U.S. Tax Benefits for Exporting

|

|

|

- Daisy Taylor

- 6 years ago

- Views:

Transcription

1 U.S. Tax Benefits for Exporting By Richard S. Lehman, Esq. TAX ATTORNEY

368-1113 Fax: (561) 368-1349 Masters in Tax Law from New York University Law School Four years of U.S. Tax Court and Internal Revenue Service experience in Washington D.")

2 Richard S. Lehman Esq. International Tax Attorney LehmanTaxLaw.com 6018 S.W. 18th Street, Suite C-1 Boca Raton, FL Tel: (561) Fax: (561) Masters in Tax Law from New York University Law School Four years of U.S. Tax Court and Internal Revenue Service experience in Washington D.C. The firm regularly works with law firms, accountants, businesses and individuals struggling to find their way through the complexities of the tax law. In short, the firm is a valuable resource to each of these audiences. With over 38 years as a tax lawyer in Florida, Lehman has built a tax law firm with a national reputation for being able to handle the toughest tax cases, structure the most sophisticated income tax and estate tax plans, and defend clients before the IRS.

3 IC-DISC A Major Tax Saving Tool

4 IC-DISC A Major Tax Saving Tool 1)Tax incentive for Americans who export product. 2)Available to manufactures, producers, wholesaler and retailer that sell export property

5 IC-DISC A Major Tax Saving Tool The U.S. Taxpayer pays 15% Tax Rate on export profits. Instead of a 35% Federal Tax Rate.

6 IC-DISC A Major Tax Saving Tool If you live in a State that has City/State Income Tax - You pay 15% tax rate NOT 50% on your export profits. Plus Taxpayer can differ export profits for many years at low interest costs.

7 Major Tax Reductions for Export Profits U.S. taxpayers that sell, lease or license export property which is manufactured, produced or grown in the United States (not more than 50% of which attributable to U.S. imports), can take advantage of strong support for their export profits in the Internal Revenue Code.

8 The United States Tax Benefits of Exporting In 2012 the business world is going to be a tough place for the American Exporter. Take advantage of the Internal Revenue Code and it s strong support for export profits.

9 Major Tax Reductions for Export Profits 1. Establish a new corporation dedicated almost exclusively to export profits; 2. a separate set of export books and records; and 3. abiding by a relatively simple set of rules that govern Domestic International Sales Corporations (now known as IC-DISC).

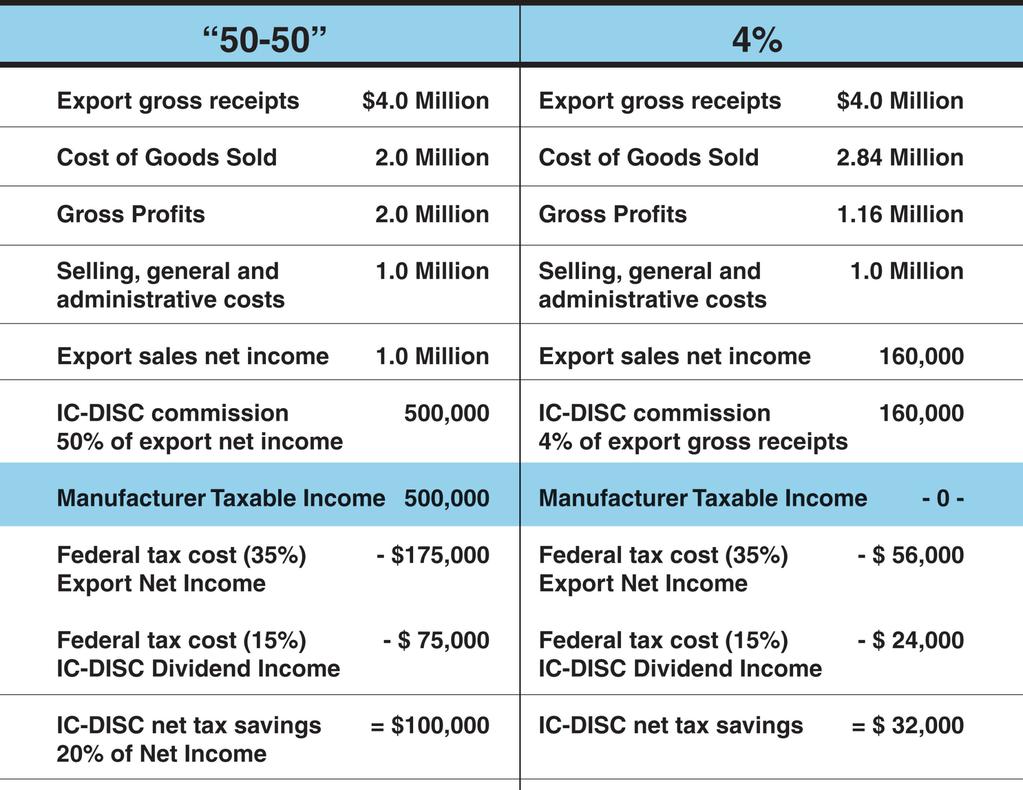

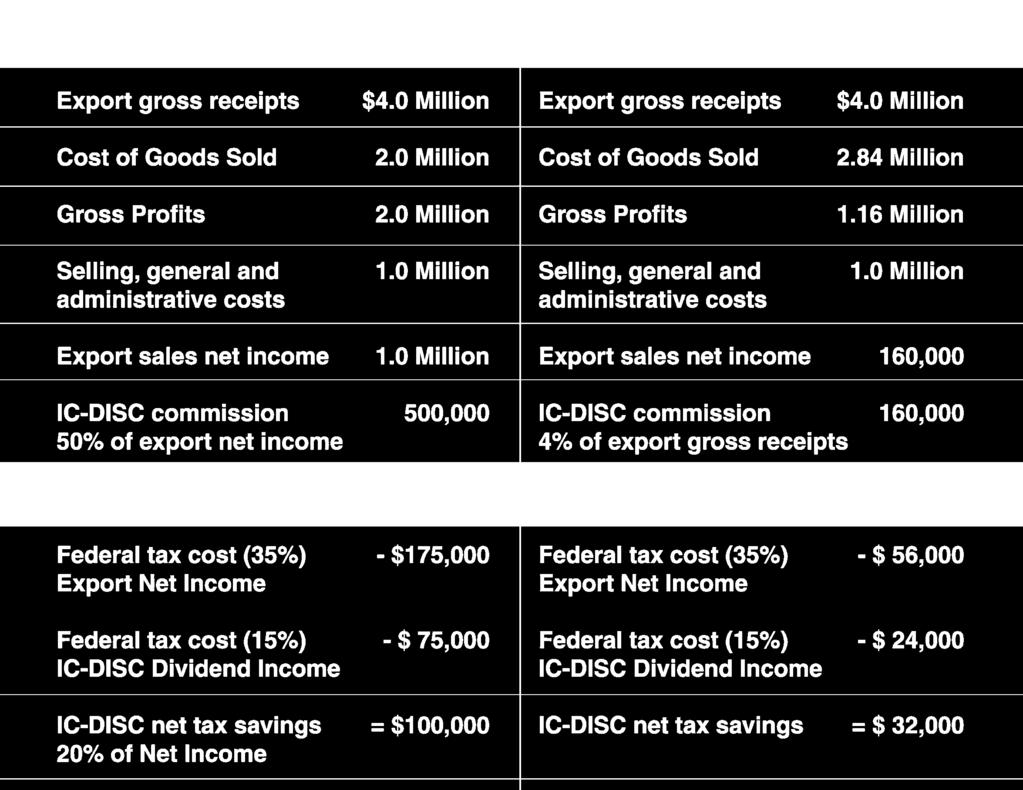

10 How does it work. Typically the U.S. taxpayer that establishes the IC-DISC will be related to the IC-DISC and even own the IC-DISC. The U.S. taxpayer agrees to pay the IC-DISC based on a Commission Agreement. A portion of the U.S. taxpayer s export profits are paid to the IC-DISC and the payment is deducted from the profits of the U.S. manufacturer, seller or licensor. The portion of the U.S. taxpayer s export profits that are paid to the IC DISC are measured under three profit scenarios. The deduction may exceed more than 50% of the U.S. Taxpayers export profits, depending upon gross income, profitability and costs.

11 IC-DISC Rules The IC-DISC must sell, lease, license or service export property Export property means property: Manufactured, produced, grown or extracted in the United States; held for sale, lease or rental, in the ordinary course of business, for use, consumption or disposition outside the United States; and Not more than 50% of the fair market value of which is attributed to articles imported into the United States.

12 IC-DISC Requirements 1. A corporation taxable as a corporation, must be formed under the laws of any State or the District of Columbia to be the IC-DISC 2. The corporation must have only one class of stock and minimum capital of $2,500. The IC-DISC shareholders may be related to the IC-DISC. 3. The IC-DISC must take a tax election to be an IC-DISC that must be filed with the Internal Revenue Service within 90 days after the beginning of the tax year of the IC-DISC. 4. The IC-DISC must maintain separate books and records. 5. The IC-DISC must have at least 95% or more of its gross receipts considered to be Qualified Receipts resulting from the DISC s export activities. 6. The IC-DISC must have at least 95% or more of its assets considered to be Qualified Export Assets.

13 The DISC Owner Typically the IC-DISC is established, by a related company that is engaged in a United States business that includes gross revenues from both domestic and international sources. The related company s principals will be the direct or indirect owners of the IC-DISC

14 The DISC Owner

15 The Tax Benefits Thus the magic of the IC-DISC is to provide both tax deferral and to apply a 15% maximum dividend tax rate to profits that would otherwise be taxable in the U.S. taxpayer s highest brackets that can range as high as 50%.

16 Tax Deferral There is a cost to take advantage of the tax deferral tax benefit available using an IC-DISC. However, in today s climate and for the foreseeable future, the cost is minimal. The IC-DISC rules provide that an interest charge must be calculated on IC-DISC distributions that are not paid as taxable dividends in the year earned.

17

18 Major Savings IC-DISC shareholders still will receive the 15% tax rate on the DISC dividends in excess of $10 Million.

19 The Commission Payments Gross Receipts Method Taxable Income Method Export promotion expenses means those expenses incurred to advance the distribution or sale of export property for use, consumption, or distributions outside of the United States but does not include income taxes. Arm s Length Method The transfer price for a sale by the related supplier to the DISC is to be determined on the basis of the sale price actually charged but subject to the rules provided by the rules of sales between related parties.

20 IC-DISC The Export Disc Corporation Computer Software, Internet Sales & Licenses

21 IC-DISC A Major Tax Saving Tool The IC-DISC has been approved as an acceptable tax planning entity for the export of American produced computer software and programs as early as 1985.

22 Computer Programs Are Usually Sold Pursuant to License or User Agreements. A computer program transaction is unlike a sale of a physical object since the value of the program copy far exceeds the value of the physical medium on which it is transferred. Often, there is no physical medium at all.

23 For purposes of determining the applicability of the DISC to computer software exports, two key analyses are often required. (1) is the software export property for DISC purposes and (2) is the software product s source of income from without the U.S.? Is the product for use, consumption or sale without the U.S.?

24 I.R.S. Guidance In 1985, the I.R.S. issued guidance that indeed certain computer software programs constituted export property for DISC purposes. In doing so the Technical Advice not only reviewed the legislative history of the DISC rules it also pointed out the distinctively different treatment that patents, inventions, models, decisions, formulas, or processes whether or not patented, copyrights, goodwill, trademarks, trade brands, franchise or other like property receive under the DISC rules, as opposed to the treatment of films, tapes, records or similar reproductions, for commercial or home use.

25 Copyright law is the basis for the Software Regulations The Regulations are based on the concept that it is possible to categorize a computer program transaction by analyzing the copyright rights transferred. The most important distinction created by the Software Regulations is the distinction between copyrighted articles and copyright rights. The Copyright Rights are not export property for DISC purposes while the Copyright Articles are export property.

26 Export Property Analysis Export property is defined to mean, in general, property that is: A. Manufactured, produced, grown or extracted in the United States by a person other than a DISC, B. Held primarily for sale, lease, or rental, in the ordinary course of trade or business, by, or to, a DISC, for direct use, consumption, or disposition outside the United States and C. Not more than 50 percent of the fair market value of which is attributable to articles imported into the United States.

27 Export Property Does Not Include patents, inventions, models, designs, formulas, or processes, whether or not patented, copyrights (other than films, tapes, records, or similar reproductions, for commercial or home use), good will, trademarks, trade brands, franchises, or other like property... Richard S. Lehman, Esq.

28 Computer software can be export property. Computer software tapes are akin to the copyrighted books, which qualify as export property. Computer programs are standardized programs that are manufactured in the United States by a person other than a DISC and then marketed outside the United States. This is not selling the source code or master recording. Those purchasing or leasing programs do not have the right to reproduce the software.

29 Copyright Rights The transfer is classified as a transfer of a copyright if, as a result of a transaction, a person acquires any one or more of the following rights: 1. the right to make copies of the computer program for purposes of distribution to the public by sale or other transfer of ownership, or by rental, lease or lending; 2. the right to prepare derivative computer programs based on the copyrighted computer program; 3. the right to make a public performance of the computer program; or 4. the right to publicly display the computer program.

30 Transfers of Computer Programs A computer program includes any media, user manuals, documentation, database or similar item if the media user manuals, documentation, database or similar item is incidental to the operation of the computer program.

31 Transfers of Computer Programs A copyrighted article is defined as a copy of a computer program from which the work can be perceived, reproduced, or otherwise communicated, either directly or with the aid of a machine or device. If a person acquires a copy of a computer program but does not acquire any of the four copyright rights, the transfer is classified as a transfer of a copyrighted article.

32 A transfer of a computer program is classified in one of the following ways. 1. A sale or exchange of the legal rights constituting a copyright (which generates income sourced according to the rules for sales of personal property); 2. A license of a copyright (which generates royalty income); 3. A sale or exchange of a copyright article produced under a copyright (which generates income sourced according to the rules for sales of personal property); 4. A lease of a copyright article produced under a copyright (which generates rental income) Additional rules allow for the classification of a transfer as partially a transfer of services or of know-how. The provision of know-how, in which the transferor retains continuing use of the know how transferred, is presumably most like a license of a copyright.

33 The Source of Income Analysis Once it is determined that a computer program is a copyright article and thus export property for DISC purposes;...then the issue is to determine whether the Software Program is being sold for use, consumption of disposition outside of the U.S. This analysis depends upon the source of income rules.

34 Income from Sales of Property Generally under the current rules, the source of income from sales of property depends to varying extents upon both the type of property and whether the property sold or leased is inventory property. Income from the lease of a copyright article must also fit this definition of non U.S. source of income. Determination of whether the transaction is a sale of inventory, a rental of property, a license or sale of intellectual property or the provision of services.

35 Income from Sales of Property Generally under the current rules, the source of income from sales of property depends to varying extents upon both the type of property and whether the property sold or leased is inventory property. Income from the lease of a copyright article must also fit this definition of non U.S. source of income. Determination of whether the transaction is a sale of inventory, a rental of property, a license or sale of intellectual property or the provision of services.

36 Income from Sales of Property The regulations focus on (i) acknowledging the special circumstances of computer programs, (ii) distinguishing between transactions in copyright rights and in copyrighted articles, and (iii) focusing on the economic substance of the transaction over the labels applied, the form and the delivery mechanism.

37 Source of Income for Sales of Copyrighted Articles The source of income generated by the sale or exchange of a copyrighted article often depends upon whether the sale took place within or without the United States. The Software Regulations provide that the place of sale is determined under the title passage rule. Richard S. Lehman, Esq.

38 Title Passage Rule There are important categories of copyrighted article transfers for DISC purposes: (i) a transfer of tangible property, such as a tangible medium in which the copyrighted article is embodied, and/or a hard copy of user manuals and documentation; (ii) (e.g., electronically transmitted copyrighted articles without any hard copy of user manuals and documentation). Either one of these can be the subject of a sale.

39 Lease and Rental Source of Income If less than all of the benefits and burdens associated with a copyrighted article have passed to the transferee, the Software Regulations treat the transaction as a lease. As a general rule, rents and royalties are sourced to the place where the leased or licensed property is located, or where the lessee or licensee uses, or is entitled to use the property.

40 Sale of Copyright Article Example 1 A U.S. corporation, (the U.S. corporation ) owns the copyright in a computer program, (the Program ). The U.S. corporation, (the U.S. Corporation ), makes the Program available, for a fee, on a World Wide Web home page on the Internet. Mr. P, a resident of Country Z, in return for payment to the U.S. Corporation, downloads the Program X (via modem) onto the hard drive of his computer. As part of the electronic communications, P signifies his assent to a license agreement. Mr. P receives the right to use the program on his own computers (for example, a laptop and a desktop). None of the copyright rights have been transferred in this transaction. P has received a copy of the Program. P has acquired solely a copyrighted article. P is properly treated as the owner of a copyrighted article. There has been a sale of a copyrighted article rather than the grant of a lease.

41 Lease of Copyright Article Example 2 The facts are the same as those in Example 1, except that the U.S. Corporation only allows Mr. P, the right to use the Program for one week. If P wishes to use the Program for a further period he must enter into a new agreement to use the program for an additional charge. P is not properly treated as the owner of a copyrighted article. There has been a lease of a copyrighted article rather than a sale.

42 Sale of Copyright Example 3 A U.S. Corporation, transfers a disk containing the Program to a Foreign Corporation (the Foreign Corporation ) and grants the Foreign Corporation an exclusive license for the remaining term of the copyright to copy and distribute an unlimited number of copies of the Program in the geographic area of the Country in which the Foreign Corporation makes public performances of the Program and publicly displays the Program. Applying the all substantial rights test, the U.S. Corporation will be treated as having sold copyright rights to the Foreign Corporation. The Foreign Corporation has acquired all of the copyright rights in the Program and has received the right to use them exclusively within the Foreign Country.

43 Lease of Copyright Rights Example 4 A U.S. corporation, transfers a disk containing the Program to a Foreign Corporation in Country X and grants the Foreign Corporation the non exclusive right to reproduce (either directly or by contracting with another person to do so) and distribute for sale to the public an unlimited number of disks at its factory in return for a payment related to the number of disks copied and sold. The term of the agreement is two years, which is less than the remaining life of the copyright. There is a lease of copyright rights since copyright right have been assigned but for a limited time period only.

44 Richard S. Lehman, Esq. TAX ATTORNEY 6018 S.W. 18th Street, Suite C-1, Boca Raton, FL Tel: Value can be lost without good professional advice.

THE IC-DISC. By Richard S. Lehman, Esq

By Richard S. Lehman, Esq The United States Tax Benefits Of Exporting THE IC-DISC The business world is going to be a tough place for the American exporter in 2012. The dollar will remain strong, keeping

By Richard S. Lehman, Esq The United States Tax Benefits Of Exporting THE IC-DISC The business world is going to be a tough place for the American exporter in 2012. The dollar will remain strong, keeping

26 CFR Ch. I ( Edition)

") 1.861 18 26 CFR Ch. I (4 1 12 Edition) erowe on DSK2VPTVN1PROD with CFR (1) Tentative Apportionment on the Basis of Sales (i) Research and experimental expense to be apportioned between statutory and residual

1.861 18 26 CFR Ch. I (4 1 12 Edition) erowe on DSK2VPTVN1PROD with CFR (1) Tentative Apportionment on the Basis of Sales (i) Research and experimental expense to be apportioned between statutory and residual

Tax Refunds from Ponzi Scheme Losses Are Extremely Valuable

Tax Refunds from Ponzi Scheme Losses Are Extremely Valuable Presented by Richard S. Lehman, Esq. www.lehmantaxlaw.com 6018 S.W. 18th Street, Suite C-1, Boca Raton, FL 33433 Tel: (561) 368-1113 Fax: (561)

Tax Refunds from Ponzi Scheme Losses Are Extremely Valuable Presented by Richard S. Lehman, Esq. www.lehmantaxlaw.com 6018 S.W. 18th Street, Suite C-1, Boca Raton, FL 33433 Tel: (561) 368-1113 Fax: (561)

INTEREST CHARGE DOMESTIC INTERNATIONAL SALES CORPORATIONS (IC-DISC) Stephen A. Lee

Stephen A. Lee") INTEREST CHARGE DOMESTIC INTERNATIONAL SALES CORPORATIONS (IC-DISC) Stephen A. Lee Lee & Desenberg, PLLC 440 Louisiana St., Ste. 2200 Houston, TX 77002 713-275-8440 March 17, 2015 Intended to encourage

INTEREST CHARGE DOMESTIC INTERNATIONAL SALES CORPORATIONS (IC-DISC) Stephen A. Lee Lee & Desenberg, PLLC 440 Louisiana St., Ste. 2200 Houston, TX 77002 713-275-8440 March 17, 2015 Intended to encourage

Reducing Taxes for Manufacturers & Related Parties

Reducing Taxes for Manufacturers & Related Parties Current & Future Savings Based On Export Sales Jonathan Glasser - BEC Partners, LLC Kimberly Rehmeyer, CPA, JD - BEC Partners, LLC Kereti Tuioti - Kereti

Reducing Taxes for Manufacturers & Related Parties Current & Future Savings Based On Export Sales Jonathan Glasser - BEC Partners, LLC Kimberly Rehmeyer, CPA, JD - BEC Partners, LLC Kereti Tuioti - Kereti

Anthony Korda, Atty, The Korda Law Firm, Naples, Fla. Richard S. Lehman, Atty, United States Taxation and Immigration Law, Boca Raton, Fla.

Presenting a live 90-minute webinar with interactive Q&A Pre-Immigration Tax and U.S. Investment Planning for High Net Worth Individuals Navigating the EB-5 Investor's Visa Program, Leveraging Tax Credits

Presenting a live 90-minute webinar with interactive Q&A Pre-Immigration Tax and U.S. Investment Planning for High Net Worth Individuals Navigating the EB-5 Investor's Visa Program, Leveraging Tax Credits

Taxation of International Computer Software Transactions under Regulation

Hastings Communications and Entertainment Law Journal Volume 22 Number 2 Article 9 1-1-1999 Taxation of International Computer Software Transactions under Regulation 1.861-18 Jonathan Purcell Follow this

Hastings Communications and Entertainment Law Journal Volume 22 Number 2 Article 9 1-1-1999 Taxation of International Computer Software Transactions under Regulation 1.861-18 Jonathan Purcell Follow this

2600 N. Military Trail, Suite 206, Boca Raton, Florida Tel

2600 N. Military Trail, Suite 206, Boca Raton, Florida 33431 Tel. 1-561-368-1113 www.lehmantaxlaw.com U.S. Taxation of Foreign Corporations And Nonresident Aliens General Rules Tax Planning Before Immigrating

2600 N. Military Trail, Suite 206, Boca Raton, Florida 33431 Tel. 1-561-368-1113 www.lehmantaxlaw.com U.S. Taxation of Foreign Corporations And Nonresident Aliens General Rules Tax Planning Before Immigrating

Reducing Taxes for Distributors

Reducing Taxes for Distributors Current & Future Savings Based On Export Sales Jonathan Glasser - BEC Partners, LLC Kimberly Rehmeyer, CPA, JD - BEC Partners, LLC Kereti Tuioti - Kereti Tuioti Partners

Reducing Taxes for Distributors Current & Future Savings Based On Export Sales Jonathan Glasser - BEC Partners, LLC Kimberly Rehmeyer, CPA, JD - BEC Partners, LLC Kereti Tuioti - Kereti Tuioti Partners

Reg. Section (f)(4)(i) Amortization of goodwill and certain other intangibles.

(4)(i) Amortization of goodwill and certain other intangibles.") Reg. Section 1.197-2(f)(4)(i) Amortization of goodwill and certain other intangibles. CLICK HERE to return to the home page (a) Overview -- (1) In general. Section 197 [26 USCS 197] allows an amortization

Reg. Section 1.197-2(f)(4)(i) Amortization of goodwill and certain other intangibles. CLICK HERE to return to the home page (a) Overview -- (1) In general. Section 197 [26 USCS 197] allows an amortization

TEI School - Houston. Intangible Property ( IP ) - Basics in IP Planning. May 3, 2017

- Basics in IP Planning. May 3, 2017") TEI School - Houston Intangible Property ( IP ) - Basics in IP Planning May 3, 2017 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global

TEI School - Houston Intangible Property ( IP ) - Basics in IP Planning May 3, 2017 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global

CFC income from software leases determined to be foreign personal holding company income

18 July 2013 CFC income from software leases determined to be foreign personal holding company income Executive summary On 15 July 2013, the Internal Revenue Service (the Service) released Field Attorney

18 July 2013 CFC income from software leases determined to be foreign personal holding company income Executive summary On 15 July 2013, the Internal Revenue Service (the Service) released Field Attorney

Internal Revenue Code Section 197 Amortization of goodwill and certain other intangibles

Internal Revenue Code Section 197 Amortization of goodwill and certain other intangibles CLICK HERE to return to the home page (a) General rule. A taxpayer shall be entitled to an amortization deduction

Internal Revenue Code Section 197 Amortization of goodwill and certain other intangibles CLICK HERE to return to the home page (a) General rule. A taxpayer shall be entitled to an amortization deduction

Chapter 12 - Exploiting Intangibles Outside U.S.

Chapter 12 - Exploiting Intangibles Outside U.S. Choices for structuring these arrangements: 1) Independent licensing for royalties. 2) Transfer of intangible property rights in an independent capital

Chapter 12 - Exploiting Intangibles Outside U.S. Choices for structuring these arrangements: 1) Independent licensing for royalties. 2) Transfer of intangible property rights in an independent capital

IBM Agreement for Services Acquired from an IBM Business Partner

IBM Agreement for Services Acquired from an IBM Business Partner This IBM Agreement for Services Acquired from an IBM Business Partner ( Agreement ) governs IBM s delivery of certain IBM Services and Product

IBM Agreement for Services Acquired from an IBM Business Partner This IBM Agreement for Services Acquired from an IBM Business Partner ( Agreement ) governs IBM s delivery of certain IBM Services and Product

Pre-Immigration Tax Planning

Pre-Immigration Tax Planning Safeguarding The Immigrant s Financial Interests Prior to Residency By Richard S. Lehman & Associates Attorneys at Law Pre-Immigration Tax Planning Safeguarding The Immigrant

Pre-Immigration Tax Planning Safeguarding The Immigrant s Financial Interests Prior to Residency By Richard S. Lehman & Associates Attorneys at Law Pre-Immigration Tax Planning Safeguarding The Immigrant

830 CMR 64H.1.3 Computer Industry Services and Products

830 CMR 64H.1.3 Computer Industry Services and Products 830 CMR: DEPARTMENT OF REVENUE 830 CMR 64H:00: SALES AND USE TAX 830 CMR 64H.1.3 is repealed and replaced with the following (1) Statement of Purpose;

830 CMR 64H.1.3 Computer Industry Services and Products 830 CMR: DEPARTMENT OF REVENUE 830 CMR 64H:00: SALES AND USE TAX 830 CMR 64H.1.3 is repealed and replaced with the following (1) Statement of Purpose;

Internal Revenue Service, Treasury

Internal Revenue Service, Treasury 1.482 3 be the basis for a separate allocation. However, if the employee continues to render services to the related entity by supervising the manufacturing operation

Internal Revenue Service, Treasury 1.482 3 be the basis for a separate allocation. However, if the employee continues to render services to the related entity by supervising the manufacturing operation

International Taxes, Credits and Deductions

1 International Taxes, Credits and Deductions P R E S E N T E D B Y : D A V I D M. W I L K E ; C P A, M B A I N C O N J U N C T I O N W I T H M A R C H 2 1, 2 0 1 7 Interest Charge Domestic International

1 International Taxes, Credits and Deductions P R E S E N T E D B Y : D A V I D M. W I L K E ; C P A, M B A I N C O N J U N C T I O N W I T H M A R C H 2 1, 2 0 1 7 Interest Charge Domestic International

Prepared by Cyberian

; and Which of the following is/are the component(s) of equity? Share Capital Reserves Share Premium In which of the following activities, a business should capitalize its incurred expenditures according

; and Which of the following is/are the component(s) of equity? Share Capital Reserves Share Premium In which of the following activities, a business should capitalize its incurred expenditures according

International Tax Update

International Tax Update AMERICAN BAR ASSOCIATION SECTION OF TAXATION 26TH ANNUAL PHILADELPHIA TAX CONFERENCE November 6, 2015 11:20 a.m. 12:35 p.m. International Tax Update The panel will discuss the

International Tax Update AMERICAN BAR ASSOCIATION SECTION OF TAXATION 26TH ANNUAL PHILADELPHIA TAX CONFERENCE November 6, 2015 11:20 a.m. 12:35 p.m. International Tax Update The panel will discuss the

Intellectual property in the age of BEPS

Intellectual property in the age of BEPS Tax Executives Institute Michigan Chapter Detroit 28 October 2015 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms

Intellectual property in the age of BEPS Tax Executives Institute Michigan Chapter Detroit 28 October 2015 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms

FINANCIAL RESEARCH ASSOCIATES PRIVATE INVESTMENT FUND TAX MASTER CLASS

FINANCIAL RESEARCH ASSOCIATES PRIVATE INVESTMENT FUND TAX MASTER CLASS EFFECTIVELY MANAGING TAX IMPLICATIONS OF FOREIGN INVESTMENTS Steven D. Bortnick May 24, 2017 Princeton Club, New York City #43410091

FINANCIAL RESEARCH ASSOCIATES PRIVATE INVESTMENT FUND TAX MASTER CLASS EFFECTIVELY MANAGING TAX IMPLICATIONS OF FOREIGN INVESTMENTS Steven D. Bortnick May 24, 2017 Princeton Club, New York City #43410091

Reducing Taxes for Farmers, Growers, Fishermen and Related Industries

Reducing Taxes for Farmers, Growers, Fishermen and Related Industries Current & Future Savings Based On Export Sales Jonathan Glasser - BEC Partners, LLC Kimberly Rehmeyer, CPA, JD - BEC Partners, LLC

Reducing Taxes for Farmers, Growers, Fishermen and Related Industries Current & Future Savings Based On Export Sales Jonathan Glasser - BEC Partners, LLC Kimberly Rehmeyer, CPA, JD - BEC Partners, LLC

Section Income Attributable to Domestic Production Activities

Part III - Administrative, Procedural, and Miscellaneous Section 199.--Income Attributable to Domestic Production Activities Notice 2005-14 CONTENTS SECTION 1. PURPOSE SECTION 2. OVERVIEW OF 199.01 In

Part III - Administrative, Procedural, and Miscellaneous Section 199.--Income Attributable to Domestic Production Activities Notice 2005-14 CONTENTS SECTION 1. PURPOSE SECTION 2. OVERVIEW OF 199.01 In

All Rights Reserved 2017 TCG

All Rights Reserved 2017 TCG 787.508.4545 www.torrescpa.com 1 Moving your Intelectual Related Business to Puerto Rico under Act 20 Act 20 offers a 4% tax rate on the net income of all services and exported

All Rights Reserved 2017 TCG 787.508.4545 www.torrescpa.com 1 Moving your Intelectual Related Business to Puerto Rico under Act 20 Act 20 offers a 4% tax rate on the net income of all services and exported

A Basic Introduction to Intellectual Property Rights. Pursuant to NASA Procurement Contracts

National Aeronautics and Space Administration A Basic Introduction to Intellectual Property Rights Pursuant to NASA Procurement Contracts 2017 Ted Ro Deputy Chief Counsel/Intellectual Property Attorney

National Aeronautics and Space Administration A Basic Introduction to Intellectual Property Rights Pursuant to NASA Procurement Contracts 2017 Ted Ro Deputy Chief Counsel/Intellectual Property Attorney

Chapter 24. Taxation of International Transactions. Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe

Chapter 24 Taxation of International Transactions Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004 South-Western/Thomson Learning Overview Of International Taxation

Chapter 24 Taxation of International Transactions Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004 South-Western/Thomson Learning Overview Of International Taxation

TAX PLANNING. Foreign Investment In United States Real Estate. By Richard S. Lehman, Esq TAX ATTORNEY

PART OF THE LEHMAN TAX LAW KNOWLEDGE BASE SERIES United States Taxation Of Investors TAX PLANNING Foreign Investment In United States Real Estate By Richard S. Lehman, Esq TAX ATTORNEY 1 FOREIGN INVESTMENT

PART OF THE LEHMAN TAX LAW KNOWLEDGE BASE SERIES United States Taxation Of Investors TAX PLANNING Foreign Investment In United States Real Estate By Richard S. Lehman, Esq TAX ATTORNEY 1 FOREIGN INVESTMENT

International Tax Impact of Business Entity Selection for Foreign Operations of U.S. Companies

FOR LIVE PROGRAM ONLY International Tax Impact of Business Entity Selection for Foreign Operations of U.S. Companies TUESDAY, DECEMBER 12, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

FOR LIVE PROGRAM ONLY International Tax Impact of Business Entity Selection for Foreign Operations of U.S. Companies TUESDAY, DECEMBER 12, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE

U.S. Tax Aspects of Technology Transfers between the United States and Canada

Canada-United States Law Journal Volume 11 Issue Article 23 January 1986 U.S. Tax Aspects of Technology Transfers between the United States and Canada George G. Goodrich Follow this and additional works

Canada-United States Law Journal Volume 11 Issue Article 23 January 1986 U.S. Tax Aspects of Technology Transfers between the United States and Canada George G. Goodrich Follow this and additional works

TAX AND STRUCTURING ANALYSIS REPORT

TAX AND STRUCTURING ANALYSIS REPORT Sample Business Somewhere, USA 813 8 th Street, Suite # 550 Wichita Falls, Texas 76301-3318 www.waa-online.com (940) 322-5086 Sample Business Report Prepared For: Mr.

TAX AND STRUCTURING ANALYSIS REPORT Sample Business Somewhere, USA 813 8 th Street, Suite # 550 Wichita Falls, Texas 76301-3318 www.waa-online.com (940) 322-5086 Sample Business Report Prepared For: Mr.

IC-DISC Strategies: Mastering the Complex Operational Challenges

IC-DISC Strategies: Mastering the Complex Operational Challenges Anticipating IRS Audit Risks, Calculating Commissions, and Tackling Computational Intricacies TUESDAY, MAY 6, 2014, 1:00-3:00 pm Eastern

IC-DISC Strategies: Mastering the Complex Operational Challenges Anticipating IRS Audit Risks, Calculating Commissions, and Tackling Computational Intricacies TUESDAY, MAY 6, 2014, 1:00-3:00 pm Eastern

lated FSCs from property acquired by the FSCs from the corporation. 6 However, this aggregate amount does not include any

252 lated FSCs from property acquired by the FSCs from the corporation. 6 However, this aggregate amount does not include any amount attributable to a transaction involving a lease by the corporation unless

252 lated FSCs from property acquired by the FSCs from the corporation. 6 However, this aggregate amount does not include any amount attributable to a transaction involving a lease by the corporation unless

TAX IMPLICATIONS RELATED TO THE IMPLEMENTATION OF FRS 138: INTANGIBLE ASSETS

The Malaysian Institute of Certified Public Accountants TAX IMPLICATIONS RELATED TO THE IMPLEMENTATION OF FRS 138: INTANGIBLE ASSETS Prepared by: Joint Tax Working Group on FRS Contents Page No. 1 Introduction

The Malaysian Institute of Certified Public Accountants TAX IMPLICATIONS RELATED TO THE IMPLEMENTATION OF FRS 138: INTANGIBLE ASSETS Prepared by: Joint Tax Working Group on FRS Contents Page No. 1 Introduction

QUESTION: WHETHER TAXPAYER S GROSS RECEIPTS EARNED FROM THE ABOVE MENTIONED REVENUE CATEGORIES SHOULD BE SOURCED TO FLORIDA.

Executive Director Marshall Stranburg QUESTION: WHETHER TAXPAYER S GROSS RECEIPTS EARNED FROM THE ABOVE MENTIONED REVENUE CATEGORIES SHOULD BE SOURCED TO FLORIDA. ANSWER: REVENUE CATEGORY 1: THIS CONSISTS

Executive Director Marshall Stranburg QUESTION: WHETHER TAXPAYER S GROSS RECEIPTS EARNED FROM THE ABOVE MENTIONED REVENUE CATEGORIES SHOULD BE SOURCED TO FLORIDA. ANSWER: REVENUE CATEGORY 1: THIS CONSISTS

THE TWILIGHT ZONE BETWEEN TRADEMARK LICENSING AND FRANCHISING

THE TWILIGHT ZONE BETWEEN TRADEMARK LICENSING AND FRANCHISING 2015 Keith J. Kanouse Kanouse & Walker, P.A. One Boca Place, Suite 324 Atrium 2255 Glades Road Boca Raton, Florida 33431 Telephone: (561) 451-8090

THE TWILIGHT ZONE BETWEEN TRADEMARK LICENSING AND FRANCHISING 2015 Keith J. Kanouse Kanouse & Walker, P.A. One Boca Place, Suite 324 Atrium 2255 Glades Road Boca Raton, Florida 33431 Telephone: (561) 451-8090

CHAPTER 05 - CORPORATE FRANCHISE, INCOME, AND INSURANCE TAXES SUBCHAPTER 05G MARKET-BASED SOURCING FOR APPORTIONMENT OF INCOME

CHAPTER 05 - CORPORATE FRANCHISE, INCOME, AND INSURANCE TAXES SUBCHAPTER 05G MARKET-BASED SOURCING FOR APPORTIONMENT OF INCOME SECTION.0100 GENERAL RULES 17 NCAC 05G.0101 SCOPE The rules in this Subchapter

CHAPTER 05 - CORPORATE FRANCHISE, INCOME, AND INSURANCE TAXES SUBCHAPTER 05G MARKET-BASED SOURCING FOR APPORTIONMENT OF INCOME SECTION.0100 GENERAL RULES 17 NCAC 05G.0101 SCOPE The rules in this Subchapter

12A Manufacturing. (1)(a) Any person who manufactures, produces, compounds, processes, or fabricates in any manner an article of tangible

(a) Any person who manufactures, produces, compounds, processes, or fabricates in any manner an article of tangible") 12A-1.043 Manufacturing. (1)(a) Any person who manufactures, produces, compounds, processes, or fabricates in any manner an article of tangible personal property for his own use shall pay a tax upon the

12A-1.043 Manufacturing. (1)(a) Any person who manufactures, produces, compounds, processes, or fabricates in any manner an article of tangible personal property for his own use shall pay a tax upon the

STATE OF RHODE ISLAND DIVISION OF TAXATION. Business Corporation Tax Corporate Nexus. Regulation CT Table of Contents

STATE OF RHODE ISLAND DIVISION OF TAXATION Business Corporation Tax Corporate Nexus Regulation CT 15-02 Table of Contents Rule 1. Rule 2. Rule 3. Rule 4. Rule 5. Rule 6. Rule 7. Purpose Authority Application

STATE OF RHODE ISLAND DIVISION OF TAXATION Business Corporation Tax Corporate Nexus Regulation CT 15-02 Table of Contents Rule 1. Rule 2. Rule 3. Rule 4. Rule 5. Rule 6. Rule 7. Purpose Authority Application

Which Cos. Are Most Likely To Benefit From Innovation Box?

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com Which Cos. Are Most Likely To Benefit From Innovation

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com Which Cos. Are Most Likely To Benefit From Innovation

26 CFR Ch. I ( Edition)

") 1.482 4 contract with Cancan, Amcan had received a bona fide offer from an independent Canadian waste disposal company, Cando, to serve as the Canadian distributor for toxicans and to purchase a similar

1.482 4 contract with Cancan, Amcan had received a bona fide offer from an independent Canadian waste disposal company, Cando, to serve as the Canadian distributor for toxicans and to purchase a similar

DISCUSSION PAPER TAX IMPLICATIONS RELATED TO THE IMPLEMENTATION OF FRS 138: INTANGIBLE ASSETS

The Malaysian Institute of Certified Public Accountants DISCUSSION PAPER TAX IMPLICATIONS RELATED TO THE IMPLEMENTATION OF FRS 138: INTANGIBLE ASSETS Prepared by: Joint Tax Working Group on FRS Date of

The Malaysian Institute of Certified Public Accountants DISCUSSION PAPER TAX IMPLICATIONS RELATED TO THE IMPLEMENTATION OF FRS 138: INTANGIBLE ASSETS Prepared by: Joint Tax Working Group on FRS Date of

IC-DISC TAX SAVINGS FOR EXPORTERS. An overlooked tax break that could be your big break. Reduce Current & Future Taxes

IC-DISC TAX SAVINGS FOR EXPORTERS An overlooked tax break that could be your big break Reduce Current & Future Taxes Interest Charge Domestic International Sales Corporation (IC-DISC) 1 What Is An IC-DISC?

IC-DISC TAX SAVINGS FOR EXPORTERS An overlooked tax break that could be your big break Reduce Current & Future Taxes Interest Charge Domestic International Sales Corporation (IC-DISC) 1 What Is An IC-DISC?

TAX PLANNING FOR THE FOREIGN REAL ESTATE INVESTOR

TAX PLANNING FOR THE FOREIGN REAL ESTATE INVESTOR Tax Benefits and Tax Traps By Richard S. Lehman & Associates Attorneys at Law TAX PLANNING FOR THE FOREIGN REAL ESTATE INVESTOR Tax Benefits and Tax Traps

TAX PLANNING FOR THE FOREIGN REAL ESTATE INVESTOR Tax Benefits and Tax Traps By Richard S. Lehman & Associates Attorneys at Law TAX PLANNING FOR THE FOREIGN REAL ESTATE INVESTOR Tax Benefits and Tax Traps

Tax Management. Using Internal Agreements to Price Intangibles Transfers

Tax Management Transfer Pricing Report Reproduced with permission from Tax Management Transfer Pricing Report, Vol. 23 No. 6, 7/10/2014. Copyright 2014 by The Bureau of National Affairs, Inc. (800-372-1033)

Tax Management Transfer Pricing Report Reproduced with permission from Tax Management Transfer Pricing Report, Vol. 23 No. 6, 7/10/2014. Copyright 2014 by The Bureau of National Affairs, Inc. (800-372-1033)

GWU Law School / IRS 30 th Annual Institute

GWU Law School / IRS 30 th Annual Institute and Washington, DC December 15, 2016 Elena Virgadamo, U.S. Department of Treasury Brian Jenn, U.S. Department of Treasury Jason Smyczek, IRS Office of Chief

GWU Law School / IRS 30 th Annual Institute and Washington, DC December 15, 2016 Elena Virgadamo, U.S. Department of Treasury Brian Jenn, U.S. Department of Treasury Jason Smyczek, IRS Office of Chief

9-1-1 PROVISIONS INCLUDED IN GENESYS LABORATORIES CANADA INC. ( GENESYS ) TERMS OF SERVICE

TERMS OF SERVICE") 9-1-1 PROVISIONS INCLUDED IN GENESYS LABORATORIES CANADA INC. ( GENESYS ) TERMS OF SERVICE ADVISORY REGARDING 911 DIALING AND LIMITATIONS OF SERVICE: THIS SECTION CONTAINS IMPORTANT PROVISIONS, INCLUDING

9-1-1 PROVISIONS INCLUDED IN GENESYS LABORATORIES CANADA INC. ( GENESYS ) TERMS OF SERVICE ADVISORY REGARDING 911 DIALING AND LIMITATIONS OF SERVICE: THIS SECTION CONTAINS IMPORTANT PROVISIONS, INCLUDING

USING INTERCOMPANY TRANSFER PRICE METHODS

Property Taxation Valuation USING INTERCOMPANY TRANSFER PRICE METHODS TO SEGREGATE TANGIBLE/INTANGIBLE ASSETS IN UNIT VALUATION PROPERTY TAX APPRAISALS Melvin R. Rodriguez and Robert F. Reilly 3 INTRODUCTION

Property Taxation Valuation USING INTERCOMPANY TRANSFER PRICE METHODS TO SEGREGATE TANGIBLE/INTANGIBLE ASSETS IN UNIT VALUATION PROPERTY TAX APPRAISALS Melvin R. Rodriguez and Robert F. Reilly 3 INTRODUCTION

BUSINESS VALUATIONS REVISED Introduction. 3.0 Definitions. 2.0 Scope INTERNATIONAL VALUATION GUIDANCE NOTE NO. 6

6.6 INTERNATIONAL VALUATION GUIDANCE NOTE NO. 6 S REVISED 2007 1.0 Introduction 1.1 The International Valuation Standards Committee (IVSC) adopted this Guidance Note (GN) to improve the consistency and

6.6 INTERNATIONAL VALUATION GUIDANCE NOTE NO. 6 S REVISED 2007 1.0 Introduction 1.1 The International Valuation Standards Committee (IVSC) adopted this Guidance Note (GN) to improve the consistency and

A guide to intellectual property and intangible assets

A guide to intellectual property and intangible assets Identifying, protecting and valuing intellectual property within your business Corporate Finance PRECISE. PROVEN. PERFORMANCE. Not surprisingly intellectual

A guide to intellectual property and intangible assets Identifying, protecting and valuing intellectual property within your business Corporate Finance PRECISE. PROVEN. PERFORMANCE. Not surprisingly intellectual

Independence- Freedom- Happiness No. 89/2002/TT-BTC Hanoi, 9 October 2002 CIRCULAR

MINISTRY OF FINANCE Socialist Republic of Vietnam Independence- Freedom- Happiness ------------------------- ----------------------------- No. 89/2002/TT-BTC Hanoi, 9 October 2002 CIRCULAR GUIDELINES ON

MINISTRY OF FINANCE Socialist Republic of Vietnam Independence- Freedom- Happiness ------------------------- ----------------------------- No. 89/2002/TT-BTC Hanoi, 9 October 2002 CIRCULAR GUIDELINES ON

IC-DISC Update for VALET Members

IC-DISC Update for VALET Members Bill Major, CPA Partner International Tax October 16, 2014 Learning Objectives 1) Explain what an IC-DISC is. 2) The IC-DISC tax benefit is tied to the differential between

IC-DISC Update for VALET Members Bill Major, CPA Partner International Tax October 16, 2014 Learning Objectives 1) Explain what an IC-DISC is. 2) The IC-DISC tax benefit is tied to the differential between

IBM Agreement for Services Excluding Maintenance

IBM Agreement for Services Excluding Maintenance This IBM Agreement for Services Excluding Maintenance (called the Agreement ) governs transactions by which Customer acquires Services (including, without

IBM Agreement for Services Excluding Maintenance This IBM Agreement for Services Excluding Maintenance (called the Agreement ) governs transactions by which Customer acquires Services (including, without

LKAS 2 Inventories. 1 P a g e

LKAS 2 Inventories This Standard prescribed the accounting treatment for inventories. It described the amount of cost to be recognized as an asset and carried forward until the related revenues are recognized.

LKAS 2 Inventories This Standard prescribed the accounting treatment for inventories. It described the amount of cost to be recognized as an asset and carried forward until the related revenues are recognized.

Transfer pricing and intangible planning

Transfer pricing and intangible planning Bob Ackerman Americas Director of Transfer Pricing Services Ernst & Young LLP Washington, DC USA Taxation Conference Mumbai 2008 Disclaimer The views reflected

Transfer pricing and intangible planning Bob Ackerman Americas Director of Transfer Pricing Services Ernst & Young LLP Washington, DC USA Taxation Conference Mumbai 2008 Disclaimer The views reflected

Internal Revenue Code Section 199(c)(4) Income attributable to domestic production activities

(4) Income attributable to domestic production activities") CLICK HERE to return to the home page Internal Revenue Code Section 199(c)(4) Income attributable to domestic production activities (a) Allowance of deduction. There shall be allowed as a deduction an

CLICK HERE to return to the home page Internal Revenue Code Section 199(c)(4) Income attributable to domestic production activities (a) Allowance of deduction. There shall be allowed as a deduction an

International Income Taxation Chapter 12: EXPLOITATION OF INTANGIBLES

Presentation: International Income Taxation Chapter 12: EXPLOITATION OF INTANGIBLES Professors Wells April 16, 2018 Chapter 12 Exploiting Intangibles Outside U.S. Choices for structuring these arrangements:

Presentation: International Income Taxation Chapter 12: EXPLOITATION OF INTANGIBLES Professors Wells April 16, 2018 Chapter 12 Exploiting Intangibles Outside U.S. Choices for structuring these arrangements:

Sports Team's Share of Broadcasting Receipts Didn't Qualify for Sec. 199 Deduction. Chief Counsel Advice

Sports Team's Share of Broadcasting Receipts Didn't Qualify for Sec. 199 Deduction Chief Counsel Advice 201545018 In Chief Counsel Advice (CCA), IRS concluded that a sports team's share of gross receipts

Sports Team's Share of Broadcasting Receipts Didn't Qualify for Sec. 199 Deduction Chief Counsel Advice 201545018 In Chief Counsel Advice (CCA), IRS concluded that a sports team's share of gross receipts

10 Steps to realising real cash value from Innovation and IC Assets. Ludo Pyis Areopa

10 Steps to realising real cash value from Innovation and IC Assets Ludo Pyis Areopa Areopa Trust Oct 2014 Topics The Fundamentals of Intellectual Capital and Intellectual Property Quick Scan of IC approach

10 Steps to realising real cash value from Innovation and IC Assets Ludo Pyis Areopa Areopa Trust Oct 2014 Topics The Fundamentals of Intellectual Capital and Intellectual Property Quick Scan of IC approach

Consolidated financial statements of. Spin Master Corp. December 31, 2015 and December 31, 2014

Consolidated financial statements of Spin Master Corp. Consolidated financial statements Table of contents Independent Auditor s Report... 1 Consolidated statements of operations and comprehensive income...

Consolidated financial statements of Spin Master Corp. Consolidated financial statements Table of contents Independent Auditor s Report... 1 Consolidated statements of operations and comprehensive income...

Small and Medium-sized Entity Financial Reporting Framework and Financial Reporting Standard

SME-FRF & SME-FRS Issued August 2005 Effective for a Qualifying Entity s financial statements that cover a period beginning on or after 1 January 2005 Small and Medium-sized Entity Financial Reporting

SME-FRF & SME-FRS Issued August 2005 Effective for a Qualifying Entity s financial statements that cover a period beginning on or after 1 January 2005 Small and Medium-sized Entity Financial Reporting

IFRS FOR SMEs ACCOMPANYING EXAMPLES AND EXERCISES. Based on the 2015 IFRS for SMEs Standard. Page 1 of 10

IFRS FOR SMEs ACCOMPANYING EXAMPLES AND EXERCISES Based on the 2015 IFRS for SMEs Standard Page 1 of 10 Section 11 Financial Instruments Examples financial assets 1. For a long-term loan made to another

IFRS FOR SMEs ACCOMPANYING EXAMPLES AND EXERCISES Based on the 2015 IFRS for SMEs Standard Page 1 of 10 Section 11 Financial Instruments Examples financial assets 1. For a long-term loan made to another

Corporations: Allocation and Apportionment of Income.

560-7-7-.03 Corporations: Allocation and Apportionment of Income. (1) What constitutes doing business. A corporation will be considered to be doing business within this state if it performs acts or consummates

560-7-7-.03 Corporations: Allocation and Apportionment of Income. (1) What constitutes doing business. A corporation will be considered to be doing business within this state if it performs acts or consummates

WEBSITE TERMS OF USE

Last Modified: November 7, 2017 WEBSITE TERMS OF USE Welcome to www.westsidememberlogin.com (this Website ), a website created by Michael L. Johnson, LLC, a California limited liability company ( Company,

Last Modified: November 7, 2017 WEBSITE TERMS OF USE Welcome to www.westsidememberlogin.com (this Website ), a website created by Michael L. Johnson, LLC, a California limited liability company ( Company,

1. Copyright, Licenses and Idea Submissions.

The Precious Richardson Web Site (the "Site") is an online information service provided by LYS Publishing Inc. ("Precious Victoria Richardson "), subject to your compliance with the terms and conditions

The Precious Richardson Web Site (the "Site") is an online information service provided by LYS Publishing Inc. ("Precious Victoria Richardson "), subject to your compliance with the terms and conditions

FAIR VALUE & TRANSFER PRICING: And the twain shall never meet? Transfer Pricing Panel ABA Fall Conf., Denver Oct. 21, 2011

FAIR VALUE & TRANSFER PRICING: And the twain shall never meet? Transfer Pricing Panel ABA Fall Conf., Denver Oct. 21, 2011 Introduction Fair Value & Transfer Pricing Panel: David Ernick, Treasury Jason

FAIR VALUE & TRANSFER PRICING: And the twain shall never meet? Transfer Pricing Panel ABA Fall Conf., Denver Oct. 21, 2011 Introduction Fair Value & Transfer Pricing Panel: David Ernick, Treasury Jason

Internal Revenue Service P.O. Box 7604 Ben Franklin Station Washington, DC Attn: CC:PA:T:CRU (ITA) Room 5529

Room 5529") Advance Payments Notice 2002 79 This notice provides a proposed revenue procedure that, if finalized, will modify and supersede Rev. Proc. 71 21, 1971 2 C.B. 549. Pursuant to the discretion granted the

Advance Payments Notice 2002 79 This notice provides a proposed revenue procedure that, if finalized, will modify and supersede Rev. Proc. 71 21, 1971 2 C.B. 549. Pursuant to the discretion granted the

Intellectual property rights in Luxembourg (IPR): tax exemption

: tax exemption") Intellectual property rights in Luxembourg (IPR): tax exemption Miami, November 3, 2011 Me Beatriz Garcia The tax attractiveness of Luxembourg regarding the intellectual property has increased by the introduction

Intellectual property rights in Luxembourg (IPR): tax exemption Miami, November 3, 2011 Me Beatriz Garcia The tax attractiveness of Luxembourg regarding the intellectual property has increased by the introduction

IFRS hot topic... Licensors enter into various types of licensing agreements with third parties. These licensing agreements may be:

1 IFRS hot topic... income from licensing intangible assets IFRS hot topic 2008-19 Issue Licensors enter into various types of licensing agreements with third parties. These licensing agreements may be:

1 IFRS hot topic... income from licensing intangible assets IFRS hot topic 2008-19 Issue Licensors enter into various types of licensing agreements with third parties. These licensing agreements may be:

OPC FOUNDATION INTELLECTUAL PROPERTY RIGHTS POLICY VERSION APR 2018

OPC FOUNDATION INTELLECTUAL PROPERTY RIGHTS POLICY VERSION 2.0 09 APR 2018 This OPC Foundation Intellectual Property Rights (IPR) Policy governs the treatment of intellectual property in the production

OPC FOUNDATION INTELLECTUAL PROPERTY RIGHTS POLICY VERSION 2.0 09 APR 2018 This OPC Foundation Intellectual Property Rights (IPR) Policy governs the treatment of intellectual property in the production

GNC-ALFA CJSC. Financial Statements for the year ended 31 December 2010

Financial Statements for the year ended 31 December 2010 Contents Statement of Comprehensive Income 3 Statement of Financial Position 4 Statement of Changes in Equity 5 Statement of Cash Flows 6 Notes

Financial Statements for the year ended 31 December 2010 Contents Statement of Comprehensive Income 3 Statement of Financial Position 4 Statement of Changes in Equity 5 Statement of Cash Flows 6 Notes

Sink or Swim, the Sales Taxation Future of Cloud Computing

Sink or Swim, the Sales Taxation Future of Cloud Computing Jennifer Jensen State & Local Tax Director PricewaterhouseCoopers McLean, VA jennifer.jensen@us.pwc.com S. Matthew McNeilly Senior Tax Manager

Sink or Swim, the Sales Taxation Future of Cloud Computing Jennifer Jensen State & Local Tax Director PricewaterhouseCoopers McLean, VA jennifer.jensen@us.pwc.com S. Matthew McNeilly Senior Tax Manager

Year End Planning and other Issues

www.pwc.com Year End Planning and other Issues December 7, 2010 Alon Sherer Manager, US Tax Josh Ashman Manager, US Tax www.pwc.com Year End Planning 1 Scope and Limitations The information contained in

www.pwc.com Year End Planning and other Issues December 7, 2010 Alon Sherer Manager, US Tax Josh Ashman Manager, US Tax www.pwc.com Year End Planning 1 Scope and Limitations The information contained in

Peculiarities of non-residents taxation in Armenia

Peculiarities of non-residents taxation in Armenia In cooperation with the RA State Revenue Committee 02 In this brochure, we would like to discuss the profit tax calculation and payment peculiarities

Peculiarities of non-residents taxation in Armenia In cooperation with the RA State Revenue Committee 02 In this brochure, we would like to discuss the profit tax calculation and payment peculiarities

Tax Management International Journal

Tax Management International Journal Reproduced with permission from Tax Management International Journal, 44 TMIJ 698, 11/13/2015. Copyright 2015 by The Bureau of National Affairs, Inc. (800-372- 1033)

Tax Management International Journal Reproduced with permission from Tax Management International Journal, 44 TMIJ 698, 11/13/2015. Copyright 2015 by The Bureau of National Affairs, Inc. (800-372- 1033)

SUGGESTED ANSWERS MARCH 2011 EXTRA ATTEMPT EXAMINATIONS 1 of 6 Business Taxation (Stage-3)

") SUGGESTED ANSWERS MARCH 2011 EXTRA ATTEMPT EXAMINATIONS 1 of 6 Q.2 (a) (i) INDUSTRIAL UNDERTAKING: (a) An undertaking which is set up in Pakistan and which employs, (i) ten or more persons in Pakistan

SUGGESTED ANSWERS MARCH 2011 EXTRA ATTEMPT EXAMINATIONS 1 of 6 Q.2 (a) (i) INDUSTRIAL UNDERTAKING: (a) An undertaking which is set up in Pakistan and which employs, (i) ten or more persons in Pakistan

MATERIALS DISCLOSED VIA THE INTERNET CONCERNING NOTICE OF CONVOCATION OF THE 33RD ANNUAL SHAREHOLDERS MEETING

[This is an English translation prepared for the convenience of non-resident shareholders. Should there be any inconsistency between the translation and the official Japanese text, the latter shall prevail.]

[This is an English translation prepared for the convenience of non-resident shareholders. Should there be any inconsistency between the translation and the official Japanese text, the latter shall prevail.]

Annual Update on California s Manufacturing Tax Incentives

Special Report for Cal-Tax Online December 1999 Annual Update on California s Manufacturing Tax Incentives by Chris Micheli I. INTRODUCTION The purpose of this article is to provide another annual update

Special Report for Cal-Tax Online December 1999 Annual Update on California s Manufacturing Tax Incentives by Chris Micheli I. INTRODUCTION The purpose of this article is to provide another annual update

INSIGHT: Aircraft Business Tax Deductions: Top Ten for 2018 and Beyond

Reproduced with permission from Daily Tax Report, 125 DTR 12, 6/28/18. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Business Expenses INSIGHT: Aircraft Business

Reproduced with permission from Daily Tax Report, 125 DTR 12, 6/28/18. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Business Expenses INSIGHT: Aircraft Business

Phillip Beutel, Bryan Ray, Steven Schwartz

TWO WORLDS COLLIDING? TRANSFER PRICING AND DAMAGES IN INTELLECTUAL PROPERTY LITIGATION Phillip Beutel, Bryan Ray, Steven Schwartz I. INTRODUCTION The profitable management of intellectual property (IP)

TWO WORLDS COLLIDING? TRANSFER PRICING AND DAMAGES IN INTELLECTUAL PROPERTY LITIGATION Phillip Beutel, Bryan Ray, Steven Schwartz I. INTRODUCTION The profitable management of intellectual property (IP)

Management & Principles of Accounting Date: 15/11/2017 Recording long-lived assets and other investments

Management & Principles of Accounting Date: 15/11/2017 Patrizia Tettamanzi Sophie Goodman Source: E-Book: (Basic accounting - how to prepare and analyze financial statements) edited by Patrizia Tettamanzi,

Management & Principles of Accounting Date: 15/11/2017 Patrizia Tettamanzi Sophie Goodman Source: E-Book: (Basic accounting - how to prepare and analyze financial statements) edited by Patrizia Tettamanzi,

Statement of Financial Accounting Standards No. 53

Statement of Financial Accounting Standards No. 53 Note: This Statement has been completely superseded FAS53 Status Page FAS53 Summary Financial Reporting by Producers and Distributors of Motion Picture

Statement of Financial Accounting Standards No. 53 Note: This Statement has been completely superseded FAS53 Status Page FAS53 Summary Financial Reporting by Producers and Distributors of Motion Picture

U.S. Taxation of Foreign Corporations

University of Miami Law School Institutional Repository University of Miami Inter-American Law Review 10-1-1976 U.S. Taxation of Foreign Corporations Follow this and additional works at: http://repository.law.miami.edu/umialr

University of Miami Law School Institutional Repository University of Miami Inter-American Law Review 10-1-1976 U.S. Taxation of Foreign Corporations Follow this and additional works at: http://repository.law.miami.edu/umialr

NATIONAL FOREIGN TRADE COUNCIL, INC.

NATIONAL FOREIGN TRADE COUNCIL, INC. 1625 K STREET, NW, WASHINGTON, DC 20006-1604 TEL: (202) 887-0278 FAX: (202) 452-8160 September 7, 2012 Organisation for Economic Cooperation and Development Centre

NATIONAL FOREIGN TRADE COUNCIL, INC. 1625 K STREET, NW, WASHINGTON, DC 20006-1604 TEL: (202) 887-0278 FAX: (202) 452-8160 September 7, 2012 Organisation for Economic Cooperation and Development Centre

INLAND REVENUE BOARD

July 18, 2003 TEC/004/07/2003 INLAND REVENUE BOARD EXTENSION OF TIME FOR SUBMISSION OF BORANG C AND BORANG R TRANSFER PRICING GUIDELINES 1. Extension of Time for Filing Borang C and Borang R for Year of

July 18, 2003 TEC/004/07/2003 INLAND REVENUE BOARD EXTENSION OF TIME FOR SUBMISSION OF BORANG C AND BORANG R TRANSFER PRICING GUIDELINES 1. Extension of Time for Filing Borang C and Borang R for Year of

Procedure and tips of registrating a trademark in China Wednesday, 23 March :52. Procedure:

Procedure: Generally we have two methods, if the applicant, for both a company and an individual, is applicant who has China nationality. First is appointing a China local trademark agency authorized by

Procedure: Generally we have two methods, if the applicant, for both a company and an individual, is applicant who has China nationality. First is appointing a China local trademark agency authorized by

Coming to America. U.S. Tax Planning for Foreign-Owned U.S. Operations. By Len Schneidman. Andersen Tax LLC, U.S.

Coming to America U.S. Tax Planning for Foreign-Owned U.S. Operations By Len Schneidman Andersen Tax LLC, U.S. January 2018 Table of Contents Introduction... 2 Tax Checklist for Foreign-Owned U.S. Operations...

Coming to America U.S. Tax Planning for Foreign-Owned U.S. Operations By Len Schneidman Andersen Tax LLC, U.S. January 2018 Table of Contents Introduction... 2 Tax Checklist for Foreign-Owned U.S. Operations...

International Income Taxation Chapter 12: EXPLOITATION OF INTANGIBLES

Presentation: International Income Taxation Chapter 12: EXPLOITATION OF INTANGIBLES Professors Wells April 20, 2016 Chapter 12 Exploiting Intangibles Outside U.S. Choices for structuring these arrangements:

Presentation: International Income Taxation Chapter 12: EXPLOITATION OF INTANGIBLES Professors Wells April 20, 2016 Chapter 12 Exploiting Intangibles Outside U.S. Choices for structuring these arrangements:

Gene Ferraro, Mazars USA LLP New York, NY William D. James, BKD, LLP St. Louis, MO

How to Plan for IP? Gene Ferraro, Mazars USA LLP New York, NY gene.ferarro@mazarsusa.com William D. James, BKD, LLP St. Louis, MO wdjames@bkd.com Cormac Kelleher, Mazars Dublin, Ireland ckelleher@mazars.ie

How to Plan for IP? Gene Ferraro, Mazars USA LLP New York, NY gene.ferarro@mazarsusa.com William D. James, BKD, LLP St. Louis, MO wdjames@bkd.com Cormac Kelleher, Mazars Dublin, Ireland ckelleher@mazars.ie

B.4. Intra-Group Services

B.4. Intra-Group Services Introduction B.4.1. This chapter considers the transfer prices for intra-group services within an MNE group. Firstly, it considers the tests for determining whether chargeable

B.4. Intra-Group Services Introduction B.4.1. This chapter considers the transfer prices for intra-group services within an MNE group. Firstly, it considers the tests for determining whether chargeable

School District of Palm Beach County

PALM BEACH COUNTY SCHOOL DISTRICT WIRELESS HOTSPOT (Wi-Fi) TERMS OF SERVICE and ACCEPTABLE USE AGREEMENT 1. Purpose The purpose of this Agreement is to set forth terms and conditions, as well as standards

PALM BEACH COUNTY SCHOOL DISTRICT WIRELESS HOTSPOT (Wi-Fi) TERMS OF SERVICE and ACCEPTABLE USE AGREEMENT 1. Purpose The purpose of this Agreement is to set forth terms and conditions, as well as standards

Obama Seeks to Tax Outbound Transfers of Workforce in Place

Checkpoint Contents International Tax Library WG&L Journals Journal of International Taxation (WG&L) Journal of International Taxation 2009 Volume 20, Number 09, September 2009 Articles Obama Seeks to

Checkpoint Contents International Tax Library WG&L Journals Journal of International Taxation (WG&L) Journal of International Taxation 2009 Volume 20, Number 09, September 2009 Articles Obama Seeks to

ILLUSTRATION 12-1 TYPES OF INTANGIBLE ASSETS

ILLUSTRATION 12-1 TYPES OF INTANGIBLE ASSETS INTANGIBLE ASSETS Identifiable Intangible Assets (Rights Type) Externally Acquired Internally Developed Financial Statement Treatment Unidentifiable Intangible

ILLUSTRATION 12-1 TYPES OF INTANGIBLE ASSETS INTANGIBLE ASSETS Identifiable Intangible Assets (Rights Type) Externally Acquired Internally Developed Financial Statement Treatment Unidentifiable Intangible

THE SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness No. 20/2017/ND-CP Hanoi, February 24, 2017 DECREE

THE GOVERNMENT -------- THE SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness --------------- No. 20/2017/ND-CP Hanoi, February 24, 2017 DECREE PRESCRIBING TAX ADMINISTRATION FOR ENTERPRISES

THE GOVERNMENT -------- THE SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom - Happiness --------------- No. 20/2017/ND-CP Hanoi, February 24, 2017 DECREE PRESCRIBING TAX ADMINISTRATION FOR ENTERPRISES

Business restructuring - depreciation on goodwill - An analysis. By Gaurav Jain, CA

DECEMBER 14, 2009 Business restructuring - depreciation on goodwill - An analysis By Gaurav Jain, CA RESTRUCTURING of existing businesses, mergers and acquisitions has become a regular feature of India

DECEMBER 14, 2009 Business restructuring - depreciation on goodwill - An analysis By Gaurav Jain, CA RESTRUCTURING of existing businesses, mergers and acquisitions has become a regular feature of India

Revenue from contracts with customers The standard is final A comprehensive look at the new revenue model

What s inside: Overview... 1 Scope...2 Licences and rights to use...2 Variable consideration and the constraint on revenue recognition...5 Sales to distributors and consignment stock...10 Collaborations

What s inside: Overview... 1 Scope...2 Licences and rights to use...2 Variable consideration and the constraint on revenue recognition...5 Sales to distributors and consignment stock...10 Collaborations

Development, Ownership and Licensing of Intellectual and Intangible Properties Including Trademarks, Trade Names and Franchises By William P.

Development, Ownership and Licensing of Intellectual and Intangible Properties Including Trademarks, Trade Names and Franchises By William P. Elliott Bill Elliott discusses the development, ownership and

Development, Ownership and Licensing of Intellectual and Intangible Properties Including Trademarks, Trade Names and Franchises By William P. Elliott Bill Elliott discusses the development, ownership and

ACCOUNTING COURSES Student Learning Outcomes 1

ACCOUNTING COURSES Student Learning Outcomes 1 ACCTG 201: Financial Accounting Fundamentals 1. Use accounting and business terminology, and understand the nature and purpose of generally accepted accounting

ACCOUNTING COURSES Student Learning Outcomes 1 ACCTG 201: Financial Accounting Fundamentals 1. Use accounting and business terminology, and understand the nature and purpose of generally accepted accounting

Tangible Property Regulations Overview Key Provisions for Small Business Taxpayers. Tim Benningfield 07/15/2015

Tangible Property Regulations Overview Key Provisions for Small Business Taxpayers Tim Benningfield 07/15/2015 Internal Revenue Code - General Rules Section 162 allows a deduction for ordinary and necessary

Tangible Property Regulations Overview Key Provisions for Small Business Taxpayers Tim Benningfield 07/15/2015 Internal Revenue Code - General Rules Section 162 allows a deduction for ordinary and necessary