EKS 3 SCENARIO-BASED TRAINING

|

|

|

- Marion Thomas

- 6 years ago

- Views:

Transcription

1 EKS 3 SCENARIO-BASED TRAINING

2 THIS LESSON YOU WILL REVIEW Filing Status Personal and Dependency Exemptions Income: W-2 Credits Child Tax Credit Additional Child Tax Credit Child and Dependent Care Credit Itemized Deductions vs. Standard Deduction ACA: 1095-C Employer Coverage Form 8888

3 TODAY YOU WILL LEARN Filing Status - Head of Household Interest Income Unemployment Income Exemptions: Dependency Adjustments: Student Loan Interest Credits Nonrefundable: CDCC, CTC, AOTC Refundable: EITC, Additional CTC, AOTC

4 LET S GET STARTED This will be you!

5 1. SCENARIO 3 CHERYL WEBSTER Let s meet the taxpayer

6 Hello! I AM CHERYL WEBSTER I volunteered with United Way in the past. This year was a bit rough when they replaced all the jobs at my work with robots. I m happy to be getting some help from other volunteers.

7 FACTS ABOUT ME: I m MARRIED, but have not lived with my spouse since June 2010 I paid all expenses and provide all support for my children I lost my job in October and had no health insurance from Nov 1 - Dec 31

8 I HAVE TWO CHILDREN Jeremy First year college student. Majoring in accounting. Future EKS volunteer? Joshua Attended 5 weeks of summer camp. Learned how to sail in the bay. It was awesome!

9 2. SCENARIO 3 CHERYL WEBSTER Let s look at the Intake/Interview Sheet

10 What question(s) should you ask Cheryl?

11 What forms should you look for in her packet?

12

13 INTERVIEW NOTES $700 Local College by check $175 Cash Donation to United Way Bay Area $625 Crossroads Child Care Center for day camp, no overnights $250 Doctor visit co-pays $969 Student Loan Interest NOT Full time student

14 BEFORE DIVING IN... Does Cheryl need to file? Is the return in scope? Tab A

15 3. SCENARIO 3 CHERYL WEBSTER 1040 step by step

16 FILING STATUS HEAD OF HOUSEHOLD Generally for unmarried taxpayers who paid more than half the cost of keeping up a home for a qualified dependent relative during the tax year. B8-B11

17 ANALYZE THE LIVING SITUATION Marital Status as of December 31st Others living in the home & their relationship/ dependency Who paid >50% cost of home upkeep Depends if qualifying person is taxpayer s dependent College students who attend school in another area often qualify as living in the home Dependent parents are not required to live with the taxpayer B8-B11

18 What is Cheryl s filing status? B-8

19 After a whirlwind love affair in college, we got married after only dating for six months. A few years after Joshua was born, he said he was going out for cigarettes and never came home.

20 WATCH instructor Enter Cheryl s main info and filing status Tab B

21 Now you try Enter Cheryl s main info and filing status Tab B

22 EXEMPTIONS: DEPENDENCY Amount that taxpayers can claim for themselves, their spouses, and eligible dependents. C1-C8

23 DEPENDENCY EXEMPTIONS Amount that taxpayers can claim for a qualifying child or qualifying relative. Each exemption reduces the income subject to tax. The exemption amount is a set amount that changes from year to year. One exemption is allowed for each qualifying child or qualifying relative claimed as a dependent. C1-C8

24 DEPENDENCY TESTS Tests used for identifying qualifying children or qualifying relatives as dependents. C1-C8

25 MUST MEET TESTS TO BE... Qualifying Child U.S. citizen or resident test, Joint return test, Dependent taxpayer test, Relationship test, Age test, Support test, Residence test, Qualifying child of more than one person Qualifying Relative U.S. citizen or resident test, Joint return test, Dependent taxpayer test, Not a qualifying child test, Member of household or relationship test, Support test, and Gross income test C1-C8

26 Can Cheryl claim any dependents? C-3

27 I love my kids to death, but they re bleeding me dry! I still have my own student loans to pay off and now I m paying for Jeremy as well. I pay for 100% of their expenses, but I know it ll all be worth it.

28 WATCH instructor Enter Cheryl s exemptions Tab C

29 Now you try Enter Cheryl s exemptions Tab C

30 INTEREST & UNEMPLOYMENT INCOME INTEREST All interest and dividend income are taxable with some exceptions (Savings bonds & Roth IRA). All Interest and dividend income must be reported! UNEMPLOYMENT Generally includes any amount received under an unemployment compensation law of the U.S. or of a state in the U.S. In most cases, unemployment compensation is taxable. D7-D8

31 Scenario 3 Interest Income

32 Scenario 3 Unemployment Income

33 WATCH instructor Enter Cheryl s income: W-2, interest and unemployment D7-D8

34 Now you try Enter Cheryl s income: W-2, interest and unemployment D7-D8

35 ADJUSTMENTS: STUDENT LOAN INTEREST Loan must have been for qualified educational expenses Taxpayer must be liable for the debt Student must have been enrolled at least half-time Maximum adjustment is $2,500 E-6

36 Scenario 3 Student Loan Interest

37 Can Cheryl claim Student Loan Interest Deduction? E-8

38 WATCH instructor Enter Cheryl s student loan interest E-1

39 Now you try Enter Cheryl s student loan interest E-1

Child Tax Credit (CTC)")

40 TAX CREDITS Child and Dependent Care Credit (CDCC) Retirement Savings Contribution Credit (RSCC) Child Tax Credit (CTC) G5-G13

41 CREDITS: CHILD & DEPENDENT CARE CREDIT A nonrefundable credit that allows taxpayers to claim a credit for paying someone to care for their qualifying dependents while they work or look for work. G5-G8

42 CDCC QUALIFYING PERSONS Qualifying Child To be identified as a qualifying child, a person must be under 13 and meet the tests to be claimed as a dependent (with some exceptions). Other Qualifying Persons To be identified as a qualifying person for CDCC, a person must be incapable of self care and live with the taxpayer more than ½ the year. G5-G8

43 CDCC WORK-RELATED EXPENSES Cost of care outside the home for dependents under 13, for example, preschool or home day care, before- or afterschool care for a child in kindergarten or higher grade Cost of care for any other qualifying person, for example, dependent care Household expenses that are at least partly for the well-being and protection of a qualifying person, for example, the services of a housekeeper or cook G5-G8

44 CHILD CARE NOTES $625 Crossroads Child Care Center Address 1648 Baylor Avenue San Francisco, CA XXXXX3 Employer Identification Number 5 Weeks Summer Camp Day Camp No overnight stays

45 Does Cheryl qualify for child and dependent care credit? G-6

46 Joshua saw Pirates of the Caribbean and now wants to be a pirate. So over the summer I signed him up for DAY camp learning how to sail in the Bay. Now I just need to find him a swashbuckling camp!

47 WATCH instructor Enter Cheryl s CDCC G7-G8

48 Now you try Enter Cheryl s CDCC G7-G8

49 CREDITS: RETIREMENT SAVINGS CONTRIBUTION CREDIT A nonrefundable credit qualifying taxpayers may claim if they made a contribution to a qualified plan G9-G11

50 RETIREMENT SAVINGS CONTRIBUTION CREDIT Nonrefundable tax credit for 10%, 20%, or 50% of eligible contributions to a retirement plan. The credit rate depends on AGI and filing status. Maximum of $1,000 ($2,000 for married filing jointly) Must meet all these qualifications: Cannot be a dependent on someone else s return Cannot be a student Must be at least 18 MAGI must be less than $30,750 ($61,500 MFJ / $46,125 HoH) Contributions through employer appear on the W-2 in Box 12 with code D, E, F, G, H, S, AA, BB, or EE Contributions to an IRA or other retirement plan appear on Form 5498 G9-G11

51 Cheryl Webster W-2

52 CALCULATING THE CREDIT The Retirement Savings Contribution Credit is calculated automatically on Form 8880 The final amount can be found on Line 12 of Form 8880 The amount is transferred to Line 51 on Page 2 of Form 1040 in the Nonrefundable Credits section G9-G11

53 Does Cheryl qualify for Retirement Savings Contribution Credit? G-9

54 When I joined the company a million years ago, they asked me if I wanted to save for retirement. I said yes but didn t think much of it. Now I m grateful to have a little something saved.

55 WATCH instructor Enter Cheryl s retirement savings contribution credit (F8880) G-10

56 Now you try Enter Cheryl s retirement savings contribution credit (F8880) G-10

57 CREDITS: CHILD TAX CREDIT A credit that may reduce tax by as much as $1,000 for each qualifying child G12-G13

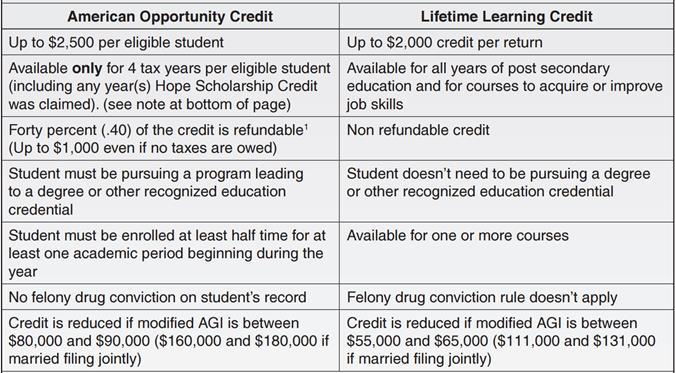

58 CHILD TAX CREDIT DETERMINING ELIGIBILITY Tests for the taxpayer Tax liability? For child tax credit (nonrefundable) Earned Income? For additional child tax credit (refundable) 3 or more children? For additional child tax credit (refundable) Tests for each child Is the child under 17 years of age? Is the child the taxpayer s dependent? G12-G13

59 CHILD TAX CREDIT CALCULATING THE CREDIT Child tax credit (nonrefundable) $1,000 for each child up to the taxpayer s tax liability Additional child tax credit (refundable) Use Schedule % of earned income over $3,000 Up to the amount of unused child tax credit Don t worry! The tax software calculates both automatically G12-G13

60 Does Cheryl qualify for CTC? G12-G13

61 WATCH instructor Cheryl s CTC is automatic

62 CREDITS: EDUCATION CREDITS Credits that reduce the amount of tax due and are based on qualified education expenses that the taxpayer paid during the tax year. Tab J

63 WHO CAN TAKE EDUCATION CREDITS? Taxpayers can take education credits for themselves, their spouse and/or dependents (claimed on the tax return) If they were attending an eligible postsecondary educational institution during the tax year Taxpayers cannot take education credits if they themselves can be claimed as dependents J-4

64 WHAT IS AN ELIGIBLE INSTITUTION? Any college, university, vocational school, or other postsecondary educational institution eligible to participate in a student aid program administered by the U.S. Department of Education A searchable database of all accredited schools is available at J-4

65 WHAT ARE QUALIFYING EXPENSES? Tuition and fees, books, supplies required for a course of study Expenses that do not qualify: Room & board, insurance, medical expenses, transportation costs, or other similar living expenses Any course involving sports, games, or hobbies Unless it is part of the student s degree program Or helps the student to acquire or improve job skills Expenses paid for using Pell grants, scholarships, etc. J-5

66 AMERICAN OPPORTUNITY TAX CREDIT A refundable credit of up to $2,500 for qualified education expenses paid for each eligible student. Forty percent of the credit is refundable, up to $1,000. Changes to this credit (formerly called the Hope credit), made it available to a broader range of taxpayers, including high income taxpayers and those who owe no tax. J2-J5

67 LIFETIME LEARNING CREDIT A nonrefundable credit of up to $2,000 for qualified education expenses for students enrolled in eligible educational institutions. It is available to students for all years of postsecondary education and for courses to acquire or improve job skills. J2-J5

68 COMPARISON J-4

69 COMPARISON QUALIFYING EXPENSES American Opportunity Expenses for books, supplies and equipment needed for a course of study, whether or not the materials are purchased from the educational institution as a condition of enrollment or attendance. Lifetime Learning Expenses for course-related books only if they are purchased directly from the educational institution. Expenses for supplies, fees, and equipment only if they are paid to the institution as a condition of enrollment or attendance. J-4

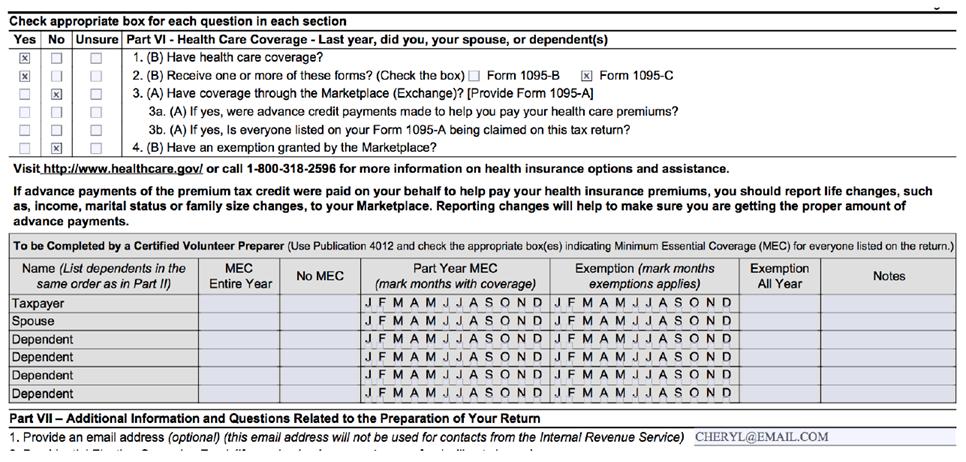

70 Does Cheryl qualify for Education Credits? J-4

71 WATCH instructor Enter Cheryl s education credit (F8863) J7-J8

72 Now you try Enter Cheryl s education credit (F8863) J7-J8

73 ACA: COVERAGE EXEMPTIONS Coverage exemptions are claimed on Form 8965, Health Care Coverage Exemptions. Tab H

74 WHAT ARE THE HEALTH COVERAGE EXEMPTIONS? Household Members of the tax household may be eligible to claim an exemption from having MEC. Some exemptions apply to the entire tax household for the year. Individual Each member of the tax household individually and generally apply on a monthly basis. H8-H17

75 HOUSEHOLD EXEMPTIONS Household income below the return filing threshold Gross income below the filing threshold H-11

76 INDIVIDUAL EXEMPTIONS Short coverage gap Citizens living abroad and certain noncitizens Incarceration Ineligible for Medicaid in a state that did not expand Medicaid (Does not apply to California) Members of federally recognized Indian tribes Members of certain religious sects Unaffordable coverage Aggregate self-only coverage considered unaffordable H-14

77 HOW TO OBTAIN A COVERAGE EXEMPTION Some exemptions are granted only by the Marketplace. Some exemptions are claimed only on a tax return. Some exemptions may be claimed from either the Marketplace or on the tax return. H-14

78 Does Cheryl qualify for any ACA Exemption? H-14

79 WATCH instructor Enter Cheryl s ACA exemption H12-H13

80 Now you try Enter Cheryl s ACA exemption H12-H13

81 Does Cheryl qualify for EITC? I-2

82 WATCH instructor Enter Cheryl s EITC Tab I

83 Now you try Enter Cheryl s EITC Tab I

84 4. SCENARIO 3 CHERYL WEBSTER Finishing the return

85 CHECK YOUR WORK QUALITY REVIEW Review entries: Main info, filing status & exemptions Income: W-2, interest, unemployment Adjustments: Student loan interest deduction Credits: RSCC, CDCC, Education, CTC, EIC ACA: Exemption Do we have matching AGI & refund?

86 $35,676 AGI (2016 calculations) $6,442 Federal Refund (2016 calculations)

87 FINISHING THE RETURN Ask the questions in the Prep Use Fields All returns must be Quality Reviewed Print return for Cheryl Review return with Cheryl Have Cheryl sign 8879s for Federal and State and remind her she is responsible for the return

BASIC CERTIFICATION STUDY GUIDE Tax Year 2018

BASIC CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents BASIC SCENARIO 1: Jeff and Linda Arnold... 1 BASIC SCENARIO 2: Ava Harvard... 2 BASIC SCENARIO 3: Ellen Santos... 3 BASIC SCENARIO 4: Christopher

BASIC CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents BASIC SCENARIO 1: Jeff and Linda Arnold... 1 BASIC SCENARIO 2: Ava Harvard... 2 BASIC SCENARIO 3: Ellen Santos... 3 BASIC SCENARIO 4: Christopher

Adjustments to Income

Adjustments to Income Pub 4491 Lesson 18 Pub 4012 Tab E Adjusted Gross Income Total Income minus Adjustments = Adjusted Gross Income (AGI) 2 1 Intake/Interview 3 A2 In-Scope Adjustments Educator expenses

Adjustments to Income Pub 4491 Lesson 18 Pub 4012 Tab E Adjusted Gross Income Total Income minus Adjustments = Adjusted Gross Income (AGI) 2 1 Intake/Interview 3 A2 In-Scope Adjustments Educator expenses

BASIC CERTIFICATION STUDY GUIDE Tax Year 2018

BASIC CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents BASIC SCENARIO 1: Jeff and Linda Arnold... 1 BASIC SCENARIO 2: Ava Harvard... 2 BASIC SCENARIO 3: Ellen Santos... 3 BASIC SCENARIO 4: Christopher

BASIC CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents BASIC SCENARIO 1: Jeff and Linda Arnold... 1 BASIC SCENARIO 2: Ava Harvard... 2 BASIC SCENARIO 3: Ellen Santos... 3 BASIC SCENARIO 4: Christopher

Nonrefundable Credits

Nonrefundable Credits TaxSlayer Navigation: Federal Section>Deductions>Credits Menu Select for Form 1116, Foreign Tax Credit Select for Form 2441 Child Tax Credit. See Child Tax Credit Tip & Interview

Nonrefundable Credits TaxSlayer Navigation: Federal Section>Deductions>Credits Menu Select for Form 1116, Foreign Tax Credit Select for Form 2441 Child Tax Credit. See Child Tax Credit Tip & Interview

REFUNDABLE TAX CREDITS NOT LIMITED TO TAX LIABILITY

REFUNDABLE TAX CREDITS NOT LIMITED TO TAX LIABILITY FORM 1040 page 2 Non-refundable credits Refundable credits Refundable credits Line 66a Earned income credit (EIC or EITC) Line 67 Additional child tax

REFUNDABLE TAX CREDITS NOT LIMITED TO TAX LIABILITY FORM 1040 page 2 Non-refundable credits Refundable credits Refundable credits Line 66a Earned income credit (EIC or EITC) Line 67 Additional child tax

Affordable Care Act. Pub 4012 ACA Tab Pub 4491 Lesson 3

Affordable Care Act Pub 4012 ACA Tab Pub 4491 Lesson 3 ACA IT s The Law Like it or not Repeal or change possible But, Applies to 2016 Deal with it The Good News Most of clients have Medicare 2 ACA Summary

Affordable Care Act Pub 4012 ACA Tab Pub 4491 Lesson 3 ACA IT s The Law Like it or not Repeal or change possible But, Applies to 2016 Deal with it The Good News Most of clients have Medicare 2 ACA Summary

1/19/2017. Agenda. Due Diligence and the Credits for 2016 Ethics (1 hours) Overview of Credits (1 hour Tax Law)

Overview of Credits (1 hour Tax Law)") Due Diligence and the Credits for 2016 Ethics (1 hours) Overview of Credits (1 hour Tax Law) January 19, 2017 Agenda Overview of the Child Tax Credit Additional Child Tax Credit American Opportunity Credit

Due Diligence and the Credits for 2016 Ethics (1 hours) Overview of Credits (1 hour Tax Law) January 19, 2017 Agenda Overview of the Child Tax Credit Additional Child Tax Credit American Opportunity Credit

City/State/Zip Relationship to Child Account Number Amount of Deposit

ESA APPLICATION Child/Student (Designated Beneficiary) Contributor (Depositor) - - - - Social Security Number Social Security Number - - Address Date of Birth Address Phone Number - - City/State/Zip Phone

ESA APPLICATION Child/Student (Designated Beneficiary) Contributor (Depositor) - - - - Social Security Number Social Security Number - - Address Date of Birth Address Phone Number - - City/State/Zip Phone

FOR DOMESTIC VIOLENCE SURVIVORS. Morgan Young Immigration and Poverty Attorney End Domestic Abuse WI

TAX PROTECTIONS FOR DOMESTIC VIOLENCE SURVIVORS Morgan Young Immigration and Poverty Attorney End Domestic Abuse WI Some materials adapted from the National Women s Law Center STARTING THE TAX RETURN 1

TAX PROTECTIONS FOR DOMESTIC VIOLENCE SURVIVORS Morgan Young Immigration and Poverty Attorney End Domestic Abuse WI Some materials adapted from the National Women s Law Center STARTING THE TAX RETURN 1

Patient Protection and Affordable Care Act (PPACA) Better known as ACA

Better known as ACA") Patient Protection and Affordable Care Act (PPACA) Better known as ACA Status The following presentation is an overview of the Affordable Care Act (ACA) Some forms and specific documentation are in draft

Patient Protection and Affordable Care Act (PPACA) Better known as ACA Status The following presentation is an overview of the Affordable Care Act (ACA) Some forms and specific documentation are in draft

VITA/TCE Basic Certification Topics on Affordable Care Act. Current as of November 20, 2017

VITA/TCE Basic Certification Topics on Affordable Care Act Current as of November 20, 2017 MEC & SRP REFRESHER What does the ACA require? 3 or or Coverage Exemption SRP Minimum Essential Coverage (MEC)

VITA/TCE Basic Certification Topics on Affordable Care Act Current as of November 20, 2017 MEC & SRP REFRESHER What does the ACA require? 3 or or Coverage Exemption SRP Minimum Essential Coverage (MEC)

Earned Income Table. Earned Income

Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from self-employment Gross income of a statutory

Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from self-employment Gross income of a statutory

2018 Instructions for Form 8965

Department of the Treasury Internal Revenue Service 2018 Instructions for Form 8965 Health Coverage Exemptions (and Instructions for Figuring Your Shared Responsibility Payment) Section references are

Department of the Treasury Internal Revenue Service 2018 Instructions for Form 8965 Health Coverage Exemptions (and Instructions for Figuring Your Shared Responsibility Payment) Section references are

Taxes and Consumer Education

Outreach and Enrollment Distance Learning Series Taxes and Consumer Education August 13, 2015 Welcome to the Outreach and Enrollment Webcast Series All lines are muted. Please use chat to ask a question

Outreach and Enrollment Distance Learning Series Taxes and Consumer Education August 13, 2015 Welcome to the Outreach and Enrollment Webcast Series All lines are muted. Please use chat to ask a question

EDUCATIONAL SAVINGS OPTIONS COMPARISON

EDUCATIONAL SAVINGS OPTIONS COMPARISON January 17, 2013 SCHOLARSHARE COVERDELL ESA ROTH IRA TRADITIONAL IRA SAVINGS BONDS GIFTS TO CHILDREN SUMMARY OF THE OPTION ScholarShare is a college savings program

EDUCATIONAL SAVINGS OPTIONS COMPARISON January 17, 2013 SCHOLARSHARE COVERDELL ESA ROTH IRA TRADITIONAL IRA SAVINGS BONDS GIFTS TO CHILDREN SUMMARY OF THE OPTION ScholarShare is a college savings program

Tips for Maximizing American Opportunity Credit

Tips for Maximizing American Opportunity Credit CFR 26 Sec. 125A-5(c) (3) Scholarships and fellowship grants Document 5311 (11-2018) Catalog Number 71763Y Department of the Treasury Internal Revenue Service

Tips for Maximizing American Opportunity Credit CFR 26 Sec. 125A-5(c) (3) Scholarships and fellowship grants Document 5311 (11-2018) Catalog Number 71763Y Department of the Treasury Internal Revenue Service

Who wants to tell us. Why do Tax Credits matter?

Who wants to tell us Why do Tax Credits matter? Non-Refundable Credits Non-Refundable Credits Other Dependent Credit Lifetime Learning (Education) Credit Credit for Child and Dependent Care Retirement

Who wants to tell us Why do Tax Credits matter? Non-Refundable Credits Non-Refundable Credits Other Dependent Credit Lifetime Learning (Education) Credit Credit for Child and Dependent Care Retirement

VITA/TCE Basic Certification Topics on Affordable Care Act. Current as of November 20, 2017

VITA/TCE Basic Certification Topics on Affordable Care Act Current as of November 20, 2017 Agenda 2 Webinar #1 Basic Certification Topics Minimum essential coverage Shared responsibility payment Exemptions

VITA/TCE Basic Certification Topics on Affordable Care Act Current as of November 20, 2017 Agenda 2 Webinar #1 Basic Certification Topics Minimum essential coverage Shared responsibility payment Exemptions

Adjustments to Income

Adjustments to Income Health Savings Account select to open Form 8889. (HSA Certification required) Must be Certified for Military. Check the box near the top of the form to indicate an Armed Forces PCS

Adjustments to Income Health Savings Account select to open Form 8889. (HSA Certification required) Must be Certified for Military. Check the box near the top of the form to indicate an Armed Forces PCS

Class 2: Basic Tax Preparation Part A (federal)

") Class 2: Basic Tax Preparation Part A (federal) Volunteer Income Tax Assistance: We love to do taxes for free. Normal? Probably not. Helpful? Absolutely! 2017-18 Curriculum 1. Introduction to VITA 2. Tax

Class 2: Basic Tax Preparation Part A (federal) Volunteer Income Tax Assistance: We love to do taxes for free. Normal? Probably not. Helpful? Absolutely! 2017-18 Curriculum 1. Introduction to VITA 2. Tax

CHILDREN EXEMPTIONS, CREDITS AND INCOME SHIFTING TECHNIQUES

CHILDREN EXEMPTIONS, CREDITS AND INCOME SHIFTING TECHNIQUES 2 STARTING A BUSINESS 3 CHILDREN: Exemptions, Credits And Income Shifting Techniques Children invariably mean you will need to incur additional,

CHILDREN EXEMPTIONS, CREDITS AND INCOME SHIFTING TECHNIQUES 2 STARTING A BUSINESS 3 CHILDREN: Exemptions, Credits And Income Shifting Techniques Children invariably mean you will need to incur additional,

Nonrefundable Credits

nrefundable Credits Link to Form 1116, Foreign Tax Credit page 1, if required. Link to Form 2441, page 1. Link to Form 8863. See Education Benefits tab. Link to Form 8880. See Child Tax Credit Tip and

nrefundable Credits Link to Form 1116, Foreign Tax Credit page 1, if required. Link to Form 2441, page 1. Link to Form 8863. See Education Benefits tab. Link to Form 8880. See Child Tax Credit Tip and

2017 Basic Certification Study and Reference Guide

2017 Basic Certification Study and Reference Guide 1 P age Basic Scenario 1: Calvin and Betty Albright 1. Qualifying health insurance coverage also known as minimum essential coverage or MEC under the

2017 Basic Certification Study and Reference Guide 1 P age Basic Scenario 1: Calvin and Betty Albright 1. Qualifying health insurance coverage also known as minimum essential coverage or MEC under the

AFFORDABLE CARE ACT SURVIVAL KIT

AFFORDABLE CARE ACT SURVIVAL KIT This tool was developed to help VITA/TCE volunteers understand the ACA-related tax provisions and how to complete a return in TaxWise. Approaching the ACA Ask each person

AFFORDABLE CARE ACT SURVIVAL KIT This tool was developed to help VITA/TCE volunteers understand the ACA-related tax provisions and how to complete a return in TaxWise. Approaching the ACA Ask each person

Basic Certification Test: Study Guide for Tax Year 2017

Basic Certification Test: Study Guide for Tax Year 2017 TRAINING PRACTICE PROBLEMS 2018 i The items in parentheses refer to sections or page numbers in Publication 4012, Volunteer Resource Guide. It s

Basic Certification Test: Study Guide for Tax Year 2017 TRAINING PRACTICE PROBLEMS 2018 i The items in parentheses refer to sections or page numbers in Publication 4012, Volunteer Resource Guide. It s

Affordable Care Act. Pub 4012 Tab H: ACA, Other Taxes & Payments Pub 4491 Lesson 3. Shared Responsibility

Affordable Care Act Pub 4012 Tab H: ACA, Other Taxes & Payments Pub 4491 Lesson 3 Shared Responsibility Individuals Purchase coverage, Claim an exemption, or Pay Shared Responsibility Payment Account for

Affordable Care Act Pub 4012 Tab H: ACA, Other Taxes & Payments Pub 4491 Lesson 3 Shared Responsibility Individuals Purchase coverage, Claim an exemption, or Pay Shared Responsibility Payment Account for

Affordable Care Act. Introduction. What is the Affordable Care Act? Objectives

Affordable Care Act Introduction This lesson covers some of the tax provisions of the Affordable Care Act (ACA). You will learn how to determine if taxpayers satisfy the individual shared responsibility

Affordable Care Act Introduction This lesson covers some of the tax provisions of the Affordable Care Act (ACA). You will learn how to determine if taxpayers satisfy the individual shared responsibility

CHILDREN EXEMPTIONS, CREDITS AND INCOME SHIFTING TECHNIQUES

CHILDREN EXEMPTIONS, CREDITS AND INCOME SHIFTING TECHNIQUES 2 STARTING A BUSINESS 3 CHILDREN: Exemptions, Credits And Income Shifting Techniques Children invariably mean making additional, often significant,

CHILDREN EXEMPTIONS, CREDITS AND INCOME SHIFTING TECHNIQUES 2 STARTING A BUSINESS 3 CHILDREN: Exemptions, Credits And Income Shifting Techniques Children invariably mean making additional, often significant,

Basic Course Scenarios and Test Questions

Basic Course Scenarios and Test Questions Directions The first six scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and resource

Basic Course Scenarios and Test Questions Directions The first six scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and resource

Child and Dependent Care Credit. Pub 4012 Tab G Pub 4491 Lesson 22

Child and Dependent Care Credit Pub 4012 Tab G Pub 4491 Lesson 22 Types of Credits Credits reduce tax liability dollar for dollar Nonrefundable (Shown on Schedule 3) Limited to tax liability Cannot reduce

Child and Dependent Care Credit Pub 4012 Tab G Pub 4491 Lesson 22 Types of Credits Credits reduce tax liability dollar for dollar Nonrefundable (Shown on Schedule 3) Limited to tax liability Cannot reduce

Form 1040 Adjustments to Income

Form 1040 Adjustments to Income Health Savings Account - link to Form 8889. (HSA Certification required) Auto calculated from Sch SE. Flows over from input of 1099- INT in Interest Statement. If the taxpayer

Form 1040 Adjustments to Income Health Savings Account - link to Form 8889. (HSA Certification required) Auto calculated from Sch SE. Flows over from input of 1099- INT in Interest Statement. If the taxpayer

2016 Instructions for Form 8965

Department of the Treasury Internal Revenue Service 2016 Instructions for Form 8965 Health Coverage Exemptions (and Instructions for Figuring Your Shared Responsibility Payment) For each month you must

Department of the Treasury Internal Revenue Service 2016 Instructions for Form 8965 Health Coverage Exemptions (and Instructions for Figuring Your Shared Responsibility Payment) For each month you must

ACA & the Tax Season

ACA & the Tax Season Common Cents Tara Straw September 9, 2014 The ACA on the Tax Return 2 Reporting health coverage For every month For everyone on the return Exemptions from the individual responsibility

ACA & the Tax Season Common Cents Tara Straw September 9, 2014 The ACA on the Tax Return 2 Reporting health coverage For every month For everyone on the return Exemptions from the individual responsibility

TY2018 VITA Advanced Certification Test - Study Guide

Scenario 1: Smith TY2018 VITA Advanced Certification Test - Study Guide Issue #1 Qualified Education Expenses, Taxable Scholarships (p4012 Tab J) When a taxpayer has more scholarships than Qualified Educational

Scenario 1: Smith TY2018 VITA Advanced Certification Test - Study Guide Issue #1 Qualified Education Expenses, Taxable Scholarships (p4012 Tab J) When a taxpayer has more scholarships than Qualified Educational

TY2018 VITA Basic Certification Test - Study Guide

Scenario 1: Arnold TY2018 VITA Basic Certification Test - Study Guide Issue #1 Minimum Essential Coverage (MEC) (p4012 Tab H) See p4012 s ACA tab for a list of what counts as MEC Issue #2 Penalties for

Scenario 1: Arnold TY2018 VITA Basic Certification Test - Study Guide Issue #1 Minimum Essential Coverage (MEC) (p4012 Tab H) See p4012 s ACA tab for a list of what counts as MEC Issue #2 Penalties for

Everyone must have Healthcare Insurance. Exemptions are available (Form 8965) No Insurance and No Exemption?

No Insurance and No Exemption?") Three Main Elements Everyone must have Healthcare Insurance Exemptions are available (Form 8965) No Insurance and No Exemption? Additional tax Individual Shared Responsibility Payment ( SRP ) Financial

Three Main Elements Everyone must have Healthcare Insurance Exemptions are available (Form 8965) No Insurance and No Exemption? Additional tax Individual Shared Responsibility Payment ( SRP ) Financial

Basic Course Scenarios and Test Questions

Basic Course Scenarios and Test Questions Directions The first six scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and resource

Basic Course Scenarios and Test Questions Directions The first six scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and resource

Exemptions and Penalties

Part IV: Exemptions and Penalties Tax Year 2017 & Coverage Year 2018 Center on Budget and Policy Priorities September 28, 2017 Shared Responsibility Payment (or Why Exemptions are Important) Individual

Part IV: Exemptions and Penalties Tax Year 2017 & Coverage Year 2018 Center on Budget and Policy Priorities September 28, 2017 Shared Responsibility Payment (or Why Exemptions are Important) Individual

CESAs Coverdell Education Savings Accounts. Questions & Answers

CESAs Coverdell Education Savings Accounts Questions & Answers What is a Coverdell Education Savings Account? A Coverdell Education Savings Account is a type of tax-preferred savings and investment account

CESAs Coverdell Education Savings Accounts Questions & Answers What is a Coverdell Education Savings Account? A Coverdell Education Savings Account is a type of tax-preferred savings and investment account

THE AFFORDABLE CARE ACT Frequently Asked Questions

THE AFFORDABLE CARE ACT Frequently Asked Questions We are providing basic information on the ACA in order for you to best prepare for your tax appointment. While we strive to give you complete and accurate

THE AFFORDABLE CARE ACT Frequently Asked Questions We are providing basic information on the ACA in order for you to best prepare for your tax appointment. While we strive to give you complete and accurate

Questions and Answers on the. Individual Shared Responsibility Provision. January 30, 2013

Questions and Answers on the Individual Shared Responsibility Provision January 30, 2013 Basic Information 1. What is the individual shared responsibility provision? Under the Affordable Care Act, the

Questions and Answers on the Individual Shared Responsibility Provision January 30, 2013 Basic Information 1. What is the individual shared responsibility provision? Under the Affordable Care Act, the

Kiddie Tax Other Taxes. Pub 4012 Tab H Pub 4491 Lessons 20 and 27

Kiddie Tax Other Taxes Pub 4012 Tab H Pub 4491 Lessons 20 and 27 Tax for Children with Unearned Income Kiddie Tax Taxpayer (refers to child) has more than $2,100 in unearned income Taxpayer has a filing

Kiddie Tax Other Taxes Pub 4012 Tab H Pub 4491 Lessons 20 and 27 Tax for Children with Unearned Income Kiddie Tax Taxpayer (refers to child) has more than $2,100 in unearned income Taxpayer has a filing

Parent and Student Guide to Federal Tax Benefits For Tuition and Fees (for Tax Year 2006) Understanding the Hope Scholarship Tax Credit

Understanding the Hope Scholarship Tax Credit") National Association of Student Financial Aid Administrators Parent and Student Guide to Federal Tax Benefits For Tuition and Fees (for Tax Year 2006) Understanding the Hope Scholarship Tax Credit What

National Association of Student Financial Aid Administrators Parent and Student Guide to Federal Tax Benefits For Tuition and Fees (for Tax Year 2006) Understanding the Hope Scholarship Tax Credit What

Basic Course Scenarios and Test Questions

Basic Course Scenarios and Test Questions Directions The first six scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and resource

Basic Course Scenarios and Test Questions Directions The first six scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and resource

Child and Dependent Care Credit. Pub 4012 Tab G Pub 4491 Lesson 22

Child and Dependent Care Credit Pub 4012 Tab G Pub 4491 Lesson 22 Child and Dependent Care Credit Pub 4012 Tab G Non-refundable credit Review Pub 4012 to Tab G Who is a qualifying person? What are Qualified

Child and Dependent Care Credit Pub 4012 Tab G Pub 4491 Lesson 22 Child and Dependent Care Credit Pub 4012 Tab G Non-refundable credit Review Pub 4012 to Tab G Who is a qualifying person? What are Qualified

The Affordable Care Act and the Income Tax. By Greg Martinez December 2013

The Affordable Care Act and the Income Tax By Greg Martinez December 2013 Overview Health insurance mandate Individual Shared Responsibility Provision Exemptions Minimum essential coverage Penalties Covered

The Affordable Care Act and the Income Tax By Greg Martinez December 2013 Overview Health insurance mandate Individual Shared Responsibility Provision Exemptions Minimum essential coverage Penalties Covered

Coverdell Education Savings Account

Coverdell Education Savings Account TABLE OF CONTENTS PART I COVERDELL ACCOUNT APPLICATION INSTRUCTIONS...3 PART II - DISCLOSURE STATEMENT...4 PART III - COVERDELL EDUCATION SAVINGS ACCOUNT CUSTODIAL AGREEMENT...

Coverdell Education Savings Account TABLE OF CONTENTS PART I COVERDELL ACCOUNT APPLICATION INSTRUCTIONS...3 PART II - DISCLOSURE STATEMENT...4 PART III - COVERDELL EDUCATION SAVINGS ACCOUNT CUSTODIAL AGREEMENT...

Course Goals: 1. Completing a tax return in Taxslayer 2. Key Tax Concepts 3. Key Credits 4. Finishing a return- bank info, consents, ready for review

Course Goals: 1. Completing a tax return in Taxslayer 2. Key Tax Concepts 3. Key Credits 4. Finishing a return- bank info, consents, ready for review Credits Refundable and Non Refundable Now we get to

Course Goals: 1. Completing a tax return in Taxslayer 2. Key Tax Concepts 3. Key Credits 4. Finishing a return- bank info, consents, ready for review Credits Refundable and Non Refundable Now we get to

Earned Income Table. Earned Income for EIC, Additional Child Tax Credit and Dependent Care Credit. Common EIC Filing Errors

Earned Income Table Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from selfemployment Gross

Earned Income Table Includes Taxable wages, salaries, and tips Union strike benefits Taxable long-term disability benefits received prior to minimum retirement age Net earnings from selfemployment Gross

AFFORDABLE CARE ACT (ACA)

") AFFORDABLE CARE ACT (ACA) Select this box if anyone in the tax household had MEC at any time during the year. (See page ACA-4) A Yes answer will prompt another question about health insurance purchased

AFFORDABLE CARE ACT (ACA) Select this box if anyone in the tax household had MEC at any time during the year. (See page ACA-4) A Yes answer will prompt another question about health insurance purchased

Training Using New NTTC Materials. Carl Kantner

Training Using New NTTC Materials Carl Kantner 2018 Workbook Revised Two Objectives Provide Instructors with tools to facilitate classroom instruction Provide volunteers with exercises for proficiency

Training Using New NTTC Materials Carl Kantner 2018 Workbook Revised Two Objectives Provide Instructors with tools to facilitate classroom instruction Provide volunteers with exercises for proficiency

Income Tax Training School. Federal & CA Pre-Season Update For Tax Preparers 2014 & 2015

A & B Office Income Tax Training School Federal & CA Pre-Season Update For Tax Preparers & 2015 Highlights: 2015 New Tax Law Recap Affordable Care Act (ACA) tax treatment (New in ) Affordable Care Act

A & B Office Income Tax Training School Federal & CA Pre-Season Update For Tax Preparers & 2015 Highlights: 2015 New Tax Law Recap Affordable Care Act (ACA) tax treatment (New in ) Affordable Care Act

HELPFUL TIPS FOR OUT OF SCOPE TOPICS ON THE 2016 IRS BASIC CERTIFICATION EXAM

HELPFUL TIPS FOR OUT OF SCOPE TOPICS ON THE 2016 IRS BASIC CERTIFICATION EXAM + H E L P F U L T I P S F O R O U T O F S C O P E T O P I C S O N T H E 2 0 1 6 I R S B A S I C C E R T I F I C A T I O N E

HELPFUL TIPS FOR OUT OF SCOPE TOPICS ON THE 2016 IRS BASIC CERTIFICATION EXAM + H E L P F U L T I P S F O R O U T O F S C O P E T O P I C S O N T H E 2 0 1 6 I R S B A S I C C E R T I F I C A T I O N E

ADVANCED CERTIFICATION STUDY GUIDE Tax Year 2018

ADVANCED CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents ADVANCED SCENARIO 1: Aiden Smith... 1 ADVANCED SCENARIO 2: Sean Yale... 2 ADVANCED SCENARIO 3: Tom and Carol Baker... 3 ADVANCED SCENARIO

ADVANCED CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents ADVANCED SCENARIO 1: Aiden Smith... 1 ADVANCED SCENARIO 2: Sean Yale... 2 ADVANCED SCENARIO 3: Tom and Carol Baker... 3 ADVANCED SCENARIO

TY2017 VITA Basic Certification Test - Study Guide

Scenario 1: Albright TY2017 VITA Basic Certification Test - Study Guide Issue #1 Minimum Essential Coverage (MEC) (p4012 Tab H) See p4012 s ACA tab for a list of what counts as MEC Issue #2 Penalties for

Scenario 1: Albright TY2017 VITA Basic Certification Test - Study Guide Issue #1 Minimum Essential Coverage (MEC) (p4012 Tab H) See p4012 s ACA tab for a list of what counts as MEC Issue #2 Penalties for

2016 vs Key Facts and Figures

2016 vs. 2017 Key Facts and Figures Keir Educational Resources compiled the following key facts and figures for the CFP Certification Examination to assist you with your preparation for this comprehensive

2016 vs. 2017 Key Facts and Figures Keir Educational Resources compiled the following key facts and figures for the CFP Certification Examination to assist you with your preparation for this comprehensive

Basic Tax Workshop for UCSF Students for the 2017 tax year

Basic Tax Workshop for UCSF Students for the 2017 tax year Tuesday February 27, from 12-1pm in N517 and Monday March 5, from 12-1pm in N217 Zoom: https://ucsf.zoom.us/j/8531229278 Daniel Roddick Resource

Basic Tax Workshop for UCSF Students for the 2017 tax year Tuesday February 27, from 12-1pm in N517 and Monday March 5, from 12-1pm in N217 Zoom: https://ucsf.zoom.us/j/8531229278 Daniel Roddick Resource

Earned Income Credit

Earned Income Credit Major update Earned Income Credit Pub 4491 Lesson 30 Pub 4012 Tab I needed for 2017 law change (disaster relief) Refundable Credit A refundable credit can generate a refund even if

Earned Income Credit Major update Earned Income Credit Pub 4491 Lesson 30 Pub 4012 Tab I needed for 2017 law change (disaster relief) Refundable Credit A refundable credit can generate a refund even if

Educational Expenses

Educational Expenses About Me H&R Block Tax Professionals Background Certifications Over 30 hours of additional training annually I love taxes! About H&R Block Client Focused Integrity Excellence Respect

Educational Expenses About Me H&R Block Tax Professionals Background Certifications Over 30 hours of additional training annually I love taxes! About H&R Block Client Focused Integrity Excellence Respect

Tax News The Annual Newsletter for the Clients of Steven P Namenye CPA PC Items impacting preparation of your 2018 tax returns - January 2019

Tax News 2018 The Annual Newsletter for the Clients of Steven P Namenye CPA PC Items impacting preparation of your 2018 tax returns - January 2019 Greetings! To our clients and friends... Happy New Year!

Tax News 2018 The Annual Newsletter for the Clients of Steven P Namenye CPA PC Items impacting preparation of your 2018 tax returns - January 2019 Greetings! To our clients and friends... Happy New Year!

Sponsored by University Student Financial Services PERSONAL TAXES. Jodi R. Kessler, LLM Tax Manager Harvard University

Sponsored by University Student Financial Services PERSONAL TAXES Jodi R. Kessler, LLM Tax Manager Harvard University 1 DISCLAIMER Federal income tax; states may differ Information is specific to US citizens

Sponsored by University Student Financial Services PERSONAL TAXES Jodi R. Kessler, LLM Tax Manager Harvard University 1 DISCLAIMER Federal income tax; states may differ Information is specific to US citizens

Advanced Course Scenarios and Test Questions

Advanced Course Scenarios and Test Questions Directions The first four scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and

Advanced Course Scenarios and Test Questions Directions The first four scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and

VITA/TCE Basic Certification Topics on Affordable Care Act. Current as of November 15, 2018

VITA/TCE Basic Certification Topics on Affordable Care Act Current as of November 15, 2018 Agenda 2 The Individual Mandate Penalty Was Repealed Everyone is Exempt Not Quite Shared Responsibility Payment

VITA/TCE Basic Certification Topics on Affordable Care Act Current as of November 15, 2018 Agenda 2 The Individual Mandate Penalty Was Repealed Everyone is Exempt Not Quite Shared Responsibility Payment

Personal Information. Present Mailing Address. [38] [39] [42] Foreign country name. [44] Foreign phone number [47] In care of addressee

![Personal Information. Present Mailing Address. [38] [39] [42] Foreign country name. [44] Foreign phone number [47] In care of addressee](/thumbs/96/126854138.jpg "Personal Information. Present Mailing Address. [38] [39] [42] Foreign country name. [44] Foreign phone number [47] In care of addressee") Form ID: 1040 Personal Information 1 Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er)) Mark if you were married

Form ID: 1040 Personal Information 1 Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er)) Mark if you were married

Preparing Taxes with TaxSlayer

Preparing Taxes with TaxSlayer Changes to Tax Law for ty 2017 What we all forget year to year Affordable Care Act New York Returns NJ non-resident returns 1 NTTC Training - TY2016 Review all docs before

Preparing Taxes with TaxSlayer Changes to Tax Law for ty 2017 What we all forget year to year Affordable Care Act New York Returns NJ non-resident returns 1 NTTC Training - TY2016 Review all docs before

2016 Year-End Tax Planning Letter

9NOV2016 2016 Year-End Tax Planning Letter Dear Vista Wealth Clients and Friends, As 2016 draws to a close, you should give consideration to year-end tax planning strategies. This letter highlights some

9NOV2016 2016 Year-End Tax Planning Letter Dear Vista Wealth Clients and Friends, As 2016 draws to a close, you should give consideration to year-end tax planning strategies. This letter highlights some

Basic Information 1. What is the individual shared responsibility provision?

Affordable Care Act Topics Individuals and Families Employers Other Organizations For Tax Pros What's Trending News Health Care Tax Tips Questions and Answers Legal Guidance and Other Resources Affordable

Affordable Care Act Topics Individuals and Families Employers Other Organizations For Tax Pros What's Trending News Health Care Tax Tips Questions and Answers Legal Guidance and Other Resources Affordable

2017 Advanced Certification Study and Reference Guide

2017 Advanced Certification Study and Reference Guide Note: Where used in the following, QRG means Quick Reference Guide ( mini manual ); Manual means the Ladder Up Volunteer Training Manual; in both cases

2017 Advanced Certification Study and Reference Guide Note: Where used in the following, QRG means Quick Reference Guide ( mini manual ); Manual means the Ladder Up Volunteer Training Manual; in both cases

Important Changes for 2017

Due Date of Return The due date for filing a 2017 return is Tuesday, April 17, 2018. This is because April 15, 2018 is a Sunday and Emancipation Day, a legal holiday in the District of Columbia, is observed

Due Date of Return The due date for filing a 2017 return is Tuesday, April 17, 2018. This is because April 15, 2018 is a Sunday and Emancipation Day, a legal holiday in the District of Columbia, is observed

Figuring your Taxes and Credits

Figuring your Taxes and Credits This self-study explains how to figure your tax and how to figure the tax of certain children who have more than $2,100 of unearned income. Also discussed are various tax

Figuring your Taxes and Credits This self-study explains how to figure your tax and how to figure the tax of certain children who have more than $2,100 of unearned income. Also discussed are various tax

FACTS ABOUT THE ACA INDIVIDUAL MANDATE

FACTS ABOUT THE ACA INDIVIDUAL MANDATE Beginning 2014, every U.S. citizen and resident alien must have health insurance (minimum essential coverage). Failure to do so will result in a penalty (an additional

FACTS ABOUT THE ACA INDIVIDUAL MANDATE Beginning 2014, every U.S. citizen and resident alien must have health insurance (minimum essential coverage). Failure to do so will result in a penalty (an additional

Coverdell Education Savings Account (ESA)

") 7. Coverdell Education Savings Account (ESA) Introduction If your modified adjusted gross income (MAGI) is less than $110,000 ($220,000 if filing a joint return), you may be able to establish a Coverdell

7. Coverdell Education Savings Account (ESA) Introduction If your modified adjusted gross income (MAGI) is less than $110,000 ($220,000 if filing a joint return), you may be able to establish a Coverdell

TOOLS AND TECHNIQUES OF INCOME TAX PLANNING 3 RD EDITION

TOOLS AND TECHNIQUES OF INCOME TAX PLANNING 3 RD EDITION 2012 Supplement Chapter 2 p. 11 In 2012 the income threshold for married person filing jointly is $19,500 (if one spouse is blind or elderly 20,650;

TOOLS AND TECHNIQUES OF INCOME TAX PLANNING 3 RD EDITION 2012 Supplement Chapter 2 p. 11 In 2012 the income threshold for married person filing jointly is $19,500 (if one spouse is blind or elderly 20,650;

Federal Income Taxes. Today s Approach. Your Tax Knowledge. Process. Process Continued. Filing Requirements. Fall 2014 VITA Training

Federal Income Taxes Fall 2014 VITA Training Dr. Cathy Bowen Dr. Barbara Yener Today s Approach Use Form 1040 and common tax forms to discuss key areas of completing a tax return for VITA taxpayers. Not

Federal Income Taxes Fall 2014 VITA Training Dr. Cathy Bowen Dr. Barbara Yener Today s Approach Use Form 1040 and common tax forms to discuss key areas of completing a tax return for VITA taxpayers. Not

EDUCATION IRA/COVERDELL EDUCATION ACCOUNT APPLICATION AND DISCLOSURE STATEMENT Account Number (if known)

") EDUCATION IRA/COVERDELL EDUCATION ACCOUNT APPLICATION AND DISCLOSURE STATEMENT Account Number (if known) Registered Representative Return your completed application to: William Blair Funds, P.O. Box 8506

EDUCATION IRA/COVERDELL EDUCATION ACCOUNT APPLICATION AND DISCLOSURE STATEMENT Account Number (if known) Registered Representative Return your completed application to: William Blair Funds, P.O. Box 8506

TAX ORGANIZER Tax Year THINGS TO BRING (or send to us if no appointment)

") TAX ORGANIZER - 2018 Tax Year THINGS TO BRING (or send to us if no appointment) NEW CLIENTS ONLY: Copy of prior year tax return. Please provide birthdates and social security numbers for all taxpayers

TAX ORGANIZER - 2018 Tax Year THINGS TO BRING (or send to us if no appointment) NEW CLIENTS ONLY: Copy of prior year tax return. Please provide birthdates and social security numbers for all taxpayers

STATE AND FEDERAL TAX BENEFITS FOR COLLEGE EXPENSES: THE CASE OF UTAH

STATE AND FEDERAL TAX BENEFITS FOR COLLEGE EXPENSES: THE CASE OF UTAH Smith, Sheldon R. Utah Valley University ABSTRACT Several different federal income tax benefits exist for higher education costs. The

STATE AND FEDERAL TAX BENEFITS FOR COLLEGE EXPENSES: THE CASE OF UTAH Smith, Sheldon R. Utah Valley University ABSTRACT Several different federal income tax benefits exist for higher education costs. The

STANDARD DEDUCTIONS MACRS RECOVERY PERIODS

217 Medical Savings Accounts (MSA) 217 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,5-6,75 Maximum Out of Pocket Self-Only Coverage 4,5 Family Coverage 8,25 STANDARD DEDUCTIONS

217 Medical Savings Accounts (MSA) 217 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,5-6,75 Maximum Out of Pocket Self-Only Coverage 4,5 Family Coverage 8,25 STANDARD DEDUCTIONS

Kiddie Tax Other Taxes. Pub 4012 Tab H Pub 4491 Lessons 20 and 27

Kiddie Tax Other Taxes Pub 4012 Tab H Pub 4491 Lessons 20 and 27 Tax for Children with Unearned Income Kiddie Tax Child has a filing requirement Find Pub 4012 Tab A Chart B For Children and Other Dependents

Kiddie Tax Other Taxes Pub 4012 Tab H Pub 4491 Lessons 20 and 27 Tax for Children with Unearned Income Kiddie Tax Child has a filing requirement Find Pub 4012 Tab A Chart B For Children and Other Dependents

2014 AFFORDABLE CARE ACT (OBAMA CARE)

") 2014 AFFORDABLE CARE ACT (OBAMA CARE) Planning for 2014 Tax Return Filings O Beginning 2014, the ACA requires all persons be covered by health insurance O Individuals not covered by Medicare, their employers,

2014 AFFORDABLE CARE ACT (OBAMA CARE) Planning for 2014 Tax Return Filings O Beginning 2014, the ACA requires all persons be covered by health insurance O Individuals not covered by Medicare, their employers,

Putting it Together: Beyond the Basics

Putting it Together: Beyond the Basics Center on Budget and Policy Priorities September 18, 2013 Topics Review and apply key concepts to three family scenarios: Household and income determinations Premium

Putting it Together: Beyond the Basics Center on Budget and Policy Priorities September 18, 2013 Topics Review and apply key concepts to three family scenarios: Household and income determinations Premium

QUESTIONS AND ANSWERS ABOUT THE EARNED INCOME TAX CREDIT TAX YEAR 2010

QUESTIONS AND ANSWERS ABOUT THE EARNED INCOME TAX CREDIT TAX YEAR 2010 The federal Earned Income Tax Credit is designed to boost the wages of working families. The following questions and answers will

QUESTIONS AND ANSWERS ABOUT THE EARNED INCOME TAX CREDIT TAX YEAR 2010 The federal Earned Income Tax Credit is designed to boost the wages of working families. The following questions and answers will

ARTICLE I ARTICLE II ARTICLE III ARTICLE IV ARTICLE V

Coverdell Education Savings Custodial Account (Under section 530 of the Internal Revenue Code) Form 5305-EA (Rev. October 2010) Department of the Treasury, Internal Revenue Service. Do not file with the

Coverdell Education Savings Custodial Account (Under section 530 of the Internal Revenue Code) Form 5305-EA (Rev. October 2010) Department of the Treasury, Internal Revenue Service. Do not file with the

Guidelines for Quality Reviewing ACA Issues

Attachment 1 Guidelines for Quality Reviewing ACA Issues Form 13614-C, Intake/Interview Sheet Is Form 13614-C complete? Every question is answered Yes or No? Unsure responses have been answered Yes or

Attachment 1 Guidelines for Quality Reviewing ACA Issues Form 13614-C, Intake/Interview Sheet Is Form 13614-C complete? Every question is answered Yes or No? Unsure responses have been answered Yes or

TAX CUT AND JOBS ACT OF INDIVIDUAL PROPOSALS

Reduction of rates Married Filing Joint () (Surviving Spouse) $0 90,000 $91,000 260,000 $260,001 1,000,000 Over $1,000,000 $0 45,000 $45,001 130,000 $130,001 500,000 Over $500,000 Head of Household ()

Reduction of rates Married Filing Joint () (Surviving Spouse) $0 90,000 $91,000 260,000 $260,001 1,000,000 Over $1,000,000 $0 45,000 $45,001 130,000 $130,001 500,000 Over $500,000 Head of Household ()

2017 INDIVIDUAL TAX PLANNING

2017 INDIVIDUAL TAX PLANNING We hope that you are looking forward to the Holiday Season. It is hard to believe that it is mid-december and this year is quickly ending. If you ve been following the news

2017 INDIVIDUAL TAX PLANNING We hope that you are looking forward to the Holiday Season. It is hard to believe that it is mid-december and this year is quickly ending. If you ve been following the news

MoneyWise Module 4 Tax and Long-term Planning: Key Issues

Discussion Topics Tax and Long-term Planning: Key Issues Module 4 1. Perspectives: Planning 2. Taxes: Learn the tax rules 3. Credits: A social tool 4. Deductions: Second price 5. Shelters & Savings: Company

Discussion Topics Tax and Long-term Planning: Key Issues Module 4 1. Perspectives: Planning 2. Taxes: Learn the tax rules 3. Credits: A social tool 4. Deductions: Second price 5. Shelters & Savings: Company

VITA/TCE Basic Certification Topics on Affordable Care Act

VITA/TCE Basic Certification Topics on Affordable Care Act What does the ACA require? 2 or or Coverage Exemption SRP Everyone has a Shared Responsibility Individuals Purchase coverage, - Claim an exemption,

VITA/TCE Basic Certification Topics on Affordable Care Act What does the ACA require? 2 or or Coverage Exemption SRP Everyone has a Shared Responsibility Individuals Purchase coverage, - Claim an exemption,

4491X. VITA/TCE Training Supplement. Volunteer Income Tax Assistance (VITA) / Tax Counseling for the Elderly (TCE)

/ Tax Counseling for the Elderly (TCE)") 4491X VITA/TCE Training Supplement Volunteer Income Tax Assistance (VITA) / Tax Counseling for the Elderly (TCE) 2010 Returns Take your VITA/TCE training online at www.irs.gov (keyword: Link and Learn

4491X VITA/TCE Training Supplement Volunteer Income Tax Assistance (VITA) / Tax Counseling for the Elderly (TCE) 2010 Returns Take your VITA/TCE training online at www.irs.gov (keyword: Link and Learn

What the New Tax Laws Mean to You

What the New Tax Laws Mean to You The American Taxpayer Relief Act of 2012 and other 2013 tax provisions January 2013 White Paper AN OVERVIEW OF THE AMERICAN TAXPAYER RELIEF ACT OF 2012 AND OTHER 2013

What the New Tax Laws Mean to You The American Taxpayer Relief Act of 2012 and other 2013 tax provisions January 2013 White Paper AN OVERVIEW OF THE AMERICAN TAXPAYER RELIEF ACT OF 2012 AND OTHER 2013

SUMMARY PLAN DESCRIPTION. for the CRETE CARRIER CORPORATION FLEXIBLE BENEFITS PLAN, DEPENDENT CARE ASSISTANCE PLAN & FLEXIBLE SPENDING ACCOUNT PLAN

SUMMARY PLAN DESCRIPTION for the CRETE CARRIER CORPORATION FLEXIBLE BENEFITS PLAN, DEPENDENT CARE ASSISTANCE PLAN & FLEXIBLE SPENDING ACCOUNT PLAN SUMMARY PLAN DESCRIPTION Introduction Crete Carrier Corporation

SUMMARY PLAN DESCRIPTION for the CRETE CARRIER CORPORATION FLEXIBLE BENEFITS PLAN, DEPENDENT CARE ASSISTANCE PLAN & FLEXIBLE SPENDING ACCOUNT PLAN SUMMARY PLAN DESCRIPTION Introduction Crete Carrier Corporation

Individual Health Insurance Marketplace FAQs Purdue Pre-65 Retiree

Individual Health Insurance Marketplace FAQs Purdue Pre-65 Retiree Maria Pearson Melva Lowry Q: What is a Health Insurance Marketplace? A: The Health Insurance Marketplace (Marketplace) is a way to find

Individual Health Insurance Marketplace FAQs Purdue Pre-65 Retiree Maria Pearson Melva Lowry Q: What is a Health Insurance Marketplace? A: The Health Insurance Marketplace (Marketplace) is a way to find

2009 Filing Requirements for Most Taxpayers

The following is a summary of 2009 tax information. Many of the most common tax deductions are explained below. Some credit s and deductions are phased out, or disallowed depending on the amount of your

The following is a summary of 2009 tax information. Many of the most common tax deductions are explained below. Some credit s and deductions are phased out, or disallowed depending on the amount of your

IRA AND EDUCATION SAVINGS. Retirement and Education Savings Accounts. TRADITIONAL IRAs Who is Eligible for a Traditional IRA?

Retirement and Education Savings Accounts This booklet is designed to highlight traditional individual retirement accounts (IRAs), Roth IRAs, and Coverdell Education Savings Accounts (CESAs). It is not

Retirement and Education Savings Accounts This booklet is designed to highlight traditional individual retirement accounts (IRAs), Roth IRAs, and Coverdell Education Savings Accounts (CESAs). It is not

ADVANCED CERTIFICATION STUDY GUIDE Tax Year 2018

ADVANCED CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents ADVANCED SCENARIO 1: Aiden Smith... 1 ADVANCED SCENARIO 2: Sean Yale... 2 ADVANCED SCENARIO 3: Tom and Carol Baker... 3 ADVANCED SCENARIO

ADVANCED CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents ADVANCED SCENARIO 1: Aiden Smith... 1 ADVANCED SCENARIO 2: Sean Yale... 2 ADVANCED SCENARIO 3: Tom and Carol Baker... 3 ADVANCED SCENARIO

The Earned Income Tax Credit

The Earned Income Tax Credit Claim the Tax Refunds You Deserve What is the Earned Income Tax Credit (EITC)? The EITC is a refundable tax-credit for working individuals who have earned income. If you are

The Earned Income Tax Credit Claim the Tax Refunds You Deserve What is the Earned Income Tax Credit (EITC)? The EITC is a refundable tax-credit for working individuals who have earned income. If you are

Your guide to Coverdell Education Savings Accounts. Coverdell Education Savings Account Disclosure Statement and Custodial Agreement

Your guide to Coverdell Education Savings Accounts Coverdell Education Savings Account Disclosure Statement and Custodial Agreement Your guide to Coverdell Education Savings Accounts This section of the

Your guide to Coverdell Education Savings Accounts Coverdell Education Savings Account Disclosure Statement and Custodial Agreement Your guide to Coverdell Education Savings Accounts This section of the

TAX FACTS AND TABLES at a glance

TAX FACTS AND TABLES 2013 at a glance Are you making smart investment decisions that can help Reduce your taxes The first step in reducing the amount of tax you pay on your investments is to get the facts.

TAX FACTS AND TABLES 2013 at a glance Are you making smart investment decisions that can help Reduce your taxes The first step in reducing the amount of tax you pay on your investments is to get the facts.

2009 Economic Stimulus Act

2009 Economic Stimulus Act On February 17, President Obama signed into law the American Recovery and Reinvestment Act of 2009 (the 2009 Economic Stimulus Act). This new legislation was passed to aid our

2009 Economic Stimulus Act On February 17, President Obama signed into law the American Recovery and Reinvestment Act of 2009 (the 2009 Economic Stimulus Act). This new legislation was passed to aid our

2018 Tax Changes. Tax Cuts and Jobs Act. STCA$H Fall Training 11/3/2018

2018 Tax Changes Tax Cuts and Jobs Act STCA$H Fall Training 11/3/2018 1 Tax Reform on IRS.gov IRS.gov/taxreform IRS.gov/getready News Releases & Fact Sheets Tax Reform Tax Tips Frequently Asked Questions

2018 Tax Changes Tax Cuts and Jobs Act STCA$H Fall Training 11/3/2018 1 Tax Reform on IRS.gov IRS.gov/taxreform IRS.gov/getready News Releases & Fact Sheets Tax Reform Tax Tips Frequently Asked Questions