FOREIGN NATIONAL PAYMENT GUIDE

|

|

|

- Thomas Ray

- 5 years ago

- Views:

Transcription

1 FOREIGN NATIONAL FOREIGN NATIONAL PAYMENT GUIDE PAYMENT GUIDE May-2018 UNIVERSITY OF PENNSYLVANIA

2 Contents Chapter 1: Foreign National Payment Guide Visa Matrix... 3 Chapter 2: Nonresident New Hire process Non-Penn Sponsored Grid Penn Sponsored Grid Quick Reference Flowchart Required Documents... 8 Foreign National Information Form (FNIF)... 8 Most recent I US Visa Passport Social Security receipt of application Immigration Documentation Form W Treaties ERN Codes Chapter 3: Non-compensatory Payments (prizes/awards, honorariums, scholarships/fellowships, independent contractors, etc.) Form W W-8BEN W-8BEN-E Income Source Foreign Source Certificate of Foreign Source Income (CFSI) Taxation US Source Honoraria Eligibility Certification Form Taxation Chapter 4: Guest Travel Reimbursements Documentation Nontaxable vs. Taxable NonTaxable P age

3 Taxable Accountable Plan Rules TIO Contact Information P age

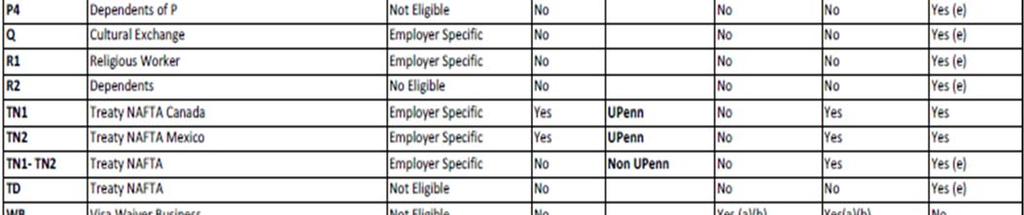

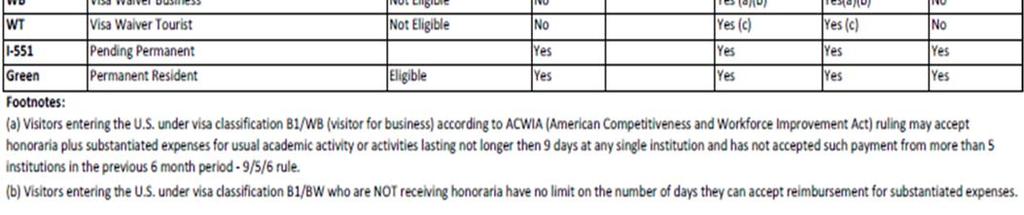

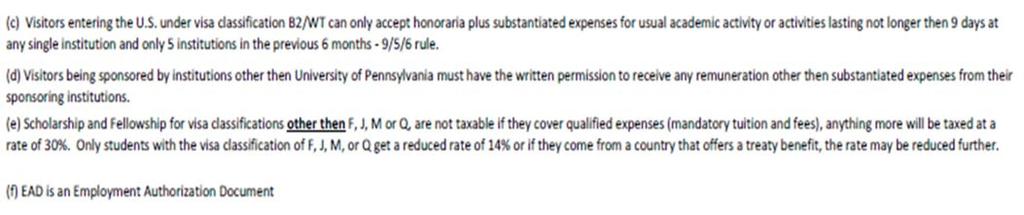

4 Chapter 1: Foreign National Payment Guide 1.1 Visa Matrix 3 P age

5 4 P age

6 Chapter 2: Nonresident New Hire process 2.1 Non-Penn Sponsored Grid 5 P age

7 2.2 Penn Sponsored Grid 6 P age

8 2.3 Quick Reference Flowchart 7 P age

8")

9 2.4 Required Documents Foreign National Information Form (FNIF) I-94 Visa Passport Social Security Receipt Immigration document Foreign National Information Form (FNIF) 8 P age

10 All foreign national (FN) new hires must complete this form. The form is a University internal document that gathers information about the individual s current and past immigration, dates of entry/exit from the US, and foreign address. The document can be found here: Page 1, the top should be completed by the department. Questions 1-15 are to be answered by the FN. 9 P age

11 Page 2, the FN must answer questions Question 20 should be completed for ALL visits to the US if they are an F, J, or H visa; this information determines if the FN will be taxed as a nonresident alien (NRA) or resident alien (RA). The form must be signed by the FN for validation. 10 P age

12 Most recent I P age

13 All individuals entering the US will have an I-94 document. FN new hires must provide a copy of the I-94. This document can be retrieved electronically on the Department of Homeland Security website US Visa 12 P age

14 Document used to enter the US. All FN new hires must provide a copy of the picture Visa. *Canadian individuals are not required to obtain a US Visa to enter the US. Passport An official document issued by a government, certifying the holder's identity and citizenship. All FN new hires must provide a copy of the picture passport. 13 P age

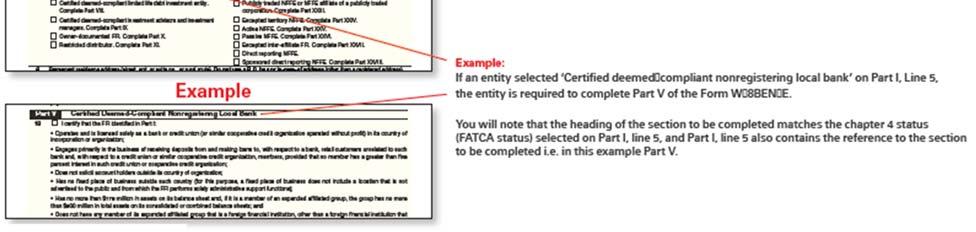

15 Social Security receipt of application If an FN new hire does not have a social security card, they must provide proof of application for an SSN. A receipt confirms that an individual successfully completed an application for a SSN card AND the applicant is approved to receive an SSN card. 14 P age

16 Immigration Documentation An FN would need to provide one of the following immigration documents. 15 P age

17 I-20 An F-1 student immigration document. Please copy pages 1 & 2. This document identifies the sponsoring institution and the dates of the program. If a student is on OPT, this is noted on page 2 of the document. DS-2019 An immigration document for a J-1 Student/Scholar. Identifies the sponsoring institution and the date of the program. Must be current. 16 P age

18 I-797 An immigration document for an H-1 visa holder. Identifies the sponsoring institution and the dates covered. Must be current. 17 P age

19 EAD Card Employment authorization document (EAD) proves an individual is eligible to work. The dates must be current. Please copy the front and back of the card. *Not all FN s will have an EAD card. We are specifically looking for this card when an FN on an F-1 visa that is not sponsored by Penn and does not have Penn listed on a CPT/OPT appointment on page 2 of the I-20 document. 18 P age

20 Permanent Resident Card (aka Green Card Holder) Card allows an individual to work and live permanently in the US. The card is typically valid for 10 years after date of issue. These individuals are taxed the same as a US citizen. Form W-4 A FN must complete sections 1,2,3,5 & sign the form. NRA individuals may only claim single on line 3 and either 0 or 1 on line 5. If the form is completed incorrectly and deemed invalid, the payroll department will automatically default to single and 0 allowance. The form can be found here 19 P age

21 2.5 Treaties Tax treaty eligibility is determined by Tax & International Operations (TIO). To be eligible, the individual must have a valid SSN or ITIN and their visa type, income type, tax status, permanent residence country, and time base or limit base must meet the criteria for the tax treaty exemption. The requirements vary by treaty country and must be renewed on a calendar year basis. Please advise FN employees to visit the TIO office for a treaty analysis. 2.6 ERN Codes When a FN employee signs a tax treaty or is receiving a nonservice fellowship that requires tax withholding, TIO will change the ERN code of these individuals to allow the payroll system to eliminate/compute tax on their compensation. When a department makes changes to an ERN code or adds a distribution line in Pennworks, it will negatively affect the individual s compensation if a NRA ERN code is not applied. Please do not change the following ERN codes, which can only be placed on the record by TIO: Nonresident Alien ERN codes- NR3, NO4, NAO, NCO, and/or NRO GF2 = NR3 treaty or NO4 tax (14% withholding) PD4 & PD3 = NAO treaty GF6 = NCO treaty 20 P age

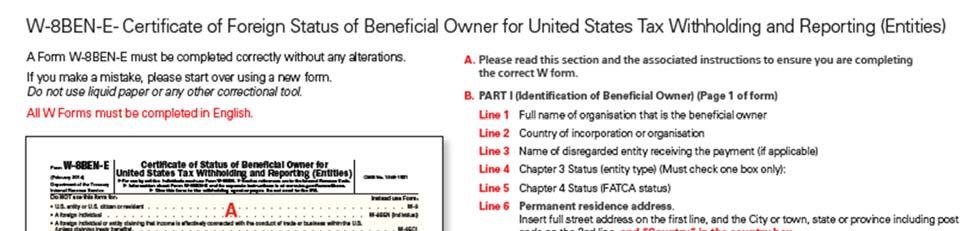

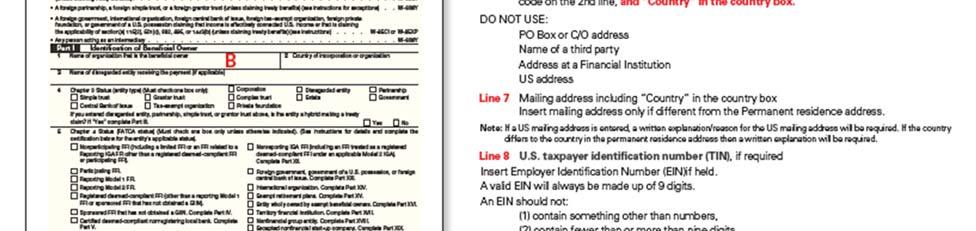

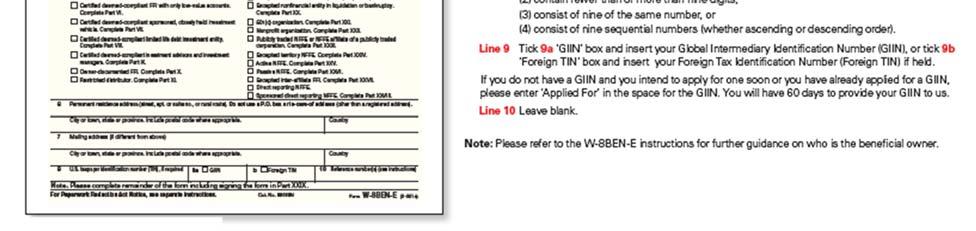

22 GF5 = NRO treaty RMO = NAO treaty If a new distribution line is added and the ERN code immediately preceding is one of the NRA ERN codes listed, please notify TIO so that we can update the ERN code. Chapter 3: Non-compensatory Payments (prizes/awards, honorariums, scholarships/fellowships, independent contractors, etc.) 3.1 Form W-8 Must be completed to certify that the recipient is foreign. W-8 forms and instructions can be found here: 8&criteria=formNumber The form expires 3 years after the year it is signed; we require an updated form when a W-8 is expired. There are many versions of the W-8 form, but the two most commonly used are: W-8BEN To be completed by a foreign individual. Guidelines for filling out form W-8BEN are provided below. If the individual is not claiming any withholding exemptions, they fill out all sections highlighted in YELLOW. If you will be claiming treaty-based withholding exemptions, you must ALSO fill out the sections highlighted in ORANGE. It is not required that you fill in any other fields. 21 P age

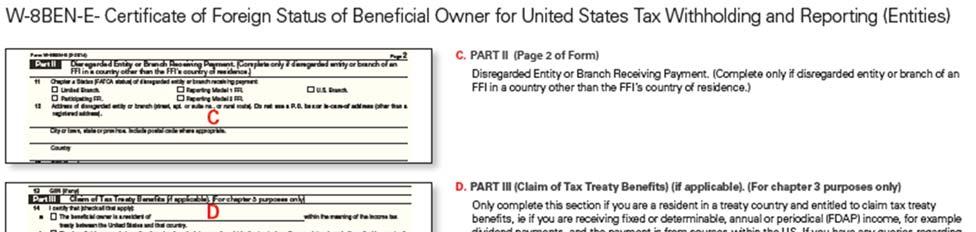

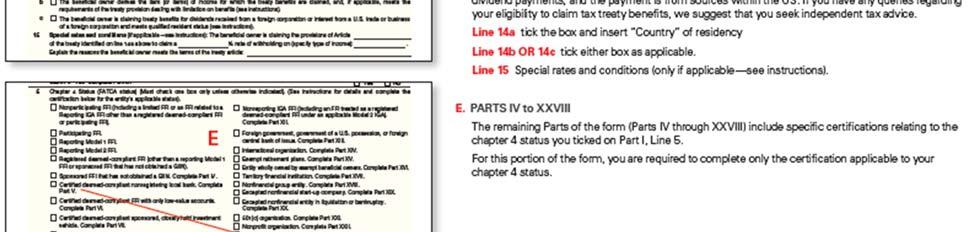

23 W-8BEN-E To be completed by a foreign entity. Please see guide below. 22 P age

24 23 P age

25 24 P age

26 3.2 Income Source Foreign Source Documentation required: 25 P age

27 Certificate of Foreign Source Income (CFSI) This is a University form used to certify that a payment is for services performed outside of the US. It is important to identify the location of services on the invoice. If TIO cannot determine the location, this can delay the payment or result in tax being withheld. This form can be found here: 26 P age

28 Taxation Generally, all services performed outside of the US are not US source, therefore not taxable. US Source Documentation required: 27 P age

29 Payments made to a FN individual located in the US require a completed W-8BEN, FNIF, and a copy of their I-94, Visa, Passport, and immigration document. Please see Chapter 2 for a description of each document. Honoraria Eligibility Certification Form Any foreign visitor receiving an honoraria must complete this form to certify that they meet the 9/5/6 rule. If they do not meet the 9/5/6 rule, they cannot be paid an honorarium. This is a University form and can be found on our website here: 28 P age

30 Taxation Payments to foreign nationals who are considered nonresident for tax purposes are subject to a 30% NRA tax unless exempted under a tax treaty. NRAs will receive Form 1042-S at year end for these payments. Payments to US citizens, permanent residents, and NRAs who are considered to be resident aliens for tax purposes will not have federal tax withheld. Payments of $600 or more in a calendar year will be reported on Form 1099-Misc. Chapter 4: Guest Travel Reimbursements 4.1 Documentation FNIF Visa Passport I P age

31 W-8BEN Immigration document (I-20, I-797, DS-2019, EAD) 4.2 Nontaxable vs. Taxable NonTaxable Any guest travel reimbursement connected to a business purpose (speaker/presenter, panelist, recruit, etc.) is generally nontaxable, as it is covered by the accountable plan rules as defined by the IRS see definition of accountable plan rules in 4.2. Taxable Any guest travel reimbursement not connected to a business purpose is generally taxable. Examples of when a guest travel reimbursement is taxable is a guest invited to merely attend a workshop on campus or sending a non-penn sponsored individual to an off-campus conference. Both instances do not directly benefit the University and do not meet the rules of accountable plan see definition of accountable plan rules in 4.2. Nonresident Alien Taxable guest travel reimbursement to foreign nationals who are considered nonresident aliens for tax purposes are subject to a 30% nonresident tax unless exempted under a tax treaty or reduced rate of 14% for F,J, or M visa holders. Payments are reported on Form 1042-S for the calendar year. US Citizen/Resident Alien/Permanent Residents Taxable guest travel reimbursement to foreign nationals who are considered resident aliens for tax purposes or who are permanent residents are not required to have tax withheld. Payments of $600 or more in a calendar year will be reported on Form Misc. 4.3 Accountable Plan Rules The requirements of the accountable plan rules are found in Treasury Regulation ; and they require that the payee: (1) establish the business purpose and connection of the expenses; (2) substantiate the expenses claimed to the payer within a reasonable period of time; and (3) return any amounts to the payer which are over and above the substantiated business expenses within a reasonable period of time. 30 P age

32 TIO Contact Information Phone Helpdesk P age

University of Utah Payments to Non Resident Aliens

University of Utah Payments to Non Resident Aliens Nonresident Alien Visitors Non-Employee Payments Visa Types: B-1 Business visitor B-2 Tourist visitor WB Business visitor (through visa waiver program)

University of Utah Payments to Non Resident Aliens Nonresident Alien Visitors Non-Employee Payments Visa Types: B-1 Business visitor B-2 Tourist visitor WB Business visitor (through visa waiver program)

FOREIGN NATIONAL TAX PROCEDURES GUIDE FOR DEPARTMENTS. Document created and modified by Financial Services Revised February 8, 2018

FOREIGN NATIONAL TAX PROCEDURES GUIDE FOR DEPARTMENTS Document created and modified by Financial Services Revised February 8, 2018 Table of Contents Pages Introduction 1 Definition of Terms 2-5 Frequently

FOREIGN NATIONAL TAX PROCEDURES GUIDE FOR DEPARTMENTS Document created and modified by Financial Services Revised February 8, 2018 Table of Contents Pages Introduction 1 Definition of Terms 2-5 Frequently

RUTGERS POLICY. Responsible Executive: Senior Vice President for Finance and Administration

RUTGERS POLICY Section: 40.2.5 Section Title: Fiscal Management Policy Name: Policies and Procedures for Payment for Intellectual Property, Honoraria or other Miscellaneous Services, and Payments to Nonresident

RUTGERS POLICY Section: 40.2.5 Section Title: Fiscal Management Policy Name: Policies and Procedures for Payment for Intellectual Property, Honoraria or other Miscellaneous Services, and Payments to Nonresident

RULES GOVERNING PAYMENT PROCESSING FOR FOREIGN NATIONALS

RULES GOVERNING PAYMENT PROCESSING FOR FOREIGN NATIONALS PAYMENT ELIGIBILITY Eligibility to receive specific types of payments is determined by the foreign national s visa status https://www.obfs.uillinois.edu/obfshome.cfm?path=foreignsecure

RULES GOVERNING PAYMENT PROCESSING FOR FOREIGN NATIONALS PAYMENT ELIGIBILITY Eligibility to receive specific types of payments is determined by the foreign national s visa status https://www.obfs.uillinois.edu/obfshome.cfm?path=foreignsecure

NONRESIDENT ALIEN TAX COMPLIANCE. A Policy and Procedure Manual. University of Nevada Reno (UNR) Nonresident Alien Tax Specialist Kellie Grahmann

Nonresident Alien Tax Specialist Kellie Grahmann") NONRESIDENT ALIEN TAX COMPLIANCE A Policy and Procedure Manual University of Nevada Reno (UNR) Nonresident Alien Tax Specialist Kellie Grahmann CONTENTS Nonresident Alien Tax Compliance Summary Taxation

NONRESIDENT ALIEN TAX COMPLIANCE A Policy and Procedure Manual University of Nevada Reno (UNR) Nonresident Alien Tax Specialist Kellie Grahmann CONTENTS Nonresident Alien Tax Compliance Summary Taxation

Princeton University International Graduate Student Tax Compliance Overview. Presented By Karen Murphy-Gordon September 9, 2011

Princeton University International Graduate Student Tax Compliance Overview Presented By Karen Murphy-Gordon September 9, 2011 Agenda Who we are and what we do What is expected of you How you are paid

Princeton University International Graduate Student Tax Compliance Overview Presented By Karen Murphy-Gordon September 9, 2011 Agenda Who we are and what we do What is expected of you How you are paid

This policy outlines circumstances in which payment of honoraria is appropriate, defines eligibility, tax implications and payment procedures.

Honorariums Summary This policy outlines circumstances in which payment of honoraria is appropriate, defines eligibility, tax implications and payment procedures. Applicability and Authority This procedure

Honorariums Summary This policy outlines circumstances in which payment of honoraria is appropriate, defines eligibility, tax implications and payment procedures. Applicability and Authority This procedure

Princeton University International Undergraduate Student Tax Compliance Overview. Presented By Karen Murphy-Gordon September 2, 2011

Princeton University International Undergraduate Student Tax Compliance Overview Presented By Karen Murphy-Gordon September 2, 2011 Agenda Who we are and what we do What is expected of you How you are

Princeton University International Undergraduate Student Tax Compliance Overview Presented By Karen Murphy-Gordon September 2, 2011 Agenda Who we are and what we do What is expected of you How you are

Nonresident Alien Tax Compliance

www.arcticintl.com ARCTIC INTERNATIONAL LLC Nonresident Alien Tax Compliance A Closer Look The Who, What When, How and Why... NACUBO Tax Forum 2013 Who... is required to withhold and report?... is a Nonresident

www.arcticintl.com ARCTIC INTERNATIONAL LLC Nonresident Alien Tax Compliance A Closer Look The Who, What When, How and Why... NACUBO Tax Forum 2013 Who... is required to withhold and report?... is a Nonresident

UNIVERSITY OF DAYTON NONRESIDENT ALIEN TAX GUIDE CONTENTS COMMON VISA TYPES AND THEIR TREATMENTS

UNIVERSITY OF DAYTON NONRESIDENT ALIEN TAX GUIDE CONTENTS I. RESPONSIBILITIES II. III. IV. SOCIAL SECURITY NUMBER REQUIREMENT DEFINITIONS TAX TREATIES V. PAYMENTS TO NONRESIDENT ALIENS VI. COMMON VISA

UNIVERSITY OF DAYTON NONRESIDENT ALIEN TAX GUIDE CONTENTS I. RESPONSIBILITIES II. III. IV. SOCIAL SECURITY NUMBER REQUIREMENT DEFINITIONS TAX TREATIES V. PAYMENTS TO NONRESIDENT ALIENS VI. COMMON VISA

Payments to Foreign Nationals. March 11, 2013

Payments to Foreign Nationals March 11, 2013 Workshop Presenters Denise Esworthy University Payroll and Benefits Assistant Payroll Manager Kami Van Bellehem University Payroll and Benefits Payroll Specialist

Payments to Foreign Nationals March 11, 2013 Workshop Presenters Denise Esworthy University Payroll and Benefits Assistant Payroll Manager Kami Van Bellehem University Payroll and Benefits Payroll Specialist

SUBJECT: Payments to Nonresident Aliens

Number 43 UNIVERSITY OF MAINE SYSTEM Issue 1 Page 1 of 2 Date 1/18/02 ADMINISTRATIVE PRACTICE LETTER INTRODUCTION SUBJECT: Payments to Nonresident Aliens United States tax law requires the University of

Number 43 UNIVERSITY OF MAINE SYSTEM Issue 1 Page 1 of 2 Date 1/18/02 ADMINISTRATIVE PRACTICE LETTER INTRODUCTION SUBJECT: Payments to Nonresident Aliens United States tax law requires the University of

Vendor Set-Up Process

Vendor Set-Up Process Office of the Controller April 26, 2018 Karen Kittredge, Manager, Policy and Business Process Teri DeLeon, Procure to Pay Manager Sharon Henry-Bell, Accounts Payable Operations Supervisor

Vendor Set-Up Process Office of the Controller April 26, 2018 Karen Kittredge, Manager, Policy and Business Process Teri DeLeon, Procure to Pay Manager Sharon Henry-Bell, Accounts Payable Operations Supervisor

Payments to Foreign Nationals. March 9, 2015

Payments to Foreign Nationals March 9, 2015 Workshop Presenters Kelly Sellers University Payroll and Benefits Assistant Payroll Manager Kami Van Bellehem University Payroll and Benefits Payroll Specialist

Payments to Foreign Nationals March 9, 2015 Workshop Presenters Kelly Sellers University Payroll and Benefits Assistant Payroll Manager Kami Van Bellehem University Payroll and Benefits Payroll Specialist

FOREIGN VISITOR TAX GUIDE

FOREIGN VISITOR TAX GUIDE University of Missouri-St. Louis The Foreign Visitor Tax Guide (Rev February 2017) is consistent with UMSL s policies and procedures for making payments to nonresident aliens.

FOREIGN VISITOR TAX GUIDE University of Missouri-St. Louis The Foreign Visitor Tax Guide (Rev February 2017) is consistent with UMSL s policies and procedures for making payments to nonresident aliens.

Tax Information for Foreign National Students, Scholars and Staff

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

Information for Foreign National Students, Scholars and Staff I. Introduction For federal income tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien

INTERNATIONAL TAX. Presented by Fiscal Services

INTERNATIONAL TAX Presented by Fiscal Services Agenda Overview Definitions Travel Reimbursements Scholarships/Fellowships Self-Employment Income Payments Vendor Payments Objectives Understand International

INTERNATIONAL TAX Presented by Fiscal Services Agenda Overview Definitions Travel Reimbursements Scholarships/Fellowships Self-Employment Income Payments Vendor Payments Objectives Understand International

Payments to Non-Resident Aliens

Payments to Non-Resident Aliens Finance and Administration Financial Operations The Office of Disbursements Who Is a Non-Resident Alien? Index Why Are Payments to Non-Resident Aliens Subject to Tax Withholding?

Payments to Non-Resident Aliens Finance and Administration Financial Operations The Office of Disbursements Who Is a Non-Resident Alien? Index Why Are Payments to Non-Resident Aliens Subject to Tax Withholding?

Taxability of Prizes and Awards President s Engagement Prizes. December 9, Office of the Comptroller

Taxability of Prizes and Awards President s Engagement Prizes December 9, 2015 1 Disclaimer The University is not permitted to provide personal tax advice. This presentation is an overview of what to expect.

Taxability of Prizes and Awards President s Engagement Prizes December 9, 2015 1 Disclaimer The University is not permitted to provide personal tax advice. This presentation is an overview of what to expect.

Tax Information for Foreign National Students, Scholars and Staff

Information for Foreign National Students, Scholars and Staff I. Introduction For federal tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien for

Information for Foreign National Students, Scholars and Staff I. Introduction For federal tax purposes, foreign national students and scholars are categorized in one of two ways: Nonresident alien for

Foreign Nationals Tax Compliance Boot Camp Employees, Vendors & Students

Foreign Nationals Tax Compliance Boot Camp Employees, Vendors & Students April 22, 2015 2015 Training Curriculum Jennifer Pacheco, Foreign Nationals Tax Compliance Program NC Office of the State Controller

Foreign Nationals Tax Compliance Boot Camp Employees, Vendors & Students April 22, 2015 2015 Training Curriculum Jennifer Pacheco, Foreign Nationals Tax Compliance Program NC Office of the State Controller

Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services

University of Washington Student Fiscal Services") Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services 1 Agenda U. S. Source of Income Scholarships Fellowships Tuition Waivers Prizes Stipends Social Security Number Tax Related

Non U.S. Resident Taxes (NRA) University of Washington Student Fiscal Services 1 Agenda U. S. Source of Income Scholarships Fellowships Tuition Waivers Prizes Stipends Social Security Number Tax Related

International Students and Scholars Nonresident Tax Orientation. February 14, 2018

International Students and Scholars Nonresident Tax Orientation February 14, 2018 Nonresident Tax Orientation Agenda General Overview of U.S. Tax and Tax Forms Items subject to tax NRA Documentation Requirements

International Students and Scholars Nonresident Tax Orientation February 14, 2018 Nonresident Tax Orientation Agenda General Overview of U.S. Tax and Tax Forms Items subject to tax NRA Documentation Requirements

TAX GUIDE FOR FOREIGN VISITORS. Anne E. Davenport, CPA October 2012

TAX GUIDE FOR FOREIGN VISITORS FOR USE BY: All Employees and Students Anne E. Davenport, CPA October 2012 Updated June 24, 2016 Table of Contents Introduction...1 Section 1: Definition of Terms...2 1.1

TAX GUIDE FOR FOREIGN VISITORS FOR USE BY: All Employees and Students Anne E. Davenport, CPA October 2012 Updated June 24, 2016 Table of Contents Introduction...1 Section 1: Definition of Terms...2 1.1

Table of Contents. Table of Contents 1. AP Information 2. Foreign Nationals Definitions 3-4. Policy Overview 5. What to Ask 6 10

Table of Contents Table of Contents 1 AP Information 2 Foreign Nationals Definitions 3-4 Policy Overview 5 What to Ask 6 10 Example Documents 11 14 Papers, Papers, and More Papers 15 Payment Information

Table of Contents Table of Contents 1 AP Information 2 Foreign Nationals Definitions 3-4 Policy Overview 5 What to Ask 6 10 Example Documents 11 14 Papers, Papers, and More Papers 15 Payment Information

Receiving payments in the U.S. Angela Gwinn

Receiving payments in the U.S. Angela Gwinn Payroll Payroll Department is part of the Office of Human Resources. 720 University Place, 2 nd floor in Evanston Abbott Hall, 8 th floor in Chicago 1071532

Receiving payments in the U.S. Angela Gwinn Payroll Payroll Department is part of the Office of Human Resources. 720 University Place, 2 nd floor in Evanston Abbott Hall, 8 th floor in Chicago 1071532

PLEASE PRESS *6 ON YOUR PHONE TO MUTE

Immigration Services Year End Tax Presentation December, 2011 PLEASE PRESS *6 ON YOUR PHONE TO MUTE Please Note the Following To listen to the session Call 508-856-8222 at the prompt enter the Participant

Immigration Services Year End Tax Presentation December, 2011 PLEASE PRESS *6 ON YOUR PHONE TO MUTE Please Note the Following To listen to the session Call 508-856-8222 at the prompt enter the Participant

I. Policy: All other University Finance policies and procedures apply in addition to those stated in this document.

Page 1 of 5 Subject: Applies to: Payments to Foreign Nationals (except salary/wage payments) For information regarding Employment of Foreign Nationals please see Personnel Policy 124: http://www.rochester.edu/working/hr/policies/pdfpolicies/124.pdf.

Page 1 of 5 Subject: Applies to: Payments to Foreign Nationals (except salary/wage payments) For information regarding Employment of Foreign Nationals please see Personnel Policy 124: http://www.rochester.edu/working/hr/policies/pdfpolicies/124.pdf.

Foreign National Tax Responsibilities

1 Cali California State University, Sacramento Foreign National Tax Responsibilities 2 What is FNIS? Foreign National Information System (FNIS) is a web-based, data-entry software application used to analyze

1 Cali California State University, Sacramento Foreign National Tax Responsibilities 2 What is FNIS? Foreign National Information System (FNIS) is a web-based, data-entry software application used to analyze

PLEASE PRESS *6 ON YOUR PHONE TO MUTE

Immigration Services Year End Tax Presentation December, 2013 PLEASE PRESS *6 ON YOUR PHONE TO MUTE Please Note the Following Keep your phone-line muted throughout the session to minimize background noise

Immigration Services Year End Tax Presentation December, 2013 PLEASE PRESS *6 ON YOUR PHONE TO MUTE Please Note the Following Keep your phone-line muted throughout the session to minimize background noise

Glacier Guide for Departments, v. 3.3 Page 1 GLACIER ONLINE NONRESIDENT ALIEN TAX COMPLIANCE SYSTEM. Glacier Guide for Departments

Glacier Guide for Departments, v. 3.3 Page 1 GLACIER ONLINE NONRESIDENT ALIEN TAX COMPLIANCE SYSTEM Glacier Guide for Departments All Glacier-related documents & forms are available in electronic format.

Glacier Guide for Departments, v. 3.3 Page 1 GLACIER ONLINE NONRESIDENT ALIEN TAX COMPLIANCE SYSTEM Glacier Guide for Departments All Glacier-related documents & forms are available in electronic format.

Financial Accounting & Reporting. Foreign National Tax Responsibilities

Foreign National Tax Responsibilities What is FNIS? Foreign National Information System (FNIS) is a web based, data entry software application used to analyze tax status, determine treaty eligibility,

Foreign National Tax Responsibilities What is FNIS? Foreign National Information System (FNIS) is a web based, data entry software application used to analyze tax status, determine treaty eligibility,

Glacier Quick Guide. You will receive an similar to the one below. Please read and follow the directions

Glacier Quick Guide You will receive an email similar to the one below. Please read and follow the directions Website from link in email Copy login information from email Create your own login information

Glacier Quick Guide You will receive an email similar to the one below. Please read and follow the directions Website from link in email Copy login information from email Create your own login information

Non-Resident Tax Workshop February 28, 2013 UTSA, Business Building Room Presented by:

Non-Resident Tax Workshop February 28, 2013 UTSA, Business Building Room 2.06.04 Presented by: Christine Bodily, Payroll Department, 458-4283 Christine.Bodily@utsa.edu Cherilyn Patteson, Office of International

Non-Resident Tax Workshop February 28, 2013 UTSA, Business Building Room 2.06.04 Presented by: Christine Bodily, Payroll Department, 458-4283 Christine.Bodily@utsa.edu Cherilyn Patteson, Office of International

FOREIGN NATIONALS TAX COMPLIANCE TRAINING Foreign Nationals Tax Compliance

FOREIGN NATIONALS TAX COMPLIANCE TRAINING 2015 Foreign Nationals Tax Compliance March 19, 2015 Presenters Jennifer Trivette Pacheco OSC s Foreign Nationals Tax Compliance Program Michelle Anderson NCSU

FOREIGN NATIONALS TAX COMPLIANCE TRAINING 2015 Foreign Nationals Tax Compliance March 19, 2015 Presenters Jennifer Trivette Pacheco OSC s Foreign Nationals Tax Compliance Program Michelle Anderson NCSU

Payments Made to Nonresident Aliens

Payments Made to Nonresident Aliens A Policies and Procedures Manual This Procedures for Payments Made to Nonresident Aliens guide was prepared by Arctic International LLC in connection with Occidental

Payments Made to Nonresident Aliens A Policies and Procedures Manual This Procedures for Payments Made to Nonresident Aliens guide was prepared by Arctic International LLC in connection with Occidental

TAX FILING FOR STUDENTS AND SCHOLARS 101. Columbus Community Legal Services

TAX FILING FOR STUDENTS AND SCHOLARS 101 Columbus Community Legal Services INTRODUCTION Who are we? Part of the Catholic University of America s Columbus School of Law Columbus Community Legal Services

TAX FILING FOR STUDENTS AND SCHOLARS 101 Columbus Community Legal Services INTRODUCTION Who are we? Part of the Catholic University of America s Columbus School of Law Columbus Community Legal Services

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University 1 Before we begin Filing taxes means submitting tax forms (or

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University 1 Before we begin Filing taxes means submitting tax forms (or

INVITING & PAYING AN HONORARIUM TO A FOREIGN NATIONAL FOR ACADEMIC ACTIVITIES AT THE UW

INVITING & PAYING AN HONORARIUM TO A FOREIGN NATIONAL FOR ACADEMIC ACTIVITIES AT THE UW Name of Foreign National: Title of Activity: Date of Activity: Notes: Pre-arrival planning: Finalize the activity

INVITING & PAYING AN HONORARIUM TO A FOREIGN NATIONAL FOR ACADEMIC ACTIVITIES AT THE UW Name of Foreign National: Title of Activity: Date of Activity: Notes: Pre-arrival planning: Finalize the activity

The hardest thing in the world to understand is the income tax. Albert Einstein FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX

The hardest thing in the world to understand is the income tax. Albert Einstein FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX University Tax Cassandra Franks, CPA Director, University Tax Services Financial

The hardest thing in the world to understand is the income tax. Albert Einstein FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX University Tax Cassandra Franks, CPA Director, University Tax Services Financial

Glacier Vendor View The Glacier Administrator for the department will enter the name and of the vendor into Glacier.

Glacier Vendor View The Glacier Administrator for the department will enter the name and email of the vendor into Glacier. The vendor will receive an email from Glacier providing them with the login information.

Glacier Vendor View The Glacier Administrator for the department will enter the name and email of the vendor into Glacier. The vendor will receive an email from Glacier providing them with the login information.

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University Before we begin Filing taxes means submitting tax forms (or

Tax Workshop for Foreign Nationals Preparing 2018 Forms Douglas Kelley Guest Lecturer Lamden School of Accountancy San Diego State University Before we begin Filing taxes means submitting tax forms (or

Webinar Tax Treatment for Scholarships and Fellowships

1 Financial Management Office May 1, 2014 Updated as of 5/16/2014 Webinar Tax Treatment for Scholarships and Fellowships 2 Webinar Instructions Web conference login: URL: http://www.hawaii.edu/halawai/login.htm

1 Financial Management Office May 1, 2014 Updated as of 5/16/2014 Webinar Tax Treatment for Scholarships and Fellowships 2 Webinar Instructions Web conference login: URL: http://www.hawaii.edu/halawai/login.htm

The ABC s s of Hosting an International Speaker or Entertainer: A Team Approach formerly The ABC s s of Inviting a Foreign Speaker

The ABC s s of Hosting an International Speaker or Entertainer: A Team Approach formerly The ABC s s of Inviting a Foreign Speaker Presenters: Minnesota State University, Mankato: Julie Rabaey, Assistant

The ABC s s of Hosting an International Speaker or Entertainer: A Team Approach formerly The ABC s s of Inviting a Foreign Speaker Presenters: Minnesota State University, Mankato: Julie Rabaey, Assistant

Nonresident Alien Federal Tax Workshop

Nonresident Alien Federal Tax Workshop Using GLACIER Tax Prep (GTP) as a tool for self-preparation of 2017 Federal Income Tax Return (Form 1040NR or Form 1040NR-EZ) and Form 8843, Payroll Tax Workshop

Nonresident Alien Federal Tax Workshop Using GLACIER Tax Prep (GTP) as a tool for self-preparation of 2017 Federal Income Tax Return (Form 1040NR or Form 1040NR-EZ) and Form 8843, Payroll Tax Workshop

Page 1 of 6 UC Santa Barbara Policy 5145 Policies Issuing Unit: Administrative Services Date: May 1, 1985 I. REFERENCES: Under Revision Contact Accounting PAYMENTS TO ALIENS A. U.S. Tax Reform Act of 1984,

Page 1 of 6 UC Santa Barbara Policy 5145 Policies Issuing Unit: Administrative Services Date: May 1, 1985 I. REFERENCES: Under Revision Contact Accounting PAYMENTS TO ALIENS A. U.S. Tax Reform Act of 1984,

International Student Taxes. Information compiled by International Student Services

International Student Taxes Information compiled by International Student Services International Student Taxes The Basics Specific Tax Scenarios What You Can Do Now Resolving Tax Issues Top Ten Tax Myths

International Student Taxes Information compiled by International Student Services International Student Taxes The Basics Specific Tax Scenarios What You Can Do Now Resolving Tax Issues Top Ten Tax Myths

International Student Taxes

International Student Taxes Information compiled by International Student Services (ISS) Important Disclaimer! ISS staff members are NOT Tax Professionals or Certified Public Accountants. ANY ADVICE IN

International Student Taxes Information compiled by International Student Services (ISS) Important Disclaimer! ISS staff members are NOT Tax Professionals or Certified Public Accountants. ANY ADVICE IN

Nonresident Alien Tax Compliance Workshop Comprehensive Overview and Update of the Issues

Day One: Monday October 17, 2016 Comprehensive Overview and Update of the Issues 8:00 8:30 Registration 8:30 8:45 Welcome, Introduction and Workshop Goals 8:45 10:30 Getting Started: An Overview of the

Day One: Monday October 17, 2016 Comprehensive Overview and Update of the Issues 8:00 8:30 Registration 8:30 8:45 Welcome, Introduction and Workshop Goals 8:45 10:30 Getting Started: An Overview of the

NEW VENDOR REQUEST NEW VENDOR INFORMATION INTERNATIONAL VENDOR REQUEST INDIVIDUAL

INTERNATIONAL VENDOR REQUEST INDIVIDUAL NEW VENDOR REQUEST This form, in conjunction with the attached taxpayer identification document, must be completed to add a new vendor to our accounting software

INTERNATIONAL VENDOR REQUEST INDIVIDUAL NEW VENDOR REQUEST This form, in conjunction with the attached taxpayer identification document, must be completed to add a new vendor to our accounting software

West Chester University. Taxation Issues Nonresident Aliens

West Chester University Taxation Issues Nonresident Aliens Agenda Tax Compliance Issues Nonresident aliens (NRA) o Vendor Payments o Scholarships o Tuition Waivers o Prizes o Stipends Tax related Forms

West Chester University Taxation Issues Nonresident Aliens Agenda Tax Compliance Issues Nonresident aliens (NRA) o Vendor Payments o Scholarships o Tuition Waivers o Prizes o Stipends Tax related Forms

HCM Specialists User Group. May 10, 2018

HCM Specialists User Group May 10, 2018 Agenda Resource updates Hiring Payroll Transfers Terminations Payments to International Students/Scholars 2 3 Resource Updates Updated Resources Available 4 www.vanderbilt.edu

HCM Specialists User Group May 10, 2018 Agenda Resource updates Hiring Payroll Transfers Terminations Payments to International Students/Scholars 2 3 Resource Updates Updated Resources Available 4 www.vanderbilt.edu

Welcome to Tax Filing Information for International Students and Scholars

Welcome to Tax Filing Information for International Students and Scholars Presented by Office of International Student & Scholar Services Florida Institute of Technology DISCLAIMER ISSS staff are not licensed

Welcome to Tax Filing Information for International Students and Scholars Presented by Office of International Student & Scholar Services Florida Institute of Technology DISCLAIMER ISSS staff are not licensed

Employment of H-2A Workers Employer Federal Withholding Requirements/ H-2A Worker Federal Income Tax Filing Requirements

Employment of H-2A Workers Employer Federal Withholding Requirements/ H-2A Worker Federal Income Tax Filing Requirements The guidance provided in this document pertains to federal tax implications only.

Employment of H-2A Workers Employer Federal Withholding Requirements/ H-2A Worker Federal Income Tax Filing Requirements The guidance provided in this document pertains to federal tax implications only.

Worker Classification/ Independent Contractor

Worker Classification/ Independent Contractor Policy Update June 2016 Contents Policy Update Objective Current Policies and Proposed Updates Overview of Proposed Updates to Policies Summary of Updates

Worker Classification/ Independent Contractor Policy Update June 2016 Contents Policy Update Objective Current Policies and Proposed Updates Overview of Proposed Updates to Policies Summary of Updates

Instructions for Form W-7

Instructions for Form W-7 (January 2010) Application for IRS Individual Taxpayer Identification Number Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

Instructions for Form W-7 (January 2010) Application for IRS Individual Taxpayer Identification Number Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue

INDEPENDENT CONTRACTORS

Responsible University Administrator: Vice President for Finance and Administration Responsible Officer: Director of the Office of Budget and Tax Compliance Origination Date: N/A Current Revision Date:

Responsible University Administrator: Vice President for Finance and Administration Responsible Officer: Director of the Office of Budget and Tax Compliance Origination Date: N/A Current Revision Date:

The hardest thing in the world to understand is the income tax. Albert Einstein FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX

The hardest thing in the world to understand is the income tax. Albert Einstein FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX University Tax Cassandra Franks, CPA Director, University Tax Services Financial

The hardest thing in the world to understand is the income tax. Albert Einstein FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX University Tax Cassandra Franks, CPA Director, University Tax Services Financial

Glacier Employee View The Glacier Administrator for the department will enter the name and of the employee into Glacier.

Glacier Employee View The Glacier Administrator for the department will enter the name and email of the employee into Glacier. The employee will receive an email from Glacier providing them with the login

Glacier Employee View The Glacier Administrator for the department will enter the name and email of the employee into Glacier. The employee will receive an email from Glacier providing them with the login

Guide to Paying for Consulting Services

Guide to Paying for Consulting Services Purpose: This guide has been created with the intention to help clarify the documentation requirements for hiring consulting services via independent contractors

Guide to Paying for Consulting Services Purpose: This guide has been created with the intention to help clarify the documentation requirements for hiring consulting services via independent contractors

US Tax Information for Diplomatic Families at the Canadian Embassy

US Tax Information for Diplomatic Families at the Canadian Rick Ward LLC January 16, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of January

US Tax Information for Diplomatic Families at the Canadian Rick Ward LLC January 16, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of January

US Tax Information for Diplomatic Families at the British Embassy

US Tax Information for Diplomatic Families at the British Rick Ward LLC February 22, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of February

US Tax Information for Diplomatic Families at the British Rick Ward LLC February 22, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of February

Foreign National Taxation and Compliance Guide October 2002 Revised May 2008

Foreign National Taxation and Compliance Guide October 2002 Revised May 2008 American University Payroll Office Mailing Address: 4400 Massachusetts Ave. NW Washington, D.C. 20016-8054 Office Location:

Foreign National Taxation and Compliance Guide October 2002 Revised May 2008 American University Payroll Office Mailing Address: 4400 Massachusetts Ave. NW Washington, D.C. 20016-8054 Office Location:

Non-Resident Alien Frequently Asked Questions

Materials Management: Payroll Time and Attendance Unit Non-Resident Alien Frequently Asked Questions TAX FILING: DO I NEED TO FILE / WHEN DO I FILE? What happens if I fail to file my taxes? If you owe

Materials Management: Payroll Time and Attendance Unit Non-Resident Alien Frequently Asked Questions TAX FILING: DO I NEED TO FILE / WHEN DO I FILE? What happens if I fail to file my taxes? If you owe

U.S. Taxation for International Students. by Sau-Wing Lam

U.S. Taxation for International Students by Sau-Wing Lam January 2018 Resident Alien or Non-Resident Alien? In American taxation there is a difference between a resident alien and a non-resident alien.

U.S. Taxation for International Students by Sau-Wing Lam January 2018 Resident Alien or Non-Resident Alien? In American taxation there is a difference between a resident alien and a non-resident alien.

ence Session date: Monday, November 12, 2007 Location: Kansas City, Missouri

Navigating the Financial Logistics of Hosting International Speakers A Team Approach NAFSA: Association of International Educators Region IV Conference ence Session date: Monday, November 12, 2007 Location:

Navigating the Financial Logistics of Hosting International Speakers A Team Approach NAFSA: Association of International Educators Region IV Conference ence Session date: Monday, November 12, 2007 Location:

Procedures for Payments Made to or on Behalf of International Students, Visitors and Vendors

Procedures for Payments Made to or on Behalf of International Students, Visitors and Vendors General Information All payments made to or on behalf of an international visitor, student orvendor have potential

Procedures for Payments Made to or on Behalf of International Students, Visitors and Vendors General Information All payments made to or on behalf of an international visitor, student orvendor have potential

US Tax Information for Diplomatic Families at the Australian Embassy

US Tax Information for Diplomatic Families at the Australian Rick Ward LLC January 25, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of

US Tax Information for Diplomatic Families at the Australian Rick Ward LLC January 25, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of

FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX

FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX University Tax Cassandra Franks Director, University Tax Services Financial Management Services Participant Outcomes Recognize when payment situations have

FOUNDATIONS IN UNIVERSITY FINANCE UNIVERSITY TAX University Tax Cassandra Franks Director, University Tax Services Financial Management Services Participant Outcomes Recognize when payment situations have

CAMP IPPS August 21, 2018

CAMP IPPS 2018 August 21, 2018 WELCOME CAMPERS A few things to remember West Ballroom Stop by the ballroom to ask us questions after the class! Meet Connexxus travel vendors in honor of the Connexxus 10

CAMP IPPS 2018 August 21, 2018 WELCOME CAMPERS A few things to remember West Ballroom Stop by the ballroom to ask us questions after the class! Meet Connexxus travel vendors in honor of the Connexxus 10

Basic Tax Information for F and J Immigration Status

1 Basic Tax Information for F and J Immigration Status International Student Services Who Should Be Here Today If you were not in the USA during 2009, you do not need to file taxes until next year. You

1 Basic Tax Information for F and J Immigration Status International Student Services Who Should Be Here Today If you were not in the USA during 2009, you do not need to file taxes until next year. You

University of Oregon Paying for and Reimbursing Travel for International Visitors 09/16/2015

The University of Oregon (UO) invites International visitors (Intl. visitor) to the United States for many reasons. Employment, presentations, collaboration, speaking engagements, research, training, and

The University of Oregon (UO) invites International visitors (Intl. visitor) to the United States for many reasons. Employment, presentations, collaboration, speaking engagements, research, training, and

AGENDA TIME TOPIC PRESENTER. 10am- 10:20am Introduc1on & Overview Kate Zheng

1 AGENDA 2 TIME TOPIC PRESENTER 10am- 10:20am Introduc1on & Overview Kate Zheng 10:20am- 11:10am Visa Type Employment Eligibility Q&A Interna'onal Center Linda Kentes Michael Olech Interna'onal Center

1 AGENDA 2 TIME TOPIC PRESENTER 10am- 10:20am Introduc1on & Overview Kate Zheng 10:20am- 11:10am Visa Type Employment Eligibility Q&A Interna'onal Center Linda Kentes Michael Olech Interna'onal Center

GENERAL ACCOUNTING GLACIER STEP BY STEP GUIDE FOR FOREIGN NATIONALS

GENERAL ACCOUNTING GLACIER STEP BY STEP GUIDE FOR FOREIGN NATIONALS Nonresident Alien Tax Compliance WHO SHOULD USE THIS GUIDE? All Foreign Nationals who are: Student Workers Graduate Assistants Interns

GENERAL ACCOUNTING GLACIER STEP BY STEP GUIDE FOR FOREIGN NATIONALS Nonresident Alien Tax Compliance WHO SHOULD USE THIS GUIDE? All Foreign Nationals who are: Student Workers Graduate Assistants Interns

TAX POLICY AND PROCEDURE GUIDE FOR PAYMENTS TO ALIEN INDIVIDUALS

TAX POLICY AND PROCEDURE GUIDE FOR PAYMENTS TO ALIEN INDIVIDUALS Revised as of July 2017 University of Alabama at Birmingham PREFACE The Tax Policy and Procedure Guide for Income Payments to Alien Individuals

TAX POLICY AND PROCEDURE GUIDE FOR PAYMENTS TO ALIEN INDIVIDUALS Revised as of July 2017 University of Alabama at Birmingham PREFACE The Tax Policy and Procedure Guide for Income Payments to Alien Individuals

US Tax Information for Diplomatic Families at the German Embassy

US Tax Information for Diplomatic Families at the German Rick Ward LLC February 26, 2018 Disclosure This presentation has been prepared for employees of the World Bank by LLC. The information in this presentation

US Tax Information for Diplomatic Families at the German Rick Ward LLC February 26, 2018 Disclosure This presentation has been prepared for employees of the World Bank by LLC. The information in this presentation

US Tax Information for Diplomatic Families at the Swiss Embassy

US Tax Information for Diplomatic Families at the Swiss Rick Ward LLC October 18, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of October

US Tax Information for Diplomatic Families at the Swiss Rick Ward LLC October 18, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of October

TAX POLICY AND PROCEDURE GUIDE FOR INCOME PAYMENTS TO ALIEN INDIVIDUALS

TAX POLICY AND PROCEDURE GUIDE FOR INCOME PAYMENTS TO ALIEN INDIVIDUALS Revised as of November 2007 University of Alabama at Birmingham Revision Date: November 2007 PREFACE The Tax Policy and Procedure

TAX POLICY AND PROCEDURE GUIDE FOR INCOME PAYMENTS TO ALIEN INDIVIDUALS Revised as of November 2007 University of Alabama at Birmingham Revision Date: November 2007 PREFACE The Tax Policy and Procedure

If you do not have all of the above forms, please call Junn De Guzman at (732)

") To: Non-Resident Aliens Requesting Special Tax Treatment From: Junn De Guzman, Sr. Accountant Payroll Department Date: December 31, 2011 Re: Requirements for Tax Benefits for Calendar Year 2012 Enclosed

To: Non-Resident Aliens Requesting Special Tax Treatment From: Junn De Guzman, Sr. Accountant Payroll Department Date: December 31, 2011 Re: Requirements for Tax Benefits for Calendar Year 2012 Enclosed

Tax information. International Students in the United States

Tax information International Students in the United States Friday workshop for MC International 1 Why Should I File Tax Forms? To keep Legal in the United States If you ever apply for Permanent Residency

Tax information International Students in the United States Friday workshop for MC International 1 Why Should I File Tax Forms? To keep Legal in the United States If you ever apply for Permanent Residency

CSU 101 Tax Discussion Monterey 2011

CSU 101 Tax Discussion Monterey 2011 Marc F. Benadiba Assistant Director Fiscal Services Cal Poly San Luis Obispo CSU Tax Discussion Contrary to popular belief, there are significant tax issues on CSU

CSU 101 Tax Discussion Monterey 2011 Marc F. Benadiba Assistant Director Fiscal Services Cal Poly San Luis Obispo CSU Tax Discussion Contrary to popular belief, there are significant tax issues on CSU

BASIC TAX WORKSHOP FOR INT L STUDENTS. Tax Information Session for MIT International Students in Non-Resident Status for Tax Purposes March 2017

BASIC TAX WORKSHOP FOR INT L STUDENTS Tax Information Session for MIT International Students in Non-Resident Status for Tax Purposes March 2017 MIT International Students Office & Office of the Vice President

BASIC TAX WORKSHOP FOR INT L STUDENTS Tax Information Session for MIT International Students in Non-Resident Status for Tax Purposes March 2017 MIT International Students Office & Office of the Vice President

Addendum: An addition to an existing document, such as additional terms or a modification of terms.

Research Corporation of the University of Hawai i 2.002 Definitions Accountable Plan: A business reimbursement expense plan for the payment of business expenses incurred by a service provider (such as

Research Corporation of the University of Hawai i 2.002 Definitions Accountable Plan: A business reimbursement expense plan for the payment of business expenses incurred by a service provider (such as

The United States Government defines an alien as any individual who is not

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 22, 2017 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

To-Be Process Review Workshop

1 To-Be Process Review Workshop Human Resources Taxes Location: ROSS Building Room: 130 Time: 8:00 am - 12:00 pm Date: 9/19/05 2 Workshop Logistics Tent Cards Rest Rooms Break Parking Lot 3 Workshop Agenda

1 To-Be Process Review Workshop Human Resources Taxes Location: ROSS Building Room: 130 Time: 8:00 am - 12:00 pm Date: 9/19/05 2 Workshop Logistics Tent Cards Rest Rooms Break Parking Lot 3 Workshop Agenda

Frequently Asked Tax Questions 2018 Tax Returns

Frequently Asked Tax Questions 2018 Tax Returns Q. When is my tax return due? A. 2018 Federal (U.S. government) tax returns are due by April 15, 2019. State of Iowa tax returns are due by May 1, 2019.

Frequently Asked Tax Questions 2018 Tax Returns Q. When is my tax return due? A. 2018 Federal (U.S. government) tax returns are due by April 15, 2019. State of Iowa tax returns are due by May 1, 2019.

1 Introduction Work Authorization Taxpayer Identification Numbers... 2

1 Introduction... 1 1.1 Work Authorization... 1 1.2 Taxpayer Identification Numbers... 2 2 U.S. Tax Residency Rules... 3 2.1 Residency Status Based on U.S. Presence... 3 2.2 U.S. Days That Do Not Count...

1 Introduction... 1 1.1 Work Authorization... 1 1.2 Taxpayer Identification Numbers... 2 2 U.S. Tax Residency Rules... 3 2.1 Residency Status Based on U.S. Presence... 3 2.2 U.S. Days That Do Not Count...

WINDSTAR: Foreign National Tax Resource User Guide

International Center 20 Sawyer Avenue, Medford, MA 02155 I TEL: 617.627.3458 I FAX: 617-627.6076 internationalcenter@tufts.edu I http://ase.tufts.edu/icenter Tax Return Resource for Returning Users WINDSTAR:

International Center 20 Sawyer Avenue, Medford, MA 02155 I TEL: 617.627.3458 I FAX: 617-627.6076 internationalcenter@tufts.edu I http://ase.tufts.edu/icenter Tax Return Resource for Returning Users WINDSTAR:

3. On the login screen, click the Login Now link or the system logo.

Overview For payments made to a foreign national, Harvard University utilizes a third-party system, called GLACIER Online Tax Compliance System, to calculate the tax withholding. This document provides

Overview For payments made to a foreign national, Harvard University utilizes a third-party system, called GLACIER Online Tax Compliance System, to calculate the tax withholding. This document provides

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014 Federal Income Tax Withholding 14.1-1 U.S. citizens & resident aliens are subject to income tax withholding

Payroll for U.S. Employees Abroad and Aliens in the U.S. Charlotte N. Hodges, CPP August 23, 2014 Federal Income Tax Withholding 14.1-1 U.S. citizens & resident aliens are subject to income tax withholding

Americans Living Abroad. 61 Tax Questions you should know.

Americans Living Abroad 61 Tax Questions you should know 1 General FAQs 1. I m a U.S. citizen living and working outside of the United States for many years. Do I still need to file a U.S. tax return?

Americans Living Abroad 61 Tax Questions you should know 1 General FAQs 1. I m a U.S. citizen living and working outside of the United States for many years. Do I still need to file a U.S. tax return?

Red Light: Dealing with the IRS Enforcement Action

SESSION 4.3 Red Light: Dealing with the IRS Enforcement Action Michael Guerra, EASi Lori Nichols, Internal Revenue Service Carol Rutlen, Partner, GTN/Rutlen Associates LLC B SESSION 4.3 Red Light: Dealing

SESSION 4.3 Red Light: Dealing with the IRS Enforcement Action Michael Guerra, EASi Lori Nichols, Internal Revenue Service Carol Rutlen, Partner, GTN/Rutlen Associates LLC B SESSION 4.3 Red Light: Dealing

Supplier Information Form Instructions

Purpose of Form. An organization that is required to file an information return with the IRS must obtain your correct Federal Taxpayer Identification Number in order to report income paid to you. The Tax

Purpose of Form. An organization that is required to file an information return with the IRS must obtain your correct Federal Taxpayer Identification Number in order to report income paid to you. The Tax

UCSF Postdoc Scholars. Revised March 20, 2013

UCSF Postdoc Scholars Revised March 20, 2013 Agenda Introduction Hiring Checklist Required Keying Practices Dues/Fees Taxation Financials Appendix: Taxation 2 Hiring Checklist Postdoc Scholars 3 Postdoc

UCSF Postdoc Scholars Revised March 20, 2013 Agenda Introduction Hiring Checklist Required Keying Practices Dues/Fees Taxation Financials Appendix: Taxation 2 Hiring Checklist Postdoc Scholars 3 Postdoc

RESTRICTED ACCOUNT POLICY TABLE OF CONTENTS

RESTRICTED ACCOUNT POLICY TABLE OF CONTENTS Page Number I. FUNDING SOURCES A. Income 1 B. Honorariums 3 C. Royalties 4 D. Grants 4 E. Contributions by Account Administrators 5 F. Undocumented Gifts 5 G.

RESTRICTED ACCOUNT POLICY TABLE OF CONTENTS Page Number I. FUNDING SOURCES A. Income 1 B. Honorariums 3 C. Royalties 4 D. Grants 4 E. Contributions by Account Administrators 5 F. Undocumented Gifts 5 G.

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 25, 2016 Presented by

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 25, 2016 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

U.S. Income Tax Workshop for Foreign Students & Scholars Rice University Office of International Students & Scholars February 25, 2016 Presented by Crystal C. Gates, Tax Principal Kelley C. Heng, Tax Supervisor

Information Reporting on Form 1042-S, A New Challenge for Accounts Payable

Information Reporting on Form 1042-S, A New Challenge for Accounts Payable By Paula N. Singer 1 This article was originally published in Tax Notes International WINDSTAR TECHNOLOGIES A THOMSON REUTERS

Information Reporting on Form 1042-S, A New Challenge for Accounts Payable By Paula N. Singer 1 This article was originally published in Tax Notes International WINDSTAR TECHNOLOGIES A THOMSON REUTERS

Employees: Employees may only access and complete Glacier after their arrival in the US.

Administrator 3 View General Information and Getting Started Administrator is the term Glacier uses to describe departmental level access. The Payroll Office will provide Administrator 3 access to the

Administrator 3 View General Information and Getting Started Administrator is the term Glacier uses to describe departmental level access. The Payroll Office will provide Administrator 3 access to the

Tax Issues Associated with Reporting Fellowships

Tax Issues Associated with Reporting Fellowships John Barrett Tax Manager-University of California Office of the President-CFO Division Benjamin Tsai Senior Tax Analyst Arthur Quilao Tax Compliance Analyst

Tax Issues Associated with Reporting Fellowships John Barrett Tax Manager-University of California Office of the President-CFO Division Benjamin Tsai Senior Tax Analyst Arthur Quilao Tax Compliance Analyst