DEPARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE WASHINGTON, D.C September 5, 2014

|

|

|

- Cynthia Barker

- 6 years ago

- Views:

Transcription

and the 99 religious organizations referenced in your letter.")

1 DEPARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE WASHINGTON, D.C COMMISSIONER September 5, 2014 The Honorable Scott Garrett U.S. House of Representatives Washington, DC Dear Mr. Garrett: I am responding to your letter dated August 25, 2014, about litigation with the Freedom From Religion Foundation (FFRF) and the 99 religious organizations referenced in your letter. 1 Your questions about the FFRF case involve litigation handled by the Department of Justice, which is in a better posture to answer your inquiries. We are, however, able to provide information related to church tax inquiries and examinations. Under the Internal Revenue Code (the Code), all section 501(c)(3) organizations are prohibited from directly or indirectly participating in, or intervening in, any political campaign on behalf of (or in opposition to) any candidate for elective public office. Contributions to political campaigns or public statements (verbal or written) made by an organization in favor of or in opposition to any candidate for public office violate the prohibition against political campaign intervention activity. Violating this prohibition may result in denial or revocation of tax-exempt status and the imposition of certain excise taxes. Certain other activities or expenditures also may be prohibited depending on the facts and circumstances. Over a period of time, we identified the 99 churches as having potential impermissible political campaign intervention activities based on referrals received by our Exempt Organizations (EO) Examination function. The Political Activity Referral Committee (PARC), which consists of career civil service managers, reviews each referral and determines whether the case should be selected for further compliance review. For cases involving churches, compliance with section 7611 of the Code, which sets forth certain restrictions applicable to church tax inquiries and examinations, is also required. Procedures under section 7611 have been in the Code of Federal Regulations since In 2009, proposed amendments to these regulations were published in the Federal Register. Public comments on the proposed regulations are at Final regulations under section 7611 are on the Treasury Department and IRS Priority Guidance 1 We assumed that the 99 religious organizations referenced in your letter were the 99 churches mentioned in the June 27, 2014, Jetter to Acting Assistant Attorney General Tamara Ashford.

at http://www.irs.gov/irm/part4/irm 04-076-007.")

2 2 Plan (available at In addition, the Internal Revenue Manual , Church Tax Inquiries and Examinations (updated June 1, 2004, August 20, 2010, and currently in the process of being updated in the normal course) at html provide guidelines for conducting church tax inquiries and examinations. I am enclosing Publication 1828, Tax Guide for Churches & Religious Organizations, for your reference. This publication explains the benefits and responsibilities for these organizations under the federal tax laws. In 1998, the Congress passed section 1203 of the Code as part of the IRS Restructuring and Reform Act of Section 1203(b)(3) provides that an IRS employee may be terminated if they violate a taxpayer's constitutional rights. In addition, we have established procedures in our Internal Revenue Manual to ensure employees do not violate any taxpayer right, including specific laws such as section 7611 regarding church tax inquiries and examinations. Regarding the PARC, our systems do not track the actual cost of the PARC or what was spent in total for the preliminary compliance assessment of the 99 organizations reviewed. In 2012, we incurred costs associated with initial PARC member training. In FY 2012, the PARC began reviews. We estimate that each committee member spends approximately 6 hours per week on PARC matters, which resulted in approximately 360 hours in FY 2012, 936 hours in FY 2013, and 828 hours in FY In responding to your letter, we are mindful that the Congress enacted section 6103 of the Code to preserve the confidentiality of the tax information of American taxpayers, including tax-exempt organizations, unless the disclosure is authorized by some provision of the Code. Section 6103(f) sets forth the means by which only the Chairmen of the House Committee on Ways and Means, the Senate Finance Committee, and the Joint Committee on Taxation may authorize access to returns and return information of a taxpayer without a confidentiality waiver from that taxpayer. Therefore, we cannot provide information on the process or even the existence of an examination of a particular organization without a confidentiality waiver from that taxpayer. I hope this information is helpful. If you have any questions, please contact me, or a member of your staff can contact Leonard Oursler, Director, Legislative Affairs, at (202) Enclosure John A. Koskinen

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

DEPARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE WASHINGTON, D.C August 24,2012

DEPARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE WASHINGTON, D.C. 20224 DEPUTY COMMISSIONER August 24,2012 The Honorable Carl Levin Chairman Permanent Subcommittee on Investigations Senate Committee

DEPARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE WASHINGTON, D.C. 20224 DEPUTY COMMISSIONER August 24,2012 The Honorable Carl Levin Chairman Permanent Subcommittee on Investigations Senate Committee

September 8, Dear Mr. Miller:

September 8, 2008 Mr. Steven T. Miller Commissioner, Tax Exempt and Government Entities Internal Revenue Service 1111 Constitution Ave NW Washington, DC 20224 Dear Mr. Miller: We, the undersigned clergy

September 8, 2008 Mr. Steven T. Miller Commissioner, Tax Exempt and Government Entities Internal Revenue Service 1111 Constitution Ave NW Washington, DC 20224 Dear Mr. Miller: We, the undersigned clergy

IRS and Legislative Update for Nonprofit Organizations. Presented by Ira Nevelow, CPA, JD, AEP

IRS and Legislative Update for Nonprofit Organizations Presented by Ira Nevelow, CPA, JD, AEP Exempt Organizations Examination Work Plan 2017 EO EXAM Five Strategic Issue Areas Exemption Protection of

IRS and Legislative Update for Nonprofit Organizations Presented by Ira Nevelow, CPA, JD, AEP Exempt Organizations Examination Work Plan 2017 EO EXAM Five Strategic Issue Areas Exemption Protection of

IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF COLUMBIA

IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF COLUMBIA ) Z STREET, ) ) Plaintiff, ) ) v. ) Civil No. 1:12-cv-401-KBJ ) DAVID KAUTTER, ) IN HIS OFFICIAL CAPACITY AS ) ACTING COMMISSIONER OF INTERNAL

IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF COLUMBIA ) Z STREET, ) ) Plaintiff, ) ) v. ) Civil No. 1:12-cv-401-KBJ ) DAVID KAUTTER, ) IN HIS OFFICIAL CAPACITY AS ) ACTING COMMISSIONER OF INTERNAL

DEPARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE WASHINGTON, D.C June 4, 2012

DEPARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE WASHINGTON, D.C. 20224 DEPUTY COMMISSIONER June 4, 2012 The Honorable Carl Levin Chairman Permanent Subcommittee on Investigations Senate Committee on

DEPARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE WASHINGTON, D.C. 20224 DEPUTY COMMISSIONER June 4, 2012 The Honorable Carl Levin Chairman Permanent Subcommittee on Investigations Senate Committee on

fj) IRS Department of the Treasury Internal Revenue Service 1111 Constitution Ave., NW Washington, DC Dear

IRS Department of the Treasury Internal Revenue Service 1111 Constitution Ave., NW Washington, DC Dear") fj) IRS Department of the Treasury Internal Revenue Service 1111 Constitution Ave., NW Washington, DC 20224 Date: October 2, 2015 Number: 201552032 Release Date: 12/24/2015 Employer ID number: Contact

fj) IRS Department of the Treasury Internal Revenue Service 1111 Constitution Ave., NW Washington, DC 20224 Date: October 2, 2015 Number: 201552032 Release Date: 12/24/2015 Employer ID number: Contact

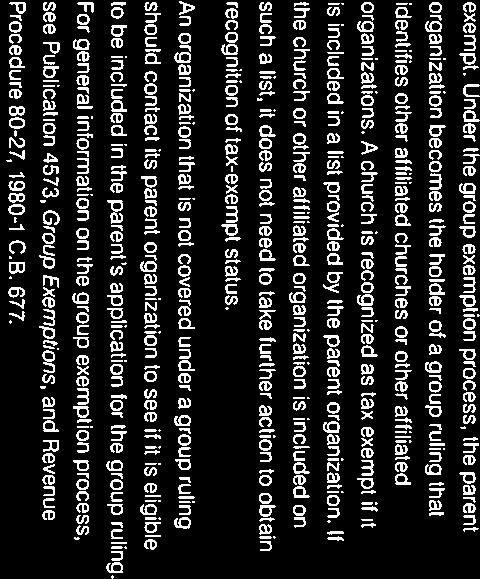

United States Catholic Conference Group Ruling and the Official Catholic Directory

United States Catholic Conference Group Ruling and the Official Catholic Directory Introduction The USCC Group Ruling is important for establishing the following: 1. The exemption of Catholic organizations

United States Catholic Conference Group Ruling and the Official Catholic Directory Introduction The USCC Group Ruling is important for establishing the following: 1. The exemption of Catholic organizations

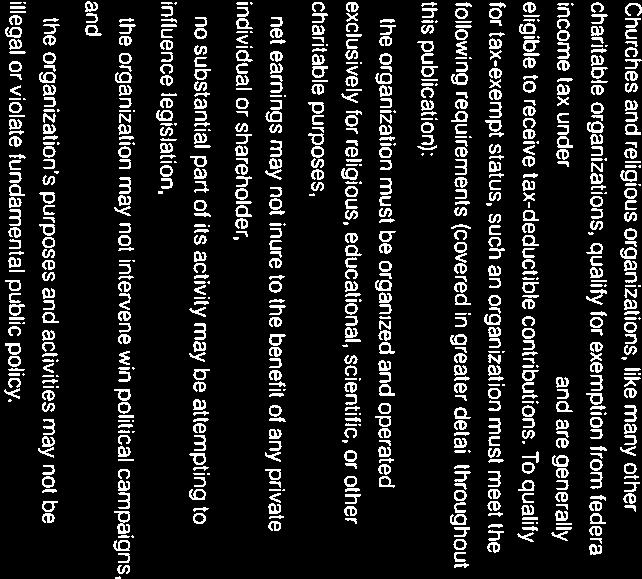

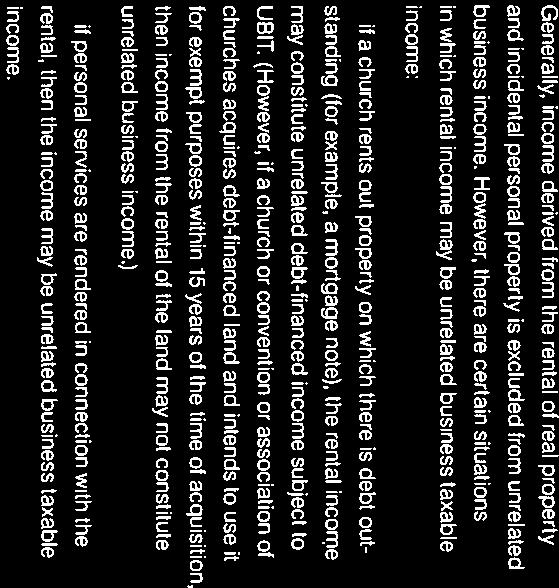

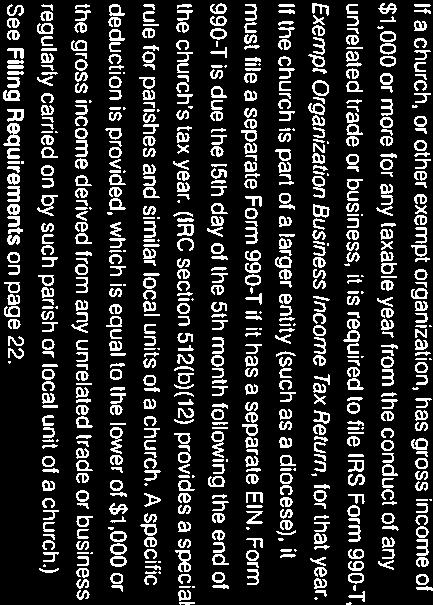

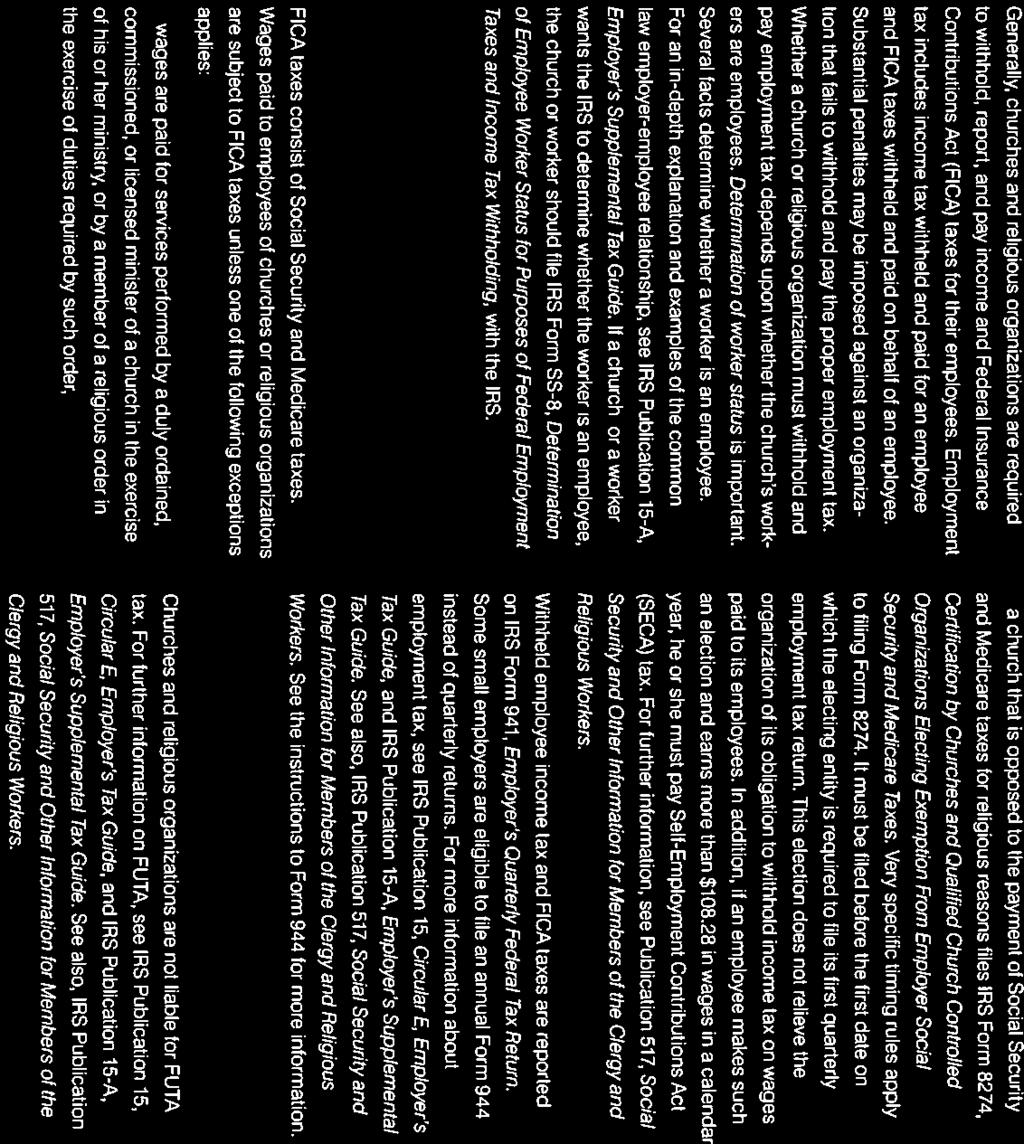

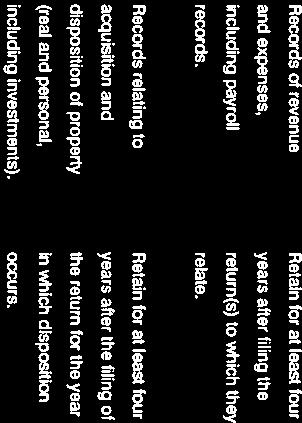

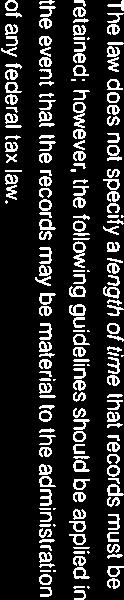

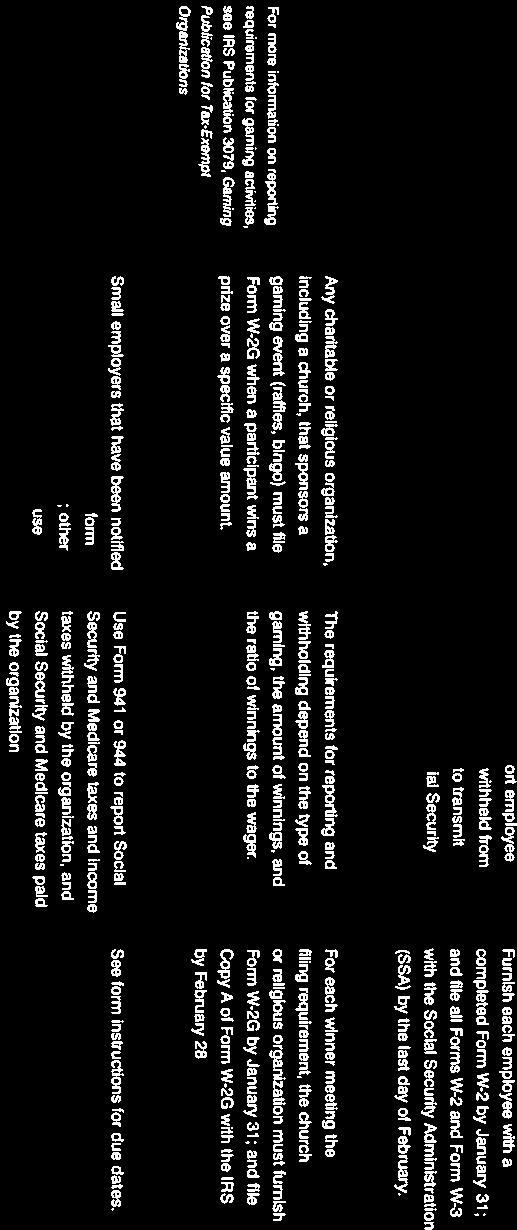

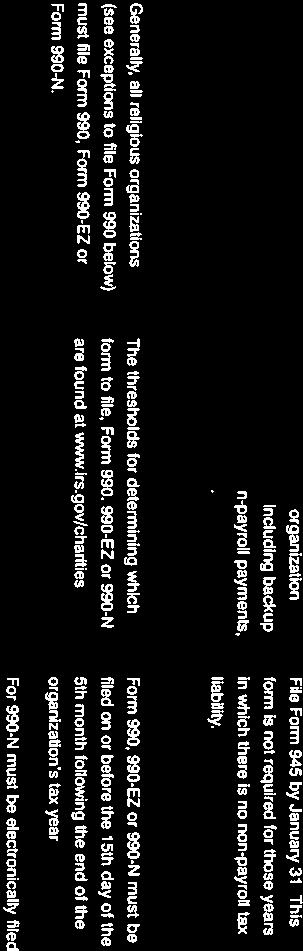

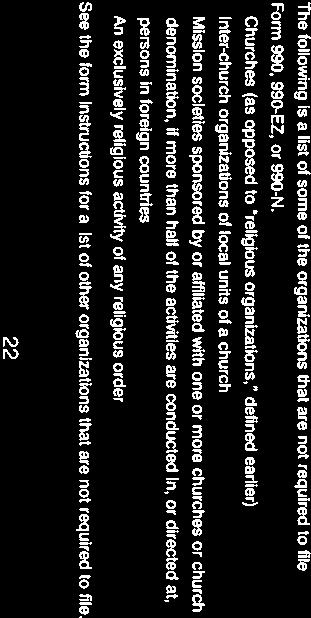

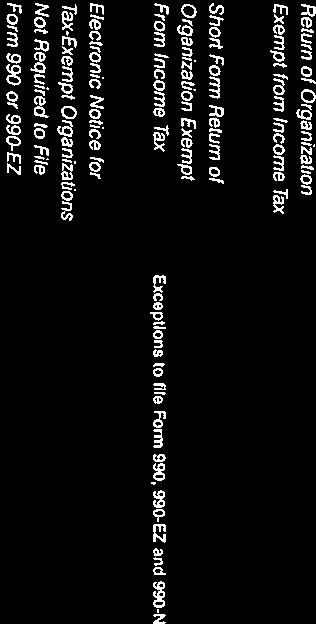

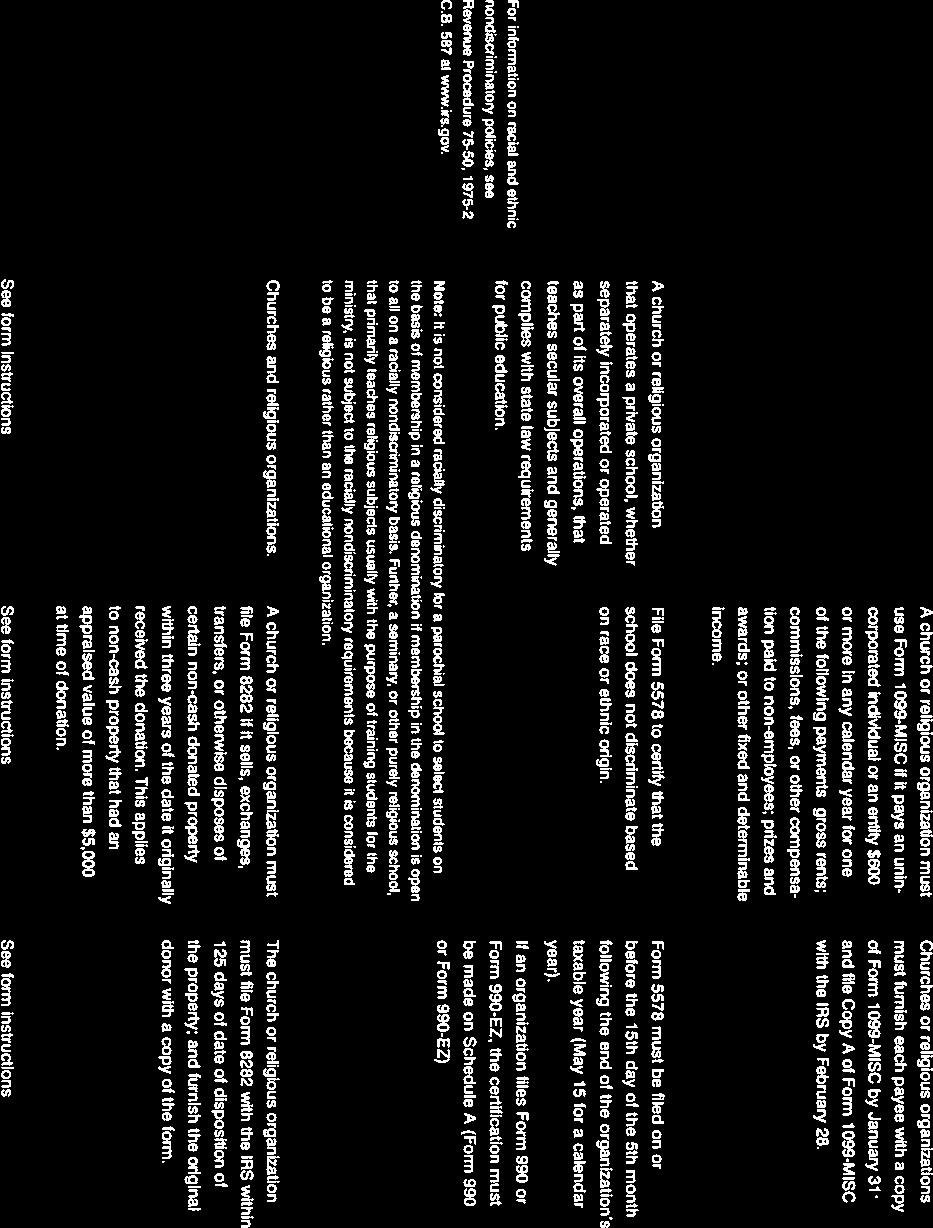

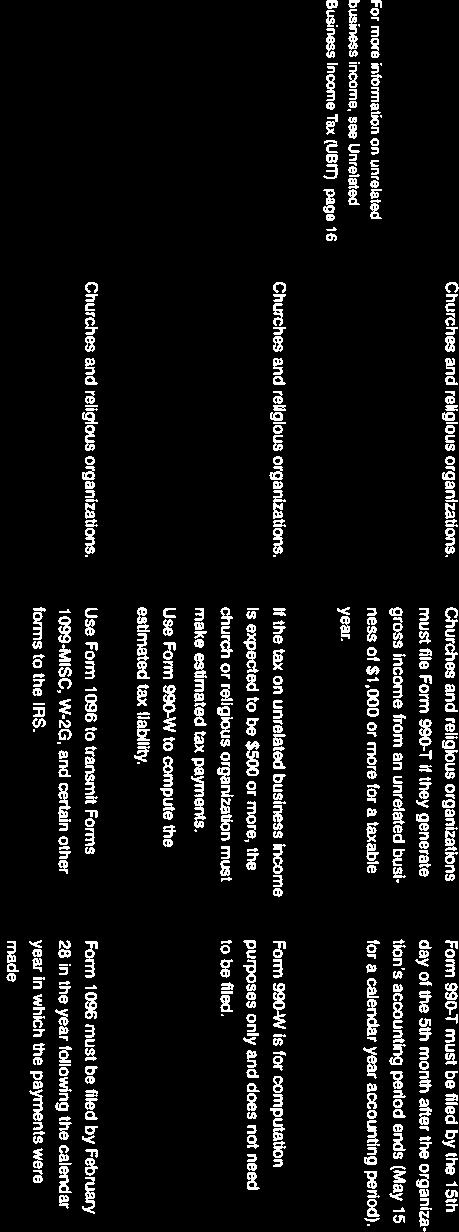

Churches and Religious Organizations

Internal Revenue Service Service Tax Tax Exempt Exempt and and Government Government Entities Entities Exempt Organizations Exempt Organizations tax guide for Churches and Religious Organizations benefits

Internal Revenue Service Service Tax Tax Exempt Exempt and and Government Government Entities Entities Exempt Organizations Exempt Organizations tax guide for Churches and Religious Organizations benefits

TAX-EXEMPT ORGANIZATIONS: EFFECTIVE GOVERNANCE AND LEGAL COMPLIANCE VICTOR J. FERGUSON SUZANNE R. GALYARDT VORYS, SATER, SEYMOUR AND PEASE LLP

TAX-EXEMPT ORGANIZATIONS: EFFECTIVE GOVERNANCE AND LEGAL COMPLIANCE VICTOR J. FERGUSON SUZANNE R. GALYARDT VORYS, SATER, SEYMOUR AND PEASE LLP OVERVIEW 1. Organizational Test 2. Operational Test 3. Private

TAX-EXEMPT ORGANIZATIONS: EFFECTIVE GOVERNANCE AND LEGAL COMPLIANCE VICTOR J. FERGUSON SUZANNE R. GALYARDT VORYS, SATER, SEYMOUR AND PEASE LLP OVERVIEW 1. Organizational Test 2. Operational Test 3. Private

Internal Revenue Code Section 501(q) and Its Critical Implications for the Nonprofit Housing Counseling Industry in Light of Recent IRS Guidance

and Its Critical Implications for the Nonprofit Housing Counseling Industry in Light of Recent IRS Guidance") 1 Internal Revenue Code Section 501(q) and Its Critical Implications for the Nonprofit Housing Counseling Industry in Light of Recent IRS Guidance Affordable Housing and Community Development Corporation

1 Internal Revenue Code Section 501(q) and Its Critical Implications for the Nonprofit Housing Counseling Industry in Light of Recent IRS Guidance Affordable Housing and Community Development Corporation

Housing Counseling Agencies and Internal Revenue Code Section 501(q): What the New IRS Guidance Means for the Housing Counseling Industry

: What the New IRS Guidance Means for the Housing Counseling Industry") 1 Housing Counseling Agencies and Internal Revenue Code Section 501(q): What the New IRS Guidance Means for the Housing Counseling Industry An Audioconference Sponsored by the HUD Counseling Intermediaries

1 Housing Counseling Agencies and Internal Revenue Code Section 501(q): What the New IRS Guidance Means for the Housing Counseling Industry An Audioconference Sponsored by the HUD Counseling Intermediaries

[ p] Amendments to the Regulations Regarding Questions and Answers Relating to Church Tax Inquiries and Examinations

![[ p] Amendments to the Regulations Regarding Questions and Answers Relating to Church Tax Inquiries and Examinations](/thumbs/90/103690088.jpg "[ p] Amendments to the Regulations Regarding Questions and Answers Relating to Church Tax Inquiries and Examinations") [4830-01-p] DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 301 [REG-112756-09] RIN 1545-BI60 Amendments to the Regulations Regarding Questions and Answers Relating to Church Tax Inquiries

[4830-01-p] DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 301 [REG-112756-09] RIN 1545-BI60 Amendments to the Regulations Regarding Questions and Answers Relating to Church Tax Inquiries

DE:PARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE WASHINGTON, D.C. ZOZZ4 OCT

DE:PARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE WASHINGTON, D.C. ZOZZ4 OCT 2 1996 Dear Mr. & Ms. Given, Sr.: This is in response to your letter, dated September 5, 1996, concerning questions posed

DE:PARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE WASHINGTON, D.C. ZOZZ4 OCT 2 1996 Dear Mr. & Ms. Given, Sr.: This is in response to your letter, dated September 5, 1996, concerning questions posed

September 13 th, 2015

Internal Revenue Service ID: LFG-2015-IRS-0012 Attn: Christie A. Preston 1111 Constitution Avenue NW, Rm 6129 Washington, DC 20224 Christie.A.Preston@irs.gov Sent via: Mail and Email September 13 th, 2015

Internal Revenue Service ID: LFG-2015-IRS-0012 Attn: Christie A. Preston 1111 Constitution Avenue NW, Rm 6129 Washington, DC 20224 Christie.A.Preston@irs.gov Sent via: Mail and Email September 13 th, 2015

Intermediate Sanctions (IRC 4958) Update. By Lawrence M. Brauer and Leonard J. Henzke

Update. By Lawrence M. Brauer and Leonard J. Henzke") Intermediate Sanctions (IRC 4958) Update By Lawrence M. Brauer and Leonard J. Henzke Intermediate Sanctions (IRC 4958) Update By Lawrence M. Brauer and Leonard J. Henzke Overview Purpose This article

Intermediate Sanctions (IRC 4958) Update By Lawrence M. Brauer and Leonard J. Henzke Intermediate Sanctions (IRC 4958) Update By Lawrence M. Brauer and Leonard J. Henzke Overview Purpose This article

Evangelical Council for Financial Accountability

Evangelical Council for Financial Accountability 440 West Jubal Early Drive, Suite 100 Winchester, VA 22601 April 5, 2013 The Honorable David Reichert United States House of Representatives Committee on

Evangelical Council for Financial Accountability 440 West Jubal Early Drive, Suite 100 Winchester, VA 22601 April 5, 2013 The Honorable David Reichert United States House of Representatives Committee on

1111 Constitution Avenue, NW 1111 Constitution Avenue, N W Washington, DC Washington, DC 20224

The Honorable John Koskinen The Honorable William J. Wilkins Commissioner Chief Counsel Internal Revenue Service Internal Revenue Service 1111 Constitution Avenue, NW 1111 Constitution Avenue, N W Washington,

The Honorable John Koskinen The Honorable William J. Wilkins Commissioner Chief Counsel Internal Revenue Service Internal Revenue Service 1111 Constitution Avenue, NW 1111 Constitution Avenue, N W Washington,

Revenue Procedure , Changes in Methods of Accounting

Mr. Scott Dinwiddie Associate Chief Counsel Income Tax & Accounting Internal Revenue Service 1111 Constitution Avenue, NW Washington, DC 20224 Re: Revenue Procedure 2015-13, Changes in Methods of Accounting

Mr. Scott Dinwiddie Associate Chief Counsel Income Tax & Accounting Internal Revenue Service 1111 Constitution Avenue, NW Washington, DC 20224 Re: Revenue Procedure 2015-13, Changes in Methods of Accounting

Appeals NOTICE. ALI CLE - Handling a Tax Controversy: Audit, Appeals, Litigation and Collections October 8-9, 2015

205 Appeals ALI CLE - Handling a Tax Controversy: Audit, Appeals, Litigation and Collections October 8-9, 2015 NOTICE The following information is not intended to be written advice concerning one or more

205 Appeals ALI CLE - Handling a Tax Controversy: Audit, Appeals, Litigation and Collections October 8-9, 2015 NOTICE The following information is not intended to be written advice concerning one or more

Office of the General Counsel

Office of the General Counsel 3211 FOURTH STREET, NE WASHINGTON, DC 20017-1194 202-541-3300 FAX 202-541-3337 June 27, 2014 TO: SUBJECT: Subordinate Organizations under USCCB Group Ruling (GEN: 0928) 2014

Office of the General Counsel 3211 FOURTH STREET, NE WASHINGTON, DC 20017-1194 202-541-3300 FAX 202-541-3337 June 27, 2014 TO: SUBJECT: Subordinate Organizations under USCCB Group Ruling (GEN: 0928) 2014

DEPARTMENT OF THE TREASURY WASHINGTON, D.C June 26, 2013

DEPARTMENT OF THE TREASURY WASHINGTON, D.C. 20005 INSPECTOR GENERAL FOR TAX ADMINISTRATION June 26, 2013 The Honorable Sander M. Levin Ranking Member Committee on Ways and Means U.S. House of Representatives

DEPARTMENT OF THE TREASURY WASHINGTON, D.C. 20005 INSPECTOR GENERAL FOR TAX ADMINISTRATION June 26, 2013 The Honorable Sander M. Levin Ranking Member Committee on Ways and Means U.S. House of Representatives

BAUCUS-GRASSLEY BILL ADDRESSES PUBLICLY TRADED PARTNERSHIPS Senators seek to clarify tax treatment for partnerships acting as corporations

For Immediate Release Contact: Carol Guthrie (Baucus) June 14, 2007 Jill Gerber (Grassley) (202) 224-4515 BAUCUS-GRASSLEY BILL ADDRESSES PUBLICLY TRADED PARTNERSHIPS Senators seek to clarify tax treatment

For Immediate Release Contact: Carol Guthrie (Baucus) June 14, 2007 Jill Gerber (Grassley) (202) 224-4515 BAUCUS-GRASSLEY BILL ADDRESSES PUBLICLY TRADED PARTNERSHIPS Senators seek to clarify tax treatment

Office of the General Counsel

Office of the General Counsel 3211 FOURTH STREET, NE WASHINGTON, DC 20017-1194 202-541-3300 FAX 202-541-3337 June 4, 2015 TO: Subordinate Organizations under USCCB Group Ruling (GEN: 0928) SUBJECT: 2015

Office of the General Counsel 3211 FOURTH STREET, NE WASHINGTON, DC 20017-1194 202-541-3300 FAX 202-541-3337 June 4, 2015 TO: Subordinate Organizations under USCCB Group Ruling (GEN: 0928) SUBJECT: 2015

Office of the General Counsel

Office of the General Counsel 3211 FOURTH STREET, NE WASHINGTON, DC 20017-1194 202-541-3300 FAX 202-541-3337 June 8, 2017 TO: Subordinate Organizations under USCCB Group Ruling (GEN: 0928) SUBJECT: 2017

Office of the General Counsel 3211 FOURTH STREET, NE WASHINGTON, DC 20017-1194 202-541-3300 FAX 202-541-3337 June 8, 2017 TO: Subordinate Organizations under USCCB Group Ruling (GEN: 0928) SUBJECT: 2017

Community Benefit Webinar

Community Benefit Webinar IRS: Form 990, Schedule H: A Review of 2014 2015 Form and Instructions Feb. 23, 2016 1 2 p.m. ET The Catholic Health Association of the United States The Catholic Health Association

Community Benefit Webinar IRS: Form 990, Schedule H: A Review of 2014 2015 Form and Instructions Feb. 23, 2016 1 2 p.m. ET The Catholic Health Association of the United States The Catholic Health Association

RE: Ethical and Possible Criminal Violations Relating to Scott Pruitt Legal Defense Fund

May 30, 2018 Attorney General Jeff Sessions U.S. Department of Justice 950 Pennsylvania Avenue, NW Washington, DC 20530-0001 Mr. David J. Apol Acting Director U.S. Office of Government Ethics 1201 New

May 30, 2018 Attorney General Jeff Sessions U.S. Department of Justice 950 Pennsylvania Avenue, NW Washington, DC 20530-0001 Mr. David J. Apol Acting Director U.S. Office of Government Ethics 1201 New

Office of the General Counsel

Office of the General Counsel 3211 FOURTH STREET, NE WASHINGTON, DC 20017-1194 202-541-3300 FAX 202-541-3337 December 6, 2018 TO: Subordinate Organizations under USCCB Group Ruling (GEN: 0928) SUBJECT:

Office of the General Counsel 3211 FOURTH STREET, NE WASHINGTON, DC 20017-1194 202-541-3300 FAX 202-541-3337 December 6, 2018 TO: Subordinate Organizations under USCCB Group Ruling (GEN: 0928) SUBJECT:

ELECTION LAW, TAX LAW, AND FUNDING A 'CONNECTED' PAC

ELECTION LAW, TAX LAW, AND FUNDING A 'CONNECTED' PAC Author: ELIZABETH J. KINGSLEY (Originally published in the journal Taxation of Exempts, Volume 21, Number 03, November/December 2009) Restrictions imposed

ELECTION LAW, TAX LAW, AND FUNDING A 'CONNECTED' PAC Author: ELIZABETH J. KINGSLEY (Originally published in the journal Taxation of Exempts, Volume 21, Number 03, November/December 2009) Restrictions imposed

Office of the General Counsel 3211 FOURTH STREET, NE WASHINGTON, DC 20017-1194 202-541-3300 FAX 202-541-3337 June 27, 2014 TO: SUBJECT: Subordinate Organizations under USCCB Group Ruling (GEN: 0928) 2014

Office of the General Counsel 3211 FOURTH STREET, NE WASHINGTON, DC 20017-1194 202-541-3300 FAX 202-541-3337 June 27, 2014 TO: SUBJECT: Subordinate Organizations under USCCB Group Ruling (GEN: 0928) 2014

1102 Longworth House Office Building 1102 Longworth House Office Building Washington, DC Washington, DC 20515

The Honorable Lynn Jenkins Chairwoman Ranking Member Subcommittee on Oversight Subcommittee on Oversight House Committee on Ways and Means House Committee on Ways and Means United States House of Representatives

The Honorable Lynn Jenkins Chairwoman Ranking Member Subcommittee on Oversight Subcommittee on Oversight House Committee on Ways and Means House Committee on Ways and Means United States House of Representatives

Office of the General Counsel

Office of the General Counsel 3211 FOURTH STREET NE WASHINGTON DC 20017-1194 202-541-3300 FAX 202-541-3337 July 22, 2010 TO: SUBJECT: Subordinate Organizations under USCCB Group Ruling [GEN: 0928] 2010

Office of the General Counsel 3211 FOURTH STREET NE WASHINGTON DC 20017-1194 202-541-3300 FAX 202-541-3337 July 22, 2010 TO: SUBJECT: Subordinate Organizations under USCCB Group Ruling [GEN: 0928] 2010

Office of the General Counsel

Office of the General Counsel 3211 FOURTH STREET NE WASHINGTON DC 20017-1194 202-541-3300 FAX 202-541-3337 July 6, 2012 TO: SUBJECT: Subordinate Organizations under USCCB Group Ruling [GEN: 0928] 2012

Office of the General Counsel 3211 FOURTH STREET NE WASHINGTON DC 20017-1194 202-541-3300 FAX 202-541-3337 July 6, 2012 TO: SUBJECT: Subordinate Organizations under USCCB Group Ruling [GEN: 0928] 2012

Gift Tax on Transfers to Section 501(c)(4) Organizations

(4) Organizations") Gift Tax on Transfers to Section 501(c)(4) Organizations ABA Tax/RPTE Joint Fall Meeting Denver, Colorado October 21, 2011 Preliminary Matter: Why are 501(c)(4)s hot? 2008 Elections Contribution Limits

Gift Tax on Transfers to Section 501(c)(4) Organizations ABA Tax/RPTE Joint Fall Meeting Denver, Colorado October 21, 2011 Preliminary Matter: Why are 501(c)(4)s hot? 2008 Elections Contribution Limits

Dear Chairmen Baucus and Camp, and Ranking Members Hatch and Levin:

April 25, 2013 The Honorable Max Baucus, Chairman Senate Committee on Finance 219 Dirksen Senate Office Building Washington, DC 20510 The Honorable Dave Camp, Chairman House Committee on Ways & Means 1102

April 25, 2013 The Honorable Max Baucus, Chairman Senate Committee on Finance 219 Dirksen Senate Office Building Washington, DC 20510 The Honorable Dave Camp, Chairman House Committee on Ways & Means 1102

Treasury Inspector General for Tax Administration Reports - October, 2018

Treasury Inspector General for Tax Administration Reports - October, 2018 TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Office of Audit Highlights THE TAXPAYER PROTECTION PROGRAM INCLUDES PROCESSES

Treasury Inspector General for Tax Administration Reports - October, 2018 TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Office of Audit Highlights THE TAXPAYER PROTECTION PROGRAM INCLUDES PROCESSES

STATEMENT OF JENNIFER E. BREEN ON BEHALF OF THE AMERICAN BAR ASSOCIATION SECTION OF TAXATION BEFORE THE COMMITTEE ON SMALL BUSINESS OF THE

STATEMENT OF JENNIFER E. BREEN ON BEHALF OF THE AMERICAN BAR ASSOCIATION SECTION OF TAXATION BEFORE THE COMMITTEE ON SMALL BUSINESS OF THE UNITED STATES HOUSE OF REPRESENTATIVES FOR THE HEARING ON IRS

STATEMENT OF JENNIFER E. BREEN ON BEHALF OF THE AMERICAN BAR ASSOCIATION SECTION OF TAXATION BEFORE THE COMMITTEE ON SMALL BUSINESS OF THE UNITED STATES HOUSE OF REPRESENTATIVES FOR THE HEARING ON IRS

Instructions for Reinstatement of Tax-Exempt Status

Instructions for Reinstatement of Tax-Exempt Status Dear Local PTA: The IRS has issued letters revoking the tax-exempt status of numerous organizations, including many local PTAs, for failure to file information

Instructions for Reinstatement of Tax-Exempt Status Dear Local PTA: The IRS has issued letters revoking the tax-exempt status of numerous organizations, including many local PTAs, for failure to file information

IRS Ogden, UT Certified Mail #

IRS Ogden, UT 84404 Certified Mail # 7006-3450-0000-7523-8440 August 20, 2008 To Whom it may concern: I am writing under the Freedom of Information Act, (FOIA) requesting documentation clarifying, specifically,

IRS Ogden, UT 84404 Certified Mail # 7006-3450-0000-7523-8440 August 20, 2008 To Whom it may concern: I am writing under the Freedom of Information Act, (FOIA) requesting documentation clarifying, specifically,

Top Legal and Tax Issues Facing Christian Not-for-Profits

Top Legal and Tax Issues Facing Christian Not-for-Profits Dave Moja, Partner John Butler, Tax Counsel 10.22.15 Tightening of Definitions 1 Definition Examples Related Organization Integrated Auxiliary

Top Legal and Tax Issues Facing Christian Not-for-Profits Dave Moja, Partner John Butler, Tax Counsel 10.22.15 Tightening of Definitions 1 Definition Examples Related Organization Integrated Auxiliary

WikiLeaks Document Release

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS21892 Application Process for Seeking Section 501(c)(3) Tax Exempt Status Erika Lunder, American Law Division December

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RS21892 Application Process for Seeking Section 501(c)(3) Tax Exempt Status Erika Lunder, American Law Division December

Case: 3:16-cv slc Document #: 1 Filed: 04/06/16 Page 1 of 13 UNITED STATES DISTRICT COURT WESTERN DISTRICT OF WISCONSIN. v. Case No.

Case: 3:16-cv-00215-slc Document #: 1 Filed: 04/06/16 Page 1 of 13 UNITED STATES DISTRICT COURT WESTERN DISTRICT OF WISCONSIN ANNIE LAURIE GAYLOR; DAN BARKER; IAN GAYLOR, PERSONAL REPRESENTATIVE OF THE

Case: 3:16-cv-00215-slc Document #: 1 Filed: 04/06/16 Page 1 of 13 UNITED STATES DISTRICT COURT WESTERN DISTRICT OF WISCONSIN ANNIE LAURIE GAYLOR; DAN BARKER; IAN GAYLOR, PERSONAL REPRESENTATIVE OF THE

SECTION 5. SMALL CASE PROCEDURE FOR REQUESTING COMPETENT AUTHORITY ASSISTANCE.01 General.02 Small Case Standards.03 Small Case Filing Procedure

Rev. Proc. 2002 52 SECTION 1. PURPOSE OF THE REVENUE PROCEDURE SECTION 2. SCOPE.01 In General.02 Requests for Assistance.03 Authority of the U.S. Competent Authority.04 General Process.05 Failure to Request

Rev. Proc. 2002 52 SECTION 1. PURPOSE OF THE REVENUE PROCEDURE SECTION 2. SCOPE.01 In General.02 Requests for Assistance.03 Authority of the U.S. Competent Authority.04 General Process.05 Failure to Request

OREGON DEPARTMENT OF JUSTICE CHARITABLE ACTIVITIES SECTION

OREGON DEPARTMENT OF JUSTICE CHARITABLE ACTIVITIES SECTION APPLICATION FOR A NEW CLASS A AND B LICENSE TO OPERATE BINGO GAMES INSTRUCTIONS This form is to be filed by organizations applying for a new class

OREGON DEPARTMENT OF JUSTICE CHARITABLE ACTIVITIES SECTION APPLICATION FOR A NEW CLASS A AND B LICENSE TO OPERATE BINGO GAMES INSTRUCTIONS This form is to be filed by organizations applying for a new class

Office of Chief Counsel Disclosure Branch

Description of document: Requested date: Released date: Posted date: Source of document: Treasury Inspector General for Tax Administration (TIGTA) Additional Options to Collect Tax Debts Need To Be Explored,

Description of document: Requested date: Released date: Posted date: Source of document: Treasury Inspector General for Tax Administration (TIGTA) Additional Options to Collect Tax Debts Need To Be Explored,

SAFARI CLUB INTERNATIONAL

SAFARI CLUB INTERNATIONAL Form 990 Compliance - Sample Governance Policies These sample policies may be adopted by a Chapter that is tax-exempt under Section 501(c)(4) of the Code in order to comply with

SAFARI CLUB INTERNATIONAL Form 990 Compliance - Sample Governance Policies These sample policies may be adopted by a Chapter that is tax-exempt under Section 501(c)(4) of the Code in order to comply with

Berke Farah LLP Attorneys at Law

Berke Farah LLP Attorneys at Law 1200 New Hampshire Ave. NW Suite 800 Washington, DC 20036 eberke@berkefarah.com 202.517.0585 www.berkefarah.com Jeff S. Jordan, Esq. Assistant General Counsel Complaints

Berke Farah LLP Attorneys at Law 1200 New Hampshire Ave. NW Suite 800 Washington, DC 20036 eberke@berkefarah.com 202.517.0585 www.berkefarah.com Jeff S. Jordan, Esq. Assistant General Counsel Complaints

The Housing Allowance Remains Under Attack

Tax Update The Housing Allowance Remains Under Attack Housing Allowance In 2011, the Freedom From Religion Foundation withdrew its first lawsuit against the Ministers Housing Allowance However, on September

Tax Update The Housing Allowance Remains Under Attack Housing Allowance In 2011, the Freedom From Religion Foundation withdrew its first lawsuit against the Ministers Housing Allowance However, on September

AMERICAN SOCIETY OF ASSOCIATION EXECUTIVES. Exempt Organization Tax Issues Compliance and Risk Avoidance in 2002

AMERICAN SOCIETY OF ASSOCIATION EXECUTIVES 2002 DC LEGAL SYMPOSIUM Exempt Organization Tax Issues Compliance and Risk Avoidance in 2002 September 25, 2002 Suzanne Ross McDowell Steptoe & Johnson LLP 1330

AMERICAN SOCIETY OF ASSOCIATION EXECUTIVES 2002 DC LEGAL SYMPOSIUM Exempt Organization Tax Issues Compliance and Risk Avoidance in 2002 September 25, 2002 Suzanne Ross McDowell Steptoe & Johnson LLP 1330

SMDL# ACA # 14

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard, Mail Stop S2-26-12 Baltimore, Maryland 21244-1850 Center for Medicaid, CHIP and Survey & Certification

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard, Mail Stop S2-26-12 Baltimore, Maryland 21244-1850 Center for Medicaid, CHIP and Survey & Certification

September 28, Authority for purchases of $250 billion in assets would be available upon enactment;

CONGRESSIONAL BUDGET OFFICE U.S. Congress Washington, DC 20515 Peter R. Orszag, Director September 28, 2008 Honorable Barney Frank Chairman Committee on Financial Services U.S. House of Representatives

CONGRESSIONAL BUDGET OFFICE U.S. Congress Washington, DC 20515 Peter R. Orszag, Director September 28, 2008 Honorable Barney Frank Chairman Committee on Financial Services U.S. House of Representatives

THE NASDAQ STOCK MARKET LLC NOTICE OF ACCEPTANCE OF AWC

THE NASDAQ STOCK MARKET LLC NOTICE OF ACCEPTANCE OF AWC Certified, Return Receipt Requested TO: FROM: Janney Montgomery Scott, LLC Mr. Eliot Duhan Vice President, Compliance 1717 Arch Street Philadelphia,

THE NASDAQ STOCK MARKET LLC NOTICE OF ACCEPTANCE OF AWC Certified, Return Receipt Requested TO: FROM: Janney Montgomery Scott, LLC Mr. Eliot Duhan Vice President, Compliance 1717 Arch Street Philadelphia,

Office of Chief Counsel

Department of the Treasury Internal Revenue Service 1 Office of Chief Counsel Notice CC-2005-009 May 19, 2005 Subject: Change in Pre-Review Requirements for Suit Letters Requesting Judicial Approval of

Department of the Treasury Internal Revenue Service 1 Office of Chief Counsel Notice CC-2005-009 May 19, 2005 Subject: Change in Pre-Review Requirements for Suit Letters Requesting Judicial Approval of

Internal Revenue Service

Internal Revenue Service Department of the Treasury Number: 200116007 Release Date: 4/20/2001 Index Number: 2055.00-00; 501.00-00 Washington, DC 20224 Person to Contact: Telephone Number: Refer Reply To:

Internal Revenue Service Department of the Treasury Number: 200116007 Release Date: 4/20/2001 Index Number: 2055.00-00; 501.00-00 Washington, DC 20224 Person to Contact: Telephone Number: Refer Reply To:

OPA Preparatory Academy Charter Schools

OPA Preparatory Academy Charter Schools 4740 Green River Road, Suite 210, Corona, CA 92880 Office: 951-496-4964 FAX: 951-496-4943 www.oxfordpreparatoryacademy.com Andrew Crowe, Managing Director September

OPA Preparatory Academy Charter Schools 4740 Green River Road, Suite 210, Corona, CA 92880 Office: 951-496-4964 FAX: 951-496-4943 www.oxfordpreparatoryacademy.com Andrew Crowe, Managing Director September

Comments Regarding the Application of Section 470 to Partnerships Solely as a Result of Section 168(h)(6)

(6)") July 26, 2006 The Honorable Charles E. Grassley Chairman Senate Finance Committee 219 Senate Dirksen Office Building Washington, D.C. 20515 The Honorable Max Baucus Ranking Minority Member Senate Finance

July 26, 2006 The Honorable Charles E. Grassley Chairman Senate Finance Committee 219 Senate Dirksen Office Building Washington, D.C. 20515 The Honorable Max Baucus Ranking Minority Member Senate Finance

NASDAQ OMX BX, INC. NOTICE OF ACCEPTANCE OF AWC

NASDAQ OMX BX, INC. NOTICE OF ACCEPTANCE OF AWC Certified, Return Receipt Requested TO: FROM: Timber Hill, LLC Mr. David M. Battan Executive Vice President and General Counsel One Pickwick Plaza Suite

NASDAQ OMX BX, INC. NOTICE OF ACCEPTANCE OF AWC Certified, Return Receipt Requested TO: FROM: Timber Hill, LLC Mr. David M. Battan Executive Vice President and General Counsel One Pickwick Plaza Suite

Re: Recommendations for Priority Guidance Plan (Notice )

") Courier s Desk Internal Revenue Service Attn: CC:PA:LPD:PR (Notice 2018-43) 1111 Constitution Avenue, N.W. Washington, DC 20224 Re: Recommendations for 2018-2019 Priority Guidance Plan (Notice 2018-43)

Courier s Desk Internal Revenue Service Attn: CC:PA:LPD:PR (Notice 2018-43) 1111 Constitution Avenue, N.W. Washington, DC 20224 Re: Recommendations for 2018-2019 Priority Guidance Plan (Notice 2018-43)

Irs Form Instructions 2012 >>>CLICK HERE<<<

Irs Form 8283 2008 Instructions 2012 contribution, you must file Form 1040 and item forms and instructions. Schedule A (Form 1040). 8283 tell you. Or go to IRS.gov. Click on Tools and then. Name. Title.

Irs Form 8283 2008 Instructions 2012 contribution, you must file Form 1040 and item forms and instructions. Schedule A (Form 1040). 8283 tell you. Or go to IRS.gov. Click on Tools and then. Name. Title.

1500 Pennsylvania Avenue, NW 1111 Constitution Ave, NW Washington, DC Washington, DC Constitution Ave, NW Internal Revenue Service

Page 1 of 5 The Honorable David J. Kautter Assistant Secretary for Tax Policy Commissioner Department of the Treasury Internal Revenue Service 1500 Pennsylvania Avenue, NW 1111 Constitution Ave, NW Washington,

Page 1 of 5 The Honorable David J. Kautter Assistant Secretary for Tax Policy Commissioner Department of the Treasury Internal Revenue Service 1500 Pennsylvania Avenue, NW 1111 Constitution Ave, NW Washington,

IN A MATTER BEFORE THE COMMISSIONER OF BANKS DOCKET NO. 06:035:RAL ) ) ) ) )

) ) ) )") STATE OF NORTH CAROLINA WAKE COUNTY IN A MATTER BEFORE THE COMMISSIONER OF BANKS DOCKET NO. 06:035:RAL IN RE: APPEAL OF PEARL McCAULEY d/b/a ACE ACCOUNTING TAX & FINANCIAL SERVICES REGISTRATION NUMBER

STATE OF NORTH CAROLINA WAKE COUNTY IN A MATTER BEFORE THE COMMISSIONER OF BANKS DOCKET NO. 06:035:RAL IN RE: APPEAL OF PEARL McCAULEY d/b/a ACE ACCOUNTING TAX & FINANCIAL SERVICES REGISTRATION NUMBER

November 6, Honorable Tom Harkin Chairman Committee on Agriculture, Nutrition, and Forestry United States Senate Washington, DC 20510

CONGRESSIONAL BUDGET OFFICE U.S. Congress Washington, DC 20515 Peter R. Orszag, Director November 6, 2007 Honorable Tom Harkin Committee on Agriculture, Nutrition, and Forestry United States Senate Washington,

CONGRESSIONAL BUDGET OFFICE U.S. Congress Washington, DC 20515 Peter R. Orszag, Director November 6, 2007 Honorable Tom Harkin Committee on Agriculture, Nutrition, and Forestry United States Senate Washington,

The Honorable Ronald L. Wyden, Chairman The Honorable Dave Camp, Chairman

The Honorable Ronald L. Wyden, Chairman The Honorable Dave Camp, Chairman Senate Committee on Finance House Committee on Ways and Means 219 Dirksen Senate Office Building 1102 Longworth House Office Building

The Honorable Ronald L. Wyden, Chairman The Honorable Dave Camp, Chairman Senate Committee on Finance House Committee on Ways and Means 219 Dirksen Senate Office Building 1102 Longworth House Office Building

AMENDED AND RESTATED ARTICLES OF INCORPORATION LAKEVILLE HOCKEY BOOSTERS

AMENDED AND RESTATED ARTICLES OF INCORPORATION OF LAKEVILLE HOCKEY BOOSTERS Pursuant to Minn. Stat. 317A.131, 317A.133 and 317A.139, LAKEVILLE HOCKEY BOOSTERS, by action of its Directors on September 14,

AMENDED AND RESTATED ARTICLES OF INCORPORATION OF LAKEVILLE HOCKEY BOOSTERS Pursuant to Minn. Stat. 317A.131, 317A.133 and 317A.139, LAKEVILLE HOCKEY BOOSTERS, by action of its Directors on September 14,

YOUR RIGHTS UNDER USERRA

REEMPLOYMENT RIGHTS YOUR RIGHTS UNDER USERRA THE UNIFORMED SERVICES EMPLOYMENT AND REEMPLOYMENT RIGHTS ACT USERRA protects the job rights of individuals who voluntarily or involuntarily leave employment

REEMPLOYMENT RIGHTS YOUR RIGHTS UNDER USERRA THE UNIFORMED SERVICES EMPLOYMENT AND REEMPLOYMENT RIGHTS ACT USERRA protects the job rights of individuals who voluntarily or involuntarily leave employment

Case 2:09-cv WBS-DAD Document 66 Filed 06/18/2010 Page 1 of 14 IN THE UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OF CALIFORNIA

Case :0-cv-0-WBS-DAD Document Filed 0//0 Page of 0 0 0 Richard L. Bolton (SBN: ) Boardman, Suhr, Curry & Field LLP P.O. Box Madison, Wisconsin 0-0 Pro Hac Vice Michael A. Newdow (SBN: 0) NEWDOWLAW P.O.

Case :0-cv-0-WBS-DAD Document Filed 0//0 Page of 0 0 0 Richard L. Bolton (SBN: ) Boardman, Suhr, Curry & Field LLP P.O. Box Madison, Wisconsin 0-0 Pro Hac Vice Michael A. Newdow (SBN: 0) NEWDOWLAW P.O.

THE INCORPORATION OF TENNESSEE BAPTIST CHURCHES

THE INCORPORATION OF TENNESSEE BAPTIST CHURCHES A church considering incorporation is very strongly encouraged to utilize the advice and assistance of an attorney experienced in Tennessee nonprofit corporation

THE INCORPORATION OF TENNESSEE BAPTIST CHURCHES A church considering incorporation is very strongly encouraged to utilize the advice and assistance of an attorney experienced in Tennessee nonprofit corporation

Attorney Advertising

Attorney Advertising For half a century, Caplin & Drysdale has been a leading provider of tax and related legal services to businesses, nonprofits, and individuals throughout the United States and around

Attorney Advertising For half a century, Caplin & Drysdale has been a leading provider of tax and related legal services to businesses, nonprofits, and individuals throughout the United States and around

United States District Court for the Southern District of Ohio NOTICE OF CLASS ACTION SETTLEMENT

United States District Court for the Southern District of Ohio NOTICE OF CLASS ACTION SETTLEMENT A court authorized this notice. This is not a solicitation from a lawyer. Please read this Notice carefully.

United States District Court for the Southern District of Ohio NOTICE OF CLASS ACTION SETTLEMENT A court authorized this notice. This is not a solicitation from a lawyer. Please read this Notice carefully.

1111 Constitution Avenue, NW 1111 Constitution Avenue, NW Washington, DC Washington, DC 20224

Mr. Scott Dinwiddie Mr. John Moriarty June 13, 2018 Page 2 of 2 June 13, 2018 Mr. Scott Dinwiddie Mr. John Moriarty Associate Chief Counsel Deputy Associate Chief Counsel Income Tax & Accounting Income

Mr. Scott Dinwiddie Mr. John Moriarty June 13, 2018 Page 2 of 2 June 13, 2018 Mr. Scott Dinwiddie Mr. John Moriarty Associate Chief Counsel Deputy Associate Chief Counsel Income Tax & Accounting Income

tinitro ~tatrs ~rnatr WASHINGTON, DC 20510

tinitro ~tatrs ~rnatr WASHINGTON, DC 20510 June 23, 2017 Jeff Mersmann President Pioneer Credit Recovery P.O. Box 100 Arcade, NY 14009 John Remondi President and CEO Navient P.O. Box 9640 Wilkes-Barre,

tinitro ~tatrs ~rnatr WASHINGTON, DC 20510 June 23, 2017 Jeff Mersmann President Pioneer Credit Recovery P.O. Box 100 Arcade, NY 14009 John Remondi President and CEO Navient P.O. Box 9640 Wilkes-Barre,

NYSE AMERICAN LLC LETTER OF ACCEPTANCE, WAIVER, AND CONSENT NO

NYSE AMERICAN LLC LETTER OF ACCEPTANCE, WAIVER, AND CONSENT NO. 2016-07-01304 TO: RE: NYSE AMERICAN LLC Merrill Lynch, Pierce, Fenner & Smith Incorporated, Respondent CRD No. 7691 Merrill Lynch, Pierce,

NYSE AMERICAN LLC LETTER OF ACCEPTANCE, WAIVER, AND CONSENT NO. 2016-07-01304 TO: RE: NYSE AMERICAN LLC Merrill Lynch, Pierce, Fenner & Smith Incorporated, Respondent CRD No. 7691 Merrill Lynch, Pierce,

February 13, Honorable Nancy Pelosi Speaker U.S. House of Representatives Washington, DC Dear Madam Speaker:

CONGRESSIONAL BUDGET OFFICE U.S. Congress Washington, DC 20515 February 13, 2009 Honorable Nancy Pelosi Speaker U.S. House of Representatives Washington, DC 20515 Dear Madam Speaker: The Congressional

CONGRESSIONAL BUDGET OFFICE U.S. Congress Washington, DC 20515 February 13, 2009 Honorable Nancy Pelosi Speaker U.S. House of Representatives Washington, DC 20515 Dear Madam Speaker: The Congressional

June 9, Honorable John McCain Chairman Committee on Armed Services United States Senate Washington, DC Dear Mr.

CONGRESSIONAL BUDGET OFFICE U.S. Congress Washington, DC 20515 Keith Hall, Director June 9, 2016 Honorable John McCain Chairman Committee on Armed Services United States Senate Washington, DC 20510 Dear

CONGRESSIONAL BUDGET OFFICE U.S. Congress Washington, DC 20515 Keith Hall, Director June 9, 2016 Honorable John McCain Chairman Committee on Armed Services United States Senate Washington, DC 20510 Dear

Section 2 Federal and State Tax Matters

Section 2 Federal and State Tax Matters Chapter 8: Tax-Exempt Status INTRODUCTION... 100 Political Campaign Prohibition... 101 Congregations... 105 Lutheran Schools... 110 Early Childhood Centers... 115

Section 2 Federal and State Tax Matters Chapter 8: Tax-Exempt Status INTRODUCTION... 100 Political Campaign Prohibition... 101 Congregations... 105 Lutheran Schools... 110 Early Childhood Centers... 115

CRS Report for Congress Received through the CRS Web

Order Code RL30877 CRS Report for Congress Received through the CRS Web Characteristics of and Reporting Requirements for Selected Tax-Exempt Organizations March 8, 2001 Marie B. Morris Legislative Attorney

Order Code RL30877 CRS Report for Congress Received through the CRS Web Characteristics of and Reporting Requirements for Selected Tax-Exempt Organizations March 8, 2001 Marie B. Morris Legislative Attorney

Audit and Tax Engagement Letters

GAVI Alliance Board Meeting, 30 November 1 December 2010 Doc #09a Audit and Tax Engagement Ltrs FOR DECISION The Board is responsible for appointing GAVI s independent auditor. At its meeting on 29 November

GAVI Alliance Board Meeting, 30 November 1 December 2010 Doc #09a Audit and Tax Engagement Ltrs FOR DECISION The Board is responsible for appointing GAVI s independent auditor. At its meeting on 29 November

Mar. 31, 2011 (202) Federal agencies address legal issues regarding Accountable Care Organizations

Federal agencies address legal issues regarding Accountable Care Organizations") DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services Room 352-G 200 Independence Avenue, SW Washington, DC 20201 Office of Media Affairs MEDICARE FACT SHEET FOR IMMEDIATE RELEASE

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services Room 352-G 200 Independence Avenue, SW Washington, DC 20201 Office of Media Affairs MEDICARE FACT SHEET FOR IMMEDIATE RELEASE

House tax bill what nonprofits need to know

NONPROFIT ORGANIZATIONS Alert House tax bill what nonprofits need to know November 6, 2017 By Michael J. Cooney and Anita Pelletier On November 2, 2017, the House Republicans released the proposed Tax

NONPROFIT ORGANIZATIONS Alert House tax bill what nonprofits need to know November 6, 2017 By Michael J. Cooney and Anita Pelletier On November 2, 2017, the House Republicans released the proposed Tax

UNITED STATES TAX COURT WASHINGTON, D.C December 28, 2011 PRESS RELEASE

UNITED STATES TAX COURT WASHINGTON, D.C. 20217 December 28, 2011 PRESS RELEASE Chief Judge John O. Colvin announced today that the United States Tax Court has proposed amendments to its Rules of Practice

UNITED STATES TAX COURT WASHINGTON, D.C. 20217 December 28, 2011 PRESS RELEASE Chief Judge John O. Colvin announced today that the United States Tax Court has proposed amendments to its Rules of Practice

IC Chapter 5. Employment Discrimination Against Disabled Persons

IC 22-9-5 Chapter 5. Employment Discrimination Against Disabled Persons IC 22-9-5-1 "Auxiliary aids and services" defined Sec. 1. As used in this chapter, "auxiliary aids and services" includes the following:

IC 22-9-5 Chapter 5. Employment Discrimination Against Disabled Persons IC 22-9-5-1 "Auxiliary aids and services" defined Sec. 1. As used in this chapter, "auxiliary aids and services" includes the following:

PROFESSIONAL ETHICS OF THE FLORIDA BAR OPINION 00 3 March 15, 2002

PROFESSIONAL ETHICS OF THE FLORIDA BAR OPINION 00 3 March 15, 2002 An attorney may provide a client with information about companies that offer non recourse advance funding and other financial assistance

PROFESSIONAL ETHICS OF THE FLORIDA BAR OPINION 00 3 March 15, 2002 An attorney may provide a client with information about companies that offer non recourse advance funding and other financial assistance

October 10, Paul Watkins, Director, Office of Innovation Bureau of Consumer Financial Protection 1700 G Street NW Washington, DC 20552

Paul Watkins, Director, Office of Innovation Bureau of Consumer Financial Protection 1700 G Street NW Washington, DC 20552 RE: Policy to Encourage Trial Disclosure Programs (Docket No. CFPB-2018-0023)

Paul Watkins, Director, Office of Innovation Bureau of Consumer Financial Protection 1700 G Street NW Washington, DC 20552 RE: Policy to Encourage Trial Disclosure Programs (Docket No. CFPB-2018-0023)

ROCKY MOUNTAIN TAX SEMINAR FOR PRIVATE FOUNDATIONS WHAT SHOULD WE EXPECT NOW FROM THE IRS?

ROCKY MOUNTAIN TAX SEMINAR FOR PRIVATE FOUNDATIONS September 16-18, 2015 Colorado Springs, Colorado WHAT SHOULD WE EXPECT NOW FROM THE IRS? by Celia Roady Morgan, Lewis & Bockius LLP 1111 Pennsylvania

ROCKY MOUNTAIN TAX SEMINAR FOR PRIVATE FOUNDATIONS September 16-18, 2015 Colorado Springs, Colorado WHAT SHOULD WE EXPECT NOW FROM THE IRS? by Celia Roady Morgan, Lewis & Bockius LLP 1111 Pennsylvania

THE PRINCIPAL FINANCIAL GROUP IS ASKING YOU TO MAKE AN IMPORTANT DECISION ABOUT OUR ORGANIZATION S FUTURE

POLICYHOLDER GUIDE FOR GROUP INSURANCE CUSTOMERS THE PRINCIPAL FINANCIAL GROUP IS ASKING YOU TO MAKE AN IMPORTANT DECISION ABOUT OUR ORGANIZATION S FUTURE THIS SPECIAL GUIDE ADDRESSES THE ISSUES OF PARTICULAR

POLICYHOLDER GUIDE FOR GROUP INSURANCE CUSTOMERS THE PRINCIPAL FINANCIAL GROUP IS ASKING YOU TO MAKE AN IMPORTANT DECISION ABOUT OUR ORGANIZATION S FUTURE THIS SPECIAL GUIDE ADDRESSES THE ISSUES OF PARTICULAR

EASIER COMPLIANCE IS GOAL OF NEW INTERMEDIATE SANCTION REGULATIONS

EASIER COMPLIANCE IS GOAL OF NEW INTERMEDIATE SANCTION REGULATIONS By Steven T. Miller 1 On January 10, 2001, the Treasury Department issued Temporary Regulations interpreting the benefit limitation provisions

EASIER COMPLIANCE IS GOAL OF NEW INTERMEDIATE SANCTION REGULATIONS By Steven T. Miller 1 On January 10, 2001, the Treasury Department issued Temporary Regulations interpreting the benefit limitation provisions

THE NASDAQ STOCK MARKET LLC NOTICE OF ACCEPTANCE OF Awe

THE NASDAQ STOCK MARKET LLC NOTICE OF ACCEPTANCE OF Awe Certified, Return Receipt Requested TO: Archipelago Securities L.L.C. Mr. Paul D. Adcock Executive Principal 100 South Wacker Drive Suite 1800 Chicago,

THE NASDAQ STOCK MARKET LLC NOTICE OF ACCEPTANCE OF Awe Certified, Return Receipt Requested TO: Archipelago Securities L.L.C. Mr. Paul D. Adcock Executive Principal 100 South Wacker Drive Suite 1800 Chicago,

January 6, Honorable John Boehner Speaker of the House U.S. House of Representatives Washington, DC Dear Mr. Speaker:

CONGRESSIONAL BUDGET OFFICE U.S. Congress Washington, DC 20515 Douglas W. Elmendorf, Director January 6, 2011 Honorable John Boehner Speaker of the House U.S. House of Representatives Washington, DC 20515

CONGRESSIONAL BUDGET OFFICE U.S. Congress Washington, DC 20515 Douglas W. Elmendorf, Director January 6, 2011 Honorable John Boehner Speaker of the House U.S. House of Representatives Washington, DC 20515

Qualified Domestic Relations Order (QDRO)

") Retirement Solutions Qualified Domestic Relations Order (QDRO) Employer s Administrative Manual This manual was prepared to assist in the processing of Qualified Domestic Relations Orders. The information

Retirement Solutions Qualified Domestic Relations Order (QDRO) Employer s Administrative Manual This manual was prepared to assist in the processing of Qualified Domestic Relations Orders. The information

GREATER INDIANA COMBINED FEDERAL CAMPAIGN

GREATER INDIANA COMBINED FEDERAL CAMPAIGN 2015 Application Instructions for Local Federations OMB APPROVED No. 3206-0131 BACKGROUND Enclosed is the approved application by the Local Federal Coordinating

GREATER INDIANA COMBINED FEDERAL CAMPAIGN 2015 Application Instructions for Local Federations OMB APPROVED No. 3206-0131 BACKGROUND Enclosed is the approved application by the Local Federal Coordinating

Behavioral Health Claims and Mental Health Parity

Behavioral Health Claims and Mental Health Parity Alan Tawshunsky Tawshunsky Law Firm PLLC Willard Office Building 1455 Pennsylvania Avenue NW, Suite 400 Washington, DC 20004 (202) 621-1781 alan@tawshunsky.com

Behavioral Health Claims and Mental Health Parity Alan Tawshunsky Tawshunsky Law Firm PLLC Willard Office Building 1455 Pennsylvania Avenue NW, Suite 400 Washington, DC 20004 (202) 621-1781 alan@tawshunsky.com

Walk Like An Exemption: Fast-Track and Maintain the Right Tax Exemption

Walk Like An Exemption: Fast-Track and Maintain the Right Tax Exemption California Charter Schools Conference March 17, 2015 Kevin M. Davis Greta A. Proctor 1 What We Will Cover in This Program What Is

Walk Like An Exemption: Fast-Track and Maintain the Right Tax Exemption California Charter Schools Conference March 17, 2015 Kevin M. Davis Greta A. Proctor 1 What We Will Cover in This Program What Is

Section 280G. Golden Parachute Payments T.D DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Parts 1. Golden Parachute Payments

DATES: Effective Date: August 4, 2003. These regulations apply to any payment that is contingent on a change in ownership or control if the change in ownership or control occurs on or after January 1,

DATES: Effective Date: August 4, 2003. These regulations apply to any payment that is contingent on a change in ownership or control if the change in ownership or control occurs on or after January 1,

Internal Revenue Service Number: Release Date: 3/2/2007 Index Number:

Internal Revenue Service Number: 200709036 Release Date: 3/2/2007 Index Number: 1031.06-00 ---------------- ------------------------------------------------------- -------------------------------------------------

Internal Revenue Service Number: 200709036 Release Date: 3/2/2007 Index Number: 1031.06-00 ---------------- ------------------------------------------------------- -------------------------------------------------

CFPB Supervision and Examination Process

Background Title X of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the Act) 1 established the Consumer Financial Protection Bureau (CFPB) and authorizes it to supervise certain

Background Title X of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the Act) 1 established the Consumer Financial Protection Bureau (CFPB) and authorizes it to supervise certain

CITY OF SOUTH MIAMI OFFICE OF THE CITY ATTORNEY INTER-OFFICE MEMORANDUM. The Honorable Mayor, Vice Mayor and Members of the City Commission

CITY OF SOUTH MIAMI OFFICE OF THE CITY ATTORNEY INTER-OFFICE MEMORANDUM To: Cc: From: Date: The Honorable Mayor, Vice Mayor and Members of the City Commission Maria Menendez, City Clerk Thomas F. Pepe,

CITY OF SOUTH MIAMI OFFICE OF THE CITY ATTORNEY INTER-OFFICE MEMORANDUM To: Cc: From: Date: The Honorable Mayor, Vice Mayor and Members of the City Commission Maria Menendez, City Clerk Thomas F. Pepe,

Significant Actions Were Taken to Address Small Corporations Erroneously Paying the Alternative Minimum Tax, but Additional Actions Are Still Needed

Significant Actions Were Taken to Address Small Corporations Erroneously Paying the Alternative Minimum Tax, but Additional Actions Are Still Needed May 2003 Reference Number: 2003-30-114 This report has

Significant Actions Were Taken to Address Small Corporations Erroneously Paying the Alternative Minimum Tax, but Additional Actions Are Still Needed May 2003 Reference Number: 2003-30-114 This report has

GAO SOCIAL SECURITY ADMINISTRATION. Revision to the Government Pension Offset Exemption Should Be Considered

GAO United States General Accounting Office Report to the Chairman, Subcommittee on Social Security, Committee on Ways and Means, House of Representatives August 2002 SOCIAL SECURITY ADMINISTRATION Revision

GAO United States General Accounting Office Report to the Chairman, Subcommittee on Social Security, Committee on Ways and Means, House of Representatives August 2002 SOCIAL SECURITY ADMINISTRATION Revision

UNITED STATES DISTRICT COURT WESTERN DISTRICT OF WISCONSIN. V. Case No. 11-CV-626 COMPLAINT

UNITED STATES DISTRICT COURT WESTERN DISTRICT OF WISCONSIN FREEDOM FROM RELIGION FOUNDATION, INC.; ANNIE LAURIE GAYLOR; ANNE NICOL GAYLOR; and DAN BARKER, Plaintiffs, V. Case No. 11-CV-626 TIMOTHY GEITHNER,

UNITED STATES DISTRICT COURT WESTERN DISTRICT OF WISCONSIN FREEDOM FROM RELIGION FOUNDATION, INC.; ANNIE LAURIE GAYLOR; ANNE NICOL GAYLOR; and DAN BARKER, Plaintiffs, V. Case No. 11-CV-626 TIMOTHY GEITHNER,

October 26, Agreed to Review Process

October 26, 2009 Compliance Review and Interpretations Committee {Sent Via E-Mail} C/O Scott Peterson, Executive Director 4205 Hillsboro Pike, Suite 305 Nashville, TN 37215 Re: Public Comment on State

October 26, 2009 Compliance Review and Interpretations Committee {Sent Via E-Mail} C/O Scott Peterson, Executive Director 4205 Hillsboro Pike, Suite 305 Nashville, TN 37215 Re: Public Comment on State

Consequences Of EU's Belgium Tax Scheme Decision

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com Consequences Of EU's Belgium Tax Scheme Decision Law360,

Portfolio Media. Inc. 860 Broadway, 6th Floor New York, NY 10003 www.law360.com Phone: +1 646 783 7100 Fax: +1 646 783 7161 customerservice@law360.com Consequences Of EU's Belgium Tax Scheme Decision Law360,