Advance Pricing Agreements (APA)

|

|

|

- Rolf Lambert

- 6 years ago

- Views:

Transcription

A")

1 Advance Pricing Agreements (APA) A welcome step in transfer pricing disputes Edition

2 Contents: Introduction What is APA? Different types of APA International scenario Key benefits of APA Overview of APA process Pre-filing consultation Application for APA Preliminary processing and procedure Annual Compliance Report Withdrawal/ cancellation of application Renewal/ revision of APA Rollback provision Safe Harbour Rules 2

3 Introduction In an environment where the government has been trying to attract multinational enterprises to Make in India, it is time to introduce initiatives or measures to signal a clear focus on making doing business in India easier. One such initiative has been the introduction of APA programme. Tax authorities in India have become increasingly proactive and vigilant while scrutinizing multinational company transfer pricing with Indian affiliates and correspondingly increasing the intensity of audits. The domestic appeal and dispute resolution process in India is slow and very time consuming. Therefore, the need for an alternative dispute resolution mechanism such as the Advance Pricing Agreement (APA) program, which provides a proactive opportunity for taxpayers to not only prevent future tax controversies but also to provide a rational basis for settling past disputes where an APA outcome may have a significant persuasive value. Advance Pricing Agreement (APA) provisions were introduced in the Income-tax Act, 1961 (Act) w.e.f. 1 July The rules in respect of the APA scheme have been notified by the Central Board of Direct Taxes (CBDT) by way of insertion of Rule 10F to Rule 10T and Rule 44GA in the Income-tax Rules, 1962 (Rules). The various aspects of rules/ guidelines governing APA and certain operational matters relating to APA are analysed below: 3

4 What is an Advance Pricing Agreement (APA)? An APA is an agreement between a tax payer and tax authority determining the transfer pricing methodology for pricing the tax payer s international transactions with its associated enterprises (AE s) for future years. The methodology is to be applied for a certain period of time based on the fulfillment of certain terms and conditions. These programmes are designed to help taxpayers voluntarily resolve actual or potential transfer pricing disputes in a proactive, cooperative manner, as an alternative to the traditional examination process. An APA offers a company several other benefits. It provides greater certainty on the transfer pricing method adopted, mitigating the possibility of disputes and facilitating the financial reporting of potential tax liabilities. Importantly, an APA also reduces the incidence of double taxation, and the costs associated with both audit defense and documentation preparation. An APA defines the arm s length price for a covered transaction. It is binding on the person in whose case the agreement has been entered into and on the Commissioner and the income-tax authorities subordinate to him [Direct Taxes Code (the DTC, Sec. 118(5)] unless there is a change in law or facts relating to the agreement. At present, a parallel mechanism exists i.e. advance rulings from the Authority for Advance Rulings (AAR). AAR is empowered to examine a prospective contract of a resident taxpayer with a non-resident in order to determine the taxability thereof. The main difference is that under the APA scheme, the tax authorities may determine/quantify the value of the international transaction or profits, whereas the Authority for Advance Rulings does not have a power to do so. In India, the Board limits the term of an APA to five years (DTC, Sec. 118(4)), as in China (3-5 years; (Implementation Measures of Special Tax Adjustments (Trial Version)[ the IMSTA ], Chapter 6, Article 49), rather than establish an expected minimum term, as in the United States (5 years; Revenue Procedure [the RP ], Sec. 4.07). Flexibility in the number of years may be a particularly important feature at the launch of an APA program, as APAs with long terms are sometimes necessary to accommodate a business cycle for a particular taxpayer, or for other reasons. 4

5 What are the different types of APAs? An APA can be unilateral, bilateral, or multilateral. Unilateral APA: an APA that involves only the tax payer and the tax authority of the country where the tax payer is located. Bilateral APA (BAPA): an APA that involves the tax payer, associated enterprise (AE) of the tax payer in the foreign country, tax authority of the country where the tax payer is located, and the foreign tax authority. Multilateral APA (MAPA): an APA that involves the tax payer, two or more AEs of the tax payer in different foreign countries, tax authority of the country where the tax payer is located, and the tax authorities of AEs. Some areas of prolific transfer pricing disputes where APA is likely to be useful: Business restructuring transactions Captive intra-group services Payments for use in intellectual property Agency services or commission agents Sales supply chain structures Procurement services and sales support services Limited risk distributors Allocation of headquarter and management fee Financial transactions such as loans and guarantees Commodity trading Low margin companies with significant inter-company transactions Contract manufacturing 5

6 International Scenario Country Year of introduction Type of APA Term of agreement Pre-filing Japan 1987 Unilateral & Bilateral 3-5 years Optional USA 1991 Unilateral, Bilateral & Multilateral 3-5 years Mandatory UK 1999 Unilateral, Bilateral (No distinction in bi and multilateral 18 to 21 months Optional China 2004 Unilateral, Bilateral & Multilateral 3-5 years Mandatory India 2012 Unilateral, Bilateral & Multilateral Upto 5 years Mandatory 6

7 What are the key benefits of APA? An APA provides the following benefits: Certainty with respect to tax outcome of the tax payer s international transactions, by agreeing in advance the arm s length pricing or pricing methodology(ies) to be applied to the tax payer s international transactions covered by the APA; Substantial reduction of compliance costs over the term of the APA; and For tax authorities, an APA reduces cost of administration and also frees scarce resources. Consequently, APAs provide a win-win situation for all the stakeholders involved. Removal of an audit threat (minimize rigours of audit), and deliverance of a particular tax outcome based on the terms of the agreement. Who is eligible to file for an APA? Any tax payer who has undertaken an international transaction or is contemplating to undertake an international transaction is eligible to file for an APA. Do the APA rules prescribe any criteria for accepting an APA? There are no monetary limits or other prescribed criteria for a tax payer to be eligible for applying for an APA. Can tax payers opt to cover some of the several international transactions in an APA? Yes, the taxpayers have the option covering all or some of the international transactions in an APA. 7

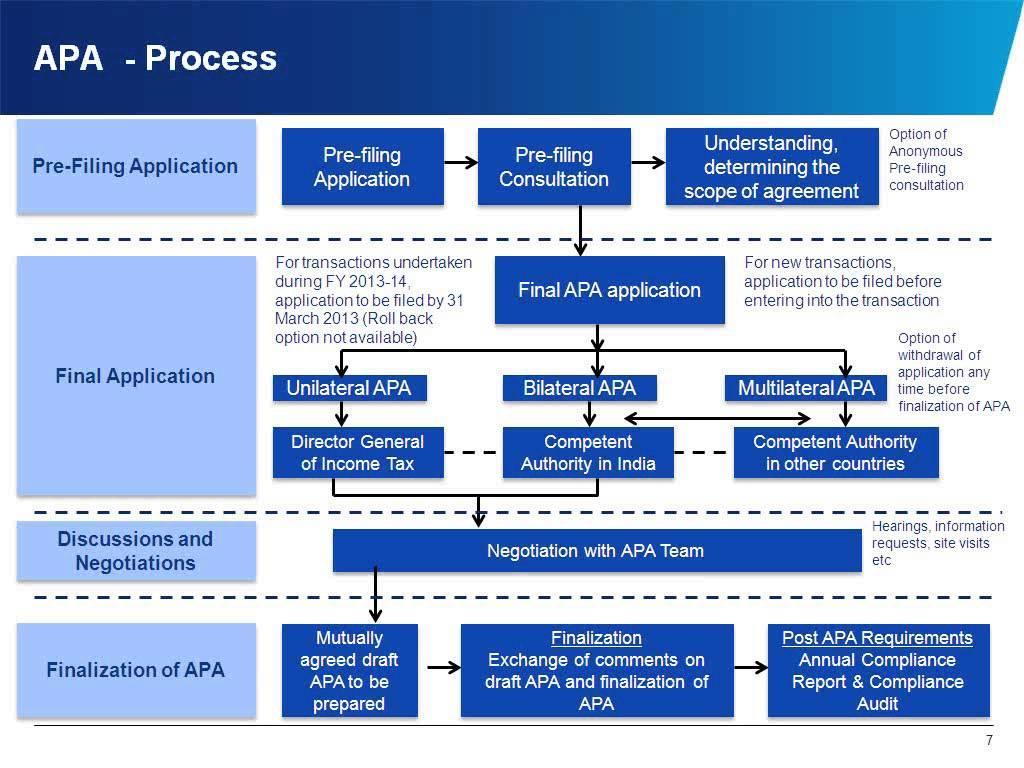

8 APA Process- An Overview Pre-filing APA request/ application Evaluation and negotiation- agreement Execution and monitoring Strategy develop ment Unilateral vs bilateral Rollback evaluatio n Optional pre-filing meeting Business overview and proposed internatio nal transacti on Industry overview Supply chain overview FAR analysis Economic analysis proposed terms processin g of applicatio n Field work Further documen ts and informati on Governm ent-togovernm ent process Critical assumpti ons Drafting and concludin g APAs Annual complian ce report, recordkeeping Complian ce audit Revision or cancellati on Renewal 8

9 9

10 Pre-filing consultation The APA Rules provide for a preliminary consultation before formally lodging an APA application. In such consultation, the tax payer and the APA team will discuss and clarify the scope of the APA, the transfer pricing issues involved and whether an APA can be executed or not. The pre-filing consultation is mandatory, and specified information has to be filed as part of the pre-filing application to Director General of Income Tax (DGIT) in form 3CEC. However, the discussion during the pre-filing meeting is not binding on either the tax payer or the tax authorities. Pre-filing conferences can be held on a named or anonymous basis. Particularly in the beginning of the program, it would be useful if taxpayers are given an opportunity to meet the Board personnel, who will process their case. This will help build trust in the process. In particular, offering anonymous pre-filing conferences provides taxpayers the opportunity to determine the receptivity of the Board to the issues in its particular case without fear of inviting an audit or identifying possible areas of audit, should the taxpayer decide not to proceed with an APA. Can tax authorities reject any APA application based on the outcome of the pre-filing discussions? The pre-filing consultation would not bind the CBDT or the tax payer to either initiate the APA process or to enter into an APA. However, it may be possible that in a prefiling meeting the authorities may indicate their reluctance to accept the proposed methodology which could influence the negotiation process. It is expected that that understanding reached at this stage will be communicated in writing. 10

in India. The CA will send the application to DG-IT who in turn will send it to respective APA teams.")

11 Application for APA An application for a unilateral agreement should be made to the Director General of Income Tax (international taxation) (DG-IT). For BAPA/MAPA, application should be made to the Competent Authority (CA) in India. The CA will send the application to DG-IT who in turn will send it to respective APA teams. In the case of BAPA/MAPA, negotiations between the CAs of India and other country (ies) shall be carried out in accordance with the provisions of the tax treaties. Further, the process in India will be initiated, only after filing the application with the CAs in the AEs jurisdiction and evidence to that effect is provided to the Indian CA. An APA application is required to be accompanied with the filing fees as below: Amount of International Transaction entered into or proposed to be undertaken in respect of which agreement is proposed during the proposed period of agreement Amount not exceeding Rs. 1 billion Amount not exceeding Rs. 2 billion Amount exceeding Rs. 2 billion Fee (INR) 1 million 1.5 million 2 million 11

12 Preliminary processing and procedure It includes vetting the application for any deficiencies. If the application is allowed in the preliminary processing phase, the main processing of applications would be conducted by the APA team in the following manner: holding meetings with applicant calling for additional documents/ information/material from the applicant visiting applicant s business premises making inquiries as may deems fit in the circumstances of the case Agreement and terms APA requires approval of the Central Government. It should include international transactions covered, agreed methodology, Arm s Length Price if any, critical assumptions, time period, definition of terms and other conditions if not covered in the prescribed APA scheme. Annual Compliance Report Compliance report shall be filed annually as below: Form 3CEF to be furnished in quadruplicate to DGIT for each of the years covered in the agreement One copy each would be sent by the DGIT to the CA India, to the jurisdictional CIT and one copy to the TPO Withdrawal If any defect is noticed in the application filed by the applicant following a successful pre-filing consultation and if the application is withdrawn at this stage, then the fee paid by the applicant shall be refunded. Further, the tax payer may withdraw an application at any time before its finalization, by filing a request in a prescribed Form 3CEE. However, in case of such withdrawal, the tax payer would not be eligible for receiving a refund of filing fee. The procedure is no different for BAPA/MAPA. Cancellation The CBDT has the powers to cancel an APA if the results of the compliance audit indicate that: the applicant has failed to comply with the terms of the agreement, there is a failure to file the annual compliance report within the stipulated timeline, there are material errors in the annual compliance report filed by the applicant, or if the applicant is in disagreement with the proposed revision in the APA. If an agreement is cancelled based on the discovery of fraud or misrepresentation of facts on the part of the applicant the same shall be deemed cancelled ab-initio and audit will take place accordingly. To be filed within thirty days of the due date of filing the income tax return for that year, or within ninety days of entering into an agreement, whichever is later 12

13 Renewal In case of renewal of an agreement, all the procedures other than the pre-filing procedures will be followed by the applicant treating the application at par with a new applicant. It is expected that where the circumstances do not change materially getting a renewal of an APA would be a lot easier than getting an APA for the first time. Renewed APA can be on new terms depending on the facts of the case. Revision of an APA An APA can be revised in case of change in critical underlying assumptions, change in such law other than that which renders it non-binding or on request from CA in the other country. The revision order is required to be in writing citing reasons of revision required and revisions can be initiated by the Board / DGIT/ CA/ taxpayer. Opportunity of being heard shall be provided and nonagreement by the taxpayer on the proposed revisions may result in cancellation of the APA. Rollback provision The recently notified APA Rollback rules also provide an option to the taxpayer to roll back the APA for prior four years to the same international transaction, subject to certain conditions. Thus, based on the amendment, an APA could be made applicable for five prospective years as well as the immediately preceding four years, thereby providing certainty to the taxpayer for a maximum period of nine years Conditions applicable for availing rollback provisions, as notified by the CBDT, are: (a) the international transaction must be the same as the one to which the APA is applicable; (b) the return of income for the relevant rollback year has been filed; (c) the report in respect of the international transaction has been furnished as required under Section 92E; (d) the rollback is requested for all rollback years in which the international transaction has taken place; and (e) the application has been made in the prescribed format of Form 3CEDA. 13

14 Safe Harbour Rules To reduce increasing number of transfer pricing audits and prolonged disputes, the Central Board of Direct Taxes (CBDT) had issued the draft Safe Harbour rules (SHR) on 14 August 2013, inviting public comments. SHRs are applicable for a period of 5 years starting with Financial Year for the prescribed sectors. The option of being governed by SHRs shall continue to remain in force for the period specified by the taxpayer in the prescribed form (Form No. 3CEFA) or a period of five years whichever is less. The notification of the safe harbour rules is a welcome development and yet another conciliatory step towards minimising transfer pricing disputes and improving the overall investment climate in India from a tax perspective. Safe harbours are generally considered incompatible with the arm s length principle. However, even internationally, safe harbours rules have been evaluated favourably where the benefits of simplified transfer pricing compliance and administration outweigh the possible concerns. Therefore, the safe harbour regime to successfully work in India would need effective implementation measures by the tax department. This is to ensure that the primary objective for introduction of safe harbours, which is reduction in transfer pricing litigation and related uncertainty, is effectively achieved. Larger captive players may still not find the revised Safe Harbour rates lucrative enough to opt for the same. In such cases, opting for an Advance Pricing Agreement (APA), which could result in closer approximation of the arm s length price, may be rather preferable option. While bilateral APAs would completely mitigate the risk of double taxation, a tax payer opting for safe harbour rules will not be able to avoid possibility of economic double taxation. 14

, Mumbai - 400086 (India) Phone : + 91 98202-63544 : + 91 22-25110016 E-mail : info@neerajbhagat.")

15 Our Offices in India New Delhi: S-13, St. Soldier Tower, G-Block Commercial Complex, Vikas Puri, New Delhi Phone : : : Fax : Gurgaon: 1156, Tower B2, 11th Floor, Spaze i- Tech Park, Sohna Road, Sector 49, Gurgaon Phone : Fax : Mumbai: Unit No.3, 1st Floor, New Laxmi Shopping Centre, A-Wing, H.D.Road, Ghatkopar (W), Mumbai (India) Phone : : info@neerajbhagat.com Web site : Neeraj Bhagat & Company is a team of distinguished chartered accountant, corporate financial advisors and tax consultants in India. Our firm of chartered accountants represents a coalition of specialized skills that is geared to offer sound financial solutions and advices. The organization is a congregation of professionally qualified and experienced persons who are committed to add value and optimize the benefits accruing to clients. We are prominent Chartered Accountants in India. We offer services of accounts outsourcing, auditing, company formation in India, Business taxation, corporate compliance, starting business in India, registration of foreign companies, transfer pricing, tax due diligence, taxation of expatriates etc. Neeraj Bhagat is a member of the Institute of Chartered Accountants of India (ICAI) since He is also an Associate member of Association of International Accountants, United Kingdom. He is founder of Neeraj Bhagat & Co, an Indian Chartered Accountancy firm serving various MNC S from across the globe. Neeraj Bhagat & Co. has its offices at New Delhi, Gurgaon and Mumbai. They are part of Allinial Global Accounting Association which is one of the World's Top 10 in accounting associations. 15

Place of Effective Management [PoEM]

![Place of Effective Management [PoEM]](/thumbs/80/80494161.jpg "Place of Effective Management [PoEM]") Place of Effective Management [PoEM] Test of tax residency for foreign companies Edition 2017 1 Contents: Introduction Residential status for companies- change in definition Likely trigger of PoEM Implications

Place of Effective Management [PoEM] Test of tax residency for foreign companies Edition 2017 1 Contents: Introduction Residential status for companies- change in definition Likely trigger of PoEM Implications

GST: Transitional Provisions

GST: Transitional Provisions Edition 3 Contents POT Transition Phase [S.188 and S. 189] Credit with ISD [S.190 and S. 191] Goods with Agent [S.192 and S.193] Transfer of goods to branch [S.194 and S. 195]

GST: Transitional Provisions Edition 3 Contents POT Transition Phase [S.188 and S. 189] Credit with ISD [S.190 and S. 191] Goods with Agent [S.192 and S.193] Transfer of goods to branch [S.194 and S. 195]

GST: Transitional Provisions

GST: Transitional Provisions Edition 1 Contents Administration under GST [S.165] Migration of Existing taxpayers [S.166] Input Tax Credits [S.167 to 172] Goods sent for Job work [S.173 to S.177] 2 Section

GST: Transitional Provisions Edition 1 Contents Administration under GST [S.165] Migration of Existing taxpayers [S.166] Input Tax Credits [S.167 to 172] Goods sent for Job work [S.173 to S.177] 2 Section

Budget 2017 Decoding the impact on Start-ups

Budget 2017 Decoding the impact on Start-ups 1 Introduction The theme of the Budget, as articulated by the Finance Minister, is to transform and energise the country and the economy as well as a much cleaner

Budget 2017 Decoding the impact on Start-ups 1 Introduction The theme of the Budget, as articulated by the Finance Minister, is to transform and energise the country and the economy as well as a much cleaner

GST: Transitional Provisions

GST: Transitional Provisions Edition 2 Contents Debit and Credit Notes [S.178] Pending Refunds [S.179 to S.181] Pending Assessments and Appeals [S.182 to S.185] Continuing Contracts [S.186 and S. 187]

GST: Transitional Provisions Edition 2 Contents Debit and Credit Notes [S.178] Pending Refunds [S.179 to S.181] Pending Assessments and Appeals [S.182 to S.185] Continuing Contracts [S.186 and S. 187]

[Chapter IX] Edition NBC, Chartered Accountants and member of Allinial Global Accounting Association. All Rights Reserved.

![[Chapter IX] Edition NBC, Chartered Accountants and member of Allinial Global Accounting Association. All Rights Reserved.](/thumbs/90/103497091.jpg "[Chapter IX] Edition NBC, Chartered Accountants and member of Allinial Global Accounting Association. All Rights Reserved.") [Chapter IX] Edition 7 Contents Furnishing details of outward supplies [S. 37] Furnishing details of inward supplies [S. 38] Furnishing of Returns [S. 39] First Return [S. 40] Claim of input tax credit

[Chapter IX] Edition 7 Contents Furnishing details of outward supplies [S. 37] Furnishing details of inward supplies [S. 38] Furnishing of Returns [S. 39] First Return [S. 40] Claim of input tax credit

KPMG FLASH NEWS. Transfer Pricing - Safe Harbour Rules Notified. Background. 20 September 2013 KPMG IN INDIA

KPMG FLASH NEWS KPMG IN INDIA Transfer Pricing - Safe Harbour Rules Notified 20 September 2013 Background To reduce increasing number of transfer pricing audits and prolonged disputes, the Central Board

KPMG FLASH NEWS KPMG IN INDIA Transfer Pricing - Safe Harbour Rules Notified 20 September 2013 Background To reduce increasing number of transfer pricing audits and prolonged disputes, the Central Board

[Chapter XI] Edition 9

![[Chapter XI] Edition 9](/thumbs/81/84570230.jpg "[Chapter XI] Edition 9") [Chapter XI] Edition 9 Contents Refund of Tax [S. 54] Refund in certain cases [S. 55] Interest on delayed refunds [S. 56] Consumer welfare fund [S. 57] Utilization of Fund [S. 58] Related FAQs 2 Rules

[Chapter XI] Edition 9 Contents Refund of Tax [S. 54] Refund in certain cases [S. 55] Interest on delayed refunds [S. 56] Consumer welfare fund [S. 57] Utilization of Fund [S. 58] Related FAQs 2 Rules

Union Budget Analysis

Union Budget 2018-19 Analysis Employees Provident Funds and Miscellaneous Provisions Act, 1952 1 About EPFO The Employees' Provident Fund Organisation (abbreviated to EPFO), is an Organization tasked to

Union Budget 2018-19 Analysis Employees Provident Funds and Miscellaneous Provisions Act, 1952 1 About EPFO The Employees' Provident Fund Organisation (abbreviated to EPFO), is an Organization tasked to

[TO BE PUBLISHED IN THE GAZETTE OF INDIA EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (ii)]

![[TO BE PUBLISHED IN THE GAZETTE OF INDIA EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (ii)]](/thumbs/85/91544243.jpg "[TO BE PUBLISHED IN THE GAZETTE OF INDIA EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (ii)]") [TO BE PUBLISHED IN THE GAZETTE OF INDIA EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] Notification

[TO BE PUBLISHED IN THE GAZETTE OF INDIA EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] Notification

Transfer Pricing in India Examining inter-company cross-border transactions

Transfer Pricing in India Examining inter-company cross-border transactions 1 Contents Background and history Meaning of International transaction Specified Domestic Transaction Arm s Length Price Associated

Transfer Pricing in India Examining inter-company cross-border transactions 1 Contents Background and history Meaning of International transaction Specified Domestic Transaction Arm s Length Price Associated

GST Input Tax Credit [Chapter V]

![GST Input Tax Credit [Chapter V]](/thumbs/82/84970219.jpg "GST Input Tax Credit [Chapter V]") GST Input Tax Credit [Chapter V] Edition 5 Contents GST Regime Eligibility and conditions for taking input tax credit [S. 16] Apportionment of credit and blocked credits [S. 17] Availability of credit

GST Input Tax Credit [Chapter V] Edition 5 Contents GST Regime Eligibility and conditions for taking input tax credit [S. 16] Apportionment of credit and blocked credits [S. 17] Availability of credit

Indian Advance Pricing Agreement Regime The Game Changer

Indian Advance Pricing Agreement Regime The Game Changer 2012 Disclaimer: The information contained in this document has been compiled or arrived at from discussions with various stakeholders, industry

Indian Advance Pricing Agreement Regime The Game Changer 2012 Disclaimer: The information contained in this document has been compiled or arrived at from discussions with various stakeholders, industry

[Chapter VI] Edition NBC, Chartered Accountants and member of Allinial Global Accounting Association. All Rights Reserved.

![[Chapter VI] Edition NBC, Chartered Accountants and member of Allinial Global Accounting Association. All Rights Reserved.](/thumbs/85/91917713.jpg "[Chapter VI] Edition NBC, Chartered Accountants and member of Allinial Global Accounting Association. All Rights Reserved.") [Chapter VI] Edition 6 Contents Persons liable for Registration [S. 22] Persons not liable for Registration [S. 23] Compulsory Registration In Certain Cases [S. 24] Procedure for Registration [S. 25] Deemed

[Chapter VI] Edition 6 Contents Persons liable for Registration [S. 22] Persons not liable for Registration [S. 23] Compulsory Registration In Certain Cases [S. 24] Procedure for Registration [S. 25] Deemed

Overview of Transfer Pricing

Overview of Transfer Pricing Contents Legislative framework Transfer pricing study Assessment and Litigation Key Recent Developments Page 2 Transfer Pricing in India- Background April 1, 2001 onwards Comprehensive

Overview of Transfer Pricing Contents Legislative framework Transfer pricing study Assessment and Litigation Key Recent Developments Page 2 Transfer Pricing in India- Background April 1, 2001 onwards Comprehensive

By---Kamlesh C Varshney, Commissioner of Income Tax(APA), Delhi

, Delhi") By---Kamlesh C Varshney, Commissioner of Income Tax(APA), Delhi 1 There have been two key developments during recent times; which are part of Finance Minister s policy of implementing non adversarial tax

By---Kamlesh C Varshney, Commissioner of Income Tax(APA), Delhi 1 There have been two key developments during recent times; which are part of Finance Minister s policy of implementing non adversarial tax

Goods and Services Tax A benchmark transformation from present tax regime to the unified tax framework

Goods and Services Tax A benchmark transformation from present tax regime to the unified tax framework Edition 2 September 15, 2016 Introduction GST Regime The much-awaited GST now becomes a law with President

Goods and Services Tax A benchmark transformation from present tax regime to the unified tax framework Edition 2 September 15, 2016 Introduction GST Regime The much-awaited GST now becomes a law with President

Issues in Transfer Pricing

Issues in Transfer Pricing Vaishali Mane Chartered Accountant, Mumbai 2017 Grant Thornton India LLP. All rights reserved. 1 Contents 1 Transfer Pricing - Basic 2 Recent Developments in Transfer Pricing

Issues in Transfer Pricing Vaishali Mane Chartered Accountant, Mumbai 2017 Grant Thornton India LLP. All rights reserved. 1 Contents 1 Transfer Pricing - Basic 2 Recent Developments in Transfer Pricing

Current TP Litigation Scenario Alternative Resolution Mechanisms MAP & APA August 2010

Current TP Litigation Scenario Alternative Resolution Mechanisms MAP & APA Agenda Increasing focus on Transfer Pricing Current litigation status in India Experiences in TP Litigation Alternatives to Litigation

Current TP Litigation Scenario Alternative Resolution Mechanisms MAP & APA Agenda Increasing focus on Transfer Pricing Current litigation status in India Experiences in TP Litigation Alternatives to Litigation

Advance Pricing Agreement Scope & Procedure Will it mitigate Litigation?

SPECIAL STORY Advance Rulings & Settlement Commission CA. Rajesh S. Athavale Advance Pricing Agreement Scope & Procedure Will it mitigate Litigation? Globally, transfer pricing has emerged as one of the

SPECIAL STORY Advance Rulings & Settlement Commission CA. Rajesh S. Athavale Advance Pricing Agreement Scope & Procedure Will it mitigate Litigation? Globally, transfer pricing has emerged as one of the

Did you know! Transactions M.2 Safe harbour rules M.3 Dispute resolution panel

M Transfer pricing Doing business in India 209 Did you know! India has emerged as the world s number one, along with the US, in annual solar power generation. In wind power production, when it comes to

M Transfer pricing Doing business in India 209 Did you know! India has emerged as the world s number one, along with the US, in annual solar power generation. In wind power production, when it comes to

APA roll back rules announced

from India Tax & Regulatory Services APA roll back rules announced March 17, 2015 In brief Provisions relating to Advance Pricing Agreements (APAs) were introduced in the Indian Income-tax Act, 1961 (the

from India Tax & Regulatory Services APA roll back rules announced March 17, 2015 In brief Provisions relating to Advance Pricing Agreements (APAs) were introduced in the Indian Income-tax Act, 1961 (the

Transfer Pricing Country Summary India

Page 1 of 13 Transfer Pricing Country Summary India April 2018 Page 2 of 13 Legislation Existence of Transfer Pricing Laws/Guidelines Section 92 of the Income-tax Act, 1961 requires international transactions

Page 1 of 13 Transfer Pricing Country Summary India April 2018 Page 2 of 13 Legislation Existence of Transfer Pricing Laws/Guidelines Section 92 of the Income-tax Act, 1961 requires international transactions

Introduction to Transfer Pricing Regulations

Introduction to Transfer Pricing Regulations January 24, 2015 Vispi T. Patel Vispi T. Patel & Associates 1 Agenda Transfer Pricing Regulations in India Practical applicability of Transfer Pricing Regulations

Introduction to Transfer Pricing Regulations January 24, 2015 Vispi T. Patel Vispi T. Patel & Associates 1 Agenda Transfer Pricing Regulations in India Practical applicability of Transfer Pricing Regulations

Contents. Introduction. International Transfer Pricing: Advance Pricing Arrangements (APAs)

") NO.: 94-4R DATE: March 16, 2001 SUBJECT: International Transfer Pricing: Advance Pricing Arrangements (APAs) This circular cancels and replaces Information Circular 94-4, dated December 30, 1994. This

NO.: 94-4R DATE: March 16, 2001 SUBJECT: International Transfer Pricing: Advance Pricing Arrangements (APAs) This circular cancels and replaces Information Circular 94-4, dated December 30, 1994. This

Secondary Adjustments What Lies beneath

Secondary Adjustments What Lies beneath UTPAL DOSHI June 2017 Contents -Transfer Pricing Adjustments - Secondary Adjustment - provisions - Global practice / OECD - Key issues - Illustrations - Way forward

Secondary Adjustments What Lies beneath UTPAL DOSHI June 2017 Contents -Transfer Pricing Adjustments - Secondary Adjustment - provisions - Global practice / OECD - Key issues - Illustrations - Way forward

Advance Pricing Agreements in India - Addressing the taxpayers needs

Advance Pricing Agreements in India - Addressing the taxpayers needs Transfer pricing (TP) the means by which income is allocated between taxing jurisdictions has emerged as the preeminent international

Advance Pricing Agreements in India - Addressing the taxpayers needs Transfer pricing (TP) the means by which income is allocated between taxing jurisdictions has emerged as the preeminent international

An overview of Transfer Pricing

An overview of Transfer Pricing WIRC of ICAI Vispi T. Patel Vispi T. Patel & Associates 19 th June, 2013 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer

An overview of Transfer Pricing WIRC of ICAI Vispi T. Patel Vispi T. Patel & Associates 19 th June, 2013 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer

Advance Pricing Agreement in India Practical Insights

APA, SAFE HARBOUR & MAP Advance Pricing Agreement in India Practical Insights 1. Background Since the Transfer Pricing Regulations were introduced in India in April 2001, Transfer Pricing ( TP ) has emerged

APA, SAFE HARBOUR & MAP Advance Pricing Agreement in India Practical Insights 1. Background Since the Transfer Pricing Regulations were introduced in India in April 2001, Transfer Pricing ( TP ) has emerged

Recent Transfer Pricing Developments

Recent Transfer Pricing Developments CA Rachesh Kotak September 08, 2017 Setting the context Old world New world Compliance driven Reliance on local documentation One-sided approaches Protracted litigation

Recent Transfer Pricing Developments CA Rachesh Kotak September 08, 2017 Setting the context Old world New world Compliance driven Reliance on local documentation One-sided approaches Protracted litigation

2 nd All India Tax Summit. - Achromic Point. Transfer Pricing. CA Sachin Kumar B P

2 nd All India Tax Summit - Achromic Point Transfer Pricing CA Sachin Kumar B P 2001: TP regulations introduced -Mandatory compliance agreement - Stringent penalty provisions 2005: First TP audit cycle

2 nd All India Tax Summit - Achromic Point Transfer Pricing CA Sachin Kumar B P 2001: TP regulations introduced -Mandatory compliance agreement - Stringent penalty provisions 2005: First TP audit cycle

Union Budget 2014 Analysis of Major Direct tax proposals

RATES OF INCOME TAX Union Budget 2014 Analysis of Major Direct tax proposals Basic exemption limit has been increased from Rs 2 lacs to Rs 2.50 lacs for resident individuals or HUF. Income slabs Income

RATES OF INCOME TAX Union Budget 2014 Analysis of Major Direct tax proposals Basic exemption limit has been increased from Rs 2 lacs to Rs 2.50 lacs for resident individuals or HUF. Income slabs Income

COUNTRY CHAPTER EXCERPT. India

COUNTRY CHAPTER EXCERPT India Mukesh Butani and Sanjiv Malhotra, Taxand India. The authors can be contacted at +91 124 339 5000, mukesh.butani@bmrlegal.in / sanjiv.malhotra@bmradvisors.com 1. Tax Authority

COUNTRY CHAPTER EXCERPT India Mukesh Butani and Sanjiv Malhotra, Taxand India. The authors can be contacted at +91 124 339 5000, mukesh.butani@bmrlegal.in / sanjiv.malhotra@bmradvisors.com 1. Tax Authority

Expatriates working in India. - Indian Regulations and Requirements Edition 2

Expatriates working in India - Indian Regulations and Requirements 2016 Edition 2 2016 NBC, Chartered Accountants and member of INAA Group. All Rights Reserved. 1 Contents: Applying for work visas business

Expatriates working in India - Indian Regulations and Requirements 2016 Edition 2 2016 NBC, Chartered Accountants and member of INAA Group. All Rights Reserved. 1 Contents: Applying for work visas business

An overview of Transfer Pricing

An overview of Transfer Pricing CTC Vispi T. Patel Vispi T. Patel & Associates Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations v OECD

An overview of Transfer Pricing CTC Vispi T. Patel Vispi T. Patel & Associates Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations v OECD

Sharing insights. News Alert 20 March, Key amendments in TP Regulations by the Union Budget Introduction of Advance Pricing Agreement

www.pwc.com/in Sharing insights News Alert 20 March, 2012 Key amendments in TP Regulations by the Union Budget 2012 The Finance Minister presented the Finance Bill 2012 (Finance Bill) in the Parliament

www.pwc.com/in Sharing insights News Alert 20 March, 2012 Key amendments in TP Regulations by the Union Budget 2012 The Finance Minister presented the Finance Bill 2012 (Finance Bill) in the Parliament

An overview of Transfer Pricing

An overview of Transfer Pricing WIRC of ICAI Vispi T. Patel 19th June, 2013 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations v OECD

An overview of Transfer Pricing WIRC of ICAI Vispi T. Patel 19th June, 2013 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations v OECD

CS Professional Programme Solution June Paper - 6 Module-III Advanced Tax Laws and Practice Part-A

CS Professional Programme Solution June - 2013 Paper - 6 Module-III Advanced Tax Laws and Practice Part-A Answer: 2013 - June [1] (a) (i) Ch-14 The statement is True. As per Section 115 BBD, dividend from

CS Professional Programme Solution June - 2013 Paper - 6 Module-III Advanced Tax Laws and Practice Part-A Answer: 2013 - June [1] (a) (i) Ch-14 The statement is True. As per Section 115 BBD, dividend from

ADVANCE PRICING ARRANGEMENT PROGRAM REPORT

ADVANCE PRICING ARRANGEMENT PROGRAM REPORT 2017 Competent Authority Services Division International and Large Business Directorate International, Large Business and Investigation Branch Canada Revenue

ADVANCE PRICING ARRANGEMENT PROGRAM REPORT 2017 Competent Authority Services Division International and Large Business Directorate International, Large Business and Investigation Branch Canada Revenue

India's New Advance Pricing Agreement (APA) Program

Program") cutting through complexity / India's New Advance Pricing Agreement (APA) Program Presenter r Alpana Saksena International Tax Conference Mumbai Dec 7, 2012 ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED

cutting through complexity / India's New Advance Pricing Agreement (APA) Program Presenter r Alpana Saksena International Tax Conference Mumbai Dec 7, 2012 ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED

White Paper June Recommendations for a model Advance Pricing Agreement scheme in India

White Paper www.deloitte.com/in June 2011 Recommendations for a model Advance Pricing Agreement scheme in India 2 Contents Table of Abbreviations 5 Executive summary 6 Introduction 7 Oecd transfer pricing

White Paper www.deloitte.com/in June 2011 Recommendations for a model Advance Pricing Agreement scheme in India 2 Contents Table of Abbreviations 5 Executive summary 6 Introduction 7 Oecd transfer pricing

CBDT Instruction No. 3/2016 : A game-changer for TP audits? - Part I

CBDT Instruction No. 3/2016 : A game-changer for TP audits? - Part I Date: Fri, 04/22/2016-15:02 Ajay Kering (Direct or, Grant Thornt on India LLP) Dinesh Ramnani (Manager, Grant Thornt on India LLP) This

CBDT Instruction No. 3/2016 : A game-changer for TP audits? - Part I Date: Fri, 04/22/2016-15:02 Ajay Kering (Direct or, Grant Thornt on India LLP) Dinesh Ramnani (Manager, Grant Thornt on India LLP) This

Indian tax administration issues revised guidance on transfer pricing audit procedures

11 March 2016 Global Tax Alert News from Transfer Pricing Indian tax administration issues revised guidance on transfer pricing audit procedures EY Global Tax Alert Library Access both online and pdf versions

11 March 2016 Global Tax Alert News from Transfer Pricing Indian tax administration issues revised guidance on transfer pricing audit procedures EY Global Tax Alert Library Access both online and pdf versions

Appeal, Set comm., DRP Etc Mock Test IGP-CS CA Vivek Gaba

1. Taking full advantage of loopholes of law so as to attract least incidence of tax is known as a) Tax planning b) Tax evasion c) Tax avoidance d) Tax management 2. Which is the relevant Form No. for

1. Taking full advantage of loopholes of law so as to attract least incidence of tax is known as a) Tax planning b) Tax evasion c) Tax avoidance d) Tax management 2. Which is the relevant Form No. for

Fundamental principles of Transfer Pricing and Transfer Pricing audit under the Income-tax Act, 1961

Fundamental principles of Transfer Pricing and Transfer Pricing audit under the Income-tax Act, 1961 Borivali (Central) CPE Study Circle of WIRC of The Institute Of Chartered Accountants Of India Vispi

Fundamental principles of Transfer Pricing and Transfer Pricing audit under the Income-tax Act, 1961 Borivali (Central) CPE Study Circle of WIRC of The Institute Of Chartered Accountants Of India Vispi

ROMANIA. minimum of 25% of the number/value of shares or voting rights in the two entities.

ROMANIA TRANSFER PRICING COUNTRY PROFILE 1. Reference to the Arm s Length Principle The arm's length principle was introduced in the domestic tax law in 1994 and is applicable to all related party transactions,

ROMANIA TRANSFER PRICING COUNTRY PROFILE 1. Reference to the Arm s Length Principle The arm's length principle was introduced in the domestic tax law in 1994 and is applicable to all related party transactions,

Tax Dispute Resolution in India - How to effectively handle? Sanjay Sanghvi 29 April 2017

Tax Dispute Resolution in India - How to effectively handle? Sanjay Sanghvi 29 April 2017 Income Tax in India An overview Residents taxed on worldwide income Non-residents taxed on Indian sourced income

Tax Dispute Resolution in India - How to effectively handle? Sanjay Sanghvi 29 April 2017 Income Tax in India An overview Residents taxed on worldwide income Non-residents taxed on Indian sourced income

ADVANCE PRICING ARRANGEMENT PROGRAM REPORT

ADVANCE PRICING ARRANGEMENT PROGRAM REPORT 2016 Competent Authority Services Division International and Large Business Directorate International, Large Business and Investigations Branch Canada Revenue

ADVANCE PRICING ARRANGEMENT PROGRAM REPORT 2016 Competent Authority Services Division International and Large Business Directorate International, Large Business and Investigations Branch Canada Revenue

Transfer Pricing. Recent Trends & Key Developments. PHD Chamber International Tax Conference September 04, 2014 New Delhi. Statement of Credentials 1

Transfer Pricing Recent Trends & Key Developments PHD Chamber International Tax Conference September 04, 2014 New Delhi Statement of Credentials 1 SESSION DETAILS Topic: Transfer Pricing Recent Trends

Transfer Pricing Recent Trends & Key Developments PHD Chamber International Tax Conference September 04, 2014 New Delhi Statement of Credentials 1 SESSION DETAILS Topic: Transfer Pricing Recent Trends

September WHAT'S INSIDE... Direct Tax Transfer Pricing Indirect Tax

September 16-30 WHAT'S INSIDE... Direct Tax Transfer Pricing Indirect Tax What s inside DIRECT TAX 1. Payment for technical services made for earning future source of income outside India is covered by

September 16-30 WHAT'S INSIDE... Direct Tax Transfer Pricing Indirect Tax What s inside DIRECT TAX 1. Payment for technical services made for earning future source of income outside India is covered by

Transfer Pricing Audits Indian experience.

Transfer Pricing Audits Indian experience. International Tax Conference - 2005 Vispi T. Patel Deloitte Haskins & Sells. Background of Indian TPR OECD s View Transfer pricing can deprive governments of

Transfer Pricing Audits Indian experience. International Tax Conference - 2005 Vispi T. Patel Deloitte Haskins & Sells. Background of Indian TPR OECD s View Transfer pricing can deprive governments of

EY Tax Alert. Executive summary. CBDT notifies guidelines for onshore management of offshore funds. 17 March 2016

17 March 2016 EY Tax Alert CBDT notifies guidelines for onshore management of offshore funds Executive summary Tax Alerts cover significant tax news, developments and changes in legislation that affect

17 March 2016 EY Tax Alert CBDT notifies guidelines for onshore management of offshore funds Executive summary Tax Alerts cover significant tax news, developments and changes in legislation that affect

Mutual agreement procedure Answering queries

www.pwc.in Mutual agreement procedure Answering queries What is a mutual agreement procedure (MAP)? MAP is an alternative available to taxpayers to resolve disputes giving rise to double taxation, whether

www.pwc.in Mutual agreement procedure Answering queries What is a mutual agreement procedure (MAP)? MAP is an alternative available to taxpayers to resolve disputes giving rise to double taxation, whether

d e vreser st ighr lla

Article 7 and 9 of the model conventions including International and Domestic TP Beginners Study Course on International Taxation July 4, 2015 Neha Arora 2 Contents Article 7 of the Model Convention Approaches

Article 7 and 9 of the model conventions including International and Domestic TP Beginners Study Course on International Taxation July 4, 2015 Neha Arora 2 Contents Article 7 of the Model Convention Approaches

Guidance for Taxpayers on the Mutual Agreement Procedure (Q&A)

") Guidance for Taxpayers on the Mutual Agreement Procedure (Q&A) July, 2017 Office of the Mutual Agreement Procedure National Tax Agency, Japan This guidance is to complement the contents of the Commissioner

Guidance for Taxpayers on the Mutual Agreement Procedure (Q&A) July, 2017 Office of the Mutual Agreement Procedure National Tax Agency, Japan This guidance is to complement the contents of the Commissioner

TAX CONTROVERSIES AND LITIGATION IN INDIA - AVOIDANCE AND THE SOLUTIONS. S.R. Wadhwa, Advocate 1

TAX CONTROVERSIES AND LITIGATION IN INDIA - AVOIDANCE AND THE SOLUTIONS S.R. Wadhwa, Advocate 1 BY: S.R. Wadhwa Ph. No. 9810414433 Email: wadhwasr@hotmail.com Website: wadhwataxconsultant.com S.R. Wadhwa,

TAX CONTROVERSIES AND LITIGATION IN INDIA - AVOIDANCE AND THE SOLUTIONS S.R. Wadhwa, Advocate 1 BY: S.R. Wadhwa Ph. No. 9810414433 Email: wadhwasr@hotmail.com Website: wadhwataxconsultant.com S.R. Wadhwa,

Comments on the United Nations Practical Manual on Transfer Pricing Countries for Developing Countries

To: United Nations From: Repsol, S.A. Date: 02/28/2014 Comments on the United Nations Practical Manual on Transfer Pricing Countries for Developing Countries REPSOL appreciates the opportunity to contribute

To: United Nations From: Repsol, S.A. Date: 02/28/2014 Comments on the United Nations Practical Manual on Transfer Pricing Countries for Developing Countries REPSOL appreciates the opportunity to contribute

Indian Tax Administration announces draft rules on transfer pricing safe harbors

19 August 2013 Global Tax Alert News from Transfer Pricing Indian Tax Administration announces draft rules on transfer pricing safe harbors Executive summary India s Finance (No 2) Act (FA), 2009 introduced

19 August 2013 Global Tax Alert News from Transfer Pricing Indian Tax Administration announces draft rules on transfer pricing safe harbors Executive summary India s Finance (No 2) Act (FA), 2009 introduced

July WHAT'S INSIDE... Direct Tax Transfer Pricing Indirect Tax

July 16-31 WHAT'S INSIDE... Direct Tax Transfer Pricing Indirect Tax What s inside DIRECT TAX 1. CBDT issues draft Buy-back tax rules for public comments 2. Export commission not taxable, applying Explanation

July 16-31 WHAT'S INSIDE... Direct Tax Transfer Pricing Indirect Tax What s inside DIRECT TAX 1. CBDT issues draft Buy-back tax rules for public comments 2. Export commission not taxable, applying Explanation

TRANSFER PRICING IN INDIA A REVENUE PERSPECTIVE

TRANSFER PRICING IN INDIA A REVENUE PERSPECTIVE A PRESENTATION BY AKHILESH RANJAN DIRECTOR OF INCOME TAX (INTERNATIONAL TAXATION), NEW DELHI 02.12.2005 HISTORICALLY Concept of transfer pricing always there

TRANSFER PRICING IN INDIA A REVENUE PERSPECTIVE A PRESENTATION BY AKHILESH RANJAN DIRECTOR OF INCOME TAX (INTERNATIONAL TAXATION), NEW DELHI 02.12.2005 HISTORICALLY Concept of transfer pricing always there

INDIA IMPORTANT CORPORATE TAX UPDATES

INDIA IMPORTANT CORPORATE TAX UPDATES Introduction Reducing tax litigation has been a key focus area for the Modi government. Several initiatives have been taken by the Central Board of Direct Taxes (the

INDIA IMPORTANT CORPORATE TAX UPDATES Introduction Reducing tax litigation has been a key focus area for the Modi government. Several initiatives have been taken by the Central Board of Direct Taxes (the

WIRC INTENSIVE COURSE ON TRANSFER PRICING

1 WIRC INTENSIVE COURSE ON TRANSFER PRICING (From 1.08.2011 to 12.08.2011) I. INTRODUCTION What is Transfer Pricing? OVERVIEW OF TRANSFER PRICING By Nilesh Patel; Ex-IRS Officer, CPA(USA) Ph: 9819060323

1 WIRC INTENSIVE COURSE ON TRANSFER PRICING (From 1.08.2011 to 12.08.2011) I. INTRODUCTION What is Transfer Pricing? OVERVIEW OF TRANSFER PRICING By Nilesh Patel; Ex-IRS Officer, CPA(USA) Ph: 9819060323

OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations

OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations 2009 Edition B 366258 TABLE OF CONTENTS - 5 Table of Contents Preface 11 Glossary 17 Chapter I The Arm's Length Principle

OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations 2009 Edition B 366258 TABLE OF CONTENTS - 5 Table of Contents Preface 11 Glossary 17 Chapter I The Arm's Length Principle

Bilateral Advance Pricing Agreement Guidelines

September 2016 Bilateral Advance Pricing Agreement Guidelines Page 1 Contents PART 1 INTRODUCTION...5 PART 2 BILATERAL APA PROGRAMME OVERVIEW...5 PART 3 PURPOSE AND SCOPE OF APA...7 What is an APA?...7

September 2016 Bilateral Advance Pricing Agreement Guidelines Page 1 Contents PART 1 INTRODUCTION...5 PART 2 BILATERAL APA PROGRAMME OVERVIEW...5 PART 3 PURPOSE AND SCOPE OF APA...7 What is an APA?...7

Advance Ruling. Chapter XV. FAQ s

FAQ s Chapter XV Advance Ruling Chapter-XVII of the CGST Act, 2017 (Section 95 to Section 106) read with Chapter XII - Advance Ruling of the CGST Rules, 2017 and Chapter-VII of the UGST Act, 2017(Section

FAQ s Chapter XV Advance Ruling Chapter-XVII of the CGST Act, 2017 (Section 95 to Section 106) read with Chapter XII - Advance Ruling of the CGST Rules, 2017 and Chapter-VII of the UGST Act, 2017(Section

Subject: Revised and Updated Guidance for Implementation of Transfer Pricing Provisions-Regarding

Instruction No. 15/2015 F.No. 500/9/2015-APA-11 Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes Foreign Tax and Tax Research Division-I APA-II Section New Delhi,

Instruction No. 15/2015 F.No. 500/9/2015-APA-11 Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes Foreign Tax and Tax Research Division-I APA-II Section New Delhi,

Arm s length principle in India: selected issues

Arm s length principle in India: selected issues 1 Timing issues OECD perspective Different country approaches: the arm s length price setting and the arm s length outcome testing approaches: Year Y-1

Arm s length principle in India: selected issues 1 Timing issues OECD perspective Different country approaches: the arm s length price setting and the arm s length outcome testing approaches: Year Y-1

INTERNATIONAL TAXATION

By CA. SANJAY D. SONAWANE M.COM; LLB; FICWA; DISA(ICAI); FCA INTERNATIONAL TAXATION International taxation is a study of determination of a tax on income earned in different countries, of a person or of

By CA. SANJAY D. SONAWANE M.COM; LLB; FICWA; DISA(ICAI); FCA INTERNATIONAL TAXATION International taxation is a study of determination of a tax on income earned in different countries, of a person or of

E/C.18/2016/CRP.2 Attachment 9

Distr.: General * October 2016 Original: English Committee of Experts on International Cooperation in Tax Matters Twelfth Session Geneva, 11-14 October 2016 Agenda item 3 (b) (i) Update of the United Nations

Distr.: General * October 2016 Original: English Committee of Experts on International Cooperation in Tax Matters Twelfth Session Geneva, 11-14 October 2016 Agenda item 3 (b) (i) Update of the United Nations

Competent Authority Resolutions and APAs

Competent Authority Resolutions and APAs Tom Akin Senior Partner, McCarthy Tétrault LLP, Toronto Patricia Spice - Director, Competent Authority Services Division, CRA, Ottawa Introduction 2 A taxpayer

Competent Authority Resolutions and APAs Tom Akin Senior Partner, McCarthy Tétrault LLP, Toronto Patricia Spice - Director, Competent Authority Services Division, CRA, Ottawa Introduction 2 A taxpayer

Domestic Transfer Pricing Provisions

Domestic Transfer Pricing Provisions Ameya Kunte April 4, 2014 ameya.kunte@taxsutra.com Contents Background why domestic TP? SC observations in Glaxo ruling Amendments by Finance Act, 2012 Domestic TP

Domestic Transfer Pricing Provisions Ameya Kunte April 4, 2014 ameya.kunte@taxsutra.com Contents Background why domestic TP? SC observations in Glaxo ruling Amendments by Finance Act, 2012 Domestic TP

ACCA 31 st August Transfer pricing

ACCA 31 st August 2015 Transfer pricing Background Objective: to enhance services to Hong Kong taxpayers and to align with international practice Topics: 1. Transfer Pricing Documentation 2. Unilateral

ACCA 31 st August 2015 Transfer pricing Background Objective: to enhance services to Hong Kong taxpayers and to align with international practice Topics: 1. Transfer Pricing Documentation 2. Unilateral

Republic of Korea Dispute Resolution Profile. (Last updated: 30 August 2017) General Information

General Information") 1 Republic of Korea Dispute Resolution Profile (Last updated: 30 August 2017) General Information Korea tax treaties are available at: www.nts.go.kr/eng/ [Please see Resources-Tax Law/Treaty] MAP request

1 Republic of Korea Dispute Resolution Profile (Last updated: 30 August 2017) General Information Korea tax treaties are available at: www.nts.go.kr/eng/ [Please see Resources-Tax Law/Treaty] MAP request

WESTERN INDIAN REGIONAL COUNCIL, THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA. Workshop on Transfer Pricing. Safe Harbour Rules- An Overview

WESTERN INDIAN REGIONAL COUNCIL, THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA Workshop on Transfer Pricing Safe Harbour Rules- An Overview Sanjay Kapadia Background Introduced in Finance (No 2) Act,

WESTERN INDIAN REGIONAL COUNCIL, THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA Workshop on Transfer Pricing Safe Harbour Rules- An Overview Sanjay Kapadia Background Introduced in Finance (No 2) Act,

Domestic Transfer Pricing

Domestic Transfer Pricing Ameya Kunte 20 March 2015 ameya.kunte@taxsutra.com Contents Background why domestic TP? SC observations in Glaxo ruling Amendments by Finance Act, 2012 Domestic TP Framework SDT

Domestic Transfer Pricing Ameya Kunte 20 March 2015 ameya.kunte@taxsutra.com Contents Background why domestic TP? SC observations in Glaxo ruling Amendments by Finance Act, 2012 Domestic TP Framework SDT

Strategic Dispute Resolution in a Post-BEPS World

Tax Management International Journal TM Reproduced with permission from Tax Management International Journal, 46 TM International Journal 317, 6/9/17. Copyright 2017 by The Bureau of National Affairs,

Tax Management International Journal TM Reproduced with permission from Tax Management International Journal, 46 TM International Journal 317, 6/9/17. Copyright 2017 by The Bureau of National Affairs,

ROMANIA TRANSFER PRICING COUNTRY PROFILE

ROMANIA TRANSFER PRICING COUNTRY PROFILE 1. Reference to the Arm s Length Principle Latest update April 2018 The arm's length principle was introduced in the domestic tax law in 1994 and is applicable

ROMANIA TRANSFER PRICING COUNTRY PROFILE 1. Reference to the Arm s Length Principle Latest update April 2018 The arm's length principle was introduced in the domestic tax law in 1994 and is applicable

TRANSFER PRICING UNDER INCOME TAX ACT, N.Madhan B.Com., CA & Grad CWA. 22 August 2015

TRANSFER PRICING UNDER INCOME TAX ACT, 1961 N.Madhan B.Com., CA & Grad CWA 1 22 August 2015 Contents Concept of Transfer Pricing Important Terminologies Nature of Methods & its Applicability Importance

TRANSFER PRICING UNDER INCOME TAX ACT, 1961 N.Madhan B.Com., CA & Grad CWA 1 22 August 2015 Contents Concept of Transfer Pricing Important Terminologies Nature of Methods & its Applicability Importance

Transfer Pricing in India Searching for stability in uncertain times

Transfer Pricing in Searching for stability in uncertain times For private circulation only October 2013 www.deloitte.com/in 2 Addressing your needs Today multinationals are operating in an environment

Transfer Pricing in Searching for stability in uncertain times For private circulation only October 2013 www.deloitte.com/in 2 Addressing your needs Today multinationals are operating in an environment

India introduces secondary adjustment and interest limitation rules

6 April 2017 Global Tax Alert News from Transfer Pricing India introduces secondary adjustment and interest limitation rules EY Global Tax Alert Library Access both online and pdf versions of all EY Global

6 April 2017 Global Tax Alert News from Transfer Pricing India introduces secondary adjustment and interest limitation rules EY Global Tax Alert Library Access both online and pdf versions of all EY Global

Tax Management Transfer Pricing Report

Tax Management Transfer Pricing Report Source: Transfer Pricing Report: News Archive > 2015 > 10/01/2015 > BNA Insights > Rev. Proc. 2015-41: A Needed Reboot of the IRS Advance Pricing Agreement Process

Tax Management Transfer Pricing Report Source: Transfer Pricing Report: News Archive > 2015 > 10/01/2015 > BNA Insights > Rev. Proc. 2015-41: A Needed Reboot of the IRS Advance Pricing Agreement Process

Time allowed : 3 hours Maximum marks : 100. Total number of questions : 8 Total number of printed pages : 7

: 1 : Roll No... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 7 NOTE : All references to sections mentioned in Part-A of the Question Paper relate

: 1 : Roll No... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 7 NOTE : All references to sections mentioned in Part-A of the Question Paper relate

Resolving transfer pricing controversies, handling audits and queries, and best practices in TP documentation: A practical guide

Resolving transfer pricing controversies, handling audits and queries, and best practices in TP documentation: A practical guide Douglas Fone Global Partner, Transfer Pricing Associates 1 Content 1. Introduction

Resolving transfer pricing controversies, handling audits and queries, and best practices in TP documentation: A practical guide Douglas Fone Global Partner, Transfer Pricing Associates 1 Content 1. Introduction

GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] INCOME TAX

![GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] INCOME TAX](/thumbs/90/104493159.jpg "GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] INCOME TAX") [TO BE PUBLSIHED IN THE GAZETTE OF INDIA EXTRAORDINARY, PART II, SECTION 3, SUB SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] Notification

[TO BE PUBLSIHED IN THE GAZETTE OF INDIA EXTRAORDINARY, PART II, SECTION 3, SUB SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE [CENTRAL BOARD OF DIRECT TAXES] Notification

Key changes / amendments to take effect from June 1, 2016

1. Equalisation Levy Section 10 Key changes / amendments to take effect from June 1, 2016 Under section 10, a new Clause 50 has been inserted that provides for exemption of income from specified services

1. Equalisation Levy Section 10 Key changes / amendments to take effect from June 1, 2016 Under section 10, a new Clause 50 has been inserted that provides for exemption of income from specified services

Foreign Tax Credit. June 2016

Foreign Tax Credit June 2016 Table of content 1 Introduction 2 Types of Relief 3 Exemption Method 4 Credit Method 5 Double non-taxation 6 Excess FTC 7 Documentation 8 Cases where FTC not available 9 Case

Foreign Tax Credit June 2016 Table of content 1 Introduction 2 Types of Relief 3 Exemption Method 4 Credit Method 5 Double non-taxation 6 Excess FTC 7 Documentation 8 Cases where FTC not available 9 Case

CBEC releases draft rules on Assessment and Audit under GST and E-Way Bill. The key highlights of the rules are as under:

18 April 2017 EY GST News Alert CBEC releases draft rules on Assessment and Audit under GST and E-Way Bill Executive summary This Alert provides an insightful coverage of news related to GST and recent

18 April 2017 EY GST News Alert CBEC releases draft rules on Assessment and Audit under GST and E-Way Bill Executive summary This Alert provides an insightful coverage of news related to GST and recent

The Centre of Excellence for GST. GST: Returns. JULY 09, 2017 ICAI Tower, BKC MUMBAI. CA. Hemant P. Vastani. The Centre of Excellence for GST

GST: Returns JULY 09, 2017 ICAI Tower, BKC MUMBAI CA. Hemant P. Vastani 1 Sections Covering Returns 37. Furnishing details of outward supplies. 38. Furnishing details of inward supplies. 39. Furnishing

GST: Returns JULY 09, 2017 ICAI Tower, BKC MUMBAI CA. Hemant P. Vastani 1 Sections Covering Returns 37. Furnishing details of outward supplies. 38. Furnishing details of inward supplies. 39. Furnishing

TRANSFER PRICING. By Yethi Remella

TRANSFER PRICING By Yethi Remella 1. INTRODUCTION 2. INCOME TAX ACT, SECTION 92 3. FORM 3CEB Introduction What is Transfer Pricing? What is the Importance of TP in Income Tax? Transfer Pricing - Term Costing

TRANSFER PRICING By Yethi Remella 1. INTRODUCTION 2. INCOME TAX ACT, SECTION 92 3. FORM 3CEB Introduction What is Transfer Pricing? What is the Importance of TP in Income Tax? Transfer Pricing - Term Costing

Transfer Pricing Issues - IT/ITES Industry - Financial Services Industry. Darpan Mehta March 20, 2015

Transfer Pricing Issues - IT/ITES Industry - Financial Services Industry Darpan Mehta March 20, 2015 Agenda IT/ITES Industry 1 Financial Services Industry 2 Slide 2 IT/ITES Industry 1 Issues and challenges

Transfer Pricing Issues - IT/ITES Industry - Financial Services Industry Darpan Mehta March 20, 2015 Agenda IT/ITES Industry 1 Financial Services Industry 2 Slide 2 IT/ITES Industry 1 Issues and challenges

India revises Country Chapter comments in UN Practical Manual on Transfer Pricing Issues for Developing Countries

14 November 2016 Global Tax Alert News from Transfer Pricing India revises Country Chapter comments in UN Practical Manual on Transfer Pricing Issues for Developing Countries EY Global Tax Alert Library

14 November 2016 Global Tax Alert News from Transfer Pricing India revises Country Chapter comments in UN Practical Manual on Transfer Pricing Issues for Developing Countries EY Global Tax Alert Library

Current Work of Interest to Developing Countries. Michelle Levac Chair Working Party 6

Current Work of Interest to Developing Countries Michelle Levac Chair Working Party 6 Current work and recent initiatives 1. 1 st Annual International Meeting on Transfer Pricing under the auspices of

Current Work of Interest to Developing Countries Michelle Levac Chair Working Party 6 Current work and recent initiatives 1. 1 st Annual International Meeting on Transfer Pricing under the auspices of

Representation to Ministry of Finance On issues faced by Private Equity / Venture Capital industry. 7 January, 2015

Representation to Ministry of Finance On issues faced by Private Equity / Venture Capital industry 7 January, 2015 1 PE/VC Industry has contributed to Indian economy across multiple dimensions 200+ active

Representation to Ministry of Finance On issues faced by Private Equity / Venture Capital industry 7 January, 2015 1 PE/VC Industry has contributed to Indian economy across multiple dimensions 200+ active

India. Vispi T. Patel and Kejal P. Visharia*

India Vispi T. Patel and Kejal P. Visharia* Ruling in Marubeni Case on Benchmarking and Determining Arm s Length Consideration for the International Provision of Agency and Marketing Support Services The

India Vispi T. Patel and Kejal P. Visharia* Ruling in Marubeni Case on Benchmarking and Determining Arm s Length Consideration for the International Provision of Agency and Marketing Support Services The

Malaysia News: Malaysia Transfer Pricing Profile Published By The OECD. November Corporate Services

Malaysia News: Malaysia Transfer Pricing Profile Published By The OECD November 2017 Corporate Services www.luther-services.com Malaysia Luther News, November 2017 Malaysia Transfer Pricing Profile Published

Malaysia News: Malaysia Transfer Pricing Profile Published By The OECD November 2017 Corporate Services www.luther-services.com Malaysia Luther News, November 2017 Malaysia Transfer Pricing Profile Published

Union Budget Fundamental Reforms in Indian Transfer Pricing Regulations. Mumbai Pune Hyderabad New Delhi Chennai Bangalore

Union Budget 2014-15 Fundamental Reforms in n Transfer Pricing Regulations Mumbai Pune Hyderabad New Delhi Chennai Bangalore 1 Budget 2014-15 Transfer Pricing Proposals 1 Roll-back provisions introduced

Union Budget 2014-15 Fundamental Reforms in n Transfer Pricing Regulations Mumbai Pune Hyderabad New Delhi Chennai Bangalore 1 Budget 2014-15 Transfer Pricing Proposals 1 Roll-back provisions introduced

Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria

![Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria](/thumbs/90/101594279.jpg "Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria") Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria Key Amendments to Form 3CD. The Central Board of Direct Taxes (CBDT) via Notification No. 33/2018 dated 20th July, 2018 has

Key Amendments to Form 3CD [Effective from August 20, 2018] Nihar Jambusaria Key Amendments to Form 3CD. The Central Board of Direct Taxes (CBDT) via Notification No. 33/2018 dated 20th July, 2018 has

IRAS release of e-tax guide: Transfer Pricing Guidelines (Fourth edition)

") Issue 9 17 January 2017 Transfer pricing alert IRAS release of e-tax guide: Transfer Pricing Guidelines (Fourth edition) Overview On 12 January 2017, the Inland Revenue Authority of Singapore (IRAS) released

Issue 9 17 January 2017 Transfer pricing alert IRAS release of e-tax guide: Transfer Pricing Guidelines (Fourth edition) Overview On 12 January 2017, the Inland Revenue Authority of Singapore (IRAS) released

INDIA BUDGET,2009 Analysis of important provisions July 13, 2009 (Budget presented on 6 th July 2009)

") INDIA BUDGET,2009 Analysis of important provisions July 13, 2009 (Budget presented on 6 th July 2009) Doing common things, Uncommonly well. July 13 2009 A Finance & Accounts Outsourcing Company A Finance

INDIA BUDGET,2009 Analysis of important provisions July 13, 2009 (Budget presented on 6 th July 2009) Doing common things, Uncommonly well. July 13 2009 A Finance & Accounts Outsourcing Company A Finance

IFA MUNICH. Strategic Approaches to Global Transfer Pricing Risk: the use of tax treaties through APA and MAP. 18 January 2018

IFA MUNICH Strategic Approaches to Global Transfer Pricing Risk: the use of tax treaties through APA and MAP 18 January 2018 www.dlapiper.com 86879547 18 January 2018 0 Agenda Current Environment / Current

IFA MUNICH Strategic Approaches to Global Transfer Pricing Risk: the use of tax treaties through APA and MAP 18 January 2018 www.dlapiper.com 86879547 18 January 2018 0 Agenda Current Environment / Current