The development and current situation of ICPAC and the Accountancy profession in Cyprus. September 2017

|

|

|

- Victoria Mitchell

- 6 years ago

- Views:

Transcription

1 The development and current situation of ICPAC and the Accountancy profession in Cyprus September 2017

2 Agenda 1. ICPAC in brief 2. Milestones in the Institute s / profession s development 3. Current position of ICPAC 4. ICPAC as a competent authority 5. Regulating the profession 6. Training accountants 7. Continuous Professional Development 8. Accounting & Audit profession in Cyprus 9. AML & Compliance 10.Economy and Business

3 1. ICPAC in brief ICPAC is the professional association for all professional accountants. Established in 1961 Numbers around 4.ooo members and around another students and graduate accountants The only recognized body of accountants in Cyprus by the Council of Ministers in Designated as a competent authority under Cyprus legislation for the professional activities of its members.

4 ICPAC s aims: To provide an organisational framework to all professional accountants of Cyprus To provide professional training, guidance and education to its members To regulate the profession, by means of issuing the practising licences and monitoring the work performed by the practising members and their firms To ensure adherence to the Code of Ethics To promote the interests of the members and the profession.

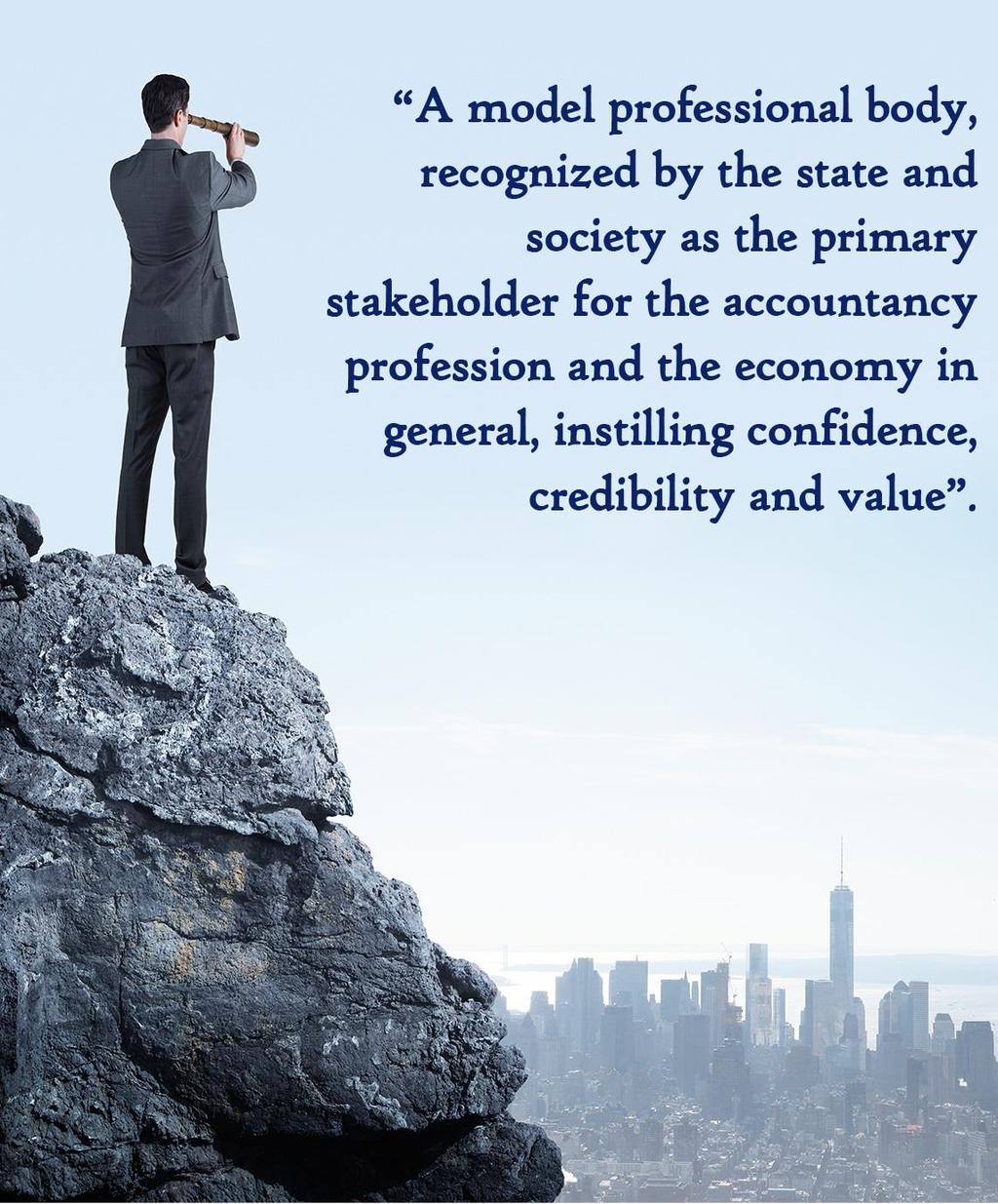

5 Vision

6 Mission To Empower its members by providing appropriate knowledge, training, guidance and support. To Promote the highest professional & ethical ideals. To Be the essential partner of the State for the matters relating to the economy. To Advance the public interest.

7 Strategic Plan Strengthen the organizational structure and the efficiency of the Institute. 2. Strengthen the role, reputation and credibility of the Institute. 3. Strengthen the accountancy profession in Cyprus and abroad. 4. Boost the economy of the country and its position as a credible international business centre of good repute.

8 ICPAC s governance Directed by a Council of 14 members Council s committees following corporate governance framework Managed by the General Manager and the office team Works through 23 specialized committees made up of members Uses the services of other professional bodies and external associates.

9 ICPAC s committees 1. Accounting Standards 2.Administrative Service 3.Advisory Services 4.Auditing Standards 5.Chief Financial Officers 6.Compliance 7.Economic Crime and Forensic Accounting 8.Education 9.Energy 10.Financial Services 11. Insolvency 12.International Business and Foreign Investment 13.Larnaca Ammochostos Coordinating Committee 14.Limassol Paphos Coordinating Committee 15.Functions 16.Public Sector 17. Shipping 18.Listed Companies 19.Taxation 20.VAT 21.Specialized Working Group for Ethics & Institutions Committee 22.Specialized working Group for Investment Funds 23.Consultative Committee for SMPs

10 International Memberships International Federation of Accountants European Federation of Accountants Mediterranean Federation of Accountants

11 International Affiliations

12 Main functions of ICPAC Council matters CyPAOA Insolvency Matters Admin ve Services Law Conferences Registration of Members Committees Reporting Communicati on & media Accountancy Europe Registers admin n FCM Promotion of the profession SMPs Management Seminars Training - Presentations IFAC Auditing matters Members support Co s Law Social Responsibility Administration Joint Exam Scheme Ministries & Gov dps IFRSs Coop with local Institutions Auditors Law IT & systems Licensing Members CPD Parliament Tax / VAT Coop with foreign bodies Public Sector Matters Acountancy Cyprus Regulation & Monitoring Disciplining Assessments & Evaluations Compliance & AML New Ventures AML Law Other events

13 2. Milestones in the Institute s / profession s development Establish ment of ICPAC Adoption of IASs Recognised as an accountancy body Auditors Law [L.42(I)/2009] Financial Crisis in Cyprus - Troika New Auditors Law (EU D & R for pie s) [L.53(I)/2017] Turkish invasion in Cyprus Co Law amendment, allowing self-regulation of the profession Move to own premises ASP New Law General Manager Insolvency Law Recognised as competent authority for AML

14 3. ICPAC in numbers (at 31/12/2016) Number of members for the last six years Members per Gender Members per professional body

15 Practitioners vs Non- Practitioners P s Non - P s Type of Practising Certificates Members Firms General Practising Certificate Auditing ASP Insolvency Practitioners 88 -

16 Practitioners Firms, per no. of partners/directors No. % Firms, per legal form No. % Between Between Sole practitioners Partnerships 36 5 Between Between Total Limited Lability Companies Total

17 4. ICPAC as a competent authority Delegated authority under the law, as follows: The Auditors and Statutory Audits of Annual and Consolidated Accounts Law (L.53(I)/2017) Prevention and Suppression of Money Laundering Activities Laws (L.188(I)/2007 and L.58(I)/2010) Law Regulating Companies Providing Administrative Services and Related Matters (L.196(I)/2012) The Insolvency Practitioners Law (L.64(I)/2015) Resolutions or Decisions of the United Nations Security Council (Sanctions) and the Decisions and Regulations of the Council of the European Union (Restrictive Measures) Law of 2016 [Law 58(I)/2016].

18 5. Regulating the profession Licensing Guiding Training Supporting Practice Monitoring Disciplining

General")

19 Licensing ICPAC issues the following practicing certificates to: Individuals (4) General P/C Firms (3) Insolvency ASP Auditing General Auditing ASP

20 Licensing Practising Certificates issued by ICPAC To obtain a practicing certificate, certain additional criteria need to be met: For the General and ASP license: - three (3) more years of working experience - Succeed in the Aptitude Tests (Cyprus Co Law and Cyprus Taxation) For the Audit Qualification, in excess of the above: must possess 3 post-qualification years of work experience in an audit firm in accordance with IES8. Succeed in Advance Audit paper (P7), for ACCA members only under specific circumstances. Additional specialized criteria needed for the Insolvency Practitioners, as imposed by the law.

21 Guiding Notifications for: ANNUAL COMPLIANCE OFFICER S REPORT Guidance for the completion and submission of the Annual Compliance Officers Report to ICPAC - Tax compliance - Company law - Sanctions - Competition - AML - Specific other matters November 2016

22 Training Seminars Workshops Presentations Circulars Webinars / e-courses Website

23 Supporting ICPAC office Help Desks External consultants Specialised Committees E-courses Collective offers from other organisations

24 Practice Monitoring Off-site surveillance On-site inspections

25 Practice Monitoring Off-site surveillance Risk Based process Questionnaire Process results Medium Risk High Risk Calculate a risk score Low Risk Assign a risk category

26 Practice Monitoring Onsite visits Monitoring tools: Audit Monitoring AML / Rules and Regulations Review Focus on auditors and audit firms On ALL Licensed entities ICPAC has outsourced the task of the on-site monitoring visits to ACCA since 2005.

27 Disciplining Disciplinary Committee: for breaches of law, the Regulations and the Code of Ethics. Regulatory Committee: for unsatisfactory results and matters arising from the on-site monitoring visits to members and firms.

28 6. Training accountants ACCA and ICPAC are partners in a Joint Examination Scheme (JES) since 2004: All ACCA students who are Cyprus residents are automatically included in the JES The JES follows the same exams as ACCA internationally The JES has 3 variant papers out of 14 papers: F4 Cyprus company law F6 Cyprus taxation P6 Cyprus advance taxation

CPD evidence review (upon request) 7.")

29 ICPAC operates its own CPD scheme, in cooperation with ACCA. Valid CPD activity, is any training activity which is RELEVANT to the work and duties of each member. Required amount of CPD units = 40 p.a., of which 21 units must be verifiable. One net hour of training is equivalent to 1 CPD unit Submissions: Annual CPD declaration (mandatory) CPD evidence review (upon request) 7. Continuous Professional Development

30 CPD Members activities ICPAC s training activities exceed attendees per year. More than 30 activities, including seminars, conferences, presentations, workshops, roadshows, are organised by ICPAC on a variety of topics, all relevant to the professional activities of the members. ICPAC s website facilitates the online members maintenance of the personal cpd records.

31 CPD Members activities E-learning platform on AML and Compliance issues

ICPAC, via ACCA, monitors the Approved Employer Schemes on a regular basis.")

32 CPD Approved Employer Schemes There are also 3 CPD schemes for employers: Approved Employer (trainee development) Approved Employer (professional development) Approved Employers (practising certificate development audit) ICPAC, via ACCA, monitors the Approved Employer Schemes on a regular basis. All members holding an Audit Qualification are required to abide by the provisions of IES8.

33 8. Accounting & Audit profession in Cyprus Companies Law, Cap 113 Assessment and Collection of Taxes Laws Auditors Law of 2017 Directives issued by the Central Bank of Cyprus

: Directors of the companies shall cause proper books of accounts to be kept which are deemed necessary for")

34 Companies Law Keeping of accounting records (art. 141): Directors of the companies shall cause proper books of accounts to be kept which are deemed necessary for the preparation of financial statements in accordance with the Law. Annual & Consolidated financial statements (art.142): Directors shall cause to be made, for every company, a full set of financial statements as this set is prescribed on the basis of International Accounting Standards.

] Article 151 A (1) Public Interest Entities which are large undertakings exceeding 500 employees, 6.")

35 Article 152 Α (1)(a) Companies Law All companies shall submit their financial statements for statutory audit. [EU Accounting Directive (2013/34/EU)] Article 151 A (1) Public Interest Entities which are large undertakings exceeding 500 employees, 6. as from [ financial years commencing on 1/1/2017 and onwards must issue a Statement on non-financial and diversity information. [EU Directive 2014/95/EU]

36 Tax Legislation (Assessment and Collection of Taxes laws) All companies and all sole traders with turnover more than p.a. must file their tax returns to the Tax Department accompanied by audited financial statements.

/2017] Article 67 All statutory auditors perform the statutory audit in accordance with the International Standards on")

37 Auditors Law of 2017 [L.53(I)/2017] Article 67 All statutory auditors perform the statutory audit in accordance with the International Standards on Auditing, as adopted by the European Commission as per article 26, paragraphs 1 of the Directive 2006/43/EU.

38 Auditors Law Directive 2014/56/EU on statutory audits of annual accounts and consolidated accounts Regulation (EU) No 537/2014 on specific requirements regarding statutory audit of public-interest entities Effective on 17 June 2016 Auditors Law of 2017 L.53(I)/2017 (enacted on 2/6/2017)

39 Cyprus Public Audit Oversight Authority (CyPAOA) is the ultimate competent authority of the audit profession responsible for the supervision of the: - Approval and registration of auditors in the official register - Adoption of ethical standards, quality control standards and auditing standards - Continual professional development of auditors - Quality control systems of the auditors and audit firms - Disciplinary procedures (investigation, referral for disciplinary action, imposition of penalties) Ultimate Competent Authority: CyPAOA

40 Delegation of tasks to Recognised Bodies of Auditors CyPAOA may delegate to Recognised Bodies of Auditors some or all of its duties mentioned before, with the exception of: Monitoring of the quality control systems of the auditors and audit firms with PIE clients Investigations relating to auditors and audit firms with PIE clients for matters arising from the monitoring of quality control systems Disciplinary proceedings and imposition of penalties to auditors and audit firms with PIE clients for matters arising from the monitoring of quality control systems.

41 ICPAC as a Recognised Body of Auditors The Law explicitly recognizes ICPAC by name as a Recognised Body of Auditors (art.113). On 12 September 2017, CyPAOB and ICPAC signed a Delegation Agreement, whereby ICPAC undertakes to carry out the delegated tasks as stipulated in the Agreement and allowed by the Law.

42 Public Interest Entities (PIE s) entities governed by the law of a Member State whose transferable securities are admitted to trading on a regulated market of any Member State; Licensed credit institutions; insurance and re-insurance undertakings; entities designated by the Council of Minister as public-interest entities. Main provisions of the Auditors Law for PIE Auditors

43 Audit Committee Main provisions of the Auditors Law for PIE Auditors Mandatory for every public-interest entity. Defined composition, independent of the audited entity. Ultimately responsible with respect to the auditors and the audit work performed.

44 Duration of the audit engagement Main provisions of the Auditors Law for PIE Auditors Initial engagement of at least one year. The engagement may be renewed for PIEs, other than Banks: Max consecutive engagement duration: 10 years. Where a public tendering process for the statutory audit is conducted, maximum duration extends to 20 years. Where there is a joint audit engagement, maximum duration extends to 24 years.

45 Duration of the audit engagement for Banks o Max consecutive engagement duration: 9 years. o No extension after the initial 9 year period, unless there is a cooling off of 4 years. o The appointment of the appointment of the statutory auditor as well as the above points for banks, is subject to the approval of the Central Bank of Cyprus. Main provisions of the Auditors Law for PIE Auditors

46 Non-Audit Services Main provisions of the Auditors Law for PIE Auditors A statutory auditor of a PIE, or any member of the network to which the statutory auditor or the audit firm belongs, shall NOT directly or indirectly provide to the audited entity, to its parent undertaking or to its controlled undertakings within the Union, any prohibited non-audit services.

47 Non-audit services to PIE s Tax Management and decision making Payroll Bookkeeping & preparation of Financial Statements Legal Human Resource Internal control, risk management & internal audit Valuations Financing, Investment strategy Promotion and dealings in shares of the client Main provisions of the Auditors Law for PIE Auditors - Tax services, relating to: Preparation of tax forms; Identification of public subsidies and tax incentives; Support regarding tax inspections by tax authorities; Calculation of direct and indirect tax and deferred tax; Provision of tax advice. - Valuation services

48 Audit fees Main provisions of the Auditors Law for PIE Auditors Fees for the provision of statutory audits to PIE s shall not be contingent fees. Fees from the provision of Non-Audit Services are limited to 70% of the average of the fees paid in the last three consecutive financial years for the statutory audit.

49 9. AML & Compliance - Competent authority since Issues its own AML Directive. - In 2015, introduced a specific monitoring tool for the off-site surveillance and onsite inspection of its members solely on aml and compliance matters. - Probably the only accountancy body in Europe that has adopted such mechanisms. - Provides dedicated training and other supporting offers to its members. - Envisages cooperation with the Police and the Economic Crime department.

50 - Dedicated committee for all Compliance matters (ie AML, Corporate Governance and Regulatory Compliance). - Enhanced its internal resources on the specific matters. - Produces and disseminates updates and guidance to the members. AML & Compliance - Seminars and participates in conferences on AML and compliance. - E-courses on AML & Compliance via a specifically designed e-learning platform, free of any charge. - Close cooperation with all competent authorities and especially with the FIU.

The process of transposing the 4 th EU AML Directive into national law The processes for implementing FATCA")

51 AML & Compliance ICPAC participates in: The Advisory Authority for the Prevention and Suppression of Money Laundering Activities A Special Technical Committee AML/CFT at the Central Bank of Cyprus The National Risk Assessment project (World Bank) The process of transposing the 4 th EU AML Directive into national law The processes for implementing FATCA and CRS

52 ICPAC: AML & Compliance - Has successfully completed the AML Action Plan of TROIKA, within the scope of the Adjustment Programme in Underwent more than 20 evaluations, assessments and other encounters with Troika, OECD, IMF, European Commission, MONEYVAL, as well as international rating agencies between Entered into a number of affiliations with international organisations that specialise on compliance matters

53 Evaluations by international organisations

54 10. Economy and Business Cyprus has developed over the years as an international business centre: - Common law legal regime - Favourable and easy to apply tax system - Good infrastructure - Trained and competent human capital - Quality, client-centred, services - Competitive cost for the services rendered - Adaptability to global changes - Pleasant conditions - Stability and security of the country

55 Contribution ICPAC and the Accountancy Profession have a vast contribution to the economic development and activity: Greatly involved in the promotion of Cyprus as an International Business Centre Attract businesses and investors to Cyprus Provide various services to international clients Give significant support to the government, ministries and various departments on a constant basis. Massively involved in the Double Tax Treaties negotiations Works closely with all productive stakeholders and sectors of the public sector.

56 Institutional Co-operations State Ministries Parliament CIPA - CIFA CyPAOA CySEC Central Bank of Cyprus MOKAS Tax Department Auditor General Accountant General Cyprus Stock Exchange CCCI OEB Private sector Cyprus Shipping Chamber Cyprus Bar Association Association of Cyprus Banks Association of Insurance Companies Association of Investment firms Universities International organisations International accountancy bodies Accountancy bodies of other countries Other international professional bodies

57 ICPAC is dedicated to servicing its Members, the accountancy profession, the economy and, in general, the public interest!

58 For more information, contact: Kyriakos Iordanou General Manager The Institute of Certified Public Accountants of Cyprus Tel: [+357] Fax: [+357] Website:

ICPAC Presentation 2016

ICPAC Presentation 2016 Agenda PART A: General info about ICPAC 1. ICPAC in brief 2. Milestones in the Institute s / profession s development 3. Current position of ICPAC 4. ICPAC as a competent authority

ICPAC Presentation 2016 Agenda PART A: General info about ICPAC 1. ICPAC in brief 2. Milestones in the Institute s / profession s development 3. Current position of ICPAC 4. ICPAC as a competent authority

Latest Developments of ICPAC

Latest Developments of ICPAC Larnaka (seminar 20/2016) 18 Nov 2016 Agenda 1. Part A Brief overview of ICPAC 2. Break 3. Part B Latest key developments 4. Q&A Discussion Agenda PART A 1. ICPAC in brief

Latest Developments of ICPAC Larnaka (seminar 20/2016) 18 Nov 2016 Agenda 1. Part A Brief overview of ICPAC 2. Break 3. Part B Latest key developments 4. Q&A Discussion Agenda PART A 1. ICPAC in brief

The Institute of Certified Public Accountants of Cyprus

The Institute of Certified Public Accountants of Cyprus 1 ICPAC Overview Joint Examination Scheme ACCA-ICPAC Continuing Professional Development ICPAC as regulatory and supervisory authority Capacities

The Institute of Certified Public Accountants of Cyprus 1 ICPAC Overview Joint Examination Scheme ACCA-ICPAC Continuing Professional Development ICPAC as regulatory and supervisory authority Capacities

New Auditors Law and the responsibilities of the Audit Committee

New Auditors Law and the responsibilities of the Audit Committee Sept 2017 Nicosia Agenda: 1. Legal background 2. EU Audit Directive and Regulation 3. Audit Committee Role Governance Responsibilities 4.

New Auditors Law and the responsibilities of the Audit Committee Sept 2017 Nicosia Agenda: 1. Legal background 2. EU Audit Directive and Regulation 3. Audit Committee Role Governance Responsibilities 4.

The value of good governance Services offered by ICPAC to its Members for compliance matters

The value of good governance Services offered by ICPAC to its Members for compliance matters (seminar 18/2016) 3-4 Nov 2016 Seminar Agenda 1. Presentation on ICPAC s latest developments and key information

The value of good governance Services offered by ICPAC to its Members for compliance matters (seminar 18/2016) 3-4 Nov 2016 Seminar Agenda 1. Presentation on ICPAC s latest developments and key information

Cyprus, a prominent and credible international business centre.

Cyprus, a prominent and credible international business centre. Marios Skandalis President of the Institute of Certified 2 nd EU Arab World Summit, Athens 9-10 Nov 2017 1 Public Accountants of Cyprus 2

Cyprus, a prominent and credible international business centre. Marios Skandalis President of the Institute of Certified 2 nd EU Arab World Summit, Athens 9-10 Nov 2017 1 Public Accountants of Cyprus 2

Additional Practising Regulations for the United Kingdom, Jersey, Guernsey and Dependencies and the Isle of Man

Additional Practising Regulations for the United Kingdom, Jersey, Guernsey and Dependencies and the Isle of Man Annex 1 to The Chartered Certified Accountants Global Practising Regulations 2003 1. Application

Additional Practising Regulations for the United Kingdom, Jersey, Guernsey and Dependencies and the Isle of Man Annex 1 to The Chartered Certified Accountants Global Practising Regulations 2003 1. Application

Audit Reform in Luxembourg what role will the Audit Committee play?

Audit Reform in Luxembourg what role will the Audit Committee play? The Law of 23 July 2016 on the audit profession transposing European Directive 2014/56/EU and implementing European Regulation n 537/2014,

Audit Reform in Luxembourg what role will the Audit Committee play? The Law of 23 July 2016 on the audit profession transposing European Directive 2014/56/EU and implementing European Regulation n 537/2014,

Continuing Professional Development (CPD)

") Continuing Professional Development (CPD) Regulations and Guidance Notes November 2016 CONTENTS CPD REGULATIONS 5 1. MEMBERSHIP OBLIGATIONS...5 2. PRINCIPLES OF CPD...5 3. RECORDING CPD...6 4. COMPLIANCE...6

Continuing Professional Development (CPD) Regulations and Guidance Notes November 2016 CONTENTS CPD REGULATIONS 5 1. MEMBERSHIP OBLIGATIONS...5 2. PRINCIPLES OF CPD...5 3. RECORDING CPD...6 4. COMPLIANCE...6

ANTI-MONEY LAUNDERING QUESTIONNAIRE. Guidance for the completion and submission of the Anti-Money Laundering Questionnaire to ICPAC

ANTI-MONEY LAUNDERING QUESTIONNAIRE Guidance for the completion and submission of the Anti-Money Laundering Questionnaire to ICPAC October 2017 1 Introduction ICPAC is the competent Supervisory Authority

ANTI-MONEY LAUNDERING QUESTIONNAIRE Guidance for the completion and submission of the Anti-Money Laundering Questionnaire to ICPAC October 2017 1 Introduction ICPAC is the competent Supervisory Authority

COMMITTEE OF EXPERTS ON THE EVALUATION OF ANTI-MONEY LAUNDERING MEASURES AND THE FINANCING OF TERRORISM. 4th round evaluation of CYPRUS

MONEYVAL(2015)47 COMMITTEE OF EXPERTS ON THE EVALUATION OF ANTI-MONEY LAUNDERING MEASURES AND THE FINANCING OF TERRORISM 4th round evaluation of CYPRUS Biennial update 16 November, 2015 Table of contents

MONEYVAL(2015)47 COMMITTEE OF EXPERTS ON THE EVALUATION OF ANTI-MONEY LAUNDERING MEASURES AND THE FINANCING OF TERRORISM 4th round evaluation of CYPRUS Biennial update 16 November, 2015 Table of contents

Profile of the Profession 2015

Profile of the Profession 2015 MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and promoting high quality financial reporting, auditing and

Profile of the Profession 2015 MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and promoting high quality financial reporting, auditing and

Tax Agent Services Regulations

Tax Agent Services Regulations 2009 1 Select Legislative Instrument 2009 No. 314 I, QUENTIN BRYCE, Governor-General of the Commonwealth of Australia, acting with the advice of the Federal Executive Council,

Tax Agent Services Regulations 2009 1 Select Legislative Instrument 2009 No. 314 I, QUENTIN BRYCE, Governor-General of the Commonwealth of Australia, acting with the advice of the Federal Executive Council,

Response to the IFAC Part 2, SMO Self-Assessment Questionnaire

Response to the IFAC Part 2, SMO Self-Assessment Questionnaire Member Name: Country: Published Date: August 2006 Disclaimer: Please refer to the Disclaimer published on IFAC s website about this assessment.

Response to the IFAC Part 2, SMO Self-Assessment Questionnaire Member Name: Country: Published Date: August 2006 Disclaimer: Please refer to the Disclaimer published on IFAC s website about this assessment.

Republika e Kosovës Republika Kosovo - Republic of Kosovo Kuvendi - Skupština - Assembly

Republika e Kosovës Republika Kosovo - Republic of Kosovo Kuvendi - Skupština - Assembly Law No. 06/L 032 ON ACCOUNTING, FINANCIAL REPORTING AND AUDITING Assembly of the Republic of Kosovo, Based on Article

Republika e Kosovës Republika Kosovo - Republic of Kosovo Kuvendi - Skupština - Assembly Law No. 06/L 032 ON ACCOUNTING, FINANCIAL REPORTING AND AUDITING Assembly of the Republic of Kosovo, Based on Article

Are you ready for an AML monitoring review?

Are you ready for an AML monitoring review? Haroulla Arkade Nicolaou Louis Theodotou Kyriacos Karaolis ACCA Senior Practice Reviewers AGENDA 1. Scope of an AML monitoring visit 2. The Prevention and Suppression

Are you ready for an AML monitoring review? Haroulla Arkade Nicolaou Louis Theodotou Kyriacos Karaolis ACCA Senior Practice Reviewers AGENDA 1. Scope of an AML monitoring visit 2. The Prevention and Suppression

LATEST DEVELOPMENTS ON THE NEW EUROPEAN UNION (EU) AUDITING FRAMEWORK

AUDITING FRAMEWORK") LATEST DEVELOPMENTS ON THE NEW EUROPEAN UNION (EU) AUDITING FRAMEWORK IAASB-CAG Meeting New York, 12 March 2014 Agenda Item I Juan Maria ARTEAGOITIA European Commission Disclaimer: The views expressed

LATEST DEVELOPMENTS ON THE NEW EUROPEAN UNION (EU) AUDITING FRAMEWORK IAASB-CAG Meeting New York, 12 March 2014 Agenda Item I Juan Maria ARTEAGOITIA European Commission Disclaimer: The views expressed

Part D: Part E: Part F:

PROFILE OF THE PROFESSION 2014 Mission To promote high quality financial reporting and effective regulation of accountants and auditors through the delivery of independent and effective supervision which

PROFILE OF THE PROFESSION 2014 Mission To promote high quality financial reporting and effective regulation of accountants and auditors through the delivery of independent and effective supervision which

Profile of the Profession 2016

Profile of the Profession 2016 MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and promoting high quality financial reporting, auditing and

Profile of the Profession 2016 MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and promoting high quality financial reporting, auditing and

LAW OF MONGOLIA ON AUDITING CHAPTER ONE GENERAL PROVISIONS. Article 1. Purpose of the law

LAW OF MONGOLIA ON AUDITING Unofficial Translation CHAPTER ONE GENERAL PROVISIONS Article 1. Purpose of the law 1.1 The purpose of the law is to determine the principles of auditing activities and organizational

LAW OF MONGOLIA ON AUDITING Unofficial Translation CHAPTER ONE GENERAL PROVISIONS Article 1. Purpose of the law 1.1 The purpose of the law is to determine the principles of auditing activities and organizational

CZECH REPUBLIC. Radek Neužil Member of Presidium

CZECH REPUBLIC Member of Presidium Structure of the Czech Audit Public Oversight Council Council Structure 6 Presidium members appointed by the Minister of Finance 2 auditors (exception for one auditor

CZECH REPUBLIC Member of Presidium Structure of the Czech Audit Public Oversight Council Council Structure 6 Presidium members appointed by the Minister of Finance 2 auditors (exception for one auditor

JC /05/2017. Final Report

JC 2017 08 30/05/2017 Final Report On Joint draft regulatory technical standards on the criteria for determining the circumstances in which the appointment of a central contact point pursuant to Article

JC 2017 08 30/05/2017 Final Report On Joint draft regulatory technical standards on the criteria for determining the circumstances in which the appointment of a central contact point pursuant to Article

Disclaimer: Please refer to the Disclaimer published on IFAC s website about this assessment. Number Question Title/Text/Help text Answer Comments

Response to the IFAC Part 2, SMO Self-Assessment Questionnaire Member Name: Country: Published Date: October 2006 Disclaimer: Please refer to the Disclaimer published on IFAC s website about this assessment.

Response to the IFAC Part 2, SMO Self-Assessment Questionnaire Member Name: Country: Published Date: October 2006 Disclaimer: Please refer to the Disclaimer published on IFAC s website about this assessment.

STAREP Accounting and Auditing Standards Community of Practice (A&A CoP) Public Oversight and Quality Assurance in Armenia: Current Status

Public Oversight and Quality Assurance in Armenia: Current Status") STAREP Accounting and Auditing Standards Community of Practice (A&A CoP) Public Oversight and Quality Assurance in Armenia: Current Status Background Auditing Market Condition Number of auditors: 309 persons

STAREP Accounting and Auditing Standards Community of Practice (A&A CoP) Public Oversight and Quality Assurance in Armenia: Current Status Background Auditing Market Condition Number of auditors: 309 persons

THE FINANCIAL REPORTING ACT 2004

THE FINANCIAL REPORTING ACT 2004 Act No. 45 of 2004 I assent SIR ANEROOD JUGNAUTH 10 th December 2004 President of the Republic Section 1. Short title 2. Interpretation PART I-PRELIMINARY ARRANGEMENT OF

THE FINANCIAL REPORTING ACT 2004 Act No. 45 of 2004 I assent SIR ANEROOD JUGNAUTH 10 th December 2004 President of the Republic Section 1. Short title 2. Interpretation PART I-PRELIMINARY ARRANGEMENT OF

EUROPEAN UNION. Brussels, 4 April 2014 (OR. en) 2011/0359 (COD) PE-CONS 5/14 DRS 2 CODEC 36

2011/0359 (COD) PE-CONS 5/14 DRS 2 CODEC 36") EUROPEAN UNION THE EUROPEAN PARLIAMT THE COUNCIL Brussels, 4 April 2014 (OR. en) 2011/0359 (COD) PE-CONS 5/14 DRS 2 CODEC 36 LEGISLATIVE ACTS AND OTHER INSTRUMTS Subject: REGULATION OF THE EUROPEAN PARLIAMT

EUROPEAN UNION THE EUROPEAN PARLIAMT THE COUNCIL Brussels, 4 April 2014 (OR. en) 2011/0359 (COD) PE-CONS 5/14 DRS 2 CODEC 36 LEGISLATIVE ACTS AND OTHER INSTRUMTS Subject: REGULATION OF THE EUROPEAN PARLIAMT

CHALLENGES FOR LITHUANIA S AUDITORS: PUSH FORWARD, HOLD BACK OR FLY ALONGSIDE?

CHALLENGES FOR LITHUANIA S AUDITORS: PUSH FORWARD, HOLD BACK OR FLY ALONGSIDE? Aurelija Lauruševičiūtė, director of The Lithuanian Chamber of Auditors STARTING POINT Audit system i 1990 by the Lithuanian

CHALLENGES FOR LITHUANIA S AUDITORS: PUSH FORWARD, HOLD BACK OR FLY ALONGSIDE? Aurelija Lauruševičiūtė, director of The Lithuanian Chamber of Auditors STARTING POINT Audit system i 1990 by the Lithuanian

Competency standards for Fellows of the NTAA auditing SMSFs

Competency standards for Fellows of the NTAA auditing SMSFs National Tax & Accountants Association Ltd. 1 Contents Introduction.. 3 Background. 4 Auditing an SMSF.. 5 The planning phase of the audit ASA

Competency standards for Fellows of the NTAA auditing SMSFs National Tax & Accountants Association Ltd. 1 Contents Introduction.. 3 Background. 4 Auditing an SMSF.. 5 The planning phase of the audit ASA

Action Plan Developed by The Chamber of Auditors of Azerbaijan Republic (CAAR) BACKGROUND NOTE ON ACTION PLANS

BACKGROUND NOTE ON ACTION PLANS") The Chamber of Auditors of Azerbaijan Republic () BACKGROUND NOTE ON ACTION PLANS Action Plans are developed by IFAC members and associates to address policy matters identified through their responses

The Chamber of Auditors of Azerbaijan Republic () BACKGROUND NOTE ON ACTION PLANS Action Plans are developed by IFAC members and associates to address policy matters identified through their responses

2018 SMO Action Plan Update. Institut des réviseurs d entreprises - Luxembourg BACKGROUND NOTE ON ACTION PLANS

BACKGROUND NOTE ON ACTION PLANS SMO Action Plans are developed by IFAC Members and Associates to demonstrate fulfillment of IFAC Statements of Membership Obligations (SMOs). SMOs require IFAC Members and

BACKGROUND NOTE ON ACTION PLANS SMO Action Plans are developed by IFAC Members and Associates to demonstrate fulfillment of IFAC Statements of Membership Obligations (SMOs). SMOs require IFAC Members and

Financial Intelligence Centre Amendment Bill [B ]

![Financial Intelligence Centre Amendment Bill [B ]](/thumbs/89/98141695.jpg "Financial Intelligence Centre Amendment Bill [B ]") Financial Intelligence Centre Amendment Bill [B 33 2015] Briefing of the Select Committee on Finance 20 May 2016 Presentation by National Treasury and Financial Intelligence Centre financial intelligence

Financial Intelligence Centre Amendment Bill [B 33 2015] Briefing of the Select Committee on Finance 20 May 2016 Presentation by National Treasury and Financial Intelligence Centre financial intelligence

European Commission Proposed Directive on Statutory Audit of Annual Accounts and Consolidated Accounts

Policy on EC Proposed Directive Fédération des Experts Comptables Européens 31 March 2004 European Commission Proposed Directive on Statutory Audit of Annual Accounts and Consolidated Accounts On 16 March

Policy on EC Proposed Directive Fédération des Experts Comptables Européens 31 March 2004 European Commission Proposed Directive on Statutory Audit of Annual Accounts and Consolidated Accounts On 16 March

GP GLOBAL LTD. Business and Finance Consulting Services COMPANY PROFILE

G P Global GP GLOBAL LTD Business and Finance Consulting Services COMPANY PROFILE Alkaios str., 7 Alkaios Court, Flat 103 Tel.: +357-25755911 3090 Limassol - CYPRUS Fax: +357-25755660 P.O. Box 59565, 4010

G P Global GP GLOBAL LTD Business and Finance Consulting Services COMPANY PROFILE Alkaios str., 7 Alkaios Court, Flat 103 Tel.: +357-25755911 3090 Limassol - CYPRUS Fax: +357-25755660 P.O. Box 59565, 4010

CONSULTATION PAPER NO JUNE 2016 PROPOSED CHANGES TO THE ANTI MONEY LAUNDERING, COUNTER- TERRORIST FINANCING AND SANCTIONS MODULE

CONSULTATION PAPER NO. 107 20 JUNE 2016 PROPOSED CHANGES TO THE ANTI MONEY LAUNDERING, COUNTER- TERRORIST FINANCING AND SANCTIONS MODULE CONSULTATION PAPER NO. 107 PROPOSED CHANGES TO THE ANTI MONEY LAUNDERING,

CONSULTATION PAPER NO. 107 20 JUNE 2016 PROPOSED CHANGES TO THE ANTI MONEY LAUNDERING, COUNTER- TERRORIST FINANCING AND SANCTIONS MODULE CONSULTATION PAPER NO. 107 PROPOSED CHANGES TO THE ANTI MONEY LAUNDERING,

THE FRAMEWORK OF SUPERVISION FOR FINANCIAL INSTITUTIONS

THE FRAMEWORK OF SUPERVISION FOR FINANCIAL INSTITUTIONS BANKING SUPERVISION UNIT TABLE OF CONTENTS 1.0.0 INTRODUCTION... 1 2.0.0 REGULATED ENTITIES... 1 3.0.0 THE BANKING SUPERVISION UNIT... 2 3.1.0 OBJECTIVES...

THE FRAMEWORK OF SUPERVISION FOR FINANCIAL INSTITUTIONS BANKING SUPERVISION UNIT TABLE OF CONTENTS 1.0.0 INTRODUCTION... 1 2.0.0 REGULATED ENTITIES... 1 3.0.0 THE BANKING SUPERVISION UNIT... 2 3.1.0 OBJECTIVES...

International Monetary Fund s Financial Sector Stability Assessment. Force Report

International Monetary Fund s Financial Sector Stability Assessment and Caribbean Financial Task Force Report Cherno Jallow,QC Director, Policy, Research and Statistics Meet The Regulator 16 March 2011

International Monetary Fund s Financial Sector Stability Assessment and Caribbean Financial Task Force Report Cherno Jallow,QC Director, Policy, Research and Statistics Meet The Regulator 16 March 2011

DECREE 247 of 24 July on Applications According to the Act on Management Companies and Investment Funds

DECREE 247 of 24 July 2013 on Applications According to the Act on Management Companies and Investment Funds as amended by Decree No. 344/2014 Coll. The Czech National Bank stipulates pursuant to Article

DECREE 247 of 24 July 2013 on Applications According to the Act on Management Companies and Investment Funds as amended by Decree No. 344/2014 Coll. The Czech National Bank stipulates pursuant to Article

An AIF shall be managed by a single AIFM responsible for ensuring compliance with the AIFM Law which shall either be:

THE DELEGATION UNDER THE AIFM LAW The law of July 12, 2013 on alternative investment fund managers (the AIFM Law ) 1 regulates the authorisation, activities and transparency requirements of managers qualifying

THE DELEGATION UNDER THE AIFM LAW The law of July 12, 2013 on alternative investment fund managers (the AIFM Law ) 1 regulates the authorisation, activities and transparency requirements of managers qualifying

MANDATORY CONTINUOUS PROFESSIONAL DEVELOPMENT PROGRAMME ICAG THE INSTITUTE OF CHARTERED ACCOUNTANTS (GHANA)

") MANDATORY CONTINUOUS PROFESSIONAL DEVELOPMENT PROGRAMME ICAG THE INSTITUTE OF CHARTERED ACCOUNTANTS (GHANA) CONTENT 2-12 13-14 15-23 CPD Brochure ICAG 2019 CPD Calendar Sypnosis 1 1 WHAT IS CPD? CPD is

MANDATORY CONTINUOUS PROFESSIONAL DEVELOPMENT PROGRAMME ICAG THE INSTITUTE OF CHARTERED ACCOUNTANTS (GHANA) CONTENT 2-12 13-14 15-23 CPD Brochure ICAG 2019 CPD Calendar Sypnosis 1 1 WHAT IS CPD? CPD is

Proceeds of Crime (Supervisory Bodies) (Jersey) Law 2008: Fees for registered persons

(Jersey) Law 2008: Fees for registered persons") Consultation Paper No. 10 2017 Proceeds of Crime (Supervisory Bodies) (Jersey) Law 2008: Fees for registered persons A consultation on proposals regarding fee rates and associated issues. Issued: October

Consultation Paper No. 10 2017 Proceeds of Crime (Supervisory Bodies) (Jersey) Law 2008: Fees for registered persons A consultation on proposals regarding fee rates and associated issues. Issued: October

Practice Information Handbook

Practice Information Handbook Contents Introduction 4 1 The practising certificate 6 Who requires a practising certificate? 6 What is public practice? 6 What is not considered to be public practice? 7

Practice Information Handbook Contents Introduction 4 1 The practising certificate 6 Who requires a practising certificate? 6 What is public practice? 6 What is not considered to be public practice? 7

Acquiring the Cypriot Citizenship

Acquiring the Cypriot Citizenship Cyprus Investment Programme The existing Cyprus Citizenship Program, updated in September 2016, enables non-cypriot citizens, entrepreneurs, investors and their immediate

Acquiring the Cypriot Citizenship Cyprus Investment Programme The existing Cyprus Citizenship Program, updated in September 2016, enables non-cypriot citizens, entrepreneurs, investors and their immediate

CYPRUS BAR ASSOCIATION

Significant amendments to the Prevention and Suppression of Money Laundering and Terrorist Financing Law (188 (I)/2007). 1. Article (2) Definitions: politically exposed persons (PEP) The definition of

Significant amendments to the Prevention and Suppression of Money Laundering and Terrorist Financing Law (188 (I)/2007). 1. Article (2) Definitions: politically exposed persons (PEP) The definition of

TRANSPARENCY PRACTICES FOR MONETARY POLICY AT THE EASTERN CARIBBEAN CENTRAL BANK

TRANSPARENCY PRACTICES FOR MONETARY POLICY AT THE EASTERN CARIBBEAN CENTRAL BANK Prepared for the 59 th Meeting of the Monetary Council 21 July 2007 Anguilla EASTERN CARIBBEAN CENTRAL BANK ST KITTS TABLE

TRANSPARENCY PRACTICES FOR MONETARY POLICY AT THE EASTERN CARIBBEAN CENTRAL BANK Prepared for the 59 th Meeting of the Monetary Council 21 July 2007 Anguilla EASTERN CARIBBEAN CENTRAL BANK ST KITTS TABLE

THE FINANCIAL REPORTING ACT 2004

THE FINANCIAL REPORTING ACT 2004 Act No. 43 of 2004 I assent 10th December, 2004 SIR ANEROOD JUGNAUTH President of the Republic Date in Force: Not Proclaimed ARRANGEMENT OF SECTIONS Section PART I-PRELIMINARY

THE FINANCIAL REPORTING ACT 2004 Act No. 43 of 2004 I assent 10th December, 2004 SIR ANEROOD JUGNAUTH President of the Republic Date in Force: Not Proclaimed ARRANGEMENT OF SECTIONS Section PART I-PRELIMINARY

SWEDEN. Mutual Evaluation Fourth Follow-Up Report - annexes. Anti-Money Laundering and Combating the Financing of Terrorism

FINANCIAL ACTION TASK FORCE Mutual Evaluation Fourth Follow-Up Report - annexes Anti-Money Laundering and Combating the Financing of Terrorism SWEDEN 22 October 2010 ANNEX 1 LIST OF LAWS, REGULATIONS,

FINANCIAL ACTION TASK FORCE Mutual Evaluation Fourth Follow-Up Report - annexes Anti-Money Laundering and Combating the Financing of Terrorism SWEDEN 22 October 2010 ANNEX 1 LIST OF LAWS, REGULATIONS,

APPLICATION FOR ACCREDITATION OR RE-ACCREDITATION AS A MEDIATOR

Current as at 1 July 2015 Office use only Date approved Approved by Payment date ABN 78 009 717 739 APPLICATION FOR ACCREDITATION OR RE-ACCREDITATION AS A MEDIATOR Before completing this form you need

Current as at 1 July 2015 Office use only Date approved Approved by Payment date ABN 78 009 717 739 APPLICATION FOR ACCREDITATION OR RE-ACCREDITATION AS A MEDIATOR Before completing this form you need

Question 1 - Money Laundering: Definition

Question 1 - Money Laundering: Definition Money Laundering is criminalised under the Prevention of Money Laundering Act (Chapter 373 of the Laws of Malta). In terms of article 2 of the Prevention of Money

Question 1 - Money Laundering: Definition Money Laundering is criminalised under the Prevention of Money Laundering Act (Chapter 373 of the Laws of Malta). In terms of article 2 of the Prevention of Money

CYPRUS: AN EMERGING FUNDS JURISDICTION. Marios Tannousis Board Member & Secretary

CYPRUS: AN EMERGING FUNDS JURISDICTION Marios Tannousis Board Member & Secretary Cyprus as Business Expansion Platform In addition to the favorable tax regime, Cyprus offers many other advantages: Strategic

CYPRUS: AN EMERGING FUNDS JURISDICTION Marios Tannousis Board Member & Secretary Cyprus as Business Expansion Platform In addition to the favorable tax regime, Cyprus offers many other advantages: Strategic

CYPRUS INVESTMENT FIRM CIF

CYPRUS INVESTMENT FIRM CIF The Applicable Legislation The Law governing the Cyprus Investment Firms (the CIF ) is the Law 144(I)/2007 as amended (the Law ). The Law has adopted a number of the EU Directives

CYPRUS INVESTMENT FIRM CIF The Applicable Legislation The Law governing the Cyprus Investment Firms (the CIF ) is the Law 144(I)/2007 as amended (the Law ). The Law has adopted a number of the EU Directives

Acquiring the Cypriot Citizenship Cyprus Investment Programme

Acquiring the Cypriot Citizenship Cyprus Investment Programme The existing Cyprus Citizenship Program, updated in September 2016, enables non-cypriot citizens, entrepreneurs, investors and their immediate

Acquiring the Cypriot Citizenship Cyprus Investment Programme The existing Cyprus Citizenship Program, updated in September 2016, enables non-cypriot citizens, entrepreneurs, investors and their immediate

STATUTORY INSTRUMENTS. S.I. No. 604 of 2017 CENTRAL BANK (SUPERVISION AND ENFORCEMENT) ACT 2013 (SECTION 48(1)) (INVESTMENT FIRMS) REGULATIONS 2017

ACT 2013 (SECTION 48(1)) (INVESTMENT FIRMS) REGULATIONS 2017") STATUTORY INSTRUMENTS. S.I. No. 604 of 2017 CENTRAL BANK (SUPERVISION AND ENFORCEMENT) ACT 2013 (SECTION 48(1)) (INVESTMENT FIRMS) REGULATIONS 2017 2 [604] S.I. No. 604 of 2017 CENTRAL BANK (SUPERVISION

STATUTORY INSTRUMENTS. S.I. No. 604 of 2017 CENTRAL BANK (SUPERVISION AND ENFORCEMENT) ACT 2013 (SECTION 48(1)) (INVESTMENT FIRMS) REGULATIONS 2017 2 [604] S.I. No. 604 of 2017 CENTRAL BANK (SUPERVISION

BOLSAS Y MERCADOS ESPAÑOLES, SISTEMAS DE NEGOCIACIÓN, S.A. ALTERNATIVE EQUITY MARKET GENERAL REGULATIONS

ALTERNATIVE EQUITY MARKET GENERAL REGULATIONS 1 CONTENTS Title I - General provisions - Article 1 - Purpose and scope of application - Article 2 - Name - Article 3 - Governing bodies - Article 4 - Legal

ALTERNATIVE EQUITY MARKET GENERAL REGULATIONS 1 CONTENTS Title I - General provisions - Article 1 - Purpose and scope of application - Article 2 - Name - Article 3 - Governing bodies - Article 4 - Legal

Your 2015 insolvency licence renewal must be completed in all circumstances and should be submitted as soon as possible.

Renewal of your insolvency licence for 2015 Your 2015 insolvency licence renewal must be completed in all circumstances and should be submitted as soon as possible. Please ensure that you read the following

Renewal of your insolvency licence for 2015 Your 2015 insolvency licence renewal must be completed in all circumstances and should be submitted as soon as possible. Please ensure that you read the following

GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES

. GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES November 2013 GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES Introduction 1. Promoting good governance has been at the

. GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES November 2013 GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES Introduction 1. Promoting good governance has been at the

ACT. ii Supplement to the Sierra Leone Gazette Vol. CXLVII, No. 11 PART IV ADMINISTRATIVE PROVISIONS. dated 3rd March, 2016

ACT ii Supplement to the Sierra Leone Gazette Vol. CXLVII, No. 11 Sections. THE SIERRA LEONE SMALL AND MEDIUM ENTERPRISES DEVELOPMENT AGENCY ACT, 2016 1. Interpretation. dated 3rd March, 2016 ARRANGEMENT

ACT ii Supplement to the Sierra Leone Gazette Vol. CXLVII, No. 11 Sections. THE SIERRA LEONE SMALL AND MEDIUM ENTERPRISES DEVELOPMENT AGENCY ACT, 2016 1. Interpretation. dated 3rd March, 2016 ARRANGEMENT

STRATEGY OF PUBLIC INTERNAL FINANCIAL CONTROL DEVELOPMENT IN THE REPUBLIC OF SERBIA FOR THE PERIOD OF

Ministry of Finance STRATEGY OF PUBLIC INTERNAL FINANCIAL CONTROL DEVELOPMENT IN THE REPUBLIC OF SERBIA FOR THE PERIOD OF 2017-2020 www.mfin.gov.rs REPUBLIC OF SERBIA MINISTRY OF FINANCE TABLE OF CONTENTS

Ministry of Finance STRATEGY OF PUBLIC INTERNAL FINANCIAL CONTROL DEVELOPMENT IN THE REPUBLIC OF SERBIA FOR THE PERIOD OF 2017-2020 www.mfin.gov.rs REPUBLIC OF SERBIA MINISTRY OF FINANCE TABLE OF CONTENTS

Practice information Handbook

Practice information Handbook 2 Practice information handbook Contents Introduction 4 1 The practising certificate 6 Who requires a practising certificate? 6 What is public practice? 6 What is not considered

Practice information Handbook 2 Practice information handbook Contents Introduction 4 1 The practising certificate 6 Who requires a practising certificate? 6 What is public practice? 6 What is not considered

IOPS Technical Committee DRAFT GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES. Version for public consultation

IOPS Technical Committee DRAFT GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES Version for public consultation DRAFT GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES Introduction:

IOPS Technical Committee DRAFT GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES Version for public consultation DRAFT GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES Introduction:

Appendix 2. In this Appendix underlining indicates new text and striking through indicates deleted text. The DFSA Rulebook

Appendix 2 In this Appendix underlining indicates new text and striking through indicates deleted text. The DFSA Rulebook Anti-Money Laundering, Counter-Terrorist Financing and Sanctions Module (AML) 1

Appendix 2 In this Appendix underlining indicates new text and striking through indicates deleted text. The DFSA Rulebook Anti-Money Laundering, Counter-Terrorist Financing and Sanctions Module (AML) 1

Taxation Vietnam (TX-VNM) (F6)

(F6)") June and December 2018 Taxation Vietnam (TX-VNM) (F6) Syllabus and study guide Guide to structure of the syllabus and study guide Overall aim of the syllabus This explains briefly the overall objective

June and December 2018 Taxation Vietnam (TX-VNM) (F6) Syllabus and study guide Guide to structure of the syllabus and study guide Overall aim of the syllabus This explains briefly the overall objective

Internal Control in Poland. Monika Kos Lima, 30 March 2016

Internal Control in Poland Monika Kos Lima, 30 March 2016 Plan of the presentation Poland in numbers Factors of reforms Reference models Legal basic and definition Implementation and reporting Role of

Internal Control in Poland Monika Kos Lima, 30 March 2016 Plan of the presentation Poland in numbers Factors of reforms Reference models Legal basic and definition Implementation and reporting Role of

GUIDANCE FOR REGULATORY ORDERS

GUIDANCE FOR REGULATORY ORDERS APPLICATIONS FOR WAIVERS OF REGULATIONS Published by The Association of Chartered Certified Accountants on 2 February 2009 Updated: February 2013 CONTENTS SECTION 1: INTRODUCTION

GUIDANCE FOR REGULATORY ORDERS APPLICATIONS FOR WAIVERS OF REGULATIONS Published by The Association of Chartered Certified Accountants on 2 February 2009 Updated: February 2013 CONTENTS SECTION 1: INTRODUCTION

Reform of the EU Statutory Audit Market - Frequently Asked Questions

EUROPEAN COMMISSION MEMO Brussels, 3 April 2014 Reform of the EU Statutory Audit Market - Frequently Asked Questions WHERE DOES THE REFORM STAND? On 17 December 2013, the European Parliament and the Member

EUROPEAN COMMISSION MEMO Brussels, 3 April 2014 Reform of the EU Statutory Audit Market - Frequently Asked Questions WHERE DOES THE REFORM STAND? On 17 December 2013, the European Parliament and the Member

OFFICE OF THE MINISTER OF COMMERCE. The Chair CABINET ECONOMIC DEVELOPMENT COMMITTEE REGULATION OF FINANCIAL INTERMEDIARIES PROPOSAL

OFFICE OF THE MINISTER OF COMMERCE The Chair CABINET ECONOMIC DEVELOPMENT COMMITTEE REGULATION OF FINANCIAL INTERMEDIARIES PROPOSAL 1 This paper outlines the final report of the Financial Intermediaries

OFFICE OF THE MINISTER OF COMMERCE The Chair CABINET ECONOMIC DEVELOPMENT COMMITTEE REGULATION OF FINANCIAL INTERMEDIARIES PROPOSAL 1 This paper outlines the final report of the Financial Intermediaries

Content. 1. Introduction of AML/CFT Legislation

ANNUAL REPORT On 2008 Activities of the Financial Monitoring Center of the Republic of Armenia Central Bank in the Field of Combating Money Laundering and Terrorism Financing Yerevan, 2009 Content This

ANNUAL REPORT On 2008 Activities of the Financial Monitoring Center of the Republic of Armenia Central Bank in the Field of Combating Money Laundering and Terrorism Financing Yerevan, 2009 Content This

Code of Professional Ethics: independence provisions relating to review and assurance engagements

Code of Professional Ethics: independence provisions relating to review and assurance engagements AAT is a registered charity. No. 1050724 Contents Foreword... 4 Introduction... 5 Glossary of Terms...

Code of Professional Ethics: independence provisions relating to review and assurance engagements AAT is a registered charity. No. 1050724 Contents Foreword... 4 Introduction... 5 Glossary of Terms...

Regulation and Supervision of the Financial Services Sector. Mdina The Silent City, Malta

Regulation and Supervision of the Financial Services Sector Mdina The Silent City, Malta Contents Introduction... 3 1 Regulation and Supervision of Financial Services Companies... 4 1.1 Jurisdiction who

Regulation and Supervision of the Financial Services Sector Mdina The Silent City, Malta Contents Introduction... 3 1 Regulation and Supervision of Financial Services Companies... 4 1.1 Jurisdiction who

Audit Regulations and Guidance

Audit Regulations and Guidance EFFECTIVE FROM 1 APRIL 2017 icaew.com AUDIT REGULATIONS AND GUIDANCE Institute of Chartered Accountants in England and Wales Institute of Chartered Accountants of Scotland

Audit Regulations and Guidance EFFECTIVE FROM 1 APRIL 2017 icaew.com AUDIT REGULATIONS AND GUIDANCE Institute of Chartered Accountants in England and Wales Institute of Chartered Accountants of Scotland

I) CONSOB REGULATION ADOPTED BY RESOLUTION NO OF 12 MARCH 2010 AS SUBSEQUENTLY AMENDED

CONSOB REGULATION ADOPTED BY RESOLUTION NO OF 12 MARCH 2010 AS SUBSEQUENTLY AMENDED") GROUP PROCEDURES REGULATING THE CONDUCT OF TRANSACTIONS WITH RELATED PARTIES OF INTESA SANPAOLO S.P.A., ASSOCIATED ENTITIES OF THE GROUP AND RELEVANT PARTIES PURSUANT TO ART. 136 OF THE CONSOLIDATED LAW

GROUP PROCEDURES REGULATING THE CONDUCT OF TRANSACTIONS WITH RELATED PARTIES OF INTESA SANPAOLO S.P.A., ASSOCIATED ENTITIES OF THE GROUP AND RELEVANT PARTIES PURSUANT TO ART. 136 OF THE CONSOLIDATED LAW

LAW OF GEORGIA ON DEPOSIT INSURANCE SYSTEM. Chapter I. General Provisions. Article 1. Scope of the Law

LAW OF GEORGIA ON DEPOSIT INSURANCE SYSTEM Chapter I General Provisions Article 1. Scope of the Law 1. The present Law defines legal framework for establishment of the Deposit Insurance System, governance

LAW OF GEORGIA ON DEPOSIT INSURANCE SYSTEM Chapter I General Provisions Article 1. Scope of the Law 1. The present Law defines legal framework for establishment of the Deposit Insurance System, governance

ANNEX XX. GUIDELINES FOR MRAs

Disclaimer: In view of the Commission's transparency policy, the Commission is publishing the texts of the Trade Part of the Agreement following the agreement in principle announced on 21 April 2018. The

Disclaimer: In view of the Commission's transparency policy, the Commission is publishing the texts of the Trade Part of the Agreement following the agreement in principle announced on 21 April 2018. The

Action Plan Developed by Ordre des Experts Comptables et Comptables Agréés du Burkina Faso (ONECCA BF) BACKGROUND NOTE ON ACTION PLANS

BACKGROUND NOTE ON ACTION PLANS") BACKGROUND NOTE ON ACTION PLANS SMO Action Plans are developed by IFAC and Associates to demonstrate fulfillment of IFAC Statements of hip Obligations (SMOs). SMOs require IFAC and Associates to support

BACKGROUND NOTE ON ACTION PLANS SMO Action Plans are developed by IFAC and Associates to demonstrate fulfillment of IFAC Statements of hip Obligations (SMOs). SMOs require IFAC and Associates to support

Fathom Wealth Management Advisors Ltd Risk Management Disclosures Year Ended 31 December 2016

Fathom Wealth Management Advisors Ltd Risk Management Disclosures Year Ended 31 December 2016 According to Directives DI144-2014-14 and DI144-2014-15 of the Cyprus Securities & Exchange Commission for

Fathom Wealth Management Advisors Ltd Risk Management Disclosures Year Ended 31 December 2016 According to Directives DI144-2014-14 and DI144-2014-15 of the Cyprus Securities & Exchange Commission for

Cyprus EU Citizenship By Investment

Cyprus EU Citizenship By Investment CYPRUS EU CITIZENSHIP BY INVESTMENT Cyprus became a member of the European Union in May 2004 and joined the EU Monetary Union in 2008 Cyprus has a stable legal and tax

Cyprus EU Citizenship By Investment CYPRUS EU CITIZENSHIP BY INVESTMENT Cyprus became a member of the European Union in May 2004 and joined the EU Monetary Union in 2008 Cyprus has a stable legal and tax

Ordinance No. 20. (title amended; Darjaven Vestnik, issue 40 of 2014) Subject

Subject") Ordinance No. 20 1 Ordinance No. 20 of 28 April 2009 on the Issuance of Approvals to the Members of the Management Board (Board of Directors) and Supervisory Board of a Credit Institution and Requirements

Ordinance No. 20 1 Ordinance No. 20 of 28 April 2009 on the Issuance of Approvals to the Members of the Management Board (Board of Directors) and Supervisory Board of a Credit Institution and Requirements

Quality Assurance Scheme for Organisations

Quality Assurance Scheme for Organisations New policy proposals by the Professional Regulation Executive Committee Exposure Draft ED 30 Consultation paper May 2013 Contents 1. Introduction and background

Quality Assurance Scheme for Organisations New policy proposals by the Professional Regulation Executive Committee Exposure Draft ED 30 Consultation paper May 2013 Contents 1. Introduction and background

Law No. 116 of 2013 Regarding the Promotion of Direct Investment in the State of Kuwait

Law No. 116 of 2013 Regarding the Promotion of Direct Investment in the State of Kuwait Law No. 116 of 2013 Regarding the Promotion of Direct Investment in the State of Kuwait - Having reviewed the Constitution;

Law No. 116 of 2013 Regarding the Promotion of Direct Investment in the State of Kuwait Law No. 116 of 2013 Regarding the Promotion of Direct Investment in the State of Kuwait - Having reviewed the Constitution;

Accountancy Profession Act 1979 Cap 281

2015 Code of Ethics for Warrant Holders Accountancy Profession Act 1979 Cap 281 Directive Number 2 issued in terms of the Accountancy Profession Act (Cap 281) and of the Accountancy Profession Regulations

2015 Code of Ethics for Warrant Holders Accountancy Profession Act 1979 Cap 281 Directive Number 2 issued in terms of the Accountancy Profession Act (Cap 281) and of the Accountancy Profession Regulations

Definition of Public Interest Entities (PIEs) in Europe

in Europe") Definition of Public Interest Entities (PIEs) in Europe FEE Survey October 2014 This document has been prepared by FEE to the best of its knowledge and ability to ensure that it is accurate and complete.

Definition of Public Interest Entities (PIEs) in Europe FEE Survey October 2014 This document has been prepared by FEE to the best of its knowledge and ability to ensure that it is accurate and complete.

CHARTERED PROFESSIONAL ACCOUNTANTS AND PUBLIC ACCOUNTING ACT

c t CHARTERED PROFESSIONAL ACCOUNTANTS AND PUBLIC ACCOUNTING ACT PLEASE NOTE This document, prepared by the Legislative Counsel Office, is an office consolidation of this Act, current to December 23, 2017.

c t CHARTERED PROFESSIONAL ACCOUNTANTS AND PUBLIC ACCOUNTING ACT PLEASE NOTE This document, prepared by the Legislative Counsel Office, is an office consolidation of this Act, current to December 23, 2017.

AML Challenges and Developments and Sanctions Compliance

The Cyprus Fiduciary Association the Institute of Certified Public Accountants of Cyprus proudly present: AML Challenges Developments Monday, 9 October 2017 09:00-13:00 St Raphael Resort Limassol Speakers

The Cyprus Fiduciary Association the Institute of Certified Public Accountants of Cyprus proudly present: AML Challenges Developments Monday, 9 October 2017 09:00-13:00 St Raphael Resort Limassol Speakers

THEMATIC COMPILATION OF RELEVANT INFORMATION SUBMITTED BY THE RUSSIAN FEDERATION ARTICLE 12 UNCAC PRIVATE SECTOR AND PUBLIC-PRIVATE PARTNERSHIPS

THEMATIC COMPILATION OF RELEVANT INFORMATION SUBMITTED BY THE RUSSIAN FEDERATION ARTICLE 12 UNCAC PRIVATE SECTOR AND PUBLIC-PRIVATE PARTNERSHIPS RUSSIAN FEDERATION (THIRD MEETING) Ministry of Finance The

THEMATIC COMPILATION OF RELEVANT INFORMATION SUBMITTED BY THE RUSSIAN FEDERATION ARTICLE 12 UNCAC PRIVATE SECTOR AND PUBLIC-PRIVATE PARTNERSHIPS RUSSIAN FEDERATION (THIRD MEETING) Ministry of Finance The

Discussion Paper. Proposed Statutory Framework For Actuaries in Hong Kong

Discussion Paper Proposed Statutory Framework For Actuaries in Hong Kong November 2013 The proposal It is proposed that the Society promote the introduction of a statutory framework for the regulation

Discussion Paper Proposed Statutory Framework For Actuaries in Hong Kong November 2013 The proposal It is proposed that the Society promote the introduction of a statutory framework for the regulation

Action Plan Developed by Chamber of Auditors of the Republic of Kazakhstan (CoA) BACKGROUND NOTE ON ACTION PLANS

BACKGROUND NOTE ON ACTION PLANS") BACKGROUND NOTE ON ACTION PLANS SMO Action Plans are developed by IFAC Members and Associates to demonstrate fulfillment of IFAC Statements of Membership Obligations (SMOs). SMOs require IFAC Members and

BACKGROUND NOTE ON ACTION PLANS SMO Action Plans are developed by IFAC Members and Associates to demonstrate fulfillment of IFAC Statements of Membership Obligations (SMOs). SMOs require IFAC Members and

Seminar Cyprus a Maritime centre: The future of the shipping industry in Cyprus Industry, Tax, VAT, and accounting related issues

Educational Seminar No 14/2015 Seminar Industry, Tax, VAT, and accounting related issues 9:00 17:30 The Education Committee in cooperation with the Limassol Paphos Coordinating Committee and the Shipping

Educational Seminar No 14/2015 Seminar Industry, Tax, VAT, and accounting related issues 9:00 17:30 The Education Committee in cooperation with the Limassol Paphos Coordinating Committee and the Shipping

VAT Seminar Holding Companies and VAT: From A to Z

The Cyprus Fiduciary Association proudly presents: VAT Seminar Holding Companies and VAT: From A to Z Wednesday, 21 February 2018 09:00 13:30 Columbia Plaza Venue Centre Limassol Speaker Alexis Tsielepis

The Cyprus Fiduciary Association proudly presents: VAT Seminar Holding Companies and VAT: From A to Z Wednesday, 21 February 2018 09:00 13:30 Columbia Plaza Venue Centre Limassol Speaker Alexis Tsielepis

impact OUTSIDE THE EUROPEAN UNION

EU impact OUTSIDE THE EUROPEAN UNION AUDIT REFORM On the 17 June 2016, 28 EU Member States, followed by Norway and Iceland implemented new regulation regarding statutory audits of Public Interest Entities

EU impact OUTSIDE THE EUROPEAN UNION AUDIT REFORM On the 17 June 2016, 28 EU Member States, followed by Norway and Iceland implemented new regulation regarding statutory audits of Public Interest Entities

CENTRAL BANK OF CYPRUS EUROSYSTEM

POLICY STATEMENT ON THE LICENSING OF BANKS IN THE REPUBLIC OF CYPRUS AND GUIDELINES ON THE INFORMATION WHICH MUST BE INCLUDED IN AN APPLICATION FOR A LICENCE BANKING SUPERVISION AND REGULATION DIVISION

POLICY STATEMENT ON THE LICENSING OF BANKS IN THE REPUBLIC OF CYPRUS AND GUIDELINES ON THE INFORMATION WHICH MUST BE INCLUDED IN AN APPLICATION FOR A LICENCE BANKING SUPERVISION AND REGULATION DIVISION

DRAFT AUDITING LAW LATEST DEVELOPMENTS IN AUDIT REGULATION IN SERBIA. Zlatko Milikić, Assistant Minister,

Republic of Serbia Ministry of Finance and Economy LATEST DEVELOPMENTS IN AUDIT REGULATION IN SERBIA DRAFT AUDITING LAW Zlatko Milikić, Assistant Minister, REPARIS CFRCoP Workshop on audit regulation,

Republic of Serbia Ministry of Finance and Economy LATEST DEVELOPMENTS IN AUDIT REGULATION IN SERBIA DRAFT AUDITING LAW Zlatko Milikić, Assistant Minister, REPARIS CFRCoP Workshop on audit regulation,

Rules relating to Practising Certificate for Public Accountants

18 Rules relating to Practising Certificate for Public Accountants Rules governing members registered with the MIPA as Professional Accountants or Public Accountants as well as to Member Firms. 1. These

18 Rules relating to Practising Certificate for Public Accountants Rules governing members registered with the MIPA as Professional Accountants or Public Accountants as well as to Member Firms. 1. These

GUIDELINES ON AUTHORISATION AND REGISTRATION UNDER PSD2 EBA/GL/2017/09 08/11/2017. Guidelines

EBA/GL/2017/09 08/11/2017 Guidelines on the information to be provided for the authorisation of payment institutions and e-money institutions and for the registration of account information service providers

EBA/GL/2017/09 08/11/2017 Guidelines on the information to be provided for the authorisation of payment institutions and e-money institutions and for the registration of account information service providers

Licensing. AAT is a registered charity. No

Licensing AAT is a registered charity. No. 1050724 Licensing Contents Purpose... 3 Policy statement... 3 Terminology... 3 Policy detail... 3 Applicable to all hip types... 3 Additional requirements applicable

Licensing AAT is a registered charity. No. 1050724 Licensing Contents Purpose... 3 Policy statement... 3 Terminology... 3 Policy detail... 3 Applicable to all hip types... 3 Additional requirements applicable

Crown Dependencies Audit Rules and Guidance

Crown Dependencies Audit Rules and Guidance CHANGES FROM 2010 TO 31 AUGUST 2018 The Crown Dependencies Audit Rules and Guidance were first introduced on 5 April 2010. The rules were based upon those applicable

Crown Dependencies Audit Rules and Guidance CHANGES FROM 2010 TO 31 AUGUST 2018 The Crown Dependencies Audit Rules and Guidance were first introduced on 5 April 2010. The rules were based upon those applicable

BERMUDA CHARTERED PROFESSIONAL ACCOUNTANTS OF BERMUDA ACT : 93

QUO FA T A F U E R N T BERMUDA CHARTERED PROFESSIONAL ACCOUNTANTS OF BERMUDA ACT 1973 1973 : 93 TABLE OF CONTENTS 1 2 3 4 5 6 7 7A 8 8A 8B 8C 8D 8E 9 9A 10 10A 11 12 13 Interpretation Chartered Professional

QUO FA T A F U E R N T BERMUDA CHARTERED PROFESSIONAL ACCOUNTANTS OF BERMUDA ACT 1973 1973 : 93 TABLE OF CONTENTS 1 2 3 4 5 6 7 7A 8 8A 8B 8C 8D 8E 9 9A 10 10A 11 12 13 Interpretation Chartered Professional

Assessment Methodology on the implementation of the objectives and principles of securities regulation. Principles relating to market intermediaries

Assessment Methodology on the implementation of the objectives and principles of securities regulation Principles relating to market intermediaries Completed by Jersey Financial Services Commission In

Assessment Methodology on the implementation of the objectives and principles of securities regulation Principles relating to market intermediaries Completed by Jersey Financial Services Commission In

STATUTORY INSTRUMENTS. S.I. No. 60 of 2017 CENTRAL BANK (SUPERVISION AND ENFORCEMENT) ACT 2013 (SECTION 48(1)) (INVESTMENT FIRMS) REGULATIONS 2017

ACT 2013 (SECTION 48(1)) (INVESTMENT FIRMS) REGULATIONS 2017") STATUTORY INSTRUMENTS. S.I. No. 60 of 2017 CENTRAL BANK (SUPERVISION AND ENFORCEMENT) ACT 2013 (SECTION 48(1)) (INVESTMENT FIRMS) REGULATIONS 2017 2 [60] S.I. No. 60 of 2017 CENTRAL BANK (SUPERVISION AND

STATUTORY INSTRUMENTS. S.I. No. 60 of 2017 CENTRAL BANK (SUPERVISION AND ENFORCEMENT) ACT 2013 (SECTION 48(1)) (INVESTMENT FIRMS) REGULATIONS 2017 2 [60] S.I. No. 60 of 2017 CENTRAL BANK (SUPERVISION AND

STATEMENT OF ANTI-MONEY LAUNDERING (AML) AND COMBATING THE FINANCING OF TERRORISM (CFT) POLICIES AND PRINCIPLES

AND COMBATING THE FINANCING OF TERRORISM (CFT) POLICIES AND PRINCIPLES") STATEMENT OF ANTI-MONEY LAUNDERING (AML) AND COMBATING THE FINANCING OF TERRORISM (CFT) POLICIES AND PRINCIPLES Scope AstroBank Limited (the Bank ) has established and implemented appropriate policies

STATEMENT OF ANTI-MONEY LAUNDERING (AML) AND COMBATING THE FINANCING OF TERRORISM (CFT) POLICIES AND PRINCIPLES Scope AstroBank Limited (the Bank ) has established and implemented appropriate policies

Eva Rossidou Papakyriacou Senior Counsel of the Republic Head of the Unit for Combating Money Laundering (MOKAS)

") Eva Rossidou Papakyriacou Senior Counsel of the Republic Head of the Unit for Combating Money Laundering (MOKAS) The process by which criminals conceal the true origin and ownership of the proceeds of

Eva Rossidou Papakyriacou Senior Counsel of the Republic Head of the Unit for Combating Money Laundering (MOKAS) The process by which criminals conceal the true origin and ownership of the proceeds of

REFORMS IN PUBLIC FINANCIAL MANAGEMENT IN THE CONTEXT OF GREECE'S ECONOMIC ADJUSTMENT PROGRAMMES

REFORMS IN PUBLIC FINANCIAL MANAGEMENT IN THE CONTEXT OF GREECE'S ECONOMIC ADJUSTMENT PROGRAMMES Hellenic Republic Ministry of Finance General Accounting Office of the State The Economic Adjustment Programmes

REFORMS IN PUBLIC FINANCIAL MANAGEMENT IN THE CONTEXT OF GREECE'S ECONOMIC ADJUSTMENT PROGRAMMES Hellenic Republic Ministry of Finance General Accounting Office of the State The Economic Adjustment Programmes