Post Assessment Work & Appeals before CIT (Appeals) under Income Tax Act Organized by: Agra Branch of CIRC 26 th December,2018. C.

|

|

|

- Francis Powell

- 5 years ago

- Views:

Transcription

1 Post Assessment Work & Appeals before CIT (Appeals) under Income Tax Act Organized by: Agra Branch of CIRC 26 th December,2018 C.A Prarthana Jalan

2 How Was The Experience Of E-Assessments? C.A Prarthana Jalan

3 Assessment Orders Acceptable to Assessee or Non Acceptable to Assessee C.A Prarthana Jalan

4 ORDER IS ACCEPTABLE Read the order carefully Computation Check Interest Component Check File application for rectification of error u/s 154 of the I.T Act. C.A Prarthana Jalan

5 Penalty notice reply. Pay the demand/stay application. Pending 143(1) or 154 to pursue again Proper Filing of file & Ack of E-proceedings Professional Fees Collection C.A Prarthana Jalan

6 STAY OF DEMAND OFFICE MEMORANDUM [F.NO.404/72/93- ITCC], DATED CBDT hikes standard rate of disputed tax payment to 20% to get stay of demand from AO C.A Prarthana Jalan

7 SCOPE OF LITIGATION IN AGRA

8 APPEAL Appeal - a remedy for redressal of grievances against unjust, erroneous, undesirable or invalid Orders passed by an Authority. No inherent right to appeal but conferred by the Statute.

9 This right is conferred by the statute, hence subject to the terms and conditions specified therein. An appeal is a continuation of assessment proceedings. The right to appeal is a substantive right which gets crystallized when assessment proceedings are initiated C.A Prarthana Jalan

10 Appellate Forum: AUTHORITHY Commissioner (Appeals) (First Appeal) u/s 246 A Income Tax Appellate Tribunal (ITAT) (Final Fact Finding Authority) 253 High Court (only if substantial question of law is involved) 260A Supreme Court of India 261 C.A Prarthana Jalan

11 MONETORY LIMIT: AUTHORITHY TAX EFFECT Income Tax Appellate Tribunal (ITAT) (Final Fact Finding Authority) 20 lakhs High Court (only if substantial question of law is involved) 50 lakhs Supreme Court of India 1 crore C.A Prarthana Jalan

12 Orders which can be appealed against before CIT (Appeals) As per section 246A, some of the common orders which can be appealed against are as under : an order where the assessee denies his liability to be assessed under the Act; an intimation u/s. 143(1); processing of TDS return u/s. 200A; order u/s. 143(3) (except an order passed in pursuance of directions of the Dispute Resolution Panel) or 144; order denying tax determined;

13 order computing loss; order whereby the status of an assessee is changed; order u/s. 115WE(3) or 115WB Fringe benefit tax order u/s. 115WG tonnage tax order u/s. 147 or 150 reopening the assessment (except an order passed in pursuance of directions of the Dispute Resolution Panel); order u/s. 153A (new search proceedings); an order of assessment or reassessment u/s. 92CD(3) i.e. an order to give effect to advance pricing agreement;

14 order of rectification u/s. 154 or 155 (except where it is in respect of an order giving effect to General Anti Avoidance Regulations (GAAR)); order u/s. 163 treating the assesse an agent of a non-resident; an order under sub-sections (2) and (3) of section 170 i.e. liability of predecessor fastened on successor;; an order u/s. 171 i.e assessment after partition of HUF; an order u/s. 237 i.e. refunds;

15 an order under sub-section (6A) of section 206C i.e. liability in case of person not collecting tax at source; order of block assessment where search initiated or requisition made on or after 1/1/1997; order levying penalty u/s. 158BFA(2); order u/s. 201 order of penalty u/s. 221, 271, 271A, 271B, 271BB, 271C, 271CA, 271D, 271E, 271F, 271FB, 272AA or 272BB C.A Deependra Mohan

16 Whether an order u/s. 263 passed by the Commissioner of Income Tax can be appealed against before CIT(A)?

17 No. As the Commissioner of Income Tax and the CIT(A) are of the same rank, an appeal against an order u/s. 263 would not lie before the CIT(A) but would lie before the Tribunal, which is a superior authority C.A Prarthana Jalan

18 Whether an order passed u/s. 143(3) r.w.s. 263 can be appealed against before CIT(A)?

19 Yes. An order passed by an AO giving effect to the CIT s order u/s. 263 is appealable. C.A Prarthana Jalan

20 Non-Appealable Order Order of refusal to grant stay of demand. Order to levy interest u/s 234 A, 234 B, 234C. Certificate granted u/s. 197(1). C.A Prarthana Jalan

21 Interest charged u/s. 220(2). Orders passed u/s 264 rejecting Revision Petition. Orders with agreed additions (No one can be aggrieved by own admission) C.A Prarthana Jalan

22 Appeals which cannot be filed with CIT (A) An Order passed by the CIT u/s 12 AA, or 80 G (5) (vi) An Order passed by the CIT u/s 263 or u/s. 271 or an order passed by him u/s 154 amending his order u/s 263. Order passed by Chief Commissioner or Director General or a Director u/s 272 A C.A Prarthana Jalan

23 Time Limit for filing of Appeal: The appeal shall be presented within 30 days of the following date, that is to say: Where the appeal relates to any TDS U/S 195(1), from the date of payment of tax. Where the appeal relates to any assessment or penalty; the date of service of the notice of demand. In other cases; the date on which such intimation of the order is served. C.A Prarthana Jalan

24 The day on which the Order appealed against was served is to be excluded If the assessee was not furnished with a copy of the order, the requisite time for obtaining a copy of such order shall be excluded.

25 Condonation of delay Application for condonation of delay must be made specifying that there was a Sufficient Cause for delay. The CIT(A) can condone delay in filing of appeal under section 249(3) if satisfied that delay was due to sufficient cause. The CIT has discretionary powers of condonation which should be exercised judiciously. C.A Prarthana Jalan

26 Anil Kumar Nehru vs. ACIT (Supreme Court) dated 3 rd December,2018, delay of 1662 days condoned It is a matter of record that on the identical issue raised by the appellant in respect of earlier assessment, the appeal is pending before the High Court. In these circumstances, the High Court should not have taken such a technical view of dismissing the appeal in the instant case on the ground of delay, when it has to decide the question of law between the parties in any case in respect of earlierassessment year. For this reason we set aside the order of the High Court; condone the delay for filing the appeal and direct to decide the appeal on merits.

27 The CIT should have a pragmatic and liberal approach. [Collector Land Acquisition Vs Mst. Katiji 167 ITR 471 SC] The Supreme Court in N. Balkrishnan vs. M. Krishnamurthy (1998) 7 SCC 123 had condoned a delay of 833 days. It was observed that condonation of delay is a matter of discretion of the Court and the only criterion is the acceptability of explanation irrespective of the length of delay.

28 The Courts have also held that the mistake of an Advocate or Chartered Accountant is a reasonable cause for delay in filing an appeal. [Rafiq C. Munshilal AIR 1981 SC 1400 (1401), Mahavir Prasad Jain vs. CIT (1988) 172 ITR 331 (MP), Concord of India Insurance Co. Ltd. vs. Smt. Nirmaladevi & Sons (1979) 118 ITR 507 (SC). Punam Singh vs. ITO (2002) 257 ITR 38 (Chennai) ( Trib). Shakti Clearing Agency P. Ltd. vs. ITO (127 Taxman 49 (Mag) (Raj.)].

29 Appeal Fee: Particulars Amount (Rs.) Total income computed by AO Rs 250/- Upto Rs. 1,00,000/- Between Rs. 1,00,000/- to Rs. Rs 500/- 2,00,000/- Above Rs. 2,00,000/- Rs 1000/- Cases not covered above Rs 250/- Loss Minimum Fees C.A Prarthana Jalan

30 C.A Deependra Mohan

31 Check list for filing a CIT appeal o On receipt of order and notice of demand, note the date of service of order and notice of demand. o Find the point of grievance. Prepare a reconciliation of return income and assessed income. o List out the additions made, disallowances, whether a notice was issued u/s. 143(2) for assessment and the order passed are within the prescribed time limit

32 o o o Pay appropriate appeal-filing fees. Grounds of appeal should be simple, concise, aptly worded, and serially numbered issue-wise. Statement of facts should highlight each and every fact, since there is only one opportunity for filing the statementof facts.

33 o Ensure to incorporate all additions, disallowances made in the assessment order from different angles i.e. put alternative claims with the words Without prejudice to above. o After raising all the grounds of appeal, crave leave to add, to amend, alter, modify, delete, etc. any of the grounds of appeal without which the CIT(A) may not allow to take some additional grounds or evenwithdraw the appeal.

34 o Ensure that the audit memo, grounds of appeal, statement of facts, etc. are signed and verified by the person who is authorised to sign the return of income u/s 140 of the Income-Tax Act. o Ensure that the appeal is filed with the jurisdictional CIT (A) as mentioned on the rear side of the demand notice.

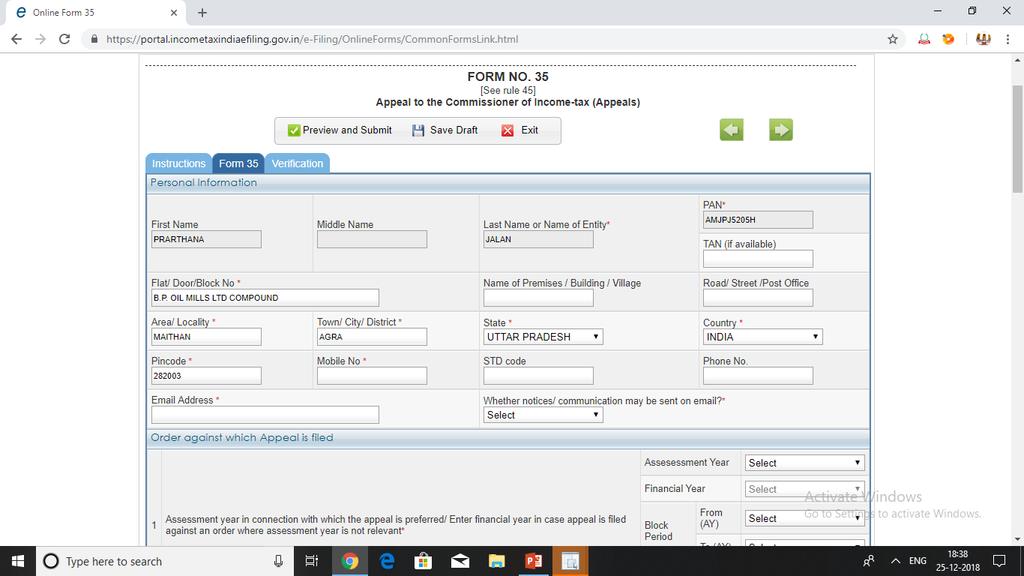

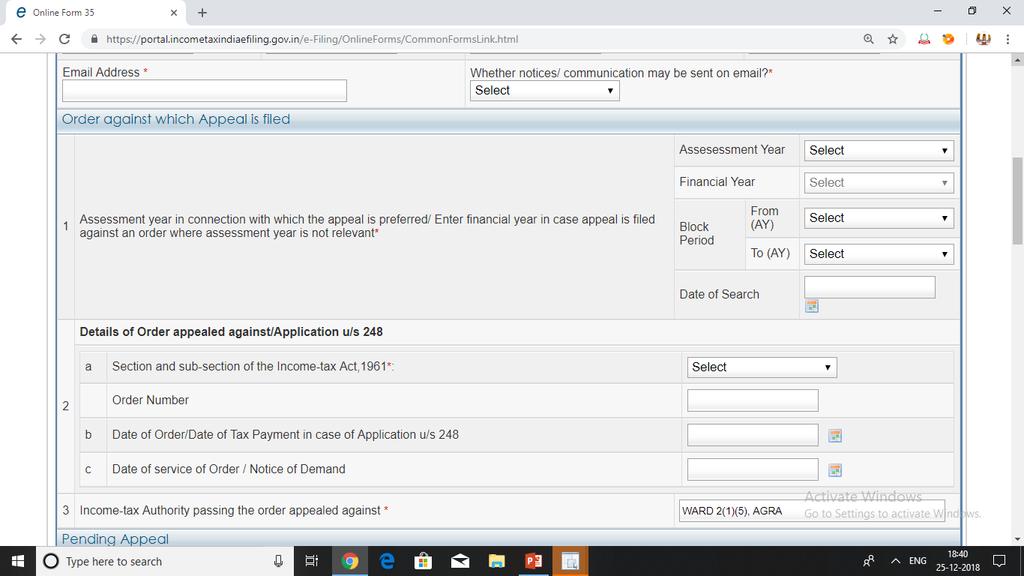

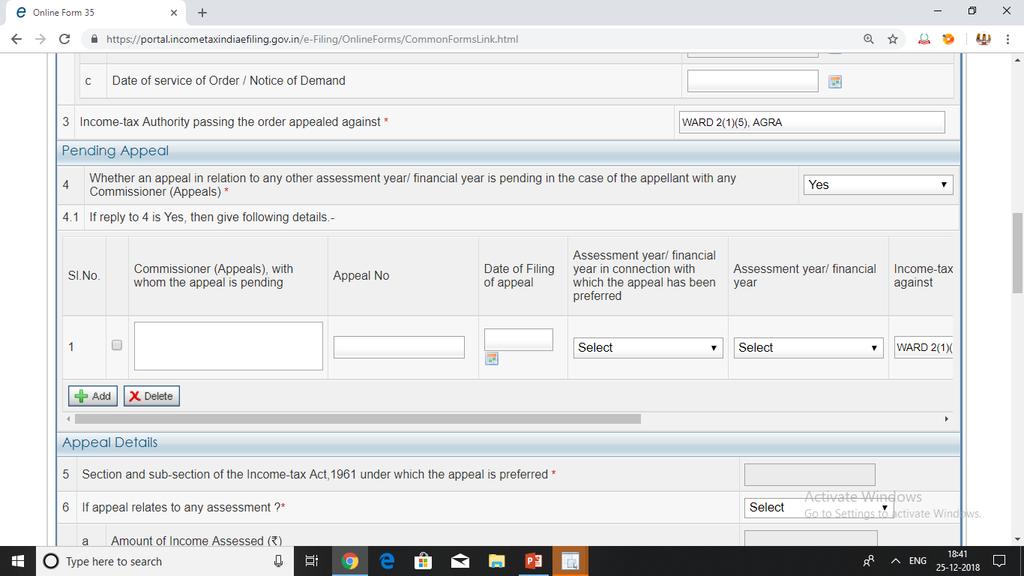

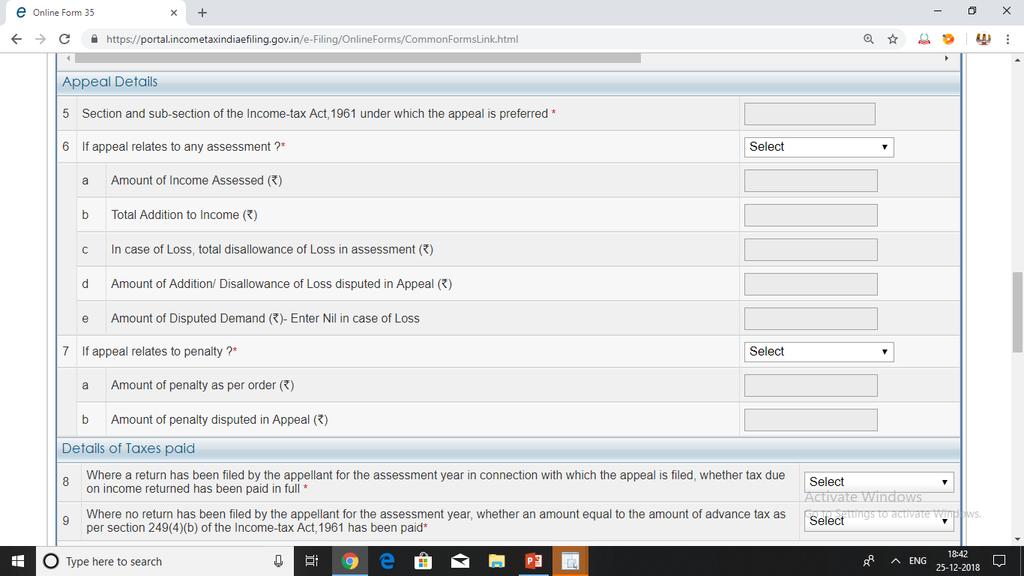

35 MODE OF FILING OF APPEAL Manual Or Electronic C.A Prarthana Jalan

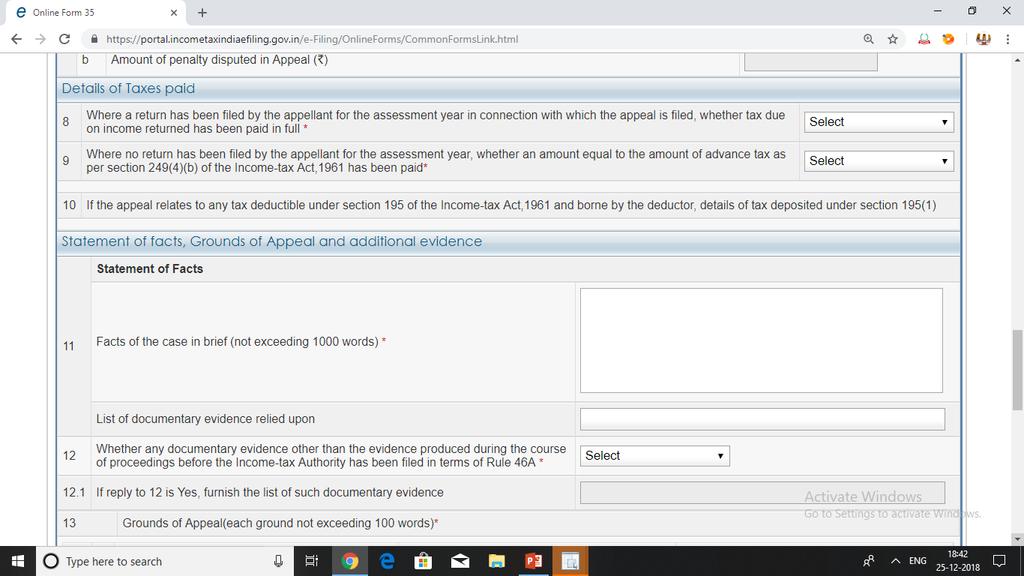

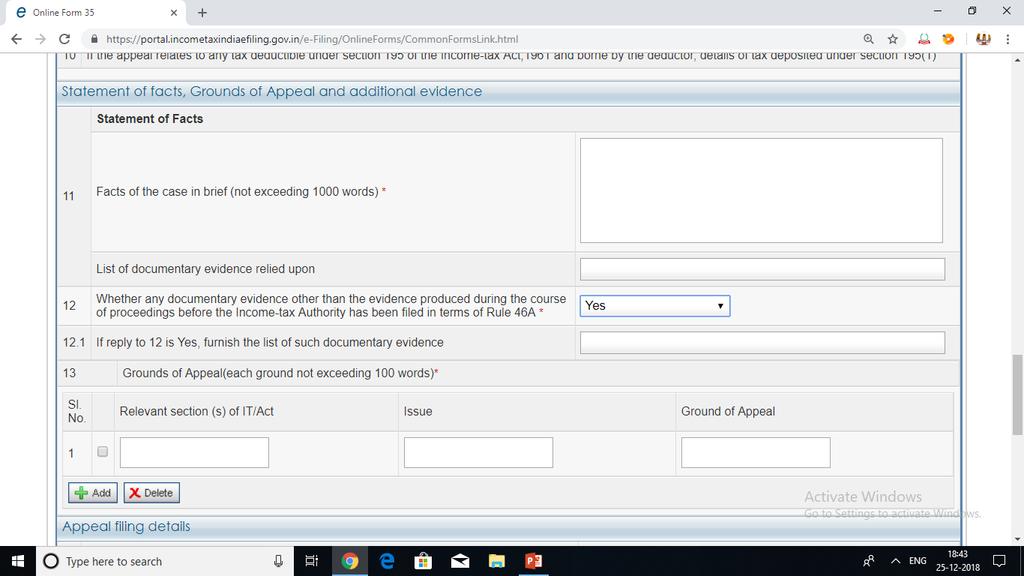

36 Documents to be filed with the Appeal Covering letter addressed to the CIT (A) Form 35 (In duplicate) Statement of Facts (In duplicate) Grounds of Appeal (In duplicate) Copy of order against which appeal preferred (In duplicate) Original notice of demand (u/s 156) Copy of challan for payment of Appeal Filing Fees Power of Attorney C.A Prarthana Jalan

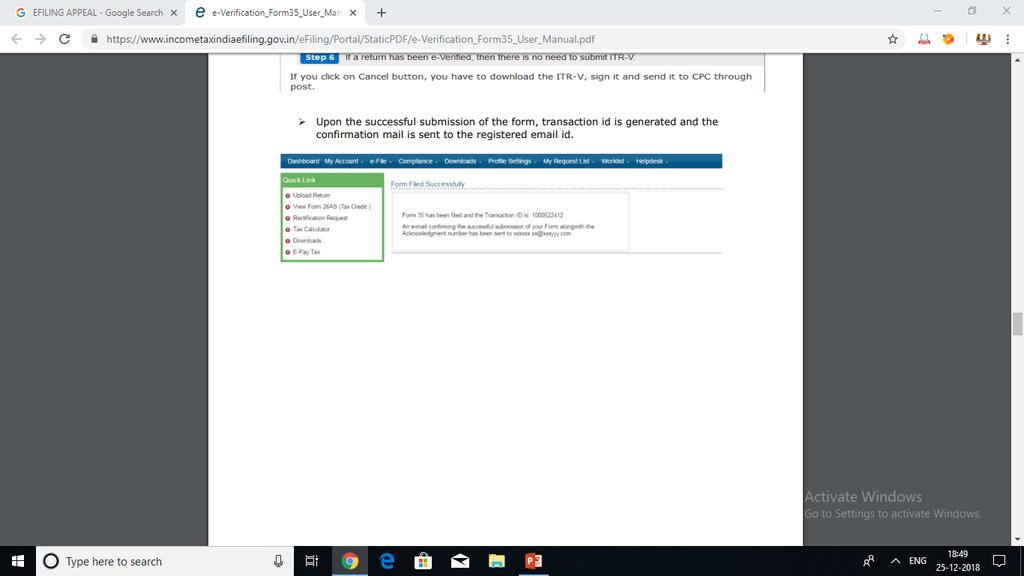

37 To digitise the Appeal function, the Income Tax Department/ CBDT has decided to make electronic filing (e- Filing) of appeals before CIT(Appeals) as mandatory for persons who are already required to file the return of income electronically C.A Prarthana Jalan

38 C.A Prarthana Jalan

39 C.A Prarthana Jalan

40 C.A Prarthana Jalan

41 C.A Deependra Mohan

42 C.A Deependra Mohan

43

44

45

46

47

48

49 C.A Deependra Mohan

50 C.A Deependra Mohan

51 C.A Deependra Mohan

52

53 Requirement Of Digital Signatures : (a) If the return form has been furnished electronically under the Digital Signatures, then form no. 35 will also have to be filed electronically under Digital Signatures. (b) If the return has been furnished electronically without Digital Signatures, then form no. 35 will have to filed electronically through the electronic verification code. (c) Where the e filing of form no. 35 is not mandatory, but is being e filed optionally, then it can be filed either under Digital Signatures or through Electronic Verification Code (as per convenience).

54 Withdrawal of Appeal: Appeal once filed cannot be withdrawn by the appellant. However the appellate authority in its discretion may allow withdrawal of appeal and dismiss the same as not pressed.

55 Although the assessee has no power to withdraw the appeal filed before the CIT(A) but the CIT(A) or Appellate Authority is satisfied that there will be no prejudice to revenue may allow to withdraw. [Bhartia Steel & Engineering Co. P. Ltd. Vs. ITO 97 ITR 154(Cal)]

56 Production of additional evidence (Rule 46A): Appellant is not entitled to produce additional evidence except in the following circumstances: Where the AO refused to admit the said evidence which ought to have been admitted. Where appellant was prevented by sufficient cause from producing evidence called upon by the AO.

57 Where the appellant was prevented by sufficient cause from producing before the AO any evidence which is relevant to any ground of appeal. Where AO passed the impugned order without giving sufficient opportunity to appellant to adduce evidence relevant to any ground of appeal.

58 The CIT (A) must record in writing the reasons for admission of additional evidence. Before considering the additional evidence, the CIT(A) must : Allow the AO a reasonable opportunity to examine the evidence or document or to cross examine the witness produced by the appellant, or To produce any evidence or document or any witness in rebuttal of the additional evidence produced by the appellant.

59 Section 250: Procedure in Appeal Notice to AO and Assessee fixing a day and place of hearing. Following shall have right to be heard: a) the appellant in person or through his AR b) the AO or his AR. CIT (A) has powers to adjourn the hearing from time to time.

60 Before disposing of the appeal, the CIT (A) has power to make further inquiry or may direct the AO to further inquire and report i.e. remand report. Additional ground may be allowed, at the time hearing of an appeal, if satisfied that the omission was not willful or unreasonable.

61 Section 251: Powers of CIT (A) To confirm, reduce, enhance or annul the assessment; or In an appeal against the order of assessment in respect of which the proceedings before the settlement commission abates under section 245 HA, confirm, reduce, enhance or annul the assessment. In Penalty matters, to confirm or cancel such order or vary it so as either to enhance or to reduce the penalty;

62 In any other case he may pass such orders in the appeal as he thinks fit. Power to consider and decide any matter arising out of the proceedings in which the order appealed against was passed, notwithstanding that such matter was not raised by the appellant.

63 Power of Enhancement O The CIT(A) can enhance assessment in respect of matters which could be considered by ITO, but which he failed to consider. However, the CIT(A) has to restrict himself to the material before the ITO. O Where the A.O. on the basis of material before him had failed to make due enquiry, the CIT(A) has powers to cause such enquiry, and make the enhancement.

64 Incentive To CIT(Appeals) CBDT in the Central Action Plan 2018 has sought to offer incentives to CITs(A) for passing quality orders. The incentives have been offered where the CIT(A) in appellate proceedings, passes an order where :- (a) enhancement has been made, (b) order has been strengthened, in the opinion of the CCIT, or (c) penalty u/s 271(1) has been levied by the CIT(A)

65 Limitations No power to review except power of rectification u/s No power to consider validity of Act or Rules [CIT Vs. Straw Products Ltd. 60 ITR 156 (SC)]

66 Commissioner (Appeals) has no power to set aside an order and refer the case back to AO for fresh assessment [w.e.f ] Commissioner (Appeals) cannot award costs to parties.

67 Appeal Order and appeal effect: After conclusion of hearing the CIT (A) will issue a order of the appeal. If it is in favour of the A, either in full or partial, he has to file a request with AO for appeal effect. In case of against the A, he has to decide to file second appeal file an appeal before jurisdictional ITAT within 60 days.

68 Presentation before the CIT(A) o Study the assessment order in depth and carefully and understand the facts of the case and the background involved in each addition. o Study all the replies filed before the AO during the assessment proceedings o Identify the weak points in relation to each additions made.

69 Examine whether any additional evidence is to be taken. If so, draft an appropriate application under Rule 46- A. o Prepare paper book with index containing all written submissions filed, evidences in support of assertions made in the written submissions. o Prepare exhaustive written submissions relevant to each ground of appeal. Highlightthe important submissions in bold or italics.

70 Make special efforts in emphasizing as to how and why the AO was wrong based on actual facts and legal issues. Controvert the stand taken by the AO duly supported by documentary evidences, legal position and decided cases by the courts.

71 o Reliance be placed on the decisions of the Apex Courts, Jurisdiction High Court and ITAT. o Revenue authorities have to follow decision of jurisdictional High Court. o [CIT Vs. G. M. Mittal Stainless Steel (P) Ltd. (2003) 130 Tax man 67 / 263 ITR 255 (SC)] o Care need to be taken while placing reliance on case laws. Examine the cases for and against. As far as possible, distinction be made between the cases which are against.

72 Distinguish the cases relied upon by the AO. o Maintain calm and be peaceful and confident. o Have proper knowledge of all facts of the case. Reply to the queries raised by the CIT (A) be offered promptly and to the point.

73 o Do not get provoked with the seemingly irrelevant queries by the CIT(A). o Avoid unnecessary arguments and altercations in case if the CIT(A) is not satisfied with your arguments.

74 Thank You!! Wishing You All A Very Happy & Prosperous New YEAR CA Prarthana Jalan prarthanajalan@gmail.com #

APPEAL BEFORE CIT(A) CA TORAL SHAH

CA TORAL SHAH") APPEAL BEFORE CIT(A) CA TORAL SHAH Meaning of Appeal The expression appeal has been defined in Black s law dictionary as A proceeding undertaken to have decision reconsidered by a higher authority. The

APPEAL BEFORE CIT(A) CA TORAL SHAH Meaning of Appeal The expression appeal has been defined in Black s law dictionary as A proceeding undertaken to have decision reconsidered by a higher authority. The

BY CA. ROHIT BHALLA (B.COM (HONS), FCA, LL.B)

, FCA, LL.B)") BY CA. ROHIT BHALLA (B.COM (HONS), FCA, LL.B) Hargovind Dayal Srivastav Vs. G.N. Verma AIR 1977 S.C. 1334: It is the duty of the lawyers to protect the dignity & decorum of the judiciary. If lawyers fail

BY CA. ROHIT BHALLA (B.COM (HONS), FCA, LL.B) Hargovind Dayal Srivastav Vs. G.N. Verma AIR 1977 S.C. 1334: It is the duty of the lawyers to protect the dignity & decorum of the judiciary. If lawyers fail

MULUND CA CPE STUDY CIRCLE

MULUND CA CPE STUDY CIRCLE Post Assessment Measures & Appellate procedures Aspects covered: - Dharan V. Gandhi, Advocate, Bombay High Court 17 April 2016 1. First Appellate Forum: a. CIT(A) - Procedures

MULUND CA CPE STUDY CIRCLE Post Assessment Measures & Appellate procedures Aspects covered: - Dharan V. Gandhi, Advocate, Bombay High Court 17 April 2016 1. First Appellate Forum: a. CIT(A) - Procedures

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH D, NEW DELHI Before Sh. N. K. Saini, AM And Smt. Beena A. Pillai, JM

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH D, NEW DELHI Before Sh. N. K. Saini, AM And Smt. Beena A. Pillai, JM : Asstt. Year : 2010-11 Income Tax Officer, TDS Rohtak (APPELLANT) PAN No. RTKPO1586E

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH D, NEW DELHI Before Sh. N. K. Saini, AM And Smt. Beena A. Pillai, JM : Asstt. Year : 2010-11 Income Tax Officer, TDS Rohtak (APPELLANT) PAN No. RTKPO1586E

2 2. Whether in the facts and circumstances of the case the Ld. CIT(A) has erred in law in holding hat there was no negative cash balance and that the

has erred in law in holding hat there was no negative cash balance and that the") IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH: B NEW DELHI BEFORE SHRI G. D. AGRAWAL, HON BLE VICE-PRESIDENT AND SHRI C. M. GARG, HON BLE JUDICIAL MEMBER (Assessment Year-2009-10) Income Tax Officer

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH: B NEW DELHI BEFORE SHRI G. D. AGRAWAL, HON BLE VICE-PRESIDENT AND SHRI C. M. GARG, HON BLE JUDICIAL MEMBER (Assessment Year-2009-10) Income Tax Officer

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH: F NEW DELHI BEFORE SH. G.C. GUPTA, VICE PRESIDENT AND SH. INTURI RAMA RAO, ACCOUNTANT MEMBER.

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH: F NEW DELHI BEFORE SH. G.C. GUPTA, VICE PRESIDENT AND SH. INTURI RAMA RAO, ACCOUNTANT MEMBER. I.T.A Nos. 1766 to 1768/Del/2015 Assessment Years-2011-12

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH: F NEW DELHI BEFORE SH. G.C. GUPTA, VICE PRESIDENT AND SH. INTURI RAMA RAO, ACCOUNTANT MEMBER. I.T.A Nos. 1766 to 1768/Del/2015 Assessment Years-2011-12

PROCEDURE FOR ASSESSMENT. -- By CA Mahendra Sanghvi

PROCEDURE FOR ASSESSMENT -- By CA Mahendra Sanghvi RETURN OF INCOME & SELF ASSESSMENT 2 Procedure assessment covered of is by Chapter XIV of RETURN OF INCOME & SELF 3 ASSESSMENT Shall furnish, on or before

PROCEDURE FOR ASSESSMENT -- By CA Mahendra Sanghvi RETURN OF INCOME & SELF ASSESSMENT 2 Procedure assessment covered of is by Chapter XIV of RETURN OF INCOME & SELF 3 ASSESSMENT Shall furnish, on or before

DIRECT TAXES Tribunal

Jitendra singh & sameer dalal Advocates DIRECT TAXES Tribunal REPORTED 1. TDS under section 194I provision for rent vis-à-vis actual payment assessee making provisions for disputed rent payable to landlord

Jitendra singh & sameer dalal Advocates DIRECT TAXES Tribunal REPORTED 1. TDS under section 194I provision for rent vis-à-vis actual payment assessee making provisions for disputed rent payable to landlord

APPEALS & REVISIONS. PART I (For CAF-6 and ICMAP students)

") Chapter 18 APPEALS & REVISIONS Section Rule Topic covered (Part - I for CAF-6 & ICMAP students) PART I 127 76 Appeal to the Commissioner Inland Revenue (Appeals) 128 Procedure in appeal 129 Decision in

Chapter 18 APPEALS & REVISIONS Section Rule Topic covered (Part - I for CAF-6 & ICMAP students) PART I 127 76 Appeal to the Commissioner Inland Revenue (Appeals) 128 Procedure in appeal 129 Decision in

IN THE INCOME TAX APPELLATE TRIBUNAL AGRA BENCH, AGRA. ITA No.450/Ag/2015 Assessment Year:

1 IN THE INCOME TAX APPELLATE TRIBUNAL AGRA BENCH, AGRA BEFORE SHRI BHAVNESH SAINI, JUDICIAL MEMBER AND MS. ANNAPURNA MEHROTRA, ACCOUNTANT MEMBER ITA No.450/Ag/2015 Assessment Year:2009-2010 ITO (TDS),

1 IN THE INCOME TAX APPELLATE TRIBUNAL AGRA BENCH, AGRA BEFORE SHRI BHAVNESH SAINI, JUDICIAL MEMBER AND MS. ANNAPURNA MEHROTRA, ACCOUNTANT MEMBER ITA No.450/Ag/2015 Assessment Year:2009-2010 ITO (TDS),

Q 8. Where only certain items of addition are in dispute can the assessee take advantage of the Scheme for the entire demand of the year?

REPRESENTATION IN RESPECT OF DIRECT TAX DISPUTE RESOLUTION SCHEME 2016 1. Eligibility 1.1 Partial disputed amounts Issue Where part of the demand determined for a year is undisputed and remains unpaid,

REPRESENTATION IN RESPECT OF DIRECT TAX DISPUTE RESOLUTION SCHEME 2016 1. Eligibility 1.1 Partial disputed amounts Issue Where part of the demand determined for a year is undisputed and remains unpaid,

IN THE INCOME TAX APPELLATE TRIBUNAL, MUMBAI BENCH B BENCH BEFORE SHRI B.R.MITTAL(JUDICIAL MEMBER) AND SHRI RAJENDRA (ACCOUNTANT MEMBER)

AND SHRI RAJENDRA (ACCOUNTANT MEMBER)") IN THE INCOME TAX APPELLATE TRIBUNAL, MUMBAI BENCH B BENCH BEFORE SHRI B.R.MITTAL(JUDICIAL MEMBER) AND SHRI RAJENDRA (ACCOUNTANT MEMBER) Assessment Year: 1999-2000 Bennett Coleman & Co.Ltd., The Times

IN THE INCOME TAX APPELLATE TRIBUNAL, MUMBAI BENCH B BENCH BEFORE SHRI B.R.MITTAL(JUDICIAL MEMBER) AND SHRI RAJENDRA (ACCOUNTANT MEMBER) Assessment Year: 1999-2000 Bennett Coleman & Co.Ltd., The Times

This is an appeal by the department against the order dated of ld. CIT(A)-XXII, New Delhi.

-XXII, New Delhi.") IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH G, NEW DELHI Before Sh. D. Manmohan, Vice President And Sh. N. K. Saini, AM ITA No. 519/Del/2013 : Asstt. Year : 2003-04 Income Tax Officer, Ward 20(3),

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH G, NEW DELHI Before Sh. D. Manmohan, Vice President And Sh. N. K. Saini, AM ITA No. 519/Del/2013 : Asstt. Year : 2003-04 Income Tax Officer, Ward 20(3),

IN THE HIGH COURT OF DELHI : NEW DELHI SUBJECT : INCOME TAX MATTER. ITA No-160/2005. Judgment reserved on: 12th March, 2007

IN THE HIGH COURT OF DELHI : NEW DELHI SUBJECT : INCOME TAX MATTER ITA No-160/2005 Judgment reserved on: 12th March, 2007 Judgment delivered on: 24th May, 2007 COMMISSIONER OF INCOME TAX DELHI-I, NEW DELHI...

IN THE HIGH COURT OF DELHI : NEW DELHI SUBJECT : INCOME TAX MATTER ITA No-160/2005 Judgment reserved on: 12th March, 2007 Judgment delivered on: 24th May, 2007 COMMISSIONER OF INCOME TAX DELHI-I, NEW DELHI...

IN THE HIGH COURT OF JUDICATURE AT BOMBAY ORDINARY ORIGINAL CIVIL JURISDICTION. WRIT PETITION No OF 2004

IN THE HIGH COURT OF JUDICATURE AT BOMBAY ORDINARY ORIGINAL CIVIL JURISDICTION WRIT PETITION No. 3314 OF 2004 wp-3314-2004.sxw M/s. Eskay K'n' IT (India) Ltd... Petitioner. V/s. Dy. Commissioner of Income

IN THE HIGH COURT OF JUDICATURE AT BOMBAY ORDINARY ORIGINAL CIVIL JURISDICTION WRIT PETITION No. 3314 OF 2004 wp-3314-2004.sxw M/s. Eskay K'n' IT (India) Ltd... Petitioner. V/s. Dy. Commissioner of Income

1 RETURN OF INCOME & ASSESSMENT PROCEDURE

1 RETURN OF INCOME & ASSESSMENT PROCEDURE THIS CHAPTER INCLUDES Return of Income Assessment Procedure Annual Information Return Income Computation and Disclosure Standards (ICDS) Marks of Short Notes,

1 RETURN OF INCOME & ASSESSMENT PROCEDURE THIS CHAPTER INCLUDES Return of Income Assessment Procedure Annual Information Return Income Computation and Disclosure Standards (ICDS) Marks of Short Notes,

April 2017 CA K Prasanna and ca Abhinaya Ramanujam

Assessment Procedure April 2017 CA K Prasanna and ca Abhinaya Ramanujam Topics Covered Return of Income Self-Assessment (S 140A) Enquiry before Assessment (S 142(1)) Summary Assessment (S 143(1)) Scrutiny

Assessment Procedure April 2017 CA K Prasanna and ca Abhinaya Ramanujam Topics Covered Return of Income Self-Assessment (S 140A) Enquiry before Assessment (S 142(1)) Summary Assessment (S 143(1)) Scrutiny

IN THE HIGH COURT OF KARNATAKA AT BANGALORE PRESENT THE HON'BLE MR.JUSTICE DILIP B.BHOSALE AND THE HON'BLE MR.JUSTICE B.MANOHAR ITA NO.

1 IN THE HIGH COURT OF KARNATAKA AT BANGALORE DATED THIS THE 05 TH DAY OF MARCH 2014 PRESENT THE HON'BLE MR.JUSTICE DILIP B.BHOSALE AND THE HON'BLE MR.JUSTICE B.MANOHAR BETWEEN: ITA NO.828/2007 H.Raghavendra

1 IN THE HIGH COURT OF KARNATAKA AT BANGALORE DATED THIS THE 05 TH DAY OF MARCH 2014 PRESENT THE HON'BLE MR.JUSTICE DILIP B.BHOSALE AND THE HON'BLE MR.JUSTICE B.MANOHAR BETWEEN: ITA NO.828/2007 H.Raghavendra

DIRECT TAX REVIEW VERENDRA KALRA & CO OCTOBER Inside this edition. Like always, Like never before

VERENDRA KALRA & CO CHARTERED A CCOUNTANTS Like always, Like never before DIRECT TAX REVIEW OCTOBER 2018 Inside this edition AO's order rejecting ITR without providing opportunity to rectify defect u/s

VERENDRA KALRA & CO CHARTERED A CCOUNTANTS Like always, Like never before DIRECT TAX REVIEW OCTOBER 2018 Inside this edition AO's order rejecting ITR without providing opportunity to rectify defect u/s

Appellant :- Commissioner Of Income Tax, Meerut And Another

HIGH COURT OF JUDICATURE AT ALLAHABAD Court No. - 33 Case:- INCOME TAX APPEAL No. - 73 of 2001 Appellant :- Commissioner Of Income Tax, Meerut And Another Respondent :- M/S Jindal Polyester & Steel Ltd.

HIGH COURT OF JUDICATURE AT ALLAHABAD Court No. - 33 Case:- INCOME TAX APPEAL No. - 73 of 2001 Appellant :- Commissioner Of Income Tax, Meerut And Another Respondent :- M/S Jindal Polyester & Steel Ltd.

more than the capital gains and the new residential asset was purchased within 2 years from the date of sale of residential property. 3. The Learned C

IN THE INCOME TAX APPELLATE TRIBUNAL Hyderabad B Bench, Hyderabad Before Smt. P. Madhavi Devi, Judicial Member AND Shri S.Rifaur Rahman, Accountant Member ITA No.1707/Hyd/2016 (Assessment Year: 2013-14)

IN THE INCOME TAX APPELLATE TRIBUNAL Hyderabad B Bench, Hyderabad Before Smt. P. Madhavi Devi, Judicial Member AND Shri S.Rifaur Rahman, Accountant Member ITA No.1707/Hyd/2016 (Assessment Year: 2013-14)

IN THE INCOME TAX APPELLATE TRIBUNAL Hyderabad A Bench, Hyderabad

IN THE INCOME TAX APPELLATE TRIBUNAL Hyderabad A Bench, Hyderabad Before Smt. P. Madhavi Devi, Judicial Member AND Shri S.Rifaur Rahman, Accountant Member Smt. Nama Chinnamma Hyderabad PAN: ABKPW 1887

IN THE INCOME TAX APPELLATE TRIBUNAL Hyderabad A Bench, Hyderabad Before Smt. P. Madhavi Devi, Judicial Member AND Shri S.Rifaur Rahman, Accountant Member Smt. Nama Chinnamma Hyderabad PAN: ABKPW 1887

Summons, Investigation, Audit, Special Audit, Show cause Notice, Appeals. Bharat Raichandani Advocate

Summons, Investigation, Audit, Special Audit, Show cause Notice, Appeals Bharat Raichandani Advocate Section 14 of CEA, 1944 - Power to summon persons to give evidence and produce documents in inquiries

Summons, Investigation, Audit, Special Audit, Show cause Notice, Appeals Bharat Raichandani Advocate Section 14 of CEA, 1944 - Power to summon persons to give evidence and produce documents in inquiries

(50 Marks) Particulars ` ` Indian Income 42,00,000 Foreign Income 6,00,000 Gross Total Income 48,00,000 Less:

Particulars ` ` Indian Income 42,00,000 Foreign Income 6,00,000 Gross Total Income 48,00,000 Less:") FINAL November 2017 DIRECT TAXATION Test Code P 34 Branch (MULTIPLE) (Date : 23.07.2017) (50 Marks) Note: All questions are compulsory. Question 1(6 Marks) Computation of tax liability of Ms. Swarnalatha

FINAL November 2017 DIRECT TAXATION Test Code P 34 Branch (MULTIPLE) (Date : 23.07.2017) (50 Marks) Note: All questions are compulsory. Question 1(6 Marks) Computation of tax liability of Ms. Swarnalatha

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH: G NEW DELHI BEFORE SHRI G. D. AGRAWAL, PRESIDENT AND MS SUCHITRA KAMBLE, JUDICIAL MEMBER

1 ITA Nos. 6675 & 6676/Del/2015 IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH: G NEW DELHI BEFORE SHRI G. D. AGRAWAL, PRESIDENT AND MS SUCHITRA KAMBLE, JUDICIAL MEMBER ITA No. 6675/DEL/2015 ( A.Y 2013-14)

1 ITA Nos. 6675 & 6676/Del/2015 IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH: G NEW DELHI BEFORE SHRI G. D. AGRAWAL, PRESIDENT AND MS SUCHITRA KAMBLE, JUDICIAL MEMBER ITA No. 6675/DEL/2015 ( A.Y 2013-14)

IN THE INCOME TAX APPELLATE TRIBUNAL LUCKNOW BENCH B, LUCKNOW. ITA No.486/LKW/2016 Assessment Year:

IN THE INCOME TAX APPELLATE TRIBUNAL LUCKNOW BENCH B, LUCKNOW BEFORE SHRI. T.S. KAPOOR, ACCOUNTANT MEMBER AND SHRI PARTHA SARATHI CHAUDHURY,JUDICIAL MEMBER ITA No.486/LKW/2016 Assessment Year:2012-13 Pankaj

IN THE INCOME TAX APPELLATE TRIBUNAL LUCKNOW BENCH B, LUCKNOW BEFORE SHRI. T.S. KAPOOR, ACCOUNTANT MEMBER AND SHRI PARTHA SARATHI CHAUDHURY,JUDICIAL MEMBER ITA No.486/LKW/2016 Assessment Year:2012-13 Pankaj

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH H : NEW DELHI VICE PRESIDENT AND SHRI CHANDRA MOHAN GARG, JUDICIAL MEMBER

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH H : NEW DELHI BEFORE SHRI G.D.AGRAWAL, VICE PRESIDENT AND SHRI CHANDRA MOHAN GARG, JUDICIAL MEMBER ITA No.1580/Del/2010 Assessment Year : 2004-05 05 M/s

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH H : NEW DELHI BEFORE SHRI G.D.AGRAWAL, VICE PRESIDENT AND SHRI CHANDRA MOHAN GARG, JUDICIAL MEMBER ITA No.1580/Del/2010 Assessment Year : 2004-05 05 M/s

Before Sh. J. S. Reddy, AM And Sh. George George K., JM

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH A, NEW DELHI Before Sh. J. S. Reddy, AM And Sh. George George K., JM : Asstt. Year : 2007-08 Dy. Commissioner of Income Tax, Central Circle-7 New Delhi

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH A, NEW DELHI Before Sh. J. S. Reddy, AM And Sh. George George K., JM : Asstt. Year : 2007-08 Dy. Commissioner of Income Tax, Central Circle-7 New Delhi

IN THE INCOME TAX APPELLATE TRIBUNAL MUMBAI BENCHES A, MUMBAI. Before Shri G S Pannu, Accountant Member & Shri Ram Lal Negi, Judicial Member

IN THE INCOME TAX APPELLATE TRIBUNAL MUMBAI BENCHES A, MUMBAI Before Shri G S Pannu, Accountant Member & Shri Ram Lal Negi, Judicial Member Assessment Year : 2010-11 Ambuja Cements Limited (Formerly known

IN THE INCOME TAX APPELLATE TRIBUNAL MUMBAI BENCHES A, MUMBAI Before Shri G S Pannu, Accountant Member & Shri Ram Lal Negi, Judicial Member Assessment Year : 2010-11 Ambuja Cements Limited (Formerly known

C.R. Building, I.P. Estate

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH: D NEW DELHI BEFORE SHRI R. P. TOLANI, JUDICIAL MEMBER AND SHRI J. S. REDDY, ACCOUNTANT MEMBER I.T.A. No. 364/Del/2012 Assessment Years: 2008-09 ACIT Vs.

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH: D NEW DELHI BEFORE SHRI R. P. TOLANI, JUDICIAL MEMBER AND SHRI J. S. REDDY, ACCOUNTANT MEMBER I.T.A. No. 364/Del/2012 Assessment Years: 2008-09 ACIT Vs.

SUPREME COURT RULING (INCOME TAX)

") SUPREME COURT RULING (INCOME TAX) 2016-TIOL-245-SC-IT MM Aqua Technologies Ltd Vs CIT (Dated: December 5, The assessee preferred this SLP challenging the judgment of High Court, whereby it was held that

SUPREME COURT RULING (INCOME TAX) 2016-TIOL-245-SC-IT MM Aqua Technologies Ltd Vs CIT (Dated: December 5, The assessee preferred this SLP challenging the judgment of High Court, whereby it was held that

HIGH COURT OF JUDICATURE AT ALLAHABAD. Judgment reserved on Judgment delivered on Income Tax Appeal No.

HIGH COURT OF JUDICATURE AT ALLAHABAD Judgment reserved on 10.10.2011 Judgment delivered on 25.11.2011 Income Tax Appeal No.241 of 2008 Commissioner of Income-tax (Central), Kanpur v. Smt. Shaila Agarwal

HIGH COURT OF JUDICATURE AT ALLAHABAD Judgment reserved on 10.10.2011 Judgment delivered on 25.11.2011 Income Tax Appeal No.241 of 2008 Commissioner of Income-tax (Central), Kanpur v. Smt. Shaila Agarwal

A legitimate expenditure or relief not claimed in the return of income can be claimed ONLY by revising the return of income under section

Fresh Claim Outside The Return of Income BY:- CA. (Dr.) Gurmeet S. Grewal B. Com (Hons.), FCA, PhD., CLA (IIAM) Grewal & Singh Chartered Accountants New Delhi, Chandigarh, Yamuna Nagar, Jammu Phones: 09811242856

Fresh Claim Outside The Return of Income BY:- CA. (Dr.) Gurmeet S. Grewal B. Com (Hons.), FCA, PhD., CLA (IIAM) Grewal & Singh Chartered Accountants New Delhi, Chandigarh, Yamuna Nagar, Jammu Phones: 09811242856

IN THE INCOME TAX APPELLATE TRIBUNAL HYDERABAD BENCHES A, HYDERABAD BEFORE SHRI D. MANMOHAN, VICE PRESIDENT AND SHRI B. RAMAKOTAIAH, ACCOUNTANT MEMBER

IN THE INCOME TAX APPELLATE TRIBUNAL HYDERABAD BENCHES A, HYDERABAD BEFORE SHRI D. MANMOHAN, VICE PRESIDENT AND SHRI B. RAMAKOTAIAH, ACCOUNTANT MEMBER I.T.A. No. 1149/HYD/2015 Assessment Year: 2008-09,

IN THE INCOME TAX APPELLATE TRIBUNAL HYDERABAD BENCHES A, HYDERABAD BEFORE SHRI D. MANMOHAN, VICE PRESIDENT AND SHRI B. RAMAKOTAIAH, ACCOUNTANT MEMBER I.T.A. No. 1149/HYD/2015 Assessment Year: 2008-09,

IN THE INCOME TAX APPELLATE TRIBUNAL HYDERABAD BENCH B, HYDERABAD BEFORE SHRI B. RAMAKOTAIAH, ACCOUNTANT MEMBER AND SHRI SAKTIJIT DEY, JUDICIAL MEMBER

IN THE INCOME TAX APPELLATE TRIBUNAL HYDERABAD BENCH B, HYDERABAD BEFORE SHRI B. RAMAKOTAIAH, ACCOUNTANT MEMBER AND SHRI SAKTIJIT DEY, JUDICIAL MEMBER ITA No. 1743/Hyd/2013 Assessment Year : 2009-10 Bellwether

IN THE INCOME TAX APPELLATE TRIBUNAL HYDERABAD BENCH B, HYDERABAD BEFORE SHRI B. RAMAKOTAIAH, ACCOUNTANT MEMBER AND SHRI SAKTIJIT DEY, JUDICIAL MEMBER ITA No. 1743/Hyd/2013 Assessment Year : 2009-10 Bellwether

CIVIL APPELLATE/ORIGINAL JURISDICTION CIVIL APPEAL Nos OF 2004

IN THE SUPREME COURT OF INDIA CIVIL APPELLATE/ORIGINAL JURISDICTION CIVIL APPEAL Nos. 516-527 OF 2004 Brij Lal & Ors.... Appellants versus Commissioner of Income Tax, Jalandhar... Respondents with Civil

IN THE SUPREME COURT OF INDIA CIVIL APPELLATE/ORIGINAL JURISDICTION CIVIL APPEAL Nos. 516-527 OF 2004 Brij Lal & Ors.... Appellants versus Commissioner of Income Tax, Jalandhar... Respondents with Civil

CA SHARAD A SHAH. 21/06/2014 DTRC - Pune WIRC

CA SHARAD A SHAH 21/06/2014 DTRC - Pune WIRC-2014 1 Relevant Part of Section 271 (1) If the Assessing Officer] or the [Commissioner (Appeals)][or the Commissioner] in the course of any proceedings under

CA SHARAD A SHAH 21/06/2014 DTRC - Pune WIRC-2014 1 Relevant Part of Section 271 (1) If the Assessing Officer] or the [Commissioner (Appeals)][or the Commissioner] in the course of any proceedings under

GLIMPSE INTO AMENDMENTS BY THE FINANCE ACT, 2015 TO INCOME TAX ACT, Amendments w.e.f

GLIMPSE INTO AMENDMENTS BY THE FINANCE ACT, 2015 TO INCOME TAX ACT, 1961 Amendments w.e.f 1.4.2015 SN Section Provision 1 4(1) {r/w Sec. 2(4) of the Finance Act, 2015} {Surcharge} In cases in which tax

GLIMPSE INTO AMENDMENTS BY THE FINANCE ACT, 2015 TO INCOME TAX ACT, 1961 Amendments w.e.f 1.4.2015 SN Section Provision 1 4(1) {r/w Sec. 2(4) of the Finance Act, 2015} {Surcharge} In cases in which tax

M/s. Ultratech Cement Ltd. The Additional Commissioner of

IN THE HIGH COURT OF JUDICATURE AT BOMBAY ORDINARY ORIGINAL CIVIL JURISDICTION INCOME TAX APPEAL NO. 1060 OF 2014 M/s. Ultratech Cement Ltd... Appellant v/s. The Additional Commissioner of Income Tax,

IN THE HIGH COURT OF JUDICATURE AT BOMBAY ORDINARY ORIGINAL CIVIL JURISDICTION INCOME TAX APPEAL NO. 1060 OF 2014 M/s. Ultratech Cement Ltd... Appellant v/s. The Additional Commissioner of Income Tax,

IN THE HIGH COURT OF DELHI AT NEW DELHI SUBJECT : INCOME TAX ACT RESERVED ON: PRONOUNCED ON: ITA No.119/2012

IN THE HIGH COURT OF DELHI AT NEW DELHI SUBJECT : INCOME TAX ACT RESERVED ON: 09.10.2012 PRONOUNCED ON: 20.11.2012 ITA No.119/2012 CIT... Appellant Through : Ms. Rashmi Chopra, Sr. Standing counsel versus

IN THE HIGH COURT OF DELHI AT NEW DELHI SUBJECT : INCOME TAX ACT RESERVED ON: 09.10.2012 PRONOUNCED ON: 20.11.2012 ITA No.119/2012 CIT... Appellant Through : Ms. Rashmi Chopra, Sr. Standing counsel versus

Bharat Raichandani Advocate

Bharat Raichandani Advocate Section 14 of CEA, 1944 - Power to summon persons to give evidence and produce documents in inquiries under this Act Section 73 of FA, 1994 - Recovery of service tax not levied

Bharat Raichandani Advocate Section 14 of CEA, 1944 - Power to summon persons to give evidence and produce documents in inquiries under this Act Section 73 of FA, 1994 - Recovery of service tax not levied

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH: H : NEW DELHI BEFORE SHRI I.C. SUDHIR, JUDICIAL MEMBER AND SHRI INTURI RAMA RAO, ACCOUNTANT MEMBER

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH: H : NEW DELHI BEFORE SHRI I.C. SUDHIR, JUDICIAL MEMBER AND SHRI INTURI RAMA RAO, ACCOUNTANT MEMBER ITA No. 1322 /Del/2012 Assessment Year: 2003-04 Asstt.

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH: H : NEW DELHI BEFORE SHRI I.C. SUDHIR, JUDICIAL MEMBER AND SHRI INTURI RAMA RAO, ACCOUNTANT MEMBER ITA No. 1322 /Del/2012 Assessment Year: 2003-04 Asstt.

Chapter IV Assessments, Payment, Recovery and Collection of Tax 24. Submission of return

Chapter IV Assessments, Payment, Recovery and Collection of Tax 24. Submission of return (1) Every dealer liable to pay tax under this Act including a dealer from whom any amount of tax has been deducted

Chapter IV Assessments, Payment, Recovery and Collection of Tax 24. Submission of return (1) Every dealer liable to pay tax under this Act including a dealer from whom any amount of tax has been deducted

CS- FINAL- DIRECT TAX Return of Income and Procedure of Assessment

CS- FINAL- DIRECT TAX Return of Income and Procedure of Assessment Section 139(1): Submission of return of income: Every person, if his or any person in respect of whom he is liable to tax and whose total

CS- FINAL- DIRECT TAX Return of Income and Procedure of Assessment Section 139(1): Submission of return of income: Every person, if his or any person in respect of whom he is liable to tax and whose total

IN THE HIGH COURT OF DELHI AT NEW DELHI SUBJECT : INCOME TAX ACT, 1961 Date of decision: ITA 232/2012

IN THE HIGH COURT OF DELHI AT NEW DELHI SUBJECT : INCOME TAX ACT, 1961 Date of decision: 22.11.2012 ITA 232/2012 COMMISSIONER OF INCOME TAX IV Through Mr. Kamal Sawhney, Sr. Standing Counsel... Appellant

IN THE HIGH COURT OF DELHI AT NEW DELHI SUBJECT : INCOME TAX ACT, 1961 Date of decision: 22.11.2012 ITA 232/2012 COMMISSIONER OF INCOME TAX IV Through Mr. Kamal Sawhney, Sr. Standing Counsel... Appellant

ADMISSION OF ADDITIONAL EVIDENCE BY THE CIT(A)- BACK TO SQUARE ONE AT TRIBUNAL STAGE By Subash Agarwal, Advocate

- BACK TO SQUARE ONE AT TRIBUNAL STAGE By Subash Agarwal, Advocate") ADMISSION OF ADDITIONAL EVIDENCE BY THE CIT(A)- BACK TO SQUARE ONE AT TRIBUNAL STAGE By Subash Agarwal, Advocate Introduction 1. The first appellate authority viz., CIT(A) enjoys wide powers under the

ADMISSION OF ADDITIONAL EVIDENCE BY THE CIT(A)- BACK TO SQUARE ONE AT TRIBUNAL STAGE By Subash Agarwal, Advocate Introduction 1. The first appellate authority viz., CIT(A) enjoys wide powers under the

Section 44AD of The Income Tax Act,1961

Section 44AD of The Income Tax Act,1961 Special provision for computing profits and gains of business on presumptive basis By: CA Sanjay Kumar Agarwal CA Sidharth Jain Assisted By : CA Neha khurana Applicability

Section 44AD of The Income Tax Act,1961 Special provision for computing profits and gains of business on presumptive basis By: CA Sanjay Kumar Agarwal CA Sidharth Jain Assisted By : CA Neha khurana Applicability

Pravin Balubhai Zala v. ITO ()

") (2010) 129 TTJ 0373 :(2010) 033 (II) ITCL 0318 :(2010) 036 DTR 0290 :ITAT Mumbai C Bench Pravin Balubhai Zala v. ITO () INCOME TAX ACT, 1961 --Assessment--ValidityNotice under section 142(1) by non-jurisdictional

(2010) 129 TTJ 0373 :(2010) 033 (II) ITCL 0318 :(2010) 036 DTR 0290 :ITAT Mumbai C Bench Pravin Balubhai Zala v. ITO () INCOME TAX ACT, 1961 --Assessment--ValidityNotice under section 142(1) by non-jurisdictional

LUNAWAT & CO. CA. PRAMOD JAIN. Chartered Accountants. 30 th January 2015 FCA, FCS, FCMA, LL.B, MIMA, DISA

LUNAWAT & CO. Chartered Accountants 30 th January 2015 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Assessment Regular [143(3)] Best Judgment [144] Reopening [147] Block [158BC] PROCEDURE AFTER FILING

LUNAWAT & CO. Chartered Accountants 30 th January 2015 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Assessment Regular [143(3)] Best Judgment [144] Reopening [147] Block [158BC] PROCEDURE AFTER FILING

THE HIGH COURT OF DELHI AT NEW DELHI. % Judgment delivered on: THE COMMISSIONER OF INCOME TAX. - versus M/S ZORAVAR VANASPATI LIMITED

THE HIGH COURT OF DELHI AT NEW DELHI % Judgment delivered on: 24.07.2009 + ITA 596/2005 THE COMMISSIONER OF INCOME TAX Appellant - versus M/S ZORAVAR VANASPATI LIMITED... Respondent Advocates who appeared

THE HIGH COURT OF DELHI AT NEW DELHI % Judgment delivered on: 24.07.2009 + ITA 596/2005 THE COMMISSIONER OF INCOME TAX Appellant - versus M/S ZORAVAR VANASPATI LIMITED... Respondent Advocates who appeared

HIGH COURT OF GUJARAT

HIGH COURT OF GUJARAT Commissioner of Income-tax-I v. Aditya Medisales Ltd. M.R. SHAH AND MS. SONIA GOKANI, JJ. TAX APPEAL NO. 730 OF 2013 SEPTEMBER 2, 2013 JUDGMENT Ms. Sonia Gokani, J. - The Tax Appeal

HIGH COURT OF GUJARAT Commissioner of Income-tax-I v. Aditya Medisales Ltd. M.R. SHAH AND MS. SONIA GOKANI, JJ. TAX APPEAL NO. 730 OF 2013 SEPTEMBER 2, 2013 JUDGMENT Ms. Sonia Gokani, J. - The Tax Appeal

25 Penalties Introduction Penalties

25 Penalties 25.1 Introduction The Income-tax Act, 1961 provides for the imposition of a penalty on an assessee who wilfully commits any offence under the provisions of the Act. Penalty is levied over

25 Penalties 25.1 Introduction The Income-tax Act, 1961 provides for the imposition of a penalty on an assessee who wilfully commits any offence under the provisions of the Act. Penalty is levied over

IN THE INCOME TAX APPELLATE TRIBUNAL BENCH 'B' NEW DELHI. ITA Nos.2337 & 4337/Del/2010 Assessment Years: &

IN THE INCOME TAX APPELLATE TRIBUNAL BENCH 'B' NEW DELHI ITA Nos.2337 & 4337/Del/2010 Assessment Years: 2006-07 & 2007-2008 DEPUTY COMMISSIONER OF INCOME TAX CIRCLE-11(1), NEW DELHI Vs M/s ENERGY INFRASTRUCTURE

IN THE INCOME TAX APPELLATE TRIBUNAL BENCH 'B' NEW DELHI ITA Nos.2337 & 4337/Del/2010 Assessment Years: 2006-07 & 2007-2008 DEPUTY COMMISSIONER OF INCOME TAX CIRCLE-11(1), NEW DELHI Vs M/s ENERGY INFRASTRUCTURE

A COMPLETE ANALYSIS OF THE FINANCE ACT, 2013 PART - VI (Chapter XIII & XIV of the IT Act)

") A COMPLETE ANALYSIS OF THE FINANCE ACT, 2013 PART - VI (Chapter XIII & XIV of the IT Act) Prepared by Advocates of M/s Subbaraya Aiyar, Padmanabhan & Ramamani (SAPR) Advocates 13. CHAPTER XIII Income Tax

A COMPLETE ANALYSIS OF THE FINANCE ACT, 2013 PART - VI (Chapter XIII & XIV of the IT Act) Prepared by Advocates of M/s Subbaraya Aiyar, Padmanabhan & Ramamani (SAPR) Advocates 13. CHAPTER XIII Income Tax

Income Tax Appeals. Revenue Division Federal Board of Revenue Government of Pakistan ,

Income Tax Appeals (Taxpayers Facilitation Guide) September 2011 Revenue Division Federal Board of Revenue Government of Pakistan helpline@cbr.gov.pk 0800-00-227, 051-111-227-227 www.fbr.gov.pk Our Vision

Income Tax Appeals (Taxpayers Facilitation Guide) September 2011 Revenue Division Federal Board of Revenue Government of Pakistan helpline@cbr.gov.pk 0800-00-227, 051-111-227-227 www.fbr.gov.pk Our Vision

IN THE INCOME TAX APPELLATE TRIBUNAL MUMBAI BENCHES, D, MUMBAI BEFORE SHRI R.S.SYAL, ACCOUNTANT MEMBER AND SHRI VIJAY PAL RAO, JUDICIAL MEMBER

IN THE INCOME TAX APPELLATE TRIBUNAL MUMBAI BENCHES, D, MUMBAI BEFORE SHRI R.S.SYAL, ACCOUNTANT MEMBER AND SHRI VIJAY PAL RAO, JUDICIAL MEMBER ITA No. 2210/Mum/2010 (Assessment Years: 2006-07) Renu Hingorani

IN THE INCOME TAX APPELLATE TRIBUNAL MUMBAI BENCHES, D, MUMBAI BEFORE SHRI R.S.SYAL, ACCOUNTANT MEMBER AND SHRI VIJAY PAL RAO, JUDICIAL MEMBER ITA No. 2210/Mum/2010 (Assessment Years: 2006-07) Renu Hingorani

Vs. Date of hearing : Date of Pronouncement : O R D E R

IN THE INCOME TAX APPELLATE TRIBUNAL, MUMBAI BENCH F, MUMBAI BEFORE SHRI RAJENDRA SINGH, ACCOUNTANT MEMBER AND SHRI AMIT SHUKLA, JUDICIAL MEMBER ITA No. 5720/Mum/2011 Assessment Year : 2004-05 M/s. Forever

IN THE INCOME TAX APPELLATE TRIBUNAL, MUMBAI BENCH F, MUMBAI BEFORE SHRI RAJENDRA SINGH, ACCOUNTANT MEMBER AND SHRI AMIT SHUKLA, JUDICIAL MEMBER ITA No. 5720/Mum/2011 Assessment Year : 2004-05 M/s. Forever

IN THE HIGH COURT OF DELHI AT NEW DELHI SUBJECT : INCOME TAX ACT. Decided on : ITA 195/2012, C.M. APPL.5434/2012

IN THE HIGH COURT OF DELHI AT NEW DELHI SUBJECT : INCOME TAX ACT Decided on : 27.07.2012 ITA 195/2012, C.M. APPL.5434/2012 ITA 196/2012, C.M. APPL. 5436/2012 ITA 197/2012, C.M. APPL.5437/2012 ITA 198/2012,

IN THE HIGH COURT OF DELHI AT NEW DELHI SUBJECT : INCOME TAX ACT Decided on : 27.07.2012 ITA 195/2012, C.M. APPL.5434/2012 ITA 196/2012, C.M. APPL. 5436/2012 ITA 197/2012, C.M. APPL.5437/2012 ITA 198/2012,

IN THE HIGH COURT AT CALCUTTA Special Jurisdiction (Income-tax) Original Side. I.T.A. No.201 of 2003

Original Side. I.T.A. No.201 of 2003") IN THE HIGH COURT AT CALCUTTA Special Jurisdiction (Income-tax) Original Side PRESENT: The Hon ble JUSTICE KALYAN JYOTI SENGUPTA AND The Hon ble JUSTICE JOYMALYA BAGCHI I.T.A. No.201 of 2003 Md. Serajuddin

IN THE HIGH COURT AT CALCUTTA Special Jurisdiction (Income-tax) Original Side PRESENT: The Hon ble JUSTICE KALYAN JYOTI SENGUPTA AND The Hon ble JUSTICE JOYMALYA BAGCHI I.T.A. No.201 of 2003 Md. Serajuddin

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH H, NEW DELHI BEFORE SH. G.C.GUPTA, V.P. AND SH. PRASHANT MAHARISHI, AM

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH H, NEW DELHI BEFORE SH. G.C.GUPTA, V.P. AND SH. PRASHANT MAHARISHI, AM : Asstt. Year: 2008-09 Universal Product (P) Ltd., Dholki Mohalla, Sadar Meerut (APPELLANT)

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH H, NEW DELHI BEFORE SH. G.C.GUPTA, V.P. AND SH. PRASHANT MAHARISHI, AM : Asstt. Year: 2008-09 Universal Product (P) Ltd., Dholki Mohalla, Sadar Meerut (APPELLANT)

At the time of Sec. 80G approval object of trust needs to be examined without considering application of income

At the time of Sec. 80G approval object of trust needs to be examined without considering application of income Citation: Commissioner of Income-tax, Rajkot-III v. Vipassana Trust Court: HIGH COURT OF

At the time of Sec. 80G approval object of trust needs to be examined without considering application of income Citation: Commissioner of Income-tax, Rajkot-III v. Vipassana Trust Court: HIGH COURT OF

DATED: 9th January, 2009

(-1-) MGN IN THE HIGH COURT OF JUDICATURE AT BOMBAY ORDINARY ORIGINAL CIVIL JURISDICTION INCOME TAX APPEAL NO.1398 OF 2008 The Commissioner of Income ) Tax-3 Aayakar Bhavan, M.K. ) Road, Mumbai-400 020.

(-1-) MGN IN THE HIGH COURT OF JUDICATURE AT BOMBAY ORDINARY ORIGINAL CIVIL JURISDICTION INCOME TAX APPEAL NO.1398 OF 2008 The Commissioner of Income ) Tax-3 Aayakar Bhavan, M.K. ) Road, Mumbai-400 020.

Page 1 of 5 IN THE INCOME TAX APPELLATE TRIBUNAL AGRA SMC BENCH, AGRA [Coram: Pramod Kumar AM] M/s Vijay Veer Singh Saiyan Road, Kheragarh Agra [PAN:AAEFV6250G].Appellant Vs. Income Tax Officer Ward 4(4),

Page 1 of 5 IN THE INCOME TAX APPELLATE TRIBUNAL AGRA SMC BENCH, AGRA [Coram: Pramod Kumar AM] M/s Vijay Veer Singh Saiyan Road, Kheragarh Agra [PAN:AAEFV6250G].Appellant Vs. Income Tax Officer Ward 4(4),

Penalty provisions under Income Tax Act Unlearning and relearning consequent to Finance bill 2016 By K.K.Chhaparia, FCA

Penalty provisions under Income Tax Act Unlearning and relearning consequent to Finance bill 2016 By K.K.Chhaparia, FCA As we know, penal provisions in any statute are intended to have deterrent effect

Penalty provisions under Income Tax Act Unlearning and relearning consequent to Finance bill 2016 By K.K.Chhaparia, FCA As we know, penal provisions in any statute are intended to have deterrent effect

IN THE INCOME TAX APPELLATE TRIBUNAL, MUMBAI BENCH A, MUMBAI BEFORE SHRI D. KARUNAKARA RAO, ACCOUNTANT MEMBER AND SHRI SANJAY GARG, JUDICIAL MEMBER

IN THE INCOME TAX APPELLATE TRIBUNAL, MUMBAI BENCH A, MUMBAI BEFORE SHRI D. KARUNAKARA RAO, ACCOUNTANT MEMBER AND SHRI SANJAY GARG, JUDICIAL MEMBER Assessment Year: 2008-09, 41-A, Film Center, 38, Tardeo

IN THE INCOME TAX APPELLATE TRIBUNAL, MUMBAI BENCH A, MUMBAI BEFORE SHRI D. KARUNAKARA RAO, ACCOUNTANT MEMBER AND SHRI SANJAY GARG, JUDICIAL MEMBER Assessment Year: 2008-09, 41-A, Film Center, 38, Tardeo

Government Law College, Mumbai

Government Law College, Mumbai 10 th Nani Palkhivala National Tax Moot Court Competition 2013 3 rd 5 th October, 2013 In association with ITAT Bar Association Mumbai All India Federation of Tax Practitioners

Government Law College, Mumbai 10 th Nani Palkhivala National Tax Moot Court Competition 2013 3 rd 5 th October, 2013 In association with ITAT Bar Association Mumbai All India Federation of Tax Practitioners

IN THE INCOME TAX APPELLATE TRIBUNAL AMRITSAR BENCH, AMRITSAR. [Coram: Pramod Kumar AM and A.D. Jain JM]

![IN THE INCOME TAX APPELLATE TRIBUNAL AMRITSAR BENCH, AMRITSAR. [Coram: Pramod Kumar AM and A.D. Jain JM]](/thumbs/77/75515091.jpg "IN THE INCOME TAX APPELLATE TRIBUNAL AMRITSAR BENCH, AMRITSAR. [Coram: Pramod Kumar AM and A.D. Jain JM]") Page 1 of 7 IN THE INCOME TAX APPELLATE TRIBUNAL AMRITSAR BENCH, AMRITSAR [Coram: Pramod Kumar AM and A.D. Jain JM] I.T.A. No.90/Asr /2015 Assessment year: 2013-14 Sibia Healthcare Private Limited..Appellant

Page 1 of 7 IN THE INCOME TAX APPELLATE TRIBUNAL AMRITSAR BENCH, AMRITSAR [Coram: Pramod Kumar AM and A.D. Jain JM] I.T.A. No.90/Asr /2015 Assessment year: 2013-14 Sibia Healthcare Private Limited..Appellant

of the CIT(A)- 16, New Delhi relating to assessment year

- 16, New Delhi relating to assessment year") IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH E, NEW DELHI BEFORE SHRI R. K. PANDA, ACCOUNTANT MEMBER AND SMT. BEENA A. PILLAI, JUDICIAL MEMBER Assessment Year : 2011-12 Smt. Prem Jain, 2683/85, Gali

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH E, NEW DELHI BEFORE SHRI R. K. PANDA, ACCOUNTANT MEMBER AND SMT. BEENA A. PILLAI, JUDICIAL MEMBER Assessment Year : 2011-12 Smt. Prem Jain, 2683/85, Gali

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH: E : NEW DELHI BEFORE SMT. DIVA SINGH, JUDICIAL MEMBER AND SH. O.P. KANT, ACCOUNTANT MEMBER

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH: E : NEW DELHI BEFORE SMT. DIVA SINGH, JUDICIAL MEMBER AND SH. O.P. KANT, ACCOUNTANT MEMBER Assessment Year: 2006-07 M/s. Ujagar Holdings Pvt. Ltd., 8-D,

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH: E : NEW DELHI BEFORE SMT. DIVA SINGH, JUDICIAL MEMBER AND SH. O.P. KANT, ACCOUNTANT MEMBER Assessment Year: 2006-07 M/s. Ujagar Holdings Pvt. Ltd., 8-D,

IN THE INCOME TAX APPELLATE TRIBUNAL (DELHI BENCH G, NEW DELHI)

") IN THE INCOME TAX APPELLATE TRIBUNAL (DELHI BENCH G, NEW DELHI) BEFORE SHRI J. S. REDDY, ACCOUNTANT MEMBER AND SHRI A. T. VARKEY, JUDICIAL MEMBER I.T.A. No.1423 /Del/2013 Assessment year : 2008-09 Simran

IN THE INCOME TAX APPELLATE TRIBUNAL (DELHI BENCH G, NEW DELHI) BEFORE SHRI J. S. REDDY, ACCOUNTANT MEMBER AND SHRI A. T. VARKEY, JUDICIAL MEMBER I.T.A. No.1423 /Del/2013 Assessment year : 2008-09 Simran

IN THE HIGH COURT OF KARNATAKA AT BANGALORE. Dated this the 17 th day of June 2014 PRESENT THE HON BLE MR. JUSTICE N KUMAR

IN THE HIGH COURT OF KARNATAKA AT BANGALORE Dated this the 17 th day of June 2014 PRESENT THE HON BLE MR. JUSTICE N KUMAR AND THE HON BLE MR. JUSTICE B. MANOHAR ITA No. 578 of 2008 BETWEEN: 1. The Commissioner

IN THE HIGH COURT OF KARNATAKA AT BANGALORE Dated this the 17 th day of June 2014 PRESENT THE HON BLE MR. JUSTICE N KUMAR AND THE HON BLE MR. JUSTICE B. MANOHAR ITA No. 578 of 2008 BETWEEN: 1. The Commissioner

Commissioner of Income-Tax Vs. Punjab Chemical & Crop Protection Ltd

Commissioner of Income-Tax Vs. Punjab Chemical & Crop Protection Ltd Judgement: 1. Ajay Kumar Mittal, J. - This appeal has been preferred by the Revenue under section 260A of the Income-tax Act, 1961 (in

Commissioner of Income-Tax Vs. Punjab Chemical & Crop Protection Ltd Judgement: 1. Ajay Kumar Mittal, J. - This appeal has been preferred by the Revenue under section 260A of the Income-tax Act, 1961 (in

The Institute of Cost Accountants of India. (Statutory body under an Act of Parliament)

") The Institute of Cost Accountants of India (Statutory body under an Act of Parliament) Suggestions and Feedback from Stakeholders and General Public submitted to CBDT on New Direct Tax Law General Information

The Institute of Cost Accountants of India (Statutory body under an Act of Parliament) Suggestions and Feedback from Stakeholders and General Public submitted to CBDT on New Direct Tax Law General Information

Short title, extent and commencement. Definitions.

PART I GOVERNMENT OF PUNJAB DEPARTMENT OF LEGAL AND LEGISLATIVE AFFAIRS, PUNJAB NOTIFICATION The 19th April, 2018 No.12-Leg./2018.-The following Act of the Legislature of the State of Punjab received the

PART I GOVERNMENT OF PUNJAB DEPARTMENT OF LEGAL AND LEGISLATIVE AFFAIRS, PUNJAB NOTIFICATION The 19th April, 2018 No.12-Leg./2018.-The following Act of the Legislature of the State of Punjab received the

IN THE INCOME TAX APPELLATE TRIBUNAL LUCKNOW BENCH B, LUCKNOW BEFORE SHRI SUNIL KUMAR YADAV, JUDICIAL MEMBER AND SHRI. A. K. GARODIA, ACCOUNTANT MEMBE

IN THE INCOME TAX APPELLATE TRIBUNAL LUCKNOW BENCH B, LUCKNOW BEFORE SHRI SUNIL KUMAR YADAV, JUDICIAL MEMBER AND SHRI. A. K. GARODIA, ACCOUNTANT MEMBER ITA No.195/LKW/2011 Assessment Year:2006-07 Income

IN THE INCOME TAX APPELLATE TRIBUNAL LUCKNOW BENCH B, LUCKNOW BEFORE SHRI SUNIL KUMAR YADAV, JUDICIAL MEMBER AND SHRI. A. K. GARODIA, ACCOUNTANT MEMBER ITA No.195/LKW/2011 Assessment Year:2006-07 Income

IN THE HIGH COURT OF DELHI AT NEW DELHI SUBJECT : INCOME TAX ACT. Judgment delivered on : ITA Nos. 697/2007, 698/2007 & 699/2007.

IN THE HIGH COURT OF DELHI AT NEW DELHI SUBJECT : INCOME TAX ACT Judgment delivered on : 06.03.2009 ITA Nos. 697/2007, 698/2007 & 699/2007 ESTER INDUSTRIES LIMITED... Appellant versus COMMISSIONER OF INCOME

IN THE HIGH COURT OF DELHI AT NEW DELHI SUBJECT : INCOME TAX ACT Judgment delivered on : 06.03.2009 ITA Nos. 697/2007, 698/2007 & 699/2007 ESTER INDUSTRIES LIMITED... Appellant versus COMMISSIONER OF INCOME

Income Tax Appeal No. 6 of M/s. Shiv Shakti Flour Mills (P) Ltd., Makum Road, Tinsukia Versus-

Ltd., Makum Road, Tinsukia Versus-") THE GAUHATI HIGH COURT (The High Court of Assam, Nagaland, Mizoram & Arunachal Pradesh) Income Tax Appeal No. 6 of 2014 M/s. Shiv Shakti Flour Mills (P) Ltd., Makum Road, Tinsukia 786125. -Versus- Commissioner

THE GAUHATI HIGH COURT (The High Court of Assam, Nagaland, Mizoram & Arunachal Pradesh) Income Tax Appeal No. 6 of 2014 M/s. Shiv Shakti Flour Mills (P) Ltd., Makum Road, Tinsukia 786125. -Versus- Commissioner

DIRECT TAX REVIEW AUGUST 2016 VERENDRA KALRA & CO. Inside this edition. Like always, Like never before

VERENDRA KALRA & CO CHARTERED A CCOUNTANTS Like always, Like never before DIRECT TAX REVIEW AUGUST 2016 Inside this edition CBDT clarifies on Income Declaration Scheme, 2016. Sum received from developer

VERENDRA KALRA & CO CHARTERED A CCOUNTANTS Like always, Like never before DIRECT TAX REVIEW AUGUST 2016 Inside this edition CBDT clarifies on Income Declaration Scheme, 2016. Sum received from developer

IN THE HIGH COURT OF KARNATAKA, BENGALURU PRESENT THE HON BLE MR.JUSTICE JAYANT PATEL AND THE HON BLE MR.JUSTICE ARAVIND KUMAR

1 IN THE HIGH COURT OF KARNATAKA, BENGALURU DATED THIS THE 21 ST DAY OF SEPTEMBER 2016 PRESENT THE HON BLE MR.JUSTICE JAYANT PATEL AND THE HON BLE MR.JUSTICE ARAVIND KUMAR BETWEEN: ITA NOS.251/2016 & 390/2016

1 IN THE HIGH COURT OF KARNATAKA, BENGALURU DATED THIS THE 21 ST DAY OF SEPTEMBER 2016 PRESENT THE HON BLE MR.JUSTICE JAYANT PATEL AND THE HON BLE MR.JUSTICE ARAVIND KUMAR BETWEEN: ITA NOS.251/2016 & 390/2016

2 sake of congruence, brevity and convenience these are being disposed off by this common order. 2. Briefly stated, the facts of the case are that Lat

IN THE INCOME TAX APPELLATE TRIBUNAL, JODHPUR BENCH: JODHPUR (BEFORE SHRI HARI OM MARATHA, JUDICIAL MEMBER AND SHRI N.K. SAINI, ACCOUNTANT MEMBER) ITA No. 228/Jodh/2014 [A.Y. 1998-1999] ITA No. 229/Jodh/2014

IN THE INCOME TAX APPELLATE TRIBUNAL, JODHPUR BENCH: JODHPUR (BEFORE SHRI HARI OM MARATHA, JUDICIAL MEMBER AND SHRI N.K. SAINI, ACCOUNTANT MEMBER) ITA No. 228/Jodh/2014 [A.Y. 1998-1999] ITA No. 229/Jodh/2014

IN THE INCOME TAX APPELLATE TRIBUNAL, MUMBAI BENCH I, MUMBAI BEFORE SHRI SANJAY GARG, JUDICIAL MEMBER AND SHRI ASHWANI TANEJA, ACCOUNTANT MEMBER

IN THE INCOME TAX APPELLATE TRIBUNAL, MUMBAI BENCH I, MUMBAI BEFORE SHRI SANJAY GARG, JUDICIAL MEMBER AND SHRI ASHWANI TANEJA, ACCOUNTANT MEMBER Assessment Year: 2005-06 DCIT, Cir. 6(1), R.No.506, 5 th

IN THE INCOME TAX APPELLATE TRIBUNAL, MUMBAI BENCH I, MUMBAI BEFORE SHRI SANJAY GARG, JUDICIAL MEMBER AND SHRI ASHWANI TANEJA, ACCOUNTANT MEMBER Assessment Year: 2005-06 DCIT, Cir. 6(1), R.No.506, 5 th

IN THE INCOME TAX APPELLATE TRIBUNAL "F" Bench, Mumbai. Before Shri B.R. Baskaran, Accountant Member and Shri Pawan Singh, Judicial Member

IN THE INCOME TAX APPELLATE TRIBUNAL "F" Bench, Mumbai Before Shri B.R. Baskaran, Accountant Member and Shri Pawan Singh, Judicial Member (Assessment Year: 2014-15) 801/806, 8th Floor, Elite Square 274,

IN THE INCOME TAX APPELLATE TRIBUNAL "F" Bench, Mumbai Before Shri B.R. Baskaran, Accountant Member and Shri Pawan Singh, Judicial Member (Assessment Year: 2014-15) 801/806, 8th Floor, Elite Square 274,

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH "F : NEW DELHI. Before Shri. G. E. Veerabhadrappa, VP and Shri. George Mathan, JM

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH "F : NEW DELHI Before Shri. G. E. Veerabhadrappa, VP and Shri. George Mathan, JM ITA No. 3198/D/2004 Asst Year: 1999-2000 GE Capital Services India, AIFACS

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH "F : NEW DELHI Before Shri. G. E. Veerabhadrappa, VP and Shri. George Mathan, JM ITA No. 3198/D/2004 Asst Year: 1999-2000 GE Capital Services India, AIFACS

RECOVERY PROCEEDINGS UNDER INCOME TAX ACT, 1961

RECOVERY PROCEEDINGS UNDER INCOME TAX ACT, 1961 By Shri Jitendra Singh, Advocate M-3, Mezzanine Floor, Court Chambers, 35, New Marine Lines, Mumbai 400020 Telephone No: (022) 49737379 Mobile No.: +91 9975750130

RECOVERY PROCEEDINGS UNDER INCOME TAX ACT, 1961 By Shri Jitendra Singh, Advocate M-3, Mezzanine Floor, Court Chambers, 35, New Marine Lines, Mumbai 400020 Telephone No: (022) 49737379 Mobile No.: +91 9975750130

Administering GST: Disputed Resolutions- Appeals and Revisions adjudication, Demand and Recovery. Porus Kaka Sr Advocate

Administering GST: Disputed Resolutions- Appeals and Revisions adjudication, Demand and Recovery. Porus Kaka Sr Advocate 1 Relevant Provisions of Constitution of India that were amended Article 264A- Special

Administering GST: Disputed Resolutions- Appeals and Revisions adjudication, Demand and Recovery. Porus Kaka Sr Advocate 1 Relevant Provisions of Constitution of India that were amended Article 264A- Special

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH A : NEW DELHI BEFORE SHRI G.D. AGRAWAL, VICE PRESIDENT AND SHRI H.S. SIDHU, JUDICIAL MEMBER ITA No.49

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH A : NEW DELHI BEFORE SHRI G.D. AGRAWAL, VICE PRESIDENT AND SHRI H.S. SIDHU, JUDICIAL MEMBER ITA No.4980/Del/2013 Assessment Year : 2008-09 09 Assistant

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH A : NEW DELHI BEFORE SHRI G.D. AGRAWAL, VICE PRESIDENT AND SHRI H.S. SIDHU, JUDICIAL MEMBER ITA No.4980/Del/2013 Assessment Year : 2008-09 09 Assistant

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH: C NEW DELHI BEFORE SHRI H. S. SIDHU, JUDICIAL MEMBER AND SHRI L.P. SAHU, ACCOUNTANT MEMBER ORDER

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH: C NEW DELHI BEFORE SHRI H. S. SIDHU, JUDICIAL MEMBER AND SHRI L.P. SAHU, ACCOUNTANT MEMBER I.T.A. No. 100/Del/2015 Assessment Year: 2010-11 HARISH NARINDER

IN THE INCOME TAX APPELLATE TRIBUNAL DELHI BENCH: C NEW DELHI BEFORE SHRI H. S. SIDHU, JUDICIAL MEMBER AND SHRI L.P. SAHU, ACCOUNTANT MEMBER I.T.A. No. 100/Del/2015 Assessment Year: 2010-11 HARISH NARINDER

IN THE INCOME TAX APPELLATE TRIBUNAL HYDERABAD BENCH B, HYDERABAD

IN THE INCOME TAX APPELLATE TRIBUNAL HYDERABAD BENCH B, HYDERABAD BEFORE SHRI P.MADHAVI DEVI, JUDICIAL MEMBER AND SHRI S. RIFAUR RAHMAN, ACCOUNTANT MEMBER ITA No. 503/Hyd/2012 Assessment Year: 2008-09,

IN THE INCOME TAX APPELLATE TRIBUNAL HYDERABAD BENCH B, HYDERABAD BEFORE SHRI P.MADHAVI DEVI, JUDICIAL MEMBER AND SHRI S. RIFAUR RAHMAN, ACCOUNTANT MEMBER ITA No. 503/Hyd/2012 Assessment Year: 2008-09,

BEFORE SHRI VIJAY PAL RAO, JM & SHRI RAJENDRA, AM

IN THE INCOME TAX APPELLATE TRIBUNAL MUMBAI G BENCH MUMBAI BENCHES, MUMBAI BEFORE SHRI VIJAY PAL RAO, JM & SHRI RAJENDRA, AM ITA No. 5994/Mum/2010 (Asst Year 2005-06) 23 Atlanta - Nariman Point Mumbai

IN THE INCOME TAX APPELLATE TRIBUNAL MUMBAI G BENCH MUMBAI BENCHES, MUMBAI BEFORE SHRI VIJAY PAL RAO, JM & SHRI RAJENDRA, AM ITA No. 5994/Mum/2010 (Asst Year 2005-06) 23 Atlanta - Nariman Point Mumbai

IN THE HIGH COURT OF JHARKHAND AT RANCHI Tax Appeal No. 7 of 2005

IN THE HIGH COURT OF JHARKHAND AT RANCHI Tax Appeal No. 7 of 2005 Commissioner of Income Tax, Jamshedpur Versus Appellant M/s. Hitech Chemical (P) Ltd., Jamshedpur Respondent CORAM : HON'BLE THE CHIEF

IN THE HIGH COURT OF JHARKHAND AT RANCHI Tax Appeal No. 7 of 2005 Commissioner of Income Tax, Jamshedpur Versus Appellant M/s. Hitech Chemical (P) Ltd., Jamshedpur Respondent CORAM : HON'BLE THE CHIEF

2. Introduction IFCI has six subsidiaries and six step down subsidiaries. 3. Scope of work - Advisory services

TENDER No. IFCI/Accts/2016-17/02 Clarification/Queries on tender document for Appointment of Consultant for Direct Tax Matters SN Reference Clarification/Queries Response 1. Declaration We do not have

TENDER No. IFCI/Accts/2016-17/02 Clarification/Queries on tender document for Appointment of Consultant for Direct Tax Matters SN Reference Clarification/Queries Response 1. Declaration We do not have

Tax Dispute Resolution in India - How to effectively handle? Sanjay Sanghvi 29 April 2017

Tax Dispute Resolution in India - How to effectively handle? Sanjay Sanghvi 29 April 2017 Income Tax in India An overview Residents taxed on worldwide income Non-residents taxed on Indian sourced income

Tax Dispute Resolution in India - How to effectively handle? Sanjay Sanghvi 29 April 2017 Income Tax in India An overview Residents taxed on worldwide income Non-residents taxed on Indian sourced income

Key changes / amendments to take effect from June 1, 2016

1. Equalisation Levy Section 10 Key changes / amendments to take effect from June 1, 2016 Under section 10, a new Clause 50 has been inserted that provides for exemption of income from specified services

1. Equalisation Levy Section 10 Key changes / amendments to take effect from June 1, 2016 Under section 10, a new Clause 50 has been inserted that provides for exemption of income from specified services

ITA No.681 & 824/Kol/2015-M/s. Kalyani Barter (P)Ltd. A.Y

Ltd. A.Y") ITA No.681 & 824/Kol/2015-M/s. Kalyani Barter (P)Ltd. A.Y.2010-11 1 IN THE INCOME TAX APPELLATE TRIBUNAL KOLKATA BENCH D KOLKATA Before Hon ble Shri Waseem Ahmed, Accountant Member and Shri S.S.Viswanethra

ITA No.681 & 824/Kol/2015-M/s. Kalyani Barter (P)Ltd. A.Y.2010-11 1 IN THE INCOME TAX APPELLATE TRIBUNAL KOLKATA BENCH D KOLKATA Before Hon ble Shri Waseem Ahmed, Accountant Member and Shri S.S.Viswanethra

CIT v. Reliance Petroproducts (P) Ltd. ()

Ltd. ()") (2010) 322 ITR 0158 :(2010) 032 (I) ITCL 0600 :(2010) 230 CTR 0320 :(2010) 036 DTR 0449 CIT v. Reliance Petroproducts (P) Ltd. () INCOME TAX ACT, 1961 --Penalty under section 271(1)(c)--Inaccurate particulars

(2010) 322 ITR 0158 :(2010) 032 (I) ITCL 0600 :(2010) 230 CTR 0320 :(2010) 036 DTR 0449 CIT v. Reliance Petroproducts (P) Ltd. () INCOME TAX ACT, 1961 --Penalty under section 271(1)(c)--Inaccurate particulars

F.NO. 380/1/2019-IT(B) Government of India/ Ministry of Finance/ Department of Revenue/ Central Board Direct Taxes / ( ) *********

Government of India/ Ministry of Finance/ Department of Revenue/ Central Board Direct Taxes / ( ) *********") Page 1 of 5 MOST IMMEDIATE BY FAX F.NO. 380/1/2019-IT(B) Government of India/ Ministry of Finance/ Department of Revenue/ Central Board Direct Taxes / ( ) ********* To North Block, New Delhi 12 th April

Page 1 of 5 MOST IMMEDIATE BY FAX F.NO. 380/1/2019-IT(B) Government of India/ Ministry of Finance/ Department of Revenue/ Central Board Direct Taxes / ( ) ********* To North Block, New Delhi 12 th April

ITA NO.3352/MUM/2010(A.Y )

") IN THE INCOME TAX APPELLATE TRIBUNAL, MUMBAI BENCH H, MUMBAI BEFORE SHRI N.V.VASUDEVAN(J.M) & SHRI R.K.PANDA (A.M) Hindustan Platinum Pvt. Ltd., C-122, TTC Indusrial Area, Pawane Village, Rabale, Navi

IN THE INCOME TAX APPELLATE TRIBUNAL, MUMBAI BENCH H, MUMBAI BEFORE SHRI N.V.VASUDEVAN(J.M) & SHRI R.K.PANDA (A.M) Hindustan Platinum Pvt. Ltd., C-122, TTC Indusrial Area, Pawane Village, Rabale, Navi

ALL GUJARAT FEDERATION OF TAX CONSULTANTS

ALL GUJARAT FEDERATION OF TAX CONSULTANTS PRE-BUDGET MEMORANDUM FOR 2015-16 1. Section 2(22)(e) : Deemed Dividend As per the present provision, even if advance or loan is given to a share holder for one

ALL GUJARAT FEDERATION OF TAX CONSULTANTS PRE-BUDGET MEMORANDUM FOR 2015-16 1. Section 2(22)(e) : Deemed Dividend As per the present provision, even if advance or loan is given to a share holder for one

$~ * IN THE HIGH COURT OF DELHI AT NEW DELHI 9. + W.P.(C) 6422/2013 & CM No.14002/2013 (Stay) versus. With W.P.(C) 4558/2014.

6422/2013 & CM No.14002/2013 (Stay) versus. With W.P.(C) 4558/2014.") $~ * IN THE HIGH COURT OF DELHI AT NEW DELHI 9. + W.P.(C) 6422/2013 & CM No.14002/2013 (Stay) INDORAMA SYNTHETICS (INDIA) LTD.... Petitioner Through: Mr. Ajay Vohra, Senior Advocate with Ms. Kavita Jha

$~ * IN THE HIGH COURT OF DELHI AT NEW DELHI 9. + W.P.(C) 6422/2013 & CM No.14002/2013 (Stay) INDORAMA SYNTHETICS (INDIA) LTD.... Petitioner Through: Mr. Ajay Vohra, Senior Advocate with Ms. Kavita Jha

IN THE HIGH COURT OF GUJARAT AT AHMEDABAD

IN THE HIGH COURT OF GUJARAT AT AHMEDABAD TAX APPEAL NO. 637 of 2013 With TAX APPEAL NO. 1711 of 2009 With TAX APPEAL NO. 2577 of 2009 With TAX APPEAL NO. 925 of 2010 With TAX APPEAL NO. 949 of 2010 With

IN THE HIGH COURT OF GUJARAT AT AHMEDABAD TAX APPEAL NO. 637 of 2013 With TAX APPEAL NO. 1711 of 2009 With TAX APPEAL NO. 2577 of 2009 With TAX APPEAL NO. 925 of 2010 With TAX APPEAL NO. 949 of 2010 With