Net Operating Losses. Presented by: Keith Altobelli, EA

|

|

|

- Ambrose Chapman

- 6 years ago

- Views:

Transcription

1 Presented by: Keith Altobelli, EA

2

3 Net Operating Losses Objectives In this webinar the student will learn to: Calculate an NOL Determine whether to carry an NOL back or forward To claim an NOL deduction Figure an NOL carryover.

4 Learn how to complete the following forms and worksheets Form 1045, Application for a Tentative Refund Form 1045, Schedule A - NOL Form 1045, Schedule B - NOL Carryover Worksheet for NOL Carryover From

5

6 Definitions: Net Operating Losses NOL Year The tax year in which a net operating loss occurs. NOL Carryback The net operating loss that is initially carried back to year(s) preceding the loss year. These years are known as the carryback period. NOL Carryforward The net operating loss that is carried to the year(s) after the loss. These years are known as the carryforward period. NOL Carryover A carryover occurs when a net operating loss exceeds the taxable income of the year to which it was carried. Carryback Year Any tax year preceding the net operating loss year, to which a net operating loss is carried. Carryover Year Any succeeding year to which the remainder of a prior net operating loss is carried.

7 It is vital for practitioners to be aware of the opportunities and pitfalls created by an NOL. Practitioners must be able to explain NOL-related choices to their clients so that taxpayers can accurately decide what is best for them. Too many taxpayers lose the benefits of the special provisions of the Code relating to NOLs because their practitioners fail to present all options or simply fail to apply an NOL to other tax years.

8 When deductions exceed income, a net operating loss may occur.

9 Deductions from a trade or business, From working as an employee, From casualty and theft losses, moving expenses, or rental property. The most common NOL is caused by a business loss.

.")

10 An NOL can be used by deducting the NOL from the taxpayer s income in another year (or years). This may result in a refund of prior years taxes.

11 Positive Or Negative?

12 The following items are not allowed when figuring an NOL: Deduction for personal exemptions Capital losses in excess of gains The section 1202 exclusion of 50% of the gain from the sale or exchange of qualified small business stock Nonbusiness deductions in excess of nonbusiness income. Net operating loss deduction from a prior year The domestic production activities deduction

13 The following items are not allowed when figuring an NOL: Deduction for personal exemptions Capital losses in excess of gains The section 1202 exclusion of 50% of the gain from the sale or exchange of qualified small business stock Nonbusiness deductions in excess of nonbusiness income. Net operating loss deduction from a prior year The domestic production activities deduction

14 2014 Net Operating Losses

15

16 Glenn Johnson is in the retail record business. He is single and has the following income and deductions on his Form 1040 for INCOME Wages from part-time job $1,225 Interest on savings 425 Net long-term capital gain on sale of real estate used in business 2,000 Glenn's total income $3,650 DEDUCTIONS Net loss from business (gross income of $67,000 minus expenses of $72,000) $5,000 Net short-term capital loss on sale of stock 1,000 Standard deduction 5,950 Personal exemption 3,800 Glenn's total deductions $15,750

17

18 The following items are not allowed when figuring an NOL: Deduction for personal exemptions Capital losses in excess of gains The section 1202 exclusion of 50% of the gain from the sale or exchange of qualified small business stock Nonbusiness deductions in excess of nonbusiness income. Net operating loss deduction from a prior year The domestic production activities deduction Therefore, Glenn's NOL for 2014 is figured as follows: Glenn's total 2014 income $3,650 Less: Glenn's original 2014 total deductions $15,750 Reduced by the disallowed items 10,325 5,425 Glenn's NOL for 2014 $1,775

19 Back: 2 Years Or not Forward: 20 Years

The election must be made on a timely filed return (including extensions) for the NOL year.")

20 Waiving the Carryback Period An election can be made to waive the carryback years and only use the NOL in the 20-year carryforward period. (This choice also means that no alternative NOL is carried back.) The election must be made on a timely filed return (including extensions) for the NOL year. To make this election, the following statement must be attached to the return: The taxpayer elects to waive the net operating loss carryback period under section 172(b)(3) of the Internal Revenue Code. Once this election is made, it generally is irrevocable. If the taxpayer chooses to waive the carryback period for more than one NOL, a separate choice must be made and a separate statement attached for each NOL year.

21

22 Eligible loss. The carryback period for eligible losses is 3 years. Only the eligible loss portion of the NOL can be carried back 3 years. An eligible loss is any part of an NOL that: Is from a fire, storm, shipwreck, casualty or theft, or Is attributable to a federally declared disaster for a qualified small business or certain qualified farming businesses.

23 Qualified small business: A qualified small business is a sole proprietorship or a partnership Average annual gross receipts (reduced by returns and allowances) of $5 million or less during the 3-year period ending with the tax year of the NOL. If the business did not exist for this entire 3-year period, use the period the business was in existence.

24 Farming loss: Only the farming loss portion A farming loss is the smaller of: The amount which would be the NOL for the tax year if only income and deductions attributable to farming businesses were taken into account, or The NOL for the tax year.

25 Farming business: Cultivation of land, raising or harvesting of any agricultural or horticultural commodity, operating a nursery or sod farm, raising or harvesting of trees bearing fruit, nuts, or other crops, or ornamental trees. The raising, shearing, feeding, caring for, training and management of animals is also considered a farming business. A farming business does not include contract harvesting of an agricultural or horticultural commodity grown or raised by someone else. It also does not include a business in which you merely buy or sell plants or animals grown or raised entirely by someone else.

, or The NOL for the tax")

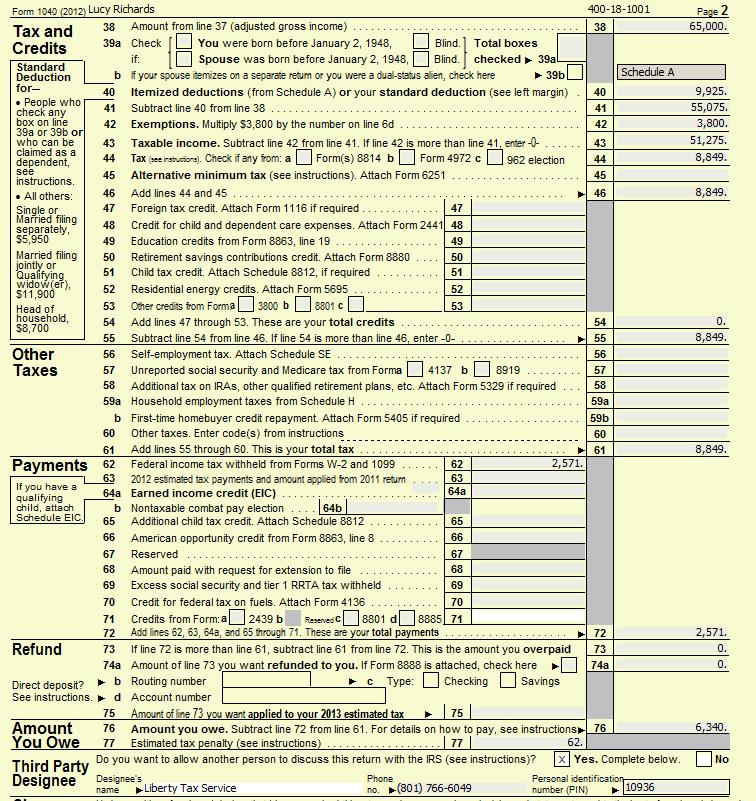

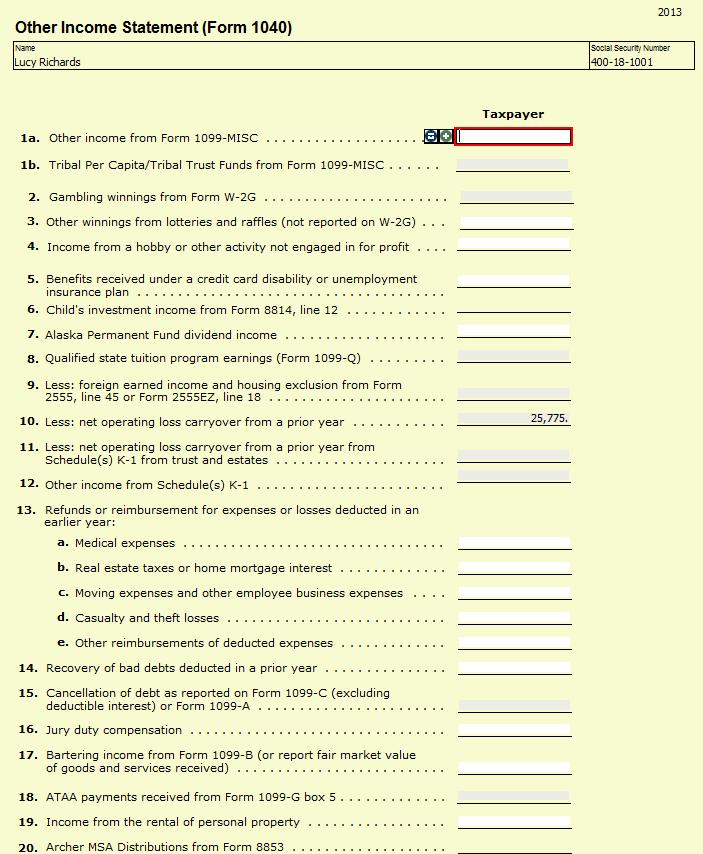

26 Qualified disaster loss: Only the qualified disaster loss portion A qualified disaster loss is the smaller of the sum of: Any losses attributable to a federally declared disaster and occurring before January 1, 2010 in the disaster area, plus any allowable qualified disaster expenses (even if you did not choose to treat those expenses as deductions in the current year), or The NOL for the tax year.

27 Private or commercial golf course, Country club, Massage parlor, Hot tub facility, Suntan facility, Any store for which the principal business is the sale of alcoholic beverages for consumption off premises. Gambling or animal racing property. Gambling or animal racing property is any property used directly in connection with gambling, the racing of animals, or the on-site viewing of such racing, unless this portion is less than 100 square feet.

28 Qualified GO Zone loss: Only the qualified GO Zone loss portion A qualified GO Zone loss is the smaller of: The excess of the NOL for the year over the specified liability loss for the year to which a 10-year carryback applies, or The total of any qualified GO Zone casualty loss and any depreciation allowable for any specified GO Zone extension property for the year such property is placed in service (even if you elected not to claim the special GO Zone depreciation allowance for such property). In most cases, specified GO Zone extension property must have been placed in service before December 31, 2011.

29 Waiving the 5-year carryback: A taxpayer can choose to figure the carryback period for a farming loss without regard to the special 5-year carryback rule. To make this choice for 2014, attach to the 2014 tax return filed by the due date (including extensions) a statement that he or she is choosing to treat any 2014 farming losses without regard to the special 5-year carryback rule. If the return is filed on time but the statement was not filed with it, the choice can be made on an amended return filed within 6 months after the due date of the return (excluding extensions). Attach an election statement to the amended return, and write Filed pursuant to section at the top of the statement. Once made, this choice is irrevocable.

that occurred at least 3 years before the beginning of the loss year and resulted in a liability under a federal or state law")

30 Specified liability loss: Only the specified liability loss portion A specified liability loss is a loss arising from: Product liability and expenses incurred in the investigation or settlement of, or opposition to, product liability claims, or An act (or failure to act) that occurred at least 3 years before the beginning of the loss year and resulted in a liability under a federal or state law requiring: Reclamation of land, Dismantling of a drilling platform, Remediation of environmental contamination, or Payment under any workers compensation act.

31 Waiving the 10-year carryback: A taxpayer can choose to figure the carryback period for a specified liability loss without regard to the special 10-year carryback rule. To make this choice for 2013, attach to the 2013 tax return filed by the due date (including extensions) a statement that he or she is choosing to treat any 2013 specified liability loss without regard to the special 10-year carryback rule. If the return is filed on time but the statement was not filed with it, the choice can be made on an amended return filed within 6 months after the due date of the return (excluding extensions). Attach a statement to the amended return, and write Filed pursuant to section at the top of the statement. Once made, this choice is irrevocable

32

33 Farmer John had a $50K loss: $25K from farming $10K from fire in home How Many Years Can He Carry Back the Losses? $15K from wife employee loss

34 Use it or lose it

35

36 Pertinent Info: Aspiring entertainer Head of Household Self-Employed Lucy Richards Had a bad year

37

38 Non-Business Non-Business Now-Business Schedule D Section 1202 Small Business Stock Final NOL

39

40 Pros: IRS has 90 days One claim for up to 3 years Better overall picture Cons: Must be filed within 1 year Payment no guarantee No TC if disallowed; 1040X IRS may bill for errors

41 Pros: Same deadline as original 6 months to process or court 2 years to appeal disallowance Cons: Separate form for each year Taxes more than 90 days Must adjust for deductions based on AGI

42 Applying the NOL to Past Returns The following items are adjusted in the order listed: 1. The special allowance for passive activity losses from rental real estate activities 2. Taxable social security and tier 1 railroad retirement benefits 3. IRA deductions 4. Excludable savings bond interest 5. Excludable employer-provided adoption benefits 6. The student loan interest deduction 7. The tuition and fees deduction

43 After all items are refigured: the following deductions are recalculated based on AGI: 1. Medical expenses 2. Qualified mortgage insurance premiums 3. Casualty losses 4. Miscellaneous itemized deductions 5. Overall limit on itemized deductions 6. Phaseout of exemptions The deduction for charitable contributions is not recalculated.

44 The final step in the applying the NOL to past returns is that taxes and credits are recalculated. SE tax is not affected by NOL carrybacks and carryforwards.

45

46 1 st year only!

47 NOL Adjustment

48 2014 NOL $80, NOL Used $55, Carryover $25,775

49 All Subsequent Years

50

51

52

53

54 1. Answer any question before they know they have one! 2. Form st 2 pages 3. IRA Contributions Schedule A 5. Any other forms that have changed

55 Recreate each year separately Carryover Line 13 if negative after Tax refund on Line 27

56 Disallowance of the Application: Your application is not treated as a claim for credit or refund. It may be disallowed if it has material omissions or math errors that are not corrected within the 90-day period. If the application is disallowed in whole or in part, no suit challenging the disallowance can be brought in any court. But you can file Form 1040X

57 Deducting a Carry-forward If a taxpayer carries forward an NOL to a tax year after the NOL year, list the NOL deduction as a negative figure on the Other income line of Form 1040 or Form 1040NR (line 21 for 2013). Estates and trusts include an NOL deduction on Form 1041 with other deductions not subject to the 2% limit (line 15a for 2013). When a taxpayer carries forward an NOL, a statement must be attached to the return showing all the important facts about the NOL. The statement should include a computation as to how the NOL deduction was figured. If the taxpayer is deducting more than one NOL in the same year, your statement must cover each of them separately.

58

59 If you carry two or more NOLs to a tax year, figure your modified taxable income by deducting the NOLs in the order in which they were incurred. First, deduct the NOL from the earliest year, then the NOL from the next earliest year, etc. After you deduct each NOL, there will be a new, smaller, modified taxable income to compare to any remaining NOL.

60

61 All Subsequent Years

62

63 Liz has 2014 NOL of $200,000 In 2012 filed MFJ They are now divorced Liz and Michael NOL is limited to her wages

64 1. Calculate the tax in the carryback year for each spouse as if they filed MFS. 2. Figure each spouse s percentage of the total tax from the two MFS returns. 3. Multiply the recomputed tax on the joint return after the NOL carryback by the taxpayer s percentage of the total MFS tax. 4. The result is the taxpayer s share of the joint tax liability.

65

66

67

$5000 X ($3000/$4800) Shared NOL $1,875 $3,125 Mark and Nancy")

68 Married to Separate Returns Example 1 Example 2 Mark Nancy Income $50,000 $7,500 Expenses $11,500 $12,500 Net $38,500 -$5,000 Mark Nancy Total NOL $1,800 $3,000 $4,800 $5000 X ($1800/$4800) $5000 X ($3000/$4800) Shared NOL $1,875 $3,125 Mark and Nancy

69 MFS to MFJ Sam Wanda Totals NOL 2014 $18,000 $2,000 $20,000 MTI 2012 $15,000 $15,000 $0 $15,000 Carryover to 2013 $3,000 $2,000 $5,000 Step 1 - Separate 2014 Modified Taxable Income $9,000 $3,000 $12,000 Step 2 - Each Joint Share Modified Taxable Income 75% $11,250 $3,750 $15,000 Step 3 - NOL Deduction $2,000 $2,000 Sam and Wanda 2012: MFJ 2013: MFS 2014: MFS Step 4 - Joint MTI to Offset $11,250 $1,750 $13,000 Step 5 - Figure Carryover NOL $18,000 Joint MTI $13,000 Carryover $5,000 $0

70

71 Pass-Through Entities Entity Decision: Gross Receipts Test Nature of Loss (special carryback years) Individual Decision: Carryback or Waive Carryback Decision A copy of K1 and any related calculations from NOL year should be attached to carry back and carry forward returns. Caution: Although the pass-through entity may generate NOLs for the partner or shareholder, the loss for any particular year may be limited by: Basis At-Risk Rules Passive Activity Rules. TC Dean vs. IRS lost because he could not prove 500 hours working in partnership

Positive Or")

72 If line 21 is negative: + Charitable Contributions + Income Distributions + The exempt amount = NOL (or not) Positive Or Negative?

73 FINAL YEAR OF THE ESTATE OR TRUST Only on the final return of the estate or trust does any unused NOL flow to the beneficiaries. The instructions for Form 1041, Schedule K-1, Beneficiary s Share of Income, Deductions, Credits, etc., advise beneficiaries filing Form 1040 how to report the NOL on their returns. However, the preparer of Form 1041 must use the proper codes on the K-1 in order to apply the instructions correctly. Generally, an unused NOL from the current year and from any carryforward years is reported to the beneficiaries on the Schedule K-1 as a Code D on line 11, Final year deductions. For individual beneficiaries, these deductions flow to Form 1040, line 21. However, if the final year of the estate or trust is also the last year of the NOL carryforward period, the unused NOL is classified as an excess deduction and reported as a Code A on line 11 of Schedule K-1. Code A deductions flow to Form 1040, Schedule A, line 23 (miscellaneous itemized deductions subject to the 2% limitation).

74 Corporate Net Operating Losses (NOLs) A corporation generally figures and deducts a net operating loss (NOL) the same way an individual, estate, or trust does. The same 2-year carryback and up to 20-year carryforward periods apply, and the same sequence applies when the corporation carries two or more NOLs to the same year. For more information on these general rules, see Publication 536, Net Operating Losses (NOLs) for Individuals, Estates, and Trusts. A corporation s NOL generally differs from individual, estate, and trust NOLs in the following ways. 1. A corporation can take different deductions when figuring an NOL. 2. A corporation must make different modifications to its taxable income in the carryback or carryforward year when figuring how much of the NOL is used and how much is carried over to the next year. 3. A corporation uses different forms when claiming an NOL deduction. For more information, see the Instructions for Form 1139, and the instructions for the corporation s tax return.

75 The main differences between corporate and non-corporate NOLs are that corporations: Can t use the domestic production activities deduction to create or increase an NOL Can use the deduction for dividends paid on certain preferred stock of public utilities, without limiting it to its taxable income for the year Can take the deduction for dividends received, without regard to the aggregate limits that normally apply

76 In 2010, corporation A had $500,000 of gross income from business operations and $625,000 of allowable business expenses. It also received $150,000 in dividends from a U.S. corporation for which it can take an 80 percent deduction, which normally would be limited to 80 percent of its taxable income before the deduction. Income: Income $500,000 Dividends $150,000 Gross Income $650,000 Expenses $625,000 Net Profit / Loss $25,000 Dividends -$120,000 NOL -$95,000 If the special rule wasn t there, the corporation s deduction for the dividends-received would ve been $20,000, or 80 percent of its taxable income before the deduction ($25,000 x 80 percent)

77 Ownership change: A loss corporation (one with cumulative losses) that has an ownership change is limited on the taxable income it can offset by NOL carryforwards arising before the date of the ownership change. This limit applies to any year ending after the change of ownership.

78

79 NOL Carryforward

80

81 1. Is the return for the NOL year being filed timely? If not, the taxpayer cannot elect out of the carryback. 2. What is the proper carryback period? 3. What are the projected tax savings from carrying back the NOL? 4. Has the practitioner consulted with the taxpayer concerning future plans that might affect the projections? For example, does the taxpayer plan to get married or divorced? Will the business be liquidated? 5. What are the projected tax savings from electing out of the carryback period and carrying the NOL forward instead? If the tax rates and tax laws are scheduled to change significantly in the future, are these changes incorporated into the projection? 6. Has the taxpayer been fully informed of the choices? 7. If the taxpayer chooses to carry back the NOL, is it better to use Form 1045 or file amended returns for the carryback years? 8. If there is any NOL carryforward, is it clearly documented so that it will not be overlooked next year?

82

7/6/2017. Net Operating Losses Part 1. Agenda. What is a Net Operating Loss? 172 and 56

Net Operating Losses Part 1 Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 6, 2017 Agenda Eligibility for an NOL The Form 1045 How To Figure an NOL How To Claim an NOL Deduction

Net Operating Losses Part 1 Kristy Maitre Tax Specialist Center for Agricultural Law and Taxation July 6, 2017 Agenda Eligibility for an NOL The Form 1045 How To Figure an NOL How To Claim an NOL Deduction

NET OPERATING LOSSES

TAX GUIDE FOR OWNERS AND OPERATORS OF SMALL AND MEDIUM SIZE FARMS CHAPTER 10 SYNPOSIS (click on section title to go directly there) Introduction... 10.2 Computing the NOL... 10.3 Items Not Included in

TAX GUIDE FOR OWNERS AND OPERATORS OF SMALL AND MEDIUM SIZE FARMS CHAPTER 10 SYNPOSIS (click on section title to go directly there) Introduction... 10.2 Computing the NOL... 10.3 Items Not Included in

NET OPERATING LOSSES FINAL COPYRIGHT 2015 LGUTEF. Learning Objectives. Introduction

NET OPERATING LOSSES Steps for NOL Deduction...... 40 NOL Carried between Joint and Separate Returns...... 50 Special Issues in NOL Calculations.......... 53 Making Optimal Use of an NOL Deduction.........

NET OPERATING LOSSES Steps for NOL Deduction...... 40 NOL Carried between Joint and Separate Returns...... 50 Special Issues in NOL Calculations.......... 53 Making Optimal Use of an NOL Deduction.........

Net Operating Losses

Net Operating Losses Edward K. Zollars, CPA Nichols Patrick CPE, Incorporated edzollars@currentfederaltaxdevelopments.com www.currentfederaltaxdevelopments.com Basic Issues Net Operating Loss rules are

Net Operating Losses Edward K. Zollars, CPA Nichols Patrick CPE, Incorporated edzollars@currentfederaltaxdevelopments.com www.currentfederaltaxdevelopments.com Basic Issues Net Operating Loss rules are

Instructions for Form 1139 (Rev. August 2010)

") Instructions for Form 1139 (Rev. August 2010) (Use with the August 2006 revision of Form 1139.) Corporation Application for Tentative Refund Department of the Treasury Internal Revenue Service Section

Instructions for Form 1139 (Rev. August 2010) (Use with the August 2006 revision of Form 1139.) Corporation Application for Tentative Refund Department of the Treasury Internal Revenue Service Section

Revenue Chapter ALABAMA DEPARTMENT OF REVENUE ADMINISTRATIVE CODE CHAPTER NET OPERATING LOSS TABLE OF CONTENTS

Revenue Chapter 810 3 15.2 ALABAMA DEPARTMENT OF REVENUE ADMINISTRATIVE CODE CHAPTER 810 3 15.2 NET OPERATING LOSS TABLE OF CONTENTS 810 3 15.2.01 Net Operating Loss Carryback Or Carryover 810 3 15.2.01

Revenue Chapter 810 3 15.2 ALABAMA DEPARTMENT OF REVENUE ADMINISTRATIVE CODE CHAPTER 810 3 15.2 NET OPERATING LOSS TABLE OF CONTENTS 810 3 15.2.01 Net Operating Loss Carryback Or Carryover 810 3 15.2.01

for Individuals, Estates, and Contents What s New For use in preparing 2008 Returns

Publication 536 Cat. No. 46569U Contents What s New... 1 Department of the Reminder... 2 Treasury Net Operating Introduction... 2 Internal Revenue NOL Steps... 2 Service Losses (NOLs) for How To Figure

Publication 536 Cat. No. 46569U Contents What s New... 1 Department of the Reminder... 2 Treasury Net Operating Introduction... 2 Internal Revenue NOL Steps... 2 Service Losses (NOLs) for How To Figure

First We Calculate the NOL 7/7/2017. NOL Part 2 Examples. NOL Importance

NOL Part 2 Examples June 21, 2017 NOL Importance Allows taxpayers to maximize the use of deductions and losses not limiting them to a single year A bit of history 2 First We Calculate the NOL 3 1 Example

NOL Part 2 Examples June 21, 2017 NOL Importance Allows taxpayers to maximize the use of deductions and losses not limiting them to a single year A bit of history 2 First We Calculate the NOL 3 1 Example

SENATE FINANCE COMMITTEE REPUBLICAN TAX STAFF SUMMARY OF MIDWESTERN DISASTER TAX RELIEF BILL (S. 3322)

") SENATE FINANCE COMMITTEE REPUBLICAN TAX STAFF SUMMARY OF MIDWESTERN DISASTER TAX RELIEF BILL (S. 3322) A request for a revenue estimate for all of the following proposals has been made to the Joint Committee

SENATE FINANCE COMMITTEE REPUBLICAN TAX STAFF SUMMARY OF MIDWESTERN DISASTER TAX RELIEF BILL (S. 3322) A request for a revenue estimate for all of the following proposals has been made to the Joint Committee

Highlights. Tax Cuts and Jobs Act of 2017

Highlights Tax Cuts and Jobs Act of 2017 Individual Taxes and s 2018 Tax s (Single) $0 to $9,525 $0 to $9,525 $9,525 to $38,700 $9,525 to $38,700 12% $38,700 to $93,700 25% $38,700 to $82,500 22% $93,700

Highlights Tax Cuts and Jobs Act of 2017 Individual Taxes and s 2018 Tax s (Single) $0 to $9,525 $0 to $9,525 $9,525 to $38,700 $9,525 to $38,700 12% $38,700 to $93,700 25% $38,700 to $82,500 22% $93,700

Integrity Accounting

Integrity Accounting Tax Reform Special Report Updated 8/15/2018 On Friday, December 22, 2017, the "Tax Cuts and Jobs Act" (H.R. 1) was signed into law by President Trump. Almost all of these provisions

Integrity Accounting Tax Reform Special Report Updated 8/15/2018 On Friday, December 22, 2017, the "Tax Cuts and Jobs Act" (H.R. 1) was signed into law by President Trump. Almost all of these provisions

PRESENT LAW. Sec. 163(e). But see section 267 (dealing in part with interest paid to a related or foreign party). 680

. But see section 267 (dealing in part with interest paid to a related or foreign party). 680") 385 D. Reform of Business Related Exclusions, Deductions, etc. 1. Interest (secs. 3203 and 3301 of the House bill, secs. 13301 and 13311 of the Senate amendment, and sec. 163(j) of the Code) Interest deduction

385 D. Reform of Business Related Exclusions, Deductions, etc. 1. Interest (secs. 3203 and 3301 of the House bill, secs. 13301 and 13311 of the Senate amendment, and sec. 163(j) of the Code) Interest deduction

I TAX REFORM FOR INDIVIDUALS

I TAX REFORM FOR INDIVIDUALS A. Simplification and Reform of Rates, Standard Deductions, and Exemptions 1. Reduction and simplification of individual income tax rates and modification of inflation adjustment

I TAX REFORM FOR INDIVIDUALS A. Simplification and Reform of Rates, Standard Deductions, and Exemptions 1. Reduction and simplification of individual income tax rates and modification of inflation adjustment

2017 Agricultural Tax Issues. Greg Bouchard for The Ohio State University

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

2017 Agricultural Tax Issues Greg Bouchard for The Ohio State University A. Income and Deductions p. 1 1. Ag. Income and Expenses 2. NOLs 3. Rental Property 4. Demolition of Structures 5. Marijuana and

TAX UPDATE TAX CUTS & JOBS ACT (2018) Add l Elderly & Blind Joint & Surviving Spouse: $1,300

Add l Elderly & Blind Joint & Surviving Spouse: $1,300") TAX UPDATE 2019 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2019 to the tax law as it was during 2017 for individuals and small businesses. Exemptions 2017 TAX CUTS

TAX UPDATE 2019 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2019 to the tax law as it was during 2017 for individuals and small businesses. Exemptions 2017 TAX CUTS

TAX CUTS AND JOBS ACT OF 2017

Scott Varon, CFP svaron@wealthmd.com 404.926.1312 www.wealthmd.com TAX CUTS AND JOBS ACT OF 2017 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2017 to the tax law as

Scott Varon, CFP svaron@wealthmd.com 404.926.1312 www.wealthmd.com TAX CUTS AND JOBS ACT OF 2017 This table compares the predominate changes made by the Tax Cuts and Jobs Act of 2017 to the tax law as

BUSINESS DEDUCTIONS 510 Limitation on Deduction of Business Interest

BUSINESS DEDUCTIONS 510 Limitation on Deduction of Business Interest NEW LAW EXPLAINED Limitation on deduction of business interest for all taxpayers. The deduction of interest paid or accrued on a debt

BUSINESS DEDUCTIONS 510 Limitation on Deduction of Business Interest NEW LAW EXPLAINED Limitation on deduction of business interest for all taxpayers. The deduction of interest paid or accrued on a debt

Year (YYYY) Month-Year (MM-YYYY) Month-Year (MM-YYYY)

Month-Year (MM-YYYY) Month-Year (MM-YYYY)") Michigan Department of Treasury (Rev. 06-17), Page 1 of 3 Application for Michigan Net Operating Loss Refund MI-1045 Issued under authority of Public Act 281 of 1967, as amended. Type or print in blue

Michigan Department of Treasury (Rev. 06-17), Page 1 of 3 Application for Michigan Net Operating Loss Refund MI-1045 Issued under authority of Public Act 281 of 1967, as amended. Type or print in blue

Tax Cuts and Jobs Act of 2017 (TCJA) Key Individual Tax Provisions

Key Individual Tax Provisions") Income Tax Rates and Exemptions Tax Rates and Brackets (TCJA) Key Individual Tax Provisions 1(j) 2018 2025 The following seven tax brackets apply for individuals: 10%, 12%, 22%, 24%, 32%, 35% and 37%.

Income Tax Rates and Exemptions Tax Rates and Brackets (TCJA) Key Individual Tax Provisions 1(j) 2018 2025 The following seven tax brackets apply for individuals: 10%, 12%, 22%, 24%, 32%, 35% and 37%.

Instructions for Schedule I (Form 1041) Alternative Minimum Tax Estates and Trusts

Alternative Minimum Tax Estates and Trusts") 2009 Instructions for Schedule I (Form 1041) Alternative Minimum Tax Estates and Trusts Department of the Treasury Internal Revenue Service Section references are to the Internal deduction (NOLD), a capital

2009 Instructions for Schedule I (Form 1041) Alternative Minimum Tax Estates and Trusts Department of the Treasury Internal Revenue Service Section references are to the Internal deduction (NOLD), a capital

2010 Instructions for Form 6251 Alternative Minimum Tax Individuals

This form is referenced in an endnote at the Bradford Tax Institute. CLICK HERE to go to the home page. 2010 Instructions for Form 6251 Alternative Minimum Tax Individuals Department of the Treasury Internal

This form is referenced in an endnote at the Bradford Tax Institute. CLICK HERE to go to the home page. 2010 Instructions for Form 6251 Alternative Minimum Tax Individuals Department of the Treasury Internal

News. Tax Cuts and Jobs Act

News Release Date: 12/26/17 Cross References H.R. 1 Tax Cuts and Jobs Act On December 22, 2017 the President signed into law H.R. 1 (officially titled An Act to Provide for Reconciliation Pursuant to Titles

News Release Date: 12/26/17 Cross References H.R. 1 Tax Cuts and Jobs Act On December 22, 2017 the President signed into law H.R. 1 (officially titled An Act to Provide for Reconciliation Pursuant to Titles

HIGHLIGHTS OF TAX CUTS AND JOBS ACT OF 2017

HIGHLIGHTS OF TAX CUTS AND JOBS ACT OF 2017 SELECTED CHANGES PRIMARILY IMPACTING INDIVIDUALS INDIVIDUAL INCOME TAX RATES (Effective for tax years beginning after 2017 and before 2026) Single Individuals

HIGHLIGHTS OF TAX CUTS AND JOBS ACT OF 2017 SELECTED CHANGES PRIMARILY IMPACTING INDIVIDUALS INDIVIDUAL INCOME TAX RATES (Effective for tax years beginning after 2017 and before 2026) Single Individuals

Instructions for Form 6251

2017 Instructions for Form 6251 Alternative Minimum Tax Individuals Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. General

2017 Instructions for Form 6251 Alternative Minimum Tax Individuals Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. General

The Tax Cuts and Jobs Act of 2017

The Tax Cuts and Jobs Act of 2017 is the most comprehensive revision to the Internal Revenue Code Since 1986. This new Tax Act reduces tax rates for individuals and corporations, repeals exemptions, eliminates

The Tax Cuts and Jobs Act of 2017 is the most comprehensive revision to the Internal Revenue Code Since 1986. This new Tax Act reduces tax rates for individuals and corporations, repeals exemptions, eliminates

5 Qualifying widow(er) (see instructions) 6a Yourself. If someone can claim you as a dependent, do not check box 6a...

(see instructions) 6a Yourself. If someone can claim you as a dependent, do not check box 6a...") Form 1040 Department of the Treasury Internal Revenue Service (99) US Individual Income Tax Return OMB No 1545-0074 IRS Use Only Do not write or staple in this space For the year Jan 1 Dec 31,, or other

Form 1040 Department of the Treasury Internal Revenue Service (99) US Individual Income Tax Return OMB No 1545-0074 IRS Use Only Do not write or staple in this space For the year Jan 1 Dec 31,, or other

Understanding the Alternative Minimum Tax. Course #6510/QAS6510 Course Material

Understanding the Alternative Minimum Tax Course #6510/QAS6510 Course Material Understanding the Alternative Minimum Tax (Course #6510/QAS6510) Table of Contents Chapter 1: Introduction 1-1 A Brief History

Understanding the Alternative Minimum Tax Course #6510/QAS6510 Course Material Understanding the Alternative Minimum Tax (Course #6510/QAS6510) Table of Contents Chapter 1: Introduction 1-1 A Brief History

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE New Individual Tax Rates New rate structure with seven tax brackets 10% (same as 2017)

TAX REFORM TCJA TAX CUTS AND JOBS ACT AL NELLA & CO, LLP CHRIS KOLLAJA & KEVIN TUSING HONE MAXWELL LLP AUBREY HONE New Individual Tax Rates New rate structure with seven tax brackets 10% (same as 2017)

How Tax Reforms Impacts Your Vineyard February 8, Presented by: Kathy Freshwater, CPA Craig Anderson, CPA

How Tax Reforms Impacts Your Vineyard February 8, 2018 Presented by: Kathy Freshwater, CPA Craig Anderson, CPA Presenters Kathy Freshwater Tax Senior Manager Yakima Craig Anderson Tax Partner Yakima High

How Tax Reforms Impacts Your Vineyard February 8, 2018 Presented by: Kathy Freshwater, CPA Craig Anderson, CPA Presenters Kathy Freshwater Tax Senior Manager Yakima Craig Anderson Tax Partner Yakima High

UNITED STATES PUBLIC LAWS 109th Congress - First Session Convening January 7, 2005 GULF OPPORTUNITY ZONE ACT OF 2005

UNITED STATES PUBLIC LAWS 109th Congress - First Session Convening January 7, 2005 PL 109-135 (HR 4440) December 21, 2005 GULF OPPORTUNITY ZONE ACT OF 2005 An Act To amend the Internal Revenue Code of

UNITED STATES PUBLIC LAWS 109th Congress - First Session Convening January 7, 2005 PL 109-135 (HR 4440) December 21, 2005 GULF OPPORTUNITY ZONE ACT OF 2005 An Act To amend the Internal Revenue Code of

PUBLIC INSPECTION COPY

Form 990-T Department of the Treasury Internal Revenue Service A Check box if address changed Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) For calendar year 2011

Form 990-T Department of the Treasury Internal Revenue Service A Check box if address changed Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) For calendar year 2011

Tax Cuts and Jobs Act 2017 HR 1

Tax Cuts and Jobs Act 2017 HR 1 The Tax Cuts and Jobs Act is arguably the most significant change to the Internal Revenue Code in decades, the law reduces tax rates for individuals and corporations and

Tax Cuts and Jobs Act 2017 HR 1 The Tax Cuts and Jobs Act is arguably the most significant change to the Internal Revenue Code in decades, the law reduces tax rates for individuals and corporations and

NEW LEGISLATION BUSINESS

NEW LEGISLATION BUSINESS 2 Land Grant University Tax Education Foundation Corporate Tax Rate... 24 Employer Credit for Paid Family and Medical Leave.... 25 Credit for Prior-Year Minimum Tax Liability of

NEW LEGISLATION BUSINESS 2 Land Grant University Tax Education Foundation Corporate Tax Rate... 24 Employer Credit for Paid Family and Medical Leave.... 25 Credit for Prior-Year Minimum Tax Liability of

AGRICULTURAL TAX. i n c o m e t a x e s

AGRICULTURAL TAX ISSUES c r i t i c a l i n f o r m a t i o n t o k n o w f o r 2 0 1 8 i n c o m e t a x e s The difference between death and taxes is death doesn t get worse every time Congress meets.

AGRICULTURAL TAX ISSUES c r i t i c a l i n f o r m a t i o n t o k n o w f o r 2 0 1 8 i n c o m e t a x e s The difference between death and taxes is death doesn t get worse every time Congress meets.

for 501(c)(3) Organizations Only Check box if Name of organization ( Check box if name changed and see instructions.)

(3) Organizations Only Check box if Name of organization ( Check box if name changed and see instructions.)") 99-T OMB No. 1545-687 Exempt Organization Business Income Tax Return(and proxy tax under section 633(e)) Form For calendar year 21 or other tax year beginning, 21, and Department of the Treasury Internal

99-T OMB No. 1545-687 Exempt Organization Business Income Tax Return(and proxy tax under section 633(e)) Form For calendar year 21 or other tax year beginning, 21, and Department of the Treasury Internal

TAX CUTS AND JOB ACT OF 2017 Highlights

2017 TAX CUTS AND JOB ACT OF 2017 Highlights UPDATED January 9, 2018 www.cordascocpa.com TAX CUTS AND JOBS ACT OF 2017 INTRODUCTION After months of intense negotiations, the President signed the Tax Cuts

2017 TAX CUTS AND JOB ACT OF 2017 Highlights UPDATED January 9, 2018 www.cordascocpa.com TAX CUTS AND JOBS ACT OF 2017 INTRODUCTION After months of intense negotiations, the President signed the Tax Cuts

Tax Bill Comparison. December 2017

Tax Bill Comparison December 2017 Individual Taxes and s 2018 Tax s (Single) $0 to $9,525 $0 to $45,000 $0 to $9,525 $9,525 to $38,700 $45,000 to $200,000 $9,325 to $38,700 $38,700 to $93,700 $200,000

Tax Bill Comparison December 2017 Individual Taxes and s 2018 Tax s (Single) $0 to $9,525 $0 to $45,000 $0 to $9,525 $9,525 to $38,700 $45,000 to $200,000 $9,325 to $38,700 $38,700 to $93,700 $200,000

Tax Law Changes 2018

Tax Law Changes 2018 Standard Deduction Standard deduction increased to $24,000 MFJ and QW $18,000 HoH $12,000 Single and MFS Pub 4012 Tab F-1 Additional standard deduction amount for age 65 and older

Tax Law Changes 2018 Standard Deduction Standard deduction increased to $24,000 MFJ and QW $18,000 HoH $12,000 Single and MFS Pub 4012 Tab F-1 Additional standard deduction amount for age 65 and older

IRC 199A Deduction for Qualified Business Income

IRC 199A Deduction for Qualified Business Income What is it? 20% deduction against qualified business income Designed to provide a tax break to owners of pass through entities, in light of substantial

IRC 199A Deduction for Qualified Business Income What is it? 20% deduction against qualified business income Designed to provide a tax break to owners of pass through entities, in light of substantial

Tax Cuts and Jobs Act of 2017

On December 22, 2017, President Donald Trump signed into law H.R. 1, the Tax Cuts and Jobs Act of 2017 (TCJA). This new tax legislation, slightly over 500 pages in length, is the most significant revision

On December 22, 2017, President Donald Trump signed into law H.R. 1, the Tax Cuts and Jobs Act of 2017 (TCJA). This new tax legislation, slightly over 500 pages in length, is the most significant revision

November 6, Comprehensive Tax Reform Proposal Released HR1 Tax Cuts and Jobs Bill, November 2,

November 6, 2017 Comprehensive Tax Reform Proposal Released... 2 HR1 Tax Cuts and Jobs Bill, November 2, 2017... 2 2017 Loscalzo Institute, a Kaplan Company Current Federal Tax Developments 2 Comprehensive

November 6, 2017 Comprehensive Tax Reform Proposal Released... 2 HR1 Tax Cuts and Jobs Bill, November 2, 2017... 2 2017 Loscalzo Institute, a Kaplan Company Current Federal Tax Developments 2 Comprehensive

Answers to Selected PAK Problems Unit07. PAK Chapter I:8. Losses and Bad Debts

Discussion Questions Answers to Selected PAK Problems Unit07. PAK Chapter I:8. Losses and Bad Debts I:0-1 If the worthless securities consist of securities of an affiliated corporation held by a domestic

Discussion Questions Answers to Selected PAK Problems Unit07. PAK Chapter I:8. Losses and Bad Debts I:0-1 If the worthless securities consist of securities of an affiliated corporation held by a domestic

Tax Reform: What You Need To Know

Tax Reform: What You Need To Know January 24, 2018 Presented by: Blake Harrison, CPA/PFS Senior Tax Manager LBMC Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on

Tax Reform: What You Need To Know January 24, 2018 Presented by: Blake Harrison, CPA/PFS Senior Tax Manager LBMC Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on

Page 2 Page 7 Page 10 Page 12 ONLY $449. Save $200 Off Retail!

All seven of the following tests must be met in order for a taxpayer to claim another person as a dependent in 0. Test numbers through vary depending joint return with a spouse. This rule does not apply

All seven of the following tests must be met in order for a taxpayer to claim another person as a dependent in 0. Test numbers through vary depending joint return with a spouse. This rule does not apply

For Better or Worse? Individual, Estate, and Presented Trust by: Taxes Under the New Tax Reform [Date] Act

![For Better or Worse? Individual, Estate, and Presented Trust by: Taxes Under the New Tax Reform [Date] Act](/thumbs/84/89476432.jpg "For Better or Worse? Individual, Estate, and Presented Trust by: Taxes Under the New Tax Reform [Date] Act") Abbott, Stringham & Lynch Tax Group For Better or Worse? Individual, Estate, and Presented Trust by: Taxes Under the New Tax Reform [Date] Act Presented by: Julie Malekhedayat, CPA Chris Madrid, CPA Anu

Abbott, Stringham & Lynch Tax Group For Better or Worse? Individual, Estate, and Presented Trust by: Taxes Under the New Tax Reform [Date] Act Presented by: Julie Malekhedayat, CPA Chris Madrid, CPA Anu

2013 Schedule M1M, Income Additions and Subtractions

2013 Schedule M1M, Income Additions and Subtractions Sequence #3 201355 Complete this schedule to determine line 3 and line 6 of Form M1. Your First Name and Initial Last Name Your Social Security Number

2013 Schedule M1M, Income Additions and Subtractions Sequence #3 201355 Complete this schedule to determine line 3 and line 6 of Form M1. Your First Name and Initial Last Name Your Social Security Number

Impact of Tax Reform on Farmers. Tax and Accounting Department Fall 2018

Impact of Tax Reform on Farmers Tax and Accounting Department Fall 2018 Agenda Summary of Tax Reform Individual Business Tax Planning with Business Structure Important Items on a Farm Tax Return Disclaimer

Impact of Tax Reform on Farmers Tax and Accounting Department Fall 2018 Agenda Summary of Tax Reform Individual Business Tax Planning with Business Structure Important Items on a Farm Tax Return Disclaimer

Tax Cuts and Jobs Act of 2017

Tax Cuts and Jobs Act of 2017 Introduction After months of intense negotiations, the President signed the Tax Cuts And Jobs Act Of 2017 (the New Law ) on December 22, 2017 - the most significant tax reform

Tax Cuts and Jobs Act of 2017 Introduction After months of intense negotiations, the President signed the Tax Cuts And Jobs Act Of 2017 (the New Law ) on December 22, 2017 - the most significant tax reform

TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University Tax Planning

1 TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2014 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

1 TAX MANAGEMENT TIPS FOR FARMERS L.R. Borton Michigan State University 2014 - Tax Planning 1. The basic management guideline is to avoid wide fluctuations in taxable income because a relatively uniform

Re: 2017 Tax Cuts Act: What it Means For Individuals

Re: 2017 Tax Cuts Act: What it Means For Individuals The Tax Cuts and Jobs Act was signed by President Trump on December 22. The Act makes sweeping changes to the U.S. tax code and impacts virtually every

Re: 2017 Tax Cuts Act: What it Means For Individuals The Tax Cuts and Jobs Act was signed by President Trump on December 22. The Act makes sweeping changes to the U.S. tax code and impacts virtually every

2017 TAX CUTS AND JOBS ACT

2017 TAX CUTS AND JOBS ACT The Tax Cuts and Jobs Act was signed by President Trump on December 22, 2017. The Act makes sweeping changes to the U.S. tax code and impacts most taxpayers; especially individuals

2017 TAX CUTS AND JOBS ACT The Tax Cuts and Jobs Act was signed by President Trump on December 22, 2017. The Act makes sweeping changes to the U.S. tax code and impacts most taxpayers; especially individuals

N/A. Kiddie Tax Various bracket thresholds Ordinary and capital gains rates applicable to trusts and estates

We have prepared a summary of the House and the Senate versions of the proposed tax reform bill. Once they reach an agreement on a final bill, we will update the summary as needed. House Bill (H. R. 1)

We have prepared a summary of the House and the Senate versions of the proposed tax reform bill. Once they reach an agreement on a final bill, we will update the summary as needed. House Bill (H. R. 1)

Tax Cuts and Jobs Act. Durham Chamber of Commerce Public Policy Meeting January 9, 2018

Tax Cuts and Jobs Act Durham Chamber of Commerce Public Policy Meeting January 9, 2018 Tax Cuts in Billions Corporate/Business ($653) S-Corps/Partnership/Sole Proprietor ($414) International Tax Changes

Tax Cuts and Jobs Act Durham Chamber of Commerce Public Policy Meeting January 9, 2018 Tax Cuts in Billions Corporate/Business ($653) S-Corps/Partnership/Sole Proprietor ($414) International Tax Changes

Quick Facts. Comprehensive Calculations. Prior Year Comparisons Software Updates Delivered Online Alerts Ability to Returns to Support

Quick Facts Access State Data Entry from Federal Data Entry Federal Information Flows to State Returns Auto-fill Available for Amended Returns Group Sales of Depreciable Assets Many Credit Forms Available

Quick Facts Access State Data Entry from Federal Data Entry Federal Information Flows to State Returns Auto-fill Available for Amended Returns Group Sales of Depreciable Assets Many Credit Forms Available

2011 Schedule M1M, Income Additions and Subtractions. Your First Name and Initial Last Name Your Social Security Number

2011 Schedule M1M Income Additions and Subtractions Sequence #3 Complete this schedule to determine line 3 and line 6 of Form M1. 201155 Your First Name and Initial Last Name Your Social Security Number

2011 Schedule M1M Income Additions and Subtractions Sequence #3 Complete this schedule to determine line 3 and line 6 of Form M1. 201155 Your First Name and Initial Last Name Your Social Security Number

TAX REFORM: IMPACT ON BUSINESSES AND INDIVIDUALS. February 8, 2018 Bruce I. Booken Rose K. Wilson

TAX REFORM: IMPACT ON BUSINESSES AND INDIVIDUALS February 8, 2018 Bruce I. Booken Rose K. Wilson The 2017 Tax Act Signed into law on December 22, 2017 Provisions apply NOW to taxable years beginning after

TAX REFORM: IMPACT ON BUSINESSES AND INDIVIDUALS February 8, 2018 Bruce I. Booken Rose K. Wilson The 2017 Tax Act Signed into law on December 22, 2017 Provisions apply NOW to taxable years beginning after

Internal Revenue Code Section 172(b)(3) Net operating loss deduction.

(3) Net operating loss deduction.") Internal Revenue Code Section 172(b)(3) Net operating loss deduction. CLICK HERE to return to the home page (a) Deduction allowed. There shall be allowed as a deduction for the taxable year an amount equal

Internal Revenue Code Section 172(b)(3) Net operating loss deduction. CLICK HERE to return to the home page (a) Deduction allowed. There shall be allowed as a deduction for the taxable year an amount equal

DUAL-STATUS RETURN U.S. Nonresident Alien Income Tax Return LEE F DUT X. MN Foreign province/county

DUAL-STATUS RETURN U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1-December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning,

DUAL-STATUS RETURN U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1-December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning,

Tax Cuts and Jobs Act February 8, 2018

Tax Cuts and Jobs Act 2017 February 8, 2018 Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax advice to any specific taxpayer

Tax Cuts and Jobs Act 2017 February 8, 2018 Disclaimer This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax advice to any specific taxpayer

Personal Exemp ons. Standard Deduc on

Personal Exemp ons Taxpayer, Spouse, Qualified Child Qualified Rela ve $4,050 for each person in the household All Personal Exemp ons are Eliminated Standard Deduc on If your filing status is... Single

Personal Exemp ons Taxpayer, Spouse, Qualified Child Qualified Rela ve $4,050 for each person in the household All Personal Exemp ons are Eliminated Standard Deduc on If your filing status is... Single

Table of Contents EA Exam Part

Table of Contents EA Exam Part 1 2017-18 Introduction... 2 Examination Content Outline... 8 Course Content... 11 Preliminary Work and Taxpayer Data... 12 Preliminary work to prepare tax returns... 12 Use

Table of Contents EA Exam Part 1 2017-18 Introduction... 2 Examination Content Outline... 8 Course Content... 11 Preliminary Work and Taxpayer Data... 12 Preliminary work to prepare tax returns... 12 Use

TAX REFORM INDIVIDUALS

The following chart sets forth some of the provisions affecting individuals in the Tax Reform Act of 2017 (the Act). This chart highlights only some of the key issues and is not intended to address all

The following chart sets forth some of the provisions affecting individuals in the Tax Reform Act of 2017 (the Act). This chart highlights only some of the key issues and is not intended to address all

Instructions for Form 4626

2004 Instructions for Form 4626 Alternative Minimum Tax Corporations Section references are to the Internal Revenue Code unless otherwise noted. Department of the Treasury Internal Revenue Service General

2004 Instructions for Form 4626 Alternative Minimum Tax Corporations Section references are to the Internal Revenue Code unless otherwise noted. Department of the Treasury Internal Revenue Service General

2017 Schedule M1NC, Federal Adjustments

2017 Schedule M1NC, Federal Adjustments *171341* Minnesota has not adopted the federal law changes made after December 16, 2016, that affect federal taxable income for tax year 2017. Your First Name and

2017 Schedule M1NC, Federal Adjustments *171341* Minnesota has not adopted the federal law changes made after December 16, 2016, that affect federal taxable income for tax year 2017. Your First Name and

5/29/ TAX CUTS AND JOBS ACT OVERVIEW. Individual Tax. Introduction-Individual Provisions. Dauphin County Bar Association May 30, 2018

2017 TAX CUTS AND JOBS ACT OVERVIEW Dauphin County Bar Association May 30, 2018 Individual Tax 2 Introduction-Individual Provisions In general, the individual provisions go into effect starting on January

2017 TAX CUTS AND JOBS ACT OVERVIEW Dauphin County Bar Association May 30, 2018 Individual Tax 2 Introduction-Individual Provisions In general, the individual provisions go into effect starting on January

Tax Update for 2018 and 2019

Tax Update for 2018 and 2019 Individual Tax Changes Business Tax Changes Depreciation Changes Inflation Adjustments IRS Mileage Rates Affordable Care Act Partnership Audit Rules The following is a summary

Tax Update for 2018 and 2019 Individual Tax Changes Business Tax Changes Depreciation Changes Inflation Adjustments IRS Mileage Rates Affordable Care Act Partnership Audit Rules The following is a summary

9033 CREDIT FOR QUALIFIED RETIREMENT SAVINGS

Tax Credits, Prepayments, and Alternative Minimum Tax 9 7 EXAMPLE 9.4 Arleta Kern is single and has two qualifying children. If Arleta has gross income of $18,000, she will have a child tax credit of $4,000.

Tax Credits, Prepayments, and Alternative Minimum Tax 9 7 EXAMPLE 9.4 Arleta Kern is single and has two qualifying children. If Arleta has gross income of $18,000, she will have a child tax credit of $4,000.

Corporate and Business Provision House Bill (HR 1) Senate Bill Final Bill

Senate Bill Final Bill") Selected provisions of the House and Senate tax reform bills as passed by both houses of Congress which resulted in the final bill in the far right column. Introduction: This summary contains what ZLQ

Selected provisions of the House and Senate tax reform bills as passed by both houses of Congress which resulted in the final bill in the far right column. Introduction: This summary contains what ZLQ

1040 U.S. Individual Income Tax Return 2011

F or Department of the Treasury Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 211 m OMB. 1545-74 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31, 211,

F or Department of the Treasury Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 211 m OMB. 1545-74 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31, 211,

Year-end Year-Round Tax Planning Guide

Year-end Year-Round Tax Planning Guide 2014 Individual Taxes What you need to know 2 2014 Business Taxes Another set of considerations 12 Are you confident you are doing everything you can to minimize

Year-end Year-Round Tax Planning Guide 2014 Individual Taxes What you need to know 2 2014 Business Taxes Another set of considerations 12 Are you confident you are doing everything you can to minimize

The Tax Treatment of Net Operating Losses: In Brief

Page: 1 of 10 The Tax Treatment of Net Operating Losses: In Brief Mark P. Keightley Specialist in Economics October 4, 2017 7-5700 www.crs.gov R44976 Page: 2 of 10 Summary Tax reform could result in any

Page: 1 of 10 The Tax Treatment of Net Operating Losses: In Brief Mark P. Keightley Specialist in Economics October 4, 2017 7-5700 www.crs.gov R44976 Page: 2 of 10 Summary Tax reform could result in any

Tax Law & Scope Changes Carl Kantner As of December 3, 2018

Tax Law & Scope Changes 2018 Carl Kantner As of December 3, 2018 Tax-Aide Scope Manual The authority for Tax-Aide scope questions Manual for Tax Year 2018 issued November 28 Located in Portal Library under

Tax Law & Scope Changes 2018 Carl Kantner As of December 3, 2018 Tax-Aide Scope Manual The authority for Tax-Aide scope questions Manual for Tax Year 2018 issued November 28 Located in Portal Library under

NATIONAL SOCIETY OF TAX PROFESSIONALS TAX CUTS AND JOBS ACT H.R.1 COMPARISON OF HOUSE AND SENATE BILLS AS OF DECEMBER 6, 2017

NATIONAL SOCIETY OF TAX PROFESSIONALS TAX CUTS AND JOBS ACT H.R.1 COMPARISON OF HOUSE AND SENATE BILLS AS OF DECEMBER 6, 2017 PROVISION: HOUSE BILL SENATE BILL 1. Individual Tax Rates 12%, 25%, 35%, 39.6%.

NATIONAL SOCIETY OF TAX PROFESSIONALS TAX CUTS AND JOBS ACT H.R.1 COMPARISON OF HOUSE AND SENATE BILLS AS OF DECEMBER 6, 2017 PROVISION: HOUSE BILL SENATE BILL 1. Individual Tax Rates 12%, 25%, 35%, 39.6%.

2017 Ohio IT 1040 Individual Income Tax Return

Do not staple or paper clip Rev 9/17 2017 Ohio IT 1040 Individual Income Tax Return Use only black ink and UPPERCASE letters 17000102 1 Check here if this is an amended return Include the Ohio IT RE (do

Do not staple or paper clip Rev 9/17 2017 Ohio IT 1040 Individual Income Tax Return Use only black ink and UPPERCASE letters 17000102 1 Check here if this is an amended return Include the Ohio IT RE (do

Bob Smith Betty Smith Home address (number and street). If you have a P.O.box, see instructions. J Important!

. If you have a P.O.box, see instructions. J Important!") Presidential Lakeview WA 99999 Election Campaign Note: Checking Yes will not change your tax or reduce your refund. You Spouse (See instructions.) A Do you, or your spouse if filing a joint return, want

Presidential Lakeview WA 99999 Election Campaign Note: Checking Yes will not change your tax or reduce your refund. You Spouse (See instructions.) A Do you, or your spouse if filing a joint return, want

Schedule M1M, Income Additions and Subtractions 2016 Sequence #3

201655 Schedule M1M, Income Additions and Subtractions 2016 Sequence #3 Complete this schedule to determine line 3 and line 6 of Form M1. Your First Name and Initial Last Name Your Social Security Number

201655 Schedule M1M, Income Additions and Subtractions 2016 Sequence #3 Complete this schedule to determine line 3 and line 6 of Form M1. Your First Name and Initial Last Name Your Social Security Number

IRS Federal Income Tax Publications provided by efile.com

IRS Federal Income Tax Publications provided by efile.com This publication should serve as a relevant source for up to date tax answers to your tax questions. Unlike most tax forms, many tax publications

IRS Federal Income Tax Publications provided by efile.com This publication should serve as a relevant source for up to date tax answers to your tax questions. Unlike most tax forms, many tax publications

TAX CUTS AND JOBS ACT

TAX CUTS AND JOBS ACT Businesses Corporate tax rate will now be a flat 21% beginning January 1, 2018. Corporate alternative minimum tax has been repealed. Effective for tax years beginning after December

TAX CUTS AND JOBS ACT Businesses Corporate tax rate will now be a flat 21% beginning January 1, 2018. Corporate alternative minimum tax has been repealed. Effective for tax years beginning after December

Benefits. and Expenses. Your Home

Recommended IRS Publication Reading Listt for Part 1: Individuals Publication 17, Your Federal Income Tax Publication 501, Exemptions, Standard Deduction, and Filing Information Publication 971, Innocent

Recommended IRS Publication Reading Listt for Part 1: Individuals Publication 17, Your Federal Income Tax Publication 501, Exemptions, Standard Deduction, and Filing Information Publication 971, Innocent

Instructions for Form 4626

1999 Department Instructions for Form 4626 Alternative Minimum Tax Corporations Section references are to the Internal Revenue Code unless otherwise noted. of the Treasury Internal Revenue Service General

1999 Department Instructions for Form 4626 Alternative Minimum Tax Corporations Section references are to the Internal Revenue Code unless otherwise noted. of the Treasury Internal Revenue Service General

Tax Reform Proposals and Year-End Planning Strategies

Tax Reform Proposals and Year-End Planning Strategies December 8, 2017 Troy D. Hogan, CPA The information presented herein is general in nature and should not be acted upon without the advice of a professional.

Tax Reform Proposals and Year-End Planning Strategies December 8, 2017 Troy D. Hogan, CPA The information presented herein is general in nature and should not be acted upon without the advice of a professional.

Tax cuts and jobs act

1 Tax cuts and jobs act BUSINESS & INDIVIDUAL TAX PROVISIONS PRESENTED BY: MIKE AMERIO & MIKE SOVIK (2017): MFJ Bracket $0 - $18,500 10% $18,501 - $75,900 15% $75,901 - $153,100 25% $153,101 - $233,350

1 Tax cuts and jobs act BUSINESS & INDIVIDUAL TAX PROVISIONS PRESENTED BY: MIKE AMERIO & MIKE SOVIK (2017): MFJ Bracket $0 - $18,500 10% $18,501 - $75,900 15% $75,901 - $153,100 25% $153,101 - $233,350

New Tax Rules. For You and Your Business Owners

New Tax Rules For You and Your Business Owners 199A-The 20% Deduction for Pass Throughs The New Rules for Meals & Entertainment QSBS-Qualified Small Business Stock And the New Depreciation Rules Presented

New Tax Rules For You and Your Business Owners 199A-The 20% Deduction for Pass Throughs The New Rules for Meals & Entertainment QSBS-Qualified Small Business Stock And the New Depreciation Rules Presented

SENATE TAX REFORM PROPOSAL INDIVIDUALS

The following chart sets forth some of the provisions affecting individuals in the Senate s version of the Tax Cuts and Jobs Act, as approved by the Senate on December 2, 2017. This chart highlights only

The following chart sets forth some of the provisions affecting individuals in the Senate s version of the Tax Cuts and Jobs Act, as approved by the Senate on December 2, 2017. This chart highlights only

TAX CUTS AND JOBS ACT SUMMARY

TAX CUTS AND JOBS ACT SUMMARY Mariner Retirement Advisors The Tax Cuts and Jobs Act ( TCJA ) was signed by President Trump on December 22, 2017. The Act makes sweeping changes to the U.S. tax code and

TAX CUTS AND JOBS ACT SUMMARY Mariner Retirement Advisors The Tax Cuts and Jobs Act ( TCJA ) was signed by President Trump on December 22, 2017. The Act makes sweeping changes to the U.S. tax code and

Your first name and initial Last name Your social security number

1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. Filing status: Single X Married filing

1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. Filing status: Single X Married filing

2001 Instructions for Schedule D, Capital Gains and Losses

2001 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

2001 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

Tax Cuts and Jobs Act Key Implications for Individuals

Tax Cuts and Jobs Act Key Implications for Individuals Overview The 2017 Tax Reform legislation, the most significant federal tax law reform in over 30 years, was passed by both the House of Representatives

Tax Cuts and Jobs Act Key Implications for Individuals Overview The 2017 Tax Reform legislation, the most significant federal tax law reform in over 30 years, was passed by both the House of Representatives

Navigating the Complexities of Tax Simplification PART 1 TAX CUTS & JOBS ACT (TCJA)

") Navigating the Complexities of Tax Simplification PART 1 TAX CUTS & JOBS ACT (TCJA) 2 1 2 1 TCJA BACKGROUND An act to provide for reconciliation pursuant to titles II and V of the concurrent resolution

Navigating the Complexities of Tax Simplification PART 1 TAX CUTS & JOBS ACT (TCJA) 2 1 2 1 TCJA BACKGROUND An act to provide for reconciliation pursuant to titles II and V of the concurrent resolution

Advance Draft. Form 100W Booklet 2011 Page 29

Instructions for Schedule P (100W) Alternative Minimum Tax and Credit Limitations Water s-edge Filers References in these instructions are to the Internal Revenue Code (IRC) as of January 1, 2009, and

Instructions for Schedule P (100W) Alternative Minimum Tax and Credit Limitations Water s-edge Filers References in these instructions are to the Internal Revenue Code (IRC) as of January 1, 2009, and

DEVELOPMENTS FILING DEADLINES

CPE Credit Service Sidney Kess and Barbara Weltman FOCUS: Loss Limitations for Individuals PRACTICE MANAGEMENT TIP: Helping Business Clients with Benefit Plans RECENT DEVELOPMENTS FILING DEADLINES and

CPE Credit Service Sidney Kess and Barbara Weltman FOCUS: Loss Limitations for Individuals PRACTICE MANAGEMENT TIP: Helping Business Clients with Benefit Plans RECENT DEVELOPMENTS FILING DEADLINES and

Business Provisions Under the Tax Cuts and Jobs Act Compared to Previous Tax Law

Tax Rates Corporate tax rate Top rate of 35 percent Flat rate of 21 percent (effective 1/1/2018) Alternative minimum tax (AMT) 20 percent Repealed; AMT credits refundable from 2018 through 2021 (1) Personal

Tax Rates Corporate tax rate Top rate of 35 percent Flat rate of 21 percent (effective 1/1/2018) Alternative minimum tax (AMT) 20 percent Repealed; AMT credits refundable from 2018 through 2021 (1) Personal

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC's 1040 Deskbook. Twenty ninth Edition (October 2016)

") Route To: Partners Managers Staff File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC's 1040 Deskbook Twenty ninth Edition (October 2016) Highlights of this Edition The following are some of the important

Route To: Partners Managers Staff File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC's 1040 Deskbook Twenty ninth Edition (October 2016) Highlights of this Edition The following are some of the important

Tax Cuts and Jobs Act Construction Industry Impact

Tax Cuts and Jobs Act Construction Industry Impact Presented By: Sean M. Auger, Partner 1 Introduction Most but not all provisions effective for tax periods beginning after December 31, 2017 2 General

Tax Cuts and Jobs Act Construction Industry Impact Presented By: Sean M. Auger, Partner 1 Introduction Most but not all provisions effective for tax periods beginning after December 31, 2017 2 General

Tax Cuts and Jobs Act of 2017 (TCJA) Key Individual Tax Provisions. 151(d) The deduction for personal exemptions is eliminated.

Key Individual Tax Provisions. 151(d) The deduction for personal exemptions is eliminated.") Income Tax Rates and Exemptions Tax Rates and Brackets Key Individual Tax Provisions Quickfinder 1(j) 2018 2025 The following seven tax brackets apply for individuals: 10%, 12%, 22%, 24%, 32%, 35% and

Income Tax Rates and Exemptions Tax Rates and Brackets Key Individual Tax Provisions Quickfinder 1(j) 2018 2025 The following seven tax brackets apply for individuals: 10%, 12%, 22%, 24%, 32%, 35% and

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2013

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2013 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION January 8, 2013 JCX-2-13R I. SUMMARY OF PRESENT-LAW FEDERAL TAX SYSTEM A. Individual Income

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2013 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION January 8, 2013 JCX-2-13R I. SUMMARY OF PRESENT-LAW FEDERAL TAX SYSTEM A. Individual Income

OTHER TOOLS TO MANAGE TAX LIABILITY

TAX GUIDE FOR OWNERS AND OPERATORS OF SMALL AND MEDIUM SIZE FARMS CHAPTER 7 OTHER TOOLS TO MANAGE TAX LIABILITY SYNPOSIS (click on section title to go directly there) Introduction... 7.2 Farm Income Averaging...

TAX GUIDE FOR OWNERS AND OPERATORS OF SMALL AND MEDIUM SIZE FARMS CHAPTER 7 OTHER TOOLS TO MANAGE TAX LIABILITY SYNPOSIS (click on section title to go directly there) Introduction... 7.2 Farm Income Averaging...

Law Offices of Bradley J. Frigon 6500 S. Quebec St. Suite 330 Englewood, CO

2018 National Conference on Special Needs Planning and Special Needs Trusts Tax Reform and Year End Tax Planning for Self Settled and Third Party Trusts Bradley J. Frigon October 18, 2018 Law Offices of

2018 National Conference on Special Needs Planning and Special Needs Trusts Tax Reform and Year End Tax Planning for Self Settled and Third Party Trusts Bradley J. Frigon October 18, 2018 Law Offices of

Tax Update Focusing on the Tax Cuts and Jobs Act of John F. Ermer, CPA Israel O. Perez, CPA

Tax Update Focusing on the Tax Cuts and Jobs Act of 2017 John F. Ermer, CPA Israel O. Perez, CPA Contact Information John F. Ermer, CPA E-mail: jermer@bhcbcpa.com Telephone: 203) 787-6527 Israel O. Perez,

Tax Update Focusing on the Tax Cuts and Jobs Act of 2017 John F. Ermer, CPA Israel O. Perez, CPA Contact Information John F. Ermer, CPA E-mail: jermer@bhcbcpa.com Telephone: 203) 787-6527 Israel O. Perez,

SENATE TAX REFORM PROPOSAL INDIVIDUALS

The following chart sets forth some of the provisions affecting individuals in the Senate Finance Committee s version of the Tax Cuts and Jobs Act bill, as approved by the Senate Finance Committee on November

The following chart sets forth some of the provisions affecting individuals in the Senate Finance Committee s version of the Tax Cuts and Jobs Act bill, as approved by the Senate Finance Committee on November