IMPORTANT NOTICE IMPORTANT:

|

|

|

- Marcia Clark

- 6 years ago

- Views:

Transcription

1 IMPORTANT NOTICE IMPORTANT: You must read the following disclaimer before continuing. The following disclaimer applies to the Prospectus attached to this electronic transmission and you are therefore advised to read this disclaimer carefully before reading, accessing or making any other use of the attached Prospectus. In accessing the attached Prospectus, you agree to be bound by the following terms and conditions, including any modifications to them from time to time, each time you receive any information from us as a result of such access. Confirmation of your representation: By accessing this Prospectus you have confirmed to the Managers, the Company and the Selling Shareholder, that (i) you have understood and agree to the terms set out herein, (ii) (a) you and the electronic mail address you have given to us are not located in the United States, its territories and possessions or (b) you are a person that is a qualified institutional buyer within the meaning of Rule 144A under the U.S. Securities Act, (iii) you consent to delivery by electronic transmission, (iv) you will not transmit the attached Prospectus (or any copy of it or part thereof) or disclose, whether orally or in writing, any of its contents to any other person except with the consent of the Managers and (v) you acknowledge that you will make your own assessment regarding any legal, taxation or other economic considerations with respect to your decision to purchase the Offer Shares. You are reminded that the attached Prospectus has been delivered to you on the basis that you are a person into whose possession this Prospectus may be lawfully delivered in accordance with the laws of the jurisdiction in which you are located and you may not, nor are you authorized to, deliver this Prospectus, electronically or otherwise, to any other person and in particular to any U.S. address. Failure to comply with this directive may result in a violation of the U.S. Securities Act of 1933 (the U.S. Securities Act ) or the applicable laws of other jurisdictions. Restrictions: NOTHING IN THIS ELECTRONIC TRANSMISSION CONSTITUTES AN OFFER OF SECURITIES FOR SALE IN THE UNITED STATES OR ANY OTHER JURISDICTION WHERE IT IS UNLAWFUL TO DO SO. ANY OFFER SHARES BEING SOLD HAVE NOT BEEN AND WILL NOT BE REGISTERED UNDER THE U.S. SECURITIES ACT OR WITH ANY SECURITIES REGULATORY AUTHORITY OF ANY STATE OR OTHER JURISDICTION OF THE UNITED STATES AND MAY NOT BE OFFERED, SOLD, PLEDGED OR OTHERWISE TRANSFERRED WITHIN THE UNITED STATES EXCEPT (1) IN ACCORDANCE WITH RULE 144A UNDER THE U.S. SECURITIES ACT TO A PERSON THAT THE HOLDER AND ANY PERSON ACTING ON ITS BEHALF REASONABLY BELIEVES IS A QIB THAT IS ACQUIRING SUCH OFFER SHARES FOR ITS OWN ACCOUNT OR FOR THE ACCOUNT OF ONE OR MORE QIBs, OR (2) IN AN OFFSHORE TRANSACTION IN ACCORDANCE WITH RULE 903 OR RULE 904 OF REGULATION S UNDER THE U.S. SECURITIES ACT, IN EACH CASE IN ACCORDANCE WITH ANY APPLICABLE SECURITIES LAWS OF ANY STATE OF THE UNITED STATES OR PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE U.S. SECURITIES ACT AND APPLICABLE STATE OR LOCAL SECURITIES LAWS. THE ATTACHED PROSPECTUS MAY NOT BE FORWARDED OR DISTRIBUTED TO ANY OTHER PERSON AND MAY NOT BE REPRODUCED IN ANY MANNER WHATSOEVER. DISTRIBUTION OR REPRODUCTION OF THE ATTACHED PROSPECTUS IN WHOLE OR IN PART IS UNAUTHORIZED. FAILURE TO COMPLY WITH THIS DIRECTIVE MAY RESULT IN A VIOLATION OF THE U.S. SECURITIES ACT OR THE APPLICABLE SECURITIES LAWS OF OTHER JURISDICTIONS. Under no circumstances shall this Prospectus constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the Offer Shares in any jurisdiction in which such offer, solicitation or sale would be unlawful. Recipients of this Prospectus who intend to purchase any Offer Shares are reminded that any such purchase may only be made on the basis of the information contained in the Prospectus.

2 This Prospectus is being distributed only to and is directed only at persons in member states of the European Economic Area (with the exception of Norway) who are qualified investors within the meaning of Article 2(1)(e) of the Prospectus Directive (Directive 2003/71/EC), as amended, and any relevant implementing measure in each Member State of the European Economic Area. This Prospectus is being distributed only to and is directed only at (i) persons who are outside the United Kingdom; or (ii) investment professionals falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the Order ); or (iii) high net worth entities, and other persons to whom it may lawfully be communicated, falling within Article 49(2)(a) to (d) of the Order (all such persons in (ii) and (iii) being referred to as relevant persons ). The Offer Shares are available only to, and any invitation, offer or agreement to purchase or otherwise acquire the Offer Shares will be engaged in only with, relevant persons. Any person who is within the United Kingdom and not a relevant person should not act or rely on this Prospectus or any of its contents. This Prospectus has been sent to you in an electronic form. You are reminded that documents transmitted via this medium may be altered or changed during the process of electronic transmission and consequently none of the Managers, any person who controls any of the Managers, the Company or the Selling Shareholder, any director, officer, employee or agent of any of them or any affiliate of any such person accepts any liability or responsibility whatsoever in respect of any difference between the Prospectus distributed to you in electronic format and the hard copy version of the Prospectus. The materials relating to the offering do not constitute, and may not be used in connection with, an offer or solicitation in any place where offers or solicitations are not permitted by law. If a jurisdiction requires that the offering be made by a licensed broker or dealer and the Managers or any affiliate of the Managers is a licensed broker or dealer in that jurisdiction, the offering shall be deemed to be made by the Managers or such affiliate on behalf of the Selling Shareholder in such jurisdiction. None of the Managers or any of their respective affiliates or any of their respective directors, officers, employees or agents accepts any responsibility whatsoever as to the accuracy, completeness or verification of the information in this document. The Managers and any of their respective affiliates accordingly disclaim all and any liability whether arising in tort, contract or otherwise which they might otherwise have in respect of such document. Any decision to purchase the Offer Shares in the offer should be made solely on the basis of information contained in this document. No representation or warranty, express or implied, is made by any of the Managers or any of their respective affiliates as to the accuracy, completeness or verification of the information set out in this document. The Managers are acting exclusively for Odfjell Drilling Ltd and BCB Paragon Trust Limited as trustee of the Larine Trust (as the Selling Shareholder) and no one else in connection with the offer. They will not regard any other person (whether or not a recipient of this document) as their client in relation to the offer and will not be responsible to any other person for providing the protections afforded to their clients nor for giving advice in relation to the offer or any transaction or arrangement referred to herein.

3 ODFJELL DRILLING LTD (An exempted company limited by shares incorporated under the laws of Bermuda) Initial public offering of up to 56,000,000 Shares with an indicative price range of NOK 37 to NOK 48 per Share Listing of the Company s shares on the Oslo Stock Exchange This prospectus (the Prospectus ) has been prepared in connection with the initial public offering (the Offering ) of up to 56,000,000 common shares (the Sale Shares ) of Odfjell Drilling Ltd (the Company ), an exempted company limited by shares incorporated under the laws of Bermuda (together with its consolidated subsidiaries, Odfjell Drilling or the Group ), and the related listing (the Listing ) on Oslo Børs, a stock exchange operated by Oslo Børs ASA (the Oslo Stock Exchange ) of the Company s shares, each with a par value of USD 0.01 (the Shares ). The Offer Shares (as defined below) are offered by BCB Paragon Trust Limited, as trustee of the Larine Trust (the Selling Shareholder ). The Company will not receive any of the proceeds of the Offering. The Offering consists of: (i) a private placement to (a) investors in Norway, (b) investors outside Norway and the United States of America (the U.S. or the United States ), subject to applicable exemptions from the prospectus requirements, and (c) qualified institutional buyers ( QIBs ) in the United States as defined in, and in reliance on, Rule 144A ( Rule 144A ) under the U.S. Securities Act of 1933, as amended (the U.S. Securities Act ) (the Institutional Offering ), and (ii) a retail offering to the public in Norway (the Retail Offering ). All offers and sales outside the United States will be made in compliance with Regulation S under the U.S. Securities Act ( Regulation S ). In addition, the Selling Shareholder has granted DNB Markets, on behalf of the Managers (as defined below), an option to purchase up to 4,000,000 additional Shares (the Additional Shares and, together with the Sale Shares, the Offer Shares ), equal to up to approximately 7% of the number of Sale Shares sold in the Offering (representing up to 2% of the Shares in issue in the Company), exercisable, in whole or in part, within a 30-day period commencing at the time at which if sold trading in the Shares commences on the Oslo Stock Exchange, expected to be on 30 September 2013, to cover any over-allotments made in connection with the Offering on the terms and subject to the conditions described in this Prospectus (the Over-Allotment Option ). Assuming the Over-Allotment Option is exercised in full, the Offering will amount to 60,000,000 Shares. The price (the Offer Price ) at which the Offer Shares are expected to be sold will be between NOK 37 and NOK 48 per Offer Share (the Indicative Price Range ). The Offer Price may be set within, below or above the Indicative Price Range. The Offer Price will be determined through a bookbuilding process and will be set by the Selling Shareholder in consultation with the Company and the Joint Bookrunners. Investors in the Retail Offering will receive a discount of NOK 1,000 on their aggregate amount payable for the Offer Shares allocated to such investors. The Offer Price, and the number of Offer Shares sold in the Offering, is expected to be announced through a stock exchange notice on or before 30 September 2013 at 07:30 hours (Central European Time, CET ). The offer period for the Institutional Offering (the Bookbuilding Period ) will commence at 09:00 hours (CET) on 16 September 2013 and close at 15:00 hours (CET) on 27 September The application period for the Retail Offering (the Application Period ) will commence at 09:00 hours (CET) on 16 September 2013 and close at 12:00 hours (CET) on 27 September The Bookbuilding Period and the Application Period may be shortened or extended beyond the set times by the Company, in consultation with the Selling Shareholder and the Joint Bookrunners, but will in no event be shortened to expire prior to 12:00 hours (CET) on 23 September 2013 or extended beyond 15:00 hours (CET) on 11 October The Shares, including the Sale Shares and any Additional Shares, will be registered in the Norwegian Central Securities Depository (the VPS ) in book-entry form. All Shares will rank in parity with one another and carry one vote per Share. Investing in the Offer Shares involves a high degree of risk. See Section 2 Risk factors beginning on page 17. The Offer Shares have not been, and will not be, registered under the U.S. Securities Act or with any securities regulatory authority of any state or other jurisdiction in the United States, and are being offered and sold: (i) in the United States only to persons who are QIBs in reliance on Rule 144A or another exemption from the registration requirements under the U.S. Securities Act; and (ii) outside the United States in compliance with Regulation S. The distribution of this Prospectus and the offer and sale of the Offer Shares in certain jurisdictions may be restricted by law. Persons in possession of this Prospectus are required to inform themselves about and to observe any such restrictions. See Section 19 Selling and transfer restrictions. Prior to the Offering, the Shares have not been publicly traded. The Company applied for the Shares to be admitted for trading and listing on the Oslo Stock Exchange on 12 September 2013, and completion of the Offering is subject to the approval of the listing application by the board of directors of the Oslo Stock Exchange. The due date for the payment of the Offer Shares is expected to be on or about 2 October 2013 and 3 October 2013 in the Retail Offering and the Institutional Offering, respectively. Delivery of the Offer Shares is expected to take place on or about 2 October 2013 and 3 October 2013 in the Retail Offering and the Institutional Offering, respectively, through the facilities of the VPS, Euroclear Bank S.A./N.V. as operator of the Euroclear System and Clearstream Banking S.A. Trading in the Shares on the Oslo Stock Exchange is expected to commence on or about 30 September 2013, on an if sold basis, under the ticker code ODL. If closing of the Offering does not take place on such dates or at all, the Offering may be withdrawn, resulting in all applications for Offer Shares being disregarded, any allocations made being deemed not to have been made and any payments made being annulled. All dealings in Shares prior to settlement and delivery are at the sole risk of the parties concerned. Joint Global Coordinators and Joint Bookrunners ABG Sundal Collier DNB Markets Goldman Sachs International Co-Lead Managers Arctic Securities Danske Bank Markets Swedbank First Securities The date of this Prospectus is 13 September 2013

4 Odfjell Drilling Ltd - Prospectus IMPORTANT INFORMATION This Prospectus has been prepared in connection with the Offering of the Offer Shares and the Listing of the Shares on the Oslo Stock Exchange. For the definitions of certain technical terms and other terms used in this Prospectus, see Section 22 Definitions and glossary. This Prospectus has been prepared to comply with the Norwegian Securities Trading Act of 29 June 2007 no. 75 (the Norwegian Securities Trading Act ) and related secondary legislation, including the Commission Regulation (EC) no. 809/2004 implementing Directive 2003/71/EC of the European Parliament and of the Council of 4 November 2003 regarding information contained in prospectuses, as amended (the EU Prospectus Directive ), and as implemented in Norway. This Prospectus has been prepared solely in the English language. However, a summary in Norwegian has been prepared in Section 21 Norwegian Summary (Norsk Sammendrag). The Financial Supervisory Authority of Norway (Nw.: Finanstilsynet) (the Norwegian FSA ) has reviewed and approved this Prospectus in accordance with Sections 7-7 and 7-8 of the Norwegian Securities Trading Act. The Norwegian FSA has not controlled or approved the accuracy or completeness of the information included in this Prospectus. The approval by the Norwegian FSA only relates to the information included in accordance with pre-defined disclosure requirements. The Norwegian FSA has not made any form of control or approval relating to corporate matters described or referred to in this Prospectus. The Company has engaged ABG Sundal Collier, DNB Markets, part of DNB Bank ASA, and Goldman Sachs International as Joint Global Coordinators and Joint Bookrunners (together, the Joint Bookrunners ) and Arctic Securities, Danske Bank Markets and Swedbank First Securities, as Co-Lead Managers (together, the Co-Lead Managers ). The Joint Bookrunners and the Co-Lead Managers are jointly referred to as the Managers. The distribution of this Prospectus and the offer and sale of the Offer Shares in certain jurisdictions may be restricted by law. This Prospectus does not constitute an offer of, or an invitation to purchase, any of the Offer Shares in any jurisdiction in which such offer or sale would be unlawful. Neither this Prospectus nor any advertisement or any other offering material may be distributed or published in any jurisdiction except under circumstances that will result in compliance with applicable laws and regulations. Persons in possession of this Prospectus are required to inform themselves about and to observe any such restrictions. In addition, the Shares are subject to restrictions on transferability and resale and may not be transferred or resold except as permitted under applicable securities laws and regulations. Investors should be aware that they may be required to bear the financial risks of this investment for an indefinite period of time. Any failure to comply with these restrictions may constitute a violation of applicable securities laws. See Section 19 Selling and transfer restrictions. This Prospectus and the terms and conditions of the Offering as set out herein and any sale and purchase of Offer Shares hereunder shall be governed by and construed in accordance with Norwegian law. The courts of Norway, with Oslo as legal venue, shall have exclusive jurisdiction to settle any dispute which may arise out of or in connection with the Offering or this Prospectus. In making an investment decision, prospective investors must rely on their own examination, and analysis of, and enquiry into the Group and the terms of the Offering, including the merits and risks involved. None of the Company, the Selling Shareholder or the Managers, or any of their respective representatives or advisers, is making any representation to any offeree or purchaser of the Offer Shares regarding the legality of an investment in the Offer Shares by such offeree or purchaser under the laws applicable to such offeree or purchaser. Each investor should consult with his or her own advisors as to the legal, tax, business, financial and related aspects of a purchase of the Offer Shares. All Sections of the Prospectus should be read in context with the information included in Section 4 General information. Consent under the Exchange Control Act 1972 (and its related regulations) has been obtained from the Bermuda Monetary Authority for the issue and transfer of the Shares to and between residents and non-residents of Bermuda for exchange control purposes provided that the Shares are listed on the Oslo Stock Exchange. In granting such consent, neither the Bermuda Monetary Authority nor any other relevant Bermuda authority or government body accepts any responsibility for the Company s financial soundness or the correctness of any of the statements made or opinions expressed in this Prospectus. NOTICE TO NEW HAMPSHIRE RESIDENTS NEITHER THE FACT THAT A REGISTRATION STATEMENT OR AN APPLICATION FOR A LICENSE HAS BEEN FILED UNDER CHAPTER 421-B OF THE NEW HAMPSHIRE REVISED STATUTES WITH THE STATE OF NEW HAMPSHIRE NOR THE FACT THAT A SECURITY IS EFFECTIVELY REGISTERED OR A PERSON IS LICENSED IN THE STATE OF NEW HAMPSHIRE CONSTITUTES A FINDING BY THE SECRETARY OF STATE OF NEW HAMPSHIRE THAT ANY DOCUMENT FILED UNDER RSA 421-B IS TRUE, COMPLETE AND NOT MISLEADING. NEITHER ANY SUCH FACT NOR THE FACT THAT AN EXEMPTION OR EXCEPTION IS AVAILABLE FOR A SECURITY OR A TRANSACTION MEANS THAT THE SECRETARY OF STATE HAS PASSED IN ANY WAY UPON THE MERITS OR QUALIFICATIONS OF, OR RECOMMENDED OR GIVEN APPROVAL TO, ANY PERSON, SECURITY OR TRANSACTION. IT IS UNLAWFUL TO MAKE, OR CAUSE TO BE MADE, TO ANY PROSPECTIVE PURCHASER, CUSTOMER OR CLIENT ANY REPRESENTATION INCONSISTENT WITH THE PROVISIONS OF THIS PARAGRAPH. NOTICE TO INVESTORS IN THE UNITED STATES Because of the following restrictions, prospective investors are advised to consult legal counsel prior to making any offer, resale, pledge or other transfer of the Shares. The Offer Shares have not been and will not be registered under the U.S. Securities Act or with any securities regulatory authority of any state or other jurisdiction in the United States and may not be offered, sold, pledged or otherwise transferred within the United States except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the U.S. Securities Act and in compliance with any applicable state securities laws. Accordingly, the Offer Shares will not be offered or sold within the United States, except in reliance on the exemption from the registration requirements of the U.S. Securities Act under Rule 144A. The Offer Shares will be offered outside the United States in compliance with Regulation S. Prospective purchasers are hereby notified that sellers of Offer Shares may be relying on the exemption from the provisions of Section 5 of the U.S. Securities Act provided by Rule 144A under the U.S. Securities Act. See Section United States. Any Shares offered or sold in the United States will be subject to certain transfer restrictions as set forth under Section United States. The securities offered hereby have not been recommended by any United States federal or state securities commission or regulatory authority. Furthermore, the foregoing authorities have not passed upon the merits of the Offering or confirmed the accuracy or determined the adequacy of this Prospectus. Any representation to the contrary is a criminal offense under the laws of the United States. In the United States, this Prospectus is being furnished on a confidential basis solely for the purposes of enabling a prospective investor to consider purchasing the particular securities described herein. The information contained in this Prospectus has been provided by the Company and other sources ii

5 Odfjell Drilling Ltd - Prospectus identified herein. Distribution of this Prospectus to any person other than the offeree specified by the Managers or their representatives, and those persons, if any, retained to advise such offeree with respect thereto, is unauthorised and any disclosure of its contents, without prior written consent of the Company, is prohibited. This Prospectus is personal to each offeree and does not constitute an offer to any other person or to the public generally to purchase Offer Shares or subscribe for or otherwise acquire any Shares. ENFORCEMENT OF CIVIL LIABILITIES The Company is an exempted company limited by shares incorporated under the laws of Bermuda. As a result, the rights of holders of the Shares will be governed by Bermuda law and the Company s memorandum of association and Bye-Laws. The rights of shareholders under Bermuda law may differ from the rights of shareholders of companies incorporated in other jurisdictions. With one exception, none of the Interim Directors or members of the New Board of Directors are residents of the United States, and a substantial portion of the Company s assets are located outside the United States. As a result, it may be difficult for investors in the United States to effect service of process on the Company or its directors and executive officers in the United States or to enforce in the United States judgments obtained in U.S. courts against the Company or those persons, including judgments based on the civil liability provisions of the securities laws of the United States or any State or territory within the United States. It is doubtful whether courts in Norway or Bermuda will enforce judgments obtained in other jurisdictions, including the United States, against the Company or its directors or officers under the securities laws of those jurisdictions or entertain actions in Bermuda against the Company or its directors or officers under the securities laws of other jurisdictions. In addition, awards of punitive damages in actions brought in the United States or elsewhere may not be enforceable in Norway or Bermuda. The United States does not currently have a treaty providing for reciprocal recognition and enforcement of judgments (other than arbitral awards) in civil and commercial matters with either Norway or Bermuda. AVAILABLE INFORMATION The Company has agreed that, for so long as any of the Offer Shares are restricted securities within the meaning of Rule 144(a)(3) under the U.S. Securities Act, it will during any period in which it is neither subject to Sections 13 or 15(d) of the U.S. Securities Exchange Act of 1934, as amended (the U.S. Exchange Act ), nor exempt from reporting pursuant to Rule 12g3-2(b) under the U.S. Exchange Act, provide to any holder or beneficial owners of Shares, or to any prospective purchaser designated by any such registered holder, upon the request of such holder, beneficial owner or prospective owner, the information required to be delivered pursuant to Rule 144A(d)(4) of the U.S. Securities Act. NOTICE TO UNITED KINGDOM INVESTORS This Prospectus is only being distributed to and is only directed at (i) persons who are outside the United Kingdom or (ii) investment professionals falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the Order ) or (iii) high net worth entities, and other persons to whom it may lawfully be communicated, falling within Article 49(2)(a) to (d) of the Order (all such persons together being referred to as Relevant Persons ). The Offer Shares are only available to, and any invitation, offer or agreement to subscribe, purchase or otherwise acquire such Shares will be engaged in only with, Relevant Persons. Any person who is not a Relevant Person should not act or rely on this document or any of its contents. NOTICE TO INVESTORS IN THE EEA In any member state of the European Economic Area (the EEA ) that has implemented the EU Prospectus Directive, other than Norway (each, a Relevant Member State ), this communication is only addressed to and is only directed at qualified investors in that Member State within the meaning of the EU Prospectus Directive. The Prospectus has been prepared on the basis that all offers of Offer Shares in any Relevant Member State outside Norway will be made pursuant to an exemption under the EU Prospectus Directive from the requirement to produce a prospectus for offers of shares. Accordingly, any person making or intending to make any offer within any Relevant Member State (other than Norway) of Offer Shares which are the subject of the Offering contemplated in this Prospectus may only do so in circumstances in which no obligation arises for the Company or any of the Managers to publish a prospectus or a supplement to a prospectus under the EU Prospectus Directive for such offer. Neither the Company nor the Managers have authorised, nor do they authorise, the making of any offer of Shares through any financial intermediary, other than offers made by Managers which constitute the final placement of Offer Shares contemplated in this Prospectus. Each person in a Relevant Member State other than, in the case of paragraph (a), persons receiving offers contemplated in this Prospectus in Norway, who receives any communication in respect of, or who acquires any Offer Shares under, the offers contemplated in this Prospectus will be deemed to have represented, warranted and agreed to and with the Managers and the Company that: a) it is a qualified investor as defined in the EU Prospectus Directive, and b) in the case of any Offer Shares acquired by it as a financial intermediary, as that term is used in Article 3(2) of the EU Prospectus Directive, (i) such Offer Shares acquired by it in the Offering have not been acquired on behalf of, nor have they been acquired with a view to their offer or resale to, persons in any Relevant Member State other than qualified investors, as that term is defined in the EU Prospectus Directive, or in circumstances in which the prior consent of the Managers has been given to the offer or resale; or (ii) where such Offer Shares have been acquired by it on behalf of persons in any Relevant Member State other than qualified investors, the offer of those Offer Shares to it is not treated under the EU Prospectus Directive as having been made to such persons. For the purposes of this provision, the expression an offer to the public in relation to any of the Offer Shares in any Relevant Member State means the communication in any form and by any means of sufficient information on the terms of the offer and any Shares to be offered so as to enable an investor to decide to purchase any of the Offer Shares, as the same may be varied in that Relevant Member State by any measure implementing the EU Prospectus Directive in that Relevant Member State, and the expression EU Prospectus Directive means Directive 2003/71/EC (and amendments thereto, including the 2010 PD Amending Directive, to the extent implemented in the Relevant Member State), and includes any relevant implementing measure in each Relevant Member State and the expression 2010 PD Amending Directive means Directive 2010/73/EU. See Section 19 Selling and transfer restrictions for certain other notices to investors. iii

6 Odfjell Drilling Ltd - Prospectus STABILISATION In connection with the Offering, DNB Markets (the Stabilisation Manager ), or its agents, on behalf of the Managers, may engage in transactions that stabilise, maintain or otherwise affect the price of the Shares for up to 30 days from the commencement of if sold trading of the Offer Shares on the Oslo Stock Exchange. Specifically, the Stabilisation Manager may over-allot Offer Shares or effect transactions with a view to supporting the market price of the Offer Shares at a level higher than that which might otherwise prevail. The Stabilisation Manager and its agents are not required to engage in any of these activities and, as such, there is no assurance that these activities will be undertaken; if undertaken, the Stabilisation Manager or its agents may end any of these activities at any time but in any case must end at the end of the 30-day period mentioned above. Save as required by law or regulation, the Stabilisation Manager does not intend to disclose the extent of any stabilisation transactions under the Offering. ADDITIONAL IMPORTANT INFORMATION For additional important information, including on the presentation of financial information in this Prospectus, forward-looking statements and the sourcing of industry data included herein, and exchange rate data, see Section 4 General information. iv

7 Odfjell Drilling Ltd - Prospectus TABLE OF CONTENTS Section Page 1 SUMMARY RISK FACTORS RESPONSIBILITY FOR THE PROSPECTUS GENERAL INFORMATION REASONS FOR THE OFFERING AND THE LISTING DIVIDENDS AND DIVIDEND POLICY INDUSTRY AND MARKET OVERVIEW BUSINESS OF THE GROUP CAPITALISATION AND INDEBTEDNESS SELECTED FINANCIAL INFORMATION OPERATING AND FINANCIAL REVIEW BOARD OF DIRECTORS, MANAGEMENT, EMPLOYEES AND CORPORATE GOVERNANCE THE SELLING SHAREHOLDER RELATED PARTY TRANSACTIONS CORPORATE INFORMATION AND DESCRIPTION OF SHARE CAPITAL SECURITIES TRADING IN NORWAY TAXATION TERMS OF THE OFFERING SELLING AND TRANSFER RESTRICTIONS ADDITIONAL INFORMATION NORWEGIAN SUMMARY (NORSK SAMMENDRAG) DEFINITIONS AND GLOSSARY Appendix A: Appendix B: Appendix C: Appendix D: Appendix E: Bye-Laws of Odfjell Drilling Ltd... A1 Financial statements for the years ended 31 December 2012, 2011 and B1 Interim financial information for the three and six month periods ended 30 June 2013 and C1 Application form for the Retail Offering... D1 Application form for the Retail Offering in Norwegian... E1 1

8 Odfjell Drilling Ltd - Prospectus 1 SUMMARY Summaries are made up of disclosure requirements known as Elements. These Elements are numbered in Sections A E (A.1 E.7) below. This summary contains all the Elements required to be included in a summary for this type of securities and the issuer. Because some Elements are not required to be addressed, there may be gaps in the numbering sequence of the Elements. Even though an Element may be required to be inserted in the summary because of the type of securities and issuer, it is possible that no relevant information can be given regarding the Element. In this case a short description of the Element is included in the summary with the mention of not applicable. Section A Introduction and Warnings A.1 Warning This summary should be read as introduction to the Prospectus; any decision to invest in the securities should be based on consideration of the Prospectus as a whole by the investor; where a claim relating to the information contained in the Prospectus is brought before a court, the plaintiff investor might, under the national legislation of the Member States, have to bear the costs of translating the Prospectus before the legal proceedings are initiated; and civil liability attaches only to those persons who have tabled the summary including any translation thereof, but only if the summary is misleading, inaccurate or inconsistent when read together with the other parts of the Prospectus or it does not provide, when read together with the other parts of the Prospectus, key information in order to aid investors when considering whether to invest in such securities. Section B - Issuer B.1 Legal and commercial name B.2 Domicile and legal form, legislation and country of incorporation B.3 Current operations, principal activities and markets Odfjell Drilling Ltd Odfjell Drilling Ltd was incorporated on 16 November 2005 as an exempted company limited by shares under the laws of Bermuda and in accordance with the Bermuda Companies Act. Odfjell Drilling is an integrated drilling, engineering and well services provider with more than 40 years of experience focusing on the offshore harsh environment and deepwater markets. Today the Group has approximately 3,100 employees operating in more than 20 countries worldwide. Odfjell Drilling operates through three segments: Mobile Offshore Drilling Units (MODU), Well Services and Drilling & Technology. Odfjell Drilling s clients are primarily major oil and gas companies. (i) Mobile Offshore Drilling Units (MODU) In the MODU segment, the Group operates drilling units owned by the Group and by third parties. Odfjell Drilling currently owns the three harsh environment semisubmersible drilling rigs Deepsea Atlantic, Deepsea Stavanger and Deepsea Bergen. Deepsea Atlantic and Deepsea Stavanger were delivered in 2009 and 2010, respectively, and are both sixth-generation ultradeepwater semisubmersible drilling rigs. Deepsea Bergen is a third-generation semisubmersible drilling rig built in 1983 and has been continually upgraded to meet changes in regulatory requirements and client demands. Further, through a joint venture, Deep Sea Metro, the Group has a 40% ownership 2

9 Odfjell Drilling Ltd - Prospectus interest in two sixth-generation ultra-deepwater drillships, Deepsea Metro I and Deepsea Metro II, which were delivered in The Group charters its drillings rigs through a mixture of medium- and long-term contracts with major oil and gas companies, which include Statoil, BP, BG and Petrobras. The Group has one harsh environment ultra-deepwater semisubmersible drilling rig under construction with expected delivery from DSME in May The rig will be named Deepsea Aberdeen and is contracted to BP Exploration for a period of seven years with expected commencement of operations in the fourth quarter of In addition, the Group holds a 50% ownership interest in Odfjell Galvão B.V., a joint-venture company established with Galvão Oil and Gas Holding B.V. Odfjell Galvão B.V. holds 20% of the shares in three Dutch special purpose companies, each of which has entered into an engineering, procurement and construction contract for the construction of a drillship mainly at Estaleiro Jurong Aracruz in Brazil. The drillships are expected to be delivered in the period from July 2016 to December The MODU segment also offers management services to other owners of semisubmersibles, drillships and jack-ups, mainly operational management, management of regulatory requirements, marketing, contract negotiations and client relations, preparations for operation and mobilisation. Odfjell Drilling is currently responsible for the management of the following mobile offshore drilling units owned by third parties or owned jointly by the Group and third parties: (i) Deepsea Metro I and Deepsea Metro II and (ii) Island Innovator. In addition, Odfjell Galvão Perfurações Ltda, a subsidiary of Odfjell Galvão B.V., is to provide management services to Petrobras in connection with the fifteen-year rig contracts on the three drillships to be delivered under the Brazilian joint-venture mentioned above. (ii) Well Services The Well Services segment provides casing and tubular running services (both automated and conventional) as well as drilling tool and tubular rental services, both for exploration wells and for production purposes. The Group provides services in more than 20 countries and to more than 50 drilling rigs. Odfjell Drilling has more than 30 years of experience in the global well services market, and the Company is of the opinion that it is one of the leaders in remote operated handling equipment for casing and tubular running services. In the drilling tool rental business, the Group benefits from a well-developed supplier base, and offers a large inventory of modern and high quality drilling tools and equipment, which have been manufactured and certified in accordance with applicable industry standards. It aims to be a single supply source for drillers and operators and also has the capacity to design custom-made equipment. The Well Services segment currently serves approximately 50 clients, of which 10 constitute material volumes. 3

10 Odfjell Drilling Ltd - Prospectus (iii) Drilling & Technology The Drilling & Technology segment is divided into two business areas: Platform Drilling and Technology. The main service offering of the Platform Drilling business area is production drilling and well completion on client s rigs. Other types of services offered are slot recovery, plug and abandonment, workovers and maintenance activities. The Group has 35 years of experience in platform drilling operation and has been one of the leading platform drilling service providers in the North Sea since the 1980s, focusing on the high-end of the market for platform drilling services. The Technology business area offers engineering services ranging from design and engineering to building supervision, project management and operational support for newbuild projects, SPS certifications and yard stays. The Technology business area performs smaller or medium sized stand alone projects, including engineering, procurement, construction and installation projects. The Technology business area has a successful track record of MODU newbuild projects and yard stays spanning 40 years. It also occupies a strong position in the North Sea market. The Technology business area has approximately 400 employees and 90 contractors in total. Its offices are located close to its key clients in Norway, the UK and the Philippines. B.4a Significant recent trends affecting the issuer and the industry in which it operates Growth and demand within the offshore oil and gas services industry are affected by the following key factors: (i) Oil and gas prices and demand: Oil and gas E&P spending is the key driver of demand in the oil and gas services industry. E&P spending is directly linked to the earnings of oil and gas companies which are, in turn, dependent on average oil and gas prices. Volatility in oil prices can therefore reduce the ability of oil and gas companies to budget for increased E&P spending. However, while market expectations of a potential decline in oil prices will affect E&P spending and activity, ultra-deepwater projects, being large projects with longer lead times and longterm outlooks, are less affected by short-term changes in oil price. (ii) Reserve replacements: The future production capacity of the oil and gas industry depends on the ability of oil and gas companies to maintain a sustainable reserve replacement ratio through the discovery and development of new reservoirs or improvements in oil recovery techniques. Currently, oil and gas companies are barely able to fully replace the hydrocarbons they produce, and the IEA reports that proven reserves of oil worldwide (an indication of the near- to medium-term potential for new production) increased slightly by 1,523 billion barrels, or 3.6%, at the end of 2011, compared to the year before (IEA, World Energy Outlook 2012, 12 November 2012). (iii) Increased emphasis on E&P spending: Oil and gas companies are increasing both their total E&P spending as well as their proportion of E&P spending on offshore activities. The largest growth in E&P spending in recent years has been in deepwater exploration and production, partly driven by the lack of new, 4

11 Odfjell Drilling Ltd - Prospectus large, onshore and shallow water discoveries. Future upstream investments will have an increased offshore focus, as exploration and development continues to move towards harsher and deeper waters. (iv) Drilling technology and innovation: Recent advances in offshore technology have improved the ability of oil and gas companies to develop reservoirs in deeper waters, and in harsh and more remote locations. A new class of drilling rigs has emerged, with the ability to drill wells of up to 40,000 feet, in water depths of up to 12,000 feet, and with them, new types of subsea construction vessels and production facilities. (v) General political and economic environment: Changes in the political, economic and regulatory environment across regions affect global demand for oil services. The political and regulatory regimes of a country also have a significant impact on the level of oil and gas extraction activity within its territory. Changes in tax rules could also alter the profitability of certain projects and accordingly, E&P spending. (vi) Increased focus on QHSE: Due to the potentially serious consequences of an accident within the offshore oil and gas industry, the industry has developed high standards to mitigate risks associated with QHSE. There has been increased focus on this area after the Macondo incident in 2010, and, to an increasing extent, oil and gas companies will contract only with oil and gas companies that have the procedures and know-how to adequately manage these risks. This trend has increased the barriers to entry in the industry. The Group has experienced generally good market conditions and operating performance during the first half of The Group believes that the current revenue backlog provides a relatively high degree of financial visibility for the next few years. The Group believes the outlook for its three business segments is positive. The MODU segment has a strong medium- to long-term outlook in the drilling market. Deepsea Aberdeen, which is expected to commence operations in the fourth quarter of 2014, and potential incremental investment opportunities are expected to drive the Group s growth. Although the Deep Sea Metro joint venture so far has been loss-making due to relatively high financing cost in this joint venture and low financial utilisation of Deepsea Metro II, the Group expects this joint venture to contribute positively in the future due to Deepsea Metro I s contract extension at higher day rates in combination with a more normalised financial utilisation of Deepsea Metro II. The Group also expects continued strong growth in the Well Services segment in the coming years in-line with recent years. Finally, in the Drilling & Technology segment, the Group expects modest growth for the Platform Drilling business area based on existing backlog and growth in the Technology business area as a consequence of expected high activity in the drilling industry in the coming years. The Group s management contract for Dalian Developer was terminated by Dalian Deepwater Developer Ltd on 4 September 2013 following a 30-day grace period as a result of Dalian Deepwater Developer Ltd s 5

12 Odfjell Drilling Ltd - Prospectus termination of its construction contract for the drillship. B.5 Description of the Group Odfjell Drilling Ltd, the parent company of the Group, is a holding company. The operations of the Group are carried out by the Group s operating subsidiaries. Odfjell Drilling Ltd has two directly wholly-owned subsidiaries, Odfjell Offshore Ltd. (holding company for the Drilling Units) and Odfjell Drilling Services Ltd. (holding company for the Group s MODU Management business area and the Drilling & Technology and Well Services segments), both incorporated in Bermuda. B.6 Interests in the Company and voting rights Shareholders owning 5% or more of the Shares have an interest in the Company s share capital which is notifiable pursuant to the Norwegian Securities Trading Act. The table below shows the ownership percentage held by such notifiable shareholders. Shareholders Number of Shares Percent Odfjell Partners Ltd ,000, BCB Paragon Trust Limited, as trustee of the Larine Trust... 60,000, Total ,000, There are no differences in voting rights between the shareholders. Following the completion of the Offering, Odfjell Partners Ltd. will control a majority of the Shares. The Company is not aware of any arrangements the operation of which may at a subsequent date result in a change of control of the Company. B.7 Selected historical key financial information The following selected financial information is derived from the Group s audited financial statements (including the notes thereto) as of and for the years ended 31 December 2012, 2011 and 2010 (the Financial Statements), as well as the unaudited interim consolidated financial information as of and for the three and six month periods ended 30 June 2013 and 2012 (the Interim Financial Statements). The Financial Statements for the year ended 31 December 2012, with comparable figures for the year ended 31 December 2011, have been prepared in accordance with IFRS, as adopted by the EU, while the Financial Statements for the year ended 31 December 2011 and 2010 have been prepared in accordance with NGAAP. The Interim Financial Statements, combined with relevant information in the financial review, have been prepared in accordance with IAS 34. The selected financial information presented herein should be read in connection with Section 11 Operating and financial review and the Financial Statements and Interim Financial Statements (included in Appendix B and Appendix C to the Prospectus). As of and for the three months ended 30 June As of and for the six months ended 30 June As of and for the year ended 31 December (In USD millions) 2013 (IFRS) (unaudited) 2012 (IFRS) (unaudited) 2013 (IFRS) (unaudited) 2012 (IFRS) (unaudited) 2012 (IFRS) (audited) 2011 (IFRS) (audited) Consolidated statement of income Operating revenue , ,056.7 EBITDA Operating profit (EBIT) Profit/(loss) for the period... (9.2)

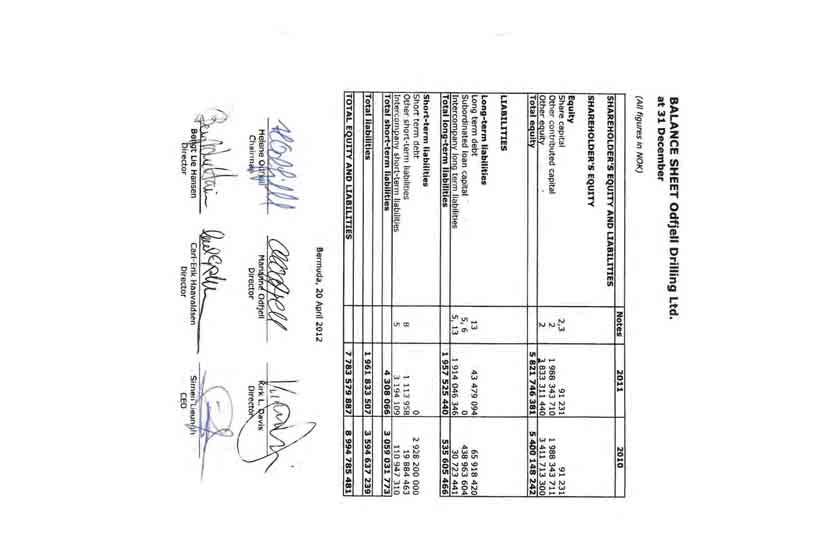

13 Odfjell Drilling Ltd - Prospectus As of and for the three months ended 30 June As of and for the six months ended 30 June As of and for the year ended 31 December (In USD millions) 2013 (IFRS) (unaudited) 2012 (IFRS) (unaudited) 2013 (IFRS) (unaudited) 2012 (IFRS) (unaudited) 2012 (IFRS) (audited) 2011 (IFRS) (audited) Consolidated statement of financial position Total non-current assets , , , ,158.4 Total current assets Total assets , , , ,740.6 Total equity , , , ,032.8 Total non-current liabilities , , , ,410.6 Total current liabilities Total liabilities , , , ,707.8 Total equity and liabilities , , , ,740.6 Consolidated statement of cash flow Net cash generated from operating activities Net cash used in investing activities (155.0) 4.4 (237.6) (305.9) (213.0) Net cash used in financing activities... (60.2) (49.7) (78.0) (49.7) (61.0) 66.0 Net change in cash and cash equivalents (142.1) 42.3 (141.9) (99.7) 50.6 Cash and cash equivalents at period end As of and for the year ended 31 December (In NOK millions) 2011 (NGAAP) (audited) 2010 (NGAAP) (audited) Consolidated statement of income Total operating income... 5, ,750.9 Total operating expenses... 4, ,756.2 Operating profit/loss... 1,106.1 (5.3) Net profit for the year Consolidated statement of financial position Total fixed assets... 12, ,144.4 Total current assets... 3, ,159.1 Total assets... 16, ,303.4 Total equity... 6, ,944.7 Total non-current liabilities... 8, ,033.8 Total current liabilities... 1, ,325.0 Total liabilities... 9, ,358.7 Total equity and liabilities... 16, ,303.4 Consolidated statement of cash flow Net cash generated from operating activities Net cash used in investing activities... (957.5) (3,025.4) Net cash used in financing activities ,567.0 Net change in cash and cash equivalents (1,323.8) Cash and cash equivalents at , ,605.3 B.8 Selected key pro forma financial information Not applicable. There is no pro forma financial information. B.9 Profit forecast or estimate Not applicable. No profit forecast or estimate is made. 7

14 Odfjell Drilling Ltd - Prospectus B.10 Audit report qualifications Not applicable. There are no qualifications in the audit reports. B.11 Insufficient working capital Not applicable. The Company is of the opinion that the working capital available to the Group is sufficient for the Group s present requirements, for the period covering at least 12 months from the date of this Prospectus. Section C - Securities C.1 Type and class of securities admitted to trading and identification number The Company has one class of shares in issue, and all shares in that class have equal rights to all such other shares in that class as set out in the Company s Bye-Laws. The Shares have been created under the Bermuda Companies Act and are registered in the VPS under ISIN BMG C.2 Currency of issue The Shares are issued in USD, but will be quoted and traded in NOK on the Oslo Stock Exchange. C.3 Number of shares in issue and par value C.4 Rights attaching to the securities At the date of this Prospectus, the Company s authorised share capital is USD 2,300,000 consisting of 230,000,000 Shares with a par value of USD 0.01 each, of which 200,000,000 Shares have been issued. Pursuant to the Bye-Laws, the holders of Shares have no pre-emptive, redemption, conversion or sinking fund rights. The holders of Shares are entitled to one vote per Share on all matters submitted to a vote of the holders of Shares. Under Bermuda law, a company may not declare or pay dividends if there are reasonable grounds for believing that: (i) the company is, or would after the payment be, unable to pay its liabilities as they become due; or (ii) that the realisable value of its assets would thereby be less than its liabilities. Under the Company s Bye-Laws, each of the Shares are entitled to dividends, as and when dividends are declared by the Board of Directors, subject to any preferred dividend right of the holders of any preference shares. C.5 Restrictions on transfer The Bye-Laws provide that the Board of Directors may decline to register the transfer of any interest in any Share in the register of members or decline to direct any registrar, appointed by the Company, to register the transfer where such transfer would result in 50% or more of the shares or votes in the Company being held, controlled or owned directly or indirectly by individuals or legal persons resident for tax purposes in Norway or connected to a Norwegian business activity, in order to avoid the Company being deemed a Controlled Foreign Company as such term is defined under the Norwegian tax rules. Subject to the above, but notwithstanding anything else contrary in the Bye-Laws, shares that are listed or admitted to trading on an Appointed Stock Exchange may be transferred in accordance with the rules and regulations of such exchange. All transfers of uncertificated shares shall be made in accordance with and be subject to the facilities and requirements of the transfer of title to shares in that class by means of the VPS or any other relevant system concerned and, subject thereto, in accordance with any arrangements made by the Board of Directors in accordance with the Bye-Laws. The Board of Directors shall refuse any transfer unless the registration of such transfer satisfies all applicable consents, authorisations and permissions of any governmental body or 8

15 Odfjell Drilling Ltd - Prospectus agency in Bermuda. The Board of Directors may also refuse to recognise an instrument of transfer of a share unless it is accompanied by the relevant share certificate (if one has been issued) and such other evidence of the transferor's right to make the transfer as the Board of Directors shall reasonably require. Please also see Section 19 Selling and transfer restrictions. C.6 Admission to trading On 12 September 2013, the Company applied for admission to trading of its Shares on the Oslo Stock Exchange. It is expected that the board of directors of the Oslo Stock Exchange will approve the listing application of the Company on 25 September 2013, subject to certain conditions being met. See Section Conditions for completion of the Offering Listing and trading of the Offer Shares. The Company currently expects commencement of trading in the Shares on the Oslo Stock Exchange on an if sold basis, on or around 30 September 2013, and on an ordinary basis on or around 3 October The Company has not applied for admission to trading of the Shares on any other stock exchange or regulated market. C.7 Dividend policy The Company aims to ensure that shareholder returns reflect the Company s value creation and will consist of both dividends and a positive share price development. The Company will target a long term dividend annual pay-out representing approximately 30 40% of its net profit on a consolidated basis. Since the Company is in a phase involving considerable investments, there is no plan for dividend payment for the financial year ended 31 December The Company has a high focus on value creation and will have a dividend policy that will preserve the interest of the Company and its shareholders. When deciding whether to declare and pay an annual dividend, the Board of Directors will take into consideration market outlook, contract backlog, cash flow generation, capital expenditure plans and funding requirements whilst maintaining adequate financial flexibility. The Board of Directors may revisit the dividend policy from time to time. The proposal in any year to pay any dividend is subject to: (i) the limitations found in the terms of certain loans made to the Group and (ii) sufficiency of distributable reserves. Section D - Risks D.1 Key risks specific to the Company or its industry Risks relating to the industry in which the Group operates (i) The Group s business depends on the level of activity in oil and gas exploration, as well as the identification and development of oil and gas reserves and production in offshore areas worldwide, particularly in harsh and ultra-deep water environments. In particular, oil and gas prices and market expectations of potential changes in these prices significantly affect the level of exploration and production activity by oil and gas companies. Due to the significant investments in exploration and, often, production made by the Group s clients at or before the time they contract for services provided by the MODU segment and the Platform Drilling business area, these businesses are typically impacted by longer term E&P spending decisions based on long-term price trends, whereas the Technology business area and the Well Services segment are more sensitive to E&P spending decisions 9

16 Odfjell Drilling Ltd - Prospectus by clients made in response to short-term fluctuations in oil and gas prices. Any decrease in demand for any of the Group s business segments services could have a material adverse effect on the Group s business, results of operations, cash flow and financial condition. (ii) Uncertainty relating to global economic conditions and development may reduce demand for the Group s Drilling Units and services or result in contract delays or cancellations. Any decrease in demand caused by this uncertainty could have a material adverse effect on the Group s results of operations, cash flow and financial condition. (iii) An over-supply of drilling units or rental equipment may lead to a reduction in day rates for the MODU segment and prices for the Well Services segment. Periods of excess drilling unit supply intensify the competition in the industry and can result in drilling units being idle for long periods of time. An over-supply of drilling units could be caused by the entry into service of new and upgraded units or by competitors shifting drilling units into those regions where the Group s Drilling Units operate. Oversupply of the equipment that the Group rents to clients (Rental Equipment), as offered by the Well Services segment, could lead to that segment experiencing decreased prices and/or client orders for its Rental Equipment. Either of these occurrences may materially impact the Group s results of operations. (iv) The oil and gas services industry in which the Group operates is highly competitive and fragmented and includes both large and small competitors that compete with the Group. The Group s operations may be materially adversely affected if its current competitors or new market entrants introduce new products or services with characteristics similar to, or better than, the Group s products and services or expand into service areas where the Group operates. Competitive pressures or other factors that result in significant price competition, particularly during industry downturns, could have a material adverse effect on the Group s business, results of operations, cash flow and financial condition. (v) The Group s business is subject to numerous operating hazards the occurrence of which could also subject the Group to property, environmental and other damage claims by third parties. The Group s insurance policies and contractual rights to indemnity may not adequately cover losses and the Group does not have insurance coverage or rights to an indemnity for all risks. The occurrence of a significant accident or other adverse event which is not fully covered by the Group s insurance or any enforceable or recoverable indemnity from a client could result in substantial losses for the Group. (vi) The Group s segments operate in various jurisdictions which subjects the Group to risks inherent in international operations that may be beyond the Group s control such as war, natural disasters, political unrest, public health threats and the inconsistent application of foreign laws and regulations. Some of these risks could disrupt the Group s operations and thereby have a material adverse effect on the Group s business, results of 10

17 Odfjell Drilling Ltd - Prospectus operations, cash flow and financial condition. Moreover, the Group operates in many developing market countries which brings with it the inherent risks associated with fraud, bribery, corruption and international sanctions regimes. Failure to comply with such laws could result in material fines and penalties and damage the Group s reputation. Risks relating to the Group (i) The Group s backlog may not be realised due to a number of reasons including the actions of its clients or its own inability to perform its obligations under its contracts. The Group s backlog represents the contracted future revenue under contracts for Drilling Units and services provided by its MODU segment and Platform Drilling business area. The Group presents backlog both inclusive and exclusive of any priced optional periods exercisable by clients calculated to reflect the nominal value of the contract, as detailed in Section Backlog. Backlog does not provide a precise indication of the time period over which the Group is contractually entitled to receive such revenues and there is no assurance that such revenue will be actually realised in the time frames anticipated, or at all. If the Group is unable to realise backlog amounts this could have a material adverse effect on the Group s results of operations, cash flows and financial condition. (ii) The Group s future performance depends on its ability to renew and extend existing contracts and to win new contracts. The Group s ability to renew or extend existing contracts or sign new contracts will largely depend on prevailing market conditions. If the Group is unable to sign new contracts that start immediately after the end of its current contracts, or in the case of the MODU segment or the Platform Drilling business area, if new contracts are entered into at day rates or prices substantially below the existing day rates or prices, or on terms otherwise less favourable compared to existing contract terms, or which leave the Group with mobilisation or demobilisation costs that cannot be fully recovered, the Group s business, results of operations, cash flow and financial condition may be adversely affected. Risks relating to operations (i) The Group, in particular the MODU segment and the Platform Drilling business area, is subject to client concentration risk. If any of the Group s major clients fail to compensate the Group, terminate their contracts, fail to renew their existing contracts or refuse to award new contracts to the Group, and the Group is unable to enter into contracts with new clients at comparable day rates, this could have a material adverse effect on the Group s results of operations. (ii) The Group s operating and maintenance costs will not necessarily fluctuate in proportion to changes in operating revenues. In a situation where a Drilling Unit faces longer idle periods, reductions in costs may not be immediate as some of the crew may be required to prepare Drilling Units for the idle period. Thus, there can be no assurance that the Group will be successful in reducing its operating costs under circumstances where its revenues may also have decreased. To the extent changes in the Group s operating and maintenance costs are not proportionate 11

18 Odfjell Drilling Ltd - Prospectus to changes in operating revenues it could have a material adverse effect on the Group s business, results of operations, cash flow and financial condition. (iii) The Group s newbuild drilling unit construction projects are subject to risks of delay, quality issues, damage to personnel, equipment and environment or cost overruns inherent in any large construction project due to numerous factors. The Group also provides consultancy and project management services on other newbuild projects where it may or may not have an ownership interest. Significant cost overruns or delays in projects may result in loss of revenue, potential penalties from the client or cancellation by the client. If any of these risks materialises, this could have a material adverse effect on the Group s results of operations, cash flow and financial condition. (iv) The Group conducts a portion of its operations through joint ventures and is, therefore, subject to the risks and uncertainties associated with participating in joint ventures. Differences in views among joint venture partners may result in delayed decisions or failures to agree on major issues. Should a joint venture partner sell its shares in the joint venture, a change of control event may be triggered under the bonds used to the finance the joint ventures, unless the Group purchases those shares. Further, if the Group s partners do not meet their contractual obligations, the respective joint venture may be unable to adequately perform and deliver its contracted services, requiring the Group to make additional investments or perform additional services. The Group could be liable for both its own obligations and those of its partners, which may result in reduced profits or, in some cases, significant losses on the project. These factors could have a material adverse effect on the business operations of the joint venture and, in turn, the Group s business operations and reputation. (v) The operation and development of the Group s business depends on its retention of key personnel and its ability to recruit, retain and develop skilled personnel for its business. Shortages of qualified personnel or the Group s inability to obtain and retain qualified personnel could have a material adverse effect on the Group s business. (vi) A loss of a major tax dispute or a successful tax challenge to the Group s operating structure or to the Group s tax payments, among other things, could result in a higher tax rate on the Group s earnings, which could have a material adverse effect on the Group s earnings and cash flows. From time to time, the Group s tax payments may be subject to review or investigation by tax authorities of the jurisdictions in which the Group operates. Specifically, the Group is currently subject to an ongoing tax audit pertaining to Deepsea Atlantic (which may have a negative impact on liquidity in the amount of approximately USD 50 million) and a tax dispute pertaining to Deepsea Bergen (where if the district court s verdict is upheld on appeal, the USD 62.8 million loss (already expensed as of 30 June 2013) for the Group will be final). 12

19 Odfjell Drilling Ltd - Prospectus Risks related to Group structure (i) The Group currently conducts its operations through, and most of the Group s assets are owned by, the Group s subsidiaries. As such, the cash that the Group obtains from its subsidiaries is the principal source of funds necessary to meet its obligations. The inability to transfer cash from the Group s subsidiaries or joint ventures may mean that the Group may not be permitted to make the necessary transfers from its subsidiaries or joint ventures to meet its obligations or pay dividends to its shareholders. A payment default by the Group, or any of the Group s subsidiaries, on any debt instruments would have a material adverse effect on the Group s business, results of operations, cash flow and financial condition. D.3 Key risks specific to the securities Risks relating to the Shares (i) Following completion of the Offering, it is expected that Odfjell Partners Ltd. will remain the major shareholder of the Group and will, accordingly, continue to have a majority of the shareholder vote. Thereby, it is expected that Odfjell Partners Ltd. will have the ability to significantly influence the outcome of matters submitted for a vote of the Company s shareholders, including election of members of the Board of Directors. There can be no assurance that the commercial goals of Odfjell Partners Ltd. and the Company will always remain aligned, and that this concentration of ownership will always be in the best interest of the Group s other shareholders. Further, while it is expected that Odfjell Partners Ltd. will remain the major shareholder of the Company after the Offering, no assurance can be given that this will continue on a permanent basis. If Odfjell Partners Ltd. was not to remain a major shareholder of the Company, or if its commercial goals were not in the best interest of the Group, this could have a material adverse effect on the market value of the Shares. (ii) After completion of the Offering there will only be a limited free float of the Shares. The limited free float may have a negative impact on the liquidity of the Shares and may result in a low trading volume of the Shares, which could have an adverse effect on the then prevailing market price for the Shares. Risks related to the Company s incorporation in Bermuda (i) The Bye-Laws contain provisions that could make it more difficult for a third party to acquire the Company without the consent of the Board of Directors. These provisions could make it more difficult for a third party to acquire the Company, even if the third party s offer may be considered beneficial by many shareholders. Section E - Offer E.1 Net proceeds and estimated expenses The Selling Shareholder will receive the proceeds of the Offering. The total costs and expenses of, and incidental to, the Listing and the Offering are estimated to amount to NOK 89 million (excluding VAT) if all Offer Shares are sold by the Selling Shareholder and the Company decides to pay the discretionary fee in full (based on a price of NOK 13

20 Odfjell Drilling Ltd - Prospectus per Share which is the mid-point of the Indicative Price Range). The costs and expenses will be paid by the Company. E.2a Reasons for the Offering and use of proceeds (i) To facilitate a sustainable shareholding structure which supports the Company s long-term strategy, by offering the Selling Shareholder an opportunity to sell all of its Shares. (ii) To enhance the Company s financing sources, thereby increasing its strategic flexibility for future growth opportunities. (iii) To enhance the Company s ability to attract talent by raising the profile of the Group and its brand. The estimated net amount of proceeds of the Offering is NOK 2,461 million. The Selling Shareholder will receive the proceeds of the Offering. The Company will not receive any of the proceeds of the Offering. E.3 Terms and conditions of the Offering The Offering consists of up to 56,000,000 Sale Shares, all of which are existing, validly issued and fully paid-up registered Shares with a par value of USD 0.01, offered by the Selling Shareholder. The Sale Shares represent, and will upon completion of the Offering represent, up to 28% of the Shares in issue in the Company. In addition, the Joint Bookrunners may elect to over-allot up to 4,000,000 Additional Shares, equalling up to approximately 7% of the number of Sale Shares (representing up to 2% of the Shares in issue in the Company). The Selling Shareholder has granted DNB Markets, on behalf of the Managers, an Over-Allotment Option to purchase a corresponding number of Additional Shares to cover any such over-allotments. Assuming the Over-Allotment Option is exercised in full, the Offering will amount to up to 60,000,000 Shares, representing up to 30% of the Shares. The Offering consists of: An Institutional Offering, in which Offer Shares are being offered (a) to investors in Norway, (b) investors outside Norway and the United States, subject to applicable exemptions from the prospectus requirements, and (c) in the United States to QIBs, as defined in, and in reliance on Rule 144A of the U.S. Securities Act. The Institutional Offering is subject to a lower limit per application of NOK 2,500,000. A Retail Offering, in which Offer Shares are being offered to the public in Norway subject to a lower limit per application of an amount of NOK 10,500 and an upper limit per application of NOK 2,499,999 for each investor. Investors in the Retail Offering will receive a discount of NOK 1,000 on their aggregate amount payable for the Offer Shares allocated to such investors. Investors who intend to place an order in excess of NOK 2,499,999 must do so in the Institutional Offering. Multiple applications by one applicant in the Retail Offering will be treated as one application with respect to the maximum application limit and the discount. All offers and sales outside the United States will be made in compliance with Regulation S. 14

21 Odfjell Drilling Ltd - Prospectus The Bookbuilding Period for the Institutional Offering is expected to take place from 16 September 2013 at 09:00 hours (CET) to 27 September 2013 at 15:00 hours (CET). The Application Period for the Retail Offering will take place from 16 September 2013 at 09:00 hours (CET) to 27 September 2013 at 12:00 hours (CET). The Company, in consultation with the Selling Shareholder and the Joint Bookrunners, reserves the right to shorten or extend the Bookbuilding Period and Application Period at any time. The Managers expect to issue notifications of allocation of Offer Shares in the Institutional Offering on or about 30 September 2013, by issuing contract notes to the applicants by mail or otherwise. DNB Markets, acting as settlement agent for the Retail Offering, expects to issue notifications of allocation of Offer Shares in the Retail Offering on or about 30 September 2013, by issuing allocation notes to the applicants by mail or otherwise. Payment by applicants in the Institutional Offering will take place against delivery of Offer Shares. Delivery and payment for Offer Shares in the Institutional Offering is expected to take place on or about 3 October The due date of payment in the Retail Offering is on or about 2 October Subject to timely payment by the applicant, delivery of the Offer Shares allocated in the Retail Offering is expected to take place on or about 2 October E.4 Material and conflicting interests The Managers or their affiliates have provided from time to time, and may provide in the future, investment and commercial banking services to the Company and its affiliates in the ordinary course of business, for which they may have received and may continue to receive customary fees and commissions. The Managers do not intend to disclose the extent of any such investments or transactions otherwise than in accordance with any legal or regulatory obligation to do so. The Selling Shareholder will receive the proceeds of the Offering. Beyond the abovementioned, the Company is not aware of any interest of natural and legal persons involved in the Offering. E.5 Selling shareholders and lock-up agreements The Selling Shareholder is BCB Paragon Trust Limited, as trustee of the Larine Trust. Marianne Odfjell is a beneficiary of the trust. As of the date of this Prospectus, the Selling Shareholder holds 60,000,000 Shares in the Company, corresponding to 30% of the issued and outstanding Shares. Following completion of the Offering, the Selling Shareholder will not hold any Shares, assuming (i) the Offering is fully subscribed, (ii) the Additional Shares are allotted and (iii) the Over-Allotment Option is exercised in full. To the extent the Stabilisation Manager, on behalf of the Managers, redelivers any of the Shares borrowed pursuant to the Lending Option to the Selling Shareholder at the end of the stabilisation period, the Selling Shareholder has the right to require Odfjell Partners Ltd. to purchase 50% of such redelivered Shares from the Selling Shareholder and Odfjell Partners Ltd. has a corresponding right to require the Selling Shareholder to sell 50% of any redelivered Shares. In connection with the Purchase Agreement, Odfjell Partners Ltd., the 15

22 Odfjell Drilling Ltd - Prospectus Selling Shareholder, the Company and Simen Lieungh (the President and CEO of Odfjell Drilling) will give an undertaking that will restrict their ability to issue, sell or transfer Shares for nine months after the date of the Purchase Agreement. For more information about these restrictions, please see Section Lock-up. E.6 Dilution resulting from the Offering E.7 Estimated expenses charged to investor Not applicable. No new shares will be issued in the Offering. Not applicable. The expenses related to the Offering will be paid by the Company. 16

23 Odfjell Drilling Ltd - Prospectus 2 RISK FACTORS Investing in the Shares involves inherent risks. Before deciding whether or not to participate in the Offering, an investor should consider carefully all of the information set forth in this Prospectus, and in particular, the specific risk factors set out below. An investment in the Shares is suitable only for investors who understand the risk factors associated with this type of investment and who can afford a loss of all or part of their investment. If any of the risks described below materialise, individually or together with other circumstances, they may have a material adverse effect on the Group s business, results of operations, cash flow and financial condition, which may cause a decline in the value and trading price of the Shares that could result in a loss of all or part of any investment in the Shares. The order in which the risks are presented below is not intended to provide an indication of the likelihood of their occurrence or of their severity or significance. 2.1 Risks relating to the industry in which the Group operates Market conditions The Group s business, results of operations and financial condition depend on the level of exploration, development and production activity in the oil and gas industry, which is significantly affected by, among other things, volatile oil and gas prices The Group s business depends on the level of activity in oil and gas exploration, as well as the identification and development of oil and gas reserves and production in offshore areas worldwide, particularly in harsh and ultradeepwater environments. The availability of quality drilling prospects, exploration success, relative production costs, the stage of reservoir development, political concerns and regulatory requirements all affect the Group s clients levels of expenditure and drilling campaigns. In particular, oil and gas prices and market expectations of potential changes in these prices significantly affect the level of exploration and production ( E&P ) activity by oil and gas companies. Oil and gas prices are volatile and cyclical and are affected by numerous factors beyond the Group s control, including, but not limited to: worldwide demand for oil and gas as well as industrial services and power generation and the competitive position of oil and gas as an energy source compared with alternative fuels; the cost of exploring for, developing, producing and delivering oil and gas; capital expenditures by major national and international oil companies; current oil and gas production, consumer capacity and price levels and expectations regarding future energy prices; the ability of the Organisation of Petroleum Exporting Countries ( OPEC ) to set and maintain production levels and impact pricing, as well as the level of production in non-opec countries; government laws and regulations; political, economic and weather conditions and incidents, including conflicts and natural disasters in oil producing countries and their impact on the world s financial and commercial markets; major accidents in the industry, including major spills, blowouts and explosions, and any resulting changes to regulations, or client safety requirements; and technological advances affecting both exploration, development and production technology and energy consumption. 17