SELECTED PARTNERSHIP & LLC TAX PROBLEMS

|

|

|

- Wendy Parsons

- 5 years ago

- Views:

Transcription

1 SELECTED PARTNERSHIP & LLC TAX PROBLEMS All Rights Reserved Handouts pages. Slides begin on page 50. If printing for the purpose of taking notes, print only through slide 379 (page 320). Mark A. Vogel Tax Education Services Denver, Colorado

: 1) Handouts file contains the PowerPoint presentation 3. Questions for the Instructor: a.")

2 SELECTED PARTNERSHIP & LLC TAX PROBLEMS Administrative Matters 1. Schedule: a. Lunch Break in four hours, for one hour (12:30 1:30 p.m. Mountain Time) 2. Reference Materials: a. Download (within three days from your Personal Page): 1) Handouts file contains the PowerPoint presentation 3. Questions for the Instructor: a. LIVE Questions During the Seminar: 1) Voice: ) Typewritten: a) Click: On next to Live Course Link on your Personal Page b) Click: On the Speech Bubble in the bottom right corner of the seminar viewing screen b. Post-Seminar Questions: 1) OR 4. Computer Problems: a. Call the Office: VOGEL.SEM/SP&LPROB.18

3 SELECTED PARTNERSHIP & LLC TAX PROBLEMS Course Objectives 1. Formation a. Balance sheet b. Tax & book capital account c. Recourse & nonrecourse debt d. Rewarding a service person with an interest in the entity 2. Operations a. Filing Form 1065 b. Basis and at-risk for losses c. Maximum amount of loss that is deductible d. Discussion of special allocations and substantial economic effect e. Disguised sales (c) Issues, including a Reverse 704(c) Allocation 4. SE Problems 5. Transactions Between a Member and the LLC 6. Deduction under 199A of 20% of qualified business income (QBI) 7. Termination Issues 8. Sale of Interest a. With and without a 754 election 9. Payments to a Retiring Member for that Member s Interest in Unrealized Receivables and Goodwill VOGEL.SEM/SP&LPROB.18

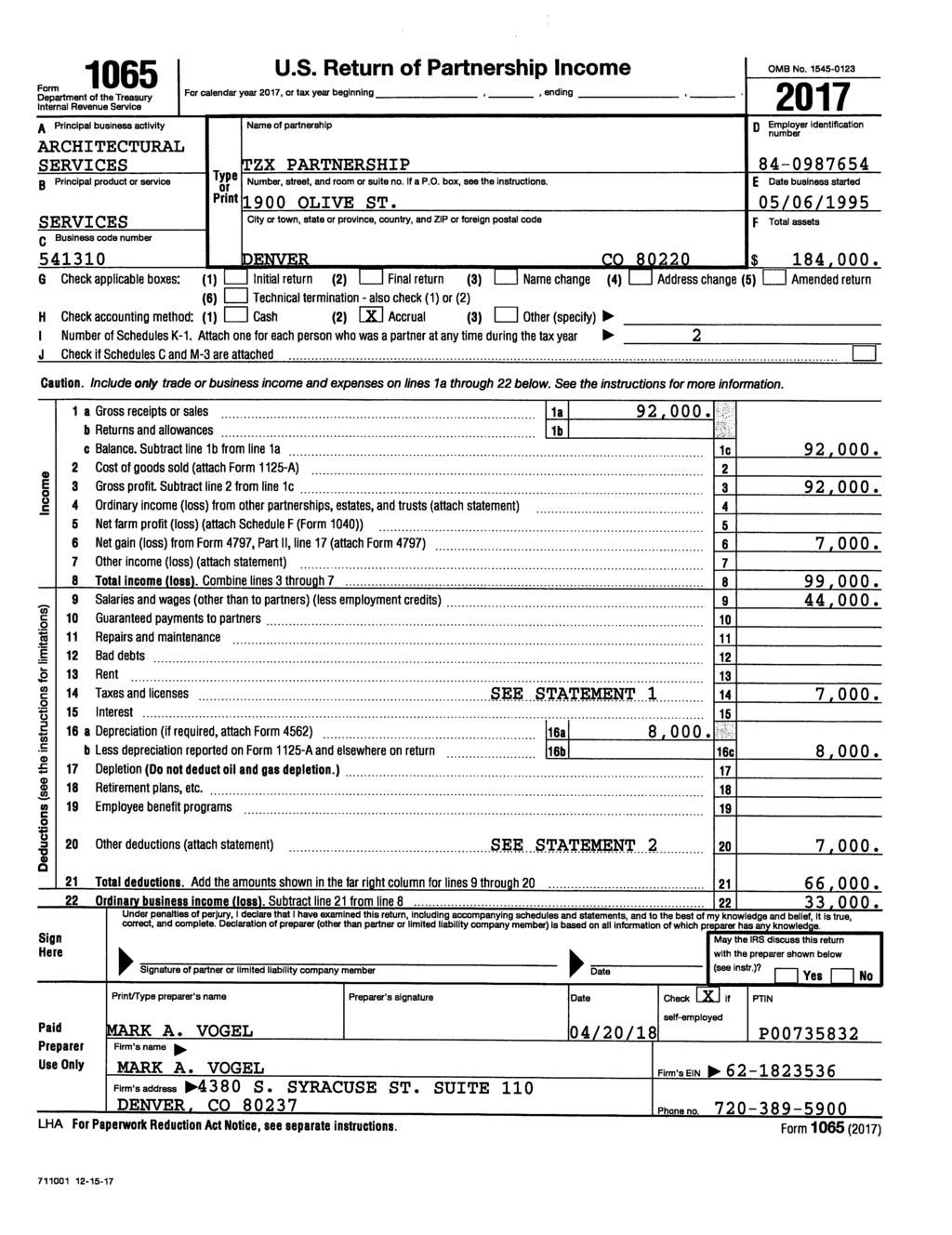

4 Form 1065 Department of the Treasury Internal Revenue Service A Principal business activity U.S. Return of Partnership Income For calendar year 2017, or tax year beginning, 2017, ending, 20. Go to for instructions and the latest information. Name of partnership OMB No D Employer identification number B Principal product or service C Business code number Type or Print Number, street, and room or suite no. If a P.O. box, see the instructions. City or town, state or province, country, and ZIP or foreign postal code E Date business started F Total assets (see the instructions) $ G Check applicable boxes: (1) Initial return (2) Final return (3) Name change (4) Address change (5) Amended return (6) Technical termination - also check (1) or (2) H Check accounting method: (1) Cash (2) Accrual (3) Other (specify) I Number of Schedules K-1. Attach one for each person who was a partner at any time during the tax year J Check if Schedules C and M-3 are attached Caution. Include only trade or business income and expenses on lines 1a through 22 below. See the instructions for more information. Income Deductions (see the instructions for limitations) Sign Here 1a Gross receipts or sales a b Returns and allowances b c Balance. Subtract line 1b from line 1a c 2 Cost of goods sold (attach Form 1125-A) Gross profit. Subtract line 2 from line 1c Ordinary income (loss) from other partnerships, estates, and trusts (attach statement) Net farm profit (loss) (attach Schedule F (Form 1040)) Net gain (loss) from Form 4797, Part II, line 17 (attach Form 4797) Other income (loss) (attach statement) Total income (loss). Combine lines 3 through Salaries and wages (other than to partners) (less employment credits) Guaranteed payments to partners Repairs and maintenance Bad debts Rent Taxes and licenses Interest a Depreciation (if required, attach Form 4562) a b Less depreciation reported on Form 1125-A and elsewhere on return 16b 16c 17 Depletion (Do not deduct oil and gas depletion.) Retirement plans, etc Employee benefit programs Other deductions (attach statement) Total deductions. Add the amounts shown in the far right column for lines 9 through Ordinary business income (loss). Subtract line 21 from line Paid Preparer Use Only Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than partner or limited liability company member) is based on all information of which preparer has any knowledge. May the IRS discuss this return with the preparer shown below (see instructions)? Yes No Signature of partner or limited liability company member Date Print/Type preparer s name Preparer s signature Date PTIN Check if self-employed Firm s name Firm s EIN Firm s address Phone no. For Paperwork Reduction Act Notice, see separate instructions. Cat. No Z Form 1065 (2017)

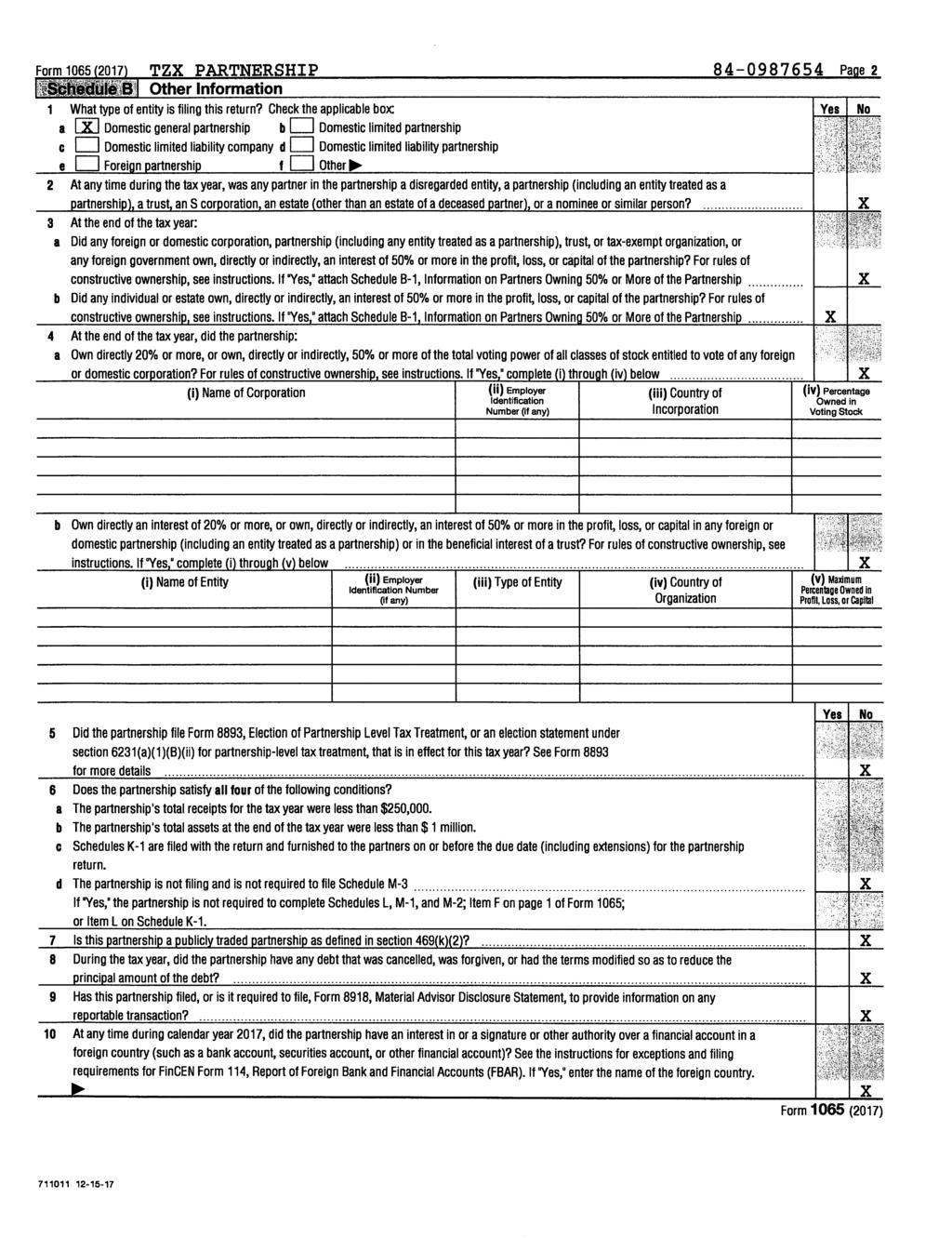

5 Form 1065 (2017) Page 2 Schedule B Other Information 1 What type of entity is filing this return? Check the applicable box: Yes No a Domestic general partnership b Domestic limited partnership c Domestic limited liability company d Domestic limited liability partnership e Foreign partnership f Other 2 At any time during the tax year, was any partner in the partnership a disregarded entity, a partnership (including an entity treated as a partnership), a trust, an S corporation, an estate (other than an estate of a deceased partner), or a nominee or similar person? At the end of the tax year: a Did any foreign or domestic corporation, partnership (including any entity treated as a partnership), trust, or taxexempt organization, or any foreign government own, directly or indirectly, an interest of 50% or more in the profit, loss, or capital of the partnership? For rules of constructive ownership, see instructions. If Yes, attach Schedule B-1, Information on Partners Owning 50% or More of the Partnership b Did any individual or estate own, directly or indirectly, an interest of 50% or more in the profit, loss, or capital of the partnership? For rules of constructive ownership, see instructions. If Yes, attach Schedule B-1, Information on Partners Owning 50% or More of the Partnership At the end of the tax year, did the partnership: a Own directly 20% or more, or own, directly or indirectly, 50% or more of the total voting power of all classes of stock entitled to vote of any foreign or domestic corporation? For rules of constructive ownership, see instructions. If Yes, complete (i) through (iv) below (i) Name of Corporation (ii) Employer Identification Number (if any) (iii) Country of Incorporation (iv) Percentage Owned in Voting Stock b Own directly an interest of 20% or more, or own, directly or indirectly, an interest of 50% or more in the profit, loss, or capital in any foreign or domestic partnership (including an entity treated as a partnership) or in the beneficial interest of a trust? For rules of constructive ownership, see instructions. If Yes, complete (i) through (v) below.. (i) Name of Entity (ii) Employer Identification Number (if any) (iii) Type of Entity (iv) Country of Organization (v) Maximum Percentage Owned in Profit, Loss, or Capital 5 Did the partnership file Form 8893, Election of Partnership Level Tax Treatment, or an election statement under section 6231(a)(1)(B)(ii) for partnership-level tax treatment, that is in effect for this tax year? See Form 8893 for more details Does the partnership satisfy all four of the following conditions? a The partnership s total receipts for the tax year were less than $250,000. b The partnership s total assets at the end of the tax year were less than $1 million. c Schedules K-1 are filed with the return and furnished to the partners on or before the due date (including extensions) for the partnership return. d The partnership is not filing and is not required to file Schedule M If Yes, the partnership is not required to complete Schedules L, M-1, and M-2; Item F on page 1 of Form 1065; or Item L on Schedule K-1. 7 Is this partnership a publicly traded partnership as defined in section 469(k)(2)? During the tax year, did the partnership have any debt that was cancelled, was forgiven, or had the terms modified so as to reduce the principal amount of the debt? Has this partnership filed, or is it required to file, Form 8918, Material Advisor Disclosure Statement, to provide information on any reportable transaction? At any time during calendar year 2017, did the partnership have an interest in or a signature or other authority over a financial account in a foreign country (such as a bank account, securities account, or other financial account)? See the instructions for exceptions and filing requirements for FinCEN Form 114, Report of Foreign Bank and Financial Accounts (FBAR). If Yes, enter the name of the foreign country. Yes No Form 1065 (2017)

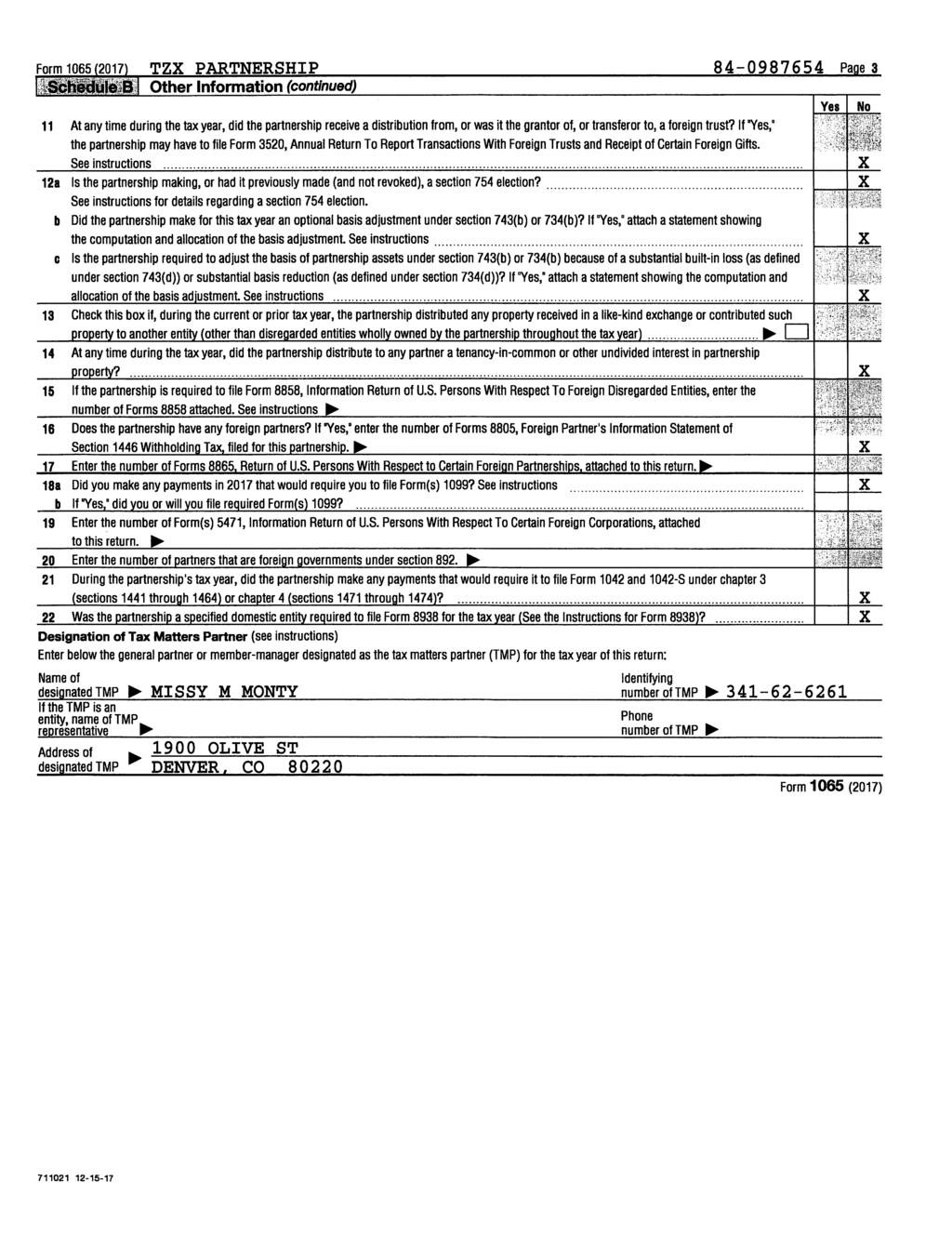

6 Form 1065 (2017) Page 3 Schedule B Other Information (continued) 11 At any time during the tax year, did the partnership receive a distribution from, or was it the grantor of, or transferor to, a foreign trust? If Yes, the partnership may have to file Form 3520, Annual Return To Report Transactions With Foreign Trusts and Receipt of Certain Foreign Gifts. See instructions a Is the partnership making, or had it previously made (and not revoked), a section 754 election? See instructions for details regarding a section 754 election. b Did the partnership make for this tax year an optional basis adjustment under section 743(b) or 734(b)? If Yes, attach a statement showing the computation and allocation of the basis adjustment. See instructions.... c Is the partnership required to adjust the basis of partnership assets under section 743(b) or 734(b) because of a substantial built-in loss (as defined under section 743(d)) or substantial basis reduction (as defined under section 734(d))? If Yes, attach a statement showing the computation and allocation of the basis adjustment. See instructions 13 Check this box if, during the current or prior tax year, the partnership distributed any property received in a like-kind exchange or contributed such property to another entity (other than disregarded entities wholly owned by the partnership throughout the tax year) At any time during the tax year, did the partnership distribute to any partner a tenancy-in-common or other undivided interest in partnership property? If the partnership is required to file Form 8858, Information Return of U.S. Persons With Respect To Foreign Disregarded Entities, enter the number of Forms 8858 attached. See instructions 16 Does the partnership have any foreign partners? If Yes, enter the number of Forms 8805, Foreign Partner s Information Statement of Section 1446 Withholding Tax, filed for this partnership. 17 Enter the number of Forms 8865, Return of U.S. Persons With Respect to Certain Foreign Partnerships, attached to this return. 18 a Did you make any payments in 2017 that would require you to file Form(s) 1099? See instructions..... b If Yes, did you or will you file required Form(s) 1099? Enter the number of Form(s) 5471, Information Return of U.S. Persons With Respect To Certain Foreign Corporations, attached to this return. 20 Enter the number of partners that are foreign governments under section During the partnership s tax year, did the partnership make any payments that would require it to file Form 1042 and 1042-S under chapter 3 (sections 1441 through 1464) or chapter 4 (sections 1471 through 1474)? Was the partnership a specified domestic entity required to file Form 8938 for the tax year (See the Instructions for Form 8938)? Designation of Tax Matters Partner (see instructions) Enter below the general partner or member-manager designated as the tax matters partner (TMP) for the tax year of this return: Yes No Name of designated TMP Identifying number of TMP If the TMP is an entity, name of TMP representative Phone number of TMP Address of designated TMP Form 1065 (2017)

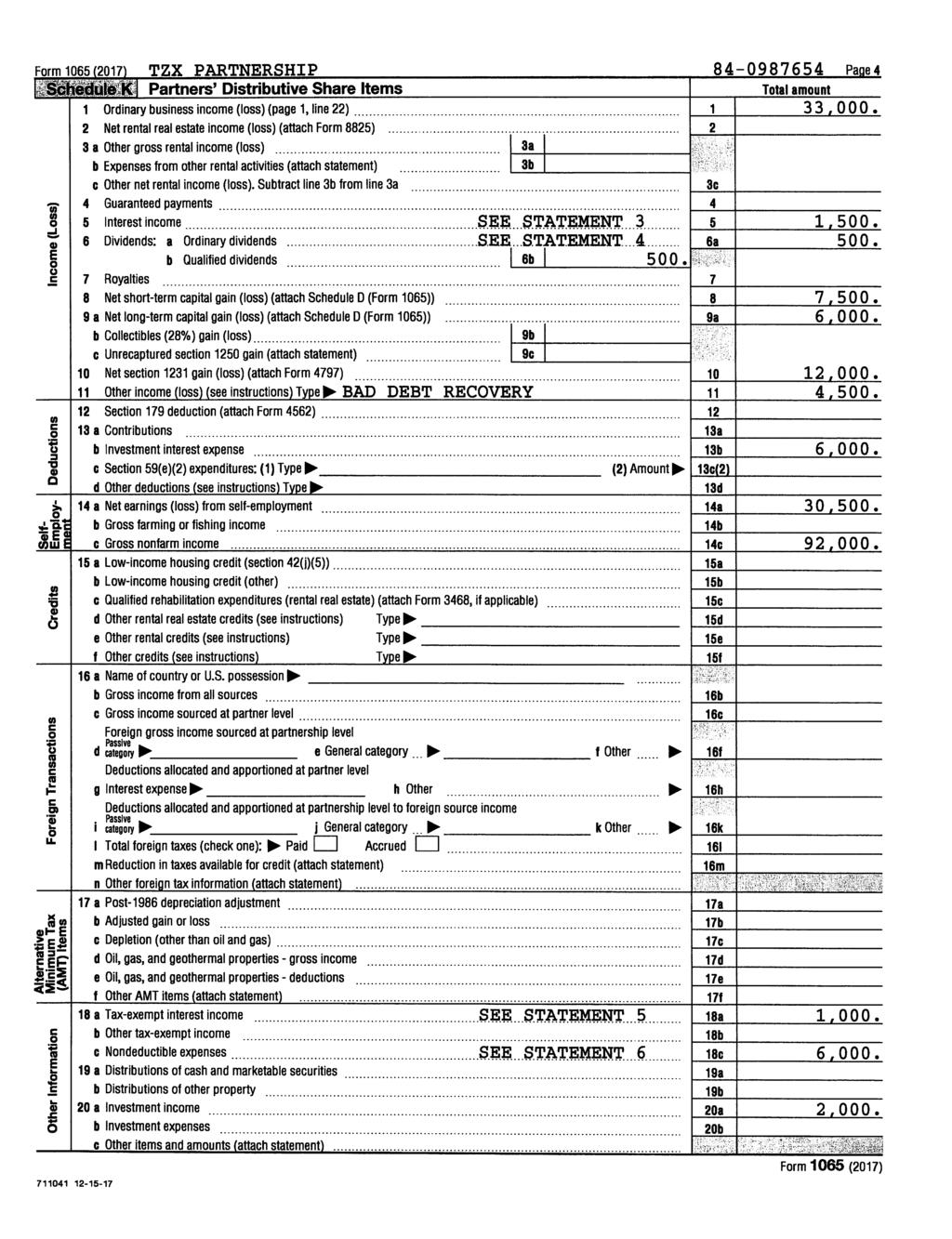

7 Form 1065 (2017) Page 4 Schedule K Partners Distributive Share Items Total amount 1 Ordinary business income (loss) (page 1, line 22) Net rental real estate income (loss) (attach Form 8825) a Other gross rental income (loss) a b Expenses from other rental activities (attach statement) 3b c Other net rental income (loss). Subtract line 3b from line 3a c 4 Guaranteed payments Interest income Dividends: a Ordinary dividends a b Qualified dividends b 7 Royalties Net short-term capital gain (loss) (attach Schedule D (Form 1065)) a Net long-term capital gain (loss) (attach Schedule D (Form 1065)) a b Collectibles (28%) gain (loss) b c Unrecaptured section 1250 gain (attach statement).. 9c 10 Net section 1231 gain (loss) (attach Form 4797) Other income (loss) (see instructions) Type Section 179 deduction (attach Form 4562) a Contributions a b Investment interest expense b c Section 59(e)(2) expenditures: (1) Type (2) Amount 13c(2) d Other deductions (see instructions) Type 13d 14a Net earnings (loss) from self-employment a b Gross farming or fishing income b c Gross nonfarm income c Income (Loss) Deductions Self- Employment Credits Foreign Transactions Alternative Minimum Tax (AMT) Items Other Information 15a Low-income housing credit (section 42(j)(5)) a b Low-income housing credit (other) b c Qualified rehabilitation expenditures (rental real estate) (attach Form 3468, if applicable) 15c d Other rental real estate credits (see instructions) Type 15d e Other rental credits (see instructions) Type 15e f Other credits (see instructions) Type 15f 16a Name of country or U.S. possession b Gross income from all sources b c Gross income sourced at partner level c Foreign gross income sourced at partnership level d Passive category e General category f Other 16f Deductions allocated and apportioned at partner level g Interest expense h Other h Deductions allocated and apportioned at partnership level to foreign source income i Passive category j General category k Other 16k l Total foreign taxes (check one): Paid Accrued l m Reduction in taxes available for credit (attach statement) m n Other foreign tax information (attach statement) a Post-1986 depreciation adjustment a b Adjusted gain or loss b c Depletion (other than oil and gas) c d Oil, gas, and geothermal properties gross income d e Oil, gas, and geothermal properties deductions e f Other AMT items (attach statement) f 18a Tax-exempt interest income a b Other tax-exempt income b c Nondeductible expenses c 19a Distributions of cash and marketable securities a b Distributions of other property b 20a Investment income a b Investment expenses b c Other items and amounts (attach statement) Form 1065 (2017)

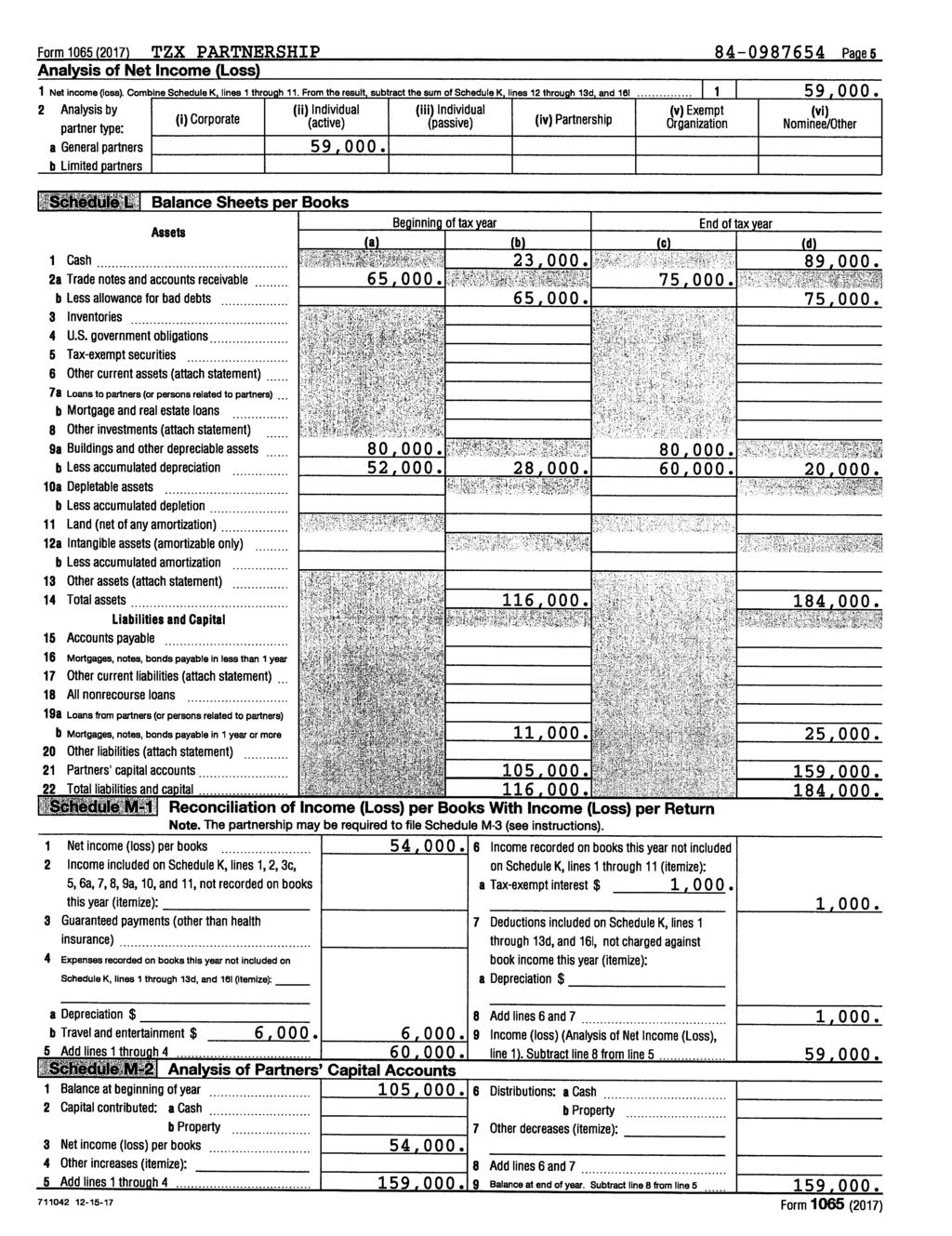

8 Form 1065 (2017) Page 5 Analysis of Net Income (Loss) 1 Net income (loss). Combine Schedule K, lines 1 through 11. From the result, subtract the sum of Schedule K, lines 12 through 13d, and 16l Analysis by partner type: (i) Corporate (ii) Individual (active) (iii) Individual (passive) (iv) Partnership (v) Exempt Organization (vi) Nominee/Other a General partners b Limited partners Schedule L Balance Sheets per Books Beginning of tax year End of tax year Assets (a) (b) (c) (d) 1 Cash a Trade notes and accounts receivable... b Less allowance for bad debts Inventories U.S. government obligations Tax-exempt securities Other current assets (attach statement).. 7a Loans to partners (or persons related to partners) b Mortgage and real estate loans Other investments (attach statement)... 9a Buildings and other depreciable assets.. b Less accumulated depreciation a Depletable assets b Less accumulated depletion Land (net of any amortization) a Intangible assets (amortizable only)... b Less accumulated amortization Other assets (attach statement) Total assets Liabilities and Capital 15 Accounts payable Mortgages, notes, bonds payable in less than 1 year 17 Other current liabilities (attach statement). 18 All nonrecourse loans a Loans from partners (or persons related to partners) b Mortgages, notes, bonds payable in 1 year or more 20 Other liabilities (attach statement) Partners capital accounts Total liabilities and capital Schedule M-1 Reconciliation of Income (Loss) per Books With Income (Loss) per Return Note. The partnership may be required to file Schedule M-3 (see instructions). 1 Net income (loss) per books Income included on Schedule K, lines 1, 2, 3c, 5, 6a, 7, 8, 9a, 10, and 11, not recorded on books this year (itemize): 3 Guaranteed payments (other than health insurance) Expenses recorded on books this year not included on Schedule K, lines 1 through 13d, and 16l (itemize): a Depreciation $ b Travel and entertainment $ 5 Add lines 1 through Schedule M-2 1 Balance at beginning of year... 2 Capital contributed: a Cash... b Property.. 3 Net income (loss) per books Other increases (itemize): 5 Add lines 1 through Analysis of Partners Capital Accounts 6 Income recorded on books this year not included on Schedule K, lines 1 through 11 (itemize): a Tax-exempt interest $ 7 Deductions included on Schedule K, lines 1 through 13d, and 16l, not charged against book income this year (itemize): a Depreciation $ 8 Add lines 6 and Income (loss) (Analysis of Net Income (Loss), line 1). Subtract line 8 from line 5. 6 Distributions: a Cash b Property Other decreases (itemize): 8 Add lines 6 and Balance at end of year. Subtract line 8 from line 5 Form 1065 (2017)

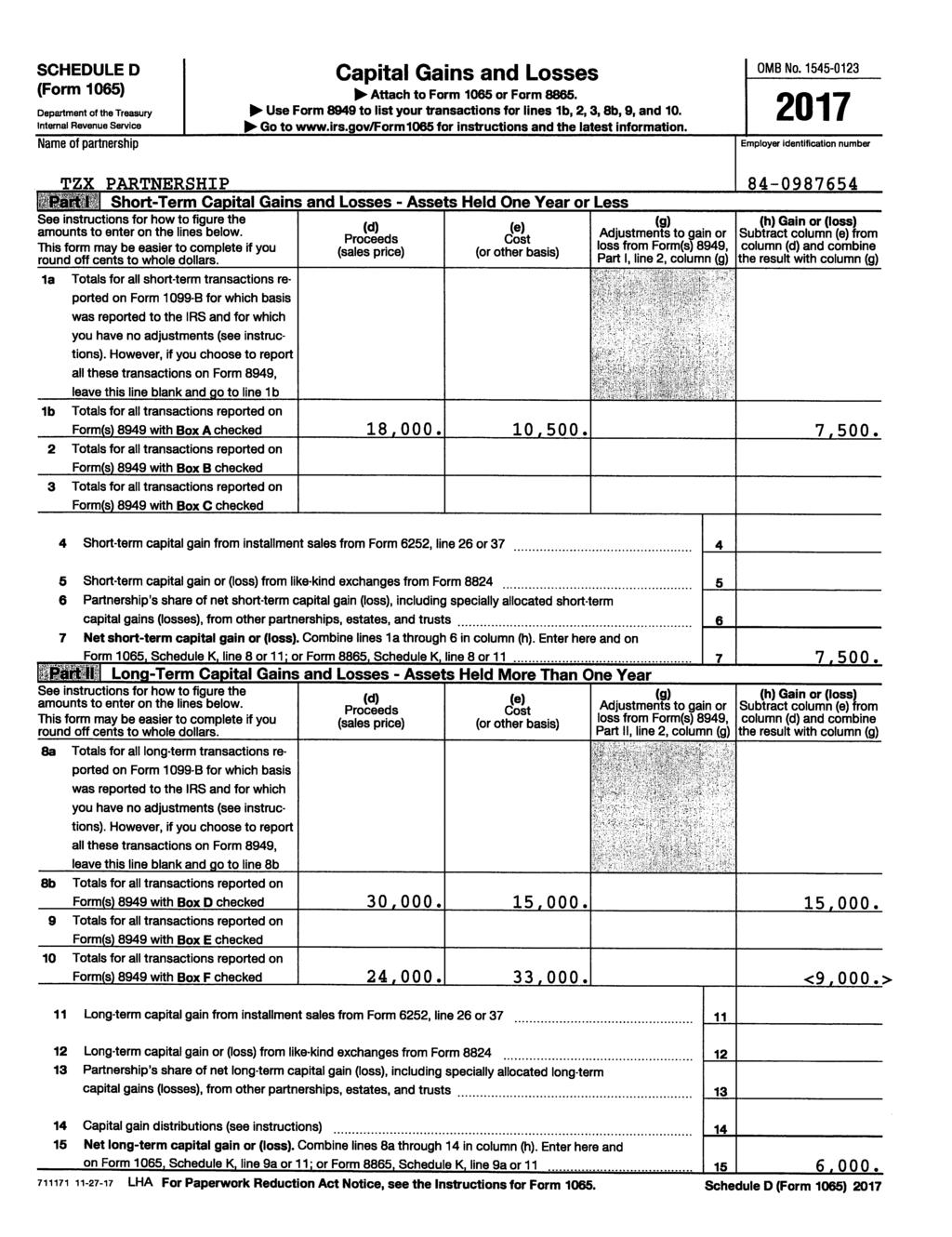

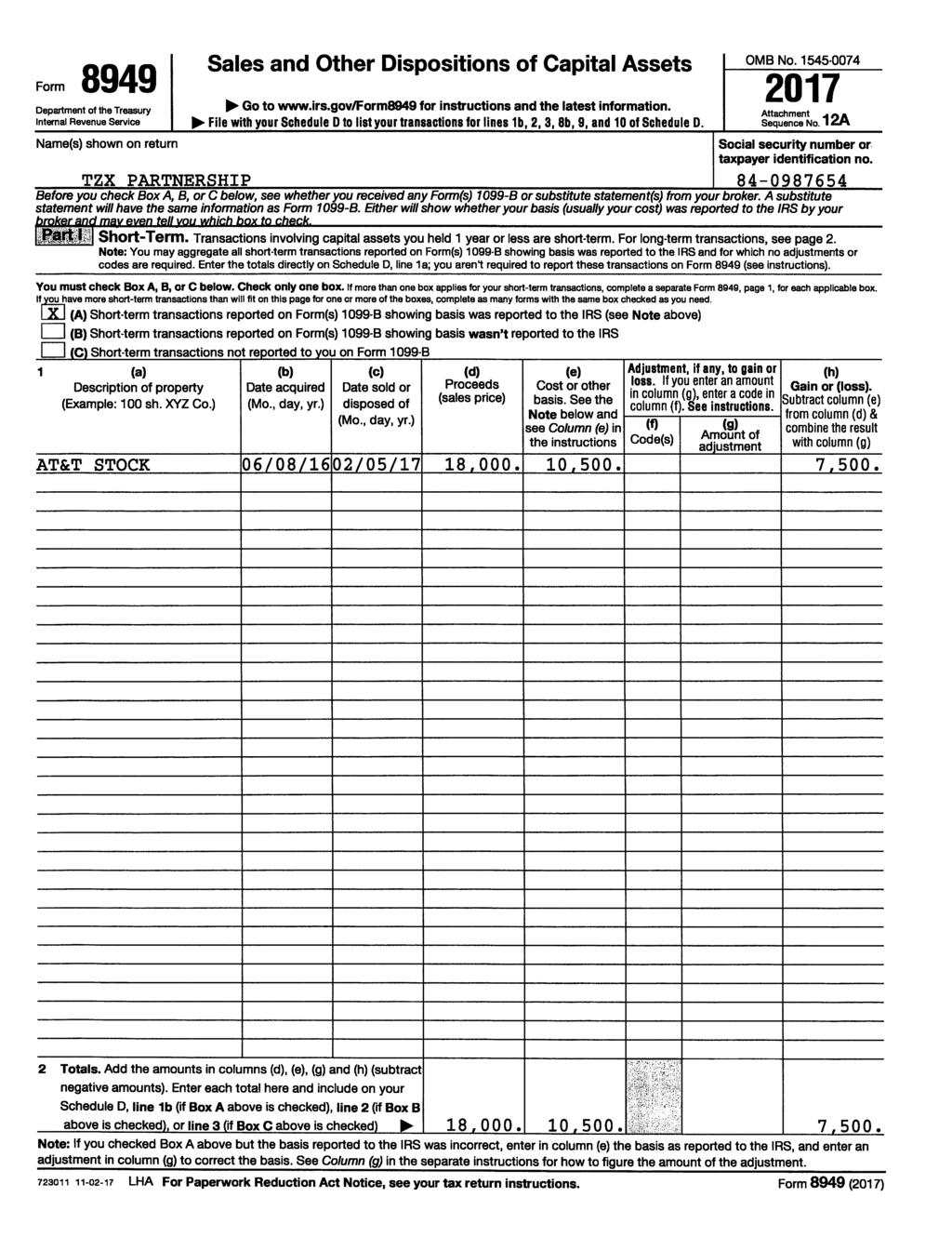

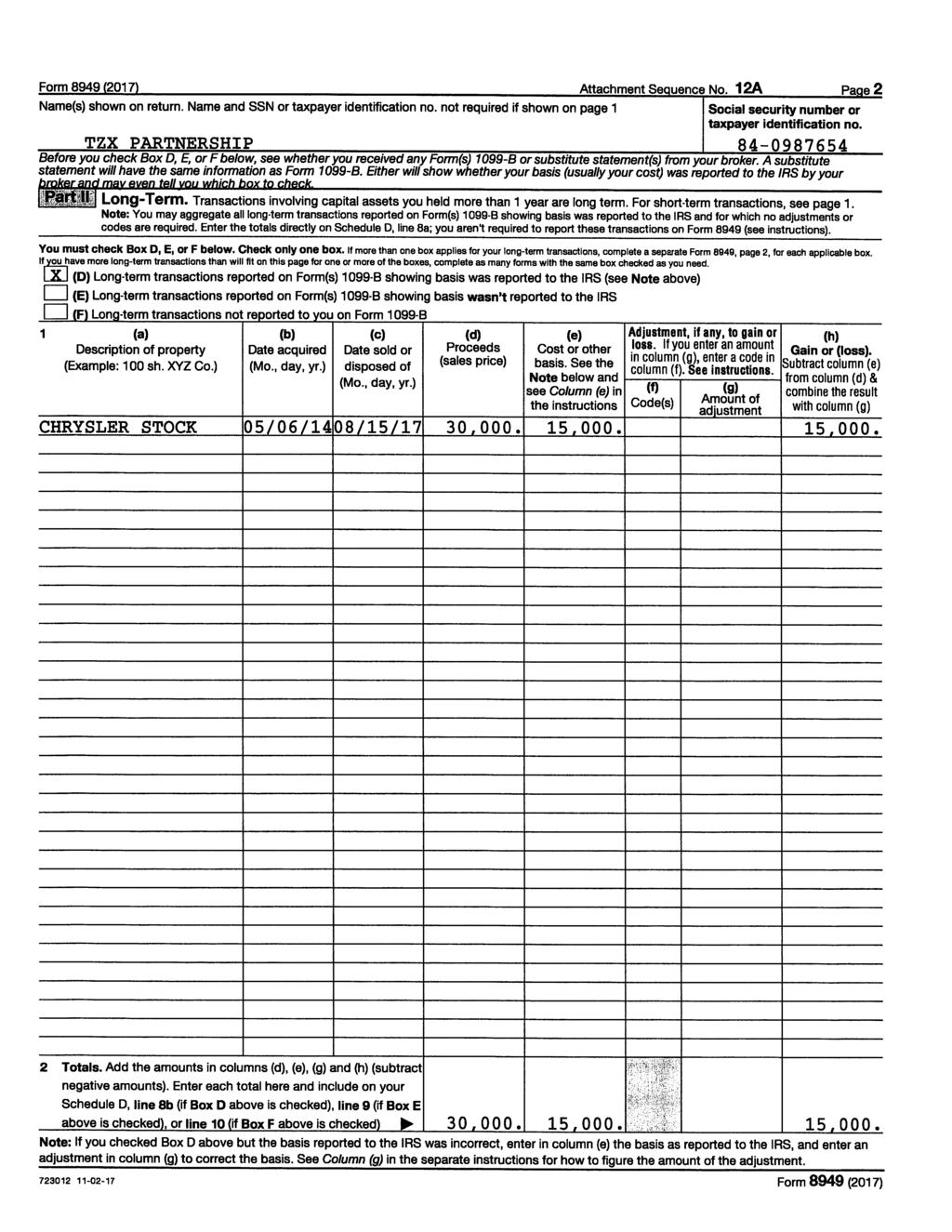

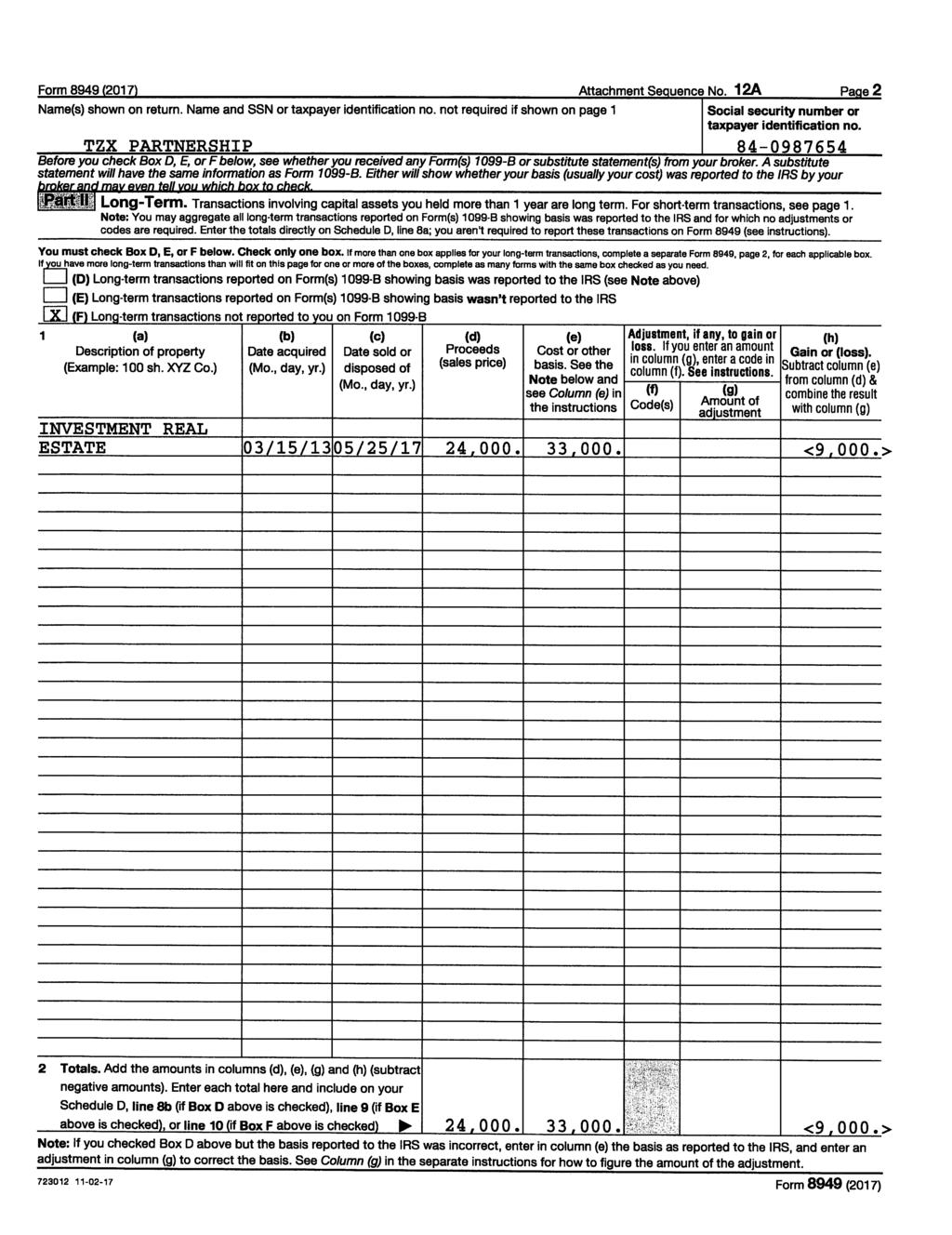

9 SCHEDULE D (Form 1065) Capital Gains and Losses Attach to Form 1065 or Form Use Form 8949 to list your transactions for lines 1b, 2, 3, 8b, 9, and 10. Go to for instructions and the latest information. Department DRAFT of the Treasury AS OF Internal Revenue Service Name of partnership OMB No Employer identification number Part I Short-Term Capital Gains and Losses (See instructions) August 3, 2018 DO NOT FILE See instructions for how to figure the amounts to enter on the lines below. This form may be easier to complete if you round off cents to whole dollars. 1a Totals for all short-term transactions reported on Form 1099-B for which basis was reported to the IRS and for which you have no adjustments (see instructions). However, if you choose to report all these transactions on Form 8949, leave this line blank and go to line 1b. 1b Totals for all transactions reported on Form(s) 8949 with Box A checked Totals for all transactions reported on Form(s) 8949 with Box B checked Totals for all transactions reported on Form(s) 8949 with Box C checked (d) Proceeds (sales price) (e) Cost (or other basis) (g) Adjustments to gain or loss from Form(s) 8949, Part I, line 2, column (g) (h) Gain or (loss) Subtract column (e) from column (d) and combine the result with column (g) 4 Short-term capital gain from installment sales from Form 6252, line 26 or Short-term capital gain or (loss) from like-kind exchanges from Form Partnership s share of net short-term capital gain (loss), including specially allocated short-term capital gains (losses), from other partnerships, estates, and trusts Net short-term capital gain or (loss). Combine lines 1a through 6 in column (h). Enter here and on Form 1065, Schedule K, line 8 or 11; or Form 8865, Schedule K, line 8 or Part II Long-Term Capital Gains and Losses (See instructions) See instructions for how to figure the amounts to enter on the lines below. This form may be easier to complete if you round off cents to whole dollars. 8a Totals for all long-term transactions reported on Form 1099-B for which basis was reported to the IRS and for which you have no adjustments (see instructions). However, if you choose to report all these transactions on Form 8949, leave this line blank and go to line 8b. 8b Totals for all transactions reported on Form(s) 8949 with Box D checked Totals for all transactions reported on Form(s) 8949 with Box E checked Totals for all transactions reported on Form(s) 8949 with Box F checked (d) Proceeds (sales price) (e) Cost (or other basis) (g) Adjustments to gain or loss from Form(s) 8949, Part II, line 2, column (g) 11 Long-term capital gain from installment sales from Form 6252, line 26 or Long-term capital gain or (loss) from like-kind exchanges from Form Partnership s share of net long-term capital gain (loss), including specially allocated long-term capital gains (losses), from other partnerships, estates, and trusts Capital gain distributions (see instructions) Net long-term capital gain or (loss). Combine lines 8a through 14 in column (h). Enter here and on Form 1065, Schedule K, line 9a or 11; or Form 8865, Schedule K, line 9a or (h) Gain or (loss) Subtract column (e) from column (d) and combine the result with column (g) For Paperwork Reduction Act Notice, see the Instructions for Form Cat. No G Schedule D (Form 1065) 2018

10 Schedule K-1 (Form 1065) 2018 Department of the Treasury Internal Revenue Service For calendar year 2018, or tax year Part III Final K-1 Amended K OMB No Partner s Share of Current Year Income, Deductions, Credits, and Other Items 1 Ordinary business income (loss) 15 Credits beginning / / 2018 ending / / Partner s Share of Income, Deductions, Credits, etc. See back of form and separate instructions. A Part I DRAFT AS OF Information About the Partnership Partnership s employer identification number 2 Net rental real estate income (loss) 3 Other net rental income (loss) 4 Guaranteed payments 5 Interest income 16 Foreign transactions B Partnership s name, July address, city, state, and ZIP code 30, a 6b Ordinary dividends Qualified dividends C D E IRS Center where partnership filed return DO NOT FILE Part II Check if this is a publicly traded partnership (PTP) Information About the Partner Partner s identifying number 6c Dividend equivalents 7 Royalties 8 Net short-term capital gain (loss) 9a Net long-term capital gain (loss) 17 Alternative minimum tax (AMT) items F Partner s name, address, city, state, and ZIP code 9b Collectibles (28%) gain (loss) 9c Unrecaptured section 1250 gain 18 Tax-exempt income and nondeductible expenses G General partner or LLC member-manager Limited partner or other LLC member H Domestic partner Foreign partner 10 Net section 1231 gain (loss) 11 Other income (loss) I1 I2 What type of entity is this partner? If this partner is a retirement plan (IRA/SEP/Keogh/etc.), check here 19 Distributions J Partner s share of profit, loss, and capital (see instructions): Beginning Ending Profit % % Loss % % Capital % % 12 Section 179 deduction 13 Other deductions 20 Other information K Partner s share of liabilities: Beginning Ending L M Nonrecourse.. $ $ Qualified nonrecourse financing... $ $ Recourse... $ $ Partner s capital account analysis: Beginning capital account... $ Capital contributed during the year $ Current year increase (decrease). $ Withdrawals & distributions.. $ ( ) Ending capital account.... $ Tax basis GAAP Section 704(b) book Other (explain) Did the partner contribute property with a built-in gain or loss? Yes No If Yes, attach statement (see instructions) 14 Self-employment earnings (loss) *See attached statement for additional information. For IRS Use Only For Paperwork Reduction Act Notice, see Instructions for Form Cat. No R Schedule K-1 (Form 1065) 2018

11 Schedule K-1 (Form 1065) 2018 Page 2 This list identifies the codes used on Schedule K-1 for all partners and provides summarized reporting information for partners who file Form For detailed reporting and filing information, see the separate Partner s Instructions for Schedule K-1 and the instructions for your income tax return. 1. Ordinary business income (loss). Determine whether the income (loss) is Code Report on passive or nonpassive and enter on your return as follows. J Work opportunity credit Report on K Disabled access credit Passive loss See the Partner s Instructions L Empowerment zone Passive income Schedule E, line 28, column (h) employment credit M Credit for increasing research Nonpassive loss See the Partner s Instructions activities See the Partner s Instructions Nonpassive income Schedule E, line 28, column (k) N Credit for employer social 2. Net rental real estate income (loss) See the Partner s Instructions security and Medicare taxes 3. Other net rental income (loss) O Backup withholding Net income Schedule E, line 28, column (h) P Other credits Net loss See the Partner s Instructions 16. Foreign transactions 4. Guaranteed payments Schedule E, line 28, column (k) A Name of country or U.S. } 5. Interest income Form 1040, line 2b possession 6a. Ordinary dividends Form 1040, line 3b B Gross income from all sources Form 1116, Part I 6b. Qualified dividends Form 1040, line 3a C Gross income sourced at 6c. Dividend equivalents See the Partner s Instructions partner level 7. Royalties Schedule E, line 4 Foreign gross income sourced at partnership level 8. Net short-term capital gain (loss) Schedule D, line 5 D Section 951A category 9a. Net long-term capital gain (loss) Schedule D, line 12 E Foreign branch category 9b. Collectibles (28%) gain (loss) 28% Rate Gain Worksheet, line 4 F Passive category }Form 1116, Part I (Schedule D instructions) G General category 9c. Unrecaptured section 1250 gain See the Partner s Instructions H Other 10. Net section 1231 gain (loss) See the Partner s Instructions 11. Other income (loss) Code DRAFT AS OF July 30, 2018 DO NOT FILE A Other portfolio income (loss) See the Partner s Instructions B Involuntary conversions See the Partner s Instructions C Sec contracts & straddles Form 6781, line 1 D Mining exploration costs recapture See Pub. 535 E Cancellation of debt Schedule 1 (Form 1040), line 21 or Form 982 } F Section 951A income G Section 965(a) inclusion H Subpart F income other than See the Partner s Instructions sections 951A and 965 inclusion I Other income (loss) 12. Section 179 deduction See the Partner s Instructions 13. Other deductions A Cash contributions (60%) B Cash contributions (30%) C Noncash contributions (60%) D Noncash contributions (30%) }See the Partner s E Capital gain property to a 50% Instructions organization (30%) F Capital gain property (20%) G Contributions (100%) H Investment interest expense Form 4952, line 1 I Deductions royalty income Schedule E, line 19 J Section 59(e)(2) expenditures See the Partner s Instructions K Excess business interest expense See the Partner s Instructions L Deductions portfolio (other) Schedule A, line 13 M Amounts paid for medical insurance Schedule A, line 1 or Schedule 1 (Form 1040), line 29 N Educational assistance benefits See the Partner s Instructions O Dependent care benefits Form 2441, line 12 P Preproductive period expenses See the Partner s Instructions Q Commercial revitalization deduction from rental real estate activities See Form 8582 instructions R Pensions and IRAs See the Partner s Instructions S Reforestation expense deduction See the Partner s Instructions T through V Reserved for future use W Other deductions See the Partner s Instructions X Section 965(c) deduction See the Partner s Instructions 14. Self-employment earnings (loss) Note: If you have a section 179 deduction or any partner-level deductions, see the Partner s Instructions before completing Schedule SE. A Net earnings (loss) from self-employment B Gross farming or fishing income C Gross non-farm income } 15. Credits A Low-income housing credit (section 42(j)(5)) from pre-2008 buildings B Low-income housing credit (other) from pre-2008 buildings C Low-income housing credit (section 42(j)(5)) from post-2007 buildings See D Low-income housing credit (other) from post-2007 buildings E Qualified rehabilitation expenditures (rental real estate) F Other rental real estate credits G Other rental credits H Undistributed capital gains credit I Biofuel producer credit Schedule SE, Section A or B See the Partner s Instructions See the Partner s Instructions the Partner s Instructions Schedule 5 (Form 1040), line 74, box a See the Partner s Instructions } Deductions allocated and apportioned at partner level I Interest expense Form 1116, Part I J Other Form 1116, Part I Deductions allocated and apportioned at partnership level to foreign source income K Section 951A category L Foreign branch category M Passive category }Form 1116, Part I N General category O Other Other information P Total foreign taxes paid Form 1116, Part II Q Total foreign taxes accrued Form 1116, Part II R Reduction in taxes available for credit Form 1116, line 12 S Foreign trading gross receipts Form 8873 T Extraterritorial income exclusion Form 8873 U Section 951A(c)(1)(A) tested income } V Tested foreign income tax W Section 965 information X Other foreign transactions See the Partner s Instructions 17. Alternative minimum tax (AMT) items } A Post-1986 depreciation adjustment B Adjusted gain or loss See the Partner s C Depletion (other than oil & gas) Instructions and D Oil, gas, & geothermal gross income the Instructions for E Oil, gas, & geothermal deductions Form 6251 F Other AMT items 18. Tax-exempt income and nondeductible expenses A Tax-exempt interest income Form 1040, line 2a B Other tax-exempt income See the Partner s Instructions C Nondeductible expenses See the Partner s Instructions 19. Distributions A Cash and marketable securities B Distribution subject to section 737 C Other property } See the Partner s Instructions 20. Other information A Investment income Form 4952, line 4a B Investment expenses Form 4952, line 5 C Fuel tax credit information Form 4136 D Qualified rehabilitation expenditures See the Partner s Instructions (other than rental real estate) E Basis of energy property See the Partner s Instructions F Recapture of low-income housing Form 8611, line 8 credit (section 42(j)(5)) G Recapture of low-income housing credit (other) Form 8611, line 8 H Recapture of investment credit See Form 4255 I Recapture of other credits See the Partner s Instructions J Look-back interest completed See Form 8697 long-term contracts K Look-back interest income forecast } See Form 8866 method L Dispositions of property with section 179 deductions M Recapture of section 179 deduction N Interest expense for corporate partners O through Y Z Section 199A income AA Section 199A W-2 wages See the Partner s AB Section 199A unadjusted basis Instructions AC Section 199A REIT dividends AD Section 199A PTP income AE Excess taxable income AF Excess business interest income AG Gross receipts for section 59A(e) AH Other information

12 SAMPLE OPERATING AGREEMENT th THIS OPERATING AGREEMENT is made and entered into as of the 15 day of April, 2018 by and among the persons executing this Agreement as the initial Members of KBAR LLC, a Colorado limited liability company (the Company ), and any other person who subsequently agrees to be bound by the terms of this Agreement. I. DEFINITIONS. The following terms used in this Agreement shall have the following meanings (unless otherwise expressly provided herein): 1.1 Act means the Colorado Limited Liability Company Act and any successor statute thereto, as amended from time to time. 1.2 Adjusted Capital Account Deficit means, with respect to any Member, the deficit balance, if any, in such Member s Capital Account as of the end of the relevant taxable year after giving effect to the following adjustments: (a) Credit to such Capital Account any amounts that such Member is obligated to restore or is deemed to be obligated to restore pursuant to the penultimate sentences of Reg (g)(1) and Reg (i)(5); and (b) Debit to such Capital Account the items described in Reg (b)(2)(ii)(d)(4), Reg (b)(2)(ii)(d)(5) and Reg (b)(2)(ii)(d)(6). The foregoing definition of Adjusted Capital Account Deficit is intended to comply with the provisions of Reg (b)(2)(ii)(d) and shall be interpreted consistently therewith. 1.3 Agreement means this Operating Agreement. 1.4 Articles of Organization means the articles of organization of the Company, as amended from time to time. 1.5 Capital Account means, with respect to any Member, the capital account maintained for such Member in accordance with the following provisions: (a) To each Member s Capital Account there shall be credited such Member s Capital Contributions, such Member s distributive share of Profits and any items in the nature of income or gain which are specially allocated to such Member, and the amount of any Company liabilities assumed by such Member, or which are secured by any Company property distributed to such Member. (b) To each Member s Capital Account there shall be debited the amount of cash and the Gross Asset Value of any Company property distributed to such Member pursuant to any provision of this Agreement, such Member s distributive share of losses and any items in the nature of expenses or losses which are specially allocated to such Member, and the amount of any liabilities of such Member assumed by the Company or which are secured by any property contributed by such Member to the Company Page 1 of 18 VOGEL.SEM/SP&LPROB.18

13 (c) In the event units are transferred and the transferee becomes the owner of such units, the transferee shall succeed to the Capital Account of the transferor to the extent it relates to such units. (d) Capital Accounts shall otherwise be maintained as provided elsewhere in this Agreement and in Reg (b)(2)(iv). The foregoing provisions and the other provisions of this Agreement relating to the maintenance of Capital Accounts are intended to comply with Reg (b)(2)(iv) and shall be interpreted and applied in a manner consistent with such Regulations. In the event any of the provisions of this Agreement relating to the maintenance of Capital Accounts are deemed to be inconsistent with the requirements of Reg (b)(2)(iv), the manner in which the Capital Accounts are maintained may be modified to comply with such Regulations section, provided that such modification does not materially affect the amount distributable to any Member under the provisions of this Agreement relating to the dissolution of the Company. 1.6 Code means the Internal Revenue Code of 1986 or corresponding provisions of subsequent superseding federal revenue laws. 1.7 Company has the meaning set forth in the first paragraph of this Agreement. 1.8 Gross Asset Value means, with respect to any asset, the asset s adjusted basis for federal income tax purposes, except as follows: (a) The initial Gross Asset Value of any asset contributed by a Member to the Company shall be the gross fair market value of such asset; (b) The Gross Asset Values of all Company assets shall be adjusted to equal their respective gross fair market values (i) in connection with an acquisition of an interest in the Company by any new or existing Member in exchange for more than a de minimis Capital Contribution, or (ii) in connection with the liquidation of the Company or a distribution by the Company to a Member of more than a de minimis amount of Company property as consideration for an interest in the Company, provided, however, that the foregoing adjustments shall be made only if they are necessary or appropriate to reflect the relative economic interests of the Members in the Company; (c) The Gross Asset Value of any Company asset distributed to any Member shall be adjusted to equal the gross fair market value of such asset on the date of distribution; (d) The Gross Asset Values of Company assets shall be increased (or decreased) to reflect any adjustments to the Adjusted basis of such assets pursuant to 734(b) or 743(b), but only to the extent that such adjustments are taken into account in determining Capital Accounts pursuant to Reg (b)(2)(iv)(m); provided, however, that Gross Asset Values shall not be adjusted pursuant to this subsection to the extent that an adjustment is required pursuant to subsection (b) above in connection with a transaction that would otherwise result in an adjustment under this subsection (d); (e) The Gross Asset Value of any Company asset shall be adjusted to reflect any cost recovery deductions claimed with respect to such asset as described in the definition of Profits and Losses Page 2 of 18 VOGEL.SEM/SP&LPROB.18

14 1.9 Managers means the Managers of the Company. So long as there is a single Manager of the Company, any reference to Managers in this Agreement (or any plural pronouns referring to the Managers) shall be understood to refer to the sole Manager Member means each person listed on Schedule A as an initial member and each other person who is admitted as a Member pursuant to the terms and conditions of this Agreement. The term Member as used herein shall include a Manager to the extent he is a Member. A person must be a Member to be a Member Pro Rata means in proportion to the relevant Members ownership of units of any class, unless a specific class is specified Profits and Losses means for any taxable year or other accounting period an amount equal to the Company s taxable income or loss for such year or period, determined in accordance with 703(a) (for this purpose, all items of income, gain, loss, or deduction required to be stated separately pursuant to 703(a)(1) shall be included in taxable income or loss), with the following adjustments: (a) Any income of the Company that is exempt from federal income tax and not otherwise taken into account in computing Profits and Losses pursuant to this Section 1.12 shall be added to such taxable income or loss; (b) Any expenditures of the Company described in 705(a)(2)(B) or treated as 705(a)(2)(B) expenditures pursuant to Reg (b)(2)(iv)(i), and not otherwise taken into account in computing Profits or Losses pursuant to this Section 1.12 shall be subtracted from such taxable income or loss; (c) In the even the Gross Asset Value of any Company asset is adjusted as provided in subsections (b) or (c) of the definition of Gross Asset Value, the amount of such adjustment shall be taken into account as gain or loss from the disposition of such asset for purposes of computing Profits and Losses; (d) Gain or loss resulting from any disposition of Company property with respect to which gain or loss is recognized for federal income tax purposes shall be computed by reference to the Gross Asset Value of the property disposed of, notwithstanding that the adjusted tax basis of such property differs from its Gross Asset Value; (e) If the Gross Asset Value of an asset differs from its adjusted basis for federal income tax purposes at the beginning of a fiscal year, cost recovery deductions with respect to such asset shall be computed by reference to the asset s Gross Asset Value using the same method as is used to compute cost recovery deductions for federal income tax purposes, provided, however, that if the adjusted basis for federal income tax purposes of the asset at the beginning of such fiscal year is zero, cost recovery deductions shall be computed by reference to the asset s Gross Asset Value using any reasonable method; (f) Notwithstanding any other provision of this Section 1.12, any items of income, gain, loss, or deduction which are specially allocated to a Member shall not be taken into account in computing Profits or Losses Page 3 of 18 VOGEL.SEM/SP&LPROB.18

15 The amounts of the items of Company income, gain, loss or deduction available to be specially allocated under the provisions of this Agreement (if any) shall be determined by applying rules analogous to those set forth in Sections 1.12(a) through 1.12(e) above Regulations means the Income Tax Regulations, including Temporary Regulations, promulgated under the Code, as such regulations may be amended from time to time (including corresponding provisions of succeeding regulations) Transfer means, as a noun, any voluntary or involuntary transfer, sale, pledge, hypothecation, or other disposition and, as a verb, voluntarily or involuntarily to transfer, sell, pledge, hypothecate, or otherwise dispose of. II. THE COMPANY. 2.1 Formation. The Company has been organized as a Colorado limited liability company by the filing of the Articles of Organization under and pursuant to the Act and the issuance of a certificate of organization for the Company by the Secretary of State of the state of Colorado. The rights and liabilities of the Members shall be determined pursuant to the Act and this Agreement. To the extent that the rights or obligations of any Member are different by reason of any provision of this Agreement than they would be in the absence of such provision, this Agreement shall, to the extent permitted by the Act, control. 2.2 Name. The name of the Company is KBAR, LLC, and all Company business shall be conducted in that name or such other names that comply with applicable law as the Managers may select from time to time. 2.3 Term. The Company shall commence on the date the Articles of Organization are filed with the Secretary of State of the state of Colorado and shall continue in existence in accordance with the terms and provisions hereof. 2.4 Registered Agent; Principal Office in the United States; Other Offices. The registered agent of the Company in the state of Colorado shall be the initial registered agent named in the Articles of Organization or such other person or persons as the Managers may designate from time to time in the manner provided by law. The principal office of the Company in the United States shall be at such place as the Managers may designate from time to time, which need not be in the state of Colorado. The Company may have such other offices as the Managers may designate from time to time. 2.5 Purpose of the Company. The purpose of the Company shall be to engage in any activity in which a limited liability company may engage, as determined by the Members. 2.6 Title to Property. All real and personal property owned by the Company shall be owned by the Company as an entity, and no Member shall have any ownership interest in such property in his individual name or right, and each member s interest in the Company shall be personal property for all purposes. Except as otherwise provided in this Agreement, the Company shall hold all of its real and personal property in the name of the Company and not in the name of any Manager or Member Page 4 of 18 VOGEL.SEM/SP&LPROB.18

16 III. GENERAL PROVISIONS RELATING TO MEMBERS AND OTHER MEMBERS. 3.1 Initial Members. The names, addresses, initial Capital Contributions, and initial units of the initial Members are set forth on Schedule A. 3.2 Authority. Unless authorized to do so by this Agreement or by the Managers of the Company, no Member of the Company, in his capacity as a Member, shall have any power or authority to bind the Company in any way, to pledge its credit, or to render it liable for any purpose. 3.3 Limitation of Liability for Company Debts. Each Member s liability for the debts and obligations of the Company shall be limited as set forth in the Act and other applicable law. 3.4 Priority and Return of Capital. Except as expressly provided herein, no Member shall have priority over any other Member, either as to the return of Capital Contributions or as to allocations or distributions; provided that this Section 3.4 shall not apply to loans (as distinguished from Capital Contributions) that a Member has made to the Company. 3.5 Competing Activities. Members and their officers, directors, shareholders, partners, members, managers, agents, employees, and Affiliates may engage or invest in, independently or with others, any business activity of any type or description, including, without limitation, those that might be the same as or similar to the Company s business and that might be in direct or indirect competition with the Company. Further, neither the Company nor any Member shall have any right in or to such other ventures or activities or to the income or proceeds derived therefrom by virtue of this Agreement or the Member s status as a Member or other Member. The Members shall not be obligated to present any investment opportunity or prospective economic advantage for their own account or to recommend such opportunity to persons other than the Company or the Members. Each Member acknowledges that the other Members and their Affiliates may own and/or manage other businesses, including businesses that may compete with the Company and for the Members time. Each Member hereby waives any and all rights and claims which he may otherwise have against the other Members and their officers, directors, shareholders, partners, members, managers, agents, employees, and Affiliates as a result of any of such activities. 3.6 Creation and Issuance of Units and Other Interests. (a) The Managers are authorized to cause the issuance of additional units beyond those initially issued to the initial Members, including units in one or more classes, or one or more series of such classes, which classes or series shall have, subject to the provisions of applicable law, such designations, preferences and relative, participating, optional, or other special rights as shall be fixed by the Managers, including, without limitation, with respect to: (i) the Capital Contribution to be required by each such class or series; (ii) the allocation of Profits or Losses to each such class or series; (iii) the right of each such class or series to share in distributions; (iv) the rights of each such class or series upon dissolution and liquidation of the Company; (v) the price at which, and the terms and conditions upon which, each such class or series of units may be redeemed by the Company, if any such class or series is so redeemable; (vi) the rate at which, and the terms and conditions upon which, each such class or series may be converted into another class or series of units; and (vii) the right of each such class or series to vote on, or take action with respect to, Company matters, including matters relating to the relative rights, preferences, and privileges of such class or series, to the extent permitted by applicable law, if any such class or series is granted such voting rights Page 5 of 18 VOGEL.SEM/SP&LPROB.18

17 (b) In the event that the Managers exercise their right to issue additional units having special rights, (i) this Agreement shall be deemed to be amended as may be necessary to reflect the designations, preferences, and relative participating, optional, or other special rights of such units and (ii) any units having rights identical to those originally issued to the initial Members pursuant to this Agreement shall be referred to as Class A units and units carrying other rights shall be otherwise designated as the Managers determine. (c) The Company is authorized to cause the issuance of any other types of interest in the Company from time to time to Members or others persons on terms and conditions established by the Managers. Such interests may include, without limitation, unsecured and secured debt obligations of the Company, debt obligations of the Company convertible into units, and options, rights, or warrants to purchase any such units. IV. MEETINGS OF, AND ACTIONS BY, MEMBERS. 4.1 Actions by Members. Except as otherwise provided herein, all actions required or permitted to be taken by the Members shall only be taken at a meeting held in accordance with the provisions of this Agreement. Members holding, personally or by proxy, at least a majority of the total votes held by all Members shall constitute a quorum at any meeting of Members. If a quorum is present at such meeting, the affirmative vote of members holding a majority of the votes held by all members represented at such meeting, in person or by proxy, and entitled to vote on the subject matter shall be the act of the Members. Members may participate in any meeting by conference telephone or similar communications equipment by means of which all persons participating in the meeting can hear each other, and participation by such means in such meeting shall constitute attendance and presence in person at such meeting. Unless otherwise agreed by the Members, the Managers shall preside over all meetings of the Members. 4.2 Voting Power. Each Member shall have one vote for each unit held by the Member, determined as of the relevant record date. 4.3 Action Without a Meeting. Action required or permitted to be taken by the Members as a group may be taken without a meeting if the action is evidenced by one or more written consents describing the action taken, signed by each Member entitled to vote and delivered to the Company for inclusion in the minutes or for filing with the Company records. Action taken pursuant to this Section 4.3 is effective when all Members entitled to vote have signed the consent unless the consent specifies a different effective date. The record date for determining Members entitled to take action without a meeting shall be the date the first Member signs a written consent. V. MANAGEMENT OF THE COMPANY. 5.1 Management of the Company by Managers. The business and affairs of the Company shall be managed by one or more Managers. The number of Managers of the Company shall be fixed from time to time by vote of the Members, but in no instance shall there be less than one Manager. 5.2 Term, Election, and Qualification of Managers. Each Manager shall hold office for such term as the Members may designate or until his successor shall have been elected and qualified. Managers shall be elected by the vote of the members pursuant to the provisions of Article IV Page 6 of 18 VOGEL.SEM/SP&LPROB.18

18 Cumulative voting for Managers shall not be permitted. The Managers may, but need not, be Members. 5.3 Resignation. Any Manager of the Company may resign at any time by giving written notice to the Company. The resignation of any Manager shall take effect upon receipt of notice thereof by the Company or at such later time as shall be specified in such notice. Unless otherwise specified therein, the acceptance of such resignation shall not be necessary to make it effective. 5.4 Removal. All or any lesser number of Managers may be removed at any time, with or without cause, at a meeting called expressly for that purpose, by the affirmative vote of the Members then entitled to vote at an election of Managers. 5.5 Vacancies. Any vacancy occurring for any reason in the group of Managers may be filled by vote of the Members. A Manager chosen to fill a vacancy shall serve the unexpired term of his or her predecessor in office. Any Manager s position to be filled by reason of an increase in the number of Managers shall be filled by vote of the Members. A Manager chosen to fill a position resulting from an increase in the number of Managers shall hold office for such term as the Members may designate or until his successor has been elected and qualified. 5.6 Actions by the Managers. Any action that may be taken by the Managers shall require the consent of a majority of the Mangers, provided, however, that the Managers may delegate to one or more of their number the right and power to deal with any aspect of the Company s business and/or take any action that the Managers are authorized to take without the further consent of the other Managers. To the extent that circumstances reasonably permit, each Manager shall have a reasonable opportunity to participate in any management decision of the Managers unless the right and power to make that decision has been delegated to other Managers pursuant to the foregoing sentence. 5.7 Action Without a Meeting. Action required or permitted to be take by the Managers as a group may be taken without a meeting if the action is evidenced by one or more written consents describing the action taken, signed by each Manager and delivered to the Company for inclusion in the minutes or for filing with the Company records. Action taken pursuant to this Section 5.7 is effective when all Managers entitled to vote have signed the consent unless the consent specifies a different effective date. The record date for determining Managers entitled to take action without a meeting shall be the date the first Manager signs a written consent. 5.8 Time Devoted; Other Activities. The Managers shall be required to manage the Company as their primary business function and may not participate in any other business activity, provided, however, that nothing in this Section 5.8 shall be construed to prohibit a Manager from owning and managing essentially passive investments (including investments in enterprises that compete with the business of Company so long as the Manager and the Affiliates of the Manager do not collectively own more than 5% of the equity in such competing enterprises), to the extent that such ownership and management do not materially interfere with the Manager s duties of managing the business of the Company, and nothing in this Agreement shall be construed to give the Company or any Member an interest in such investments. 5.9 Standards of Care. Each Manager shall discharge his duties in good faith, in a manner he reasonably believes to be in the best interests of the Company Page 7 of 18 VOGEL.SEM/SP&LPROB.18

19 VI. CAPITAL. 6.1 Members Initial Capital Contributions. The amount of cash and the nature and agreed value of any property initially contributed or to be contributed to the Company by each initial Member are set forth on Schedule A hereto. 6.2 Additional Capital Contributions. The Members may contribute additional cash and property to the Company in such amounts and at such times as they shall determine No Obligation to Restore Negative or Deficit Capital Account Balances. Except as otherwise provided in the Agreement, no Member shall have any liability to restore all or any portion of the negative or deficit balance in the Member s Capital Account, and the negative or deficit balance of the member s Capital Account shall not be considered to be a debt owed by the Member to the Company or to any other person for any purpose whatsoever. This provision shall apply, without limitation, to a winding up, liquidation, and dissolution of the Company. 6.4 Interest On and Return of Capital Contributions. No Member shall be entitled to interest on the Member s Capital Contributions, except with the consent of the other Members or as provided by this Agreement. No Member shall be entitled to a return of the Member s Capital Contributions, as such, but only to such distributions as are provided for in this Agreement. VII. ALLOCATIONS. 7.1 General Allocation of Profits and Losses. Subject to the special allocations, limitations, and other provisions of this Article VII, the Profits and Losses of the Company will be allocated to and shared by the Members Pro Rata. 7.2 Special Allocations. The Company shall make the following special allocations: (a) Limitation on Allocation of Losses. Notwithstanding any other provision of this Agreement, no allocation of Losses, or any item in the nature of expenses or losses shall be made to a Member if such allocation would cause or increase an Adjusted Capital Account Deficit for such Member. The amount otherwise allocable to a Member but for the foregoing sentence shall instead be allocated to the other members in the manner, order, and priority set forth in this Agreement, subject again to the first sentence of this Section 7.2(a). (b) Qualified Income Offset. In the event a Member receives any adjustments, allocations, or distributions described in Reg (b)(2)(ii)(d)(4), (5), or (6) items of Company income and gain (consisting of a pro rata portion of each item of Company income, including gross income, and gain for such year) shall be specially allocated to that Member in an amount and manner sufficient to eliminate, to the extent required by the Regulations, and Adjusted Capital Account Deficit of that Member as quickly as possible, provided that an allocation pursuant to the Section 7.2(b) shall be made only if and to the extent that the Member would have an Adjusted Capital Account Deficit after all other allocations provided for in this Agreement have been tentatively made as if this Section 7.2(b) were not in this Agreement. The provisions of this Section 7.2(b) are intended to comply with the requirements of Reg (b)(2)(ii)(d) and shall be interpreted consistently therewith Page 8 of 18 VOGEL.SEM/SP&LPROB.18

20 (c) Special Provisions Applicable in the Event of Nonrecourse Borrowings. Capitalized terms used in this Section 7.2(c) and not otherwise defined shall have the meaning given them in Reg (1) Nonrecourse Deductions. Nonrecourse Deductions of the Company for any taxable year or other period shall be allocated among the Members Pro Rata. (2) Partner Nonrecourse Deductions. Any Partner Nonrecourse Deductions for any taxable year shall be specially allocated to the Member who bears the economic risk of loss with respect to the Partner Nonrecourse Debt to which such Partner Nonrecourse Deductions are attributable in accordance with Reg (i)(1). (3) Minimum Gain Chargeback. Except as otherwise provided in Reg (f), notwithstanding any other provision of this Article VII, if there is a net decrease in Partnership Minimum Gain during any Company fiscal year, each Member shall be specially allocated items of Company income and gain for such fiscal year (and, if necessary, subsequent fiscal years) in an amount equal to such Member s share of the net decrease in Partnership Minimum Gain, determined in accordance with Reg (g). Allocations pursuant to the previous sentence shall be made in proportion to the respective amounts required to be allocated to each member pursuant thereto. The items to be so allocated shall be determined in accordance with Reg (f)(6) and Reg (j)(2). This Section 7.1(d)(3) is intended to comply with the minimum gain chargeback requirement in Reg (f) and shall be interpreted consistently therewith. (4) Partner Minimum Gain Chargeback. Except as otherwise provided in Reg (i)(4), notwithstanding any other provision of this Article VII, if there is a net decrease in Partner Nonrecourse Debt Minimum Gain attributable to a Partner Nonrecourse Debt during any Company fiscal year, each Member who has a share of the Partner Nonrecourse Debt Minimum Gain attributable to such Partner Nonrecourse Debt, determined in accordance with Reg (i)(5), shall be specially allocated items of Company income and gain for such taxable year (and, if necessary, subsequent taxable years) in an amount equal to such Member s share of the net decrease in Partner Nonrecourse Debt Minimum Gain attributable to such Partner Nonrecourse Debt, determined in accordance with Reg (i)(4). Allocations pursuant to the previous sentence shall be made in proportion to the respective amounts required to be allocated to each Member pursuant thereto. The items to be so allocated shall be determined in accordance with Reg (i)(4) and Reg (j)(2). This Section 7.1(d)(4) is intended to comply with the minimum gain chargeback requirement in Reg (i)(4) and shall be interpreted consistently therewith. (5) Excess Nonrecourse Liabilities. Solely for purposes of determining a Member s proportionate share of the excess nonrecourse liabilities of the Company within the meaning of Reg (a)(3), the Members interest in the Company Profits are Pro Rata. (6) Distributions. To the extent permitted by Reg (h)(3), the Company shall endeavor to treat distributions of cash as having liability only to the extent that such distributions would cause or increase an Adjusted Capital Account Deficit for any Member Page 9 of 18 VOGEL.SEM/SP&LPROB.18

21 7.3 Curative Allocations. The allocations set forth in Section 7.2 (the Regulatory Allocations ) are intended to comply with certain requirements of the Regulations. It is the intent of the Unitholders that, to the extent possible, all Regulatory Allocations shall be offset either with other Regulatory Allocations or with special allocations of other items of Company income, gain, loss, or deduction pursuant to this Section 7.3. Therefore, notwithstanding any other provision of this Article VII (other than the Regulatory Allocations), to the extent possible offsetting special allocations of Company income, gain, loss, or deduction shall be made so that, after such offsetting allocations are made, each Unitholder s Capital Account balance is equal to the Capital Account balance such Unitholder would have had if the Regulatory Allocations were not part of this Agreement and all Company items were allocated pursuant to the other Sections of this Article VII. 7.4 Allocation in the Event of a Change in Interest. In the event that a Unitholder s interest in the Profits and Losses of the Company changes during any Fiscal Year, whether because of an initial or subsequent acquisition of Units, a Transfer of Units, a redemption of Units, or other reason, the Managers shall determine such Unitholder s distributive share of any item of income, gain, loss, deduction, or credit for such Fiscal Year by reference to this Agreement and by using any convention permitted by 706 and the Regulations thereunder, provided, however, that in no event shall a new Unitholder be entitled to any retroactive allocation of income, gain, loss, deduction or credit. 7.5 Tax Allocations: 704(c). (a) In accordance with 704(c) and the Regulations thereunder, income, gain, loss, and deduction with respect to any property contributed to the capital of the Company shall, solely for tax purposes, be allocated among the Members so as to take account of any variation between the adjusted basis of such property to the Company for federal income tax purposes and its initial Gross Asset Value, using any method authorized by Reg as determined by the Managers. (b) In the event the Gross Asset Value of any Company asset is adjusted pursuant to subsection (b) of the definition of Gross Asset Value, subsequent allocations of income, gain, loss, and deduction with respect to such asset shall take account of any variation between the adjusted basis of such asset for federal income tax purposes and its Gross Asset Value in the same manner as under 704(c), using any method described in Reg as determined by the Managers. 7.6 Curative Allocations Regarding Payments to Unitholders. To the extent that any compensation or guaranteed payment paid to a Unitholder or its Affiliate is ultimately not determined to be either a guaranteed payment under 707(c) or a payment to a Member other than his capacity as a Member under 707(a), such Unitholder shall be specially allocated gross income of the Company for the year in which such compensation or payment was made in an amount equal to the amount of such compensation or payment. If the Company s income for the year in which the compensation or payment was made is insufficient to satisfy this allocation, similar special allocations of income shall be made in subsequent years until the full amount of the allocation required by this Section 7.6 has been made. In the event that a distribution to a Member is ultimately recharacterized as a guaranteed payment under 707(c) or a payment to a Member other than in his capacity as a Member under 707(a), and if such recharacterization gives rise to a deduction, such deduction shall be allocated to the Member receiving the distribution Page 10 of 18 VOGEL.SEM/SP&LPROB.18

22 VIII. DISTRIBUTIONS. 8.1 Distributions. The Managers shall distribute the net Cash Flow of the Company not less than quarterly. For these purposes, the term Net Cash Flow for any period means (i) the Profits or Losses of the Company from operations (including investments of cash reserves), plus (ii) depreciation and other non-cash charges deducted in computing such Profits and Losses, less (iii) payments made in amortization of indebtedness of the Company, and less (iv) payments made to property replacement, contingency, capital expenditure, and other reserves as determined by the Managers. Except as otherwise provided in this Agreement, all distributions shall be made to the Members Pro Rata. 8.2 Tax Distributions. During each Taxable Year of the Company, and in any event no later than March 31 of the following Taxable Year, each Unitholders who has been allocated net taxable income of the Company (determined in accordance with 703(a)) for such Taxable Year shall be entitled to receive a cash distribution (or distributions) equal to his allocable share of such net taxable income multiplied by a percentage equal to the highest rate of tax imposed on individuals for federal income tax purposes for such Taxable Year (without regard to alternative minimum taxes or tax surcharges), plus five percent (a Tax Distribution ). Any Tax Distributions shall be deemed to be an advance distribution of amounts otherwise distributable to the Unitholders pursuant to Section 8.1, and will reduce the amounts that would subsequently otherwise be distributable to the Unitholders pursuant to Section 8.1 in the order distributions would otherwise have been made. The Company may distribute Tax Distributions in quarterly installments on an estimated basis prior to the end of a Taxable Year, but if the amounts distributed by the Company to a Unitholder as estimated quarterly Tax Distributions exceed the greater of (a) the amount of Tax Distributions to which such Unitholders entitled for such Taxable Year, or (b) the total amount of distributions to which such Unitholder is otherwise entitled in such Taxable Year, the Unitholder will, within fifteen (15) days after the tax return for such Taxable Year is filed, return such excess to the Company, and such excess shall be treated as a distribution to such Unitholder pursuant to Section 8.1 until it is returned (or if for any reason such excess is not returned, then such excess shall be set off against any future distributions to which such Unitholder otherwise would be entitled). 8.3 General Distribution Rules. (a) All amounts withheld pursuant to the Code or any provision of any state or local tax law with respect to any distribution shall be treated as amounts actually distributed to the Members. The Managers are authorized to withhold from distributions, or with respect to allocations, to the Members and to pay over to federal, state, or local government any amounts required to be so withheld pursuant to the Code or any provisions of any other federal, state, or local law and shall allocate such amounts to the Members with respect to which such amount was withheld. In the event that the Company is obligated to withhold in respect of an allocation to a Member, and such withholding obligation is in excess of the amount otherwise distributable to such Member, such excess withholding obligation shall be treated as an interest-free loan to the Member by the Company. Such loan shall be repaid out of future distributions frm the Company to the Member. If such distributions are insufficient to repay such loan, the Member shall be obligated to repay the remaining balance of such loan to the Company upon the withdrawal of the Member or upon dissolution of the Company, whichever comes first. (b) No distribution shall be made by the Company to the extent that, after giving effect to the distribution, the Company would not be able to pay its debts as they become due in the Page 11 of 18 VOGEL.SEM/SP&LPROB.18

23 usual course of business or the liabilities of the Company would exceed the fair market value of the Company s assets. IX. ADMINISTRATIVE MATTERS 9.1 Books and Records. At the expense of the Company, the Managers shall maintain at the principal place of business of the Company separate books and records of all operations and expenditures of the Company. The books and records of the Company shall be maintained using reasonable and proper accounting methods. 9.2 Returns and Elections. (a) The Managers shall cause the preparation and timely filing of all tax returns required to be filed by the Company pursuant to the Code and all other tax returns deemed necessary and required in each jurisdiction in which the Company does business. Copies of such returns, or pertinent information therefrom, shall be furnished to the Members within a reasonable time after the end of the Company s taxable year. (b) All elections permitted to be made by the Company under federal or state laws shall be made by the Managers in such manner as they deem appropriate and in the best interests of the Members. 9.3 Tax Matters Partner. The Managers shall select the tax matters partner as defined in 6231(a)(7) of the Code. The tax matters partner is authorized and required to represent the Company, at the Company s expense, in connection with all examinations of the Company s affairs by tax authorities, including resulting judicial and administrative proceedings, and to expend Company funds for professional services and costs associated therewith. 9.4 Transactions With Members and Managers. To the extent permitted by applicable law and except as otherwise provided in this Agreement, the Managers are hereby authorized to purchase property from, sell property to, borrow money from, or otherwise deal with any Member or Manager acting on its own behalf, or any Affiliate of any Member of Manager, provided that any such purchase, sale, loan, or other transaction shall be made on terms and conditions which are no less favorable to the Company than if the sale, purchase, loan, or other transaction had been entered into with an independent third party. X. TRANSFER OF INTERESTS General. Except as otherwise permitted or required by this Agreement a Unitholder shall not have the right or power to Transfer all or any part of his Units. In the event of a Transfer of Units, the transferee in all cases shall be bound by the terms of this Agreement, including, without limitation, the provisions of this Article X Permitted Transfers. Subject to the conditions and restrictions set forth in Section 10.3 hereof, a Unitholder may at any time Transfer all or any portion of its Units: (a) With the express written consent of the Managers, which consent may be withheld, or conditionally or unconditionally granted, as they shall determine in their absolute discretion; Page 12 of 18 VOGEL.SEM/SP&LPROB.18

24 (b) (c) To a Unitholder; To any members of such Unitholder s Immediate Family; (d) To a trust the current beneficiaries of which are solely the Unitholder or members of the Unitholder s Immediate Family, provided, however, that if any of the current beneficiaries are not the Unitholder or members of the Unitholder s Immediate Family, the trust shall be deemed to have withdrawn from the Company. (e) To an entity that is wholly owned by Persons to whom Units may be Transferred under the foregoing paragraphs of this Section 10.2, provided, however, that if such an interest in such entity ceases to be so owned, the entity shall be deemed to have withdrawn from the Company. (f) In the case of a trust or entity described in Section 10.2(d) or Section 10.2(e) that has not deemed to have withdrawn from the Company, to any beneficiary or owner of such trust or entity. (g) To the estate of the Unitholder, provided that under the terms of the estate the Units pass to, or are held for the benefit of, Persons to whom Units may have been Transferred directly by the Unitholder under foregoing paragraphs of this Section Any such Transfer is referred to in this Agreement as a Permitted Transfer Conditions to Permitted Transfers. A Transfer shall not be treated as a Permitted Transfer under Section 10.2 hereof unless and until the following conditions are satisfied; provided, however, that any such conditions may be waived in writing by the Company: (a) The transferor and transferee shall execute and deliver to the Company such documents and instruments of conveyance as may be necessary or appropriate in the opinion of counsel to the Company to effect or confirm such Transfer and to confirm the agreement of the transferee to be bound by the provisions of this Agreement. In all cases, the Company shall be reimbursed by the transferor and/or transferee for all costs and expenses that it reasonably incurs in connection with such Transfer including reasonable attorney s fees. (b) Except in the case of a Transfer involuntarily by operation of law, the transferor shall furnish to the Company an opinion of counsel, at the transferor s expense, which counsel and opinion shall be satisfactory to the Company, that the Transfer will not cause the Company to terminate for federal income tax purposes. (c) The transferor and transferee shall furnish the Company with the transferee s taxpayer identification number and any other information reasonably necessary to permit the Company to file all required federal, state, and local tax returns and other legally required information statements or returns. Without limiting the generality of the foregoing, the Company shall not be required to make any distribution otherwise provided for in this Agreement with respect to any Transferred Units until it has received such information. (d) Except in the case of a Transfer of Units involuntarily by operation of law, either (i) such Units shall be registered under the Securities Act of 1933, as amended, and any applicable state securities laws, or (ii) the transferor shall provide an opinion of counsel, at transferor s expense, which opinion and counsel shall be satisfactory to the Company, to the Page 13 of 18 VOGEL.SEM/SP&LPROB.18

25 effect that such Transfer is exempt from all applicable registration requirements and that such Transfer will not violate any applicable laws regulating the Transfer of securities Prohibited Transfers. Any purported Transfer of Units that is not a Permitted Transfer shall be null and void and of no effect whatsoever. In the case of a Transfer or attempted Transfer of Units that is not a Permitted Transfer, the parties engaging or attempting to engage in such Transfer shall be liable to indemnify and hold the Company and the other Unitholders harmless from all costs, liabilities, and damages that any of such indemnified Persons may incur (including, without limitation, incremental tax liability and attorneys fees and expenses) as a result of such Transfer or attempted Transfer and efforts to enforce the indemnity granted hereby. In the event that the Company is required to recognize a Transfer that is not a Permitted Transfer, the transferee of the Transferred Units shall be only a Unitholder Rights of Unadmitted Transferee. A person who acquires one or more Units through a Permitted Transfer shall be only a Unitholder and shall not have any of the rights of a Member under the Act or this Agreement (including, without limitation, any voting rights) unless such Person is admitted as a Member pursuant to the provisions of Article XI Rights and Duties of Transferor. Any Unitholder who has Transferred all of its Units (regardless of whether such Transfer was a Permitted Transfer) shall automatically cease to have any rights it held as a Member in the Company (if any) and, if applicable, shall be deemed to have resigned as a Manager, provided, however, that if the Company is not required to recognize such Transfer, such Transferor shall continue to be treated as a mere Unitholder. In no event will any Transfer relieve any Unitholder of any obligation or duty imposed by this Agreement, without the express consent of [all the other members] [a Required Interest of the Members] [the Managers]. st 10.7 Effective Date of Transfer. Any Transfer shall be deemed effective as of the 1 day of the calendar month in which the Transfer occurs. XI. ADDITIONAL MEMBERS Admission of New Members. From the date of the formation of the Company, any Person acceptable to the Managers may become a Member of the Company subject to the terms and conditions of this Agreement. No Person shall become a Member unless and until such Person has explicitly accepted, assumed, and agreed to be subject to and bound by all of the terms, obligations, and conditions of this Agreement, as the same may have been further amended Documentation of Admission. As a condition to the admission of a Person as an additional Member, the Managers may require the new member to execute, acknowledge and deliver to the Company such certificates, representations, and documents and to perform all such other acts that the Managers may deem necessary or desirable to (a) constitute such Person as an additional Member; (b) confirm that the person to be admitted as an additional Member has accepted, assumed and agreed to be subject and bound by all of the terms, obligations, and conditions of this Agreement, as the same may have been further amended; and (c) assure compliance with any applicable state and federal securities laws and regulations Page 14 of 18 VOGEL.SEM/SP&LPROB.18

26 XII. WITHDRAWAL Withdrawal. A Unitholder shall be deemed to have withdrawn from the Company upon the resignation, Bankruptcy, death, termination of existence, dissolution and commencement of winding-up, [or] incompetency (as determined by decree of a court of competent jurisdiction) [or expulsion (by a vote of a Required Interest of the Members)] of the Unitholder, or upon the occurrence of any other event that cause the Unitholder to be deemed to have withdrawn from the Company under the terms of this Agreement (an Event of Withdrawal ). Notwithstanding the foregoing, in no event shall an Event of Withdrawal be deemed to have occurred merely by reason of a Permitted Transfer by a Unitholder. A Unitholder who has withdrawn from the Company is referred to herein as a Withdrawing Unitholder Status of a Holder of Withdrawing Unitholder s Units. Any holder of a Withdrawing Unitholder s Units (including, without limitation, a Member who withdraws and continues to own Units) shall be treated as a Unitholder unless admitted to the Company as a Member under the provisions of Article XI. If a Withdrawing Unitholder is a Manager, he shall be deemed to have resigned as a Manager Economic Consequence of Withdrawal. In the event any Unitholder withdraws, the following provisions shall apply: (a) Within sixty (60) days following the date upon which the Company receives notice of an Event of Withdrawal, the Managers may elect to redeem all of the Units which were held by the Withdrawing Unitholder (regardless of the present owner of such Units), for an amount equal to the net amount that the Unitholder of such Units would have received if (i) all items of Company property (which, for this purpose, shall not be considered to include any goodwill or going concern value) were sold for fair market value as of the last day of the month in which the Event of Withdrawal occurred, (ii) the liabilities of the Company as of such date were paid, and (iii) the Company was liquidated in accordance with the provisions of Section For this purpose, the amount which would be realized pursuant to clause (1) of the foregoing sentence shall be determined by the Managers, which determination shall be binding provided it is reasonable and made in good faith. (b) The amount due the Unitholder whose Units are to be acquired under the provisions of Section 12.3(a) shall be paid in eight (8) semi-annual installments, without interest, with the first such payment due on the last day of the sixth month following the Event of Withdrawal, provided, however, that if the Company is subsequently dissolved pursuant to Section 13.1, all remaining amounts due to the Unitholder shall become due and payable upon the final distribution to the Company s Unitholders pursuant to Section 13.2 XIII. DISSOLUTION AND TERMINATION Dissolution. The Company shall be dissolved only upon the vote of a Majority in Interest of the Members or entry of a decree of involuntary dissolution by a court of competent jurisdiction (an Event of Dissolution ) Page 15 of 18 VOGEL.SEM/SP&LPROB.18