Prospectus Requirements and Review Process

|

|

|

- Archibald Todd

- 6 years ago

- Views:

Transcription

1 Prospectus Requirements and Review Process Corporate Finance Branch October 23, 2012

2 SME Disclaimer The views expressed in this presentation are the personal views of the presenting staff and do not necessarily represent the views of the Commission or other Commission staff. The presentation is provided for general information purposes only and does not constitute legal or accounting advice. Information has been summarized and paraphrased for presentation purposes and the examples have been provided for illustration purposes only. Responsibility for making sufficient and appropriate disclosure and complying with applicable securities legislation remains with the company. Information in this presentation reflects securities legislation and other relevant standards that are in effect as of the date of the presentation. The contents of this presentation should not be modified without the express written permission of the presenters. 2

3 Presentation Outline Time Topic Page 1:30 1:35 Welcome and Introduction to the 4 1:35 1:45 Overview 6 1:45 2:30 Offering Securities to the Public in Ontario 13 2:30 2:35 Break 2:35 2:40 Phases of the Prospectus Offering 49 2:40 3:05 Prospectus Filing and Review Process 52 3:05 3:25 Illustrative Case Study Going concern issue 65 3:25 3:30 Questions 76 3

4 Welcome and introduction to the 4

5 - Objectives Our goal is to: Help SMEs navigate the regulatory waters Demystify disclosure requirements so companies can focus on building their business Reduce SMEs cost of compliance so that this money can be better spent on strategic initiatives Provide an opportunity for informal dialogue with staff Disclosure requirements, including those for financial reporting, are a cornerstone of investor confidence 5

6 Overview 6

7 IPO Outlook and Trends Factors impacting confidence in/attractiveness of equity financing: 1. Continuing concerns in the global economy U.S. economy continues to grow slowly which will impact Canadian businesses exporting south of the border Increasingly worrying signs of economic weakness in emerging markets slower growth will lessen demand in the commodity markets which will impact commodity producers and will probably dampen demand for new issues in mining sector 2. Continuing low interest rate environment will make debt markets a more attractive option for companies that have access to debt 3. Data shows investors are still not putting their money in equities markets focus has been on passive ETF type products and those that generate yield 7

8 Access to Capital Toronto Stock Exchange and TSX Venture Exchange Total Financings (C$Billions) Toronto Stock Exchange TSX Venture Exchange * Sept. 30, 2012 Source: TMX Group * TSX Venture Exchange commenced operations on November 29,

9 Access to Capital Equity Financings by Sector Diversified Industries 28% Oil and Gas & Energy Services 26% Structured Products & ETFs 8% Mining 17% Financial Services 15% Clean Technology 2% Life Sciences 1% Technology 3% $51.1B Value of Financings by Sector TSX and TSXV 2011 $41.7B Value of Financings by Sector TSX and TSXV September 2012 Source: TMX Group 9

10 Importance of Today s Seminar Topic Prospectus Requirements and Review Process 10

11 Why this Topic? De-mystify the regulatory requirements and share staff s expectations Provide tips to help accelerate the time to complete the regulatory review process which will save time and costs for companies Companies need to provide meaningful disclosure in the prospectus to tell their story to prospective investors 11

12 Meaningful Disclosure A prospectus is a key investor protection tool Provides investors with important information about the company and the securities being offered The information disclosed within must be entity-specific and comprehensive to provide meaningful information Should help investors evaluate the performance and risks of the company so they can make an informed investment decision Can only do that if the information is balanced and not boilerplate 12

13 Offering Securities to the Public in Ontario 13

14 Offering Securities to the Public in Ontario Distribution of Securities Prospectus-Exempt Offerings Types of Prospectus Offerings Types of Prospectuses Long Form Prospectus Content Requirements 14

15 Distribution of Securities 15

16 Distribution of Securities If you are selling securities to an investor in a distribution, you must do so under a prospectus unless you are relying on an exemption A distribution includes: a trade in securities of an issuer that have not been previously issued a trade in previously issued securities of an issuer from the holdings of any control person deemed distributions under securities legislation 16

17 Prospectus-Exempt Offerings 17

18 Prospectus-Exempt Offerings Key Prospectus Exemptions in NI Capital raising exemptions Accredited investor Founder, control person and family Minimum amount investment Transaction exemptions Business combination and reorganization Asset acquisition Securities for debt Employee, executive officer, director and consultant exemptions Primary exemptions used in Ontario are accredited investor and minimum amount investment 18

19 Prospectus-Exempt Offerings Exemptions in NI that do not Apply in Ontario Family, friends and business associates Offering memorandum 19

20 Types of Offerings 20

21 Types of Offerings Generally six types of offerings that may be available Bought deal Overnight marketed deal Fully marketed underwritten deal Best efforts agency offering Special warrant offering Non-offering prospectus Consult your legal and financial advisors as to which type of offering works for your purposes 21

22 Types of Offerings Bought deal Underwriters price the deal and sign a firm commitment to buy base amount of the offering 4 days prior to filing the preliminary prospectus Overnight marketed deal Underwriters market the deal overnight after preliminary receipt is issued at the close of the market The next morning the underwriters price the deal and sign a firm commitment to buy a base amount of the offering An amended and restated prelim prospectus is filed with size and pricing information provided 22

23 Types of Offerings Fully marketed underwritten deal On eve of filing the final prospectus, the underwriters will price the deal and sign a firm commitment to buy base amount of the offering Best efforts agency offering Two types a minimum/maximum offering and a best efforts with no minimum Agents price the deal on the eve of the final prospectus Agents are not liable to buy any unsold securities When purchasers are obtained after final receipt a closing date is scheduled 23

24 Types of Offerings Special warrant offering Prior to filing preliminary, special warrants are issued to investors pursuant to an exemption from the prospectus requirements The special warrants are convertible into underlying securities (i.e. common shares) Issuer required to file a prospectus to qualify the distribution of underlying securities Non-offering prospectus Purpose is primarily to become a reporting issuer Does not involve the selling of any securities to the public 24

25 Types of Prospectuses 25

26 Types of Prospectuses Type Characteristics Who uses it? Long Form NI General Prospectus Requirements and Form F1 Information Required in a Prospectus sets out in detail the information required Short Form NI Shortform Prospectus Distributions sets out the eligibility criteria and disclosure requirements for this type of prospectus All disclosure contained directly within the prospectus Allows existing reporting issuers to incorporate certain information into a prospectus by reference including: Financial statements & MD&A Annual information form Material Change reports Used by a company undertaking an initial offering of its securities (commonly referred to as an Initial Public Offering, or IPO), or A company that is not eligible to use a short-form prospectus Used by a company that is already a reporting issuer in a Canadian jurisdiction Must be qualified under NI to file a short form prospectus Generally quicker review time than long form 26

27 Types of Prospectuses Type Characteristics Who uses it? Shelf Required disclosure is essentially the same as for a short-form prospectus, modified in accordance with NI Shelf Distributions Post-Receipt Pricing NI Post- Receipt Pricing sets out the criteria Certain information relating to the particular offering may be omitted from a base shelf prospectus, provided it is included in the shelf supplement that is filed and delivered when the actual distribution of securities occurs Once pricing is determined, a supplemented PREP prospectus that contains all of the omitted information is filed with the and provided to purchasers A PREP prospectus can be based on a long-form or short-form prospectus Form of prospectus used by a company that is already a reporting issuer. It allows companies to access the capital markets quickly because they can drawdown using a supplement with details of the offering Cost effective way of accessing the markets Allows issuers to file a final prospectus that omits pricing and related information Any issuer can use this, not limited to issuers qualified to file a short form 27

28 Long Form Prospectus Content Requirements 28

29 The Prospectus Tells the Story Overriding Principle A prospectus shall provide full, true and plain disclosure of all material facts relating to the securities issued or proposed to be distributed and shall comply with the requirements of Ontario securities law Provides a clear understanding of the company including its history, performance and future expectations Explains the nature of the securities being offered Sets out the risks associated with the security and the company 29

30 Key Considerations for Full, True and Plain Disclosure FULL sufficient facts to permit investors to make an informed investment decision TRUE disclosure: is accurate is not misleading does not omit a fact that is either material itself or is necessary to understand the facts that have been disclosed PLAIN disclosure must be understandable to investors and be written in plain language Consider whether all material facts have been included in the prospectus 30

31 Prospectus Content Requirements Topic General Disclosure about the issuer Governance disclosure Detailed requirements Cover page disclosure Table of contents Summary of prospectus Experts Rights of withdrawal and rescission List of exemptions from Instrument Certificates Corporate structure Description of the business of the issuer Principal securityholders and selling securityholders Risk factors Legal proceedings and regulatory actions Auditors, transfer agents and registrars Material contracts Other material facts Probable reverse takeovers Mineral property/oil & Gas technical disclosures Directors and executive officers Executive compensation Indebtedness of directors and executive officers Audit committees and corporate governance Interests of management and others in material transactions 31

32 Prospectus Content Requirements Topic Disclosure about the securities being offered Financial disclosure Other financial information Detailed requirements Use of proceeds of the offering Dividends or distributions Earnings coverage ratios Description of the securities distributed Prior sales Options to purchase securities Escrowed securities and securities subject to contractual restriction on transfer Plan of distribution Promoters Relationship between issuer or selling securityholder and underwriter Financial statements Significant aquisitions MD&A Consolidated capitalization of the issuer Credit supporter disclosure, including financial statements Exemptions for certain issues of guaranteed securities 32

33 Prospectus Content Requirements Areas of focus today General hot button prospectus issues Financial disclosure requirements MD&A General requirements for resource issuers 33

34 General Prospectus Hot Buttons Areas Financial condition of Issuer and sufficiency of proceeds from offering Issuers operating in an emerging market Novel, hybrid or derivative securities Considerations Whether the company has sufficient resources to continue its operations Whether proceeds from the offering are sufficient to meet the stated purpose of the offering Whether there are concerns about titles and ownerships of assets Whether there are language barriers for officers and directors Governance structure Whether complex securities should be offered to retail investors What disclosure should be required for complex securities Whether an undertaking is required 34

35 General Prospectus Hot Buttons Areas Considerations Involvement of promoters in an offering and promoter certificates Equity lines of credit and at the market prospectus distributions Whether a person or company should be signing the prospectus certificate as promoter Whether a person or company who previously signed the prospectus certificate as promoter should continue to sign as promoter Whether the issuer has received relief from the requirement to deliver a prospectus Whether there are sufficient risk factors disclosures of the investment intentions of the equity line or at-the-market investors Whether there is sufficient disclosure about the dilution as a result of draw downs made by equity line or at-the-market investors Failure to address the above issues may delay your offering or result in receipt refusal 35

36 Financial Disclosure Requirements In general, an issuer s prospectus must include the following: Annual: For the three most recent annual periods: Statement of comprehensive income Statement of changes in equity Statement of cash flows For the two most recent annual periods: Statement of financial position Interim: Comparative interim financial report for most recent interim period (subsequent to most recent financial year end. In cases of a reverse take-over transaction or other transactions, know who the issuer is For more information, see: Item 32 of Form F1 36

37 Financial Disclosure Requirements (continued) Financial statements also required for any significant or probable business acquisitions Generally, the same financial disclosure requirements as required by NI , Part 8 Business Acquisition Reports Two years of financial statements Most recent year audited Interim financial statements if necessary Pro-forma financial statements For more information, see: Item 35 of Form F1 37

38 Significance Tests Determination of significance An acquisition of a business is a significant acquisition if any one of the significance tests apply Venture/IPO Venture Non-Venture Asset test > 40% > 20% Investment test > 40% > 20% Profit or loss test N/A > 20% 38

39 Acceptable Accounting and Auditing Standards For a domestic issuer: Issuer SEC Issuer Accounting Standards Canadian GAAP applicable to publicly accountable enterprises (IFRS as of January 1, 2011) - NI s. 3.2 Can also use U.S. GAAP - NI s. 3.7 Auditing Standards Canadian GAAS - NI s. 3.3 Can also use U.S. PCAOB GAAS - NI s. 3.8 Special rules apply in NI for foreign issuers 39

40 Acceptable Accounting and Auditing Standards For financial statements of acquisitions: Accounting standards Auditing standards Requirement Choice of: IFRS U.S. GAAP Canadian GAAP applicable to private enterprises, subject to conditions Choice of: Canadian GAAS International Standards on Auditing U.S. PCAOB 1 GAAS U.S. AICPA 2 GAAS Reference NI s NI s Special rules apply in for certain foreign acquisitions 1 PCAOB Public Company Accounting Oversight Board 2 AICPA American Institute of Certified Public Accountants 40

41 Financial Disclosure Hot Buttons Area Considerations Financial statements for the issuer Disclosure for significant acquisitions Requirements relating to Auditors report and Auditor s consent Has historical financial information been provided in substance for the issuer? Use of acceptable accounting or auditing standards Whether there should be a going concern note in the financial statements Whether significance tests have been applied appropriately Whether a proposed acquisition is probable Complexity in preparing pro forma financial statements with non-coterminous year ends Have all auditors consents been included in the prospectus 41

42 MD&A Background MD&A is a narrative explanation through the eyes of management which: Provides a balanced discussion of company s results, financial condition and future prospects openly reporting bad news as well as good news Helps current and prospective investors understand what the financial statements show and do not show Discusses trends and risks that have affected or are reasonably likely to affect the financial statements in the future Provides information about the quality and potential variability of company s earnings and cash flow To be meaningful for investors, MD&A disclosure should not be boilerplate 42

43 Annual MD&A Critical accounting estimates Fourth quarter analysis Financial instruments Selected annual information Annual MD&A Discussion of operations Liquidity and capital resources Summary of quarterly results Related party transactions Off-balance sheet arrangements 43

44 Management Discussion & Analysis MD&A relating to annual and interim financial statements must be included in the prospectus Must be reviewed/approved by issuer s audit committee/board of directors Additional disclosure required for: venture issuers without significant revenue reporting issuers with significant equity investees previously disclosed material forward-looking information Must be prepared in accordance with Form F1 44

45 Common MD&A Hot Buttons Area Considerations Discussion of operations Disclosure simply repeats differences in the financial statements without explanation of why changes occurred Liquidity and capital resources Few details on the performance by business segments or lines of business Incomplete working capital discussion Unclear disclosure of liquidity needs and how funded Going concern uncertainty in financial statements unaccompanied by MD&A discussion Risk disclosure Laundry list of risks no detail or discussion included on impact on business Irrelevant risks not relevant to entity s business or circumstances Unclear discussion of how risks are managed 45

46 General Requirements for Resource Issuers NI Standards of Disclosure for Mineral Projects contains disclosure requirements for mining technical reports NI Standards of Disclosure for Oil and Gas Activities contains disclosure requirements for reserves data and other information for oil and gas issuers 46

47 Mining Technical Report Hot Buttons Area Considerations Complete and current information Provide information which is currently material to the entire property, not just for a project on the property Verification of data Ensure that qualified person(s) has: conducted data verification and provided an opinion on the adequacy of the data used in the report Mineral resources and reserves Disclose and justify key information related to how estimates were determined such as: assumptions on metal prices mining methods 47

48 Five Ws (& one H) of Mining Technical Reports Who Prepared by qualified persons who are (often) independent What When Where Why How Current summary of material information on a material property Triggered by milestone events and filed within a specific timeframe Filed publicly on SEDAR Supports the company s technical disclosure and assists investors Must follow prescribed requirements 48

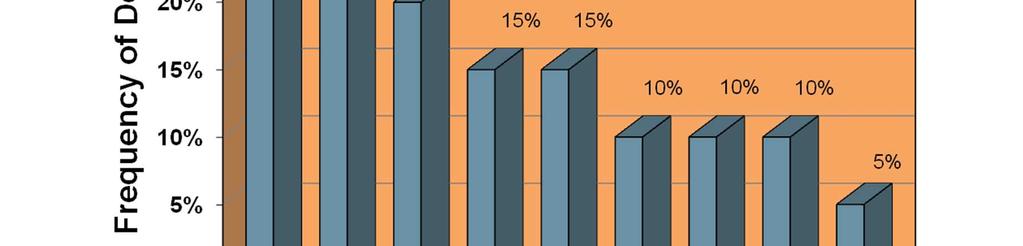

49 Common Technical Report Deficiencies 49

50 Phases of the Prospectus Offering 50

51 Phases of the Prospectus Offering Soliciting expressions of interest on a bought deal Pre-Marketing Period A B-4 B Sufficient specificity occurs/ distribution commences Bought deal agreement signed and announced by press release Preliminary prospectus receipt Waiting Period C Final prospectus receipt Post Final Receipt Period D Closing of prospectus offering 51

52 Prospectus Filing and Review Process 52

53 Prospectus Filing and Review Process Principal Regulator Prospectus Pre-filing and Waiver Applications Filing Preliminary Prospectus Review Process Filing Final Prospectus 53

54 Prospectus Filing and Review Process Activity Issuer determines Principal Regulator Issuer files prefile and waiver applications if required Issuer files preliminary prospectus reviews preliminary prospectus and issues comments Issuer files final prospectus Final Receipt Issued Time period 54

55 Principal Regulator Principal Regulator determination Issuer s head office if it is located in a specified jurisdiction (BC, AB, SK, MB, ON, QC, NB, NS) Location of management, assets and operations, trading market, securityholders, underwriter, legal counsel, and transfer agent For more information, see: National Policy Process for Prospectus Reviews in Multiple Jurisdictions 55

56 Why Pre-File To seek relief from a requirement under securities law To consult with staff as to how securities legislation may be interpreted in particular circumstances Done prior to or concurrently with filing of preliminary prospectus To avoid surprises during the comment period Length of time required depends on the complexity and the novelty of the issue Start preliminary conversations with regulator if novel structure 56

57 Prospectus Pre-Filing and Applications Applications reviewed on a case-by-case basis Depends on the facts and circumstances. Time and costs are not considered as reasons for non-compliance with prospectus requirements Consultation with other CSA jurisdictions for novel issues Description of relief disclosed in the prospectus 57

58 Filing Preliminary Prospectus Documents required to be filed English and French translation of the prospectus Qualification certificate (Short-Form prospectus) Material incorporated by reference (Short-Form prospectus) Documents affecting the rights of securityholders Material contracts Reports, valuations, and mining reports Failure to file above documents will delay preliminary receipt 58

59 Filing Preliminary Prospectus Documents required to be delivered Personal Information Forms and related authorizations Auditors comfort letter Issuer confirmation letter pursuant to section 7.2 of NP

60 Filing Preliminary Prospectus Substantive compliance with requirements Date of the prospectus and date of filing Time of filing and time of receipt Amendment to the preliminary prospectus material adverse change 60

61 Comment Letters and Response Letters Timing of first comment letter Long Form Prospectus: 10 business days Tips for responding Short Form Prospectus: 3 business days make sure response comprehensively addresses staff s comments cite authoritative references where appropriate, especially when responding to technical accounting comments provide proposed disclosure to be included in the prospectus to address staff s comments, where appropriate 61

62 Filing Final Prospectus Documents required to be filed English and French translation of the prospectus Material incorporated by reference (Short-Form prospectus) Documents affecting the rights of securityholders Material contracts Reports and valuations Undertakings, submission to jurisdiction, and expert s consents 62

63 Filing Final Prospectus Documents required to be delivered Blackline to show changes from preliminary prospectus Conditional approval letter from the exchange 63

64 Filing Final Prospectus Date of the prospectus and date of filing (90-Day deadline) Time of filing and time of receipt Amendment to the final prospectus material change If date between preliminary and final is greater than 90 days, will need to update the financial statements 64

65 Illustrative Case Study Going Concern Issue 65

66 Facts From Disclosure Contained in the Issuer s Prospectus Background ABC Inc. operates in the technology industry and is continuing to enhance its proprietary technology with the goal of increasing sales of its core product Core product sales have been low and cash burn rate has been increasing in recent quarters The company states that sales are expected to increase in the second half of the year as market penetration increases and product enhancements are made 66

67 Facts From Disclosure Contained in the Issuer s Prospectus Offering Has filed a best efforts short-form prospectus with a minimum offering to raise funds for operations and further product enhancement Use of proceeds disclosure in the prospectus does not include a discussion of milestones and does not break down how funds will be spent 67

68 Facts From Disclosure Contained in the Issuer s Prospectus Financial Information Experienced significant negative operating cash flows of $15M in its most recent annual period Has working capital deficiency with minimal cash on hand Company has represented that they will be able to continue operations for a period of 12 months Boilerplate risk factor disclosure and going concern note included in the annual financial statements 68

69 Facts From Disclosure Contained in the Issuer s Prospectus Excerpt of disclosure included in the prospectus: Risk Factors ABC Inc. has experienced continuing operating losses over the past several years. We will require additional financing in order to continue enhancing our proprietary technology. The ability of the company to obtain financing in the future will depend on capital market conditions as well as the company s operating performance. There can be no assurance that the company will be successful in its efforts to obtain financings and if available, may not be on favourable terms. 69

70 Facts From Disclosure Contained in the Issuer s Prospectus Use of proceeds disclosure Use of Proceeds (000's) Minimum Offering Amount Product enhancement 5,000 Selling, general and admin (S,G&A) 4,000 General working capital 1,500 Total 10,500 70

71 Notes From Regulatory Review Prospectus disclosure Risk factor disclosure is boilerplate Provides the principal purposes of the funds being raised but does not provide breakdown of S,G&A and product enhancement costs and does not discuss relevant milestones Staff considerations Enhance the risk factor disclosure to include negative operating cash flows from operations, quantification (e.g., amount of negative cash flows from operations and working capital deficiency) as well as the impact on the issuer s operations Enhance use of proceeds disclosures to clearly identify any milestones in the product enhancement stage and a breakdown of the associated costs for each milestone provide a detailed breakdown of S,G&A costs prominently disclose that issuer has negative cash flows from operations disclose working capital and cash balance as at most recent month end 71

72 Notes From Regulatory Review Prospectus disclosure Staff considerations Issuer has represented that they will be able to continue operations for a period of 12 months Unclear how management has arrived at the expectation that funds will be sufficient for the next 12 month period, given: Issuer has not been able to raise money in financings over the last 12 months (no private placements completed) Issuer has had significant negative operating cash flows, has a working capital deficit and minimal cash on hand Issuer is not raising sufficient proceeds to fund operations for a 12 month period and may not be able to achieve the stated objective of the prospectus 72

73 Notes From Regulatory Review Prospectus disclosure Staff considerations The issuer states that sales are expected to increase in the second half of the year as market penetration increases and product enhancements are made with a portion of the proceeds of the current offering and is expecting to become cash flow positive during the year Stated expectations for future not consistent with past performance: historically, core product sales have been low cash outflows in recent quarters have been increasing How reasonable is the conclusion that funds will be sufficient for operations over the next 12 months? 73

74 SME Potential Outcomes Staff are concerned that the proceeds from the offering together with the resources of the issuer, may not be sufficient to fund operations for the 12 month period represented Given that the issuer has stated that the future cash flows from operations will be positive (inconsistent with past performance), we may request: A detailed cash flow analysis with supportable assumptions that clearly demonstrate the ability to continue operations over the next 12 month period (Staff will review assumptions and may raise further comments) 74

75 Potential Outcomes Staff may request the cash flow forecast to be included in the final prospectus to support the issuer s representations regarding ability to continue operations Staff may request issuer to increase minimum offering amount in order for the issuer to raise sufficient proceeds to fund operations over the period represented If cash flow analysis does not appear reasonable or is not supportable and/or the issuer does not increase the minimum offering amount, Staff may have receipt refusal concerns Refer to CSA Staff Notice Concerns regarding an issuer s financial condition and the sufficiency of proceeds from a prospectus offering, for further information 75

76 Questions 76

77 Appendices 77

78 Appendix A Securities Requirements 78

79 Appendix A Securities Requirements Subject Long Form Short Form Shelf PREP Prospectus exemptions Other references Instrument, Rule or Policy General Prospectus Requirements Short Form Prospectus Offerings Shelf Distributions Post Receipt Pricing Prospectus and Registration Exemptions Ontario Prospectus and Registration Exemptions Corporate Finance Prospectus Guidance Concerns regarding and issuer s financial condition and the sufficiency of proceeds from a prospectus offering Issuance of Receipts for Preliminary Prospectuses and Prospectuses 79

80 Appendix B Contact Information 80

81 Appendix B Contact Kelly Gorman Deputy Director, Corporate Finance kgorman@osc.gov.on.ca Phone: Matthew Au Senior Accountant, Corporate Finance mau@osc.gov.on.ca Phone: Viraj Trivedi Accountant, Corporate Finance vtrivedi@osc.gov.on.ca Phone: Lisa Enright Manager, Corporate Finance lenright@osc.gov.on.ca Phone: Neeti Varma Senior Accountant, Corporate Finance nvarma@osc.gov.on.ca Phone: Nicole Stephenson Legal Counsel, Corporate Finance nstephenson@osc.gov.on.ca Phone:

Raising capital A Primer for SMEs

Raising capital A Primer for SMEs Corporate Finance Branch November 15, 2012 Disclaimer The views expressed in this presentation are the personal views of the presenting staff and do not necessarily represent

Raising capital A Primer for SMEs Corporate Finance Branch November 15, 2012 Disclaimer The views expressed in this presentation are the personal views of the presenting staff and do not necessarily represent

Continuous Disclosure Special Topics I Risk and Cash Flows

Continuous Disclosure Special Topics I Risk and Cash Flows Corporate Finance Branch September 18, 2012 Disclaimer The views expressed in this presentation are the personal views of the presenting staff

Continuous Disclosure Special Topics I Risk and Cash Flows Corporate Finance Branch September 18, 2012 Disclaimer The views expressed in this presentation are the personal views of the presenting staff

National Instrument General Prospectus Requirements. Table of Contents

This document is an unofficial consolidation of all amendments to National Instrument 41-101 General Prospectus Requirements, effective as of March 8, 2017. This document is for reference purposes only.

This document is an unofficial consolidation of all amendments to National Instrument 41-101 General Prospectus Requirements, effective as of March 8, 2017. This document is for reference purposes only.

National Instrument General Prospectus Requirements. Table of Contents

This document is an unofficial consolidation of all amendments to National Instrument 41-101 General Prospectus Requirements, effective as of September 1, 2017. This document is for reference purposes

This document is an unofficial consolidation of all amendments to National Instrument 41-101 General Prospectus Requirements, effective as of September 1, 2017. This document is for reference purposes

Form F1 Information Required in a Prospectus

Form 41-101F1 Information Required in a Prospectus GENERAL INSTRUCTIONS Item 1 Cover Page Disclosure 1.1 Required statement 1.2 Preliminary prospectus disclosure 1.3 Basic disclosure about the distribution

Form 41-101F1 Information Required in a Prospectus GENERAL INSTRUCTIONS Item 1 Cover Page Disclosure 1.1 Required statement 1.2 Preliminary prospectus disclosure 1.3 Basic disclosure about the distribution

NATIONAL INSTRUMENT SHORT FORM PROSPECTUS DISTRIBUTIONS TABLE OF CONTENTS

5.1.3 NI 44-101 Short Form Prospectus Distributions NATIONAL INSTRUMENT 44-101 SHORT FORM PROSPECTUS DISTRIBUTIONS TABLE OF CONTENTS Part 1 Part 2 Part 3 Part 4 Part 5 Part 6 Part 7 Part 8 Part 9 DEFINITIONS

5.1.3 NI 44-101 Short Form Prospectus Distributions NATIONAL INSTRUMENT 44-101 SHORT FORM PROSPECTUS DISTRIBUTIONS TABLE OF CONTENTS Part 1 Part 2 Part 3 Part 4 Part 5 Part 6 Part 7 Part 8 Part 9 DEFINITIONS

National Instrument Short Form Prospectus Distributions

This is an unofficial consolidation of National Instrument 44-101 Short Form Prospectus Distributions reflecting amendments made effective January 1, 2011 in connection with Canada s changeover to IFRS.

This is an unofficial consolidation of National Instrument 44-101 Short Form Prospectus Distributions reflecting amendments made effective January 1, 2011 in connection with Canada s changeover to IFRS.

National Instrument Short Form Prospectus Distributions. Table of Contents

This document is an unofficial consolidation of all amendments to National Instrument 44-101 Short Form Prospectus Distributions, effective as of December 8, 2015. This document is for reference purposes

This document is an unofficial consolidation of all amendments to National Instrument 44-101 Short Form Prospectus Distributions, effective as of December 8, 2015. This document is for reference purposes

Companion Policy CP Continuous Disclosure Obligations. Table of Contents

This document is an unofficial consolidation of all changes to Companion Policy 51-102CP Continuous Disclosure Obligations, effective as of June 30, 2015. This document is for reference purposes only Companion

This document is an unofficial consolidation of all changes to Companion Policy 51-102CP Continuous Disclosure Obligations, effective as of June 30, 2015. This document is for reference purposes only Companion

Industry Series: Mining

Industry Series: Mining Corporate Finance Branch December 5, 2012 Disclaimer The views expressed in this presentation are the personal views of the presenting staff and do not necessarily represent the

Industry Series: Mining Corporate Finance Branch December 5, 2012 Disclaimer The views expressed in this presentation are the personal views of the presenting staff and do not necessarily represent the

National Instrument Shelf Distributions. Table of Contents

National Instrument 44-102 Shelf Distributions Table of Contents PART 1 PART 2 PART 3 PART 4 PART 5 DEFINITIONS AND INTERPRETATION 1.1 Definitions 1.2 Amendments SHELF QUALIFICATION AND PERIOD OF RECEIPT

National Instrument 44-102 Shelf Distributions Table of Contents PART 1 PART 2 PART 3 PART 4 PART 5 DEFINITIONS AND INTERPRETATION 1.1 Definitions 1.2 Amendments SHELF QUALIFICATION AND PERIOD OF RECEIPT

Companion Policy CP to National Instrument Shelf Distributions. Table of Contents

Companion Policy 44-102CP to National Instrument 44-102 Shelf Distributions Table of Contents PART PART 1 PART 2 PART 3 PART 4 TITLE GENERAL 1.1 Relationship of the National Instrument to Securities Legislation

Companion Policy 44-102CP to National Instrument 44-102 Shelf Distributions Table of Contents PART PART 1 PART 2 PART 3 PART 4 TITLE GENERAL 1.1 Relationship of the National Instrument to Securities Legislation

Code Updates NI CANADA. Deborah McCombe, P.Geo Past Chairperson CRIRSCO Annual Meeting Bogota, Columbia November 21, 2013

Code Updates NI43-101 CANADA Deborah McCombe, P.Geo Past Chairperson CRIRSCO Annual Meeting Bogota, Columbia November 21, 2013 Agenda Background on NI43-101 Technical Reports Issues Identified by Regulators

Code Updates NI43-101 CANADA Deborah McCombe, P.Geo Past Chairperson CRIRSCO Annual Meeting Bogota, Columbia November 21, 2013 Agenda Background on NI43-101 Technical Reports Issues Identified by Regulators

PROPOSED NATIONAL POLICY INCOME TRUSTS AND OTHER INDIRECT OFFERINGS

6.1.2 Proposed National Policy 41-201 Income Trusts and Other Indirect Offerings Part 1 - Introduction 1.1 What is the purpose of the policy? PROPOSED NATIONAL POLICY 41-201 INCOME TRUSTS AND OTHER INDIRECT

6.1.2 Proposed National Policy 41-201 Income Trusts and Other Indirect Offerings Part 1 - Introduction 1.1 What is the purpose of the policy? PROPOSED NATIONAL POLICY 41-201 INCOME TRUSTS AND OTHER INDIRECT

Unofficial consolidation in effect as of January 1, 2011 for financial years beginning on or after January 1, 2011

This document is one of two versions of unofficial consolidations of National Instrument 44-102 Shelf Distributions and its companion policy prepared as of January 1, 2011. This version generally applies

This document is one of two versions of unofficial consolidations of National Instrument 44-102 Shelf Distributions and its companion policy prepared as of January 1, 2011. This version generally applies

REGULATION RESPECTING SHORT FORM PROSPECTUS DISTRIBUTIONS TABLE OF CONTENTS PART TITLE PAGE PART 1 DEFINITIONS AND INTERPRETATION 1

AS PUBLISHED IN THE SUPPLEMENT OF THE BULLETIN OF JANUARY 7, 2005, VOL. 2 N 1 REGULATION 44-101 RESPECTING SHORT FORM PROSPECTUS DISTRIBUTIONS TABLE OF CONTENTS PART TITLE PAGE PART 1 DEFINITIONS AND INTERPRETATION

AS PUBLISHED IN THE SUPPLEMENT OF THE BULLETIN OF JANUARY 7, 2005, VOL. 2 N 1 REGULATION 44-101 RESPECTING SHORT FORM PROSPECTUS DISTRIBUTIONS TABLE OF CONTENTS PART TITLE PAGE PART 1 DEFINITIONS AND INTERPRETATION

Companion Policy CP Continuous Disclosure Obligations. Table of Contents

Companion Policy 51-102CP Continuous Disclosure Obligations Table of Contents PART 1 INTRODUCTION AND DEFINITIONS 1.1 Introduction and Purpose 1.2 Filing Obligations 1.3 Corporate Law Requirements 1.4

Companion Policy 51-102CP Continuous Disclosure Obligations Table of Contents PART 1 INTRODUCTION AND DEFINITIONS 1.1 Introduction and Purpose 1.2 Filing Obligations 1.3 Corporate Law Requirements 1.4

POLICY 5.2 CHANGES OF BUSINESS AND REVERSE TAKEOVERS

POLICY 5.2 CHANGES OF BUSINESS AND REVERSE TAKEOVERS Scope of Policy This Policy applies to any transaction or series of transactions entered into by an Issuer or a NEX Company that will result in a Change

POLICY 5.2 CHANGES OF BUSINESS AND REVERSE TAKEOVERS Scope of Policy This Policy applies to any transaction or series of transactions entered into by an Issuer or a NEX Company that will result in a Change

FORM F1 MANAGEMENT S DISCUSSION & ANALYSIS TABLE OF CONTENTS

Note: [30 Jun 2015] - The following is a consolidation of 51-102F1. It incorporates the amendments to this document that came into effect on December 29, 2006, December 31, 2007, December 15, 2008, January

Note: [30 Jun 2015] - The following is a consolidation of 51-102F1. It incorporates the amendments to this document that came into effect on December 29, 2006, December 31, 2007, December 15, 2008, January

Document Type : National Instrument Document N o. : Subject : Short Form Prospectus Distributions Notes : Consolidated up to 31 December 2007

Document Type : National Instrument Document N o. : 44-101 Subject : Short Form Prospectus Distributions Notes : Consolidated up to 31 December 2007 Published Date : 21 February 2008 Effective Date : 20

Document Type : National Instrument Document N o. : 44-101 Subject : Short Form Prospectus Distributions Notes : Consolidated up to 31 December 2007 Published Date : 21 February 2008 Effective Date : 20

CORPORATE FINANCE AND MERGERS & ACQUISITIONS

Introduction 31 Public Offerings and Private Placements 33 Mergers & Acquisitions 36 Business Combinations 38 Related-Party Transactions 39 By Robert Hansen INTRODUCTION Corporate Finance and Mergers &

Introduction 31 Public Offerings and Private Placements 33 Mergers & Acquisitions 36 Business Combinations 38 Related-Party Transactions 39 By Robert Hansen INTRODUCTION Corporate Finance and Mergers &

OSC THE INVESTMENT FUNDS PRACTITIONER

1.1.3 The Investment Funds Practitioner April 2012 April 2012 OSC THE INVESTMENT FUNDS PRACTITIONER From the Investment Funds Branch, Ontario Securities Commission What is the Investment Funds Practitioner?

1.1.3 The Investment Funds Practitioner April 2012 April 2012 OSC THE INVESTMENT FUNDS PRACTITIONER From the Investment Funds Branch, Ontario Securities Commission What is the Investment Funds Practitioner?

COMPANION POLICY CP PASSPORT SYSTEM

Note: [20 Apr 2012] - The following is a consolidation of Companion Policy 11-102CP. It incorporates the amendments to this document that came into effect on September 28, 2009, January 01, 2011 and April

Note: [20 Apr 2012] - The following is a consolidation of Companion Policy 11-102CP. It incorporates the amendments to this document that came into effect on September 28, 2009, January 01, 2011 and April

Calculating Participation Fees

Calculating Participation Fees Corporate Finance Branch February 11, 2015 Disclaimer The views expressed in this presentation are the personal views of the presenting staff and do not necessarily represent

Calculating Participation Fees Corporate Finance Branch February 11, 2015 Disclaimer The views expressed in this presentation are the personal views of the presenting staff and do not necessarily represent

Guide to Going Public in Canada

Guide to Going Public in Canada July 2017 TABLE OF CONTENTS Introduction...1 Executive Summary...2 Canadian Regulatory Framework and Exchanges...3 Prerequisites to Listing...4 The Deal Team...5 Getting

Guide to Going Public in Canada July 2017 TABLE OF CONTENTS Introduction...1 Executive Summary...2 Canadian Regulatory Framework and Exchanges...3 Prerequisites to Listing...4 The Deal Team...5 Getting

Unofficial consolidation in effect as of October 31, 2011 for financial years beginning before January 1, 2011

This document is one of two versions of unofficial consolidations of National Instrument 51-102 Continuous Disclosure Obligations and its companion policy prepared as of October 31, 2011. This version

This document is one of two versions of unofficial consolidations of National Instrument 51-102 Continuous Disclosure Obligations and its companion policy prepared as of October 31, 2011. This version

Appendix C. Blackline of the Proposed Instrument

Appendix C Blackline of the Proposed Instrument National Instrument 52-107 Acceptable Accounting Principles, and Auditing Standards and Reporting Currency PART 1: DEFINITIONS AND INTERPRETATION 1.1 Definitions

Appendix C Blackline of the Proposed Instrument National Instrument 52-107 Acceptable Accounting Principles, and Auditing Standards and Reporting Currency PART 1: DEFINITIONS AND INTERPRETATION 1.1 Definitions

PUBLIC OFFERINGS IN CANADA

PUBLIC OFFERINGS IN CANADA At Davies, we focus on the matters that are the most important to our clients, in Canada and around the world. The more complex the challenge, the better. Our strength is our

PUBLIC OFFERINGS IN CANADA At Davies, we focus on the matters that are the most important to our clients, in Canada and around the world. The more complex the challenge, the better. Our strength is our

Going Public: The Art of the Prospectus

Going Public: The Art of the Prospectus Stikeman Elliott LLP Going Public: The Art of the Prospectus Prospectus Requirement... 2 Prospectus Preparation... 2 Prospectus disclosure... 3 Historical Financial

Going Public: The Art of the Prospectus Stikeman Elliott LLP Going Public: The Art of the Prospectus Prospectus Requirement... 2 Prospectus Preparation... 2 Prospectus disclosure... 3 Historical Financial

Unofficial consolidation for financial years beginning on or after January 1, 2011

This is an unofficial consolidation of National Policy 41-201 Income Trusts and other Indirect Offerings reflecting amendments made effective January 1, 2011 in connection with Canada s changeover to IFRS.

This is an unofficial consolidation of National Policy 41-201 Income Trusts and other Indirect Offerings reflecting amendments made effective January 1, 2011 in connection with Canada s changeover to IFRS.

TOP 10 PRACTICE TIPS: COMFORT LETTERS. Lexis Practice Advisor 1. REVIEW AS 6101 AND RELEVANT COMFORT LETTER PRECEDENTS

Lexis Practice Advisor TOP 10 PRACTICE TIPS: COMFORT LETTERS by Anna T. Pinedo and Ryan Castillo, Mayer Brown LLP A comfort letter is a letter delivered by an issuer s independent accountants to the underwriters

Lexis Practice Advisor TOP 10 PRACTICE TIPS: COMFORT LETTERS by Anna T. Pinedo and Ryan Castillo, Mayer Brown LLP A comfort letter is a letter delivered by an issuer s independent accountants to the underwriters

Continuous Disclosure Best Practices

Continuous Disclosure Best Practices Corporate Finance Branch January 21, 2014 Disclaimer The views expressed in this presentation are the personal views of the presenting staff and do not necessarily

Continuous Disclosure Best Practices Corporate Finance Branch January 21, 2014 Disclaimer The views expressed in this presentation are the personal views of the presenting staff and do not necessarily

Corporate Finance Branch Report

OSC Staff Notice 51-706 Corporate Finance Branch Report October 20, 2010 Fiscal 2010 2 Contents 1. Introduction 1. 1.1 Role of the Corporate Finance Branch 1.2 Purpose of this report 1.3 Ontario s capital

OSC Staff Notice 51-706 Corporate Finance Branch Report October 20, 2010 Fiscal 2010 2 Contents 1. Introduction 1. 1.1 Role of the Corporate Finance Branch 1.2 Purpose of this report 1.3 Ontario s capital

Companion Policy CP Continuous Disclosure Obligations. Table of Contents

Companion Policy 51-102CP Continuous Disclosure Obligations Table of Contents PART 1 INTRODUCTION AND DEFINITIONS 1.1 Introduction and Purpose 1.2 Filing Obligations 1.3 Corporate Law Requirements 1.4

Companion Policy 51-102CP Continuous Disclosure Obligations Table of Contents PART 1 INTRODUCTION AND DEFINITIONS 1.1 Introduction and Purpose 1.2 Filing Obligations 1.3 Corporate Law Requirements 1.4

OSC SME Institute. Continuous Disclosure Best Practices. December 10, 2014 Corporate Finance Branch

OSC SME Institute Continuous Disclosure Best Practices December 10, 2014 Corporate Finance Branch Disclaimer The views expressed in this presentation are the personal views of the presenting staff and

OSC SME Institute Continuous Disclosure Best Practices December 10, 2014 Corporate Finance Branch Disclaimer The views expressed in this presentation are the personal views of the presenting staff and

OSC Staff Notice Report on Staff s Review of Non-GAAP Financial Measures and Additional GAAP Measures. t: November 10, 2010

OSC Staff Notice 52-722 Report on Staff s Review of Non-GAAP Financial Measures and Additional GAAP Measures t: November 10, 2010 Publication date: December 11, 2013 OSC Staff Notice 52-722 Report on Staff

OSC Staff Notice 52-722 Report on Staff s Review of Non-GAAP Financial Measures and Additional GAAP Measures t: November 10, 2010 Publication date: December 11, 2013 OSC Staff Notice 52-722 Report on Staff

1.1 What is the purpose of the policy?

CONSOLIDATED UP TO 13 August 2013 This consolidation is provided for your convenience and should not be relied on as authoritative NATIONAL POLICY 41-201 INCOME TRUSTS AND OTHER INDIRECT OFFERINGS Part

CONSOLIDATED UP TO 13 August 2013 This consolidation is provided for your convenience and should not be relied on as authoritative NATIONAL POLICY 41-201 INCOME TRUSTS AND OTHER INDIRECT OFFERINGS Part

AND AND AMENDMENTS TO NATIONAL INSTRUMENT SHELF DISTRIBUTIONS

NOTICE OF AMENDMENTS TO NATIONAL INSTRUMENT 41-101 GENERAL PROSPECTUS REQUIREMENTS AND COMPANION POLICY 41-101CP COMPANION POLICY TO NATIONAL INSTRUMENT 41-101 GENERAL PROSPECTUS REQUIREMENTS AND AMENDMENTS

NOTICE OF AMENDMENTS TO NATIONAL INSTRUMENT 41-101 GENERAL PROSPECTUS REQUIREMENTS AND COMPANION POLICY 41-101CP COMPANION POLICY TO NATIONAL INSTRUMENT 41-101 GENERAL PROSPECTUS REQUIREMENTS AND AMENDMENTS

Mineral Disclosure Best Practices

OSC SME Institute Mineral Disclosure Best Practices Craig Waldie, P.Geo., Senior Geologist, Corporate Finance Jim Whyte, P.Geo., Senior Geologist, Corporate Finance Sandra Heldman, CPA, CA, Senior Accountant,

OSC SME Institute Mineral Disclosure Best Practices Craig Waldie, P.Geo., Senior Geologist, Corporate Finance Jim Whyte, P.Geo., Senior Geologist, Corporate Finance Sandra Heldman, CPA, CA, Senior Accountant,

U.S. SECURITIES LAW ISSUES RAISED BY ACQUISITIONS BY NON-U.S. COMPANIES OF COMPANIES WITH U.S. SHAREHOLDERS

P A U L, W E I S S, R I F K I N D, W H A R T O N & G A R R I S O N U.S. SECURITIES LAW ISSUES RAISED BY ACQUISITIONS BY NON-U.S. COMPANIES OF COMPANIES WITH U.S. SHAREHOLDERS MARK S. BERGMAN SEPTEMBER

P A U L, W E I S S, R I F K I N D, W H A R T O N & G A R R I S O N U.S. SECURITIES LAW ISSUES RAISED BY ACQUISITIONS BY NON-U.S. COMPANIES OF COMPANIES WITH U.S. SHAREHOLDERS MARK S. BERGMAN SEPTEMBER

going public in Canada

table of contents going public in Canada 1 about Canada's exchanges 1 methods of going public on the TSXV 1 1. reverse takeover 2. initial public offering 3. capital pool corporation CPC formation the

table of contents going public in Canada 1 about Canada's exchanges 1 methods of going public on the TSXV 1 1. reverse takeover 2. initial public offering 3. capital pool corporation CPC formation the

IIAC CORPORATE FINANCE DUE DILIGENCE GUIDELINES

IIAC CORPORATE FINANCE DUE DILIGENCE GUIDELINES February 2006 February 2006 IDA DUE DILIGENCE GUIDELINES The purpose of these Guidelines is to provide guidance to Member firms regarding the planning and

IIAC CORPORATE FINANCE DUE DILIGENCE GUIDELINES February 2006 February 2006 IDA DUE DILIGENCE GUIDELINES The purpose of these Guidelines is to provide guidance to Member firms regarding the planning and

Appendix A. Summary of Changes to Accounting Terms and Phrases and Other Changes for the Continuous Disclosure Rules

A. TERMINOLOGY CHANGES Appendix A Summary of Changes to Accounting Terms and Phrases and Other Changes for the Continuous Disclosure Rules Accounting Terms or Phrases We replaced the following terms or

A. TERMINOLOGY CHANGES Appendix A Summary of Changes to Accounting Terms and Phrases and Other Changes for the Continuous Disclosure Rules Accounting Terms or Phrases We replaced the following terms or

Form F1 Short Form Prospectus. Table of Contents

Form 44-101F1 Short Form Prospectus Table of Contents Item 1 Item 2 Item 3 Item 4 Item 5 Cover Page Disclosure 1.1 Required Language 1.2 Preliminary Short Form Prospectus Disclosure 1.3 Disclosure Concerning

Form 44-101F1 Short Form Prospectus Table of Contents Item 1 Item 2 Item 3 Item 4 Item 5 Cover Page Disclosure 1.1 Required Language 1.2 Preliminary Short Form Prospectus Disclosure 1.3 Disclosure Concerning

SECURITIES LAW NEWSLETTER

SECURITIES LAW NEWSLETTER Q4 2015 FOR MORE INFORMATION OR INQUIRIES Michael Dolphin 416.947.5005» full bio Zachary Goldenberg 416.619.6291» full bio A Newsletter Providing Concise Updates on Securities

SECURITIES LAW NEWSLETTER Q4 2015 FOR MORE INFORMATION OR INQUIRIES Michael Dolphin 416.947.5005» full bio Zachary Goldenberg 416.619.6291» full bio A Newsletter Providing Concise Updates on Securities

REGULATION RESPECTING MUTUAL FUND PROSPECTUS DISCLOSURE

Last amendment in force on September 1, 2017 This document has official status chapter V-1.1, r. 38 REGULATION 81-101 RESPECTING MUTUAL FUND PROSPECTUS DISCLOSURE Decision 2001-C-0283, Title; M.O. 2004-01,

Last amendment in force on September 1, 2017 This document has official status chapter V-1.1, r. 38 REGULATION 81-101 RESPECTING MUTUAL FUND PROSPECTUS DISCLOSURE Decision 2001-C-0283, Title; M.O. 2004-01,

Continuous Disclosure: Hot Topics and More

The OSC SME Institute Continuous Disclosure: Hot Topics and More (for non-investment fund reporting issuers) Jonathan Blackwell Senior Accountant, Corporate Finance Marija Loubser Accountant, Corporate

The OSC SME Institute Continuous Disclosure: Hot Topics and More (for non-investment fund reporting issuers) Jonathan Blackwell Senior Accountant, Corporate Finance Marija Loubser Accountant, Corporate

AND AND AMENDMENTS TO NATIONAL INSTRUMENT SHELF DISTRIBUTIONS

Notice of IFRS-Related Amendments to Prospectus Rules NOTICE OF AMENDMENTS TO NATIONAL INSTRUMENT 41-101 GENERAL PROSPECTUS REQUIREMENTS AND COMPANION POLICY 41-101CP COMPANION POLICY TO NATIONAL INSTRUMENT

Notice of IFRS-Related Amendments to Prospectus Rules NOTICE OF AMENDMENTS TO NATIONAL INSTRUMENT 41-101 GENERAL PROSPECTUS REQUIREMENTS AND COMPANION POLICY 41-101CP COMPANION POLICY TO NATIONAL INSTRUMENT

TECHNICAL GUIDE TO LISTING

TECHNICAL GUIDE TO LISTING 2 INTRODUCTION This guide provides information about the process of listing on Toronto Stock Exchange ("TSX") or TSX Venture Exchange ("TSXV") (collectively "the Exchanges")

TECHNICAL GUIDE TO LISTING 2 INTRODUCTION This guide provides information about the process of listing on Toronto Stock Exchange ("TSX") or TSX Venture Exchange ("TSXV") (collectively "the Exchanges")

For additional guidance see OSC Staff Notice Going Concern Disclosure Review (OSC Staff Notice ). 2

. 2") CORPORATE FINANCE PROSPECTUS GUIDANCE Concerns regarding an issuer s financial condition and the sufficiency of proceeds from a prospectus offering CSA Staff Notice 41-307 March 2, 2012 The purpose of

CORPORATE FINANCE PROSPECTUS GUIDANCE Concerns regarding an issuer s financial condition and the sufficiency of proceeds from a prospectus offering CSA Staff Notice 41-307 March 2, 2012 The purpose of

IFRS Discussion Group Report on the Public Meeting January 12, 2012

IFRS Discussion Group Report on the Public Meeting January 12, 2012 The IFRS Discussion Group is a discussion forum only. The Group s purpose is to assist the Accounting Standards Board (AcSB) regarding

IFRS Discussion Group Report on the Public Meeting January 12, 2012 The IFRS Discussion Group is a discussion forum only. The Group s purpose is to assist the Accounting Standards Board (AcSB) regarding

NATIONAL INSTRUMENT CONTINUOUS DISCLOSURE AND OTHER EXEMPTIONS RELATING TO FOREIGN ISSUERS

This document is an unofficial consolidation of all amendments to National Instrument 71-102 Continuous Disclosure And Other Exemptions Relating To Foreign Issuers and its companion policy current to October

This document is an unofficial consolidation of all amendments to National Instrument 71-102 Continuous Disclosure And Other Exemptions Relating To Foreign Issuers and its companion policy current to October

SEC Financial Reporting Series SEC quarterly reports Form 10-Q

SEC Financial Reporting Series 2018 SEC quarterly reports Form 10-Q Contents 1 Overview... 1 1.1 Section highlights... 1 1.2 EY publications and checklists... 2 1.3 Other considerations in preparing Form

SEC Financial Reporting Series 2018 SEC quarterly reports Form 10-Q Contents 1 Overview... 1 1.1 Section highlights... 1 1.2 EY publications and checklists... 2 1.3 Other considerations in preparing Form

POLICY REFORMULATION TABLE OF CONCORDANCE AND LIST OF NEW INSTRUMENTS

POLICY REFORMULATION TABLE OF CONCORDANCE AND LIST OF Policy Reformulation Table of Concordance To assist market participants in identifying the status of instruments that existed before the Policy Reformulation

POLICY REFORMULATION TABLE OF CONCORDANCE AND LIST OF Policy Reformulation Table of Concordance To assist market participants in identifying the status of instruments that existed before the Policy Reformulation

PRE-MARKETING AND MARKETING AMENDMENTS TO PROSPECTUS RULES (FINAL) Supplement to the OSC Bulletin

Supplement to the OSC Bulletin") The Ontario Securities Commission PRE-MARKETING AND MARKETING AMENDMENTS TO PROSPECTUS RULES (FINAL) May 30, 2013 Volume 36, Issue 22 (Supp-4) (2013), 36 OSCB The Ontario Securities Commission administers

The Ontario Securities Commission PRE-MARKETING AND MARKETING AMENDMENTS TO PROSPECTUS RULES (FINAL) May 30, 2013 Volume 36, Issue 22 (Supp-4) (2013), 36 OSCB The Ontario Securities Commission administers

POLICY REFORMULATION TABLE OF CONCORDANCE AND LIST OF NEW INSTRUMENTS

POLICY REFORMULATION TABLE OF CONCORDANCE AND LIST OF Policy Reformulation Table of Concordance To assist market participants in identifying the status of instruments that existed before the Policy Reformulation

POLICY REFORMULATION TABLE OF CONCORDANCE AND LIST OF Policy Reformulation Table of Concordance To assist market participants in identifying the status of instruments that existed before the Policy Reformulation

FREQUENTLY ASKED QUESTIONS ABOUT PERIODIC REPORTING REQUIREMENTS FOR U.S. ISSUERS PRINCIPAL EXCHANGE ACT REPORTS

FREQUENTLY ASKED QUESTIONS ABOUT PERIODIC REPORTING REQUIREMENTS FOR U.S. ISSUERS PRINCIPAL EXCHANGE ACT REPORTS These Frequently Asked Questions should be read together with our Frequently Asked Questions

FREQUENTLY ASKED QUESTIONS ABOUT PERIODIC REPORTING REQUIREMENTS FOR U.S. ISSUERS PRINCIPAL EXCHANGE ACT REPORTS These Frequently Asked Questions should be read together with our Frequently Asked Questions

National Instrument Mutual Fund Prospectus Disclosure. Table of Contents

National Instrument 81-101 Mutual Fund Prospectus Disclosure Table of Contents PART PART1 PART 2 PART 3 PART 4 PART 5 PART 6 PART 7 TITLE DEFINITIONS, INTERPRETATION AND APPLICATION 1.1 Definitions 1.2

National Instrument 81-101 Mutual Fund Prospectus Disclosure Table of Contents PART PART1 PART 2 PART 3 PART 4 PART 5 PART 6 PART 7 TITLE DEFINITIONS, INTERPRETATION AND APPLICATION 1.1 Definitions 1.2

MANULIFE MUTUAL FUNDS

MANULIFE MUTUAL FUNDS Annual Information Form (OFFERING ADVISOR SERIES, SERIES F, SERIES I, SERIES IT, SERIES T5 AND SERIES T6 SECURITIES, AS INDICATED) MANULIFE FUNDS Manulife Opportunities Funds Manulife

MANULIFE MUTUAL FUNDS Annual Information Form (OFFERING ADVISOR SERIES, SERIES F, SERIES I, SERIES IT, SERIES T5 AND SERIES T6 SECURITIES, AS INDICATED) MANULIFE FUNDS Manulife Opportunities Funds Manulife

GOING PUBLIC IN CANADA

GOING PUBLIC IN CANADA Added experience. Added clarity. Added value. Miller Thomson is one of Canada s most respected national business law firms, committed to delivering what matters most added experience,

GOING PUBLIC IN CANADA Added experience. Added clarity. Added value. Miller Thomson is one of Canada s most respected national business law firms, committed to delivering what matters most added experience,

SEC Proposes Amendments to Rule 12g3-2(b) and Foreign Issuer Reporting Requirements

and Foreign Issuer Reporting Requirements") SEC Proposes Amendments to Rule 12g3-2(b) and Foreign Issuer Reporting Requirements April 1, 2008 On February 19, 2008, the U.S. Securities and Exchange Commission proposed amendments to Rule 12g3-2(b)

SEC Proposes Amendments to Rule 12g3-2(b) and Foreign Issuer Reporting Requirements April 1, 2008 On February 19, 2008, the U.S. Securities and Exchange Commission proposed amendments to Rule 12g3-2(b)

Companion Policy CP Passport System

This document is an unofficial consolidation of all changes to Companion Policy 11-102CP Passport System, effective as of June 23, 2016. This document is for reference purposes only. Companion Policy 11-102CP

This document is an unofficial consolidation of all changes to Companion Policy 11-102CP Passport System, effective as of June 23, 2016. This document is for reference purposes only. Companion Policy 11-102CP

This Amendment No. 1 amends the Prospectus in respect of the exchange-traded funds listed below (collectively, the ishares Funds ).

.") Amendment No. 1 dated September 2, 2016 to the prospectus dated March 29, 2016 (the Prospectus ). This Amendment No. 1 amends the Prospectus in respect of the exchange-traded funds listed below (collectively,

Amendment No. 1 dated September 2, 2016 to the prospectus dated March 29, 2016 (the Prospectus ). This Amendment No. 1 amends the Prospectus in respect of the exchange-traded funds listed below (collectively,

Canada: Capital Markets and Securities Law Overview

Canada: Capital Markets and Securities Law Overview Stikeman Elliott LLP Canada: Capital Markets and Securities Law Overview Securities Legislation... 2 Registration Requirements... 2 Prospectus Requirement...

Canada: Capital Markets and Securities Law Overview Stikeman Elliott LLP Canada: Capital Markets and Securities Law Overview Securities Legislation... 2 Registration Requirements... 2 Prospectus Requirement...

RAISING CAPITAL IN THE UNITED STATES July 2013

RAISING CAPITAL IN THE UNITED STATES July 2013 A Guide to Using MJDS for U.S. Public Offerings and Periodic Reporting Osler, Hoskin & Harcourt LLP Osler, Hoskin & Harcourt LLP Raising Capital in the United

RAISING CAPITAL IN THE UNITED STATES July 2013 A Guide to Using MJDS for U.S. Public Offerings and Periodic Reporting Osler, Hoskin & Harcourt LLP Osler, Hoskin & Harcourt LLP Raising Capital in the United

Securities Law Update (August 2003) Southbound Multijurisdictional Disclosure System: The Basics

Southbound Multijurisdictional Disclosure System: The Basics") Securities Law Update (August 2003) Southbound Multijurisdictional Disclosure System: The Basics Introduction The multijurisdictional disclosure system (the "MJDS") was adopted in 1991 by the United States

Securities Law Update (August 2003) Southbound Multijurisdictional Disclosure System: The Basics Introduction The multijurisdictional disclosure system (the "MJDS") was adopted in 1991 by the United States

NATIONAL INSTRUMENT INVESTMENT FUND CONTINUOUS DISCLOSURE

Note: [08 Mar 2017] - The following is a consolidation of NI 81-106. It incorporates the amendments to this document that came into effect on November 1, 2006, July 4, 2008, September 8, 2008, January

Note: [08 Mar 2017] - The following is a consolidation of NI 81-106. It incorporates the amendments to this document that came into effect on November 1, 2006, July 4, 2008, September 8, 2008, January

SECURITIES LAW AND CORPORATE GOVERNANCE

Doing Business in Canada 1 C: SECURITIES LAW AND CORPORATE GOVERNANCE Canada currently does not have a federal securities regulator, as other major capital markets do. Rather, each province and territory

Doing Business in Canada 1 C: SECURITIES LAW AND CORPORATE GOVERNANCE Canada currently does not have a federal securities regulator, as other major capital markets do. Rather, each province and territory

CSA Staff Notice Continuous Disclosure Review Program Activities for the fiscal year ended March 31, 2014

CSA Staff Notice 51-341 Continuous Disclosure Review Program Activities for the fiscal year ended March 31, 2014 July 17, 2014 Introduction This notice contains the results of the reviews conducted by

CSA Staff Notice 51-341 Continuous Disclosure Review Program Activities for the fiscal year ended March 31, 2014 July 17, 2014 Introduction This notice contains the results of the reviews conducted by

CSA Staff Notice Continuous Disclosure Review Program Activities for the fiscal year ended March 31, 2015

CSA Staff Notice 51-344 Continuous Disclosure Review Program Activities for the fiscal year ended March 31, 2015 July 16, 2015 Introduction This notice contains the results of the reviews conducted by

CSA Staff Notice 51-344 Continuous Disclosure Review Program Activities for the fiscal year ended March 31, 2015 July 16, 2015 Introduction This notice contains the results of the reviews conducted by

PRELIMINARY AND PRO FORMA PROSPECTUS. Initial Public Offering and Continuous Distribution May 9, 2014

This is a preliminary prospectus in respect of each of Vanguard FTSE All-World ex Canada Index ETF, Vanguard FTSE Developed Europe Index ETF, Vanguard FTSE Developed Asia Pacific Index ETF, Vanguard U.S.

This is a preliminary prospectus in respect of each of Vanguard FTSE All-World ex Canada Index ETF, Vanguard FTSE Developed Europe Index ETF, Vanguard FTSE Developed Asia Pacific Index ETF, Vanguard U.S.

CSA Staff Notice Continuous Disclosure Considerations Related to Current Economic Conditions

CSA Staff Notice 51-328 Continuous Disclosure Considerations Related to Current Economic Conditions Purpose of Notice Current economic conditions present more than normal challenges for many issuers in

CSA Staff Notice 51-328 Continuous Disclosure Considerations Related to Current Economic Conditions Purpose of Notice Current economic conditions present more than normal challenges for many issuers in

Form F2 Information Required in an Investment Fund Prospectus. Table of Contents

This document is an unofficial consolidation of all amendments to National Instrument 41-101F2 Information Required in an Investment Fund Prospectus, effective as of September 1, 2017. This document is

This document is an unofficial consolidation of all amendments to National Instrument 41-101F2 Information Required in an Investment Fund Prospectus, effective as of September 1, 2017. This document is

NYSE MKT (formerly known as the American Stock Exchange) - IPO Overview

- IPO Overview") NYSE MKT (formerly known as the American Stock Exchange) - IPO Overview 1 Regulatory Background On 1 October 2008 NYSE Euronext, which operates exchanges, including the New York Stock Exchange, completed

NYSE MKT (formerly known as the American Stock Exchange) - IPO Overview 1 Regulatory Background On 1 October 2008 NYSE Euronext, which operates exchanges, including the New York Stock Exchange, completed

ONTARIO EXEMPT MARKET REPORT

ONTARIO EXEMPT MARKET REPORT OSC Staff Notice 45-716 2018 ONTARIO EXEMPT MARKET REPORT 2018 TABLE OF CONTENTS EXECUTIVE SUMMARY... 2 BACKGROUND... 4 ANNUAL GROWTH AND MARKET COMPOSITION... 7 INVESTOR TRENDS...

ONTARIO EXEMPT MARKET REPORT OSC Staff Notice 45-716 2018 ONTARIO EXEMPT MARKET REPORT 2018 TABLE OF CONTENTS EXECUTIVE SUMMARY... 2 BACKGROUND... 4 ANNUAL GROWTH AND MARKET COMPOSITION... 7 INVESTOR TRENDS...

Current Developments: Canadian Securities and Auditing Matters

Current Developments: Canadian Securities and Auditing Matters September 2017 kpmg.ca Canadian Securities and Auditing Matters This edition provides a summary of newly effective and forthcoming regulatory

Current Developments: Canadian Securities and Auditing Matters September 2017 kpmg.ca Canadian Securities and Auditing Matters This edition provides a summary of newly effective and forthcoming regulatory

PROSPECTUS. Initial Public Offering April 25, 2018

No securities regulatory authority has expressed an opinion about these securities and it is an offence to claim otherwise. This prospectus constitutes a public offering of these securities in those jurisdictions

No securities regulatory authority has expressed an opinion about these securities and it is an offence to claim otherwise. This prospectus constitutes a public offering of these securities in those jurisdictions

GOLD STANDARD VENTURES CORP. (formerly Devonshire Resources Ltd.)

") GOLD STANDARD VENTURES CORP. (formerly Devonshire Resources Ltd.) Financial Statements For the Quarter ended March 31, 2010, Management Discussion and Analysis General The purpose of this Management Discussion

GOLD STANDARD VENTURES CORP. (formerly Devonshire Resources Ltd.) Financial Statements For the Quarter ended March 31, 2010, Management Discussion and Analysis General The purpose of this Management Discussion

Tentative Disclosures about Investments in Another Investment Company Operationality Feedback Summary

Financial Accounting Standards Board Investment Companies Project Tentative Disclosures about Investments in Another Investment Company Operationality Feedback Summary Introduction 1. In October 2011,

Financial Accounting Standards Board Investment Companies Project Tentative Disclosures about Investments in Another Investment Company Operationality Feedback Summary Introduction 1. In October 2011,

Management and Discussion Analysis Interim Consolidated Financial Statements (In US dollars) COALCORP MINING INC. Six months ended December 31, 2010

COALCORP MINING INC. Six months ended December 31, 2010") Management and Discussion Analysis Interim Consolidated Financial Statements (In US dollars) COALCORP MINING INC. Six months ended December 31, 2010 1 COALCORP MINING INC. (the Company ) Management s Discussion

Management and Discussion Analysis Interim Consolidated Financial Statements (In US dollars) COALCORP MINING INC. Six months ended December 31, 2010 1 COALCORP MINING INC. (the Company ) Management s Discussion

DECEMBER Corporate Finance Disclosure Report

DECEMBER 2018 Corporate Finance Disclosure Report TABLE OF CONTENTS Letter 3 1. The Alberta Capital Market 4 2. Review Process & Outcomes 5 3. Notable Review Observations 6 Unbalanced and Promotional

DECEMBER 2018 Corporate Finance Disclosure Report TABLE OF CONTENTS Letter 3 1. The Alberta Capital Market 4 2. Review Process & Outcomes 5 3. Notable Review Observations 6 Unbalanced and Promotional

UNDERWRITING AGREEMENT. Sylvain Girard, Executive Vice President and Chief Financial Officer. Offering of Subscription Receipts

Execution Version UNDERWRITING AGREEMENT April 24, 2017 SNC-Lavalin Group Inc. 455, René-Lévesque Blvd., West Montreal, Québec H2Z 1Z3 Attention: Sylvain Girard, Executive Vice President and Chief Financial

Execution Version UNDERWRITING AGREEMENT April 24, 2017 SNC-Lavalin Group Inc. 455, René-Lévesque Blvd., West Montreal, Québec H2Z 1Z3 Attention: Sylvain Girard, Executive Vice President and Chief Financial

April 26, Introduction and Purpose

Multilateral CSA Staff Notice 45-309 Guidance for Preparing and Filing an Offering Memorandum under National Instrument 45-106 Prospectus and Registration Exemptions April 26, 2012 Introduction and Purpose

Multilateral CSA Staff Notice 45-309 Guidance for Preparing and Filing an Offering Memorandum under National Instrument 45-106 Prospectus and Registration Exemptions April 26, 2012 Introduction and Purpose

PROSPECTUS. Initial Public Offering and Continuous Offering January 31, 2018 Blockchain Technologies ETF (the Harvest ETF )

") No securities regulatory authority has expressed an opinion about these securities and it is an offence to claim otherwise. This prospectus constitutes a public offering of these securities only in those

No securities regulatory authority has expressed an opinion about these securities and it is an offence to claim otherwise. This prospectus constitutes a public offering of these securities only in those

Financing Alternatives for Mid-size or Smaller Public Companies

Financing Alternatives for Mid-size or Smaller Public Companies Capital raising alternatives Underwritten offering (marketed) Public deal with lead investors or anchor investors Public deal that is pre-marketed

Financing Alternatives for Mid-size or Smaller Public Companies Capital raising alternatives Underwritten offering (marketed) Public deal with lead investors or anchor investors Public deal that is pre-marketed

Companion Policy CP to National Instrument Standards of Disclosure for Mineral Projects. Table of Contents

Companion Policy 43-101CP to National Instrument 43-101 Standards of Disclosure for Mineral Projects Table of Contents PART TITLE GENERAL GUIDANCE PART 1 PART 2 PART 3 PART 4 PART 5 PART 6 PART 7 PART

Companion Policy 43-101CP to National Instrument 43-101 Standards of Disclosure for Mineral Projects Table of Contents PART TITLE GENERAL GUIDANCE PART 1 PART 2 PART 3 PART 4 PART 5 PART 6 PART 7 PART

6.1.3 Multilateral Instrument Certification of Disclosure in Issuers Annual and Interim Filings

6.1.3 Multilateral Instrument 52-109 Certification of Disclosure in Issuers and Interim Filings TABLE OF CONTENTS MULTILATERAL INSTRUMENT 52-109 CERTIFICATION OF DISCLOSURE IN ISSUERS ANNUAL AND INTERIM

6.1.3 Multilateral Instrument 52-109 Certification of Disclosure in Issuers and Interim Filings TABLE OF CONTENTS MULTILATERAL INSTRUMENT 52-109 CERTIFICATION OF DISCLOSURE IN ISSUERS ANNUAL AND INTERIM

Notices / News Releases

Chapter 1 Notices / News Releases 1.1 Notices 1.1.1 CSA Staff Notice 51-344 Continuous Disclosure Review Program Activities for the fiscal year ended March 31, 2015 CSA Staff Notice 51-344 Continuous Disclosure

Chapter 1 Notices / News Releases 1.1 Notices 1.1.1 CSA Staff Notice 51-344 Continuous Disclosure Review Program Activities for the fiscal year ended March 31, 2015 CSA Staff Notice 51-344 Continuous Disclosure

Going Public in Canada

Going Public in Canada Issues and considerations Asssociated with an Initial Public Offering Stikeman Elliott LLP Going Public in Canada Issues and Considerations Associated with an Initial Public Offering

Going Public in Canada Issues and considerations Asssociated with an Initial Public Offering Stikeman Elliott LLP Going Public in Canada Issues and Considerations Associated with an Initial Public Offering

Initial Public Offerings vs Reverse Takeovers

Initial Public Offerings vs Reverse Takeovers August 2018 TABLE OF CONTENTS INTRODUCTION... 1 INITIAL PUBLIC OFFERING... 2 Advantages... 2 Dilution 2 Stronger Retail Distribution 2 Limits Liability 2 Timeliness

Initial Public Offerings vs Reverse Takeovers August 2018 TABLE OF CONTENTS INTRODUCTION... 1 INITIAL PUBLIC OFFERING... 2 Advantages... 2 Dilution 2 Stronger Retail Distribution 2 Limits Liability 2 Timeliness

CSA Staff Notice Disclosure of Expected Changes in Accounting Policies Relating to Changeover to International Financial Reporting Standards

. CSA Staff Notice 52-320 Disclosure of Expected Changes in Accounting Policies Relating to Changeover to International Financial Reporting Standards Purpose This notice provides guidance to an issuer

. CSA Staff Notice 52-320 Disclosure of Expected Changes in Accounting Policies Relating to Changeover to International Financial Reporting Standards Purpose This notice provides guidance to an issuer

PRELIMINARY AND PRO FORMA PROSPECTUS. Initial Public Offering and Continuous Distribution September 4, 2012

This is a preliminary prospectus in respect of each of Vanguard FTSE Canadian High Dividend Yield Index ETF, Vanguard FTSE Canadian Capped REIT Index ETF, Vanguard Canadian Short-Term Corporate Bond Index

This is a preliminary prospectus in respect of each of Vanguard FTSE Canadian High Dividend Yield Index ETF, Vanguard FTSE Canadian Capped REIT Index ETF, Vanguard Canadian Short-Term Corporate Bond Index

NATIONAL INSTRUMENT RULE UNDERWRITING CONFLICTS

This document is an unofficial consolidation of all amendments to National Instrument 33-105 Underwriting Conflicts and Companion Policy 33-105CP, applying from September 28, 2009. This document is for

This document is an unofficial consolidation of all amendments to National Instrument 33-105 Underwriting Conflicts and Companion Policy 33-105CP, applying from September 28, 2009. This document is for

SEC Comments and Trends

SEC Comments and Trends An analysis of current reporting issues Media and entertainment industry supplement December 2016 To our clients and other friends We are pleased to issue this supplement to EY

SEC Comments and Trends An analysis of current reporting issues Media and entertainment industry supplement December 2016 To our clients and other friends We are pleased to issue this supplement to EY

Cross Border Seminar Series

Cross Border Seminar Series Seminar Four Cross Border Financing: Private Placements December 5, 2006 Welcome 2 Why a cross-border seminar series? Acceleration in cross-border business activity Driven by

Cross Border Seminar Series Seminar Four Cross Border Financing: Private Placements December 5, 2006 Welcome 2 Why a cross-border seminar series? Acceleration in cross-border business activity Driven by

OSC Staff Notice , Continuous Disclosure Review Program Report - November 2001

OSC Staff Notice 51-706, Continuous Disclosure Review Program Report - November 2001 1. Introduction The Continuous Disclosure Team of the Ontario Securities Commission's Corporate Finance Branch intends

OSC Staff Notice 51-706, Continuous Disclosure Review Program Report - November 2001 1. Introduction The Continuous Disclosure Team of the Ontario Securities Commission's Corporate Finance Branch intends

National Instrument Acceptable Accounting Principles, Auditing Standards and Reporting Currency

National Instrument 52-107 Acceptable Accounting Principles, Auditing Standards and Reporting Currency PART 1 DEFINITIONS AND INTERPRETATION 1.1 Definitions 1.2 Determination of Canadian Shareholders for

National Instrument 52-107 Acceptable Accounting Principles, Auditing Standards and Reporting Currency PART 1 DEFINITIONS AND INTERPRETATION 1.1 Definitions 1.2 Determination of Canadian Shareholders for

Regulation A+: New Financing Opportunities for the Canadian Markets

Regulation A+: New Financing Opportunities for the Canadian Markets Christopher Doerksen Partner, Seattle Richard Raymer Partner, Toronto Kenneth Sam Partner, Denver 1 Old Regulation A Public offering

Regulation A+: New Financing Opportunities for the Canadian Markets Christopher Doerksen Partner, Seattle Richard Raymer Partner, Toronto Kenneth Sam Partner, Denver 1 Old Regulation A Public offering