Explanation of Items

|

|

|

- Cody Cummings

- 5 years ago

- Views:

Transcription

1

2

3 Form 886-A (Rev. January 1994) Name of Taxpayer College ofdupage Explanation of Items Tax Identification Number Schedule No. Or Exhibit Year/Period Ended 2013 Issue: Were the meals employees received at the Waterleaftaxable as a fringe benefit? Facts: When certain employees of the College or Foundation dine at the Waterleaf (an on campus culinary school restaurant), the meal is charged to four different "house accounts" so the employee does not need to pay. The four house accounts are: 1. House Account # 10 - President Breuder' s office 2. House Account #20-Foundation 3. House Account #30 - All other internal college departments 4. House Account # Waterleaf department internal charges At the end of each month, the Waterleaf general manager collects all house account receipts for the month and delivers copies to the Finance office as well as the College department. The authorized signers send Finance the GL accounts to use in the journal entry. Finance prepares the journal to credit the Waterleaf for the revenue and debit the GL accounts that the authorized signers have decided to charge. The College provided some documentation that included the receipts of the meals and, in some situations, a business expense report that documented business purpose and attendees. The majority of the documentation was receipts and handwritten notes or signatures without business related documentation. There was no documentation that supported employees reimbursing the college for any of the meals or drinks. Law: Internal Revenue Code (IRC) section 61 provides that, except as otherwise provided, gross income means all income from whatever source derived - including fringe benefits. Under the provisions of sections 61(a)(l) and 3121(a) of the Internal Revenue Code, the value of employer provided meals and reimbursements for meals are included in an employee's income and wages for employment tax purposes unless there is some provision that allows for their exclusion. The Internal Revenue Code contains several provisions that might exclude the value of employer provided meals and reimbursements for meals from the recipient's income and wages. Section 119 of the Code provides for the exclusion of the value of employer provided meals if the meals are provided on the employer's business premises and if the meals are provided for the convenience of the employer. Under the provisions of section 1. l 19-l(a)(2)(i) of the income tax regulations, meals furnished by an employer without charge to the employee will be regarded as furnished for the convenience of the employer if such meals are furnished for a substantial noncompensatory business reason of the employer. In determining the reason of an employer for furnishing meals, the mere declaration that meals are furnished for a noncompensatory business reason is not sufficient to prove that meals are furnished for the convenience of the Department of the Treasury - Internal Revenue Service Form 886-A Page 1 of8

4

5

6

7

8

9 Form 886-A (Rev. January 1994) Name of Taxpayer College ofdupage Explanation of Items Tax Identification Number Schedule No. Or Exhibit Year/Period Ended 2013 This analysis reaches the following conclusions: Meals furnished by an employer can be excluded from wages if they are provided on the employer's business premises and if the meals are furnished for the convenience of the employers; Furnishing meals before, during, or after an employee meeting would generally not be considered for the convenience of the employer, unless there is some reason which causes the employees to be unable to leave the business premises for sufficient time to have a meal; Meals may be excluded from wages as de minimis fringe benefits if they are furnished so infrequently and if are so small in value that accounting for the meals would be administratively impracticable. Generally, accounting for meals provided to employees who attend a meeting would not be administratively impracticable. Conclusion: A few meals did meet the rules for exclusion under the Internal Revenue Code. However, a significant and substantial number of meals at the Waterleaf (attached on related spreadsheet) would be taxable because: The meals were not de minimis in nature in accordance with Internal Revenue Code Section 132; The meals would be considered "day meals" under relation to Internal Revenue Code Section 162(a)(2); The meals did not meet accountable plan rules under Internal Revenue Code Section l.62-2(c). Specifically, the meals did not meet all the requirements as entertainment expense, because the employee did not substantiate by adequate records (A) the amount of such expense or other item, (B) the time and place of the travel or entertainment, (C) the business purpose of the expense or other item, and (D) the business relationship to the taxpayer of persons entertained. All elements must be present for exclusion. The meals do not meet exclusion under Internal Revenue Code Section 119. The College did not show that there was some business purpose that either prevented the employees from leaving the premises for lunch/dinner or that prevented the employees from having sufficient time to have lunch/dinner during the allotted time. The situations in which meals were provided do not meet the intended exclusion under Section 119 nor is there any equivalence to the College meals at Waterleaf to the excluded meals in the court cases cited. As there was no documentation that the employees reimbursed the college for the meals, the meals are taxable as a fringe benefit. Income withholding wage adjustment is subject to tax at 25% under Internal Revenue Code Under Internal Revenue Code 3403 the employer is liable for the tax not withheld under Internal Revenue Code FITW $ 18, x.25 = $ 4, Medicare $ 18, x.029 = $ Department of the Treasury- Internal Revenue Service Form 886-A Page 7 of8

10 Form 886-A (Rev. January 1994) Name of Taxpayer College ofdupage Explanation of Items Tax Identification Number Schedule No. Or Exhibit Year/Period Ended 2013 Total $ 5, Not all employees can be identified who received the meals. Those employees who can be identified were not in social security, and there would be no benefit to the government nor benefit gained or lost to the employee to have the TP issue corrected Forms W-2c for each of these employees, Internal Revenue Agent asked and IRS Group manager agreed that individual corrected Forms W-2c would be a burden to both the TP and individuals. Per IRM the College ofdupage will not have to issue Forms W-2c or Form W-3c for the fringe benefit because: 1) Not all employee's can be identified with the documentation presented; 2) it reduces the taxpayer's burden for multiple entries on Forms W-2c and reduces the burden on the individual to prepare an amended return that will not affect any benefit as: 3) the individuals do not participate in social security and would not have any benefit increase or decrease by filing an amended return (which would be an expense to the individual) 4) and Medicare benefits are unaffected. Department of the Treasury - Internal Revenue Service Form 886-A Page 8 of8

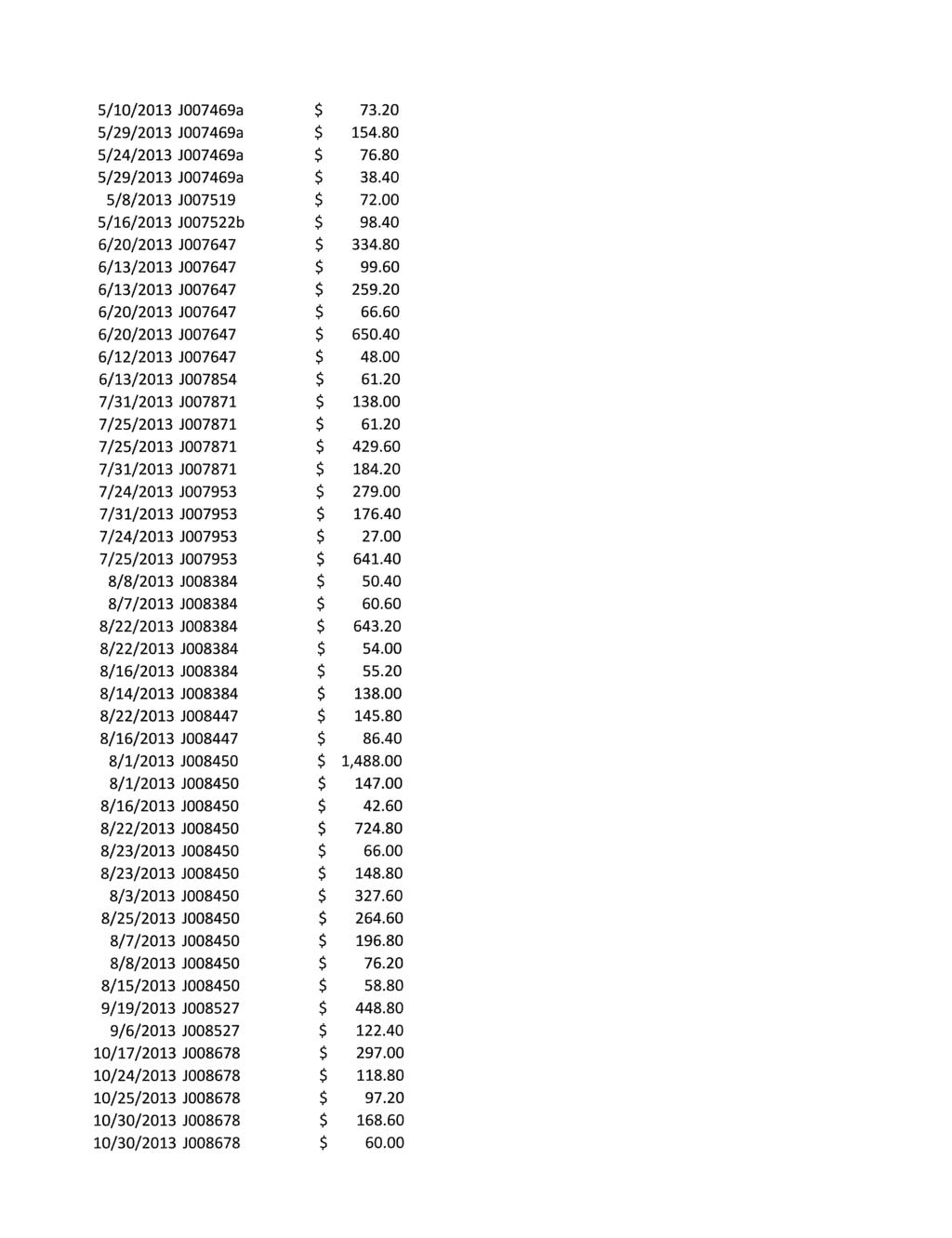

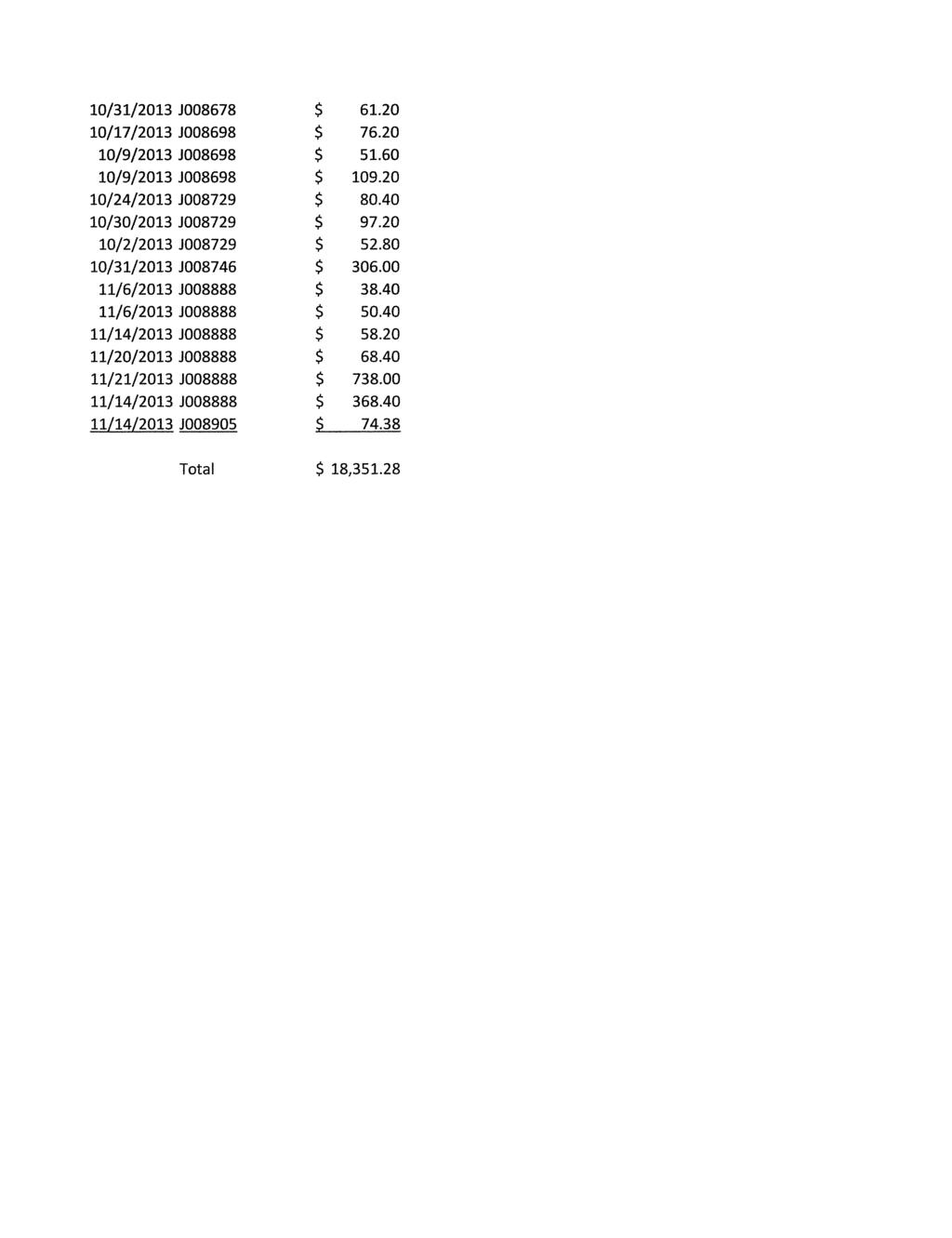

11 College of Dupage Meals at Waterleaf Meals TY 2013 Below are a list of meals that do not have the documentation to be considered exempt from taxability as a fringe benefit. The meals are day meals; documents do not support accountable plans; and do not meet exemption under IRC 119. Sorted by invoice Date Invoice number Amount 1/24/2013 J006813b $ /9/2013 J $ /9/2013 J $ /9/2013 J $ /16/2013 J $ /30/2013 J $ /31/2013 J $ /14/2013 J $ /1/2013 J $ /28/2013 J $ /21/2013 J $ /22/2013 J $ /27 /2013 J $ /28/2013 J $ /8/2013 J $ /6/2013 J007138b $ /17 /2013 J007203c $ /10/2013 J007203c $ /4/2013 J $ /12/2013 J007295a $ /24/2013 J007295a $ /26/2013 J007295a $ /19/2013 J007295a $ /12/2013 J007295a $ /12/2013 J007295b $ /18/2013 J007295b $ /26/2013 J007295b $ /24/2013 J $ /24/2013 J $ /25/2013 J $ /25/2013 J $ /12/2013 J $ /10/2013 J $

12

13

Pay_910 Gift Cards, Gifts, Prizes and Awards Prepared By: Associate Controller Disbursements Approved By: John Kirsits Effective Date: 4/12/2016

Pay_910 Gift Cards, Gifts, Prizes and Awards Prepared By: Associate Controller Disbursements Approved By: John Kirsits Effective Date: 4/12/2016 Purpose The policy provides University departments with

Pay_910 Gift Cards, Gifts, Prizes and Awards Prepared By: Associate Controller Disbursements Approved By: John Kirsits Effective Date: 4/12/2016 Purpose The policy provides University departments with

INTERNAL REVENUE SERVICE NATIONAL OFFICE TECHNICAL ADVICE MEMORANDUM. April 30, 2004

INTERNAL REVENUE SERVICE NATIONAL OFFICE TECHNICAL ADVICE MEMORANDUM April 30, 2004 Number: 200437030 Release Date: 9/10/04 Index (UIL) No.: 132.04-01 CASE-MIS No.: TAM-108577-04/CC:TEGE:EOEG:ET2 -----------------------

INTERNAL REVENUE SERVICE NATIONAL OFFICE TECHNICAL ADVICE MEMORANDUM April 30, 2004 Number: 200437030 Release Date: 9/10/04 Index (UIL) No.: 132.04-01 CASE-MIS No.: TAM-108577-04/CC:TEGE:EOEG:ET2 -----------------------

Tax Update for State and Local Governments

Tax Update for State and Local Governments Fringe Benefit and Tax Reporting Overview Presented by: Ashley M. Summers, CPA Tax Manager Sales & Use Tax Reminder Retail Sales and Use tax exemptions can now

Tax Update for State and Local Governments Fringe Benefit and Tax Reporting Overview Presented by: Ashley M. Summers, CPA Tax Manager Sales & Use Tax Reminder Retail Sales and Use tax exemptions can now

Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing:

The following are various types of income commonly found on a priest s tax filing:") Diocese of Madison Policy for Priest Compensation Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing: A. Salary and Supplements

Diocese of Madison Policy for Priest Compensation Taxable income (Federal and Social Security) The following are various types of income commonly found on a priest s tax filing: A. Salary and Supplements

608 Taxability of Employee Benefits

Page 1 of 9 608 Taxability of Employee Benefits Approved by President Sidney A. McPhee, President Effective Date: January 1, 2019 Responsible Division: Business and Finance Responsible Office: Business

Page 1 of 9 608 Taxability of Employee Benefits Approved by President Sidney A. McPhee, President Effective Date: January 1, 2019 Responsible Division: Business and Finance Responsible Office: Business

Preparing for an Internal Revenue Service Review for a Housing Authority

Preparing for an Internal Revenue Service Review for a Housing Authority Prepared by Urlaub & Co., PLLC, Certified Public Accountants (580) 332-4802 Presented by Ronald Urlaub, CPA 1 Objectives To understand

Preparing for an Internal Revenue Service Review for a Housing Authority Prepared by Urlaub & Co., PLLC, Certified Public Accountants (580) 332-4802 Presented by Ronald Urlaub, CPA 1 Objectives To understand

Simplifying the complexities of payroll taxes and year-end planning November 7, 2013

Simplifying the complexities of payroll taxes and year-end planning November 7, 2013 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International.

Simplifying the complexities of payroll taxes and year-end planning November 7, 2013 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International.

INTERNAL REVENUE SERVICE NATIONAL OFFICE TECHNICAL ADVICE MEMORANDUM April 6, 2000

INTERNAL REVENUE SERVICE NATIONAL OFFICE TECHNICAL ADVICE MEMORANDUM April 6, 2000 Number: 200030001 Release Date: 7/28/2000 Third Party Contact: Index (UIL) No.: 274.14-00 CASE MIS No.: TAM-117215-99/CC:DOM:IT&A:B2

INTERNAL REVENUE SERVICE NATIONAL OFFICE TECHNICAL ADVICE MEMORANDUM April 6, 2000 Number: 200030001 Release Date: 7/28/2000 Third Party Contact: Index (UIL) No.: 274.14-00 CASE MIS No.: TAM-117215-99/CC:DOM:IT&A:B2

FRINGE BENEFITS. Federal, State and Local Governments (FSLG) FRINGE BENEFITS GENERAL RULES. FSLG Specialist Clark Fletcher

FRINGE BENEFITS GENERAL RULES. FSLG Specialist Clark Fletcher") FRINGE BENEFITS Sponsored by Commonwealth of Northern Marianas Islands, Division of Revenue & Taxation March 2, 2010 1 Federal, State and Local Governments (FSLG) FSLG Specialist Clark Fletcher Tel: 425.489.4042

FRINGE BENEFITS Sponsored by Commonwealth of Northern Marianas Islands, Division of Revenue & Taxation March 2, 2010 1 Federal, State and Local Governments (FSLG) FSLG Specialist Clark Fletcher Tel: 425.489.4042

Tax Update April 23, 2013

Presentation to SPRING 2013 FOCUS CONFERENCE Tax Update April 23, 2013 Presentation by Donald E. Dee Rich, Jr. Partner, KPMG LLP Exempt Organizations Tax Practice derichjr@kpmg.com (336) 433-7071 KPMG

Presentation to SPRING 2013 FOCUS CONFERENCE Tax Update April 23, 2013 Presentation by Donald E. Dee Rich, Jr. Partner, KPMG LLP Exempt Organizations Tax Practice derichjr@kpmg.com (336) 433-7071 KPMG

NERC/NAHRO Mashantucket, CT

NERC/NAHRO 2-9-10 Mashantucket, CT Intro to FSLG Exam Procedures Payroll Issues W4 and withholdings Medicare- rehired annuitants Accounts Payable and Disbursement Issues Accountable v Non accountable Plans

NERC/NAHRO 2-9-10 Mashantucket, CT Intro to FSLG Exam Procedures Payroll Issues W4 and withholdings Medicare- rehired annuitants Accounts Payable and Disbursement Issues Accountable v Non accountable Plans

DINWIDDIE COUNTY DIVISION OF FINANCE & GENERAL SERVICES POLICIES AND PROCEDURES TAXABLE FRINGE BENEFITS. Adopted March 1, 2015, Revised March 18, 2015

Adopted March 1, 2015, Revised March 18, 2015 DINWIDDIE COUNTY DIVISION OF FINANCE & GENERAL SERVICES POLICIES AND PROCEDURES TAXABLE FRINGE BENEFITS POLICY Dinwiddie County strives to adhere to all federal

Adopted March 1, 2015, Revised March 18, 2015 DINWIDDIE COUNTY DIVISION OF FINANCE & GENERAL SERVICES POLICIES AND PROCEDURES TAXABLE FRINGE BENEFITS POLICY Dinwiddie County strives to adhere to all federal

Development of year-end work plan Create the year-end team (e.g., Payroll, HR, IT, and Accounting) and focus on the following tasks:

and focus on the following tasks:") Presentation topics > Development of year-end work plan > Management and completion of year-end tasks > Form W-4 compliance > Social Security number (SSN) verification > Form W-2 reporting > IRS Publication

Presentation topics > Development of year-end work plan > Management and completion of year-end tasks > Form W-4 compliance > Social Security number (SSN) verification > Form W-2 reporting > IRS Publication

Award Safety.... with the award that changes behavior. Income Tax Treatment of Safety Awards

Award Safety... with the award that changes behavior. Income Tax Treatment of Safety Awards Federal Income Tax Treatment of Employee Recognition and Safety Awards Following is a primer on the Federal Income

Award Safety... with the award that changes behavior. Income Tax Treatment of Safety Awards Federal Income Tax Treatment of Employee Recognition and Safety Awards Following is a primer on the Federal Income

TEXAS SOUTHERN UNIVERSITY MANUAL OF ADMINISTRATIVE POLICIES AND PROCEDURES. SECTION: Fiscal Affairs NUMBER:

TEXAS SOUTHERN UNIVERSITY MANUAL OF ADMINISTRATIVE POLICIES AND PROCEDURES SECTION: Fiscal Affairs NUMBER: 03.04.04 AREA: SUBJECT: Payroll Taxable Fringe Benefits I. PURPOSE AND SCOPE Texas Southern University

TEXAS SOUTHERN UNIVERSITY MANUAL OF ADMINISTRATIVE POLICIES AND PROCEDURES SECTION: Fiscal Affairs NUMBER: 03.04.04 AREA: SUBJECT: Payroll Taxable Fringe Benefits I. PURPOSE AND SCOPE Texas Southern University

named 2018 Year End Packet Action Items that summarizes the required steps to be taken for each item.

HUTS N G BBLE LLC Important - Time Sensitive Dear Clients, As the end of the year approaches, there are several important items that are required to be reported on employee and employee-owner W-2 s. These

HUTS N G BBLE LLC Important - Time Sensitive Dear Clients, As the end of the year approaches, there are several important items that are required to be reported on employee and employee-owner W-2 s. These

2017 Guide to Valuation of Personal Use of Employer-Provided Vehicles and Other Select Taxable Fringe Benefits

2017 Guide to Valuation of Personal Use of Employer-Provided Vehicles and Other Select Taxable Fringe Benefits Changes to note: The automobile mileage rates are: 53.5 cents for 2017 54.5 cents for every

2017 Guide to Valuation of Personal Use of Employer-Provided Vehicles and Other Select Taxable Fringe Benefits Changes to note: The automobile mileage rates are: 53.5 cents for 2017 54.5 cents for every

MINNESOTA STATE COLLEGES AND UNIVERSITIES January 2005 Notice of Employer-Provided Educational Assistance

MINNESOTA STATE COLLEGES AND UNIVERSITIES January 2005 Notice of Employer-Provided Educational Assistance The Minnesota State Colleges & Universities System has a written educational assistance plan to

MINNESOTA STATE COLLEGES AND UNIVERSITIES January 2005 Notice of Employer-Provided Educational Assistance The Minnesota State Colleges & Universities System has a written educational assistance plan to

UNIVERSITY OF HOUSTON SYSTEM ADMINISTRATIVE MEMORANDUM. SECTION: Fiscal Affairs NUMBER: 03.D.06

UNIVERSITY OF HOUSTON SYSTEM ADMINISTRATIVE MEMORANDUM SECTION: Fiscal Affairs NUMBER: 03.D.06 AREA: Payroll SUBJECT: Taxable Fringe Benefits 1. PURPOSE 1.1. The University of Houston System provides a

UNIVERSITY OF HOUSTON SYSTEM ADMINISTRATIVE MEMORANDUM SECTION: Fiscal Affairs NUMBER: 03.D.06 AREA: Payroll SUBJECT: Taxable Fringe Benefits 1. PURPOSE 1.1. The University of Houston System provides a

Comprehensive W-2 Review Presented by: Jacob Franklin, CPA

Comprehensive W-2 Review Presented by: Jacob Franklin, CPA Presenter Information Jacob Franklin, CPA Senior Tax Manager Grand Forks, ND Overview 1. Tying Out Year-End Payroll Reports 2. W-2 Example 3.

Comprehensive W-2 Review Presented by: Jacob Franklin, CPA Presenter Information Jacob Franklin, CPA Senior Tax Manager Grand Forks, ND Overview 1. Tying Out Year-End Payroll Reports 2. W-2 Example 3.

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS. 16th Edition (March 2015)

") Route To: Partners Managers Staff File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC's Guide to Compensation and Benefits 16th Edition (March 2015) Highlights of this Edition The following are some of

Route To: Partners Managers Staff File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC's Guide to Compensation and Benefits 16th Edition (March 2015) Highlights of this Edition The following are some of

ACCOUNTS PAYABLE POLICIES AND PROCEDURES

ACCOUNTS PAYABLE POLICIES AND PROCEDURES...... Accounts Payable Payment Processing x General Information x Overview of the Disbursement Voucher x Disbursement Voucher Approval x Payments Against Purchase

ACCOUNTS PAYABLE POLICIES AND PROCEDURES...... Accounts Payable Payment Processing x General Information x Overview of the Disbursement Voucher x Disbursement Voucher Approval x Payments Against Purchase

LESSON Recording A Payroll. CENTURY 21 ACCOUNTING 2009 South-Western, Cengage Learning

LESSON 13-1 Recording A Payroll 2 PAYROLL REGISTER page 369 Use the payroll register to record the payment of the payroll. The payment of the payroll is recorded in the cash payments journal. LESSON 13-1

LESSON 13-1 Recording A Payroll 2 PAYROLL REGISTER page 369 Use the payroll register to record the payment of the payroll. The payment of the payroll is recorded in the cash payments journal. LESSON 13-1

ACCOUNTING FOR EMPLOYEE FRINGE BENEFITS. All campuses served by Louisiana State University (LSU) Office of Accounting Services

Office of Accounting Services") Louisiana State University Finance and Administration Operating Procedure FASOP: AS-12 ACCOUNTING FOR EMPLOYEE FRINGE BENEFITS Scope: Effective: Purpose: All campuses served by Louisiana State University

Louisiana State University Finance and Administration Operating Procedure FASOP: AS-12 ACCOUNTING FOR EMPLOYEE FRINGE BENEFITS Scope: Effective: Purpose: All campuses served by Louisiana State University

(See also Publication 15-B irs.gov)

") Fringe Benefits Fringe and Special Benefits Reporting (See also Publication 15-B irs.gov) Any fringe benefit provided is taxable and must be included in the recipients pay unless the law specifically excludes

Fringe Benefits Fringe and Special Benefits Reporting (See also Publication 15-B irs.gov) Any fringe benefit provided is taxable and must be included in the recipients pay unless the law specifically excludes

2016 Automobile Rules. Computation of Personal Use

2016 Automobile Rules Computation of Personal Use 2016 Automobile Rules: Computation of Personal Use... 2 Exhibit 1A... 8 Exhibit 1B... 9 Exhibit 1C... 10 Exhibit 1D... 11 LEGAL NOTICE: The contents of

2016 Automobile Rules Computation of Personal Use 2016 Automobile Rules: Computation of Personal Use... 2 Exhibit 1A... 8 Exhibit 1B... 9 Exhibit 1C... 10 Exhibit 1D... 11 LEGAL NOTICE: The contents of

Chapter 13 Payroll Accounting, Taxes, and Reports

Chapter 13 Payroll Accounting, Taxes, and Reports -- The payroll register and employee earnings records provide all the payroll information needed to prepare a payroll and payroll tax reports. Journal

Chapter 13 Payroll Accounting, Taxes, and Reports -- The payroll register and employee earnings records provide all the payroll information needed to prepare a payroll and payroll tax reports. Journal

Employer's Tax Guide to Fringe Benefits

Department of the Treasury Internal Revenue Service Publication 15-B Cat. No. 29744N Employer's Tax Guide to Fringe Benefits For use in 2014 Contents What's New... 1 Reminders... 2 Introduction... 2 1.

Department of the Treasury Internal Revenue Service Publication 15-B Cat. No. 29744N Employer's Tax Guide to Fringe Benefits For use in 2014 Contents What's New... 1 Reminders... 2 Introduction... 2 1.

Application of Retroactive Increase in Transit Benefits

Legislative Brief Application of Retroactive Increase in Transit Benefits The American Taxpayer Relief Act increased the maximum monthly transit benefit for employees from $125 per participating employee

Legislative Brief Application of Retroactive Increase in Transit Benefits The American Taxpayer Relief Act increased the maximum monthly transit benefit for employees from $125 per participating employee

Navigating Fringe Benefits: Exempt Organization Overview Q&A

Navigating Fringe Benefits: Exempt Organization Overview Q&A Below is a summary of the questions we have received from tax-exempt organizations regarding fringe benefits with answers from our tax team.

Navigating Fringe Benefits: Exempt Organization Overview Q&A Below is a summary of the questions we have received from tax-exempt organizations regarding fringe benefits with answers from our tax team.

2017 TAX CUTS AND JOBS ACT

2017 TAX CUTS AND JOBS ACT The Tax Cuts and Jobs Act was signed by President Trump on December 22, 2017. The Act makes sweeping changes to the U.S. tax code and impacts most taxpayers; especially individuals

2017 TAX CUTS AND JOBS ACT The Tax Cuts and Jobs Act was signed by President Trump on December 22, 2017. The Act makes sweeping changes to the U.S. tax code and impacts most taxpayers; especially individuals

Payments on Behalf of or Reimbursements Made to Employees Under an Accountable Plan

Payments on Behalf of or Reimbursements Made to Employees Under an Accountable Plan Introduction Under Reg. 1.62 2(c)(4), payments on behalf of or reimbursements to employees that are treated as paid under

Payments on Behalf of or Reimbursements Made to Employees Under an Accountable Plan Introduction Under Reg. 1.62 2(c)(4), payments on behalf of or reimbursements to employees that are treated as paid under

Internal Revenue Service

Internal Revenue Service Federal, State and Local Governments February 2013 QUICK REFERENCE GUIDE FOR PUBLIC EMPLOYERS CONTENTS INTRODUCTION -2-1 COMPENSATION -3-2 SOCIAL SECURITY AND MEDICARE COVERAGE

Internal Revenue Service Federal, State and Local Governments February 2013 QUICK REFERENCE GUIDE FOR PUBLIC EMPLOYERS CONTENTS INTRODUCTION -2-1 COMPENSATION -3-2 SOCIAL SECURITY AND MEDICARE COVERAGE

LESSON Recording A Payroll. CENTURY 21 ACCOUNTING Thomson/South-Western

Recording A Payroll 2 Different Forms of Payroll Information Payroll information for each pay period is recorded in a payroll register Each pay period the payroll information for each employee is also

Recording A Payroll 2 Different Forms of Payroll Information Payroll information for each pay period is recorded in a payroll register Each pay period the payroll information for each employee is also

Sports & Entertainment Tickets & Suites Tax Questions

Background H.R. 1 (the 2017 Act ) includes numerous revisions to section 274 impacting deductions for entertainment and recreation expenses that are directly related to the conduct of an employer s trade

Background H.R. 1 (the 2017 Act ) includes numerous revisions to section 274 impacting deductions for entertainment and recreation expenses that are directly related to the conduct of an employer s trade

Chapter 2 p.39 Income In Kind

Chapter 2 p.39 Income In Kind How is the concept of income defined? Consider the Haig-Simons (economist s) definition of income: Accession to wealth consisting of: 1) Consumption (occurring during the

Chapter 2 p.39 Income In Kind How is the concept of income defined? Consider the Haig-Simons (economist s) definition of income: Accession to wealth consisting of: 1) Consumption (occurring during the

EMPLOYEE VS CONTRACTOR

INTERNAL REVENUE SERVICE EMPLOYEE VS CONTRACTOR Presented By: Deishun Garmon-Robinson Badge Number: FSLG Specialist Tax Exempt and Government Entities Internal Revenue Service 1110 Montlimar Drive, Suite

INTERNAL REVENUE SERVICE EMPLOYEE VS CONTRACTOR Presented By: Deishun Garmon-Robinson Badge Number: FSLG Specialist Tax Exempt and Government Entities Internal Revenue Service 1110 Montlimar Drive, Suite

Provided Cell Phones But Questions Remain

IRS Provides Tax Relief for Employer - Provided Cell Phones But Questions Remain October 4, 2011 Presenters: www.morganlewis.com David Fuller Mary Hevener Vicki Nielsen Taxation of Cell Phones and Other

IRS Provides Tax Relief for Employer - Provided Cell Phones But Questions Remain October 4, 2011 Presenters: www.morganlewis.com David Fuller Mary Hevener Vicki Nielsen Taxation of Cell Phones and Other

FSLG Fringe Benefit Guide FEDERAL, STATE, AND LOCAL GOVERNMENTS THE INTERNAL REVENUE SERVICE

FSLG Fringe Benefit Guide FEDERAL, STATE, AND LOCAL GOVERNMENTS THE INTERNAL REVENUE SERVICE January 2013 TABLE OF CONTENTS 1 Introduction 2 Reporting and Withholding on Fringe Benefits 3 Working Condition

FSLG Fringe Benefit Guide FEDERAL, STATE, AND LOCAL GOVERNMENTS THE INTERNAL REVENUE SERVICE January 2013 TABLE OF CONTENTS 1 Introduction 2 Reporting and Withholding on Fringe Benefits 3 Working Condition

IRS EMPLOYMENT TAX ISSUES

IRS EMPLOYMENT TAX ISSUES vgfoa Conference October 22, 2009 Christina Chang Federal State & Local Government Topics: Current Issues ARRA (COBRA) Subsidy Reporting Form 94X Corrections Military Differential

IRS EMPLOYMENT TAX ISSUES vgfoa Conference October 22, 2009 Christina Chang Federal State & Local Government Topics: Current Issues ARRA (COBRA) Subsidy Reporting Form 94X Corrections Military Differential

Employer's Tax Guide to Fringe Benefits

Department of the Treasury Internal Revenue Service Publication 15-B Cat. No. 29744N Employer's Tax Guide to Fringe Benefits For use in 2013 Contents What's New... 1 Reminders... 2 Introduction... 2 1.

Department of the Treasury Internal Revenue Service Publication 15-B Cat. No. 29744N Employer's Tax Guide to Fringe Benefits For use in 2013 Contents What's New... 1 Reminders... 2 Introduction... 2 1.

Making sense of the new tax law: How it impacts corporate sponsorships & tickets

Making sense of the new tax law: How it impacts corporate sponsorships & tickets KPMG / TicketManager 2 Background Overview of Relevant Rules under H.R. 1 H.R. 1 (the 2017 Act ) includes numerous revisions

Making sense of the new tax law: How it impacts corporate sponsorships & tickets KPMG / TicketManager 2 Background Overview of Relevant Rules under H.R. 1 H.R. 1 (the 2017 Act ) includes numerous revisions

TAXABLE AND NONTAXABLE COMPENSATON. CHAPTER 3, Part I (2016)

") TAXABLE AND NONTAXABLE COMPENSATON CHAPTER 3, Part I (2016) 1 GROSS INCOME The IRC uses the term gross income to determine a taxpayer s federal tax bill and defines it as compensation for services, including

TAXABLE AND NONTAXABLE COMPENSATON CHAPTER 3, Part I (2016) 1 GROSS INCOME The IRC uses the term gross income to determine a taxpayer s federal tax bill and defines it as compensation for services, including

OFFICIAL POLICY. Policy Statement

OFFICIAL POLICY 4.1 COLLEGE OF CHARLESTON FOUNDATION EXPENSE REIMBURSEMENT POLICY 2/5/16 Policy Statement The College of Charleston Foundation is a non-profit corporation that operates within the provisions

OFFICIAL POLICY 4.1 COLLEGE OF CHARLESTON FOUNDATION EXPENSE REIMBURSEMENT POLICY 2/5/16 Policy Statement The College of Charleston Foundation is a non-profit corporation that operates within the provisions

Non Tax Levy Guidelines

Non Tax Levy Guidelines Before You Begin: Please be sure that there are sufficient funds in your budget to cover the request. Email FBSC@brooklyn.cuny.edu if you are unsure of your account balance. Requests

Non Tax Levy Guidelines Before You Begin: Please be sure that there are sufficient funds in your budget to cover the request. Email FBSC@brooklyn.cuny.edu if you are unsure of your account balance. Requests

Consultant/Trainer Independent Contractor Agreement

P.O. Box 2770 La Plata, Maryland 20646-0170 Switchboard: (301) 932-6610 (301) 870-3814 Recorded Information 24 Hours a Day: (301) 934-7410 NOTE: Contract shall be used for goods and or services delivered

P.O. Box 2770 La Plata, Maryland 20646-0170 Switchboard: (301) 932-6610 (301) 870-3814 Recorded Information 24 Hours a Day: (301) 934-7410 NOTE: Contract shall be used for goods and or services delivered

Franchise Tax Board. 3. Is the Amount to be withheld based on net or gross rent? The Franchise Tax Board Guidelines uses the term gross.

Franchise Tax Board Resident & Nonresident Withholding Guidelines November 2009 On February 9, 2009, the Franchise Tax Board (FTB) issued new franchise tax nonresident withholding guidelines. California

Franchise Tax Board Resident & Nonresident Withholding Guidelines November 2009 On February 9, 2009, the Franchise Tax Board (FTB) issued new franchise tax nonresident withholding guidelines. California

All travelers are to comply with the following travel and business expense reimbursement policies and procedural guidelines.

Title: Travel and Business Expense Reimbursement Policy Code: 5-200-050 Date: 1-18-06rev Approved: WPL Policy General The Boston College Travel and Business Expense Reimbursement Policy provides guidelines

Title: Travel and Business Expense Reimbursement Policy Code: 5-200-050 Date: 1-18-06rev Approved: WPL Policy General The Boston College Travel and Business Expense Reimbursement Policy provides guidelines

Relocation Expenses Policy

Relocation Expenses Policy 2.1.26 January 1, 2018 The Relocation Expenses policy is being updated to reflect changes to the taxability of reimbursements per the 2018 Federal Tax Cuts and Jobs Act. Moving

Relocation Expenses Policy 2.1.26 January 1, 2018 The Relocation Expenses policy is being updated to reflect changes to the taxability of reimbursements per the 2018 Federal Tax Cuts and Jobs Act. Moving

Tax Impact of Entertainment

Tax Impact of Entertainment Peter C. Adams October 2017 Entertainment The provision of to employees, associates and clients has income tax, fringe benefits tax and GST implications Identifying what amounts

Tax Impact of Entertainment Peter C. Adams October 2017 Entertainment The provision of to employees, associates and clients has income tax, fringe benefits tax and GST implications Identifying what amounts

Texas Hotel Occupancy Tax Exemption Certificate

12-302 (Rev.4-14/18) Texas Hotel Occupancy Tax Exemption Certificate Provide completed certificate to hotel to claim exemption from hotel tax. Hotel operators should request a photo ID, business card or

12-302 (Rev.4-14/18) Texas Hotel Occupancy Tax Exemption Certificate Provide completed certificate to hotel to claim exemption from hotel tax. Hotel operators should request a photo ID, business card or

Glossary of Terms. Accrual ACH. Advance. Allowable Expense

Term Glossary of Terms Definition The recognition of revenue and expenses when incurred, not paid. An example is an expense purchasing supplies on June 28th but not paying the expense until July 15th.

Term Glossary of Terms Definition The recognition of revenue and expenses when incurred, not paid. An example is an expense purchasing supplies on June 28th but not paying the expense until July 15th.

RE: W-2 REPORTING REQUIREMENTS FOR FRINGE BENEFITS TO BE ADDED TO EMPLOYEES' W-2 AS COMPENSATION

December 2017 To Our Clients: RE: - 2017 W-2 REPORTING REQUIREMENTS FOR FRINGE BENEFITS TO BE ADDED TO EMPLOYEES' W-2 AS COMPENSATION - SPECIAL RULES FOR S-CORPORATION SHAREHOLDERS In this letter, we will

December 2017 To Our Clients: RE: - 2017 W-2 REPORTING REQUIREMENTS FOR FRINGE BENEFITS TO BE ADDED TO EMPLOYEES' W-2 AS COMPENSATION - SPECIAL RULES FOR S-CORPORATION SHAREHOLDERS In this letter, we will

S Corporation Health Insurance Modification

S Corporation Owner Health Insurance Deduction December 26, 2007 Feed address for Podcast subscription: http://feeds.feedburner.com/edzollarstaxupdate Home page for Podcast: http://ezollars.libsyn.com

S Corporation Owner Health Insurance Deduction December 26, 2007 Feed address for Podcast subscription: http://feeds.feedburner.com/edzollarstaxupdate Home page for Podcast: http://ezollars.libsyn.com

Gross Income Exclusions and Adjustments to Income

CCH Essentials of Federal Income Taxation Gross Income Exclusions and Adjustments to Income 2001, CCH INCORPORATED 4025 West Peterson Ave. Chicago, IL 60646-6085 http://tax.cchgroup.com Gross Income Exclusions

CCH Essentials of Federal Income Taxation Gross Income Exclusions and Adjustments to Income 2001, CCH INCORPORATED 4025 West Peterson Ave. Chicago, IL 60646-6085 http://tax.cchgroup.com Gross Income Exclusions

Part 4. Comprehensive Examples and Forms Example One: Active minister

Part 4. Comprehensive Examples and Forms Example One: Active minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the minister

Part 4. Comprehensive Examples and Forms Example One: Active minister Note: This example is based on an illustrated example contained at the end of IRS Publication 517. Rev. John Michaels is the minister

This is your Social Security number. Double check to ensure it is correct.

2017 Year End W-2 Box Descriptions for Employees Knowing how to read a Form W-2, or Wage and Tax Statement, can help you understand your total overall compensation, and also help you get a head start when

2017 Year End W-2 Box Descriptions for Employees Knowing how to read a Form W-2, or Wage and Tax Statement, can help you understand your total overall compensation, and also help you get a head start when

Christmas party decision tree

Christmas party decision tree provides a Christmas party (meals and drinks) On business premises during a working day to: Offsite (eg a restaurant) regardless of the time of day to: 2 Associate of employee

Christmas party decision tree provides a Christmas party (meals and drinks) On business premises during a working day to: Offsite (eg a restaurant) regardless of the time of day to: 2 Associate of employee

Taxable Fringe Benefit Guide

Note: This document contains information on qualified commuter tax benefits only. The entire document, "Tax Fringe Benefit Guide" is available at http://www.irs.gov/pub/irs-tege/fringe_benefit_fslg.pdf.

Note: This document contains information on qualified commuter tax benefits only. The entire document, "Tax Fringe Benefit Guide" is available at http://www.irs.gov/pub/irs-tege/fringe_benefit_fslg.pdf.

Impact of US Tax Reform on Employee Compensation and Benefits Programs

Rutgers NJ/NY Center for Employee Ownership Impact of US Tax Reform on Employee Compensation and Benefits Programs October 26, 2018 Sharmon Priaulx, Global Human Resource Services Agenda Tax Reform Changes

Rutgers NJ/NY Center for Employee Ownership Impact of US Tax Reform on Employee Compensation and Benefits Programs October 26, 2018 Sharmon Priaulx, Global Human Resource Services Agenda Tax Reform Changes

JOYNER, KIRKHAM, KEEL & ROBERTSON, P.C INDIVIDUAL TAX ORGANIZER

Please provide a copy of your 2013 federal and state tax returns, and complete pages 1 through 3. Other pages: complete only those sections that apply to you. Your Name SS# Occupation Birth Date Spouse

Please provide a copy of your 2013 federal and state tax returns, and complete pages 1 through 3. Other pages: complete only those sections that apply to you. Your Name SS# Occupation Birth Date Spouse

Fringe Benefits and Employment Tax Update: A Potpourri of Issues Certain to Annoy Tax Departments American Gas Association Tax Meeting

Fringe Benefits and Employment Tax Update: A Potpourri of Issues Certain to Annoy Tax Departments American Gas Association Tax Meeting Marianna G. Dyson June 22, 2016 Topics du Jour Current employment

Fringe Benefits and Employment Tax Update: A Potpourri of Issues Certain to Annoy Tax Departments American Gas Association Tax Meeting Marianna G. Dyson June 22, 2016 Topics du Jour Current employment

Fringe Benefit Client Questionnaire

Fringe Benefit Client Questionnaire This attachment has been prepared to aid you in completing your Fringe Benefit Client Questionnaire. The purpose of this attachment is to provide you with more information

Fringe Benefit Client Questionnaire This attachment has been prepared to aid you in completing your Fringe Benefit Client Questionnaire. The purpose of this attachment is to provide you with more information

Fringe Benefits That May Affect Your Payroll Reporting and Tax Withholding

Anchin Alert Anchin, Block & Anchin LLP Accountants and Advisors November 2018 Fringe Benefits That May Affect Your Payroll Reporting and Tax Withholding To Our Business Clients: Attached for your convenience

Anchin Alert Anchin, Block & Anchin LLP Accountants and Advisors November 2018 Fringe Benefits That May Affect Your Payroll Reporting and Tax Withholding To Our Business Clients: Attached for your convenience

This policy outlines circumstances in which payment of honoraria is appropriate, defines eligibility, tax implications and payment procedures.

Honorariums Summary This policy outlines circumstances in which payment of honoraria is appropriate, defines eligibility, tax implications and payment procedures. Applicability and Authority This procedure

Honorariums Summary This policy outlines circumstances in which payment of honoraria is appropriate, defines eligibility, tax implications and payment procedures. Applicability and Authority This procedure

A Federal. Income Tax. Guide. for College & University Presidents. Published with generous support from TIAA-CREF. American Council on Education

A Federal Income Tax Guide for College & University Presidents American Council on Education Published with generous support from TIAA-CREF A Federal Income Tax Guide for College & University Presidents

A Federal Income Tax Guide for College & University Presidents American Council on Education Published with generous support from TIAA-CREF A Federal Income Tax Guide for College & University Presidents

Dear Clients and Business Friends:

Dear Clients and Business Friends: All employers who furnish vehicles to employees for the employee s personal use are required to add the personal use value of the vehicle to the employee s W-2. As an

Dear Clients and Business Friends: All employers who furnish vehicles to employees for the employee s personal use are required to add the personal use value of the vehicle to the employee s W-2. As an

Clergy Compensation Archdiocese of Baltimore Parish/School Management Training April/May 2008

Clergy Compensation Archdiocese of Baltimore Parish/School Management Training April/May 2008 Archdiocese of Baltimore ~ Parish/School Management Training Agenda 1. Tax Treatment 2. Taxable Income 3. Administrative

Clergy Compensation Archdiocese of Baltimore Parish/School Management Training April/May 2008 Archdiocese of Baltimore ~ Parish/School Management Training Agenda 1. Tax Treatment 2. Taxable Income 3. Administrative

CSU 101 Tax Discussion Monterey 2011

CSU 101 Tax Discussion Monterey 2011 Marc F. Benadiba Assistant Director Fiscal Services Cal Poly San Luis Obispo CSU Tax Discussion Contrary to popular belief, there are significant tax issues on CSU

CSU 101 Tax Discussion Monterey 2011 Marc F. Benadiba Assistant Director Fiscal Services Cal Poly San Luis Obispo CSU Tax Discussion Contrary to popular belief, there are significant tax issues on CSU

Dear Clients and Business Friends:

Dear Clients and Business Friends: All employers who furnish vehicles to employees for the employee s personal use are required to add the personal use value of the vehicle to the employee s W-2. As an

Dear Clients and Business Friends: All employers who furnish vehicles to employees for the employee s personal use are required to add the personal use value of the vehicle to the employee s W-2. As an

Lackland ISD Accounts Payable Procedures

Accounts payable checks should be processed on a weekly basis for release by Friday morning, or earlier dependent upon work schedules or holidays. General Instructions: All invoices shall be entered separately

Accounts payable checks should be processed on a weekly basis for release by Friday morning, or earlier dependent upon work schedules or holidays. General Instructions: All invoices shall be entered separately

GENERAL INSTRUCTIONS FOR PREPARING 2015 CITY OF XENIA INDIVIDUAL RETURNS *

Who must file? It is mandatory that you file an annual City of Xenia tax return EVEN IF NO TAX IS DUE: All Xenia residents and partial year residents between the ages of 18 and 65. All Xenia residents

Who must file? It is mandatory that you file an annual City of Xenia tax return EVEN IF NO TAX IS DUE: All Xenia residents and partial year residents between the ages of 18 and 65. All Xenia residents

RECOGNITIONS, REFRESHMENTS, AND MISCELLANEOUS REIMBURSEMENTS POLICY 504

RECOGNITIONS, REFRESHMENTS, AND MISCELLANEOUS REIMBURSEMENTS POLICY 504.1 PURPOSE This policy authorizes and provides regulations on activities to recognize employees and volunteers, on providing refreshments/meals

RECOGNITIONS, REFRESHMENTS, AND MISCELLANEOUS REIMBURSEMENTS POLICY 504.1 PURPOSE This policy authorizes and provides regulations on activities to recognize employees and volunteers, on providing refreshments/meals

1099 vs. W2 1/30/ vs. W 2. Classifying Independent Contractors and Employees

1099 vs. W2 Classifying Independent Contractors and Employees February 23, 2019 1099 vs. W 2 In this webinar we will discuss the classification criteria used to identify an individual/worker as an independent

1099 vs. W2 Classifying Independent Contractors and Employees February 23, 2019 1099 vs. W 2 In this webinar we will discuss the classification criteria used to identify an individual/worker as an independent

2016 S CORPORATION INCOME TAX RETURN CHECKLIST (form 1120S) (SHORT)

(SHORT)") Client name and number: Prepared by: Date: Reviewed by: Date: 100) GENERAL 101) Identify the authorized officer who will sign the return. 102) Obtain a signed engagement letter. 103) Confirm the taxpayer

Client name and number: Prepared by: Date: Reviewed by: Date: 100) GENERAL 101) Identify the authorized officer who will sign the return. 102) Obtain a signed engagement letter. 103) Confirm the taxpayer

December In addition, we have enclosed some additional materials for your guidance including:

Dear Client December 2011 It is time again to prepare for year-end payroll processing specifically the preparation of Forms W-2 and 1099. To assist you in the preparation of these forms, we offer the following

Dear Client December 2011 It is time again to prepare for year-end payroll processing specifically the preparation of Forms W-2 and 1099. To assist you in the preparation of these forms, we offer the following

Tax Cuts and Jobs Act: Mobility and Rewards House and Senate proposals side-by-side comparison November 13, 2017

Tax Cuts and Jobs Act: Mobility and Rewards House and Senate proposals side-by-side comparison November 13, 2017 Overview On November 2, 2017, the House Ways and Means Committee released details of their

Tax Cuts and Jobs Act: Mobility and Rewards House and Senate proposals side-by-side comparison November 13, 2017 Overview On November 2, 2017, the House Ways and Means Committee released details of their

Relocation Policy. 01 Policy Statement Reason for Policy Who Needs to Know This Policy Eligibility... 2

Relocation Policy Table of Contents 01 Policy Statement... 2 02 Reason for Policy... 2 03 Who Needs to Know This Policy... 2 04 Eligibility... 2 05 Explanation Reimbursable Relocation Expenses... 2 06

Relocation Policy Table of Contents 01 Policy Statement... 2 02 Reason for Policy... 2 03 Who Needs to Know This Policy... 2 04 Eligibility... 2 05 Explanation Reimbursable Relocation Expenses... 2 06

GENERAL INSTRUCTIONS FOR PREPARING 2017 CITY OF XENIA INDIVIDUAL RETURNS *

Who must file? It is mandatory that you file an annual City of Xenia tax return EVEN IF NO TAX IS DUE: All Xenia residents and partial year residents between the ages of 18 and 65. All Xenia residents

Who must file? It is mandatory that you file an annual City of Xenia tax return EVEN IF NO TAX IS DUE: All Xenia residents and partial year residents between the ages of 18 and 65. All Xenia residents

JANUARY 2017 EMPLOYEE OR INDEPENDENT CONTRACTOR

JANUARY 2017 GUIDELINES TO OBLIGATIONS OF BRANCH CHURCHES AND SOCIETIES TO WITHHOLD FEDERAL INCOME AND SOCIAL SECURITY TAXES AND TO REPORT COMPENSATION; AND OTHER INFORMATION EMPLOYEE OR INDEPENDENT CONTRACTOR

JANUARY 2017 GUIDELINES TO OBLIGATIONS OF BRANCH CHURCHES AND SOCIETIES TO WITHHOLD FEDERAL INCOME AND SOCIAL SECURITY TAXES AND TO REPORT COMPENSATION; AND OTHER INFORMATION EMPLOYEE OR INDEPENDENT CONTRACTOR

How to Contain Your Employee Award Program Costs

How to Contain Your Employee Award Program Costs How to Contain Your Employee Award Program Costs by Craig Ainsworth In today s economy, reducing expenses is at the forefront of every business plan. Human

How to Contain Your Employee Award Program Costs How to Contain Your Employee Award Program Costs by Craig Ainsworth In today s economy, reducing expenses is at the forefront of every business plan. Human

Accountable Plans as per the IRS Code Section 62(c) and IRS Regulation

and IRS Regulation") Accountable Plans as per the IRS Code Section 62(c) and IRS Regulation 1.62-2. To save yourself and your employees some payroll tax expenses, the Internal Revenue Code and the IRS regulations allow expenses

Accountable Plans as per the IRS Code Section 62(c) and IRS Regulation 1.62-2. To save yourself and your employees some payroll tax expenses, the Internal Revenue Code and the IRS regulations allow expenses

OLD DOMININION UNIVERSITY DEPARTMENTAL FINANCIAL AND ADMINISTRATIVE PROCEDURES AND PRACTICES MANUAL

A. PURPOSE The purpose of this procedure is to outline the process for reconciling and reimbursing a departmental petty cash fund. B. DESIGNATED STAFF Accounts Payable Travel Supervisor Accounts Payable

A. PURPOSE The purpose of this procedure is to outline the process for reconciling and reimbursing a departmental petty cash fund. B. DESIGNATED STAFF Accounts Payable Travel Supervisor Accounts Payable

CR 2017/38. Summary what this ruling is about

Page status: legally binding Page 1 of 12 Class Ruling Fringe benefits tax: employer clients of Community Sector Banking Pty Limited who are subject to the provisions of either section 57A or 65J of the

Page status: legally binding Page 1 of 12 Class Ruling Fringe benefits tax: employer clients of Community Sector Banking Pty Limited who are subject to the provisions of either section 57A or 65J of the

MISSOURI INTERGOVERNMENTAL RISK MANAGEMENT ASSOCIATION PAYROLL VERIFICATION PROGRAM

MISSOURI INTERGOVERNMENTAL RISK MANAGEMENT ASSOCIATION PAYROLL VERIFICATION PROGRAM Verification of reported member city payrolls is vital to the financial integrity of the association. As set forth under

MISSOURI INTERGOVERNMENTAL RISK MANAGEMENT ASSOCIATION PAYROLL VERIFICATION PROGRAM Verification of reported member city payrolls is vital to the financial integrity of the association. As set forth under

Business meals. Convenience of the employer.

Dear Client: The following is a summary of important tax developments that occurred in October, November, and December of 2018 that may affect you, your family, your investments, and your livelihood. Please

Dear Client: The following is a summary of important tax developments that occurred in October, November, and December of 2018 that may affect you, your family, your investments, and your livelihood. Please

Ovals must be filled in completely. Example RETURN WITH CHECK (PLEASE ATTACH CHECK HERE)

") Form 481.0 Rev. 05.03 SHORT FORM Liquidator Reviewer Ovals must be filled in completely. Example RETURN WITH CHECK (PLEASE ATTACH CHECK HERE) 23 23 COMMONWEALTH OF PUERTO RICO DEPARTMENT OF THE TREASURY

Form 481.0 Rev. 05.03 SHORT FORM Liquidator Reviewer Ovals must be filled in completely. Example RETURN WITH CHECK (PLEASE ATTACH CHECK HERE) 23 23 COMMONWEALTH OF PUERTO RICO DEPARTMENT OF THE TREASURY

JOYNER, KIRKHAM, KEEL & ROBERTSON, P.C INDIVIDUAL TAX ORGANIZER

Please provide a copy of your 2017 federal and state tax returns, and complete pages 1 through 3. Other pages: complete only those sections that apply to you. Taxpayer Name SS# Occupation Birth Date Spouse

Please provide a copy of your 2017 federal and state tax returns, and complete pages 1 through 3. Other pages: complete only those sections that apply to you. Taxpayer Name SS# Occupation Birth Date Spouse

SECTION C: Tax Manual I MISC

SECTION C: Tax Manual I. 1099-MISC The Internal Revenue Service requires a 1099-MISC form be issued to independent contractors, other individuals, LLCs, and unincorporated businesses that have received

SECTION C: Tax Manual I. 1099-MISC The Internal Revenue Service requires a 1099-MISC form be issued to independent contractors, other individuals, LLCs, and unincorporated businesses that have received

Notice Meals, Entertainment, and Travel Expenses

Notice 87-23 Meals, Entertainment, and Travel Expenses CLICK HERE to return to the home page January 1987 The Tax Reform Act of 1986 (the Act) made significant changes to the rules for deducting meals,

Notice 87-23 Meals, Entertainment, and Travel Expenses CLICK HERE to return to the home page January 1987 The Tax Reform Act of 1986 (the Act) made significant changes to the rules for deducting meals,

SAS (the payer) has the responsibility to comply with the withholding tax provisions and not the non-resident recipient.

has the responsibility to comply with the withholding tax provisions and not the non-resident recipient.") The Singapore Actuarial Society (SAS) Process for Payments to Non-Singapore Tax Resident Entities (Corporates or Individuals) Date: 21 June 2018 Tax information below is of a general nature and may not

The Singapore Actuarial Society (SAS) Process for Payments to Non-Singapore Tax Resident Entities (Corporates or Individuals) Date: 21 June 2018 Tax information below is of a general nature and may not

STATE OF ALABAMA Department of Finance Office of the State Comptroller

STATE OF ALABAMA Department of Finance Office of the State Comptroller 100 North Union Street, Suite 220 Montgomery, Alabama 36130-2620 Telephone (334) 242-7050 Fax (334) 242-7466 wwwcomptrollcr.alabama.gov

STATE OF ALABAMA Department of Finance Office of the State Comptroller 100 North Union Street, Suite 220 Montgomery, Alabama 36130-2620 Telephone (334) 242-7050 Fax (334) 242-7466 wwwcomptrollcr.alabama.gov

2018 Payroll Update Reference Guide

2018 Payroll Update Reference Guide Jones & Roth is providing this Payroll Update as a reference guide for you. It is not meant to be all-inclusive. If there is a payroll item that you have questions about,

2018 Payroll Update Reference Guide Jones & Roth is providing this Payroll Update as a reference guide for you. It is not meant to be all-inclusive. If there is a payroll item that you have questions about,

KENNETH M. WEINSTEIN,

Dear Client: KENNETH M. WEINSTEIN, CPA AND CFP 1450 Niagara Falls Boulevard, Suite #202 Tonawanda, NY 14150-8440 (716) 837-2525 ~ FAX (716) 837-2527 E-Mail: kweinsteincpa@gmail.com The enclosed 2015 Tax

Dear Client: KENNETH M. WEINSTEIN, CPA AND CFP 1450 Niagara Falls Boulevard, Suite #202 Tonawanda, NY 14150-8440 (716) 837-2525 ~ FAX (716) 837-2527 E-Mail: kweinsteincpa@gmail.com The enclosed 2015 Tax

SOUTH CAROLINA STATE FIREFIGHTERS ASSOCIATION. AGREED UPON PROCEDURES-Periods ending December 30, 2015 SUMMARY OF FINDINGS

SOUTH CAROLINA STATE FIREFIGHTERS ASSOCIATION AGREED UPON PROCEDURES-Periods ending December 30, 2015 SUMMARY OF FINDINGS Note-the number in parentheses represents the number of departments that received

SOUTH CAROLINA STATE FIREFIGHTERS ASSOCIATION AGREED UPON PROCEDURES-Periods ending December 30, 2015 SUMMARY OF FINDINGS Note-the number in parentheses represents the number of departments that received

The College of Idaho

The College of Idaho Policy Name: Business Travel, Entertainment and Expense Reimbursement Policy Responsible Department: Business Office Approved By: President and Senior Staff Approval Date: 05/07/14

The College of Idaho Policy Name: Business Travel, Entertainment and Expense Reimbursement Policy Responsible Department: Business Office Approved By: President and Senior Staff Approval Date: 05/07/14

BELMONT COUNTY BOARD OF COMMISSIONERS PERSONNEL POLICY MANUAL SECTION 5 CLASSIFICATION AND COMPENSATION

SECTION 5 CLASSIFICATION AND COMPENSATION 5.1 Compensation Plan 5.2 Overtime 5.3 Pay Period 5.4 Compensatory Time 5.5 Payroll Deductions 5.6 Retirement Plan and Deferred Compensation 5.7 Workers= Compensation

SECTION 5 CLASSIFICATION AND COMPENSATION 5.1 Compensation Plan 5.2 Overtime 5.3 Pay Period 5.4 Compensatory Time 5.5 Payroll Deductions 5.6 Retirement Plan and Deferred Compensation 5.7 Workers= Compensation

MANUAL OF PROCEDURE. Contracts, Agreements, and Leases - Signature Requirements and Procedures CHAPTER 6A STATE BOARD OF EDUCATION RULES

MANUAL OF PROCEDURE PROCEDURE NUMBER: 6300 PAGE 1 of 6 PROCEDURE TITLE: Contracts, Agreements, and Leases - Signature Requirements and Procedures STATUTORY REFERENCE: FLORIDA STATUTE 287.017 CHAPTER 6A-14.0734

MANUAL OF PROCEDURE PROCEDURE NUMBER: 6300 PAGE 1 of 6 PROCEDURE TITLE: Contracts, Agreements, and Leases - Signature Requirements and Procedures STATUTORY REFERENCE: FLORIDA STATUTE 287.017 CHAPTER 6A-14.0734

Examination Issues. Resources. Public Employers Toolkit

Tax Exempt Government Entities IRS Examination Issues Examination Issues Public Employers Toolkit Resources Publication 963 Federal State Reference Guide Publication 5137 Fringe Benefit Guide Publication

Tax Exempt Government Entities IRS Examination Issues Examination Issues Public Employers Toolkit Resources Publication 963 Federal State Reference Guide Publication 5137 Fringe Benefit Guide Publication

Increases to unrelated business taxable income by amount of certain fringe benefit expenses for which deduction is disallowed

Increases to unrelated business taxable income by amount of certain fringe benefit expenses for which deduction is disallowed Prepared by: James P. Sweeney, Partner, RSM US LLP, National Leader, National

Increases to unrelated business taxable income by amount of certain fringe benefit expenses for which deduction is disallowed Prepared by: James P. Sweeney, Partner, RSM US LLP, National Leader, National