WHAT ELSE YOU SHOULD KNOW ABOUT DONOR ADVISED FUNDS AND THEIR ALTERNATIVES or Where Have All The Dollars Gone?

|

|

|

- Johnathan Garrett

- 5 years ago

- Views:

Transcription

1 WHAT ELSE YOU SHOULD KNOW ABOUT DONOR ADVISED FUNDS AND THEIR ALTERNATIVES or Where Have All The Dollars Gone? David S. Rosen, Senior Vice President, Legacies and Endowments Rose L. Jagust, Associate Vice President, Donor Advised Programs

2 Outline Donor Advised Fund Basics Other Public Charity Alternatives Handling DAF Grants and Administration DAFs As Part Of Estate Planning and/or Used With Other Giving Vehicles

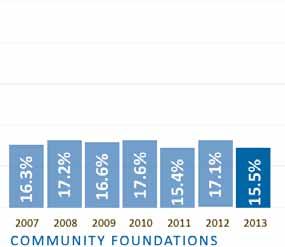

3 Donor Advised Funds Basics Growth Gifts to DAFs were 5.2% of all gifts to charitable organizations or $17.28 billion of the $ billion given to charities in Gifts to DAFs generally increased each year since 2007 (besides downturn in 2008/9) 217, 367 accounts $53.74 billion in assets $9.66 billion in grants

4 Total DAF Accounts Aggregate Assets in DAFs Grants from DAFs Aggregate Contributions to DAFs National Philanthropic Trust, 2014

5 PROVIDERS Community Foundations Single-Issue Charities Commercial Entities

6 Why do People Like Donor Advised Funds? Easy Set Up Tax Advantages Flexibility Fewer Rules No Administrative Burdens Anonymity

7 History A. First started in 1930 s with community foundations, Jewish Federations; grew with Tax Acts of 1969 and 1986 and with entrance of commercial organizations (e.g. Fidelity) in 1990 s. B. Codified by Pension Protection Act of 2006 (PPA).

8 History (cont d) C. Donor advised fund now defined in Internal Revenue Code (IRC) Section 4966 as any fund or account: 1. Which is owned and controlled by a sponsoring organization ; 2. Which is separately identified by reference to contributions of a donor or donors; and 3. Which a donor or person appointed by the donor had advisory rights with respect to investments or distributions.

9 Private Foundation vs. Public Charity Private foundations and public charities are both included under Section 501(c)(3) of Internal Revenue Code. Public charities generally receive a greater portion of their financial support from the general public or governmental units, and have greater interaction with the public. Private foundations are typically controlled by members of a family or by a small group of individuals, and derive much of their support from a small number of sources and from investment income.

10 Private Foundation vs. Public Charity Continued A private foundation is a Section 501(c)(3) organization that does not qualify as a public charity under one of the following Sections: 509(a)(1) A church, school, hospital, medical research organization operated in conjunction with a hospital, a governmental unit, college or university endowment organization, public charity, or an organization that normally receives a substantial part of its support from a governmental unit or from the general public. 509(a)(2) An organization that receives substantial support from grants, gifts, and contributions, and fees for services. 509(a)(3) Supporting organizations. Section 509(a)(4) Public safety testing organizations.

11 Private Foundation Rules & Regulations Grantmaking: Must give out at least 5% of fair market value of the foundation s non-charitable assets in the previous year. 30% tax on any undistributed income and additional 100% tax if foundation doesn t make up the deficient distribution within 90 days of receiving notification from the IRS. Also, an excise tax of 1 to 2% on net investment depending on amount of grants.

12 Rules & Regulations Continued Self Dealing: no sales, exchanges or leases of property, most loans, or the provision of goods, services or facilities between a disqualified person and a private foundation. Excess Business Holdings: private foundation and its disqualified persons together may own no more than 20 percent of the voting or ownership interest in a business enterprise.

13 Do Donor Advised Funds Give Out Enough Money? Arguments that they don t are: Commercial companies are just making money off DAFs by sitting on funds and charging fees. Donor gets a tax advantage for money that doesn t necessarily go to charities. BUT

14 DAFs Give Out A Lot

15 Other Public Charity Alternatives Field of Interest Funds Designated & Scholarship Funds Giving Circles Supporting Organizations

16 Field of Interest Funds Established for specific area of donor s interest: Distributions can be set amount or as donor recommends Can last in perpetuity/cy pres doctrine

17 Designated & Scholarship Funds These are types of Field of Interest Funds: Designated funds support one or more specific charities Scholarship fund: donor can sit on larger committee that chooses who gets the scholarship, but cannot control/direct who gets scholarship

18 Giving Circles Group of donors band together to contribute to a defined cause and work together to make grants to programs that address that cause.

19 Supporting Foundations To be supporting organization, you must meet four tests Organizational Test Operational Test Relationship Test: One of the three defined relationships and each one is a type supporting organization. Type I Operated, supervised or controlled by, which means supported organization designates a majority of the board. Type II Supervised or controlled in connection with same individual supervise both organizations. Type III Operated in connection with, which has its own complicated tests to meet, the first being a responsiveness test, the other and integral part test. Control Test

20 Benefits of a supporting organization Public charity status, bypassing a number of private foundation limitations Subtle bootstrapping of future descendants Forcing a clear direction of the grantmaking by affiliating with donor s favorite charity to ensure that significant support continues to that charity and others closely related to its purposes Very flexible vehicle

21 Common uses of a supporting organization: As a fundraising arm of public charity As a family grant-making entity under the control and supervision of a like-minded public charity As an endowment or asset holding company As a scholarship fund Problematic holdings or operations with liability problems

22 DAF Grants & Administration Or My Life As a Paper Pusher

23 No grants: Some Rules for DAFs (like Private Foundations) to individuals, private foundations, for expense reimbursement, non-charitable purpose, certain supporting organizations (all considered taxable distribution). where the donor (or his/her family member) receives more than an incidental benefit: things like events, memberships, tuition, payment of a legally enforceable pledge. No excess benefit transaction: automatic excess benefit for ANY grant, loan, compensation, or similar payment from a DAF to a disqualified person; also can be where value of the economic benefit provided by the charity to disqualified person exceeds the value of the consideration received for providing the benefit.

24 Some Rules for DAFs (continued) No Excess Business Holdings (same as private foundation): DAF and its disqualified persons together may own no more than 20 percent of the voting or ownership interest in a business enterprise.

25 Some Rules for DAFS (Penalty Phase) Big Penalties for everyone: For taxable distributions: 20% tax on sponsoring organization and 5% on fund manager For grants where donor gets more than incidental benefit: a 125% on the donor or donor advisor and 10% excise tax on fund manager For excess benefits: 25% of the excess portion on the person who received the benefit; if uncorrected, tax equal to 200% of the excess benefit on the disqualified person and 10% on fund manager; for automatic excess benefit cases, entire payment is considered excess benefit For excess business holdings: An excise tax of ten percent of the value of the excess holdings an excise tax of 200 percent of the excess holdings is imposed on the foundation if it has not disposed of the remaining excess business holdings by the end of the taxable period.

26 So. Some things, you just can t do, but: What if your donor has pledged a gift and wants to pay it from a DAF? What if your donor wants to come to your fundraising dinner and pay for it from a DAF? What if your donor wants to make a multi-year commitment and pay for it from a DAF? What about all those posters, mugs and keychains?

27 Best Defense Is A Good Offense Know Your Donor And Work With Sponsoring Organization Find out how the donor wants to make payment when planning the gift to: Avoid compliance problems before the gift Learn useful information about the donor Gain an opportunity for planning and stewardship Work with the sponsoring organization to: Address questions in advance Educate the donor

28 What do you do with this?

29

30 What That Letter Means What Do You Do About The Letter? Read it! Is there a pledge, incidental benefit? Thank the donor Acknowledge the donor Your Donor Is Thinking About Philanthropy Why did he/she open the DAF? What are the donor s intentions with it?

31 How Families Work Together (or not) with DAFs Children can be part of fund either while parents are alive or after they re gone What happens when: A couple gets divorced Siblings stop talking to each other Kids just don t think similarly about philanthropy

32 DAFs As Part Of Estate Planning and/or Used With Other Giving Vehicles

33 Key Times for Donors to Think about DAFs High Income Years Retirement Planning Capital Transaction

34 DAF as a Bequest Alternative Provides enhanced flexibility to make testamentary gifts. Super-charge a DAF.

35 Retirement Assets to a Donor Advised Fund Does not qualify for on again off again income tax exclusion. Can leave to DAF Significant tax savings Nice and tax efficient way to encourage descendants to be generous.

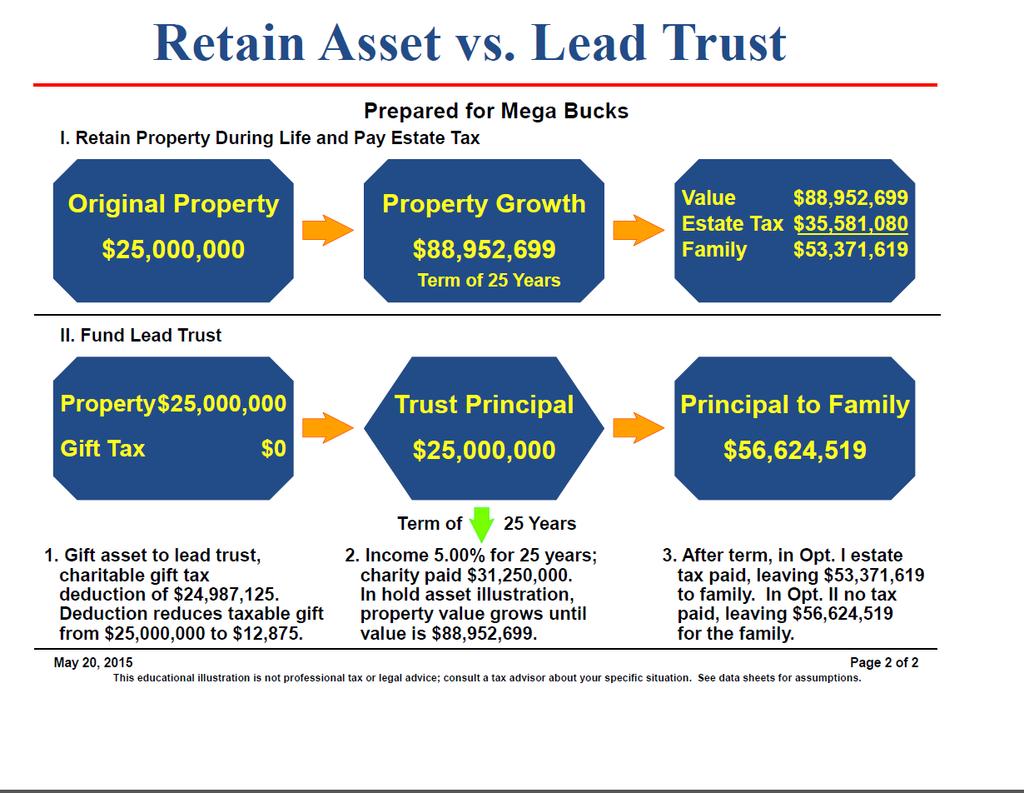

36 Donor Advised Fund Case Study Maker and Lotta Bucks Maker and Lotta Bucks married in college. Maker started a small candy company that grew to a name brand manufacturer. Lotta became a partner at an investment house. They had three children, Mega, Caring and Simple. As the family grew, the Bucks fortune grew, especially with Lotta s financial acumen. The Bucks wanted to give back and decided to create a giving vehicle. They give to 20 charities a year ($1,000 each). Assets: Stock in Makers Candy Lotta s Partnership in Investment Co. 2 Retirement IRA s each with 1,000,000 in them Stock portfolio 3,000,000 Explore the Bucks Family s Options

37 The Saga Continues... The three sons marry and start their families: Mega marries Minnie, have 6 kids. Mega starts a hedge Fund in college and makes at least $10 million a year. Caring marries Caren, have 2 kids, and both are city high school teachers. Simple who works at Maker s marries Simpler, an aspiring yoga instructor. Maker and Lotta want to get the kids and grandkids involved in giving.

38 And The Saga Continues... Maker and Lotta Bucks decide to revise their planning. Lotta joins the Board of the local Art Museum, and she is immediately solicited to leave a major endowment.

39

40 As the World Turns Siblings have disagreements and very different charitable interests. This is exacerbated by Simpler running off to the Himalayas with her meditation teacher. Mega wants to go his own way.

41

42

43 CLT Issues Lead interest to private foundations vs DAF organization: If private foundation, there are control issues which could lead to an argument that this was not a completed gift if the settlor was on the board of the private foundation.

MAKE THE MOST OF YOUR DONOR ADVISED FUND

MAKE THE MOST OF YOUR DONOR ADVISED FUND GUIDELINES, TIPS, DOS AND DON TS More and more individuals and families are using donor advised funds (DAFs) either as their primary charitable giving vehicle or

MAKE THE MOST OF YOUR DONOR ADVISED FUND GUIDELINES, TIPS, DOS AND DON TS More and more individuals and families are using donor advised funds (DAFs) either as their primary charitable giving vehicle or

Guidelines for Donor Advised Funds

Guidelines for Donor Advised Funds 901 Route 10 PO Box 929 Whippany, New Jersey 07981-0929 Phone 973.929.3113 Fax 973.884.9316 SStone@jfedgmw.org www.jcfmetrowest.org Revised 12/14/2016 Creating a Donor

Guidelines for Donor Advised Funds 901 Route 10 PO Box 929 Whippany, New Jersey 07981-0929 Phone 973.929.3113 Fax 973.884.9316 SStone@jfedgmw.org www.jcfmetrowest.org Revised 12/14/2016 Creating a Donor

When Your Donor has a Donor Advised Fund

When Your Donor has a Donor Advised Fund Sindy L. Craig, J.D.,LL.M. Northern California Planned Giving Conference May 5, 2017 When Your Donor Has a Donor Advised Fund Overview Case Study: Framework for

When Your Donor has a Donor Advised Fund Sindy L. Craig, J.D.,LL.M. Northern California Planned Giving Conference May 5, 2017 When Your Donor Has a Donor Advised Fund Overview Case Study: Framework for

Why Donor Advised Funds and Supporting Organizations are a Gift Planner s Friend WENDY CHOU & BRIGIT KAVANAGH

Why Donor Advised Funds and Supporting Organizations are a Gift Planner s Friend WENDY CHOU & BRIGIT KAVANAGH Donor Advised Funds and Supporting Organizations The Other Grantmakers by Wendy Chou and Brigit

Why Donor Advised Funds and Supporting Organizations are a Gift Planner s Friend WENDY CHOU & BRIGIT KAVANAGH Donor Advised Funds and Supporting Organizations The Other Grantmakers by Wendy Chou and Brigit

Making Your Charitable Gifts Last Turn year-end giving into a longer-term strategy

Making Your Charitable Gifts Last Turn year-end giving into a longer-term strategy b y c ar ol g. k r o c h National Director of Philanthropic Planning Wilmington Trust Company ke y p oin t s Even as you

Making Your Charitable Gifts Last Turn year-end giving into a longer-term strategy b y c ar ol g. k r o c h National Director of Philanthropic Planning Wilmington Trust Company ke y p oin t s Even as you

Donor Advised Funds Through Donors Eyes

Presented by: Carlos S. Byrne, CAP Director of Relationship Management 617-722-7191 carlos.byrne@bnymellon.com Donor Advised Funds Through Donors Eyes May 24, 2018 Donor Advised Funds Through Donors Eyes

Presented by: Carlos S. Byrne, CAP Director of Relationship Management 617-722-7191 carlos.byrne@bnymellon.com Donor Advised Funds Through Donors Eyes May 24, 2018 Donor Advised Funds Through Donors Eyes

Your Guide to Gifts & Giving GIVE NOW. GIVE LATER. GIVE & RECEIVE.

Your Guide to Gifts & Giving GIVE NOW. GIVE LATER. GIVE & RECEIVE. GIVING SOLUTIONS TAILORED TO YOUR NEEDS At InFaith Community Foundation, we re committed to helping you give in ways that are right for

Your Guide to Gifts & Giving GIVE NOW. GIVE LATER. GIVE & RECEIVE. GIVING SOLUTIONS TAILORED TO YOUR NEEDS At InFaith Community Foundation, we re committed to helping you give in ways that are right for

Creating Philanthropy using Noncash Assets: Community Foundation Case Studies

Creating Philanthropy using Noncash Assets: Community Foundation Case Studies 1 Agenda Quick Intros Benefits to using Community Foundations Donor-Advised Funds Noncash Assets Statistics Case Studies 2

Creating Philanthropy using Noncash Assets: Community Foundation Case Studies 1 Agenda Quick Intros Benefits to using Community Foundations Donor-Advised Funds Noncash Assets Statistics Case Studies 2

Tax Reform and Its Impact on Nonprofits

Wednesday, April 11, 2018 Tax Reform and Its Impact on Nonprofits Jeff Chapman Mike Engle Chris Hoyt Corey Ziegler Presented by Tax Reform and Its Impact on Nonprofits Welcome Dana Knapp Luann Feehan Presented

Wednesday, April 11, 2018 Tax Reform and Its Impact on Nonprofits Jeff Chapman Mike Engle Chris Hoyt Corey Ziegler Presented by Tax Reform and Its Impact on Nonprofits Welcome Dana Knapp Luann Feehan Presented

Creative Philanthropy: Noncash Assets

Creative Philanthropy: Noncash Assets Dallas/Fort Worth FPA January 26 th, 2018 Dallas Foundation: Gary Garcia, CAP, Senior Director of Development Rod Riggins, CFA, CAP, Advisor Relations Officer 1 Agenda

Creative Philanthropy: Noncash Assets Dallas/Fort Worth FPA January 26 th, 2018 Dallas Foundation: Gary Garcia, CAP, Senior Director of Development Rod Riggins, CFA, CAP, Advisor Relations Officer 1 Agenda

The UBS Donor-Advised Fund. Program guide

The UBS Donor-Advised Fund Program guide Contents Creating a donor-advised fund...1 Assets accepted...1 Tax benefits...2 Contributions...2 Account valuation...3 Grantmaking...3 Administration...4 Investments...4

The UBS Donor-Advised Fund Program guide Contents Creating a donor-advised fund...1 Assets accepted...1 Tax benefits...2 Contributions...2 Account valuation...3 Grantmaking...3 Administration...4 Investments...4

Professional Notes SPRING 2019

Professional Notes SPRING 2019 TAX & ESTATE PLANNING : An Examination of Their Popularity and Legal Underpinnings This series of Professional Notes focuses on donor-advised funds. This first column examines

Professional Notes SPRING 2019 TAX & ESTATE PLANNING : An Examination of Their Popularity and Legal Underpinnings This series of Professional Notes focuses on donor-advised funds. This first column examines

Charitable Giving: Tax Benefits and Strategies

Charitable Giving: Tax Benefits and Strategies CPAs Attorneys Enrolled Agents Tax Professionals Professional Education Network TM Contents 1 Introduction 2 Overview of Tax Benefits 3 Tax Treatment of Gifts

Charitable Giving: Tax Benefits and Strategies CPAs Attorneys Enrolled Agents Tax Professionals Professional Education Network TM Contents 1 Introduction 2 Overview of Tax Benefits 3 Tax Treatment of Gifts

Issues AND. Tax-Powered Philanthropy: Doing well by doing good

Issues AND INSIGHTS February 2015 Tax-Powered Philanthropy: Doing well by doing good IN THIS ARTICLE Higher tax rates offer greater potential savings from charitable giving Strategies such as outright

Issues AND INSIGHTS February 2015 Tax-Powered Philanthropy: Doing well by doing good IN THIS ARTICLE Higher tax rates offer greater potential savings from charitable giving Strategies such as outright

2016 Estate Planning and Community Property Law Journal CLE & Expo March 4, 2016 Lubbock, Texas

2016 Estate Planning and Community Property Law Journal CLE & Expo March 4, 2016 Lubbock, Texas Darren B. Moore Bourland, Wall & Wenzel, P.C. Attorneys and Counselors 301 Commerce Street, Suite 1500 Fort

2016 Estate Planning and Community Property Law Journal CLE & Expo March 4, 2016 Lubbock, Texas Darren B. Moore Bourland, Wall & Wenzel, P.C. Attorneys and Counselors 301 Commerce Street, Suite 1500 Fort

The Center for Jewish Philanthropy Jewish Federation of Metropolitan Chicago. DONOR ADVISED FUNDS: Policies & Procedures

The Center for Jewish Philanthropy Jewish Federation of Metropolitan Chicago DONOR ADVISED FUNDS: Policies & Procedures Sec. 1 ESTABLISHMENT and PURPOSE 1.1 Establishment of Funds. Donor Advised Funds

The Center for Jewish Philanthropy Jewish Federation of Metropolitan Chicago DONOR ADVISED FUNDS: Policies & Procedures Sec. 1 ESTABLISHMENT and PURPOSE 1.1 Establishment of Funds. Donor Advised Funds

From Lindsey W. Duvall. Duvall Law Firm, LLC. 147 Old Solomons Island Road Suite 306 Annapolis MD

Uncovering Charitable Planning Opportunities Volume 7, Issue 11 Charitable giving is discretionary spending. It is affected by both the economy and the income tax rates. Not surprisingly, charitable giving

Uncovering Charitable Planning Opportunities Volume 7, Issue 11 Charitable giving is discretionary spending. It is affected by both the economy and the income tax rates. Not surprisingly, charitable giving

Giving is a part of life. Charitable Giving With Life Insurance

Giving is a part of life Charitable Giving With Life Insurance If you are interested in giving more to charity, life insurance may be able to help. When properly implemented, a life insurance policy may

Giving is a part of life Charitable Giving With Life Insurance If you are interested in giving more to charity, life insurance may be able to help. When properly implemented, a life insurance policy may

Planned Giving 201. Presented by Christy Eckoff, JD, LL.M. Director of Gift Planning

Planned Giving 201 Presented by Christy Eckoff, JD, LL.M. Director of Gift Planning The Community Foundation for Greater Atlanta Bullet Mission information here To be the most trusted resource for growing

Planned Giving 201 Presented by Christy Eckoff, JD, LL.M. Director of Gift Planning The Community Foundation for Greater Atlanta Bullet Mission information here To be the most trusted resource for growing

Charitable Gift Fund Program Circular. December 2017

Charitable Gift Fund Program Circular December 2017 Introduction The J.P. Morgan Securities Charitable Gift Fund ( JPMSCGF ) is a donor-advised fund that facilitates charitable giving by individuals and

Charitable Gift Fund Program Circular December 2017 Introduction The J.P. Morgan Securities Charitable Gift Fund ( JPMSCGF ) is a donor-advised fund that facilitates charitable giving by individuals and

Private foundations Establishing a vehicle for your charitable vision

Private foundations Establishing a vehicle for your charitable vision I didn t know where to start. The advice I received on creating a private foundation pointed me in the right direction, and now I m

Private foundations Establishing a vehicle for your charitable vision I didn t know where to start. The advice I received on creating a private foundation pointed me in the right direction, and now I m

Philanthropy as a Family Affair: Using a Private Foundation to Achieve Your Charitable Goals ~ Susan B. Hecker

Philanthropy as a Family Affair: Using a Private Foundation to Achieve Your Charitable Goals ~ Susan B. Hecker Establishing a private foundation can be a fulfilling way to work with charities, but be prepared

Philanthropy as a Family Affair: Using a Private Foundation to Achieve Your Charitable Goals ~ Susan B. Hecker Establishing a private foundation can be a fulfilling way to work with charities, but be prepared

DONOR ADVISED FUND POLICIES AND GUIDELINES

DONOR ADVISED FUND POLICIES AND GUIDELINES March 2017 BNY MELLON CHARITABLE GIFT FUND is a service mark of The Bank of New York Mellon Corporation. 2017 BNY MELLON CHARITABLE GIFT FUND. All rights reserved.

DONOR ADVISED FUND POLICIES AND GUIDELINES March 2017 BNY MELLON CHARITABLE GIFT FUND is a service mark of The Bank of New York Mellon Corporation. 2017 BNY MELLON CHARITABLE GIFT FUND. All rights reserved.

Donor Advised Fund Guidelines

Policy Revised Dec 2011 Reviewed Nov 2013 Donor Advised Fund Guidelines Donor Advised Funds give donors an unparalleled opportunity to: play an active, personal role in their charitable giving; enhance

Policy Revised Dec 2011 Reviewed Nov 2013 Donor Advised Fund Guidelines Donor Advised Funds give donors an unparalleled opportunity to: play an active, personal role in their charitable giving; enhance

2018 Options and Opportunities: Charitable Giving and the New Tax Rules

2018 Options and Opportunities: Charitable Giving and the New Tax Rules Page 1 Single filers (2018 2025): Joint filers (2018 2025): Page 2 In 2017, the standard deduction combined with the personal exemption

2018 Options and Opportunities: Charitable Giving and the New Tax Rules Page 1 Single filers (2018 2025): Joint filers (2018 2025): Page 2 In 2017, the standard deduction combined with the personal exemption

Charitable Giving Options for 2018 and Beyond. Tama Brooks Klosek Klosek & Associates PLLC Planned Giving Council of Houston April 26, 2018

Charitable Giving Options for 2018 and Beyond Tama Brooks Klosek Klosek & Associates PLLC Planned Giving Council of Houston April 26, 2018 TAMA BROOKS KLOSEK Tama has a tax practice focused on both the

Charitable Giving Options for 2018 and Beyond Tama Brooks Klosek Klosek & Associates PLLC Planned Giving Council of Houston April 26, 2018 TAMA BROOKS KLOSEK Tama has a tax practice focused on both the

The UBS Donor-Advised Fund program guide

The UBS Donor-Advised Fund program guide Contents Creating a donor-advised fund...1 Assets accepted...2 Tax benefits...2 Contributions...2 Account valuation...3 Grantmaking...3 Administration...4 Investments...4

The UBS Donor-Advised Fund program guide Contents Creating a donor-advised fund...1 Assets accepted...2 Tax benefits...2 Contributions...2 Account valuation...3 Grantmaking...3 Administration...4 Investments...4

A Guide to Your Donor-Advised Fund

A Guide to Your Donor-Advised Fund Introduction Thank you for your interest in establishing a donor-advised fund (DAF) with National Philanthropic Trust (NPT). NPT is a tax-exempt public charity under

A Guide to Your Donor-Advised Fund Introduction Thank you for your interest in establishing a donor-advised fund (DAF) with National Philanthropic Trust (NPT). NPT is a tax-exempt public charity under

Tax Relief and Giving Your Way

Tax Relief and Giving Your Way The Donor Advised Fund Presented by: Scott Talbot, CFP, CAP Director of Planned Giving The Great Commission Foundation & Michael Occhipinti, MBT Gift Planning Advisor Wycliffe

Tax Relief and Giving Your Way The Donor Advised Fund Presented by: Scott Talbot, CFP, CAP Director of Planned Giving The Great Commission Foundation & Michael Occhipinti, MBT Gift Planning Advisor Wycliffe

Program Description. Purpose

Program Description Purpose The following sections describe policies, rules and regulations of the GuideStream Charitable Gift Fund (GuideStream). GuideStream s primary activities consist of assisting

Program Description Purpose The following sections describe policies, rules and regulations of the GuideStream Charitable Gift Fund (GuideStream). GuideStream s primary activities consist of assisting

Charitable Conversations...

Welcome The Community Foundation of the Holland/Zeeland Area is a public charity that as of 2015 manages over $55 million in charitable assets spread across 475 different funds that have been established

Welcome The Community Foundation of the Holland/Zeeland Area is a public charity that as of 2015 manages over $55 million in charitable assets spread across 475 different funds that have been established

PNC CENTER FOR FINANCIAL INSIGHT

PNC CENTER FOR FINANCIAL INSIGHT Tax Reform and Philanthropy: Exploring Why and How You Give The new tax law will have sweeping implications on charitable giving, creating a greater urgency to examine

PNC CENTER FOR FINANCIAL INSIGHT Tax Reform and Philanthropy: Exploring Why and How You Give The new tax law will have sweeping implications on charitable giving, creating a greater urgency to examine

Charitable Planning Guide

Charitable Planning Guide Purpose of this Guide This guide is designed to provide an overview of the benefits of incorporating charitable giving into your financial planning including common techniques

Charitable Planning Guide Purpose of this Guide This guide is designed to provide an overview of the benefits of incorporating charitable giving into your financial planning including common techniques

Private Foundations Deeper Dive

Private Foundations Deeper Dive David Lawson, Davis Wright Tremaine November 2, 2017 Seattle, Washington What is a private foundation? Can be a nonprofit corporation or a charitable trust Nonprofit corporation

Private Foundations Deeper Dive David Lawson, Davis Wright Tremaine November 2, 2017 Seattle, Washington What is a private foundation? Can be a nonprofit corporation or a charitable trust Nonprofit corporation

Advised Fund Policy Statement LEGACY FUND

Advised Fund Policy Statement LEGACY FUND A Legacy Fund at the Oklahoma City Community Foundation is an extremely simple way for an individual, family or even a corporation to create a permanent fund,

Advised Fund Policy Statement LEGACY FUND A Legacy Fund at the Oklahoma City Community Foundation is an extremely simple way for an individual, family or even a corporation to create a permanent fund,

Frequently Asked Questions About Company Foundations and Corporate Giving

Welcome to Our 2006 Seminar Series: Frequently Asked Questions About Company Foundations and Corporate Giving May 23, 2006 1 Speakers: Victoria Bjorklund David Shevlin 2006 Simpson Thacher & Bartlett LLP.

Welcome to Our 2006 Seminar Series: Frequently Asked Questions About Company Foundations and Corporate Giving May 23, 2006 1 Speakers: Victoria Bjorklund David Shevlin 2006 Simpson Thacher & Bartlett LLP.

The Tax Act of 2017: What Just Happened? And What Does It Mean for Charities? Ruth Madrigal

The Tax Act of 2017: What Just Happened? And What Does It Mean for Charities? Ruth Madrigal The Tax Act of 2017: H.R. 1 The Tax Cuts and Jobs Act short title was stricken An Act to provide for reconciliation

The Tax Act of 2017: What Just Happened? And What Does It Mean for Charities? Ruth Madrigal The Tax Act of 2017: H.R. 1 The Tax Cuts and Jobs Act short title was stricken An Act to provide for reconciliation

Client Advisory. Changes for Charities and Donors in the Pension Protection Act By Douglas D. Thomson. Corporate and Business

Client Advisory www.frostbrowntodd.com Corporate and Business August 30, 2006 Changes for Charities and Donors in the Pension Protection Act By Douglas D. Thomson On August 17, 2006, President Bush signed

Client Advisory www.frostbrowntodd.com Corporate and Business August 30, 2006 Changes for Charities and Donors in the Pension Protection Act By Douglas D. Thomson On August 17, 2006, President Bush signed

QUALIFYING FOR PUBLIC CHARITY STATUS: The Section 170(b)(1)(A)(vi) and 509(a)(1) Test and the Section 509(a)(2) Test

(1)(A)(vi) and 509(a)(1) Test and the Section 509(a)(2) Test") QUALIFYING FOR PUBLIC CHARITY STATUS: The Section 170(b)(1)(A)(vi) and 509(a)(1) Test and the Section 509(a)(2) Test Tax-exempt status under Section 501(c)(3) of the Internal Revenue Code permits a charitable

QUALIFYING FOR PUBLIC CHARITY STATUS: The Section 170(b)(1)(A)(vi) and 509(a)(1) Test and the Section 509(a)(2) Test Tax-exempt status under Section 501(c)(3) of the Internal Revenue Code permits a charitable

DONOR ADVISED FUND PROGRAM CIRCULAR. An Overview, Rules and Regulations of Rotary s Donor Advised Fund

DONOR ADVISED FUND PROGRAM CIRCULAR An Overview, Rules and Regulations of Rotary s Donor Advised Fund Updated 1 July 2014 Welcome to Rotary s Donor Advised Fund. Please read this Program Circular carefully.

DONOR ADVISED FUND PROGRAM CIRCULAR An Overview, Rules and Regulations of Rotary s Donor Advised Fund Updated 1 July 2014 Welcome to Rotary s Donor Advised Fund. Please read this Program Circular carefully.

Donor-Advised Fund Agreement

Donor-Advised Fund Agreement Date: This Agreement updates and supersedes any previous Donor-Advised Fund Agreement with Jewish Federation of Greater Atlanta. Delivery is hereby made by the undersigned

Donor-Advised Fund Agreement Date: This Agreement updates and supersedes any previous Donor-Advised Fund Agreement with Jewish Federation of Greater Atlanta. Delivery is hereby made by the undersigned

IRS Issues Interim Guidance on Provisions in Pension Protection Act of 2006 Relating to Supporting Organizations & Donor Advised Funds

IRS Issues Interim Guidance on Provisions in Pension Protection Act of 2006 Relating to Supporting Organizations & Donor Advised Funds By Suzanne Ross McDowell Catherine W. Wilkinson Randal T. Evans On

IRS Issues Interim Guidance on Provisions in Pension Protection Act of 2006 Relating to Supporting Organizations & Donor Advised Funds By Suzanne Ross McDowell Catherine W. Wilkinson Randal T. Evans On

Kingdom Advisors Charitable Giving Tool Kit

I. Outright charitable gift arrangements Kingdom Advisors Charitable Giving Tool Kit Gifts of appreciated publicly-traded stock or real estate: For most donors, gifts of appreciated assets are more beneficial

I. Outright charitable gift arrangements Kingdom Advisors Charitable Giving Tool Kit Gifts of appreciated publicly-traded stock or real estate: For most donors, gifts of appreciated assets are more beneficial

Wealth structuring and estate planning. Your vision and your legacy. Life s better when we re connected

Wealth structuring and estate planning Your vision and your legacy Life s better when we re connected Inside 1 Helping you shape the future 2 The elements of wealth structuring 4 The power and flexibility

Wealth structuring and estate planning Your vision and your legacy Life s better when we re connected Inside 1 Helping you shape the future 2 The elements of wealth structuring 4 The power and flexibility

Private foundations Establishing a vehicle for your charitable vision

Private foundations Establishing a vehicle for your charitable vision I didn t know where to start. The advice I received on creating a private foundation pointed me in the right direction, and now I m

Private foundations Establishing a vehicle for your charitable vision I didn t know where to start. The advice I received on creating a private foundation pointed me in the right direction, and now I m

PRIVATE FOUNDATION VERSUS PUBLIC CHARITY (Non Profit Advisory No. 5)

") PRIVATE FOUNDATION VERSUS PUBLIC CHARITY (Non Profit Advisory No. 5) Most nonprofit entities -- and especially their primary donors -- want to insure that they have public charity status for the 50% deduction

PRIVATE FOUNDATION VERSUS PUBLIC CHARITY (Non Profit Advisory No. 5) Most nonprofit entities -- and especially their primary donors -- want to insure that they have public charity status for the 50% deduction

Charitable Gifts II: Deferred Giving Techniques

Charitable Gifts II: Deferred Giving Techniques Susan Berkman, J.D. Assistant Vice President, Gift Planning California State University, Long Beach This information is for educational purposes only and

Charitable Gifts II: Deferred Giving Techniques Susan Berkman, J.D. Assistant Vice President, Gift Planning California State University, Long Beach This information is for educational purposes only and

What is Planned Giving?

What is Planned Giving? Church of the Nazarene Foundation 17001 Prairie Star Parkway, Suite 200 Lenexa, KS 66220 (913) 577-2983 info@nazarenefoundation.org www.nazarenefoundation.org Planned Giving: A

What is Planned Giving? Church of the Nazarene Foundation 17001 Prairie Star Parkway, Suite 200 Lenexa, KS 66220 (913) 577-2983 info@nazarenefoundation.org www.nazarenefoundation.org Planned Giving: A

Six Alternatives to Traditional Holiday Gifts. Member FINRA/SIPC

Six Alternatives to Traditional Holiday Gifts Gifts That Pay Off We ve all been there. A holiday is approaching, and you need to purchase a holiday gift. Or maybe it s a present to mark a special occasion

Six Alternatives to Traditional Holiday Gifts Gifts That Pay Off We ve all been there. A holiday is approaching, and you need to purchase a holiday gift. Or maybe it s a present to mark a special occasion

PROCEDURES FOR OPERATION OF DONOR-ADVISED/PHILANTHROPIC FUNDS

PROCEDURES FOR OPERATION OF DONOR-ADVISED/PHILANTHROPIC FUNDS Sec.1. ESTABLISHMENT AND PURPOSE 1.1. Authorization. The Jewish Federation of Cincinnati ( JFC ) authorized the establishment of Philanthropic

PROCEDURES FOR OPERATION OF DONOR-ADVISED/PHILANTHROPIC FUNDS Sec.1. ESTABLISHMENT AND PURPOSE 1.1. Authorization. The Jewish Federation of Cincinnati ( JFC ) authorized the establishment of Philanthropic

2016 Charitable Giving Review

2016 Charitable Giving Review SUMMARY TABLE OF CONTENTS With the end of the year approaching rapidly, Morgan Stanley Global Impact Funding Trust, Inc. ( Morgan Stanley GIFT ) would like to take this opportunity

2016 Charitable Giving Review SUMMARY TABLE OF CONTENTS With the end of the year approaching rapidly, Morgan Stanley Global Impact Funding Trust, Inc. ( Morgan Stanley GIFT ) would like to take this opportunity

The 2008 Bank of America Study of High Net Worth Philanthropy Issues Driving Charitable Activities Among Affluent Households

The 2008 Bank of America Study of High Net Worth Philanthropy Issues Driving Charitable Activities Among Affluent Households April 20, 2010 Ramsay H. Slugg Senior Vice President National Wealth Strategies

The 2008 Bank of America Study of High Net Worth Philanthropy Issues Driving Charitable Activities Among Affluent Households April 20, 2010 Ramsay H. Slugg Senior Vice President National Wealth Strategies

A DONOR S GUIDE. https://rcf.reninc.com RCF A DONOR S GUIDE 1 RCF_DG_

A DONOR S GUIDE RCF A DONOR S GUIDE 1 Helping your philanthropy go further You know how gratifying it is to support a worthy cause. What if you could create an enduring legacy through your charitable contributions?

A DONOR S GUIDE RCF A DONOR S GUIDE 1 Helping your philanthropy go further You know how gratifying it is to support a worthy cause. What if you could create an enduring legacy through your charitable contributions?

Wealth Advisors and JCF: An Opportunity in Common

Wealth Advisors and JCF: An Opportunity in Common A New Advice Premium Focused on Philanthropy: With recent market tailwinds and concern about rising tax rates, the appeal of strategic charitable giving

Wealth Advisors and JCF: An Opportunity in Common A New Advice Premium Focused on Philanthropy: With recent market tailwinds and concern about rising tax rates, the appeal of strategic charitable giving

A DONOR S GUIDE. https://rcf.reninc.com RCF A DONOR S GUIDE 1 RCF_DG_

A DONOR S GUIDE RCF A DONOR S GUIDE 1 Helping your philanthropy go further You know how gratifying it is to support a worthy cause. What if you could create an enduring legacy through your charitable contributions?

A DONOR S GUIDE RCF A DONOR S GUIDE 1 Helping your philanthropy go further You know how gratifying it is to support a worthy cause. What if you could create an enduring legacy through your charitable contributions?

Donor Advised Fund. New Bremen Foundation Fund Agreement. P.O. Box 97, New Bremen, Ohio 45869

03-19-14 Donor Advised Fund New Bremen Foundation Fund Agreement P.O. Box 97, New Bremen, Ohio 45869 I. General Information A. FUND DONOR Fill in all areas. Individual Trust/Foundation Estate Corporation

03-19-14 Donor Advised Fund New Bremen Foundation Fund Agreement P.O. Box 97, New Bremen, Ohio 45869 I. General Information A. FUND DONOR Fill in all areas. Individual Trust/Foundation Estate Corporation

Donor-Advised Fund Report

2010 Donor-Advised Fund Report This report was edited and compiled by Andrew W. Hastings, Vice President of Business Development at National Philanthropic Trust. Research assistance was provided by Paul

2010 Donor-Advised Fund Report This report was edited and compiled by Andrew W. Hastings, Vice President of Business Development at National Philanthropic Trust. Research assistance was provided by Paul

Program Guidelines. Bank of America Charitable Gift Fund CONTRIBUTIONS TO THE BANK OF AMERICA CHARITABLE GIFT FUND

Bank of America Charitable Gift Fund Program Guidelines The following document outlines the Guidelines that govern the Bank of America Charitable Gift Fund (Charitable Gift Fund) including contributions,

Bank of America Charitable Gift Fund Program Guidelines The following document outlines the Guidelines that govern the Bank of America Charitable Gift Fund (Charitable Gift Fund) including contributions,

RECENT DEVELOPMENTS AFFECTING TAX-EXEMPT ORGANIZATIONS

BEYOND THE 990 Recent Developments, Unrelated Business Income Tax and Other Taxes Affecting Nonprofit Organizations David S. Rosen, Esq., CPA RS&F MACPA 2012 Government and Not For Profit Conference April

BEYOND THE 990 Recent Developments, Unrelated Business Income Tax and Other Taxes Affecting Nonprofit Organizations David S. Rosen, Esq., CPA RS&F MACPA 2012 Government and Not For Profit Conference April

DONOR ADVISED FUND AGREEMENT between and The Virginia United Methodist Foundation

DONOR ADVISED FUND AGREEMENT between and The Virginia United Methodist Foundation This Agreement is effective the day of, 20 between (Donor) of (address) and the Virginia United Methodist Foundation of

DONOR ADVISED FUND AGREEMENT between and The Virginia United Methodist Foundation This Agreement is effective the day of, 20 between (Donor) of (address) and the Virginia United Methodist Foundation of

Summary of Charitable Provisions in H.R. 4 Pension Protection Act of 2006

Summary of Charitable Provisions in H.R. 4 Pension Protection Act of 2006 This is a summary of the provisions in the Pension Protection Act of 2006 (H.R. 4) that most directly affect grantmakers. It is

Summary of Charitable Provisions in H.R. 4 Pension Protection Act of 2006 This is a summary of the provisions in the Pension Protection Act of 2006 (H.R. 4) that most directly affect grantmakers. It is

FIDELITY CHARITABLE POLICY GUIDELINES: Program Circular

FIDELITY CHARITABLE POLICY GUIDELINES: Program Circular FIDELITY CHARITABLE POLICY GUIDELINES This Program Circular ( Circular ) describes the donor-advised fund program of Fidelity Charitable, as well

FIDELITY CHARITABLE POLICY GUIDELINES: Program Circular FIDELITY CHARITABLE POLICY GUIDELINES This Program Circular ( Circular ) describes the donor-advised fund program of Fidelity Charitable, as well

Charitable Gifting: Overview and Tax Implications. Overview. Tax Implications - Charitable Deduction Rules

Overview Charitable Gifting: Overview and Tax Implications The desire to assist a charitable organization must be a primary motive for making a gift; if no charitable inclination exists, charitable giving

Overview Charitable Gifting: Overview and Tax Implications The desire to assist a charitable organization must be a primary motive for making a gift; if no charitable inclination exists, charitable giving

Planned Giving Made Simple

The webinar will begin at 12 p.m. Central Daylight Time Planned Giving Made Simple April 29, 2015 PRESENTED BY Lynn M. Gaumer, J.D. Senior Technical Consultant The Stelter Company Philip Purcell, J.D.

The webinar will begin at 12 p.m. Central Daylight Time Planned Giving Made Simple April 29, 2015 PRESENTED BY Lynn M. Gaumer, J.D. Senior Technical Consultant The Stelter Company Philip Purcell, J.D.

Giving Today to Guarantee Tomorrow: A Lesson in Charitable Giving

Giving Today to Guarantee Tomorrow: A Lesson in Charitable Giving A careful review of the various ways to structure charitable gifts can help make your gifts more meaningful, both to you and to the charities

Giving Today to Guarantee Tomorrow: A Lesson in Charitable Giving A careful review of the various ways to structure charitable gifts can help make your gifts more meaningful, both to you and to the charities

March 5, CC:PA:LPD:PR (Notice ) Room 5203 P.O. Box 7604 Ben Franklin Station Washington, DC RE: Comments Regarding Notice

Room 5203 P.O. Box 7604 Ben Franklin Station Washington, DC RE: Comments Regarding Notice") March 5, 2018 Internal Revenue Service CC:PA:LPD:PR (Notice 2017-73) Room 5203 P.O. Box 7604 Ben Franklin Station Washington, DC 20044 Via Email: Notice.Comments@irscounsel.treas.gov RE: Comments Regarding

March 5, 2018 Internal Revenue Service CC:PA:LPD:PR (Notice 2017-73) Room 5203 P.O. Box 7604 Ben Franklin Station Washington, DC 20044 Via Email: Notice.Comments@irscounsel.treas.gov RE: Comments Regarding

Year-End Planning 2017

Wealth Management Year-End Planning Executive Summary As we approach the end of, it is time to review traditional year-end planning decisions. We are aware of the significant changes in the tax code currently

Wealth Management Year-End Planning Executive Summary As we approach the end of, it is time to review traditional year-end planning decisions. We are aware of the significant changes in the tax code currently

THE AMERICAN LAW INSTITUTE Continuing Legal Education. Estate Planning for the Family Business Owner

473 THE AMERICAN LAW INSTITUTE Continuing Legal Education Estate Planning for the Family Business Owner Cosponsored by the ABA Section of Real Property, Trust and Estate Law and ABA Section of Taxation

473 THE AMERICAN LAW INSTITUTE Continuing Legal Education Estate Planning for the Family Business Owner Cosponsored by the ABA Section of Real Property, Trust and Estate Law and ABA Section of Taxation

Private Foundations vs. Donor Advised Funds

The Path of Least Resistance Converting Private Foundations to Donor Advised Funds Cherie Evans Evans & Rosen LLP Berkeley, California 415.703.0300 cherie@evansrosen.com www.evansrosen.com 2016 Evans &

The Path of Least Resistance Converting Private Foundations to Donor Advised Funds Cherie Evans Evans & Rosen LLP Berkeley, California 415.703.0300 cherie@evansrosen.com www.evansrosen.com 2016 Evans &

Endowment funds at the Catholic Foundation can support things like:

HOW TO GIVE Making a Gift Why give to the Foundation? The Catholic Foundation of Maine offers donors several gifting opportunities to help them fulfill their charitable intentions. By creating a legacy

HOW TO GIVE Making a Gift Why give to the Foundation? The Catholic Foundation of Maine offers donors several gifting opportunities to help them fulfill their charitable intentions. By creating a legacy

Tax Exempt and Charitable Planning

Tax Exempt and Charitable Planning Bryan Cave lawyers routinely assist numerous nonprofit and tax-exempt organizations to achieve their missions. Our lawyers also routinely assist individuals interested

Tax Exempt and Charitable Planning Bryan Cave lawyers routinely assist numerous nonprofit and tax-exempt organizations to achieve their missions. Our lawyers also routinely assist individuals interested

A Resource for Charitable Giving

A Resource for Charitable Giving Your clients care about giving. At the Community Foundation we help people contribute to their community during their lifetime, and through planned giving. Partnering with

A Resource for Charitable Giving Your clients care about giving. At the Community Foundation we help people contribute to their community during their lifetime, and through planned giving. Partnering with

Accounting, Counting & Recognition Beyond the Annual Fund

Accounting, Counting & Recognition Beyond the Annual Fund April 11, 2019 Marie Ruzek Senior Philanthropic Specialist, Wells Fargo Philanthropic Services Athena Mihas Vice President, Finance, Greater Twin

Accounting, Counting & Recognition Beyond the Annual Fund April 11, 2019 Marie Ruzek Senior Philanthropic Specialist, Wells Fargo Philanthropic Services Athena Mihas Vice President, Finance, Greater Twin

SOFTWARE FREEDOM CONSERVANCY, INC

SOFTWARE FREEDOM CONSERVANCY, INC. 41-2203632 SOFTWARE FREEDOM CONSERVANCY, INC. 41-2203632 SOFTWARE FREEDOM CONSERVANCY, INC. 41-2203632 SOFTWARE FREEDOM CONSERVANCY, INC. 41-2203632 SOFTWARE FREEDOM

SOFTWARE FREEDOM CONSERVANCY, INC. 41-2203632 SOFTWARE FREEDOM CONSERVANCY, INC. 41-2203632 SOFTWARE FREEDOM CONSERVANCY, INC. 41-2203632 SOFTWARE FREEDOM CONSERVANCY, INC. 41-2203632 SOFTWARE FREEDOM

Couple choo Simplicity combines enduring c Art and Ginger Nowak s first planned gift to the Community Foundation of Johnson County (CFJC) followed a financial planning discussion with their attorney, who

Couple choo Simplicity combines enduring c Art and Ginger Nowak s first planned gift to the Community Foundation of Johnson County (CFJC) followed a financial planning discussion with their attorney, who

23 rd Annual Health Sciences Tax Conference

23 rd Annual Health Sciences Tax Conference and public charity status December 9, 2013 Disclaimer Any US tax advice contained herein was not intended or written to be used, and cannot be used, for the

23 rd Annual Health Sciences Tax Conference and public charity status December 9, 2013 Disclaimer Any US tax advice contained herein was not intended or written to be used, and cannot be used, for the

Charity Issues Threshold for Foundations

Charity Issues Threshold for Foundations 2016 Loyola Estate Planning Conference December 1, 2016 Pan American Life Center New Orleans, LA Bonnie M. Wyllie Lukinovich A Professional Law Corporation 4415

Charity Issues Threshold for Foundations 2016 Loyola Estate Planning Conference December 1, 2016 Pan American Life Center New Orleans, LA Bonnie M. Wyllie Lukinovich A Professional Law Corporation 4415

University Fund. Why I Give

University Fund MAKE A TANGIBLE IMPACT ON OUR STUDENTS. Funding from the commonwealth addresses less than 35% of the real cost associated with educating a student today, and tuition and fees alone do not

University Fund MAKE A TANGIBLE IMPACT ON OUR STUDENTS. Funding from the commonwealth addresses less than 35% of the real cost associated with educating a student today, and tuition and fees alone do not

Fund Agreements: Best Practices. Phil Purcell, JD Consultant for Philanthropy, LLC Copyright rights reserved

Fund Agreements: Best Practices Phil Purcell, JD Consultant for Philanthropy, LLC pmpurcell@outlook.com Copyright 2017@All rights reserved Outline Fund Agreement (FA) Basics What should a FA say? Special

Fund Agreements: Best Practices Phil Purcell, JD Consultant for Philanthropy, LLC pmpurcell@outlook.com Copyright 2017@All rights reserved Outline Fund Agreement (FA) Basics What should a FA say? Special

A Guide to Your Donor-Advised Fund

A Guide to Your Donor-Advised Fund Contents Introduction 1 About National Philanthropic Trust 1 About Hollencrest Securities 1 The Independent Charitable Gift Fund 1 Creating a Donor-Advised Fund 2 Contributions

A Guide to Your Donor-Advised Fund Contents Introduction 1 About National Philanthropic Trust 1 About Hollencrest Securities 1 The Independent Charitable Gift Fund 1 Creating a Donor-Advised Fund 2 Contributions

Internal Revenue Service CC:PA:LPD:PR (Notice ), Room 5203 P.O. Box 7604 Ben Franklin Station, Washington, DC 20044,

, Room 5203 P.O. Box 7604 Ben Franklin Station, Washington, DC 20044,") March 5, 2018 Internal Revenue Service CC:PA:LPD:PR (Notice 2017-73), Room 5203 P.O. Box 7604 Ben Franklin Station, Washington, DC 20044, Attn: Amber L. MacKenzie and Ward L. Thomas Office of Associate

March 5, 2018 Internal Revenue Service CC:PA:LPD:PR (Notice 2017-73), Room 5203 P.O. Box 7604 Ben Franklin Station, Washington, DC 20044, Attn: Amber L. MacKenzie and Ward L. Thomas Office of Associate

Please understand that this podcast is not intended to be legal advice. As always, you should contact your WEALTH TRANSFER STRATEGIES

WEALTH TRANSFER STRATEGIES Hello and welcome. Northern Trust is proud to sponsor this podcast, Wealth Transfer Strategies, the third in a series based on our book titled Legacy: Conversations about Wealth

WEALTH TRANSFER STRATEGIES Hello and welcome. Northern Trust is proud to sponsor this podcast, Wealth Transfer Strategies, the third in a series based on our book titled Legacy: Conversations about Wealth

How to Make a Difference Now and in the Future

How to Make a Difference Now and in the Future Josh D. McDowell Founder Josh McDowell Ministry Jay R. Link, CGPA Senior Planned Giving Consultant The Great Commission Foundation What We Will Cover What

How to Make a Difference Now and in the Future Josh D. McDowell Founder Josh McDowell Ministry Jay R. Link, CGPA Senior Planned Giving Consultant The Great Commission Foundation What We Will Cover What

A. There is no more estate tax, so the use of private foundations is not motivated by tax avoidance.

Rocky Mountain Tax Seminar for Private Foundations Estate Taxes, Donor Advised Funds, and Supporting Organizations: Are Private Foundations Obsolete? September 1, 2010 James K. Hasson, Jr. I. Arguments

Rocky Mountain Tax Seminar for Private Foundations Estate Taxes, Donor Advised Funds, and Supporting Organizations: Are Private Foundations Obsolete? September 1, 2010 James K. Hasson, Jr. I. Arguments

CHARITABLE GIFT FUND USER S GUIDE

CHARITABLE GIFT FUND USER S GUIDE CHARITABLE GIFT FUND USER'S GUIDE Thank you for your interest in Anabaptist Foundation s Charitable Gift Fund (CGF) Program. We have collected the most frequently asked

CHARITABLE GIFT FUND USER S GUIDE CHARITABLE GIFT FUND USER'S GUIDE Thank you for your interest in Anabaptist Foundation s Charitable Gift Fund (CGF) Program. We have collected the most frequently asked

ESTATE PLANNING 1 / 11

2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 What happens to my money and assets after I die? No matter what your age or income, you need to

2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 What happens to my money and assets after I die? No matter what your age or income, you need to

CGP Legislative Update. November 6, 2017

CGP Legislative Update November 6, 2017 House I N T R O D U C T I O N M A R K - UP F L O O R A C T I O N Individuals Creates individual tax brackets of 12%, 25%, 35%, and maintains 39.6% for higher-income

CGP Legislative Update November 6, 2017 House I N T R O D U C T I O N M A R K - UP F L O O R A C T I O N Individuals Creates individual tax brackets of 12%, 25%, 35%, and maintains 39.6% for higher-income

Donor-Advised Fund Program Guide

Donor-Advised Fund Program Guide In accordance with the Pension Protection Act of 2006, the U.S. Department of Treasury and the Internal Revenue Service may update regulations for donor-advised funds.

Donor-Advised Fund Program Guide In accordance with the Pension Protection Act of 2006, the U.S. Department of Treasury and the Internal Revenue Service may update regulations for donor-advised funds.

Estate Planning Through Charitable Gifting

Donna Sheehy, CFP 29605 US Highway 19 Suite 250 Clearwater, FL 33761 727-943-8813 dsheehy@harborfs.com www.investdonna.com Estate Planning Through Charitable Gifting Call today for a personal consultation

Donna Sheehy, CFP 29605 US Highway 19 Suite 250 Clearwater, FL 33761 727-943-8813 dsheehy@harborfs.com www.investdonna.com Estate Planning Through Charitable Gifting Call today for a personal consultation

What Must a Tax-Exempt Organization Do To Acknowledge Donations?

What Must a Tax-Exempt Organization Do To Acknowledge Donations? An important feature of being a tax-exempt organization under Section 501(c)(3) of the Internal Revenue Code is the ability to accept tax-deductible

What Must a Tax-Exempt Organization Do To Acknowledge Donations? An important feature of being a tax-exempt organization under Section 501(c)(3) of the Internal Revenue Code is the ability to accept tax-deductible

DONOR-ADVISED FUND PROGRAM GUIDE

DONOR-ADVISED FUND PROGRAM GUIDE In accordance with the Pension Protection Act of 2006, the U.S. Department of Treasury and the Internal Revenue Service will soon be updating regulations for donor advised

DONOR-ADVISED FUND PROGRAM GUIDE In accordance with the Pension Protection Act of 2006, the U.S. Department of Treasury and the Internal Revenue Service will soon be updating regulations for donor advised

PLANNED GIVING ESSENTIALS

PLANNED GIVING ESSENTIALS PRESENTED BY: ELISA M. SMITH, CPA/PFS PRESENTED FOR: COMMUNITY FOUNDATION OF GREATER FORT WAYNE PRESENTED ON: OCTOBER 7, 2015 OVERVIEW OF PRESENTATION Why you NEED a Planned

PLANNED GIVING ESSENTIALS PRESENTED BY: ELISA M. SMITH, CPA/PFS PRESENTED FOR: COMMUNITY FOUNDATION OF GREATER FORT WAYNE PRESENTED ON: OCTOBER 7, 2015 OVERVIEW OF PRESENTATION Why you NEED a Planned

Basic Certification Test: Study Guide for Tax Year 2017

Basic Certification Test: Study Guide for Tax Year 2017 TRAINING PRACTICE PROBLEMS 2018 i The items in parentheses refer to sections or page numbers in Publication 4012, Volunteer Resource Guide. It s

Basic Certification Test: Study Guide for Tax Year 2017 TRAINING PRACTICE PROBLEMS 2018 i The items in parentheses refer to sections or page numbers in Publication 4012, Volunteer Resource Guide. It s

Asset Protection. A planning, conversation, and resource guide

Asset Protection A planning, conversation, and resource guide LOREM IPSUM A PLANNING, CONVERSATION, AND RESOURCE GUIDE Use this guide to help create a plan for protecting those you love and what you have.

Asset Protection A planning, conversation, and resource guide LOREM IPSUM A PLANNING, CONVERSATION, AND RESOURCE GUIDE Use this guide to help create a plan for protecting those you love and what you have.

A Guide to Planned Giving

A Guide to Planned Giving - A Guide to Plan Giving What is Planned Giving? The integration of personal, financial and estate planning goals with lifetime or testamentary charitable giving. An opportunity

A Guide to Planned Giving - A Guide to Plan Giving What is Planned Giving? The integration of personal, financial and estate planning goals with lifetime or testamentary charitable giving. An opportunity

Introduction of Advisors Charitable Gift Fund Page 3. Advantages Page 5. Definitions Page 6. Contributions Page 9. Investment of the Endowment Page 11

TABLE OF CONTENTS Introduction of Advisors Charitable Gift Fund Page 3 Advantages Page 5 Definitions Page 6 Contributions Page 9 Investment of the Endowment Page 11 Grant Making Page 12 Creating a Legacy

TABLE OF CONTENTS Introduction of Advisors Charitable Gift Fund Page 3 Advantages Page 5 Definitions Page 6 Contributions Page 9 Investment of the Endowment Page 11 Grant Making Page 12 Creating a Legacy

Federal Tax Law Changes Affecting 501(c)(3) Nonprofits

(3) Nonprofits") Federal Tax Law Changes Affecting 501(c)(3) Nonprofits David Heinen North Carolina Center for Nonprofits Connect Learn Advocate Important Disclaimers If you can read this fine print, you are sitting too

Federal Tax Law Changes Affecting 501(c)(3) Nonprofits David Heinen North Carolina Center for Nonprofits Connect Learn Advocate Important Disclaimers If you can read this fine print, you are sitting too

Donor Advised Funds: The Swiss Army Knife of Charitable Planning. Bryan Clontz, Ph.D., CFP Charitable Solutions, LLC

Donor Advised Funds: The Swiss Army Knife of Charitable Planning Bryan Clontz, Ph.D., CFP Charitable Solutions, LLC 1 HIGH NET WORTH HOUSEHOLDS WHO HAVE OR WOULD CONSIDER ESTABLISHING IN THREE YEARS Will

Donor Advised Funds: The Swiss Army Knife of Charitable Planning Bryan Clontz, Ph.D., CFP Charitable Solutions, LLC 1 HIGH NET WORTH HOUSEHOLDS WHO HAVE OR WOULD CONSIDER ESTABLISHING IN THREE YEARS Will

MILLIKIN UNIVERSITY CONFLICT AND DUALITY OF INTEREST QUESTIONNAIRE

MILLIKIN UNIVERSITY CONFLICT AND DUALITY OF INTEREST QUESTIONNAIRE Please complete the following questions, sign and return in the enclosed envelope. Refer to Schedules 1 and 2 for examples and definitions.

MILLIKIN UNIVERSITY CONFLICT AND DUALITY OF INTEREST QUESTIONNAIRE Please complete the following questions, sign and return in the enclosed envelope. Refer to Schedules 1 and 2 for examples and definitions.

DONOR ADVISED FUND FUND AGREEMENT

DONOR ADVISED FUND FUND AGREEMENT Please Complete This Form to Establish a D O N O R A DV I S E D F U N D at the Boston Foundation, Inc. Return to: Donor Services 75 Arlington Street Boston, MA 02116 2

DONOR ADVISED FUND FUND AGREEMENT Please Complete This Form to Establish a D O N O R A DV I S E D F U N D at the Boston Foundation, Inc. Return to: Donor Services 75 Arlington Street Boston, MA 02116 2