FASB Taxonomy Advisory Group Meeting. Date: June 8, 2017 Location: Web Conference

|

|

|

- Stephen Ford

- 5 years ago

- Views:

Transcription

1 FASB Taxonomy Advisory Group Meeting Date: June 8, 2017 Location: Web Conference 1

2 Contents I. Agenda... 3 II. Sessions and Highlights... 4 Session 1 FAQ Reporting Unit... 5 A. Meeting Highlights... 5 B. FAQ Reporting Unit... 5 Session 2 Reference Project A. Meeting Highlights B. Reference Project Session 3 Retirement Benefits Plan Assets (Phase 2) A. Meeting Highlights B. Retirement Benefits Plan Assets (Phase 2) Session 4 Review of May 18, 2017 Meeting Highlights A. Meeting Highlights B. Review of May 18, 2017 Meeting Highlights Session 5 Accounting Standards Updates (ASU) Report A. Meeting Highlights B. Accounting Standards Updates (ASU) Report

3 I. Agenda Session Presenter 1 FAQ Reporting Unit 2 Reference Project 3 Retirement Benefit Plan Assets (Phase 2) 4 Review of May 18, 2017 Meeting Highlights 5 Accounting Standards Updates (ASU) Report Melissa Vickie Melissa 3

![II. Sessions and Highlights Proposed changes were provided and reviewed for the intended and appropriate usage of the Reporting Unit [Axis], Segments [Axis] and Subsegments [Axis].](/docs-images/86/93636066/images/4-1.jpg "Taxonomy staff presented three alternatives for the inclusion and appropriateness of references to Taxonomy elements in the codification and further discussed pros and cons of each approach.")

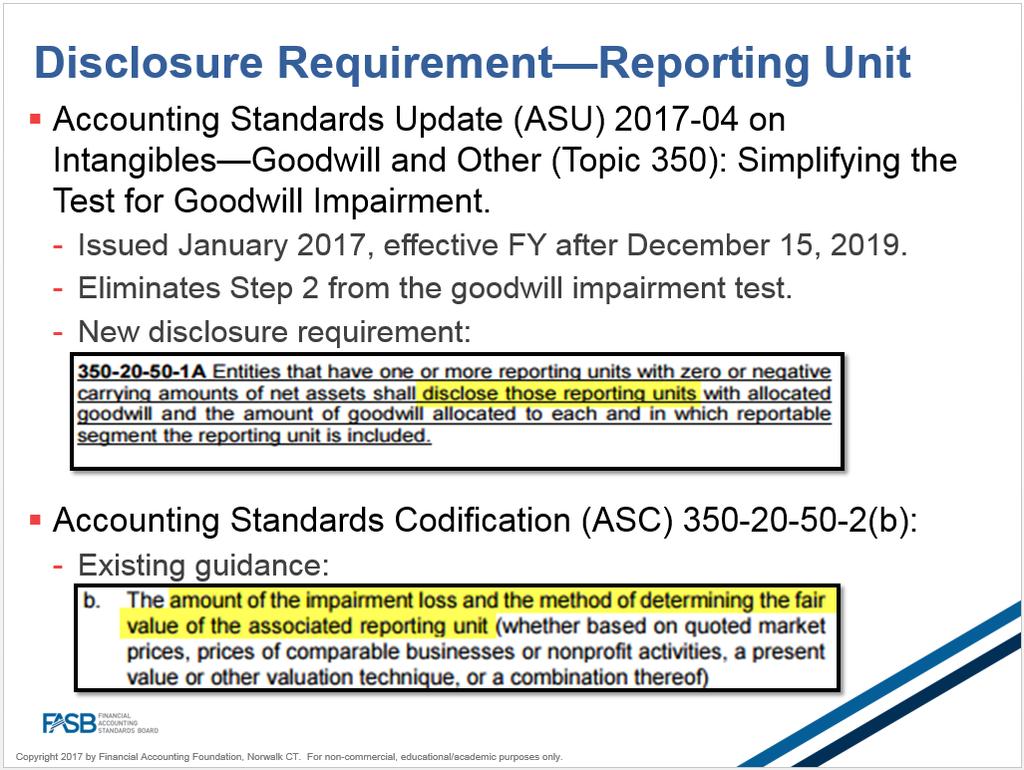

4 II. Sessions and Highlights Proposed changes were provided and reviewed for the intended and appropriate usage of the Reporting Unit [Axis], Segments [Axis] and Subsegments [Axis]. Taxonomy staff presented three alternatives for the inclusion and appropriateness of references to Taxonomy elements in the codification and further discussed pros and cons of each approach. The memo related to retirement benefits plan assets (phase 2 discussion of line items only) was provided but not reviewed. This topic will be discussed in future TAG meeting. The May 18, 2017 meeting highlights were not reviewed, but Taxonomy Advisory Group (TAG) members were asked to provide comments by June 15, The Accounting Standards Update (ASU) report was provided but not discussed. 4

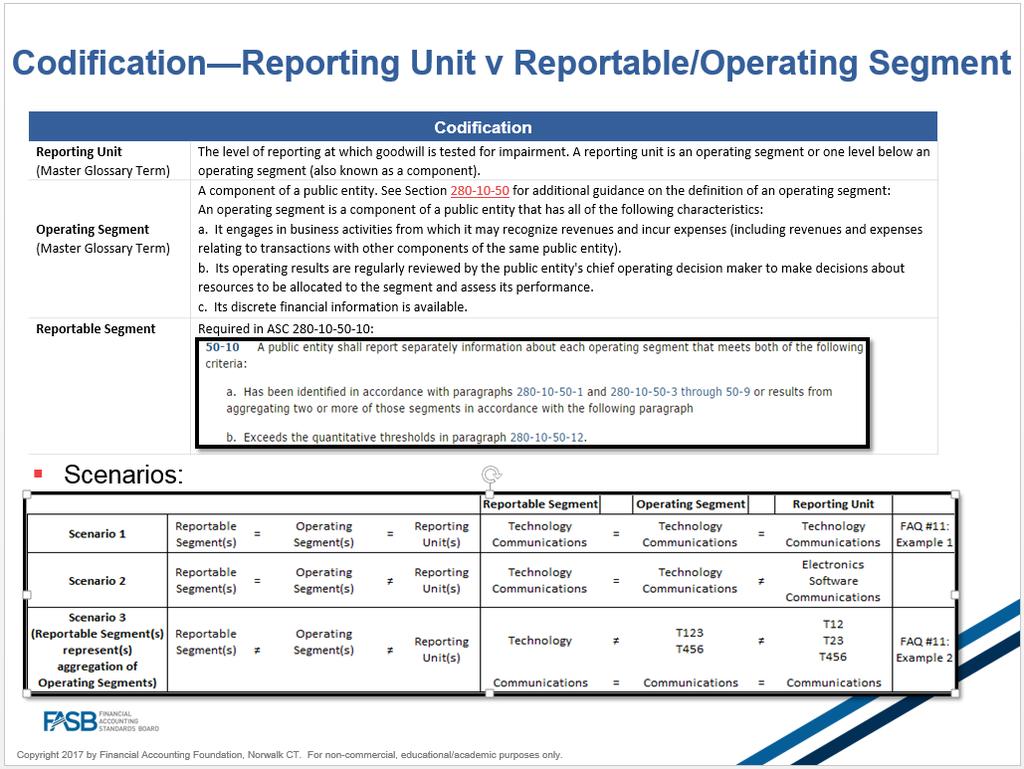

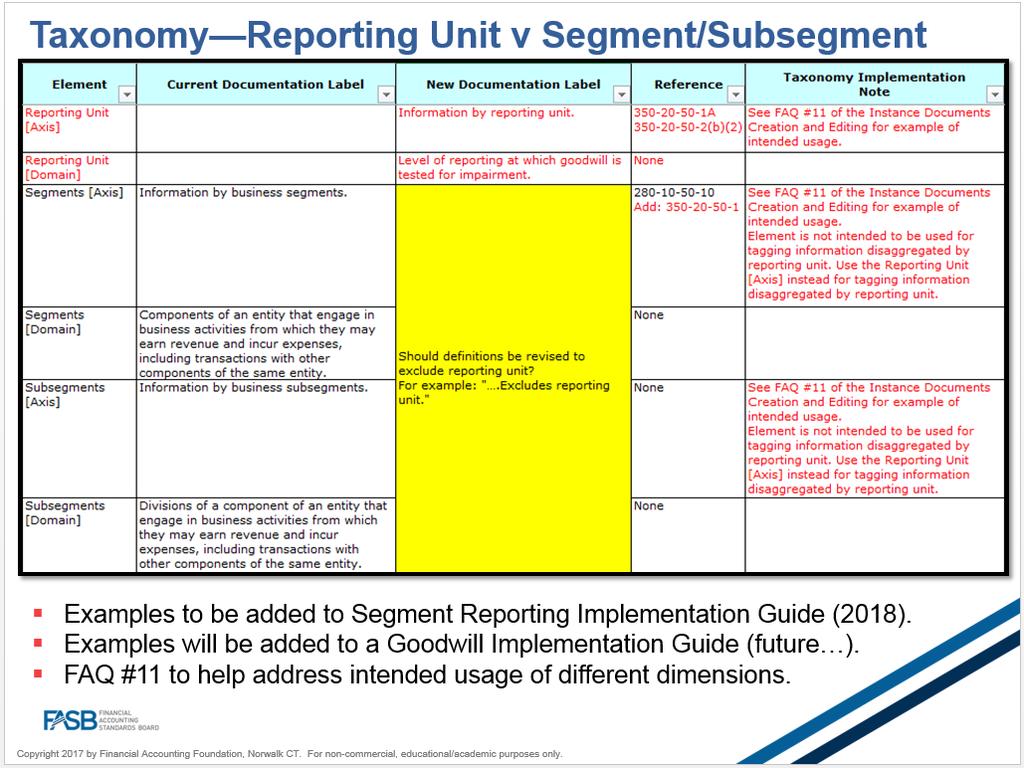

5 Session 1 FAQ Reporting Unit A. Meeting Highlights The Taxonomy staff sought feeding on examples of intended usage of the Reporting Unit [Axis], Segments [Axis] and Subsegments [Axis] to be included as FAQ #11 in the Instance Documents Creation and Editing FAQs for posting to the Taxonomy (XBRL) page of the FASB s website. There were two issues for discussion: (1) Whether the FAQ should be used as a resource to illustrate the intended usage of these axes or whether a Taxonomy Implementation Guide should be created instead? (2) Whether the existing definitions of the Segments [Axis] and Subsegments [Axis] should be revised to exclude reporting units or whether the following Taxonomy Implementation Note is sufficient to differentiate intended usage: Element is not intended to be used for tagging information disaggregated by reporting unit. The Reporting Unit [Axis] is intended to be used for tagging information disaggregated by reporting unit. The Taxonomy staff provided background on why a Reporting Unit [Axis] and this FAQ was created, illustrated several scenarios where there could be overlap with these axes, and walked through the two examples in FAQ #11. Feedback provided from the TAG memebers focused on whether the Reporting Unit [Axis] should be a separate axis or should the existing Segments [Axis] be broadened to include reporting unit information in a hierarchical domain. The Reporting Unit [Axis] is dependent on the segment to which it belongs, which indicates that the Segment [Axis] and the Reporting Unit [Axis] are not orthogonal. The Taxonomy staff historically has viewed the Segments [Axis] as a distinct domain and not intended to be modeled as a hierarchical domain because segment is specifically defined by GAAP. Disaggregations of segment information in a hierarchical structure may distort the actual reportable segments required to be disclosed. The TAG member discussion suggested that the Segments [Axis] should be broadened to include reporting unit information in a hierarchical domain. The Taxonomy staff considered this option, however, the dimension design principles, applied in creating the Reporting Unit [Axis], view the modeling of the Segments [Axis] with a distinct domain as an exception because there is a specific GAAP definition of segments. In light of the feedback provided, the Taxonomy staff will re-consider this dimension design principle and whether the Segments [Axis] should be broadened to include reporting unit information. Such considerations will be discussed at a future meeting. B. FAQ Reporting Unit 5

6 6

7 7

8 8

9 9

10 10

11 11

12 12

13 13

.")

14 Session 2 Reference Project A. Meeting Highlights The Taxonomy staff sought feedback on the inclusion and appropriateness of references to Taxonomy elements in the Accounting Standards Codification (ASC). The Taxonomy staff presented three alternatives for developing the criteria for associating references related to Policy Text Blocks with ASC requirements and the pros and cons of each approach. The three alternatives under consideration were: (1) the topic/subtopic alternative, (2) the Topic 235 Approach, and (3) the Hybrid Approach which was a combination of Alternatives 1 and 2. The Taxonomy staff asked if TAG members objected to the Taxonomy staff pursuing the Hybrid Approach. There were no objections. The TAG members were also asked to consider the order and content of the steps within the approach and to provide any comments or concerns to the Taxonomy staff as soon as possible to incorporate into the flowchart outlining the Hybrid Approach. A question of whether the project could benefit data aggregators was raised. The Taxonomy staff indicated that improving references would benefit all data users. The Taxonomy staff also presented two issues related to disclosures in recently issued Accounting Standards Updates (ASU) that have been codified. The first relates to ASC paragraphs that combine distinct but related requirements associated with retirement benefit plan disclosures. The TAG members discussed the disclosure in ASU which requires either the components of net periodic benefits be separately recognized or disclosure of the line item(s) used in the income statement in which those components are included if not presently separately. The Taxonomy staff indicated that the disclosure is currently modeled with references to the individual components containing the subparagraph and sub-subparagraphs and the location in the income statement containing only the subparagraph. There were no other reference alternatives suggested. The second issue related to ASC paragraphs that have GAAP requirements that are required but are not expected to be separately reported. In that case, the Taxonomy staff suggested no reference for the concept be associated with the paragraph. TAG members agreed that inclusion of a reference for that concept would not be useful and that treating those paragraphs similar to informational paragraphs would be appropriate. B. Reference Project Purpose of This Memo 1. The Taxonomy staff is seeking feedback to determine inclusion and appropriateness of references on elements to improve usability for element selection and achieve the objective of identifying elements from the stated disclosure requirements in the Accounting Standards Codification (ASC) by providing the specific paragraph in which the disclosure is required. 2. At this meeting, the Taxonomy staff is asking for feedback on the most appropriate approach to reference: 14

15 (a) Policy Text Block, including those covering multiple topics (Topic 1) (i) (ii) Topic 1a-References for Policy Text Blocks not specifically required in the ASC Topic 1b-Policy Text Blocks that cover more than one topic (b) ASC paragraphs that combine two distinct but related requirements (Topic 2) (c) Requirement in GAAP that may have many appropriate elements (Topic 3) Background Information 3. The Taxonomy staff has undertaken a project to review and evaluate references for completeness and appropriateness to assist with element selection. Feedback from constituents and internal review suggested that element selection could be simpler and data quality could be improved if the element selection process started with the disclosure requirements rather than navigating through a Taxonomy view that may be time consuming and confusing. 4. In meeting the requirements for XBRL filings (levels 1-4), elements for text blocks, policy text blocks and table text blocks are needed in addition to the level 4 element to meet the specific disclosure requirement. The project to evaluate the references will consider what references will assist in element selection elements for all four levels to meet the disclosure requirements. 5. This project is expected to be completed in phases. The following table illustrates the proposed phases and their status: Phase Target Status 1. Establish format for reference Complete 2. Establish criteria for reference addition In process 3. Assign every element to a Topic (subtopic) (internal) In process 15

16 Phase Target Status 4. Identify missing references on explicit disclosure requirements 5. Review elements with more than a certain number of references 6. Review references with more than a certain number of elements 7. Update categories of elements based on criteria (i.e. text blocks, table text blocks) In process Not started* Not started* In process 8. Review references topically for appropriateness By topic review 9. Review common reporting elements Not started* 10. Develop tool to search by reference In process *Topical projects include review of references but this phase has not started at a broad level 6. The Taxonomy staff introduced the reference project at the September 22, 2016, TAG meeting. At that meeting, the Taxonomy staff discussed the criteria for including references on elements to improve usability. The Taxonomy staff also asked for feedback on the format of the references. The TAG was supportive of providing a consistent format and the Taxonomy staff recommendation to indicate when an element is a common reporting practice. The TAG generally agreed that text blocks, table text blocks, and policy text blocks that were not explicitly required in the literature should be referenced to their topic/subtopic only. In review of the text blocks and policy text blocks, additional considerations for discussion were identified (Issue 1). Issue 1a References for Policy Text Blocks not specifically required in the ASC Analysis 16

17 7. The Taxonomy staff's research found that of the 296 policy text block approximately 65 are specifically required in the ASC. When there is not specific policy language in the ASC, the Taxonomy staff believes there are three alternatives that could accomplish the objective of the reference project. Alternative 1 is to adopt the Topic/Subtopic Approach which was mentioned in the September 22, 2016 memorandum. Alternative 2 is to apply the criteria in ASC to existing ASC paragraphs that currently have policy text blocks associated with them. Alternative 3 is to apply a Hybrid Approach (a combination of Alternatives 1 and 2). 8. Under all alternatives, references to Topic 235 would be removed because constituent feedback indicated that these general references were not helpful. In addition, there would be no action taken to update references to paragraphs that will be superseded as a result of a final Accounting Standards Update (ASU) as they will be updated with transition. Finally, if an element has multiple references, the Taxonomy staff would review and remove references if they are ineffective. Editing the references in this manner will reduce the number of references and make the references more focused. However, there are requirements in multiple places within the ASC that contain more than a link to a specific requirement. For example, Inventory Finished Goods [Policy Text Block] is associated with ASC (Inventory), (Balance Sheet) and S99-1 references which are provided below. In this case, following the most appropriate topical reference would result in keeping the 330 reference and removing the 210 references. However, this may result in paragraphs with specific requirements not having a reference The basis of stating inventories shall be consistently applied and shall be disclosed in the financial statements; whenever a significant change is made therein, there shall be disclosure of the nature of the change and, if material, the effect on income. A change of such basis may have an important effect upon the interpretation of the financial statements both before and after that change, and hence, in the event of a change, a full disclosure of its nature and of its effect, if material, upon income shall be made. See paragraph It is important that the amounts at which current assets are stated be supplemented by information that reveals, for the various classifications of inventory items, the basis upon which their amounts are stated and, where 17

18 practicable, indication of the method of determining the cost for example, average cost, first-in first-out (FIFO), last-in first-out (LIFO), and so forth S99-1 The following is the text of Regulation S-X Rule 5-02, Balance Sheets. 6. Inventories (b) The basis of determining the amounts shall be stated. If cost is used to determine any portion of the inventory amounts, the description of this method shall include the nature of the cost elements included in inventory. Elements of cost include, among other items, retained costs representing the excess of manufacturing or production costs over the amounts charged to cost of sales or delivered or in-process units, initial tooling or other deferred startup costs, or general and administrative costs. The method by which amounts are removed from inventory (e. g., average cost, first-in, first-out, last-in, first-out, estimated average cost per unit) shall be described. If the estimated average cost per unit is used as a basis to determine amounts removed from inventory under a total program or similar basis of accounting, the principal assumptions (including, where meaningful, the aggregate number of units expected to be delivered under the program, the number of units delivered to date and the number of units on order) shall be disclosed. If any general and administrative costs are charged to inventory, state in a note to the financial statements the aggregate amount of the general and administrative costs incurred in each period and the actual or estimated amount remaining in inventory at the date of each balance sheet. 9. Alternative 1 (referred to as the "Topic/subtopic" Approach) results in three topic/subtopic combinations that have more than 20 elements associated with them using current associated references. Those topics and the number of elements associated with them are: (Balance Sheet, Overall), 26 elements: (Receivables, Overall), 20 elements; and (Revenue Recognition): 34. See Appendix A. 10. Alternative 2 (referred to as the "Topic 235" Approach) involves the review of all ASC paragraphs that have policy text blocks associated with them and applies the criteria in ASC to assess whether language present in that paragraph implies that a policy is required. 18

19 11. Alternative 3 (referred to as the "Hybrid" Approach) would consider the number of policy text blocks in an area and evaluate whether the reference or references to the concepts should be to a topic/subtopic or a specific paragraph that either directly or indirectly (using guidance based on Topic 235) may require a disclosure of a policy. Alternative 1 Topic/subtopic Approach 12. The advantages of Alternative 1 are that it (1) does not refer to a specific paragraph if there is not a specific requirement to provide a policy text block, (2) eliminates references that are nonsensical such as those related to non-presentation/disclosure paragraphs (for example, Business Combination Policy which is referenced to ), (3) places all of the policy text blocks related to a topic in one place which makes searching for a policy text block easier, and (4) it removes policy text blocks from paragraphs that are broader than the policy text block as defined. However, Alternative 1 does not always provide relevant requirements that may be available in the ASC based on Topic 235 requirements for choices and methods. 13. Alternative 1 works well when there is not a requirement in the disclosure section that mentions policy and there are multiple paragraphs without a clear requirement based on Topic 235. However, it may result in several policy text blocks referenced to the same topic/subtopic. 14. There are some elements for which a Topic/subtopic approach does not work well such as concepts contained within a more general topic or subtopic. Four examples of these types of policy text blocks are provided in Appendix B. In these cases, the usage appears to be low and may be based on preparers interpretation of the ASC requirement. Providing a reference to only the topic or topic/subtopic may be too broad to be useful. Alternative 2 Topic 235 Approach 15. Paragraph ASC states Disclosure of accounting policies shall identify and describe the accounting principles followed by the entity and the methods of applying those principles that materially affect the determination of financial position, cash flows, or results of operations. In general, the disclosure shall encompass important judgments as to appropriateness of principles relating to recognition of revenue and allocation of 19

20 asset costs to current and future periods; in particular, it shall encompass those accounting principles and methods that involve any of the following: a. A selection from existing acceptable alternatives b. Principles and methods peculiar to the industry in which the entity operates, even if such principles and methods are predominantly followed in that industry c. Unusual or innovative applications of GAAP. [italics added for emphasis] 16. Under Alternative 2 (the "Topic 235 Approach"), the Taxonomy staff would apply the criteria in ASC to ASC paragraphs with policy text blocks that did not specifically mention disclose policy and focus on key phrases such as (ASC paragraphs provided in their entirety in Appendix C): (i) (ii) The basis of presentation Long-Duration Contracts, Policy [Policy Text Block] The method of amortizing Deferred Policy Acquisition Costs, Policy [Policy Text Block (iii) Using estimates based on past experience [Insurance Premiums Revenue Recognition, Policy [Policy Text Block] (iv) Use a variety of methods to estimate Utility, Revenue and Expense Recognition, Policy [Policy Text Block] 17. Other phrases that could be used to locate a reference for a policy include, but are not limited to, methods and assumptions, qualitative and quantitative information, a general description, and method of accounting. 18. The principle advantage of Alternative 2 is that is it provides a specific paragraph reference in the ASC and targets an element for selection rather than a list to evaluate. However, the application is subject to judgement and the associated reference may not be the one expected by a broader constituency. 19. One example of a paragraph that would be used as a reference for a policy text block under the Topic 235 Approach is found in ASC , Deferred Policy Acquisition Costs, Policy [Policy Text Block] which reads Insurance entities shall disclose all of the following in their financial statements: a. The nature and type of acquisition costs capitalized 20

21 b. The method of amortizing capitalized acquisition costs c. The amount of acquisition costs amortized for the period. 20. Another example of a paragraph that would be used as a reference for a policy text block under the Topic 235 Approach is found in ASC , Property, Plant and Equipment, Policy [Policy Text Block]). ASC reads Because of the significant effects on financial position and results of operations of the depreciation method or methods used, all of the following disclosures shall be made in the financial statements or in notes thereto: a. Depreciation expense for the period b. Balances of major classes of depreciable assets, by nature or function, at the balance sheet date c. Accumulated depreciation, either by major classes of depreciable assets or in total, at the balance sheet date d. A general description of the method or methods used in computing depreciation with respect to major classes of depreciable assets. Alternative 3 Hybrid Approach 21. If Alternative 2 is the desired approach, there may be policy text block elements that cannot be linked to a specific paragraph and may only be able to be related to a topic/subtopic. Also, where there is only one policy text block for a topic/subtopic, selection may be easier if found by the topic/subtopic. This may result in a hybrid approach a combination of Alternatives 1 and Under the Hybrid Approach, the Taxonomy staff would go through a series of steps to determine the reference or references that are most appropriate and meet the goal of the reference project providing the specific paragraph in which the disclosure is required. A flowchart outlining the Hybrid Approach is included as Appendix D. 23. If there is a specific policy required in the ASC, then the policy note would be associated with that paragraph (Step 1). If not, the Taxonomy staff would evaluate whether there is a topic/subtopic that the element should be associated with (Step 2). If the topic/subtopic is too broad or the concept is only part of a topic, then the Taxonomy staff would apply the Topic 235 Approach and evaluate whether there is language consistent with the guidance in ASC (Step 3) that suggests the reference could be used for the policy text 21

22 block. The order and application of these two steps may need to be reordered to be most usable for element selection. 24. The Taxonomy staff would review Sections 45 and 50 (which relate to presentation and disclosures) first using the Topic 235 Approach (Step 3) and if there were no paragraphs in the presentation and disclosure sections that include the key phrases that signal a policy should be disclosed, then Section 55 paragraphs (implementation guidance and illustrations) would be reviewed for illustrations or guidance of policy text blocks (Step 4). Only after that review is complete would the Taxonomy staff consider guidance outside of Sections 45, 50, or 55 (Step 5). 25. Under this approach, if the Taxonomy staff could not locate an appropriate paragraph to associate with the policy text block then the policy text block would be assigned a topic and the Taxonomy staff would consider (1) adding that reference to the policy text block or (2) evaluating the need for the policy text block. The course of action would depend on the number of policy text blocks associated with a topic and evaluation after research. 26. The principle advantage of this approach is that it blends the simplicity of Alternative 1 with the comprehensiveness of Alternative 2 to provide references and it provides a process of steps that can be used consistently. 27. The principal disadvantage of this approach is that it has the same disadvantages as the individual approaches which is that it may result in many policy text blocks being associated with a single topic and the 235 Approach criteria is somewhat subjective (key phrases are subject to interpretation by the Taxonomy staff). Staff Recommendation 28. The Taxonomy staff recommends that the Hybrid Approach be adopted and removal of all references to Topic 235. Additional work may be needed to refine the approach as the Taxonomy staff applies the approach to the current policy text blocks and future requirements necessitated by ASUs. 22

23 Questions for the TAG Members 1. Does the TAG member support the Hybrid Approach? If not, why not? 2. Does the TAG members think that a Topic/subtopic approach (Step 2) should be performed after the Topic 235 approach (Step 3) under the Hybrid Approach? If not, why not? 3. Does the TAG member think that references to separate paragraphs that may be redundant to specific topics be included or excluded? 4. Does the TAG member agree that Section 55 (illustrative examples) and other non-presentation/disclosure sections should be used as a reference under the Hybrid Approach for policy text blocks? If not, why not? 5. Does the TAG member have other suggestions for references on policy text blocks? Issue 1b Policy Text Blocks that Cover More than One Topic Analysis 29. In reviewing the ASC, the Taxonomy staff noted a number of instances where more than one topic has been included in a policy text block. Some examples are: (a) Compensation Related Costs, Policy [Policy Text Block] {854} (b) Research, Development, and Computer Software, Policy [Policy Text Block] {410} (c) Asset Retirement Obligation and Environmental Cost [Policy Text Block] {0} (d) Equity and Cost Method Investments, Policy [Policy Text Block] {147} 30. In these cases, the policy text blocks are shown in Presentation Group as having "children" that are separate and distinct components of the "parent" but do not necessarily include all the same ASC paragraphs. 31. For example, Compensation Related Costs, Policy [Policy Text Block] covers more than one topic yet it is only referenced to ASC (b)(f(1)) which covers Compensation Stock Compensation. It is defined as: Disclosure of accounting policy for salaries, bonuses, incentive awards, postretirement and postemployment benefits granted to 23

24 employees, including equity-based arrangements; discloses methodologies for measurement, and the bases for recognizing related assets and liabilities and recognizing and reporting compensation expense. 32. This element does not include any references for postretirement or postemployment benefits. In addition, the reference is not to a specific policy disclosure requirement but includes language based on Topic 235 requirements (emphasis added): b. The method it uses for measuring compensation cost from share-based payment arrangements with employees. f. For each year for which an income statement is presented, both of the following (An entity that uses the intrinsic value method pursuant to paragraphs through is not required to disclose the following information for awards accounted for under that method): 1. A description of the method used during the year to estimate the fair value (or calculated value) of awards under share-based payment arrangements 33. Another policy text block that appears to be a comprehensive policy text block, but either does not refer to the ASC paragraphs of its "children" or refers to a different ASC paragraph in the same topic, is Research, Development, and Computer Software, Policy [Policy Text Block]. This policy text block has the following four children: (i) (ii) Research and Development Expense, Policy [Policy Text Block] Internal Use Software, Policy [Policy Text Block] (iii) Software to be Sold, Leased, or Otherwise Marketed, Policy [Policy Text Block] (iv) In Process Research and Development, Policy [Policy Text Block] 34. The "parent" policy text block refers specifically to ASC , website development cost; , intangibles-goodwill and other-internal use software; , costs of software to be sold, leased, or marketed; and S99-1, balance sheet S99-SEC materials. While the definitions appear consistent, the references are not consistent and are referenced to disclosure paragraphs that do not have specific policy requirements or language based on Topic 235 (other than basis mentioned in SEC materials). 35. Research, Development, and Computer Software, Policy [Policy Text Block] is defined as "Disclosure of accounting policy for its research and development and computer software activities including the accounting treatment for costs incurred 24

25 for (1) research and development activities, (2) development of computer software for internal use, (3) computer software to be sold, leased or otherwise marketed as a separate product or as part of a product or process and (4) in-process research and development acquired in a purchase business combination." [italics added for emphasis] 36. "Research and Development Expense, Policy [Policy Text Block]" the first "child" is defined as Disclosure of accounting policy for costs it has incurred (1) in a planned search or critical investigation aimed at discovery of new knowledge with the hope that such knowledge will be useful in developing a new product or service, a new process or technique, or in bringing about a significant improvement to an existing product or process; or (2) to translate research findings or other knowledge into a plan or design for a new product or process or for a significant improvement to an existing product or process. 37. "Internal Use Software, Policy [Policy Text Block]" the second "child" is defined as Disclosure of accounting policy for costs incurred when both (1) the software is acquired, internally developed, or modified solely to meet the entity's internal needs, and (2) during the software's development or modification, no substantive plan exists or is being developed to market the software externally. 38. "Software to be Sold, Leased, or Otherwise Marketed, Policy [Policy Text Block]" the third "child" is defined as Disclosure of accounting policy for costs incurred to (1) establish the technological feasibility of a computer software product to be sold, leased, or otherwise marketed; and (2) produce product masters after establishing technological feasibility. This accounting policy also may apply to purchased computer software. This policy also may address the entity's amortization policy for its capitalized computer software costs and how it evaluates such capitalized costs for impairment. 39. And, finally "In Process Research and Development, Policy [Policy Text Block]" the fourth "child" is defined as Disclosure of accounting policy for costs assigned to identifiable tangible and intangible assets of an acquired entity to be used in the research and development activities of the combined enterprise. An entity also may disclose the appraisal method or significant assumptions used to value acquired research and development assets. 40. The Taxonomy staff reviewed filings for the 2015 year and found that: 25

26 (a) (b) (c) (d) Six companies applied both the "Research, Development, and Computer Software, Policy [Policy Text Block]" and the "In Process Research and Development, Policy [Policy Text Block]." 30 companies applied both the "Research, Development, and Computer Software, Policy [Policy Text Block]" and "Internal Use Software, Policy [Policy Text Block]" Eight companies applied both "Research, Development, and Computer Software, Policy [Policy Text Block]" and "Software to be Sold, Leased, or Otherwise Marketed, Policy [Policy Text Block]." 72 companies applied both "Research, Development, and Computer Software, Policy [Policy Text Block]" and "Research and Development Expense, Policy [Policy Text Block]." 41. In a number of those cases, the information in the combined research and development policy text block overlaps with the more specific policy text blocks or should be tagged with "Research and Development Expense, Policy [Policy Text Block]." 42. The variability in use of the policy text blocks makes discovery and comparability difficult between entities. 43. "Asset Retirement Obligation and Environmental Cost [Policy Text Block]" is not referenced to a specific policy requirement and contains references to both Topics (Asset Retirement Obligations) and (Environmental Obligations) however the specific references include an illustrative example which focuses solely on environmental remediation costs. 44. In other cases, policy text blocks in Presentation Group appear to have children in that presentation group that are refinements of the same concept. Example of those policy text blocks are: (a) Cash and Cash Equivalents, Policy [Policy Text Block] (i) "Cash and Cash Equivalents, Unrestricted Cash and Cash Equivalents, Policy [Policy Text Block]" (ii) "Cash and Cash Equivalents, Restricted Cash and Cash Equivalents, Policy [Policy Text Block] 26

27 (b) Environmental Costs, Policy [Policy Text Block]" (i) (ii) "Environmental Cost, Expense Policy [Policy Text Block]" "Environmental Costs, Capitalization Policy [Policy Text Block]" 45. Some filers used Cash and Cash Equivalents, Policy [Policy Text Block] and Cash and Cash Equivalents, Restricted Cash and Cash Equivalents, Policy [Policy Text Block] in the same filing and others used Cash and Cash Equivalents, Unrestricted Cash and Cash Equivalents, Policy [Policy Text Block]" and Cash and Cash Equivalents, Restricted Cash and Cash Equivalents, Policy [Policy Text Block] in the same filing. 46. "Environmental Cost, Expense Policy [Policy Text Block]" is also an example of a policy text block that is based on the illustration in ASC This Example illustrates the guidance in paragraph for accounting policies note disclosure for environmental remediation-related costs (information that is enclosed in brackets is not required). Environmental Remediation Costs [Entity A accrues for losses associated with environmental remediation obligations when such losses are probable and reasonably estimable. Accruals for estimated losses from environmental remediation obligations generally are recognized no later than completion of the remedial feasibility study. Such accruals are adjusted as further information develops or circumstances change.] Costs of future expenditures for environmental remediation obligations are not discounted to their present value. [Recoveries of environmental remediation costs from other parties are recorded as assets when their receipt is deemed probable.] 47. ASC does not specifically require the policy be disclosed but includes language based on Topic 235: With respect to environmental remediation obligations, financial statements shall disclose whether the accrual for environmental remediation liabilities is measured on a discounted basis. If an entity utilizes present-value measurement techniques, additional disclosures are appropriate, and are discussed further in paragraph (see paragraph ). 48. Given the illustration is Implementation Guidance and Illustrations, it is not clear whether the reference should be included when there may be a more appropriate reference. 49. Policy text blocks that cover more than one topic were added to accommodate the way filers were reporting the information. Combining multiple topics can make the policy text block disclosure less effective for users because it they may be more difficult to locate and not as 27

28 comparable. This is complicated when the combined policy text block is used in addition to a more specific policy text block that is included as part of the combined policy text block. Removing the combined policy text blocks could result in filers extending for these concepts if they were not available in the Taxonomy and would require communication and education that multiple policy text blocks can be used on a single disclosure. Staff Recommendation 50. The Taxonomy staff recommends that after research and evaluation, policy text blocks that contain multiple topics be deprecated from the Taxonomy and communication provided that (1) multiple policy text blocks can be used to tag portions of a single paragraph/note, and (2) single topic policy text blocks provide users of the data with more consistent information that can be compared across companies. Question for the TAG Members 6. Does the TAG member agree that policy text blocks should not contain multiple topics? If not, why not?? 7. Does the TAG member have other suggestions for references on policy text blocks? Issue 2 ASC Paragraphs that combine two distinct but related requirements Analysis 51. In Accounting Standards Update , Retirement Benefits (Topic 715): Improving the Presentation of Net Periodic Pension Costs and Net Periodic Postretirement Benefit Costs (ASU ), the Board required that an employer disclose the location of the other components of net benefit cost (other than the service cost component) in the income statement, if they are not separately presented. In ASU , the requirement to disclose the individual concepts or their location is combined in one paragraph ASC for annual financial statements (ASC for interim financial statements). A copy of the paragraphs is included in Appendix E to this memorandum. 52. The disclosures are "connected" or "related" but both may not be required (because if an element is separately reported, the location disclosure is not required). The individual components of net periodic benefit cost have separate subparagraphs, but the location 28

29 requirement is one sentence within the requirement. The Taxonomy staff has modelled the separate components of net periodic benefit cost recognized and referenced them to paragraph ASC (h) (1-7) as follows (1) Defined Benefit Plan, Service Cost (2) Defined Benefit Plan, Interest Cost (3) Defined Benefit Plan, Expected Return (Loss) on Plan Assets (4) Defined Benefit Plan, Amortization of Gain (Loss) (5) Defined Benefit Plan, Amortization of Prior Service Cost (Credit) (6) Defined Benefit Plan, Amortization of Transition Asset (Obligation) (7) Defined Benefit Plan, Net Periodic Benefit Cost (Credit), Gain (Loss) Due to Settlement and Curtailment 53. The Taxonomy staff has included an element for each component's location for example, "Defined Benefit Plan, Net Periodic Benefit (Cost) Credit, Settlement Gain (Loss), Statement of Income or Comprehensive Income [Extensible List]" in the Taxonomy when a company chooses not to separately report the component in the statement of income which is referenced to ASC (h). 54. The Taxonomy staff did not include the subparagraph (1-7) to each element for the location of component as the reference, while related, is for the component itself. The result is the ten location elements all have the same reference. The filer will need to review the labels to identify the appropriate element, the reference will not be enough to initially identify the most appropriate element. 55. Placing a reference to both the sub-paragraph (h) and the sub-subparagraphs ASC (h)(1-7) is contradictory to the objective of the reference project; that is, providing the specific paragraph in which the disclosure is required. In addition, providing both references (a reference for the location and the component) for the separate component would not make selection of the appropriate element for disclosure of the component easier as two elements would be referenced and only one is appropriate. 56. The Taxonomy staff has referenced the location elements only to the subparagraph as that paragraph does not identify the individual components associated with the location requirement. Therefore, there will be ten elements with the same reference. The labels indicate the particular component for which the location is being disclosed, however, there 29

30 is only a reference to the location language and not to the specific component for which the location is being disclosed. Question for the TAG Members 1. Does the TAG member agree that a reference to the individual subsubparagraphs is not appropriate for the location element? If not, why not? Issue 3 Requirements in GAAP that do not have one appropriate element or will not be reported separately because of that same GAAP requirement Analysis 57. Paragraph ASC A of ASU , Compensation Retirement Benefits (Topic 715): Improving the Presentation of Net Periodic Pension Cost and Net Periodic Postretirement Benefit Cost, requires that an employer report in the income statement the service cost component of net periodic pension cost and periodic postretirement benefit cost in the same line item or items as other compensation costs. The requirement in this paragraph is to report the service cost component together with other compensation costs which can be reported in a number of different line items. Given that the goal of the reference project is to associate an element to a specific paragraph where it is required by GAAP, it seems that this objective may not be met ASC A as there is not one specific element associated with this paragraph. 58. There is a similar example in the ASC (also included in Appendix F) of a requirement to report a specific concept in "the same line" as a broader concept that may be found in a number of locations. In that case, the Taxonomy staff did not create an element for the broader concept. 59. In that example, there is a requirement to report the cumulative effect of the change resulting from either the timing or amount of estimated cash flows in the same lines in the income statement used when the initial costs for exit or disposal activities was recognized (ASC ). No element was created for this requirement because the requirement lacked specificity about what lines in the income statement it would be reported within. 60. Given the variability of the line item location in these cases, it is difficult to associate all the possible elements that the required disclosure could be contained in. Thus, this type of 30

31 guidance would be treated in the same manner as "informational paragraphs" that are not referenced to a specific element. Question for the TAG Members 1. Does the TAG member agree with the Taxonomy staff's position in ASU that the requirement should be treated similar to an informational paragraph? If not, why not? 2. Does the TAG member have any suggestions for handling referencing for this type of presentation requirement? Next Steps 61. The Taxonomy staff will consider the feedback from the TAG members and other constituents as changes are made through the various phases of the reference project. 31

32 Appendix A Statistics Number of Topics with 3 or more policy text block elements Number of Number of Elements Topics or more elements 4 30 or more elements 5 20 or more elements or more elements 40 3 or more elements Number of policy text block element with 2 or more references Number of Elements Number of References 2 7 or more 4 6 or more 10 5 or more 27 4 or more 60 3 or more 32

33 Appendix B Policy text block elements that contain concepts that do not have specific topics/subtopics "Anticipated Investment Income as Component of Premium Deficiency on Short Duration Contracts, Policy [Policy Text Block]" {2} Reference Number Reference Text An insurance entity shall disclose in its financial statements whether it considers anticipated investment income in determining if a premium deficiency relating to shortduration contracts exists. "Allowance for Funds Used During Construction, Policy [Policy Text Block]" {56} Reference Number Reference Text Paragraph requires an allowance for funds used during construction, including a designated cost of equity funds, to be capitalized in specified circumstances as part of the acquisition cost of the related asset. That cost shall be capitalized under those circumstances only if its subsequent inclusion in allowable costs for rate-making purposes is probable. "Industry Specific Policies, Broker Dealer [Policy Text Block]" {8} Reference Number Reference Text The Financial Services Brokers and Dealers Topic includes the following Subtopics relating specifically to brokers and dealers in securities (broker-dealers): a. Overall b. Broker-Dealer Activities c. Receivables 33

34 d. Investments Debt and Equity Securities e. Investments All Other f. Other Assets and Deferred Costs g. Liabilities h. Subparagraph superseded by Accounting Standards Update No i. Consolidation j. Fair Value Measurements. " Closed Block Accounting Policy [Policy Text Block]" {9} Reference Number Reference Text An insurance entity shall disclose all of the following: a. The nature and terms of a demutualization or formation of a mutual insurance holding entity b. The basis of presentation and terms of operation of the closed block c. A general description of all of the following: 1. The method of emergence of earnings from the closed block 2. Presentation of assets and liabilities of the closed block 3. The policyholder dividend obligation. 34

35 Appendix C Topic 235 Approach "Long-Duration Contracts, Policy [Policy Text Block]" Reference Number Reference Text The following information shall be disclosed in the financial statements of the insurance entity: a. The general nature of the contracts reported in separate accounts, including the extent and terms of minimum guarantees b. The basis of presentation for both of the following: 1. Separate account assets and liabilities 2. Related separate account activity. c. A description of the liability valuation methods and assumptions used in estimating the liabilities for additional insurance benefits and minimum guarantees d. All of the following amounts related to minimum guarantees: 1. The separate account liability balances subject to various types of benefits, for example: a. Guaranteed minimum death benefit b. Guaranteed minimum income benefit c. Guaranteed minimum accumulation benefit. 2. Disclosures within the categories of benefits identified in (d)(1) for the types of guarantees provided may also be appropriate, for example, all of the following: a. Return of net deposit b. Return of net deposits accrued at a stated rate c. Return of highest anniversary value. 3. The amount of liability reported for additional insurance benefits, annuitization benefits and other minimum guarantees, by type of benefit, for the most recent balance sheet date 4. The incurred and paid amounts related to (d)(3) for all periods presented 5. For contracts for which an additional liability is disclosed in (d)(3), the net amount at risk and weighted average attained age of contract holders. e. The aggregate fair value of assets, by major investment asset category, supporting separate accounts with additional insurance benefits and minimum investment return guarantees as of each date for which a statement of financial position is presented f. The amount of gains and losses recognized on assets transferred to separate accounts for the periods presented 35

36 "Long-Duration Contracts, Policy [Policy Text Block]" Reference Number Reference Text This Subtopic provides guidance to insurance entities on accounting for and financial reporting of revenue from insurance contracts. The guidance in this Subtopic is presented in the following five Subsections: a. General b. Short-Duration Contracts c. Long-Duration Contracts d. Reinsurance Contracts e. Financial Guarantee Insurance Contracts. "Insurance Premiums Revenue Recognition, Policy [Policy Text Block]" Reference Number Reference Text If premiums are subject to adjustment (for example, retrospectively rated or other experience-rated insurance contracts for which the premium is determined after the period of the contract based on claim experience or reporting-form contracts for which the premium is adjusted after the period of the contract based on the value of insured property), premium revenue shall be recognized as follows: a. If the ultimate premium is reasonably estimable, the estimated ultimate premium shall be recognized as revenue over the period of the contract. The estimated ultimate premium shall be revised to reflect current experience. b. If the ultimate premium cannot be reasonably estimated, the cost recovery method or the deposit method may be used until the ultimate premium becomes reasonably estimable If reasonably estimable, premium revenue and costs relating to title insurance contracts issued by agents shall be recognized when the agents are legally or contractually entitled to the premiums, using estimates based on past experience and other sources. If not reasonably estimable, premium revenue and costs shall be recognized when agents report the issuance of title insurance contracts. 36

37 "Deferred Policy Acquisition Costs, Policy [Policy Text Block]" Reference Number Reference Text Insurance entities shall disclose all of the following in their financial statements: a. The nature and type of acquisition costs capitalized b. The method of amortizing capitalized acquisition costs c. The amount of acquisition costs amortized for the period. 37

38 "Consolidation, Subsidiaries or Other Investments, Consolidated Entities, Policy [Policy Text Block]" Reference Number 810-s99-4 Reference Text The following is the text of Regulation S-X Rule 3A-04, Intercompany Items and Transactions. In general, there shall be eliminated intercompany items and transactions between persons included in the (a) consolidated financial statements being filed and, as appropriate, (b) unrealized intercompany profits and losses on transactions between persons for which financial statements are being filed and persons the investment in which is presented in such statements by the equity method. If such eliminations are not made, a statement of the reasons and the methods of treatment shall be made. o [37 FR 14597, July 21, Redesignated at 46 FR 56179, Nov. 16, 1981] The text of Regulation S-X Rule 3A-05 can be found at S99-1. "Consolidation, Subsidiaries or Other Investments, Consolidated Entities, Policy [Policy Text Block]" Reference Number Reference Text Regulation of an entity's rates (also referred to as prices) is sometimes based on the entity's costs. Regulators use a variety of mechanisms to estimate a regulated entity's allowable costs, and they allow the entity to charge rates that are intended to produce revenue approximately equal to those allowable costs. Specific costs that are allowable for rate-making purposes result in revenue approximately equal to the costs. 38

39 Appendix D The "Hybrid" Approach Step 1 Is there a specific requirement for a policy note? No Yes Should the Topic 235 approach be applied first for a Topic with only one policy note? That is, perform Step 3 before Step 2? Associate the policy note to the paragraph that contains the specific requirement Step 2 Is there only one policy note for a concept/subject? Yes Is there a Topic/Subtopic that a filer would look to that can be associated with that policy note? Use that Topic/Subtopic as appropriate No No Step 3 Can you apply the Topic 235 Approach to one of the ASC paragraphs? Yes Is the language in a presentation/disclosure paragraph (ASC section 45/50)? Yes Associate that paragraph (or paragraphs) with the policy text block No No Step 4 Is there an illustration in Section 55 that illustrates a policy note? Yes Associate that paragraph in Section 55 with the policy text block No How many elements make the reference less useful? Step 5 Yes Are there more than X number of elements that would be associated with the related Topic? No Is there language in Sections that are unrelated to either presentation/disclosure (Topics 45 and 50)? No Yes Step 6 Evaluate the need to either deprecate the policy text block because it (1) does not seem to be a GAAP requirement. Associate the policy note with the most appropriate Topic (only) Associate ASC nonpresentation/ disclosre section paragraph to element 39

40 Appendix E Providing references for paragraphs that combine two distinct but related requirements in single ASC paragraph ASU Compensation-Retirement Benefits (Topic 715): Improving the Presentation of Net Periodic Pension Costs and Net Periodic Postretirement Benefit Costs, requires that an employer provide the components of net benefit costs separately or its location in the income statement, however both requirements are found in the same paragraph as shown below: Annual and Interim Disclosures Annual An employer that sponsors one or more defined benefit pension plans or one or more defined benefit other postretirement plans shall provide the following information, separately for pension plans and other postretirement benefit plans. Amounts related to the employer s results of operations shall be disclosed for each period for which a statement of income is presented. Amounts related to the employer s statement of financial position shall be disclosed as of the date of each statement of financial position presented. All of the following shall be disclosed: h. The amount of net benefit cost recognized, showing separately all of the following: 1. The service cost component 2. The interest cost component 3. The expected return on plan assets for the period 4. The gain or loss component 5. The prior service cost or credit component 6. The transition asset or obligation component 7. The gain or loss recognized due to settlements or curtailments. The line item(s) used in the income statement to present the components other than the service cost component shall be disclosed if the other components are not presented in a separate line item or items in the income statement. 40

41 Interim A publicly traded entity shall disclose the following information for its interim financial statements that include a statement of income: a. The amount of net benefit cost recognized, for each period for which a statement of income is presented, showing separately each of the following: 1. The service cost component 2. The interest cost component 3. The expected return on plan assets for the period 4. The gain or loss component 5. The prior service cost or credit component 6. The transition asset or obligation component 7. The gain or loss recognized due to a settlement or curtailment. The line item(s) used in the income statement to present the components other than the service cost component shall be disclosed if the other components are not presented in a separate line item or items in the income statement. b. The total amount of the employer s contributions paid, and expected to be paid, during the current fiscal year, if significantly different from amounts previously disclosed pursuant to paragraph (g). Estimated contributions may be presented in the aggregate combining all of the following: 1. Contributions required by funding regulations or laws 2. Discretionary contributions 3. Noncash contributions 41

42 A An employer shall report in the income statement: a. The service cost component of net periodic pension cost and net periodic postretirement benefit cost in the same line item or items as other compensation costs arising from services rendered by the pertinent employees during the period (except for the amount being capitalized, if appropriate, in connection with the production or construction of an asset such as inventory or property, plant, and equipment) b. The other components as defined in paragraphs and separately from the service cost component and outside a subtotal of income from operations, if one is presented. If a separate line item or items are used to present the other components, that line item or items shall be described appropriately. For the purpose of applying the guidance in this paragraph, a gain or loss from a settlement or curtailment or the cost of certain termination benefits accounted for under this Topic shall be reported in the same way as the other components in (b). 420 Exit or Disposal Cost Obligations 10 Overall 45 Other Presentation Matters The cumulative effect of a change resulting from a revision to either the timing or the amount of estimated cash flows shall be reported in the same line item(s) in the income statement (statement of activities) used when the related costs were recognized initially in the period of change. [No XBRL elements associated with this paragraph] 42

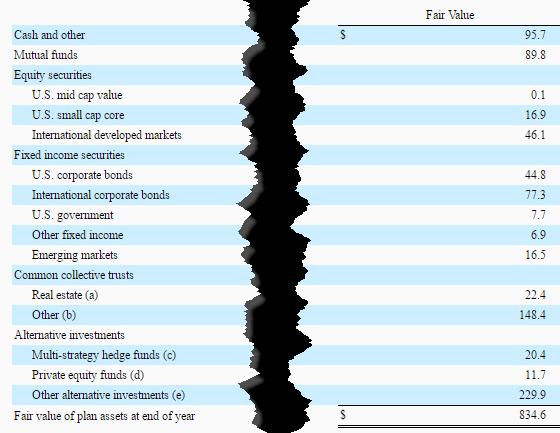

43 Session 3 Retirement Benefits Plan Assets (Phase 2) A. Meeting Highlights The memo related to retirement benefits plan assets (phase 2 discussion of line items only) was provided but not reviewed. This topic will be discussed in a future TAG meeting. B. Retirement Benefits Plan Assets (Phase 2) Purpose of This Memo 1. The Taxonomy staff is seeking feedback on modeling certain line item elements for plan asset disclosures in connection with the Retirement Benefits Topical Focus Project. Issues to be discussed: (a) (b) Modeling multiple line items or a single line item. Design principles for modeling different ways of tagging similar information in the Taxonomy (for example, cash or investments in equity securities). Background Information 2. The elements for retirement benefit disclosures continue to be examined in connection with the Retirement Benefits Topical Focus Project. Phase 1 of this project resulted in changes to the 2017 Taxonomy. Phase 2 of this project is expected to result in changes to the 2018 Taxonomy. The focus of Phase 2 of this project consists primarily of elements for plan asset disclosures. 3. Topic 715 of the Accounting Standards Codification (ASC), Compensation Retirement Benefits, specifically ASC (d) currently provides guidance for plan asset disclosures. Plan assets are required to be disaggregated by asset class and by level within the fair value hierarchy/nav practical expedient. The requirement to disaggregate plan assets by asset class is in ASC (d)(ii). The following table outlines the required disclosures in ASC (d)(ii) with emphasis added for the current modeling of different attributes. The color coding is as follows: blue represents information intended to be tagged with monetary elements, red represents dimensions and purple represents members. Appendix A includes the entire listing of 43

While class is the terminology used in the ASC, the Taxonomy uses the term category because there is diversity in the presentation of plan asset information.")

(ii): three options under a principles-based model and one")

44 Plan Asset elements in Presentation Group that are within the scope of phase 2 of the Retirement Benefits Topical Focus Project. (a) While class is the terminology used in the ASC, the Taxonomy uses the term category because there is diversity in the presentation of plan asset information. Category is appropriate when disaggregations are not expected to be homogeneous. 4. At the May 18 th TAG meeting, four options were discussed for modeling elements for plan asset disclosures required in ASC (d)(ii): three options under a principles-based model and one option under a practical expedient model. The principles-based model aligns with dimension modeling design principles and would be applicable across the Taxonomy, with certain exceptions for member elements, while the practical expedient model does not fully align with the dimension modeling design principles, but it is intended to serve as an alternative to applying multiple dimensions to the same disclosure. The options were as follows: (a) Option #1 (Line Items Approach): Model plan asset categories as line items specific to defined benefit plans, consistent with the financial instruments model, 44

45 and deprecate the Defined Benefit Plan, Asset Categories [Axis]. For example, plan assets cash, plan asset equity securities, plan asset debt securities, plan asset alternative/other investments, plan asset real estate monetary line items would be modeled. Any further disaggregations of these line items would be tagged with general dimensions for a single attribute, such as investment type (pending remodeling for financial instruments), sector or issuer location. (i) This approach is intended to align with the modeling of line items for financial instruments in connection with ASU , Financial Instruments Overall (Subtopic 321): Recognition and Measurement of Financial Assets and Financial Liabilities (ASU ). The intent of aligning these models is to consistently tag the same information in the Taxonomy. For example, elements intended for tagging cash, investments in equity securities or investments in real estate would be modeled as line items throughout the Taxonomy. (b) (c) Option #2 (Retirement Plan Identifier Approach): Model a dimension similar to the Legal Entity [Axis] for defined benefit plans, such as a retirement plan [axis]. The attribute for defined benefit plans would be modeled in this dimension rather than in the line item. The same line items used for tagging the balance sheet would apply to tagging plan asset category information, such as cash and cash equivalents, investment in equity securities and investment in debt securities, etc. Under this model, financial instruments owned by a company or by a defined benefit plan or included as in separate accounts for an insurance company would be tagged with the same line item elements. This model was introduced as an option, but then removed because the perceived advantages do not appear to outweigh the perceived disadvantages associated with unintended consequences. It was removed as an option for consideration. Option #3 (1 Line Item, Multiple Dimensions for plan asset category information): The same line item (Defined Benefit Plan, Fair Value of Plan Assets) and general dimensions for a single attribute, such as investment type, sector or issuer location, would be used for tagging plan asset category 45

Option #4 (1 Line Item, 1 Dimension for plan asset category information): The same line item (Defined Benefit Plan, Fair Value of Plan Assets) and the same dimension (Defined Benefit Plan, Asset")

46 information. Certain member elements would be specific to defined benefit plans because these members would be modeled as line items elsewhere in the Taxonomy. (d) Option #4 (1 Line Item, 1 Dimension for plan asset category information): The same line item (Defined Benefit Plan, Fair Value of Plan Assets) and the same dimension (Defined Benefit Plan, Asset Categories [Axis]) would be used for tagging plan asset category information. Certain member elements would be specific to defined benefit plans because these members would be modeled as line items elsewhere in the Taxonomy. 5. Since option #2 was removed, the three options under consideration are outlined in the following tables, along with an excerpt of the sample disclosure and related modeling, for the elements highlighted in yellow. 46

rather than option #1 (multiple line items).")

47 6. At the May 8 th meeting, the TAG members provided feedback on all options. However, the TAG members were not ready for a poll. Of the TAG members that indicated a preference at the May 8 th meeting, most were leaning toward option #3 (single line item) rather than option #1 (multiple line items). (a) To use a single line item approach provides an inconsistent modeling approach in the Taxonomy. For example, elements intended for tagging cash, investments in equity securities or investments in real estate in the balance sheet would be modeled as line items, but for defined benefit plans, such elements would be modeled as members. 7. To limit the issues (options) for discussion, at the June 8 th TAG meeting, the intent is to focus on the line item(s) for tagging plan asset disclosures (as illustrated in sample disclosure in paragraph 5). The issue for discussion is whether multiple line items or a 47

48 single line item should be modeled for plan asset disclosures. The Taxonomy staff is also seeking feedback on why different ways of tagging similar information should exist in the Taxonomy. (a) The dimension(s) intended to be applied to these line item(s) for plan asset information will be discussed at a future TAG meeting. 48

49 Modeling Issue Should multiple line items or a single line item be modeled for tagging plan asset amounts? 8. Upon further analysis and consideration, two options are being considered for modeling certain plan asset disclosures. These options are intended to focus on the line item(s) for tagging plan asset amounts disaggregated by asset category. The line item elements under options #1 and #2 are outlined in the following table for certain plan asset elements. Option 1 Multiple Line Items 9. Option #1 is to consider plan assets as the form, outlined in ASU , in order to align the modeling of financial instrument line items throughout the Taxonomy. There would be monetaryitemtype elements for plan asset category for cash and cash equivalents, plan asset category for equity securities, plan asset category for debt securities, plan asset category for alternative investments (or other investments), plan asset category for real estate, etc., which would have a calculation relationship with Defined Benefit Plan, Fair Value of Plan Assets. Further disaggregations of plan asset category for equity securities would be dimensionalized. These monetary elements would participate in a calculation relationship as children of the existing element for fair value of plan assets. Option 2 Single Line Item 10. Option #2 does not consider the underlying form of plan assets as financial instruments, as outlined in ASU , because plan assets are scoped out of ASU 49

50 and would not appear in a primary financial statement. The element, Defined Benefit Plan, Fair Value of Plan Assets, would be used for plan asset category amounts and disaggregations would be tagged with dimension(s). There are two modeling decisions inherent in this option: (a) (b) The element, Defined Benefit Plan, Fair Value of Plan Asset, would be a twoway element. Specific defined benefit plan members would be needed because certain elements would be modeled elsewhere in the Taxonomy as line items, such as Defined Benefit Plan, Cash and Cash Equivalents [Member] and Defined Benefit Plan, Equity Securities [Member]. Analysis of Option #1 versus Option #2 11. This section covers considerations to help determine the appropriate design principles for modeling attributes in line item elements for plan asset disclosures. Option 1 Multiple Line Items 12. Further analysis and consideration of the feedback provided about option #1 (multiple line items for plan asset categories similar to the financial instruments model) indicates that aligning the modeling in the Taxonomy has more perceived challenges than benefits. The reasons are outlined as follows and discussed in more detail in paragraphs 13 through 16: (a) (b) (c) (d) Form is not consistently presented in plan asset categories. This model potentially creates multiple ways of tagging the same information. Existing guidance does not address certain forms of plan asset categories. A multiple line item model raises additional questions that preparers need to address compared with a single line item model. 13. Given the diversity in plan asset category information, form is not presented consistently. Plan asset categories could represent investments that are directly, indirectly or directly and indirectly owned by the defined benefit plan. In other words, the plan asset categories could represent the actual investments owned, the underlying 50

51 investments owned or a combination of the two. The distinction as to whether such investments are directly or indirectly owned seems less relevant to defined benefit plans and more relevant to investments belonging to an employer or investments in separate accounts of an insurance company because such amounts could be presented separately in the balance sheet. Investments owned by an employer would be included as assets, depending on materiality, in a separate line item in the balance sheet. For investments in separate accounts of an insurance company, the employer may or may not directly own some of the investments which determines the line items in which they would be included in the balance sheet. If the employer owns none, then all investments would be included in Separate Accounts, Asset. If the employer owns some, then only the investments not owned by the employer would be included in Separate Accounts, Asset, and the rest would be included in the same line item(s) as other investments owned by the employer. For investments owned by defined benefit plans, these assets would never appear as a separate line item in the employer s balance sheet. Therefore, to distinguish whether certain plan asset categories should be tagged as line items or as line items with dimension/member does not add value to maintaining separate lines, but contributes to complexity for preparers and users. (a) The following examples illustrate how the same equity and debt information could be presented differently by preparers. (i) This example includes plan asset categories, which may or may not be directly owned by the defined benefit plan, and how this information is intended to be tagged under option #1 versus option #2. (ii) In contrast, the next example illustrates plan assets that are directly owned and the underlying investments within each plan asset category, 51

52 and how this information is intended to be tagged under option #1 versus option # An unintended consequence of option #1 is that it could contribute to multiple ways of tagging the same information, which may or may not represent appropriate ways to tag the information, but syntactically possible in XBRL. Using the second example from paragraph 13, alternative, unintended methods to tag the disclosure is illustrated in the following table. (a) The feedback provided at the May 18 th TAG meeting from consumption indicated that option #1 could pose a challenge for distinguishing totals from subtotals, if the same line items could participate in different subtotals. The 52

53 calculation and presentation relationships could be lost if line items and dimensions are used versus only using line items or only using dimensions to tag the information. 15. There is limited guidance in ASU to determine how form should be applied, which is problematic given the diversity in presentation of plan asset category information. (a) Under ASU , a mutual fund may be considered an equity security even if it only invests in U.S. government debt securities. How should plan asset categories that contain both equity securities and mutual funds be tagged? (i) As illustrated in the following example, these plan asset categories consist of equity securities, mutual funds and money market mutual funds. If the same line item for plan asset, equity securities is used, then what members should be applied to tag the amounts being disaggregated? (ii) What if plan asset categories contain both equity mutual funds and fixed income mutual funds as the following example illustrates? How should the different mutual fund plan asset categories be tagged? 53

54 (iii) While mutual funds that invest only in U.S. government debt securities may be presented separately rather than grouped with other equity securities under ASU , that presentation may not be possible to apply to defined benefit plans because plan asset categories could combine this information. As the following example illustrates, mutual funds could be disclosed based on investment objective, which could combine equities, bonds and other types of assets. Should the $4,512 fact value be tagged with a line item, while the other types of mutual funds be tagged dimensionally? (b) The guidance in ASU does not address the appropriate form that would be applicable to certain plan asset categories, such as common/collective trusts 54

The following example classifies some of these as other versus alternative investments.")

55 or collective investment funds. Should these be their own form or considered alternative investments or just other types of investments? There is diversity in how this information is presented as illustrated in the following examples. (i) The following example classifies common/collective trusts as alternative investments. (ii) The following example classifies some of these as other versus alternative investments. (iii) The following examples classifies these as neither. Should these types of investments be their own form as illustrated in the following examples? 55

56 56

57 (c) Under ASU , there is no looking through the form of the investment to the instruments held by the investment. For defined benefit plan disclosures, by not looking-through the form of the investment, the same information could be tagged in different ways. (i) Under option #1, the following example would be tagged with line items for plan asset, equity securities and plan asset, debt securities. (ii) Under option #1, the same information would be tagged differently if presented as the underlying investments in common/collective trusts. The fact that the underlying investments are in debt and equity securities is more important to a user of defined benefit plan information than the fact that the form of the plan asset category is common/collective trust. (iii) This point is also illustrated in paragraph Option #1 would raise more questions for preparers to address in order to determine the appropriate line item for tagging that may not otherwise have to be addressed if a single line item model were to be followed. (a) Are the plan assets invested in derivatives subject to a master netting arrangement or not? Should a derivatives, net element be used, a derivative asset element be used or both? Such questions may be more relevant to required disclosures about risk that are qualitative rather than quantitative in nature. 57

58 (b) Are mutual funds considered funds or securities? When is a mutual fund considered a fund rather than an equity security? Preparers tend to use these terms interchangeably as illustrated in the following examples. 17. Another option considered, but also discarded, was to model all plan asset categories as line items. The reason for discarding this option was not only does it create modeling inconsistencies in the Taxonomy, without adding much value, it also contributes to more extension line item elements than extension member elements. Data users have indicated that it is easier to consume extension members rather than extension line items. Option 2 Single Line Item 18. Certain attributes to be included in the monetary line item under option #2 are outlined in the following table. 58

FASB Taxonomy Advisory Group Meeting. Date: May 28, 2015 Location: FASB Board Room

FASB Taxonomy Advisory Group Meeting Date: May 28, 2015 Location: FASB Board Room 1 Contents I. Agenda... 4 II. Sessions and Highlights... 6 Session 1a(i) Modeling Comparative Periods for Discontinued

FASB Taxonomy Advisory Group Meeting Date: May 28, 2015 Location: FASB Board Room 1 Contents I. Agenda... 4 II. Sessions and Highlights... 6 Session 1a(i) Modeling Comparative Periods for Discontinued

Fair value measurement

Fair value measurement Questions and answers US GAAP and IFRS $ December 2017 kpmg.com Contents Contents Comparability is the challenge 1 About the standards 2 About this publication 4 A. An introduction

Fair value measurement Questions and answers US GAAP and IFRS $ December 2017 kpmg.com Contents Contents Comparability is the challenge 1 About the standards 2 About this publication 4 A. An introduction

Accounting changes and error corrections

Financial reporting developments A comprehensive guide Accounting changes and error corrections Revised May 2017 To our clients and other friends This guide is designed to summarize the accounting literature

Financial reporting developments A comprehensive guide Accounting changes and error corrections Revised May 2017 To our clients and other friends This guide is designed to summarize the accounting literature

FASB Proposes Targeted Improvements for Long-Duration Insurance Contracts

Issues & Trends In Insurance October 2016, No. 16-6 FASB Proposes Targeted Improvements for Long-Duration Insurance Contracts The FASB recently proposed changing how insurance entities recognize, measure,

Issues & Trends In Insurance October 2016, No. 16-6 FASB Proposes Targeted Improvements for Long-Duration Insurance Contracts The FASB recently proposed changing how insurance entities recognize, measure,

Brighthouse Financial, Inc.

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q þ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q þ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C FORM 10-Q. For the quarterly period ended September 30, 2018

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q (Mark One) x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q (Mark One) x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly

SIGNIFICANT ACCOUNTING & REPORTING MATTERS FIRST QUARTER 2017

SIGNIFICANT ACCOUNTING & REPORTING MATTERS FIRST QUARTER 2017 Significant Accounting & Reporting Matters First Quarter 2017 2 TABLE OF CONTENTS Financial Accounting Standards Board (FASB)... 3 Final FASB

SIGNIFICANT ACCOUNTING & REPORTING MATTERS FIRST QUARTER 2017 Significant Accounting & Reporting Matters First Quarter 2017 2 TABLE OF CONTENTS Financial Accounting Standards Board (FASB)... 3 Final FASB

Harley-Davidson, Inc. (Exact name of registrant as specified in its charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D. C. 20549 FORM 10-Q x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D. C. 20549 FORM 10-Q x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

ISG Bulletin. FASB Accounting Standard Codification

ISG Bulletin FASB Accounting Standard Codification FASB Accounting Standard Codification Introduction The purpose of this document is to familiarise the audit teams with the content and the structure of

ISG Bulletin FASB Accounting Standard Codification FASB Accounting Standard Codification Introduction The purpose of this document is to familiarise the audit teams with the content and the structure of

Consolidated and other financial statements

Financial reporting developments A comprehensive guide Consolidated and other financial statements Presentation and accounting for changes in ownership interests Revised August 2015 To our clients and

Financial reporting developments A comprehensive guide Consolidated and other financial statements Presentation and accounting for changes in ownership interests Revised August 2015 To our clients and

Derivatives and Hedging (Topic 815)

") No. 2017-12 August 2017 Derivatives and Hedging (Topic 815) Targeted Improvements to Accounting for Hedging Activities An Amendment of the FASB Accounting Standards Codification The FASB Accounting Standards

No. 2017-12 August 2017 Derivatives and Hedging (Topic 815) Targeted Improvements to Accounting for Hedging Activities An Amendment of the FASB Accounting Standards Codification The FASB Accounting Standards