WORK DISINCENTIVES IN THE TAXATION OF CAPITAL GAINS AND THE TARGETING OF SOCIAL SECURITY BENEFITS

|

|

|

- Clifford Montgomery

- 5 years ago

- Views:

Transcription

1 WORK DISINCENTIVES IN THE TAXATION OF CAPITAL GAINS AND THE TARGETING OF SOCIAL SECURITY BENEFITS By Ross Guest, Kim Wyatt and Peter Schuwalow This article compares the implications of the very high effective marginal tax rates ( EMTRs ) created by the taxation of capital gains on the one hand and the targeting of social security benefits on the other hand. The empirical evidence from labour economics suggests that such high EMTRs are a disincentive to work, particularly for some groups such as married women, lone parents and those on low incomes. An example is provided of the high EMTRs arising from targeted social security entitlements by comparing the EMTRs faced by a hypothetical family. In the case of assessable capital gains, simulations show that the EMTR on other (noncapital gain) income can be over 200% and that the EMTR is higher the smaller the amount of other income and the higher the capital gain. it is argued that work disincentive effects, in particular those arising from the taxation of capital gains, cannot be clearly justified in terms of equity and efficiency. An alternative to the existing method for taxing capital gains is suggested which would overcome the work disincentive problem and may therefore provide benefits to both the Commonwealth government and the taxpayer. 1. INTRODUCTION An effective marginal tax rate ( EMTR ) is the proportion of an extra dollar of taxable income that is lost to income tax and reductions in social security entitlements. A targeted (or means-tested) social security system necessarily implies higher effective EMTRs. This is because social security payments are reduced as the income of the recipient increases. In extreme cases this can lead to poverty traps in which the EMTR is greater than 100%. 1 This phenomenon is well known and has been widely reported. 2 Less well known is the fact that capital gains tax ( CGT ) can also create EMTRs on other income well above 100%. This is purely a design feature of the tax treatment of capital gains 3 which has nothing to do with the social security system. Cleaver 4 has identified this feature in the taxation of capital gains and called it the CGT trap. However, the implications for work disincentives and equity have not yet been explored. The economic case against high EMTRs is that the evidence suggests that on balance they reduce labour supply by creating a disincentive to work. 5 In the case of the social security system this cost must be weighed against the benefits of targeting payments to the most needy, namely, that it improves equity and reduces government budget outlays. In the case of CGT, however, it is not clear what benefits in terms of equity or efficiency can be traded off against the work disincentive effects of the high EMTRs. The purpose of this article is to compare examples of EMTRs from both of these sources and to compare the implications for the incentive to work and equity. The article provides an example of the high EMTRs arising from narrowly targeted social security payments by considering the EMTRs faced by a typical family. The article then shows, with respect to the taxation of capital gains, that the EMTRs are higher the lower the amount of other income earned and the larger the capital gain. 1 Poverty traps are so named because of the disincentive to accept additional work which would increase taxable income, hence trapping the individual into accepting a lower income. The marginal costs of accepting additional work can also include workrelated expenses such as child care, clothing and transport. 2 See eg, references cited in part 2 of this article. 3 Income Tax Rates Act 1986 (Cth) ( ITRA ), Sch 7. 4 B Cleaver, A CGT Trap: 235% Marginal Tax Rates (1993) April New Accountant See eg, references cited in part 2 of this article. 188 JOURNAL OF AUSTRALIAN TAXATION

2 WORK DISINCENTIVES: TAXATION OF CAPITAL GAINS & SOCIAL SECURITY BENEFITS It is shown that the work disincentive effects in the taxation of capital gains could be overcome by alternative methods whilst retaining the benefit to the taxpayer in the existing concessional treatment of capital gains. These alternative methods would not tax the whole of the capital gain in the one year of assessment. The article argues that this may provide benefits to all parties - the taxpayer, the Commonwealth government and the wider community - by encouraging taxpayers to earn additional amounts of other income while holding a taxable capital gain. The remainder of the article is organised as follows. Part 2 provides a brief review of the theoretical and empirical evidence of the work disincentive effects of high EMTRs. Part 3 determines the EMTRs for 1997/98 faced by a typical family as its taxable income increases, where no capital gains are assessable. This illustrates the high EMTRs created by the interaction of the social security system and the income tax rate scales. Part 4 provides the results of simulations of EMTRs on other income where capital gains are assessable. Part 5 asks whether the high EMTRs can be justified and Part 6 offers a suggested alternative method of taxing capital gains. Part 7 concludes the article. 2. THE WORK DISINCENTIVE EFFECT OF HIGH EMTRS The arguments presented here are well established in the public finance literature and so the purpose here is a non-technical outline. For a more thorough treatment see for example, Brown. 6 For workers who have some discretion over their work hours and productivity, the impact of an increase in the EMTR is in theory ambiguous. On the one hand, workers have to work longer or more productively to earn the same disposable (that is, after tax) income. This is the income effect. On the other hand, they have less incentive to do so because they retain a smaller proportion of the last dollar earned. This is the work disincentive effect (or substitution effect) 7 which therefore has an opposite effect on work effort to that of the income effect. Both effects can be illustrated by plotting on a graph disposable (after tax) income against taxable income. This is done in Appendix A. Whether the income or the work disincentive effect dominates and hence whether workers choose to work more or less hours depends on how much the taxpayer enjoys extra work compared to the alternative. This cannot be known a priori and hence is an empirical question. 8 As noted above, the weight of empirical evidence is that there is a negative net impact of high EMTRs on labour supply, implying that the disincentive effect dominates. However, the size of the net labour supply response varies considerably between categories of workers - for instance, between married men and married women, part-time and full-time workers, lone parents and coupled parents, low and high income earners. In his survey of the literature on effects of taxation on labour supply, Blundell 9 finds that married women are the group whose labour supply is most (negatively) responsive to EMTRs, while the least responsive is that of married, full-time male workers. Recent evidence for Australia presented by Mitchell and Dowrick 10 show that the labour force participation rates of the wives of unemployed and low income men is systematically lower than for middle and higher income earners. It is likely that the high EMTRs faced by these groups explain their lower participation rates. The overseas evidence indicates that groups of workers who are entitled to receive social security payments, such as lone mothers and 6 CV Brown, Taxation and the Incentive to Work (2nd ed, 1983). 7 The term substitution effect comes from the idea that an increase in EMTRs lowers the cost of not working (or enjoying leisure) and hence encourages the substitution of leisure for work. 8 Although one can reason a priori that the work disincentive effect is more likely to outweigh the income effect for higher income earners. 9 R Blundell, Labour Supply and Taxation: A Survey (1992) 13(3) Fiscal Studies D Mitchell and S Dowrick, Women s Increasing Participation in the Labour Force: Implications for Equity and Efficiency (1994) Research Discussion Paper No. 308, Centre for Economic Policy, ANU. NOVEMBER/DECEMBER 189

3 R GUEST, K WYATT & P SCHUWALOW the unemployed, have the highest negative labour supply responsiveness to EMTRs. 11 Work disincentive effects have macroeconomic implications. To the extent that work disincentive effects operate to reduce labour supply, average real wages are higher, employment and national output of goods and services is lower; national saving is lower and therefore the growth of national wealth is also lower. An analysis and empirical evaluation of the extent of these effects is beyond the scope of this article. Nevertheless, the point is made that work disincentives do impose economic costs on the community. The overwhelming evidence that targeted social security payments generate negative work incentives is one reason for the increasing consideration being given in Australia and overseas to an alternative income support system, namely the universal transfer system or negative income tax system. 12 Under this system a minimum income is guaranteed to all individuals. There is no targeting whatsoever. 13 Income tax is only payable on additional income above the guaranteed minimum. The problem with this system is that in order to generate the same budgetary cost as a targeted system, either the minimum income may have to be set too low to provide adequate income support or the tax rate may have to be set too high thereby creating significant work disincentives that would be spread across the whole population. Hence, the choice may be between having work disincentives spread across all groups in the population, under a universal transfer system, or concentrating them in certain groups under a targeted system. See Lambert 14 for a comparison of the key features of the targeted and universal transfer systems. 3. THE IMPACT OF TARGETED SOCIAL SECURITY BENEFITS ON EMTRS: AN EXAMPLE This part determines the EMTRs that apply to a typical family as its taxable income increases, where no capital gains are assessable. The typical family chosen is a couple with one child over 5 years old and under 13 years old, and where one of the couple is a dependant spouse who does not receive any income. 15 The EMTRs are determined by the interaction of the income tax rate scales, including the Medicare Levy, and the following tax and social security benefits: Family Tax Assistance ( FTA ), Parenting Payment ( PP ), Family Payment ( FP ) and the Low Income Rebate ( LIR ). The details of these benefits and the calculations of tax payable are described in Appendix B. As a number of the payments are paid directly by the government rather than through the tax system and indeed they are paid to the dependant spouse, our analysis looks at the effect additional earned income has on the EMTR of the family as opposed to one of the individual partners. The results are illustrated in Charts 1 and 2 from which the following picture emerges: EMTRs in excess of 80% apply for taxable incomes in the range approximately 13,000 to 11 See eg, LM Powell, The Impact of Child Care Costs in the Labour Supply of Married Mothers: Evidence from Canada (1997) 30(3) Canadian Journal of Economics ; M Kell and J Wright, Benefits and the Labour Supply of Women Married to Unemployed Men (1990) 100(400) Economic Journal ; R Blundell, A Duncan and C Meaghir, Taxation in Empirical Labour Supply Models: Lone Mothers in the UK (1992) 102(411) Economic Journal ; HJ Gensler and WD Walls, Labour Supply Impacts of Effective Welfare Programme Parameters: A Reanalysis (1995) 27(5) Applied Economics ; N Smith, A Panel Study of Labour Supply and Taxes in Denmark (1995) 27(5) Applied Economics Consideration of this system is mainly at the academic level at this stage. It is not yet on the policy agenda of any major political party. 13 In terms of Figure 1 in Appendix A, there are no kinks in the budget constraint and hence no jumps in work disincentives as income increases. 14 S Lambert, Social Policy: Poverty Traps and Alternative Income Support Systems (1995) 3rd Qtr Australian Economic Review Our simulations (not reported) show that there is very little difference in the overall pattern of EMTRs for couples with more than one child. 190 JOURNAL OF AUSTRALIAN TAXATION

4 WORK DISINCENTIVES: TAXATION OF CAPITAL GAINS & SOCIAL SECURITY BENEFITS 27,000. The number of couples in this taxable income range can be estimated at 320,000 in 1995/ Moreover, taxable incomes in the range 20,700 to 23,400 attract an EMTR of 108%. Approximately 70,000 couples had taxable incomes in this range in 1995/96. For these people another dollar of income would have cost them 1.08, leaving them worse off by 8 cents. It seems reasonable to conclude from these figures that there are a large number of couples facing significant work disincentives arising from the interaction of the income tax scales and the various social security entitlements. The extent to which this is actually reducing labour supply and the extent of the resulting economic costs on the community are empirical questions for further investigation. 4. THE TAXATION OF CAPITAL GAINS AND EMTRS In this part simulations show the high EMTRs on other taxable income 17 that can arise when capital gains are assessable. This design feature in the taxation of capital gains has been identified by Cleaver. 18 The purpose here is to explore the implications for work disincentives and equity; and to suggest alternatives that could leave all parties better off - the taxpayer, the Commonwealth and the wider community. The method of calculating the total tax payable for an individual earning a taxable capital gain and other taxable income is given in Appendix C using the terminology in the Income Tax Rates Act 1986 ( ITRA ). The method is described alternatively here with an example to follow. 20% of the capital gain is added to other taxable income and the resulting notional taxable income is taxed at ordinary rates. The tax payable on the other income is then subtracted to arrive at the tax attributable to the 20% capital gain. This amount is then multiplied by five to give the total tax payable on the capital gain, which is then added to the tax on other taxable income to give the total tax payable on both the capital gain and other income. Consider the following example. Suppose a taxpayer sells an asset and derives a net capital gain of 100,000 and has a salary of 35,000 with no deductions. 20% of the capital gain equals 20,000 which is added to 35,000 to give a notional taxable income of 55,000. The tax payable on 55,000 is 16,452 and from this is subtracted the tax payable on 35,000 which is 7,922 to give a tax attributable to the capital gain of 8, This amount is multiplied by 5 to give a total tax payable on the capital gain of 42,650, which is added to 7,922 to give the total tax payable on taxable income of 50,572. This method effectively recognises that capital gains accrue over time whilst taxing the whole of the capital gain in the year in which it is realised. In the above example, there is a benefit to the taxpayer in that the total capital gain is taxed at a concessional average rate of (42,650/100,000) instead of if the 100,000 capital gain had been taxed at ordinary rates. However, this benefit comes at the cost of an EMTR of 99% on additional salary income. To explain, if this taxpayer were to earn an extra dollar of salary income (so that the salary is 35,001) the total tax payable would increase to 50, This can be verified by repeating the above calculation given the new salary level. The EMTR is 99%. As explained algebraically in Appendix C, the 99% rate in this example is equal to the tax rate applying to 35,001, plus 5 times the gap between that rate and the tax rate applying to the notional income. It is this gap multiplied by 5 which creates the high EMTRs. Multiplying the gap by 5 is the way in which the whole of the capital gain is taxed in the one year. 16 Australian Bureau of Statistics, Cat. No , Income Distribution 1995/96, Table This refers to income other than capital gains and is called the reduced taxable income in the ITRA (see Appendix C). 18 Cleaver, above n 4, All tax calculations exclude the Medicare Levy. NOVEMBER/DECEMBER 191

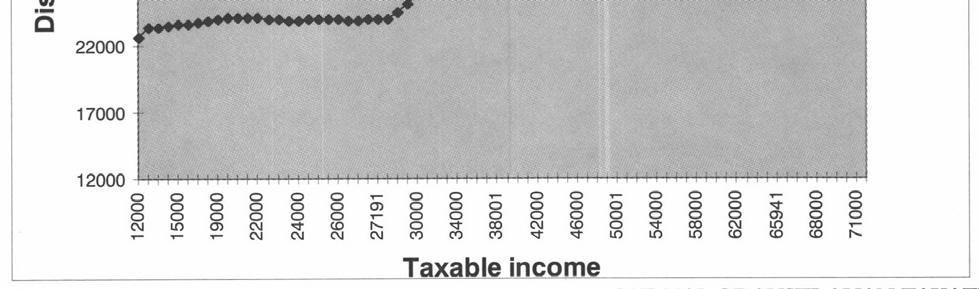

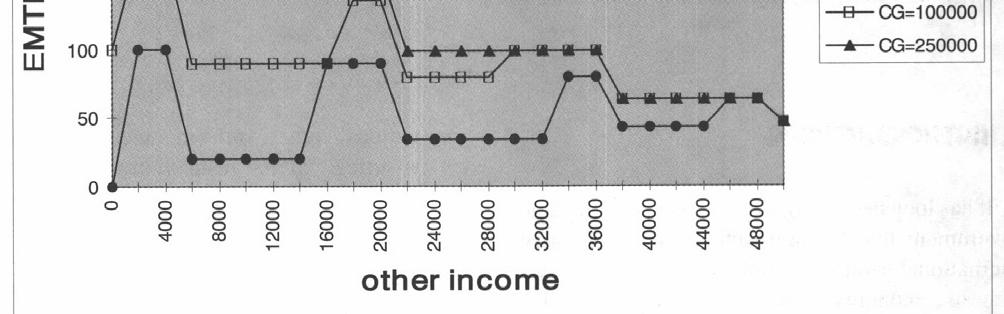

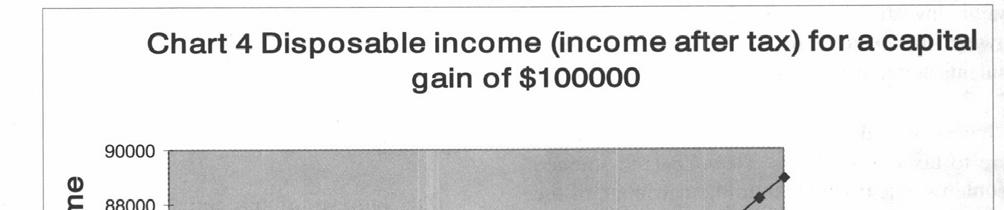

5 R GUEST, K WYATT & P SCHUWALOW Chart 3 shows simulations of the EMTRs on other income as other income increases for capital gains of 25,000, 100,000 and 250,000. All calculations in this part do not include the medicare levy. The chart shows that the EMTRs are higher the lower the amount of other income and the higher the capital gain. Consider two examples of this result. A relatively modest capital gain of 25,000 attracts an EMTR of 100% for other income earned in the range 400 to 5,400. A similar EMTR (99%) is payable in the range of other income from 20,700 to 38,000 on a capital gain of 250,000. The taxpayers in these examples are effectively paying 100% and 99%, respectively, of marginal taxable income to the Commonwealth. Chart 3 shows that the EMTR can be as high as 235% in the case where the other income is below the tax free threshold (5,400) and the capital gain is at least 250,000 (so that 20% of the capital gain attracts the top marginal rate of 47%). Chart 4 shows disposable income as a function of total taxable income for the case of a 100,000 capital gain. 20 The kinks at which disposable income flattens out are points at which the EMTR jumps and hence points at which the disincentive to work jumps. For a practical example of the effect on work incentives, and also expenditure incentives, consider the following scenario. A taxpayer has sold a business in July and made a net capital gain of 80, During the financial year the taxpayer is offered a 6 month consulting contract for 20,000. Should the taxpayer accept the work? If the only income is the 80,000 capital gain, the income tax payable is 10,600. With the 20,000 additional consulting income the total tax payable is 29, That means 19,030 of the additional 20,000 income is payable in tax - a tax rate of 95.15% on the 20,000 income. Arguably not many taxpayers would accept additional work attracting a tax rate of 95%. Suppose that, instead, an opportunity to earn only 5,000 rather than 20,000 of other income is being contemplated by the taxpayer. In this case the EMTR on the 5,000 would be 104.2%. 23 In an alternative scenario this taxpayer may be considering starting another business in the same year. If the taxable profit for the new business venture in the first year is expected to be 20,000 then, given the tax effect of the capital gain, the taxpayer could spend an additional 20,000 on a marketing campaign at an after tax cost of only approximately 1,000. The marketing campaign would presumably increase sales in the following year at an after tax cost of only 1,000. Hence, not only does CGT distort the decision to work, it also distorts the decision to spend. In general terms, these distortions lead to an inefficient allocation of resources which lowers national economic welfare. This concept of efficiency is discussed further below. 5. CAN THE HIGH EMTRS BE JUSTIFIED? High EMTRs may be justified if they are a consequence of achieving other objectives of the tax and social welfare system. From a social perspective, these objectives are to achieve equity - horizontal and vertical, efficiency, simplicity and revenue-raising. A thorough treatment of these objectives can be found in the public finance literature - see in the Australian context for example, Groenwegen. 24 The purpose here is a brief sketch only. Vertical equity is the principle that those with a higher capacity to pay should pay proportionately more tax. Horizontal equity is the principle that people with equal capacity to pay tax 20 This is a numerical example of Figure 1 in Appendix A. 21 This is not an uncommon amount of capital gain. In 1995/96 there were 67,159 taxpayers who had assessable capital gains in the range 50,000 to 99,999 and a further 18,433 taxpayers had assessable capital gains greater than 100,000. (Australian Taxation Office, Taxation Statistics 1995/96 70). 22 Other income is taxable income (that is, there are no deductions). 23 The total tax payable would be 15,810, 5,210 of which is a result of the additional 5,000 income, giving an EMTR of 104.2%. 24 PD Groenwegen, Public Finance In Australia (3rd ed, 1990). 192 JOURNAL OF AUSTRALIAN TAXATION

6 WORK DISINCENTIVES: TAXATION OF CAPITAL GAINS & SOCIAL SECURITY BENEFITS ought to pay equal tax. An efficient tax system is one which does not distort economic choices about, for example, consumption, saving, investment and labour supply. Simplicity refers to transparency and ease of administering the tax. A further consideration is that governments aim to achieve their objectives with lowest cost to their budgets. This is one justification for the targeting of social security entitlements and the need to raise revenue through taxes, including CGT. Inevitably, there is conflict between the objectives of efficiency, equity, simplicity and government budgetary cost minimisation. The high EMTRs on other income resulting from both the taxation of capital gains and the targeting of social security entitlements are a violation of the efficiency criterion by creating work disincentives which distort labour supply decisions. In the case of the social security system, this inefficiency is a result of the attempt to meet the objective of vertical equity by providing a lower tax payable by those in greater need. However, the method of taxing capital gains cannot be so clearly justified in terms of meeting equity objectives. Indeed, the principle of horizontal equity is violated in the sense that capital gains are taxed at a concessional rate relative to other income. To see this, consider two taxpayers who both earn income of 135,000. For one taxpayer this consists of 100,000 of capital gains and 35,000 of other taxable income. The other taxpayer earns the whole 135,000 in other taxable income. The tax payable in each case is 50,572 and 54,052. The taxpayer receiving capital gains pays 3,480 less tax. In order to avoid violating the principle of horizontal equity, a case would have to be made that capital gains confer a lesser capacity to pay tax than an equivalent amount of other income. It is difficult to see how such a case could be made. Work disincentives also have implications for the amount of tax revenue raised and hence implications for the Commonwealth government s budgetary outcome. To the extent that work effort is discouraged, taxable income is lower, tax revenues are lower and the budget deficit is higher with implications for macroeconomic management. This is an additional problem with taxes that create high work disincentives and another reason why such taxes must be shown to be superior in achieving other objectives. Finally, it is sometimes argued that the costs of high EMTRs are grossly exaggerated because the proportion of people who actually face high EMTRs is very small. See for examples in the Australian context, Mitchell, Harding, Gruen 25 and Pollette, 26 who find that only 5% of people have EMTRs in excess of 60% arising from the social security system. The implication is that the economic costs imposed on the community are small. The argument could equally be applied to the high EMTRs resulting from the taxation of capital gains. In 1995/96, 4.5% of all individual taxpayers had assessable capital gains. 27 However, these relatively low percentages may simply prove the point that high EMTRs distort labour supply decisions. It is likely that rational people adjust their labour supply or other circumstances in order to avoid high EMTRs. Therefore, the fact that not many people actually have high EMTRs may simply be because people have avoided them by reducing their labour supply. It would be incorrect to conclude that this is evidence that high EMTRs do not distort labour supply D Mitchell, A Harding and A & F Gruen, Targeting Welfare (1994) 70(210) Economic Record J Pollette, Distribution of Effective Marginal Tax Rates Across the Australian Labour Force (1995) Discussion Paper No. 6, National Centre for Social and Economic Modelling. 27 Australian Taxation Office, Taxation Statistics 1995/ The general point can be illustrated with reference to Figure 1 in Appendix A. A taxpayer who has the opportunity to earn taxable income of V may choose to reduce work effort and hence earn less, say T, because the EMTR at T is less than the EMTR at V. This is simply the work disincentive effect dominating the income effect. To the extent that this occurs, we can expect to find fewer people earning income of V and more earning income of T than would otherwise be the case. NOVEMBER/DECEMBER 193

7 R GUEST, K WYATT & P SCHUWALOW Moreover, in the case of capital gains, the view that the costs are small because so few people pay capital gains, apart from being logically flawed as explained above, is based on an increasingly false premise because of the rapid increase in the numbers of taxpayers who derive capital gains. In 1995/96, 369,189 individuals had assessable capital gains and in the five years from 1991/92 to 1995/96 the number had increased by 82%. This trend looks set to continue, not least as a result of the privatisation programme of the Commonwealth and State governments. 6. ALTERNATIVE TREATMENT OF CAPITAL GAINS It is possible to retain the concessional tax treatment of capital gains whilst reducing the work disincentive effect. This could be achieved by simply assessing a proportion, say 20%, of the capital gain in the current year and in each of the subsequent four years. This 20% amount would be added to other income earned for the year and taxed at normal rates. The result will be that where the other income is constant over the five years, then the same amount of tax will be paid; however the EMTR of the taxpayer on additional income will now be in line with the current tax rates. This will eliminate the very high EMTRs that can apply to additional income where capital gains are derived (as demonstrated in this article). The taxpayer would also receive a concession determined by the time value of the deferred tax. The idea is illustrated below using our previous example of a taxpayer receiving a 100,000 capital gain in Year 1. We will further assume that the taxpayer will receive an additional salary income of 35,000 in Years 1-5. Under the present concessional treatment of capital gains, the taxpayer s tax liability and EMTR on additional salary (or other) income excluding the medicare levy is calculated in the table below: Years Capital Gain Present Concessional Treatment of Capital Gains Other Income Tax Paid EMTR on 5% Discount Additional Factor Income Present Value Tax Paid 1 100,000 35,000 50,572 99c , ,000 7,922 34c , ,000 7,922 34c , ,000 7,922 34c , ,000 7,922 34c , ,260 78, JOURNAL OF AUSTRALIAN TAXATION

8 WORK DISINCENTIVES: TAXATION OF CAPITAL GAINS & SOCIAL SECURITY BENEFITS Applying our suggested alternative, the taxpayer s tax liability and EMTR on additional income excluding the medicare levy is determined as follows: Years 20% Capital Gain Spread over 5 Years Other Income Alternative Treatment of Capital Gains Tax Paid EMTRs - similar to those that are well known to result from the targeting of social security benefits; and that such high EMTRs are a disincentive to work which imposes efficiency costs on the EMTR on Additional Income 5% Discount Factor Present Value Tax Paid 1 20,000 35,000 16,452 47c , ,000 35,000 16,452 47c , ,000 35,000 16,452 47c , ,000 35,000 16,452 47c , ,000 35,000 16,452 47c , ,260 74, Given the assumed discount factor of 5%, the present value of tax paid using our alternative method is less and therefore better for the taxpayer. The high EMTR in Year 1 of 99c on additional salary income under the current treatment of capital gains has been reduced to 47c under our alternative method. This would reduce the work disincentive effect in Year 1 and provide a steady EMTR over the remaining four years, although years 2 to 4 do show a higher EMTR in our alternative. This alternative would not necessarily imply a loss of tax revenue to the Commonwealth if the improved work incentives translated into higher taxable income earned and therefore higher tax payable, at least over the five year period. Indeed, it is possible that tax revenues would increase in which case all parties would be better off - the taxpayer, the Commonwealth government and the wider community. 7. CONCLUSION This article has established that the taxation of capital gains (ITRA, Sch 7) can create very high community in terms of loss of potential output. Also, while the high EMTRs arising from the social security system may be able to be justified in terms of equity objectives, the concessional tax treatment of capital gains violates the principle of horizontal equity. It is at least hoped that the arguments presented in this article warrant an empirical study of the impact of the current tax treatment of capital gains and the targeting of social security benefits on labour supply choices and hence government revenue. APPENDIX A This appendix illustrates both the income and work disincentive effects of EMTRs for the general case by plotting disposable income against taxable income. In figure 1 below the vertical intercept, X, represents the level of social security entitlements where taxable income is zero. At each of the concave kinks in the budget constraints, A and C, NOVEMBER/DECEMBER 195

9 R GUEST, K WYATT & P SCHUWALOW there is a jump in the EMTR, while at each of the convex kinks, B and D, there is a drop in the EMTR. Consider a taxpayer facing the segment BC and currently earning taxable income of Y and disposable income of Z. An increase in the EMTR represented by the budget segment BD implies that the taxpayer would have to increase work effort and earn W in order to maintain disposable income of Z. This is the income effect. However, there is a work disincentive effect represented by the flatter slope of BD than BC. As explained in this article, whether the income or the work disincentive effect dominates and hence whether workers choose to work more or less hours cannot be known a priori and hence is an empirical question. The empirical evidence is that the work disincentive effect tends to dominate, especially for some groups with high EMTRs such as welfare recipients. One might argue that high EMTRs in an intermediate range such as AB in Figure 1 may actually encourage the work effort of people who would otherwise be in this range in order that they place themselves in the higher range BC which has a lower EMTR. Even if this were true, it probably does not represent a net economic benefit to the community. It is a well-established economic principle that differential tax rates distort economic behaviour and lead to lower national output from the nation s resources. A similar principle applies to differential rates of indirect taxes such as sales taxes and rates of tariff on imports. Such differential tax rates are sometimes justified on equity grounds but again economic principles show 1997/98 Taxable Income Income Tax Rate Scales for the 1997/98 Financial Year Tax on Taxable Income % on Excess (Marginal Rate) 5,400 Nil 20 20,700 3, ,000 8, ,000 14, JOURNAL OF AUSTRALIAN TAXATION

10 WORK DISINCENTIVES: TAXATION OF CAPITAL GAINS & SOCIAL SECURITY BENEFITS that equity objectives would be better achieved by other means such as a universal transfer system (see the brief discussion in the article above). APPENDIX B This Appendix gives the income tax rate scales and social security entitlements required to calculate the EMTRs discussed in Part 3. The Medicare Levy of 1.5% of taxable income is also applied to the above rates. However, there are income thresholds and shading-in ranges. The Family Tax Assistance ( FTA ) provides financial assistance to eligible families with dependant children under the age of 16 or, if in fulltime secondary education, aged 16 or 17. The FTA comes in the form of either an increase in the taxfree threshold or a non-taxable payment equal in value through the Department of Social Security. There are two parts of FTA. Part A applies where there is at least one dependant child and the family income is less than 70,000 (increasing by 3,000 for each dependant child after the first). Where this applies, the standard taxfree threshold of 5,400 for one partner of a couple or for a sole parent is increased by 1,000 for each dependant child. As the marginal tax rate is 20% at this point, it effectively reduces a person s tax by 200 per child per year. Part B provides an additional benefit directed at families with one primary income earner and at least one dependant child under 5 years. This is not applicable to the example chosen in this article since the child is assumed to be over 5 years. Parenting Payments are made by the government and paid to a dependant spouse. There are two payments. The basic rate of per fortnight ( pa) is paid to all dependant spouses whose income is less than 60 per fortnight and the family have a child under 16 years old. This amount is fixed and is irrespective of how many children are in the family and how much the income earner s income is. Once the dependant spouse s income is beyond 60 per fortnight, then the basic rate reduces by 50c for each extra dollar between 60 and 140 per fortnight and then the basic rate reduces by a further 70c for each dollar above 140 per fortnight. The basic rate cuts out once the dependant spouse earns more than per fortnight. As our article is assuming that the dependant spouse does not earn an income, then the entitlement to the basic rate will be per fortnight or 1, per annum. Where the income earner s income is less than 498 per fortnight (12,948 pa), and the dependant spouse does not receive any income, then an additional parenting payment of per fortnight (7, pa) will be paid. This additional parenting payment reduces by 70c for each dollar of income over 498 per fortnight effectively eliminating an entitlement to any part payment of the additional rate once the income earner s income is greater than per fortnight (23,723 pa). The additional parenting payment is paid to the dependant spouse and as distinct from the basic parenting payment, is taxable. However, in our example we are assuming that the dependant spouse is receiving no other income. Therefore, with the tax-free threshold, the low income rebate and an entitlement to a beneficiary rebate, no tax will be payable by the dependant spouse in our example No. of Children Allowable Income 1 65, , , , ,132 NOVEMBER/DECEMBER 197

11 R GUEST, K WYATT & P SCHUWALOW The Family Payment is a tax-free payment paid by the government to help parents, single or couples, with the cost of raising children. There are two payments; a basic rate of per child per fortnight (611 pa) for each of the first 3 children, and then at a rate of per fortnight for each additional child. There are no shading-in provisions, that is no withdrawal of FP as income increases. However, once the family income is beyond a certain level, then the FP is not paid. The allowable income levels for 1998 before the basic payment ceased is provided for in the table on the previous page. An additional tax-free FP is also made by the government to low income families. In 1998, the maximum rates for a low income family were: per fortnight ( pa) for each dependant child under 13 years; per fortnight ( pa) for each dependant child aged between 13 and 15 years; and per fortnight ( pa) for dependant students aged between who are not receiving a Commonwealth Student Assistance Scheme payment like AUSTUDY or ABSTUDY. The allowable income limit for this additional FP for a single parent or couple with one dependant child is 23,400 pa. This amount is increased by 624 a year for each additional dependant child. For example, a person with 3 children would have an allowable income limit of 24,648 [23,400 + (624 x 2)]. This additional FP is reduced by 50c for every additional dollar above the allowable income limits. The cut-off point as detailed below depends on the number and age of the children: 1 child under 13: 27,191 pa; 1 child 13-15: 28,699 pa; 1 student 16-18: 25,309 pa. For each additional child under 13, add 4,415 pa. For each additional child 13 to 15, add 5,923 pa. For each additional student 16 to 18, add 2,533 pa. The Low Income Rebate is available to taxpayers whose taxable income in a year of income is less than 24,450. For 1997/98 the maximum rebate is 150, reduced by 4 cents for every dollar by which the taxpayer s taxable income exceeds 20,700. APPENDIX C This Appendix describes the calculation of the total tax payable where capital gains are assessable using the method and terminology in the ITRA, Sch 7. The total tax payable is equal to A + B. A is the amount of tax that would be payable at the ordinary rates applicable to the taxpayer on a taxable income equal to the reduced taxable income (RTI), which is essentially the taxpayer s other taxable income. B is five times the difference between (i) the amount of tax that would be payable at the taxpayer s ordinary rates on a taxable income equal to the sum of the RTI and 20% of the special income component (SIC) which is essentially the net capital gain; and (ii) the amount equal to A. Consider the example given in Part 4. Suppose a taxpayer sells an asset and derives a net capital gain of 100,000 and has a salary of 35,000 with no deductions. The total taxable income = 135,000, the SIC = 100,000 and the RTI = 135,000-SIC = 35,000. The taxpayer s total tax payable is A + B, where A = tax on RTI = tax on 35,000 = 7,922; and B = 5 x (tax on (RTI + 20% SIC) - A) = 42,650. Hence A + B = 50,572. The EMTR can be derived algebraically using this terminology. Let RTI + 20%SIC = notional income. Let t not =marginal tax rate on notional income; t RTI =marginal tax rate on RTI (or other income); EMTR RTI = EMTR on RTI. Then EMTR RTI = 5(tnot - t RTI ) + t RTI. If tnot = t RTI then EMTR RTI = t RTI ; that is, the capital gains do not push the taxpayer into a higher tax bracket and do not create a higher EMTR on other income. In this case, the CGT is benign in its effect on work 198 JOURNAL OF AUSTRALIAN TAXATION

12 WORK DISINCENTIVES: TAXATION OF CAPITAL GAINS & SOCIAL SECURITY BENEFITS top marginal rate but is not the case for lower values of t RTI where t not > t RTI, implying that the 20% capital gain pushes the taxpayer into a higher tax bracket. The maximum EMTR that can arise is 235% in the case where t RTI = 0 and t not = 47%. Applying this formula to the above example, the notional income = RTI + 20%SIC = 55,000 and RTI =other income = 35,000. The marginal tax rate on the notional income and other income is 47% and 34%, respectively. Therefore, using the formula given in the text, the EMTR is (5 x [47-34] + 34)% = 99%. Ross Guest is a Senior Lecturer in Economics in the School of Accounting and Finance at Griffith University. His research has concentrated on empirical applications of representative agent models of optimal national saving, investment and the current account balance, with reference to Australia and South East Asia. Other research has included applied financial economics and income distribution. Kim Wyatt is a Senior Lecturer in the Department of Accounting and Finance at Monash University. His professional experience is in the area of capital expenditure analysis, budgeting, company reporting and taxation. He has wide experience in accounting and tax consulting and has authored and coauthored a number of publications in other law and accounting journals. Kim was a recipient of the Monash University Award for Excellence in First Year Undergraduate Teaching. Peter Schuwalow is the Course Director of the Bachelor of Business (International Trade) and is a Lecturer in the Department of Economics at Monash University. He has co-authored and contributed to a number of economic books and has previously published in other journals. NOVEMBER/DECEMBER 199

13 R GUEST, K WYATT & P SCHUWALOW 200 JOURNAL OF AUSTRALIAN TAXATION

14 WORK DISINCENTIVES: TAXATION OF CAPITAL GAINS & SOCIAL SECURITY BENEFITS NOVEMBER/DECEMBER 201

REFORM OF INCOME TAX IN AUSTRALIA: A LONG-TERM AGENDA

DEMOGRAPHY AND SOCIOLOGY PROGRAM RESEARCH SCHOOL OF SOCIAL SCIENCES REFORM OF INCOME TAX IN AUSTRALIA: A LONG-TERM AGENDA Peter McDonald Rebecca Kippen Working Papers in Demography No. 95 March 2005 Working

DEMOGRAPHY AND SOCIOLOGY PROGRAM RESEARCH SCHOOL OF SOCIAL SCIENCES REFORM OF INCOME TAX IN AUSTRALIA: A LONG-TERM AGENDA Peter McDonald Rebecca Kippen Working Papers in Demography No. 95 March 2005 Working

EVIDENCE ON INEQUALITY AND THE NEED FOR A MORE PROGRESSIVE TAX SYSTEM

EVIDENCE ON INEQUALITY AND THE NEED FOR A MORE PROGRESSIVE TAX SYSTEM Revenue Summit 17 October 2018 The Australia Institute Patricia Apps The University of Sydney Law School, ANU, UTS and IZA ABSTRACT

EVIDENCE ON INEQUALITY AND THE NEED FOR A MORE PROGRESSIVE TAX SYSTEM Revenue Summit 17 October 2018 The Australia Institute Patricia Apps The University of Sydney Law School, ANU, UTS and IZA ABSTRACT

An Education Bond Co-contribution Scheme:

An Education Bond Co-contribution Scheme: Estimating the Budgetary Cost 12 th December, 2012 An independent report prepared for Abacus by the Australian Centre for Financial Studies. Principal authors

An Education Bond Co-contribution Scheme: Estimating the Budgetary Cost 12 th December, 2012 An independent report prepared for Abacus by the Australian Centre for Financial Studies. Principal authors

Exploring the Personal Income Tax System

www.pwc.com.au 22 October 2018 Exploring the Personal Income Tax System Paper Two Separate taxation of labour and capital income Paper Two Separate taxation of labour and capital income Exploring the Personal

www.pwc.com.au 22 October 2018 Exploring the Personal Income Tax System Paper Two Separate taxation of labour and capital income Paper Two Separate taxation of labour and capital income Exploring the Personal

Deadweight Loss and the Cost of Public Funds in Australia

Notes and Topics 231 Deadweight Loss and the Cost of Public Funds in Australia Harry Campbell \ ECENT studies of productivity and economic growth have stressed the importance of infrastructure such as

Notes and Topics 231 Deadweight Loss and the Cost of Public Funds in Australia Harry Campbell \ ECENT studies of productivity and economic growth have stressed the importance of infrastructure such as

Public Economics (ECON 131) Section #4: Labor Income Taxation

Section #4: Labor Income Taxation") Public Economics (ECON 131) Section #4: Labor Income Taxation September 22 to 27, 2016 Contents 1 Implications of Tax Inefficiencies for Optimal Taxation 2 1.1 Key concepts..........................................

Public Economics (ECON 131) Section #4: Labor Income Taxation September 22 to 27, 2016 Contents 1 Implications of Tax Inefficiencies for Optimal Taxation 2 1.1 Key concepts..........................................

The Melbourne Institute Report on the 2004 Federal Budget Hielke Buddelmeyer, Peter Dawkins, and Guyonne Kalb

The Melbourne Institute Report on the 2004 Federal Budget Hielke Buddelmeyer, Peter Dawkins, and Guyonne Kalb The Melbourne Institute of Applied Economic and Social Research University of Melbourne May

The Melbourne Institute Report on the 2004 Federal Budget Hielke Buddelmeyer, Peter Dawkins, and Guyonne Kalb The Melbourne Institute of Applied Economic and Social Research University of Melbourne May

Exploring the Personal Income Tax System

www.pwc.com.au 19 November 2018 Exploring the Personal Income Tax System Paper Three Removal of the Tax-Free Threshold Exploring the Personal Income Tax System November 2018 Paper Three Removal of the

www.pwc.com.au 19 November 2018 Exploring the Personal Income Tax System Paper Three Removal of the Tax-Free Threshold Exploring the Personal Income Tax System November 2018 Paper Three Removal of the

Practice Problem Set 2 (ANSWERS)

") Economics 370 Professor H.J. Schuetze Practice Problem Set 2 (NSWERS) 1. See the figure below, where the initial budget constraint is given by E. fter the new legislation is passed, the budget constraint

Economics 370 Professor H.J. Schuetze Practice Problem Set 2 (NSWERS) 1. See the figure below, where the initial budget constraint is given by E. fter the new legislation is passed, the budget constraint

Basic income as a policy option: Technical Background Note Illustrating costs and distributional implications for selected countries

May 2017 Basic income as a policy option: Technical Background Note Illustrating costs and distributional implications for selected countries May 2017 The concept of a Basic Income (BI), an unconditional

May 2017 Basic income as a policy option: Technical Background Note Illustrating costs and distributional implications for selected countries May 2017 The concept of a Basic Income (BI), an unconditional

Macroeconomics Review Course LECTURE NOTES

Macroeconomics Review Course LECTURE NOTES Lorenzo Ferrari frrlnz01@uniroma2.it August 11, 2018 Disclaimer: These notes are for exclusive use of the students of the Macroeconomics Review Course, M.Sc.

Macroeconomics Review Course LECTURE NOTES Lorenzo Ferrari frrlnz01@uniroma2.it August 11, 2018 Disclaimer: These notes are for exclusive use of the students of the Macroeconomics Review Course, M.Sc.

Income Trends for Selected Single Parent Families 1

Income Trends for Selected Single Parent Families 1 Ben Phillips and Cukkoo Joseph 2 ANU Centre for Social Research and Methods November 2016 1 This work was funded by National Council for Single Mothers

Income Trends for Selected Single Parent Families 1 Ben Phillips and Cukkoo Joseph 2 ANU Centre for Social Research and Methods November 2016 1 This work was funded by National Council for Single Mothers

A Clear Direction Financial Planning Level 19, 10 Eagle Street, Brisbane QLD 4000 (07) ABN:

ABN:") A Clear Direction Financial Planning Level 19, 10 Eagle Street, Brisbane QLD 4000 scottk@acleardirection.com.au (07) 3379 6068 ABN: 85 147 572 870 The budget has provided a number of significant changes

A Clear Direction Financial Planning Level 19, 10 Eagle Street, Brisbane QLD 4000 scottk@acleardirection.com.au (07) 3379 6068 ABN: 85 147 572 870 The budget has provided a number of significant changes

Personal Income Tax Cuts and the new Child Care Subsidy: Do They Address High Effective Marginal Tax Rates on Women s Work?

Personal Income Tax Cuts and the new Child Care Subsidy: Do They Address High Effective Marginal Tax Rates on Women s Work? Miranda Stewart 1 Summary In Australia s tax and social welfare system, many

Personal Income Tax Cuts and the new Child Care Subsidy: Do They Address High Effective Marginal Tax Rates on Women s Work? Miranda Stewart 1 Summary In Australia s tax and social welfare system, many

A gender impact assessment of Australia s retirement income policy

A gender impact assessment of Australia s retirement income policy Siobhan Austen*, Helen Hodgson & Rhonda Sharp TTPI, Crawford School of Public Policy, ANU, Canberra, Tuesday 28 April 2015 Plan of presentation

A gender impact assessment of Australia s retirement income policy Siobhan Austen*, Helen Hodgson & Rhonda Sharp TTPI, Crawford School of Public Policy, ANU, Canberra, Tuesday 28 April 2015 Plan of presentation

AUSTRALIA Overview of the tax-benefit system

AUSTRALIA 2007 1. Overview of the tax-benefit system The Australian social security system is funded from general taxation revenue and not from employer or employee social security contributions. The system

AUSTRALIA 2007 1. Overview of the tax-benefit system The Australian social security system is funded from general taxation revenue and not from employer or employee social security contributions. The system

CRS-2 as the preferential tax treatment accorded Social Security and railroad retirement benefits and the favorable tax treatment accorded long-term c

Order Code RS20342 Updated May 7, 2008 Additional Standard Tax Deduction for the Elderly: A Description and Assessment Summary Pamela J. Jackson Specialist in Public Finance Government and Finance Division

Order Code RS20342 Updated May 7, 2008 Additional Standard Tax Deduction for the Elderly: A Description and Assessment Summary Pamela J. Jackson Specialist in Public Finance Government and Finance Division

STATUS QUO AND PROBLEM

STATUS QUO AND PROBLEM 3 1. This statement considers detailed design options for implementing legislation to provide for an income-sharing tax credit for couples with dependent children in New Zealand.

STATUS QUO AND PROBLEM 3 1. This statement considers detailed design options for implementing legislation to provide for an income-sharing tax credit for couples with dependent children in New Zealand.

Answers To Chapter 7. Review Questions

Answers To Chapter 7 Review Questions 1. Answer d. In the household production model, income is assumed to be spent on market-purchased goods and services. Time spent in home production yields commodities

Answers To Chapter 7 Review Questions 1. Answer d. In the household production model, income is assumed to be spent on market-purchased goods and services. Time spent in home production yields commodities

THE CENTRAL ROLE OF A WELL-DESIGNED INCOME TAX IN THE MODERN ECONOMY

THE CENTRAL ROLE OF A WELL-DESIGNED INCOME TAX IN THE MODERN ECONOMY Income tax conference: Looking forward at 100 Years: Where next for the Income Tax? 27-28 April 2015 Tax and Transfer Policy Institute

THE CENTRAL ROLE OF A WELL-DESIGNED INCOME TAX IN THE MODERN ECONOMY Income tax conference: Looking forward at 100 Years: Where next for the Income Tax? 27-28 April 2015 Tax and Transfer Policy Institute

2006 Economics GA 3: Written examination

2006 Economics GA 3: Written examination GENERAL COMMENTS The standard generally displayed in student responses this year was improved over previous years. The performance on the multiple-choice section

2006 Economics GA 3: Written examination GENERAL COMMENTS The standard generally displayed in student responses this year was improved over previous years. The performance on the multiple-choice section

ECONOMIC SURVEY OF NEW ZEALAND 2007: TWO BROAD APPROACHES FOR TAX REFORM

ECONOMIC SURVEY OF NEW ZEALAND 2007: TWO BROAD APPROACHES FOR TAX REFORM This is an excerpt of the OECD Economic Survey of New Zealand, 2007, from Chapter 4 www.oecd.org/eco/surveys/nz This section discusses

ECONOMIC SURVEY OF NEW ZEALAND 2007: TWO BROAD APPROACHES FOR TAX REFORM This is an excerpt of the OECD Economic Survey of New Zealand, 2007, from Chapter 4 www.oecd.org/eco/surveys/nz This section discusses

Would the Senate Democrats proposed excise tax on highcost employer-paid health insurance benefits be progressive?

Citizens for Tax Justice December 11, 2009 Would the Senate Democrats proposed excise tax on highcost employer-paid health insurance benefits be progressive? Summary Senate Democrats have proposed a new,

Citizens for Tax Justice December 11, 2009 Would the Senate Democrats proposed excise tax on highcost employer-paid health insurance benefits be progressive? Summary Senate Democrats have proposed a new,

Comparison of the Coalition Federal Budget Income Tax Measures and the Labor Proposal

Comparison of the Coalition 2018-19 Federal Budget Income Tax Measures and the Labor Proposal Associate Professor Ben Phillips, Richard Webster, Professor Matthew Gray ANU Centre for Social Research and

Comparison of the Coalition 2018-19 Federal Budget Income Tax Measures and the Labor Proposal Associate Professor Ben Phillips, Richard Webster, Professor Matthew Gray ANU Centre for Social Research and

On Tax-Transfer Integration: Let Us Return to the Ability-To-Pay Principle

On Tax-Transfer Integration: Let Us Return to the Ability-To-Pay Principle Thomas A. Wilson* The attempt to replace the type of welfare or means-tested support for the poor with a much simpler system through

On Tax-Transfer Integration: Let Us Return to the Ability-To-Pay Principle Thomas A. Wilson* The attempt to replace the type of welfare or means-tested support for the poor with a much simpler system through

Economics 602 Macroeconomic Theory and Policy Problem Set 3 Suggested Solutions Professor Sanjay Chugh Spring 2012

Department of Applied Economics Johns Hopkins University Economics 60 Macroeconomic Theory and Policy Problem Set 3 Suggested Solutions Professor Sanjay Chugh Spring 0. The Wealth Effect on Consumption.

Department of Applied Economics Johns Hopkins University Economics 60 Macroeconomic Theory and Policy Problem Set 3 Suggested Solutions Professor Sanjay Chugh Spring 0. The Wealth Effect on Consumption.

WELFARE AND TAXATION (1987)

") WELFARE AND TAXATION (1987) This paper to the Liberal Forum concentrates on cash transfer and income redistribution. It does not deal specifically with provision of services. Three main questions arise.

WELFARE AND TAXATION (1987) This paper to the Liberal Forum concentrates on cash transfer and income redistribution. It does not deal specifically with provision of services. Three main questions arise.

Fair tax and welfare for older workers. Older Australians at work summit John Daley Grattan Institute 24 February 2015

Fair tax and welfare for older workers Older Australians at work summit John Daley Grattan Institute 24 February 215 Fair tax and welfare for older workers Government budgets are unsustainable: spending

Fair tax and welfare for older workers Older Australians at work summit John Daley Grattan Institute 24 February 215 Fair tax and welfare for older workers Government budgets are unsustainable: spending

The equity and sustainability of government assistance for retirement income in Australia

The equity and sustainability of government assistance for retirement income in Australia Ross Clare Director of Research July 2014 1 of 15 The Association of Superannuation Funds of Australia Limited

The equity and sustainability of government assistance for retirement income in Australia Ross Clare Director of Research July 2014 1 of 15 The Association of Superannuation Funds of Australia Limited

Gender equity in the tax-transfer system for fiscal sustainability 1

3 Gender equity in the tax-transfer system for fiscal sustainability 1 Patricia Apps There has been a significant focus in recent years on the persistent gender pay gap in Australia. According to Australian

3 Gender equity in the tax-transfer system for fiscal sustainability 1 Patricia Apps There has been a significant focus in recent years on the persistent gender pay gap in Australia. According to Australian

V. MAKING WORK PAY. The economic situation of persons with low skills

V. MAKING WORK PAY There has recently been increased interest in policies that subsidise work at low pay in order to make work pay. 1 Such policies operate either by reducing employers cost of employing

V. MAKING WORK PAY There has recently been increased interest in policies that subsidise work at low pay in order to make work pay. 1 Such policies operate either by reducing employers cost of employing

Distributional Modelling of Effective Marginal Tax Rates: Work-in-progress only

Distributional Modelling of Effective Marginal Tax Rates: 2000-2015 Work-in-progress only Ben Phillips: ANU Centre for Social Research and Methods (CSRM) August, 2017 What is an EMTR? The percentage of

Distributional Modelling of Effective Marginal Tax Rates: 2000-2015 Work-in-progress only Ben Phillips: ANU Centre for Social Research and Methods (CSRM) August, 2017 What is an EMTR? The percentage of

Melbourne Economic Forum, 13 April Lower Personal Income Tax Rates. John Freebairn. University of Melbourne

Melbourne Economic Forum, 13 April 2016 Lower Personal Income Tax Rates John Freebairn University of Melbourne Current personal income taxation Collect $170 b in 2013-14, and 40% of total government taxation

Melbourne Economic Forum, 13 April 2016 Lower Personal Income Tax Rates John Freebairn University of Melbourne Current personal income taxation Collect $170 b in 2013-14, and 40% of total government taxation

RETIREMENT INCOME GETTING STARTED

RETIREMENT INCOME GETTING STARTED A regular income stream from an account-based or an annuity can be an effective way to fund your retirement. Some retirees may also be eligible for social security benefits

RETIREMENT INCOME GETTING STARTED A regular income stream from an account-based or an annuity can be an effective way to fund your retirement. Some retirees may also be eligible for social security benefits

Capping Pensions Tax Relief

Capping Pensions Tax Relief An Overview of Proposals Considered by the Taxation Policy (Pensions) Group Patrick Burke Background Establishment and Composition of the Taxation Policy (Pensions) Group Requirement

Capping Pensions Tax Relief An Overview of Proposals Considered by the Taxation Policy (Pensions) Group Patrick Burke Background Establishment and Composition of the Taxation Policy (Pensions) Group Requirement

ABSTRACT. Exchange Rates and Macroeconomic Policy with Income-sensitive Capital Flows. J.O.N. Perkins, University of Melbourne

1 ABSTRACT Exchange Rates and Macroeconomic Policy with Income-sensitive Capital Flows J.O.N. Perkins, University of Melbourne This paper considers some implications for macroeconomic policy in an open

1 ABSTRACT Exchange Rates and Macroeconomic Policy with Income-sensitive Capital Flows J.O.N. Perkins, University of Melbourne This paper considers some implications for macroeconomic policy in an open

Modelling of the Federal Budget Personal Income Tax Measures

Modelling of the 2018-19 Federal Budget Personal Income Tax Measures Associate Professor Ben Phillips, Richard Webster, Professor Matthew Gray ANU Centre for Social Research and Methods 10 May 2018 CSRM

Modelling of the 2018-19 Federal Budget Personal Income Tax Measures Associate Professor Ben Phillips, Richard Webster, Professor Matthew Gray ANU Centre for Social Research and Methods 10 May 2018 CSRM

Financial Management Bachelors of Business Administration Study Notes & Tutorial Questions Chapter 3: Capital Structure

Financial Management Bachelors of Business Administration Study Notes & Tutorial Questions Chapter 3: Capital Structure Ibrahim Sameer AVID College Page 1 Chapter 3: Capital Structure Introduction Capital

Financial Management Bachelors of Business Administration Study Notes & Tutorial Questions Chapter 3: Capital Structure Ibrahim Sameer AVID College Page 1 Chapter 3: Capital Structure Introduction Capital

Until recently not much was known about the distribution of

The Australian Journal of Financial Planning annuation & the self-employed By Ross Clare Ross Clare has degrees in Economics and Law from the Australian National University. Prior to joining the staff

The Australian Journal of Financial Planning annuation & the self-employed By Ross Clare Ross Clare has degrees in Economics and Law from the Australian National University. Prior to joining the staff

PAYROLL TAX INCREASE FOR LARGE WA EMPLOYERS Economic Analysis

PAYROLL TAX INCREASE FOR LARGE WA EMPLOYERS Economic Analysis SUMMARY This study investigates the impact of increasing the payroll tax burden to 6 per cent for payrolls that exceed $100 million, and to

PAYROLL TAX INCREASE FOR LARGE WA EMPLOYERS Economic Analysis SUMMARY This study investigates the impact of increasing the payroll tax burden to 6 per cent for payrolls that exceed $100 million, and to

The Impact of Penalty Rate Cuts on Personal Tax Revenue and Welfare

The Impact of Penalty Rate Cuts on Personal Tax Revenue and Welfare Briefing note Richard Denniss March 2017 ABOUT THE AUSTRALIA INSTITUTE The Australia Institute is an independent public policy think

The Impact of Penalty Rate Cuts on Personal Tax Revenue and Welfare Briefing note Richard Denniss March 2017 ABOUT THE AUSTRALIA INSTITUTE The Australia Institute is an independent public policy think

Testimony to the President s Tax Reform Panel

Testimony to the President s Tax Reform Panel John D. Podesta President Center for American Progress May 11, 2005 Overview The Center for American Progress Tax Reform Plan Fair and Responsible Reform The

Testimony to the President s Tax Reform Panel John D. Podesta President Center for American Progress May 11, 2005 Overview The Center for American Progress Tax Reform Plan Fair and Responsible Reform The

Economics Lecture Sebastiano Vitali

Economics Lecture 6 2016-17 Sebastiano Vitali Course Outline 1 Consumer theory and its applications 1.1 Preferences and utility 1.2 Utility maximization and uncompensated demand 1.3 Expenditure minimization

Economics Lecture 6 2016-17 Sebastiano Vitali Course Outline 1 Consumer theory and its applications 1.1 Preferences and utility 1.2 Utility maximization and uncompensated demand 1.3 Expenditure minimization

Labour Market Responses to the Abolition of Compulsory Superannuation

Author: Australian Paper Journal title of Labour Economics, Vol. 8, No. 4, December 2005, pp 351-364 351 Labour Market Responses to the Abolition of Compulsory Superannuation Louise Carter Economics Program,

Author: Australian Paper Journal title of Labour Economics, Vol. 8, No. 4, December 2005, pp 351-364 351 Labour Market Responses to the Abolition of Compulsory Superannuation Louise Carter Economics Program,

2016/17 Budget. 1. Effective Budget Night 7.30pm (AEST) 3 May New lifetime cap for non-concessional superannuation contributions

3 May New lifetime cap for non-concessional superannuation contributions") 2016/17 Budget Superannuation reform changes 1. Effective Budget Night 7.30pm (AEST) 3 May 2016 1.1 New lifetime cap for non-concessional superannuation contributions The government will introduce a $500,000

2016/17 Budget Superannuation reform changes 1. Effective Budget Night 7.30pm (AEST) 3 May 2016 1.1 New lifetime cap for non-concessional superannuation contributions The government will introduce a $500,000

Effects of the Australian New Tax System on Government Expenditure; With and without Accounting for Behavioural Changes

Effects of the Australian New Tax System on Government Expenditure; With and without Accounting for Behavioural Changes Guyonne Kalb, Hsein Kew and Rosanna Scutella Melbourne Institute of Applied Economic

Effects of the Australian New Tax System on Government Expenditure; With and without Accounting for Behavioural Changes Guyonne Kalb, Hsein Kew and Rosanna Scutella Melbourne Institute of Applied Economic

Payroll giving: providing a real-time benefit for charitable giving

Payroll giving: providing a real-time benefit for charitable giving A government discussion document Hon Dr Michael Cullen Minister of Finance Hon Peter Dunne Minister of Revenue First published in November

Payroll giving: providing a real-time benefit for charitable giving A government discussion document Hon Dr Michael Cullen Minister of Finance Hon Peter Dunne Minister of Revenue First published in November

Lesson 7 - Tax Offsets

Tax Training School Contents Tax Offsets 2 Refundable Tax Offsets 2 Tax Offsets on the return 2 T1 - Senior and Pensioners (including self-funded retirees) 4 T2 - Australian Superannuation Income Stream

Tax Training School Contents Tax Offsets 2 Refundable Tax Offsets 2 Tax Offsets on the return 2 T1 - Senior and Pensioners (including self-funded retirees) 4 T2 - Australian Superannuation Income Stream

Retirement income getting started

Retirement getting started A regular stream from an account-based or an annuity can be an effective way to fund your retirement. Some retirees may also be eligible for social security benefits from the

Retirement getting started A regular stream from an account-based or an annuity can be an effective way to fund your retirement. Some retirees may also be eligible for social security benefits from the

The principles of GIA and their application to an analysis of Australia s retirement incomes and savings policies

The principles of GIA and their application to an analysis of Australia s retirement incomes and savings policies Siobhan Austin, Rhonda Sharp and Helen Hodgson This presentation Sets out key principles

The principles of GIA and their application to an analysis of Australia s retirement incomes and savings policies Siobhan Austin, Rhonda Sharp and Helen Hodgson This presentation Sets out key principles

Household Stimulus Package

of 13/02/2009 Fact Sheet 2009 Updated Economic and Fiscal Outlook Household Stimulus Package The Government will provide $12.2 billion to assist households and support economic growth in 2008-09. The measures

of 13/02/2009 Fact Sheet 2009 Updated Economic and Fiscal Outlook Household Stimulus Package The Government will provide $12.2 billion to assist households and support economic growth in 2008-09. The measures

National saving and population ageing. Author. Published. Journal Title. Copyright Statement. Downloaded from. Link to published version

National saving and population ageing Author Guest, Ross, McDonald, Ian M. Published 2001 Journal Title Agenda Copyright Statement The Author(s) 2001. The attached file is reproduced here in accordance

National saving and population ageing Author Guest, Ross, McDonald, Ian M. Published 2001 Journal Title Agenda Copyright Statement The Author(s) 2001. The attached file is reproduced here in accordance

DISCUSSION PAPERS. Reforming the Australian Tax Transfer System

CENTRE FOR ECONOMIC POLICY RESEARCH Australian National University DISCUSSION PAPERS Reforming the Australian Tax Transfer System Patricia Apps Faculty of Law, University of Sydney and Economics Program

CENTRE FOR ECONOMIC POLICY RESEARCH Australian National University DISCUSSION PAPERS Reforming the Australian Tax Transfer System Patricia Apps Faculty of Law, University of Sydney and Economics Program

DEPARTMENT OF ECONOMICS

ISSN 0819-2642 ISBN 0 7340 2588 2 THE UNIVERSITY OF MELBOURNE DEPARTMENT OF ECONOMICS RESEARCH PAPER NUMBER 932 MARCH 2005 BEHAVIOURAL MICROSIMULATION MODELLING WITH THE MELBOURNE INSTITUTE TAX AND TRANSFER

ISSN 0819-2642 ISBN 0 7340 2588 2 THE UNIVERSITY OF MELBOURNE DEPARTMENT OF ECONOMICS RESEARCH PAPER NUMBER 932 MARCH 2005 BEHAVIOURAL MICROSIMULATION MODELLING WITH THE MELBOURNE INSTITUTE TAX AND TRANSFER

NORWAY Overview of the system

NORWAY 1997 1. Overview of the system In Norway, the unemployment insurance scheme is part of the National Insurance Scheme (NIS). Unemployment benefits are calculated as a percentage of previous earnings,

NORWAY 1997 1. Overview of the system In Norway, the unemployment insurance scheme is part of the National Insurance Scheme (NIS). Unemployment benefits are calculated as a percentage of previous earnings,

A Review of Funding Measures for Urban Infrastructure with Special Reference to Developer Charges, Betterment (Value Uplift) Taxes and Turnover Taxes

Taxes and Turnover Taxes") A Review of Funding Measures for Urban Infrastructure with Special Reference to Developer Charges, Betterment (Value Uplift) Taxes and Turnover Taxes Peter Abelson Department of Economics, University of

A Review of Funding Measures for Urban Infrastructure with Special Reference to Developer Charges, Betterment (Value Uplift) Taxes and Turnover Taxes Peter Abelson Department of Economics, University of

AIST. 22 October Sex Discrimination Commissioner Australian Human Rights Commission Level 3, 175 Pitt St SYDNEY NSW 200. Dear Ms Broderick,

22 October 2012 Sex Discrimination Commissioner Australian Human Rights Commission Level 3, 175 Pitt St SYDNEY NSW 200 Dear Ms Broderick, Application by Rice Warner Thank you for the opportunity to comment

22 October 2012 Sex Discrimination Commissioner Australian Human Rights Commission Level 3, 175 Pitt St SYDNEY NSW 200 Dear Ms Broderick, Application by Rice Warner Thank you for the opportunity to comment

Most performance surveys for Australian sector funds are presented in

The Australian Journal of Financial Planning 43 Portfolio turnover s impact on the tax efficiency of active equity strategies By Dr Don Hamson Plato Investment Management Dr Don Hamson is managing director

The Australian Journal of Financial Planning 43 Portfolio turnover s impact on the tax efficiency of active equity strategies By Dr Don Hamson Plato Investment Management Dr Don Hamson is managing director

Chapter 1 Microeconomics of Consumer Theory

Chapter Microeconomics of Consumer Theory The two broad categories of decision-makers in an economy are consumers and firms. Each individual in each of these groups makes its decisions in order to achieve

Chapter Microeconomics of Consumer Theory The two broad categories of decision-makers in an economy are consumers and firms. Each individual in each of these groups makes its decisions in order to achieve

The Economy Wide Benefits of Increasing the Proportion of Students Achieving Year 12 Equivalent Education

January 2003 A Report prepared for the Business Council of Australia by The Economy Wide Benefits of Increasing the Proportion of Students Achieving Year 12 Equivalent Education Modelling Results The

January 2003 A Report prepared for the Business Council of Australia by The Economy Wide Benefits of Increasing the Proportion of Students Achieving Year 12 Equivalent Education Modelling Results The

Estimating the Distortionary Costs of Income Taxation in New Zealand

Estimating the Distortionary Costs of Income Taxation in New Zealand Background paper for Session 5 of the Victoria University of Wellington Tax Working Group October 2009 Prepared by the New Zealand Treasury

Estimating the Distortionary Costs of Income Taxation in New Zealand Background paper for Session 5 of the Victoria University of Wellington Tax Working Group October 2009 Prepared by the New Zealand Treasury

Chapter 19: Compensating and Equivalent Variations

Chapter 19: Compensating and Equivalent Variations 19.1: Introduction This chapter is interesting and important. It also helps to answer a question you may well have been asking ever since we studied quasi-linear

Chapter 19: Compensating and Equivalent Variations 19.1: Introduction This chapter is interesting and important. It also helps to answer a question you may well have been asking ever since we studied quasi-linear

GENDER EQUITY IN THE TAX SYSTEM FOR FISCAL SUSTAINABILITY

GENDER EQUITY IN THE TAX SYSTEM FOR FISCAL SUSTAINABILITY Workshop: Gender Equity in Australia s Tax and Transfer System 4-5 November 2015 Patricia Apps University of Sydney Law School and IZA Introduction

GENDER EQUITY IN THE TAX SYSTEM FOR FISCAL SUSTAINABILITY Workshop: Gender Equity in Australia s Tax and Transfer System 4-5 November 2015 Patricia Apps University of Sydney Law School and IZA Introduction

Reference date for all information is June 30th 2008 Country chapter for OECD series Benefits and Wages (www.oecd.org/els/social/workincentives)

") AUSTRALIA 2008 Table of Contents Introduction... 1 1. Overview of the tax-benefit system... 2 2. Unemployment insurance... 3 3. Unemployment assistance... 3 4. Social assistance... 9 5. Housing benefits

AUSTRALIA 2008 Table of Contents Introduction... 1 1. Overview of the tax-benefit system... 2 2. Unemployment insurance... 3 3. Unemployment assistance... 3 4. Social assistance... 9 5. Housing benefits

Establishing the right price for electricity in South Africa. Brian Kantor with assistance from Andrew Kenny and Graham Barr

Establishing the right price for electricity in South Africa Brian Kantor with assistance from Andrew Kenny and Graham Barr This exercise is designed to answer the essential question of relevance for consumers

Establishing the right price for electricity in South Africa Brian Kantor with assistance from Andrew Kenny and Graham Barr This exercise is designed to answer the essential question of relevance for consumers

A Clear Direction Financial Planning Level 19, 10 Eagle Street, Brisbane QLD 4000 (07) ABN:

ABN:") A Clear Direction Financial Planning Level 19, 10 Eagle Street, Brisbane QLD 4000 scottk@acleardirection.com.au (07) 3379 6068 ABN: 85 147 572 870 The budget has provided a number of significant changes

A Clear Direction Financial Planning Level 19, 10 Eagle Street, Brisbane QLD 4000 scottk@acleardirection.com.au (07) 3379 6068 ABN: 85 147 572 870 The budget has provided a number of significant changes

Account-based pensions: making your super go further in retirement

Booklet 3 Account-based pensions: making your super go further in retirement MAStech Smart technical solutions made simple Contents Introduction 01 Introduction 03 What are account-based pensions? 05 Investing

Booklet 3 Account-based pensions: making your super go further in retirement MAStech Smart technical solutions made simple Contents Introduction 01 Introduction 03 What are account-based pensions? 05 Investing

Age Discrimination in Superannuation. Submission to. The Hon Susan Ryan AO Age Discrimination Commissioner

Association of Independent Retirees (A.I.R.) Ltd ACN 102 164 385 Age Discrimination in Superannuation Submission to The Hon Susan Ryan AO Age Discrimination Commissioner December 2011 Summary The Association

Association of Independent Retirees (A.I.R.) Ltd ACN 102 164 385 Age Discrimination in Superannuation Submission to The Hon Susan Ryan AO Age Discrimination Commissioner December 2011 Summary The Association

Understanding Income Distribution and Poverty

Understanding Distribution and Poverty : Understanding the Lingo market income: quantifies total before-tax income paid to factor markets from the market (i.e. wages, interest, rent, and profit) total

Understanding Distribution and Poverty : Understanding the Lingo market income: quantifies total before-tax income paid to factor markets from the market (i.e. wages, interest, rent, and profit) total

SOLUTION ECO 202Y - L5101 MACROECONOMIC THEORY. Term Test #1 LAST NAME FIRST NAME STUDENT NUMBER. University of Toronto June 18, 2002 INSTRUCTIONS:

Department of Economics Prof. Gustavo Indart University of Toronto June 18, 2002 SOLUTION ECO 202Y - L5101 MACROECONOMIC THEORY Term Test #1 LAST NAME FIRST NAME STUDENT NUMBER INSTRUCTIONS: 1. The total

Department of Economics Prof. Gustavo Indart University of Toronto June 18, 2002 SOLUTION ECO 202Y - L5101 MACROECONOMIC THEORY Term Test #1 LAST NAME FIRST NAME STUDENT NUMBER INSTRUCTIONS: 1. The total

BUEC 280 LECTURE 6. Individual Labour Supply Continued

BUEC 280 ECTURE 6 Individual abour Supply Continued ast day Defined budget constraint Defined optimal allocation of leisure and consumption Changes in non-labour income generate a pure income effect Change

BUEC 280 ECTURE 6 Individual abour Supply Continued ast day Defined budget constraint Defined optimal allocation of leisure and consumption Changes in non-labour income generate a pure income effect Change

Economics 2002 HIGHER SCHOOL CERTIFICATE EXAMINATION. Total marks 100. Section I. Pages 2 8

2002 HIGHER SCHOOL CERTIFICATE EXAMINATION Economics Total marks 100 Section I Pages 2 8 General Instructions Reading time 5 minutes Working time 3 hours Write using black or blue pen Board-approved calculators

2002 HIGHER SCHOOL CERTIFICATE EXAMINATION Economics Total marks 100 Section I Pages 2 8 General Instructions Reading time 5 minutes Working time 3 hours Write using black or blue pen Board-approved calculators

NEW ZEALAND. 1. Overview of the tax-benefit system

NEW ZEALAND 2006 1. Overview of the tax-benefit system The provision of social security benefits in New Zealand is funded from general taxation and not specific social security contributions. Social security

NEW ZEALAND 2006 1. Overview of the tax-benefit system The provision of social security benefits in New Zealand is funded from general taxation and not specific social security contributions. Social security

Parliament of Australia Department of Parliamentary Services

Parliament of Australia Department of Parliamentary Services Parliamentary Library Information, analysis and advice for the Parliament RESEARCH PAPER www.aph.gov.au/library 4 September 2009, no. 4, 2009

Parliament of Australia Department of Parliamentary Services Parliamentary Library Information, analysis and advice for the Parliament RESEARCH PAPER www.aph.gov.au/library 4 September 2009, no. 4, 2009

CHAPTER 2. A TOUR OF THE BOOK

CHAPTER 2. A TOUR OF THE BOOK I. MOTIVATING QUESTIONS 1. How do economists define output, the unemployment rate, and the inflation rate, and why do economists care about these variables? Output and the

CHAPTER 2. A TOUR OF THE BOOK I. MOTIVATING QUESTIONS 1. How do economists define output, the unemployment rate, and the inflation rate, and why do economists care about these variables? Output and the

Empirical Evidence and Earnings Taxation:

Empirical Evidence and Earnings Taxation: Lessons from the Mirrlees Review ES World Congress August 2010 Richard Blundell University College London and Institute for Fiscal Studies Institute for Fiscal

Empirical Evidence and Earnings Taxation: Lessons from the Mirrlees Review ES World Congress August 2010 Richard Blundell University College London and Institute for Fiscal Studies Institute for Fiscal

c x y = U 2 a x U 1 earned income, per Angle with tangent w = wage rate 168 l = leisure (hours pw)

") Money for everyone? An appendi to chapter 10 The utility - or otherwise of being employed for a few hours a week 1 This appendi employs the concepts of utility or indifference curves to evaluate a change

Money for everyone? An appendi to chapter 10 The utility - or otherwise of being employed for a few hours a week 1 This appendi employs the concepts of utility or indifference curves to evaluate a change

Final. Mark Scheme ECON2. Economics. (Specification 2140) Unit 2: The National Economy. General Certificate of Education (A-level) January 2013 PMT