and ARS (50)

20 HARDWARE & SOFTWARE SERVICES Computer services such as analysis, design, repair, and support engineering: Not taxable Maintenance and warranty agreement for hardware and software: Generally not taxable if: Sold as a separate item, and Does not include TPP, and The price is stated separately Software agreement including updates, upgrades, modification or revisions to a standard software: Taxable as purchase of TPP

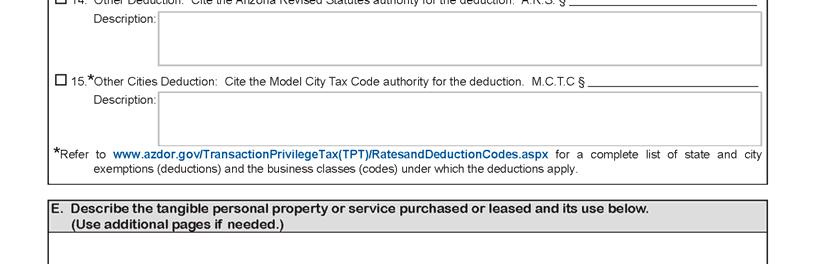

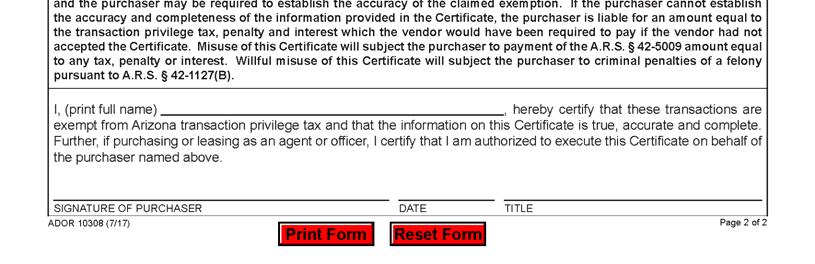

21 CLAIMING TAX EXEMPTION FROM A VENDOR Vendors must document tax exempt transactions: Tax exemption certificates (Arizona Form 5000 and Arizona Form 5000A) are required and provide: University s Federal Tax ID ( ), AZ TPT License Number ( ), Reason for exemption, and The signature of the individual authorizing the purchase Arizona Form 5000 (and 5000A for resale purchases) for a PCard purchase: Provided to the vendor (prior to transaction) by the department Signed by the departmental individual who authorizes the purchase Certificates and instructions are located the Financial Services Office Tax Services webpage:

22 ARIZONA FORM 5000

23 ARIZONA FORM 5000

24 UNIVERSITY AS A BUYER

25 PCARD USE TAX EXEMPTION PCard reconcilers avoid erroneous assessment of use tax by: Entering the sales tax amount in the Enter Sales Tax field when sales tax is charged by the vendor, or Checking the Tax Exempt Indicator box in UAccess Financials when the transaction is sales or use tax exempt, or Checking the Tax Exempt Indicator box in UAccess Financials when sales tax is charged but amount cannot be identified Taxes are always included in the total price for the following: Airline tickets Telecommunication charges (Verizon/ AT&T / Sprint, etc.) Use tax is not automatically assessed on the following object codes: 3820 (Postage & Mailing), 3870 (Express Shipping), 5520 (Conference Registration Fees), 5540 (Dues), 5560 (Freight In/Out noncapital), 5810 (Resale), 5830 (Resale), 7810 (Library Acquisitions Books), 7820 (Library Acquisitions Periodicals), and 7830 (Library Acquisitions Other)

26 USE TAX GENERAL ERROR CORRECTION Step 1 Review transactions where use tax was assessed UAccess Analytics> Dashboards> Financial> General Financial Management > Transactions Include relevant period, account and organization information Doc Type = PCDO Use Report View Detail by Fund Group by Account and Object Code Export data and sort to see if use tax was charged and whether it needs correction If use tax was erroneously assessed, see Step 2

27 GENERAL ERROR CORRECTION FOR USE TAX Step 2 GEC UAccess Financials> Main Menu> Transactions> Financial> General Error Correction

28 GENERAL ERROR CORRECTION FOR USE TAX Step 2 continued Description Reversal of use tax Explanation Brief explanation why Org. Doc. # - Original doc # All entries would be in the From section Reducing expense and liability from the account Chart UA Reducing expenses Account # - Account # in which the expense was charged Object code Object code in which the expense was charged Reference Origin Code 01 Reference Number Original doc # where the expense was charged Line Description Reversal of use tax Amount Use tax charged Click Add

29 GENERAL ERROR CORRECTION FOR USE TAX Step 2 continued Reducing liability Account # Object code 9190 Reference Origin Code 01 Reference Number Original doc # where the expense was charged Line Description Reversal of use tax Amount Use tax charged Click Add Notes and Attachments - Include detailed explanation why the transaction is not taxable Optional if details are included in Explanation box Submit Please note Use tax can be reversed with a GEC only for prior periods in the current fiscal year

30 IN REVIEW: THE GENERAL RULES Purchases and sales of tangible personal property and services are generally taxable, unless specifically exempt Many services are specifically exempt If taxable goods are purchased from an out of state vendor without Arizona nexus, self-assess use tax At the UA, if an item does not fit into machinery or equipment used in research or chemical used in research, it generally DOES NOT qualify for an exemption from tax

31 RESOURCES AND CONTACT INFORMATION Tax Services Arizona Sales and Use Tax page: For assistance to determine the taxability of a purchase/sale: taxservices@fso.arizona.edu FSO-Tax Compliance: For assistance to record the purchase, sales and related tax, or correction of use tax: FSO-Financial Management: or

ARIZONA TRANSACTION PRIVILEGE AND USE TAX

ARIZONA TRANSACTION PRIVILEGE AND USE TAX DEFINITION TRANSACTION PRIVILEGE TAX (TPT) Commonly referred to as sales tax, TPT is tax on the retail sale of tangible personal property AND services. Retail

ARIZONA TRANSACTION PRIVILEGE AND USE TAX DEFINITION TRANSACTION PRIVILEGE TAX (TPT) Commonly referred to as sales tax, TPT is tax on the retail sale of tangible personal property AND services. Retail

Sales and Use Tax Information Session

Sales/Use Tax Information Session Sales and Use Tax Information Session By A/P & Tax Sales/Use Tax Information Session For 2014, UCD collected and remitted sales and use tax in the amount of? to the State

Sales/Use Tax Information Session Sales and Use Tax Information Session By A/P & Tax Sales/Use Tax Information Session For 2014, UCD collected and remitted sales and use tax in the amount of? to the State

Managing Sales Tax Exemptions

Managing Sales Tax Exemptions Diane Yetter May 11, 2017 Introduction Sales are taxable unless a specific exemption or exclusion Proceed with caution when determining which transactions qualify Careful

Managing Sales Tax Exemptions Diane Yetter May 11, 2017 Introduction Sales are taxable unless a specific exemption or exclusion Proceed with caution when determining which transactions qualify Careful

GENERAL INSTRUCTIONS FOR ARIZONA JOINT TAX APPLICATION (JT-1)

") ARIZONA DEPARTMENT OF REVENUE GENERAL FOR ARIZONA JOINT TAX APPLICATION (JT-1) Online Application Go to www.aztaxes.gov Notice for Construction Contractors: Due to bonding requirements, construction contractors

ARIZONA DEPARTMENT OF REVENUE GENERAL FOR ARIZONA JOINT TAX APPLICATION (JT-1) Online Application Go to www.aztaxes.gov Notice for Construction Contractors: Due to bonding requirements, construction contractors

GLOSSARY. IPT Sales and Use Tax Symposium Beginner Basics

GLOSSARY IPT Sales and Use Tax Symposium Beginner Basics GLOSSARY The following definitions have been developed to facilitate an understanding of the course material. They tend to be generic in nature,

GLOSSARY IPT Sales and Use Tax Symposium Beginner Basics GLOSSARY The following definitions have been developed to facilitate an understanding of the course material. They tend to be generic in nature,

Navigating Sales & Use Tax w/ Microsoft Dynamics & CCH. Andrew Phillips. Channel Sales Representative, Corporate. May 2, 2014

Navigating Sales & Use Tax w/ Microsoft Dynamics & CCH Andrew Phillips Channel Sales Representative, Corporate May 2, 2014 May 2, 2014 2 Sales & Use Tax Today s Climate May 2, 2014 - USA 3 Sales & Use

Navigating Sales & Use Tax w/ Microsoft Dynamics & CCH Andrew Phillips Channel Sales Representative, Corporate May 2, 2014 May 2, 2014 2 Sales & Use Tax Today s Climate May 2, 2014 - USA 3 Sales & Use

SALES & USE TAX FOR PUBLIC PROCUREMENT THE BASICS OF SALES TAX

SALES & USE TAX FOR PUBLIC PROCUREMENT SC ASSOCIATION OF GOVERNMENTAL PURCHASING OFFICIALS SEPTEMBER 14, 2017 1 THE BASICS OF SALES TAX South Carolina imposes a sales tax equal to 6%, plus applicable local

SALES & USE TAX FOR PUBLIC PROCUREMENT SC ASSOCIATION OF GOVERNMENTAL PURCHASING OFFICIALS SEPTEMBER 14, 2017 1 THE BASICS OF SALES TAX South Carolina imposes a sales tax equal to 6%, plus applicable local

STATE & LOCAL TAX SOLUTIONS: Understanding Sales & Use Taxes for Construction, Real Estate & Manufacturing Industries

STATE & LOCAL TAX SOLUTIONS: Understanding Sales & Use Taxes for Construction, Real Estate & Manufacturing Industries November 8, 2017 PRESENTED BY: KENNETH TAYLOR, SENIOR MANAGING CONSULTANT, STATE &

STATE & LOCAL TAX SOLUTIONS: Understanding Sales & Use Taxes for Construction, Real Estate & Manufacturing Industries November 8, 2017 PRESENTED BY: KENNETH TAYLOR, SENIOR MANAGING CONSULTANT, STATE &

830 CMR 64H.1.3 Computer Industry Services and Products

830 CMR 64H.1.3 Computer Industry Services and Products 830 CMR: DEPARTMENT OF REVENUE 830 CMR 64H:00: SALES AND USE TAX 830 CMR 64H.1.3 is repealed and replaced with the following (1) Statement of Purpose;

830 CMR 64H.1.3 Computer Industry Services and Products 830 CMR: DEPARTMENT OF REVENUE 830 CMR 64H:00: SALES AND USE TAX 830 CMR 64H.1.3 is repealed and replaced with the following (1) Statement of Purpose;

Department of Finance and Administration

STATE OF ARKANSAS Department of Finance and Administration REVENUE LEGAL COUNSEL Post Office Box 1272, Room 2380 Little Rock, Arkansas 72203-1272 Phone: (501) 682-7030 Fax: (501) 682-7599 http://www.dfa.arkansas.gov

STATE OF ARKANSAS Department of Finance and Administration REVENUE LEGAL COUNSEL Post Office Box 1272, Room 2380 Little Rock, Arkansas 72203-1272 Phone: (501) 682-7030 Fax: (501) 682-7599 http://www.dfa.arkansas.gov

MAINE REVENUE SERVICES SALES, FUEL & SPECIAL TAX DIVISION SALES TAX INSTRUCTIONAL BULLETIN 54

MAINE REVENUE SERVICES SALES, FUEL & SPECIAL TAX DIVISION SALES TAX INSTRUCTIONAL BULLETIN 54 RESALE CERTIFICATES This Bulletin is intended solely as advice to assist persons in determining, exercising

MAINE REVENUE SERVICES SALES, FUEL & SPECIAL TAX DIVISION SALES TAX INSTRUCTIONAL BULLETIN 54 RESALE CERTIFICATES This Bulletin is intended solely as advice to assist persons in determining, exercising

Intro to Sales and Use Tax. City of Wheat Ridge Basics 2017

Intro to Sales and Use Tax City of Wheat Ridge Basics 2017 This Class Briefing on licensing An overview of sales and use tax for those with little, no or rusty knowledge of them. Definition, history and

Intro to Sales and Use Tax City of Wheat Ridge Basics 2017 This Class Briefing on licensing An overview of sales and use tax for those with little, no or rusty knowledge of them. Definition, history and

GLOSSARY. IPT 2016 Sales and Use Tax Symposium Beginner Basics

GLOSSARY IPT 2016 Sales and Use Tax Symposium Beginner Basics GLOSSARY The following definitions have been developed to facilitate an understanding of the course material. They tend to be generic in nature,

GLOSSARY IPT 2016 Sales and Use Tax Symposium Beginner Basics GLOSSARY The following definitions have been developed to facilitate an understanding of the course material. They tend to be generic in nature,

10 Sales Tax Rules to Live By

10 Sales Tax Rules to Live By Chuck Marcouiller, Tax Technology Expert Avalara Avalara Chuck Marcouiller Tax Technology Expert, Avalara 20 Years in tax technology and education Held operational and training

10 Sales Tax Rules to Live By Chuck Marcouiller, Tax Technology Expert Avalara Avalara Chuck Marcouiller Tax Technology Expert, Avalara 20 Years in tax technology and education Held operational and training

Changes in Arkansas Sales and Use Tax Law Effective January 1, 2008

STATE OF ARKANSAS Department of Finance and Administration http://www.state.ar.us/dfa SALES & USE TAX SECTION P. O. BOX 1272 LITTLE ROCK, AR 72203-1272 PHONE: (501) 682-7104 FAX: (501) 682-7904 sales.tax@rev.state.ar.us

STATE OF ARKANSAS Department of Finance and Administration http://www.state.ar.us/dfa SALES & USE TAX SECTION P. O. BOX 1272 LITTLE ROCK, AR 72203-1272 PHONE: (501) 682-7104 FAX: (501) 682-7904 sales.tax@rev.state.ar.us

Sales & Use Tax for Government & Municipalities

Sales & Use Tax for Government & Municipalities Sales Tax 12-36- 910(A) reads: A sales tax, equal to [six] percent of the gross proceeds of sales, is imposed upon every person engaged or continuing within

Sales & Use Tax for Government & Municipalities Sales Tax 12-36- 910(A) reads: A sales tax, equal to [six] percent of the gross proceeds of sales, is imposed upon every person engaged or continuing within

THE UNIVERSITY OF TEXAS SYSTEM

THE UNIVERSITY OF TEXAS SYSTEM PERMANENT UNIVERSITY FUND (PUF) BOND PROCEEDS FOR LIBRARY, EQUIPMENT, REPAIR AND REHABILITATION (LERR) AND FACULTY SCIENCE AND TECHNOLOGY ACQUISITION AND RETENTION (STARS)

THE UNIVERSITY OF TEXAS SYSTEM PERMANENT UNIVERSITY FUND (PUF) BOND PROCEEDS FOR LIBRARY, EQUIPMENT, REPAIR AND REHABILITATION (LERR) AND FACULTY SCIENCE AND TECHNOLOGY ACQUISITION AND RETENTION (STARS)

Photography and Video Production

www.revenue.state.mn.us Photography and Video Production Sales Tax Fact Sheet 169 169 Fact Sheet What s New in 2015 Starting July 1, 2015, the capital equipment refund is an up-front sales tax exemption.

www.revenue.state.mn.us Photography and Video Production Sales Tax Fact Sheet 169 169 Fact Sheet What s New in 2015 Starting July 1, 2015, the capital equipment refund is an up-front sales tax exemption.

Common Sales Tax Pitfalls for Contractors

Common Sales Tax Pitfalls for Contractors Rob Wollfarth, Esq. Baker, Donelson, Bearman, Caldwell & Berkowitz, PC 201 St. Charles Avenue, Suite 3600 New Orleans, LA 70170 Direct: 504.566.8623 E-mail: rwollfarth@bakerdonelson.com

Common Sales Tax Pitfalls for Contractors Rob Wollfarth, Esq. Baker, Donelson, Bearman, Caldwell & Berkowitz, PC 201 St. Charles Avenue, Suite 3600 New Orleans, LA 70170 Direct: 504.566.8623 E-mail: rwollfarth@bakerdonelson.com

PURCHASING CARD PROCEDURES

EDGEWOOD INDEPENDENT SCHOOL DISTRICT PURCHASING CARD PROCEDURES September 2017 5358 West Commerce Street San Antonio, Texas 78237 Table of Contents Page Table of Contents... 1 Introduction... 2 Card Holder...

EDGEWOOD INDEPENDENT SCHOOL DISTRICT PURCHASING CARD PROCEDURES September 2017 5358 West Commerce Street San Antonio, Texas 78237 Table of Contents Page Table of Contents... 1 Introduction... 2 Card Holder...

Sales and Use Tax Information Session

Sales/Use Tax Information Session Sales and Use Tax Information Session By A/P & Tax Quick Quiz: Sales/Use Tax Information Session In 2013, how much sales and use tax did UCD collect and remit to the State

Sales/Use Tax Information Session Sales and Use Tax Information Session By A/P & Tax Quick Quiz: Sales/Use Tax Information Session In 2013, how much sales and use tax did UCD collect and remit to the State

Introduction to Washington Business Taxes

Introduction to Washington Business Taxes Washington State Department of Revenue Maureen O Connell, September 30, 2017 Objectives Provide information on major taxes in Washington Provide helpful contacts

Introduction to Washington Business Taxes Washington State Department of Revenue Maureen O Connell, September 30, 2017 Objectives Provide information on major taxes in Washington Provide helpful contacts

CITY REVITALIZATION AND IMPROVEMENT ZONE PROGRAM ELECTRONIC TAX REPORT INSTRUCTIONS

CITY REVITALIZATION AND IMPROVEMENT ZONE PROGRAM ELECTRONIC TAX REPORT INSTRUCTIONS Contents Report Changes for 2018... 1 Report Filing Criteria... 2 Help and Assistance... 2 Accessing the CRIZ Report

CITY REVITALIZATION AND IMPROVEMENT ZONE PROGRAM ELECTRONIC TAX REPORT INSTRUCTIONS Contents Report Changes for 2018... 1 Report Filing Criteria... 2 Help and Assistance... 2 Accessing the CRIZ Report

Sales and Use Tax Introduction

Sales and Use Tax Introduction Carlos Hernandez Ernst & Young LLP Chicago, IL Lauren Tallman KPMG LLP Seattle, WA Presenters Carlos Hernandez Ernst & Young LLP Indirect Tax Services 115 N Wacker Drive

Sales and Use Tax Introduction Carlos Hernandez Ernst & Young LLP Chicago, IL Lauren Tallman KPMG LLP Seattle, WA Presenters Carlos Hernandez Ernst & Young LLP Indirect Tax Services 115 N Wacker Drive

PURCHASING CARD MANUAL

PURCHASING CARD MANUAL Revised 11/2016 Page 1 of 6 OVERVIEW Palm Beach State has implemented a Purchasing Card (P-Card) Program to serve as an alternate and more efficient method for purchasing small dollar

PURCHASING CARD MANUAL Revised 11/2016 Page 1 of 6 OVERVIEW Palm Beach State has implemented a Purchasing Card (P-Card) Program to serve as an alternate and more efficient method for purchasing small dollar

For Fiscal Year Ending August 31, 2016

THE UNIVERSITY OF TEXAS SYSTEM LIBRARY, EQUIPMENT, REPAIR AND REHABILITATION AND FACULTY SCIENCE AND TECHNOLOGY ACQUISITION AND RETENTION (STARS) AND SIMILAR FUNDED PROGRAMS BUDGET RULES AND PROCEDURES

THE UNIVERSITY OF TEXAS SYSTEM LIBRARY, EQUIPMENT, REPAIR AND REHABILITATION AND FACULTY SCIENCE AND TECHNOLOGY ACQUISITION AND RETENTION (STARS) AND SIMILAR FUNDED PROGRAMS BUDGET RULES AND PROCEDURES

Frequently Asked Questions (FAQ s) Use Tax Collection Requirements Due to Wayfair Decision

Use Tax Collection Requirements Due to Wayfair Decision") Frequently Asked Questions (FAQ s) Use Tax Collection Requirements Due to Wayfair Decision IMPORTANT NOTE The requirements to register and collect the California use tax prior to the Wayfair decision remain

Frequently Asked Questions (FAQ s) Use Tax Collection Requirements Due to Wayfair Decision IMPORTANT NOTE The requirements to register and collect the California use tax prior to the Wayfair decision remain

Welcome! Agenda. Background re: the Partial Exemption Procedure Q&A Next Steps

Welcome! Agenda Background re: the Partial Exemption Procedure Q&A Next Steps State of California Partial Exemption From Sales and Use Tax In an effort to promote and keep Manufacturing and Research and

Welcome! Agenda Background re: the Partial Exemption Procedure Q&A Next Steps State of California Partial Exemption From Sales and Use Tax In an effort to promote and keep Manufacturing and Research and

Sales and Use Tax Information Session

Sales/Use Tax Information Session Sales and Use Tax Information Session By A/P & Tax Sales/Use Tax Information Session For 2013, UCD collected and remitted sales and use tax in the amount of? to the State

Sales/Use Tax Information Session Sales and Use Tax Information Session By A/P & Tax Sales/Use Tax Information Session For 2013, UCD collected and remitted sales and use tax in the amount of? to the State

Purchasing Card Allocation Using Banner Admin:

Purchasing Card Allocation Using Banner Admin: Purchasing card allocations are an important part of a department's regular weekly duties to ensure purchases made by department cardholders are recorded

Purchasing Card Allocation Using Banner Admin: Purchasing card allocations are an important part of a department's regular weekly duties to ensure purchases made by department cardholders are recorded

Use Tax for Businesses 146

www.revenue.state.mn.us Use Tax for Businesses 146 Sales Tax Fact Sheet 146 What s new in 2017 We updated the layout to make this fact sheet easier to use. Minnesota Use Tax applies when you buy, lease,

www.revenue.state.mn.us Use Tax for Businesses 146 Sales Tax Fact Sheet 146 What s new in 2017 We updated the layout to make this fact sheet easier to use. Minnesota Use Tax applies when you buy, lease,

SENATE, No STATE OF NEW JERSEY. 209th LEGISLATURE INTRODUCED MAY 14, 2001

SENATE, No. 0 STATE OF NEW JERSEY 0th LEGISLATURE INTRODUCED MAY, 00 Sponsored by: Senator JOSEPH A. PALAIA District (Monmouth) SYNOPSIS Raises threshold for public advertisement of contracts under "County

SENATE, No. 0 STATE OF NEW JERSEY 0th LEGISLATURE INTRODUCED MAY, 00 Sponsored by: Senator JOSEPH A. PALAIA District (Monmouth) SYNOPSIS Raises threshold for public advertisement of contracts under "County

The taxpayer must not have misstated or omitted material facts involved in the transaction;

Letter rulings are binding on the Department only with respect to the individual taxpayer being addressed in the ruling. This ruling is based on the particular facts and circumstances presented, and is

Letter rulings are binding on the Department only with respect to the individual taxpayer being addressed in the ruling. This ruling is based on the particular facts and circumstances presented, and is

Tax Treatment of Digital Goods and Services: Overview and Cross-State Comparison

Tax Treatment of Digital Goods and Services: Overview and Cross-State Comparison Arizona State Legislature Ad Hoc Joint Committee on the Tax Treatment of Digital Goods and Services July 31, 2017 Taxation

Tax Treatment of Digital Goods and Services: Overview and Cross-State Comparison Arizona State Legislature Ad Hoc Joint Committee on the Tax Treatment of Digital Goods and Services July 31, 2017 Taxation

Procurement Card Training

Procurement Card Training University of Connecticut Procurement Services Revised April 19, 2017 TOPICS Section 1: Responsibilities Understand the responsibilities of the cardholder, record manager, and

Procurement Card Training University of Connecticut Procurement Services Revised April 19, 2017 TOPICS Section 1: Responsibilities Understand the responsibilities of the cardholder, record manager, and

Arizona State and Local Sales Taxes

Arizona State and Local Sales Taxes Arizona House Ways and Means Committee Kevin McCarthy Total State and Local Taxes in Arizona FY 2010 Sales $7,364,083,841 Property $7,043,999,906 Income $2,836,408,014

Arizona State and Local Sales Taxes Arizona House Ways and Means Committee Kevin McCarthy Total State and Local Taxes in Arizona FY 2010 Sales $7,364,083,841 Property $7,043,999,906 Income $2,836,408,014

Sharing may be caring, but is it also taxable?

Sharing may be caring, but is it also taxable? State Taxation of the Sharing Economy 23 rd Annual Paul J. Hartman State and Local Tax Forum Vanderbilt University Law School October 25-27, 2016 Agenda I.

Sharing may be caring, but is it also taxable? State Taxation of the Sharing Economy 23 rd Annual Paul J. Hartman State and Local Tax Forum Vanderbilt University Law School October 25-27, 2016 Agenda I.

CAMP PAYING: INNOVATIVE SOLUTIONS

CAMP IPPS 2016 CAMP PAYING: INNOVATIVE SOLUTIONS Spelunking in the Cave of Tax Topics Presented by Heather Vinograd PC West: Eleanor Roosevelt College Room 2:30 3:15 TAX TOPICS Non-payroll Payments SALES

CAMP IPPS 2016 CAMP PAYING: INNOVATIVE SOLUTIONS Spelunking in the Cave of Tax Topics Presented by Heather Vinograd PC West: Eleanor Roosevelt College Room 2:30 3:15 TAX TOPICS Non-payroll Payments SALES

STREAMLINED SALES TAX GOVERNING BOARD, INC.

STREAMLINED SALES TAX GOVERNING BOARD, INC. RULES AND PROCEDURES Approved October 1, 2005 (Amended January 13, 2006, April 18, 2006, August 30, 2006, December 14, 2006, March 17, 2007, June 23, 2007, and

STREAMLINED SALES TAX GOVERNING BOARD, INC. RULES AND PROCEDURES Approved October 1, 2005 (Amended January 13, 2006, April 18, 2006, August 30, 2006, December 14, 2006, March 17, 2007, June 23, 2007, and

Unallowable Cost Policy Revision Date: 8/18/17

Reason for Policy The Office of Management and Budget (OMB) Uniform Guidance prohibits the University from charging federally funded agreements or requesting federal reimbursement for the following costs

Reason for Policy The Office of Management and Budget (OMB) Uniform Guidance prohibits the University from charging federally funded agreements or requesting federal reimbursement for the following costs

QUESTION: IS THE SALE OF THE SERVICES (BOTH, SOFTWARE AND CLOUD-COMPUTING) SOLD BY [THE TAXPAYER] TO ITS CLIENTS SUBJECT TO SALES TAX?

![QUESTION: IS THE SALE OF THE SERVICES (BOTH, SOFTWARE AND CLOUD-COMPUTING) SOLD BY [THE TAXPAYER] TO ITS CLIENTS SUBJECT TO SALES TAX?](/thumbs/73/68253707.jpg "QUESTION: IS THE SALE OF THE SERVICES (BOTH, SOFTWARE AND CLOUD-COMPUTING) SOLD BY [THE TAXPAYER] TO ITS CLIENTS SUBJECT TO SALES TAX?") Executive Director Leon M. Biegalski QUESTION: IS THE SALE OF THE SERVICES (BOTH, SOFTWARE AND CLOUD-COMPUTING) SOLD BY [THE TAXPAYER] TO ITS CLIENTS SUBJECT TO SALES TAX? ANSWER BASED ON THE FACTS BELOW:

Executive Director Leon M. Biegalski QUESTION: IS THE SALE OF THE SERVICES (BOTH, SOFTWARE AND CLOUD-COMPUTING) SOLD BY [THE TAXPAYER] TO ITS CLIENTS SUBJECT TO SALES TAX? ANSWER BASED ON THE FACTS BELOW:

Sales Tax 101 For The Small Business Owner

Sales Tax 101 For The Small Business Owner Presented by Brian Mackin Sales Manager Avalara About the Presenter Brian Mackin Small business owner for over 30 years Joined Avalara 5 years ago as a project

Sales Tax 101 For The Small Business Owner Presented by Brian Mackin Sales Manager Avalara About the Presenter Brian Mackin Small business owner for over 30 years Joined Avalara 5 years ago as a project

SALES AND USE TAX TECHNICAL BULLETINS SECTION 12 SECTION 12 - HOSPITALS, SANITARIUMS, NURSING HOMES, AND REST HOMES

SECTION 12 - HOSPITALS, SANITARIUMS, NURSING HOMES, AND REST HOMES 12-1 SALES TO AND BY HOSPITALS, SANITARIUMS, NURSING HOMES, AND REST HOMES A. Purchases of Tangible Personal Property Hospitals, sanitariums,

SECTION 12 - HOSPITALS, SANITARIUMS, NURSING HOMES, AND REST HOMES 12-1 SALES TO AND BY HOSPITALS, SANITARIUMS, NURSING HOMES, AND REST HOMES A. Purchases of Tangible Personal Property Hospitals, sanitariums,

ruling ( TIR ) on certain transaction processing through the

on certain transaction processing through the") S TATE OF ARIZONA Department of Revenuee TAXPAYER INFORMATION RULING LR16-011 Douglas A. Ducey D Governor David Briant Directorr Thank you for your letter dated June 1, 2016, requesting a taxpayer information

S TATE OF ARIZONA Department of Revenuee TAXPAYER INFORMATION RULING LR16-011 Douglas A. Ducey D Governor David Briant Directorr Thank you for your letter dated June 1, 2016, requesting a taxpayer information

State Tax Return. Out With The Old And In With The New: Ohio Abandons Its Corporate Franchise Tax And Enacts A Commercial Activities Tax

June 2005 Volume 12 Number 6 State Tax Return Out With The Old And In With The New: Ohio Abandons Its Corporate Franchise Tax And Enacts A Commercial Activities Tax Maryann B. Gall Jason R. Grove Columbus

June 2005 Volume 12 Number 6 State Tax Return Out With The Old And In With The New: Ohio Abandons Its Corporate Franchise Tax And Enacts A Commercial Activities Tax Maryann B. Gall Jason R. Grove Columbus

UNIFORM SALES & USE TAX EXEMPTION/RESALE CERTIFICATE MULTIJURISDICTION

UNIFORM SALES & USE TAX EXEMPTION/RESALE CERTIFICATE MULTIJURISDICTION The below-listed states have indicated that this certificate is acceptable as a resale/exemption certificate for sales and use tax,

UNIFORM SALES & USE TAX EXEMPTION/RESALE CERTIFICATE MULTIJURISDICTION The below-listed states have indicated that this certificate is acceptable as a resale/exemption certificate for sales and use tax,

Administrative Assistant and Athletic Assistant Training. February 10, 2017

Administrative Assistant and Athletic Assistant Training February 10, 2017 Welcome and Introductions Who s Who? Topics for today: Uniform System of Financial Records (USFR) Questionnaire Fees and Waivers

Administrative Assistant and Athletic Assistant Training February 10, 2017 Welcome and Introductions Who s Who? Topics for today: Uniform System of Financial Records (USFR) Questionnaire Fees and Waivers

You have requested a legal opinion on behalf of dated September 14, 2018 states:

STATE OF ARKANSAS REVENUE LEGAL COUNSEL Department of Finance Post Office Box 1272, Room 2380 Little Rock, Arkansas 72203-1272 and Administration Phone: (501) 682-7030 Fax: (501) 682-7599 http://www.arkansas.gov/dfa

STATE OF ARKANSAS REVENUE LEGAL COUNSEL Department of Finance Post Office Box 1272, Room 2380 Little Rock, Arkansas 72203-1272 and Administration Phone: (501) 682-7030 Fax: (501) 682-7599 http://www.arkansas.gov/dfa

UNIFORM SALES & USE TAX CERTIFICATE MULTIJURISDICTION

Please fax to 336-719-8114 or email to buyers@renfro.com UNIFORM SALES & USE TAX CERTIFICATE MULTIJURISDICTION The below-listed states have indicated that this form of certificate is acceptable, subject

Please fax to 336-719-8114 or email to buyers@renfro.com UNIFORM SALES & USE TAX CERTIFICATE MULTIJURISDICTION The below-listed states have indicated that this form of certificate is acceptable, subject

PURCHASING CARD USER S GUIDE

PURCHASING CARD USER S GUIDE 1. OVERVIEW OF THE PURCHASING CARD (P-Card) PROGRAM 1.1 Purpose This program is designed to dramatically improve efficiency in purchasing low dollar goods and services for

PURCHASING CARD USER S GUIDE 1. OVERVIEW OF THE PURCHASING CARD (P-Card) PROGRAM 1.1 Purpose This program is designed to dramatically improve efficiency in purchasing low dollar goods and services for

Fiscal Year End Quick Guide. Financial Services

Fiscal Year End Quick Guide http://finance.wfu.edu Table of Contents Importance of Fiscal Year End & Accrual Accounting Process.. 1 Payroll, SFS, and Accounting & Treasury. 5 Procurement Services. 7 Accounts

Fiscal Year End Quick Guide http://finance.wfu.edu Table of Contents Importance of Fiscal Year End & Accrual Accounting Process.. 1 Payroll, SFS, and Accounting & Treasury. 5 Procurement Services. 7 Accounts

Policies and Procedures Date: June 28, 2012

No. 4304 Rev.: 0 Policies and Procedures Date: June 28, 2012 Subject: Payment for Goods and Services 1. Purpose... 1 2. Policy... 2 2.1. General Guidelines... 2 2.2. Source of Funding... 2 2.3. Payment

No. 4304 Rev.: 0 Policies and Procedures Date: June 28, 2012 Subject: Payment for Goods and Services 1. Purpose... 1 2. Policy... 2 2.1. General Guidelines... 2 2.2. Source of Funding... 2 2.3. Payment

Connecticut. Connecticut Will Implement App and Cookie Nexus. November 2017

November 2017 Connecticut Connecticut Will Implement App and Cookie Nexus Commissioner Kevin B. Sullivan stated that the Connecticut Department of Revenue Services will issue revised guidance early in

November 2017 Connecticut Connecticut Will Implement App and Cookie Nexus Commissioner Kevin B. Sullivan stated that the Connecticut Department of Revenue Services will issue revised guidance early in

1/25/2018. Disclaimer. Course Objectives. Basic Sales and Use Tax

Basic Sales and Use Tax Minnesota Business Tax Education February 2018 Disclaimer This presentation is for educational purposes only. It is meant to accompany an oral presentation and not to be used as

Basic Sales and Use Tax Minnesota Business Tax Education February 2018 Disclaimer This presentation is for educational purposes only. It is meant to accompany an oral presentation and not to be used as

Department of Finance Post Office Box 1272, Room and Administration Phone: (501) REVENUE LEGAL COUNSEL.

REVENUE LEGAL COUNSEL.") STATE OF ARKANSAS REVENUE LEGAL COUNSEL Department of Finance Post Office Box 1272, Room 2380 Little Rock, Arkansas 72203-1272 and Administration Phone: (501) 682-7030 Fax: (501) 682-7599 http://www.arkansas.gov/dfa

STATE OF ARKANSAS REVENUE LEGAL COUNSEL Department of Finance Post Office Box 1272, Room 2380 Little Rock, Arkansas 72203-1272 and Administration Phone: (501) 682-7030 Fax: (501) 682-7599 http://www.arkansas.gov/dfa

OBJECT CODE GUIDELINES. Revised: 12/3/2013

OBJECT CODE GUIDELINES Revised: 12/3/2013 Purpose: The purpose of this document is to provide general guidance to users on appropriate object code use for the procurement of goods or services. These guidelines

OBJECT CODE GUIDELINES Revised: 12/3/2013 Purpose: The purpose of this document is to provide general guidance to users on appropriate object code use for the procurement of goods or services. These guidelines

SALES TAX INFORMATION GUIDE. Town of Snowmass Village P.O. Box 5010 Snowmass Village, CO (970)

") SALES TA INFORMATION GUIDE Town of Snowmass Village P.O. Box 5010 Snowmass Village, CO 81615 www.tosv.com (970) 923-3796 Table of Contents *You will be taken directly to any section in this document by

SALES TA INFORMATION GUIDE Town of Snowmass Village P.O. Box 5010 Snowmass Village, CO 81615 www.tosv.com (970) 923-3796 Table of Contents *You will be taken directly to any section in this document by

October 25, requests a legal opinion on how each of the main practices performed within the company fits within the established rules.

STATE OF ARKANSAS REVENUE LEGAL COUNSEL Department of Finance Post Office Box 1272, Room 2380 Little Rock, Arkansas 72203-1272 and Administration Phone: (501) 682-7030 Fax: (501) 682-7599 http://www.arkansas.gov/dfa

STATE OF ARKANSAS REVENUE LEGAL COUNSEL Department of Finance Post Office Box 1272, Room 2380 Little Rock, Arkansas 72203-1272 and Administration Phone: (501) 682-7030 Fax: (501) 682-7599 http://www.arkansas.gov/dfa

Sparta Area School District Purchasing Card Program and Employee Use Agreement

All employees responsible for the use or custodial responsibilities of the PCard must read, understand, and sign this agreement before a card may be checked out to them. Introduction and Purpose A Purchasing

All employees responsible for the use or custodial responsibilities of the PCard must read, understand, and sign this agreement before a card may be checked out to them. Introduction and Purpose A Purchasing

Dear New Business Owner,

Dear New Business Owner, The City of Beckley would like to take this opportunity to welcome you! The city believes that all business is important not only to our city but to the overall economy. I would

Dear New Business Owner, The City of Beckley would like to take this opportunity to welcome you! The city believes that all business is important not only to our city but to the overall economy. I would

How to Avoid E-Commerce Tax Pitfalls

How to Avoid E-Commerce Tax Pitfalls Featuring: Shane Ratigan, Avalara Inc. Eric Smith, Modern Distribution Management Sponsored by: July 27, 2017 Avalara helps make sales tax compliance simple and automatic

How to Avoid E-Commerce Tax Pitfalls Featuring: Shane Ratigan, Avalara Inc. Eric Smith, Modern Distribution Management Sponsored by: July 27, 2017 Avalara helps make sales tax compliance simple and automatic

Table of Contents. A. Income Tax Legislation B. Transaction Privilege ( Sales ) and Use Tax Legislation C. Property Tax Legislation...

and Use Tax Legislation C. Property Tax Legislation...") Important information about this Summary This document briefly summarizes recent substantive changes to Arizona s tax laws. The bills addressed herein were approved by both houses of Arizona s Legislature

Important information about this Summary This document briefly summarizes recent substantive changes to Arizona s tax laws. The bills addressed herein were approved by both houses of Arizona s Legislature

UNIFORM SALES & USE TAX EXEMPTION/RESALE CERTIFICATE MULTIJURISDICTION

UNIFORM SALES & USE TAX EXEMPTION/RESALE CERTIFICATE MULTIJURISDICTION The below-listed states have indicated that this certificate is acceptable as a resale/exemption certificate for sales and use tax,

UNIFORM SALES & USE TAX EXEMPTION/RESALE CERTIFICATE MULTIJURISDICTION The below-listed states have indicated that this certificate is acceptable as a resale/exemption certificate for sales and use tax,

Reseller Application

Reseller Application Legal Name: Trade Name: State of Incorporation: (if applicable) Federal Employer I.D.#: (if applicable) Address: City: State: County: Zip Code: Phone No.: Fax No.: Company Email Address:

Reseller Application Legal Name: Trade Name: State of Incorporation: (if applicable) Federal Employer I.D.#: (if applicable) Address: City: State: County: Zip Code: Phone No.: Fax No.: Company Email Address:

Kirkwood Accounting Colleague/Datatel

Kirkwood Accounting Colleague/Datatel The GL (General Ledger) Code: Fund Location Function Unit Object Fund Code: 11 Unrestricted General Fund 13 Auxiliary Fund 17 Unexpended Plant Fund 22 Restricted General

Kirkwood Accounting Colleague/Datatel The GL (General Ledger) Code: Fund Location Function Unit Object Fund Code: 11 Unrestricted General Fund 13 Auxiliary Fund 17 Unexpended Plant Fund 22 Restricted General

UC MERCED PROCUREMENT CARD APPLICATION

UC MERCED PROCUREMENT CARD APPLICATION Return completed and signed application to: PCard Administrator, UC Merced, 1715 Canal Street, Merced, CA 95340 Tel: 209-228-4669 Fax: 209-228-2925 Email: pcard@ucmerced.edu

UC MERCED PROCUREMENT CARD APPLICATION Return completed and signed application to: PCard Administrator, UC Merced, 1715 Canal Street, Merced, CA 95340 Tel: 209-228-4669 Fax: 209-228-2925 Email: pcard@ucmerced.edu

2013 Tax Law Changes Overview: Sales and Use Tax

2013 Tax Law Changes Overview: Sales and Use Tax Tax Type Statute Brief Description Effective Date 116J.3738, Subd. 1 : Provides a definition and method of certification for businesses in Greater Minnesota

2013 Tax Law Changes Overview: Sales and Use Tax Tax Type Statute Brief Description Effective Date 116J.3738, Subd. 1 : Provides a definition and method of certification for businesses in Greater Minnesota

PimaCountyCommunityCollegeDistrict Board of Governors 4905C East Broadway/Tucson, Arizona INFORMATION REPORT

PimaCountyCommunityCollegeDistrict Board of Governors 4905C East Broadway/Tucson, Arizona 85709-1010 INFORMATION REPORT Meeting Date: 9/14/16 Item Number: 2.1 Item Title Financial Report July 2016 Financial

PimaCountyCommunityCollegeDistrict Board of Governors 4905C East Broadway/Tucson, Arizona 85709-1010 INFORMATION REPORT Meeting Date: 9/14/16 Item Number: 2.1 Item Title Financial Report July 2016 Financial

Tax Implications and Best Practices for Conducting Business in the Cloud. Subrina L. Wood, CPA Senior Director

Tax Implications and Best Practices for Conducting Business in the Cloud Subrina L. Wood, CPA Senior Director Welcome! SUBRINA L. WOOD, CPA Senior Director Subrina has been in public accounting for over

Tax Implications and Best Practices for Conducting Business in the Cloud Subrina L. Wood, CPA Senior Director Welcome! SUBRINA L. WOOD, CPA Senior Director Subrina has been in public accounting for over

Florida. Sales Tax Tales:

Sales Tax Tales: Objectives Registration and Account Maintenance Sales Tax Transactions Use Tax Tax Rates How to File and Pay Fact or Fiction New businesses must register at their nearest service center.

Sales Tax Tales: Objectives Registration and Account Maintenance Sales Tax Transactions Use Tax Tax Rates How to File and Pay Fact or Fiction New businesses must register at their nearest service center.

Sales/Use Tax Discussion

Sales/Use Tax Discussion Spring 2013 Last Updated 2/28/2013 Clemson University is NOT tax exempt You are responsible in determining tax applicability. Some specific items/commodities are tax exempt. View

Sales/Use Tax Discussion Spring 2013 Last Updated 2/28/2013 Clemson University is NOT tax exempt You are responsible in determining tax applicability. Some specific items/commodities are tax exempt. View

Selected Consumer Taxes in the City of Chicago

Selected Consumer Taxes in the City of Chicago A Civic Federation Issue Brief This brief provides a compilation of selected consumer taxes, including rates and descriptions, in place in the City of Chicago

Selected Consumer Taxes in the City of Chicago A Civic Federation Issue Brief This brief provides a compilation of selected consumer taxes, including rates and descriptions, in place in the City of Chicago

PURCHASING CARD GUIDE

Southern Utah University PURCHASING CARD GUIDE The Southern Utah University Purchasing Card is a campus owned credit card issued to an employee to assist in their daily purchasing activities. The Purchasing

Southern Utah University PURCHASING CARD GUIDE The Southern Utah University Purchasing Card is a campus owned credit card issued to an employee to assist in their daily purchasing activities. The Purchasing

Purchaser's Obligations to Pay Sales and Use Taxes Directly to the Tax Department Questions and Answers

New York State Department of Taxation and Finance Publication 774 (1/10) Purchaser's Obligations to Pay Sales and Use Taxes Directly to the Tax Department Questions and Answers About this publication

New York State Department of Taxation and Finance Publication 774 (1/10) Purchaser's Obligations to Pay Sales and Use Taxes Directly to the Tax Department Questions and Answers About this publication

FISCAL POLICY MANUAL SUMMER 2018

FISCAL POLICY MANUAL SUMMER 2018 Children s Services Council of St. Lucie County 546 NW University Boulevard, Suite 201 Port St. Lucie, Florida 34986 772.408.1100 (PHONE) 772.408.1111 (FAX) Web site: www.cscslc.org

FISCAL POLICY MANUAL SUMMER 2018 Children s Services Council of St. Lucie County 546 NW University Boulevard, Suite 201 Port St. Lucie, Florida 34986 772.408.1100 (PHONE) 772.408.1111 (FAX) Web site: www.cscslc.org

PURCHASING CARD MANUAL

MOREHEAD STATE UNIVERSITY PURCHASING CARD MANUAL OFFICE OF PROCUREMENT SERVICES INTRODUCTION Welcome to the Morehead State University Purchasing Card (Pcard) Program Cardholder Manual. This program has

MOREHEAD STATE UNIVERSITY PURCHASING CARD MANUAL OFFICE OF PROCUREMENT SERVICES INTRODUCTION Welcome to the Morehead State University Purchasing Card (Pcard) Program Cardholder Manual. This program has

DECISION OF MUNICIPAL TAX HEARING OFFICER

DECISION OF MUNICIPAL TAX HEARING OFFICER Decision Date: August 13, 2004 Decision: MTHO #151 Tax Collector: Cities of Peoria, Tempe, and Scottsdale Hearing Date: April 5, 2004 Introduction DISCUSSION On

DECISION OF MUNICIPAL TAX HEARING OFFICER Decision Date: August 13, 2004 Decision: MTHO #151 Tax Collector: Cities of Peoria, Tempe, and Scottsdale Hearing Date: April 5, 2004 Introduction DISCUSSION On

Introducing the Purchasing Card Program

Introducing the Purchasing Card (P-card) Program at Boston College Uses Becoming a Cardholder How it Works Restricted Commodities Sponsored Funding Restrictions Reconciliation and Documentation Transaction

Introducing the Purchasing Card (P-card) Program at Boston College Uses Becoming a Cardholder How it Works Restricted Commodities Sponsored Funding Restrictions Reconciliation and Documentation Transaction

Faxed & ed responses are not acceptable - Return bid form in a sealed envelope with the bid number noted on the outside.

4905 East Broadway, D-232 Bid No. B15/9903 Tucson, AZ 85709-1420 Requisition No. R0054391 Telephone (520) 206-4759 Buyer Philip Quintanilla Date 4/22/15 Page 1 Of 4 Bid must be in this office on or before:

4905 East Broadway, D-232 Bid No. B15/9903 Tucson, AZ 85709-1420 Requisition No. R0054391 Telephone (520) 206-4759 Buyer Philip Quintanilla Date 4/22/15 Page 1 Of 4 Bid must be in this office on or before:

WHAT IS TAX BASE? DEFINING THE SALE.

WHAT IS TAX BASE? DEFINING THE SALE. IPT SALES TAX SYMPOSIUM 2013 Presented by: B.J. Pritchett, CMI Pritchett Sales & Use Tax Consulting Susan Haffield, CPA PriceWaterhouseCoopers, LLP TAX BASE Sales and

WHAT IS TAX BASE? DEFINING THE SALE. IPT SALES TAX SYMPOSIUM 2013 Presented by: B.J. Pritchett, CMI Pritchett Sales & Use Tax Consulting Susan Haffield, CPA PriceWaterhouseCoopers, LLP TAX BASE Sales and

2017 Year-End State and Local Tax Update Jason Sneeringer, CPA Tax Manager

2017 Year-End State and Local Tax Update Jason Sneeringer, CPA Tax Manager Agenda Current state and local tax (SALT) atmosphere Nexus Sales & use tax Unclaimed property Property tax Income & Franchise

2017 Year-End State and Local Tax Update Jason Sneeringer, CPA Tax Manager Agenda Current state and local tax (SALT) atmosphere Nexus Sales & use tax Unclaimed property Property tax Income & Franchise

Part I Handset Protection Programs Overview of Insurance and Service Contract Regulation

Part I Handset Protection Programs Overview of Insurance and Service Contract Regulation Gerald Gary Mize Chair, Handset Protection and Insurance Practice Gerald.Mize@alston.com Direct: (404) 881-7579

Part I Handset Protection Programs Overview of Insurance and Service Contract Regulation Gerald Gary Mize Chair, Handset Protection and Insurance Practice Gerald.Mize@alston.com Direct: (404) 881-7579

Lansing Community College Internal Expense Account Dictionary

Lansing Community College Internal Expense Account Dictionary Account Account Title Usage Definition 71000 Bond Administrative Fees 71001 Bond Interest Payments 71002 Bond Principal Payments Expenses for

Lansing Community College Internal Expense Account Dictionary Account Account Title Usage Definition 71000 Bond Administrative Fees 71001 Bond Interest Payments 71002 Bond Principal Payments Expenses for

CARBON COUNTY MASTERCARD PURCHASE CARD PROGRAM

CARBON COUNTY MASTERCARD PURCHASE CARD PROGRAM Procedures Manual for Carbon County Program Card Administration Name: Carbon County Clerk (307) 328-2668 Address: 415 West Pine Street, PO Box 6, Rawlins,

CARBON COUNTY MASTERCARD PURCHASE CARD PROGRAM Procedures Manual for Carbon County Program Card Administration Name: Carbon County Clerk (307) 328-2668 Address: 415 West Pine Street, PO Box 6, Rawlins,

South Carolina Department of Revenue

SMALL BUSINESS TAX WORKSHOP South Carolina Department of Revenue Topics To Be Covered Today Checklist for New Businesses in South Carolina Purchasing the Assets of a Business The Retail License Sales &

SMALL BUSINESS TAX WORKSHOP South Carolina Department of Revenue Topics To Be Covered Today Checklist for New Businesses in South Carolina Purchasing the Assets of a Business The Retail License Sales &

Sales/Use Tax Updates & Developments - Texas & Louisiana - Streamlined Sales Tax - Affiliate Nexus. IPT - San Antonio March 28, 2012

Sales/Use Tax Updates & Developments - Texas & Louisiana - Streamlined Sales Tax - Affiliate Nexus IPT - San Antonio March 28, 2012 Scott Steinbring David Somerville Tracy Watts Overview Updates & Developments

Sales/Use Tax Updates & Developments - Texas & Louisiana - Streamlined Sales Tax - Affiliate Nexus IPT - San Antonio March 28, 2012 Scott Steinbring David Somerville Tracy Watts Overview Updates & Developments

Michael Silver & Company CPAs Comprehensive Automobile Dealer Sales Tax Checklist

5750 Old Orchard Road Suite 200 Skokie, IL 60077 Main: 847-982-0333 Fax: 847-982-0219 www.msco.net Michael Silver & Company CPAs Comprehensive Automobile Dealer Sales Tax Checklist Sales Taxable Trade

5750 Old Orchard Road Suite 200 Skokie, IL 60077 Main: 847-982-0333 Fax: 847-982-0219 www.msco.net Michael Silver & Company CPAs Comprehensive Automobile Dealer Sales Tax Checklist Sales Taxable Trade

Expenditure Objects and Subobjects

70.09.1 ENTER CODING Departments are responsible for including object and subobject with the account coding on expenditure documents, e.g., IRI, Departmental Requisition, Departmental Purchase Order, State

70.09.1 ENTER CODING Departments are responsible for including object and subobject with the account coding on expenditure documents, e.g., IRI, Departmental Requisition, Departmental Purchase Order, State

UNIVERSITY OF OREGON PURCHASING AND CONTRACTING PROCEDURES

UNIVERSITY OF OREGON PURCHASING AND CONTRACTING PROCEDURES Purchasing and Contracting Services (PCS) facilitates the procurement of goods and services necessary to support the University s core business

UNIVERSITY OF OREGON PURCHASING AND CONTRACTING PROCEDURES Purchasing and Contracting Services (PCS) facilitates the procurement of goods and services necessary to support the University s core business

HYDRAULIC INSTITUTE REPORT 2015 ANNUAL REPORT OF OPERATING RATIOS

COMPANY NAME: #A02 HYDRAULIC INSTITUTE REPORT REPORT RATIOS FOR PUMP DIVISION ONLY IN COLUMN I. IF THE ACCOUNTING SYSTEM OF THAT DIVISION INCLUDES ALLIED OPERATIONS SUCH AS A FOUNDRY, EXPENSES, SALES PROFITS,

COMPANY NAME: #A02 HYDRAULIC INSTITUTE REPORT REPORT RATIOS FOR PUMP DIVISION ONLY IN COLUMN I. IF THE ACCOUNTING SYSTEM OF THAT DIVISION INCLUDES ALLIED OPERATIONS SUCH AS A FOUNDRY, EXPENSES, SALES PROFITS,

3. How can I contact the Department of Taxation with questions about the CAT?

1. What is the Commercial Activity Tax ("CAT")? The CAT is an annual tax imposed on the privilege of doing business in Ohio, measured by taxable gross receipts from most business activities. Most receipts

1. What is the Commercial Activity Tax ("CAT")? The CAT is an annual tax imposed on the privilege of doing business in Ohio, measured by taxable gross receipts from most business activities. Most receipts

Stetson University PCARD. MasterCard Purchasing/Travel Card Program

Stetson University PCARD MasterCard Purchasing/Travel Card Program Updated July 14, 2016 TABLE OF CONTENTS Contents 1 Overview 3 General Information 4 To Obtain a Card 5 Some Built In Restrictions 6 Unacceptable/Acceptable

Stetson University PCARD MasterCard Purchasing/Travel Card Program Updated July 14, 2016 TABLE OF CONTENTS Contents 1 Overview 3 General Information 4 To Obtain a Card 5 Some Built In Restrictions 6 Unacceptable/Acceptable

MooreCo New Dealer Application

MooreCo Inc 2885 Lorraine Avenue Temple, TX 76501 P.O. Drawer D Temple, TX 76503 p: 800.749.2258 f: 866.888.7483 www.moorecoinc.com MooreCo New Dealer Application Please type or print all information using

MooreCo Inc 2885 Lorraine Avenue Temple, TX 76501 P.O. Drawer D Temple, TX 76503 p: 800.749.2258 f: 866.888.7483 www.moorecoinc.com MooreCo New Dealer Application Please type or print all information using

TITLE DEPARTMENT OF REVENUE CHAPTER 20 - DIVISION OF TAXATION Purpose Authority Application. 25.

280-RICR-20-70-25 TITLE 280 - DEPARTMENT OF REVENUE CHAPTER 20 - DIVISION OF TAXATION SUBCHAPTER 70 - SALES AND USE TAX Part 25 - Use Tax Generally 25.1 Purpose This regulation implements R.I. Gen. Laws

280-RICR-20-70-25 TITLE 280 - DEPARTMENT OF REVENUE CHAPTER 20 - DIVISION OF TAXATION SUBCHAPTER 70 - SALES AND USE TAX Part 25 - Use Tax Generally 25.1 Purpose This regulation implements R.I. Gen. Laws

Sales, storage, use tax.--it is hereby declared to be the legislative intent that every person is exercising a taxable privilege who engages

212.05 Sales, storage, use tax.--it is hereby declared to be the legislative intent that every person is exercising a taxable privilege who engages in the business of selling tangible personal property

212.05 Sales, storage, use tax.--it is hereby declared to be the legislative intent that every person is exercising a taxable privilege who engages in the business of selling tangible personal property

UNIFORM SALES & USE TAX CERTIFICATE

UNIFORM SALES & USE TAX CERTIFICATE The issuer and the recipient have the responsibility of determining the proper use of this certificate under applicable laws in each state, as these may change from

UNIFORM SALES & USE TAX CERTIFICATE The issuer and the recipient have the responsibility of determining the proper use of this certificate under applicable laws in each state, as these may change from

Overview of Southwestern States Construction Sales Tax Structure Prepared for the Construction Financial Management Association

Overview of Southwestern States Construction Sales Tax Structure Prepared for the Construction Financial Management Association Pat Derdenger, Partner Steptoe & Johnson LLP pderdenger@steptoe.com (602)

Overview of Southwestern States Construction Sales Tax Structure Prepared for the Construction Financial Management Association Pat Derdenger, Partner Steptoe & Johnson LLP pderdenger@steptoe.com (602)

9/15/2017. State and Local Tax. State and Local Taxes

State and Local Tax State and Local Taxes 1 The Wonderful World of SALT Gross Receipts Tax Income Tax Property Tax Franchise Tax Payroll Tax Sales Tax Unclaimed Property Use Tax Why It s Important! Financial

State and Local Tax State and Local Taxes 1 The Wonderful World of SALT Gross Receipts Tax Income Tax Property Tax Franchise Tax Payroll Tax Sales Tax Unclaimed Property Use Tax Why It s Important! Financial

State Tax Chart Results

State Tax Chart Results Tax Type: Sales/Use Legend: N/A - Not Applicable Software as a Service (SaaS) This chart shows whether or not the state imposes a tax on the sales of Software as a Service (SaaS).

State Tax Chart Results Tax Type: Sales/Use Legend: N/A - Not Applicable Software as a Service (SaaS) This chart shows whether or not the state imposes a tax on the sales of Software as a Service (SaaS).

Web Claim Voucher Instructions

Web Claim Voucher Instructions Logging In To login in to the Claim Voucher Web Forms open a web browser and go to the UI Home Page at http://www.uidaho.edu/ to logon to the Employee Web Login. Once logged

Web Claim Voucher Instructions Logging In To login in to the Claim Voucher Web Forms open a web browser and go to the UI Home Page at http://www.uidaho.edu/ to logon to the Employee Web Login. Once logged