Income Capital Gain or Loss; Form 1040, Line 13

|

|

|

- Gwendolyn Morton

- 6 years ago

- Views:

Transcription

1 Income Capital Gain or Loss; Form 1040, Line 13

2 Objectives Capital Gain or Loss Determine if the asset s holding period is long-term or short-term Calculate the taxable gain or deductible loss from the sale of capital assets Determine whether a home is the taxpayer s main home Determine if a taxpayer meets the ownership and use tests Income Capital Gain or Loss; Form 1040, Line 13 2

3 Capital Gain or Loss Definitions Capital gain (or loss) = Proceeds Basis Proceeds = sales price sales commissions Basis = purchase price + purchase commissions Holding period = Time from purchase of asset to sale Short term = less than or equal to 1 year Long term = greater than 1 year Covered/not covered Covered = proceeds and basis are reported to IRS Not covered = proceeds only are reported to IRS 3 rd possibility = no 1099-B for transaction (neither proceeds nor basis are reported to IRS) 3

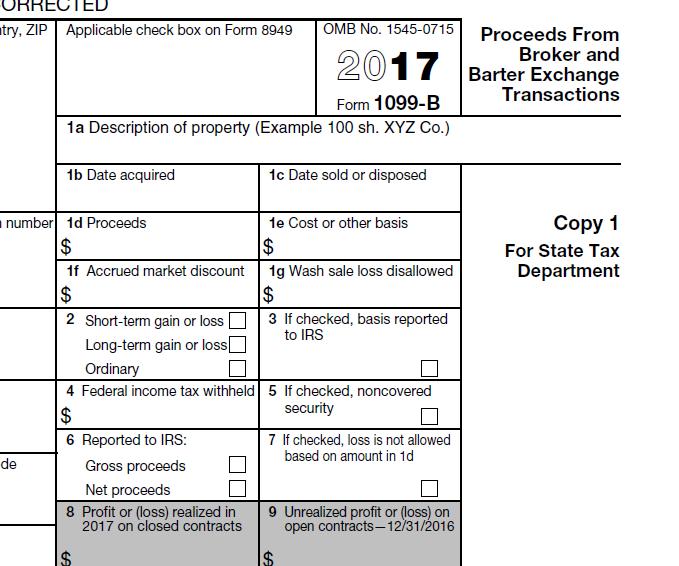

4 Proceeds from the Sale Brokers report information about sale of stock on Form 1099-B Entries in boxes 8 through 13 are out of scope Unless securities sold were noncovered securities, brokers must report: Cost or other basis Whether gain/loss is short-term or long-term Income Capital Gain or Loss; Form 1040, Line 13 4

5 1099-B 5

6 Basis of Stock If Form 1099-B does not provide the basis, taxpayers must provide this information. If taxpayers received property as a gift or inheritance, and do not know the basis and holding period, refer them to a professional tax preparer. Income Capital Gain or Loss; Form 1040, Line 13 6

7 1099-B on Summary Statement from Broker 7

8 Six possible combinations of holding and reporting Short term, covered Short term, not covered Short term, no 1099-B Long term, covered Long term, not covered Long term, no 1099-B 8

9 Capital Gains Reporting 1099-B 1099-B 1099-B 8949 LONG TERM, COVERED 8949 SHORT TERM, COVERED SCH D B 1099-B 8949 LONG TERM, NOT COVERED TaxSlayer 9

10 TaxSlayer Capital Gains Reporting (4012 D-22 to D-27) 10

11 TaxSlayer Capital Gains Reporting (4012 D-22 to D-27) 11

12 TaxSlayer Capital Gains Reporting (4012 D-22 to D-27) 12

13 TaxSlayer Capital Gains Reporting (4012 D-22 to D-27) 13

14 TaxSlayer Capital Gains Reporting (4012 D-22 to D-27) 14

15 Capital Gains Adjustments (4012 D-26 to D-27) 15

16 TaxSlayer Capital Gains Reporting (4012 D-22 to D-27) 16

17 Capital Loss Carryovers $3000 ($1,500 for Married Filing Separately) is the maximum net capital loss a taxpayer can take in a single year? Unused losses can be carried over to later years until gone Previous year return is needed to figure capital loss carryover. If the loss is over the limit, the tax software reports the maximum allowable deduction. The remainder can be carried over. Income Capital Gain or Loss; Form 1040, Line 13 17

18 TaxSlayer Capital Loss Carryover (4012 D-22) Federal Section > Income > Capital Gain and Losses 18

19 TaxSlayer Capital Loss Carryover (4012 D-22) 19

20 Sale of Main Home (4012 D-28 to D-32) Taxpayers may be able to exclude from taxable income the gain from sale of a main home. Up to a maximum of $250,000 ($500,0000 for Married Filing Jointly) Volunteers need to confirm the home sold was the taxpayer s main home, and the taxpayer meets the ownership and use tests. For help in making this determination, see Pub 17 or Pub 523. Income Capital Gain or Loss; Form 1040, Line 13 20

21 Ownership and Use Tests (4012 D-28) During the five-year period ending on the date of the sale, the taxpayer must have: Owned the home for at least two years (the ownership test), and Lived in the home as his or her main home for at least two years (the use test) In addition, during the two-year period ending on the date of the sale, the taxpayer must not have claimed an exclusion on a gain from the sale of another home. Income Capital Gain or Loss; Form 1040, Line 13 21

22 Gain on Sale of Home (4012 D-28 to D-32) Figuring the gain or loss on the sale of a home is based on: Selling price Amount realized Basis Adjusted basis See the worksheet examples in Pub 523 Adjusted Basis of Home Sold Remember loss on the sale of a personal residence is not deductible. Income Capital Gain or Loss; Form 1040, Line 13 22

23 Reporting Gain from the Sale of Home Gain must be reported when Amount is greater than the allowed exclusion Home is not the taxpayer s main home If taxpayer received Form 1099-S for their gain or loss on the sale of a main home, it must be reported on Form 8949 and Schedule D Income Capital Gain or Loss; Form 1040, Line 13 23

24 5-Year Test Period Suspension 5-Year ownership and use period may be suspended during any period of qualified official extended duty for a taxpayer who is: Member of uniformed services or Foreign Service of the U.S. Intelligence community employee Employee or volunteer of the Peace Corps Qualified official extended duty: Serve at a duty station at least 50 miles from their main home, or Live in government quarters under government order Called to active duty for more than 90 days or an indefinite period Income Capital Gain or Loss; Form 1040, Line 13 24

25 Out of Scope for this Lesson: Taxpayers who have sold any assets other than stock, mutual funds, or a personal residence Taxpayers who trade in options, futures, or other commodities, whether or not they bought or sold Determination of basis issues: Basis of any asset acquired other than by purchase or inheritance, such as a gift or employee stock option, unless the taxpayer provides the basis and holding period Basis of inherited property determined by method other than the fair market value (FMV) of the property on the date of the decedent's death, unless the taxpayer provides the basis and holding period Like-kind exchanges and worthless securities Form 1099-B, boxes on Bartering: Profit or (loss) realized on closed contracts; Unrealized profit (loss) on open contracts prior year; Unrealized profit or (loss) on open contracts current year; or Aggregate profit (loss) on contracts; Proceeds from collectibles; or FATCA filing requirement Income Capital Gain or Loss; Form 1040, Line 13 25

26 Out of Scope for this Lesson: Reduced exclusion computations/determinations in the sale of a home Married homeowners who do not meet all requirements to claim the maximum exclusion on sale of home Decreases to basis, including: Deductible casualty losses and gains a taxpayer postponed from the sale of a previous home before May 7, 1997 Depreciation during the time the home was used for business purposes or as rental property Taxpayers with nonqualified use issues Sale of a home used for business purposes or as rental property Income Capital Gain or Loss; Form 1040, Line 13 26

27 Summary Capital Gains and Losses In this lesson, you learned how to identify an asset s holding period, adjusted basis, net short-term and long-term capital gains or losses, the taxable gain or deductible loss, and the amount of capital loss carryover. Taxpayers must use Form 8949 and Schedule D to report capital gains and losses. Completion of Form 8949 and Schedule D requires information from Form 1099-B and Form 1099-DIV or a 1099 Consolidated Statement and from taxpayer records. Information from a taxpayer s prior year return is needed to compute a loss carryover amount. Income Capital Gain or Loss; Form 1040, Line 13 27

28 Summary Sale of a Main Home This lesson covered how to report the sale of a taxpayer s principal residence. To exclude gain from sale of a home : The home sold was taxpayer s main home (place the taxpayer lived most of the time) Owned the home for at least two years (the ownership test), and Lived in the home as their main home for at least two years (the use test) The required two years of ownership/use need not be continuous Taxpayer did not exclude gain in the two years before the current sale of the home 5-Year test period can be suspended for taxpayers serving on qualified official extended duty. Income Capital Gain or Loss; Form 1040, Line 13 28

29 Foreign Tax Credit and Schedule K-1

30 Foreign Tax Credit (4012 G-2) Taxpayers who receive form 1099-INT 1099-DIV or Sched K-1 may have amounts indicating that foriegn taxes have been paid. Taxpayers can elect to report foreign tax on Form 1040, page 2 without filing form 1116 when the following conditions are met: All of the foreign source income was from interest and dividends and all that income and foreign tax paid is reported on Form 1099-INT, 1099-DIV or Schedule K-1 If dividend income is from shares they must have been held for at least 15 days Not filing form 4563 (Samoa income) or excluding income from Puerto Rico Total of all foreign taxes is not more that $300 (or $600 if married filing jointly) Legally owed, paid to a country recognized by the United States, paid to a country that does not support terrorism 30

31 TaxSlayer Foreign Tax Credit (4012 G-1 & G-2) Federal Section > Deductions 31

32 TaxSlayer Foreign Tax Credit (4012 G-1 & G-2) 32

33 TaxSlayer Foreign Tax Credit (4012 G-1 & G-2) 33

34 Schedule K-1 (4012 D-47 to D-49) Reports taxpayer s share of income and other distributions, deductions, and credits from partnerships, S corporations, and some estates and trusts Limited Schedule K-1 income topics (and reporting forms) are in scope Interest income (Form 1040, line 8a, unless Schedule B is required) Dividend income (Form 1040, line 9a, unless Schedule B is required) Qualified Dividends income (1040, line 9b) Net short-term capital gains and losses (Schedule D, line 5) Net long-term capital gains and losses (Schedule D, line 12) Tax-exempt interest income (Form 1040, line 8b) Royalty income (Schedule E) only in scope if the source document is a Schedule K-1 or Form 1099-MISC, Box 2, Royalties, with no associated expenses Foreign tax paid Income Schedules K-1 and Rental 34

35 Schedule K-1 (4012 D-47 to D-49)... 35

36 Schedule K-1 (4012 D-47 to D-49) 36

37 Schedule K-1 (4012 D-47 to D-49) 37

38 Schedule K-1 (4012 D-47 to D-49) 38

39 Summary Foreign Tax Credit and Schedule K-1 In this lesson, you learned how volunteers with Advanced certification can claim a foreign tax credit for a client when the foreign tax paid is reported on a 1099-INT, 1099-DIV or Schedule K-1. Volunteers can report income from Schedule K-1 when the Sched K-1 contains only limited types of income: Interest income Dividend income Qualified Dividends income Net short-term capital gains and losses Net long-term capital gains and losses Tax-exempt interest income Royalty income Otherwise, return is out of scope. Income Capital Gain or Loss; Form 1040, Line 13 39

OUT OF SCOPE - VITA 2017 TAX YEAR The following are out of scope. While this list may not be all inclusive, it is provided for your awareness only.

The following are out of scope. While this list may not be all inclusive, it is provided for your awareness only. Legislative Extenders Residential energy-efficient property credit (Form 5695, Part I)

The following are out of scope. While this list may not be all inclusive, it is provided for your awareness only. Legislative Extenders Residential energy-efficient property credit (Form 5695, Part I)

Sale of Personal Residence. Form 1040 Line 13 Pub 4012 Tab D Pg Pub 4491 Part 3 Lesson 11

Sale of Personal Residence Form 1040 Line 13 Pub 4012 Tab D Pg 28-32 Pub 4491 Part 3 Lesson 11 The Interview Question 3 in Life Events section COD is out of scope this tax season Home can be a second home

Sale of Personal Residence Form 1040 Line 13 Pub 4012 Tab D Pg 28-32 Pub 4491 Part 3 Lesson 11 The Interview Question 3 in Life Events section COD is out of scope this tax season Home can be a second home

Capital Gain or Loss. Introduction. Capital Asset Taxation. Introduction. Capital Asset Taxation. What is a Capital Asset

Introduction Capital Gain or Loss Form 1040 Line 13 Pub 4012 Tab D Pub 4491 Part 3 Lesson 11 What is a capital gain? It s the taxpayer s profit when they sell a capital asset for more than they have in

Introduction Capital Gain or Loss Form 1040 Line 13 Pub 4012 Tab D Pub 4491 Part 3 Lesson 11 What is a capital gain? It s the taxpayer s profit when they sell a capital asset for more than they have in

Capital Asset Taxation Introduction

Capital Asset Taxation Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually 0% or 15% rate Could be 20% rate for very high incomes NTTC Training

Capital Asset Taxation Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually 0% or 15% rate Could be 20% rate for very high incomes NTTC Training

Capital Gain or Loss

Capital Gain or Loss Form 1040 Line 13 Pub 4012 Tab D Pages 22-27 Pub 4491 Part 3 Lesson 11 The Interview Question 9 in Income section Question 3 in Life Events section 2 1 In Scope Capital Assets Stocks

Capital Gain or Loss Form 1040 Line 13 Pub 4012 Tab D Pages 22-27 Pub 4491 Part 3 Lesson 11 The Interview Question 9 in Income section Question 3 in Life Events section 2 1 In Scope Capital Assets Stocks

Capital Gain or Loss

Capital Gain or Loss Form 1040 Line 13 Pub 4012 D 13 Pub 4491 Page 89 Capital Asset Taxation Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually

Capital Gain or Loss Form 1040 Line 13 Pub 4012 D 13 Pub 4491 Page 89 Capital Asset Taxation Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually

Capital Gain or Loss. Form 1040 Line 13 Pub 4012 Tab D Pages Pub 4491 Part 3 Lesson 11

Capital Gain or Loss Form 1040 Line 13 Pub 4012 Tab D Pages 22-27 Pub 4491 Part 3 Lesson 11 Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually

Capital Gain or Loss Form 1040 Line 13 Pub 4012 Tab D Pages 22-27 Pub 4491 Part 3 Lesson 11 Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually

Sale of Personal Residence. Pub 4012 Tab D Pub 4491 Lesson 11

Sale of Personal Residence Pub 4012 Tab D Pub 4491 Lesson 11 The Interview Question 9 in Income section: 9. (A) Income (or loss) from the sale of Stocks, Bonds or Real Estate? (including your home) (Forms

Sale of Personal Residence Pub 4012 Tab D Pub 4491 Lesson 11 The Interview Question 9 in Income section: 9. (A) Income (or loss) from the sale of Stocks, Bonds or Real Estate? (including your home) (Forms

Capital Gain or Loss. Pub 4012 Tab D Pub 4491 Lesson 11

Capital Gain or Loss Pub 4012 Tab D Pub 4491 Lesson 11 Introduction Ordinary income tax rates range from 10% to 37% Capital gain tax rates are much lower Usually 0% or 15% rate Could be 20% rate for very

Capital Gain or Loss Pub 4012 Tab D Pub 4491 Lesson 11 Introduction Ordinary income tax rates range from 10% to 37% Capital gain tax rates are much lower Usually 0% or 15% rate Could be 20% rate for very

Instructions for Form 5405 (Rev. March 2011) First-Time Homebuyer Credit and Repayment of the Credit For use with Form 5405 (Rev.

First-Time Homebuyer Credit and Repayment of the Credit For use with Form 5405 (Rev.") Instructions for Form 5405 (Rev. March 2011) First-Time Homebuyer Credit and Repayment of the Credit For use with Form 5405 (Rev. December 2010) Department of the Treasury Internal Revenue Service Section

Instructions for Form 5405 (Rev. March 2011) First-Time Homebuyer Credit and Repayment of the Credit For use with Form 5405 (Rev. December 2010) Department of the Treasury Internal Revenue Service Section

Helpful Tips. for Out of Scope Topics. on the 2014 IRS Advanced Certification Exam

Helpful Tips for Out of Scope Topics on the 2014 IRS Advanced Certification Exam HELPFUL TIPS FOR OUT OF SCOPE TOPICS ON 2014 IRS ADVANCED CERTIFICATION EXAM (Out Of Scope For SaveFirst Intermediate Volunteer

Helpful Tips for Out of Scope Topics on the 2014 IRS Advanced Certification Exam HELPFUL TIPS FOR OUT OF SCOPE TOPICS ON 2014 IRS ADVANCED CERTIFICATION EXAM (Out Of Scope For SaveFirst Intermediate Volunteer

H E L P F U L T I P S F O R O U T O F S C O P E T O P I C S O N T H E I R S A D V A N C E D C E R T I F I C A T I O N E X A M

H E L P F U L T I P S F O R O U T O F S C O P E T O P I C S O N T H E 2 0 1 7 I R S A D V A N C E D C E R T I F I C A T I O N E X A M OUT OF S COPE FOR S AV EFIRST INTERMEDIATE VOLUNTEERS AT TAX PR EPAR

H E L P F U L T I P S F O R O U T O F S C O P E T O P I C S O N T H E 2 0 1 7 I R S A D V A N C E D C E R T I F I C A T I O N E X A M OUT OF S COPE FOR S AV EFIRST INTERMEDIATE VOLUNTEERS AT TAX PR EPAR

2017 Instructions for Schedule D

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule D Capital Gains and Losses These instructions explain how to complete Schedule D (Form 1040). Complete Form 8949 before

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule D Capital Gains and Losses These instructions explain how to complete Schedule D (Form 1040). Complete Form 8949 before

Internal Revenue Code Section 121(d)(10) Exclusion of gain from sale of principal residence.

(10) Exclusion of gain from sale of principal residence.") Internal Revenue Code Section 121(d)(10) Exclusion of gain from sale of principal residence. CLICK HERE to return to the home page (a) Exclusion. Gross income shall not include gain from the sale or exchange

Internal Revenue Code Section 121(d)(10) Exclusion of gain from sale of principal residence. CLICK HERE to return to the home page (a) Exclusion. Gross income shall not include gain from the sale or exchange

The VITA TaxSlayer Map

The purpose of this tool is to help tax preparers and reviewers locate most tax return items in TaxSlayer Pro Online. The objective is to lay out the menu structures of each section of a return so that

The purpose of this tool is to help tax preparers and reviewers locate most tax return items in TaxSlayer Pro Online. The objective is to lay out the menu structures of each section of a return so that

A Comprehensive Guide to your Composite Tax Statement

A Comprehensive Guide to your Composite Tax Statement Hilltop Securities does not provide tax advice. This material is presented for informational purposes only. You should consult your tax advisor on

A Comprehensive Guide to your Composite Tax Statement Hilltop Securities does not provide tax advice. This material is presented for informational purposes only. You should consult your tax advisor on

Itemized Deductions. Attach to Form See Instructions for Schedule A (Form 1040). Your social security number ROBERT RAMOS

. Your social security number ROBERT RAMOS") SCHEDULE A (Form 14) Name(s) shown on Form 14 Itemized Deductions Attach to Form 14. See Instructions for Schedule A (Form 14). Medical Caution. Do not include expenses reimbursed or paid by others. and

SCHEDULE A (Form 14) Name(s) shown on Form 14 Itemized Deductions Attach to Form 14. See Instructions for Schedule A (Form 14). Medical Caution. Do not include expenses reimbursed or paid by others. and

State Income Tax Refunds

State Income Tax Refunds Form 1040 Line 10 Pub 4491 Part 3 Lesson 9 Pub 4012 Page D 12 The Interview Point of awareness From 2016 returns 2 1 State Income Tax Refunds Form 1099-G State or local income

State Income Tax Refunds Form 1040 Line 10 Pub 4491 Part 3 Lesson 9 Pub 4012 Page D 12 The Interview Point of awareness From 2016 returns 2 1 State Income Tax Refunds Form 1099-G State or local income

Tax Organizer. Please Complete And Bring This Organizer To Your Tax Appointment. Tax Year

Affix Address Label Tax Organizer Tax Year Please Complete And Bring This Organizer To Your Tax Appointment We are pleased to have you joining us this tax season. Thank you for completing your tax organizer,

Affix Address Label Tax Organizer Tax Year Please Complete And Bring This Organizer To Your Tax Appointment We are pleased to have you joining us this tax season. Thank you for completing your tax organizer,

Name of Fiduciary - Compliance Test Acco Name of Fiduciary - Continued Line Midway Rd Carrollton, TX 75006

+ DIAGNOSTIC REPORT TRUST NAME: FEDERAL EIN: TRUST NUMBER: DIOBREF ** No Severe Diagnostics Detected ** ** No Informational Diagnostics Detected ** XD571 1000 SV0631 L605 01/18/2016 19:19:08 DIOBREF +

+ DIAGNOSTIC REPORT TRUST NAME: FEDERAL EIN: TRUST NUMBER: DIOBREF ** No Severe Diagnostics Detected ** ** No Informational Diagnostics Detected ** XD571 1000 SV0631 L605 01/18/2016 19:19:08 DIOBREF +

AARP FOUNDATION TAX-AIDE SCOPE MANUAL WHAT S IN WHAT S OUT

AARP Foundation Tax-Aide helps low and moderate income taxpayers, with special attention to those 60 and older. Volunteers are trained to assist in filing Form 1040 and certain other schedules and forms.

AARP Foundation Tax-Aide helps low and moderate income taxpayers, with special attention to those 60 and older. Volunteers are trained to assist in filing Form 1040 and certain other schedules and forms.

2001 Instructions for Schedule D, Capital Gains and Losses

2001 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

2001 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

Summary Unless Congress acts to extend the first-time homebuyer tax credit, November 30, 2009, is the last day on which a taxpayer may purchase a prin

Carol A. Pettit Legislative Attorney September 30, 2009 Congressional Research Service CRS Report for Congress Prepared for Members and Committees of Congress 7-5700 www.crs.gov RL34664 c11173008 Summary

Carol A. Pettit Legislative Attorney September 30, 2009 Congressional Research Service CRS Report for Congress Prepared for Members and Committees of Congress 7-5700 www.crs.gov RL34664 c11173008 Summary

Impact of Tax Reform on Farmers. Tax and Accounting Department Fall 2018

Impact of Tax Reform on Farmers Tax and Accounting Department Fall 2018 Agenda Summary of Tax Reform Individual Business Tax Planning with Business Structure Important Items on a Farm Tax Return Disclaimer

Impact of Tax Reform on Farmers Tax and Accounting Department Fall 2018 Agenda Summary of Tax Reform Individual Business Tax Planning with Business Structure Important Items on a Farm Tax Return Disclaimer

THE NEW YORK TAX GROUP

Important Federal Tax Due Dates 2018 Tax Returns for Taxpayers subject to Unlimited Tax Liability (Page 3) Information Returns & Reporting for Taxpayers subject to Unlimited Tax Liability (Page 4) Tax

Important Federal Tax Due Dates 2018 Tax Returns for Taxpayers subject to Unlimited Tax Liability (Page 3) Information Returns & Reporting for Taxpayers subject to Unlimited Tax Liability (Page 4) Tax

FIDUCIARY TAX ORGANIZER FORM 1041

FIDUCIARY TAX ORGANIZER FORM 1041 Enclosed is an organizer that I provide to my tax clients in order to assist them in gathering the information necessary to prepare their fiduciary income tax returns.

FIDUCIARY TAX ORGANIZER FORM 1041 Enclosed is an organizer that I provide to my tax clients in order to assist them in gathering the information necessary to prepare their fiduciary income tax returns.

Welcome & Happy New Year Refresher Training 5-8 Jan 2016 Part 2

Welcome & Happy New Year Refresher Training 5-8 Jan 2016 Part 2 1 Review of Tax Laws and TaxWise Use 2 Elements of Fed 1040 & MA Form 1 Tax Returns Taxpayer information (incl health ins.) Dependents Filing

Welcome & Happy New Year Refresher Training 5-8 Jan 2016 Part 2 1 Review of Tax Laws and TaxWise Use 2 Elements of Fed 1040 & MA Form 1 Tax Returns Taxpayer information (incl health ins.) Dependents Filing

Instructions for Form 1116

Department of the Treasury Internal Revenue Service Instructions for Form 1116 Foreign Tax Credit (Individual, Estate, Trust, or Nonresident Alien Individual) Section references are to the Internal Revenue

Department of the Treasury Internal Revenue Service Instructions for Form 1116 Foreign Tax Credit (Individual, Estate, Trust, or Nonresident Alien Individual) Section references are to the Internal Revenue

LINE 13 CAPITAL GAIN AND LOSSES (SCHEDULE D) LINE 16 PENSIONS AND ANNUITIES LINE 17 RENTAL REAL ESTATE, ROYALTIES LINE 20 SOCIAL SECURITY BENEFITS

LINE 16 PENSIONS AND ANNUITIES LINE 17 RENTAL REAL ESTATE, ROYALTIES LINE 20 SOCIAL SECURITY BENEFITS") LINE 13 CAPITAL GAIN AND LOSSES (SCHEDULE D) LINE 15 IRA DISTRIBUTIONS LINE 16 PENSIONS AND ANNUITIES LINE 17 RENTAL REAL ESTATE, ROYALTIES LINE 19 UNEMPLOYMENT LINE 20 SOCIAL SECURITY BENEFITS LINE 21

LINE 13 CAPITAL GAIN AND LOSSES (SCHEDULE D) LINE 15 IRA DISTRIBUTIONS LINE 16 PENSIONS AND ANNUITIES LINE 17 RENTAL REAL ESTATE, ROYALTIES LINE 19 UNEMPLOYMENT LINE 20 SOCIAL SECURITY BENEFITS LINE 21

Income. Taxwise Online. IRS Training Workbook

Income Taxwise Online IRS Training Workbook I N C O ME IRS Training Workbook 2012 CCH Small Firm Services. All rights reserved. 225 Chastain Meadows Court NW Suite 200 Kennesaw, Georgia 30144 Information

Income Taxwise Online IRS Training Workbook I N C O ME IRS Training Workbook 2012 CCH Small Firm Services. All rights reserved. 225 Chastain Meadows Court NW Suite 200 Kennesaw, Georgia 30144 Information

Changes to Fall 2018 Mass Manual

Changes to Fall 2018 Mass Manual Changes and errata to the Fall 2018 Mass Manual are listed below. These resulted from changes to the TaxSlayer 2018 Massachusetts software which was released on 5 January

Changes to Fall 2018 Mass Manual Changes and errata to the Fall 2018 Mass Manual are listed below. These resulted from changes to the TaxSlayer 2018 Massachusetts software which was released on 5 January

Shareholder's Instructions for Schedule K-1 (Form 1120S)

") 2017 Shareholder's Instructions for Schedule K-1 (Form 1120S) Shareholder's Share of Income, Deductions, Credits, etc. (For Shareholder's Use Only) Department of the Treasury Internal Revenue Service Section

2017 Shareholder's Instructions for Schedule K-1 (Form 1120S) Shareholder's Share of Income, Deductions, Credits, etc. (For Shareholder's Use Only) Department of the Treasury Internal Revenue Service Section

State/Local Income Tax Refunds and Other Recoveries. Pub 4012 Tab D Pub 4491 Lesson 9

State/Local Income Tax Refunds and Other Recoveries Pub 4012 Tab D Pub 4491 Lesson 9 State Tax Refund Point of awareness Form 1099-G State or local income tax refund 2 Recoveries in General In a prior

State/Local Income Tax Refunds and Other Recoveries Pub 4012 Tab D Pub 4491 Lesson 9 State Tax Refund Point of awareness Form 1099-G State or local income tax refund 2 Recoveries in General In a prior

Personal Information 3

Personal Information 3 Taxpayer: First Name and Initial Last Name Social Security Number Occupation Date of Birth (Mo/Da/Yr) Date of Death (Mo/Da/Yr) Spouse: First Name and Initial Last Name Social Security

Personal Information 3 Taxpayer: First Name and Initial Last Name Social Security Number Occupation Date of Birth (Mo/Da/Yr) Date of Death (Mo/Da/Yr) Spouse: First Name and Initial Last Name Social Security

Volunteer Income Tax Assistance Part 3. Income

Volunteer Income Tax Assistance Part 3 Income Gross Income The Tax Return Get to know the 1040 page one and two Who NEEDS to file? Consider their age, filing status, and income: Filing Status Gross Income

Volunteer Income Tax Assistance Part 3 Income Gross Income The Tax Return Get to know the 1040 page one and two Who NEEDS to file? Consider their age, filing status, and income: Filing Status Gross Income

Tax Year 2017 Form 1099-DIV/B Guide

Tax Year 2017 Form 1099-DIV/B Guide Form 1099 FAQs Q: WHAT SHOULD I DO UPON RECEIVING MY FORM 1099? A: Upon receiving your form please review the data carefully. Also be sure to check the tax identification

Tax Year 2017 Form 1099-DIV/B Guide Form 1099 FAQs Q: WHAT SHOULD I DO UPON RECEIVING MY FORM 1099? A: Upon receiving your form please review the data carefully. Also be sure to check the tax identification

1040 Quickfinder Handbook (2010 Tax Year) Page Updates for the 2010 Tax Relief Act

Page Updates for the 2010 Tax Relief Act") 040 Quickfinder Handbook (200 Tax Year) Page Updates for the 200 Tax Relief Act Instructions: This packet contains marked up changes to the pages in the 040 Quickfinder Handbook that were affected by the

040 Quickfinder Handbook (200 Tax Year) Page Updates for the 200 Tax Relief Act Instructions: This packet contains marked up changes to the pages in the 040 Quickfinder Handbook that were affected by the

State/Local Income Tax Refunds. Form 1040 Line 10 Pub 4491 Part 3 Lesson 9 Pub 4012 Page D 12

State/Local Income Tax Refunds Form 1040 Line 10 Pub 4491 Part 3 Lesson 9 Pub 4012 Page D 12 Recoveries In a prior year, you Paid an expense, and Deducted the expense, and Your taxes were reduced. In current

State/Local Income Tax Refunds Form 1040 Line 10 Pub 4491 Part 3 Lesson 9 Pub 4012 Page D 12 Recoveries In a prior year, you Paid an expense, and Deducted the expense, and Your taxes were reduced. In current

1998 Instructions for Schedule D, Capital Gains and Losses

1998 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report: The sale or exchange of a capital asset (defined on this page). Gains from involuntary conversions (other

1998 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report: The sale or exchange of a capital asset (defined on this page). Gains from involuntary conversions (other

Interest and Dividend Income. Pub 4012 Tab D Pub 4491 Lesson 9

Interest and Dividend Income Pub 4012 Tab D Pub 4491 Lesson 9 Interest and Dividend Income Interest Income US Savings Bonds and Treasury Obligation Interest Tax exempt interest Interest in a foreign bank

Interest and Dividend Income Pub 4012 Tab D Pub 4491 Lesson 9 Interest and Dividend Income Interest Income US Savings Bonds and Treasury Obligation Interest Tax exempt interest Interest in a foreign bank

. Your completed tax organizer needs to be received no later than

Organizer Estate and trust This organizer is designed to assist you in gathering the information required for preparation of fiduciary tax returns. Please complete it in full and provide details and documentation

Organizer Estate and trust This organizer is designed to assist you in gathering the information required for preparation of fiduciary tax returns. Please complete it in full and provide details and documentation

Shareholder's Instructions for Schedule K-1 (Form 1120S)

") 2016 Shareholder's Instructions for Schedule K-1 (Form 1120S) Shareholder's Share of Income, Deductions, Credits, etc. (For Shareholder's Use Only) Department of the Treasury Internal Revenue Service Section

2016 Shareholder's Instructions for Schedule K-1 (Form 1120S) Shareholder's Share of Income, Deductions, Credits, etc. (For Shareholder's Use Only) Department of the Treasury Internal Revenue Service Section

THE TAXATION OF INDIVIDUALS AND FAMILIES

THE TAXATION OF INDIVIDUALS AND FAMILIES Scheduled for a Public Hearing Before the TAX POLICY SUBCOMMITTEE of the HOUSE COMMITTEE ON WAYS AND MEANS on July 19, 2017 Prepared by the Staff of the JOINT COMMITTEE

THE TAXATION OF INDIVIDUALS AND FAMILIES Scheduled for a Public Hearing Before the TAX POLICY SUBCOMMITTEE of the HOUSE COMMITTEE ON WAYS AND MEANS on July 19, 2017 Prepared by the Staff of the JOINT COMMITTEE

2018 TAX ORGANIZER. This tax organizer has been prepared for your use in gathering the information needed for your 2018 tax return.

F R O M 2018 TAX ORGANIZER T O This tax organizer has been prepared for your use in gathering the information needed for your 2018 tax return. To save you time, selected information from your 2017 tax

F R O M 2018 TAX ORGANIZER T O This tax organizer has been prepared for your use in gathering the information needed for your 2018 tax return. To save you time, selected information from your 2017 tax

Welcome December Tax Training For New Volunteers. 6-8 Dec 2016

Welcome December Tax Training For New Volunteers 6-8 Dec 2016 1 Handouts Presentation charts Instructions for logging into 2015 TaxSlayer Practice Lab (training) are included IRS Pubs or excerpts for studying

Welcome December Tax Training For New Volunteers 6-8 Dec 2016 1 Handouts Presentation charts Instructions for logging into 2015 TaxSlayer Practice Lab (training) are included IRS Pubs or excerpts for studying

NORTHERN FUNDS TA X GUIDE 2O14

NORTHERN FUNDS TA X GUIDE 2O14 Contents 1 Mutual Fund Distributions 2 Forms & Statements 4 Form 1099 DIV 5 Form 1099 B 6 Form 1099 R WELCOME TO YOUR NORTHERN FUNDS TAX GUIDE To help you prepare your tax

NORTHERN FUNDS TA X GUIDE 2O14 Contents 1 Mutual Fund Distributions 2 Forms & Statements 4 Form 1099 DIV 5 Form 1099 B 6 Form 1099 R WELCOME TO YOUR NORTHERN FUNDS TAX GUIDE To help you prepare your tax

A & B Office. Education Benefits. A Self-Improvement Mini-Course. Student Loan Interest & Education Expenses. Income Tax Training School

A & B Office Income Tax Training School Education Benefits Student Loan Interest & Education Expenses Key Features: Learn how to properly calculate education expenses. Step-by-step description of the education

A & B Office Income Tax Training School Education Benefits Student Loan Interest & Education Expenses Key Features: Learn how to properly calculate education expenses. Step-by-step description of the education

Income Tax Organizer Instructions

Income Tax Organizer Instructions Our Tax Organizer is designed to help you gather the proper tax information required to prepare your tax return. Please fill out completely all areas that pertain to you.

Income Tax Organizer Instructions Our Tax Organizer is designed to help you gather the proper tax information required to prepare your tax return. Please fill out completely all areas that pertain to you.

Selling Your Home. Future Developments. Reminders. Contents. Publication 523 Cat. No W. For use in preparing 2013 Returns

This publication is cited in an endnote in an article on the Bradford Tax Institute. Department of the Treasury Internal Revenue Service Publication 523 Cat. No. 15044W Selling Your Home For use in preparing

This publication is cited in an endnote in an article on the Bradford Tax Institute. Department of the Treasury Internal Revenue Service Publication 523 Cat. No. 15044W Selling Your Home For use in preparing

NTTC Modifications to the IRS Training Guide 2018 Returns Publication 4491

For volunteers using the hard copy of Pub 4491, the following recaps the modifications that were made to the electronic version available on the Volunteer Portal Library. Use this document in conjunction

For volunteers using the hard copy of Pub 4491, the following recaps the modifications that were made to the electronic version available on the Volunteer Portal Library. Use this document in conjunction

Hickman & Hickman, PLLC 1248 Freiheit Rd, #200, New Braunfels, TX 78130

Hickman & Hickman, PLLC 1248 Freiheit Rd, #200, New Braunfels, TX 78130 This organizer is designed to help clients identify items needed to thoroughly prepare individual income tax returns. Please check

Hickman & Hickman, PLLC 1248 Freiheit Rd, #200, New Braunfels, TX 78130 This organizer is designed to help clients identify items needed to thoroughly prepare individual income tax returns. Please check

Income Tax Organizer Instructions

Income Tax Organizer Instructions Our Tax Organizer is designed to help you gather the proper tax information required to prepare your tax return. Please fill out completely all areas that pertain to you.

Income Tax Organizer Instructions Our Tax Organizer is designed to help you gather the proper tax information required to prepare your tax return. Please fill out completely all areas that pertain to you.

Amended Returns Prior Year Returns. Pub 4012 Tab M Pub 4491 Part 9 Lesson 34

Amended Returns Prior Year Returns Pub 4012 Tab M Pub 4491 Part 9 Lesson 34 Why Amend a Return Something not correctly reported on original return New/updated information received by taxpayer Should or

Amended Returns Prior Year Returns Pub 4012 Tab M Pub 4491 Part 9 Lesson 34 Why Amend a Return Something not correctly reported on original return New/updated information received by taxpayer Should or

Partner's Instructions for Schedule K-1 (Form 1065)

") 2017 Partner's Instructions for Schedule K-1 (Form 1065) Partner's Share of Income, Deductions, Credits, etc. (For Partner's Use Only) Department of the Treasury Internal Revenue Service Section references

2017 Partner's Instructions for Schedule K-1 (Form 1065) Partner's Share of Income, Deductions, Credits, etc. (For Partner's Use Only) Department of the Treasury Internal Revenue Service Section references

1. Determination of gain or loss. 2. Basis considerations. 3. Definition of a capital asset. 6. Sale or exchange. 7.

Outline 1 Unit09. Property Transactions: Capital Gains and Losses (PAK Chap. 5) This unit examines the tax consequences of property transactions. A property transaction includes sale, exchange, or abandonment

Outline 1 Unit09. Property Transactions: Capital Gains and Losses (PAK Chap. 5) This unit examines the tax consequences of property transactions. A property transaction includes sale, exchange, or abandonment

Shareholder s Share of Income, Deductions, Credits, etc.

Schedule K-1 (Form 1120S) Department of the Treasury Internal Revenue Service 2010 For calendar year 2010, or tax year beginning, 2010 ending, 20 Shareholder s Share of Income, Deductions, Credits, etc.

Schedule K-1 (Form 1120S) Department of the Treasury Internal Revenue Service 2010 For calendar year 2010, or tax year beginning, 2010 ending, 20 Shareholder s Share of Income, Deductions, Credits, etc.

Instructions for Form 8949

This form is referenced in an endnote at the Bradford Tax Institute. CLICK HERE to go to the home page. 2015 Instructions for Form 8949 Sales and Other Dispositions of Capital Assets Department of the

This form is referenced in an endnote at the Bradford Tax Institute. CLICK HERE to go to the home page. 2015 Instructions for Form 8949 Sales and Other Dispositions of Capital Assets Department of the

FIDUCIARY TAX ORGANIZER (FORM 1041)

") Trust/Estate Name(s) Federal ID# Address City, Town, or Post Office County State ZIP Code Telephone Number Telephone Number Fax Number E-mail Address Home/Mobile Office Fiduciary Name(s) and Title(s) Federal

Trust/Estate Name(s) Federal ID# Address City, Town, or Post Office County State ZIP Code Telephone Number Telephone Number Fax Number E-mail Address Home/Mobile Office Fiduciary Name(s) and Title(s) Federal

A Comprehensive Guide to Your Composite 1099 Tax Statement

A Comprehensive Guide to Your 2016 Composite 1099 Tax Statement Table of Contents A Note from Hilliard Lyons... 1 Tax Information Reporting and Our Obligation to Clients... 2 What s New This Year and Important

A Comprehensive Guide to Your 2016 Composite 1099 Tax Statement Table of Contents A Note from Hilliard Lyons... 1 Tax Information Reporting and Our Obligation to Clients... 2 What s New This Year and Important

Personal Information

Form ID: 1040 Personal Information 1 Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er)) Mark if you were married

Form ID: 1040 Personal Information 1 Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er)) Mark if you were married

TAX ORGANIZER. If you answer 'Yes' to any of the General Business and Investment questions, please provide detailed information with your answer.

TAX ORGANIZER Enclosed is your Tax Organizer for tax year 2011. Your Organizer contains several sections that include common expenses and deductions that many taxpayers overlook. Please review these sections

TAX ORGANIZER Enclosed is your Tax Organizer for tax year 2011. Your Organizer contains several sections that include common expenses and deductions that many taxpayers overlook. Please review these sections

ESTATE OR TRUST TAX ORGANIZER FORM New Estate or Trust Administrators Information Needed

ESTATE OR TRUST TAX ORGANIZER FORM 1041 New Estate or Trust Administrators Information Needed This is a list of information which will be typically needed for us to work with you on tax issues for an estate

ESTATE OR TRUST TAX ORGANIZER FORM 1041 New Estate or Trust Administrators Information Needed This is a list of information which will be typically needed for us to work with you on tax issues for an estate

97 Partner's Instructions for Schedule K-1 (Form 1065)

") 97 Department Partner's Instructions for Schedule K-1 (Form 1065) Partner's Share of Income, Credits, Deductions, etc. (For Partner's Use Only) Section references are to the Internal Revenue Code unless

97 Department Partner's Instructions for Schedule K-1 (Form 1065) Partner's Share of Income, Credits, Deductions, etc. (For Partner's Use Only) Section references are to the Internal Revenue Code unless

DeSain Financial Services 2018 Tax Questionnaire

Last Name: Last Name: Taxpayer First Name & Middle Initial: Taxpayer Social Security Number: Taxpayer First Name & Middle Initial: Social Security Number: Address: City, State, Zip: Home Phone: Work Phone:

Last Name: Last Name: Taxpayer First Name & Middle Initial: Taxpayer Social Security Number: Taxpayer First Name & Middle Initial: Social Security Number: Address: City, State, Zip: Home Phone: Work Phone:

2002 Instructions for Schedule D, Capital Gains and Losses

2002 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

2002 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

Selling Your Home. Future Developments. Reminders. Contents. Publication 523 Cat. No W. For use in preparing 2012 Returns

Department of the Treasury Internal Revenue Service Publication 523 Cat. No. 15044W Selling Your Home For use in preparing 2012 Returns Contents Reminders... 1 Introduction... 2 Main Home... 3 Figuring

Department of the Treasury Internal Revenue Service Publication 523 Cat. No. 15044W Selling Your Home For use in preparing 2012 Returns Contents Reminders... 1 Introduction... 2 Main Home... 3 Figuring

Small Business Accounting & Complete Income Tax Services

Small Business Accounting & Complete Income Tax Services email: info@accountingconsortium.com www.accountingconsortium.com Bay Creek Business Center 305 Cooper Road, Ste 200 Loganville, GA 30052 Ph: 678.696.0829

Small Business Accounting & Complete Income Tax Services email: info@accountingconsortium.com www.accountingconsortium.com Bay Creek Business Center 305 Cooper Road, Ste 200 Loganville, GA 30052 Ph: 678.696.0829

PARTNERSHIP/LLC TAX ORGANIZER Form 1065

Enclosed is an organizer that I (we) provide to our tax clients to assist in gathering the information necessary to prepare the current year tax returns. The Internal Revenue Service matches information

Enclosed is an organizer that I (we) provide to our tax clients to assist in gathering the information necessary to prepare the current year tax returns. The Internal Revenue Service matches information

Attention: See IRS Publications 1141, 1167, 1179 and other IRS resources for information about printing these tax forms.

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

Attention: This form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. Do not file copy A downloaded from this website. The official printed version

2018 tax planning guide

Advanced Planning 2018 tax planning guide We are committed to helping you confirm that your current and future tax strategy supports your larger financial goals. Advice. Beyond investing. Your financial

Advanced Planning 2018 tax planning guide We are committed to helping you confirm that your current and future tax strategy supports your larger financial goals. Advice. Beyond investing. Your financial

TAX YEAR 2017 FORM 1099 COMPOSITE & YEAR-END SUMMARY

FORM 1099 COMPOSITE & Recipient s Name and Address Your Consultant C/O SAMPLE GLOBAL ENTERPRISE 3RD FLOOR, SUITE 1800 1234 MAIN STREET ANYTOWN, US 12345 JOHN Q. ADVISOR VP FINANCIAL CONSULTANT 1 (907)

FORM 1099 COMPOSITE & Recipient s Name and Address Your Consultant C/O SAMPLE GLOBAL ENTERPRISE 3RD FLOOR, SUITE 1800 1234 MAIN STREET ANYTOWN, US 12345 JOHN Q. ADVISOR VP FINANCIAL CONSULTANT 1 (907)

Partner s Instructions for Schedule K-1 (Form 1065-B) Partner s Share of Income (Loss) From an Electing Large Partnership (For Partner s Use Only)

Partner s Share of Income (Loss) From an Electing Large Partnership (For Partner s Use Only)") 2008 Partner s Instructions for Schedule K-1 (Form 1065-B) Partner s Share of Income (Loss) From an Electing Large Partnership (For Partner s Use Only) Section references are to the Internal Revenue Code

2008 Partner s Instructions for Schedule K-1 (Form 1065-B) Partner s Share of Income (Loss) From an Electing Large Partnership (For Partner s Use Only) Section references are to the Internal Revenue Code

NORTHERN FUNDS TA X GUIDE 2O12

NORTHERN FUNDS TA X GUIDE 2O12 Contents 1 Mutual Fund Distributions 2 Forms & Statements 4 Form 1099 DIV 5 Form 1099 B/Cost Basis 6 Form 1099 R 7 Form 1099 Q 8 Form 5498 IRA 9 Form 5498 ESA WELCOME TO

NORTHERN FUNDS TA X GUIDE 2O12 Contents 1 Mutual Fund Distributions 2 Forms & Statements 4 Form 1099 DIV 5 Form 1099 B/Cost Basis 6 Form 1099 R 7 Form 1099 Q 8 Form 5498 IRA 9 Form 5498 ESA WELCOME TO

Attention: See IRS Publications 1141, 1167, 1179, and other IRS resources for information about printing these tax forms.

Attention: Do not download, print, and file Copy A with the IRS. Copy A appears in red, similar to the official IRS form, but is for informational purposes only. A penalty of 50 per information return

Attention: Do not download, print, and file Copy A with the IRS. Copy A appears in red, similar to the official IRS form, but is for informational purposes only. A penalty of 50 per information return

Determining your 2017 stock plan tax requirements a step-by-step guide

Determining your 2017 stock plan tax requirements a step-by-step guide Alert: The tax-reform legislation adopted in December 2017 does not affect the 2017 tax year or the federal tax return for 2017 that

Determining your 2017 stock plan tax requirements a step-by-step guide Alert: The tax-reform legislation adopted in December 2017 does not affect the 2017 tax year or the federal tax return for 2017 that

TAX PLANNING GUIDE 2002/ A065977

2002/2003 TAX PLANNING GUIDE www.prudential.com Prudential Financial is a service mark of The Prudential Insurance Company of America, Newark, NJ, and its affiliates. August 2002 TAX100 A065977 Securities

2002/2003 TAX PLANNING GUIDE www.prudential.com Prudential Financial is a service mark of The Prudential Insurance Company of America, Newark, NJ, and its affiliates. August 2002 TAX100 A065977 Securities

Instructions for Form 1099-B

2013 Instructions for Form 1099-B Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. Future Developments For the latest information

2013 Instructions for Form 1099-B Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. Future Developments For the latest information

PROSHARES SAMPLE TAX PACKAGE 7501 WISCONSIN AVE SUITE 1000 BETHESDA, MD PROSHARES. K-1 Account Number:

PROSHARES 750 WISCONSIN AVE SUITE 000 BETHESDA, MD 2084 PROSHARES K- Account Number: 207 SCHEDULE K- SUPPLEMENTAL INFORMATION % of the amount of interest income included on your Schedule K- is from US

PROSHARES 750 WISCONSIN AVE SUITE 000 BETHESDA, MD 2084 PROSHARES K- Account Number: 207 SCHEDULE K- SUPPLEMENTAL INFORMATION % of the amount of interest income included on your Schedule K- is from US

Premium Quickfinder Handbook (2010 Tax Year) Page Updates for the 2010 Tax Relief Act

Page Updates for the 2010 Tax Relief Act") Premium Quickfinder Handbook (2010 Tax Year) Page Updates for the 2010 Tax Relief Act Instructions: This packet contains marked up changes to the pages in the Premium Quickfinder Handbook that were affected

Premium Quickfinder Handbook (2010 Tax Year) Page Updates for the 2010 Tax Relief Act Instructions: This packet contains marked up changes to the pages in the Premium Quickfinder Handbook that were affected

2011 Partner s Instructions for Schedule K-1 (Form 1065) Partner s Share of Income, Deductions, Credits, etc.

Partner s Share of Income, Deductions, Credits, etc.") 2011 Partner s Instructions for Schedule K-1 (Form 1065) Partner s Share of Income, Deductions, Credits, etc. (For Partner s Use Only) Department of the Treasury Internal Revenue Service Section references

2011 Partner s Instructions for Schedule K-1 (Form 1065) Partner s Share of Income, Deductions, Credits, etc. (For Partner s Use Only) Department of the Treasury Internal Revenue Service Section references

Filing Final Income Tax Return for Deceased Person: Mastering Allocations, Understanding IRD and More

Filing Final Income Tax Return for Deceased Person: Mastering Allocations, Understanding IRD and More FOR LIVE PROGRAM ONLY TUESDAY, SEPTEMBER 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Filing Final Income Tax Return for Deceased Person: Mastering Allocations, Understanding IRD and More FOR LIVE PROGRAM ONLY TUESDAY, SEPTEMBER 18, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Partner s Instructions for Schedule K-1 (Form 1065-B)

") 2001 Partner s Instructions for Schedule K-1 (Form 1065-B) Partner s Share of Income (Loss) From an Electing Large Partnership (For Partner s Use Only) Section references are to the Internal Revenue Code

2001 Partner s Instructions for Schedule K-1 (Form 1065-B) Partner s Share of Income (Loss) From an Electing Large Partnership (For Partner s Use Only) Section references are to the Internal Revenue Code

Guide To Your USAA Investment Management Company Mutual Fund Forms 1099 For Tax Year 2017

Guide To Your USAA Investment Management Company Mutual Fund Forms 1099 For Tax Year 2017 We are committed to providing accuracy in reporting tax information related to your USAA mutual fund account(s)

Guide To Your USAA Investment Management Company Mutual Fund Forms 1099 For Tax Year 2017 We are committed to providing accuracy in reporting tax information related to your USAA mutual fund account(s)

Tax Law & Scope Changes Carl Kantner As of December 3, 2018

Tax Law & Scope Changes 2018 Carl Kantner As of December 3, 2018 Tax-Aide Scope Manual The authority for Tax-Aide scope questions Manual for Tax Year 2018 issued November 28 Located in Portal Library under

Tax Law & Scope Changes 2018 Carl Kantner As of December 3, 2018 Tax-Aide Scope Manual The authority for Tax-Aide scope questions Manual for Tax Year 2018 issued November 28 Located in Portal Library under

Instructions for Form 8949

2012 Instructions for Form 8949 Sales and Other Dispositions of Capital Assets Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted.

2012 Instructions for Form 8949 Sales and Other Dispositions of Capital Assets Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted.

Traditional Individual Retirement Account (Trust) Disclosure Statement

Disclosure Statement") Traditional Individual Retirement Account (Trust) Disclosure Statement This Disclosure Statement contains important information about traditional Individual Retirement Accounts ( traditional IRA ) described

Traditional Individual Retirement Account (Trust) Disclosure Statement This Disclosure Statement contains important information about traditional Individual Retirement Accounts ( traditional IRA ) described

Table of Contents EA Exam Part

Table of Contents EA Exam Part 1 2017-18 Introduction... 2 Examination Content Outline... 8 Course Content... 11 Preliminary Work and Taxpayer Data... 12 Preliminary work to prepare tax returns... 12 Use

Table of Contents EA Exam Part 1 2017-18 Introduction... 2 Examination Content Outline... 8 Course Content... 11 Preliminary Work and Taxpayer Data... 12 Preliminary work to prepare tax returns... 12 Use

Americans Living Abroad. 61 Tax Questions you should know.

Americans Living Abroad 61 Tax Questions you should know 1 General FAQs 1. I m a U.S. citizen living and working outside of the United States for many years. Do I still need to file a U.S. tax return?

Americans Living Abroad 61 Tax Questions you should know 1 General FAQs 1. I m a U.S. citizen living and working outside of the United States for many years. Do I still need to file a U.S. tax return?

Chapter 12. Property Transactions: Determination of Gain or Loss,Basis Considerations, and Nontaxable Exchanges

Chapter 12 Property Transactions: Determination of Gain or Loss,Basis Considerations, and Nontaxable Exchanges Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004

Chapter 12 Property Transactions: Determination of Gain or Loss,Basis Considerations, and Nontaxable Exchanges Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004

Taxpayer Questionnaire

Personal Information Select Filing Status (select ONE) Single Married Filing Joint Married Filing Separately Head of Household Qualifying Widow(er). Year spouse died: Help Me Choose Enter Personal Information

Personal Information Select Filing Status (select ONE) Single Married Filing Joint Married Filing Separately Head of Household Qualifying Widow(er). Year spouse died: Help Me Choose Enter Personal Information

Interactive Brokers presents:

Interactive Brokers presents: Understanding your US tax forms - What does your Consolidated 1099 tell you? Nancy A. Nelson CPA Tax Director nnelson@interactivebrokers.com Webinar begins @ 12:00 pm Disclosures

Interactive Brokers presents: Understanding your US tax forms - What does your Consolidated 1099 tell you? Nancy A. Nelson CPA Tax Director nnelson@interactivebrokers.com Webinar begins @ 12:00 pm Disclosures

Tax Organizer For 2014 Income Tax Return

Prepared By: Tax Organizer For 2014 Income Tax Return Prepared For: This Tax Organizer can be used to help identify information needed to prepare your 2014 income tax return. Enter your 2014 tax information

Prepared By: Tax Organizer For 2014 Income Tax Return Prepared For: This Tax Organizer can be used to help identify information needed to prepare your 2014 income tax return. Enter your 2014 tax information

Part 1 - Account Information. Date moved out of city. Filing Status Married filing separately

07LF Return with attachments due by April 7, 08 Account Part - Account Information Social Security Number Name Resident Address Mailing Address Phone Date moved into city Email Spouse Date moved out of

07LF Return with attachments due by April 7, 08 Account Part - Account Information Social Security Number Name Resident Address Mailing Address Phone Date moved into city Email Spouse Date moved out of

Tax Law Changes 2018

Tax Law Changes 2018 Standard Deduction Standard deduction increased to $24,000 MFJ and QW $18,000 HoH $12,000 Single and MFS Pub 4012 Tab F-1 Additional standard deduction amount for age 65 and older

Tax Law Changes 2018 Standard Deduction Standard deduction increased to $24,000 MFJ and QW $18,000 HoH $12,000 Single and MFS Pub 4012 Tab F-1 Additional standard deduction amount for age 65 and older

See Tax-Aide Scope Summary from OneSupport>Tax Training>Scope for differences between Tax-Aide scope and VITA scope.

This document provides how-to information for those items that are in scope for Tax-Aide but out of scope for VITA (and therefore not covered in Pub 4012.) See Tax-Aide Scope Summary from OneSupport>Tax

This document provides how-to information for those items that are in scope for Tax-Aide but out of scope for VITA (and therefore not covered in Pub 4012.) See Tax-Aide Scope Summary from OneSupport>Tax

Itemized Deductions Tax Computation. Pub 4012 Tab F Pub 4491 Part 5 Lessons 20 & 21

Itemized Deductions Tax Computation Pub 4012 Tab F Pub 4491 Part 5 Lessons 20 & 21 Deductions May claim larger of Standard deduction Increased if at least 65 or blind -OR- Itemized deductions If itemized

Itemized Deductions Tax Computation Pub 4012 Tab F Pub 4491 Part 5 Lessons 20 & 21 Deductions May claim larger of Standard deduction Increased if at least 65 or blind -OR- Itemized deductions If itemized

Tax Considerations for Seniors - General Outline

BRAD BORNCAMP, CPA, LLC CERTIFIED PUBLIC ACCOUNTANT CERTIFIED VALUATION ANALYST CERTIFIED FINANCIAL PLANNER Tax Considerations for Seniors - General Outline This outline illustrates some of the areas we

BRAD BORNCAMP, CPA, LLC CERTIFIED PUBLIC ACCOUNTANT CERTIFIED VALUATION ANALYST CERTIFIED FINANCIAL PLANNER Tax Considerations for Seniors - General Outline This outline illustrates some of the areas we

Tax Cuts and Jobs Act of 2017

On December 22, 2017, President Donald Trump signed into law H.R. 1, the Tax Cuts and Jobs Act of 2017 (TCJA). This new tax legislation, slightly over 500 pages in length, is the most significant revision

On December 22, 2017, President Donald Trump signed into law H.R. 1, the Tax Cuts and Jobs Act of 2017 (TCJA). This new tax legislation, slightly over 500 pages in length, is the most significant revision

Hemminger & Associates, Inc. Income Tax Service Please Read!

Dear Client; Hemminger & Associates, Inc. Income Tax Service Please Read! This organizer is for the tax year 2018. Please use it as a guide in gathering together your 2018 tax information. Bring it with

Dear Client; Hemminger & Associates, Inc. Income Tax Service Please Read! This organizer is for the tax year 2018. Please use it as a guide in gathering together your 2018 tax information. Bring it with

7th Correction Run October 10. ***Prior year corrections are included in the above schedule if requested.

Tax Reporting Q: LPL mails the majority of the 1099-C forms on February 15. Isn t this considered late? A: No. In the fall of 2008, the IRS recognized that there was not sufficient time to make the necessary

Tax Reporting Q: LPL mails the majority of the 1099-C forms on February 15. Isn t this considered late? A: No. In the fall of 2008, the IRS recognized that there was not sufficient time to make the necessary