Arizona Withholding Liability/Payment Schedule. B. Alternate Arizona Withholding Liability/Payment Schedule Computation

|

|

|

- Reginald Houston

- 5 years ago

- Views:

Transcription

1

2

3

4 C. Additional Failure to Pay Penalty. An employer is required to withhold Arizona income tax from compensation paid to an employee for services performed in Arizona, unless the compensation is exempt from Arizona withholding by Arizona law. The department may impose a penalty if the amount of tax required to be withheld, whether the amount of tax is determined by the employer or the department, is not paid to the department by the date prescribed for its payment. The amount of the penalty is 25 percent of the amount of tax required to be withheld and paid to the department. D. Payroll Service Company Penalty. A payroll service company, as defined in Arizona Revised Statutes (ARS) (E)(3), is subject to a $25 penalty for failure to make withholding payments electronically and a $25 penalty for failure to file withholding returns electronically. Multiple $25 penalties could apply to the same client on one return. For example, if Client A is required to make four payments in the 3rd quarter, and none of the payments are made electronically, the payroll service company would be subject to four $25 penalties, a total of $100. If the payroll service company files the quarterly reconciliation for Client A by paper, an additional penalty of $25 would apply for a grand total of $125 in penalties assessed toward the payroll service company related to Client A for the 3rd quarter. E. Interest. The department assesses interest on any portion of the tax, whether determined by the department or the employer/taxpayer, not paid by the date prescribed for its payment. The department applies interest, compounded annually, in the same manner and at the same times as prescribed by Internal Revenue Code (IRC) 6621 with the following exception. Exception: The Arizona rate of interest for both underpayments and overpayments for all taxpayers is the federal underpayment rate under IRC 6621(a)(2) [the federal short-term rate, determined pursuant to IRC 6621(b), plus three percentage points]. On January 1 of each year, the department adds any interest outstanding as of that date to the principal amount of the tax. It is then a part of the principal amount of the tax and accrues interest until paid. Arizona Withholding Liability/Payment Schedule Arizona law requires an employer to compute its average Arizona withholding tax liability for the preceding four calendar quarters at the beginning of each new quarter. This calculation is performed to determine the correct Arizona withholding payment An employer that has four full consecutive calendar quarters of Arizona withholding liability historical data must use the regular withholding payment schedule computation. An employer that does not have four full consecutive calendar quarters of Arizona withholding liability historical data must use the alternate withholding payment schedule computation. A. Regular Arizona Withholding Liability/Payment Schedule Computation An employer required to use the regular computation must add its withholding liabilities for the preceding four calendar quarters and divide the total by four. An employer must make its Arizona withholding payments on a quarterly basis if the average amount of Arizona income taxes withheld during the preceding four calendar quarters does not exceed $1, Arizona Form A1-QRT An employer must make its Arizona withholding tax payments at the same time as its federal withholding deposits if the average amount of Arizona income taxes withheld during the preceding four calendar quarters exceeds $1,500. Example 1 An employer is trying to determine the correct Arizona withholding payment schedule for the second calendar quarter The employer would make the following calculation to compute the average amount of Arizona income taxes withheld in the preceding four calendar quarters. First quarter 2013 withholding $ 1,100 Fourth quarter 2012 withholding + 1,600 Third quarter 2012 withholding + 1,000 Second quarter 2012 withholding + 1,200 Total withholding = $ 4,900 Divide by 4 Average withholding = $ 1,225 This example illustrates a four-quarter average of Arizona income taxes withheld that does not exceed $1,500. Therefore, the employer is required to make Arizona withholding payments on a quarterly basis. Example 2 An employer is trying to determine the correct Arizona withholding payment schedule for the third calendar quarter The employer would make the following calculation to compute the average amount of Arizona income taxes withheld in the preceding four calendar quarters. Second quarter 2013 withholding $ 1,800 First quarter 2013 withholding + 1,400 Fourth quarter 2012 withholding + 1,900 Third quarter 2012 withholding + 1,300 Total withholding = $ 6,400 Divide by 4 Average withholding = $ 1,600 This example illustrates a four-quarter average of Arizona income taxes withheld that exceeds $1,500. Therefore, the employer is required to make Arizona withholding payments at the same time as its federal withholding deposits. B. Alternate Arizona Withholding Liability/Payment Schedule Computation An employer must make its Arizona withholding payments on a quarterly basis if the average amount of Arizona income taxes withheld during the preceding four calendar quarters does not exceed $1,500. An employer must make its Arizona withholding tax payments at the same time as its federal withholding deposits (monthly, semi-weekly, or one-banking day), if the average amount of Arizona income taxes withheld during the preceding four calendar quarters exceeds $1,500. An employer required to use the alternate computation must use one of the following methods. An employer that purchases an existing business must determine its Arizona withholding payment schedule for each calendar quarter by calculating the average amount withheld in the four preceding calendar quarters as follows: For the first quarter of withholding, the employer must calculate the previous owner's average amount of Arizona income taxes withheld in the four preceding calendar quarters.

5 For the second through fourth quarters of withholding, the employer must calculate the average amount withheld in the four preceding calendar quarters by combining its prior quarters of withholding with the previous owner's quarters of withholding. For subsequent quarters of withholding, the employer must add the amounts it withheld in the four preceding calendar quarters and then divide that sum by four. A newly formed business must determine its Arizona withholding payment schedule as follows: For the first quarter of withholding, the employer must make its Arizona withholding payments on a quarterly basis. For the second quarter of withholding, the employer must determine its Arizona withholding payment schedule based on the amount withheld in the first quarter of withholding. For the third quarter of withholding, the employer must determine its Arizona withholding payment schedule by adding the amounts withheld in the first and second quarters and dividing by two. For the fourth quarter of withholding, the employer must determine its Arizona withholding payment schedule by adding the amounts withheld in the first, second, and third quarters and dividing by three. For subsequent quarters of withholding, the employer must determine its Arizona withholding payment schedule by adding the amounts withheld in the four preceding calendar quarters and dividing by four. When two or more employers consolidate their business activities to form one entity, the new employer must determine its Arizona withholding payment schedule based on the combined withholding of the prior employers for the preceding four full quarters. Any prior employer with fewer than four full quarters of withholding activity must annualize the amounts withheld and divide by four. The new employer must determine its Arizona withholding payment schedule by combining this amount with the quarterly averages of the other prior employers with four full quarters of withholding activity. C. Withholding Payment Due Dates Internet payments: Registered employers may make their withholding payments on the Internet. Go to to register or for further information. Quarterly Arizona withholding payments are due on the following dates: First calendar quarter - April 30; Second calendar quarter - July 31; Third calendar quarter - October 31; Fourth calendar quarter - January 31. If the quarterly withholding payment due date is a non-banking day (Saturday, Sunday, or a legal holiday), the withholding payment is timely if made on the next banking day. An employer required to make its Arizona withholding payments at the same time as its federal withholding deposits must make its Arizona withholding payments on a monthly, semi-weekly, or one-banking day basis. Monthly Arizona withholding payments are due on the fifteenth day of the month following the calendar month in which the taxes accumulated. 3 Arizona Form A1-QRT If the fifteenth day of the following month is a non-banking day (Saturday, Sunday, or a legal holiday), the withholding payment is timely if made on the next banking day. Semi-weekly Arizona withholding payments are due on the following schedule: Wednesday through Friday semi-weekly period - on or before the following Wednesday. Saturday through Tuesday semi-weekly period - on or before the following Friday. If any of the three weekdays following the close of a semi-weekly period is a non-banking day (a legal holiday), an additional banking day is granted to make the required payment. If a calendar quarter ends during a semi-weekly period (on a day other than Tuesday or Friday), the following rules apply: Taxes accumulated on the days in the current calendar quarter are subject to one payment obligation. Taxes accumulated on the days in the next calendar quarter are subject to a separate payment obligation. The payment(s) is (are) due at the normal payment due date for the semi-weekly period. One-banking day Arizona withholding payments are due on the first banking day following the day that an employer incurs a federal one-banking day deposit obligation. The employer must make a one-banking day federal withholding deposit if federal taxes accumulate to $100,000 or more on any day during a monthly or semi-weekly deposit period. The Arizona withholding payment is due the same day as the federal withholding deposit although the Arizona withholding tax liability may not have reached $100,000 for the same monthly or semi-weekly period. A monthly liability payer that incurs an Arizona one-banking day withholding payment obligation during the calendar quarter immediately becomes an Arizona semiweekly liability payer for the remainder of the calendar quarter. Extended Form A1-QRT due dates available to taxpayers who have made every payment on time. ARS (C) allows some employers additional time to file Form A1-QRT. Employers who have made every payment on time during the preceding calendar quarter may have ten additional days in which to file Form A1-QRT. Form A1-QRT, for employers who have not made every payment on time during the preceding calendar quarter, are considered timely if filed by the following dates: First calendar quarter - April 30; Second calendar quarter - July 31; Third calendar quarter - October 31; Fourth calendar quarter - January 31. Form A1-QRT filing due dates for employers who have made every payment on time during the preceding calendar quarter are: First calendar quarter - May 10; Second calendar quarter - August 12; Third calendar quarter - November 12; Fourth calendar quarter - February 10. Because August 10, 2013, and November 10, 2013, are each on a weekend day, the return is considered to be timely for those quarters if it is made on the next day that is not a Saturday, Sunday, or legal holiday.

6

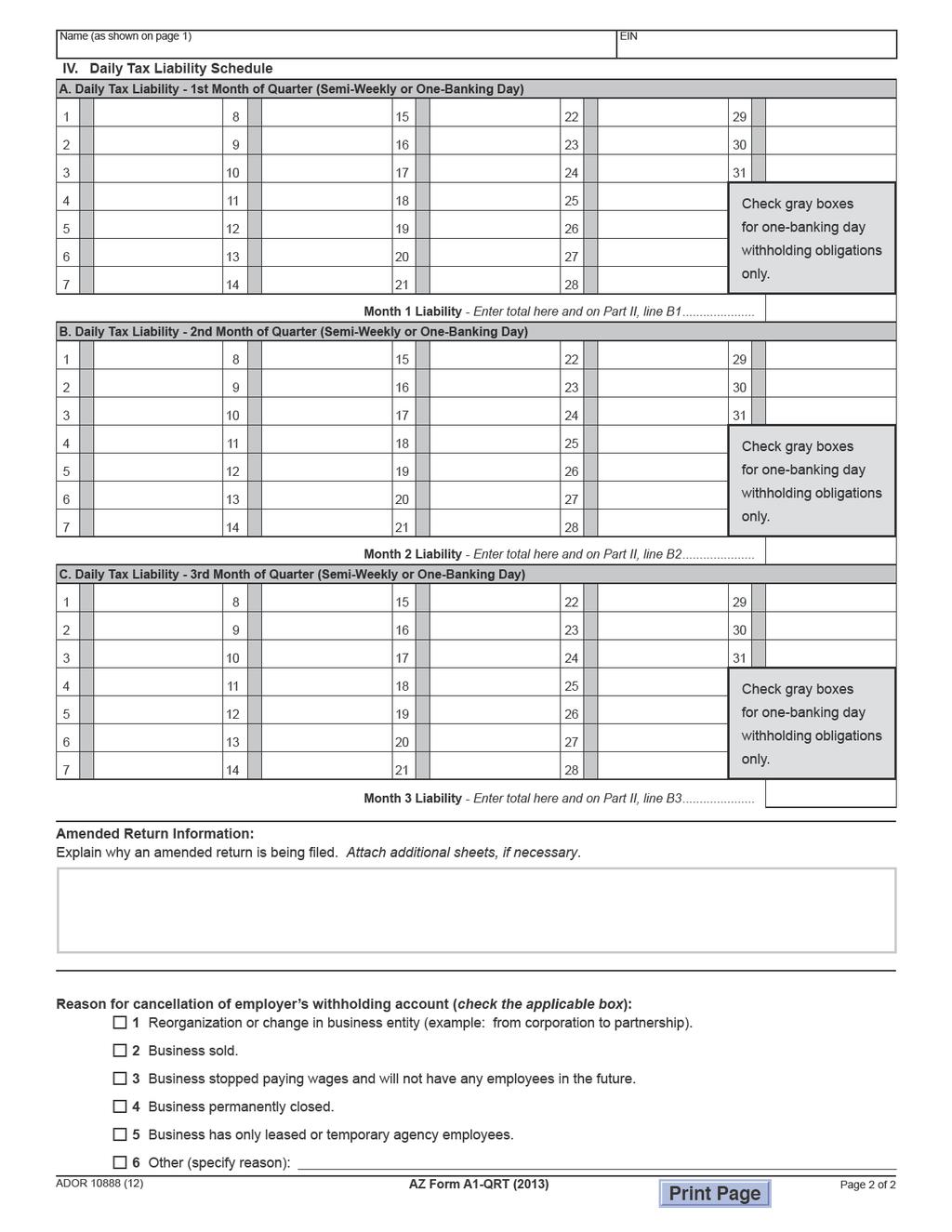

7 monthly subtotals. Enter the total Arizona tax liability for the calendar quarter on Part IIB, line B4 and Part III, line 1. NOTE: Be sure to check the box on page 1, in Part IIB, if the taxpayer is required to complete section A, B, and/or C of the Daily Tax Liability Schedule on page 2. IF AN EMPLOYER INCURS A ONE-BANKING DAY OBLIGATION DURING THE FIRST MONTH: First month - complete section A of the daily tax liability Second month - complete section B of the daily tax liability Third month - complete section C of the daily tax liability IF AN EMPLOYER INCURS A ONE-BANKING DAY OBLIGATION DURING THE SECOND MONTH: First month - complete Part IIB, line B1, month 1 liability. Second month - complete section B of the daily tax liability Third month - complete section C of the daily tax liability IF AN EMPLOYER INCURS A ONE-BANKING DAY OBLIGATION DURING THE THIRD MONTH: First month - complete Part IIB, line B1, month 1 liability. Second month - complete Part IIB, line B2, month 2 liability. Third month - complete section C of the daily tax liability Daily Tax Liability (Semi-Weekly or One-Banking Day) NOTE: Be sure to check the box on page 1, in Part IIB, if the taxpayer is required to complete section A, B, and/or C of the Daily Tax Liability Schedule on page 2. Complete sections A, B, and C, of the Daily Tax Liability Schedule; lines B1 through B4 of Part IIB, Monthly Tax Liability; and Part III, line 1. On lines A1 through A31, B1 through B31, and C1 through C31, of the Daily Tax Liability Schedule, make entries on the day that an Arizona withholding tax liability was incurred. Enter the amount of Arizona withholding tax liability for each applicable day, not the amount of Arizona withholding payments. Add the amounts entered on the daily liability schedule for each month. Enter the total for each month on sections A, B, and C, and on Part IIB, lines B1 through B3. Add the amounts entered on Part IIB, lines B1 through B3. Enter the total Arizona tax liability for the calendar quarter on Part IIB, line B4 and Part III, line 1. Important note for one-banking day obligations: Check the small gray box to the right of the number that corresponds to the day that the employer incurred an Arizona one-banking day withholding obligation. Leave this box blank unless a onebanking day withholding obligation was incurred. III. Tax Computation Section Line 1 - Liability Quarterly tax liability employer - enter the amount from Part IIA, line A1. 5 Arizona Form A1-QRT Monthly tax liability employer (all three months of quarter) - enter the total from Part IIB, line B4. Monthly tax liability (less than three months)/daily tax liability employer - enter the total from Part IIB, line B4. Daily tax liability employer (all three months of quarter) - enter the total from Part IIB, line B4. Line 2 - Prior Payments Made for This Quarter Enter the total amount of prior payments made for this quarter in this field. If no payments were made prior to filing this return for this quarter, enter -0- in this field. Do NOT include the payment made with or for this return. Line 3 - Total Amount Due Subtract the amount on line 2 from the amount on line 1. Enter the difference. If line 3 is a positive number, this is the amount of tax remaining due. Payments can be made via check, electronic check, money order, or credit card. The department will calculate the amount of interest, apply any applicable penalties, and send a billing notice after the return is processed. Check or Money Order Make checks payable to Arizona Department of Revenue. Write the taxpayer's EIN on the front of the check or money order. Include the check or money order with the return. Internet Payments Employers must be registered with the Department of Revenue before they can register to pay taxes online. Go to to register or to make payments over the internet. Electronic payment from checking or savings account Payments can be made electronically from a checking or savings account. Go to and choose the e- check option. There is no fee to use this method. This payment method will debit the amount from the specified checking or savings account on the date specified. If an electronic payment is made from a checking or savings account, a confirmation number will be generated. Please keep this confirmation number as proof of payment. Credit card payment Payments can be made via American Express, Discover, MasterCard or VISA credit cards. Go to and choose the credit card option. This will take you to the website of the credit card payment service provider. The service provider will charge a convenience fee based on the amount of the tax payment. The service provider will disclose the amount of the convenience fee during the transaction and the option to continue or cancel the transaction will be presented. If you accept the convenience fee and complete the credit card transaction, a confirmation number will be generated. Please keep this confirmation number as proof of payment. If line 3 is a negative number (an amount less than zero), this is the overpayment for the quarter. After the return is processed and payments are confirmed, the overpayment will be applied to any outstanding liabilities, possibly in another tax type. If the overpayment exceeds the outstanding liabilities or the employer has no outstanding liabilities, a refund check will be issued and mailed to the employer. A refund will not be issued once the overpayment is applied to a liability.

8

9 Name (as shown on page 1) EIN IV. Daily Tax Liability Schedule A. Daily Tax Liability - 1st Month of Quarter (Semi-Weekly or One-Banking Day) Check gray boxes for one-banking day withholding obligations only. Month 1 Liability - Enter total here and on Part II, line B1... B. Daily Tax Liability - 2nd Month of Quarter (Semi-Weekly or One-Banking Day) Check gray boxes for one-banking day withholding obligations only. Month 2 Liability - Enter total here and on Part II, line B2... C. Daily Tax Liability - 3rd Month of Quarter (Semi-Weekly or One-Banking Day) Check gray boxes for one-banking day withholding obligations only. Month 3 Liability - Enter total here and on Part II, line B3... Amended Return Information: Explain why an amended return is being fi led. Attach additional sheets, if necessary. 2 Reason for cancellation of employer s withholding account (check the applicable box): 3 1 Reorganization or change in business entity (example: from corporation to partnership). 2 Business sold. 3 Business stopped paying wages and will not have any employees in the future. 4 Business permanently closed. 5 Business has only leased or temporary agency employees. 6 Other (specify reason): ADOR (12) AZ Form A1-QRT (2013) Page 2 of 2 7

This booklet contains: FORM 140ES WORKSHEET

Arizona Booklet 40ES Individual Estimated Tax Payment 202 This booklet contains: FORM 40ES WORKSHEET 202 Individual Estimated Arizona Form Tax Payment Instructions 40ES Phone Numbers If you have questions,

Arizona Booklet 40ES Individual Estimated Tax Payment 202 This booklet contains: FORM 40ES WORKSHEET 202 Individual Estimated Arizona Form Tax Payment Instructions 40ES Phone Numbers If you have questions,

Arizona Form 2012 Arizona Exempt Organization Business Income Tax Return 99T

Arizona Form 2012 Arizona Exempt Organization Business Income Tax Return 99T Obtain additional information or assistance by calling one of the numbers listed below: Phoenix (602) 255-3381 From area codes

Arizona Form 2012 Arizona Exempt Organization Business Income Tax Return 99T Obtain additional information or assistance by calling one of the numbers listed below: Phoenix (602) 255-3381 From area codes

SECTION 8: Depositing and Reporting Withheld Taxes

SECTION 8: Depositing and Reporting Withheld Taxes 1 Employer Identification Numbers (EIN) All employers are assigned an Employer Identification Number (EIN) The EIN is a nine-digit number, expressed as

SECTION 8: Depositing and Reporting Withheld Taxes 1 Employer Identification Numbers (EIN) All employers are assigned an Employer Identification Number (EIN) The EIN is a nine-digit number, expressed as

WITHHOLDING TABLES MAINE INDIVIDUAL INCOME TAX

WITHHOLDING TABLES MAINE INDIVIDUAL INCOME TAX 2000 Effective January 1, 2000 REMEMBER: A person required to withhold must continue to file quarterly withholding tax returns until the account is canceled,

WITHHOLDING TABLES MAINE INDIVIDUAL INCOME TAX 2000 Effective January 1, 2000 REMEMBER: A person required to withhold must continue to file quarterly withholding tax returns until the account is canceled,

New Mexico Taxation and Revenue Department 2013 Calculation of Estimated Personal Income Tax Underpayment Penalty

Print your name (first, middle, last) Enter your social security number HOW TO USE THIS FORM You need to complete this form only if you have elected to use an alternative method of computing estimated

Print your name (first, middle, last) Enter your social security number HOW TO USE THIS FORM You need to complete this form only if you have elected to use an alternative method of computing estimated

Form 941/C1-ME. Questions regarding: Important

State of Maine Maine Revenue Services and Department of Labor 2001 Combined Filing for Income Tax Withholding and Unemployment Contributions Form 941/C1-ME Questions regarding: Income Tax Withholding 207-626-8475

State of Maine Maine Revenue Services and Department of Labor 2001 Combined Filing for Income Tax Withholding and Unemployment Contributions Form 941/C1-ME Questions regarding: Income Tax Withholding 207-626-8475

SECTION 8: Employer Identification Numbers (EIN) Employer Identification Number (EIN) Cont

Employer Identification Number (EIN) Cont") SECTION 8: Depositing and Reporting Withheld Taxes 1 Employer Identification Numbers (EIN) All employers are assigned an Employer Identification Number (EIN) to ensure that all payments are credited to

SECTION 8: Depositing and Reporting Withheld Taxes 1 Employer Identification Numbers (EIN) All employers are assigned an Employer Identification Number (EIN) to ensure that all payments are credited to

Form CT-1040ES Estimated Connecticut Income Tax Payment Coupon for Individuals

Department of Revenue Services State of Connecticut Form CT-1040ES 2017 Estimated Connecticut Income Tax Payment Coupon for Individuals 2017 (Rev. 01/17) Complete this form in blue or black ink only. Who

Department of Revenue Services State of Connecticut Form CT-1040ES 2017 Estimated Connecticut Income Tax Payment Coupon for Individuals 2017 (Rev. 01/17) Complete this form in blue or black ink only. Who

Chapter 13 Payroll Accounting, Taxes, and Reports

Chapter 13 Payroll Accounting, Taxes, and Reports -- The payroll register and employee earnings records provide all the payroll information needed to prepare a payroll and payroll tax reports. Journal

Chapter 13 Payroll Accounting, Taxes, and Reports -- The payroll register and employee earnings records provide all the payroll information needed to prepare a payroll and payroll tax reports. Journal

Minnesota Income Tax Withholding

2010 Minnesota Income Tax Withholding Instruction Booklet and Tax Tables Start using this booklet January 1, 2010 Contents Fact sheets...2 Directory... 2 What s new... 3 Register for a Minnesota tax ID

2010 Minnesota Income Tax Withholding Instruction Booklet and Tax Tables Start using this booklet January 1, 2010 Contents Fact sheets...2 Directory... 2 What s new... 3 Register for a Minnesota tax ID

Newark Income Tax Office Payroll Withholding

Newark Income Tax Office Payroll Withholding Filed Period Must be postmarked on or before Pay Period 1st 05-01-17 January 1 -March 31 2nd 07-31-17 April 1 - June 30 3rd 10-31-17 July 1 - September 30 4th

Newark Income Tax Office Payroll Withholding Filed Period Must be postmarked on or before Pay Period 1st 05-01-17 January 1 -March 31 2nd 07-31-17 April 1 - June 30 3rd 10-31-17 July 1 - September 30 4th

Colorado Income Tax Withholding Tables For Employers

DR 1098 (12/23/16) Colorado Income Tax Withholding Tables For Employers What s Inside? Electronic Filing Information Filing periods and requirements effective January 1, 2017 Income Tax Withholding Tables

DR 1098 (12/23/16) Colorado Income Tax Withholding Tables For Employers What s Inside? Electronic Filing Information Filing periods and requirements effective January 1, 2017 Income Tax Withholding Tables

Electronic Filing and Payment Requirements

Maine Revenue Services 2018 Filing for Maine Income Tax Withholding Form 941ME Stay current with the latest tax news and information. Subscribe to the online Maine Tax Alert newsletter. It s free! Sign

Maine Revenue Services 2018 Filing for Maine Income Tax Withholding Form 941ME Stay current with the latest tax news and information. Subscribe to the online Maine Tax Alert newsletter. It s free! Sign

RI-1040X-NR Amended Rhode Island Nonresident Individual Income Tax Return 2011 NAME AND ADDRESS

RI-1040X-NR Amended Rhode Island Nonresident Individual Income Tax Return 2011 NAME AND ADDRESS First name Spouse s first name (To be used by nonresident and part-year resident taxpayers only) Initial

RI-1040X-NR Amended Rhode Island Nonresident Individual Income Tax Return 2011 NAME AND ADDRESS First name Spouse s first name (To be used by nonresident and part-year resident taxpayers only) Initial

STATE OF ARKANSAS Estimated Tax Declaration Vouchers and Instructions for Tax Year 2007

STATE OF ARKANSAS Estimated Tax Declaration s and Instructions for Tax Year 27 INSTRUCTIONS FOR COMPLETION OF DECLARATION-VOUCHER 1. Fill out the 27 Estimated Tax Worksheet to figure your estimated tax

STATE OF ARKANSAS Estimated Tax Declaration s and Instructions for Tax Year 27 INSTRUCTIONS FOR COMPLETION OF DECLARATION-VOUCHER 1. Fill out the 27 Estimated Tax Worksheet to figure your estimated tax

CITY OF KENTON EMPLOYER S WITHHOLDING BOOKLET

Income Tax Division 555 W Franklin St Kenton, OH 43326 IMPORTANT TAX INFORMATION Phone: 419-673-1355 (8:30-4:30, M-F, EST) W-3 2019 RECONCILIATION Fax: 419-675-3200 Email: W-1 2019 WITHHOLDING RETURNS

Income Tax Division 555 W Franklin St Kenton, OH 43326 IMPORTANT TAX INFORMATION Phone: 419-673-1355 (8:30-4:30, M-F, EST) W-3 2019 RECONCILIATION Fax: 419-675-3200 Email: W-1 2019 WITHHOLDING RETURNS

COMMISSIONER OF TAXATION CITY OF MAUMEE 400 CONANT STREET PHONE:

00 CONANT ST. MAUMEE OH 7-00 HOURS MONDAY FRIDAY 8:00 AM :0 PM TELEPHONE: (9) 897-70 FAX: (9) 897-89 WWW.MAUMEE.ORG EMAIL: TAX@MAUMEE.ORG EMPLOYER S MUNICIPAL INCOME TAX WITHHOLDING FORMS FORM MW (MONTHLY

00 CONANT ST. MAUMEE OH 7-00 HOURS MONDAY FRIDAY 8:00 AM :0 PM TELEPHONE: (9) 897-70 FAX: (9) 897-89 WWW.MAUMEE.ORG EMAIL: TAX@MAUMEE.ORG EMPLOYER S MUNICIPAL INCOME TAX WITHHOLDING FORMS FORM MW (MONTHLY

RI-1040X-R Amended Rhode Island Resident Individual Income Tax Return 2011 NAME AND ADDRESS

RI-1040X-R Amended Rhode Island Resident Individual Income Tax Return 2011 NAME AND ADDRESS First name Spouse s first name (To be used by resident taxpayers only) Initial Initial Last name Last name Your

RI-1040X-R Amended Rhode Island Resident Individual Income Tax Return 2011 NAME AND ADDRESS First name Spouse s first name (To be used by resident taxpayers only) Initial Initial Last name Last name Your

Instructions for Form City of Detroit Income Tax Withholding Monthly/Quarterly Return

Instructions for Form 5323 2017 City of Detroit Income Tax Withholding Monthly/Quarterly Return Purpose The purpose of this form is for an employer to file a City of Detroit Income Tax Withholding return

Instructions for Form 5323 2017 City of Detroit Income Tax Withholding Monthly/Quarterly Return Purpose The purpose of this form is for an employer to file a City of Detroit Income Tax Withholding return

Division of Employer Accounts Hotline (609) Division of Taxation Hotline (609)

Division of Taxation Hotline (609)") Instructions for Completing Employer Payroll Tax Form NJ-927W General Instructions The NJ-927W Form has been revised for reporting periods starting with the report for the 3rd quarter of 1998 (report due

Instructions for Completing Employer Payroll Tax Form NJ-927W General Instructions The NJ-927W Form has been revised for reporting periods starting with the report for the 3rd quarter of 1998 (report due

Pataskala JEDD Income Tax Payroll Withholding

Pataskala JEDD Income Tax Payroll Withholding Filed Period Must be postmarked on or before Pay Period 1st 04-30-18 January 1 -March 31 2nd 07-31-18 April 1 - June 30 3rd 10-31-18 July 1 - September 30

Pataskala JEDD Income Tax Payroll Withholding Filed Period Must be postmarked on or before Pay Period 1st 04-30-18 January 1 -March 31 2nd 07-31-18 April 1 - June 30 3rd 10-31-18 July 1 - September 30

8Great Reasons to. Faster Refunds: With Direct Deposit Filing Confirmation Provided Error/Math Checking Feature If You Qualify, It s Free

2 16 Arizona Form 140PY Part-Year Resident Personal Income Tax This Booklet Contains: Form 140PY Part-Year Resident Personal Income Tax Return Schedule A(PY) Itemized Deductions Form 204 Extension Request

2 16 Arizona Form 140PY Part-Year Resident Personal Income Tax This Booklet Contains: Form 140PY Part-Year Resident Personal Income Tax Return Schedule A(PY) Itemized Deductions Form 204 Extension Request

2008 Tax Rates and Information Bulletin

Albin, Randall & Bennett, CPAs 2008 Tax Rates and Information Bulletin 06/08 2008 TAX UPDATE BULLETIN TABLE OF CONTENTS Topic Page Number Payroll Withholding Rates and Limits...1 Backup Withholding...2

Albin, Randall & Bennett, CPAs 2008 Tax Rates and Information Bulletin 06/08 2008 TAX UPDATE BULLETIN TABLE OF CONTENTS Topic Page Number Payroll Withholding Rates and Limits...1 Backup Withholding...2

NOTICE OF NET WAGES PAID & TAX DUE

PAY-DATE PAYROLL SUMMARY Check Date: Period Covered: 01/01/2018 To: Enclosed: List of Paychecks. Payroll Checks. Payroll Summary & Cash Requirements. Payroll Register. Payroll Journal Report. Employer's

PAY-DATE PAYROLL SUMMARY Check Date: Period Covered: 01/01/2018 To: Enclosed: List of Paychecks. Payroll Checks. Payroll Summary & Cash Requirements. Payroll Register. Payroll Journal Report. Employer's

Small Business Tax and Form Calendar

BONUS CHAPTER 2 Small Business Tax and Form Calendar Here we ve assembled all the key tax dates you need to know and the federal forms that must be submitted on those dates. The dates listed are the actual

BONUS CHAPTER 2 Small Business Tax and Form Calendar Here we ve assembled all the key tax dates you need to know and the federal forms that must be submitted on those dates. The dates listed are the actual

Maine Revenue Services Withholding Tables for Individual Income Tax

Maine Revenue Services Withholding Tables for Individual Income Tax The tables in this book have been adjusted for inf ation. 2008 Make Electronic Withholding Payments at www.maine.gov/revenue Income Tax

Maine Revenue Services Withholding Tables for Individual Income Tax The tables in this book have been adjusted for inf ation. 2008 Make Electronic Withholding Payments at www.maine.gov/revenue Income Tax

OPIC. Estimating Income Taxes

New Jersey Division of Taxation TAX OPIC Estimating Income Taxes Bulletin GIT-8 Introduction Individuals (residents and nonresidents) and certain estates and trusts who have income that is not subject

New Jersey Division of Taxation TAX OPIC Estimating Income Taxes Bulletin GIT-8 Introduction Individuals (residents and nonresidents) and certain estates and trusts who have income that is not subject

Property Tax Refund (Credit) Claim. You must file this form, or Arizona Form 204, by April 17, 2018.

Claim. You must file this form, or Arizona Form 204, by April 17, 2018.") DO NOT STAPLE ANY ITEMS TO THE CLAIM. Arizona Form 140PTC You must file this form, or Arizona Form 204, by April 17, 2018. 82F Check box 82F if filing under extension 95 Check box 95 if amending claim

DO NOT STAPLE ANY ITEMS TO THE CLAIM. Arizona Form 140PTC You must file this form, or Arizona Form 204, by April 17, 2018. 82F Check box 82F if filing under extension 95 Check box 95 if amending claim

Accounting for Payroll: Employer Taxes and Reports

Ch.12 Accounting for Payroll: Employer Taxes and Reports o Calculate Employer s Payroll Taxes o Record Employer s Payroll Taxes o Forms 8109 & 941 o Form 940 o Forms W-2 & W-3 o Account For Workers Compensation

Ch.12 Accounting for Payroll: Employer Taxes and Reports o Calculate Employer s Payroll Taxes o Record Employer s Payroll Taxes o Forms 8109 & 941 o Form 940 o Forms W-2 & W-3 o Account For Workers Compensation

Estimating Income Taxes

Tax Topic Bulletin GIT-8 Estimating Income Taxes Introduction Residents, nonresidents, and certain estates and trusts must make estimated tax payments if they expect their New Jersey Income Tax liability

Tax Topic Bulletin GIT-8 Estimating Income Taxes Introduction Residents, nonresidents, and certain estates and trusts must make estimated tax payments if they expect their New Jersey Income Tax liability

EMPLOYMENT TAXES UNDERSTANDING AND PAYING PAYROLL TAXES

EMPLOYMENT TAXES UNDERSTANDING AND PAYING PAYROLL TAXES 2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 Understanding and Paying Payroll Taxes

EMPLOYMENT TAXES UNDERSTANDING AND PAYING PAYROLL TAXES 2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 Understanding and Paying Payroll Taxes

2017 Ohio IT 1040ES, Voucher 1 Due April 18, Electronic Payment Available

2017 Ohio IT 1040ES, Voucher 1 Due April 18, 2017 Electronic Available Cut on the dotted lines. DO NOT USE PENCIL to complete this form. (Voucher 1) Due April 18, 2017 0 0 2017 Ohio IT 1040ES, Voucher

2017 Ohio IT 1040ES, Voucher 1 Due April 18, 2017 Electronic Available Cut on the dotted lines. DO NOT USE PENCIL to complete this form. (Voucher 1) Due April 18, 2017 0 0 2017 Ohio IT 1040ES, Voucher

QUARTERLY STATEMENT OF ESTIMATED INCOME TAX DUE D-1/I. VOUCHER 2 (CALENDAR YEAR-DUE JULY 31st) NOTE: DO NOT SEND CASH THROUGH U.S.

NOTE: DO NOT SEND CASH THROUGH U.S.") QUARTERLY STATEMENT VOUCHER 2 (CALENDAR YEAR-DUE JULY 31st) 2nd QUARTER PAYMENT DUE JULY 31 QUARTERLY STATEMENT VOUCHER 3 (CALENDAR YEAR-DUE OCTOBER 31st) 3rd QUARTER PAYMENT DUE OCT. 31 QUARTERLY STATEMENT

QUARTERLY STATEMENT VOUCHER 2 (CALENDAR YEAR-DUE JULY 31st) 2nd QUARTER PAYMENT DUE JULY 31 QUARTERLY STATEMENT VOUCHER 3 (CALENDAR YEAR-DUE OCTOBER 31st) 3rd QUARTER PAYMENT DUE OCT. 31 QUARTERLY STATEMENT

Oregon Withholding Tax Formulas

Oregon Withholding Tax Formulas Effective January 1, 2014 To: Oregon employers The Oregon Withholding Tax Formulas include: Things you need to know. Phase-out information for high income employees. Frequently

Oregon Withholding Tax Formulas Effective January 1, 2014 To: Oregon employers The Oregon Withholding Tax Formulas include: Things you need to know. Phase-out information for high income employees. Frequently

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS Department of Administration DIVISION OF TAXATION One Capitol Hill Providence, RI 02908-5800 Tel: (401) 222-3911 Fax: (401) 222-5134 Forms (401) 222-1111

STATE OF RHODE ISLAND AND PROVIDENCE PLANTATIONS Department of Administration DIVISION OF TAXATION One Capitol Hill Providence, RI 02908-5800 Tel: (401) 222-3911 Fax: (401) 222-5134 Forms (401) 222-1111

CITY OF KENTON EMPLOYER S WITHHOLDING BOOKLET

Income Tax Division 555 W Franklin St Kenton, OH 43326 IMPORTANT TAX INFORMATION Phone: 419-673-1355 (8:30-4:30, M-F, EST) W-3 2019 RECONCILIATION Fax: 419-675-3200 Email: incometax@kentoncity.com W-1

Income Tax Division 555 W Franklin St Kenton, OH 43326 IMPORTANT TAX INFORMATION Phone: 419-673-1355 (8:30-4:30, M-F, EST) W-3 2019 RECONCILIATION Fax: 419-675-3200 Email: incometax@kentoncity.com W-1

Introduction. Important. Changes Coming for Tax Year General Information. Tax Topic Bulletin GIT-8 Estimating Income Taxes

Tax Topic Bulletin GIT-8 Estimating Income Taxes Introduction Residents, nonresidents, and certain estates and trusts must make estimated tax payments if they expect their New Jersey Income Tax liability

Tax Topic Bulletin GIT-8 Estimating Income Taxes Introduction Residents, nonresidents, and certain estates and trusts must make estimated tax payments if they expect their New Jersey Income Tax liability

County. (indicate state) (indicate state)

(indicate state)") IT 1040X Please Print Payments Calendar Year Ohio Amended Individual Income Tax Return for Year 2014 20 Your fi rst name M.I. Last name If a joint return, spouse's first name M.I. Last name Current address

IT 1040X Please Print Payments Calendar Year Ohio Amended Individual Income Tax Return for Year 2014 20 Your fi rst name M.I. Last name If a joint return, spouse's first name M.I. Last name Current address

SC REVENUE RULING #13-1. General Rules for Limitations on Filing a Claim for Refund

State of South Carolina Department of Revenue 300A Outlet Pointe Blvd., Columbia, South Carolina 29210 P.O. Box 125, Columbia, South Carolina 29214 SC REVENUE RULING #13-1 SUBJECT: SUPERSEDES: General

State of South Carolina Department of Revenue 300A Outlet Pointe Blvd., Columbia, South Carolina 29210 P.O. Box 125, Columbia, South Carolina 29214 SC REVENUE RULING #13-1 SUBJECT: SUPERSEDES: General

Connecticut Combined Unitary Corporation Business Tax Return

2016 FORM CT-1120CU This booklet contains instructions for the following forms: Form CT-1120CU Form CT-1120CU-MI Form CT-1120CU-NI Form CT-1120CU-MTB Form CT-1120A-CU Form CT-1120CU-NCB Tax information

2016 FORM CT-1120CU This booklet contains instructions for the following forms: Form CT-1120CU Form CT-1120CU-MI Form CT-1120CU-NI Form CT-1120CU-MTB Form CT-1120A-CU Form CT-1120CU-NCB Tax information

RI-1040X-NR Amended Rhode Island Nonresident Individual Income Tax Return 2013 NAME AND ADDRESS

RI-1040X-NR Amended Rhode Island Nonresident Individual Income Tax Return 2013 NAME AND ADDRESS First name Spouse s first name (To be used by nonresident and part-year resident taxpayers only) Initial

RI-1040X-NR Amended Rhode Island Nonresident Individual Income Tax Return 2013 NAME AND ADDRESS First name Spouse s first name (To be used by nonresident and part-year resident taxpayers only) Initial

Form 941 for 2017: All You Need to Know Presented on Thursday, September 28, 2017

Form 941 for 2017: All You Need to Know Presented on Thursday, September 28, 2017 1 2016 The Payroll Advisor 2 Housekeeping 3 Credit Questions Today s topic Speaker 2016 The Payroll Advisor To earn RCH

Form 941 for 2017: All You Need to Know Presented on Thursday, September 28, 2017 1 2016 The Payroll Advisor 2 Housekeeping 3 Credit Questions Today s topic Speaker 2016 The Payroll Advisor To earn RCH

CONSUMER DEPOSIT ACCOUNT TERMS AND CONDITIONS

CONSUMER DEPOSIT ACCOUNT TERMS AND CONDITIONS WELCOME TO M&T A GUIDE TO THE TERMS OF YOUR PERSONAL DEPOSIT ACCOUNTS On November 1, 2015, Hudson City Savings Bank ( HCSB ) merged into and became part of

CONSUMER DEPOSIT ACCOUNT TERMS AND CONDITIONS WELCOME TO M&T A GUIDE TO THE TERMS OF YOUR PERSONAL DEPOSIT ACCOUNTS On November 1, 2015, Hudson City Savings Bank ( HCSB ) merged into and became part of

- 1 - assigned FEIN by filing a Notice of Change or Discontinuance, Form S-6-IT.

SAGINAW, MICHIGAN WITHHOLDING TAX GUIDE PLEASE NOTE: EFFECTIVE JANUARY 1, 2005, THE PERSONAL AND DEPENDENCY EXEMPTION ALLOWANCE OF THE SAGINAW INCOME TAX WILL CHANGE FROM $1000 TO $750. THE INSTRUCTIONS

SAGINAW, MICHIGAN WITHHOLDING TAX GUIDE PLEASE NOTE: EFFECTIVE JANUARY 1, 2005, THE PERSONAL AND DEPENDENCY EXEMPTION ALLOWANCE OF THE SAGINAW INCOME TAX WILL CHANGE FROM $1000 TO $750. THE INSTRUCTIONS

PAYROLL PROCESSING COMPANIES

Maine Revenue Services 2018 Withholding Tables for Individual Income Tax Reflects Maine tax law as of December 31, 2017. Income Tax Withholding Questions? Email: withholding.tax@maine.gov Call: (207) 626-8475

Maine Revenue Services 2018 Withholding Tables for Individual Income Tax Reflects Maine tax law as of December 31, 2017. Income Tax Withholding Questions? Email: withholding.tax@maine.gov Call: (207) 626-8475

federal tax deposits

The ABCs of FTDs Resource Guide for Understanding federal tax deposits The ABCs of FTDs It s a great feeling to have your own small business, isn t it? You re the boss! You have a lot of responsibility

The ABCs of FTDs Resource Guide for Understanding federal tax deposits The ABCs of FTDs It s a great feeling to have your own small business, isn t it? You re the boss! You have a lot of responsibility

Arizona Form 2016 Property Tax Refund (Credit) Claim 140PTC

Claim 140PTC") Arizona Form 2016 Property Tax Refund (Credit) Claim 140PTC NOTICE: If you are age 70 or over and meet certain tests, you may be able to defer the payment of your property taxes on your home. You should

Arizona Form 2016 Property Tax Refund (Credit) Claim 140PTC NOTICE: If you are age 70 or over and meet certain tests, you may be able to defer the payment of your property taxes on your home. You should

2018 Payroll Update Reference Guide

2018 Payroll Update Reference Guide Jones & Roth is providing this Payroll Update as a reference guide for you. It is not meant to be all-inclusive. If there is a payroll item that you have questions about,

2018 Payroll Update Reference Guide Jones & Roth is providing this Payroll Update as a reference guide for you. It is not meant to be all-inclusive. If there is a payroll item that you have questions about,

CITY OF CUYAHOGA FALLS INCOME TAX DIVISION nd Street CUYAHOGA FALLS, OHIO IMPORTANT TAX INFORMATION EMPLOYER MUNICIPAL WITHHOLDING BOOKLET

CITY OF CUYAHOGA FALLS INCOME TAX DIVISION CUYAHOGA FALLS, OHIO 44221 IMPORTANT TAX INFORMATION EMPLOYER MUNICIPAL WITHHOLDING BOOKLET THIS BOOKLET INCLUDES THE FOLLOWING: CW-1 Forms CW-3 Form 2018 Used

CITY OF CUYAHOGA FALLS INCOME TAX DIVISION CUYAHOGA FALLS, OHIO 44221 IMPORTANT TAX INFORMATION EMPLOYER MUNICIPAL WITHHOLDING BOOKLET THIS BOOKLET INCLUDES THE FOLLOWING: CW-1 Forms CW-3 Form 2018 Used

F-1120 INSTRUCTIONS. What s Inside. Florida Department of Revenue

F-1120 INSTRUCTIONS Corporate Income/Franchise Tax Return for taxable years beginning on or after January 1, 2012. F-1120N R. 01/13 Rule 12C-1.051 Florida Administrative Code Effective 01/13 All installment

F-1120 INSTRUCTIONS Corporate Income/Franchise Tax Return for taxable years beginning on or after January 1, 2012. F-1120N R. 01/13 Rule 12C-1.051 Florida Administrative Code Effective 01/13 All installment

2018 CITY OF BENTON HARBOR 2018 EMPLOYER'S WITHHOLDING TAX FORMS AND INSTRUCTIONS

RETURN TO: BENTON HARBOR PO BOX 597 BENTON HARBOR, MI 49023 ADDRESS SERVICE REQUESTED MAIL TO: 2018 CITY OF BENTON HARBOR 2018 EMPLOYER'S WITHHOLDING TAX FORMS AND INSTRUCTIONS ONLINE FILING AND PAYMENT

RETURN TO: BENTON HARBOR PO BOX 597 BENTON HARBOR, MI 49023 ADDRESS SERVICE REQUESTED MAIL TO: 2018 CITY OF BENTON HARBOR 2018 EMPLOYER'S WITHHOLDING TAX FORMS AND INSTRUCTIONS ONLINE FILING AND PAYMENT

EMPLOYER MUNICIPAL QUARTERLY WITHHOLDING BOOKLET

INCOME TAX DIVISION P.O. BOX 385 MARYSVILLE, OHIO 43040-0385 PHONE: (937) 645-1090 FAX: (937) 645-1105 IMPORTANT TAX INFORMATION EMPLOYER MUNICIPAL QUARTERLY WITHHOLDING BOOKLET This Booklet Contains the

INCOME TAX DIVISION P.O. BOX 385 MARYSVILLE, OHIO 43040-0385 PHONE: (937) 645-1090 FAX: (937) 645-1105 IMPORTANT TAX INFORMATION EMPLOYER MUNICIPAL QUARTERLY WITHHOLDING BOOKLET This Booklet Contains the

IT 1040X Ohio Amended Individual Income Tax Return Rev. 1/10

Ohio Amended Individual Income Tax Return Please Print Payments Your fi rst name M.I. Last name If a joint return, spouse's fi rst name M.I. Last name Home address (number and street) City, town or post

Ohio Amended Individual Income Tax Return Please Print Payments Your fi rst name M.I. Last name If a joint return, spouse's fi rst name M.I. Last name Home address (number and street) City, town or post

RI-1040X-R Amended Rhode Island Resident Individual Income Tax Return 2012 NAME AND ADDRESS

RI-1040X-R Amended Rhode Island Resident Individual Income Tax Return 2012 NAME AND ADDRESS First name Spouse s first name (To be used by resident taxpayers only) Initial Initial Last name Last name Your

RI-1040X-R Amended Rhode Island Resident Individual Income Tax Return 2012 NAME AND ADDRESS First name Spouse s first name (To be used by resident taxpayers only) Initial Initial Last name Last name Your

INSTRUCTIONS FOR PREPARING THE PAYROLL TAX DEPOSIT (DE 88/DE 88ALL) COUPON

COUPON") INSTRUCTIONS FOR PREPARING THE PAYROLL TA DEPOSIT (DE 88/DE 88ALL) COUPON The Employment Development Department (EDD) Taxpayer Assistance Center agents are available to answer your general state payroll

INSTRUCTIONS FOR PREPARING THE PAYROLL TA DEPOSIT (DE 88/DE 88ALL) COUPON The Employment Development Department (EDD) Taxpayer Assistance Center agents are available to answer your general state payroll

AGENCY: Internal Revenue Service (IRS), Treasury. ACTION: Notice of proposed rulemaking and notice of public

, Treasury. ACTION: Notice of proposed rulemaking and notice of public") [4830-01-p] DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Parts 1, 31, 40, and 301 [REG-153340-09] RIN 1545-BJ13 Electronic Funds Transfer of Depository Taxes AGENCY: Internal Revenue Service

[4830-01-p] DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Parts 1, 31, 40, and 301 [REG-153340-09] RIN 1545-BJ13 Electronic Funds Transfer of Depository Taxes AGENCY: Internal Revenue Service

Minnesota Income Tax Withholding

2019 Minnesota Income Tax Withholding Instruction Booklet and Tax Tables Start using this booklet Jan. 1, 2019 Inside This Booklet Forms and Fact Sheets.... 2 Directory.... 2 Free Business Tax Workshops...

2019 Minnesota Income Tax Withholding Instruction Booklet and Tax Tables Start using this booklet Jan. 1, 2019 Inside This Booklet Forms and Fact Sheets.... 2 Directory.... 2 Free Business Tax Workshops...

North Carolina. Includes Forms: NC - 30 Web Income Tax Withholding Tables and Instructions for Employers

North Carolina www.dornc.com NC - 30 Web Income Tax Withholding Tables and Instructions for Employers (Revised 11/11) You can file your return and pay your tax online at www.dornc.com. Click on Electronic

North Carolina www.dornc.com NC - 30 Web Income Tax Withholding Tables and Instructions for Employers (Revised 11/11) You can file your return and pay your tax online at www.dornc.com. Click on Electronic

CITY OF CUYAHOGA FALLS INCOME TAX DIVISION nd Street CUYAHOGA FALLS, OHIO IMPORTANT TAX INFORMATION EMPLOYER MUNICIPAL WITHHOLDING BOOKLET

CITY OF CUYAHOGA FALLS INCOME TAX DIVISION CUYAHOGA FALLS, OHIO 44221 IMPORTANT TAX INFORMATION EMPLOYER MUNICIPAL WITHHOLDING BOOKLET THIS BOOKLET INCLUDES THE FOLLOWING: s CW-3 2018 Used for the remittance

CITY OF CUYAHOGA FALLS INCOME TAX DIVISION CUYAHOGA FALLS, OHIO 44221 IMPORTANT TAX INFORMATION EMPLOYER MUNICIPAL WITHHOLDING BOOKLET THIS BOOKLET INCLUDES THE FOLLOWING: s CW-3 2018 Used for the remittance

Minnesota Income Tax Withholding

2018 Minnesota Income Tax Withholding Instruction Booklet and Tax Tables Start using this booklet Jan. 1, 2018 Inside This Booklet Forms and Fact Sheets.... 2 Directory.... 2 Free Business Tax Workshops...

2018 Minnesota Income Tax Withholding Instruction Booklet and Tax Tables Start using this booklet Jan. 1, 2018 Inside This Booklet Forms and Fact Sheets.... 2 Directory.... 2 Free Business Tax Workshops...

Arizona Form 2017 Resident Personal Income Tax Return 140

Arizona Form 2017 Resident Personal Income Tax Return 140 For information or help, call one of the numbers listed: Phoenix (602) 255-3381 From area codes 520 and 928, toll-free (800) 352-4090 Tax forms,

Arizona Form 2017 Resident Personal Income Tax Return 140 For information or help, call one of the numbers listed: Phoenix (602) 255-3381 From area codes 520 and 928, toll-free (800) 352-4090 Tax forms,

H.B. 133 As Passed by the House

AM2070 H.B. 133 As Passed by the House Topic: Estimated income tax underpayment penalty 1 moved to amend as follows: In line 2 of the title, after "5747.01," insert "5747.09, 5747.43," In line 10 of the

AM2070 H.B. 133 As Passed by the House Topic: Estimated income tax underpayment penalty 1 moved to amend as follows: In line 2 of the title, after "5747.01," insert "5747.09, 5747.43," In line 10 of the

2019 Taxbrief. Paychex Tax Facts

2019 Taxbrief 1 2019 Taxbrief This section includes 2019 payroll tax deposit rules, regulations, and deadlines. For additional information on any of the topics discussed in this Taxbrief, please consult

2019 Taxbrief 1 2019 Taxbrief This section includes 2019 payroll tax deposit rules, regulations, and deadlines. For additional information on any of the topics discussed in this Taxbrief, please consult

CITY OF FOREST PARK 2016 INCOME TAX RETURN - FORM IR DUE ON OR BEFORE APRIL 18, 2017

City of Forest Park Income Tax Division 1201 West Kemper Road Forest Park, Ohio 45240 Phone (513) 595-5211 Fax (513) 595-5293 IF TAXPAYER AND SPOUSE ARE FULLY RETIRED AND WITHOUT TAXABLE INCOME, PLACE

City of Forest Park Income Tax Division 1201 West Kemper Road Forest Park, Ohio 45240 Phone (513) 595-5211 Fax (513) 595-5293 IF TAXPAYER AND SPOUSE ARE FULLY RETIRED AND WITHOUT TAXABLE INCOME, PLACE

Income Tax Guide for Electing Under Section 216

Income Tax Guide for Electing Under Section 216 2016 T4144(E) Rev. 16 Is this guide for you? T his guide is for you if you were a non-resident of Canada (see the definition below) for all or part of 2016

Income Tax Guide for Electing Under Section 216 2016 T4144(E) Rev. 16 Is this guide for you? T his guide is for you if you were a non-resident of Canada (see the definition below) for all or part of 2016

January 7, Medicare Rate 1.45% [.0145]* 1.45% [.0145] Maximum wage NO MAXIMUM NO MAXIMUM Maximum withholding NO MAXIMUM NO MAXIMUM

![January 7, Medicare Rate 1.45% [.0145]* 1.45% [.0145] Maximum wage NO MAXIMUM NO MAXIMUM Maximum withholding NO MAXIMUM NO MAXIMUM](/thumbs/93/112509111.jpg "January 7, Medicare Rate 1.45% [.0145]* 1.45% [.0145] Maximum wage NO MAXIMUM NO MAXIMUM Maximum withholding NO MAXIMUM NO MAXIMUM") January 7, 2019 Dear Client: We want to take this opportunity to thank you for your continued support of our firm. As we move forward to 2019, we want to update you on relevant changes to payroll and general

January 7, 2019 Dear Client: We want to take this opportunity to thank you for your continued support of our firm. As we move forward to 2019, we want to update you on relevant changes to payroll and general

Instructions for Form 941 (Rev. April 2005)

") Instructions for Form 941 (Rev. April 2005) For use with Form 941 (Rev. January 2005) Employer s Quarterly Federal Tax Return Section references are to the Internal Revenue Code unless otherwise indicated.

Instructions for Form 941 (Rev. April 2005) For use with Form 941 (Rev. January 2005) Employer s Quarterly Federal Tax Return Section references are to the Internal Revenue Code unless otherwise indicated.

Provincial Remittances and Reconciliations

Chapter 5 Provincial Remittances and Reconciliations Learning Objectives: Upon completion of this chapter, you should be able to: 1. apply Québec statutory remittance schedules 2. calculate Québec statutory

Chapter 5 Provincial Remittances and Reconciliations Learning Objectives: Upon completion of this chapter, you should be able to: 1. apply Québec statutory remittance schedules 2. calculate Québec statutory

Form RI-1041ES Rhode Island Fiduciary Estimated Payment Coupons

2008 Form RI- Rhode Island Fiduciary Estimated Payment Coupons PURPOSE OF FORM This form provides a means of paying your Rhode Island income tax on a current basis on income other than salaries or wages

2008 Form RI- Rhode Island Fiduciary Estimated Payment Coupons PURPOSE OF FORM This form provides a means of paying your Rhode Island income tax on a current basis on income other than salaries or wages

2019 Tax Calendar This day 2019 Tax Return Due Dates Jan. 15th Estimated Tax. Jan. 31st Employers' Taxes. Withholding. Individuals.

2019 Tax Calendar This day 2019 Tax Return Due Dates Jan. 15th Jan. 31st Estimated Tax. Final installment of 2018 estimated tax ( Form 1040-ES) by individuals unless income tax return is filed with final

2019 Tax Calendar This day 2019 Tax Return Due Dates Jan. 15th Jan. 31st Estimated Tax. Final installment of 2018 estimated tax ( Form 1040-ES) by individuals unless income tax return is filed with final

RHODE ISLAND EMPLOYER S INCOME TAX WITHHOLDING TABLES

2008 RHODE ISLAND EMPLOYER S INCOME TAX WITHHOLDING TABLES www.tax.ri.gov CONTENTS Page Employer s Tax Calendar... 3 Instructions... 4-6 WITHHOLDING METHODS AND TABLES Withholding Percentage Method...

2008 RHODE ISLAND EMPLOYER S INCOME TAX WITHHOLDING TABLES www.tax.ri.gov CONTENTS Page Employer s Tax Calendar... 3 Instructions... 4-6 WITHHOLDING METHODS AND TABLES Withholding Percentage Method...

Must be postmarked not later than. Jan January 1 - January 31. Feb February 1 - February 28. Mar March 1 - March 31

Etna Newark JEDZ South Income Office Payroll Withholding Payroll Withholding Filed Period not later than Pay Period Jan 02-15-18 January 1 - January 31 Feb 03-15-18 February 1 - February 28 Mar 04-17-18

Etna Newark JEDZ South Income Office Payroll Withholding Payroll Withholding Filed Period not later than Pay Period Jan 02-15-18 January 1 - January 31 Feb 03-15-18 February 1 - February 28 Mar 04-17-18

Oregon Withholding Tax Formulas

Oregon Withholding Tax Formulas Effective January 1, 2013 To Oregon employers: The Oregon Withholding Tax Formulas include: Things you need to know. Phase-out information for high income employees. Frequently

Oregon Withholding Tax Formulas Effective January 1, 2013 To Oregon employers: The Oregon Withholding Tax Formulas include: Things you need to know. Phase-out information for high income employees. Frequently

The ABCs and XYZs of Correcting IRS Forms Presented on Tuesday, March 1, 2016

The ABCs and XYZs of Correcting IRS Forms Presented on Tuesday, March 1, 2016 1 2015 The Payroll Advisor 2 Housekeeping 3 Credit Questions Today s topic Speaker 2015 The Payroll Advisor To earn RCH credit

The ABCs and XYZs of Correcting IRS Forms Presented on Tuesday, March 1, 2016 1 2015 The Payroll Advisor 2 Housekeeping 3 Credit Questions Today s topic Speaker 2015 The Payroll Advisor To earn RCH credit

EMPLOYER MUNICIPAL QUARTERLY WITHHOLDING BOOKLET

INCOME TAX DIVISION 209 S. MAIN ST., P.O. BOX 385 MARYSVILLE, OHIO 43040 PHONE: (937) 645-7350 FAX: (937) 645-7351 IMPORTANT TAX INFORMATION EMPLOYER MUNICIPAL QUARTERLY WITHHOLDING BOOKLET This Booklet

INCOME TAX DIVISION 209 S. MAIN ST., P.O. BOX 385 MARYSVILLE, OHIO 43040 PHONE: (937) 645-7350 FAX: (937) 645-7351 IMPORTANT TAX INFORMATION EMPLOYER MUNICIPAL QUARTERLY WITHHOLDING BOOKLET This Booklet

Newark Income Tax Office Payroll Withholding

Newark Income Tax Office Payroll Withholding Filed Period not later than Pay Period Jan 02-15-17 January 1 - January 31 Feb 03-15-17 February 1 - February 28 Mar 04-18-17 March 1 - March 31 Apr 05-15-17

Newark Income Tax Office Payroll Withholding Filed Period not later than Pay Period Jan 02-15-17 January 1 - January 31 Feb 03-15-17 February 1 - February 28 Mar 04-18-17 March 1 - March 31 Apr 05-15-17

Chapter 7 Contribution Reporting

IN THIS CHAPTER: Tax-Sheltered Deductions Contribution Rates Compensation or Contribution Limits Social Security and Medicare Coverage Remitting Payments Salary Deduction Reports Special Situations Wrongful

IN THIS CHAPTER: Tax-Sheltered Deductions Contribution Rates Compensation or Contribution Limits Social Security and Medicare Coverage Remitting Payments Salary Deduction Reports Special Situations Wrongful

Electronic Funds Transfer, Credit Card Payments, and Electronic Filing.

560-3-2-.26 Electronic Funds Transfer, Credit Card Payments, and Electronic Filing. (1) Purpose. The purpose of this rule is to provide guidance concerning the administration of O.C.G.A. 48-2-32(f), which

560-3-2-.26 Electronic Funds Transfer, Credit Card Payments, and Electronic Filing. (1) Purpose. The purpose of this rule is to provide guidance concerning the administration of O.C.G.A. 48-2-32(f), which

2017 New Mexico Instructions for Form FID-1 Fiduciary Income Tax Return

STATE OF NEW MEXICO Taxation and Revenue Department P.O. Box 25127 Santa Fe, New Mexico 87504-5127 2017 New Mexico Instructions for Form FID-1 Fiduciary Income Tax Return READ THE INSTRUCTIONS CAREFULLY.

STATE OF NEW MEXICO Taxation and Revenue Department P.O. Box 25127 Santa Fe, New Mexico 87504-5127 2017 New Mexico Instructions for Form FID-1 Fiduciary Income Tax Return READ THE INSTRUCTIONS CAREFULLY.

2018 Payroll Withholding and Payroll Tax Changes

Below is our annual summary of specific provisions relating to payroll and information reporting. The provisions will be effective January 1, 2018. Please review this information carefully and share it

Below is our annual summary of specific provisions relating to payroll and information reporting. The provisions will be effective January 1, 2018. Please review this information carefully and share it

QuickSuper. Paying for contributions.

QuickSuper Paying for contributions www.clearinghouse.australiansuper.com QuickSuper Paying for contributions Document History Date Description 15 May 2011 Initial release to include Direct Debit and EFT

QuickSuper Paying for contributions www.clearinghouse.australiansuper.com QuickSuper Paying for contributions Document History Date Description 15 May 2011 Initial release to include Direct Debit and EFT

Activity Summary. New Balance $ Minimum Payment Due $ Payment Due Date 02/03/2016. Reward Points. January 2016 Statement

Page 1 of 4 Open Date: 12/08/2015 Closing Date: 01/07/2016 Account: 4798 5100 5300 3857 Visa Business Bonus Rewards Card BATTLE ROCK CHARTER New Balance $117.31 Minimum Payment Due $17.00 Payment Due Date

Page 1 of 4 Open Date: 12/08/2015 Closing Date: 01/07/2016 Account: 4798 5100 5300 3857 Visa Business Bonus Rewards Card BATTLE ROCK CHARTER New Balance $117.31 Minimum Payment Due $17.00 Payment Due Date

January 3, Medicare Rate 1.45% [.0145]* 1.45% [.0145] Maximum wage NO MAXIMUM NO MAXIMUM Maximum withholding NO MAXIMUM NO MAXIMUM

![January 3, Medicare Rate 1.45% [.0145]* 1.45% [.0145] Maximum wage NO MAXIMUM NO MAXIMUM Maximum withholding NO MAXIMUM NO MAXIMUM](/thumbs/74/69630893.jpg "January 3, Medicare Rate 1.45% [.0145]* 1.45% [.0145] Maximum wage NO MAXIMUM NO MAXIMUM Maximum withholding NO MAXIMUM NO MAXIMUM") January 3, 2017 Dear Client: We want to take this opportunity to thank you for your continued support of our firm. As we move forward to 2017, we want to update you on relevant changes to payroll and general

January 3, 2017 Dear Client: We want to take this opportunity to thank you for your continued support of our firm. As we move forward to 2017, we want to update you on relevant changes to payroll and general

Additional Disclosures. Definitions. Revolving Credit Limit. APRs

Additional Disclosures These Additional Disclosures include the Citi Disclosures on the accompanying promotional offer. Keep both documents for your records. If you are approved for credit, you will receive

Additional Disclosures These Additional Disclosures include the Citi Disclosures on the accompanying promotional offer. Keep both documents for your records. If you are approved for credit, you will receive

2019 Ohio IT 1040ES Voucher 1 Due April 15, 2019

Voucher 1 Due April 15, 2019 Electronic Options Cut on the dotted lines. Use only black ink. (Voucher 1) Due April 15, 2019 Spouse s first name M.I. Last name Spouse s P.O. Box 1460, Columbus, OH 432161460

Voucher 1 Due April 15, 2019 Electronic Options Cut on the dotted lines. Use only black ink. (Voucher 1) Due April 15, 2019 Spouse s first name M.I. Last name Spouse s P.O. Box 1460, Columbus, OH 432161460

2017 Insurance Premium Tax Return for Life and Health Companies

2017 Insurance Premium Tax Return for Life and Health Companies Due March 1, 2018 M11L Page 1 Check if: Amended Return Name of Insurance Company FEIN Minnesota Tax ID (required) Mailing Address Check if

2017 Insurance Premium Tax Return for Life and Health Companies Due March 1, 2018 M11L Page 1 Check if: Amended Return Name of Insurance Company FEIN Minnesota Tax ID (required) Mailing Address Check if

Amendment to the Personal Deposit Account Agreement (Dated January 2, 2014)

") Effective February 28, 2017 Amendment to the Personal Deposit Account Agreement (Dated January 2, 2014) Beginning February 28, 2017 cash deposited at an Eastern Bank ATM will be available for withdrawal

Effective February 28, 2017 Amendment to the Personal Deposit Account Agreement (Dated January 2, 2014) Beginning February 28, 2017 cash deposited at an Eastern Bank ATM will be available for withdrawal

Form 2-ES Massachusetts Estimated Income Tax for Filers of Forms 2 and 2G

Form 2-ES Massachusetts Estimated Income Tax for Filers of Forms 2 and 2G 2018 Massachusetts Department of Revenue General Information What is the purpose of estimated tax payment vouchers? The purpose

Form 2-ES Massachusetts Estimated Income Tax for Filers of Forms 2 and 2G 2018 Massachusetts Department of Revenue General Information What is the purpose of estimated tax payment vouchers? The purpose

Form1040-ES/V (OCR) Department of the Treasury Internal Revenue Service

Department of the Treasury Internal Revenue Service") Form1040-ES/V (OCR) Department Treasury Internal Revenue Service Purpose of This Package Use this package to figure and pay your estimated tax. If you are not required to make estimated tax payments for

Form1040-ES/V (OCR) Department Treasury Internal Revenue Service Purpose of This Package Use this package to figure and pay your estimated tax. If you are not required to make estimated tax payments for

2013 Insurance Premium Tax Return for Life and Health Companies

2013 Insurance Premium Tax Return for Life and Health Companies Due March 1, 2014 Check if: Amended return No activity Name of insurance company FEIN Minnesota tax ID (required) M11L Page 1 Mailing address

2013 Insurance Premium Tax Return for Life and Health Companies Due March 1, 2014 Check if: Amended return No activity Name of insurance company FEIN Minnesota tax ID (required) M11L Page 1 Mailing address

BMA Payroll is designed to help you with payroll every step of the way.

Payroll 101: An Introduction to Payroll and Taxes As a new employer, you probably have questions about what it means to "do payroll." This document will provide you with an introduction to payroll processing

Payroll 101: An Introduction to Payroll and Taxes As a new employer, you probably have questions about what it means to "do payroll." This document will provide you with an introduction to payroll processing

2018 Insurance Premium Tax Return for Life and Health Companies

1 1 2 1 2 2 2 0 2 0 2 0 2 ML Page 1 1 1 1 1 2 2 2 2 2 2 2 0 1 2 1 Insurance Premium Tax Return for Life and Health Companies Due March 1, 1 Sign Here Amount Due/Overpaid Part 2 Deductions Premiums Print

1 1 2 1 2 2 2 0 2 0 2 0 2 ML Page 1 1 1 1 1 2 2 2 2 2 2 2 0 1 2 1 Insurance Premium Tax Return for Life and Health Companies Due March 1, 1 Sign Here Amount Due/Overpaid Part 2 Deductions Premiums Print

F-1120 on or after January 1, 2009.

Corporate Income/Franchise and Emergency Excise Tax Return for taxable years beginning F-1120 on or after January 1, 2009. INSTRUCTIONS F-1120N R. 01/10 Rule 12C-1.051 Florida Administrative Code Effective

Corporate Income/Franchise and Emergency Excise Tax Return for taxable years beginning F-1120 on or after January 1, 2009. INSTRUCTIONS F-1120N R. 01/10 Rule 12C-1.051 Florida Administrative Code Effective

NR4 Non-Resident Tax Withholding, Remitting, and Reporting

NR4 Non-Resident Tax Withholding, Remitting, and Reporting 2013 T4061 (E) Rev. 13 Is this guide for you? T his guide provides information for payers and agents who make payments to non-residents of Canada

NR4 Non-Resident Tax Withholding, Remitting, and Reporting 2013 T4061 (E) Rev. 13 Is this guide for you? T his guide provides information for payers and agents who make payments to non-residents of Canada

SC DEPARTMENT OF REVENUE 2018 INDIVIDUAL DECLARATION OF ESTIMATED TAX PAY YOUR SOUTH CAROLINA ESTIMATED TAX PAYMENTS FREE OF CHARGE

SC DEPARTMENT OF REVENUE PAY YOUR SOUTH CAROLINA ESTIMATED TAX S FREE OF CHARGE Through our website MyDORWAY.dor.sc.gov Safe, Secure, and Convenient! Available 24 hours a day/7 days a week Pay by credit

SC DEPARTMENT OF REVENUE PAY YOUR SOUTH CAROLINA ESTIMATED TAX S FREE OF CHARGE Through our website MyDORWAY.dor.sc.gov Safe, Secure, and Convenient! Available 24 hours a day/7 days a week Pay by credit

CITY OF CUYAHOGA FALLS INCOME TAX DIVISION nd Street CUYAHOGA FALLS, OHIO IMPORTANT TAX INFORMATION EMPLOYER MUNICIPAL WITHHOLDING BOOKLET

CITY OF CUYAHOGA FALLS INCOME TAX DIVISION CUYAHOGA FALLS, OHIO 44221 IMPORTANT TAX INFORMATION EMPLOYER MUNICIPAL WITHHOLDING BOOKLET IMPORTANT WITHHOLDING TAX CHANGES EFFECTIVE FOR TAX YEARS BEGINNING

CITY OF CUYAHOGA FALLS INCOME TAX DIVISION CUYAHOGA FALLS, OHIO 44221 IMPORTANT TAX INFORMATION EMPLOYER MUNICIPAL WITHHOLDING BOOKLET IMPORTANT WITHHOLDING TAX CHANGES EFFECTIVE FOR TAX YEARS BEGINNING

TSB-M-09(1)MCTMT begins on page 2 below.

MCTMT begins on page 2 below.") Note: Please see TSB-M-09(1.1)MCTMT, Correction to TSB-M-09(1)MCTMT Metropolitan Commuter Transportation Mobility Tax, for a correction to the definition of net earnings from self-employment that appears

Note: Please see TSB-M-09(1.1)MCTMT, Correction to TSB-M-09(1)MCTMT Metropolitan Commuter Transportation Mobility Tax, for a correction to the definition of net earnings from self-employment that appears

Estimated Tax on Unrelated Business Taxable Income for Tax-Exempt Organizations. (Keep for Your Records Do Not Send to the Internal Revenue Service)

") Form 0-W (WORKSHEET) Department of the Treasury Internal Revenue Service Estimated Tax on Unrelated Business Taxable Income for Tax-Exempt Organizations (Keep for Your Records Do Not Send to the Internal

Form 0-W (WORKSHEET) Department of the Treasury Internal Revenue Service Estimated Tax on Unrelated Business Taxable Income for Tax-Exempt Organizations (Keep for Your Records Do Not Send to the Internal

2017 RI-1041 FIDUCIARY INCOME TAX RETURN GENERAL INSTRUCTIONS

2017 RI-1041 FIDUCIARY INCOME TAX RETURN GENERAL INSTRUCTIONS WHO MUST FILE The fiduciary of a RESIDENT estate or trust must file a return on Form RI-1041 if the estate or trust: (1) is required to file

2017 RI-1041 FIDUCIARY INCOME TAX RETURN GENERAL INSTRUCTIONS WHO MUST FILE The fiduciary of a RESIDENT estate or trust must file a return on Form RI-1041 if the estate or trust: (1) is required to file

SC1040X (Rev. 8/23/12) 3083

3083") Do not write in this space - OFFICE USE 50 STATE OF SOUTH CAROLINA DEPARTMENT OF REVENUE AMENDED INDIVIDUAL INCOME TAX Fiscal year Ended of, OR CALENDAR YEAR Tax Year SC00X (Rev. 8//) 08 PART I Print Your

Do not write in this space - OFFICE USE 50 STATE OF SOUTH CAROLINA DEPARTMENT OF REVENUE AMENDED INDIVIDUAL INCOME TAX Fiscal year Ended of, OR CALENDAR YEAR Tax Year SC00X (Rev. 8//) 08 PART I Print Your