Section 6 Depreciation (Cost Recovery)

|

|

|

- Adelia Chandler

- 6 years ago

- Views:

Transcription

1 Section 6 Depreciation (Cost Recovery) Federal tax law uses Modified Accelerated Cost Recovery System (MACRS; tax treatment) which is different from GAAP depreciation (financial accounting; book purpose). IRS Publication 946, Form

2 Depreciation Real Property (Section 1250) Tangible Personal Property (Sec 1245) Land & anything fixed to land Non-realty 27.5 years: Residential rental 3 years Small tools, software 39 years: Commercial real estate 5 years Auto, light trucks, computers, a. Salvage value ignored other office equipment 7 years Office furniture, desks, most other personal prop 10 years Barges, vessels, water transport equipment b. MACRS SL MACRS - DDB 15 years Muni wwtr treatment plants 20 years Municipal sewer buildings c. Mid-month Convention: Mid-year (Half-year) Convention bought/sold in the mid of mo. ½ the month of purchase ½ the mo of disposal Mid-quarter Convention: 40% or more of pers prop are acquired in the last QTR of the yr: ½ of the ½ of half-year. Half QTR = 1.5 mo

3 Depreciation Depreciation Conventions Half-year Convention One half year s depreciation is allowed in first and last year of an asset s life An IRS depreciation tables automatically account for the half-year convention in year of purchase and disposition (P 6-3) If an asset is disposed of before it is fully depreciated, only one-half of the table s applicable depreciation percentage is allowed in the year of disposition

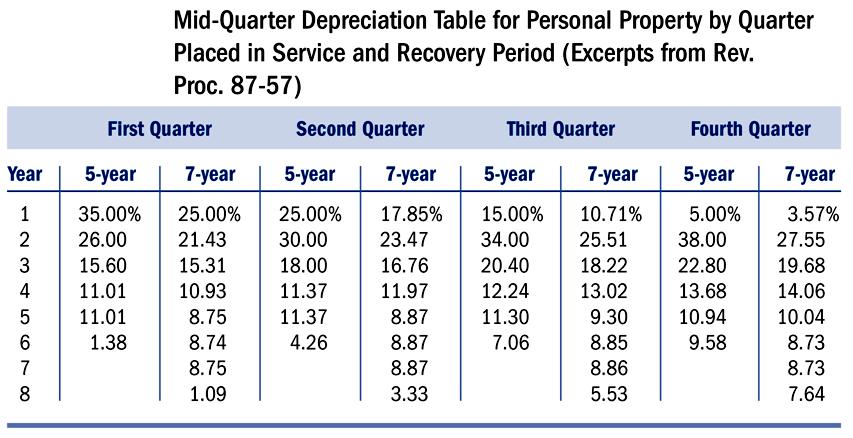

4 Depreciation Mid Quarter Convention Steps to determine whether the mid quarter convention applies 1) Sum of the total basis of tangible personal property that was placed in service during the year 2) Sum of the total basis of tangible personal property that was placed in service during the fourth quarter 3) Divide step (2) by step (1), if the quotient is > 40%, then the business must use this method or else half year convention is used

5 Depreciation 5

6 Depreciation

7 Depreciation 9-7

8 Depreciation - Example In 2015, Scrap-Pro purchased and placed in service the following assets: Asset Cost Date placed in service Di-Cut Machine $3,500 February 2 (1 st Qtr.) Computer $1,200 October 25 (4 th Qtr.) What is the recovery period for each of the assets? Computer = 5 years Di-Cut Machine = 7 years Which convention should Scrap-Pro use to determine depreciation for 2015? Answer: Half-year $1,200 4 th qtr. assets/$4,700 total assets = 25.53% < 40%

9 Depreciation Example Now assume all the same facts, except that the computer was purchased in February and the machine in October, as shown: Asset Cost Date placed in service Recovery Period Computer $1,200 February 2 (1 st Qtr.) 5 Years Di-Cut Machine $3,500 October 25 (4 th Qtr.) 7 Years What convention should be used in computing depreciation for the year? Answer: Mid-quarter $3,500 4 th qtr. assets/$4,700 total assets = 74.46% > 40% How much depreciation can they take for each of the assets in 2015? Computer: $1,200 x 35%* = $420 Di-Cut Machine: 3,500 x 3.57%* = $125 *See respective mid-quarter MACRS tables for rates 9-9

10 Section 179 Deduction Intended for smaller business to immediately expense certain new & used depreciable prop instead of capitalizing & depreciating it. a. Max. expense amount: $500,000 for b. Phase out begins at $2,000,000 of purchase, reduced dollar for dollar by purchases > $2,000,000. c. Not available if purchases > $2,500,000 e.g., Following are 4 separate/independent scenarios for the total property purchase in 2015 at ABC Partnership: (a) $40,000, (b) $590,000, (c) $2,400,000, (d) $2,800,000. What is the max Sec 179 deduction under each scenario? Solution: Qualified purchases 40, ,000 2,400,000 2,800,000 Max election 40, , ,000* 0 Remaining basis 0 90,000 2,300,000 2,800,000 *It is over $2,000,000 by $400,000 so it looses 400,000 of 500,000. Can only elect 100,000 and 2,300,000 goes to 3, 5, or 7 years depreciation. Note: SUV max expense is $25,000.

11 Additional 1 st -Year Depreciation A Bonus depreciation to stimulate economy For qualified new assets (tangible 1245 property & MACRS = or < 20 years) 50% bonus depreciation after reduction for any Sec 179 elections. e.g., 590, ,000 90,000 x ½ = 45,000 bonus; total = 500, ,000

12 Intangibles (Section 197) For not self-created properties: e.g., acquired goodwill, franchises, trademarks, patent, copyright, formula, process, design, pattern, knowhow, format, customer-based intangibles (composition of market, market share); no land or computer software. MACRS SL 15 years (180 months) Must begin amortization in month of purchase (Use it or lose it) Pub 535, Form 4562

13 Depletion For natural resources, e.g., timber, minerals, oil & gas Cost method: Adjusted basis x units sold Estimated Recoverable Units Percentage method: a statutory % x gross income (% generally ranges from 5% to 20%, never > 50%)

14 Domestic Production Activities Deduction (DPAD; Section 199) A Manufacturers Deduction to encourage production in the U S. Calculated on the basis of Qualified Production Activities Income (QPAI). DPAD = 9% of the lesser of QPAI or taxable income.

ATCF w/ Depreciation. Tax Savings Due to Depreciation. Timing of Expenses. PW of Tax Savings. Why Study Depreciation Methods?

13: Depreciation and Basic Tax Considerations Taxes are a major component of any project's cash flows, particularly income tax Taxable income (TI) is the income on which taxes are paid Not reduced by initial

13: Depreciation and Basic Tax Considerations Taxes are a major component of any project's cash flows, particularly income tax Taxable income (TI) is the income on which taxes are paid Not reduced by initial

Chapter 7 Accounting Periods and Methods and Depreciation

Chapter 7 Accounting Periods and Methods and Depreciation Income Tax Fundamentals 2011 Gerald E. Whittenburg & Martha Altus-Buller Learning Objectives Determine different accounting periods and methods

Chapter 7 Accounting Periods and Methods and Depreciation Income Tax Fundamentals 2011 Gerald E. Whittenburg & Martha Altus-Buller Learning Objectives Determine different accounting periods and methods

(Refer Slide Time: 01:02)

") Engineering Economic Analysis Professor Dr. Pradeep K Jha Department of Mechanical and Industrial Engineering Indian Institute of Technology Roorkee Lecture 24 Modified Accelerated Cost Recovery System

Engineering Economic Analysis Professor Dr. Pradeep K Jha Department of Mechanical and Industrial Engineering Indian Institute of Technology Roorkee Lecture 24 Modified Accelerated Cost Recovery System

Taxable Income. Lecture notes for PET 472 Spring 2013 Prepared by: Thomas W. Engler, Ph.D., P.E.

Taxable Income Lecture notes for PET 472 Spring 2013 Prepared by: Thomas W. Engler, Ph.D., P.E. Taxable Income Components Taxable Income = Net Revenue Gross operating expenses state/local production taxes

Taxable Income Lecture notes for PET 472 Spring 2013 Prepared by: Thomas W. Engler, Ph.D., P.E. Taxable Income Components Taxable Income = Net Revenue Gross operating expenses state/local production taxes

Construction Accounting and Financial Management

Construction Accounting and Financial Management Chapter 5 Depreciation Purpose Financial statements Cost allocation of equipment Taxes 1 Variables P = Purchase price F = Salvage Value Zero for tax purposes

Construction Accounting and Financial Management Chapter 5 Depreciation Purpose Financial statements Cost allocation of equipment Taxes 1 Variables P = Purchase price F = Salvage Value Zero for tax purposes

Chapter 15 p.869 Capital Cost Recovery

Chapter 15 p.869 Capital Cost Recovery Code 167(a) allows a depreciation deduction for a reasonable allowance for the exhaustion, wear and tear (including for obsolescence) of property: (1) used in a trade

Chapter 15 p.869 Capital Cost Recovery Code 167(a) allows a depreciation deduction for a reasonable allowance for the exhaustion, wear and tear (including for obsolescence) of property: (1) used in a trade

Internal Revenue Code Section 197 Amortization of goodwill and certain other intangibles

Internal Revenue Code Section 197 Amortization of goodwill and certain other intangibles CLICK HERE to return to the home page (a) General rule. A taxpayer shall be entitled to an amortization deduction

Internal Revenue Code Section 197 Amortization of goodwill and certain other intangibles CLICK HERE to return to the home page (a) General rule. A taxpayer shall be entitled to an amortization deduction

Depreciation, Cost Recovery, Amortization, and Depletion

C H A P T E R 8 Depreciation, Cost Recovery, Amortization, and Depletion L E A R N I N G O B J E C T I V E S : After completing Chapter 8, you should be able to: LO.1 LO.2 LO.3 LO.4 State the rationale

C H A P T E R 8 Depreciation, Cost Recovery, Amortization, and Depletion L E A R N I N G O B J E C T I V E S : After completing Chapter 8, you should be able to: LO.1 LO.2 LO.3 LO.4 State the rationale

Federal Income Taxation Chapter 15 Capital Cost Recovery

Presentation: Federal Income Taxation Chapter 15 Capital Cost Recovery Professors Wells October 24, 2017 Antiques p.870 Richard L. Simon Simon acquired two Tourte bows for $30,000 and $21,000, respectively.

Presentation: Federal Income Taxation Chapter 15 Capital Cost Recovery Professors Wells October 24, 2017 Antiques p.870 Richard L. Simon Simon acquired two Tourte bows for $30,000 and $21,000, respectively.

TAX ESSENTIALS For the Tax Year 2010

TAX ESSENTIALS For the Tax Year 2010 TAX ESSENTIALS WAS NOT INTENDED OR WRITTEN TO BE USED, AND IT CANNOT BE USED, FOR THE PURPOSE OF AVOIDING U.S. FEDERAL, STATE OR LOCAL TAX PENALTIES. Form 4562 Depreciation

TAX ESSENTIALS For the Tax Year 2010 TAX ESSENTIALS WAS NOT INTENDED OR WRITTEN TO BE USED, AND IT CANNOT BE USED, FOR THE PURPOSE OF AVOIDING U.S. FEDERAL, STATE OR LOCAL TAX PENALTIES. Form 4562 Depreciation

Fixed Asset Accounting

Fixed Asset Accounting 4 th Edition Steven M. Bragg Chapter 1 Introduction to Fixed Assets... 1 Learning Objectives... 1 Introduction... 1 What are Fixed Assets?... 1 The Fixed Asset Designation... 2 Fixed

Fixed Asset Accounting 4 th Edition Steven M. Bragg Chapter 1 Introduction to Fixed Assets... 1 Learning Objectives... 1 Introduction... 1 What are Fixed Assets?... 1 The Fixed Asset Designation... 2 Fixed

Instructions for Form 4562

2002 Instructions for Form 4562 Depreciation and Amortization (Including Information on Listed Property) Section references are to the Internal Revenue Code unless otherwise noted. Department of the Treasury

2002 Instructions for Form 4562 Depreciation and Amortization (Including Information on Listed Property) Section references are to the Internal Revenue Code unless otherwise noted. Department of the Treasury

Accounting What the Numbers Mean. Cash. What are Current Assets? Cash Equivalents. Cash Management Goals 5-1

5-1 Accounting What the Numbers Mean CHAPTER 5: Accounting for and Presentation of Current Assets Marshall, McManus, and Viele 11th Edition 5-1 5-2 What are Current Assets? Current assets include cash

5-1 Accounting What the Numbers Mean CHAPTER 5: Accounting for and Presentation of Current Assets Marshall, McManus, and Viele 11th Edition 5-1 5-2 What are Current Assets? Current assets include cash

Chapter 2 Property Acquisition and Cost Recovery SOLUTIONS MANUAL

Chapter 2 Property Acquisition and Cost Recovery SOLUTIONS MANUAL Discussion Questions 1. [LO 1] Explain why the tax laws require the cost of certain assets to be capitalized and recovered over time rather

Chapter 2 Property Acquisition and Cost Recovery SOLUTIONS MANUAL Discussion Questions 1. [LO 1] Explain why the tax laws require the cost of certain assets to be capitalized and recovered over time rather

Full file at

Chapter 2 Property Acquisition and Cost Recovery SOLUTIONS MANUAL Discussion Questions 1. [LO 1] Explain the reasoning why the tax laws require the cost of certain assets to be capitalized and recovered

Chapter 2 Property Acquisition and Cost Recovery SOLUTIONS MANUAL Discussion Questions 1. [LO 1] Explain the reasoning why the tax laws require the cost of certain assets to be capitalized and recovered

12/3/2014. Key Issues in Oil & Gas Taxation. Agenda. Methods of accounting. General Discussion of Oil and Gas GAAP vs Tax Treatment

Key Issues in Oil & Gas Taxation December 5, 2014 Agenda General Discussion of Oil and Gas GAAP vs Tax Treatment Depletion Differences Asset Retirement Obligations ( ARO ) Intangible Drilling Costs ( IDC

Key Issues in Oil & Gas Taxation December 5, 2014 Agenda General Discussion of Oil and Gas GAAP vs Tax Treatment Depletion Differences Asset Retirement Obligations ( ARO ) Intangible Drilling Costs ( IDC

Chapter 16 Depreciation Methods

Chapter 16 Depreciation Methods Lecture slides to accompany Engineering Economy 7 th edition Leland Blank Anthony Tarquin 16-1 LEARNING OUTCOMES 1. Understand basic terms of asset depreciation 2. Apply

Chapter 16 Depreciation Methods Lecture slides to accompany Engineering Economy 7 th edition Leland Blank Anthony Tarquin 16-1 LEARNING OUTCOMES 1. Understand basic terms of asset depreciation 2. Apply

Final Examination (Optional) MASTERING DEPRECIATION

MASTERING DEPRECIATION") Final Examination (Optional) MASTERING DEPRECIATION Instructions: Detach the Final Examination Answer Sheet on page 247 before beginning your final examination. Select the correct letter for the answer

Final Examination (Optional) MASTERING DEPRECIATION Instructions: Detach the Final Examination Answer Sheet on page 247 before beginning your final examination. Select the correct letter for the answer

2003 ELA Lease Accountants Conference

2003 ELA Lease Accountants Conference Basics of Tax Leasing (1) September 9, 2003 Speakers: Suresh Makam CitiCapital Bankers Leasing Roger Idnani Boeing Capital Corporation Single Investor Lease Lessor

2003 ELA Lease Accountants Conference Basics of Tax Leasing (1) September 9, 2003 Speakers: Suresh Makam CitiCapital Bankers Leasing Roger Idnani Boeing Capital Corporation Single Investor Lease Lessor

Instructions for Form 4562

2000 Department Instructions for Form 4562 Depreciation and Amortization (Including Information on Listed Property) Section references are to the Internal Revenue Code unless otherwise noted. of the Treasury

2000 Department Instructions for Form 4562 Depreciation and Amortization (Including Information on Listed Property) Section references are to the Internal Revenue Code unless otherwise noted. of the Treasury

Instructions for Form 4562

2016 Instructions for Form 4562 Depreciation and Amortization (Including Information on Listed Property) Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

2016 Instructions for Form 4562 Depreciation and Amortization (Including Information on Listed Property) Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

b. What is the largest category of property, plant, and equipment?

BUS512M Accounting for Investment Decisions: Property, Plant, & Equipment & Intangibles; Long-term Investments including Available for Sale, Equity, and Consolidations Module 8 ID9-13 Google 10-K Disclosures

BUS512M Accounting for Investment Decisions: Property, Plant, & Equipment & Intangibles; Long-term Investments including Available for Sale, Equity, and Consolidations Module 8 ID9-13 Google 10-K Disclosures

Green Income Tax Incentives. By Colleen M. Berndt, CPA Meyers Brothers Kalicka, P.C. MBKCPA.COM

Green Income Tax Incentives By Colleen M. Berndt, CPA Meyers Brothers Kalicka, P.C. MBKCPA.COM Residential Energy Property Credit Tax Credit: 30% of cost up to $1,500 Expires: December 31, 2010 Details:

Green Income Tax Incentives By Colleen M. Berndt, CPA Meyers Brothers Kalicka, P.C. MBKCPA.COM Residential Energy Property Credit Tax Credit: 30% of cost up to $1,500 Expires: December 31, 2010 Details:

BACKGROUND AND PRESENT LAW RELATING TO COST RECOVERY AND DOMESTIC PRODUCTION ACTIVITIES

BACKGROUND AND PRESENT LAW RELATING TO COST RECOVERY AND DOMESTIC PRODUCTION ACTIVITIES Scheduled for a Public Hearing Before the SENATE COMMITTEE ON FINANCE on March 6, 2012 Prepared by the Staff of the

BACKGROUND AND PRESENT LAW RELATING TO COST RECOVERY AND DOMESTIC PRODUCTION ACTIVITIES Scheduled for a Public Hearing Before the SENATE COMMITTEE ON FINANCE on March 6, 2012 Prepared by the Staff of the

Instructions for Form 4562 Depreciation and Amortization (Section references are to the Internal Revenue Code, unless otherwise noted.

Department of the Treasury Internal Revenue Service Instructions for Form 4562 Depreciation and Amortization (Section references are to the Internal Revenue Code, unless otherwise noted.) General Instructions

Department of the Treasury Internal Revenue Service Instructions for Form 4562 Depreciation and Amortization (Section references are to the Internal Revenue Code, unless otherwise noted.) General Instructions

Chapter Review Problems

Chapter Review Problems Unit 19.1 Depreciation for financial accounting 1. Depreciation for financial accounting is identical to depreciation for federal income tax purposes. (T or F) False For Problems

Chapter Review Problems Unit 19.1 Depreciation for financial accounting 1. Depreciation for financial accounting is identical to depreciation for federal income tax purposes. (T or F) False For Problems

ILLUSTRATION 12-1 TYPES OF INTANGIBLE ASSETS

ILLUSTRATION 12-1 TYPES OF INTANGIBLE ASSETS INTANGIBLE ASSETS Identifiable Intangible Assets (Rights Type) Externally Acquired Internally Developed Financial Statement Treatment Unidentifiable Intangible

ILLUSTRATION 12-1 TYPES OF INTANGIBLE ASSETS INTANGIBLE ASSETS Identifiable Intangible Assets (Rights Type) Externally Acquired Internally Developed Financial Statement Treatment Unidentifiable Intangible

Tax Cuts and Jobs Act of 2017 (TCJA) Key General Business Tax Provisions

Key General Business Tax Provisions") Item IRC Expensing and Depreciating Section 179 Limits 179(b) For property service in For property service in The maximum Section 179 deduction and phaseout threshold are increased to $1 million and $2.5

Item IRC Expensing and Depreciating Section 179 Limits 179(b) For property service in For property service in The maximum Section 179 deduction and phaseout threshold are increased to $1 million and $2.5

U.S. Income Tax Return for an S Corporation. OMB No Form 1120S. Do not file this form unless the corporation has filed or is

U.S. Income Tax Return for an S Corporation OMB No. 1545-0130 Form 1120S Do not file this form unless the corporation has filed or is Department of the Treasury attaching Form 2553 to elect to be an S

U.S. Income Tax Return for an S Corporation OMB No. 1545-0130 Form 1120S Do not file this form unless the corporation has filed or is Department of the Treasury attaching Form 2553 to elect to be an S

Full file at

Chapter 2 Property Acquisition and Cost Recovery SOLUTIONS MANUAL Discussion Questions 1. [LO 1] Explain the reasoning why the tax laws require the cost of certain assets to be capitalized and recovered

Chapter 2 Property Acquisition and Cost Recovery SOLUTIONS MANUAL Discussion Questions 1. [LO 1] Explain the reasoning why the tax laws require the cost of certain assets to be capitalized and recovered

Section 8 TAX DEPRECIATION OF PASSENGER CARS AND OTHER VEHICLES

Section 8 TAX DEPRECIATION OF PASSENGER CARS AND OTHER VEHICLES Introduction There are special dollar limits on annual depreciation that apply only to a passenger automobile, defined under tax law as any

Section 8 TAX DEPRECIATION OF PASSENGER CARS AND OTHER VEHICLES Introduction There are special dollar limits on annual depreciation that apply only to a passenger automobile, defined under tax law as any

Glossary of Business Valuation Terms

Adjusted Net Assets Method Asset-Based Approach Beta Blockage Discount Business Business Risk Business Valuation Capital Asset Pricing Model (CAPM) Capitalization Capitalization of Earnings Method Capital

Adjusted Net Assets Method Asset-Based Approach Beta Blockage Discount Business Business Risk Business Valuation Capital Asset Pricing Model (CAPM) Capitalization Capitalization of Earnings Method Capital

Tax Cuts and Jobs Act

Tax Cuts and Jobs Act 1. Deduction For Qualified Business Income IRC 199A a. The Tax Cuts and Jobs Act permits pass-through business owners, including partners of partnerships, S corporation shareholders

Tax Cuts and Jobs Act 1. Deduction For Qualified Business Income IRC 199A a. The Tax Cuts and Jobs Act permits pass-through business owners, including partners of partnerships, S corporation shareholders

Notes. 351 Spring Accounting. Cost Allocation of Operational Assets. Partial Periods. Chapter 11. Depreciation (tangibles)

") Notes Chapter 11 Accounting 351 Spring 2011 California State University, Northridge 1 Cost Allocation of Operational Assets Depreciation (tangibles) Product Cost or Period Cost Time-Based Methods Sum-of

Notes Chapter 11 Accounting 351 Spring 2011 California State University, Northridge 1 Cost Allocation of Operational Assets Depreciation (tangibles) Product Cost or Period Cost Time-Based Methods Sum-of

ANSWER SHEET EXAMINATION #1

ANSWER SHEET EXAMINATION #1 NAME: DATE: 1) 29) Multiple-choice (38) 2) 30) Matching (46) 3) 31) Problems (16) 4) 32) Total (100) / Grade 5) 33) 6) 34) 7) 35) 8) 36) 9) 37) 10) 38) 11) 12) 13) 14) 15) 16)

ANSWER SHEET EXAMINATION #1 NAME: DATE: 1) 29) Multiple-choice (38) 2) 30) Matching (46) 3) 31) Problems (16) 4) 32) Total (100) / Grade 5) 33) 6) 34) 7) 35) 8) 36) 9) 37) 10) 38) 11) 12) 13) 14) 15) 16)

Fixed Assets Management: What You Need to Know

Fixed Assets Management: What You Need to Know Fixed Assets Management: What You Need to Know by Nancy Faussett, CPA 1.0 Introduction 3 2.0 Defining a Fixed Asset 4 2.1 Defining a Fixed Asset 4 3.0 Critical

Fixed Assets Management: What You Need to Know Fixed Assets Management: What You Need to Know by Nancy Faussett, CPA 1.0 Introduction 3 2.0 Defining a Fixed Asset 4 2.1 Defining a Fixed Asset 4 3.0 Critical

Page 1 of 10 Ehab Abdou ( )

") Statement of Financial Position, also referred to as the balance sheet: 1. Reports assets, liabilities, and equity at a specific date. 2. Provides information about resources, obligations to creditors,

Statement of Financial Position, also referred to as the balance sheet: 1. Reports assets, liabilities, and equity at a specific date. 2. Provides information about resources, obligations to creditors,

UW Cover Page. AFM of 21

UW Cover Page 1 of 21 Intermediate Financial Accounting I Part Instructions: 1. This is a closed note, closed book examination. You may use pen/pencil and a calculator during the examination. 2. The examination

UW Cover Page 1 of 21 Intermediate Financial Accounting I Part Instructions: 1. This is a closed note, closed book examination. You may use pen/pencil and a calculator during the examination. 2. The examination

DEPRECIATION $350K $100K $425K - $25K $75K $450K - $50K $50K HIGH- STAKES TAX DEFENSE & COMPLEX CRIMINAL DEFENSE

HIGH- STAKES TAX DEFENSE & COMPLEX CRIMINAL DEFENSE 1012 Broad Street, 2nd Fl Bloomfield, NJ 07003 Tel (973) 783-7000 Fax (973) 338-3955 www.deblislaw.com DEPRECIATION I. Depreciation groups a. Tangible

HIGH- STAKES TAX DEFENSE & COMPLEX CRIMINAL DEFENSE 1012 Broad Street, 2nd Fl Bloomfield, NJ 07003 Tel (973) 783-7000 Fax (973) 338-3955 www.deblislaw.com DEPRECIATION I. Depreciation groups a. Tangible

CHAPTER 11. Depreciation, Impairments, and Depletion 1, 2, 3, 4, 5, 6, 10, 13, 19, 20, 28 7, 8, 9, 12, 30

CHAPTER 11 Depreciation, Impairments, and Depletion ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Depreciation methods; meaning

CHAPTER 11 Depreciation, Impairments, and Depletion ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Depreciation methods; meaning

ANSWER SHEET EXAMINATION #1 29) Problem 1 30) 31) 32) 33) 34) 35) 36) 37) 10) 38) 11) 12) Problem 2 Problem 3 Problem 4 13) 14) 15) 16) 17) 18) 19)

Problem 1 30) 31) 32) 33) 34) 35) 36) 37) 10) 38) 11) 12) Problem 2 Problem 3 Problem 4 13) 14) 15) 16) 17) 18) 19)") ANSWER SHEET EXAMINATION #1 1) B 29) A Problem 1 2) B 30) D B 01 3) D 31) B A 02 4) D 32) B D 03 5) C 33) A A 04 6) C 34) C B 05 7) B 35) B A 06 8) B 36) B B 07 9) D 37) D C 08 10) B 38) D C 09 11) D D

ANSWER SHEET EXAMINATION #1 1) B 29) A Problem 1 2) B 30) D B 01 3) D 31) B A 02 4) D 32) B D 03 5) C 33) A A 04 6) C 34) C B 05 7) B 35) B A 06 8) B 36) B B 07 9) D 37) D C 08 10) B 38) D C 09 11) D D

Depreciation Process 1. Depreciate by Component: o By useful lives and patterns of consumption group similar o By depreciation method

Depreciation - means of cost allocation to match expense with revenue - not a method of valuation - involves allocating the depreciable amount of property, plant, and equipment over the periods expected

Depreciation - means of cost allocation to match expense with revenue - not a method of valuation - involves allocating the depreciable amount of property, plant, and equipment over the periods expected

Corporate Finance. Prof. Dr. Frank Andreas Schittenhelm. Introduction to Financial Accounting. Prof. Dr. Frank Andreas Schittenhelm

Corporate Finance Introduction to Financial Accounting Corporate Finance slide 1 Literature Basic Literature Anthony/Hawkins/Merchant: Accounting, 11 th ed., McGraw-Hill Additional Literature Dyckman/Dukes/Davis:

Corporate Finance Introduction to Financial Accounting Corporate Finance slide 1 Literature Basic Literature Anthony/Hawkins/Merchant: Accounting, 11 th ed., McGraw-Hill Additional Literature Dyckman/Dukes/Davis:

Profit or loss recorded to Retained Earnings

Cash basis Recognizes transactions when cash or equivalents DIAGRAM OF T-ACCOUNTS METHODS & ORGS Balance Sheet as of 12/31/2100 Accrual basis Follows the matching principle and recognizes Assets = Liabilities

Cash basis Recognizes transactions when cash or equivalents DIAGRAM OF T-ACCOUNTS METHODS & ORGS Balance Sheet as of 12/31/2100 Accrual basis Follows the matching principle and recognizes Assets = Liabilities

Tax Cuts and Jobs Act - Cost Recovery Provisions, Expensing, and Like-kind Exchanges last updated

Tax Cuts and Jobs Act - Cost Recovery Provisions, Expensing, and Like-kind Exchanges last updated 12.27.2017 The Tax Cuts and Jobs Act was signed into law by the President on Friday, December 22, 2017.

Tax Cuts and Jobs Act - Cost Recovery Provisions, Expensing, and Like-kind Exchanges last updated 12.27.2017 The Tax Cuts and Jobs Act was signed into law by the President on Friday, December 22, 2017.

TAX CUTS AND JOBS ACT

TAX CUTS AND JOBS ACT Public Law 115-97 December 22, 2017 TABLE OF CONTENTS BUSINESS PROVISIONS... 1-5 C CORPORATION TAX RATES REDUCED... 1 DIVIDENDS-RECEIVED DEDUCTION... 1 ALTERNATIVE MINIMUM TAX REPEALED

TAX CUTS AND JOBS ACT Public Law 115-97 December 22, 2017 TABLE OF CONTENTS BUSINESS PROVISIONS... 1-5 C CORPORATION TAX RATES REDUCED... 1 DIVIDENDS-RECEIVED DEDUCTION... 1 ALTERNATIVE MINIMUM TAX REPEALED

Instructions for Form 4562

2017 Instructions for Form 4562 Department of the Treasury Internal Revenue Service Depreciation and Amortization (Including Information on Listed Property) Section references are to the Internal Revenue

2017 Instructions for Form 4562 Department of the Treasury Internal Revenue Service Depreciation and Amortization (Including Information on Listed Property) Section references are to the Internal Revenue

Reg. Section (f)(4)(i) Amortization of goodwill and certain other intangibles.

(4)(i) Amortization of goodwill and certain other intangibles.") Reg. Section 1.197-2(f)(4)(i) Amortization of goodwill and certain other intangibles. CLICK HERE to return to the home page (a) Overview -- (1) In general. Section 197 [26 USCS 197] allows an amortization

Reg. Section 1.197-2(f)(4)(i) Amortization of goodwill and certain other intangibles. CLICK HERE to return to the home page (a) Overview -- (1) In general. Section 197 [26 USCS 197] allows an amortization

Sports Team's Share of Broadcasting Receipts Didn't Qualify for Sec. 199 Deduction. Chief Counsel Advice

Sports Team's Share of Broadcasting Receipts Didn't Qualify for Sec. 199 Deduction Chief Counsel Advice 201545018 In Chief Counsel Advice (CCA), IRS concluded that a sports team's share of gross receipts

Sports Team's Share of Broadcasting Receipts Didn't Qualify for Sec. 199 Deduction Chief Counsel Advice 201545018 In Chief Counsel Advice (CCA), IRS concluded that a sports team's share of gross receipts

NINE. Depreciation and Corporate Taxes CHAPTER

CHAPTER NINE Depreciation and Corporate Taxes Know What It Costs to Own a Piece of Equipment: A Hospital Pharmacy Gets a Robotic Helper 1 When most patients at Kirkland s Evergreen Hospital Medical Center

CHAPTER NINE Depreciation and Corporate Taxes Know What It Costs to Own a Piece of Equipment: A Hospital Pharmacy Gets a Robotic Helper 1 When most patients at Kirkland s Evergreen Hospital Medical Center

Accounting Cheat Sheet

DIAGRAM OF TACCOUNTS Assets = Balance Sheet as of 12/31/20 Liabilit ies + = + Equity METHODS & ORGS Accrual basis Follows the matching principle and recognizes transactions as they occur (GAAP Method)

DIAGRAM OF TACCOUNTS Assets = Balance Sheet as of 12/31/20 Liabilit ies + = + Equity METHODS & ORGS Accrual basis Follows the matching principle and recognizes transactions as they occur (GAAP Method)

Business Changes in the Tax Cuts and Jobs Act. Alan D. Sobel, CPA December 27,

Business Changes in the Tax Cuts and Jobs Act Alan D. Sobel, CPA December 27, 2017 Alan.sobel@sobelcollc.com 973-994-9494 Background Most significant tax legislation since 1986 503 pages of legislation

Business Changes in the Tax Cuts and Jobs Act Alan D. Sobel, CPA December 27, 2017 Alan.sobel@sobelcollc.com 973-994-9494 Background Most significant tax legislation since 1986 503 pages of legislation

Exercises Corporate Finance

Exercises Financial Accounting I) Consider the following business case. Prepare the financial statements (balance sheet, income statement, cash flow statement) for the year 01. You decide to open a beverage

Exercises Financial Accounting I) Consider the following business case. Prepare the financial statements (balance sheet, income statement, cash flow statement) for the year 01. You decide to open a beverage

Legal Alert: The Tax Cuts and Jobs Act, Take One: A Methods-Based Overview of the Initial Draft of the House Tax Bill

Jobs Act, Take One: A the Initial Draft of the House November 7, 2017 In the Tax Cuts and Jobs Act (the Act) released by the House Ways & Means Committee on Thursday, November 2, 2017, a number of reforms

Jobs Act, Take One: A the Initial Draft of the House November 7, 2017 In the Tax Cuts and Jobs Act (the Act) released by the House Ways & Means Committee on Thursday, November 2, 2017, a number of reforms

Tax Reform Changes Businesses & Business Owners

8 Tax Brackets: Business Rates Taxable income is taxed at a flat 20% Taxable income is taxed at a flat 20%. C Corporations (Non-Personal Service) C Corporations (Personal Service Corporations) 15% 25%

8 Tax Brackets: Business Rates Taxable income is taxed at a flat 20% Taxable income is taxed at a flat 20%. C Corporations (Non-Personal Service) C Corporations (Personal Service Corporations) 15% 25%

SU 3.1 Property, Plant, and Equipment

Part 1 Study Unit 3 SU 3.1 Property, Plant, and Equipment Overview Property, plant and equipment are also referred to as fixed assets, or capital assets. Last more than 1 year. Are for production or benefit

Part 1 Study Unit 3 SU 3.1 Property, Plant, and Equipment Overview Property, plant and equipment are also referred to as fixed assets, or capital assets. Last more than 1 year. Are for production or benefit

IRD Tax Information Bulletin - Appendix to Volume Four, No. 9 - April Depreciation

IRD Tax Information Bulletin - Appendix to Volume Four, No. 9 - April 1993 We've mailed this appendix separately in advance of the main Tax Information Bulletin, to get the depreciation information to

IRD Tax Information Bulletin - Appendix to Volume Four, No. 9 - April 1993 We've mailed this appendix separately in advance of the main Tax Information Bulletin, to get the depreciation information to

The RMA Guide to Spreading Financial Statements

1 The RMA Guide to Spreading Financial Statements Enterprise 2321.6 v.4 Risk Credit Risk Market Risk Operational Risk Regulatory Affairs Securities Lending 2 SPREADING FINANCIAL STATEMENTS "Spreading"

1 The RMA Guide to Spreading Financial Statements Enterprise 2321.6 v.4 Risk Credit Risk Market Risk Operational Risk Regulatory Affairs Securities Lending 2 SPREADING FINANCIAL STATEMENTS "Spreading"

Prepared by Cyberian

; and Which of the following is/are the component(s) of equity? Share Capital Reserves Share Premium In which of the following activities, a business should capitalize its incurred expenditures according

; and Which of the following is/are the component(s) of equity? Share Capital Reserves Share Premium In which of the following activities, a business should capitalize its incurred expenditures according

CAPITAL BUDGETING Shenandoah Furniture, Inc.

CAPITAL BUDGETING Shenandoah Furniture, Inc. Shenandoah Furniture is considering replacing one of the machines in its manufacturing facility. The cost of the new machine will be $76,120. Transportation

CAPITAL BUDGETING Shenandoah Furniture, Inc. Shenandoah Furniture is considering replacing one of the machines in its manufacturing facility. The cost of the new machine will be $76,120. Transportation

CHAPTER 1 UNDERSTANDING THE ISSUES

CHAPTER 1 UNDERSTANDING THE ISSUES 1. (a) Product extension manufacturer expands product lines in boating industry. (b) Vertical forward manufacturer buys distribution outlets (c) Conglomerate unrelated

CHAPTER 1 UNDERSTANDING THE ISSUES 1. (a) Product extension manufacturer expands product lines in boating industry. (b) Vertical forward manufacturer buys distribution outlets (c) Conglomerate unrelated

Property Transactions Business Assets

Property Transactions Business Assets Introduction & Review of Asset Categorization In prior chapters, we learned about the general rules governing the taxation of property transactions, and how the sale

Property Transactions Business Assets Introduction & Review of Asset Categorization In prior chapters, we learned about the general rules governing the taxation of property transactions, and how the sale

Statement of Financial Position Module 1 Topic 2

Sourced from: https://www.dreamstime.com/illustration/balance-sheet.html Statement of Financial Position Module 1 Topic 2 Learning Objectives Describe the characteristics of business transactions Identify

Sourced from: https://www.dreamstime.com/illustration/balance-sheet.html Statement of Financial Position Module 1 Topic 2 Learning Objectives Describe the characteristics of business transactions Identify

THE PROGRESSIVE CORPORATION. Notice of Annual Meeting of Shareholders and 2018 Proxy Statement including the 2017 Annual Report to Shareholders

THE PROGRESSIVE CORPORATION Notice of Annual Meeting of Shareholders and 2018 Proxy Statement including the 2017 Annual Report to Shareholders THE PROGRESSIVE CORPORATION 2017 ANNUAL REPORT TO SHAREHOLDERS

THE PROGRESSIVE CORPORATION Notice of Annual Meeting of Shareholders and 2018 Proxy Statement including the 2017 Annual Report to Shareholders THE PROGRESSIVE CORPORATION 2017 ANNUAL REPORT TO SHAREHOLDERS

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Sarbanes-Oxley was passed in response to which of the following? 1) A) The mounting government

Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Sarbanes-Oxley was passed in response to which of the following? 1) A) The mounting government

Basic Legal Accounting outline, Fall Professor MacDonald. I. Accounting A. Foundations 1. Assumptions a) The separate entity assumption: you

The separate entity assumption: you") Basic Legal Accounting outline, Fall 2004. Professor MacDonald. I. Accounting A. Foundations 1. Assumptions a) The separate entity assumption: you regard the entity you are reporting about as distinct

Basic Legal Accounting outline, Fall 2004. Professor MacDonald. I. Accounting A. Foundations 1. Assumptions a) The separate entity assumption: you regard the entity you are reporting about as distinct

Review for the June 2008 Level 1 CFA Exam Study Session 9 Tuesday, February 26, 2008 Assets and Liabilities

Review for the June 2008 Level 1 CFA Exam Study Session 9 Tuesday, February 26, 2008 Assets and Liabilities Kris Clark 404.413.7208 or kjclark@gsu.edu Reading 35: Analysis of Inventories LOS 35a: Compute

Review for the June 2008 Level 1 CFA Exam Study Session 9 Tuesday, February 26, 2008 Assets and Liabilities Kris Clark 404.413.7208 or kjclark@gsu.edu Reading 35: Analysis of Inventories LOS 35a: Compute

ACC100 Introduction to Accounting

ACC100 Introduction to Accounting Week 8 Accounting for Non-Current Assets Chapter 15 Non-Current Assets: Revaluation, Disposal and Other Aspects Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning

ACC100 Introduction to Accounting Week 8 Accounting for Non-Current Assets Chapter 15 Non-Current Assets: Revaluation, Disposal and Other Aspects Study Group Australia Pty Limited, SGA1286-F2/10/12 2 Learning

IFRS-compliant accounting principles

IFRS-compliant accounting principles Since 1 January 2005, Uponor Corporation has prepared its consolidated financial statements in compliance with the following accounting principles: Main functions Uponor

IFRS-compliant accounting principles Since 1 January 2005, Uponor Corporation has prepared its consolidated financial statements in compliance with the following accounting principles: Main functions Uponor

TAX IMPLICATIONS RELATED TO THE IMPLEMENTATION OF FRS 138: INTANGIBLE ASSETS

The Malaysian Institute of Certified Public Accountants TAX IMPLICATIONS RELATED TO THE IMPLEMENTATION OF FRS 138: INTANGIBLE ASSETS Prepared by: Joint Tax Working Group on FRS Contents Page No. 1 Introduction

The Malaysian Institute of Certified Public Accountants TAX IMPLICATIONS RELATED TO THE IMPLEMENTATION OF FRS 138: INTANGIBLE ASSETS Prepared by: Joint Tax Working Group on FRS Contents Page No. 1 Introduction

TAX REFORM CORPORATE & BUSINESS

The following chart sets forth some of the provisions affecting businesses in H.R. 1, originally called the Tax Cuts and Jobs Act (the Act), as signed by President Donald Trump on December 22, 2017. This

The following chart sets forth some of the provisions affecting businesses in H.R. 1, originally called the Tax Cuts and Jobs Act (the Act), as signed by President Donald Trump on December 22, 2017. This

Chapter 9. Depreciation. Principles of Engineering Economic Analysis, 5th edition

Chapter 9 Depreciation Systematic Economic Analysis Technique 1. Identify the investment alternatives 2. Define the planning horizon 3. Specify the discount rate 4. Estimate the cash flows 5. Compare the

Chapter 9 Depreciation Systematic Economic Analysis Technique 1. Identify the investment alternatives 2. Define the planning horizon 3. Specify the discount rate 4. Estimate the cash flows 5. Compare the

Accounting for Business Decisions B

Accounting for Business Decisions B Non-current assets Describe non-current assets and how they are recorded, expensed, and reported Resource that is expected to be used in the normal course of operations

Accounting for Business Decisions B Non-current assets Describe non-current assets and how they are recorded, expensed, and reported Resource that is expected to be used in the normal course of operations

TAX REFORM CORPORATE & BUSINESS

The following chart sets forth some of the provisions affecting businesses in the Tax Reform Act of 2017 (the Act). This chart highlights only some of the key issues and is not intended to address all

The following chart sets forth some of the provisions affecting businesses in the Tax Reform Act of 2017 (the Act). This chart highlights only some of the key issues and is not intended to address all

FAIR VALUE & TRANSFER PRICING: And the twain shall never meet? Transfer Pricing Panel ABA Fall Conf., Denver Oct. 21, 2011

FAIR VALUE & TRANSFER PRICING: And the twain shall never meet? Transfer Pricing Panel ABA Fall Conf., Denver Oct. 21, 2011 Introduction Fair Value & Transfer Pricing Panel: David Ernick, Treasury Jason

FAIR VALUE & TRANSFER PRICING: And the twain shall never meet? Transfer Pricing Panel ABA Fall Conf., Denver Oct. 21, 2011 Introduction Fair Value & Transfer Pricing Panel: David Ernick, Treasury Jason

GAINING MOMENTUM IN OUR NEW TAX ENVIRONMENT: Moving Forward with Confidence

CLICK TO EDIT MASTER TEXT STYLES GAINING MOMENTUM IN OUR NEW TAX ENVIRONMENT: Moving Forward with Confidence Sno L. Barry, CPA, MST Cathy Jackson, CPA, MST CLICK TO EDIT MASTER AREAS TEXT OF INTEREST STYLES

CLICK TO EDIT MASTER TEXT STYLES GAINING MOMENTUM IN OUR NEW TAX ENVIRONMENT: Moving Forward with Confidence Sno L. Barry, CPA, MST Cathy Jackson, CPA, MST CLICK TO EDIT MASTER AREAS TEXT OF INTEREST STYLES

Instructions for Form 4626

1999 Department Instructions for Form 4626 Alternative Minimum Tax Corporations Section references are to the Internal Revenue Code unless otherwise noted. of the Treasury Internal Revenue Service General

1999 Department Instructions for Form 4626 Alternative Minimum Tax Corporations Section references are to the Internal Revenue Code unless otherwise noted. of the Treasury Internal Revenue Service General

total fair market value in 2003 is $550. The fair market *In addition to the 80% nonbusiness part of the expense.

Expense Amount Schedule A amount of the section deduction ($) for a total Deductible mortgage interest $,500 Line or * business income of $7,7. This amount goes on line Real estate taxes $,000 Line * since

Expense Amount Schedule A amount of the section deduction ($) for a total Deductible mortgage interest $,500 Line or * business income of $7,7. This amount goes on line Real estate taxes $,000 Line * since

Self-Employed Borrower Basics

Self-Employed Borrower Basics Part I - Personal Tax Return Review October 2016 Genworth Mortgage Insurance Corporation 2016 Genworth Financial, Inc. All rights reserved. Agenda Business Income Concepts

Self-Employed Borrower Basics Part I - Personal Tax Return Review October 2016 Genworth Mortgage Insurance Corporation 2016 Genworth Financial, Inc. All rights reserved. Agenda Business Income Concepts

ACCOUNTING STANDARDS BY D.S. RAWAT FCA

ACCOUNTING STANDARDS BY D.S. RAWAT FCA Accounting Standards Rules (2006) Notified on 07.12.2006 Two types of Companies -SMC - Non- SMC Accounting Standards Rules (2006) Some relaxation to SMC All the AS

ACCOUNTING STANDARDS BY D.S. RAWAT FCA Accounting Standards Rules (2006) Notified on 07.12.2006 Two types of Companies -SMC - Non- SMC Accounting Standards Rules (2006) Some relaxation to SMC All the AS

Form 3115 Application for Change in Accounting Method

Form 3115 Application for Change in Accounting Method (Rev. December 2015) Department of the Treasury Information about Form 3115 and its separate instructions is at www.irs.gov/form3115. Internal Revenue

Form 3115 Application for Change in Accounting Method (Rev. December 2015) Department of the Treasury Information about Form 3115 and its separate instructions is at www.irs.gov/form3115. Internal Revenue

Engineering Economics and Financial Accounting

Engineering Economics and Financial Accounting Unit 5: Accounting Major Topics are: Balance Sheet - Profit & Loss Statement - Evaluation of Investment decisions Average Rate of Return - Payback Period

Engineering Economics and Financial Accounting Unit 5: Accounting Major Topics are: Balance Sheet - Profit & Loss Statement - Evaluation of Investment decisions Average Rate of Return - Payback Period

PREVIEW OF CHAPTER 5-2

5-1 PREVIEW OF CHAPTER 5 5-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 5 and Statement of Cash Flows Statement of Financial Position LEARNING OBJECTIVES After studying this

5-1 PREVIEW OF CHAPTER 5 5-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 5 and Statement of Cash Flows Statement of Financial Position LEARNING OBJECTIVES After studying this

Bottomline Technologies Reconciliation to Non GAAP Measures Three Months Ended June 30, 2013

Reconciliation to Measures Three Months Ended June 30, 2013 Non Cash Amortization of Equity Based Integration Restructuring Interest GAAP Intangible Assets Compensation Related Expenses Expenses Expense

Reconciliation to Measures Three Months Ended June 30, 2013 Non Cash Amortization of Equity Based Integration Restructuring Interest GAAP Intangible Assets Compensation Related Expenses Expenses Expense

COPYRIGHTED MATERIAL. Index

Index Accelerated depreciation, 34 38 asset acquisition and, 76 77 declining balance method, 34, 35 Modified Accelerated Cost Recovery System (MACRS) method, 35 38 sum of the year s digits method, 34 35

Index Accelerated depreciation, 34 38 asset acquisition and, 76 77 declining balance method, 34, 35 Modified Accelerated Cost Recovery System (MACRS) method, 35 38 sum of the year s digits method, 34 35

VILLAGE OF CROOKSVILLE INCOME TAX RETURN FOR THE CALENDAR YEAR 2012

FORM R, Page 1 RETURN MUST BE FILED ON OR BEFORE APRIL 15, 2013, OR WITHIN 4 MONTHS OF END OF TAX PERIOD. VILLAGE OF CROOKSVILLE INCOME TAX RETURN FOR THE CALENDAR YEAR 2012 OR OTHER TAXABLE PERIOD BEGINNING

FORM R, Page 1 RETURN MUST BE FILED ON OR BEFORE APRIL 15, 2013, OR WITHIN 4 MONTHS OF END OF TAX PERIOD. VILLAGE OF CROOKSVILLE INCOME TAX RETURN FOR THE CALENDAR YEAR 2012 OR OTHER TAXABLE PERIOD BEGINNING

FUNDAMENTAL FINANCIAL CONCEPTS OF MEDICAL PRACTICE MANAGEMENT. [Top 25 Most Urgent Questions Answered by imba, Inc.]

![FUNDAMENTAL FINANCIAL CONCEPTS OF MEDICAL PRACTICE MANAGEMENT. [Top 25 Most Urgent Questions Answered by imba, Inc.]](/thumbs/83/87666602.jpg "FUNDAMENTAL FINANCIAL CONCEPTS OF MEDICAL PRACTICE MANAGEMENT. [Top 25 Most Urgent Questions Answered by imba, Inc.]") FUNDAMENTAL FINANCIAL CONCEPTS OF MEDICAL PRACTICE MANAGEMENT [Top 25 Most Urgent Questions Answered by imba, Inc.] ### WHY A MEDICAL PRACTICE IS CONSIDERED A FINANCIAL ASSET? A medical practice is a valuable

FUNDAMENTAL FINANCIAL CONCEPTS OF MEDICAL PRACTICE MANAGEMENT [Top 25 Most Urgent Questions Answered by imba, Inc.] ### WHY A MEDICAL PRACTICE IS CONSIDERED A FINANCIAL ASSET? A medical practice is a valuable

Basis Rules, Depreciation, and Asset Categorization Chapter 10

Basis Rules, Depreciation, and Asset Categorization Chapter 10 Tax is levied on income, not capital Capital is income that has already been taxed The Tax Toll-Booth 10-2 Gains must be realized before they

Basis Rules, Depreciation, and Asset Categorization Chapter 10 Tax is levied on income, not capital Capital is income that has already been taxed The Tax Toll-Booth 10-2 Gains must be realized before they

Financial Summary and Key Metrics (Unaudited) (In Thousands, Except Share Data and % )

(In Thousands, Except Share Data and % )") Second Quarter Page 1 Financial Summary and Key Metrics (In Thousands, Except Share Data and % ) Second Quarter First Quarter Fourth Quarter Third Quarter Second Quarter Statement of Income Data Total

Second Quarter Page 1 Financial Summary and Key Metrics (In Thousands, Except Share Data and % ) Second Quarter First Quarter Fourth Quarter Third Quarter Second Quarter Statement of Income Data Total

VILLAGE OF NEW LONDON, OHIO INCOME TAX RETURN AND DECLARATION

VILLAGE OF NEW LONDON Return Service Requested TO: INCOME TAX DEPARTMENT 115 EAST MAIN STREET NEW LONDON, OHIO 44851 PRE-SORTED FIRST CLASS MAIL U.S. POSTAGE PAID NEW LONDON, OHIO Permit No. 5 VILLAGE

VILLAGE OF NEW LONDON Return Service Requested TO: INCOME TAX DEPARTMENT 115 EAST MAIN STREET NEW LONDON, OHIO 44851 PRE-SORTED FIRST CLASS MAIL U.S. POSTAGE PAID NEW LONDON, OHIO Permit No. 5 VILLAGE

TECHNICAL EXPLANATION OF THE INNOVATION PROMOTION ACT OF 2015

TECHNICAL EXPLANATION OF THE INNOVATION PROMOTION ACT OF 2015 July 28, 2015 CONTENTS Page A. Deduction for Innovation Box Profits... 1 B. Special Rules for Transfers of Intangible Property From Controlled

TECHNICAL EXPLANATION OF THE INNOVATION PROMOTION ACT OF 2015 July 28, 2015 CONTENTS Page A. Deduction for Innovation Box Profits... 1 B. Special Rules for Transfers of Intangible Property From Controlled

Rent Payments vs. Installment Purchases

Rent Payments vs. Installment Purchases If a business rents anything necessary for the business, such as an office, a copier, machinery, etc., 100% of the rent can usually be deducted as an ordinary business

Rent Payments vs. Installment Purchases If a business rents anything necessary for the business, such as an office, a copier, machinery, etc., 100% of the rent can usually be deducted as an ordinary business

Limit on business interest deduction. Under the new law, every business, regardless of its form, is limited to a deduction for business interest equal

Dear Client, The recently enacted Tax Cuts and Jobs Act ("TCJA") is a sweeping tax package. Here's an overview of some of the more important business tax changes in the new law. Unless otherwise noted,

Dear Client, The recently enacted Tax Cuts and Jobs Act ("TCJA") is a sweeping tax package. Here's an overview of some of the more important business tax changes in the new law. Unless otherwise noted,

Aviation Tax Issues From The New Tax Changes: Opportunities, Challenges & Questions Sue Folkringa, CPA

Aviation Tax Issues From The New Tax Changes: Opportunities, Challenges & Questions Sue Folkringa, CPA 2018 NBAA Regional Forum San Jose, CA September 6, 2018 Wolcott & Associates, P.A. - What We Do We

Aviation Tax Issues From The New Tax Changes: Opportunities, Challenges & Questions Sue Folkringa, CPA 2018 NBAA Regional Forum San Jose, CA September 6, 2018 Wolcott & Associates, P.A. - What We Do We

Page 669 TITLE 26 INTERNAL REVENUE CODE 167

Page 669 TITLE 26 INTERNAL REVENUE CODE 167 in section 166(g)(1)(A) of such Code (as amended by the first section of this Act), and (2) the assessment of a deficiency of the tax imposed by chapter 1 of

Page 669 TITLE 26 INTERNAL REVENUE CODE 167 in section 166(g)(1)(A) of such Code (as amended by the first section of this Act), and (2) the assessment of a deficiency of the tax imposed by chapter 1 of

Oil and Gas Tax Issues. Don Nestor, CPA Ryan Nestor, CPA, CGMA Bill Phillips, CPA J. Marlin Witt, CPA, CFP

Oil and Gas Tax Issues Don Nestor, CPA Ryan Nestor, CPA, CGMA Bill Phillips, CPA J. Marlin Witt, CPA, CFP Arnett Carbis Toothman llp 2018 Depletion and Ways to Compute What is depletion and what is its

Oil and Gas Tax Issues Don Nestor, CPA Ryan Nestor, CPA, CGMA Bill Phillips, CPA J. Marlin Witt, CPA, CFP Arnett Carbis Toothman llp 2018 Depletion and Ways to Compute What is depletion and what is its

The Tax Cuts and Jobs Act of 2017 and Internal Revenue Code Section

The Tax Cuts and Jobs Act of 2017 and Internal Revenue Code Section 1031 1 David M. Sengstock, JD Mick Law P.C. LLO November 23, 2018 How does one manage an Internal Revenue Code Section 199A qualified

The Tax Cuts and Jobs Act of 2017 and Internal Revenue Code Section 1031 1 David M. Sengstock, JD Mick Law P.C. LLO November 23, 2018 How does one manage an Internal Revenue Code Section 199A qualified

Failure to follow instructions below will result in a 5 point reduction in your grade.

T15F-Chp-00-Tst-3-Exam-Prb-WORD-FALL-2015-Nov-17 - Page 1 of 4 FEDERAL TAX - TEST No. 3. Chapters 8-10 Test No. Fall, 2015. The University of North Carolina at Charlotte Name Row In Class Instructions:

T15F-Chp-00-Tst-3-Exam-Prb-WORD-FALL-2015-Nov-17 - Page 1 of 4 FEDERAL TAX - TEST No. 3. Chapters 8-10 Test No. Fall, 2015. The University of North Carolina at Charlotte Name Row In Class Instructions:

Instructions for Form 4626

2004 Instructions for Form 4626 Alternative Minimum Tax Corporations Section references are to the Internal Revenue Code unless otherwise noted. Department of the Treasury Internal Revenue Service General

2004 Instructions for Form 4626 Alternative Minimum Tax Corporations Section references are to the Internal Revenue Code unless otherwise noted. Department of the Treasury Internal Revenue Service General

Chapter 3 TCJA: Depreciation, Bonus Dep., 179, NOLs, and 461(L) Depreciation

Depreciation") Chapter 3 TCJA: Depreciation, Bonus Dep., 179, NOLs, and 461(L) Depreciation ADS Recovery Period for Residential Property is Shortened (Section 168(g)(2)(C)) ADS recovery period for residential rental

Chapter 3 TCJA: Depreciation, Bonus Dep., 179, NOLs, and 461(L) Depreciation ADS Recovery Period for Residential Property is Shortened (Section 168(g)(2)(C)) ADS recovery period for residential rental