TRANSFER PRICING. 19 th July, July-14 1

|

|

|

- Bernard Tucker

- 6 years ago

- Views:

Transcription

1 TRANSFER PRICING 19 th July, July-14 1

2 TRANSFER PRICING AND ITS FUTURE PROSPECTS Due to the increasing trend in globalization of Indian business, transfer pricing will remain foremost on the agenda of Indian income-tax authorities into the foreseeable future. 19-July-14 2

3 Top 10 Toughest Tax Authorities For Transfer Pricing Risk * 1. Japan 2. India 3. China 4. Canada 5. United States 6. France 7. Germany 8. Australia 9. Korea 10. United Kingdom * FICCI presentation on transfer pricing, October, July-14 3

4 TAX TREATY/ DOUBLE TAX RESOLUTION What is the extent of the double tax treaty network? India has an extensive tax treaty network and has entered into comprehensive tax treaties with 85 countries. India is also party to a series of treaties under negotiation. Other agreements The basic objective of DTAA : Avoid double taxation of income in both the countries. Promote and foster economic trade and investment between the two countries. 19-July-14 4

5 Agreements DTAA * India has the following agreements except the comprehensive agreements with 85 countries : DTAA Limited agreements With respect to income of airlines/ merchant shipping with 8 countries. Limited Multilateral Agreement with 8 countries. DTAA Other Agreements/Double Taxation Relief Rules 3. Specified Associations Agreement with Taipei. Tax Information Exchange Agreement with 10 countries. *as per income tax authority, India 19-July-14 5

6 CONTENTS Transfer Pricing Outline International Transactions Associated Enterprises Domestic Transfer Pricing Related Parties Debatable Issues International TP vs Domestic TP FAR Analysis Methods of Computation Documentation Dispute Resolution Panel Assessment Procedure Transfer of Intangibles Safe Harbour Advance Pricing Agreement Mutual Agreement Procedure Budget 2014 OECD & India Transfer Pricing vs Other Statutes Recent Rulings Bibliography 19-July-14 6

7 Transfer Pricing: Outline 19-July-14 7

8 WHAT IS TRANSFER PRICING? DEFINITION Transfer Pricing is a term used to refer to all inter- company pricing. The prices at which an enterprise transfers physical goods and intangibles or provide services to associated enterprises. Transfer Pricing provisions were introduced in India in 2001 to prevent shifting of profits by Large Corporates from high tax rate jurisdiction to low tax rate jurisdictions to minimize tax cost at group level. 19-July-14 8

9 19-July-14 9

10 Tax authority name Central Board of Direct Taxes (CBDT). Effective date of transfer pricing rules Revenue Transactions :1 April 2001 Capital Transactions : 1 April 2011 Domestic Transactions : 1 April July-14 10

11 RELEVENT SETIONS OF THE INCOME TAX ACT Computation of income from international transaction having regard to arm s length price 92A Meaning of associated enterprise 92B Meaning of international transaction 92BA Meaning of domestic transaction 92C Computation of arm s length price 19-July-14 11

12 92CA Reference to Transfer Pricing Officer 92CB Power of Board to make Safe Harbour Rules 92CC Advance Pricing Agreement 92CD Effect to Advance Pricing Agreement 92D Maintenance and keeping of information and document by persons entering into an international transaction 92E Report from an accountant to be furnished by persons entering into international transaction 92F Definitions of certain terms relevant to computation of arm s length price, etc 19-July-14 12

13 INCOME TAX RULES Rule 10A : Definitions. Rule 10B : Determination of Arm s Length Price. Rule 10C : Most Appropriate method. Rule 10D : Documents to be kept and maintained. Rule10E : Furnishing report from Chartered Accountant in Form 3CEB. 19-July-14 13

14 SECTION 92 Where a business is carried on between a resident and a nonresident and it appears to the Assessing Officer that, owing to the close connection between them, the course of business is so arranged that the business transacted between them produces to the resident either no profits or less than the ordinary profits which might be expected to arise in that business, the Assessing Officer shall determine the amount of profits which may reasonably be deemed to have been derived there from and include such amount in the total income of the resident. 19-July-14 14

15 TRANSFER PRICING PROCESS 19-July-14 15

16 International Transfer Pricing 19-July-14 16

17 INTERNATIONAL TRANSACTIONS: SECTION 92B An international transaction is essentially a cross border transaction between associated enterprises. At least one of the parties to the transaction must be a non-resident. The definition also covers a transaction between two nonresidents. E.g. One of them has a permanent establishment whose income is taxable in India. Thus in conclusion, it is a transaction between two or more associated enterprises, either or both of who are non-residents. 19-July-14 17

18 NATURE OF TRANSACTIONS COVERED UNDER SECTION 92B Purchase, sale, transfer, use, lease of tangible or intangible property. Provision of services. Capital financing(short and long term), marketable security exchange or debts arising in course of business. Transactions of business restructuring or reorganization irrespective of the bearing on profits, incomes, losses or assets. 19-July-14 18

19 19-July-14 19

20 ASSOCIATED ENTERPRISES The basic criterion to determine associated enterprises is the participation in management, control or capital (ownership) of one enterprise by another enterprise. The participation may be direct or indirect or through one or more intermediaries. 19-July-14 20

21 ASSOCIATED ENTERPRISES Direct Control Enterprise X Enterprise Y If Enterprise Y is managed, controlled or owned by Enterprise X directly as above then, Enterprise Y is said to be an Associated Enterprise of Enterprise X. 19-July-14 21

22 ASSOCIATED ENTERPRISES Indirect Control through Intermediary Enterprise X Intermediary Enterprise Y If Enterprise Y is managed, controlled or owned by Enterprise X through a intermediary as above then, Enterprise Y is said to be an Associated Enterprise of Enterprise X. 19-July-14 22

23 ASSOCIATED ENTERPRISES Participation/ Control/ Management Mr. X & Mr. Y Enterprise X Enterprise Y Mr. X & Mr. Y control Enterprise X & Enterprise Y. Therefore, Enterprise X & Enterprise Y are AEs. 19-July-14 23

24 ASSOCIATED ENTERPRISES DEEMING SITUATIONS Control Of Voting Power Enterprise X Enterprise Y Enterprise X controls 26 % OR MORE of shares carrying voting rights of Enterprise Y whether directly or indirectly. Enterprise X and Enterprise Y are AE s. 19-July-14 24

25 ASSOCIATED ENTERPRISES DEEMING SITUATIONS Control Of Voting Power Mr. X/ Enterprise X Controls 26% of voting power directly or indirectly Enterprise Y Enterprise Z Enterprise Y and Enterprise Z are AE s. 19-July-14 25

26 ASSOCIATED ENTERPRISES DEEMING SITUATIONS Enterprise X has given a loan Enterprise Y. Loan by X to Y is not less than 51 % of the book value of Assets of Y. Enterprise X Enterprise Y Therefore, X & Y are AE s. 19-July-14 26

27 ASSOCIATED ENTERPRISES DEEMING SITUATIONS Guarantee of Debts not Less than 10%. Total Borrowing of Enterprise Y is Rs /-. Guaranteed by Enterprise X is Rs. 1000/-. Therefore, Enterprise X and Enterprise Y are AE s. Enterprise X Enterprise Y 19-July-14 27

28 ASSOCIATED ENTERPRISES DEEMING SITUATIONS Control over Board of Directors (MORE THAN 50%). Total number of Board of Directors of Y is 10. Enterprise X appoints 6 of them. Therefore, X & Y are AE s. Enterprise X Enterprise Y 19-July-14 28

29 ASSOCIATED ENTERPRISES DEEMING SITUATIONS Control over Board of Directors/ Governing Board Members (MORE THAN 50%) or Executive Directors or both. Enterprise X or Mr. X appoints more than 50 % of directors/governing board members or one or more Executive Director or governing Board Members of both of two enterprises. Therefore, Y and Z are AEs. Enterprise Y Mr. X/ Enterprise X Enterprise Z 19-July-14 29

30 ASSOCIATED ENTERPRISES DEEMING SITUATIONS Dependence on Enterprise for use of brand, know-how, patents, etc. Enterprise Y manufactures product A under a brand owned by Enterprise X Therefore, Enterprise X & Y are AEs. Enterprise X Only technology transfer from X to Y. No financial participation. Enterprise Y 19-July-14 30

31 ASSOCIATED ENTERPRISES DEEMING SITUATIONS Dependence on Enterprise for raw materials. Enterprise X procures 90% OR MORE of its raw materials from Enterprise Y. Therefore, Enterprise X and Enterprise Y are AEs. Enterprise Y Enterprise X 19-July-14 31

32 ASSOCIATED ENTERPRISES DEEMING SITUATIONS Dependence on Enterprise for raw materials. Enterprise X procures 90% OR MORE of its raw materials from Enterprise Y who in turn supplies it at such price as influenced by Enterprise Z. Therefore, Enterprise X and Enterprise Z are AEs. Enterprise Z Enterprise X Enterprise Y 19-July-14 32

33 ASSOCIATED ENTERPRISES DEEMING SITUATIONS Control over Sale Price. If price is influenced by Enterprise Y, then X & Y are AEs. If instead of Enterprise Y, Enterprise X sells to Enterprise Z at a price influenced by Y, then still X & Y are related AEs. Enterprise X Enterprise Y 19-July-14 33

34 19-July-14 34

35 19-July-14 35

36 DOMESTIC TRANSFER PRICING Effective from 1st April, 2012 Domestic Transfer Pricing is applicable only where value of Specified Domestic Transactions in aggregate crosses 5 Crores. The threshold for substantial interest to qualify as specified persons is 20% or more, as compared to the threshold limit of 26% or more for international transfer pricing. Sec 92BA of The Income tax Act, 1961 covers provisions for Domestic Transfer Pricing. 19-July-14 36

37 India now part of DTP 19-July-14 37

38 PURPOSE OF INTRODUCING DOMESTIC TRANSFER PRICING It was realized by the government that: Presently, there is no method prescribed to determine reasonableness of expenditure to re-compute the income in related party transactions. There is need to provide objectivity in determination of income and determination of reasonableness of expenditure in domestic related party transactions. There is need to create legally enforceable obligation on assessee to maintain proper documentation Based on the above observations of the Honorable Supreme Court, the Finance Act, 2012 has extended the applicability of the transfer pricing provisions for specified domestic related party transactions 19-July-14 38

(b); any transaction referred to in sec 80A; any transfer of goods or services referred to in sec 80-IA(8); any business")

39 MEANING OF SPECIFIED DOMESTIC TRANSACTION SECTION 92BA Specified Domestic Transaction" means any transaction, not being international transaction, namely: an i. ii. iii. iv. v. vi. any expenditure for which payment is to a person referred to in sec 40A(2)(b); any transaction referred to in sec 80A; any transfer of goods or services referred to in sec 80-IA(8); any business transacted between the assessee and other person sec 80-IA(10); any transaction, under Chapter VI-A or s.10aa, if sec 80-IA(8) or sec 80- IA(10) is applicable; or any other transaction as may be prescribed, and the aggregate of such transactions entered into in the previous year exceeds INR 5 Crores 19-July-14 39

40 OVERVIEW OF PROVISIONS OF SECTION 92BA Inter unit transfer of goods & services by undertakings to which profit-linked deductions apply Expenditure incurred between related parties defined under section 40A SDT Transactions between undertakings, to which profit-linked deductions apply, having close connection Any other transaction that may be specified 19-July-14 40

41 19-July-14 41

Tax Exemption Tax @ 32.")

42 DOMESTIC TRANSFER PRICING India Shifting of expenses India Indian Co. Tax Holiday undertaking Related Enterprise in Domestic Tariff Area (DTA) Tax Exemption 32.45% Shifting of income Tax Saving for the Group Loss to Indian revenue 19-July-14 42

43 SECTION 40A(2)(b) The persons referred to in clause (a) are the following, namely : where the assessee is a relative; where the assessee is a member of HUF / director of the company / partner of the firm; any individual who has a substantial interest; a company, firm, AOP or HUF having a substantial interest or whose director, partner or member has substantial interest in the business of the assessee; any person who carries on a business or profession where the assessee being an individual, director of company, partner of a firm or member of an HUF which has a substantial interest in the business or profession of that person; 19-July-14 43

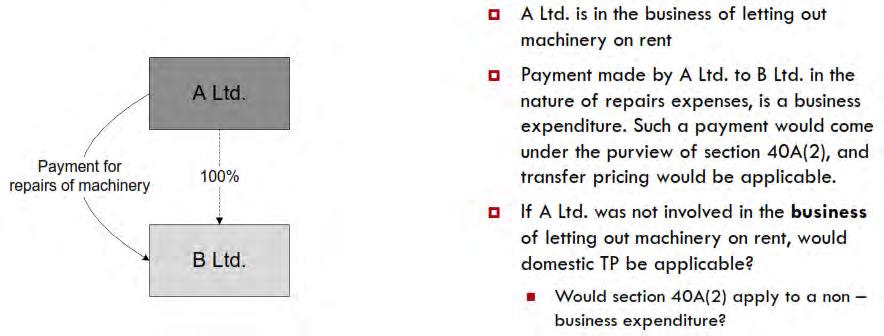

Beneficial ownership >20% Any payment towards expenditure by: X Co to A Co/B Co A co(indian Company) B co(indian Company) 19-July-14")

44 SEC 40A(2)(B)-PAYMENT TO RELATED PARTIES Any payment towards expenditure by : A Co to its own directors as remuneration, salary, bonus etc A Co to X Co A Co to directors of X Co A Co to Relatives of directors of A Co and X Co A Co to B Co X Co (Indian Company) Beneficial ownership >20% Any payment towards expenditure by: X Co to A Co/B Co A co(indian Company) B co(indian Company) 19-July-14 44

45 TYPE OF TRANSACTIONS COVERED (ILLUSTRATIONS FOR PAYMENTS MADE BY A COMPANY) Case 1 - Director or any relative of the Director of the taxpayer Section 40A(2)(b)(ii) Assessee (Taxpayer) Director Mr. A Mr. D Relative Mr. C Covered transactions Holding Structure 19-July-14 45

46 TYPE OF TRANSACTIONS COVERED (ILLUSTRATIONS FOR PAYMENTS MADE BY A COMPANY) Case 2 - To an individual who has substantial interest in the business or profession of the taxpayer or relative of such individual Section 40A(2)(b)(iii) Assessee (Taxpayer) Substantial interest >20% Mr. A Covered transactions Relative Mr. D Relative Mr. C Holding Structure 19-July-14 46

47 TYPE OF TRANSACTIONS COVERED (ILLUSTRATIONS FOR PAYMENTS MADE BY A COMPANY) Case 3 To a Company having substantial interest in the business of the taxpayer or any director of such company or relative of the director Section 40A(2)(b)(iv) Mr. D Relative Director A Ltd Substantial interest >20% Assessee (Taxpayer) Mr. C Covered transactions Holding Structure 19-July-14 47

48 TYPE OF TRANSACTIONS COVERED (ILLUSTRATIONS FOR PAYMENTS MADE BY A COMPANY) Case 4 Any other company carrying on business in which the first mentioned company has substantial interest Section 40A(2)(b)(iv) Assessee (Taxpayer) Substantial interest >20% A Ltd Covered transactions Holding Structure Substantial interest >20% B Ltd 19-July-14 48

49 TYPE OF TRANSACTIONS COVERED (ILLUSTRATIONS FOR PAYMENTS MADE BY A COMPANY) Case 5 To a Company of which a director has a substantial interest in the business of the taxpayer or any director of such company or relative of the director Section 40A(2)(b)(v) B Ltd Director Mr. C Mr. A Substantial interest >20% Assessee (Taxpayer) Relative Relative Mr. D Covered transactions Holding Structure 19-July-14 49

50 TYPE OF TRANSACTIONS COVERED (ILLUSTRATIONS FOR PAYMENTS MADE BY A COMPANY) Case 6 To a person in which the taxpayer(individual) has substantial interest Section 40A(2)(b)(vi)(A) Assessee (Individual) Relative B Ltd 19-July-14 Covered transactions Holding Structure 50

51 TYPE OF TRANSACTIONS COVERED (ILLUSTRATIONS FOR PAYMENTS MADE BY A COMPANY) Case 7 To a Company in which the taxpayer has substantial interest in the business of the company Section 40A(2)(b)(vi)(B) Assessee (Company) Director Relative Substantial interest >20% B Ltd 19-July-14 Covered transactions Holding Structure 51

52 40A(2) ISSUES AND CHALLENGES Whether indirect shareholding is covered? Whether Capital Expenditure or corresponding depreciation is covered? Whether shareholding of individual Directors can be aggregated for determining substantial interest? Directors Remuneration- Benchmarking Issues Interest free Loans to Group Companies Granting of Corporate Guarantees/Performance Guarantees by Parent Company to its subsidiaries 19-July-14 52

53 ANY TRANSACTION REFERRED IN SECTION 80A Section 80A applies to profit linked deductions to be made in computing total income under Chapter VI-A. Though the reference in section 92BA is to section 80A in general, on a closer examination, it becomes clear that the reference is merely to subsection (6) of section 80A and not to any other sub-section since other subsection of section 80A merely regulates the quantum of deduction and does not involve fair pricing of any transaction. This is also supported by corresponding amendment made to section 80A(6) by Finance Act 2012 to amend the meaning of expression market value referred to in that sub-section and to provide that in case of specified domestic transactions, the market value shall be computed at arm s length price. 19-July-14 53

54 19-July-14 54

55 ANY TRANSACTION REFERRED IN SECTION 80A Explanation of Section 80A(6): Internal transactions between various units / undertakings of the assessee in respect of goods or services. This clause covers any transactions of goods or services. And hence covers income as well as expenditure. 19-July-14 55

56 APPLICABILITY OF DOMESTIC TP- INTER UNIT TRANSFER Particulars Income GTI Deduction Total Unit P Unit M Unit P Unit M Income AS returned by the taxpayer If AO enhances income of Unit P If AO reduces income of Unit P Power Unit(Tax Holiday 100%) A Co Manufacturing Unit (Tax Holiday 100%) Nil (100?) (100?) 80 Nil (20?) (20?) FACTS: Both units of A co are tax holiday qualifying 100%. Power unit transfers power to the Manufacturing unit. ISSUE: Whether application of Domestic TP can result in adverse impact for taxpayers despite there being no potential for tax arbitrage between two units? 10-Jan July-14 56

57 19-July-14 57

(b) or Section 80A(6) relating to transfer of goods between two units of the same assessee?")

58 ISSUES/CHALLENGES RELATING TO 80A(6) TRANSACTIONS If both tax holiday units of the same assessee enter into transaction inter unit transfer will that be part of specified domestic transfer pricing? Will the purchase of goods from a related party be covered under Section 40A(2)(b) or Section 80A(6) relating to transfer of goods between two units of the same assessee? 19-July-14 58

59 PURPOSE OF INTRODUCING 80-IA(8) A Ltd. Unit 1 (Eligible Unit) Particulars Unit 1 Unit 2 Tax Rate 0% 30% Sales to Ineligible Unit Sales to third parties Purchase from Eligible Unit Other expenses Profit/Loss Tax Nil 300 Total Tax for the Group 300 Sale of Goods Scenario 1 Scenario 2 A Ltd.-Unit 2 (Ineligible Unit) Particulars Unit 1 Unit 2 Tax Rate 0% 30% Sales to Ineligible Unit Sales to third parties Purchase from Eligible Unit Other Expenses Profit/Loss Tax Nil Nil Total Tax for the group 19-July Nil

60 ANY TRANSFER OF GOODS OR SERVICES REFERRED TO IN SUB-SECTION (8) OF SECTION 80-IA; Where any goods [or services] held for the purposes of any other business carried on by the assessee are transferred to the eligible business and, the consideration does not correspond to the market value of such goods [or services]. When the computation of the profits and gains of the eligible business in the manner hereinbefore specified presents exceptional difficulties, the Assessing Officer may compute such profits and gains on such reasonable basis as he may deem fit. Explanation of Section 80-IA(8): Deals with the internal transactions with more than one undertaking / units of the assessee, out of which one or more undertaking is enjoying the tax holiday. Onus is on the taxpayer to prove that the internal transfer is at Arms Length Price. 19-July-14 60

61 TRANSACTIONS COVERED UNDER SECTION 80IA (8) A Ltd Unit A Telecom Business 80IA- Eligible Unit Goods & Services Unit B Manufacturing Business Taxable Unit Transfer at Rs. 120 Market value of above goods and services is Rs. 100 So, ALP of above transaction is Rs July-14 61

62 SECTION 80-IA(8) COVERAGE Contextually covers intra division transfers not being a transaction. Inter unit transfer between two non-eligible units has no TP implications. Section requires any other business carried on by assessee and dealings between businesses. Restricted to goods and services of marketable nature. 19-July-14 62

63 ANY BUSINESS TRANSACTED BETWEEN THE ASSESSEE AND OTHER PERSON AS REFERRED TO IN SUB-SECTION (10) OF SECTION 80-IA; As per this clause, when due to close connection between assessee and any other person the eligible business of the assessee produces more than the ordinary profit, then for the purpose of deduction under this section, profit of the eligible business shall be determined by taking ALP of the transaction. 19-July-14 63

64 TRANSACTIONS COVERED UNDER SECTION 80IA(10) A Ltd Infrastructure Business 80IA- Eligible Unit Goods and Services Close connection B Ltd Trading Business Taxable Unit Operating Profit: 40% (Extraordinary profits) Industry Average: 10% Hence, Arm s length profit margin would be taken as 10% 19-July-14 64

65 COVERAGE OF SEC 80IA (10) For A Co A Co Sale of goods at cost < FMV Corporate Guarantee : NIL cost Free use of TM and KHW or HO resources Related Parties B Co (WOS) Tax Holiday Unit Domestic TP not applicable transaction is of income receipt, 40A(2) not triggered For B Co Covered by s. 40A(2)(b) and hence SDT. But, payment is at < FMV, no TP adjustments required. S. 80-IA(10) may still be invoked on the ground that arrangement leads to more than ordinary profits? 19-July-14 65

66 80IA(10) ISSUES AND CHALLENGES The term Close Connection not defined and subject to litigation. Whether the term more than ordinary profit can be equated with ALP. Whether Capital account transactions are covered? 19-July-14 66

67 The term close connection has not been expressly defined in the Act. Accordingly, reference could be drawn from conjoint reading of the other provisions of the Act as well as the Accounting Standards to define close connection as under. Particulars Substantial interest- Section 40A(2)(b) Associated enterprise- Section 92A(2) Voting power >=20% >=26% >=50% Related party as per AS-18 as issued by ICAI Direct or indirect holding covered Only Direct Holding Both Both Director s covered Covered Covered Key managerial personnel covered Key suppliers covered Not covered Supplying more than 90% Specifically excluded 19-July-14 67

68 19-July-14 68

69 Unit 1 Eligible Unit Sale of goods Head Office Party with Close Connection Unit 2 Non Eligible Unit Sale of goods Will Domestic TP be applicable to such a transaction structure? Close Connection under Section 80-IA(10) What if the intermediary does not have a close connection with the taxpayer? any other reason section 80-IA(10) Is the business transacted so arranged? Which transaction to report in Form 3CEB / justify arm s length pricing? 19-July-14 69

70 Will Domestic TP be applicable for the transaction involving transfer of funds? Does Unit 1 need to pay Unit 2 an arm s length interest on the funds transferred? Head Office What will be the scenario if the funds were transferred to bank account of Unit 1 from the bank account of a party having close connection with the taxpayer? What will be the scenario if the funds were transferred to bank account of Unit 1 from the bank account of a third party? Unit 1 Eligible Unit u/s 80-IA Transfer of Funds Unit 2 19-July-14 70

71 19-July-14 71

72 COST ALLOCATIONS Allocation of common expenditures to tax holiday undertakings has been a highly litigated issue. Under the Act, tax holiday undertakings are required to maintain separate accounts. The costs directly relatable to the undertakings are charged to such undertakings. However, common expenses benefit all the undertakings of the taxpayer. These expenses could be in the nature of general administrative expenses or research, marketing and finance expenses. In this regard following approach may be considered: Issue Approach Whether allocation of costs is a SDT Determination of allocable costs Determining reasonable allocation keys Allocation of costswhether at actual or at mark-up Relying on judicial precedent taxpayers may argue that pure cost allocations to determine appropriate profits of the undertaking do not entail a service and accordingly, are not covered under DTP provisions. An ideal costs allocation policy would entail allocation of all common costs based on rational allocation keys. Expenses ought to be allocated on a reasonable and scientific basis (say, on the basis of ratio of turnover, head-count, cost of sales, etc) Where the services are of a marketable nature, the relevant costs could be charged at the mark-up and reported in Form 3CEB. 19-July-14 72

73 ORDINARY PROFITS VS ARM S LENGTH Under section 80IA(10), ordinary profits for tax holiday undertakings will need to be determined by using prescribed transfer pricing methods. The challenges likely to be faced by taxpayers in this regard have been illustrated below: Transactions with closely connected person Particulars Profit level Indicator Total income 130 Cost(TC) 100 Profits(OP) 30 OP/TC 30% Comparables Particulars OP/TC Company A 35% Company B 10% Company C 25% Company D 14% Company E -8% Arithmetic mean 15% 19-July-14 73

74 Sec 92BA(iv): any transaction, referred to in any other section under Chapter VI-A or section 10AA, to which provisions of sub-section (8) or sub-section (10) of section 80-IA are applicable; or The following profit linked incentive provisions under Chapter VI-A are also governed by provisions of section 80-IA(8) and section 80-IA(10) and hence will be subject to Domestic TP:- 80-IAB- Deductions in respect of profits and gains by an undertaking or enterprise engaged in development of Special Economic Zone. 80-IB- Deduction in respect of profits and gains from certain industrial undertakings other than infrastructure development undertakings. 80-IC- Special provisions in respect of certain undertakings or enterprises in certain special category States. 80-ID- Deduction in respect of profits and gains from business of hotels and convention centres in specified area. 80-IE- Special provisions in respect of certain undertakings in Northeastern States. 19-July-14 74

.")

75 CIT VS. GLAXO SMITH KLINE ASIA (P) LTD. Facts: The assessee-company was engaged in the business of manufacture and sale of fast moving consumer products. Administrative services relating to marketing, finance, human resources, secretarial services, etc., were provided by Glaxo Smith Kline Consumer Healthcare Ltd. ( GSKCH ). The assessee had entered into agreement with GSKCH for reimbursement of the costs incurred for various services plus 5% by GSKCH. 19-July-14 75

76 Facts: The costs towards services provided to the assessee were allocated on the basis suggested by a firm of CAs. The administrative expenses/ cross charges were worked out on the basis of the report of the CA and same was claimed by the assessee. The Assessing Officer disallowed the same and raised a demand. 19-July-14 76

77 Decision: As far as this SLP is concerned no interference is called for as the entire exercise is a revenue neutral exercise. The Tribunal observed that "there is no provision to disallow any expenditure on the ground that such expenditure is excessive or unreasonable unless the case of the assessee falls within the scope of section 40A(2). It was held that as it was not the case of the Department that s. 40A(2) was attracted, the disallowance could not be made. 19-July-14 77

by making amendments to the Act.")

78 CIT VS. GLAXO SMITH KLINE ASIA (P) LTD. Issues: Whether TP Regulations should be limited to cross-border transactions or be extended to domestic transactions. The CBDT should examine whether TP Regulations can be applied to domestic transactions between related parties u/s 40A(2) by making amendments to the Act. The CBDT should examine whether Transfer Pricing Regulations can be applied to domestic transactions between related parties u/s 40A(2) by making amendments to the Act. 19-July-14 78

79 19-July-14 79

80 GENERAL CHALLENGES IN DTP 19-July-14 80

81 Arm s Length Principle Arm s length principle may be difficult to apply to associated enterprises engage in transactions that independent enterprises would not undertake. Arm s length principle, in some cases, may result in an administrative burden for taxpayers./tax admin. of evaluating significant number / type of cross border transactions There are difficulties in finding and interpreting evidence from which arm's length prices can be deduced. There may be no, or very little, evidence on which to base a determination of an arm's length price, and what evidence there is may be difficult to interpret or may indicate only that the arm's length price is within a certain range of prices. A flexible approach is, thus the requirement. Notwithstanding the above, this is superior to any other approach because it is essentially simple, aligns the comparatively exceptional kind of transaction with the normal kind, is equitable between taxpayers of different kinds, and, unlike other approaches, is widely accepted. 19-July-14 81

82 CHALLENGES Type of payments/ transactions Salary and Bonuses paid to the partners Remuneration paid to the Directors Transfer of land Joint Development agreements Project management fees Allocation of expenses between the same taxpayer having an eligible unit and noneligible unit Definition of Related Party Challenges Benchmarking? Whether the limit as mentioned in section 40 (b) would be the ALP? Benchmarking? Whether the limit as mentioned in Schedule XIII would be the ALP? Whether the rates mentioned in the ready reckoner be considered as ALP? Benchmarking? Benchmarking? Whether these allocation would be SDT Sec 80-IA(10)? Directly v/s Indirectly 19-July-14 82

83 19-July-14 83

322 ITR 678 (AAR)] b) Provisions of section 40A(2) are not applicable to a co-operative society. [CIT vs. Manjara Shetkari Sahakari Sakhar Karkhana Ltd.(2008) 301 ITR 191 (Bom.")

84 Something to consider a) Transfer pricing provisions are not applicable in case where income is not chargeable to tax at all. [Amiantit International Holding Ltd., (2010) 322 ITR 678 (AAR)] b) Provisions of section 40A(2) are not applicable to a co-operative society. [CIT vs. Manjara Shetkari Sahakari Sakhar Karkhana Ltd.(2008) 301 ITR 191 (Bom.)] c) Correlative adjustments - if excessive or unreasonable expenses are disallowed in the hands of tax payer at time of the assessment then corresponding adjustment to the income of the recipient will not be allowed in the hands of recipient of income. Hence, it would lead to double taxation in India. 19-July-14 84

85 Outsourcing by a Special Economic Zone (SEZ) unit to a non-sez unit of the taxpayer In this case, the rates charged by the non-sez unit to the SEZ unit can be compared with the rates charged to third-party customers; or the profit earned by the non-sez unit can be compared with the profit earned by the non-sez unit from services rendered to third-party customers; or the profit earned by the non-sez unit can be compared with the profit earned by third-party companies in rendering similar services using external databases. The development of intellectual property by the units may add to the complexity. 19-July-14 85

86 Some other provisions The provisions currently in force which grant profit linked tax holiday deductions and which are regulated by section 80A(6) and, consequently, subject to Domestic transfer pricing are as follows:- 80-IA Infrastructure development, etc 80-IAB SEZ development 80-IB Industrial undertakings 80-IC Industrial undertakings or enterprises in special category states 80-ID Hotels and convention centres in specified area 80-IE Undertakings in North-Eastern states 80JJA Collection and processing of bio-degradable waste 80JJAA Employment of new workmen 80LA Offshore Banking units and International Financial Services Centre 80P Co-operative societies 19-July-14 86

87 Debatable issues Income part of transactions are not touched in DTP provisions? Intra group loans? Interest free loans? Whether a taxpayer entitled to investment linked tax holiday (section 35AD) is covered by DTP? 19-July-14 87

88 Debatable issues Company XYZ Mr. A 10% Shares Mr. B 10% Shares Mr. C 10% Shares Mr. D 10% Shares Mr. E 10% Shares For Substantial Interest, Shareholding to be considered individually or aggregate?? 19-July-14 88

or Section")

89 Debatable issues Unit A- Eligible Unit AB Company Transfer of goods Unit B Non eligible Unit A Ltd Eligible Unit Transfer of goods B Ltd Non Eligible Unit Transfer of goods and services must be of same ASSESSEE and inter-unit transfer for the purpose Section 80A(6) or Section 80-IA(8) 19-July-14 89

90 Debatable issues Transactions not covered Assessee (Taxpayer) C Ltd Substantial interest >20% A Ltd Substantial interest >20% Substantial interest >20% B Ltd Transactions covered 19-July-14 90

Will this transaction come under the ambit of International transfer pricing or")

91 Debatable issues A LTD less than 20% Shareholding Payment of Director s Remuneration Mr. A (Director of A Ltd- Non Resident) Will this transaction come under the ambit of International transfer pricing or Domestic transfer pricing??? 19-July-14 91

92 Debatable issues Corporate Guarantee? Purchase or sale of marketable securities? Business restructuring transactions? Repayment of loan taken? 19-July-14 92

93 Debatable issues If deduction on account of payment to a related party, is reduced by application of Domestic TP provisions, whether the related party s income will automatically stand reduced to that extent? What is the impact on profit linked tax holiday claimed under Chapter VI-A or s. 10AA on the amount of addition due to Domestic TP adjustment (other than on account of payment to related party under s. 40A(2)(b)? Will higher deduction be permissible including on such adjustments made? 19-July-14 93

94 Debatable issues Transactions entered into with related parties without consideration? For determining substantial interest of a related party, indirect holding is not covered? Will presumptive taxation rule out transfer pricing rules? Why threshold limit of 5 crores? 19-July-14 94

95 19-July-14 95

96 INTERNATIONAL vs DOMESTIC TP Particulars International TP Domestic TP Threshold No limit Above Rs. 5 Crore Applicability Associated Enterprises Ownership threshold 26% 20% Related Parties Transactions covered All transactions Limited transactions APA Available Not available 19-July-14 96

97 INTERNATIONAL vs DOMESTIC TP Particulars International TP Domestic TP Safe Harbour Applicable Not Applicable Tested Party Preferably Taxpayer Taxpayer or other party ALP options for interest LIBOR / EURIBOR / RUPEE Only Domestic Rates 19-July-14 97

98 19-July-14 98

. Therefore, in determining whether controlled and uncontrolled transactions are comparable, comparison of the functions performed, assets used and risks assumed by the parties is necessary.")

99 TRANSFER PRICING ANALYSIS In dealing between two independent enterprises, the price charged, usually reflects the functions that each enterprise performs ( taking into account assets used and risks assumed). Therefore, in determining whether controlled and uncontrolled transactions are comparable, comparison of the functions performed, assets used and risks assumed by the parties is necessary. This comparison is based on a FAR Study. Functional study thus forms the basis, and provides a framework for comparability study and subsequent determination of the most appropriate method. It assists in proper assessment of comparability for the purpose of arm s length study. 19-July-14 99

100 Assets Funtions Risks FAR Analysis 19-July

101 PURPOSE OF FAR Gathering and organizing facts needed to analyze intercompany prices To identify an appropriate level of profit that related parties should earn with respect to intercompany transactions under review. To identify effects of functions, risks and assets on its profitability. To determine the economic characterization of the entities in the transaction. To determine the most appropriate method for benchmarking the transaction. To identify any uncontrolled transaction involving one of the controlled parties. 19-July

102 Business Process Forecasts / Business Plans Organisation / Staff Markets / Competition Financial Result Products FAR ANALYSIS Agreements / Terms Entities Assets Transactions Risks Functions 19-July

103 WHAT GOES INTO FAR ANALYSIS Transactions Entities Functions Risks Assets Products Markets/ Competition Business Processes FAR ANALYSIS Agreements Financial Results Forecasts/ Business Plans Organisation/ Staff 19-July

104 WHAT COMES OUT FUNCTIONAL ANALYSIS Understanding of the Business Documentation Characterization of entities Internal Comparables FAR ANALYSIS Basis to search for external comparable Risk and opportunity assessment Determination of the MAP 19-July

105 19-July-14 Chokshi Training & Educational Services, LLP 105

106 COMPONENT OF FAR ANALYSIS Functions performed Activities carried out by each of the parties to the Transaction. Focus should be on identification of critical functions which add value to the transactions. Principal functions performed by the entities in a controlled transaction are compared with the functions performed in uncontrolled transactions. 19-July

107 COMPONENT OF FAR ANALYSIS. Assets employed The type of assets and their nature needs to be understood. Helps in determination of their contribution to the business process / economic activity. Facilitates understanding of respective roles played by the entities participating in the transaction. Knowledge of assets owned and employed by the entities facilitates determination of the profit margin to be earned by them. 19-July

108 COMPONENT OF FAR ANALYSIS. Risks Assumed Probable variability of future outcomes or returns. As the risk increases, the expected return should increase as well. The potential risks are company and industry specific. Only important risks should be described and quantified. Important to distinguish between which entity bears risks as per legal terms and which one bears as per the economic substance of the transaction. 19-July

109 FUNCTIONS ASSETS RISKS Manufacturing/Processing R&D Quality Control Advertising/Marketing Sales Ordering and Distribution Invoicing and collection Warranty Service, warranty and spare parts Administrative, Financial and Legal Matter Tangible Assets e.g. Building, Plant & Machinery etc. Intangible Assets e.g. Patents, Copyrights and Trade Marks etc. Risks Analysis Product Liability Risk Inventory Risk Technology Risk R&D Risk Credit Risk Manpower Risk 19-July

are: Distinctive nature of property transferred or services provided.")

110 COMPARABILITY PRINCIPLES Rule 10B (2), lays down the criteria for comparability between international or domestic transactions and uncontrolled transactions. This process is not quantitative but qualitative and involves exercise of judgment. The criteria listed in Rule 10B(2) are: Distinctive nature of property transferred or services provided. Functions performed taking into account assets employed and to be employed. Risk assumed by respective parties. Contractual terms of the transaction. 19-July

111 19-July-14 Chokshi Training & Educational Services, LLP 111

112 SEARCH OF UNCONTROLLED TRANSACTIONS Internal uncontrolled transactions Transactions between assessee and third party External uncontrolled transactions Transactions by and between third parties 19-July

113 POINTS TO BE CONSIDERED IN SEARCH. Internal uncontrolled transactions External uncontrolled transactions Same transaction with third party must be considered. Accurate and reliable data must be available for benchmarking. Search from external databases of comparables must be undertaken. Same Industry and enterprises having same business. Year of data must be of current year in which such transaction has taken place or 2 years preceding such financial year. 19-July

114 19-July

115 19-July

116 The selection of the tested party influences the selection of the most appropriate method to benchmark the international or domestic transaction and consequently on the comparables selected. The comparables performing similar functions as the AE in the territory in which the AE operates will have to be selected as comparables. The term tested party has not been defined in the Indian transfer pricing regulations. Entity performing simpler functions and not owning any valuable intangibles is normally selected as the tested party Availability of the reliable financial information of the comparable companies Normally least complex entity is selected as tested party as testing the margins of such entity would involve least adjustments. 19-July

117 ABC Inc Owner of IP Contract Risk R & D Marketing & Sales USA INDIA Provision of Services Payment of Services ABC India Subsidiary Back Office, Accounting Least Complex Entity. No ownership of IP Tested Party 19-July

118 KEY TAKEAWAYS Robust FAR analysis is the foundation of a sound Transfer Pricing Analysis. Choice of the tested party should be consistent with the functional analysis of the controlled transaction. Selection of Tested Party, plays a central role in the overall application of the arm's- length principle. Enough documentation to substantiate. 19-July

119 19-July

120 19-July

121 1. Comparable Uncontrolled Price Method ( CUP Method) The CUP Method compares the price charged for property or services transferred in a controlled transaction with the same with unrelated party. Such price is adjusted to account for differences in nature of functions, characteristics of property or contractual terms or geographical indices, etc. Such adjusted price is considered to be an arm s length price in respect of the property transferred or services provided. 19-July

122 Strengths & Weaknesses of CUP STRENGTHS Two sided Analysis. Avoids tested party selection. Involves a direct transactional comparison. Less susceptible to differences in non transfer pricing factors WEAKNESSES Finding comparables is a difficult task as it is specific in nature. Comparables availability is less common as specific transactions are not available on public domain. 19-July

123 2. Resale price method (RPM) RPM is a method based on the price at which a product that has been purchased from a related party is resold to an unrelated enterprise. The resale price is reduced by the resale price margin/ gross profit margin. This is further reduced by the expenses incurred in connection with the purchase of product or obtaining of services. The price so arrived is adjusted price, considered as the Arm s length price. 19-July

124 Strengths & Weaknesses of RPM STRENGTHS Demand driven method. Reliable when demand is inelastic. WEAKNESSES Accounting inconsistencies. One sided analysis. Can lead to extreme results. 19-July

125 3. Cost Plus Method (CPM) CPM uses the costs incurred by the supplier of the property (or services) in a controlled transaction. Direct and indirect costs of production incurred by the enterprise in respect of the property or service to a related party are determined. A gross profit mark up in the same or similar comparable uncontrolled transaction by the enterprise or an unrelated enterprise is added. Used where raw materials or semi-finished goods are sold; where joint facility agreements or long term buy-and-supply arrangements, or the provision or services are involved. 19-July

126 Strengths & Weaknesses of CPM STRENGTHS Based on internal costs. Information is usually readily available. WEAKNESSES Data on mark-up may be difficult to find. Weak link between level of costs and market price. Consistency required between controlled and uncontrolled transaction. Focus only on related party manufacturer. 19-July

127 19-July

128 4. Profit Split Method PSM first identifies the combined profit of the related parties arising from the domestic transaction in which they are engaged. The relative contribution made by each related party is then evaluated on the basis of the FAR Analysis. The combined profit is then split amongst the parties in proportion to their respective contributions. The profit thus apportioned is taken into account to arrive at arm s length price in relation to the domestic transaction. 19-July

129 Strengths & Weaknesses of PSM STRENGTHS Suitable for highly integrated operations. Suitable when comparables not readily available. Two-sided approach hence no extreme result to the parties. WEAKNESSES Dependence on data from foreign affiliates. Certain measurement problems due to difference in accounting practices. Allocation of costs may be difficult. 19-July

130 5. Transactional Net Margin Method(TNMM) Comparison of the net profit margin computed on an appropriate base (for e.g. costs, sales, assets, etc.); Used in majority of the cases including transfer of semi-finished goods, distribution of finished products where applicability of resale price method appears to be inappropriate. And transaction involving provision of services. 6. Other Method Used for which accurate comparable data in respect of similar transactions is easily available. 19-July

131 Strengths & Weaknesses of TNMM STRENGTHS Less affected by transactional differences. More tolerant to some functional differences. Advantageous when it is difficult to obtain reliable information about one of the parties. WEAKNESSES Can be influenced by some factors that do not have an effect, or have a less substantial effect. It leads to difficulty in determination of arm's length net margins difficult. TNMM method is applied only to one of the controlled taxpayer. 19-July

132 TRANSACTION NET MARGIN METHOD (TNMM) Identify the net profit margin realized by the enterprise from a transaction with regard to an appropriate base. Identify net profit margin from a comparable uncontrolled transaction or a number of such transactions having regard to the same base. Adjust for differences that could affect net profit in the open market. 19-July

- Any abnormal income (xx) - XX")

133 TNMM Adjustment PBT xx + Depreciation xx + Interest xx + Any one-time expense paid xx + Any abnormal expenditure xx - Any one-time income received (xx) - Any abnormal income (xx) - XX 19-July

134 Choice of Profit Level Indicator (PLI) Each method, with the exception of the CUP method, examines a profit level indicator (PLI) relevant to the method of analysis. Specified financial ratio of the tested party is compared to the results of independent, functionally comparable companies. 19-July

135 Profit Level Indicators (PLI) and Methods CUP PSM RPM CPM TNMM Other Method Prices Generally, operating profit margins Gross Margin on Operating Revenue Gross Margin (mark-up) on Operating Cost In case transaction of a tested party pertain to receipt of income Operating Margin on Operating Cost. In case transaction of a tested party pertain to payment of expenses Operating Margin on Operating Revenue Would be price 19-July

136 19-July

137 Selection Of Most Appropriate Method [Rule 10C(2)] Factors Determining Most Appropriate Method Nature & class of transaction. Class of associated enterprise and functions performed. Availability and reliability of data. Degree of comparability. Extent and reliability of adjustments. Nature, extent and reliability of assumptions. 19-July

138 Selection Of Most Appropriate Method [Rule 10C(2)] RPM CUP TNMM CPM PSM Other 19-July

139 TRANSFER PRICING METHODS Any Other Method 7% CPM/TNMM 79% PSM 9% CUP Method 9% 19-July

140 19-July

141 19-July

142 ACCOUNTANTS REPORT Section 92: Requires every person entering into an international transaction to obtain an accountants report. To be Submitted on or before the due date for filing the tax return. 19-July

143 SECTION 139: DUE DATE FOR FILING RETURN IN FORM 3CEB 30 th November for ALL Assessees. Corporate : 30 th November. Other than Corporate assesses: 30 th November. 19-July

Transfer Pricing Report TP Report is required")

144 FILING OF TRANSFER PRICING REPORT Manual (A.Y ) Transfer Pricing Report TP Report is required to be filed (uploaded) before the filing of the Income Tax Return E-Filing (A.Y ) 3CEB Template 19-July

145 Preparation of Form 3CEB The Central Board of Direct Taxes ( CBDT ) issued a notification on 10 June 2013, amending the Accountant s Report (also referred to as Form No. 3CEB of the Income-tax Rules, 1962) with effect from 1 April 2013 to ensure that the same corresponds to the amended Indian TPR. Overview of the amendments The amended Form No. 3CEB contains 25 clauses requiring disclosure of the details of the various international transactions and SDT. It is divided into the following three parts: Part A: Requires the taxpayer to provide general information about itself along with the aggregate value of international transactions and SDT Part B: Requires the taxpayer to provide the details of the international transactions entered into during the FY Part C: Requires the taxpayer to provide the details of SDT entered into during the FY Part C requiring disclosure of SDT is an addition to the earlier Form No. 3CEB; whereas, Part A and Part B have been amended, primarily to incorporate the changes made in the definition of the term international transactions. 19-July

146 MANAGEMENT REPRESENTATION An Example of Certificate to Form 3CEB 19-July

147 19-July-14 Can I write Chokshi off Training last & year s Educational Services, taxes LLP as bad investments 147

148 HOW TO PREPARE TP STUDY/DOCUMENTATION?? Brief business profile of the tested party and the AEs Identification and analysis of transactions Planning & Budgeting Industry & Market Analysis FAR Analysis Selection & Characterization of entities Economic Analysis Selection & Application of MAM 19-July

149 DOCUMENTATION Under Section? Section 92D of Income-tax Act, Maintenance and keeping of information and document by persons entering into international transaction or specified domestic transaction. Who has to Maintain? Every person who has entered into an international transaction or specified domestic transaction. 19-July

150 DOCUMENTATION NEED For Proper documentation For Assessee: Because of legislation. To be prepared for TP Audit. To show that ALP has been followed. For the department: Selection for cases for scrutiny. Arriving at the correct result. Thus, it is an important tool for enforcing TP Regulations. 19-July

says that the required I&D would be prescribed by the CBDT.")

151 DOCUMENTATION Statutory Obligations: Section 92D lays down statutory requirement for maintenance and keeping of information and document by persons entering into International Transaction or Specified Domestic Transaction. Sub section (1) says that the required I&D would be prescribed by the CBDT. Sub section (2) requires the board to prescribe the period for which such I&D are to be kept and maintained. 19-July

152 DOCUMENTATION Sub section (3) prescribes that the requisitioned I&D should be produced before tax authorities. Section 92E requires submission of report from accountant by persons entering into International Transaction or specified domestic Transactions. DETAILS OF I&D Basically of 2 Types: Those to be furnished along with the return : FORM 3CEB Those to be maintained and kept for production before tax authorities : Report/Documents under Income Tax Rules (10D Documentation) 19-July

153 DOCUMENTATION General Requirements: Documentation should be contemporaneous. Should be in place as on the due date for filing of return of income. Should be kept for 8 years.. Threshold limits Before After Documentation 1 Crore 1 Crore Scrutiny 5 Crore 15 Crore 19-July

154 COMMON TRANSACTIONS DOCUMENTATION Transaction entered Purchase/ Sale of raw material -Invoices - purchase/ Sale order - product details - Sale Details if sold to 3 rd Party Documents to be maintained -Pricing strategy - proof of price negotiation - Quotes from competitors - Terms of payment Remuneration to Directors -Qualification - Work experience & profile - Minutes of Meeting authorizing - the Director s remuneration - Data from HR firms for Directors in the same line of Business Corporate Cost sharing -Nature of expenses - Auditor s certificate allocating the expenses -Basis of allocation between the companies - proof of usage (rendering) of services - Cost Benefit analysis 19-July

155 COMMON TRANSACTIONS DOCUMENTATION Transaction entered Documents to be maintained Rent paid toward use of premises Reimbursement of expenses - Rent receipts - Documents suggesting the rent of the surrounding area -Nature of expenses with detailed break up - reason of expense incurred for -Rental agreement - Fair market Value of the property (municipal Valuation, only if higher than actual rent paid) -Employee Details -Actual invoice of the expense Interest on loan (non financial service company) - Basis of determination of Interest rate - Interest rate card for the period of loan -Loan agreement - Basis on which the interest rate is pegged above standard rate 19-July

156 19-July

157 TPO TRANSFER PRICING ADJUSTMENTS 19-July

158 An adjustment in Tax when it is determined that the pricing scheme of an enterprise falls outside the range of what is considered to be an arm's length transaction between associated enterprises. Taxpayer disputes over the adjustment may be argued before a court but the burden of proof lies with the taxpayer to prove the authorities acted incorrectly. 19-July

159 TREND OF ADJUSTMENTS OVER THE YEARS TP Audit trends indicate greater scrutinity, leading to increased adjustments and resultant litigation. Financial Year No. of TP Number of % of Audits Adjustment Adjustment Completed Cases Cases Amount of Adjustment (Rs. in Crore) , , , , , , , , , , ,301 1, , ,638 1, ,531 Source: White Paper May 2012, Ministry Of Finance, Department Of Revenue 19-July

160 19-July

19-July-14")

161 AVAILABLE DATABASES Indian Databases: Prowess Capitaline Ace Technology Foreign Databases: Compustat OneSource Database Moody s Electronic Data Gathering, Analysis, and Retrieval System (EDGAR) 19-July

162 19-July

163 19-July

164 TRANSFER PRICING AUDIT CONSIDERATIONS IN AUDIT Agreements Ledgers AS 18 Tax Audit Report Supporting Documents 19-July

165 TRANSFER PRICING AUDIT ISSUES Data for comparability analysis: Current year s data i.e., the year in which the transaction has taken place needs to compared with that of comparables. Data of comparables can be of previous two years. Royalties/ management charges: These are of significant focus of the revenue authorities. In many cases, the authorities have rejected the taxpayer s analysis and disallowed payments. Hence, extensive documentation is required, failing which they could face significant adjustments on account of intellectual property or services fee payments made to group concerns. Use of nonpublic comparables: In some cases, TPOs seek pricing information from competitors of the taxpayers. The use of competitor data not in the public domain is not only unjust from the taxpayer s point of view, but may also harm the business interests of the competitor once such strategic pricing information is shared with the taxpayer. Such information is also not enough to undertake a detailed comparability or functional analysis of the enterprises/transactions, thus leading to an inappropriate TP analysis. 19-July

166 19-July

167 DISPUTE RESOLUTION PANEL (DRP) 19-July

168 DISPUTE RESOLUTION PANEL Introduced with the policy objective of expediting dispute resolution. Expectation from panel of 3 Commissioners more judicious orders. Higher comfort level to taxpayers. Complex TP case would be resolved confidently by a team of 3 Commissioners as opposed to a single person. Result expected fewer cases being filed in the ITAT. 19-July

against order passed by AO.")

169 DISPUTE RESOLUTION PANEL Set up for Speedy resolutions. Investor-friendly mechanism & expected to reduce taxpayer grievance and litigation. Choice of the assessee to file an objection before the DRP or file an appeal before CIT (Appeals) against order passed by AO. 19-July

170 DISPUTE RESOLUTION PANEL Conform, reduce or enhance the variations as proposed by TA. Cannot set aside the variation to TA. Cannot leave adjudication of issue of TA by directing the TA to pass order of assessment by conducting further inquiry. Powers & Duties 19-July

171 DISPUTE RESOLUTION PANEL Decision to be based on opinion of the majority of members. No direction can be issued by DRP after 9 months from the end of the month in which draft order is forwarded to the assessee. Has powers as vested in a court under the Code of Civil Procedure, Powers & Duties 19-July

172 PENALTIES Nature of Default Failure to maintain prescribed information or documents. Penalty Prescribed 2 % of value of Transactions. Failure to furnish information/documents during audit. Concealment of income 2 % of value Transactions. 100 to 300 % on tax evaded. Failure to furnish accountants report. INR 100, July

173 19-July

174 DTP ASSESSMENTS The Indian revenue authorities have not issued any clarification on the selection of cases for DTP assessments. Assessment of DTP compliances would fall within the jurisdiction of the same TPOs who presently review ITP compliances. 19-July

175 FIRST DTP AUDIT CYCLE (Estimated) File Tax Return and accountant s report (30 Nov 2013) TP Order (31 Jan 2017) Draft AO Order (31 March 2017) AO passes final order (31 Jan 2018) DRP Order (31 Dec 2017) ITAT final fact finding authority High Court on questions of law Supreme Court 19-July

176 Examination of International Transactions not reported by the Assessee Section 92CA has been amended retrospectively from 1 st June, It empowers TPO to determine ALP of an international transaction noticed by him in the course of proceedings before him, even if the said transaction was not referred to him by the AO. But no reopening of any proceeding would be undertaken only on account of such an amendment. 19-July

.")

177 ASSESSMENT PROCEDURE Audit teams- cities: 1. Delhi 2. Mumbai 3. Bangalore 4. Chennai 5. Kolkata Team: Director of International Tax and Joint / Additional Commissioners as Transfer Pricing Officers (TPO). The TPO receives reference from Assessing Officer. Aggregate value of international transactions > Rs 15 crores: compulsory TP audit. AO refer Determination to TPO with approval of commissioner. TPO notify taxpayer to produce evidence. TPO will determine ALP by passing an order. AO proceeds to calculate IT on basis of ALP determined by TPO. 19-July

178 19-July

179 19-July

180 TRANSFER OF INTANGIBLES 19-July

181 Intangibles related to marketing and technology have become crucial sources of value and of competitive distinctiveness and now play a greater role in a company s profitability. 19-July

182 TRANSFER OF INTANGIBLES As per Erstwhile RBI circular on Miscellaneous Remittances from India: Any payment under a technical collaboration agreement where amount of royalty exceeds 5% on local sales and 8% on exports. Lump-sum payment exceeds USD $ 2 million. Then one needs to approach Ministry of Industry and Commerce for Approval. 19-July

183 Comparative Chart on the Remittance of Technology Fees and the Royalty Payments. Details Before issue of Press Note 8 (2009 series) Prior to Lump sum payments Not exceeding US$ 2 million. After issue of Press Note 8 (2009 series) with effect from No limit now. Royalty payable Duration of royalty payments 5% on domestic sales and 8 % on export. No restrictions. No restrictions - subject to FEMA (Current Account Transactions) Rules, No restrictions. Royalty limits are Net of taxes and are calculated according to standard conditions. Net of taxes and are calculated according to standard conditions. 19-July

184 ISSUES RELATING TO TRANSFER OF INTANGIBLES Lack of external comparables. Comparability analysis may reveal that transactions in addition to, or different from, the transactions described in the registrations and contracts actually occurred. Incase when transfer of Intangible provides the enterprise with a unique competitive advantage in the market, purportedly comparable intangibles or transactions should be carefully scrutinized. It is critical to assess whether potential comparables in fact exhibit similar profit potential. 19-July

185 Safe Harbour Rules in India 19-July

186 OVERVIEW A Safe Harbour can be any statutory provision or regulatory approach directed at simplifying transfer pricing compliance. The Central Board of Direct Taxes notified the Safe Harbour Rules by Press Release on 18 th September, 2013 vide Notification No. 73/2013. Safe Harbour is a Transfer Pricing provision applying to a specific category of tax payers/transactions. These rules are optional in nature and can be opted for by filling Form 3CEFA. The assessee can opt for the safe harbor regime for a period of his choice but not exceeding 5 AYs beginning from AY by filing Form 3CEFA. Once the option exercise by the assessee has been held valid it shall remain so for the period opted unless the assessee voluntarily opts out of safe harbor regime by furnishing a statement to this effect. 19-July

187 Once Safe Harbour rules are chosen, the assessee is not eligible for comparability adjustment or for a +/-3% benefit while adjusting the ALP (Arm s Length Price). Safe Harbour rules are not applicable for Specific Domestic Transactions. The Safe Harbour rates or margins specified therein cannot be considered as a benchmark by the TPO in cases not covered by Safe Harbour Rules and also where the assessee has not opted for Safe Harbour Rules. 19-July

188 RULES FOR SAFE HARBOUR RULES Rule 10TA Definitions Rule 10TB Eligible Assessee Rule 10TC Eligible International Transaction Rule 10TD Safe Harbour Benchmarks Rule 10TE Procedure Rule 10TF Non-Applicability 19-July

189 Sr. No. Eligible International Transaction Circumstances 1. Provision of software development services referred to in clause (i) of rule 10TC. Transactions upto Rs. 500 crore: The operating profit margin declared by the eligible assessee from the eligible international transaction in relation to operating expense is 20 per cent or more. Transactions above Rs. 500 crore: The operating profit margin declared by the eligible assessee from the eligible international transaction in relation to operating expense is 22 per cent or more 2. Provision of information technology enabled services referred to in clause (ii) of rule 10TC. Transactions upto Rs. 500 crore: The operating profit margin declared by the eligible assessee from the eligible international transaction in relation to operating expense is 20 per cent or more. Transactions above Rs. 500 crore: The operating profit margin declared by the eligible assessee from the eligible international transaction in relation to operating expense is 22 per cent or more. 19-July

190 Sr. No. Eligible International Transaction Circumstances 3. Provision of knowledge process outsourcing services referred to in clause (iii) of rule 10TC. The operating profit margin declared by the eligible assessee from the eligible international transaction in relation to operating expense is 25 per cent or more. 4. Advancing of intragroup loans referred to in clause (iv) of rule 10TC to wholly owned subsidiaries where the amount of loan does not exceed fifty crore rupees. The Interest rate declared in relation to the eligible international transaction is equal to or greater than the base rate of State Bank of India (SBI) as on 30th June of the relevant previous year plus 150 basis points. 5. Advancing of intragroup loans referred to in clause (iv) of rule 10TC to wholly owned subsidiaries where the amount of loan exceeds fifty crore rupees. The Interest rate declared in relation to the eligible international transaction is equal to or greater than the base rate of SBI as on 30th June of the relevant previous year plus 300 basis points. 19-July

191 Sr. No. Eligible International Transaction 6. Providing corporate guarantee referred to in clause (v) of rule 10TC to wholly owned subsidiaries where the amount guaranteed does not exceed Rs. 100 crore. 7. Providing corporate guarantee referred to in clause (v) of rule 10TC to wholly owned subsidiaries where the amount guaranteed exceeds Rs. 100 crore. 8. Provision of contract research and development services wholly or partly relating to software development referred to in clause (vi) of rule 10TC. Circumstances The commission or fee declared in relation to the eligible international transaction is at the rate of 2 per cent or more per annum on the amount guaranteed. The commission or fee declared in relation to the eligible international transaction is at the rate of 1.75 per cent or more per annum on the amount guaranteed. The operating profit margin declared by the eligible assessee from the eligible international transaction in relation to operating expense incurred is 30 per cent or more. 19-July

192 Sr. No. Eligible International Transaction Circumstances 9. Provision of contract research and development services wholly or partly relating to generic pharmaceutical drugs referred to clause (vii) of rule 10TC. The operating profit margin declared by the eligible assessee from the eligible international transaction in relation to operating expense incurred is 29 per cent or more. 10. Manufacture and export of core auto components. The operating profit margin declared by the eligible assessee from the eligible international transaction in relation to operating expense is 12 per cent or more. 11. Manufacture and export of non- core auto components. The operating profit margin declared by the eligible assessee from the eligible international transaction in relation to operating expense is 8.5 per cent or more. 19-July

193 Advance Pricing Agreement 19-July

194 Advance Pricing Agreement (APA) APA is an agreement between a taxpayer and a taxing authority on an appropriate transfer pricing methodology for a set of transactions over a fixed period of time in future. The APAs offer better assurance on transfer pricing methods and are conducive in providing certainty and unanimity of approach. New sections 92CC and 92CD in the Act have been inserted to provide a framework for APA. 19-July

195 Advance Pricing Agreement (APA) 1. Such APAs shall include determination of the ALP or specify the manner in which ALP shall be determined. 2. The manner of determination of ALP shall be any method including those provided in sub- section (1) of section 92C, with necessary adjustments or variations. 3. The ALP of any international transaction, which is covered under such APA, which normally apply for determination of arm s length price would be modified to this extent and arm s length price shall be determined in accordance with APA. 4. APA would be valid for a period of time not exceeding five consecutive years. 19-July

196 Advance Pricing Agreement (APA) 5. The CBDT is empowered to rescind the APA if it is found to be obtained by fraud or misrepresentation of fact. 6. The Board is empowered to prescribe a Scheme providing for the manner, form, procedure and any other matter generally in respect of the APA. 19-July

197 Advance Pricing Agreement (APA) Timeline for making the application of the APA For an International Transaction of a Continuous Nature- Before the first day of the previous year relevant to the first assessment year for which the application is made. In any other case- Before undertaking the international transaction under consideration. Contents of an APA Terms of the Agreement Details of the Transaction intended to be covered Details of the other International Transactions Agreed TP Methodology Determination of the Arm s Length Price (ALP) Critical Assumptions Case Specific details, if any. 19-July

198 Advance Pricing Agreement (APA) Benefits: 1. APAs are seen as dispute resolution vehicles that helps in attaining certainty on transfer pricing. 2. Agreement on the TP method and the price for various transactions for a fixed period of time prospectively is expected to reduce the burden associated with annual audit examinations and litigation. 3. The tax administration can channelize its resources more constructively and focus on better enforcement. 4. A well designed program can also provide a collaborative and cooperative setting to find mutually beneficial solutions to contentious transfer pricing issues. 19-July

199 Advance Pricing Agreement (APA) 5. This endows a strong foundation for evolving unambiguous laws which feeds into a virtuous circle of clarity, minimized interpretational differences, and greater acceptance by the tax authority and lowered need to litigate on the part of both the taxpayer and the tax administration. 19-July

200 Advance Pricing Agreement (APA) Bilateral APA's Unilateral APA's Multilateral APA's Types of APA's Unilateral APA entered into between a taxpayer and the tax administration of the country where it is subject to taxation. Suitability A unilateral APA may be best suited in the following cases: Where it is either unnecessary to involve a foreign tax authority in the APA process - where the counter-party to an Indian resident s international related party transaction is a taxpayer in a country which does not have a tax treaty with India. A unilateral APA would also be appropriate where a foreign tax authority declines to participate in case of a bilateral APA. 19-July

201 Advance Pricing Agreement (APA) Bilateral APA entered into between the taxpayers, the tax administration of the host country and the foreign tax administration. Multilateral APA entered between the taxpayers, the tax administration of the host country and more than one foreign tax administrations. Bilateral and multilateral APAs are often referred to as Mutual Agreement Procedures (MAP APA). Suitability A MAP APA is best suited where the Indian resident s international related party transaction(s) occurs with a related party that is a taxpayer in a tax treaty partner country. The agreement with the foreign tax authority ensures there is no economic double taxation in respect of the transaction(s) covered by the APA by ensuring that the benefits of the DTAA provisions are thoroughly taken into consideration. 19-July

202 Advance Pricing Agreement (APA) Process of filing an APA: Stage I : Pre-filing consultation (Form 3CEC) Stage II : Filing of an application for an APA (Form 3CED) Stage III : Preliminary Processing of Application Stage IV : Processing of the Application Discussions / negotiations for bilateral / multilateral APAs and their outcome Drafting of an APA 19-July

203 Advance Pricing Agreement (APA) Stage V : Post APA Compliances Revision of tax return Filing of an Annual Compliance Report (Form 3CEF) Audit of the Compliance Report Withdrawal of the application seeking an APA (Form 3CEE) Revision of an APA Cancellation of the APA Renewal of the APA 19-July

204 FEES PAYABLE IN APA Amount of International Transactions entered or to proposed to be entered Fee Amount not exceeding Rs. 100 crores Amount not exceeding Rs. 200 crores Amount exceeding Rs. 200 crores 10 lakhs 15 lakhs 20 lakhs 19-July

205 Mutual Agreement Procedure 19-July

206 Mutual Agreement Procedure (MAP) What is Mutual Agreement Procedure (MAP)? MAP is an alternative available to taxpayers for resolving disputes giving rise to double taxation. The agreement for avoidance of double taxation between the countries would give authorization for assistance of Competent Authorities in the respective jurisdiction under MAP. In the context of OECD Model Convention for the Avoidance of Double Taxation, Article 25 provide for assistance of Competent Authorities under MAP. 19-July

207 Mutual Agreement Procedure (MAP) What are the Key Benefits of Pursuing MAP? Elimination of double taxation (either juridical or economic). It is very rare that a case under MAP is not resolved. Also, cases involving certain jurisdictions (US, UK and Denmark), the Indian authorities have entered into an agreement under which the taxpayer can choose to provide a bank guarantee for the outstanding tax demand. In such cases, the tax demand would not be pursued by the tax authorities until disposal of the MAP application. The MAP resolution, once accepted, eliminates the need for protracted litigation.. 19-July

208 Mutual Agreement Procedure (MAP) What kind of issues can be taken for resolution under MAP? Generally, the issues giving rise to double taxation are submitted by the taxpayers for resolution under MAP: Adjustment arising from Transfer Pricing assessment. Issues relating to existence of Permanent Establishment. Characterization of income. Attribution of profits to Permanent Establishment. 19-July

209 Mutual Agreement Procedure (MAP) What is the time limit for filing of MAP? Generally, the time limit ranges between two to three years from the date of the notice giving rise to double taxation. In cases where the Convention for Avoidance of Double Taxation does not provide for time limit the domestic tax provision on time limit has to be looked into for filing an application for assistance of Competent Authorities under MAP. E.g., the Convention for Avoidance of Double Taxation between India and UK does not provide time limit for filing for assistance under MAP. However, the UK domestic regulation provides a time limit of six years from the end of the relevant financial year to which adjustment relates. 19-July

210 Mutual Agreement Procedure (MAP) Can an application for assistance of Competent Authorities under MAP be made? The tax Conventions allow the taxpayers to apply for MAP even in anticipation of a dispute giving rise to double taxation. Technically, one can file a MAP application upon receipt of the draft Assessment Order. However, from a practical perspective, the Competent Authority might not begin the negotiation process until the final Assessment Order has been issued as the tax demand would only crystallize upon issuance of the final Assessment Order. 19-July

211 Mutual Agreement Procedure (MAP) Does the taxpayer have to exhaust the appeal options available under the domestic litigation route to apply for assistance under MAP? Option of resolution under MAP is an additional dispute resolution option available to the taxpayer. It can be pursued simultaneously with the dispute resolution options available under domestic regulation. 19-July

212 Mutual Agreement Procedure (MAP) Can a taxpayer participate in the negotiation process between the Competent Authorities? The negotiation process between the Competent Authorities of countries under MAP, are generally a closed door event. Thus, the taxpayer would not have access to and cannot participate in the negotiation process between the Competent Authorities. Taxpayers can work with the Competent Authorities to explain their own case and positions prior to the negotiation meetings between the Competent Authorities. 19-July

there is no timeline for disposal of application for assistance of Competent Authorities under MAP.")

213 Mutual Agreement Procedure (MAP) How soon the taxpayer can expect the outcome under MAP? Under the Indian tax Conventions (entered into with other countries) there is no timeline for disposal of application for assistance of Competent Authorities under MAP. Based on experience, the resolution under MAP can be expected within a period of two years from the filing of an application. 19-July

214 Mutual Agreement Procedure (MAP) Is the outcome under MAP binding on the taxpayer and the Revenue? While the taxpayers have the option of either accepting or rejecting the resolution arrived under MAP, should the taxpayer opt to accept the MAP resolution, it will be binding on the Revenue for that international transaction and for that Assessment Year. Rule 44H (4) of the Indian Income Tax Rules, 1962 provided that the Assessing Officer shall, within 90 days of receipt of the resolution by the Chief Commissioner or Director General of Income Tax, give effect to the resolution provided: The taxpayer gives his acceptance to the resolution arrived at under MAP; and withdraw the appeal filed under the domestic litigation provisions. 19-July

215 Mutual Agreement Procedure (MAP) Can outcome under MAP for a year be applied even for subsequent years? The resolutions under MAP are for the particular issues and the Assessment Years covered in the application for assistance of Competent Authorities under MAP. Thus, strictly speaking, the resolution under MAP for one year cannot be applied for the subsequent year. That said, the principle agreed upon for one year is likely to be followed in MAP proceedings for the subsequent years should the taxpayer choose to apply for MAP for the those years. However, since the MAP resolution is in the nature of settlement between two Competent authorities, it cannot be used as a basis for supporting arm s length nature under the domestic litigation process. 19-July

216 Mutual Agreement Procedure (MAP) Can a resolution under MAP be treated as an Arm s Length Price? The resolution arrived at by the Competent Authorities under MAP are based on the negotiation with the objective of settlement of issues. The negotiated settlement cannot be considered as an Arm s Length Price which needs to be based on principles of Transfer. 19-July

217 Mutual Agreement Procedure (MAP) What is the procedure for withdrawal of domestic appeal in case the settlement under MAP is accepted? If the taxpayer accepts the resolution arrived at under MAP, a letter indicating the acceptance of resolution under MAP, and withdrawal of appeal (to the extent of the issues covered under the MAP resolution) need to be made to the Assessing Officer and the Appellate Authorities before whom an appeal is filed under domestic litigation provisions. 19-July

218 July

219 Roll Back of APAs Likely to settle and resolve pending disputes/ litigation. The roll back provisions would apply to APAs signed after 1 st October, Rules still to be framed by government. If an APA application was filed on 31 st March, 2013 and is signed after 1 st October, 2014, it may still provide for its rollback applicability for the four fiscal years prior to fiscal year Gives total cover of nine years.[four years in the past and five years in the future] 19-July

220 Deeming TP Provisions Deeming TP provisions are proposed to be applied to transactions between an enterprise and an independent person irrespective of whether such persons are non-resident or not. The proposed amendment now effectively includes domestic transactions with third parties in India as international transactions. This amendment shall take effect from 1st April, July