ICDS - 2 CHANGES IN ITR FOR AY COMPANIES (AMENDMENT) ACT 2017 CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA

|

|

|

- Wendy Stafford

- 5 years ago

- Views:

Transcription

, FCA, FCS, FCMA, LL.")

1 ICDS - 2 CHANGES IN ITR FOR AY COMPANIES (AMENDMENT) ACT 2017 CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Sonepat Branch of NIRC of ICAI 3 rd June 2018

2 CRITICAL ISSUES CA. Pramod Jain Companies (Amendment) Act 2017

3 SUMMARY CA. Pramod Jain 93 Amendments in all This ppt contains major amendments 3 Provisions applicable from 3 rd January 2018 related to IBC 43 Provisions applicable from 9 th February Provisions applicable from 7 th May 2018 Compliances emphasized Penalties rationalized

4 AMENDMENTS IMPORTANT DEFINITIONS 2(51) KMP to include 1 level below director who is in whole time employment, designated as KMP by Board 2(57) Net worth to include debit / credit balance of Profit Loss Account 2(76) Related party to include Investing co. or Venturer of the company i.e., a body corporate whose investment in company would result in the company becoming an associate company of the body corporate

5 AMENDMENTS IMPORTANT DEFINITIONS 2(85) - Small co- upper limit of capital 5 Cr to 10 Cr & turnover 20 Cr to 100 Cr 2(87) Subsidiary voting power now 2(91) Turnover realization confusion removed - means the gross amount of revenue recognised in the profit and loss account from the sale, supply, or distribution of goods or on account of services rendered, or both, by a company during a financial year

6 AMENDMENTS PRIVATE PLACEMENT S. 42 to be substituted PP offer not to contain right of renunciation Can have more than one offer at one time, however offer to no. of persons to be within limit of 50 identified persons Amount cannot be utilized unless shares allotted and Form PAS-3 is filed PAS-3 is to be filed within 15 days of allotment Late filing of PAS 3 Penalty on company, promoters & directors for each default - Rs. 1k p. d. Max 25L

7 AMENDMENTS PRIVATE PLACEMENT Penalty for contravention changed to amount involved or Rs. 2 Cr whichever is lower. Amount to be refunded within 30 days of imposing penalty along with interest If offer not as per ss.(2) 50 limit public offer SEBI Act would also apply

8 AMENDMENTS SHARES CA. Pramod Jain S Preferential issue Chapter III (s. 42) also to be complied -( ) S Right Issue Offer letter allowed to be given by courier or any other mode of having proof of delivery. Earlier only speed post or electronic mode -( )

9 AMENDMENTS DEPOSITS S. 73(2) From members: CA. Pramod Jain Amount to be deposited 20 20% (E-15%) by 30th April Deposit insurance not required now In case of default in repayment of deposits which is made good later and 5 years has elapsed can raise deposits Existing deposits period increased from 1 yr to 3 years. Renewal to be done as per Chapter V Penalty u/s 76A - lower limit changed 1 Cr or twice the amount of deposit whichever is lower. Officer in default Imp. 7 yrs & fine (earlier or) 25 L to 2 Cr -( )

10 AMENDMENTS CHARGES S Section may not apply to such charges as prescribed by RBI -( ) S Registrar may allow on application reporting of satisfaction of charge within 300 days with additional fee -( )

11 AMENDMENTS MANAGEMENT Beneficial interest defined in S. 89(10) - ( ) CA. Pramod Jain Beneficial interest in a share includes, directly or indirectly, through any contract, arrangement or otherwise, the right or entitlement of a person alone or together with any other person to Exercise or cause to be exercised any or all of the rights attached to such share; or Receive or participate in any dividend or other distribution in respect of such share. S. 90 substituted to provide for Register of significant beneficial owners in a company

12 AMENDMENTS MANAGEMENT S Every individual, who acting alone or together, or through one or more persons or trust, including a trust and persons resident outside India, holds beneficial interests, of not less than 25% or such other % as may be prescribed, in shares of a company or the right to exercise, or the actual exercising of significant influence or control as defined in s. 2(27), over the company (herein referred to as "significant beneficial owner"), shall make a declaration to the company, specifying the nature of his interest and other particulars.

13 AMENDMENTS MANAGEMENT S. 90 Register of beneficial ownership to be maintained by co file return. Penalty: On person not making declaration Min. 1 L to 10 L continuing 1k p.d. On Co. for not maintaining register and filing return Min. 10 L to 50 L continuing 1k p.d. Willfully False or incorrect information or suppress s. 447 S Abridged Annual Return for OPC & small Co. to exclude indebtness and details of name address, etc of FIIs -( ( )

14 AMENDMENTS MANAGEMENT S AR on website, if any - link in B. Report Listed Co. change in shareholding by top 10 shareholders reporting omitted (S. 93) S. 94 Place to keep registers & AR if to be kept at other than R.O. i.e. where more than 1/10 members no need to give copy of the proposed special resolution in advance to RoC now. AOC-5 for separate place. Certain particulars of register or index or return as may be prescribed not to be available for inspection u/s 94(2)

15 AMENDMENTS ACCOUNTS S. 129(3) CFS substituted -( ( ): To specifically include associate companies CFS to be in accordance with applicable AS CA. Pramod Jain S. 130 Reopening on Court or NCLT order - ( ) : NCLT to give notice to any other person concerned also No reopening for period earlier than 8 FYs immediately preceding the current FYs unless direction issued u/s 128(5) Proviso to keep books of accounts for more than 8 years

16 AMENDMENTS NFRA S ( ) Firm minimum penalty reduced from Rs. 10L to 5 L Appellate authority not to be constituted now ss. 6,7,8 7 9 omitted Appeal now to Appellate Tribunal

17 AMENDMENT FILING OF FS S. 137 ( ) While filing AOC-4 accounts of foreign subsidiary(s) is also to be attached in case of unaudited attached unaudited. If in other language, translate in English and attach

18 AMENDMENTS AUDIT CA. Pramod Jain S. 139(1) 1 st Proviso - Annual Ratification of auditors not required -( ) S ADT 3 Auditor resignation minimum penalty reduced to 50k or the audit fee whichever is less -( ) S. 143(1) - Auditor to have access to records of associate companies also as it relates to CFS -( ) S. 143(3)(i) - Auditor to report on Internal Financial Controls with reference to Financial Statements -( ( )

19 AMENDMENTS AUDIT CA. Pramod Jain 141(3)(i) ) disqualification changed from - ( ) any person whose subsidiary or associate company or other form of entity is engaged on the date of appointment in consulting and specialized services u/s 144 to a person who, directly or indirectly, renders any service referred to in s.144 to the company or its holding company or its subsidiary company. Directly, Indirectly same as in s. 144

20 AMENDMENTS AUDIT -( ( ) 147(2) maximum penalty reduced to 5 L or 4 times the audit fee whichever is less Where default with intention to deceive penalty reduced from 1 L - 25L to 50k - 25L or 8 times the audit fee whichever is less 147(3) - For damages (class action) any other person substituted (restricted to) - members or creditors of company 147 (5) - Criminal liability restricted to the concerned partner who acted in fraudulent manner or abetted or colluded..

21 AMENDMENTS DIRECTORS ( ) S. 149 (3) - Resident director (182 days) requirement changed from calendar year to FY. In case of co. incorporated during year proportionate. S. 149 (6) - Pecuniary relationship for independent director to exclude director remuneration or transactions > 10% of his total income or prescribed amount. Relatives pecuniary limits also specified holding, indebtness & gaurantee-wise

22 AMENDMENTS DIRECTORS In case of relative who is an employee, the restriction shall not apply for his employment during preceding 3 Fys ( ) S. 152 / CG may prescribe any other identification no. which shall be treated as DIN - ( ) S Requirement of deposit Rs. 1 L for standing for directorship shall not apply in case of independent director or dir. recommended by Nomination & Remuneration Comm. or by Board, in case of No Nomn. /Rem. Comm. -( )

23 AMENDMENTS DIRECTORS S. 161 (2) A person holding directorship in company cannot be appointed as alternate director in same company -( ) S. 161 (4) Casual vacancy in office of director may be filled by Board to be approved in next GM in case of all companies (earlier only Public companies) -( ) S. 164(2) - Disqualification not applicable for 6 months of new appointment in defaulting co. Existing director disqualified in all Cos except said Co. [S. 167(1)] -( ( )

24 AMENDMENTS DIRECTORS S. 164(3) - Disqualification related to conviction, by tribunal or not paid calls (6 months) shall continue to apply even if the appeal or petition has been filed against order of conviction or disqualification -( ) S limit to exclude D Cos -( ) S. 167(1) Vacation due to conviction not applicable for 30 days from conviction, if appeal preferred until 7 days appeal or further appeal is disposed off -( ) S DIR 11 made optional -( )

25 AMENDMENTS BOARD MEETINGS S. 173(2) In case where certain matters cannot be dealt in Board meeting through video conferencing - If directors physical present form quorum then other director can attend by video conference or other audio video means too. -( ) S. 177(1) - Audit committee for listed public company and others prescribed -( ) S. 177(4)(iv) - AC to recommend transaction with related party other than 188 to Board if AC does not approve -( )

26 AMENDMENTS BOARD MEETINGS S. 177(4)(iv) - If transaction > 1Cr with related party without AC approval or ratification within 3 months, voidable at option of AC, director to indemnify. Such provisions shall not apply to a transaction, other than a transaction referred to in s. 188, between a holding & WOS -( ) S. 180(1)(c) to include sec. premium -( ) Non-compliance penalty of s. 184(1)/(2) [MBP1, etc] minimum penalty 50k removed max remains at 1 L S.184-For 2 % limit body corp. included

27 AMENDMENTS LOAN TO DIRECTORS -( ( ) S. 185 substituted. Following restriction on giving loan etc. continues: Director of Company Director of holding Company Partner or relative of Director Firm in which director or relative is partner CA. Pramod Jain Others including to Private Co. in which director is director or member allowed, subject to: SR, with complete details in Explanatory statement and proposed utilization by recipient Loans to be utilized for principal business activities

28 AMENDMENTS LOAN TO DIRECTORS -( ) Exemption to a company which in the ordinary course of business gives loans or guarantees or securities in respect of loan if interest is charged not less than bank rate --- changed to 1,3, 5 or 10 year govt. securities prevailing yield (similar to s. 186) All other conditions same Penalty same on giver and receiver Officer in default added Imprisonment upto six months or fine min Rs. 5 L & Max 25 L or both

29 AMENDMENTS LOAN BY COMPANY -( ( ) S. 186(2) - Loan to employees excluded S. 186(3) Limits - aggregating past loans, investments, etc and proposed loans investments, etc. No requirement of SR if loan, guarantee or security is given to WOS or JV Co or investment in WOS. Disclosure u/s 186(4) in FS required S. 186 not applicable to investment made by Invt nvt. co. Investment Co. means whose asset in investments is not less than 50% of total assets or income therefrom is not less than 50% of total income Not applicable on loan etc given by Cos, established with object of and engaged in business of financing Industrial enterprises (earlier Cos)

30 AMENDMENTS FEE S ( ) If not filed within the due period of section: Annual Return CA. Pramod Jain Financial Statements to be filed with ROC Additional Fee not less than Rs. 100 p.d Others additional fee (12 times) other than s. 92, 137 & increase in nominal capital Fee payable - at actual time of filing applicable Higher additional fee not less than twice the additional fee in case of default on 2 or more occasions

31 S. 403 AMENDMENT & IMPACT Within the time specified u/s 403 omitted S. 89 MGT 6 declaration by beneficial owner within 30 days of declaration received S. 92 MGT 7 - Annual return S. 117 MGT 14 - Filing of resolutions S. 121 MGT 15 Report on AGM by listed Cos S. 137 AOC-4 Filing of FS S. 157 Furnishing of DIN

32 AMENDMENTS FEE S. 403 Shall without prejudice to the liability for the payment of fee and additional fee, be liable for the penalty or punishment provided under this Act for such failure or default Declaration by beneficial owner (89): Rs. 500 p.d.. if continuing Rs p.d. AR (92) : Co Rs. 50 K to Rs. 5 L OID Imp upto 6 Months or fine 50K to 5 L or both FS (137) Rs p.d.. max 10 L CA. Pramod Jain

33 AMENDMENTS FEE S. 403 Filing of resolution amended (117): Co - 1 L to 25 L OID 50K to 5 L Report on AGM by listed Cos (121): Co 1 L to 5 L OID 25k to 1 L Furnishing of DIN (157) Co 25k to 1 L OID 25k to 1 L CA. Pramod Jain

34 AMENDMENTS OTHERS S. 247 Registered valuer not to undertake valuation if has direct / indirect interest 3 years prior or 3 years post valuation -( ) S Conversion of firm, LLP etc into company allowed if having 2 or more members (earlier 7). Such co to be registered as Pvt Co S. 374 LLP converted into Co. LLP deemed to be dissolved under LLP Act without further act S CSR applicable to Foreign Cos

35 AMENDMENT - OTHERS CA. Pramod Jain S Compounding allowed if imprisonment not mandatory or punishable with imprisonment and also with fine New S. 446A Due regard to be given for imposing fine or imprisonment -( ) : Size of the company; Nature of business carried on by the company; Injury to public interest; Nature of the default; and Repetition of the default.

36 AMENDMENT - OTHERS CA. Pramod Jain New S. 446B - OPC & SC only ½ of fine/imp. -s. 92, 117& 137 -( ) S If amount involved in fraud is less than Rs. 10L or 1% of turnover imprisonment upto 5 years or fine upto Rs. 25 Lacs or with both. No minimum term or amount -( )

37 RATIONALIZATION OF PENALTIES CA. Pramod Jain Sec. Particulars Old Penalty New Penalty 42 Filing of PAS 3 after 15 days Nil Min - Rs p. d. Max Rs. 25 L 42 Contravention of s. 42 Higher of Rs. 2 Crores or Lower of Rs. 2 Crores or Amount involved Amt involved 76A Deposits Co 1 Cr to 10 Cr OID Imp upto 7 Yrs or fine 25L to 2 Cr Co Lower of 1 Cr or twice amount of deposit to 10 Cr OID Imp upto 7 Yrs AND fine 25L to 2 Cr 117 Filing of Resolutions C- 5 L to 25 L OID 1 L to 5 L C- 1 L to 25 L OID 50K L to 5 L 132 NRFA for Firms Rs. 10 L to 10 times of fee Rs. 5 L to 10 times of fee

38 RATIONALIZATION OF PENALTIES CA. Pramod Jain Sec. Particulars 140 Auditor non filing of ADT-3 on resignation 147(2) Auditor contravention of ss. 139 / 143 / 144 / 145 Provis Auditor knowingly or o to wilfully to deceive by 147(2) contravention of ss. 139 /143 / 144 / Non-compliance of s. 184 (1) / (2) Old Penalty Min - Rs. 50 K Max - Rs. 5 Lakhs Min - Rs. 25 K Max - Rs. 5 Lakhs Imp. Upto 1 year & Min - Rs. 1 L Max - Rs. 25 L Min Rs. 50K Max Rs. 1 L New Penalty Min - Rs. 50 K or remuneration of auditor whichever is less Max - Rs. 5 Lakhs Min - Rs. 50 K Max - Rs. 5 Lakhs or 4 times the audit fee whichever is less Imp upto 1 Yr & Min - Rs. 50 K Max Lower of Rs. 25 L or 8 times the audit fee Min Nil Max Rs. 1 L

39 II VALUATION OF INVENTORIES

40 ICDS II VALUATION OF INVENTORIES Inventory to be valued at cost or NRV whichever is lower. By-products, scrap or waste material are immaterial, they shall be measured at NRV and this value shall be deducted from the cost of the main product. Cost of inventories to include: Cost of purchases; Includes all duties & taxes. AS 2 excludes refundable from taxing authorities

41 ICDS II VALUATION OF INVENTORIES Costs of services - Includes labour and other costs of personnel directly engaged in providing the service including supervisory personnel and attributable overheads Costs of conversion; and Other costs incurred in bringing the inventories to their present location and condition Cost Formulae Specific identification of cost FIFO Weighted Average CA. Pramod Jain

42 ICDS II VALUATION OF INVENTORIES Techniques for measurement of cost: CA. Pramod Jain Standard Cost Retail method (An average percentage for each retail department is to be used ) ICDS - Machinery spares, which can be used only in connection with a tangible fixed asset and their use is expected to be irregular, to be dealt with in accordance with the ICDS V (Tangible fixed assets) The New AS 10 PPE read with new AS 2 FA if expected to be used for more than 12 months

43 ICDS II TAX DUTIES CA. Pramod Jain AS: The costs of purchase shall consist of purchase price including duties & taxes (other than those subsequently recoverable by the enterprise from the taxing authorities), freight inwards & other expenditure directly attributable to the acquisition. (Exclusive method). ICDS: The costs of purchase shall consist of purchase price including duties and taxes, freight inwards & other expenditure directly attributable to the acquisition. (Inclusive method) Already u/s. 145A since amended now

44 ICDS II TAX DUTIES CA. Pramod Jain Assuming that the assessee has opening stock of Rs.3,30,000/- on which input tax rebate of Rs.30,000/- is available. During the year three items Rs.3,00,000/- per item. VAT on 10%. There is no opening stock. Two items are Rs.4,50,000/- per item. VAT on 10%

45 ICDS II TAX DUTIES

46 Sl. No. ADJUSTMENT U/S 145A Particulars CA. Pramod Jain Increase Decrease in profit in profit (Rs Rs) (Rs Rs) 1 Increase in Opening Stock on inclusion of VAT 2 Increase in Purchases on inclusion of VAT Increase in Sales on inclusion of VAT Increase in Closing Stock on inclusion of VAT VAT paid on sales VAT credit availed on cost of goods sold

47 COMPUTATION OF INCOME CA. Pramod Jain

48 ICDS II PARTNERSHIP FIRMS In case of dissolution of a partnership firm or AOP / BOI, notwithstanding whether business is discontinued or not, the inventory on the date of dissolution shall be valued at the NRV. Judicial Precedents: At prevailing market price while preparing a/cs if the business of firm is discontinued- A.L.A. Firm v. CIT [1991] 55 Taxman 497(SC) Business continued without any interruption after death - closing stock was to be valued at cost or MP, whichever was lower, & not at market value -Sakthi Trading Co. v. CIT [2001] 118 Taxman 301 (SC)

49 DHC CA. Pramod Jain ICDS Contrary to DHC Finance Act 2018 Stock-in in-trade in case of dissolution of firm to be valued at market price irrespective of whether the business discontinues. Shakti Trading Co. 250 ITR 871 (SC) Section 145A of the IT Act providing valuation of inventory in accordance with the method of accounting regularly employed by the taxpayer is independent and irrespective of section 145(2) (ICDS). Section 145A amended

50 FINANCE ACT 2018 S. 145A Valuation of inventory shall be made at lower of actual cost or NRV in accordance with ICDS notified u/s 145(2) Valuation of purchase and sale of goods or services and of inventory shall be adjusted to include the amount of any tax, duty, cess or fee actually paid or incurred by the assessee to bring the goods or services to the place of its location and condition as on the date of valuation.

51 ICDS II VALUATION OF INVENTORIES No Interest /borrowing cost unless as per ICDS IX Where inventories require a period of 12 months or more to bring them to a saleable condition Value of the inventory as on beginning of PY shall be: Cost of inventory available, if any, on day of commencement of business when the business has commenced during the PY; Value of the inventory as on the close of the immediately preceding PY, in any other case.

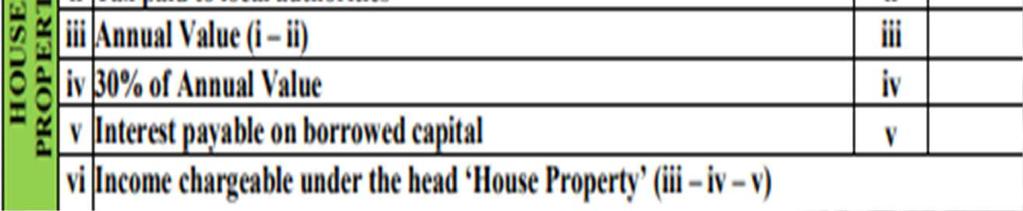

52 ICDS II DISCLOSURES CA. Pramod Jain Accounting policies adopted in measuring inventories including the cost formulae used. Where Standard Costing has been used as a measurement of cost, details of such inventories and a confirmation of the fact that standard cost approximates the actual cost; The total carrying amount of inventories and its classification appropriate to a person. AS same as above except underlined content

53 ICDS II PRACTICAL IMPLICATION Disclosures Same as per AS 2, but if standard cost used.. State whether it approximates the actual cost Carrying amount?? If there is change in method of valuation of inventory its change in accounting policy follow AS 1 disclosure Take care at time of dissolution of partnership firm

54 ICDS II PRACTICAL IMPLICATION Disclosure for not following inclusive method of valuation of inventory non-compliance of s. 145A Already reporting at Para 14(b) of Form 3CD refer Para 23 of ICAI Tax Audit Guidance Note (After GST refer Paras to 23.24) ITR for AY says to disclose other than 145A?? Form 3CD?? Borrowing costs for inventories only if they require a period of 12 months or more to bring them to a saleable condition

55 FORM 3CD CLAUSE 13(E) ICD S II Name of ICDS Valuation of Inventories Increase Decrease Net (Rs ( Rs.) Description in Profit in Profit Difference over cost to NRV in case of dissolution of firm. Valued at lower in books Total 10000

56 FORM 3CD CLAUSE 13(F) ICDS II Name of ICDS Valuation of Inventories Disclosures Refer to Note No. _ to Financial Statements For carrying amount & classification refer Note No. _ to Balance Sheet Inventories are not inclusive of duties and taxes, yet there is no effect on profits, refer to clause 14(b) of Form 3CD Assessee is following Standard Costing as a measurement of cost, and that approximates the actual cost

57

58 WHICH ITR CA. Pramod Jain No major change except ITR 1, 2 & 3 Form AY AY ITR- 1 For Individuals having Income from Salaries, one house property, other sources (Interest etc.) having total income up to Rs.50 lakh For individuals being a resident other than not ordinarily resident having Income from Salaries, one house property, other sources (Interest etc.) having total income up to Rs.50 lakh ITR-2 For Individuals and HUFs not carrying out business or profession Being a partner received Salary, bonus, interest, commission or remuneration from the firm treats as business Income For Individuals and HUFs not carrying out business or profession

59 S. 234F FEE CA. Pramod Jain

60 DETAILS INCREASED SALARY & HP DETAILS

61 GENDER EQUALITY CA. Pramod Jain

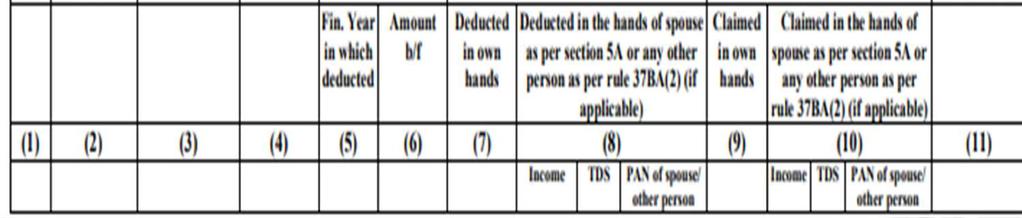

62 CREDIT TRANSFER OF TDS CREDIT

63 GSTR DETAILS ITR 4

64 PRESUMPTIVE NO BOOKS???

65 PRESUMPTIVE NO BOOKS???

66 GSTR DETAILS ITR 3, 5 &

67 RESIDENTS REFUND BANK NON-RESIDENTS

68 RELIEF NON-RESIDENTS LTCG DTAA RELIEF

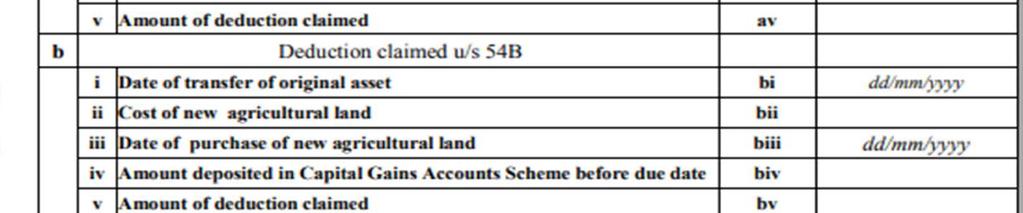

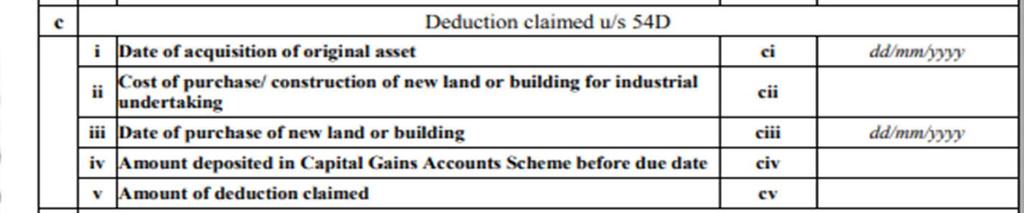

69 MORE DETAILS FOR CG DEDUCTIONS 2017

70 MORE DETAILS FOR CG DEDUCTIONS 2018

71 SHARES TRANSFER OF UNQUOTED SHARES

72 SHARES TRANSFER OF UNQUOTED SHARES

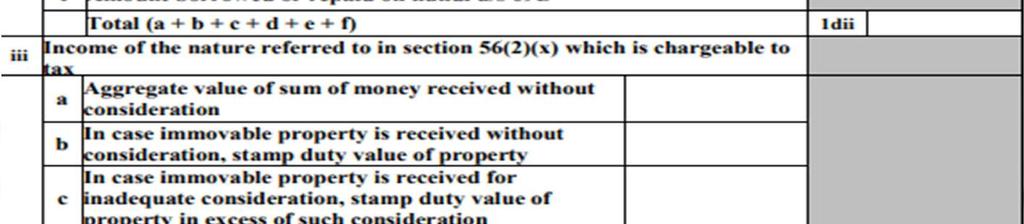

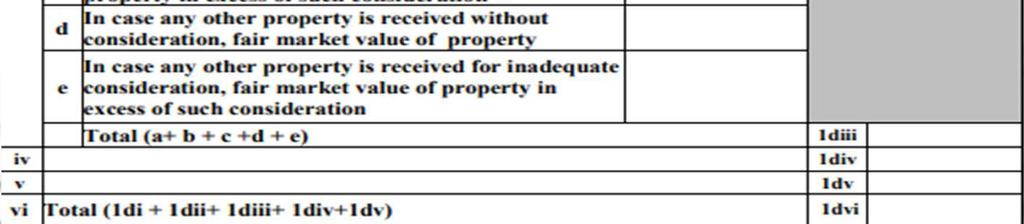

73 ADDITIONAL DETAILS FOR S. 56(2)

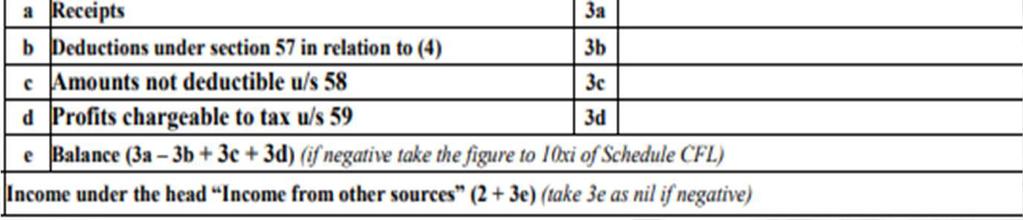

74 S. 58 & S. 59 CA. Pramod Jain

75 S. 115BBG TRANSFER OF CARBON CREDITS

76 ICDS IMPACT CA. Pramod Jain

77 ICDS IMPACT CA. Pramod Jain

78 REVISED DEPRECIATION CA. Pramod Jain

79 ITR-6 SPECIFIC CHANGES CA. Pramod Jain Separate Format for Balance Sheet and Profit & Loss Account has provided for companies on which Ind-AS is applicable in ITR-6 CSR appropriation

80 GST ITR-6 SPECIFIC CHANGES - GST

81 ITR-6 FOREIGN CURRENCY

82 ITR-6 OWNERSHIP UNLISTED CO

83 ITR 7 CHANGES CHANGE IN OBJECTS 2017

84 ITR 7 CHANGES CHANGE IN OBJECTS 2018

85 ITR 7 CHANGES CORPUS DONATION 2017

86 ITR 7 CHANGES CORPUS DONATION 2018

87 This Presentation would be available on Also may download free mobile app LUNAWAT For all updates & Ready to use Charts since year 2007

88 A one stop place where all your Queries can be answered by various Experts throughout the Country

89 Together we shall make it. CA. Pramod Jain CA. Pramod Jain

CHANGES IN ITR FOR AY COMPANIES (AMENDMENT) ACT 2017 SIGNIFICANT BENEFICIAL OWNERSHIP CA. PRAMOD JAIN

ACT 2017 SIGNIFICANT BENEFICIAL OWNERSHIP CA. PRAMOD JAIN") CHANGES IN ITR FOR AY 2018-19 COMPANIES (AMENDMENT) ACT 2017 SIGNIFICANT BENEFICIAL OWNERSHIP CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at West Delhi Study Circle of NIRC of ICAI

CHANGES IN ITR FOR AY 2018-19 COMPANIES (AMENDMENT) ACT 2017 SIGNIFICANT BENEFICIAL OWNERSHIP CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at West Delhi Study Circle of NIRC of ICAI

ICDS Overview & ICDS I & II

ICDS Overview & ICDS I & II CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at NIRC of ICAI jointly with CPE Study Circles: North Campus North-Ex Netaji Subhash Place Rohini 11 th May

ICDS Overview & ICDS I & II CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at NIRC of ICAI jointly with CPE Study Circles: North Campus North-Ex Netaji Subhash Place Rohini 11 th May

ICDS Overview & ICDS I, II & IV

ICDS Overview & ICDS I, II & IV CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at NIRC of ICAI 28 th April 2018 BASICS CA. Pramod Jain Source Effective Date Heads of Income No. of

ICDS Overview & ICDS I, II & IV CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at NIRC of ICAI 28 th April 2018 BASICS CA. Pramod Jain Source Effective Date Heads of Income No. of

ICDS Disclosures & Reporting ICDS I, II, III, IV & IX

ICDS Disclosures & Reporting ICDS I, II, III, IV & IX CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Eagle Group 24 th September 2017 WHAT TO DO CA. Pramod Jain Get the FS prepared complying

ICDS Disclosures & Reporting ICDS I, II, III, IV & IX CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Eagle Group 24 th September 2017 WHAT TO DO CA. Pramod Jain Get the FS prepared complying

Practical Aspects of Audit under Income Tax Act and Companies Act

Practical Aspects of Audit under Income Tax Act and Companies Act LUNAWAT & CO. Chartered Accountants 16 th January 2016, Gurgaon CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA AUDIT PROCESS APPOINTMENT

Practical Aspects of Audit under Income Tax Act and Companies Act LUNAWAT & CO. Chartered Accountants 16 th January 2016, Gurgaon CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA AUDIT PROCESS APPOINTMENT

Loans & Deposits. Companies Act 2013 Audit Reports CA. PRAMOD JAIN. under

Loans & Deposits under Companies Act 2013 Audit Reports CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Pusa Road CPE Study Circle of NIRC of ICAI 30 th December 2018 CA. Pramod

Loans & Deposits under Companies Act 2013 Audit Reports CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Pusa Road CPE Study Circle of NIRC of ICAI 30 th December 2018 CA. Pramod

Practical Aspects of Audit under Income Tax Act and Companies Act (Including CARO 2016 & IFC / ICFR)

") Practical Aspects of Audit under Income Tax Act and Companies Act (Including CARO 2016 & IFC / ICFR) LUNAWAT & CO. Chartered Accountants 20 th February 2016, North Campus CA. PRAMOD JAIN FCA, FCS, FCMA,

Practical Aspects of Audit under Income Tax Act and Companies Act (Including CARO 2016 & IFC / ICFR) LUNAWAT & CO. Chartered Accountants 20 th February 2016, North Campus CA. PRAMOD JAIN FCA, FCS, FCMA,

AN OVERVIEW OF THE COMPANIES (AMENDMENT) BILL, As passed by the Parliament

BILL, As passed by the Parliament") AN OVERVIEW OF THE COMPANIES (AMENDMENT) BILL, 2017 As passed by the Parliament BRIEF SUMMARY The Companies (Amendment) Bill, 2017, introduced in Lok Sabha on 16 March, 2016 as The Companies (Amendment)

AN OVERVIEW OF THE COMPANIES (AMENDMENT) BILL, 2017 As passed by the Parliament BRIEF SUMMARY The Companies (Amendment) Bill, 2017, introduced in Lok Sabha on 16 March, 2016 as The Companies (Amendment)

The Companies (Amendment) Act, 2017

Act, 2017") The Companies (Amendment) Act, 2017 - Strengthening Corporate Governance - Action against Defaulting Companies AND - Helps Improve Ease of Doing Business JOURNEY The Companies (Amendment) Bill 2016, introduced

The Companies (Amendment) Act, 2017 - Strengthening Corporate Governance - Action against Defaulting Companies AND - Helps Improve Ease of Doing Business JOURNEY The Companies (Amendment) Bill 2016, introduced

11 th April 2018 IIBF CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA

, FCA, FCS, FCMA, LL.B, MIMA, DISA") 11 th April 2018 IIBF CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA AGENDA BANKERS PERSPECTIVE Corporate Balance sheet Annual Report Directors Report Auditors Report Aspects of Accounting

11 th April 2018 IIBF CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA AGENDA BANKERS PERSPECTIVE Corporate Balance sheet Annual Report Directors Report Auditors Report Aspects of Accounting

LUNAWAT & CO. Chartered Accountants 16 th April 2016, Pune CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA

SHARE CAPITAL & DEPOSITS LUNAWAT & CO. Chartered Accountants 16 th April 2016, Pune CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Lunawat & Co. ISSUE OF SECURITIES Lunawat & Co. Public Public Issue

SHARE CAPITAL & DEPOSITS LUNAWAT & CO. Chartered Accountants 16 th April 2016, Pune CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Lunawat & Co. ISSUE OF SECURITIES Lunawat & Co. Public Public Issue

PRACTICAL IMPLICATIONS OF ICDS (Except ICDS VI, VII & X)

") PRACTICAL IMPLICATIONS OF ICDS (Except ICDS VI, VII & X) CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Trinagar Keshav Puram CPE Study Circle of NIRC of ICAI 4 th September 2017 SUMMARY CA.

PRACTICAL IMPLICATIONS OF ICDS (Except ICDS VI, VII & X) CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Trinagar Keshav Puram CPE Study Circle of NIRC of ICAI 4 th September 2017 SUMMARY CA.

Interim Union Budget 2019 Important changes for AY Recent Amendments in Companies Act CA. PRAMOD JAIN

Interim Union Budget 2019 Important changes for AY 2019-20 Recent Amendments in Companies Act CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA, IP Shared at Agra Branch of CIRC of ICAI 9 th

Interim Union Budget 2019 Important changes for AY 2019-20 Recent Amendments in Companies Act CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA, IP Shared at Agra Branch of CIRC of ICAI 9 th

CRITICAL ISSUES in TAX AUDIT & ICDS I & II

CRITICAL ISSUES in TAX AUDIT & ICDS I & II CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Panchkuin Road CPE of NIRC of ICAI 15 th September 2017 LEGISLATION FOR AY 2017-18 18 S. 44AB Rule

CRITICAL ISSUES in TAX AUDIT & ICDS I & II CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Panchkuin Road CPE of NIRC of ICAI 15 th September 2017 LEGISLATION FOR AY 2017-18 18 S. 44AB Rule

Critical Issues in ICDS I to V & IX

Critical Issues in ICDS I to V & IX CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Gurugram Branch of NIRC of ICAI 18 th May 2018 BASICS CA. Pramod Jain Source Effective Date No.

Critical Issues in ICDS I to V & IX CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Gurugram Branch of NIRC of ICAI 18 th May 2018 BASICS CA. Pramod Jain Source Effective Date No.

TAX AUDIT & ICDS CA. PRAMOD JAIN. B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Dehradun Branch of CIRC of ICAI 15 th July 2018

, FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Dehradun Branch of CIRC of ICAI 15 th July 2018") TAX AUDIT & ICDS CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Dehradun Branch of CIRC of ICAI 15 th July 2018 CA. Pramod Jain LEGISLATION FOR AY 2017-18 18 S. 44AB Rule 6G Form

TAX AUDIT & ICDS CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Dehradun Branch of CIRC of ICAI 15 th July 2018 CA. Pramod Jain LEGISLATION FOR AY 2017-18 18 S. 44AB Rule 6G Form

Basics of Tax Audit and ICDS I, II & IV

Basics of Tax Audit and ICDS I, II & IV CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at East Delhi Study Circle of NIRC of ICAI 19 th August 2017 LEGISLATION FOR AY 2017-18 18 S. 44AB Rule

Basics of Tax Audit and ICDS I, II & IV CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at East Delhi Study Circle of NIRC of ICAI 19 th August 2017 LEGISLATION FOR AY 2017-18 18 S. 44AB Rule

PRACTICAL IMPLICATIONS

PRACTICAL IMPLICATIONS West Delhi Study Circle of NIRC of ICAI 29 th May 2017 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA WHO TO FOLLOW ICDS Assessee having PGBP & Other Source income having Method

PRACTICAL IMPLICATIONS West Delhi Study Circle of NIRC of ICAI 29 th May 2017 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA WHO TO FOLLOW ICDS Assessee having PGBP & Other Source income having Method

Chartered Accountants

LUNAWAT & CO. Chartered Accountants CA. PRAMOD JAIN FCA, FCS, FCMA, MIMA, DISA THE COMPANIES ACT, 2013 18/12/2012 Lok Sabha 08/08/2013 Rajya Sabha 29/08/2013 President Assent 30/08/2013 Companies Act 2013

LUNAWAT & CO. Chartered Accountants CA. PRAMOD JAIN FCA, FCS, FCMA, MIMA, DISA THE COMPANIES ACT, 2013 18/12/2012 Lok Sabha 08/08/2013 Rajya Sabha 29/08/2013 President Assent 30/08/2013 Companies Act 2013

COMPANIES ACT LUNAWAT & CO. Chartered Accountants

COMPANIES ACT 2013 LUNAWAT & CO. Chartered Accountants CA. PRAMOD JAIN FCA, FCS, FCMA, MIMA, DISA GENERAL It applies to the whole of India and is also applicable to certain companies or bodies corporate

COMPANIES ACT 2013 LUNAWAT & CO. Chartered Accountants CA. PRAMOD JAIN FCA, FCS, FCMA, MIMA, DISA GENERAL It applies to the whole of India and is also applicable to certain companies or bodies corporate

Specific issues in Audit for FY under Companies Act, 2013

Specific issues in Audit for FY 2014-15 under Companies Act, 2013 LUNAWAT & CO. Chartered Accountants 24 th April 2015 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA ????? Why so many Seminars on Companies

Specific issues in Audit for FY 2014-15 under Companies Act, 2013 LUNAWAT & CO. Chartered Accountants 24 th April 2015 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA ????? Why so many Seminars on Companies

COMPANIES(AMENDMENT) ACT, 2017 CS.DESIKAN BALAJI ADVOCATE

ACT, 2017 CS.DESIKAN BALAJI ADVOCATE") COMPANIES(AMENDMENT) ACT, 2017 CS.DESIKAN BALAJI ADVOCATE desikan.b@gmail.com +91 98840 61064 AMENDMENT IS MANDATORY FOR EVERY LAW No organic law can ever be framed with a provision specifically applicable

COMPANIES(AMENDMENT) ACT, 2017 CS.DESIKAN BALAJI ADVOCATE desikan.b@gmail.com +91 98840 61064 AMENDMENT IS MANDATORY FOR EVERY LAW No organic law can ever be framed with a provision specifically applicable

Finalization of Audit for FY ALWAR

Finalization of Audit for FY 2014-15 ALWAR LUNAWAT & CO. Chartered Accountants 3 rd May 2015 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA ????? Why so many Seminars on Companies Act 2013? What has

Finalization of Audit for FY 2014-15 ALWAR LUNAWAT & CO. Chartered Accountants 3 rd May 2015 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA ????? Why so many Seminars on Companies Act 2013? What has

Auditors Reporting Requirements

Auditors Reporting Requirements LUNAWAT & CO. Chartered Accountants 21 st June 2015 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA ????? Why so many Seminars on Companies Act 2013? What has changed so

Auditors Reporting Requirements LUNAWAT & CO. Chartered Accountants 21 st June 2015 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA ????? Why so many Seminars on Companies Act 2013? What has changed so

Loans & Deposits Under Companies Act 2013

Loans & Deposits Under Companies Act 2013 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at CICASA, Ranchi of CIRC of ICAI 26 th November 2017 What is first thing to be SUCCESSFULL?? RECEIVING

Loans & Deposits Under Companies Act 2013 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at CICASA, Ranchi of CIRC of ICAI 26 th November 2017 What is first thing to be SUCCESSFULL?? RECEIVING

Interim Union Budget 2019 & Important changes for AY CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA, IP

, FCA, FCS, FCMA, LL.B, MIMA, DISA, IP") Interim Union Budget 2019 & Important changes for AY 2019-20 CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA, IP Shared at Nehru Place CPE Study Circle of NIRC of ICAI 7 th February 2019 INCOME

Interim Union Budget 2019 & Important changes for AY 2019-20 CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA, IP Shared at Nehru Place CPE Study Circle of NIRC of ICAI 7 th February 2019 INCOME

Note on Companies (Amendment) Bill, 2017

Bill, 2017") Note on Companies (Amendment) Bill, 2017 By: G Usha, Practising Company Secretary E-Mail: cs.ushaganapathy@gmail.com, Contact: 9741097191 December 20, 2017 This article presents a Chapter-wise note on

Note on Companies (Amendment) Bill, 2017 By: G Usha, Practising Company Secretary E-Mail: cs.ushaganapathy@gmail.com, Contact: 9741097191 December 20, 2017 This article presents a Chapter-wise note on

FINANCIAL LITERACY FOR DIRECTORS CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA. 16 th December 2017, IOD

FINANCIAL LITERACY FOR DIRECTORS 16 th December 2017, IOD CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA CA. Pramod Jain Annual Report Director s Report Auditor s Report Financial Statements Balance

FINANCIAL LITERACY FOR DIRECTORS 16 th December 2017, IOD CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA CA. Pramod Jain Annual Report Director s Report Auditor s Report Financial Statements Balance

Committed to quality and excellence

Committed to quality and excellence www.rsmindia.in Newsflash: Companies (Amendment) Bill 2017 The Companies (Amendment) Bill, 2016, (Old Bill) was introduced in Lok Sabha on 16 March, 2016. It was then

Committed to quality and excellence www.rsmindia.in Newsflash: Companies (Amendment) Bill 2017 The Companies (Amendment) Bill, 2016, (Old Bill) was introduced in Lok Sabha on 16 March, 2016. It was then

CA. PRAMOD JAIN. B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Laxmi Nagar CPE Study Circle of NIRC of ICAI 16 th February 2018

, FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Laxmi Nagar CPE Study Circle of NIRC of ICAI 16 th February 2018") Union Budget 2018 CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Laxmi Nagar CPE Study Circle of NIRC of ICAI 16 th February 2018 INCOME TAX PROPOSALS TAX RATES No change in tax

Union Budget 2018 CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Laxmi Nagar CPE Study Circle of NIRC of ICAI 16 th February 2018 INCOME TAX PROPOSALS TAX RATES No change in tax

Practical issues in Finalization of Audit for FY

Practical issues in Finalization of Audit for FY 2014-2015 LUNAWAT & CO. Chartered Accountants 22 nd August 2015, Faridabad CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA AGENDA Filing of Resolutions

Practical issues in Finalization of Audit for FY 2014-2015 LUNAWAT & CO. Chartered Accountants 22 nd August 2015, Faridabad CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA AGENDA Filing of Resolutions

CS SAROJ KUMAR RAY, FCS

COMPANIES ACT 2013 CS SAROJ KUMAR RAY, FCS FOCUS AREAS AUDIT & AUDITORS CHAPTER X : AUDITORS Appointment/ Eligibility etc. Removal/ Resignation Penal Provisions Others Sec. 139 : Appointment of Auditors

COMPANIES ACT 2013 CS SAROJ KUMAR RAY, FCS FOCUS AREAS AUDIT & AUDITORS CHAPTER X : AUDITORS Appointment/ Eligibility etc. Removal/ Resignation Penal Provisions Others Sec. 139 : Appointment of Auditors

Deposits. CA. Pramod Jain_. This document would assist in understanding the requirements for accepting / renewing DEPOSITS under Companies Act, 2013

Deposits CA. Pramod Jain_ B. Com (H), FCA, FCS, FCMA, LL.B. DISA, MIMA This document would assist in understanding the requirements for accepting / renewing DEPOSITS under Companies Act, 2013 17-Aug-15

Deposits CA. Pramod Jain_ B. Com (H), FCA, FCS, FCMA, LL.B. DISA, MIMA This document would assist in understanding the requirements for accepting / renewing DEPOSITS under Companies Act, 2013 17-Aug-15

Shell Companies Strike-off Companies Director Disqualification CODS 2018

Shell Companies Strike-off Companies Director Disqualification CODS 2018 Shared at Vikas Marg CA Study Circle NIRC of ICAI 26 th December 2017 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA SHELL COMPANY

Shell Companies Strike-off Companies Director Disqualification CODS 2018 Shared at Vikas Marg CA Study Circle NIRC of ICAI 26 th December 2017 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA SHELL COMPANY

e-form ACTIVE BUDS Ordinance 2019 DPT- 3 & MSME Compliance Significant Beneficial Ownership Recent Amendments in Companies Act CA.

e-form ACTIVE BUDS Ordinance 2019 DPT- 3 & MSME Compliance Significant Beneficial Ownership Recent Amendments in Companies Act CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA, IP Shared at

e-form ACTIVE BUDS Ordinance 2019 DPT- 3 & MSME Compliance Significant Beneficial Ownership Recent Amendments in Companies Act CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA, IP Shared at

PRACTICAL IMPLICATIONS

PRACTICAL IMPLICATIONS CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at South Delhi CA Study Circle of NIRC of ICAI 22 nd June 2017 ICDS BACKGROUND CA. Pramod Jain CG notified 10 ICDS vide notification

PRACTICAL IMPLICATIONS CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at South Delhi CA Study Circle of NIRC of ICAI 22 nd June 2017 ICDS BACKGROUND CA. Pramod Jain CG notified 10 ICDS vide notification

Nehru Place CPE Study Circle 21 st November 2017 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA

Nehru Place CPE Study Circle 21 st November 2017 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Incorporate / Convert Partners Individual Body Corporate Designated Partners Min - 2 Max NA DPIN / DIN

Nehru Place CPE Study Circle 21 st November 2017 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Incorporate / Convert Partners Individual Body Corporate Designated Partners Min - 2 Max NA DPIN / DIN

PRACTICAL IMPLICATIONS

PRACTICAL IMPLICATIONS CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Ludhiana Branch of NIRC of ICAI 10 th June 2017 WHO TO FOLLOW ICDS Assessee having PGBP & Other Source income having Method

PRACTICAL IMPLICATIONS CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Ludhiana Branch of NIRC of ICAI 10 th June 2017 WHO TO FOLLOW ICDS Assessee having PGBP & Other Source income having Method

LUNAWAT & CO. Chartered Accountants 15 th April 2017, Janakpuri CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA

APPLICABILITY OVERVIEW LUNAWAT & CO. Chartered Accountants 15 th April 2017, Janakpuri CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA ICDS BACKGROUND CG notified 10 ICDS vide notification no. 32 of 2015

APPLICABILITY OVERVIEW LUNAWAT & CO. Chartered Accountants 15 th April 2017, Janakpuri CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA ICDS BACKGROUND CG notified 10 ICDS vide notification no. 32 of 2015

Voices on Reporting. Quarterly updates. January Contents. Updates relating to the Companies Act, Updates relating to Ind AS

Voices on Reporting Quarterly updates January 2018 Contents Updates relating to the Companies Act, 2013 Updates relating to Ind AS Updates relating to SEBI regulations Other regulatory updates 01 19 25

Voices on Reporting Quarterly updates January 2018 Contents Updates relating to the Companies Act, 2013 Updates relating to Ind AS Updates relating to SEBI regulations Other regulatory updates 01 19 25

THE COMPANIES ACT, 2013

THE COMPANIES ACT, 2013 A Presentation by: Rajeev Goel B Com (Hons), LLB, FCS, MIMA Corporate Lawyer 93124 09354 rajeev391@gmail.com The Companies Act, 2013 Overview of Changes Accounts, Audit & Auditors

THE COMPANIES ACT, 2013 A Presentation by: Rajeev Goel B Com (Hons), LLB, FCS, MIMA Corporate Lawyer 93124 09354 rajeev391@gmail.com The Companies Act, 2013 Overview of Changes Accounts, Audit & Auditors

Presentation by CA M.R.HUNDIWALA M.R.HUNDIWALA & CO. CHARTERED ACCOUNTANTS AURANGABAD/PUNE

Presentation by CA M.R.HUNDIWALA M.R.HUNDIWALA & CO. CHARTERED ACCOUNTANTS AURANGABAD/PUNE 2 Synopsis of Contents Background of Section 145 Journey of notified standards under Section 145 Notified ICDS

Presentation by CA M.R.HUNDIWALA M.R.HUNDIWALA & CO. CHARTERED ACCOUNTANTS AURANGABAD/PUNE 2 Synopsis of Contents Background of Section 145 Journey of notified standards under Section 145 Notified ICDS

Satwinder Singh Partner, Vaish Associates Advocates Central Council Member-ICSI

Satwinder Singh Partner, Vaish Associates Advocates Central Council Member-ICSI Satwinder@vaishlaw.com Chapter 1: Definitions Section No. Companies Act, 2013 Companies (Amendment) Bill, 2017 Section 2(6)

Satwinder Singh Partner, Vaish Associates Advocates Central Council Member-ICSI Satwinder@vaishlaw.com Chapter 1: Definitions Section No. Companies Act, 2013 Companies (Amendment) Bill, 2017 Section 2(6)

INCOME COMPUTATION AND DISCLOSURE STANDARDS. CA. P T JOY, BCom, LLB, FCA, DISA

INCOME COMPUTATION AND DISCLOSURE STANDARDS CA. P T JOY, BCom, LLB, FCA, DISA DISCLAIMER This power point presentation contains professional view of certain legal or statutory provisions. The ownership

INCOME COMPUTATION AND DISCLOSURE STANDARDS CA. P T JOY, BCom, LLB, FCA, DISA DISCLAIMER This power point presentation contains professional view of certain legal or statutory provisions. The ownership

Whether there is ease of doing business for Private Companies under Company Law?

Whether there is ease of doing business for Private Companies under Company Law? The Ministry of Corporate Affairs ( MCA ) has exempted private companies from the compliance of certain provisions of Company

Whether there is ease of doing business for Private Companies under Company Law? The Ministry of Corporate Affairs ( MCA ) has exempted private companies from the compliance of certain provisions of Company

Draft Disclosures of ICDS in Clause 13(f) of Form 3CD

of Form 3CD") 2017 Draft Disclosures of ICDS in Clause 13(f) of Form 3CD CA. Pramod Jain B. Com (H), FCA, FCS, FCMA, LL.B, MIMA, DISA 9 th October 2017 CONTENTS S. No Content Page No(s) 1 Statutory Summary 3 2 To Whom

2017 Draft Disclosures of ICDS in Clause 13(f) of Form 3CD CA. Pramod Jain B. Com (H), FCA, FCS, FCMA, LL.B, MIMA, DISA 9 th October 2017 CONTENTS S. No Content Page No(s) 1 Statutory Summary 3 2 To Whom

LATEST IN INCOME TAX. LUNAWAT & CO. Chartered Accountants CA. PRAMOD JAIN. (From Businessmen s Point of View) 3 rd June, Phagwara

3 rd June, Phagwara") LATEST IN INCOME TAX (From Businessmen s Point of View) LUNAWAT & CO. Chartered Accountants 3 rd June, Phagwara CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA AGENDA Lunawat & Co. PAN Quoting AIR Reporting

LATEST IN INCOME TAX (From Businessmen s Point of View) LUNAWAT & CO. Chartered Accountants 3 rd June, Phagwara CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA AGENDA Lunawat & Co. PAN Quoting AIR Reporting

Updates/Amendments in Companies Act, CS DHARMENDRA GANATRA PRACTISING COMPANY SECRETARY Saturday

Updates/Amendments in Companies Act, 2013 CS DHARMENDRA GANATRA PRACTISING COMPANY SECRETARY Saturday- 07.10.2017 CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA

Updates/Amendments in Companies Act, 2013 CS DHARMENDRA GANATRA PRACTISING COMPANY SECRETARY Saturday- 07.10.2017 CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA

MAJOR Income Tax Proposals in UNION BUDGET 2017

MAJOR Income Tax Proposals in UNION BUDGET 2017 LUNAWAT & CO. Chartered Accountants 3 rd February 2017, Nehru Place CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA THE CRUX TIMELY FILING OF RETURNS No

MAJOR Income Tax Proposals in UNION BUDGET 2017 LUNAWAT & CO. Chartered Accountants 3 rd February 2017, Nehru Place CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA THE CRUX TIMELY FILING OF RETURNS No

CA Paresh Vakharia. Standards (ICDS) Accounting Policies, Inventories & Government Grants. A Workshop organized by

Accounting Policies, Inventories & Government Grants. A Workshop organized by") CA Paresh Vakharia On Income Computation and Disclosure Standards (ICDS) Accounting Policies, Inventories & Government Grants A Workshop organized by Western India Regional Council of ICAI, Mumbai 31 October

CA Paresh Vakharia On Income Computation and Disclosure Standards (ICDS) Accounting Policies, Inventories & Government Grants A Workshop organized by Western India Regional Council of ICAI, Mumbai 31 October

ACCOUNTS & AUDIT UNDER COMPANIES ACT,2013

ACCOUNTS & AUDIT UNDER COMPANIES ACT,2013 Advocate Arun Saxena Advocates & Attorneys 603-604, New Delhi House, 27, Barakhamba Road, New Delhi 110 001. Ph: 43044999, Mob.: 9810037364 E-mail : advisor@sslclegal.in

ACCOUNTS & AUDIT UNDER COMPANIES ACT,2013 Advocate Arun Saxena Advocates & Attorneys 603-604, New Delhi House, 27, Barakhamba Road, New Delhi 110 001. Ph: 43044999, Mob.: 9810037364 E-mail : advisor@sslclegal.in

DRIVING FINANCIAL PERFORMANCE

DRIVING FINANCIAL PERFORMANCE 26 th October 2017, IOD, Kolkata CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA BOD / DIRECTORS RESPONSIBILITIES To act with due diligence and care in the best interest

DRIVING FINANCIAL PERFORMANCE 26 th October 2017, IOD, Kolkata CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA BOD / DIRECTORS RESPONSIBILITIES To act with due diligence and care in the best interest

APPOINTMENT OF AUDITOR (Section -139) Particulars Non Government Company Government Company

Particulars Non Government Company Government Company") Appointment of 1 st Audit After Incpation (Till the conclusion of first AGM) {139 (6 & 7)} [AUDIT AND AUDITORS ] (Section 139 to 148) APPOINTMENT OF AUDITOR (Section -139) Particulars Non Government Company

Appointment of 1 st Audit After Incpation (Till the conclusion of first AGM) {139 (6 & 7)} [AUDIT AND AUDITORS ] (Section 139 to 148) APPOINTMENT OF AUDITOR (Section -139) Particulars Non Government Company

REPLYING TO IT NOTICES & CASH RESTRICTIONS

REPLYING TO IT NOTICES & CASH RESTRICTIONS CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Advocate Forum, Delhi 30 th June 2018 INQUIRY NOTICES Simple letter 133(6) 131 131 (1A)

REPLYING TO IT NOTICES & CASH RESTRICTIONS CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Advocate Forum, Delhi 30 th June 2018 INQUIRY NOTICES Simple letter 133(6) 131 131 (1A)

Cash Restrictions Recent Amendments for FS for FY & ICDS OVERVIEW ICDS VIII - SECURITIES

Cash Restrictions Recent Amendments for FS for FY 2016-17 & ICDS OVERVIEW ICDS VIII - SECURITIES LUNAWAT & CO. Chartered Accountants 21 st April 2017, Rohini CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA,

Cash Restrictions Recent Amendments for FS for FY 2016-17 & ICDS OVERVIEW ICDS VIII - SECURITIES LUNAWAT & CO. Chartered Accountants 21 st April 2017, Rohini CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA,

ICDS (I V & IX) AS AMENDMENTS TAX AUDIT ISSUES SCHEDULE III AMENDMENTS

AS AMENDMENTS TAX AUDIT ISSUES SCHEDULE III AMENDMENTS") ICDS (I V & IX) AS AMENDMENTS TAX AUDIT ISSUES SCHEDULE III AMENDMENTS CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Indore Branch of CIRC of ICAI 30 th August 2017 CA. Pramod Jain SCHEDULE

ICDS (I V & IX) AS AMENDMENTS TAX AUDIT ISSUES SCHEDULE III AMENDMENTS CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Indore Branch of CIRC of ICAI 30 th August 2017 CA. Pramod Jain SCHEDULE

Companies Act Provisions Related to Private Limited Companies. Udyog Software (India) Ltd. 20/08/2014

Ltd. 20/08/2014") Companies Act 2013 Provisions Related to Private Limited Companies Udyog Software (India) Ltd. 20/08/2014 This document contains a brief on Provisions Related to Private Limited Companies under Companies

Companies Act 2013 Provisions Related to Private Limited Companies Udyog Software (India) Ltd. 20/08/2014 This document contains a brief on Provisions Related to Private Limited Companies under Companies

Actionables pursuant to passing of Companies (Amendment) Act, 2017

Act, 2017") Actionables pursuant to passing of Companies (Amendment) Act, 2017 Team Vinod Kothari & Company corplaw@vinodkothari.com Pursuant to the assent granted by Lok Sabha on July 27, 2017 to the Companies (Amendment)

Actionables pursuant to passing of Companies (Amendment) Act, 2017 Team Vinod Kothari & Company corplaw@vinodkothari.com Pursuant to the assent granted by Lok Sabha on July 27, 2017 to the Companies (Amendment)

PREVENTION OF CORPORATE FRAUDS & RISK MANAGEMENT

PREVENTION OF CORPORATE FRAUDS & RISK MANAGEMENT 16 th December 2017, IOD CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA CA. Pramod Jain RISK MANAGEMENT CA. Pramod Jain Risks are potential events that

PREVENTION OF CORPORATE FRAUDS & RISK MANAGEMENT 16 th December 2017, IOD CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA CA. Pramod Jain RISK MANAGEMENT CA. Pramod Jain Risks are potential events that

LUNAWAT & CO. Chartered Accountants 13 th February2016, Faridabad CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA

Chartered Accountants 13 th February2016, Faridabad CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA An Intro. LUNAWAT & CO. What is Limited Liability Partnership? A body corporate formed & incorporated

Chartered Accountants 13 th February2016, Faridabad CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA An Intro. LUNAWAT & CO. What is Limited Liability Partnership? A body corporate formed & incorporated

IFC REPORTING. LUNAWAT & CO. Chartered Accountants 17 th June 2016, Rohini CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA

CARO 2016 IFC REPORTING LUNAWAT & CO. Chartered Accountants 17 th June 2016, Rohini CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA AGENDA CARO 2016 Internal Financial Controls AUDIT REPORTS Under Companies

CARO 2016 IFC REPORTING LUNAWAT & CO. Chartered Accountants 17 th June 2016, Rohini CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA AGENDA CARO 2016 Internal Financial Controls AUDIT REPORTS Under Companies

LUNAWAT & CO. Chartered Accountants 26 th June 2016, Kota CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA

LUNAWAT & CO. Chartered Accountants 26 th June 2016, Kota CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA An Intro. Lunawat & Co. What is Limited Liability Partnership? A body corporate formed & incorporated

LUNAWAT & CO. Chartered Accountants 26 th June 2016, Kota CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA An Intro. Lunawat & Co. What is Limited Liability Partnership? A body corporate formed & incorporated

ICDS Workshop: ICDS I III 11 May 2018

ICDS Workshop: ICDS I III 11 An introduction to ICDS ```` 2 Introduction to ICDS Framework for computation of taxable income; 10 ICDS notified; mandatory from AY 2017-18 Applicable on all tax payers following

ICDS Workshop: ICDS I III 11 An introduction to ICDS ```` 2 Introduction to ICDS Framework for computation of taxable income; 10 ICDS notified; mandatory from AY 2017-18 Applicable on all tax payers following

Income Computation And Disclosure Standards (ICDS) Overview CA. MehulofShah. Care, Pair, and Share

Overview CA. MehulofShah. Care, Pair, and Share") Income Computation And Disclosure Standards (ICDS) Overview CA. MehulofShah Act B.Companies Com, F.C.A., DISA (ICAI). 2013 Care, Pair, and Share Agenda ICDS Holistic View Accounting Policies ICDS 1 vis-à-vis

Income Computation And Disclosure Standards (ICDS) Overview CA. MehulofShah Act B.Companies Com, F.C.A., DISA (ICAI). 2013 Care, Pair, and Share Agenda ICDS Holistic View Accounting Policies ICDS 1 vis-à-vis

25 Key takeaways from Companies Amendment bill passed by Rajya Sabha

25 Key takeaways from Companies Amendment bill passed by Rajya Sabha The Companies (Amendment) Bill, 2017 has been passed by both the houses of parliament and is awaiting President's assent. The proposed

25 Key takeaways from Companies Amendment bill passed by Rajya Sabha The Companies (Amendment) Bill, 2017 has been passed by both the houses of parliament and is awaiting President's assent. The proposed

Audit & Auditors. Sec 139 Appointment of Auditors

Audit, Auditors And Fraud Reporting under Companies Act 2013 Audit & Auditors 2 Sec 139 Appointment of Auditors For Companies other than Government Companies Board to appoint 1 st auditors within 30 days

Audit, Auditors And Fraud Reporting under Companies Act 2013 Audit & Auditors 2 Sec 139 Appointment of Auditors For Companies other than Government Companies Board to appoint 1 st auditors within 30 days

PUNE. CA. Pramod Jain LUNAWAT & CO. FCA, FCS, FCMA, LL.B, MIMA, DISA. 6 th December 2014

PUNE CA. Pramod Jain FCA, FCS, FCMA, LL.B, MIMA, DISA 6 th December 2014 LUNAWAT & CO. Close Merge Options Run Convert An Intro. LUNAWAT & CO. What is Limited Liability Partnership? A body corporate formed

PUNE CA. Pramod Jain FCA, FCS, FCMA, LL.B, MIMA, DISA 6 th December 2014 LUNAWAT & CO. Close Merge Options Run Convert An Intro. LUNAWAT & CO. What is Limited Liability Partnership? A body corporate formed

Compliance Under Companies Act 2013 GMJ & Associates

Compliance Under Companies Act 2013 GMJ & Associates Andheri (East), Mumbai - 400 069. Tel No. 61919222 Email id : cs@gmj.co.in Speaker: CS Bijal Gada Incorporation Topics to be covered Issue and allotment

Compliance Under Companies Act 2013 GMJ & Associates Andheri (East), Mumbai - 400 069. Tel No. 61919222 Email id : cs@gmj.co.in Speaker: CS Bijal Gada Incorporation Topics to be covered Issue and allotment

Income Computation And Disclosure Standards (ICDS) Sanjeev Pandit CA P. D. Kunte & Co.

Sanjeev Pandit CA P. D. Kunte & Co.") Income Computation And Disclosure Standards (ICDS) Sanjeev Pandit CA P. D. Kunte & Co. Background History Section 145 substituted by the Finance Act, 1995. Section 145(1) Use of hybrid method of accounting

Income Computation And Disclosure Standards (ICDS) Sanjeev Pandit CA P. D. Kunte & Co. Background History Section 145 substituted by the Finance Act, 1995. Section 145(1) Use of hybrid method of accounting

Finalization of Balance Sheet, Tax Audit & ICDS (I, II, IV, V & IX)

") Finalization of Balance Sheet, Tax Audit & ICDS (I, II, IV, V & IX) CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at KGCA, Khanna, Punjab of Ludhiana Branch of NIRC of ICAI 17 th August 2017

Finalization of Balance Sheet, Tax Audit & ICDS (I, II, IV, V & IX) CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at KGCA, Khanna, Punjab of Ludhiana Branch of NIRC of ICAI 17 th August 2017

DIRECTORS & THEIR REMUNERATION IMPLICATIONS UNDER THE COMPANIES (AMENDMENT) ACT, 2017

ACT, 2017") DIRECTORS & THEIR REMUNERATION IMPLICATIONS UNDER THE COMPANIES (AMENDMENT) ACT, 2017 SECTION 2(49) INTERESTED DIRECTOR Interested Director means a director who is in any way, whether by himself or through

DIRECTORS & THEIR REMUNERATION IMPLICATIONS UNDER THE COMPANIES (AMENDMENT) ACT, 2017 SECTION 2(49) INTERESTED DIRECTOR Interested Director means a director who is in any way, whether by himself or through

THE COMPANIES ACT, 2013 Union Budget 2018

THE COMPANIES ACT, 2013 Union Budget 2018 INDEX 10-11 12-13 14-15 16-18 7 8 9 Chapter V: Acceptance Of Deposits Sample text Sample text 19-22 3-6 Table of Contents Sample text 23 Note: All the provisions

THE COMPANIES ACT, 2013 Union Budget 2018 INDEX 10-11 12-13 14-15 16-18 7 8 9 Chapter V: Acceptance Of Deposits Sample text Sample text 19-22 3-6 Table of Contents Sample text 23 Note: All the provisions

ICDS Reporting under Tax Audit

ICDS Reporting under Tax Audit Pune West Study Circle Western India Regional Council - Pune Branch The Institute of Chartered Accountants of India 1 st October, 2017 CA Ganesh Rajgopalan Computation of

ICDS Reporting under Tax Audit Pune West Study Circle Western India Regional Council - Pune Branch The Institute of Chartered Accountants of India 1 st October, 2017 CA Ganesh Rajgopalan Computation of

Seminar on Important Aspects on Companies Act,2013 by WIRC, ICAI. Acceptance of Deposits, Loans & Investment by Companies

Seminar on Important Aspects on Companies Act,2013 by WIRC, ICAI Acceptance of Deposits, Loans & Investment by Companies Pankaj Tiwari C N K & Associates LLP 28 th April 2018 Today s Agenda: Acceptance

Seminar on Important Aspects on Companies Act,2013 by WIRC, ICAI Acceptance of Deposits, Loans & Investment by Companies Pankaj Tiwari C N K & Associates LLP 28 th April 2018 Today s Agenda: Acceptance

INCOME TAX PROPOSALS in UNION BUDGET 2017

INCOME TAX PROPOSALS in UNION BUDGET 2017 LUNAWAT & CO. Chartered Accountants 10 th February 2017, Bhiwani CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA THE CRUX TIMELY FILING OF RETURNS No exemptions

INCOME TAX PROPOSALS in UNION BUDGET 2017 LUNAWAT & CO. Chartered Accountants 10 th February 2017, Bhiwani CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA THE CRUX TIMELY FILING OF RETURNS No exemptions

ICDS OVERVIEW IV Revenue Recognition V Tangible Fixed Assets VII Government Grants VIII Securities X Provisions, Contingent Liabilities & Assets

ICDS OVERVIEW IV Revenue Recognition V Tangible Fixed Assets VII Government Grants VIII Securities X Provisions, Contingent Liabilities & Assets 4 th May 2017 KCASSC, CIRC Kanpur CA. PRAMOD JAIN FCA, FCS,

ICDS OVERVIEW IV Revenue Recognition V Tangible Fixed Assets VII Government Grants VIII Securities X Provisions, Contingent Liabilities & Assets 4 th May 2017 KCASSC, CIRC Kanpur CA. PRAMOD JAIN FCA, FCS,

PRESENTATION BY. CA. (DR.) DEBASHIS MITRA M.COM, LL.B, F.C.A., A.C.M.A., A.C.S., DISA(ICA), PhD.

DEBASHIS MITRA M.COM, LL.B, F.C.A., A.C.M.A., A.C.S., DISA(ICA), PhD.") PRESENTATION BY CA. (DR.) DEBASHIS MITRA M.COM, LL.B, F.C.A., A.C.M.A., A.C.S., DISA(ICA), PhD. LOANS TO DIRECTORS ETC. According to section 185 of the Act save as otherwise provided in this Act, no company

PRESENTATION BY CA. (DR.) DEBASHIS MITRA M.COM, LL.B, F.C.A., A.C.M.A., A.C.S., DISA(ICA), PhD. LOANS TO DIRECTORS ETC. According to section 185 of the Act save as otherwise provided in this Act, no company

Companies Act 2013 Impact on Accounting and Auditing. CA. Aniruddh Sankaran

Impact on Accounting and Auditing CA. Aniruddh Sankaran Agenda Key provisions of the relating to: Financial Statements Consolidation Audit and Auditors Page 2 Effective Date Accounts, audit and auditor

Impact on Accounting and Auditing CA. Aniruddh Sankaran Agenda Key provisions of the relating to: Financial Statements Consolidation Audit and Auditors Page 2 Effective Date Accounts, audit and auditor

District Centre Janakpuri CPE Study Circle 23 rd June 2018 CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA

, FCA, FCS, FCMA, LL.B, MIMA, DISA") District Centre Janakpuri CPE Study Circle 23 rd June 2018 CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA An Intro. CA. Pramod Jain Incorporate / convert Partners Individual Body Corporate

District Centre Janakpuri CPE Study Circle 23 rd June 2018 CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA An Intro. CA. Pramod Jain Incorporate / convert Partners Individual Body Corporate

Income Computation & Disclosure Standards

2017 Income Computation & Disclosure Standards B D Jokhakar & Company Chartered Accountants 08/09/2017 Sr. No. Chapter Head Page No. 1 Overview 2-5 2 ICDS-I: Accounting Policies 6-8 3 ICDS-II: Valuation

2017 Income Computation & Disclosure Standards B D Jokhakar & Company Chartered Accountants 08/09/2017 Sr. No. Chapter Head Page No. 1 Overview 2-5 2 ICDS-I: Accounting Policies 6-8 3 ICDS-II: Valuation

Impact on Private Companies & Independent Directors

Impact on Private Companies & Independent Directors National CPE Conference, Chennai Organized by: Corporate Laws and Corporate Governance Committee, ICAI Hosted By: SIRC of ICAI December 27, 2013 Passage

Impact on Private Companies & Independent Directors National CPE Conference, Chennai Organized by: Corporate Laws and Corporate Governance Committee, ICAI Hosted By: SIRC of ICAI December 27, 2013 Passage

INCOME COMPUTATION & DISCLOSURE STANDARDS. H. N. Motiwalla 1

INCOME COMPUTATION & DISCLOSURE STANDARDS ICDS ICDS H. N. Motiwalla 1 BACK GROUND (Section 145) S. 145 Method of Accounting: Subject to provisions of Sub S. (2) Applicable to Income chargeable under the

INCOME COMPUTATION & DISCLOSURE STANDARDS ICDS ICDS H. N. Motiwalla 1 BACK GROUND (Section 145) S. 145 Method of Accounting: Subject to provisions of Sub S. (2) Applicable to Income chargeable under the

Income Computation and Disclosure Standards. CA Parul Mittal

Income Computation and Disclosure Standards CA Parul Mittal ICDS Overview In Finance Act 2014, vide amendment made in section 145(2), power granted to Central Government to notify income computation and

Income Computation and Disclosure Standards CA Parul Mittal ICDS Overview In Finance Act 2014, vide amendment made in section 145(2), power granted to Central Government to notify income computation and

PAN Quoting and AIR Reporting

PAN Quoting and AIR Reporting LUNAWAT & CO. Chartered Accountants 20 th February 2016, North Campus CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA MANDATORY TO APPLY PAN Total Income exceeds maximum

PAN Quoting and AIR Reporting LUNAWAT & CO. Chartered Accountants 20 th February 2016, North Campus CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA MANDATORY TO APPLY PAN Total Income exceeds maximum

AN OVERVIEW OF THE COMPANIES (AMENDMENT) ACT, 2017

ACT, 2017") AN OVERVIEW OF THE COMPANIES (AMENDMENT) ACT, 2017 Information in the following slides is intended to provide only a general outline of the subjects covered. It should neither be regarded as comprehensive

AN OVERVIEW OF THE COMPANIES (AMENDMENT) ACT, 2017 Information in the following slides is intended to provide only a general outline of the subjects covered. It should neither be regarded as comprehensive

INCOME COMPUTATION AND DISCLOSURE STANDARDS (ICDS) Notification No.32/2015, F. No. 134/48/2010 TPL, dated 31st March, 2015 INTRODUCTION

Notification No.32/2015, F. No. 134/48/2010 TPL, dated 31st March, 2015 INTRODUCTION") INCOME COMPUTATION AND DISCLOSURE STANDARDS (ICDS) Notification No.32/2015, F. No. 134/48/2010 TPL, dated 31st March, 2015 INTRODUCTION Section 145 of the Income-tax Act relates to method of accounting.

INCOME COMPUTATION AND DISCLOSURE STANDARDS (ICDS) Notification No.32/2015, F. No. 134/48/2010 TPL, dated 31st March, 2015 INTRODUCTION Section 145 of the Income-tax Act relates to method of accounting.

CA Mehul Shah B. Com, F.C.A., DISA (ICAI).

.") Management and Administration provisions under the Companies Act 2013 CA Mehul Shah B. Com, F.C.A., DISA (ICAI). # : 2510 0861; 2510 9990 Email : mehulshah@shah3ca.com Agenda Management and Administration

Management and Administration provisions under the Companies Act 2013 CA Mehul Shah B. Com, F.C.A., DISA (ICAI). # : 2510 0861; 2510 9990 Email : mehulshah@shah3ca.com Agenda Management and Administration

The Companies (Amendment) Bill, Overview

Bill, Overview") www.vinodkothari.com / www.india-financing.com Email: info@vinodkothari.com / vinod@vinodkothari.com The Companies (Amendment) Bill, 2017 - Overview Vinod Kothari & Company Kolkata 1006-1009 Krishna Building

www.vinodkothari.com / www.india-financing.com Email: info@vinodkothari.com / vinod@vinodkothari.com The Companies (Amendment) Bill, 2017 - Overview Vinod Kothari & Company Kolkata 1006-1009 Krishna Building

ANALYSIS OF COMPANIES ACT AMENDMENT 2017 BY: CS ANIL KUMAR PANCHARIYA BENGALURU

ANALYSIS OF COMPANIES ACT AMENDMENT 2017 BY: CS ANIL KUMAR PANCHARIYA BENGALURU 2 AT A GLANCE COMPANIES (AMENDMENT) BILL 2017 THE JOURNEY The Bill was introduced in the Lok Sabha on March 16, 2016. The

ANALYSIS OF COMPANIES ACT AMENDMENT 2017 BY: CS ANIL KUMAR PANCHARIYA BENGALURU 2 AT A GLANCE COMPANIES (AMENDMENT) BILL 2017 THE JOURNEY The Bill was introduced in the Lok Sabha on March 16, 2016. The

INCOME COMPUTATION & DISCLOSURE STANDARDS. H. N. Motiwalla 1

INCOME COMPUTATION & DISCLOSURE STANDARDS ICDS ICDS H. N. Motiwalla 1 BACK GROUND (Section 145) S. 145 Method of Accounting: Subject to provisions of Sub S. (2) Applicable to Income chargeable under the

INCOME COMPUTATION & DISCLOSURE STANDARDS ICDS ICDS H. N. Motiwalla 1 BACK GROUND (Section 145) S. 145 Method of Accounting: Subject to provisions of Sub S. (2) Applicable to Income chargeable under the

CNK & Associates LLP. Provisions relating to Loans, Borrowings and Deposits. Chartered Accountants

& Associates LLP Chartered Accountants Provisions relating to Loans, Borrowings and Deposits (Practical issues and reporting requirements, Impact on Private Limited Companies) Manish Sampat June 9, 2018

& Associates LLP Chartered Accountants Provisions relating to Loans, Borrowings and Deposits (Practical issues and reporting requirements, Impact on Private Limited Companies) Manish Sampat June 9, 2018

Tax Audit Series 20 S. Nos

Namaste In series - 20 we would discuss S. Nos. 40 to 44 of Form 3CD. Reporting under S. Nos. 42 to 44 have been inserted w.e.f. 20 th August 2018. However S. No. 44 has been deferred till 31 st March

Namaste In series - 20 we would discuss S. Nos. 40 to 44 of Form 3CD. Reporting under S. Nos. 42 to 44 have been inserted w.e.f. 20 th August 2018. However S. No. 44 has been deferred till 31 st March

ICDS Impact on Computation of Income

ICDS Impact on Computation of Income Ajinkya Jagoje Partner abm & associates LLP Chartered Accountants 1 Background in brief Introduction ICDS notified by Central Government (CG) as a delegated legislation

ICDS Impact on Computation of Income Ajinkya Jagoje Partner abm & associates LLP Chartered Accountants 1 Background in brief Introduction ICDS notified by Central Government (CG) as a delegated legislation

Practical Aspects of Companies Act, 2013 on Midsized Companies.

Presentation on Practical Aspects of Companies Act, 2013 on Midsized Companies. ByC.S.Kelkar Partner C. S. Kelkar& Associates, Company Secretaries Points covered in the Presentation 1. Types of Companies

Presentation on Practical Aspects of Companies Act, 2013 on Midsized Companies. ByC.S.Kelkar Partner C. S. Kelkar& Associates, Company Secretaries Points covered in the Presentation 1. Types of Companies

IMPACT ON PRIVATE & UNLISTED PUBLIC COMPANIES OF NEW COMPANIES ACT, Organized by J.B. Nagar CPE Study Circle of WIRC

IMPACT ON PRIVATE & UNLISTED PUBLIC COMPANIES OF NEW COMPANIES ACT, 2013 Organized by J.B. Nagar CPE Study Circle of WIRC Hasmukh B Dedhia February 3, 2014 1 Passage of Companies Bill Co. s Bill, 2008

IMPACT ON PRIVATE & UNLISTED PUBLIC COMPANIES OF NEW COMPANIES ACT, 2013 Organized by J.B. Nagar CPE Study Circle of WIRC Hasmukh B Dedhia February 3, 2014 1 Passage of Companies Bill Co. s Bill, 2008

Form 61A AS AMENDMENTS CASH RESTRICTIONS ICDS OVERVIEW, ICDS I & V SCHEDULE III AMENDMENTS

Form 61A AS AMENDMENTS CASH RESTRICTIONS ICDS OVERVIEW, ICDS I & V SCHEDULE III AMENDMENTS Sonepat Branch of NIRC of ICAI 20 th May 2017 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA FORM 61A Section

Form 61A AS AMENDMENTS CASH RESTRICTIONS ICDS OVERVIEW, ICDS I & V SCHEDULE III AMENDMENTS Sonepat Branch of NIRC of ICAI 20 th May 2017 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA FORM 61A Section

Private Companies, OPC, Small Company, Section 8 Company. Study Course on the Companies Act, June 2014

Private Companies, OPC, Small Company, Section 8 Company Study Course on the Companies Act, 2013 12 June 2014 1 Contents Background Private Companies One Person Company Small Companies Section 8 Companies

Private Companies, OPC, Small Company, Section 8 Company Study Course on the Companies Act, 2013 12 June 2014 1 Contents Background Private Companies One Person Company Small Companies Section 8 Companies

Regulatory Alert Stay Ahead

India Tax & Regulatory For private circulation only 10 January 2018 p Regulatory Alert Stay Ahead Companies (Amendment) Act 2017 Issue no: RA/01/2018 In this issue: Background Highlights Conclusion Do

India Tax & Regulatory For private circulation only 10 January 2018 p Regulatory Alert Stay Ahead Companies (Amendment) Act 2017 Issue no: RA/01/2018 In this issue: Background Highlights Conclusion Do

Key Amendments in Cos. (Amendment) Bill, 2017 & E-Filing. Gaurav N Pingle, Practising Co. Secretary, Pune.

Bill, 2017 & E-Filing. Gaurav N Pingle, Practising Co. Secretary, Pune.") Key Amendments in Cos. (Amendment) Bill, 2017 & E-Filing Gaurav N Pingle, Practising Co. Secretary, Pune. ICAI WIRC Seminar on Important Aspects on Cos. Act, 2013 Key Amendments in Cos. (Amendment) Bill,

Key Amendments in Cos. (Amendment) Bill, 2017 & E-Filing Gaurav N Pingle, Practising Co. Secretary, Pune. ICAI WIRC Seminar on Important Aspects on Cos. Act, 2013 Key Amendments in Cos. (Amendment) Bill,

AS AMENDMENTS CASH RESTRICTIONS ICDS OVERVIEW & ICDS I SCHEDULE III AMENDMENTS

AS AMENDMENTS CASH RESTRICTIONS ICDS OVERVIEW & ICDS I SCHEDULE III AMENDMENTS Meerut Branch of CIRC of ICAI 15 th May 2017 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA CASH RESTRICTIONS DEDUCTION

AS AMENDMENTS CASH RESTRICTIONS ICDS OVERVIEW & ICDS I SCHEDULE III AMENDMENTS Meerut Branch of CIRC of ICAI 15 th May 2017 CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA CASH RESTRICTIONS DEDUCTION