BOARD OF SUPERVISORS BUSINESS MEETING ACTION ITEM

|

|

|

- Adele Marion Summers

- 6 years ago

- Views:

Transcription

1 Date of Meeting: November 4, 2015 BOARD OF SUPERVISORS BUSINESS MEETING ACTION ITEM # 8 SUBJECT: ELECTION DISTRICT: Real Estate Tax Relief for the Elderly and Permanently Disabled/Proposed Amendments to Chapter 872 of the Codified Ordinances Countywide CRITICAL ACTION DATE: November 4, 2015 CONTACTS: Robert S. Wertz, Jr., Commissioner of the Revenue Darya Thompson, Deputy Commissioner of the Revenue, Tax Exemptions and Deferrals PURPOSE: This Board initiated Item is to increase the net worth limit of the Tax Relief for the Elderly or Totally and Permanently Disabled Program by implementing a net worth tier system which will allow those with a higher net worth to benefit from the program. RECOMMENDATIONS: Board of Supervisors: At the October 14, 2015, Board of Supervisors Public Hearing, Vice Chairman Buona moved that the Board of Supervisors forward the Proposed Amendments to Chapter 872 of the Codified Ordinances of Loudoun County Real Estate Tax Relief for the Elderly or Totally and Permanently Disabled, as shown in Attachment 1 to this item, to become effective January 1, 2016, to the November 4, 2015, Board of Supervisors Business Meeting for action. (Seconded by Supervisor Volpe. The motion passed 8-1, Supervisor Delgaudio opposed.) Commissioner of the Revenue: Extending real property tax relief to those with a higher net worth is at the discretion of the Board of Supervisors. The Commissioner recommends that Board action be prompt, if changes are to go into effect on January 1, 2016, since system and form changes will be necessary. BACKGROUND: At the November 6, 2013, Finance/Government Services and Operations Committee Meeting, revising the applicable sections of Chapter 827 of the Codified Ordinances of Loudoun County, Real Estate Tax Relief for the Elderly or Totally and Permanently Disabled, to benefit the portion of Loudoun s population who have a higher net worth was

2 Item #8, Real Estate Tax Relief for the Elderly and Permanently Disabled/Proposed Amendment to Chapter 872 Board of Supervisors Business Meeting November 4, 2015 Page 2 discussed. This included several methods of calculating tax relief, including instituting tiers of tax relief based on net worth ranges and annual income. The item was tabled to be discussed during the FY15 budget process. However, this did not take place. The previous items are provided in to this item. Supervisor Buona brought a Board Member Initiative forward on September 17, 2014 regarding a tiered system of net worth ranges and corresponding percentages of relief as seen below in the table. Further, he suggested relief be capped at $1,000,000 (one million dollars) in assessed value on the applicants dwelling. Tier Net Worth Range % Relief 1 $0 - $450, $450, $600, $600, $750, $750, $900, $900, Supervisor Buona moved that the Board of Supervisors direct staff to prepare amendments to the applicable sections of Chapter 872 of the Codified Ordinances of Loudoun County to become effective January 1, 2016, using the figures in the table above and providing tax relief on only the first $1,000,000 (one million dollars) of assessed value, which passed (Supervisors Delgaudio, Letourneau, and Williams - No; Supervisor Clarke Absent). ISSUES: The changes will not directly affect the tax programs in the towns since the towns enact their own qualifying criteria for Tax Relief for the Elderly or Totally and Permanently Disabled. Some of the towns, however, have adopted ordinances which mirror Loudoun County s criteria. Any amendments to Chapter 872 shall be communicated to the towns by the Office of the Commissioner of the Revenue. Currently, the program provides relief on a person s dwelling and up to three acres upon which it is situated. The proposed changes to Chapter 872 would provide relief on the first one million dollars ($1,000,000) of assessed value, thus increasing to ten acres the acreage eligible for relief, which is the maximum acreage eligible for relief under the Code of Virginia. The increase of applications may require additional resources to administer the program once we can quantify the effects of the changes.

3 Item #8, Real Estate Tax Relief for the Elderly and Permanently Disabled/Proposed Amendment to Chapter 872 Board of Supervisors Business Meeting November 4, 2015 Page 3 FISCAL IMPACT: The result of the increase in the net worth criteria is that more elderly and disabled individuals will qualify for tax relief under the program. Unfortunately, it is impossible, using currently available data, to quantify with accuracy the fiscal impact of raising the net worth threshold, since net worth information is not public information or readily available. However, a decrease in the County s total real property tax revenue is inevitable. The use of data on homeownership rates for the elderly and disabled, comparative household wealth and income statistics for the target population, and the location and values of parcels owned by potentially eligible citizens is speculative at best. It is not until applications for relief have been received under the revised criteria that the impact of the changes be quantified. The impact of any proposed changes should be known in the first quarter of calendar year ALTERNATIVES: 1. Adopt alternative net worth tier ranges which correspond with percentages of relief and cap of relief on the first $1,000,000 (one million dollars) of assessed value. 2. Increase the maximum qualifying net worth threshold. 3. Maintain the current net worth threshold of $440,000. DRAFT MOTIONS: 1. I move that the Board of Supervisors approve the Proposed Amendments to Chapter 872 of the Codified Ordinances of Loudoun County Real Estate Tax Relief for the Elderly or Totally and Permanently Disabled, as shown in Attachment 1 to this item, to become effective January 1, OR 2. I move an alternate motion. ATTACHMENTS: 1. Proposed Changes to Chapter 872 of the Codified Ordinances. 2. 9/17/14 Board of Supervisors Action Item: Real Estate Tax Relief for the Elderly and Permanently Disabled/Proposed Amendment to the Chapter 872 of the Codified Ordinances.

4 CHAPTER 872 Real Estate Tax Relief for Elderly or Totally and Permanently Disabled EDITOR'S NOTE: Unless otherwise indicated, this chapter was enacted on November 21, 1972, and was amended on October 21, 1975, June 6, 1977, July 17, 1978, August 7, 1979, September 19, 1989,and June 4, 1991, November 19, 1991,, November 4, 1998, September 17, 2001, December 14, 2004, December 5, 2006, January 3, 2007, December 18, 2007, December 12, 2011, and December 10, Definitions Exemption authorized; effective date Administration of exemptions Requirements for full exemptions Requirements for pro-rated exemption Requirements for full exemptions and partial prorated exemptions Claiming an exemption Amount Percentage of exemption Adjustment upon change in eligibility Changes in status False claims Penalty. CROSS REFERENCES Exemptions for elderly and handicapped - see Code of Va et seq. Agricultural, Horticultural, Forest or Newly Annexed Real Estate Tax - see B.R. & T. Ch. 848 Personal Property and Real Estate Tax - see B.R. & T. Ch. 860 Exemptions and refunds generally - see B.R. & T. Ch. 864 Exemption for certified solar energy equipment - see B.R. & T. Ch. 868 Personal property tax relief for elderly or totally and permanently disabled - see B.R. & T. Ch DEFINITIONS. As used in this chapter: (a) Affidavit means the Real Estate Tax Exemption Affidavit. ATTACHMENT 1

5 (b) County means Loudoun County, Virginia. (c) County Board means the Board of Supervisors of the County. (d) Commissioner of the Revenue means the Commissioner of the Revenue of the County or any of his duly authorized deputies or agents. (e) Dwelling means the sole residence owned and occupied by the person or persons claiming exemption, and includes a manufactured home used as the sole residence owned and occupied by the person(s) claiming an exemption hereunder. (f) Exemption means exemption from the County Real Estate Tax according to the provisions of this chapter. (g) Manufactured Home means a structure subject to federal regulation which is transportable in one or more sections; is eight body feet or more in width and forty body feet or more in length in the traveling more, or is 320 or more square feet when erected on site; is built on a permanent chassis; is designed to be used as a single-family dwelling, with or without a permanent foundation when connected to the required utilities; and includes the plumbing, heating, air-conditioning, and electrical systems contained in the structure. (h) Net worth means the amount by which assets (including the present value of all equitable interests) exceed liabilities. (i) Net Worth Tier 1 means a person or persons applying for exemption under this Chapter, who have a combined net worth between zero dollars ($0) and four hundred fifty thousand dollars ($450,000.00) excluding the fair market value of their dwelling and the land, not exceeding ten (10) acres, upon which it is situated. (j) Net Worth Tier 2 means a person or persons applying for exemption who have a combined net worth between four hundred fifty thousand dollars and one cent ($450,000.01) and six hundred thousand dollars ($ ) excluding the fair market value of their dwelling and the land, not exceeding ten (10) acres, upon which it is situated. (k) Net Worth Tier 3 means a person or persons applying for exemption who have a combined net worth between six-hundred thousand dollars and one cent ($ ) and seven-hundred fifty thousand dollars ($750,000.00) excluding the fair market value of their dwelling and the land, not exceeding ten (10) acres, upon which it is situated. (l) Net Worth Tier 4 means a person or persons applying for exemption who have a combined net worth between seven-hundred fifty thousand dollars and one cent ($ ) and ninehundred thousand dollars ($900,000.00) excluding the fair market value of their dwelling and the land, not exceeding ten (10) acres, upon which it is situated. (m) Net Worth Tier 5 means a person or persons applying for exemption who have a combined net worth of nine-hundred thousand dollars and one cent ($900,000.01) or more, excluding the fair market value of their dwelling and the land, not exceeding ten (10) acres, upon which it is situated. (ni) Person means a natural person. ATTACHMENT 1

6 (oj) Permanently and totally disabled means a person who has been certified by the Social Security Administration, the Department of Veterans Affairs or the Railroad Retirement Board, or if such person is not eligible for certification by any of these agencies, by a sworn affidavit by two medical doctors who either are licensed to practice medicine in the Commonwealth or are military officers on active duty who practice medicine with the United States Armed Forces, to the effect that the person is permanently and totally disabled, and, in addition, who has been found by the Commissioner of the Revenue to be unable to engage in any substantial gainful activity by reason of any medically determinable physical or mental impairment or deformity which can be expected to result in death or can be expected to last for the duration of such person's life. (pk) Property means real property. (ql) Taxable year means the calendar year, from January 1 until December 31, for which exemption is claimed. (Ord Passed ; Ord Passed ; Ord Passed ; Ord Passed _-_-15..) EXEMPTION AUTHORIZED. (a) Full Exemption. Real estate tax exemption is provided for qualified property owners who are not less than sixty-five years of age or who are permanently and totally disabled and who are eligible according to state law and the provisions of this chapter. The percentage of the exemption shall correspond with the person or person(s) applying for relief Net Worth Tier range as defined in , above. (b) Pro-Rated Exemption. A pro-rated exemption from real estate tax is provided for the real estate (and dwelling) property which is (i) jointly owned by two or more persons and (ii) occupied as the sole dwelling of each such person(s), at least one of whom is at least age 65 or permanently and totally disabled, and who are eligible according to state law and the provisions of this chapter. (c) Cap to the Exemption and the ProRated Exemption. If the assessed fair market value as determined by the Commissioner of the Revenue of the dwelling and land upon which is it situated is more than one million dollars ($1,000,000.00) as of January 1 of the year for which the tax exemption is requested, then only the portion of such fair market value up to one million dollars ($1,000,000.00) will qualify for the tax exemption, while the portion of such fair market value in excess of one million dollars ($1,000,000.00) will be subject to real property taxes. (c) Persons qualifying for exemption under this chapter shall also be exempt from the special tax levied on property within the Loudoun County Fire and Emergency Medical Services Tax District. (Ord Passed ; Ord Passed ; Ord Passed ; Ord Passed Ord Passed _-_-15) ADMINISTRATION OF EXEMPTIONS. ATTACHMENT 1

7 The exemptions shall be administered by the Commissioner of the Revenue according to the provisions of this chapter. The Commissioner is hereby authorized to make an inquiry of persons seeking such exemption in conformity with the provisions of this chapter, including the requiring of answers under oath, as may be reasonably necessary to determine qualifications for exemption as specified by this chapter. The Commissioner may require the production of certified income tax returns, appraisal reports, financial statements and any other pertinent documents to reasonably necessary to establish qualification. (Ord Passed ; Ord Passed Ord Passed _-_-15) REQUIREMENTS FOR FULL EXEMPTIONS. An full eexemptions shall be granted subject to the following provisions: (a) Ownership. The title of the property for which an exemption is claimed must be held on January 1 of the taxable year, by the person or persons claiming the exemption, each of whom must also be (i) 65 years of age or older, or (ii) permanently and totally disabled on December 31 of the year immediately preceding the taxable year. A dwelling jointly owned by spousesa husband and wife, with no other joint owners, may qualify if either spouse is 65 years of age or older or is permanently and totally disabled. Real property owned and occupied as the sole dwelling of an eligible person includes real property (i) held by the eligible person alone or in conjunction with his spouse as tenant or tenants for life or joint lives, (ii) held in a revocable inter vivos trust over which the eligible person or the eligible person and his spouse hold the power of revocation, or (iii) held in an irrevocable trust under which an eligible person alone or in conjunction with his spouse possesses a life estate or an estate for joint lives or enjoys a continuing right of use or support. (b) Occupancy. The property must be occupied as the sole dwelling of the person or persons claiming the exemption, each of whom must also be (i) 65 years of age or older, or (ii) permanently and totally disabled on December 31 of the year immediately preceding the taxable year. The primary residence owned by a person otherwise qualified for exemption under this chapter who is not actually occupying the same while a patient in a hospital, nursing home, convalescent home or other facility for physical or mental care for an extended period of time shall continue to be deemed such qualifying owner's dwelling; provided, however, that such residence is not used by or leased to others for consideration. (c) Income. The gross combined income of the person or persons claiming the exemption during the calendar year immediately preceding the taxable year did not exceed seventy-two thousand dollars ($72,000), provided that all disability income received by an owner or owner s spouse during the calendar year immediately preceding the taxable year shall be excluded not be included in such total. Gross combined income shall be computed by adding together the total income received during the preceding calendar year, without regard to whether a tax return is actually filed, by (i) owners of the dwelling who use it as their principal residence and (ii) owners relatives who live in the dwelling provided that the first ten thousand dollars ($10,000) of income of the owner s spouse and each relative of the owner or owners, who is living in the dwelling, shall be excluded not be included in such total. Owners relatives include any member of the owners family, except those relatives living in the dwelling for the purpose of providing bona fide caregiving services to the owner, whether such relatives are compensated or not ATTACHMENT 1

8 (d) Net Worth. The total net financial worth of the person or persons claiming the exemption as of December 31 of the calendar year immediately preceding the taxable year did not exceed four hundred forty thousand dollars ($440,000). Total net financial worth shall include the value of all assets, including the present value of all equitable interests of the owner or owners and the owner's spouse, and shall exclude the fair market value of the dwelling and the land, not exceeding ten (10) acres, upon which it is so situated. The percentage of relief as set out in (a) shall correspond with the person or person(s) applying for relief Net Worth Tier range as defined in , above.. In addition, the value of the land upon which the dwelling is situated, up to a maximum of 10 acres, shall also be excluded. (Ord Passed ; Ord Passed ; Ord Passed ; Ord Passed ; Ord Passed ; Ord Passed ; Ord Passed Ord Passed ) REQUIREMENTS FOR PRO-RATED EXEMPTION A pro-rated exemption shall be granted subject to the following provisions: (a) Ownership. Property for which a pro-rated exemption is claimed may be jointly owned on January 1 of the taxable year by two or more individuals not all of whom are at least 65 years of age or older; however, the person or persons claiming the pro-rated exemption must be (i) 65 years of age or older, or (ii) permanently and totally disabled on December 31 of the year immediately preceding the taxable year. The joint owners shall furnish the Commissioner of the Revenue with sufficient evidence of each joint owner's ownership interest in the dwelling. Real property that is a dwelling jointly held by two or more individuals includes real property (i) held by an eligible person in conjunction with one or more other people as tenant or tenants for life or joint lives, (ii) held in a revocable inter vivos trust over which an eligible person with one or more other people hold the power of revocation, or (iii) held in an irrevocable trust under which an eligible person in conjunction with one or more other people possesses a life estate or an estate for joint lives or enjoys a continuing right of use or support. (b) Occupancy. The property must be occupied as the sole dwelling of all the joint owners. The primary residence owned by a person otherwise qualified for exemption under this chapter who is not actually occupying the same while a patient in a hospital, nursing home, convalescent home or other facility for physical or mental care for an extended period of time shall continue to be deemed such qualifying owner's dwelling; provided, however, that such residence is not used by or leased to others for consideration. (c) Income. The gross combined income of all joint owners during the calendar year immediately preceding the taxable year did not exceed seventy-two thousand dollars ($72,000), provided that the disability income received by an owner or owner s spouse during the calendar year immediately preceding the taxable year shall be excluded not be included in from such total. Gross combined income shall be computed by adding together the total income received during the preceding calendar year, without regard to whether a return is actually filed, by (i) owners of the dwelling who use it as their principal residence and (ii) owners' relatives who live in the dwelling provided that the first ten thousand dollars ($10,000) of income of the owner s spouse and each relative of the owner or owners, who is living in the dwelling, shall be excluded not be included in from such total. ATTACHMENT 1

9 (d) Net Worth. The total net financial worth of all joint owners as of December 31 of the calendar year immediately preceding the taxable year did not exceed five hundred thousand dollars ($500,000). Beginning as of December 31, 2008, and as of December 31st of each year thereafter, the limit on combined net financial worth shall be increased by an amount equivalent to the percentage increase in the Consumer Price Index. Total net financial worth shall include the value of all assets, including the present value of all equitable interests, of the owners and the owners' spouses, and shall include the fair market value of the dwelling, the land, and any other asset. (Ord Passed ; Ord Passed ; Ord Passed ) REQUIREMENTS FOR EXEMPTIONS AND PRORATED EXEMPTIONSFULL AND PARTIAL EXEMPTIONS. For purposes of either Section or an eligible person does not include a person with an interest held under a leasehold or for a term of years is not eligible to seek an exemption under this chapter. (Ord Passed Ord Passed - -15) CLAIMING AN EXEMPTION. (a) The person or persons claiming an exemption must file an Application for Real Estate Tax Exemption and Affidavit with the Commissioner of the Revenue, on forms supplied by the Commissioner, on or before April 1 of the tax year for which relief is sought. Those applying for an exemption for the first time must file on or before December 31 of the tax year for which relief is sought. Every third year from the date of the original Application, the person or persons claiming an exemption must file a new Application and Affidavit with the Commissioner. For the two years following the date of the original Application and all subsequent Applications, the person or persons claiming an exemption must file a Certification, on forms supplied by the Commissioner, stating that no information contained on the last preceding Affidavit, Application, or Certification filed has changed to violate the limitations or conditions provided herein. The Commissioner shall have the discretion to permit applicants to file after these deadlines in cases of genuine hardship. (b) The Application and Affidavit shall set forth, in a manner prescribed by the Commissioner, the names of the related persons occupying the dwelling for which the exemption is claimed, their gross combined income and the total combined net worth of the all owners and spouses. (c) If, after audit and investigation, the Commissioner determines that the person or persons are qualified for an exemption, he the Commissioner shall so certify to the County Treasurer who shall deduct the amount of the exemption from the claimant's real estate tax liability. (Ord Passed ; Ord Passed ; Ord Passed ; Ord Passed Ord Passed - -15) AMOUNT PERCENTAGE OF EXEMPTION. (a) AmountPercentage of Full Exemption. A person must satisfy the ownership requirement as set forth in (a), occupy the property as set forth in (b), and not exceed the ATTACHMENT 1

10 income limits as set forth in (c). The person or persons who satisfy the ownership, occupancy and income limits shall be entitled to a percentage of relief on the dwelling and the land, not exceeding ten (10) acres on which it is situated, determined by the Net Worth Tier range for such person(s) as defined in , in which such persons are in, as set forth below: Tier Net Worth Range Exemption % 1 $0 - $450, $450, $600, $600, $750, $750, $900, $900, The person or persons qualifying for and claiming full exemption shall be relieved of liability for the real estate tax levied on the qualifying dwelling and the land on which it is situated as set forth below. Annual Household Income (not including allowable deductions) Up to and including $72,000 Amount of Exemption 100% Extent of Exemption Dwelling and the land on which it is situated, not to exceed 3 acres Over $72,000 0% None (b) Amount of Pro-Rated Exemption. The amount by which the person or persons qualifying for and claiming the pro-rated exemption shall be relieved of liability for real estate taxes levied on the qualifying dwelling and the land, not exceeding ten (10), on which it is situated shall be calculated by multiplying the amount of the full exemption based upon (a) that would otherwise have been provided by a fraction that has as the numerator the percentage of ownership interest in the qualifying dwelling and the land, not exceeding ten (10) acres on which it is situated held by all such joint owners who are at least 65 years of age and as the denominator, 100%. (Ord Passed ; Ord Passed ; Ord Passed ; Ord Passed ; Ord Passed Ord Passed - -15) ADJUSTMENT UPON CHANGE IN ELIGIBILITY. If the qualifying property is sold, ceases to be the primary residence of the qualifying owner(s), or if the last qualifying owner dies during the taxable year, the exemption granted hereunder shall be adjusted by prorating it for that portion of the taxable year prior to the date on which the property was sold or ceased to be the qualifying owner's primary residence, or the date of death ATTACHMENT 1

11 of the last qualifying owner. Such prorated adjustment shall be based upon the number of complete months of the year that such property was properly eligible for the relief granted by this chapter. (Ord Passed ; Ord Passed ; Ord Passed ; Ord Passed ) CHANGES IN STATUS. (a) The primary residence owned by a person otherwise qualified for exemption under this chapter who is not actually occupying the same while a patient in a hospital, nursing home, convalescent home or other facility for physical or mental care for an extended period of time, not intended to be permanent, shall continue to be deemed such qualifying owner's dwelling; provided, however, that such residence isshall not be used by or leased to others for consideration. (b) Except as provided in Section (a), above, changes with respect to income, financial net worth, ownership of property, occupancy, medical status or other factors occurring during the taxable year for which the Affidavit is filed, and having the effect of exceeding or violating the limitations and conditions provided in this chapter, shall nullify any relief of real estate tax liability for the then current taxable year and the taxable year immediately following. (Ord Passed ; Ord Passed Ord Passed - -15) FALSE CLAIMS. No person shall intentionally make a false claim for an exemption. (Ord Passed ) PENALTY. In addition to any other penalties provided by law, any person who intentionally makes a false claim for an exemption shall not be entitled to the exemption from taxation, if granted, but shall be liable for the full amount of tax due. In addition, such person shall be disqualified from reapplying for an exemption for a period of two years. (Ord Passed ) ATTACHMENT 1

12 BOARD OF SUPERVISORS ACTION ITEM BOARD MEMBER INITIATIVE Date of Meeting: September 17, 2014 # 11 SUBJECT: ELECTION DISTRICT: Real Estate Tax Relief for the Elderly and Permanently Disabled/Proposed Amendment to the Chapter 872 of the Codified Ordinance Countywide CRITICAL ACTION DATE: September 17, 2014 STAFF CONTACT: Dorri O Brien, Staff Aide to Supervisor Buona PURPOSE: The purpose of this item is to direct staff to prepare an amendment to the applicable sections of Chapter 827 of the Codified Ordinance of Loudoun County, Real Estate Tax Relief for the Elderly or Totally and Permanently Disabled to correct inequities in the current system. RECOMMENDTION: Supervisor Buona recommends that the Board of Supervisors direct staff to prepare an amendment to the applicable sections of Chapter 827 of the Codified Ordinance of Loudoun County, Real Estate Tax Relief for the Elderly or Totally and Permanently Disabled, to be effective in FY16 to also benefit the portion of Loudoun s elderly and the totally and permanently disabled who have a higher net worth. BACKGROUND: At the November 6, 2013 Finance, Government Services and Operations Committee, the topic of revising the applicable sections of Chapter 827 of the Codified Ordinance of Loudoun County, Real Estate Tax Relief for the Elderly or Totally and Permanently Disabled to benefit the portion of Loudoun s population who have a higher net Worth was discussed. Several methods of calculating tax relief were discussed, including instituting tiers of tax relief based on net worth and annual income. The item was tabled to be discussed later during the FY15 budget process. However, this did not take place. The previous items are provided as attachments to this item. Supervisor Buona would like to revisit this initiative with a refined method of calculating tax relief. A cap would be placed on the value of the home which would qualify for relief. Supervisor Buona suggests that cap be one million dollars. This cap would be based on assessed

13 value regardless of parcel acreage. Relief could be granted in a fashion represented in the chart below: Category Net Worth Range % Relief 1 $0 - $450, $450, $600, $600, $750, $750, $900, $900, ISSUES: Concern has been raised that existing net worth limits penalize seniors who have low incomes but high net worth. A discussion of Loudoun s existing program is provided in Attachment 1. FISCAL IMPACT: It is not possible to estimate the fiscal impact of the proposed tax relief changes because data on net worth of residents is not readily available. Only once applications are received, will the impact of the changes be known. DRAFT MOTIONS: 1. I move that the Board of Supervisors direct staff to prepare an amendment to the applicable sections of Chapter 827 of the Codified Ordinance of Loudoun County, Real Estate Tax Relief for the Elderly or Totally and Permanently Disabled, to be effective in FY16 to also benefit the portion of Loudoun s elderly and the totally and permanently disabled who have a higher net worth. AND OR I further move that staff use the table provided in the Action Item for the September 17, 2014, Board of Supervisors Business Meeting to guide the revisions. 2. I move and alternate motion.

14 ATTACHMENTS: 1. 11/6/2013 Board of Supervisors Action Item: FGSOC Report: Real Estate Tax Relief for the Elderly or Totally and Permanently Disabled/Proposed Amendment to Chapter 872 of the Codified Ordinances. 2. 5/14/2012 FGSOC Information Item: Loudoun County/Real Estate Tax Relief for the Elderly or Totally and Permanently Disabled /12/2011 Board of Supervisors Public Hearing: Proposed Amendments to Chapter 872 of the Codified Ordinances of Loudoun County/Real Estate Tax Relief for the Elderly or Totally and Permanently Disabled.

15 BOARD OF SUPERVISORS ACTION ITEM Date of Meeting: November 6, 2013 #21a SUBJECT: FINANCE/GOVERNMENT SERVICES AND OPERATIONS COMMITTEE REPORT: Real Estate Tax Relief for the Elderly and Totally and Permanently Disabled/Proposed Amendment to Chapter 872 of the Codified Ordinances ELECTION DISTRICT: STAFF CONTACTS: Countywide Robert Wertz, Commissioner of the Revenue Heather MacSorley, County Administration RECOMMENDATIONS: Committee: On October 8, 2013, the Finance/Government Services and Operations Committee voted (York absent, Letourneau opposed) to recommend to the Board of Supervisors that an amendment be prepared for the applicable sections of Chapter 872 of the Codified Ordinance of Loudoun County, Real Estate Tax Relief for the Elderly or Totally and Permanently Disabled to also benefit the portion of our elderly population who have higher net worth, by providing 100% real property tax relief to owners that fit into one of the four categories described in this item. Staff: As this is a Board member initiative, staff does not have a recommendation but will be present to answer questions. BACKGROUND: At the September 4, 2013 Board of Supervisors Business meeting Supervisor Volpe presented a Board Initiated Item, Proposed Amendment to Chapter 872 of the Codified Ordnance/Real Estate Tax Relief for the Elderly (Attachment 1). The Board voted 9-0 to forward the item to Finance/Government Services and Operations (FGSO) Committee for further review. At their October 8, 2013 meeting, the FGSO Committee discussed the topic. Supervisor Buona proposed a new motion, which was approved (York absent, Letourneau opposed). This motion recommended the Board of Supervisors direct staff to prepare an amendment to the applicable sections of Chapter 872 of the Codified Ordinance of Loudoun County, Real Estate Tax Relief for the Elderly or Totally and Permanently Disabled, to be effective FY 2015, to also benefit the portion of Loudoun s elderly population who have higher net worth, by providing 100% real property relief to owners that fit within one of the following four categories: Category Annual Income Limit Net Worth Range 1 $72,000 $0 - $450,000 2 $62,000 $450, $600,000 3 $52,000 $600, $750,000 4 $42,000 $750, $900,000 This topic was also previously considered by the Board in This item is provided in for the Board s reference in its discussion.

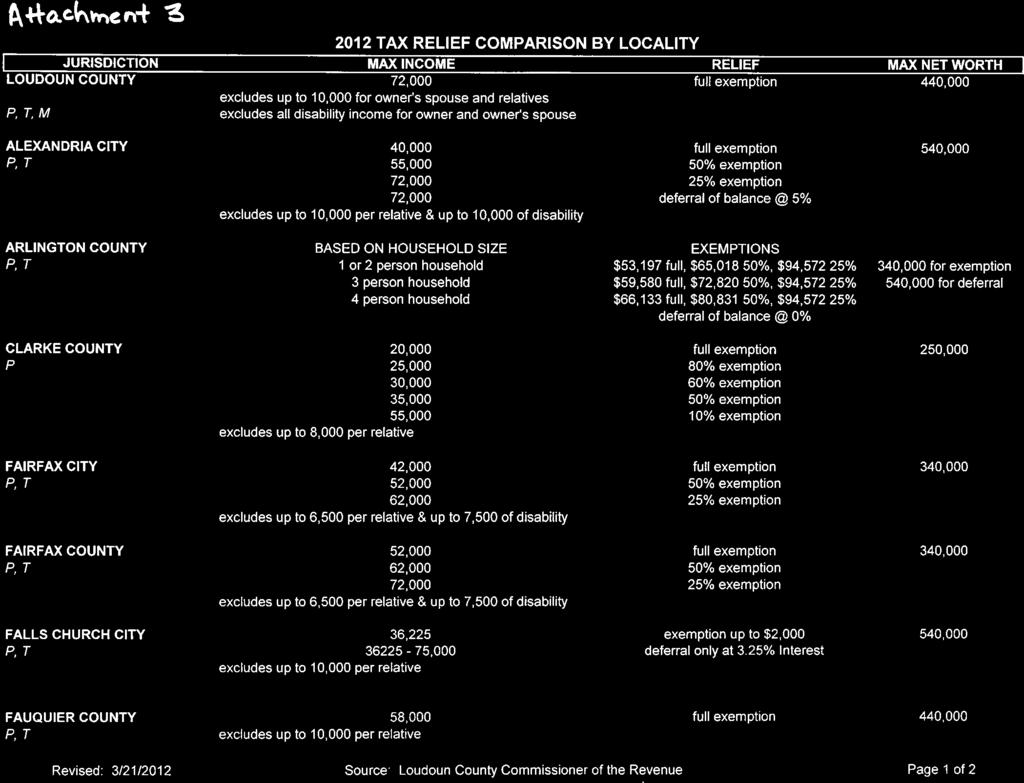

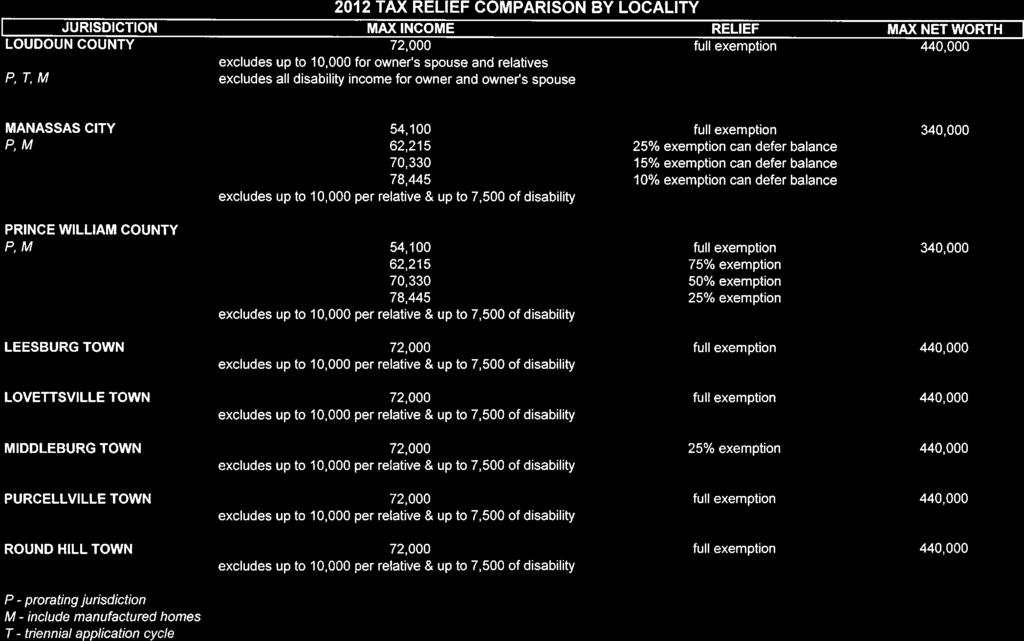

16 ISSUES: Concern has been raised that the net worth limit prevents seniors who may have little to no income, but high net worth from qualifying for tax relief. Opposition has voiced that the current qualification criteria punishes those who have responsibly saved and invested to amass sufficient resources for retirement. This section summarizes the current criteria used by Loudoun County and compares it to other localities in the region. Loudoun s Current Criteria Chapter 872 of the Codified Ordinances of Loudoun County currently stipulates that a full real estate tax exemption be granted when the following four criteria are met 1 : Ownership (i) 65 years of age or older or (ii) permanently and totally disabled Occupancy Occupied as the sole dwelling Income Combined gross income cannot exceed $72,000 Net Worth Combined net worth cannot exceed $440,000, excluding the value of the dwelling Comparison of Tax Relief by Locality An inventory of tax relief by locality was provided to the Board by the Commissioner of the Revenue at their September 4, 2013 meeting (see Attachment 1). Information on criteria for full exemption is summarized below. Falls Church City is not included, as it only offers a maximum exemption of $2,000. Criteria for Full Exemption by Locality Locality Max Income Max Net Worth Other Clarke County $ 20,000 $ 250,000 Fairfax City $ 42,000 $ 340,000 Fairfax County $ 52,000 $ 340,000 Arlington County $ 55,953 $ 340,000 1 or 2 person household Manassas City $ 56,200 $ 340,000 Prince William County $ 56,200 $ 340,000 Fauquier County $ 58,000 $ 440,000 Loudoun County (current) $ 72,000 $ 440,000 Type of Exemption All of the localities compared offer full exemption. However, only Loudoun and Fauquier counties offer only full exemption. The other seven localities vary the amount of relief by income level. Type of Criteria All localities use income and net worth limits as their criteria for tax relief. Arlington County also combines these limits with ranges of household size. Max Income Varies from $20,000 to $72,000 for full exemption. Loudoun County has the highest income limit among the eight localities ($72,000). Max Net Worth Varies from $250,000 to $440,000. Loudoun and Fauquier counties have the highest net worth limit ($440,000). No locality in the region currently uses net worth ranges. Towns within Loudoun County must use the same criteria for qualifying for tax relief as the County. However, towns may choose to set different amounts of tax relief given to qualifying applicants. 1 This item summarizes this section of the ordinance for ease of reference. For complete information on qualifications for exemption, please consult Section 872 of the Codified Ordinances of Loudoun County.

17 Currently, all five towns in Loudoun County provide the same level of relief (full exemption) as the County. FISCAL IMPACT: It is not possible to estimate the fiscal impact of the tax relief changes recommended by the FGSO Committee. This is because data on the net worth of residents is not readily available. Only once applications for relief have been received, will the impact of the changes be realized. ALTERNATIVES: The Board of Supervisors may choose further discuss the issue, propose new criteria for consideration, or approve or reject the recommendation to prepare an amendment changing the qualification criteria for tax relief for the elderly or totally and permanently disabled. DRAFT MOTION: 1. I move the recommendation of the Finance/Government Services and Operations Committee that the Board of Supervisors direct staff to prepare an amendment to the applicable sections of Chapter 872 of the Codified Ordinance of Loudoun County, Real Estate Tax Relief for the Elderly or Totally and Permanently Disabled, to be effective FY 2015, to also benefit the portion of Loudoun s elderly population who have higher net worth, by providing 100% real property relief to owners that fit within one of the following four categories: 1) Max Income of $72,000 and Net Worth $0-$450,000.00; 2) Max Income of $62,000 and Net Worth $450, $600,000.00; 3) Max Income of $52,000 and Net Worth $600, $750,000.00; 4) Max Income of $62,000 and Net Worth $750, $900, I move an alternate motion. ATTACHMENTS: OR 1. Board of Supervisors Action Item 21: Proposed Amendment to Chapter 872 of the Codified Ordnance/Real Estate Tax Relief for the Elderly or Totally and Permanently Disabled. September 4, Board of Supervisors Action Item 4: Proposed Amendment to Chapter 872 of the Codified Ordnance/Real Estate Tax Relief for the Elderly or Totally and Permanently Disabled. October 12, 2011.

18 Date of Meeting September 4, 2013 BOARD OF SUPERVISORS ACTION ITEM BOARD MEMBER INITIATIVE #21 SUBJECT: INTENT TO AMEND CHAPTER 872 OF THE CODIFIED ORDINANCES OF LOUDOUN COUNTY/REAL ESTATE TAX RELIEF FOR THE ELDERLY OR TOTALLY AND PERMANENTLY DISABLED ELECTION DISTRICTS: Countywide CRITICAL ACTION DATE: September 4, 2013 CONTACT: Benjamin M. Fornwalt, Staff Aide Algonkian District RECOMMENDATION: Supervisor Volpe recommends that Chapter 872 if the Codified Ordinance of Loudoun County Real Estate Tax Relief for the Elderly or Totally and Permanently Disaled be amended to increase the maximum qualifying net worth threshold by $110,000 (from $440,000 to $550,000). Qualifying applicants in the $440, $500,000 range will receive 50% relief in real estate taxes. Qualifying applicants in the $500, $500,000 range will receive 25% relief in real estate taxes. BACKGROUND: Establishing the qualifying income and net worth criteria for the real estate tax relief program is solely at the discretion of the Board of Supervisors. The County s real estate tax relief program for persons 65 or older or with disabilities, reflected in Chapter 872 of its Codified Ordinances (Attachment #1), is administered by the Commissioner of the Revenue. Since 1972 many changes have been made to Chapter 872 of its Codified Ordinances. The last changes were made by the Board of Supervisors in their September 7, 2011 business meeting. The Board then decided to fully exempt disability income for the Elderly or Disabled Tax Relief program. No changes have been made in regards to income or net worth limits since 2007, which was prior to the economic downturn. On March 15, 2012, Supervisor Bouna asked the Commissioner of the Revenue to present an information item to the Finance/Government Services and Operations Committee regarding the program. The Finance/Government Services and Operations Committee suggested no changes to

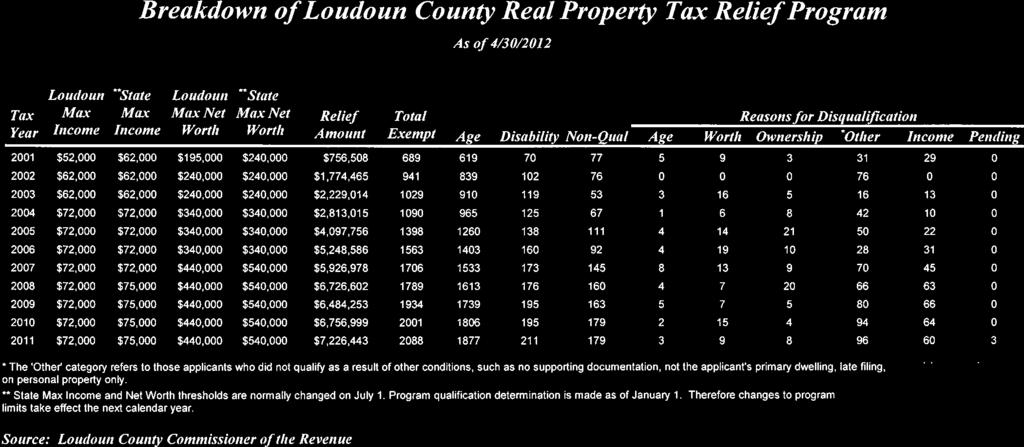

19 Board of Supervisor Meeting Item #21 September 4, 2013 Page 2 of 4 the Board of Supervisors at that time. However, Supervisor Volpe has been working with the Commission on Aging and other Supervisors in order to create possible changes to the program. FISCAL IMPACT: Currently, the County s real property tax relief program provides complete relief from real property taxes for eligible applicants as to the applicants primary dwelling and up to ten acres of land. If Loudoun adopts this new financial worth limit, there will be an additional revenue loss and additional administrative expenses. Current program statistics using existing criteria for qualification are shown in Attachment #2 Tax Relief by Magisterial District. According to the Commissioner of the Revenue, it is impossible, using currently available data, to predict with accuracy the fiscal impact of an increase in the qualifying net worth limit. There is no known available data on the net worth of all Loudoun County households with individuals eligible for the real property tax relief program by virtue of age or disability, nor on the average value of the real property owned by such individuals. The use of data on homeownership rates for the elderly and disabled, comparative household wealth and income statistics for the target population, and the location of parcels owned by potentially eligible citizens, is speculative at best. However, a decrease in the County s total real property tax revenues is inevitable since it is likely that more elderly and disabled individuals will be able to qualify for tax relief under the higher financial worth threshold. Historical data supports this conclusion. Increases in the value of real estate exempted by the real property tax relief program and the continual growth in the number of residents utilizing the program directly impacts total real property tax revenue on a yearly basis, as seen in Attachment #2. From , the program has been greatly expanded in terms of qualifying criteria (net worth and max income). These program increases combined with increased constituent interest, has resulted in substantial growth in program use. For example, in 2001 a total of 689 Loudoun residents were exempt under the 2001 program criteria, causing a revenue loss of $756,508. This year, 2108 people were exempt under the current 2006/2011 criteria, causing a revenue loss of $7,256,941. Further increase in the net worth threshold of the Tax Relief for the Elderly and Disabled Program would no doubt increase the number of qualifying participants as well as the amount of revenue loss to the County. Loudoun County s current qualifying criteria for the Tax Relief for the Elderly and Disabled Program is comparable with many of the surrounding localities, as seen in Attachment #3. The County s current program is less rigorous than many of the surrounding localities. The Towns of Leesburg, Lovettsville, Purcellville, Middleburg, Round Hill, and Hillsboro have tax relief programs similar to Loudoun County. Each of the towns utilizes the same program criteria and qualification determination made by the Commissioner s Office. Any change in net worth will need to be promptly communicated to the incorporated towns since they may need to amend their ordinances to mirror the County s amendments and will need to project decreases in

20 Board of Supervisor Meeting Item #21 September 4, 2013 Page 3 of 4 real estate tax revenue. The Town of Hamilton currently does not participate in any tax relief programs for the elderly and disabled. ISSUES: - Loudoun County has the lowest senior population per capita out of the surrounding localities. Living on a fixed income, rising healthcare costs, and rising real estate assessments have put strain on Loudoun s senior population to the point where senior citizens can no longer afford to live in the County. - Senior citizens utilize an average of $0.38 cents of every tax dollar they pay in services, according to previous accounts by County Staff. - Currently, Loudoun County schools have overcrowding issues. This overcrowding is partly caused by a low senior population in already established areas. Current communities aren t aging. Rather, senior citizens are leaving the County, causing a greater influx of families with children in areas currently at build-out. These established schools cannot handle this influx, causing greater strain on the equalized tax rate. ALTERNATIVES: 1) Increase the maximum qualifying net worth threshold by 110,000 (from $440,000 to $550,000).Qualifying applicants in the 440, $500,000 range will receive 50% relief in real estate taxes. Qualifying applicants in the $500, $550,000 range will receive 25% relief in real estate taxes. 2) Increase the maximum qualifying net worth threshold to $550,000, but adjust the percentage of relief. 3) Increase the maximum qualifying net worth threshold by another amount. 4) Keep the maximum household net worth threshold at $440,000. DRAFT MOTIONS: 1. I move that Chapter 872 of the Codified Ordinance of Loudoun County Real Estate Tax Relief for the Elderly or Totally and Permanently Disabled be amended to increase the maximum qualifying net worth threshold by $110,000 (from $440,000 to $550,000). Qualifying applicants in the $440, $500,000 range will receive 50% relief in real estate taxes. Qualifying applicants in the $500, $500,000 range will receive 25% relief in real estate taxes. OR

21 Board of Supervisor Meeting Item #21 September 4, 2013 Page 4 of 4 2. I move that Chapter 872 of the Codified Ordinance of Loudoun County Real Estate Tax Relief for the Elderly or Totally and Permanently Disabled be amended to increase the maximum qualifying net worth threshold by the amount of. OR 3. I move to place this item be sent to Finance/Government Services and Operations Committee for further review. OR 4. I move an alternate motion. ATTACHMENTS: Attachment 1 - Chapter 872- Real Estate Tax Relief for Elderly or Totally and Permanently Disabled Breakdown of Loudoun County Real Property Tax Relief Program Attachment Tax Relief Comparison by Locality Attachment Qualifications for Tax Relief for the Elderly and/or Totally and Permanently Disabled Attachment 5 - FGSO Committee May 14, 2012 Presentation

22 Attachment 1 87 CHAPTER 872 Real Estate Tax Relief for Elderly or Totally and Permanently Disabled EDITOR'S NOTE: Unless otherwise indicated, this chapter was enacted on November 21, 1972, and was amended on October 21, 1975, June 6, 1977, July 17, 1978, August 7, 1979, and November 19, Definitions Exemption authorized; effective date Administration of exemption Requirements for full exemption Requirements for pro-rated exemption Claiming an exemption Amount of exemption Adjustment upon change in Changes in status False claims Penalty. CROSS REFERENCES Exemptions for elderly and handicapped - see Code of Va et seq. Agricultural, Horticultural, Forest or Newly Annexed Real Estate Tax - see B.R. & T. Ch. 848 Personal Property and Real Estate Tax - see B.R. & T. Ch. 860 Exemptions and refunds generally - see B.R. & T. Ch. 864 Exemption for certified solar energy equipment - see B.R. & T. Ch. 868 Personal property tax relief for elderly or totally and permanently disabled - see B.R. & T. Ch DEFINITIONS. As used in this chapter: (a) Affidavit means the Real Estate Tax Exemption Affidavit. (b) County means Loudoun County, Virginia. (c) County Board means the Board of Supervisors of the County. (d) Commissioner of the Revenue means the Commissioner of the Revenue of the

23 Attachment 1 County or any of his duly authorized deputies or agents. (e) Dwelling means the sole residence owned and occupied by the person or persons claiming exemption, and includes a manufactured home used as the sole residence owned and occupied by the person(s) claiming an exemption hereunder. (f) Exemption means exemption from the County Real Estate Tax according to the provisions of this chapter. (g) Manufactured Home means a structure subject to federal regulation which is transportable in one or more sections; is eight body feet or more in width and forty body feet or more in length in the traveling more, or is 320 or more square feet when erected on site; is built on a permanent chassis; is designed to be used as a singlefamily dwelling, 2011 Replacement

24 Attachment BUSINESS REGULATION AND TAXATION CODE ) with or without a permanent foundation when connected to the required utilities; and includes the plumbing, heating, air-conditioning, and electrical systems contained in the structure. (h) Net worth means the amount by which assets (including the present value of all equitable interests) exceed liabilities. (i) Person means a natural person. (j) Permanently and totally disabled means a person who has been certified by the Social Security Administration, the Department of Veterans Affairs or the Railroad Retirement Board, or if such person is not eligible for certification by any of these agencies, by a sworn affidavit by two medical doctors who either are licensed to practice medicine in the Commonwealth or are military officers on active duty who practice medicine with the United States Armed Forces, to the effect that the person is permanently and totally disabled, and, in addition, who has been found by the Commissioner of the Revenue to be unable to engage in any substantial gainful activity by reason of any medically determinable physical or mental impairment or deformity which can be expected to result in death or can be expected to last for the duration of such person's life. (k) Property means real property. (l) Taxable year means the calendar year, from January 1 until December 31, for which exemption is claimed. (Ord Passed ; Ord Passed ; Ord Passed EXEMPTION AUTHORIZED. (a) Full Exemption. Real estate tax exemption is provided for qualified property owners who are not less than sixty-five years of age or who are permanently and totally disabled and who are eligible according to state law and the provisions of this chapter. (b) Pro-Rated Exemption. A pro-rated exemption from real estate tax is provided for the real estate (and dwelling) which is (i) jointly owned by two or more persons and (ii) occupied as the sole dwelling of each such person, at least one of whom is at least age 65 or permanently and totally disabled, and who are eligible according to state law and the provisions of this chapter. (c) Persons qualifying for exemption under this chapter shall also be exempt from the special tax levied on property within the Loudoun County Fire and Emergency Medical Services Tax District. (Ord Passed ; Ord Passed ; Ord Passed ; Ord Passed ) ADMINISTRATION OF EXEMPTION. The exemption shall be administered by the Commissioner of the Revenue according to the provisions of this chapter. The Commissioner is hereby authorized to make an inquiry of persons

25 Attachment Replacement

26 Attachment 1 Relief Estate Tax Relief for Elderly 88A or Totally and Permanently Disabled seeking such exemption in conformity with the provisions of this chapter, including the requiring of answers under oath, as may be reasonably necessary to determine qualifications for exemption as specified by this chapter. The Commissioner may require the production of certified income tax returns, appraisal reports and any other pertinent documents to establish qualification. (Ord Passed ; Ord Passed ) REQUIREMENTS FOR FULL EXEMPTION. A full exemption shall be granted subject to the following provisions: (a) Ownership. The title of the property for which an exemption is claimed must be held on January 1 of the taxable year, by the person or persons claiming the exemption, each of whom must also be (i) 65 years of age or older, or (ii) permanently and totally disabled on December 31 of the year immediately preceding the taxable year. A dwelling jointly owned by a husband and wife, with no other joint owners, may qualify if either spouse is 65 years of age or older or is permanently and totally disabled. (b) Occupancy. The property must be occupied as the sole dwelling of the person or persons claiming the exemption, each of whom must also be (i) 65 years of age or older, or (ii) permanently and totally disabled on December 31 of the year immediately preceding the taxable year. The primary residence owned by a person otherwise qualified for exemption under this chapter who is not actually occupying the same while a patient in a hospital, nursing home, convalescent home or other facility for physical or mental care for an extended period of time shall continue to be deemed such qualifying owner's dwelling; provided, however, that such residence is not used by or leased to others for consideration. (c) Income. The gross combined income of the person or persons claiming the exemption during the calendar year immediately preceding the taxable year did not exceed seventy-two thousand dollars ($72,000), provided that all disability income received by an owner or owner s spouse during the calendar year immediately preceding the taxable year shall not be included in such total. Gross combined income shall be computed by adding together the total income received during the preceding calendar year, without regard to whether a tax return is actually filed, by (i) owners of the dwelling who use it as their principal residence and (ii) owners relatives who live in the dwelling provided that the first ten thousand dollars ($10,000) of income of the owner s spouse and each relative of the owner or owners, who is living in the dwelling, shall not be included in such total. (d) Net Worth. The total net financial worth of the person or persons claiming the exemption as of December 31 of the calendar year immediately preceding the taxable year did not exceed four hundred forty thousand dollars ($440,000). Total net financial worth shall include the value of all assets, including the present value of all equitable interests of the owner or owners and the owner's spouse, and shall exclude the fair market value of the dwelling. In addition, the value of the land upon which the dwelling is situated, up to a maximum of 10 acres, shall also be excluded. (Ord Passed ; Ord Passed ; Ord Passed

27 Attachment ; Ord Passed ; Ord Passed ; Ord Passed ) 2011 Replacement

28 Attachment BUSINESS REGULATION AND TAXATION CODE 88B REQUIREMENTS FOR PRO-RATED EXEMPTION A pro-rated exemption shall be granted subject to the following provisions: (a) Ownership. Property for which a pro-rated exemption is claimed may be jointly owned on January 1 of the taxable year by two or more individuals not all of whom are at least 65 years of age or older; however, the person or persons claiming the prorated exemption must be (i) 65 years of age or older, or (ii) permanently and totally disabled on December 31 of the year immediately preceding the taxable year. The joint owners shall furnish the Commissioner of the Revenue with sufficient evidence of each joint owner's ownership interest in the dwelling. (b) Occupancy. The property must be occupied as the sole dwelling of all the joint owners. The primary residence owned by a person otherwise qualified for exemption under this chapter who is not actually occupying the same while a patient in a hospital, nursing home, convalescent home or other facility for physical or mental care for an extended period of time shall continue to be deemed such qualifying owner's dwelling; provided, however, that such residence is not used by or leased to others for consideration. (c) Income. The gross combined income of all joint owners during the calendar year immediately preceding the taxable year did not exceed seventy-two thousand dollars ($72,000), provided that the disability income received by an owner or owner s spouse during the calendar year immediately preceding the taxable year shall not be included in such total. Gross combined income shall be computed by adding together the total income received during the preceding calendar year, without regard to whether a return is actually filed, by (i) owners of the dwelling who use it as their principal residence and (ii) owners' relatives who live in the dwelling provided that the first ten thousand dollars ($10,000) of income of the owner s spouse and each relative of the owner or owners, who is living in the dwelling, shall not be included in such total. (d) Net Worth. The total net financial worth of all joint owners as of December 31 of the calendar year immediately preceding the taxable year did not exceed five hundred thousand dollars ($500,000). Beginning as of December 31, 2008, and as of December 31st of each year thereafter, the limit on combined net financial worth shall be increased by an amount equivalent to the percentage increase in the Consumer Price Index. Total net financial worth shall include the value of all assets, including the present value of all equitable interests, of the owners and the owners' spouses, and shall include the fair market value of the dwelling, the land, and any other asset. (Ord Passed ; Ord Passed ) CLAIMING AN EXEMPTION. (a) The person or persons claiming an exemption must file an Application for Real Estate Tax Exemption and Affidavit with the Commissioner of the Revenue, on forms supplied by the Commissioner, on or before April 1 of the tax year for which relief is sought. Those applying for an exemption for the first time must file on or before December 31 of the tax year for which relief is sought. Every third year from the date of the original Application, the person or persons claiming an exemption must file a new Application and Affidavit with the Commissioner. For the two years

29 Attachment Replacement

30 Attachment 1 Relief Estate Tax Relief for Elderly 89 or Totally and Permanently Disabled following the date of the original Application and all subsequent Applications, the person or persons claiming an exemption must file a Certification, on forms supplied by the Commissioner, stating that no information contained on the last preceding Affidavit, Application, or Certification filed has changed to violate the limitations or conditions provided herein. The Commissioner shall have the discretion to permit applicants to file after these deadlines in cases of genuine hardship. (b) The Application and Affidavit shall set forth, in a manner prescribed by the Commissioner, the names of the related persons occupying the dwelling for which the exemption is claimed, their gross combined income and the total combined net worth of the owners and spouses. (c) If, after audit and investigation, the Commissioner determines that the person or persons are qualified for an exemption, he shall so certify to the County Treasurer who shall deduct the amount of the exemption from the claimant's real estate tax liability. (Ord Passed ; Ord Passed ; Ord Passed ; Ord Passed ) AMOUNT OF EXEMPTION. (a) Amount of Full Exemption. The person or persons qualifying for and claiming full exemption shall be relieved of liability for the real estate tax levied on the qualifying dwelling and the land on which it is situated as set forth below. Annual Household Income (not including allowable deductions) Amount of Exemption Extent of Exemption Up to and including $72, % Dwelling and the land on which it is situated, not to exceed 3 acres Over $72,000 0% None (b) Amount of Pro-Rated Exemption. The amount by which the person or persons qualifying for and claiming the pro-rated exemption shall be relieved of liability for real estate taxes levied on the qualifying dwelling and the land on which it is situated shall be calculated by multiplying the amount of the full exemption that would otherwise have been provided by a fraction that has as the numerator the percentage of ownership interest in the qualifying dwelling and the land on which it is situated held by all such joint owners who are at least 65 years of age and as the denominator, 100%. (Ord Passed ; Ord Passed ; Ord Passed ; Ord Passed ; Ord Passed )

31 Attachment Replacement

32 Attachment BUSINESS REGULATION AND TAXATION CODE ADJUSTMENT UPON CHANGE IN ELIGIBILITY. If the qualifying property is sold, ceases to be the primary residence of the qualifying owner(s), or if the last qualifying owner dies during the taxable year, the exemption granted hereunder shall be adjusted by prorating it for that portion of the taxable year prior to the date on which the property was sold or ceased to be the qualifying owner's primary residence, or the date of death of the last qualifying owner. Such prorated adjustment shall be based upon the number of complete months of the year that such property was properly eligible for the relief granted by this chapter. (Ord Passed ; Ord Passed ; Ord Passed ; Ord Passed ) CHANGES IN STATUS. (a) The primary residence owned by a person otherwise qualified for exemption under this chapter who is not actually occupying the same while a patient in a hospital, nursing home, convalescent home or other facility for physical or mental care for an extended period of time, not intended to be permanent, shall continue to be deemed such qualifying owner's dwelling; provided, however, that such residence is not used by or leased to others for consideration. (b) Except as provided in Section (a), above, changes with respect to income, financial worth, ownership of property, occupancy, medical status or other factors occurring during the taxable year for which the Affidavit is filed, and having the effect of exceeding or violating the limitations and conditions provided in this chapter, shall nullify any relief of real estate tax liability for the then current taxable year and the taxable year immediately following. (Ord Passed ; Ord Passed ) FALSE CLAIMS. No person shall intentionally make a false claim for an exemption. (Ord Passed ) PENALTY. In addition to any other penalties provided by law, any person who intentionally makes a false claim for an exemption shall not be entitled to the exemption from taxation, if granted, but shall be liable for the full amount of tax due. In addition, such person shall be disqualified from re-applying for an exemption for a period of two years. (Ord Passed )

33 Attachment Replacement

34 Breakdown of Loudoun County Real Property Tax Relief Program As of 7/30/2013 Loudoun ** State Loudoun ** State Tax Max Max Max Net Max Net Relief Total Reasons for Disqualification Year Income Income Worth Worth Amount Exempt Age Disability Non-Qual Age Worth Ownership * Other Income Pending 2001 $52,000 $62,000 $195,000 $240,000 $756, $62,000 $62,000 $240,000 $240,000 $1,774, $62,000 $62,000 $240,000 $240,000 $2,229, $72,000 $72,000 $340,000 $340,000 $2,813, $72,000 $72,000 $340,000 $340,000 $4,097, $72,000 $72,000 $340,000 $340,000 $5,248, $72,000 $72,000 $440,000 $540,000 $5,926, $72,000 $75,000 $440,000 $540,000 $6,726, $72,000 $75,000 $440,000 $540,000 $6,484, $72,000 $75,000 $440,000 $540,000 $6,757, $72,000 $75,000 $440,000 $540,000 $7,322, $72,000 $0 $440,000 $0 $7,459, $72,000 $0 $440,000 $0 $7,256, * The 'Other' category refers to those applicants who did not qualify as a result of other conditions, such as no supporting documentation, not the applicant's primary dwelling, late filing, or receiving tax relief on personal property only. ** State Max Income and Net Worth thresholds are normally changed on July 1. Program qualification determination is made as of January 1. Therefore changes to program limits take effect the next calendar year. Beginning in 2012 the state no longer mandates maximum income or net worth thresholds. Source: Loudoun County Commissioner of the Revenue Tuesday, July 30, 2013 Page 1 of 1

35 2013 TAX RELIEF COMPARISON BY LOCALITY JURISDICTION MAX INCOME RELIEF MAX NET WORTH LOUDOUN COUNTY 72,000 full exemption 440,000 excludes up to 10,000 for owner's spouse and relatives P, T, M excludes all disability income for owner and owner's spouse ALEXANDRIA CITY 40,000 full exemption 540,000 P, T 55,000 50% exemption 72,000 25% exemption 72,000 deferral of 5% excludes up to 10,000 per relative & up to 10,000 of disability ARLINGTON COUNTY BASED ON HOUSEHOLD SIZE EXEMPTIONS P, T 1 or 2 person household $55,953 full, $68,387 50%, $99,472 25% 340,000 for exemption 3 person household $66,667 full, $76,593 50%, $99,472 25% 540,000 for deferral 4 person household $69,560 full, $85,018 50%, $99,472 25% deferral of 0% CLARKE COUNTY 20,000 full exemption 250,000 P 25,000 80% exemption 30,000 60% exemption 35,000 50% exemption 55,000 10% exemption excludes up to 8,000 per relative FAIRFAX CITY 42,000 full exemption 340,000 P, T 52,000 50% exemption 62,000 25% exemption excludes up to 6,500 per relative & up to 7,500 of disability FAIRFAX COUNTY 52,000 full exemption 340,000 P, T 62,000 50% exemption 72,000 25% exemption excludes up to 6,500 per relative & up to 7,500 of disability FALLS CHURCH CITY 37,650 exemption up to $2, ,000 P, T 37,651-75,000 deferral only at 3.25% Interest excludes up to 10,000 per relative FAUQUIER COUNTY 58,000 full exemption 440,000 P, T excludes up to 10,000 per relative Revised: 3/21/2012 Source: Loudoun County Commissioner of the Revenue Page 1 of 2

36 2013 TAX RELIEF COMPARISON BY LOCALITY JURISDICTION MAX INCOME RELIEF MAX NET WORTH LOUDOUN COUNTY 72,000 full exemption 440,000 excludes up to 10,000 for owner's spouse and relatives P, T, M excludes all disability income for owner and owner's spouse MANASSAS CITY 56,200 full exemption 340,000 P, M 64,630 25% exemption can defer balance 73,060 15% exemption can defer balance 81,490 10% exemption can defer balance excludes up to 10,000 per relative & up to 7,500 of disability PRINCE WILLIAM COUNTY P, M 56,200 full exemption 340,000 64,630 75% exemption 73,060 50% exemption 81,490 25% exemption excludes up to 10,000 per relative & up to 7,500 of disability LEESBURG TOWN 72,000 full exemption 440,000 excludes up to 10,000 per relative & up to 7,500 of disability LOVETTSVILLE TOWN 72,000 full exemption 440,000 excludes up to 10,000 per relative & up to 7,500 of disability MIDDLEBURG TOWN 72,000 full exemption 440,000 excludes up to 10,000 per relative & up to 7,500 of disability PURCELLVILLE TOWN 72,000 full exemption 440,000 excludes up to 10,000 per relative & up to 7,500 of disability ROUND HILL TOWN 72,000 full exemption 440,000 excludes up to 10,000 per relative & up to 7,500 of disability P - prorating jurisdiction M - include manufactured homes T - triennial application cycle Revised: 3/21/2012 Source: Loudoun County Commissioner of the Revenue Page 2 of 2

37 2013 TAX RELIEF COMPARISON BY LOCALITY JURISDICTION MAX INCOME RELIEF MAX NET WORTH LOUDOUN COUNTY 72,000 full exemption 440,000 excludes up to 10,000 for owner's spouse and relatives P, T, M excludes all disability income for owner and owner's spouse ALEXANDRIA CITY 40,000 full exemption 540,000 P, T 55,000 50% exemption 72,000 25% exemption 72,000 deferral of 5% excludes up to 10,000 per relative & up to 10,000 of disability ARLINGTON COUNTY BASED ON HOUSEHOLD SIZE EXEMPTIONS P, T 1 or 2 person household $55,953 full, $68,387 50%, $99,472 25% 340,000 for exemption 3 person household $66,667 full, $76,593 50%, $99,472 25% 540,000 for deferral 4 person household $69,560 full, $85,018 50%, $99,472 25% deferral of 0% CLARKE COUNTY 20,000 full exemption 250,000 P 25,000 80% exemption 30,000 60% exemption 35,000 50% exemption 55,000 10% exemption excludes up to 8,000 per relative FAIRFAX CITY 42,000 full exemption 340,000 P, T 52,000 50% exemption 62,000 25% exemption excludes up to 6,500 per relative & up to 7,500 of disability FAIRFAX COUNTY 52,000 full exemption 340,000 P, T 62,000 50% exemption 72,000 25% exemption excludes up to 6,500 per relative & up to 7,500 of disability FALLS CHURCH CITY 37,650 exemption up to $2, ,000 P, T 37,651-75,000 deferral only at 3.25% Interest excludes up to 10,000 per relative FAUQUIER COUNTY 58,000 full exemption 440,000 P, T excludes up to 10,000 per relative Revised: 3/21/2012 Source: Loudoun County Commissioner of the Revenue Page 1 of 2

38 2013 TAX RELIEF COMPARISON BY LOCALITY JURISDICTION MAX INCOME RELIEF MAX NET WORTH LOUDOUN COUNTY 72,000 full exemption 440,000 excludes up to 10,000 for owner's spouse and relatives P, T, M excludes all disability income for owner and owner's spouse MANASSAS CITY 56,200 full exemption 340,000 P, M 64,630 25% exemption can defer balance 73,060 15% exemption can defer balance 81,490 10% exemption can defer balance excludes up to 10,000 per relative & up to 7,500 of disability PRINCE WILLIAM COUNTY P, M 56,200 full exemption 340,000 64,630 75% exemption 73,060 50% exemption 81,490 25% exemption excludes up to 10,000 per relative & up to 7,500 of disability LEESBURG TOWN 72,000 full exemption 440,000 excludes up to 10,000 per relative & up to 7,500 of disability LOVETTSVILLE TOWN 72,000 full exemption 440,000 excludes up to 10,000 per relative & up to 7,500 of disability MIDDLEBURG TOWN 72,000 full exemption 440,000 excludes up to 10,000 per relative & up to 7,500 of disability PURCELLVILLE TOWN 72,000 full exemption 440,000 excludes up to 10,000 per relative & up to 7,500 of disability ROUND HILL TOWN 72,000 full exemption 440,000 excludes up to 10,000 per relative & up to 7,500 of disability P - prorating jurisdiction M - include manufactured homes T - triennial application cycle Revised: 3/21/2012 Source: Loudoun County Commissioner of the Revenue Page 2 of 2

39 Date of Meeting: October 12, 2011 BOARD OF SUPERVISORS FINANCE/GOVERNMENT SERVICES AND OPERATIONS COMMITTEE ACTION ITEM # 4 SUBJECT: ELECTION DISTRICT: CRITICAL ACTION DATE: CONTACT: Proposed Amendments to Chapter 872 of the Codified Ordinances of Loudoun County/Real Estate Tax Relief for the Elderly or Totally and Permanently Disabled Countywide November 2, 2011 (to advertise for December Public Hearing) Robert S. Wertz, Jr., Commissioner of the Revenue RECOMMENDATIONS: Commission on Aging (COA): The Commission on Aging recommends that the Board of Supervisors amend Loudoun s real estate tax relief ordinance to allow the owner s spouse to exclude his or her first $10,000 of income from the qualifying income calculation. Disability Services Board (DSB): The DSB recommends that the Board of Supervisors increase the qualifying income limit and either increase or eliminate all together the net worth qualification criteria. The DSB also recommends that the Board exempt all of the income received by an owner during the calendar year as compensation for permanent disability. In addition, the DSB recommends that the real estate tax relief ordinance be changed in order to comply with the amended provisions of the Code of Virginia pertaining to this program. Commissioner of the Revenue: Establishing qualifying income and net worth criteria for the real estate tax relief program is at the discretion of the Board of Supervisors. However, the Commissioner proposes that a number of administrative changes be made to ordinances governing the administration of the program. The Commissioner of the Revenue recommends that these administrative changes and any changes to the qualifying income and net worth criteria, if so desired by the Board, be effective January 1, As a result, the Committee will need to provide guidance at this meeting to allow sufficient time for a draft of the amended real estate tax relief ordinance to be prepared for the Board s approval and to advertise the proposed ordinance amendments for the December 12, 2011 public hearing.

40 Proposed Amendment to Chapter 872 of the Loudoun County Codified Ordinances October 12, 2011 Page 2 BACKGROUND The County s real estate tax relief program for persons 65 or older or with disabilities, reflected in Chapter 872 of its Codified Ordinances, is administered by the Commissioner of the Revenue. During its April 19, 2011 business meeting, the Board of Supervisors supported a Board-initiated item to direct the COA and the DSB to review the qualifying criteria for the County s real estate tax relief program and make recommendations for changes to the Board by September 7, 2011 so that any ordinance amendments can be adopted to take effect January 1, (The motion passed , Supervisor Delgaudio voted no and Vice Chairman Buckley was absent for the vote.). At that meeting, Commissioner Wertz agreed to compile the recommendations from the COA and DSB and transmit them to the Board of Supervisors. At its September 20, 2011 business meeting, the Board of Supervisors unanimously supported a motion to send the item to the October 12, 2011 Finance/Government Services and Operations Committee meeting. At that meeting, the Board asked the Commissioner of the Revenue to bring to the Committee the following additional information regarding the real estate tax relief program: Supervisor McGimsey requested a comparison of Loudoun s real estate tax relief program with similar programs in other localities (see Attachment 1). Supervisor Kurtz requested the average amount of tax forgiven per qualifying applicant (see ). Supervisor Delgaudio requested a breakdown of real estate tax relief granted within the various magisterial districts (see Attachment 3), a summary of when applicants arrived in the County as compared to when they first applied for tax relief, and the implication of raising the net worth threshold (see Fiscal Impact section of this item). The chart below provides a breakdown of the number of years that applicants who qualified for real estate tax relief in tax year 2010 owned their property prior to receiving tax relief for the first time. However, since the County s tax assessment system does not currently have the date an applicant first purchased a parcel in the County, some anomalies may exist in the data. Number of Years Property Owned Prior to Receiving Tax Relief for First Time Percentage of Applicants that Qualified in Tax Year % % % % Supervisor Delgaudio also wanted the Committee to have a discussion regarding the correctness of the net worth threshold since residents who have accumulated savings over their lifetime are frequently unable to qualify for the real estate tax relief program.

41 Proposed Amendment to Chapter 872 of the Loudoun County Codified Ordinances October 12, 2011 Page 3 Supervisor Miller asked if the Commissioner of the Revenue and representatives from the DSB and COA could attend the Finance/Government Services and Operations Committee meeting at which this item is scheduled to be discussed. Immediately following the Board s business meeting, the Commissioner notified representatives from both the DSB and COA of the Board s actions and invited them to attend the October 12 th Finance/Government Services and Operations Committee meeting. Additionally, Supervisor Miller inquired about whether localities could institute a length of residency requirement as a condition of qualifying for the real estate tax relief program. This was addressed by the General Assembly during its 1989 session, wherein House Bill 1526 added the following language to Code of Virginia , No local ordinance shall require that a citizen reside in the jurisdiction for a designated period of time as a condition for qualifying for any real estate tax exemption or deferral program established pursuant to This item summarizes the recommendations of the COA, DSB and the Commissioner of the Revenue that were presented to the Board of Supervisors at its September 20, 2011 business meeting. The full item from that meeting is available in Attachment 4 of this item. The COA recommends that the Board extend Loudoun s current $10,000 income exclusion for nonspousal relatives who reside in the same house as the elderly person(s) to the income of the spouse as well. When the General Assembly amended the Commonwealth s enabling real estate tax relief legislation during its 2011 session, the language which previously prohibited localities from excluding any amount of a spouse s income was removed. The DSB recommends that the Board exclude, for income qualification purposes, all of the income received by an owner or owner s spouse during the calendar year as compensation for permanent disability. This exclusion however, would not be limited solely to those who qualify for relief based on a disability but would encompass disability income when the owner qualifies for relief based on age, not disability, and the disability is less than 100% or total. Currently, the County excludes the first $7,500 of disability income. In addition to a full exclusion of disability income, the DSB recommends increasing the income limit and either increasing or eliminating all together the net worth limit. The DSB provides a number of options for calculating the income and net worth limits for qualifying purposes and further suggests that those criteria could be automatically adjusted annually for inflation through the use of the Consumer Price Index (CPI). For purposes of providing income and net worth qualification figures as adjusted for inflation in the charts below, staff has used the Bureau of Labor Statistics (BLS s) HALF1 figure for the All Items Consumer Price Index for All Urban Consumers (CPI-U) for the Washington-Baltimore area for base period NOVEMBER 1996=100. The options presented by the DSB for increasing the income qualification criteria and the associated limit amounts calculated using their proposed methodology are provided in the chart below. The

42 Proposed Amendment to Chapter 872 of the Loudoun County Codified Ordinances October 12, 2011 Page 4 County s current real estate tax relief income limit is $72,000. DSB Recommended Proposed Qualifying Income Limit Options Income Limit(s) 1. $75,000 cap set by the General Assembly in 2008 plus inflation based on CPI through the present $76, Latest married median adjusted gross income for Loudoun County of $121,300 as published by the Weldon Cooper Center for Public Excellence adjusted for inflation based on CPI through the present $129, Median household income based on the 2010 US Census (Loudoun) $114,204 The options presented by the DSB for increasing the net worth qualification criteria and the net worth limits calculated using their proposed methodology are provided in the chart below. The County s current real estate tax relief net worth limits are $440,000 for property owned by an individual or jointly owned by a husband and wife, and $530,270 (adjusted annually by CPI) for property owned by two or more individuals, not all of whom are 65 of age or permanently or totally disabled. DSB Recommended Proposed Qualifying Net Worth Limit Options Net Worth Limit(s) 1. $540,000 cap set by the General Assembly in 2008 plus inflation based on CPI through the present $550, $440,000 cap set by Loudoun County in 2007 plus inflation based on CPI through the present $468, Eliminate the net worth limitation in its entirety None Much of the enabling legislation that forms the basis of the real estate tax relief program was amended during the 2011 General Assembly session in the process of enacting last year s constitutional amendment to provide a real estate tax exemption for 100 percent service-connected, permanently disabled property owners (or their unmarried surviving spouses).. This resulted in changes to the basic framework upon which the program is based. As an example, the income and net worth computations have been significantly altered. Consequently, the Commissioner is recommending a number of administrative changes to the program to comply with the recently enacted legislation (Attachment 5).