Momentum in Imperial Russia

|

|

|

- Mildred Bates

- 6 years ago

- Views:

Transcription

1 Momentum in Imperial Russia William Goetzmann 1 Simon Huang 2 1 Yale School of Management 2 Independent May 15,2017 Goetzmann & Huang Momentum in Imperial Russia May 15, /33

2 Momentum: robust puzzle - Buy last year s winners & short last year s losers. Hold 6 months. Make excess profits. Jegadeesh & Titman (1993) US International evidence (Rouwenhorst, 1998, 1999) - Historical evidence: US, Geczy & Samonov (2016) - UK 19 th century Chabot et al. (2008) - Other asset markets (everywhere) Asness & Moskowitz (2013) - High Sharpe ratio - Signs of reversal after a year - Occasional extreme crashes

3 Theories - Time-varying expected returns - Compensation for risk - Prevalent (or salient) behavioral biases - Under-reaction - Over-reaction - Institutional and/or informational frictions

4

5 This paper: Test some theories with old (new) data The St. Petersburg Stock Exchange in Un-snooped sample No evidence of delegated management Financial crises in the sample period Regulatory change in 1893 exogenous to momentum changes market participation Main findings: Momentum profits as high as 77 bps per month (t-stat = 6.25) Significantly stronger momentum effect after 1893 No evidence of momentum crashes in this sample of almost 50 years Reject some theories: Data-snooping Institutional Crash risk correlation Under-reaction to information Goetzmann & Huang Momentum in Imperial Russia May 15, /33

6 Explanation I: delegated management Lou (2012) and Vayanos and Woolley (2013): flows into and between institutional money managers = weak momentum profits in our entire sample due to lack of delegated management Goetzmann & Huang Momentum in Imperial Russia May 15, /33

7 Explanations II & III: Behavioral On June 8, 1893, PSZ removed all restrictions prohibiting purchases of stock in the absence of cash and with future delivery. A national speculative episode followed. Many people bought stocks for the first time. Daniel, Hirshleifer, and Subrahmanyam (1998): investor overconfidence about the precision of private information = lower momentum profits pre-1893 due to (proportionally) more sophisticated investors Hong and Stein (1999): slow diffusion of information = lower momentum profits post-1893 due to lower informational frictions Goetzmann & Huang Momentum in Imperial Russia May 15, /33

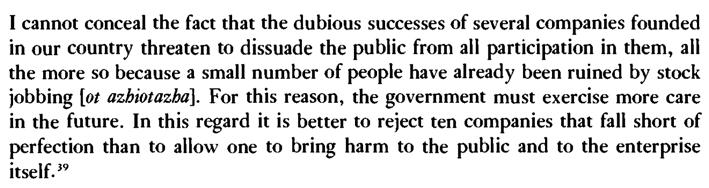

8 Regulatory Background 1836 debate & law

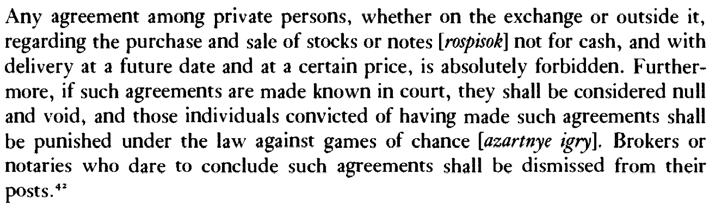

9 June, 1893 Law

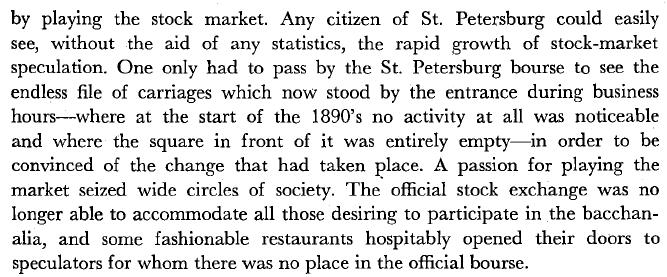

10 Speculation in 1893

11 Data ( ) End-of-month stock prices and annual dividends from various historical archives 543 firms 38,090 monthly returns Price-weighted SPSE index as market portfolio Goetzmann & Huang Momentum in Imperial Russia May 15, /33

12 Goetzmann & Huang Momentum in Imperial Russia May 15, /33

13 Goetzmann & Huang Momentum in Imperial Russia May 15, /33

14 The SPSE index Goetzmann & Huang Momentum in Imperial Russia May 15, /33

15 Summary statistics of the SPSE index (Table 1) Goetzmann & Huang Momentum in Imperial Russia May 15, /33

16 Returns of momentum portfolios (Table 2) There is a one-month gap between the formation period and the holding period in Panel B Goetzmann & Huang Momentum in Imperial Russia May 15, /33

17 Returns of momentum portfolios (Table 2), cont d There is a one-month gap between the formation period and the holding period in Panel B Goetzmann & Huang Momentum in Imperial Russia May 15, /33

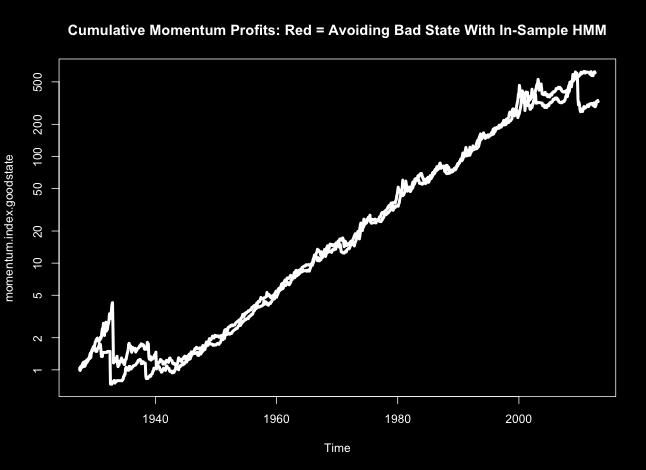

18 Performance of 6-month/6-month momentum Goetzmann & Huang Momentum in Imperial Russia May 15, /33

19 Risk-adjusted returns: CAPM alphas Goetzmann & Huang Momentum in Imperial Russia May 15, /33

20 Market dependent risk-adjusted returns (Table 3) Adjust returns by running regressions of the form r t = α + β + U t r M,t + β (1 U t )r M,t + E t Goetzmann & Huang Momentum in Imperial Russia May 15, /33

21 The effects of PSZ on momentum Daniel, Hirshleifer, and Subrahmanyam (1998): lower momentum profitspre-1893 Hong and Stein (1999): lower momentum profitspost-1893 Goetzmann & Huang Momentum in Imperial Russia May 15, /33

22 Test for structural change on momentum profits supf -statistic = (p = 0.01) Goetzmann & Huang Momentum in Imperial Russia May 15, /33

23 Did composition of market participants change? This 1893 regulatory change removed constraints that were presumably more binding for small, less sophisticated investors = did it increase market participation by these investors? We investigate its effects on liquidity to test this argument Glosten and Milgrom (1985): risk-neutral market maker sets bid-ask spread allowing expected noise-trading profits to offset expected informed-trading losses = liquidity should improve when there are more noise traders Goetzmann & Huang Momentum in Imperial Russia May 15, /33

24 The effects of PSZ on liquidity (Table 4) Following Bekaert, Harvey, and Lundblad (2007), our (inverse) liquidity measure is the price-weighted proportion of zero monthly returns Goetzmann & Huang Momentum in Imperial Russia May 15, /33

25 Crash risk compensation? Daniel and Moskowitz (2016) document momentum crashes in the U.S. from 1927 to 2010 Skewness = Ten worst monthly returns range from -28% to -79% Could momentum profits be compensating for bearing crash risk? Important to know more about their frequency andmagnitude Goetzmann & Huang Momentum in Imperial Russia May 15, /33

26 Skewness (Table 6) Goetzmann & Huang Momentum in Imperial Russia May 15, /33

27 Minimum & maximum (Table 6) Goetzmann & Huang Momentum in Imperial Russia May 15, /33

28 In search of momentum crashes Daniel and Moskowitz (2013) document momentum crashes in the U.S. from 1927 to 2010 Skewness = Ten worst monthly returns range from -28% to -79% Could momentum profits be compensating for bearing crash risk? Important to know more about their frequency and magnitude Goetzmann & Huang Momentum in 23 / 33

29 Over-reaction or under-reaction? Goetzmann & Huang Momentum in Imperial Russia May 15, /33

30 Big stocks vs. small stocks Goetzmann & Huang Momentum in Imperial Russia May 15, /33

31 Conclusion Eliminates data-snooping theory Eliminates institutional theory Weakens crash risk theory Weakens under-reaction theory Goetzmann & Huang Momentum in Imperial Russia May 15, /33

Momentum Crashes. Kent Daniel. Columbia University Graduate School of Business. Columbia University Quantitative Trading & Asset Management Conference

Crashes Kent Daniel Columbia University Graduate School of Business Columbia University Quantitative Trading & Asset Management Conference 9 November 2010 Kent Daniel, Crashes Columbia - Quant. Trading

Crashes Kent Daniel Columbia University Graduate School of Business Columbia University Quantitative Trading & Asset Management Conference 9 November 2010 Kent Daniel, Crashes Columbia - Quant. Trading

The Role of Industry Effect and Market States in Taiwanese Momentum

The Role of Industry Effect and Market States in Taiwanese Momentum Hsiao-Peng Fu 1 1 Department of Finance, Providence University, Taiwan, R.O.C. Correspondence: Hsiao-Peng Fu, Department of Finance,

The Role of Industry Effect and Market States in Taiwanese Momentum Hsiao-Peng Fu 1 1 Department of Finance, Providence University, Taiwan, R.O.C. Correspondence: Hsiao-Peng Fu, Department of Finance,

April 13, Abstract

R 2 and Momentum Kewei Hou, Lin Peng, and Wei Xiong April 13, 2005 Abstract This paper examines the relationship between price momentum and investors private information, using R 2 -based information measures.

R 2 and Momentum Kewei Hou, Lin Peng, and Wei Xiong April 13, 2005 Abstract This paper examines the relationship between price momentum and investors private information, using R 2 -based information measures.

Underreaction, Trading Volume, and Momentum Profits in Taiwan Stock Market

Underreaction, Trading Volume, and Momentum Profits in Taiwan Stock Market Mei-Chen Lin * Abstract This paper uses a very short period to reexamine the momentum effect in Taiwan stock market, focusing

Underreaction, Trading Volume, and Momentum Profits in Taiwan Stock Market Mei-Chen Lin * Abstract This paper uses a very short period to reexamine the momentum effect in Taiwan stock market, focusing

NBER WORKING PAPER SERIES MOMENTUM CYCLES AND LIMITS TO ARBITRAGE EVIDENCE FROM VICTORIAN ENGLAND AND POST-DEPRESSION US STOCK MARKETS

NBER WORKING PAPER SERIES MOMENTUM CYCLES AND LIMITS TO ARBITRAGE EVIDENCE FROM VICTORIAN ENGLAND AND POST-DEPRESSION US STOCK MARKETS Benjamin Chabot Eric Ghysels Ravi Jagannathan Working Paper 15591

NBER WORKING PAPER SERIES MOMENTUM CYCLES AND LIMITS TO ARBITRAGE EVIDENCE FROM VICTORIAN ENGLAND AND POST-DEPRESSION US STOCK MARKETS Benjamin Chabot Eric Ghysels Ravi Jagannathan Working Paper 15591

Fundamental, Technical, and Combined Information for Separating Winners from Losers

Fundamental, Technical, and Combined Information for Separating Winners from Losers Prof. Cheng-Few Lee and Wei-Kang Shih Rutgers Business School Oct. 16, 2009 Outline of Presentation Introduction and

Fundamental, Technical, and Combined Information for Separating Winners from Losers Prof. Cheng-Few Lee and Wei-Kang Shih Rutgers Business School Oct. 16, 2009 Outline of Presentation Introduction and

Economics of Behavioral Finance. Lecture 3

Economics of Behavioral Finance Lecture 3 Security Market Line CAPM predicts a linear relationship between a stock s Beta and its excess return. E[r i ] r f = β i E r m r f Practically, testing CAPM empirically

Economics of Behavioral Finance Lecture 3 Security Market Line CAPM predicts a linear relationship between a stock s Beta and its excess return. E[r i ] r f = β i E r m r f Practically, testing CAPM empirically

Momentum Crashes. The Q -GROUP: FALL SEMINAR. 17 October Kent Daniel & Tobias Moskowitz. Columbia Business School & Chicago-Booth

Momentum Crashes Kent Daniel & Tobias Moskowitz Columbia Business School & Chicago-Booth The Q -GROUP: FALL SEMINAR 17 October 2012 Momentum Introduction This paper does a deep-dive into one particular

Momentum Crashes Kent Daniel & Tobias Moskowitz Columbia Business School & Chicago-Booth The Q -GROUP: FALL SEMINAR 17 October 2012 Momentum Introduction This paper does a deep-dive into one particular

International Journal of Management Sciences and Business Research, 2013 ISSN ( ) Vol-2, Issue 12

Vol-2, Issue 12") Momentum and industry-dependence: the case of Shanghai stock exchange market. Author Detail: Dongbei University of Finance and Economics, Liaoning, Dalian, China Salvio.Elias. Macha Abstract A number of

Momentum and industry-dependence: the case of Shanghai stock exchange market. Author Detail: Dongbei University of Finance and Economics, Liaoning, Dalian, China Salvio.Elias. Macha Abstract A number of

Economic Fundamentals, Risk, and Momentum Profits

Economic Fundamentals, Risk, and Momentum Profits Laura X.L. Liu, Jerold B. Warner, and Lu Zhang September 2003 Abstract We study empirically the changes in economic fundamentals for firms with recent

Economic Fundamentals, Risk, and Momentum Profits Laura X.L. Liu, Jerold B. Warner, and Lu Zhang September 2003 Abstract We study empirically the changes in economic fundamentals for firms with recent

The Trend is Your Friend: Time-series Momentum Strategies across Equity and Commodity Markets

The Trend is Your Friend: Time-series Momentum Strategies across Equity and Commodity Markets Athina Georgopoulou *, George Jiaguo Wang This version, June 2015 Abstract Using a dataset of 67 equity and

The Trend is Your Friend: Time-series Momentum Strategies across Equity and Commodity Markets Athina Georgopoulou *, George Jiaguo Wang This version, June 2015 Abstract Using a dataset of 67 equity and

Monotonicity in Asset Returns: New Tests with Applications to the Term Structure, the CAPM and Portfolio Sorts

Monotonicity in Asset Returns: New Tests with Applications to the Term Structure, the CAPM and Portfolio Sorts Andrew Patton and Allan Timmermann Oxford/Duke and UC-San Diego June 2009 Motivation Many

Monotonicity in Asset Returns: New Tests with Applications to the Term Structure, the CAPM and Portfolio Sorts Andrew Patton and Allan Timmermann Oxford/Duke and UC-San Diego June 2009 Motivation Many

PROFITABILITY OF CAPM MOMENTUM STRATEGIES IN THE US STOCK MARKET

International Journal of Business and Society, Vol. 18 No. 2, 2017, 347-362 PROFITABILITY OF CAPM MOMENTUM STRATEGIES IN THE US STOCK MARKET Terence Tai-Leung Chong The Chinese University of Hong Kong

International Journal of Business and Society, Vol. 18 No. 2, 2017, 347-362 PROFITABILITY OF CAPM MOMENTUM STRATEGIES IN THE US STOCK MARKET Terence Tai-Leung Chong The Chinese University of Hong Kong

Stocks with Extreme Past Returns: Lotteries or Insurance?

Stocks with Extreme Past Returns: Lotteries or Insurance? Alexander Barinov Terry College of Business University of Georgia June 14, 2013 Alexander Barinov (UGA) Stocks with Extreme Past Returns June 14,

Stocks with Extreme Past Returns: Lotteries or Insurance? Alexander Barinov Terry College of Business University of Georgia June 14, 2013 Alexander Barinov (UGA) Stocks with Extreme Past Returns June 14,

Time-series and Cross-sectional Momentum in the Saudi Arabia Stock Market Returns

International Research Journal of Finance and Economics ISSN 1450-2887 Issue 164 November, 2017 http://www.internationalresearchjournaloffinanceandeconomics.com Time-series and Cross-sectional Momentum

International Research Journal of Finance and Economics ISSN 1450-2887 Issue 164 November, 2017 http://www.internationalresearchjournaloffinanceandeconomics.com Time-series and Cross-sectional Momentum

Optimal Debt-to-Equity Ratios and Stock Returns

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2014 Optimal Debt-to-Equity Ratios and Stock Returns Courtney D. Winn Utah State University Follow this

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2014 Optimal Debt-to-Equity Ratios and Stock Returns Courtney D. Winn Utah State University Follow this

One Brief Shining Moment(um): Past Momentum Performance and Momentum Reversals

: Past Momentum Performance and Momentum Reversals") One Brief Shining Moment(um): Past Momentum Performance and Momentum Reversals Usman Ali, Kent Daniel, and David Hirshleifer Preliminary Draft: May 15, 2017 This Draft: December 27, 2017 Abstract Following

One Brief Shining Moment(um): Past Momentum Performance and Momentum Reversals Usman Ali, Kent Daniel, and David Hirshleifer Preliminary Draft: May 15, 2017 This Draft: December 27, 2017 Abstract Following

Momentum Crashes. Kent Daniel and Tobias J. Moskowitz. - Abstract -

August 08, 2014 Comments Welcome Momentum Crashes Kent Daniel and Tobias J. Moskowitz - Abstract - Despite their strong positive average returns across numerous asset classes, momentum strategies can experience

August 08, 2014 Comments Welcome Momentum Crashes Kent Daniel and Tobias J. Moskowitz - Abstract - Despite their strong positive average returns across numerous asset classes, momentum strategies can experience

Momentum During Intraday Trading

Momentum During Intraday Trading Evidence from US NASDAQ Kristoffer Frösing Supervisor: Hans Jeppsson Master of Science in Finance thesis Graduate School June 2017 Abstract Both momentum and contrarian

Momentum During Intraday Trading Evidence from US NASDAQ Kristoffer Frösing Supervisor: Hans Jeppsson Master of Science in Finance thesis Graduate School June 2017 Abstract Both momentum and contrarian

Chapter 13: Investor Behavior and Capital Market Efficiency

Chapter 13: Investor Behavior and Capital Market Efficiency -1 Chapter 13: Investor Behavior and Capital Market Efficiency Note: Only responsible for sections 13.1 through 13.6 Fundamental question: Is

Chapter 13: Investor Behavior and Capital Market Efficiency -1 Chapter 13: Investor Behavior and Capital Market Efficiency Note: Only responsible for sections 13.1 through 13.6 Fundamental question: Is

Momentum and Downside Risk

Momentum and Downside Risk Abstract We examine whether time-variation in the profitability of momentum strategies is related to variation in macroeconomic conditions. We find reliable evidence that the

Momentum and Downside Risk Abstract We examine whether time-variation in the profitability of momentum strategies is related to variation in macroeconomic conditions. We find reliable evidence that the

Behavioral Finance. Nicholas Barberis Yale School of Management October 2016

Behavioral Finance Nicholas Barberis Yale School of Management October 2016 Overview from the 1950 s to the 1990 s, finance research was dominated by the rational agent framework assumes that all market

Behavioral Finance Nicholas Barberis Yale School of Management October 2016 Overview from the 1950 s to the 1990 s, finance research was dominated by the rational agent framework assumes that all market

Momentum Crashes. Society of Quantitative Analysts SQA Fall Seminar 16 October Kent Daniel & Tobias Moskowitz

Momentum Crashes Kent Daniel & Tobias Moskowitz Columbia Business School & NBER Chicago Booth & NBER Society of Quantitative Analysts Fall Seminar October 16, 2014 Momentum Momentum in Investment Strategies

Momentum Crashes Kent Daniel & Tobias Moskowitz Columbia Business School & NBER Chicago Booth & NBER Society of Quantitative Analysts Fall Seminar October 16, 2014 Momentum Momentum in Investment Strategies

Momentum Strategies in Futures Markets and Trend-following Funds

Momentum Strategies in Futures Markets and Trend-following Funds Akindynos-Nikolaos Baltas and Robert Kosowski Imperial College London 2012 BK (Imperial College London) Momentum Strategies in Futures Markets

Momentum Strategies in Futures Markets and Trend-following Funds Akindynos-Nikolaos Baltas and Robert Kosowski Imperial College London 2012 BK (Imperial College London) Momentum Strategies in Futures Markets

Behavioral Finance 1-1. Chapter 4 Challenges to Market Efficiency

Behavioral Finance 1-1 Chapter 4 Challenges to Market Efficiency 1 Introduction 1-2 Early tests of market efficiency were largely positive However, more recent empirical evidence has uncovered a series

Behavioral Finance 1-1 Chapter 4 Challenges to Market Efficiency 1 Introduction 1-2 Early tests of market efficiency were largely positive However, more recent empirical evidence has uncovered a series

Heterogeneous Beliefs and Momentum Profits

JOURNAL OF FINANCIAL AND QUANTITATIVE ANALYSIS Vol. 44, No. 4, Aug. 2009, pp. 795 822 COPYRIGHT 2009, MICHAEL G. FOSTER SCHOOL OF BUSINESS, UNIVERSITY OF WASHINGTON, SEATTLE, WA 98195 doi:10.1017/s0022109009990214

JOURNAL OF FINANCIAL AND QUANTITATIVE ANALYSIS Vol. 44, No. 4, Aug. 2009, pp. 795 822 COPYRIGHT 2009, MICHAEL G. FOSTER SCHOOL OF BUSINESS, UNIVERSITY OF WASHINGTON, SEATTLE, WA 98195 doi:10.1017/s0022109009990214

The Effect of Kurtosis on the Cross-Section of Stock Returns

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2012 The Effect of Kurtosis on the Cross-Section of Stock Returns Abdullah Al Masud Utah State University

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 5-2012 The Effect of Kurtosis on the Cross-Section of Stock Returns Abdullah Al Masud Utah State University

Risk-Adjusted Momentum: A Superior Approach to Momentum Investing

Bridgeway Capital Management, Inc. Rasool Shaik, CFA Portfolio Manager Fall 2011 : A Superior Approach to Investing Synopsis This paper summarizes our methodology and findings on a risk-adjusted momentum

Bridgeway Capital Management, Inc. Rasool Shaik, CFA Portfolio Manager Fall 2011 : A Superior Approach to Investing Synopsis This paper summarizes our methodology and findings on a risk-adjusted momentum

Ulaş ÜNLÜ Assistant Professor, Department of Accounting and Finance, Nevsehir University, Nevsehir / Turkey.

Size, Book to Market Ratio and Momentum Strategies: Evidence from Istanbul Stock Exchange Ersan ERSOY* Assistant Professor, Faculty of Economics and Administrative Sciences, Department of Business Administration,

Size, Book to Market Ratio and Momentum Strategies: Evidence from Istanbul Stock Exchange Ersan ERSOY* Assistant Professor, Faculty of Economics and Administrative Sciences, Department of Business Administration,

Momentum and Credit Rating

Momentum and Credit Rating Doron Avramov, Tarun Chordia, Gergana Jostova, and Alexander Philipov Abstract This paper establishes a robust link between momentum and credit rating. Momentum profitability

Momentum and Credit Rating Doron Avramov, Tarun Chordia, Gergana Jostova, and Alexander Philipov Abstract This paper establishes a robust link between momentum and credit rating. Momentum profitability

Profitability of CAPM Momentum Strategies in the US Stock Market

MPRA Munich Personal RePEc Archive Profitability of CAPM Momentum Strategies in the US Stock Market Terence Tai Leung Chong and Qing He and Hugo Tak Sang Ip and Jonathan T. Siu The Chinese University of

MPRA Munich Personal RePEc Archive Profitability of CAPM Momentum Strategies in the US Stock Market Terence Tai Leung Chong and Qing He and Hugo Tak Sang Ip and Jonathan T. Siu The Chinese University of

Known to financial academics

Momentum Investing Finally Accessible for Individual Investors By Tobias J. Moskowitz, PhD Known to financial academics for many years, momentum investing is a powerful tool for building portfolio efficiency,

Momentum Investing Finally Accessible for Individual Investors By Tobias J. Moskowitz, PhD Known to financial academics for many years, momentum investing is a powerful tool for building portfolio efficiency,

EXPLANATIONS FOR THE MOMENTUM PREMIUM

Tobias Moskowitz, Ph.D. Summer 2010 Fama Family Professor of Finance University of Chicago Booth School of Business EXPLANATIONS FOR THE MOMENTUM PREMIUM Momentum is a well established empirical fact whose

Tobias Moskowitz, Ph.D. Summer 2010 Fama Family Professor of Finance University of Chicago Booth School of Business EXPLANATIONS FOR THE MOMENTUM PREMIUM Momentum is a well established empirical fact whose

HIGHER ORDER SYSTEMATIC CO-MOMENTS AND ASSET-PRICING: NEW EVIDENCE. Duong Nguyen* Tribhuvan N. Puri*

HIGHER ORDER SYSTEMATIC CO-MOMENTS AND ASSET-PRICING: NEW EVIDENCE Duong Nguyen* Tribhuvan N. Puri* Address for correspondence: Tribhuvan N. Puri, Professor of Finance Chair, Department of Accounting and

HIGHER ORDER SYSTEMATIC CO-MOMENTS AND ASSET-PRICING: NEW EVIDENCE Duong Nguyen* Tribhuvan N. Puri* Address for correspondence: Tribhuvan N. Puri, Professor of Finance Chair, Department of Accounting and

Time-Varying Momentum Payoffs and Illiquidity*

Time-Varying Momentum Payoffs and Illiquidity* Doron Avramov Si Cheng and Allaudeen Hameed Current Draft: August, 2013 * Doron Avramov is from The Hebrew University of Jerusalem (email: doron.avromov@huji.ac.il).

Time-Varying Momentum Payoffs and Illiquidity* Doron Avramov Si Cheng and Allaudeen Hameed Current Draft: August, 2013 * Doron Avramov is from The Hebrew University of Jerusalem (email: doron.avromov@huji.ac.il).

Sources of Momentum Profits

Journal of Internet Banking and Commerce An open access Internet journal (http://www.icommercecentral.com) Journal of Internet Banking and Commerce, April 2016, vol. 21, no. 2 Sources of Momentum Profits

Journal of Internet Banking and Commerce An open access Internet journal (http://www.icommercecentral.com) Journal of Internet Banking and Commerce, April 2016, vol. 21, no. 2 Sources of Momentum Profits

Systematic liquidity risk and stock price reaction to shocks: Evidence from London Stock Exchange

Systematic liquidity risk and stock price reaction to shocks: Evidence from London Stock Exchange Khelifa Mazouz a,*, Dima W.H. Alrabadi a, and Shuxing Yin b a Bradford University School of Management,

Systematic liquidity risk and stock price reaction to shocks: Evidence from London Stock Exchange Khelifa Mazouz a,*, Dima W.H. Alrabadi a, and Shuxing Yin b a Bradford University School of Management,

Market Liquidity. Theory, Evidence, and Policy OXFORD UNIVERSITY PRESS THIERRY FOUCAULT MARCO PAGANO AILSA ROELL

Market Liquidity Theory, Evidence, and Policy THIERRY FOUCAULT MARCO PAGANO AILSA ROELL OXFORD UNIVERSITY PRESS CONTENTS Preface xii ' -. Introduction 1 0.1 What is This Book About? 1 0.2 Why Should We

Market Liquidity Theory, Evidence, and Policy THIERRY FOUCAULT MARCO PAGANO AILSA ROELL OXFORD UNIVERSITY PRESS CONTENTS Preface xii ' -. Introduction 1 0.1 What is This Book About? 1 0.2 Why Should We

Cards. Joseph Engelberg Linh Le Jared Williams. Department of Finance, University of California at San Diego

Stock Market Joseph Engelberg Linh Le Jared Williams Department of Finance, University of California at San Diego Department of Finance, University of South Florida Basic finance theory suggests that stock

Stock Market Joseph Engelberg Linh Le Jared Williams Department of Finance, University of California at San Diego Department of Finance, University of South Florida Basic finance theory suggests that stock

LECTURE 3. Market Efficiency & Investment Valuation - EMH and Behavioral Analysis. The Quants Book Eugene Fama and Cliff Asnes

Baruch College Executive MS in Financial Statement Analysis CHAPTER 6 (PARTIAL) LECTURE 3 Market Efficiency & Investment Valuation - EMH and Behavioral Analysis Professor s Notes Are markets efficient?????

Baruch College Executive MS in Financial Statement Analysis CHAPTER 6 (PARTIAL) LECTURE 3 Market Efficiency & Investment Valuation - EMH and Behavioral Analysis Professor s Notes Are markets efficient?????

Momentum Crashes. Kent Daniel and Tobias Moskowitz. - Abstract -

Comments Welcome Momentum Crashes Kent Daniel and Tobias Moskowitz - Abstract - Across numerous asset classes, momentum strategies have historically generated high returns, high Sharpe ratios, and strong

Comments Welcome Momentum Crashes Kent Daniel and Tobias Moskowitz - Abstract - Across numerous asset classes, momentum strategies have historically generated high returns, high Sharpe ratios, and strong

Separating Up from Down: New Evidence on the Idiosyncratic Volatility Return Relation

Separating Up from Down: New Evidence on the Idiosyncratic Volatility Return Relation Laura Frieder and George J. Jiang 1 March 2007 1 Frieder is from Krannert School of Management, Purdue University,

Separating Up from Down: New Evidence on the Idiosyncratic Volatility Return Relation Laura Frieder and George J. Jiang 1 March 2007 1 Frieder is from Krannert School of Management, Purdue University,

Momentum Crashes. Kent Daniel and Tobias Moskowitz. - Abstract -

April 12, 2013 Comments Welcome Momentum Crashes Kent Daniel and Tobias Moskowitz - Abstract - Across numerous asset classes, momentum strategies have historically generated high returns, high Sharpe ratios,

April 12, 2013 Comments Welcome Momentum Crashes Kent Daniel and Tobias Moskowitz - Abstract - Across numerous asset classes, momentum strategies have historically generated high returns, high Sharpe ratios,

Time-Varying Momentum Payoffs and Illiquidity*

Time-Varying Momentum Payoffs and Illiquidity* Doron Avramov Si Cheng and Allaudeen Hameed Current Draft: January 28, 2014 * Doron Avramov is from The Hebrew University of Jerusalem (email: doron.avromov@huji.ac.il);

Time-Varying Momentum Payoffs and Illiquidity* Doron Avramov Si Cheng and Allaudeen Hameed Current Draft: January 28, 2014 * Doron Avramov is from The Hebrew University of Jerusalem (email: doron.avromov@huji.ac.il);

Momentum Effect: Evidence from the Vietnamese Stock Market

Momentum Effect: Evidence from the Vietnamese Stock Market Pascal Alphonse Professor, University of Lille North of France - Skema Business School - LSMRC Thu Hang Nguyen PhD Candidate, University of Lille

Momentum Effect: Evidence from the Vietnamese Stock Market Pascal Alphonse Professor, University of Lille North of France - Skema Business School - LSMRC Thu Hang Nguyen PhD Candidate, University of Lille

Time-Varying Momentum Payoffs and Illiquidity*

Time-Varying Momentum Payoffs and Illiquidity* Doron Avramov Si Cheng and Allaudeen Hameed Current Draft: July 5, 2013 * Doron Avramov is from The Hebrew University of Jerusalem (email: doron.avromov@huji.ac.il).

Time-Varying Momentum Payoffs and Illiquidity* Doron Avramov Si Cheng and Allaudeen Hameed Current Draft: July 5, 2013 * Doron Avramov is from The Hebrew University of Jerusalem (email: doron.avromov@huji.ac.il).

Daily Stock Returns: Momentum, Reversal, or Both. Steven D. Dolvin * and Mark K. Pyles **

Daily Stock Returns: Momentum, Reversal, or Both Steven D. Dolvin * and Mark K. Pyles ** * Butler University ** College of Charleston Abstract Much attention has been given to the momentum and reversal

Daily Stock Returns: Momentum, Reversal, or Both Steven D. Dolvin * and Mark K. Pyles ** * Butler University ** College of Charleston Abstract Much attention has been given to the momentum and reversal

PRICE REVERSAL AND MOMENTUM STRATEGIES

PRICE REVERSAL AND MOMENTUM STRATEGIES Kalok Chan Department of Finance Hong Kong University of Science and Technology Clear Water Bay, Hong Kong Phone: (852) 2358 7680 Fax: (852) 2358 1749 E-mail: kachan@ust.hk

PRICE REVERSAL AND MOMENTUM STRATEGIES Kalok Chan Department of Finance Hong Kong University of Science and Technology Clear Water Bay, Hong Kong Phone: (852) 2358 7680 Fax: (852) 2358 1749 E-mail: kachan@ust.hk

On the Profitability of Volume-Augmented Momentum Trading Strategies: Evidence from the UK

On the Profitability of Volume-Augmented Momentum Trading Strategies: Evidence from the UK AUTHORS ARTICLE INFO JOURNAL FOUNDER Sam Agyei-Ampomah Sam Agyei-Ampomah (2006). On the Profitability of Volume-Augmented

On the Profitability of Volume-Augmented Momentum Trading Strategies: Evidence from the UK AUTHORS ARTICLE INFO JOURNAL FOUNDER Sam Agyei-Ampomah Sam Agyei-Ampomah (2006). On the Profitability of Volume-Augmented

Risk-managed 52-week high industry momentum, momentum crashes, and hedging macroeconomic risk

Risk-managed 52-week high industry momentum, momentum crashes, and hedging macroeconomic risk Klaus Grobys¹ This draft: January 23, 2017 Abstract This is the first study that investigates the profitability

Risk-managed 52-week high industry momentum, momentum crashes, and hedging macroeconomic risk Klaus Grobys¹ This draft: January 23, 2017 Abstract This is the first study that investigates the profitability

Momentum Profits and Macroeconomic Risk 1

Momentum Profits and Macroeconomic Risk 1 Susan Ji 2, J. Spencer Martin 3, Chelsea Yao 4 Abstract We propose that measurement problems are responsible for existing findings associating macroeconomic risk

Momentum Profits and Macroeconomic Risk 1 Susan Ji 2, J. Spencer Martin 3, Chelsea Yao 4 Abstract We propose that measurement problems are responsible for existing findings associating macroeconomic risk

Mutual Fund Performance and Performance Persistence

Peter Luckoff Mutual Fund Performance and Performance Persistence The Impact of Fund Flows and Manager Changes With a foreword by Prof. Dr. Wolfgang Bessler GABLER RESEARCH List of Tables List of Figures

Peter Luckoff Mutual Fund Performance and Performance Persistence The Impact of Fund Flows and Manager Changes With a foreword by Prof. Dr. Wolfgang Bessler GABLER RESEARCH List of Tables List of Figures

Momentum Loses Its Momentum: Implications for Market Efficiency

Momentum Loses Its Momentum: Implications for Market Efficiency Debarati Bhattacharya, Raman Kumar, and Gokhan Sonaer ABSTRACT We evaluate the robustness of momentum returns in the US stock market over

Momentum Loses Its Momentum: Implications for Market Efficiency Debarati Bhattacharya, Raman Kumar, and Gokhan Sonaer ABSTRACT We evaluate the robustness of momentum returns in the US stock market over

Market Conditions and Momentum in Japanese Stock Returns*

30 Journal of Behavioral Economics and Finance, Vol. 9 (2016), 30 41 Market Conditions and Momentum in Japanese Stock Returns* Mostafa Saidur Rahim Khan a Abstract This study examines the momentum effect

30 Journal of Behavioral Economics and Finance, Vol. 9 (2016), 30 41 Market Conditions and Momentum in Japanese Stock Returns* Mostafa Saidur Rahim Khan a Abstract This study examines the momentum effect

Momentum, Business Cycle, and Time-varying Expected Returns

THE JOURNAL OF FINANCE VOL. LVII, NO. 2 APRIL 2002 Momentum, Business Cycle, and Time-varying Expected Returns TARUN CHORDIA and LAKSHMANAN SHIVAKUMAR* ABSTRACT A growing number of researchers argue that

THE JOURNAL OF FINANCE VOL. LVII, NO. 2 APRIL 2002 Momentum, Business Cycle, and Time-varying Expected Returns TARUN CHORDIA and LAKSHMANAN SHIVAKUMAR* ABSTRACT A growing number of researchers argue that

CHAPTER 2. Contrarian/Momentum Strategy and Different Segments across Indian Stock Market

CHAPTER 2 Contrarian/Momentum Strategy and Different Segments across Indian Stock Market 2.1 Introduction Long-term reversal behavior and short-term momentum behavior in stock price are two of the most

CHAPTER 2 Contrarian/Momentum Strategy and Different Segments across Indian Stock Market 2.1 Introduction Long-term reversal behavior and short-term momentum behavior in stock price are two of the most

Optimal Financial Education. Avanidhar Subrahmanyam

Optimal Financial Education Avanidhar Subrahmanyam Motivation The notion that irrational investors may be prevalent in financial markets has taken on increased impetus in recent years. For example, Daniel

Optimal Financial Education Avanidhar Subrahmanyam Motivation The notion that irrational investors may be prevalent in financial markets has taken on increased impetus in recent years. For example, Daniel

Momentum and Market Correlation

Momentum and Market Correlation Ihsan Badshah, James W. Kolari*, Wei Liu, and Sang-Ook Shin August 15, 2015 Abstract This paper proposes that an important source of momentum profits is market information

Momentum and Market Correlation Ihsan Badshah, James W. Kolari*, Wei Liu, and Sang-Ook Shin August 15, 2015 Abstract This paper proposes that an important source of momentum profits is market information

REVIEW OF OVERREACTION AND UNDERREACTION IN STOCK MARKETS

International Journal of Economics, Commerce and Management United Kingdom Vol. IV, Issue 12, December 2016 http://ijecm.co.uk/ ISSN 2348 0386 REVIEW OF OVERREACTION AND UNDERREACTION IN STOCK MARKETS

International Journal of Economics, Commerce and Management United Kingdom Vol. IV, Issue 12, December 2016 http://ijecm.co.uk/ ISSN 2348 0386 REVIEW OF OVERREACTION AND UNDERREACTION IN STOCK MARKETS

Impact of business cycle on investors preferences and trading strategies

[January effect, business cycle, lottery-type stocks and cross-section of expected returns (old name)] Impact of business cycle on investors preferences and trading strategies Yuxing Yan a,* and Shaojun

[January effect, business cycle, lottery-type stocks and cross-section of expected returns (old name)] Impact of business cycle on investors preferences and trading strategies Yuxing Yan a,* and Shaojun

Momentum crashes. Kent Daniel a,b and Tobias J. Moskowitz b,c, ABSTRACT:

Momentum crashes Kent Daniel a,b and Tobias J. Moskowitz b,c, a Columbia Business School, New York, NY, USA b National Bureau of Economic Research, Cambridge, MA, USA c Booth School of Business, University

Momentum crashes Kent Daniel a,b and Tobias J. Moskowitz b,c, a Columbia Business School, New York, NY, USA b National Bureau of Economic Research, Cambridge, MA, USA c Booth School of Business, University

Existence of short term momentum effect and stock market of Turkey

Existence of short term momentum effect and stock market of Turkey AUTHORS ARTICLE INFO JOURNAL FOUNDER Abdullah Ejaz Petr Polak https://orcid.org/0000-0003-4825-7553 https://orcid.org/0000-0002-2434-4540

Existence of short term momentum effect and stock market of Turkey AUTHORS ARTICLE INFO JOURNAL FOUNDER Abdullah Ejaz Petr Polak https://orcid.org/0000-0003-4825-7553 https://orcid.org/0000-0002-2434-4540

MOMENTUM, MARKET STATES AND INVESTOR BEHAVIOR

DOCUMENTO DE TRABAJO WORKING PAPERS SERIES MOMENTUM, MARKET STATES AND INVESTOR BEHAVIOR Autor Luis Muga Rafael Santamaría DT 68/05 DEPARTAMENTO DE GESTIÓN DE EMPRESAS Universidad Pública de Navarra Nafarroako

DOCUMENTO DE TRABAJO WORKING PAPERS SERIES MOMENTUM, MARKET STATES AND INVESTOR BEHAVIOR Autor Luis Muga Rafael Santamaría DT 68/05 DEPARTAMENTO DE GESTIÓN DE EMPRESAS Universidad Pública de Navarra Nafarroako

Quantitative Analysis in Finance

*** This syllabus is tentative and subject to change as needed. Quantitative Analysis in Finance Professor: E-mail: sean.shin@aalto.fi Phone: +358-50-304-3004 Office: G2.10 (Office hours: by appointment)

*** This syllabus is tentative and subject to change as needed. Quantitative Analysis in Finance Professor: E-mail: sean.shin@aalto.fi Phone: +358-50-304-3004 Office: G2.10 (Office hours: by appointment)

Price Momentum and Idiosyncratic Volatility

Marquette University e-publications@marquette Finance Faculty Research and Publications Finance, Department of 5-1-2008 Price Momentum and Idiosyncratic Volatility Matteo Arena Marquette University, matteo.arena@marquette.edu

Marquette University e-publications@marquette Finance Faculty Research and Publications Finance, Department of 5-1-2008 Price Momentum and Idiosyncratic Volatility Matteo Arena Marquette University, matteo.arena@marquette.edu

Liquidity Skewness. Richard Roll and Avanidhar Subrahmanyam. October 28, Abstract

Liquidity Skewness by Richard Roll and Avanidhar Subrahmanyam October 28, 2009 Abstract Bid-ask spreads have declined on average but have become increasingly right-skewed. Higher right-skewness is consistent

Liquidity Skewness by Richard Roll and Avanidhar Subrahmanyam October 28, 2009 Abstract Bid-ask spreads have declined on average but have become increasingly right-skewed. Higher right-skewness is consistent

Does market liquidity explain the idiosyncratic volatility puzzle in the Chinese stock market?

Does market liquidity explain the idiosyncratic volatility puzzle in the Chinese stock market? Xiaoxing Liu Guangping Shi Southeast University, China Bin Shi Acadian-Asset Management Disclosure The views

Does market liquidity explain the idiosyncratic volatility puzzle in the Chinese stock market? Xiaoxing Liu Guangping Shi Southeast University, China Bin Shi Acadian-Asset Management Disclosure The views

Market States and Momentum

Market States and Momentum MICHAEL J. COOPER, ROBERTO C. GUTIERREZ JR., and ALLAUDEEN HAMEED * * Cooper is from the Krannert Graduate School of Management, Purdue University; Gutierrez is from the Lundquist

Market States and Momentum MICHAEL J. COOPER, ROBERTO C. GUTIERREZ JR., and ALLAUDEEN HAMEED * * Cooper is from the Krannert Graduate School of Management, Purdue University; Gutierrez is from the Lundquist

ALTERNATIVE MOMENTUM STRATEGIES. Faculdade de Economia da Universidade do Porto Rua Dr. Roberto Frias Porto Portugal

FINANCIAL MARKETS ALTERNATIVE MOMENTUM STRATEGIES António de Melo da Costa Cerqueira, amelo@fep.up.pt, Faculdade de Economia da UP Elísio Fernando Moreira Brandão, ebrandao@fep.up.pt, Faculdade de Economia

FINANCIAL MARKETS ALTERNATIVE MOMENTUM STRATEGIES António de Melo da Costa Cerqueira, amelo@fep.up.pt, Faculdade de Economia da UP Elísio Fernando Moreira Brandão, ebrandao@fep.up.pt, Faculdade de Economia

Behavioral Finance. Understanding the Social, Cognitive, and Economic Debates EDWIN T. BURTON SUNIT N. SHAH

Behavioral Finance Understanding the Social, Cognitive, and Economic Debates EDWIN T. BURTON SUNIT N. SHAH Contents Preface xi Introduction 1 PART ONE Introduction to Behavioral Finance CHAPTER 1 What

Behavioral Finance Understanding the Social, Cognitive, and Economic Debates EDWIN T. BURTON SUNIT N. SHAH Contents Preface xi Introduction 1 PART ONE Introduction to Behavioral Finance CHAPTER 1 What

Momentum pricing and trading, and economic uncertainty regimes

Momentum pricing and trading, and economic uncertainty regimes Jorge M. Uribe Riskcenter and UB School of Economics, University of Barcelona, Barcelona, Spain. Contact: juribegi9@alumnes.ub.edu This version

Momentum pricing and trading, and economic uncertainty regimes Jorge M. Uribe Riskcenter and UB School of Economics, University of Barcelona, Barcelona, Spain. Contact: juribegi9@alumnes.ub.edu This version

Fresh Momentum. Engin Kose. Washington University in St. Louis. First version: October 2009

Long Chen Washington University in St. Louis Fresh Momentum Engin Kose Washington University in St. Louis First version: October 2009 Ohad Kadan Washington University in St. Louis Abstract We demonstrate

Long Chen Washington University in St. Louis Fresh Momentum Engin Kose Washington University in St. Louis First version: October 2009 Ohad Kadan Washington University in St. Louis Abstract We demonstrate

NCER Working Paper Series

NCER Working Paper Series Momentum in Australian Stock Returns: An Update A. S. Hurn and V. Pavlov Working Paper #23 February 2008 Momentum in Australian Stock Returns: An Update A. S. Hurn and V. Pavlov

NCER Working Paper Series Momentum in Australian Stock Returns: An Update A. S. Hurn and V. Pavlov Working Paper #23 February 2008 Momentum in Australian Stock Returns: An Update A. S. Hurn and V. Pavlov

Investor Sentiment and Price Momentum

Investor Sentiment and Price Momentum Constantinos Antoniou John A. Doukas Avanidhar Subrahmanyam This version: January 10, 2010 Abstract This paper sheds empirical light on whether investor sentiment

Investor Sentiment and Price Momentum Constantinos Antoniou John A. Doukas Avanidhar Subrahmanyam This version: January 10, 2010 Abstract This paper sheds empirical light on whether investor sentiment

Liquidity Creation as Volatility Risk

Liquidity Creation as Volatility Risk Itamar Drechsler Alan Moreira Alexi Savov Wharton Rochester NYU Chicago November 2018 1 Liquidity and Volatility 1. Liquidity creation - makes it cheaper to pledge

Liquidity Creation as Volatility Risk Itamar Drechsler Alan Moreira Alexi Savov Wharton Rochester NYU Chicago November 2018 1 Liquidity and Volatility 1. Liquidity creation - makes it cheaper to pledge

Discussion Paper No. DP 07/02

SCHOOL OF ACCOUNTING, FINANCE AND MANAGEMENT Essex Finance Centre Can the Cross-Section Variation in Expected Stock Returns Explain Momentum George Bulkley University of Exeter Vivekanand Nawosah University

SCHOOL OF ACCOUNTING, FINANCE AND MANAGEMENT Essex Finance Centre Can the Cross-Section Variation in Expected Stock Returns Explain Momentum George Bulkley University of Exeter Vivekanand Nawosah University

Time-Varying Momentum Payoffs and Illiquidity*

Time-Varying Momentum Payoffs and Illiquidity* Doron Avramov Si Cheng and Allaudeen Hameed Version: September 23, 2013 * Doron Avramov is from The Hebrew University of Jerusalem (email: davramov@huji.ac.il);

Time-Varying Momentum Payoffs and Illiquidity* Doron Avramov Si Cheng and Allaudeen Hameed Version: September 23, 2013 * Doron Avramov is from The Hebrew University of Jerusalem (email: davramov@huji.ac.il);

A comparison of the technical moving average strategy, the momentum strategy and the short term reversal

ERASMUS UNIVERSITY ROTTERDAM ERASMUS SCHOOL OF ECONOMICS MSc Economics & Business Master Specialization Financial Economics A comparison of the technical moving average strategy, the momentum strategy

ERASMUS UNIVERSITY ROTTERDAM ERASMUS SCHOOL OF ECONOMICS MSc Economics & Business Master Specialization Financial Economics A comparison of the technical moving average strategy, the momentum strategy

Comparison in Measuring Effectiveness of Momentum and Contrarian Trading Strategy in Indonesian Stock Exchange

Comparison in Measuring Effectiveness of Momentum and Contrarian Trading Strategy in Indonesian Stock Exchange Rizky Luxianto* This paper wants to explore the effectiveness of momentum or contrarian strategy

Comparison in Measuring Effectiveness of Momentum and Contrarian Trading Strategy in Indonesian Stock Exchange Rizky Luxianto* This paper wants to explore the effectiveness of momentum or contrarian strategy

Crowding and the Moments of Momentum

Crowding and the Moments of Momentum Pedro Barroso, Roger M. Edelen, and Paul Karehnke May 5, 2017 Abstract We develop a model of crowding as in Stein (2009), applied to momentum. The model demonstrates

Crowding and the Moments of Momentum Pedro Barroso, Roger M. Edelen, and Paul Karehnke May 5, 2017 Abstract We develop a model of crowding as in Stein (2009), applied to momentum. The model demonstrates

Master Thesis. Risk Measures of Momentum Strategy And Linkage with Macroeconomic Factors. 12 May FENG Ting 1 and LI Zhen 2. Thesis Supervisor:

12 May 2015 Master Thesis Risk Measures of Momentum Strategy And Linkage with Macroeconomic Factors By FENG Ting 1 and LI Zhen 2 Thesis Supervisor: Prof. LANGLOIS Hugues, PhD 1 Ting FENG: HEC Paris Grande

12 May 2015 Master Thesis Risk Measures of Momentum Strategy And Linkage with Macroeconomic Factors By FENG Ting 1 and LI Zhen 2 Thesis Supervisor: Prof. LANGLOIS Hugues, PhD 1 Ting FENG: HEC Paris Grande

Alpha Momentum and Price Momentum*

Alpha Momentum and Price Momentum* Hannah Lea Huehn 1 Friedrich-Alexander-Universität (FAU) Erlangen-Nürnberg Hendrik Scholz 2 Friedrich-Alexander-Universität (FAU) Erlangen-Nürnberg First Version: July

Alpha Momentum and Price Momentum* Hannah Lea Huehn 1 Friedrich-Alexander-Universität (FAU) Erlangen-Nürnberg Hendrik Scholz 2 Friedrich-Alexander-Universität (FAU) Erlangen-Nürnberg First Version: July

Persistence in Mutual Fund Performance: Analysis of Holdings Returns

Persistence in Mutual Fund Performance: Analysis of Holdings Returns Samuel Kruger * June 2007 Abstract: Do mutual funds that performed well in the past select stocks that perform well in the future? I

Persistence in Mutual Fund Performance: Analysis of Holdings Returns Samuel Kruger * June 2007 Abstract: Do mutual funds that performed well in the past select stocks that perform well in the future? I

Slow Diffusion of Information and Price Momentum in Stocks: Evidence from Options Markets

Slow Diffusion of Information and Price Momentum in Stocks: Evidence from Options Markets Zhuo Chen Andrea Lu November 10, 2014 Abstract This paper investigates the source of price momentum in the stock

Slow Diffusion of Information and Price Momentum in Stocks: Evidence from Options Markets Zhuo Chen Andrea Lu November 10, 2014 Abstract This paper investigates the source of price momentum in the stock

Chris Brightman, CFA, Feifei Li, Ph.D., FRM, and Xi Liu, CFA

Chasing Performance with ETFs Chris Brightman, CFA, Feifei Li, Ph.D., FRM, and Xi Liu, CFA Chris Brightman, CFA What s hot may change abruptly, but investors penchant for what s hot is steady. KEY POINTS

Chasing Performance with ETFs Chris Brightman, CFA, Feifei Li, Ph.D., FRM, and Xi Liu, CFA Chris Brightman, CFA What s hot may change abruptly, but investors penchant for what s hot is steady. KEY POINTS

Trade Size and the Cross-Sectional Relation to Future Returns

Trade Size and the Cross-Sectional Relation to Future Returns David A. Lesmond and Xue Wang February 1, 2016 1 David Lesmond (dlesmond@tulane.edu) is from the Freeman School of Business and Xue Wang is

Trade Size and the Cross-Sectional Relation to Future Returns David A. Lesmond and Xue Wang February 1, 2016 1 David Lesmond (dlesmond@tulane.edu) is from the Freeman School of Business and Xue Wang is

ALPHA ANALYSIS - A MOMENTUM AND PERFORMANCE

Department of Economics Master Thesis January 2012 ALPHA ANALYSIS - A MOMENTUM AND PERFORMANCE METRICS STUDY OF THE EFFICIENT MARKET HYPOTHESIS Authors Mikael Lindberg Supervisor Hossein Asgharian Andreas

Department of Economics Master Thesis January 2012 ALPHA ANALYSIS - A MOMENTUM AND PERFORMANCE METRICS STUDY OF THE EFFICIENT MARKET HYPOTHESIS Authors Mikael Lindberg Supervisor Hossein Asgharian Andreas

Realized Skewness for Information Uncertainty

Realized Skewness for Information Uncertainty Youngmin Choi Suzanne S. Lee December 2015 Abstract We examine realized daily skewness as a measure of information uncertainty concerning a firm s fundamentals.

Realized Skewness for Information Uncertainty Youngmin Choi Suzanne S. Lee December 2015 Abstract We examine realized daily skewness as a measure of information uncertainty concerning a firm s fundamentals.

Notes. 1 Fundamental versus Technical Analysis. 2 Investment Performance. 4 Performance Sensitivity

Notes 1 Fundamental versus Technical Analysis 1. Further findings using cash-flow-to-price, earnings-to-price, dividend-price, past return, and industry are broadly consistent with those reported in the

Notes 1 Fundamental versus Technical Analysis 1. Further findings using cash-flow-to-price, earnings-to-price, dividend-price, past return, and industry are broadly consistent with those reported in the

The Worst, The Best, Ignoring All the Rest: The Rank Effect and Trading Behavior

: The Rank Effect and Trading Behavior Samuel M. Hartzmark The Q-Group October 19 th, 2014 Motivation How do investors form and trade portfolios? o Normative: Optimal portfolios Combine many assets into

: The Rank Effect and Trading Behavior Samuel M. Hartzmark The Q-Group October 19 th, 2014 Motivation How do investors form and trade portfolios? o Normative: Optimal portfolios Combine many assets into

MULTI FACTOR PRICING MODEL: AN ALTERNATIVE APPROACH TO CAPM

MULTI FACTOR PRICING MODEL: AN ALTERNATIVE APPROACH TO CAPM Samit Majumdar Virginia Commonwealth University majumdars@vcu.edu Frank W. Bacon Longwood University baconfw@longwood.edu ABSTRACT: This study

MULTI FACTOR PRICING MODEL: AN ALTERNATIVE APPROACH TO CAPM Samit Majumdar Virginia Commonwealth University majumdars@vcu.edu Frank W. Bacon Longwood University baconfw@longwood.edu ABSTRACT: This study

The V-shaped Disposition Effect

The V-shaped Disposition Effect Li An December 9, 2013 Abstract This study investigates the asset pricing implications of the V-shaped disposition effect, a newly-documented behavior pattern characterized

The V-shaped Disposition Effect Li An December 9, 2013 Abstract This study investigates the asset pricing implications of the V-shaped disposition effect, a newly-documented behavior pattern characterized

Mispriced Index Option Portfolios George Constantinides University of Chicago

George Constantinides University of Chicago (with Michal Czerwonko and Stylianos Perrakis) We consider 2 generic traders: Introduction the Index Trader (IT) holds the S&P 500 index and T-bills and maximizes

George Constantinides University of Chicago (with Michal Czerwonko and Stylianos Perrakis) We consider 2 generic traders: Introduction the Index Trader (IT) holds the S&P 500 index and T-bills and maximizes

The performance of mutual funds on French stock market:do star funds managers exist or do funds have to hire chimpanzees?

MPRA Munich Personal RePEc Archive The performance of mutual funds on French stock market:do star funds managers exist or do funds have to hire chimpanzees? Michel Blanchard and philippe Bernard INALCO,

MPRA Munich Personal RePEc Archive The performance of mutual funds on French stock market:do star funds managers exist or do funds have to hire chimpanzees? Michel Blanchard and philippe Bernard INALCO,

The 52-Week High and Momentum Investing

THE JOURNAL OF FINANCE VOL. LIX, NO. 5 OCTOBER 2004 The 52-Week High and Momentum Investing THOMAS J. GEORGE and CHUAN-YANG HWANG ABSTRACT When coupled with a stock s current price, a readily available

THE JOURNAL OF FINANCE VOL. LIX, NO. 5 OCTOBER 2004 The 52-Week High and Momentum Investing THOMAS J. GEORGE and CHUAN-YANG HWANG ABSTRACT When coupled with a stock s current price, a readily available

Time-Series Momentum versus Technical Analysis

Time-Series Momentum versus Technical Analysis Abstract Time-series momentum and technical analysis are closely related. The returns generated by these two hitherto distinct return predictability techniques

Time-Series Momentum versus Technical Analysis Abstract Time-series momentum and technical analysis are closely related. The returns generated by these two hitherto distinct return predictability techniques

Size Matters, if You Control Your Junk

Discussion of: Size Matters, if You Control Your Junk by: Cliff Asness, Andrea Frazzini, Ronen Israel, Tobias Moskowitz, and Lasse H. Pedersen Kent Daniel Columbia Business School & NBER AFA Meetings 7

Discussion of: Size Matters, if You Control Your Junk by: Cliff Asness, Andrea Frazzini, Ronen Israel, Tobias Moskowitz, and Lasse H. Pedersen Kent Daniel Columbia Business School & NBER AFA Meetings 7

An analysis of momentum and contrarian strategies using an optimal orthogonal portfolio approach

An analysis of momentum and contrarian strategies using an optimal orthogonal portfolio approach Hossein Asgharian and Björn Hansson Department of Economics, Lund University Box 7082 S-22007 Lund, Sweden

An analysis of momentum and contrarian strategies using an optimal orthogonal portfolio approach Hossein Asgharian and Björn Hansson Department of Economics, Lund University Box 7082 S-22007 Lund, Sweden

Do Retail Trades Move Markets? Brad Barber Terrance Odean Ning Zhu

Do Retail Trades Move Markets? Brad Barber Terrance Odean Ning Zhu Do Noise Traders Move Markets? 1. Small trades are proxy for individual investors trades. 2. Individual investors trading is correlated:

Do Retail Trades Move Markets? Brad Barber Terrance Odean Ning Zhu Do Noise Traders Move Markets? 1. Small trades are proxy for individual investors trades. 2. Individual investors trading is correlated:

Another Look at Market Responses to Tangible and Intangible Information

Critical Finance Review, 2016, 5: 165 175 Another Look at Market Responses to Tangible and Intangible Information Kent Daniel Sheridan Titman 1 Columbia Business School, Columbia University, New York,

Critical Finance Review, 2016, 5: 165 175 Another Look at Market Responses to Tangible and Intangible Information Kent Daniel Sheridan Titman 1 Columbia Business School, Columbia University, New York,