Dilip Buildcon Ltd. 1 P a g e. Stock Details. Dilip Buildcon 2.1% Sensex 0.9%

|

|

|

- Hester Martin

- 6 years ago

- Views:

Transcription

1

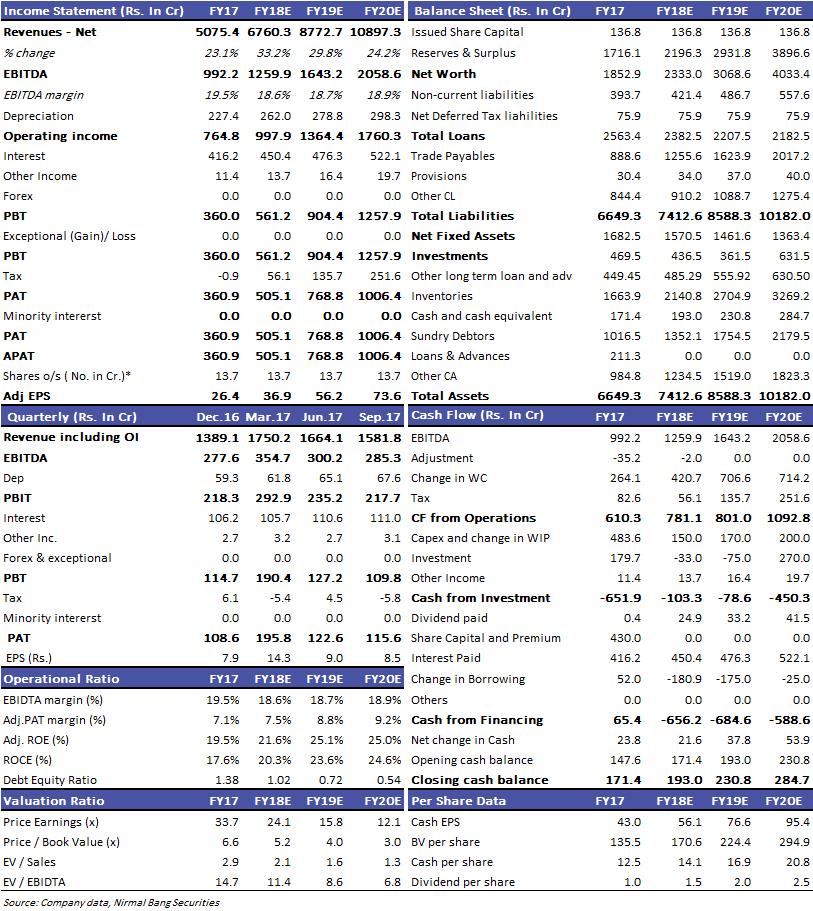

2 Recommendation BUY CMP 889 Target Price 1324 Sector Stock Details Construction-Roads BSE Code NSE Code Bloomberg Code DBL DBL IN Market Cap (Rs cr) Free Float (%) wk HI/Lo (Rs) 1009/217 Avg. volume (BSE+NSE) (Quarterly) Face Value (Rs) 10 Dividend (FY 17) Rs.1 Shares o/s (Crs) 13.7 Relative Performance 1Mth 3Mth 1Yr Dilip Buildcon 2.1% Sensex 0.9% Shareholding Pattern Sept 17 Promoters Holding 75.6% Institutional (Incl. FII) 16.6% Corporate Bodies 2.8% Public & others 5.0% Sunil Jain ( ) Head-Research Nandish Shah-( ) Research On a High growth road (DBL) is one of the largest road construction company in India. Started as sole proprietorship firm in 1988, DBL has an outstanding track record of early completion of road projects. Its clientele in the road segment includes NHAI, state governments and private companies. DBL also diversified into segment like irrigation, urban development and mining. Investment Rationale Sales of BOT/HAM projects will free capital for growth: DBL entered into agreement with Chhatwal Group Trust (Shrem Group) to sell 24 projects comprising of 14 operational projects, 4 under construction projects & 6 recently won HAM projects. EPC work of under construction projects will be done by DBL while the ownership of the BOT asset will shift. DBL has already received Rs. 195Cr till date and expect to receive Rs. 550Cr in FY18 and the balance in FY19. The debts relating to BOT and HAM projects will also get transferred. Consistent track record of early completion of Projects: DBL focus has always remained execution and for this it has won early completion bonus from various authorities from time to time. DBL has till date won Rs.345Cr as early completion bonus since inception. Industry leading margin and ROE: DBL continuous focus on execution and planning led to earning higher operating margins and in turn higher ROE compared to its industry peers. Improvement in Working capital Cycle: DBL plans to bring down its working capital cycle by focusing more on EPC projects. From the working capital cycle of 5.85 months in FY15, DBL has brought it down to 4.47 months in FY17 and plans to further reduce by days. Capitalizing on market opportunities in Road sector: The road construction push by NHAI and the Bharatmala Pariyojana will entail total investment of Rs Trillion. Players like DBL will be able to garner a larger pie of these orders on the back of their execution skills, owned equipment and higher borrowing power on the back of healthy balance sheet. Valuation & Recommendation DBL reported Revenues, EBIDTA and PAT of Rs. 5075Cr, 992Cr and Rs. 361Cr in FY17, growth of 25%, 45% and 21% respectively over FY16. With healthy order books, owned equipments, in-house execution capabilities, strong bid pipeline we expect revenues, EBIDTA and PAT to grow at CAGR of 30%, 27.5% and 41% respectively during FY17 FY20E. We expect EBIDTA margin to remain stable in the range of 18-19%. With the recent sale of BOT assets and reduction in working capital requirement, debt is likely to come down further which in turn will help ROE and ROCE to improve. We expect ROE and ROCE to improve from 19.5% in FY17 to 25% in FY20 and 17.6% in FY17 to 24.6% in FY20 respectively. At CMP, DBL is trading at 12.1x FY20 EPS. We recommend a BUY on DBL with a target price of Rs. 1324, based on 18x FY20E EPS. (Upside of 49%). Year Net Sales Growth % EBITDA Margin % PAT Margin EPS PE EV/EBITDA ROE % FY % % % % FY18E % % % % FY19E % % % % FY20E % % % % 1 P a g e

3 Chart 1: Order Book Background (DBL) is one of the leading private sector road focused EPC contractors in India. Their core business is undertaking construction projects across India in the road and irrigation sectors. They specialize in constructing state and national highways, city roads, culverts and bridges. Initially started with presence in Madhya Pradesh, DBL ventured out into other states in India and currently has presence in almost 16 states. DBL strength lies in its ability to execute projects on time, within costs, and of the highest quality. Its clientele in the road segment includes NHAI, state governments and private companies. Witnessing opportunities in other space, DBL also diversified into segment like irrigation, urban development and mining in 2014 and As on 30 th September 2017, 53% of their order book is from NHAI, 27% from Ministry of Road transport and Highways, 10% from Northern Coalfields, 6% from Singareni collieries Co ltd, 3% from state governments and rest from others. In last 5 years DBL has completed 73 projects with lane km in road portfolio with lane km being operational. As on 30 th September2017, DBL has an order book of Rs Cr, as compared Rs Cr as on 30 st Jun-17. Chart 2: Order book-by Sector Source: Company data, NBRR Chart 3: Order book-by state Source: Company data, NBRR Chart 4: Order book-by Clients Source: Company data, NBRR Source: Company data, NBRR 2 P a g e

and Devendra Jain (Executive Director and Chief Executive officer), DBL s revenue, EBIDTA and PAT grew by 28%, 25% and 10% CAGR from FY13 to FY17")

4 Under the leadership of Mr. Dilip Suryavanshi (Chairman and Managing Director) and Devendra Jain (Executive Director and Chief Executive officer), DBL s revenue, EBIDTA and PAT grew by 28%, 25% and 10% CAGR from FY13 to FY17 respectively. In August 2016, DBL came out with a public issue of Rs.654 Cr at Rs. 219 per share offering 2.98 Cr shares. Out of 2.98 Cr shares, 1.96 Cr shares were fresh issue while the rest was offer for sale. Investment Rationale Sales of BOT/HAM projects will free capital for growth Recently Company entered into agreement with Chhatwal Group Trust (Shrem Group) to sell 24 projects comprising of 14 operational projects, 4 under construction projects & 6 recently won HAM projects. Company has invested Rs. 682cr in all these projects. Whereas company was supposed to invest Rs.842cr in under construction and HAM projects in next 1-2 years. DBL will get around Rs.1600cr as consideration on sale of these projects and will be making nominal profit (Rs.75cr) but will free up the capital to bid for more and more project under emerging opportunity in road sector. DBL has already received Rs. 195 Cr towards part payment for the above sale. Management expects Rs. 550Cr to be received in FY18 and the remaining by FY19. HAM are at initial stage of construction and will be transferred post completion and receipt of COP. Apart from this Loan related to operational 14 BOT project of Rs.1251cr, current and future loan of Rs.965cr related to 4 under construction BOT projects and current and future loan of Rs.2571cr related to recently won HAM project will also be transferred to the acquirer. Company has increased its guidance of Order intake during FY18 from Rs.6000cr to Rs cr post this deal. Though the order booking by company in H1 was very low as Q1 is generally inactive quarter and Q2 got impacted by GST implementation. But presently the Bid pipe line is very strong (over Rs.50000cr) and considering relatively low competitive scenario company is hopeful of achieving its order intake target in FY18 Consistent track record of early completion of Projects DBL has earned Rs.345cr till 30 th September2017 as early completion bonus and completed 47 road projects, on or ahead of schedule. Source: Company report, Nirmal Bang Retail Research This company is able to achieve this on account of careful selection of projects, efficient project planning and management, project tracking to minimize the delay, owning sand and stone mines, apart from largest owner of construction equipment and one of the largest employer of construction manpower. DBL owns one of the largest fleet of Construction equipment (around 9000) and is one of the largest employers in construction industry (27,000 employees). 3 P a g e

5 Industry leading margin and ROE Early completion bonus along with own construction and own asset base leading to one of the highest operating margin for DBL and effective utilization of assets leading to even one of the highest ROE in the industry. Source: Company report, Nirmal Bang Retail Research DBL has implemented live tracking system to keep control of its large feel of construction equipment and has implemented effective HRD policy to reduce attrition. DBL is now implementing SAP and Data analytics tool from IBM which will help it to more effectively utilize its large resources. This is likely to have positive impact on margin and capital deployment. Improvement in Working capital Cycle Construction business is working capital intensive where in around 50% of capital employed is in working capital. DBL has shown impressive improvement in working capital cycle from 5.85 months of sales in FY15 to 4.47 months of sales in FY17. This was mainly driven by Inventory holding which reduced from 4.3 months to 3.7 months and Receivable from 5.2 months to 2.4 months in the same period. Creditor also declined from 3.8 months to 2.1 months in similar period. Working capital cycle in number of months. Source: Company report, Nirmal Bang Retail Research Company is further pursuing to improve working capital cycles mainly inventory with the implementation of SAP and Data analytical tools of IBM. 4 P a g e

6 Diversifying to other but related infrastructure sectors Till FY13 DBL order booking was solely from Road sector. In FY14 DBL diversified into Irrigation and Urban Infra projects. In FY16 DBL further diversified to Mining and Cable suspension Bridge area. At the end of FY17 though Road continue to dominant DBL order book with 80% share but DBL is establishing its foot in other Sector like Mining, Cable Bridges, Irrigation etc. DBL has diversified in the area where it can utilize its skill and Assets more effectively without sacrificing on margin and same principle will be followed to diversify in any other area. Capitalizing on market opportunities in Road sector Recently Government of India announced investment of Rs Trillion for building an km road network over the next 5 years. The road construction push includes the Bharatmala Pariyojana with a Rs5.35 trillion investment to construct 34,800km of roads. In addition, Rs1.57 trillion will be spent on the construction of 48,877km of roads by the state-run National Highway Authority of India (NHAI) and the ministry of road transport and highways. To expedite the Bharatmala projects, apart from ministry of road transport and highways and state-run firms NHAI and National Highways and Infrastructure Development Corporation Ltd (NHIDCL) even respective state public works departments (PWDs) will be roped in for timely execution. With lot of work in the road segment, DBL will be able to garner large pie of the same given it higher execution capabilities, owned equipment and higher borrowing power after the recent sell-off of the BOT assets. Industry Roads: Investments in roads is expected to increase to Rs. 5.8 trillion in the ( ) 13th Five-Year Plan, as against Rs.5.3 trillion ( ) (actual) in the 12th Five-Year Plan (marking a 11% increase). NHAI awards projects under different modes - EPC, build-operate-transfer, or BOT, and the recently introduced HAM. In the last two years, BOT projects have lost out to EPC projects because the latter requires limited upfront capital and involves lower risk.since , cash contracts have dominated NHAI awarding as a result of low appetite of road players for BOT projects.to boost private participation further, the government introduced HAM in , wherein 40% of the total project cost is to be funded by the government and the remaining by the private developer. The equity requirement in these projects is only about 12-15% of the project cost, which is much lower than a BOT project, and the developer is immune to traffic, inflation and interest rate risk. In , this model took off at a rather slower than-expected pace and only about 350 km were awarded mostly due to the apprehensions of various stakeholders towards a new, untested model. However, the participation of players in these projects improved significantly towards the end of In , almost half of the projects were awarded on HAM. Between and , Crisil research expect investment of Rs. 3.8 trillion, up by 3.2 times in the next 5 years compared to the past 5 years. Notably, the government will account for more than half of the investment as against 44% in the previous five years. Key Risks and concerns Any hurdle in the completion of the deal for sale of assets can have a negative impact on the financial of the company. Any delays in execution of the projects due to lack of land acquisition or other issues can risk the revenues recognition. With lot of investment in plant and equipment, lack of order with DBL can put pressure on margins of the Co. 5 P a g e

7 Valuation and Recommendation DBL reported Revenues, EBIDTA and PAT of Rs. 5075Cr, 992Cr and Rs. 361Cr in FY17, growth of 25%, 45% and 21% respectively from FY16. With healthy order books, owned equipments, in-house execution capabilities, strong bid pipeline we expect revenues, EBIDTA and PAT to grow at CAGR of 30%, 27.5% and 41% respectively during FY17 to FY20E. We expect EBIDTA margin to remain stable in the range of 18-19%. With the recent sale of BOT assets and reduction in working capital requirement, debt is likely to come down further which in turn will help ROE and ROCE to improve. We expect ROE and ROCE to improve from 19.5% in FY17 to 25% in FY20 and 17.6% in FY17 to 24.6% in FY20 respectively. We have compared DBL with 4 others players in the industry. DBL enjoy one of the best EBIDTA margins and ROE as compared to others. On the valuation it is still available at a discount to all the other players. Peer Comparison Revenues EBIDTA EBIDTA Net EPS P/E ROE % FY20(Rs in cr) margins Profit Dilip Buildcon Ashoka Buildcon Sadbhav Engineering PNC Infra KNR Constructions Source: Bloomberg estimate, Nirmal Bang Retail Research, Standalone numbers At CMP, DBL is trading at 12.1x FY20E EPS. We recommend a BUY on DBL with a target price of Rs. 1324, based on 18x FY20E EPS. (Upside of 49%). 6 P a g e

8 Quarterly Financials Particulars Q2FY18 Q1FY18 QoQ% Q2FY17 YoY% Net Sales % % Other Operating Income Total Income % % Cost of raw material consumed % % Gross Profit % % Gross Margin (% of net sales) 22.6% 23.3% % Employee Expenses % % Other Expenses % % Total Expenditure % % EBITDA % % % of net sales 18.0% 18.0% % Depreciation % % EBIT % % Interest % % PBT & OI % % Other Income % % PBT % % Tax % % Tax / PBT -5.3% 3.6% 24.7% Net Profit % % % of net sales 7.3% 7.4% 0.8% Equity EPS (Unit Curr.) Source: Company data, Nirmal Bang Securities Revenues grew by 73% YoY on the back of strong execution of roads and mining EPC orders. EBIDTA increased by 83% YoY on the back of higher revenues. EBIDTA margins increased by 100 bps YoY on the back of lower other expenses. Interest cost remained flat QoQ on the back of improving working capital cycle. Other income grew by 18% QoQ while YoY decreased by 12%. PBT grew by 1088% YoY while QoQ decreased by 14%. PAT grew by 1560% YoY and decreased 6% QoQ. 7 P a g e

9 Financials 8 P a g e

10 Disclaimer: Nirmal Bang Securities Private Limited (hereinafter referred to as NBSPL ) is a registered Member of National Stock Exchange of India Limited, Bombay Stock Exchange Limited and MCX stock Exchange Limited. We have been granted certificate of Registration as a Research Analyst with SEBI. Registration no. is INH for the period to NBSPL or its associates including its relatives/analyst do not hold any financial interest/beneficial ownership of more than 1% in the company covered by Analyst (in case any financial interest is held kindly disclose) NBSPL or its associates/analyst has not received any compensation from the company covered by Analyst during the past twelve months. NBSPL /analyst has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity of the company covered by Analyst. The views expressed are based solely on information available publicly and believed to be true. Investors are advised to independently evaluate the market conditions/risks involved before making any investment decision. Nirmal Bang Research (Division of Nirmal Bang Securities Pvt. Ltd.) B-2, 301/302, Marathon Innova, Opp. Peninsula Corporate Park Off. Ganpatrao Kadam Marg Lower Parel (W), Mumbai Board No. : /8001 Fax. : P a g e

Phillips Carbon Black Ltd

4 Recommendation BOOK PROFITS Pain not yet over CMP (09/02/2015)* Rs. 131 Phillips Carbon Black (PCB) reported results in line with expectations; with EBITDA margins at 10.0% vs 9.3% in Q2FY15. The company

4 Recommendation BOOK PROFITS Pain not yet over CMP (09/02/2015)* Rs. 131 Phillips Carbon Black (PCB) reported results in line with expectations; with EBITDA margins at 10.0% vs 9.3% in Q2FY15. The company

Margin (%) PAT (Rs cr)

PAT (Rs cr)") 4 Recommendation HOLD Reiterating positive outlook CMP (27/7/2015) Rs. 115 Target Price Rs. 125 Sector Stock Details Pharmaceuticals BSE Code 532482 NSE Code Bloomberg Code GRANULES GRAN IN Market Cap

4 Recommendation HOLD Reiterating positive outlook CMP (27/7/2015) Rs. 115 Target Price Rs. 125 Sector Stock Details Pharmaceuticals BSE Code 532482 NSE Code Bloomberg Code GRANULES GRAN IN Market Cap

LIC Housing Finance Ltd

4 Recommendation BUY In line results; asset quality improves CMP (27/4/215) Rs. 421 Target Price Rs. 518 Sector Stock Details Housing Finance BSE Code 5253 NSE Code Bloomberg Code LICHSGFIN LICF IN Market

4 Recommendation BUY In line results; asset quality improves CMP (27/4/215) Rs. 421 Target Price Rs. 518 Sector Stock Details Housing Finance BSE Code 5253 NSE Code Bloomberg Code LICHSGFIN LICF IN Market

DCB Bank Ltd. 1 P a g e

4 Recommendation HOLD Another strong quarter CMP (16/04/2015) Rs. 120 Target Price Rs. 140 Sector Stock Details Banking BSE Code 532772 NSE Code Bloomberg Code DCB DEVB IN Market Cap (Rs cr) 3383 Free

4 Recommendation HOLD Another strong quarter CMP (16/04/2015) Rs. 120 Target Price Rs. 140 Sector Stock Details Banking BSE Code 532772 NSE Code Bloomberg Code DCB DEVB IN Market Cap (Rs cr) 3383 Free

PSP Projects Ltd. 1 P a g e. Subscribe with Long Recommendation. Term View BACKGROUND

Subscribe with Long Recommendation Term View BACKGROUND Price Band Rs. 205 Rs. 210 (PSP) is a multidisciplinary construction company Bidding Date 17 th Sep - 19 th May 2017 Book Running Lead Manager Registrar

Subscribe with Long Recommendation Term View BACKGROUND Price Band Rs. 205 Rs. 210 (PSP) is a multidisciplinary construction company Bidding Date 17 th Sep - 19 th May 2017 Book Running Lead Manager Registrar

Pennar Industries Ltd.

4 Recommendation CMP Target Price Sector Stock Details BUY Rs. 25 Rs.31 Metals Moderate Quarter Pennar Industries has reported a moderate consolidated quarter due to lower demand in the auto, engineering,

4 Recommendation CMP Target Price Sector Stock Details BUY Rs. 25 Rs.31 Metals Moderate Quarter Pennar Industries has reported a moderate consolidated quarter due to lower demand in the auto, engineering,

Consolidated Sales (Cr) Growth EBITDA (Cr) Margin PAT Margin EPS (Rs) P/E RoE

Growth EBITDA (Cr) Margin PAT Margin EPS (Rs) P/E RoE") Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 2904 Recommendation CMP Target Price BUY Rs. 312 Rs. 443 Better times ahead! reported a good set of numbers in

Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 2904 Recommendation CMP Target Price BUY Rs. 312 Rs. 443 Better times ahead! reported a good set of numbers in

Navkar Corporation Ltd

27 June 2016 Recommendation BUY Expansion on cards which will drive the future growth Navkar Corporation,incorporated in the year 2008, purely focused at JNPT, is a CMP Rs. 203 CFS(Container freight station)

27 June 2016 Recommendation BUY Expansion on cards which will drive the future growth Navkar Corporation,incorporated in the year 2008, purely focused at JNPT, is a CMP Rs. 203 CFS(Container freight station)

Bajaj Electricals Ltd.

4 Recommendation CMP Target Price Sector Stock Details Book Profit Rs. 197 Rs. 178 Consumer Durable Quarterly Analysis Bajaj Electricals has reported a dismal performance where the EBIDTA margin was down

4 Recommendation CMP Target Price Sector Stock Details Book Profit Rs. 197 Rs. 178 Consumer Durable Quarterly Analysis Bajaj Electricals has reported a dismal performance where the EBIDTA margin was down

Phillips Carbon Black Ltd

4 Recommendation BUY Snail Pace Recovery CMP (06/02/2013) Rs. 85 Target Price Rs. 110 Sector Stock Details Carbon Black BSE Code 506590 NSE Code Bloomberg Code PHILIPCARB PHCB IN Market Cap (Rs crs) 293

4 Recommendation BUY Snail Pace Recovery CMP (06/02/2013) Rs. 85 Target Price Rs. 110 Sector Stock Details Carbon Black BSE Code 506590 NSE Code Bloomberg Code PHILIPCARB PHCB IN Market Cap (Rs crs) 293

Initiating Coverage. Uflex Ltd.

2904 Recommendation CMP Target Price BUY Rs. 283 Rs. 444 Better times ahead! reported a good set of numbers for the year FY18 and for Q4. Sales for the quarter increase by 11.8% YoY to Rs 1809.8 Cr and

2904 Recommendation CMP Target Price BUY Rs. 283 Rs. 444 Better times ahead! reported a good set of numbers for the year FY18 and for Q4. Sales for the quarter increase by 11.8% YoY to Rs 1809.8 Cr and

KPIT Cummins Infosystems Ltd

4 Recommendation HOLD Q1FY13 results above expectations; onsite volume growth of 7%, pricing stable. CMP Target Price Sector Stock Details Rs.126 Rs.137 IT Software products BSE Code 532400 NSE Code Bloomberg

4 Recommendation HOLD Q1FY13 results above expectations; onsite volume growth of 7%, pricing stable. CMP Target Price Sector Stock Details Rs.126 Rs.137 IT Software products BSE Code 532400 NSE Code Bloomberg

Initiating Coverage. Dr Lal Path Labs Ltd. 1 P a g e. related healthcare tests and services in India. Dr Lal Path Labs has strong.

4 Recommendation BUY Dr Lal Path Labs (DLPL) is India s second largest provider of diagnostic and related healthcare tests and services in India. Dr Lal Path Labs has strong CMP Rs 973 pedigree of promoters.

4 Recommendation BUY Dr Lal Path Labs (DLPL) is India s second largest provider of diagnostic and related healthcare tests and services in India. Dr Lal Path Labs has strong CMP Rs 973 pedigree of promoters.

Investment Rationale. Strong Parentage. Renewed focus of Ricoh Japan in India. Margin (%) Adj PAT

Adj PAT") 0 4 Recommendation BUY Delisting Offer Price - Still a long way CMP Rs. 73 Target Price Rs. 89 Sector Stock Details Comm. Trading & Distribution BSE Code 517496 NSE Code Bloomberg Code NA RPGR IN Market

0 4 Recommendation BUY Delisting Offer Price - Still a long way CMP Rs. 73 Target Price Rs. 89 Sector Stock Details Comm. Trading & Distribution BSE Code 517496 NSE Code Bloomberg Code NA RPGR IN Market

Investment Rationale: Adj PAT (Rs cr)

") 4 Recommendation CMP BUY Rs 92 Cementing the Turnaround NCL Industries Limited is a south based small cement company. The Target Price Rs 131 company operates through four related business divisions such

4 Recommendation CMP BUY Rs 92 Cementing the Turnaround NCL Industries Limited is a south based small cement company. The Target Price Rs 131 company operates through four related business divisions such

Result Analysis. Recommendation CMP (09/02/2010) Rs. 212

Rs. 212") Recommendation BUY CMP (09/02/2010) Rs. 212 Sector Stock Details BSE Code NSE Code Bloomberg Market Cap (Rs. cr) Free Float (%) 52- wk HI/Lo Avg. volume BSE (Quarterly) Face Value Dividend (FY09) Shares

Recommendation BUY CMP (09/02/2010) Rs. 212 Sector Stock Details BSE Code NSE Code Bloomberg Market Cap (Rs. cr) Free Float (%) 52- wk HI/Lo Avg. volume BSE (Quarterly) Face Value Dividend (FY09) Shares

Honeywell Automation India Ltd

4 Recommendation SUBSCRIBE SUBSCRIBE FROM A LONG TERM VIEW CMP (14/12/2012) Rs. 2,335 Target Price Sector Stock Details N/A Automation BSE Code 500033 NSE Code Bloomberg Code HONAUT HWA IN Market Cap (Rs

4 Recommendation SUBSCRIBE SUBSCRIBE FROM A LONG TERM VIEW CMP (14/12/2012) Rs. 2,335 Target Price Sector Stock Details N/A Automation BSE Code 500033 NSE Code Bloomberg Code HONAUT HWA IN Market Cap (Rs

S Chand and Company Ltd

h e t G g rowth n i d i R Recommendation BUY Riding the growth!!! CMP 489 Target Price 632 Sector Stock Details Education BSE Code 54097 NSE Code Bloomberg Code SCHAND SCHAND IN Market Cap (Rs cr) 1704

h e t G g rowth n i d i R Recommendation BUY Riding the growth!!! CMP 489 Target Price 632 Sector Stock Details Education BSE Code 54097 NSE Code Bloomberg Code SCHAND SCHAND IN Market Cap (Rs cr) 1704

Bajaj Electricals. Institutional Equities. 3QFY15 Result Update

3QFY15 Result Update Institutional Equities Bajaj Electricals 13 February 2015 Reuters: BJEL.BO; Bloomberg: BJE IN Final Phase Of Transition Pain; Retain Buy Bajaj Electricals (BJE) posted 3QFY15 revenue

3QFY15 Result Update Institutional Equities Bajaj Electricals 13 February 2015 Reuters: BJEL.BO; Bloomberg: BJE IN Final Phase Of Transition Pain; Retain Buy Bajaj Electricals (BJE) posted 3QFY15 revenue

Power Mech Projects. Institutional Equities. 2QFY18 Result Update BUY. Strong Business Scalability Likely; Retain Buy

2QFY18 Result Update Power Mech Projects 23 November 217 Reuters: POMP.BO; Bloomberg: POWM IN Strong Business Scalability Likely; Retain Buy Power Mech Projects (PMPL) posted 2QFY18 consolidated revenues

2QFY18 Result Update Power Mech Projects 23 November 217 Reuters: POMP.BO; Bloomberg: POWM IN Strong Business Scalability Likely; Retain Buy Power Mech Projects (PMPL) posted 2QFY18 consolidated revenues

SUBSCRIBE to H.G. Infra Engineering Ltd. Strong player in government s renewed focus sector

SUBSCRIBE to H.G. Infra Engineering Ltd. Strong player in government s renewed focus sector 19 th Feb. 2018 Salient features of the IPO: H.G. Infra Engineering Ltd. (HGIEL) is an infrastructure construction,

SUBSCRIBE to H.G. Infra Engineering Ltd. Strong player in government s renewed focus sector 19 th Feb. 2018 Salient features of the IPO: H.G. Infra Engineering Ltd. (HGIEL) is an infrastructure construction,

Minda Industries Ltd.

Recommendation BUY Riding On Growth!!! CMP 810 Target Price 1,193 Sector Stock Details Auto Parts & Equipment BSE Code 532539 NSE Code Bloomberg Code MINDAIND MNDA IN Market Cap (Rs cr) 1,284 Free Float

Recommendation BUY Riding On Growth!!! CMP 810 Target Price 1,193 Sector Stock Details Auto Parts & Equipment BSE Code 532539 NSE Code Bloomberg Code MINDAIND MNDA IN Market Cap (Rs cr) 1,284 Free Float

Grindwell Norton Ltd

Grindwell Norton Ltd 4 Recommendation BUY Company Overview Grindwell Norton Ltd (GNO) is India s leading manufacturer of Abrasives (Bonded, CMP (11/07/2012) Rs. 258 Coated, Non-Woven, Superabrasives and

Grindwell Norton Ltd 4 Recommendation BUY Company Overview Grindwell Norton Ltd (GNO) is India s leading manufacturer of Abrasives (Bonded, CMP (11/07/2012) Rs. 258 Coated, Non-Woven, Superabrasives and

Margin PAT (Rs Margin

4 Recommendation BUY Best bet at current FMCG space, Attractive Valuations; BUY CMP Rs. 345 ITC posted a good quarter in terms of Net Sales/Gross Profit/EBITDA/PAT increased by 11.8%/13.9%/18.4%/18.2%

4 Recommendation BUY Best bet at current FMCG space, Attractive Valuations; BUY CMP Rs. 345 ITC posted a good quarter in terms of Net Sales/Gross Profit/EBITDA/PAT increased by 11.8%/13.9%/18.4%/18.2%

Initiating Coverage. Vaibhav Global Ltd. (VGL) BUY Back On Track Huge Potential Ahead. 1 P a g e

BUY Back On Track Huge Potential Ahead. 1 P a g e") 4 Recommendation CMP Rs. 725 Target Price Rs. 887 Sector Stock Details BUY Back On Track Huge Potential Ahead Vaibhav Global Ltd s (VGL) journey has been a roller coaster ride since its inception. After

4 Recommendation CMP Rs. 725 Target Price Rs. 887 Sector Stock Details BUY Back On Track Huge Potential Ahead Vaibhav Global Ltd s (VGL) journey has been a roller coaster ride since its inception. After

HG Infra Engineering Ltd.

Recommendation Subscribe BACKGROUND Price Band Rs.263 Rs.270 Incorporated in 2003, HG Infra Engineering Ltd mainly provides Bidding Date Book Running Lead Manager Registrar Sector 26-28 February SBI Capital

Recommendation Subscribe BACKGROUND Price Band Rs.263 Rs.270 Incorporated in 2003, HG Infra Engineering Ltd mainly provides Bidding Date Book Running Lead Manager Registrar Sector 26-28 February SBI Capital

Financials/Valu FY15 FY16 FY17 FY18E FY19E

29Aug17 INDUSTRY Eng. & Cons. BSE Code 540047 NSE Code NIFTY DBL 9912 Company Data CMP 625 Target Price 6 Previous Target Price 595 Upside 9% 52wk Range H/L Mkt Capital (Rs Cr) Av. Volume (,000) Superior

29Aug17 INDUSTRY Eng. & Cons. BSE Code 540047 NSE Code NIFTY DBL 9912 Company Data CMP 625 Target Price 6 Previous Target Price 595 Upside 9% 52wk Range H/L Mkt Capital (Rs Cr) Av. Volume (,000) Superior

Recommendation BUY Snapshot CMP (01/08/2011) Rs. 85 Target Rs. 129

Rs. 85 Target Rs. 129") Recommendation BUY Snapshot CMP (01/08/2011) Rs. 85 Target Rs. 129 Sector Banking Stock Details BSE Code NSE Code Bloomberg Code Market Cap (Rs. Crs) Free Float (%) 52 wk HI/Low Avg. volume BSE (Quarterly)

Recommendation BUY Snapshot CMP (01/08/2011) Rs. 85 Target Rs. 129 Sector Banking Stock Details BSE Code NSE Code Bloomberg Code Market Cap (Rs. Crs) Free Float (%) 52 wk HI/Low Avg. volume BSE (Quarterly)

Institutional Equities

2QFY18 Result Update Institutional Equities KCP 5 December 2017 Reuters: KCP.BO; Bloomberg: KCPL IN Other Income Drives PAT; High International Coal Price Is Cause For Concern KCP reported a weak set of

2QFY18 Result Update Institutional Equities KCP 5 December 2017 Reuters: KCP.BO; Bloomberg: KCPL IN Other Income Drives PAT; High International Coal Price Is Cause For Concern KCP reported a weak set of

Swaraj Engines. Institutional Equities. 2QFY18 Result Update ACCUMULATE

2QFY18 Result Update Institutional Equities Swaraj Engines 13 November 2017 Reuters: SWAR.BO; Bloomberg: SWE IN Strong Realisation Drives Earnings Growth Swaraj Engines (SEL) 2QFY18 earnings were 5% above

2QFY18 Result Update Institutional Equities Swaraj Engines 13 November 2017 Reuters: SWAR.BO; Bloomberg: SWE IN Strong Realisation Drives Earnings Growth Swaraj Engines (SEL) 2QFY18 earnings were 5% above

E&P To Stay Strong; Consumer Segment To Revive

Management Meet Update Institutional Equities Bajaj Electricals 30 August 2017 Reuters: BJEL.BO; Bloomberg: BJE IN E&P To Stay Strong; Consumer Segment To Revive We had a meeting with the management of

Management Meet Update Institutional Equities Bajaj Electricals 30 August 2017 Reuters: BJEL.BO; Bloomberg: BJE IN E&P To Stay Strong; Consumer Segment To Revive We had a meeting with the management of

Institutional Equities

Management Meet Update Institutional Equities Kaya Reuters: KAYA.NS; Bloomberg: KAYA IN We interacted with the management of Kaya at an investor conference held by us recently. Following are the key takeaways:

Management Meet Update Institutional Equities Kaya Reuters: KAYA.NS; Bloomberg: KAYA IN We interacted with the management of Kaya at an investor conference held by us recently. Following are the key takeaways:

Inox Wind BUY. Performance Highlights. CMP Target Price `242 `286. 4QFY2016 Result Update Capital Goods. 3 year price chart

4QFY216 Result Update Capital Goods May 11, 216 Inox Wind Performance Highlights Quarterly Data (Consolidated) ( ` cr) 4QFY16 4QFY15 % chg (yoy) 3QFY16 % chg (qoq) Total Income 1,829 93 96.6 941 94.2 EBITDA

4QFY216 Result Update Capital Goods May 11, 216 Inox Wind Performance Highlights Quarterly Data (Consolidated) ( ` cr) 4QFY16 4QFY15 % chg (yoy) 3QFY16 % chg (qoq) Total Income 1,829 93 96.6 941 94.2 EBITDA

Crisil. Institutional Equities. 3QCY17 Result Update ACCUMULATE. Weak SME Rating Revenues & Currency Movement Play Spoilsport

3QCY17 Result Update Institutional Equities Crisil 18 October 2017 Reuters: CRSL.BO; Bloomberg: CRISIL IN Weak SME Rating Revenues & Currency Movement Play Spoilsport Crisil s 3QCY17 performance was below

3QCY17 Result Update Institutional Equities Crisil 18 October 2017 Reuters: CRSL.BO; Bloomberg: CRISIL IN Weak SME Rating Revenues & Currency Movement Play Spoilsport Crisil s 3QCY17 performance was below

Inox Wind BUY. Performance Highlights. CMP Target Price `390 `505. 2QFY2016 Result Update Capital Goods. 3 year price chart

2QFY2016 Result Update Capital Goods October 27, 2015 Inox Wind Performance Highlights Quarterly Data (Consolidated) ( ` cr) 2QFY16 2QFY15 % chg (yoy) 1QFY16 % chg (qoq) Revenues 1,008 543 85.6 636 58.6

2QFY2016 Result Update Capital Goods October 27, 2015 Inox Wind Performance Highlights Quarterly Data (Consolidated) ( ` cr) 2QFY16 2QFY15 % chg (yoy) 1QFY16 % chg (qoq) Revenues 1,008 543 85.6 636 58.6

Quarterly Result Analysis

Recommendation BUY Snapshot CMP (04/02/2011) Rs. 640 Sector Stock Details BSE Code NSE Code Bloomberg Code Market Cap (Rs. cr) Free Float (%) 52 wk HI/Lo Avg. volume BSE (Monthly) Shares o/s (Crs) Metals

Recommendation BUY Snapshot CMP (04/02/2011) Rs. 640 Sector Stock Details BSE Code NSE Code Bloomberg Code Market Cap (Rs. cr) Free Float (%) 52 wk HI/Lo Avg. volume BSE (Monthly) Shares o/s (Crs) Metals

Timken India. Institutional Equities. 4QFY16 Result Update BUY. Margin Expansion Leads To Huge Growth In Profit; Retain Buy

4QFY16 Result Update Institutional Equities Timken India 23 May 2016 Reuters: TMKN.BO; Bloomberg: TIMK IN Margin Expansion Leads To Huge Growth In Profit; Retain Buy Timken India (TIL), the leading manufacturer

4QFY16 Result Update Institutional Equities Timken India 23 May 2016 Reuters: TMKN.BO; Bloomberg: TIMK IN Margin Expansion Leads To Huge Growth In Profit; Retain Buy Timken India (TIL), the leading manufacturer

Institutional Equities

3QFY15 Result Update Institutional Equities GlaxoSmithKline Consumer Healthcare Reuters: GLSM.BO; Bloomberg: SKB IN 4 February 2015 Price Hike Leads To Sales Growth Glaxo SmithKline Consumer Healthcare

3QFY15 Result Update Institutional Equities GlaxoSmithKline Consumer Healthcare Reuters: GLSM.BO; Bloomberg: SKB IN 4 February 2015 Price Hike Leads To Sales Growth Glaxo SmithKline Consumer Healthcare

Shemaroo Entertainment Ltd

Recommendation BUY CMP 356 Target Price 485 Sector Stock Details Media BSE Code 538685 NSE Code Bloomberg Code SHEMAROO SHEM IN Market Cap (Rs cr) 968 Free Float (%) 34.18 52- wk HI/Lo (Rs) 439/294 Avg.

Recommendation BUY CMP 356 Target Price 485 Sector Stock Details Media BSE Code 538685 NSE Code Bloomberg Code SHEMAROO SHEM IN Market Cap (Rs cr) 968 Free Float (%) 34.18 52- wk HI/Lo (Rs) 439/294 Avg.

CARE Ratings. Institutional Equities. 2QFY18 Result Update BUY

2QFY18 Result Update Institutional Equities CARE Ratings 17 November 217 Reuters: CREI.BO; Bloomberg: CARE IN Mixed Performance CARE Ratings (CARE) reported an increase of 12.3% in revenues for 2QFY18

2QFY18 Result Update Institutional Equities CARE Ratings 17 November 217 Reuters: CREI.BO; Bloomberg: CARE IN Mixed Performance CARE Ratings (CARE) reported an increase of 12.3% in revenues for 2QFY18

Recommendation Not Rated Snapshot Bajaj Finance Ltd (BFL), earlier known as Bajaj Auto Finance Ltd is a

, earlier known as Bajaj Auto Finance Ltd is a") Recommendation Not Rated Snapshot (BFL), earlier known as Bajaj Auto Finance Ltd is a CMP (13/07/2011) Rs. 686 Bajaj group company and was incorporated in 1987. BFL started its Sector NBFC operations as

Recommendation Not Rated Snapshot (BFL), earlier known as Bajaj Auto Finance Ltd is a CMP (13/07/2011) Rs. 686 Bajaj group company and was incorporated in 1987. BFL started its Sector NBFC operations as

Recommendation HOLD Dismal performance drags margins Appreciating Japanese Yen, drop in volumes and increase in. Rs. 1,126.

Recommendation HOLD Dismal performance drags margins Appreciating Japanese Yen, drop in volumes and increase in Rs. 1,126 Raw material costs pulled down Maruti s EBITDA margin to Rs 1,200 6.5% in Q2FY12

Recommendation HOLD Dismal performance drags margins Appreciating Japanese Yen, drop in volumes and increase in Rs. 1,126 Raw material costs pulled down Maruti s EBITDA margin to Rs 1,200 6.5% in Q2FY12

Dilip Buildcon. Strong comeback BUY RESULT REVIEW 1QFY19 16 AUG Highlights of the quarter. CMP (as on 16 Aug 2018) Rs 847 Target Price Rs 1,434

Rs 847 Target Price Rs 1,434") INDUSTRY INFRASTRUCTURE CMP (as on 16 Aug 2018) Rs 847 Target Price Rs 1,434 Nifty 11,385 Sensex 37,664 KEY STOCK DATA Bloomberg DBL IN No. of Shares (mn) 137 MCap (Rs bn) / ($ mn) 116/1,656 5m avg traded

INDUSTRY INFRASTRUCTURE CMP (as on 16 Aug 2018) Rs 847 Target Price Rs 1,434 Nifty 11,385 Sensex 37,664 KEY STOCK DATA Bloomberg DBL IN No. of Shares (mn) 137 MCap (Rs bn) / ($ mn) 116/1,656 5m avg traded

HUDCO Ltd. 1 P a g e. Recommendation Subscribe BACKGROUND

Recommendation Subscribe BACKGROUND Price Band Rs. 56 Rs. 60 Housing and Urban Development Finance Corporation Ltd. (HUDCO) was Bidding Date 8 th May 11 th May 2017 Book Running Lead Manager Registrar

Recommendation Subscribe BACKGROUND Price Band Rs. 56 Rs. 60 Housing and Urban Development Finance Corporation Ltd. (HUDCO) was Bidding Date 8 th May 11 th May 2017 Book Running Lead Manager Registrar

Crompton Greaves. Institutional Equities. 4QFY15 Result Update ACCUMULATE. Overseas Losses Continue; More Business Exits Likely

4QFY15 Result Update Crompton Greaves 29 May 2015 Reuters: CROM.BO; Bloomberg: CRG IN Overseas Losses Continue; More Business Exits Likely The 4QFY15 performance of Crompton Greaves (CGL) was below expectation

4QFY15 Result Update Crompton Greaves 29 May 2015 Reuters: CROM.BO; Bloomberg: CRG IN Overseas Losses Continue; More Business Exits Likely The 4QFY15 performance of Crompton Greaves (CGL) was below expectation

Key highlights for the year

Recommendation Not Rated Snapshot CMP (26/04/2010) Rs. 693 Sector IT & Software Stock Details BSE Code NSE Code Bloomberg Code Market Cap (Rs. Crs) Free Float (%) 52- wk HI/Lo Avg. volume BSE (Quarterly)

Recommendation Not Rated Snapshot CMP (26/04/2010) Rs. 693 Sector IT & Software Stock Details BSE Code NSE Code Bloomberg Code Market Cap (Rs. Crs) Free Float (%) 52- wk HI/Lo Avg. volume BSE (Quarterly)

Recommendation HOLD Results in line with our expectations CMP (15/10/2010) Rs Target Rs Sector

Rs Target Rs Sector") Recommendation HOLD Results in line with our expectations CMP (15/10/2010) Rs. 3212 Target Rs. 3208 Sector IT & Software BSE Code NSE Code Bloomberg Code Market Cap (Rs. cr) Free Float (%) 52- wk HI/Lo

Recommendation HOLD Results in line with our expectations CMP (15/10/2010) Rs. 3212 Target Rs. 3208 Sector IT & Software BSE Code NSE Code Bloomberg Code Market Cap (Rs. cr) Free Float (%) 52- wk HI/Lo

Muthoot Finance. Institutional Equities. 2QFY18 Result Update BUY

2QFY18 Result Update Institutional Equities Muthoot Finance 10 November 2017 Reuters: MUTT.BO; Bloomberg: MUTH IN Gold Loan Business Really Glitters Strong profitability numbers of Muthoot Finance (MFL)

2QFY18 Result Update Institutional Equities Muthoot Finance 10 November 2017 Reuters: MUTT.BO; Bloomberg: MUTH IN Gold Loan Business Really Glitters Strong profitability numbers of Muthoot Finance (MFL)

EBITDA 5,019 4,211 5, EBITDA

Result Update Institutional Equities Dalmia Bharat Reuters: DALA.BO; Bloomberg: DBEL IN Outperformance Likely To Continue Dalmia Bharat (DBL) reported a good set of numbers for, given the challenging environment

Result Update Institutional Equities Dalmia Bharat Reuters: DALA.BO; Bloomberg: DBEL IN Outperformance Likely To Continue Dalmia Bharat (DBL) reported a good set of numbers for, given the challenging environment

Colgate-Palmolive (India)

") Result Update Colgate-Palmolive (India) 27 July 218 Reuters: COLG.BO; Bloomberg: CLGT IN Tough Times Continue Colgate-Palmolive (India) or CLGT reported a mixed earnings performance in. Volume and revenue

Result Update Colgate-Palmolive (India) 27 July 218 Reuters: COLG.BO; Bloomberg: CLGT IN Tough Times Continue Colgate-Palmolive (India) or CLGT reported a mixed earnings performance in. Volume and revenue

3,746 2,551 3, NIM

4QFY17 Result Update Institutional Equities Capital First 11 May 2017 Reuters: CAPF.BO; Bloomberg: CAFL IN Net Interest Income Up, But Offset By Elevated Credit Costs Although the net interest income or

4QFY17 Result Update Institutional Equities Capital First 11 May 2017 Reuters: CAPF.BO; Bloomberg: CAFL IN Net Interest Income Up, But Offset By Elevated Credit Costs Although the net interest income or

Power Mech Projects. Institutional Equities. 2QFY19 Result Update BUY. Strong Order Book Drives Robust Execution

2QFY19 Result Update Power Mech Projects 21 November 218 Reuters: POMP.BO; Bloomberg: POWM IN Strong Order Book Drives Robust Execution Power Mech Projects (PMPL) posted 2QFY19 consolidated revenues of

2QFY19 Result Update Power Mech Projects 21 November 218 Reuters: POMP.BO; Bloomberg: POWM IN Strong Order Book Drives Robust Execution Power Mech Projects (PMPL) posted 2QFY19 consolidated revenues of

Shankara Building Products Ltd.

Recommendation Subscribe BACKGROUND Price Band Rs.440 Rs. 460 Promoted by Mr. Sukumar Srinivas, Shankara Building Products (SBPL) is Bidding Date Book Running Lead Manager Registrar Sector 22 March - 24

Recommendation Subscribe BACKGROUND Price Band Rs.440 Rs. 460 Promoted by Mr. Sukumar Srinivas, Shankara Building Products (SBPL) is Bidding Date Book Running Lead Manager Registrar Sector 22 March - 24

Bata India. Institutional Equities. Management Meet Update. On Right Track ACCUMULATE. Sector: Retail CMP: Rs692 Target Price: 696 Upside: 1%

Management Meet Update Bata India Reuters: BATA.BO; Bloomberg: BATA IN On Right Track We had a meeting recently with Mr. R. K. Gupta, Chief Financial Officer (CFO) of Bata India (BIL) to understand recent

Management Meet Update Bata India Reuters: BATA.BO; Bloomberg: BATA IN On Right Track We had a meeting recently with Mr. R. K. Gupta, Chief Financial Officer (CFO) of Bata India (BIL) to understand recent

Hindustan Media Ventures

2QFY216 Result Update Media October 27, 215 Hindustan Media Ventures Performance Highlights Quarterly Data (` cr) 2QFY16 2QFY15 % yoy 1QFY15 % qoq Revenue 227 2 13.7 224 1.4 EBITDA 52 39 33.1 55 (4.5)

2QFY216 Result Update Media October 27, 215 Hindustan Media Ventures Performance Highlights Quarterly Data (` cr) 2QFY16 2QFY15 % yoy 1QFY15 % qoq Revenue 227 2 13.7 224 1.4 EBITDA 52 39 33.1 55 (4.5)

Minda Industries Ltd.

e Recommendation BUY Another Good Performance... CMP Rs. 1, 278 Taret Price Rs. 1,635 Sector Stock Details Auto Parts & Equipments BSE de 532539 NSE de Bloomber de MINDAIND MNDA IN Market Cap 2,028 Free

e Recommendation BUY Another Good Performance... CMP Rs. 1, 278 Taret Price Rs. 1,635 Sector Stock Details Auto Parts & Equipments BSE de 532539 NSE de Bloomber de MINDAIND MNDA IN Market Cap 2,028 Free

La Opala RG. Institutional Equities. 4QFY17 Result Update UNDER REVIEW. Revenues Soar, But Margins Take A Hit. Sector: Tableware CMP: Rs536

4QFY17 Result Update La Opala RG 11 May 217 Reuters: LAOP.BO; Bloomberg: LOG IN Revenues Soar, But Margins Take A Hit La Opala RG (LORL) reported revenues of Rs761mn for 4QFY17, up 41% YoY. The stellar

4QFY17 Result Update La Opala RG 11 May 217 Reuters: LAOP.BO; Bloomberg: LOG IN Revenues Soar, But Margins Take A Hit La Opala RG (LORL) reported revenues of Rs761mn for 4QFY17, up 41% YoY. The stellar

Garware Wall Ropes ACCUMULATE. Performance Highlights CMP. `550 Target Price `618. 2QFY2017 Result Update Textile. Investment Period 12 months

2QFY217 Result Update Textile November 16, 216 Garware Wall Ropes Performance Highlights Quarterly Data (`cr) 2QFY17 2QFY16 % yoy 1QFY17 % qoq Revenue 232 214 8.5 225 3.3 EBITDA 4 26 5.9 31 29.4 Margin

2QFY217 Result Update Textile November 16, 216 Garware Wall Ropes Performance Highlights Quarterly Data (`cr) 2QFY17 2QFY16 % yoy 1QFY17 % qoq Revenue 232 214 8.5 225 3.3 EBITDA 4 26 5.9 31 29.4 Margin

Tata Steel NEUTRAL. Performance Highlights CMP. `226 Target Price - 2QFY2016 Result Update Steel. Investment Period - 3-year price chart

2QFY2016 Result Update Steel November 6, 2015 Tata Steel Performance Highlights Standalone (` cr) 2QFY16 2QFY15 yoy % 1QFY16 qoq % Net revenue 9,531 10,785 (11.6) 9,094 4.8 EBITDA 1,862 3,094 (39.8) 1,689

2QFY2016 Result Update Steel November 6, 2015 Tata Steel Performance Highlights Standalone (` cr) 2QFY16 2QFY15 yoy % 1QFY16 qoq % Net revenue 9,531 10,785 (11.6) 9,094 4.8 EBITDA 1,862 3,094 (39.8) 1,689

Coal India ACCUMULATE. Performance Highlights CMP. `338 Target Price `380. Outlook and valuation. 2QFY2016 Result Update Mining

Coal India Performance Highlights (` cr) % yoy % qoq Net Sales 16,958 15,678 8.2 18,956 (1.5) EBITDA 3,8 2,556 17.7 4,944 (39.2) % margin 17.2 15.8 139bp 25.3 (813bp) Net Profit 2,519 2,188 15.2 3,787

Coal India Performance Highlights (` cr) % yoy % qoq Net Sales 16,958 15,678 8.2 18,956 (1.5) EBITDA 3,8 2,556 17.7 4,944 (39.2) % margin 17.2 15.8 139bp 25.3 (813bp) Net Profit 2,519 2,188 15.2 3,787

ITC ACCUMULATE. Performance Highlights CMP. `257 Target Price `284. 3QFY2017 Result Update FMCG. Investment Period 12 Months

3QFY2017 Result Update FMCG January 30, 2017 ITC Performance Highlights Quarterly result (Standalone) (` cr) 3QFY17 3QFY16 % yoy 2QFY17 %qoq Revenue 9,248 8,867 4.3 9,661 (4.3) EBITDA 3,546 3,475 2.1 3,630

3QFY2017 Result Update FMCG January 30, 2017 ITC Performance Highlights Quarterly result (Standalone) (` cr) 3QFY17 3QFY16 % yoy 2QFY17 %qoq Revenue 9,248 8,867 4.3 9,661 (4.3) EBITDA 3,546 3,475 2.1 3,630

Cadila Healthcare. Institutional Equities. 3QFY15 Result Update UNDER REVIEW. Stable Performance. Sector: Pharmaceuticals CMP: Rs1,514

3QFY15 Result Update Institutional Equities Cadila Healthcare 11 February 2015 Reuters: CADI.BO; Bloomberg: CDH IN Stable Performance Cadila Healthcare s (CHL) 3QFY15 earnings were in line with our expectations

3QFY15 Result Update Institutional Equities Cadila Healthcare 11 February 2015 Reuters: CADI.BO; Bloomberg: CDH IN Stable Performance Cadila Healthcare s (CHL) 3QFY15 earnings were in line with our expectations

Gillette India. Institutional Equities. 2QFY19 Result Update BUY. Marketing Investments Mask Improved Top-line Performance

2QFY19 Result Update Gillette India 13 February 2019 Reuters: GILE.NS; Bloomberg: GILL IN Marketing Investments Mask Improved Top-line Performance Gillette India s (GILL) 2QFY19 operating and net earnings

2QFY19 Result Update Gillette India 13 February 2019 Reuters: GILE.NS; Bloomberg: GILL IN Marketing Investments Mask Improved Top-line Performance Gillette India s (GILL) 2QFY19 operating and net earnings

Valuation and Outlook. Growth (%) PAT (Rs cr)

PAT (Rs cr)") Feb-18 May-18 Aug-18 Nov-18 Feb-19 4 Recommendation Hold CMP Rs. 67 Target Price Rs. 90 Sector Stock Details Banking BSE Code 590003 NSE Code Bloomberg Code KARURVYSYA KVB IN Market Cap (Rs Cr) Rs. 5,355

Feb-18 May-18 Aug-18 Nov-18 Feb-19 4 Recommendation Hold CMP Rs. 67 Target Price Rs. 90 Sector Stock Details Banking BSE Code 590003 NSE Code Bloomberg Code KARURVYSYA KVB IN Market Cap (Rs Cr) Rs. 5,355

19 th, September, Kwality Ltd. On Strong Profitability Growth Path

19 th, September, 2016 Kwality Ltd On Strong Profitability Growth Path 15-Sep-15 06-Oct-15 27-Oct-15 17-Nov-15 08-Dec-15 29-Dec-15 19-Jan-16 09-Feb-16 01-Mar-16 22-Mar-16 12-Apr-16 03-May-16 24-May-16

19 th, September, 2016 Kwality Ltd On Strong Profitability Growth Path 15-Sep-15 06-Oct-15 27-Oct-15 17-Nov-15 08-Dec-15 29-Dec-15 19-Jan-16 09-Feb-16 01-Mar-16 22-Mar-16 12-Apr-16 03-May-16 24-May-16

Punjab National Bank

4QFY15 Result Update Institutional Equities Punjab National Bank 11 May 2015 Reuters: PNB.BO; Bloomberg: PNB IN Asset Quality Disappointment Continues Punjab National Bank (PNB) posted dismal 4QFY15 performance,

4QFY15 Result Update Institutional Equities Punjab National Bank 11 May 2015 Reuters: PNB.BO; Bloomberg: PNB IN Asset Quality Disappointment Continues Punjab National Bank (PNB) posted dismal 4QFY15 performance,

Key highlights of the quarter

Recommendation BUY Results above expectations CMP (25/01/2010) Rs. 159 Target Rs. 186 Sector IT Consulting & Software Stock Details BSE Code NSE Code Bloomberg Code Market Cap (Rs. cr) Free Float (%) 52-

Recommendation BUY Results above expectations CMP (25/01/2010) Rs. 159 Target Rs. 186 Sector IT Consulting & Software Stock Details BSE Code NSE Code Bloomberg Code Market Cap (Rs. cr) Free Float (%) 52-

Construction. 4QFY18E Results Preview 14 APR Parikshit D Kandpal

Construction 4QFY18E Results Preview 14 APR 2018 Parikshit D Kandpal parikshit.kandpal@hdfcsec.com +91-22-6171 7317 Kunal Bhandari kunal.bhandari@hdfcsec.com +91-22-6639 3035 4QFY15 1QFY16 2QFY16 3QFY16

Construction 4QFY18E Results Preview 14 APR 2018 Parikshit D Kandpal parikshit.kandpal@hdfcsec.com +91-22-6171 7317 Kunal Bhandari kunal.bhandari@hdfcsec.com +91-22-6639 3035 4QFY15 1QFY16 2QFY16 3QFY16

Symphony Ltd. RESULT UPDATE 31st October 2017

. RESULT UPDATE 31st October 2017 Oct-14 Apr-15 Oct-15 Apr-16 Oct-16 Apr-17 Oct-17 India Equity Institutional Research II Result Update Q2FY18 II 31st October 2017. CMP INR 1,465 Target INR 1,700 Potential

. RESULT UPDATE 31st October 2017 Oct-14 Apr-15 Oct-15 Apr-16 Oct-16 Apr-17 Oct-17 India Equity Institutional Research II Result Update Q2FY18 II 31st October 2017. CMP INR 1,465 Target INR 1,700 Potential

Swiss Glascoat Equipments

Management Meet Update Institutional Equities Swiss Glascoat Equipments 28 December 17 Reuters: SWGE.BO; Bloomberg: SWGE IN We had a meeting with the management of Swiss Glascoat Equipments (SGEL) recently

Management Meet Update Institutional Equities Swiss Glascoat Equipments 28 December 17 Reuters: SWGE.BO; Bloomberg: SWGE IN We had a meeting with the management of Swiss Glascoat Equipments (SGEL) recently

Muthoot Finance. Institutional Equities. 1QFY18 Result Update. Gold Loan Business Continues To Glitter BUY. 10 August 2017

1QFY18 Result Update Institutional Equities Muthoot Finance 10 August 2017 Reuters: MUTT.BO; Bloomberg: MUTH IN Gold Loan Business Continues To Glitter Strong profitability numbers of Muthoot Finance (MFL)

1QFY18 Result Update Institutional Equities Muthoot Finance 10 August 2017 Reuters: MUTT.BO; Bloomberg: MUTH IN Gold Loan Business Continues To Glitter Strong profitability numbers of Muthoot Finance (MFL)

Religare Investment Call

v-17 v-17 Dec-17 Jan-18 Jan-18 Feb-18 Mar-18 Mar-18 Apr-18 May-18 May-18 Jun-18 Jul-18 Aug-18 Aug-18 Sep-18 Oct-18 Oct-18 Q2FY19 Result Update Q2FY19 Result Update BUY CMP (Rs) 282 Target Price (Rs) 321

v-17 v-17 Dec-17 Jan-18 Jan-18 Feb-18 Mar-18 Mar-18 Apr-18 May-18 May-18 Jun-18 Jul-18 Aug-18 Aug-18 Sep-18 Oct-18 Oct-18 Q2FY19 Result Update Q2FY19 Result Update BUY CMP (Rs) 282 Target Price (Rs) 321

Goodyear India BUY. Company Update. CMP Target Price `515 `631. Company Update Tyres. 3-year Daily Price Chart. Key Financials

Company Update Tyres June 10, 2016 Goodyear India Company Update Expectation of normal monsoon to energize stagnant tractor demand: Goodyear India (GIL) is a leader in the farm tyre segment in India with

Company Update Tyres June 10, 2016 Goodyear India Company Update Expectation of normal monsoon to energize stagnant tractor demand: Goodyear India (GIL) is a leader in the farm tyre segment in India with

Mahindra & Mahindra Ltd.

Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17 Jul-17 Oct-17 Jan-18 Apr-18 Jul-18 Oct-18 Jan-19 3QFY2019 Result Update Automobile February 15, 2019 Mahindra & Mahindra Ltd. Performance Update Y/E March (` cr)

Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17 Jul-17 Oct-17 Jan-18 Apr-18 Jul-18 Oct-18 Jan-19 3QFY2019 Result Update Automobile February 15, 2019 Mahindra & Mahindra Ltd. Performance Update Y/E March (` cr)

Gillette India. Institutional Equities. 1QFY18 Result Update

1QFY18 Result Update Institutional Equities Gillette India 14 November 2017 Reuters: GILE.NS; Bloomberg: GILL IN Robust Growth In Operating Margin Gillette India s or GIL s overall top-line performance

1QFY18 Result Update Institutional Equities Gillette India 14 November 2017 Reuters: GILE.NS; Bloomberg: GILL IN Robust Growth In Operating Margin Gillette India s or GIL s overall top-line performance

Punjab National Bank

1QFY16 Result Update Institutional Equities Punjab National Bank 29 July 2015 Reuters: PNB.BO; Bloomberg: PNB IN Some Respite On Asset Quality Front Punjab National Bank (PNB) reported moderate 1QFY16

1QFY16 Result Update Institutional Equities Punjab National Bank 29 July 2015 Reuters: PNB.BO; Bloomberg: PNB IN Some Respite On Asset Quality Front Punjab National Bank (PNB) reported moderate 1QFY16

ITC Ltd. RESULT UPDATE 27th October, 2017

. RESULT UPDATE 27th October, 2017 Oct-14 Apr-15 Oct-15 Apr-16 Oct-16 Apr-17 Oct-17 India Equity Institutional Research II Result Update - II 27th October, 2017 CMP INR 269 Target INR 349 Potential Upside

. RESULT UPDATE 27th October, 2017 Oct-14 Apr-15 Oct-15 Apr-16 Oct-16 Apr-17 Oct-17 India Equity Institutional Research II Result Update - II 27th October, 2017 CMP INR 269 Target INR 349 Potential Upside

Institutional Equities

Company Update Institutional Equities Dr. Reddy s Laboratories 5 September 2017 Reuters: REDY.BO; Bloomberg: DRRD IN Suboxone Generic Opportunity To Be Lucrative, Can Sustain For Longer Time The district

Company Update Institutional Equities Dr. Reddy s Laboratories 5 September 2017 Reuters: REDY.BO; Bloomberg: DRRD IN Suboxone Generic Opportunity To Be Lucrative, Can Sustain For Longer Time The district

Prabhat Dairy Ltd. RESULT UPDATE 8th June, 2018

RESULT UPDATE 8 th June, 2018 Sep-15 Jan-16 May-16 Sep-16 Jan-17 May-17 Sep-17 Jan-18 May-18 India Equity Institutional Research II Result Update - Q4FY18 II 8 th June, 2018 2 Under Expansion Mode CMP

RESULT UPDATE 8 th June, 2018 Sep-15 Jan-16 May-16 Sep-16 Jan-17 May-17 Sep-17 Jan-18 May-18 India Equity Institutional Research II Result Update - Q4FY18 II 8 th June, 2018 2 Under Expansion Mode CMP

Jamna Auto Industries

2QFY19 Result Update Institutional Equities Jamna Auto Industries Reuters: JMNA.NS; Bloomberg: JMNA IN Performance Below Expectations; Retain Buy Due To Strong Outlook Jamna Auto s 2QFY19 earnings were

2QFY19 Result Update Institutional Equities Jamna Auto Industries Reuters: JMNA.NS; Bloomberg: JMNA IN Performance Below Expectations; Retain Buy Due To Strong Outlook Jamna Auto s 2QFY19 earnings were

Atul Auto. Institutional Equities. Management Meet Update ACCUMULATE. Sector: Automobile CMP: Rs445 Target Price: Rs489 Upside: 10% 23 August 2017

Management Meet Update Atul Auto 23 August 2017 Reuters: ATUL.BO; Bloomberg: ATUL IN We had a meeting with the management of Atul Auto (AAL) recently to gauge its performance in the aftermath of a relatively

Management Meet Update Atul Auto 23 August 2017 Reuters: ATUL.BO; Bloomberg: ATUL IN We had a meeting with the management of Atul Auto (AAL) recently to gauge its performance in the aftermath of a relatively

Parag Milk Foods BUY. Performance Update CMP. `256 Target Price `330. 2QFY2019 Result Update Dairy Products. Investment Period 12 Months

2QFY2019 Result Update Dairy Products November 6, 2018 Parag Milk Foods Performance Update Y/E March (` cr) Q2FY19 Q2FY18 % yoy Q1FY19 % qoq Net sales 573 505 13.7% 549 4.4% EBITDA 58 50 16.3% 60-2.7%

2QFY2019 Result Update Dairy Products November 6, 2018 Parag Milk Foods Performance Update Y/E March (` cr) Q2FY19 Q2FY18 % yoy Q1FY19 % qoq Net sales 573 505 13.7% 549 4.4% EBITDA 58 50 16.3% 60-2.7%

Quarterly result- Revenues in line with our Expectations, Profits Disappoint.

Recommendation HOLD Snapshot CMP (09/06/2010) Rs. 1295 Maruti Suzuki India Limited, a subsidiary of Suzuki Motor Corporation Sector Auto of Japan, is the leader in the Indian car market with 54% market

Recommendation HOLD Snapshot CMP (09/06/2010) Rs. 1295 Maruti Suzuki India Limited, a subsidiary of Suzuki Motor Corporation Sector Auto of Japan, is the leader in the Indian car market with 54% market

Kalpataru Power Transmission Ltd.

Change in Estimates Rating Target Q1 FY16 Kalpataru Power Transmission Ltd. KPTL s standalone results were quite stronger than our expectations due to higher execution in the infrastructure segment Topline

Change in Estimates Rating Target Q1 FY16 Kalpataru Power Transmission Ltd. KPTL s standalone results were quite stronger than our expectations due to higher execution in the infrastructure segment Topline

Mahindra & Mahindra Ltd.

Nov-15 Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17 Jul-17 Oct-17 Jan-18 Apr-18 Jul-18 Oct-18 2QFY2019 Result Update Automobile November 15, 2018 Mahindra & Mahindra Ltd. Performance Update Y/E March (` cr)

Nov-15 Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17 Jul-17 Oct-17 Jan-18 Apr-18 Jul-18 Oct-18 2QFY2019 Result Update Automobile November 15, 2018 Mahindra & Mahindra Ltd. Performance Update Y/E March (` cr)

Voltas. Institutional Equities. Management Meet Update ACCUMULATE. Sector: Capital Goods CMP: Rs309 Target Price: Rs325 Upside: 5% 23 December 2016

Management Meet Update Institutional Equities Voltas Reuters: VOLT.BO; Bloomberg: VOLT IN We had a meeting with the management of Voltas recently to get the latest business update. While the management

Management Meet Update Institutional Equities Voltas Reuters: VOLT.BO; Bloomberg: VOLT IN We had a meeting with the management of Voltas recently to get the latest business update. While the management

Dilip Buildcon Ltd.: Q3FY18 Result Update

Edelweiss Investment Research Dilip Buildcon Ltd.: Q3FY18 Result Update From Sub-contractor to Marquee EPC Play CMP INR: 981 Rating: BUY Target Price INR: 1,204 Upside: 22% Dilip Buildcon (DBL), the largest

Edelweiss Investment Research Dilip Buildcon Ltd.: Q3FY18 Result Update From Sub-contractor to Marquee EPC Play CMP INR: 981 Rating: BUY Target Price INR: 1,204 Upside: 22% Dilip Buildcon (DBL), the largest

Capacity expansion to drive growth and profitability

STOCK POINTER Swaraj Engines Ltd. BUY Target Price `656 CMP `41 FY14 PE 6.9x Index Details Sensex 17,853 Nifty 5,39 BSE 1 5,367 Industry Auto parts Scrip Details Mkt Cap (` cr) 59 BVPS (`) 161 O/s Shares

STOCK POINTER Swaraj Engines Ltd. BUY Target Price `656 CMP `41 FY14 PE 6.9x Index Details Sensex 17,853 Nifty 5,39 BSE 1 5,367 Industry Auto parts Scrip Details Mkt Cap (` cr) 59 BVPS (`) 161 O/s Shares

ITC. Institutional Equities. 4QFY18 Result Update. Tracking Expectations ACCUMULATE. Sector: FMCG CMP: Rs286 Target Price: Rs290 Upside: 1%

4QFY18 Result Update Institutional Equities ITC 17 May 2018 Reuters: ITC.NS; Bloomberg: ITC IN Tracking Expectations ITC s growth in 4QFY18 was modest and in line with expectations. On the revenue side,

4QFY18 Result Update Institutional Equities ITC 17 May 2018 Reuters: ITC.NS; Bloomberg: ITC IN Tracking Expectations ITC s growth in 4QFY18 was modest and in line with expectations. On the revenue side,

Parag Milk Foods BUY. Performance Update CMP. `324 Target Price `410. 1QFY2019 Result Update Dairy Products. Investment Period 12 Months

1QFY2019 Result Update Dairy Products August 8, 2018 Parag Milk Foods Performance Update Y/E March (` cr) Q1FY19 Q1FY18 % yoy Q4FY18 % qoq Net sales 549 413 32.9 518 5.9 EBITDA 60 29 103% 55 8.4% EBITDA

1QFY2019 Result Update Dairy Products August 8, 2018 Parag Milk Foods Performance Update Y/E March (` cr) Q1FY19 Q1FY18 % yoy Q4FY18 % qoq Net sales 549 413 32.9 518 5.9 EBITDA 60 29 103% 55 8.4% EBITDA

Institutional Equities

4QFY18 Result Update Institutional Equities Atul Auto 30 May 2018 Reuters: ATUL.BO; Bloomberg: ATUL IN Higher Expenses Mar Profitability Atul Auto s (AAL) 4QFY18 earnings missed our expectations on account

4QFY18 Result Update Institutional Equities Atul Auto 30 May 2018 Reuters: ATUL.BO; Bloomberg: ATUL IN Higher Expenses Mar Profitability Atul Auto s (AAL) 4QFY18 earnings missed our expectations on account

9,251 7,812 8, NIM

4QFY15 Result Update Institutional Equities IndusInd Bank 17 April 2015 Reuters: INBK.BO; Bloomberg: IIB IN Yet Another Robust Performance IndusInd Bank s 4QFY15 profit beat our estimate by 12%. Its bottom-line

4QFY15 Result Update Institutional Equities IndusInd Bank 17 April 2015 Reuters: INBK.BO; Bloomberg: IIB IN Yet Another Robust Performance IndusInd Bank s 4QFY15 profit beat our estimate by 12%. Its bottom-line

Procter & Gamble Hygiene & Health Care

3QFY216 Result Update FMCG May 6, 216 Procter & Gamble Hygiene & Health Care Performance Highlights Quarterly Data (` cr) 3QFY16 3QFY15 % yoy 2QFY16 % qoq Revenue 614 555 1.5 714 (14.) EBITDA 133 123 8.5

3QFY216 Result Update FMCG May 6, 216 Procter & Gamble Hygiene & Health Care Performance Highlights Quarterly Data (` cr) 3QFY16 3QFY15 % yoy 2QFY16 % qoq Revenue 614 555 1.5 714 (14.) EBITDA 133 123 8.5

Blue Star Ltd BUY. Performance Update. CMP Target Price `703 `867. 1QFY2019 Result Update Cons. Durable. 3-year price chart.

Aug-15 Oct-15 Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16 Dec-16 Jan-17 Apr-17 May-17 Jul-17 Sep-17 Nov-17 Jan-18 Mar-18 May-18 Jul-18 1QFY2019 Result Update Cons. Durable August 10, 2018 Blue Star Ltd Performance

Aug-15 Oct-15 Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16 Dec-16 Jan-17 Apr-17 May-17 Jul-17 Sep-17 Nov-17 Jan-18 Mar-18 May-18 Jul-18 1QFY2019 Result Update Cons. Durable August 10, 2018 Blue Star Ltd Performance

KNR CONSTRUCTIONS LTD

14 June 2017 KNR CONSTRUCTIONS LTD CMP INR 210 Initiating Coverage (BUY) Target Price INR 242 Stock Details Industry Construction & Engineering Bloomberg Code KNRC:IN BSE Code 532942 Face Value (Rs.) 2.00

14 June 2017 KNR CONSTRUCTIONS LTD CMP INR 210 Initiating Coverage (BUY) Target Price INR 242 Stock Details Industry Construction & Engineering Bloomberg Code KNRC:IN BSE Code 532942 Face Value (Rs.) 2.00

Everest Kanto Cylinder Ltd.

Industrial Goods CMP Rs. 82 August 16, 2011 BSE Code 532684 BSE ID EKC High/Low 1Y (Rs.) 133 / 68 Avg. vol (3m) 98,219 Market Cap (Rs Cr) 879 Net IB Debt (Rs Cr) 286 Enterprise value(rs Cr) 1,166 Shareholding

Industrial Goods CMP Rs. 82 August 16, 2011 BSE Code 532684 BSE ID EKC High/Low 1Y (Rs.) 133 / 68 Avg. vol (3m) 98,219 Market Cap (Rs Cr) 879 Net IB Debt (Rs Cr) 286 Enterprise value(rs Cr) 1,166 Shareholding

9,807 8,007 9, NIM

1QFY16 Result Update Institutional Equities IndusInd Bank Reuters: INBK.BO; Bloomberg: IIB IN Yet Another Stellar Performance IndusInd Bank s 1QFY16 profit beat our estimate by 4%. Its bottom-line grew

1QFY16 Result Update Institutional Equities IndusInd Bank Reuters: INBK.BO; Bloomberg: IIB IN Yet Another Stellar Performance IndusInd Bank s 1QFY16 profit beat our estimate by 4%. Its bottom-line grew

production (a return to Q1FY11 production level of 120ktons meeting ( ) E mail:

E mail:") Recommendation BUY Investment Rationale CMP (23/12/2010) Sector Stock Details BSE Code NSE Code Market Cap (Rs. cr) Free Float (%) 52 wk HI/Lo Avg. volume BSE (Monthly) Dividend Shares o/s (Crs) Rs.70

Recommendation BUY Investment Rationale CMP (23/12/2010) Sector Stock Details BSE Code NSE Code Market Cap (Rs. cr) Free Float (%) 52 wk HI/Lo Avg. volume BSE (Monthly) Dividend Shares o/s (Crs) Rs.70

93,707 77,814 90, NIM

1QFY18 Result Update Institutional Equities HDFC Bank Reuters: HDBK.BO; Bloomberg: HDFCB IN Higher Fee Income Offsets Higher Provisioning HDFC Bank s net interest income or NII grew 20% in 1QFY18 driven

1QFY18 Result Update Institutional Equities HDFC Bank Reuters: HDBK.BO; Bloomberg: HDFCB IN Higher Fee Income Offsets Higher Provisioning HDFC Bank s net interest income or NII grew 20% in 1QFY18 driven

Amber Enterprises India Ltd

3QFY2019 Result Update Consumer Durable February 16, 2019 Amber Enterprises India Ltd Performance Update (` cr) 3QFY19 3QFY18 % yoy 2QFY19 % qoq Revenue 388.8 338.4 14.9 226.3 71.8 EBITDA 22.1 24.1 (8.2)

3QFY2019 Result Update Consumer Durable February 16, 2019 Amber Enterprises India Ltd Performance Update (` cr) 3QFY19 3QFY18 % yoy 2QFY19 % qoq Revenue 388.8 338.4 14.9 226.3 71.8 EBITDA 22.1 24.1 (8.2)