CHOICE OF ENTITY: AN OVERVIEW. Steven G. Thomas, JD, LL.M. Lavelle & Finn, LLP

|

|

|

- Brenda Bailey

- 6 years ago

- Views:

Transcription

1 CHOICE OF ENTITY: AN OVERVIEW by Steven G. Thomas, JD, LL.M. Lavelle & Finn, LLP 1

2 2

3 BUSINESS ORGANIZATIONS: Tax and Legal Aspects Compared Choice of Entity: An Overview November 4, 2015 Steven G. Thomas, JD, LL.M. 3

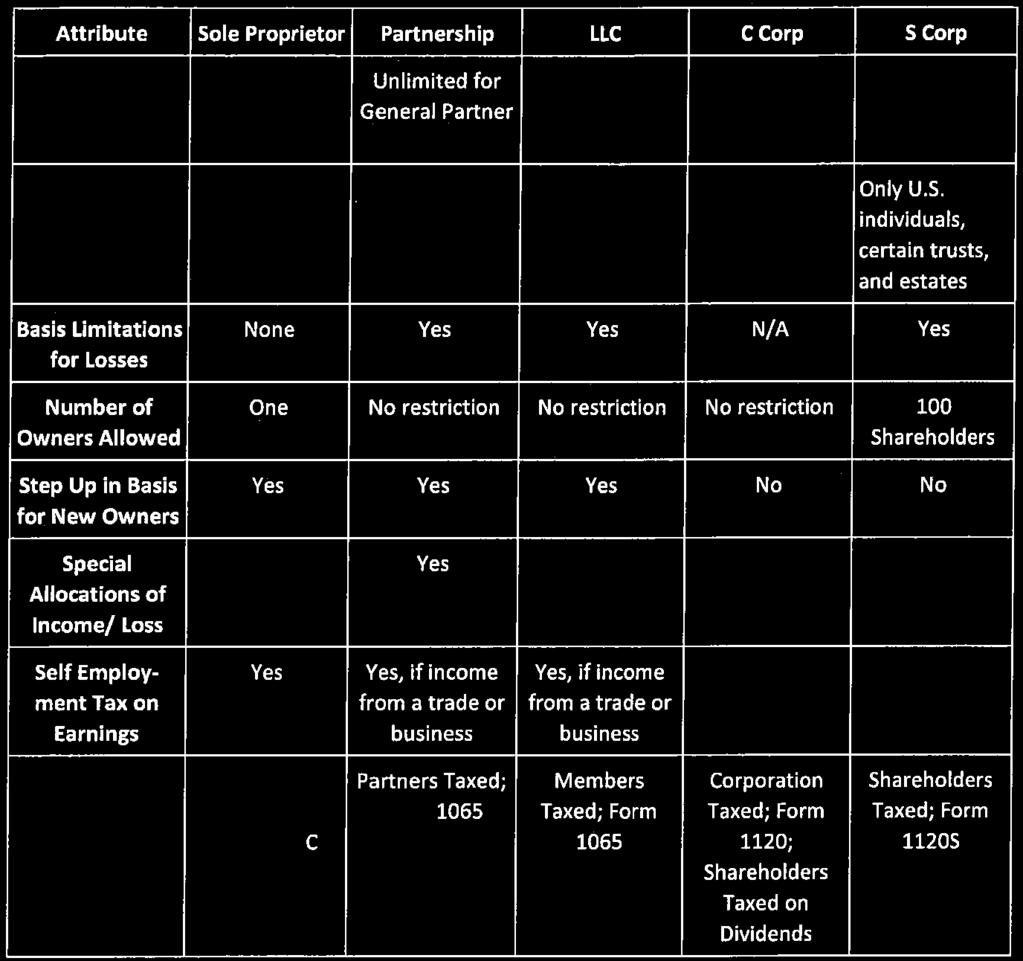

4 Choice of Entity Considerations Prior to establishing a new business, an entrepreneur is faced with the crucial task of choosing the appropriate business vehicle. There are several issues of organizational structure which should be considered by the business owner, both tax and non tax related. In selecting the appropriate business structure, one must take into account several factors, including the need for flexibility, tax advantages of different types of entities and the way that each business vehicle exposes an owner to liability. Formation I. Procedural/Formation Requirements A. Considerations: 1. Ease of formation 2. Costs of organization and doing business 3. Simplicity v. formality of operations 4. State of formation B. Requirements of Different Types of Entities: 1. Sole Proprietorship: a) No formal organization required. b) Operated under name of individual owner. c) Least Expensive formation costs. d) Can file a "doing business as" (DBA) name, if doing business under an assumed name, a sole proprietor must file with the County Clerk in each County in which the business is transacted [NY GBL 130(1)]. 2. General Partnership: a) Similar to a sole proprietorship, but has more than one owner. b) Doesn't require a formal agreement, informal agreement arises from sharing profits and losses of a business. c) Must file a certificate with clerk of each county in which partnership transacts business, or with the Secretary of State, setting forth name, address and nature of business [NY GBL 130 (1)). 4

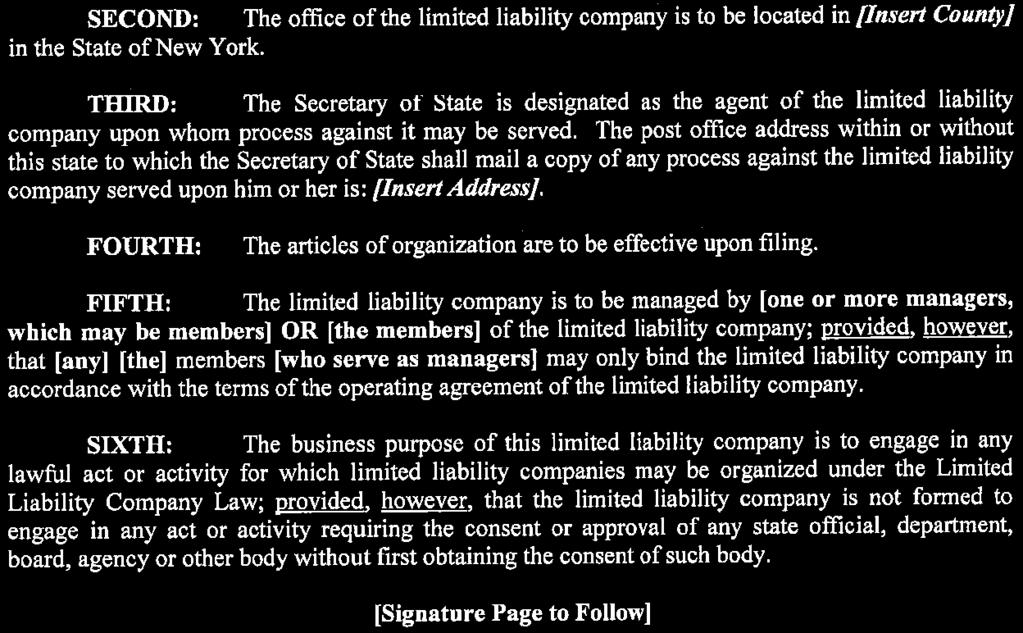

5 d) Partner does not need to be an individual (i.e. can be a Corporation [NY BCL 202(a)(15)]). e) Duration: the death of any partner usually causes dissolution [NY Partnership Law 62(4)], although a partnership agreement can provide for continuation after the death of a partner. 3. Limited Partnership: a) Requires certificate of formation to be filed with Department of State [NY Partnership Law , ]. b) Requires a written partnership agreement [NY Partnership Law ], which must be signed by all general partners. c) Name of the entity must contain "LP" or "Limited Partnership" [NY Partnership Law (a)(1)]. d) A partner need not be an individual (A corporation may be a limited partner [NY BCL 202(a)(15)]. e) Requires at least one general partner [NY Partnership Law (h)]. f) Publication Requirement: A limited partnership must publish a notice containing the substance of the certificate of limited partnership, once a week for six consecutive weeks, in two newspapers in the county in which the original certificate is filed [NY Partnership Law (c)(i)]. 4. Limited Liability Company (LLC): a) Requires Articles of Organization to be filed with the Department of State [NY LLCL 203(a)] (See Attachment A). (1) An LLC is formed at the time of filing, or at another time stated in the articles of organization, but not to exceed 60 days from the filing of initial articles [NY LLCL 203(d)]. (2) An organizer may be an individual or another entity [NY LLCL 102(w); NY LLCL 203(a)]. (3) The name of the organization must include LLC or "Limited Liability Company" [NY LLCL 204(a)]. 5

6 (4) Articles of Organization must contain the company name, the county of the principal office, and the events necessitating dissolution. Additionally, it must designate the Secretary of State as an agent for the service of process [NY LLCL 203(e)]. b) Publication Requirement: An LLC must publish a notice containing the substance of the articles of organization, once a week for six consecutive weeks, in two newspapers in the county in which the LLC is located [NY LLCL 206(a)]. c) No limit on number or character of members, except that there must be at least one member [NY LLCL 203(c)]. Can provide for future classes of members in the articles of organization [NY LLCL 418(a)]. d) Operating Agreement: A written operating agreement is required under NYS law (compare with Delaware, which does not require an operating agreement) [NY LLCL 417(a)]. (1) Must be entered into within 90 days of formation, but may be entered into prior to formation of the LLC [NY LLCL 417(c)]. (2) An operating agreement must be consistent with law and the articles of organization. Generally governs the business of the LLC, the conduct of the affairs, and the rights, powers, preferences, limitations or responsibilities of its members, managers, employees or agents. (i) (ii) Provisions in an operating agreement can override statutory default provisions Provisions that should be in an Operating Agreement: (a) Name of LLC and names of members; Location of principal office; (b) Duration of LLC; (c) Rights and responsibilities of members; 6

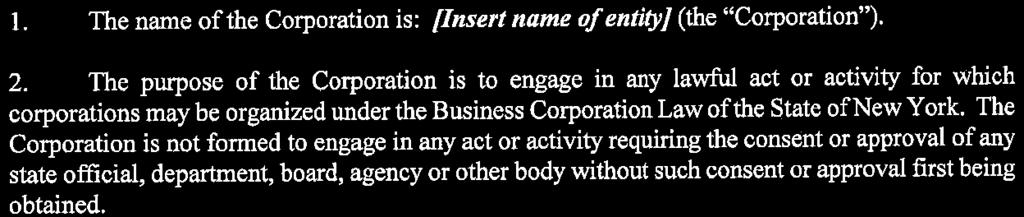

7 (d) Management Structure (including procedures for change of managers); (e) Accounting protocols; (f) Voting procedures and agreements (g) Capital Contributions (h) Admission of members (i) Indemnification; (j) Provisions for change of membershipdissolution, winding up, consolidation, death or disability of member; (k) Transfer rights, etc. 5. Corporations: a) Requires Certificate of Incorporation to be filed with the Department of State [NY BCL 104]. b) Must file a Certificate of Incorporation (Certificate) detailing the corporate name, corporate purpose or purposes, place of office, duration (only if not perpetual), aggregate number of shares authorized to be issued (including a description of classes and series of shares, if any), and name and address of the registered agent, if any, for service of process [NY BCL 402] (See Attachment B). (1) The Certificate may include any other provision that is consistent with law [NY BCL 402(c)]. c) Certificate must designate the Secretary of State as agent for service of process and should include the address to which the Secretary of State shall address any such process. d) Must state a lawful business purpose [NY BCL 201(a)]. e) Same requirements for C and S Corporations, (i.e. state filings/fees; S Corporation differences come from federal tax law). f) If an S Corporation (discussed hereunder "Taxation"), must file with both New York State (Form CT 6, Attachment C) and with 7

8 the IRS (Form 2553, Attachment D). g) The Organizational Instruments of the corporation (the Certificate of Incorporation and the By laws) govern the corporate existence, the operations and management of the corporation and the relationships between the owners and employees of the corporation. (1) Initial By laws: Upon formation of a corporation, initial by laws must be adopted by the incorporators at the organization meeting [NY BCL 601(a)]. Such by laws may include any provision pertaining to the business of the corporation, the rights and responsibilities of shareholders, directors or officers, and any matter related to the operations of the business, so long as the by laws do not conflict with the Certificate of Incorporation or law [NY BCL 601(b)]. h) Organizational Meeting: Generally, an organizational meeting is held by the incorporators to select an initial board of directors. Operational Issues II. Control/Operational Issues A. Considerations: 1. Who will be the owners? 2. Statutory restrictions on types of owners in certain entities 3. Who will make Management and control considerations a) Some entities require more formalities in setting up management structure 4. Will you want Different classes of ownership a) One or more classes of stock b) Voting and non voting interests c) Flexibility in allocating income and losses B. Differences between Entities: 1. Sole Proprietorship Complete Control over the company. Can sell business, although a partial sale will result in a partnership. 8

9 2. General Partnership All partners share in management unless otherwise provided in partnership agreement. 3. Limited Partnership General Partner controls and Limited Partners have no say in management. 4. Limited Liability Company a) Management by statutory default is vested in the members, but the articles of organization can place management responsibilities in a certain class of members or delegate management to a manager [NY LLCL 401(a), 408(a)]. (1) If management is vested in members by statutory default, all members are agents of the LLC [NY LLCL 412(a)]. (2) Managers (including member managers) must perform their duties in good faith. The duty of care standard is that of an ordinary prudent person [NY LLCL 409(a)]. (3) A manager doesn't have to be a member [NY LLCL 410(a)]. (4) Voting Rights are generally tied to members' shares of profits. (5) Meetings: Annual meeting of the members required [NY LLCL 403]. Note that the minimum quorum by statute is 1/3 of members in interest (cannot lower by terms of the operating agreement [NY LLCL 404]). (a) Statutory notice requirements of meetings [see NY LLCL 405, 406]. (6) New members may be admitted to an LLC, however, such admittance must comply with the operating agreement. If the operating agreement is silent on the issue, then a majority vote of the interests is required to admit the new member. (7) Neither a member, manager nor agent is liable for the debts, obligations or liabilities of the LLC. 9

10 b) Operating Agreement (1) Statutorily Required [NY LLCL 417(a)]. (2) Profits and losses may be allocated as mandated by the agreement. If there is no such allocation, profits and losses are distributed in accordance with the value of the contributions of each member [NY LLCL 504]. (3) Although a member manager will be shielded from liability if his or her actions are performed in good faith [NY LLCL 409(c)], the operating agreement may not protect a manager against intentional bad faith acts or misconduct [NY LLCL 417(a)(i)]. c) Distributions to Members: (1) Do not have to be pro rata (unless operating agreement stipulates otherwise). (2) Cannot be made if liabilities of the company exceed assets [NY LLCL 508(a)]. (3) Interest is personal property, thus a member has no interest in actual assets of LLC [NY LLCL 601]. (4) A member has no right to distribution other than cash (not in other assets) [NY LLCL 505]. 5. Corporations: a) Management and control of a corporation is stratified: (1) Shareholders elect a board of directors to oversee the management and operations of the corporation. (2) The board of directors then elects officers to handle dayto day operations. (3) For smaller corporations, management is typically exercised by the owners in various capacities. May have voting and nonvoting shareholders to isolate management and control to a certain group. b) The Shareholder's Agreement governs the relationships between the shareholders. Notably, no such agreement is statutorily required. 10

11 c) Bylaws: Bylaws are the rules and regulations of the corporation and govern its internal affairs, including matters relating to its shareholders, directors and officers [NY BCL 601(b)]. They are not public and thus do not need to be filed with or approved by the Secretary of State. They can be altered by a shareholder vote. (1) Typically by laws address the time and manner of holding shareholders' meetings; those authorized to call special shareholder meetings; requirements for quorum; election, qualifications, duties, terms and removal of officers and directors; place and time of meetings of board of directors; the number of directors; dividends and distributions; and any other matter relating to the management of the entity [NY BCL ]. C. Continuity/Business Succession 1. Considerations: a) Estate and business succession planning. b) What happens to the entity on death of a member can the interests be transferred easily? 2. Continuity of Different Entities: a) Sole Proprietorship: (1) It terminates on death of owner but can be sold prior to death. b) General Partnership: (1) Terminates on death of any partner unless otherwise provided in partnership agreement [NY Partnership Law 62(4)]. (2) Transfer of partnership interest requires consent of other partners unless otherwise stated [NY Partnership Law 40(7)]. c) Limited Partnership: (1) Continuity depends largely on the partnership agreement, but there must always be at least one general 11

12 partner and one limited partner. (2) In NY, unless otherwise provided by the partnership agreement, a limited partner cannot withdraw from the partnership prior to dissolution [NY Partnership Law (a)]. (3) Good opportunities for estate planning, a partner can gift limited partnership shares but keep control of entity. d) Limited Liability Company: (1) In general, a membership interest can be assigned, but assignee needs the consent of a majority of the nonassigning members to become a member [NY LLCL 604(a)]. (2) Good for estate planning especially because there can be varying classes of interest. (3) Death or Disability of a Member: (a) The representative of the member's estate has the same rights as the member for purposes of settling estate [NY LLCL 608]. e) Corporations: (1) The life of a corporation is unlimited. Shares are generally freely transferable (although transferability can be restricted by a shareholder agreement). Taxation Ill. Tax Issues A. Considerations: 1. How will entity be taxed a) "Double tax" issue? 2. Taxation of the owners a) "Pass through" taxation? B. Taxation of Various Entities: 1. Sole Proprietorship: Income of business is reported on tax return of owner (i.e., Schedule C). 12

13 2. General Partnership: a) Must file a tax return for the partnership, but partnership income passes through to partners (and the partners are taxed on their share regardless of whether income is actually distributed). Losses can be deducted up to partner's basis. b) Must pay self employment tax on income from a trade or business. 3. Limited Partnership: a) Income passes through to partners (similar to General Partnership). 4. Limited Liability Company: a) An LLC can be taxed as partnership or corporation (must elect to be taxed as a corporation [Treas. Reg ]). If the LLC is taxed as a partnership: (1) Income is taxed directly to the members. (2) Services rendered by a member to an LLC may be structured so that they are not taxed (if the ownership interest is merely a profits interest). (3) A member can deduct losses up to level of basis in the entity. (4) Any income derived by the member from the LLC is subject to employment taxes. (5) Upon liquidation, member is not taxed on amounts up to the member's basis. 5. Corporations: a) C Corporation: (1) Double tax Situation: Entity is taxed on the net income and shareholders are taxed on Corporation distributions [IRC 11, 301). (2) A shareholder will be taxed on services performed for the corporation in exchange for ownership interests. Such services will be taxed on their fair market value. 13

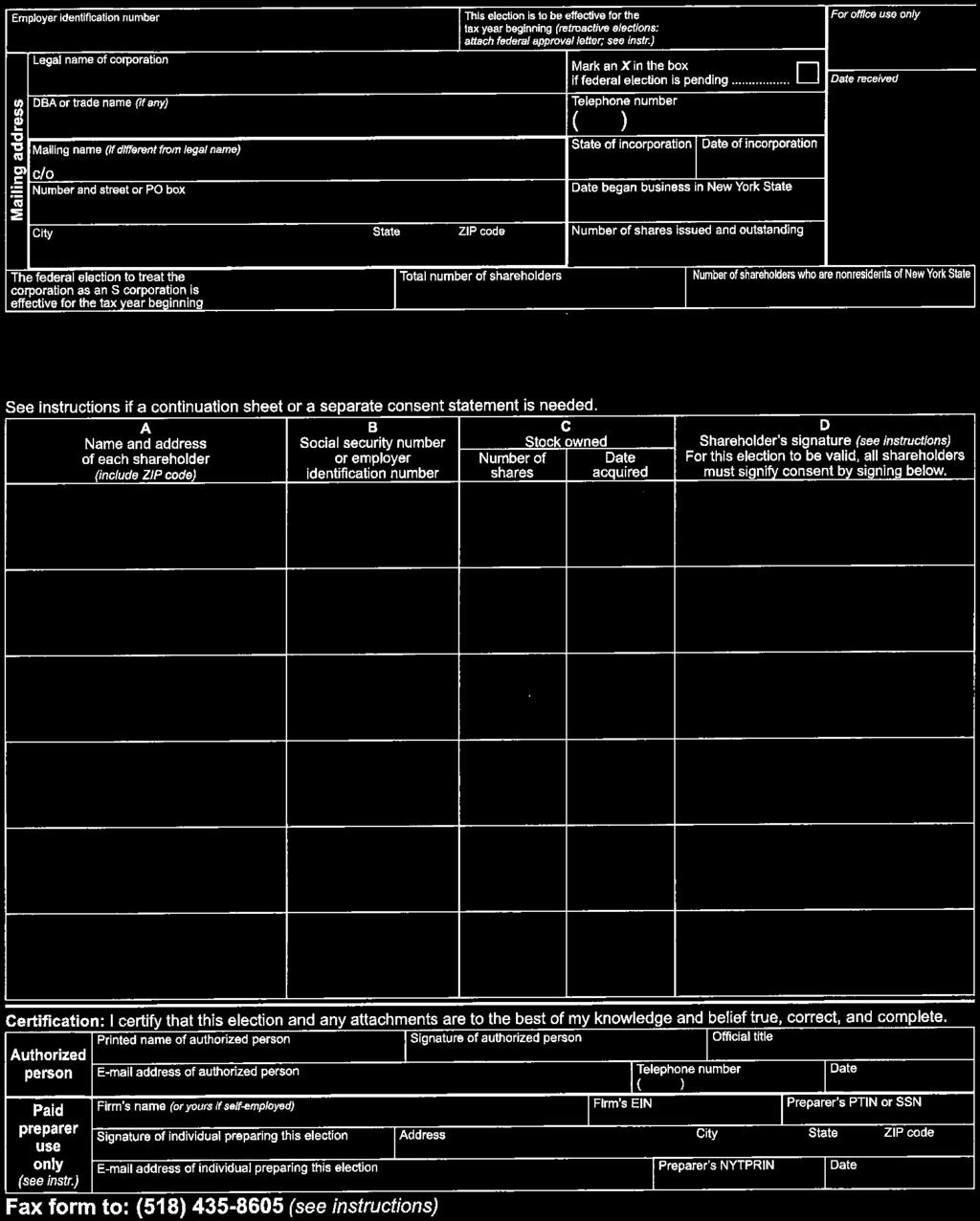

14 (3) Tax advantage of corporation over LLC's: (a) The graduated corporate tax rates are lower than those of individual rates. (b) There is no self employment tax on profits drawn by shareholder. (c) A shareholder employee may enjoy greater fringe benefits. b) S Corporation: (1) An election under IRC 1362 (See Attachment C) and NY Tax Law 660 (See Attachment D) must be timely filed for the entity to be treated as an S corporation. The following requirements must be met in order to qualify for the election: (a) Maximum of 100 shareholders. (b) Only U.S. citizens, resident aliens and certain trusts are eligible shareholders. (c) Single class of stock. (d) Can be formed by one or more natural persons 18 years or older. (2) Pass through taxation applies so long as a valid S Corporation election is made. (a) Losses are deductible to the extent of the shareholder's basis. (b) As with a ( Corporation, an individual who performs services for the entity in exchange for an ownership interest will be subject to tax on the fair market value of such services. (c) Medicare Tax on passive income If a shareholder is not active in the business, there may be up to a 3.8% surtax depending upon the shareholders' tax bracket. (d) shareholder employee is only subject to self 14

15 employment tax on "reasonable wages." Any profits derived from the corporation beyond "reasonable wages" are not subject to employment tax. Jurisdictional lssues I. Jurisdiction: A. Important to decide in which STATE to form your company. Every state has its own set of laws regarding how entities are governed. Some are more favorable than others depending on your particular circumstances. For example: 1. NY Rule Protecting 20% Shareholders In New York, BCL 1104 a gives the holders of 20% or more of the outstanding shares of a corporation the right, when the other shareholders or directors engage in oppressive conduct, to petition the court for dissolution. Delaware does not provide similar protection, leaving minority shareholders to rely on case law regarding oppression and breach of fiduciary duty. 2. Corporate Liability for Wages: a) In New York, the ten largest shareholders of a corporation are liable for wage claims [NY BCL 630]. 3. Business Purpose: a) New York Limited Liability Company Law 201requires a lawful business purpose to form a Limited Liability Company in New York, for example, owning and operating business assets. A lawful business purpose is also required to form a Corporation in New York, as required by New York Business Corporation Law 201. Other activities like maintaining an investment portfolio or owning residential property may not constitute a valid business purpose in New York. b) To form a Limited Liability Company in Delaware, of the Delaware Limited Liability Act states that the entity only needs a lawful purpose. Additionally, one only needs lawful purpose to form a Corporation in Delaware pursuant to Delaware General Corporations Law 101. Therefore, holding an investment 15

16 portfolio and owning residential property will constitute a valid entity purpose in Delaware. B. Consider the rights of personal creditors which are governed by state law. 1. Charging orders. A charging order is a creditor's remedy by which the creditor can attach a partner's or member's right to distributions. A charging order is used by a personal creditor of the owner of the entity (not a creditor of the entity itself). Note that a creditor of a shareholder cannot obtain a charging order against a corporation. a) In Delaware, charging orders are the exclusive remedy for creditors of the member/partner [DE LLCA (d)]. It prevents the creditor from attaching the member's or partner's membership/or partnership interest, or from forcing dissolution of the entity. b) Unlike the Delaware statute, the New York statute does not clearly indicate that a charging order is an exclusive remedy for the creditor of an LLC member [NY LLCL 607]. However, consider NY LLCL 603, which governs assignments of membership interests. Unless otherwise stated in the operating agreement, "the only effect of an assignment... is to entitle the assignee to receive... distributions" [NY LLCL 603(a) (3}]. (1) With regard to partnerships, New York is explicit that the charging order is not the exclusive remedy of a creditor of a partner [NY Partnership 111]. 2. Piercing the Corporate Veil: a) Under Delaware law, the corporate veil may be pierced "in the interest of justice, when such matters as fraud, contravention of law or contract, public wrong, or where equitable consideration among members of the corporation require it, are involved." [See Pauley Petroleum Inc. v. Continental Oil Co., 43 Del. Ch. 516, 521, 239 A. 2d 629, 633 (1968}]. b) In contrast, New York courts disregard a party's corporate veil more "reluctantly". New York law requires a part seeking to 16

17 pierce the corporate veil to show that the owners, through their domination, abused the privilege of doing business in the corporate form to commit a wrong or fraud. 3. Taking Ownership: a) In a corporation, a creditor may attach the shares of a debtor's stock to gain all the rights that the debtor had in the corporation, including rights to sell the shares, voting rights, the right to view books and records, and rights to bring derivative actions against errant corporate officers and directors. b) If the corporation is an "S" corporation, and the creditor is not an individual, then the creditor's attachment of the stock may cause the "S" election to be terminated, which would possibly result in unwanted tax consequences to the remaining shareholders. c) A similar change in ownership with a Partnership or LLC may disrupt the operations of the entity and force non debtor partners into an involuntary partnership with the creditor. C. Formation Requirements may also be more costly in one state over another: 1. States available for formation are usually where the business of the company will be conducted, where the assets of the company will be held, and then several states such as Delaware and Nevada that have advanced corporation laws and whose courts tend to respect the sanctity of the corporate entity against those who would set it aside. 2. Small businesses benefit most from incorporating or forming their LLC in the state where the business is physically located or operating, by avoiding additional costs and paperwork associated with forming in one state and then having to qualify their corporation or LLC to do business as a foreign entity in another state. 3. Additional costs to file in a foreign state: a) State fee required to file foreign qualifications; b) Registered agent service fees; c) The company will have to pay an annual fee and possibly franchise taxes in both states. 17

18 4. Additional paperwork to file in a foreign state: a) Foreign qualification filing with the state; b) Will have to file tax returns in both states; c) Will have to file annual reports in both states. 18

19 19

20 20

21 21

22 22

23 23

24 24

25 25

26 26

27 27

28 28

29 29

30 30

31 31

32 32

33 33

34 34

35 35

36 36

Sole Proprietorship Limited Liability Co. (LLC) C-Corp S-Corp Fairly Easy Fairly Easy Fairly Easy Moderately Difficult

C-Corp S-Corp Fairly Easy Fairly Easy Fairly Easy Moderately Difficult") Estimated Ease of Formation Fairly Easy Fairly Easy Fairly Easy Moderately Difficult Formation Procedure Key Documents for Formation No Filing Required -DBA Filing (Give the business a name other than

Estimated Ease of Formation Fairly Easy Fairly Easy Fairly Easy Moderately Difficult Formation Procedure Key Documents for Formation No Filing Required -DBA Filing (Give the business a name other than

CHOICE OF ENTITY COMPARISON AND CONTRASTS. The Tax Section of The Florida Bar. Cristin Keane, Carlton Fields, Tampa

CHOICE OF ENTITY COMPARISON AND CONTRASTS The Tax Section of The Florida Bar Cristin Keane, Carlton Fields, Tampa Guy Whitesman, Henderson Franklin, Fort Myers November 16, 2016 1) Introduction-Overview

CHOICE OF ENTITY COMPARISON AND CONTRASTS The Tax Section of The Florida Bar Cristin Keane, Carlton Fields, Tampa Guy Whitesman, Henderson Franklin, Fort Myers November 16, 2016 1) Introduction-Overview

GUIDE TO SELECTING YOUR SMALL BUSINESS LEGAL STRUCTURE. To make your business #CPAPOWERED, call today and let s get started.

GUIDE TO SELECTING YOUR SMALL BUSINESS LEGAL STRUCTURE To make your business #CPAPOWERED, call today and let s get started. One important consideration when starting your business is determining the best

GUIDE TO SELECTING YOUR SMALL BUSINESS LEGAL STRUCTURE To make your business #CPAPOWERED, call today and let s get started. One important consideration when starting your business is determining the best

CHOOSING THE RIGHT LEGAL ENTITY FOR A STARTUP BUSINESS

CHOOSING THE RIGHT LEGAL ENTITY FOR A STARTUP BUSINESS by MAUREEN CRUSH, Esq. Crush & Varma Law Group P.C. Fishkill, NY 1 2 CHOOSING THE RIGHT LEGAL ENTITY FOR A STARTUP BUSINESS Presented by: Maureen

CHOOSING THE RIGHT LEGAL ENTITY FOR A STARTUP BUSINESS by MAUREEN CRUSH, Esq. Crush & Varma Law Group P.C. Fishkill, NY 1 2 CHOOSING THE RIGHT LEGAL ENTITY FOR A STARTUP BUSINESS Presented by: Maureen

a guide to forming your business

a guide to forming your business table of contents entity descriptions, advantages & disadvantages... 2 sole proprietorship.... 2 general partnership................................. 2 limited partnership...3

a guide to forming your business table of contents entity descriptions, advantages & disadvantages... 2 sole proprietorship.... 2 general partnership................................. 2 limited partnership...3

Desirable Characteristics for the Business Entity

Desirable Characteristics for the Business Entity Maintain control while giving interests to family members (unity of management) Avoiding veto power of small owners Preventing interests in family property

Desirable Characteristics for the Business Entity Maintain control while giving interests to family members (unity of management) Avoiding veto power of small owners Preventing interests in family property

Business Entities GENERAL PARTNERSHIP

THE PRUDENTIAL INSURANCE OF AMERICA Business Entities General Entity Tax Characteristics and Executive Benefits Using Life Insurance LIABILITY EASE OF FORMATION State law requirements for incorporation

THE PRUDENTIAL INSURANCE OF AMERICA Business Entities General Entity Tax Characteristics and Executive Benefits Using Life Insurance LIABILITY EASE OF FORMATION State law requirements for incorporation

Business Entities GENERAL PARTNERSHIP

Business Entities General Entity Tax Characteristics and Executive Benefits Using Life Insurance LIABILITY EASE OF FORMATION State law requirements for incorporation must be met. Implementation expenses

Business Entities General Entity Tax Characteristics and Executive Benefits Using Life Insurance LIABILITY EASE OF FORMATION State law requirements for incorporation must be met. Implementation expenses

The Corporation Handbook

The Corporation Handbook 2016 Edition CTcorporation.com 2016 C T Corporation System and its affiliates and/or licensors. All rights reserved. CT THE CORPORATION HANDBOOK AN INTRODUCTION TO CORPORATIONS

The Corporation Handbook 2016 Edition CTcorporation.com 2016 C T Corporation System and its affiliates and/or licensors. All rights reserved. CT THE CORPORATION HANDBOOK AN INTRODUCTION TO CORPORATIONS

23041 Mill Creek Dr. Laguna Hills, California April 12, Protecting Your Business

TAXATION CORPORATE & BUSINESS LAW ESTATE PLANNING MICHAEL R. BROWN, A LAW CORPORATION MASTER OF BUSINESS ADMINISTRATION CERTIFIED PUBLIC ACCOUNTANT CERTIFIED TAX SPECIALIST (State Bar of California Board

TAXATION CORPORATE & BUSINESS LAW ESTATE PLANNING MICHAEL R. BROWN, A LAW CORPORATION MASTER OF BUSINESS ADMINISTRATION CERTIFIED PUBLIC ACCOUNTANT CERTIFIED TAX SPECIALIST (State Bar of California Board

Choosing the Right Legal Entity for a Startup Business

NEW YORK STATE BAR ASSOCIATION Choosing the Right Legal Entity for a Startup Business Maureen Crush, Esq. FACTORS TO CONSIDER: º COST (What the Client is worried about) - Including filing fees, annual

NEW YORK STATE BAR ASSOCIATION Choosing the Right Legal Entity for a Startup Business Maureen Crush, Esq. FACTORS TO CONSIDER: º COST (What the Client is worried about) - Including filing fees, annual

Entrepreneurs may choose from a myriad of entities, including:

TABLE OF CONTENTS Choices Available... 3 Entities Defined... 4 Tax Differences... 5 Legal Distinctions... 6 Liability Concerns... 6 Insurance versus Limited Liability... 7 Protect Using LLCs, LLPs, and

TABLE OF CONTENTS Choices Available... 3 Entities Defined... 4 Tax Differences... 5 Legal Distinctions... 6 Liability Concerns... 6 Insurance versus Limited Liability... 7 Protect Using LLCs, LLPs, and

Farm Business Arrangement Alternatives

Farm Business Arrangement Alternatives Introduction If the new and established operators decide to farm together after the testing stage, they are ready to move from the beginning farm business arrangement

Farm Business Arrangement Alternatives Introduction If the new and established operators decide to farm together after the testing stage, they are ready to move from the beginning farm business arrangement

Knowledge Share. Alternative. Navigating New choices for business formations

Knowledge Share Alternative ENTITIES Navigating New choices for business formations 2016 SEMINAR REFERENCE BOOK NAVIGATING NEW CHOICES FOR BUSINESS FORMATIONS Seminar Reference Book TABLE OF CONTENTS INTRODUCTION

Knowledge Share Alternative ENTITIES Navigating New choices for business formations 2016 SEMINAR REFERENCE BOOK NAVIGATING NEW CHOICES FOR BUSINESS FORMATIONS Seminar Reference Book TABLE OF CONTENTS INTRODUCTION

Shared Aspirations, Satisfied Expectations and Cooperation. Robert M. Gottschalk, Esq.

Shared Aspirations, Satisfied Expectations and Cooperation Robert M. Gottschalk, Esq. June 13, 2013 1 Congratulations! Mazel tov! The affiliation between owners is very much like a marriage IT S A RELATIONSHIP.

Shared Aspirations, Satisfied Expectations and Cooperation Robert M. Gottschalk, Esq. June 13, 2013 1 Congratulations! Mazel tov! The affiliation between owners is very much like a marriage IT S A RELATIONSHIP.

Estate Planning Strategies Using LLC's, Part One. By Jim Gulseth

Estate Planning Strategies Using LLC's, Part One By Jim Gulseth Why and how do we use LP s (limited partnerships) and LLC-P s (limited liability companies taxed as a partnership) for estate planning? (a)

Estate Planning Strategies Using LLC's, Part One By Jim Gulseth Why and how do we use LP s (limited partnerships) and LLC-P s (limited liability companies taxed as a partnership) for estate planning? (a)

Choosing the Legal Structure of Your Business

Brief #02.00 Latest Revision: 09/2013 Southern Ohio Chapters Choosing the Legal Structure of Your Business Sole Proprietorship "C" Corporation Limited Liability Partnership Partnership "S" Corporation

Brief #02.00 Latest Revision: 09/2013 Southern Ohio Chapters Choosing the Legal Structure of Your Business Sole Proprietorship "C" Corporation Limited Liability Partnership Partnership "S" Corporation

OPERATING AGREEMENT DMF IRA, LLC ARTICLE 1 ORGANIZATIONAL MATTERS. 1.1 Name. The name of the limited liability company is DMF IRA, LLC (the "LLC").

.") OPERATING AGREEMENT OF DMF IRA, LLC The parties to this Operating Agreement are the Member identified in Section 1.6, the Manager identified in Section 6.1 and the LLC, who agree to form a limited liability

OPERATING AGREEMENT OF DMF IRA, LLC The parties to this Operating Agreement are the Member identified in Section 1.6, the Manager identified in Section 6.1 and the LLC, who agree to form a limited liability

2014 Nuts & Bolts Seminar Coralville

2014 Nuts & Bolts Seminar Coralville TRANSACTIONAL TRACK Business Formation 12:30 p.m.- 1:30 p.m. Presented by Sean W. Wandro Meardon, Sueppel & Downer P.L.C. 122 S. Linn St. Iowa City, IA 52240 Phone:

2014 Nuts & Bolts Seminar Coralville TRANSACTIONAL TRACK Business Formation 12:30 p.m.- 1:30 p.m. Presented by Sean W. Wandro Meardon, Sueppel & Downer P.L.C. 122 S. Linn St. Iowa City, IA 52240 Phone:

Legal Basis for Smooth Transfer of Property

Legal Basis for Smooth Transfer of Property Robert A. Tufts Attorney and Associate Professor School of Forestry and Wildlife Sciences Auburn University (334) 844-1011 Form of ownership Entities other than

Legal Basis for Smooth Transfer of Property Robert A. Tufts Attorney and Associate Professor School of Forestry and Wildlife Sciences Auburn University (334) 844-1011 Form of ownership Entities other than

Farm Business Arrangement Alternatives. Introduction. Sole Proprietorships. Partnerships. Farm Business Arrangements Page 1

Farm Business Arrangement Alternatives Philip E. Harris Department of Agricultural and Applied Economics and Center for Dairy Profitability University of Wisconsin-Madison/Extension (Revised 14 January

Farm Business Arrangement Alternatives Philip E. Harris Department of Agricultural and Applied Economics and Center for Dairy Profitability University of Wisconsin-Madison/Extension (Revised 14 January

florida ARECS Florida s New Revised Limited Liability Company ( LLC ) Act

Act") Florida s New Revised Limited Liability Company ( LLC ) Act James A Marx, Esq., Marx Rosenthal PLLC, Miami, Florida Previously published in the spring 2015 edition of Action Line Revised May 2016 Florida

Florida s New Revised Limited Liability Company ( LLC ) Act James A Marx, Esq., Marx Rosenthal PLLC, Miami, Florida Previously published in the spring 2015 edition of Action Line Revised May 2016 Florida

Entity Selection. Presented to the ISBA 9 th Annual Solo & Small Firm Conference by: Miriam Leskovar Burkland and Mark B. Ryerson October 5, 2013

Entity Selection Presented to the ISBA 9 th Annual Solo & Small Firm Conference by: Miriam Leskovar Burkland and Mark B. Ryerson October 5, 2013 I. OWNERSHIP / INVESTMENT A. Nature of Contribution in Exchange

Entity Selection Presented to the ISBA 9 th Annual Solo & Small Firm Conference by: Miriam Leskovar Burkland and Mark B. Ryerson October 5, 2013 I. OWNERSHIP / INVESTMENT A. Nature of Contribution in Exchange

C Corporation S Corporation LLC. and LLLP. Legal Entity? Same entity as owner Separate entity from owner. Taxed separate from Owner

Legal Entity? Same entity as owner Separate entity from owner Taxed separate from Owner Separate entity from owner, unless piercing or reverse piercing applies Separate entity from owner, unless piercing

Legal Entity? Same entity as owner Separate entity from owner Taxed separate from Owner Separate entity from owner, unless piercing or reverse piercing applies Separate entity from owner, unless piercing

The Virginia Limited Liability Company

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 1995 The Virginia Limited Liability Company

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 1995 The Virginia Limited Liability Company

For Preview Only - Please Do Not Copy

Company Agreement, Operating agreement of a limited liability company. 1. The affairs of a limited liability company are governed by its Company Agreement or operating agreement. The term regulations has

Company Agreement, Operating agreement of a limited liability company. 1. The affairs of a limited liability company are governed by its Company Agreement or operating agreement. The term regulations has

LIMITED PARTNERSHIP LAW

LIMITED PARTNERSHIP LAW DIFC LAW No. 4 of 2006 Consolidated Version (May 2017) As Amended by DIFC Law Amendment Law DIFC Law No. 1 of 2017 LIMITED PARTNERSHIP LAW AMENDMENT LAW CONTENTS PART 1: GENERAL...

LIMITED PARTNERSHIP LAW DIFC LAW No. 4 of 2006 Consolidated Version (May 2017) As Amended by DIFC Law Amendment Law DIFC Law No. 1 of 2017 LIMITED PARTNERSHIP LAW AMENDMENT LAW CONTENTS PART 1: GENERAL...

(5) "Person" means individuals, partnerships, corporations, limited liability companies, and other associations. NC General Statutes - Chapter 59 1

Person means individuals, partnerships, corporations, limited liability companies, and other associations. NC General Statutes - Chapter 59 1") Chapter 59. Partnership. Article 1. Uniform Limited Partnership Act. 59-1 through 59-30.1: Repealed by Session Laws 1985 (Regular Session, 1986), c. 989, s. 2. Article 2. Uniform Partnership Act. Part

Chapter 59. Partnership. Article 1. Uniform Limited Partnership Act. 59-1 through 59-30.1: Repealed by Session Laws 1985 (Regular Session, 1986), c. 989, s. 2. Article 2. Uniform Partnership Act. Part

Choice of Entity. 69 th Annual Program of the West Virginia Tax Institute October 28-30, 2018 Marriott Morgantown Morgantown, West Virginia

Choice of Entity 69 th Annual Program of the West Virginia Tax Institute October 28-30, 2018 Marriott Morgantown Morgantown, West Virginia John F. Allevato Spilman Thomas & Battle, PLLC 300 Kanawha Boulevard,

Choice of Entity 69 th Annual Program of the West Virginia Tax Institute October 28-30, 2018 Marriott Morgantown Morgantown, West Virginia John F. Allevato Spilman Thomas & Battle, PLLC 300 Kanawha Boulevard,

BUSINESS ENTITIES: Schedule C Requirements

BUSINESS ENTITIES: Schedule C Requirements 2015 Texas Land Title Institute Stephen R. Streiff Texas State Counsel Old Republic National Title Insurance Company Houston, TX Stephen R. Streiff is the Texas

BUSINESS ENTITIES: Schedule C Requirements 2015 Texas Land Title Institute Stephen R. Streiff Texas State Counsel Old Republic National Title Insurance Company Houston, TX Stephen R. Streiff is the Texas

OPERATING AGREEMENT OF {NAME}

OPERATING AGREEMENT OF {NAME} THIS OPERATING AGREEMENT (the Agreement ) is made this day of, 20, by and among {Name}, an Ohio limited liability company (the Company ), and the undersigned members of the

OPERATING AGREEMENT OF {NAME} THIS OPERATING AGREEMENT (the Agreement ) is made this day of, 20, by and among {Name}, an Ohio limited liability company (the Company ), and the undersigned members of the

LAWS OF MALAYSIA. Act 707 LABUAN LIMITED PARTNERSHIPS AND LIMITED LIABILITY PARTNERSHIPS ACT 2010

LAWS OF MALAYSIA Act 707 LABUAN LIMITED PARTNERSHIPS AND LIMITED LIABILITY PARTNERSHIPS ACT 2010 Date of Royal Assent...... 31 January 2010 Date of publication in the Gazette......... 11 February 2010

LAWS OF MALAYSIA Act 707 LABUAN LIMITED PARTNERSHIPS AND LIMITED LIABILITY PARTNERSHIPS ACT 2010 Date of Royal Assent...... 31 January 2010 Date of publication in the Gazette......... 11 February 2010

CHOICE OF BUSINESS ENTITY

CHOICE OF BUSINESS ENTITY Business, Legal and Tax Implications A Primer Presented for BALTIMORE COUNTY SMALL BUSINESS RESOURCE CENTER Whiteford, Taylor & Preston L.L.P. 2005 Whiteford, Taylor & Preston

CHOICE OF BUSINESS ENTITY Business, Legal and Tax Implications A Primer Presented for BALTIMORE COUNTY SMALL BUSINESS RESOURCE CENTER Whiteford, Taylor & Preston L.L.P. 2005 Whiteford, Taylor & Preston

Comparison of S Corporations and LLCs

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 2006 Comparison of S Corporations and LLCs Stefan

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 2006 Comparison of S Corporations and LLCs Stefan

OPERATING AGREEMENT OF A GEORGIA LIMITED LIABILITY COMPANY

OPERATING AGREEMENT OF A GEORGIA LIMITED LIABILITY COMPANY THIS OPERATING AGREEMENT ("Agreement") is entered into the day of, 20, by and between the following persons: 1. 2. 3. 4. hereinafter, ("Members"

OPERATING AGREEMENT OF A GEORGIA LIMITED LIABILITY COMPANY THIS OPERATING AGREEMENT ("Agreement") is entered into the day of, 20, by and between the following persons: 1. 2. 3. 4. hereinafter, ("Members"

BUSINESS ORGANIZATIONS UPDATE

BUSINESS ORGANIZATIONS UPDATE Frank J. Carroll, JD Beverly Evans, JD Davis, Brown, Koehn, Shors & Roberts, P.C. 215 10th Street, Suite 1300 Des Moines, IA 50309 Phone: (515) 288-2500 Fax: (515) 243-0654

BUSINESS ORGANIZATIONS UPDATE Frank J. Carroll, JD Beverly Evans, JD Davis, Brown, Koehn, Shors & Roberts, P.C. 215 10th Street, Suite 1300 Des Moines, IA 50309 Phone: (515) 288-2500 Fax: (515) 243-0654

LLC, LLP, PC, LP Business Formation Rules

Vertex Wealth Management LLC Michael Aluotto President Private Wealth Manager 1325 Franklin Ave., Ste. 335 Garden City, NY 11530 516-294-8200 mjaluotto@1stallied.com LLC, LLP, PC, LP Business Formation

Vertex Wealth Management LLC Michael Aluotto President Private Wealth Manager 1325 Franklin Ave., Ste. 335 Garden City, NY 11530 516-294-8200 mjaluotto@1stallied.com LLC, LLP, PC, LP Business Formation

THE AMERICAN LAW INSTITUTE Continuing Legal Education

1 THE AMERICAN LAW INSTITUTE Continuing Legal Education Practical LLC and LP Opinions: What They Mean and How To Prepare Them June 23, 2014 Telephone Seminar/Audio Webcast Practical LLC and LP Opinions:

1 THE AMERICAN LAW INSTITUTE Continuing Legal Education Practical LLC and LP Opinions: What They Mean and How To Prepare Them June 23, 2014 Telephone Seminar/Audio Webcast Practical LLC and LP Opinions:

Uses and Advantages of Delaware Statutory Trusts and Delaware Limited Liability Companies in Structured Finance Transactions

Uses and Advantages of Delaware Statutory Trusts and Delaware Limited Liability Companies in Structured Finance Transactions Business Transactions, Strategic Planning and Counseling Group Introduction

Uses and Advantages of Delaware Statutory Trusts and Delaware Limited Liability Companies in Structured Finance Transactions Business Transactions, Strategic Planning and Counseling Group Introduction

TITLE 26. Limited Liability Company Code. Chapter General Provisions

TITLE 26 Limited Liability Company Code Chapter 26.01 General Provisions 26.01.01 Short Title...1 26.01.02 Authority...1 26.01.03 Scope...1 26.01.04 Purpose and Construction...1 26.01.05 Definitions...2

TITLE 26 Limited Liability Company Code Chapter 26.01 General Provisions 26.01.01 Short Title...1 26.01.02 Authority...1 26.01.03 Scope...1 26.01.04 Purpose and Construction...1 26.01.05 Definitions...2

AMENDED AND RESTATED CERTIFICATE OF INCORPORATION OF MASTERCARD INTERNATIONAL INCORPORATED

AMENDED AND RESTATED CERTIFICATE OF INCORPORATION OF MASTERCARD INTERNATIONAL INCORPORATED The present name of the corporation is Mastercard International Incorporated. The corporation was incorporated

AMENDED AND RESTATED CERTIFICATE OF INCORPORATION OF MASTERCARD INTERNATIONAL INCORPORATED The present name of the corporation is Mastercard International Incorporated. The corporation was incorporated

TRI-COUNTY SCHOOLS INSURANCE GROUP AMENDED JOINT POWERS AGREEMENT FOR THE OPERATION OF COMMON RISK MANAGEMENT AND RISK POOLING PROGRAMS

TRI-COUNTY SCHOOLS INSURANCE GROUP AMENDED JOINT POWERS AGREEMENT FOR THE OPERATION OF COMMON RISK MANAGEMENT AND RISK POOLING PROGRAMS TRI-COUNTY SCHOOLS INSURANCE GROUP Amended Joint Powers Agreement

TRI-COUNTY SCHOOLS INSURANCE GROUP AMENDED JOINT POWERS AGREEMENT FOR THE OPERATION OF COMMON RISK MANAGEMENT AND RISK POOLING PROGRAMS TRI-COUNTY SCHOOLS INSURANCE GROUP Amended Joint Powers Agreement

A. INTRODUCTION B. PARTNERSHIPS

Part IV Choosing the Appropriate Business Entity by Richard M. Baskett, J.D., C.P.A. Baskett Law Offices 1001 South Higgins Avenue Missoula, Montana 59801 (406) 549-1110 A. INTRODUCTION Limited liability

Part IV Choosing the Appropriate Business Entity by Richard M. Baskett, J.D., C.P.A. Baskett Law Offices 1001 South Higgins Avenue Missoula, Montana 59801 (406) 549-1110 A. INTRODUCTION Limited liability

AMENDED AND RESTATED ARTICLES OF INCORPORATION PODS ASSOCIATION, INC.

AMENDED AND RESTATED ARTICLES OF INCORPORATION OF PODS ASSOCIATION, INC. These Amended and Restated Articles of Incorporation (the Articles ) constitute the Articles of Incorporation of PODS Association,

AMENDED AND RESTATED ARTICLES OF INCORPORATION OF PODS ASSOCIATION, INC. These Amended and Restated Articles of Incorporation (the Articles ) constitute the Articles of Incorporation of PODS Association,

Last Updated: November SOUTH CAROLINA FORMS OF ORGANIZATION Wyche, P.A. Eric K. Graben, Esquire

Last Updated: November 2013 SOUTH CAROLINA FORMS OF ORGANIZATION Wyche, P.A. Eric K. Graben, Esquire Table of Contents 1. Nonprofit Corporations 2. For-Profit Corporations 3. Benefit Corporations 4. Limited

Last Updated: November 2013 SOUTH CAROLINA FORMS OF ORGANIZATION Wyche, P.A. Eric K. Graben, Esquire Table of Contents 1. Nonprofit Corporations 2. For-Profit Corporations 3. Benefit Corporations 4. Limited

LIMITED LIABILITY COMPANY OPERATING AGREEMENT OF RECOUP FITNESS, LLC

LIMITED LIABILITY COMPANY OPERATING AGREEMENT OF RECOUP FITNESS, LLC This Limited Liability Company Agreement of Recoup Fitness, LLC, a Colorado limited liability company ( the Company ), dated and effective

LIMITED LIABILITY COMPANY OPERATING AGREEMENT OF RECOUP FITNESS, LLC This Limited Liability Company Agreement of Recoup Fitness, LLC, a Colorado limited liability company ( the Company ), dated and effective

Tax reform and the choice of business entity

The Adviser s Guide to Financial and Estate Planning: Tax reform and the choice of business entity Presented by: Steven G. Siegel, JD, LLM About the PFP Section & PFS Credential The AICPA Personal Financial

The Adviser s Guide to Financial and Estate Planning: Tax reform and the choice of business entity Presented by: Steven G. Siegel, JD, LLM About the PFP Section & PFS Credential The AICPA Personal Financial

Using Business Dollars to Fund S.O.L.A.R. Insurance Arrangements

Using Business Dollars to Fund S.O.L.A.R. Insurance Arrangements A Self Owned Life And Retirement (S.O.L.A.R.) Insurance Arrangement is an arrangement where an employee purchases a Voya Indexed Universal

Using Business Dollars to Fund S.O.L.A.R. Insurance Arrangements A Self Owned Life And Retirement (S.O.L.A.R.) Insurance Arrangement is an arrangement where an employee purchases a Voya Indexed Universal

The Choice is Yours Revised November 2016

The Choice is Yours Sole Proprietorship General Partnership Limited Partnership Corporation Close Corporation Limited Liability Company Close Limited Liability Supplement Statutory Trust Limited Liability

The Choice is Yours Sole Proprietorship General Partnership Limited Partnership Corporation Close Corporation Limited Liability Company Close Limited Liability Supplement Statutory Trust Limited Liability

LIMITED LIABILITY COMPANY CODE (As adopted January 13, 2010) SUMMARY OF CONTENTS. 1. TABLE OF REVISIONS ii. 2. TABLE OF CONTENTS iii

SUMMARY OF CONTENTS. 1. TABLE OF REVISIONS ii. 2. TABLE OF CONTENTS iii") TITLE 11B TITLE 11B LIMITED LIABILITY COMPANY CODE (As adopted January 13, 2010) SUMMARY OF CONTENTS SECTION ARTICLE-PAGE 1. TABLE OF REVISIONS ii 2. TABLE OF CONTENTS iii 3. ARTICLE 1: GENERAL PROVISIONS

TITLE 11B TITLE 11B LIMITED LIABILITY COMPANY CODE (As adopted January 13, 2010) SUMMARY OF CONTENTS SECTION ARTICLE-PAGE 1. TABLE OF REVISIONS ii 2. TABLE OF CONTENTS iii 3. ARTICLE 1: GENERAL PROVISIONS

CERTIFICATE OF INCORPORATION KKR & CO. INC. ARTICLE I NAME. The name of the Corporation is KKR & Co. Inc. (the Corporation ).

.") CERTIFICATE OF INCORPORATION OF KKR & CO. INC. ARTICLE I NAME The name of the Corporation is KKR & Co. Inc. (the Corporation ). ARTICLE II REGISTERED OFFICE AND AGENT The address of the Corporation s registered

CERTIFICATE OF INCORPORATION OF KKR & CO. INC. ARTICLE I NAME The name of the Corporation is KKR & Co. Inc. (the Corporation ). ARTICLE II REGISTERED OFFICE AND AGENT The address of the Corporation s registered

CORPORATE ENTITY MANAGEMENT

CORPORATE ENTITY MANAGEMENT Melinda Brown Former General Counsel, Draper Laboratory Jesse R. Moore Deputy General Counsel, Corporate & Regional INC Research/inVentiv Health Maggie Palen Director, Subsidiary

CORPORATE ENTITY MANAGEMENT Melinda Brown Former General Counsel, Draper Laboratory Jesse R. Moore Deputy General Counsel, Corporate & Regional INC Research/inVentiv Health Maggie Palen Director, Subsidiary

The New LLC Law in Pennsylvania 24 TH ANNUAL HEALTH LAW INSTITUTE MARCH 14, 2018 LISA JACOBS, ESQUIRE TIM HOY, ESQUIRE

The New LLC Law in Pennsylvania 24 TH ANNUAL HEALTH LAW INSTITUTE MARCH 14, 2018 LISA JACOBS, ESQUIRE TIM HOY, ESQUIRE Background The new LLC law is part of Act 170, which became effective in early 2017.

The New LLC Law in Pennsylvania 24 TH ANNUAL HEALTH LAW INSTITUTE MARCH 14, 2018 LISA JACOBS, ESQUIRE TIM HOY, ESQUIRE Background The new LLC law is part of Act 170, which became effective in early 2017.

Considerations in Selecting Business Entities

Considerations in Selecting Business Entities 2014 Outline prepared by David J. Dietrich Dietrich & Associates, P.C. 401 North 31 st Street, Ste 1650 P.O. Box 7054 Billings, MT 59103 Phone: 406-255-7150

Considerations in Selecting Business Entities 2014 Outline prepared by David J. Dietrich Dietrich & Associates, P.C. 401 North 31 st Street, Ste 1650 P.O. Box 7054 Billings, MT 59103 Phone: 406-255-7150

THE ROLE OF DELAWARE STATUTORY TRUSTS AND DELAWARE LIMITED LIABILITY COMPANIES LIKE-KIND EXCHANGE TRANSACTIONS

THE ROLE OF DELAWARE STATUTORY TRUSTS AND DELAWARE LIMITED LIABILITY COMPANIES IN LIKE-KIND EXCHANGE TRANSACTIONS presented to The American Bar Association s Section of Real Property, Trust & Estate Law

THE ROLE OF DELAWARE STATUTORY TRUSTS AND DELAWARE LIMITED LIABILITY COMPANIES IN LIKE-KIND EXCHANGE TRANSACTIONS presented to The American Bar Association s Section of Real Property, Trust & Estate Law

Chapter No. 353] PUBLIC ACTS, CHAPTER NO. 353 SENATE BILL NO By Jackson. Substituted for: House Bill No

![Chapter No. 353] PUBLIC ACTS, CHAPTER NO. 353 SENATE BILL NO By Jackson. Substituted for: House Bill No](/thumbs/85/92708382.jpg "Chapter No. 353] PUBLIC ACTS, CHAPTER NO. 353 SENATE BILL NO By Jackson. Substituted for: House Bill No") Chapter No. 353] PUBLIC ACTS, 2001 1 CHAPTER NO. 353 SENATE BILL NO. 1276 By Jackson Substituted for: House Bill No. 1328 By McMillan AN ACT To enact the Revised Uniform Partnership Act "RUPA of 2001,

Chapter No. 353] PUBLIC ACTS, 2001 1 CHAPTER NO. 353 SENATE BILL NO. 1276 By Jackson Substituted for: House Bill No. 1328 By McMillan AN ACT To enact the Revised Uniform Partnership Act "RUPA of 2001,

NC General Statutes - Chapter 57D 1

Chapter 57D. North Carolina Limited Liability Company Act. Article 1. General Provisions. Part 1. Short Title; Reservation of Power; Definitions. 57D-1-01. Short title. This Chapter is the "North Carolina

Chapter 57D. North Carolina Limited Liability Company Act. Article 1. General Provisions. Part 1. Short Title; Reservation of Power; Definitions. 57D-1-01. Short title. This Chapter is the "North Carolina

LIMITED LIABILITY COMPANY AGREEMENT FOR BLACKBURNE & BROWN EQUITY PRESERVATION FUND, LLC

LIMITED LIABILITY COMPANY AGREEMENT FOR BLACKBURNE & BROWN EQUITY PRESERVATION FUND, LLC THIS LIMITED LIABILITY COMPANY AGREEMENT ( Agreement ) is made as of, 20, by and among Blackburne & Brown Mortgage

LIMITED LIABILITY COMPANY AGREEMENT FOR BLACKBURNE & BROWN EQUITY PRESERVATION FUND, LLC THIS LIMITED LIABILITY COMPANY AGREEMENT ( Agreement ) is made as of, 20, by and among Blackburne & Brown Mortgage

Issues Relating To Organizational Forms And Taxation. U.S.A. - GEORGIA Alston & Bird LLP

Issues Relating To Organizational Forms And Taxation U.S.A. - GEORGIA Alston & Bird LLP CONTACT INFORMATION Jeffrey C. Glickman/ Edward Tanenbaum/ Susan J. Wilson Alston & Bird LLP One Atlantic Center

Issues Relating To Organizational Forms And Taxation U.S.A. - GEORGIA Alston & Bird LLP CONTACT INFORMATION Jeffrey C. Glickman/ Edward Tanenbaum/ Susan J. Wilson Alston & Bird LLP One Atlantic Center

Professional Corporation (PC)

") Vertex Wealth Management, LLC Michael J. Aluotto, CRPC President Private Wealth Manager 1325 Franklin Ave., Ste. 335 Garden City, NY 11530 516-294-8200 mjaluotto@1stallied.com Professional Corporation

Vertex Wealth Management, LLC Michael J. Aluotto, CRPC President Private Wealth Manager 1325 Franklin Ave., Ste. 335 Garden City, NY 11530 516-294-8200 mjaluotto@1stallied.com Professional Corporation

ENTREPRENEUR S ENTITY FORMATION QUICK-GUIDE

Natoli-Lapin, LLC 304 Park Avenue South 11 th Floor New York, NY 10010 (212) 537-4436 (866) 871-8655 Support@LanternLegal.com www.lanternlegal.com ENTREPRENEUR S ENTITY FORMATION QUICK-GUIDE The following

Natoli-Lapin, LLC 304 Park Avenue South 11 th Floor New York, NY 10010 (212) 537-4436 (866) 871-8655 Support@LanternLegal.com www.lanternlegal.com ENTREPRENEUR S ENTITY FORMATION QUICK-GUIDE The following

Estate Planning for the Closely-Held Business. Presented By: Thomas J. Collura, Esq. and Joseph T. La Ferlita, Esq.

Estate Planning for the Closely-Held Business Presented By: Thomas J. Collura, Esq. and Joseph T. La Ferlita, Esq. NEW YORK STATE BAR ASSOCIATION Trusts and Estates Law Section Fall Meeting September

Estate Planning for the Closely-Held Business Presented By: Thomas J. Collura, Esq. and Joseph T. La Ferlita, Esq. NEW YORK STATE BAR ASSOCIATION Trusts and Estates Law Section Fall Meeting September

HO-CHUNK NATION CODE (HCC) TITLE 5 BUSINESS AND FINANCE CODE SECTION 2 BUSINESS CORPORATION ORDINANCE ENACTED BY LEGISLATURE: OCTOBER 4, 2005

TITLE 5 BUSINESS AND FINANCE CODE SECTION 2 BUSINESS CORPORATION ORDINANCE ENACTED BY LEGISLATURE: OCTOBER 4, 2005") HO-CHUNK NATION CODE (HCC) TITLE 5 BUSINESS AND FINANCE CODE SECTION 2 BUSINESS CORPORATION ORDINANCE ENACTED BY LEGISLATURE: OCTOBER 4, 2005 CITE AS: 5 HCC 2 This Ordinance supersedes the Ho-Chunk Nation

HO-CHUNK NATION CODE (HCC) TITLE 5 BUSINESS AND FINANCE CODE SECTION 2 BUSINESS CORPORATION ORDINANCE ENACTED BY LEGISLATURE: OCTOBER 4, 2005 CITE AS: 5 HCC 2 This Ordinance supersedes the Ho-Chunk Nation

(f) Act as the repository for all certified and approved records pertaining to the sport;

Act as the repository for all certified and approved records pertaining to the sport;") SECOND AMENDED AND RESTATED ARTICLES OF INCORPORATION OF USA CYCLING, INC. ARTICLE I. NAME The name of the nonprofit corporation is USA Cycling, Inc. (hereinafter called the Corporation ). ARTICLE II.

SECOND AMENDED AND RESTATED ARTICLES OF INCORPORATION OF USA CYCLING, INC. ARTICLE I. NAME The name of the nonprofit corporation is USA Cycling, Inc. (hereinafter called the Corporation ). ARTICLE II.

RESTATED ARTICLES OF INCORPORATION WITH AMENDMENTS OF FRIENDS OF THE COLORADO TALKING BOOK LIBRARY ARTICLE I NAME

RESTATED ARTICLES OF INCORPORATION WITH AMENDMENTS OF FRIENDS OF THE COLORADO TALKING BOOK LIBRARY The name of the Corporation is: ARTICLE I NAME FRIENDS OF THE COLORADO TALKING BOOK LIBRARY ARTICLE II

RESTATED ARTICLES OF INCORPORATION WITH AMENDMENTS OF FRIENDS OF THE COLORADO TALKING BOOK LIBRARY The name of the Corporation is: ARTICLE I NAME FRIENDS OF THE COLORADO TALKING BOOK LIBRARY ARTICLE II

CERTIFICATE OF INCORPORATION OF ARCONIC INC. ARTICLE I NAME OF CORPORATION ARTICLE II REGISTERED OFFICE; REGISTERED AGENT

CERTIFICATE OF INCORPORATION OF ARCONIC INC. ARTICLE I NAME OF CORPORATION The name of the corporation is: Arconic Inc. (the Corporation ). ARTICLE II REGISTERED OFFICE; REGISTERED AGENT The address of

CERTIFICATE OF INCORPORATION OF ARCONIC INC. ARTICLE I NAME OF CORPORATION The name of the corporation is: Arconic Inc. (the Corporation ). ARTICLE II REGISTERED OFFICE; REGISTERED AGENT The address of

ARTICLES OF INCORPORATION. Professional Association of Therapeutic Horsemanship International. A Nonprofit Corporation

ARTICLES OF INCORPORATION OF Professional Association of Therapeutic Horsemanship International A Nonprofit Corporation Pursuant to C.R.S. 7-122-102 and part 3 of Article 90 of Title 7, Colorado Revised

ARTICLES OF INCORPORATION OF Professional Association of Therapeutic Horsemanship International A Nonprofit Corporation Pursuant to C.R.S. 7-122-102 and part 3 of Article 90 of Title 7, Colorado Revised

Limited Liability Companies

New York Lawyers Practical Skills Series Limited Liability Companies Michele A. Santucci, Esq.* 2017 2018 * The author wishes to thank Frederick P. Korkosz for his assistance with the sections on foreign

New York Lawyers Practical Skills Series Limited Liability Companies Michele A. Santucci, Esq.* 2017 2018 * The author wishes to thank Frederick P. Korkosz for his assistance with the sections on foreign

Third-Party Closing Opinions: Limited Partnerships

Third-Party Closing Opinions: Limited Partnerships By the TriBar Opinion Committee* The TriBar Opinion Committee has published two reports on opinions on limited liability companies ( LLCs ). 1 This report

Third-Party Closing Opinions: Limited Partnerships By the TriBar Opinion Committee* The TriBar Opinion Committee has published two reports on opinions on limited liability companies ( LLCs ). 1 This report

Controlling Legal Risk: Business Formation, Taxes and Intellectual Property

Controlling Legal Risk: Business Formation, Taxes and Intellectual Property Presented by: Frank P. Nagorney, Esq., Cowden & Humphrey Co. LPA Thunderbird School of Global Management March 18, 2013 Copyright

Controlling Legal Risk: Business Formation, Taxes and Intellectual Property Presented by: Frank P. Nagorney, Esq., Cowden & Humphrey Co. LPA Thunderbird School of Global Management March 18, 2013 Copyright

1. A LLC is formed by filing Certificate of Formation by an organizer.

Certificate of Formation for a Limited liability company 1. A LLC is formed by filing Certificate of Formation by an organizer. 2. An organizer is the person who signs the Certificate of Formation and

Certificate of Formation for a Limited liability company 1. A LLC is formed by filing Certificate of Formation by an organizer. 2. An organizer is the person who signs the Certificate of Formation and

No. 36 Limited Liability Companies 2008 SAINT VINCENT AND THE GRENADINES LIMITED LIABILITY COMPANIES ACT, 2008 ARRANGEMENT OF SECTIONS PART I

785 i SAINT VINCENT AND THE GRENADINES LIMITED LIABILITY COMPANIES ACT, 2008 ARRANGEMENT OF SECTIONS PART I PRELIMINARY SECTION 1. Short Title and Commencement 2. Definitions 3. Name of LLC 4. Reservation

785 i SAINT VINCENT AND THE GRENADINES LIMITED LIABILITY COMPANIES ACT, 2008 ARRANGEMENT OF SECTIONS PART I PRELIMINARY SECTION 1. Short Title and Commencement 2. Definitions 3. Name of LLC 4. Reservation

Regulation Study Notes Business Structure

Regulation 2014 Study Notes Business Structure How To Use These Notes These study notes are strategically broken down into the most important topics related to Business Structure on the Regulation (REG)

Regulation 2014 Study Notes Business Structure How To Use These Notes These study notes are strategically broken down into the most important topics related to Business Structure on the Regulation (REG)

Nonprofit Insurance Trust. Workers Compensation Pool Bylaws

Nonprofit Insurance Trust Workers Compensation Pool Bylaws Preamble: The Minnesota employers which previously met all membership qualifications and were admitted to this Pool, and the Minnesota employers

Nonprofit Insurance Trust Workers Compensation Pool Bylaws Preamble: The Minnesota employers which previously met all membership qualifications and were admitted to this Pool, and the Minnesota employers

Contents. Table of Statutes. Table of Secondary Legislation. Table of Cases. Glossary. Overview of the Subject and the Nature of Partnership

Contents Table of Statutes Table of Secondary Legislation Table of Cases Glossary Chapter 1: Overview of the Subject and the Nature of Partnership 1.1 Introduction 1.2 The partnership and the company contrasted

Contents Table of Statutes Table of Secondary Legislation Table of Cases Glossary Chapter 1: Overview of the Subject and the Nature of Partnership 1.1 Introduction 1.2 The partnership and the company contrasted

PS Business Parks, Inc.

The information in this preliminary prospectus supplement is not complete and may be changed. This preliminary prospectus supplement and the accompanying prospectus are not an offer to sell these securities

The information in this preliminary prospectus supplement is not complete and may be changed. This preliminary prospectus supplement and the accompanying prospectus are not an offer to sell these securities

ADVISING STARTUPS AND ENTREPRENEURS

ADVISING STARTUPS AND ENTREPRENEURS T. Joshua Wu www.jwlawdc.com Sponsored by ADVISING STARTUPS AND ENTREPRENEURS 2 T. Joshua Wu www.jwlawdc.com OVERVIEW Starting a new business venture Choosing the business

ADVISING STARTUPS AND ENTREPRENEURS T. Joshua Wu www.jwlawdc.com Sponsored by ADVISING STARTUPS AND ENTREPRENEURS 2 T. Joshua Wu www.jwlawdc.com OVERVIEW Starting a new business venture Choosing the business

The Foundation: Structuring Your New Venture

TAKE YOUR TECHNOLOGY TO THE LIMIT! Center for Innovation and Technology Entrepreneurship Technology Entrepreneurship from Innovation to Business Venture The Foundation: Structuring Your New Venture Patrick

TAKE YOUR TECHNOLOGY TO THE LIMIT! Center for Innovation and Technology Entrepreneurship Technology Entrepreneurship from Innovation to Business Venture The Foundation: Structuring Your New Venture Patrick

Contents PART I ORGANIZATION

Contents PART I ORGANIZATION CHAPTER 1: INTRODUCTION......................... 1-1 1.1. Nature and Use of This Practice Manual.................. 1-2 1.2. Comparison of the LLC with Other Entities..............

Contents PART I ORGANIZATION CHAPTER 1: INTRODUCTION......................... 1-1 1.1. Nature and Use of This Practice Manual.................. 1-2 1.2. Comparison of the LLC with Other Entities..............

LIMITED LIABILITY COMPANY OPERATING AGREEMENT FOR. A, LIMITED LIABILITY COMPANY State

LIMITED LIABILITY COMPANY OPERATING AGREEMENT FOR Name Of LLC A, LIMITED LIABILITY COMPANY THIS OPERATING AGREEMENT ( Agreement ) is entered into this day of, 20, by and between the following person(s):

LIMITED LIABILITY COMPANY OPERATING AGREEMENT FOR Name Of LLC A, LIMITED LIABILITY COMPANY THIS OPERATING AGREEMENT ( Agreement ) is entered into this day of, 20, by and between the following person(s):

FAQ s. Coworker Stock Purchase Plan

FAQ s Coworker Stock Purchase Plan Q: What is CDW s Coworker Stock Purchase Plan? A: CDW s Coworker Stock Purchase Plan (CSPP) provides the opportunity for eligible coworkers to acquire shares of CDW Corporation

FAQ s Coworker Stock Purchase Plan Q: What is CDW s Coworker Stock Purchase Plan? A: CDW s Coworker Stock Purchase Plan (CSPP) provides the opportunity for eligible coworkers to acquire shares of CDW Corporation

SHATTERING THREE COMMON MYTHS ABOUT MISSOURI LIMITED LIABILITY COMPANIES

DANIEL R. SCHRAMM, L.L.C. Attorney at Law 121 Chesterfield Business Parkway Chesterfield, Missouri 63005 Phone: (636) 532-2300 Fax: (636) 532-6002 Email: daniel@dschrammlaw.com Web site: www.dschrammlaw.com

DANIEL R. SCHRAMM, L.L.C. Attorney at Law 121 Chesterfield Business Parkway Chesterfield, Missouri 63005 Phone: (636) 532-2300 Fax: (636) 532-6002 Email: daniel@dschrammlaw.com Web site: www.dschrammlaw.com

NORTH CAROLINA State Decanting Summary 1

NORTH CAROLINA State Decanting Summary 1 STATUTORY HISTORY Statutory citation N.C. GEN. STAT. 36C-8-816.1 Effective Date 10/1/09 Amendment Date(s) 7/20/10; 6/12/13; 10/1/15 ABILITY TO DECANT 1. Discretionary

NORTH CAROLINA State Decanting Summary 1 STATUTORY HISTORY Statutory citation N.C. GEN. STAT. 36C-8-816.1 Effective Date 10/1/09 Amendment Date(s) 7/20/10; 6/12/13; 10/1/15 ABILITY TO DECANT 1. Discretionary

Issues Relating To Organizational Forms And Taxation. FINLAND Roschier, Attorneys Ltd.

Issues Relating To Organizational Forms And Taxation FINLAND Roschier, Attorneys Ltd. CONTACT INFORMATION Manne Airaksinen & Mia Hukkinen Roschier, Attorneys Ltd. Keskuskatu 7 A, 00100 Helsinki, Finland

Issues Relating To Organizational Forms And Taxation FINLAND Roschier, Attorneys Ltd. CONTACT INFORMATION Manne Airaksinen & Mia Hukkinen Roschier, Attorneys Ltd. Keskuskatu 7 A, 00100 Helsinki, Finland

Contents. Table of Statutes. Table of Secondary Legislation. Table of Cases. Glossary. Formation of Partnerships. Relations Between Partners

Contents Table of Statutes Table of Secondary Legislation Table of Cases Glossary Chapter 1: Business Media 1.1 Introduction 1.2 Partnerships, limited liability partnerships and companies compared 1.2.1

Contents Table of Statutes Table of Secondary Legislation Table of Cases Glossary Chapter 1: Business Media 1.1 Introduction 1.2 Partnerships, limited liability partnerships and companies compared 1.2.1

AFFILIATED HEALTHCARE SYSTEMS NONQUALIFIED DEFERRED COMPENSATION PLAN ARTICLE I PURPOSE

AFFILIATED HEALTHCARE SYSTEMS NONQUALIFIED DEFERRED COMPENSATION PLAN ARTICLE I PURPOSE 1.1 Purpose of Plan. Effective as of the 1st day of January, 2018, Affiliated Healthcare Systems ( AHS ), a Maine

AFFILIATED HEALTHCARE SYSTEMS NONQUALIFIED DEFERRED COMPENSATION PLAN ARTICLE I PURPOSE 1.1 Purpose of Plan. Effective as of the 1st day of January, 2018, Affiliated Healthcare Systems ( AHS ), a Maine

GENERAL PARTNERSHIP AGREEMENT

GENERAL PARTNERSHIP AGREEMENT 1. FORMATION This partnership agreement is entered into and effective as of (Date), 2001, by (Names), hereafter referred to as "the partners." The partners desire to form

GENERAL PARTNERSHIP AGREEMENT 1. FORMATION This partnership agreement is entered into and effective as of (Date), 2001, by (Names), hereafter referred to as "the partners." The partners desire to form

Understanding Legal Organization Structures

Understanding Legal Organization Structures Presented by Lisa A. Waligorski, CLM FM33 5/5/2018 3:00 PM The handout(s) and presentation(s) attached are copyright and trademark protected and provided for

Understanding Legal Organization Structures Presented by Lisa A. Waligorski, CLM FM33 5/5/2018 3:00 PM The handout(s) and presentation(s) attached are copyright and trademark protected and provided for

COMPARISON OF LEGAL STRUCTURES FOR SOCIAL ENTERPRISES 1

COMPARISON OF LEGAL STRUCTURES FOR SOCIAL ENTERPRISES 1 INDEX 1. Comparison of HK, UK and Singapore legal structures... 2 2. Principal Legal Forms in US... 8 3. Legal Innovations in US and UK... 11 3.1

COMPARISON OF LEGAL STRUCTURES FOR SOCIAL ENTERPRISES 1 INDEX 1. Comparison of HK, UK and Singapore legal structures... 2 2. Principal Legal Forms in US... 8 3. Legal Innovations in US and UK... 11 3.1

To LLC or Not to LLC: That is the Question!

To LLC or Not to LLC: That is the Question! by Jordan N. Uditsky Limited Liability Companies, or LLC as they are more commonly known, have been the entity du jour over the past decade, and I ve been asked

To LLC or Not to LLC: That is the Question! by Jordan N. Uditsky Limited Liability Companies, or LLC as they are more commonly known, have been the entity du jour over the past decade, and I ve been asked

HANDBOOK. Glenwood Springs, Colorado

HANDBOOK on The Law of Small Business: A Practice Guide for Attorneys By C. Jonathan Lee, Esq. ARGYLE PUBLISHING COMPANY Glenwood Springs, Colorado Other books published by Argyle Publishing Company: The

HANDBOOK on The Law of Small Business: A Practice Guide for Attorneys By C. Jonathan Lee, Esq. ARGYLE PUBLISHING COMPANY Glenwood Springs, Colorado Other books published by Argyle Publishing Company: The

CHAPTER 15 LIMITED LIABILITY COMPANIES

CHAPTER 15 LIMITED LIABILITY COMPANIES SOURCE: Entire Chapter added by P.L. 23-125:2 (Sept. 9, 1996). 15101. Short Title. 15102. Definitions. 15103. Purpose. 15104. Powers. 15105. Formation. 15106. Limited

CHAPTER 15 LIMITED LIABILITY COMPANIES SOURCE: Entire Chapter added by P.L. 23-125:2 (Sept. 9, 1996). 15101. Short Title. 15102. Definitions. 15103. Purpose. 15104. Powers. 15105. Formation. 15106. Limited

ALABAMA LIMITED LIABILITY COMPANY LAW OF 2014

ALABAMA LIMITED LIABILITY COMPANY LAW OF 2014 September 9, 2015 Robert J. Riccio, J.D., LL.M., CPA Hand Arendall LLC (251) 694-6216 P.O. Box 123 Mobile, Alabama 36601 IN GENERAL Result of a five year project

ALABAMA LIMITED LIABILITY COMPANY LAW OF 2014 September 9, 2015 Robert J. Riccio, J.D., LL.M., CPA Hand Arendall LLC (251) 694-6216 P.O. Box 123 Mobile, Alabama 36601 IN GENERAL Result of a five year project

FORT POINT CABINET MAKERS, LLC OPERATING AGREEMENT

FORT POINT CABINET MAKERS, LLC OPERATING AGREEMENT THIS OPERATING AGREEMENT of Fort Point Cabinet Makers, LLC (the LLC ), dated as of February 17, 2006, is among xxx,xxx,xxx,xxx,,, (collectively, the Members,

FORT POINT CABINET MAKERS, LLC OPERATING AGREEMENT THIS OPERATING AGREEMENT of Fort Point Cabinet Makers, LLC (the LLC ), dated as of February 17, 2006, is among xxx,xxx,xxx,xxx,,, (collectively, the Members,

SUMMARY OF PRINCIPAL TERMS. Jennifer J. Burleigh Debevoise & Plimpton LLP

From PLI s Course Handbook Ninth Annual Private Equity Forum #14028 8 SUMMARY OF PRINCIPAL TERMS Jennifer J. Burleigh Debevoise & Plimpton LLP Copyright 2007 Attachment I: Copyright 2006 Peter K. Yu. Reprinted

From PLI s Course Handbook Ninth Annual Private Equity Forum #14028 8 SUMMARY OF PRINCIPAL TERMS Jennifer J. Burleigh Debevoise & Plimpton LLP Copyright 2007 Attachment I: Copyright 2006 Peter K. Yu. Reprinted

DRAFT APRIL 13, 2015 LIMITED LIABILITY COMPANY AGREEMENT OF PALADIN-AVANTI MANAGEMENT, LLC APRIL, 2015

DRAFT APRIL 13, 2015 LIMITED LIABILITY COMPANY AGREEMENT OF PALADIN-AVANTI MANAGEMENT, LLC APRIL, 2015 DRAFT April 13, 2015 TABLE OF CONTENTS Page ARTICLE I GENERAL COMPANY MATTERS... 1 Section 1.1 Formation

DRAFT APRIL 13, 2015 LIMITED LIABILITY COMPANY AGREEMENT OF PALADIN-AVANTI MANAGEMENT, LLC APRIL, 2015 DRAFT April 13, 2015 TABLE OF CONTENTS Page ARTICLE I GENERAL COMPANY MATTERS... 1 Section 1.1 Formation

Company Agreement SAMPLE. XYZ Company, LLC., a Texas Professional Limited Liability Company

Company Agreement XYZ Company, LLC., a Texas Professional Limited Liability Company THIS COMPANY AGREEMENT of XYZ Company, LLC. (the Company ) is entered into as of the date set forth on the signature

Company Agreement XYZ Company, LLC., a Texas Professional Limited Liability Company THIS COMPANY AGREEMENT of XYZ Company, LLC. (the Company ) is entered into as of the date set forth on the signature

GUIDE TO LIMITED LIABILITY COMPANIES IN THE CAYMAN ISLANDS

GUIDE TO LIMITED LIABILITY COMPANIES IN THE CAYMAN ISLANDS CONTENTS PREFACE 1 1. Limited Liability Companies 2 2. Formation and Registration 2 3. Nature of a Limited Liability Company 2 4. Members 2 5.

GUIDE TO LIMITED LIABILITY COMPANIES IN THE CAYMAN ISLANDS CONTENTS PREFACE 1 1. Limited Liability Companies 2 2. Formation and Registration 2 3. Nature of a Limited Liability Company 2 4. Members 2 5.

RESTATED CERTIFICATE OF INCORPORATION OF SUPERVALU INC.

RESTATED CERTIFICATE OF INCORPORATION OF SUPERVALU INC. SUPERVALU INC., a corporation organized and existing under the laws of the State of Delaware, hereby certifies as follows: (1) The name under which

RESTATED CERTIFICATE OF INCORPORATION OF SUPERVALU INC. SUPERVALU INC., a corporation organized and existing under the laws of the State of Delaware, hereby certifies as follows: (1) The name under which

Instructions Forming an Alabama Limited Liability Company

Contact Information State Business Entities Department: Alabama Secretary of State Business Services Mailing Address: PO Box 5616 Montgomery, AL 36130-5616 Physical Address: RSA Union Building Suite 770

Contact Information State Business Entities Department: Alabama Secretary of State Business Services Mailing Address: PO Box 5616 Montgomery, AL 36130-5616 Physical Address: RSA Union Building Suite 770