i. On or before the due date of furnishing the return for the month of September 2018 i.e (unless extended). OR

|

|

|

- Dulcie Lawrence

- 5 years ago

- Views:

Transcription

1 Points to consider before filing GSTR-3B/GSTR-1 for September 1. Pending Input Tax Credit to be availed before filing GSTR- 3B of Sept 18: Section 16 (4) of Central Goods and Services Tax Act, 2017 provides that the Input Tax Credit (ITC) on the invoices raised during July 2017 to March can be availed by the registered person on earliest of the following dates: i. On or before the due date of furnishing the return for the month of September i.e (unless extended). OR ii. Before filing of annual return for July 2017 to March. Therefore, the last date of availing the ITC on invoices pertaining to the period July 2017 to March shall be the due date of filing of GSTR-3B for September i.e (unless extended). Therefore, the registered person is advised to avail the pending ITC pertaining to invoices raised in July 2017 to March by the vendor within the due date of filing the return of September. Therefore, all registered persons are advised that the return in Form GSTR- 3B for September should be filed within the due date i.e. 20 th October (for availment of credit on invoices / debit note of ) to avoid any action of reversal of credit from the department. The following activities has to be carried out by the company for each GST registration before filing the GSTR-3B of September and avail the pending eligible ITC otherwise the ITC on the same shall lapse. A. Reconciliation of ITC availed in GSTR-3B with the books: Reconciliation of ITC availed in books and that availed in GSTR-3B. There may be instances where due to human/system error, the ITC has not been availed in GSTR-3B. Such invoices are required to be traced so that the ITC can be availed within the time frame. B. Reconciliation of ITC availed in GSTR-3B with ITC available as per GSTR-2A: Presently, there is no requirement to file or verify GSTR 2A return. However, there may be many reasons for difference between credit availed under GSTR-3B & credit appearing under GSTR-2A. Page 1

2 For example: There may be cases where vendor has sent the invoice which the company has not received at all. In such cases, the company is required to follow up with the vendor and get the invoices and then avail ITC within the time prescribed above. In many cases, ITC on bank charges have not been taken as invoice may not be received from Bank. In such cases, the company is required to follow up with the bank and get the invoices and then avail ITC within the time prescribed above. There have been instances where GSTIN number was not provided to the vendors initially resulting in issuance of invoice as B2C. In such cases, the company must get the invoices amended from the vendor as B2B before availing the ITC and assure that the vendor rectifies the same in his GSTR-1 not later than GSTR-1 for the month of September. There may be instances where the goods have been received in but the same has not yet been cleared by the quality & inspection department and thus the purchases have not yet been booked. In such case, the quality & inspection department must take place immediately so that the ITC can be availed within the time frame. A reconciliation between ITC as per GSTR-2A and as per books will reveal such differences (if any). Hence, such activity may be carried out to avail credit at the time of filing September return within the due date. C. ITC available on distribution by ISD: All the recipient units are required to avail the ISD credit based on the invoices issued by ISD. It is advised that all such ITC distributed on ISD invoices issued in July 2017 to March, shall be availed on or before due date of Sept return. D. Debit note issued during -19 by vendor for invoices issued in : As per section 16 (4) of Central Goods and Services Tax Act, ITC on debit note issued by vendor during the current year i.e. -19 which is pertaining to invoices raised in has to be availed before due date of filing of annual return OR before due date of filing GSTR-3B for the month of September 18, whichever is earlier. Therefore, the company has to evaluate all the debit notes issued during the period to pertaining to the original invoices issued during the period to E.g. ITC on debit note issued by vendor in April 18 against the original invoice pertaining to March 18 has to be availed on or before due date of Sept return. Page 2

3 2. Other important points to be considered before filing GSTR- 3B/GSTR-1 of Sept 18: i. Rectification of error or omission of invoices: In case of any errors made while uploading Invoices in GSTR-1, the company can rectify in GSTR-1 in subsequent months. However, as per section 37, rectification of such invoices can be made before filing GSTR-1 for the month of September OR before filing annual return, whichever is earlier. Similarly, the invoices which have been missed in GSTR-1 for July 17 to March 18 can be uploaded in GSTR-1 of September. Further corrections in GSTR-3B should also be done till the return of September. ii. Credit Notes: The credit notes for the period to have to be issued & uploaded in GSTR-1 before filing annual return OR before filing GSTR-1 for the month of September, whichever is earlier. If such credit notes are not uploaded on or before filing GSTR-1, then the liability cannot be reduced to that extent. 3. Other Important Points: i. Cross-charging: The Head office provides administration/business support services (Tax/HR/Legal/Finance Team) to other units/branches located in different states or different registrations i.e. distinct persons which is considered as supply of services and accordingly GST has to be charged on the same. Therefore, Head office has to cross charge and pay GST on the same (if not done) to all distinct persons at the earliest. ii. Reverse charge liability paid under normal registration on behalf of ISD unit: Reverse charge liability cannot be discharged under ISD and therefore the same has to be paid under the normal registration in the state in which ISD is registered. Thereafter, an invoice has to be raised on ISD as per rule 54 (1A) for common input services so that the same can be distributed to distinct persons at the earliest. It is advisable that the invoice shall be raised on ISD in the month in which ITC is availed under the normal registration. Page 3

4 Analysis of GST Notifications Dated 10th September : CBIC has issued the various Notifications related to the GST Returns and Amendment in CGST, Rules 2017 on 10th September. In this article we will see the detailed analysis about the Notification No. 43/ Central Tax to Notification No. 48/ Central Tax. Analysis is as follows:- 1. Extension of the due-date of TRANS-1: The Commissioner may, on the recommendations of the Council, extend the date for submitting the declaration electronically in FORM GST TRAN-1 by a further period not beyond 31st March, 2019, in respect of registered persons who could not submit the said declaration by the due date on account of technical difficulties on the common portal and in respect of whom the Council has made a recommendation for such extension. 2. Extension of the due-date of TRANS-2: The registered persons filing the declaration in FORM GST TRAN-1 in accordance with point (1), may submit the statement in FORM GST TRAN-2 by 30th April, Extension of the due-date of GSTR-3B for newly migrated taxpayers as per Notification No 31/-Central Tax,dt : The newly migrated taxpayers can file GSTR-3B for the period from July, 2017 to November, electronically through the common portal on or before the 31st day of December,. 4. Extension of the due date for filing of FORM GSTR 1 for taxpayers having aggregate turnover above Rs 1.5 crores: The registered persons having aggregate turnover of more than 1.5 crore rupees in the preceding financial year or the current financial year, for the months from July, 2017 to September, till the 31st day of October, and for the months from October, to March, 2019 till the eleventh day of the succeeding month. Provided that the time limit for furnishing the details of outward supplies in FORM GSTR-1 for the months from July, 2017 to November, for newly migrated taxpayers, shall be extended till the 31st day of December,. 5. Extension of the due date for filing of FORM GSTR 1 for taxpayers having aggregate turnover upto Rs 1.5 crores: The Central Government, on the recommendations of the Council, hereby notifies the Page 4

5 registered persons having aggregate turnover of up to 1.5 crore rupees in the preceding financial year or the current financial year, as the class of registered persons who shall follow the special procedure as mentioned below for furnishing the details of outward supply of goods or services or both. The said persons may furnish the details of outward supply of goods or services or both in FORM GSTR-1 of the Central Goods and Services Tax Rules, 2017, effected during the quarter as specified in column (2) of the Table below till the time period as specified in the corresponding entry in column (3) of the said Table, namely:- S.No Quarter for which details in Time period for furnishing FORM GSTR-1 are furnished details in FORM GSTR-1 (1) (2) (3) 1. July September, st October, 2. October December, st October, 3. January March, 31st October, 4. April June, 31st October, 5. July September, 31st October, 6. October December, 31st January, January March, th April, 2019 Remarks: Please note that this extension to file GSTR-1 does not alter the time limit under section 16(4) to claim input tax credit. 6. The outward supply of goods or services or both in FORM GSTR-1 for the quarter from July, to September, by: a) registered persons in the State of Kerala; b) registered persons whose principal place of business is in Kodagu district in the State of Karnataka; and c) registered persons whose principal place of business is in Mahe in the Union territory of Puducherry shall be furnished electronically through the common portal, on or before the 15 th day of November,. 7. The details of outward supply of goods or services or both in FORM GSTR- 1 to be filed for the quarters from July, 2017 to September, furnished by newly migrated taxpayers, electronically through the common portal, on or before the 31st day of December,. The Link for the notifications are mentioned below: Page 5

6 Title Notification No. Date Extension of Due date of TRAN-1 and TRAN-2- Notification No. 48/ Power of Commissioner Central Tax 10/09/ Due date to file FORM GSTR-3B for recently Notification No. 47/ Migrated taxpayers Central Tax 10/09/ Due date to file FORM GSTR-3B for newly Notification No. 46/ Migrated taxpayers Central Tax 10/09/ CBIC extends due date for filing of FORM Notification No. 45/ GSTR-3B for newly migrated taxpayers Central Tax 10/09/ Extended due date to file Form GSTR-1 Notification No. 44/ if T.O. more than Rs 1.5 crores Central Tax 10/09/ Extended due date to file Form GSTR-1 Notification No. 43/ if T.O. up to Rs 1.5 crores Central Tax 10/09/ Page 6

7 Due Date of TRAN-1 is Not Extended but Power of Commissioner is extended: Due date of Filing of TRAN-1 is Not Extended by Notification No. 48/ Central Tax Dated Government has issued Notification No. 48/ Central Tax Dated which empowers the Commissioner to Extend the due date of Filing of TRAN-1 in case of Technical Glitches. However, this Notification does not extend the due date but only gives the powers to the Commissioner to extend the due date. Originally Proviso to sub rule 1 of Rule 117 of CGST Rules, 2017 empowered the Commissioner to extend the due date of Filing of TRAN-1 and Commissioner by issuing the order extended the due date to 27th Dec-2017 and beyond which commissioner was not empowered to extend. By issuing the aforementioned Notification Sub Rule 1A inserted in Rule 117 through which Power to Extend the due date of TRAN-1 is again given to the commissioner who may exercise the power on the recommendation of GST Council up to 31st March Thus, to extend the due date commissioner is required to Issue an order and conditions of Technical Glitches may also be specified in this order. Page 7

8 The Central Government vide Notification No. 39 / CT dated 4th September, has notified following rules further to amend the Central Goods and Service Tax Rules, Insertion in Rule : 22 Cancellation of registration New proviso in sub- rule (4) of Rule 22 has been inserted to provide that where the person instead of replying to the notice served for cancellation of registration for contravention of the provisions contained in clause (b) or clause (c) of sub-section (2) of section 29, furnishes all the pending returns and makes full payment of the tax dues along with applicable interest and late fee, the proper officer shall drop the proceedings and pass an order in FORM GST-REG 20. Remarks: With the insertion of this proviso proper officer shall drop the proceedings initiated on person paying tax under section 10 who has not furnished returns for 3 consecutive tax periods or any other registered person who has not furnished return for a continuous period of 6 months and pass an order in FORM GST-REG 20 to such person on furnishing all the pending returns and making full payment of the tax dues along with applicable interest and late fee by him. Insertion in Rule : 36 Documentary requirements and conditions for claiming input tax credit New proviso in sub- rule (2) of Rule 36 has been inserted to provide that if the invoice does not contain all the specified particulars but contains the details of the amount of tax charged, description of goods or services, total value of supply of goods or services or both, GSTIN of the supplier and recipient and place of supply in case of inter-state supply, input tax credit may be availed by such registered person. Remarks: With the insertion of this proviso a relief has been given to registered person by allowing ITC on the basis of invoice if that invoice contains not all the necessary but following particulars: 1. value of goods and tax thereon, 2. description of goods or services 3. GSTIN of the supplier and recipient and 4. Place of supply in case of inter-state supply. Insertion in Rule 138 A: Information to be furnished prior to commencement of movement of goods and generation of e- way bill. New proviso in sub- rule (1) of Rule 138A has been inserted to provide that in case of imported goods, the person in charge of a conveyance shall also carry a copy of the bill of entry filed by the importer of such goods and shall indicate the number and date of the bill of entry in Part A of FORM GST EWB-01. Page 8

9 Remarks: It would seem that any kind of bill of entry (into-bond, ex-bond, home consumption, re warehousing and SEZ-cargo) may be carried by the transporter Substitution in sub-rule 10 of Rule 96 The persons claiming refund of integrated tax paid on exports of goods or services should not have 1. Received supplies on which the following benefits of the Government of India has been received: Notification No. 48/2017-Central Tax, dated the 18th October, 2017: It covers domestic supplies made against advance authorization, supply of capital goods against EPCG authorization, supply of goods to EOU & supply of gold by a bank or PSU against advance authorization. Notification No. 40/2017-Central Tax (Rate), dated the 23rd October or notification No. 41/2017-Integrated Tax (Rate), dated the 23rd October, 2017: This notification covers supplies made to merchant exporter at the rate of 0.1% in case of IGST or 0.05% each in case of CGST & SGST. Hence in above cases, exporter has to export only under LUT and claim refund of accumulated ITC. 3. Availed the benefit under following notifications: Notification No. 78/2017-Customs, dated the 13th October, 2017: This notification provides exemption from Customs Duty & IGST under Customs on goods imported or procured from Public or Private Warehouse or from International Exhibition by Hundred per cent EOU, STP or EHTP units. Notification No. 79/2017- Customs, dated the 13th October, 2017: This notification provides exemption from Customs Duty & IGST under Customs on imports under EPCG, Advance Authorization, Advance Authorization for Annual Requirements, Advance Authorization for Deemed Export, Advance Authorization for export of Prohibited Goods and Narrow Woven Fabrics, etc. Remarks: The latest amendment now carves out such cases referred above by way of a separate clause and provides that if the benefit has been availed by an exporter, he cannot export with payment of IGST. Exporter must compulsorily export under LUT and claim refund of the accumulated ITC. Said amendment is applied retrospectively w.e.f. 23 October, This would adversely affect claim of transition credit and credit on capital goods to EOUs. Insertion of Forms after Form GSR 8: 1. Form GSTR 9 Annual Return 2. Form GSTR 9 A Annual Return (For Composition Taxpayer) Page 9

10 Existing provision Substitution in Rule: 55 Transportation of goods without issue of invoice. (5) Where the goods are being transported in a semi knocked down or completely knocked down condition Revised provision Where the goods are being transported in a semi knocked down or completely knocked down condition or in batches or lots -. (a) the supplier shall issue the complete invoice before dispatch of the first consignment; (b) the supplier shall issue a delivery challan for each of the subsequent consignments, giving reference of the invoice; (c) each consignment shall be accompanied by copies of the corresponding delivery challan along with a duly certified copy of the invoice; and (d) the original copy of the invoice shall be sent along with the last consignment. Remarks: With insertion of these words or in batches or lots the manner prescribed for transportation of goods in a semi knocked down or completely knocked down condition shall also apply to the transportation of goods in batches or lots. Page 10

11 Extension of time limit for making declaration in Form GST ITC-04 The Central Government vide Notification No. 40 / CT dated 4th September,; Notification No. 42 / CT dated 4th September, has extended the time limit of filing various declarations upto the date as shown in the table below: Sl.no Form and Purpose Due date 1. GST ITC-04 Form for declaration in respect of goods dispatched to a job worker or received from a job worker or sent from one job worker to another, during the period from July, 2017 to June, 30th September, 2. GST ITC-01 Form containing details of the stock of inputs and inputs contained in semi finished or finished goods held in stock by him on the date on which the option of availing composition is withdrawn or denied to the effect that he is eligible to avail the input tax credit (Only for registered persons who have filed the application in Form GST-CMP- 04 between the period from 2ndMarch, to 31st March,) 3rd October, Page 11

12 Recovery of arrears of wrongly availed CENVAT credit under the existing Law and inadmissible transitional credit The Central Government vide Circular No. 58/32/-GST dated 4th September, has clarified an alternative method of recovery of the arrears of wrongly availed CENVAT credit under the existing Law and inadmissible transitional credit. In this method of recovery, taxpayers may reverse the wrongly availed CENVAT credit under the existing law and inadmissible transitional credit through Table 4(B)(2) of FORM GSTR-3B. The applicable interest and penalty shall apply on all such reversals which shall be paid through entry in column 9 of Table 6.1 of FORM GSTR-3B. 4. Eligible ITC Details Integrated Central State/UT Tax tax tax Cess A) ITC available full or part 1. Import of goods 2. Import of services 3. Inward supplies liable to reverse charge other than 1 & 2 above 4. Inward supplies from ISD 5. All other ITC B) ITC reversed 1. As per Rule 42 & 43 of CGST Rules 2. Others 6.1 Payment of Tax Description Tax Payable IGST Amount pd as ITC CGST SGST Cess Tax pd TDS/TCS Tax/Cess pd in Cash Interest Integrated tax Central Tax State/UT tax Cess Remarks: Earlier the Circular no. 46/16/-GST dated 13th April, has clarified that that the recovery of arrears arising under the existing law shall be made as central tax liability to be paid through the utilization of the amount available in the electronic credit ledger or electronic cash ledger of the registered person, and the same shall be recorded in Part II of the Electronic Liability Register (FORM GST PMT-01). However, the functionality to record this liability in the Late Fee Page 12

13 electronic liability register is not available on the common portal. Therefore, alternative method of recovery has been provided. [Circular No. 58/32/-GST dated 4th September, ] Page 13

14 Page 14

15 Page 15

16 Page 16

17 Page 17

18 Page 18

19 Page 19

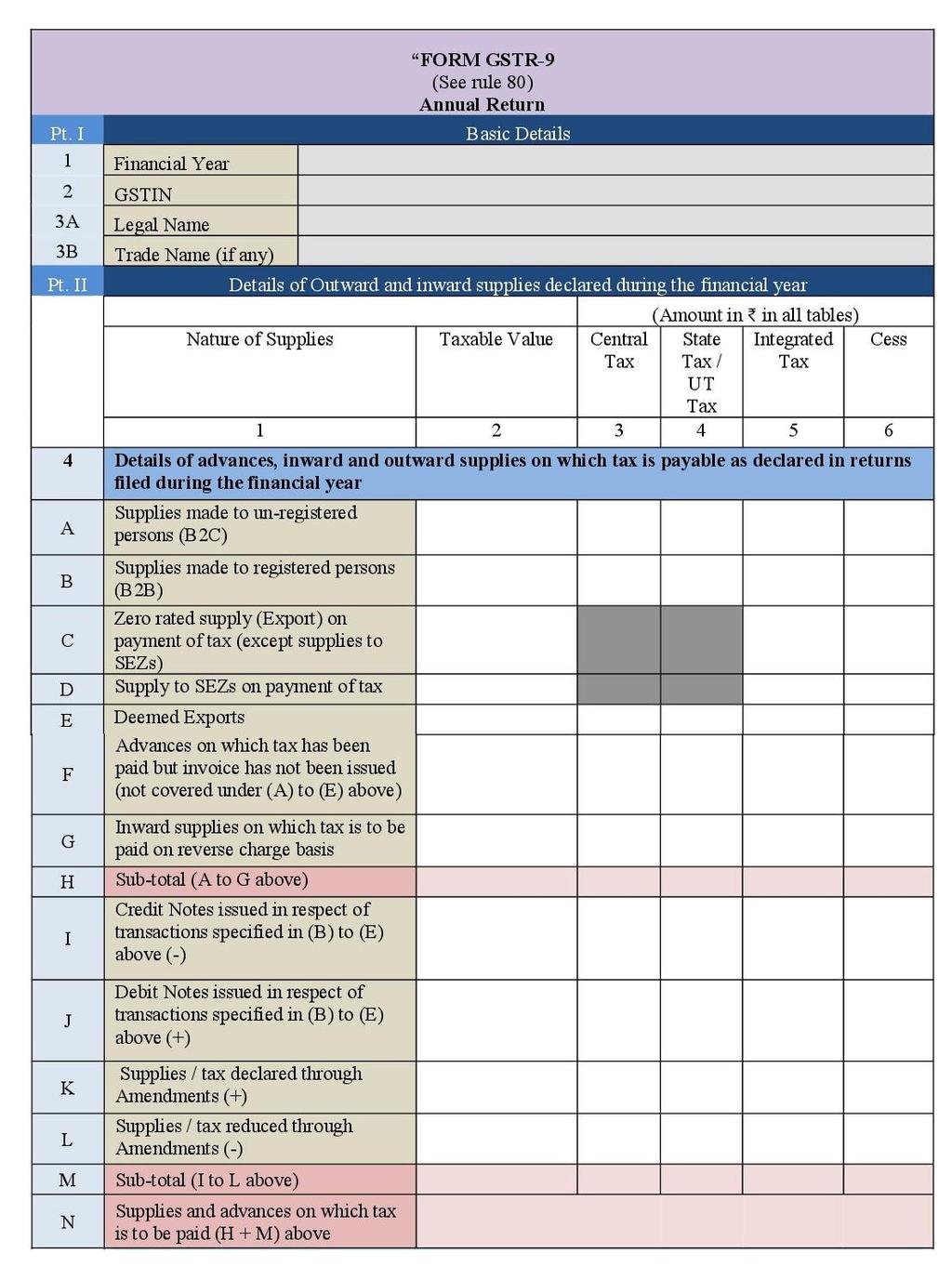

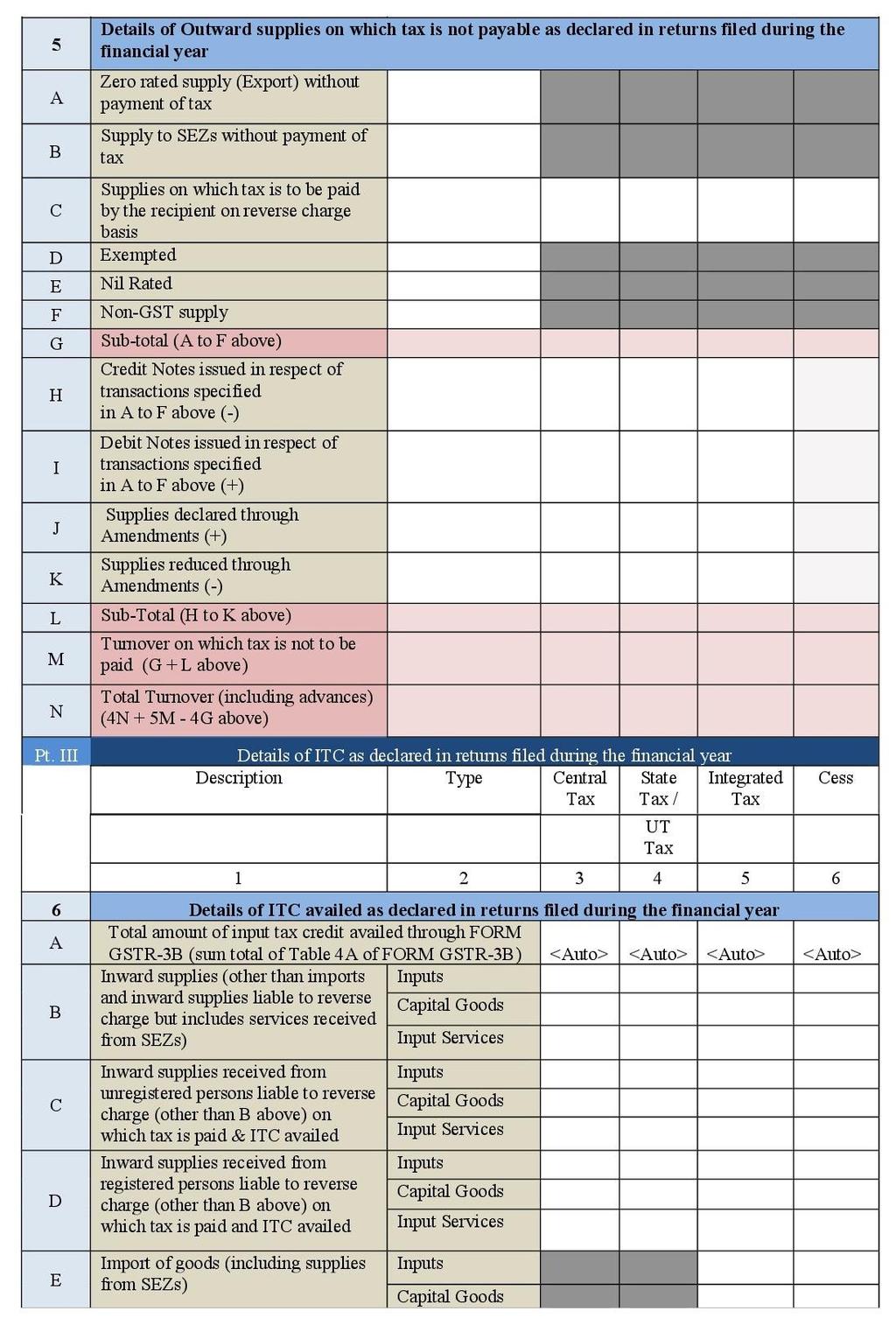

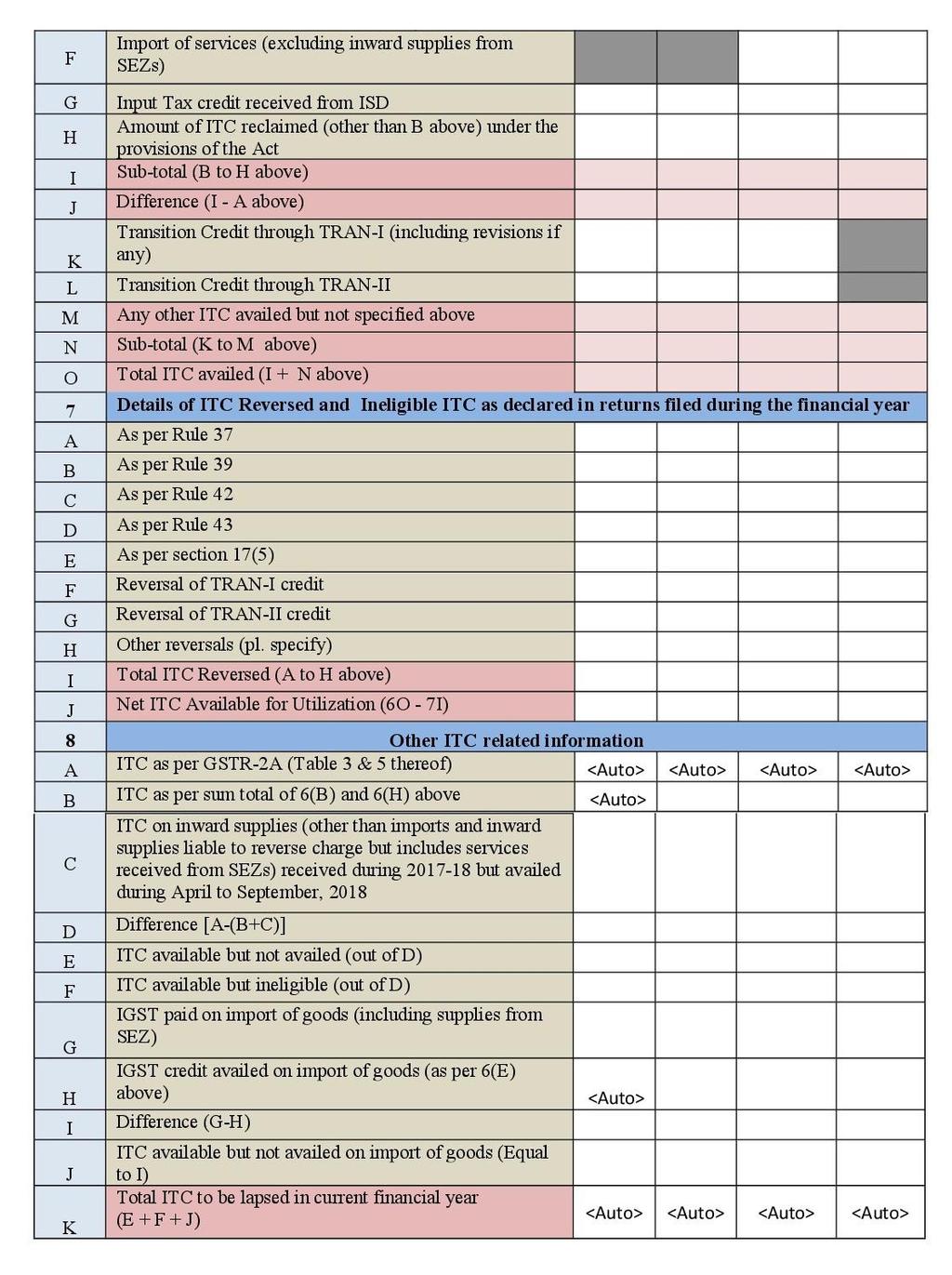

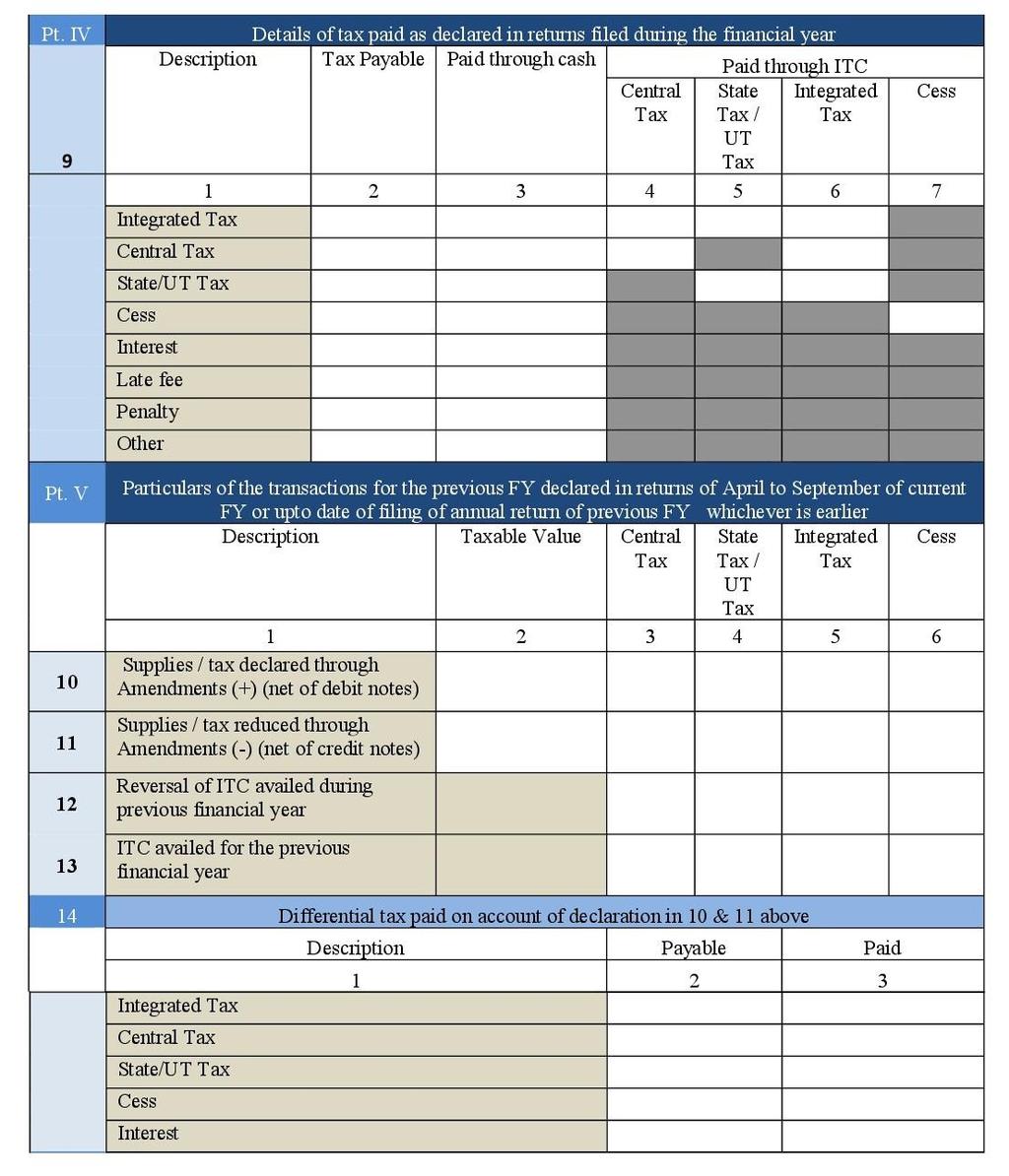

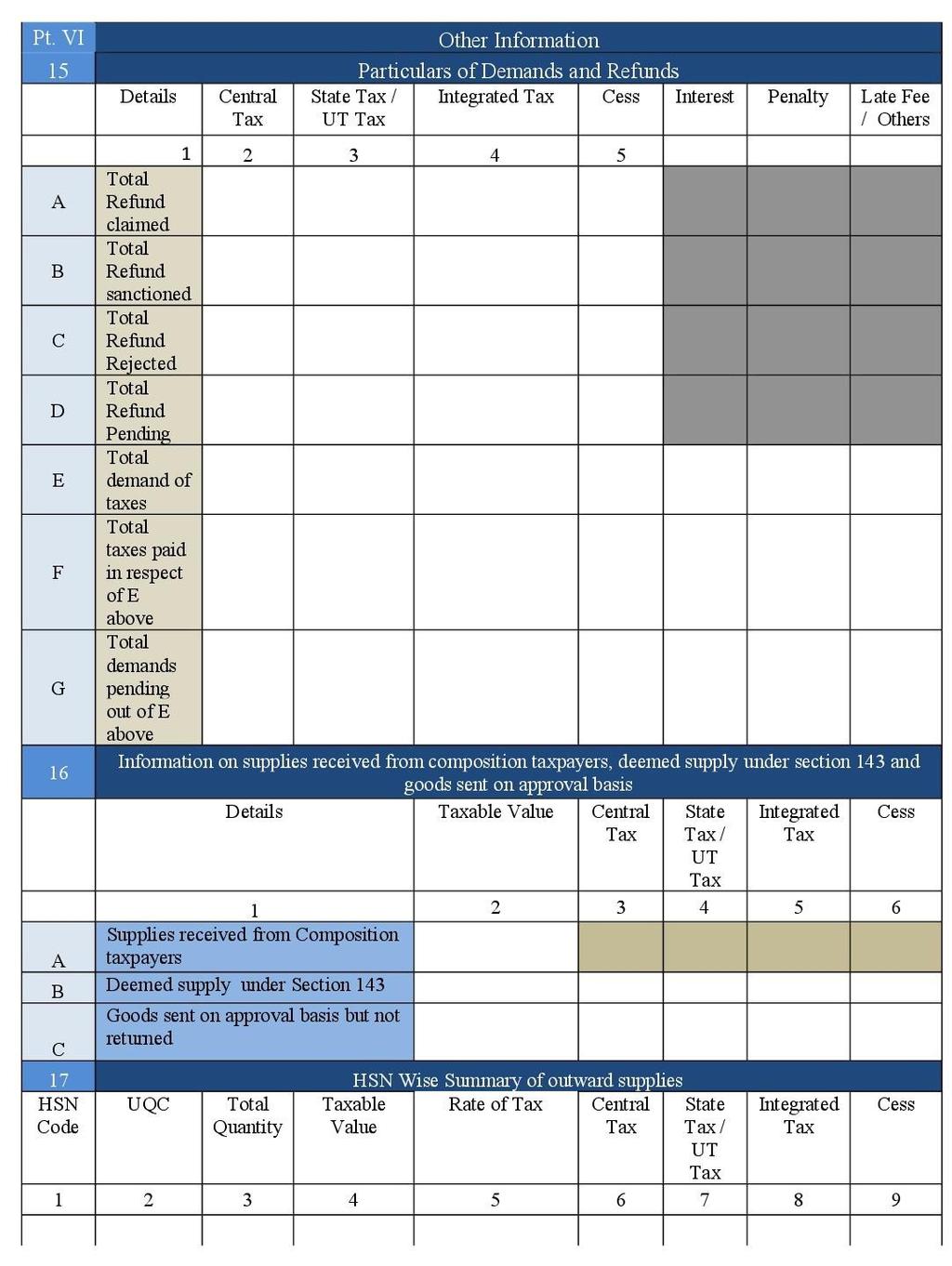

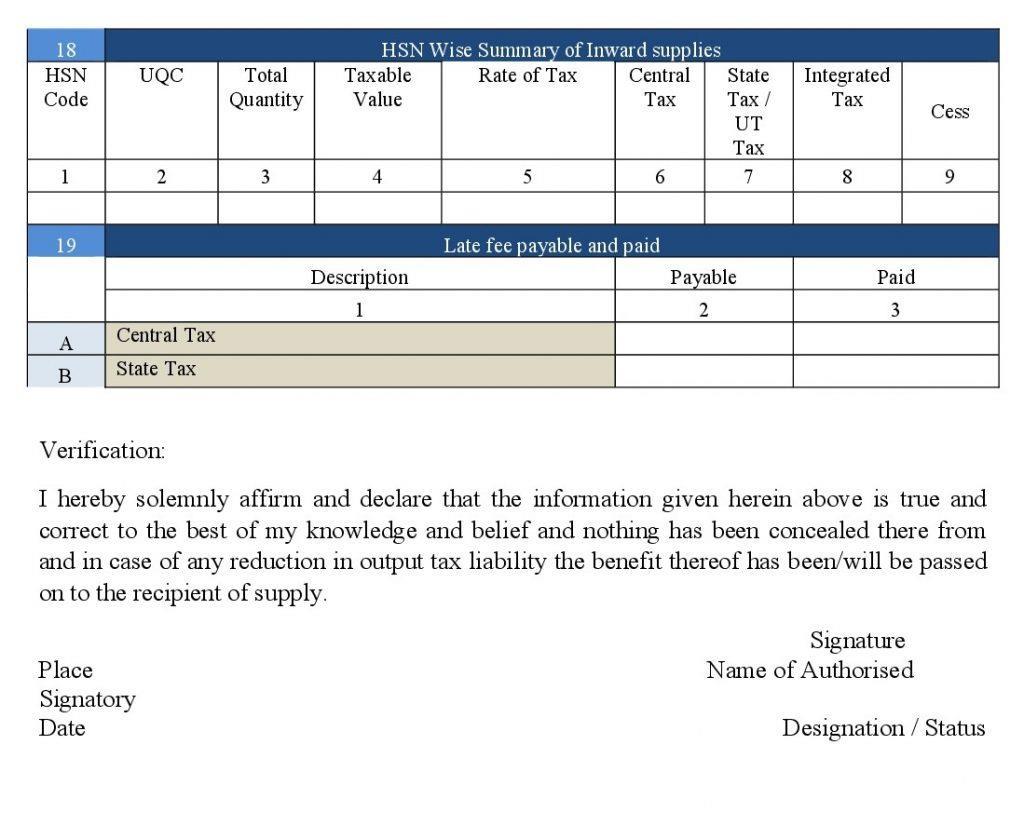

20 6. DETAILS TO BE PROVIDED IN GSTR-9 Sl No Parts of the GSTR-9 Information required 1 Part-I Basic details of the taxpayer. This detail will be auto populated. 2 Part-II Details of Outward and Inward supplies declared during the financial year(fy). This detail must be picked up by consolidating summary from all GST returns filed in previous FY. 3 Part-III Details of ITC declared in returns filed during the FY. This will be summarized values picked up from all the GST returns filed in previous FY. 4 Part-IV Details of tax paid as declared in returns filed during the FY. 5 Part-V Particulars of the transactions for the previous FY declared in returns of April to September of current FY or up to the date of filing of annual return of previous FY whichever is earlier. Usually, the summary of amendment or omission entries belonging to previous FY but reported in Current FY would be segregated and declared here. 6 Part-VI Other Information comprising details of: -GST Demands and refunds, -HSN wise summary information of the quantity of goods supplied and received with its corresponding Tax details against each HSN code, -Late fees payable and paid details and -Segregation of inward supplies received from different categories of taxpayers like Composition dealers, deemed supply and goods supplied on approval basis. Page 20

21 1. What is GSTR 9 GSTR 9 is an annual return to be filed once in a year by the registered taxpayers under GST including those registered under composition levy scheme. It consists of details regarding the supplies made and received during the year under different tax heads i.e. CGST, SGST and IGST. It consolidates the information furnished in the monthly/quarterly returns during the year. 2. Who should File GSTR 9 All the registered taxable persons under GST must file GSTR 9. However, following persons are not required to file GSTR 9 Casual Taxable Person. Input Service Distributors Non-resident taxable persons Persons paying TDS under section 51 of GST Act 3. What are different types of Return under GSTR - 9 There are 4 types of return under GSTR 9 : 1. GSTR 9 -- GSTR 9 should be filed by the regular taxpayers filing GSTR 1, GSTR 2, GSTR GSTR 9A GSTR 9A should be filed by the persons registered under composition scheme under GST. 3. GSTR 9B GSTR 9B should be filed by the e-commerce operators who have filed GSTR 8 during the financial year. 4. GSTR 9C GSTR 9C should be filed by the taxpayers whose annual turnover exceeds Rs 2 crores during the financial year. All such taxpayers are also required to get their accounts audited and file a copy of audited annual accounts and reconciliation statement of tax already paid and tax payable as per audited accounts along with GSTR 9C. 4. When is GSTR 9 Due? GSTR-9 shall be filed on or before 31st December of the subsequent financial year. For instance for FY , the due date for filing GSTR 9 is 31st December,. 5. What is the Penalty for the Late filing of GSTR 9 Return? Late fees for not filing the GSTR 9 within the due date is Rs. 100 per day per act up to a maximum of an amount calculated at a quarter percent of the taxpayer turnover in the state or union territory. Thus it is Rs 100 under CGST & 100 under SGST, total penalty is Rs 200 per day of default. There is no late fee on IGST. Page 21

GOODS & SERVICES TAX / IDT UPDATE 58 GST. Central Goods and Services tax (Eighth Amendment ) Rules, 2018

Rules, 2018") GOODS & SERVICES TAX / IDT UPDATE 58 GST Central Goods and Services tax (Eighth Amendment ) Rules, 2018 The Central Government vide Notification No. 39 /2018 CT dated 4 th September, 2018 has notified

GOODS & SERVICES TAX / IDT UPDATE 58 GST Central Goods and Services tax (Eighth Amendment ) Rules, 2018 The Central Government vide Notification No. 39 /2018 CT dated 4 th September, 2018 has notified

Presentation on GST Annual Return & GST Audit

Optitax s R Presentation on GST Annual Return & GST Audit 25th Nov 2018 1 1 Legal provisions 2 Legal provision Applicability Section 44 (1) - Every registered person, other than an Input Service Distributor,

Optitax s R Presentation on GST Annual Return & GST Audit 25th Nov 2018 1 1 Legal provisions 2 Legal provision Applicability Section 44 (1) - Every registered person, other than an Input Service Distributor,

FAQ s on Form GSTR-9 Annual Return

FAQ s on Form GSTR-9 Annual Return DISCLAIMER The views expressed in this write up are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed

FAQ s on Form GSTR-9 Annual Return DISCLAIMER The views expressed in this write up are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed

Chapter IX Returns Statutory Provision 37. Furnishing details of outward supplies

Chapter IX Returns Statutory Provision 37. Furnishing details of outward supplies (1) Every registered taxable person, other than an input service distributor, a non-resident taxable person and a person

Chapter IX Returns Statutory Provision 37. Furnishing details of outward supplies (1) Every registered taxable person, other than an input service distributor, a non-resident taxable person and a person

ISSUES IN COMPOSITION SCHEME UNDER GST PGS & ASSOCIATES

ISSUES IN COMPOSITION SCHEME UNDER GST PGS & ASSOCIATES DEFINITIONS:- Aggregate Turnover means the aggregate value of all taxable supplies, exempt supplies, exports of goods or services or both and Inter-State

ISSUES IN COMPOSITION SCHEME UNDER GST PGS & ASSOCIATES DEFINITIONS:- Aggregate Turnover means the aggregate value of all taxable supplies, exempt supplies, exports of goods or services or both and Inter-State

The Centre of Excellence for GST. GST: Returns. JULY 09, 2017 ICAI Tower, BKC MUMBAI. CA. Hemant P. Vastani. The Centre of Excellence for GST

GST: Returns JULY 09, 2017 ICAI Tower, BKC MUMBAI CA. Hemant P. Vastani 1 Sections Covering Returns 37. Furnishing details of outward supplies. 38. Furnishing details of inward supplies. 39. Furnishing

GST: Returns JULY 09, 2017 ICAI Tower, BKC MUMBAI CA. Hemant P. Vastani 1 Sections Covering Returns 37. Furnishing details of outward supplies. 38. Furnishing details of inward supplies. 39. Furnishing

GST Update. Weekly Update N a t i o n a l A c a d e m y o f C u s t o m s, I n d i r e c t T a x e s a n d N a r c o t i c s ( N A C I N )

") GST Update Weekly Update 02.02.2019 1 Background This Presentation covers the GST changes / observations/ press releases/ Tweet FAQs/ Sectoral FAQs released by CBEC since the last update on 26.01.2019.

GST Update Weekly Update 02.02.2019 1 Background This Presentation covers the GST changes / observations/ press releases/ Tweet FAQs/ Sectoral FAQs released by CBEC since the last update on 26.01.2019.

GOODS AND SERVICE TAX FILING OF RETURN. Prepared by Dharmendra Academy of GST Awareness

GOODS AND SERVICE TAX FILING OF RETURN 1 Returns Chapter IX of the CGST/SGST Act, 2017 GST Return Rules, 2017 2 RETURNS: SALIENT FEATURES A return is a statement of specified particulars relating to business

GOODS AND SERVICE TAX FILING OF RETURN 1 Returns Chapter IX of the CGST/SGST Act, 2017 GST Return Rules, 2017 2 RETURNS: SALIENT FEATURES A return is a statement of specified particulars relating to business

Procedures under GST BY CA LAKSHMI G K. Hiregange & Associates

Procedures under GST BY CA LAKSHMI G K 1 Coverage Procedure to register under GST Procedure to supply goods Books of accounts to be maintained under GST Procedure to pay GST Procedure to file returns under

Procedures under GST BY CA LAKSHMI G K 1 Coverage Procedure to register under GST Procedure to supply goods Books of accounts to be maintained under GST Procedure to pay GST Procedure to file returns under

FILING OF RETURNS UNDER GST INCLUDING MATCHING OF INPUT TAX CREDIT

FILING OF RETURNS UNDER GST INCLUDING MATCHING OF INPUT TAX CREDIT DRAFT RETURN FORMS FORM NO DETAILS 1. GSTR 1 Details of outward supplies of taxable goods and/or services effected 2. GSTR 01A Details

FILING OF RETURNS UNDER GST INCLUDING MATCHING OF INPUT TAX CREDIT DRAFT RETURN FORMS FORM NO DETAILS 1. GSTR 1 Details of outward supplies of taxable goods and/or services effected 2. GSTR 01A Details

GST Annual Return: Introduction

Annual Return (Relevant Provisions) CGST Act Sections: 35(5), 44 and 47(2) D R Gupta: GSTR-9 CGST Rules Rule: 80 1 GST Annual Return: Introduction GST annual return (i.e. GSTR-9) is be filed by the regular

Annual Return (Relevant Provisions) CGST Act Sections: 35(5), 44 and 47(2) D R Gupta: GSTR-9 CGST Rules Rule: 80 1 GST Annual Return: Introduction GST annual return (i.e. GSTR-9) is be filed by the regular

EXECUTIVE PROGRAMME (NEW SYLLABUS) SUPPLEMENT FOR TAX LAWS (PART II - INDIRECT TAXES) MODULE 1- PAPER 4

SUPPLEMENT FOR TAX LAWS (PART II - INDIRECT TAXES) MODULE 1- PAPER 4") EXECUTIVE PROGRAMME (NEW SYLLABUS) SUPPLEMENT FOR TAX LAWS (PART II - INDIRECT TAXES) (Relevant for Students appearing in June, 2019 Examination) MODULE 1- PAPER 4 Disclaimer- This document has been prepared

EXECUTIVE PROGRAMME (NEW SYLLABUS) SUPPLEMENT FOR TAX LAWS (PART II - INDIRECT TAXES) (Relevant for Students appearing in June, 2019 Examination) MODULE 1- PAPER 4 Disclaimer- This document has been prepared

Notification No. 39/2018 Central Tax

[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)] Government of India Ministry of Finance Department of Revenue entral Board of Indirect es and ustoms Notification

[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)] Government of India Ministry of Finance Department of Revenue entral Board of Indirect es and ustoms Notification

Name What does it relate to When to be filed

Name What does it relate to When to be filed GSTR-1 GSTR-2 GSTR-3 Outward Supplies made for a month by a regular taxpayer Inward Supplies made for the month by a regular taxpayer Consolidated return by

Name What does it relate to When to be filed GSTR-1 GSTR-2 GSTR-3 Outward Supplies made for a month by a regular taxpayer Inward Supplies made for the month by a regular taxpayer Consolidated return by

10. In the said rules, after FORM GSTR-8, the following FORMS shall be inserted, namely:-

3. Columns (7) & (8) in Table (A), Table (B) and Table (C) may not be filled where one-to-one correspondence between goods sent for job work and goods received back after job work is not possible. 6. Verification

3. Columns (7) & (8) in Table (A), Table (B) and Table (C) may not be filled where one-to-one correspondence between goods sent for job work and goods received back after job work is not possible. 6. Verification

Input Tax Credit. work and GSTR-9 other aspects. CA Lakshmi G K

Input Tax Credit Annual Availment, Returns Restrictions, under GSTJob- work and GSTR-9 other aspects CA Lakshmi G K Coverage Understanding legal provisions Step by step filing of Annual Return Action plan

Input Tax Credit Annual Availment, Returns Restrictions, under GSTJob- work and GSTR-9 other aspects CA Lakshmi G K Coverage Understanding legal provisions Step by step filing of Annual Return Action plan

GOODS & SERVICES TAX / IDT UPDATE 67

GOODS & SERVICES TAX / IDT UPDATE 67 Amendment in the meaning Advance Authorisation The Central Government vide N No. 1/2019- CT dt 15 th Jan, 2019 made the following amendments in the N No. 48/2018- CT

GOODS & SERVICES TAX / IDT UPDATE 67 Amendment in the meaning Advance Authorisation The Central Government vide N No. 1/2019- CT dt 15 th Jan, 2019 made the following amendments in the N No. 48/2018- CT

GOODS AND SERVICES TAX

GOODS AND SERVICES TAX TRANSITIONAL CREDITS AND DEMONSTRATION OF FILING OF TRAN-1 Two days webcast on GST Organised by: Indirect Taxes Committee GENERAL PRINCIPLES RELATING TO TRANSITION a) Every person

GOODS AND SERVICES TAX TRANSITIONAL CREDITS AND DEMONSTRATION OF FILING OF TRAN-1 Two days webcast on GST Organised by: Indirect Taxes Committee GENERAL PRINCIPLES RELATING TO TRANSITION a) Every person

Bhavani Associates welcomes you all

Bhavani Associates welcomes you all Annual Returns under GST GSTR 9 Mysore Bhavani Associates Venu and Vinay Chartered Accountants Agenda for Discussion Provisions of Annual Returns Understanding GSTR

Bhavani Associates welcomes you all Annual Returns under GST GSTR 9 Mysore Bhavani Associates Venu and Vinay Chartered Accountants Agenda for Discussion Provisions of Annual Returns Understanding GSTR

ॐ सह न ववत सह न भ नक त सह व र य करव वह त जस वव न वध तमवत म ववद ववष वह ॐ श स त श स त श स त

ॐ सह न ववत सह न भ नक त सह व र य करव वह त जस वव न वध तमवत म ववद ववष वह ॐ श स त श स त श स त Om, May God Protect us Both (the Teacher and the Members), May God Nourish us Both, May we Work Together with Energy

ॐ सह न ववत सह न भ नक त सह व र य करव वह त जस वव न वध तमवत म ववद ववष वह ॐ श स त श स त श स त Om, May God Protect us Both (the Teacher and the Members), May God Nourish us Both, May we Work Together with Energy

Composition Levy Under GST- A Boon or Bane

Composition Levy Under GST- A Boon or Bane INTRODUCTION T he appointed date for Goods and Services Tax Law (GST Law or GST) role out is 1st of July, 2017. GST Law will affect, directly and indirectly,

Composition Levy Under GST- A Boon or Bane INTRODUCTION T he appointed date for Goods and Services Tax Law (GST Law or GST) role out is 1st of July, 2017. GST Law will affect, directly and indirectly,

GOODS AND SERVICES TAX RULES, 2017 RETURN FORMATS

GOODS AND SERVICES TAX RULES, 2017 RETURN FORMATS 1 List of Forms Sr. No. Form No. Title of the Form 1 2 3 1. GSTR-1 2. GSTR-1A 3. GSTR-2 4. GSTR-2A 5. GSTR-3 6. GSTR-3A Details of outwards supplies of

GOODS AND SERVICES TAX RULES, 2017 RETURN FORMATS 1 List of Forms Sr. No. Form No. Title of the Form 1 2 3 1. GSTR-1 2. GSTR-1A 3. GSTR-2 4. GSTR-2A 5. GSTR-3 6. GSTR-3A Details of outwards supplies of

F. No. CBEC/20/16/4/2018-GST Government of India Ministry of Finance Department of Revenue Central Board of Indirect Taxes and Customs GST Policy Wing

Circular No. 45/19/2018-GST F. No. CBEC/20/16/4/2018-GST Government of India Ministry of Finance Department of Revenue Central Board of Indirect Taxes and Customs GST Policy Wing New Delhi, Dated the 30

Circular No. 45/19/2018-GST F. No. CBEC/20/16/4/2018-GST Government of India Ministry of Finance Department of Revenue Central Board of Indirect Taxes and Customs GST Policy Wing New Delhi, Dated the 30

GST: Frequently Asked Questions(FAQs) for Traders

for Traders") GST: Frequently Asked Questions(FAQs) for Traders Q 1. How will GST benefit the Trading Community? Under GST, a trader would be entitled to avail input tax credit paid on their domestic procurements of

GST: Frequently Asked Questions(FAQs) for Traders Q 1. How will GST benefit the Trading Community? Under GST, a trader would be entitled to avail input tax credit paid on their domestic procurements of

Tax Invoice, Credit and Debit Notes

Chapter VII Tax Invoice, Credit and Debit Notes Sections 31. Tax Invoice 32. Prohibition of unauthorized collection of tax 33. Amount of tax to be indicated in tax invoice and other documents 34. Credit

Chapter VII Tax Invoice, Credit and Debit Notes Sections 31. Tax Invoice 32. Prohibition of unauthorized collection of tax 33. Amount of tax to be indicated in tax invoice and other documents 34. Credit

Input Tax Credit Rules

Input Tax Credit Rules Rule 1 of ITC - Documentary requirements and conditions for claiming ITC:- Input Tax Credit shall be availed by a registered person, including the Input Service Distributor, on the

Input Tax Credit Rules Rule 1 of ITC - Documentary requirements and conditions for claiming ITC:- Input Tax Credit shall be availed by a registered person, including the Input Service Distributor, on the

GST: FREQUENTLY ASKED QUESTIONS [FAQS] FOR COMPOSITION SCHEME

![GST: FREQUENTLY ASKED QUESTIONS [FAQS] FOR COMPOSITION SCHEME](/thumbs/79/79563057.jpg "GST: FREQUENTLY ASKED QUESTIONS [FAQS] FOR COMPOSITION SCHEME") Q 1. What is composition levy under GST? Ans. The composition levy is an alternative method of levy of tax designed for small taxpayers whose turnover is up to Rs. 75 lakhs (Rs. 50 lakhs in case of few

Q 1. What is composition levy under GST? Ans. The composition levy is an alternative method of levy of tax designed for small taxpayers whose turnover is up to Rs. 75 lakhs (Rs. 50 lakhs in case of few

Composition. Exports

Email FAQs The emails were received by the GST Policy Wing from various sources and were scrutinized and developed into a short FAQ of 100 emails. It should be noted that the emails received or the replies

Email FAQs The emails were received by the GST Policy Wing from various sources and were scrutinized and developed into a short FAQ of 100 emails. It should be noted that the emails received or the replies

Draft suggestions on GST -Form GSTR- 9

Draft suggestions on GST -Form GSTR- 9 Indirect es Committee THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA NEW DELHI INTRODUCTION 1. The Institute of Chartered Accountants of India considers it a privilege

Draft suggestions on GST -Form GSTR- 9 Indirect es Committee THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA NEW DELHI INTRODUCTION 1. The Institute of Chartered Accountants of India considers it a privilege

UPDATE ON AMENDMENTS TO CGST ACT, 2017

UPDATE ON AMENDMENTS TO CGST ACT, 2017 Dear Person, August 31, 2018 TEAM TRD An amendment to CGST Act, 2017 has been introduced on 29 th August, 2018 with the following objective by The Central Government:-

UPDATE ON AMENDMENTS TO CGST ACT, 2017 Dear Person, August 31, 2018 TEAM TRD An amendment to CGST Act, 2017 has been introduced on 29 th August, 2018 with the following objective by The Central Government:-

GSTR 9 ANNUAL RETURN UNDER GST

GSTR 9 ANNUAL RETURN UNDER GST What is the Annual return? Consolidation of information furnished in the forms GSTR 1, GSTR 2, GSTR 3 & GSTR 3B Details of Outward Supplies made and Inward Supplies received,

GSTR 9 ANNUAL RETURN UNDER GST What is the Annual return? Consolidation of information furnished in the forms GSTR 1, GSTR 2, GSTR 3 & GSTR 3B Details of Outward Supplies made and Inward Supplies received,

Master class on GST. Institute of Company Secretaries of India - WIRC. CA Ashit Shah. Shah & Savla LLP. Chartered Accountants

Master class on GST Institute of Company Secretaries of India - WIRC CA Ashit Shah Chartered Accountants Matters to be covered Job work E-Commerce Valuation of Goods and Services Accounts & Records Tax

Master class on GST Institute of Company Secretaries of India - WIRC CA Ashit Shah Chartered Accountants Matters to be covered Job work E-Commerce Valuation of Goods and Services Accounts & Records Tax

1 Introduction 2 Tax Return 3 Goods and Services Tax Return 4 GST Model Law and Draft GST Rules 5 Outward supplies return (GSTR-1)

") Topic 1 Introduction 2 Tax Return 3 Goods and Services Tax Return 4 GST Model Law and Draft GST Rules 5 Outward supplies return (GSTR-1) Page 6 Outward Supply details 7 Post ling of GSTR-1 8 Inward Supply

Topic 1 Introduction 2 Tax Return 3 Goods and Services Tax Return 4 GST Model Law and Draft GST Rules 5 Outward supplies return (GSTR-1) Page 6 Outward Supply details 7 Post ling of GSTR-1 8 Inward Supply

GSTR 9- Annual Overview Engagement. pack

GSTR 9- Annual Overview Engagement Return pack TYPES of GSTR 9 GSTR 9 : GSTR 9 should be filed by the regular taxpayers filing GSTR 1, GSTR 2, GSTR 3. GSTR 9A GSTR 9A should be filed by the persons registered

GSTR 9- Annual Overview Engagement Return pack TYPES of GSTR 9 GSTR 9 : GSTR 9 should be filed by the regular taxpayers filing GSTR 1, GSTR 2, GSTR 3. GSTR 9A GSTR 9A should be filed by the persons registered

A COMPREHENSIVE GST CHECKLIST BEFORE FINALISATION OF BALANCE SHEET FOR THE FY FOR REGISTERED PERSONS - PART 3

A COMPREHENSIVE GST CHECKLIST BEFORE FINALISATION OF BALANCE SHEET FOR THE FY 2017-2018 FOR REGISTERED PERSONS - PART 3 CMA SUSANTA KUMAR SAHA GST Consultant This being the concluding part of this series

A COMPREHENSIVE GST CHECKLIST BEFORE FINALISATION OF BALANCE SHEET FOR THE FY 2017-2018 FOR REGISTERED PERSONS - PART 3 CMA SUSANTA KUMAR SAHA GST Consultant This being the concluding part of this series

Annual Returns GST Index

DISCLAIMER The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s). The information

DISCLAIMER The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s). The information

RETURNS TIME PERIOD OF FILING RETURN UNDER GST

RETURNS Introduction: Every registered taxable person shall himself assess the tax payable and furnished return for each tax period under Self-Assessment as per Section 57 of the Revised Model GST Act.

RETURNS Introduction: Every registered taxable person shall himself assess the tax payable and furnished return for each tax period under Self-Assessment as per Section 57 of the Revised Model GST Act.

[Chapter IX] Edition NBC, Chartered Accountants and member of Allinial Global Accounting Association. All Rights Reserved.

![[Chapter IX] Edition NBC, Chartered Accountants and member of Allinial Global Accounting Association. All Rights Reserved.](/thumbs/90/103497091.jpg "[Chapter IX] Edition NBC, Chartered Accountants and member of Allinial Global Accounting Association. All Rights Reserved.") [Chapter IX] Edition 7 Contents Furnishing details of outward supplies [S. 37] Furnishing details of inward supplies [S. 38] Furnishing of Returns [S. 39] First Return [S. 40] Claim of input tax credit

[Chapter IX] Edition 7 Contents Furnishing details of outward supplies [S. 37] Furnishing details of inward supplies [S. 38] Furnishing of Returns [S. 39] First Return [S. 40] Claim of input tax credit

Input Tax Credit Rules

Input Tax Credit Rules Rule# Rule title Form # Time Limit Section Reference Text of the Provision Analysis 1 (1) Documentary requirements and conditions for claiming input tax credit 1 (2) Documentary

Input Tax Credit Rules Rule# Rule title Form # Time Limit Section Reference Text of the Provision Analysis 1 (1) Documentary requirements and conditions for claiming input tax credit 1 (2) Documentary

Returns in goods and services tax

Returns in goods and services tax A brief overview by Shri Sunil Lahane, Dy Commissioner, Sales Tax Outline What s special about GST return? Overview of Returns to be submitted by regular tax payers Process

Returns in goods and services tax A brief overview by Shri Sunil Lahane, Dy Commissioner, Sales Tax Outline What s special about GST return? Overview of Returns to be submitted by regular tax payers Process

GSTR - 3B Dec 3B Jan 3B Feb 3B Mar 3B Apr 3B GSTR -1 July to Nov 2017 Dec 2017 Jan 2018 Feb 2018 Mar 2018

Circular No. 26/26/2017-GST F. No. 349/164/2017/-GST Government of India Ministry of Finance Department of Revenue Central Board of Excise and Customs GST Policy Wing New Delhi, Dated the 29 th December,

Circular No. 26/26/2017-GST F. No. 349/164/2017/-GST Government of India Ministry of Finance Department of Revenue Central Board of Excise and Customs GST Policy Wing New Delhi, Dated the 29 th December,

BUSINESS PROCESSES ON GST RETURN

Content provided by Mr. Vineet Bhatia, Advocate BUSINESS PROCESSES ON GST RETURN Proposed returns in the GST regime are quite detailed in nature, with emphasis on cross-matching of data submitted by various

Content provided by Mr. Vineet Bhatia, Advocate BUSINESS PROCESSES ON GST RETURN Proposed returns in the GST regime are quite detailed in nature, with emphasis on cross-matching of data submitted by various

Input Tax Credit Rules

Input Tax Credit Rules Rule# Rule title Form # Time Limit Section Reference Text of the Provision Bizsol Analysis 1 (1) Documentary requirements and conditions for claiming input tax credit 1 (2) Documentary

Input Tax Credit Rules Rule# Rule title Form # Time Limit Section Reference Text of the Provision Bizsol Analysis 1 (1) Documentary requirements and conditions for claiming input tax credit 1 (2) Documentary

GOODS AND SERVICE TAX (GST) TRANSITIONAL PROVISIONS COMPILED AND PREPARED BY : CA SAGAR THAKKAR

TRANSITIONAL PROVISIONS COMPILED AND PREPARED BY : CA SAGAR THAKKAR") GOODS AND SERVICE TAX (GST) TRANSITIONAL PROVISIONS COMPILED AND PREPARED BY : CA SAGAR THAKKAR PRESENTATION COVERAGE TRANSITIONAL PROVISIONS UNDER CGST/SGST ACT SEC. 139 TO 142 OF CGST ACT TRANSITIONAL

GOODS AND SERVICE TAX (GST) TRANSITIONAL PROVISIONS COMPILED AND PREPARED BY : CA SAGAR THAKKAR PRESENTATION COVERAGE TRANSITIONAL PROVISIONS UNDER CGST/SGST ACT SEC. 139 TO 142 OF CGST ACT TRANSITIONAL

Returns, Matching Concept, Accounts & Records, under GST Law. Presentation by CA. Gaurav V Save GST Course for CA Students WIRC of ICAI June 07, 2017

Returns, Matching Concept, Accounts & Records, under GST Law Presentation by CA. Gaurav V Save GST Course for CA Students WIRC of ICAI June 07, 2017 Agenda Returns & Matching Concept Accounts & Records

Returns, Matching Concept, Accounts & Records, under GST Law Presentation by CA. Gaurav V Save GST Course for CA Students WIRC of ICAI June 07, 2017 Agenda Returns & Matching Concept Accounts & Records

GOODS & SERVICES TAX / IDT UPDATE 51

GOODS & SERVICES TAX / IDT UPDATE 51 Central Goods and Services tax (Fifth Amendment ) Rules, 2018 The Central Government vide Notification No. 46 /20/2018 GST dated 13 th June, 2018 notified following

GOODS & SERVICES TAX / IDT UPDATE 51 Central Goods and Services tax (Fifth Amendment ) Rules, 2018 The Central Government vide Notification No. 46 /20/2018 GST dated 13 th June, 2018 notified following

Note on Simplified Returns and Return Formats July, 2018

Note on Simplified Returns and Return Formats July, 2018 1 INDEX Sr. Name Description Page 1 2 3 4 1. Features Key Features of Monthly Returns 3-9 2. Features Key Features of Quarterly Returns 10-11 3.

Note on Simplified Returns and Return Formats July, 2018 1 INDEX Sr. Name Description Page 1 2 3 4 1. Features Key Features of Monthly Returns 3-9 2. Features Key Features of Quarterly Returns 10-11 3.

GST Update. Weekly Update N a t i o n a l A c a d e m y o f C u s t o m s, I n d i r e c t T a x e s a n d N a r c o t i c s ( N A C I N )

") GST Update Weekly Update 21.10.2017 1 Background This Presentation covers the GST changes / observations/ press releases/ Tweet FAQs/ Sectoral FAQs released by CBEC since the last update on 14.10.2017.

GST Update Weekly Update 21.10.2017 1 Background This Presentation covers the GST changes / observations/ press releases/ Tweet FAQs/ Sectoral FAQs released by CBEC since the last update on 14.10.2017.

Frequently Asked Questions on Composition Levy

Frequently Asked Questions on Composition Levy Q 1. What is composition levy under GST? Ans. The composition levy is an alternative method of levy of tax designed for small taxpayers whose turnover is

Frequently Asked Questions on Composition Levy Q 1. What is composition levy under GST? Ans. The composition levy is an alternative method of levy of tax designed for small taxpayers whose turnover is

Chapter - RETURNS. 1. Form and manner of furnishing details of outward supplies

Chapter - RETURNS 1. Form and manner of furnishing details of outward supplies (1) Every registered person (other than a person referred to in section 14 of the Integrated Goods and Services Tax Act, 2017)

Chapter - RETURNS 1. Form and manner of furnishing details of outward supplies (1) Every registered person (other than a person referred to in section 14 of the Integrated Goods and Services Tax Act, 2017)

GST Returns. Law and procedure

GST Returns Law and procedure Objectives Brief overview of Act and rules Category of return filers Frequency and Timelines Content, relationships and data flow of returns Mismatches and credit reversal

GST Returns Law and procedure Objectives Brief overview of Act and rules Category of return filers Frequency and Timelines Content, relationships and data flow of returns Mismatches and credit reversal

GST Overview. ~CA Unmesh G. Patwardhan~ Mobile No Unmesh Patwardhan Mobile No

GST Overview ~CA Unmesh G. Patwardhan~ Mobile No.98224 24968 Unmesh Patwardhan Mobile No.98224 24968 1 Brief History & Concept of GST Unmesh Patwardhan Mobile No.98224 24968 2 1 st Jul 2017 The D Day Journey

GST Overview ~CA Unmesh G. Patwardhan~ Mobile No.98224 24968 Unmesh Patwardhan Mobile No.98224 24968 1 Brief History & Concept of GST Unmesh Patwardhan Mobile No.98224 24968 2 1 st Jul 2017 The D Day Journey

Input Tax Credit (ITC)

") FAQ s Chapter III Input Tax Credit (ITC) Eligibility and Conditions for taking Input Tax Credit (Section 16) Section 16 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017

FAQ s Chapter III Input Tax Credit (ITC) Eligibility and Conditions for taking Input Tax Credit (Section 16) Section 16 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017

WIRC of ICAI. Understanding Annual Returns & Reconciliation Statement. Presented By CA. Kevin Shah

WIRC of ICAI Understanding Annual Returns & Reconciliation Statement Presented By CA. Kevin Shah STATUTORY PROVISIONS Section 35 (5) of the CGST Act, 2017 (5) Every registered person whose turnover during

WIRC of ICAI Understanding Annual Returns & Reconciliation Statement Presented By CA. Kevin Shah STATUTORY PROVISIONS Section 35 (5) of the CGST Act, 2017 (5) Every registered person whose turnover during

GST MSME SECTORAL SERIES CENTRAL BOARD OF EXCISE & CUSTOMS. Directorate General of Taxpayer Services. Follow

GST SECTORAL SERIES MSME Directorate General of Taxpayer Services CENTRAL BOARD OF EXCISE & CUSTOMS www.cbec.gov.in Question 55: Whether a registered person under the composition scheme needs to learn

GST SECTORAL SERIES MSME Directorate General of Taxpayer Services CENTRAL BOARD OF EXCISE & CUSTOMS www.cbec.gov.in Question 55: Whether a registered person under the composition scheme needs to learn

Payment of tax, interest, penalty and other amounts (Section 49)

") FAQ s Chapter VIII Payment of Tax Payment of tax, interest, penalty and other amounts (Section 49) Section 49 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017 and UTGST

FAQ s Chapter VIII Payment of Tax Payment of tax, interest, penalty and other amounts (Section 49) Section 49 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017 and UTGST

All you should know while filing GSTR - 3B Return

All you should know while filing GSTR - 3B Return Filing of GSTR-3B return is the first formal communication of business transactions with the government machinery in the GST era. It holds lot of importance

All you should know while filing GSTR - 3B Return Filing of GSTR-3B return is the first formal communication of business transactions with the government machinery in the GST era. It holds lot of importance

Transitional Provisions

Transitional Provisions Udayan Choksi 17 May 2017 18-05-2017 1 S139 - Migration of Existing Taxpayers» Migration is for Every existing registered person Having a PAN Shall be issued a certificate of registration

Transitional Provisions Udayan Choksi 17 May 2017 18-05-2017 1 S139 - Migration of Existing Taxpayers» Migration is for Every existing registered person Having a PAN Shall be issued a certificate of registration

[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)]

![[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)]](/thumbs/93/111735181.jpg "[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)]") [To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)] Government of India Ministry of Finance (Department of Revenue) Central Board of Indirect es and Customs Notification

[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)] Government of India Ministry of Finance (Department of Revenue) Central Board of Indirect es and Customs Notification

COMPOSITION LEVY DISCLAIMER: Threshold limit for Composition scheme: Act

COMPOSITION LEVY DISCLAIMER: The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s).

COMPOSITION LEVY DISCLAIMER: The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s).

Transitional Provisions

FAQ s Migration of Existing Tax Payers (Section 139) Similar provisions have been specified in the UTGST Act, 2017 Chapter XVIII Transitional Provisions Q1. What is the primary condition for provisional

FAQ s Migration of Existing Tax Payers (Section 139) Similar provisions have been specified in the UTGST Act, 2017 Chapter XVIII Transitional Provisions Q1. What is the primary condition for provisional

Transition Returns. Tran 1 + Tran 2

Transition Returns Tran 1 + Tran 2 1 Transition Returns Tran 1 Entitled to Input tax credit u/140 Final One Time Transition Return Entitled for Actual Credit Tran 2 Not Registered Under Existing Law 140(3)

Transition Returns Tran 1 + Tran 2 1 Transition Returns Tran 1 Entitled to Input tax credit u/140 Final One Time Transition Return Entitled for Actual Credit Tran 2 Not Registered Under Existing Law 140(3)

REVENUE (COMMERCIAL TAXES-II) DEPARTMENT G.O.MS.No. 179 Dated: Read the following:

DEPARTMENT G.O.MS.No. 179 Dated: Read the following:") GOVERNMENT OF ANDHRA PRADESH ABSTRACT The Andhra Pradesh Goods and Services Act, 2017 (Act No.16 of 2017) Amendment of Rules - Notification- Orders - Issued. REVENUE (COMMERCIAL TAXES-II) DEPARTMENT G.O.MS.No.

GOVERNMENT OF ANDHRA PRADESH ABSTRACT The Andhra Pradesh Goods and Services Act, 2017 (Act No.16 of 2017) Amendment of Rules - Notification- Orders - Issued. REVENUE (COMMERCIAL TAXES-II) DEPARTMENT G.O.MS.No.

Response to questions raised by members in relation to Goods and Services Tax ( GST )

") Response to questions raised by members in relation to Goods and Services Tax ( GST ) 1. What will be the treatment for hallmarking charges recovered from Customer? As per Section 15 of the CGST Act, 2017,

Response to questions raised by members in relation to Goods and Services Tax ( GST ) 1. What will be the treatment for hallmarking charges recovered from Customer? As per Section 15 of the CGST Act, 2017,

Beginners Course on GST (Registration, Returns, Payment & Documentation) organised by WIRC 3rd October Presenter CA Mandar Telang

organised by WIRC 3rd October Presenter CA Mandar Telang") Beginners Course on GST (Registration, Returns, Payment & Documentation) organised by WIRC Presenter CA Mandar Telang 1 Registration 2 Registration Legal Framework v Taxable Person means a person who carries

Beginners Course on GST (Registration, Returns, Payment & Documentation) organised by WIRC Presenter CA Mandar Telang 1 Registration 2 Registration Legal Framework v Taxable Person means a person who carries

CHAPTER---- Input Tax Credit. 1. Documentary requirements and conditions for claiming input tax credit

CHAPTER---- Input Tax Credit 1. Documentary requirements and conditions for claiming input tax credit (1) The input tax credit shall be availed by a registered person, including the Input Service Distributor,

CHAPTER---- Input Tax Credit 1. Documentary requirements and conditions for claiming input tax credit (1) The input tax credit shall be availed by a registered person, including the Input Service Distributor,

Tax Invoice, Credit and Debit Notes

FAQ s Chapter VII Tax Invoice, Credit and Debit Notes Tax Invoice, Credit and Debit Notes (Section 31 Section 34) Section 31 to 34 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST

FAQ s Chapter VII Tax Invoice, Credit and Debit Notes Tax Invoice, Credit and Debit Notes (Section 31 Section 34) Section 31 to 34 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST

GOODS & SERVICES TAX / IDT UPDATE 61

GOODS & SERVICES TAX / IDT UPDATE 61 Collection of Tax at source by Tea Board of India Tea Board of India (electronic commerce operator) pays to the sellers (i.e. tea producers) for the supply of goods

GOODS & SERVICES TAX / IDT UPDATE 61 Collection of Tax at source by Tea Board of India Tea Board of India (electronic commerce operator) pays to the sellers (i.e. tea producers) for the supply of goods

Designation /Status. Instructions:

Date Designation /Status Instructions: 1. Terms used: (a) GSTIN: (b) TDS: Goods and Services Identification Number Deducted at Source 2. The details in GSTR-4 should be furnished between 11 th and 18 th

Date Designation /Status Instructions: 1. Terms used: (a) GSTIN: (b) TDS: Goods and Services Identification Number Deducted at Source 2. The details in GSTR-4 should be furnished between 11 th and 18 th

Proposed Amendments in GST Law

Proposed Amendments in GST Law On 09.07.2018, the Goods and Service Tax Council has issued draft proposal for the amendment in the "Goods and Services Tax" Law. The entire proposal gives brief view on

Proposed Amendments in GST Law On 09.07.2018, the Goods and Service Tax Council has issued draft proposal for the amendment in the "Goods and Services Tax" Law. The entire proposal gives brief view on

Addendum to Background Material on GST updated till

(Composition levy) Notification No. 21/2018 Central Tax dated 18 th April, 2018 Explanation to Form GST ITC- 03 revised- the registered person who has availed ITC and later on opt for composition scheme

(Composition levy) Notification No. 21/2018 Central Tax dated 18 th April, 2018 Explanation to Form GST ITC- 03 revised- the registered person who has availed ITC and later on opt for composition scheme

GSTR-3. (figures in Rs) Value IGST Additional Tax (1) (2) (3) (4) (5) Goods

Value IGST Additional Tax (1) (2) (3) (4) (5) Goods") GSTR-3 ANNEXURE-IV TAXPAYER DETAILS 1. GSTIN. GST RETURN [To be furnished by the 20 th of the month] [Other than compounding taxpayer / ISD] 2. Name of Taxpayer. 3. Address [S. Nos. 1, 2 and 3 shall be

GSTR-3 ANNEXURE-IV TAXPAYER DETAILS 1. GSTIN. GST RETURN [To be furnished by the 20 th of the month] [Other than compounding taxpayer / ISD] 2. Name of Taxpayer. 3. Address [S. Nos. 1, 2 and 3 shall be

ITC Concepts. Features of ITC Provisions. ISD & its Features

Legal Provisions ITC Concepts Eligibility for ITC Features of ITC Provisions Transitional Provisions ISD & its Features Cross Utilization Does Law define Input 2 (59) means any goods other than capital

Legal Provisions ITC Concepts Eligibility for ITC Features of ITC Provisions Transitional Provisions ISD & its Features Cross Utilization Does Law define Input 2 (59) means any goods other than capital

[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section

[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)] Government of India Ministry of Finance (Department of Revenue) Central Board of Indirect es and Customs Notification

[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)] Government of India Ministry of Finance (Department of Revenue) Central Board of Indirect es and Customs Notification

Invoice IGST Addl Tax # POS

GSTR-1 OUTWARD SUPPLIES MADE BY THE TAXPAYER 1. GSTIN:.. 2. Name of the taxpayer:.. (S. No. 1 and 2 will be auto-populated on logging) ANNEXURE-II [To be furnished by the 10 th of the month] [Not to be

GSTR-1 OUTWARD SUPPLIES MADE BY THE TAXPAYER 1. GSTIN:.. 2. Name of the taxpayer:.. (S. No. 1 and 2 will be auto-populated on logging) ANNEXURE-II [To be furnished by the 10 th of the month] [Not to be

Analysis of Recent Amendments in GST law. - CA Ravi Kumar Somani

Analysis of Recent Amendments in GST law - CA Ravi Kumar Somani Extension of due dates Coverage of the PPT Waiver of late fees in respect of delay in filing of returns to be furnished Changes in the format

Analysis of Recent Amendments in GST law - CA Ravi Kumar Somani Extension of due dates Coverage of the PPT Waiver of late fees in respect of delay in filing of returns to be furnished Changes in the format

Issues relating to SEZ

Issues relating to SEZ DISCLAIMER The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s).

Issues relating to SEZ DISCLAIMER The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s).

The Central Goods and Services Tax Bill, Returns. Arun Kumar Agarwal. 5-May-17

The Central Goods and Services Tax Bill, 2017 Returns Arun Kumar Agarwal info@arsconsultants.net www.arsconsultants.net 1 Statutory Provisions: Chapter Sections 37 to 48 VIII info@arsconsultants.net www.arsconsultants.net

The Central Goods and Services Tax Bill, 2017 Returns Arun Kumar Agarwal info@arsconsultants.net www.arsconsultants.net 1 Statutory Provisions: Chapter Sections 37 to 48 VIII info@arsconsultants.net www.arsconsultants.net

Reverse Charge. Section 9 (3) of CGST Act, 2017 Section 9 (4) of CGST Act, Section 5(3) of IGST Act, 2017 Section 5(4) of IGST Act, 2017

of CGST Act, 2017 Section 9 (4) of CGST Act, Section 5(3) of IGST Act, 2017 Section 5(4) of IGST Act, 2017") GST RETURNS Reverse Charge Section 9 (3) of CGST Act, 2017 Section 9 (4) of CGST Act, 2017 Section 5(3) of IGST Act, 2017 Section 5(4) of IGST Act, 2017 Reverse Charge Sl No. Category of Supply of Services

GST RETURNS Reverse Charge Section 9 (3) of CGST Act, 2017 Section 9 (4) of CGST Act, 2017 Section 5(3) of IGST Act, 2017 Section 5(4) of IGST Act, 2017 Reverse Charge Sl No. Category of Supply of Services

Input Tax Credit & Refunds under GST Law. Presentation by CA. Gaurav V Save WIRC of ICAI June 28, 2017

Input Tax Credit & Refunds under GST Law Presentation by CA. Gaurav V Save WIRC of ICAI June 28, 2017 Agenda Definitions in ITC Eligibility & Conditions for ITC Apportionment & Blocked Credits Input Service

Input Tax Credit & Refunds under GST Law Presentation by CA. Gaurav V Save WIRC of ICAI June 28, 2017 Agenda Definitions in ITC Eligibility & Conditions for ITC Apportionment & Blocked Credits Input Service

Analysis of draft Composition Rules:

of draft Composition Rules: Rule 1 Intimation for CMP- 01 Any person who has been granted registration on a provisional basis under sub-rule (1) of rule Registration.16 and who opts to pay tax under section

of draft Composition Rules: Rule 1 Intimation for CMP- 01 Any person who has been granted registration on a provisional basis under sub-rule (1) of rule Registration.16 and who opts to pay tax under section

Points of discussion with the Group of Ministers on 17th April 2018 on " Return filing under GST-Issues and Challenges"

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Annexure - A Points of discussion with the Group of Ministers on 17th April 2018 on " Return filing under GST-Issues

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Annexure - A Points of discussion with the Group of Ministers on 17th April 2018 on " Return filing under GST-Issues

S. No. Questions / Tweets Received Replies Registration 1. Does aggregate turnover include value of inward supplies Refer Section 2(6) of CGST Act.

of CGST Act.") S. No. Questions / Tweets Received Replies Registration 1. Does aggregate turnover include value of inward supplies Refer Section 2(6) of CGST Act. received on which RCM is payable? Aggregate turnover

S. No. Questions / Tweets Received Replies Registration 1. Does aggregate turnover include value of inward supplies Refer Section 2(6) of CGST Act. received on which RCM is payable? Aggregate turnover

Tax Liability Ledger, will reflect the total tax liability of a tax payer (after netting) for the particular month.

for the particular month.") ELECTRONIC LEDGERS & PAYMENTS Once a tax payer is registered on the common portal GSTN, two e-ledgers Cash Ledger & Input Tax Credit Ledger and an Electronic Tax liability ledger will be automatically

ELECTRONIC LEDGERS & PAYMENTS Once a tax payer is registered on the common portal GSTN, two e-ledgers Cash Ledger & Input Tax Credit Ledger and an Electronic Tax liability ledger will be automatically

DRAFT GOODS AND SERVICES TAX - REFUND RULES, 20--

DRAFT GOODS AND SERVICES TAX - REFUND RULES, 20-- Note: Corresponding changes in the Model GST Law are being carried out separately. Comments, if any may kindly be given by 28 th September, 2016. Chapter-

DRAFT GOODS AND SERVICES TAX - REFUND RULES, 20-- Note: Corresponding changes in the Model GST Law are being carried out separately. Comments, if any may kindly be given by 28 th September, 2016. Chapter-

4. Inward supplies on which tax is to be paid on reverse charge

Form GSTR-2 [See Rule..] Details inward supplies goods or services Year Month 1. GSTIN 2. (a) Legal name the registered person Auto populated (b) Trade name, if any Auto populated 3. Inward supplies received

Form GSTR-2 [See Rule..] Details inward supplies goods or services Year Month 1. GSTIN 2. (a) Legal name the registered person Auto populated (b) Trade name, if any Auto populated 3. Inward supplies received

CPE Meeting on Input Tax Credit & Rules DATE: , Chennai INPUT TAX CREDIT CA. M. SELVAKUMAR KV & CO, CHARTERED ACCOUNTANTS

CPE Meeting on Input Tax Credit & Rules DATE: 12.10.2017, Chennai INPUT TAX CREDIT CA. M. SELVAKUMAR KEY UPDATES Refund claimed by Exporters for July 2017 will be granted by 10 th Oct and Aug 2017 by 18

CPE Meeting on Input Tax Credit & Rules DATE: 12.10.2017, Chennai INPUT TAX CREDIT CA. M. SELVAKUMAR KEY UPDATES Refund claimed by Exporters for July 2017 will be granted by 10 th Oct and Aug 2017 by 18

fgekpy izns'k ljdkj 30th June, 2017 Shimla , the

jkti=] fgekpy izns'k fgekpy izns'k jkt; 'kklu }kjk izdkf'kr 'kqøokj] 30 twu] 2017@9 vk"kk

jkti=] fgekpy izns'k fgekpy izns'k jkt; 'kklu }kjk izdkf'kr 'kqøokj] 30 twu] 2017@9 vk"kk

Input tax credit under GST regime

Input tax credit under GST regime 1 ü Matching, Reversal and Reclaim of Input tax credit ü Availability of credit in certain special circumstances CA V Vijay Anand PART A 2 Matching, Reversal and Reclaim

Input tax credit under GST regime 1 ü Matching, Reversal and Reclaim of Input tax credit ü Availability of credit in certain special circumstances CA V Vijay Anand PART A 2 Matching, Reversal and Reclaim

GST MATCHING & REVERSAL

GST MATCHING & REVERSAL CA. Rohit R. Bora M.com, FCA, DISA, SAP(FI/CO) rohit@rcnco.net Rohit Bora, All rights reserved Returns Process Upload GSTR-1 Can include missing invoice upto 17 th Auto-drafted

GST MATCHING & REVERSAL CA. Rohit R. Bora M.com, FCA, DISA, SAP(FI/CO) rohit@rcnco.net Rohit Bora, All rights reserved Returns Process Upload GSTR-1 Can include missing invoice upto 17 th Auto-drafted

GST. Concept & Roadmap By CA. Ashwarya Agarwal

GST Concept & Roadmap By CA. Ashwarya Agarwal 1 What is GST?? GST Goods and Services Tax Clause 12A of Article 366 of The Constitution of India goods and services tax means any tax on supply of goods,

GST Concept & Roadmap By CA. Ashwarya Agarwal 1 What is GST?? GST Goods and Services Tax Clause 12A of Article 366 of The Constitution of India goods and services tax means any tax on supply of goods,

Filling of GSTR 2 on GST Portal

Webinar on Filling of GSTR 2 on GST Portal 06/09/2017 Presented By Rajeev Agarwal, IRS, SVP, GSTN in collaboration with NeGD (National E Governance Division) Digital India & My Gov Portal 1 Acknowledgements

Webinar on Filling of GSTR 2 on GST Portal 06/09/2017 Presented By Rajeev Agarwal, IRS, SVP, GSTN in collaboration with NeGD (National E Governance Division) Digital India & My Gov Portal 1 Acknowledgements

under RCM How composition dealer will be affected by RCM? What if the supplier is not registered?

Step by step compliances under RCM How composition dealer will be affected by RCM? He may have to prepare self tax invoice being a recipient He will have to put such inward supply in GSTR 2 Also to ensure

Step by step compliances under RCM How composition dealer will be affected by RCM? He may have to prepare self tax invoice being a recipient He will have to put such inward supply in GSTR 2 Also to ensure

GST ISSUES IN ACCOUNT CLOSING AND RECONCILIATION CA VIKRAM MEHTA

GST ISSUES IN ACCOUNT CLOSING AND RECONCILIATION CA ACCOUNT CLOSING Account closing necessitates making of provisions for expenses and liability and recording of incomes and assets at its correct and appropriate

GST ISSUES IN ACCOUNT CLOSING AND RECONCILIATION CA ACCOUNT CLOSING Account closing necessitates making of provisions for expenses and liability and recording of incomes and assets at its correct and appropriate

GST:TAX INVOICE, DEBIT OR CREDIT NOTES, RETURNS, PAYMENT OF TAX (PROVISION & PROCEDURE) AND ELECTRONIC COMMERCE OPERATOR,

AND ELECTRONIC COMMERCE OPERATOR,") GST:TAX INVOICE, DEBIT OR CREDIT NOTES, RETURNS, PAYMENT OF TAX (PROVISION & PROCEDURE) AND ELECTRONIC COMMERCE OPERATOR, Baroda Branch of WIRC of ICAI Dated 26/04/2017 A Presentation by CA. (Dr.) Shailendra

GST:TAX INVOICE, DEBIT OR CREDIT NOTES, RETURNS, PAYMENT OF TAX (PROVISION & PROCEDURE) AND ELECTRONIC COMMERCE OPERATOR, Baroda Branch of WIRC of ICAI Dated 26/04/2017 A Presentation by CA. (Dr.) Shailendra

Filling of GSTR 2 on GST Portal and Offline tool

WebEx on Filling of GSTR 2 on GST Portal and Offline tool 12/10/2017 Presented By GSTN Team 1 Agenda for Webinar on 11/10/2017 Overview of GSTR 2A Overview of GSTR 2 Instructions to fill GSTR 2 Demo of

WebEx on Filling of GSTR 2 on GST Portal and Offline tool 12/10/2017 Presented By GSTN Team 1 Agenda for Webinar on 11/10/2017 Overview of GSTR 2A Overview of GSTR 2 Instructions to fill GSTR 2 Demo of

Tweet FAQs. The tweets received by askgst_goi handle were scrutinized and developed into a short FAQ of 100 tweets.

Tweet FAQs The tweets received by askgst_goi handle were scrutinized and developed into a short FAQ of 100 tweets. S. No. Questions / Tweets Received Replies Registration 1. Does aggregate turnover include

Tweet FAQs The tweets received by askgst_goi handle were scrutinized and developed into a short FAQ of 100 tweets. S. No. Questions / Tweets Received Replies Registration 1. Does aggregate turnover include

Input Tax Credit. Chapter III FAQS. Eligibility and conditions for taking Input Tax credit (Section 16)

") FAQS Chapter III Input Tax Credit Eligibility and conditions for taking Input Tax credit (Section 16) Section 16 of CGST Act, made applicable to IGST vide Section 20 of IGST Act and Section 21 of UTGST

FAQS Chapter III Input Tax Credit Eligibility and conditions for taking Input Tax credit (Section 16) Section 16 of CGST Act, made applicable to IGST vide Section 20 of IGST Act and Section 21 of UTGST

Registration. Chapter IV. FAQ s. Registration (Section 22 to 30)

") Chapter IV Registration FAQ s Registration (Section 22 to 30) Section 22 to 30 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017 and UTGST vide Section 21 of the UTGST

Chapter IV Registration FAQ s Registration (Section 22 to 30) Section 22 to 30 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017 and UTGST vide Section 21 of the UTGST

Accounts and Records. Chapter VI. FAQ s. Accounts and other records (Section 35)

") FAQ s Accounts and other records (Section 35) Chapter VI Accounts and Records Section 35 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017 and UTGST vide Section 21 of

FAQ s Accounts and other records (Section 35) Chapter VI Accounts and Records Section 35 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017 and UTGST vide Section 21 of