INDIVIDUAL INCOME TAX Schedule NR Worksheet A Worksheet B. for Part-year Residents/Nonresidents/Safe Harbor Residents GUIDANCE DOCUMENT

|

|

|

- Lynn Johnston

- 6 years ago

- Views:

Transcription

1 INDIVIDUAL INCOME TAX Schedule NR Worksheet A Worksheet B for Part-year Residents/Nonresidents/Safe Harbor Residents GUIDANCE DOCUMENT Maine Revenue Services, Income/Estate Tax Division Last Revised: January, 2018

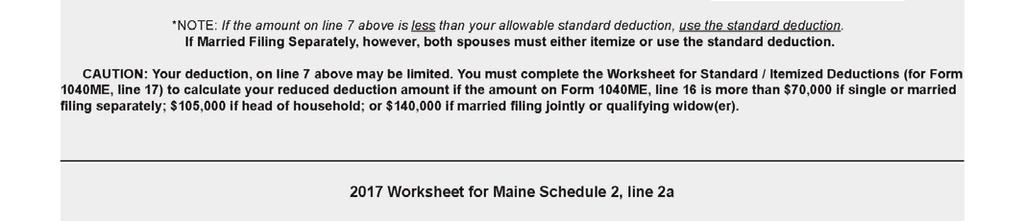

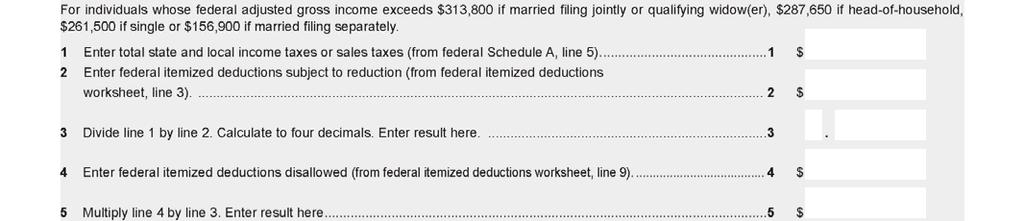

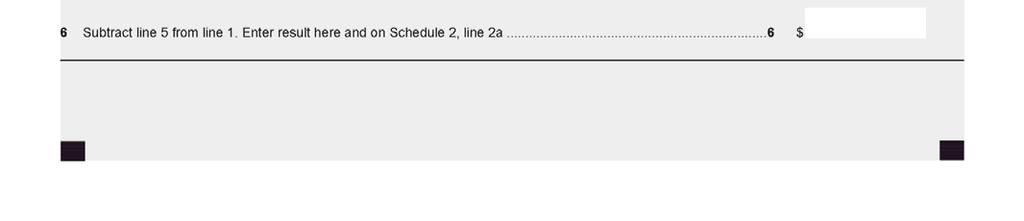

2 SCHEDULE NR PART-YEAR RESIDENTS, NONRESIDENTS and SAFE HARBOR RESIDENTS ONLY If you are a part-year resident of Maine and received income during that part of the year you were a resident of Maine, or, during any period of nonresidency, had income from Maine sources resulting in a Maine income tax liability, you must file Maine Form 1040ME. Exceptions Minimum taxability thresholds. A nonresident individual working in Maine as an employee is not required to pay a Maine tax or file a Maine return on income from personal services unless that individual works in Maine for more than 12 days or, having worked in Maine for more than 12 days, earns or derives income from all Maine sources totaling more than $3,000. Up to 24 days performing certain personal services, such as training and site inspections, are not counted against the 12-day threshold. Also, generally, a nonresident individual present in Maine for business for no more than 12 days and earning no more than $3,000 from business activity in Maine is not required to pay a Maine tax or file a Maine return on that income. Political subdivision employee. Income earned by a nonresident employee of a political subdivision of an adjoining state performing services in Maine in accordance with an interlocal agreement under 30-A M.R.S., Chapter 115 is not considered Maine-source income, so long as the work performed does not displace a Maine resident employee. Declared state disaster or emergency. Compensation or income directly related to a declared state disaster or emergency is exempt from Maine tax if the taxpayer s only presence in Maine during the tax year is for the sole purpose of providing disaster relief. See 36 M.R.S. 5142(8-B) and 5142(9) and Rule 806. For more information regarding residency status, please refer to the Guidance to Residency Status brochure and the Guidance to Residency Safe Harbors brochure at Part-year residents, nonresidents and safe harbor residents who receive income from outside Maine during the period of nonresidence may be able to claim a nonresident credit. This credit is calculated on Schedule NR using Worksheet A, Worksheet B and, if necessary, Worksheet C. Full year residents of Maine may not claim a nonresident credit and should not complete Schedule NR. Do not file Schedule NR if all your income is taxable by Maine. Part-year residents, nonresidents and safe harbor residents must include a complete copy of their federal return (including all schedules and worksheets) with the Maine return, even if they are not eligible to claim a nonresident credit. Part-year residents, nonresidents and safe harbor residents must file a Maine return using the same filing status as properly used on the federal return and must complete Form 1040ME and Schedule NR. However, do not use Schedule NR if all your income is taxable to Maine. If one spouse is a full-year Maine resident and the other spouse is not, and a joint federal return was filed, you have two options: 1) You can choose to file a joint Maine return as if both were full-year Maine residents, in which case, you may qualify for the Credit for Income Tax Paid to Other Jurisdictions; OR 2

3 2) Each can file a Maine return as a single individual using Form 1040ME with Schedule NRH. For more information, see Form 1040ME, Schedule NRH and the Instructional Pamphlet for Schedule NRH at Each return must show the proper residency status. You may choose this option only if you filed a joint federal return. If the nonresident, or safe harbor resident spouse has no Maine-source income, that spouse does not have to file a Maine Return. If one spouse is a full-year Maine resident and the other spouse is a nonresident, the Maine resident spouse must file as a single individual using Schedule NRH. See the Instructional Pamphlet for Schedule NRH at for examples of when to file Schedule NRH. If both spouses are nonresidents or safe harbor residents, and a joint federal return was filed, but only one spouse has Maine-source income, you have two options: 1) You can choose to file a joint Maine return and determine your joint tax liability as nonresidents using Form 1040ME with Schedule NR; OR 2) The spouse who has Maine-source income can choose to file a return as a single individual using Form 1040ME with Schedule NRH. For more information, see Form 1040ME, Schedule NRH. Maine taxable income is equal to federal adjusted gross income adjusted by Maine modifications, exemptions and deductions. Your tax is first calculated as if you were a resident of Maine for the entire year. Part-year residents, nonresidents and safe harbor residents must then claim a nonresident credit calculated on Schedule NR using Worksheets A and B, and if necessary, Worksheet C based on the income that was earned outside Maine while a nonresident of Maine. NOTE: Nonresident or safe harbor resident service members, see below for special instructions. Do not begin the Maine return with only the income earned in Maine. You must begin your Maine return with the total federal adjusted gross income. Unless specifically instructed, do not subtract the income earned outside Maine as a negative income modification on Form 1040ME, Schedule 1. Schedule NR is designed to separate a part-year resident s, nonresident s or safe harbor resident s income between Maine source income and non-maine source income. Maine source income includes the following: 1) All income received while a resident of Maine; 2) Salaries and wages earned working in Maine, including any taxable benefits related to those earnings, such as annual and sick leave unless otherwise excepted. See Exceptions above. Also see 36 M.R.S. 5142(8-B) and 5142(9) and Rule 806; 3) Income derived from or connected with the carrying on of a trade or business within Maine (including distributive share of income (loss) from partnerships and S corporations operating in Maine) unless otherwise excepted. See Exceptions above. See 36 M.R.S. 5142(8-B) and 5142(9) and Rule 806; 3

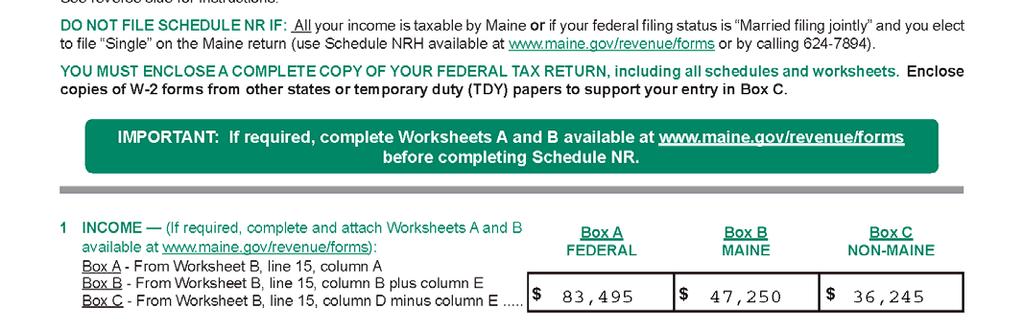

4 4) Shares of trust and estate income derived from Maine sources; 5) Income (loss) attributed to the ownership or disposition of real or tangible personal property in Maine; 6) Maine-source gain (or loss) from sale of a partnership interest. NOTE: To determine the gain or loss from the sale of a partnership interest attributable to Maine, divide the original cost of all tangible property of the partnership located in Maine by tangible property everywhere. Tangible property includes real estate, inventory and equipment. If you don t know these amounts, contact the partnership. If more than 50% of the partnership s assets consist of intangibles, the gain (or loss) is allocated to Maine based on the sales factor of the partnership. Divide the sales in Maine for the last full tax year of the partnership preceding the year of sale by the total sales for that same year. Multiply the result by the gain or loss on the sale of the partnership interest reported on your federal return. Sales for purposes of computing the sales factor are defined in Rule No Include the gain (or loss) from the sales of a partnership interest on Worksheet B, Column E, line 6; and 7) Maine State Lottery or Tri-State Lottery winnings from tickets purchased within Maine, including payments received from third parties for the transfer of rights to future proceeds related to Maine State Lottery or Tri-state Lotto tickets purchased in Maine, plus all other income from gambling activity conducted in Maine on or after June 29, Except for Item #6 above, income from intangible sources, such as interest, dividends, annuities, most pensions and gains or losses attributable to intangible personal property, received by a nonresident of Maine is not Maine-source income unless it is attributable to a business, trade, profession or occupation carried on in Maine. Instructions for completing Form 1040ME, Schedule NR A part-year resident is subject to Maine income tax on all income derived while a resident of Maine, even if the income is received from out-of-state sources, plus any income derived from Maine sources during the period of nonresidence. Form 1040ME, Worksheets A and B, available at must be completed prior to completing Schedule NR. Follow the step-by-step instructions for completing Schedule NR available at Form 1040ME, Schedule NR, line 1. (Nonresident and Safe Harbor resident service members, see below for special instructions.) After you complete the Maine return through line 24 based on your total federal adjusted gross income, complete Schedule NR to calculate the amount of your nonresident credit. To complete Schedule NR, line 1: 1) Enter your total federal income in Box A (from Worksheet B, column A, line 15). 2) Enter all Maine source income in Box B, including any income earned in Maine while a nonresident or safe harbor resident of Maine (Worksheet B, column B, line 15 plus Worksheet B, column E, line 15). 4

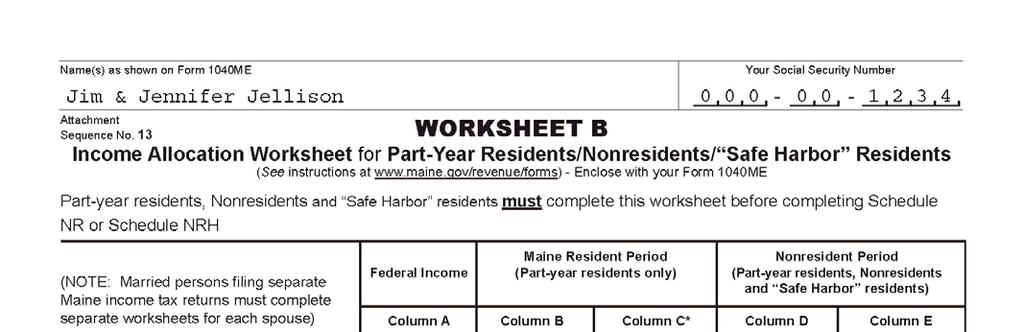

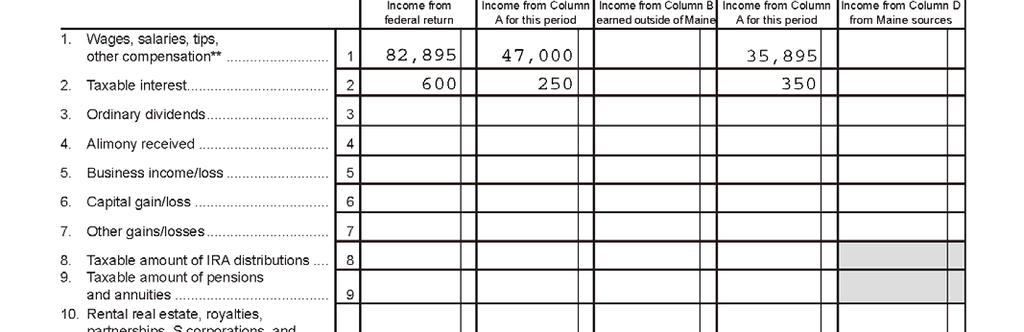

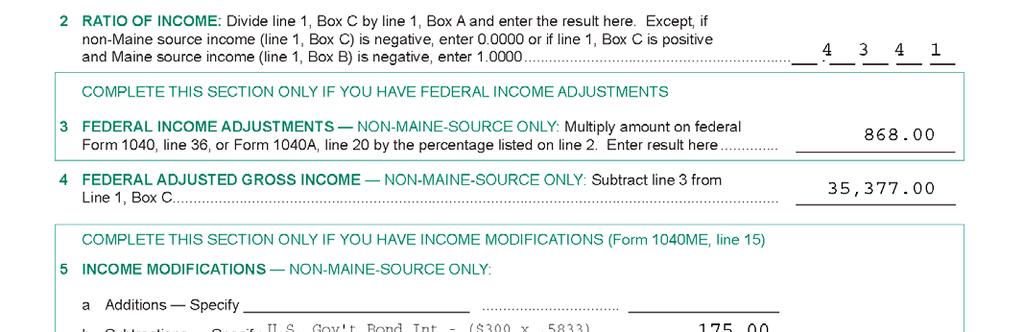

5 3) Enter all non-maine source income in Box C (Worksheet B, column D, line 15 minus Worksheet B, column E, line 15). If you included a taxable state income tax refund on your federal return, do not include that refund when completing Worksheet B or Schedule NR. Form 1040ME, Schedule NR, line 2. If the ratio of non-maine income to total income calculated on Schedule NR, line 2, is less than 0%, enter If the ratio is 100% or greater, enter the ratio like this: You may not claim a negative nonresident credit or a nonresident credit that is more than your tax liability otherwise due to Maine. You should always extend the percentage calculations four digits beyond the decimal point; for example, 5.00% (.0500), 25.25% (.2525) or % (1.0000). Form 1040ME, Schedule NR, line 3. To complete Schedule NR, line 3, Federal Income Adjustments, multiply the amount of federal income adjustments listed on federal Form 1040, line 36 or federal Form 1040A, line 20, by the percentage calculated on Schedule NR, line 2. Form 1040ME, Schedule NR, line 5. (Nonresident and Safe Harbor resident service members, see below for special instructions.) If you have completed Form 1040ME, Schedule 1, Income Modifications, you must complete Schedule NR, line 5. Enter the amount of income modifications from non-maine sources on Schedule NR, lines 5a and 5b as they apply. Generally, for a part-year resident, the amount of the non-maine source income modification that is from intangible sources (interest, dividends, annuities, etc.) is calculated by multiplying the income by the percentage of the year you were a nonresident. For example, if you were a nonresident for 9 months of the year, you would enter on Schedule NR, lines 5a and 5b as applicable, 75% (9 months divided by 12 months) of the income modifications reported on Maine Schedule 1. Do not include taxable refunds of state and local taxes. Prorate the pension deduction (Form 1040ME, Schedule 1, line 2d) based on the percentage of qualified pension income received as a nonresident. Form 1040ME, Schedule NR, line 9. After completing Schedule NR, any nonresident credit on line 9 is entered on Form 1040ME, line 23. This credit will reduce your Maine taxes for income not taxable to Maine. If you are a nonresident of Maine, and your only income from Maine sources are losses, you do not need to file an income tax return with Maine, because you have no Maine income tax liability. However, you may choose to file a return with Maine if you expect to have positive income from Maine sources in future years and want to avoid having gaps in your filing history. You may not use Maine losses in a prior year to offset Maine income in the current year, unless those losses also appear on the federal return for the current year or the loss relates to NOLs disallowed in or to a federal NOL carryback disallowed for Maine income tax purposes. (Federal NOL carrybacks with respect to NOLs realized in tax years beginning after 2001 are not allowed for Maine purposes. The disallowed NOL carryback may be recovered in the allowable carryover period.) For additional information on determining what types of income are subject to Maine tax when received by a nonresident, see Rule 806 available at Attached is a sample return for a part-year resident. The instructions in the Form 1040ME booklet and this pamphlet are used to complete a Maine return for the Jellisons based on the information below: 5

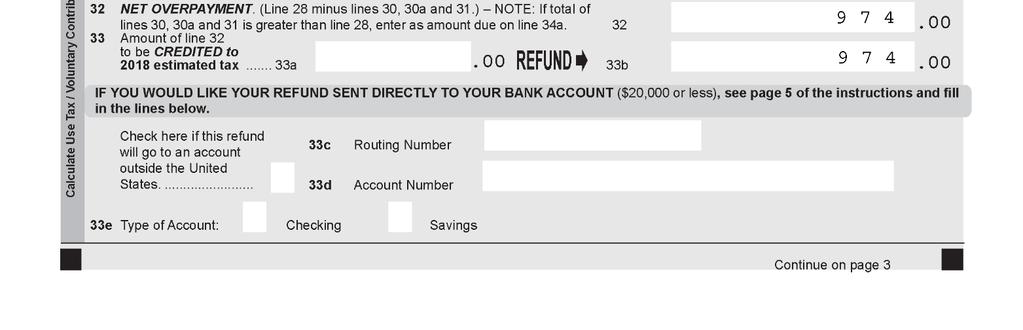

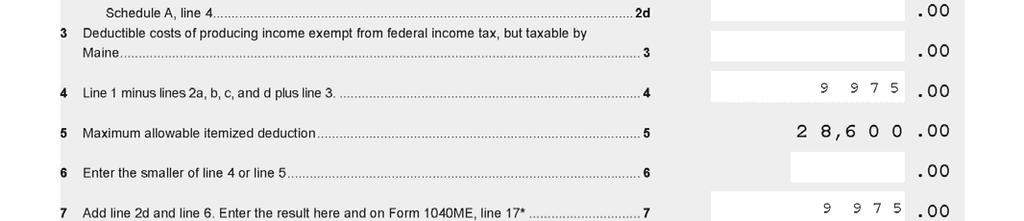

6 Jim and Jennifer Jellison are from New York. They have a six-year-old daughter named Jessica. Jim works as an analyst for a large bank. Effective August 1, 2017, Jim was transferred to Maine while working for the same employer. Jim and his family moved to Maine and became residents of Maine on August 1, After coming to Maine, Jennifer got a job as a supervisor in a local production facility. In 2017, Jim earned a total of $57,895 in wages from the bank. He earned $35,895 in New York and $22,000 in Maine. Jennifer earned $25,000 from her job in Maine. From Jim s pay, $2,050 was withheld for New York income taxes and $1,250 was withheld for Maine income tax. Jennifer had $1,250 withheld from her pay for Maine. The Jellisons had $600 in interest income throughout the year, $300 of which came from U.S. Government bonds. The Jellisons filed a married joint federal income tax return for 2017 and reported federal adjusted gross income of $81,495. They contributed $2,000 to their IRA for the tax year and had total federal itemized deductions of $14,525, which included state income taxes of $4,550. 6

7 7

8 8

9 9

10 10

11 11

12 12

13 13

14 NONRESIDENT & SAFE HARBOR RESIDENT SERVICE MEMBERS: The Servicemembers Civil Relief Act SCRA (Public Law No ) provisions offset the computation of Maine individual income tax for certain nonresidents (including Safe Harbor residents) as follows: 1) Section 511(d) of the Act prevents states from including the military compensation of nonresident service members in the total income when computing the applicable rate of tax imposed on other income earned by the nonresident service member, or their spouse, that is subject to tax by the state. These changes affect Maine returns beginning on or after January 1, 2003 for some military taxpayers (Maine returns beginning on or after January 1, 2007 for Safe Harbor residents.) 2) Amendments were made to the SCRA in 2009 to provide that a spouse of a service member may retain residency in their home state for voting and tax purposes if the spouse is in Maine solely to be with the service member who is in the state due to military orders. Income earned in Maine by a nonresident service member s spouse who is domiciled in another state may not be considered Maine-source income. These changes affect Maine tax years beginning on or after January 1, Since the 2017 Maine income tax return includes income of the nonresident service member, a deduction must be made on the Maine return for a nonresident (or Safe Harbor resident) service member. To deduct the military income of a nonresident (or Safe Harbor resident) service member from the Maine taxable income in 2017, use the following instructions: 1) Enter the total federal adjusted gross income on Form 1040ME, line 14. 2) Complete Form 1040ME, Schedule 1 and the Worksheet for Form 1040ME, Schedule 1, Line 2i (line 3). Include the amount of military compensation of the nonresident service member on Form 1040ME, Schedule 1, line 2i, Other. 3) Complete Form 1040ME, lines 15 through 22. 4) Complete Form 1040ME, Worksheet A (if applicable) and Worksheet B for Part-Year Residents/Nonresidents / Safe Harbor Residents. NOTE: When completing Worksheet B, include the military compensation received by the nonresident ( Safe Harbor resident) service member and the Maine earned income of the service member s spouse on line 1, columns A and D. This procedure will ensure the proper determination of non-maine-source income. 5) Complete Form 1040ME, Schedule NR. NOTE: The military income of a nonresident ( Safe Harbor resident) service member should be included on both line 1, boxes A and C and line 5b of Schedule NR. On line 5b, write NR military compensation in the space provided. The Maine earned income of the service member s spouse should be included on line 1, boxes A and C of Schedule NR. This procedure will ensure the proper ratio for the determination of the non-resident credit. If you are completing Schedule NRH, see the Guidance Document titled Instructional Pamphlet for Individual Income Tax, Schedule NRH for more information. 14

15 6) Complete Form 1040ME, lines 23 through 34. A service member is defined as a member of the United States Army, Navy, Air Force, Marine Corps, Coast Guard, a commissioned officer of the Public Health Service or the National Oceanic and Atmospheric Administration. It also includes a member of the National Guard who is under a call to active service authorized by the President or the Secretary of Defense for a period of more than 30 consecutive days for purposes of responding to a national emergency declared by the President and supported by Federal funds. Any further questions about the computation of Maine individual income tax for certain nonresidents should be directed to the Income/Estate Tax Division of Maine Revenue Services at: income.tax@maine.gov or call

INDIVIDUAL INCOME TAX. Schedule NRH Worksheet A Worksheet B Worksheet C. for Part-year Residents/Nonresidents/Safe Harbor Residents GUIDANCE DOCUMENT

INDIVIDUAL INCOME TAX Schedule NRH Worksheet A Worksheet B Worksheet C for Part-year Residents/Nonresidents/Safe Harbor Residents GUIDANCE DOCUMENT Maine Revenue Services, Income/Estate Tax Division Last

INDIVIDUAL INCOME TAX Schedule NRH Worksheet A Worksheet B Worksheet C for Part-year Residents/Nonresidents/Safe Harbor Residents GUIDANCE DOCUMENT Maine Revenue Services, Income/Estate Tax Division Last

INDIVIDUAL INCOME TAX

INDIVIDUAL INCOME TAX Credit for Income Taxes Paid to Other Jurisdictions GUIDANCE DOCUMENT Maine Revenue Services, Income/Estate Tax Division Last Revised: December, 2015 CREDIT FOR INCOME TAXES PAID

INDIVIDUAL INCOME TAX Credit for Income Taxes Paid to Other Jurisdictions GUIDANCE DOCUMENT Maine Revenue Services, Income/Estate Tax Division Last Revised: December, 2015 CREDIT FOR INCOME TAXES PAID

GIT-1, Pensions and Annuities

GIT-1, Pensions and Annuities Introduction This bulletin explains how to report pension and annuity income on your New Jersey gross income tax return. It also describes the income exclusions which qualified

GIT-1, Pensions and Annuities Introduction This bulletin explains how to report pension and annuity income on your New Jersey gross income tax return. It also describes the income exclusions which qualified

2018 INSTRUCTIONS FOR FILING RI-1040NR (FOR RHODE ISLAND NONRESIDENTS OR PART-YEAR RESIDENTS FILING FORM RI-1040NR)

") 2018 INSTRUCTIONS FOR FILING RI-1040NR (FOR RHODE ISLAND NONRESIDENTS OR PART-YEAR RESIDENTS FILING FORM RI-1040NR) The RI-1040NR Nonresident booklet contains returns and instructions for filing the 2018

2018 INSTRUCTIONS FOR FILING RI-1040NR (FOR RHODE ISLAND NONRESIDENTS OR PART-YEAR RESIDENTS FILING FORM RI-1040NR) The RI-1040NR Nonresident booklet contains returns and instructions for filing the 2018

2011 INSTRUCTIONS FOR FILING RI-1040NR

2011 INSTRUCTIONS FOR FILING RI-1040NR (FOR RHODE ISLAND NONRESIDENTS OR PART-YEAR RESIDENTS FILING FORM RI-1040NR) This booklet contains returns and instructions for filing the 2011 Rhode Island Nonresident

2011 INSTRUCTIONS FOR FILING RI-1040NR (FOR RHODE ISLAND NONRESIDENTS OR PART-YEAR RESIDENTS FILING FORM RI-1040NR) This booklet contains returns and instructions for filing the 2011 Rhode Island Nonresident

State of Rhode Island and Providence Plantations 2017 Form RI-1040NR Nonresident Individual Income Tax Return

State of Rhode Island and Providence Plantations 2017 Form RI-1040NR Nonresident Individual Income Tax Return 17100499990101 Your social security number Spouse s social security number Your first name

State of Rhode Island and Providence Plantations 2017 Form RI-1040NR Nonresident Individual Income Tax Return 17100499990101 Your social security number Spouse s social security number Your first name

2017 INSTRUCTIONS FOR FILING RI-1040NR (FOR RHODE ISLAND NONRESIDENTS OR PART-YEAR RESIDENTS FILING FORM RI-1040NR)

") 2017 INSTRUCTIONS FOR FILING RI-1040NR (FOR RHODE ISLAND NONRESIDENTS OR PART-YEAR RESIDENTS FILING FORM RI-1040NR) This booklet contains returns and instructions for filing the 2017 Rhode Island Nonresident

2017 INSTRUCTIONS FOR FILING RI-1040NR (FOR RHODE ISLAND NONRESIDENTS OR PART-YEAR RESIDENTS FILING FORM RI-1040NR) This booklet contains returns and instructions for filing the 2017 Rhode Island Nonresident

2010 MAINE. Individual Income Tax Booklet

Visit www.maine.gov/revenue to learn the status your refund and obtain the latest tax updates, frequently asked questions (FAQs), electronic tax assistance, download Maine tax forms and instructions, pay

Visit www.maine.gov/revenue to learn the status your refund and obtain the latest tax updates, frequently asked questions (FAQs), electronic tax assistance, download Maine tax forms and instructions, pay

NEW MEXICO DEDUCTIONS AND EXEMPTIONS FROM FEDERAL ADJUSTED GROSS INCOME 6. New Mexico tax-exempt interest and dividends...

2017 PIT-ADJ NEW MEXICO SCHEDULE OF ADDITIONS, DEDUCTIONS, AND EXEMPTIONS *170280200* We cannot accept statements instead of this schedule. Print your name (first, middle, last) YOUR SOCIAL SECURITY NUMBER

2017 PIT-ADJ NEW MEXICO SCHEDULE OF ADDITIONS, DEDUCTIONS, AND EXEMPTIONS *170280200* We cannot accept statements instead of this schedule. Print your name (first, middle, last) YOUR SOCIAL SECURITY NUMBER

Spouse s driver s license number and state. Yes

State of Rhode Island and Providence Plantations 2016 Form RI-1040NR Nonresident Individual Income Tax Return Your first name MI Last name Suffix Deceased? Your social security number Spouse s first name

State of Rhode Island and Providence Plantations 2016 Form RI-1040NR Nonresident Individual Income Tax Return Your first name MI Last name Suffix Deceased? Your social security number Spouse s first name

ONLINE TAX PREPARATION TOOL

CITY OF GRAND RAPIDS 2008 RESIDENT INCOME TAX FORMS AND INSTRUCTIONS FORM GR-1040R USE OF MAILING LABEL: Do not use the label on computer prepared tax forms. Use the label on manually prepared tax forms.

CITY OF GRAND RAPIDS 2008 RESIDENT INCOME TAX FORMS AND INSTRUCTIONS FORM GR-1040R USE OF MAILING LABEL: Do not use the label on computer prepared tax forms. Use the label on manually prepared tax forms.

SCHEDULE NR (Rev. 7/12/16)

") 1350 STATE OF SOUTH CAROLINA DEPARTMENT OF REVENUE 2016 NONRESIDENT SCHEDULE SCHEDULE NR (Rev. 7/12/16) For the year January 1 - December 31, 2016, or fiscal tax year beginning 2016 and ending 2017 Print

1350 STATE OF SOUTH CAROLINA DEPARTMENT OF REVENUE 2016 NONRESIDENT SCHEDULE SCHEDULE NR (Rev. 7/12/16) For the year January 1 - December 31, 2016, or fiscal tax year beginning 2016 and ending 2017 Print

Maine Revenue Services

Maine Revenue Services Guidance to Residency Safe Harbors for Residents Spending Time Outside Maine 1 As explained in the Maine Revenue Services Guidance to Residency Status, an individual who is domiciled

Maine Revenue Services Guidance to Residency Safe Harbors for Residents Spending Time Outside Maine 1 As explained in the Maine Revenue Services Guidance to Residency Status, an individual who is domiciled

ONLINE TAX PREPARATION TOOL

CITY OF GRAND RAPIDS 2008 NONRESIDENT INCOME TAX FORM AND INSTRUCTIONS, FORM GR-1040NR USE OF MAILING LABEL: Do not use the label on computer prepared tax forms. Use the label on manually prepared tax

CITY OF GRAND RAPIDS 2008 NONRESIDENT INCOME TAX FORM AND INSTRUCTIONS, FORM GR-1040NR USE OF MAILING LABEL: Do not use the label on computer prepared tax forms. Use the label on manually prepared tax

2011 PIT-B NEW MEXICO ALLOCATION AND APPORTIONMENT OF INCOME SCHEDULE

2011 PIT-B NEW MEXICO ALLOCATION AND APPORTIONMENT OF INCOME SCHEDULE YOUR SOCIAL SECURITY NUMBER This schedule must be completed by taxpayers who allocate and apportion income from both within and outside

2011 PIT-B NEW MEXICO ALLOCATION AND APPORTIONMENT OF INCOME SCHEDULE YOUR SOCIAL SECURITY NUMBER This schedule must be completed by taxpayers who allocate and apportion income from both within and outside

Retirement Facts 2. Military Service Credit Under the Civil Service Retirement System

Retirement Facts 2 Military Service Credit Under the Civil Service Retirement System This is a non-technical summary of the laws and regulations on the subject. It should not be relied upon as a sole source

Retirement Facts 2 Military Service Credit Under the Civil Service Retirement System This is a non-technical summary of the laws and regulations on the subject. It should not be relied upon as a sole source

VILLAGE OF NEW LONDON, OHIO INCOME TAX RETURN AND DECLARATION

VILLAGE OF NEW LONDON Return Service Requested TO: INCOME TAX DEPARTMENT 115 EAST MAIN STREET NEW LONDON, OHIO 44851 PRE-SORTED FIRST CLASS MAIL U.S. POSTAGE PAID NEW LONDON, OHIO Permit No. 5 VILLAGE

VILLAGE OF NEW LONDON Return Service Requested TO: INCOME TAX DEPARTMENT 115 EAST MAIN STREET NEW LONDON, OHIO 44851 PRE-SORTED FIRST CLASS MAIL U.S. POSTAGE PAID NEW LONDON, OHIO Permit No. 5 VILLAGE

Introduction...2. Purpose of the Credit...2. How to Claim the Credit...3. Proportional Credit Limitation Formula...4

Tax Topic Bulletin GIT-3W Credit for Taxes Paid to Other Jurisdictions (Wage Income) Contents Introduction...2 Purpose of the Credit...2 How to Claim the Credit...3 Proportional Credit Limitation Formula...4

Tax Topic Bulletin GIT-3W Credit for Taxes Paid to Other Jurisdictions (Wage Income) Contents Introduction...2 Purpose of the Credit...2 How to Claim the Credit...3 Proportional Credit Limitation Formula...4

Pensions and Annuities

Tax Topic Bulletin GIT-1 Pensions and Annuities Introduction This bulletin explains how to report pension and annuity income on your New Jersey Income Tax return. It also describes the income exclusions

Tax Topic Bulletin GIT-1 Pensions and Annuities Introduction This bulletin explains how to report pension and annuity income on your New Jersey Income Tax return. It also describes the income exclusions

Introduction...2. Purpose of the Credit...2. How to Claim the Credit...3. Proportional Credit Limitation Formula...4

Tax Topic Bulletin GIT-3B Credit for Income Tax Paid to Other Jurisdictions (Business/Nonwage Income) Contents Introduction...2 Purpose of the Credit...2 How to Claim the Credit...3 Proportional Credit

Tax Topic Bulletin GIT-3B Credit for Income Tax Paid to Other Jurisdictions (Business/Nonwage Income) Contents Introduction...2 Purpose of the Credit...2 How to Claim the Credit...3 Proportional Credit

Form CT-6251 Connecticut Alternative Minimum Tax Return - Individuals

Department of Revenue Services State of Connecticut (Rev. 12/17) Page 1 of 2 6251 1217W 01 9999 Form CT-6251 Connecticut Alternative Minimum Tax Return - Individuals 2017 You must attach this form to the

Department of Revenue Services State of Connecticut (Rev. 12/17) Page 1 of 2 6251 1217W 01 9999 Form CT-6251 Connecticut Alternative Minimum Tax Return - Individuals 2017 You must attach this form to the

2013 Schedule M1M, Income Additions and Subtractions

2013 Schedule M1M, Income Additions and Subtractions Sequence #3 201355 Complete this schedule to determine line 3 and line 6 of Form M1. Your First Name and Initial Last Name Your Social Security Number

2013 Schedule M1M, Income Additions and Subtractions Sequence #3 201355 Complete this schedule to determine line 3 and line 6 of Form M1. Your First Name and Initial Last Name Your Social Security Number

opics Pensions and Annuities

New Jersey Division of Taxation Tax opics Pensions and Annuities Bulletin GIT-1 Introduction This bulletin explains how to report pen sion and annuity income on your New Jersey gross income tax return

New Jersey Division of Taxation Tax opics Pensions and Annuities Bulletin GIT-1 Introduction This bulletin explains how to report pen sion and annuity income on your New Jersey gross income tax return

Department of Revenue

Page 1 of 6 The Official Website of the Department of Revenue (DOR) Mass.Gov Department of Revenue Home > Businesses > Help & Resources > Legal Library > Technical Information Releases > TIRs - By Year(s)

Page 1 of 6 The Official Website of the Department of Revenue (DOR) Mass.Gov Department of Revenue Home > Businesses > Help & Resources > Legal Library > Technical Information Releases > TIRs - By Year(s)

2017 Schedule M1M, Income Additions and Subtractions

2017 Schedule M1M, Income Additions and Subtractions *171551* Complete this schedule to determine line 3 and line 6 of Form M1. Your First Name and Initial Last Name Your Social Security Number Additions

2017 Schedule M1M, Income Additions and Subtractions *171551* Complete this schedule to determine line 3 and line 6 of Form M1. Your First Name and Initial Last Name Your Social Security Number Additions

Above lists are not all-inclusive. For more information, contact (937)

") In this packet you, will find general tax information about the City of Springboro Income Tax Return. We encourage you to bring your income tax information to our office and we will gladly prepare your

In this packet you, will find general tax information about the City of Springboro Income Tax Return. We encourage you to bring your income tax information to our office and we will gladly prepare your

Instructions for Form 6251

2017 Instructions for Form 6251 Alternative Minimum Tax Individuals Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. General

2017 Instructions for Form 6251 Alternative Minimum Tax Individuals Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. General

opics Pensions and Annuities

New Jersey Division of Taxation Tax opics Pensions and Annuities Bulletin GIT-1 Introduction This bulletin explains how to report pen sion and annuity income on your New Jersey income tax return. It also

New Jersey Division of Taxation Tax opics Pensions and Annuities Bulletin GIT-1 Introduction This bulletin explains how to report pen sion and annuity income on your New Jersey income tax return. It also

2017 FLINT INDIVIDUAL INCOME TAX FORMS AND INSTRUCTIONS

City of Flint Income Tax Department 1101 S Saginaw St Flint, Michigan 48502 Form F-1040 2017 FLINT INDIVIDUAL INCOME TAX FORMS AND INSTRUCTIONS For use by individual residents, part-year residents and

City of Flint Income Tax Department 1101 S Saginaw St Flint, Michigan 48502 Form F-1040 2017 FLINT INDIVIDUAL INCOME TAX FORMS AND INSTRUCTIONS For use by individual residents, part-year residents and

2011 Schedule M1M, Income Additions and Subtractions. Your First Name and Initial Last Name Your Social Security Number

2011 Schedule M1M Income Additions and Subtractions Sequence #3 Complete this schedule to determine line 3 and line 6 of Form M1. 201155 Your First Name and Initial Last Name Your Social Security Number

2011 Schedule M1M Income Additions and Subtractions Sequence #3 Complete this schedule to determine line 3 and line 6 of Form M1. 201155 Your First Name and Initial Last Name Your Social Security Number

Schedule M1M, Income Additions and Subtractions 2016 Sequence #3

201655 Schedule M1M, Income Additions and Subtractions 2016 Sequence #3 Complete this schedule to determine line 3 and line 6 of Form M1. Your First Name and Initial Last Name Your Social Security Number

201655 Schedule M1M, Income Additions and Subtractions 2016 Sequence #3 Complete this schedule to determine line 3 and line 6 of Form M1. Your First Name and Initial Last Name Your Social Security Number

Introduction Definitions Filing Requirements Filing Status Considerations How Residents and Nonresidents Are Taxed...

Tax Topic Bulletin GIT-6 Part-Year Residents Contents Introduction... 1 Definitions... 2 Filing Requirements... 3 Filing Status Considerations... 7 How Residents and Nonresidents Are Taxed... 8 Completing

Tax Topic Bulletin GIT-6 Part-Year Residents Contents Introduction... 1 Definitions... 2 Filing Requirements... 3 Filing Status Considerations... 7 How Residents and Nonresidents Are Taxed... 8 Completing

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS Department of Administration DIVISION OF TAXATION One Capitol Hill Providence, RI 02908-5800 Tel: (401) 222-3911 Fax: (401) 222-5134 Forms (401) 222-1111

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS Department of Administration DIVISION OF TAXATION One Capitol Hill Providence, RI 02908-5800 Tel: (401) 222-3911 Fax: (401) 222-5134 Forms (401) 222-1111

Qualifying widow(er) with dependent child Is an amended Federal return being filed? If yes, submit copy.

with dependent child Is an amended Federal return being filed? If yes, submit copy.") FORM AMENDED MARYLAND TAX RETURN Your first name and initial Last name Social security number Check here if you are: 65 or Blind over Spouse s first name and initial Last name Social security number Check

FORM AMENDED MARYLAND TAX RETURN Your first name and initial Last name Social security number Check here if you are: 65 or Blind over Spouse s first name and initial Last name Social security number Check

City of Detroit City of Detroit. Forms and Instructions. Filing Due Date: April 18, 2016

City of Detroit 2015 City of Detroit aa aa Income Tax Returns Forms and Instructions Starting with tax year 2015, the Michigan Department of Treasury will begin processing City of Detroit Individual Income

City of Detroit 2015 City of Detroit aa aa Income Tax Returns Forms and Instructions Starting with tax year 2015, the Michigan Department of Treasury will begin processing City of Detroit Individual Income

As Introduced. 132nd General Assembly Regular Session H. B. No

132nd General Assembly Regular Session H. B. No. 751 2017-2018 Representative Smith, T. A B I L L To amend sections 5747.01 and 5747.06 of the Revised Code to authorize an income tax deduction for volunteer

132nd General Assembly Regular Session H. B. No. 751 2017-2018 Representative Smith, T. A B I L L To amend sections 5747.01 and 5747.06 of the Revised Code to authorize an income tax deduction for volunteer

If a joint return, spouse s first name and initial Last name Spouse s social security number

Form Department of the Treasury Internal Revenue Service 1040A U.S. Individual Income Tax Return (99) 2016 Your first name and initial Last name IRS Use Only Do not write or staple in this space. OMB No.

Form Department of the Treasury Internal Revenue Service 1040A U.S. Individual Income Tax Return (99) 2016 Your first name and initial Last name IRS Use Only Do not write or staple in this space. OMB No.

2018 INSTRUCTIONS FOR FILING RI-1040

2018 INSTRUCTIONS FOR FILING RI-1040 The RI-1040 Resident booklet contains returns and instructions for filing the 2018 Rhode Island Resident Individual Income Tax Return. Read the instructions in this

2018 INSTRUCTIONS FOR FILING RI-1040 The RI-1040 Resident booklet contains returns and instructions for filing the 2018 Rhode Island Resident Individual Income Tax Return. Read the instructions in this

Credit for Tax Paid to Other States. Step 2: Figure the Illinois and non-illinois portions of your federal adjusted gross income

Illinois Department of Revenue Attach to your Form IL-1040 Read this information first You should file Schedule CR if you were either a resident or a part-year resident of Illinois during the tax year;

Illinois Department of Revenue Attach to your Form IL-1040 Read this information first You should file Schedule CR if you were either a resident or a part-year resident of Illinois during the tax year;

State of Rhode Island and Providence Plantations 2017 Form RI-1040 Resident Individual Income Tax Return

State of Rhode Island and Providence Plantations 2017 Form RI-1040 Resident Individual Income Tax Return 17100199990101 Your social security number Spouse s social security number Your first name MI Last

State of Rhode Island and Providence Plantations 2017 Form RI-1040 Resident Individual Income Tax Return 17100199990101 Your social security number Spouse s social security number Your first name MI Last

2018 RI-1041 FIDUCIARY INCOME TAX RETURN GENERAL INSTRUCTIONS

2018 RI-1041 FIDUCIARY INCOME TAX RETURN GENERAL INSTRUCTIONS WHO MUST FILE The fiduciary of a RESIDENT estate or trust must file a return on Form RI-1041 if the estate or trust: (1) is required to file

2018 RI-1041 FIDUCIARY INCOME TAX RETURN GENERAL INSTRUCTIONS WHO MUST FILE The fiduciary of a RESIDENT estate or trust must file a return on Form RI-1041 if the estate or trust: (1) is required to file

Amended Returns 3 Line-by-Line Instructions... 5 U.S. Obligations

2018 DELAWARE 2018 Non-Resident Individual Income Tax Return FOR A LIGHTNING-FAST DELAWARE REFUND, SUBMIT YOUR RETURN ELECTRONICALLY. Advantages of electronic submission: Refunds as quick as 5 days, if

2018 DELAWARE 2018 Non-Resident Individual Income Tax Return FOR A LIGHTNING-FAST DELAWARE REFUND, SUBMIT YOUR RETURN ELECTRONICALLY. Advantages of electronic submission: Refunds as quick as 5 days, if

2017 Educational Opportunity Tax Credit Worksheet

2017 Educational Opportunity Tax Credit Worksheet for Maine Resident & Part-year Resident Individuals 36 M.R.S. 5217-D IMPORTANT NOTE: Use this worksheet if you paid all of your education loan payments

2017 Educational Opportunity Tax Credit Worksheet for Maine Resident & Part-year Resident Individuals 36 M.R.S. 5217-D IMPORTANT NOTE: Use this worksheet if you paid all of your education loan payments

Chapter 4 NON-CORPORATE INCOME TAXES. By Kevin A. Highlander and J. Marlin Witt

Chapter 4 NON-CORPORATE INCOME TAXES By Kevin A. Highlander and J. Marlin Witt Kevin A. Highlander, CPA is a senior manager in the Charleston, West Virginia office of Arnett Carbis Toothman LLP. He serves

Chapter 4 NON-CORPORATE INCOME TAXES By Kevin A. Highlander and J. Marlin Witt Kevin A. Highlander, CPA is a senior manager in the Charleston, West Virginia office of Arnett Carbis Toothman LLP. He serves

Facts 2. Mili tary. Serv ice. Civil Service Retirement System CSRS. Re tire ment. Re tire ment and In sur ance

CSRS Civil Service Retirement System Re tire ment Facts 2 Mili tary Service Credit Under the Civil Service Retirement System United States Of fice of Per son nel Man age ment Re tire ment and In sur ance

CSRS Civil Service Retirement System Re tire ment Facts 2 Mili tary Service Credit Under the Civil Service Retirement System United States Of fice of Per son nel Man age ment Re tire ment and In sur ance

FINAL DRAFT 10/14/2010

GENERAL INFORMATION If you qualify, you are required to make certain additions to your federal adjusted gross income, and you can take certain deductions and exemptions from your federal adjusted gross

GENERAL INFORMATION If you qualify, you are required to make certain additions to your federal adjusted gross income, and you can take certain deductions and exemptions from your federal adjusted gross

5 Qualifying widow(er) (see instructions) 6a Yourself. If someone can claim you as a dependent, do not check box 6a...

(see instructions) 6a Yourself. If someone can claim you as a dependent, do not check box 6a...") Form 1040 Department of the Treasury Internal Revenue Service (99) US Individual Income Tax Return OMB No 1545-0074 IRS Use Only Do not write or staple in this space For the year Jan 1 Dec 31,, or other

Form 1040 Department of the Treasury Internal Revenue Service (99) US Individual Income Tax Return OMB No 1545-0074 IRS Use Only Do not write or staple in this space For the year Jan 1 Dec 31,, or other

First-Time Homebuyer Tax Credit

AKD Consultants Adam Dworkin CPA 188 Whiting Street Suite 10 Hingham, MA 02043 781-556-5554 Adam@AKDConsultants.com First-Time Homebuyer Tax Credit Page 1 of 6, see disclaimer on final page First-Time

AKD Consultants Adam Dworkin CPA 188 Whiting Street Suite 10 Hingham, MA 02043 781-556-5554 Adam@AKDConsultants.com First-Time Homebuyer Tax Credit Page 1 of 6, see disclaimer on final page First-Time

CITY OF HAMTRAMCK INCOME TAX 2014

City of Hamtramck Income Tax Department P.O. Box 209 Eaton Rapids, MI 48827-0209 Form H-1040 2014 HAMTRAMCK INDIVIDUAL INCOME TAX FORMS AND INSTRUCTIONS For use by individual residents, part-year residents

City of Hamtramck Income Tax Department P.O. Box 209 Eaton Rapids, MI 48827-0209 Form H-1040 2014 HAMTRAMCK INDIVIDUAL INCOME TAX FORMS AND INSTRUCTIONS For use by individual residents, part-year residents

2017 RI-1041 FIDUCIARY INCOME TAX RETURN GENERAL INSTRUCTIONS

2017 RI-1041 FIDUCIARY INCOME TAX RETURN GENERAL INSTRUCTIONS WHO MUST FILE The fiduciary of a RESIDENT estate or trust must file a return on Form RI-1041 if the estate or trust: (1) is required to file

2017 RI-1041 FIDUCIARY INCOME TAX RETURN GENERAL INSTRUCTIONS WHO MUST FILE The fiduciary of a RESIDENT estate or trust must file a return on Form RI-1041 if the estate or trust: (1) is required to file

2018 IONIA INDIVIDUAL INCOME TAX INSTRUCTIONS For use by individual residents, partyear residents and nonresidents

City of Ionia Income Tax Division PO Box 512 Ionia, Michigan 48846 Form I-1040 INDIVIDUAL INCOME TAX INSTRUCTIONS For use by individual residents, partyear residents and nonresidents ALL PERSONS HAVING

City of Ionia Income Tax Division PO Box 512 Ionia, Michigan 48846 Form I-1040 INDIVIDUAL INCOME TAX INSTRUCTIONS For use by individual residents, partyear residents and nonresidents ALL PERSONS HAVING

2018 CITY OF GRAYLING INDIVIDUAL INCOME TAX INSTRUCTIONS For use by individual residents, part-year residents and nonresidents

City of Grayling Income Tax Department 1020 City Blvd PO BOX 549 Grayling, Michigan 49738 Form GR-1040 2018 CITY OF GRAYLING INDIVIDUAL INCOME TAX INSTRUCTIONS For use by individual residents, part-year

City of Grayling Income Tax Department 1020 City Blvd PO BOX 549 Grayling, Michigan 49738 Form GR-1040 2018 CITY OF GRAYLING INDIVIDUAL INCOME TAX INSTRUCTIONS For use by individual residents, part-year

Spouse s driver s license number and state. Yes

State of Rhode Island and Providence Plantations 2016 Form RI-1040 Resident Individual Income Tax Return Your first name MI Last name Suffix Deceased? Your social security number Spouse s first name MI

State of Rhode Island and Providence Plantations 2016 Form RI-1040 Resident Individual Income Tax Return Your first name MI Last name Suffix Deceased? Your social security number Spouse s first name MI

2013 INSTRUCTIONS FOR FILING RI-1040

2013 INSTRUCTIONS FOR FILING RI-1040 GENERAL INSTRUCTIONS This booklet contains returns and instructions for filing the 2013 Rhode Island Resident Individual Income Tax Return. Read the instructions in

2013 INSTRUCTIONS FOR FILING RI-1040 GENERAL INSTRUCTIONS This booklet contains returns and instructions for filing the 2013 Rhode Island Resident Individual Income Tax Return. Read the instructions in

DRAFT AS OF August 7, 2013

Form 8960 Department of the Treasury Internal Revenue Service (99) Name(s) shown on Form 1040 or Form 1041 Net Investment Income Tax Individuals, Estates, and Trusts Attach to Form 1040 or Form 1041. Information

Form 8960 Department of the Treasury Internal Revenue Service (99) Name(s) shown on Form 1040 or Form 1041 Net Investment Income Tax Individuals, Estates, and Trusts Attach to Form 1040 or Form 1041. Information

2010 Instructions for Form 6251 Alternative Minimum Tax Individuals

This form is referenced in an endnote at the Bradford Tax Institute. CLICK HERE to go to the home page. 2010 Instructions for Form 6251 Alternative Minimum Tax Individuals Department of the Treasury Internal

This form is referenced in an endnote at the Bradford Tax Institute. CLICK HERE to go to the home page. 2010 Instructions for Form 6251 Alternative Minimum Tax Individuals Department of the Treasury Internal

2016 IONIA INDIVIDUAL INCOME TAX FORMS AND INSTRUCTIONS

INDIVIDUAL INCOME TAX FORMS AND INSTRUCTIONS City of Ionia Income Tax Division PO Box 512 Ionia, Michigan 48846 For use by individual residents, part-year residents and nonresidents Form I-1040 ALL PERSONS

INDIVIDUAL INCOME TAX FORMS AND INSTRUCTIONS City of Ionia Income Tax Division PO Box 512 Ionia, Michigan 48846 For use by individual residents, part-year residents and nonresidents Form I-1040 ALL PERSONS

FORM AMENDED MARYLAND TAX RETURN. Tax year Spouse s first name and initial Last name Social security number Check here if your spouse is:

FORM AMENDED MARYLAND TAX RETURN Your first name and initial Last name Social security number Check here if you are: 65 or Blind over Tax year Spouse s first name and initial Last name Social security

FORM AMENDED MARYLAND TAX RETURN Your first name and initial Last name Social security number Check here if you are: 65 or Blind over Tax year Spouse s first name and initial Last name Social security

2017 INSTRUCTIONS FOR FILING RI-1040

2017 INSTRUCTIONS FOR FILING RI-1040 This booklet contains returns and instructions for filing the 2017 Rhode Island Resident Individual Income Tax Return. Read the instructions in this booklet carefully.

2017 INSTRUCTIONS FOR FILING RI-1040 This booklet contains returns and instructions for filing the 2017 Rhode Island Resident Individual Income Tax Return. Read the instructions in this booklet carefully.

As Introduced. 132nd General Assembly Regular Session H. B. No Representative Young A B I L L

132nd General Assembly Regular Session H. B. No. 317 2017-2018 Representative Young A B I L L To amend section 5747.01 and to enact section 5747.014 of the Revised Code to authorize, for six years, a personal

132nd General Assembly Regular Session H. B. No. 317 2017-2018 Representative Young A B I L L To amend section 5747.01 and to enact section 5747.014 of the Revised Code to authorize, for six years, a personal

Instructions for Form 5405 (Rev. March 2011) First-Time Homebuyer Credit and Repayment of the Credit For use with Form 5405 (Rev.

First-Time Homebuyer Credit and Repayment of the Credit For use with Form 5405 (Rev.") Instructions for Form 5405 (Rev. March 2011) First-Time Homebuyer Credit and Repayment of the Credit For use with Form 5405 (Rev. December 2010) Department of the Treasury Internal Revenue Service Section

Instructions for Form 5405 (Rev. March 2011) First-Time Homebuyer Credit and Repayment of the Credit For use with Form 5405 (Rev. December 2010) Department of the Treasury Internal Revenue Service Section

Uniform Loss Mitigation Request Form

ACCOUNT OR LOAN NUMBER: MEMBER Member s Name: (Please Print) Uniform Loss Mitigation Request Form Co-Member s Name: (Please Print) CO-MEMBER Social Security No.: Date of Birth: Social Security No.: Date

ACCOUNT OR LOAN NUMBER: MEMBER Member s Name: (Please Print) Uniform Loss Mitigation Request Form Co-Member s Name: (Please Print) CO-MEMBER Social Security No.: Date of Birth: Social Security No.: Date

* * MM DD YYYY MM DD YYYY

FORM 1120ME For calendar year or tax year to *1400100* MM DD YYYY MM DD YYYY Name of Corporation Federal Business Code Check if you filed federal Form 0-T Address Federal Employer ID Number State of Incorporation

FORM 1120ME For calendar year or tax year to *1400100* MM DD YYYY MM DD YYYY Name of Corporation Federal Business Code Check if you filed federal Form 0-T Address Federal Employer ID Number State of Incorporation

IDAHO PART-YEAR RESIDENT & NONRESIDENT INCOME TAX RETURN State Use Only. Idaho Resident on Active Military Duty

PLEASE PRINT OR TYPE 43 F O R M EFO091 08-01-2016 AMENDED RETURN, check the box See instructions, page 12, for the reasons for amending and enter the number For calendar year 2016, or fiscal year beginning

PLEASE PRINT OR TYPE 43 F O R M EFO091 08-01-2016 AMENDED RETURN, check the box See instructions, page 12, for the reasons for amending and enter the number For calendar year 2016, or fiscal year beginning

PA-20S/PA-65 PA S Corporation/Partnership Information Return PAGE 1 of 3 (05-10) (FI) 2010

(FI) 2010") Business Name C 1006010050 PLEASE PRINT. USE BLACK INK. Filing Status: PA-20S PA-65 PA-KOZ PS First Line of Address - Street Address - If Address has Apartment Number, Suite, RR No. - Place on this Line.

Business Name C 1006010050 PLEASE PRINT. USE BLACK INK. Filing Status: PA-20S PA-65 PA-KOZ PS First Line of Address - Street Address - If Address has Apartment Number, Suite, RR No. - Place on this Line.

SEPARATE RETURNS: Individuals filing separate federal income tax returns must file separate Rhode Island income tax returns.

2011 INSTRUCTIONS FOR FILING RI-1040 GENERAL INSTRUCTIONS This booklet contains returns and instructions for filing the 2011 Rhode Island Resident Individual Income Tax Return. Read the instructions in

2011 INSTRUCTIONS FOR FILING RI-1040 GENERAL INSTRUCTIONS This booklet contains returns and instructions for filing the 2011 Rhode Island Resident Individual Income Tax Return. Read the instructions in

WITHHOLDING TABLES MAINE INDIVIDUAL INCOME TAX

WITHHOLDING TABLES MAINE INDIVIDUAL INCOME TAX 2000 Effective January 1, 2000 REMEMBER: A person required to withhold must continue to file quarterly withholding tax returns until the account is canceled,

WITHHOLDING TABLES MAINE INDIVIDUAL INCOME TAX 2000 Effective January 1, 2000 REMEMBER: A person required to withhold must continue to file quarterly withholding tax returns until the account is canceled,

Instructions for Form 8960

2017 Instructions for Form 8960 Department of the Treasury Internal Revenue Service Net Investment Income Tax Individuals, Estates, and Trusts Section references are to the Internal Revenue Code unless

2017 Instructions for Form 8960 Department of the Treasury Internal Revenue Service Net Investment Income Tax Individuals, Estates, and Trusts Section references are to the Internal Revenue Code unless

2008 KANSAS. Fiduciary Income Tax. Forms and Instructions. Page 1

2008 KANSAS Fiduciary Income Tax Forms and Instructions www.ksrevenue.org Page 1 What s New... The following changes are effective for the 2008 tax year: WHAT S IN THIS BOOKLET? What s New Tips to Improve

2008 KANSAS Fiduciary Income Tax Forms and Instructions www.ksrevenue.org Page 1 What s New... The following changes are effective for the 2008 tax year: WHAT S IN THIS BOOKLET? What s New Tips to Improve

Indiana Corporate Adjusted. Form IT-20. Gross Income Tax Booklet For Tax Year. and Fiscal Years Ending in

Indiana Corporate Adjusted Form IT-20 Gross Income Tax Booklet For Tax Year 2005 and Fiscal Years Ending in 2006 2005 Indiana Corporate Adjusted Gross Income Tax Booklet Legislative and Administrative

Indiana Corporate Adjusted Form IT-20 Gross Income Tax Booklet For Tax Year 2005 and Fiscal Years Ending in 2006 2005 Indiana Corporate Adjusted Gross Income Tax Booklet Legislative and Administrative

Nonresident Alien State of Hawaii Tax Workshop

Nonresident Alien State of Hawaii Tax Workshop University of Hawaii J-1 State of Hawaii Tax Workshop March 23, 2017 Major Differences: Federal & Hawaii Federal Tax treaties Green card test Substantial

Nonresident Alien State of Hawaii Tax Workshop University of Hawaii J-1 State of Hawaii Tax Workshop March 23, 2017 Major Differences: Federal & Hawaii Federal Tax treaties Green card test Substantial

Booklet IL-700-T. Illinois Withholding. Tax Tables. Effective January 1, Tax rate 3.75%* *This rate has not changed from tax year 2016.

Illinois Department of Revenue Tax rate 3.75%* Booklet IL-700-T Illinois Withholding Tax Tables Effective January 1, 2017 *This rate has not changed from tax year 2016. Table of Contents General Information

Illinois Department of Revenue Tax rate 3.75%* Booklet IL-700-T Illinois Withholding Tax Tables Effective January 1, 2017 *This rate has not changed from tax year 2016. Table of Contents General Information

SC1040 (Rev. 7/28/16) 3075

3075") 1350 STATE OF SOUTH CAROLINA DEPARTMENT OF REVENUE 2016 INDIVIDUAL INCOME TAX RETURN SC1040 (Rev. 7/28/16) 3075 Your social security number Check if deceased Spouse's social security number Check if deceased

1350 STATE OF SOUTH CAROLINA DEPARTMENT OF REVENUE 2016 INDIVIDUAL INCOME TAX RETURN SC1040 (Rev. 7/28/16) 3075 Your social security number Check if deceased Spouse's social security number Check if deceased

New York State Department of Taxation and Finance Instructions for Form IT-205. Fiduciary Income Tax Return New York State New York City Yonkers

New York State Department of Taxation and Finance Instructions for Form IT-205 Fiduciary Income Tax Return New York State New York City Yonkers IT-205-I Form IT-205 highlights for tax year 2012 General

New York State Department of Taxation and Finance Instructions for Form IT-205 Fiduciary Income Tax Return New York State New York City Yonkers IT-205-I Form IT-205 highlights for tax year 2012 General

8Great Reasons to. Faster Refunds: With Direct Deposit Filing Confirmation Provided Error/Math Checking Feature If You Qualify, It s Free

2 16 Arizona Form 140PY Part-Year Resident Personal Income Tax This Booklet Contains: Form 140PY Part-Year Resident Personal Income Tax Return Schedule A(PY) Itemized Deductions Form 204 Extension Request

2 16 Arizona Form 140PY Part-Year Resident Personal Income Tax This Booklet Contains: Form 140PY Part-Year Resident Personal Income Tax Return Schedule A(PY) Itemized Deductions Form 204 Extension Request

502X Final 10/27/15 FORM IF THIS IS BEING FILED TO CLAIM A NET OPERATING LOSS, CHECK. Check here if your spouse is: Check here if you are:

MARYLAND AMENDED TAX RETURN 502X OR FISCAL YEAR BEGINNING, ENDING Your Social Security Number Your First Name Your Last Name Spouse's First Name Spouse's Social Security Number Initial Initial Maryland

MARYLAND AMENDED TAX RETURN 502X OR FISCAL YEAR BEGINNING, ENDING Your Social Security Number Your First Name Your Last Name Spouse's First Name Spouse's Social Security Number Initial Initial Maryland

GENERAL INSTRUCTIONS - ALL FILERS

GENERAL INSTRUCTIONS - ALL FILERS WHO MUST FILE A RETURN Everyone who has income that is subject to City tax must file a return. You do not have to file a return if your total income subject to tax is

GENERAL INSTRUCTIONS - ALL FILERS WHO MUST FILE A RETURN Everyone who has income that is subject to City tax must file a return. You do not have to file a return if your total income subject to tax is

Arizona Form 2012 Part-Year Resident Personal Income Tax Return 140PY

Arizona Form 2012 Part-Year Resident Personal Income Tax Return 140PY Leave the Paper Behind - e-file! Quick Refunds Accurate Proof of Acceptance Free ** No more paper, math errors, or mailing delays when

Arizona Form 2012 Part-Year Resident Personal Income Tax Return 140PY Leave the Paper Behind - e-file! Quick Refunds Accurate Proof of Acceptance Free ** No more paper, math errors, or mailing delays when

PUBLIC INSPECTION COPY

Form 990-T Department of the Treasury Internal Revenue Service A Check box if address changed Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) For calendar year 2011

Form 990-T Department of the Treasury Internal Revenue Service A Check box if address changed Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) For calendar year 2011

Personal Income Tax Forms and Instructions NEW FOR TAX YEAR 2008

2008 West Virginia Personal Income Tax Forms and Instructions NEW FOR TAX YEAR 2008 Expanded Form - The 2008 Income Tax form has been expanded to allow larger spaces for entries. This will permit our scanning

2008 West Virginia Personal Income Tax Forms and Instructions NEW FOR TAX YEAR 2008 Expanded Form - The 2008 Income Tax form has been expanded to allow larger spaces for entries. This will permit our scanning

SOUTH DAKOTA DEPARTMENT OF LABOR, JOB SERVICE, UNEMPLOYMENT DIVISION, AND OFFICE OF ADMINISTRATIVE SERVICES RETIREMENT PLAN A Summary Plan Description

SOUTH DAKOTA DEPARTMENT OF LABOR, JOB SERVICE, UNEMPLOYMENT DIVISION, AND OFFICE OF ADMINISTRATIVE SERVICES RETIREMENT PLAN A Summary Plan Description (11/2013) PLAN HIGHLIGHTS 4-15193 (CL2012) Plan Highlights

SOUTH DAKOTA DEPARTMENT OF LABOR, JOB SERVICE, UNEMPLOYMENT DIVISION, AND OFFICE OF ADMINISTRATIVE SERVICES RETIREMENT PLAN A Summary Plan Description (11/2013) PLAN HIGHLIGHTS 4-15193 (CL2012) Plan Highlights

SC1040X (Rev. 8/23/12) 3083

3083") Do not write in this space - OFFICE USE 50 STATE OF SOUTH CAROLINA DEPARTMENT OF REVENUE AMENDED INDIVIDUAL INCOME TAX Fiscal year Ended of, OR CALENDAR YEAR Tax Year SC00X (Rev. 8//) 08 PART I Print Your

Do not write in this space - OFFICE USE 50 STATE OF SOUTH CAROLINA DEPARTMENT OF REVENUE AMENDED INDIVIDUAL INCOME TAX Fiscal year Ended of, OR CALENDAR YEAR Tax Year SC00X (Rev. 8//) 08 PART I Print Your

Instructions for Forms 40N and 40P

Instructions for Forms 40N and 40P Step 1: Select the appropriate form. Please determine which form was designed for your situation. This will help ensure the proper calculation of your Oregon income,

Instructions for Forms 40N and 40P Step 1: Select the appropriate form. Please determine which form was designed for your situation. This will help ensure the proper calculation of your Oregon income,

SC1040X (Rev. 6/30/15) 3083

3083") 1350 Print Your first name and Initial Spouse's first name and Initial, if married filing jointly Mailing address (number and street, or P. O. Box) STATE OF SOUTH CAROLINA DEPARTMENT OF REVENUE AMENDED

1350 Print Your first name and Initial Spouse's first name and Initial, if married filing jointly Mailing address (number and street, or P. O. Box) STATE OF SOUTH CAROLINA DEPARTMENT OF REVENUE AMENDED

Arizona Form 2012 Nonresident Personal Income Tax Return 140NR

Arizona Form 2012 Nonresident Personal Income Tax Return 140NR Leave the Paper Behind - e-file! Quick Refunds Accurate Proof of Acceptance Free ** No more paper, math errors, or mailing delays! Refunds

Arizona Form 2012 Nonresident Personal Income Tax Return 140NR Leave the Paper Behind - e-file! Quick Refunds Accurate Proof of Acceptance Free ** No more paper, math errors, or mailing delays! Refunds

ATTENTION: NEW NC-4 WITHHOLDING FORMS ENCLOSED

North Carolina Department of Revenue ATTENTION: NEW NC-4 WITHHOLDING FORMS ENCLOSED IMMEDIATE ACTION REQUIRED North Carolina Department of Revenue TO: IMPORTANT NOTICE: NEW NC-4 REQUIRED FOR PAYMENTS BEGINNING

North Carolina Department of Revenue ATTENTION: NEW NC-4 WITHHOLDING FORMS ENCLOSED IMMEDIATE ACTION REQUIRED North Carolina Department of Revenue TO: IMPORTANT NOTICE: NEW NC-4 REQUIRED FOR PAYMENTS BEGINNING

2017 Ohio IT 1040 Individual Income Tax Return

Do not staple or paper clip Rev 9/17 2017 Ohio IT 1040 Individual Income Tax Return Use only black ink and UPPERCASE letters 17000102 1 Check here if this is an amended return Include the Ohio IT RE (do

Do not staple or paper clip Rev 9/17 2017 Ohio IT 1040 Individual Income Tax Return Use only black ink and UPPERCASE letters 17000102 1 Check here if this is an amended return Include the Ohio IT RE (do

Year (YYYY) Month-Year (MM-YYYY) Month-Year (MM-YYYY)

Month-Year (MM-YYYY) Month-Year (MM-YYYY)") Michigan Department of Treasury (Rev. 06-17), Page 1 of 3 Application for Michigan Net Operating Loss Refund MI-1045 Issued under authority of Public Act 281 of 1967, as amended. Type or print in blue

Michigan Department of Treasury (Rev. 06-17), Page 1 of 3 Application for Michigan Net Operating Loss Refund MI-1045 Issued under authority of Public Act 281 of 1967, as amended. Type or print in blue

K-40 Instructions. WORKSHEET I - Standard Deduction for People 65 or Older and/or Blind

K-40 Instructions TAXPAYER INFORMATION Complete all information at the top of the K-40 by printing neatly. If your name or address changed, or if you are filing with or for a deceased taxpayer, indicate

K-40 Instructions TAXPAYER INFORMATION Complete all information at the top of the K-40 by printing neatly. If your name or address changed, or if you are filing with or for a deceased taxpayer, indicate

CITY OF SIDNEY BUSINESS RETURN INSTRUCTIONS

GENERAL TAX INFORMATION FOR 2015 BUSINESS RETURNS * WHO MUST FILE: EVERY BUSINESS ENTITY conducting business in, performing services in, or deriving income (or loss) from activities in the City of Sidney.

GENERAL TAX INFORMATION FOR 2015 BUSINESS RETURNS * WHO MUST FILE: EVERY BUSINESS ENTITY conducting business in, performing services in, or deriving income (or loss) from activities in the City of Sidney.

ACTIVE TRADE OR BUSINESS INCOME REDUCED RATE COMPUTATION (Complete one I-335 for each return) Enter amount from Worksheet 1, line 3...

Enter amount from Worksheet 1, line 3...") 1350 Print your name STATE OF SOUTH CAROLINA DEPARTMENT OF REVENUE I-335 (Rev. 3/22/16) ACTIVE TRADE OR BUSINESS INCOME REDUCED RATE COMPUTATION (Complete one I-335 for each return) 3410 (Attach I-335

1350 Print your name STATE OF SOUTH CAROLINA DEPARTMENT OF REVENUE I-335 (Rev. 3/22/16) ACTIVE TRADE OR BUSINESS INCOME REDUCED RATE COMPUTATION (Complete one I-335 for each return) 3410 (Attach I-335

, ending. child tax credit (1) First name Last name

First name Last name") Department of the Treasury Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return 2016 OMB No. 1545-0074 For the year Jan. 1-Dec. 31, 2016, or other tax year beginning, ending Form Your first

Department of the Treasury Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return 2016 OMB No. 1545-0074 For the year Jan. 1-Dec. 31, 2016, or other tax year beginning, ending Form Your first

THIS BOOKLET CONTAINS INSTRUCTIONS FOR FORMS D-400, D-400 SCHEDULE S, D-400 SCHEDULE PN, D-400TC, AND D-400 SCHEDULE AM FOR TAX YEAR 2017

Form D-401 North Carolina Individual Income Tax INSTRUCTIONS THIS BOOKLET CONTAINS INSTRUCTIONS FOR FORMS D-400, D-400 SCHEDULE S, D-400 SCHEDULE PN, D-400TC, AND D-400 SCHEDULE AM FOR TAX YEAR 2017 efile

Form D-401 North Carolina Individual Income Tax INSTRUCTIONS THIS BOOKLET CONTAINS INSTRUCTIONS FOR FORMS D-400, D-400 SCHEDULE S, D-400 SCHEDULE PN, D-400TC, AND D-400 SCHEDULE AM FOR TAX YEAR 2017 efile

Fiduciary Income Tax. File your fiduciary return electronically! webtax.org. See back cover for details.

2014 Fiduciary Income Tax File your fiduciary return electronically! See back cover for details. webtax.org GENERAL INFORMATION If any due date falls on a Saturday, Sunday, or legal holiday, substitute

2014 Fiduciary Income Tax File your fiduciary return electronically! See back cover for details. webtax.org GENERAL INFORMATION If any due date falls on a Saturday, Sunday, or legal holiday, substitute

2017 City of GraylinG individual income tax returns (Resident and Nonresident)

") CITY OF GRAYLING 2017 City of GraylinG individual income tax returns (Resident and Nonresident) This booklet contains the following forms and instructions: GR-1040 Individual Income Tax Return GR-1040ES

CITY OF GRAYLING 2017 City of GraylinG individual income tax returns (Resident and Nonresident) This booklet contains the following forms and instructions: GR-1040 Individual Income Tax Return GR-1040ES

Married Filing Combined. Yourself Spouse Yourself Spouse Yourself Spouse Yourself Spouse. in Last Name

Form MO-1040 Department of Revenue 2018 Individual Income Tax Return - Long Form For Calendar Year January 1 - December 31, 2018 Print in BLACK ink only and DO NOT STAPLE Amended Return Composite Return

Form MO-1040 Department of Revenue 2018 Individual Income Tax Return - Long Form For Calendar Year January 1 - December 31, 2018 Print in BLACK ink only and DO NOT STAPLE Amended Return Composite Return

GENERAL INSTRUCTIONS FOR PREPARING 2017 CITY OF XENIA INDIVIDUAL RETURNS *

Who must file? It is mandatory that you file an annual City of Xenia tax return EVEN IF NO TAX IS DUE: All Xenia residents and partial year residents between the ages of 18 and 65. All Xenia residents

Who must file? It is mandatory that you file an annual City of Xenia tax return EVEN IF NO TAX IS DUE: All Xenia residents and partial year residents between the ages of 18 and 65. All Xenia residents

California Forms & Instructions

2017 Local Agency Military Base Recovery Area Business Booklet 3807 California Forms & Instructions Members of the Franchise Tax Board Betty T. Yee, Chair Diane L. Harkey, Member Michael Cohen, Member

2017 Local Agency Military Base Recovery Area Business Booklet 3807 California Forms & Instructions Members of the Franchise Tax Board Betty T. Yee, Chair Diane L. Harkey, Member Michael Cohen, Member

Part 1 - Account Information. Date moved out of city. Filing Status Married filing separately

07LF Return with attachments due by April 7, 08 Account Part - Account Information Social Security Number Name Resident Address Mailing Address Phone Date moved into city Email Spouse Date moved out of

07LF Return with attachments due by April 7, 08 Account Part - Account Information Social Security Number Name Resident Address Mailing Address Phone Date moved into city Email Spouse Date moved out of

MAINE CORPORATE INCOME TAX RETURN FORM 1120ME 99 MM DD YYYY MM DD YYYY. Address Federal Employer ID Number State of Incorporation

For calendar year or tax year FORM 1120ME MM DD YYYY MM DD YYYY to *1700100* Name of Corporation Federal Business Code Check if you filed federal Form 0-T Address Federal Employer ID Number State of Incorporation

For calendar year or tax year FORM 1120ME MM DD YYYY MM DD YYYY to *1700100* Name of Corporation Federal Business Code Check if you filed federal Form 0-T Address Federal Employer ID Number State of Incorporation