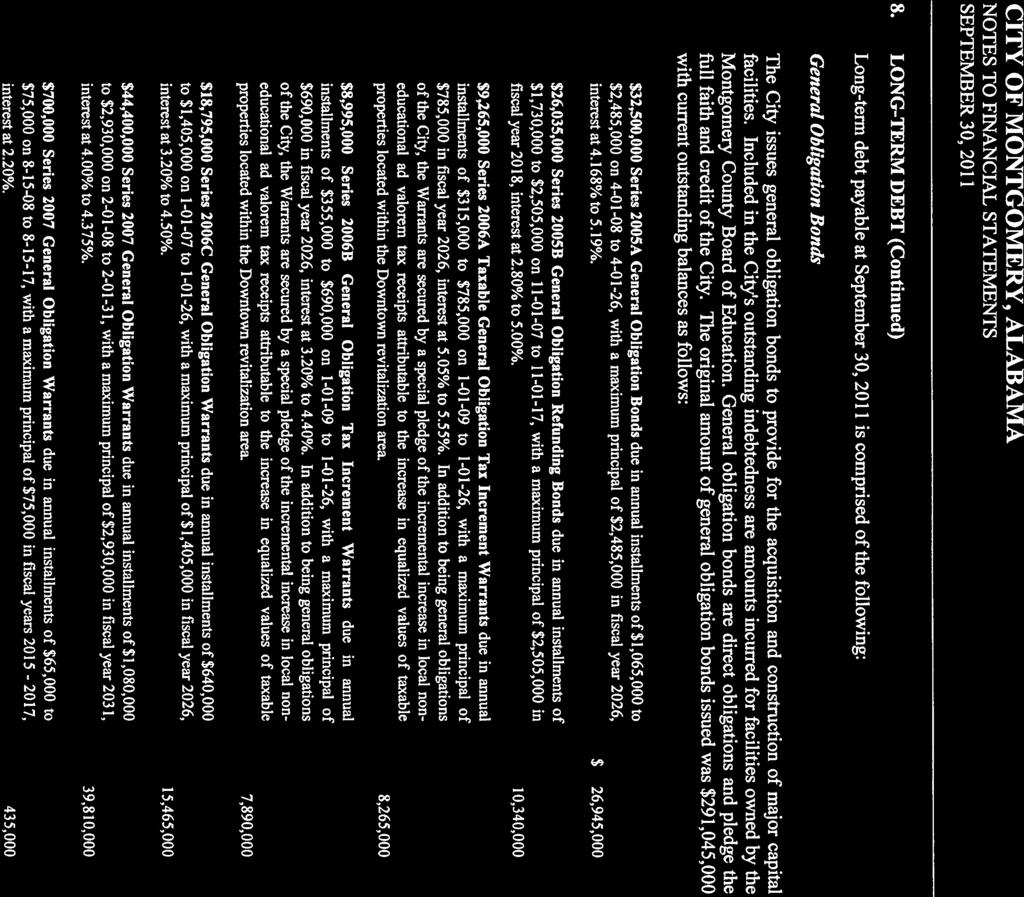

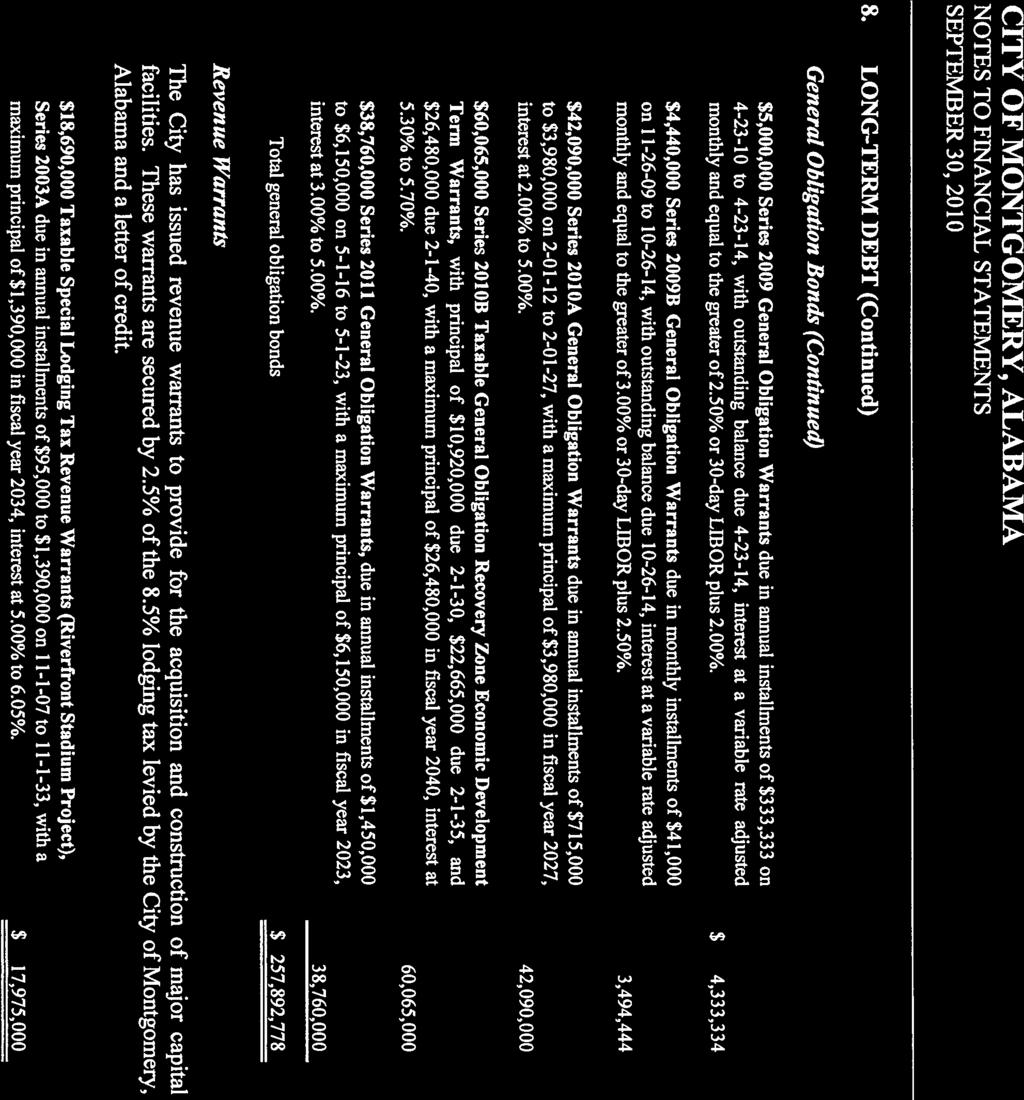

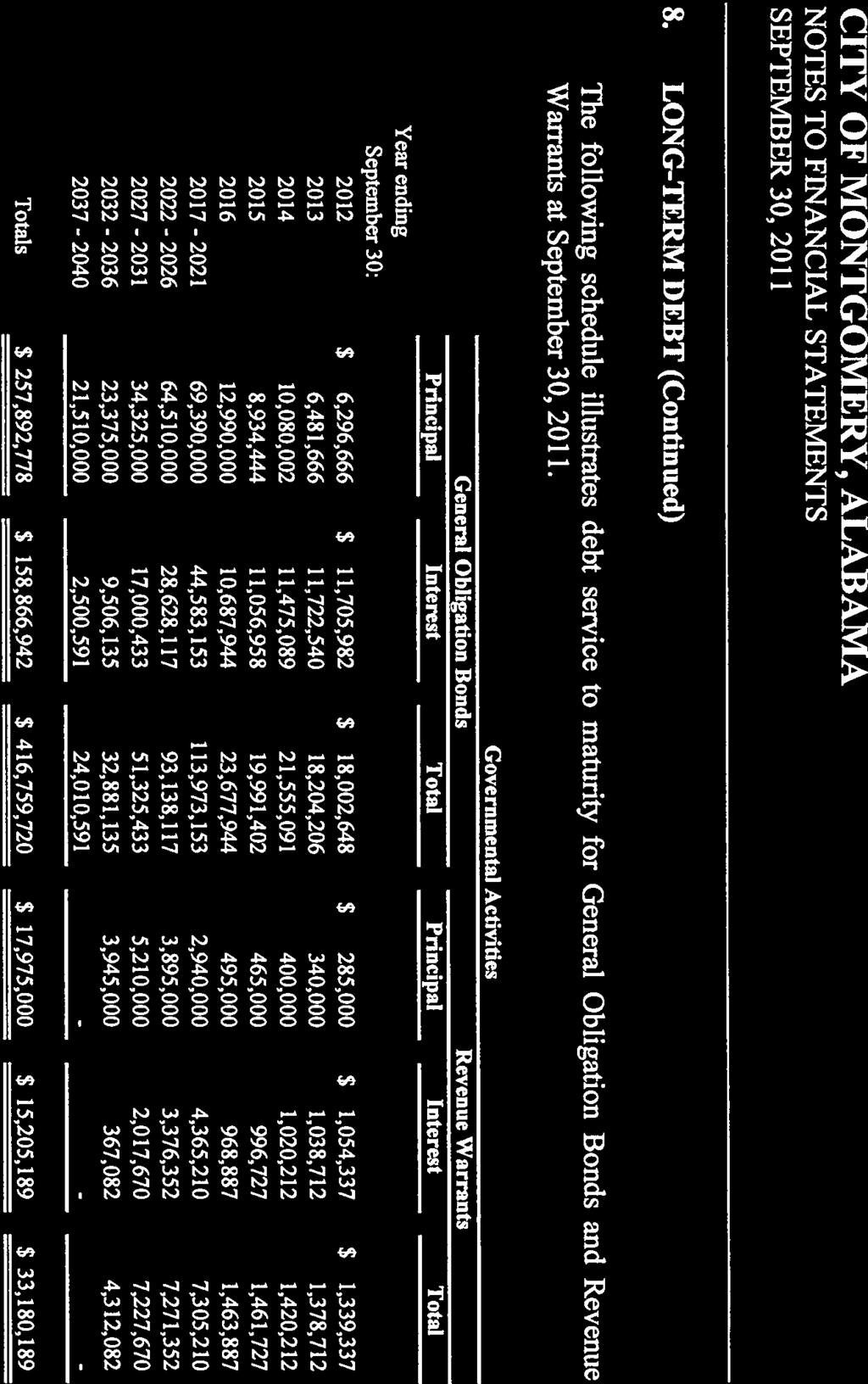

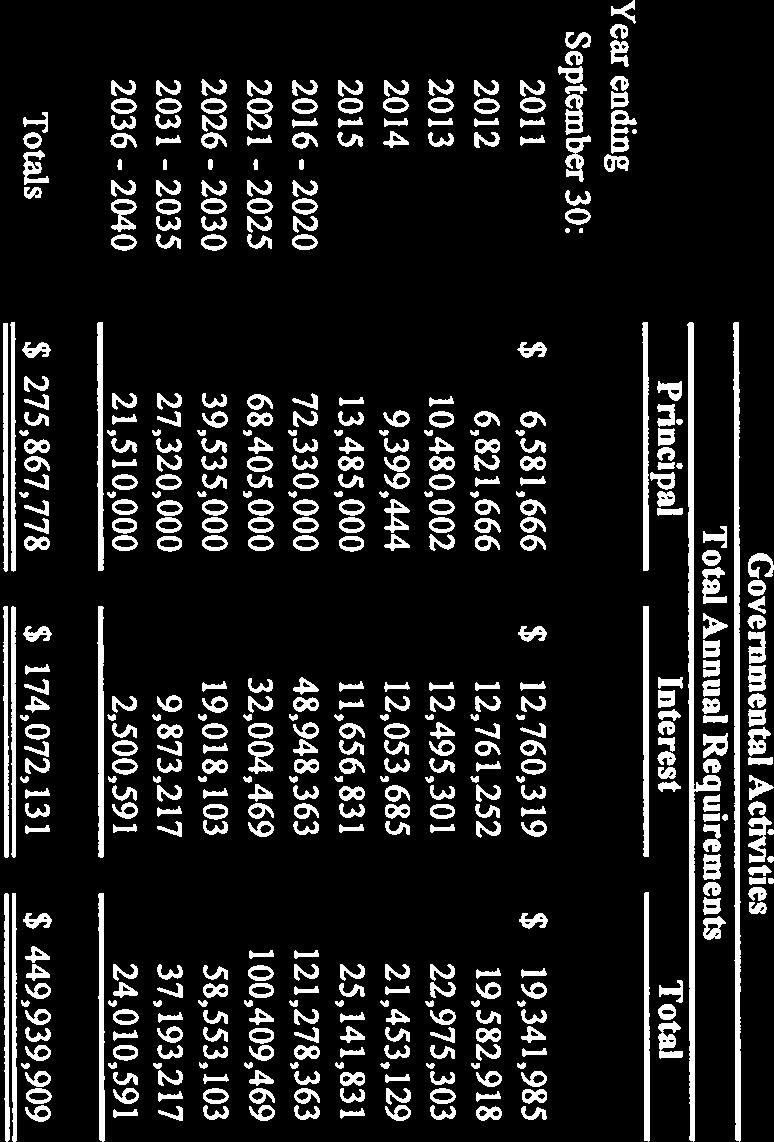

$9,835,000 CITY. Series 2012-A. Series S&P: AA+ + NEW. Series. an item of tax 2012-B WARRANTS 2012-B. York, check. issued, subject

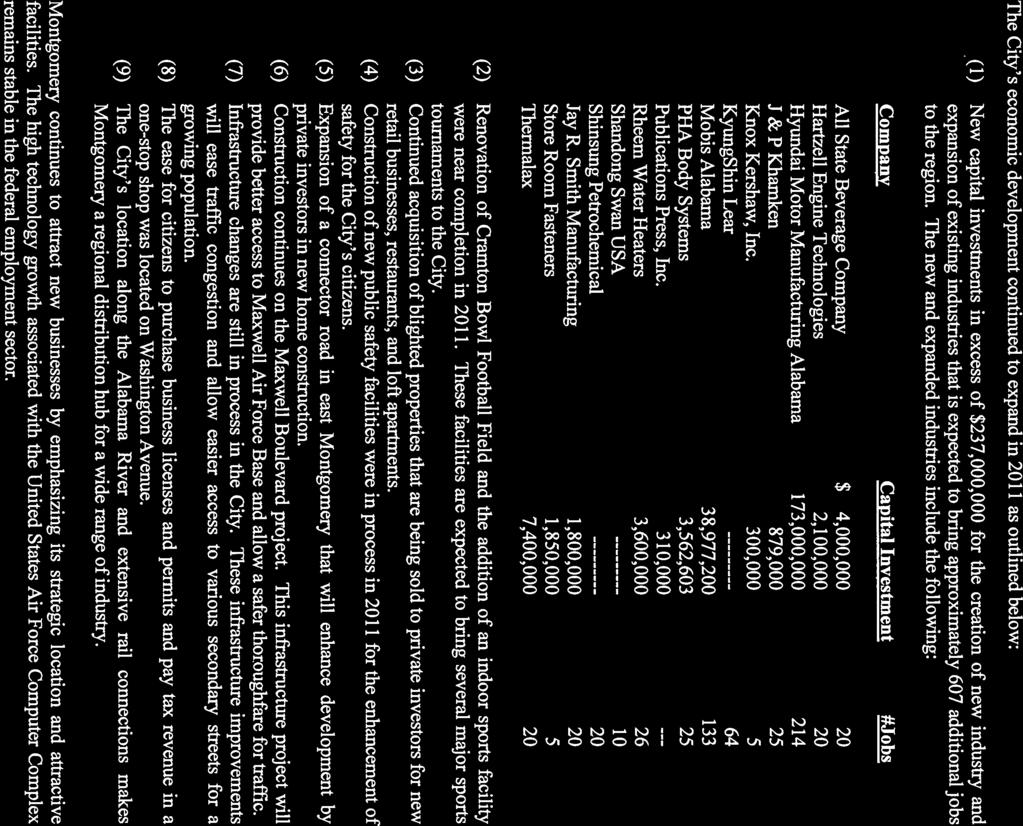

|

|

|

- Jeremy Wilkins

- 5 years ago

- Views:

Transcription

1 Ratings: Moody's: Aa2 S&P: AA+ + NEW ISSUE BOOK ENTRY ONLY (See "RATINGS" Herein) ) In the opinion of Bond Counsel based on existing law, and assuming the accuracy of certain representations and certifications and compliance with certain tax covenants, interest on the Series 2012-A Warrants (i) will be excluded from grosss income for federal income tax purposes if the City complies with all requirements of the Internal Revenue Code that must be satisfied subsequent to the issuance of the Series 2012-A Warrants in order that interest thereon be and remain excluded from gross income, and (ii) will not be an item of tax preference for purposes of the federal alternative minimum tax on individuals and corporations; such interest, however, is included in adjusted current earnings in computing the federal alternative minimum tax imposed on certainn corporations. INTEREST ON THE SERIESS 2012-B WARRANTS IS NOT EXCLUDED FROM GROSS INCOME FOR FEDERAL INCOME TAX PURPOSES. Bond Counsel is also of o the opinion that, under existing law, interest on the Series 2012-A Warrants and Series 2012-B Warrants will be exempt from State of o Alabama income taxation. See "TAX MATTERS" herein for further information and certainn other federal tax consequences arising with respect to the Warrants. $9,835,000 CITY OF MONTGOMERY, ALABAMA General Obligation Warrants, Series 2012-A $65,150,000 CITY OF MONTGOMERY, ALABAMA Taxable General Obligation Warrants, Series 2012-B Dated: Date of delivery Due: As shown on inside coverr The Warrants are issuable as fully registered warrants, without coupons, in denominations of $5,000 or any integral multiple thereof, and will initially be registered in the name of Cede & Co., as registered owner and nominee for The Depository Trust Company, Neww York, New York, which will act as initial securities depository for the Warrants. Individual purchases will be made in book-entry form only, and purchasers will not receive certificates representing their interest in the Warrants purchased. Interest on the Warrants due on each interest payment date (each April 1 and October 1, beginning April 1, 2013) will be payable byy check or draft mailed on such interest payment date to the persons who were registered owners of the Warrants on the record date for such interest payment date. The principal of the Warrants and redemption premium,, if any, thereonn shall be payable only upon presentation and surrender of the Warrants at the designated corporate trust office of Regions Bank. THE WARRANTS WILL CONSTITUTE GENERAL OBLIGATIONS OF THE CITY OF MONTGOMERY, ALABAMA, FOR THE PAYMENT OF WHICH ITS FULL FAITH AND CREDIT ARE IRREVOCABLY PLEDGED. The Warrants do not constitute an indebtedness of the State of Alabamaa or Montgomery County, Alabama, or give rise to a pecuniary liability or charge against the general credit or taxing powers of the State of Alabama or Montgomery County, Alabama. The Warrants are subject to redemption prior to their respective maturities as describedd herein. FOR MATURITY SCHEDULES, SEEE INSIDE COVER This cover page contains certain information for quick reference only. It is not a summary of these issues. Investors must read the entiree official statement to obtain information essential to the making of an informed investmentt decision. The Warrants are offered when, as and if issued, subject to approval off validity by Capell & Howard, P.C., Montgomery, Alabama, Bond Counsel. Certain legal matters will be passed upon for the City by its counsel, Davis & Hatcher, L.L.C., Montgomery, Alabama, and for the Underwriters by their counsel, Balch & Bingham LLP, Birmingham, Alabama. It is expected that the Warrants in definitive form will be available for delivery through the facilities of DTC in New York, New York onn or about November 29, STERNE, AGEE & LEACH, INC. FIRST TUSKEGEE CAPITAL MARKETS November 15, 2012

2 Dated: As of their date of delivery $9,835,000 City of Montgomery, Alabama General Obligation Warrants, Series 2012-A Serial Warrants Due: April 1, as shown below Maturity Principal Amount Interest Rate Yield CUSIP No. Maturity Principal Amount Interest Rate Yield CUSIP No $300, % 0.450% M $ 365, % 1.390% c J , % 0.550% M ,280, % 1.570% c J , % 0.670% M ,310, % 1.750% K , % 0.770% J ,335, % 1.890% K , % 0.900% J ,355, % 1.960% K , % 1.000% J ,380, % 2.030% K , % 1.180% c J ,400, % 2.100% K60 All Warrants priced to produce the yield indicated. c Priced to April 1, 2018 optional call date. Dated: As of their date of delivery $65,150,000 City of Montgomery, Alabama Taxable General Obligation Warrants, Series 2012-B Serial Warrants Due: April 1, as shown below Maturity Principal Amount Interest Rate Yield CUSIP No. Maturity Principal Amount Interest Rate Yield CUSIP No $1,090, % 0.480% K $3,735, % 2.150% L ,775, % 0.620% K ,820, % 2.350% L ,995, % 0.740% K ,905, % 2.500% L ,535, % 1.070% L ,000, % 2.700% L ,060, % 1.270% L ,110, % 2.850% M ,140, % 1.570% L ,220, % 3.000% M ,675, % 1.770% L ,090, % 3.150% M43 Term Warrants $10,000, % Term Warrants maturing April 1, 2034; Yield: 3.730% c ; CUSIP: M68 All Warrants priced to produce the yield indicated. c Priced to April 1, 2022 optional call date.

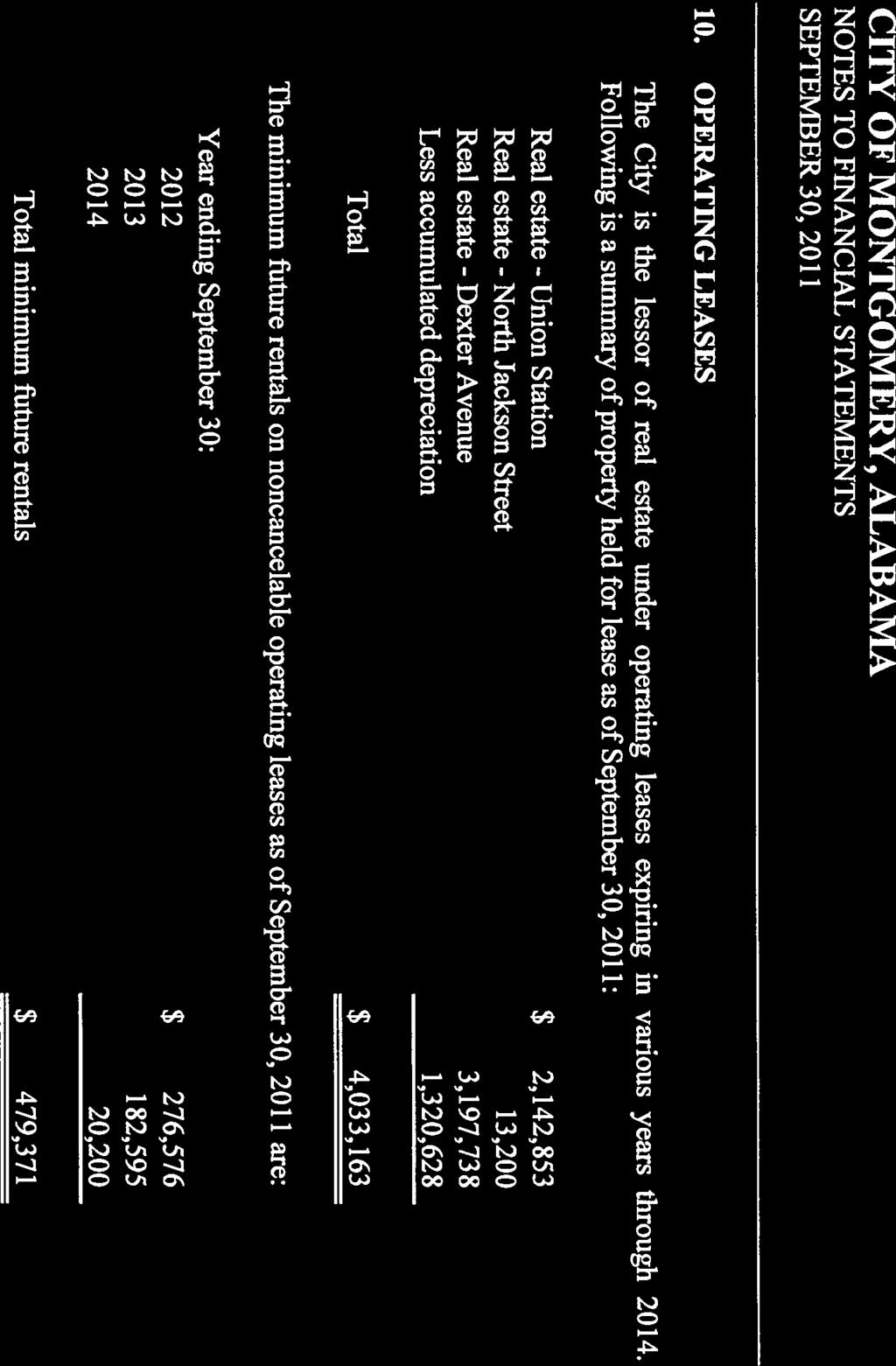

3 CITY OF MONTGOMERY MAYOR Todd Strange CITY COUNCIL Richard Bollinger Charles W. Smith Tracy Larkin David Burkette Cornelius C. C. Calhoun Jon Dow Arch Lee Glen O. Pruitt, Jr. Charles W. Jinright DIRECTOR OF FINANCE E. Lloyd Faulkner BOND COUNSEL Capell & Howard, P.C. Montgomery, Alabama ISSUER'S COUNSEL Davis & Hatcher, L.L.C. Montgomery, Alabama UNDERWRITING GROUP Merchant Capital, L.L.C. First Tuskegee Bank Sterne, Agee & Leach, Inc. UNDERWRITERS' COUNSEL Balch & Bingham LLP Birmingham, Alabama PAYING AGENT Regions Bank Birmingham, Alabama

4 NO DEALER, BROKER, SALESMAN OR OTHER PERSON HAS BEEN AUTHORIZED BY THE CITY OR THE UNDERWRITERS TO GIVE ANY INFORMATION OR TO MAKE ANY REPRESENTATIONS IN CONNECTION WITH THE OFFERING OF THE WARRANTS, OTHER THAN THOSE CONTAINED IN THIS OFFICIAL STATEMENT, AND, IF GIVEN OR MADE, SUCH OTHER INFORMATION OR REPRESENTATIONS MUST NOT BE RELIED UPON. THIS OFFICIAL STATEMENT DOES NOT CONSTITUTE ANY OFFER TO SELL OR THE SOLICITATION OF ANY OFFER TO BUY, NOR SHALL THERE BE ANY SALE OF THE WARRANTS BY ANY PERSON, IN ANY JURISDICTION IN WHICH SUCH OFFER, SALE OR SOLICITATION IS UNLAWFUL. THIS OFFICIAL STATEMENT IS NOT TO BE CONSTRUED AS A CONTRACT WITH THE PURCHASERS OF THE WARRANTS. STATEMENTS CONTAINED IN THIS OFFICIAL STATEMENT WHICH INVOLVE ESTIMATES, FORECASTS OR MATTERS OF OPINION, WHETHER OR NOT EXPRESSLY SO DESCRIBED HEREIN, ARE INTENDED SOLELY AS SUCH AND ARE NOT TO BE CONSTRUED AS REPRESENTATIONS OF FACT. THE UNDERWRITERS HAVE PROVIDED THE FOLLOWING SENTENCE FOR INCLUSION IN THIS OFFICIAL STATEMENT. THE UNDERWRITERS HAVE REVIEWED THE INFORMATION IN THIS OFFICIAL STATEMENT IN ACCORDANCE WITH, AND AS A PART OF, THEIR RESPONSIBILITIES TO INVESTORS UNDER THE FEDERAL SECURITIES LAWS AS APPLIED TO THE FACTS AND CIRCUMSTANCES OF THIS TRANSACTION, BUT THE UNDERWRITERS DO NOT GUARANTEE THE ACCURACY OR COMPLETENESS OF SUCH INFORMATION. THIS OFFICIAL STATEMENT IS INTENDED TO REFLECT INFORMATION AS OF THE DATE OF THIS OFFICIAL STATEMENT. THE DELIVERY OF THIS OFFICIAL STATEMENT DOES NOT IMPLY THAT THE INFORMATION CONTAINED HEREIN IS CORRECT ON ANY DATE SUBSEQUENT TO THE DATE OF THIS OFFICIAL STATEMENT. IN CONNECTION WITH THE OFFERING OF THE WARRANTS, THE UNDERWRITERS MAY OVERALLOT OR EFFECT TRANSACTIONS THAT STABILIZE OR MAINTAIN THE MARKET PRICE OF THE WARRANTS AT LEVELS ABOVE THOSE THAT MIGHT OTHERWISE PREVAIL IN THE OPEN MARKET. SUCH STABILIZING, IF COMMENCED, MAY BE DISCONTINUED AT ANY TIME. THE CITY HAS NO CONTROL OVER THE TRADING OF THE WARRANTS AFTER THEIR SALE BY THE CITY. INFORMATION REGARDING REOFFERING YIELDS OR PRICES IS THE RESPONSIBILITY OF THE UNDERWRITERS.

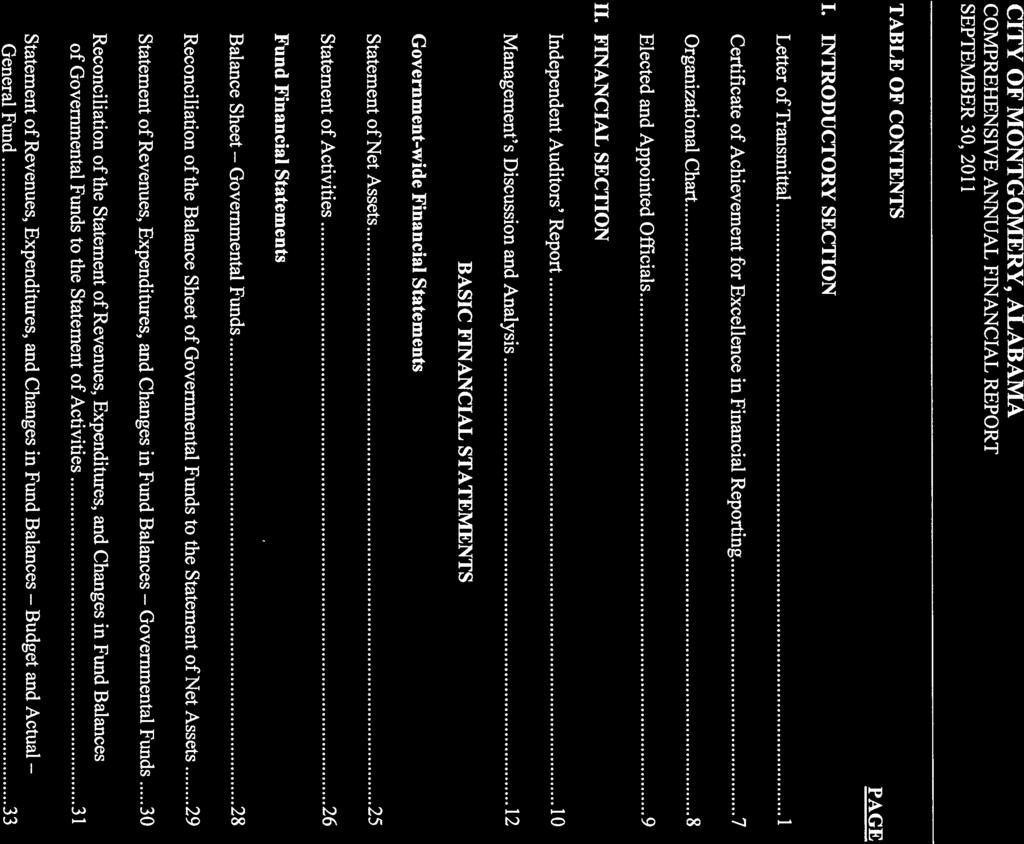

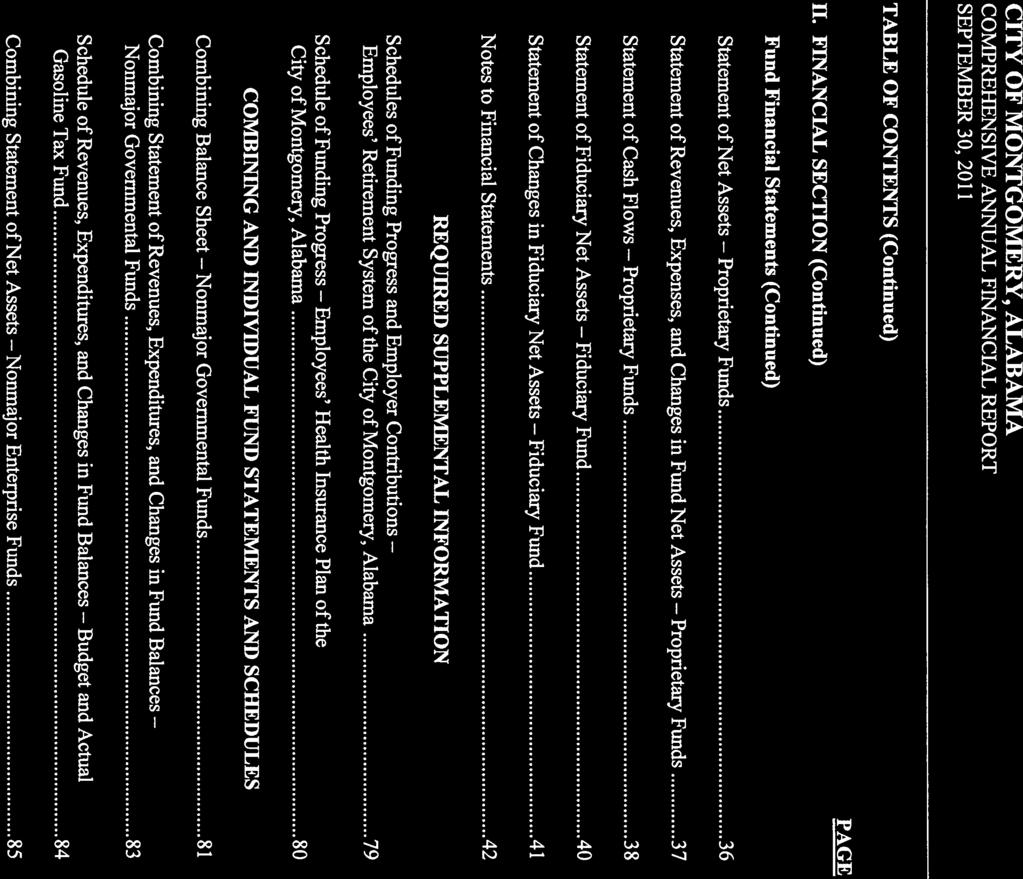

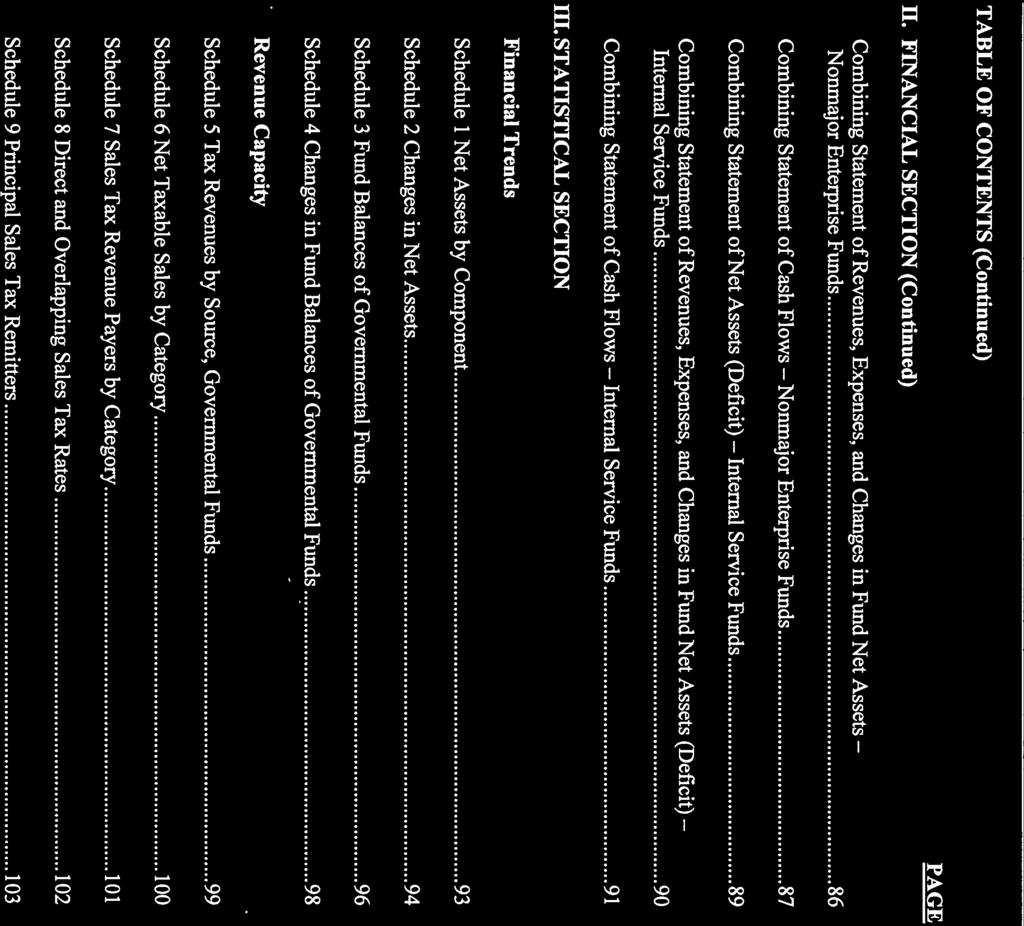

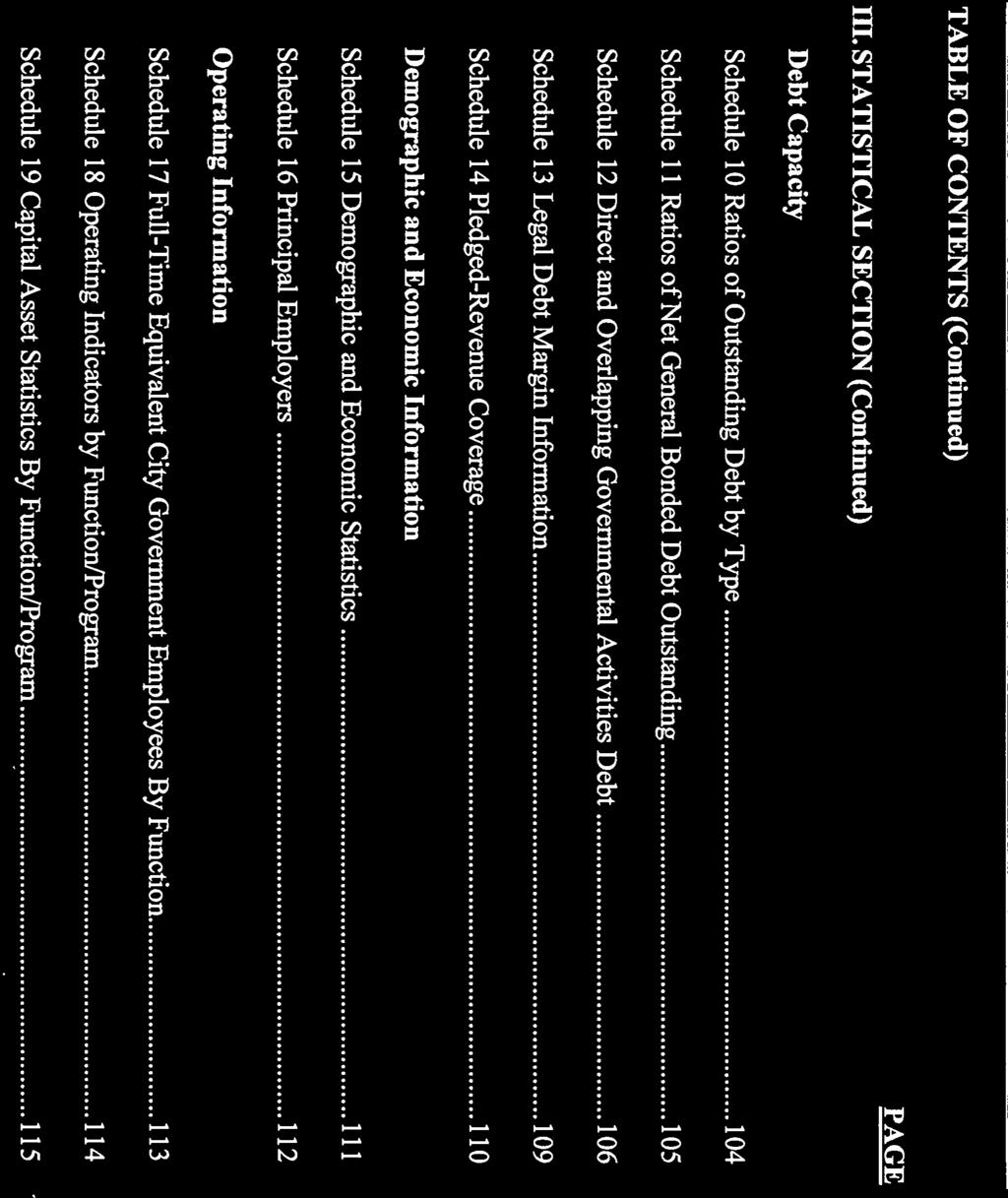

5 TABLE OF CONTENTS INTRODUCTION... 1 THE WARRANTS... 2 General Description... 2 Registration, Transfer, Exchange and Replacement... 2 Redemption Prior to Maturity... 3 SOURCE OF PAYMENT AND SECURITY... 4 General... 4 Authority for Issuance... 5 Remedies... 5 SUMMARY OF CERTAIN PROVISIONS OF THE WARRANT ORDINANCE... 5 Warrant Funds... 5 Provisions for Payment of Warrants... 5 THE FINANCING PLAN... 7 SOURCES AND USES OF FUNDS... 7 Series 2012-A Warrants... 7 Series 2012-B Warrants... 8 DEBT SERVICE REQUIREMENTS... 9 BOOK-ENTRY ONLY SYSTEM THE CITY General Employee Relations Personnel and Retirement System Other Post-Employment Benefits FINANCIAL SYSTEM General Budgetary System Accounting System Governmental Funds Description of Major Sources of General Fund Revenues RESULTS OF OPERATIONS Comparative Statement of General Fund Revenues and Expenditures Summary of the Operating Budget for Fiscal Year ending September 30, Tax Collections DEBT MANAGEMENT General Outstanding Indebtedness Constitutional Debt Limit Direct and Overlapping Debt Debt Ratios Page

6 SALES AND USE TAXATION AD VALOREM TAXATION General Assessed Valuation of Taxable Property Largest Ad Valorem Taxpayers of City Limitations on City's Imposition of Ad Valorem Taxes LITIGATION WARRANTHOLDER RISK FACTORS BANKRUPTCY ECONOMIC AND DEMOGRAPHIC INFORMATION Location Historical Population Business Climate Healthcare Military Community Transportation Agriculture Wholesale Sales Trade Area Employment Statistics Income Levels Major Employers Education Utilities Telecommunications Construction Statistics LEGAL MATTERS TAX MATTERS FEDERAL TAX ACCOUNTING TREATMENT OF ORIGINAL ISSUE DISCOUNT FEDERAL TAX ACCOUNTING TREATMENT OF ORIGINAL ISSUE PREMIUM UNDERWRITING VERIFICATION REPORT CONTINUING DISCLOSURE INDEPENDENT AUDITORS RATINGS APPENDICES FORWARD-LOOKING STATEMENTS ii

7 ADDITIONAL INFORMATION MISCELLANEOUS APPENDIX A Comprehensive Annual Financial Report of the City as of and for the Fiscal Year ended September 30, 2011 APPENDIX B Proposed Forms of Opinions of Bond Counsel iii

8

9 $9,835,000 CITY OF MONTGOMERY, ALABAMA General Obligation Warrants, Series 2012-A $65,150,000 CITY OF MONTGOMERY, ALABAMA Taxable General Obligation Warrants, Series 2012-B INTRODUCTION This Official Statement is furnished by the City of Montgomery, Alabama (the "City") in order to provide information to prospective purchasers regarding its $9,835,000 principal amount of General Obligation Warrants, Series 2012-A (the "Series 2012-A Warrants") and its $65,150,000 Taxable General Obligation Warrants, Series 2012-B (the "Series 2012-B Warrants" and together with the Series 2012-A Warrants herein the "Warrants"). The City is a municipal body politic and corporate organized under the laws of the State of Alabama. The Warrants will be issued by the City under the authority of the Constitution and laws of the State of Alabama, including particularly and of the Code of Alabama (1975), as amended, and that certain ordinance and other proceedings adopted by the City in connection with the issuance thereof (herein referred to as the "Warrant Ordinance"). The Warrants will constitute general obligations of the City for the payment of which its full faith and credit are irrevocably pledged. See "SOURCE OF PAYMENT AND SECURITY" herein. The Warrants are being issued by the City for the purposes of (i) advance refunding the following outstanding warrants - the City's Taxable Special Lodging Tax Revenue Warrants (Riverfront Stadium Project), Series 2003A (the "Series 2003A Warrants"), a portion of the Taxable General Obligation Warrants, Series 2005A (the portion being refunded herein the "Refunded Series 2005A Warrants"), a portion of the General Obligation Refunding Warrants, Series 2005B (the portion being refunded herein the "Refunded Series 2005B Warrants"), a portion of the Taxable General Obligation Tax Increment Warrants, Series 2006A (the portion being refunded herein the "Refunded Series 2006A Warrants") and a portion of the General Obligation Warrants, Series 2006C (the portion being refunded herein the "Refunded Series 2006C Warrants" and together with the Series 2003A Warrants, Refunded Series 2005A Warrants, Refunded Series 2005B Warrants and Refunded Series 2006A Warrants herein the "Refunded Warrants") (ii) funding certain capital expenditures and (iii) paying the costs of issuing the Warrants. See "THE FINANCING PLAN" herein. This Official Statement contains brief descriptions of the City, the financing plan, information respecting the use of the proceeds of the Warrants, summaries of certain provisions of the Warrants and the Warrant Ordinance, and a description of certain of the risks associated with an investment in the Warrants. The summaries of the documents herein contained are not complete or definitive, and each and every statement made in this Official Statement concerning any provision of any document or instrument is qualified by reference to such document or instrument in its entirety. The City has covenanted and agreed to undertake certain continuing disclosure pursuant to Rule 15c2-12 of the United States Securities and Exchange Commission. See "CONTINUING DISCLOSURE" herein. This Official Statement speaks only as of its date, and the information contained herein is subject to change.

10 THE WARRANTS General Description The Warrants will be issued as fully registered warrants, without coupons, in the denominations of $5,000 or any integral multiple thereof. The Warrants shall be issued solely in fully registered form, and shall initially be registered in the name of Cede & Co., as registered owner and nominee for DTC. Payments of principal, interest, and redemption premium, if any, shall be governed by procedures established by DTC (the "Securities Depository"). See "BOOK-ENTRY ONLY SYSTEM" herein. The Warrants will be dated the date of their delivery, will bear interest from such date payable on April 1, 2013, and semiannually on each October 1 and April 1 thereafter at the rates set forth on the inside front cover hereof and will mature on the dates and in the principal amounts set forth on the inside front cover hereof. The principal of and the interest on any Warrant will bear interest from their respective due dates until paid at the rate of interest borne by the principal of such Warrant prior to maturity. The principal of and the premium, if any, on the Warrants will be payable, with par clearance guaranteed, at the designated corporate trust agency office of Regions Bank, the registrar, transfer agent and paying agent for the Warrants (said bank acting in such capacity, together with any successor thereto, being herein called the "Registrar" or "Paying Agent"). The interest payable on the Warrants on each interest payment date will be paid by check or draft mailed by the Registrar on such interest payment date to the registered holders thereof as of the March 15 or September 15 immediately preceding such interest payment date. If any interest payment date shall fall on a Saturday, Sunday or other date on which the Registrar is not open for business, or on which the Federal Reserve Bank is closed, such payment shall be made on the next following business day. Upon the written request of the registered holder of any Warrants of a single series in an aggregate principal amount of not less than $100,000, the Paying Agent will make payment of interest due on such Warrants upon any interest payment date by wire transfer to an account of such holder maintained at a bank in the continental United States or by any other method providing for payment in same-day funds that is acceptable to the Paying Agent, provided that payment of the principal of and redemption premium (if any) on such Warrants shall be made only upon surrender of such Warrants to the Paying Agent. Registration, Transfer, Exchange and Replacement Subject to the provisions herein with respect to the book-entry system, the Warrants shall be registered as to both principal and interest and may be transferred only on the registry books of the Paying Agent pertaining to the Warrants. No transfer of the Warrants shall be permitted except upon presentation and surrender of such Warrant at the office of the Paying Agent with written power to transfer signed by the registered owner thereof in person or by a duly authorized attorney in form and with guaranty of signature satisfactory to the Paying Agent. The Paying Agent will not be required to register or transfer any Warrant during the period of fifteen (15) calendar days next preceding any interest payment date and shall not be required to transfer or exchange any Warrant during the period of forty-five (45) calendar days next preceding the date for redemption or prepayment of any Warrant. The holder of one or more of the Warrants may, upon request, and upon the surrender to the Paying Agent of such Warrant, exchange such Warrant for Warrants of other authorized denominations of the series, maturity and interest rate and together aggregating the same principal amount as the Warrant so surrendered. Any registration, transfer and exchange of Warrants shall be without expense to the holder thereof, except that the holder shall pay all taxes and other governmental charges, if any, required to be paid in connection 2

11 with such transfer, registration or exchange. The holder of any Warrant will be required to pay any expenses incurred in connection with the replacement of a mutilated, lost, stolen or destroyed Warrant. The Warrant Ordinance provides that each holder of the Warrants, by receiving or accepting the Warrants, consents and agrees and is estopped to deny that, insofar as the City and the Paying Agent are concerned, the Warrants may be transferred only in accordance with the provisions of the Warrant Ordinance. The Warrant Ordinance also provides that each transferee of the Warrants takes them subject to all principal and interest payments in fact made with respect to the Warrants. Redemption Prior to Maturity Series 2012-A Warrants. The Series 2012-A Warrants are subject to redemption prior to maturity as provided below. Optional Redemption. The Series 2012-A Warrants, maturing on or after April 1, 2019 will be subject to redemption prior to their maturity, at the option of the City, in whole or in part, on April 1, 2018 and on any date thereafter (in principal amounts of $5,000 and any integral multiple thereof and if less than all of the Series 2012-A Warrants are to be redeemed, those maturities or portions thereof to be called for redemption shall be selected by the City in its discretion, and if less than all the Series 2012-A Warrants of a single maturity are to be redeemed, those to be called for redemption shall be selected by lot), at a redemption price equal to 100% of the principal amount of each Series 2012-A Warrant or portion thereof redeemed, plus accrued interest to the date fixed for redemption. Series 2012-B Warrants. The Series 2012-B Warrants are subject to redemption prior to maturity as provided below. Optional Redemption. The Series 2012-B Warrants, maturing on or after April 1, 2023 will be subject to redemption prior to their maturity, at the option of the City, in whole or in part, on April 1, 2022 and on any date thereafter (in principal amounts of $5,000 and any integral multiple thereof and if less than all of the Series 2012-B Warrants are to be redeemed, those maturities or portions thereof to be called for redemption shall be selected by the City in its discretion, and if less than all the Series 2012-B Warrants of a single maturity are to be redeemed, those to be called for redemption shall be selected by lot), at a redemption price equal to 100% of the principal amount of each Series 2012-B Warrant or portion thereof redeemed, plus accrued interest to the date fixed for redemption. Mandatory Redemption. Those of the Series 2012-B Warrants having a stated maturity in 2034 shall be subject to mandatory redemption prior to maturity, at a redemption price equal to 100% of the principal amount redeemed, plus accrued interest thereon to the redemption date, with those to be redeemed to be selected by the Paying Agent by lot, on the dates and in the principal amounts set forth below: 3

12 PRINCIPAL REDEMPTION DATE * AMOUNT * April 1, 2026 $ 255,000 April 1, ,070,000 April 1, ,110,000 April 1, ,150,000 April 1, ,190,000 April 1, ,235,000 April 1, ,285,000 April 1, ,330,000 April 1, 2034 (final maturity) 1,375,000 The City may, not less than 60 days prior to any such mandatory redemption date, direct that any or all of the following amounts be credited against the Series 2012-B Warrants scheduled for redemption on such date: (i) the principal amount of Series 2012-B Warrants of such maturity delivered by the City to the Paying Agent for cancellation and not previously claimed as a credit; (ii) the principal amount of Series 2012-B Warrants of such maturity previously redeemed (other than Series 2012-B Warrants of such maturity redeemed pursuant to mandatory redemption) and not previously claimed as credit; and (iii) the principal amount of Series 2012-B Warrants of such maturity otherwise deemed paid in full and not previously claimed as credit. General Provisions Regarding Redemptions. Upon any partial redemption of a Warrant, such Warrant shall be surrendered to the Paying Agent in exchange for one or more new Warrants of the same series and maturity and bearing the same interest rate in an authorized denomination of $5,000 or any multiple thereof in fully registered form, without coupons, for the unredeemed portion in principal. Any Warrant or portion thereof which is to be redeemed must be surrendered to the Paying Agent for payment of the redemption price. Notice of any such redemption is required to be given, not more than 60 nor less than thirty (30) days prior to the date fixed for redemption, by United States registered or certified mail to the registered holder of any Warrant called for redemption. After any specified redemption date, the Warrants so called for redemption shall cease to bear or to accrue interest if funds have been deposited with the Paying Agent for the payment thereof and if the redemption notice has been duly given as provided in the Warrant Ordinance. General SOURCE OF PAYMENT AND SECURITY The Warrants will constitute general obligations of the City for the payment of which the full faith and credit of the City will be irrevocably pledged. None of the general revenues of the City that will be legally available for the payment of debt service on the Warrants have been specially pledged for payment of debt service on the Warrants, nor has any lien been placed on such general revenues for payment of debt service on the Warrants. The Warrants are not secured by a mortgage or lien on, or a security interest in, any real or personal property. Information describing the taxes collected by the City and other revenues of the City is set forth below under "FINANCIAL SYSTEM", "RESULTS OF OPERATIONS", "SALES AND USE TAXATION" AND "AD VALOREM TAXATION". 4

13 Authority for Issuance The Warrants are being issued by the City under the authority of the Constitution and laws of the State of Alabama, including particularly Sections and of the Code of Alabama (1975), as amended, which authorize any municipality in the State of Alabama to borrow money for any lawful purpose and to issue, without an election, evidences of indebtedness, in the form of interest-bearing warrants, notes or bills payable, maturing not later than 30 years from the date of issue. The Warrants have been authorized to be issued pursuant to the Warrant Ordinance. See "DEBT MANAGEMENT". Remedies The Director of Finance, as Treasurer of the City, is, under existing law, subject to mandamus by a court of competent jurisdiction in the event that he has money available for payment of debt service on the Warrants and does not apply such money as and to the extent provided in the Warrant Ordinance. However, Alabama law provides that necessary and legitimate governmental expenses may be paid by the City before payment of debt service. See "WARRANTHOLDER RISK FACTORS". Warrant Funds SUMMARY OF CERTAIN PROVISIONS OF THE WARRANT ORDINANCE General. The Warrant Ordinance will provide for the maintenance of special funds for each series of the Warrants, designated the "City of Montgomery Warrant Fund, 2012-A" and the "City of Montgomery Warrant Fund, 2012-B" (collectively, the "Warrant Funds"). Regions Bank will be designated in the Warrant Ordinance as the depository, custodian and disbursing agent for the Warrant Funds. In addition, there is created under the Warrant Ordinance an issuance costs account designated the "2012 Issuance Expense Account". Regions Bank will be designated in the Warrant Ordinance as the depository for the 2012 Issuance Expense Account. The Warrant Funds. The City will be required to transfer to each of the Warrant Funds, on or before the business day next preceding each April 1 and October 1, commencing April 1, 2013, an amount equal to the sum of (i) the semiannual installment of interest that will mature with respect to the respective series of the Warrants on the then next succeeding interest payment date, plus (ii) the principal, if any, of the respective series of the Warrants that will mature or be due for mandatory redemption on the then next succeeding interest payment date. Moneys on deposit in the Warrant Funds are to be used for the payment of the principal of and interest on the respective series of the Warrants. Provisions for Payment of Warrants Provision for Payment the Warrants. (a) If the principal of and interest and redemption premium (if any) on the Series 2012-A Warrants or the Series 2012-B Warrants is paid in accordance with the terms set forth in the Warrant Ordinance, then all covenants, agreements and other obligations of the City to the holders of such series of Warrants shall thereupon cease, terminate and become void and be discharged and satisfied. In the event the Series 2012-A Warrants or the Series 2012-B Warrants are so paid, the Paying Agent shall pay to the City any surplus remaining in the corresponding Warrant Fund. (b) The Series 2012-A Warrants or the Series 2012-B Warrants shall, prior to the maturity or redemption date thereof, be deemed to have been paid within the meaning and with the effect expressed in subsection (a) of this Section if: 5

14 (1) the City and the Paying Agent enter into an appropriate trust agreement under which there shall be deposited, for payment or redemption of such Warrants and for payment of the interest to accrue thereon until maturity or redemption, and any redemption premium thereon, securities that are direct obligations of the United States of America or securities with respect to which payment of the principal thereof and the interest thereon is unconditionally guaranteed by the United States of America ("Federal Securities") and cash or any combination of cash and Federal Securities which, together with the income to be derived from such, will produce monies sufficient to provide for the payment, redemption and retirement of such Warrants as and when the same become due; (2) the City shall have adopted all necessary proceedings providing for the redemption of any such Warrants that are required to be redeemed prior to their respective maturities and shall have instructed the Paying Agent under the aforesaid trust agreement to provide such notices of redemption as are required under the Warrant Ordinance; (3) the City and the Paying Agent shall have been furnished a certificate of a firm of certified public accountants satisfactory to the Paying Agent stating that such trust will produce monies sufficient to provide for the full payment and retirement of such Warrants as and when the principal of and interest and redemption premium (if any) on such Warrants shall come due; and (4) in the case of the Series 2012-A Warrants, the City and the Paying Agent shall have been furnished with an opinion of nationally recognized bond counsel to the effect that the creation of any such trust will not result in subjecting to federal income taxation the interest on any of the Series 2012-A Warrants that are to be paid in accordance with such trust. Interest After Payment Due Date. The Warrants, any premium thereon and, to the extent legally enforceable, overdue installments of interest thereon, shall bear interest after the maturity dates thereof or such earlier date as they may be called for redemption, until paid or until money sufficient for the payment thereof shall have been deposited for that purpose with the Paying Agent, at the respective rates borne thereby. Any provision hereof to the contrary notwithstanding, overdue interest shall not be payable to the holder solely by reason of such holder having been the holder on the record date next preceding the interest payment date on which such interest became due and payable, but shall be payable by the Paying Agent as follows: (a) Not less than ten (10) days following receipt by the Paying Agent of immediately available funds in an amount sufficient to enable the Paying Agent to pay all overdue interest, the Paying Agent shall fix an overdue interest payment date for payment of such overdue interest, which date shall be not more than twenty (20) days following the expiration of the ten-day period after receipt of funds by the Paying Agent; and (b) Overdue interest shall be paid by check or draft mailed by the Paying Agent to the persons in whose names the Warrants were registered in the registry books of the Registrar pertaining to the Warrants on the overdue interest payment date. 6

15 Payment of overdue interest in the manner herein prescribed to the persons in whose names the Warrants were registered on the overdue interest payment date shall fully discharge and satisfy all liability for the same. THE FINANCING PLAN The Series 2012-A Warrants are being issued by the City to provide funds for the purposes of (i) advance refunding the Refunded Series 2006C Warrants and (ii) paying the costs of issuance of the Series 2012-A Warrants. The Series 2012-B Warrants are being issued by the City to provide funds for the purposes of (i) advance refunding the Series 2003A Warrants, Refunded Series 2005A Warrants, Refunded Series 2005B Warrants and Refunded Series 2006A Warrants and (ii) paying the costs of issuance of the Series 2012-B Warrants. In order to effect the refunding of the Refunded Warrants, the City will enter into an Escrow Trust Agreement (the "Escrow Agreement") with Regions Bank (the "Escrow Trustee"). The City will deposit, from the proceeds of the Series 2012-A Warrants, the sum of $8,899, into the Series 2012-A Account of the Escrow Fund (the "Escrow Fund") established pursuant to the Escrow Agreement. The City will also deposit, from the proceeds of the Series 2012-B Warrants, the sum of $58,894, into the Series 2012-B Account of the Escrow Fund. Money in the Escrow Fund will be invested in direct obligations of the United States Treasury or other permitted investments (herein referred to as the "Escrow Securities") for the benefit of the holders of the Refunded Warrants and will not be available under any circumstances to pay principal of or interest on the Warrants. The maturing principal and interest on the Escrow Securities, without reinvestment, together with the initial cash balances remaining in each account of the Escrow Fund after purchase of the Escrow Securities, will be sufficient to pay the principal, interest and redemption price maturing or coming due on the Refunded Warrants. Series 2012-A Warrants SOURCES AND USES OF FUNDS The estimated sources and uses of proceeds from the sale of the Series 2012-A Warrants are as follows: Sources of Funds Principal amount of Series 2012-A Warrants... $9,835, Net Original Issue Premium... 33, Total... $9,868, Uses of Funds Deposit to Escrow Fund... $8,899, Underwriters' Discount... 72, Costs of Issuance... 25, Capital Projects. 870, Total... $9,868,

16 Series 2012-B Warrants The estimated sources and uses of proceeds from the sale of the Series 2012-B Warrants are as follows: Sources of Funds Principal amount of Series 2012-B Warrants... $65,150, Net Original Issue Premium , Debt Service Reserve Fund from Series 2003A Warrants. 1,479, Total... $66,742, Uses of Funds Deposit to Escrow Fund... $58,894, Underwriters' Discount , Costs of Issuance , Capital Projects.. 7,199, Total... $66,742, [Balance of page intentionally left blank] 8

17 DEBT SERVICE REQUIREMENTS The table below sets forth the debt service requirements on the City's long-term general obligation indebtedness following the issuance of the Warrants and refunding of the Refunded Warrants. Fiscal Year Ending September 30 Other Outstanding Warrants (1)(2) Series 2012-A Warrants Series 2012-B Warrants Total 2013 $15,175,578 $ 365,148 $1,588,776 $17,129, ,315, ,240 3,241,568 22,913, ,627, ,840 4,450,563 21,441, ,796, ,240 6,968,400 25,129, ,311, ,540 7,434,175 25,106, ,238, ,840 7,437,213 25,037, ,062, ,040 4,875,815 23,306, ,481, ,040 4,870,768 23,881, ,575,995 1,434,915 4,875,465 23,886, ,583,695 1,432,915 4,870,695 23,887, ,579,911 1,436,628 4,868,070 23,884, ,227,778 1,433,265 4,870,070 17,531, ,230,356 1,433,875 4,862,935 17,527, ,227,515 1,428,000 4,861,335 17,516, ,143, ,447,619 12,591, ,171, ,446,156 11,617, ,090, ,443,144 11,533, ,006, ,438,581 11,445, ,913, ,437,469 11,350, ,807, ,439,613 8,246, ,697, ,434,819 8,132, ,579, ,428,281 8,008, ,459, ,459, ,337, ,337, ,205, ,205, ,073, ,073, ,936, ,936, ,795, ,795,598 Source: City Finance Department. (1) Assumes an interest rate of 2.50% on the Taxable General Obligation Warrants, Series 2009, which bear interest at a variable rate. Assumes an interest rate of 3.00% on the Taxable General Obligation Warrants, Series 2009B, which bear interest at a variable rate. Reflects the gross amount of interest payable on the General Obligation Recovery Zone Economic Development Warrants, Series 2010-B, without deduction for the forty-five percent (45%) subsidy payment the City expects to receive from the United States Treasury with respect to each interest payment. See "DEBT MANAGEMENT - Outstanding Indebtedness - Long-Term Indebtedness" herein for additional information regarding the City's outstanding indebtedness. (2) Future payments under the City's outstanding capital leases in the approximate aggregate principal amount of $12,500,000 are not included. Does not include operating leases which are funded on a year-to-year basis. Also, does not include amounts payable under the City's line of credit. See "DEBT MANAGEMENT - Outstanding Indebtedness" herein for additional information. 9

18 BOOK-ENTRY ONLY SYSTEM The information in this section concerning The Depository Trust Company ("DTC"), New York, NY, and DTC's book-entry system has been obtained from sources the City and the Underwriters believe to be reliable, but neither the City nor the Underwriters take responsibility for the accuracy or completeness thereof. There can be no assurance that DTC will abide by its procedures or that such procedures will not be changed from time to time. The Warrants will be issued as fully-registered warrants in the name of Cede & Co., as nominee of DTC, as registered owner of the Warrants. Purchasers of such Warrants will not receive physical delivery of warrant certificates. For purposes of this Official Statement, so long as all of the Warrants of a series are in the custody of DTC, references to the warrantholder or owner of Warrants of such series shall mean DTC or its nominee. DTC will act as securities depository for the Warrants. The Warrants will be issued as fullyregistered securities in the name of Cede & Co. (DTC's partnership nominee herein "Cede") or such other name as may be requested by an authorized representative of DTC. One fully-registered Warrant certificate will be issued for each maturity of each series of Warrants, in the aggregate principal amount of such maturity, and will be deposited with DTC. DTC, the world's largest securities depository, is a limited-purpose trust company organized under the New York Banking Law, a "banking organization" within the meaning of the New York Banking Law, a member of the Federal Reserve System, a "clearing corporation" within the meaning of the New York Uniform Commercial Code and a "clearing agency" registered pursuant to the provisions of Section 17A of the Securities Exchange Act of 1934, as amended. DTC holds and provides asset servicing for over 3.5 million issues of U.S. and non-u.s. equity issues, corporate and municipal debt issues, and money market instruments (from over 100 countries) that DTC's participants ("Direct Participants") deposit with DTC. DTC also facilitates post-trade settlement among Direct Participants of sales and other securities transactions in deposited securities, through electronic computerized book-entry transfers and pledges between Direct Participants' accounts. This eliminates the need for physical movement of securities certificates. Direct Participants include both U.S. and non-u.s. securities brokers and dealers, banks, trust companies, clearing corporations and certain other organizations. DTC is a wholly-owned subsidiary of The Depository Trust & Clearing Corporation ("DTCC"). DTCC is the holding company for DTC, National Securities Clearing Corporation and Fixed Income Clearing Corporation, all of which are registered clearing agencies. DTCC is owned by the users of its regulated subsidiaries. Access to the DTC system is also available to others such as both U.S. and non-u.s. securities brokers and dealers, banks, trust companies and clearing corporations that clear through or maintain a custodial relationship with a Direct Participant, either directly or indirectly ("Indirect Participants"). DTC has a Standard & Poor's rating of AA+. The DTC Rules applicable to its Direct and Indirect Participants are on file with the Securities and Exchange Commission. More information on DTC can be found at Purchases of Warrants, in the denomination of $5,000 principal amount or any integral multiple of $5,000 in excess thereof, under the DTC system must be made by or through Direct Participants, which will receive a credit for the Warrants on DTC's records. The ownership interest of each actual purchaser of each Warrant ("Beneficial Owner") is in turn to be recorded on the Direct and Indirect Participants' records. Beneficial Owners will not receive written confirmation from DTC of their purchase. Beneficial Owners are expected, however, to receive written confirmations providing details of the transaction, as well as periodic statements of their holdings, from the Direct or Indirect Participant through which the Beneficial Owner entered into the transaction. Transfers of ownership interests in the Warrants are to be accomplished by entries made on the books of Direct and Indirect Participants acting on behalf of 10

19 Beneficial Owners. Beneficial Owners will not receive certificates representing their ownership interests in Warrants, except in the event that use of the book-entry system for the Warrants is discontinued. To facilitate subsequent transfers, all Warrants deposited by Direct Participants with DTC are registered in the name of DTC's partnership nominee, Cede, or such other name as may be requested by an authorized representative of DTC. The deposit of Warrants with DTC and their registration in the name of Cede or such other DTC nominee does not effect any change in beneficial ownership. DTC has no knowledge of the actual Beneficial Owners of the Warrants; DTC's records reflect only the identity of the Direct Participants to whose accounts such Warrants are credited, which may or may not be the Beneficial Owners. The Direct and Indirect Participants will remain responsible for keeping account of their holdings on behalf of their customers. Conveyance of notices and other communications by DTC to Direct Participants, by Direct Participants to Indirect Participants, and by Direct Participants and Indirect Participants to Beneficial Owners will be governed by arrangements among them, subject to any statutory or regulatory requirements as may be in effect from time to time. Beneficial Owners of Warrants may wish to take certain steps to augment the transmission to them of notices of significant events with respect to the Warrants, such as redemptions, defaults, and proposed amendments to the Warrant documents. For example, Beneficial Owners of Warrants may wish to ascertain that the nominee holding the Warrants for their benefit has agreed to obtain and transmit notices to Beneficial Owners. In the alternative, Beneficial Owners may wish to provide their names and addresses to the registrar and request that copies of notices be provided directly to them. Redemption notices shall be sent to DTC. If less than all of the Warrants of a series are being redeemed, DTC's practice is to determine by lot the amount of the interest of each Direct Participant in such Warrants to be redeemed. Neither DTC nor Cede (nor any other DTC nominee) will consent or vote with respect to Warrants unless authorized by a Direct Participant in accordance with DTC's MMI Procedures. Under its usual procedures, DTC mails an Omnibus Proxy to the City as soon as possible after the record date. The Omnibus Proxy assigns Cede's consenting or voting rights to those Direct Participants to whose accounts the Warrants are credited on the record date (identified in a listing attached to the Omnibus Proxy). Principal, redemption price and interest payments on the Warrants will be made by the Paying Agent to Cede or such other nominee as may be requested by an authorized representative of DTC. DTC's practice is to credit Direct Participants' accounts, upon DTC's receipt of funds and corresponding detail information from the City or Paying Agent, on a payment date in accordance with their respective holdings shown on DTC's records. Payments by Participants to Beneficial Owners will be governed by standing instructions and customary practices, as in the case with securities held for the accounts of customers in bearer form or registered in "street name," and will be the responsibility of such Participant and not of DTC, the Paying Agent or the City, subject to any statutory or regulatory requirements as may be in effect from time to time. Payment of principal, redemption price and interest to Cede (or such other nominee as may be requested by an authorized representative of DTC) is the responsibility of the City or the Paying Agent, disbursement of such payments to Direct Participants will be the responsibility of DTC, and disbursement of such payments to the Beneficial Owners will be the responsibility of Direct and Indirect Participants. THE CITY, THE PAYING AGENT AND THE UNDERWRITERS WILL NOT HAVE ANY RESPONSIBILITY OR OBLIGATION TO SUCH PARTICIPANTS, OR TO THE PERSONS FOR WHOM THEY ACT AS NOMINEES WITH RESPECT TO THE WARRANTS, OR TO ANY BENEFICIAL OWNER IN RESPECT OF THE ACCURACY OF ANY RECORDS MAINTAINED BY 11

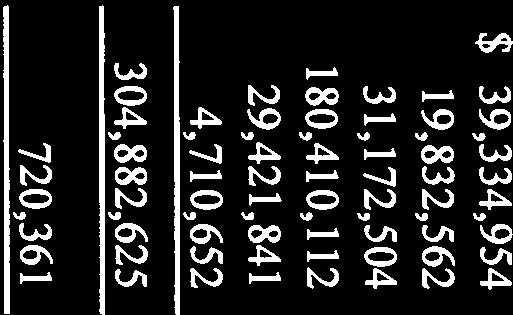

20 DTC OR ANY DIRECT PARTICIPANT OR INDIRECT PARTICIPANT, THE PAYMENT BY DTC OR ANY DIRECT PARTICIPANT OR INDIRECT PARTICIPANT OF ANY AMOUNT IN RESPECT OF THE PRINCIPAL OR REDEMPTION PRICE OF OR INTEREST ON THE WARRANTS, ANY NOTICE WHICH IS PERMITTED OR REQUIRED TO BE GIVEN TO WARRANTHOLDERS UNDER THE WARRANT ORDINANCE, THE SELECTION BY DTC OR ANY DIRECT PARTICIPANT OR INDIRECT PARTICIPANT OF ANY PERSON TO RECEIVE PAYMENT IN THE EVENT OF PARTIAL REDEMPTION OF THE WARRANTS WITH RESPECT TO LESS THAN ALL OF THE WARRANTS, OR ANY OTHER ACTION TAKEN BY DTC AS REGISTERED WARRANTHOLDER. DTC may discontinue providing its services as depository with respect to the Warrants at any time by giving reasonable notice to the City or the Paying Agent. Under such circumstances, in the event that a successor depository is not obtained, warrant certificates are required to be printed and delivered. The City may decide to discontinue use of the system of book-entry-only transfers through DTC (or a successor securities depository). In that event, warrant certificates will be printed and delivered to DTC. General THE CITY The City is a body politic and corporate and political subdivision of the State of Alabama organized under the laws of the State of Alabama in Since 1975, the City has been governed under a Mayor-Council form of government, which was established pursuant to Act No adopted on August 28, 1973 at a 1973 Session of the Legislature of Alabama. The Mayor is elected in a City-wide vote to a four-year term, and the members of the City Council are elected from each of nine single member districts throughout the City to four-year terms. The City Council elects from among its members a President of the Council who serves at the pleasure of the City Council. The Mayor is charged with the administration of the day-to-day activities of the City, while the City Council exercises legislative powers and institutes policy decisions. The current terms of the Mayor and all nine Council Members end in November The City operates on a fiscal year from October 1 of a calendar year to September 30 of the following calendar year. Employee Relations The City considers relations with its employees to be satisfactory. No employees of the City are represented by labor unions or similar employee organizations. The City does not bargain collectively with any labor union or employee organization. As of September 30, 2012, the City had approximately 2,638 employees. Personnel and Retirement System The City contributes to the Employees' Retirement System of the City of Montgomery, which is a cost-sharing, multiple-employer defined benefit plan (the "Retirement System"). The Retirement System is not in any way related to the State of Alabama's retirement system. The Retirement System was established by the City to provide retirement allowances to City employees and the employees of The City of Montgomery Airport Authority. As of October 1, 2005, the Water Works Board opted out of the Retirement System and has elected to be included under the State of Alabama's retirement system. The employees covered under the Retirement System are broken into two (2) separate groups as follows: (1) Group I most general employees of the City and The City of Montgomery Airport Authority and 12

21 (2) Group II members of the City's Fire Department and Police Department. The Retirement System is administered by a separate nine-member Board of Trustees each of whom is appointed by the City. Under the law authorizing the establishment of the Retirement System, the authority to establish and amend benefit provisions (including cost-of-living increases) is granted to such Board of Trustees. Benefits under the Retirement System are funded through contributions made by both covered employees and the participating employers. Covered employees are required to contribute six percent (6%) of their "earnable compensation" to the Retirement System each payroll period. The participating employers are required to make annual contributions in amounts which, together with contributions of covered employees (and earnings thereon), will be sufficient to permit the payment of benefits as they come due. The participating employers' annual contributions consist of (i) "normal contributions," which are intended to cover the currently accruing cost of benefits not covered by employee contributions, and (ii) "accrued liability contributions" which are intended to cover the cost of benefits not covered by "normal contributions" and employee contributions. The "normal contributions" and "accrued liability contributions" are stated as percentages of the compensation of covered employees. The appropriate accrued liability percentage is determined as provided in the governing act and ordinance, and the appropriate normal contribution percentage is determined annually on the basis of annual actuarial valuation of the assets and liabilities of the Retirement System. As of October 1, 2012, the City's rate of contribution for Group I and Group II employees was 9.29% and 19.48% of annual covered payroll, respectively. The contributions required of the plan members and the City are established, and may be amended by, the Board of Trustees for the Retirement System. For the fiscal year ended September 30, 2012 the City's actual contribution was $13,843,183, which was equal to the City's required contribution for that year. Based on actuarial analysis, the Retirement System determines the value of its assets and the value of the accrued liabilities to make benefit payments. Based on such actuarial analysis, as of the December 31, 2011, the City's unfunded actuarial accrued liability relating to the Retirement System was $163,954,143. [Balance of page intentionally left blank] 13

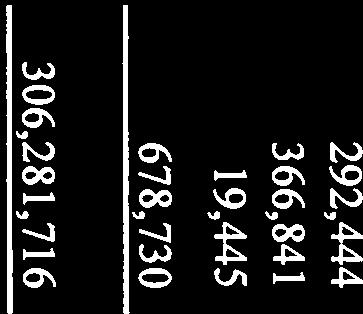

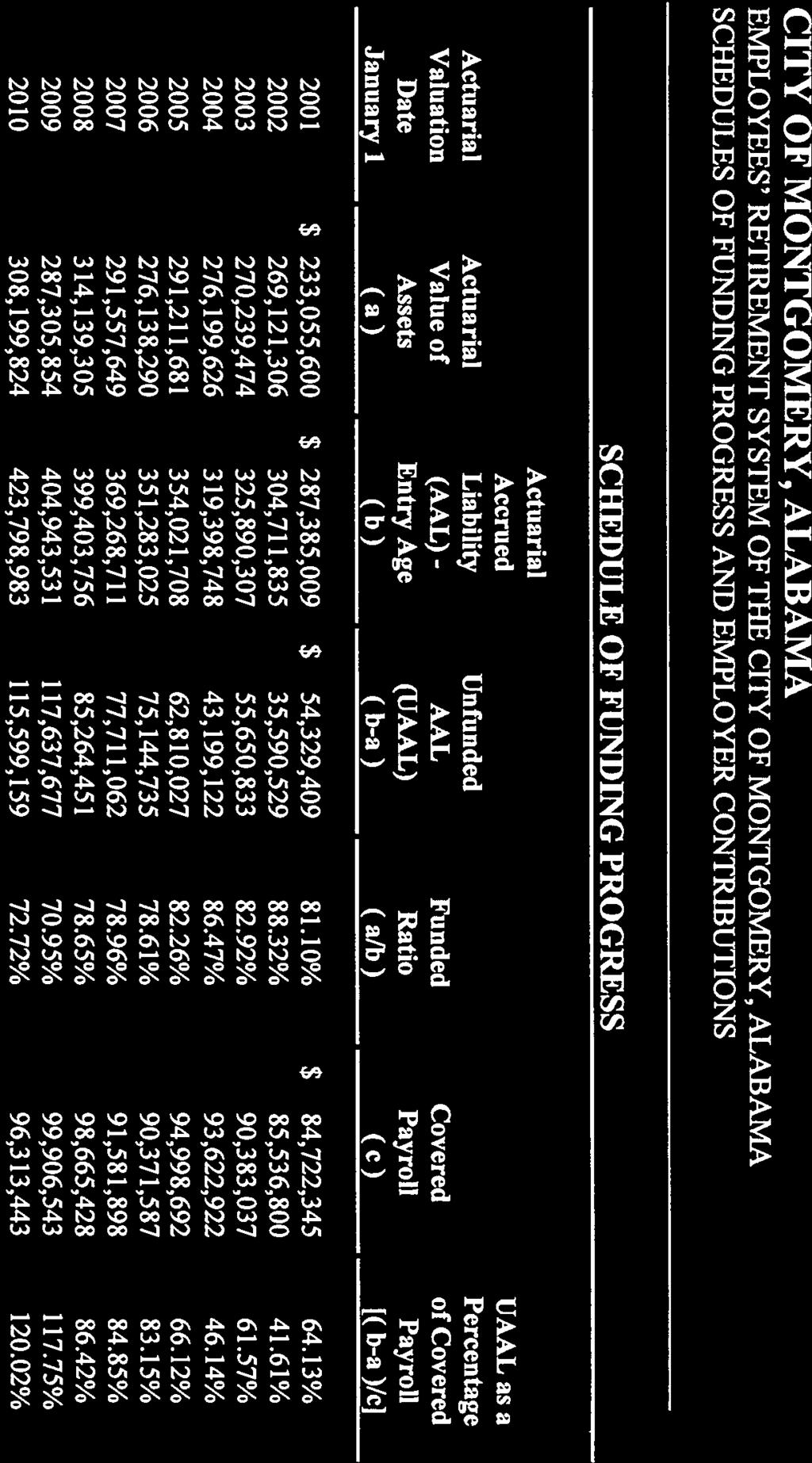

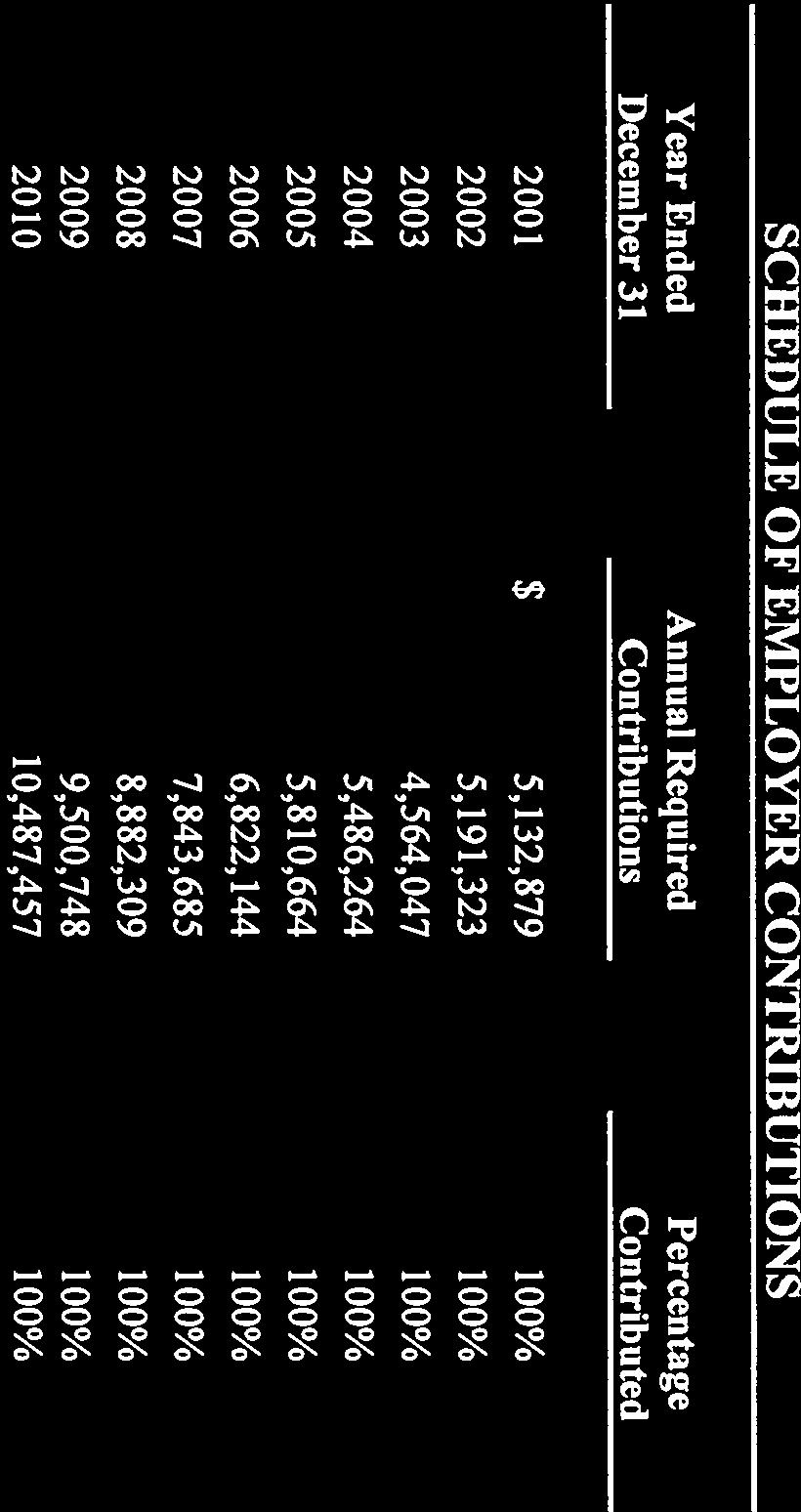

22 The following table contains certain funding trend information for the Retirement System: Actuarial Valuation Date Actuarial Value of Assets Actuarial Accrued Liability Entry Age Unfunded Actuarial Accrued Liability Funded Ratio Covered Payroll Unfunded Actuarial Accrued Liability as of % of Covered Payroll 12/31/2000 $233,055,600 $287,385,009 $ 54,329, % $84,722, % 12/31/ ,121, ,711,835 35,590, % 85,536, % 12/31/ ,239, ,890,307 55,650, % 90,383, % 12/31/ ,199, ,398,748 43,199, % 93,622, % 12/31/ ,211, ,021,708 62,810, % 94,998, % 12/31/ ,138, ,283,025 75,144, % 90,371, % 12/31/ ,557, ,268,711 77,711, % 91,581, % 12/31/ ,139, ,403,756 85,264, % 98,665, % 12/31/ ,305, ,943, ,637, % 99,906, % 12/31/ ,199, ,798, ,599, % 96,313, % 12/31/ ,019, ,662, ,643, % 98,456, % 12/31/ ,508, ,462, ,954, % 99,195, % The following table shows certain contribution information for the Retirement System: Year Ended Annual Required Contribution Actual Contribution Percentage Contributed 12/31/2000 $ 5,282,064 $ 5,282, % 12/31/2001 5,132,879 5,132, % 12/31/2002 5,191,323 5,191, % 12/31/2003 4,564,047 4,564, % 12/31/2004 5,486,264 5,486, % 12/31/2005 5,810,664 5,810, % 12/31/2006 6,822,144 6,822, % 12/31/2007 7,843,686 7,843, % 12/31/2008 8,936,193 8,936, % 12/31/2009 9,572,795 9,572, % 12/31/ ,487,458 10,487, % 12/31/ ,971,544 11,971, % 14

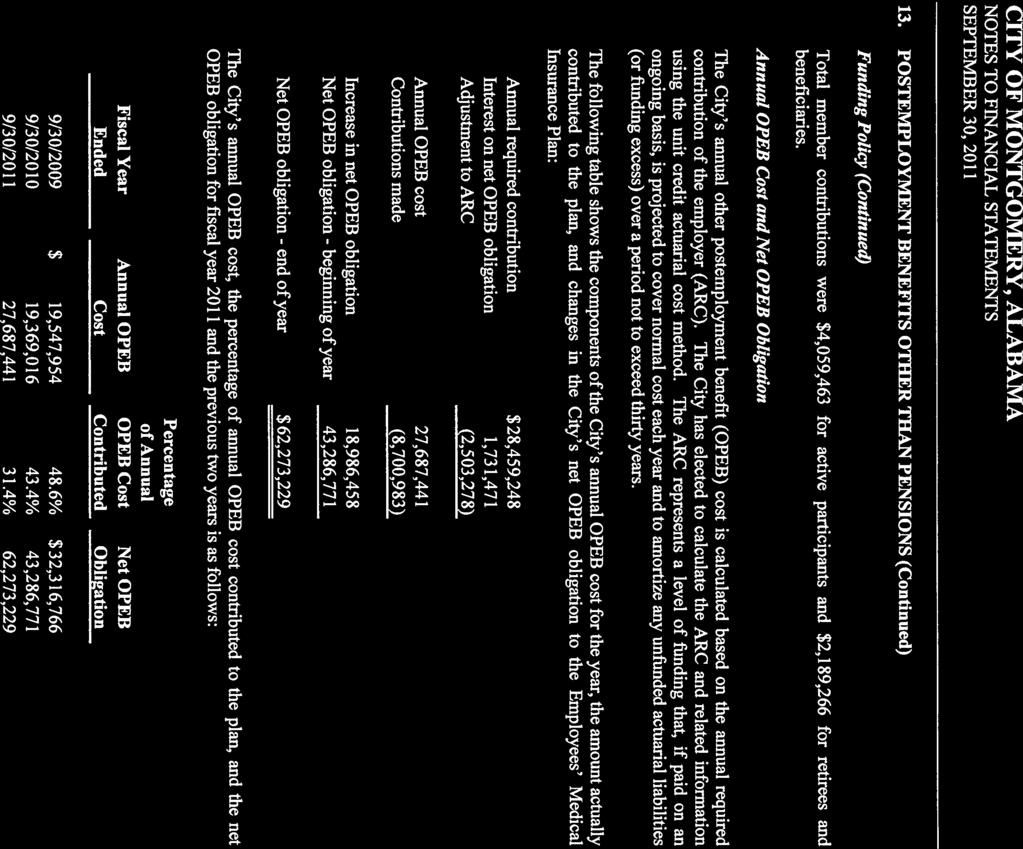

23 As of the January 1, 2012 actuarial valuation date, the entry age (level percentage of pay) cost method was used to determine contributions. The remaining amortization period as of January 1, 2012 was 24 years. The five-year smoothing method is used to determine the actuarial value of assets. A seven percent (7%) rate of return on investments is assumed. Certain other assumptions regarding future employment of covered employees, payroll increases, mortality and other factors have also been made in determining the actuarial valuations. Actuarial assessments are based upon a variety of assumptions, one or more of which may prove to be inaccurate or be changed in the future, and will change with the future experience of the Retirement System. Actuarial assessments are "forward-looking" information that reflect the judgment of those performing such assessments. Other Post-Employment Benefits. The City administers a multi-employer defined benefit healthcare plan (the "Employees' Medical Insurance Plan") for employees of the City and one other participating governmental unit. The plan provides lifetime healthcare insurance for eligible retirees and their spouses through the City's group health insurance plan, which covers both active and retired members. The Employees' Medical Insurance Plan does not issue a publicly available financial report. At September 30, 2012, the plan had approximately 1,465 active participants and 1,682 retired members and beneficiaries. The plan requires monthly contributions ranging from $46 to $206 from active participants. Retirees' or their beneficiaries are required to contribute certain amounts based on level of coverage and date of retirement. The City's annual other postemployment benefit (OPEB) cost is calculated based on the annual required contribution of the employer (ARC). The City has elected to calculate the ARC and related information using the unit credit actuarial cost method. The ARC represents a level of funding that, if paid on an ongoing basis, is projected to cover normal cost each year and to amortize any unfunded actuarial liabilities (or funding excess) over a period not to exceed thirty years. The following tables contain certain information regarding the City's OPEB cost, contributions to the Employees' Medical Insurance Plan and actuarial valuations. Fiscal Year Ended Annual OPEB Cost Percentage of Annual OPEB Cost Contributed Net OPEB Obligation 9/30/2009 $19,547, % $32,316,766 9/30/ ,369, % 43,286,771 9/30/ ,687, % 62,273,229 [Balance of page intentionally left blank] 15

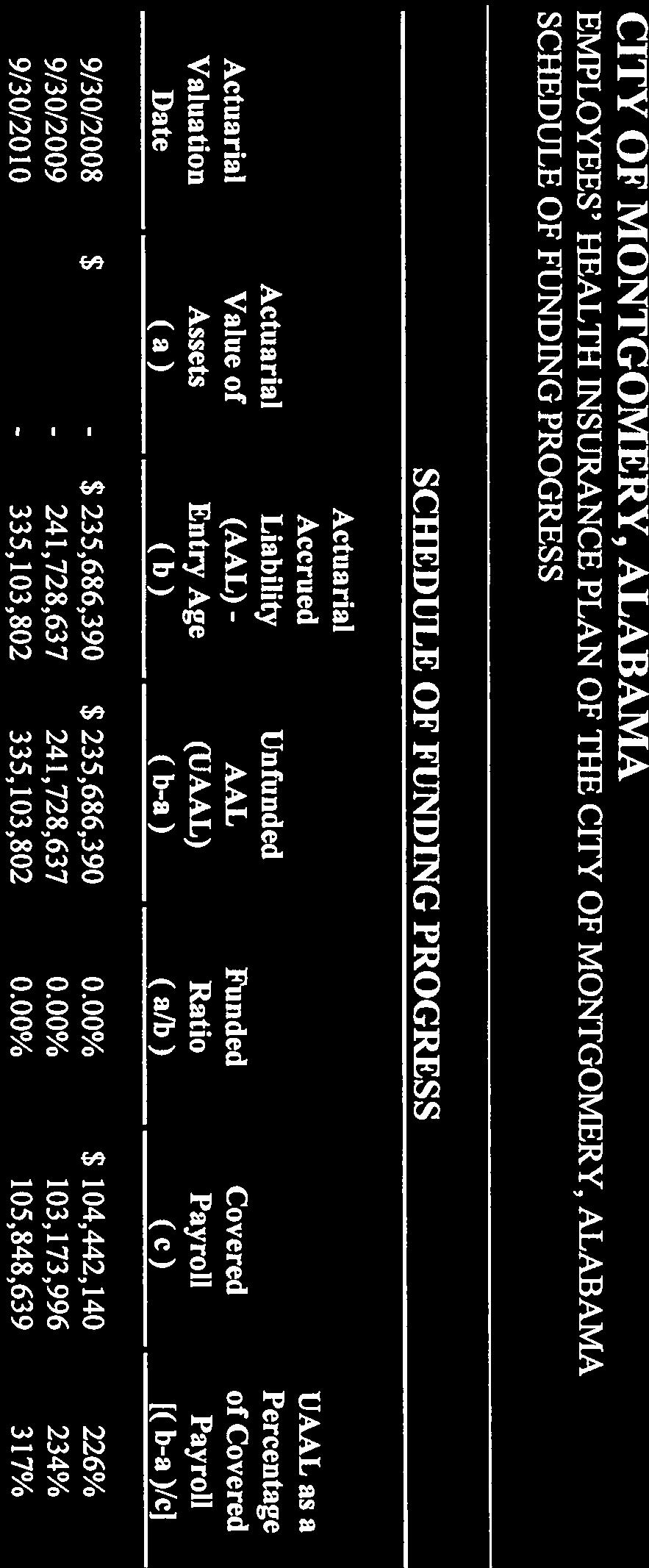

24 Actuarial Valuation Date Actuarial Value of Assets (a) SCHEDULE OF FUNDING PROGRESS Actuarial Accrued Liability (AAL) Entry Age (b) Unfunded AAL (UAAL) (b-a) Funded Ratio (a/b) Covered Payroll (c) UAAL as a Percentage of Covered Payroll [(b-a)/c)] 9/30/2008 $0 $235,686,390 $235,686, % $104,442, % 9/30/ ,728, ,728, % 103,173, % 9/30/ ,103, ,103, % 105,848, % See Note 13 to the City's audited financial statements included in the CAFR for the fiscal year ended September 30, 2011 attached hereto as APPENDIX A for additional information regarding the City's OPEB costs and certain assumptions made in connection with the actuarial assessments. Actuarial assessments are based upon a variety of assumptions, one or more of which may prove to be inaccurate or be changed in the future, and will change with the future experience of the Retirement System. Actuarial assessments are "forward-looking" information that reflect the judgment of those performing such assessments. General FINANCIAL SYSTEM The City maintains a financial reporting system providing reports of receipts and expenditures. Internal accounting controls are designed to provide reasonable, but not absolute, assurance regarding (1) the safeguarding of assets against loss from unauthorized use or disposition, and (2) the reliability of financial records for preparing financial statements and maintaining accountability for assets. Activities of the City are monitored internally on a monthly basis and are audited annually, as required by law, by independent certified public accountants. Budgetary System By applicable law, the City follows the following procedures in establishing a budget: 1. Not later than August 20th of each year, the Mayor submits to the City Council a proposed balanced operating budget for the City's general fund and a capital budget for the fiscal year commencing the following October 1. The operating budget for the general fund includes proposed revenues and expenditures and the means of financing them for the upcoming year. The level of control for the detailed budgets is at the government function category level. 2. Public hearings are conducted to obtain taxpayer comments. The City Council may add to or delete from the budget proposed so long as the budget remains in balance. 3. The budget is legally enacted through passage of a resolution receiving the approving majority vote of five members of the City Council. 16

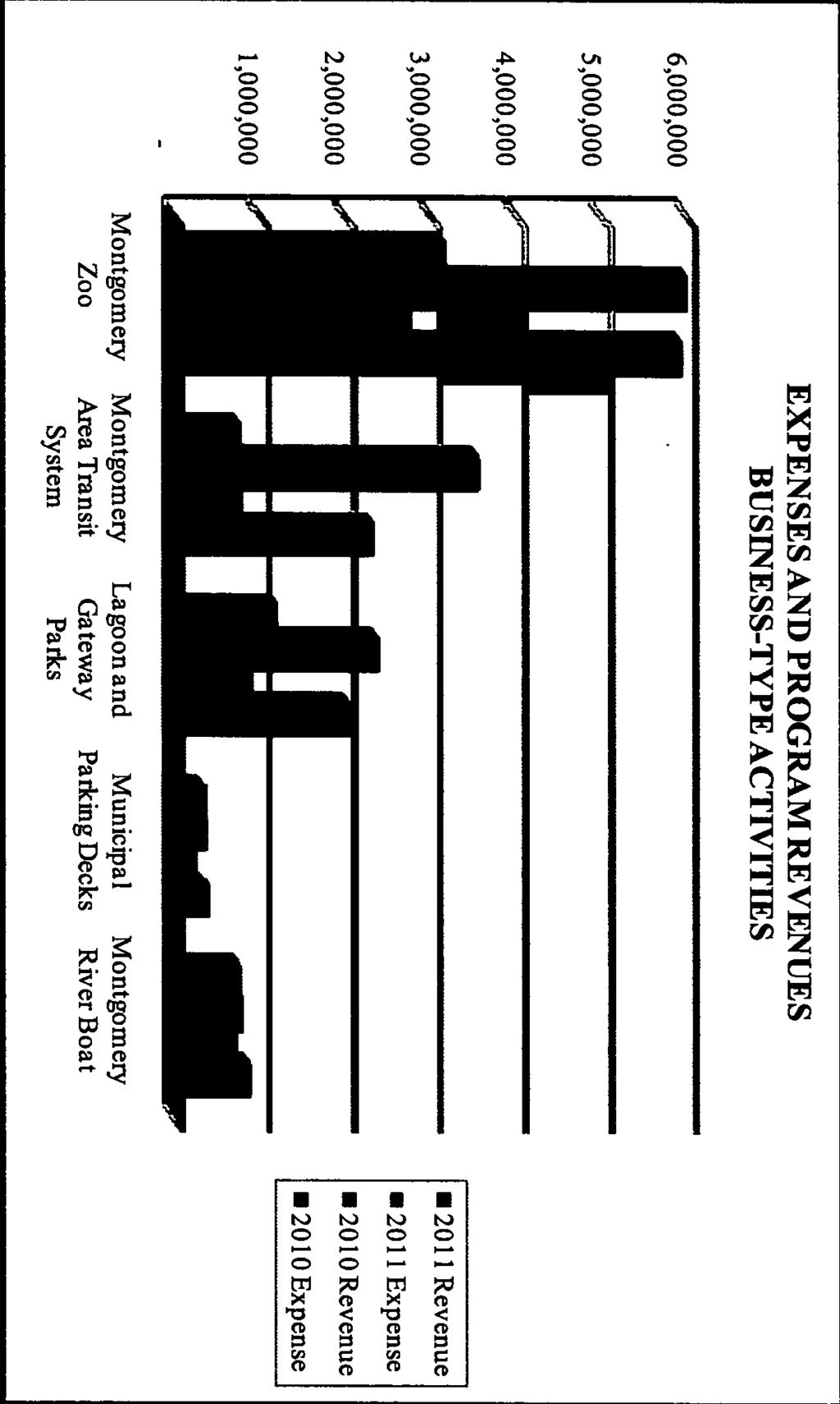

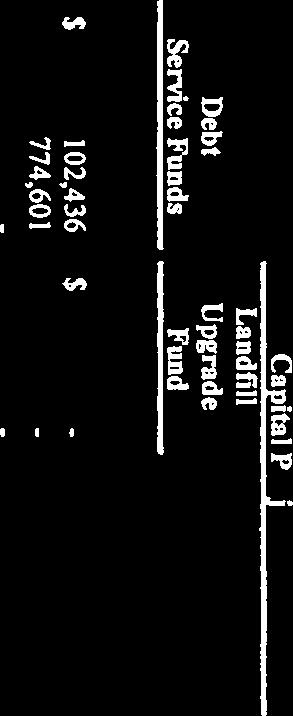

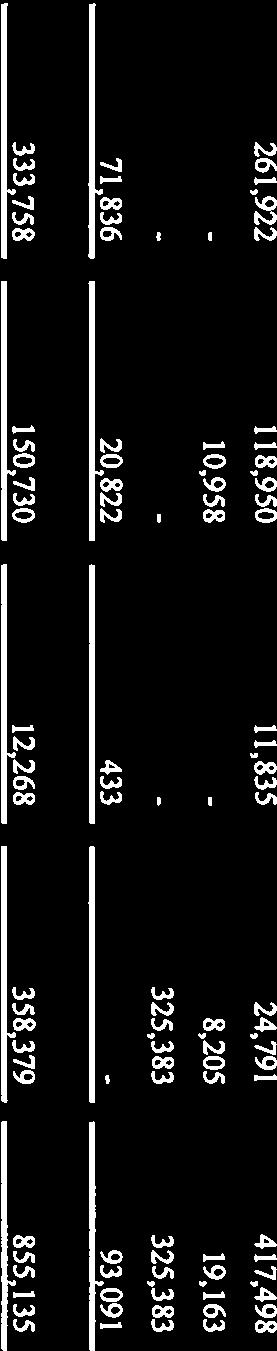

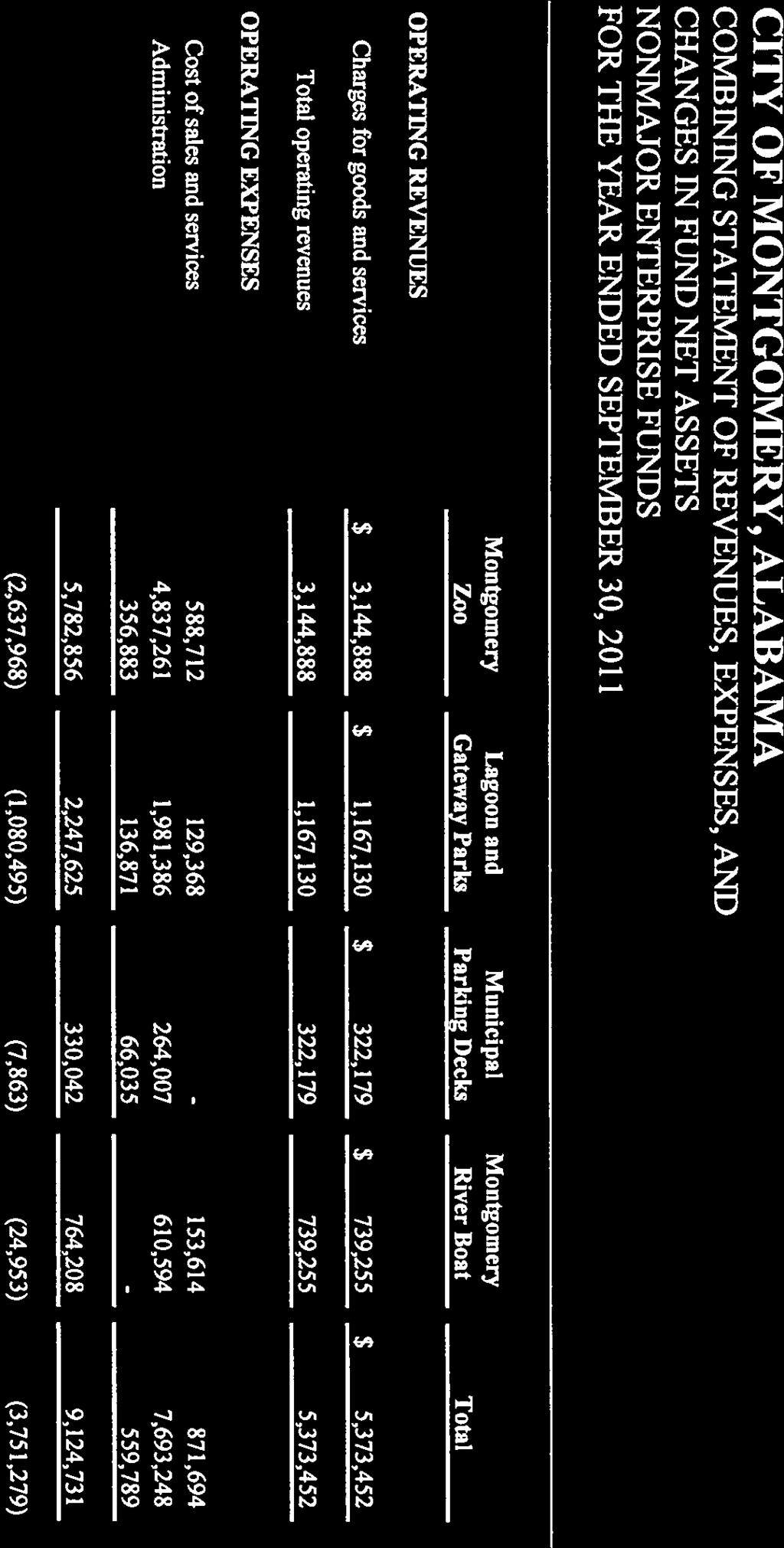

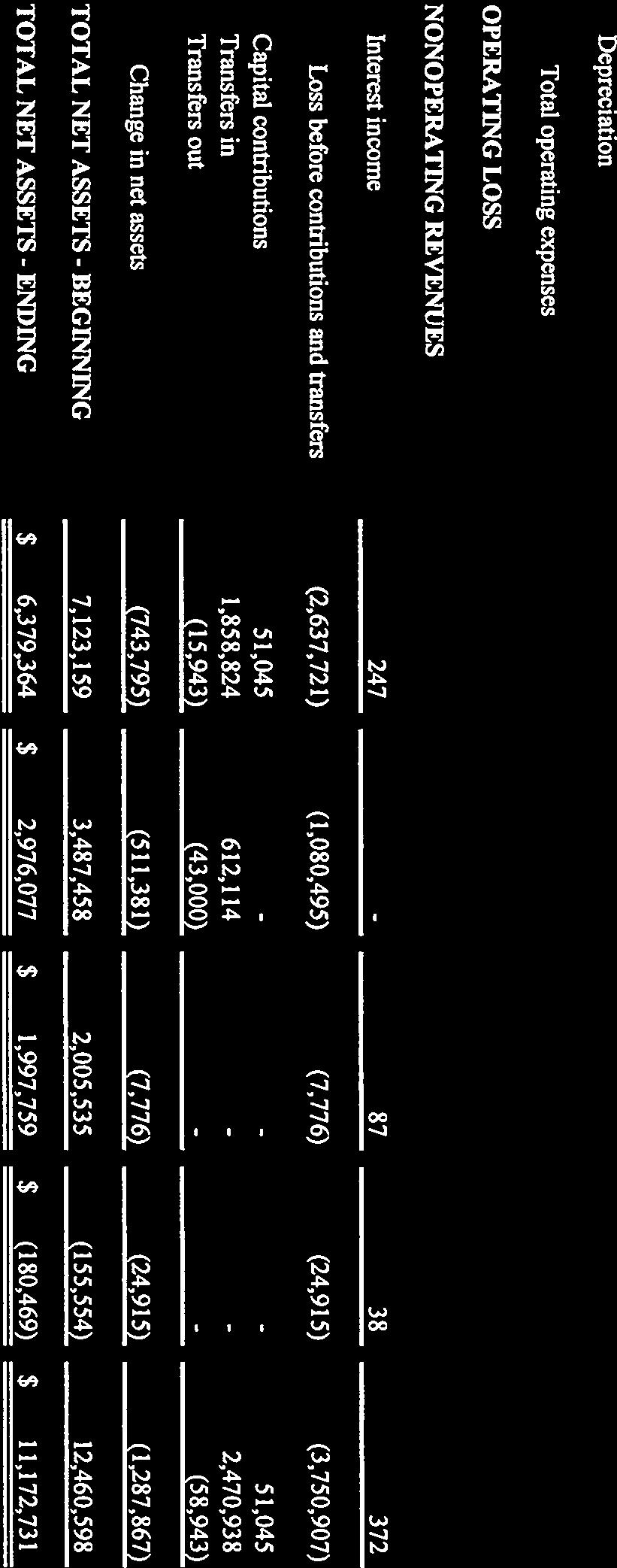

25 4. The Mayor is authorized to transfer budgeted amounts within the same departments within the general fund; however, any revisions or transfers of appropriations in the general fund from one department, office or agency to another department, office or agency must be approved by the City Council. 5. Budgets are adopted on a modified accrual basis which differs from generally accepted accounting principles (GAAP) insofar as encumbrances are included with expenditures. The City's operating budget for its fiscal year ending September 30, 2013, is summarized under "RESULTS OF OPERATIONS - Summary of the Operating Budget for Fiscal Year Ending September 30, 2013." Accounting System The accounting system of the City is organized on the basis of funds (and account groups under such funds), with each considered as a separate accounting entity. The operations of each fund are accounted for with a separate set of self-balancing accounts that comprise its assets, liabilities, fund equity, revenues and expenditures, or expenses, as appropriate. Government resources are allocated to and accounted for in individual funds based upon the purposes for which they are to be spent and the means by which spending activities are controlled. Each of these categories is divided into separate fund types as follows. Governmental Funds General Fund. The General Fund is the primary operating fund of the City. It is used to account for all financial resources except those required to be accounted for in another fund. As discussed above, the City adopts an annual appropriated operating budget for its General Fund. Debt Service Fund. This fund is used to account for the resources accumulated and payments made for principal and interest on long-term general obligation debt. Although not required by applicable law, the City Council for the City also formally approves a Debt Service budget for the fiscal year. Capital Projects Fund. The Capital Projects Fund accounts for the acquisition and construction of major capital facilities other than those financed by proprietary funds and trust funds. An example of the specific projects accounted for are school construction, recreational facilities and miscellaneous projects. As discussed above, the Capital Projects Fund is annually budgeted pursuant to a capital budget submitted by the Mayor and approved by the City Council. Proprietary Funds. The City also maintains five (5) significant proprietary funds: (i) the Montgomery Zoo Fund which accounts for the operations of the City-owned and operated Zoo, (ii) the Montgomery Area Transit System Fund which accounts for the operations of the public transportation system within the City, (iii) the Lagoon and Gateway Parks Fund which accounts for operations of the City's recreational complexes, (iv) the Montgomery River Boat Fund which accounts for operations of the City riverboat attraction and (v) the Municipal Parking Decks Fund which accounts for the operations of the City-owned parking decks. Proprietary funds distinguish operating revenues and expenses from nonoperating items. Operating revenues and expenses generally result from providing services and producing goods in connection with a Proprietary Funds' principal on-going operations. The principal operating revenues of the proprietary funds are charges to customers for sales and services. Operating expenses for the proprietary funds are the costs of sales and services, administrative expenses, and depreciation on capital assets. 17

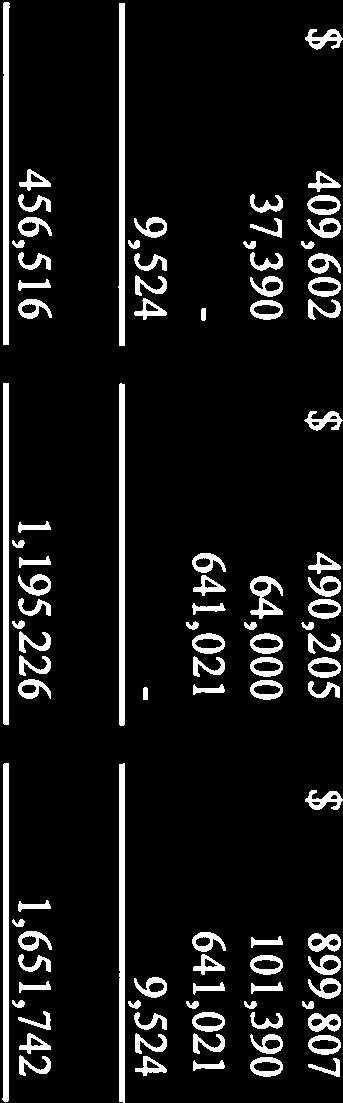

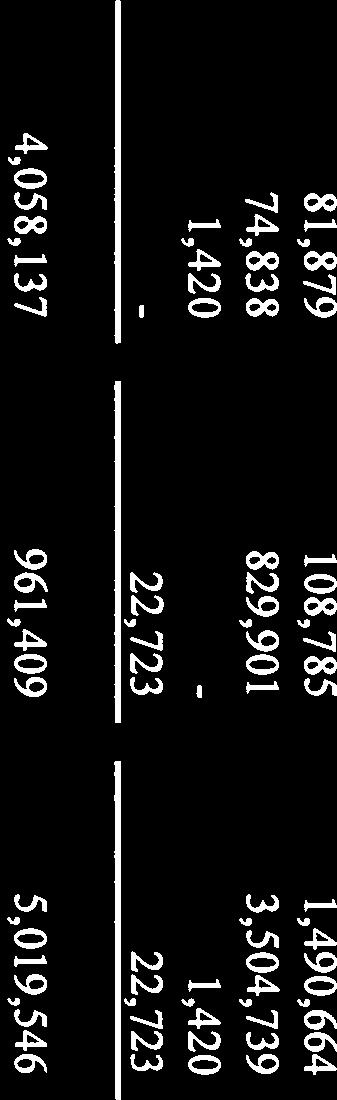

26 Internal Service Funds. The Internal Service Funds account for the operations of the selfinsured medical insurance plan (i.e., Employees Medical Insurance Fund), the workers' compensation plan and the self-insured liability insurance plan (i.e., Liability Insurance Fund) provided to other departments of the City on a cost reimbursement basis. The Liability Insurance Fund accounts for the operations of the self-insured liability insurance fund of the City including general liability, public officials' liability and law enforcement officers' liability. Pension Trust Fund. The Pension Trust Fund accounts for the activities of the Employees' Retirement System of the City of Montgomery, Alabama, which accumulates resources for pension benefits to qualified City employees and the employees of the other participating employers. See "THE CITY - Personnel and Retirement System" herein. Special Revenue Funds. Special revenue funds are used to account for the proceeds of specific revenue sources (other than special assessments, expendable trusts, or major capital projects) that are legally restricted to expenditures for specified purposes. The City has established the following Special Revenue Funds: State Gasoline Tax Fund. The State Gasoline Tax Fund accounts for the proceeds received by the City from certain state imposed gasoline taxes. The use of this money is restricted to expenditures related to construction, improvement and maintenance of highways, bridges and streets. Alabama Trust Fund. The Alabama Trust Fund accounts for funds received by the City from the Municipal Government Capital Improvement Fund funded by the State of Alabama's Alabama Trust Fund, which funds are required to be used solely for capital improvements and the renovation of capital improvements determined by the municipal governing body. Riverfront Stadium Fund. The Riverfront Stadium Fund accounts for proceeds received from lodging tax receipts. Two and one-half (2½ percent of total lodging tax collections are earmarked for the fund). Collections from the Montgomery Pro Baseball Club for leasing and concessions sales are also accounted for in this fund. All proceeds are used for capital improvements, repairs, and maintenance on the stadium and debt service payments. Municipal Court Corrections Fund. The Municipal Court Corrections Fund accounts for funds restricted for the municipal court and jail. These funds may be used for capital improvements or operations. Miscellaneous Special Revenue Fund. The Miscellaneous Special Revenue Fund accounts for funding arising from miscellaneous federal and state government sources. Montgomery Area Transit System Grant Fund. The Montgomery Area Transit System Grant Fund accounts for grant funding received primarily from the Federal Transit Administration to be used for the Montgomery Area Transit System. Housing and Urban Development Grant Fund. The Housing and Urban Development Grant Fund accounts for grant funding used for community development block grant programs and housing development action grant programs. 18

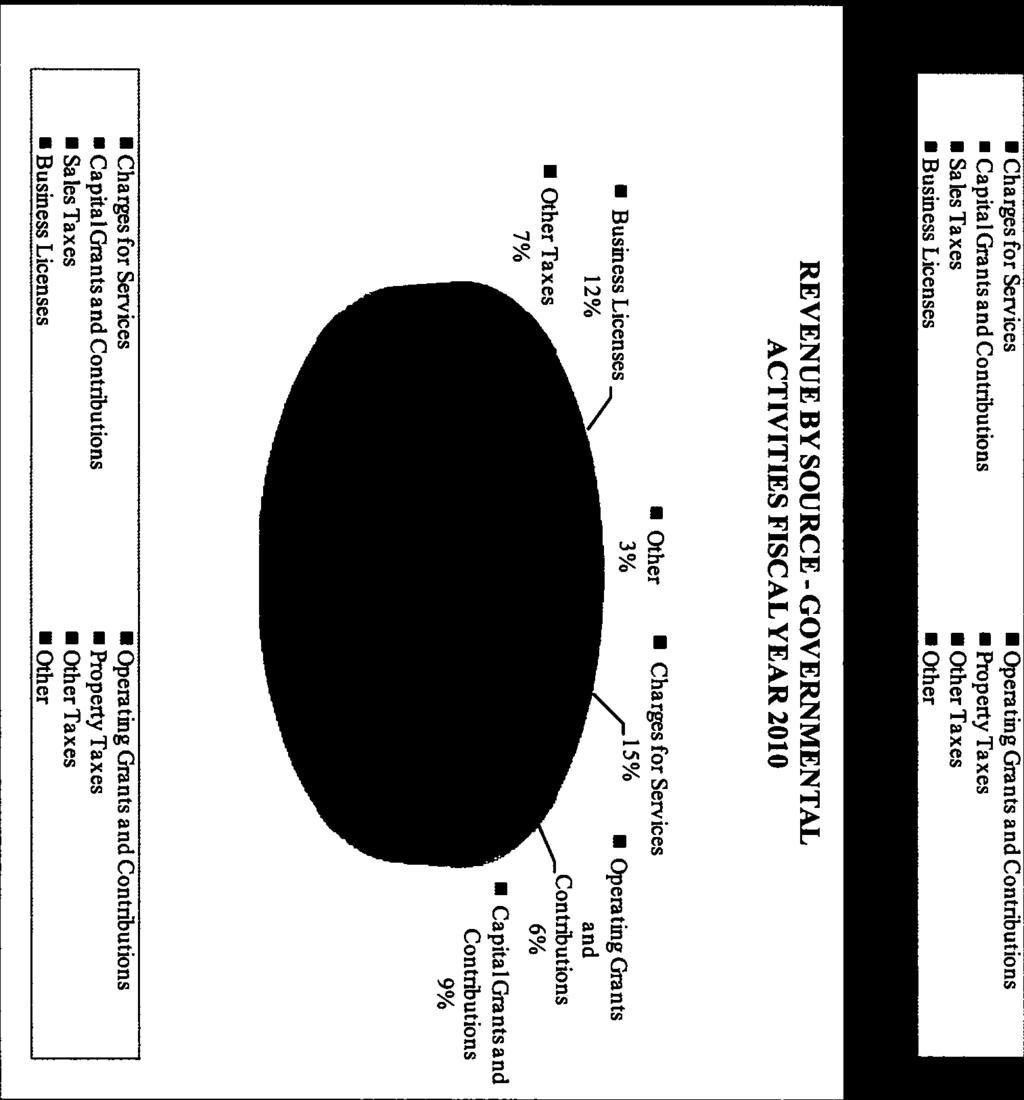

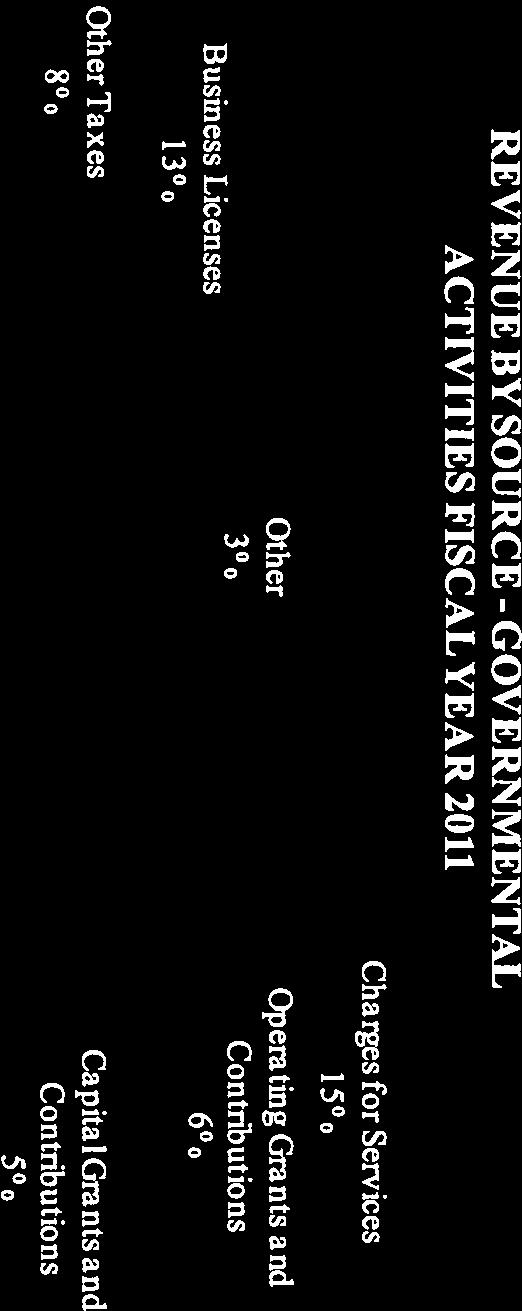

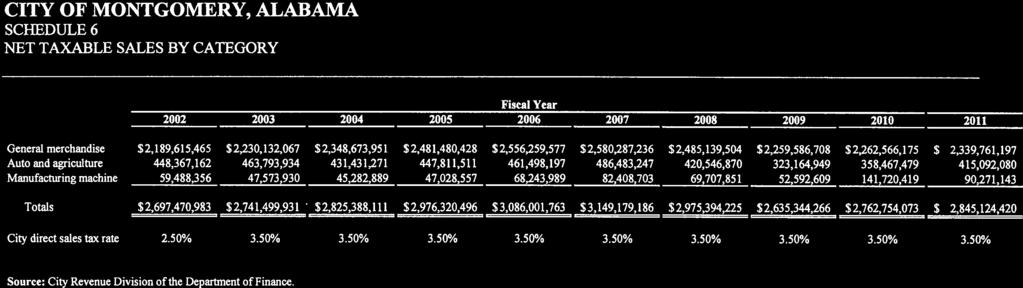

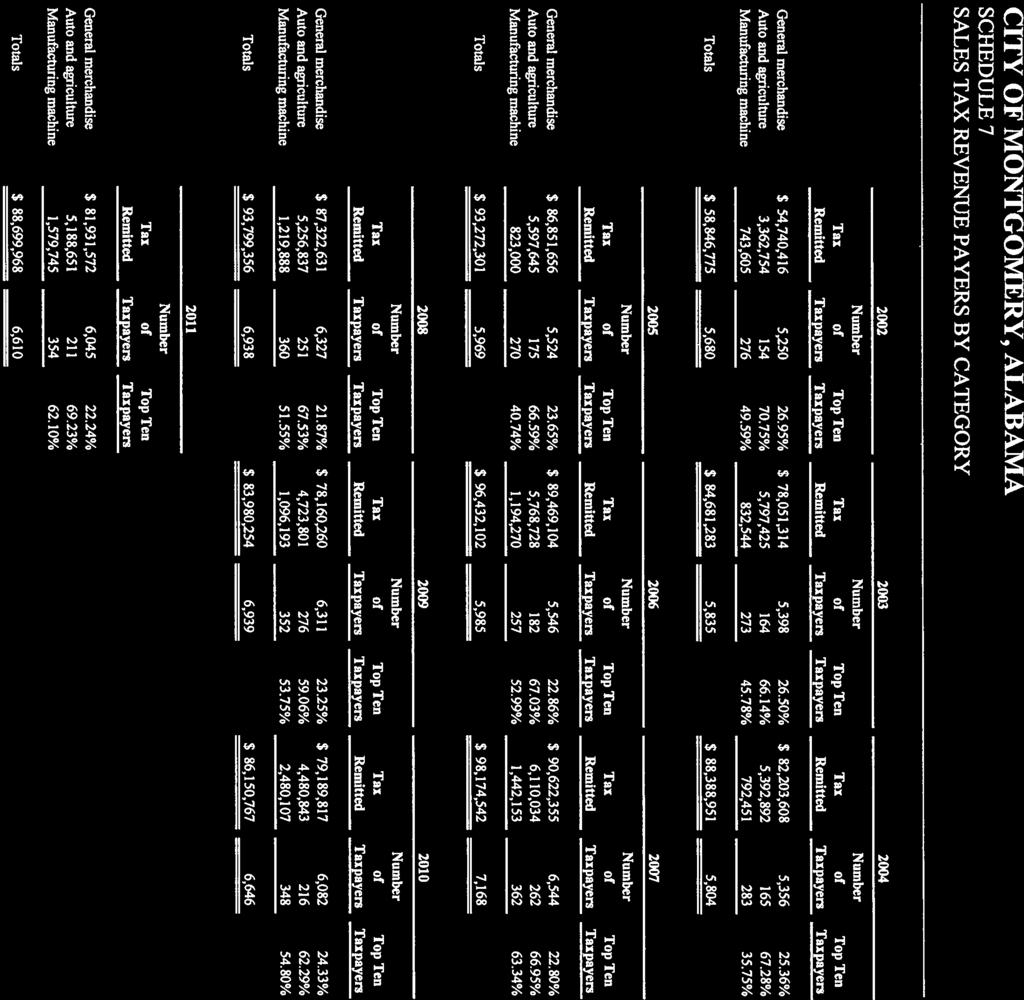

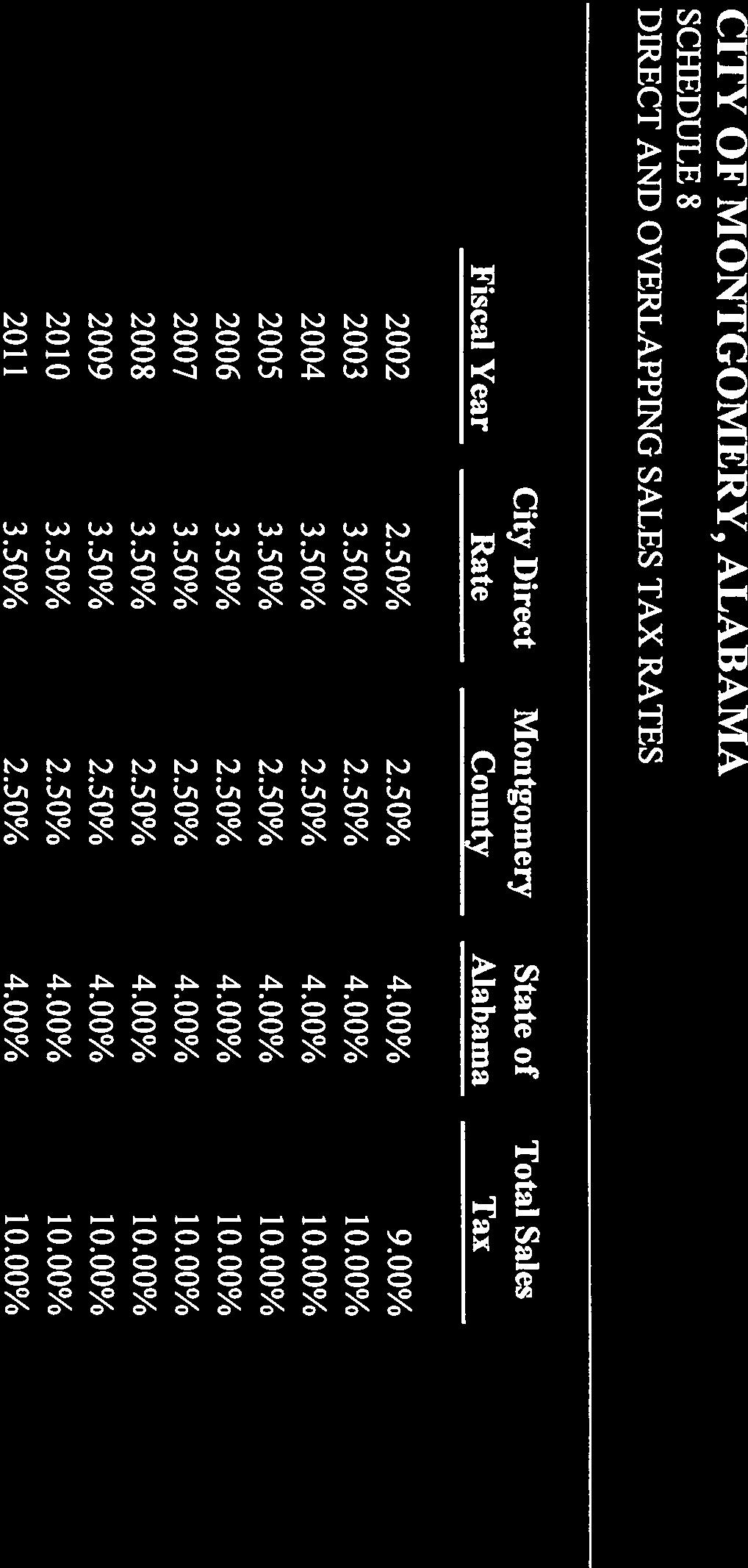

27 Description of Major Sources of General Fund Revenues The City's major sources of revenue for its General Fund are as follows: Sales and Use Tax. The City levies and collects sales and use taxes generally parallel to the State sales and use tax, except for the respective rates, consisting of (1) privilege, license taxes on every person, firm or corporation engaged or continuing within the corporate limits of the City or its police jurisdiction in the business of selling tangible personal property at retail, (2) privilege, license taxes on every person, firm or corporation engaged or continuing within the corporate limits of the City or its police jurisdiction in the business of conducting or operating places of amusement or entertainment and (3) excise taxes on persons, firms or corporations storing, using or otherwise consuming tangible personal property within the corporate limits of the City or its police jurisdiction. See "SALES AND USE TAXATION" herein. The proceeds of the City's sales and use taxes are not earmarked or specifically pledged to any outstanding indebtedness of the City and are used for general governmental purposes. Under applicable judicial precedents, sales and use taxes may not be levied at rates that are confiscatory or unreasonable. Further, the rates of any such taxes in the police jurisdiction of the City may not be fixed at rates in excess of one-half the rates levied for like business, sales or uses conducted within the corporate limits of the City. Lodgings Tax. The City levies a lodgings tax at the rate of eight and one-half percent (8.5%) on the gross revenues derived from the renting of rooms or apartments within the City by persons, firms, associations or corporations engaged in the business of operating hotels, motels, tourists courts, tourists cabins, lodging houses and rooming houses renting to transients. The lodgings tax was increased from six percent (6%) to eight and one-half percent (8.5%) effective October 1, The 2.5% increase was pledged to secure the City's Taxable Special Lodging Tax Revenue Warrants (Riverfront Stadium Project), Series 2003A, which will be refunded and no longer treated as outstanding upon the issuance of the Warrants. The remaining portion of the Lodgings Tax (6%) is not earmarked or specifically pledged to any outstanding indebtedness of the City and such remaining portion (as well as the 2.5% portion following refunding of the Series 2003A Warrants) is used for general governmental purposes. Business Licenses and Permits. The City levies license and permit fees on the privilege of engaging in certain businesses and professions within the corporate limits of the City. License and permit fees are computed either as a percentage of gross receipts or as a flat stated amount and in some cases is a combination of both a percentage of gross receipts and a flat stated amount. In addition, the City also charges an issuance fee. The receipts from business licenses and permits are not earmarked or specifically pledged to any outstanding indebtedness and are used for general governmental purposes. Under applicable judicial precedents, business license taxes may not be levied at rates that are confiscatory or unreasonable. Further, the rates of any such taxes in the police jurisdiction of the City may not be fixed at rates in excess of one-half the amount charged for like businesses, trades or professions conducted within the corporate limits of the City or at rates that will yield an amount in excess of the cost of furnishing police and fire protection and other essential services in such police jurisdiction. City Gasoline Tax. The City levies a gasoline tax on the business of selling gasoline to customers, irrespective of the use for which it is sold. These taxes are also levied on motor fuels other than gasoline for use in powering motor vehicles and aircraft. The receipts from this tax are not earmarked or specifically pledged to any outstanding indebtedness and are used for general governmental purposes. 19

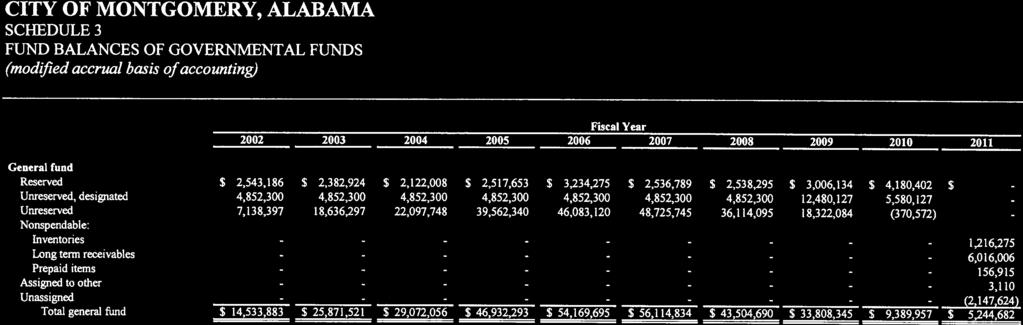

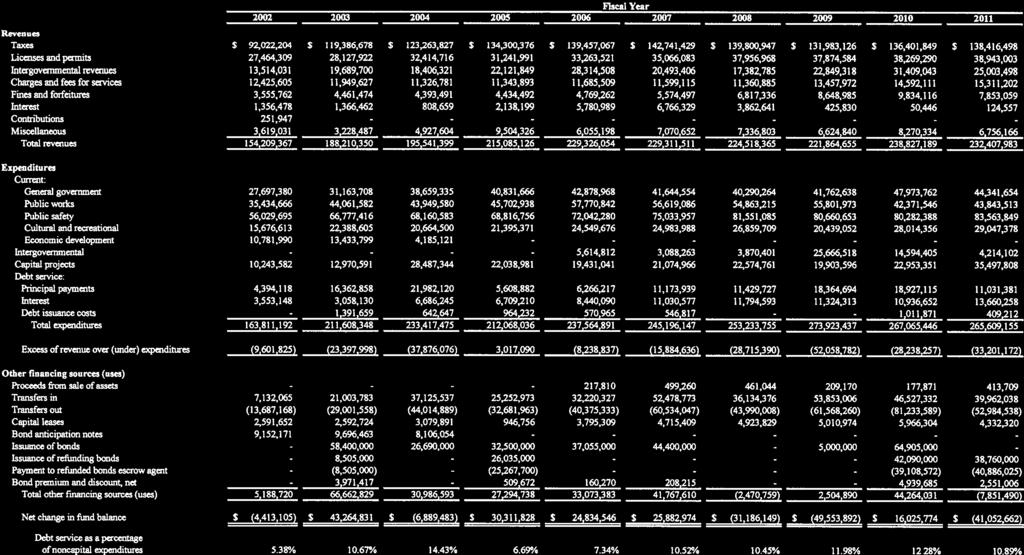

28 Ad Valorem Taxes. Property or ad valorem taxes are levied under various provisions of the constitution and statutes of the State of Alabama and may be used only for the purpose or purposes for which they are levied. The City levies a 12.5-mill tax for general municipal purposes, the proceeds of which are deposited in the City's General Fund. Under present law, the rates at which local ad valorem taxes are levied may be increased only after approval by the legislature and a majority vote of the qualified electors of the affected jurisdiction. See "AD VALOREM TAXATION". Except for the tax increment arising within the City's Downtown Tax Increment Financing District which is pledged for the City's Series 2006A Warrants and Series 2006B Warrants, portions of each of which are expected to remain outstanding following the issuance of the Warrants, the City's ad valorem tax receipts are not earmarked or specifically pledged to any indebtedness. See "SOURCE OF PAYMENT AND SECURITY" herein. Rental Tax. The City levies a rental tax on the gross revenues of persons engaged in the business of renting property at a rate of four percent (4%) on rentals of personal property, linens and garments and one and one-half percent (1.5%) on rentals of vehicles, truck trailers and house trailers. The receipts from this tax are not earmarked or specifically pledged to any outstanding indebtedness and are used for general governmental purposes. Charges and Fees for Services. The City also imposes various charges for services such as fees for admittance to the Montgomery Zoo and charges for utilizing the City's public transportation system and recreational complexes. Inter-Governmental Revenues. The City also receives from the State of Alabama and the federal government operating grants and contributions and capital grants and contributions. The grants and contributions refer to revenues restricted for specific programs whose use may be restricted from other operational or capital items. Although such grant money and contributions have historically been made available to the City, no assurance is given nor is any representation made that such grants or contributions will continue to be available. It should be noted that the continued availability of grant contribution monies from both State and Federal governments is dependent upon the ability and willingness of said governmental entities to continue to provide such moneys and contributions for needed programs, and is not assured to continue. See ''RESULTS OF OPERATIONS" for information regarding receipts from the City's major sources of revenue. See also the City's Comprehensive Annual Financial Report for the fiscal year ending September 30, 2011 attached hereto as APPENDIX A. RESULTS OF OPERATIONS This section of the Official Statement presents certain historical financial information concerning the City. Comparative Statement of General Fund Revenues and Expenditures The table below sets forth revenues, expenditures and changes in fund balance for the City's General Fund for the fiscal years indicated. The information for each of the fiscal years shown was extracted from the audited financial statements of the City for such fiscal years. The audited financial statements for the fiscal year ended September 30, 2011, are included in the City's Comprehensive Annual Financial Report attached hereto as APPENDIX A, and audited financial statements for prior fiscal years may be obtained from the City upon request. 20

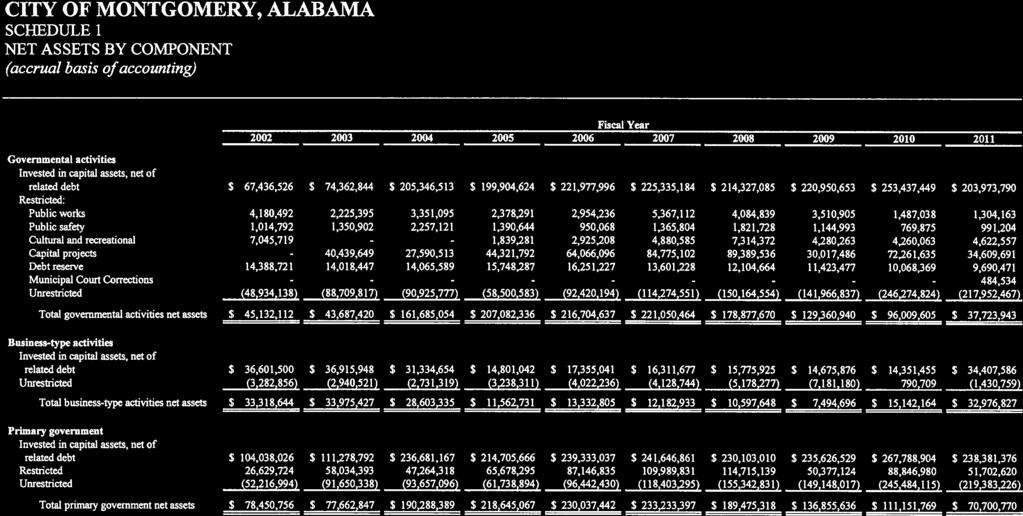

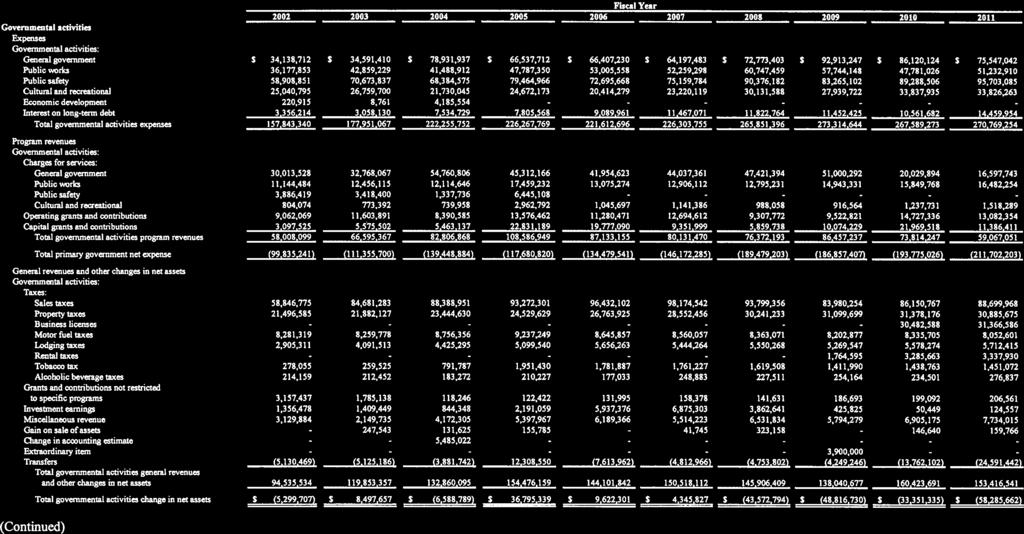

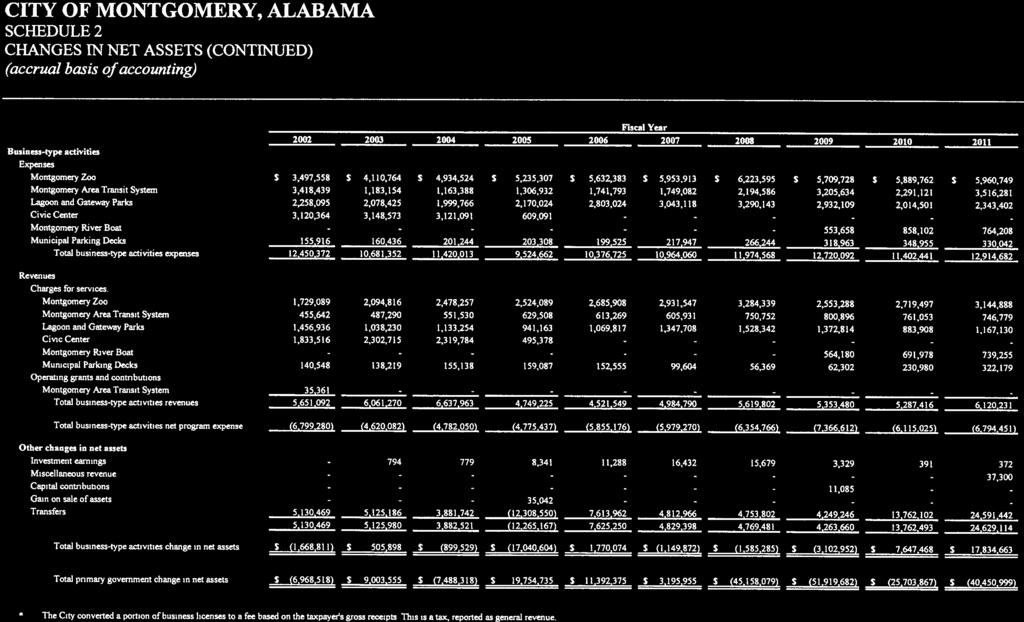

29 In June of 1999, the Governmental Accounting Standards Board ("GASB") issued Statement Number 34, Basic Financial Statements and Management's Discussion and Analysis for State and Local Governments ("GASB 34"), which substantially revised the financial reporting requirements for state and local governments in the United States, including the City. The City's audited financial statements for the fiscal years ended on or after September 30, 2002 were prepared in accordance with GASB 34. For more information concerning GASB 34, contact GASB, at 401 Merritt 7, Post Office Box 5116, Norwalk, Connecticut , Telephone (203) The City's operating budget for fiscal year ending September 30, 2013 is summarized in the subsection below entitled "Summary of the Operating Budget for Fiscal Year Ending September 30, 2013". [Balance of page intentionally left blank] 21

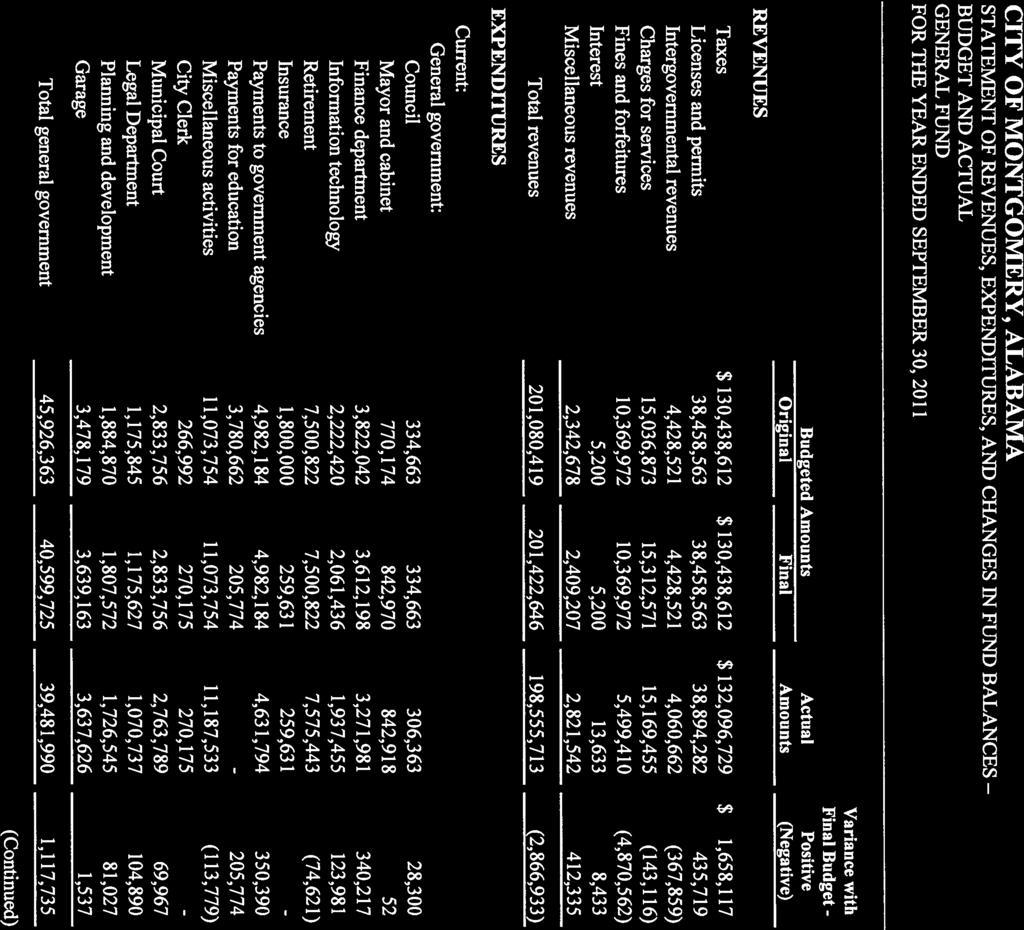

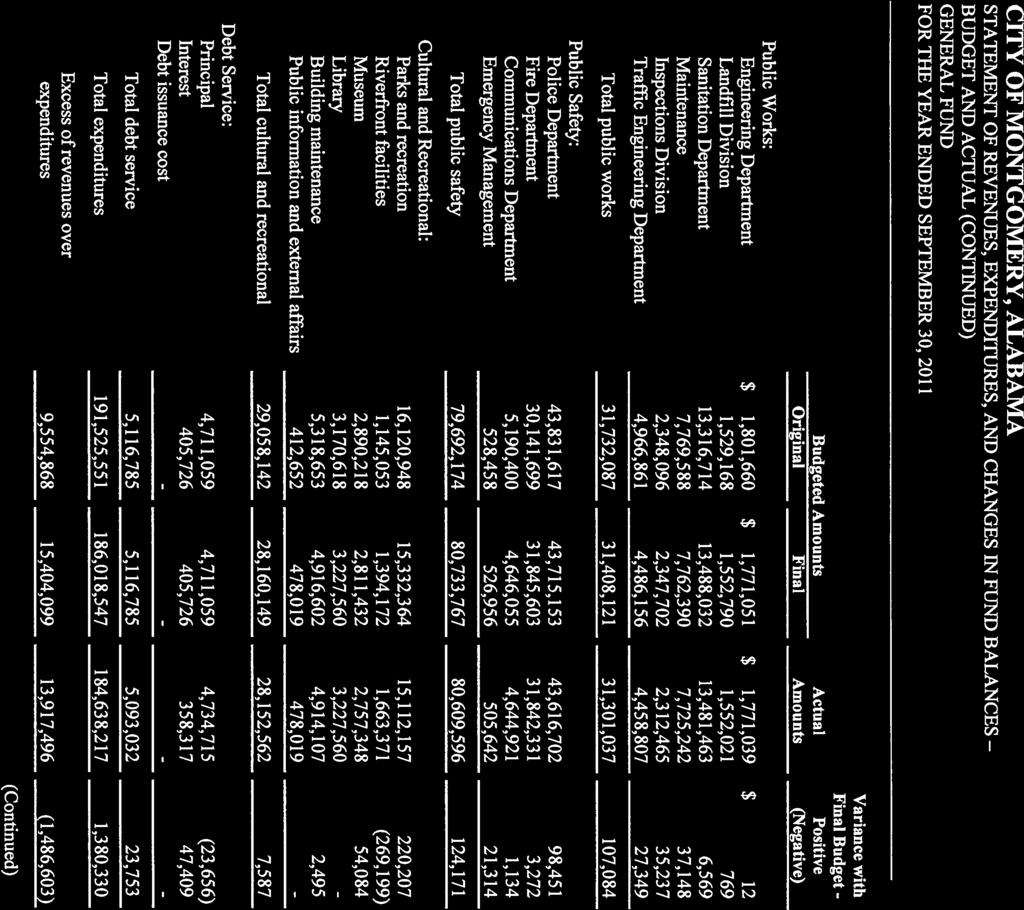

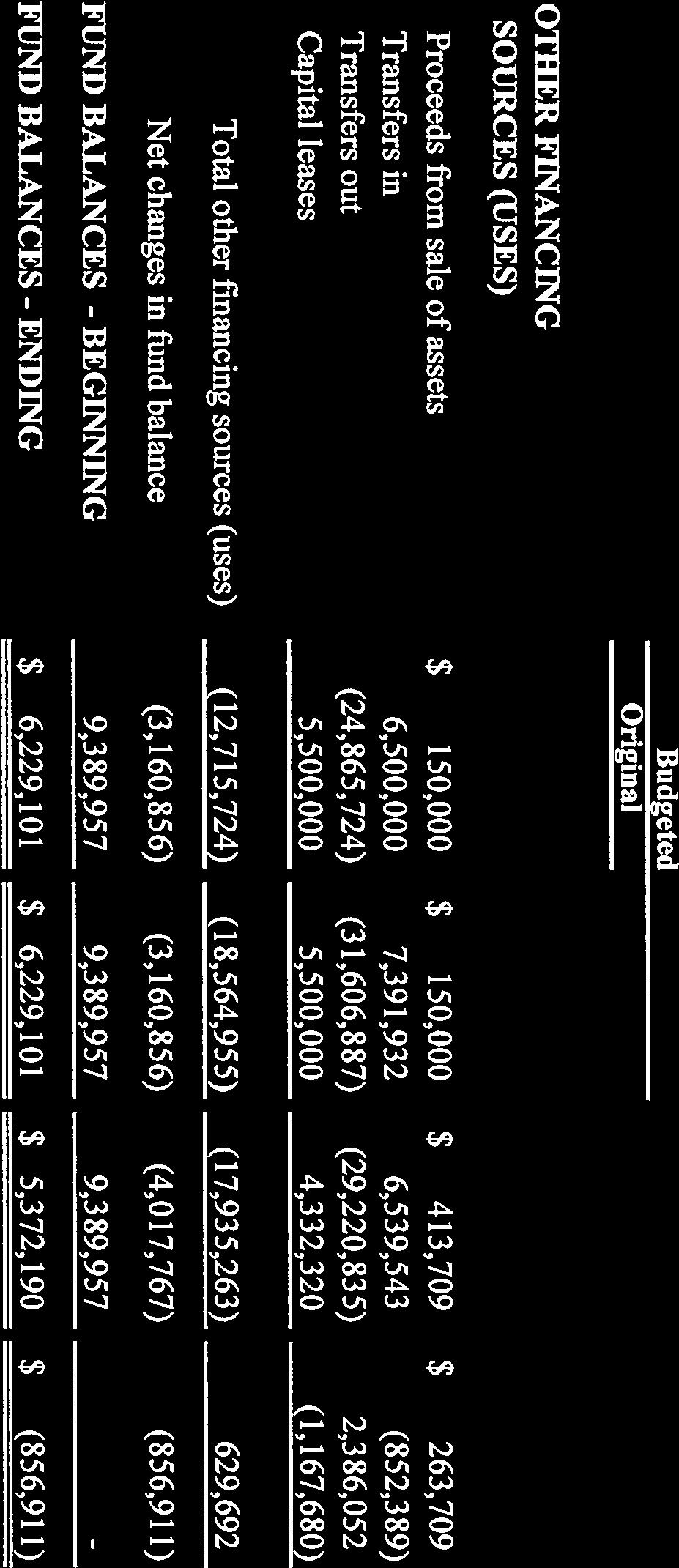

30 Comparative Statement of General Fund Revenues, Expenditures and Changes in Fund Balance Fiscal Year Ended September Revenues Taxes $137,828,097 $135,099,339 $127,489,528 $131,837,921 $132,096,729 Licenses and permits 34,973,866 37,878,497 37,845,467 38,203,350 38,894,282 Intergovernmental Revenues 4,640,144 3,783,812 4,628,057 3,782,033 4,060,662 Charges for Services 11,598,277 11,230,500 13,319,163 14,444,392 15,169,455 Fines and Forfeitures 5,574,497 6,817,336 8,648,985 9,834,116 5,499,410 Interest 2,593,274 1,144,300 49,892 16,151 13,633 Miscellaneous revenues 3,467,881 2,767,965 2,488,777 3,490,075 2,821,542 Total revenues 200,676, ,721, ,469, ,608, ,555,713 Expenditures Current: General Government 34,800,385 36,232,930 36,035,732 39,753,028 39,524,223 Public Works 40,189,677 42,497,589 38,659,217 30,688,028 31,322,781 Public Safety 73,792,084 79,562,346 78,897,150 77,948,144 80,669,397 Cultural and Recreational 20,612,254 21,419,153 19,835,274 27,210,590 28,156,292 Debt Service: Principal 2,863,943 3,394,729 4,864,694 4,871,560 4,734,715 Interest 677, , , , ,317 Total expenditures 172,935, ,744, ,888, ,820, ,765,725 Excess of revenues over (under) expenditures 27,740,520 14,977,167 15,581,783 20,787,516 13,789,988 Other financing sources (uses) Proceeds From Sale of Capital Assets 388, , , , ,709 Transfers In 0 296,067 4,035,000 8,660,607 6,539,543 Transfers Out (30,899,390) (33,267,251) (33,085,840) (59,999,537) (29,220,835) Capital Leases 4,715,409 4,923,829 3,657,542 5,966,304 4,332,320 Total Other Financing Sources (Uses) (25,795,381) (27,587,311) (25,278,128) (45,194,755) (17,935,263) Net Change in Fund Balances 1,945,139 (12,610,144) (9,696,345) (24,407,239) (4,145,275) Fund Balance - Beginning 54,169,695 56,114,834 43,504,690 33,808,345 9,389,957 1 Fund Balance - Ending $ 56,114,834 $ 43,504,690 $ 33,808,345 $ 9,401,106 $ 5,244,682 Source: City's CAFRs for the fiscal years ended September 30, 2007, 2008, 2009, 2010 and Restated. 22

31 The following table sets forth unaudited revenues, expenditures and changes in fund balance for the City's General Fund for the fiscal year ended September 30, Revenues Taxes $135,153,695 Licenses and permits 39,456,369 Intergovernmental Revenues 4,407,714 Charges for Services 14,845,041 Fines and Forfeitures 9,105,630 Interest 3,166 Miscellaneous revenues 2,228,067 Total revenues 205,199,682 Expenditures General Government 40,844,056 Public Works 29,795,194 Public Safety 81,393,815 Cultural and Recreational 29,279,466 Debt Service 5,103,050 Total expenditures 186,415,581 Excess of revenues over (under) expenditures 18,784,101 Other financing sources (uses) Proceeds From Sale of Capital Assets 407,094 Transfers In 5,134,154 Transfers Out (29,756,693) Capital Leases 6,242,540 Total Other Financing Sources (Uses) (17,972,905) Net Change in Fund Balance 811,196 Fund Balance - Beginning 5,255,831 Fund Balance - Ending $ 6,067,027 [Balance of page intentionally left blank] 23

32 Summary of the Operating Budget for Fiscal Year ending September 30, 2013 The following table is a summary of the operating budget for the City's General Fund for the fiscal year ending September 30, 2013: Budgeted Revenues Taxes $137,625,464 Business License and Permits 41,754,000 Intergovernmental 5,297,065 Charges for Services 16,005,366 Fines and Forfeitures 10,522,538 Other 1,762,388 Total 212,966,821 Expenditures General Government 42,371,142 Public Safety 81,987,373 Public Works 33,054,502 Cultural and Recreational 29,608,259 Debt Service 4,907,207 Total 191,928,483 Excess (Deficiency) 21,038,338 Other Financing Sources (Uses) Proceeds from sale of assets 1,017,000 Transfers from other funds 3,500,000 Transfers to other funds (30,055,338) Capital leases 4,500,000 Total (21,038,338) Net Change in Fund Balance 0 [Balance of page intentionally left blank] 24

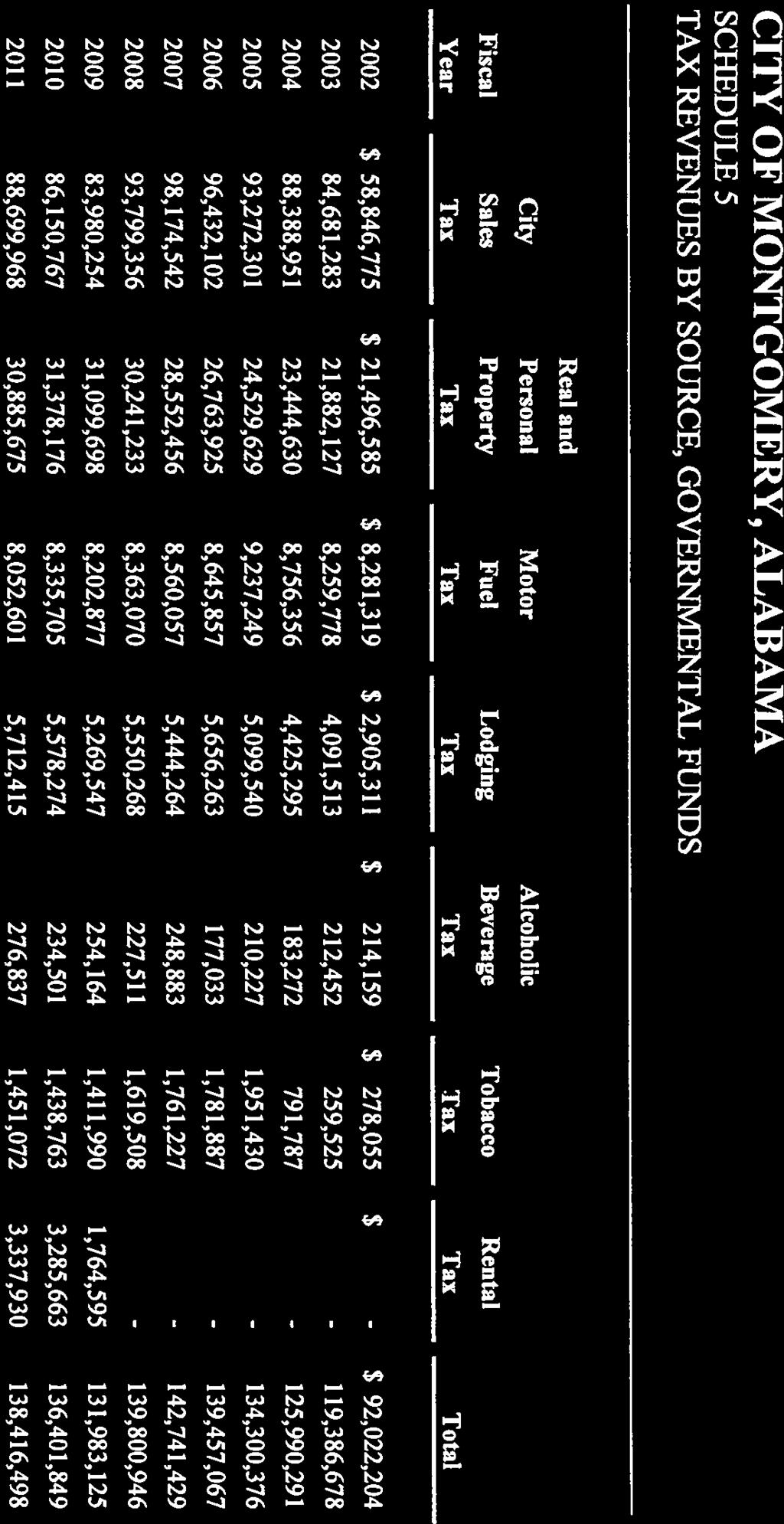

33 Tax Collections The City's collections from its major sources of tax revenue are shown in the table below on a cash basis for the fiscal years indicated: Fiscal year ended September Sales Tax (1) $98,305,775 $94,323,759 $84,412,059 $84,884,050 $89,004,278 $91,297,837 Ad Valorem Tax (2) 28,552,456 30,241,233 31,099,698 31,378,176 30,885,675 30,799,146 Lodgings Tax (3) 5,487,158 5,516,785 5,367,667 5,503,209 5,734,191 6,049,431 Alcoholic Beverage & Tobacco Tax 2,010,110 1,847,019 1,666,154 1,673,261 1,727,910 1,717,802 City Gasoline Tax (4) 5,453,401 5,276,386 5,172,022 5,175,114 5,040,673 4,855,356 Rental Tax (5) 0 0 1,764,595 3,285,666 3,337,930 3,354,828 Source: City Finance Department. (1) Sales tax receipts based on 3.5% general sales tax rate. (2) Includes ad valorem tax on motor vehicles. (3) The amounts shown reflect the total collections of the 8.5% lodgings tax. (4) Reflects collections of the City's gasoline tax, which amounts are deposited in the City's General Fund. Does not include the City's share of certain county and State gasoline taxes received by the City which are restricted as to use and maintained in a special revenue fund. (5) The City instituted a rental tax in 2009 of four percent (4%) for tangible personal property, linens and garments and one and one-half percent (1.5%) for vehicles, truck trailers and house trailers. The tobacco tax receipts are not general fund revenues and are earmarked for capital improvement projects and may not be used to pay debt service on the City's bonds, warrants and other indebtedness. [Balance of page intentionally left blank] 25

34 DEBT MANAGEMENT General The principal forms of indebtedness that the City is authorized to incur include general obligation bonds, general obligation warrants, general obligation bond anticipation notes, revenue anticipation notes, gasoline tax anticipation bonds, and various revenue anticipation bonds and warrants relating to enterprises. In addition, the City has the power to enter into certain leases which constitute a charge upon the general credit of the City and to guarantee obligations of certain public corporations affiliated with the City. In general, the issuance of general obligation bonds requires voter approval, The following types of obligations may be issued or incurred by the City without voter approval: (1) general obligation warrants; (2) general obligation refunding bonds; (3) certain revenue anticipation bonds, warrants and notes; (4) general and special obligation bonds financing street, sidewalk and sewer improvements supported, in whole or in part, by assessments; and (5) capitalized lease obligations that are funded on a "year-to-year basis". The City has never defaulted in the payment of debt service on its bonds, warrants or other funded indebtedness, nor has the City ever refunded any funded indebtedness for the purpose of preventing or avoiding such a default. [Balance of page intentionally left blank] 26

35 Outstanding Indebtedness Long-Term Indebtedness. As of December 1, 2012, the City will have the following long-term indebtedness outstanding (taking into account the issuance of the Warrants and the refunding of the Refunded Warrants): Outstanding Principal Description of Indebtedness Source of Payment Balance Taxable General Obligation Warrants, Series 2012-B General Obligation Warrants, Series 2012-A General Obligation Refunding Warrants, Series 2011 General Obligation Recovery Zone Economic Development Warrants, Series 2010-B General Obligation Warrants, Series 2010-A Taxable General Obligation Warrants, Series 2009B Taxable General Obligation Warrants, Series 2009 General Obligation Warrants, Series 2007B General Obligation School Warrants, Series 2007 General Obligation Warrants, Series 2006C full faith and credit $65,150,000 full faith and credit 9,835,000 full faith and credit 38,760,000 full faith and credit 60,065,000 full faith and credit 41,375,000 full faith and credit 3,001,111 full faith and credit 4,000,001 full faith and credit 365,000 full faith and credit 38,545,000 full faith and credit 7,020,000 General Obligation Tax Increment Warrants, Series 2006B Taxable General Obligation Tax Increment Warrants, Series 2006A full faith and credit and pledge of tax increment receipts full faith and credit and pledge of tax increment receipts 7,495,000 1,685,000 General Obligation Refunding Warrants, Series 2005B Taxable General Obligation Warrants, Series 2005A full faith and credit 710,000 full faith and credit 4,145,000 Capital Leases full faith and credit 12,518,037 (1) Total $294,669,148 Source: City Finance Department (1) Outstanding principal amount only. Excludes operating leases. 27