Farm Taxes. David L. Marrison, Associate Professor

|

|

|

- Arnold Wilson

- 6 years ago

- Views:

Transcription

1 Farm Taxes David L. Marrison, Associate Professor

2 Session Objectives Provide a background on how to manage your farm records for ease in completing Schedule F tax returns. Discuss additional federal tax concerns.

3

4

5 Circular 230 Disclosure Pursuant to the requirements of the Internal Revenue Service Circular 230, we inform you that, to the extent any advice relating to a Federal tax issue is contained in this communication, it was not written or intended to be used, and cannot be used, for the purpose of (a) avoiding any tax related penalties that may be imposed on you or any other person under the Internal Revenue Code, or (b) promoting, marketing or recommending to another person any transaction or matter addressed in this communication. The information provided in this presentation is for educational purposes only. This presentation is designed to provide accurate and authoritative information concerning the subject matter covered, but it is communicated with the understanding that the publisher is not engaged in rendering legal, accounting, or other professional services. If legal advice or other expert assistance is required, the services of a competent professional person should be sought.

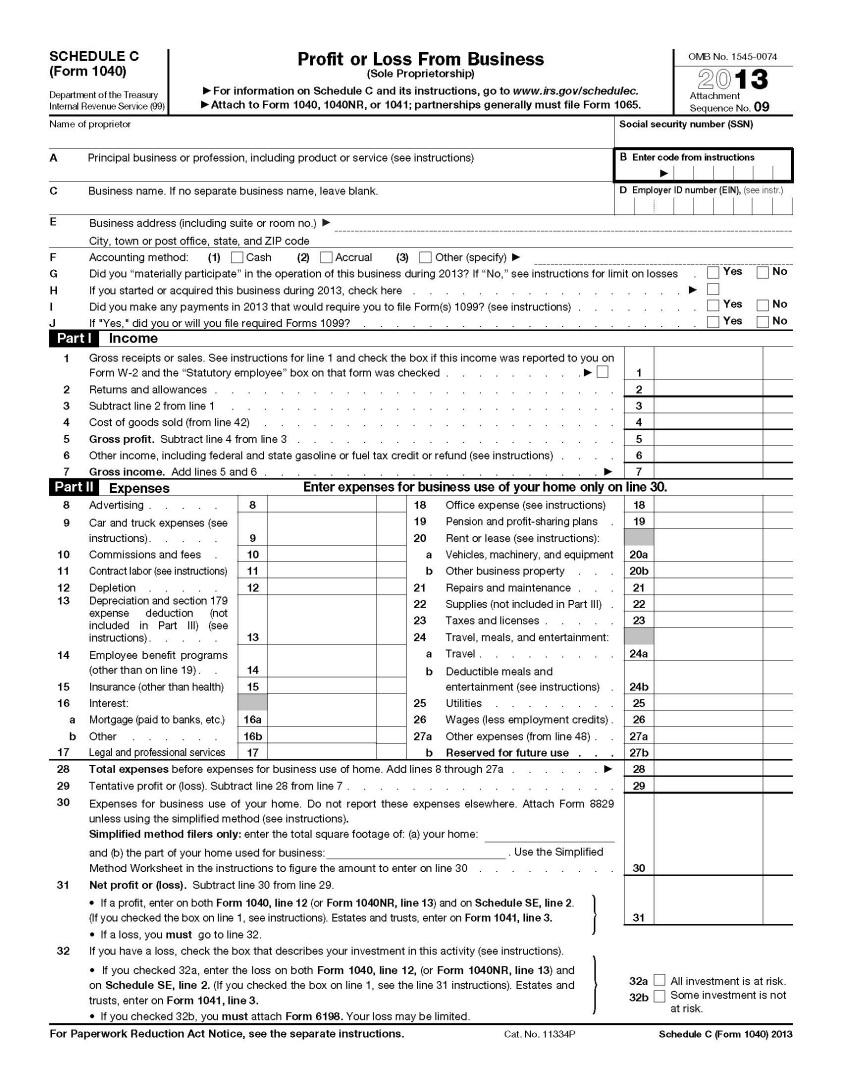

6 Schedule C Schedule E Schedule F W2 Income 1040 Schedule A Deductions

7 It all begins with a good record keeping system Find a way to keep farm receipts, invoices, cancelled checks and documentation of expense transactions. These records should be kept until the period of limitation expires for a tax return. For assessment of tax you owe, this generally is 3 years from the date you filed the return. Use Excel, Quicken, Ohio Commercial Farm Account Book, shoe box or custom design your own.

8 Design your system to keep income & expenses by the lines on the Schedule F

9

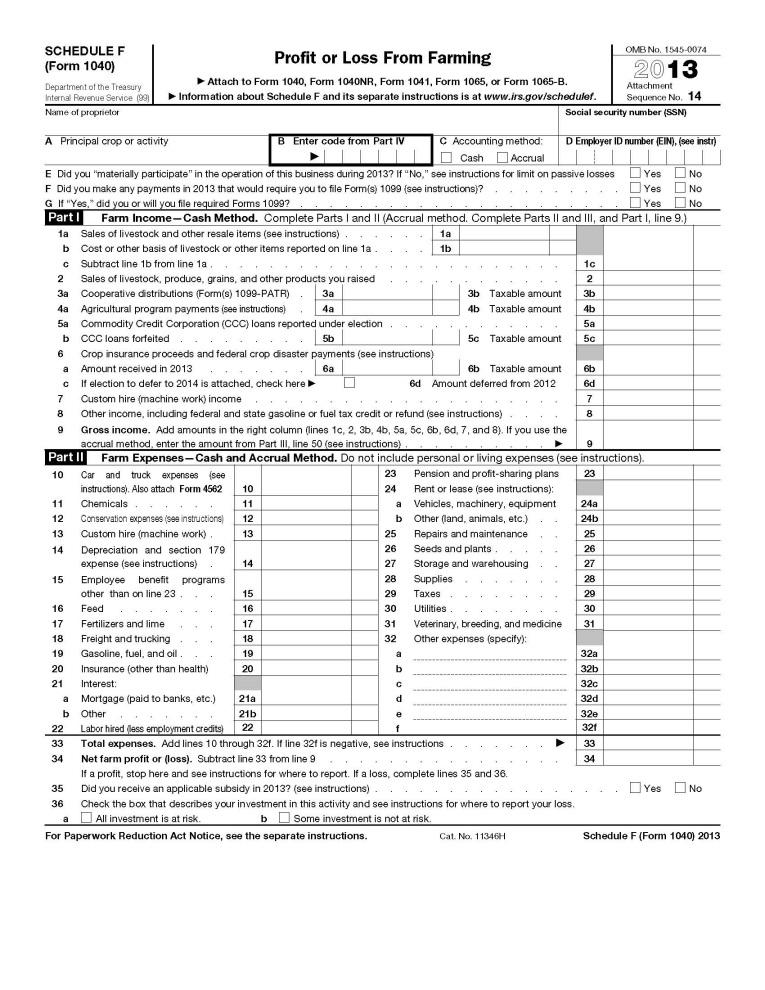

10 Schedule F Income Sales of livestock & other resale items Sale of livestock, produce, grains and other products you raised Crop insurance proceeds Custom hire income Other farm income

11 Schedule F Expenses Car & truck expenses Chemicals Conservation Expenses Custom Hire Depreciation Employee Benefit programs Feed Fertilizers & Lime

12 Schedule F Expenses Freight & Trucking Gasoline, Fuel & Oil Insurance Interest Hired Labor Pension Rents or Leases Repairs & Maintenance

13 Schedule F Expenses Seeds & Plants Storage & Warehousing Supplies Taxes Utilities Vet, breeding & medicine Other Expenses

14 A Farm Classified by the I.R.S The Internal Revenue Service indicates you are in the business of farming if you cultivate, operate, or manage a farm for profit either as an owner or tenant. A farm includes stock, dairy, poultry, fish, and truck farms. It also includes plantations, nurseries, ranches, ranges and orchards. Complete Schedule F (Form 1040)

15 Schedule F Can deduct the current costs of operating your farm. Some deductions include: hired labor, fertilizer and lime, depreciation on farm property, accounting fees, farm fuels and oils, feed, custom hire, trucking, veterinary fees, farm magazines and farm related attorney fees

16 Farming for Hobby or Profit? Why does it matter? Expenses are deductible beyond income if you are operating for profit. And are not deductible beyond income if you operating as a hobby or not-for-profit. I.e., cannot report a loss. Ensuring that your operation qualifies as a for profit business according to the IRS will reduce your income tax burden.

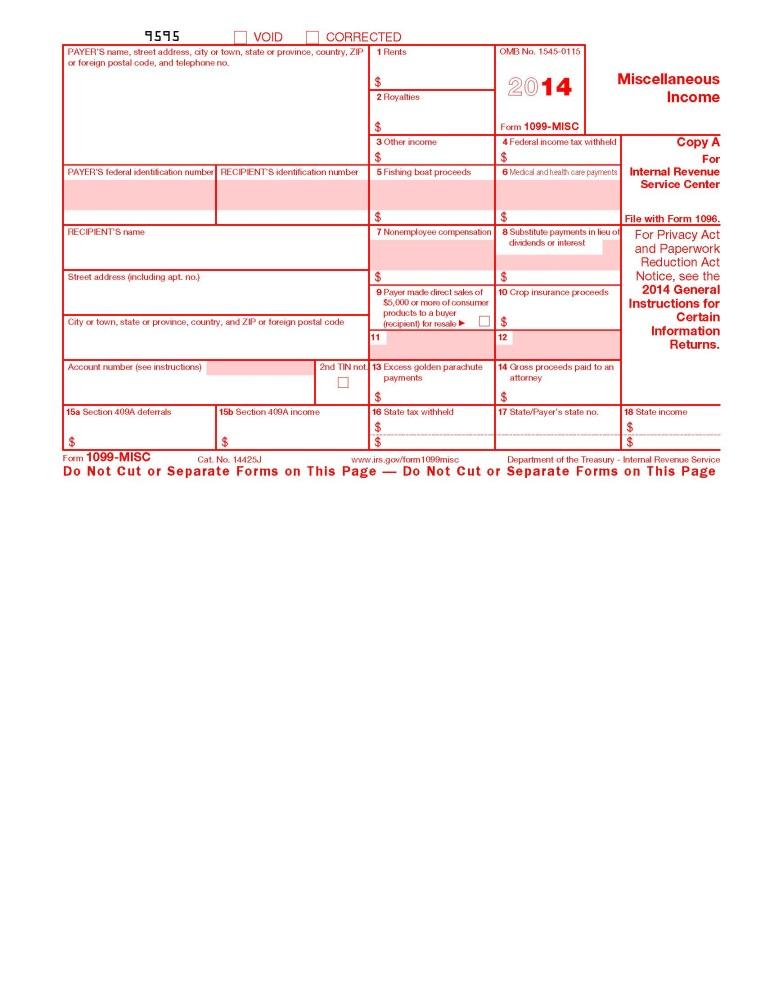

17 Schedule F Note Form 1099 reporting question. Under reporting Misc. Income is a emphasis point for IRS. Required if you paid at least $600 in rents, services, prizes, medical & health care payments, and other income payments.

18

19 1099 Reporting Requirements 1099s were designed to increase tax compliance. The 1099 is a series of 17 different forms. Due to the recipient by January 31 of each year and the forms need to be sent to the IRS by February 28. If a business spends $600 or more for services from an unincorporated business (s-corps, LLCs, sole proprietors, etc.) during a tax year, the total is reported on a 1099-MISC.

20 1099-Misc

21 Typical 1099s which are issued 1099 G for government payments, unemployment, state/local tax refunds, & taxable grants MISC for miscellaneous income INT for interest income DIV- for dividends & distributions R for retirement distributions.

22 When is a 1099 Issued? Farm rental payments which are over $600 to an individual (combined or individual). Crop Insurance proceeds over $600 or royalties over $10. Payments for services performed valued at $600 or more. These could include someone painting the barn, hoof trimmers or certified crop consultants. If a contractor who is not a dealer in supplies performs a service and also provides the supplies required, the farmer must report the entire payment for supplies and services on the Form 1099 that is prepared for the contractor.

23 1099 Reporting Requirements What does not need reported: Most payments made to a corporation. Payments made to a government agency or tax-exempt organization. Payments for merchandise. Payments made in connection with the trucking or hauling of livestock, grain or other farm produce forms are not required for the purchase of feed, seed, fertilizer or equipment parts.

24 Questions Another fellow urban farmer has a small two row planter. So he plants your green beans and corn. He supplies the fertilizer and seed. The cost to do this $625. Do you have to send him a 1099? A friend fixes your rotiller. With parts and labor it costs $250. Do you have to send him a 1099?

25 Questions When doing silage bagging, they charge for the operation of renting the bagger and bagging the silage, and then they also charge for the bag they provide/sell. The farmer who paid the bill is arguing with the custom silage bagger over whether the cost of the bag goes on the 1099.

26 Questions Another fellow custom plants for the neighbor and also supplies the seed and planter fertilizer. They are arguing whether the value of the seed and fertilizer must go on the They planted something like 35 acres for $15 per acre which is only $525 and does not require a BUT, when you add the seed and fertilizer expense you re suddenly talking about a 1099 with around $5000 reported on it.

27 Questions In another case the neighbor did some repairs on a tractor. The labor was less than $600, but IF the parts are included it s way over $600.

28 Questions What about the landowner who rents their hay ground for $50/acre rent for first cutting and then the landowner gets ½ of the 2 nd cutting. So if the farmer sells the hay for the landowner after he bales it, does his 1099 now include the rent of $50/acre plus the value of the hay sold?

29

30 Reporting Requirements Payments shown on Form 1099-MISC are generally not subject to FICA. If the party receiving payment does not provide the farmer with a valid social security number, the farmer is required to withhold 28% of the payment in the form of backup withholding for income tax.

31 Depreciation Develop machinery & equipment depreciation schedules to recapture their cost. Example: fruit trees, single purpose ag structures & greenhouses are depreciated over 10 years. Farm machinery & equipment over 7 years (MACRS). Can use Section 179 as a form of accelerated depreciation limit is $25,000 (unless Congress increases back to 2014 limit of $500,000).

32 Special Bonus Depreciation (AFYD) Was set to be eliminated in 2013 with a 50% limit in Fiscal cliff legislation extended the 50% depreciation through the end of Eliminated in 2014 but brought back in December for 2014 (only) New Equipment.

33 Section 179-Equipment Expensing Farmers have been aggressive in using AFYD and I.R.C. 179 to purchase equipment. I.R.C. 179 deduction was $500,000 in 2013 and dropped to $25,000 for 2014 with $200,000 phase-out. Late year legislation returned to $500,000 with $2 million phaseout for Back to $25,000 in 2015.

34 Farm or nonfarm business income? Farming: Significant involvement in growing, raising, harvesting agricultural product Excludes most processing of crops

35

36 Processing of commodities Farming includes handling, shearing, packing, grading, storing on a farm any agricultural or horticulture commodity in its unmanufactured state. Farm owner or operator must produce > 50% of the commodity. End point is considered when commodity is prepared for its initial sale. Sole proprietor s further activities are reported on Schedule C. Example: Crushing grapes and marketing juice or making wine are not farming activities.

37

38 Sales at Farmers Markets Report sales of produce on Schedule F; report sales of processed items on Schedule C Vendor may supplement own produce with items purchased from another farmer. Value of swapped items treated as sale and purchase for resale; net effect is a wash. For produce donated to charities the deduction is limited to basis in donated crops; basis in raised crops is usually zero.

39 Schedule F Basics Bartering is income which should be reported. Cost of purchasing or raising produce or livestock consumed by you or family is not deductible. See Qualified Farmer (2/3 test) definition in Chapter 15. Deals with paying estimated tax. If you are a qualified farmer you do not need to pay estimated taxes. However, if you do not pay estimated taxes then you need to file and pay taxes by March 1.

40 Other Annual Adjustments Annual Exclusion for gifts remains at $14,000 per person. Standard mileage rate deduction was $0.56 per mile in 2014 and$0.575 in 2015.

41 Business Tax Deductions Start-up- can deduct business start up fees ($5,000). Home office-can deduct home office if you are using for the business. Includes direct, indirect and depreciation costs. Understand the ramifications of selling your home and the tax consequences such as depreciation recapture that result from using this deduction. Business Travel- can deduct business travel. Business Use of Vehicle-standard mileage or actual expense method.

42 Deductible Travel Expenses Travel by airplane, train, bus, or car between your home and your business destination. Using your car while at your business destination. Fares for taxis or other types of transportation between the airport or train station and your hotel. Meals and lodging. Tips you pay for services related to any of these expenses. Dry cleaning and laundry. Business calls while on your business trip.

43 Self-Employment Tax Schedule F income is subject to Self Employment Tax Tax rates. SE Tax is 15.3% (6.2% employee portion and 6.2% employer portion + 2.9% Medicare) on Maximum net earnings. The maximum net selfemployment earnings subject to the social security part (12.4%) of the self-employment tax is $113,700 for There is no maximum limit on earnings subject to the Medicare part (2.9%). Medicare surtax. Tax of 0.9% applies to the net income in excess of $200,000 for singles and $250,000 for couples filing jointly.

44 Reminder on Estate Tax Changes

45 Federal Estate & Gift Tax The fiscal cliff was good for estate planning. Sets permanent limit indexed for inflation. Limit in 2014 is $5,340,000 and 2015 limit will be $5,430,000. Excess taxed at maximum of 40%. Includes portability.to spouse.

Capital Gains NIIT Medicare")

46 Other Federal Taxes Federal Income Tax Brackets Income Averaging for Farmers Schedule C (Not F) Capital Gains NIIT Medicare Surtax

47 Income Tax Brackets

48 Federal Income Tax Rates 2014 (Married Filing Jointly) Income Level Tax Rate <$18,150 10% $18,150 - $73,800 15% $73,800 -$148,850 25% $148,850 - $226,850 28% $226,850 -$405,100 33% $405,100 - $457,600 35% > $457, %

49 Federal Income Tax Rates 2015 (Married Filing Jointly) Income Level Tax Rate <$18,450 10% $18,450 - $74,900 15% $74,900 -$151,200 25% $151,200 - $230,450 28% $230,450 - $411,500 33% $411,500 - $464,850 35% > $464, %

50 Federal Income Tax Rates 2014 (Single) Income Level Tax Rate <$9,075 10% $9,075 - $36,900 15% $36,900 -$89,350 25% $89,350 - $186,350 28% $186,350 -$405,100 33% $405,100 - $406,750 35% > $406, %

51 Federal Income Tax Rates 2015 (Single) Income Level Tax Rate <$9,225 10% $9,225 - $37,450 15% $37,450 -$90,750 25% $90,750 - $189,300 28% $189,300 -$411,500 33% $411,500 - $413,200 35% > $413, %

52 Capital Gains Capital gains rates were adjusted in fiscal cliff legislation. 0% applies to capital gains income if a person is in the 10% and 15% tax brackets. 15% applies to capital gains income if a person is in the 25%, 28%, 33%, or 35% tax brackets. 20% applies to capital gain income if a person is in the 39.6% tax bracket.

53 Net Investment Income Tax A new 3.8% surtax began January 1, 2013 on investment income for $ amount over $200,000 (single) or $250,000 (MFJ). 3.8% tax on smaller of net investment income or excess of adjusted gross income. Investment income includes: interest, dividends, capital gains, annuities, royalties, passive rental income.

54 Additional Medicare Surtax An additional 0.9% medicare tax was added in 2013, if over the threshold. Threshold amounts are $200,000 (single) or $250,000 (MFJ). No employer match required to the amount owed by the employee.

55 Strategies for Year End Tax Management Farmers hate paying taxes, so what can we do?

56 Major Tax Planning Methods Prepaid expenses Deferred payment contracts AFYD and I.R.C. 179 Postpone crop insurance Gain on weather-related sales

57 Prepaid Expenses Purchase inputs before close of year. Payment, not deposit Business purpose Income not materially distorted Deduction limited to 50% of other farm expenses, unless qualified taxpayer.

58 Deferred Payment Contract Installment sale can defer income from crop or livestock sales until year payment is made Need to avoid constructive receipt

59 Income Averaging Income averaging rules in IRC 1301 is a very powerful tool for farmers. Allows farmers to take advantage of lower tax rates from 3 prior years. Does not reduce SE tax; Medicare Surtax, NIIT; or phase outs of personal exemptions & itemized deductions.

60 Using Income Averaging to Overcome New Taxes Higher effective rate on high income 39.6% bracket for ordinary income 20% bracket for capital gain 3.8% net investment income tax 0.9% Medicare surtax Phase-out of personal exemptions deduction and itemized deductions

61 Questions?

62 For More Information David Marrison OSU Extension-Ashtabula County 39 Wall Street Jefferson, Ohio

TAX ORGANIZER Page 3

TAX ORGANIZER Page Basic Taxpayer Information Taxpayer Spouse Taxpayer Spouse First Name Initial Last Name Social Security No. Check if Date of Occupation Dependent Presidential Birth Disabled Blind of

TAX ORGANIZER Page Basic Taxpayer Information Taxpayer Spouse Taxpayer Spouse First Name Initial Last Name Social Security No. Check if Date of Occupation Dependent Presidential Birth Disabled Blind of

TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University Tax Planning

1 TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2014 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

1 TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2014 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

OHIO STATE UNIVERSITY EXTENSION. OSU EXTENSION TAXATION PROGRAM January 2014

OHIO STATE UNIVERSITY EXTENSION Tax Bulletin OSU EXTENSION TAXATION PROGRAM January 2014 FUEL TAX CREDITS AND REFUNDS FOR FARMERS INTRODUCTION Farming can be a fuel- intensive business. Both the federal

OHIO STATE UNIVERSITY EXTENSION Tax Bulletin OSU EXTENSION TAXATION PROGRAM January 2014 FUEL TAX CREDITS AND REFUNDS FOR FARMERS INTRODUCTION Farming can be a fuel- intensive business. Both the federal

CHAPTER 3 FARM INCOME

MANAGING THE TIMING OF INCOME AND DEDUCTIONS CHAPTER 3 SYNPOSIS (click on section title to go directly there) Introduction... 3.2 Defining Farm and Farming... 3.2 Definition of Farm... 3.2 Definition of

MANAGING THE TIMING OF INCOME AND DEDUCTIONS CHAPTER 3 SYNPOSIS (click on section title to go directly there) Introduction... 3.2 Defining Farm and Farming... 3.2 Definition of Farm... 3.2 Definition of

TAX REPORTING AND PAYMENT

CHAPTER 13 SYNPOSIS (click on section title to go directly there) Introduction... 13.2 Filing Requirements for Individual Income Tax Returns... 13.2 Filing Threshold... 13.2 Due Dates... 13.3 Penalties...

CHAPTER 13 SYNPOSIS (click on section title to go directly there) Introduction... 13.2 Filing Requirements for Individual Income Tax Returns... 13.2 Filing Threshold... 13.2 Due Dates... 13.3 Penalties...

2017 Agricultural Tax Issues. Greg Bouchard for The Ohio State University

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

Presented by: Peggy Hall, Legacy Accounting and Software Training Sponsored by: KCAA (Kitsap Community and Agricultural Alliance) WSU Regional Small

WSU Regional Small") Presented by: Peggy Hall, Legacy Accounting and Software Training Sponsored by: KCAA (Kitsap Community and Agricultural Alliance) WSU Regional Small Farms Program Useful Resources Start Up Decisions/Farm

Presented by: Peggy Hall, Legacy Accounting and Software Training Sponsored by: KCAA (Kitsap Community and Agricultural Alliance) WSU Regional Small Farms Program Useful Resources Start Up Decisions/Farm

Prepare, print, and e-file your federal tax return for free!

Prepare, print, and e-file your federal tax return for free! www.freetaxusa.com SCHEDULE F (Form 1040) Department of the Treasury Internal Revenue Service (99) Name of proprietor Profit or Loss From Farming

Prepare, print, and e-file your federal tax return for free! www.freetaxusa.com SCHEDULE F (Form 1040) Department of the Treasury Internal Revenue Service (99) Name of proprietor Profit or Loss From Farming

A. Scott Colby, PC Tax Organizer

A. Scott Colby, PC Tax Organizer ***YOU MUST DOWNLOAD THIS ORGANIZER TO YOUR COMPUTER AND OPEN IT IN ADOBE SOFTWARE BEFORE FILLING OUT ANY INFORMATION OR ELSE YOUR INFORMATION WILL NOT BE SAVED.*** ***DO

A. Scott Colby, PC Tax Organizer ***YOU MUST DOWNLOAD THIS ORGANIZER TO YOUR COMPUTER AND OPEN IT IN ADOBE SOFTWARE BEFORE FILLING OUT ANY INFORMATION OR ELSE YOUR INFORMATION WILL NOT BE SAVED.*** ***DO

Balance Sheet and Schedules

Balance Sheet and Schedules CURRENT ASSET SCHEDULE DOLLAR VALUE CASH AND EQUIVALENTS A $ MARKETABLE EQUITIES B $ ACCOUNTS RECEIVABLE C $ MARKET LIVESTOCK $ PRODUCE OR BY-PRODUCTS $ CROP INVENTORY D $ CROP

Balance Sheet and Schedules CURRENT ASSET SCHEDULE DOLLAR VALUE CASH AND EQUIVALENTS A $ MARKETABLE EQUITIES B $ ACCOUNTS RECEIVABLE C $ MARKET LIVESTOCK $ PRODUCE OR BY-PRODUCTS $ CROP INVENTORY D $ CROP

2017 TAX PROFORMA/ORGANIZER

2017 TAX PROFORMA/ORGANIZER This Tax Proforma/Organizer package was designed to assist you in collecting the information we need for the preparation of your 2017 income tax return. The following pages

2017 TAX PROFORMA/ORGANIZER This Tax Proforma/Organizer package was designed to assist you in collecting the information we need for the preparation of your 2017 income tax return. The following pages

National Society of Accountants Tax Organizer for Tax Year 2012

National Society of Accountants Tax Organizer for Tax Year 2012 Compliments of: Name: Taxpayer SS No. Birthdate/Age Spouse SS No. Birthdate/Age Address: Telephone (Home) ( ) Telephone (Work) ( ) Cell Phone:

National Society of Accountants Tax Organizer for Tax Year 2012 Compliments of: Name: Taxpayer SS No. Birthdate/Age Spouse SS No. Birthdate/Age Address: Telephone (Home) ( ) Telephone (Work) ( ) Cell Phone:

Tax Return Questionnaire Tax Year

Tax Return Questionnaire - 2018 Tax Year - Page 1 of 18 Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money and help

Tax Return Questionnaire - 2018 Tax Year - Page 1 of 18 Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money and help

Farm Tax Update 1/21/2019. Teaching Objectives. Circular 230 Disclosure. Thank You Farmers Tax Guide

Circular 230 Disclosure Farm Tax Update David Marrison, OSU Extension The information provided in this presentation is for educational purposes only. This presentation is designed to provide accurate and

Circular 230 Disclosure Farm Tax Update David Marrison, OSU Extension The information provided in this presentation is for educational purposes only. This presentation is designed to provide accurate and

INCOME TAX CHECKLIST TAXPAYER SSN NAME BIRTHDATE OCCUPATION SPOUSE SSN NAME BIRTHDATE OCCUPATION ADDRESS CITY STATE ZIP CODE

INCOME TAX CHECKLIST All last names must match the name listed on the Social Security Card TAXPAYER SSN NAME BIRTHDATE OCCUPATION SPOUSE SSN NAME BIRTHDATE OCCUPATION ADDRESS CITY STATE ZIP CODE TELEPHONE

INCOME TAX CHECKLIST All last names must match the name listed on the Social Security Card TAXPAYER SSN NAME BIRTHDATE OCCUPATION SPOUSE SSN NAME BIRTHDATE OCCUPATION ADDRESS CITY STATE ZIP CODE TELEPHONE

INCOME TAX CHECKLIST TAXPAYER SSN NAME BIRTHDATE OCCUPATION SPOUSE SSN NAME BIRTHDATE OCCUPATION ADDRESS CITY STATE ZIP CODE

INCOME TAX CHECKLIST All last names must match the name listed on the Social Security Card. TAXPAYER SSN NAME BIRTHDATE OCCUPATION SPOUSE SSN NAME BIRTHDATE OCCUPATION ADDRESS CITY STATE ZIP CODE TELEPHONE

INCOME TAX CHECKLIST All last names must match the name listed on the Social Security Card. TAXPAYER SSN NAME BIRTHDATE OCCUPATION SPOUSE SSN NAME BIRTHDATE OCCUPATION ADDRESS CITY STATE ZIP CODE TELEPHONE

Income Tax Management for Farmers in 2011

Income Tax Management for Farmers in 2011 George Patrick Purdue University 765-494-4241 gpatrick@purdue.edu and David Frette, CPA, Washington, IN 812-254-3442 1 Reference Materials Income Tax Management

Income Tax Management for Farmers in 2011 George Patrick Purdue University 765-494-4241 gpatrick@purdue.edu and David Frette, CPA, Washington, IN 812-254-3442 1 Reference Materials Income Tax Management

Total Tax If you have church employee income, see page 2 of the instructions before you begin.

Form 00-SS U.S. Self-Employment Tax Return (Including the Additional Child Tax Credit for Bona Fide Residents of Puerto Rico) Virgin Islands, Guam, American Samoa, the Commonwealth of the Northern Department

Form 00-SS U.S. Self-Employment Tax Return (Including the Additional Child Tax Credit for Bona Fide Residents of Puerto Rico) Virgin Islands, Guam, American Samoa, the Commonwealth of the Northern Department

Tax Return Questionnaire Tax Year

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

Managerial Accounting Using QuickBooks Pro TM

Managerial Accounting Using QuickBooks Pro TM This manual is intended as a reference in furthering knowledge of management accounting for agricultural producers using QuickBooks Pro TM. Historically, agricultural

Managerial Accounting Using QuickBooks Pro TM This manual is intended as a reference in furthering knowledge of management accounting for agricultural producers using QuickBooks Pro TM. Historically, agricultural

Cattle Enterprise Tax and Financial Management

Cattle Enterprise Tax and Financial Management T. Bryant, CPA 1 1 Senior Tax Partner, Beasley, Bryant & Company, CPA s, P.A. Owner/Operator, Overkill Hill Farms, LLC I. Current tax situation for farmers

Cattle Enterprise Tax and Financial Management T. Bryant, CPA 1 1 Senior Tax Partner, Beasley, Bryant & Company, CPA s, P.A. Owner/Operator, Overkill Hill Farms, LLC I. Current tax situation for farmers

National Society of Accountants Tax Organizer for Tax Year 2018

National Society of Accountants Tax Organizer for Tax Year 2018 Compliments of: Are you Are interested you interested IRS in account IRS monitoring? Yes No Name: Taxpayer SS No. Birthdate/Age Spouse SS

National Society of Accountants Tax Organizer for Tax Year 2018 Compliments of: Are you Are interested you interested IRS in account IRS monitoring? Yes No Name: Taxpayer SS No. Birthdate/Age Spouse SS

Allen L. Kockler Company 2018 Tax Organizer

Client Information: Returning Client New Client If a new client, please bring a copy of your 2017 tax return 2017 Preparer Allen Kockler Jon Augustus Mark Moore Taxpayer Name Spouse Name Taxpayer DOB Spouse

Client Information: Returning Client New Client If a new client, please bring a copy of your 2017 tax return 2017 Preparer Allen Kockler Jon Augustus Mark Moore Taxpayer Name Spouse Name Taxpayer DOB Spouse

AGRICULTURAL TAX. i n c o m e t a x e s

AGRICULTURAL TAX ISSUES c r i t i c a l i n f o r m a t i o n t o k n o w f o r 2 0 1 8 i n c o m e t a x e s The difference between death and taxes is death doesn t get worse every time Congress meets.

AGRICULTURAL TAX ISSUES c r i t i c a l i n f o r m a t i o n t o k n o w f o r 2 0 1 8 i n c o m e t a x e s The difference between death and taxes is death doesn t get worse every time Congress meets.

Tax Organizer For 2014 Income Tax Return

Prepared By: Tax Organizer For 2014 Income Tax Return Prepared For: This Tax Organizer can be used to help identify information needed to prepare your 2014 income tax return. Enter your 2014 tax information

Prepared By: Tax Organizer For 2014 Income Tax Return Prepared For: This Tax Organizer can be used to help identify information needed to prepare your 2014 income tax return. Enter your 2014 tax information

2017 Farm Tax Organizer Gurr & Company LLC

2017 Farm Tax Organizer Gurr & Company LLC Here is your tax organizer to assist you in gathering the information necessary information for your Schedule F "Farm" tax return for 2017. The Internal Revenue

2017 Farm Tax Organizer Gurr & Company LLC Here is your tax organizer to assist you in gathering the information necessary information for your Schedule F "Farm" tax return for 2017. The Internal Revenue

2014 Conversion Instructions UltraTax 1040 to TaxWise

2014 Conversion Instructions UltraTax 1040 to TaxWise Important Notice Please Read!!! The data contained in these returns is minimal and contains ONLY the items needed to pass through to the 2014 return.

2014 Conversion Instructions UltraTax 1040 to TaxWise Important Notice Please Read!!! The data contained in these returns is minimal and contains ONLY the items needed to pass through to the 2014 return.

National Society of Accountants Tax Organizer for Tax Year 2017

National Society of Accountants Tax Organizer for Tax Year 2017 Compliments of: Berman and Sons, LTD Accountants and Consultants Name: Taxpayer SS No. Birthdate/Age Spouse SS No. Birthdate/Age Address:

National Society of Accountants Tax Organizer for Tax Year 2017 Compliments of: Berman and Sons, LTD Accountants and Consultants Name: Taxpayer SS No. Birthdate/Age Spouse SS No. Birthdate/Age Address:

BYRT CPAs, LLC Tax Organizer

BYRT CPAs, LLC 2017 Tax Organizer General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household,

BYRT CPAs, LLC 2017 Tax Organizer General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household,

PERSONAL TAX INFORMATION WORKSHEET

PERSONAL TAX INFORMATION WORKSHEET Please check the appropriate box: Date Received: I need my taxes done early for my child s financial aid. Most of the information needed to complete this form can be

PERSONAL TAX INFORMATION WORKSHEET Please check the appropriate box: Date Received: I need my taxes done early for my child s financial aid. Most of the information needed to complete this form can be

2017 Conversion Instructions TaxACT to ATX Individual

Updated 08/27/2017 2017 Conversion Instructions TaxACT to ATX Individual TaxACT is a registered trademark of 2nd Story Software, Inc.2nd Story Software, Inc. does not sanction nor participate in this conversion

Updated 08/27/2017 2017 Conversion Instructions TaxACT to ATX Individual TaxACT is a registered trademark of 2nd Story Software, Inc.2nd Story Software, Inc. does not sanction nor participate in this conversion

2002 Instructions for Schedule F, Profit or Loss From Farming

2002 Instructions for Schedule F, Profit or Loss From Farming Use Schedule F (Form 1040) to report farm income and expenses. File it with Form 1040, 1041, 1065, or 1065-B. This activity may subject you

2002 Instructions for Schedule F, Profit or Loss From Farming Use Schedule F (Form 1040) to report farm income and expenses. File it with Form 1040, 1041, 1065, or 1065-B. This activity may subject you

Farmer and Farmland Owner Income Tax Webinar. Chris Bruynis, Davis Marrison, and Barry Ward OSU Extension

Farmer and Farmland Owner Income Tax Webinar Chris Bruynis, Davis Marrison, and Barry Ward OSU Extension Chris Bruynis Circular 230 Disclosure The information provided in this presentation is for educational

Farmer and Farmland Owner Income Tax Webinar Chris Bruynis, Davis Marrison, and Barry Ward OSU Extension Chris Bruynis Circular 230 Disclosure The information provided in this presentation is for educational

BYRT CPAs, LLC Tax Organizer

BYRT CPAs, LLC 2016 Tax Organizer General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household,

BYRT CPAs, LLC 2016 Tax Organizer General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household,

Agricultural & Natural Resource Issues Chapter 10 pp National Income Tax Workbook

Agricultural & Natural Resources Tax Issues Chris Bruynis David Marrison Barry Ward Associate Professor Associate Professor Assistant Professor bruynis.1@osu.edu marrison.2@osu.edu ward.8@osu.edu 740-702-3200

Agricultural & Natural Resources Tax Issues Chris Bruynis David Marrison Barry Ward Associate Professor Associate Professor Assistant Professor bruynis.1@osu.edu marrison.2@osu.edu ward.8@osu.edu 740-702-3200

Farm/Ranch Accounting and Tax 101

2013 CliftonLarsonAllen LLP 2013 CliftonLarsonAllen LLP Farm/Ranch Accounting and Tax 101 Randy Netek, CPA & Brandt Self, CPA May 2018 CLAconnect.com The Agenda Tax Reform Basics of Accounting Documentation

2013 CliftonLarsonAllen LLP 2013 CliftonLarsonAllen LLP Farm/Ranch Accounting and Tax 101 Randy Netek, CPA & Brandt Self, CPA May 2018 CLAconnect.com The Agenda Tax Reform Basics of Accounting Documentation

ESTATE AND TRUST INCOME

ESTATE AND TRUST INCOME 2017 (K-1 E/T) Your 2016 K-1 information is shown below. Name of Estate, Trust If any rental real estate, are you an active participant? Name of Estate, Trust If any rental real

ESTATE AND TRUST INCOME 2017 (K-1 E/T) Your 2016 K-1 information is shown below. Name of Estate, Trust If any rental real estate, are you an active participant? Name of Estate, Trust If any rental real

Income Tax Organizer

Income Tax Organizer 1200 W. Cherry Lane, Suite 100 Meridian, ID 83642 208-888-6501 office 866-408-1836 fax 1. Personal Information Roberts Hart and Company, CPA's Income Tax Organizer Taxpayer Last Name

Income Tax Organizer 1200 W. Cherry Lane, Suite 100 Meridian, ID 83642 208-888-6501 office 866-408-1836 fax 1. Personal Information Roberts Hart and Company, CPA's Income Tax Organizer Taxpayer Last Name

Crop Cash Flow and Enterprise Information - step two for your 2017 farm analysis

Name Address County Phone Email Operator #1 Year Born Year Started Farming Operator #2 Year Born Year Started Farming Operator #3 Year Born Year Started Farming Crop Cash Flow and Enterprise Information

Name Address County Phone Email Operator #1 Year Born Year Started Farming Operator #2 Year Born Year Started Farming Operator #3 Year Born Year Started Farming Crop Cash Flow and Enterprise Information

TAX ORGANIZER. If you answer 'Yes' to any of the General Business and Investment questions, please provide detailed information with your answer.

TAX ORGANIZER Enclosed is your Tax Organizer for tax year 2012. Your Organizer contains several sections that include common expenses and deductions that many taxpayers overlook. Please review these sections

TAX ORGANIZER Enclosed is your Tax Organizer for tax year 2012. Your Organizer contains several sections that include common expenses and deductions that many taxpayers overlook. Please review these sections

Please also attach copies of your individual income tax returns for the past two years. About you: Name (First, MI, Last): Taxpayer Social Security #

: Taxpayer Social Security #") JOHN D. GALLO, C.P.A., LLC CERTIFIED PUBLIC ACCOUNTANT 2500 EAST 168TH AVENUE BRIGHTON, COLORADO 80602 (303) 817-7855 www.johngallocpa.com email: john@johngallocpa.com Organizer for individual income tax

JOHN D. GALLO, C.P.A., LLC CERTIFIED PUBLIC ACCOUNTANT 2500 EAST 168TH AVENUE BRIGHTON, COLORADO 80602 (303) 817-7855 www.johngallocpa.com email: john@johngallocpa.com Organizer for individual income tax

2017 JAMES J. TOWEY, P.C. Information Summarizer for Self Employed

2017 JAMES J. TOWEY, P.C. Information Summarizer for Self Employed 11555 Beamer Road, Ste. 100 Houston, TX 77089 (281)484-5561 (Tel.) (281)481-0987 (Fax) pcjjt76@gmail.com www.jamesjtoweycpa.com CLIENT:

2017 JAMES J. TOWEY, P.C. Information Summarizer for Self Employed 11555 Beamer Road, Ste. 100 Houston, TX 77089 (281)484-5561 (Tel.) (281)481-0987 (Fax) pcjjt76@gmail.com www.jamesjtoweycpa.com CLIENT:

US Topical Index

2010 1040 US Topical Index Page 1 TOPIC FORM Adoption expenses........................... 37 Alimony paid................................. 24 Alimony received............................. 14.1 Business

2010 1040 US Topical Index Page 1 TOPIC FORM Adoption expenses........................... 37 Alimony paid................................. 24 Alimony received............................. 14.1 Business

Individual Items to Note (1040)

") Individual Items to Note (1040) Items to Note This list provides details about how ProSeries converts the following 1040 calculated carryovers. The 2015 converted client file is not intended to duplicate

Individual Items to Note (1040) Items to Note This list provides details about how ProSeries converts the following 1040 calculated carryovers. The 2015 converted client file is not intended to duplicate

ROLAND & DIELEMAN 2018 TAX WORKSHEET

ROLAND & DIELEMAN 2018 TAX WORKSHEET FARM 808 4 TH Ave. Grinnell, IA 50112 (641) 236-6558 126 West 3 rd Street Tama, IA 52339 (641) 484-2970 (Grinnell) (641) 484-5622 (Mon./Sat.) 612 4 th St. Sully, IA

ROLAND & DIELEMAN 2018 TAX WORKSHEET FARM 808 4 TH Ave. Grinnell, IA 50112 (641) 236-6558 126 West 3 rd Street Tama, IA 52339 (641) 484-2970 (Grinnell) (641) 484-5622 (Mon./Sat.) 612 4 th St. Sully, IA

Individual Items to Note (1040)

") Individual Items to Note (1040) Items to Note This list provides details about how ProSeries converts the following 1040 calculated carryovers. The 2013 converted client file is not intended to duplicate

Individual Items to Note (1040) Items to Note This list provides details about how ProSeries converts the following 1040 calculated carryovers. The 2013 converted client file is not intended to duplicate

Tax Organizer For 2017 Income Tax Return

Tax Organizer For 2017 Income Tax Return Prepared For:,,, Prepared By: Strategic Tax & Accounting LLC 3650 Canton Road Marietta, GA 30066 This Tax Organizer can be used to help identify information needed

Tax Organizer For 2017 Income Tax Return Prepared For:,,, Prepared By: Strategic Tax & Accounting LLC 3650 Canton Road Marietta, GA 30066 This Tax Organizer can be used to help identify information needed

2017 TAX ORGANIZER F R O M T O

F R O M TAX ORGANIZER T O I (We) have submitted this information for the sole purpose of preparing my (our) tax return(s). Each item can be substantiated by receipts, canceled checks or other documents.

F R O M TAX ORGANIZER T O I (We) have submitted this information for the sole purpose of preparing my (our) tax return(s). Each item can be substantiated by receipts, canceled checks or other documents.

INCOME TAX MANAGEMENT FOR FARMERS IN 2011

INCOME TAX MANAGEMENT FOR FARMERS IN 2011 George F. Patrick Department of Agricultural Economics Purdue University DRAFT DECEMBER 2011 DRAFT 2011 version has not been peer-reviewed. Comments are welcome.

INCOME TAX MANAGEMENT FOR FARMERS IN 2011 George F. Patrick Department of Agricultural Economics Purdue University DRAFT DECEMBER 2011 DRAFT 2011 version has not been peer-reviewed. Comments are welcome.

1040 U.S. Individual Income Tax Return 2011

F or Department of the Treasury Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 211 m OMB. 1545-74 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31, 211,

F or Department of the Treasury Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 211 m OMB. 1545-74 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31, 211,

Miscellaneous Information

Miscellaneous Information Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your address

Miscellaneous Information Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your address

2015 Iowa Farm Business Management Career Development Event. INDIVIDUAL EXAM (150 pts.)

") 2015 Iowa Farm Business Management Career Development Event INDIVIDUAL EXAM (150 pts.) Select the best answer to each of the 75 questions to follow (2 pts. ea.). Code your answers on the answer sheet provided.

2015 Iowa Farm Business Management Career Development Event INDIVIDUAL EXAM (150 pts.) Select the best answer to each of the 75 questions to follow (2 pts. ea.). Code your answers on the answer sheet provided.

Farm Income Statement 2015 Moorhead Farm Business Management Annual Report (Farms Sorted By Net Farm Income) Number of farms

Number of farms") Farm Income Statement Cash Farm Income Barley 5,929 2,010 - - 12,581 14,753 Beans, Black Turtle 350 - - - - 1,723 Beans, Navy 3,627 13,512 - - 5,385 - Corn 168,160 172,777 84,655 79,253 289,902 214,568

Farm Income Statement Cash Farm Income Barley 5,929 2,010 - - 12,581 14,753 Beans, Black Turtle 350 - - - - 1,723 Beans, Navy 3,627 13,512 - - 5,385 - Corn 168,160 172,777 84,655 79,253 289,902 214,568

Individual Items to Note (1040)

") Items to Note Individual Items to Note (1040) During the conversion process, the following Form 1040 carryover information will NOT be converted to your 2016 ProSeries data files. To ensure your calculated

Items to Note Individual Items to Note (1040) During the conversion process, the following Form 1040 carryover information will NOT be converted to your 2016 ProSeries data files. To ensure your calculated

Who Blinked? The American Taxpayer Relief Act of Winter 2013 A 45,000 foot view of Recent Tax Law Changes affecting Agriculture

Who Blinked? The American Taxpayer Relief Act of 2012 Winter 2013 A 45,000 foot view of Recent Tax Law Changes affecting Agriculture Federal Income Tax Changes Affecting Agriculture Individual Income Tax

Who Blinked? The American Taxpayer Relief Act of 2012 Winter 2013 A 45,000 foot view of Recent Tax Law Changes affecting Agriculture Federal Income Tax Changes Affecting Agriculture Individual Income Tax

2017 Farm Tax Worksheet For Clients of Erpelding, Voigt & Co., L.L.P.

2017 Farm Tax Worksheet For Clients of Erpelding, Voigt & Co., L.L.P. INCOME WORKSHEET SALES/COSTS OF LIVESTOCK PURCHASED FOR RESALE: Sold Proceeds Bought Cost Net Calves/fat cattle $ $ $ Calves/fat cattle

2017 Farm Tax Worksheet For Clients of Erpelding, Voigt & Co., L.L.P. INCOME WORKSHEET SALES/COSTS OF LIVESTOCK PURCHASED FOR RESALE: Sold Proceeds Bought Cost Net Calves/fat cattle $ $ $ Calves/fat cattle

Tax Planning. and. Management Considerations. for Farmers in George F. Patrick Extension Agricultural Economist Purdue University

DRAFT 11/15/00 Tax Planning and Management Considerations for Farmers in 2000 by George F. Patrick Extension Agricultural Economist Purdue University Cooperative Extension Service Paper No. CES- December

DRAFT 11/15/00 Tax Planning and Management Considerations for Farmers in 2000 by George F. Patrick Extension Agricultural Economist Purdue University Cooperative Extension Service Paper No. CES- December

Developing a Cash Flow Plan

Oklahoma Cooperative Extension Service AGEC-751 Developing a Cash Flow Plan Damona G. Doye Extension Economist and Professor A cash flow plan is a recorded projection of the amount and timing of all cash

Oklahoma Cooperative Extension Service AGEC-751 Developing a Cash Flow Plan Damona G. Doye Extension Economist and Professor A cash flow plan is a recorded projection of the amount and timing of all cash

Miscellaneous Information

Miscellaneous Information Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your address

Miscellaneous Information Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your address

US Client Information 1

1040 US Client Information 1 Page 6 Russell CPAs 5530 Birdcage Street, Suite 105 Citrus Heights, CA 95610 Telephone number: Fax number: E-mail address: (916) 966-9366 (916) 966-8743 Chad@RussellCPAs.com

1040 US Client Information 1 Page 6 Russell CPAs 5530 Birdcage Street, Suite 105 Citrus Heights, CA 95610 Telephone number: Fax number: E-mail address: (916) 966-9366 (916) 966-8743 Chad@RussellCPAs.com

1040 US Tax Organizer

1040 US Tax Organizer Page 1 Please enter all pertinent information. If you have attached a government form for an item, check the box and do not enter a amount. WAGES, SALARIES AND TIPS Employer name:

1040 US Tax Organizer Page 1 Please enter all pertinent information. If you have attached a government form for an item, check the box and do not enter a amount. WAGES, SALARIES AND TIPS Employer name:

Agricultural and Natural Resource Issues Chapter 9 pp National Income Tax Workbook

Agricultural and Natural Resource Issues Chapter 9 pp. 287-327 2018 National Income Tax Workbook Agricultural and Natural Resources Issues Chris Bruynis, David Marrison, and Barry Ward Ag Economy Update

Agricultural and Natural Resource Issues Chapter 9 pp. 287-327 2018 National Income Tax Workbook Agricultural and Natural Resources Issues Chris Bruynis, David Marrison, and Barry Ward Ag Economy Update

2018 Tax Organizer Personal and Dependent Information

Tax Organizer Personal and Dependent Information Personal Information Name SSN Date of birth Healthcare coverage ALL year Taxpayer Spouse Street address, city, state, and ZIP Occupation Daytime phone Evening

Tax Organizer Personal and Dependent Information Personal Information Name SSN Date of birth Healthcare coverage ALL year Taxpayer Spouse Street address, city, state, and ZIP Occupation Daytime phone Evening

US Client Information 1

2009 1040 US Client Information 1 Page 1 Soukup, Bush & Associates, PC 2032 Caribou Drive, Suite 200 Fort Collins, CO 80525 Telephone number: (970) 223-2727 Fax number: (970) 226-0813 E-mail address: jenny@soukupbush.com

2009 1040 US Client Information 1 Page 1 Soukup, Bush & Associates, PC 2032 Caribou Drive, Suite 200 Fort Collins, CO 80525 Telephone number: (970) 223-2727 Fax number: (970) 226-0813 E-mail address: jenny@soukupbush.com

2015 CALT Tax Schools Day 2. Contact Information. Day 2 Topics 12/15/2015. Dave Repp. Paul Neiffer.

2015 CALT Tax Schools Day 2 David Repp and Paul Neiffer Contact Information Dave Repp drepp@dickinsonlaw.com Paul Neiffer Paul.neiffer@claconnect.com 509 823 2920 www.farmcpatoday.com @farmcpa Day 2 Topics

2015 CALT Tax Schools Day 2 David Repp and Paul Neiffer Contact Information Dave Repp drepp@dickinsonlaw.com Paul Neiffer Paul.neiffer@claconnect.com 509 823 2920 www.farmcpatoday.com @farmcpa Day 2 Topics

2015 ProSystem Tax Line Conversion Chart by Input Form. Individual. January 2015

2015 ProSystem Conversion Chart by Input Form Individual January 2015 The following chart provides Individual tax line conversion data sorted by form and box number. te: CCH ProSystem fx allows tax lines

2015 ProSystem Conversion Chart by Input Form Individual January 2015 The following chart provides Individual tax line conversion data sorted by form and box number. te: CCH ProSystem fx allows tax lines

Promoting Innovation in Maryland Agricultural and Resource-Based Business. * Now includes financing for tree fruit orchards and hopyards *

Promoting Innovation in Maryland Agricultural and Resource-Based Business Application for the Maryland Vineyard Planting Loan Fund * Now includes financing for tree fruit orchards and hopyards * Program

Promoting Innovation in Maryland Agricultural and Resource-Based Business Application for the Maryland Vineyard Planting Loan Fund * Now includes financing for tree fruit orchards and hopyards * Program

Developing a Cash Flow Plan

Developing a Cash Flow Plan Oklahoma Cooperative Extension Service Division of Agricultural Sciences and Natural Resources F-751 Damona G. Doye Extension Economist and Professor Acash flow plan is a recorded

Developing a Cash Flow Plan Oklahoma Cooperative Extension Service Division of Agricultural Sciences and Natural Resources F-751 Damona G. Doye Extension Economist and Professor Acash flow plan is a recorded

Additional Information

Charles Brown 2015 Farm Income Tax Webinar Field Specialist - Farm Management crbrown@iastate.edu 641-673-5841 515-240-9214 Additional Information Tax Summary Social Security Wage Base Entity Comparison

Charles Brown 2015 Farm Income Tax Webinar Field Specialist - Farm Management crbrown@iastate.edu 641-673-5841 515-240-9214 Additional Information Tax Summary Social Security Wage Base Entity Comparison

Also, you may write the addresses below and fax or mail this letter back to us.

To Our Valued Customers: In an effort to continually improve our service to you, our valued customers, Brabazon Pump Company is preparing to initiate electronic delivery of invoices. We are presently building

To Our Valued Customers: In an effort to continually improve our service to you, our valued customers, Brabazon Pump Company is preparing to initiate electronic delivery of invoices. We are presently building

Common Deductions For Business Owners

Common Deductions For Business Owners Within the day-to-day life of your small business, you will incur ordinary and necessary expenses that you can deduct when filing your taxes. So what does that mean?

Common Deductions For Business Owners Within the day-to-day life of your small business, you will incur ordinary and necessary expenses that you can deduct when filing your taxes. So what does that mean?

Developing a Cash Flow Plan

Oklahoma Cooperative Extension Service AGEC-751 Developing a Cash Flow Plan Damona Doye Regents Professor and Extension Economist Brent Ladd Extension Assistant Oklahoma Cooperative Extension Fact Sheets

Oklahoma Cooperative Extension Service AGEC-751 Developing a Cash Flow Plan Damona Doye Regents Professor and Extension Economist Brent Ladd Extension Assistant Oklahoma Cooperative Extension Fact Sheets

New Customer Questionnaire and Credit Application

Remit all payments to: CMA/Flodyne/Hydradyne, Inc., 3265 Gateway Road, Suite 300, Brookfield, WI 53045 Phone: 262-781-1815 Fax: 262-781-2521 New Customer Questionnaire and Credit Application As you are

Remit all payments to: CMA/Flodyne/Hydradyne, Inc., 3265 Gateway Road, Suite 300, Brookfield, WI 53045 Phone: 262-781-1815 Fax: 262-781-2521 New Customer Questionnaire and Credit Application As you are

OTHER TOOLS TO MANAGE TAX LIABILITY

TAX GUIDE FOR OWNERS AND OPERATORS OF SMALL AND MEDIUM SIZE FARMS CHAPTER 7 OTHER TOOLS TO MANAGE TAX LIABILITY SYNPOSIS (click on section title to go directly there) Introduction... 7.2 Farm Income Averaging...

TAX GUIDE FOR OWNERS AND OPERATORS OF SMALL AND MEDIUM SIZE FARMS CHAPTER 7 OTHER TOOLS TO MANAGE TAX LIABILITY SYNPOSIS (click on section title to go directly there) Introduction... 7.2 Farm Income Averaging...

Miscellaneous Information

Miscellaneous Information Page 1 Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your

Miscellaneous Information Page 1 Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your

Miscellaneous Information

Miscellaneous Information Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your address

Miscellaneous Information Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your address

Miscellaneous Information

Miscellaneous Information Page 1 Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your

Miscellaneous Information Page 1 Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your

2011 ProSystem Tax Line Conversion Chart by Input Form. Individual. November 2011

2011 ProSystem Conversion Chart by Input Form Individual vember 2011 The following chart provides Individual tax line conversion data sorted by form and box number. te: ProSystem FX allows tax lines to

2011 ProSystem Conversion Chart by Input Form Individual vember 2011 The following chart provides Individual tax line conversion data sorted by form and box number. te: ProSystem FX allows tax lines to

Miscellaneous Information

Miscellaneous Information Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your address

Miscellaneous Information Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your address

2017 Instructions for Schedule F

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule F Profit or Loss From Farming Use Schedule F (Form 1040) to report farm income and expenses. File it with Form 1040, 1040NR,

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule F Profit or Loss From Farming Use Schedule F (Form 1040) to report farm income and expenses. File it with Form 1040, 1040NR,

2014 Income Tax Webinar

2014 Income Tax Webinar Charles Brown ISU Farm Management Specialist 515 240 9214 crbrown@iastate.edu Expired Tax Provisions Above the line deduction for certain expenses of school teachers Above the line

2014 Income Tax Webinar Charles Brown ISU Farm Management Specialist 515 240 9214 crbrown@iastate.edu Expired Tax Provisions Above the line deduction for certain expenses of school teachers Above the line

Welcome to a brief discussion of income statements. The income statement is a critical record-keeping tool in evaluating the profitability of your

Welcome to a brief discussion of income statements. The income statement is a critical record-keeping tool in evaluating the profitability of your business. As with the other statements, you may choose

Welcome to a brief discussion of income statements. The income statement is a critical record-keeping tool in evaluating the profitability of your business. As with the other statements, you may choose

Miscellaneous Information

Miscellaneous Information Page 1 Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your

Miscellaneous Information Page 1 Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your

2017 Farm Income Tax Webinar

2017 Farm Income Tax Webinar Charles Brown Field Specialist - Farm Management crbrown@iastate.edu 641-673-5841 515-240-9214 Additional Information Tax Bracket Tables Standard Deduction Social Security

2017 Farm Income Tax Webinar Charles Brown Field Specialist - Farm Management crbrown@iastate.edu 641-673-5841 515-240-9214 Additional Information Tax Bracket Tables Standard Deduction Social Security

Batten Down the Hatches and Protect the Hen House Keeping the Government Foxes (IRS) at Bay

at Bay") Batten Down the Hatches and Protect the Hen House Keeping the Government Foxes (IRS) at Bay Orman R. Wilson, CPA October 20, 2016 Birmingham, Selma & Tuscaloosa, Alabama USA Today s Outline You are a timber

Batten Down the Hatches and Protect the Hen House Keeping the Government Foxes (IRS) at Bay Orman R. Wilson, CPA October 20, 2016 Birmingham, Selma & Tuscaloosa, Alabama USA Today s Outline You are a timber

US Topical Index

2010 1040 US Topical Index TOPIC FORM Adoption expenses........................... 37 Alimony paid................................. 24 Alimony received............................. 14.1 Business income

2010 1040 US Topical Index TOPIC FORM Adoption expenses........................... 37 Alimony paid................................. 24 Alimony received............................. 14.1 Business income

You may wish to carefully examine your records to determine if you may be missing any of these deductions.

2018 tax planning and tax changes Re: Planning 2018: Tax Consequences for Self-Employed Individuals Dear Client: Owning your own business can be very rewarding, both personally and financially. Being the

2018 tax planning and tax changes Re: Planning 2018: Tax Consequences for Self-Employed Individuals Dear Client: Owning your own business can be very rewarding, both personally and financially. Being the

Personal Legal Plans Client Organizer 2018

TAXPAYER NAME SOCIAL SECURITY NUMBER OCCUPATION DATE OF BIRTH EMAIL ADDRESS CELL PHONE SPOUSE Address: Home Phone: City: State: Zip: County: DEPENDENT CHILDREN & OTHER DEPENDENTS NAME SOCIAL SECURITY NUMBER

TAXPAYER NAME SOCIAL SECURITY NUMBER OCCUPATION DATE OF BIRTH EMAIL ADDRESS CELL PHONE SPOUSE Address: Home Phone: City: State: Zip: County: DEPENDENT CHILDREN & OTHER DEPENDENTS NAME SOCIAL SECURITY NUMBER

2017 TAX ORGANIZER. This tax organizer has been prepared for your use in gathering the information needed for your 2017 tax return.

F R O M 2017 TAX ORGANIZER T O This tax organizer has been prepared for your use in gathering the information needed for your 2017 tax return. To save you time, selected information from your 2016 tax

F R O M 2017 TAX ORGANIZER T O This tax organizer has been prepared for your use in gathering the information needed for your 2017 tax return. To save you time, selected information from your 2016 tax

Miscellaneous Information

Miscellaneous Information Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your address

Miscellaneous Information Personal Information Yes No Did your marital status change during the year? If "Yes," explain Can you or your spouse be claimed as a dependent by someone else? Did your address

2017 Year-End Tax Memo

2017 Year-End Tax Memo An Annual Publication of Large & Gilbert, Inc. January 2018 Large & Gilbert, Inc., is a full service CPA firm specializing in Accounting, Tax, Consulting, Business Advisory, Wealth

2017 Year-End Tax Memo An Annual Publication of Large & Gilbert, Inc. January 2018 Large & Gilbert, Inc., is a full service CPA firm specializing in Accounting, Tax, Consulting, Business Advisory, Wealth

10/24/2017. Farm Expenses. 26 CFR Expenses of Farmers. Ordinary and Necessary

Farm Expenses Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 24, 2017 26 CFR 1.162 12 Expenses of Farmers Farms engaged in for profit activities A farmer who operates a farm

Farm Expenses Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation October 24, 2017 26 CFR 1.162 12 Expenses of Farmers Farms engaged in for profit activities A farmer who operates a farm

1040 US Miscellaneous Questions

1040 US Miscellaneous Questions Page 1 If any of the following items pertain to you or your spouse for, please check the appropriate box and provide additional information if necessary. YES NO PERSONAL

1040 US Miscellaneous Questions Page 1 If any of the following items pertain to you or your spouse for, please check the appropriate box and provide additional information if necessary. YES NO PERSONAL

2013 Instructions for Schedule E (Form 1040)

") Department of the Treasury Internal Revenue Service 2013 Instructions for Schedule E (Form 1040) Supplemental Income and Loss Use Schedule E (Form 1040) to report income or loss from rental real estate,

Department of the Treasury Internal Revenue Service 2013 Instructions for Schedule E (Form 1040) Supplemental Income and Loss Use Schedule E (Form 1040) to report income or loss from rental real estate,

WAHL, WILLEMSE & WILSON, LLP CERTIFIED PUBLIC ACCOUNTANTS 2018 TAX ORGANIZER

FILING STATUS FILING STATUS (See table) Filing Status MARRIED FILING SEPARATE AND LIVED WITH SPOUSE? 1 = Single SPOUSE'S DATE OF DEATH (mm/dd/yy), IF QUALIFYING WIDOW(ER) - 2017 or 2018 2 = Married filing

FILING STATUS FILING STATUS (See table) Filing Status MARRIED FILING SEPARATE AND LIVED WITH SPOUSE? 1 = Single SPOUSE'S DATE OF DEATH (mm/dd/yy), IF QUALIFYING WIDOW(ER) - 2017 or 2018 2 = Married filing

2017 NATIONAL FFA FARM AND AGRIBUSINESS MANAGEMENT CAREER DEVELOPMENT EVENT

Participant s Name (please print clearly). Important: Before you start this portion of the event, please write your participant number and state abbreviation on the blanks provided at the top of each page.

Participant s Name (please print clearly). Important: Before you start this portion of the event, please write your participant number and state abbreviation on the blanks provided at the top of each page.

Individual. Tax Organizer. Hibbs and Associates, PLLC 713 North Third Street Bardstown, KY Phone: (502) Fax: (877)

Fax: (877)") Individual 2016 Tax Organizer Hibbs and Associates, PLLC 713 North Third Street Bardstown, KY 40004 Phone: (502) 348-0276 Fax: (877) 344-0735 THIS ORGANIZER IS PROVIDED TO ASSIST YOU IN GATHERING YOUR

Individual 2016 Tax Organizer Hibbs and Associates, PLLC 713 North Third Street Bardstown, KY 40004 Phone: (502) 348-0276 Fax: (877) 344-0735 THIS ORGANIZER IS PROVIDED TO ASSIST YOU IN GATHERING YOUR

STORMS & ALPAUGH, PLLC CERTIFIED PUBLIC ACCOUNTANTS P. O. Box Tower Blvd Suite 212 Victoria, Minnesota 55386

December 18, STORMS & ALPAUGH, PLLC CERTIFIED PUBLIC ACCOUNTANTS P. O. Box 446 1750 Tower Blvd Suite 212 Victoria, Minnesota 55386 Phone (952) 443-2200 Fax (952) 443-2279 Serving Clients since 1972 Dear

December 18, STORMS & ALPAUGH, PLLC CERTIFIED PUBLIC ACCOUNTANTS P. O. Box 446 1750 Tower Blvd Suite 212 Victoria, Minnesota 55386 Phone (952) 443-2200 Fax (952) 443-2279 Serving Clients since 1972 Dear

SELFEMPLOYMENT. Self employment Income/Expense Tracking Worksheet. Tax strategies for the self-employed

ADVANTAXADVANTAXADVANTAX Self employment Income/Expense Tracking Worksheet (Use the worksheet below to track your income and allowable expenses by quarter to assist in deriving your net earnings and estimated

ADVANTAXADVANTAXADVANTAX Self employment Income/Expense Tracking Worksheet (Use the worksheet below to track your income and allowable expenses by quarter to assist in deriving your net earnings and estimated

Client Organizer Topical Index

Form ID: INDX Client Organizer Topical Index This client organizer topical index is designed to help you quickly locate the items listed. To use the index just locate the topic and refer to the page number

Form ID: INDX Client Organizer Topical Index This client organizer topical index is designed to help you quickly locate the items listed. To use the index just locate the topic and refer to the page number