Form 1041 Preparation: Estates & Trusts. Presented by J. William Strickland, Esq., CPA, MBA (864)

|

|

|

- Cecily Grant

- 5 years ago

- Views:

Transcription

1 Form 1041 Preparation: Estates & Trusts Presented by J. William Strickland, Esq., CPA, MBA (864)

2 Form 1041 Preparation Tax Rates 26 U.S. Code 1 - Tax imposed (E) Estates and trusts The following table shall be applied in lieu of the table contained in subsection (e): If taxable income is: The tax is: Not over $2,550 10% of taxable income. Over $2,550 but not over $9,150 $255, plus 24% of the excess over $2,550. Over $9,150 but not over $12,500 $1,839, plus 35% of the excess over $9,150. Over $12,500 $3,011.50, plus 37% of the excess over $12,500.

3 Form 1041 Preparation Look at the Internal Revenue Code Look at Trust Documents Get Information on Grantor and Beneficiaries SSN/EIN Current Address Look at Financial Information Income Expenses Distributions

4 Form 1041 Preparation What is an Estate? Someone has died What is the date of death? Get copies of Probate Forms Application Inventory Testate or Non-testate? Know the rules for intestate succession Know the rules for spousal election Read the Will and any Associated Trusts Look at multiple marriages Who is the Personal Representative? What is the Year End?

5 Form 1041 Preparation What is a Trust? Trust Document Grantor Beneficiaries Trustee

6 Form 1041 Preparation What is a Trust? Income Principal Distributions Allocations to Income and Principal

7 Form 1041 Preparation What is in a Trust Document? Identification of Grantor Revocability Initial Assets Identification of Beneficiaries Present interests Contingent interests Survivorship Identification of Trustee Succession Fees

8 Form 1041 Preparation What is in a Trust Document? Trustees: Multiple Trustees Unanimity or Majority Delegation of Authority Individual Family Non-family Corporate Ancillary

9 Form 1041 Preparation What is in a Trust Document? Investment and Distribution Provisions Trust Protector Applicable State Law

10 Form 1041 Preparation What is in a Trust Document? Trustee Powers Gifting Modification of Estate Plan Provisions for Tax Purposes Allocation of Capital Gains S Corporation Charitable Provisions Coordination with Personal Representative

11 Form 1041 Preparation Internal Revenue Code Subchapter J SUBPART A - General Rules for Taxation of Estates & Trusts ( 641 to 646) SUBPART B - Trusts Which Distribute Current Income Only ( 651 to 652) SUBPART C - Estates and Trusts Which May Accumulate Income or Which Distribute Corpus ( 661 to 664) SUBPART E - Grantors & Others Treated as Substantial Owners ( 671 to 679)

12 Form 1041 Preparation The Internal Revenue Code 642 Exemptions Complex Trust = $100 Simple Trust = $300 Estate = $600

13 643 Definitions: DISTRIBUTABLE NET INCOME Taxable year of trusts Deduction for trusts distributing current income only Inclusion of amounts in gross income of beneficiaries of trusts distributing current income only [Character of Income] [Taxable Year] Deduction for estates and trusts accumulating income or distributing corpus Inclusion of amounts in gross income of beneficiaries of estates and trusts accumulating income or distributing corpus Special rules: Distributions in first sixty-five days of taxable year Trust income, deductions, and credits attributable to grantors and others as substantial owners

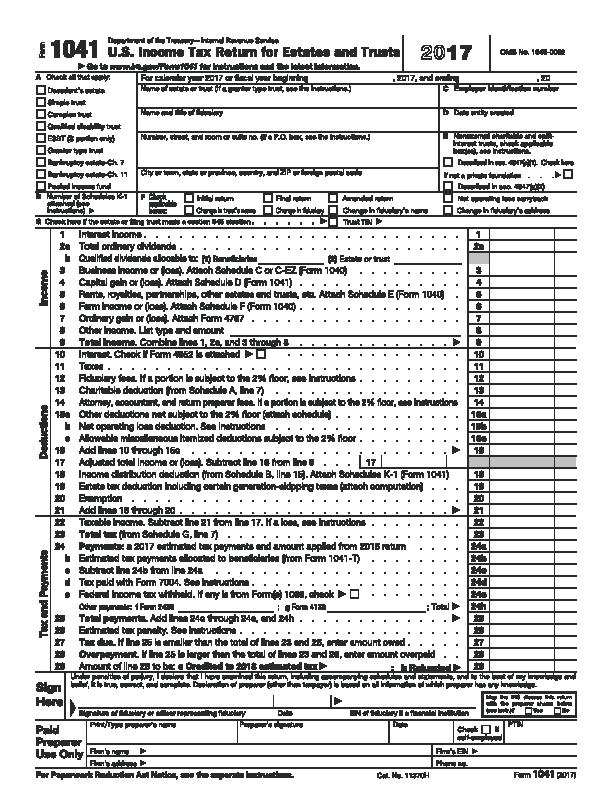

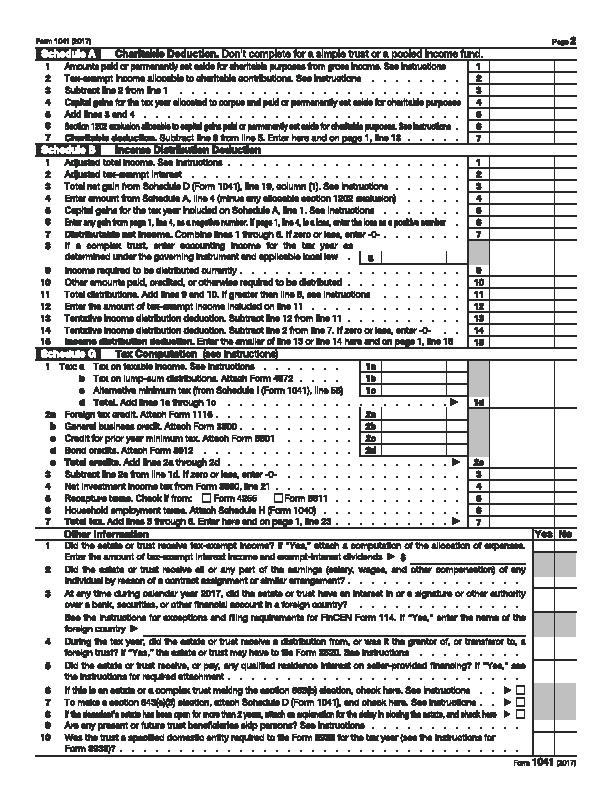

14 FORM 1041

15

16

17

18

19

20

21

22

23 Form 1041 Preparation

24

25 26 U.S. Code 1 - Tax imposed (E) Estates and trusts The following table shall be applied in lieu of the table contained in subsection (e): If taxable income is: Not over $2,550 The tax is: 10% of taxable income. Over $2,550 but not over $9,150 $255, plus 24% of the excess over $2,550. Over $9,150 but not over $12,500 Over $12,500 $1,839, plus 35% of the excess over $9,150. $3,011.50, plus 37% of the excess over $12,500.

26 26 U.S. Code Part I - ESTATES, TRUSTS, AND BENEFICIARIES SUBPART A - General Rules for Taxation of Estates and Trusts ( 641 to 646) SUBPART B - Trusts Which Distribute Current Income Only ( 651 to 652) SUBPART C - Estates and Trusts Which May Accumulate Income or Which Distribute Corpus ( 661 to 664) SUBPART D - Treatment of Excess Distributions by Trusts ( 665 to 669) SUBPART E - Grantors and Others Treated as Substantial Owners ( 671 to 679) SUBPART F - Miscellaneous ( 681 to 685)

27 26 U.S. Code Special rules for credits and deductions (b) DEDUCTION FOR PERSONAL EXEMPTION (2) TRUSTS (A) In general Except as otherwise provided in this paragraph, a trust shall be allowed a deduction of $100. (B) Trusts distributing income currently A trust which, under its governing instrument, is required to distribute all of its income currently shall be allowed a deduction of $ U.S. Code Definitions applicable to subparts A, B, C, and D (a) DISTRIBUTABLE NET INCOME For purposes of this part, the term distributable net income means, with respect to any taxable year, the taxable income of the estate or trust computed with the following modifications (1) DEDUCTION FOR DISTRIBUTIONS No deduction shall be taken under sections 651 and 661 (relating to additional deductions). (2) DEDUCTION FOR PERSONAL EXEMPTION No deduction shall be taken under section 642(b) (relating to deduction for personal exemptions). (3) CAPITAL GAINS AND LOSSES Gains from the sale or exchange of capital assets shall be excluded to the extent that such gains are allocated to corpus and are not (A) paid, credited, or required to be distributed to any beneficiary during the taxable year, or (B) paid, permanently set aside, or to be used for the purposes specified in section 642(c). Losses from the sale or exchange of capital assets shall be excluded, except to the extent such losses are taken into account in determining the amount of gains from the sale or exchange of capital assets which are paid, credited, or required to be distributed to any beneficiary during the taxable year. The exclusion under section 1202 shall not be taken into account. (4) EXTRAORDINARY DIVIDENDS AND TAXABLE STOCK DIVIDENDS For purposes only of subpart B (relating to trusts which distribute current income only), there shall be excluded those items of gross income constituting extraordinary dividends or taxable stock dividends which the fiduciary, acting in good faith, does not pay or credit to any beneficiary by

28 reason of his determination that such dividends are allocable to corpus under the terms of the governing instrument and applicable local law. (5) TAX-EXEMPT INTEREST There shall be included any tax-exempt interest to which section 103 applies, reduced by any amounts which would be deductible in respect of disbursements allocable to such interest but for the provisions of section 265 (relating to disallowance of certain deductions). 26 U.S. Code Taxable year of trusts (a) IN GENERAL For purposes of this subtitle, the taxable year of any trust shall be the calendar year. 26 U.S. Code Deduction for trusts distributing current income only (a) DEDUCTION In the case of any trust the terms of which (1) provide that all of its income is required to be distributed currently, and (2) do not provide that any amounts are to be paid, permanently set aside, or used for the purposes specified in section 642(c) (relating to deduction for charitable, etc., purposes), there shall be allowed as a deduction in computing the taxable income of the trust the amount of the income for the taxable year which is required to be distributed currently. This section shall not apply in any taxable year in which the trust distributes amounts other than amounts of income described in paragraph (1). (b) LIMITATION ON DEDUCTION If the amount of income required to be distributed currently exceeds the distributable net income of the trust for the taxable year, the deduction shall be limited to the amount of the distributable net income. For this purpose, the computation of distributable net income shall not include items of income which are not included in the gross income of the trust and the deductions allocable thereto.

29 26 U.S. Code Inclusion of amounts in gross income of beneficiaries of trusts distributing current income only (a) INCLUSION Subject to subsection (b), the amount of income for the taxable year required to be distributed currently by a trust described in section 651 shall be included in the gross income of the beneficiaries to whom the income is required to be distributed, whether distributed or not. If such amount exceeds the distributable net income, there shall be included in the gross income of each beneficiary an amount which bears the same ratio to distributable net income as the amount of income required to be distributed to such beneficiary bears to the amount of income required to be distributed to all beneficiaries. (b) CHARACTER OF AMOUNTS The amounts specified in subsection (a) shall have the same character in the hands of the beneficiary as in the hands of the trust. For this purpose, the amounts shall be treated as consisting of the same proportion of each class of items entering into the computation of distributable net income of the trust as the total of each class bears to the total distributable net income of the trust, unless the terms of the trust specifically allocate different classes of income to different beneficiaries. In the application of the preceding sentence, the items of deduction entering into the computation of distributable net income shall be allocated among the items of distributable net income in accordance with regulations prescribed by the Secretary. (c) DIFFERENT TAXABLE YEARS If the taxable year of a beneficiary is different from that of the trust, the amount which the beneficiary is required to include in gross income in accordance with the provisions of this section shall be based upon the amount of income of the trust for any taxable year or years of the trust ending within or with his taxable year. 26 U.S. Code Deduction for estates and trusts accumulating income or distributing corpus (a) DEDUCTION In any taxable year there shall be allowed as a deduction in computing the taxable income of an estate or trust (other than a trust to which subpart B applies), the sum of (1) any amount of income for such taxable year required to be distributed currently (including any amount required to be distributed which may be

30 paid out of income or corpus to the extent such amount is paid out of income for such taxable year); and (2) any other amounts properly paid or credited or required to be distributed for such taxable year; but such deduction shall not exceed the distributable net income of the estate or trust. (b) CHARACTER OF AMOUNTS DISTRIBUTED The amount determined under subsection (a) shall be treated as consisting of the same proportion of each class of items entering into the computation of distributable net income of the estate or trust as the total of each class bears to the total distributable net income of the estate or trust in the absence of the allocation of different classes of income under the specific terms of the governing instrument. In the application of the preceding sentence, the items of deduction entering into the computation of distributable net income (including the deduction allowed under section 642(c)) shall be allocated among the items of distributable net income in accordance with regulations prescribed by the Secretary. (c) LIMITATION ON DEDUCTION No deduction shall be allowed under subsection (a) in respect of any portion of the amount allowed as a deduction under that subsection (without regard to this subsection) which is treated under subsection (b) as consisting of any item of distributable net income which is not included in the gross income of the estate or trust. 26 U.S. Code Inclusion of amounts in gross income of beneficiaries of estates and trusts accumulating income or distributing corpus (a) INCLUSION Subject to subsection (b), there shall be included in the gross income of a beneficiary to whom an amount specified in section 661(a) is paid, credited, or required to be distributed (by an estate or trust described in section 661), the sum of the following amounts: (1) AMOUNTS REQUIRED TO BE DISTRIBUTED CURRENTLY The amount of income for the taxable year required to be distributed currently to such beneficiary, whether distributed or not. If the amount of income required to be distributed currently to all beneficiaries exceeds the distributable net income (computed without the deduction allowed by section 642(c), relating to deduction for charitable, etc., purposes) of the estate or trust, then, in lieu of the amount provided in the preceding sentence, there shall be included in the gross income of the beneficiary an amount which bears the same ratio to distributable net income (as so computed) as the

31 amount of income required to be distributed currently to such beneficiary bears to the amount required to be distributed currently to all beneficiaries. For purposes of this section, the phrase the amount of income for the taxable year required to be distributed currently includes any amount required to be paid out of income or corpus to the extent such amount is paid out of income for such taxable year. (2) OTHER AMOUNTS DISTRIBUTED All other amounts properly paid, credited, or required to be distributed to such beneficiary for the taxable year. If the sum of (A) the amount of income for the taxable year required to be distributed currently to all beneficiaries, and (B) all other amounts properly paid, credited, or required to be distributed to all beneficiaries exceeds the distributable net income of the estate or trust, then, in lieu of the amount provided in the preceding sentence, there shall be included in the gross income of the beneficiary an amount which bears the same ratio to distributable net income (reduced by the amounts specified in (A)) as the other amounts properly paid, credited or required to be distributed to the beneficiary bear to the other amounts properly paid, credited, or required to be distributed to all beneficiaries. (b) CHARACTER OF AMOUNTS The amounts determined under subsection (a) shall have the same character in the hands of the beneficiary as in the hands of the estate or trust. For this purpose, the amounts shall be treated as consisting of the same proportion of each class of items entering into the computation of distributable net income as the total of each class bears to the total distributable net income of the estate or trust unless the terms of the governing instrument specifically allocate different classes of income to different beneficiaries. In the application of the preceding sentence, the items of deduction entering into the computation of distributable net income (including the deduction allowed under section 642(c)) shall be allocated among the items of distributable net income in accordance with regulations prescribed by the Secretary. In the application of this subsection to the amount determined under paragraph (1) of subsection (a), distributable net income shall be computed without regard to any portion of the deduction under section 642(c) which is not attributable to income of the taxable year. (c) DIFFERENT TAXABLE YEARS If the taxable year of a beneficiary is different from that of the estate or trust, the amount to be included in the gross income of the beneficiary shall be based on the distributable net income of the estate or trust and the amounts properly paid, credited, or required to be distributed to the beneficiary during any taxable year or years of the estate or trust ending within or with his taxable year.

32 26 U.S. Code Special rules applicable to sections 661 and 662 (b) DISTRIBUTIONS IN FIRST SIXTY-FIVE DAYS OF TAXABLE YEAR (1) GENERAL RULE If within the first 65 days of any taxable year of an estate or a trust, an amount is properly paid or credited, such amount shall be considered paid or credited on the last day of the preceding taxable year. (2) LIMITATION Paragraph (1) shall apply with respect to any taxable year of an estate or a trust only if the executor of such estate or the fiduciary of such trust (as the case may be) elects, in such manner and at such time as the Secretary prescribes by regulations, to have paragraph (1) apply for such taxable year. (c) SEPARATE SHARES TREATED AS SEPARATE ESTATES OR TRUSTS For the sole purpose of determining the amount of distributable net income in the application of sections 661 and 662, in the case of a single trust having more than one beneficiary, substantially separate and independent shares of different beneficiaries in the trust shall be treated as separate trusts. Rules similar to the rules of the preceding provisions of this subsection shall apply to treat substantially separate and independent shares of different beneficiaries in an estate having more than 1 beneficiary as separate estates. The existence of such substantially separate and independent shares and the manner of treatment as separate trusts or estates, including the application of subpart D, shall be determined in accordance with regulations prescribed by the Secretary. 26 U.S. Code Trust income, deductions, and credits attributable to grantors and others as substantial owners Where it is specified in this subpart that the grantor or another person shall be treated as the owner of any portion of a trust, there shall then be included in computing the taxable income and credits of the grantor or the other person those items of income, deductions, and credits against tax of the trust which are attributable to that portion of the trust to the extent that such items would be taken into account under this chapter in computing taxable income or credits against the tax of an individual. Any remaining portion of the trust shall be subject to subparts A through D. No items of a trust shall be included in computing the taxable income and credits of the grantor or of any other person solely on the grounds of his dominion and control over the trust under section 61 (relating to

33 definition of gross income) or any other provision of this title, except as specified in this subpart.

34

35

36

37

38

39 ACCOUNTING INCOME WORKSHEET Part A Name of Trust Tax Year Ending December 31, 2017 Employer ID Number INCOME DESCRIPTION Dividends ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ Nondividend Distributions~~~~~~~~~~~~~~~~~~~~~~~ Interest ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ U.S. Obligations ~~~~~~~~~~~~~~~~~~~~~~~~~~ Net Rent/Royalty ~~~~~~~~~~~~~~~~~~~~~~~~~~~ Net Business/Farm ~~~~~~~~~~~~~~~~~~~~~~~~~~ Partnership/S Corporation~~~~~~~~~~~~~~~~~~~~~~~ Estate/Trust ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ Ordinary Gains ~~~~~~~~~~~~~~~~~~~~~~~~~~~ Other Nontaxable Income ~~~~~~~~~~~~~~~~~~~~~~~ Net Short-term Capital Gain ~~~~~~~~~~~~~~~~~~~~~~ Net Long-term Capital Gain ~~~~~~~~~~~~~~~~~~~~~~ Other Income INCOME PRINCIPAL TOTAL 6,469. 6, ,511. 2,511. Totals ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ 6,470. 2,560. 9,030. SUMMARY Accounting Income Distributable Net Income Total Income Taxable Tax-Exempt NAI 6,470. Taxable 6,470. Taxable 6,451. 6,793. Tax-Exempt 6,793. Tax-Exempt 6, ,263. DNI 13,263. TOTAL 13,

40 ACCOUNTING INCOME WORKSHEET Part B Name of Trust Tax Year Ending December 31, 2017 Employer ID Number DEDUCTIONS DESCRIPTION INCOME PRINCIPAL TOTAL Interest Expense ~~~~~~~~~~~~~~~~~~~~~~~~~~~ Taxes ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ Less: Amount Allocated to Tax-Exempt Interest ~~~~~~~~~~~~~ Fiduciary Fees ~~~~~~~~~~~~~~~~~~~~~~~~~~~ Less: Amount Allocated to Tax-Exempt Interest ~~~~~~~~~~~~~ Attorney, Accountant, and Return Preparer Fees ~~~~~~~~~~~~ Less: Amount Allocated to Tax-Exempt Interest ~~~~~~~~~~~~~ Tax on Income in Respect of a Decedent ~~~~~~~~~~~~~~~~ Other Deductions Total Deductions ~~~~~~~~~~~~~~~~~~~~~~~~~~~ TAX-EXEMPT INTEREST SUMMARY DESCRIPTION INCOME PRINCIPAL TOTAL Tax-Exempt Interest ~~~~~~~~~~~~~~~~~~~~~~~~~ 6,793. 6,793. Allocated Direct Expenses Allocated Indirect Expenses ~~~~~~~~~~~~~~~~~~~~~~ ~~~~~~~~~~~~~~~~~~~~~ Net Tax-Exempt Interest ~~~~~~~~~~~~~~~~~~~~~~~ 6,793. 6,

41 2017 Expense Allocation by Income Type Income Type Income Charity Direct Expenses Specifically Allocated Indirect and Direct Expenses not Specifically Allocated Net Income Other Taxable Non-Passive Ordinary Business Net Rental Real Estate Other Rental Interest Non-qualified Dividends Passive Ordinary Business Net Rental Real Estate Other Rental U.S. Interest U.S. Interest/Dividends Qualified Dividends 5,671. 5,671. Short-term Capital Gains Long-term Capital Gains Tax-exempt Interest 6,793. 6,793. Total 13, ,

42 Alternative Minimum Tax 2017 Expense Allocation by Income Type Income Type Income Charity Direct Expenses Specifically Allocated Indirect and Direct Expenses not Specifically Allocated Net Income Other Taxable Non-Passive Ordinary Business Net Rental Real Estate Other Rental Interest Non-qualified Dividends Passive Ordinary Business Net Rental Real Estate Other Rental U.S. Interest U.S. Interest/Dividends Qualified Dividends 5,671. 5,671. Short-term Capital Gains Long-term Capital Gains Tax-exempt Interest 6,773. 6,773. Total 13, ,

43 Schedule K-1 Distribution Workpaper 1 - Amount of Income DNI Amount available 13,263. Accounting Income 13,263. to distribute 6,470. Amount to be Distributed from Form 1041, Schedule B, line 15 ~~~~~~~~~~~~~~~~~~~~~~~~~~~ Amount specifically allocated for ordinary income ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ Remaining amount for distributions ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ Beginning column is from: Expense Allocation Worksheet 6, ,470. Income Type Other Taxable Net Income Percentage of Sch B, line 15 to be Distributed Amount to be Distributed Non-passive Ordinary Business Net Rental Real Estate Other Rental Interest Non-qualified Dividends Passive Ordinary Business Net Rental Real Estate Other Rental U.S. Interest U.S. Interest/Dividends Qualified Dividends Subtotal 5, ,671. 6, ,470. Short-term Capital Gains Long-term Capital Gains Total Tax-Exempt Interest 6,793. 6,793. Amount required to be distributed (Tier I) ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ Discretionary amount to be distributed (Tier II) ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ 13,263. Note: Tax exempt interest is assumed to be in the amounts entered to be distributed to beneficiaries

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

2017 National Conference on Special Needs Planning. Trust Income, Trust Expenses and Calculating Distributable Net Income Bradley J.

2017 National Conference on Special Needs Planning and Special Needs Trusts Trust Income, Trust Expenses and Calculating Distributable Net Income Bradley J. Frigon Law Offices of Bradley J. Frigon 6500

2017 National Conference on Special Needs Planning and Special Needs Trusts Trust Income, Trust Expenses and Calculating Distributable Net Income Bradley J. Frigon Law Offices of Bradley J. Frigon 6500

Internal Revenue Code Section 1296(e) Election of mark to market for marketable stock

Election of mark to market for marketable stock") CLICK HERE to return to the home page Internal Revenue Code Section 1296(e) Election of mark to market for marketable stock (a) General rule. In the case of marketable stock in a passive foreign investment

CLICK HERE to return to the home page Internal Revenue Code Section 1296(e) Election of mark to market for marketable stock (a) General rule. In the case of marketable stock in a passive foreign investment

26 USC 643. NB: This unofficial compilation of the U.S. Code is current as of Jan. 7, 2011 (see

TITLE 26 - INTERNAL REVENUE CODE Subtitle A - Income Taxes CHAPTER 1 - NORMAL TAXES AND SURTAXES Subchapter J - Estates, Trusts, Beneficiaries, and Decedents PART I - ESTATES, TRUSTS, AND BENEFICIARIES

TITLE 26 - INTERNAL REVENUE CODE Subtitle A - Income Taxes CHAPTER 1 - NORMAL TAXES AND SURTAXES Subchapter J - Estates, Trusts, Beneficiaries, and Decedents PART I - ESTATES, TRUSTS, AND BENEFICIARIES

MICKEY R. DAVIS DAVIS & WILLMS, PLLC HOUSTON, TEXAS JULY 9, 2018

MICKEY R. DAVIS DAVIS & WILLMS, PLLC HOUSTON, TEXAS JULY 9, 2018 Trusts and estates are not entities Tax laws treat them as though they were Rules applicable to individuals apply to trusts and estates

MICKEY R. DAVIS DAVIS & WILLMS, PLLC HOUSTON, TEXAS JULY 9, 2018 Trusts and estates are not entities Tax laws treat them as though they were Rules applicable to individuals apply to trusts and estates

Internal Revenue Code Section 664(d)(1) Charitable remainder trusts.

(1) Charitable remainder trusts.") Internal Revenue Code Section 664(d)(1) Charitable remainder trusts. CLICK HERE to return to the home page (a) General rule. Notwithstanding any other provision of this subchapter, the provisions of this

Internal Revenue Code Section 664(d)(1) Charitable remainder trusts. CLICK HERE to return to the home page (a) General rule. Notwithstanding any other provision of this subchapter, the provisions of this

MICKEY R. DAVIS DAVIS & WILLMS, PLLC HOUSTON, TEXAS JULY 18, 2016

MICKEY R. DAVIS DAVIS & WILLMS, PLLC HOUSTON, TEXAS JULY 18, 2016 Trusts and estates are not entities Tax laws treat them as though they were Rules applicable to individuals apply to trusts and estates

MICKEY R. DAVIS DAVIS & WILLMS, PLLC HOUSTON, TEXAS JULY 18, 2016 Trusts and estates are not entities Tax laws treat them as though they were Rules applicable to individuals apply to trusts and estates

Estate (cont.) IRC 2033 includes in the gross estate all probate assets IRC includes in the gross estate all non-probate assets

IRC 2033 includes in the gross estate all probate assets IRC includes in the gross estate all non-probate assets") Overview Certain entities are created for planning purposes. These entities are separate and apart from individuals or businesses. Income in these entities needs to be accounted for and taxed if held within

Overview Certain entities are created for planning purposes. These entities are separate and apart from individuals or businesses. Income in these entities needs to be accounted for and taxed if held within

Internal Revenue Code Section 338(g) Certain stock purchases treated as asset acquisitions

Certain stock purchases treated as asset acquisitions") Internal Revenue Code Section 338(g) Certain stock purchases treated as asset acquisitions CLICK HERE to return to the home page (a) General rule. For purposes of this subtitle, if a purchasing corporation

Internal Revenue Code Section 338(g) Certain stock purchases treated as asset acquisitions CLICK HERE to return to the home page (a) General rule. For purposes of this subtitle, if a purchasing corporation

Internal Revenue Code Section 469(h)(2) Passive activity losses and credits limited.

(2) Passive activity losses and credits limited.") CLICK HERE to return to the home page Internal Revenue Code Section 469(h)(2) Passive activity losses and credits limited. (a) Disallowance. If for any taxable year the taxpayer is described in paragraph

CLICK HERE to return to the home page Internal Revenue Code Section 469(h)(2) Passive activity losses and credits limited. (a) Disallowance. If for any taxable year the taxpayer is described in paragraph

Introduction to the Federal Income Tax Issues of Filing Form 1041 for Estates and Trusts

National Society of Tax Professionals presents Introduction to the Federal Income Tax Issues of Filing Form 1041 for Estates and Trusts Developed and Written by Paul La Monaca, CPA, MST NSTP Director of

National Society of Tax Professionals presents Introduction to the Federal Income Tax Issues of Filing Form 1041 for Estates and Trusts Developed and Written by Paul La Monaca, CPA, MST NSTP Director of

LEXISNEXIS' CODE OF FEDERAL REGULATIONS Copyright (c) 2011, by Matthew Bender & Company, a member of the LexisNexis Group. All rights reserved.

2011, by Matthew Bender & Company, a member of the LexisNexis Group. All rights reserved.") LEXISNEXIS' CODE OF FEDERAL REGULATIONS Copyright (c) 2011, by Matthew Bender & Company, a member of the LexisNexis Group. All rights reserved. *** THIS SECTION IS CURRENT THROUGH THE MARCH 30, 2011 ***

LEXISNEXIS' CODE OF FEDERAL REGULATIONS Copyright (c) 2011, by Matthew Bender & Company, a member of the LexisNexis Group. All rights reserved. *** THIS SECTION IS CURRENT THROUGH THE MARCH 30, 2011 ***

Internal Revenue Code Section 1022 (REPEALED) Treatment of property acquired from a decedent dying after December 31, 2009.

Treatment of property acquired from a decedent dying after December 31, 2009.") CLICK HERE to return to the home page Internal Revenue Code Section 1022 (REPEALED) Treatment of property acquired from a decedent dying after December 31, 2009. (a) In general. Except as otherwise provided

CLICK HERE to return to the home page Internal Revenue Code Section 1022 (REPEALED) Treatment of property acquired from a decedent dying after December 31, 2009. (a) In general. Except as otherwise provided

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018 Alan S. Halperin Paul, Weiss, Rifkind, Wharton & Garrison LLP Amy E. Heller

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018 Alan S. Halperin Paul, Weiss, Rifkind, Wharton & Garrison LLP Amy E. Heller

Bring SPF. Take CPE. JULY 6, 7, & 8. Ocean City, MD Clarion Resort Fontainebleau Hotel

Bring SPF. Take CPE. JULY 6, 7, & 8 Ocean City, MD Clarion Resort Fontainebleau Hotel It s not about climbing the ladder. It s about serving your team, your organization, and yourself. It s about being

Bring SPF. Take CPE. JULY 6, 7, & 8 Ocean City, MD Clarion Resort Fontainebleau Hotel It s not about climbing the ladder. It s about serving your team, your organization, and yourself. It s about being

Deductions in a Proposed Calculation and Allocation of Distributable Net Income to the Separate Shares of a Trust or Estate

California Western School of Law CWSL Scholarly Commons Faculty Scholarship 2008 Deductions in a Proposed Calculation and Allocation of Distributable Net Income to the Separate Shares of a Trust or Estate

California Western School of Law CWSL Scholarly Commons Faculty Scholarship 2008 Deductions in a Proposed Calculation and Allocation of Distributable Net Income to the Separate Shares of a Trust or Estate

Internal Revenue Code Section 469(j)(8) Passive activity losses and credits limited

(8) Passive activity losses and credits limited") Internal Revenue Code Section 469(j)(8) Passive activity losses and credits limited CLICK HERE to return to the home page (a) Disallowance. (1) In general. If for any taxable year the taxpayer is described

Internal Revenue Code Section 469(j)(8) Passive activity losses and credits limited CLICK HERE to return to the home page (a) Disallowance. (1) In general. If for any taxable year the taxpayer is described

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates FOR LIVE PROGRAM ONLY THURSDAY, SEPTEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates FOR LIVE PROGRAM ONLY THURSDAY, SEPTEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

A CPA s Guide to Trusts

A CPA s Guide to Trusts Edward K. Zollars, CPA Phoenix, Arizona ed@tzlcpas.com www.cperesources.com CPA s Guide to Trusts KEY PLAYERS IN A TRUST 1 Purposes of Trusts Parties Involved in a Trust 2 Advisers

A CPA s Guide to Trusts Edward K. Zollars, CPA Phoenix, Arizona ed@tzlcpas.com www.cperesources.com CPA s Guide to Trusts KEY PLAYERS IN A TRUST 1 Purposes of Trusts Parties Involved in a Trust 2 Advisers

Internal Revenue Code Section 1291 Interest on tax deferral

Internal Revenue Code Section 1291 Interest on tax deferral (a) Treatment of distributions and stock dispositions. CLICK HERE to return to the home page (1) Distributions. If a United States person receives

Internal Revenue Code Section 1291 Interest on tax deferral (a) Treatment of distributions and stock dispositions. CLICK HERE to return to the home page (1) Distributions. If a United States person receives

Third-Party Special Needs Trusts: Asset Protection Benefits and Tax Burdens

Third-Party Special Needs Trusts: Asset Protection Benefits and Tax Burdens Presented by I. Richard Gershon University of Mississippi School of Law I. What is a Third-Party Special Needs Trust? A. Difference

Third-Party Special Needs Trusts: Asset Protection Benefits and Tax Burdens Presented by I. Richard Gershon University of Mississippi School of Law I. What is a Third-Party Special Needs Trust? A. Difference

Reg. Section (b) Charitable remainder annuity trust.

Charitable remainder annuity trust.") CLICK HERE to return to the home page Reg. Section 1.664-2(b) Charitable remainder annuity trust. (a) Description. A charitable remainder annuity trust is a trust which complies with the applicable provisions

CLICK HERE to return to the home page Reg. Section 1.664-2(b) Charitable remainder annuity trust. (a) Description. A charitable remainder annuity trust is a trust which complies with the applicable provisions

ESTATE OR TRUST TAX ORGANIZER FORM New Estate or Trust Administrators Information Needed

ESTATE OR TRUST TAX ORGANIZER FORM 1041 New Estate or Trust Administrators Information Needed This is a list of information which will be typically needed for us to work with you on tax issues for an estate

ESTATE OR TRUST TAX ORGANIZER FORM 1041 New Estate or Trust Administrators Information Needed This is a list of information which will be typically needed for us to work with you on tax issues for an estate

CHAPTER 13 INCOME TAXATION OF TRUSTS AND ESTATES LECTURE NOTES

CHAPTER 13 INCOME TAXATION OF TRUSTS AND ESTATES LECTURE NOTES 13.1 AN OVERVIEW OF SUBCHAPTER J What is a Trust? 1. A trust is an arrangement created by a will or by a lifetime declaration, through which

CHAPTER 13 INCOME TAXATION OF TRUSTS AND ESTATES LECTURE NOTES 13.1 AN OVERVIEW OF SUBCHAPTER J What is a Trust? 1. A trust is an arrangement created by a will or by a lifetime declaration, through which

CHAPTER SIX Income Tax Non-grantor Trusts

CHAPTER SIX Income Tax Non-grantor Trusts What is the income tax treatment of a true trust income allocation between: (1) the trust, (2) the beneficiaries (but not the grantor)? Subchap. J, Subparts A-D

CHAPTER SIX Income Tax Non-grantor Trusts What is the income tax treatment of a true trust income allocation between: (1) the trust, (2) the beneficiaries (but not the grantor)? Subchap. J, Subparts A-D

Chapter 27. Income Taxation of Trusts and Estates. Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe

Chapter 27 Income Taxation of Trusts and Estates Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004 South-Western/Thomson Learning Using Trusts (slide 1 of 5)

Chapter 27 Income Taxation of Trusts and Estates Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004 South-Western/Thomson Learning Using Trusts (slide 1 of 5)

Gift Planning Glossary of Terms

Gift Planning Glossary of Terms Annual Exclusion The amount of property (presently $14,000 or $28,000 for a married couple in 2013) that may annually be given to a donee, regardless of the donee s relationship

Gift Planning Glossary of Terms Annual Exclusion The amount of property (presently $14,000 or $28,000 for a married couple in 2013) that may annually be given to a donee, regardless of the donee s relationship

Federal Income Tax Concepts Needed to Prepare Fiduciary Form 1041 and the Final Form 1040 of the Decedent

Michigan Society of Enrolled Agents MiSEA presents Federal Income Tax Concepts Needed to Prepare Fiduciary Form 1041 and the Final Form 1040 of the Decedent at the Bavarian Inn Lodge and Conference Center

Michigan Society of Enrolled Agents MiSEA presents Federal Income Tax Concepts Needed to Prepare Fiduciary Form 1041 and the Final Form 1040 of the Decedent at the Bavarian Inn Lodge and Conference Center

Internal Revenue Code Section 1374 Tax imposed on certain built-in gains.

Internal Revenue Code Section 1374 Tax imposed on certain built-in gains. CLICK HERE to return to the home page (a) General rule. If for any taxable year beginning in the recognition period an S corporation

Internal Revenue Code Section 1374 Tax imposed on certain built-in gains. CLICK HERE to return to the home page (a) General rule. If for any taxable year beginning in the recognition period an S corporation

FIDUCIARY TAX ORGANIZER (FORM 1041)

") Trust/Estate Name(s) Federal ID# Address City, Town, or Post Office County State ZIP Code Telephone Number Telephone Number Fax Number E-mail Address Home/Mobile Office Fiduciary Name(s) and Title(s) Federal

Trust/Estate Name(s) Federal ID# Address City, Town, or Post Office County State ZIP Code Telephone Number Telephone Number Fax Number E-mail Address Home/Mobile Office Fiduciary Name(s) and Title(s) Federal

Irrevocable Trust Seminar Presented by Anthony L. Barney, Esq. March 11, 2014

Irrevocable Trust Seminar Presented by Anthony L. Barney, Esq. March 11, 2014 I. Irrevocable Trust A. Definition: Unless a trust is defined as a revocable trust, the presumption is that a trust is irrevocable

Irrevocable Trust Seminar Presented by Anthony L. Barney, Esq. March 11, 2014 I. Irrevocable Trust A. Definition: Unless a trust is defined as a revocable trust, the presumption is that a trust is irrevocable

CHAPTER SIX Income Tax Non-grantor Trusts

CHAPTER SIX Income Tax Non-grantor Trusts What is federal income tax treatment of a true trust? Income allocation is to be made between: (1) trust & (2) the beneficiaries (but not grantor)? Subchap. J,

CHAPTER SIX Income Tax Non-grantor Trusts What is federal income tax treatment of a true trust? Income allocation is to be made between: (1) trust & (2) the beneficiaries (but not grantor)? Subchap. J,

Southern Arizona Estate Planning Council FIDUCIARY INCOME TAX BOOT CAMP

Southern Arizona Estate Planning Council FIDUCIARY INCOME TAX BOOT CAMP November 9, 2016 1 FIDUCIARY INCOME TAX BOOT CAMP INCOME TAXATION OF TRUSTS AND ESTATES Presenters: Gregory V. Gadarian Steven W.

Southern Arizona Estate Planning Council FIDUCIARY INCOME TAX BOOT CAMP November 9, 2016 1 FIDUCIARY INCOME TAX BOOT CAMP INCOME TAXATION OF TRUSTS AND ESTATES Presenters: Gregory V. Gadarian Steven W.

CHAPTER SIX Income Tax Non-grantor Trusts

CHAPTER SIX Income Tax Non-grantor Trusts What is the federal income tax treatment of a true trust income allocation is to be made between: (1) trust & (2) the beneficiaries (but not grantor)? Subchap.

CHAPTER SIX Income Tax Non-grantor Trusts What is the federal income tax treatment of a true trust income allocation is to be made between: (1) trust & (2) the beneficiaries (but not grantor)? Subchap.

FIDUCIARY TAX ORGANIZER FORM 1041

FIDUCIARY TAX ORGANIZER FORM 1041 Enclosed is an organizer that I provide to my tax clients in order to assist them in gathering the information necessary to prepare their fiduciary income tax returns.

FIDUCIARY TAX ORGANIZER FORM 1041 Enclosed is an organizer that I provide to my tax clients in order to assist them in gathering the information necessary to prepare their fiduciary income tax returns.

Part 91 REGISTRATION AND REPORTING BY TRUSTEES PURSUANT TO ARTICLE 8 OF THE ESTATES, POWERS AND TRUSTS LAW

Chapter V Charitable Uses and Purposes Title 13 New York Code of Rules and Regulations Part 90 - Definitions 90.1 Trustees RULES AND REGULATIONS FOR REGISTRATION OF CHARITABLE TRUSTEES, INCLUDING TRUSTS,

Chapter V Charitable Uses and Purposes Title 13 New York Code of Rules and Regulations Part 90 - Definitions 90.1 Trustees RULES AND REGULATIONS FOR REGISTRATION OF CHARITABLE TRUSTEES, INCLUDING TRUSTS,

If for any taxable year the taxpayer is described in paragraph (2), neither-- (A) the passive activity loss, nor (B) the passive activity credit,

, neither-- (A) the passive activity loss, nor (B) the passive activity credit,") From the U.S. Code Online via GPO Access [wais.access.gpo.gov] [Laws in effect as of January 3, 2006] [Document affected by Public Law 7 Section (5)] [Document affected by Public Law 7] [Document affected

From the U.S. Code Online via GPO Access [wais.access.gpo.gov] [Laws in effect as of January 3, 2006] [Document affected by Public Law 7 Section (5)] [Document affected by Public Law 7] [Document affected

Dual National Beneficiaries of Foreign Trusts: UNI, PFICs and GILTI Tax. Juan Pablo G. Zaragoza - Procopio

Dual National Beneficiaries of Foreign Trusts: UNI, PFICs and GILTI Tax Juan Pablo G. Zaragoza - Procopio U.S. Federal Income Taxation of Trusts Domestic Trusts (U.S. Person Trust) World-wide income Foreign

Dual National Beneficiaries of Foreign Trusts: UNI, PFICs and GILTI Tax Juan Pablo G. Zaragoza - Procopio U.S. Federal Income Taxation of Trusts Domestic Trusts (U.S. Person Trust) World-wide income Foreign

Page 1431 TITLE 26 INTERNAL REVENUE CODE 469

Page 1431 TITLE 26 INTERNAL REVENUE CODE 469 fund established after Aug. 16, 1986, not be subject to current income tax and that if contributions to such account or fund are not deductible then the account

Page 1431 TITLE 26 INTERNAL REVENUE CODE 469 fund established after Aug. 16, 1986, not be subject to current income tax and that if contributions to such account or fund are not deductible then the account

Taxation of Estate and Trust Income under the Internal Revenue Code of 1954

Notre Dame Law Review Volume 30 Issue 1 Article 3 12-1-1954 Taxation of Estate and Trust Income under the Internal Revenue Code of 1954 Roger Paul Peters Follow this and additional works at: http://scholarship.law.nd.edu/ndlr

Notre Dame Law Review Volume 30 Issue 1 Article 3 12-1-1954 Taxation of Estate and Trust Income under the Internal Revenue Code of 1954 Roger Paul Peters Follow this and additional works at: http://scholarship.law.nd.edu/ndlr

H.R. 4 Pension Protection Act of 2006 (Enrolled as Agreed to or Passed by Both House and Senate)

") H.R. 4 Pension Protection Act of 2006 (Enrolled as Agreed to or Passed by Both House and Senate) TITLE XII--PROVISIONS RELATING TO EXEMPT ORGANIZATIONS Subtitle A--Charitable Giving Incentives SEC. 1201.

H.R. 4 Pension Protection Act of 2006 (Enrolled as Agreed to or Passed by Both House and Senate) TITLE XII--PROVISIONS RELATING TO EXEMPT ORGANIZATIONS Subtitle A--Charitable Giving Incentives SEC. 1201.

CHAPTER 27 INCOME TAXATION OF TRUSTS AND ESTATES SOLUTIONS TO PROBLEM MATERIALS. Status: Q/P Question/ Present in Prior Problem Topic Edition Edition

CHAPTER 27 INCOME TAATION OF TRUSTS AND ESTATES SOLUTIONS TO PROBLEM MATERIALS Status: Q/P Question/ Present in Prior Problem Topic Edition Edition 1 Issue ID Unchanged 1 2 Parties to a fiduciary entity

CHAPTER 27 INCOME TAATION OF TRUSTS AND ESTATES SOLUTIONS TO PROBLEM MATERIALS Status: Q/P Question/ Present in Prior Problem Topic Edition Edition 1 Issue ID Unchanged 1 2 Parties to a fiduciary entity

Title 18-A: PROBATE CODE

Title 18-A: PROBATE CODE Article 7: Trust Administration Table of Contents Part 1. TRUST REGISTRATION... 5 Section 7-101. REGISTRATION OF TRUSTS... 5 Section 7-102. REGISTRATION PROCEDURES... 5 Section

Title 18-A: PROBATE CODE Article 7: Trust Administration Table of Contents Part 1. TRUST REGISTRATION... 5 Section 7-101. REGISTRATION OF TRUSTS... 5 Section 7-102. REGISTRATION PROCEDURES... 5 Section

Distributable Net Income: Mastering Difficult DNI Calculations for Estates and Complex Trusts

FOR LIVE PROGRAM ONLY Distributable Net Income: Mastering Difficult DNI Calculations for Estates and Complex Trusts TUESDAY, DECEMBER 5, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FOR LIVE PROGRAM ONLY Distributable Net Income: Mastering Difficult DNI Calculations for Estates and Complex Trusts TUESDAY, DECEMBER 5, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM

FIDUCIARY INCOME TAXES

FIDUCIARY INCOME TAXES 12 Miscellaneous Itemized Deductions.............. 362 Qualified Revocable Trust.... 365 Case Study................. 367 Appendix: Treasury Regulation 1.67-4................ 389

FIDUCIARY INCOME TAXES 12 Miscellaneous Itemized Deductions.............. 362 Qualified Revocable Trust.... 365 Case Study................. 367 Appendix: Treasury Regulation 1.67-4................ 389

INCOME AND FIDUCIARY TAX ISSUES FOR ESTATE PLANNERS, PART 1 & PART

INCOME AND FIDUCIARY TAX ISSUES FOR ESTATE PLANNERS, PART 1 & PART 2 First Run Broadcast: September 19 & 20, 2018 1:00 p.m. E.T./12:00 p.m. C.T./11:00 a.m. M.T./10:00 a.m. P.T. (60 minutes each day) Understanding

INCOME AND FIDUCIARY TAX ISSUES FOR ESTATE PLANNERS, PART 1 & PART 2 First Run Broadcast: September 19 & 20, 2018 1:00 p.m. E.T./12:00 p.m. C.T./11:00 a.m. M.T./10:00 a.m. P.T. (60 minutes each day) Understanding

WHAT A BENEFICIARY NEEDS TO KNOW ABOUT THE PROBATE PROCESS April 19, INTRODUCTION.

WHAT A BENEFICIARY NEEDS TO KNOW ABOUT THE PROBATE PROCESS April 19, 2011 1. INTRODUCTION. Many Decedents make gifts to persons that take effect upon their deaths. These gifts may take the form of a designation

WHAT A BENEFICIARY NEEDS TO KNOW ABOUT THE PROBATE PROCESS April 19, 2011 1. INTRODUCTION. Many Decedents make gifts to persons that take effect upon their deaths. These gifts may take the form of a designation

New York State Department of Taxation and Finance Instructions for Form IT-205. Fiduciary Income Tax Return New York State New York City Yonkers

New York State Department of Taxation and Finance Instructions for Form IT-205 Fiduciary Income Tax Return New York State New York City Yonkers IT-205-I Form IT-205 highlights for tax year 2012 General

New York State Department of Taxation and Finance Instructions for Form IT-205 Fiduciary Income Tax Return New York State New York City Yonkers IT-205-I Form IT-205 highlights for tax year 2012 General

. Your completed tax organizer needs to be received no later than

Organizer Estate and trust This organizer is designed to assist you in gathering the information required for preparation of fiduciary tax returns. Please complete it in full and provide details and documentation

Organizer Estate and trust This organizer is designed to assist you in gathering the information required for preparation of fiduciary tax returns. Please complete it in full and provide details and documentation

Title 12 - Decedents' Estates and Fiduciary Relations. Part VI Allocation of Principal and Income

Part VI Allocation of Principal and Income Chapter 61 DELAWARE UNIFORM PRINCIPAL AND INCOME ACT Subchapter I Definitions and General Principles 61-101 Short title. Subchapters I through VI of this chapter

Part VI Allocation of Principal and Income Chapter 61 DELAWARE UNIFORM PRINCIPAL AND INCOME ACT Subchapter I Definitions and General Principles 61-101 Short title. Subchapters I through VI of this chapter

UNIFORM FIDUCIARY INCOME AND PRINCIPAL ACT*

UNIFORM FIDUCIARY INCOME AND PRINCIPAL ACT* Drafted by the NATIONAL CONFERENCE OF COMMISSIONERS ON UNIFORM STATE LAWS and by it APPROVED AND RECOMMENDED FOR ENACTMENT IN ALL THE STATES at its ANNUAL CONFERENCE

UNIFORM FIDUCIARY INCOME AND PRINCIPAL ACT* Drafted by the NATIONAL CONFERENCE OF COMMISSIONERS ON UNIFORM STATE LAWS and by it APPROVED AND RECOMMENDED FOR ENACTMENT IN ALL THE STATES at its ANNUAL CONFERENCE

Chapter 37A. Uniform Principal and Income Act. 37A Short title. 37A Definitions.

Chapter 37A. Uniform Principal and Income Act. Article 1. Definitions and Fiduciary Duties; Conversion to Unitrust; Judicial Control of Discretionary Power. Part 1. Definitions. 37A-1-101. Short title.

Chapter 37A. Uniform Principal and Income Act. Article 1. Definitions and Fiduciary Duties; Conversion to Unitrust; Judicial Control of Discretionary Power. Part 1. Definitions. 37A-1-101. Short title.

Internal Revenue Code Section 172(c) Net operating loss deduction.

Net operating loss deduction.") Note: This document has been updated to reflect amendments by the TCJA, Pub. L. No. 115-97. CLICK HERE to return to the home page Internal Revenue Code Section 172(c) Net operating loss deduction. (a)

Note: This document has been updated to reflect amendments by the TCJA, Pub. L. No. 115-97. CLICK HERE to return to the home page Internal Revenue Code Section 172(c) Net operating loss deduction. (a)

2018 National Conference on Special Needs Planning and Special Needs Trusts Taxation of Third Party SNT s I. Richard Gershon 10/17/2018

2018 National Conference on Special Needs Planning and Special Needs Trusts Taxation of Third Party SNT s I. Richard Gershon 10/17/2018 Professor of Law University of Mississippi (Ole Miss) School of Law

2018 National Conference on Special Needs Planning and Special Needs Trusts Taxation of Third Party SNT s I. Richard Gershon 10/17/2018 Professor of Law University of Mississippi (Ole Miss) School of Law

TITLE 26 INTERNAL REVENUE CODE. specified in any of the paragraphs of subsection

266 TITLE 26 INTERNAL REVENUE CODE Page 922 section 2137(e) of Pub. L. 94 455, set out as a note under section 852 of this title. EFFECTIVE DATE OF 1964 AMENDMENT Pub. L. 88 272, title II, 216(b), Feb.

266 TITLE 26 INTERNAL REVENUE CODE Page 922 section 2137(e) of Pub. L. 94 455, set out as a note under section 852 of this title. EFFECTIVE DATE OF 1964 AMENDMENT Pub. L. 88 272, title II, 216(b), Feb.

MELISSA J. WILLMS DAVIS & WILLMS, PLLC HOUSTON, TEXAS JULY 9, 2018

MELISSA J. WILLMS DAVIS & WILLMS, PLLC HOUSTON, TEXAS JULY 9, 2018 Unified transfer tax system $10,000,000 exclusion/exemption for gift, estate and GST tax for years 2018 2025 Indexed for inflation: $11.18

MELISSA J. WILLMS DAVIS & WILLMS, PLLC HOUSTON, TEXAS JULY 9, 2018 Unified transfer tax system $10,000,000 exclusion/exemption for gift, estate and GST tax for years 2018 2025 Indexed for inflation: $11.18

GLOSSARY OF FIDUCIARY TERMS

The terminology used when discussing trusts and estates can often be unfamiliar and our glossary of fiduciary terms is designed to help you understand it better. If you have a question about the glossary

The terminology used when discussing trusts and estates can often be unfamiliar and our glossary of fiduciary terms is designed to help you understand it better. If you have a question about the glossary

Estate and Trust Income Taxation. Course #5185J/QAS5185J Exam Packet

Estate and Trust Income Taxation Course #5185J/QAS5185J Exam Packet ESTATE AND TRUST INCOME TAXATION (COURSE #5185J/QAS5185J) COURSE DESCRIPTION This course has two major components. The first component

Estate and Trust Income Taxation Course #5185J/QAS5185J Exam Packet ESTATE AND TRUST INCOME TAXATION (COURSE #5185J/QAS5185J) COURSE DESCRIPTION This course has two major components. The first component

1a. Analyze the dollar amount of D's 1978 Taxable Gifts (TC).

.") Searcy Estate and Gift Tax Fall 1983 Problem 1 For simplification purposes, throughout this Problem disregard the 2503 PDE, and disregard the Generation Skipping Tax, and assume that there are no ascertainable

Searcy Estate and Gift Tax Fall 1983 Problem 1 For simplification purposes, throughout this Problem disregard the 2503 PDE, and disregard the Generation Skipping Tax, and assume that there are no ascertainable

1500 Pennsylvania Avenue, NW 1111 Constitution Ave, NW Washington, DC Washington, DC 20224

The Honorable David J. Kautter Assistant Secretary for Tax Policy Acting Chief Counsel Department of the Treasury Internal Revenue Service 1500 Pennsylvania Avenue, NW 1111 Constitution Ave, NW Washington,

The Honorable David J. Kautter Assistant Secretary for Tax Policy Acting Chief Counsel Department of the Treasury Internal Revenue Service 1500 Pennsylvania Avenue, NW 1111 Constitution Ave, NW Washington,

Estate Planning. Farm Credit East, ACA Stephen Makarevich

Estate Planning Farm Credit East, ACA Stephen Makarevich Farm Business Consultant 9 County Road 618 Lebanon, NJ 08833 1.800.787.3276 stephen.makarevich@farmcrediteast.com 1 What is Estate Planning? 2 Estate

Estate Planning Farm Credit East, ACA Stephen Makarevich Farm Business Consultant 9 County Road 618 Lebanon, NJ 08833 1.800.787.3276 stephen.makarevich@farmcrediteast.com 1 What is Estate Planning? 2 Estate

Section 11 Probate Glossary

Section 11 Probate Glossary 2012 Investors Empowerment Academy, LLC 119 Abatement A proportional diminution or reduction of the pecuniary legacies, when there are not sufficient funds to pay them in full.

Section 11 Probate Glossary 2012 Investors Empowerment Academy, LLC 119 Abatement A proportional diminution or reduction of the pecuniary legacies, when there are not sufficient funds to pay them in full.

The Truth About Trusts To Trust or not to Trust: That is the Question

The Truth About Trusts To Trust or not to Trust: That is the Question Tim Mezhlumov, EA Melissa Simmons, CPA, EA Presented to North Texas Chapter of EAs, August 5, 2017 What is a Trust? A. A trust is traditionally

The Truth About Trusts To Trust or not to Trust: That is the Question Tim Mezhlumov, EA Melissa Simmons, CPA, EA Presented to North Texas Chapter of EAs, August 5, 2017 What is a Trust? A. A trust is traditionally

26 USC NB: This unofficial compilation of the U.S. Code is current as of Jan. 7, 2011 (see

TITLE 26 - INTERNAL REVENUE CODE Subtitle A - Income Taxes CHAPTER 1 - NORMAL TAXES AND SURTAXES Subchapter S - Tax Treatment of S Corporations and Their Shareholders PART I - IN GENERAL 1361. S corporation

TITLE 26 - INTERNAL REVENUE CODE Subtitle A - Income Taxes CHAPTER 1 - NORMAL TAXES AND SURTAXES Subchapter S - Tax Treatment of S Corporations and Their Shareholders PART I - IN GENERAL 1361. S corporation

Internal Revenue Code Section 2056 Bequests, etc., to surviving spouse.

Internal Revenue Code Section 2056 Bequests, etc., to surviving spouse. CLICK HERE to return to the home page (a) Allowance of marital deduction. For purposes of the tax imposed by section 2001 [IRC Sec.

Internal Revenue Code Section 2056 Bequests, etc., to surviving spouse. CLICK HERE to return to the home page (a) Allowance of marital deduction. For purposes of the tax imposed by section 2001 [IRC Sec.

Page 1715 TITLE 26 INTERNAL REVENUE CODE 856

Page 1715 TITLE 26 INTERNAL REVENUE CODE 856 tribution as provided in subsection (a) of this section, the shareholders shall consider the amounts described in section 853(b)(2) allocable to such distribution

Page 1715 TITLE 26 INTERNAL REVENUE CODE 856 tribution as provided in subsection (a) of this section, the shareholders shall consider the amounts described in section 853(b)(2) allocable to such distribution

ALI-ABA Course of Study Estate Planning for the Family Business Owner

1089 ALI-ABA Course of Study Estate Planning for the Family Business Owner Cosponsored by the ABA Section of Real Property, Trust and Estate Law - ABA Section of Taxation July 9-11, 2008 Boston, Massachusetts

1089 ALI-ABA Course of Study Estate Planning for the Family Business Owner Cosponsored by the ABA Section of Real Property, Trust and Estate Law - ABA Section of Taxation July 9-11, 2008 Boston, Massachusetts

IRREVOCABLE TRUSTS Memorandum to the Settlor and the Trustee

Memorandum to the Settlor and the Trustee by Layne T. Rushforth 1. GENERALLY This memorandum is for the settlor (creator) and the trustee (manager) of an irrevocable trust. There is a section for each

Memorandum to the Settlor and the Trustee by Layne T. Rushforth 1. GENERALLY This memorandum is for the settlor (creator) and the trustee (manager) of an irrevocable trust. There is a section for each

Internal Revenue Code Section 954(c) Foreign base company income

Foreign base company income") CLICK HERE to return to the home page Internal Revenue Code Section 954(c) Foreign base company income (a) Foreign base company income. For purposes of section 952(a)(2), the term "foreign base company

CLICK HERE to return to the home page Internal Revenue Code Section 954(c) Foreign base company income (a) Foreign base company income. For purposes of section 952(a)(2), the term "foreign base company

Taxes and the Decedent s Estate 2010 A Year of Change. A New Start

Taxes and the Decedent s Estate 2010 A Year of Change Rebecca A. Pace, CPA Estate Accountant Vorys, Sater, Seymour and Pease LLP 614.545-6632 RAPace@vorys.com A New Start January 1, 2010, Federal Estate

Taxes and the Decedent s Estate 2010 A Year of Change Rebecca A. Pace, CPA Estate Accountant Vorys, Sater, Seymour and Pease LLP 614.545-6632 RAPace@vorys.com A New Start January 1, 2010, Federal Estate

IMPACT OF THE TAX CUTS AND JOBS ACT ON ESTATE PLANNING

IMPACT OF THE TAX CUTS AND JOBS ACT ON ESTATE PLANNING By: Dean Mead P.A. Matthew J. Ahearn, Esq. David J. Akins, Esq. Lauren Y. Detzel, Esq. Kyle C. Griffin, Esq. Brian M. Malec, Esq. TABLE OF CONTENTS

IMPACT OF THE TAX CUTS AND JOBS ACT ON ESTATE PLANNING By: Dean Mead P.A. Matthew J. Ahearn, Esq. David J. Akins, Esq. Lauren Y. Detzel, Esq. Kyle C. Griffin, Esq. Brian M. Malec, Esq. TABLE OF CONTENTS

IRREVOCABLE TRUSTS Memorandum to the Settlor and the Trustee

Memorandum to the Settlor and the Trustee by Layne T. Rushforth 1. GENERALLY This memorandum is for the settlor (creator) and the trustee (manager) of an irrevocable trust. There is a section for each

Memorandum to the Settlor and the Trustee by Layne T. Rushforth 1. GENERALLY This memorandum is for the settlor (creator) and the trustee (manager) of an irrevocable trust. There is a section for each

UNIFORM PRINCIPAL AND INCOME ACT (1997) [ARTICLE] 1 DEFINITIONS AND FIDUCIARY DUTIES

![UNIFORM PRINCIPAL AND INCOME ACT (1997) [ARTICLE] 1 DEFINITIONS AND FIDUCIARY DUTIES](/thumbs/82/85139689.jpg "UNIFORM PRINCIPAL AND INCOME ACT (1997) [ARTICLE] 1 DEFINITIONS AND FIDUCIARY DUTIES") UNIFORM PRINCIPAL AND INCOME ACT (1997) [ARTICLE] 1 DEFINITIONS AND FIDUCIARY DUTIES SECTION 101. SHORT TITLE. This [Act] may be cited as the Uniform Principal and Income Act (1997). SECTION 102. DEFINITIONS.

UNIFORM PRINCIPAL AND INCOME ACT (1997) [ARTICLE] 1 DEFINITIONS AND FIDUCIARY DUTIES SECTION 101. SHORT TITLE. This [Act] may be cited as the Uniform Principal and Income Act (1997). SECTION 102. DEFINITIONS.

New IRC Section 67(g) and Form 1041 Trust Deduction Rules Post-Tax Reform

and Form 1041 Trust Deduction Rules Post-Tax Reform") New IRC Section 67(g) and Form 1041 Trust Deduction Rules Post-Tax Reform FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

New IRC Section 67(g) and Form 1041 Trust Deduction Rules Post-Tax Reform FOR LIVE PROGRAM ONLY TUESDAY, MAY 22, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved

Understanding TRUSTS. A Summary of Trusts for Estate Planning VLC

Understanding TRUSTS A Summary of Trusts for Estate Planning VLC0009-0417 TABLE OF CONTENTS What Is a Trust.... 1 Who s Who in a Trust.... 2 Types of Trusts... 3 Taxation.... 4 Frequently Asked Questions....

Understanding TRUSTS A Summary of Trusts for Estate Planning VLC0009-0417 TABLE OF CONTENTS What Is a Trust.... 1 Who s Who in a Trust.... 2 Types of Trusts... 3 Taxation.... 4 Frequently Asked Questions....

6. The legal home where a person has a true, fixed, and permanent place of dwelling and to which the person intends to return when absent

CHAPTER 7: THE PARTICIPANTS AND THE PROPER COURT MATCHING a. Letters Testamentary b. tickler system c. registrar d. probate (of a will) e. jurisdiction f. in rem jurisdiction g. disbursements h. venue

CHAPTER 7: THE PARTICIPANTS AND THE PROPER COURT MATCHING a. Letters Testamentary b. tickler system c. registrar d. probate (of a will) e. jurisdiction f. in rem jurisdiction g. disbursements h. venue

Internal Revenue Code Section 475(c)(2) Mark to market accounting method for dealers in securities

(2) Mark to market accounting method for dealers in securities") CLICK HERE to return to the home page Internal Revenue Code Section 475(c)(2) Mark to market accounting method for dealers in securities (a) General rule. Notwithstanding any other provision of this subpart,

CLICK HERE to return to the home page Internal Revenue Code Section 475(c)(2) Mark to market accounting method for dealers in securities (a) General rule. Notwithstanding any other provision of this subpart,

CPAs & ADVISORS FIDUCIARY TAX COMPLIANCE. Kevin G. Horn, CPA. experience ideas //

CPAs & ADVISORS experience ideas // FIDUCIARY TAX COMPLIANCE Kevin G. Horn, CPA PRESENTATION AGENDA General Terminology Types of Trusts Reporting for Grantor Trust Ficuciary Accounting Rules Reporting

CPAs & ADVISORS experience ideas // FIDUCIARY TAX COMPLIANCE Kevin G. Horn, CPA PRESENTATION AGENDA General Terminology Types of Trusts Reporting for Grantor Trust Ficuciary Accounting Rules Reporting

BLAZING TRAILS AROUND PEAKS AND VALLEYS TOTAL RETURN TRUST STRUCTURING

BLAZING TRAILS AROUND PEAKS AND VALLEYS TOTAL RETURN TRUST STRUCTURING Estate Planning Council of Birmingham February 6, 2014 C. Fred Daniels (205) 716-5232 cfd@cabaniss.com Leonard Wertheimer (205) 716-5254

BLAZING TRAILS AROUND PEAKS AND VALLEYS TOTAL RETURN TRUST STRUCTURING Estate Planning Council of Birmingham February 6, 2014 C. Fred Daniels (205) 716-5232 cfd@cabaniss.com Leonard Wertheimer (205) 716-5254

ENGINEERED CAPITAL GAINS TRANSACTIONS THE ULTIMATE TRANSACTION The Numbers - California

Copyright 2013: United Wealth Protection Concepts, Presentation Chart #6.20 R04/13 The Numbers - California Ultimate Straight Sale Cost Basis $100,000 $100,000 Sale Price $1,000,000 $1,000,000 Capital

Copyright 2013: United Wealth Protection Concepts, Presentation Chart #6.20 R04/13 The Numbers - California Ultimate Straight Sale Cost Basis $100,000 $100,000 Sale Price $1,000,000 $1,000,000 Capital

No An act relating to the uniform principal and income act. (H.327) It is hereby enacted by the General Assembly of the State of Vermont:

It is hereby enacted by the General Assembly of the State of Vermont:") No. 114. An act relating to the uniform principal and income act. (H.327) It is hereby enacted by the General Assembly of the State of Vermont: Sec. 1. 14 V.S.A. chapter 118 is added to read: CHAPTER 118.

No. 114. An act relating to the uniform principal and income act. (H.327) It is hereby enacted by the General Assembly of the State of Vermont: Sec. 1. 14 V.S.A. chapter 118 is added to read: CHAPTER 118.

TRUST OVERVIEW. Patricia J. Shevy, Esq. The Shevy Law Firm, LLC

TRUST OVERVIEW Patricia J. Shevy, Esq. The Shevy Law Firm, LLC 518-456-6705 What is a Trust? A Trust is a written, formal agreement between: The Grantor (settlor, creator)- the person who makes the contribution

TRUST OVERVIEW Patricia J. Shevy, Esq. The Shevy Law Firm, LLC 518-456-6705 What is a Trust? A Trust is a written, formal agreement between: The Grantor (settlor, creator)- the person who makes the contribution

The Funding of Children's Educational Costs

University of Michigan Law School University of Michigan Law School Scholarship Repository Articles Faculty Scholarship 1985 The Funding of Children's Educational Costs Douglas A. Kahn University of Michigan

University of Michigan Law School University of Michigan Law School Scholarship Repository Articles Faculty Scholarship 1985 The Funding of Children's Educational Costs Douglas A. Kahn University of Michigan

GOALS OF ESTATE PLANNING 12/12/2011 SUCCESSION PLANNING SUCCESSION PLANNING IMPEDIMENTS TO ACHIEVING ESTATE PLANNING GOALS

SUCCESSION PLANNING Why is succession planning so important Avoid sacrificing land for liquidity http://bit.ly/vwx5jn SUCCESSION PLANNING 1. Discuss your vision and goals for the land with your spouse

SUCCESSION PLANNING Why is succession planning so important Avoid sacrificing land for liquidity http://bit.ly/vwx5jn SUCCESSION PLANNING 1. Discuss your vision and goals for the land with your spouse

2) An estate represents a deceased person's assets after all debts are paid. Answer: TRUE Diff: 1 Question Status: Previous edition

An estate represents a deceased person's assets after all debts are paid. Answer: TRUE Diff: 1 Question Status: Previous edition") Personal Finance, 6e (Madura) Chapter 20 Estate Planning 20.1 Purpose of a Will 1) Two key goals of estate planning are to ensure that your estate passes to the proper beneficiaries and to ensure that

Personal Finance, 6e (Madura) Chapter 20 Estate Planning 20.1 Purpose of a Will 1) Two key goals of estate planning are to ensure that your estate passes to the proper beneficiaries and to ensure that

Glossary of Charitable Giving Terms

Glossary of Charitable Giving Terms (Adapted, revised and updated based on material presented in Planned Giving for Canadians, by Frank Minton and Lorna Somers, 2nd Edition, 1997). Below are definitions

Glossary of Charitable Giving Terms (Adapted, revised and updated based on material presented in Planned Giving for Canadians, by Frank Minton and Lorna Somers, 2nd Edition, 1997). Below are definitions

856 version date: July 30, 2008.

856 version date: July 30, 2008. 856 Page 1774 856. Definition of real estate investment trust (a) In general For purposes of this title, the term real estate investment trust means a corporation, trust,

856 version date: July 30, 2008. 856 Page 1774 856. Definition of real estate investment trust (a) In general For purposes of this title, the term real estate investment trust means a corporation, trust,

Internal Revenue Code Section 6654 Failure by individual to pay estimated income tax.

Internal Revenue Code Section 6654 Failure by individual to pay estimated income tax. CLICK HERE to return to the home page (a) Addition to the tax. Except as otherwise provided in this section, in the

Internal Revenue Code Section 6654 Failure by individual to pay estimated income tax. CLICK HERE to return to the home page (a) Addition to the tax. Except as otherwise provided in this section, in the

Internal Revenue Code Section 1(h) Tax imposed.

Tax imposed.") Internal Revenue Code Section 1(h) Tax imposed.... (h) Maximum capital gains rate. CLICK HERE to return to the home page (1) In general. If a taxpayer has a net capital gain for any taxable year, the tax

Internal Revenue Code Section 1(h) Tax imposed.... (h) Maximum capital gains rate. CLICK HERE to return to the home page (1) In general. If a taxpayer has a net capital gain for any taxable year, the tax

Beat the estate tax blow: with deferred annuities and an irrevocable trust

Beat the estate tax blow: with deferred annuities and an irrevocable trust JAN 01, 2012 BY The hinge around which estate planning revolves is gifting. The future growth in value of the asset from the date

Beat the estate tax blow: with deferred annuities and an irrevocable trust JAN 01, 2012 BY The hinge around which estate planning revolves is gifting. The future growth in value of the asset from the date

Personal Trust Services

Personal Trust Services Morgan Stanley Trust National Association 1 Morgan Stanley Trust, N.A. is dedicated to providing comprehensive and customized trustee services to wealthy families. As an experienced

Personal Trust Services Morgan Stanley Trust National Association 1 Morgan Stanley Trust, N.A. is dedicated to providing comprehensive and customized trustee services to wealthy families. As an experienced

(a) an inter vivos CRUT providing for unitrust payments for a term of years (see Rev. Proc );

an inter vivos CRUT providing for unitrust payments for a term of years (see Rev. Proc );") Rev. Proc. 2005-52 [2005-34 I.R.B. ] SECTION 1. PURPOSE This revenue procedure contains an annotated sample declaration of trust and alternate provisions that meet the requirements of 664(d)(2) and (d)(3)

Rev. Proc. 2005-52 [2005-34 I.R.B. ] SECTION 1. PURPOSE This revenue procedure contains an annotated sample declaration of trust and alternate provisions that meet the requirements of 664(d)(2) and (d)(3)

Tax Implications of Family Wealth Transfers

Tax Implications of Family Wealth Transfers Jill Choate Beier, Esq. Federal and Estate Gift Tax Overview Estate Tax Formula: Less: Plus: Equals: Decedent s Gross Estate Allowable Deductions Adjusted Taxable

Tax Implications of Family Wealth Transfers Jill Choate Beier, Esq. Federal and Estate Gift Tax Overview Estate Tax Formula: Less: Plus: Equals: Decedent s Gross Estate Allowable Deductions Adjusted Taxable

(e) a testamentary CRUT providing for unitrust payments for a term of years (see Rev. Proc );

a testamentary CRUT providing for unitrust payments for a term of years (see Rev. Proc );") Rev. Proc. 2005-53 [2005-34 I.R.B. ] SECTION 1. PURPOSE This revenue procedure contains an annotated sample declaration of trust and alternate provisions that meet the requirements of 664(d)(2) and (d)(3)

Rev. Proc. 2005-53 [2005-34 I.R.B. ] SECTION 1. PURPOSE This revenue procedure contains an annotated sample declaration of trust and alternate provisions that meet the requirements of 664(d)(2) and (d)(3)

Introduction. Definitions. Tax Topic Bulletin GIT-12 Estates and Trusts

Tax Topic Bulletin GIT-12 Estates and Trusts Introduction Estates and trusts are taxpayers under the Gross Income Tax Act (N.J.S.A. 54A:1-1 et seq.) and are required to file a return and pay taxes (including

Tax Topic Bulletin GIT-12 Estates and Trusts Introduction Estates and trusts are taxpayers under the Gross Income Tax Act (N.J.S.A. 54A:1-1 et seq.) and are required to file a return and pay taxes (including

NEW MEXICO 46A-1-10 to 46A Effective: July 1, Omits [UTC] subsection (2), defining ascertainable standard. (2004 amendment not adopted).

![NEW MEXICO 46A-1-10 to 46A Effective: July 1, Omits [UTC] subsection (2), defining ascertainable standard. (2004 amendment not adopted).](/thumbs/84/90614818.jpg "NEW MEXICO 46A-1-10 to 46A Effective: July 1, Omits [UTC] subsection (2), defining ascertainable standard. (2004 amendment not adopted).") Significant Differences in States Enacted Uniform Trust Codes This chart was created as an unofficial in-house NCCUSL document and is not for general publication. To report a typo or omission, please contact

Significant Differences in States Enacted Uniform Trust Codes This chart was created as an unofficial in-house NCCUSL document and is not for general publication. To report a typo or omission, please contact

2002 Rhode Island Fiduciary Income Tax Return

QUESTIONS? Forms and taxpayer information are available: In Person One Capitol Hill Providence, RI The Telephone (401) 222-1040 The web www.tax.ri.us 2002 Rhode Island Fiduciary Income Tax Return 2002

QUESTIONS? Forms and taxpayer information are available: In Person One Capitol Hill Providence, RI The Telephone (401) 222-1040 The web www.tax.ri.us 2002 Rhode Island Fiduciary Income Tax Return 2002

A WILL IS NOT ENOUGH by Kelly A. Thompson

A WILL IS NOT ENOUGH by Kelly A. Thompson kelly@twplc.com DISCLAIMER: This outline is for information purposes only and is not a substitute for legal counsel. assumes no liability for errors or admissions,

A WILL IS NOT ENOUGH by Kelly A. Thompson kelly@twplc.com DISCLAIMER: This outline is for information purposes only and is not a substitute for legal counsel. assumes no liability for errors or admissions,

Non-Probate vs. Probate Assets Why You Should Care

Chapter 17 Non-Probate vs. Probate Why You Should Care Susan McMakin (Richmond, Virginia) When you die, like most other people, you will probably leave assets that need to be transferred to the person,

Chapter 17 Non-Probate vs. Probate Why You Should Care Susan McMakin (Richmond, Virginia) When you die, like most other people, you will probably leave assets that need to be transferred to the person,

IRS Guidance on the 2-Percent of AGI Floor for Trusts and Estates The Final Regulations under IRC 67(e)

") KEVIN MATZ & ASSOCIATES PLLC IRS Guidance on the 2-Percent of AGI Floor for Trusts and Estates The Final Regulations under IRC 67(e) Kevin Matz, Esq., CPA, LL.M. (Taxation) Trusts and Estates Lawyer, Tax

KEVIN MATZ & ASSOCIATES PLLC IRS Guidance on the 2-Percent of AGI Floor for Trusts and Estates The Final Regulations under IRC 67(e) Kevin Matz, Esq., CPA, LL.M. (Taxation) Trusts and Estates Lawyer, Tax

THE LIVING TRUST. TRUST AGREEMENT signed this day of, 20 by. (hereafter "Settlor,"), and trustee. (hereafter "trustee). ESTABLISHMENT OF TRUST

, and trustee. (hereafter trustee). ESTABLISHMENT OF TRUST") THE LIVING TRUST OF TRUST AGREEMENT signed this day of, 20 by (hereafter "Settlor,"), and trustee (hereafter "trustee). (Note: Generally, to begin with, the 'settlor' and the 'trustee' are the same person(s)

THE LIVING TRUST OF TRUST AGREEMENT signed this day of, 20 by (hereafter "Settlor,"), and trustee (hereafter "trustee). (Note: Generally, to begin with, the 'settlor' and the 'trustee' are the same person(s)