Belfast Region Committee. South Region Committee presents. "Mind Your Own Business" an evening with Bryan Johnson. Welcome

|

|

|

- Willis Norman

- 5 years ago

- Views:

Transcription

1 Belfast Region Committee South Region Committee presents "Mind Your Own Business" an evening with Bryan Johnson Welcome

2 Retirement Planning CPD 17 Bryan Johnston

3 This evening Challenges facing Irish Pensions The OECD view How the State has changed the State Pension How much should you be putting into your pension How easing back is the new retirement 1.5 hour CPD

4 Bryan Johnston QFA FLIA Progressive Life. Sales / marketing Management. Training. Irish Permanent. Business Champions Ltd QFA Public Lectures Webinars In house Personal coaching Consultancy Financial DNA Sales CPD events

5 Anyone fancy a glass of wine?

Relatively modest tastes")

6 Happy Retirement! One bottle of wine per day between you and your partner (both aged 40 and wishing to retire at 65) Relatively modest tastes say per bottle OK bottle of New Zealand Sauvignon Blanc How much would you need to save to pay for it?

7 Assumptions Inflation at 2% Investment Return of 5% (gross) Management Charge 1% Current Annuity Rates prevail Current Tax and PRSI Rates remain constant Retirement income will be liable to tax at top rate (40%)

8 Required Fund at bottle will then cost A bottle a day will cost 7786 per annum Pre tax income required Fund required to buy a pension of that amount will be 432,555 If you opt for a level annual amount ( not increasing) the required saving will be 850 Annuity 3%

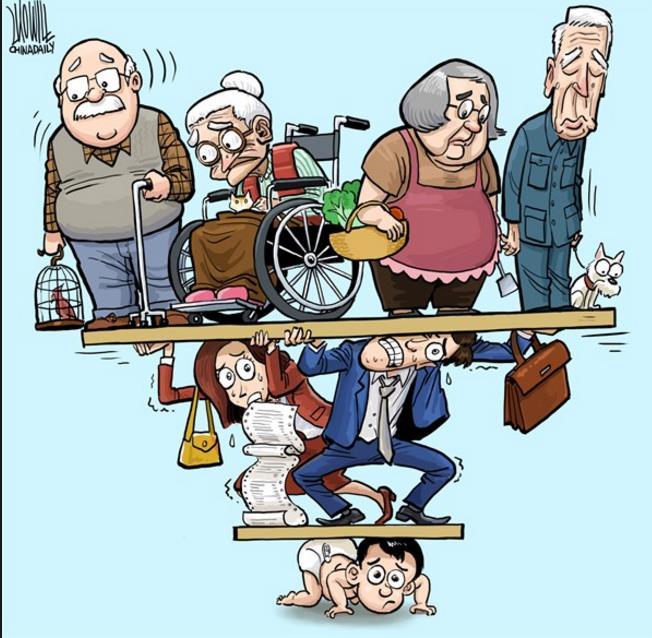

9 We are facing a Retirement Income Crisis! We are living longer We are healthier for longer We are likely to be ill for longer Annuity rates are at historically low levels We will have less children to support us Having children later means that we won't have enough disposable income to save We can no longer rely on the State for any help

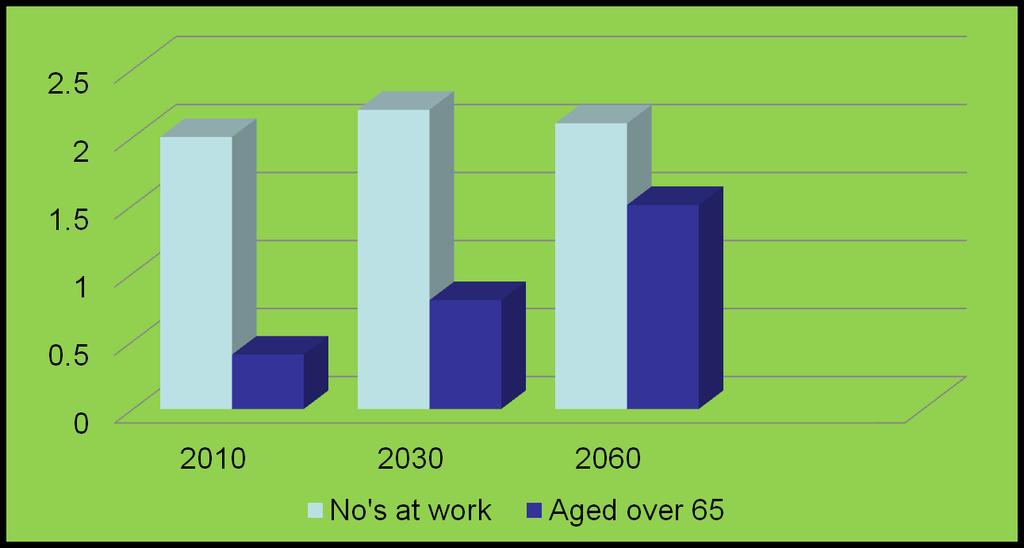

10 Pensions coverage in the Irish workforce

11 Changing Demographics

12 Issues Defined benefit schemes underfunded Pension contribution slow down People living longer State Pension age Annuities low Charges and pension plans Investing your money

13 The Pensions Authority in 2016 published proposals to change the private pensions system which, if implemented, will have a significant impact on the pensions market, particularly individual pensions. The target date for implementation is September 2018.

14 Pensions developments Proposed.. no new RACs or Buy Out Bonds and The PRSA would be the single DC accumulation contract available for: 1. The self employed 2. AVCs outside a scheme 3. Accepting transfers from other arrangements, such as occupational pension schemes, RACs, and Buy Out Bonds

15 Transfers RACs will be allowed to transfer to an occupational pension scheme, as well as to a PRSA; BOBs will be allowed to transfer to a PRSA as well as to an occupational pension scheme; The current max 15 years service limit on transfers from an occupational pension scheme to a PRSA will be lifted.

16 One member DC schemes Enhanced authorisation and regulations More difficult and harder to set up including 1. Scheme structure and formation; 2. Governance and management; 3. Investment 4. Business Plan Also includes SSAPS

17 Trustees Cannot be employer and financial advisors The scheme trustees will have to be: At least two individuals, one with a mandatory trustee qualification (NFQ Level 7 upwards) and another with appropriate trustee experience (at least 2 years), OR A corporate trustee acting as sole trustee with at least two directors, one with a mandatory trustee qualification and another with appropriate trustee experience

18 Trustees 1. Will have to undergo fitness and probity verification by the Pensions Authority. 2. ALL scheme trustees will have to meet an ongoing CPD requirement. 3. Mandatory codes of practice for trustees; 4. The Pensions Authority will have enhanced supervisory powers to intervene in the operation of schemes. 5. Will also apply to all existing large DC schemes after May 18

19 Master Trusts The Pensions Authority wants to encourage the development of master trusts, i.e. one large multi-employer scheme and trust. The hope is that the scale of such larger schemes will lead to better outcomes for members 1. Lower charges, 2. Better governance and 3. Better advice provided to members

20 Proprietary directors choices 1. PRSA; May be subject to the current age related tax relief limits (combined employer and member) with no facility for funding back service, etc. The scope for contributions may be far lower than at present under a one member DC scheme; 2. One member DC scheme; More expensive and difficult to set up and operate than at present, 3. Master trust scheme. Investment options in such a scheme are likely to be more limited than available currently to one member DC schemes. No self directed funds

21 Think about If you have deferred benefits in a DB scheme transfer to a BOB or PRSA Will allow ARF and traditional options Proprietary directors If not started start new and have much bigger potential contributions Some may have reached contribution levels and could put fund into BOB and future funding could be done through cheaper PRSA route

22

23 OECD Ireland faces challenges on the financial sustainability of its pension system as the population ages;. The economic situation of pensioners in Ireland is comparatively good, both with respect to other age groups in the population and internationally. Ireland and New Zealand are the only OECD countries that do not have a mandatory earning-related pillar to complement the State pension at basic level, Private pension coverage, both in occupational and personal pensions, is uneven and needs to be increased urgently.

24 OECD Pension charges are expensive for small occupational schemes and personal pension schemes. The existing tax deferral structure in Ireland provides greater incentives for those with high incomes to save for retirement. The Irish legislation regarding the protection of defined-benefit (DB) plan members is weak. There is unequal treatment of public and private sector workers due to the prevalence of DB plans in the public sector and DC plans in the private sector. The State pension system lacks transparency, both with respect to the calculation of benefit entitlements and to the interplay of the contributory and non-contributory pensions. The link between contributions and benefits in the Irish State pension scheme is very weak.

25 Their recommendations

26 Change the parameters of the State pension system in order to improve financial sustainability 1. The long-term retirement age, which at 68 is relatively high in international comparison, could be linked to life expectancy after To provide incentives for workers to remain in the labour market longer and on the other hand provide more flexibility in deciding when to retire, increments and decrements of the State pension could be introduced for late and early retirement. 3. More flexibility could also be provided in allowing retirees to combine work income and pension receipt; this could also ensure more adequate retirement income. 4. The adjustment of pensions which have been frozen in recent years also needs to be considered; various options of combining indexation to wage growth and price inflation could be considered.

27 Structural reform of the State pension system to eliminate inequities Current inequities in the treatment of workers contributions to the system should be removed The best two options for a structural reform of the State pension scheme are 1. a universal basic pension 2. or a means-tested basic pension..

28 Reform of the public service pension scheme At a minimum, a faster phase-in of the new rules of the occupational scheme for public servants should be considered; this would entail including existing public servants in the new scheme based either on a certain cut-off age or on length of service. Any new private pension scheme for private sector workers should also be extended to public servants, at a minimum for new entrants but ideally also for some of the existing public servants.

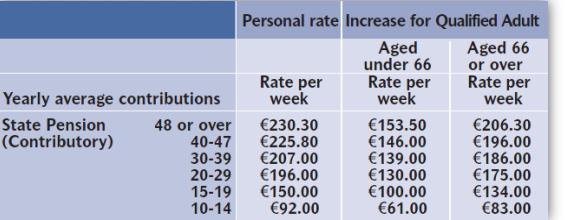

29 Expand private pensions coverage and retirement savings Compulsion is the less costly and most effective approach to increase coverage of private pensions. Automatic enrolment is a second-best option. Its success depends on how it is designed and on its interaction with incentives in the system. Existing private schemes need to be subject to the same rules as the new schemes under auto-enrolment or compulsion.

30 Enhancing benefit security in DB schemes Strengthen the Irish legislation regarding the protection of DB plan members Introduce more flexible DB plans that allow for accrued benefits to be cut in case of underfunding and for risks to be shared Establish a clear framework to facilitate domestic investment in infrastructure projects Revise the new funding standards,

31 Trends Defined benefit schemes being wound up Enhanced benefits being offered in some cases Retirement for State pension effectively 68 How do you bridge that gap

32 Retirement Landing Choices 1. Tax free cash 2. Annuity 3. ARF 4. Mixture of these

33 DC Scheme Members Choice Options Standard benefit options OR Alternative benefit options Tax Free Lump Sum related to service and final remuneration, max 150% x final remuneration Tax Free Lump Sum of 25% x accumulated fund AND Balance of fund must buy Pension AND Balance of fund: Buy annuity ARF Taxable lump sum

34 Retirement options Take 25% as a tax free lump sum (Max 200,000) Balance Buy annuity with life company, Invest in ARF, OR * Take as taxable cash sum* Restriction * 63,500 must be invested in annuity or AMRF Unless Guaranteed Income of 12,700 +

35 Effect of charges

36 Income in retirement Three ways of providing your income in retirement 1. State Pension 2. Private Pension provision 3. Accumulated Wealth and Savings State Pension? May depend on PRSI contributions Qualifying age increasing (68 if born after 1961) Home Reversions and Lifetime loans set to make a comeback

37 State Pension Contributory How to? PRSI contribution record (A and S ) At 66, if born before 1954, no retirement necessary If born between now age 67 If born after 61 now 68 Level of benefit? Personal rate Personal rate + adult dependant Maximum pw Taxation? Liable to PAYE but not directly taken However if individual has other income Other income / pensions reduced to collect tax due on Above How long? Life

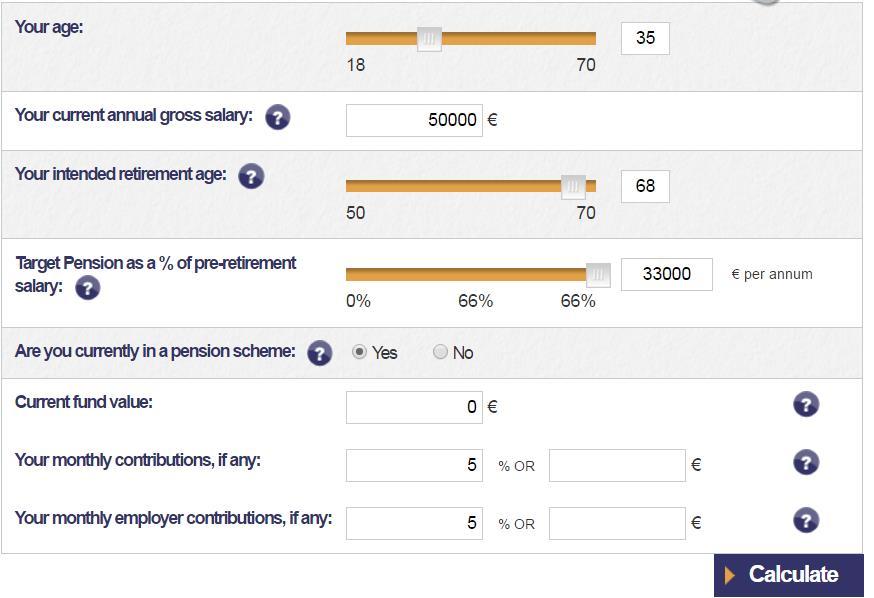

38 Contributions

39 Income in retirement There are 2 considerations 1. Drop in income in retirement 2. Increase in life expectancy

40 Drop in income at retirement solely relying on current state pension 40,000 60,000 80,000 Income -71% -45% -81% -64% -85% -72% Drop in income if single Drop in income if dependant spouse

41 From Increase in Life Expectancy - people are living longer! Age Age Female Male Age Years

42 Life Expectancy Living longer Most people under estimate their life expectancy Men at 65 by at least 5 years Women at 65 by 6 years Life expectancy at birth often thought to be a given age less expectancy at birth E.g. in 2000 men at birth could expect to live to 75 however when they reach 65 on average will live to 80 Irish men aged 65 today..83 and women 86 Born in 1980 at 65 men 86 and women 89

43 How much do you need in retirement Basic living costs annually 12400

44 What else would you like

45 How do you want retirement to be? Cost That s after tax 20% Tax = % tax = 58333

46 Age 35 and 10% salary going into pension

47

48 How much extra per month needed Need to increase to 25.3% salary Fund only Expected fund if left at 10% of salary Fund in todays terms Contributions increase by 2..5% Investment return 4%

49

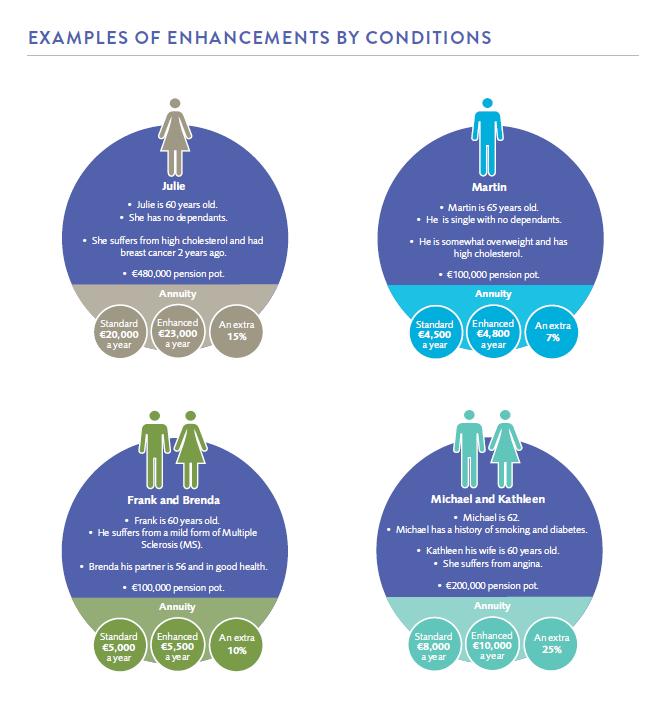

50 Extra 35% needed Fund only Expected fund if left at 10% of salary Fund in todays terms Contributions increase by 2..5% Investment return 4%

51 45 and in pension already

52 45 and in pension already Extra 30% needed Fund only Fund in todays terms Contributions increase by 2..5% Investment return 4%

53 55 and 100,000

54 55 and fund of 100,000 now Need to increase to about 57% salary Fund only Expected fund 168,000 if left at 10% of salary

55 An ideal world Ideally pa State Pension pa Lets look at some funds Irish men aged 65 today..83 and women 86 Born in 1980 at 65 men 86 and women 89

56 Age 65 getting pa ARF pa needed pre tax Age Last year residue Annuity years years years years years

57 Shop around for annuity rates 50000

58 Enhanced annuities Standard annuity Regular payment for life Enhanced Takes account of your health status and lifestyle health risks (e.g. smoking) in determining the level of regular income payable to you. With an enhanced annuity you may be entitled to a higher regular income than you would under a standard annuity.

59

60

61 Start now - cost of delay

62 Tax Relief in Practice Example - assume 40% Income Tax Rate Salary 50,000 Monthly Pension Contribution (10%) Less tax relief: Income 40% Net cost to you Amount invested in pension

63 Maximum contribution levels Age Attained in Year Under 30 15% % % % % 60 Plus 40% % Of Salary (to a max salary of 115,000)

64 Start now - cost of delay Example Contribution 1,000 p.m. Retiring at age 60 Level contributions Assume 6% growth Age Fund at age , , , , ,000

65 Major Survey

66 Retirement is changing along with the pensions landscape The nature of retirement is changing along with the pensions landscape in Ireland. As a result, people s attitudes towards retirement are shifting. The concept of gradual retirement is becoming more prevalent as people slowly reduce the amount of time they spend working, a fact that is evidenced by the 37% of respondents in our survey who indicated that they plan to continue working during retirement. This reflects the widespread move away from Defined Benefit to Defined Contribution pension plans.

67

68 In a Nutshell More than half of people surveyed (52%) did not feel completely ready to retire and just two-fifths believed that 65 was the right age to retire. Over 61% felt they had more to contribute to the workforce, but most would not choose to remain on with their current employer if given the option. People were overwhelmingly looking forward to the free time they would gain, the time they could spend with family and the chance to travel when they retired.

69 In a Nutshell 34% of respondents had not put any kind of healthy living plan in place for when they retire. A strong majority of those surveyed had social networks in place outside of work Almost two-thirds of those surveyed already held membership of clubs and organisations that they intended to continue into retirement Nearly 60% of survey participants intended to engage in volunteer work

70 Finances While most of those surveyed (67%) had been preparing financially for retirement through saving, 55% of those surveyed had not prepared any kind of personal budget to address the future change in their financial circumstance

71 Is 65 the right age % Before 60 16%

72 Ready for retirement Stay with current employer if they could No 54% Yes 24% 61% More to give

73 Most Looking forward to Relaxing more Taking up new things Being stress free Farming Having freedom

74 Financial Planning for Retirement 50% have a plan for retirement 66% saving 13% have an annual budget 50% no budget at all 66% happy they will be ok financially 80% plan to ski!

75 Steps for a Successful Retirement 1. Begin planning early 2. Consult with your family and your spouse or partner 3. Consult with your employer & signal well in advance 4. Plan to hand over your responsibilities your succession plan. 5. Take time to understand your financial situation and options available to you 6. Take a pro-active approach to minding your health. 7. Don t let your financial future be your only consideration 8. Think about ways in which you can re-apply your skills. 9. Make sure you have a strong social network outside the workplace 10. Give yourself some structure and routine. 11. Take care of your psychological well-being. 12. Enjoy your time in retirement.

76 Finally The day will come If you retire at 65 what happens until state pension kicks in Look at charges Start saving early Ease back Happy retirement Thank you The tragedy of growing old is not that one is old but that one is young. Oscar Wilde

77 Questions 77

AN ADVISER S GUIDE TO PENSIONS UPDATED FOR FINANCE ACT 2016

PENSIONS INVESTMENTS LIFE INSURANCE AN ADVISER S GUIDE TO PENSIONS UPDATED FOR FINANCE ACT 2016 This is a technical guide for financial advisers only and is not intended as an advertisement. AN ADVISER

PENSIONS INVESTMENTS LIFE INSURANCE AN ADVISER S GUIDE TO PENSIONS UPDATED FOR FINANCE ACT 2016 This is a technical guide for financial advisers only and is not intended as an advertisement. AN ADVISER

The Citizens Assembly

Paper of Mr. Andrew Nugent The Pensions Authority of Ireland delivered to The Citizens Assembly on 08 July 2017 Pension Provision in Ireland A paper for the Citizens Assembly 8 July 2017 Introduction The

Paper of Mr. Andrew Nugent The Pensions Authority of Ireland delivered to The Citizens Assembly on 08 July 2017 Pension Provision in Ireland A paper for the Citizens Assembly 8 July 2017 Introduction The

AN ADVISER S GUIDE TO PENSIONS 2018 UPDATED FOR FINANCE ACT 2017

PENSIONS INVESTMENTS LIFE INSURANCE AN ADVISER S GUIDE TO PENSIONS 2018 UPDATED FOR FINANCE ACT 2017 This is a technical guide for financial brokers or advisers only and is not intended as an advertisement.

PENSIONS INVESTMENTS LIFE INSURANCE AN ADVISER S GUIDE TO PENSIONS 2018 UPDATED FOR FINANCE ACT 2017 This is a technical guide for financial brokers or advisers only and is not intended as an advertisement.

COMPANY PENSION RETIREMENT OPTIONS

PENSIONS INVESTMENTS LIFE INSURANCE AN ADVISERS GUIDE TO: COMPANY PENSION RETIREMENT OPTIONS UPDATED FOR FINANCE ACT 2016 This is a technical guide for financial advisers only and is not intended as an

PENSIONS INVESTMENTS LIFE INSURANCE AN ADVISERS GUIDE TO: COMPANY PENSION RETIREMENT OPTIONS UPDATED FOR FINANCE ACT 2016 This is a technical guide for financial advisers only and is not intended as an

Initial Response of the Irish Congress of Trade Unions to the OECD Review of the Irish Pension System (Preliminary Version) - April 2013

- April 2013") Initial Response of the Irish Congress of Trade Unions to the OECD Review of the Irish Pension System (Preliminary Version) - April 2013 This report of almost 160 pages took 12 OECD consultants more than

Initial Response of the Irish Congress of Trade Unions to the OECD Review of the Irish Pension System (Preliminary Version) - April 2013 This report of almost 160 pages took 12 OECD consultants more than

At Retirement. A guide to your choices. Retirement Investments Insurance

At Retirement A guide to your choices Retirement Investments Insurance 2 Why choose Aviva? Around the world, Aviva provides around 34 million customers with life assurance, savings and investment products*.

At Retirement A guide to your choices Retirement Investments Insurance 2 Why choose Aviva? Around the world, Aviva provides around 34 million customers with life assurance, savings and investment products*.

D&B (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION

Pension Plan DEFINED CONTRIBUTION (DC) SECTION") D&B (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION Contents 1 Welcome to the D&B (UK) Pension Plan Defined Contribution (DC) section The DC section of the D&B (UK) Pension Plan (the Plan ) provides

D&B (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION Contents 1 Welcome to the D&B (UK) Pension Plan Defined Contribution (DC) section The DC section of the D&B (UK) Pension Plan (the Plan ) provides

COMPLETE SOLUTIONS COMPANY PENSION 1

PENSIONS INVESTMENTS LIFE INSURANCE COMPLETE SOLUTIONS COMPANY PENSION 1 YOUR COMPLETE RETIREMENT PLAN PRODUCT SNAPSHOT This booklet will give you details of the benefits available under the Complete Solutions

PENSIONS INVESTMENTS LIFE INSURANCE COMPLETE SOLUTIONS COMPANY PENSION 1 YOUR COMPLETE RETIREMENT PLAN PRODUCT SNAPSHOT This booklet will give you details of the benefits available under the Complete Solutions

COMPLETE SOLUTIONS COMPANY PENSION 2

PENSIONS INVESTMENTS LIFE INSURANCE COMPLETE SOLUTIONS COMPANY PENSION 2 YOUR COMPLETE RETIREMENT PLAN PRODUCT SNAPSHOT This booklet will give you details of the benefits available under the Complete Solutions

PENSIONS INVESTMENTS LIFE INSURANCE COMPLETE SOLUTIONS COMPANY PENSION 2 YOUR COMPLETE RETIREMENT PLAN PRODUCT SNAPSHOT This booklet will give you details of the benefits available under the Complete Solutions

D&B (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION

Pension Plan DEFINED CONTRIBUTION (DC) SECTION") D&B (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION Contents 1 Welcome to the D&B (UK) Pension Plan Defined Contribution (DC) section The DC section of the D&B (UK) Pension Plan (the Plan ) provides

D&B (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION Contents 1 Welcome to the D&B (UK) Pension Plan Defined Contribution (DC) section The DC section of the D&B (UK) Pension Plan (the Plan ) provides

AER LINGUS DEFINED CONTRIBUTION PENSION SCHEME

PENSIONS INVESTMENTS LIFE INSURANCE AER LINGUS DEFINED CONTRIBUTION PENSION SCHEME MEMBER GUIDE CONTENTS INTRODUCTION 2 WHAT IS A DEFINED CONTRIBUTION SCHEME? 3 COMMUNICATION 7 IMPORTANT INFORMATION TO

PENSIONS INVESTMENTS LIFE INSURANCE AER LINGUS DEFINED CONTRIBUTION PENSION SCHEME MEMBER GUIDE CONTENTS INTRODUCTION 2 WHAT IS A DEFINED CONTRIBUTION SCHEME? 3 COMMUNICATION 7 IMPORTANT INFORMATION TO

Economics of Policy Issues EC3060 Spring 2018

Economics of Policy Issues EC3060 Spring 2018 Case Study: Irish Pension System and Challenges Michael King 1 Additional Readings Supplementary National Pensions Framework (2010) http://www.oecd.org/site/iops/research/455

Economics of Policy Issues EC3060 Spring 2018 Case Study: Irish Pension System and Challenges Michael King 1 Additional Readings Supplementary National Pensions Framework (2010) http://www.oecd.org/site/iops/research/455

Defined Contribution Pension Plan. Employee Brochure

Defined Contribution Pension Plan Employee Brochure This brochure describes your Defined Contribution Pension Plan, the aim of which is to help you provide financially for your retirement. This plan is

Defined Contribution Pension Plan Employee Brochure This brochure describes your Defined Contribution Pension Plan, the aim of which is to help you provide financially for your retirement. This plan is

GUIDE TO OPTIONS UNDER A COMPANY PENSION SCHEME ON LEAVING EMPLOYMENT OR ON WIND-UP OF SCHEME

PENSIONS INVESTMENTS LIFE INSURANCE GUIDE TO OPTIONS UNDER A COMPANY PENSION SCHEME ON LEAVING EMPLOYMENT ON WIND-UP OF SCHEME This information document must be provided by tied agents (or employees) of

PENSIONS INVESTMENTS LIFE INSURANCE GUIDE TO OPTIONS UNDER A COMPANY PENSION SCHEME ON LEAVING EMPLOYMENT ON WIND-UP OF SCHEME This information document must be provided by tied agents (or employees) of

THE UNIVERSITY OF DUBLIN TRINITY COLLEGE AVC SCHEME ADDITIONAL VOLUNTARY CONTRIBUTION BOOKLET 2011

THE UNIVERSITY OF DUBLIN TRINITY COLLEGE AVC SCHEME ADDITIONAL VOLUNTARY CONTRIBUTION BOOKLET 2011 INTRODUCTION This booklet has been prepared to explain to you, simply and concisely, the various benefits

THE UNIVERSITY OF DUBLIN TRINITY COLLEGE AVC SCHEME ADDITIONAL VOLUNTARY CONTRIBUTION BOOKLET 2011 INTRODUCTION This booklet has been prepared to explain to you, simply and concisely, the various benefits

YOUR RETIREMENT OPTIONS

PENSIONS INVESTMENTS LIFE INSURANCE YOUR RETIREMENT OPTIONS A GUIDE FROM IRISH LIFE ABOUT US Established in Ireland in 1939, Irish Life is now part of the Great-West Lifeco group of companies, one of the

PENSIONS INVESTMENTS LIFE INSURANCE YOUR RETIREMENT OPTIONS A GUIDE FROM IRISH LIFE ABOUT US Established in Ireland in 1939, Irish Life is now part of the Great-West Lifeco group of companies, one of the

D&B (UK) Pension Plan. Career Average Revalued Earnings (CARE) section

Pension Plan. Career Average Revalued Earnings (CARE) section") D&B (UK) Pension Plan Career Average Revalued Earnings (CARE) section Contents Appendix: Welcome Welcome to the D&B (UK) Pension Plan CARE section The D&B (UK) Pension Plan (the Plan ) provides you with

D&B (UK) Pension Plan Career Average Revalued Earnings (CARE) section Contents Appendix: Welcome Welcome to the D&B (UK) Pension Plan CARE section The D&B (UK) Pension Plan (the Plan ) provides you with

Irish Association of Pension Funds. Pre Budget Submission

Irish Association of Pension Funds Pre Budget Submission November 2004 1. Executive Summary The Irish Association of Pension Funds (IAPF) has prepared this submission with a view to making constructive

Irish Association of Pension Funds Pre Budget Submission November 2004 1. Executive Summary The Irish Association of Pension Funds (IAPF) has prepared this submission with a view to making constructive

Executive Pension Account Live life your way

Executive Pension Account Live life your way 2 Contents Introduction 4 A Closer Look At Our Executive Pension Account 5 Tax Benefits 7 Contributing to an Executive Pension Account 9 Investment Options

Executive Pension Account Live life your way 2 Contents Introduction 4 A Closer Look At Our Executive Pension Account 5 Tax Benefits 7 Contributing to an Executive Pension Account 9 Investment Options

The Changing Pension Landscape

The Changing Pension Landscape Cornmarket Group Financial Services Ltd. is regulated by the Central Bank of Ireland. A member of the Irish Life Group Ltd. which is part of the Great-West Lifeco Group of

The Changing Pension Landscape Cornmarket Group Financial Services Ltd. is regulated by the Central Bank of Ireland. A member of the Irish Life Group Ltd. which is part of the Great-West Lifeco Group of

Your AVC Scheme & Public Sector PRSA. Member Guide

Your AVC Scheme & Public Sector PRSA Member Guide 2 AVC and PRSA Member Guide Your AVC Scheme & Public Sector PRSA Contents How an AVC Plan works 6 Why an AVC Plan may be right for you 8 Setting up an

Your AVC Scheme & Public Sector PRSA Member Guide 2 AVC and PRSA Member Guide Your AVC Scheme & Public Sector PRSA Contents How an AVC Plan works 6 Why an AVC Plan may be right for you 8 Setting up an

Dun & Bradstreet (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION PUBLIC DUN & BRADSTREET (UK) PENSION PLAN DEFINED CONTRIBUTION (DC) SECTION

Pension Plan DEFINED CONTRIBUTION (DC) SECTION PUBLIC DUN & BRADSTREET (UK) PENSION PLAN DEFINED CONTRIBUTION (DC) SECTION") PUBLIC Dun & Bradstreet (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION 1 Welcome to the Dun & Bradstreet (UK) Pension Plan Defined Contribution (DC) section The DC section of the Dun & Bradstreet

PUBLIC Dun & Bradstreet (UK) Pension Plan DEFINED CONTRIBUTION (DC) SECTION 1 Welcome to the Dun & Bradstreet (UK) Pension Plan Defined Contribution (DC) section The DC section of the Dun & Bradstreet

Public Sector Group AVC Plan Member Booklet

Public Sector Group AVC Plan Member Booklet Sub-Title taking care of you... Group AVC Plan Contents Your Additional Voluntary Contributions (AVC) Plan 4 Contributing to the Plan 5 Tax Benefits 7 Why is

Public Sector Group AVC Plan Member Booklet Sub-Title taking care of you... Group AVC Plan Contents Your Additional Voluntary Contributions (AVC) Plan 4 Contributing to the Plan 5 Tax Benefits 7 Why is

GUIDE TO RETIREMENT PLANNING MAKING THE MOST OF THE NEW PENSION RULES TO ENJOY FREEDOM AND CHOICE IN YOUR RETIREMENT

GUIDE TO RETIREMENT PLANNING MAKING THE MOST OF THE NEW PENSION RULES TO ENJOY FREEDOM AND CHOICE IN YOUR RETIREMENT FINANCIAL GUIDE Green Financial Advice is authorised and regulated by the Financial

GUIDE TO RETIREMENT PLANNING MAKING THE MOST OF THE NEW PENSION RULES TO ENJOY FREEDOM AND CHOICE IN YOUR RETIREMENT FINANCIAL GUIDE Green Financial Advice is authorised and regulated by the Financial

PENSIONS INVESTMENTS LIFE INSURANCE IRISH LIFE EMPOWER YOUR RETIREMENT GUIDE

PENSIONS INVESTMENTS LIFE INSURANCE IRISH LIFE EMPOWER YOUR RETIREMENT GUIDE CONTENTS IT S TIME TO SAVE FOR YOUR FUTURE 2 WHAT MAKES UP YOUR RETIREMENT SAVINGS 3 HOW YOUR CONTRIBUTIONS ARE INVESTED 6 BETTER

PENSIONS INVESTMENTS LIFE INSURANCE IRISH LIFE EMPOWER YOUR RETIREMENT GUIDE CONTENTS IT S TIME TO SAVE FOR YOUR FUTURE 2 WHAT MAKES UP YOUR RETIREMENT SAVINGS 3 HOW YOUR CONTRIBUTIONS ARE INVESTED 6 BETTER

HOUSE OF FINANCE PENSIONS INVESTMENTS PROTECTION. A Guide to Annuities

HOUSE OF FINANCE PENSIONS INVESTMENTS PROTECTION Contents I m approaching retirement, what are my financial options? What is a Financial Broker? Why would I need to use a Financial Broker? What is an annuity?

HOUSE OF FINANCE PENSIONS INVESTMENTS PROTECTION Contents I m approaching retirement, what are my financial options? What is a Financial Broker? Why would I need to use a Financial Broker? What is an annuity?

COMPANY PENSION RETIREMENT OPTIONS

PENSIONS INVESTMENTS LIFE INSURANE AN ADVISERS GUIDE TO: OMPANY PENSION RETIREMENT OPTIONS UPDATED FOR FINANE AT 2014 This is a technical guide for financial advisers only and is not intended as an advertisement.

PENSIONS INVESTMENTS LIFE INSURANE AN ADVISERS GUIDE TO: OMPANY PENSION RETIREMENT OPTIONS UPDATED FOR FINANE AT 2014 This is a technical guide for financial advisers only and is not intended as an advertisement.

ADDITIONAL VOLUNTARY CONTRIBUTIONS (AVCs)

") PENSIONS INVESTMENTS LIFE INSURANCE ADDITIONAL VOLUNTARY CONTRIBUTIONS (AVCs) MEMBER GUIDE ABOUT US Established in Ireland in 1939, Irish Life is now part of the Great-West Lifeco group of companies, one

PENSIONS INVESTMENTS LIFE INSURANCE ADDITIONAL VOLUNTARY CONTRIBUTIONS (AVCs) MEMBER GUIDE ABOUT US Established in Ireland in 1939, Irish Life is now part of the Great-West Lifeco group of companies, one

A GUIDE TO PERSONAL RETIREMENT SAVINGS ACCOUNTS (PRSAs)

") A GUIDE TO PERSONAL RETIREMENT SAVINGS ACCOUNTS (PRSAs) A Guide to Personal Retirement Savings Accounts (PRSAs) Contents Why should I plan for my retirement? 02 What is a PRSA? 03 What is a? 06 Why would

A GUIDE TO PERSONAL RETIREMENT SAVINGS ACCOUNTS (PRSAs) A Guide to Personal Retirement Savings Accounts (PRSAs) Contents Why should I plan for my retirement? 02 What is a PRSA? 03 What is a? 06 Why would

Why do you need a pension? State and other types of pension schemes. Company or occupational pensions offered by Employers

Contents: What is a pension? Why do you need a pension? State and other types of pension schemes Company or occupational pensions offered by Employers Personal or private pension schemes Shopping around

Contents: What is a pension? Why do you need a pension? State and other types of pension schemes Company or occupational pensions offered by Employers Personal or private pension schemes Shopping around

Complete Solutions Personal Retirement Bond 1. your Customer Information Notice. This plan is provided by Irish Life Assurance plc.

Complete Solutions Personal Retirement Bond 1 your Customer Information Notice This plan is provided by Irish Life Assurance plc. Introduction This notice is designed to highlight some important details

Complete Solutions Personal Retirement Bond 1 your Customer Information Notice This plan is provided by Irish Life Assurance plc. Introduction This notice is designed to highlight some important details

Financial Planning Report

{{TOC}} Financial Planning Report Prepared for: ABC Company Prepared by: Mr PPOL REMOTE DEMO Independent Financial Adviser PPOL 25/11/2014 SUITABILITY REPORT Introduction and Basis of Advice I am authorised

{{TOC}} Financial Planning Report Prepared for: ABC Company Prepared by: Mr PPOL REMOTE DEMO Independent Financial Adviser PPOL 25/11/2014 SUITABILITY REPORT Introduction and Basis of Advice I am authorised

THE ITC ARF BROCHURE

www.independent-trustee.com THE ITC ARF BROCHURE The ITC ARF If you are one of those wise people who have invested in a pension, you may be under the impression that your planning for retirement is complete.

www.independent-trustee.com THE ITC ARF BROCHURE The ITC ARF If you are one of those wise people who have invested in a pension, you may be under the impression that your planning for retirement is complete.

ADDITIONAL VOLUNTARY CONTRIBUTIONS AND YOUR PERSONAL RETIREMENT SAVINGS ACCOUNT

PENSIONS INVESTMENTS LIFE INSURANCE ADDITIONAL VOLUNTARY CONTRIBUTIONS AND YOUR PERSONAL RETIREMENT SAVINGS ACCOUNT A GUIDE FOR MEMBERS OF OCCUPATIONAL PENSION SCHEMES ABOUT US Established in Ireland in

PENSIONS INVESTMENTS LIFE INSURANCE ADDITIONAL VOLUNTARY CONTRIBUTIONS AND YOUR PERSONAL RETIREMENT SAVINGS ACCOUNT A GUIDE FOR MEMBERS OF OCCUPATIONAL PENSION SCHEMES ABOUT US Established in Ireland in

Company Owners, Directors & Executives

We hope this document has given you some insight into the many things you need to think about before you retire. Our pension specialists are available to meet with you to tailor a retirement plan based

We hope this document has given you some insight into the many things you need to think about before you retire. Our pension specialists are available to meet with you to tailor a retirement plan based

Your Second Life. Your Way. A guide to planning for your retirement on your terms

Your Second Life. Your Way. A guide to planning for your retirement on your terms 2 Your Second Life. Your Way. Retirement is not an end, it s the start of something new We re living longer, which is great

Your Second Life. Your Way. A guide to planning for your retirement on your terms 2 Your Second Life. Your Way. Retirement is not an end, it s the start of something new We re living longer, which is great

your Preliminary Disclosure Certificate - Complete Solutions PRSA Standard Plan (3%) This product is provided by Irish Life Assurance plc.

This product is provided by Irish Life Assurance plc.") your Preliminary Disclosure Certificate - Complete Solutions PRSA Standard Plan (3%) This product is provided by Irish Life Assurance plc. The Complete Solutions PRSA Standard plan has been approved under

your Preliminary Disclosure Certificate - Complete Solutions PRSA Standard Plan (3%) This product is provided by Irish Life Assurance plc. The Complete Solutions PRSA Standard plan has been approved under

A GUIDE FOR MEMBERS contributing 6.5% to the First Active Pension Scheme. First Active Pension Scheme

A GUIDE FOR MEMBERS contributing 6.5% to the First Active Pension Scheme First Active Pension Scheme 1 2 A GUIDE TO YOUR PENSION SCHEME Your pension scheme is one of the most important and valuable benefits

A GUIDE FOR MEMBERS contributing 6.5% to the First Active Pension Scheme First Active Pension Scheme 1 2 A GUIDE TO YOUR PENSION SCHEME Your pension scheme is one of the most important and valuable benefits

Guide to Self-Invested Personal Pensions

NOVEMBER 2017 Guide to Self-Invested Personal Pensions Putting you in control of your financial future 02 GUIDE TO SELF-INVESTED PERSONAL PENSIONS Welcome Putting you in control of your financial future

NOVEMBER 2017 Guide to Self-Invested Personal Pensions Putting you in control of your financial future 02 GUIDE TO SELF-INVESTED PERSONAL PENSIONS Welcome Putting you in control of your financial future

Self-Invested Personal Pensions Putting you in control of your financial future

NOVEMBER 2017 Guide to Self-Invested Personal Pensions Putting you in control of your financial future 02 GUIDE TO SELF-INVESTED PERSONAL PENSIONS GUIDE TO SELF-INVESTED PERSONAL PENSIONS Contents 02 Welcome

NOVEMBER 2017 Guide to Self-Invested Personal Pensions Putting you in control of your financial future 02 GUIDE TO SELF-INVESTED PERSONAL PENSIONS GUIDE TO SELF-INVESTED PERSONAL PENSIONS Contents 02 Welcome

Member s Booklet June 2007

DEFINED BENEFIT SECTION Member s Booklet June 2007 A Glossary of special pension terms used in this booklet can be found on the fold-out flap at the back The following forms / leaflets are currently available

DEFINED BENEFIT SECTION Member s Booklet June 2007 A Glossary of special pension terms used in this booklet can be found on the fold-out flap at the back The following forms / leaflets are currently available

Pension Post. Issue 3 - Updated February 2018 For financial advisers only

Pension Post Issue 3 - Updated February 2018 For financial advisers only How the Pension Threshold limit system works For this issue of Pension Post, Tony Gilhawley of Technical Guidance Ltd explains how

Pension Post Issue 3 - Updated February 2018 For financial advisers only How the Pension Threshold limit system works For this issue of Pension Post, Tony Gilhawley of Technical Guidance Ltd explains how

AIB Invest PRSA. Saving for your retirement. AIB Retirement. This product is provided by Irish Life Assurance plc.

AIB Retirement AIB Invest PRSA Saving for your retirement This product is provided by Irish Life Assurance plc. Drop into any branch 1890 724 724 aib.ie AIB has chosen Irish Life, Ireland s leading life

AIB Retirement AIB Invest PRSA Saving for your retirement This product is provided by Irish Life Assurance plc. Drop into any branch 1890 724 724 aib.ie AIB has chosen Irish Life, Ireland s leading life

Pensions Update. Aidan McLoughlin BCL, FITI, CTA, TEP, FIIPM

Pensions Update Aidan McLoughlin BCL, FITI, CTA, TEP, FIIPM Agenda Overview of pension structures Recent Developments Future Changes Planning 2 What are the main types of arrangements? State funded or

Pensions Update Aidan McLoughlin BCL, FITI, CTA, TEP, FIIPM Agenda Overview of pension structures Recent Developments Future Changes Planning 2 What are the main types of arrangements? State funded or

COMPLETE SOLUTIONS PERSONAL PENSION 1

PENSIONS INVESTMENTS LIFE INSURANCE COMPLETE SOLUTIONS PERSONAL PENSION 1 YOUR COMPLETE RETIREMENT PLAN PRODUCT SNAPSHOT This booklet will give you details of the benefits available under the Complete

PENSIONS INVESTMENTS LIFE INSURANCE COMPLETE SOLUTIONS PERSONAL PENSION 1 YOUR COMPLETE RETIREMENT PLAN PRODUCT SNAPSHOT This booklet will give you details of the benefits available under the Complete

Sample Plan. Financial Plan

Financial Plan ... Financial Plan For Jim & Mary Moran....... a. a August 15, 2012 This Financial Plan together with your Plan of Action constitute your Statement of Suitability. Important Notice - Statement

Financial Plan ... Financial Plan For Jim & Mary Moran....... a. a August 15, 2012 This Financial Plan together with your Plan of Action constitute your Statement of Suitability. Important Notice - Statement

Self Directed Personal Retirement Bond. Personal Retirement Benefits Brochure

Self Directed Personal Retirement Bond Personal Retirement Benefits Brochure Contents Section 1: What is a Personal Retirement Bond? 2 Section 2: Definitions 3 Section 3: Contributions 4 Section 4: Charges

Self Directed Personal Retirement Bond Personal Retirement Benefits Brochure Contents Section 1: What is a Personal Retirement Bond? 2 Section 2: Definitions 3 Section 3: Contributions 4 Section 4: Charges

State Pensions and National Pensions Policy. Orlaigh Quinn Irish Institute of Pensions Management 27 April 2011

State Pensions and National Pensions Policy Orlaigh Quinn Irish Institute of Pensions Management 27 April 2011 Department of Social Protection 87 million payments made each year 2.1 million people in receipt

State Pensions and National Pensions Policy Orlaigh Quinn Irish Institute of Pensions Management 27 April 2011 Department of Social Protection 87 million payments made each year 2.1 million people in receipt

BUDGET SUMMARY FOR PUBLIC SECTOR EMPLOYEES

BUDGET SUMMARY FOR PUBLIC SECTOR EMPLOYEES Inside is a quick outline of how the budget affects public sector employees and examples of the difference it will make to their take home pay. As the days progress,

BUDGET SUMMARY FOR PUBLIC SECTOR EMPLOYEES Inside is a quick outline of how the budget affects public sector employees and examples of the difference it will make to their take home pay. As the days progress,

RETIREMENT INCOME GETTING STARTED

RETIREMENT INCOME GETTING STARTED A regular income stream from an account-based or an annuity can be an effective way to fund your retirement. Some retirees may also be eligible for social security benefits

RETIREMENT INCOME GETTING STARTED A regular income stream from an account-based or an annuity can be an effective way to fund your retirement. Some retirees may also be eligible for social security benefits

RETIREMENT PLANNING PLANNING AHEAD FOR THE FINANCIAL FUTURE YOU WANT GUIDE TO

JANUARY 2019 GUIDE TO RETIREMENT PLANNING PLANNING AHEAD FOR THE FINANCIAL FUTURE YOU WANT A E Thomson Ltd is authorised and regulated by the Financial Conduct Authority 02 GUIDE TO RETIREMENT PLANNING

JANUARY 2019 GUIDE TO RETIREMENT PLANNING PLANNING AHEAD FOR THE FINANCIAL FUTURE YOU WANT A E Thomson Ltd is authorised and regulated by the Financial Conduct Authority 02 GUIDE TO RETIREMENT PLANNING

PENSION TAX DEADLINE 2017

PENSIONS INVESTMENTS LIFE INSURANCE PENSION TAX DEADLINE 2017 31ST OCTOBER & 16TH NOVEMBER 16 This is not a customer document and is intended for Financial Advisers only Individuals who both pay and file

PENSIONS INVESTMENTS LIFE INSURANCE PENSION TAX DEADLINE 2017 31ST OCTOBER & 16TH NOVEMBER 16 This is not a customer document and is intended for Financial Advisers only Individuals who both pay and file

A GUIDE TO PERSONAL PENSION PLANS

A GUIDE TO PERSONAL PENSION PLANS A Guide to Personal Pension Plans Contents Why should I plan for my retirement? 02 What is a Personal Pension Plan? 03 How much should I invest in my Personal Pension

A GUIDE TO PERSONAL PENSION PLANS A Guide to Personal Pension Plans Contents Why should I plan for my retirement? 02 What is a Personal Pension Plan? 03 How much should I invest in my Personal Pension

Accessing your pension savings

Accessing your pension savings 2 Accessing your pension savings CONTENTS 03 About this guide 04 An important note 06 A few basics to start 06 Your options in summary 07 Tax-free cash 10 Flexible retirement

Accessing your pension savings 2 Accessing your pension savings CONTENTS 03 About this guide 04 An important note 06 A few basics to start 06 Your options in summary 07 Tax-free cash 10 Flexible retirement

CHAPTER 24. Vested PRSAs, AMRFs and ring-fenced amounts

CHAPTER 24 PERSONAL RETIREMENT SAVINGS ACCOUNTS Revised December 2015 Introduction 24.1 A Personal Retirement Savings Account (PRSA) is a long term savings account designed to assist people to save for

CHAPTER 24 PERSONAL RETIREMENT SAVINGS ACCOUNTS Revised December 2015 Introduction 24.1 A Personal Retirement Savings Account (PRSA) is a long term savings account designed to assist people to save for

Income Exemption Limits

Income Exemption Limits SEPTEMBER 2015 The information and tax rates contained in this presentation are based on Irish Life s understanding of legislation and Revenue practice as at September 2015 and

Income Exemption Limits SEPTEMBER 2015 The information and tax rates contained in this presentation are based on Irish Life s understanding of legislation and Revenue practice as at September 2015 and

Engaging with your Pension

Engaging with your Pension Tuesday 18 May 2010 David Malone Head of Information The Pensions Board The Pensions Board Established by the Pensions Act, 1990 Operations: Supervision, regulation and enforcement

Engaging with your Pension Tuesday 18 May 2010 David Malone Head of Information The Pensions Board The Pensions Board Established by the Pensions Act, 1990 Operations: Supervision, regulation and enforcement

STAKEHOLDER PENSION DECISION TREES AMENDMENT INSTRUMENT 2006

FSA 2006/12 STAKEHOLDER PENSION DECISION TREES AMENDMENT INSTRUMENT 2006 Powers exercised A. The Financial Services Authority makes this instrument in the exercise of the following powers and related provisions

FSA 2006/12 STAKEHOLDER PENSION DECISION TREES AMENDMENT INSTRUMENT 2006 Powers exercised A. The Financial Services Authority makes this instrument in the exercise of the following powers and related provisions

PENSION FUND. Information Sheet. *A GUIDE TO THE LOCAL GOVERNMENT PENSION SCHEME FOR COUNCILLORS IN SCOTLAND Administered by Aberdeen City Council

* ABERDEEN CITY COUNCIL PENSION FUND Information Sheet Aberdeen City Council Pension Fund *A GUIDE TO THE LOCAL GOVERNMENT PENSION SCHEME FOR COUNCILLORS IN SCOTLAND Administered by Aberdeen City Council

* ABERDEEN CITY COUNCIL PENSION FUND Information Sheet Aberdeen City Council Pension Fund *A GUIDE TO THE LOCAL GOVERNMENT PENSION SCHEME FOR COUNCILLORS IN SCOTLAND Administered by Aberdeen City Council

The Local Government Pension Scheme

The Local Government Pension Scheme A Guide to the Local Government Pension Scheme for Eligible Councillors in England and Wales [English and Welsh version 1.4- September 2016] 1 The Index Page Introduction

The Local Government Pension Scheme A Guide to the Local Government Pension Scheme for Eligible Councillors in England and Wales [English and Welsh version 1.4- September 2016] 1 The Index Page Introduction

The ITC ARF

www.independent-trustee.com The ITC ARF Brochure The ITC ARF If you are one of those wise people who have invested in a pension, you may be under the impression that your planning for retirement is complete.

www.independent-trustee.com The ITC ARF Brochure The ITC ARF If you are one of those wise people who have invested in a pension, you may be under the impression that your planning for retirement is complete.

PRSA Guide. Get to know the advantages of a PRSA

PRSA Guide Get to know the advantages of a PRSA Allow us to introduce ourselves. We are Zurich. We are part of a global insurance group with Swiss roots. We are one of Ireland s most successful life and

PRSA Guide Get to know the advantages of a PRSA Allow us to introduce ourselves. We are Zurich. We are part of a global insurance group with Swiss roots. We are one of Ireland s most successful life and

RETIREMENT OPTIONS REQUEST AND CLAIM FORM FOR A COMPANY PENSION, AVC, PRSA AVC AND PERSONAL RETIREMENT BOND

PENSIONS INVESTMENTS LIFE INSURANCE RETIREMENT OPTIONS REQUEST AND CLAIM FORM FOR A COMPANY PENSION, AVC, PRSA AVC AND PERSONAL RETIREMENT BOND Before you give us your personal information it is important

PENSIONS INVESTMENTS LIFE INSURANCE RETIREMENT OPTIONS REQUEST AND CLAIM FORM FOR A COMPANY PENSION, AVC, PRSA AVC AND PERSONAL RETIREMENT BOND Before you give us your personal information it is important

Five Keys to Retirement Investment. WorkplaceIncredibles

Five Keys to Retirement Investment WorkplaceIncredibles February 2018 Introduction Everybody s ideal retirement life looks different. To achieve our various goals, we work hard and save to pave the way

Five Keys to Retirement Investment WorkplaceIncredibles February 2018 Introduction Everybody s ideal retirement life looks different. To achieve our various goals, we work hard and save to pave the way

Additional Voluntary Contributions (AVCs) For independent financial brokers use only

For independent financial brokers use only") Additional Voluntary Contributions (AVCs) For independent financial brokers use only Committed to Plain English There is no financial jargon in this booklet and everything you need to know is written in

Additional Voluntary Contributions (AVCs) For independent financial brokers use only Committed to Plain English There is no financial jargon in this booklet and everything you need to know is written in

Financial Planning Report

{{TOC}} Financial Planning Report Prepared for: ABC Limited Prepared by: Independent Financial Adviser PPOL Penylan Mill Coed-y-Go Oswestry Shropshire SY10 9AF 06/04/2016 SUITABILITY REPORT Different Introductions

{{TOC}} Financial Planning Report Prepared for: ABC Limited Prepared by: Independent Financial Adviser PPOL Penylan Mill Coed-y-Go Oswestry Shropshire SY10 9AF 06/04/2016 SUITABILITY REPORT Different Introductions

Metal Box AVC Plan Member s Booklet

DEFINED BENEFIT SECTION Metal Box AVC Plan Member s Booklet June 2007 A Glossary of special pension terms used in this booklet can be found on the fold-out flap at the back Contents Planning for your

DEFINED BENEFIT SECTION Metal Box AVC Plan Member s Booklet June 2007 A Glossary of special pension terms used in this booklet can be found on the fold-out flap at the back Contents Planning for your

Submission on Automatic Enrolment Retirement Savings System. Strawman Consultation November 2018

Submission on Automatic Enrolment Retirement Savings System Strawman Consultation November 2018 Early Childhood Ireland is the largest representative of early childhood education and care settings in Ireland.

Submission on Automatic Enrolment Retirement Savings System Strawman Consultation November 2018 Early Childhood Ireland is the largest representative of early childhood education and care settings in Ireland.

Complete Solutions Approved Minimum Retirement Fund 2. your Customer Information Notice. This product is provided by Irish Life Assurance plc.

Complete Solutions Approved Minimum Retirement Fund 2 your Customer Information Notice This product is provided by Irish Life Assurance plc. Introduction This notice is designed to highlight some important

Complete Solutions Approved Minimum Retirement Fund 2 your Customer Information Notice This product is provided by Irish Life Assurance plc. Introduction This notice is designed to highlight some important

Retirement income getting started

Retirement getting started A regular stream from an account-based or an annuity can be an effective way to fund your retirement. Some retirees may also be eligible for social security benefits from the

Retirement getting started A regular stream from an account-based or an annuity can be an effective way to fund your retirement. Some retirees may also be eligible for social security benefits from the

Investing for income when you retire

KEY GUIDE Investing for income when you retire Planning the longest holiday of your life There comes a time when you stop working for your money and put your money to work for you. For most people, that

KEY GUIDE Investing for income when you retire Planning the longest holiday of your life There comes a time when you stop working for your money and put your money to work for you. For most people, that

Stakeholder pensions and decision trees

Stakeholder pensions and decision trees The Money Advice Service is here to help you manage your money better. We provide clear, unbiased advice to help you make informed choices. The information in this

Stakeholder pensions and decision trees The Money Advice Service is here to help you manage your money better. We provide clear, unbiased advice to help you make informed choices. The information in this

I m on to it one of these days

I m on to it one of these days Who will look after you in your retirement? The current State social welfare pension is 209.30 per week or 10,883 per year (as of Jan 2007) will this be enough for you to

I m on to it one of these days Who will look after you in your retirement? The current State social welfare pension is 209.30 per week or 10,883 per year (as of Jan 2007) will this be enough for you to

Your retirement. A guide for members of the defined contribution section of Pace. April 2017

Your retirement A guide for members of the defined contribution section of Pace April 0 Contents 0. Thinking about retirement?. How to decide when to retire So, when s the right time to retire? Budgeting

Your retirement A guide for members of the defined contribution section of Pace April 0 Contents 0. Thinking about retirement?. How to decide when to retire So, when s the right time to retire? Budgeting

Retirement Planning Toolkit

Retirement Planning Toolkit Planning a Financially Secure Retirement Page 1 Overview The purpose of this guide is to provide a framework to help you to plan for your retirement. Retirement is one of life

Retirement Planning Toolkit Planning a Financially Secure Retirement Page 1 Overview The purpose of this guide is to provide a framework to help you to plan for your retirement. Retirement is one of life

Your retirement. A guide for members of Pace DC. Co-operative Bank Section August 2018

Your retirement A guide for members of Pace DC Co-operative Bank Section August 2018 Contents 1. Thinking about retirement? 3 2. How to decide when to retire 4 So, when s the right time to retire? 5 Budgeting

Your retirement A guide for members of Pace DC Co-operative Bank Section August 2018 Contents 1. Thinking about retirement? 3 2. How to decide when to retire 4 So, when s the right time to retire? 5 Budgeting

Northern Foods Pension Scheme Explanatory Booklet

Northern Foods Pension Scheme Explanatory Booklet Your benefits in depth Welcome to the Northern Foods Pension Scheme an important and valuable part of your employment benefits package. Contents Introduction

Northern Foods Pension Scheme Explanatory Booklet Your benefits in depth Welcome to the Northern Foods Pension Scheme an important and valuable part of your employment benefits package. Contents Introduction

Workplace pensions AUTO ENROLMENT HAS TAKEN OFF

Workplace pensions AUTO ENROLMENT HAS TAKEN OFF INTRODUCTION The Government introduced auto enrolment to help more people save for their future. It means your employer will have to give you access to a

Workplace pensions AUTO ENROLMENT HAS TAKEN OFF INTRODUCTION The Government introduced auto enrolment to help more people save for their future. It means your employer will have to give you access to a

Benefiting you. A guide to the ITV Defined Contribution Plan For members who joined on 1 March 2017 from the DB section of the ITV Pension Scheme

Benefiting you A guide to the ITV Defined Contribution Plan For members who joined on 1 March 2017 from the DB section of the ITV Pension Scheme Welcome As someone who s built up valuable retirement benefits

Benefiting you A guide to the ITV Defined Contribution Plan For members who joined on 1 March 2017 from the DB section of the ITV Pension Scheme Welcome As someone who s built up valuable retirement benefits

Your pension choices explained

YOUR pension YOUR future OU way YOUR way November 2017 Your pension choices explained It s YOUR journey It s YOUR choice Does your future look expensive? Three different ways to save for your retirement

YOUR pension YOUR future OU way YOUR way November 2017 Your pension choices explained It s YOUR journey It s YOUR choice Does your future look expensive? Three different ways to save for your retirement

YOUR CHOICES IN A WORLD OF PENSION FREEDOM. Lee Coles

YOUR CHOICES IN A WORLD OF PENSION FREEDOM Lee Coles YOUR CHOICES IN A WORLD OF PENSION FREEDOM Welcome from CABA Wendy Saunders Recent service development in Australia caba.org.uk/australia Interactive

YOUR CHOICES IN A WORLD OF PENSION FREEDOM Lee Coles YOUR CHOICES IN A WORLD OF PENSION FREEDOM Welcome from CABA Wendy Saunders Recent service development in Australia caba.org.uk/australia Interactive

Approved Retirement Funds

Approved Retirement Funds Product providers for financial advisors A simple guide to securing your future Who are we? Wealth Options Ltd. is a leading distributor of innovative products to the Irish financial

Approved Retirement Funds Product providers for financial advisors A simple guide to securing your future Who are we? Wealth Options Ltd. is a leading distributor of innovative products to the Irish financial

A Guide to the Local Government Pension Scheme for Councillors in Scotland

A Guide to the Local Government Pension Scheme for Councillors in Scotland April 2017 Index 1. About this Booklet pg 4 2. About the Local Government Pension Scheme (LGPS) pg 5 Who runs the LGPS? LGPS rules

A Guide to the Local Government Pension Scheme for Councillors in Scotland April 2017 Index 1. About this Booklet pg 4 2. About the Local Government Pension Scheme (LGPS) pg 5 Who runs the LGPS? LGPS rules

Taking income at retirement FINANCIAL

Taking income at retirement FINANCIAL KEY GUIDE January 2019 Taking an income at retirement 2 Introduction PLANNING THE LONGEST HOLIDAY OF YOUR LIFE There comes a time when you stop working for your money

Taking income at retirement FINANCIAL KEY GUIDE January 2019 Taking an income at retirement 2 Introduction PLANNING THE LONGEST HOLIDAY OF YOUR LIFE There comes a time when you stop working for your money

Pension Adjustment Orders

Pension Adjustment Orders Chapter 22 Document last reviewed September 2017 Table of Contents Introduction...2 Options for beneficiaries in respect of designated benefits...2 Impact on Member...3 Impact

Pension Adjustment Orders Chapter 22 Document last reviewed September 2017 Table of Contents Introduction...2 Options for beneficiaries in respect of designated benefits...2 Impact on Member...3 Impact

Pension Challenges and Pension Reforms in OECD Countries

Pension Challenges and Pension Reforms in OECD Countries Peter Whiteford Social Policy Division, OECD http://www.oecd.org/els/social Email: Peter.Whiteford@oecd.org 1 Issues and Outline The challenges

Pension Challenges and Pension Reforms in OECD Countries Peter Whiteford Social Policy Division, OECD http://www.oecd.org/els/social Email: Peter.Whiteford@oecd.org 1 Issues and Outline The challenges

NEWCOURT YOUR SELF INVESTED PENSION PROVIDER SMALL SELF-ADMINISTERED PENSION SCHEME (SSAPS)

") NEWCOURT YOUR SELF INVESTED PENSION PROVIDER SMALL SELF-ADMINISTERED PENSION SCHEME (SSAPS) Who are Newcourt? Newcourt Pensioneer Trustees Limited (Newcourt) was established in 1989. Newcourt is approved

NEWCOURT YOUR SELF INVESTED PENSION PROVIDER SMALL SELF-ADMINISTERED PENSION SCHEME (SSAPS) Who are Newcourt? Newcourt Pensioneer Trustees Limited (Newcourt) was established in 1989. Newcourt is approved

Enhanced Transfer Values

Enhanced Transfer Values Page 1 BACKGROUND The difficulties currently faced by defined benefit schemes are well known at this stage. Low expected returns from investments and increasing annuity prices

Enhanced Transfer Values Page 1 BACKGROUND The difficulties currently faced by defined benefit schemes are well known at this stage. Low expected returns from investments and increasing annuity prices

THE EDF ENERGY PENSION SCHEME. A guide for new joiners

THE EDF ENERGY PENSION SCHEME A guide for new joiners January 2016 CONTENTS Welcome 3 CARE Section 4 At a glance How it works Membership and contributions Building retirement benefits today Building retirement

THE EDF ENERGY PENSION SCHEME A guide for new joiners January 2016 CONTENTS Welcome 3 CARE Section 4 At a glance How it works Membership and contributions Building retirement benefits today Building retirement

Allow us to introduce ourselves.

Allow us to introduce ourselves. We are Zurich. We are part of a global insurance group with Swiss roots. We are one of Ireland s most successful life and pension providers. We believe in building a life

Allow us to introduce ourselves. We are Zurich. We are part of a global insurance group with Swiss roots. We are one of Ireland s most successful life and pension providers. We believe in building a life

Private Client. A Guide to Occupational and Personal Pensions

Private Client A Guide to Occupational and Personal Pensions Date: Tue 01 Oct 2002 A Guide to Occupational and Personal Pensions Published: Tue 01 Oct 2002 Unless you make provisions for your retirement,

Private Client A Guide to Occupational and Personal Pensions Date: Tue 01 Oct 2002 A Guide to Occupational and Personal Pensions Published: Tue 01 Oct 2002 Unless you make provisions for your retirement,

Budget Update 2018 LIA

Budget Update 2018 LIA s mission is to enhance the knowledge, competence and skills of our members and students who work in all areas of the Financial Services industry. LIA Budget 2018 Update Main points

Budget Update 2018 LIA s mission is to enhance the knowledge, competence and skills of our members and students who work in all areas of the Financial Services industry. LIA Budget 2018 Update Main points

BT PENSION SCHEME SECTION B. Explanatory booklet for Members who joined Section B of the BT Pension Scheme between 1 December 1971 and 31 March 1986

BT PENSION SCHEME SECTION B Explanatory booklet for Members who joined Section B of the BT Pension Scheme between 1 December 1971 and 31 March 1986 (and Section A members who elected to be subject to Section

BT PENSION SCHEME SECTION B Explanatory booklet for Members who joined Section B of the BT Pension Scheme between 1 December 1971 and 31 March 1986 (and Section A members who elected to be subject to Section

Canada Report. The Future of Retirement Healthy new beginnings

The Future of Retirement Healthy new beginnings Canada Report Foreword The possibilities Key findings The doubts Overview The research Healthy living Practical steps Foreword Retirement can be an opportunity

The Future of Retirement Healthy new beginnings Canada Report Foreword The possibilities Key findings The doubts Overview The research Healthy living Practical steps Foreword Retirement can be an opportunity

PENSIONS POLICY INSTITUTE. Automatic enrolment changes

Automatic enrolment changes This report is based upon modelling commissioned by NOW: Pensions Limited. A Technical Modelling Report by Silene Capparotto and Tim Pike. Published by the Pensions Policy

Automatic enrolment changes This report is based upon modelling commissioned by NOW: Pensions Limited. A Technical Modelling Report by Silene Capparotto and Tim Pike. Published by the Pensions Policy

International Pension Systems. Germany. Australia. Sweden

appendices Appendix A (Chapter 1) 226 International Pension Systems This appendix provides examples of how pensions systems are organised in different countries. Generally speaking, these examples are

appendices Appendix A (Chapter 1) 226 International Pension Systems This appendix provides examples of how pensions systems are organised in different countries. Generally speaking, these examples are

Accurium SMSF Retirement Insights

Accurium SMSF Retirement Insights Bridging the prosperity gap Volume 3 August 2015 This paper is the first to provide a report on the changing state of SMSFs during 2014. It shows that SMSF trustees are

Accurium SMSF Retirement Insights Bridging the prosperity gap Volume 3 August 2015 This paper is the first to provide a report on the changing state of SMSFs during 2014. It shows that SMSF trustees are

CHANGES TO YOUR PENSION SCHEME FREQUENTLY ASKED QUESTIONS

CHANGES TO YOUR PENSION SCHEME FREQUENTLY ASKED QUESTIONS BACKGROUND TO THE CHANGES 1 Why is Sony Europe Limited (the Company) making these changes and why now? There are increasing requirements on employers

CHANGES TO YOUR PENSION SCHEME FREQUENTLY ASKED QUESTIONS BACKGROUND TO THE CHANGES 1 Why is Sony Europe Limited (the Company) making these changes and why now? There are increasing requirements on employers

A Guide to Financial Planning Recommendations and Statements of Suitability

A Guide to Developing Business Strategy for Financial Brokers & Guidance One - Unified Voice A Guide to Recommendations and Statements of Suitability Page 01 A Guide to Developing Business Strategy for

A Guide to Developing Business Strategy for Financial Brokers & Guidance One - Unified Voice A Guide to Recommendations and Statements of Suitability Page 01 A Guide to Developing Business Strategy for

WORKPLACE SAVINGS GUIDE

WORKPLACE SAVINGS GUIDE START HERE. We understand that pensions can be confusing and difficult to understand. That s why we ve created this guide, to explain to you how they work and why they re so important

WORKPLACE SAVINGS GUIDE START HERE. We understand that pensions can be confusing and difficult to understand. That s why we ve created this guide, to explain to you how they work and why they re so important