Bahrain Monetary Agency REGULATION GOVERNING COLLECTIVE INVESTMENT SCHEMES

|

|

|

- Dortha Rodgers

- 5 years ago

- Views:

Transcription

1 Bahrain Monetary Agency REGULATION GOVERNING COLLECTIVE INVESTMENT SCHEMES June 2003

2 Preface In pursuit of its objective of continuing to develop Bahrain as a major international financial centre for fund management business, the Agency introduced the Regulation with Respect to the General Supervision, Operation and Marketing of Collective Investment Schemes (1992). Basically the above Regulation seeks to provide an appropriate framework of supervision for schemes that are established and/pr Marketed in/from Bahrain by banks and financial institutions. This framework ensures the soundness and stability with a view to providing a firm basis for the confidence of investors. This publication has been produced for the benefit of banks and financial institutions involved or interested in establishing and/or marketing collective investment schemes in Bahrain. The Agency hopes that this publication will assist those involved in carrying out the above investment activities to better understand the requirements of the Agency in this area.

3 Table of Contents Regulation with respect to the General Supervision, Operation and Marketing of Collective Investment Schemes Agency Circular No. OG/356/92 dated 18 th November Supervision... 9 Participation in Schemes... 9 Application Authorization, Approval, and Revocation Accounts and Other General Supervisory Matters Miscellaneous Principles of Supervision, operation and Marketing with respect to Collective Investment Schemes Agency Circular No. OG/318/95 dated 4 th November General Principles Mutual Fund Investment Company Established in, and Marketed in/from Bahrain.. 16 Relevant Persons Investment Policies Repurchase, Redemption, Unit Certificates and Other Provisions Prospectus, Reports and Publication of Information Specific Powers of the Agency Schemes Established and Managed Outside Bahrain to be Marketed in Bahrain Revocation and Refusal of Authorization and Approval Advertising and Public Announcements Scheme Investigation Publication of Names of Authorised Schemes Collective Investment Schemes (Amendment to Item I.B of the Regulation) Agency Circular No. OG/121/99 dated 19 th April

4 Quarterly Information Returns for Collective Investment Schemes Agency, Circular No. BC/15/97 dated 5 th October The Quarterly Returns Guidelines on Advertising and Public Announcements for Collective Investment Schemes Agency, Circular No. BC/23/99 dated 27 th October General Matters Guarantees Comparisons Past Performance Taxation Unusual Risks Fluctuations High Volatility Investment Income Foreign Currency Schemes Carrying Contingent Liability Cancellation Forecasts or Projections Quarterly Information Return for Collective Investment Schemes Agency Circular No. BC/13/2001 dated 9 th December The Quarterly Returns Information to be Contained in the Scheme Particulars Document Agency Circular No. BC/05/02 dated 1 st June Constitution of the Scheme The Operators and Principles of the Scheme Investment Policy and Restrictions Number of Units in Issue The Characteristics of Units in the Scheme... 51

5 The Valuation of the Property of the Scheme The Sale and Redemption of Units in the Scheme Fees and Charges Distribution Policy Reports and Accounts Warnings Inspection of documents Termination of scheme Governing Law Taxation Money Laundering General Information... 56

6 Regulation with respect to the General Supervision, Operation and Marketing of Collective Investment Schemes

7 OG/356/92 18th November, 1992 The General Manager, All FCBs/IBs/OBUs and Representative Offices, Manama, Bahrain. Dear Sir, Re: Collective Investment Schemes As you are aware, the Agency has been considering the introduction of arrangements for the supervision, operation and marketing of Collective Investment Schemes which are either already established and/or marketed in Bahrain, or which intend to be so established and/or marketed in Bahrain in the future. This work is consistent with the intention of the Bahrain authorities to develop and diversify further Bahrain s financial sector. In this connection and in accordance with Resolution No. (3) of 1992 on 24 th October, 1992 signed by H.H. Sh. Khalifa Bin Salman Al Khalifa, The Prime Minister, Chairman of the Board of the Bahrain Monetary Agency, the Agency is hereby circulating the attached Regulation with respect to the general supervision, operation and marketing of Collective Investment Schemes. Banks and other financial institutions in Bahrain which have already established and/or are engaged in the marketing of Collective Investment Schemes will wish to note the requirements of the Regulation, while other such institutions may wish to consider participating in the type of activity covered by the Regulation. -7-

8 Banks and other financial institutions for which the Regulation is, or may become, relevant should feel free to contact Mr. Anwar Al-Sadah (Director of Financial Institutions Supervision) here at the Agency on for further information and guidance. Yours sincerely, Abdulla H. Saif, Governor -8-

9 REGULATION WITH RESPECT TO THE GENERAL SUPERVISION, OPERATION AND MARKETING OF COLLECTIVE INVESTMENT SCHEMES 1. Supervision A. In accordance with the powers given to it pursuant to the provisions of Articles 41 and 50 of Decree - Law No. (23) of 1973 (the BMA Law ), the Bahrain Monetary Agency (the Agency ) shall supervise and regulate all collective investment schemes (the schemes ) established and/or marketed in any manner whatsoever in the State of Bahrain ( Bahrain ). In this Regulation, the term scheme shall include any scheme, regardless of the form thereof (including, but not limited to, a mutual fund investment company with fixed or variable capital), the sole object of which is the collective investment in transferable securities (or other investments disclosed to, and agreed by, the Agency) of capital raised from the public, which operates on the principle of risk-spreading and the holdings or interests in which are, at the request of the investors in such schemes (the scheme participants ), repurchased, redeemed, reimbursed or otherwise repaid, directly or indirectly, out of the assets of the scheme. B. Only banking firms or financial institutions (herein jointly referred to as institutions ) operating in/from Bahrain and licensed by the Agency shall be entitled to apply to establish and/or market schemes in/from Bahrain. No scheme shall be established and/or marketed in/from Bahrain without the express prior written authorisation and approval of the Agency. C. The authorisation and/or approval of a scheme by the Agency shall not constitute a warranty as to the performance of a scheme and the Agency shall not be liable for the performance or default of a scheme. 2. Participation in Schemes Both Bahraini and/or non-bahraini citizens shall be entitled to become scheme participants and, for the purposes of this Regulation, the term unit shall mean any holding or interest, regardless of the form thereof -9-

10 (including, but not limited to, a share in a mutual fund investment company), by a scheme participant in a scheme. 3. Applications Authorisation, Approval, and Revocation A. Every institution shall submit a written application, in form and substance satisfactory to the Agency, to obtain (i) its authorisation to establish and/or market a scheme in/from Bahrain (and, in the case of an institution incorporated in Bahrain, to establish and/or market a scheme outside of Bahrain) and (ii) (in each case) its approval for the particulars of the scheme itself. B. The Agency may, in its discretion and having consulted with other relevant authorities, either authorise and approve (with or without conditions), or refuse its authorisation and approval for such scheme. C. Every institution shall obtain the Agency s prior approval to any material changes in the terms and conditions and other features of a scheme originally authorised and approved under this Regulation. D. In addition to the general authorisation and approval referred, the Agency s prior express written approval must be obtained as to (i) the identity of any persons involved in the management and operation of a scheme (who shall, in all cases, and unless the Agency otherwise permits, be separate and independent of each other) and (ii) the form and content of all documentation relevant to a scheme. E. The Agency may, in whole or in part, revoke or impose conditions upon any authorisation and approval given hereunder. 4. Accounts and other General Supervisory Matters A. Every institution shall at all times keep proper, complete and separate accounting systems, books and records of account for an authorised and approved scheme. B. The Agency and the relevant institution shall agree on the form and content of all reports, statements and other documentation to be -10-

11 provided to the Agency and the scheme participants, as well as the regularity of, and time periods within which, such reports, statements and documents are to be provided. C. The Agency shall be provided each year with a detailed report for each scheme authorised and approved by it. Scheme participants shall be provided each year with such a report for the scheme in which they have participated. Any report to be provided under this paragraph 4. C shall include the financial statements for such scheme, which statements shall be (i) prepared in accordance with standards acceptable to the Agency and (ii) audited by a firm of accountants approved by the Agency. Such auditors shall be and act, at all times and in all respects, independently of the scheme and any person involved in the management and operation thereof. D. Every institution shall provide to the Agency, in form and substance satisfactory to it, such information in relation to an authorised and approved scheme as the Agency may require from time to time. 5. Miscellaneous A. The Agency may make subsidiary rules and regulations and may issue principles of supervision, operation and marketing for the proper and regular enforcement of this Regulation from time to time. These subsidiary rules and regulations and principles may deal with any matter referred to herein and/or any other matters incidental or additional thereto (including, but not limited to, the principles upon which any persons involved in the management and operation of a scheme shall carry out their duties, the fees which may be charged under a scheme, the method for pricing the units in a scheme, disclosure of certain matters to scheme participants and restrictions on the investment powers of a scheme), and may be applicable to any one or all schemes authorised and approved hereunder. B. Any scheme existing on 18th November, 1992, the date of commencement of this Regulation, shall have a period of 24 months from the date in which to comply with this Regulation and any subsidiary rules, regulations and principles which the Agency may issue pursuant hereto in that period. -11-

12 C. Without prejudice to the provisions of this Regulation, the Agency may, in its discretion, exempt certain schemes, including those existing at the date of the commencement of this Regulation, from some or all of the requirements hereof. D. Save as otherwise provided by the Agency, the provisions of the BMA Law concerning banking firms shall also apply to other financial institutions authorised to establish and/or market schemes under this Regulation. -12-

13 Principles of Supervision, Operation and Marketing with respect to Collective Investment Schemes

14 OG/318/95 4th November, 1995 The General Manager All FCBs, IBs, OBUs and Representative Offices Manama Bahrain Dear Sir, Principles of Supervision, Operation and Marketing with respect to Collective Investment Schemes I now attach, for your information and attention, a copy of the above Principles, which are now issued by the Agency pursuant to Circular No. OG/356/92 dated 18th November Unless the Agency expressly gives its permission in writing to the contrary, all banks and other financial institutions which are involved in the establishment and/or marketing of Collective Investment Schemes in/from Bahrain are henceforth required to comply in full with the attached Principles which override and supercede previous directions of the Agency in this context. Schemes, the establishment and/or marketing of which have been authorised and approved by the Agency prior to the date of this letter, and which do not comply in full with the attached Principles, should be brought to the attention of the Agency without delay. The Agency will give specific directions to relevant parties on what, if anything, the Agency requires to be done in such cases. Any queries and/or clarifications sought in relation to the attached Principles should be directed to Mr. Anwar Al-Sadah, Director of Financial Institutions Supervision, at the Agency (Tel: /445). Yours faithfully, Abdulla H. Saif Governor -14-

15 PRINCIPLES OF SUPERVISION, OPERATION AND MARKETING WITH RESPECT TO COLLECTIVE INVESTMENT SCHEMES; ISSUED PURSUANT TO AGENCY CIRCULAR NO. OG/356/92 DATED 18TH NOVEMBER, 1992 General Principles 1. Unless otherwise directed by the Agency, only paragraphs 43 and 44 (and those other paragraphs of these Principles which are, in the Agency s opinion, consistent with the marketing in Bahrain thereof) shall apply to schemes established and managed outside Bahrain which are merely to be marketed in Bahrain. 2. The activities and business of the scheme, and (as may be appropriate) of persons involved in the management, operation and marketing of schemes (including, but not limited to, any person whose role in the scheme is to hold assets thereof for and on behalf of the scheme and the scheme participants), shall be supervised and regulated by the Agency. Such persons (herein referred to as the relevant persons ) shall perform such functions and have such duties in the scheme as are set out in the documents relevant to the establishment and form of the scheme (herein referred to as the scheme documents ) and shall, at all times, act in accordance with these Principles, the scheme documents and the Agency s directions. 3. At all times, all relevant persons shall act in the best interests of the scheme and the scheme participants, taking into account the stated objectives of the scheme and other relevant factors. 4. All persons involved in any way with schemes shall ensure that at all times these Principles (as amended from time to time) and any directions issued by the Agency in relation to a particular scheme and/or schemes in general, are adhered to in all respects and that no deviation therefrom occurs without the prior express written consent of the Agency. 5. No person involved in any way with a scheme in any capacity, nor any person connected therewith, shall carry out transactions for itself, or make a profit from transactions in any assets held under a scheme, which transactions shall always be carried out at arm s length. -15-

16 Mutual Fund Investment Company Established in, and Marketed in/from, Bahrain 6. A scheme in the form of a mutual fund investment company established in, and marketed in/from, Bahrain shall (at all times) have an initial paid-up share capital which is acceptable to the Agency. Unless the Agency expressly agrees otherwise in writing, the net asset value of the scheme must reach US$5 million (or equivalent) no later than 6 months after the commencement of the scheme (as agreed with the Agency and specified in the scheme documents). In the event that the net asset value fails to reach this amount within this six month period, or falls below this amount at any time thereafter, the Agency may require the scheme to be wound up, or require other action to be taken, in accordance with its instructions. The Agency may, at its discretion, require a scheme in a form other than a mutual fund investment company to meet similar requirements in this context. 7. A scheme in the form of a mutual fund investment company shall include the words investment company on all documentation and instruments, and may, from time to time and if so authorised by its constitutive documents, (i) issue (and redeem) redeemable preference shares, and/or (ii) repurchase its own shares. 8. The directors of the mutual fund investment company shall be knowledgeable and experienced in the area of collective investment schemes generally, and shall be fully conversant and acquainted with all aspects of the instant scheme in particular, bearing in mind their liabilities to the scheme and scheme participants. Relevant Persons 9. All relevant persons shall, subject to the Agency s specific prior written agreement to the contrary, be bodies corporate with their registered office in the State of Bahrain which, in the opinion of the Agency, (i) have sufficient financial resources at their disposal to enable them to conduct their business effectively and to meet their liabilities, (ii) do not engage in activities which, are inconsistent with their functions in, and duties to, such scheme, and (iii) are sufficiently experienced and qualified to carry out the duties imposed on them in relation to a particular scheme. -16-

17 10. The liability of any relevant person who holds the assets of a scheme pursuant to the scheme documents shall not be affected by the fact that such relevant person may have given possession of some or all of those assets to a third party. 11. A relevant person shall be (i) a bank licensed by the Agency, or (ii) a company approved by the Agency which is wholly owned by a licensed bank, or (iii) any other person approved by the Agency at its discretion. Such relevant person may retire, be discharged or replaced, from time to time, in accordance with the scheme documents, or by order of the Agency acting at its discretion and/or on a request from the scheme, or (as may be appropriate) any other relevant person, or the scheme participants. Any new person appointed as a replacement in this regard shall have the same powers, duties, authorities, and discretion as if it had originally held such position. 12. To ensure the safe custody of the assets of a scheme, and in order to ensure that it carries out its duties to the scheme participants, such relevant person shall: (i) act with diligence, act as would a prudent person, act to the best of its ability and skill and observe the utmost good faith; (ii) keep the assets of a scheme separate from its personal property and separately identifiable from any property of any other scheme in its possession; (iii) keep accurate accounts and records for each scheme for which it holds assets; (iv) be impartial and do, or refrain from doing, any act or deed which is, or might be, the advantage of one scheme, and/or one scheme participant, at the expense of another scheme, and/or scheme participant; (v) act in all other respects in accordance with the scheme documents and/or as the Agency may so require, including, if appropriate, providing certain information and preparing reports to the scheme and/or (as may be appropriate) other relevant persons, and the scheme participants and/or the Agency on such matters as the scheme documents and/or the Agency may specify; and (vi) use all its powers to achieve the above and have all powers reasonably -17-

18 incidental to the above. 13. Such relevant person shall be liable to the scheme, and/or (as may be appropriate) other relevant persons, and the scheme participants, for any loss suffered by any one or more of them as a result of the unjustifiable failure to perform, or the improper performance of, its obligations. This liability shall not in any way be diminished by any provision in any document, save to the extent that any release or indemnity from liability relates to a prior event and/or where not less than 75% in value of the units in issue at that date have agreed to such release or indemnity. Investment Policies 14. Subject to obtaining the prior written agreement of the Agency to the contrary, which agreement shall also be required for any variation in the investment policies and limits referred to below, a scheme may: (i) invest in transferable securities admitted to official listing on stock exchanges recognised by the Agency; (ii) invest in transferable securities, other than those referred to above, up to a maximum of 10% of its total assets; (iii) invest in transferable securities issued or guaranteed by any government (or its agencies) or public international bodies, without limitation provided that any one such issue shall not account for more than 20% of its total assets; (iv) invest in other transferable debt instruments up to a maximum of 10% of its total assets; (v) invest in options and warrants for hedging purposes. In addition, to value of a scheme s investment in warrants and options not held for such purposes may not exceed 15% of its total assets; (vi) enter into financial futures contracts for hedging purposes. In addition, a scheme may enter into futures contracts on an unhedged basis provided that the net aggregate value of contract prices, together with the net aggregate value of holdings under no. (vii) below, does not exceed 20% of total assets; -18-

19 (vii) invest in physical commodities and commodity based investments, which together with the net aggregate value of holdings under no. (vi) above, does not exceed 20% of its assets; (viii) invest in real and personal property required for its business; (ix) hold liquid assets and employ techniques and instruments in relation to transferable securities intended to provide protection against exchange risks (by reference to the base currency of the scheme) in the context of, and to assist in, the efficient use and management of its assets and liabilities; (x) invest in holdings of units in other schemes up to 10% of its assets in aggregate; (xi) save as otherwise provided herein, invest no more than 10% of its assets in transferable securities issued by any one issuer; (xii) not lend, assume, guarantee, endorse or otherwise become directly or contingently liable for, or in connection with, any obligation or indebtedness of any person, otherwise in accordance with its scheme documents. In particular, no lending etc., shall be permitted to any company into which a scheme is to make an investment. This prohibition shall also apply where the loan etc. is to be made to the parent, subsidiary or other associated company of the company in which the scheme is to make the investment; (xiii) not acquire any asset which involves the assumption of any liability which is unlimited; (xiv) not invest in any security of any class in any company or body if any director, officer or broker of the scheme and/or, as may be appropriate, any one of more of the relevant persons (or related or associated persons) owns more than 1/2% of the total nominal amount of all the issued securities of that class, or collectively the directors, officers or brokers of the scheme and/or, as may be appropriate, any one or more of the relevant persons (or related or associated persons) own more than 5% of those securities. This prohibition shall also apply where the ownership of the directors and other parsons referred to above is in the parent, subsidiary or other associated company of the company in which the scheme is to make the investment; -19-

20 (xv) not invest in any security where a call is to be made for any sum to be paid on that security unless that call could be paid in full out of cash (or near cash) by the scheme s portfolio; (xvi) not (nor may any one or more of the relevant persons or any other person, acting for and on behalf of the scheme) borrow more than 20% of its asset value; provided that: (i) its scheme documents shall expressly make provision for such investment policies and that the prospectus and any other promotional literature draw attention to such policies; (ii) the above provisions shall not apply to an umbrella fund as if it were a single scheme, but shall apply to each sub-fund of the umbrella fund as if each separate part thereof were a separate scheme; (iii) if the investment policies and limits outlined above are breached, the scheme and/or, as may be appropriate, any one or more of the relevant persons shall, in accordance with the scheme documents, take as a priority objective, all steps as are necessary to remedy the situation, taking into account the interests of the scheme and the scheme participants; (iv) if the name or particulars of a scheme indicates a specific objective, geographic region or market, the scheme should invest at least 50% of its non-cash assets in securities and other investments to reflect the specific objective, region or market; and (v) neither the scheme, nor any one or more relevant persons involved in the management, operation and marketing of a number of schemes which fall within the scope of these principles, may acquire any securities carrying voting rights which will enable it, or them, to exercise significant influence over the management of an issuing body. Repurchase, Redemption, Unit Certificates and Other Provisions 15. The Agency shall be given prior notice of, and shall be invited to attend, all ordinary and extraordinary general meetings for a scheme. 16. Units in a scheme must be redeemed, repurchased, reimbursed or repaid (as may be appropriate) at the request of the share participants and in accordance with -20-

21 the scheme documents. 17. Unless the Agency gives its specific prior written agreement, the minimum subscription price on issue for a unit shall be BD100 (or equivalent) per unit for a scheme established in Bahrain, and US$2,000 (or equivalent) per unit for a scheme established outside Bahrain. 18. Units shall be created or sold, and redeemed, repurchased, reimbursed or repaid (as may be appropriate), in accordance with the scheme documents and at a price arrived at by dividing the net asset value of the scheme by the number of units outstanding; such sale price may be increased by duties and charges as are agreed in advance with the Agency. 19. Units may not be created unless the equivalent of the net issue price is paid into the assets of the scheme. This shall not preclude the distribution of bonus units. Furthermore, units may not be created or canceled during a period of suspension thereof, or if such creation or cancellation would not be in the interests of the scheme and the scheme participants. 20. The value of the assets of a scheme shall be based, in the case of officially quoted securities, on the last known stock exchange quotation unless such quotation is not representative of such value. For securities not so quoted, and for securities which are so quoted but for which the latest quotation is not representative, the value shall be based on the estimated realisation value. The method of valuation for other types of asset shall be agreed with the Agency. 21. Scheme participants shall be informed of any significant decline in the net asset value of a scheme and the reasons therefor. 22. The scheme documents shall determine the frequency of the calculation of the issue and repurchase and other appropriate prices of the units of such scheme. 23. Without prejudice to paragraph 22 and at least once a month, an independent auditor approved by the Agency must ensure that (i) the calculation of the value of the units in a scheme is effected in accordance with the formula relevant thereto, and (ii) the schemes assets are invested in accordance with these Principles, the scheme documents and the Agency s directions. -21-

22 24. The repurchase, redemption, reimbursement or repayment (as may be appropriate) of units in a scheme may, in accordance with its scheme documents, be temporarily suspended. Suspension may be provided for only where exceptional circumstances so require it, and where justified in the interests of the scheme and the scheme participants. In addition, the Agency may permit, or require such suspension if it considers such action is, or would be, in the interests of the scheme, the scheme participants or the public. 25. The Agency, and competent authorities in States in which the units of the scheme are marketed, shall he notified, without delay, of any action taken pursuant to paragraph Scheme participants shall, in accordance with the scheme documents, either (i) be issued with registered certificates representing one or more units of the scheme or, alternatively, (ii) be provided with written confirmation of entry in a register for such units which shall be kept current and up-to-date at all times and shall contain full details of the names and addresses of the scheme participants, the number of units held thereby and the date of acquisition of such units. Such register shall be available for inspection by the scheme participants at a set place and at set times. Such certificates or written confirmation shall constitute prime facie evidence of title to units in a scheme. In all other respects, the certificates and register shall be, in form and substance, satisfactory to the Agency. 27. The scheme documents, shall amongst other things and as may be appropriate: (i) lay down the conditions for the replacement of the relevant persons and provide rules to ensure the protection of the scheme and the scheme participants on the event of such replacement; (ii) provide for the remuneration and expenditure of the relevant persons, and the method of calculation thereof; and (iii) provide for the conditions and manner of application of income. 28. The Agency shall satisfy itself as to the experience and standing of all relevant, and other, persons and shall be notified in advance of any changes in the identity thereof. 29. The Agency s prior approval must be obtained to the form and content of -22-

23 all the scheme documents. 30. Appropriate procedures shall be established to prevent conflicts of interest arising as a result of the staff of the relevant persons of a scheme dealing in the units of such scheme. Prospectus, Reports and Publication of Information 31. There shall be published, in accordance with these Principles, the scheme documents and the Agency s directions, a dated and current prospectus (regardless of its actual title) for each scheme, which shall include the necessary information to enable the scheme participants to make an informed judgment of the investment proposed to them. The prospectus must be offered to the scheme participants free of charge before the conclusion of any agreement therewith and must be sent, together with any amendments made thereto from time to time, to the Agency. 32. The Agency shall specify which of the scheme documents shall form an integral part of the prospectus and which must be annexed thereto. 33. There shall be published, in accordance with each scheme s scheme documents: (i) an Annual Report for each financial year within 3 months from the end of such year (prepared in accordance with International Accounting Standards), which report shall contain a balance sheet, a detailed income and expenditure account, a report on the activities of the scheme during the financial year (including the composition of the scheme s portfolio at the year end), as well as any significant information which will enable the scheme participants to make an informed judgment on the development of the activities of the scheme and its results; and (ii) a half-yearly report covering the first six months of the financial year within 2 months from the end of such period, which report shall contain in summary form the information referred to in (i) above; and (iii) in each of the above cases, such other information as the Agency may stipulate from time to time. -23-

24 34. The above reports must (i) be sent to the Agency, (ii) be made available to the scheme participants free of charge before the conclusion of an agreement therewith, (iii) be made available to the public at a place specified in the prospectus, and (iv) be made available to the scheme participants free of charge on request. 35. There shall be submitted to the Agency for its prior approval one pro forma copy of each document (together with any amendments made thereto from time to time) relating to a scheme which is to be made available to, or executed by, the scheme participants including, but not limited to, copies of contracts to be entered into with the scheme participants. 36. If an auditor of a scheme: (i) has reason to believe that the information provided to the scheme participants or to the Agency does not truly describe the financial situation of a scheme, or (ii) has reason to believe that there has been some breach of these Principles, the scheme documents and the Agency s directions, or (iii) has reason to believe that there exist circumstances which are likely to affect materially the ability of the scheme to fulfill its obligations to the scheme participants or to meet any of its financial obligations under these Principles, the scheme documents and the Agency s directions, or (iv) has reason to believe that there are material defects in the financial systems, controls or accounting records of the scheme, or (v) has reason to believe that there are material inaccuracies in, or omissions from, any returns of a financial nature made by the scheme and/or, as may be appropriate, any one or more of the relevant persons, to the Agency, or (vi) proposes to qualify any certificate which he is to provide in relation to the financial statements or returns of the scheme under Bahrain law and these Principles, he shall report the matter to the Agency in writing, with a copy to the scheme and/or, as may be appropriate, to the relevant persons, without delay. -24-

25 37. The auditor of a scheme shall, if requested by the Agency, furnish to it, with a copy to the scheme and/or (as may be appropriate) the relevant persons, a report stating whether in his opinion and to the best of his knowledge the scheme has complied with these Principles, the scheme documents and/or any relevant directions of the Agency. The auditor may be requested by the Agency to supply it with information available to him as a result of his audit of the scheme. 38. Subject to the Agency s directions to the contrary, in accordance with the scheme documents there shall be made public the issue, sale, and (as may be appropriate) repurchase, redemption, reimbursement or repayment price of the units in a scheme at least once a month. 39. All publicity comprising an invitation to purchase units of a scheme must indicate that a prospectus exists and include the places where such prospectus may be obtained. Specific Powers of the Agency 40. The scheme and/or (as may be appropriate) the relevant persons shall comply with such additional supervisory and reporting requirements or conditions as the Agency considers prudent and/or desirable for the scheme. 41. There shall be kept, at an office within Bahrain, such books and records relating to the scheme as may be specified by the Agency. Such books and records may be inspected, and removed to the Agency s possession, if it decides that such action is desirable and necessary. These provisions shall extend to all persons in possession of such books or records. 42. The Agency shall be provided with such information and returns concerning each scheme at such times, within such period and in such form as it may specify. No person shall furnish information or returns under these Principles which he knows to be false and/or misleading. These provisions shall extend to all persons in whose possession such information or returns lie. Schemes Established and Managed Outside Bahrain to be Marketed in Bahrain 43. Any bank or other financial institution in Bahrain through which a scheme established and managed outside Bahrain is marketed in Bahrain must obtain the authorisation and approval of the Agency prior to the commencement of such marketing. The relevant bank or other financial institution shall send to the Agency as part of its application for authorisation and approval: -25-

26 (i) confirmation from licensing authorities in the jurisdiction in which the scheme is established that the scheme is licensed in that jurisdiction; (ii) a copy of the relevant scheme s rules and other scheme documents; (iii) the prospectus; (iv) its latest yearly and half yearly reports; (v) details of the arrangements for the marketing of the scheme in Bahrain; (vi) details of the parent and other group companies of such bank or other financial institution and, if relevant, of the scheme itself; and (vii) any other documentation as may be requested by the Agency. 44. The Agency shall co-operate and co-ordinate with competent authorities in other countries in order to carry out its authorisation and supervisory duties under these Principles. Revocation and Refusal of Authorisation and Approval 45. The Agency may revoke the authorisation and approval for a scheme if: (i) any of the requirements of the scheme are not met; or (ii) deemed desirable in the interests of the scheme, the scheme participants or potential scheme participants; or (iii) these Principles or the scheme documents, have been contravened or any false, inaccurate or misleading information has been provided to the Agency or any information which should have been provided to the Agency has not been so provided; or (iv) the Agency has been so requested by the scheme and/or, as may be appropriate, any one or more of the relevant persons, of the scheme participants. 46. Where the Agency proposes to refuse or revoke authorisation of a scheme (otherwise than in the circumstances described in paragraph 45 (iv) above), it shall give the applicants, or, as the case may be, the scheme and/or, as may be -26-

27 appropriate, the relevant persons, written notice of its intention to do so and the reasons for such action. 47. If it appears to the Agency: (i) that the requirements for authorisation are no longer satisfied, or (ii) that the exercise of the powers conferred by these Principles is desirable, or (iii) that, without prejudice to (ii) above, any provision of these Principles has been contravened, or the Agency has been furnished with false, inaccurate or misleading information, it may require the cessation of the issue and/or (as may be appropriate) repurchase, redemption, reimbursement or repayment of units on a specified date and/or the winding up of the scheme by a specified date. 48. The Agency may, either of its own volition or on the application of the scheme and/or (as may be appropriate) one or more of the relevant persons, withdraw or vary a direction given under these Principles. Advertising and Public Announcements 49. Advertisements and other announcements to the public in Bahrain to invest in a scheme (whether established in Bahrain or elsewhere) shall be submitted for approval to the Agency prior to the issue or publication thereof in Bahrain. Any approval granted by the Agency may be varied or withdrawn. Once authorized, the advertisement may be used for a maximum period of 12 months, provided there are no material changes in that period to the scheme. 50. Unless the Agency s specifically otherwise agrees in writing, no radio, television or cinema advertising of a scheme is permitted in Bahrain, nor is door to door canvassing for sales of a scheme permitted. 51. If any scheme is described as having been authorised and approved by the Agency, it must be stated in all relevant documentation that, in giving this authorisation and approval, the Agency does not take responsibility for the financial soundness of the scheme or for the correctness of any statements made or expressed in relation thereto. -27-

28 52. Advertisements and other invitations to the public in Bahrain must not refer to any scheme which has not obtained the prior authorisation and approval of the Agency. 53. Advertisements should include a warning statement that: (i) the price of units (and, if appropriate, the income if dividends are to be paid from them) may go down as well as up, and that past performance is not a guide to future performance; and (ii) in certain circumstances, the right to repurchase, redeem, reimburse or repay (as may be appropriate) units may be suspended. Scheme Investigation 54. Where it appears to the Agency that it is desirable for the protection of the public, the scheme, the scheme participants or potential scheme participants, to appoint a person to investigate: (i) any alleged breach of any part of these Principles, any directions of the Agency issued pursuant hereto, a scheme, or any defalcation, fraud or misfeasance in connection with a scheme, and/or (ii) any matter concerning dealing in securities or any other assets, or the giving of investment advice, in relation to a scheme, the Agency may appoint a person to investigate the allegation or matter and to report thereon to the Agency. 55. Any person appointed by the Agency pursuant to paragraph 54 above shall be entitled to inspect and take possession of all documents in the possession of any person, to interview all persons relevant to such investigation and to be given all reasonable assistance in relation to such investigation. 56. At the conclusion of such investigation, the person appointed by the Agency to carry out the investigation shall provide to the Agency a report containing the results of such investigation. A copy of such report shall, at the Agency s discretion, be given by it to the investigated person. Any evidence produced as a result of an investigation undertaken pursuant to these Principles shall be made available to the Agency and, if the Agency so deems appropriate, to the Director of Public Prosecutions. -28-

29 57. If it appears to the Agency as a result of the investigation that the person investigated has carried out its operations in any way which contravenes these Principles, any directions issued by the Agency hereunder, the scheme documents, and/or the BMA Law, such person shall be required to take such action as the Agency deems appropriate. Publication of Names of Authorised Schemes 58. The Agency shall publish once a year, in the Annual Report of the Agency, the names of all schemes which are then currently authorised and approved by it. -29-

30 Collective Investment Schemes (Amendment to Item 1.B of the Regulation)

31 OG/121/99 19th April, 1999 The General Manager All FCBs, IBs, OBUs and Representative Offices The Managing Partner Selected Law Firms and Auditing Firms Manama Bahrain Dear Sir, Re: Collective Investment Schemes As you are aware, in accordance with Resolution No. (3) of 1992 dated 24th October, 1992 signed by H.H. Sh. Khalifa Bin Salman Al Khalifa, The Prime Minister, chairman of the Board of Directors of the Bahrain Monetary Agency, the Agency is responsible for the overall licensing and regulation of Collective Investment Schemes in Bahrain. Pursuant to this Resolution, on 18th November, 1992 the Agency issued a Regulation (Agency Circular OG/356/92) concerning the Supervision, Operation and Marketing of Schemes. As part of the process of developing Bahrain s banking and financial center, the Agency has decided that, effective as of the date of this Circular, it will consider application for authorization and approval to establish Schemes in Bahrain, and/or to market Schemes in/from Bahrain, (1) from banks and other financial institutions operating in/from Bahrain and licensed by the Agency, and (2) from banks and other financial or other institutions which are not operating in/from Bahrain (and, therefore, not licensed by the Agency), but which are institutions of high standing and good reputation and which are operating in/from other reputable international financial centers. Paragraph 1.B of the above Regulation is, therefore, amended to take account of this change. In addition to meeting the requirements set out in the Regulation (and subsidiary principles issued pursuant thereto), a local representative will to be appointed in Bahrain for Schemes falling under (2) above. This representative, who the Agency would ordinarily expect to be a law firm, accountancy firm or an Agency licensee (and who must be acceptable to the Agency in terms of experience, qualifications and abilities), will act as the person in Bahrain who is responsible for all administrative and other matters pertaining to the Scheme. -31-

32 Any authorization and approval given for a Scheme falling under (2) above will require the payment to the Agency of an annual fee of Bahraini Dinars Two Thousand (in the case of an Umbrella Scheme, Bahraini Dinars 2,000 x (1+x) where x is the number of subschemes in the Umbrella Scheme). Schemes listed on the Bahrain Stock Exchange ordinarily attract separate listing charges. For Schemes falling under (2) above for which the Agency has given its authorization and approval, however, no listing fees will be levied by the Exchange. Separate Commercial Registration fees will, however, be charged by the Ministry of Commerce for the Commercial Registration of any locally incorporated Scheme and for any expansion in the permitted activities of the local representative of a Scheme. The Ministry should be contacted directly in relation to the amount of all such fees. Queries and/or clarifications in relation to the contents of this Circular should be addressed to Anwar Al Sadah, Director Financial Institutions Supervision Directorate at the Agency on phone number Application forms for authorization and approval of Schemes can be obtained directly from the Directorate. Yours faithfully, Abdulla H. Saif Governor -32-

33 Quarterly Information Returns for Collective Investment Schemes

34 BC/15/97 5th October, 1997 The General Manager, All FCBs, IBs, OBUs & Representative Offices, Manama, Bahrain. Dear Sir, Re: Quarterly Information Returns for Collective Investment Schemes In accordance with Article 4 (D) of the Regulation with respect to the general supervision, operation and marketing of Collective Investment Schemes in/from Bahrain, you are requested to submit the attached quarterly return to the Agency no later than 20 days from the end of each quarter. The attached return replaces the return attached to Agency Circular No. BMA/487/94 dated 16th April, 1994 with effect from end For the sake of clarity, the first return using the attached form will, therefore, be for the quarter ending 31st December, 1997 and should be send to the Agency no later than 21st January, Returns should be sent to the Agency for the attention of Mr. Anwar Al-Sadah, Director of Fin. Inst. Sup. Directorate (Tel: / 445). Your co-operation in this matter is greatly appreciated. Yours faithfully, Dr. Khalid Abdulla Ateeq, Executive Director Banking Control. -34-

35 -35-

36 Guidelines on Advertising and Public Announcements for Collective Investment Schemes

37 BC/23/99 27 th October, 1999 The General Manager All FCBs, OBUs, IBs and Representative Offices Manama Bahrain Dear Sir, Collective Investment Schemes The Agency refers to Circulars No. 356/92, 318/95 and 121/99 dated 18th November, 1992, 4 th November, 1995 and 19 th April, 1999 respectively, and specifically to Paragraphs (inclusive) of the second Circular referred to above. The Agency has decided that, with effect from the date of this Circular, banks and financial institutions engaged in the marketing and/or establishment of Collective Investment Schemes in/from Bahrain may advertise Schemes in accordance with the attached Guidelines. Terms used in the Guidelines shall have the same meaning as set out in the above Circulars. Agency officials will, during the course of their normal inspection of Licensees activities, undertake a review of advertisements used by Licensees for Collective Investment Schemes. It should be noted that the Guidelines apply to all forms of advertising, regardless of the media used. Banks and financial institutions seeking clarification on any point referred to therein should contact Mr. Anwar Khalifa A1-Sadah, Director of Financial Institutions Supervision Directorate, at the Agency on Tel: / Yours faithfully, Dr. Khalid Abdulla Ateeq Executive Director -Banking Control -37-

38 GUIDELINES ON ADVERTISING AND PUBLIC ANNOUNCEMENTS FOR COLLECTIVE INVESTMENT SCHEMES 1. General Matters: (i) (ii) (iii) (iv) (v) (vi) Steps must be taken to ensure that advertisements are fair and not misleading. The purpose of advertisements must be clear and self-explanatory. The nature or type of schemes to which advertisements relate must be clear. Any assumptions on which statements in advertisements are based must be stated. Advertisements must not provide any false or misleading indications. The design and presentation of advertisements should allow them to be easily and clearly understood. (vii) Any risk warnings used in advertisements must he prominently presented and not be obscured or disguised. (viii) Advertisements must not seek to take improper advantage of any circumstance that may make investors/potential investors vulnerable. (ix) (x) Advertisements should not mislead investors/potential investors about any matter likely to influence their attitudes to the scheme in question. Advertisements should be prepared with the aim of ensuring that investors/potential investors fully grasp the nature of the scheme in question. 2. Guarantees: Advertisements must not describe schemes as guaranteed unless there is a legally enforceable guarantee in place and full details of guarantees, sufficient for a fair assessment to be made about the value of such guarantees, are given. -38-

39 3. Comparisons: Comparisons (or contrasts) must be based either on verified facts or on stated assumptions. Comparisons must not be misleading and must be presented in a fair and balanced way and not omit anything material. 4. Past Performance: Any information in the advertisement about the past performance of the scheme in question must be relevant, complete, not exaggerate the success (or disguise the lack of success) of the scheme in question, based on actual performance, and contain a warning that neither past experience nor the current situation is necessarily a guide to future performance. 5. Taxation: Advertisements must contain information on all applicable taxes and the impact of taxation for investors/potential investors. 6. Unusual Risks: Advertisements must adequately explain any unusual risks involved in the scheme in question. 7. Fluctuations: Where the scheme unit price or value can fluctuate, a statement must be made that prices or values may fall or rise. 8. High Volatility: Where appropriate, advertisements must state that sudden and large falls in value may occur and detail the effect of such falls. 9. Investment Income: Where a scheme is described as being likely to yield income or as being suitable for an investor/potential investor particularly seeking income, the -39-

40 investor/potential investor must be warned, if it is the case, that such income may fluctuate. 10. Foreign Currency: Where a scheme is denominated in a currency other than that of the country in which an advertisement is issued, the investor/potential investor must be warned that changes in rates of exchange may have an adverse effect on the value, price or income of his holding in the scheme in question. 11. Schemes carrying Contingent Liability: Where an advertisement relates to a scheme in which investors/potential investors may not only lose all of the amount originally invested, but may also have to pay more later, the advertisement must state this fact. 12. Cancellation: Where cancellation rights apply, all rights and liabilities on cancellation should be disclosed. 13. Forecasts or Projections: Where an advertisement contains any forecast or projection, it should make clear the basis upon which that forecast or projection is made. -40-

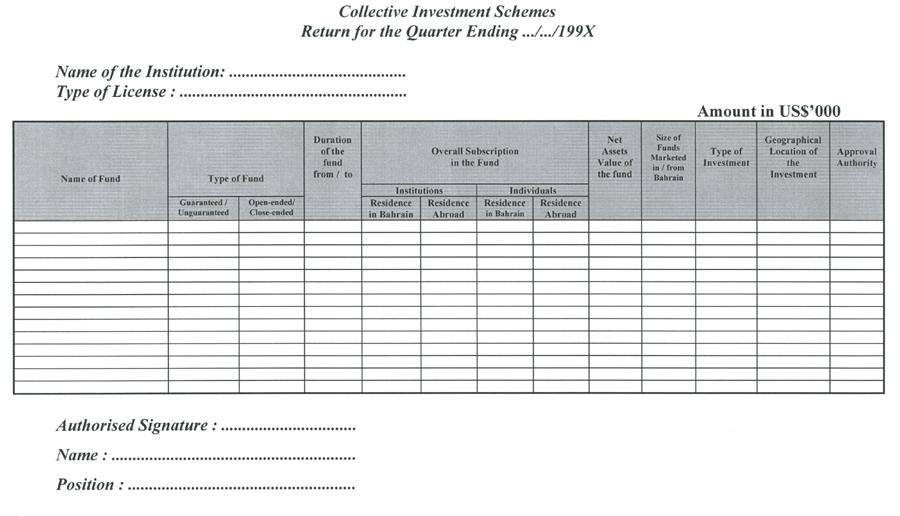

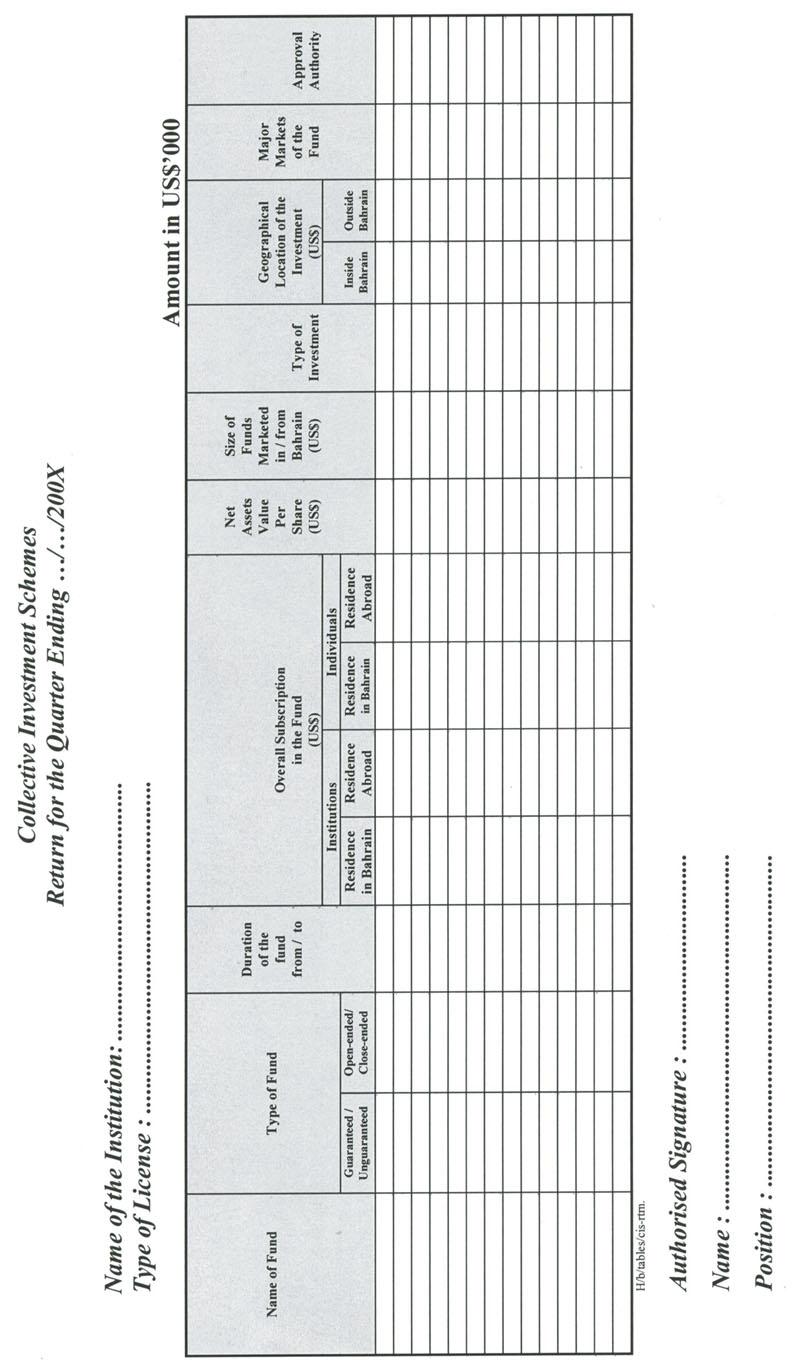

41 Quarterly Information Return for Collective Investment Schemes

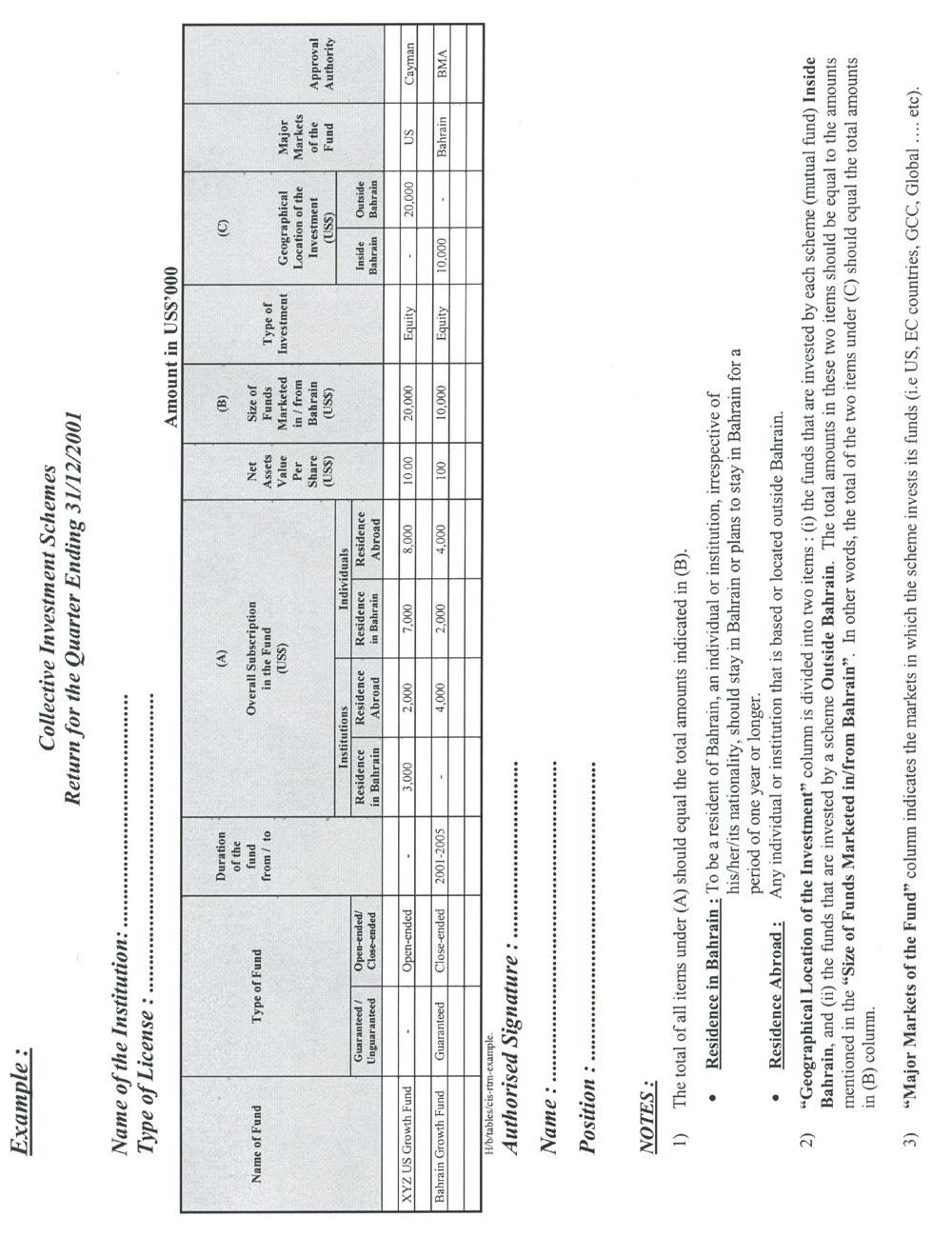

42 BC/I 3/2001 9th December, 2001 The General Manager All FCBs, IBs, OBUs and Representative Offices Manama Bahrain Dear Sir, Re: Quarterly Information Returns for Collective Investment Schemes Further to our Circular No. BC/15/97 of 5 th October 1997, regarding the Quarterly Information Returns that you are requested to be submitted to the Agency at the end of each quarter. The Agency would like to inform you that the following changes are incorporated in the above return: Geographical Location of the Investment column is divided into two items: (i) the funds that are invested by each scheme (mutual fund) Inside Bahrain, and (ii) the funds that are invested by a scheme Outside Bahrain. Major Markets of the Fund column indicates the markets in which the scheme invests its funds (i.e. US, EC countries, GCC, Global... etc). For the sake of clarity, please refer to the attached example on how to fill the return. The attached return replaces the previous return attached to the Agency s Circular No. BC/15/1997 dated 5 th October 1997 with effect from the fourth quarter of The first return using the attached form will, therefore, be for the quarter ending 31st December 2001 and should be sent to the Agency on a date not later that 21st January

43 Should you have any queries in respect of any matter referred to in this Circular, please do not hesitate to contact Mr. Abdul Rahman Al-Baker, Head of Investment Business on Tel or Fax No Yours faithfully, Dr. Khalid Abdulla Ateeq Executive Director Banking Control -43-

44 -44-

45 -45-

SECURITIES (COLLECTIVE INVESTMENT SCHEMES) REGULATIONS 2001 ARRANGEMENT OF REGULATIONS PART I PRELIMINARY

REGULATIONS 2001 ARRANGEMENT OF REGULATIONS PART I PRELIMINARY") 3 SECURITIES ACT 2001 SECURITIES (COLLECTIVE INVESTMENT SCHEMES) REGULATIONS 2001 ARRANGEMENT OF REGULATIONS PART I PRELIMINARY Regulation 1. Citation and commencement 2. Interpretation 3. Unit trusts

3 SECURITIES ACT 2001 SECURITIES (COLLECTIVE INVESTMENT SCHEMES) REGULATIONS 2001 ARRANGEMENT OF REGULATIONS PART I PRELIMINARY Regulation 1. Citation and commencement 2. Interpretation 3. Unit trusts

THE SECURITIES ACT The Securities (Collective Investment Schemes and Closed-end Funds) Regulations 2008 ARRANGEMENT OF REGULATIONS PART I

Regulations 2008 ARRANGEMENT OF REGULATIONS PART I") The text below is an internet version of the Regulations made by the Minister under the Securities Act 2005 and is for information purpose only. Whilst reasonable care has been taken to ensure its accuracy,

The text below is an internet version of the Regulations made by the Minister under the Securities Act 2005 and is for information purpose only. Whilst reasonable care has been taken to ensure its accuracy,

BERMUDA MONETARY AUTHORITY (COLLECTIVE INVESTMENT SCHEME CLASSIFICATION) REGULATIONS 1998 BR 12/1998 BERMUDA MONETARY AUTHORITY ACT : 57

REGULATIONS 1998 BR 12/1998 BERMUDA MONETARY AUTHORITY ACT : 57") BR 12/ BERMUDA MONETARY AUTHORITY ACT 1969 1969 : 57 BERMUDA MONETARY AUTHORITY (COLLECTIVE The Minister, after consultation with the Board of Directors of the Bermuda Monetary Authority, in exercise of

BR 12/ BERMUDA MONETARY AUTHORITY ACT 1969 1969 : 57 BERMUDA MONETARY AUTHORITY (COLLECTIVE The Minister, after consultation with the Board of Directors of the Bermuda Monetary Authority, in exercise of

THE COLLECTIVE INVESTMENT SCHEMES (CLASS A) RULES Index

RULES Index") THE COLLECTIVE INVESTMENT SCHEMES (CLASS A) RULES 2002 Index THE COLLECTIVE INVESTMENT SCHEMES (CLASS A) RULES 2002...1 Part 1 - Introduction... 1 1.01 Citation and commencement... 1 1.02 Interpretation...

THE COLLECTIVE INVESTMENT SCHEMES (CLASS A) RULES 2002 Index THE COLLECTIVE INVESTMENT SCHEMES (CLASS A) RULES 2002...1 Part 1 - Introduction... 1 1.01 Citation and commencement... 1 1.02 Interpretation...

THE INVESTMENT FUNDS ACT (No. 20 of 2003) THE INVESTMENT FUNDS REGULATIONS, Investment Funds Act, 2003 hereby makes the following regulations

THE INVESTMENT FUNDS REGULATIONS, Investment Funds Act, 2003 hereby makes the following regulations") THE INVESTMENT FUNDS ACT (No. 20 of 2003) THE INVESTMENT FUNDS REGULATIONS, 2003 The Minister in exercise of the powers conferred by section 62 of the Investment Funds Act, 2003 hereby makes the following

THE INVESTMENT FUNDS ACT (No. 20 of 2003) THE INVESTMENT FUNDS REGULATIONS, 2003 The Minister in exercise of the powers conferred by section 62 of the Investment Funds Act, 2003 hereby makes the following

Code on Unit Trusts and Mutual Funds

Code on Unit Trusts and Mutual Funds Third Edition December 1997 Hong Kong * Securities & Futures Commission 1997 1991 first edition 1995 second edition 1997 third edition (Amendment made in February 1999

Code on Unit Trusts and Mutual Funds Third Edition December 1997 Hong Kong * Securities & Futures Commission 1997 1991 first edition 1995 second edition 1997 third edition (Amendment made in February 1999

Supplement No. 6 published with Gazette No. 16 of 6th August, MUTUAL FUNDS LAW. (2007 Revision) RETAIL MUTUAL FUNDS (JAPAN) REGULATIONS

RETAIL MUTUAL FUNDS (JAPAN) REGULATIONS") Supplement No. 6 published with Gazette No. 16 of 6th August, 2007. Retail Mutual Funds (Japan) Regulations (2007 Revision) MUTUAL FUNDS LAW (2007 Revision) RETAIL MUTUAL FUNDS (JAPAN) REGULATIONS (2007

Supplement No. 6 published with Gazette No. 16 of 6th August, 2007. Retail Mutual Funds (Japan) Regulations (2007 Revision) MUTUAL FUNDS LAW (2007 Revision) RETAIL MUTUAL FUNDS (JAPAN) REGULATIONS (2007

INVESTMENT SERVICES RULES FOR PROFESSIONAL INVESTOR FUNDS

INVESTMENT SERVICES RULES FOR PROFESSIONAL INVESTOR FUNDS PART B: STANDARD LICENCE CONDITIONS Part APPLICABILITY OF REGULATION (EU) NO 345/2013 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL OF 17 APRIL

INVESTMENT SERVICES RULES FOR PROFESSIONAL INVESTOR FUNDS PART B: STANDARD LICENCE CONDITIONS Part APPLICABILITY OF REGULATION (EU) NO 345/2013 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL OF 17 APRIL

THE COLLECTIVE INVESTMENT SCHEMES (UNIT TRUSTS) REGULATIONS 20043

REGULATIONS 20043") THE COLLECTIVE INVESTMENT SCHEMES (UNIT TRUSTS) REGULATIONS 20043 CONTENTS Part 1 Introduction 1.01 Citation and commencement 1.02 Interpretation 1.03 Sources of powers Part 2 Constitution 2.01 The trust

THE COLLECTIVE INVESTMENT SCHEMES (UNIT TRUSTS) REGULATIONS 20043 CONTENTS Part 1 Introduction 1.01 Citation and commencement 1.02 Interpretation 1.03 Sources of powers Part 2 Constitution 2.01 The trust

Schedule 4 Guide to Jersey Open-Ended Unclassified Collective Investment Funds offered to the general public (OCIF Guide)

") Schedule 4 Guide to Jersey Open-Ended Unclassified Collective Investment Funds offered to the general public () Effective from: 2 April 2012 Last revised: 19 November 2012 Glossary of Terms Glossary of

Schedule 4 Guide to Jersey Open-Ended Unclassified Collective Investment Funds offered to the general public () Effective from: 2 April 2012 Last revised: 19 November 2012 Glossary of Terms Glossary of

GUIDELINES ON WHOLESALE FUNDS

GUIDELINES ON WHOLESALE FUNDS Issued by: Securities Commission Effective Date: 18 February 2009 CONTENTS 1.0 APPLICATION OF GUIDELINES 1 2.0 DEFINITIONS 1 3.0 ROLE AND DUTIES OF THE FUND MANAGER 6 4.0

GUIDELINES ON WHOLESALE FUNDS Issued by: Securities Commission Effective Date: 18 February 2009 CONTENTS 1.0 APPLICATION OF GUIDELINES 1 2.0 DEFINITIONS 1 3.0 ROLE AND DUTIES OF THE FUND MANAGER 6 4.0

UCITS NOTICES April 2008

UCITS NOTICES UNDERTAKINGS FOR COLLECTIVE INVESTMENT IN TRANSFERABLE SECURITIES AUTHORISED UNDER EUROPEAN COMMUNITIES (UNDERTAKINGS FOR COLLECTIVE INVESTMENT IN TRANSFERABLE SECURITIES) REGULATIONS 2003

UCITS NOTICES UNDERTAKINGS FOR COLLECTIVE INVESTMENT IN TRANSFERABLE SECURITIES AUTHORISED UNDER EUROPEAN COMMUNITIES (UNDERTAKINGS FOR COLLECTIVE INVESTMENT IN TRANSFERABLE SECURITIES) REGULATIONS 2003

POLICE AND CRIMINAL EVIDENCE BILL 2004 A BILL. entitled "BERMUDA DEPOSIT INSURANCE ACT 2010

3 September 2010 A BILL entitled "BERMUDA DEPOSIT INSURANCE ACT 2010 ARRANGEMENT OF CLAUSES PART I Preliminary 1 Short title and commencement 2 Interpretation 3 Meaning of insured deposit base and relevant

3 September 2010 A BILL entitled "BERMUDA DEPOSIT INSURANCE ACT 2010 ARRANGEMENT OF CLAUSES PART I Preliminary 1 Short title and commencement 2 Interpretation 3 Meaning of insured deposit base and relevant

Bourse de Montréal Inc. 7-1 RULE SEVEN OPERATIONS OF APPROVED PARTICIPANTS. Section Financial Conditions - General

Bourse de Montréal Inc. 7-1 7001 Compliance with Legal Requirements RULE SEVEN OPERATIONS OF APPROVED PARTICIPANTS Section 7001-7075 Financial Conditions - General Every approved participant must comply

Bourse de Montréal Inc. 7-1 7001 Compliance with Legal Requirements RULE SEVEN OPERATIONS OF APPROVED PARTICIPANTS Section 7001-7075 Financial Conditions - General Every approved participant must comply

STANDARD CONDITIONS FOR COMPANY VOLUNTARY ARRANGEMENTS

STANDARD CONDITIONS FOR COMPANY VOLUNTARY ARRANGEMENTS Version 3 January 2013 TABLE OF CONTENTS 1 COMPANY VOLUNTARY ARRANGEMENTS 1 PART I: INTERPRETATION 5 1 Miscellaneous definitions 5 2 The Conditions

STANDARD CONDITIONS FOR COMPANY VOLUNTARY ARRANGEMENTS Version 3 January 2013 TABLE OF CONTENTS 1 COMPANY VOLUNTARY ARRANGEMENTS 1 PART I: INTERPRETATION 5 1 Miscellaneous definitions 5 2 The Conditions

STATUTORY INSTRUMENTS. SI. No. 352 of 2011 EUROPEAN COMMUNITIES (UNDERTAKINGS FOR COLLECTIVE INVESTMENT IN TRANSFERABLE SECURITIES) REGULATIONS 2011

REGULATIONS 2011") STATUTORY INSTRUMENTS. SI. No. 352 of 2011 EUROPEAN COMMUNITIES (UNDERTAKINGS FOR COLLECTIVE INVESTMENT IN TRANSFERABLE SECURITIES) REGULATIONS 2011 (Prn. A11/1185) 2 [352] SI. No. 352 of 2011 EUROPEAN

STATUTORY INSTRUMENTS. SI. No. 352 of 2011 EUROPEAN COMMUNITIES (UNDERTAKINGS FOR COLLECTIVE INVESTMENT IN TRANSFERABLE SECURITIES) REGULATIONS 2011 (Prn. A11/1185) 2 [352] SI. No. 352 of 2011 EUROPEAN

COLLECTIVE INVESTMENT FUNDS (RECOGNIZED FUNDS) (RULES) (JERSEY) ORDER 2003

(RULES) (JERSEY) ORDER 2003") COLLECTIVE INVESTMENT FUNDS (RECOGNIZED FUNDS) (RULES) (JERSEY) ORDER 2003 Revised Edition Showing the law as at 1 January 2014 This is a revised edition of the law Collective Investment Funds (Recognized

COLLECTIVE INVESTMENT FUNDS (RECOGNIZED FUNDS) (RULES) (JERSEY) ORDER 2003 Revised Edition Showing the law as at 1 January 2014 This is a revised edition of the law Collective Investment Funds (Recognized

Securities Industry (Amendment) Act, Act, Act 590 ARRANGEMENT OF SECTIONS

Act, Act, Act 590 ARRANGEMENT OF SECTIONS") Securities Industry (Amendment) Act, Act, 2000 2000 Act 590 Section ARRANGEMENT OF SECTIONS 1. Section 1 of P.N.D.C.L. 333 amended 2. Section 2 of P.N.D.C.L. 333 amended 3. Section 5 of P.N.D.C.L. 333

Securities Industry (Amendment) Act, Act, 2000 2000 Act 590 Section ARRANGEMENT OF SECTIONS 1. Section 1 of P.N.D.C.L. 333 amended 2. Section 2 of P.N.D.C.L. 333 amended 3. Section 5 of P.N.D.C.L. 333

DIVISION 3 STRUCTURED WARRANT

DIVISION 3 STRUCTURED WARRANT C O N T E N T S PAGE Chapter 1 GENERAL 1 Chapter 2 FRONT COVER 2 Chapter 3 INSIDE COVER/FIRST PAGE 3 Chapter 4 TIME TABLE/DEFINITIONS/TABLE OF CONTENTS/CORPORATE DIRECTORY

DIVISION 3 STRUCTURED WARRANT C O N T E N T S PAGE Chapter 1 GENERAL 1 Chapter 2 FRONT COVER 2 Chapter 3 INSIDE COVER/FIRST PAGE 3 Chapter 4 TIME TABLE/DEFINITIONS/TABLE OF CONTENTS/CORPORATE DIRECTORY

REPORT ON INVESTMENT MANAGEMENT INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS

REPORT ON INVESTMENT MANAGEMENT INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS October 1994 PRINCIPLES FOR THE REGULATION OF COLLECTIVE INVESTMENT SCHEMES and EXPLANATORY MEMORANDUM INTRODUCTION

REPORT ON INVESTMENT MANAGEMENT INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS October 1994 PRINCIPLES FOR THE REGULATION OF COLLECTIVE INVESTMENT SCHEMES and EXPLANATORY MEMORANDUM INTRODUCTION

1 L.R.O Financial Institutions CAP. 324A FINANCIAL INSTITUTIONS

1 L.R.O. 2007 Financial Institutions CAP. 324A CHAPTER 324A FINANCIAL INSTITUTIONS ARRANGEMENT OF SECTIONS SECTION PART I Preliminary 1. Short title. 2. Interpretation. PART II COMMERCIAL BANKS Licensing

1 L.R.O. 2007 Financial Institutions CAP. 324A CHAPTER 324A FINANCIAL INSTITUTIONS ARRANGEMENT OF SECTIONS SECTION PART I Preliminary 1. Short title. 2. Interpretation. PART II COMMERCIAL BANKS Licensing

INVESTMENT SERVICES RULES FOR PROFESSIONAL INVESTOR FUNDS

INVESTMENT SERVICES RULES FOR PROFESSIONAL INVESTOR FUNDS PART B: STANDARD LICENCE CONDITIONS Part B II: Professional Investor Funds targeting Qualifying Investors APPLICABILITY OF REGULATION (EU) NO 345/2013

INVESTMENT SERVICES RULES FOR PROFESSIONAL INVESTOR FUNDS PART B: STANDARD LICENCE CONDITIONS Part B II: Professional Investor Funds targeting Qualifying Investors APPLICABILITY OF REGULATION (EU) NO 345/2013

DEPOSIT PROTECTION CORPORATION ACT

CHAPTER 24:29 DEPOSIT PROTECTION CORPORATION ACT ARRANGEMENT OF SECTIONS Acts 7/2011, 9/2011 PART I PRELIMINARY Section 1. Short title. 2. Interpretation. 3. When contributory institution becomes financially

CHAPTER 24:29 DEPOSIT PROTECTION CORPORATION ACT ARRANGEMENT OF SECTIONS Acts 7/2011, 9/2011 PART I PRELIMINARY Section 1. Short title. 2. Interpretation. 3. When contributory institution becomes financially

CAYMAN ISLANDS. Supplement No. 21 published with Extraordinary Gazette No. 53 of 17th July, MUTUAL FUNDS LAW.

CAYMAN ISLANDS Supplement No. 21 published with Extraordinary Gazette No. 53 of 17th July, 2015. MUTUAL FUNDS LAW (2015 Revision) Law 13 of 1993 consolidated with Laws 18 of 1993, 16 of 1996 (part), 9

CAYMAN ISLANDS Supplement No. 21 published with Extraordinary Gazette No. 53 of 17th July, 2015. MUTUAL FUNDS LAW (2015 Revision) Law 13 of 1993 consolidated with Laws 18 of 1993, 16 of 1996 (part), 9

OFFSHORE BANKING ACT 1990 (Act 443) ARRANGEMENT OF SECTIONS. Part I. Preliminary. Part II. Licensing Of Offshore Banks. Part III

ARRANGEMENT OF SECTIONS. Part I. Preliminary. Part II. Licensing Of Offshore Banks. Part III") OFFSHORE BANKING ACT 1990 (Act 443) ARRANGEMENT OF SECTIONS Part I Section Preliminary 1. Short title and commencement 2. Interpretation 3. Functions, powers and duties of the Bank Part II Licensing Of

OFFSHORE BANKING ACT 1990 (Act 443) ARRANGEMENT OF SECTIONS Part I Section Preliminary 1. Short title and commencement 2. Interpretation 3. Functions, powers and duties of the Bank Part II Licensing Of

PROSPECTUS OF THE KGORI CAPITAL ENHANCED CASH FUND

PROSPECTUS OF THE KGORI CAPITAL ENHANCED CASH FUND A unit portfolio of the Prescient Management Company Botswana Collective Investment Undertaking, a trust authorised to operate as a Collective Investment

PROSPECTUS OF THE KGORI CAPITAL ENHANCED CASH FUND A unit portfolio of the Prescient Management Company Botswana Collective Investment Undertaking, a trust authorised to operate as a Collective Investment

AIM opened on 19 June It is regulated by London Stock Exchange plc.

PLEASE NOTE this mark-up is provided for indicative purpose only. Please refer to the current AIM Rules for Companies for a definitive version. Mark-up in yellow indicates changes made since the version

PLEASE NOTE this mark-up is provided for indicative purpose only. Please refer to the current AIM Rules for Companies for a definitive version. Mark-up in yellow indicates changes made since the version

Draft Partnership Agreement relating to [Name of ECF] Amending and restating a partnership agreement dated [Date]

![Draft Partnership Agreement relating to [Name of ECF] Amending and restating a partnership agreement dated [Date]](/thumbs/73/69412391.jpg "Draft Partnership Agreement relating to [Name of ECF] Amending and restating a partnership agreement dated [Date]") Draft Partnership Agreement relating to [Name of ECF] Amending and restating a partnership agreement dated [Date] Dated [General Partner] (1) [Founder Partner] (2) British Business Finance Ltd (3) [Investor]

Draft Partnership Agreement relating to [Name of ECF] Amending and restating a partnership agreement dated [Date] Dated [General Partner] (1) [Founder Partner] (2) British Business Finance Ltd (3) [Investor]

CHAPTER 8 SPECIALIST DEBT SECURITIES

CHAPTER 8 SPECIALIST DEBT SECURITIES Contents This chapter sets out the conditions for listing and the information which is required to be included in the listing document for specialist debt securities

CHAPTER 8 SPECIALIST DEBT SECURITIES Contents This chapter sets out the conditions for listing and the information which is required to be included in the listing document for specialist debt securities

STANDARD CONDITIONS FOR INDIVIDUAL VOLUNTARY ARRANGEMENTS. Produced by the. Association of Business Recovery Professionals

STANDARD CONDITIONS FOR INDIVIDUAL VOLUNTARY ARRANGEMENTS Produced by the Association of Business Recovery Professionals Version 2 November 2004 TABLE OF CONTENTS FOR STANDARD CONDITIONS 1 INDIVIDUAL VOLUNTARY

STANDARD CONDITIONS FOR INDIVIDUAL VOLUNTARY ARRANGEMENTS Produced by the Association of Business Recovery Professionals Version 2 November 2004 TABLE OF CONTENTS FOR STANDARD CONDITIONS 1 INDIVIDUAL VOLUNTARY

Master Selling Group Agreement

Master Selling Group Agreement Negotiated Offerings of Municipal Securities MANAGER: DEALER: I. PURPOSE OF AGREEMENT This Master Selling Group Agreement (the Master Agreement ) is between the Manager identified

Master Selling Group Agreement Negotiated Offerings of Municipal Securities MANAGER: DEALER: I. PURPOSE OF AGREEMENT This Master Selling Group Agreement (the Master Agreement ) is between the Manager identified

The Central Bank of The Bahamas

The Central Bank of The Bahamas CONSULTATION PAPER on the Draft Banks and Trust Companies Regulation (Amendment) (No. 1) Bill, 2013 and the Draft Banks and Trust Companies (Administrative Monetary Penalties),

The Central Bank of The Bahamas CONSULTATION PAPER on the Draft Banks and Trust Companies Regulation (Amendment) (No. 1) Bill, 2013 and the Draft Banks and Trust Companies (Administrative Monetary Penalties),

DENALI INVESTORS ACCREDITED FUND, LP LIMITED PARTNERSHIP AGREEMENT

DENALI INVESTORS ACCREDITED FUND, LP LIMITED PARTNERSHIP AGREEMENT Dated as of October 1, 2007 DENALI INVESTORS ACCREDITED FUND, LP AMENDED AND RESTATED LIMITED PARTNERSHIP AGREEMENT TABLE OF CONTENTS

DENALI INVESTORS ACCREDITED FUND, LP LIMITED PARTNERSHIP AGREEMENT Dated as of October 1, 2007 DENALI INVESTORS ACCREDITED FUND, LP AMENDED AND RESTATED LIMITED PARTNERSHIP AGREEMENT TABLE OF CONTENTS

Fiscal Management & Acclountability Act N0. 20 of 2003

GUYANA ACT No. 20 of 2003 FISCAL MANAGEMENT AND ACCOUNTABILITY ACT 2003 I assent, Bharrat Jagdeo, President. 16 th December, 2003. ARRANGEMENT OF SECTIONS SECTION PART I GENERAL PROVISIONS 1. Short title

GUYANA ACT No. 20 of 2003 FISCAL MANAGEMENT AND ACCOUNTABILITY ACT 2003 I assent, Bharrat Jagdeo, President. 16 th December, 2003. ARRANGEMENT OF SECTIONS SECTION PART I GENERAL PROVISIONS 1. Short title

THE INSURANCE ACT (Consolidated version with amendments as at 07 September 2016) ARRANGEMENT OF SECTIONS

ARRANGEMENT OF SECTIONS") The text below has been prepared to reflect the text passed by the National Assembly on 25 March 2005, with subsequent amendments, and is for information purpose only. The authoritative version is the

The text below has been prepared to reflect the text passed by the National Assembly on 25 March 2005, with subsequent amendments, and is for information purpose only. The authoritative version is the

COMPOSITE STATEMENT FAX INDEMNITY

COMPOSITE STATEMENT 148. The Bank will send to the Account holder each month (or as specified by the Account holder) statements of account showing the transactions and balances in relation to all HSBC

COMPOSITE STATEMENT 148. The Bank will send to the Account holder each month (or as specified by the Account holder) statements of account showing the transactions and balances in relation to all HSBC

HSBC MSCI TURKEY UCITS ETF Supplement. 6 October 2014

HSBC MSCI TURKEY UCITS ETF Supplement 6 October 2014 The Company and the Directors of HSBC ETFs PLC (the Directors ) listed in the Prospectus in the Management and Administration section, accept responsibility

HSBC MSCI TURKEY UCITS ETF Supplement 6 October 2014 The Company and the Directors of HSBC ETFs PLC (the Directors ) listed in the Prospectus in the Management and Administration section, accept responsibility

COLLECTIVE INVESTMENT FUNDS (UNCLASSIFIED FUNDS) (PROSPECTUSES) (JERSEY) ORDER 1995

(PROSPECTUSES) (JERSEY) ORDER 1995") COLLECTIVE INVESTMENT FUNDS (UNCLASSIFIED FUNDS) (PROSPECTUSES) (JERSEY) ORDER 1995 Revised Edition Showing the law as at 1 January 2009 This is a revised edition of the law Collective Investment Funds

COLLECTIVE INVESTMENT FUNDS (UNCLASSIFIED FUNDS) (PROSPECTUSES) (JERSEY) ORDER 1995 Revised Edition Showing the law as at 1 January 2009 This is a revised edition of the law Collective Investment Funds

CHAPTER 308A EXEMPT INSURANCE

1 L.R.O. 1998 Exempt Insurance CAP. 308A CHAPTER 308A EXEMPT INSURANCE ARRANGEMENT OF SECTIONS SECTION PART I Preliminary 1. Short title. 2. Interpretation. 3. Exempt insurance business. PART II Licensing

1 L.R.O. 1998 Exempt Insurance CAP. 308A CHAPTER 308A EXEMPT INSURANCE ARRANGEMENT OF SECTIONS SECTION PART I Preliminary 1. Short title. 2. Interpretation. 3. Exempt insurance business. PART II Licensing

REVISED STATUTES OF ANGUILLA CHAPTER M107 MUTUAL FUNDS ACT. Showing the Law as at 15 December 2014

ANGUILLA REVISED STATUTES OF ANGUILLA CHAPTER M107 MUTUAL FUNDS ACT Showing the Law as at 15 December 2014 This Edition was prepared under the authority of the Revised Statutes and Regulations Act, R.S.A.

ANGUILLA REVISED STATUTES OF ANGUILLA CHAPTER M107 MUTUAL FUNDS ACT Showing the Law as at 15 December 2014 This Edition was prepared under the authority of the Revised Statutes and Regulations Act, R.S.A.

AMENDED AND RESTATED LIMITED PARTNERSHIP AGREEMENT

Execution Version AMENDED AND RESTATED LIMITED PARTNERSHIP AGREEMENT of RBC COVERED BOND GUARANTOR LIMITED PARTNERSHIP by and among RBC COVERED BOND GP INC. as Managing General Partner and 6848320 CANADA

Execution Version AMENDED AND RESTATED LIMITED PARTNERSHIP AGREEMENT of RBC COVERED BOND GUARANTOR LIMITED PARTNERSHIP by and among RBC COVERED BOND GP INC. as Managing General Partner and 6848320 CANADA

BRITISH VIRGIN ISLANDS BANKS AND TRUST COMPANIES ACT, (as amended, 2001) ARRANGEMENT OF SECTIONS. PART I - Preliminary. PART II - Licences

ARRANGEMENT OF SECTIONS. PART I - Preliminary. PART II - Licences") BRITISH VIRGIN ISLANDS BANKS AND TRUST COMPANIES ACT, 1990 1 (as amended, 2001) ARRANGEMENT OF SECTIONS 1. Short title PART I - Preliminary 2. Interpretation. PART II - Licences 3. Requirement for licence.

BRITISH VIRGIN ISLANDS BANKS AND TRUST COMPANIES ACT, 1990 1 (as amended, 2001) ARRANGEMENT OF SECTIONS 1. Short title PART I - Preliminary 2. Interpretation. PART II - Licences 3. Requirement for licence.

Rg 10 G.N. No. S 457/2002 REVISED EDITION 2004 (29th February 2004) PART I PRELIMINARY

PART I PRELIMINARY") SECURITIES AND FUTURES ACT (CHAPTER 289, SECTIONS 2(1), 84(3), 85(1) AND (4), 86(3), 87, 90(2), 91, 93(1), 94(1), 95(1), 96(2), 97(2), 97A(3), 97B(1), TO 97, 99(4), 99A(1) AND (4), [99AC(2), 99C(1),] 99D(2),

SECURITIES AND FUTURES ACT (CHAPTER 289, SECTIONS 2(1), 84(3), 85(1) AND (4), 86(3), 87, 90(2), 91, 93(1), 94(1), 95(1), 96(2), 97(2), 97A(3), 97B(1), TO 97, 99(4), 99A(1) AND (4), [99AC(2), 99C(1),] 99D(2),

LLP AGREEMENT. (As per section 23 of LLP Act, 2008) This Agreement of Limited Liability Partnership made at on this day of 2011 BETWEEN

This Agreement of Limited Liability Partnership made at on this day of 2011 BETWEEN") LLP AGREEMENT (As per section 23 of LLP Act, 2008) This Agreement of Limited Liability Partnership made at on this day of 2011 BETWEEN 1., Age- years, Occupation Business, residing at, PAN No- and hereinafter

LLP AGREEMENT (As per section 23 of LLP Act, 2008) This Agreement of Limited Liability Partnership made at on this day of 2011 BETWEEN 1., Age- years, Occupation Business, residing at, PAN No- and hereinafter

SUNCORP GROUP HOLDINGS (NZ) LIMITED SUNCORP GROUP LIMITED CRS NOMINEES LIMITED TRUST DEED CONSTITUTING THE EXEMPT EMPLOYEE SHARE PLAN

LIMITED SUNCORP GROUP LIMITED CRS NOMINEES LIMITED TRUST DEED CONSTITUTING THE EXEMPT EMPLOYEE SHARE PLAN") SUNCORP GROUP HOLDINGS (NZ) LIMITED SUNCORP GROUP LIMITED CRS NOMINEES LIMITED TRUST DEED CONSTITUTING THE EXEMPT EMPLOYEE SHARE PLAN CONTENTS PARTIES... 1 INTRODUCTION... 1 COVENANTS... 1 1. INTERPRETATION...

SUNCORP GROUP HOLDINGS (NZ) LIMITED SUNCORP GROUP LIMITED CRS NOMINEES LIMITED TRUST DEED CONSTITUTING THE EXEMPT EMPLOYEE SHARE PLAN CONTENTS PARTIES... 1 INTRODUCTION... 1 COVENANTS... 1 1. INTERPRETATION...

Regulations issued pursuant to section 34 of the Banking Laws, 1997 to 2008 PART II STATUS AND OPERATION OF THE SCHEME

24 July 2009 Unofficial consolidated text of the Establishment and Operation of the Deposit Protection Scheme Regulations of 2000 to 2009 English translation Regulations issued pursuant to section 34 of

24 July 2009 Unofficial consolidated text of the Establishment and Operation of the Deposit Protection Scheme Regulations of 2000 to 2009 English translation Regulations issued pursuant to section 34 of

BANKING ACT 2003 As amended 2004 ANALYSIS

BANKING ACT 2003 As amended 2004 ANALYSIS PART 1 PRELIMINARY 1. Short Title, commencement and application of this Act 2. Interpretation PART 2 LICENSING OF BANKING BUSINESS 3. Licence needed to carry on

BANKING ACT 2003 As amended 2004 ANALYSIS PART 1 PRELIMINARY 1. Short Title, commencement and application of this Act 2. Interpretation PART 2 LICENSING OF BANKING BUSINESS 3. Licence needed to carry on

LIMITED PARTNERSHIP AGREEMENT

Execution Copy LIMITED PARTNERSHIP AGREEMENT of NBC COVERED BOND (LEGISLATIVE) GUARANTOR LIMITED PARTNERSHIP by and among NBC COVERED BOND (LEGISLATIVE) GP INC. as Managing General Partner and 8603413

Execution Copy LIMITED PARTNERSHIP AGREEMENT of NBC COVERED BOND (LEGISLATIVE) GUARANTOR LIMITED PARTNERSHIP by and among NBC COVERED BOND (LEGISLATIVE) GP INC. as Managing General Partner and 8603413

CO-OPERATIVE BANKS ACT

REPUBLIC OF SOUTH AFRICA CO-OPERATIVE BANKS ACT IRIPHABLIKI YOMZANTSI AFRIKA UMTHETHO WEEBHANKI ZENTSEBENZISWANO No, 07 ACT To promote and advance the social and economic welfare of all South Africans

REPUBLIC OF SOUTH AFRICA CO-OPERATIVE BANKS ACT IRIPHABLIKI YOMZANTSI AFRIKA UMTHETHO WEEBHANKI ZENTSEBENZISWANO No, 07 ACT To promote and advance the social and economic welfare of all South Africans

ATLANTE FUNDS PLC FOURTH ADDENDUM TO THE PROSPECTUS DATED 27 JUNE 2014