Estate Planning for the Multinational Family. Steven L. Cantor Cantor & Webb P.A., October 15, 2015

|

|

|

- Charity Bruce

- 5 years ago

- Views:

Transcription

1 Estate Planning for the Multinational Family Steven L. Cantor Cantor & Webb P.A., October 15, 2015

2 Introduction U.S. Tax Issues Discussion Points Planning Issues and Strategies U.S. Reporting Requirements Obligations of Financial Advisor/ Planner Common Mistakes Planning for A Foreign Family Member Who Will Become A U.S. Person

3 Resident/Nonresident Domiciliary/Nondomiciliary RESIDENT DOMICILIARY NONRESIDENT NONDOMICILIARY Why a Frown? Why a Smile?

4 Resident For U.S. Income Tax Purposes Green Card Physical presence Substantial presence Election Exceptions: Closer connection Treaty-based position Days not counted

5 Resident For U.S. Estate and Gift Tax Purposes Domicile: means physical presence AND intent to remain indefinitely Facts and circumstances test Treaty-based position

6 U.S. Income Taxation of U.S. Citizens and Residents Income taxation on worldwide income

7 U.S. Income Taxation of Nonresident Aliens Passive Income Fixed or determinable annual or periodic income (i.e. interest, dividends, rents, royalties, etc.) Subject to 30% withholding tax on the gross amount at the time of payment Effectively Connected Income Taxed on a net basis (after deductions) at graduated tax rates as they apply to United States residents Capital Gains United States Real Property Interests Physically present in U.S. for 183 days and U.S. tax home

8 U.S. Ownership of Foreign Corporations Controlled Foreign Corporation ( CFC ) More than 50% of vote or value owned by United States residents Applies only to 10% shareholders - a U.S. person who owns 10% or more of the total combined voting power Passive Foreign Investment Company ( PFIC ) At least 75% of gross income is passive income or average percentage of assets which produce or are held for production of passive income is at least 50% No minimum threshold of ownership

9 U.S. Estate & Gift Tax U.S. Citizens and Residents Taxed on worldwide assets, including certain interests in trust

10 U.S. Gift Tax - Nonresident Aliens Nonresident aliens are subject to gift tax on gifts of real property and tangible personal property situated within the United States. Gifts of intangible personal property are exempt Cash is tangible personal property Wires can be problematic Jointly held real estate is a gift tax trap for the unwary

11 Income Taxation of Trusts

12 Domestic Trust vs. Foreign Trust Domestic Trust: Court Test: A court within the U.S. is able to exercise primary supervision over the administration of the trust; AND Control Test: One or more U.S. persons have the authority to control all substantial decisions of the trust. Foreign Trust: all other trusts

13 Income Taxation of Trusts and Beneficiaries Grantor Trust Person treated as owner of assets is subject to U.S. income tax on current income (grantor trust does not have accumulated income) Non-Grantor Trust Trust subject to U.S. income tax except that beneficiaries are taxed on receipt of distributions of income and income required to be distributed (whether or not actually distributed) Foreign vs. Domestic Accumulation Distributions from foreign trust subject to throwback rules U.S. income tax and interest charge Accumulated income loses character Attribution of CFCs and PFICs

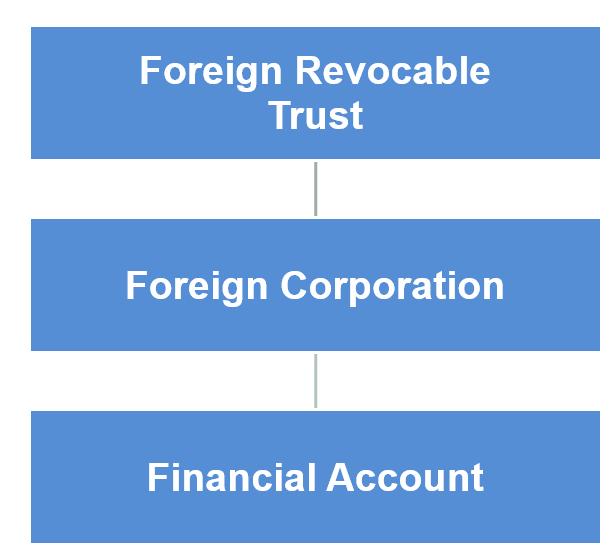

14 Examples

15 Planning Issues and Strategies

16 Funding of Trust Transfer of U.S. situs property Transfer of foreign situs property

17 Gifts During Settlor s Lifetime Transfers from foreign corporations or foreign partnerships Transfers from trust Transfers made by settlor personally

18 Step-Up in Basis Benefit How to do it?

19 Step-Up in Basis for Revocable Trusts Catch-all provision does not apply to foreign situs property acquired from NRNC Step-up in basis applies to property transferred by the decedent during his lifetime in trust to pay the income for life to or on the direction of the decedent, with the right reserved to the decedent at all times prior to his death to revoke the trust. Issues related to income Issues related to incapacity of decedent

20 Step-Up in Basis for Irrevocable Trusts Step-up in basis also applies, with respect to decedents dying after December 31, 1951, to property transferred by the decedent during his lifetime in trust to pay the income for life to or on the direction of the decedent, with the right reserved to the decedent at all times prior to his death to make any change in the enjoyment thereof through the exercise of a power to alter, amend, or terminate the trust. Issues of qualifying trust as a grantor trust when only grantor or spouse may be a beneficiary

21 Dealing with Foreign Corporations Basis Retained earnings CFC and PFIC rules

22 Incapacity of the Settlor Power to revoke or otherwise revest Dispositive provisions Pitfalls to avoid

23 Jointly-Settled Trusts General Power of Appointment for Surviving Spouse: Power must be exercised to transfer to another trust Surviving spouse must have a power over the new trust to be treated as an owner Distribution and recontribution

24 Typical method Accountings U.S. standards

25 Community Property U.S. spouse treated as owning or transferring half?

26 United States Reporting Requirements

27 FinCen Form 114 (June 30) IRS Form 3520 Important Forms IRS Form 3520-A (March 15) Foreign Grantor/Nongrantor Trust Beneficiary Statement IRS Form 5471 IRS Form 8621 IRS Form 8938 FATCA Compliance

28 Obligations of Financial Advisor Planning with PFICs Elections Exit Strategy

29 Common Mistakes Failure to spot a U.S. beneficiary Unrestricted power to remove and replace the trustee Failure to file timely reporting requirements Failure to maintain companies properly Failure to recognize and plan for the CFC or PFIC issues Transfer from account owned by foreign corporation or foreign partnership Failure to treat certain loans or property use as distributions Unintentionally creating a nongrantor trust Failure to take timely advice

30 Planning for A Foreign Family Member Who Will Become A U.S. Person

31 Objectives Minimize United States and Home Country taxes Consult with local counsel Consider interim residence Least aggregate amount of taxes in both countries and avoid double taxation to the greatest possible extent Coordinate tax and estate plan with non-tax issues Family relationships Cash flow Access to assets Understand United States financial disclosure and other relevant laws Maximize protection from creditors Address spousal rights, if any Address forced heirship rights, if any

32 Accelerate Income and Gains Income and gains realized prior to becoming a resident will not be subject to United States income tax if not ordinarily subject to such tax Identify key assets and income sources Determine expected time of ownership Difficulty in determining historic cost Appreciated marketable securities Rents and royalties Review existing life insurance and deferred compensation products/plans

33 Defer Deductions and Losses Sale of assets having built-in losses should be deferred until after becoming a resident Deductible expenses should be paid after becoming a resident Mortgage payments Charitable contributions

34 U.S. Pre-Immigration Planning Basis Step-Up Step up the basis of assets which have large built-in gains Check-the-Box Election technique for existing companies Additional gain recognition techniques

35 Gifts in Trust May avoid inclusion in donor s gross estate (depends upon powers retained or given, i.e., power to revoke or power of appointment) Donor may not be subject to tax on income from assets (i.e., if irrevocable domestic trust or foreign trust, but no U.S. beneficiaries) Not subject to United States gift tax if assets transferred to trust are not situated in the United States and donor not domiciled in the United States at time of gift

36 Gifts in Trust (Continued) Grantor can be a discretionary beneficiary of irrevocable trust Foreign vs. Domestic trusts Citizenship and residence of beneficiaries is important Reporting requirements Ensure gift is complete Dominion and control Claim of creditors

37 Action Items Make sure foreign trusts are drafted, funded and administered properly Maintain and respect structures owned by trusts as well Help foreign families spot U.S. beneficiaries to ensure accurate reporting Help foreign families identify estate planning opportunities Help foreign families identify pre-immigration planning opportunities Help foreign families plan for foreign grantor Review FATCA Compliance Plan the death and incapacity of

38 CAVEAT The information contained herein is provided for informational purposes only and is not intended to constitute the rendition of legal advice. No person should act upon this information without obtaining the opinion of United States legal counsel specializing in the area of international taxation.

39 Contact Information Steven L. Cantor Cantor & Webb P.A Brickell Bay Drive Suite 3112, Miami, FL Phone: (305) Fax: (305) Website:

Trusts with U.S. Beneficiaries Planning for The Avoidance of Costly Mistakes

Trusts with U.S. Beneficiaries Planning for The Avoidance of Costly Mistakes Steven L. Cantor October 25, 2012 Barbados Resident/Nonresident Domiciliary/Nondomiciliary RESIDENT DOMICILIARY NONRESIDENT

Trusts with U.S. Beneficiaries Planning for The Avoidance of Costly Mistakes Steven L. Cantor October 25, 2012 Barbados Resident/Nonresident Domiciliary/Nondomiciliary RESIDENT DOMICILIARY NONRESIDENT

Foreign Trusts With U.S. Beneficiaries. Mistakes Made in Drafting and Administration and How to Avoid Them. By: Kathryn von Matthiessen May 31, 2013

Foreign Trusts With U.S. Beneficiaries Mistakes Made in Drafting and Administration and How to Avoid Them By: Kathryn von Matthiessen May 31, 2013 Topics Foreign Trust Definition Grantor Trusts: Incapacity

Foreign Trusts With U.S. Beneficiaries Mistakes Made in Drafting and Administration and How to Avoid Them By: Kathryn von Matthiessen May 31, 2013 Topics Foreign Trust Definition Grantor Trusts: Incapacity

The Impact of U.S. Tax Reform on International Private Clients and Their Foreign Trusts

The Impact of U.S. Tax Reform on International Private Clients and Their Trusts Hal J. Webb: Partner Head of International Private Client Services STEP Cayman April 19, 2018 1 Gift and Estate Tax Exemption

The Impact of U.S. Tax Reform on International Private Clients and Their Trusts Hal J. Webb: Partner Head of International Private Client Services STEP Cayman April 19, 2018 1 Gift and Estate Tax Exemption

U.S. Tax Considerations for Multi-Jurisdictional Family Trust Planning

Slide 1 Slide 2 Estate Planning Council of Greater Miami February 19, 2015 U.S. Tax Considerations for Multi-Jurisdictional Family Trust Planning Presented by Todd N. Rosenberg, Esq. of Packman, Neuwahl

Slide 1 Slide 2 Estate Planning Council of Greater Miami February 19, 2015 U.S. Tax Considerations for Multi-Jurisdictional Family Trust Planning Presented by Todd N. Rosenberg, Esq. of Packman, Neuwahl

Meritas Capability Webinar U.S. Tax and Estate Planning for Foreign Persons

Meritas Capability Webinar U.S. Tax and Estate Planning for Foreign Persons Matthew R. Hillery, Director September 27, 2016 Speaker Matthew R. Hillery Director in the Private Client Department. Concentrates

Meritas Capability Webinar U.S. Tax and Estate Planning for Foreign Persons Matthew R. Hillery, Director September 27, 2016 Speaker Matthew R. Hillery Director in the Private Client Department. Concentrates

(b) TAX BENEFITS OF A HYBRID TRUST. The following are some US Federal Tax benefits of a Hybrid Grantor Trust.

TAX BENEFITS OF A HYBRID TRUST. The following are some US Federal Tax benefits of a Hybrid Grantor Trust.") NON RESIDENT ALIENS OF THE UNITED STATES AND HYBRID GRANTOR TRUSTS Last Updated: May 19, 2014 Article by Milagros Gomez Munoz of Milagros Gomez Munoz, P.A. I. HYBRID GRANTOR TRUSTS. (a) WHAT IS A HYBRID

NON RESIDENT ALIENS OF THE UNITED STATES AND HYBRID GRANTOR TRUSTS Last Updated: May 19, 2014 Article by Milagros Gomez Munoz of Milagros Gomez Munoz, P.A. I. HYBRID GRANTOR TRUSTS. (a) WHAT IS A HYBRID

Tax Planning for US Bound Clients

Tax Planning for US Bound Clients International Wealth Planners Geneva, 15 June 2011 Michael Parets Withers LLP, Zurich Office +41 44 488 8803 direct michael.parets@withersworldwide.com US-Bound Clients

Tax Planning for US Bound Clients International Wealth Planners Geneva, 15 June 2011 Michael Parets Withers LLP, Zurich Office +41 44 488 8803 direct michael.parets@withersworldwide.com US-Bound Clients

PRE-IMMIGRATION AND PRE-EXPATRIATION PLANNING

PRE-IMMIGRATION AND PRE-EXPATRIATION PLANNING A discussion about the hurdles, traps and best practices for counseling clients entering or leaving the U.S. DM2/7935921.1 The Attraction of the United States

PRE-IMMIGRATION AND PRE-EXPATRIATION PLANNING A discussion about the hurdles, traps and best practices for counseling clients entering or leaving the U.S. DM2/7935921.1 The Attraction of the United States

An Introduction to the US Estate and Gift Tax Regime

An Introduction to the US Estate and Gift Tax Regime DAVID G. ROBERTS www.crossborder.com CTF Edmonton Young Practitioners Group September 2012 Issues Who is a US person? US transfer taxes Common estate

An Introduction to the US Estate and Gift Tax Regime DAVID G. ROBERTS www.crossborder.com CTF Edmonton Young Practitioners Group September 2012 Issues Who is a US person? US transfer taxes Common estate

Filing Requirements U.S. citizens residing in Canada must file both Canadian and U.S. income tax returns every year.

RBC Wealth Management Services The Navigator Tax Planning for U.S. Citizen Residents in Canada Maximize your wealth by utilizing tax planning ideas and understanding the tax issues The United States is

RBC Wealth Management Services The Navigator Tax Planning for U.S. Citizen Residents in Canada Maximize your wealth by utilizing tax planning ideas and understanding the tax issues The United States is

Tax Guide For Foreign Investors In U.S. Residential Real Estate

A T T O R N E Y S A T L A W Tax Guide For Foreign Investors In U.S. Residential Real Estate 2018 Edition In this guide I. Introduction 2 II. The U.S. Tax System 3 A. U.S. Persons 3 1. Basic Rules 3 2.

A T T O R N E Y S A T L A W Tax Guide For Foreign Investors In U.S. Residential Real Estate 2018 Edition In this guide I. Introduction 2 II. The U.S. Tax System 3 A. U.S. Persons 3 1. Basic Rules 3 2.

Tax Planning for U.S. Citizen Residents in Canada. Maximize your wealth by utilizing tax planning ideas and understanding the tax issues

The Navigator RBC WEALTH MANAGEMENT SERVICES Tax Planning for U.S. Citizen Residents in Canada Maximize your wealth by utilizing tax planning ideas and understanding the tax issues The United States is

The Navigator RBC WEALTH MANAGEMENT SERVICES Tax Planning for U.S. Citizen Residents in Canada Maximize your wealth by utilizing tax planning ideas and understanding the tax issues The United States is

What Every Domestic Estate Planning Attorney Should Know About International Estate Planning

What Every Domestic Estate Planning Attorney Should Know About International Estate Planning October 21, 2015 Todd Angkatavanich, Esq., Withers Bergman LLP (Connecticut) Richard Cassell, Esq., Withers

What Every Domestic Estate Planning Attorney Should Know About International Estate Planning October 21, 2015 Todd Angkatavanich, Esq., Withers Bergman LLP (Connecticut) Richard Cassell, Esq., Withers

EXPAT TAX HANDBOOK. Non-Citizens and U.S. Tax Residency. Tax Year Ephraim Moss, Esq Ext 101

EXPAT TAX HANDBOOK Non-Citizens and U.S. Tax Residency Tax Year 2018 Ephraim Moss, Esq. 718-887-9933 Ext 101 emoss@expattaxprofessionals.com Joshua Ashman, CPA 718-887-9933 Ext 102 jashman@expattaxprofessionals.com

EXPAT TAX HANDBOOK Non-Citizens and U.S. Tax Residency Tax Year 2018 Ephraim Moss, Esq. 718-887-9933 Ext 101 emoss@expattaxprofessionals.com Joshua Ashman, CPA 718-887-9933 Ext 102 jashman@expattaxprofessionals.com

T he relatively strong U.S. economy continues to attract

Daily Tax Report Reproduced with permission from Daily Tax Report, 243 DTR J-1, 12/18/15. Copyright 2015 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Foreign Taxpayers Jenny

Daily Tax Report Reproduced with permission from Daily Tax Report, 243 DTR J-1, 12/18/15. Copyright 2015 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Foreign Taxpayers Jenny

I. Basic Rules. Planning for the Non- Citizen Spouse: Tips and Traps 2/25/2016. Zena M. Tamler. March 11, 2016 New York, New York

Planning for the Non- Citizen Spouse: Tips and Traps Zena M. Tamler March 11, 2016 New York, New York Attorney Advertising Prior results do not guarantee a similar outcome. Copyright 2016 2015 Sullivan

Planning for the Non- Citizen Spouse: Tips and Traps Zena M. Tamler March 11, 2016 New York, New York Attorney Advertising Prior results do not guarantee a similar outcome. Copyright 2016 2015 Sullivan

International Trade and/or Investment Affords Opportunities

Overview of International Estate Planning Issues Affecting U.S. Persons or Non-U.S. Persons with U.S. Sitused Assets 2010 Advanced Tax Institute November 3, 2010 Baltimore, Maryland Elizabeth M. Schurig

Overview of International Estate Planning Issues Affecting U.S. Persons or Non-U.S. Persons with U.S. Sitused Assets 2010 Advanced Tax Institute November 3, 2010 Baltimore, Maryland Elizabeth M. Schurig

U.S. Tax Planning for Non-U.S. Persons, Assets and Trusts An Introductory. Outline. G. Warren Whitaker Dina Kapur Sanna Day Pitney LLP, New York, NY

U.S. Tax Planning for Non-U.S. Persons, Assets and Trusts An Introductory Outline G. Warren Whitaker Dina Kapur Sanna Day Pitney LLP, New York, NY BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON,

U.S. Tax Planning for Non-U.S. Persons, Assets and Trusts An Introductory Outline G. Warren Whitaker Dina Kapur Sanna Day Pitney LLP, New York, NY BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON,

What You Don t Know Will Hurt You

What You Don t Know Will Hurt You Avoiding International Tax and Estate Planning Traps STEP Silicon Valley April 19, 2017 Richard S. Kinyon, Partner, Shartsis Friese, LLP E.J. Hong, Esq., Law Offices of

What You Don t Know Will Hurt You Avoiding International Tax and Estate Planning Traps STEP Silicon Valley April 19, 2017 Richard S. Kinyon, Partner, Shartsis Friese, LLP E.J. Hong, Esq., Law Offices of

A Guide to Estate Planning

BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON, DC www.daypitney.com A Guide to Estate Planning THE IMPORTANCE OF ESTATE PLANNING The goal of estate planning is to direct the transfer and management

BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON, DC www.daypitney.com A Guide to Estate Planning THE IMPORTANCE OF ESTATE PLANNING The goal of estate planning is to direct the transfer and management

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features: Dean C. Berry, Partner, Cadwalader Wickersham & Taft, New York

Presenting a live 90-minute webinar with interactive Q&A Estate Planning Involving Resident and Non-Resident Aliens Navigating Estate, Gift and GST Tax Rules; Leveraging Estate and Lifetime Gifting Opportunities

Presenting a live 90-minute webinar with interactive Q&A Estate Planning Involving Resident and Non-Resident Aliens Navigating Estate, Gift and GST Tax Rules; Leveraging Estate and Lifetime Gifting Opportunities

Expatriation from the United States

Expatriation from the United States Hal J. Webb November 15, 2012 Bahamas Discussion Points Tax Rules Applicable to Expatriations on or After June 17, 2008 Reporting Requirements Planning for Expatriation

Expatriation from the United States Hal J. Webb November 15, 2012 Bahamas Discussion Points Tax Rules Applicable to Expatriations on or After June 17, 2008 Reporting Requirements Planning for Expatriation

VEGAS IS NOT JUST FOR GAMBLERS: THE BENEFITS AND OPPORTUNITIES OF NEVADA DISCRETIONARY TRUSTS FOR NRAS DATAN Z. DOROT, ESQ.

TTN CONFERENCE November 30, 2017 VEGAS IS NOT JUST FOR GAMBLERS: THE BENEFITS AND OPPORTUNITIES OF NEVADA DISCRETIONARY TRUSTS FOR NRAS DATAN Z. DOROT, ESQ. 1 CIRCULAR 230 NOTICE The information contained

TTN CONFERENCE November 30, 2017 VEGAS IS NOT JUST FOR GAMBLERS: THE BENEFITS AND OPPORTUNITIES OF NEVADA DISCRETIONARY TRUSTS FOR NRAS DATAN Z. DOROT, ESQ. 1 CIRCULAR 230 NOTICE The information contained

Looking Beyond Our Borders:

Looking Beyond Our Borders: U.S. Income, Estate, and Gift Tax Implications 2017 Advanced Estate Planning Conference MGM Grand Las Vegas June 13, 2017 Peggy A. Ugent, CPA 100 CONGRESS AVENUE, SUITE 1440

Looking Beyond Our Borders: U.S. Income, Estate, and Gift Tax Implications 2017 Advanced Estate Planning Conference MGM Grand Las Vegas June 13, 2017 Peggy A. Ugent, CPA 100 CONGRESS AVENUE, SUITE 1440

Top 10 Tax Issues facing U.S. Citizens living in Canada

Top 10 Tax Issues facing U.S. Citizens living in Canada An individual may be considered a U.S. citizen if he or she: was born in the U.S.; successfully applied to become a naturalized citizen of the U.S.;

Top 10 Tax Issues facing U.S. Citizens living in Canada An individual may be considered a U.S. citizen if he or she: was born in the U.S.; successfully applied to become a naturalized citizen of the U.S.;

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA Over the past few years, there has been increased media attention in Canada with respect to the U.S. income tax filing requirements

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA Over the past few years, there has been increased media attention in Canada with respect to the U.S. income tax filing requirements

Identifying and Solving Problems in the Taxation of Non-Resident Aliens. Presented to New York Step Conference. March 10, New York, New York

Identifying and Solving Problems in the Taxation of Non-Resident Aliens Presented to New York Step Conference March 10, 2016 New York, New York By Leigh-Alexandra Basha, Partner/Private Client Group McDermott

Identifying and Solving Problems in the Taxation of Non-Resident Aliens Presented to New York Step Conference March 10, 2016 New York, New York By Leigh-Alexandra Basha, Partner/Private Client Group McDermott

RBC Wealth Management Services

RBC Wealth Management Services The Navigator C HARLES W. C ULLEN III CFP(Canada and U.S.),CIM Associate Portfolio Manager & Wealth Advisor 902-424-1092 charles.cullen@rbc.com D AYNA P ARK Associate 902-421-0244

RBC Wealth Management Services The Navigator C HARLES W. C ULLEN III CFP(Canada and U.S.),CIM Associate Portfolio Manager & Wealth Advisor 902-424-1092 charles.cullen@rbc.com D AYNA P ARK Associate 902-421-0244

Foreign Trusts Reporting Obligations

Foreign Trusts Reporting Obligations Brad Bedingfield 24270 by any measure What is a Foreign Trust? By default, all trusts are foreign trusts unless: A court within the US is able to exercise primary supervision

Foreign Trusts Reporting Obligations Brad Bedingfield 24270 by any measure What is a Foreign Trust? By default, all trusts are foreign trusts unless: A court within the US is able to exercise primary supervision

D'Amico Family Wealth Management Group Of RBC Dominion Securities

D'Amico Family Wealth Management Group Of RBC Dominion Securities Presents David Altro from Altro Levy, Lawyers "Cross Border Tax & Estate Planning for Canadians with U.S. Real Estate" Angelo D Amico FCSI,

D'Amico Family Wealth Management Group Of RBC Dominion Securities Presents David Altro from Altro Levy, Lawyers "Cross Border Tax & Estate Planning for Canadians with U.S. Real Estate" Angelo D Amico FCSI,

ABA RPTE 2016 Spring Symposia Boston, MA

Hot Topics: Foreign versus Domestic Trusts, US Trusts for Foreign Families, Migration of Trusts, FATCA Requirements, Investment in US Real Estate, and FIRPTA ABA RPTE 2016 Spring Symposia Boston, MA Brian

Hot Topics: Foreign versus Domestic Trusts, US Trusts for Foreign Families, Migration of Trusts, FATCA Requirements, Investment in US Real Estate, and FIRPTA ABA RPTE 2016 Spring Symposia Boston, MA Brian

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA

`` TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA Over the past few years, there has been increased media attention in Canada with respect to the U.S. income tax filing requirements

`` TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA Over the past few years, there has been increased media attention in Canada with respect to the U.S. income tax filing requirements

Galia Antebi, Esq. Nina Krauthamer, Esq. Ruchelman P.L.L.C. New York, NY

Nina Krauthamer, Esq. krauthamer@ruchelaw.com Ruchelman P.L.L.C. New York, NY Galia Antebi, Esq. antebi@ruchelaw.com www.ruchelaw.com +1 (212) 755 3333-1 - - 2-2017 Purchases by foreign individuals of

Nina Krauthamer, Esq. krauthamer@ruchelaw.com Ruchelman P.L.L.C. New York, NY Galia Antebi, Esq. antebi@ruchelaw.com www.ruchelaw.com +1 (212) 755 3333-1 - - 2-2017 Purchases by foreign individuals of

Article-Foreign Trusts and U.S. Estate Planning: A Client- Centered Analysis

Article-Foreign Trusts and U.S. Estate Planning: A Client- Centered Analysis I. INTRODUCTION by Michael W. Galligan In 1996, with a series of amendments to the Internal Revenue Code regarding the tax treatment

Article-Foreign Trusts and U.S. Estate Planning: A Client- Centered Analysis I. INTRODUCTION by Michael W. Galligan In 1996, with a series of amendments to the Internal Revenue Code regarding the tax treatment

"US recipients of gifts and bequests from Covered Expatriates will now incur gift and estate tax"

Steve Leimberg's Estate Planning Email Newsletter - Archive Message #1324 Date: 23-Jul-08 From: Steve Leimberg's Estate Planning Newsletter Subject: HEART Legislation Enacts New Expatriation Rules "US

Steve Leimberg's Estate Planning Email Newsletter - Archive Message #1324 Date: 23-Jul-08 From: Steve Leimberg's Estate Planning Newsletter Subject: HEART Legislation Enacts New Expatriation Rules "US

Practical Solutions to Deal with the Inconvenience of Having a Family Member Who is a U.S. Person

Practical Solutions to Deal with the Inconvenience of Having a Family Member Who is a U.S. Person! Shawn P. Wolf, Esq. Packman, Neuwahl & Rosenberg E-mail: spw@pnrlaw.com! 1500 San Remo Ave. Suite 125

Practical Solutions to Deal with the Inconvenience of Having a Family Member Who is a U.S. Person! Shawn P. Wolf, Esq. Packman, Neuwahl & Rosenberg E-mail: spw@pnrlaw.com! 1500 San Remo Ave. Suite 125

TECHNICAL EXPLANATION OF H.R

TECHNICAL EXPLANATION OF H.R. 6081, THE HEROES EARNINGS ASSISTANCE AND RELIEF TAX ACT OF 2008, AS SCHEDULED FOR CONSIDERATION BY THE HOUSE OF REPRESENTATIVES ON MAY 20, 2008 Prepared by the Staff of the

TECHNICAL EXPLANATION OF H.R. 6081, THE HEROES EARNINGS ASSISTANCE AND RELIEF TAX ACT OF 2008, AS SCHEDULED FOR CONSIDERATION BY THE HOUSE OF REPRESENTATIVES ON MAY 20, 2008 Prepared by the Staff of the

Private Company Services. U.S. Estate and Gift taxation of resident aliens and nonresident aliens

Private Company Services U.S. Estate and Gift taxation of resident aliens and nonresident aliens 2010 2012 Non-U.S. citizens, both resident and nonresident aliens, may be subject to U.S. estate and gift

Private Company Services U.S. Estate and Gift taxation of resident aliens and nonresident aliens 2010 2012 Non-U.S. citizens, both resident and nonresident aliens, may be subject to U.S. estate and gift

INFORMATION ON REVOCABLE LIVING TRUSTS

INFORMATION ON REVOCABLE LIVING TRUSTS The revocable, or living, trust is often promoted as a means of avoiding probate and saving taxes at death. The revocable trust has certain advantages over a traditional

INFORMATION ON REVOCABLE LIVING TRUSTS The revocable, or living, trust is often promoted as a means of avoiding probate and saving taxes at death. The revocable trust has certain advantages over a traditional

2600 N. Military Trail, Suite 206, Boca Raton, Florida Tel

2600 N. Military Trail, Suite 206, Boca Raton, Florida 33431 Tel. 1-561-368-1113 www.lehmantaxlaw.com U.S. Taxation of Foreign Corporations And Nonresident Aliens General Rules Tax Planning Before Immigrating

2600 N. Military Trail, Suite 206, Boca Raton, Florida 33431 Tel. 1-561-368-1113 www.lehmantaxlaw.com U.S. Taxation of Foreign Corporations And Nonresident Aliens General Rules Tax Planning Before Immigrating

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2013

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2013 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION January 8, 2013 JCX-2-13R I. SUMMARY OF PRESENT-LAW FEDERAL TAX SYSTEM A. Individual Income

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2013 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION January 8, 2013 JCX-2-13R I. SUMMARY OF PRESENT-LAW FEDERAL TAX SYSTEM A. Individual Income

QDOT-ting I's and Crossing T's: Estate Tax Planning for Non-United States Citizen Spouses

QDOT-ting I's and Crossing T's: Estate Tax Planning for Non-United States Citizen Spouses Written By John R. Cella, Jr. (jrcella@wardandsmith.com) April 17, 2017 Individual and corporate citizens from

QDOT-ting I's and Crossing T's: Estate Tax Planning for Non-United States Citizen Spouses Written By John R. Cella, Jr. (jrcella@wardandsmith.com) April 17, 2017 Individual and corporate citizens from

Reporting Requirements of U.S. Persons Connected to Foreign Trusts and of Delaware (Foreign) Trusts 1

Trusts 1") Reporting Requirements of U.S. Persons Connected to Foreign Trusts and of Delaware (Foreign) Trusts 1 Dina Kapur Sanna 2 This outline describes the reporting requirements applicable to U.S. persons who

Reporting Requirements of U.S. Persons Connected to Foreign Trusts and of Delaware (Foreign) Trusts 1 Dina Kapur Sanna 2 This outline describes the reporting requirements applicable to U.S. persons who

Complex Issues. Foreign Trusts

Complex Issues in Foreign Trusts Robert D. Colvin, Houston, TX Dina Kapur Sanna, New York, NY 13 th Annual International Estate Planning Institute March 23, 2017 Domestic vs Foreign Trusts Bias in favor

Complex Issues in Foreign Trusts Robert D. Colvin, Houston, TX Dina Kapur Sanna, New York, NY 13 th Annual International Estate Planning Institute March 23, 2017 Domestic vs Foreign Trusts Bias in favor

Non-Citizen Spouse. Estate Planning Using Qualified Domestic Trusts (QDOTs) and Irrevocable Life Insurance Trusts (ILITs)

and Irrevocable Life Insurance Trusts (ILITs)") Guiding you through life. SALES STRATEGY NEEDS ANALYSIS Non-Citizen Spouse Estate Planning Using Qualified Domestic Trusts (QDOTs) and Irrevocable Life Insurance Trusts (ILITs) As large numbers of people

Guiding you through life. SALES STRATEGY NEEDS ANALYSIS Non-Citizen Spouse Estate Planning Using Qualified Domestic Trusts (QDOTs) and Irrevocable Life Insurance Trusts (ILITs) As large numbers of people

ALIYAH FROM THE USA. STEP ISRAEL Annual Conference Tel Aviv, Israel June 20, 21, 2017

Washington, DC New York, NY New Haven, CT Chicago, IL ALIYAH FROM THE USA STEP ISRAEL Annual Conference Tel Aviv, Israel June 20, 21, 2017 Stanley A. Barg Kozusko Harris Duncan Email: sbarg@kozlaw.com

Washington, DC New York, NY New Haven, CT Chicago, IL ALIYAH FROM THE USA STEP ISRAEL Annual Conference Tel Aviv, Israel June 20, 21, 2017 Stanley A. Barg Kozusko Harris Duncan Email: sbarg@kozlaw.com

Estate Planning Council of Toronto: Estate Tax Update

www.pwc.com/ca Estate Planning Council of Toronto: Ian Macdonald November 5, 2013 Agenda US Estate and Gift Tax Update 1. New Rules 2. Implications for US Citizens Living in Canada 3. Implications for

www.pwc.com/ca Estate Planning Council of Toronto: Ian Macdonald November 5, 2013 Agenda US Estate and Gift Tax Update 1. New Rules 2. Implications for US Citizens Living in Canada 3. Implications for

Canadians with International Assets

Canadians with International Assets Presented by: Lorne Saltman May 17, 2017 Topics to Discuss 1. Introduction: Know Your Client 2. Common law vs. Civil Law Jurisdictions 3. Recognition of Trusts 4. Multiple

Canadians with International Assets Presented by: Lorne Saltman May 17, 2017 Topics to Discuss 1. Introduction: Know Your Client 2. Common law vs. Civil Law Jurisdictions 3. Recognition of Trusts 4. Multiple

GUIDANCE ON MAKING GIFTS: FOREIGN PERSONS WITH CHILDREN IN THE U.S.

FOREIGN PERSONS WITH CHILDREN IN THE U.S. GENERAL RULES A foreign person refers to someone who is not a U.S. citizen or domiciled in the U.S. Gifts of real property in the U.S. are subject to U.S. federal

FOREIGN PERSONS WITH CHILDREN IN THE U.S. GENERAL RULES A foreign person refers to someone who is not a U.S. citizen or domiciled in the U.S. Gifts of real property in the U.S. are subject to U.S. federal

Estate Planning for Foreign Nationals

Estate Planning for Foreign Nationals What Financial Professionals Need to Know www.mcnulty-law.com Tel. (212) 431-7526 What We ll Be Covering Non-Tax Estate Planning Issues US Estate Taxation of US citizens

Estate Planning for Foreign Nationals What Financial Professionals Need to Know www.mcnulty-law.com Tel. (212) 431-7526 What We ll Be Covering Non-Tax Estate Planning Issues US Estate Taxation of US citizens

Use of Bahamas Foundations and Private Trust Companies in International Planning

Use of Bahamas Foundations and Private Trust Companies in International Planning Date: March 20, 2007 Speaker: Steven L. Cantor, Esq. Wealth Management Planning Seminar Sponsored by the Bahamas Financial

Use of Bahamas Foundations and Private Trust Companies in International Planning Date: March 20, 2007 Speaker: Steven L. Cantor, Esq. Wealth Management Planning Seminar Sponsored by the Bahamas Financial

PRESENTATION FOR VAELA

ESTATE PLANNING ISSUES SPECIFIC TO NON-U.S. CITIZENS PRESENTATION FOR VAELA BY YAHNE MIORINI, ESQ. Miorini Law PLLC 1816 Opalocka Drive McLean, VA 22101 www.miorinilaw.com (703) 448-6121 Yahne.miorini@miorinilaw.com

ESTATE PLANNING ISSUES SPECIFIC TO NON-U.S. CITIZENS PRESENTATION FOR VAELA BY YAHNE MIORINI, ESQ. Miorini Law PLLC 1816 Opalocka Drive McLean, VA 22101 www.miorinilaw.com (703) 448-6121 Yahne.miorini@miorinilaw.com

International Tax Issues for the Domestic Estate Planner. N. Todd Angkatavanich Scott A. Bowman Carlyn McCaffrey Edward Vergara

International Tax Issues for the Domestic Estate Planner N. Todd Angkatavanich Scott A. Bowman Carlyn McCaffrey Edward Vergara The World is Getting Smaller And Clients Are Getting More Global Increasing

International Tax Issues for the Domestic Estate Planner N. Todd Angkatavanich Scott A. Bowman Carlyn McCaffrey Edward Vergara The World is Getting Smaller And Clients Are Getting More Global Increasing

Tax & Estate Planning for Snowbirds

Tax & Estate Planning for Snowbirds Amin Mawani Schulich School of Business York University amawani@schulich.yorku.ca Taxes do influence behaviour Windowless Castles Narrow frontages SIN & gasoline taxes

Tax & Estate Planning for Snowbirds Amin Mawani Schulich School of Business York University amawani@schulich.yorku.ca Taxes do influence behaviour Windowless Castles Narrow frontages SIN & gasoline taxes

The Navigator. RBC Wealth Management Services. Understand Your Exposure and Strategies to Minimize It

RBC Wealth Management Services The Navigator U.S. Estate Tax for Canadians in 2013 Understand Your Exposure and Strategies to Minimize It Did you know that even Canadians who die owning U.S. assets such

RBC Wealth Management Services The Navigator U.S. Estate Tax for Canadians in 2013 Understand Your Exposure and Strategies to Minimize It Did you know that even Canadians who die owning U.S. assets such

Not Your Father s U.S. Pre-Immigration Tax Plan

Slide 1 Slide 2 TTN Conference Miami 2014 Not Your Father s U.S. Pre-Immigration Tax Plan Presented by Todd N. Rosenberg, Esq. of Packman, Neuwahl & Rosenberg 1500 San Remo Avenue, Suite 125 Coral Gables,

Slide 1 Slide 2 TTN Conference Miami 2014 Not Your Father s U.S. Pre-Immigration Tax Plan Presented by Todd N. Rosenberg, Esq. of Packman, Neuwahl & Rosenberg 1500 San Remo Avenue, Suite 125 Coral Gables,

Opportunities for Guernsey trust business in the US/UK market place

Opportunities for Guernsey trust business in the US/UK market place 19 October 2016 Disclaimer This presentation reflects our understanding of US tax issues based on our experience but, for the avoidance

Opportunities for Guernsey trust business in the US/UK market place 19 October 2016 Disclaimer This presentation reflects our understanding of US tax issues based on our experience but, for the avoidance

TAX CONSEQUENCES OF U.S. INVESTMENTS FOR NON-U.S. CITIZENS

TAX CONSEQUENCES OF U.S. INVESTMENTS FOR NON-U.S. CITIZENS WHAT A GLOBAL FAMILY NEEDS TO KNOW If you are not a United States ( U.S. ) citizen (or a U.S. resident/ domiciliary) and are considering an investment

TAX CONSEQUENCES OF U.S. INVESTMENTS FOR NON-U.S. CITIZENS WHAT A GLOBAL FAMILY NEEDS TO KNOW If you are not a United States ( U.S. ) citizen (or a U.S. resident/ domiciliary) and are considering an investment

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features: W. Aaron Hawthorne, Managing Director, Andersen Tax, Dallas

Presenting a live 90-minute webinar with interactive Q&A U.S.-Mexican Tax and Estate Planning for Cross-Border Clients Reconciling U.S. and Mexican Law on Trusts, Ownership of Real Property, Situs and

Presenting a live 90-minute webinar with interactive Q&A U.S.-Mexican Tax and Estate Planning for Cross-Border Clients Reconciling U.S. and Mexican Law on Trusts, Ownership of Real Property, Situs and

A comparison of the Form filing requirements and the Form 8938 filing requirements follows:

This week Mark Jennings, Assistant Vice President of Investments, at LOM Securities (Bermuda) Ltd. hosted a conference on International Taxes and Trusts for US Citizens Living in Bermuda and US Beneficiaries

This week Mark Jennings, Assistant Vice President of Investments, at LOM Securities (Bermuda) Ltd. hosted a conference on International Taxes and Trusts for US Citizens Living in Bermuda and US Beneficiaries

U.S. Estate Tax for Canadians in 2012

The Navigator RBC WEALTH MANAGEMENT SERVICES U.S. Estate Tax for Canadians in 2012 Understand your exposure and strategies to minimize it The U.S. has a wealth transfer tax regime that imposes taxes on

The Navigator RBC WEALTH MANAGEMENT SERVICES U.S. Estate Tax for Canadians in 2012 Understand your exposure and strategies to minimize it The U.S. has a wealth transfer tax regime that imposes taxes on

U.S. Income Tax for Foreign Students, Scholars and Teachers. Arthur R. Kerr II Vacovec Mayotte & Singer LLP

U.S. Income Tax for Foreign Students, Scholars and Teachers Arthur R. Kerr II Vacovec Mayotte & Singer LLP 617-964-0500 akerr@vacovec.com Are You Resident or Nonresident? Residence for tax purposes not

U.S. Income Tax for Foreign Students, Scholars and Teachers Arthur R. Kerr II Vacovec Mayotte & Singer LLP 617-964-0500 akerr@vacovec.com Are You Resident or Nonresident? Residence for tax purposes not

Tax Planning for High Net Worth Individuals Immigrating to the United States

The Tax Adviser Tax Planning for High Net Worth Individuals Immigrating to the United States By Rolando Garcia, CPA, J.D., Houston 7 hours 42 minutes ago Editor: Mindy Tyson Weber, CPA, M.Tax. For generations,

The Tax Adviser Tax Planning for High Net Worth Individuals Immigrating to the United States By Rolando Garcia, CPA, J.D., Houston 7 hours 42 minutes ago Editor: Mindy Tyson Weber, CPA, M.Tax. For generations,

Understanding the Gift and Estate Tax Rules for MAPTs and VAPTs. General Trust Considerations. General Trust Considerations

Understanding the Gift and Estate Tax Rules for MAPTs and VAPTs 1 General Trust Considerations Gift Taxes (is the transfer taxable?) Estate Taxes (are the assets includable?) Income Taxes (who pays it?)

Understanding the Gift and Estate Tax Rules for MAPTs and VAPTs 1 General Trust Considerations Gift Taxes (is the transfer taxable?) Estate Taxes (are the assets includable?) Income Taxes (who pays it?)

BUILDING BASIS, BEYOND THE BASICS: Effective and Efficient Basis Building Strategies For Your Client

BUILDING BASIS, BEYOND THE BASICS: Effective and Efficient Basis Building Strategies For Your Client Ellen Harrison McDermott Will & Emery Washington, D.C., Turney P. Berry Wyatt Tarrant & Combs Louisville,

BUILDING BASIS, BEYOND THE BASICS: Effective and Efficient Basis Building Strategies For Your Client Ellen Harrison McDermott Will & Emery Washington, D.C., Turney P. Berry Wyatt Tarrant & Combs Louisville,

The US Ireland Connection John Gill and Lydia McCormack

The US Ireland Connection John Gill and Lydia McCormack The information in this document is provided subject to the Legal Terms and Liability Disclaimer contained on the Matheson website. The material

The US Ireland Connection John Gill and Lydia McCormack The information in this document is provided subject to the Legal Terms and Liability Disclaimer contained on the Matheson website. The material

WHAT THE FATCA IS GOING ON? NAVIGATING VARIOUS U.S. TAX IMPLICATIONS AND COMPLIANCE REQUIREMENTS FOR INTERNATIONAL CLIENTS AND ASSETS

WHAT THE FATCA IS GOING ON? NAVIGATING VARIOUS U.S. TAX IMPLICATIONS AND COMPLIANCE REQUIREMENTS FOR INTERNATIONAL CLIENTS AND ASSETS BENETTA P. JENSON is a Managing Director at J.P. Morgan Private Bank

WHAT THE FATCA IS GOING ON? NAVIGATING VARIOUS U.S. TAX IMPLICATIONS AND COMPLIANCE REQUIREMENTS FOR INTERNATIONAL CLIENTS AND ASSETS BENETTA P. JENSON is a Managing Director at J.P. Morgan Private Bank

AN ASSOCIATION OF ATTORNEYS EST BEVERLY HILLS, CALIFORNIA (310) (323)

(323)") Altshuler and and Spiro Spiro AN ASSOCIATION OF ATTORNEYS EST. 1959 ssor 9301 wtishrre WILSHIRE BouLEVARD, BOULEVARD, sutre SUITE s04 504 BEVERLY HILLS, CALIFORNIA 90210-5412 0-5412 (310) 275-4475 - (323)

Altshuler and and Spiro Spiro AN ASSOCIATION OF ATTORNEYS EST. 1959 ssor 9301 wtishrre WILSHIRE BouLEVARD, BOULEVARD, sutre SUITE s04 504 BEVERLY HILLS, CALIFORNIA 90210-5412 0-5412 (310) 275-4475 - (323)

Business Development: Trust 101

Business Development: Trust 101 The Basics of Delaware Trust Planning Commonwealth Trust Trust Company Company 29 Bancroft 29 Bancroft Mills Mills Road, Road 2 nd Floor Wilmington, Delaware 19806 P: (302)

Business Development: Trust 101 The Basics of Delaware Trust Planning Commonwealth Trust Trust Company Company 29 Bancroft 29 Bancroft Mills Mills Road, Road 2 nd Floor Wilmington, Delaware 19806 P: (302)

U.S. Estate Tax for Canadians

BMO Financial Group PAGE 1 U.S. Estate Tax for Canadians As a Canadian you may be unaware that your estate could be impacted by U.S. estate tax if you own U.S. securities or U.S. real estate. This article

BMO Financial Group PAGE 1 U.S. Estate Tax for Canadians As a Canadian you may be unaware that your estate could be impacted by U.S. estate tax if you own U.S. securities or U.S. real estate. This article

Estate Planning under the New Tax Law

Tax, Benefits, and Private Client JANUARY 2018 NO. 1 Estate Planning under the New Tax Law This client alert is part of a special series on the Tax Cuts and Jobs Act and related changes to the tax code,

Tax, Benefits, and Private Client JANUARY 2018 NO. 1 Estate Planning under the New Tax Law This client alert is part of a special series on the Tax Cuts and Jobs Act and related changes to the tax code,

Trump Change: Tax planning for US/UK individuals in a post-truth world

Trump Change: Tax planning for US/UK individuals in a post-truth world Chris McLemore Contact Information Chris.McLemore@butlersnow.com +44 (0) 203 300 3806 Practice Areas and Industry Teams Wealth Transfer

Trump Change: Tax planning for US/UK individuals in a post-truth world Chris McLemore Contact Information Chris.McLemore@butlersnow.com +44 (0) 203 300 3806 Practice Areas and Industry Teams Wealth Transfer

Estate Planning Techniques for Multinational Families

Presenting a live 90-minute teleconference with interactive Q&A Estate Planning Techniques for Multinational Families Navigating Interests in Foreign Business, Real Estate and Financial Accounts TUESDAY,

Presenting a live 90-minute teleconference with interactive Q&A Estate Planning Techniques for Multinational Families Navigating Interests in Foreign Business, Real Estate and Financial Accounts TUESDAY,

American Citizens Abroad. Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION

1 November 2017; 1 December 2017; 19 January 2018 American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION This side-by-side analysis compares Current Law (i.e.,

1 November 2017; 1 December 2017; 19 January 2018 American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION This side-by-side analysis compares Current Law (i.e.,

The confluence of several events

Estate Planning Gets More Complex for Non-U.S. Citizens Tax treaties, as well as the Internal Revenue Code, need to be reviewed when advising non-u.s. citizens about strategies to minimize transfer taxes.

Estate Planning Gets More Complex for Non-U.S. Citizens Tax treaties, as well as the Internal Revenue Code, need to be reviewed when advising non-u.s. citizens about strategies to minimize transfer taxes.

RECENT LEGISLATION INVOLVING FOREIGN TRUSTS AND GIFTS 1997 Robert L. Sommers

RECENT LEGISLATION INVOLVING FOREIGN TRUSTS AND GIFTS 1997 Robert L. Sommers I. INTRODUCTION... 1 1. Rich Immigrating Foreigners - The New Villain... 1 2. Foreign Gifts - New Reporting Requirements...

RECENT LEGISLATION INVOLVING FOREIGN TRUSTS AND GIFTS 1997 Robert L. Sommers I. INTRODUCTION... 1 1. Rich Immigrating Foreigners - The New Villain... 1 2. Foreign Gifts - New Reporting Requirements...

Did You Say You Have a U.S. Passport?

Did You Say You Have a U.S. Passport? STEP Bahamas 7 June 2012 Jack Brister, Principal International Tax Services jbrister@mbafcpa.com Introduction So you have a U.S. Passport. Welcome to the club! Your

Did You Say You Have a U.S. Passport? STEP Bahamas 7 June 2012 Jack Brister, Principal International Tax Services jbrister@mbafcpa.com Introduction So you have a U.S. Passport. Welcome to the club! Your

MANAGING TRIVIAL PURSUITS: DOMESTICATION OF FOREIGN TRUSTS

MANAGING TRIVIAL PURSUITS: DOMESTICATION OF FOREIGN TRUSTS Delaware Trust Conference October 24, 2017 Leigh-Alexandra Basha McDermott, Will & Emery 500 Capitol Street, N.W. Washington, DC 20001 lbasha@mwe.com

MANAGING TRIVIAL PURSUITS: DOMESTICATION OF FOREIGN TRUSTS Delaware Trust Conference October 24, 2017 Leigh-Alexandra Basha McDermott, Will & Emery 500 Capitol Street, N.W. Washington, DC 20001 lbasha@mwe.com

I n the first two installments of this series we discussed

Daily Tax Report Reproduced with permission from Daily Tax Report, 216 DTR J-1, 11/8/16. Copyright 2016 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Foreign Taxpayers In the

Daily Tax Report Reproduced with permission from Daily Tax Report, 216 DTR J-1, 11/8/16. Copyright 2016 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Foreign Taxpayers In the

Estate & Gift Tax Treatment for Non-Citizens

ADVANCED MARKETS Estate & Gift Tax Treatment for Non-Citizens BECAUSE YOU ASKED It goes without saying that the laws governing the U.S. estate and gift tax system are complex. When you then consider the

ADVANCED MARKETS Estate & Gift Tax Treatment for Non-Citizens BECAUSE YOU ASKED It goes without saying that the laws governing the U.S. estate and gift tax system are complex. When you then consider the

Estate planning for non-citizens.

Estate Planning Estate planning for non-citizens. The federal gift and estate tax laws that apply to non-united States citizens (aliens) are different from those for citizens. Further, there are different

Estate Planning Estate planning for non-citizens. The federal gift and estate tax laws that apply to non-united States citizens (aliens) are different from those for citizens. Further, there are different

American Citizens Abroad. Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION

American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation 5 December 2016; 1 November 2017; 1 December 2017; 18 January 2018; 19 April 2018 INTRODUCTION This side-by-side analysis

American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation 5 December 2016; 1 November 2017; 1 December 2017; 18 January 2018; 19 April 2018 INTRODUCTION This side-by-side analysis

EXPATRIATION TAX AND PLANNING

New Haven New York Geneva EXPATRIATION TAX AND PLANNING Greenwich London Speaker: Ivan A. Sacks, Esq. Chairman, Withersworldwide Partner, Withers Bergman LLP Milan May 1, 2014 Miami, Florida Hong Kong

New Haven New York Geneva EXPATRIATION TAX AND PLANNING Greenwich London Speaker: Ivan A. Sacks, Esq. Chairman, Withersworldwide Partner, Withers Bergman LLP Milan May 1, 2014 Miami, Florida Hong Kong

2014 WORLD CONFERENCE: FOREIGN GRANTOR TRUST

r u c h e l m a n 1 2014 WORLD CONFERENCE: FOREIGN GRANTOR TRUST A Foreign Grantor Trust is a Great Solution to Benefit U.S. Persons: A Look at How This is Done Thomas Lee, Chair Thomas Lee & Partners

r u c h e l m a n 1 2014 WORLD CONFERENCE: FOREIGN GRANTOR TRUST A Foreign Grantor Trust is a Great Solution to Benefit U.S. Persons: A Look at How This is Done Thomas Lee, Chair Thomas Lee & Partners

Principal Residence Rules An Update

Principal Residence Rules An Update Presented by: Josh Harnett December 7, 2016 Table of Contents 1. One Plus Rule 2. Trusts 3. Subsection 107(4.1) 4. Compliance Rules 2 One Plus Rule Current Rule Individual

Principal Residence Rules An Update Presented by: Josh Harnett December 7, 2016 Table of Contents 1. One Plus Rule 2. Trusts 3. Subsection 107(4.1) 4. Compliance Rules 2 One Plus Rule Current Rule Individual

Tax Planning Considerations for 2015

Tax Planning Considerations for 2015 Most strategies that could have an impact on your taxes need to be made by December 31 if you want them reflected on your 2015 tax return. Executive summary As the

Tax Planning Considerations for 2015 Most strategies that could have an impact on your taxes need to be made by December 31 if you want them reflected on your 2015 tax return. Executive summary As the

Controlled Foreign Corp. Restructuring For US Taxpayers By Carl Merino and Dina Kapur Sanna (August 13, 2018, 12:48 PM EDT)

") Controlled Foreign Corp Restructuring For US Taxpayers By Carl Merino and Dina Kapur Sanna (August 13, 2018, 12:48 PM EDT) Few areas of the tax law were as heavily impacted by the Tax Cuts and Jobs Act

Controlled Foreign Corp Restructuring For US Taxpayers By Carl Merino and Dina Kapur Sanna (August 13, 2018, 12:48 PM EDT) Few areas of the tax law were as heavily impacted by the Tax Cuts and Jobs Act

Introduction: recent trends... CROSS BORDER ESTATE PLANNING. Advocis Breakfast Meeting. Are you American? Is your child? Who should consider U.S. tax?

Introduction: recent trends.... CROSS BORDER ESTATE PLANNING Advocis Breakfast Meeting Will Todd Taxation / Wills, Estates & Trusts Practice Group April 4, 2013... Why pay attention now. More Canadian

Introduction: recent trends.... CROSS BORDER ESTATE PLANNING Advocis Breakfast Meeting Will Todd Taxation / Wills, Estates & Trusts Practice Group April 4, 2013... Why pay attention now. More Canadian

TAX PLANNING FOR FOREIGN INVESTORS Table of Contents

TAX PLANNING FOR FOREIGN INVESTORS Table of Contents 1. Introduction...1 1.1. Tax Planning vs. Tax Cheating...1 1.2. Legitimate Tax Planning...2 1.3. Economic Substance Doctrine...2 2. Income Tax Consequences...3

TAX PLANNING FOR FOREIGN INVESTORS Table of Contents 1. Introduction...1 1.1. Tax Planning vs. Tax Cheating...1 1.2. Legitimate Tax Planning...2 1.3. Economic Substance Doctrine...2 2. Income Tax Consequences...3

U.S. Estate Tax For Canadians

B M O N e s b i t t b u r n s U.S. Estate Tax For Canadians Introduction The intention of this article is to highlight the potential U.S. estate taxes that might apply to Canadian estates and to suggest

B M O N e s b i t t b u r n s U.S. Estate Tax For Canadians Introduction The intention of this article is to highlight the potential U.S. estate taxes that might apply to Canadian estates and to suggest

Non-US Trust with US Beneficiaries: Now What? Michael J. Legamaro (312)

") Non-US Trust with US Beneficiaries: Now What? Michael J. Legamaro michael@legamaro.com (312) 543-5181 1 Case Study: Representative Family Foreign family with substantial offshore wealth Trust structures

Non-US Trust with US Beneficiaries: Now What? Michael J. Legamaro michael@legamaro.com (312) 543-5181 1 Case Study: Representative Family Foreign family with substantial offshore wealth Trust structures

Taxation of: U.S. Foreign Nationals

Taxation of: U.S. Foreign Nationals 2017 Edition ZanderSterling.com 1 The information contained in this publication is provided for general informational purposes only and is based on U.S. income tax law

Taxation of: U.S. Foreign Nationals 2017 Edition ZanderSterling.com 1 The information contained in this publication is provided for general informational purposes only and is based on U.S. income tax law

U.S. Estate Tax For Canadians

B M O N E S B I T T B U R N S U.S. Estate Tax For Canadians Introduction There is currently great uncertainty as to the status of U.S. estate tax legislation. As a result of the failure of the U.S. federal

B M O N E S B I T T B U R N S U.S. Estate Tax For Canadians Introduction There is currently great uncertainty as to the status of U.S. estate tax legislation. As a result of the failure of the U.S. federal

AHLA. A. The Globalization of Health Care Opportunities and Potential Pitfalls. Michael Domanski Honigman Miller Schwartz and Cohn LLP Detroit, MI

AHLA A. The Globalization of Health Care Opportunities and Potential Pitfalls Michael Domanski Honigman Miller Schwartz and Cohn LLP Detroit, MI Timothy A. A. Stiles KPMG LLP New York, NY Tax Issues for

AHLA A. The Globalization of Health Care Opportunities and Potential Pitfalls Michael Domanski Honigman Miller Schwartz and Cohn LLP Detroit, MI Timothy A. A. Stiles KPMG LLP New York, NY Tax Issues for

California Society of CPAs 20 th Annual Tax and Accounting Institute. Taking Your Tax Practice International

California Society of CPAs 20 th Annual Tax and Accounting Institute Taking Your Tax Practice International November 18, 2016 Handlery Hotel 8:20 a.m. 10:00 a.m. Jon P. Schimmer, J.D., LL.M., CPA Procopio,

California Society of CPAs 20 th Annual Tax and Accounting Institute Taking Your Tax Practice International November 18, 2016 Handlery Hotel 8:20 a.m. 10:00 a.m. Jon P. Schimmer, J.D., LL.M., CPA Procopio,

Schedule B, Part III (disclosing interest in foreign financial account)

") FOREIGN TRUSTS REPORTING OBLIGATIONS FOR U.S. PERSONS BRAD BEDINGFIELD CHOATE, HALL & STEWART LLP Form Who Reports Conditions / Notes What is Reported When and 1040 U.S. taxpayer See 1040 instructions.

FOREIGN TRUSTS REPORTING OBLIGATIONS FOR U.S. PERSONS BRAD BEDINGFIELD CHOATE, HALL & STEWART LLP Form Who Reports Conditions / Notes What is Reported When and 1040 U.S. taxpayer See 1040 instructions.

Private Wealth Services

Private Wealth Services Winter 2007 Volume 5, Issue 3 Estate Planning for the International Private Client Melinda Merk The laws governing estate plans of nonresident aliens and non-citizens of the United

Private Wealth Services Winter 2007 Volume 5, Issue 3 Estate Planning for the International Private Client Melinda Merk The laws governing estate plans of nonresident aliens and non-citizens of the United

U.S. Citizens Living in Canada

BMO Wealth Management U.S. Citizens Living in Canada Income Tax Considerations Many U.S. citizens have lived in Canada most of their lives and often think of themselves as Canadians. This may be true in

BMO Wealth Management U.S. Citizens Living in Canada Income Tax Considerations Many U.S. citizens have lived in Canada most of their lives and often think of themselves as Canadians. This may be true in

Sarasota 240 South Pineapple Ave. 10th Floor Sarasota, Florida

The Estate Planner September/October 2013 The GRAT: A limited time offer? International relations Estate planning for noncitizens Avoid probate to keep your estate private Estate Planning Red Flag You

The Estate Planner September/October 2013 The GRAT: A limited time offer? International relations Estate planning for noncitizens Avoid probate to keep your estate private Estate Planning Red Flag You

STILL THINKING OF COMING TO AMERICA? ADVISING THE FOREIGN PRIVATE CLIENT ON FUNDAMENTALS OF U.S. ESTATE, GIFT AND GST TAX PLANNING

STILL THINKING OF COMING TO AMERICA? ADVISING THE FOREIGN PRIVATE CLIENT ON FUNDAMENTALS OF U.S. ESTATE, GIFT AND GST TAX PLANNING By M. Katharine Davidson, Esq. Henderson, Caverly, Pum & Charney, LLP

STILL THINKING OF COMING TO AMERICA? ADVISING THE FOREIGN PRIVATE CLIENT ON FUNDAMENTALS OF U.S. ESTATE, GIFT AND GST TAX PLANNING By M. Katharine Davidson, Esq. Henderson, Caverly, Pum & Charney, LLP