The Small Business Employment Tax Guide

|

|

|

- Erik Hicks

- 6 years ago

- Views:

Transcription

1 The Small Business Employment Tax Guide Roanoke Regional Small Business Development Center 210 S. Jefferson Street, Roanoke, Virginia Roanoke Small Business Development Center 2017

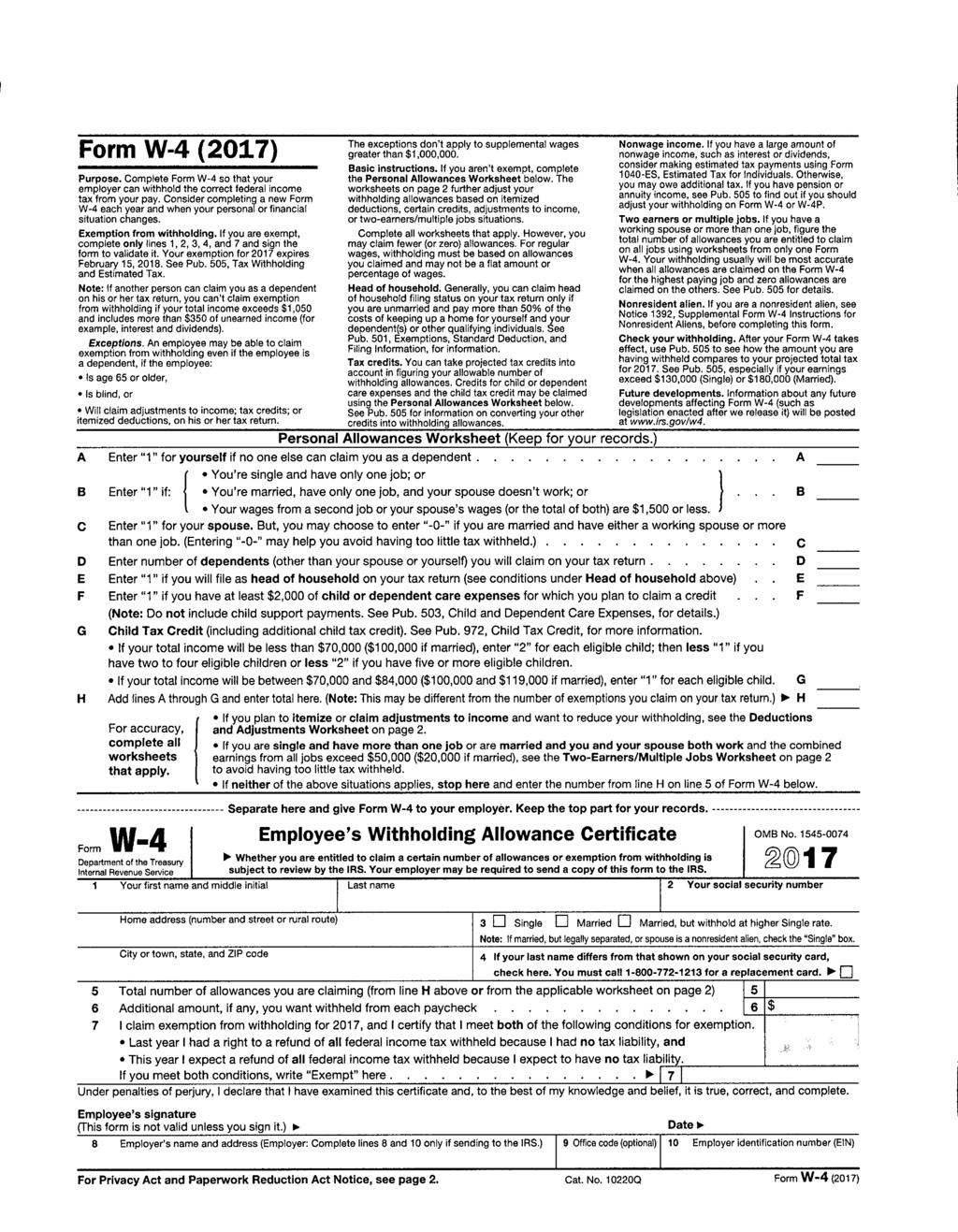

2 About this manual: This manual is divided into several sections. Section 1 Payroll Section 2 Independent Contractor Requirements Section 3 Estimated Taxes Appendix Listing of forms Note: This guidebook should be used as a guide to understanding taxes for your small business. Tax laws, rates and schedules change regularly so be sure to check with your accountant for current requirements. SECTION 1 - PAYROLL Hiring Employees: If your business will be hiring employees, there are certain tax and filing requirements you need to be aware of. Owner(s) of an S-Corporation are considered employees (even if there are no other employees) and the business is required to follow all the requirements set forth as any other company hiring employees. Before hiring a new employee, you must at a minimum have the employee complete the following: W-4 (Employee s Withholding) page 10. VA-4 (Virginia Withholding) page 11. I-9 (Employment Eligibility Verification) page Current federal forms can be downloaded from and Virginia State forms from To find the latest version of the I-9 form, go to If you wish to verify the accuracy of the applicant s information, you may use the E-Verify system. This online verification system will immediately inform you if the documentation the applicant has presented to you is accurate. To register for this service (it is free and voluntary) go to (page 9) One of the first steps you need to do before hiring employees is to obtain an Employer Identification Number (EIN). To get an EIN you will need to file Form SS-4 with the Internal Revenue Service, or file online at *Special Note to S-Corporation owners. If you are an owner of an S-Corporation you are considered an employee of the company for payroll purposes and required to complete all payroll requirements including registering and paying unemployment. As an owner of an S-Corporation you are able to receive income from the company as either payroll or distribution. Payroll is subject to FICA taxes and unemployment. Distributions are not subject to FICA or unemployment. According to IRS rules, an owner is required to be paid Reasonable Compensation before taking distributions. For further explanation, please visit or ask your accountant. Federal Tax Payments Using the EFTPS To make federal tax payments you need to register with the Electronic Federal Tax Payment System (EFTPS). Go to (see page 8) to register. This process takes several weeks, so do not wait until the last minute to register. When you request an EIN, you should automatically be registered in 1

3 the system if you stated you would be hiring employees, if not you will need to register. After registering you will receive a PIN by mail. Do not lose this PIN as you will need this number to access your account in order to make payments. All federal payments for taxes will need to be made through the EFTPS system. Virginia New Hire Requirement: When an employer hires or re-hires a full, part-time, or temporary employee, the employer must report this information within 20 days of hiring. Go to: (see page 9). Virginia State Taxes: If you have never registered in the state of Virginia for business taxes, you will first need an Employer Identification Number (EIN). You have several ways to file and pay taxes in Virginia. However; if you will be hiring employees you will need to register and use the Virginia ifile System in order to report to the Virginia Employment Commission (VEC). ifile system this allows your company to key payroll and sales tax reports and pay online. The ifile system also allows you to review past reports and payments and schedule future payments. This service is required if you will be filing VEC reports electronically. eforms system this service allows your company to key payroll and sales tax reports and then pay online. No registration is required and is a simple approach to filing and paying. With eforms you do not have the advantage of looking at past reports or payments. (Cannot use for filing VEC reports electronically). To register for business taxes in Virginia go to and register using ireg or complete form R-1 and return to the Virginia Department of Taxation. You will also want to register for ifile so you can file and pay online and complete the registration with the Virginia Employment Commission. You will not be able to register with the VEC until you have paid employees (cannot do a pre-registration). Payroll: When you are ready to pay employees, you will need to be sure each employee s Net Pay is figured correctly. The following information is needed. Employee s income (wages, bonuses, salary, commissions, etc.) Is there tip income (see tip income below) From the employee s W-4 and VA-4, you need the following: What is the filing status of the employee (state and federal) Any additional withholding Any other non-taxable deductions (retirement plan, healthcare, etc.) Other benefits to include Vacation, Sick-Pay, PTO, etc. If you are using a software program (such as QuickBooks Payroll) the tax amounts are properly calculated provided the employee and payroll system is setup correctly. The following are taxes required with all Virginia Employees: Employee Social Security 6.2% (up to wage cap of $127,200 (2017) per employee) 2

4 Employer paid portion of Social Security 6.2% (up to wage cap of $127,200) Employee Medicare 1.45% (no wage cap) Employer paid portion of Medicare 1.45% (no wage cap) Virginia Withholding taxes (based on employee VA-4) Federal Withholding taxes (based on employee W-4) Virginia State Unemployment Tax (paid by employer) Federal Unemployment Tax (paid by employer) If you do not have a payroll program or provider you will need to use the payroll tables available at the IRS and Virginia Department of Taxation website or use an online payroll calculator. There are web based payroll calculators available. One Free Payroll Calculator can be found at This free calculator allows you to enter gross pay, deductions, etc. and determine proper net pay for each employee. Another is This company also offers other inexpensive payroll solutions. There are many online payroll solutions to include your bank, local payroll vendors and be sure to check with your accounting firm. Note: Federal and State tax laws are subject to change. Check with the state, IRS, or your accountant to be sure these rates have not changed. Tip Income If an employee receives tips, they are required to report these tips to their employer no later than the 10 th of the month for tips earned in the previous month (do not need to report tips less than $20 received in a month). Tips to report include cash, credit card or checks. Employees are not required to report noncash tips such as gifts, free tickets, etc. (even though they are taxable to the employee). The employee can keep track of their tips on IRS form 4070A, but must report tips earned each month to their employer on IRS Form You may wish to have the employee report tips on the same schedule as your payroll rather than on the 10 th of each month. The employer is required to include the tip reported income into the employee s income and take out the appropriate Social Security, Medicare, State and Federal Withholding. If the employer pays the employee in cash for credit card tips, the employee must also include these tips on the monthly IRS Form If the employer has an allocated tips program, be sure to include these tips in the employee s income and take out the appropriate taxes. Failure on the part of the employee to report tips can result in penalties up to 50% to the employee and penalty to the employer for all unpaid FICA taxes. Annual Reporting Requirements: Certain restaurants have annual tip filing requirements because they are considered a large food or beverage establishment. To be considered a large food or beverage establishment all of the following must apply: Food or beverage is provided for consumption on the premises Tipping is customary practice 3

5 More than 10 employees who are employed on a typical business day. All employees count, not just tipped employees. (Owners who own 50% or more and work in business are not counted towards the 10). If this applies to your business, your business is required to file IRS Form 8027 by February 28 th of each year unless you are filing electronically in which the deadline is March 30th. If these items do not apply to your business, no annual reporting is required, but you are still responsible for reporting all employee tips and paying appropriate taxes. Note: If total tips reported do not equal 8% of total sales, you will be required to make up the difference by paying the additional amount as allocated tips. The 8% amount is a minimum and does not mean your employees do not have to report more than 8%. Note: To learn more about tip income responsibilities for employees and employers, refer to IRS Publication 531, Instructions for Form 8027, Form 4070 and Form 4070A, and Publication Taxes: Once you have determined what the correct net pay is for every employee you will need to be sure the withheld taxes are paid according to your filing status. Step 1: Federal Withholding Payments: When to deposit your business will either be a monthly or semi-weekly depositor. Determination is made each year based on tax liability reported on your Form 941 during the look back period. Look back period is the 4-quarters beginning on July 1 st and ending on June 30 th of each year. If your business reported $50,000 or less in tax liability for the entire 12-month period, your business is designated as a monthly schedule depositor. Monthly depositors must deposit by the 15th for the previous month withholding. If you reported more than $50,000 in tax liability your business will be designated as a semiweekly depositor. Semi-Weekly deposit must be made by Wednesday for any payroll made on the previous Wednesday, Thursday or Friday. All payments MUST be made electronically using the EFTPS (Electronic Federal Tax Payment System). Note: New businesses are considered monthly depositors for the first calendar year of operation. Step 2: Virginia Withholding Tax: (must be done electronically) When to deposit. Virginia employee tax withholding must be filed to the Virginia Department of Taxation based on the following schedule: Quarterly Filing Business: If the average monthly Virginia withholding amount is less than $100, your business is a quarterly filer. Use form VA-5 to make payments. Payments must be made by the last day of the month following the end of the quarter. Filing and Payment must be made by EFT (Electronic Funds Transfer using the ifile system or eforms). Also required to file VA-6 by January 31 st of each year. Monthly Filing: If the average monthly Virginia withholding amount is more than $100, but less than $1000 your business is a monthly filer. Use form VA-5 to make payments. Withholding must be made by the 25 th day of the month following the end of the preceding month. Filing and Payment must be made by 4

6 EFT (Electronic Funds Transfer using the ifile system or eforms). Also required to file VA-6 by January 31 st of each year. Semi-Weekly Filing: If the average monthly liability is greater than $1,000 your business is a semiweekly filer. Deposits must be made within three banking days of the withholding date using form VA-15 (Electronic Funds Transfer using the ifile system or eforms). At the end of the quarter Form VA- 16, quarterly reconciliation, must be filed by the last day of the month following the end of the quarter. Also required to file VA-6 by January 31 st of each year. Seasonal: When registering for taxes if you registered as a seasonal filer, you will need to complete the same requirements. Note: Regardless of your filing schedule, even if you have no withholding, a return must be filed on the correct due dates or you will be accessed a penalty. Reporting Requirements: Making tax deposits is only the first step to properly accounting for employment taxes. On a quarterly and annual basis, certain reports are required. If you are not using a payroll software program to file your reporting requirements, there are several internet based companies that charge you a minimal expense for the filing of these returns. You may also manually send in forms (Virginia requires online submission and payments), but electronic payments are required by the IRS for Federal payments. Step 1 Federal Reporting Requirements At the end of each quarter you are required to complete and file form 941 Employer s Quarterly Federal Tax Return. Form 941 includes the total number of employees, total wages paid in the quarter and the total of taxes both withheld and employer matched. If your regular deposits are being made there should be no payment required with this form. (see page 14-15). Note: See Annual Filing Requirements to see if you are required to make Quarterly 940 Payments. Step 2 Virginia Withholding Reporting Requirements If you are a semi-weekly filer then at the end of the quarter Form VA-16, quarterly reconciliation, must be filed by the last day of the month following the end of the quarter. If you are a monthly filer or quarterly filer, then no other further reporting requirements are necessary other than your regular deposit requirements. Step 3 Virginia Employment Commission Reporting Requirements Every business (note exceptions at end of section), is required to pay into the Virginia Unemployment Tax Fund (SUTA) and the Federal Unemployment Tax Fund (FUTA). At the end of the quarter, VEC form FC-21 must be completed, filed and paid by the end of the month following the end of the quarter (January 31 st, April 30 th, July 31 st, October 31 st ). This form reports each employee s wages and determines the unemployment tax owed. (see pages 18-19) Your unemployment tax rate is based on the business s historical unemployment claims (Experience Rating). This number is assigned by the Virginia Employment Commission on an annual basis. Startup businesses are assigned a rate of approximately 3% (adjusts annually). 5

7 Businesses are taxed only on the first $8,000 of wages of each employee. Once an employee reaches $8,000 in wages in a calendar year, there will be no additional unemployment taxes for that employee. NOTE: Churches are exempt from both SUTA and FUTA taxes. Non-Profit 501 c(3) are exempt from FUTA, but are required to pay SUTA if the organization has more than 3 employees for more than 20 weeks in a year. If your organization is exempt from paying into the fund, the employees will not be able to collect unemployment benefits. Annual Requirements Step 1 Federal Requirements Form 940, Employer s Annual Federal Unemployment (FUTA) Tax Return, must be filed by January 31 st of each year reporting data from the previous year. (see page 16-17) FUTA deposits must be made quarterly by the end of the month following the end of a quarter if your liability is more than $500. If liability is less than $500, you may wait until the end of the next quarter to deposit. FUTA rate is.6% on the first $7,000 of each employee s income. W-2s Must be given to employees no later than January 31 st of each year. Must be completed and submitted with a W-3 by January 31 st of each year. NOTE: The total on your W-2s must match the totals on the total of your 941s. Step 2 Virginia State Requirements Form VA-6, Employer s Annual Summary of Virginia Income Tax Withheld, must be filed by January 31st of each year. This form lists your monthly or quarterly deposits in an annual summary and must match the amount that is on your W-2s. W-2s Must be given to employees no later than January 31 st of each year. Must be completed and electronically submitted to the state by January 31 st or each year. SECTION 2 Independent Contractors The Internal Revenue Service (IRS) has defined as to whether someone is an independent contractor or employee. Be sure you understand the difference as you can be held liable for taxes in the event you misclassify an individual. Listed below is the basic information about Independent Contractor. To get more information download IRS Publication Behavioral Control - These facts show whether there is a right to direct or control how the worker does the work. A worker is an employee when the business has the right to direct and control the worker. The business does not have to actually direct or control the way the work is done as long as the employer has the right to direct and control the work. The worker is an independent contractor if the business has no rights to direct or control worker. Financial Control: 6

8 Significant Investment does the person have a significant investment in the work being done (not just a paycheck)? If so, most likely an independent contractor. Is this the only business that the person is working for and is and ongoing relationship? If so, then most likely the worker is an employee. Expenses If you are not reimbursed for your expenses since they are included in the job price. Then the worker may be an independent contractor. Opportunity for Profit or Loss If the person has an opportunity to realize a profit, or to incur a loss. Then most likely an independent contractor. Relationship of the Parties Employee Benefits A true independent contractor would not be receiving benefits from the hiring business Written Contract Is there a written contract between the parties. If so, then more likely an independent contractor. Requirements If you hire an individual as an independent contractor there are several requirements (this includes rents to landlords or payment for other services such as accountants, attorneys, etc.) Have the individual or company complete a W-9 Request for Taxpayer ID Number (page 20). You will need this in order to complete the 1099 filing requirements. If you pay any independent contractor $600 or more in a calendar year, you are required to send them a 1099-MISC. The 1099-MISC must be sent to individual or company by January 31 st of each year. The 1099-MISC along with Form 1096 to the IRS by January 31 st of each year. The 1099 must also be sent to VA Department of Taxation along with W-2s and VA-6. Note: If the Independent Contractor is taxed as a corporation there is no need to send a SECTION 4 Estimated Taxes If your business is taxed as a sole proprietor or partnership (even if legally setup as an LLC) or an S- corporation (either LLC, or Corporation) then you may be required to file individual estimated taxes. Payments must be made by April 15th, June 15th, September 15th and January 15 th. Payments must be made to the IRS using form 1040ES (page 21) and using either the appropriate voucher, or pay by EFTPS (see instructions above for info on EFTPS). Note: Pass through entities file individual estimated taxes, not business taxes, so be sure you use the owners SSN not the business s EIN. You will also be required to pay Virginia estimated taxes on the same schedule using form 760ES. Payments can be made by mail using the correct voucher, or by using the Virginia e-file system. Dates are May 1 st, June 15 th, September 15, and January 15 th. For individuals (if sole proprietor, partner or owner in S-Corp) you would file form 760ES. Do you need to file and pay estimated taxes? 1) You expect to owe at least $1,000 in tax year. 2) You expect your withholding to be less than the smaller of a) 90% of the tax on your next tax return b) 100% of the latest tax return you filed. 7

9 Even if you are a startup business, you are still required to file and pay estimated taxes based on the above criteria. Note: Be sure to keep track of your estimated taxes paid so when you file your tax return you can credit these payments towards the amount already paid. The IRS will not send you a notice of your estimated payments made. 8

10 9

11

12

13

14

15

16

17

18

19

20

21

22

Archdiocese of Baltimore- Federal, State, & Other Filing Requirements January 13, 2005

Archdiocese of Baltimore- Federal, State, & Other Filing Requirements January 13, 2005 Agenda 1. Federal Payroll Filings a. Payroll Related Forms b. Proper Completion of Federal Forms c. Federal Payroll

Archdiocese of Baltimore- Federal, State, & Other Filing Requirements January 13, 2005 Agenda 1. Federal Payroll Filings a. Payroll Related Forms b. Proper Completion of Federal Forms c. Federal Payroll

BMA Payroll is designed to help you with payroll every step of the way.

Payroll 101: An Introduction to Payroll and Taxes As a new employer, you probably have questions about what it means to "do payroll." This document will provide you with an introduction to payroll processing

Payroll 101: An Introduction to Payroll and Taxes As a new employer, you probably have questions about what it means to "do payroll." This document will provide you with an introduction to payroll processing

2018 Payroll Update Reference Guide

2018 Payroll Update Reference Guide Jones & Roth is providing this Payroll Update as a reference guide for you. It is not meant to be all-inclusive. If there is a payroll item that you have questions about,

2018 Payroll Update Reference Guide Jones & Roth is providing this Payroll Update as a reference guide for you. It is not meant to be all-inclusive. If there is a payroll item that you have questions about,

2018 Payroll Withholding and Payroll Tax Changes

Below is our annual summary of specific provisions relating to payroll and information reporting. The provisions will be effective January 1, 2018. Please review this information carefully and share it

Below is our annual summary of specific provisions relating to payroll and information reporting. The provisions will be effective January 1, 2018. Please review this information carefully and share it

Withholding, Estimated Payments & Payroll Taxes

CHAPTER 9 Withholding, Estimated Payments & Payroll Taxes Compute income tax withholding from employee wages Determine taxpayers quarterly estimated payments Understand FICA, federal deposit system and

CHAPTER 9 Withholding, Estimated Payments & Payroll Taxes Compute income tax withholding from employee wages Determine taxpayers quarterly estimated payments Understand FICA, federal deposit system and

Small Business Tax and Form Calendar

BONUS CHAPTER 2 Small Business Tax and Form Calendar Here we ve assembled all the key tax dates you need to know and the federal forms that must be submitted on those dates. The dates listed are the actual

BONUS CHAPTER 2 Small Business Tax and Form Calendar Here we ve assembled all the key tax dates you need to know and the federal forms that must be submitted on those dates. The dates listed are the actual

Form 941 for 2017: All You Need to Know Presented on Thursday, September 28, 2017

Form 941 for 2017: All You Need to Know Presented on Thursday, September 28, 2017 1 2016 The Payroll Advisor 2 Housekeeping 3 Credit Questions Today s topic Speaker 2016 The Payroll Advisor To earn RCH

Form 941 for 2017: All You Need to Know Presented on Thursday, September 28, 2017 1 2016 The Payroll Advisor 2 Housekeeping 3 Credit Questions Today s topic Speaker 2016 The Payroll Advisor To earn RCH

Paychex 2017 Employer Year-end Guide

Paychex 2017 Employer Year-end Guide Overview Paychex is committed to helping you prepare and plan for year-end. Please use this guide to help make sure you have a successful 2017 year-end. The guide contains

Paychex 2017 Employer Year-end Guide Overview Paychex is committed to helping you prepare and plan for year-end. Please use this guide to help make sure you have a successful 2017 year-end. The guide contains

federal tax deposits

The ABCs of FTDs Resource Guide for Understanding federal tax deposits The ABCs of FTDs It s a great feeling to have your own small business, isn t it? You re the boss! You have a lot of responsibility

The ABCs of FTDs Resource Guide for Understanding federal tax deposits The ABCs of FTDs It s a great feeling to have your own small business, isn t it? You re the boss! You have a lot of responsibility

Worker Classification: Employee or Independent Contractor?

Worker Classification: Employee or Independent Contractor? Doug Blade July 24, 2013 A Note Before We Begin This presentation is designed to provide information not specific determination for any situation.

Worker Classification: Employee or Independent Contractor? Doug Blade July 24, 2013 A Note Before We Begin This presentation is designed to provide information not specific determination for any situation.

Orthodox Church in America Tax Help for Parish Treasurers

Orthodox Church in America Tax Help for Parish Treasurers INTRODUCTION Taxes in the United States are complex and consequences for noncompliance can be significant. Furthermore, there are nuances in the

Orthodox Church in America Tax Help for Parish Treasurers INTRODUCTION Taxes in the United States are complex and consequences for noncompliance can be significant. Furthermore, there are nuances in the

The Secure Way. to Pay Your Federal Taxes. for Business and Individual Taxpayers ELECTRONIC FEDERAL TAX PAYMENT SYSTEM

The Secure Way to Pay Your Federal Taxes for and Taxpayers ELECTRONIC FEDERAL TAX PAYMENT SYSTEM Electronic Federal Tax Payment System... THE BASICS OF EFTPS With EFTPS, you have two payment methods that

The Secure Way to Pay Your Federal Taxes for and Taxpayers ELECTRONIC FEDERAL TAX PAYMENT SYSTEM Electronic Federal Tax Payment System... THE BASICS OF EFTPS With EFTPS, you have two payment methods that

Sage Abra HRMS I Planning Guide. The Payroll Manager s Guide to Year-End

I Planning Guide The Payroll Manager s Guide to Year-End Table of Contents Introduction... 1 What s Involved in Payroll Processing and Year-End Compliance... 1 Checklist for Year-End 2011... 2-3 Looking

I Planning Guide The Payroll Manager s Guide to Year-End Table of Contents Introduction... 1 What s Involved in Payroll Processing and Year-End Compliance... 1 Checklist for Year-End 2011... 2-3 Looking

Terms. Write down as many payroll terms or payroll taxes that you can think of in 2 minutes. Ready, Set, Go!

Payroll Unit Terms Write down as many payroll terms or payroll taxes that you can think of in 2 minutes. Ready, Set, Go! Payroll Pay Periods Weekly 52 checks a year Biweekly 26 checks a year, every other

Payroll Unit Terms Write down as many payroll terms or payroll taxes that you can think of in 2 minutes. Ready, Set, Go! Payroll Pay Periods Weekly 52 checks a year Biweekly 26 checks a year, every other

The. Easiest Way. to Pay Your. Federal. Taxes. for Individual Taxpayers

The Easiest Way to Pay Your Federal Taxes for Individual Taxpayers Welcome to the Electronic Federal Tax Payment System EFTPS EFTPS is a system provided free by the U.S. Department of the Treasury that

The Easiest Way to Pay Your Federal Taxes for Individual Taxpayers Welcome to the Electronic Federal Tax Payment System EFTPS EFTPS is a system provided free by the U.S. Department of the Treasury that

BY BROTHERHOOD MUTUAL A STRESS-FREE PROCEDURAL GUIDE. End-of-Year Payroll, Simplified 1

BY BROTHERHOOD MUTUAL BY BROTHERHOOD MUTUAL End-of-Year Payroll, Simplified A STRESS-FREE PROCEDURAL GUIDE End-of-Year Payroll, Simplified 1 Welcome to End-of-Year Payroll, Simplified The key to successfully

BY BROTHERHOOD MUTUAL BY BROTHERHOOD MUTUAL End-of-Year Payroll, Simplified A STRESS-FREE PROCEDURAL GUIDE End-of-Year Payroll, Simplified 1 Welcome to End-of-Year Payroll, Simplified The key to successfully

BOLES METZGER BROSIUS & WALBORN PC CERTIFIED PUBLIC ACCOUNTANTS AND CONSULTANTS

BOLES METZGER BROSIUS & WALBORN PC CERTIFIED PUBLIC ACCOUNTANTS AND CONSULTANTS 3601 N. FRONT STREET HARRISBURG, PA 17110 PHONE: (717) 238-0446 FAX: (717) 238-3960 www.bmbwcpa.com WILLIAM B. BOLES, CPA/ABV,

BOLES METZGER BROSIUS & WALBORN PC CERTIFIED PUBLIC ACCOUNTANTS AND CONSULTANTS 3601 N. FRONT STREET HARRISBURG, PA 17110 PHONE: (717) 238-0446 FAX: (717) 238-3960 www.bmbwcpa.com WILLIAM B. BOLES, CPA/ABV,

Accounting for Payroll: Employer Taxes and Reports

Ch.12 Accounting for Payroll: Employer Taxes and Reports o Calculate Employer s Payroll Taxes o Record Employer s Payroll Taxes o Forms 8109 & 941 o Form 940 o Forms W-2 & W-3 o Account For Workers Compensation

Ch.12 Accounting for Payroll: Employer Taxes and Reports o Calculate Employer s Payroll Taxes o Record Employer s Payroll Taxes o Forms 8109 & 941 o Form 940 o Forms W-2 & W-3 o Account For Workers Compensation

SECTION 8: Employer Identification Numbers (EIN) Employer Identification Number (EIN) Cont

Employer Identification Number (EIN) Cont") SECTION 8: Depositing and Reporting Withheld Taxes 1 Employer Identification Numbers (EIN) All employers are assigned an Employer Identification Number (EIN) to ensure that all payments are credited to

SECTION 8: Depositing and Reporting Withheld Taxes 1 Employer Identification Numbers (EIN) All employers are assigned an Employer Identification Number (EIN) to ensure that all payments are credited to

IRS FORM 941. Instructions: Select any any line or box for IRS instructions and QuickBooks information and troubleshooting steps.

IRS FORM 941 Instructions: Select any any line or box for IRS instructions and QuickBooks information and troubleshooting steps. Select to get back to the main form. For more information see: Form 941:

IRS FORM 941 Instructions: Select any any line or box for IRS instructions and QuickBooks information and troubleshooting steps. Select to get back to the main form. For more information see: Form 941:

2013 Year End Customer Guide

November 2013 Wells Fargo Business Payroll Services 2013 Year End Customer Guide 2013 Wells Fargo Bank N.A. All rights reserved. Member FDIC. Welcome to the 2013 year-end customer guide The 2013 year-end

November 2013 Wells Fargo Business Payroll Services 2013 Year End Customer Guide 2013 Wells Fargo Bank N.A. All rights reserved. Member FDIC. Welcome to the 2013 year-end customer guide The 2013 year-end

IRS FORM 944. Instructions: Select any any line or box for IRS instructions and QuickBooks information and troubleshooting steps.

IRS FORM 944 Instructions: Select any any line or box for IRS instructions and QuickBooks information and troubleshooting steps. Select to get back to the main form. For more information see: Form 944:

IRS FORM 944 Instructions: Select any any line or box for IRS instructions and QuickBooks information and troubleshooting steps. Select to get back to the main form. For more information see: Form 944:

2008 Tax Rates and Information Bulletin

Albin, Randall & Bennett, CPAs 2008 Tax Rates and Information Bulletin 06/08 2008 TAX UPDATE BULLETIN TABLE OF CONTENTS Topic Page Number Payroll Withholding Rates and Limits...1 Backup Withholding...2

Albin, Randall & Bennett, CPAs 2008 Tax Rates and Information Bulletin 06/08 2008 TAX UPDATE BULLETIN TABLE OF CONTENTS Topic Page Number Payroll Withholding Rates and Limits...1 Backup Withholding...2

Chapter 13 Payroll Accounting, Taxes, and Reports

Chapter 13 Payroll Accounting, Taxes, and Reports -- The payroll register and employee earnings records provide all the payroll information needed to prepare a payroll and payroll tax reports. Journal

Chapter 13 Payroll Accounting, Taxes, and Reports -- The payroll register and employee earnings records provide all the payroll information needed to prepare a payroll and payroll tax reports. Journal

Minnesota Income Tax Withholding

2010 Minnesota Income Tax Withholding Instruction Booklet and Tax Tables Start using this booklet January 1, 2010 Contents Fact sheets...2 Directory... 2 What s new... 3 Register for a Minnesota tax ID

2010 Minnesota Income Tax Withholding Instruction Booklet and Tax Tables Start using this booklet January 1, 2010 Contents Fact sheets...2 Directory... 2 What s new... 3 Register for a Minnesota tax ID

AS EASY AS E F T P S. Paying with EFTPS Online. Enrolling in EFTPS Online. For more information, go to

AS EASY AS 1-2 - 3 Enrolling in EFTPS Online 1. Locate Your Taxpayer Identification Number (Employer Identification Number or Social Security Number). Your financial institution routing and account numbers.

AS EASY AS 1-2 - 3 Enrolling in EFTPS Online 1. Locate Your Taxpayer Identification Number (Employer Identification Number or Social Security Number). Your financial institution routing and account numbers.

CLIENT START-UP CHECKLIST

CLIENT START-UP CHECKLIST Adding clients to PayCycle is easy. The initial step is to organize all the necessary client information so it s ready to enter into PayCycle. Please note that you will need to

CLIENT START-UP CHECKLIST Adding clients to PayCycle is easy. The initial step is to organize all the necessary client information so it s ready to enter into PayCycle. Please note that you will need to

2017 Year-End Tax Memo

2017 Year-End Tax Memo An Annual Publication of Large & Gilbert, Inc. January 2018 Large & Gilbert, Inc., is a full service CPA firm specializing in Accounting, Tax, Consulting, Business Advisory, Wealth

2017 Year-End Tax Memo An Annual Publication of Large & Gilbert, Inc. January 2018 Large & Gilbert, Inc., is a full service CPA firm specializing in Accounting, Tax, Consulting, Business Advisory, Wealth

MEMO #3. Tax and Reporting Procedures for Congregations. Pensions and Benefits USA. Caution! Determine employee classifications accurately.

MEMO #3 Tax and Reporting Procedures for Congregations Pensions and Benefits USA The tax and reporting requirements with which churches must comply often seem to complicate the task of the local church

MEMO #3 Tax and Reporting Procedures for Congregations Pensions and Benefits USA The tax and reporting requirements with which churches must comply often seem to complicate the task of the local church

YEAR-END UPDATE FOR PAYROLL AND RELATED TAXES WITH ADDITIONAL INFORMATION FOR INDIVIDUALS

YEAR-END UPDATE FOR PAYROLL AND RELATED TAXES WITH ADDITIONAL INFORMATION FOR INDIVIDUALS JANUARY 2011 This memo provides information that is useful in the annual preparation of employment related forms

YEAR-END UPDATE FOR PAYROLL AND RELATED TAXES WITH ADDITIONAL INFORMATION FOR INDIVIDUALS JANUARY 2011 This memo provides information that is useful in the annual preparation of employment related forms

An Employer s Guide To Payroll

An Employer s Guide To Payroll Solutions That Save You Time www.timeplus.com Table of Contents NEW BUSINESS CHECKLIST...2 EMPLOYER IDENTIFICATION NUMBER...3 TELE-TIN...4 FAIR LABOR STANDARDS ACT...4 Wage

An Employer s Guide To Payroll Solutions That Save You Time www.timeplus.com Table of Contents NEW BUSINESS CHECKLIST...2 EMPLOYER IDENTIFICATION NUMBER...3 TELE-TIN...4 FAIR LABOR STANDARDS ACT...4 Wage

2016 Year End Guide. Dear Valued Payroll Dynamics Client,

2016 Year End Guide Dear Valued Payroll Dynamics Client, The end of 2016 is approaching! Payroll Dynamics knows that our clients rely on us to guide them through the complexities of year-end payroll and

2016 Year End Guide Dear Valued Payroll Dynamics Client, The end of 2016 is approaching! Payroll Dynamics knows that our clients rely on us to guide them through the complexities of year-end payroll and

4 - Reporting Wages & Contributions

Illinois Municipal Retirement Fund Reporting Wages & Contributions / SECTION 4 4 - Reporting Wages & Contributions REPORTING WAGES & CONTRIBUTIONS... 119 4.00 INTRODUCTION... 119 4.10 GENERAL EXPLANATIONS...

Illinois Municipal Retirement Fund Reporting Wages & Contributions / SECTION 4 4 - Reporting Wages & Contributions REPORTING WAGES & CONTRIBUTIONS... 119 4.00 INTRODUCTION... 119 4.10 GENERAL EXPLANATIONS...

Chapter 1: Payroll Fundamentals Challenges Concepts

Table of Chapter 1: Payroll Fundamentals.... 1-1 1.1 Challenges... 1-1 1.2 Concepts.... 1-2 1.2.1 Employees vs. Independent Contractors...1-3 1.2.2 Common Law and Reasonable Basis Tests...1-4 1.2.3 Temporary

Table of Chapter 1: Payroll Fundamentals.... 1-1 1.1 Challenges... 1-1 1.2 Concepts.... 1-2 1.2.1 Employees vs. Independent Contractors...1-3 1.2.2 Common Law and Reasonable Basis Tests...1-4 1.2.3 Temporary

Chapter 11 Payroll Taxes, Deposits, and Reports

Chapter 11 - Payroll Taxes, Deposits, and Reports Chapter 11 Payroll Taxes, Deposits, and Reports TEACHING OBJECTIVES 11-1) Explain how and when payroll taxes are paid to the government. 11-2) Compute

Chapter 11 - Payroll Taxes, Deposits, and Reports Chapter 11 Payroll Taxes, Deposits, and Reports TEACHING OBJECTIVES 11-1) Explain how and when payroll taxes are paid to the government. 11-2) Compute

IRS FORM 940. Instructions: Select any any line or box for IRS instructions and QuickBooks information and troubleshooting steps.

IRS FORM 940 Instructions: Select any any line or box for IRS instructions and QuickBooks information and troubleshooting steps. Select to get back to the main form. For more information see: Form 940:

IRS FORM 940 Instructions: Select any any line or box for IRS instructions and QuickBooks information and troubleshooting steps. Select to get back to the main form. For more information see: Form 940:

2017 Year-end OptRight Customer Guide

October 2017 Business Payroll Services 2017 Year-end OptRight Customer Guide 2017 Wells Fargo Bank N.A. All rights reserved. Member FDIC. Making it easier to prepare for your year-end payroll needs This

October 2017 Business Payroll Services 2017 Year-end OptRight Customer Guide 2017 Wells Fargo Bank N.A. All rights reserved. Member FDIC. Making it easier to prepare for your year-end payroll needs This

Instructions for Form 941 (Rev. April 2005)

") Instructions for Form 941 (Rev. April 2005) For use with Form 941 (Rev. January 2005) Employer s Quarterly Federal Tax Return Section references are to the Internal Revenue Code unless otherwise indicated.

Instructions for Form 941 (Rev. April 2005) For use with Form 941 (Rev. January 2005) Employer s Quarterly Federal Tax Return Section references are to the Internal Revenue Code unless otherwise indicated.

SECTION 8: Depositing and Reporting Withheld Taxes

SECTION 8: Depositing and Reporting Withheld Taxes 1 Employer Identification Numbers (EIN) All employers are assigned an Employer Identification Number (EIN) The EIN is a nine-digit number, expressed as

SECTION 8: Depositing and Reporting Withheld Taxes 1 Employer Identification Numbers (EIN) All employers are assigned an Employer Identification Number (EIN) The EIN is a nine-digit number, expressed as

LESSON 3-1. Completing Payroll Records for Employee Earnings and Deductions. CENTURY 21 ACCOUNTING 2009 South-Western, Cengage Learning

LESSON 3-1 Completing Payroll Records for Employee Earnings and Deductions 2 Payroll Deductions pages 60-61 Salary money paid for employee services Pay period period covered by a salary payment Payroll

LESSON 3-1 Completing Payroll Records for Employee Earnings and Deductions 2 Payroll Deductions pages 60-61 Salary money paid for employee services Pay period period covered by a salary payment Payroll

This is a list of items you should gather for the Income Tax Preparation

This is a list of items you should gather for the Income Tax Preparation 1. Social Security Card(s) - Your Social Security number, which is your taxpayer identification number, is printed on your Social

This is a list of items you should gather for the Income Tax Preparation 1. Social Security Card(s) - Your Social Security number, which is your taxpayer identification number, is printed on your Social

Preparation for a Successful Payroll Year end. Presented by: Jean Domaingue, CPP

Preparation for a Successful Payroll Year end Presented by: Jean Domaingue, CPP November 15, 2012 CompuPay is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor

Preparation for a Successful Payroll Year end Presented by: Jean Domaingue, CPP November 15, 2012 CompuPay is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor

In the United States today, GTM Payroll Services estimates that there are

224 10 Managing Payroll and Taxes In the United States today, GTM Payroll Services estimates that there are more than two million household employees. Exact figures on household help are difficult to obtain.

224 10 Managing Payroll and Taxes In the United States today, GTM Payroll Services estimates that there are more than two million household employees. Exact figures on household help are difficult to obtain.

Overview. How many Town Accountant's come across payroll issues?

Eric Kinsherf, CPA Introduction There are a variety of payroll related issues that are encountered by the Town Accountant The Town Accountant's role in the payroll is shared with the Treasurer Town Accountant

Eric Kinsherf, CPA Introduction There are a variety of payroll related issues that are encountered by the Town Accountant The Town Accountant's role in the payroll is shared with the Treasurer Town Accountant

Instructions for Form 941

Instructions for Form 941 (Rev. October 2007) For use with Form 941 (Rev. January 2007) Employer s QUARTERLY Federal Tax Return What s New Department of the Treasury Internal Revenue Service 941TeleFile

Instructions for Form 941 (Rev. October 2007) For use with Form 941 (Rev. January 2007) Employer s QUARTERLY Federal Tax Return What s New Department of the Treasury Internal Revenue Service 941TeleFile

January 7, Medicare Rate 1.45% [.0145]* 1.45% [.0145] Maximum wage NO MAXIMUM NO MAXIMUM Maximum withholding NO MAXIMUM NO MAXIMUM

![January 7, Medicare Rate 1.45% [.0145]* 1.45% [.0145] Maximum wage NO MAXIMUM NO MAXIMUM Maximum withholding NO MAXIMUM NO MAXIMUM](/thumbs/93/112509111.jpg "January 7, Medicare Rate 1.45% [.0145]* 1.45% [.0145] Maximum wage NO MAXIMUM NO MAXIMUM Maximum withholding NO MAXIMUM NO MAXIMUM") January 7, 2019 Dear Client: We want to take this opportunity to thank you for your continued support of our firm. As we move forward to 2019, we want to update you on relevant changes to payroll and general

January 7, 2019 Dear Client: We want to take this opportunity to thank you for your continued support of our firm. As we move forward to 2019, we want to update you on relevant changes to payroll and general

Virginia Department of Taxation

Virginia Department of Taxation 2013 Legislative Update 1 Agenda Tips and Tools for Preparers Income Tax Legislation Tax Credits Business Tax Changes Administrative Changes Other Issues Late Payment Penalty

Virginia Department of Taxation 2013 Legislative Update 1 Agenda Tips and Tools for Preparers Income Tax Legislation Tax Credits Business Tax Changes Administrative Changes Other Issues Late Payment Penalty

Table of Contents DISCLAIMER

Table of Contents Welcome... 3 What Do You Know? Tax Planning and Reporting for a Small Business... 4 Pre-Test... 5 Tax Obligation Management... 6 Business Taxes... 6 Federal Income Tax Forms... 7 Discussion

Table of Contents Welcome... 3 What Do You Know? Tax Planning and Reporting for a Small Business... 4 Pre-Test... 5 Tax Obligation Management... 6 Business Taxes... 6 Federal Income Tax Forms... 7 Discussion

January 3, Medicare Rate 1.45% [.0145]* 1.45% [.0145] Maximum wage NO MAXIMUM NO MAXIMUM Maximum withholding NO MAXIMUM NO MAXIMUM

![January 3, Medicare Rate 1.45% [.0145]* 1.45% [.0145] Maximum wage NO MAXIMUM NO MAXIMUM Maximum withholding NO MAXIMUM NO MAXIMUM](/thumbs/74/69630893.jpg "January 3, Medicare Rate 1.45% [.0145]* 1.45% [.0145] Maximum wage NO MAXIMUM NO MAXIMUM Maximum withholding NO MAXIMUM NO MAXIMUM") January 3, 2017 Dear Client: We want to take this opportunity to thank you for your continued support of our firm. As we move forward to 2017, we want to update you on relevant changes to payroll and general

January 3, 2017 Dear Client: We want to take this opportunity to thank you for your continued support of our firm. As we move forward to 2017, we want to update you on relevant changes to payroll and general

Year End. Guide. At Your Service

Year End 2017 Guide Precision Payroll of America (PPA) would like to take this opportunity to thank you for your business and to wish you a happy holiday season and a prosperous New Year. Please review

Year End 2017 Guide Precision Payroll of America (PPA) would like to take this opportunity to thank you for your business and to wish you a happy holiday season and a prosperous New Year. Please review

We hope the following summarized payroll, sales tax and form 1099 information will be helpful to you in the coming New Year.

Dear Client: We hope the following summarized payroll, sales tax and form 1099 information will be helpful to you in the coming New Year. Rates and Limits For 2017 FEDERAL PAYROLL TAXES FICA- The Social

Dear Client: We hope the following summarized payroll, sales tax and form 1099 information will be helpful to you in the coming New Year. Rates and Limits For 2017 FEDERAL PAYROLL TAXES FICA- The Social

2014 Year End Newsletter

2014 Year End Newsletter Dear Client: Please read this year-end newsletter carefully and keep it available for reference. It contains important information to help you prepare and plan for the busy months

2014 Year End Newsletter Dear Client: Please read this year-end newsletter carefully and keep it available for reference. It contains important information to help you prepare and plan for the busy months

Form 941/C1-ME. Questions regarding: Important

State of Maine Maine Revenue Services and Department of Labor 2001 Combined Filing for Income Tax Withholding and Unemployment Contributions Form 941/C1-ME Questions regarding: Income Tax Withholding 207-626-8475

State of Maine Maine Revenue Services and Department of Labor 2001 Combined Filing for Income Tax Withholding and Unemployment Contributions Form 941/C1-ME Questions regarding: Income Tax Withholding 207-626-8475

Payroll Quarterly Reporting Connecticut

Table of Contents 1-1: Federal End of Quarter Report Options... 2 1-2: Federal End of Quarter Report 941 PDF... 3 1-3: Filing Deadlines & Address Information... 7 1-4: End of Quarter Report CT-941... 8

Table of Contents 1-1: Federal End of Quarter Report Options... 2 1-2: Federal End of Quarter Report 941 PDF... 3 1-3: Filing Deadlines & Address Information... 7 1-4: End of Quarter Report CT-941... 8

MISSOURI INTERGOVERNMENTAL RISK MANAGEMENT ASSOCIATION PAYROLL VERIFICATION PROGRAM

MISSOURI INTERGOVERNMENTAL RISK MANAGEMENT ASSOCIATION PAYROLL VERIFICATION PROGRAM Verification of reported member city payrolls is vital to the financial integrity of the association. As set forth under

MISSOURI INTERGOVERNMENTAL RISK MANAGEMENT ASSOCIATION PAYROLL VERIFICATION PROGRAM Verification of reported member city payrolls is vital to the financial integrity of the association. As set forth under

Employment Tax Laws LAUSD Small Business Boot Camp. v15a

Employment Tax Laws LAUSD Small Business Boot Camp v15a Presenters Jimmy Wong Employment Development Department (EDD) Taxpayer Assistance Center 1-888-745-3886 / www.edd.ca.gov Anthony Sykes Internal Revenue

Employment Tax Laws LAUSD Small Business Boot Camp v15a Presenters Jimmy Wong Employment Development Department (EDD) Taxpayer Assistance Center 1-888-745-3886 / www.edd.ca.gov Anthony Sykes Internal Revenue

Oregon Domestic Combined Payroll. Tax Report. Oregon Department of Revenue

Oregon Domestic Combined Payroll 2013 Tax Report Oregon Department of Revenue Oregon Employment Department Oregon Department of Consumer & Business Services Forms and Instructions For Oregon Domestic Employers

Oregon Domestic Combined Payroll 2013 Tax Report Oregon Department of Revenue Oregon Employment Department Oregon Department of Consumer & Business Services Forms and Instructions For Oregon Domestic Employers

EMPLOYMENT TAXES UNDERSTANDING AND PAYING PAYROLL TAXES

EMPLOYMENT TAXES UNDERSTANDING AND PAYING PAYROLL TAXES 2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 Understanding and Paying Payroll Taxes

EMPLOYMENT TAXES UNDERSTANDING AND PAYING PAYROLL TAXES 2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 Understanding and Paying Payroll Taxes

Instructions for Form 941

Instructions for Form 941 (Rev. February 2010) Employer s QUARTERLY Federal Tax Return Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise

Instructions for Form 941 (Rev. February 2010) Employer s QUARTERLY Federal Tax Return Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise

Federal Reporting Requirements for Churches

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, CHURCH LAW & TAX REPORT Copyright 2013 Christianity Today International. Federal Reporting Requirements

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, CHURCH LAW & TAX REPORT Copyright 2013 Christianity Today International. Federal Reporting Requirements

TAX DEPARTMENT ACCOUNTING DEPARTMENT ADMINISTRATIVE

January 2015 Dear Business Client, This annual client letter has been prepared to inform you of business rules and regulations, both old and new, that may apply to your business and to provide new 2015

January 2015 Dear Business Client, This annual client letter has been prepared to inform you of business rules and regulations, both old and new, that may apply to your business and to provide new 2015

Enclosed you will find the following information to help you prepare for year-end 2018:

Product Guide Dear Valued Deluxe Payroll Client, This guide has been designed to assist our clients through the year-end process and to meet critical deadlines. Our goal is to ensure an accurate and timely

Product Guide Dear Valued Deluxe Payroll Client, This guide has been designed to assist our clients through the year-end process and to meet critical deadlines. Our goal is to ensure an accurate and timely

Paying and Reporting Form 941 Quarterly T ax

Paying and Reporting Form 941 Quarterly T ax This guide will walk you through: Documenting tax payments in WinStabs Making tax payments through EFTPS Filing 941 tax return with the IRS Who must file Form

Paying and Reporting Form 941 Quarterly T ax This guide will walk you through: Documenting tax payments in WinStabs Making tax payments through EFTPS Filing 941 tax return with the IRS Who must file Form

2018 Year-end Processing Guide. Lancaster, Pennsylvania 1858 Charter Ln Ste 201 Lancaster, PA

2018 Year-end Processing Guide Nashville, Tennessee 636 Grassmere Park Ste 110 Nashville, TN 37211 615.921.0600 Chattanooga, Tennessee 5720 Skurlock Rd Ste 8600 Chattanooga, TN 37411 423.499.5478 Knoxville,

2018 Year-end Processing Guide Nashville, Tennessee 636 Grassmere Park Ste 110 Nashville, TN 37211 615.921.0600 Chattanooga, Tennessee 5720 Skurlock Rd Ste 8600 Chattanooga, TN 37411 423.499.5478 Knoxville,

Guide to Taxation of Employee Disability Benefits

Guide to Taxation of Employee Disability Benefits STANDARD INSURANCE COMPANY Guide to Taxation of Employee Disability Benefits Standard Insurance Company (The Standard) developed this guide to help you

Guide to Taxation of Employee Disability Benefits STANDARD INSURANCE COMPANY Guide to Taxation of Employee Disability Benefits Standard Insurance Company (The Standard) developed this guide to help you

2018 Paychex Reference Guide for Accountants

2018 Paychex Reference Guide for Accountants Paychex Promise There are too many what if moments that can disrupt your clients business. The Paychex Promise helps assure that covering payroll will never

2018 Paychex Reference Guide for Accountants Paychex Promise There are too many what if moments that can disrupt your clients business. The Paychex Promise helps assure that covering payroll will never

American Payroll Association

Chapter 9 Employer Taxes, Payments, and Reports American Payroll Association Professional association for over 22,000 payroll professionals Provides National Payroll Week Survey Training, certification,

Chapter 9 Employer Taxes, Payments, and Reports American Payroll Association Professional association for over 22,000 payroll professionals Provides National Payroll Week Survey Training, certification,

Payroll Management Edition. Steven M. Bragg

Payroll Management 2018 Edition Steven M. Bragg Chapter 1 Payroll Management... 1 Learning Objectives... 1 Introduction... 1 Payroll Cycle Duration... 1 Streamlined Timekeeping... 3 Electronic Payments...

Payroll Management 2018 Edition Steven M. Bragg Chapter 1 Payroll Management... 1 Learning Objectives... 1 Introduction... 1 Payroll Cycle Duration... 1 Streamlined Timekeeping... 3 Electronic Payments...

The guidelines do not replace existing law, regulations, forms or publications.

4/5/2005 WITHHOLDING TAX FIELD AUDIT GUIDELINES Page 1 I. INTRODUCTION These guidelines have been established to ensure uniformity and consistency in examination of withholding tax records. The procedures

4/5/2005 WITHHOLDING TAX FIELD AUDIT GUIDELINES Page 1 I. INTRODUCTION These guidelines have been established to ensure uniformity and consistency in examination of withholding tax records. The procedures

JANUARY 2017 EMPLOYEE OR INDEPENDENT CONTRACTOR

JANUARY 2017 GUIDELINES TO OBLIGATIONS OF BRANCH CHURCHES AND SOCIETIES TO WITHHOLD FEDERAL INCOME AND SOCIAL SECURITY TAXES AND TO REPORT COMPENSATION; AND OTHER INFORMATION EMPLOYEE OR INDEPENDENT CONTRACTOR

JANUARY 2017 GUIDELINES TO OBLIGATIONS OF BRANCH CHURCHES AND SOCIETIES TO WITHHOLD FEDERAL INCOME AND SOCIAL SECURITY TAXES AND TO REPORT COMPENSATION; AND OTHER INFORMATION EMPLOYEE OR INDEPENDENT CONTRACTOR

Chapter 11: Unrelated Business Income

Chapter 11: Unrelated Business Income INTRODUCTION... 100 Definition... 105 Filing Requirements... 110 Public Disclosure of Form 990-T... 111 Examples of Unrelated Business Activities... 115 Royalties

Chapter 11: Unrelated Business Income INTRODUCTION... 100 Definition... 105 Filing Requirements... 110 Public Disclosure of Form 990-T... 111 Examples of Unrelated Business Activities... 115 Royalties

P&B. Memo #3. The tax and reporting requirements with which churches must comply. Tax and Reporting Procedures for Congregations

P&B Memo #3 Pensions and Benefits USA, Church of the Nazarene Tax and Reporting Procedures for Congregations The tax and reporting requirements with which churches must comply often seem to complicate

P&B Memo #3 Pensions and Benefits USA, Church of the Nazarene Tax and Reporting Procedures for Congregations The tax and reporting requirements with which churches must comply often seem to complicate

Federal Reporting Requirements for Churches

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2014 Christianity Today International. Federal Reporting Requirements

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2014 Christianity Today International. Federal Reporting Requirements

WITHHOLDING TABLES MAINE INDIVIDUAL INCOME TAX

WITHHOLDING TABLES MAINE INDIVIDUAL INCOME TAX 2000 Effective January 1, 2000 REMEMBER: A person required to withhold must continue to file quarterly withholding tax returns until the account is canceled,

WITHHOLDING TABLES MAINE INDIVIDUAL INCOME TAX 2000 Effective January 1, 2000 REMEMBER: A person required to withhold must continue to file quarterly withholding tax returns until the account is canceled,

YEAR END GUIDE. TABLE OF CONTENTS Page 2. Page 3. Page 4 Page 5. DATES and Holidays. BEFORE YOUR LAST PAYROLL

YOUR GUIDE TO YEAR END 2013/2014 TABLE OF CONTENTS Page 2 BEFORE YOUR LAST PAYROLL W2 Edit List, Tax Letters Top 5 Items to Review Page 3 BEFORE YOUR FIRST PAYROLL Top 5 Items to Review Page 4 Page 5 2014

YOUR GUIDE TO YEAR END 2013/2014 TABLE OF CONTENTS Page 2 BEFORE YOUR LAST PAYROLL W2 Edit List, Tax Letters Top 5 Items to Review Page 3 BEFORE YOUR FIRST PAYROLL Top 5 Items to Review Page 4 Page 5 2014

Section 6 Withholding Taxes (Student Guide) Table of Contents Introduction

Table of Contents Introduction") Section 6 Withholding Taxes (Student Guide) Table of Contents Introduction... - 2 - Topics from Content Outline... - 2 - The Principle of Actual or Constructive Payment... - 2 - Social Security Numbers...

Section 6 Withholding Taxes (Student Guide) Table of Contents Introduction... - 2 - Topics from Content Outline... - 2 - The Principle of Actual or Constructive Payment... - 2 - Social Security Numbers...

Preparing for 2018: BLUE GUIDE. A Guide for Employers

BLUE GUIDE Preparing for 2018: A Guide for Employers Learn how to take the guesswork out of some of your most important year end payroll and taxation obligations, and organize everything according to this

BLUE GUIDE Preparing for 2018: A Guide for Employers Learn how to take the guesswork out of some of your most important year end payroll and taxation obligations, and organize everything according to this

PPL s Payroll Service- MA DDS Autism Waiver Program

Public Partnerships, LLC (PPL) Agency Payroll Department One Cabot rd. STE 102 Medford, MA 02155 Phone 1-866-315-3740 Admin Fax 1-866-578-0533 TS Fax 1-866-578-0536 STEP ONE - SETTING UP AN EMPLOYER ACCOUNT

Public Partnerships, LLC (PPL) Agency Payroll Department One Cabot rd. STE 102 Medford, MA 02155 Phone 1-866-315-3740 Admin Fax 1-866-578-0533 TS Fax 1-866-578-0536 STEP ONE - SETTING UP AN EMPLOYER ACCOUNT

Introduction FYI - Topics from Content Outline Employers, Wages and Employment Liable for FUTA Employers liable for FUTA...

Section 7 Unemployment Insurance (Student Guide) Table of Contents Introduction... 2 FYI - Topics from Content Outline... 2 Employers, Wages and Employment Liable for FUTA... 3 Employers liable for FUTA...

Section 7 Unemployment Insurance (Student Guide) Table of Contents Introduction... 2 FYI - Topics from Content Outline... 2 Employers, Wages and Employment Liable for FUTA... 3 Employers liable for FUTA...

EMPLOYER INFORMATION SHEET

General EMPLOYER INFORMATION SHEET Business Name: Business Address: City, State, Zip: Filing Name (if different): Filing Address (if different): City, State, Zip: Contact Name: Phone: Fax: Email: Company

General EMPLOYER INFORMATION SHEET Business Name: Business Address: City, State, Zip: Filing Name (if different): Filing Address (if different): City, State, Zip: Contact Name: Phone: Fax: Email: Company

JANUARY 2014 UPDATE ON PAYROLL, EMPLOYMENT TAXES AND INFORMATION RETURNS

JANUARY 2014 UPDATE ON PAYROLL, EMPLOYMENT TAXES AND INFORMATION RETURNS This letter sets forth employee payroll tax withholding rates, employer payroll tax rates in effect for 2014 and some pertinent

JANUARY 2014 UPDATE ON PAYROLL, EMPLOYMENT TAXES AND INFORMATION RETURNS This letter sets forth employee payroll tax withholding rates, employer payroll tax rates in effect for 2014 and some pertinent

Focus on what matters and leave the processing to us. 71 Hanover Road, Florham Park, NJ smallbusiness.adp.com. Retirement Services 401(k) Plan*

Plan*") 71 Hanover Road, Florham Park, NJ 07932 smallbusiness.adp.com Focus on what matters and leave the processing to us. ADP offers additional services that enable you to put your business first, without diverting

71 Hanover Road, Florham Park, NJ 07932 smallbusiness.adp.com Focus on what matters and leave the processing to us. ADP offers additional services that enable you to put your business first, without diverting

Local Section Finances

Local Section Finances Local sections, like the national association, must incur expenses, manage their budgets, pay bills, and deal with tax issues. The following information provides the basic requirements

Local Section Finances Local sections, like the national association, must incur expenses, manage their budgets, pay bills, and deal with tax issues. The following information provides the basic requirements

Payroll Tax Update 2014

Payroll Tax Update 2014 200 Commerce Street Montgomery, AL 36104 334.834.7660 jacksonthornton.com Table of Contents Section Page 1 Payroll Related Filing Requirements New Employee Reporting Requirements

Payroll Tax Update 2014 200 Commerce Street Montgomery, AL 36104 334.834.7660 jacksonthornton.com Table of Contents Section Page 1 Payroll Related Filing Requirements New Employee Reporting Requirements

2013 Newsletter on Form 1099 Reporting

01 Newsletter on Form 1099 Reporting 5656 E. Grant Rd., Suite 00 Tucson, Arizona 8571 50.886.181 IRS Increases Scrutiny Over 1099 Reporting Following the stated guidelines of Form 1099 will help avoid

01 Newsletter on Form 1099 Reporting 5656 E. Grant Rd., Suite 00 Tucson, Arizona 8571 50.886.181 IRS Increases Scrutiny Over 1099 Reporting Following the stated guidelines of Form 1099 will help avoid

2017 Year End Newsletter

2017 Year End Newsletter Dear Client: Please read this year-end newsletter carefully and keep it available for reference. It contains important information to help you prepare and plan for the busy months

2017 Year End Newsletter Dear Client: Please read this year-end newsletter carefully and keep it available for reference. It contains important information to help you prepare and plan for the busy months

Form 1099 Reporting and Backup Withholding Reporting. Tax Law Reporting Changes. Form 1099 General Requirements

Form 1099 Reporting and Backup Withholding Reporting Washington Association of School Business Officials Spring Conference May 10, 2012 Federal, State and Local Government Internal Revenue Service Clark

Form 1099 Reporting and Backup Withholding Reporting Washington Association of School Business Officials Spring Conference May 10, 2012 Federal, State and Local Government Internal Revenue Service Clark

ACCOUNTING POLICIES AND PROCEDURES MANUAL

ACCOUNTING POLICIES AND PROCEDURES MANUAL Accounting Policies and Procedures Manual Page 1 Table of Contents Introduction... 3 Division of Responsibilities... 4 Board of Directors... 4 Executive Director...

ACCOUNTING POLICIES AND PROCEDURES MANUAL Accounting Policies and Procedures Manual Page 1 Table of Contents Introduction... 3 Division of Responsibilities... 4 Board of Directors... 4 Executive Director...

Federal Reporting. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2019 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Click

The Pension Boards United Church of Christ, Inc. 2019 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Click

Payroll Taxes 101. Presented by Larry Holmes

Payroll Taxes 101 Presented by Larry Holmes What is payroll? The total amount of money paid by a business to its employees are payroll taxes? Taxes levied by a government agency on employees wages, tips,

Payroll Taxes 101 Presented by Larry Holmes What is payroll? The total amount of money paid by a business to its employees are payroll taxes? Taxes levied by a government agency on employees wages, tips,

Federal Tax Brackets for Startup Businesses In 2018

Federal Tax Brackets for Startup Businesses In 2018 Federal Income Tax Brackets by Business Type (Single Taxpayer) Type 2017 2018 C CORPORATION Corporate Income Tax 15% - $0 to $50,000 25% - $50,000 to

Federal Tax Brackets for Startup Businesses In 2018 Federal Income Tax Brackets by Business Type (Single Taxpayer) Type 2017 2018 C CORPORATION Corporate Income Tax 15% - $0 to $50,000 25% - $50,000 to

Chapter 6. Paying Taxes Pearson Education, Inc. All rights reserved

Chapter 6 Paying Taxes 2010 Pearson Education, Inc. All rights reserved Learning Objectives Describe the basic principles of taxation and the major categories of taxes. Explain payroll taxes Describe the

Chapter 6 Paying Taxes 2010 Pearson Education, Inc. All rights reserved Learning Objectives Describe the basic principles of taxation and the major categories of taxes. Explain payroll taxes Describe the

THE BUCK STOPS HERE: All about payroll taxes in your Local union.

THE BUCK STOPS HERE: All about payroll taxes in your Local union. Role of the Agencies involved Payroll tax basics How to Manage Payroll Taxes in WinStabs Payroll Tax Workflow Paying and Reporting Guides

THE BUCK STOPS HERE: All about payroll taxes in your Local union. Role of the Agencies involved Payroll tax basics How to Manage Payroll Taxes in WinStabs Payroll Tax Workflow Paying and Reporting Guides

PAYROLL SOURCE TABLE OF CONTENTS

PAYROLL SOURCE TABLE OF CONTENTS SECTION 1: THE EMPLOYER-EMPLOYEE RELATIONSHIP 1.1 Importance of the Determination... 1-2 1.2 Employee vs. Independent Contractor... 1-2 1.2-1 Common Law Test... 1-3 1.2-2

PAYROLL SOURCE TABLE OF CONTENTS SECTION 1: THE EMPLOYER-EMPLOYEE RELATIONSHIP 1.1 Importance of the Determination... 1-2 1.2 Employee vs. Independent Contractor... 1-2 1.2-1 Common Law Test... 1-3 1.2-2

SUMMARY OF 2016 YEAR- END PROCESSING FOR TOPS IQ & TOPS PROFESSIONAL

SUMMARY OF 2016 YEAR- END PROCESSING FOR TOPS IQ & TOPS PROFESSIONAL This document summarizes the steps required to close the books for the calendar year ending December 31, 2016. This procedure will cover

SUMMARY OF 2016 YEAR- END PROCESSING FOR TOPS IQ & TOPS PROFESSIONAL This document summarizes the steps required to close the books for the calendar year ending December 31, 2016. This procedure will cover

Minnesota Income Tax Withholding

2019 Minnesota Income Tax Withholding Instruction Booklet and Tax Tables Start using this booklet Jan. 1, 2019 Inside This Booklet Forms and Fact Sheets.... 2 Directory.... 2 Free Business Tax Workshops...

2019 Minnesota Income Tax Withholding Instruction Booklet and Tax Tables Start using this booklet Jan. 1, 2019 Inside This Booklet Forms and Fact Sheets.... 2 Directory.... 2 Free Business Tax Workshops...

FAST TRACK TAX FACTS UNEMPLOYMENT INSURANCE TAX AND COMBINED REPORTING

FAST TRACK TAX FACTS UNEMPLOYMENT INSURANCE TAX AND COMBINED REPORTING Next Back Main Menu Coverage Requirements Combined Registration Change in Status Exclusions from Coverage Reporting Requirements &

FAST TRACK TAX FACTS UNEMPLOYMENT INSURANCE TAX AND COMBINED REPORTING Next Back Main Menu Coverage Requirements Combined Registration Change in Status Exclusions from Coverage Reporting Requirements &

City of Detroit City of Detroit. Forms and Instructions. Filing Due Date: April 18, 2016

City of Detroit 2015 City of Detroit aa aa Income Tax Returns Forms and Instructions Starting with tax year 2015, the Michigan Department of Treasury will begin processing City of Detroit Individual Income

City of Detroit 2015 City of Detroit aa aa Income Tax Returns Forms and Instructions Starting with tax year 2015, the Michigan Department of Treasury will begin processing City of Detroit Individual Income

Small Business Tax Saving Strategies for the 2012 Filing Season

Small Business Tax Saving Strategies for the 2012 Filing Season Few business sectors embody today s entrepreneurial spirit, drive for innovation and unwavering perseverance more than the small business

Small Business Tax Saving Strategies for the 2012 Filing Season Few business sectors embody today s entrepreneurial spirit, drive for innovation and unwavering perseverance more than the small business

Maine Revenue Services Withholding Tables for Individual Income Tax

Maine Revenue Services Withholding Tables for Individual Income Tax The tables in this book have been adjusted for inf ation. 2008 Make Electronic Withholding Payments at www.maine.gov/revenue Income Tax

Maine Revenue Services Withholding Tables for Individual Income Tax The tables in this book have been adjusted for inf ation. 2008 Make Electronic Withholding Payments at www.maine.gov/revenue Income Tax